UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 28, 2013

Commission file number 1-12551

CENVEO, INC.

(Exact name of Registrant as specified in its charter.)

| COLORADO | 84-1250533 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

| 200 FIRST STAMFORD PLACE | ||

| STAMFORD, CT | 06902 | |

| (Address of principal executive offices) | (Zip Code) | |

| 203-595-3000 | ||

| (Registrant’s telephone number, including area code) | ||

Securities Registered Pursuant to Section 12(b) of the Act:

| Title of Each Class | Name of Each Exchange on Which Registered | |

| Common Stock, par value $0.01 per share | New York Stock Exchange | |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. Large accelerated filer o Accelerated filer ý Non-accelerated filer o Smaller reporting company o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No ý

As of June 29, 2013, the aggregate market value of the registrant’s common stock held by non-affiliates of the registrant was approximately $109,519,661 based on the closing sale price as reported on the New York Stock Exchange.

As of February 25, 2014, the registrant had 66,351,596 shares of common stock, par value $0.01 per share, outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Certain information required by Part II (Item 5) and Part III of this form (Items 11, 12, 13 and 14, and part of Item 10) is incorporated by reference from the Registrant’s Proxy Statement to be filed pursuant to Regulation 14A with respect to the Registrant’s Annual Meeting of Shareholders to be held on or about May 1, 2014.

CENVEO, INC. AND SUBSIDIARIES

TABLE OF CONTENTS

| PART I | ||

Page | ||

| PART II | ||

| PART III | ||

| PART IV | ||

1

PART I

Item 1. Business

Overview

We are a diversified manufacturing company focused on print related products. Our broad portfolio of products includes envelope converting, commercial printing, label manufacturing and specialty packaging. We operate a global network of strategically located manufacturing facilities, serving a diverse base of over 100,000 customers.

We operate our business in three complementary reportable segments: envelope, print, and label and packaging. During the fourth quarter of 2013, we completed a realignment of our segments as a result of a change in management reporting and strategy. Previously, we reported our segments as print and envelope and label and packaging.

Envelope. We are the largest envelope manufacturer in North America. On September 16, 2013, we enhanced our manufacturing capabilities and reduced capacity in the envelope industry with the acquisition of certain assets of National Envelope Corporation, which we refer to as National. Our envelope segment had net sales of $749.9 million, $658.2 million and $706.6 million and operating income of $39.8 million, $45.5 million and $46.8 million, in 2013, 2012 and 2011, respectively. Total assets for our envelope segment were $472.3 million and $376.2 million, as of the years ended 2013 and 2012, respectively. Our envelope segment represented approximately 42.2% of our consolidated net sales for the year ended 2013.

Our envelope segment offers direct mail products used for customer solicitations and transactional envelopes used for billing and remittance by end users including financial institutions, insurance companies and telecommunications companies. We also produce a broad line of specialty and stock envelopes which are sold through wholesalers, distributors and national catalogs for the office product markets and office product superstores.

Print. We are one of the leading commercial printers in North America. Our print segment had net sales of $529.8 million, $585.6 million and $627.0 million and operating (loss) income of $(6.0) million, $32.8 million and $43.7 million, in 2013, 2012 and 2011, respectively. Total assets for our print segment were $320.7 million and $378.1 million, as of the years ended 2013 and 2012, respectively. Our print segment represented approximately 29.8% of our consolidated net sales for the year ended 2013.

Our print segment primarily caters to the consumer products, automotive, travel and leisure and telecommunications industries. We provide a wide array of print offerings to our customers including electronic prepress, digital asset archiving, direct-to-plate technology, high-quality color printing on web and sheet-fed presses, digital printing and content management. The broad selection of print products we produce includes car brochures, annual reports, direct mail products, advertising literature, corporate identity materials and brand marketing materials. Our content management business offers complete solutions, including: editing, content processing, content management, electronic peer review, production, distribution and reprint marketing.

Label and Packaging. We are a leading label manufacturer, and the largest North American prescription label manufacturer for retail pharmacy chains. On December 31, 2012, we added to our label business with the acquisition of Express Label Company, which we refer to as Express Label. Our specialty packaging business currently focuses on specialty folded carton packaging and shrink-sleeve packaging. Our label and packaging segment had net sales of $498.2 million, $494.4 million and $510.8 million and operating income of $32.6 million, $54.7 million and $57.8 million in 2013, 2012 and 2011, respectively. Total assets for our label and packaging segment were $356.2 million and $370.4 million, as of the years ended 2013 and 2012, respectively. Our label and packaging segment represented approximately 28.0% of our consolidated net sales for the year ended 2013.

Our label and packaging segment produces a diverse line of custom labels for a broad range of industries including manufacturing, warehousing, packaging, food and beverage, and health and beauty, which we sell through extensive networks within the resale channels. We provide direct mail and overnight packaging labels, food and beverage labels, and shelf and scale labels for national and regional customers. We produce pressure-sensitive prescription labels for the retail pharmacy chain market. We produce premium, high-quality promotional packaging offerings including, folded carton and full body shrink sleeves. Our primary customers for our specialty packaging products are pharmaceutical, apparel, neutraceutical and other large, multinational consumer product companies.

The primary methods of distribution of the principal products for our three segments are by freight carriers, direct shipment via express mail and the United States postal system.

2

Acquisitions and Divestitures

Acquisitions

On September 16, 2013, we acquired certain assets of National. National's accounts receivable and inventory were purchased by unrelated third parties in conjunction with our acquisition. National manufactured and distributed envelope products for the wholesale, billing, financial, direct mail and office products markets and had approximately1,600 employees. We believe the acquisition of certain assets of National will enhance our manufacturing capabilities and reduce capacity in the envelope industry.

On December 31, 2012, we acquired all of the assets of Express Label, which had annual net sales of approximately $5.4 million prior to our acquisition. Express Label is a label business focusing on food and grocery customers, and was acquired to further enhance our label operations.

Divestitures

On September 28, 2013, we completed the sale of our Custom Envelope Group, which we refer to as Custom Envelope. Additionally, during the second quarter of 2013, we decided to exit the San Francisco market and closed a manufacturing facility located there. As a result, the financial results of Custom Envelope and the San Francisco facility have been accounted for as discontinued operations. Our historical, consolidated financial statements have been reclassified to reflect these discontinued operations separately from continuing operations for all periods presented. See Note 3 of our consolidated financial statements for further discussion.

In February of 2012, we completed the sale of our documents and forms business, which we refer to as the Documents Group. In January of 2012, we completed the sale of our wide-format papers business. Collectively, we refer to these businesses as the Discontinued Operations.

Our Business Strategy

Our business strategy has been, and continues to be, focused on improving sales performance, pursuing and integrating strategic acquisitions, improving our cost and capital structure, and maintaining reasonable levels of financial flexibility. We believe this strategy has allowed us to diversify our revenue base, maintain our low cost structure and deliver quality product offerings to our customers.

Improving Sales Performance

Our sales focus has been, and will continue to be, on our customers' experience across each of our businesses, ensuring we meet our customers' demands. We conduct regular reviews of our product offerings, manufacturing processes and distribution methods to ensure they meet the changing needs of our customers. By expanding our product offerings, we intend to increase cross-selling opportunities to better serve our existing customer base. Additionally, we will continue to make investments in our e-commerce platform and sales force to maintain and expand our customer base.

Pursuing Strategic Acquisitions

We continue to selectively review opportunities to expand within growing niche markets, broaden our product offerings and increase our economies of scale through acquisitions. Our acquisition strategy is focused on product expansion or expanding our position in the current markets in which we operate. We believe this focused approach to acquisitions will allow us to grow at a faster pace than the broader industries in which we do business, and continue to leverage our competitive advantage by utilizing our existing infrastructure, operating expertise and customer relationships. We intend to continue practicing acquisition disciplines and pursuing opportunities for greater expected profitability and cash flow and improved operating efficiencies, such as increased utilization of our manufacturing assets. We believe our acquisition strategy will allow us to both realize increased revenue and cost-saving synergies, and apply our management expertise to improve the operations of acquired entities.

Improving our Cost Structure

We regularly assess our operations with a view toward eliminating operations that are not aligned with our core operations, or are underperforming. Over the past seven years, we have initiated cost savings, restructuring and acquisition integration plans that have included the closure of a significant number of manufacturing facilities throughout our operating platform and a significant number of headcount reductions. We continue to work with our core suppliers to improve all aspects of our purchasing spend and

3

other logistical capabilities as well as to ensure a stable source of supply. We seek to lower costs through more favorable pricing and payment terms, more effective inventory management and improved communications with vendors.

Improving our Capital Structure

We are focused on improving our capital structure through a number of initiatives including working capital improvements, exiting underperforming or non-strategic businesses, and taking advantage of attractive leverage loan and high yield debt market conditions.

Our Industry

The overall industry for print related products is highly fragmented with excess capacity. We face price sensitivity and price pressures in many of our businesses. The information set forth below is applicable to the operating environments within our segments.

Raw Materials

The primary materials used in our businesses are paper, ink, film, offset plates, chemicals and cartons, with paper accounting for the majority of total material costs. We purchase these materials from a number of key suppliers and have not experienced any significant difficulties in obtaining the raw materials necessary for our operations. However, in times of limited supply, we have occasionally experienced minor delays in delivery. We believe we purchase our materials and supplies at competitive prices, primarily due to the size and scope of our purchasing power; however, many of our businesses experience pricing pressure related to increases in the cost of materials used in the production of our products. The uncoated freesheet paper market, which is the primary input for our envelope and certain other products, experienced supply reductions beginning in the fourth quarter of 2013 which will continue into the first quarter of 2014. As a result, our suppliers announced price increases which became effective for us during our fourth quarter of 2013 or will become effective for us in 2014. We have begun the process of negotiating these increases as well as other ancillary raw material costs, which we have not been able to pass along to our envelope customers over the past two years, with our envelope customers beginning in our fourth quarter of 2013. While we believe we will be successful in our ability to pass through our increased costs, we cannot be assured we will be successful in every effort. Moreover, any increase in price may have an adverse impact on the product volume levels our customers have ordered previously.

While we expect to pass along to our customers a substantial portion of any raw materials price increase, any price increase passed along carries the risk of an offsetting decrease in demand for our products.

Patents, Trademarks and Trade Names

Our sales do not materially depend upon any single patent or group of related patents; however, we do market products under a number of trademarks and trade names. We also hold or have rights to use various patents relating to our businesses. Our patents expire between 2014 and 2031 and our trademarks expire between 2014 and 2028. During the fourth quarter of 2013, we made the decision to retire certain trade names during 2014 as a result of rebranding our print and packaging business lines.

Seasonality

Our envelope market and certain segments of the direct mail market have historically experienced seasonality with a higher percentage of volume of products sold to these markets during the fourth quarter of the year, primarily related to holiday purchases.

Our print plants experience seasonal variations. Revenues associated with consumer publications, such as holiday catalogs and automobile brochures tend to be concentrated from July through October. Revenues from annual reports are generally concentrated from February through April. Revenues associated with the educational and scholastic market and promotional materials tend to decline in the summer. As a result of these seasonal variations, some of our print operations operate at or near capacity at certain times throughout the year.

Our general label business has historically experienced a seasonal increase in net sales during the first and second quarters of the year, primarily resulting from the release of our product catalogs to the trade channel customers and our customers’ spring advertising campaigns. Our prescription label business has historically experienced seasonality in net sales due to cold and flu seasons, generally concentrated in the fourth and first quarters of the year. As a result of these seasonal variations, some of our label operations operate at or near capacity at certain times throughout the year. Our packaging business has not historically experienced seasonal variations.

4

Backlog

Backlog generally is not considered a significant factor in our business due to the relatively short delivery periods and frequent inventory turnover many of our businesses experience. Our backlog of customer orders to be produced or shipped was approximately $119.4 million and $98.5 million as of the years ended 2013 and 2012, respectively.

Competition

We compete with a few multi-plant and many single-plant companies which primarily service regional and local markets in selling our envelope products. We also face competition from alternative sources of communication and information transfer such as electronic mail, the internet, interactive television and electronic retailing. Although these sources of communication and advertising may eliminate some domestic envelope sales in the future, we believe we will experience continued demand for envelope products due to: (i) the ability of our customers to obtain a relatively low-cost information delivery vehicle that may be customized with text, color, graphics and action devices to achieve the desired presentation effect; (ii) the ability of our direct mail customers to penetrate desired markets as a result of the widespread delivery of mail to residences and businesses through the United States Postal Service; and (iii) the ability of our direct mail customers to include return materials inside their mailings. Principal competitive factors in the envelope business are quality, service and price. Although all three factors are equally important, various customers may emphasize one or more over the others.

In selling our commercial print product offerings, we compete with large multinational commercial printing companies, as well as regional and local printers. The commercial printing industry continues to have excess capacity, and is highly competitive in most of our product categories and geographic regions. This excess capacity has resulted in a competitive pricing environment, in which companies have focused on reducing costs in order to preserve operating margins. Competition is based largely on price, quality and servicing the special needs of customers. We believe this environment, combined with recent economic trends, will continue to lead to more consolidation within the commercial print industry as companies seek economies of scale, broader customer relationships, geographic coverage and product breadth to overcome or offset excess industry capacity and pricing pressures.

In selling our printed labels products, we compete with other label manufacturers with nationwide locations as well as regional and local printers that typically sell within a few hundred mile radius of their plants. Printed labels competition is based mainly on quick-turn customization, quality of products and customer service levels.

Employees

We employed approximately 8,700 people worldwide as of the year ended 2013, approximately 25% of whom were members of various local labor unions. Collective bargaining agreements, each of which cover the workers at a particular facility, expire from time to time and are negotiated separately. Accordingly, we believe no single collective bargaining agreement is material to our operations as a whole.

Environmental Regulations

Our operations are subject to federal, state, local and foreign environmental laws and regulations, including those relating to air emissions, waste generation, handling, management and disposal, and remediation of contaminated sites. We have implemented environmental programs designed to ensure that we operate in compliance with the applicable laws and regulations governing environmental protection. We believe we are in substantial compliance with applicable laws and regulations relating to environmental protection, and we do not anticipate material capital expenditures will be required to achieve or maintain compliance with environmental laws and regulations. However, there can be no assurance newly discovered conditions, or new laws and regulations or stricter interpretations of existing laws and regulations, will not result in increased compliance or remediation costs.

5

Executive Officers

The following presents a list of our executive officers, their age, present position, the year elected to their present position and other positions they have held during the past five years. Robert G. Burton, Jr. and Michael G. Burton are the sons of Robert G. Burton, Sr. There are no undisclosed arrangements or understandings pursuant to which any person was selected as an officer. This information is presented as of the date of the Form 10-K filing.

| Name | Age | Position | Year Elected to Present Position | ||||

| Robert G. Burton, Sr. | 73 | Chairman and Chief Executive Officer | 2005 | ||||

| Robert G. Burton, Jr. | 38 | President | 2011 | ||||

| Scott J. Goodwin | 36 | Chief Financial Officer | 2012 | ||||

| Mark S. Hiltwein | 50 | President, Envelope Operations | 2012 | ||||

| Michael G. Burton | 36 | President, Print, Label & Packaging | 2013 | ||||

| Ian R. Scheinmann | 45 | Senior Vice President, Legal Affairs | 2010 | ||||

Robert G. Burton, Sr. Mr. Burton, 73, has been Cenveo’s Chairman and Chief Executive Officer since September 2005. In January 2003, he formed Burton Capital Management, LLC, a company which invests in manufacturing companies, and has been its Chairman, Chief Executive Officer and sole managing member since its formation. From December 2000 through December 2002, Mr. Burton was the Chairman, President, and Chief Executive Officer of Moore Corporation Limited, a leading printing company with over $2.0 billion in revenue for fiscal year 2002. Preceding his employment at Moore, Mr. Burton was Chairman, President, and Chief Executive Officer of Walter Industries, Inc., a diversified holding company. From April 1991 through October 1999, he was the Chairman, President, and Chief Executive Officer of World Color Press, Inc., a $3.0 billion diversified printing company. From 1981 through 1991, he held a series of senior executive positions at Capital Cities/ABC, including President of ABC Publishing. Mr. Burton was also employed for 10 years as a senior executive of SRA, the publishing division of IBM.

Robert G. Burton, Jr. Mr. Burton, Jr., 38, has served as Cenveo’s President since August 10, 2011. From December 2010 to August 2011, Mr. Burton was President of Corporate Operations, with a primary focus on M&A, Treasury, IT, Human Resources, Legal and Investor Relations. From September 2005 to December 2010, Mr. Burton was EVP of Investor Relations, Treasury, HR and Legal at Cenveo. He has been a member of the Chairman’s Executive Committee since joining Cenveo. From 2004 to 2005, Mr. Burton was also President of Burton Capital Management, LLC and was the primary investment officer before he joined Cenveo on September 12, 2005. Mr. Burton has over 16 years of business experience as an Investor Relations, M&A and financial professional. Mr. Burton also served as the Senior Vice President, Investor Relations and Corporate Communications for Moore Wallace Incorporated (and its predecessor, Moore Corporation) from December 2001 to May 2003. Mr. Burton served as Vice President, Investor Relations of Walter Industries in 2000. From 1996 through December 1999, Mr. Burton held various management positions at World Color Press, Inc., including Vice President, Investor Relations. Mr. Burton earned a Bachelor of Arts degree from Vanderbilt University.

Scott J. Goodwin. Mr. Goodwin, 36, has served as Cenveo's Chief Financial Officer since August 2012 and was Chief Accounting Officer from April 2012 to August 2012. From June 2009 to April 2012, Mr. Goodwin served as Cenveo's Corporate Controller. Mr. Goodwin joined Cenveo as its Assistant Corporate Controller in June 2006. Prior to joining Cenveo, Mr. Goodwin spent seven years in public accounting at Deloitte & Touche LLP. Mr. Goodwin is a Certified Public Accountant and received his degree in accounting from The Citadel.

Mark S. Hiltwein. Mr. Hiltwein, 50, has served as Cenveo's President, Envelope Operations since August 2012. Mr. Hiltwein was Cenveo's Chief Financial Officer from December 2009 to August 2012 and was Chief Financial Officer from July 2007 to June 2009. From June 2009 to December 2009, Mr. Hiltwein served as Cenveo's President of Field Sales and Manufacturing. From July 2005 to July 2007, he was President of Smartshipper.com, an online third party logistics company. From February 2002 through July 2005, Mr. Hiltwein was Executive Vice President and Chief Financial Officer of Moore Wallace Incorporated, a $3.5 billion printing company. Prior to that, he served as Senior Vice President and Controller from December 2000 to February 2002. Mr. Hiltwein has served in a number of financial positions from 1992 through 2000 with L.P. Thebault Company, a commercial printing company, including Chief Financial Officer from 1997 through 2000. Mr. Hiltwein began his career at Mortenson and Associates, a regional public accounting firm where he held various positions in the audit department. Mr. Hiltwein received his Bachelor's degree in accounting from Kean University and he is a CPA.

6

Michael G. Burton. Mr. Burton, 36, has served as Cenveo’s President, Print, Label and Packaging Group since July, 2013. In November 2010 Mr. Burton became President of the Label division and subsequently became responsible for the Packaging division in January 2012. From September 2005 to November 2010, Mr. Burton was Senior Vice President, Operations with a primary focus on, Procurement, Information Technology, Environmental Health & Safety, and Human Resources. From 2003 to 2005, Mr. Burton was also Executive Vice President, Operations of Burton Capital Management, LLC. He was a founding member of this group before he joined Cenveo on September 12, 2005. Mr. Burton was previously Vice President of Commercial & Subsidiary Operations, a $600 million division of Moore Corporation Limited. Mr. Burton received his Bachelor of Arts degree from the University of Connecticut where he was captain of the football team.

Ian R. Scheinmann. Mr. Scheinmann, 45, has served as Cenveo’s Senior Vice President, Legal Affairs since August 2010. From May 2010 until August 2010, he served as Cenveo’s in-house real estate counsel. Prior to joining Cenveo, Mr. Scheinmann was Cenveo’s outside real estate counsel as a member of Rudoler & DeRosa, LLC where his practice covered a wide range of real estate and business transactions. Prior to joining Rudoler & DeRosa, Mr. Scheinmann was a real estate shareholder with Greenberg Traurig, LLP from August 2002 until March 2009. From 1995 until 2002, he was engaged in private practice with (i) Dilworth Paxson, LLP (September 2000 until July 2002); (ii) Anderson, Kill and Olick, P.C. (November 1996 until May 2000); and (iii) Weiner Lesniak (October 1995 until October 1996). Mr. Scheinmann received his B.S.B.A. from the John M. Olin School of Business at Washington University, St. Louis, Missouri and his J.D. with honors from Seton Hall University School of Law.

Cautionary Statements

Certain statements in this report, particularly statements found in “Risk Factors,” “Business” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. In addition, we or our representatives have made or continue to make forward-looking statements, orally or in writing, in other contexts. These forward-looking statements generally can be identified by the use of terminology such as “may,” “will,” “expect,” “intend,” “estimate,” “anticipate,” “plan,” “foresee,” “believe” or “continue” and similar expressions, or as other statements which do not relate solely to historical facts. These statements are not guarantees of future performance and involve risks, uncertainties and assumptions which are difficult to predict or quantify. Management believes these statements to be reasonable when made. However, actual outcomes and results may differ materially from what is expressed or forecasted in these forward-looking statements. As a result, these statements speak only as of the date they were made. We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. In view of such uncertainties, investors should not place undue reliance on our forward-looking statements.

Such forward-looking statements involve known and unknown risks, including, but not limited to, those identified in Item 1A. Risk Factors along with changes in general economic, business and labor conditions. More information regarding these and other risks can be found below under “Risk Factors,” “Business,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and other sections of this report.

Available Information

Our Internet address is: www.cenveo.com. References to our website address do not constitute incorporation by reference of the information contained on the website, and the information contained on the website is not part of this document. We make available free of charge through our website our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed pursuant to Section 13(a) or 15(d) of the Exchange Act as soon as reasonably practicable after such documents are filed electronically with the Securities and Exchange Commission, which we refer to as the SEC. Our Code of Business Conduct and Ethics is also posted on our website. In addition, our earnings conference calls are archived for replay on our website. In May 2013, we submitted to the New York Stock Exchange a certificate of our Chief Executive Officer certifying he is not aware of any violation by us of New York Stock Exchange corporate governance listing standards. We also filed as exhibits to our annual report on Form 10-K for our year ended 2012 certificates of the Chief Executive Officer and Chief Financial Officer as required under Section 302 of the Sarbanes-Oxley Act.

The public may read and copy any materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, D.C. 20549. The public may obtain information about the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an Internet site (http://www.sec.gov) which contains reports, proxy and information statements and other information regarding issuers that file electronically with the SEC.

7

Item 1A. Risk Factors

Many factors which affect our business and operations involve risks and uncertainties. The factors described below are some of the risks that could materially harm our business, financial conditions, results of operations or prospects.

The recent United States and global economic conditions have adversely affected us and could continue to do so.

The current United States and global economic conditions have affected and, most likely, will continue to affect our results of operations and financial position. A significant part of our business relies on our customers’ printing spend. The prolonged downturn in the United States and global economies and an uncertain economic outlook has reduced the demand for printed materials and related offerings that we provide our customers. Consequently, the reductions and delays in our customers’ spending have adversely impacted and could continue to adversely impact our results of operations, financial position and cash flows. We believe the extended economic uncertainty will continue to impact our operating results.

Our substantial level of indebtedness could impair our financial condition, and prevent us from fulfilling our business obligations.

We currently have a substantial amount of debt, which requires significant principal and interest payments. As of our year ended 2013, our total indebtedness was approximately $1.2 billion. Our level of indebtedness could affect our future operations, for example by:

| • | requiring a substantial portion of our cash flow from operations to be dedicated to the payment of principal and interest on indebtedness instead of funding working capital, capital expenditures, acquisitions and other business purposes; |

| • | making it more difficult for us to satisfy all of our debt obligations, thereby increasing the risk of triggering a cross-default provision; |

| • | increasing our vulnerability to economic downturns or other adverse developments relative to less leveraged competitors; |

| • | limiting our ability to obtain additional financing for working capital, capital expenditures, acquisitions or other corporate purposes in the future; and |

| • | increasing our cost of borrowing to satisfy business needs. |

We may be unable to service or refinance our debt.

Our ability to make scheduled payments on, or to reduce or refinance, our indebtedness will depend on our future financial and operating performance, and prevailing market conditions. Our future performance will be affected by the impact of general economic, financial, competitive and other factors beyond our control, including the availability of financing in bank and capital markets. We cannot be certain our business will generate sufficient cash flow from operations in an amount necessary to service our debt. If we are unable to meet our debt obligations or to fund our other liquidity needs, we may be required to restructure or refinance all, or a portion of, our debt to avoid defaulting on our debt obligations or to meet other business needs. Such a refinancing of our indebtedness could result in higher interest rates, could require us to comply with more onerous covenants further restricting our business operations, could be restricted by another one of our debt instruments outstanding, or refinancing opportunities may not be available at all.

The terms of our indebtedness impose significant restrictions on our operating and financial flexibility.

The agreements governing our principal debt obligations contain various covenants which limit our ability to, among other things:

| • | incur or guarantee additional indebtedness; |

| • | make restricted payments, including dividends and prepaying indebtedness; |

| • | create or permit certain liens; |

| • | enter into business combinations and asset sale transactions; |

| • | make investments, including capital expenditures; |

| • | amend organizational documents and change accounting methods; |

| • | enter into transactions with affiliates; and, |

8

| • | enter into new businesses. |

These restrictions could limit our ability to obtain future financing, make acquisitions or incur needed capital expenditures, withstand a future downturn in our business or the economy in general, conduct operations or otherwise take advantage of business opportunities which may arise. Our senior secured term loan facility also contains a maximum consolidated leverage ratio which we must be in compliance with on a quarterly basis, and our senior secured asset-based revolving credit facility contains a minimum consolidated fixed charge coverage ratio which, under certain circumstances, we must comply with on a quarterly basis. Our ability to meet these financial ratios may be affected by events beyond our control, such as further deterioration in general economic conditions. We are also required to provide certain financial information on a quarterly basis. Our failure to maintain applicable financial ratios, in certain circumstances, or effective internal controls would prevent us from borrowing additional amounts, and could result in a default under our senior secured term loan facility and/or senior secured asset-based revolving credit facility. A default could cause the indebtedness outstanding under the senior secured term loan facility and/or the senior secured asset-based revolving credit facility, and, by reason of cross-acceleration or cross-default provisions, the senior, senior exchangeable and senior second lien notes, the senior unsecured term loan facility and any other indebtedness we may then have, to become immediately due and payable. If we are unable to repay those amounts, the lenders under our senior secured term loan facility, senior secured asset-based revolving credit facility and senior second lien notes indenture could initiate a bankruptcy or liquidation proceeding, or proceed against the collateral granted to them which secures that indebtedness. If the lenders under our senior secured term loan facility agreement, senior secured asset-based revolving credit facility agreement and/or senior second lien notes indenture were to accelerate the repayment of outstanding borrowings, we might not have sufficient assets to repay our indebtedness.

There are additional borrowings available to us which could further exacerbate our risk exposure from debt.

Despite current indebtedness levels, we may incur substantial additional indebtedness in the future. Our senior secured term loan facility, senior secured asset-based revolving credit facility, senior unsecured term loan facility and senior, senior exchangeable and senior second lien notes indentures and our other debt instruments limit, but do not prohibit, us from incurring additional debt. If we incur additional debt above our current outstanding levels, the risks associated with our substantial leverage would increase.

To the extent we make select acquisitions, we may not be able to successfully integrate the acquired businesses into our business.

In the past, we have grown rapidly through acquisitions. We intend to continue to pursue select acquisition opportunities within our core and niche businesses. To the extent we seek to pursue additional acquisitions, we cannot be certain target businesses will be available on favorable terms or that, if we are able to acquire businesses on favorable terms, we will be able to successfully integrate or profitably manage them. Successfully integrating an acquisition involves minimizing disruptions and efficiently managing substantial changes, some of which may be beyond our control. An acquisition always carries the risk that such changes, including facility and equipment location, management and employee base, policies, philosophies and procedures, could have unanticipated effects, could require more resources than intended and could cause customers to temporarily or permanently seek alternate suppliers. A failure to realize acquisition synergies and savings could negatively impact the results of both our acquired and existing operations.

A decline in our consolidated profitability or profitability within one of our individual reporting units could result in the impairment of assets, including goodwill and other long-lived assets.

We have material amounts of goodwill and other long-lived assets on our consolidated balance sheet. A decline in expected profitability, particularly the impact of an extended uncertainty in the United States and global economies, could call into question the recoverability of our related goodwill and other long-lived assets and require us to write down or write-off these assets.

The industries in which we operate our business are highly competitive and extremely fragmented.

The industries in which we compete are highly competitive and extremely fragmented. In the envelope market, we compete primarily with a few multi-plant and many single-plant companies servicing regional and local markets. In the commercial printing market, we compete against a few large, diversified and financially stronger printing companies, as well as smaller regional and local commercial printers, many of which are capable of competing with us on volume, price and production quality. We believe there currently is excess capacity in the industries in which we operate, which has resulted in substantial price competition which may continue as customers put product work out for competitive bid. We are constantly seeking ways to reduce our costs, become more efficient and attract customers. We cannot, however, be certain these efforts will be successful or our competitors will not be more successful in their similar efforts. If we fail to reduce costs and increase productivity, or to meet customer demand for new value-added products, services or technologies, we may face decreased revenues and profit margins in markets where we encounter price competition, which in turn could reduce our cash flow and profitability.

9

The printing business we compete in generally does not have long-term customer agreements, and our printing operations may be subject to quarterly and cyclical fluctuations.

The printing industry in which we compete is generally characterized by individual orders from customers or short-term contracts. A significant portion of our customers are not contractually obligated to purchase products or services from us. Most customer orders are for specific printing jobs, and repeat business largely depends on our customers’ satisfaction with our work product. Although our business does not depend on any one customer or group of customers, we cannot be sure that any particular customer will continue to do business with us for any period of time. In addition, the timing of particular jobs or types of jobs at particular times of year may cause significant fluctuations in the operating results of our operations in any given quarter. We depend to some extent on sales to certain industries, such as the financial services, advertising, pharmaceutical, automotive and office products industries. To the extent these industries experience downturns, the results of our operations may be adversely affected.

Factors affecting the United States Postal Service can impact demand for our products.

Postal costs are a significant component of many of our customers’ cost structure. Historically, increases in postal rates have resulted in reductions in the volume of mail sent, including direct mail, which is a meaningful portion of our envelope volume. As postal rate increases in the United States are outside our control, we can provide no assurance that any future increases in United States postal rates will not have a negative effect on the level of mail sent or the volume of envelopes purchased.

Factors other than postal rates which affect the volume of mail sent through the United States postal system may also negatively affect our business. Congress enacted a federal “Do Not Call” registry in response to consumer backlash against telemarketers and is contemplating enacting so-called “anti-spam” legislation in response to consumer complaints about unsolicited e-mail advertisements. If similar legislation becomes enacted for direct mail advertisers, our business could be adversely affected. Additionally, the United States Postal Service has also indicated the potential need to reduce delivery days from six to five. We can provide no assurance that such a change would not impact our customers’ decisions to use direct mail products, which may in turn cause a decrease in our revenues and profitability; however, we do not expect such an impact.

The availability of the internet and other electronic media may adversely affect our business.

Our business is highly dependent upon the demand for envelopes sent through the mail. Such demand comes from utility companies, banks and other financial institutions, among other companies. Our printing business also depends upon demand for printed advertising among other products. Consumers increasingly use the internet and other electronic media to purchase goods and services, and for other purposes, such as paying bills and obtaining electronic versions of printed product. The level of acceptance of electronic media by consumers as well as the extent that consumers are replacing traditional printed reading materials with internet hosted media content or e-reading devices is difficult to predict. Advertisers use the internet and other electronic media for targeted campaigns directed at specific electronic user groups. We cannot be certain the acceleration of the trend towards electronic media will not cause a decrease in the demand for our products. If demand for our products decreases, our cash flow or profitability could materially decrease.

Increases in paper costs and any decreases in the availability of our raw materials could have a material effect on our business.

Paper costs represent a significant portion of our cost of materials. Changes in paper pricing generally do not affect the operating margins of our commercial printing business, because the transactional nature of the business allows us to pass on most announced increases in paper prices to our customers. However, our ability to pass on increases in paper prices is dependent upon the competitive environment at any given time. Paper pricing also affects the operating margins of our envelope business. We have historically been less successful in immediately passing on such paper price increases due to several factors, including contractual restrictions in certain cases and the inability to quickly update catalog prices in other instances. Moreover, rising paper costs, and their consequent impact on our pricing, could lead to a decrease in demand for our products.

We depend on the availability of paper in manufacturing most of our products. During periods of tight paper supply, many paper producers allocate shipments of paper based on the historical purchase levels of customers. In the past, we have occasionally experienced minor delays in delivery. Any future delay in availability could negatively impact our cash flow and profitability.

We depend on good labor relations.

As of our year ended 2013, we employed approximately 8,700 people worldwide, approximately 25% of whom were members of various local labor unions. If our unionized employees were to engage in a concerted strike or other work stoppage,

10

or if other employees were to become unionized, we could experience a disruption of operations, higher labor costs or both. A lengthy strike could result in a material decrease in our cash flow or profitability.

Environmental laws may affect our business.

Our operations are subject to federal, state, local and foreign environmental laws and regulations, including those relating to air emissions, wastewater discharge, waste generation, handling, management and disposal, and remediation of contaminated sites. Currently unknown environmental conditions or matters at our existing and prior facilities, new laws and regulations, or stricter interpretations of existing laws and regulations could result in increased compliance or remediation costs which, if substantial, could have a material effect on our business or operations in the future.

We are dependent on key management personnel.

Our success will depend to a significant degree on our executive officers and other key management personnel. We cannot be certain we will be able to retain our executive officers and key personnel, or attract additional qualified management in the future. In addition, the success of any acquisitions we may pursue may depend, in part, on our ability to retain management personnel of the acquired companies. We do not carry key person insurance on any of our managerial personnel.

Our business could be materially adversely affected by any failure, interruption or security lapse of our information technology systems.

We are increasingly dependent on information technology systems to process transactions, manage inventory, purchase, sell and ship goods on a timely basis and maintain cost-efficient operations. We use information systems to support decision making and to monitor business performance. Our information technology systems depend on global communications providers, telephone systems, hardware, software and other aspects of internet infrastructure which can experience significant system failures and outages. Our systems are susceptible to outages due to fire, floods, power loss, telecommunications failures and similar events. Despite the implementation of network security measures, our systems are vulnerable to computer viruses and similar disruptions from unauthorized tampering with our systems. In addition, cybersecurity threats are evolving and include, but are not limited to, malicious software, attempts to gain unauthorized access to data, denial of service attacks and other electronic security breaches which could lead to disruptions in critical systems, unauthorized release of confidential or otherwise protected information and corruption of data. The occurrence of these or other events could disrupt or damage our information technology systems and inhibit internal operations, the ability to provide customer service or provide management with accurate financial and operational information essential for making decisions at various levels of management.

Item 1B. Unresolved Staff Comments

None.

Item 2. Properties

We currently occupy 66 manufacturing facilities, primarily in North America, of which 18 are owned and 48 are leased. We also lease our corporate headquarters space in Stamford, Connecticut. We believe we have adequate facilities to conduct our current and future operations.

Item 3. Legal Proceedings

From time to time we may be involved in claims or lawsuits that arise in the ordinary course of business. Accruals for claims or lawsuits have been provided for to the extent losses are deemed probable and estimable. Although the ultimate outcome of these claims or lawsuits cannot be ascertained, on the basis of present information and advice received from counsel, it is our opinion that the disposition or ultimate determination of such claims or lawsuits will not have a material effect on our consolidated financial statements.

In the case of administrative proceedings related to environmental matters involving governmental authorities, we do not believe that any imposition of monetary damages or fines would be material.

Item 4. Mine Safety Disclosures

Not applicable.

11

PART II

Item 5. Market for Registrant’s Common Equity, Related Shareholder Matters and Issuer Purchases of Equity Securities

The certificate of incorporation of Cenveo, Inc. and its subsidiaries, which we refer to as Cenveo, states that the total authorized capital stock is 100 million shares of common stock, $0.01 par value per share, which we refer to as Common Stock. Each share of voting Common Stock is entitled to one vote in respect of each share of Cenveo voting Common Stock held of record on all matters submitted to a vote of stockholders.

Our Common Stock is traded on the New York Stock Exchange, which we refer to as NYSE under the symbol “CVO.” As of February 5, 2014, there were 602 shareholders of record and, as of that date, we estimate there were approximately 10,582 beneficial owners holding stock in nominee or “street” name. The following table sets forth, for the periods indicated, the range of the high and low closing prices for our Common Stock as reported by the NYSE:

| 2013 | High | Low | |||||

| First Quarter | $ | 3.03 | $ | 1.98 | |||

| Second Quarter | 2.40 | 1.99 | |||||

| Third Quarter | 3.00 | 2.02 | |||||

| Fourth Quarter | 3.53 | 2.75 | |||||

| 2012 | High | Low | |||||

| First Quarter | $ | 5.23 | $ | 3.13 | |||

| Second Quarter | 3.51 | 1.57 | |||||

| Third Quarter | 2.44 | 1.80 | |||||

| Fourth Quarter | 2.70 | 1.90 | |||||

We have not paid a dividend on our Common Stock since our incorporation and do not anticipate paying dividends in the foreseeable future as the instruments governing a significant portion of our debt obligations limit our ability to pay Common Stock dividends.

See Note 12 to our consolidated financial statements included in Item 8 of this Annual Report on Form 10-K for information regarding our stock compensation plans. Compensation information required by Item II will be presented in our 2014 definitive proxy statement, which is incorporated herein by reference.

12

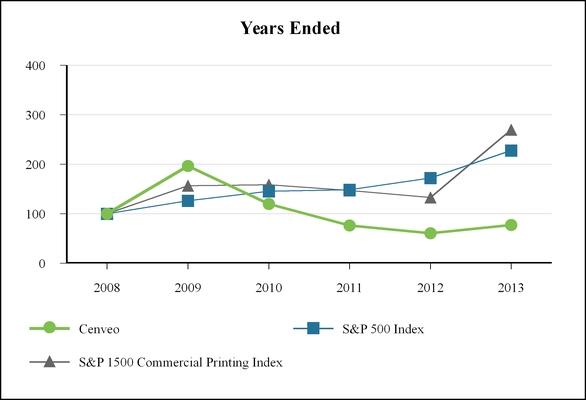

The graph below compares five-year returns of our Common Stock with those of the S&P 500 Index and the S&P 1500 Commercial Printing Index. The graph assumes that $100 was invested as of our year ended 2008 in each of our Common Stock, the S&P 500 Index, and the S&P 1500 Commercial Printing Index and that all dividends were reinvested. The S&P 1500 Commercial Printing Index is a capitalization weighted index designed to measure the performance of all NASDAQ-traded stocks in the commercial printing sector.

| Years Ended | ||||||||||||||||||

| 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | |||||||||||||

| Cenveo | 100.00 | 196.63 | 120.00 | 76.41 | 60.67 | 77.30 | ||||||||||||

| S&P 500 Index | 100.00 | 126.46 | 145.50 | 148.58 | 172.35 | 228.17 | ||||||||||||

| S&P 1500 Commercial Printing Index | 100.00 | 156.94 | 158.68 | 146.94 | 132.82 | 270.03 | ||||||||||||

13

Item 6. Selected Financial Data

The following table sets forth our selected financial and operating data for the years ended December 28, 2013, December 29, 2012, December 31, 2011, January 1, 2011 and January 2, 2010, which we refer to as the years ended 2013, 2012, 2011, 2010 and 2009, respectively.

The following consolidated selected financial data has been derived from, and should be read in conjunction with, the related consolidated financial statements, either elsewhere in this report or in reports we have previously filed with the SEC. Additionally, it reflects the reclassification of Custom Envelope, our San Francisco manufacturing facility, Documents Group and our wide-format papers business to discontinued operations, for all periods presented.

CENVEO, INC. AND SUBSIDIARIES (in thousands, except per share data) | ||||||||||||||||||||

| Years Ended | ||||||||||||||||||||

| Statement of Operations: | 2013 | 2012 | 2011 | 2010 | 2009 | |||||||||||||||

| Net sales | $ | 1,777,808 | $ | 1,738,293 | $ | 1,844,371 | $ | 1,643,286 | $ | 1,547,602 | ||||||||||

| Restructuring and other charges | 13,100 | 27,100 | 17,812 | 44,731 | 68,034 | |||||||||||||||

| Impairment of goodwill and intangible assets | 33,367 | — | — | 181,419 | — | |||||||||||||||

| Operating income (loss) | 29,363 | 101,185 | 105,162 | (130,504 | ) | 5,876 | ||||||||||||||

| Loss (gain) on early extinguishment of debt, net | 11,324 | 12,487 | (4,011 | ) | 9,592 | (16,917 | ) | |||||||||||||

| Loss from continuing operations | (85,527 | ) | (1) | (80,528 | ) | (3) | (8,694 | ) | (205,387 | ) | (55,910 | ) | ||||||||

| Income from discontinued operations, net of taxes | 16,741 | (2) | 641 | (4) | 129 | (5) | 19,011 | 24,971 | ||||||||||||

| Net loss | (68,786 | ) | (1) (2) | (79,887 | ) | (3) (4) | (8,565 | ) | (5) | (186,377 | ) | (30,939 | ) | |||||||

| Loss per share from continuing operations: | ||||||||||||||||||||

| Basic | (1.32 | ) | (1.27 | ) | (0.14 | ) | (3.29 | ) | (0.98 | ) | ||||||||||

| Diluted | (1.32 | ) | (1.27 | ) | (0.14 | ) | (3.29 | ) | (0.98 | ) | ||||||||||

| Income per share from discontinued operations: | ||||||||||||||||||||

| Basic | 0.25 | 0.01 | — | 0.30 | 0.44 | |||||||||||||||

| Diluted | 0.25 | 0.01 | — | 0.30 | 0.44 | |||||||||||||||

| Net loss per share: | ||||||||||||||||||||

| Basic | (1.07 | ) | (1.26 | ) | (0.14 | ) | (2.99 | ) | (0.54 | ) | ||||||||||

| Diluted | (1.07 | ) | (1.26 | ) | (0.14 | ) | (2.99 | ) | (0.54 | ) | ||||||||||

| Balance Sheet data: | ||||||||||||||||||||

| Total assets | $ | 1,213,704 | $ | 1,200,555 | $ | 1,391,104 | $ | 1,412,270 | $ | 1,536,185 | ||||||||||

| Total long-term debt, including current maturities | 1,185,525 | 1,183,618 | 1,246,343 | 1,294,003 | 1,233,917 | |||||||||||||||

__________________________

| (1) | Includes $40.6 million valuation allowance related to deferred tax assets. |

| (2) | Includes $14.9 million gain on sale of discontinued operations, net of tax expense of $10.7 million. |

| (3) | Includes $56.5 million valuation allowance related to deferred tax assets. |

| (4) | Includes $6.3 million loss on sale of discontinued operations, net of tax benefit of $2.6 million. |

| (5) | Includes $13.5 million goodwill impairment charges. |

14

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

This Management’s Discussion and Analysis of Financial Condition and Results of Operations, which we refer to as MD&A, of Cenveo, Inc. and its subsidiaries, which we refer to as Cenveo, should be read in conjunction with our consolidated financial statements included in Item 8 of this Annual Report on Form 10-K, which we refer to as the Form 10-K. Certain statements we make under this Item 7 constitute forward-looking statements under the Private Securities Litigation Reform Act of 1995. See Cautionary Statements regarding forward-looking statements in Item 1, and Risk Factors in Item 1A.

Introduction and Executive Overview

We are a diversified manufacturing company focused on print related products. Our broad portfolio of products includes envelope converting, commercial printing, label manufacturing and specialty packaging. We operate a global network of strategically located manufacturing facilities, serving a diverse base of over 100,000 customers.

Our business strategy has been, and continues to be, focused on improving sales performance, pursuing and integrating strategic acquisitions, improving our cost and capital structure, and maintaining reasonable levels of financial flexibility. We believe this strategy has allowed us to diversify our revenue base, maintain our low cost structure and deliver quality product offerings to our customers.

See Part 1 Item 1 of this Form 10-K for a more complete description of our business.

2013 Overview/2014 Outlook

Economy and Industry Highlights

We believe that the mild recovery of the general economy experienced in 2012 continued in 2013. We currently expect similar recovery trends for the foreseeable future, particularly in 2014. The print related industries are highly fragmented and extremely competitive due to over-capacity and pricing pressures. We believe these factors, combined with a slow general economic recovery, will continue to impact our results of operations into 2014.

Our current management focus is on the following areas:

Improving Sales Performance

Our sales focus has been, and will continue to be, on our customers' experience across each of our businesses, ensuring we meet our customers' demands. We seek to expand our relationship with them through cross-selling initiatives available within our platform. During 2013, we implemented a customer relationship management tool across our entire sales platform, and we focused on our e-commerce platform in 2013 through both capital investments and incremental headcount. We have also begun a series of sales recruiting efforts with a focus on attracting not only talented individuals with experience in our current business lines, but also individuals with experience in complementary industry channels. We expect these focus points, along with our expanded geographic presence from the acquisition of certain assets of National, will allow us to experience modest sales growth despite operating in challenging industries and an uncertain economy. In addition, the uncoated freesheet paper market, which is the primary input for our envelope and certain other products, experienced supply reductions beginning in the fourth quarter of 2013 which will continue into the first quarter of 2014. As a result, our suppliers announced price increases which became effective for us during our fourth quarter of 2013. We have begun the process of negotiating these increases as well as other ancillary raw material costs, which we have not been able to pass along to our envelope customers over the past two years, with our envelope customers beginning in our fourth quarter of 2013. While we believe we will be successful in our ability to pass through our increased costs, we cannot be assured we will be successful in every effort. Moreover, any increase in price may have an adverse impact on the product volume levels our customers have ordered previously.

Integrating Certain Assets of National

We believe our acquisition of certain assets of National will provide much needed capacity reductions within the envelope industry. We developed and began implementing our plan to integrate those assets into our existing envelope operations in the third quarter of 2013. At this time, we expect this integration to take in excess of a year to complete due to the condition of National’s operating platform and asset base at the time of acquiring these assets out of bankruptcy.

15

Improving our Cost Structure

We continue to monitor our cost structure as marketplace conditions warrant, and expect to further reduce costs as necessary. In the first quarter of 2013, as a result of margin pressures from rising input costs and price pressures experienced within our envelope and print segments, we initiated a plan to further reduce our cost structure. We also continue to focus on strategic investments, capital expenditures and acquisitions in areas that we believe will strengthen our manufacturing platform and product offerings. We continue to review strategic alternatives for business lines we believe are underperforming or non-strategic to our future operations.

Improving our Capital Structure

Since the beginning of 2011, we have been focused on improving our capital structure through a number of initiatives including working capital improvements, exiting underperforming or non-strategic businesses, and taking advantage of attractive leverage loan and high yield debt market conditions. Since we began this initiative, we have reduced our outstanding debt by over $105 million, despite our continued reinvestments of cash into our businesses via four acquisitions, focused capital expenditures, and incurring over $55 million in transaction costs associated with the improvement of our capital structure. At the beginning of 2013, we addressed a near-term maturity which was coming due at the end of 2013 by entering into an unsecured $50.0 million aggregate principal amount term loan due 2017, which we refer to as the Unsecured Term Loan. As of February 5, 2014, there is $10.0 million remaining on the Unsecured Term Loan, which we expect to repay in full in the next few months. During the second quarter of 2013, we refinanced our first lien debt, which extended our next sizable debt maturity until 2017 and resulted in increased cash flows via lower cash interest upon the completion of the refinancing. As part of the refinancing, we transitioned from a cash flow revolving credit facility to an asset-based revolving credit facility, which we refer to as our ABL Facility, to further reduce interest expense. In December of 2013, primarily due to our acquisition of certain assets of National, we increased our borrowing capacity on our ABL Facility to $230 million from $200 million, supported by over $60 million of suppressed capacity underlying our ABL Facility. The accordion feature within our ABL Facility will, subject to the satisfaction of customary conditions, permit us to borrow up to an additional $20 million to further enhance our capital structure by using this lower interest rate vehicle to address our higher interest rate debt currently outstanding.

Acquisitions

On September 16, 2013, we acquired certain assets of National. National's accounts receivable and inventory were purchased by unrelated third parties in conjunction with our acquisition. National manufactured and distributed envelope products for the billing, financial, direct mail and office products markets and had approximately 1,600 employees. We believe the acquisition of certain assets of National will enhance our manufacturing capabilities and reduce capacity in the envelope industry.

On December 31, 2012, we acquired all of the assets of Express Label, which had annual net sales of approximately $5.4 million prior to our acquisition. Express Label is a label business that focuses on food and grocery customers and was acquired to further enhance our label operations.

Discontinued Operations

In September of 2013, we completed the sale of Custom Envelope within our envelope segment and received net proceeds of $44.8 million. During the second quarter of 2013, we decided to exit the San Francisco market and closed a manufacturing facility within our print segment.

In February of 2012, we completed the sale of Documents Group within our label and packaging segment. Net cash proceeds were approximately $35.5 million. In January of 2012, we completed the sale of our wide-format papers business and received proceeds of approximately $4.7 million.

The operating results of these transactions are reported in discontinued operations in our consolidated financial statements for all periods presented.

16

Reportable Segments

We operate three complementary reportable segments: envelope, print and the label and packaging segments. During the fourth quarter of 2013, we completed a realignment of our segments as a result of a change in management reporting and strategy. Our historical financial statement disclosures have been updated to reflect the current year presentation.

Deferred Taxes

In the fourth quarter of 2013, we recorded a non-cash valuation allowance charge of $40.6 million related to the realizability of our net deferred tax assets due to excess capacity and pricing pressure combined with the decline in net sales and operating performance of our print segment during 2013.

In the fourth quarter of 2012, we recorded a non-cash valuation allowance charge of $56.5 million related to the realizability of our net deferred tax assets due to excess capacity and pricing pressure, combined with the decline in net sales of our print segment during 2012.

Goodwill and Intangible Asset Impairments

We did not record any goodwill impairment charges in 2013 or 2012.

In the fourth quarter of 2011, we recorded non-cash goodwill impairment charges of $13.5 million related to the Discontinued Operations. These charges were due to our carrying value of the assets, including goodwill and intangible assets, of the Discontinued Operations being in excess of the fair value we received from divesting these businesses.

During the fourth quarter of 2013, we made the decision to retire certain indefinite-lived trade names in 2014 as a result of rebranding our print and packaging business lines. Accordingly, based on our evaluation using a relief from royalty and other discounted cash flow methodologies, we concluded that those trade name assets were impaired. An impairment charge of $33.4 million was recorded to reduce their carrying value to their estimated fair value. Those trade names have a remaining carrying value of $1.9 million as of the year ended 2013, which will be amortized over their remaining useful life of less than one year. There were no intangible asset impairments in the years ended 2012 or 2011.

Consolidated Operating Results

This MD&A includes an overview of our consolidated results of operations for 2013, 2012 and 2011 followed by a discussion of the results of operations of each of our reportable segments for the same periods. Our results for the year ended 2013 include the operating results of Express Label for a full year and National's results of operations are included in our operating results from September 16, 2013. Our results for the year ended 2012 and 2011 do not include the operating results of National or Express Label.

A summary of our consolidated statements of operations is presented below. The summary presents reported net sales and operating income (loss). See Segment Operations below for a summary of net sales and operating income (loss) of our reportable segments we use internally to assess our operating performance. Our reporting periods for 2013, 2012 and 2011 each consisted of 52 week periods ending on the Saturday closest to the last day of the calendar month and ended on December 28, 2013, December 29, 2012 and December 31, 2011, respectively. We refer to such periods herein as: (i) the year ended 2013; (ii) the year ended 2012; and (iii) the year ended 2011. All references to years and year-ends herein relate to fiscal years rather than calendar years.

17

| For The Years Ended | ||||||||||||

| 2013 | 2012 | 2011 | ||||||||||

(in thousands, except per share amounts) | ||||||||||||

| Net sales | $ | 1,777,808 | $ | 1,738,293 | $ | 1,844,371 | ||||||

| Operating income (loss): | ||||||||||||

| Envelope | $ | 39,775 | $ | 45,485 | $ | 46,838 | ||||||

| (6,042 | ) | 32,845 | 43,709 | |||||||||

| Label and packaging | 32,644 | 54,666 | 57,768 | |||||||||

| Corporate | (37,014 | ) | (31,811 | ) | (43,153 | ) | ||||||

| Total operating income | 29,363 | 101,185 | 105,162 | |||||||||

| Gain on bargain purchase | (17,262 | ) | — | (11,720 | ) | |||||||

| Interest expense, net | 112,677 | 114,755 | 115,968 | |||||||||

| Loss (gain) on early extinguishment of debt, net | 11,324 | 12,487 | (4,011 | ) | ||||||||

| Other (income) expense, net | (5,602 | ) | (1,249 | ) | 9,074 | |||||||

| Loss from continuing operations before income taxes | (71,774 | ) | (24,808 | ) | (4,149 | ) | ||||||

| Income tax expense | 13,753 | 55,720 | 4,545 | |||||||||

| Loss from continuing operations | (85,527 | ) | (80,528 | ) | (8,694 | ) | ||||||

| Income from discontinued operations, net of taxes | 16,741 | 641 | 129 | |||||||||

| Net loss | $ | (68,786 | ) | $ | (79,887 | ) | $ | (8,565 | ) | |||

| (Loss) income per share – basic: | ||||||||||||

| Continuing operations | $ | (1.32 | ) | $ | (1.27 | ) | $ | (0.14 | ) | |||

| Discontinued operations | 0.25 | 0.01 | — | |||||||||

| Net loss | $ | (1.07 | ) | $ | (1.26 | ) | $ | (0.14 | ) | |||

| (Loss) income per share – diluted: | ||||||||||||

| Continuing operations | $ | (1.32 | ) | $ | (1.27 | ) | $ | (0.14 | ) | |||

| Discontinued operations | 0.25 | 0.01 | — | |||||||||

| Net loss | $ | (1.07 | ) | $ | (1.26 | ) | $ | (0.14 | ) | |||

18

Net Sales

Net sales increased $39.5 million, or 2.3%, in 2013, as compared to 2012, due to higher sales from our envelope segment of $91.7 million and higher sales from our label and packaging segment of $3.7 million, offset by lower sales in our print segment of $55.9 million.

Net sales decreased $106.1 million, or 5.8%, in 2012, as compared to 2011, primarily due to lower sales from our print segment of $41.4 million, $48.4 million from our envelope segment and $16.3 million from our label and packaging segment.

See Segment Operations below for a detailed discussion of the primary factors affecting the change in our net sales by reportable segment.

Operating Income

Operating income decreased $71.8 million, or 71.0%, in 2013, as compared to 2012. This decrease was due to: (i) a decrease in operating income from our print segment of $38.9 million; (ii) a decrease in operating income from our label and packaging segment of $22.0 million; (iii) a decrease in operating income from our envelope segment of $5.7 million; and (iv) higher corporate expenses of $5.2 million.

Operating income decreased $4.0 million, or 3.8%, in 2012, as compared to 2011. This decrease was primarily due to decreases from: (i) our print segment of $10.9 million; (ii) our label and packaging segment of $3.1 million; and (iii) our envelope segment of $1.4 million, partially offset by lower corporate expenses of $11.3 million.

See Segment Operations below for a more detailed discussion of the primary factors for the changes in operating income by reportable segment.

Gain on Bargain Purchase

During 2013, in connection with the acquisition of certain assets of National, we recognized a preliminary bargain purchase gain of approximately $17.3 million.

During 2011, in connection with the acquisition of MeadWestvaco Corporation's Envelope Product Group, which we refer to as EPG, we recognized a bargain purchase gain of approximately $11.7 million.

Interest Expense

Interest expense decreased $2.1 million to $112.7 million in 2013, as compared to $114.8 million in 2012. The decrease was primarily due to lower average outstanding debt balances primarily as a result of debt repayments using cash flow from operations and the proceeds from the sale of Custom Envelope, as well as lower interest rates on our revolver borrowings as a result of our refinancing of debt in the second quarter of 2013. Interest expense in 2013 reflected average outstanding debt of approximately $1.2 billion and a weighted average interest rate of 8.2%, compared to the average outstanding debt of approximately $1.3 billion and a weighted average interest rate of 8.2% in 2012.

Interest expense decreased $1.2 million to $114.8 million in 2012, as compared to $116.0 million in 2011. The decrease was primarily due to lower average outstanding debt balances primarily as a result of debt repayments using cash flow from operations and the proceeds from the sale of the Discontinued Operations, offset in part by higher interest expense as a result of our refinancing activities in 2012. Interest expense in 2012 reflected average outstanding debt of approximately $1.3 billion and a weighted average interest rate of 8.2%, as compared to average outstanding debt of $1.4 billion and a weighted average interest rate of 8.0% in 2011.

Loss on Early Extinguishment of Debt

During the year ended 2013, we recorded a total loss on early extinguishment of debt of $11.3 million. In connection with the refinancing of our $170 million revolving credit facility due 2014, which we refer to as the Revolving Credit Facility, and our existing term loan B due 2016, which we refer to as Term Loan B, and collectively with the Revolving Credit Facility we refer to as the Refinanced Facility, we recorded a loss on early extinguishment of debt of approximately $6.4 million, of which $4.1 million related to consent fees paid to consenting lenders, $2.1 million related to the write-off of unamortized debt issuance costs and $0.2 million related to the write-off of original issuance discount. We recorded a loss on early extinguishment of debt of approximately $4.0 million related to the extinguishment of $40.0 million of our Unsecured Term Loan, of which $2.2 million

19

related to the write-off of unamortized debt issuance costs and $1.8 million related to the write-off of original issuance discount. In connection with the extinguishment of $28.2 million of our secured term loan facility, which we refer to as the Term Loan Facility, we recorded a loss on early extinguishment of debt of approximately $0.8 million, of which $0.5 million related to the write-off of unamortized debt issuance costs and $0.3 million related to the write-off of original issuance discount.

During 2012, we recorded a total loss on early extinguishment of debt of $12.5 million. In connection with various refinancing activities, we incurred losses on early extinguishment of debt of $14.9 million, of which $11.7 million related to tender and consent fees paid to consenting lenders and $3.2 million related to the write-off of previously unamortized debt issuance costs. The loss on early extinguishment was partially offset by the gains on early extinguishment of debt of $2.4 million related to repurchases of: (i) our 7.875% senior subordinated notes, due 2013, which we refer to as the 7.875% Notes; (ii) our 10.5% senior notes due 2016, which we refer to as the 10.5% Notes; and (iii) our 8.375% senior subordinated notes, due 2014, which we refer to as the 8.375% Notes, plus in each case accrued and unpaid interest thereon.

During 2011, we repurchased $11.4 million of our 7.875% Notes for $9.0 million plus accrued and unpaid interest and $7.0 million of our 8.375% Notes for $5.4 million plus accrued and unpaid interest. As a result, we recognized gains on early extinguishment of debt of $4.0 million.

Income Taxes

| For The Years Ended | ||||||||||||

| 2013 | 2012 | 2011 | ||||||||||

| (in thousands) | ||||||||||||

| Income tax expense from U.S. operations | $ | 14,197 | $ | 56,173 | $ | 2,184 | ||||||

| Income tax (benefit) expense from foreign operations | (444 | ) | (453 | ) | 2,361 | |||||||

| Income tax expense | $ | 13,753 | $ | 55,720 | $ | 4,545 | ||||||