UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-08614

Brandes Investment Trust

(Exact name of registrant as specified in charter)

11988 El Camino Real, Suite 600

San Diego, CA 92130

(Address of principal executive offices) (Zip code)

Michael Glazer

Morgan, Lewis & Bockius LLP

355 South Grand Ave., Suite 4400

Los Angeles, CA 90071-3106

(Name and address of agent for service)

800-331-2979

Registrant’s telephone number, including area code

Date of fiscal year end: September 30, 2017

Date of reporting period: September 30, 2017

Item 1. Reports to Stockholders.

ANNUAL REPORT INTERNATIONAL EQUITY FUND GLOBAL EQUITY FUND GLOBAL EQUITY INCOME FUND GLOBAL OPPORTUNITIES VALUE FUND EMERGING MARKETS VALUE FUND INTERNATIONAL SMALL CAP EQUITY FUND CORE PLUS FIXED INCOME FUND CREDIT FOCUS YIELD FUND For the year ended September 30, 2017

| 2 | ||||

| 2 | ||||

| 8 | ||||

| 14 | ||||

| 21 | ||||

| 27 | ||||

| 33 | ||||

| 39 | ||||

| 46 | ||||

| 53 | ||||

| 57 | ||||

| 57 | ||||

| 60 | ||||

| 63 | ||||

| 66 | ||||

| 70 | ||||

| 75 | ||||

| 80 | ||||

| 85 | ||||

| 90 | ||||

| 92 | ||||

| 94 | ||||

| 98 | ||||

| 108 | ||||

| 132 | ||||

| 133 | ||||

| 137 |

1

Brandes International Equity Fund

The net asset value of the Brandes International Equity Fund (Class I Shares) advanced 15.33% in the 12 months ended September 30, 2017. For the same period, the MSCI EAFE Index rose 19.10%.

Holdings in industrials helped performance, driven by U.K.-based security services provider G4S and Brazilian regional jet manufacturer Embraer. Embraer benefited from higher revenue growth, cost cuts and an improved order pipeline.

Positions in financial services also aided returns, led by South Korean Hana Financial Group, Italy’s Intesa Sanpaolo and Dutch insurer Aegon, whose shares rose on improved earnings and capital position.

Other notable contributors were French pharmaceutical firm Sanofi, oil & gas companies Eni (Italy) and Repsol (Spain), as well as South Korean steel manufacturer POSCO. From a country perspective, the Fund benefited from holdings in Switzerland and off-index allocations to emerging markets, especially Brazil and South Korea.

Meanwhile, holdings in consumer discretionary appreciated, but not as much as the benchmark, thus weighing on relative returns. Similarly, positions in information technology (IT), which were flat in the period, underperformed the benchmark’s IT allocation.

The Fund’s cash position hurt relative returns in a rising market. We continue to exercise patience and caution when evaluating opportunities. Our cash will enable us to act quickly when we uncover potentially undervalued companies.

From a country standpoint, holdings in France detracted from relative returns, as did allocation to Sweden. Notable detractors included French retailer Carrefour and media company Publicis Groupe, as well as Swedish telecommunication equipment firm Ericsson. Additionally, South Korean auto components manufacturer Hyundai Mobis, Japanese pharmaceutical firm Taisho Pharmaceutical and U.K.-based home improvement retailer Kingfisher declined.

New purchases included Intesa Sanpaolo, pharmaceutical firms AstraZeneca (United Kingdom) and Astellas Pharma (Japan), as well as British advertising agency WPP Group. The investment committee also initiated positions in Russian mobile operator Mobile TeleSystems, South African bank Barclays Africa and Mexico’s Fibra Uno.

A Fibra (Fideicomiso de Infraestructura y Bienes Raíces) is an investment vehicle in Mexico that has similarities to a real estate investment trust (REIT) in the United States.

Fibra Uno (FUNO) is a Mexican trust formed primarily to acquire, own, develop and operate a broad range of commercial real estate in Mexico, including industrial, retail and office properties. FUNO has selectively assembled a

2

Brandes International Equity Fund

diversified portfolio of high-quality, well-located, income-producing commercial properties. The trust began trading on the Mexican stock exchange in 2011 and is the first — also currently the largest — publicly listed Fibra.

Over the past few years, FUNO’s shares have been under pressure, mainly due to the peso depreciation, which negatively affected the company’s real estate value and peso-denominated rental revenues. FUNO has more U.S. dollar-denominated debt than revenues; however, from a debt servicing perspective, it has what we consider solid revenue coverage of interest expense in U.S. dollars. Moreover, FUNO has predominantly long-term debt with a fixed interest rate. Hence, we believe FUNO should be relatively resilient against rising rates.

The selloff in FUNO’s shares was magnified by the election of Donald Trump as U.S. President, creating what we considered a good entry point for investment. In our view, FUNO’s positive attributes include:

| • | Strong earnings growth prospects through a sizeable development pipeline |

| • | A solid balance sheet and a seasoned management team |

| • | An income stream which is “inflation protected” as rents are contractually tied to inflation |

| • | Attractive dividend yield |

When we purchased FUNO, the company traded not only below our conservative estimate of its net assets value, but also less than its original initial public offering (IPO) price in U.S. dollars. At the time of its IPO, FUNO was less diversified than it is today and was operating in a developing industry that was untested. Moreover, while the market seems focused on U.S. policy concerns, we appreciate that the company’s property portfolio has limited direct exposure to major exporters to the United States. We also like that management continues to demonstrate strong capital allocation, with a conservative balance sheet that should enable the company to be opportunistic, in our view, if the market conditions in Mexico weaken further.

Other activity included the divestments of Japanese imaging company Canon and Irish construction materials manufacturer CRH. The investment committee also exited the Fund’s position in TIM Participacoes (TSU), the fourth-largest Brazilian telecommunications firm by sales and the second-largest by wireless subscribers.

We first took a small position in TSU in the mid 2000’s. We were attracted by its 17% free-cash-flow yield, and the fact that the Brazilian telecommunications market was still in the early stages of growth, with wireless penetration at only 30%.

At the time, TSU’s shares were under pressure from concerns about unfavorable treatment of minority shareholders by TSU’s controlling shareholder, Telecom Italia. Through multiple transactions over the last 10 years, the company was increasingly consolidated into Telecom Italia’s Brazilian holdings. Many of the

3

Brandes International Equity Fund

transactions were value destructive for minority shareholders, although not to the extent the market originally feared, in our opinion. Despite these challenges, we believed TSU’s attractive price, combined with the potential growth in TSU’s underpenetrated market, warranted an investment.

We added to our position in TSU, notably in 2008 and 2012, when valuations became more attractive. We pared our allocation in early 2014 after the company’s share price appreciated significantly. In 2015 and 2016, the company endured a deep economic recession in Brazil, sending its share price to a level that reflected a significant discount to our estimate of intrinsic value. Accordingly, we increased our position.

In the past year, TSU enjoyed renewed investor interest due largely to improved operations, which enabled the company to grow its revenue, as well as positive industry developments and rumors of a possible acquisition. As TSU’s shares became fully valued based on our analysis, we exited our position.

Outlook

As of September 30, 2017, the Fund’s largest overweight positions were in emerging markets, France, and Italy. From an industry standpoint, the Fund held key overweights in pharmaceuticals, oil, gas & consumable fuels, and food retailing.

We maintained underweight positions to companies based in Germany and Australia, as well in the industrials, materials and real estate sectors.

Meanwhile, we have increasingly found investment opportunities in the consumer discretionary sector. As of September 30, the Fund held a higher allocation to the sector than the benchmark, after having an equal weight a year prior. The automobile and auto component industries continued to represent our most significant allocations, but more recently, we have started to find new opportunities in the media industry, as exemplified by our positions in Publicis and WPP Group.

Events across the globe this year may serve as a good reminder that macroeconomic and geopolitical factors can affect individual businesses differently. As one of the first asset managers to bring a global perspective to value investing, Brandes relies on an established research infrastructure that enables us to analyze how each company may be affected by events globally. Our analyst teams have extensive knowledge of industries worldwide, and each team member’s perspective allows us to think and invest independently from the market consensus.

Thank you for your business and continued trust.

Sincerely yours,

The Brandes International Large-Cap Investment Committee

Brandes Investment Trust

Because the values of the Fund’s investments will fluctuate with market conditions, so will the value of your investment in the Fund. You could lose

4

Brandes International Equity Fund

money on your investment in the Fund, or the Fund could underperform other investments. The values of the Fund’s investments fluctuate in response to the activities of individual companies and general stock market and economic conditions. In addition, the performance of foreign securities depends on the political and economic environments and other overall economic conditions in the countries where the Fund invests. Emerging country markets involve greater risk and volatility than more developed markets. Some emerging markets countries may have fixed or managed currencies that are not free-floating against the U.S. dollar. Certain of these currencies have experienced, and may experience in the future, substantial fluctuations or a steady devaluation relative to the U.S. dollar.

Past performance is not a guarantee of future results.

Dividend Yield: Dividends per share divided by price per share.

Free Cash Flow: Total cash flow from operations less capital expenditures.

Free Cash Flow Yield: Free cash flow per share divided by price per share.

Intrinsic Value: The actual value of a company or an asset based on an underlying perception of its true value.

The declaration and payment of shareholder dividends are solely at the discretion of the issuer and are subject to change at any time.

Please refer to the Schedule of Investments in the report for complete holdings information. Fund holdings, geographic allocations and/or sector allocations are subject to change at any time and are not considered a recommendation to buy or sell any security.

The foregoing reflects the thoughts and opinions of Brandes Investment Partners® exclusively and is subject to change without notice. Brandes Investment Partners® is a registered trademark of Brandes Investment Partners, L.P. in the United States and Canada.

Must be preceded or accompanied by a prospectus.

Index Guide

The MSCI EAFE Index with net dividends captures large and mid cap representation of developed market countries excluding the U.S. and Canada.

MSCI has not approved, reviewed or produced this report, makes no express or implied warranties or representations and is not liable whatsoever for any data in the report. You may not redistribute the MSCI data or use it as a basis for other indices or investment products.

One cannot invest directly in an index.

The Brandes International Equity Fund is distributed by ALPS Distributors, LLC.

5

Brandes International Equity Fund

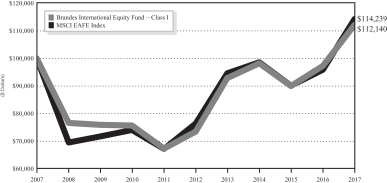

The following chart compares the value of a hypothetical $100,000 investment in the Brandes International Equity Fund – Class I from September 30, 2007 to September 30, 2017 with the value of such an investment in the MSCI EAFE (Europe, Australasia and Far East) Index for the same period.

Value of $100,000 Investment vs MSCI EAFE (Europe, Australasia and Far East) Index (Unaudited)

| Average Annual Total Return Periods Ended September 30, 2017 | ||||||||||||||||

| One Year | Five Years | Ten Years | Since Inception(1) | |||||||||||||

Brandes International Equity Fund | ||||||||||||||||

Class A* | 15.07 | % | 8.61 | % | 0.97 | % | 7.99 | % | ||||||||

Class A* (with maximum sales charge) | 8.44 | % | 7.33 | % | 0.37 | % | 7.68 | % | ||||||||

Class C* | 14.19 | % | 7.81 | % | 0.18 | % | 7.16 | % | ||||||||

Class I | 15.33 | % | 8.83 | % | 1.15 | % | 8.22 | % | ||||||||

Class R6* | 15.48 | % | 8.93 | % | 1.22 | % | 8.29 | % | ||||||||

MSCI EAFE (Europe, Australasia, and Far East) Index | 19.10 | % | 8.38 | % | 1.34 | % | 4.93 | % | ||||||||

| (1) | The inception date is January 2, 1997. |

| * | Performance shown prior to January 31, 2011 for Class A shares reflects the performance of Class I shares adjusted to reflect Class A expenses. Performance shown prior to January 31, 2013 for Class C shares reflects the performance of Class I shares adjusted to reflect Class C expenses. Performance shown prior to February 1, 2016 for Class R6 shares reflects the performance of Class I shares adjusted to reflect Class R6 expenses. |

Performance data quoted represents past performance; past performance does not indicate future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or

6

Brandes International Equity Fund

less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 800-331-2979.

The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The Advisor has a fee waiver arrangement in place to limit the Fund’s annual operating expenses.

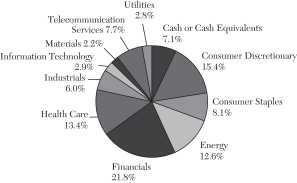

Sector Allocation as a Percentage of Total Investments as of

September 30, 2017 (Unaudited)

The sector classifications represented in the graph above and industry classifications represented in the Schedule of Investments are in accordance with Global Industry Classification Standard (GICS®), which was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor Financial Services LLC.

7

Dear Fellow Investor,

The net asset value of the Brandes Global Equity Fund (Class I Shares) rose 17.48% in the 12 months ended September 30, 2017. For the same period, the MSCI World Index increased 18.17%.

A number of U.S.-based financial services holdings significantly boosted absolute performance, most notably Citigroup, Bank of America, State Street and PNC Financial Services. These firms appreciated on the back of improved earnings and the potential benefit of U.S. interest-rate hikes.

Additionally, several U.S.-based banks announced increased dividends and share repurchase authorizations following the results of the Federal Reserve’s stress tests and comprehensive capital analysis and review, which measures the capital adequacy and planning processes of the largest U.S. banks. Citigroup announced it would double its dividend and repurchase over $15 billion of its shares.

Other top contributors included South Korea-based Samsung Electronics and France-based pharmaceutical firm Sanofi.

The Fund’s most significant return detractors relative to its benchmark were Sweden-based telecommunications equipment firm Ericsson, South Korea-based auto components manufacturer Hyundai Mobis, U.K.-based pharmaceutical firm GlaxoSmithKline and U.S.-based pharmacy benefit manager Express Scripts.

Ericsson declined after reporting weaker earnings. However, the company announced plans to reduce costs to improve margins. Hyundai Mobis’ share price fell on the back of slowing Chinese demand, which was in part due to political tensions between South Korea and China.

A significant headwind to relative performance in the first nine months of calendar year 2017 had been value stocks’ underperformance versus growth stocks, as measured by the MSCI World Value Index and the MSCI World Growth Index. Although value stocks posted strong returns in the second half of 2016, they lagged growth stocks in the first nine months of 2017 by more than 800 basis points, wiping out the relative outperformance from 2016.

While the Fund generated strong absolute performance, it underperformed the broader MSCI World Index in a significantly appreciating global market. The primary drivers of underperformance included:

| • | Holdings in the health care sector |

This was led by the share-price drop in U.S.-based Express Scripts

| • | European retailers |

The Fund’s European food retailer holdings were roughly flat for the first three quarters of 2017, thus detracting from relative returns in a rising market.

8

Brandes Global Equity Fund

| • | Conservative cash position |

Although the Fund’s cash position declined slightly after the investment committee redeployed some capital, it weighed on relative returns in a rising market. We continue to exercise patience and caution when evaluating opportunities and our cash position will enable us to act quickly when we uncover potentially undervalued companies.

In a fairly busy period for buys and sells, the Fund’s Investment Committee initiated several positions, including U.K.-based Kingfisher, Imperial Brands and WPP Group, as well as U.S.-based Cardinal Healthcare and HCA Healthcare.

Kingfisher is Europe’s largest and the world’s third-largest home improvement retailer, operating in 10 countries across Europe. The company’s most important markets are the United Kingdom, France and Poland. Kingfisher has faced challenges in the aftermath of the Brexit vote and increased competition in key markets. We took advantage of Kingfisher’s share-price decline to initiate a position in the company.

An industry leader in Europe, Kingfisher has nonetheless been less profitable than many of its peers in other regions, most notably U.S. home improvement stores Home Depot and Lowes. Additionally, the company also faces long-term challenges, most significantly from increasing competition from online and other brick-and-mortar retailers.

The company has embarked on restructuring efforts in order to improve operations. The moves have shown positive results, putting the company on course to pursue its long-term goals. We believe while it is unlikely that Kingfisher will be able to match its U.S. peers in terms of profitability, it has enough room for improvement to help offset the near-term cyclical issues in the United Kingdom.

HCA Healthcare is the largest for-profit hospital operator in the United States, where it has operations across 20 states and 5% of total hospital admissions. It also has a presence in the United Kingdom. The company has been weighed down by the uncertainty surrounding U.S. health care policy and reimbursement pressures for care and services. However, it is our view that these concerns have been more than priced into HCA, which traded at 12x free cash flow as of September 30.

We believe the company is an attractive investment due to its history of strong cash flows and returns on capital. Additionally, we are attracted to the company’s stable and recurring earnings, as well as its reasonable growth prospects.

Meanwhile, the Fund’s investment committee divested several positions that reached our estimates of intrinsic value. These included Latin American telecommunication services companies TIM Participacoes and America Movil, U.S.-based Exelon and Xilinx, as well as resorts operator Genting Malaysia.

9

Brandes Global Equity Fund

Outlook

As of September 30, the Brandes Global Equity Fund exhibited more attractive valuation characteristics, in our opinion, and a higher dividend yield than the MSCI World Index.

Allocations to emerging markets, France and the United Kingdom represented the largest overweights. From an industry standpoint, key areas of exposure were in financials, pharmaceuticals, oil & gas, food retailing and automobiles.

The Fund maintained its largest underweight in the United States. On the sector level, significant under-allocations were in industrials, materials and technology.

We continued to reduce our information technology allocation, which was less than half the benchmark’s weight as of September 30. At the same time, we increasingly found value potential in the health care sector as our allocation increased to almost 19% compared to over 12% for the MSCI World Index. While we maintained a significant exposure to pharmaceuticals, the main driver of the increased allocation has been health care service companies, such as drug distributor Cardinal Health and hospital operator HCA Healthcare (see commentary above).

As market dynamics constantly present challenges and opportunities, Brandes maintains a disciplined process of stock selection based on fundamental, detailed research on companies throughout the world. We are always focused on company valuations and margin of safety — because we believe this careful approach is the most prudent way to pursue growth for the Fund over the long term.

Thank you, as always, for your business and continued trust.

Sincerely yours,

The Brandes Global Large-Cap Investment Committee

Brandes Investment Trust

Because the values of the Fund’s investments will fluctuate with market conditions, so will the value of your investment in the Fund. You could lose money on your investment in the Fund, or the Fund could underperform other investments. The values of the Fund’s investments fluctuate in response to the activities of individual companies and general stock market and economic conditions. In addition, the performance of foreign securities depends on the political and economic environments and other overall economic conditions in the countries where the Fund invests. Emerging country markets involve greater risk and volatility than more developed markets. Some emerging markets countries may have fixed or managed currencies that are not free-floating against the U.S. dollar. Certain of these currencies have experienced, and may experience in the future, substantial fluctuations or a steady devaluation relative to the U.S. dollar.

Past performance is not a guarantee of future results.

10

Brandes Global Equity Fund

Basis Point: 1/100 of 1%.

Book Value: Assets minus liabilities. Also known as shareholders’ equity.

Free Cash Flow: Total cash flow from operations less capital expenditures.

Intrinsic Value: The actual value of a company or an asset based on an underlying perception of its true value.

Margin of Safety: The discount of a security’s market price to what the firm believes is the intrinsic value of that security.

Yield: Annual income from the investment (dividend, interest, etc.) divided by the current market price of the investment.

Please refer to the Schedule of Investments in the report for complete holdings information. Fund holdings, geographic allocations and/or sector allocations are subject to change at any time and are not considered a recommendation to buy or sell any security.

The foregoing reflects the thoughts and opinions of Brandes Investment Partners® exclusively and is subject to change without notice. Brandes Investment Partners® is a registered trademark of Brandes Investment Partners, L.P. in the United States and Canada.

Must be preceded or accompanied by a prospectus.

Index Guide

The MSCI World Index with net dividends measures equity market performance of developed markets.

The MSCI World Value Index with net dividends captures large and mid cap securities across developed market countries exhibiting value style characteristics, defined using book value to price, 12-month forward earnings to price, and dividend yield.

The MSCI World Growth Index with gross dividends captures large and mid cap securities across developed market countries exhibiting growth style characteristics, defined using long-term forward earnings per share (EPS) growth rate, short-term forward EPS growth rate, current internal growth rate, long-term historical EPS growth trend, and long-term historical sales per share growth trend.

MSCI has not approved, reviewed or produced this report, makes no express or implied warranties or representations and is not liable whatsoever for any data in the report. You may not redistribute the MSCI data or use it as a basis for other indices or investment products.

One cannot invest directly in an index

The Brandes Global Equity Fund is distributed by ALPS Distributors, LLC.

11

Brandes Global Equity Fund

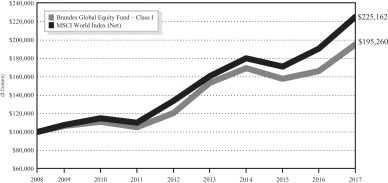

The following chart compares the value of a hypothetical $100,000 investment in the Brandes Global Equity Fund – Class I from its inception (October 6, 2008) to September 30, 2017 with the value of such an investment in the MSCI World Index for the same period.

Value of $100,000 Investment vs MSCI World Index (Unaudited)

| Average Annual Total Return Periods Ended September 30, 2017 | ||||||||||||||||

| One Year | Three Years | Five Years | Since Inception(1) | |||||||||||||

Brandes Global Equity Fund | ||||||||||||||||

Class A* | 17.20 | % | 4.61 | % | 9.85 | % | 7.50 | % | ||||||||

Class A* (with maximum sales charge) | 10.48 | % | 2.56 | % | 8.55 | % | 6.79 | % | ||||||||

Class C* | 16.31 | % | 3.84 | % | 9.04 | % | 6.67 | % | ||||||||

Class I | 17.48 | % | 4.87 | % | 10.12 | % | 7.73 | % | ||||||||

MSCI World Index | 18.17 | % | 7.69 | % | 10.99 | % | 9.46 | % | ||||||||

| (1) | The inception date is October 6, 2008. |

| * | Performance shown prior to January 31, 2011 for Class A shares reflects the performance of Class I shares adjusted to reflect Class A expenses. Performance shown prior to January 31, 2013 for Class C shares reflects the performance of Class I shares adjusted to reflect Class C expenses. |

Performance data quoted represents past performance; past performance does not indicate future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 800-331-2979.

12

Brandes Global Equity Fund

The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The Advisor has a fee waiver arrangement in place to limit the Fund’s annual operating expenses.

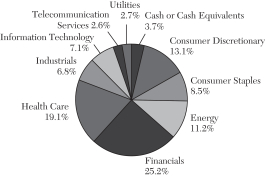

Sector Allocation as a Percentage of Total Investments as of

September 30, 2017 (Unaudited)

The sector classifications represented in the graph above and industry classifications represented in the Schedule of Investments are in accordance with Global Industry Classification Standard (GICS®), which was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor Financial Services LLC.

13

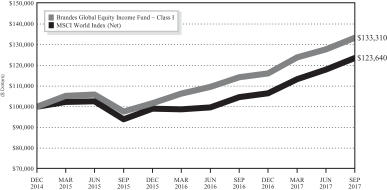

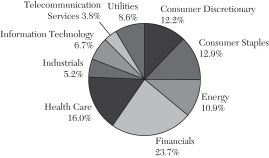

Brandes Global Equity Income Fund

Dear Fellow Investor,

The net asset value of the Brandes Global Equity Income Fund (Class I Shares) rose 16.71% in the 12 months ended September 30, 2017. For the same period, the MSCI World Index increased 18.17%.

The Fund’s holdings in emerging markets, France and in the energy sector significantly boosted absolute performance.

Within emerging markets, notable contributors included South Korea-based Samsung Electronics, Chilean electric utility Enel Chile, as well as Brazil-based telecommunications firm Telefonica Brasil and water utility Companhia Paranaense de Energia (Copel).

In France, positive contributors included pharmaceutical firm Sanofi, luxury goods company LVMH, electrical equipment supplier Schneider Electric and utility company Engie.

Several holdings in the energy sector advanced in the third quarter, offsetting the declines from the first and second quarters of 2017, as they benefited from the rise in oil prices and improved earnings. The Fund’s energy holdings outperformed the energy sector of the MSCI World Index. Top contributors were Netherlands-based Royal Dutch Shell, Italy-based ENI, U.K.-based BP, France-based Total and U.S.-based Chevron.

Other contributors included U.S.-based PNC Financial, Western Digital (sold in the second quarter), Microsoft and Wells Fargo.

A significant headwind to relative performance in the first nine months of calendar year 2017 had been value stocks’ underperformance versus growth stocks, as measured by the MSCI World Value Index and the MSCI World Growth Index. Although value stocks posted strong returns in the second half of 2016, they lagged growth stocks in the first nine months of 2017 by more than 800 basis points, wiping out the relative outperformance from 2016.

While the Fund’s absolute performance was strong, the Fund underperformed the broader MSCI World Index in a significantly appreciating global market. The primary drivers of underperformance were:

| • | Holdings in the health care sector |

Including drug distributor Cardinal Health and pharmaceutical firm GlaxoSmithKline

| • | European retailers |

The Fund’s European food retailer holdings were roughly flat for much of the period, thus detracting from relative returns in a rising market.

| • | Conservative cash position |

Although the Fund’s cash position declined slightly after the investment committee redeployed some capital, it weighed on relative returns in a

14

Brandes Global Equity Income Fund

rising market. We continue to exercise patience and caution when evaluating opportunities and our cash position will enable us to act quickly when we uncover potentially undervalued companies.

Sweden-based telecommunications equipment firm Ericsson also weighed on performance. The company’s share price declined after reporting weaker earnings on the back of a lull in demand for wireless network equipment from carriers. However, it announced plans to reduce costs to improve margins.

We believe despite the currently weak carrier spending environment, Ericsson should see its profitability pick up if spending starts to recover from its current decline. Moreover, we hold the view that the company remains well positioned to benefit from an industry consolidation that has occurred over the last several years.

Throughout the fiscal year, the Fund’s Investment Committee initiated positions in companies exhibiting appealing valuations relative to our intrinsic value estimates and those with attractive dividend yield.

New additions included WPP Group, the world’s largest ad agency holding company by revenue. Its brands include Ogilvy & Mather, JWT, Young & Rubicam, Grey, Group M and Kantar.

In our opinion, the business model of ad agencies is attractive and resilient amid changing economic conditions, given their variable-cost nature and technological neutrality (i.e., generally limited disruption from how ads are viewed). Over the past year, organic revenue growth for the ad agency industry has slowed, in part due to tough comparisons with 2016, a year that saw elevated ad spending related to the Summer Olympics in Brazil and the U.S. presidential election.

A number of factors have contributed to a contraction in valuation multiples for the ad agency industry, including:

| • | Slowing topline growth |

| • | Reduced ad spending by consumer packaged goods companies |

| • | Concerns about evolving technological and competitive landscape |

These concerns, which we view as short term in nature and overdone in magnitude, have created several potentially undervalued investment opportunities.

Among large, publicly listed ad agency holding companies, WPP has leading exposures to potential growth from the digital space and from emerging markets. We are attracted to the company’s strong business model, healthy cash flows and steady pace of shareholder returns. Moreover, the stock’s recent underperformance has led to an appealing valuation, in our view. The company traded at just 11x forward earnings as of September 30 and had a 4.0% dividend yield.

The investment committee also purchased Switzerland-based financial firm Credit Suisse (with a dividend yield of 4.5% as of September 30).

15

Brandes Global Equity Income Fund

The second-largest bank in Switzerland, Credit Suisse possesses one of the strongest private-banking and wealth-management platforms in the world, offering leverage to wealth creation in emerging markets. We are attracted to the appealing growth potential of the company’s businesses and its improved capital position. At current valuation levels, we feel Credit Suisse’s strengths are underappreciated by the market.

Other Fund activity included the sale of Switzerland-based luxury goods firm Richemont, as well as U.S.-based computer data storage firm Western Digital and semiconductor company Xilinx. These companies’ share prices rose toward our intrinsic value estimates.

Outlook

As of September 30, the Brandes Global Equity Income Fund exhibited more appealing valuations than the benchmark, in our opinion. The Fund also had a higher dividend yield of 3.9% compared to 2.4% for the MSCI World Index.

Allocations to emerging markets, France and the United Kingdom represented the Fund’s largest overweights. From an industry standpoint, key areas of exposure were in pharmaceuticals, oil & gas, food & staples retailing, capital markets and banks.

The Fund maintained its largest underweights in the United States and Japan. On the sector level, significant under-allocations were in industrials, information technology and materials.

We continued to reduce our information technology sector allocation, which was less than half the benchmark’s weight as of September 30. After having an overweight position in technology for several years, largely in what we called “boring” or mature technology companies mostly based in the United States, the Fund is now underweight the sector. Several companies from this group have had strong share-price appreciation, moving closer to or exceeding our intrinsic value estimates. Consequently, the investment committee decided to pare or sell several of our tech holdings over the past year. While the Fund’s recent underweight has hurt relative performance, it is not surprising that we are starting to find fewer value opportunities in a sector that has performed so well.

As market dynamics constantly present challenges and opportunities, Brandes maintains a disciplined process of stock selection based on fundamental, detailed research on companies throughout the world. For the Fund, we are always focused on company valuations and margin of safety with an additional consideration for yield and the potential for dividend growth. We believe this careful approach is the most prudent way to pursue growth and income for the Fund over the long term.

Thank you for your business and continued trust.

Sincerely yours,

The Brandes Global Large-Cap Investment Committee

Brandes Investment Trust

16

Brandes Global Equity Income Fund

Because the values of the Fund’s investments will fluctuate with market conditions, so will the value of your investment in the Fund. You could lose money on your investment in the Fund, or the Fund could underperform other investments. The values of the Fund’s investments fluctuate in response to the activities of individual companies and general stock market and economic conditions. In addition, the performance of foreign securities depends on the political and economic environments and other overall economic conditions in the countries where the Fund invests. Emerging country markets involve greater risk and volatility than more developed markets. Some emerging markets countries may have fixed or managed currencies that are not free-floating against the U.S. dollar. Certain of these currencies have experienced, and may experience in the future, substantial fluctuations or a steady devaluation relative to the U.S. dollar. Growth stocks typically are more volatile than value stocks; however, value stocks have a lower expected growth rate in earnings and sales.

Past performance is not a guarantee of future results.

Basis Point: 1/100 of 1%.

Book Value: Assets minus liabilities. Also known as shareholders’ equity.

Free Cash Flow: Total cash flow from operations less capital expenditures.

Intrinsic Value: The actual value of a company or an asset based on an underlying perception of its true value.

Margin of Safety: The discount of a security’s market price to what the firm believes is the intrinsic value of that security.

Yield: Annual income from the investment (dividend, interest, etc.) divided by the current market price of the investment.

SEC 30-Day Yield (Class I Shares): 2.82% (subsidized); -12.76% (unsubsidized). This calculation is based on a 30-day period ending on the last day of the month shown. It is computed by dividing the net investment income per share earned during the period by the maximum offering price per share on the last day of the period. The yield figure reflects the dividends and interest earned during the period, after the deduction of the fund expenses. A subsidized yield takes into consideration the expenses paid by the advisor.

Please refer to the Schedule of Investments in the report for complete holdings information. Fund holdings, geographic allocations and/or sector allocations are subject to change at any time and are not considered a recommendation to buy or sell any security.

The declaration and payment of shareholder dividends are solely at the discretion of the issuer and are subject to change at any time.

17

Brandes Global Equity Income Fund

The foregoing reflects the thoughts and opinions of Brandes Investment Partners® exclusively and is subject to change without notice. Brandes Investment Partners® is a registered trademark of Brandes Investment Partners, L.P. in the United States and Canada.

Must be preceded or accompanied by a prospectus.

Index Guide

The MSCI World Index with net dividends measures equity market performance of developed markets.

The MSCI World Value Index with net dividends captures large and mid cap securities across developed market countries exhibiting value style characteristics, defined using book value to price, 12-month forward earnings to price, and dividend yield.

The MSCI World Growth Index with gross dividends captures large and mid cap securities across developed market countries exhibiting growth style characteristics, defined using long-term forward earnings per share (EPS) growth rate, short-term forward EPS growth rate, current internal growth rate, long-term historical EPS growth trend, and long-term historical sales per share growth trend.

MSCI has not approved, reviewed or produced this report, makes no express or implied warranties or representations and is not liable whatsoever for any data in the report. You may not redistribute the MSCI data or use it as a basis for other indices or investment products.

One cannot invest directly in an index.

The Brandes Global Equity Income Fund is distributed by ALPS Distributors, LLC.

18

Brandes Global Equity Income Fund

The following chart compares the value of a hypothetical $100,000 investment in the Brandes Global Equity Income Fund – Class I from its inception (December 31, 2014) to September 30, 2017 with the value of such an investment in the MSCI World Index for the same period.

Value of $100,000 Investment vs MSCI World Index (Unaudited)

| Average Annual Total Return Periods Ended September 30, 2017 | ||||||||

| One Year | Since Inception(1) | |||||||

Brandes Global Equity Income Fund | ||||||||

Class A | 18.81 | % | 11.84 | % | ||||

Class A (with maximum sales charge) | 11.96 | % | 9.46 | % | ||||

Class C | 16.01 | % | 10.19 | % | ||||

Class I | 16.71 | % | 11.03 | % | ||||

MSCI World Index | 18.17 | % | 8.03 | % | ||||

| (1) | The inception date is December 31, 2014. |

Performance data quoted represents past performance; past performance does not indicate future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 800-331-2979.

19

Brandes Global Equity Income Fund

The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The Advisor has a fee waiver arrangement in place to limit the Fund’s annual operating expenses.

Sector Allocation as a Percentage of Total Investments as of September 30, 2017 (Unaudited)

The sector classifications represented in the graph above and industry classifications represented in the Schedule of Investments are in accordance with Global Industry Classification Standard (GICS®), which was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor Financial Services LLC.

20

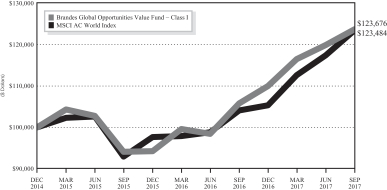

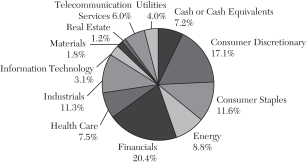

Brandes Global Opportunities Value Fund

Dear Fellow Investor,

The net asset value of the Brandes Global Opportunities Value Fund (Class I Shares) rose 16.91% in the 12 months ended September 30, 2017. For the same period, the MSCI ACWI (All Country World) Index advanced 18.65%.

Allocations to financials, especially banks, and industrials, led by holdings in machinery, helped performance significantly. The Fund also benefited from positions in health care and consumer staples. From a country standpoint, holdings in the United States, where we held a significant underweight, boosted absolute and relative returns, as did positions in Brazil.

Notable performers included U.S.-based banks Citigroup and Bank of America, as well as engine manufacturer Briggs & Stratton. Additionally, Brazilian regional jet manufacturer Embraer, South Korean Samsung, Austria-domiciled Erste Group Bank and Russian Sberbank contributed positively to returns.

Holdings in consumer discretionary appreciated, but not as much as the benchmark, thus detracting from relative returns. Similarly, positions in information technology, where we held a significant underweight, helped absolute returns but underperformed the benchmark’s sector allocation.

Moreover, the Fund’s cash position hurt performance in a rising market. The investment committee continues to exercise patience and caution when evaluating opportunities. Our cash will enable us to act quickly when we uncover potentially undervalued companies.

At the company level, notable detractors included U.K.-based real estate firm Countrywide, South Korean auto components manufacturer Hyundai Mobis, Hong Kong-based satellite operator APT Satellite Holdings and French retailer Carrefour.

New purchases included U.S.-based pharmaceuticals distributor McKesson and pharmacy benefit manager Express Scripts, Chinese telecommunication company China Mobile, Irish beverage company C&C Group, and French advertising agency Publicis Groupe.

Publicis is the world’s third-largest global advertising agency holding company. It owns many of the industry’s most valuable brands, such as Saatchi & Saatchi, Leo Burnett, Razorfish, ZenithOptimedia and Starcom MediaVest. The ad agency has historically been a well-run company with a sound balance sheet and industry-leading margins.

In our opinion, the business model of ad agencies is attractive and resilient given their variable-cost nature and technological neutrality (i.e., generally limited disruption from how ads are viewed). Over the past year, organic revenue growth for the ad agency industry has slowed, in part due to tough comparisons with 2016, a year that saw elevated ad spending related to the Summer Olympics in Brazil and the U.S. presidential election.

21

Brandes Global Opportunities Value Fund

A number of factors have contributed to a contraction in valuation multiples for the ad agency industry, including:

| • | Slowing topline growth |

| • | Reduced ad spending by fast-moving consumer goods (FMCG) companies. FMCG is composed of products that tend to have short shelf lives, such as packaged foods, beverages and toiletries. |

| • | Concerns about evolving technological and competitive landscape |

These concerns, which we view as short term in nature and overdone in magnitude, have created several potentially undervalued investment opportunities.

Market concerns for Publicis include slowing organic growth, a handful of recent account losses and its acquisition of Sapient (its largest acquisition to date), which was seen as expensive.

We believe excessive short-term pessimism centered on these recent missteps has created an attractive entry point in Publicis’ shares for long-term investors. Historically, Publicis management has displayed, in our opinion, an admirable track record of profitability, earnings growth, operational execution and successful acquisition integration. We do not view recent client losses and the potential overpayment for Sapient as evidence of permanent structural changes in the business, and we believe Publicis is well positioned to return to levels of growth in line with its peers. Given its strong free-cash-flow generation, we also expect the company will quickly de-lever its balance sheet.

During the period, the investment committee also purchased shares of Mexico-based real estate investment trust Fibra Uno and U.K.-based Kingfisher, Europe’s largest and the world’s third-largest home improvement retailer.

Kingfisher operates in 10 countries across Europe, where the company’s most important markets are the United Kingdom, France and Poland. Kingfisher has faced challenges in the aftermath of the Brexit vote (the United Kingdom’s decision to leave the European Union) and increased competition in key markets. We took advantage of Kingfisher’s share-price decline to initiate a position in the company.

An industry leader in Europe, Kingfisher has nonetheless been less profitable than many of its peers in other regions, most notably U.S. home improvement stores Home Depot and Lowes. Additionally, the company also faces long-term challenges, most significantly increasing competition from online and other brick-and-mortar retailers.

In 2008, Kingfisher appointed a new chief executive officer and began a restructuring effort to improve operations. The move has shown positive results, putting the company on course to pursue its long-term goals. We believe that while it is unlikely Kingfisher will be able to match its U.S. peers in terms of profitability, it has enough room for improvement to help offset the near-term cyclical issues in the United Kingdom.

22

Brandes Global Opportunities Value Fund

Other activity included the divestments of U.S.-based computer data storage company Western Digital and oil company Chesapeake Energy, South Korean bank KB Financial Group, and Brazilian telecommunications firm TIM Participacoes.

Outlook

As of September 30, 2017, the Fund held key overweights in real estate and consumer discretionary, and key underweights in information technology and financials.

We maintained a large underweight in the United States and a notable overweight in the United Kingdom. We also continued to find many value opportunities in emerging markets. The region accounted for about a third of the Fund as of September 30, with Brazil and South Korea representing key areas of exposure.

Events across the globe this year may serve as a good reminder that macroeconomic and geopolitical factors can affect individual businesses differently. As one of the first asset managers to bring a global perspective to value investing, Brandes relies on an established research infrastructure that enables us to analyze how each company may be affected by events globally. Our analyst teams have extensive knowledge of industries worldwide, and each team member’s perspective allows us to think and invest independently from the market consensus.

Thank you for your business and continued trust.

Sincerely yours,

The Brandes All-Cap Investment Committee

Brandes Investment Trust

Because the values of the Fund’s investments will fluctuate with market conditions, so will the value of your investment in the Fund. You could lose money on your investment in the Fund, or the Fund could underperform other investments. The values of the Fund’s investments fluctuate in response to the activities of individual companies and general stock market and economic conditions. In addition, the performance of foreign securities depends on the political and economic environments and other overall economic conditions in the countries where the Fund invests. Emerging country markets involve greater risk and volatility than more developed markets. Some emerging markets countries may have fixed or managed currencies that are not free-floating against the U.S. dollar. Certain of these currencies have experienced, and may experience in the future, substantial fluctuations or a steady devaluation relative to the U.S. dollar.

Past performance is not a guarantee of future results.

Free Cash Flow: Total cash flow from operations less capital expenditures.

23

Brandes Global Opportunities Value Fund

Please refer to the Schedule of Investments in the report for complete holdings information. Fund holdings, geographic allocations and/or sector allocations are subject to change at any time and are not considered a recommendation to buy or sell any security.

The foregoing reflects the thoughts and opinions of Brandes Investment Partners® exclusively and is subject to change without notice. Brandes Investment Partners® is a registered trademark of Brandes Investment Partners, L.P. in the United States and Canada.

Must be preceded or accompanied by a prospectus.

Index Guide

The MSCI ACWI with net dividends captures large and mid cap representation of developed and emerging markets.

MSCI has not approved, reviewed or produced this report, makes no express or implied warranties or representations and is not liable whatsoever for any data in the report. You may not redistribute the MSCI data or use it as a basis for other indices or investment products.

One cannot invest directly in an index.

The Brandes Global Opportunities Value Fund is distributed by ALPS Distributors, LLC.

24

Brandes Global Opportunities Value Fund

The following chart compares the value of a hypothetical $100,000 investment in the Brandes Global Opportunities Value Fund – Class I from its inception (December 31, 2014) to September 30, 2017 with the value of such an investment in the MSCI All Country World Index for the same period.

Value of $100,000 Investment vs MSCI All Country World Index (Unaudited)

| Average Annual Total Return Periods Ended September 30, 2017 | ||||||||

| One Year | Since Inception(1) | |||||||

Brandes Global Opportunities Value Fund | ||||||||

Class A | 16.66 | % | 7.95 | % | ||||

Class A (with maximum sales charge) | 9.95 | % | 5.65 | % | ||||

Class C | 15.80 | % | 7.14 | % | ||||

Class I | 16.91 | % | 8.04 | % | ||||

MSCI All Country World Index | 18.65 | % | 7.98 | % | ||||

| (1) | The inception date is December 31, 2014. |

Performance data quoted represents past performance; past performance does not indicate future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 800-331-2979.

25

Brandes Global Opportunities Value Fund

The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The Advisor has a fee waiver arrangement in place to limit the Fund’s annual operating expenses.

Sector Allocation as a Percentage of Total Investments as of September 30, 2017 (Unaudited)

The sector classifications represented in the graph above and industry classifications represented in the Schedule of Investments are in accordance with Global Industry Classification Standard (GICS®), which was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor Financial Services LLC.

26

Brandes Emerging Markets Value Fund

Dear Fellow Investor,

The net asset value of the Brandes Emerging Markets Value Fund (Class I shares) increased 22.07% in the 12 months ended September 30, 2017. For the same period, the Fund’s benchmark, the MSCI Emerging Markets Index, gained 22.46%.

Holdings in financials (especially banks), industrials and consumer staples contributed positively to performance. From a country perspective, allocations to Brazil, Russia and Hong Kong helped returns. At the company level, notable contributors included banks Sberbank (Russia) and Erste Group (Austria), Brazil-based educational services provider Estacio Participacoes and South Korean technology company Samsung Electronics.

Additionally, Hong Kong-based luxury goods companies Luk Fook Holdings and Chow Tai Fook Jewellery aided performance, increasing over 70% each. These retailers benefited from the Chinese demand for luxury goods, which, after a couple of years of stagnation, has grown substantially in recent quarters amid China’s improved economic environment.

A significant underweight to information technology (IT), in which our holdings rose but not as much as those in the benchmark, hurt relative returns.

Contributions to the MSCI Emerging Markets Index’s return were extremely concentrated for the period. The top five performing stocks were IT companies and the IT sector accounted for 40% of index performance. The disproportionate contributions to the index’s return highlight, in our view, the importance of being selective when investing in emerging markets. The elevated prices — and valuations — of many emerging market IT businesses were the main reason we have been significantly underweight the sector.

Other detractors included holdings in real estate and our meaningful underweight to China, as well as positions in Turkey and South Korea.

At the security level, Turkish real estate investment trust (REIT) Emlak Konut and Chinese telecommunication services provider China Mobile weighed on performance. Moreover, South Korean automotive-related companies KIA Motors and Hyundai Mobis declined.

In a relatively busy period, the Emerging Markets Investment Committee initiated positions in financial services firms Barclays Africa (South Africa), Siam Commercial Bank (Thailand) and Prosegur Cash (Spain). Other new purchases included South Korean tobacco company KT&G Corp, Mexican REIT Fibra Uno and India-based IT services provider Tech Mahindra.

Serving approximately 12.5 million customers through more than 1,200 branches across Africa, Barclays Africa (BGA) is among the four largest banks in South Africa. U.K.-based Barclays acquired a controlling stake in BGA in 2005, and until recently, controlled over 62% of the company.

27

Brandes Emerging Markets Value Fund

A number of factors have pressured BGA’s shares and provided us with an attractive opportunity to invest, in our opinion. These headwinds included:

| • | Large overhang from ongoing divestment by Barclays: Barclays announced its divestment plans in March 2016 and subsequently sold about a 12% stake in May 2017 at a 9% discount to the last closing price prior to the sale. In order to deconsolidate BGA from a regulatory perspective, Barclays needs to reduce its current stake to below 20%. Losing Barclays’ brand and support could pose business risks and negatively affect employee morale. |

| • | South Africa’s political and economic instability: Following a major cabinet reshuffle, S&P and Fitch cut the country’s credit rating below investment grade in April 2017. |

We appreciate that BGA has a solid market share in South Africa’s banking industry, which is an oligopoly with high barriers to entry and strong competition. The company is also among the top three banks by revenue in other important markets, including Kenya, Ghana, Botswana and Zambia. Moreover, BGA’s healthy profitability and capital position, as well as its good cost control can help the company navigate its challenges, in our view. At its current price, we believe BGA offers an attractive long-term risk/reward tradeoff.

Other activities included the full sale of Brazilian wireless telecommunication services provider TIM Participacoes and real-estate developer Viver Inc E Construtora, Panamanian airline Copa Holdings, and Malaysian resorts operator Genting Malaysia.

Additionally, the investment committee exited the Fund’s position in Argentina-based Arcos Dorados, McDonald’s largest franchisee that operates in 20 countries across Latin America and the Caribbean, and counts Brazil as its biggest market.

We first added Arcos in late 2014, when its shares had fallen over 40% for the year, mainly due to weak earnings results for the second quarter of 2014. Concerns included challenged near-term cash flows resulting from economic difficulties in a number of Arcos’ end markets, aggressive expansion plans, and credit and liquidity weakness.

We believed these concerns were more than accounted for in Arcos’ share price, and that the company had great flexibility to control capital expenditures from year to year. Furthermore, Arcos had renegotiated its debt covenants with Bank of America while suspending those with McDonald’s, and had done so without incurring any penalty, which alleviated concerns about its credit and liquidity.

Over our holding period, we largely saw our investment thesis play out. Economic conditions have improved in most of Arcos’ end markets, heightened political uncertainty has dissipated and currencies have stabilized. In early 2017, the market seemed to welcome Arcos’ announcement of its 2017-2019 reinvestment and restaurant opening plans, as well as a new royalty rate schedule. The company’s balance sheet leverage also improved, in part due to asset monetization initiatives that raised over $100 million in fiscal year 2016 alone.

28

Brandes Emerging Markets Value Fund

Outlook

While the return of investor optimism and the resulting strong performance of emerging markets over the past 18+ months have driven up equity valuations, we are yet to witness material improvements in company earnings or returns on equity, leading us to believe there is still ample opportunity to uncover value.

Valuations for emerging market equities remain attractive compared to those for developed markets (as represented by the MSCI World Index). Within the asset class itself, the valuations for value stocks (as represented by the MSCI Emerging Markets Value Index) continue to look attractive to us. After a solid performance in the second half of 2016, value stocks meaningfully underperformed growth stocks (as represented by the MSCI Emerging Markets Growth Index) by 16% over the last nine months. As of September 30, 2017, value stocks traded in line with their 10-year price-to-book average, while growth stocks traded significantly above their 10-year price-to-book average.

While emerging markets’ strong performance in the last several quarters can be perceived as good news, a deeper look into the MSCI Emerging Markets Index’s performance (i.e., how concentrated its return contribution has been) reveals, in our opinion, how investors may be best served by applying an active, opportunity-focused investment approach. At Brandes, our stock selection relies on a careful, bottom-up research, instead of assigning capital based on companies’ market-capitalization sizes without regard to business fundamentals.

We remain optimistic about the prospects for the Brandes Emerging Markets Value Fund and thank you for your continued trust.

Sincerely yours,

The Brandes Emerging Markets Investment Committee

Brandes Investment Trust

Because the values of the Fund’s investments will fluctuate with market conditions, so will the value of your investment in the Fund. You could lose money on your investment in the Fund, or the Fund could underperform other investments. The values of the Fund’s investments fluctuate in response to the activities of individual companies and general stock market and economic conditions. In addition, the performance of foreign securities depends on the political and economic environments and other overall economic conditions in the countries where the Fund invests. Emerging country markets involve greater risk and volatility than more developed markets. Some emerging markets countries may have fixed or managed currencies that are not free-floating against the U.S. dollar. Certain of these currencies have experienced, and may experience in the future, substantial fluctuations or a steady devaluation relative to the U.S. dollar. Investments in small and medium capitalization companies tend to have limited liquidity and greater price volatility than large capitalization companies.

29

Brandes Emerging Markets Value Fund

Past performance is not a guarantee of future results.

Cash Flow: The amount of cash generated minus the amount of cash used by a company in a given period.

Price/Book: Price per share divided by book value per share.

Return on Equity: Net income divided by shareholder’s equity.

Please refer to the Schedule of Investments in the report for complete holdings information. Fund holdings, geographic allocations and/or sector allocations are subject to change at any time and are not considered a recommendation to buy or sell any security.

The foregoing reflects the thoughts and opinions of Brandes Investment Partners® exclusively and is subject to change without notice. Brandes Investment Partners® is a registered trademark of Brandes Investment Partners, L.P. in the United States and Canada.

Must be preceded or accompanied by a prospectus.

Index Guide

The MSCI Emerging Markets Index with net dividends captures large and mid cap representation of emerging market countries. Data prior to 2001 is gross dividend and linked to the net dividend returns.

The MSCI World Index with net dividends captures large and mid cap representation of developed markets.

The MSCI Emerging Markets Growth Index with gross dividends captures large and mid cap securities exhibiting growth style characteristics, defined using long-term forward earnings per share (EPS) growth rate, short-term forward EPS growth rate, current internal growth rate, long-term historical EPS growth trend, and long-term historical sales per share growth trend.

The MSCI Emerging Markets Value Index with gross dividends captures large and mid cap securities exhibiting value style characteristics, defined using book value to price, 12-month forward earnings to price, and dividend yield.

MSCI has not approved, reviewed or produced this report, makes no express or implied warranties or representations and is not liable whatsoever for any data in the report. You may not redistribute the MSCI data or use it as a basis for other indices or investment products.

One cannot invest directly in an index.

The Brandes Emerging Markets Value Fund is distributed by ALPS Distributors, LLC.

30

Brandes Emerging Markets Value Fund

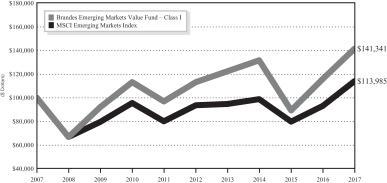

The following chart compares the value of a hypothetical $100,000 investment in the Brandes Emerging Markets Value Fund – Class I from September 30, 2007 to September 30, 2017 with the value of such an investment in the MSCI Emerging Markets Index for the same period.

Value of $100,000 Investment vs MSCI Emerging Markets Index (Unaudited)

| Average Annual Total Return Periods Ended September 30, 2017** | ||||||||||||||||

| One Year | Five Years | Ten Years | Since Inception(1) | |||||||||||||

Brandes Emerging Markets Value Fund | ||||||||||||||||

Class A | 21.78 | % | 4.30 | % | 3.27 | % | 7.87 | % | ||||||||

Class A (with maximum sales charge) | 14.77 | % | 3.07 | % | 2.66 | % | 7.56 | % | ||||||||

Class C* | 20.83 | % | 3.51 | % | 2.49 | % | 7.06 | % | ||||||||

Class I | 22.07 | % | 4.55 | % | 3.52 | % | 8.13 | % | ||||||||

Class R6* | 22.53 | % | 4.64 | % | 3.59 | % | 8.20 | % | ||||||||

MSCI Emerging Markets Index | 22.46 | % | 3.99 | % | 1.32 | % | 6.53 | % | ||||||||

| (1) | The inception date is August 20, 1996. |

| * | Performance shown prior to January 31, 2013 for Class C shares reflects the performance of Class I shares adjusted to reflect Class C expenses. Performance shown prior to July 11, 2016 for Class R6 shares reflects the performance of Class I shares adjusted to reflect Class R6 expenses. |

31

Brandes Emerging Markets Value Fund

| ** | Prior to January 31, 2011, the Advisor managed a private investment fund with an investment objective, investment policies and strategies that were, in all material respects, equivalent to those of the Brandes Emerging Markets Value Fund. The performance information shown for the Class I shares for periods before January 31, 2011 is that of the private investment fund and reflects the net expenses of the private investment fund. The performance of the private investment fund prior to January 31, 2011 is based on a calculation method that is different from the standardized calculation method prescribed by the SEC. The performance information shown for the Class A shares has been adjusted to reflect the differences in the net expense ratios between the Class I and A shares. The private investment fund was not registered under the Investment Company Act of 1940 (“1940 Act”) and was not subject to certain investment limitations, diversification requirements, and other restrictions imposed by the 1940 Act and the Internal Revenue Code of 1986, which, if applicable, may have adversely affected its performance. |

Performance data quoted represents past performance; past performance does not indicate future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 800-331-2979.

The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The Advisor has a fee waiver arrangement in place to limit the Fund’s annual operating expenses.

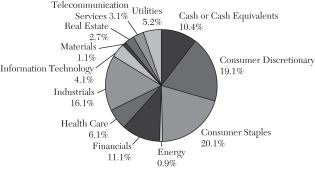

Sector Allocation as a Percentage of Total Investments as of

September 30, 2017 (Unaudited)

The sector classifications represented in the graph above and industry classifications represented in the Schedule of Investments are in accordance with Global Industry Classification Standard (GICS®), which was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor Financial Services LLC.

32

Brandes International Small Cap Equity Fund

Dear Fellow Investor,

The net asset value of the Brandes International Small Cap Equity Fund (Class I Shares) advanced 11.54% in the 12 months ended September 30, 2017. For the same period, the S&P Developed Ex-U.S. SmallCap Index rose 20.22%.

We saw positive performance across almost every sector, with holdings in industrials and health care contributing the most on an absolute basis. From a country standpoint, holdings in Japan and Brazil were strong contributors. At the company level, top performers included Japanese power tools producer Hitachi Koki, Brazilian regional jet manufacturer Embraer, German medical equipment company Draegerwerk and Canadian wood-based panel products company Norbord.

The underperformance for the period could primarily be attributed to the Fund’s underweights to cyclical sectors, including financials, industrials and information technology. In our view, these sectors currently represent increasingly risky areas of the market as many constituents are trading at what we consider elevated multiples on potentially unsustainable earnings and free-cash-flow streams. We believe our consistent value-based approach helps our fund shareholders avoid securities with potentially poor risk/reward tradeoff. We remain committed to our price disciplined philosophy, building portfolios by focusing on both the risk and reward of each individual business.

Major detractors included U.K.-based real estate firm Countrywide, Irish beverage company C&C Group and Indian electric utility Reliance Infrastructure. Additionally, the Fund’s cash position hurt performance in a rising market. The investment committee continues to exercise patience and caution when evaluating opportunities. Our cash will enable us to act quickly when we uncover potentially undervalued companies.

The investment committee divested several holdings in Japan as the shares appreciated to our estimates of intrinsic value. These included machinery companies Toshiba Machine, Fuji Machine and Hitachi Koki, game equipment company Sega Sammy Holdings and electronic components manufacturer Hosiden. Other positions sold included Israel Discount Bank and Italy-based construction materials manufacturer Buzzi Unicem.

New purchases included Japanese food product company Toyo Suisan Kaisha and apparel company Wacoal Holdings, South Korean beverage company Lotte Chilsung and Mexican Fibra Uno.

A Fibra (Fideicomiso de Infraestructura y Bienes Raíces) is an investment vehicle that has similarities to a REIT (real estate investment trust) in the United States.

Fibra Uno (FUNO) is a Mexican trust formed primarily to acquire, own, develop and operate a broad range of commercial real estate in Mexico, including industrial, retail and office properties. FUNO has selectively assembled a diversified portfolio of high-quality, well-located, income-producing commercial

33

Brandes International Small Cap Equity Fund

properties. The trust began trading on the Mexican stock exchange in 2011 and is the first — also currently the largest — publicly listed Fibra.

Having previously held the company and currently owning one of its peers (Macquarie Mexico Real Estate Management), we are very familiar with FUNO’s business. Over the past few years, FUNO’s shares have been under pressure, mainly due to the peso depreciation, which negatively affected the company’s real estate value and peso-denominated rental revenues. FUNO has more U.S. dollar-denominated debt than revenues; however, from a debt servicing perspective, it has what we consider solid revenue coverage of interest expense in U.S. dollars. Moreover, FUNO has predominantly long-term debt (expiring in six years or later) with a fixed interest rate. Hence, we believe FUNO should be relatively resilient against rising rates.

The selloff in FUNO’s shares was magnified by the election of Donald Trump as U.S. President, creating what we viewed as a good entry point for investment. In our view, FUNO’s positive attributes include:

| • | Strong earnings growth prospects through a sizeable development pipeline |

| • | A solid balance sheet and a seasoned management team |

| • | An income stream which is “inflation protected” as rents are contractually tied to inflation |

| • | Attractive dividend yield |

When we purchased FUNO, the company traded not only below our conservative estimate of its net assets value, but also less than its original IPO (initial public offering) price in U.S. dollar terms. At the time of its IPO, FUNO was less diversified than it is today and was operating in a developing industry that was untested. Moreover, while the market seems focused on U.S. policy concerns, we appreciate that the company’s property portfolio has limited direct exposure to major exporters to the United States. We also like that management continues to demonstrate strong capital allocation, with a conservative balance sheet which should enable the company to be opportunistic, in our view, if the market conditions in Mexico weaken further.

Outlook

As of September 30, 2017, the Fund’s key exposures and overweights from a country perspective remained in Japan and the United Kingdom.

Japanese companies continued to represent the Fund’s largest country weighting. The majority of our Japanese holdings have conservative financial leverage and traded below their book value as of September 30. Moreover, Japan is one of the very few countries where we have found companies with market capitalizations lower than the cash on their balance sheets, offering what we consider a particularly attractive value proposition.

34

Brandes International Small Cap Equity Fund

We also continue to see tremendous value potential in emerging markets, which accounted for approximately 25% of the Fund as of September 30. Brazil and South Korea represented our two largest allocations in the region. We continue to uncover what we believe are undervalued opportunities in South Korean businesses, with three new positions in the period (the aforementioned Lotte Chilsung, security services firm S-1 and food products company Namyang Dairy Products).

From a sector standpoint, the Fund maintained notable overweights in consumer staples and utilities, and key underweights in industrials and materials. Over the past year, the most dramatic change in the Fund has been our growing exposure to companies in consumer staples, specifically food products, and our declining position in materials companies.

Events across the globe this year may serve as a good reminder that macroeconomic and geopolitical factors can affect individual businesses differently. As one of the first asset managers to bring a global perspective to value investing, Brandes relies on an established research infrastructure that enables us to analyze how each company may be affected by events globally. Our analyst teams have extensive knowledge of industries worldwide, and each team member’s perspective allows us to think and invest independently from the market consensus.

Thank you for your business and continued trust.

Sincerely yours,

The Brandes Small-Cap Investment Committee

Brandes Investment Trust

Because the values of the Fund’s investments will fluctuate with market conditions, so will the value of your investment in the Fund. You could lose money on your investment in the Fund, or the Fund could underperform other investments. The values of the Fund’s investments fluctuate in response to the activities of individual companies and general stock market and economic conditions. In addition, the performance of foreign securities depends on the political and economic environments and other overall economic conditions in the countries where the Fund invests. Emerging country markets involve greater risk and volatility than more developed markets. Some emerging markets countries may have fixed or managed currencies that are not free-floating against the U.S. dollar. Certain of these currencies have experienced, and may experience in the future, substantial fluctuations or a steady devaluation relative to the U.S. dollar. Investments in small and medium capitalization companies tend to have limited liquidity and greater price volatility than large capitalization companies.

Past performance is not a guarantee of future results.

Book Value: Assets minus liabilities. Also known as shareholders’ equity.

35

Brandes International Small Cap Equity Fund

Dividend Yield: Dividends per share divided by price per share.

Free Cash Flow: Total cash flow from operations less capital expenditures.

Net Assets Value: A company’s total assets minus its liabilities, divided by the number of outstanding shares.

The declaration and payment of shareholder dividends are solely at the discretion of the issuer and are subject to change at any time.

Please refer to the Schedule of Investments in the report for complete holdings information. Fund holdings, geographic allocations and/or sector allocations are subject to change at any time and are not considered a recommendation to buy or sell any security.

The foregoing reflects the thoughts and opinions of Brandes Investment Partners® exclusively and is subject to change without notice. Brandes Investment Partners® is a registered trademark of Brandes Investment Partners, L.P. in the United States and Canada.

Must be preceded or accompanied by a prospectus.

Index Guide

The S&P Developed Ex-U.S. SmallCap Index with net dividends measures the equity performance of small-capitalization companies from developed markets excluding the United States. Data prior to 2001 is gross dividend and linked to the net dividend returns.

One cannot invest directly in an index.

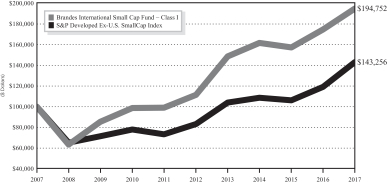

The Brandes International Small Cap Equity Fund is distributed by ALPS Distributors, LLC.