UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549FORM 10-Q |

| |

| ☒ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended June 30, 2020

OR

|

| |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ____ to ____

Commission File Number: 1-36282 LA JOLLA PHARMACEUTICAL COMPANY

(Exact name of registrant as specified in its charter) |

| | | | | |

| California | | 33-0361285 |

| (State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

| | | | | | |

| 4550 Towne Centre Court, | San Diego, | CA | | | 92121 |

| (Address of principal executive offices) | | (Zip Code) |

Registrant’s telephone number, including area code: (858) 207-4264

|

| | | | | | | | |

| | Securities registered pursuant to Section 12(b) of the Act: | |

| | Title of each class | | Trading Symbol(s) | | Name of each exchange on which registered | |

| | Common Stock, par value $0.0001 per share | | LJPC | | The | Nasdaq | Capital Market | |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

| | | |

| Large accelerated filer | ☐

| Accelerated filer | ☒

|

| Non-accelerated filer | ☐

| Smaller reporting company | ☒ |

| | | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of July 27, 2020, there were 27,362,100 shares of common stock outstanding.

TABLE OF CONTENTS

PART I. FINANCIAL INFORMATION

Item 1. Financial Statements

LA JOLLA PHARMACEUTICAL COMPANY

Condensed Consolidated Balance Sheets

(in thousands, except par value and share amounts)

|

| | | | | | | |

| | June 30,

2020 | | December 31,

2019 |

| | (Unaudited) | | |

| ASSETS | | | |

| Current assets: | | | |

| Cash | $ | 68,353 |

| | $ | 87,820 |

|

| Short-term investments | 3,062 |

| | — |

|

| Accounts receivable, net | 1,843 |

| | 2,960 |

|

| Inventory, net | 3,120 |

| | 2,211 |

|

| Prepaid expenses and other current assets | 2,792 |

| | 4,467 |

|

| Total current assets | 79,170 |

| | 97,458 |

|

| Property and equipment, net | 12,827 |

| | 18,389 |

|

| Right-of-use lease asset | 14,792 |

| | 15,491 |

|

| Restricted cash | 606 |

| | 909 |

|

| Total assets | $ | 107,395 |

| | $ | 132,247 |

|

| | | | |

| LIABILITIES AND SHAREHOLDERS’ DEFICIT | | | |

| Current liabilities: | | | |

| Accounts payable | $ | 2,481 |

| | $ | 4,177 |

|

| Accrued expenses | 6,772 |

| | 9,312 |

|

| Accrued payroll and related expenses | 5,741 |

| | 8,332 |

|

| Lease liability, current portion | 2,890 |

| | 2,766 |

|

| Total current liabilities | 17,884 |

| | 24,587 |

|

| Lease liability, less current portion | 25,000 |

| | 26,481 |

|

| Deferred royalty obligation, net | 124,406 |

| | 124,379 |

|

| Other noncurrent liabilities | 15,317 |

| | 12,790 |

|

| Total liabilities | 182,607 |

| | 188,237 |

|

| Commitments and contingencies (Note 6) | | | |

| Shareholders’ deficit: | | | |

Common Stock, $0.0001 par value; 100,000,000 shares authorized, 27,358,611 and 27,195,469 shares issued and outstanding at June 30, 2020 and December 31, 2019, respectively | 3 |

| | 3 |

|

Series C-12 Convertible Preferred Stock, $0.0001 par value; 11,000 shares authorized, 3,906 shares issued and outstanding at June 30, 2020 and December 31, 2019; and liquidation preference of $3,906 at June 30, 2020 and December 31, 2019 | 3,906 |

| | 3,906 |

|

| Additional paid-in capital | 982,393 |

| | 977,432 |

|

| Accumulated deficit | (1,061,514 | ) | | (1,037,331 | ) |

| Total shareholders’ deficit | (75,212 | ) | | (55,990 | ) |

| Total liabilities and shareholders’ deficit | $ | 107,395 |

| | $ | 132,247 |

|

See accompanying notes to the condensed consolidated financial statements.

LA JOLLA PHARMACEUTICAL COMPANY

Condensed Consolidated Statements of Operations

(Unaudited)

(in thousands, except per share amounts)

|

| | | | | | | | | | | | | | | |

| | Three Months Ended June 30, | | Six Months Ended June 30, |

| | 2020 | | 2019 | | 2020 | | 2019 |

| Revenue | | | | | | | |

| Net product sales | $ | 5,805 |

| | $ | 5,703 |

| | $ | 13,396 |

| | $ | 10,098 |

|

| Total revenue | 5,805 |

| | 5,703 |

| | 13,396 |

| | 10,098 |

|

| Operating expenses | | | | | | | |

| Cost of product sales | 808 |

| | 551 |

| | 1,524 |

| | 1,051 |

|

| Research and development | 8,781 |

| | 22,043 |

| | 17,964 |

| | 43,287 |

|

| Selling, general and administrative | 8,677 |

| | 11,323 |

| | 16,829 |

| | 23,643 |

|

| Total operating expenses | 18,266 |

| | 33,917 |

| | 36,317 |

| | 67,981 |

|

| Loss from operations | (12,461 | ) | | (28,214 | ) | | (22,921 | ) | | (57,883 | ) |

| Other income (expense) | | | | | | | |

| Interest expense | (2,470 | ) | | (2,806 | ) | | (4,876 | ) | | (5,535 | ) |

| Interest income | 32 |

| | 604 |

| | 222 |

| | 1,317 |

|

| Other income—related party | — |

| | — |

| | 4,085 |

| | — |

|

| Other expense | (693 | ) | | — |

| | (693 | ) | | — |

|

| Total other income (expense), net | (3,131 | ) | | (2,202 | ) | | (1,262 | ) | | (4,218 | ) |

| Net loss | $ | (15,592 | ) | | $ | (30,416 | ) | | $ | (24,183 | ) | | $ | (62,101 | ) |

| Net loss per share, basic and diluted | $ | (0.57 | ) | | $ | (1.12 | ) | | $ | (0.89 | ) | | $ | (2.29 | ) |

| Weighted-average common shares outstanding, basic and diluted | 27,326 |

| | 27,108 |

| | 27,282 |

| | 27,071 |

|

See accompanying notes to the condensed consolidated financial statements.

LA JOLLA PHARMACEUTICAL COMPANY

Condensed Consolidated Statements of Shareholders’ (Deficit) Equity

(Unaudited)

(in thousands)

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Series C-12 Convertible Preferred Stock | | Series F Convertible Preferred Stock | | Common Stock | | Additional Paid-in Capital | | Accumulated Deficit | | Total Shareholders’ (Deficit) Equity |

| | | Shares | | Amount | | Shares | | Amount | | Shares | | Amount | | | |

| Balance at December 31, 2019 | | 4 |

| | $ | 3,906 |

| | — |

| | $ | — |

| | 27,195 |

| | $ | 3 |

| | $ | 977,432 |

| | $ | (1,037,331 | ) | | $ | (55,990 | ) |

| Share-based compensation expense | | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 2,407 |

| | — |

| | 2,407 |

|

| Issuance of common stock under 2013 Equity Plan | | — |

| | — |

| | — |

| | — |

| | 44 |

| | — |

| | 305 |

| | — |

| | 305 |

|

| Issuance of common stock under ESPP | | — |

| | — |

| | — |

| | — |

| | 38 |

| | — |

| | 200 |

| | — |

| | 200 |

|

| Net loss | | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | (8,591 | ) | | (8,591 | ) |

| Balance at March 31, 2020 | | 4 |

| | 3,906 |

| | — |

| | — |

| | 27,277 |

| | 3 |

| | 980,344 |

| | (1,045,922 | ) | | (61,669 | ) |

| Share-based compensation expense | | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 1,590 |

| | — |

| | 1,590 |

|

| Issuance of common stock under 2013 Equity Plan | | — |

| | — |

| | — |

| | — |

| | 50 |

| | — |

| | 300 |

| | — |

| | 300 |

|

| Issuance of common stock under ESPP | | — |

| | — |

| | — |

| | — |

| | 32 |

| | — |

| | 159 |

| | — |

| | 159 |

|

| Net loss | | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | (15,592 | ) | | (15,592 | ) |

| Balance at June 30, 2020 | | 4 |

| | $ | 3,906 |

|

| — |

|

| $ | — |

|

| 27,359 |

|

| $ | 3 |

|

| $ | 982,393 |

|

| $ | (1,061,514 | ) |

| $ | (75,212 | ) |

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Series C-12 Convertible Preferred Stock | | Series F Convertible Preferred Stock | | Common Stock | | Additional Paid-in Capital | | Accumulated Deficit | | Total Shareholders’ (Deficit) Equity |

| | | Shares | | Amount | | Shares | | Amount | | Shares | | Amount | | | |

| Balance at December 31, 2018 | | 4 |

| | $ | 3,906 |

| | 3 |

| | $ | 2,737 |

| | 26,259 |

| | $ | 3 |

| | $ | 950,258 |

| | $ | (920,983 | ) | | $ | 35,921 |

|

| Share-based compensation expense | | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 6,782 |

| | — |

| | 6,782 |

|

| Issuance of common stock under ESPP | | — |

| | — |

| | — |

| | — |

| | 52 |

| | — |

| | 283 |

| | — |

| | 283 |

|

| Issuance of common stock for conversion of Series F Preferred Stock | | — |

| | — |

| | (3 | ) | | (2,737 | ) | | 782 |

| | — |

| | 2,737 |

| | — |

| | — |

|

| Cumulative-effect adjustment from adoption of ASU 2018-07 | | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | (160 | ) | | 160 |

| | — |

|

| Net loss | | — |

|

| — |

|

| — |

|

| — |

|

| — |

|

| — |

|

| — |

|

| (31,685 | ) |

| (31,685 | ) |

| Balance at March 31, 2019 | | 4 |

| | 3,906 |

| | — |

| | — |

| | 27,093 |

| | 3 |

| | 959,900 |

| | (952,508 | ) | | 11,301 |

|

| Share-based compensation expense | | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 6,321 |

| | — |

| | 6,321 |

|

| Issuance of common stock under ESPP | | — |

| | — |

| | — |

| | — |

| | 32 |

| | — |

| | 201 |

| | — |

| | 201 |

|

| Net loss | | — |

|

| — |

|

| — |

|

| — |

|

| — |

|

| — |

|

| — |

|

| (30,416 | ) |

| (30,416 | ) |

| Balance at June 30, 2019 | | 4 |

| | $ | 3,906 |

| | — |

| | $ | — |

| | 27,125 |

| | $ | 3 |

| | $ | 966,422 |

| | $ | (982,924 | ) | | $ | (12,593 | ) |

See accompanying notes to the condensed consolidated financial statements.

LA JOLLA PHARMACEUTICAL COMPANY

Condensed Consolidated Statements of Cash Flows

(Unaudited)

(in thousands) |

| | | | | | | |

| | Six Months Ended June 30, |

| | 2020 | | 2019 |

| Operating activities | | | |

| Net loss | $ | (24,183 | ) | | $ | (62,101 | ) |

| Adjustments to reconcile net loss to net cash used for operating activities: | | | |

| Share-based compensation expense | 3,997 |

| | 13,103 |

|

| Depreciation and amortization expense | 1,798 |

| | 2,263 |

|

| Loss on disposal of equipment | 904 |

| | 15 |

|

| Unrealized gains on short-term investments | (63 | ) | | — |

|

| Non-cash interest expense | 3,392 |

| | 4,678 |

|

| Non-cash rent expense | 699 |

| | 639 |

|

| Changes in operating assets and liabilities: | | | |

| Accounts receivable, net | 1,117 |

| | (512 | ) |

| Inventory, net | (909 | ) | | 52 |

|

| Prepaid expenses and other current assets | 1,675 |

| | 22 |

|

| Accounts payable | (1,696 | ) | | (3,664 | ) |

| Accrued expenses | (3,378 | ) | | 974 |

|

| Accrued payroll and related expenses | (2,591 | ) | | (3,429 | ) |

| Lease liability | (1,357 | ) | | (1,241 | ) |

| Net cash used for operating activities | (20,595 | ) | | (49,201 | ) |

| Investing activities | | | |

| Proceeds from the sale of property and equipment | 2,860 |

| | — |

|

| Purchases of property and equipment | — |

| | (441 | ) |

| Purchases of short-term investments | (2,999 | ) | | — |

|

| Net cash used for investing activities | (139 | ) | | (441 | ) |

| Financing activities | | | |

| Net proceeds from issuance of common stock under 2013 Equity Plan | 605 |

| | — |

|

| Net proceeds from issuance of common stock under ESPP | 359 |

| | 484 |

|

| Net cash provided by financing activities | 964 |

| | 484 |

|

| Net decrease in cash and restricted cash | (19,770 | ) | | (49,158 | ) |

| Cash and restricted cash at beginning of period | 88,729 |

| | 173,513 |

|

| Cash and restricted cash at end of period | $ | 68,959 |

| | $ | 124,355 |

|

| Supplemental disclosure of non-cash investing and financing activities: | | | |

| Conversion of Series F Convertible Preferred Stock into common stock | $ | — |

| | $ | 2,737 |

|

| Cumulative-effect adjustment from adoption of ASU 2018-07 | $ | — |

| | $ | (160 | ) |

| Initial recognition of right-of-use lease asset | $ | — |

| | $ | 16,798 |

|

| Reconciliation of cash and restricted cash to the condensed consolidated balance sheets |

| Cash | $ | 68,353 |

| | $ | 123,446 |

|

| Restricted cash | 606 |

| | 909 |

|

| Total cash and restricted cash | $ | 68,959 |

| | $ | 124,355 |

|

See accompanying notes to the condensed consolidated financial statements.

LA JOLLA PHARMACEUTICAL COMPANY

Notes to the Condensed Consolidated Financial Statements

(Unaudited)

1. Business

La Jolla Pharmaceutical Company (collectively with its wholly owned subsidiaries, “La Jolla” or the “Company”) is dedicated to the development and commercialization of innovative therapies that improve outcomes in patients suffering from life-threatening diseases. GIAPREZATM (angiotensin II) for injection is approved by the U.S. Food and Drug Administration (“FDA”) as a vasoconstrictor indicated to increase blood pressure in adults with septic or other distributive shock.

On July 28, 2020, La Jolla completed its acquisition of Tetraphase Pharmaceuticals, Inc. (“Tetraphase”), a biopharmaceutical company focused on commercializing its novel tetracycline, XERAVATM (eravacycline), to treat serious and life-threatening infections, for $43 million in upfront cash plus potential future cash payments of up to $16 million. XERAVA for injection is a novel fluorocycline of the tetracycline class of antibacterials that is approved by the FDA for the treatment of complicated intra-abdominal infections (“cIAI”) in patients 18 years of age and older. See Note 12.

As of June 30, 2020 and December 31, 2019, the Company had cash and short-term investments of $71.4 million and $87.8 million, respectively. Based on the Company’s current operating plans and projections, the Company expects that its existing cash and short-term investments will be sufficient to fund operations for at least one year from the date this Quarterly Report on Form 10-Q is filed with the U.S. Securities and Exchange Commission (the “SEC”).

2. Basis of Presentation and Summary of Significant Accounting Policies

Basis of Presentation and Use of Estimates

The accompanying condensed consolidated financial statements of the Company have been prepared in accordance with U.S. generally accepted accounting principles (“GAAP”) for interim financial information and with the instructions to Form 10-Q and Article 10 of SEC Regulation S-X. Accordingly, certain information and disclosures required by GAAP for annual financial statements have been omitted. In the opinion of management, all adjustments, consisting of normal recurring adjustments, considered necessary for a fair presentation have been included. These condensed consolidated financial statements should be read in conjunction with the audited consolidated financial statements and notes thereto for the year ended December 31, 2019 included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2019, filed with the SEC on March 2, 2020 (the “Form 10-K”). The accompanying condensed consolidated financial statements include the accounts of La Jolla Pharmaceutical Company and its wholly owned subsidiaries. All inter-company transactions and balances have been eliminated in consolidation.

The preparation of the Company’s condensed consolidated financial statements requires management to make estimates and assumptions that impact the reported amounts of assets, liabilities, revenue and expenses and the disclosure of contingent assets and liabilities in the Company’s condensed consolidated financial statements and the accompanying notes. Actual results may differ materially from these estimates. Certain amounts previously reported in the financial statements have been reclassified to conform to the current year presentation. Such reclassifications did not affect net loss, shareholders’ (deficit) equity or cash flows. The results of operations for the three and six months ended June 30, 2020 are not necessarily indicative of the results to be expected for the full year or any future interim periods. The accompanying condensed consolidated balance sheet as of December 31, 2019 has been derived from the audited consolidated balance sheet as of December 31, 2019 contained in the Form 10-K.

Summary of Significant Accounting Policies

During the six months ended June 30, 2020, other than the short-term investments policy described below, there have been no changes to the Company’s significant accounting policies as described in the Form 10-K.

Short-term investments

Short-term investments are comprised of marketable equity securities that are “available-for-sale,” as such term is defined by the Financial Accounting Standards Board (the “FASB”) Accounting Standards Codification (“ASC”) Topic 320. Marketable equity securities are classified as current assets. Short-term investments are measured at fair value, and unrealized gains and losses are recorded in other income (expense), net in the consolidated statements of operations.

Concentration of Credit Risk

Financial instruments that potentially subject the Company to concentration of credit risk consist of cash and accounts receivable. The Company maintains its cash in checking and savings accounts at federally insured financial institutions in excess of federally insured limits.

During the six months ended June 30, 2020, 409 hospitals in the U.S. purchased GIAPREZA. Hospitals purchase our products through a network of specialty and wholesale distributors (“Customers”). The Company does not believe that the loss of one of these distributors would significantly impact the ability to distribute GIAPREZA, as the Company expects that sales volume would be absorbed by the remaining distributors. The following table includes the percentage of U.S. net product sales and accounts receivable balances for the Company’s three major Customers, each of which comprised 10% or more of its U.S. net product sales:

|

| | | | | | | | |

| | U.S. Net Product Sales | | Accounts Receivable |

| | Three Months Ended June 30, 2020 | | Six Months Ended June 30, 2020 | | As of June 30, 2020 |

| Customer A | 38 | % | | 38 | % | | 22 | % |

| Customer B | 33 | % | | 31 | % | | 41 | % |

| Customer C | 25 | % | | 29 | % | | 33 | % |

| Total | 96 | % | | 98 | % | | 96 | % |

Revenue Recognition

The Company has adopted FASB ASC Topic 606—Revenue from Contracts with Customers (“ASC 606”). Under ASC 606, the Company recognizes revenue when its customers obtain control of the Company’s product, which typically occurs on delivery. Revenue is recognized in an amount that reflects the consideration that the Company expects to receive in exchange for those goods. To determine revenue recognition for contracts with customers within the scope of ASC 606, the Company performs the following 5 steps: (i) identify the contract(s) with a customer; (ii) identify the performance obligations in the contract; (iii) determine the transaction price; (iv) allocate the transaction price to the performance obligations in the contract; and (v) recognize revenue when (or as) the entity satisfies the relevant performance obligations. There have been no contract assets or liabilities recorded to date relating to product sales.

Revenue from product sales is recorded at the transaction price, net of estimates for variable consideration consisting of chargebacks, discounts, returns and administrative fees. Variable consideration is estimated using the expected-value amount method, which is the sum of probability-weighted amounts in a range of possible consideration amounts. Actual amounts of consideration ultimately received may differ from the Company’s estimates. If actual results vary materially from the Company’s estimates, the Company will adjust these estimates, which will affect revenue from product sales and earnings in the period such estimates are adjusted. These items include:

| |

| • | Chargebacks—Chargebacks are discounts the Company provides to distributors in the event that the sales prices to end users are below the distributors’ acquisition price. This may occur due to a direct contract with a health system, a group purchasing organization (“GPO”) agreement or a sale to a government facility. Chargebacks are estimated based on known chargeback rates and recorded as a reduction of revenue on delivery to the Company’s customers. |

| |

| • | Discounts—The Company offers customers various forms of incentives and consideration, including prompt-pay and other discounts. The Company estimates discounts primarily based on contractual terms. These discounts are recorded as a reduction of revenue on delivery to the Company’s customers. |

| |

| • | Returns—The Company offers customers a limited right of return, generally for damaged or expired product. The Company estimates returns based on an internal analysis, which includes actual experience. The estimates for returns are recorded as a reduction of revenue on delivery to the Company’s customers. |

| |

| • | Administrative Fees—The Company pays administrative fees to GPOs for services and access to data. Additionally, the Company pays an Industrial Funding Fee as part of the U.S. General Services Administration’s Federal Supply Schedules program. These fees are based on contracted terms and are paid after the quarter in which the product was purchased by the applicable GPO or government agency. |

The Company will continue to assess its estimates of variable consideration as it accumulates additional historical data and will adjust these estimates accordingly.

Recent Accounting Pronouncements

Management has considered all recent accounting pronouncements and has concluded that there are no recently issued accounting pronouncements that may have a material effect on the Company’s results of operations, financial condition or cash flows based on current information.

3. Net Loss per Share

Basic net loss per share is calculated by dividing net loss by the weighted-average number of common shares outstanding during the period, without consideration of potential common shares. Diluted net loss per share is calculated by dividing net loss by the weighted-average number of common shares outstanding plus potential common shares. Convertible preferred stock, stock options and warrants are considered potential common shares and are included in the calculation of diluted net loss per share using the treasury stock method when their effect is dilutive. Potential common shares are excluded from the calculation of diluted net loss per share when their effect is anti-dilutive. As of June 30, 2020 and 2019, there were 10.2 million and 14.0 million potential common shares, respectively, that were excluded from the calculation of diluted net loss per share because their effect was anti-dilutive.

4. Balance Sheet Details

Restricted Cash

Restricted cash as of June 30, 2020 and December 31, 2019 represents a standby letter of credit for the Company’s building lease in lieu of a security deposit during the term of such lease (see Note 6). There is a requirement to maintain $0.6 million of cash collateral in an account pledged as security for such letter of credit.

Inventory, Net

Inventory, net consisted of the following (in thousands):

|

| | | | | | | | |

| | | June 30,

2020 | | December 31,

2019 |

| Work-in-process | | $ | 1,801 |

| | $ | 1,505 |

|

| Finished goods | | 1,319 |

| | 706 |

|

| Total inventory, net | | $ | 3,120 |

| | $ | 2,211 |

|

As of June 30, 2020 and December 31, 2019, total inventory is recorded net of inventory reserves of $0.2 million and $0.1 million, respectively.

Property and Equipment, Net

Property and equipment, net consisted of the following (in thousands): |

| | | | | | | | |

| | | June 30,

2020 | | December 31,

2019 |

| Leasehold improvements | | $ | 14,504 |

| | $ | 14,504 |

|

| Furniture and fixtures | | 2,549 |

| | 2,598 |

|

| Computer hardware | | 1,296 |

| | 1,296 |

|

| Software | | 733 |

| | 733 |

|

| Lab equipment | | — |

| | 9,665 |

|

| Total property and equipment, gross | | 19,082 |

| | 28,796 |

|

| Accumulated depreciation and amortization | | (6,255 | ) | | (10,407 | ) |

| Total property and equipment, net | | $ | 12,827 |

| | $ | 18,389 |

|

Accrued Expenses

Accrued expenses consisted of the following (in thousands):

|

| | | | | | | | |

| | | June 30,

2020 | | December 31,

2019 |

| Accrued interest expense | | $ | 3,530 |

| | $ | 2,692 |

|

| Accrued manufacturing costs | | 1,369 |

| | 1,339 |

|

| Accrued clinical study costs | | 815 |

| | 3,496 |

|

| Accrued other | | 1,058 |

| | 1,785 |

|

| Total accrued expenses | | $ | 6,772 |

| | $ | 9,312 |

|

5. Deferred Royalty Obligation

In May 2018, the Company closed a $125.0 million royalty financing agreement (the “Royalty Agreement”) with HealthCare Royalty Partners (“HCR”). Under the terms of the Royalty Agreement, the Company received $125.0 million in exchange for tiered royalty payments on worldwide net sales of GIAPREZA. HCR is entitled to receive quarterly royalties on worldwide net sales of GIAPREZA beginning April 1, 2018. Quarterly payments to HCR under the Royalty Agreement start at a maximum royalty rate, with step-downs based on the achievement of annual net product sales thresholds. Through December 31, 2021, the royalty rate will be a maximum of 10%. Starting January 1, 2022, the maximum royalty rate may increase by 4% if an agreed-upon, cumulative net product sales threshold has not been met, and, starting January 1, 2024, the maximum royalty rate may increase by an additional 4% if a different agreed-upon, cumulative net product sales threshold has not been met. The Royalty Agreement is subject to maximum aggregate royalty payments to HCR of $225.0 million. The Royalty Agreement expires upon the first to occur of January 1, 2031 or when the maximum aggregate royalty payments have been made. The Royalty Agreement was entered into by the Company’s wholly owned subsidiary, La Jolla Pharma, LLC, and HCR has no recourse under the Royalty Agreement against La Jolla Pharmaceutical Company or any assets other than GIAPREZA.

On receipt of the $125.0 million payment from HCR, the Company recorded a deferred royalty obligation of $125.0 million, net of issuance costs of $0.7 million. For the three months ended June 30, 2020 and 2019, the Company recognized interest expense, including amortization of the obligation discount, of $2.5 million and $2.8 million, respectively. For the six months ended June 30, 2020 and 2019, the Company recognized interest expense, including amortization of the obligation discount, of $4.9 million and $5.5 million, respectively. The carrying value of the deferred royalty obligation as of June 30, 2020 was $124.4 million, net of unamortized obligation discount of $0.6 million, and was classified as noncurrent. The related accrued interest expense was $18.8 million and $15.5 million as of June 30, 2020 and December 31, 2019, respectively, of which $15.3 million and $12.8 million was classified as other noncurrent liabilities, respectively. During the three and six months ended June 30, 2020, the Company made royalty payments to HCR of $0.8 million and $1.5 million, respectively, and, as of June 30, 2020, the Company recorded royalty obligations payable of $0.6 million in accrued expenses. The deferred royalty obligation is classified as Level 3 in the ASC 820-10, three-tier fair value hierarchy, and its carrying value approximates fair value.

Under the terms of the Royalty Agreement, La Jolla Pharma, LLC has certain obligations, including the obligation to use commercially reasonable and diligent efforts to commercialize GIAPREZA. If La Jolla Pharma, LLC is held to not have met these obligations, HCR would have the right to terminate the Royalty Agreement and demand payment from La Jolla Pharma, LLC of either $125.0 million or $225.0 million (depending on which obligation La Jolla Pharma, LLC is held to not have met), minus aggregate royalties already paid to HCR. In the event that La Jolla Pharma, LLC fails to timely pay such amount if and when due, HCR would have the right to foreclose on the GIAPREZA-related assets. The Company concluded that certain of these contract provisions that could result in an acceleration of amounts due under the Royalty Agreement are embedded derivatives that require bifurcation from the deferred royalty obligation and fair value recognition. The Company determined the fair value of each derivative by assessing the probability of each event occurring, as well as the potential repayment amounts and timing of such repayments that would result under various scenarios. As a result of this assessment, the Company determined that the fair value of the embedded derivatives is immaterial as of June 30, 2020 and December 31, 2019. Each reporting period, the Company estimates the fair value of the embedded derivatives until the features lapse and/or the termination of the Royalty Agreement. Any change in the fair value of the embedded derivatives will be recorded as either a gain or loss on the consolidated statements of operations.

6. Commitments and Contingencies

Lease Commitments

On December 29, 2016, the Company entered into an agreement with BMR-Axiom LP (the “Landlord”) to lease office and laboratory space as its corporate headquarters located at 4550 Towne Centre Court, San Diego, California (the “Lease”) for a period of 10 years commencing on October 30, 2017 (the “Initial Lease Term”). The Company has an option to extend the Lease for an additional 5 years at the end of the Initial Lease Term.

The Company provided a standby letter of credit for $0.9 million in lieu of a security deposit. This amount decreased to $0.6 million after year two of the Initial Lease Term and will decrease to $0.3 million after year 5 of the Initial Lease Term. As of June 30, 2020, $0.6 million of cash was pledged as collateral for such letter of credit and recorded as restricted cash. The annual rent under the Lease is subject to escalation during the term. In addition to rent, the Lease requires the Company to pay certain taxes, insurance and operating costs relating to the leased premises. The Lease contains customary default provisions, representations, warranties and covenants. The Lease is classified as an operating lease.

Future minimum lease payments under the Lease as of June 30, 2020 are as follows (in thousands): |

| | | |

| 2020 | $ | 2,039 |

|

| 2021 | 4,174 |

|

| 2022 | 4,294 |

|

| 2023 | 4,417 |

|

| 2024 | 4,544 |

|

| Thereafter | 13,590 |

|

| Total future minimum lease payments | 33,058 |

|

| Less: discount | (5,168 | ) |

| Total lease liability | $ | 27,890 |

|

The Company recorded a lease liability for the Lease based on the present value of the Lease payments over the Initial Lease Term, discounted using the Company’s incremental borrowing rate. The Company recorded a corresponding right-of-use lease asset based on the lease liability, adjusted for incentives received prior to the Lease commencement date. The option to extend the Initial Lease Term was not recognized as a part of either the Company’s lease liability or right-of-use lease asset. Lease expense was $0.7 million and $1.4 million for the three and six months ended June 30, 2020, respectively, and for the same periods in 2019. Amortization for the right-of-use lease asset was $0.4 million and $0.7 million for the three and six months ended June 30, 2020, respectively, and was $0.3 million and $0.6 million for the three and six months ended June 30, 2019, respectively.

Contingencies

From time to time, the Company may become subject to claims and litigation arising in the ordinary course of business. The Company is not a party to any material legal proceedings, nor is it aware of any material pending or threatened litigation.

7. Shareholders’ Equity

Preferred Stock

As of June 30, 2020 and December 31, 2019, 3,906 shares of Series C-12 Convertible Preferred Stock (“Series C-12 Preferred”) were issued, outstanding and convertible into 6,735,378 shares of common stock. In January 2019, the Company issued 782,031 shares of common stock upon the conversion of 2,737 shares of Series F Convertible Preferred Stock. As of June 30, 2020 and December 31, 2019, there were no shares of Series F Convertible Preferred Stock issued and outstanding.

Warrants

As of June 30, 2020 and December 31, 2019, the Company had outstanding warrants to purchase 10,000 shares of common stock. The Company did not recognize share-based compensation expense for these outstanding warrants for the three and six months ended June 30, 2020 and 2019.

8. Equity Incentive Plans

2013 Equity Incentive Plan

A total of 9,600,000 shares of common stock have been reserved for issuance under the La Jolla Pharmaceutical Company 2013 Equity Incentive Plan (the “2013 Equity Plan”). As of June 30, 2020, 5,940,653 shares of common stock remained available for future grants under the 2013 Equity Plan.

2018 Employee Stock Purchase Plan

A total of 750,000 shares of common stock have been reserved for issuance under the La Jolla Pharmaceutical Company 2018 Employee Stock Purchase Plan (the “ESPP”). As of June 30, 2020, 499,805 shares of common stock remained available for future grants under the ESPP.

Equity Awards

The activity related to equity awards, which are comprised of stock options and inducement grants, during the six months ended June 30, 2020 is summarized as follows: |

| | | | | | | | | | | | |

| | Equity Awards | | Weighted- average Exercise Price per Share | | Weighted- average Remaining Contractual Term | | Aggregate

Intrinsic

Value |

| Outstanding at December 31, 2019 | 5,616,840 |

| | $ | 19.50 |

| | | | |

| Granted | 806,923 |

| | $ | 5.27 |

| | | | |

| Exercised | (94,219 | ) | | $ | 6.42 |

| | | | |

| Cancelled/forfeited | (2,883,533 | ) | | $ | 19.43 |

| | | | |

| Outstanding at June 30, 2020 | 3,446,011 |

| | $ | 16.59 |

| | 5.87 years | | $ | 35,037 |

|

| Exercisable at June 30, 2020 | 2,144,609 |

| | $ | 20.84 |

| | 4.27 years | | $ | — |

|

Share-based Compensation Expense

The classification of share-based compensation expense is summarized as follows (in thousands):

|

| | | | | | | | | | | | | | | |

| | Three Months Ended June 30, | | Six Months Ended June 30, |

| | 2020 | | 2019 | | 2020 | | 2019 |

| Research and development | $ | 964 |

| | $ | 3,960 |

| | $ | 2,527 |

| | $ | 7,893 |

|

| Selling, general and administrative | 626 |

| | 2,361 |

| | 1,470 |

| | 5,210 |

|

| Total share-based compensation expense | $ | 1,590 |

| | $ | 6,321 |

| | $ | 3,997 |

| | $ | 13,103 |

|

As of June 30, 2020, total unrecognized share-based compensation expense related to unvested equity awards was $8.6 million, which is expected to be recognized over a weighted-average period of 2.2 years. As of June 30, 2020, there was no unrecognized share-based compensation expense related to shares of common stock issued under the ESPP.

9. Other Income—Related Party

The Company has a non-voting profits interest in a related party, which provides the Company with the potential to receive a portion of the future distributions of profits, if any. Investment funds affiliated with the Chairman of the Company’s board of directors have a controlling interest in the related party. During the six months ended June 30, 2020, the Company received distributions of $4.1 million in connection with this profits interest.

10. George Washington University License

In December 2014, the Company entered into a patent license agreement with George Washington University (“GW”), which was amended and restated on March 1, 2016 (the “GW License”) and subsequently assigned to La Jolla Pharma, LLC. Pursuant to the GW License, GW exclusively licensed to the Company certain intellectual property rights relating to GIAPREZA, including the exclusive rights to certain issued patents and patent applications covering GIAPREZA. Under the GW License, the Company is obligated to use commercially reasonable efforts to develop, commercialize, market and sell GIAPREZA. The Company has paid a one-time license initiation fee, annual maintenance fees, an amendment fee, additional payments following the achievement of certain development and regulatory milestones and royalties. As a result of the EC’s approval of GIAPREZA in August 2019, the Company made a milestone payment to GW in the amount of $0.5 million in the first quarter of 2020. The Company is obligated to pay a 6% royalty on net sales of GIAPREZA. The patents and patent applications covered by the GW License are expected to expire between 2029 and 2034, and the obligation to pay royalties under this agreement extends through the last-to-expire patent covering GIAPREZA.

11. Company-wide Realignments

On December 2, 2019, the Board of Directors of the Company approved a restructuring plan (the “2019 Realignment”) that reduced the Company’s headcount. The 2019 Realignment did not result in any reductions in headcount in the Company’s commercial organization supporting GIAPREZA. For the year ended December 31, 2019, total expense was comprised of $5.8 million for one-time termination benefits to the affected employees, including severance and health care benefits, offset by a $0.9 million reversal of non-cash, share-based compensation expense related to forfeited, unvested equity awards. As of June 30, 2020, the Company had paid $4.8 million of the $5.8 million cash severance and health care benefits charges, and the remaining $1.0 million of the health care benefits charges were included in accrued payroll and related expenses.

On May 28, 2020, the Board of Directors of the Company approved a restructuring plan (the “2020 Realignment”) to align its organization with the Company’s sole focus on the commercialization of GIAPREZA. The 2020 Realignment reduced the Company’s headcount. For the three months ended June 30, 2020, total expense was comprised of $4.1 million for one-time termination benefits to the affected employees, including severance and health care benefits, offset by a $0.4 million reversal of non-cash, share-based compensation expense related to forfeited, unvested equity awards. As of June 30, 2020, the Company had paid $0.7 million of the $4.1 million cash severance and health care benefits charges, and the remaining $3.4 million of the cash severance and health care

benefits charges were included in accrued payroll and related expenses. The Company expects to make substantially all of the remaining payments resulting from the 2020 Realignment in the third quarter of 2020.

12. Subsequent Events

Acquisition of Tetraphase Pharmaceuticals, Inc.

On June 24, 2020, La Jolla entered into an Agreement and Plan of Merger (the “Merger Agreement”) with Tetraphase, a biopharmaceutical company focused on commercializing its novel tetracycline XERAVA to treat serious and life‑threatening infections, and TTP Merger Sub, Inc., a wholly owned subsidiary of La Jolla. On July 28, 2020, La Jolla completed its acquisition of Tetraphase for $43 million in upfront cash plus potential future cash payments of up to $16 million pursuant to contingent value rights (“CVRs”). The holders of the CVRs are entitled to receive potential future cash payments of up to $16 million in the aggregate upon the achievement of certain net sales of XERAVA in the U.S. as follows: (i) $2.5 million if 2021 XERAVA U.S. net sales are at least $20 million; (ii) $4.5 million if XERAVA U.S. net sales are at least $35 million during any calendar year ending on or prior to December 31, 2024; and (iii) $9 million if XERAVA U.S. net sales are at least $55 million during any calendar year ending on or prior to December 31, 2024. Following the acquisition, Tetraphase became a wholly owned subsidiary of La Jolla. The acquisition of Tetraphase will be accounted for as a business combination pursuant to FASB ASC Topic 805.

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

You should read the following discussion and analysis of our financial condition and results of operations together with our condensed consolidated financial statements and the related notes and other financial information included elsewhere in this Quarterly Report on Form 10-Q and our audited financial statements and the related notes and other financial information included in our Annual Report on Form 10-K for the year ended December 31, 2019 filed with the U.S. Securities and Exchange Commission (the “SEC”) on March 2, 2020 (the “Form 10-K”).

Forward-looking Statements

This Quarterly Report on Form 10-Q contains “forward-looking statements” within the meaning of the federal securities laws, and such statements may involve substantial risks and uncertainties. All statements, other than statements of historical facts included in this Quarterly Report on Form 10-Q, including statements concerning our plans, objectives, goals, strategies, future events, future revenues or performance, future expenses, financing needs, plans or intentions relating to acquisitions, business trends and other information referred to under this section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” are forward-looking statements. Forward-looking statements generally relate to future events or our future financial or operating performance. In some cases, you can identify forward-looking statements by terms such as “may,” “might,” “will,” “objective,” “intend,” “should,” “could,” “can,” “would,” “expect,” “believe,” “design,” “estimate,” “predict,” “potential,” “plan,” “anticipate,” “target,” “forecast” or the negative of these terms and similar expressions intended to identify forward-looking statements. Forward-looking statements are not historical facts and reflect our current views with respect to future events. Forward-looking statements are also based on assumptions and are subject to risks and uncertainties. Given these uncertainties, you should not place undue reliance on these forward-looking statements.

There are a number of risks, uncertainties and other important factors that could cause our actual results to differ materially from the forward-looking statements contained in this Quarterly Report on Form 10-Q. Such risks, uncertainties and other factors are described under “Risk Factors” in Item 1A of our Form 10-K for the year ended December 31, 2019 and under “Risk Factors” in Item 1A of this Quarterly Report on Form 10-Q. We caution you that these risks, uncertainties and other factors may not contain all of the risks, uncertainties and other factors that are important to you. In addition, we cannot assure you that we will realize the results, benefits or developments that we expect or anticipate or, even if substantially realized, that they will result in the consequences or affect us or our business in the way expected. All forward-looking statements in this Quarterly Report on Form 10-Q apply only as of the date made and are expressly qualified in their entirety by the cautionary statements included in this Quarterly Report on Form 10-Q. We undertake no obligation to publicly update or revise any forward-looking statements to reflect subsequent events or circumstances.

Business Overview

La Jolla Pharmaceutical Company is dedicated to the development and commercialization of innovative therapies that improve outcomes in patients suffering from life-threatening diseases. GIAPREZATM (angiotensin II) for injection is approved by the U.S. Food and Drug Administration (“FDA”) as a vasoconstrictor indicated to increase blood pressure in adults with septic or other distributive shock. For the three and six months ended June 30, 2020, U.S. net sales of GIAPREZA were $5.8 million and $13.4 million, up 2% and 33%, respectively, from the same periods in 2019.

On July 28, 2020, La Jolla completed its acquisition of Tetraphase Pharmaceuticals, Inc., a biopharmaceutical company focused on commercializing its novel tetracycline, XERAVATM (eravacycline), to treat serious and life-threatening infections, for $43 million in upfront cash plus potential future cash payments of up to $16 million. XERAVA for injection is a novel fluorocycline of the tetracycline class of antibacterials that is approved by the FDA for the treatment of complicated intra-abdominal infections (“cIAI”) in patients 18 years of age and older. For the three and six months ended June 30, 2020, U.S. net sales of XERAVA, which was launched in October 2018, were $1.5 million and $3.2 million, up 88% and 191%, respectively, from the same periods in 2019. Complete financial results of Tetraphase for the six months ended June 30, 2020 will be included in an amended Form 8-K to be filed by La Jolla on or before October 13, 2020. Financial results for periods ending September 30, 2020 and beyond will include Tetraphase’s financial results subsequent to the acquisition closing date of July 28, 2020.

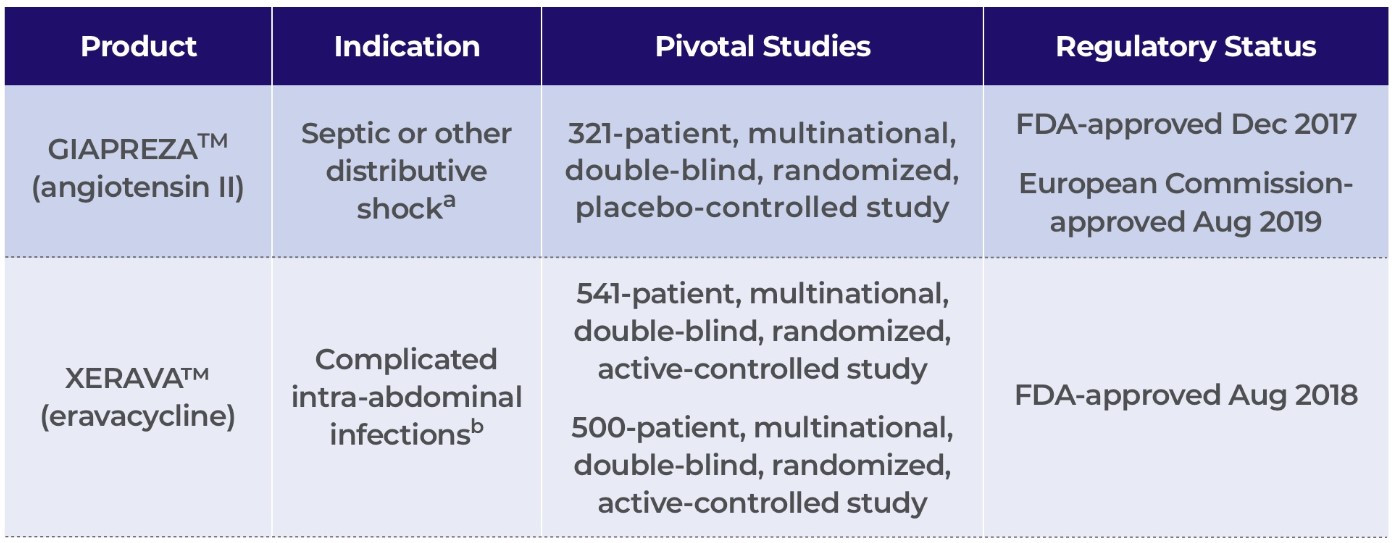

Product Portfolio

|

| |

a | U.S.: GIAPREZA is a vasoconstrictor to increase blood pressure in adults with septic or other distributive shock. |

| | European Union: GIAPREZA is indicated for the treatment of refractory hypotension in adults with septic or other distributive shock who remain hypotensive despite adequate volume restitution and application of catecholamines and other available vasopressor therapies. |

b | U.S.: XERAVA is a novel fluorocycline of the tetracycline class of antibacterials for the treatment of complicated intra-abdominal infections (“cIAI”) in patients 18 years of age and older. European Union: XERAVA is indicated for the treatment of cIAI in adults. |

GIAPREZATM (angiotensin II)

GIAPREZATM (angiotensin II) for injection is approved by the FDA as a vasoconstrictor indicated to increase blood pressure in adults with septic or other distributive shock. GIAPREZA is approved by the European Commission (“EC”) for the treatment of refractory hypotension in adults with septic or other distributive shock who remain hypotensive despite adequate volume restitution and application of catecholamines and other available vasopressor therapies. GIAPREZA mimics the body’s endogenous angiotensin II peptide, which is central to the renin-angiotensin-aldosterone system, which in turn regulates blood pressure. GIAPREZA is marketed in the U.S. by La Jolla Pharmaceutical Company on behalf of La Jolla Pharma, LLC, its wholly owned subsidiary.

XERAVATM (eravacycline)

XERAVATM (eravacycline) for injection is a novel fluorocycline of the tetracycline class of antibacterials that is approved by the FDA for the treatment of cIAI in patients 18 years of age and older. XERAVA is approved by the EC for the treatment of cIAI in adults. XERAVA is marketed in the U.S. by Tetraphase Pharmaceuticals, Inc., a wholly owned subsidiary of La Jolla.

Components of Our Results of Operations

The following table summarizes our results of operations for each of the periods below (in thousands):

|

| | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended June 30, | | Six Months Ended June 30, |

| | 2020 | | 2019 | | Change | | 2020 | | 2019 | | Change |

| Net product sales | $ | 5,805 |

| | $ | 5,703 |

| | $ | 102 |

| | $ | 13,396 |

| | $ | 10,098 |

| | $ | 3,298 |

|

| Cost of product sales | (808 | ) | | (551 | ) | | (257 | ) | | (1,524 | ) | | (1,051 | ) | | (473 | ) |

| Research and development expense | (8,781 | ) | | (22,043 | ) | | 13,262 |

| | (17,964 | ) | | (43,287 | ) | | 25,323 |

|

| Selling, general and administrative expense | (8,677 | ) | | (11,323 | ) | | 2,646 |

| | (16,829 | ) | | (23,643 | ) | | 6,814 |

|

| Other income (expense), net | (3,131 | ) | | (2,202 | ) | | (929 | ) | | (1,262 | ) | | (4,218 | ) | | 2,956 |

|

| Net loss | $ | (15,592 | ) | | $ | (30,416 | ) | | $ | 14,824 |

| | $ | (24,183 | ) | | $ | (62,101 | ) | | $ | 37,918 |

|

Net Product Sales

Net product sales consist solely of revenue recognized from sales of GIAPREZA to hospitals in the U.S. through a network of specialty and wholesaler distributors (“Customers”). GIAPREZA U.S. net sales were $5.8 million and $13.4 million for the three and six months ended June 30, 2020, respectively, compared to $5.7 million and $10.1 million, respectively, for the same periods in 2019.

Cost of Product Sales

Cost of product sales primarily consists of royalties paid or payable to George Washington University and the costs to produce, package and deliver GIAPREZA to our Customers. These costs include raw materials, labor and manufacturing and quality control, as well as shipping and distribution costs. Cost of product sales was $0.8 million and $1.5 million for the three and six months ended June 30, 2020, respectively, compared to $0.6 million and $1.1 million, respectively, for the same periods in 2019.

Research and Development Expense

Research and development expense consists of non-personnel and personnel expenses. The following table summarizes these expenses for each of the periods below (in thousands):

|

| | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended June 30, | | Six Months Ended June 30, |

| | 2020 | | 2019 | | Change | | 2020 | | 2019 | | Change |

| Non-personnel expenses: |

| | | | | | | | | | |

| GIAPREZA | $ | 1,762 |

| | $ | 1,623 |

| | $ | 139 |

| | $ | 2,843 |

| | $ | 3,021 |

| | $ | (178 | ) |

| LJPC-0118 | 404 |

| | 113 |

| | 291 |

| | 917 |

| | 1,135 |

| | (218 | ) |

| LJPC-401 | — |

| | 4,880 |

| | (4,880 | ) | | 1,531 |

| | 8,795 |

| | (7,264 | ) |

| Other programs | — |

| | 2,280 |

| | (2,280 | ) | | — |

| | 3,843 |

| | (3,843 | ) |

| Facility | 1,124 |

| | 1,785 |

| | (661 | ) | | 2,560 |

| | 3,576 |

| | (1,016 | ) |

| Other | — |

| | 992 |

| | (992 | ) | | 474 |

| | 1,918 |

| | (1,444 | ) |

| Total non-personnel expense | $ | 3,290 |

| | $ | 11,673 |

| | $ | (8,383 | ) | | $ | 8,325 |

| | $ | 22,288 |

| | $ | (13,963 | ) |

| Personnel expenses: | | | | | | | | | | | |

| Salaries, bonuses and benefits | 4,527 |

| | 6,410 |

| | (1,883 | ) | | 7,112 |

| | 13,106 |

| | (5,994 | ) |

| Share-based compensation expense | 964 |

| | 3,960 |

| | (2,996 | ) | | 2,527 |

| | 7,893 |

| | (5,366 | ) |

| Total personnel expense | $ | 5,491 |

| | $ | 10,370 |

| | $ | (4,879 | ) | | $ | 9,639 |

| | $ | 20,999 |

| | $ | (11,360 | ) |

| Total research and development expense | $ | 8,781 |

| | $ | 22,043 |

| | $ | (13,262 | ) | | $ | 17,964 |

| | $ | 43,287 |

| | $ | (25,323 | ) |

During the three and six months ended June 30, 2020, total research and development non-personnel expense decreased primarily as a result of decreases in LJPC-401- and other programs-related expenses. During the three and six months ended June 30, 2020, total research and development personnel expense, including share-based compensation expense, decreased as a result of reduced headcount in 2020 from a Company-wide

realignment in November 2019, partially offset by $2.4 million of one-time charges in 2020 resulting from another Company-wide realignment in May 2020.

Selling, General and Administrative Expense

Selling, general and administrative expense consists of non-personnel and personnel expenses. The following table summarizes these expenses for each of the periods below (in thousands):

|

| | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended June 30, | | Six Months Ended June 30, |

| | 2020 | | 2019 | | Change | | 2020 | | 2019 | | Change |

| Non-personnel expenses: |

| |

| | | |

| | | |

|

| Professional fees | $ | 1,356 |

| | $ | 1,139 |

| | $ | 217 |

| | $ | 2,227 |

| | $ | 2,095 |

| | $ | 132 |

|

| Sales and marketing | 588 |

| | 1,471 |

| | (883 | ) | | 1,811 |

| | 3,492 |

| | (1,681 | ) |

| Facility | 554 |

| | 393 |

| | 161 |

| | 1,047 |

| | 773 |

| | 274 |

|

| Other | 339 |

| | 595 |

| | (256 | ) | | 925 |

| | 1,187 |

| | (262 | ) |

| Total non-personnel expense | $ | 2,837 |

| | $ | 3,598 |

| | $ | (761 | ) | | $ | 6,010 |

| | $ | 7,547 |

| | $ | (1,537 | ) |

| Personnel expenses: | | | | | | | | | | |

|

| Salaries, bonuses and benefits | 5,214 |

| | 5,364 |

| | (150 | ) | | 9,349 |

| | 10,886 |

| | (1,537 | ) |

| Share-based compensation expense | 626 |

| | 2,361 |

| | (1,735 | ) | | 1,470 |

| | 5,210 |

| | (3,740 | ) |

| Total personnel expense | $ | 5,840 |

| | $ | 7,725 |

| | $ | (1,885 | ) | | $ | 10,819 |

| | $ | 16,096 |

| | $ | (5,277 | ) |

| Total selling, general and administrative expense | $ | 8,677 |

| | $ | 11,323 |

| | $ | (2,646 | ) | | $ | 16,829 |

| | $ | 23,643 |

| | $ | (6,814 | ) |

During the three and six months ended June 30, 2020, total selling, general and administrative non-personnel expense decreased primarily as a result of decreases in sales and marketing-related expenses. During the three months ended June 30, 2020, La Jolla incurred $0.6 million of professional fees related the acquisition of Tetraphase. During the three and six months ended June 30, 2020, total selling, general and administrative personnel expense, including share-based compensation expense, decreased as a result of reduced headcount in 2020 from a Company-wide realignment in November 2019, partially offset by $1.7 million of one-time charges in 2020 resulting from another Company-wide realignment in May 2020.

Other Income (Expense), Net

Other income (expense), net primarily consists of distributions in connection with our non-voting profits interest in a related party, interest accrued for our deferred royalty obligation and interest income generated from cash held in savings accounts. During the three months ended June 30, 2020, other expense, net increased to $3.1 million from $2.2 million for the same period in 2019, an increase of $0.9 million. This increase was primarily due to a $0.9 million loss on disposal of equipment and a $0.6 million decrease in interest income generated from cash held in savings accounts, partially offset by a $0.3 million decrease in interest expense for our deferred royalty obligation. During the six months ended June 30, 2020, other expense, net decreased to $1.3 million from $4.2 million for the same period in 2019, a decrease of $2.9 million. This decrease was primarily due to the receipt of distributions of $4.1 million in connection with the Company’s non-voting profits interest in a related party and a $0.6 million decrease in interest expense for our deferred royalty obligation, partially offset by a $1.1 million decrease in interest income generated from cash held in savings accounts and a $0.9 million loss on disposal of equipment.

Liquidity and Capital Resources

Since January 2012, when the Company was effectively restarted, through June 30, 2020, our cash used in operating activities was $447 million. As of June 30, 2020, we had an accumulated deficit of $1,062 million and have financed our operations through public and private offerings of securities, a royalty financing, revenues from net product sales, interest income on invested cash balances and other income.

As of June 30, 2020 and December 31, 2019, we had cash and short-term investments of $71.4 million and $87.8 million, respectively. On July 28, 2020, La Jolla completed the acquisition of Tetraphase for $43.0 million in upfront cash. Based on our current operating plans and projections, we believe that our existing cash and short-

term investments will be sufficient to fund operations for at least one year from the date this Quarterly Report on Form 10-Q is filed with the SEC.

Cash used for operating activities was $20.6 million and $49.2 million for the six months ended June 30, 2020 and 2019, respectively. The decrease in cash used for operating activities was a result of decreases in our net loss and changes in working capital, partially offset by decreased non-cash expenses.

Cash used for investing activities was $0.1 million and $0.4 million for the six months ended June 30, 2020 and 2019, respectively. The decrease in cash used for investing activities resulted from the sale of property and equipment, partially offset by purchases of short-term investments.

Cash provided by financing activities was $1.0 million and $0.5 million for the six months ended June 30, 2020 and 2019, respectively. The increase in cash provided by financing activities was primarily the result of net proceeds from issuance of common stock under employee stock plans.

Contractual Obligations

In May 2018, we closed a $125.0 million royalty financing agreement (the “Royalty Agreement”) with HealthCare Royalty Partners (“HCR”). Under the terms of the Royalty Agreement, we received $125.0 million in exchange for tiered royalty payments on worldwide net sales of GIAPREZA. HCR is entitled to receive quarterly royalties on worldwide net sales of GIAPREZA beginning April 1, 2018. Quarterly payments to HCR under the Royalty Agreement start at a maximum royalty rate, with step-downs based on the achievement of annual net product sales thresholds. Through December 31, 2021, the royalty rate will be a maximum of 10%. Starting January 1, 2022, the maximum royalty rate may increase by 4% if an agreed-upon, cumulative net product sales threshold has not been met, and, starting January 1, 2024, the maximum royalty rate may increase by an additional 4% if a different agreed-upon, cumulative net product sales threshold has not been met. The Royalty Agreement is subject to maximum aggregate royalty payments to HCR of $225.0 million. The Royalty Agreement expires upon the first to occur of January 1, 2031 or when the maximum aggregate royalty payments have been made. The Royalty Agreement was entered into by our wholly owned subsidiary, La Jolla Pharma, LLC, and HCR has no recourse under the Royalty Agreement against La Jolla Pharmaceutical Company or any assets other than GIAPREZA.

In December 2014, we entered into a patent license agreement with George Washington University (“GW”), which was amended and restated on March 1, 2016 (the “GW License”) and subsequently assigned to La Jolla Pharma, LLC. Pursuant to the GW License, GW exclusively licensed to us certain intellectual property rights relating to GIAPREZA, including the exclusive rights to certain issued patents and patent applications covering GIAPREZA. Under the GW License, we are obligated to use commercially reasonable efforts to develop, commercialize, market and sell GIAPREZA. We have paid a one-time license initiation fee, annual maintenance fees, an amendment fee, additional payments following the achievement of certain development and regulatory milestones and royalties. As a result of the EC’s approval of GIAPREZA in August 2019, we made a milestone payment to GW in the amount of $0.5 million in the first quarter of 2020. We are obligated to pay a 6% royalty on net sales of GIAPREZA. The patents and patent applications covered by the GW License are expected to expire between 2029 and 2034, and the obligation to pay royalties under this agreement extends through the last-to-expire patent covering GIAPREZA.

Off−Balance Sheet Arrangements

We have no off-balance sheet arrangements that have, or are reasonably likely to have, a current or future effect on our financial condition, changes in our financial condition, expenses, results of operations, liquidity, capital expenditures or capital resources.

Critical Accounting Estimates

We believe the estimates, assumptions and judgments involved in the accounting policies described in “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in Item 7 of our Form 10-K for the year ended December 31, 2019 are most critical to understanding and evaluating our reported financial results. During the three and six months ended June 30, 2020, there have been no material changes to the critical accounting policies and estimates as described in Item 7 of our Form 10-K for the year ended December 31, 2019.

Recent Accounting Pronouncements

See Note 2 to our condensed consolidated financial statements included in Item 1 of this Quarterly Report on Form 10-Q.

Item 3. Quantitative and Qualitative Disclosure about Market Risk

We are a smaller reporting company, as defined by Rule 12b-2 under the Securities and Exchange Act of 1934 and in Item 10(f)(1) of Regulation S-K, and are not required to provide the information under this item.

Item 4. Controls and Procedures

Management’s Evaluation of our Disclosure Controls and Procedures

Our management, with the participation of our principal executive officer and our principal financial officer, evaluated, as of the end of the period covered by this Quarterly Report on Form 10-Q, the effectiveness of our disclosure controls and procedures. Based on that evaluation of our disclosure controls and procedures as of June 30, 2020, our principal executive officer and principal financial officer concluded that our disclosure controls and procedures as of such date are effective at the reasonable assurance level. The term “disclosure controls and procedures,” as defined in Rules 13a-15(e) and 15d-15(e) under the Securities Exchange Act of 1934 (the “Exchange Act”), means controls and other procedures of a company that are designed to ensure that information required to be disclosed by a company in the reports that it files or submits under the Exchange Act are recorded, processed, summarized and reported within the time periods specified in the U.S. Securities and Exchange Commission’s rules and forms. Disclosure controls and procedures include, without limitation, controls and procedures designed to ensure that information required to be disclosed by us in the reports we file or submit under the Exchange Act is accumulated and communicated to our management, including our principal executive officer and principal financial officer, as appropriate to allow timely decisions regarding required disclosure. Management recognizes that any controls and procedures, no matter how well designed and operated, can provide only reasonable assurance of achieving their objectives, and our management necessarily applies its judgment in evaluating the cost-benefit relationship of possible controls and procedures.

Changes in Internal Control over Financial Reporting

There was no change in our internal control over financial reporting that occurred during our most recent quarter that has materially affected, or is reasonably likely to materially affect, our internal control over financial reporting.

PART II. OTHER INFORMATION

Item 1. Legal Proceedings

From time to time, we may become subject to claims and litigation arising in the ordinary course of business. We are not a party to any material legal proceedings, nor are we aware of any material pending or threatened litigation.

Item 1A. Risk Factors

Our business is subject to various risks, including those described in Item 1A of our Annual Report on Form 10-K for the year ended December 31, 2019. There have been no material changes from the risk factors disclosed in Item 1A of our Annual Report on Form 10-K, except for the additional risk factor set forth below.

Our ability to realize the benefits from the acquisition of Tetraphase Pharmaceuticals, Inc. is substantially dependent on the commercial success of XERAVATM (eravacycline) and the cost savings resulting from the timely and effective integration of the operations of La Jolla and Tetraphase.

Our ability to realize the benefits from the acquisition of Tetraphase is substantially dependent on our ability to successfully commercialize XERAVATM (eravacycline). Combining with La Jolla may not accelerate XERAVA’s availability to patients in need, and our presence in the hospital may not increase with a second innovative therapy. If we are unsuccessful at convincing hospitals and health care providers to increase their rate of adoption of XERAVA, our sales could be adversely affected, and our business could suffer.

Further, our ability to realize the benefits from the acquisition of Tetraphase is substantially dependent on the cost savings resulting from the timely and effective integration of the operations La Jolla and Tetraphase. The process of integrating the operations of La Jolla and Tetraphase could encounter unexpected costs and delays, which include: the loss of key personnel; the loss of key customers; the loss of key suppliers; and unanticipated issues in integrating sales, marketing and administrative functions. If we are unable to timely and effectively integrate the operations of La Jolla and Tetraphase, our costs could be adversely affected, and our business could suffer. Further, even if the integration is timely and effective, we may never realize the cost savings expected from the integration of the operations of our two companies.

The ongoing COVID-19 pandemic may disrupt our operations and affect our ability to sell GIAPREZATM (angiotensin II) and XERAVA.

We are unable to accurately predict the full impact that the ongoing Coronavirus Disease 2019 (“COVID‑19”) pandemic will have on our results from operations, financial condition and our ability to sell GIAPREZATM (angiotensin II) and XERAVA due to numerous factors that are not within our control, including its duration and severity of the outbreak. Stay-at-home orders, business closures, travel restrictions, supply chain disruptions and employee illness or quarantines could result in disruptions to our operations, which could adversely impact our results from operations and financial condition. In addition, the COVID-19 pandemic has resulted in ongoing volatility in financial markets. If our access to capital is restricted or associated borrowing costs increase as a result of developments in financial markets relating to the COVID-19 pandemic, our operations and financial condition could be adversely impacted.

Item 2. Unregistered Sales of Equity Securities and Use of Proceeds

None.

Item 3. Defaults upon Senior Securities

None.

Item 4. Mine Safety Disclosures

Not applicable.

Item 5. Other Information

None.

Item 6. Exhibits

|

| | |

| | | |

| Exhibit No. | | Exhibit Description |

| | |

| | | |

| | |

| | | |

| | |

| | | |

| | |

| | | |

| | |

| | | |

| 101.INS | | XBRL Instance Document |

| | | |

| 101.SCH | | XBRL Taxonomy Extension Schema Document |

| | | |

| 101.CAL | | XBRL Taxonomy Extension Calculation Linkbase Document |

| | | |

| 101.DEF | | XBRL Taxonomy Extension Definition Linkbase Document |

| | | |

| 101.LAB | | XBRL Taxonomy Extension Label Linkbase Document |

| | | |

| 101.PRE | | XBRL Taxonomy Extension Presentation Linkbase Document |

* Filed as an exhibit to Registrant’s Current Report on Form 8-K filed on June 24, 2020, and incorporated herein by reference.

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned thereunto duly authorized.

|

| | | |

| | | | La Jolla Pharmaceutical Company |

| | | | |

| Date: | August 6, 2020 | By: | /s/ Larry Edwards |

| | | | Larry Edwards |

| | | | President and Chief Executive Officer |

| | | | (Principal Executive Officer) |

| | | | |

| | | | /s/ Michael Hearne |

| | | | Michael Hearne |

| | | | Chief Financial Officer |

| | | | (Principal Financial and Accounting Officer) |