UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K/A

AMENDMENT NO. 3 TO FORM 10-K

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2002

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from __________ to __________

Commission File Number 0-24796

CENTRAL EUROPEAN MEDIA ENTERPRISES LTD.

(Exact name of registrant as specified in its charter)

| BERMUDA | N/A |

| (State or other jurisdiction of incorporation and organisation) | (IRS Employer Identification No.) |

| Clarendon House, Church Street, Hamilton | HM CX Bermuda |

| (Address of principal executive offices) | (Zip Code) |

Registrant's telephone number, including area code: 441-296-1431

Securities registered pursuant to Section 12(b) of the Act: NONE

Securities registered pursuant to Section 12(g) of the Act:

Class A Common Stock, $0.08 par value

93/8% Notes Due 2004

81/8% Notes Due 2004

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for each shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YESx NOo

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.x

Indicate by check mark whether the registrant is an accelerated filer (as defined in Rule 12b-2 of the Securities Exchange Act of 1934) Yesx Noo

The aggregate market value of the voting stock of registrant held by non-affiliates of the registrant as of March 3, 2003 was approximately $105 million

Number of shares of Class A Common Stock outstanding as of March 3, 2003 : 9,261,884

Number of shares of Class B Common Stock outstanding as of March 3, 2003 : 3,967,368

DOCUMENTS INCORPORATED BY REFERENCE

Document | Location in Form 10-K in Which Document is Incorporated |

| Registrant's Proxy Statement for the Annual General Meeting of Shareholders to be held on May 22, 2003 | Part III |

EXPLANATORY NOTE

This is Amendment No. 3 to the Central European Media Enterprises Ltd. Annual Report on Form 10-K/A, as originally filed on March 10, 2003. No changes have been made to our income statement, balance sheet or cash flow statements as they appeared in our March 10, 2003 Form 10-K/A, although changes have been made to the notes to our financial statements.

Modifications to the March 10, 2003 Form 10-K/A have been made to various parts of the text primarily to:

Clarify Risk Factors and remove non-specific Risk Factors.

Clarify corporate structure, consolidation policies and ownership particularly to remove confusion between legal entities and TV network names.

Provide a full quantified discussion in MD&A of our Romanian related party transactions, the internal control issues in 2002 and how they were resolved.

Reconcile Segment EBITDA and Segment Broadcast Cash Flow to Net Income rather than Operating Income and discuss why they are important to management and investors.

Discuss trends and segment results including Slovakia in the MD&A.

Discuss our treatment of the contingent interest in the Goldentree transaction.

Expand disclosure on our application of FAS142 to Goodwill and Long lived Assets.

We have not updated the Form 10-K/A to modify disclosures in the Form 10-K/A for events occurring subsequent to the original March 10, 2003 filing date. This Amendment No. 3 to Form 10-K/A continues to speak as of March 10, 2003.

| Page 2 | ||

TABLE OF CONTENTS

| Page | |||

| PART I | |||

| Item 1 | Business | 4 | |

| Item 2 | Properties | 26 | |

| Item 3 | Legal Proceedings | 27 | |

| Item 4 | Submission of Matters to a Vote of Security Holders | 30 | |

| PART II | |||

| Item 5 | Market for Registrant's Common Equity and Related Stockholder Matters | 31 | |

| Item 6 | Selected Financial Data | 31 | |

| Item 7 | Management's Discussion and Analysis of Financial Condition and Results of Operations | 34 | |

| Item 7A | Quantitative and Qualitative Disclosures About Market Risk | 56 | |

| Item 8 | Financial Statements and Supplementary Data | 58 | |

| Item 9 | Changes in and Disagreements with Accountants on Accounting and Financial Disclosures | 124 | |

| PART III | |||

| Item 10 | Directors and Executive Officers of the Registrant | 125 | |

| Item 11 | Executive Compensation | 125 | |

| Item 12 | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 125 | |

| Item 13 | Certain Relationships and Related Transactions | 125 | |

| PART IV | |||

| Item 14 | Controls and Procedures | 126 | |

| Item 15 | Exhibits, Financial Statement Schedules, and Reports on Form 8-K | 126 | |

| SIGNATURES | |||

| CERTIFICATIONS | |||

| Page 3 | ||

PART I

GENERAL

Central European Media Enterprises Ltd. is a Bermuda company that, together with its subsidiaries and affiliates, invests in, develops and operates national and regional commercial television stations and networks in Central and Eastern Europe. At present, we have operations in Romania, the Slovak Republic, Slovenia and Ukraine.

Our registered offices are located at Clarendon House, Church Street, Hamilton HM CX Bermuda, and our telephone number is 441-296-1431. We also maintain offices at 8th Floor, Aldwych House, 71-91 Aldwych, London, WC2B 4HN, England, telephone number 44-20-7430-5430/1.

Our registered offices are located at Clarendon House, Church Street, Hamilton HM CX Bermuda, and our telephone number is 441-296-1431. We also maintain offices at 8th Floor, Aldwych House, 71-91 Aldwych, London, WC2B 4HN, England, telephone number 44-20-7430-5430/1.

Unless otherwise noted, all statistical and financial information presented in this report has been converted into U.S. dollars using appropriate exchange rates. All references to '$' or 'dollars' are to U.S. dollars, all references to 'Kc' are to Czech korunas, all references to 'ROL' are to Romanian lei, all references to 'SIT' are to Slovenian tolar, all references to 'Sk' are to Slovak korunas, all references to 'Hrn' are to Ukrainian hryvna. The exchange rates as of December 31, 2002 used in this report are 33,500 ROL/$; 221.07 SIT/$; 40.04 Sk/$; 5.33 Hrn/$; 30.14 Kc/$, and 0.95 Euro/$.

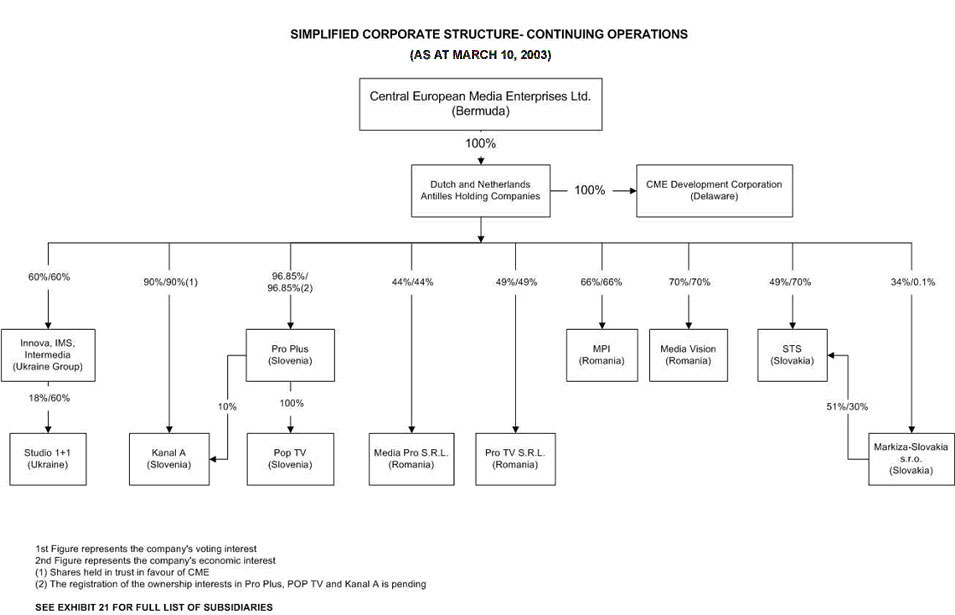

CORPORATE STRUCTURE

Central European Media Enterprises Limited was incorporated on June 15, 1994 under the laws of Bermuda. Our assets are held through a series of Dutch and Netherlands Antilles holding companies. In each market, we have interests both in license companies and in operating companies. License companies have been authorized by the relevant local regulatory authority to engage in television broadcasting in accordance with the terms of a particular license. Revenues are generated primarily through operating companies, which acquire programming for provision to the corresponding license companies and which sell advertising time that is acquired from or made available by the license companies. In Ukraine, the license company also engages directly in the acquisition of programming and the sale of some adverti sing time. Our economic interest in the operating companies corresponds with our voting interest other than in the Slovak Republic, where we are entitled by contract to a share of profits that is in excess of our voting interest. Below is an overview of our operating structure, the accounting treatment for each entity and a chart entitled “Simplified Corporate Structure - Continuing Operations”.

| Page 4 | ||

Key Subsidiaries and Affiliates | Share of Profits | Voting Interest | Subsidiary / Equity Accounted Affiliate | TV Network |

Continuing Operations | ||||

| Romania | ||||

Operating Companies: | ||||

| Media Pro International S.A. (MPI) | 66% | 66% | Subsidiary | |

| Media Vision S.R.L. (Media Vision) | 70% | 70% | Subsidiary | |

License Companies: | ||||

| Pro TV S.R.L. (Pro TV) | 49% | 49% | Equity Accounted Affiliate | PRO TV, ACASA, and PRO TV INTERNATIONAL |

| Media Pro S.R.L. (Media Pro) | 44% | 44% | Equity Accounted Affiliate | PRO TV and ACASA |

| Slovenia | ||||

Operating Companies: | ||||

| Produkcija Plus, d.o.o. (Pro Plus) | 96.85% | 96.85% | Subsidiary | |

License Companies: | ||||

| Pop TV d.o.o. (Pop TV) | 96.85% | 96.85% | Subsidiary | POP TV |

| Kanal A d.d. (Kanal A) | 99.7% | 99.7% | Subsidiary | KANAL A |

| Slovak Republic | ||||

Operating Companies: | ||||

| Slovenska Televizna Spolocnost, spol. s r.o. (STS) | 70% | 49% | Equity Accounted Affiliate | |

License Companies: | ||||

| Markiza-Slovakia s r.o. (Markiza) | 0.1% | 34% | Equity Accounted Affiliate | MARKIZA TV |

| Ukraine | ||||

Operating Companies: | ||||

| Innova Film GmbH (Innova) | 60% | 60% | Subsidiary | |

| International Media Services Ltd. (IMS) | 60% | 60% | Subsidiary | |

| Enterprise "Inter-Media" (Inter-Media) | 60% | 60% | Subsidiary | |

License Companies: | ||||

| Broadcasting Company "Studio 1+1" (Studio 1+1) | 18% | 18% | Equity Accounted Affiliate | STUDIO 1+1 |

| Czech Republic | ||||

Operating Companies: | ||||

| Ceska Nezavisla Televizni Spolecnost, spol. s r.o. (CNTS) | 93.2% | 93.2% | Subsidiary | |

License Companies: | ||||

| CET 21 spol. s r.o. (CET) | 3.125% | 3.125% | Investment | N/A |

| Page 5 | ||

Czech Republic

See Part I, Item 3, "Legal Proceedings" for a discussion on the ongoing dispute between our subsidiary in the Czech Republic CNTS and CET, our former partner and the broadcast license holder, in connection with the Nova TV network. The outcome of these legal proceedings will have a significant impact on our financial position.

| Page 6 | ||

| Page 7 | ||

License Renewal

Management believes that the licenses for the television license companies will be renewed prior to expiry. In Romania, the Slovak Republic and Slovenia local regulations do contain a qualified presumption for extensions of broadcast licenses. However, there can be no assurance that any of the licenses will be renewed upon expiration of their current terms. The failure of any such license to be renewed could adversely affect the results of our operations. However, to date, licenses have been renewed in the ordinary course of business. Access to the available frequencies is controlled by regulatory bodies in each country in which we operate.

In Ukraine, the license to broadcast is currently being challenged in the Arbit ration Court of Kiev. It is alleged that Studio 1+1 Ltd was granted two licenses by the Ukraine TV Council and that the required license fee was not paid. These and almost identical allegations have been the subject of various legal actions for over two years. We believe that these allegations are groundless. See Part I, Item 3, “Legal Proceedings”, below.

In Ukraine, the license to broadcast is currently being challenged in the Arbit ration Court of Kiev. It is alleged that Studio 1+1 Ltd was granted two licenses by the Ukraine TV Council and that the required license fee was not paid. These and almost identical allegations have been the subject of various legal actions for over two years. We believe that these allegations are groundless. See Part I, Item 3, “Legal Proceedings”, below.

Regulation

Our Form 10-K refers to broadcasting regulatory authorities or agencies as "The Media Council". These authorities or bodies are as follows:

Romania – National Audio-Visual Commission

Slovenia – Telecommunications, Radio Diffusion and Postal Agency

Slovak Republic – Council of the Slovak Republic for Broadcasting and Television Transmission

Ukraine – National Council for Television and Radio Broadcasting

Czech Republic – Council of the Czech Republic for Radio and Television Broadcasting

OPERATING ENVIRONMENT

Our television stations and networks reach an aggregate of approximately 69 million people in four countries. Our national private television stations and networks in the Slovak Republic and Slovenia had the leading nationwide audience shares for 2002 and our television network in Romania had the leading average audience share within its area of broadcast reach for 2002. In Ukraine, for 2002, our national private television station and network had the leading nationwide average audience share of television stations broadcasting in the Ukrainian language.

The market ratings of our stations in their respective markets are reflected below.

The market ratings of our stations in their respective markets are reflected below.

| Country | Station and Networks | Launch Date | Technical Reach (1) | 2002 Audience Share (2) | Market Rank (2) |

| Romania | PRO TV | December 1995 | 68% | 19.2% | 1 |

| ACASA | February 1998 | 52% | 6.2% | 4 | |

| Slovenia | POP TV | December 1995 | 87% | 29.3% | 1 |

| KANAL A | October 2000 (3) | 80% | 11.0% | 3 | |

| Slovak Republic | MARKIZA TV | August 1996 | 96% | 48.2% | 1 |

| Ukraine | STUDIO 1+1 | January 1997 | 95% | 22.2% | 2 |

(1) "Technical Reach" measures the percentage of people in the country who are able to receive the signals of the indicated stations and networks. Source: Internal estimates supplied by each station in each country. Each of our stations in the relevant country has estimated its own technical reach based on the location, power and frequency of each of its many transmitters and the local population density and geography around that transmitter. The technical reach calculation is designed to estimate the number of homes that can receive the station’s broadcast signal. This is separate from the independent third party measurement that determines viewing shares. Source: Internal estimate, supplied by each station in each country.

(2) Nationwide all day audience share and rank (except Romania and Ukraine, which is audience share and rank within coverage area). Source: (Romania: Peoplemeters CSOP Gallop/Taylor Nelson Sofres, Slovenia: Peoplemeters AGB Media Services, Slovak Republic: Visio / MVK, Ukraine: AGB Ukraine). There are seven, four, six and six significant stations ranked in Romania, Slovenia, the Slovak Republic and Ukraine, respectively.

| Page 8 | ||

(3) Kanal A was originally launched in 1991 and re-launched in October 2000 after we assumed control of the operations, economics and programming of Kanal A.

The following table sets forth the population, technical reach, number of TV households, per capita GDP and cable penetration for those countries of Central and Eastern Europe where we have broadcast operations.

Country | Population(in millions)(1) | Technical Reach (in millions) (2) | TV Households (in millions) (3) | Per Capita GDP 2001 (4) | Cable Penetration (5) |

| Romania | 22.4 | 15.3 | 7.6 | $1,695 | 51% |

| Slovenia | 2.0 | 1.7 | 0.7 | $9,780 | 52% |

| Slovak Republic | 5.4 | 5.2 | 1.9 | $3,804 | 28% |

| Ukraine | 49.1 | 46.6 | 18.6 | $766 | 27% |

| Total | 78.9 | 68.8 | 28.8 | ||

(1) Source: World Bank Group, 2001.

(2) Source: Internal estimates supplied by each station in each country. “Technical Reach” measures the percentage of people in the country who are able to receive the signals of our stations and networks in the indicated country. Each of our stations in the relevant country has estimated its own technical reach based on the location, power and frequency of each of its many transmitters and the local population density and geography around that transmitter. The technical reach calculation is designed to estimate the number of homes that can receive the station’s broadcast signal. This is separate from the independent third party measurement that determines viewing shares. Source: Internal estimate, supplied by each station in each country.

(3) Source: Kagan World Media, European Television 2001. A TV household is a residential dwelling with one or more television sets.

(4) Source: World Bank Group 2001.

(5) Source: Romania and Slovak Republic: Informa Media Group, European Television 6thEdition 2002. Slovenia and Ukraine: IP European Key Facts, Television 2001. Ukraine data refers to Urban only. Penetration refers to the percentage of TV Households who subscribe to cable television.

Television Advertising Expenditures

The following table sets out the recent levels of television advertising expenditures in those countries where we do business. (Note: All figures are internal estimates and are in $US millions).

| Country | 1998 | 1999 | 2000 | 2001 | 2002 | |||||||||||

| Romania | 87 |

|

| 69 |

|

| 69 |

|

| 63 |

|

| 66 |

| ||

| Slovenia |

|

| 51 |

|

| 49 |

|

| 47 |

|

| 47 |

|

| 48 |

|

| Slovak Republic |

|

| 56 |

|

| 43 |

|

| 42 |

|

| 42 |

|

| 47 |

|

| Ukraine |

|

| 65 |

|

| 32 |

|

| 35 |

|

| 50 |

|

| 60 | |

In Romania, the television advertising market grew by 5% showing a reversal of earlier trends. In Slovenia television advertising revenues remained constant expressed in local currency terms. In the Slovak Republic television advertising revenues increased by 3%, expressed in local currency terms. Further, the Slovenian tolar appreciated by 2% and the Slovak koruna appreciated by 7% and against the dollar. Therefore, television advertising expenditures in US Dollar terms increased by 2% in Slovenia and 11% in the Slovak Republic. In Ukraine, television advertising revenues continued their recent trend with a significant increase of 20% in US Dollar terms.

| Page 9 | ||

THE EUROPEAN UNION

If any Central or Eastern European country in which we operate becomes a member of the European Union (the "EU"), our broadcast operations in such country would be subject to relevant legislation of the EU, including programming content regulations. Slovenia, the Slovak Republic and the Czech Republic are expected to be admitted into the EU in the first wave of the enlargement process in 2004. It is currently anticipated that Romania will be admitted sometime after 2007.

The EU's Television Without Frontiers directive (the "EU Directive") sets forth the legal framework for television broadcasting in the EU. It requires broadcasters, where "practicable and by appropriate means," to reserve a majority proportion of their broadcast time for "European works." Such works are defined as originating from an EU member state or a signatory to the Council of Europe's Convention on Transfrontier Television, as well as written and produced mainly by residents of the EU or Council of Europe member states. In addition, the EU Directive provides for a 10% quota of either broadcast time or programming budget for programs made by European producers who are independent of broadcasters. News, sports, games, advertising, teletext services and teleshopping are excluded from the calculation of these quotas. Further, the EU Directive provides for regulations on advertising, including limits on the amount of time that may be devoted to advertising spots, including direct sales advertising. The necessary legislation in Romania, Slovenia and the Slovak Republic is now in line with the EU Directive and it has had no material adverse effect on our operations.

The EU's Television Without Frontiers directive (the "EU Directive") sets forth the legal framework for television broadcasting in the EU. It requires broadcasters, where "practicable and by appropriate means," to reserve a majority proportion of their broadcast time for "European works." Such works are defined as originating from an EU member state or a signatory to the Council of Europe's Convention on Transfrontier Television, as well as written and produced mainly by residents of the EU or Council of Europe member states. In addition, the EU Directive provides for a 10% quota of either broadcast time or programming budget for programs made by European producers who are independent of broadcasters. News, sports, games, advertising, teletext services and teleshopping are excluded from the calculation of these quotas. Further, the EU Directive provides for regulations on advertising, including limits on the amount of time that may be devoted to advertising spots, including direct sales advertising. The necessary legislation in Romania, Slovenia and the Slovak Republic is now in line with the EU Directive and it has had no material adverse effect on our operations.

COUNCIL OF EUROPE

Our broadcast operations are all located in countries which are members of the Council of Europe, a supranational body through which international conventions are negotiated. In 1990, the Council of Europe adopted a Convention on Transfrontier Television, which provides for European programming content quotas similar to those in the EU Directive. This Convention has been ratified by some of the countries in which we operate, but all countries in which we operate have already implemented its principles into their national media legislation.

RISK FACTORS

This annual report contains forward-looking statements that involve risks and uncertainties. See "Forward-looking Statements" in Part II, Item 7. Our actual results in the future could differ materially from those anticipated in these forward-looking statements as a result of certain factors, including the risks described below and elsewhere in this annual report.

Risks Relating to Our US$100 million 93/8% and Euro 71.6 million 81/8% (approximately US$75 million) Senior Notes Due in 2004

We may not be able to repay our US$100 million 9 3/8% and Euro 71.6 million 8 1/8% (approximately US$75 million) Senior Notes Due in 2004.

In 1997 we issued Senior Notes, denominated in part in U.S. dollars and in part in Euros. These Senior Notes, aggregating approximately $175 million in principal amount at December 31, 2002, are due on August 15, 2004. We do not expect cash on hand at December 31, 2002 plus revenues which may be generated from operations between now and August 15, 2004 to be sufficient to fund the payment of the Senior Notes at maturity. Our ability to refinance or repay the Senior Notes will depend upon the outcome of pending litigation concerning our former Czech Republic operations and our ability to collect from the Czech Republic any final award determination (see Part I, Item 3, "Legal Proceedings") and/or our ability to attra ct equity investors. If we are unsuccessful in these respects and are not able to repay or refinance the Senior Notes, we are unlikely to be able to continue operations.

| Page 10 | ||

Alternative sources of financing may include public or private debt or equity financings, sale of assets or other financing arrangements. Any additional equity or equity-linked financing may dilute our common shares. In addition, such additional financing may or may not be available or available on acceptable terms. Any future credit agreement or other debt agreement may limit our ability to incur additional debt. These limits could adversely affect our ability to finance our business plan.

Our leverage, debt service obligations and debt instrument restrictions could adversely affect our business

We are highly leveraged. As of December 31, 2002, we had total consolidated debt of $205 million and shareholders' deficit of $96 million. Our consolidated interest expense for the year ended December 31, 2002 was $15.3 million. Our operating income for the year ended December 31, 2002 was $13.4 million.

Our level of debt could have important consequences for our business, including the following:

- we may have difficulty borrowing money in the future for working capital, capital expenditures, acquisitions, general corporate purposes or other purposes; | ||

- the payment of principal and interest on debt will reduce the amount of cash available to finance our operations and other business activities; and | ||

- our debt level makes us more vulnerable to economic downturns and adverse developments in our business. |

The indenture for the Euro 71.6 million (approximately US$75 million) 81/8% and US$100 million 93/8% Senior Notes restricts our ability to, among other things, incur additional debt and make investments. In addition, our subsidiaries' ability to incur debt beyond a certain amount is limited by this indenture. These restrictions may impede our ability to finance programming expenditures, acquisitions and other business opportunities.

Our $30 million financing agreement with GoldenTree Asset Management contains negative covenants, including those restricting our ability to incur additional debt, make new investments, pledge assets or sell assets other than in the normal course of business. Security has been provided in the form of guarantees and pledges over all of the stock of our Dutch B.V. holding companies. Guarantees have been provided by Central European Media Enterprises Ltd. and Central European Media Enterprises N.V. Pledges in the amount of $15,000,000, the amount outstanding to Goldentree Asset Man agement, which are exerciseable in the event of default, secure the shares of CME Media Enterprises B.V., CME Ukraine B.V., CME Slovenia B.V. and CME Romania B.V. Should CME Media Enterprises B.V. default on its loan, shareholders would lose control of all subsidiaries and affiliates until such time as Goldentree Asset Management had been repaid. Given the illiquid nature of our shareholdings in our subsidiaries and affiliates this could result in a substantial loss in value for shareholders if such an event occurred.

Risks Relating to the Our Operations

We have a history of losses and may not be profitable in the future

We have incurred net losses since inception and we may incur additional net losses for the next several years. As of December 31, 2002, we had an accumulated deficit of $452 million.

Our future ability to generate operating profits and net profits will be dependent upon a number of factors that are difficult to predict, such as our ability to:

| - retain and renew licenses; | |

| - attract and maintain audiences; | |

| - generate advertising revenues; | |

| - develop additional revenue streams; and | |

| - control costs in all areas, but particularly programming costs. |

| Page 11 | ||

There are also a number of external factors over which we have no control, such as the level of economic growth and consumer and advertising spending in our markets.

We and our subsidiaries have a number of tax contingencies that may be material

We have accrued tax liabilities and interest and penalties on overdue tax liabilities, in the aggregate, of $23.3 million in our December 31, 2002 balance sheet. Included in accrued tax liabilities is a provision for $3 million related to our agreement with the Dutch tax authorities. The Dutch tax authorities have agreed that payment of this amount is to be made from any amount collected from the Czech Republic pursuant to the Netherlands-Czech Bilateral Investment Treaty arbitration proceedings (See Part I, Item 3 "Legal Proceedings"). We have agreed with the Dutch tax authorities that the question of taxability of any award against the Czech Republic shall be determined by the Dutch tax courts based upon an agreed statement of fact. Until that court decision, we have agreed with the Dutch tax autho rities to deposit 35% of the net proceeds of any amount collected from the Czech Republic pursuant to the Netherlands-Czech Bilateral Investment Treaty arbitration proceedings in a nominated bank account. Any such deposit will be treated as restricted cash.

The major portion of estimated interest and penalties on overdue tax liabilities relate to the outstanding tax liability at our Romanian subsidiaries. A recent agreement with the Romanian tax authorities has reduced and re-scheduled a portion of these interest and penalty charges in return for specific deposits and an agreed repayment schedule. This rescheduling is permitted under Romanian law subject to written application demonstrating compliance with a series of objective criteria. Penalties of up to $5 million may be imposed if the repayment schedule and the conditions of the agreement are not met. Should the Romanian tax authorities demand immediate payment of all potential tax liabilities, the Romanian operations would experience difficulties in continuing to operate and may have to cease operations entirely unless they can arrange financing to secure the required funds or the shareholders (including us) determine to inject equity into the business.

Our holding company structure limits our access to cash flow

We conduct all of our operations through subsidiaries and affiliated companies. Accordingly, our primary internal source of cash and our ability to service debt are dependent upon the earnings of our subsidiaries and affiliated companies and the distribution of those earnings to us, or upon loans or other payments of funds by those subsidiaries to us. We may not be able to compel certain of our subsidiaries and affiliated companies to make distributions to service the Senior Notes and other of our obligations. Our ability to obtain dividends or other distributions is subject to, among other things, restrictions on dividends under applicable local laws and foreign currency exchange regulations of the jurisdictions in which our subsidiaries operate. The subsidiaries’ or affiliated companies abilit y to make distributions to us is also subject to their having sufficient funds from their operations legally available for the payment thereof which are not needed to fund their operations, obligations or other business plans and, in some cases, the approval of the other partners, stockholders or creditors of these entities. The laws under which our operating subsidiaries and affiliated companies are organized provide generally that dividends may be declared by the partners or shareholders out of yearly profits subject to the maintenance of registered capital and required reserves and after the recovery of accumulated losses. If our subsidiaries or affiliated companies are unable or unwilling to make distributions to us and we are unable to obtain additional debt or equity financing, we may be unable to continue to service the Senior Notes.

We do not have sole management control of our unconsolidated affiliates in the Slovak Republic and Ukraine

We own certain subsidiaries and affiliated companies jointly with various strategic partners. We have management control over the subsidiaries in which we have a majority interest. However, we are not able to affirmatively control the operations, strategies and financial decisions of either Markiza, the license holding company or STS, the operating company for the MARKIZA TV network in the Slovak Republic in which we hold 34% and 49% voting interests, respectively or the license holding company for the Studio 1+1 Group in Ukraine, in which we hold only an 18% voting interest. Therefore, without the consent of the relevant partners, we may be unable to cause these affiliated companies to distribute funds, to implement strategi es or to make programming decisions that we might favor.

| Page 12 | ||

We are subject to risks relating to fluctuations in exchange rates

Our reporting currency is the US dollar but a significant portion of our consolidated revenues and costs are in other currencies, including programming rights expenses and interest on debt. Changes, mainly in the value of the Euro as compared to the US dollar, may have an adverse effect on our reported results of operations and financial condition.

We are also exposed to risks related to non-US dollar borrowings, particularly our Euro 71.6 million ($75 million) Senior Note debt. As the net position of our unhedged foreign currency transactions may fluctuate, our earnings may be negatively affected.

For a detailed analysis of our exposure to exchange rate risk, see Part II, Item 7A "Quantitative and Qualitative Disclosure about Market Risk" and to "Foreign Currency" in Part II, Item 7, "Management's Discussion and Analysis of Financial Condition and Results of Operations."

Risk Factors Relating to Our Operating Environment

Our license in Ukraine has been challenged

In 2001 AITI, a television station in Ukraine, commenced a court action in Ukraine against the Ukraine Media Council challenging certain aspects of the granting to Studio 1+1 of its television broadcast license in Ukraine. Studio 1+1 is involved in this litigation as a third party acting together with the Ukraine Media Council. The claim is almost identical to one which was previously brought by AITI and was dismissed on April 5, 2001 by the Supreme Arbitration Court of Ukraine.

AITI's allegations are that Studio 1+1 has, in effect, been granted two licenses by the Ukraine Media Council, entitling it to in excess of 32 hours of broadcast time a day on Ukraine's nationwide Channel N2 (UT-2). Further, AITI alleged that Studio 1+1 never paid the required license fee. On February 1, 2002, the Economic Court of the City of Kiev ruled in AITI's favor. The Ukraine Media Council, Studio 1+1, and the Public Prosecutor's Office of Kiev, the latter two acting as interested third parties, appealed the Economic Court's decision to the Kiev Economic Court of Appeal.

The Kiev Economic Court of Appeal upheld the Economic Court of Kiev's decision of February 1, 2002. This decision was appealed to the Court of Cassation, the same court that ruled in favor of Studio 1+1 on April 5, 2001. On November 1, 2002 the Court of Cassation ruled that the decisions taken by the two lower courts had not fully taken into consideration all the facts surrounding the matter before reaching judgment and ordered that the case be returned to the Economic Court of Kiev. The first hearing took place on February 5, 2003.

If the decision in the Ukraine court system is ultimately unfavorable, it could result in a loss of the broadcast license of Studio 1+1. Net revenues and expenses of the consolidated entities of our Ukrainian operations were $24.9 million and $19.0 million respectively in 2002.

We have regulatory challenges in our business in Romania

In September 2002, the Romanian Media Council notified all television stations in Romania that they would like to see their operations restructured by January 2003 so that the license holding companies become the main operators of the broadcasting licenses they hold. The Romanian Media Council has given some guidance on how it interprets the new audio-visual law in relation to this restructuring.

| Page 13 | ||

At a formal meeting on September 19, 2002 the Council expressed their view that exclusive operating agreements, such as exists between our subsidiary MPI and the two Romanian license holding companies, are not permissible under the new law. We are in discussions with our partners in Romania to transfer the operation of the broadcasting licenses from MPI to the main license holding company Pro TV SRL and to increase our stake in Pro TV SRL from the existing 49% to a majority 66% stake as permitted under the new Media Law that came into force on July 22, 2002. In connection with these discussions, it is expected that the secondary license holding company, Media Pro SRL, would apply to the Romanian Media Council to transfer the licenses it owns to Pro TV SRL, as this is also permitted un der the new Media Law. We are in the process of commencing the legal and regulatory steps required in order to complete this restructuring procedure.

Upon completion of this restructuring we would have majority control over all the key licenses we operate in Romania. Currently we only have minority stakes in the two Romanian license holding companies, albeit with blocking rights. We are dependent on our partners’ agreement to the restructuring in order to comply with the new audio-visual law.

In our Consolidated Balance Sheet at December 31, 2002 there are accrued tax liabilities and estimated interest and penalties on outstanding tax liabilities of $23,300,000, in the aggregate. The major portion of estimated interest and penalties on overdue tax liabilities relate to the outstanding tax liability at our Romanian subsidiaries. A recent agreement with the Romanian tax authorities has reduced and re-scheduled a portion of these interest and penalty charges in return for specific deposits and an agreed repayment schedule. This rescheduling is permitted under Romanian law subject to written application demonstrating compliance with a series of objective criteria. Penalties of up to $5 million may be imposed if the repayment schedule and the conditions of the agreement are not met. Should the Romanian tax authorities demand immediate payment of all potential tax liabilities, the Romanian operations would experience difficulties in continuing to operate and may have to cease operations entirely unless they can arrange financing to secure the required funds or the shareholders (including us) determine to inject equity into the business.

As at December 31, 2002, 33% of the Romanian subsidiaries’ accounts receivable balance was more than 360 days old and 9% was in the 180-360 day category. Subsequent to year end $7,672,000 was r eceived with $860,000 being against debt older than 360 days. Accordingly, $831,000 of our total bad debt provision was released in the fourth quarter resulting in a total decrease to our total bad debt provision of $738,000 in the twelve months ended December 31, 2002. On our Consolidated Balance Sheet at December 31, 2002, the total provision for bad debt is $7,481,000, of which our provision for Romanian bad debts is $5,733,000. The total gross accounts receivable in respect to our Romanian operations is $15,544,000 (included in “Accounts Receivable” in the Consolidated Balance Sheet, see Part II, Item 8) at December 31, 2002.

In our Consolidated Balance Sheet at December 31, 2002 there are accrued tax liabilities and estimated interest and penalties on outstanding tax liabilities of $23,300,000, in the aggregate. The major portion of estimated interest and penalties on overdue tax liabilities relate to the outstanding tax liability at our Romanian subsidiaries. A recent agreement with the Romanian tax authorities has reduced and re-scheduled a portion of these interest and penalty charges in return for specific deposits and an agreed repayment schedule. This rescheduling is permitted under Romanian law subject to written application demonstrating compliance with a series of objective criteria. Penalties of up to $5 million may be imposed if the repayment schedule and the conditions of the agreement are not met. Should the Romanian tax authorities demand immediate payment of all potential tax liabilities, the Romanian operations would experience difficulties in continuing to operate and may have to cease operations entirely unless they can arrange financing to secure the required funds or the shareholders (including us) determine to inject equity into the business.

As at December 31, 2002, 33% of the Romanian subsidiaries’ accounts receivable balance was more than 360 days old and 9% was in the 180-360 day category. Subsequent to year end $7,672,000 was r eceived with $860,000 being against debt older than 360 days. Accordingly, $831,000 of our total bad debt provision was released in the fourth quarter resulting in a total decrease to our total bad debt provision of $738,000 in the twelve months ended December 31, 2002. On our Consolidated Balance Sheet at December 31, 2002, the total provision for bad debt is $7,481,000, of which our provision for Romanian bad debts is $5,733,000. The total gross accounts receivable in respect to our Romanian operations is $15,544,000 (included in “Accounts Receivable” in the Consolidated Balance Sheet, see Part II, Item 8) at December 31, 2002.

Risks Relating to Our Industry

Our licenses may not be renewed

The licenses to operate our broadcast operations are effective for the following periods:

| Slovenia | The licenses of our operations in Slovenia expire in 2012 | |

| Slovak Republic | The license of our partner in the Slovak Republic expires in 2007 | |

| Ukraine | The license to provide programming and sell advertising to UT-2 in Ukraine expires in 2006 | |

| Romania | Licenses which cover 19% of the Romanian population, including the license for Bucharest, expire from October 2003. To date, licenses have been renewed as they expired. The remaining licenses expire on dates ranging from 2004 to 2008 |

| Page 14 | ||

In Romania, the Slovak Republic and Slovenia, local regulations do contain a qualified presumption for extensions of broadcast licenses, however, these licenses may nevertheless not be renewed upon the expiration of their current terms. The failure of any such licenses to be renewed may have a material adverse effect on our operations.

Our operating results are dependent on the sale of commercial advertising time in developing markets.

Our business relies on advertising revenues, which depends partly upon prevailing general economic conditions. Our advertising revenues also depend on our stations’ broadcast reach, television viewing levels, the relative popularity of our programming and the pricing of advertising time. Furthermore, increases in advertising spending have generally corresponded to economic recoveries, while decreases have generally corresponded to general economic downturns and recessions. Advertising spending or advertising spending growth in our markets has declined in our markets in the past and may decline in the future. If our television audience shares decline for any reason, we may not be able to maintain our current levels of advertising income or the rates we can charge advertisers. We must also compete for advertising revenues with other forms of advertising media, such as radio, newspapers, magazines, outdoor advertising, transit advertising, telephone directory advertising, on-line advertising and direct mail. Any decline in advertising revenues may adversely affect our results.

Our business relies on advertising revenues, which depends partly upon prevailing general economic conditions. Our advertising revenues also depend on our stations’ broadcast reach, television viewing levels, the relative popularity of our programming and the pricing of advertising time. Furthermore, increases in advertising spending have generally corresponded to economic recoveries, while decreases have generally corresponded to general economic downturns and recessions. Advertising spending or advertising spending growth in our markets has declined in our markets in the past and may decline in the future. If our television audience shares decline for any reason, we may not be able to maintain our current levels of advertising income or the rates we can charge advertisers. We must also compete for advertising revenues with other forms of advertising media, such as radio, newspapers, magazines, outdoor advertising, transit advertising, telephone directory advertising, on-line advertising and direct mail. Any decline in advertising revenues may adversely affect our results.

Risks Relating to the Markets in which we Operate

Our operations are in developing markets

Our revenue generating operations are located in Central and Eastern Europe, namely Romania, the Slovak Republic, Slovenia and Ukraine, and have a country risk as follows:

| Country | Rating | Detail of Rating |

| Slovenia | A2 | Default probability is still weak even in the case when one country's political and economic environment or the payment record of companies are not as good as A1-rated countries. |

| Slovak Republic | A4 | An already patchy payment record could be further worsened by a deteriorating political and economic environment. Nevertheless, the probability of a default is still acceptable. |

| Romania | B | An unsteady political and economic environment is likely to affect further an already poor payment record. |

| Ukraine | D | The high risk profile of a country's economic and political environment will further worsen further a generally very bad payment record. |

| Source : Coface USA. Country ratings issued by the Coface Group measure the average default risk on corporate payments in a given country and indicate to what extent a company's financial commitments are affected by the local business, financial and political outlook. Coface continuously monitors 140 countries using a spectrum of indicators incorporating political factors; risk of currency shortage and devaluation; ability to meet financial commitments abroad; risk of a systemic crisis in the banking sector; cyclical risk; and payment behavior for short term transactions. |

These markets have economic and legal systems, standards of corporate governance and business practices which continue to develop. Government policies could be altered significantly, especially in the event of a change in leadership, social or political disruption or unforeseen circumstances affecting economic, political or social life. Combined with legal and regulatory systems that could be subject to political pressures, these factors, given the fact that we operate with local partners in all these jurisdictions, create a risk of unfair treatment before the local courts in disputes with our local partners and, ultimately, loss of our business operations, as occurred in the Czech Republic.

Enforcement of civil liabilities and judgments may be difficult.

| Page 15 | ||

Central European Media Enterprises Ltd. is a Bermuda company, and substantially all of our assets and all of our operations are located, and all of our revenues are derived, outside the United States of America. However, it may not be possible for investors to enforce outside the United States of America judgments against us obtained in the United States of America in any civil actions, including actions predicated upon the civil liability provisions of the United States of America federal securities laws. In addition, certain of our directors and officers are non-residents of the United States of America, and all or a substantial portion of the assets of such persons are or may be located outside the United States of America . As a result, it may not be possible for investors to effect service of process within the United States of America upon such persons, or to enforce against them judgments obtained in the United States of America courts, including judgments predicated upon the civil liability provisions of the United States of America federal securities laws. There is uncertainty as to whether the courts of the countries in which we operate would enforce (i) judgments of United States of America courts obtained against us or such persons predicated upon the civil liability provisions of the United States of America federal and state securities laws or (ii) in original actions brought in such countries, as applicable, liabilities against us or such persons predicated upon the United States of America federal and state securities laws. A final and conclusive judgment in Federal or State courts of the United States of America under which a sum of money is payable (not being a sum payable in respect of taxes or other charges of a like nature or in respect of a fine or other penalty or multiple damages) may be subject to enforcement proceedings as a debt in the Supreme Court of Bermuda under the common law doctrine of obligation. Among other things, it is necessary to demonstrate that the court which gave the judgment was competent to hear the action in accordance with private law principles as applied in Bermuda and that the judgment is not contrary to public policy in error in Bermuda, has not been obtained by fraud or in proceedings contrary to natural justice and was not based on error in Bermuda law.

Risks Relating to Our Common Shares

The price of our common shares is likely to remain volatile

The market price of our common shares is likely to be volatile. Events that could cause future volatility may include, among other things:

| - Announcement of the monetary value of the Czech award or collection or failure to collect the Czech award; and | |

| - Conditions or trends in Europe and our markets. |

Many of these events are beyond our control. These factors may materially adversely affect the market price of our common shares, regardless of future operating performance.

OPERATIONS BY COUNTRY

ROMANIA

General

Romania is a parliamentary democracy of approximately 22.4 million people. Per capita GDP was an estimated $1,695 in 2001 with a GDP growth rate of 4% in 2002. Approximately 88% of Romanian households have one or more television sets, and cable penetration is approximately 51%. According to our estimates, Romanian television advertising totalled approximately $66 million in 2002.

Operating Companies : MPI and Media Vision

Our interest in our Romanian operation is governed by a Co-operation Agreement (the "Romanian Agreement") between Adrian Sarbu, Ion Tiriac and ourselves, forming Media Pro International S.A. ("MPI"), through which the PRO TV, ACASA and PRO TV INTERNATIONAL networks are operated. MPI provides programming to and sells advertising for the stations which comprise the PRO TV, ACASA and PRO TV INTERNATIONAL networks.

| Page 16 | ||

Pursuant to the Romanian Agreement, we have a 66% voting interest in MPI. Shares of profits of MPI are equal to the partners' equity interests. We have the right to appoint three of the five members of the Council of Administration which directs the affairs of MPI. Although we have majority voting power in MPI, with respect to certain financial and corporate matters, the affirmative vote of either Mr. Sarbu or Mr. Tiriac is required.

With specific reference to MPI, the financial and corporate matters which require approval of the minority shareholders are in the nature of protective rights which are not an impediment to consolidation for accounting purposes.

In addition, in Romania, we have a 70% voting interes t and share of profits in Media Vision SRL ("Media Vision"), a production and subtitling company. On November 22, 2001 we sold our 70% voting and profits interests in Video Vision International SRL ("Video Vision"), a Romanian post-production company and the gain recognized on this sale was $1.8 million.

With specific reference to MPI, the financial and corporate matters which require approval of the minority shareholders are in the nature of protective rights which are not an impediment to consolidation for accounting purposes.

In addition, in Romania, we have a 70% voting interes t and share of profits in Media Vision SRL ("Media Vision"), a production and subtitling company. On November 22, 2001 we sold our 70% voting and profits interests in Video Vision International SRL ("Video Vision"), a Romanian post-production company and the gain recognized on this sale was $1.8 million.

License Companies : Pro TV Srl and Media Pro Srl

We own a 49% voting and profits interest in Pro TV, Srl which holds 19 of the 22 licenses for the stations which comprise the PRO TV, ACASA and PRO TV INTERNATIONAL network. Messrs. Sarbu and Tiriac own substantially all of the remainder of the voting and profits interests of Pro TV, Srl. The remaining three licenses for the PRO TV network together with the licenses for the PRO FM and PRO AM radio networks are held by Media Pro Srl, in which we hold 44% of the voting interest and share of profits. The remainder is owned by Messrs. Sarbu and Tiriac.

Under an agreement between Mr. Tiriac and Mr. Sarbu, Mr. Tiriac has agreed to transfer his shareholding in the license companies and MPI to Mr. Sarbu following completion of a multi-year series of payments by Mr. Sarbu. Upon completion of these pay ments, Mr. Sarbu would control the remainder of the shares in the license companies and MPI not owned by us.

Under an agreement between Mr. Tiriac and Mr. Sarbu, Mr. Tiriac has agreed to transfer his shareholding in the license companies and MPI to Mr. Sarbu following completion of a multi-year series of payments by Mr. Sarbu. Upon completion of these pay ments, Mr. Sarbu would control the remainder of the shares in the license companies and MPI not owned by us.

Operations : PRO TV, ACASA and PRO TV INTERNATIONAL networks

PRO TV is a national television broadcast network in Romania which was launched in December 1995. PRO TV reaches approximately 68% of the Romanian population of 22.4 million, including 100% of the urban population. PRO TV broadcasts from studios located in Bucharest via digitally encoded satellite signals which deliver programming to terrestrial broadcast facilities and to approximately 674 cable systems throughout Romania. Independent research from CSOP Gallup/Taylor Nelson Sofres (peoplemeter) in Romania shows that the PRO TV network is currently the top-rated television station in its coverage area, with a nationwide all day audience share of 19.2% during the year ended December 2002.

In February 1998, MPI launched the ACASA network, a station reaching approximately 52% of the Romanian population, including approximately 100% of the urban population via satellite and cable distribution. During the year ended December 2002, ACASA had a nationwide all day audience share of 6.2%, making it the third ranked station in Romania.

The PRO TV INTERNATIONAL network rebroadcasts PRO TV and ACASA programs throughout Europe and in Israel, using the existing PRO TV and ACASA satellite infrastructure. In 2002 MPI entered into a four year agreement under which MPI will provide the Romanian language program content of PRO TV INTERNATIONAL for broadcast in the US at no direct cost to MPI.

Media Vision is a television production company in Romania and produces a significant portion of PRO TV's entertainment programming, performs dubbing and produces advertising spots for third party clients such as Coca Cola, Procter & Gamble and Unilever.

MPI also operates PRO FM, a radio network which is broadcast through owned and affiliate stations to approximately 7.0 million people in Romania. In 2002, PRO FM had an average audience share of 20.9% for the whole day and 21.6% for prime time in the Bucharest area.

Programming

| Page 17 | ||

The PRO TV network's programming strategy is to appeal to a mass market audience through a wide range of programming, including movies and series, news, sitcoms, telenovellas, soap operas and game shows. PRO TV broadcasts 24 hours of programming daily by means of cable and satellite. In excess of 40% of PRO TV's programming is comprised of locally produced programming, including top rated shows Vacanta Mare (Big Holiday), Leona si Costel and the Teo Show.

MPI has secured exclusive broadcast rights in Romania to broadcast on the PRO TV network a large number of quality American and Western European programs and films produced by such companies as Warner Bros. and Twentieth Century Fox. The PRO TV network also receives foreign news reports and film footage from Reuters, APTN and ENEX to integrate into its news programs. All foreign language programs and films are subtitled in Romanian.

The ACASA network broadcasts 24 hours of programming daily by means of cable and satellite. Its programming strategy is to target a female audience with programming including telenovellas, films and soap operas as well as news, daily local production for women and family, talk shows and entertainment. ACASA's viewer demographics are complementary to PRO TV's, providing an attractive advertising medium for small to medium sized companies that would not otherwise advertise on television. Approximately 29% of ACASA's total programming is locally produced, including top rated shows Porestiri Adevarde (Newstories) and De 3X Femie (3 Times a Lady).

Advertising

MPI derives revenues principally from the sale of commercial advertising time on the PRO TV and ACASA networks, sold both through independent agencies and media buying groups. The PRO TV network currently serves approximately 100 advertisers, including multinational companies such as Wrigley, Henkel, Mobifon and Procter & Gamble. Procter & Gamble was the largest advertiser on PRO TV and ACASA, accounting for 7% of the combined stations' revenue in 2002.

The PRO TV network is permitted to broadcast advertising for up to 15% of its broadcast time with an additional 5% of broadcast time that may be used for direct sales advertising. There is an overall hourly maximum of 12 minutes that may be allocated to advertising and teleshopping in any one hour for private broadcasters. For public broadcasters this is reduced to 8 minutes per hour. There are also restrictions on the frequency of advertising breaks (for example, news and children's programs shorter than 30 minutes cannot be interrupted). These restrictions are the same for public and private broadcasters.

Competition

Prior to the launch of the PRO TV network, TVR 1, a public station, was the dominant broadcaster in Romania. In December 2002, PRO TV achieved an average audience share of 27% in its coverage area, while TVR 1's December 2002 average audience share in PRO TV's coverage area was approximately 11%. TVR 1 reaches 99% of the Romanian population. Other competitors include the second public national station, TVR 2, with a 74% broadcast reach, and privately owned Antena 1, Tele 7 ABC and Prima TV, which reach approximately 68%, 58% and 62% of the population respectively.

Additional competitors include cable and satellite stations. Cable and satellite currently penetrate approximately 51% of the Romanian market. PRO TV competes for advertising revenues with other media such as newspapers, radio, magazines, outdoor advertising, telephone directory advertising and direct mail.

Regulation

Licenses for the television stations which show programming provided by MPI and which broadcast advertising sold by MPI are regulated by the Romanian Media Council. Pro TV 's television licenses have been granted for nine-year periods. Licenses which cover 19% of the Romanian population, including the license for Bucharest, expire from October 2003. To date, licenses have been renewed as they expired. The remaining licenses expire on dates ranging from 2004 to 2008. Under regulations established by the Romanian Media Council and the various licenses of stations which broadcast the PRO TV network, programming and advertising provided by MPI is required to comply with certain restrictions. These restrictions include a requirement that at least 40% of programming be "own" produced.

| Page 18 | ||

Regulations relating to advertising content include (i) a ban on tobacco and restrictions on alcohol advertising, (ii) advertising targeted at children or during children's programming must account for the overall sensitivity of that age group and (iii) members of the news department of PRO TV are prohibited from appearing in advertisements.

A new audio-visual law came into force in Romania on July 22, 2002, harmonizing Romanian legislation with that of the European Union. The law now permits a change in ownership of license holding companies or the transfer of the licenses to another company at the discretion of the Romanian Media Council. This was previously not permitted under the old audio-visual law. There is no restriction on foreign ownership under Romanian law.

In September 2002, the Romanian Media Council instructed all television stations in Romania to restructure their operations by January 2003 so that the license holding companies become the main operators of the broadcasting licenses they hold. The Romanian Med ia Council has given some guidance on how it interprets the new audio-visual law in relation to this restructuring. At a formal meeting on September 19, 2002 the Council expressed their view that exclusive operating agreements, such as exists between our subsidiary MPI and the two Romanian license holding companies, are not permissible under the new law. We are in discussions with our partners in Romania to transfer the operation of the broadcasting licenses from MPI to the main license holding company Pro TV SRL and to increase our stake in Pro TV Srl from the existing 49% to a majority 66% stake as permitted under the new Media Law that came into force on July 22, 2002. In connection with these discussions, it is expected that the secondary license holding company, Media Pro SRL, would apply to the Romanian Media Council to transfer the licenses it owns to Pro TV SRL, as this is also permitted under the new Media Law. We are in the process of commencing the legal and regulatory steps required in order to c omplete this restructuring procedure.

Upon completion of this restructuring we would have majority control over all the key licenses we operate in Romania. Currently we only have minority stakes in the two Romanian license holding companies, albeit with blocking rights. We are dependent on our partners’ agreement to the restructuring in order to comply with the new audio-visual law.

In September 2002, the Romanian Media Council instructed all television stations in Romania to restructure their operations by January 2003 so that the license holding companies become the main operators of the broadcasting licenses they hold. The Romanian Med ia Council has given some guidance on how it interprets the new audio-visual law in relation to this restructuring. At a formal meeting on September 19, 2002 the Council expressed their view that exclusive operating agreements, such as exists between our subsidiary MPI and the two Romanian license holding companies, are not permissible under the new law. We are in discussions with our partners in Romania to transfer the operation of the broadcasting licenses from MPI to the main license holding company Pro TV SRL and to increase our stake in Pro TV Srl from the existing 49% to a majority 66% stake as permitted under the new Media Law that came into force on July 22, 2002. In connection with these discussions, it is expected that the secondary license holding company, Media Pro SRL, would apply to the Romanian Media Council to transfer the licenses it owns to Pro TV SRL, as this is also permitted under the new Media Law. We are in the process of commencing the legal and regulatory steps required in order to c omplete this restructuring procedure.

Upon completion of this restructuring we would have majority control over all the key licenses we operate in Romania. Currently we only have minority stakes in the two Romanian license holding companies, albeit with blocking rights. We are dependent on our partners’ agreement to the restructuring in order to comply with the new audio-visual law.

License Renewal

The PRO TV network licenses consist of many local licenses, with varying expiry dates. The licensing procedure in Romania is governed by the 1992 Audiovisual Law ("Audiovisual Law"). According to the Audiovisual Law, the Romanian Media Council is in charge of issuing and renewing licenses. Renewal, as a separate procedure is not described in the Audiovisual Law and therefore expired licenses are subject to bidding procedures similar to those applicable to new licenses. A decision of the Romanian Media Council, however, provides that past broadcasting experience, is a deciding factor in the renewal procedure. All renewal applications have been granted so far by the Audiovisual Council. However there is no assurance that ProTV 's licenses will be renewed. A local Pro TV license, covering certain parts of Bucharest, will expire in 2003.

SLOVENIA

General

Slovenia, a parliamentary democracy of 2.0 million people, had an estimated per capita GDP of $9,780 in 2001 with a GDP growth rate of 3.2% in 2002, the highest per capita GDP among the former Eastern bloc countries. Approximately 96% of Slovenian households have one or more televisions. According to our estimates, Slovenian television advertising totalled $48 million in 2002.

Operating Company : Pro Plus

| Page 19 | ||

Pro Plus provides programming to and sells advertising for the broadcast license holders Pop TV and Kanal A, as well as additional affiliates. Following the receipt by Pro Plus of an approval from the Ministry of Culture of Slovenia to own more than 20% of two broadcasters, we have restructured our Slovenian operations. As of January 30, 2003 we own 96.85% of the voting and profits interests in Pro Plus with corresponding economic and voting rights. This ownership interest is subject to registration in the Commercial Registry of Slovenia. Prior to January 30, 2003 we had 78% of the voting interests in Pro Plus and an effective share of profits of 85.5%.

In connection with the restructuring of our Slovenian operations, we have entered into a put/call arrangement with the general director of Pro Plus, Marijan Jurenec, who owns the remaining 3.15% of Pro Plus. Under the terms of the agreement, Mr. Jurenec generally has the right to put his interest to us for approximately one year beginning on December 31, 2004 at a price that consists of a fixed component and a variable component based on station segment EBITDA. We have the right to call the interest held by Mr. Jurenec at any time until December 31, 2006 at a price that is the same as the put price until the end of the put period and is fixed during the remainder of 2006, after which the call expires.

In connection with the restructuring of our Slovenian operations, we have entered into a put/call arrangement with the general director of Pro Plus, Marijan Jurenec, who owns the remaining 3.15% of Pro Plus. Under the terms of the agreement, Mr. Jurenec generally has the right to put his interest to us for approximately one year beginning on December 31, 2004 at a price that consists of a fixed component and a variable component based on station segment EBITDA. We have the right to call the interest held by Mr. Jurenec at any time until December 31, 2006 at a price that is the same as the put price until the end of the put period and is fixed during the remainder of 2006, after which the call expires.

License Companies : Pop TV and Kanal A

As of January 30, 2003, Pro Plus owns 100% of Pop TV, giving us a 96.85% voting interest and share of profits in Pop TV. Pop TV holds all of the licenses for the Slovenian operations apart from those effectively held by Kanal A. Pro Plus has entered into an agreement with Pop TV, under which Pro Plus provides all programming to Pop TV and sells its advertising for the POP TV network.

We control the operations, economics and the programming of Kanal A, which is the second leading commercial television broadcaster in Slovenia. 90% of the voting and profits interest in Kanal A is being held by Superplus Holding d.d. (“Superplus”) which is owned by individuals who are holding the share of Superplus in trust for us. As of January 30, 2003, Pro Plus owns the remaining 10% of Kanal A, givin g us an effective 96.85% voting interest and share of profits in Kanal A. Pro Plus has entered into an agreement with Kanal A, under which Pro Plus provides all programming to Kanal A and sells its advertising for the KANAL A network.

We control the operations, economics and the programming of Kanal A, which is the second leading commercial television broadcaster in Slovenia. 90% of the voting and profits interest in Kanal A is being held by Superplus Holding d.d. (“Superplus”) which is owned by individuals who are holding the share of Superplus in trust for us. As of January 30, 2003, Pro Plus owns the remaining 10% of Kanal A, givin g us an effective 96.85% voting interest and share of profits in Kanal A. Pro Plus has entered into an agreement with Kanal A, under which Pro Plus provides all programming to Kanal A and sells its advertising for the KANAL A network.

Operations : POP TV and KANAL A networks

The POP TV network is the leading national commercial television broadcaster in Slovenia and reaches approximately 87% of the population of Slovenia, including Ljubljana, the capital of Slovenia, and Maribor, Slovenia's second largest city. Independent research shows that among main television programs in 2002, the POP TV network had an audience share in its coverage area of 29% all day and 32% in prime time, the largest share of television viewers in Slovenia (Media Services AGB).

The KANAL A network, a national television broadcaster, reaches 80% of the population of Slovenia, including Ljubljana and Maribor. Independent research shows that among main television programs in 2002, the KANAL A network had an audience share of 11% in its coverage area all day and in prime time, making it the third most watched television channel in Slovenia (Media Services AGB).

Programming

The POP TV network's programming strategy is to appeal to a mass market audience through a wide variety of programming including series, movies, news, variety shows and features. The POP TV network broadcasts 18 hours of programming daily, of which approximately 20% is locally produced programming, including top rated international formats, Who Wants to be a Millionaire and Popstars and local series Pod eno streho (Under One Roof) and Trafika (Newstand).

Pro Plus has secured exclusive program rights in Slovenia to a number of successful American and Western European programs and films produced by studios such as Warner Bros., Twentieth Century Fox and Paramount. Pro Plus has agreements with CNN, Reuters and APTN to receive foreign news reports and film footage to integrate into news programs. All foreign language programs and films are subtitled in Slovenian.

| Page 20 | ||

The KANAL A network's programming strategy is to complement the programming strategy of the POP TV network with a mixture of locally produced and acquired foreign programs including films and series. The KANAL A network broadcasts for 16 hours daily.

Advertising

Pro Plus derives revenues from the sale of commercial advertising time on the POP TV and KANAL A networks. Current multinational advertisers include firms such as Benckiser, Henkel, Procter & Gamble, Wrigley and Colgate, although no one advertiser dominates the market. During 1999 and 2000, "Peoplemeter" devices were placed in a number of television homes, and they are currently present in 450 homes in Slovenia. They are the primary source for the POP TV network's rating information. The POP TV network is permitted to broadcast advertising for up to 20% of its daily broadcast time (and up to 12 minutes in any hour) and there are also restrictions on the frequency of advertising breaks during films and other programs. The same rules apply to its competitors.

Competition

Historically, the television market in Slovenia has been dominated by SLO 1, a national public television station. The other national public station, SLO 2 provides programming which is complementary to SLO 1. SLO 1 reaches nearly all of Slovenia's TV households, and SLO 2 reaches 97% of Slovenia's TV households. One other private television station, TV3, competes with the POP TV and KANAL A networks in Slovenia. It has achieved a relatively small audience share, less than 1.2%, due primarily to its low budget programming and lack of extensive news programming.

The POP TV and KANAL A networks also compete with foreign television stations, particularly Croatian, Italian, German and Austrian stations. Cable penetration at 52% is similar to other countries in Central and Eastern Europe and approximately 12% of households have satellite dishes. In addition, the POP TV and KANAL A networks compete for revenues with other media, such as newspapers, radio, magazines, outdoor advertising, telephone directory advertising and direct mail.

Regulation

Under Slovenian television regulations, Pop TV , and Kanal A are required to comply with a number of restrictions on programming and advertising. These restrictions include that 20% of the station's daily broadcast time must be internally produced programming (or programming produced on order and on behalf of the broadcaster itself), of which at least 60 minutes must be broadcast between 6:00 p.m. and 10:00 p.m., and 2% of the station's annual broadcast time must be Slovenian origin films (or other works from the field of literature, science and art). In the future a majority (at present at least 40%) of the station's annual broadcast time will required to be European origin films (or other works from the field of literature, science and art); of which at least 10% of the station's annual broadcast t ime will be required to be works produced by independent producers, of which at least 50% has to be produced in the last 5 years (a broadcaster presently not broadcasting such percentage of works produced by independent European producers, must increase its present percentage each year). Certain films and other programs may only be broadcast between 12:00 p.m. and 5:00 am, and Pop TV or Kanal A news editors, journalists and correspondents on the POP TV and KANAL A networks must not reflect a biased approach toward news reporting.

In addition to the restrictions discussed above and under the sub-heading "Advertising," advertising is not permitted during news, documentary or children's programming and programming with religious content under 30 minutes in duration, or during religious ceremonials and state celebrations. Advertising is not permitted during individual programming units, unless such units are divided into independent parts (advertising is allowed between such independent parts). Restrictions on advertising content include a prohibition on tobacco advertising and on the advertising of alcoholic beverages other than low alcohol content beer.

| Page 21 | ||

License Renewals

The POP TV and KANAL A networks operate under licenses regulated pursuant to the Law on Media adopted in 2001 and pursuant to the Law on Telecommunications adopted in 2001. Following a decision by the Slovenian Media Council in July 2002, all of the licenses held by Pop TV and Kanal A have been extended until August 2012.

SLOVAK REPUBLIC

General

The Slovak Republic is a parliamentary democracy with a population of 5.4 million where nearly 99% of households have television. Per capita GDP was an estimated $3,804 in 2001 with a GDP growth rate of 3.6% in 2002. Television advertising was approximately $47 million in 2002, in the Slovak Republic according to our estimates.

Operating Company : STS

Our interest in STS is governed by a Participants Agreement (the "Slovak Agreement") between ourselves and Markiza-Slovakia s.r.o. ("Markiza") forming STS. Pursuant to the Slovak Agreement, we are required to fund all of the capital requirements of and hold a 49% voting interest and a 70% share of profits in STS. Markiza, which holds the television broadcast license, and STS have entered into a series of agreements under which STS is entitled to conduct television broadcast operations pursuant to the license. We are entitled to a 70% share of the profits of STS, except that our share in STS' profit shall be increased by 3% for every additional $1 million invested in STS by us. A Board of Representatives directs the affairs of STS, the composition of which includes two of our designees and three desig nees of Markiza. All significant financial and operational decisions of the Board of Representatives require a vote of 80% of its members. In addition, certain fundamental corporate matters are reserved for decision by a general meeting of partners and require a 67% affirmative vote of the partners.

License Company : Markiza

On January 18, 2002, we entered into an interest participation transfer agreement to acquire a 34% voting interest and a 0.1% share of profits in Markiza. As a result of this acquisition, we will be entitled to a 70% share of STS' profits as opposed to 80% prior to the acquisition. We now have the right to appoint one of three authorized co-signatories of Markiza, which gives us a blocking control over Markiza's significant activities. The ownership transfer to us was approved by the Slovak Republic Media Council at its meeting on February 11, 2002. The transfer was registered with the Slovak Commercial Registry on March 13, 2002.

As a result of the change in our entitlement to distribution of profits, we have charged the Consolidated Statement of Operations with $2,685,000 in the first quart er 2002, to reflect the reduction in the economic interest based on our value of the investment as at December 31, 2001.

As a result of the change in our entitlement to distribution of profits, we have charged the Consolidated Statement of Operations with $2,685,000 in the first quart er 2002, to reflect the reduction in the economic interest based on our value of the investment as at December 31, 2001.

Operations : MARKIZA TV network

The MARKIZA TV network was launched as a national television station in the Slovak Republic in August 1996. The MARKIZA TV network reaches approximately 96% of the Slovak Republic's population, including virtually all of its major cities. According to independent research, the MARKIZA TV network had an average national television viewer share for 2002 of approximately 48% versus 16% for its nearest competitor, STV 1 and JOJ TV had 7% audience share.

Programming