UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-08360 |

|

GUINNESS ATKINSON FUNDS |

(Exact name of registrant as specified in charter) |

|

21550 Oxnard Street, Suite 850 Woodland Hills, CA | | 91367 |

(Address of principal executive offices) | | (Zip code) |

|

James J. Atkinson, Jr. 21550 Oxnard Street, Suite 850 Woodland Hills, CA 91367 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | (800-915-6566) | |

|

Date of fiscal year end: | December 31 | |

|

Date of reporting period: | December 31, 2012 | |

| | | | | | | | |

Item 1. Reports to Stockholders.

The registrant’s annual report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the “Investment Company Act”), is as follows:

Guinness AtkinsonTM Funds

Annual Report

December 31, 2012

TABLE OF CONTENTS

| | 3 | | | Letter to Shareholders | |

| | 6 | | | Expense Example | |

| | 7 | | | Alternative Energy Fund | |

| | 15 | | | Asia Focus Fund | |

| | 21 | | | Asia Pacific Dividend Fund | |

| | 27 | | | China & Hong Kong Fund | |

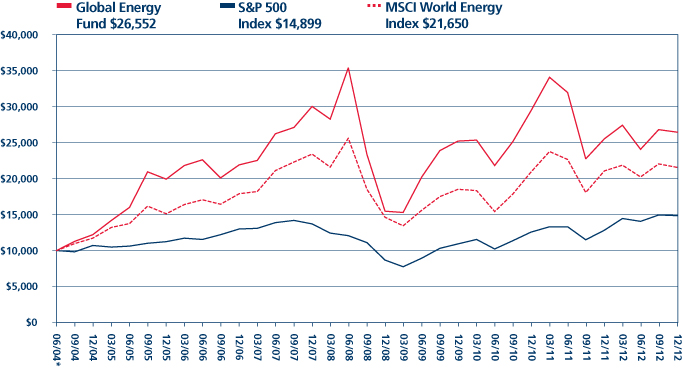

| | 33 | | | Global Energy Fund | |

| | 41 | | | Global Innovators Fund | |

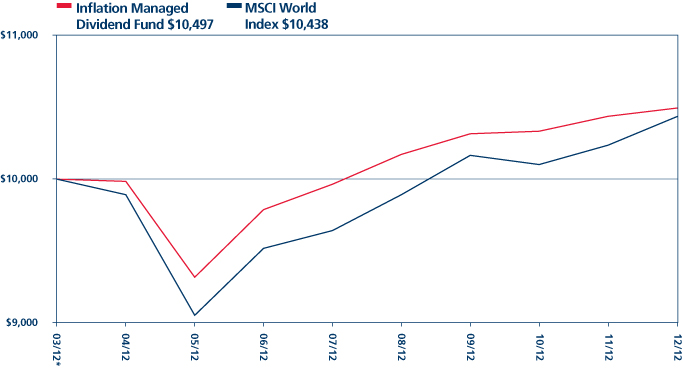

| | 48 | | | Inflation Managed Dividend FundTM | |

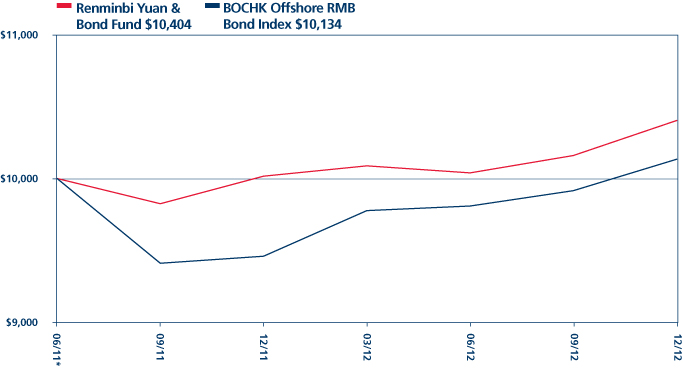

| | 55 | | | Renminbi Yuan & Bond Fund | |

| | 62 | | | Statements of Assets and Liabilities | |

| | 64 | | | Statements of Operations | |

| | 66 | | | Statements of Changes in Net Assets | |

| | 69 | | | Financial Highlights | |

| | 77 | | | Notes to Financial Statements | |

| | 91 | | | Report of Independent Registered Public Accounting Firm | |

| | 92 | | | Trustee and Officer Information | |

| | 95 | | | Privacy Notice | |

| | 99 | | | Guinness Atkinson Funds Information | |

2

Dear Guinness Atkinson Funds Shareholders,

Judging by the performance of the global equity markets in 2012 it appears the world isn't going to end soon. We're not surprised; in fact, readers of these letters will note that we've been planning on continued improvement even during the worst of times. Yes, we know, the news always seem to be negative. But as we're fond of saying, there has never been a better time to be alive and the human condition has never been better. On a global basis, life expectancy has never been higher; same for per capita income, literacy rates, access to education, health care and, frankly, by any statistical measure life on this planet has never been better. Are there intractable and serious problems? Yes, of course there are. But that doesn't diminish the fact that the human condition has improved (and continues to improve) for the vast majority of world's seven billion.

One economic fact that may surprise: Despite the global economic crisis that continues to linger, global per capita gross domestic product (GDP) has nearly doubled since the turn of the century. (Source: CIA Factbook.) Your newspaper is more likely to report on the European debt crisis, the US budget crisis or other negative economic news on the global economy. It isn't that the negative news isn't true; it is. But the dramatic improvement in global per capita GDP happens incrementally over time. The media has a short news cycle and a decade plus trend, as inexorable as it clearly is, struggles to compete with the repeated bursts of big bad news. And, let's face it, negative news is generally more newsworthy than positive news. But in the end, it is extremely clear that the constant compounding of positivity handily beats the repeated bursts of negative news. We base that assessment on the facts we cite above, namely that humans are healthier, wealthier and wiser than at any point in history.

This brings us to the themes that form the foundation of the Guinness Atkinson Funds. Asia continues its remarkable economic advance. We know that the "Asia Miracle" has become a tired cliché for many, but the fact is that the economic progress over the last 30 years in Asia is unprecedented in human history. Innovation (and we don't just mean technological innovation) has been rapidly and persistently reshaping the global business environment and is one of the keys to the steady growth in per capita GDP. Global economic growth and the aforementioned growth in per capita GDP is increasing global energy demand which in turn, has been one of the factors spurring a shift to alternative energy. Regardless of the economic cycle we believe these themes will continue to reshape the planet and those investors that understand these themes could potentially position themselves for investment success.

Outlook for 2013

Given that the global economy is in a recovery mode (albeit a slow and fitful recovery to date), and given the interest rate environment and the large amounts of economic stimulus that has been provided, it is hard to see how higher interest rates and inflation are not headed our way. While the timing may be a bit difficult to forecast, it is our opinion that we will see a return of higher interest rates and inflation. We believe two Guinness Atkinson Funds may be well-positioned to deal with higher interest rates and inflation. The Renminbi Yuan & Bond Fund may do well should the US dollar decline relative to the Renminbi Yuan in an inflationary environment. The newest addition to the Guinness Atkinson Fund family, the Inflation Managed Dividend Fund, was designed to assist investors meet their long-term income needs and is specifically designed to mitigate the effect of inflationary environments with a focus on dividend growth. The Fund seeks to invest in high quality dividend paying stocks that we believe can grow their dividend at a rate greater than inflation. While dividend paying stocks may be negatively affected by rising interest rates over a short-term period, we believe the ability to grow the dividend should, over time, help combat both rising interest rates and inflation.

Fund Performance

The performance for the Guinness Atkinson Funds for 2012 was, broadly speaking, good. With the exception of the Alternative Energy Fund all of the Funds produced a positive total return. The leader among the Guinness Atkinson Funds for 2012 was the Asia Pacific Dividend Fund which produced a total return of 23.39%. The lone negative result for the year was posted by the Alternative Energy Fund which produced a negative total return of 15.20%. It is worth noting that despite the dismal returns for this Fund the Alternative Energy Fund finished the year with a spring in its step and has gotten off to a very good start early in 2013. Clearly this Fund has a long way to go to recover but the signs point to a recovery for the beleaguered sector.

3

The table below provides total return data for each of the Funds over the one, three, five, ten and from inception periods through December 31, 2012. Also included in the table is the expense ratio data from the most recent prospectus dated May 1, 2012.

Fund (inception date) | | 1-year | | 3-year | | 5-year | | 10-year | | From Inception | | Expense Ratio | |

Alternative Energy Fund (March 31, 2006) | | | -15.20 | % | | | -27.53 | % | | | -29.64 | % | | | — | | | | -19.78 | % | | | 1.81 | % | |

Asia Focus (April 29, 1996) | | | 15.89 | % | | | 2.72 | % | | | -2.99 | % | | | 14.05 | % | | | 3.42 | % | | | 1.59 | % | |

Asia Pacific Dividend Fund (March 31, 2006) | | | 23.48 | % | | | 9.49 | % | | | 0.87 | % | | | — | | | | 5.73 | % | | | 3.26 | % gross; 1.98% net† | |

China & Hong Kong (June 30, 1994) | | | 14.42 | % | | | -1.46 | % | | | -3.43 | % | | | 14.36 | % | | | 7.75 | % | | | 1.53 | % | |

Global Energy Fund (June 30, 2004) | | | 3.53 | % | | | 1.60 | % | | | -2.51 | % | | | — | | | | 12.16 | % | | | 1.27 | % | |

Global Innovators Fund (December 15, 1998) | | | 19.91 | % | | | 9.46 | % | | | 0.78 | % | | | 9.69 | % | | | 4.79 | % | | | 1.42 | % gross; 1.44% net* | |

Inflation Managed Dividend FundTM (March 30, 2012) | | | — | | | | — | | | | — | | | | — | | | | 4.97 | % | | | 0.92 | % gross; 0.68% net† | |

Renminbi Yuan & Bond Fund (June 30, 2011) | | | 3.88 | % | | | — | | | | — | | | | — | | | | 2.67 | % | | | 0.92 | % gross; 0.90% net† | |

Periods of greater than one year are average annualized returns; one year and shorter period returns are actual returns. All returns are for the periods ending December 31, 2012.

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than the original cost. Current performance of the Funds may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.gafunds.com.

Each Fund imposes a 2% redemption fee on shares held less than 30 days. Performance data quoted does not reflect this fee. If it had, total return would be lower.

†All of the Guinness Atkinson Funds have an expense cap in place and the advisor is contractually obligated to cap the Funds' total expenses at least through June 30, 2013. For the Inflation Managed Dividend FundTM, the advisor is contractually obligated to cap total expenses at least through March 31, 2015.

*Includes 0.02% of recaptured fees previously waived by the Advisor.

Expense ratios are from the most recent prospectus (dated May 1, 2012) and are from the most recent audited financials (period ending December 31, 2011) at the time that prospectus was completed.

Our investment team has provided a detailed commentary for each of the Guinness Atkinson Funds adjacent to each Fund's financial results. Below you'll find Morningstar ratings data for the Fund range.

As usual, we appreciate the confidence you have placed in us and our management team and look forward to what will hopefully be a great 2013.

Sincerely,

| |

| |

Timothy Guinness | | James Atkinson | |

4

Morningstar Ratings (based on Morningstar risk-adjusted returns)

Below is a table listing the Morningstar star ratings as of December 31, 2012 for the six Guinness Atkinson Funds that have at least a three year history. Parenthetical numbers after the star rating indicate the number of funds in the comparison group.

Fund | | Category | | Overall | | 3-year | | 5-year | | 10-year | |

Alternative Energy | | Equity Energy | | | 1 | * | | | 1 | * | | | 1 | * | | | | | |

Fund | | | | | | | (78 | funds) | | | (78 | funds) | | | (69 | funds) | | | N/A | | |

Asia Focus | | Pacific/Asia | | | 2 | ** | | | 2 | ** | | | 2 | ** | | | 2 | ** | |

Fund | | Ex-Japan Stk | | | (51 | funds) | | | (51 | funds) | | | (37 | funds) | | | (30 | funds) | |

Asia Pacific Dividend | | Pacific/Asia | | | 3 | *** | | | 4 | **** | | | 3 | *** | | | | | |

Fund | | Ex-Japan Stk | | | (51 | funds) | | | (51 | funds) | | | (37 | funds) | | | N/A | | |

China & Hong Kong | | China Region | | | 3 | *** | | | 2 | ** | | | 2 | ** | | | 3 | *** | |

Fund | | | | | | | (81 | funds) | | | (81 | funds) | | | (60 | funds) | | | (24 | funds) | |

Global Energy | | Equity Energy | | | 3 | *** | | | 2 | ** | | | 3 | *** | | | | | |

Fund | | | | | | | (78 | funds) | | | (78 | funds) | | | (69 | funds) | | | N/A | | |

Global Innovators | | Large Growth | | | 3 | *** | | | 3 | *** | | | 2 | ** | | | 4 | **** | |

Fund | | | | | | | (1,503 | funds) | | | (1,503 | funds) | | | (1,301 | funds) | | | (863 | funds) | |

©2013 Morningstar, Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

The Funds invest in foreign securities, which involves greater volatility and political, economic and currency risks and differences in accounting methods. Non-diversified Funds' assets may be concentrated in fewer individual holdings than diversified funds. Therefore, these Funds are more exposed to individual stock volatility than diversified funds. Investments in smaller companies involve additional risks such as limited liquidity and greater volatility. Investments focused in a single geographic region may be exposed to greater risk than investments diversified among various geographies. Investments focused on the energy sector may be exposed to greater risk than an investments diversified among various sectors.

For each fund with at least a three-year history, Morningstar calculates a Morningstar RatingTM based on a Morningstar Risk-Adjusted Return measure that accounts for variation in a fund's monthly performance (including the effects of sales charges, loads, and redemption fees), placing more emphasis on downward variations and rewarding consistent performance. The top 10% of funds in each category receive 5 stars, the next 22.5% receive 4 stars the next 35% receive 3 stars, the next 22.5% receive 2 stars and the bottom 10% receive 1 star. (Each share class is counted as a fraction of one fund within this scale and rated separately, which may cause slight variations in distribution percentages.)

5

Expense Examples (Unaudited)

As a shareholder of the Funds, you incur two types of costs: (1) redemption fees; and (2) ongoing costs, including advisory fees and other Fund expenses. The examples below are intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds.

The examples are based on an investment of $1,000 invested at the beginning of the period shown and held for the entire period from July 1, 2012 to December 31, 2012.

Actual Expenses

For each Fund, the first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled "Expenses Paid during Period" to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

For each Fund, the second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund's actual expense ratios and an assumed rate of return of 5% per year before expenses, which is not the Fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any redemption fees. Therefore, the second line for each Fund of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these redemption fees were included, your costs would have been higher.

| | | Beginning

Account

Value

(07/01/12) | | Ending

Account

Value

(12/31/12) | | Expenses Paid

During Period*

(07/01/12 to

12/31/12) | | Expense Ratios

During Period*

(07/01/12 to

12/31/12) | |

Guinness Atkinson Alternative Energy Fund Actual | | $ | 1,000.00 | | | $ | 1,014.90 | | | $ | 10.03 | | | | 1.98 | %† | |

Guinness Atkinson Alternative Energy Fund Hypothetical

(5% return before expenses) | | $ | 1,000.00 | | | $ | 1,015.18 | | | $ | 10.03 | | | | 1.98 | %† | |

Guinness Atkinson Asia Focus Fund Actual | | $ | 1,000.00 | | | $ | 1,178.10 | | | $ | 9.25 | | | | 1.69 | % | |

Guinness Atkinson Asia Focus Fund Hypothetical

(5% return before expenses) | | $ | 1,000.00 | | | $ | 1,016.64 | | | $ | 8.57 | | | | 1.69 | % | |

Guinness Atkinson Asia Pacific Dividend Fund Actual | | $ | 1,000.00 | | | $ | 1,159.50 | | | $ | 10.75 | | | | 1.98 | %† | |

Guinness Atkinson Asia Pacific Dividend Fund Hypothetical

(5% return before expenses) | | $ | 1,000.00 | | | $ | 1,015.18 | | | $ | 10.03 | | | | 1.98 | %† | |

Guinness Atkinson China & Hong Kong Fund Actual | | $ | 1,000.00 | | | $ | 1,110.40 | | | $ | 8.01 | | | | 1.51 | % | |

Guinness Atkinson China & Hong Kong Fund Hypothetical

(5% return before expenses) | | $ | 1,000.00 | | | $ | 1,017.55 | | | $ | 7.66 | | | | 1.51 | % | |

Guinness Atkinson Global Energy Fund Actual | | $ | 1,000.00 | | | $ | 1,098.20 | | | $ | 7.23 | | | | 1.37 | % | |

Guinness Atkinson Global Energy Fund Hypothetical

(5% return before expenses) | | $ | 1,000.00 | | | $ | 1,018.25 | | | $ | 6.95 | | | | 1.37 | % | |

Guinness Atkinson Global Innovators Fund Actual | | $ | 1,000.00 | | | $ | 1,089.10 | | | $ | 8.09 | | | | 1.54 | % | |

Guinness Atkinson Global Innovators Fund Hypothetical

(5% return before expenses) | | $ | 1,000.00 | | | $ | 1,017.39 | | | $ | 7.81 | | | | 1.54 | % | |

Guinness Atkinson Inflation Managed Dividend Fund Actual | | $ | 1,000.00 | | | $ | 1,071.80 | | | $ | 3.54 | | | | 0.68 | %† | |

Guinness Atkinson Inflation Managed Dividend Fund Hypothetical

(5% return before expenses) | | $ | 1,000.00 | | | $ | 1,021.72 | | | $ | 3.46 | | | | 0.68 | %† | |

Guinness Atkinson Renminbi Yuan & Bond Fund Actual | | $ | 1,000.00 | | | $ | 1,036.30 | | | $ | 4.61 | | | | 0.90 | % | |

Guinness Atkinson Renminbi Yuan & Bond Fund Hypothetical

(5% return before expenses) | | $ | 1,000.00 | | | $ | 1,020.61 | | | $ | 4.57 | | | | 0.90 | % | |

*Expenses are equal to the Funds' annualized expense ratio as indicated, multiplied by the average account value over the period, multiplied by the number of days in most recent fiscal half-year period (184), then divided by the number of days in the fiscal year (366) (to reflect the one-half year period).

†Net of fee waivers and/or expense reimbursements. If those fee waivers and/or expense reimbursements had not been in effect, the Fund's actual expenses would have been higher.

6

1. Performance

AVERAGE ANNUALISED TOTAL RETURNS

| | | 1 Year

(actual) | | 3 years | | 5 Years | | Since

Inception

(March 31, 2006) | |

Fund | | | -15.20 | % | | | -27.53 | % | | | -29.64 | | | | -19.78 | % | |

Benchmark indices | |

Wilderhill New Energy Global Innovation Index | | | -4.23 | % | | | -20.67 | % | | | -22.57 | % | | | -10.42 | % | |

Wilderhill Clean Energy Index | | | -17.58 | % | | | -26.99 | % | | | -31.37 | % | | | -21.50 | % | |

MSCI World Index | | | 16.60 | % | | | 7.59 | % | | | -0.55 | % | | | 2.82 | % | |

The Fund's gross expense ratio is 1.81% per the Summary Prospectus dated May 1, 2012. The Advisor has contractually agreed to waive a portion of its advisory fees and/or reimburse other Fund expenses so that the Fund's ratio of expenses to average daily net assets will not exceed 1.98% (excluding Acquired Fund Fees and Expenses, interest, taxes, dividends on short positions and extraordinary expenses) through at least June 30, 2013. To the extent that the Advisor waives fees, it may seek repayment of a portion or all of such amounts at any time within the three fiscal years after the fiscal year in which such amounts were waived and/or reimbursed, subject to the applicable cap.

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.gafunds.com, or calling (800) 916-6566.

The Fund imposes a 2% redemption fee on the sale of shares held less than 30 days. Performance data quoted does not reflect this redemption fee. Total returns for certain periods reflect fee limitations in effect and in the absence of these limitations total returns would have been lower.

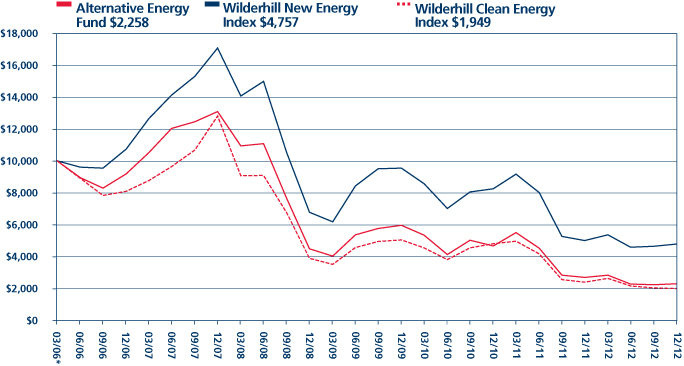

The Guinness Atkinson Alternative Energy Fund was down -15.20% in 2012. This compared to a fall in the Wilderhill New Energy Global Innovation Index of -4.23% and in the Wilderhill Clean Energy Index of -17.58%. The Fund underperformed the Wilderhill New Energy Global Innovation Index as this index has little solar exposure compared to the Fund. The sector has not recovered with broad markets as shown by the underperformance versus the MSCI World Index.

As in a number of previous years, the first quarter saw strong performance but this tailed off for the rest of the year. The Fund's performance turned in November to end the year well up from its low.

The portfolios efficiency stocks were the best performing subsector, with strong performances from Canada Lithium, Good Energy, Elster and Itron. Canada Lithium and Good Energy were acquired during the year and the performance partly reflected the Fund taking advantage of discounted share issuance by the company. Elster was acquired by Melrose Industrials. Powerone, Boralex and Ormat Technologies all further contributed. The portfolios solar and wind stocks were the main source of underperformance. The worst solar performers were STR Holdings, LDK Solar, SMA Solar and the worst wind performers were Greentech, Theolia and Vestas. They hydro holdings also underperformed.

The main reasons that alternative energy has underperformed versus global equities are that the alternative energy sector currently faces the headwinds of falling subsidies and lower availability of finance for alternative energy projects. Importantly, we believe the long term drivers for alternative energy remain broadly intact and the prices of stocks in the sector reflect the challenges the sector faces.

7

2. Portfolio

Sector | | % of Assets | |

Solar | | | 26.76 | % | |

Wind | | | 49.38 | % | |

Efficiency | | | 15.15 | % | |

Geothermal | | | 3.26 | % | |

Hydro | | | 5.24 | % | |

Biomass Energy | | | 0.00 | % | |

Cash | | | 0.21 | % | |

| | | | 100.00 | % | |

Domicile* | | % of Assets | |

Europe | | | 36.60 | % | |

North America | | | 31.57 | % | |

Asia | | | 29.54 | % | |

Latin America | | | 2.08 | % | |

Australasia | | | 0.00 | % | |

Cash | | | 0.21 | % | |

| | | | 100.00 | % | |

* region is as per company domicile.

The Fund uses a structure of 30 equally weighted holdings.

The portfolio is focused in the wind and solar sectors, with 26.76% in solar and 49.38% in Wind. We believe these sectors have the best long-term growth potential of the alternative energy space.

Within the solar sector, most of our holdings have Asian manufacturing capabilities as this is essential for a competitive cost structure today. Further solar holdings are in leading installers with good exposure to the end market volume growth and we hold two companies that manufacture inverters.

For our wind exposure we are invested in both turbine manufacturers and wind farm developers.

Further investments are in hydroelectric power producers in Europe and Latin America, a geothermal energy company, a ground source heat company and a lithium mining company.

The Fund has 36.61% of its holdings in companies domiciled in Europe, reflecting the more mature European industry. North America accounts for 31.57% of the Fund. The Fund's 31.62% of emerging markets holdings is principally in Asia, with our investments in Chinese companies making up 29.54% of the Fund.

Mkt Cap $m | | Positions | | % of Assets | |

>1000 | | | 9 | | | | 28.21 | % | |

500-1000 | | | 6 | | | | 18.26 | % | |

250-500 | | | 6 | | | | 18.75 | % | |

100-250 | | | 8 | | | | 25.83 | % | |

50-100 | | | — | | | | 0.00 | % | |

<50 | | | 4 | | | | 8.74 | % | |

8

Position size | | Positions | | % of Assets | |

Full | | | 30 | | | | 97.50 | % | |

Half | | | 0 | | | | 0.00 | % | |

Research | | | 3 | | | | 2.29 | % | |

The liquidity of The Fund is good, with 28.21% of The Fund in companies with a market capitalization over US$1,000 million. The Fund now has 30 full units and 3 research holdings.

3. Activity

The Fund acquired new positions in Canada Lithium and Good Energy Group plc. Canada Lithium is a lithium mining company that supports the global lithium battery industry. Good Energy Group is a renewables utility with wind generation assets and a customer base in the UK.

The Fund sold its holdings in Elster which was acquired by Melrose Industrials.

4. Outlook

The outlook for 2013 remains challenging from a macroeconomic perspective and visibility on 2013 earnings for most companies is limited. However, this is offset by stock prices that reflect the uncertainty and the negative investor sentiment for the sector.

Longer term, the investment case is still intact but there are grounds for near term caution. Reviewing the drivers of energy security, rising fossil fuel prices and environmental concerns (including climate change) we see specific challenges for each.

Energy security is an important driver for promotion of alternative energy. However, increasing oil and gas production in the US is moving the country closer towards a notional energy independence. However, even if the US produces as much oil as is consumed domestically, its energy security is still impacted by events in oil producing nations. Instability in the Middle east will continue to be a concern for the US notwithstanding increased fossil fuel production. On the natural gas side, we think that once liquefied natural gas (LNG) exports from the US commence in 2015, we will move closer to a global gas market which is likely to lead to higher US natural gas prices.

Given the experience of the US in increasing oil and gas supply and the many announcements of new oil and gas discoveries, there is an implication that supply is not a long term concern. However, the discoveries are more than offset by increasing emerging markets demand and declines in production in existing fields. Ultimately fossil fuels are a finite resource, nothwithstanding that at higher prices we will find new ways to produce them.

The environmental case for moving to alternative energy remains fully intact, but there is a lower political will towards addressing climate change as witnessed by the Republican position in the US. However, the visible increasing numbers of "extreme" weather events underpins popular support for alternative energy and we expect policy support to continue globally albeit focused on the least expensive solutions.

We believe the long term outlook for the alternative energy sector remains positive and continues to improve as costs of alternative energy technologies become more competitive and global demand for energy continues to rise, pushing fossil fuel prices higher.

Edward Guinness

The Fund invests in foreign securities, which will involve political, economic and currency risks, greater volatility, and differences in accounting methods. The Fund is non-diversified, meaning that its assets may be concentrated in fewer individual holdings than diversified funds. Therefore, the Fund is more exposed to individual stock volatility than diversified funds. The Fund invests in smaller companies, which will involve additional risks such as limited liquidity and greater volatility. The Fund's focus on the energy sector to the exclusion of other sectors exposes the Fund to greater market risk and potential monetary losses than if the Fund's assets were diversified among various sectors. Should the prices of energy (oil, gas, electricity) or alternative energy decline, this would likely have a negative affect on the Fund's holdings. Investing in this Fund may be more risky than investing in a fund that invests in U.S. securities due to increased volatility of foreign or emerging markets. Specific risks include the risk of expropriation of assets and higher volatility among other risks.

9

The Wilderhill New Energy Global Innovation Index (NEX) is a modified dollar-weighted index of publicly traded companies that are active in renewable and low-carbon energy, and that stand to benefit from responses to climate change and energy security concerns. The Wilderhill Clean Energy Index (ECO) is a modified equal dollar weighted index comprised of publicly traded companies whose businesses stand to benefit substantially from societal transition toward the use of cleaner energy and conservation. The MSCI World Energy Index is an unmanaged index composed of more than 1,400 stocks listed on exchanges in the U.S. Europe, Canada, Australia, New Zealand, and the Far East. These indices are unmanaged, not available for investment and do not incur expenses.

Please refer to the Schedule of Investments for details on fund holdings. Current and future portfolio holdings are subject to risk.

The information provided herein represents the opinion of Guinness Atkinson Asset Management, Inc. for the period stated and is not intended to be a forecast of future events, a guarantee of future results, or investment advice. Opinions, fund holdings and sector allocations are subject to change at any time and are not recommendations to buy or sell any security.

10

GUINNESS ATKINSON ALTERNATIVE ENERGY FUND

Growth of $10,000

Average Annual Total Return

Periods Ended December 31, 2012

| One Year | | Five Year | | Since Inception

(03/31/06) | |

| | -15.20 | % | | | -29.64 | % | | | -19.78 | % | |

*Inception date 03/31/06.

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.gafunds.com.

Total returns reflect a fee waiver in effect and in the absence of this waiver, the total returns would be lower. The Fund imposes a 2% redemption fee on shares held less than 30 days.

The Wilderhill New Energy Global Innovations Index (NEX) is a modified dollar weighted index of publicly traded companies, which are active in renewable and low-carbon energy, and which stand to benefit from responses to climate change and energy security concern. The Wilderhill Clean Energy Index (ECO) is a modified equal dollar weighted index comprised of publicly traded companies whose businesses stand to benefit substantially from societal transition toward the use of cleaner energy and conservation.

11

FUND HIGHLIGHTS at December 31, 2012

GUINNESS ATKINSON ALTERNATIVE ENERGY FUND

# of Holdings in Portfolio: | | | 33 | | |

Portfolio Turnover: | | | 7.8 | % | |

% of Stocks in Top 10: | | | 43.0 | % | |

Fund Managers:

Edward Guinness | |

Matthew Page | |

Top 10 Holdings (% of net assets) | | | | Sector Breakdown (% of net assets) | | | |

Canada Lithium Corp. | | | 6.7 | % | | Wind | | | 49.5 | % | |

Good Energy Group PLC | | | 6.5 | % | | Solar | | | 26.8 | % | |

China Longyuan Power Group Corp. - H Shares | | | 4.1 | % | | Efficiency | | | 15.2 | % | |

China Suntien Green Energy Corp. Ltd. - H Shares | | | 4.0 | % | | Hydro | | | 5.3 | % | |

Boralex, Inc. - Class A | | | 3.9 | % | | Geothermal | | | 3.3 | % | |

Enel Green Power SpA | | | 3.8 | % | | | | | | | |

Acciona, S.A. | | | 3.6 | % | | | | | | | |

Power-One Inc. | | | 3.6 | % | | | | | | | |

SunPower Corp. | | | 3.5 | % | | | | | | | |

Theolia SA | | | 3.3 | % | | | | | | | |

12

SCHEDULE OF INVESTMENTS

December 31, 2012

GUINNESS ATKINSON ALTERNATIVE ENERGY FUND

Shares | | COMMON STOCKS: 100.1% | | Value | |

Efficiency: 15.2% | | | |

| | 146,000 | | | Applied Intellectual Capital Ltd.*†^ | | $ | — | | |

| | 1,310,000 | | | Canada Lithium Corp. | | | 869,207 | | |

| | 760,987 | | | Carmanah Technologies Corp.* | | | 206,561 | | |

| | 9,000 | | | Itron, Inc.* | | | 400,950 | | |

| | 2,306,792 | | | Thermal Energy International, Inc.* | | | 92,763 | | |

| | 28,400 | | | WaterFurnace Renewable Energy Inc | | | 412,281 | | |

| | | | | | | | 1,981,762 | | |

Geothermal: 3.3% | | | |

| | 22,119 | | | Ormat Technologies, Inc. | | | 426,454 | | |

Hydro: 5.3% | | | |

| | 25,066 | | | Cia Energetica de Minas Gerais ADR | | | 272,217 | | |

| | 16,700 | | | Verbund AG | | | 413,532 | | |

| | | | | | | | 685,749 | | |

Solar: 26.8% | | | |

| | 85,700 | | | JA Solar Holdings Co., Ltd.* | | | 365,939 | | |

| | 155,800 | | | LDK Solar Co., Ltd. - ADR* | | | 224,352 | | |

| | 113,000 | | | Power-One Inc.* | | | 464,227 | | |

| | 252,000 | | | Renesola Ltd. - ADR* | | | 388,080 | | |

| | 10,560 | | | SMA Solar Technology AG | | | 265,564 | | |

| | 114,200 | | | STR Holdings, Inc.* | | | 287,784 | | |

| | 81,205 | | | SunPower Corp. - Class B* | | | 456,372 | | |

| | 247,291 | | | Suntech Power Holdings Co., Ltd. - ADR* | | | 378,355 | | |

| | 80,500 | | | Trina Solar Ltd. - ADR* | | | 349,370 | | |

| | 136,500 | | | Yingli Green Energy Holding Co., Ltd. - ADR* | | | 320,775 | | |

| | | | | | | | 3,500,818 | | |

Wind: 49.5% | | | |

| | 6,200 | | | Acciona S.A. | | | 470,161 | | |

| | 55,627 | | | Boralex Inc. - Class A* | | | 512,818 | | |

| | 2,946,000 | | | China Datang Corp. Renewable Power Co. Ltd. - H Shares* | | | 377,588 | | |

| | 763,000 | | | China Longyuan Power Group Corp. - H Shares | | | 535,987 | | |

| | 2,356,000 | | | China Suntien Green Energy Corp. Ltd. - H Shares | | | 518,199 | | |

| | 75,400 | | | EDP Renovaveis SA* | | | 402,083 | | |

| | 264,600 | | | Enel Green Power SpA | | | 494,868 | | |

| | 156,831 | | | Gamesa Corporation Tecnologica S.A. | | | 346,958 | | |

| | 332,941 | | | Good Energy Group PLC | | | 843,724 | | |

| | 221,100 | | | Greentech Energy Systems* | | | 396,975 | | |

| | 2,264,000 | | | Huaneng Renewables Corp. Ltd. - H Shares* | | | 408,210 | | |

| | 108,400 | | | Nordex SE* | | | 428,008 | | |

| | 245,708 | | | Theolia SA* | | | 435,091 | | |

| | 51,315 | | | Vestas Wind Systems A/S* | | | 290,939 | | |

| | | | | | | | 6,461,609 | | |

| | | | | Total Common Stocks

(cost $31,039,852) | | | 13,056,392 | | |

The accompanying notes are an integral part of these financial statements.

13

| | | | | Value | |

| | | | | Total Investments in Securities

(cost $ $31,039,852): 100.1% | | $ | 13,056,392 | | |

| | | | | Liabilities in Excess of Other Assets: (0.1%) | | | (15,889 | ) | |

| | | Net Assets: 100.0% | | $ | 13,040,503 | | |

* Non-income producing security.

† Illiquid. Illiquid securities represent 0.0% of net assets.

^ Fair value under direction of the Board of Trustees. Fair valued securities represent 0.0% of net assets.

ADR - American Depository Receipt

The accompanying notes are an integral part of these financial statements.

14

ASIA FOCUS FUND for the period ended December 31, 2012

1. Performance

AVERAGE ANNUALIZED TOTAL RETURNS

| | 1 Year

(actual) | | 3 Years | | 5 Years | | 10 Years | |

Fund | | | 15.89 | % | | | 2.72 | % | | | -2.99 | % | | | 14.05 | % | |

Benchmark Index: | |

MSCI AC Far East Free Ex Japan Index | | | 22.06 | % | | | 7.56 | % | | | 0.85 | % | | | 14.42 | % | |

S&P 500 Index | | | 15.99 | % | | | 10.86 | % | | | 1.66 | % | | | 7.09 | % | |

The Fund's gross expense ratio is 1.59% per the Summary Prospectus dated May 1, 2012. The Advisor has contractually agreed to waive a portion of its advisory fees and/or reimburse other Fund expenses so that the Fund's ratio of expenses to average daily net assets will not exceed 1.98% (excluding Acquired Fund Fees and Expenses, interest, taxes, dividends on short positions and extraordinary expenses) through at least June 30, 2013. To the extent that the Advisor waives fees and/or reimburses expenses, it may seek repayment of a portion or all of such amounts at any time within the three fiscal years after the fiscal year in which such amounts were waived and/or reimbursed, subject to the applicable cap.

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by visiting www.gafunds.com, or calling (800) 916-6566.

The Fund imposes a 2% redemption fee on the sale of shares held less than 30 days. Performance data quoted does not reflect this redemption fee. Total returns for certain periods reflect fee limitations in effect and, in the absence of these limitations, total returns would have been lower.

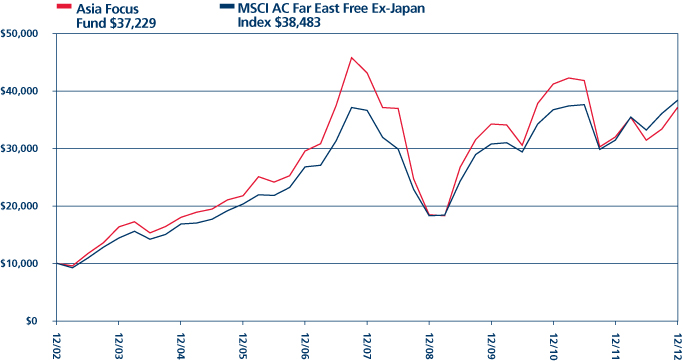

The Fund ended the year up 15.89%, with a strong period of performance from the beginning of August through to the end of the year compared to a return of 22.06% for the benchmark, the MSCI AC Far East Free Ex Japan Index. There is still ground to be made up, however.

The performance of cyclical stocks, especially those in the Energy, Materials and Industrials sectors, were the main drivers of overall Fund performance. In the first part of the year markets were concerned about slowing Chinese growth and fears, exacerbated by weakness in the developed world, that Chinese exports might sharply contract. This did not happen. Tighter policies designed to counteract the inflationary effects of the 2009/10 credit expansion remained in place for longer than expected as the political transition in China encountered unexpected turbulence in the middle of the year. By August, however, there were signs of monetary loosening and a number of new investment projects were given formal approval to proceed. By the end September the Renminbi resumed its appreciation against the US Dollar.

While Chinese stocks languished in the first half of the year, money moved to South-East Asia, where Singapore, Thailand and the Philippines all had a particularly good year. In Singapore, economic growth slowed given its high exposure to trade, but in spite of this, the stock market did well. Earnings forecasts for 2012 stayed largely unchanged in contrast to most other countries, which were supported by material upgrades to bank sector earnings forecasts. Thailand's economy rebounded from the widespread damage cause by flooding in late 2011 and the stock market rallied strongly on the back of it. The Philippines too saw a strong performance as economic growth picked up and national finances were such as to warrant an upgrade to its sovereign debt investment rating, with S&P raising the rating to a nine-year high of B+ in July, and Moody's following suit in October to Ba1.

Indonesia and Malaysia were relatively weaker performers. The Indonesian market has performed well over the past few years, but 2012 saw more modest returns and a weaker exchange rate against the U.S. dollar. After a number of years of strong economic growth, inflationary pressures have risen, as have political concerns, now that the popular president SB Yudhoyono is nearing the end of his term and cannot seek re-election.

The past year has seen political developments assume much greater significance than in prior years, as sovereign debt and budget issues persisted in Europe and the U.S. By the end of the year, however, (right at the end, in the case of the U.S.) the immediacy of the problems had retreated. In Asia, there was a change in China's leadership, and also new governments in Japan and South Korea. All three have emphasized their focus on domestic economic growth and stimulus. Discussion about reflation efforts in

15

Japan have perhaps been the most eye-catching, since they represent a significant change. This has been reflected in strong Japanese stock market performance (in yen terms) and a significant weakening of the yen against the U.S. dollar.

2. Portfolio Position

The position of the Fund at the year-end remains largely unchanged, with overweight positions in China/Hong Kong and Thailand, and underweight in South Korea, Singapore and Taiwan. On a sector basis, the focus has been on Energy and Materials at the expense of banks, insurance, real estate and Consumer Staples. The portfolio also has been overweight in technology, with the bulk of this concentrated the consumer-related segments of tablet computers and smartphones.

3. Outlook

We see a better likelihood for stronger economic growth to come from Asia in the coming year. In part, this is based on an expectation of a continued cyclical recovery in developed markets, which, although not expected to drive growth through an export rebound, is at least likely to be supportive. Efforts to support domestic growth in China and South Korea also are positive in our view. Elsewhere, there are upcoming elections in Malaysia and Indonesia that may result in some pre-election giveaways. This should not, however, detract from the fact that there is a marked increase in investment which appears to be already underway.

Malaysia's economic transformation plan is designed to push it into becoming a high-income country. The Plan was begun three years ago and calls for significant new investment in sectors such as not only agribusiness, technology, oil & gas, but also in infrastructure and education. Efforts to develop southern Malaysia into an economic hinterland with Singapore, much the same as Shenzhen does for Hong Kong could benefit both Malaysia and Singapore. Progress clearly is being made, and Malaysian economic growth looks like it has the potential to sustain the 5% growth rate that surprised the market in 2012.

The Asian domestic investment story is not just confined to Malaysia. Investment in Indonesia is sorely needed and has increased, directed not only at mining, but also at power, transportation, communications, motor vehicles and agriculture. Furthermore, if the new governments of South Korea and Japan are to deliver on their election promises, further stimulus and reflation policies can be expected there too.

Asian currencies were strong in 2012 and it seems likely they will remain so in 2013. Emerging markets is still an attractive asset class and there is also some mild inflation, which at current levels suggests decent underlying economic activity and would also likely be supportive of stronger local currencies. The weakness of the yen is the major standout, with Taiwan and South Korea as the two countries most vulnerable to this weakness, given their export competition. A cyclical recovery in world trade, however, which is forecast by the World Trade Organization to grow 4.5% in 2013, combined with increasing sales into emerging markets, may offset some of the currency effect.

Edmund Harriss James Weir

The Fund invests in foreign securities, which involves political, economic and currency risks, greater volatility, and differences in accounting methods. The Fund is non-diversified, meaning that its assets may be concentrated in fewer individual holdings than diversified funds. Therefore, the Fund is more exposed to individual stock volatility than diversified funds. Investments focused in a single geographic region may be exposed to greater risk and more volatility than investments diversified among various geographies. The Fund invests in smaller companies, which involves additional risks such as limited liquidity and greater volatility.

The MSCI All Country Far East Free ex-Japan Index (MSCI AC Far East Free ex-Japan Index) is a free float-adjusted, capitalization-weighted index that is designed to measure equity market performance in the Asia region, excluding Japan. The Standard & Poor's 500 Index is a market capitalization-weighted index composed of 500 widely held common stocks of U.S. companies. These indices are unmanaged, not available for investment and do not incur expenses.

Please refer to the Schedule of Investments for details on Fund holdings. Current and future portfolio holdings are subject to risk.

The information provided herein represents the opinion of Guinness Atkinson Asset Management, Inc. for the period stated and is not intended to be a forecast of future events, a guarantee of future results, or investment advice. Opinions, Fund holdings and sector allocations are subject to change at any time, and are not recommendations to buy or sell any security.

16

GUINNESS ATKINSON ASIA FOCUS FUND

Growth of $10,000

Average Annual Total Return

Periods Ended December 31, 2012

| One Year | | Five Year | | Ten Year | |

| | 15.89 | % | | | -2.99 | % | | | 14.05 | % | |

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.gafunds.com.

Total returns reflect a fee waiver in effect and in the absence of this waiver, the total returns would be lower. The Fund imposes a 2% redemption fee on shares held less than 30 days.

The MSCI All Country Far East Free ex-Japan Index (MSCI AC Far East Free ex-Japan Index) is a free float-adjusted, capitalization-weighted index that is designed to measure equity market performance in the Asia region excluding Japan. The index referenced in this chart is not available for investment and does not incur expenses.

17

FUND HIGHLIGHTS at December 31, 2012

GUINNESS ATKINSON ASIA FOCUS FUND

# of Holdings in Portfolio: | | | 37 | | |

Portfolio Turnover: | | | 10.9 | % | |

% of Stocks in Top 10: | | | 41.3 | % | |

Fund Managers:

Edmund Harriss | |

James Weir | |

Top 10 Holdings (% of net assets) | | | |

Samsung Electronics Co. Ltd. | | | 6.4 | % | | Glow Energy PCL/Foreign | | | 3.4 | % | |

Taiwan Semiconductor Manufacturing Co., Ltd. | | | 5.6 | % | | PetroChina Co. Ltd. - H Shares | | | 3.3 | % | |

DiGi.Com Bhd | | | 5.3 | % | | Jiangxi Copper Co. Ltd. - H Shares | | | 3.3 | % | |

Kunlun Energy Co., Ltd. | | | 4.2 | % | | China Shenhua Energy Co. Ltd. - H Shares | | | 3.2 | % | |

Weichai Power Co. Ltd. - H Shares | | | 3.4 | % | | CNOOC Ltd | | | 3.2 | % | |

Sector Breakdown (% of net assets) | | | | | | | |

Oil Company - Exploration & Production | | | 10.0 | % | | Commercial Banks | | | 2.6 | % | |

Coal | | | 9.0 | % | | Engineering/R&D Services | | | 2.5 | % | |

Semiconductor Components - Integrated Circuits | | | 8.8 | % | | Chemicals - Other | | | 2.3 | % | |

Auto/Truck Parts & Equipment | | | 6.4 | % | | Auto-Cars/Light Trucks | | | 2.3 | % | |

Electronic Components - Semiconductor | | | 6.4 | % | | Exchange Traded Funds | | | 2.2 | % | |

Electric - Generation | | | 6.0 | % | | Building Products - Air&Heating | | | 2.2 | % | |

Oil Company - Integrated | | | 5.8 | % | | Casino Hotels | | | 2.1 | % | |

Telecommunication Services | | | 5.3 | % | | Steel - Producers | | | 1.8 | % | |

Metal - Copper | | | 3.3 | % | | Web Portals/ISP | | | 1.8 | % | |

Real Estate Operations/Development | | | 3.1 | % | | Power Converson/Supply Equipment | | | 1.7 | % | |

Cellular Telecommunications | | | 2.9 | % | | Public Thoroughfares | | | 1.3 | % | |

Computers | | | 2.7 | % | | Non-Ferrous Metals | | | 0.9 | % | |

Electronic Components - Miscellaneous | | | 2.7 | % | | Machinery | | | 0.4 | % | |

Building & Construction Products | | | 2.6 | % | | Metal Processors & Fabricators | | | 0.0 | % | |

18

SCHEDULE OF INVESTMENTS

December 31, 2012

GUINNESS ATKINSON ASIA FOCUS FUND

Shares | | COMMON STOCKS: 99.1% | | Value | |

China: 35.1% | | | |

| | 263,000 | | | Anhui Conch Cement Co Ltd - H Shares | | $ | 978,515 | | |

| | 1,671,000 | | | China Liansu Group Holdings Ltd | | | 1,165,380 | | |

| | 321,000 | | | China Shenhua Energy Co., Ltd. - H Shares | | | 1,432,084 | | |

| | 645,000 | | | CNOOC Ltd | | | 1,416,263 | | |

| | 1,209,900 | | | db x-trackers - CSI300 INDEX ETF - 2D | | | 980,839 | | |

| | 382,000 | | | Dongfang Electric Corp. Ltd. - H Shares | | | 785,302 | | |

| | 145,950 | | | Inner Mongolia Yitai - B Shares | | | 832,547 | | |

| | 550,000 | | | Jiangxi Copper Co., Ltd. - H Shares | | | 1,478,501 | | |

| | 1,030,000 | | | PetroChina Co., Ltd. - H Shares | | | 1,479,385 | | |

| | 1,492,000 | | | Shenzhen Expressway Co., Ltd. - H Shares | | | 579,911 | | |

| | 1,694,000 | | | Soho China, Ltd. | | | 1,372,822 | | |

| | 16,650 | | | Sohu.com Inc.* | | | 788,211 | | |

| | 336,000 | | | Weichai Power Co., Ltd. - H Shares | | | 1,525,777 | | |

| | 544,800 | | | Yanzhou Coal Mining Co., Ltd. - H Shares | | | 920,076 | | |

| | | | | | | | 15,735,613 | | |

Hong Kong: 14.5% | | | |

| | 618,000 | | | Chen Hsong Holdings | | | 188,024 | | |

| | 110,500 | | | China Mobile Ltd. | | | 1,294,381 | | |

| | 240,000 | | | Galaxy Entertainment Group Ltd | | | 957,325 | | |

| | 109,266 | | | HSBC Holdings PLC | | | 1,159,938 | | |

| | 286,000 | | | Kingboard Chemical Holdings Ltd. | | | 1,029,761 | | |

| | 904,000 | | | Kunlun Energy Co., Ltd. | | | 1,897,783 | | |

| | | | | | | | 6,527,212 | | |

Indonesia: 2.9% | | | |

| | 198,000 | | | Indo Tambangraya Megah PT | | | 854,890 | | |

| | 1,747,000 | | | Vale Indonesia Tbk | | | 428,622 | | |

| | | | | | | | 1,283,512 | | |

Malaysia: 7.6% | | | |

| | 1,375,000 | | | DiGi.Com Bhd | | | 2,380,457 | | |

| | 262,000 | | | UMW Holdings Bhd | | | 1,022,982 | | |

| | | | | | | | 3,403,439 | | |

South Korea: 13.8% | | | |

| | 4,962 | | | Hyundai Mobis | | | 1,345,827 | | |

| | 2,525 | | | POSCO | | | 825,597 | | |

| | 2,010 | | | Samsung Electronics Co., Ltd. | | | 2,876,764 | | |

| | 7,373 | | | Samsung Engineering Co., Ltd. | | | 1,149,037 | | |

| | | | | | | | 6,197,225 | | |

The accompanying notes are an integral part of these financial statements.

19

Shares | | COMMON STOCKS: 99.1% (Continued) | | Value | |

Taiwan: 14.1% | | | |

| | 108,000 | | | Asustek Computer Inc. | | $ | 1,219,509 | | |

| | 343,000 | | | Novatek Microelectronics Corp. Ltd. | | | 1,408,410 | | |

| | 2 | | | Shin Zu Shing Co., Ltd. | | | 6 | | |

| | 750,000 | | | Taiwan Semiconductor Manufacturing Co., Ltd. | | | 2,510,184 | | |

| | 67,000 | | | TPK Holding Co. Ltd. | | | 1,196,693 | | |

| | | | | | | | 6,334,802 | | |

Thailand: 11.1% | | | |

| | 234,500 | | | Electricity Generating PCL/Foreign | | | 1,159,007 | | |

| | 595,000 | | | Glow Energy PCL/Foreign | | | 1,511,319 | | |

| | 216,198 | | | PTT Exploration & Production PCL/Foreign | | | 1,165,105 | | |

| | 103,700 | | | PTT PCL/Foreign | | | 1,130,746 | | |

| | | | | | | | 4,966,177 | | |

| | | | | Total Common Stocks

(cost $32,224,702) | | | 44,447,980 | | |

| | | | | Total Investments in Securities

(cost $32,224,702): 99.1% | | | 44,447,980 | | |

| | | | | Other Assets less Liabilities: 0.9% | | | 405,441 | | |

| | | | | Net Assets: 100.0% | | $ | 44,853,421 | | |

* Non-income producing security.

ADR - American Depository Receipt

The accompanying notes are an integral part of these financial statements.

20

ASIA PACIFIC DIVIDEND FUND for the period ended December 31, 2012

1. Performance

AVERAGE ANNUALIZED TOTAL RETURNS

| | 1 Year

(actual) | | 3 Year | | 5 Year | | Since

Launch

(March 31, 2006) | |

Fund | | | 23.48 | % | | | 9.49 | % | | | 0.87 | % | | | 5.74 | % | |

Benchmark Index: | |

MSCI Pacific Ex Japan Index | | | 22.72 | % | | | 8.08 | % | | | 1.60 | % | | | 9.13 | % | |

S&P 500 Index | | | 15.99 | % | | | 10.86 | % | | | 1.66 | % | | | 3.63 | % | |

The Fund's gross expense ratio is 3.26% and net expense ratio is 1.98% per the Summary Prospectus dated May 1, 2012. The Advisor has contractually agreed to waive a portion of its advisory fees and/or reimburse other Fund expenses so that the Fund's ratio of expenses to average daily net assets will not exceed 1.98% (excluding Acquired Fund Fees and Expenses, interest, taxes, dividends on short positions and extraordinary expenses) through at least June 30, 2013. To the extent that the Advisor waives fees and/or reimburses expenses, it may seek repayment of a portion or all of such amounts at any time within the three fiscal years after the fiscal year in which such amounts were waived and/or reimbursed, subject to the applicable cap.

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by visiting www.gafunds.com, or calling (800) 916-6566.

The Fund imposes a 2% redemption fee on the sale of shares held less than 30 days. Performance data quoted does not reflect this redemption fee. Total returns for certain periods reflect expense limitations in effect and, in the absence of these imitations, total returns would have been lower.

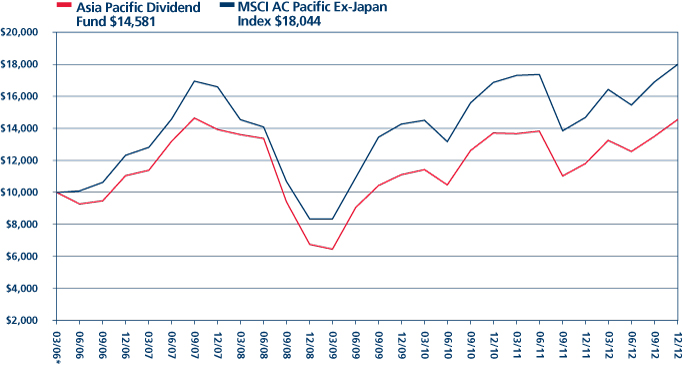

2012 was a decent year for the Fund, which finished up 23.48%, 0.76% ahead of its benchmark, the MSCI Pacific Ex Japan Index, which returned 22.72%. Over the longer term, the Fund is now ahead of the benchmark for three years, although it remains behind over five and since inception time periods. This has been a good year for Asian equities, and a good year for the dividend-producing stocks favoured by our strategy, as they tend to have relatively defensive cash flows.

The first half of the year was dominated by fears over a slowdown in Chinese growth, with concerns that excessive tightening in the property market had done permanent damage to China's economy. Decent economic growth in China in the second half of the year demonstrated that the government appeared to have successfully engineered a 'soft landing' for growth, and a sharp contraction of activity was not in progress. It is becoming clear, however, that part of the slowdown in China's growth this year was structural, rather than just cyclical, and the hyper-growth period of double digit annual gross domestic product (GDP) growth for the economy is likely coming to an end.

There are also fears that China's growth is facing a 'middle income trap' and that it will not be able to keep growing its per capita GDP. We believe that, while there is some danger of this, the available evidence suggests to us that the government's medium term target of 7-8% real GDP growth per annum is achievable. A new administration came to power in China in October 2012, and this was a catalyst for improved performance in Chinese equities, and helped to spread confidence across the region.

The economies of South East Asia performed well in 2012, and some of the smaller countries, such as the Philippines and Thailand, were the best-performing Asian equity markets over the period. The growth in these economies is founded on material improvements in household incomes as a result of better employment prospects. The governments of these countries have helped create the conditions for recovery by leading crackdowns on corruption in business and public life, and creating a degree of stability based on genuine political mandates. The improvements have been recognised by international investors, both through the equity market and through inflows to sovereign debt markets, which help lower borrowing costs for governments in these countries.

21

ASIA PACIFIC DIVIDEND FUND

2. Portfolio Position

In our view, China remains central to economic activity in Asia, and this is reflected in an overweight position in the portfolio in China and Hong Kong. Although Chinese growth has slowed in recent quarters, the growth in middle-class households there continues, and this theme has the potential to re-shape the Chinese economy. The new Chinese administration seems to recognise this, and has highlighted urbanisation is its key message for economic development. This is of benefit not only to direct consumption stocks, but also to indirect beneficiaries, such as those involved in construction and infrastructure, given that a home is often an early purchase for a household with improved incomes. The Fund is overweight in Energy, as a direct proxy for Asia growth, and in Information Technology, particularly those firms that can benefit from domestic Asian growth.

The Fund also has a significant relative weighting in Thailand, which saw a strong year of economic activity in 2012, and still looks to offer reasonable value. Thailand's growth has helped it achieve full employment, with the availability of labour now a serious issue for many employers. Firms in Thailand have a good propensity to pay dividends, as this is expected by local investors. This has meant that we have been able to find stocks there offering a compelling combination of value, earnings growth and attractive dividend yields.

3. Outlook

The challenge for the Fund in 2013 is to find decent value and dividends, given this theme was favoured by investors looking for defensive cash flows during the cyclical slowdown. Good stock returns in 2012 have led to some yield compression, but as the northern economies of Asia, such as China and South Korea, recover and offer better growth potential, so we anticipate that dividend yields could improve further. This is mainly due to a propensity to pay dividends based on a payout ratio, that is, as a percentage of net income. As economic growth improves and confidence returns to north Asia, firms can potentially grow the absolute level of their dividends as earnings grow, and some may even improve their payout ratios to further improve dividends.

We believe tapping into domestic growth remains the key to equity returns in Asia, and we anticipate that the export economy is likely to remain sluggish in the coming year. The changes underway in Asia have not been swept away by a financial crisis in the Western world, nor were they simply created by leverage, unlike some of the economic growth elsewhere in the world over the last decade. Rather, Asian growth is due to steady, and sometimes rapid, improvement of household incomes and living standards as a result of demographics, urbanisation and the improving ability of Asian countries to trade with one another. The prospect of a recovery in Chinese growth, albeit a measured one, is helpful, but the story of the growing middle-class is a pan-Asian story that can drive decent equity returns for some years to come.

Edmund Harriss James Weir

The Fund invests in foreign securities, which involves political, economic and currency risks, greater volatility, and differences in accounting methods. The Fund is non-diversified, meaning that its assets may be concentrated in fewer individual holdings than diversified funds. Therefore, the Fund is more exposed to individual stock volatility than diversified funds. Investments focused in a single geographic region may be exposed to greater risk and more volatility than investments diversified among various geographies. The Fund invests in smaller companies, which involves additional risks such as limited liquidity and greater volatility.

The MSCI Pacific ex-Japan Index is a free float-adjusted, capitalization-weighted index that is designed to measure equity market performance in the Pacific region excluding Japan. The Standard & Poor's 500 Index is a market capitalization-weighted index composed of 500 widely held common stocks of U.S. companies. These indices are unmanaged and not available for investment. and do not incur expenses.

Cash flow measures the cash generating capability of a company by adding non-cash charges (e.g., depreciation) and interest expense to pretax income.

Please refer to the Schedule of Investments for details on Fund holdings. Current and future portfolio holdings are subject to risk.

The information provided herein represents the opinion of Guinness Atkinson Asset Management, Inc. for the period stated and is not intended to be a forecast of future events, a guarantee of future results, or investment advice. Opinions, Fund holdings and sector allocations are subject to change at any time, and are not recommendations to buy or sell any security.

22

GUINNESS ATKINSON ASIA PACIFIC DIVIDEND FUND

Growth of $10,000

Average Annual Total Return

Periods Ended December 31, 2012

| One Year | | Five Year | | Since Inception

(03/31/06) | |

| | 23.48 | % | | | 0.87 | % | | | 5.74 | % | |

*Inception date 03/31/06.

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.gafunds.com.

Total returns reflect a fee waiver in effect and in the absence of this waiver, the total returns would be lower. The Fund imposes a 2% redemption fee on shares held less than 30 days.

The MSCI All Country Pacific Free ex-Japan Index (MSCI AC Pacific ex-Japan Index) is a free float-adjusted, capitalization-weighted index that is designed to measure equity market performance in the Pacific region including Japan.

23

FUND HIGHLIGHTS at December 31, 2012

GUINNESS ATKINSON ASIA PACIFIC DIVIDEND FUND

# of Holdings in Portfolio: | | | 30 | | |

Portfolio Turnover: | | | 10.2 | % | |

% of Stocks in Top 10: | | | 42.5 | % | |

Fund Managers:

Edmund Harriss | |

James Weir | |

Top 10 Holdings (% of net assets) | | | | | | | |

Taiwan Semiconductor Manufacturing Co., Ltd. | | | 4.9 | % | | China Mobile Ltd. | | | 4.1 | % | |

DiGi.Com Bhd | | | 4.6 | % | | BOC Hong Kong Holdings Ltd. | | | 4.1 | % | |

KT&G Corp. | | | 4.5 | % | | Novatek Microelectronics Corp. Ltd. | | | 4.0 | % | |

HSBC Holdings PLC - ADR | | | 4.3 | % | | PTT PCL/Foreign | | | 3.9 | % | |

PetroChina Co., Ltd. - ADR | | | 4.2 | % | | VTech Holdings Ltd. | | | 3.9 | % | |

Sector Breakdown (% of net assets) | | | | | | | |

Commercial Banks | | | 15.0 | % | | Electric - Generation | | | 3.1 | % | |

Semiconductor Components - Integrated Circuits | | | 8.9 | % | | Textile - Apparel | | | 3.1 | % | |

Coal | | | 8.4 | % | | Real Estate Operations/Development | | | 2.9 | % | |

Telecommunication Services | | | 8.1 | % | | Electric - Integrated | | | 2.9 | % | |

Oil Company - Integrated | | | 8.1 | % | | Chemical Diversified | | | 2.7 | % | |

Electronic Component-Miscellaneous | | | 5.5 | % | | Computers | | | 2.6 | % | |

Tobacco | | | 4.5 | % | | Computers - Peripheral Equipment | | | 2.4 | % | |

Cellular Telecommunications | | | 4.1 | % | | Building Products - Air & Heating | | | 2.3 | % | |

Telecommunication Equipment | | | 3.9 | % | | Agricultural Chemicals | | | 2.0 | % | |

Optical Supplies | | | 3.8 | % | | Steel - Producers | | | 1.8 | % | |

Water | | 3.5% | |

24

SCHEDULE OF INVESTMENTS

December 31, 2012

GUINNESS ATKINSON ASIA PACIFIC DIVIDEND FUND

Shares | | COMMON STOCKS: 99.6% | | Value | |

Australia: 2.0% | | | |

| | 28,849 | | | Incitec Pivot Ltd. | | $ | 98,048 | | |

China: 21.4% | | | |

| | 152,000 | | | China Shanshui Cement Group Ltd. | | | 113,996 | | |

| | 218,000 | | | Industrial & Commercial Bank of China - H Shares | | | 157,215 | | |

| | 23,915 | | | Inner Mongolia Yitai - B Shares | | | 136,060 | | |

| | 1,400 | | | PetroChina Co., Ltd. - ADR | | | 201,292 | | |

| | 67,000 | | | Shenzhou Int'l Group | | | 151,274 | | |

| | 171,000 | | | Soho China Ltd. | | | 138,579 | | |

| | 80,000 | | | Yanzhou Coal Mining Co., Ltd. - H Shares | | | 135,107 | | |

| | | | | | | | 1,033,523 | | |

Hong Kong: 19.2% | | | |

| | 62,500 | | | BOC Hong Kong Holdings Ltd. | | | 196,080 | | |

| | 17,000 | | | China Mobile Ltd. | | | 199,135 | | |

| | 16,500 | | | CLP Holdings Ltd. | | | 138,555 | | |

| | 3,924 | | | HSBC Holdings PLC - ADR | | | 208,247 | | |

| | 16,600 | | | VTech Holdings Ltd. | | | 186,514 | | |

| | | | | | | | 928,531 | | |

Indonesia: 6.3% | | | |

| | 30,500 | | | Indo Tambangraya Megah PT | | | 131,687 | | |

| | 179,500 | | | Telekomunikasi Indonesia Tbk PT | | | 168,892 | | |

| | | | | | | | 300,579 | | |

Malaysia: 4.6% | | | |

| | 129,000 | | | DiGi.Com Bhd | | | 223,330 | | |

Singapore: 3.4% | | | |

| | 10,000 | | | United Overseas Bank Ltd. | | | 163,784 | | |

South Korea: 6.3% | | | |

| | 2,840 | | | KT&G Corp. | | | 215,377 | | |

| | 270 | | | POSCO | | | 88,282 | | |

| | | | | | | | 303,659 | | |

Taiwan: 19.8% | | | |

| | 11,000 | | | Asustek Computer Inc. | | | 124,209 | | |

| | 86,126 | | | Lite-On Technology Corp. | | | 114,648 | | |

| | 47,000 | | | Novatek Microelectronics Corp. Ltd. | | | 192,989 | | |

| | 12,000 | | | St Shine Optical Co., Ltd. | | | 182,650 | | |

| | 70,000 | | | Taiwan Semiconductor Manufacturing Co., Ltd. | | | 234,284 | | |

| | 6,000 | | | TPK Holding Co. Ltd. | | | 107,166 | | |

| | | | | | | | 955,946 | | |

The accompanying notes are an integral part of these financial statements.

25

Shares | | COMMON STOCKS: 99.6% (Continued) | | Value | |

Thailand: 16.6% | | | |

| | 151,400 | | | Delta Electronics Thai PCL/Foreign | | $ | 159,000 | | |

| | 60,100 | | | Glow Energy PCL/Foreign | | | 152,656 | | |

| | 56,820 | | | PTT Global Chemical PCL/Foreign | | | 131,636 | | |

| | 17,200 | | | PTT PCL/Foreign | | | 187,549 | | |

| | 560,600 | | | Thai Tap Water Supply PCL/Foreign | | | 168,821 | | |

| | | | | | | | 799,662 | | |

| | | | | Total Common Stocks

(cost $3,738,257) | | | 4,807,062 | | |

| | | | | Total Investments in Securities

(cost $3,738,257): 99.6% | | | 4,807,062 | | |

| | | | | Other Assets less Liabilities: 0.4% | | | 18,400 | | |

| | | | | Net Assets: 100.0% | | $ | 4,825,462 | | |

ADR - American Depository Receipt

The accompanying notes are an integral part of these financial statements.

26

CHINA & HONG KONG FUND for the period ended December 31, 2012

1. Performance

AVERAGE ANNUALIZED TOTAL RETURNS

| | 1 Year

(actual) | | 3 Years | | 5 Years | | 10 Years | |

Fund | | | 14.42 | % | | | -1.46 | % | | | -3.43 | % | | | 14.36 | % | |

Benchmark Index: | |

Hang Seng Composite Index | | | 26.34 | % | | | 3.67 | % | | | -1.53 | % | | | 14.32 | % | |

Hang Seng Index | | | 27.64 | % | | | 4.56 | % | | | -0.71 | % | | | 13.15 | % | |

S&P 500 Index | | | 15.99 | % | | | 10.86 | % | | | 1.66 | % | | | 7.09 | % | |

The Fund's gross expense ratio is 1.53% per the Summary Prospectus dated May 1, 2012. The Advisor has contractually agreed to waive a portion of its advisory fees and/or reimburse other Fund expenses so that the Fund's ratio of expenses to average daily net assets will not exceed 1.98% (excluding Acquired Fund Fees and Expenses, interest, taxes, dividends on short positions and extraordinary expenses) through at least June 30, 2013. To the extent that the Advisor waives fees and/or reimburses expenses, it may seek repayment of a portion or all of such amounts at any time within the three fiscal years after the fiscal year in which such amounts were waived and/or reimbursed, subject to the applicable cap.

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by visiting www.gafunds.com, or calling (800) 916-6566.

The Fund imposes a 2% redemption fee on the sale of shares held less than 30 days. Performance data quoted does not reflect this redemption fee. Total returns for certain periods reflect expense limitations in effect and, in the absence of these limitations, total returns would have been lower.

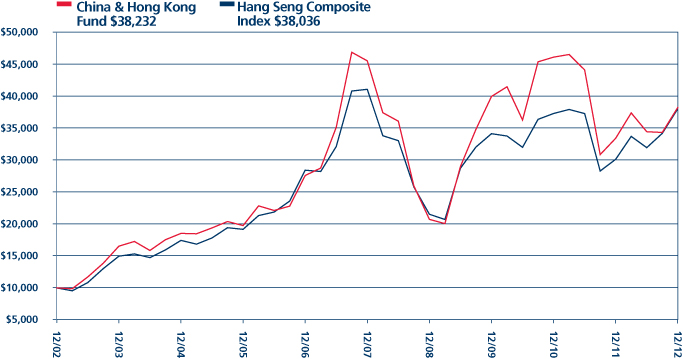

During 2012 the Fund returned 14.42%, compared to a return of 26.34% for the benchmark, the Hang Seng Composite Index. This was a mixed year for the Fund, with a slowdown in economic growth in China affecting the performance of some of our holdings, particularly in the first half of the year. The second half of the year was more favourable to Fund performance, with a cyclical recovery in growth in progress, and even early signs of an improvement in China's export economy.

At the beginning of 2012, the Chinese authorities attempted to restart economic growth, having slowed the economy in 2011 through monetary tightening to deal with inflation in the property market. This led to concerns over China's development model, and there was a slowdown in activity in construction for infrastructure and private housing, which negatively affected investor confidence., By mid-2012, however, the impact of the pro-growth policies was felt, and the economy reported a soft landing in Q3 (7.4% real GDP growth) and a decent recovery in Q4 (7.9% real GDP growth). The improved economic outlook was positive for cyclical stocks, in particular those related to construction and property development.

Chinese equities were given a further boost in October with the announcement of a new political leadership at the 18th People's Congress. The Congress marked a significant change of leadership, with the two most senior leaders and most of the politburo being replaced. The new leadership quickly set out its economic agenda, with a renewed commitment to economic growth-led development. The emphasis of this growth will change, however, with urbanisation now the central tenet of policy.

2. Portfolio Position

The Fund's focus is on stocks that can benefit from the domestic-led growth underway in China, with less emphasis on exporters. The Fund is overweight in Energy, Materials and Industrials stocks, and is underweight in Real Estate and Financials stocks. The rationale for this positioning is that infrastructure spending has been used as a driving force for economic growth in recent years, and this has been of benefit to earnings in our favoured sectors. We believe these sectors also offer reasonable value for investment, although they are cyclical. As a result of good economic growth, there is now a growing middle-class in China, and the expectations of this middle class are rising as household income and living standards improve. This has positively reinforced the need for further infrastructure spending, as the middle-class demand better roads, railways, retail centres and housing to reflect their greater spending power and higher status.

27

Increasingly, although the government is prioritising policies that encourage consumption over investment, investment and construction remain the bedrocks of the Chinese economy. In response to rising property prices, the government also has been keen to encourage the construction of affordable housing, and this has helped create additional demand for building materials such as cement and pipes, which has been of benefit to some of the Fund's holdings.

Real Estate and Financials stocks have suffered in recent quarters, as the government has tightened monetary policy as a result of excess price rises in the property sector. This process reversed during 2012, and the government encouraged greater loan growth from the banks, and eased some of the administrative restrictions on Real Estate companies. Banking remains a relatively controlled sector, and its returns are primarily defined by government policy, rather than free competition between the banks. Similarly, the government is keen to control private property development, as it wishes to avoid social discontent if property price rises become excessive.

3. Outlook

For the coming year, we anticipate that the recovery in Chinese growth should continue, although we are cautious that it may not accelerate back to the previous exceptionally high levels of growth. Our view of the fundamental data is that there could be a structural element to the recent growth slowdown, and that the benefit of China's demographic composition is coming to an end. We are not concerned that Chinese growth will fall sharply, but that a future real GDP growth rate of 7-8% per annum seems realistic. There will also be a greater emphasis on the quality, rather than just the quantity, of growth, with a focus on improving productivity and encouraging consumption. Infrastructure spending and construction will remain significant elements in China's growth, but adding further pillars to the China growth story is a healthy development.

This thinking is reflected in the new government's economic agenda, with urbanisation named as central to its growth strategy. In the Chinese context, urbanisation encompasses not just the act of moving to urban areas, but improving living standards in the cities, and easing the official burden on individuals in order to make relocation easier. In our view, this is likely to be positive for housing construction and infrastructure spending, as well as middle-class spending to help set up those homes and purchase other capital goods such as cars, computers and mobile phones.

Our investment focus remains on the recovery in China's domestic economy, but there has also been good data on the export sector in recent months. There are early signs of recovery in the U.S., and the Japanese economy also is looking better than it has in some time. Europe is still stuck in the process of deleveraging, but there may be some selected opportunities for us to add more export-related exposure to the portfolio.

Edmund Harriss James Weir

The Fund invests in foreign securities, which involves political, economic and currency risks, greater volatility, and differences in accounting methods. The Fund is non-diversified, meaning that its assets may be concentrated in fewer individual holdings than diversified funds. Therefore, the Fund is more exposed to individual stock volatility than diversified funds. Investments focused in a single geographic region may be exposed to greater risk and more volatility than investments diversified among various geographies. The Fund invests in smaller companies, which involves additional risks such as limited liquidity and greater volatility.

The Hang Seng Composite Index is a market capitalization-weighted index that is comprised of the top 200 companies listed on the Hong Kong Stock Exchange, based on the average market capitalization for the past twelve months. The Hang Seng Index is a barometer of the Hong Kong Stock Market, whose aggregate market capitalization accounts for about 70% of the total market-capitalization of the Stock Exchange of Hong Kong Limited. The Standard & Poor's 500 Index is a market capitalization-weighted index composed of 500 widely held common stocks of U.S. companies. These indices are unmanaged and not available for investment, and do not incur expenses.

Please refer to the Schedule of Investments for details on Fund holdings. Current and future portfolio holdings are subject to risk.

The information provided herein represents the opinion of Guinness Atkinson Asset Management, Inc. for the period stated and is not intended to be a forecast of future events, a guarantee of future results, or investment advice. Opinions, Fund holdings and sector allocations are subject to change at any time, and are not recommendations to buy or sell any security.

28

GUINNESS ATKINSON CHINA & HONG KONG FUND

Growth of $10,000

Average Annual Total Return

Periods Ended December 31, 2012

| One Year | | Five Year | | Ten Year | |

| | 14.42 | % | | | -3.43 | % | | | 14.36 | % | |