UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the quarterly period ended June 30, 2006

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the transition period from __________ to __________

Commission File Number: 0-24796

CENTRAL EUROPEAN MEDIA ENTERPRISES LTD.

(Exact name of registrant as specified in its charter)

BERMUDA | 98-0438382 |

| (State or other jurisdiction of incorporation and organization) | (IRS Employer Identification No.) |

| | |

Clarendon House, Church Street, Hamilton | HM 11 Bermuda |

| (Address of principal executive offices) | (Zip Code) |

Registrant's telephone number, including area code: 441-296-1431

Indicate by check mark whether registrant: (1) has filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for each shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act.

Large accelerated filer x | Accelerated filer o | Non-accelerated filer o |

Indicate by check mark whether the registrant is a shell company (as defined by Rule 12b-2 of the Exchange Act) Yes o No x

Indicate the number of shares outstanding of each of the issuer's classes of common stock, as of the latest practicable date.

Class | Outstanding as of July 31, 2006 |

| Class A Common Stock, par value $0.08 | 34,393,938 |

| Class B Common Stock, par value $0.08 | 6,212,839 |

CENTRAL EUROPEAN MEDIA ENTERPRISES LTD.

FORM 10-Q

For the quarterly period ended June 30, 2006

INDEX

| | | | Page |

Part I. Financial information | |

| | | |

| | | | 2 |

| | | | 4 |

| | | | 6 |

| | | | 7 |

| | | | 8 |

| | | 40 |

| | | 77 |

| | | 79 |

Part II. Other Information | |

| | | 80 |

| | | 83 |

| | | 90 |

| | | 91 |

| | | 91 |

| | | 92 |

| 93 |

| 94 |

Part I. Financial Information

Item 1. Financial Statements

CENTRAL EUROPEAN MEDIA ENTERPRISES LTD. CONDENSED CONSOLIDATED BALANCE SHEETS

(US$ 000’s)

(Unaudited)

| | | June 30, 2006 | | December 31, 2005 | |

ASSETS | | | | | | | |

Current assets | | | | | | | |

| Cash and cash equivalents | | $ | 158,998 | | $ | 71,658 | |

| Restricted cash (Note 6) | | | 14,290 | | | 34,172 | |

| Accounts receivable, net (Note 7) | | | 120,183 | | | 97,396 | |

| Income taxes receivable | | | 5,772 | | | 9,930 | |

| Program rights, net | | | 47,960 | | | 34,914 | |

| Other current assets (Note 8) | | | 32,169 | | | 38,856 | |

Total current assets | | | 379,372 | | | 286,926 | |

Non-current assets | | | | | | | |

| Investments | | | 65 | | | 23,936 | |

| Acquisition costs (Note 3) | | | - | | | 5,118 | |

| Property, plant and equipment, net (Note 9) | | | 84,913 | | | 58,897 | |

| Program rights, net | | | 52,967 | | | 33,081 | |

| Goodwill (Note 4) | | | 846,147 | | | 746,583 | |

| Broadcast licenses, net (Note 4) | | | 193,310 | | | 171,591 | |

| Other intangible assets, net (Note 4) | | | 69,508 | | | 47,658 | |

| Other non-current assets (Note 8) | | | 15,233 | | | 15,060 | |

Total non-current assets | | | 1,262,143 | | | 1,101,924 | |

Total assets | | $ | 1,641,515 | | $ | 1,388,850 | |

The accompanying notes are an integral part of these condensed consolidated financial statements.

CENTRAL EUROPEAN MEDIA ENTERPRISES LTD.

CONDENSED CONSOLIDATED BALANCE SHEETS (continued)

(US$ 000’s)

(Unaudited)

| | | June 30, 2006 | | December 31, 2005 | |

LIABILITIES AND SHAREHOLDERS’ EQUITY | | | | | | | |

Current liabilities | | | | | | | |

| Accounts payable and accrued liabilities (Note 10) | | $ | 97,190 | | $ | 84,849 | |

| Duties and other taxes payable | | | 32,160 | | | 27,654 | |

| Income taxes payable | | | 9,206 | | | 21,894 | |

| Credit facilities and obligations under capital leases (Note 11) | | | 18,350 | | | 43,566 | |

| Deferred consideration - Croatia | | | 3,893 | | | 3,591 | |

| Deferred consideration - Czech Republic | | | - | | | 24,402 | |

| Deferred consideration - Ukraine | | | 200 | | | - | |

| Deferred tax | | | 365 | | | 1,005 | |

Total current liabilities | | | 161,364 | | | 206,961 | |

Non-current liabilities | | | | | | | |

| Credit facilities and obligations under capital leases (Note 11) | | | 4,985 | | | 4,740 | |

| Senior Notes (Note 5) | | | 473,085 | | | 436,424 | |

| Income taxes payable | | | 2,196 | | | 681 | |

| Deferred tax | | | 53,661 | | | 42,149 | |

| Other non-current liabilities | | | 7,075 | | | 4,105 | |

Total non-current liabilities | | | 541,002 | | | 488,099 | |

| Commitments and contingencies (Note 18) | | | | | | | |

Minority interests in consolidated subsidiaries | | | 20,089 | | | 13,237 | |

SHAREHOLDERS' EQUITY: | | | | | | | |

| Nil shares of Preferred Stock of $0.08 each (December 31, 2005 - nil) | | | - | | | - | |

| 34,393,938 shares of Class A Common Stock of $0.08 each (December 31, 2005 - 31,032,994) | | | 2,752 | | | 2,482 | |

| 6,212,839 shares of Class B Common Stock of $0.08 each (December 31, 2005 - 6,966,533) | | | 497 | | | 558 | |

| Additional paid-in capital | | | 917,755 | | | 746,880 | |

| Accumulated deficit | | | (54,715 | ) | | (44,973 | ) |

| Accumulated other comprehensive income / (loss) | | | 52,771 | | | (24,394 | ) |

Total shareholders’ equity | | | 919,060 | | | 680,553 | |

Total liabilities and shareholders’ equity | | $ | 1,641,515 | | $ | 1,388,850 | |

The accompanying notes are an integral part of these condensed consolidated financial statements.

CENTRAL EUROPEAN MEDIA ENTERPRISES LTD. CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE INCOME

(US$ 000’s, except share and per share data)

(Unaudited)

| | | For the Three Months Ended June 30, | | For the Six Months Ended June 30, | |

| | | 2006 | | 2005 | | 2006 | | 2005 | |

| | | | | | | | | | |

Net revenues | | $ | 156,589 | | $ | 113,109 | | $ | 276,343 | | $ | 161,413 | |

| Operating costs | | | 26,042 | | | 18,117 | | | 49,014 | | | 29,402 | |

| Cost of programming | | | 52,850 | | | 32,081 | | | 101,268 | | | 54,403 | |

| Depreciation of station property, plant and equipment | | | 6,059 | | | 3,161 | | | 11,761 | | | 5,062 | |

| Amortization of broadcast licenses and other intangibles (Note 4) | | | 4,620 | | | 1,544 | | | 8,952 | | | 1,933 | |

Cost of revenues | | | 89,571 | | | 54,903 | | | 170,995 | | | 90,800 | |

| Station selling, general and administrative expenses | | | 14,541 | | | 12,562 | | | 28,707 | | | 19,490 | |

| Corporate operating costs | | | 7,696 | | | 3,451 | | | 15,677 | | | 11,182 | |

| Impairment charge (Note 4) | | | 748 | | | 35,331 | | | 748 | | | 35,331 | |

Operating income | | | 44,033 | | | 6,862 | | | 60,216 | | | 4,610 | |

| Interest income | | | 1,741 | | | 559 | | | 3,194 | | | 1,638 | |

| Interest expense | | | (11,337 | ) | | (6,424 | ) | | (21,855 | ) | | (6,731 | ) |

| Foreign currency exchange gain / (loss), net | | | (20,625 | ) | | 30,159 | | | (31,487 | ) | | 29,430 | |

| Change in fair value of derivatives (Note 12) | | | (1,876 | ) | | - | | | (1,876 | ) | | - | |

| Other income / (expense) | | | 167 | | | 312 | | | (381 | ) | | (3,689 | ) |

Income before provision for income taxes, minority interest, equity in income of unconsolidated affiliates and discontinued operations | | | 12,103 | | | 31,468 | | | 7,811 | | | 25,258 | |

| Provision for income taxes | | | (3,582 | ) | | (3,565 | ) | | (7,576 | ) | | (5,906 | ) |

Income before minority interest, equity in income of unconsolidated affiliates and discontinued operations | | | 8,521 | | | 27,903 | | | 235 | | | 19,352 | |

| Minority interest in income of consolidated subsidiaries | | | (1,276 | ) | | (4,104 | ) | | (6,717 | ) | | (4,681 | ) |

| Equity in income / (loss) of unconsolidated affiliates | | | - | | | 4,049 | | | (730 | ) | | 4,883 | |

Net income / (loss) from continuing operations | | | 7,245 | | | 27,848 | | | (7,212 | ) | | 19,554 | |

Discontinued operations (Note 17): | | | | | | | | | | | | | |

| Pre-tax income from discontinued operations (Czech Republic) | | | - | | | 46 | | | - | | | 164 | |

| Tax on disposal of discontinued operations (Czech Republic) | | | 1,277 | | | (2,435 | ) | | (2,530 | ) | | (2,208 | ) |

Net income / (loss) from discontinued operations | | | 1,277 | | | (2,389 | ) | | (2,530 | ) | | (2,044 | ) |

Net income / (loss) | | $ | 8,522 | | $ | 25,459 | | $ | (9,742 | ) | $ | 17,510 | |

| Currency translation adjustment, net | | | 44,706 | | | (42,767 | ) | | 77,165 | | | (45,018 | ) |

Total comprehensive income / (loss) | | $ | 53,228 | | $ | (17,308 | ) | $ | 67,423 | | $ | (27,508 | ) |

The accompanying notes are an integral part of these condensed consolidated financial statements.

CENTRAL EUROPEAN MEDIA ENTERPRISES LTD.

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE INCOME (continued)

(US$ 000’s, except share and per share data)

(Unaudited)

| | | For the Three Months Ended June 30, | | For the Six Months Ended June 30, | |

| | | 2006 | | 2005 | | 2006 | | 2005 | |

PER SHARE DATA (Note 15): | | | | | | | | | | | | | |

Net income / (loss) per share: | | | | | | | | | | | | | |

| Continuing operations - Basic | | $ | 0.18 | | $ | 0.81 | | $ | (0.18 | ) | $ | 0.62 | |

| Continuing operations - Diluted | | | 0.18 | | | 0.79 | | | (0.18 | ) | | 0.61 | |

| Discontinued operations - Basic | | | 0.03 | | | (0.07 | ) | | (0.07 | ) | | (0.06 | ) |

| Discontinued operations - Diluted | | | 0.03 | | | (0.07 | ) | | (0.07 | ) | | (0.07 | ) |

| Net income / (loss) - Basic | | | 0.21 | | | 0.74 | | | (0.25 | ) | | 0.56 | |

| Net income / (loss) - Diluted | | $ | 0.21 | | $ | 0.72 | | $ | (0.25 | ) | $ | 0.54 | |

| | | | | | | | | | | | | | |

Weighted average common shares used in computing per share amounts (000’s): | | | | | | | | | | | | | |

| Basic | | | 40,597 | | | 34,274 | | | 39,355 | | | 31,345 | |

| Diluted | | | 41,186 | | | 35,145 | | | 39,355 | | | 32,288 | |

The accompanying notes are an integral part of these condensed consolidated financial statements.

CENTRAL EUROPEAN MEDIA ENTERPRISES LTD. CONDENSED CONSOLIDATED STATEMENTS OF SHAREHOLDERS' EQUITY

(US$ 000’s)

(Unaudited)

| | | Class A Common Stock | | Class B Common Stock | | | | | | | | | |

| | | Number of Shares | | Par Value | | Number of Shares | | Par Value | | Additional Paid-In Capital | | Accumulated Deficit | | Accumulated Other Comprehensive Income / (Loss) | | Total Shareholders' Equity | |

BALANCE, December 31, 2005 | | | 31,032,994 | | $ | 2,482 | | | 6,966,533 | | $ | 558 | | $ | 746,880 | | $ | (44,973 | ) | $ | (24,394 | ) | $ | 680,553 | |

| Stock-based compensation | | | - | | | - | | | - | | | - | | | 1,418 | | | - | | | - | | | 1,418 | |

| Stock options exercised | | | 77,250 | | | 7 | | | - | | | - | | | 1,060 | | | - | | | - | | | 1,067 | |

| Shares issued, net of fees | | | 2,530,000 | | | 202 | | | - | | | - | | | 168,397 | | | - | | | - | | | 168,599 | |

| Conversion of Class B to Class A Common Shares | | | 753,694 | | | 61 | | | (753,694 | ) | | (61 | ) | | - | | | - | | | - | | | - | |

| Net loss | | | - | | | - | | | - | | | - | | | - | | | (9,742 | ) | | - | | | (9,742 | ) |

| Currency translation adjustment | | | - | | | - | | | - | | | - | | | - | | | - | | | 77,165 | | | 77,165 | |

BALANCE, June 30, 2006 | | | 34,393,938 | | $ | 2,752 | | | 6,212,839 | | $ | 497 | | $ | 917,755 | | $ | (54,715 | ) | $ | 52,771 | | $ | 919,060 | |

| | | Class A Common Stock | | Class B Common Stock | | | | | | | | | |

| | | Number of Shares | | Par Value | | Number of Shares | | Par Value | | Additional Paid-In Capital | | Accumulated Deficit | | Accumulated Other Comprehensive Income / (Loss) | | Total Shareholders' Equity | |

BALANCE, December 31, 2004 | | | 21,049,400 | | $ | 1,684 | | | 7,334,768 | | $ | 587 | | $ | 387,305 | | $ | (87,468 | ) | $ | 8,960 | | $ | 311,068 | |

| Stock-based compensation | | | - | | | - | | | - | | | - | | | 1,690 | | | - | | | - | | | 1,690 | |

| Stock options exercised | | | 552,334 | | | 45 | | | - | | | - | | | 2,898 | | | - | | | - | | | 2,943 | |

| Shares issued, net of fees | | | 5,405,000 | | | 432 | | | - | | | - | | | 230,172 | | | - | | | - | | | 230,604 | |

| Shares issued to PPF | | | 3,500,000 | | | 280 | | | - | | | - | | | 120,603 | | | - | | | - | | | 120,883 | |

| Net income | | | - | | | - | | | - | | | - | | | - | | | 17,510 | | | - | | | 17,510 | |

| Currency translation adjustment | | | - | | | - | | | - | | | - | | | - | | | - | | | (45,018 | ) | | (45,018 | ) |

BALANCE, June 30, 2005 | | | 30,506,734 | | $ | 2,441 | | | 7,334,768 | | $ | 587 | | $ | 742,668 | | $ | (69,958 | ) | $ | (36,058 | ) | $ | 639,680 | |

The accompanying notes are an integral part of these condensed consolidated financial statements.

CENTRAL EUROPEAN MEDIA ENTERPRISES LTD. CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(US$ 000’s)

(Unaudited)

| | | For the Six Months Ended June 30, | |

| | | 2006 | | 2005 | |

CASH FLOWS FROM OPERATING ACTIVITIES: | | | | | |

Net (loss) / income | | $ | (9,742 | ) | $ | 17,510 | |

| Adjustments to reconcile net (loss) / income to net cash generated from operating activities: | | | | | | | |

| Loss from discontinued operations (Note 17) | | | 2,530 | | | 2,044 | |

| Equity in loss / (income) of unconsolidated affiliates, net of dividends received | | | 730 | | | (720 | ) |

| Depreciation and amortization | | | 74,429 | | | 38,363 | |

| Impairment charge | | | 748 | | | 35,331 | |

| Loss on disposal of fixed asset | | | 1,171 | | | 389 | |

| Interest receivable, net | | | (95 | ) | | (84 | ) |

| Stock-based compensation (Note 14) | | | 1,418 | | | 1,690 | |

| Minority interest in income of consolidated subsidiaries | | | 6,717 | | | 4,681 | |

| Foreign currency exchange loss / (gain), net | | | 31,487 | | | (29,430 | ) |

| Net change in (net of effects of acquisitions and disposals of businesses): | | | | | | | |

| Accounts receivable | | | (7,875 | ) | | (6,432 | ) |

| Program rights | | | (69,836 | ) | | (37,056 | ) |

| Other assets | | | 1,963 | | | (4,082 | ) |

| Settlement liability (Note 10) | | | (10,007 | ) | | - | |

| Other accounts payable and accrued liabilities | | | 2,114 | | | (2,679 | ) |

| Change in fair value of derivative instruments | | | 1,876 | | | (643 | ) |

| Income taxes payable | | | (6,922 | ) | | 4,523 | |

| Deferred taxes | | | 5,352 | | | (1,818 | ) |

| VAT and other taxes payable | | | 11,217 | | | 1,816 | |

Net cash generated from continuing operating activities | | | 37,275 | | | 23,403 | |

| | | | | | | | |

CASH FLOWS FROM INVESTING ACTIVITIES: | | | | | | | |

| Net change in restricted cash | | | (4,068 | ) | | (18,677 | ) |

| Purchase of property, plant and equipment | | | (18,461 | ) | | (8,539 | ) |

| Proceeds from disposal of property, plant and equipment | | | 19 | | | 124 | |

| Investments in subsidiaries and unconsolidated affiliates | | | (59,308 | ) | | (12,884 | ) |

| Partial consideration for acquisition of TV Nova (Czech Republic) group | | | - | | | (218,381 | ) |

| Repayment of loans and advances to related parties | | | 250 | | | - | |

Net cash used in continuing investing activities | | | (81,568 | ) | | (258,357 | ) |

| | | | | | | | |

CASH FLOWS FROM FINANCING ACTIVITIES: | | | | | | | |

| Proceeds from credit facilities | | | 34,765 | | | - | |

| Payment of credit facilities and capital leases | | | (65,519 | ) | | (9,942 | ) |

| Net proceeds from issuance of Senior Notes | | | - | | | 476,188 | |

| Repayment of notes for acquisition of TV Nova (Czech Republic) group | | | - | | | (491,703 | ) |

| Issuance of shares of Class A Common Stock | | | 169,666 | | | 233,547 | |

| Dividends paid to minority shareholders | | | (679 | ) | | (77 | ) |

Net cash received from continuing financing activities | | | 138,233 | | | 208,013 | |

| | | | | | | | |

| NET CASH USED IN DISCONTINUED OPERATIONS - OPERATING ACTIVITIES | | | (1,690 | ) | | (2,000 | ) |

Impact of exchange rate fluctuations on cash | | | (4,910 | ) | | (9,830 | ) |

| | | | | | | | |

| Net increase / (decrease) in cash and cash equivalents | | | 87,340 | | | (38,771 | ) |

CASH AND CASH EQUIVALENTS, beginning of period | | | 71,658 | | | 152,568 | |

CASH AND CASH EQUIVALENTS, end of period | | $ | 158,998 | | $ | 113,797 | |

The accompanying notes are an integral part of these condensed consolidated financial statements.

CENTRAL EUROPEAN MEDIA ENTERPRISES LTD. NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Tabular amounts in US$ 000’s, except per share data)

(Unaudited)

1. ORGANIZATION AND BUSINESS

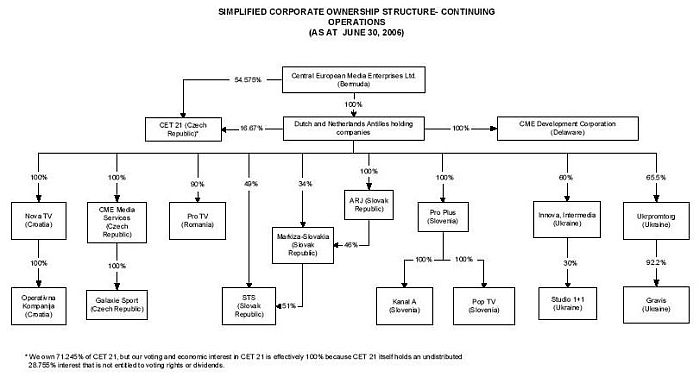

Central European Media Enterprises Ltd., a Bermuda corporation, was formed in June 1994. Our assets are held through a series of Dutch and Netherlands Antilles holding companies. We invest in, develop and operate national and regional commercial television stations and channels in Central and Eastern Europe. At June 30, 2006, we had operations in Croatia, the Czech Republic, Romania, the Slovak Republic, Slovenia and Ukraine.

Our principal subsidiaries and equity-accounted affiliates as at June 30, 2006 were:

Company Name | Voting Interest | Jurisdiction of Organization | Subsidiary / Equity-Accounted Affiliate (1) |

| | | | |

| Nova TV d.d. (“Nova TV (Croatia)”) | 100.0% | Croatia | Subsidiary |

| Operativna Kompanija d.o.o. (“OK”) | 100.0% | Croatia | Subsidiary |

| Media House d.o.o. | 100.0% | Croatia | Subsidiary |

| | | | |

| CME Media Investments s.r.o. | 100.0% | Czech Republic | Subsidiary |

| Vilja a.s. (“Vilja”) | 100.0% | Czech Republic | Subsidiary |

| CET 21 s.r.o. (“CET 21”) | 100.0% | Czech Republic | Subsidiary |

| CME Media Services s.r.o. (“CME Media Services”) | 100.0% | Czech Republic | Subsidiary |

| ERIKA a.s. | 100.0% | Czech Republic | Subsidiary |

| Media Capitol, a.s. | 100.0% | Czech Republic | Subsidiary |

| NOVA-V.I.P., a.s. | 100.0% | Czech Republic | Subsidiary (in liquidation) |

| HARTIC, a.s. | 100.0% | Czech Republic | Subsidiary |

| Galaxie Sport s.r.o. (“Galaxie Sport”) | 100.0% | Czech Republic | Subsidiary |

| | | | |

| Media Pro International S.A. (“MPI”) | 90.0% | Romania | Subsidiary |

| Media Vision S.R.L. (“Media Vision”) | 75.0% | Romania | Subsidiary |

| MPI Romania B.V. | 90.0% | Netherlands | Subsidiary |

| Pro TV S.A. (“Pro TV”) | 90.0% | Romania | Subsidiary |

| Radio Pro S.R.L | 20.0% | Romania | Equity Accounted Affiliate |

| | | | |

| A.R.J. a.s. (“ARJ”) | 100.0% | Slovak Republic | Subsidiary |

| Slovenska Televizna Spolocnost s.r.o. (“STS”) | 89.8% | Slovak Republic | Subsidiary |

| Markiza-Slovakia s.r.o. (“Markiza”) | 80.0% | Slovak Republic | Subsidiary |

| Gamatex s.r.o. | 89.8% | Slovak Republic | Subsidiary |

| ADAM a.s. | 89.8% | Slovak Republic | Subsidiary |

| | | | |

| MM TV 1 d.o.o. | 100.0% | Slovenia | Subsidiary |

| Produkcija Plus d.o.o. (“Pro Plus”) | 100.0% | Slovenia | Subsidiary |

| POP TV d.o.o. (“Pop TV”) | 100.0% | Slovenia | Subsidiary |

| Kanal A d.o.o. (“Kanal A”) | 100.0% | Slovenia | Subsidiary |

| Euro 3 TV d.o.o. | 33.0% | Slovenia | Equity Accounted Affiliate |

CENTRAL EUROPEAN MEDIA ENTERPRISES LTD.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Tabular amounts in US$ 000’s, except per share data)

(Unaudited)

Company Name | Voting Interest | Jurisdiction of Organization | Subsidiary / Equity-Accounted Affiliate (1) |

| | | | |

| Super Plus Holding d.d. | 100.0% | Slovenia | Subsidiary (in liquidation) |

| MTC Holding d.o.o. | 24.0% | Slovenia | Equity-Accounted Affiliate (in liquidation) |

| | | | |

| International Media Services Ltd. (“IMS”) | 60.0% | Bermuda | Subsidiary |

| Innova Film GmbH (“Innova”) | 60.0% | Germany | Subsidiary |

| Enterprise “Inter-Media” (“Inter-Media”) | 60.0% | Ukraine | Subsidiary |

| TV Media Planet Ltd. | 60.0% | Cyprus | Subsidiary |

| Broadcasting Company “Studio 1+1” LLC (“Studio 1+1”) | 18.0% | Ukraine | Consolidated Variable Interest Entity |

| Ukraine Media Services LLC | 99.0% | Ukraine | Subsidiary |

| Ukrpromtorg 2003 LLC | 65.5% | Ukraine | Subsidiary |

| Gravis LLC | 60.4% | Ukraine | Subsidiary |

| Delta ZAO | 60.4% | Ukraine | Subsidiary |

| Nart LLC | 65.5% | Ukraine | Subsidiary |

| TV Stimul LLC | 49.1% | Ukraine | Equity Accounted Affiliate |

| | | | |

| CME Media Enterprises B.V. | 100.0% | Netherlands | Subsidiary |

| CME Czech Republic B.V. | 100.0% | Netherlands | Subsidiary |

| CME Czech Republic II B.V. | 100.0% | Netherlands | Subsidiary |

| CME Germany B.V. | 100.0% | Netherlands | Subsidiary |

| CME Hungary B.V. | 100.0% | Netherlands | Subsidiary |

| CME Poland B.V. | 100.0% | Netherlands | Subsidiary |

| CME Romania B.V. | 100.0% | Netherlands | Subsidiary |

| | | | |

| Central European Media Enterprises N.V. | 100.0% | Netherlands Antilles | Subsidiary |

| Central European Media Enterprises II B.V. | 100.0% | Netherlands Antilles | Subsidiary |

| | | | |

| CME Ukraine Holding GmbH | 100.0% | Austria | Subsidiary |

| CME Cyprus Holding Ltd. | 100.0% | Cyprus | Subsidiary |

| CME Germany GmbH | 100.0% | Germany | Subsidiary (in liquidation) |

| CME Development Corporation | 100.0% | USA | Subsidiary |

| (1) | All subsidiaries have been consolidated in our Condensed Consolidated Financial Statements. All equity-accounted affiliates have been accounted for using the equity method. |

CENTRAL EUROPEAN MEDIA ENTERPRISES LTD.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Tabular amounts in US$ 000’s, except per share data)

(Unaudited)

CENTRAL EUROPEAN MEDIA ENTERPRISES LTD.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Tabular amounts in US$ 000’s, except per share data)

(Unaudited)

Croatia

We own 100% of Nova TV (Croatia), which holds a national terrestrial broadcast license for Croatia which expires in April 2010. Nova TV (Croatia) owns 100% of OK.

Czech Republic

We own 71.245% of CET 21, which holds the national terrestrial broadcast license for TV NOVA (Czech Republic) which expires in 2017. Our voting and economic interest in CET 21 is effectively 100% because CET 21 itself holds an undistributed 28.755% interest that is not entitled to voting rights or dividends. We own 100% of CME Media Services which provides services related to programming, production and advertising to CET 21.

Romania

We have a voting and economic interest of 90% in Pro TV and MPI and a 75% voting and economic interest in Media Vision, a production, dubbing and subtitling company. In addition, Pro TV holds the licenses for ACASA, PRO TV INTERNATIONAL and PRO CINEMA. These licenses expire on various dates from October 2006 until July 2015.

We have a 20% voting and economic interest in Radio Pro, which holds the licenses for the PRO FM and INFOPRO radio networks.

Slovak Republic

We have an 89.9% voting interest and are entitled to 80% of the profits in STS, the operating company for the MARKIZA TV network, and an 80% voting interest and a 0.1% economic interest in Markiza, the license holding company for the MARKIZA TV network, which holds a 51% voting interest in STS. The Markiza license expires in September 2019.

Slovenia

We own 100% of Pro Plus, the operating company for our Slovenian operations. Pro Plus has a 100% voting and economic interest in Pop TV, which holds the licenses for the POP TV network, and Kanal A, which holds the licenses for the KANAL A network, which expire in August 2012.

Ukraine

The Studio 1+1 Group consists of several entities in which we hold direct or indirect interests. We hold a 60% ownership and economic interest in each of Innova and IMS. Innova owns 100% of Inter-Media, a Ukrainian company, which in turn holds a 30% voting and economic interest in Studio 1+1, which holds the licenses for the STUDIO 1+1 network. The first of these licenses which covers fifteen hours including prime time expires in December 2006. On July 19, 2006, the Ukrainian Media Council issued a decision to extend the 15-hour broadcasting license of Studio 1+1 for a 10-year period from January 1, 2007. Issuance of the license itself is subject to the payment of a fee of approximately UAH 5.9 million (approximately US$ 1.2 million), which has been paid, and the registration by October 1, 2006 of amendments to the charter of Studio 1+1 to conform with the recent amendments to the Ukrainian Media Law (see Part II, Item 1A Risk Factors). The second license for the remaining nine hours expires in 2014.

Our indirect ownership interest in Studio 1+1 is only 18%. We entered into an additional agreement on December 30, 2004 with Boris Fuchsmann, Alexander Rodnyansky and Studio 1+1 which re-affirms our entitlement to 60% of any distribution from Studio 1+1 to its shareholders.

CENTRAL EUROPEAN MEDIA ENTERPRISES LTD.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Tabular amounts in US$ 000’s, except per share data)

(Unaudited)

We have a 65.5% interest in Ukrpromtorg 2003 LLC, which owns 92.2% of Gravis LLC, the operator of the GRAVIS television channel in Kiev as well as two other local channels in Ukraine, collectively referred to as the GRAVIS channels. The GRAVIS licenses expire between 2008 and 2012.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of Presentation

The interim financial statements for the three and six months ended June 30, 2006 should be read in conjunction with the Notes to the Consolidated Financial Statements contained in our Annual Report of Form 10-K for the period ended December 31, 2005, as amended by our Form 10-K/A filed with the SEC on March 15, 2006. Our significant accounting policies have not changed since December 31, 2005, except as noted below.

In the opinion of management, the accompanying interim unaudited financial statements reflect all adjustments, consisting only of normal recurring items, necessary for their fair presentation in conformity with accounting principles generally accepted in the United States of America (“US GAAP”). The consolidated results of operations for interim periods are not necessarily indicative of the results to be expected for a full year.

The preparation of financial statements in conformity with US GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting year. Actual results could differ from those estimates and assumptions.

The condensed consolidated financial statements include the accounts of Central European Media Enterprises Ltd. and our subsidiaries, after the elimination of intercompany accounts and transactions. We consolidate the financial statements of entities in which we hold at least a majority voting interest and also those entities which are deemed to be a Variable Interest Entity of which we are the primary beneficiary as defined by FASB Interpretation No. 46 (revised December 2003), “Consolidation of Variable Interest Entities” ("FIN 46(R)"). Entities in which we hold less than a majority voting interest but over which we have the ability to exercise significant influence are accounted for using the equity method. Other investments are accounted for using the cost method.

We, like other television operators, experience seasonality, with advertising sales tending to be lower during the first and third quarters of each calendar year, particularly during the summer holiday period (typically July and August) and higher during the second and fourth quarters of each calendar year, particularly toward the end of the year.

The terms “Company”, “we”, “us”, and “our” are used in this Form 10-Q to refer collectively to the parent company and the subsidiaries through which our various businesses are actually conducted.

Unless otherwise noted, all statistical and financial information presented in this report has been converted into US dollars using appropriate exchange rates. All references to 'US$' or 'dollars' are to US dollars, all references to 'HRK' are to Croatian kuna, all references to 'CZK' are to Czech korunas, all references to 'RON' are to the New Romanian lei, all references to 'SIT' are to Slovenian tolars, all references to 'SKK' are to Slovak korunas, all references to 'UAH' are to Ukrainian hryvna, all references to 'Euro or EUR' are to the European Union Euro and all references to 'GBP' are to British Pounds.

Stock-based Compensation

On January 1, 2006, we adopted SFAS 123(R), “Share-Based Payment” (“SFAS 123(R)”), which requires the recognition of stock-based compensation at fair value, using the modified prospective transition method. Under that method, we recognized compensation cost for the requisite service rendered in the six months ended June 30, 2006, for (a) awards granted prior to, but not vested as of, January 1, 2006, based on the grant-date fair value of those awards as calculated for either recognition or pro forma disclosures under SFAS 123, “Accounting for Stock-Based Compensation (“SFAS 123”) and (b) awards granted after January 1, 2006, based on the grant-date fair value estimated in accordance with the provisions of SFAS 123(R). We did not restate prior periods. Our adoption of SFAS 123(R) did not have a material impact on our condensed consolidated statements of operations or cash flows because we had previously adopted the fair value recognition provisions of SFAS 123 prospectively for employee stock option awards granted, modified, or settled beginning January 1, 2003, as contemplated by SFAS 148, “Accounting for Stock-Based Compensation - Transition & Disclosure”. Prior to January 1, 2003, we used the intrinsic method of accounting as defined in APB 25, “Accounting for Stock Issued to Employees”.

CENTRAL EUROPEAN MEDIA ENTERPRISES LTD.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Tabular amounts in US$ 000’s, except per share data)

(Unaudited)

Pro Forma Disclosures

Had compensation costs for employee stock option awards granted, modified or settled prior to January 1, 2003 been determined consistent with the fair value approach required by SFAS 123(R) for the three months and six months ended June 30, 2005, using the Black-Scholes option pricing model with the assumptions as estimated on the date of each grant, our net loss and net loss per common share would decrease on a pro forma basis as follows:

| | | | | For the Three Months Ended June 30, | | For the Six Months Ended June 30, | |

| | | | | 2005 | | 2005 | |

| | | | | | | | |

Net income | | | As Reported | | $ | 25,459 | | $ | 17,510 | |

| Add / (deduct): Stock-based compensation expense / (income) included in reported net income, net of related tax effects | | | As Reported | | | (1,411 | ) | | 1,690 | |

| Deduct: Total stock-based compensation expense determined under fair value based method for all awards, net of related tax effects | | | Pro Forma Expense | | | 1,384 | | | (1,727 | ) |

Net income | | | Pro Forma | | $ | 25,432 | | $ | 17,473 | |

| | | | | | | | | | | |

| Net income per share - Basic: | | | As Reported | | $ | 0.74 | | $ | 0.56 | |

| | | | Pro Forma | | $ | 0.74 | | $ | 0.56 | |

| Net income per share - Diluted: | | | As Reported | | $ | 0.72 | | $ | 0.54 | |

| | | | Pro Forma | | $ | 0.72 | | $ | 0.54 | |

Reclassifications

Certain reclassifications were made to prior period amounts to conform to current period presentation.

Recent Accounting Pronouncements

In May 2005, the Financial Accounting Standards Board (FASB) issued SFAS No. 154, “Accounting for Changes and Error Corrections” (“FAS 154”), which replaces APB Opinion No. 20 “Accounting Changes” (“APB 20”), and SFAS No. 3, “Reporting Accounting Changes in Interim Financial Statements”, and changes the requirements for the accounting for and reporting of a change in accounting principle. APB 20 previously required that most voluntary changes in accounting principle be recognized by including in net income of the period of the change the cumulative effect of changing to the new accounting principle. FAS 154 requires that the new accounting principle be applied to the balances of assets and liabilities as of the beginning of the earliest period for which retrospective application is practicable and that a corresponding adjustment be made to the opening balance of retained earnings for that period rather than being reported in the income statement. We adopted the provisions of FAS 154 on January 1, 2006 and it did not have a material impact on our financial position or results of operations.

CENTRAL EUROPEAN MEDIA ENTERPRISES LTD.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Tabular amounts in US$ 000’s, except per share data)

(Unaudited)

In July 2006, the Financial Accounting Standards Board (‘FASB’) issued FASB Interpretation No. 48, Accounting for Uncertainty in Income Taxes—an interpretation of FASB Statement No. 109 (‘FIN 48’), which clarifies the accounting for uncertainty in tax positions. The evaluation of a tax position under FIN 48 is a two-step process. The first step is recognition: Tax positions taken or expected to be taken in a tax return should be recognized only if those positions are more likely than not of being sustained upon examination, based on the technical merits of the position. In evaluating whether a tax position has met the more likely than not recognition threshold, it should be presumed that the position will be examined by the relevant taxing authority that would have full knowledge of all relevant information. The second step is measurement: Tax positions that meet the recognition criteria are measured at the largest amount of benefit that is greater than 50 percent likely of being recognized upon ultimate settlement.

FIN 48 also provides guidance on derecognition, classification, interest and penalties, accounting in interim periods, disclosure and transition. FIN 48 is effective for fiscal years beginning after December 15, 2006 and we will adopt it in the first quarter of the year beginning January 1, 2007. We are currently assessing FIN 48 and have not yet determined the impact that the adoption of this interpretation will have on our financial position or results of operations.

3. ACQUISITIONS AND DISPOSALS

Czech Republic

On April 3, 2006, the Czech Republic Media Council approved the transfer of the 1.25% interest in CET 21 held by Ceska Sporitelna, a.s. to Vilja and the transfer of the 1.25% interest in CET 21 held by CEDC to PPF (Cyprus) Ltd. (“PPF”). On May 5, 2006 the Czech Republic Media Council approved the transfer of the PPF interest to Vilja and on May 16, 2006, Vilja acquired such interest after fulfillment of all conditions precedent set forth in the relevant transfer agreement. We now have a voting and economic interest in CET 21 of 100%. Both of these transactions took place for nominal consideration.

On May 26, 2006, following the registration of our subsidiary CME Media Enterprises B.V. as the owner of 16.67% of CET 21, we paid the final CZK 600.0 million (approximately US$ 27.3 million at the payment date) installment of the consideration due to Peter Krsak for his 16.67% interest in CET 21. This amount had been held in escrow, and disclosed in restricted cash (see Note 6) since May 27, 2005, with a corresponding amount reported as deferred consideration.

Romania

Acquisition of additional interest - MPI and Pro TV

On February 17, 2006, we purchased an additional 5.0% of Pro TV, MPI and Media Vision from Adrian Sarbu, the General Director of our Romania operations, for consideration of US$ 27.2 million. We now own a 90.0% voting and economic interest in Pro TV and MPI and a 75.0% voting and economic interest in Media Vision. We completed a fair value exercise to allocate the purchase price to the acquired assets and liabilities, and identified separately identifiable assets. The following table summarizes the fair values of the assets acquired and liabilities assumed at the date of acquisition:

CENTRAL EUROPEAN MEDIA ENTERPRISES LTD.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Tabular amounts in US$ 000’s, except per share data)

(Unaudited)

| | | Fair Value on Acquisition | |

| | | | |

| Intangible assets subject to amortization (1) | | $ | 4,655 | |

| Intangible assets not subject to amortization (2) | | | 12,947 | |

| Goodwill | | | 11,376 | |

| Deferred tax liability | | | (2,816 | ) |

| Minority interest | | | 1,038 | |

Total purchase price | | $ | 27,200 | |

(1) The intangible assets subject to amortization comprise customer relationships, which are being amortized over one to ten years (weighted average: 8.3 years).

(2) Intangible assets not subject to amortization comprise approximately US$ 6.5 million in trademarks and US$ 6.5 million relating to television broadcast licenses.

Mr. Sarbu has the right to sell his remaining 10.0% shareholding in Pro TV and MPI to us under a put option agreement entered into in July 2004 at a price to be determined by an independent valuation, subject to a floor price of US$ 1.45 million for each 1.0% interest sold. This put is exercisable from March 1, 2009 for a twenty-year period thereafter. As at June 30, 2006, we consider the fair value of the put option to be approximately US$ nil.

Slovak Republic

Acquisition - A.R.J. a.s.

On January 23, 2006, we completed the acquisition of a controlling interest in Markiza, the license-holding company for MARKIZA TV, by purchasing 100.0% of the share capital of ARJ. ARJ owns 46.0% of the voting rights in Markiza.

This acquisition consisted of our acquiring a 34.0% interest in ARJ from Pavol Rusko for total consideration of SKK 575.0 million (approximately US$ 18.5 million at the date of acquisition) of which SKK 494.0 million (US$ 15.9 million at the date of acquisition) was paid on closing and SKK 81.0 million (US$ 2.6 million at the date of acquisition) was paid on April 25, 2006. In addition, we acquired the remaining 66.0% in ARJ from Media Partners s.r.o. and Salis s.r.o. for consideration of approximately US$ 11.0 million, of which EUR 7.0 million (approximately US$ 8.5 million at the date of acquisition) was paid on closing and SKK 78.0 million (approximately US$ 2.5 million at the date of acquisition) was paid on May 2, 2006.

As of January 23, 2006, we hold an 80.0% voting interest in Markiza and an 89.8% voting interest in STS, and have increased our economic interest in the Slovak operations from 70.0% to 80.0%. The remaining minority interests in Markiza are held by our partners Jan Kovacik and Milan Fil’o through Media Invest s.r.o. Markiza and STS have been consolidated from the date of acquisition of ARJ.

We completed a fair value exercise to allocate the purchase price to the acquired assets and liabilities, and identified separately identifiable assets. The following table summarizes the fair values of the assets acquired and liabilities assumed at the date of acquisition:

CENTRAL EUROPEAN MEDIA ENTERPRISES LTD.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Tabular amounts in US$ 000’s, except per share data)

(Unaudited)

| | | Fair Value on Acquisition | |

| | | | |

| Property, plant and equipment | | $ | 870 | |

| Program library | | | 185 | |

| Intangible assets subject to amortization (1) | | | 8,128 | |

| Intangible assets not subject to amortization (2) | | | 530 | |

| Goodwill | | | 22,021 | |

| Deferred tax liability | | | (1,893 | ) |

Total purchase price (3) | | $ | 29,841 | |

(1) The intangible assets subject to amortization comprise approximately US$ 7.2 million in customer relationships, which are being amortized over three to fourteen years (weighted average: 13.8 years), and US$ 0.9 million relating to television broadcast licenses, which are being amortized over fourteen years.

(2) Intangible assets not subject to amortization comprise trademarks.

(3) Total purchase price includes US$ 0.3 million of capitalized acquisition costs.

Ukraine

Acquisition - Ukrpromtorg 2003 LLC

On January 11, 2006, we completed the acquisition of a 65.5% interest in Ukrpromtorg 2003 LLC (“Ukrpromtorg”), which owns 92.2% of Gravis LLC, the operator of the GRAVIS television channel in Kiev as well as two other local channels in Ukraine, for consideration of approximately US$ 7.4 million including acquisition costs. US$ 5.1 million of the consideration was paid in 2005 and reported as acquisition costs on the consolidated balance sheet as at December 31, 2005, US$ 1.5 million was paid in January 2006, and US$ 0.3 million was paid in May 2006. The remainder of the purchase price was outstanding at June 30, 2006.

We completed a fair value exercise to allocate the purchase price to the acquired assets and liabilities, and identified separately identifiable assets. The following table summarizes the fair values of the assets acquired and liabilities assumed at the date of acquisition:

| | | Fair Value on Acquisition | |

| | | | |

| Property, plant and equipment | | $ | 2,615 | |

| Intangible assets subject to amortization (1) | | | 968 | |

| Other assets | | | 239 | |

| Goodwill | | | 4,627 | |

| Deferred tax liability | | | (724 | ) |

| Other liabilities | | | (373 | ) |

Total purchase price (2) | | $ | 7,352 | |

(1) The intangible assets subject to amortization comprise approximately US$ 0.6 million relating to television broadcast licenses, which are being amortized over 9 years, approximately US$ 0.3 million relating to a favorable lease contract, which is being amortized over 19 years, and approximately US$ 0.1 million relating to order backlog, which was amortized during the year.

(2) Total purchase price includes US$ 0.4 million of capitalized acquisition costs.

CENTRAL EUROPEAN MEDIA ENTERPRISES LTD.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Tabular amounts in US$ 000’s, except per share data)

(Unaudited)

4. GOODWILL AND INTANGIBLE ASSETS

Our goodwill and intangible asset additions are the result of acquisitions in Croatia, the Czech Republic, Romania, the Slovak Republic, Slovenia and Ukraine. No goodwill is expected to be deductible for tax purposes.

Goodwill:

Goodwill by operating segment as at June 30, 2006, and December 31, 2005 is summarized as follows:

| | | Croatia | | Czech Republic | | Romania | | Slovak Republic | | Slovenia | | Ukraine | | Total | |

| | | | | | | | | | | | | | | | |

Balance, December 31, 2005 | | $ | 695 | | $ | 706,950 | | $ | 19,754 | | $ | - | | $ | 15,088 | | $ | 4,096 | | $ | 746,583 | |

| Additions | | | - | | | - | | | 11,376 | | | 22,021 | | | - | | | 4,627 | | | 38,024 | |

| Other adjustments | | | - | | | (7,580 | ) | | - | | | - | | | - | | | - | | | (7,580 | ) |

| Impairment charge | | | (748 | ) | | - | | | - | | | - | | | - | | | - | | | (748 | ) |

| Foreign currency movements | | | 53 | | | 68,605 | | | - | | | 349 | | | 861 | | | - | | | 69,868 | |

Balance, June 30, 2006 | | $ | - | | $ | 767,975 | | $ | 31,130 | | $ | 22,370 | | $ | 15,949 | | $ | 8,723 | | $ | 846,147 | |

When we updated our medium-term forecast models at June 30, 2006, we determined that the forecast future cash flows of our Croatia operations had decreased compared to our previous forecast. In such circumstances, SFAS 142 “Goodwill and Other Intangible Assets” requires that the carrying value of the intangible assets with indefinite lives are compared to their fair value to determine whether an impairment exists. If an asset is determined to be impaired, the loss is measured as the excess of the carrying value over the fair value. As a result of our analysis, we have recognized an impairment charge of US$ 0.7 million relating to goodwill. A further impairment charge relating to other Long-Lived assets was not deemed necessary under the requirements of SFAS 144 “Accounting for the Impairment or Disposal of Long-Lived Assets”.

Broadcast licenses:

The net book value of our broadcast licenses as at June 30, 2006, and December 31, 2005 is summarized as follows:

| | | Indefinite-Lived Broadcast Licenses | | Amortized Broadcast Licenses | | Total | |

| | | | | | | | |

Balance, December 31, 2005 | | $ | 18,936 | | $ | 152,655 | | $ | 171,591 | |

| Additions | | | 7,390 | | | 6,960 | | | 14,350 | |

| Amortization | | | - | | | (7,605 | ) | | (7,605 | ) |

| Foreign currency movements | | | 468 | | | 14,506 | | | 14,974 | |

Balance, June 30, 2006 | | $ | 26,794 | | $ | 166,516 | | $ | 193,310 | |

CENTRAL EUROPEAN MEDIA ENTERPRISES LTD.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Tabular amounts in US$ 000’s, except per share data)

(Unaudited)

With the exception of our broadcast licenses in the Czech Republic, Slovak Republic and Ukraine, our broadcast licenses primarily have indefinite lives and are subject to annual impairment reviews. The licenses in Ukraine have economic useful lives of, and are amortized on a straight-line basis over, between seven and ten years. The license in the Czech Republic has an economic useful life of, and is amortized on a straight-line basis over, twelve years. The license in the Slovak Republic has an economic useful life of, and is amortized on a straight-line basis over, fourteen years.

The gross value and accumulated amortization of amortized broadcast licenses was as follows at June 30, 2006 and December 31, 2005:

| | | June 30, 2006 | | December 31, 2005 | |

| | | | | | |

| Gross value | | $ | 186,199 | | $ | 163,628 | |

| Accumulated amortization | | | (19,683 | ) | | (10,973 | ) |

Total net book value | | $ | 166,516 | | $ | 152,655 | |

Other intangible assets:

The net book value of our other intangible assets as at June 30, 2006 and December 31, 2005 is summarized as follows:

| | | Trademarks | | Customer Relationships | | Other | | Total | |

| | | | | | | | | | |

Balance, December 31, 2005 | | $ | 32,560 | | $ | 15,098 | | $ | - | | $ | 47,658 | |

| Additions | | | 7,698 | | | 11,868 | | | 321 | | | 19,887 | |

| Amortization | | | - | | | (1,341 | ) | | (6 | ) | | (1,347 | ) |

| Foreign currency movements | | | 1,972 | | | 1,338 | | | - | | | 3,310 | |

Balance, June 30, 2006 | | $ | 42,230 | | $ | 26,963 | | $ | 315 | | $ | 69,508 | |

Customer relationships are deemed to have an economic useful life of, and are amortized on a straight-line basis over, five to fourteen years. Trademarks have an indefinite life.

The gross value and accumulated amortization of customer relationships and other intangible assets was as follows at June 30, 2006 and December 31, 2005:

| | | June 30, 2006 | | December 31, 2005 | |

| | | | | | |

| Gross value | | $ | 30,027 | | $ | 17,038 | |

| Accumulated amortization | | | (2,749 | ) | | (1,940 | ) |

Total net book value | | $ | 27,278 | | $ | 15,098 | |

5. SENIOR NOTES

Our Senior Notes consist of the following:

| | | Carrying Value | | Fair Value | |

| | | June 30, 2006 | | December 31, 2005 | | June 30, 2006 | | December 31, 2005 | |

| | | | | | | | | | |

| EUR 245.0 million 8.25% Senior Notes | | $ | 313,259 | | $ | 288,984 | | $ | 343,351 | | $ | 323,737 | |

| EUR 125.0 million floating rate Senior Notes | | | 159,826 | | | 147,440 | | | 169,416 | | | 156,324 | |

| | | $ | 473,085 | | $ | 436,424 | | $ | 512,767 | | $ | 480,061 | |

CENTRAL EUROPEAN MEDIA ENTERPRISES LTD.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Tabular amounts in US$ 000’s, except per share data)

(Unaudited)

On May 5, 2005, we issued Senior Notes in the aggregate principal amount of EUR 370.0 million consisting of EUR 245.0 million of 8.25% Senior Notes due May 2012 and EUR 125.0 million of floating rate Senior Notes due May 2012, which bear interest at six-month Euro Inter-Bank Offered Rate (“EURIBOR”) plus 5.50% (8.57% was applicable at June 30, 2006). Interest is payable semi-annually in arrears on each May 15 and November 15. The fair value of the Senior Notes as at June 30, 2006 and December 31, 2005 was calculated by multiplying the outstanding debt by the traded market price at the relevant date.

The Senior Notes are secured senior obligations and rank pari passu with all existing and future senior indebtedness and are effectively subordinated to all existing and future indebtedness of our subsidiaries. The amounts outstanding are guaranteed by certain of our subsidiaries and are secured by a pledge of shares of those subsidiaries and an assignment of certain contractual rights. The terms of our indebtedness restrict the manner in which our business is conducted, including the incurrence of additional indebtedness, the making of investments, the payment of dividends or the making of other distributions, entering into certain affiliate transactions and the sale of assets.

In the event that (A) there is a change in control by which (i) any party other than our present shareholders becomes the beneficial owner of more than 35.0% of our total voting power; (ii) we agree to sell substantially all of our operating assets; or (iii) there is a change in the composition of a majority of our Board of Directors; and (B) on the 60th day following any such change of control the rating of the Senior Notes is either withdrawn or downgraded from the rating in effect prior to the announcement of such change of control, we can be required to repurchase the Senior Notes at a purchase price in cash equal to 101.0% of the principal amount of the Senior Notes plus accrued and unpaid interest to the date of purchase.

The Senior Notes are redeemable at our option, in whole or in part, at the redemption prices set forth below:

From: | EUR 245.0 Million 8.25% Senior Notes Redemption Price | | From: | EUR 125.0 Million Floating Rate Senior Notes Redemption Price |

| | | | | |

| May 15, 2009 to May 14, 2010 | 104.125% | | May 15, 2007 to May 14, 2008 | 102.000% |

| May 15, 2010 to May 14, 2011 | 102.063% | | May 15, 2008 to May 14, 2009 | 101.000% |

| May 15, 2011 and thereafter | 100.000% | | May 15, 2009 and thereafter | 100.000% |

In addition, at any time prior to May 15, 2008, we may redeem up to 35.0% of the fixed rate notes with the proceeds of any public equity offering at a price of 108.250% of the principal amount of such notes, plus accrued and unpaid interest, if any, to the redemption date.

In addition, prior to May 15, 2009, we may redeem all or a part of the fixed rate notes at a redemption price equal to 100.0% of the principal amount of such notes, plus a “make-whole” premium and accrued and unpaid interest to the redemption date.

Certain derivative instruments, including redemption call options and change of control and asset disposition put options, have been identified as being embedded in the Senior Notes; but as they are considered clearly and closely related to the Senior Notes, they are not accounted for separately.

CENTRAL EUROPEAN MEDIA ENTERPRISES LTD.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Tabular amounts in US$ 000’s, except per share data)

(Unaudited)

6. RESTRICTED CASH

Restricted cash consists of the following at June 30, 2006 and December 31, 2005:

| | | June 30, 2006 | | December 31, 2005 | |

| | | | | | |

| Czech Republic | | $ | - | | $ | 24,554 | |

| Croatia | | | 3,988 | | | 3,640 | |

| Romania | | | 4,164 | | | - | |

| Directors’ and officers’ insurance | | | 5,404 | | | 5,285 | |

| Other | | | 734 | | | 693 | |

Total restricted cash | | $ | 14,290 | | $ | 34,172 | |

The restricted cash balances in Czech Republic and Croatia at December 31, 2005 represented amounts held in escrow that are payable to certain former owners of our businesses in those countries. The amount due to one of the former owners of our Czech Republic operations was paid on May 26, 2006. Directors’ and officers’ insurance relates to a balance being held in a captive insurance company to underwrite a part of our directors’ and officers’ insurance program. The restricted cash balance in Romania represents cash collateral for an overdraft facility (see note 11).

7. ACCOUNTS RECEIVABLE

Accounts receivable consist of the following at June 30, 2006 and December 31, 2005:

| | | June 30, 2006 | | December 31, 2005 | |

Trading: | | | | | | | |

| Third-party customers | | $ | 128,161 | | $ | 103,921 | |

| Less: allowance for bad debts and credit notes | | | (10,569 | ) | | (8,612 | ) |

| Related parties | | | 2,432 | | | 2,034 | |

| Less: allowance for bad debts and credit notes | | | (245 | ) | | (265 | ) |

Total trading | | $ | 119,779 | | $ | 97,078 | |

| | | | | | | | |

Other: | | | | | | | |

| Third-party customers | | $ | 349 | | $ | 257 | |

| Less: allowance for bad debts and credit notes | | | (96 | ) | | (83 | ) |

| Related parties | | | 441 | | | 434 | |

| Less: allowance for bad debts and credit notes | | | (290 | ) | | (290 | ) |

Total other | | $ | 404 | | $ | 318 | |

| | | | | | | | |

Total accounts receivable | | $ | 120,183 | | $ | 97,396 | |

CENTRAL EUROPEAN MEDIA ENTERPRISES LTD.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Tabular amounts in US$ 000’s, except per share data)

(Unaudited)

8. OTHER ASSETS

Other current and non-current assets consist of the following at June 30, 2006 and December 31, 2005:

| | | June 30, 2006 | | December 31, 2005 | |

Current: | | | | | | | |

| Prepaid programming | | $ | 15,719 | | $ | 17,534 | |

| Other prepaid expenses | | | 6,762 | | | 6,009 | |

| Deferred tax | | | 2,578 | | | 3,025 | |

| VAT recoverable | | | 877 | | | 7,888 | |

| Loan to related party | | | 600 | | | 600 | |

| Capitalized debt costs | | | 2,250 | | | 2,250 | |

| Assets held-for-sale | | | 367 | | | 341 | |

| Other | | | 3,016 | | | 1,209 | |

Total other current assets | | $ | 32,169 | | $ | 38,856 | |

| | | | | | | | |

Non-current: | | | | | | | |

| Capitalized debt costs | | $ | 10,745 | | $ | 11,618 | |

| Loan to related party | | | 1,754 | | | 1,910 | |

| Deferred tax | | | 1,552 | | | 779 | |

| Other | | | 1,182 | | | 753 | |

Total other non-current assets | | $ | 15,233 | | $ | 15,060 | |

Capitalized debt costs primarily comprise the costs incurred in connection with the issuance of our Senior Notes in May 2005 (see Note 5), and are being amortized over the term of the Senior Notes using the effective interest method. The assets held-for-sale relate to land and buildings in our Croatia operations.

CENTRAL EUROPEAN MEDIA ENTERPRISES LTD.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Tabular amounts in US$ 000’s, except per share data)

(Unaudited)

9. PROPERTY, PLANT AND EQUIPMENT

Property, plant and equipment consists of the following:

| | | June 30, 2006 | | December 31, 2005 | |

| | | | | | |

| Land and buildings | | $ | 36,430 | | $ | 17,548 | |

| Station machinery, fixtures and equipment | | | 89,279 | | | 72,017 | |

| Other equipment | | | 19,985 | | | 20,447 | |

| Software licenses | | | 12,976 | | | 8,360 | |

| Construction in progress | | | 6,194 | | | 5,180 | |

Total cost | | | 164,864 | | | 123,552 | |

| Less: Accumulated depreciation | | | (79,951 | ) | | (64,655 | ) |

Total net book value | | $ | 84,913 | | $ | 58,897 | |

| | | | | | | | |

Assets held under capital leases (included in the above) | | | | | | | |

| Land and buildings | | $ | 5,270 | | $ | 4,980 | |

| Station machinery, fixtures and equipment | | | 1,791 | | | 1,434 | |

Total cost | | | 7,061 | | | 6,414 | |

| Less: Accumulated depreciation | | | (1,438 | ) | | (1,167 | ) |

Net book value | | $ | 5,623 | | $ | 5,247 | |

10. ACCOUNTS PAYABLE AND ACCRUED LIABILITIES

Accounts payable and accrued liabilities consist of the following:

| | | June 30, 2006 | | December 31, 2005 | |

| | | | | | |

| Accounts payable | | $ | 22,573 | | $ | 21,533 | |

| Programming liabilities | | | 24,800 | | | 18,891 | |

| Deferred income | | | 15,577 | | | 7,202 | |

| Settlement liability | | | - | | | 10,007 | |

| Accrued staff costs | | | 9,501 | | | 9,402 | |

| Accrued production costs | | | 6,504 | | | 5,882 | |

| Accrued interest payable | | | 4,988 | | | 4,483 | |

| Accrued legal costs | | | 3,863 | | | 3,620 | |

| Accrued rent costs | | | 1,435 | | | 82 | |

| Other accrued liabilities | | | 7,949 | | | 3,747 | |

Total accounts payable and accrued liabilities | | $ | 97,190 | | $ | 84,849 | |

CENTRAL EUROPEAN MEDIA ENTERPRISES LTD.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Tabular amounts in US$ 000’s, except per share data)

(Unaudited)

The settlement liability represented an amount owed by CET 21 under a settlement agreement among CET 21, Ceska nezavisla televizni spolecnost ("CNTS") and the PPF Group dated December 19, 2003 following a mediation. This liability was assumed as part of the TV Nova (Czech Republic) group acquisition and was fully repaid in January 2006.

The accrued interest payable balance relates primarily to interest calculated on our Senior Notes.

11. CREDIT FACILITIES AND OBLIGATIONS UNDER CAPITAL LEASES

Group loan obligations and overdraft facilities consist of the following:

| | | | | June 30, 2006 | | December 31, 2005 | |

Credit facilities: | | | | | | | |

| Croatia operations | | | (a) - (c) | | $ | 1,021 | | $ | 1,135 | |

| Czech Republic operations | | | (d) - (f) | | | 17,642 | | | 42,703 | |

| Romania operations | | | (g) | | | - | | | - | |

| Slovenia operations | | | (h) | | | - | | | - | |

Total credit facilities | | | | | $ | 18,663 | | $ | 43,838 | |

| | | | | | | | | | | |

Capital leases | | | | | | | | | | |

| Croatia operations, net of interest | | | | | $ | 39 | | $ | 132 | |

| Czech Republic operations, net of interest | | | | | | 3 | | | 6 | |

| Romania operations, net of interest | | | | | | 326 | | | 290 | |

| Slovenia operations, net of interest | | | | | | 4,145 | | | 4,040 | |

| Slovak Republic operations, net of interest | | | | | | 159 | | | - | |

Total capital leases | | | | | $ | 4,672 | | $ | 4,468 | |

| | | | | | | | | | | |

Total credit facilities and capital leases | | | | | $ | 23,335 | | $ | 48,306 | |

Less current maturities | | | | | | (18,350 | ) | | (43,566 | ) |

Total non-current maturities | | | | | $ | 4,985 | | $ | 4,740 | |

Croatia

(a) A total of EUR 0.7 million (approximately US$ 0.9 million) was drawn down on three agreements our Croatia operations have with Hypo Alpe-Adria-Bank d.d. These loans bear a variable interest rate of the European Inter Bank Official Rate (“EURIBOR”) three-month rate plus 2.50% and are repayable in quarterly installments until April 1, 2011. As at June 30, 2006, a rate of 5.50% applied to these loans. These loans are secured by certain fixed assets of OK, which as at June 30, 2006 have a carrying value of approximately US$ 0.1 million.

(b) An amount of EUR 0.004 million (approximately US$ 0.005 million) was drawn down on an agreement our Croatia operations had with Hypo Alpe-Adria-Bank d.d. that bore interest at a rate of 7.25% with the final installment due July 31, 2006.

(c) EUR 0.1 million (approximately US$ 0.1 million) was drawn down by our Croatia operations under a loan agreement with BKS Bank fur Karnten and Steiermark AG. This loan bears a variable interest rate of EURIBOR three-month rate plus 3.00% and is repayable on October 1, 2006. As at June 30, 2006 a rate of 5.75% applied to this loan.

CENTRAL EUROPEAN MEDIA ENTERPRISES LTD.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Tabular amounts in US$ 000’s, except per share data)

(Unaudited)

Czech Republic

(d) As at June 30, 2006, there were no drawings by CET 21 under a four-year credit facility of CZK 1.2 billion (approximately US$ 53.5 million) with Ceska Sporitelna, a.s. (“CS”). This facility is secured by a guarantee of CME Media Services and a pledge of receivables, which are also subject to a factoring arrangement between CME Media Services and Factoring Ceska Sporitelna, a.s., a subsidiary of CS.

(e) CZK 250.0 million (approximately US$ 11.2 million), the full amount of the facility, has been drawn by CET 21 and CME Media Services under a working capital facility agreement with CS which matures on October 31, 2006 and bears interest at the three-month PRIBOR rate plus 1.65% (three-month PRIBOR relevant to drawings under this facility at June 30, 2006 was 2.09%). This working capital facility is secured by a pledge of receivables, which are also subject to a factoring arrangement between CME Media Services and Factoring Ceska Sporitelna.

(f) CZK 145.4 million (approximately US$ 6.5 million) was drawn under a CZK 600.0 million (approximately US$ 26.8 million) factoring facility between CME Media Services and Factoring Ceska Sporitelna. The facility bears interest at one-month PRIBOR plus 1.40% for the period that actively assigned accounts receivable are outstanding.

Romania

(g) As at June 30, 2006 and December 31, 2005, there were no drawings under a EUR 6.0 million (approximately US$ 7.7 million) overdraft facility with ING Bank N.V. Amsterdam. This facility is secured by cash collateral of New Romania Lei 11.7 million (approximately US$ 4.2 million) and the assignment of certain accounts receivable and allows drawings to be made in US dollars (bearing interest at one-month LIBOR plus 2.00%), Euro (bearing interest at one-month EURIBOR plus 2.00%) or New Romanian Lei (bearing interest at 'best market rate').

Slovenia

(h) On July 29, 2005, Pro Plus entered into a revolving facility agreement for up to EUR 37.5 million (approximately US$ 47.9 million) in aggregate principal amount with ING Bank N.V., Nova Ljubljanska Banka d.d., Ljubljana and Bank Austria Creditanstalt d.d., Ljubljana. The facility availability amortizes by 10.0% each year for four years commencing one year after signing, with 60.0% repayable after five years. This facility is secured by a pledge of the bank accounts of Pro Plus, the assignment of certain receivables, a pledge of our interest in Pro Plus and a guarantee of our wholly owned subsidiary CME Media Enterprises B.V.. Loans drawn under this facility will bear interest at a rate of EURIBOR for the period of drawing plus a margin of between 2.10% and 3.60% that varies according to the ratio of consolidated net debt to consolidated broadcasting cash flow for Pro Plus. As at June 30, 2006 and December 31, 2005, there were no drawings under this revolving facility.

CENTRAL EUROPEAN MEDIA ENTERPRISES LTD.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Tabular amounts in US$ 000’s, except per share data)

(Unaudited)

Total Group

At June 30, 2006, the maturity of our debt (including our Senior Notes) is as follows:

| 2006 | | $ | 17,852 | |

| 2007 | | | 164 | |

| 2008 | | | 172 | |

| 2009 | | | 182 | |

| 2010 | | | 193 | |

| 2011 and thereafter | | | 473,185 | |

Total | | $ | 491,748 | |

Capital Lease Commitments

We lease certain of our office and broadcast facilities as well as machinery and equipment under various leasing arrangements. The future minimum lease payments from continuing operations, by year and in the aggregate, under capital leases with initial or remaining non-cancelable lease terms in excess of one year, consisted of the following at June 30, 2006:

| 2006 | | $ | 619 | |

| 2007 | | | 647 | |

| 2008 | | | 647 | |

| 2009 | | | 496 | |

| 2010 | | | 496 | |

| 2011 and thereafter | | | 3,450 | |

| | | | 6,355 | |

| Less: amount representing interest | | | (1,683 | ) |

Present value of net minimum lease payments | | $ | 4,672 | |

12. FINANCIAL INSTRUMENTS

On April 27, 2006, we entered into currency swap agreements with two counterparties whereby we swapped a fixed annual coupon interest rate (of 9.0%) on notional principal of CZK 10.7 billion (approximately US$ 477.4 million), payable on July 15, October 15, January 15, and April 15, to the termination date of April 15, 2012 for a fixed annual coupon interest rate (of 9.0%) on notional principal of EUR 375.9 million (approximately US$ 480.6 million) receivable on July 15, October 15, January 15, and April 15, to the termination date of April 15, 2012.

The fair value of these financial instruments as at June 30, 2006 is a US$ 1.9 million liability.

These currency swap agreements reduce our exposure to movements in foreign exchange rates on a part of the CZK-denominated cash flows generated by our Czech Republic operations that is approximately equivalent in value to the Euro-denominated interest payments on our Senior Notes (see Note 5). They are financial instruments that are used to minimize currency risk and are considered an economic hedge of foreign exchange rates. These instruments have not been designated as hedging instruments as defined under SFAS No. 133, “Accounting for Derivative Instruments and Hedging Activities”, and so changes in their fair value are recorded in the consolidated statement of operations and in the consolidated balance sheet in other non-current liabilities.

CENTRAL EUROPEAN MEDIA ENTERPRISES LTD.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Tabular amounts in US$ 000’s, except per share data)

(Unaudited)

13. SHAREHOLDERS’ EQUITY

Preferred Stock

5,000,000 shares of Preferred Stock, with a $0.08 par value, were authorized as at June 30, 2006 and December 31, 2005. None were issued and outstanding as at June 30, 2006, and December 31, 2005.

Class A and B Common Stock

100,000,000 shares of Class A Common Stock and 15,000,000 shares of Class B Common Stock were authorized as at June 30, 2006 and December 31, 2005. The rights of the holders of Class A Common Stock and Class B Common Stock are identical except for voting rights. The shares of Class A Common Stock are entitled to one vote per share and the shares of Class B Common Stock are entitled to ten votes per share. Class B Common Stock is convertible into Class A Common Stock for no additional consideration on a one-for-one basis. Holders of each class of shares are entitled to receive dividends and upon liquidation or dissolution are entitled to receive all assets available for distribution to shareholders. The holders of each class have no preemptive or other subscription rights and there are no redemption or sinking fund provisions with respect to such shares.

On May 3, 2006, EL/RSLG Media Inc. converted 336,000 shares of Class B Common Stock, on May 9, 2006, Leonard A. Lauder converted 140,000 and LWG Family Partners L.P. converted 215,000 shares of Class B Common Stock, on May 11, 2006, EL/RSLG Media Inc. converted 4,895 shares of Class B Common Stock, and on June 23, 2006, Ronald Lauder converted 57,799 shares of Class B Common Stock into a total of 753,694 shares of Class A Common Stock (par value of US$ 0.1 million), which decreased Class B Common Stock to US$ 0.5 million.

On March 29, 2006, we sold 2,530,000 shares of our Class A Common Stock (including 330,000 sold pursuant to an underwriters’ option) and received net proceeds of approximately US$ 168.6 million.

14. STOCK-BASED COMPENSATION

The charge for stock-based compensation in our condensed consolidated statements of operations is as follows:

| | | For the Three Months Ended June 30, | | For the Six Months Ended June 30, | |

| | | 2006 | | 2005 | | 2006 | | 2005 | |

| | | | | | | | | | |

| Stock-based compensation charged under FIN 44 | | $ | - | | $ | (1,910 | ) | $ | - | | $ | 746 | |

| Stock-based compensation charged under SFAS 123(R) (2005: SFAS 123) | | | 730 | | | 499 | | | 1,418 | | | 944 | |

Total stock-based compensation | | $ | 730 | | $ | (1,411 | ) | $ | 1,418 | | $ | 1,690 | |

Stock-based compensation under FIN 44

For certain options issued in 2000, our stock-based compensation charge was calculated according to FASB Interpretation 44, “Accounting for Certain Transactions involving Stock Compensation" ("FIN 44"). This requires that compensation costs for modified awards are adjusted for increases and decreases in the intrinsic value in subsequent periods until that award is exercised, forfeited or expires unexercised, subject to a minimum of the original intrinsic value at the original measurement date. The last of these options were exercised on May 11, 2005.

CENTRAL EUROPEAN MEDIA ENTERPRISES LTD.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Tabular amounts in US$ 000’s, except per share data)

(Unaudited)

Stock-based compensation under SFAS 123(R)

Under the provisions of SFAS 123(R), the fair value of stock options is estimated on the grant date using the Black-Scholes option-pricing model and recognized ratably over the requisite service period.

2006 Option Grants

Pursuant to the Amended and Restated 1995 Stock Incentive Plan, the Compensation Committee of our Board of Directors awarded grant of options to employees to purchase 22,000 shares of our Class A Common Stock, with a vesting period of four years, on February 1, 2006, 12,500 such options, with a vesting period of four years, on May 1, 2006, and 50,000 such options, with a vesting period of four years, on June 8, 2006. Pursuant to the Amended and Restated 1995 Stock Incentive Plan, the Compensation Committee of our Board of Directors awarded grant of options to non-executive directors to purchase 48,000 shares of our Common Stock with a vesting period of four years. The exercise price of the granted options ranges from US$ 56.42 to US$ 64.81 per share. The fair value of the option grants was estimated on the date of the grant using the Black-Scholes option-pricing model, with the following assumptions used:

Date of Option Grant | | Number of Options Granted | | Risk-free interest rate (%) | | Expected term (years) | | Expected volatility (%) | | Dividend yield (%) | | Weighted-average fair value ($/share) | |

| | | | | | | | | | | | | | |

| February 1, 2006 | | | 22,000 | | | 4.52 | % | | 6.25 | | | 45.87 | % | | 0 | % | $ | 30.74 | |

| May 1, 2006 | | | 12,500 | | | 5.04 | % | | 6.25 | | | 44.55 | % | | 0 | % | $ | 33.21 | |

| June 7, 2006 | | | 48,000 | | | 4.98 | % | | 6.25 | | | 44.46 | % | | 0 | % | $ | 29.96 | |

| June 8, 2006 | | | 50,000 | | | 4.96 | % | | 6.25 | | | 44.53 | % | | 0 | % | $ | 28.83 | |

The expected stock price volatility was calculated based on an analysis of the historical stock price volatility of our shares and its peers for the preceding 6.25-year period. We consider this basis to represent the best indicator of expected volatility over the life of the option. The expected dividend yield for these grants was assumed to be 0%. The weighted average fair value of all the grants made in the three months ended June 30, 2006 was US$ 29.82 per option. The weighted average fair value of all the grants made in the six months ended June 30, 2006 was US$ 29.97 per option. In accordance with SFAS 123(R), the total fair value of the option grants made in the six months ended June 30, 2006 of US$ 4.0 million is being recognized as an expense in the consolidated statement of operations over the requisite service period of the award.

2005 Option Grants

Pursuant to the Amended and Restated 1995 Stock Incentive Plan, the Compensation Committee of our Board of Directors awarded a grant of options to non-executive directors and employees to purchase 122,000 shares of our Common Stock on June 2, 2005. These options vest in equal installments over 4 years. The exercise price of the granted options ranges from US$ 44.50 to US$ 46.73 per share, with a weighted average exercise price of US$ 44.61. The total fair value of the option grants was estimated on the date of the grant using the Black-Scholes option-pricing model, with the following assumptions used:

Date of Option Grant | | Number of Options Granted | | Risk-free interest rate (%) | | Expected term (years) | | Expected volatility (%) | | Dividend yield (%) | | Weighted-average fair value ($/share) | |

| | | | | | | | | | | | | | |

| June 2, 2005 | | | 122,000 | | | 3.74 | % | | 6.25 | | | 53.24 | % | | 0 | % | $ | 24.56 | |

The expected stock price volatility was calculated as 53.24% based on an analysis of the historical stock price volatility of the Company and its peers for the preceding 6.25-year period. The total fair value of these options of US$ 3.0 million is being recognized in the consolidated Statement of Operations over the requisite service period of the award.

CENTRAL EUROPEAN MEDIA ENTERPRISES LTD.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Tabular amounts in US$ 000’s, except per share data)

(Unaudited)

A summary of option activity for the six months ended June 30, 2006 is presented below:

| | | Shares | | Weighted Average Exercise Price per Share | | Weighted Average Remaining Contractual Term (years) | | Aggregate Intrinsic Value | |

| | | | | | | | | | |

| Outstanding at January 1, 2006 | | | 1,118,275 | | $ | 22.23 | | | 7.11 | | $ | 39,763 | |

| Granted | | | 132,500 | | | 58.82 | | | | | | | |

| Exercised | | | (77,250 | ) | | 13.85 | | | | | | | |

| Forfeited | | | (17,750 | ) | | 35.70 | | | | | | | |

Outstanding at June 30, 2006 | | | 1,155,775 | | $ | 26.90 | | | 7.18 | | $ | 41,958 | |

| Vested or expected to vest at June 30, 2006 | | | 1,062,902 | | | 25.83 | | | 7.11 | | | 39,715 | |

Exercisable at June 30, 2006 | | | 605,850 | | $ | 16.06 | | | 5.82 | | $ | 28,573 | |

The aggregate intrinsic value (the difference between the stock price on the last day of trading of the second quarter of 2006 and the exercise prices multiplied by the number of in-the-money options) represents the total intrinsic value that would have been received by the option holders had all option holders exercised their options as of June 30, 2006. This amount changes based on the fair value of our Common Stock. The total intrinsic value of options exercised during the six months ended June 30, 2006 and 2005, respectively, was US$ 4.0 million and US$ 21.4 million, respectively. As of June 30, 2006, there was US$ 9.1 million of total unrecognized compensation expense related to options. The expense is expected to be recognized over a weighted average period of 3.0 years. Proceeds received from the exercise of stock options was US$ 1.1 million and US$ 2.9 million for the six months ended June 30, 2006 and 2005, respectively.

15. EARNINGS PER SHARE

The components of basic and diluted earnings per share are as follows:

| | | For the Three Months Ended June 30, | | For the Six Months Ended June 30, | |

| | | 2006 | | 2005 | | 2006 | | 2005 | |

| | | | | | | | | | |

Net income / (loss) available for common shareholders | | $ | 8,522 | | $ | 25,459 | | $ | (9,742 | ) | $ | 17,510 | |

| | | | | | | | | | | | | | |

Weighted average outstanding shares of common stock (000’s) | | | 40,597 | | | 34,274 | | | 39,355 | | | 31,345 | |

| Dilutive effect of employee stock options (000’s) | | | 589 | | | 871 | | | - | | | 943 | |

Common stock and common stock equivalents (000’s) | | | 41,186 | | | 35,145 | | | 39,355 | | | 32,288 | |

| | | | | | | | | | | | | | |

Net income / (loss) per share: | | | | | | | | | | | | | |

| Basic | | $ | 0.21 | | $ | 0.74 | | $ | (0.25 | ) | $ | 0.56 | |

| Diluted | | $ | 0.21 | | $ | 0.72 | | $ | (0.25 | ) | $ | 0.54 | |

At June 30, 2006 and 2005, we did not include stock options to purchase 327,000 shares and 122,000 shares of Common Stock, respectively, in the calculations of diluted income / (loss) per share because their inclusion would be anti-dilutive.

CENTRAL EUROPEAN MEDIA ENTERPRISES LTD.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Tabular amounts in US$ 000’s, except per share data)

(Unaudited)

16. SEGMENT DATA