UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-8372

Travelers Series Fund Inc.

(Exact name of registrant as specified in charter)

| | |

| 125 Broad Street, New York, NY | | 10004 |

| (Address of principal executive offices) | | (Zip code) |

Robert I. Frenkel, Esq.

Smith Barney Fund Management LLC

300 First Stamford Place

Stamford, CT 06902

(Name and address of agent for service)

Registrant’s telephone number, including area code: (800) 451-2010

Date of fiscal year end: October 31

Date of reporting period: October 31, 2004

| ITEM 1. | REPORT TO STOCKHOLDERS. |

The Annual Report to Stockholders is filed herewith.

TRAVELERS SERIES FUND INC.

SMITH BARNEY

INTERNATIONAL ALL CAP

GROWTH PORTFOLIO

SALOMON BROTHERS

STRATEGIC TOTAL RETURN

BOND PORTFOLIO

SB ADJUSTABLE RATE

INCOME PORTFOLIO

ANNUAL REPORT | OCTOBER 31, 2004

NOT FDIC INSURED • NOT BANK GUARANTEED • MAY LOSE VALUE

WHAT’S INSIDE

LETTER FROM THE CHAIRMAN

R. JAY GERKEN, CFA

Chairman, President and Chief Executive Officer

Dear Shareholder,

Stock prices collectively advanced over the 12 months ended October 31, 2004, although performance varied sharply among sectors and investment styles. The equity market also shifted gears during the period due to investors’ reaction to mixed signals about the economy.

Last fall, stocks continued to rise as many geopolitical concerns began to ease, and a spate of mortgage refinancings freed up investable cash for investors. Despite positive corporate earnings results, stocks traded in a narrow range during the first quarter of this year due to concerns about anemic job growth. During this time, the economy grew at a moderate pace,i albeit at significantly stronger levels than during the first half of 2003.

In the spring, the economic recovery became broader based as labor market growth improved dramatically in March and April, although signs suggested a pickup in inflation in the spring as well. As widely anticipated, the Federal Reserve Board (“Fed”)ii proceeded to push short-term interest rates higher, marking its first hike in four years. The Fed raised its target for the closely watched federal funds rateiii by 0.25% on three occasions during the reporting period, increasing it from a four-decade low of 1.00% in June to 1.75% in September, and then again to 2.00% on November 10th, after the fund’s reporting period had ended. Higher rates can help slow a potential acceleration of economic growth and thereby help maintain a balance between that growth and the inflation that can generally accompany it.

As the period came to a close, inflation figures were benign while labor market growth, which had tapered off during the summer, exceeded consensus estimates for October. Crude oil prices, which had risen to record highs in the third quarter, when coupled with investors’ reaction to terrorism concerns, weakened investor sentiment toward the equity markets. However, reports of a pullback in oil prices and strong third-quarter corporate profits gave stock prices a boost in the final month of the period.

Over the past 12 months, stocks of small- and mid-capitalization companies continued to outperform large-caps in general. Value-oriented stocks handily outpaced growth-oriented stocks. International stock markets beat out the broad domestic U.S. market by a wide margin.

Following a sharp sell-off in the spring in anticipation that rates were poised to rise, bond prices rose later in the period. The bond market benefited in the third

1 Travelers Series Fund Inc. | 2004 Annual Report

quarter when investors reallocated assets from stocks into bonds. However, the fixed-income markets experienced some downward pricing pressures after the reporting period as interest rate concerns resurfaced. Over the 12 months, however, bonds finished in modestly positive territory on a total return basis.

Within this environment, the portfolios performed as follows:1

PERFORMANCE SNAPSHOT

AS OF OCTOBER 31, 2004

| | | | | | |

| | | 6 Months | | | 12 Months | |

| | | | | | | |

Smith Barney International All Cap Growth Portfolio | | 3.79 | % | | 13.90 | % |

| | | | | | | |

MSCI EAFE Growth Index | | 2.80 | % | | 14.00 | % |

| | | | | | | |

MSCI EAFE Index | | 5.74 | % | | 18.84 | % |

| | | | | | | |

Lipper Variable International Growth Funds Category Average | | 3.91 | % | | 14.40 | % |

| | | | | | | |

Salomon Brothers Strategic Total Return Bond Portfolio | | 4.69 | % | | 6.83 | % |

| | | | | | | |

J.P. Morgan Global Government Bond Index — Unhedged | | 7.29 | % | | 10.54 | % |

| | | | | | | |

Lehman Brothers Aggregate Bond Index | | 4.23 | % | | 5.53 | % |

| | | | | | | |

Lipper Variable Global Income Funds Category Average | | 6.82 | % | | 9.13 | % |

| | | | | | | |

SB Adjustable Rate Income Portfolio | | 0.50 | % | | 1.24 | % |

| | | | | | | |

Citigroup 6-Month U.S. Treasury Bill Index | | 0.65 | % | | 1.16 | % |

| | | | | | | |

Lipper Variable Short-lntermediate Investment Grade Debt Funds Category Average | | 1.41 | % | | 2.25 | % |

| | | | | | | |

30 Day SEC Yield | | 1.59 | % | | 1.59 | % |

The performance shown represents past performance. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown above. Principal value and investment returns will fluctuate and investors’ shares, when redeemed, may be worth more or less than their original cost.

Returns assume the reinvestment of income dividends and capital gains distributions at net asset value and the deduction of all fund expenses.

Performance figures for both Smith Barney International All Cap Growth Portfolio and Salomon Brothers Strategic Total Return Bond Portfolio may reflect reimbursements or fee waivers, without which the performance would have been lower. The reimbursements and/or fee waivers are voluntary and may be reduced or terminated at any time.

For SB Adjustable Rate Income Portfolio, the yields reflect fee waivers and/or expense reimbursements in effect through the period of 12 months from October 31, 2003. Without these fee waivers and reimbursements the fund’s yield would have been 1.50%.

Lipper, Inc. is a major independent mutual-fund tracking organization. Returns are based on the period ended October 31, 2004 and include the reinvestment of dividends and capital gains, if any. Returns in the variable international growth funds category were calculated among the 50 funds for the six-month period and among the 50 funds for the 12-month period. Returns in the variable global income funds category were calculated among the 31 funds for the six-month period and among the 31 funds for the 12-month period. Returns in the variable short-intermediate investment grade debt funds category were calculated among the 32 funds for the six-month period and among the 31 funds for the 12-month period.

| 1 | The fund is an underlying investment option of various variable annuity products. A variable annuity product is a contract issued by an insurance company where the annuity premiums (a set amount of dollars) is immediately turned into units of a portfolio of securities. Upon retirement, the policyholder is paid according to accumulated units whose dollar value varies according to the performance of the securities within the sub accounts. Its objective is to preserve, through investment, the purchasing value of the annuity, which otherwise is subject to erosion through inflation. The fund’s performance returns do not reflect the deduction of initial sales charges and expenses imposed in connection with investing in variable annuity contracts such as administrative fees, account charges and surrender charges, which if reflected, would reduce the performance of the fund. Past performance is no guarantee of future results. |

2 Travelers Series Fund Inc. | 2004 Annual Report

Please read on for a more detailed look at prevailing economic and market conditions during the fund’s fiscal year and to learn how those conditions have affected fund performance.

Information About Your Funds

As you may be aware, several issues in the mutual fund industry have recently come under the scrutiny of federal and state regulators. The fund’s Adviser and some of its affiliates have received requests for information from various government regulators regarding market timing, late trading, fees, and other mutual fund issues in connection with various investigations. The regulators appear to be examining, among other things, the fund’s response to market timing and shareholder exchange activity, including compliance with prospectus disclosure related to these subjects. The fund has been informed that the Adviser and its affiliates are responding to those information requests, but are not in a position to predict the outcome of these requests and investigations.

In November 2003, Citigroup Asset Management (“CAM”) disclosed an investigation by the Securities and Exchange Commission (“SEC”) and the U.S. Attorney relating to Citigroup Asset Management’s entry into the transfer agency business during 1997-1999. Citigroup has disclosed that the Staff of the SEC is considering recommending a civil injunctive action and/or an administrative proceeding against certain advisory and transfer agent entities affiliated with Citigroup, the former CEO of CAM, two former employees and a current employee of CAM, relating to the creation, operation and fees of its internal transfer agent unit that serves various CAM-managed funds. Citigroup is cooperating with the SEC and will seek to resolve this matter in discussion with the SEC Staff. Although there can be no assurance, Citigroup does not believe that this matter will have a material adverse effect on the fund.

As always, thank you for your confidence in our stewardship of your assets. We look forward to helping you continue to meet your financial goals.

Sincerely,

/s/ R. Jay Gerken

R. Jay Gerken, CFA

Chairman, President and Chief Executive Officer

December 13, 2004

3 Travelers Series Fund Inc. | 2004 Annual Report

MANAGER OVERVIEW

Smith Barney International All Cap Growth Portfolio

Special Shareholder Notice

Effective June 30, 2004, the benchmark was changed from the Morgan Stanley Capital International Europe, Australasia and the Far East Index (“MSCI EAFE” Index)iv to the Morgan Stanley Capital International Europe, Australasia and the Far East Growth Index (“MSCI EAFE Growth Index”).v

Effective July 1, 2004, the management fee payable by Smith Barney International All Cap Growth Portfolio was reduced to 0.85% of the portfolio’s average daily net assets.

Performance Review

For the 12 months ended October 31, 2004, the Smith Barney International All Cap Growth Portfolio returned 13.90%.1 In comparison, the fund’s unmanaged benchmark, the MSCI EAFE Growth Index,v returned 14.00% while the MSCI EAFE Indexiv returned 18.84% for the same period. The Lipper variable international growth funds category average2 was 14.40% for the same period.

Market Review

Equity markets rewarded many international growth investors for the twelve months ended October 31, 2004 with positive returns. The global economic recovery unfolded well as the fiscal year progressed, providing good corporate earnings gains in many sectors and markets. Improving cash flows and balance sheets were further positive influences.

Despite the somber news from the Middle East, significantly higher energy prices, terrorist activities and uncertainties heading into the U.S. elections, international growth stocks experienced strong double-digit growth over the past year.

International stocks substantially outperformed U.S. equities during the year. Those returns were augmented by the decline of the U.S. dollar versus the

| 1 | The fund is an underlying investment option of various variable annuity products. A variable annuity product is a contract issued by an insurance company where the annuity premium (a set amount of dollars) is immediately turned into units of a portfolio of securities. Upon retirement, the policyholder is paid according to accumulated units whose dollar value varies according to the performance of the securities within the sub accounts. Its objective is to preserve, through investment, the purchasing value of the annuity, which otherwise is subject to erosion through inflation. The fund’s performance returns do not reflect the deduction of initial sales charges and expenses imposed in connection with investing in variable annuity contracts such as administrative fees, account charges and surrender charges, which if reflected, would reduce the performance of the fund. Past performance is no guarantee of future results. |

| 2 | Lipper, Inc. is a major independent mutual-fund tracking organization. Returns are based on the 12-month period ended October 31, 2004, calculated among the 50 funds in the funds Lipper category, including the reinvestment of dividends and capital gains, if any. |

4 Travelers Series Fund Inc. | 2004 Annual Report

currencies underlying the benchmark index during the fiscal year. The dollar’s decline increased the return of the benchmark from 5.90% in local currencies to 14.00% as measured in U.S. dollars.

Portfolio Overview

The portfolio performed in line with the benchmark this past fiscal year. European markets were the strongest benchmark performers with an 18.00% return (in U.S. dollars) compared with 5.20% for the Pacific markets. Returns from the Pacific markets were restrained by the modest decline of the Japanese market, which slid nearly 3.00% in yen terms, and increased less than 1.00% as measured in dollars. The portfolio was modestly overweight in European markets for most of the fiscal year and was modestly underweight in Japanese equities.

Stock selection made a positive contribution during this fiscal year, offsetting the negative impact from sector selection. The top three contributors to overall portfolio return were the U.K.’s Vodafone Group PLC (+24%), the U.K.’s Capita Group PLC (+55%) and Ireland’s Grafton Group PLC (+44%). The three largest detractors to portfolio return were the U.K.’s Compass Group PLC (-27%), Japan’s Nomura Holdings, Inc. (-28%), and Japan’s NTT DoCoMo, Inc. (-18%).vi

Sector selection detracted from portfolio performance. The sector weights in the portfolio are derived from stock selection, with a risk control limit versus the benchmark weight. The portfolio had no exposure to the strong-performing utilities sector; most utilities do not meet the portfolio team’s qualitative criteria for growth companies. The overweight exposure to the information technology sector also detracted from sector attribution. Our overweight position in energy sector stocks was contributory to the portfolio’s return.vii

Portfolio Composition

Our top holdings in the portfolio reflect an eclectic mix of investment themes and portfolio emphasis. These holdings are illustrative of our growth-oriented stock selection criteria, which include what we believe are strong financial structures, large business opportunities and stable, visionary management. The portfolio ended the fiscal year with approximately 67% of its assets in European stocks, 25% in Asian stocks, and 8% in other markets and cash.

Thank you for your investment in the Smith Barney International All Cap Growth Portfolio. As ever, we appreciate that you have chosen us to manage your assets and we remain focused on seeking to achieve the fund’s investment goals.

Sincerely,

Jeffrey J. Russell, CFA

Vice President and Investment Officer

December 13, 2004

5 Travelers Series Fund Inc. | 2004 Annual Report

MANAGER OVERVIEW

Salomon Brothers Strategic Total Return Bond Portfolio

Special Shareholder Notice

Effective December 31, 2004, the Lehman Brothers Aggregate Bond Index, a broad-based bond index comprised of Government, Corporate, Mortgage, Asset-backed issues, rated investment-grade or higher, and having at least one year to maturity, will replace the J.P. Morgan Global Government Bond Index — Unhedged as the fund’s sole benchmark. The manager has determined that the Lehman Brothers Aggregate Bond Index more closely reflects the composition of the portfolio and the management style.

Performance Review

For the 12 months ended October 31, 2004, the Salomon Brothers Strategic Total Return Bond Portfolio, returned 6.83%.1 In comparison, the fund’s unmanaged benchmarks, the J.P. Morgan Global Government Bond Index — Unhedgedviii and the Lehman Brothers Aggregate Bond Index,ix returned 10.54% and 5.53%, respectively, for the same period.

Investment Grade Market Overview

U.S. government securities collectively generated positive total returns over the 12 months ended October 31, 2004, despite some market volatility as investors dissected language from the Fed for clues on its assessment of the U.S. economy and an indication when rates would begin to creep higher. The first five months were relatively stable as the economy showed signs of a turnaround, with the economic outlook for 2004 as encouraging as it has been since 1999. Nevertheless, despite the apparent strength of the economy, the Fed held fast to its 1.00% short-term lending rate, attributing the economic growth more to increases in productivity than to jobs. The Fed did, however, alter its policy

| 1 | The fund is an underlying investment option of various variable annuity products. A variable annuity product is a contract issued by an insurance company where the annuity premium (a set amount of dollars) is immediately turned into units of a portfolio of securities. Upon retirement, the policyholder is paid according to accumulated units whose dollar value varies according to the performance of the securities within the sub accounts. Its objective is to preserve, through investment, the purchasing value of the annuity, which otherwise is subject to erosion through inflation. The fund’s performance returns do not reflect the deduction of initial sales charges and expenses imposed in connection with investing in variable annuity contracts such as administrative fees, account charges and surrender charges, which if reflected, would reduce the performance of the fund. Past performance is no guarantee of future results. |

6 Travelers Series Fund Inc. | 2004 Annual Report

language after its January meeting from the open-ended “considerable period” to simply state that it wished to show “patience” in “removing” the accommodation. Following the May policy meeting, the Fed again altered its accommodation language from “patience” in “removing” the accommodation to “a pace that is likely to be measured”. We viewed this as an attempt by the Fed to signal that it was intending to raise rates incrementally and deliberately over the months to come.

Signs of inflation and strong non-farm payroll numbers began to appear in March and April of 2004. Strong job numbers combined with inflation fighting language from the Fed, led to a rise in U.S. treasury yields, with 10-year yields gaining more than 100 basis points from their early March lows. Yields on most fixed-income instruments, particularly those on shorter-maturity issues, began moving up and continued their ascent as it became more evident that the improving economy and higher inflation would compel the Fed to act in June. The Fed finally raised its federal funds rate target to 1.25% in June off the stronger employment numbers.

Against this backdrop, fixed income markets finished on a somewhat more stable note in June and July. The Fed raised its federal funds target rate by an additional 0.25% at each subsequent meeting in July, August, and September, despite significant softening of many economic indicators during the late summer months, bringing the target rate to 1.75% at the end of the reporting cycle for the portfolio. Following the end of the fund’s reporting period, at its November meeting, the Fed once again raised its target for the federal funds rate by 0.25% to 2.00%.

Over the period, U.S. treasuries, as represented by the Citigroup U.S. Treasury Bond Index,x returned 4.98%, rebounding in the third quarter after the worst quarter in more than two decades. U.S. Agencies, as represented by the Citigroup U.S. Agency Index,xi also had positive returns during the period of 4.78%. The sector saw widening in the third quarter of 2004, as the Office of Federal Housing Enterprise Oversight (OFHEO) and the SEC continued to look closely at the accounting practices of the Federal National Mortgage Association (“FNMA”). The market had been expecting no headline risk for the agencies until after the election. The mortgage-backed sector as represented by the Citigroup Mortgage Indexxii returned 5.68%. Early in the third quarter of 2004, the environment looked favorable for mortgage-backed securities with light supply, low volatility and positive technicals. As the 10-year U.S. treasury note approached 4.10% later in the quarter, convexity started to become a concern and supply from originators increased.

7 Travelers Series Fund Inc. | 2004 Annual Report

High Yield Market Overview

The high-yield bond market, as represented by the Citigroup High Yield Market Index,xiii returned 12.28% for the 12 months ended October 31, 2004. The rally that began in the second half of August 2003 continued for the remainder of the 2003 calendar year as lower U.S. treasury yields and positive mutual fund inflows propelled the high-yield market higher. Fundamentals also supported the market, with the improving economy, strong earnings and declining default rates contributing to the market’s advance. Corporate bond issuers took advantage of the low interest rates to improve their balance sheets and liquidity.

Following a strong run over 2003, high-yield bond priced began to retreat early in 2004 due to profit-taking as investors became concerned that company fundamentals did not warrant such gains and the low yields did not offer enough compensation for the risk. Additionally, the Fed’s removal of the “considerable period” language from its policy statement during this time sparked concerns that the Fed would begin raising interest rates sooner than had been expected. The high-yield market continued to decline in February, with lower-quality issues leading the way down amid large fund outflows, continued profit taking and greater focus on company fundamentals.

In March, investors sought haven in higher-rated bonds in the non-investment-grade universe as terrorism fears and weak employment numbers exerted pressure on stock markets and drove yields on U.S. treasury bonds lower. However, economic data released in April showing an improving labor market and signs of higher inflation sparked another sell-off in U.S. treasury bonds as investors shifted their expectations of Fed tightening from 2005 to the summer of 2004. Additionally, economic data in May sparked increased inflation fears, with concern over Fed tightening transitioning from timing to size and pace of the expected interest rate increases. Once again, the volatility in the U.S. treasury market spilled into the high-yield market, resulting in negative returns and large mutual fund redemptions. However, the high-yield bond market rallied for the remainder of the fiscal year due to positive mutual fund flows and a strong rally in U.S. treasuries as the economy showed signs of slowing. Additionally, default rates remained low as the improving economy and the low interest rate environment enabled companies to extend their debt maturities on new issues at favorable rates and improve their liquidity.

Based on the 7.46% yield of the Citigroup High Yield Market Indexxiii as of October 31, 2004, high-yield bonds continued to offer competitive yields relative to U.S. treasury notes.xiv However, high-yield issues are subject to additional risks, such as the increased possibility of default because of their lower credit quality, and yields and prices will fluctuate.

8 Travelers Series Fund Inc. | 2004 Annual Report

Emerging Markets Overview

Emerging markets debt performed positively through the 12 months ended October 31, 2004, returning 12.94% as represented by the J.P. Morgan Emerging Markets Bond Index Plus (“EMBI+”).xv Sovereign debt markets exhibited strong performance from the start of the fund’s fiscal year in November through March 2004 amid a relatively benign stretch in the U.S. Treasury bond markets; hedge funds joined crossover buyers in adding to their emerging markets debt allocations. However, markets were disrupted in April and May following a sharp sell-off in U.S. Treasury bonds caused by an extremely strong March U.S. jobs report. April saw the EMBI+’s largest sell-off since July of 2001, and May saw yield spreadsxvi over U.S. treasuries widening to 569 during the month, a level not seen since August of 2003. Markets rallied over the next few months — taking back all the losses of April and May — and performing strongly through the end of the period. Good country fundamentals, commodity price strength and the absence of U.S. Treasury market volatility supported emerging markets debt returns.

Through all of this, emerging markets debt fundamentals remained strong, and the markets benefited from increasing signs of a global economic turnaround. Continued strength in commodity prices, including metals, agriculture, and oil provided positive support for many emerging market countries. Oil prices, in particular, remained high favoring oil exporters, but fears remained that high-energy prices might dampen the global recovery. Revenues from oil production contributed to positive performance in Ecuador, Russia, and Venezuela. The markets also benefited from higher-than-expected global economic growth and higher-than-expected inflation.

Spreads tightened 57 basis pointsxvii during the 12-month period ended October 31, 2004, closing at 413 basis points over U.S. Treasuries. Over the same period, 12-month return volatility stood at 8.09%,xviii substantially below long-term, historical levels of approximately 16.00%.

Continued progress on political and economic reforms in many emerging countries, combined with the positive macro environment, led to a spate of upgrades or improved outlook changes during the period; Moody’s and Standard & Poor’s collectively upgraded 12 countries during the last 12 months, representing more than 56.00% of the J.P. Morgan Emerging Markets Bond Index Global, (“EMBI Global”).xix The improving credit quality in emerging markets encouraged broader investor participation and may have caused some long-term investors to change their allocation to emerging markets from tactical to strategic, providing some technical support for the market.

9 Travelers Series Fund Inc. | 2004 Annual Report

Factors Influencing Fund Performance

During the period, the fund benefited from its strategic allocations to high yield and emerging markets debt, which returned 12.28% and 12.94%, respectively, for the 12 months ended October 31, 2004, as represented by the Citigroup High Yield Market Indexxiii and the EMBI+.xv We increased our allocations to mortgage-backed securities, asset-backed securities and emerging markets debt during the 12 months and decreased our allocations to U.S. high yield and non-U.S. investment grade securities. Our decision to allocate assets out of high yield and the defensive positioning of the portfolio somewhat muted our performance during the reporting period.

We remained defensive throughout the period being shorter duration, which somewhat hampered performance as interest rates declined in the longer end of the curve. We will continue to position the portfolio defensively until we see a slowdown in the back up of rates on the short end of the curve.

Thank you for your investment in the Salomon Brothers Strategic Total Return Bond Portfolio. As ever, we appreciate that you have chosen us to manage your assets and we remain focused on achieving the fund’s investment goals.

Sincerely,

| | |

Peter J. Wilby, CFA Vice President and Investment Officer | |

Beth A. Semmel, CFA Vice President and Investment Officer |

December 13, 2004

10 Travelers Series Fund Inc. | 2004 Annual Report

MANAGER OVERVIEW

SB Adjustable Rate Income Portfolio

Performance Review

For the 12 months ended October 31, 2004, the SB Adjustable Rate Income Portfolio returned 1.24%.1 In comparison, the portfolio’s unmanaged benchmark, the Citigroup 6-Month U.S. Treasury Bill Index,xx returned 1.16% for the same period. The Lipper variable short-intermediate investment grade debt funds category average2 was 2.25%.

Market Overview

U.S. government securities collectively generated positive total returns over the 12 months ended October 31, 2004, despite some market volatility as investors dissected language from the Fed for clues on its assessment of the U.S. economy and an indication when rates would begin to creep higher. The first five months were relatively stable as the economy showed signs of a turnaround, with the economic outlook for 2004 as encouraging as it has been since 1999. Nevertheless, despite the apparent strength of the economy, the Fed held fast to its 1.00% short-term lending rate, attributing the economic growth more to increases in productivity than to jobs. The Fed did, however, alter its policy language after its January meeting from the open-ended “considerable period” to simply state that it wished to show “patience” in “removing” the accommodation. Following the May policy meeting, the Fed again altered its accommodation language from “patience” in “removing” the accommodation to “a pace that is likely to measured”. We view this as an attempt by the Fed to signal that it intends to raise rates incrementally and deliberately over the months to come.

| 1 | The fund is an underlying investment option of various variable annuity products. A variable annuity product is a contract issued by an insurance company where the annuity premium (a set amount of dollars) is immediately turned into units of a portfolio of securities. Upon retirement, the policyholder is paid according to accumulated units whose dollar value varies according to the performance of the securities within the sub accounts. Its objective is to preserve, through investment, the purchasing value of the annuity, which otherwise is subject to erosion through inflation. The fund’s performance returns do not reflect the deduction of initial sales charges and expenses imposed in connection with investing in variable annuity contracts such as administrative fees, account charges and surrender charges, which if reflected, would reduce the performance of the fund. Past performance is no guarantee of future results. |

| 2 | Lipper, Inc. is a major independent mutual-fund tracking organization. Returns are based on the 12-month period ended October 31, 2004, calculated among the 31 funds in the fund’s Lipper category, including the reinvestment of dividends and capital gains, if any. |

11 Travelers Series Fund Inc. | 2004 Annual Report

Signs of inflation and strong non-farm payroll numbers began to appear in March and April of 2004. Strong job numbers, combined with inflation fighting language from the Fed, led to a rise in U.S. treasury yields, with 10-year yields gaining more than 100 basis points from their early March lows. Yields on most fixed-income instruments, particularly those on shorter-maturity issues, began moving up and continued their ascent as it became more evident that the improving economy and higher inflation would compel the Fed to act in June. The Fed finally raised its federal funds rate target to 1.25% in June off the stronger employment numbers.

Against this backdrop, fixed income markets finished on a somewhat more stable note in June and July. The Fed raised its federal funds target rate by an additional 0.25% at each subsequent meeting in July, August, and September, despite significant softening of many economic indicators during the late summer months, bringing the target rate to 1.75% at the end of the reporting cycle for the fund. Following the end of the fund’s reporting period, at its November meeting, the Fed once again raised its target for the federal funds rate by 0.25% to 2.00%.

Over the period, U.S. Treasuries, as represented by the Citigroup U.S. Treasury Bond Index,x returned 4.98%, rebounding in the third quarter after the worst quarter in more than two decades. U.S. Agencies, as represented by the Citigroup U.S. Agency Index,xi also had positive returns during the period of 4.78%. The sector saw widening in the third quarter of 2004, as the Office of Federal Housing Enterprise Oversight (OFHEO) and the SEC continued to look closely at the accounting practices of the Federal National Mortgage Association (“FNMA “). The market had been expecting no headline risk for the agencies until after the election. The mortgage-backed sector, as represented by the Citigroup Mortgage Index,xii returned 5.68%. Early in the third quarter of 2004, the environment looked favorable for mortgage-backed securities with light supply, low volatility and positive technicals. As the 10-year U.S. treasury note approached 4.10% later in the quarter, convexity started to become a concern and supply from originators increased.

Factors Influencing Fund Performance

Despite the volatility of the yield curve during the period, the fund outperformed its benchmark, the Citigroup 6-Month U.S. Treasury Bill Indexxx providing 8 basis points of excess returns. Our strategic allocation to mortgage-backed securities, specifically mortgage pass-throughs and, to a lesser extent collateralized mortgage obligations, and U.S. Treasury securities, benefited the fund during the period. Our substantial allocation to asset-backed securities provided diversification and attributed to NAV stability during periods of volatility within

12 Travelers Series Fund Inc. | 2004 Annual Report

the mortgage sector. We continued to invest fund assets primarily in mortgage-backed and asset-backed securities, with strategic allocations to commercial mortgage backed securities. We increased our allocation to adjustable rate securities during the period as a defensive measure against upward pressure on the short end of the yield curve as rates continued to rise.xxi

We plan to maintain our current allocation to mortgage-backed securities and asset-backed securities in an effort to provide diversification and achieve greater total return.

Thank you for your investment in the SB Adjustable Rate Income Portfolio. As ever, we appreciate that you have chosen us to manage your assets and we remain focused on achieving the fund’s investment goals.

Sincerely,

| | |

| |  |

| David A. Torchia | | Theresa M. Veres |

| Vice President and Investment Officer | | Vice President and Investment Officer |

December 13, 2004

The information provided is not intended to be a forecast of future events, a guarantee of future results or investment advice. Views expressed may differ from those of the firm as a whole.

RISKS:

Smith Barney International AIl Cap Growth Portfolio: Keep in mind, the fund is subject to certain risks of overseas investing, not associated with domestic investing, including currency fluctuations, change in political and economic conditions, differing securities regulations and periods of illiquidity, which could result in significant market fluctuations. These risks are magnified in emerging markets. The fund may use derivatives, such as options and futures, which can be illiquid, may disproportionately increase losses, and have a potentially large impact on fund performance.

Salomon Brothers Strategic Total Return Bond Portfolio: Investments in high-yield securities and foreign companies and governments, including emerging markets involve risks beyond those inherent solely in higher-rated and domestic investments. The risks of high-yield securities include, but are not limited to, price volatility and the possibility of default in the timely payment of interest and principal. Foreign stocks are subject to certain risks of overseas investing including currency fluctuations and changes in political and economic conditions, which could result in significant market fluctuations. The fund may use derivatives, such as options and futures, which can be illiquid, may disproportionately increase losses, and have a potentially large impact on fund performance. The fund is not diversified, which may magnify the fund’s losses from adverse events affecting a particular issuer.

SB Adjustable Rate Income Portfolio: Keep in mind, the fund is subject to fluctuations in share price as interest rates rise and fall. Adjustable rate securities are subject to additional risks such as prepayment risk. The fund may use derivatives, such as options and futures, which can be illiquid, may disproportionately increase losses, and have a potentially large impact on fund performance.

13 Travelers Series Fund Inc. | 2004 Annual Report

All index performance reflects no deduction for fees, expenses or taxes. Please note that an investor cannot invest directly in an index.

| i | Source: Commerce Department (Bureau of Economic Analysis). Refers to quarterly growth of Gross Domestic Product ("GDP"). Gross domestic product is a market value of goods and services produced by labor and property in a given country. |

| ii | Source: U.S. Federal Reserve Board. The Fed is responsible for the formulation of a policy designed to promote economic growth, full employment, stable prices, and a sustainable pattern of international trade and payments. |

| iii | The federal funds rate is the interest rate that banks with excess reserves at a Federal Reserve district bank charge other banks that need overnight loans. |

| iv | The MSCI EAFE Index is an unmanaged index of common stocks of companies located in Europe, Australasia and the Far East. |

| v | The MSCI EAFE Growth Index is an unmanaged index of growth stocks of companies located in Europe, Australasia and the Far East. |

14 Travelers Series Fund Inc. | 2004 Annual Report

| vi | Portfolio holdings and breakdowns are as of October 31, 2004 and are subject to change and may not be representative of the portfolio manager’s current or future investments. The fund’s top ten holdings as of this date were: Vodafone Group PLC (5.1%), Mettler-Toledo International, Inc. (A) (3.5%), Grafton Group PLC (3.3%), Roche Holdings AG (2.9%), Serco Group PLC (2.8%), Capita Group PLC (2.8%), CRH PLC (2.5%), Nokia Oyj (2.4%), CANON INC. (2.4%), UBS AG (2.3%). Please refer to pages 27 through 30 for a list and percentage breakdown of the fund’s holdings. |

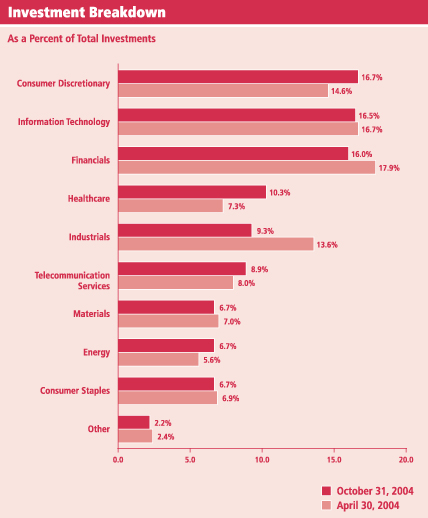

| vii | The mention of sector breakdowns is for informational purposes only and should not be construed as a recommendation to purchase or sell any securities. The information provided regarding such sectors is not a sufficient basis upon which to make an investment decision. Investors seeking financial advice regarding the appropriateness of investing in any securities or investment strategies discussed should consult their financial professional. Portfolio holdings are subject to change at any time and may not be representative of the portfolio manager’s current or future investments. The fund’s top five sector holdings as of October 31, 2004 were: Consumer Discretionary (16.4%); Information Technology (16.3%); Financials (15.7%); Healthcare (10.2%); Industrials (9.1%). The fund’s portfolio composition is subject to change at any time. |

| viii | The J.P. Morgan Global Government Bond Index — Unhedged is a daily, market capitalization-weighted, international fixed-income index consisting of 13 countries. |

| ix | The Lehman Brothers Aggregate Bond Index is a broad-based bond index comprised of Government, Corporate, Mortgage and Asset-backed issues, rated investment-grade or higher, and having at least one year to maturity. Effective December 31, 2004, The Lehman Brothers Aggregate Bond Index will replace the J.P. Morgan Global Government Bond Index — Unhedged as the fund’s sole benchmark. |

| x | The Citigroup U.S. Treasury Bond Index is a broad measure of the performance of U.S. Treasury securities. |

| xi | The Citigroup U.S. Agency Index is the U.S. Agency component of the Citigroup Broad Investment-Grade Bond Index. |

| xii | The Citigroup Mortgage Index is the mortgage component of the Citigroup Broad Investment-Grade Bond Index. It includes 30- and 15-year GNMA, Fannie Mae and Freddie Mac pass-throughs, and Fannie Mae and Freddie Mac balloon mortgages. |

| xiii | The Citigroup High Yield Market Index is a broad-based unmanaged index of high yield securities. |

| xiv | Yields are subject to change and will fluctuate. |

| xv | The J.P. Morgan Emerging Markets Bond Index Plus is a total return index that tracks the traded market for U.S. dollar-denominated Brady and other similar sovereign restructured bonds traded in the emerging markets. |

| xvi | Yield spread is the difference between yields on securities of the same quality but different maturities or the difference between yields on securities of the same maturity but different quality. |

| xvii | A basis point is one one-hundredth ( 1/100 or 0.01) of one percent. |

| xviii | Source: J.P. Morgan Chase. China. Columbia, Cote d'Ivoire, Croatia, Ecuador, Greece, Hungary, Lebanon, Malaysia, Mexico, Morocco, Nigeria, Panama, Peru, the Philippines, Poland, Russia, South Africa, South Korea. Thailand, Turkey and Venezuela. |

| xix | J.P. Morgan Emerging Markets Bond Index Global tracks total returns for U.S. dollar denominated debt instruments issued by emerging market sovereign and quasi-sovereign entities: Brady bonds, loans, Eurobonds, and local market instruments. Countries covered are Algeria, Argentina, Brazil, Bulgaria, Chile, |

| xx | The Citigroup 6-Month U.S. Treasury Bill Index performance is an average of the last 6-Month Treasury Bill issues. 6-Month U.S. Treasury Bills are guaranteed by the U.S. government and provide a fixed rate of return when held to maturity. |

| xxi | Portfolio holdings and breakdowns are as of October 31, 2004 and are subject to change and may not be representative of the portfolio manager’s current or future investments. The fund’s top ten holdings as of this date were: FNMA Six Month LIBOR, 4.810% due 10/1/34 (2.1%), MASTR Alternative Loan Trust, Series 2003-7, Class 7AI, 2.333% due 11/25/33 (1.9%), FNMA, 30 Year, 12.000% due 4/20/16 (1.6%), Credit Acceptance Auto Dealer Loan Trust, Series 2004-1, Class A, 2.530% due 8/17/09 (1.7%), Structured Asset Securities Corp., Series 2002-8A, Class 7A1, 3.319% due 5/25/32 (1.6%), FNMA Six Month Libor, 4.366% due 4/1/33 (1.6%), FNMA One Year LIBOR, 4.068% due 7/1/33 (1.6%), Renaissance Home Equity Loan Trust, Series 2003-3, Class A, 2.433% due 12/25/33 (1.5%), Fannie Mae REMIC Trust, Series 2003-W15, Class 3A, 4.027% due 12/25/42 (1.4%), Amortizing Residential Collateral Trust, Series 2002-BC10, Class A3, 2.363% due 1/25/33 (1.4%). Please refer to pages 42 through 47 for a list and percentage breakdown. |

15 Travelers Series Fund Inc. | 2004 Annual Report

International All Cap Growth Portfolio

Fund at a Glance (unaudited)

16 Travelers Series Fund Inc. | 2004 Annual Report

Salomon Brothers Strategic Total Return Bond Portfolio

Fund at a Glance (unaudited)

17 Travelers Series Fund Inc. | 2004 Annual Report

SB Adjustable Rate Income Portfolio

Fund at a Glance (unaudited)

18 Travelers Series Fund Inc. | 2004 Annual Report

Fund Expenses (unaudited)

Example

As a shareholder of the Fund, you may incur two types of costs: (1) transaction costs, including front-end and back-end sales charges (loads) on purchase payments, reinvested dividends, or other distributions; and (2) ongoing costs, including management fees; distribution and/or service (12b-1) fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

This example is based on an investment of $1,000 invested on May 1, 2004 and held for the six months ended October 31, 2004.

Actual Expenses

The table below titled “Based on Actual Total Return” provides information about actual account values and actual expenses. You may use the information provided in this table, together with the amount you invested, to estimate the expenses that you paid over the period. To estimate the expenses you paid on your account, divide your ending account value by $1,000 (for example, an $8,600 ending account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled “Expenses Paid During the Period”.

| | | | | | | | | | | | | | | |

| Based on Actual Total Return(1) | | | |

| | | | | | | | | | | | | | | | |

| | | Actual

Total Return(2) | | | Beginning

Account

Value | | Ending

Account

Value | | Annualized

Expense

Ratio | | | Expenses

Paid During

the Period(3) |

Smith Barney International All Cap Growth Portfolio | | 3.79 | % | | $ | 1,000.00 | | $ | 1,037.90 | | 1.01 | % | | $ | 5.17 |

|

Salomon Brothers Strategic Total Return Bond Portfolio | | 4.69 | | | | 1,000.00 | | | 1,046.90 | | 1.27 | | | | 6.53 |

|

SB Adjustable Rate Income Portfolio | | 0.50 | | | | 1,000.00 | | | 1,005.00 | | 1.00 | | | | 5.04 |

|

| (1) | | For the six months ended October 31, 2004. |

| (2) | | Assumes reinvestment of all dividends and capital gain distributions, if any, at net asset value. Total return is not annualized, as it may not be representative of the total return for the year. Total returns do not reflect expenses associated with the separate account such as administrative fees, account charges and surrender charges which, if reflected, would reduce the total returns. Performance figures may reflect fee waivers and/or expense reimbursements. Past performance is no guarantee of future results. In the absence of fee waivers and/or expense reimbursements, the total return would have been lower. |

| (3) | | Expenses (net of voluntary waiver) are equal to each Fund’s respective annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year, then divided by 366. |

19 Travelers Series Fund Inc. | 2004 Annual Report

Fund Expenses (unaudited) (continued)

Hypothetical Example for Comparison Purposes

The table below titled “Based on Hypothetical Total Return” provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio and an assumed rate of return of 5.00% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use the information provided in this table to compare the ongoing costs of investing in the Fund and other funds. To do so, compare the 5.00% hypothetical example relating to the Fund with the 5.00% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table below are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as front-end or back-end sales charges (loads). Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

| | | | | | | | | | | | | | | |

| Based on Hypothetical Total Return(1) | | | |

| | | | | | | | | | | | | | | | |

| | | Hypothetical

Total Return | | | Beginning

Account

Value | | Ending

Account

Value | | Annualized

Expense

Ratios | | | Expenses

Paid During

the Period(2) |

Smith Barney International All Cap Growth Portfolio | | 5.00 | % | | $ | 1,000.00 | | $ | 1,020.06 | | 1.01 | % | | $ | 5.13 |

|

Salomon Brothers Strategic Total Return Bond Portfolio | | 5.00 | | | | 1,000.00 | | | 1,018.75 | | 1.27 | | | | 6.44 |

|

SB Adjustable Rate Income Portfolio | | 5.00 | | | | 1,000.00 | | | 1,020.11 | | 1.00 | | | | 5.08 |

|

| (1) | | For the six months ended October 31, 2004. |

| (2) | | Expenses (net of voluntary waiver) are equal each Fund’s respective annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year, then divided by 366. |

20 Travelers Series Fund Inc. | 2004 Annual Report

Smith Barney International All Cap Growth Portfolio

Average Annual Total Returns† (unaudited)

| | | |

Twelve Months Ended 10/31/04 | | 13.90 | % |

|

|

Five Years Ended 10/31/04 | | (6.48 | ) |

|

|

Ten Years Ended 10/31/04 | | 1.44 | |

|

|

6/16/94* through 10/31/04 | | 1.91 | |

|

|

Cumulative Total Return† (unaudited)

| | | |

10/31/94 through 10/31/04 | | 15.33 | % |

|

|

| † | | Assumes the reinvestment of dividends and capital gains distributions, if any, at net asset value. All figures represent past performance and are not a guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Total returns do not reflect expenses associated with the separate account such as administrative fees, account charges and surrender charges which, if reflected, would reduce the total returns. Performance figures may reflect fee waivers and/or expense reimbursements. In the absence of fee waivers and/or expense reimbursements, the total return would have been lower. |

| * | | Commencement of operations. |

21 Travelers Series Fund Inc. | 2004 Annual Report

Historical Performance (unaudited)

Value of $10,000 Invested in Shares of the

Smith Barney International All Cap Growth Portfolio vs.

MSCI EAFE Index and MSCI EAFE Growth Index†

October 1994 — October 2004

| † | Hypothetical illustration of $10,000 invested in shares of the Smith Barney International All Cap Growth Portfolio on October 31, 1994, assuming reinvestment of dividends and capital gains, if any, at net asset value through October 31, 2004. The Morgan Stanley Capital International Europe, Australasia and the Far East Growth Index (“MSCI EAFE Growth Index”) is an unmanaged index composed of growth stocks of companies located in Europe, Australasia and the Far East. The Morgan Stanley Capital International Europe, Australasia and the Far East Index (“MSCI EAFE Index”) is an unmanaged index of common stocks of companies located in Europe, Australasia and the Far East. The MSCI EAFE Index is weighted based on each company’s market capitalization. The indexes are not subject to the same management and trading expenses of a mutual fund. Please note that an investor cannot invest directly in an index. |

All figures represent past performance and are not a guarantee of future results. Investment return and principal value of an investment, which will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The graph does not reflect expenses associated with the separate account such as administrative fees, account charges and surrender charges which, if reflected, would reduce the total returns. Performance figures may reflect fee waivers and/or expense reimbursements. In the absence of fee waivers and/or expense reimbursements, the total return would have been lower.

It is the opinion of management that the MSCI EAFE Growth Index more accurately reflects the current composition of the Fund than the MSCI EAFE Index. In future reports, the MSCI EAFE Growth Index will be used as the basis of comparison of total returns for all periods shown.

22 Travelers Series Fund Inc. | 2004 Annual Report

Salomon Brothers Strategic Total Return Bond Portfolio

Average Annual Total Returns† (unaudited)

| | | |

Twelve Months Ended 10/31/04 | | 6.83 | % |

|

|

Five Years Ended 10/31/04 | | 8.04 | |

|

|

Ten Years Ended 10/31/04 | | 7.39 | |

|

|

6/16/94* through 10/31/04 | | 7.06 | |

|

|

Cumulative Total Return† (unaudited)

| | | |

10/31/94 through 10/31/04 | | 104.03 | % |

|

|

| † | | Assumes the reinvestment of all dividends and capital gains distributions, if any, at net asset value. All figures represent past performance and are not a guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Total returns do not reflect expenses associated with the separate account such as administrative fees, account charges and surrender charges which, if reflected, would reduce the total returns. Performance figures may reflect fee waivers and/or expense reimbursements. In the absence of fee waivers and/or expense reimbursements, the total return would have been lower. |

| * | | Commencement of operations. |

23 Travelers Series Fund Inc. | 2004 Annual Report

Historical Performance (unaudited)

Value of $10,000 Invested in Shares of the

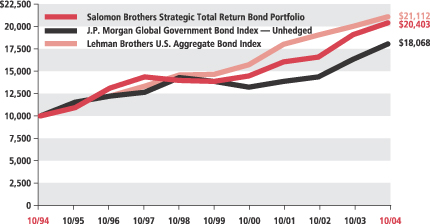

Salomon Brothers Strategic Total Return Bond Portfolio vs.

J.P. Morgan Global Government Bond Index — Unhedged and Lehman Brothers U.S. Aggregate Bond Index†

October 1994 — October 2004

| † | Hypothetical illustration of $10,000 invested in shares of the Salomon Brothers Strategic Total Return Bond Portfolio on October 31, 1994, assuming reinvestment of dividends and capital gains, if any, at net asset value through October 31, 2004. The J.P. Morgan Global Government Bond Index — Unhedged is a daily, market capitalization weighted international fixed-income index consisting of 13 countries. The Lehman Brothers U.S. Aggregate Bond Index is a broad-based bond index comprised of Government, Corporate, Mortgage and Asset-backed issues, rated investment-grade or higher, and having at least one year to maturity. The Indexes are unmanaged and are not subject to the same management and trading expenses of a mutual fund. Please note that an investor cannot invest directly in an index. |

All figures represent past performance and are not a guarantee of future results. Investment return and principal value of an investment which will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The graph does not reflect expenses associated with the separate account such as administrative fees, account charges and surrender charges which, if reflected, would reduce the total returns. Performance figures may reflect fee waivers and/or expense reimbursements. In the absence of fee waivers and/or expense reimbursements, the total return would have been lower.

24 Travelers Series Fund Inc. | 2004 Annual Report

SB Adjustable Rate Income Portfolio

Average Annual Total Returns† (unaudited)

| | | |

Twelve Months Ended 10/31/04 | | 1.24 | % |

|

|

9/12/03* through 10/31/04 | | 1.18 | |

|

|

Cumulative Total Return† (unaudited)

| | | |

9/12/03* through 10/31/04 | | 1.34 | % |

|

|

| † | | Assumes the reinvestment of all dividends and capital gains distributions, if any, at net asset value. All figures represent past performance and are not a guarantee of future results. Investment return and principal value of an investment will fluctuate so that an Investor’s shares, when redeemed, may be worth more or less than their original cost. Total returns do not reflect expenses associated with the separate account such as administrative fees, account charges and surrender charges which, if reflected, would reduce the total returns. Performance figures may reflect fee waivers and/or expense reimbursements. In the absence of fee waivers and/or expense reimbursements, the total return would have been lower. |

| * | | Commencement of operations. |

25 Travelers Series Fund Inc. | 2004 Annual Report

Historical Performance (unaudited)

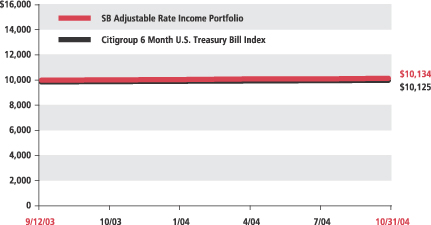

Value of $10,000 Invested in Shares of the

SB Adjustable Rate Income Portfolio vs.

Citigroup 6 Month U.S. Treasury Bill Index†

September 2003 — October 2004

| † | Hypothetical illustration of $10,000 invested in shares of the SB Adjustable Rate Income Portfolio on September 12, 2003 (commencement of operations), assuming reinvestment of dividends and capital gains, if any, at net asset value through October 31, 2004. The Citigroup 6 Month U.S. Treasury Bill Index includes 6-Month Treasury Bills that are guaranteed by the U.S. government and provide a fixed rate of return when held to maturity. The Index is unmanaged and is not subject to the same management and trading expenses of a mutual fund. Please note that an investor cannot invest directly in an index. |

All figures represent past performance and are not a guarantee of future results. Investment return and principal value of an investment, which will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The graph does not reflect expenses associated with the separate account such as administrative fees, account charges and surrender charges which, if reflected, would reduce the total returns. Performance figures may reflect fee waivers and/or expense reimbursements. In the absence of fee waivers and/or expense reimbursements, the total return would have been lower.

26 Travelers Series Fund Inc. | 2004 Annual Report

| | |

| Schedules of Investments | | October 31, 2004 |

SMITH BARNEY INTERNATIONAL ALL CAP GROWTH PORTFOLIO

| | | | | |

| SHARES | | SECURITY | | VALUE |

| | | | | | |

| STOCKS — 97.8% | | | |

| Australia — 2.5% | | | |

| 69,000 | | Macquarie Bank Ltd. (a) | | $ | 2,040,178 |

| 200,024 | | The News Corp. Ltd. (a) | | | 1,608,908 |

| 27,000 | | Westpac Banking Corp. | | | 380,714 |

|

| | | | | | 4,029,800 |

|

| Denmark — 1.4.% | | | |

| 44,000 | | Novo Nordisk A/S, Class B Shares | | | 2,185,206 |

|

| Finland — 2.4% | | | |

| 248,000 | | Nokia Oyj | | | 3,822,257 |

|

| France — 6.7% | | | |

| 154,000 | | Axa | | | 3,311,904 |

| 32,000 | | Essilor International SA (a) | | | 2,170,219 |

| 30,000 | | Groupe Danone (a) | | | 2,508,806 |

| 13,000 | | Total SA (a) | | | 2,701,300 |

|

| | | | | | 10,692,229 |

|

| Germany — 3.0% | | | |

| 25,300 | | BASF AG (a) | | | 1,577,144 |

| 12,500 | | SAP AG (a) | | | 2,127,800 |

| 50,000 | | Stada Arzneimittel AG (a) | | | 1,040,874 |

|

| | | | | | 4,745,818 |

|

| Hong Kong — 2.3% | | | |

| 118,000 | | Hutchinson Whampoa Ltd. | | | 909,616 |

| 826,000 | | Li & Fung Ltd. (a) | | | 1,225,708 |

| 525,000 | | Luen Thai Holdings Ltd. (b) | | | 269,802 |

| 191,000 | | Swire Pacific Ltd. | | | 1,355,785 |

|

| | | | | | 3,760,911 |

|

| Ireland — 8.4% | | | |

| 128,000 | | Bank of Ireland | | | 1,754,124 |

| 168,000 | | CRH PLC | | | 4,004,911 |

| 584,000 | | Grafton Group PLC (b) | | | 5,248,605 |

| 180,740 | | Irish Continental Group PLC | | | 2,338,634 |

|

| | | | | | 13,346,274 |

|

| Italy — 1.1% | | | |

| 150,000 | | Saipem S.p.A. | | | 1,728,628 |

|

| Japan — 17.7% | | | |

| 77,000 | | CANON INC. | | | 3,798,434 |

| 30,000 | | DaiichiKosho Co., Ltd. | | | 911,149 |

| 300 | | Dentsu Inc. | | | 803,622 |

| 179,000 | | Dowa Mining Co., Ltd. | | | 1,080,551 |

| 44,500 | | Honda Motor Co., Ltd. | | | 2,149,028 |

See Notes to Financial Statements.

27 Travelers Series Fund Inc. | 2004 Annual Report

| | |

| Schedules of Investments (continued) | | October 31, 2004 |

SMITH BARNEY INTERNATIONAL ALL CAP GROWTH PORTFOLIO

| | | | | |

| SHARES | | SECURITY | | VALUE |

| | | | | | |

| Japan — 17.7% (continued) | | | |

| 16,000 | | Hoya Corp. | | $ | 1,641,954 |

| 58,000 | | Ito-Yokado Co., Ltd. | | | 2,078,853 |

| 298 | | Mitsubishi Tokyo Financial Group, Inc. | | | 2,529,711 |

| 14,000 | | Nichii Gakkan Co. | | | 377,665 |

| 8,500 | | Nidec Corp. (a) | | | 920,392 |

| 159,000 | | Nomura Holdings, Inc. | | | 1,949,632 |

| 580 | | NTT DoCoMo, Inc. | | | 1,023,015 |

| 120 | | Rakuten, Inc. (a) | | | 899,830 |

| 12,000 | | Rohm Co., Ltd. | | | 1,231,466 |

| 26,000 | | Seven-Eleven Japan Co., Ltd. | | | 752,877 |

| 100,000 | | Sharp Corp. | | | 1,380,872 |

| 34,000 | | Shin-Etsu Chemical Co., Ltd. | | | 1,292,398 |

| 100,000 | | Terumo Corp. | | | 2,490,096 |

| 18,600 | | Tokyo Electron Ltd. | | | 1,008,772 |

|

| | | | | | 28,320,317 |

|

| Mexico — 2.0% | | | |

| 995,000 | | Wal-Mart De Mexico S.A. de C.V. | | | 3,255,439 |

|

| The Netherlands — 3.0% | | | |

| 39,351 | | ING Groep N.V. | | | 1,040,916 |

| 72,000 | | Randstad Holdings N.V. (a) | | | 2,424,057 |

| 25,000 | | Royal Dutch Petroleum Co. | | | 1,357,343 |

|

| | | | | | 4,822,316 |

|

| Norway — 0.9% | | | |

| 297,000 | | Stolt Offshore S.A. (a)(b) | | | 1,468,043 |

|

| Singapore — 2.3% | | | |

| 200,000 | | DBS Group Holdings, Ltd. | | | 1,875,282 |

| 289,000 | | Singapore Press Holdings, Ltd. | | | 816,409 |

| 104,000 | | Venture Corp., Ltd. | | | 987,648 |

|

| | | | | | 3,679,339 |

|

| Spain — 5.4% | | | |

| 136,000 | | Banco Bilbao Vizcaya Argentaria, S.A. (a) | | | 2,132,485 |

| 226,000 | | Indra Sistemas, S.A. | | | 3,347,777 |

| 190,000 | | Telefonica S.A. (b) | | | 3,134,222 |

|

| | | | | | 8,614,484 |

|

| Sweden — 2.2% | | | |

| 46,500 | | Atlas Copco AB (a) | | | 1,922,624 |

| 534,000 | | Telefonaktiebolaget LM Ericsson (b) | | | 1,549,680 |

|

| | | | | | 3,472,304 |

|

| Switzerland — 11.4% | | | |

| 115,500 | | Mettler-Toledo International Inc. (b) | | | 5,532,450 |

| 6,500 | | Nestle SA | | | 1,536,191 |

| 41,000 | | Novartis AG | | | 1,953,358 |

See Notes to Financial Statements.

28 Travelers Series Fund Inc. | 2004 Annual Report

| | |

| Schedules of Investments (continued) | | October 31, 2004 |

SMITH BARNEY INTERNATIONAL ALL CAP GROWTH PORTFOLIO

| | | | | |

| SHARES | | SECURITY | | VALUE |

| | | | | | |

| Switzerland — 11.4% (continued) | | | |

| 45,000 | | Roche Holdings AG | | $ | 4,595,745 |

| 8,800 | | Synthes, Inc. (b) | | | 936,904 |

| 50,600 | | UBS AG | | | 3,643,538 |

|

| | | | | | 18,198,186 |

|

| United Kingdom — 25.1% | | | |

| 50,000 | | BOC Group PLC | | | 804,472 |

| 330,700 | | BP PLC | | | 3,200,354 |

| 681,000 | | Capita Group PLC | | | 4,394,632 |

| 535,000 | | Compass Group PLC | | | 2,208,400 |

| 184,000 | | Diageo PLC | | | 2,459,171 |

| 87,538 | | HSBC Holdings PLC | | | 1,417,073 |

| 326,470 | | Kingfisher PLC | | | 1,810,302 |

| 880,000 | | mm02 PLC (b) | | | 1,699,206 |

| 70,000 | | Rio Tinto PLC | | | 1,828,729 |

| 57,647 | | Royal Bank of Scotland Group PLC | | | 1,697,435 |

| 1,137,000 | | Serco Group PLC | | | 4,547,349 |

| 100,000 | | Smith & Nephew PLC | | | 848,502 |

| 605,145 | | Tesco PLC | | | 3,186,271 |

| 3,196,000 | | Vodafone Group PLC | | | 8,179,416 |

| 178,000 | | WPP Group PLC | | | 1,784,644 |

|

| | | | | | 40,065,956 |

|

| | | TOTAL STOCKS

(Cost — $125,575,033) | | | 156,207,507 |

|

| | |

FACE

AMOUNT | | | | |

| REPURCHASE AGREEMENT — 0.6% | | | |

| $ 884,000 | | Goldman, Sachs & Co. dated 10/29/04, 1.840% due 11/1/04; Proceeds at maturity — $884,136; (Fully collateralized by various U.S. government agency obligations, 0.000% to 10.625% due 12/2/04 to 4/15/29; Market value — $901,680) (Cost — $884,000) | | | 884,000 |

|

| | | TOTAL INVESTMENTS — 98.4% (Cost — $126,459,033*) | | | 157,091,507 |

| | | Other Assets in Excess of Liabilities — 1.6% | | | 2,630,140 |

|

| | | TOTAL NET ASSETS — 100.0% | | $ | 159,721,647 |

|

| LOANED SECURITIES COLLATERAL | | | |

| 21,892,934 | | State Street Navigator Securities Lending Trust Prime Portfolio

(Cost — $21,892,934) | | $ | 21,892,934 |

|

| (a) | | All or a portion of this security is on loan (See Notes 1 and 3). |

| (b) | | Non-income producing security. |

| * | | Aggregate cost for federal income tax purposes is $126,490,649. |

See Notes to Financial Statements.

29 Travelers Series Fund Inc. | 2004 Annual Report

| | |

| Schedules of Investments (continued) | | October 31, 2004 |

| | | |

| Summary of Investments by Sector* | | | |

Consumer Discretionary | | 16.7 | % |

Information Technology | | 16.5 | |

Financials | | 16.0 | |

Healthcare | | 10.3 | |

Industrials | | 9.3 | |

Telecommunication Services | | 8.9 | |

Materials | | 6.7 | |

Energy | | 6.7 | |

Consumer Staples | | 6.7 | |

Other | | 2.2 | |

|

|

| | | 100.0 | % |

|

|

| * | | As a percentage of total investments. |

See Notes to Financial Statements.

30 Travelers Series Fund Inc. | 2004 Annual Report

| | |

| Schedules of Investments (continued) | | October 31, 2004 |

| | | | | | | |

| SALOMON BROTHERS STRATEGIC TOTAL RETURN BOND PORTFOLIO |

FACE

AMOUNT† | | RATING(e) | | SECURITY | | VALUE |

| U.S. GOVERNMENT OBLIGATIONS AND AGENCIES — 38.4% | | | |

| | | | | U.S. Treasury Notes: | | | |

| $ 450,000 | | | | 4.875% due 2/15/12 (a)(b) | | $ | 482,397 |

| 205,000 | | | | 4.000% due 2/15/14 (a) | | | 205,072 |

| 400,000 | | | | U.S. Treasury Bonds, 6.250% due 5/15/30 (a)(b) | | | 481,125 |

| | | | | Federal Home Loan Mortgage Corp.: | | | |

| 1,000,000 | | | | 5.000% due 11/1/34 (c)(d) | | | 997,188 |

| 1,250,000 | | | | 6.000% due 11/1/34 (c)(d) | | | 1,294,531 |

| | | | | Federal National Mortgage Association: | | | |

| 250,000 | | | | 5.000% due 11/1/34 (c)(d) | | | 249,140 |

| 500,000 | | | | 6.500% due 11/1/34 (c)(d) | | | 525,781 |

| 2,000,000 | | | | 7.000% due 11/1/34 (c)(d) | | | 2,123,750 |

|

| | | | | TOTAL U.S. GOVERNMENT OBLIGATIONS

AND AGENCIES (Cost — $6,225,662) | | | 6,358,984 |

|

| COLLATERALIZED MORTGAGE OBLIGATIONS — 1.1% | | | |

| 57,873 | | A+ | | Commercial Mortgage Pass-Through Certificates, Series 2003-FL9, Class E, 2.870% due 11/15/15 (f)(g) | | | 58,233 |

| 125,000 | | A2* | | Merit Securities Corp., Series 11PA, Class B2, 3.459% due 9/28/32 (f)(g) | | | 120,742 |

|

| | | | | TOTAL COLLATERALIZED MORTGAGE OBLIGATIONS (Cost — $170,339) | | | 178,975 |

|

| ASSET-BACKED SECURITIES — 4.9% | | | |

| 150,000 | | A | | Amortizing Residential Collateral Trust, Series 2002-BC6, Class M2, 3.132% due 8/25/32 (g) | | | 150,750 |

| 250,000 | | A2* | | Bayview Financial Acquisition Trust, Series 2001-CA, Class M3, 3.182% due 8/25/36 (f)(g) | | | 248,281 |

| | | | | Bear Stearns Asset Backed Securities: | | | |

| 18,509 | | BBB | | Series 2003-HE1N, Class N1, 6.500% due 8/25/05 (f) | | | 18,636 |

| 32,890 | | BBB | | Series 2004-FR1N, Class A1, 5.000% due 5/25/34 (f) | | | 32,821 |

| 33,035 | | BBB | | Series 2004-HE6, Class A1, 5.250% due 8/25/34 (f) | | | 33,000 |

| | | | | Countrywide Asset-Backed Certificates: | | | |

| 50,000 | | AA | | Series 2004-5, Class M4, 3.182% due 6/25/34 (g) | | | 50,029 |

| 33,290 | | BBB | | Series 2004-5N, Class N1, 5.500% due 10/25/35 (f) | | | 33,369 |

| 71,790 | | B | | First Consumers Master Trust, Series 2001-A, Class A, 2.180% due 9/15/08 (g) | | | 69,873 |

| 50,183 | | AAA | | Green Tree Home Equity Loan Trust, Series 1999-D, Class A5, 7.880% due 9/15/30 | | | 50,671 |

| 70,000 | | BBB | | Metris Master Trust, Series 2001-2, Class B,

2.990% due 11/20/09 (g) | | | 69,475 |

| 20,000 | | A | | Novastar Home Equity Loan Trust, Series 2003-4, Class M2, 3.557% due 2/25/34 (g) | | | 20,456 |

See Notes to Financial Statements.

31 Travelers Series Fund Inc. | 2004 Annual Report

| | |

| Schedules of Investments (continued) | | October 31, 2004 |

| | | | | | | |

| SALOMON BROTHERS STRATEGIC TOTAL RETURN BOND PORTFOLIO |

FACE

AMOUNT | | RATING(e) | | SECURITY | | VALUE |

| ASSET-BACKED SECURITIES — 4.9% (continued) | | | |

| | | | | Sail Net Interest Margin Notes: | | | |

| $ 6,184 | | BBB | | Series 2003-3, Class A, 7.750% due 4/27/33 (f) | | $ | 6,221 |

| 32,844 | | BBB+ | | Series 2004-4A, Class A, 5.000% due 4/27/34 (f) | | | 32,896 |

|

| | | | | TOTAL ASSET-BACKED SECURITIES (Cost $802,700) | | | 816,478 |

|

| CORPORATE BONDS AND NOTES — 25.6% | | | |

| Aerospace/Defense — 0.3% | | | |

| 25,000 | | B | | Alliant Techsystems Inc., Sr. Sub. Notes, 8.500% due 5/15/11 (a) | | | 27,688 |

| 25,000 | | BB- | | Sequa Corp., Sr. Notes, 9.000% due 8/1/09 | | | 28,062 |

|

| | | | | | | | 55,750 |

|

| Airlines — 0.1% | | | |

| 25,000 | | BB- | | Continental Airlines, Inc., Pass-Through Certificates, Series 98-3, Class C-2, 7.250% due 11/1/05 (a) | | | 22,142 |

|

| Automotive — 0.3% | | | |

| 25,000 | | B- | | EaglePicher Inc., Sr. Notes, 9.750% due 9/1/13 | | | 25,500 |

| 22,000 | | BB- | | TRW Automotive Inc., Sr. Notes, 9.375% due 2/15/13 | | | 25,410 |

|

| | | | | | | | 50,910 |

|

| Business Services — 0.2% | | | |

| 25,000 | | CCC | | SITEL Corp., Sr. Sub. Notes, 9.250% due 3/15/06 | | | 25,125 |

|

| Chemicals — 1.8% | | | |

| 15,000 | | Caa3* | | Applied Extrusion Technologies, Inc., Sr. Notes, Series B, 10.750% due 7/1/11 (h) | | | 9,075 |

| 25,000 | | BB+ | | FMC Corp., Sr. Debentures, 7.750% due 7/1/11 | | | 26,625 |

| 25,000 | | B | | Huntsman Advanced Materials LLC., Sr. Secured Second Lien Notes, 11.000% due 7/15/10 (a)(f) | | | 29,000 |

| 25,000 | | CCC+ | | Huntsman ICI Chemicals LLC, Sr. Sub. Notes, 10.125% due 7/1/09 | | | 26,375 |

| 25,000 | | BB- | | ISP Chemco Inc., Sr. Sub. Notes, Series B, 10.250% due 7/1/11 | | | 28,000 |

| 25,000 | | B+ | | Lyondell Chemical Co., Sr. Secured Notes, 11.125% due 7/15/12 | | | 29,594 |

| 25,000 | | BBB- | | Methanex Corp., Sr. Notes, 8.750% due 8/15/12 | | | 29,375 |

| 25,000 | | BB- | | Millenium America Inc., Sr. Notes, 9.250% due 6/15/08 (f) | | | 28,000 |

| 25,000 | | CCC | | Resolution Performance Products LLC, Sr. Sub. Notes, 13.500% due 11/15/10 | | | 24,875 |

| 25,000 | | CCC+ | | Rhodia S.A., Sr. Sub. Notes, 8.875% due 6/1/11 | | | 23,500 |

| 25,000 | | B- | | United Industries Corp., Sr. Sub. Notes, Series D, 9.875% due 4/1/09 | | | 26,375 |

| 16,000 | | BB- | | Westlake Chemical Corp., Sr. Notes, 8.750% due 7/15/11 | | | 18,120 |

|

| | | | | | | | 298,914 |

|

| Consumer Products & Services — 1.0% | | | |

| 1,000 | | CCC | | Applica Inc., Sr. Sub. Notes, 10.000% due 7/31/08 | | | 980 |

| 25,000 | | C* | | Brown Jordan International, Inc., Sr. Sub. Notes, Series B, 12.750% due 8/15/07 | | | 20,750 |

See Notes to Financial Statements.

32 Travelers Series Fund Inc. | 2004 Annual Report

| | |

| Schedules of Investments (continued) | | October 31, 2004 |

| | | | | | | |

| SALOMON BROTHERS STRATEGIC TOTAL RETURN BOND PORTFOLIO |

FACE

AMOUNT | | RATING(e) | | SECURITY | | VALUE |

| Consumer Products & Services — 1.0% (continued) | | | |

| $ 50,000 | | CCC+ | | Home Interiors & Gifts, Inc., Sr. Sub. Notes, 10.125% due 6/1/08 | | $ | 43,250 |

| 25,000 | | B- | | ICON Health & Fitness, Inc., Sr. Sub. Notes, 11.250% due 4/1/12 | | | 20,875 |

| 25,000 | | B- | | Jafra Cosmetics International, Inc./Distribuidora Comercial Jafra, S.A. de C.V., Sr. Sub. Notes, 10.750% due 5/15/11 | | | 28,625 |

| 20,000 | | CCC | | Levi Strauss & Co., Sr. Notes, 12.250% due 12/15/12 | | | 20,750 |

| 16,000 | | B | | Tempur-Pedic, Inc./Tempur Production USA, Inc., Sr. Sub. Notes, 10.250% due 8/15/10 | | | 18,600 |

|

| | | | | | | | 153,830 |

|

| Energy — 1.3% | | | |

| 50,000 | | BBB | | Devon Financing Corp., ULC., Notes, 6.875% due 9/30/11 | | | 57,332 |

| 16,000 | | B+ | | Magnum Hunter Resources, Inc., Sr. Notes, 9.600% due 3/15/12 | | | 18,360 |

| 75,000 | | BBB- | | Petróleos Mexicanos, Global Bonds, 9.500% due 9/15/27 | | | 92,625 |

| 25,000 | | B+ | | Stone Energy Corp., Sr. Sub. Notes, 8.250% due 12/15/11 | | | 27,250 |

| 25,000 | | B | | Vintage Petroleum, Inc., Sr. Sub. Notes, 7.875% due 5/15/11 | | | 27,125 |

|

| | | | | | | | 222,692 |

|

| Environmental Services — 0.3% | | | |

| 25,000 | | BB- | | Allied Waste North America, Inc., Sr. Notes, Series B, 9.250% due 9/1/12 (a) | | | 27,125 |

| 25,000 | | B- | | IMCO Recycling Inc., Sr. Secured Notes, Series B, 10.375% due 10/15/10 | | | 28,000 |

|

| | | | | | | | 55,125 |

|

| Financial Services — 4.8% | | | |

| 80,000 | | A+ | | Bank of America Corp., Sr. Notes, 4.875% due 9/15/12 | | | 82,293 |

| 25,000 | | B- | | BCP Caylux Holdings Luxembourg S.C.A., Sr. Sub. Notes, 9.625% due 6/15/14 (f) | | | 28,125 |

| 100,000 | | BBB- | | Capital One Financial Corp., Notes, 7.250% due 5/1/06 | | | 105,989 |

| 75,000 | | A | | CIT Group Inc., Sr. Notes, 7.750% due 4/2/12 | | | 89,409 |

| 100,000 | | AAA | | General Electric Capital Corp., Global Medium-Term Notes, Series A, 6.000% due 6/15/12 | | | 109,965 |

| 75,000 | | A | | Household Finance Corp., Notes, 6.375% due 11/27/12 | | | 83,862 |

| 50,000 | | AA- | | International Lease Finance Corp., Medium-Term Notes,

Series O, 4.375% due 11/1/09 | | | 50,171 |

| 70,000 | | A | | JPMorgan Chase & Co., Sub. Notes, 6.625% due 3/15/12 | | | 79,152 |

| 25,000 | | A | | Lehman Brothers Holdings Inc., Notes, 3.500% due 8/7/08 | | | 24,903 |

| 55,000 | | BBB | | MBNA Corp., Sr. Medium-Term Notes, 4.625% due 9/15/08 | | | 56,587 |

| 75,000 | | A+ | | Morgan Stanley, Notes, 6.600% due 4/1/12 | | | 84,655 |

|

| | | | | | | | 795,111 |

|

| Food & Beverage — 0.4% | | | |

| 25,000 | | B | | Del Monte Corp., Sr. Sub. Notes, Series B, 9.250% due 5/15/11 | | | 27,750 |

| 40,000 | | BBB+ | | Kraft Foods Inc., Notes, 5.625% due 11/1/11 | | | 42,681 |

|

| | | | | | | | 70,431 |

|

See Notes to Financial Statements.

33 Travelers Series Fund Inc. | 2004 Annual Report

| | |

| Schedules of Investments (continued) | | October 31, 2004 |

| | | | | | | |

| SALOMON BROTHERS STRATEGIC TOTAL RETURN BOND PORTFOLIO |

FACE

AMOUNT | | RATING(e) | | SECURITY | | VALUE |

| Healthcare — 0.4% | | | |

| $ 25,000 | | CC | | aaiPharma Inc., Sr. Sub. Notes, 12.000% due 4/1/10 (a)(g) | | $ | 19,250 |

| 25,000 | | B | | Extendicare Health Services, Inc., Sr. Notes, 9.500% due 7/1/10 | | | 28,250 |

| 25,000 | | B- | | Tenet Healthcare Corp., Sr. Notes, 9.875% due 7/1/14 (f) | | | 26,312 |

|

| | | | | | | | 73,812 |

|

| Hotel/Casino — 0.7% | | | |

| 25,000 | | B+ | | Host Marriott, L.P., Sr. Notes, 7.125% due 11/1/13 | | | 27,125 |

| 25,000 | | B | | John Q. Hammons Hotels L.P./John Q. Hammons Hotels Finance Corp. III, First Mortgage Notes, Series B,

8.875% due 5/15/12 | | | 28,875 |

| 25,000 | | BB+ | | MGM Mirage Inc., Sr. Notes, 6.750% due 9/1/12 (f) | | | 26,625 |

| 25,000 | | B+ | | Turning Stone Casino Resort Enterprise, Sr. Notes, 9.125% due 12/15/10 (f) | | | 27,250 |

|

| | | | | | | | 109,875 |

|

| Machinery — 0.5% | | | |

| 25,000 | | BB- | | Case New Holland Inc., Sr. Notes, 9.250% due 8/1/11 (f) | | | 28,625 |

| 25,000 | | B+ | | NMHG Holding Co., Sr. Notes, 10.000% due 5/15/09 | | | 27,781 |

| 25,000 | | B | | Terex Corp., Sr. Sub. Notes, Series B, 10.375% due 4/1/11 | | | 28,250 |

|

| | | | | | | | 84,656 |

|

| Manufacturing — 0.2% | | | |

| 25,000 | | B- | | Medical Device Manufacturing Inc., Sr. Sub. Notes, 10.000% due 7/15/12 (f) | | | 26,875 |

|

| Media — 2.8% | | | |

| | | | | Charter Communications Holdings, LLC/Charter Communications Holdings Capital Corp.: | | | |

| 15,000 | | CCC- | | Sr. Discount Notes, step bond to yield 18.168% due 5/15/11 | | | 9,750 |

| | | | | Sr. Notes: | | | |

| 25,000 | | CCC- | | 8.250% due 4/1/07 | | | 23,750 |

| 25,000 | | CCC- | | 10.250% due 1/15/10 | | | 20,625 |

| 10,000 | | CCC- | | 10.000% due 5/15/11 | | | 8,050 |

| 50,000 | | BBB | | Comcast Cable Communications Holdings, Notes, 8.375% due 3/15/13 (a) | | | 61,441 |

| 100,000 | | BBB | | Cox Communications, Inc., Notes, 7.750% due 11/1/10 (a) | | | 114,894 |

| 25,000 | | B+ | | CSC Holdings, Inc., Sr. Sub. Debentures, 10.500% due 5/15/16 | | | 28,688 |

| 25,000 | | BB- | | DIRECTV Holdings LLC/DIRECTV Financing Co., Inc., Sr. Notes, 8.375% due 3/15/13 | | | 28,625 |