UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-08360 |

|

GUINNESS ATKINSON FUNDS |

(Exact name of registrant as specified in charter) |

|

21550 Oxnard Street, Suite 750 Woodland Hills, CA | | 91367 |

(Address of principal executive offices) | | (Zip code) |

|

James J. Atkinson, Jr. 21550 Oxnard Street, Suite 750 Woodland Hills, CA 91367 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | (800-915-6566) - | |

|

Date of fiscal year end: | December 31 | |

|

Date of reporting period: | December 31, 2011 | |

| | | | | | | | |

Item 1. Reports to Stockholders.

The registrant’s annual report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the “Investment Company Act”), is as follows:

Annual

Report

December 31, 2011

• Alternative Energy Fund

• Asia Focus Fund

• Asia Pacific Dividend Fund

• China & Hong Kong Fund

• Global Energy Fund

• Global Innovators Fund

• Renminbi Yuan & Bond Fund

Guinness Atkinson Funds

Annual Report

December 31, 2011

TABLE OF CONTENTS

| 4 | | | Letter to Shareholders | |

|

| 7 | | | Expense Example | |

|

| 8 | | | Alternative Energy Fund | |

|

| 16 | | | Asia Focus Fund | |

|

| 23 | | | Asia Pacific Dividend Fund | |

|

| 29 | | | China & Hong Kong Fund | |

|

| 35 | | | Global Energy Fund | |

|

| 42 | | | Global Innovators Fund | |

|

| 50 | | | Renminbi Yuan & Bond Fund | |

|

| 56 | | | Statements of Assets and Liabilities | |

|

| 58 | | | Statements of Operations | |

|

| 60 | | | Statements of Changes in Net Assets | |

|

| 63 | | | Financial Highlights | |

|

| 70 | | | Notes to Financial Statements | |

|

| 83 | | | Report of Independent Registered Public Accounting Firm | |

|

| 84 | | | Trustee and Officer Information | |

|

| 86 | | | Privacy Notice | |

|

| 87 | | | Guinness Atkinson Funds Information | |

|

3

Dear Guinness Atkinson Funds Shareholders,

To acknowledge the obvious, 2011 will not be among our favorite years. All of the Guinness Atkinson Funds with a full year track record produced negative total returns during the year. The newest member of the Guinness Atkinson Fund family, the Renminbi Yuan & Bond Fund, did manage to produce a positive return during its first six months which ended December 31, 2011. Despite the generally disappointing performance for the year we feel many of the Funds still have had excellent longer term results. The most obvious exception to that statement is the Alternative Energy Fund; more on that in a moment. Notwithstanding the performance of the Guinness Atkinson Funds or the global stock markets of late, we're still optimistic about the themes that underlie our fund range and look forward to improving performance both for the markets, our Funds and the global economy. And while it is still early in 2012, the year is starting off quite well for each of the Funds.

The performance of the Alternative Energy Fund pains all of us. We are still strongly of the opinion that alternative energy will play a major role in meeting the world's energy needs in coming years. In fact, it seems to us to be an inescapable conclusion. But, short term issues have swamped the long term potential. These short term issues include a weak global economy, reduced government support for alternative energy and a scarcity of capital at a time when much of the industry is still in its development years. Despite these short term negatives there are some positive developments. Most importantly solar technology continues to improve and the cost of solar panels continues to drop as efficiency increases. We believe we are not far from the day when solar power (without subsidy) is fully competitive with grid delivered electricity. If you live in the sunnier portions of the US you may have noticed more and more solar installations in your neighborhood. Our view is that within a few years neighborhood solar panels will be the norm.

As in past letters, we continue to advise investors to focus on the long term. In many ways it seems that we are alone in this long term orientation. We understand that global markets have become volatile and that for many sectors the buy and hold strategy has not worked well. Two points are worth making here. First, the themes that underlie the Guinness Atkinson Funds are by their very definition long term. We see more velocity in and out of the Guinness Atkinson Funds than seems appropriate, particularly given the long term nature of the Funds. Second, the Guinness Atkinson Funds with long term track records have generally done quite well. We don't mean to boast here; our point is more that we believe that the Guinness Atkinson Funds are meant to be long term investments and despite some very volatile periods, including a very weak 2011, the Funds have generally done well over the long term.

Fund Performance

The table below provides total return data for each of the Funds over the one, three, five, ten and from inception periods through December 31, 2011. Also included in the table is the expense ratio data from the most recent prospectus dated May 1, 2011. Astute readers will recognize that these expense ratios are inconsistent with the expense ratios found elsewhere in this report. By rule we are required to provide this expense ratio data whenever standardized performance data is provided and, further, the rule requires data from the most recent prospectus, which is sourcing its data from the 2010 annual report.

| Fund (inception date) | | 1-year | | 3-year | | 5-year | | 10-year | | From Inception | | Expense Ratio | |

| Alternative Energy Fund (March 31, 2006) | | | -42.53 | % | | | -15.71 | % | | | -21.93 | % | | | N/A | | | | -20.55 | % | | 1.76% | |

| Asia Focus (April 29, 1996) | | | -22.35 | % | | | 20.27 | % | | | 1.60 | % | | | 11.67 | % | | | 2.67 | % | | 1.67% | |

| Asia Pacific Dividend Fund (March 31, 2006) | | | -14.04 | % | | | 20.55 | % | | | 1.32 | % | | | N/A | | | | 2.93 | % | | 2.92% gross; 2.01% net† | |

| China & Hong Kong (June 30, 1994) | | | -27.52 | % | | | 17.25 | % | | | 3.91 | % | | | 11.29 | % | | | 7.38 | % | | 1.48% | |

| Global Energy Fund (June 30, 2004) | | | -13.16 | % | | | 18.25 | % | | | 3.15 | % | | | N/A | | | | 13.37 | % | | 1.25% | |

| Global Innovators Fund (December 15, 1998) | | | -6.51 | % | | | 16.67 | % | | | 0.99 | % | | | 3.77 | % | | | 3.72 | % | | 1.47% gross; 1.55% net† | |

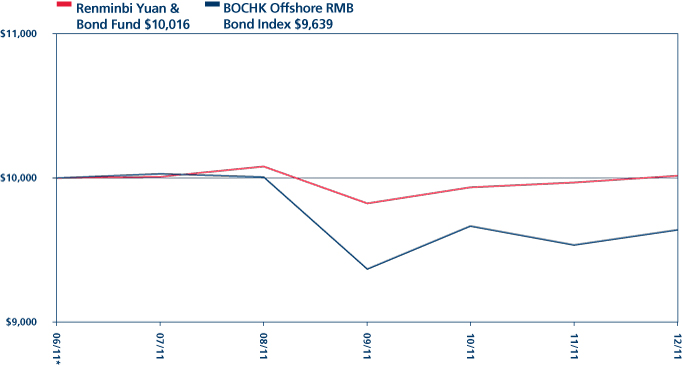

| Renminbi Yuan & Bond Fund (June 30, 2011) | | | N/A | | | | N/A | | | | N/A | | | | N/A | | | | 0.16 | % | | .90%* | |

Periods of greater than one year are average annualized returns; one year and shorter period returns are actual returns. All returns are for the periods ending December 31, 2011.

4

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than the original cost. Current performance of the Funds may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.gafunds.com. Each Fund imposes a 2% redemption fee on shares held less than 30 days. Performance data quoted does not reflect this fee. If it had, total return would be lower.

†All of the Guinness Atkinson Funds have an expense cap in place and the advisor is contractually obligated to cap the total expenses at least through June 30, 2012 and June 30, 2013 for the Renminbi Yuan & Bond Fund.

Expense ratios are from the most recent prospectus (dated May 1, 2011) and are from the most recent audited financials (period ending December 31, 2010) at the time that prospectus was completed.

*The Fund commenced operations on June 30, 2011.

Our investment team has provided a detailed commentary for each of the Guinness Atkinson Funds adjacent to each Fund's financial results. Below you'll find Morningstar ratings data for the Fund range.

As usual, we appreciate the confidence you have placed in us and our management team and look forward to what will hopefully be a great 2012.

Sincerely,

Timothy Guinness James Atkinson

5

Morningstar Ratings (based on Morningstar risk adjusted returns)

Below is a table listing the Morningstar star ratings as of December 31, 2011 for the six Guinness Atkinson Funds that have at least a three year history. Parenthetical numbers after the star rating indicate the number of funds in the comparison group.

| Fund | | Category | | Overall | | 3-year | | 5-year | | 10-year | |

Alternative Energy

Fund | | Equity Energy

| | | 1

(75 funds) | * | | | 1

(75 funds) | * | | | 1

(61 funds) | * | | | N/A

| | |

Asia Focus

Fund | | Pacific/Asia

Ex-Japan Stk | | | 2

(65 funds) | ** | | | 3

(65 funds) | *** | | | 2

(41 funds) | ** | | | 2

(35 funds) | ** | |

Asia Pacific Dividend

Fund | | Pacific/Asia

Ex-Japan Stk | | | 3

(65 funds) | *** | | | 4

(65 funds) | **** | | | 3

(41 funds) | *** | | | N/A

| | |

China & Hong Kong

Fund | | China Region | | | 3

(80 funds) | *** | | | 3

(80funds) | *** | | | 3

(61 funds) | *** | | | 3

(29 funds) | *** | |

Global Energy

Fund | | Equity Energy

| | | 3

(75 funds) | *** | | | 4

(75 funds) | **** | | | 3

(61 funds) | *** | | | N/A

| | |

Global Innovators

Fund | | Large Growth

| | | 3

(1,478 funds) | *** | | | 3

(1,478 funds) | *** | | | 2

(1,279 funds) | ** | | | 3

(804 funds) | *** | |

©2012 Morningstar, Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

The Funds invest in foreign securities which involves greater volatility and political, economic and currency risks and differences in accounting methods. Non-diversified Funds' assets may be concentrated in fewer individual holdings than diversified funds. Therefore, these Funds are more exposed to individual stock volatility than diversified funds. Investments in smaller companies involve additional risks such as limited liquidity and greater volatility. Investments in debt securities typically decrease in value when interest rates rise, which can be greater for long-term debt securities. The Funds may invest in derivatives which involves risks different from, and in certain cases, greater than the risks presented by traditional investments.

For each fund with at least a three-year history, Morningstar calculates a Morningstar RatingTM based on a Morningstar Risk-Adjusted Return measure that accounts for variation in a fund's monthly performance (including the effects of sales charges, loads, and redemption fees), placing more emphasis on downward variations and rewarding consistent performance. The top 10% of funds in each category receive 5 stars, the next 22.5% receive 4 stars the next 35% receive 3 stars, the next 22.5% receive 2 stars and the bottom 10% receive 1 star. (Each share class is counted as a fraction of one fund within this scale and rated separately, which may cause slight variations in distribution percentages.)

6

GUINNESS ATKINSON FUNDS

Expense Examples (Unaudited)

As a shareholder of the Funds, you incur two types of costs: (1) redemption fees; and (2) ongoing costs, including advisory fees; and other Fund expenses. The examples below are intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds.

The examples are based on an investment of $1,000 invested at the beginning of the period shown and held for the entire period from July 1, 2011 to December 31, 2011.

Actual Expenses

For each Fund, the first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled "Expenses Paid during Period" to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

For each Fund, the second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund's actual expense ratios and an assumed rate of return of 5% per year before expenses, which is not the Fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any redemption fees. Therefore, the second line for each Fund of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these redemption fees were included, your costs would have been higher.

| | | Beginning

Account

Value

(07/01/11) | | Ending

Account

Value

(12/31/11) | | Expenses Paid

During Period*

(07/01/11 to

12/31/11) | | Expense Ratios

During Period*

(07/01/11 to

12/31/11) | |

| Guinness Atkinson Alternative Energy Fund Actual | | $ | 1,000.00 | | | $ | 591.90 | | | $ | 7.34 | | | | 1.83 | % | |

Guinness Atkinson Alternative Energy Fund Hypothetical

(5% return before expenses) | | $ | 1,000.00 | | | $ | 1,015.98 | | | $ | 9.30 | | | | 1.83 | % | |

| Guinness Atkinson Asia Focus Fund Actual | | $ | 1,000.00 | | | $ | 765.20 | | | $ | 7.12 | | | | 1.60 | % | |

Guinness Atkinson Asia Focus Fund Hypothetical

(5% return before expenses) | | $ | 1,000.00 | | | $ | 1,017.14 | | | $ | 8.13 | | | | 1.60 | % | |

| Guinness Atkinson Asia Pacific Dividend Fund Actual | | $ | 1,000.00 | | | $ | 851.90 | | | $ | 9.24 | | | | 1.98 | %† | |

Guinness Atkinson Asia Pacific Dividend Fund Hypothetical

(5% return before expenses) | | $ | 1,000.00 | | | $ | 1,015.22 | | | $ | 10.06 | | | | 1.98 | %† | |

| Guinness Atkinson China & Hong Kong Fund Actual | | $ | 1,000.00 | | | $ | 757.70 | | | $ | 6.82 | | | | 1.54 | % | |

Guinness Atkinson China & Hong Kong Fund Hypothetical

(5% return before expenses) | | $ | 1,000.00 | | | $ | 1,017.44 | | | $ | 7.83 | | | | 1.54 | % | |

| Guinness Atkinson Global Energy Fund Actual | | $ | 1,000.00 | | | $ | 798.10 | | | $ | 6.21 | | | | 1.37 | % | |

Guinness Atkinson Global Energy Fund Hypothetical

(5% return before expenses) | | $ | 1,000.00 | | | $ | 1,018.30 | | | $ | 6.97 | | | | 1.37 | % | |

| Guinness Atkinson Global Innovators Fund Actual | | $ | 1,000.00 | | | $ | 909.10 | | | $ | 6.78 | | | | 1.41 | % | |

Guinness Atkinson Global Innovators Fund Hypothetical

(5% return before expenses) | | $ | 1,000.00 | | | $ | 1,018.10 | | | $ | 7.17 | | | | 1.41 | % | |

| Guinness Atkinson Renminbi Yuan & Bond Fund Actual | | $ | 1,000.00 | | | $ | 1,001.60 | | | $ | 4.54 | | | | 0.90 | %† | |

Guinness Atkinson Renminbi Yuan & Bond Fund Hypothetical

(5% return before expenses) | | $ | 1,000.00 | | | $ | 1,020.67 | | | $ | 4.58 | | | | 0.90 | %† | |

*Expenses are equal to the Funds' annualized expense ratio as indicated, multiplied by the average account value over the period, multiplied by the number of days in most recent fiscal half-year period (184), then divided by the number of days in the fiscal year (365) (to reflect the one-half year period).

†Net of fee waivers and/or expense reimbursements. If those fee waivers and/or expense reimbursements had not been in effect, the Fund's actual expenses would have been higher.

7

ALTERNATIVE ENERGY FUND for the period ended December 31, 2011

1. Performance

AVERAGE ANNUALIZED TOTAL RETURNS

| | | 1 Year

(actual) | | 3 Years | | 5 Years | | Since

inception

(March 31, 2006) | |

| Fund | | | -42.53 | % | | | -15.71 | % | | | -21.93 | % | | | -20.55 | % | |

| Benchmark Indices: | |

| Wilderhill New Energy Global Innovation Index | | | -39.61 | % | | | -9.75 | % | | | -14.27 | % | | | -11.46 | % | |

| Wilderhill Clean Energy Index | | | -50.48 | % | | | -15.11 | % | | | -21.76 | % | | | -22.18 | % | |

| MSCI World Index | | | -5.01 | % | | | 11.81 | % | | | -1.76 | % | | | 0.60 | % | |

The Fund's gross expense ratio is 1.76% per the Summary Prospectus dated May 1, 2011. Guinness Atkinson Asset Management has contractually agreed to waive a portion of its advisory fees so that the Fund's ratio of expenses to average daily net assets will not exceed 1.98% (excluding Acquired Fund Fees and Expenses, interest, taxes, dividends on short positions and extraordinary expenses) through at least June 30, 2012. To the extent that the Advisor waives fees it may seek repayment of a portion or all of such amounts at any time within the three fiscal years after the fiscal year in which such amounts were waived, subject to the applicable cap.

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.gafunds.com, or calling (800) 916-6566.

The Fund imposes a 2% redemption fee on shares held less than 30 days. Performance data quoted does not reflect the 2% redemption fee on shares held less than 30 days. Total returns for certain periods reflect a fee waiver in effect and in the absence of this waiver, the total returns would have been lower.

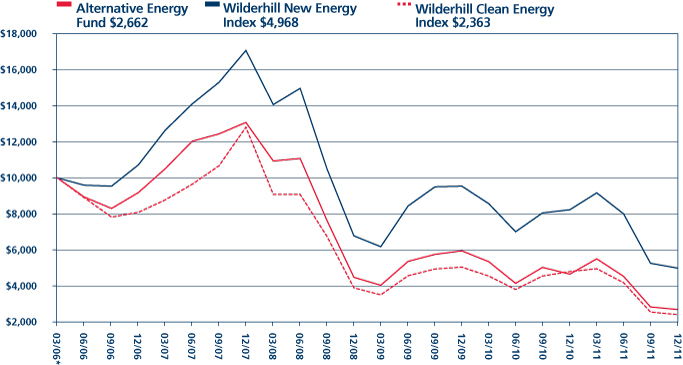

The Guinness Atkinson Alternative Energy Fund was down 42.53% in 2011. This compared to a fall in the Wilderhill New Energy Global Innovation Index of 39.61% and in the Wilderhill Clean Energy Index of 50.48%. The year was particularly disappointing given the strong first quarter. The alternative energy industry appeared to be getting back on track but the European debt crisis set the recovery back dramatically.

As a result of the crisis, demand for alternative energy was weaker in key European markets which was compounded by the difficulty investors faced in procuring bank financing. The ensuing oversupply in both the wind and solar sectors saw pricing pressure and lower volumes than expected which significantly eroded profitability and hurt share prices.

The Fund has been positioned in the lower cost solar manufacturers, and while we believe these companies are positioned to emerge as leaders in the next cycle of the industry, 2012 saw indiscriminate poor performance from all solar stocks and notwithstanding the Fund's sales of some solar holdings in the first quarter, the remaining solar holdings were the main driver of the Fund's weak performance.

The wind sector also experienced a difficult year, with installations levels plateauing in most market and continued pricing pressure, which weighed on the stock prices of the turbine manufacturers.

The Fund's better performing stocks were mainly the renewables utility holdings, with a notable outperformance from one of the Fund's ground source heat pump stocks – LSB Industries.

Stock performance numbers taken as the price return of the stocks when included in the fund; Source: Bloomberg

8

ALTERNATIVE ENERGY FUND

2. Portfolio

| Sector | | % of Assets | |

| Wind | | | 38.89 | % | |

| Solar | | | 35.19 | % | |

| Efficiency | | | 11.30 | % | |

| Geothermal | | | 3.18 | % | |

| Hydro | | | 6.40 | % | |

| Biomass Energy | | | 0.00 | % | |

| Cash | | | 1.46 | % | |

| | | | 100.00 | % | |

| Domicile* | | % of Assets | |

| Europe | | | 36.28 | % | |

| Asia | | | 30.88 | % | |

| North America | | | 28.31 | % | |

| Latin America | | | 3.07 | % | |

| Australasia | | | 0.00 | % | |

| Cash | | | 1.46 | % | |

| | | | 100.00 | % | |

* region is as per company domicile.

The portfolio is concentrated in the wind and solar sectors, with 38.89% in Wind and 35.19% in Solar. We believe these sectors have the best long-term growth potential of the alternative energy space.

Within the Solar sector, most of our holdings have Asian manufacturing capabilities, as we believe that this is essential for a competitive cost structure today. Further solar holdings are in leading installers with good exposure to the end market volume growth and we hold one company that manufactures inverters.

For our Wind exposure we are invested in both turbine manufacturers and wind farm developers. In the long run, we believe that there are good potential returns both from owning Wind assets and investing in the turbine value chain as the Wind industry becomes more mainstream and as offshore Wind gains traction.

Further investments are in a hydroelectric power producer in Latin America, a geothermal company, a ground source heat pump company two metering companies and two inverter manufacturers.

The Fund has 36.28% of its holdings in companies domiciled in Europe, reflecting the more mature European industry. North America accounts for 28.31% of the Fund. The Fund's 33.96% of emerging markets holdings is principally in Asia, with our investments in Chinese companies making up 30.88% of the Fund.

| Mkt Cap $m | | Positions | | % of Assets | |

| >1000 | | | 13 | | | | 41.99 | % | |

| 500-1000 | | | 6 | | | | 18.60 | % | |

| 250-500 | | | 6 | | | | 20.44 | % | |

| 100-250 | | | 4 | | | | 14.12 | % | |

| 50-100 | | | 0 | | | | 0.00 | % | |

| <50 | | | 3 | | | | 3.39 | % | |

9

ALTERNATIVE ENERGY FUND

| Position size | | Positions | | % of Assets | |

| Full | | | 29 | | | | 95.15 | % | |

| Half | | | 0 | | | | 0.00 | % | |

| Research | | | 3 | | | | 3.39 | % | |

The liquidity of the Fund remains excellent, with 41.99% of the Fund in companies with a market capitalization over US$1,000 million. The Fund now has 29 full units and 3 research holdings.

3. Activity

The Fund uses a structure of 30 equally weighted holdings, a small number of which are split into two half holdings. The Fund has also historically held a small number of research holdings. The Fund has moved away from holding half-units in stocks in favour of holding full units in stocks and there has been a reduction in the number of research holdings. The Fund should continue to hold around 30 equally weighted holdings.

The Fund acquired new positions in Enel Green Power, Nordex, Verbund, China Datang, China Longyuan, China Suntien, Huaneng Renewables, Elster, Power One. As a result the Fund has increased its exposure to utility stocks in both Europe and China. Elster is a metering company that complements the fund's holding in Itron and Power One increases the Fund's holdings in inverter manufacturers.

The Fund sold its holdings in Iberdrola Renovables, Phoenix Solar, Solarworld, Clipper Windpower, Hansen Transmissions, PV Crystalox, Renewable Energy Corporation, Canadian Solar, First Solar, LSB Industries and MEMC Electronics. The main emphasis has been on reducing the Fund's exposure to solar companies, in our view, that do not have a competitive cost structure in the current pricing environment, which has principally involved selling the Fund's remaining European solar holdings.

4. Outlook

We believe that 2012 should be a challenging year for companies in the sector as a result of the current economic environment. The sector is vulnerable to lack of financing and reductions in subsidies. However, we would point out that the share prices and valuations reflect this challenging environment and there is potential for earnings expectations for 2012 to be exceeded given how low they have been set and for the outlook for 2013 to improve, both of which would be positive for share prices.

It is our view that there should be a demand response to the current low price of solar modules that could see demand exceed expectations. The low cost solar manufacturers should be able to operate plants at capacities that allow them to continue lowering costs further, which, in our view, should lead to higher margins and a better ability to compete. Headwinds include further German tariff reductions and the potential imposition of import tariffs on solar modules by the US. However, a major difference between today and three years ago is that Germany is now less than 30% of the market, having been over half of the market and the main countries experiencing growth in demand are emerging markets and those with high electricity prices. In our view, this provides better diversification of the sources of solar demand.

In our view, key markets for 2012 will be China and the US. China has introduced a feed-in tariff that is leading to demand far in excess of that expected and based on Edward Guinness's visit to China in early 2011, we do not think that China will look to constrain the volumes of installations. The US is emerging as a serious market with utility scale installations leading the way. We also note the emergence of the rent-a-roof model in the US that is likely to lead to rapid deployment of residential installations that provide a firmer foundation for demand. We also believe that we will start to see installations in Germany and Italy being made that do not rely on Feed-in Tariffs for their economics, which should begin the transition away from subsidies.

We expect that the key drivers of growth in the wind market will be emerging markets and the construction of large new offshore wind installations. The US market has been hurt by the low natural gas price caused by the production of high volumes of shale gas. There is an expectation that 2012 could be a relatively strong year for US installations as the Production Tax Credit expires at the end of 2012, but expectations for installations in 2013 are low unless it is extended. Previously this credit has been extended on expiration, but the freeze in legislative activity caused by the US presidential election and the aggressive positioning of the Republican Party against alternative energy means that wind developers in the US are not expecting an extension and are preparing for low levels of installations in the US from 2013.

10

ALTERNATIVE ENERGY FUND

The Chinese electricity market has grown dramatically over the last five years to over 20GW of annual installations. However, the level of new installations is now expected to plateau at this high level as a result of grid constraints. There has been a sharp reduction in turbine prices as the domestic manufacturers – Dongfang Electric, Sinovel and Goldwind – compete hard. The main beneficiaries of this have been the Chinese Wind developers, which are able to generate higher returns from newly constructed assets.

We have begun to see the first indications of improvement in the US housing market, which should improve the outlook for ground source heat pump installations, and we see good opportunities for companies in the metering sector as utilities execute upgrades to their networks.

The long term outlook for the sector remains positive and continues to improve as costs of alternative energy technologies become more competitive and global demand for energy continues to rise, pushing fossil fuel prices higher.

| |  | |

|

| Edward Guinness | | Matthew Page | |

|

The Fund invests in foreign securities, which will involve political, economic and currency risks, greater volatility, and differences in accounting methods. The Fund is non-diversified, meaning that its assets may be concentrated in fewer individual holdings than diversified funds. Therefore, the Fund is more exposed to individual stock volatility than diversified funds. The Fund invests in smaller companies, which will involve additional risks such as limited liquidity and greater volatility.

The Wilderhill New Energy Global Innovation Index (NEX) is a modified dollar-weighted index of publicly traded companies that are active in renewable and low-carbon energy, and that stand to benefit from responses to climate change and energy security concerns. The Wilderhill Clean Energy Index (ECO) is a modified equal dollar weighted index comprised of publicly traded companies whose businesses stand to benefit substantially from societal transition toward the use of cleaner energy and conservation. The MSCI World Energy Index is an unmanaged index composed of more than 1,400 stocks listed on exchanges in the U.S., Europe, Canada, Australia, New Zealand, and the Far East. These indices are unmanaged, not available for investment and do not incur expenses.

Please refer to the Schedule of Investments for details on fund holdings. Current and future portfolio holdings are subject to risk.

The information provided herein represents the opinion of Guinness Atkinson Management for the period stated and is not intended to be a forecast of future events, a guarantee of future results, or investment advice. Opinions, fund holdings and sector allocations are subject to change at any time and are not recommendations to buy or sell any security.

11

GUINNESS ATKINSON ALTERNATIVE ENERGY FUND

Growth of $10,000

Average Annual Total Return

Periods Ended December 31, 2011

| One Year | | Five Year | | Since Inception

(03/31/06)* | |

| | (42.53 | )% | | | (21.93 | )% | | | (20.55 | )% | |

* Inception date 3/31/06.

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.gafunds.com.

Total returns reflect a fee waiver in effect and in the absence of this waiver, the total returns would be lower. The Fund imposes a 2% redemption fee on shares held less than 30 days.

The Wilderhill New Energy Global Innovations Index (NEX) is a modified dollar weighted index of publicly traded companies, which are active in renewable and low-carbon energy, and which stand to benefit from responses to climate change and energy security concern. The Wilderhill Clean Energy Index (ECO) is a modified equal dollar weighted index comprised of publicly traded companies whose businesses stand to benefit substantially from societal transition toward the use of cleaner energy and conservation.

12

FUND HIGHLIGHTS at December 31, 2011

GUINNESS ATKINSON ALTERNATIVE ENERGY FUND

| # of Holdings in Portfolio: | | 33 | |

| Portfolio Turnover: | | 43.1% | |

| % of Stocks in Top 10: | | 36.3% | |

| Fund Managers: | |

| Edward Guinness | | | |

| Top 10 Holdings (% of net assets) | | | | Sector Breakdown (% of net assets) | | | |

| WaterFurnace Renewable Energy, Inc. | | 4.7% | | Wind | | 42.6% | |

| Greentech Energy Systems | | 3.9% | | Solar | | 32.1% | |

| Boralex, Inc. | | 3.6% | | Efficiency | | 14.5% | |

| Gamesa Corporacion Tecnologica S.A. | | 3.6% | | Hydro | | 6.4% | |

| SunPower Corp. - Class B | | 3.6% | | Geothermal | | 3.2% | |

| STR Holdings, Inc. | | 3.5% | | | | | |

| China Longyuan Power Group Corp. - H Shares | | 3.4% | | | | | |

| SMA Solar Technology AG | | 3.4% | | | | | |

| Verbund AG | | 3.3% | | | | | |

| EDP Renovaveis SA | | 3.3% | | | | | |

13

SCHEDULE OF INVESTMENTS

at December 31, 2011

GUINNESS ATKINSON ALTERNATIVE ENERGY FUND

| Shares | | COMMON STOCKS: 98.8% | | Value | |

| Efficiency: 14.5% | | | |

| | 146,000 | | | Applied Intellectual Capital Ltd.*†^ | | $ | — | | |

| | 760,987 | | | Carmanah Technologies Corp.*† | | | 336,141 | | |

| | 44,000 | | | Elster Group SE - ADR* | | | 572,000 | | |

| | 16,000 | | | Itron, Inc.* | | | 572,320 | | |

| | 4,445,888 | | | Thermal Energy International, Inc.*† | | | 250,934 | | |

| | 53,700 | | | WaterFurnace Renewable Energy, Inc. | | | 820,193 | | |

| | | | | | | | 2,551,588 | | |

| Geothermal: 3.2% | | | |

| | 31,119 | | | Ormat Technologies, Inc. | | | 561,076 | | |

| Hydro: 6.4% | | | |

| | 30,453 | | | Cia Energetica de Minas Gerais ADR | | | 541,759 | | |

| | 21,800 | | | Verbund AG | | | 585,029 | | |

| | | | | | | | 1,126,788 | | |

| Solar: 32.1% | | | |

| | 428,500 | | | JA Solar Holdings Co., Ltd.* | | | 574,190 | | |

| | 122,200 | | | LDK Solar Co., Ltd. - ADR* | | | 512,018 | | |

| | 143,000 | | | Power-One Inc.* | | | 559,130 | | |

| | 356,600 | | | Renesola Ltd. - ADR* | | | 545,598 | | |

| | 10,560 | | | SMA Solar Technology AG | | | 589,947 | | |

| | 74,900 | | | STR Holdings, Inc.* | | | 616,427 | | |

| | 100,705 | | | SunPower Corp. - Class B* | | | 627,392 | | |

| | 247,291 | | | Suntech Power Holdings Co., Ltd. - ADR* | | | 546,513 | | |

| | 80,500 | | | Trina Solar Ltd. - ADR* | | | 537,740 | | |

| | 136,500 | | | Yingli Green Energy Holding Co., Ltd. - ADR* | | | 518,700 | | |

| | | | | | | | 5,627,655 | | |

| Wind: 42.6% | | | |

| | 6,200 | | | Acciona S.A. | | | 535,464 | | |

| | 90,387 | | | Boralex, Inc.* | | | 632,598 | | |

| | 2,946,000 | | | China Datang Corp. Renewable Power Co. Ltd. - H Shares* | | | 531,043 | | |

| | 763,000 | | | China Longyuan Power Group Corp. - H Shares | | | 596,324 | | |

| | 2,967,000 | | | China Suntien Green Energy Corp. Ltd. - H Shares | | | 519,548 | | |

| | 94,300 | | | EDP Renovaveis SA* | | | 577,040 | | |

| | 264,600 | | | Enel Green Power SpA | | | 552,727 | | |

| | 152,219 | | | Gamesa Corporacion Tecnologica S.A. | | | 632,399 | | |

| | 221,100 | | | Greentech Energy Systems* | | | 692,946 | | |

| | 2,264,000 | | | Huaneng Renewables Corp. Ltd. - H Shares* | | | 559,689 | | |

| | 108,400 | | | Nordex SE* | | | 554,171 | | |

| | 491,416 | | | Theolia SA* | | | 546,972 | | |

| | 51,315 | | | Vestas Wind Systems A/S* | | | 553,955 | | |

| | | | | | | | 7,484,876 | | |

| | | | | Total Common Stocks

(cost $33,674,278) | | | 17,351,983 | | |

The accompanying notes are an integral part of these financial statements.

14

| | | | Value | |

| | | | | Total Investments in Securities

(cost $ $33,674,278): 98.8% | | $ | 17,351,983 | | |

| | | | | Other Assets less Liabilities: 1.2% | | | 208,520 | | |

| | | Net Assets: 100.0% | | $ | 17,560,503 | | |

* Non-income producing security.

† Illiquid. Illiquid securities represent 3.3% of net assets.

^ Fair value under direction of the Board of Trustees. Fair valued securities represent 0.0% of net assets.

ADR - American Depository Receipt

The accompanying notes are an integral part of these financial statements.

15

ASIA FOCUS FUND for the period ended December 31, 2011

1. Performance

AVERAGE ANNUALIZED TOTAL RETURNS

| | | 6 Months

(actual) | | 1 Year

(actual) | | 3 Years | | 5 Years | | 10 Years | |

| Fund | | | -23.48 | % | | | -22.35 | % | | | 20.27 | % | | | 1.60 | % | | | 11.67 | % | |

| Benchmark Index: | |

| MSCI AC Far East Free Ex Japan | | | -16.60 | % | | | -14.68 | % | | | 19.84 | % | | | 3.19 | % | | | 11.46 | % | |

| S&P 500 | | | -3.70 | % | | | 2.09 | % | | | 14.12 | % | | | -0.25 | % | | | 2.92 | % | |

The Fund's gross expense ratio is 1.67% per the Summary Prospectus dated May 1, 2011. Guinness Atkinson Asset Management has contractually agreed to waive a portion of its advisory fees so that the Fund's ratio of expenses to average daily net assets will not exceed 1.98% (excluding Acquired Fund Fees and Expenses, interest, taxes, dividends on short positions and extraordinary expenses) through at least June 30, 2012. To the extent that the Advisor waives fees it may seek repayment of a portion or all of such amounts at any time within the three fiscal years after the fiscal year in which such amounts were waived, subject to the applicable cap.

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.gafunds.com, or calling (800) 916-6566.

The Fund imposes a 2% redemption fee on shares held less than 30 days. Performance data quoted does not reflect the 2% redemption fee on shares held less than 30 days. Total returns for certain periods reflect a fee waiver in effect and in the absence of this waiver, the total returns would have been lower.

The Fund had a disappointing year in 2011, and suffered as a result of volatility in Asian equity markets, particularly in the third quarter of the year. During the third quarter, there was a fall in global risk appetite as a result of fears over excess sovereign debt in the Eurozone countries, and this caused volatility in global equity markets. Emerging markets equities, including Asian equities, suffered relative to developed world equities as investors considered them to be riskier than their counterparts in the US or Europe. In our view, the flight to developed world assets reflects a misunderstanding of the real risks in the financial world at present, given much of the excess leverage, and the risk to sovereign finances, lies in the developed world and not in Asia. In our view, some of the selling was based on fear, and was detached from the reality of balance sheet strength and faster growth in Asia, relative to the US and Europe.

In addition to these macro issues, the construction of the portfolio is driven by bottom-up stock selection, and we have overweight positions in some sectors which suffered on a relative basis this year. The Fund is overweight in Materials, Energy and Industrials stocks, and is underweight in Consumer Staples and Utilities, sectors which are traditionally considered as having 'defensive' earnings. In our view, Materials, Energy and Industrials stocks offer a good combination of earnings growth, and a reasonable valuation, although their earnings can be considered reasonably cyclical. These stocks have suffered excessively, in our view, given there are also investor concerns about a slowdown in Chinese growth, partly due to slowing growth globally, and partly due to the monetary tightening policies of the Chinese authorities.

Although global growth is clearly slowing, the Chinese authorities seem to have changed course on monetary policy, and have already started some limited loosening. The loosening reflects a shift to more pro-growth policies, but also their view that inflation and the property market are coming under control. If this trend continues, it is likely to be positive for the construction industry in China, and this could help confidence return to some of our holdings in Materials, Energy and Industrials.

Elsewhere in Asia, there was a decent performance from Thai equities, where the Fund is well represented. Thailand held a successful transfer of power following its general election in July, and this helped improve confidence with international investors. However, there was widespread flooding in October, and as a result there was disruption and dislocation of economic activity. It seems, though, that there was little permanent damage to Thailand's infrastructure as a result, and the market was one of the better performers over the full year.

16

ASIA FOCUS FUND

2. Portfolio Position

The Fund remains overweight in Chinese equities, and the rise of domestic consumption there is the central theme in the portfolio. Portfolio construction is driven principally by stock selection, but the portfolio is managed to reflect our view of the macro circumstances. Although Chinese economic growth has slowed in recent quarters, it is still rapid for a country of its size, and China should continue to suck in goods and services from elsewhere in Asia.

The Fund is also overweight in Thailand and Indonesia, and both of these countries have continued to grow well in the last year, despite facing challenges. We did not change positioning as a result of the flooding in Thailand, and we have been rewarded with a decent bounce in our equity holdings there. Growth in Indonesia has been consistently impressive in the last two years, and the market has attracted more foreign capital as a result. Indeed, Indonesia was one of the select few equity indices in Asia to finish 2011 in positive territory. We are looking more closely at Indonesia in the light of the Land Acquisition Act, which passed into law in December 2011. This Act is designed to encourage infrastructure development by making it easier to acquire land for government projects.

By sector, the Fund is overweight in Energy, Materials, Industrials and Information Technology stocks. This makes the Fund sensitive to domestic construction and infrastructure projects, which we see as a good way to benefit from domestic consumption growth whilst avoiding Consumer stocks, which we feel have insufficient value to be attractive. The portfolio is also underweight in Financials and Real Estate stocks, which have been under pressure due to monetary tightening in the last year, particularly in China.

3. Outlook

Looking forward, we remain concerned that the fundamental problem of excess leverage in the developed world has not been resolved, and this could cause further equity instability in the future. Economic growth remains slow in Europe, although there are some signs that growth may be beginning to bottom out in the US. In Asia, Chinese growth is clearly slowing, but the most recent economic data suggest that a gradual slowdown is underway, rather than the 'hard landing' which has been suggested by some commentators.

In our view, China remains central to the economic welfare of Asia, and we think that the prospects for this market are good for the coming year. Chinese equities have suffered a de-rating over the course of the last two years, and a range of blue-chip stocks have effectively remained below their medium-term ratings since the financial crisis of 2008/9. We think that this situation will not persist, and that investors will recognise the superior prospects of these stocks, relative to their indebted cousins in the developed world.

Elsewhere in Asia, we have been underweight in South Korea for a number of quarters, but we feel that prospects there are as bright as they have been for some time, and we are considering adding to our holdings. South Korea was down in line with the benchmark last year, but we believe its stocks have reasonable earnings momentum, and on a valuation basis we feel this is one of the more attractive markets in the region. Although South Korea has significant exports, these are spread across a range of sectors including shipbuilding, engineering, petrochemicals, electronics and mobile phone handsets. Exports to emerging markets, particularly China, are now making up a bigger part of the mix. This diversity of trading partners and sectors has helped to smooth out economic growth, whilst domestic consumption is also becoming more significant.

Edmund Harriss

The Fund invests in foreign securities, which involves political, economic and currency risks, greater volatility, and differences in accounting methods. The Fund is non-diversified, meaning its assets may be concentrated in fewer individual holdings than diversified funds. Therefore, the Fund is more exposed to individual stock volatility than diversified funds. The Fund invests in smaller companies, which involves additional risks such as limited liquidity and greater volatility.

The MSCI All Country Far East Free ex-Japan Index (MSCI AC Far East Free ex-Japan Index) is a free float-adjusted, capitalization-weighted index that is designed to measure equity market performance in the Asia region excluding Japan. The

17

ASIA FOCUS FUND

Standard & Poor's 500 Index is a market-capitalization weighted index composed of 500 widely held common stocks of U.S. companies. These indices are unmanaged, not available for investment and do not incur expenses.

Please refer to the Schedule of Investments for details on Fund holdings. Current and future portfolio holdings are subject to risk.

The information provided herein represents the opinion of Guinness Atkinson Management for the period stated and is not intended to be a forecast of future events, a guarantee of future results, or investment advice. Opinions, Fund holdings and sector allocations are subject to change at any time, and are not recommendations to buy or sell any security.

18

GUINNESS ATKINSON ASIA FOCUS FUND

Growth of $10,000

Periods Ended December 31, 2011

| One Year | | Five Year | | Ten Year | |

| | (22.35 | )% | | | 1.60 | % | | | 11.67 | % | |

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.gafunds.com.

Total returns reflect a fee waiver in effect and in the absence of this waiver, the total returns would be lower. The Fund imposes a 2% redemption fee on shares held less than 30 days.

The MSCI All Country Far East Free ex-Japan Index (MSCI AC Far East Free ex-Japan Index) is a free float-adjusted, capitalization-weighted index that is designed to measure equity market performance in the Asia region excluding Japan. The index referenced in this chart is not available for investment and does not incur expenses.

19

FUND HIGHLIGHTS at December 31, 2011

GUINNESS ATKINSON ASIA FOCUS FUND

| # of Holdings in Portfolio: | | 39 | |

| Portfolio Turnover: | | 7.8% | |

| % of Stocks in Top 10: | | 41.4% | |

| Fund Managers: | |

| Edmund Harriss | |

| James Weir | |

| Top 10 Holdings (% of net assets) | | | |

| Hyundai Mobis | | 6.0% | |

| Samsung Electronics Co., Ltd. | | 5.0% | |

| Taiwan Semiconductor Manufacturing Co., Ltd. | | 4.5% | |

| Weichai Power Co., Ltd. - H Shares | | 4.3% | |

| Digi.Com Bhd | | 4.2% | |

| PetroChina Co., Ltd. - H Shares | | 4.0% | |

| HTC Corp. | | 3.7% | |

| Kunlun Energy Co., Ltd. | | 3.3% | |

| Dongfang Electric Corp. Ltd. - H Shares | | 3.2% | |

| Jiangxi Copper Co., Ltd. - H Shares | | 3.2% | |

| Sector Breakdown (% of net assets) | | | | | | | |

| Coal | | 10.8% | | Computers | | 2.4% | |

| Oil Company - Exploration & Production | | 8.8% | | Cellular Telecommunications | | 2.4% | |

| Oil Company - Integrated | | 6.9% | | Steel - Producers | | 2.2% | |

| Semiconductor Components - Integrated Circuits | | 6.8% | | Commercial Banks | | 2.1% | |

| Auto/Truck Parts & Equipment - Original | | 6.0% | | Exchange Traded Funds | | 2.1% | |

| Electronic Components - Semiconductor | | 5.0% | | Auto-Cars/Light Trucks | | 2.0% | |

| Electric - Generation | | 4.3% | | Building Products - Cement/Aggregate | | 2.0% | |

| Auto/Truck Parts & Equipment - Replacements | | 4.2% | | Chemicals - Other | | 1.8% | |

| Telecommunication Services | | 4.2% | | Web Portals/ISP | | 1.8% | |

| Wireless Equipment | | 3.7% | | Non-Ferrous Metals | | 1.6% | |

| Power Converson/Supply Equipment | | 3.2% | | Building & Construction Products | | 1.6% | |

| Metal - Copper | | 3.2% | | Public Thoroughfares | | 1.6% | |

| Engineering/R&D Services | | 3.1% | | Energy - Alternate Sources | | 1.3% | |

| Computers - Peripheral Equipment | | 2.5% | | Machinery - General Industry | | 0.4% | |

| Real Estate Operations/Development | | 2.5% | | | | | | | |

20

SCHEDULE OF INVESTMENTS

at December 31, 2011

GUINNESS ATKINSON ASIA FOCUS FUND

| Shares | | COMMON STOCKS: 100.5% | | Value | |

| China: 33.8% | | | |

| | 309,000 | | | Anhui Conch Cement Co Ltd - H Shares | | $ | 917,062 | | |

| | 321,000 | | | China Shenhua Energy Co., Ltd. - H Shares | | | 1,392,849 | | |

| | 1,209,900 | | | db x-trackers - CSI300 INDEX ETF - 2D | | | 959,620 | | |

| | 490,000 | | | Dongfang Electric Corp. Ltd. - H Shares | | | 1,451,085 | | |

| | 1,104,636 | | | Guangzhou Automobile Group Co., Ltd. - H Shares | | | 921,644 | | |

| | 168,300 | | | JA Solar Holdings Co., Ltd. - ADR* | | | 225,522 | | |

| | 670,000 | | | Jiangxi Copper Co., Ltd. - H Shares | | | 1,447,558 | | |

| | 1,490,000 | | | PetroChina Co., Ltd. - H Shares | | | 1,855,162 | | |

| | 1,714,000 | | | Shenzhen Expressway Co., Ltd. - H Shares | | | 723,859 | | |

| | 1,694,000 | | | Soho China, Ltd. | | | 1,127,647 | | |

| | 16,650 | | | Sohu.com Inc.* | | | 832,500 | | |

| | 54,000 | | | Trina Solar Ltd. - ADR* | | | 360,720 | | |

| | 396,000 | | | Weichai Power Co., Ltd. - H Shares | | | 1,947,725 | | |

| | 616,800 | | | Yanzhou Coal Mining Co., Ltd. - H Shares | | | 1,316,734 | | |

| | | | 15,479,687 | | |

| Hong Kong: 14.4% | | | |

| | 618,000 | | | Chen Hsong Holdings † | | | 191,767 | | |

| | 1,671,000 | | | China Liansu Group Holdings Ltd. | | | 725,062 | | |

| | 110,500 | | | China Mobile Ltd. | | | 1,079,874 | | |

| | 715,000 | | | CNOOC Ltd. | | | 1,250,187 | | |

| | 129,266 | | | HSBC Holdings PLC | | | 981,986 | | |

| | 286,000 | | | Kingboard Chemical Holdings Ltd. | | | 846,960 | | |

| | 1,048,000 | | | Kunlun Energy Co., Ltd. | | | 1,492,401 | | |

| | | | 6,568,237 | | |

| Indonesia: 3.7% | | | |

| | 225,000 | | | Indo Tambangraya Megah PT | | | 959,057 | | |

| | 2,111,000 | | | International Nickel Indonesia Tbk PT | | | 744,990 | | |

| | | | 1,704,047 | | |

| Malaysia: 4.2% | | | |

| | 1,588,000 | | | DiGi.Com Bhd | | | 1,943,672 | | |

| Singapore: 2.8% | | | |

| | 901,000 | | | Sakari Resources Ltd. | | | 1,278,162 | | |

| South Korea: 16.3% | | | |

| | 10,730 | | | Hyundai Mobis | | | 2,733,965 | | |

| | 3,055 | | | POSCO | | | 1,011,842 | | |

| | 2,500 | | | Samsung Electronics Co., Ltd. | | | 2,300,773 | | |

| | 8,000 | | | Samsung Engineering Co., Ltd. | | | 1,407,547 | | |

| | | | 7,454,127 | | |

The accompanying notes are an integral part of these financial statements.

21

| Shares | | COMMON STOCKS: 100.5% (Continued) | | Value | |

| Taiwan: 15.4% | | | |

| | 103,411 | | | HTC Corp. | | $ | 1,697,390 | | |

| | 1,039,314 | | | Lite-On Technology Corp. | | | 1,170,468 | | |

| | 407,000 | | | Novatek Microelectronics Corp. Ltd. | | | 1,020,222 | | |

| | 2 | | | Shin Zu Shing Co., Ltd. | | | 4 | | |

| | 830,000 | | | Taiwan Semiconductor Manufacturing Co., Ltd. | | | 2,077,810 | | |

| | 863,324 | | | Wistron Corp. | | | 1,093,447 | | |

| | | | 7,059,341 | | |

| Thailand: 9.9% | | | |

| | 234,500 | | | Electricity Generating PCL/Foreign | | | 715,392 | | |

| | 685,000 | | | Glow Energy PCL/Foreign | | | 1,237,559 | | |

| | 239,000 | | | PTT Exploration & Production PCL/Foreign | | | 1,276,434 | | |

| | 130,700 | | | PTT PCL/Foreign | | | 1,317,357 | | |

| | | | 4,546,742 | | |

| | | | | Total Common Stocks

(cost $40,369,746) | | | 46,034,015 | | |

| | | | | Total Investments in Securities

(cost $40,369,746): 100.5% | | | 46,034,015 | | |

| | | | | Liabilities in Excess of Other Assets: (0.5%) | | | (216,979 | ) | |

| | | | | Net Assets: 100.0% | | $ | 45,817,036 | | |

* Non-income producing security.

† Illiquid. Illiquid securities represent 0.4% of net assets.

ADR - American Depository Receipt

The accompanying notes are an integral part of these financial statements.

22

ASIA PACIFIC DIVIDEND FUND for the period ended December 31, 2011

1. Performance

ANNUALIZED TOTAL RETURNS

| | | 6 Months

(actual) | | 1 Year

(actual) | | 3 Years | | 5 Years | | Since Launch

(March 31, 2006) | |

| Fund | | | -14.81 | % | | | -14.04 | % | | | 20.55 | % | | | 1.32 | % | | | 2.93 | % | |

| Benchmark Index: | |

| MSCI Pacific Ex Japan | | | -15.65 | % | | | -13.18 | % | | | 20.86 | % | | | 3.55 | % | | | 6.93 | % | |

| S&P 500 | | | -3.70 | % | | | 2.09 | % | | | 14.12 | % | | | -0.25 | % | | | 1.63 | % | |

The Fund's gross expense ratio is 2.92% per the Summary Prospectus dated May 1, 2011. Guinness Atkinson Asset Management has contractually agreed to waive a portion of its advisory fees so that the Fund's ratio of expenses to average daily net assets will not exceed 1.98% (excluding Acquired Fund Fees and Expenses, interest, taxes, dividends on short positions and extraordinary expenses) through at least June 30, 2012. To the extent that the Advisor waives fees it may seek repayment of a portion or all of such amounts at any time within the three fiscal years after the fiscal year in which such amounts were waived, subject to the applicable cap.

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.gafunds.com, or calling (800) 916-6566.

The Fund imposes a 2% redemption fee on shares held less than 30 days. Performance data quoted does not reflect the 2% redemption fee on shares held less than 30 days. Total returns for certain periods reflect a fee waiver in effect and in the absence of this waiver, total returns would have been lower.

2011 was a difficult year for Asian equities, and a fall in investor risk appetite has affected the performance of Asian markets. Although we feel that the fundamentals of Asian countries and equities are in many cases better than their developed world counterparts, there has been a flight to perceived 'safety', which has been negative for our holdings. On a relative basis, the Fund has fallen almost in line with the wider market, reflecting our overweight position in cash-flow generative companies. Our overweight position in Telecoms worked well last year, whilst our Utility and Healthcare holdings have also outperformed. However, some of our sector allocations have hurt performance, with Industrials, Materials and Energy all falling more than the benchmark during 2011. There were also mixed performances from our holdings in Technology stocks, with performance much more stock, than sector, driven.

China has been a mixed performer in 2011, with concerns over the property market, and the continuation of monetary tightening, weighing on equities. This marks the second consecutive year where China has underperformed the broader Asian market, and in our view, there is now considerable value in the equity market there. In the final quarter of 2011, the Chinese central bank began to change course on monetary policy, and reduced the banks' reserve requirement ratio, to release more liquidity back into the financial system. If this trend continues, this should be supportive for Chinese equities in 2012, and should improve investor comfort with the region as a whole.

Our overweight position in Thailand worked well this year, with a change of government successfully taking place in July, and despite heavy flooding in the Bangkok area in October. There was a widespread impact on industrial production in the third quarter, but Thailand showed remarkable resilience, and there was, in fact, little lasting damage to infrastructure. Indonesia was also a stand-out performer in 2011, and was one of the very few equity indices in our universe to finish the year in positive territory.

2. Portfolio Position

The Fund's positioning is constructed primarily from the bottom-up, with a focus on finding stocks with a good combination of earnings growth and cash flow generation, allied to a management willingness to pay dividends. These stocks might be available in any Asian nation, but we also have a macroeconomic view which helps to keep the Fund's allocation reasonable.

23

ASIA PACIFIC DIVIDEND FUND

From a top down perspective, we remain focused on benefiting from Chinese growth as the key driver of economic growth in the Asian region. The Fund is skewed towards China and Hong Kong, with also significant overweight positions in Taiwan, Thailand and Indonesia. As well as a good combination of growth and cash flow, we have found stocks in these markets that have a propensity to pay dividends, as, in our view, management sees this as a good way to manage capital structure and to incentivise shareholders.

The Fund is well underweight Australia, as we feel there are fewer stocks that benefit directly from Asian economic growth, and the market is focused on domestic large cap stocks, such as banks and insurance companies. We are also well underweight South Korea, mainly given the low propensity for firms to pay dividends to their shareholders.

By sector, the Fund is focused on cash-generative firms that can benefit from increased consumer spending, such as Telecoms, Utilities, Consumer Staples and some in Healthcare. We also have significant positions in Information Technology companies in Taiwan, which have been paying very good dividends, and are decent value, even in the face of a slowdown in export orders. The Fund is particularly underweight in Financials, which have suffered due to monetary tightening in Asia over the last two years.

3. Outlook

There is still considerable uncertainty in the developed world over economic growth, and over the financial future of the eurozone countries. There is some evidence that economic growth might be bottoming in the US, and that is certainly encouraging for better prospects for equities in 2012. We continue to prefer companies that derive their profits from domestic growth in Asia, and are less keen on exporters, unless we can make a strong argument on grounds of attractive valuations or good, sustainable dividends.

Looking forward, we believe that economic growth in China is slowing to what we think are more sustainable rates, and that in response the central bank has shifted to a loosening stance on monetary policy. We are not alarmed by this slower growth in China, as we believe that Chinese equities have underperformed for two years now, and that there is substantial value in this market. The looser monetary policy is likely to be more positive for financials, and we are looking critically at this sector and actively looking for opportunities.

Elsewhere in the region, South Korea is looking increasingly attractive from a valuation and growth point of view, but it remains difficult to find many stocks with sufficiently high dividends to add to the Fund. There seems to be an unwillingness in South Korea to pay dividends, and many firms have little or no interest in optimizing capital structure to the benefit of the shareholders.

Indonesia is also a market of interest for the coming year, as the domestic economy is growing at a steady pace and the government seems committed to encouraging spending on infrastructure. The country also has a range of materials exporters selling coal, nickel, oil and palm oil to the growing countries of Asia, and the tax and earnings from these companies could help to support the rest of the economy.

| |  | |

|

| Edmund Harriss | | James Weir | |

|

The Fund invests in foreign securities, which involves political, economic and currency risks, greater volatility, and differences in accounting methods. The Fund is non-diversified, meaning that its assets may be concentrated in fewer individual holdings than diversified funds. Therefore, the Fund is more exposed to individual stock volatility than diversified funds. The Fund invests in smaller companies, which involves additional risks such as limited liquidity and greater volatility.

The MSCI Pacific ex-Japan Index is a free float-adjusted, capitalization-weighted index that is designed to measure equity market performance in the Pacific region excluding Japan. The Standard & Poor's 500 Index is a market capitalization-weighted index composed of 500 widely held common stocks of U.S. companies. These indices are unmanaged, not available for investment and do not incur expenses.

Please refer to the Schedule of Investments for details on Fund holdings. Current and future portfolio holdings are subject to risk.

The information provided herein represents the opinion of Guinness Atkinson Management for the period stated and is not intended to be a forecast of future events, a guarantee of future results, or investment advice. Opinions, Fund holdings and sector allocations are subject to change at any time, and are not recommendations to buy or sell any security.

24

GUINNESS ATKINSON ASIA PACIFIC DIVIDEND FUND

Growth of $10,000

Average Annual Total Return

Periods Ended December 31, 2011

| One Year | | Five Year | | Since Inception

(03/31/06)* | |

| | (14.04 | )% | | | 1.32 | % | | | 2.93 | % | |

* Inception date 3/31/06.

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.gafunds.com.

Total returns reflect a fee waiver in effect and in the absence of this waiver, the total returns would be lower. The Fund imposes a 2% redemption fee on shares held less than 30 days.

The MSCI All Country Pacific Free ex-Japan Index (MSCI AC Pacific ex-Japan Index) is a free float-adjusted, capitalization-weighted index that is designed to measure equity market performance in the Pacific region including Japan.

25

FUND HIGHLIGHTS at December 31, 2011

GUINNESS ATKINSON ASIA PACIFIC DIVIDEND FUND

| # of Holdings in Portfolio: | | 31 | |

| Portfolio Turnover: | | 10.7% | |

| % of Stocks in Top 10: | | 41.8% | |

| Fund Managers: | |

| Edmund Harriss | |

| James Weir | |

| Top 10 Holdings (% of net assets) | | | | | | | |

| Digi.Com BHD | | 5.2% | | CLP Holdings Ltd. | | 3.9% | |

| KT&G Corporation | | 5.0% | | Yanzhou Coal Mining Co., Ltd. - H Shares | | 3.8% | |

| PTT PCL Foreign | | 4.7% | | Vtech Holdings Ltd. | | 3.7% | |

| PetroChina Co., Ltd. - ADR | | 4.3% | | China Mobile Ltd. | | 3.7% | |

| Taiwan Semiconductor Manufacturing Co., Ltd. | | 4.1% | | Compal Electronics, Inc. | | 3.4% | |

| Sector Breakdown (% of net assets) | | | | | | | |

| Commercial Banks | | 12.0% | | Textile - Products | | 3.0% | |

| Oil Company - Integrated | | 9.0% | | Agricultural Chemicals | | 3.0% | |

| Telecommunication Services | | 8.3% | | Chemical Diversified | | 2.9% | |

| Semiconductor Components - Integrated Circuits | | 6.7% | | Optical Supplies | | 2.8% | |

| Coal | | 6.6% | | Steel - Producers | | 2.7% | |

| Tobacco | | 5.0% | | Electric - Generation | | 2.7% | |

| Electric - Integrated | | 4.0% | | Water | | 2.7% | |

| Telecommunication Equipment | | 3.7% | | Auto/Truck Parts & Equipment - Replacements | | 2.5% | |

| Cellular Telecommunications | | 3.7% | | Real Estate Operations/Development | | 2.5% | |

| Computers | | 3.4% | | Wireless Equipment | | 2.5% | |

| Computers - Peripheral Equipment | | 3.3% | | Electronic Component - Miscellaneous | | 2.3% | |

| Chemicals - Plastics | | 3.1% | | Building Products - Cement/Aggregate | | 2.2% | |

26

SCHEDULE OF INVESTMENTS

at December 31, 2011

GUINNESS ATKINSON ASIA PACIFIC DIVIDEND FUND

| Shares | | COMMON STOCKS: 100.6% | | Value | |

| Australia: 3.0% | | | |

| | 42,787 | | | Incitec Pivot Ltd. | | $ | 136,101 | | |

| China: 15.6% | | | |

| | 152,000 | | | China Shanshui Cement Group Ltd | | | 101,182 | | |

| | 218,000 | | | Industrial & Commercial Bank of China - H Shares | | | 129,398 | | |

| | 1,560 | | | PetroChina Co., Ltd. - ADR | | | 193,924 | | |

| | 171,000 | | | Soho China Ltd | | | 113,830 | | |

| | 80,000 | | | Yanzhou Coal Mining Co., Ltd. - H Shares | | | 170,783 | | |

| | | | 709,117 | | |

| Hong Kong: 20.9% | | | |

| | 62,500 | | | BOC Hong Kong Holdings Ltd. | | | 148,070 | | |

| | 17,000 | | | China Mobile Ltd. | | | 166,134 | | |

| | 21,000 | | | CLP Holdings Ltd. | | | 178,592 | | |

| | 3,924 | | | HSBC Holdings PLC - ADR | | | 149,504 | | |

| | 241,000 | | | Pacific Textile Holdings Ltd | | | 136,844 | | |

| | 16,600 | | | VTech Holdings Ltd. | | | 166,286 | | |

| | | | 945,430 | | |

| Indonesia: 6.0% | | | |

| | 30,500 | | | Indo Tambangraya Megah PT | | | 130,006 | | |

| | 179,500 | | | Telekomunikasi Indonesia Tbk PT | | | 139,562 | | |

| | | | 269,568 | | |

| Malaysia: 5.2% | | | |

| | 194,200 | | | DiGi.Com Bhd | | | 237,696 | | |

| Singapore: 2.6% | | | |

| | 10,000 | | | United Overseas Bank Ltd. | | | 117,729 | | |

| South Korea: 7.7% | | | |

| | 3,220 | | | KT&G Corp | | | 227,524 | | |

| | 370 | | | POSCO | | | 122,547 | | |

| | | | 350,071 | | |

| Taiwan: 21.2% | | | |

| | 155,394 | | | Compal Electronics, Inc. | | | 154,989 | | |

| | 60,400 | | | Depo Auto Parts Ind Co., Ltd. | | | 115,697 | | |

| | 6,854 | | | HTC Corp. | | | 112,502 | | |

| | 130,633 | | | Lite-On Technology Corp. | | | 147,118 | | |

| | 47,000 | | | Novatek Microelectronics Corp. Ltd. | | | 117,814 | | |

| | 12,000 | | | St Shine Optical Co., Ltd. | | | 126,821 | | |

| | 74,000 | | | Taiwan Semiconductor Manufacturing Co., Ltd. | | | 185,250 | | |

| | | | 960,191 | | |

The accompanying notes are an integral part of these financial statements.

27

| Shares | | COMMON STOCKS: 100.6% (Continued) | | Value | |

| Thailand: 18.4% | | | |

| | 151,400 | | | Delta Electronics Thai PCL/Foreign | | $ | 104,132 | | |

| | 67,800 | | | Glow Energy PCL/Foreign | | | 122,491 | | |

| | 67,720 | | | PTT Chemical PCL/Foreign | | | 130,932 | | |

| | 21,200 | | | PTT PCL/Foreign | | | 213,680 | | |

| | 152,100 | | | Thai Plastic & Chemical PCL/Foreign | | | 142,217 | | |

| | 760,600 | | | Thai Tap Water Supply PCL/Foreign | | | 121,744 | | |

| | | | 835,196 | | |

| | | | | Total Common Stocks

(cost $4,244,950) | | | 4,561,099 | | |

| | | | | Total Investments in Securities

(cost $4,244,950): 100.6% | | | 4,561,099 | | |

| | | | | Liabilities in Excess of Other Assets: (0.6%) | | | (29,145 | ) | |

| | | | | Net Assets: 100.0% | | $ | 4,531,954 | | |

ADR - American Depository Receipt

The accompanying notes are an integral part of these financial statements.

28

CHINA & HONG KONG FUND for the period ended December 31, 2011

1. Performance

AVERAGE ANNUALIZED TOTAL RETURNS

| | | 6 Months

(actual) | | 1 Year

(actual) | | 3 Years | | 5 Years | | 10 Years | |

| Fund | | | -24.23 | % | | | -27.52 | % | | | 17.25 | % | | | 3.91 | % | | | 11.29 | % | |

| Benchmark Index: | |

| Hang Seng Composite | | | -19.23 | % | | | -19.29 | % | | | 11.86 | % | | | 1.17 | % | | | 10.12 | % | |

| Hang Seng | | | -16.49 | % | | | -17.27 | % | | | 11.92 | % | | | 1.55 | % | | | 8.57 | % | |

| S&P 500 | | | -3.70 | % | | | 2.09 | % | | | 14.12 | % | | | -0.25 | % | | | 2.92 | % | |

The Fund's gross expense ratio is 1.48% per the Summary Prospectus dated May 1, 2011. Guinness Atkinson Asset Management has contractually agreed to waive a portion of its advisory fees so that the Fund's ratio of expenses to average daily net assets will not exceed 1.98% (excluding Acquired Fund Fees and Expenses, interest, taxes, dividends on short positions and extraordinary expenses) through at least June 30, 2012. To the extent that the Advisor waives fees it may seek repayment of a portion or all of such amounts at any time within the three fiscal years after the fiscal year in which such amounts were waived, subject to the applicable cap.

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.gafunds.com, or calling (800) 916-6566.

The Fund imposes a 2% redemption fee on shares held less than 30 days. Performance data quoted does not reflect the 2% redemption fee on shares held less than 30 days. Total returns for certain periods reflect a fee waiver in effect and in the absence of this waiver, total returns would have been lower.

During the year investor sentiment has been very bearish toward China as inflation remained high and as a consequence, the measures put in place to tighten liquidity looked unlikely to ease any time soon. This was compounded by increasing fears for the property market which has been particular focus of monetary tightening. In the last three months of the year the China and Hong Kong markets rebounded as investors' fears about European debt receded somewhat and Chinese inflation began to ease. The Fund finished the year down 27.52%, compared to a fall in the Hang Seng Composite Index of 19.29%

The portfolio is positioned with higher exposure toward energy, industrials and materials which reflects our belief that China's domestic economy offers the best investment prospects. During the year investor sentiment has been very bearish toward China as inflation remained high and as a consequence, the measures put in place to tighten liquidity looked unlikely to ease any time soon. This was compounded by increasing fears for the property market which has been particular focus of monetary tightening. This meant that stocks related to construction such as steelmaking and cement did poorly for much of the year but rebounded strongly on signs of policy easing.

The last three months of the year brought some relief to policymakers as inflation began to come down in the food, non-food and industrial products categories. This has provided more policy flexibility at a time when external demand was deteriorating. We therefore saw increased bank lending, a cut in banks' required reserve ratios and an increase in money supply. While the authorities are wary about providing actual stimulus, since they are trying to correct the ill-effects of the last stimulus package, the mood has certainly changed to one that is supportive of growth.

2. Portfolio Position

The portfolio positioning was substantially unchanged this year, with our overweight positions in Energy, Materials and Industrials stocks remaining in place. The portfolio is also underweight in Financials, Insurance and Real Estate stocks, and this has been supportive to performance as these sectors have been under pressure due to monetary tightening for most of 2011.

29

CHINA & HONG KONG FUND

3. Outlook

We expect inflation in China will continue to fall and we also expect external demand for Chinese-manufactured goods will continue to weaken. China's measures to put downward pressure on residential property prices are also likely to continue and this should depress construction activity. However, policy makers now have the flexibility and the resources to tailor policy to support domestic growth while maintaining a grip on those sectors of the economy that overheated following the stimulus policies of 2009/10.

We have already seen moves to support growth with increased liquidity being made available and we expect this continue with additional cuts to the required reserve ratio over the course of the year. Fiscal measures are likely to be preferred rather than direct stimulus which could take the form of tax cuts, rebates and/or subsidies. There is also a big social housing construction programme underway which is likely to ramp up this year.

We believe these measures may cushion, but not prevent, a deceleration of growth. In our view, the reality is that the days of double digit growth are almost certainly behind us and the focus now is on the quality and sustainability of growth. The social housing programme should help preserve jobs in the construction industry while at the same time provide an adequate supply of affordable housing which would help take the heat out of the residential property market.

From an investment perspective we believe that stable growth, albeit slower than in 2009-11, is still better than investors were expecting. Stock market valuations are currently very cheap and we believe will close up toward the regional average supported by a steady stream of low level supportive policy moves.

Edmund Harriss

The Fund invests in foreign securities, which involves political, economic and currency risks, greater volatility, and differences in accounting methods. The Fund is non-diversified, meaning its assets may be concentrated in fewer individual holdings than diversified funds. Therefore, the Fund is more exposed to individual stock volatility than diversified funds. The Fund invests in smaller companies, which involves additional risks such as limited liquidity and greater volatility.

The Hang Seng Composite Index is a market capitalization-weighted index that is comprised of the top 200 companies listed on the Hong Kong Stock Exchange, based on the average market capitalization for the past twelve months. The Hang Seng Composite Index commenced operations on January 3, 2000 and therefore does not have returns since the Fund's inception. The Hang Seng Index is a barometer of the Hong Kong Stock Market, whose aggregate market capitalization accounts for about 70% of the total market-capitalization of the Stock Exchange of Hong Kong Limited. The Standard & Poor's 500 Index is a market capitalization-weighted index composed of 500 widely held common stocks of U.S. companies. These indices are unmanaged, not available for investment and do not incur expenses.

Please refer to the Schedule of Investments for details on Fund holdings. Current and future portfolio holdings are subject to risk.

The information provided herein represents the opinion of Guinness Atkinson Management for the period stated and is not intended to be a forecast of future events, a guarantee of future results, or investment advice. Opinions, Fund holdings and sector allocations are subject to change at any time, and are not recommendations to buy or sell any security.

30

GUINNESS ATKINSON CHINA & HONG KONG FUND

Growth of $10,000

Average Annual Total Return

Periods Ended December 31, 2011

| One Year | | Five Year | | Ten Year | |

| | (27.52 | )% | | | 3.91 | % | | | 11.29 | % | |

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.gafunds.com.

Total returns reflect a fee waiver in effect and in the absence of this waiver, the total returns would be lower. The Fund imposes a 2% redemption fee on shares held less than 30 days.