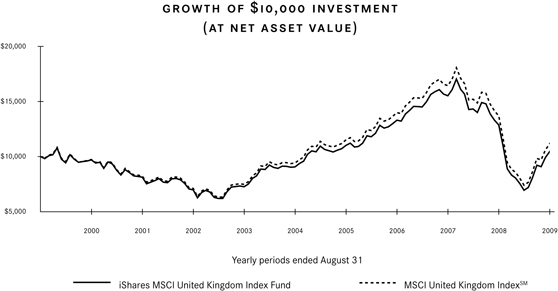

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-09102

iShares, Inc.

(Exact name of registrant as specified in charter)

c/o: State Street Bank and Trust Company

200 Clarendon Street, Boston, MA 02116

(Address of principal executive offices) (Zip code)

The Corporation Trust Company

300 East Lombard Street, Baltimore, MD 21202

(Name and address of agent for service)

Registrant’s telephone number, including area code: 1-800-474-2737

Date of fiscal year end: August 31, 2009

Date of reporting period: August 31, 2009

Table of Contents

Item 1. Reports to Stockholders.

2009 ANNUAL REPORT TO SHAREHOLDERS

iSHARES® MSCI SERIES

AUGUST 31, 2009

Would you prefer to receive materials like this electronically?

See inside cover for details.

iShares MSCI Austria Investable Market Index Fund

iShares MSCI Belgium Investable Market Index Fund

iShares MSCI EMU Index Fund

iShares MSCI France Index Fund

iShares MSCI Germany Index Fund

iShares MSCI Italy Index Fund

iShares MSCI Netherlands Investable Market Index Fund

iShares MSCI Spain Index Fund

iShares MSCI Sweden Index Fund

iShares MSCI Switzerland Index Fund

iShares MSCI United Kingdom Index Fund

iShares®

Table of Contents

iShares

Dear iShares Shareholder:

Electronic delivery is the easiest, most convenient way to receive reporting on your iShares holdings. In addition, it’s a way we can all care for our environment. To that end, we are pleased to offer shareholder reports and prospectuses online.

To sign up for electronic delivery, please follow these simple steps:

1. Go to www.icsdelivery.com.

2. From the main page, select the first letter of your brokerage firm’s name.

3. Select your brokerage institution from the list that follows. If your brokerage firm is not listed, electronic delivery may not be available. Please contact your brokerage firm or financial adviser.

4. Fill out the appropriate information and provide the e-mail address where you would like your information sent.

Your information and email address will be kept confidential and only used to deliver documents to you. If at any time you are not satisfied, you can cancel electronic delivery at www.icsdelivery.com and once again receive physical delivery of your materials. If you have any questions, please contact your brokerage firm or financial adviser.

Once you have enrolled, you will no longer receive prospectuses and shareholder reports in the mail. Instead, you will receive e-mail notifications announcing that the shareholder report or prospectuses has been posted on the iShares website at www.iShares.com.

Table of Contents

| 1 | ||

| 34 | ||

| 36 | ||

| 36 | ||

| 38 | ||

| 40 | ||

| 45 | ||

| 48 | ||

| �� | 50 | |

| 52 | ||

| 54 | ||

| 56 | ||

| 58 | ||

| 60 | ||

| 63 | ||

| 75 | ||

| 86 | ||

| 96 | ||

| 97 | ||

Board Review and Approval of Current Investment Advisory Contract (Unaudited) | 98 | |

Board Review and Approval of New Investment Advisory Agreements (Unaudited) | 101 | |

| 107 | ||

| 116 | ||

| 124 |

Table of Contents

Management’s Discussion of Fund Performance

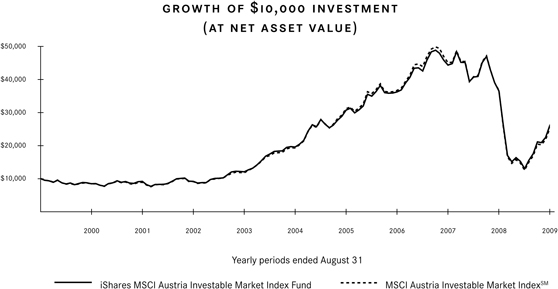

iSHARES® MSCI AUSTRIA INVESTABLE MARKET INDEX FUND

(TICKER: EWO)

INVESTMENT OBJECTIVE

The iShares MSCI Austria Investable Market Index Fund (the “Fund”) seeks to provide investment results that correspond generally to the price and yield performance, before fees and expenses, of publicly traded securities in the aggregate in the Austrian market, as measured by the MSCI Austria Investable Market IndexSM (the “Index”). The Fund invests in a representative sample of securities included in the Index that collectively has an investment profile similar to the Index. Due to the use of representative sampling, the Fund may or may not hold all of the securities that are included in the Index. For the 12-month period ended August 31, 2009 (the “reporting period”), the total return for the Fund was (28.52)%, while the total return for the Index was (31.11)%.

MARKET OVERVIEW AND DISCUSSION OF PERFORMANCE

A slowing global economic environment and ongoing credit crisis weighed on stock markets around the world during much of the reporting period. Early in the reporting period, the credit crisis that had begun with problems within the U.S. mortgage industry spurred extreme turmoil in the global financial sector, leading to a series of bankruptcies and takeovers among several major financial institutions in late 2008. The events impacted markets worldwide, pushing major indices downward and sapping strength from already weak economies. Unemployment rates climbed in most major economies as industrial output declined and levels of imports and exports fell. In an effort to stabilize markets, key central banks around the world took decisive steps, initiating debt purchase programs and easing monetary policy. In the U.S., the Federal Reserve Board cut the federal funds rate to an unprecedented range of 0.00% – 0.25% during the course of the reporting period. The European Central Bank echoed these actions, lowering its key lending rate from 4.25% to a historically low 1.00%.

After dipping to multi-year lows in early March 2009, most international markets rebounded strongly, as many investors appeared confident that the threats surrounding financial markets were beginning to recede. European markets followed these trends. Market strength continued through the end of the reporting period as early, yet uneven, signs of economic recovery emerged in key European markets. Germany and the U.K. experienced increases in industrial output, while consumer spending increased in France. In Switzerland, the KOF broad measure of economic activity reported large jumps in July and August.

Austria’s equity market finished the reporting period with a double-digit decline, despite rebounding sharply in the second half of the reporting period. Austria relies on its European neighbors for most of its exports, and it is vulnerable to the economic health of the constituent markets of the European Union. During the reporting period, Austria’s economic conditions slowed along with the economies of its trading partners, but appeared to be nearing the end of a slowdown as the health of its partners improved. In particular, shifting economic conditions in Germany, Europe’s largest economy and Austria’s leading export market, significantly affected Austria’s GDP growth. For the first quarter of 2009, annual GDP growth declined 2.6%, followed by a decline of a more modest 1.8% for the second quarter of 2009. The U.S dollar depreciated against the euro in the final months of the reporting period, benefiting dollar-denominated performance returns.

All of the Fund’s ten largest holdings as of August 31, 2009 declined for the reporting period. Raiffeisen International Bank Holding AG experienced the steepest decline among the ten largest holdings. Steel maker voestalpine AG, and oil and gas company OMV AG also delivered significant negative returns, as did the Fund’s largest holding, retail bank Erste Group Bank AG. Telecommunications company Telekom Austria AG logged more modest, although double-digit, declines. Vienna Insurance Group and Wienerberger AG, the world’s largest producer of bricks, also experienced relatively modest declines.

| MANAGEMENT’S DISCUSSIONSOF FUND PERFORMANCE | 1 |

Table of Contents

Management’s Discussion of Fund Performance (Continued)

iSHARES® MSCI AUSTRIA INVESTABLE MARKET INDEX FUND

Performance as of August 31, 2009

| Average Annual Total Returns | ||||||||||||||||

| Year Ended 8/31/09 | Five Years Ended 8/31/09 | Ten Years Ended 8/31/09 | ||||||||||||||

| NAV | MARKET | INDEX | NAV | MARKET | INDEX | NAV | MARKET | INDEX | ||||||||

| (28.52)% | (27.71)% | (31.11)% | 5.92% | 5.79% | 5.54% | 10.06% | 10.08% | 9.71% | ||||||||

| Cumulative Total Returns | ||||||||||||||||

| Year Ended 8/31/09 | Five Years Ended 8/31/09 | Ten Years Ended 8/31/09 | ||||||||||||||

| NAV | MARKET | INDEX | NAV | MARKET | INDEX | NAV | MARKET | INDEX | ||||||||

| (28.52)% | (27.71)% | (31.11)% | 33.30% | 32.49% | 30.94% | 160.82% | 161.21% | 152.62% | ||||||||

“Average Annual Total Returns” represent the average annual change in value of an investment over the period(s) indicated. “Cumulative Total Returns” represent the total change in value of an investment over the period(s) indicated.

The Fund’s per share net asset value or “NAV” is the value of one share of the Fund as calculated in accordance with the standard formula for valuing mutual fund shares. The NAV return is based on the NAV of the Fund and the market return is based on the market price per share of the Fund. The price used to calculate market return (“Market Price”) is determined by using the midpoint between the highest bid and the lowest offer on the primary stock exchange on which the shares of the Fund are listed for trading, as of the time that the Fund’s NAV is calculated. Market and NAV returns assume that dividends and capital gain distributions have been reinvested in the Fund at Market Price and NAV, respectively.

An index is a statistical composite that tracks a specified financial market or sector. Unlike the Fund, an index does not actually hold a portfolio of securities and therefore does not incur the expenses incurred by the Fund. These expenses negatively impact the performance of the Fund. Also, market returns do not include brokerage commissions that may be payable on secondary market transactions. If brokerage commissions were included, market returns would be lower. The performance shown in the table(s) and chart(s) above assumes reinvestment of all dividends and capital gain distributions and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption or sale of fund shares. The investment return and principal value of shares of the Fund will vary with changes in market conditions. Shares of the Fund may be worth more or less than their original cost when they are redeemed or sold in the market. The Fund’s past performance is no guarantee of future results.

| 2 | 2009 iSHARES ANNUAL REPORT TO SHAREHOLDERS |

Table of Contents

Management’s Discussion of Fund Performance (Continued)

iSHARES® MSCI AUSTRIA INVESTABLE MARKET INDEX FUND

PORTFOLIO ALLOCATION As of 8/31/09 | |||

| Sector | Percentage of Net Assets | ||

Financial | 37.17 | % | |

Industrial | 16.63 | ||

Energy | 12.21 | ||

Communications | 10.25 | ||

Basic Materials | 8.85 | ||

Utilities | 7.08 | ||

Consumer Non-Cyclical | 4.36 | ||

Consumer Cyclical | 2.66 | ||

Short-Term and Other Net Assets | 0.79 | ||

TOTAL | 100.00 | % | |

TEN LARGEST FUND HOLDINGS As of 8/31/09 | |||

| Security | Percentage of Net Assets | ||

Erste Group Bank AG | 14.23 | % | |

OMV AG | 11.06 | ||

Telekom Austria AG | 10.25 | ||

voestalpine AG | 7.10 | ||

Oesterreichische Elektrizitaetswirtschafts AG Class A | 6.68 | ||

Raiffeisen International Bank Holding AG | 4.70 | ||

Vienna Insurance Group | 4.33 | ||

Wienerberger AG | 3.97 | ||

Andritz AG | 3.45 | ||

Immoeast AG | 3.06 | ||

TOTAL | 68.83 | % | |

| MANAGEMENT’S DISCUSSIONSOF FUND PERFORMANCE | 3 |

Table of Contents

Management’s Discussion of Fund Performance

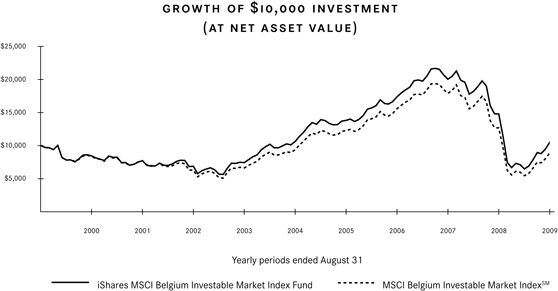

iSHARES® MSCI BELGIUM INVESTABLE MARKET INDEX FUND

(TICKER: EWK)

INVESTMENT OBJECTIVE

The iShares MSCI Belgium Investable Market Index Fund (the “Fund”) seeks to provide investment results that correspond generally to the price and yield performance, before fees and expenses, of publicly traded securities in the aggregate in the Belgian market, as measured by the MSCI Belgium Investable Market IndexSM (the “Index”). The Fund invests in a representative sample of securities included in the Index that collectively has an investment profile similar to the Index. Due to the use of representative sampling, the Fund may or may not hold all of the securities that are included in the Index. For the 12-month period ended August 31, 2009 (the “reporting period”), the total return for the Fund was (29.15)%, while the total return for the Index was (29.98)%.

MARKET OVERVIEW AND DISCUSSION OF PERFORMANCE

A slowing global economic environment and ongoing credit crisis weighed on stock markets around the world during much of the reporting period. Early in the reporting period, the credit crisis that had begun with problems within the U.S. mortgage industry spurred extreme turmoil in the global financial sector, leading to a series of bankruptcies and takeovers among several major financial institutions in late 2008. The events impacted markets worldwide, pushing major indices downward and sapping strength from already weak economies. Unemployment rates climbed in most major economies as industrial output declined and levels of imports and exports fell. In an effort to stabilize markets, key central banks around the world took decisive steps, initiating debt purchase programs and easing monetary policy. In the U.S., the Federal Reserve Board cut the federal funds rate to an unprecedented range of 0.00% - 0.25% during the course of the reporting period. The European Central Bank echoed these actions, lowering its key lending rate from 4.25% to a historically low 1.00%.

After dipping to multi-year lows in early March 2009, most international markets rebounded strongly, as many investors appeared confident that the threats surrounding financial markets were beginning to recede. European markets followed these trends. Market strength continued through the end of the reporting period as early, yet uneven, signs of economic recovery emerged in key European markets. Germany and the U.K. experienced increases in industrial output, while consumer spending increased in France. In Switzerland, the KOF broad measure of economic activity reported large jumps in July and August.

Belgium’s equity market experienced a double-digit decline during the reporting period, despite a sharp rebound in the final months of the period. With few natural resources, Belgium imports raw materials and exports end products, and is highly sensitive to the economic state of its trading partners. Sluggish economic conditions in Europe and the U.S., Belgium’s largest export destinations, hurt Belgium’s economy during the reporting period. High commodity prices further dampened economic conditions, as evidenced by GDP rates. In the first two quarters of 2009, Belgium’s GDP fell at annualized rates of 3.1% and 3.7%, respectively, as its export levels dropped sharply, the unemployment rate topped 8% and industrial production decreased. Consumer confidence levels sank to their lowest levels in more than 10 years. The U.S dollar depreciated against the euro in the final months of the reporting period, benefiting dollar-denominated performance returns.

Seven of the ten largest Fund holdings as of August 31, 2009 delivered negative performance for the reporting period. Four financial companies among the Fund’s ten largest holdings declined for the reporting period, including the Fund’s second largest holding, Fortis and KBC Groep NV. The Fund’s largest holding, Anheuser-Busch InBev NV, the world’s largest brewer, posted only a slight decline. Retail food chain Delhaize Group logged a gain for the reporting period, as did biopharmaceutical company UCB SA. Telecommunications company Belgacom SA finished the reporting period with a slight gain.

| 4 | 2009 iSHARES ANNUAL REPORT TO SHAREHOLDERS |

Table of Contents

Management’s Discussion of Fund Performance (Continued)

iSHARES® MSCI BELGIUM INVESTABLE MARKET INDEX FUND

Performance as of August 31, 2009

| Average Annual Total Returns | ||||||||||||||||

| Year Ended 8/31/09 | Five Years Ended 8/31/09 | Ten Years Ended 8/31/09 | ||||||||||||||

| NAV | MARKET | INDEX | NAV | MARKET | INDEX | NAV | MARKET | INDEX | ||||||||

| (29.15)% | (28.62)% | (29.98)% | (0.26)% | (0.44)% | (1.08)% | 0.46% | 0.37% | (1.20)% | ||||||||

| Cumulative Total Returns | ||||||||||||||||

| Year Ended 8/31/09 | Five Years Ended 8/31/09 | Ten Years Ended 8/31/09 | ||||||||||||||

| NAV | MARKET | INDEX | NAV | MARKET | INDEX | NAV | MARKET | INDEX | ||||||||

| (29.15)% | (28.62)% | (29.98)% | (1.29)% | (2.16)% | (5.28)% | 4.67% | 3.81% | (11.37)% | ||||||||

“Average Annual Total Returns” represent the average annual change in value of an investment over the period(s) indicated. “Cumulative Total Returns” represent the total change in value of an investment over the period(s) indicated.

The Fund’s per share net asset value or “NAV” is the value of one share of the Fund as calculated in accordance with the standard formula for valuing mutual fund shares. The NAV return is based on the NAV of the Fund and the market return is based on the market price per share of the Fund. The price used to calculate market return (“Market Price”) is determined by using the midpoint between the highest bid and the lowest offer on the primary stock exchange on which the shares of the Fund are listed for trading, as of the time that the Fund’s NAV is calculated. Market and NAV returns assume that dividends and capital gain distributions have been reinvested in the Fund at Market Price and NAV, respectively.

An index is a statistical composite that tracks a specified financial market or sector. Unlike the Fund, an index does not actually hold a portfolio of securities and therefore does not incur the expenses incurred by the Fund. These expenses negatively impact the performance of the Fund. Also, market returns do not include brokerage commissions that may be payable on secondary market transactions. If brokerage commissions were included, market returns would be lower. The performance shown in the table(s) and chart(s) above assumes reinvestment of all dividends and capital gain distributions and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption or sale of fund shares. The investment return and principal value of shares of the Fund will vary with changes in market conditions. Shares of the Fund may be worth more or less than their original cost when they are redeemed or sold in the market. The Fund’s past performance is no guarantee of future results.

| MANAGEMENT’S DISCUSSIONSOF FUND PERFORMANCE | 5 |

Table of Contents

Management’s Discussion of Fund Performance (Continued)

iSHARES® MSCI BELGIUM INVESTABLE MARKET INDEX FUND

PORTFOLIO ALLOCATION As of 8/31/09 | |||

| Sector | Percentage of Net Asset | ||

Consumer Non-Cyclical | 40.62 | % | |

Financial | 22.64 | ||

Diversified | 10.71 | ||

Basic Materials | 9.66 | ||

Communications | 8.51 | ||

Industrial | 4.62 | ||

Consumer Cyclical | 1.24 | ||

Technology | 0.17 | ||

Short-Term and Other Net Assets | 1.83 | ||

TOTAL | 100.00 | % | |

TEN LARGEST FUND HOLDINGS As of 8/31/09 | |||

| Security | Percentage of Net Assets | ||

Anheuser-Busch InBev NV | 24.16 | % | |

Fortis | 8.64 | ||

Groupe Bruxelles Lambert SA | 7.14 | ||

Delhaize Group | 6.26 | ||

Solvay SA | 4.87 | ||

Belgacom SA | 4.67 | ||

KBC Groep NV | 4.61 | ||

Dexia SA | 4.23 | ||

UCB SA | 3.80 | ||

Colruyt SA | 3.76 | ||

TOTAL | 72.14 | % | |

| 6 | 2009 iSHARES ANNUAL REPORTTO SHAREHOLDERS |

Table of Contents

Management’s Discussion of Fund Performance

iSHARES® MSCI EMU INDEX FUND

(TICKER: EZU)

INVESTMENT OBJECTIVE

The iShares MSCI EMU Index Fund (the “Fund”) seeks to provide investment results that correspond generally to the price and yield performance, before fees and expenses, of publicly traded securities in the aggregate in the EMU markets, as measured by the MSCI EMU IndexSM (the “Index”). The Fund invests in a representative sample of securities included in the Index that collectively has an investment profile similar to the Index. Due to the use of representative sampling, the Fund may or may not hold all of the securities that are included in the Index. For the 12-month period ended August 31, 2009 (the “reporting period”), the total return for the Fund was (19.05)%, while the total return for the Index was (19.02)%.

MARKET OVERVIEW AND DISCUSSION OF PERFORMANCE

A slowing global economic environment and ongoing credit crisis weighed on stock markets around the world during much of the reporting period. Early in the reporting period, the credit crisis that had begun within the U.S. mortgage industry spurred turmoil in the global financial sector, leading to a series of bankruptcies and takeovers among several major financial institutions in late 2008. The events negatively affected markets in the United States and throughout Europe, pushing major indices downward and sapping strength from already weak economies. Unemployment rates climbed in most major economies as industrial output declined and levels of imports and exports fell. In an effort to stabilize markets, key central banks took decisive steps, initiating debt purchase programs and easing monetary policy. In the U.S., the Federal Reserve Board cut the federal funds rate to an unprecedented range of 0.00% - 0.25% during the course of the reporting period. The European Central Bank echoed these actions, lowering its key lending rate from 4.25% to a historically low 1.00%.

Countries across the European Monetary Union endured a difficult economic environment, with several key nations experiencing recessions. The German economy faced a challenging recession during the reporting period, as evidenced by a contraction in annualized GDP levels for the third and fourth quarters of 2008 and first quarter of 2009. Industrial production declined and the unemployment rate surpassed 8%. The U.K. also struggled with recession during the reporting period. For the fourth quarter of 2008, in particular, annualized GDP declined by its largest level since 1980. Consumer confidence fell to a near record low, and the unemployment rate climbed above 7%. In an effort to stimulate economic activity, the Bank of England cut its key lending rate, the repo rate, aggressively throughout the period, bringing the rate from 5.00% to an unprecedented 0.50%. France experienced its first recession in 16 years. Economic activity, as measured by annualized GDP, contracted for the third and fourth quarters of 2008 and for the first quarter of 2009 as industrial production dropped and the unemployment rate surpassed 9%.

After dipping to multi-year lows in early March 2009, major European markets rebounded, as many investors appeared confident that the threats surrounding financial markets had begun to be mitigated. Market strength continued through the end of the reporting period as early, yet uneven, signs of economic recovery emerged in key European markets. For example, Germany and the U.K. experienced increases in industrial output, while consumer spending climbed in France.

The Fund’s ten largest holdings represented approximately 26% of Fund net assets as of August 31, 2009. Among the Fund’s ten largest holdings performance was mixed for the reporting period. Two financial companies, Allianz SE (Germany) and BNP Paribas (France) both declined. Utility companies E.ON AG (Germany) and ENI SpA (Italy) also lost ground during the period, as did Europe’s largest engineering company, Siemens AG (Germany). On the positive side, two of the four financial companies among the ten largest holdings posted gains: Banco Bilbao Vizcaya Argentaria SA (Spain) delivered a double-digit gain, and the Fund’s largest holding, Banco Santander SA (Spain) also finished the reporting period in positive territory. Telecommunications company Telefonica SA (Spain) also gained ground.

| MANAGEMENT’S DISCUSSIONSOF FUND PERFORMANCE | 7 |

Table of Contents

Management’s Discussion of Fund Performance (Continued)

iSHARES® MSCI EMU INDEX FUND

Performance as of August 31, 2009

| Average Annual Total Returns | ||||||||||||||||

| Year Ended 8/31/09 | Five Years Ended 8/31/09 | Inception to 8/31/09 | ||||||||||||||

| NAV | MARKET | INDEX | NAV | MARKET | INDEX | NAV | MARKET | INDEX | ||||||||

| (19.05)% | (18.31)% | (19.02)% | 7.02% | 6.88% | 7.22% | 0.74% | 0.77% | 1.01% | ||||||||

| Cumulative Total Returns | ||||||||||||||||

| Year Ended 8/31/09 | Five Years Ended 8/31/09 | Inception to 8/31/09 | ||||||||||||||

| NAV | MARKET | INDEX | NAV | MARKET | INDEX | NAV | MARKET | INDEX | ||||||||

| (19.05)% | (18.31)% | (19.02)% | 40.38% | 39.48% | 41.70% | 6.95% | 7.20% | 9.54% | ||||||||

Total returns for the period since inception are calculated from the inception date of the Fund (7/25/00). “Average Annual Total Returns” represent the average annual change in value of an investment over the period(s) indicated. “Cumulative Total Returns” represent the total change in value of an investment over the period(s) indicated.

The Fund’s per share net asset value or “NAV” is the value of one share of the Fund as calculated in accordance with the standard formula for valuing mutual fund shares. The NAV return is based on the NAV of the Fund and the market return is based on the market price per share of the Fund. The price used to calculate market return (“Market Price”) is determined by using the midpoint between the highest bid and the lowest offer on the primary stock exchange on which the shares of the Fund are listed for trading, as of the time that the Fund’s NAV is calculated. Since shares of the Fund did not trade in the secondary market until after the Fund’s inception, for the period from inception to the first day of secondary market trading in shares of the Fund (7/31/00), the NAV of the Fund is used as a proxy for the Market Price to calculate market returns. Market and NAV returns assume that dividends and capital gain distributions have been reinvested in the Fund at Market Price and NAV, respectively.

An index is a statistical composite that tracks a specified financial market or sector. Unlike the Fund, an index does not actually hold a portfolio of securities and therefore does not incur the expenses incurred by the Fund. These expenses negatively impact the performance of the Fund. Also, market returns do not include brokerage commissions that may be payable on secondary market transactions. If brokerage commissions were included, market returns would be lower. The performance shown in the table(s) and chart(s) above assumes reinvestment of all dividends and capital gain distributions and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption or sale of fund shares. The investment return and principal value of shares of the Fund will vary with changes in market conditions. Shares of the Fund may be worth more or less than their original cost when they are redeemed or sold in the market. The Fund’s past performance is no guarantee of future results.

| 8 | 2009 iSHARES ANNUAL REPORT TO SHAREHOLDERS |

Table of Contents

Management’s Discussion of Fund Performance (Continued)

iSHARES® MSCI EMU INDEX FUND

PORTFOLIO ALLOCATION As of 8/31/09 | |||

| Sector | Percentage of Net Assets | ||

Financial | 26.96 | % | |

Consumer Non-Cyclical | 13.36 | ||

Communications | 12.85 | ||

Industrial | 10.97 | ||

Utilities | 10.33 | ||

Energy | 7.94 | ||

Basic Materials | 7.31 | ||

Consumer Cyclical | 6.13 | ||

Technology | 2.60 | ||

Diversified | 1.21 | ||

Short-Term and Other Net Assets | 0.34 | ||

TOTAL | 100.00 | % | |

TEN LARGEST FUND HOLDINGS As of 8/31/09 | |||

| Security | Percentage of Net Assets | ||

Banco Santander SA (Spain) | 3.99 | % | |

Total SA (France) | 3.86 | ||

Telefonica SA (Spain) | 3.35 | ||

E.ON AG (Germany) | 2.54 | ||

Siemens AG Registered (Germany) | 2.26 | ||

Sanofi-Aventis (France) | 2.25 | ||

BNP Paribas (France) | 2.13 | ||

Banco Bilbao Vizcaya Argentaria SA (Spain) | 2.04 | ||

Eni SpA (Italy) | 1.95 | ||

Allianz SE Registered (Germany) | 1.66 | ||

TOTAL | 26.03 | % | |

| MANAGEMENT’S DISCUSSIONSOF FUND PERFORMANCE | 9 |

Table of Contents

Management’s Discussion of Fund Performance

iSHARES® MSCI FRANCE INDEX FUND

(TICKER: EWQ)

INVESTMENT OBJECTIVE

The iShares MSCI France Index Fund (the “Fund”) seeks to provide investment results that correspond generally to the price and yield performance, before fees and expenses, of publicly traded securities in the aggregate in the French market, as measured by the MSCI France IndexSM (the “Index”). The Fund invests in a representative sample of securities included in the Index that collectively has an investment profile similar to the Index. Due to the use of representative sampling, the Fund may or may not hold all of the securities that are included in the Index. For the 12-month period ended August 31, 2009 (the “reporting period”), the total return for both the Fund and the Index was (17.11)%.

MARKET OVERVIEW AND DISCUSSION OF PERFORMANCE

A slowing global economic environment and ongoing credit crisis weighed on stock markets around the world during much of the reporting period. Early in the reporting period, the credit crisis that had begun with problems within the U.S. mortgage industry spurred extreme turmoil in the global financial sector, leading to a series of bankruptcies and takeovers among several major financial institutions in late 2008. The events impacted markets worldwide, pushing major indices downward and sapping strength from already weak economies. Unemployment rates climbed in most major economies as industrial output declined and levels of imports and exports fell. In an effort to stabilize markets, key central banks around the world took decisive steps, initiating debt purchase programs and easing monetary policy. In the U.S., the Federal Reserve Board cut the federal funds rate to an unprecedented range of 0.00% - 0.25% during the course of the reporting period. The European Central Bank echoed these actions, lowering its key lending rate from 4.25% to a historically low 1.00%.

After dipping to multi-year lows in early March 2009, most international markets rebounded strongly, as many investors appeared confident that the threats surrounding financial markets were beginning to recede. European markets followed these trends. Market strength continued through the end of the reporting period as early, yet uneven, signs of economic recovery emerged in key European markets. Germany and the U.K. experienced increases in industrial output, while consumer spending increased in France. In Switzerland, the KOF broad measure of economic activity reported large jumps in July and August.

French equity markets declined during the reporting period, despite a strong rebound in the second half of the period. During the reporting period, France experienced its first recession in 16 years. Economic activity, as measured by annualized GDP, contracted for the third and fourth quarters of 2008 and for the first quarter of 2009 as industrial production dropped and the unemployment rate surpassed 9%. In the final months of the reporting period, however, early signs of economic recovery emerged. By June, consumer spending levels rose, the contraction in manufacturing and services slowed, and industrial production increased. For the second quarter of 2009, GDP grew at an annualized 0.3% rate, its first gain in five quarters. The U.S dollar depreciated against the euro in the final months of the reporting period, benefiting dollar-denominated performance returns.

Nine of the Fund’s ten largest holdings as of August 31, 2009 experienced share price declines for the reporting period. Steelmaker ArcelorMittal posted the largest decline of the ten largest holdings during the reporting period. Financial companies, including insurer AXA and investment bank Societe Generale, also suffered double-digit declines in share prices, as did natural gas producer GDF Suez. The Fund’s largest holding, oil company Total SA, declined for the reporting period. Media conglomerate Vivendi SA also lost ground. On the positive side, pharmaceutical company Sanofi-Aventis delivered a slight gain.

| 10 | 2009 iSHARES ANNUAL REPORT TO SHAREHOLDERS |

Table of Contents

Management’s Discussion of Fund Performance (Continued)

iSHARES® MSCI FRANCE INDEX FUND

Performance as of August 31, 2009

| Average Annual Total Returns | ||||||||||||||||

| Year Ended 8/31/09 | Five Years Ended 8/31/09 | Ten Years Ended 8/31/09 | ||||||||||||||

| NAV | MARKET | INDEX | NAV | MARKET | INDEX | NAV | MARKET | INDEX | ||||||||

| (17.11)% | (16.44)% | (17.11)% | 6.31% | 6.25% | 6.53% | 2.91% | 2.90% | 3.27% | ||||||||

| Cumulative Total Returns | ||||||||||||||||

| Year Ended 8/31/09 | Five Years Ended 8/31/09 | Ten Years Ended 8/31/09 | ||||||||||||||

| NAV | MARKET | INDEX | NAV | MARKET | INDEX | NAV | MARKET | INDEX | ||||||||

| (17.11)% | (16.44)% | (17.11)% | 35.77% | 35.40% | 37.20% | 33.26% | 33.08% | 37.96% | ||||||||

“Average Annual Total Returns” represent the average annual change in value of an investment over the period(s) indicated. “Cumulative Total Returns” represent the total change in value of an investment over the period(s) indicated.

The Fund’s per share net asset value or “NAV” is the value of one share of the Fund as calculated in accordance with the standard formula for valuing mutual fund shares. The NAV return is based on the NAV of the Fund and the market return is based on the market price per share of the Fund. The price used to calculate market return (“Market Price”) is determined by using the midpoint between the highest bid and the lowest offer on the primary stock exchange on which the shares of the Fund are listed for trading, as of the time that the Fund’s NAV is calculated. Market and NAV returns assume that dividends and capital gain distributions have been reinvested in the Fund at Market Price and NAV, respectively.

An index is a statistical composite that tracks a specified financial market or sector. Unlike the Fund, an index does not actually hold a portfolio of securities and therefore does not incur the expenses incurred by the Fund. These expenses negatively impact the performance of the Fund. Also, market returns do not include brokerage commissions that may be payable on secondary market transactions. If brokerage commissions were included, market returns would be lower. The performance shown in the table(s) and chart(s) above assumes reinvestment of all dividends and capital gain distributions and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption or sale of fund shares. The investment return and principal value of shares of the Fund will vary with changes in market conditions. Shares of the Fund may be worth more or less than their original cost when they are redeemed or sold in the market. The Fund’s past performance is no guarantee of future results.

| MANAGEMENT’S DISCUSSIONSOF FUND PERFORMANCE | 11 |

Table of Contents

Management’s Discussion of Fund Performance (Continued)

iSHARES® MSCI FRANCE INDEX FUND

PORTFOLIO ALLOCATION As of 8/31/09 | |||

| Sector | Percentage of Net Assets | ||

Consumer Non-Cyclical | 19.49 | % | |

Financial | 19.21 | ||

Industrial | 13.39 | ||

Energy | 12.90 | ||

Communications | 11.17 | ||

Utilities | 8.00 | ||

Basic Materials | 5.79 | ||

Consumer Cyclical | 5.41 | ||

Diversified | 2.29 | ||

Technology | 2.05 | ||

Short-Term and Other Net Assets | 0.30 | ||

TOTAL | 100.00 | % | |

TEN LARGEST FUND HOLDINGS As of 8/31/09 | |||

| Security | Percentage of Net Assets | ||

Total SA | 11.97 | % | |

Sanofi-Aventis | 6.99 | ||

BNP Paribas | 6.59 | ||

GDF Suez | 4.97 | ||

France Telecom SA | 4.56 | ||

Societe Generale | 3.67 | ||

AXA | 3.49 | ||

Vivendi SA | 3.27 | ||

ArcelorMittal | 3.01 | ||

Danone SA | 2.93 | ||

TOTAL | 51.45 | % | |

| �� | |||

| 12 | 2009 iSHARES ANNUAL REPORTTO SHAREHOLDERS |

Table of Contents

Management’s Discussion of Fund Performance

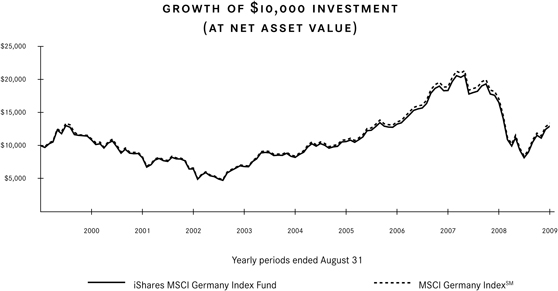

iSHARES® MSCI GERMANY INDEX FUND

(TICKER: EWG)

INVESTMENT OBJECTIVE

The iShares MSCI Germany Index Fund (the “Fund”) seeks to provide investment results that correspond generally to the price and yield performance, before fees and expenses, of publicly traded securities in the aggregate in the German market, as measured by the MSCI Germany IndexSM (the “Index”). The Fund invests in a representative sample of securities included in the Index that collectively has an investment profile similar to the Index. Due to the use of representative sampling, the Fund may or may not hold all of the securities that are included in the Index. For the 12-month period ended August 31, 2009 (the “reporting period”), the total return for the Fund was (21.62)%, while the total return for the Index was (21.71)%.

MARKET OVERVIEW AND DISCUSSION OF PERFORMANCE

A slowing global economic environment and ongoing credit crisis weighed on stock markets around the world during much of the reporting period. Early in the reporting period, the credit crisis that had begun with problems within the U.S. mortgage industry spurred extreme turmoil in the global financial sector, leading to a series of bankruptcies and takeovers among several major financial institutions in late 2008. The events impacted markets worldwide, pushing major indices downward and sapping strength from already weak economies. Unemployment rates climbed in most major economies as industrial output declined and levels of imports and exports fell. In an effort to stabilize markets, key central banks around the world took decisive steps, initiating debt purchase programs and easing monetary policy. In the U.S., the Federal Reserve Board cut the federal funds rate to an unprecedented range of 0.00% - 0.25% during the course of the reporting period. The European Central Bank echoed these actions, lowering its key lending rate from 4.25% to a historically low 1.00%.

After dipping to multi-year lows in early March 2009, most international markets rebounded strongly, as many investors appeared confident that the threats surrounding financial markets were beginning to recede. European markets followed these trends. Market strength continued through the end of the reporting period as early, yet uneven, signs of economic recovery emerged in key European markets. Germany and the U.K. experienced increases in industrial output, while consumer spending increased in France. In Switzerland, the KOF broad measure of economic activity reported large jumps in July and August.

Germany’s market finished the reporting period with a double-digit decline, despite rebounding sharply in the second half of the reporting period. The German economy was challenged with a recession during the reporting period, as evidenced by a contraction in annualized GDP levels for the third and fourth quarters of 2008 and first quarter of 2009. Industrial production declined throughout the period, and the unemployment rate surpassed 8%. In the final months of the reporting period, though, early signs of economic recovery began to surface. Industrial production improved and the unemployment rate stabilized at 8.3%. German retail sales rose as consumer confidence reached its highest level in more than a year. For the second quarter of 2009, GDP grew at an annualized 0.3% rate. The U.S dollar depreciated against the euro in the final months of the reporting period, benefiting dollar-denominated performance returns.

All of the Fund’s ten largest holdings as of August 31, 2009 delivered negative returns for the reporting period. Financial companies Allianz SE and Deutsche Bank AG both posted double-digit declines, as did the Fund’s largest holding, utility company E.ON AG. Bayer AG, Germany’s largest drug maker, and car maker Daimler AG also experienced significant declines. Telecommunications company Deutsche Telekom AG lost ground as well. Chemical company BASF SE posted only a modest drop in share price for the reporting period.

| MANAGEMENT’S DISCUSSIONSOF FUND PERFORMANCE | 13 |

Table of Contents

Management’s Discussion of Fund Performance (Continued)

iSHARES® MSCI GERMANY INDEX FUND

Performance as of August 31, 2009

| Average Annual Total Returns | ||||||||||||||||

| Year Ended 8/31/09 | Five Years Ended 8/31/09 | Ten Years Ended 8/31/09 | ||||||||||||||

| NAV | MARKET | INDEX | NAV | MARKET | INDEX | NAV | MARKET | INDEX | ||||||||

| (21.62)% | (21.00)% | (21.71)% | 9.51% | 9.46% | 9.73% | 2.62% | 2.70% | 2.94% | ||||||||

| Cumulative Total Returns | ||||||||||||||||

| Year Ended 8/31/09 | Five Years Ended 8/31/09 | Ten Years Ended 8/31/09 | ||||||||||||||

| NAV | MARKET | INDEX | NAV | MARKET | INDEX | NAV | MARKET | INDEX | ||||||||

| (21.62)% | (21.00)% | (21.71)% | 57.47% | 57.14% | 59.08% | 29.51% | 30.53% | 33.61% | ||||||||

“Average Annual Total Returns” represent the average annual change in value of an investment over the period(s) indicated. “Cumulative Total Returns” represent the total change in value of an investment over the period(s) indicated.

The Fund’s per share net asset value or “NAV” is the value of one share of the Fund as calculated in accordance with the standard formula for valuing mutual fund shares. The NAV return is based on the NAV of the Fund and the market return is based on the market price per share of the Fund. The price used to calculate market return (“Market Price”) is determined by using the midpoint between the highest bid and the lowest offer on the primary stock exchange on which the shares of the Fund are listed for trading, as of the time that the Fund’s NAV is calculated. Market and NAV returns assume that dividends and capital gain distributions have been reinvested in the Fund at Market Price and NAV, respectively.

An index is a statistical composite that tracks a specified financial market or sector. Unlike the Fund, an index does not actually hold a portfolio of securities and therefore does not incur the expenses incurred by the Fund. These expenses negatively impact the performance of the Fund. Also, market returns do not include brokerage commissions that may be payable on secondary market transactions. If brokerage commissions were included, market returns would be lower. The performance shown in the table(s) and chart(s) above assumes reinvestment of all dividends and capital gain distributions and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption or sale of fund shares. The investment return and principal value of shares of the Fund will vary with changes in market conditions. Shares of the Fund may be worth more or less than their original cost when they are redeemed or sold in the market. The Fund’s past performance is no guarantee of future results.

| 14 | 2009 iSHARES ANNUAL REPORT TO SHAREHOLDERS |

Table of Contents

Management’s Discussion of Fund Performance (Continued)

iSHARES® MSCI GERMANY INDEX FUND

PORTFOLIO ALLOCATION As of 8/31/09 | |||

| Sector | Percentage of Net Assets | ||

Financial | 19.63 | % | |

Basic Materials | 15.63 | ||

Utilities | 15.60 | ||

Industrial | 15.36 | ||

Consumer Cyclical | 14.18 | ||

Consumer Non-Cyclical | 7.64 | ||

Technology | 5.94 | ||

Communications | 5.06 | ||

Diversified | 0.35 | ||

Energy | 0.24 | ||

Short-Term and Other Net Assets | 0.37 | ||

TOTAL | 100.00 | % | |

TEN LARGEST FUND HOLDINGS As of 8/31/09 | |||

| Security | Percentage of Net Assets | ||

E.ON AG | 10.71 | % | |

Siemens AG Registered | 9.37 | ||

Allianz SE Registered | 6.85 | ||

BASF SE | 6.21 | ||

Bayer AG | 6.11 | ||

Daimler AG Registered | 5.24 | ||

SAP AG | 5.22 | ||

Deutsche Telekom AG Registered | 4.79 | ||

RWE AG | 4.71 | ||

Deutsche Bank AG Registered | 4.70 | ||

TOTAL | 63.91 | % | |

| MANAGEMENT’S DISCUSSIONSOF FUND PERFORMANCE | 15 |

Table of Contents

Management’s Discussion of Fund Performance

iSHARES® MSCI ITALY INDEX FUND

(TICKER: EWI)

INVESTMENT OBJECTIVE

The iShares MSCI Italy Index Fund (the “Fund”) seeks to provide investment results that correspond generally to the price and yield performance, before fees and expenses, of publicly traded securities in the aggregate in the Italian market, as measured by the MSCI Italy IndexSM (the “Index”). The Fund invests in a representative sample of securities included in the Index that collectively has an investment profile similar to the Index. Due to the use of representative sampling, the Fund may or may not hold all of the securities that are included in the Index. For the 12-month period ended August 31, 2009 (the “reporting period”), the total return for the Fund was (20.78)%, while the total return for the Index was (20.48)%.

MARKET OVERVIEW AND DISCUSSION OF PERFORMANCE

A slowing global economic environment and ongoing credit crisis weighed on stock markets around the world during much of the reporting period. Early in the reporting period, the credit crisis that had begun with problems within the U.S. mortgage industry spurred extreme turmoil in the global financial sector, leading to a series of bankruptcies and takeovers among several major financial institutions in late 2008. The events impacted markets worldwide, pushing major indices downward and sapping strength from already weak economies. Unemployment rates climbed in most major economies as industrial output declined and levels of imports and exports fell. In an effort to stabilize markets, key central banks around the world took decisive steps, initiating debt purchase programs and easing monetary policy. In the U.S., the Federal Reserve Board cut the federal funds rate to an unprecedented range of 0.00% - 0.25% during the course of the reporting period. The European Central Bank echoed these actions, lowering its key lending rate from 4.25% to a historically low 1.00%.

After dipping to multi-year lows in early March 2009, most international markets rebounded strongly, as many investors appeared confident that the threats surrounding financial markets were beginning to recede. European markets followed these trends. Market strength continued through the end of the reporting period as early, yet uneven, signs of economic recovery emerged in key European markets. Germany and the U.K. experienced increases in industrial output, while consumer spending increased in France. In Switzerland, the KOF broad measure of economic activity reported large jumps in July and August.

Italy’s equity market finished the reporting period with a double-digit decline, despite rebounding sharply in the second half of the reporting period. Already one of the slowest economies in the euro zone, Italy’s economic growth declined further during the reporting period. Annualized GDP contracted for the third and fourth quarters of 2008, as well as the first two quarters of 2009, as industrial production declined and unemployment levels rose above 7%. For the second quarter of 2009, though, the decline in GDP was a relatively modest 0.5%, compared to declines of 2.1% and 2.7% for the fourth quarter of 2008 and first quarter of 2009, respectively. The U.S dollar depreciated against the euro in the final months of the reporting period, benefiting dollar-denominated performance returns.

For the reporting period, performance was mostly negative among the Fund’s ten largest holdings. The Fund’s largest holding, utility company ENI SpA, detracted significantly from performance. Financial companies Assicurazioni Generali SpA, UniCredit SpA, and Intesa Sanpaolo SpA all posted double-digit declines, as did car maker Fiat SpA. Enel SpA, Italy’s largest power company, also delivered negative returns for the period. On the positive side, telecommunications company Telecom Italia SpA and financial company Mediobanca SpA both produced positive returns for the reporting period.

| 16 | 2009 iSHARES ANNUAL REPORT TO SHAREHOLDERS |

Table of Contents

Management’s Discussion of Fund Performance (Continued)

iSHARES® MSCI ITALY INDEX FUND

Performance as of August 31, 2009

| Average Annual Total Returns | ||||||||||||||||

| Year Ended 8/31/09 | Five Years Ended 8/31/09 | Ten Years Ended 8/31/09 | ||||||||||||||

| NAV | MARKET | INDEX | NAV | MARKET | INDEX | NAV | MARKET | INDEX | ||||||||

| (20.78)% | (19.43)% | (20.48)% | 2.65% | 2.53% | 2.51% | 2.36% | 2.39% | 2.17% | ||||||||

| Cumulative Total Returns | ||||||||||||||||

| Year Ended 8/31/09 | Five Years Ended 8/31/09 | Ten Years Ended 8/31/09 | ||||||||||||||

| NAV | MARKET | INDEX | NAV | MARKET | INDEX | NAV | MARKET | INDEX | ||||||||

| (20.78)% | (19.43)% | (20.48)% | 13.94% | 13.30% | 13.20% | 26.32% | 26.64% | 23.95% | ||||||||

“Average Annual Total Returns” represent the average annual change in value of an investment over the period(s) indicated. “Cumulative Total Returns” represent the total change in value of an investment over the period(s) indicated.

The Fund’s per share net asset value or “NAV” is the value of one share of the Fund as calculated in accordance with the standard formula for valuing mutual fund shares. The NAV return is based on the NAV of the Fund and the market return is based on the market price per share of the Fund. The price used to calculate market return (“Market Price”) is determined by using the midpoint between the highest bid and the lowest offer on the primary stock exchange on which the shares of the Fund are listed for trading, as of the time that the Fund’s NAV is calculated. Market and NAV returns assume that dividends and capital gain distributions have been reinvested in the Fund at Market Price and NAV, respectively.

An index is a statistical composite that tracks a specified financial market or sector. Unlike the Fund, an index does not actually hold a portfolio of securities and therefore does not incur the expenses incurred by the Fund. These expenses negatively impact the performance of the Fund. Also, market returns do not include brokerage commissions that may be payable on secondary market transactions. If brokerage commissions were included, market returns would be lower. The performance shown in the table(s) and chart(s) above assumes reinvestment of all dividends and capital gain distributions and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption or sale of fund shares. The investment return and principal value of shares of the Fund will vary with changes in market conditions. Shares of the Fund may be worth more or less than their original cost when they are redeemed or sold in the market. The Fund’s past performance is no guarantee of future results.

| MANAGEMENT’S DISCUSSIONSOF FUND PERFORMANCE | 17 |

Table of Contents

Management’s Discussion of Fund Performance (Continued)

iSHARES® MSCI ITALY INDEX FUND

PORTFOLIO ALLOCATION As of 8/31/09 | |||

| Sector | Percentage of Net Assets | ||

Financial | 43.01 | % | |

Energy | 20.07 | ||

Utilities | 14.43 | ||

Communications | 7.09 | ||

Industrial | 5.66 | ||

Consumer Non-Cyclical | 5.25 | ||

Consumer Cyclical | 3.88 | ||

Diversified | 0.46 | ||

Short-Term and Other Net Assets | 0.15 | ||

TOTAL | 100.00 | % | |

TEN LARGEST FUND HOLDINGS As of 8/31/09 | |||

| Security | Percentage of Net Assets | ||

Eni SpA | 17.00 | % | |

UniCredit SpA | 14.43 | ||

Enel SpA | 9.76 | ||

Intesa Sanpaolo SpA | 8.35 | ||

Assicurazioni Generali SpA | 4.75 | ||

Telecom Italia SpA | 3.78 | ||

Unione di Banche Italiane ScpA | 3.29 | ||

Terna SpA | 3.29 | ||

Mediobanca SpA | 2.71 | ||

Fiat SpA | 2.68 | ||

TOTAL | 70.04 | % | |

| 18 | 2009 iSHARES ANNUAL REPORTTO SHAREHOLDERS |

Table of Contents

Management’s Discussion of Fund Performance

iSHARES® MSCI NETHERLANDS INVESTABLE MARKET INDEX FUND

(TICKER: EWN)

INVESTMENT OBJECTIVE

The iShares MSCI Netherlands Investable Market Index Fund (the “Fund”) seeks to provide investment results that correspond generally to the price and yield performance, before fees and expenses, of publicly traded securities in the aggregate in the Dutch market, as measured by the MSCI Netherlands Investable Market IndexSM (the “Index”). The Fund invests in a representative sample of securities included in the Index that collectively has an investment profile similar to the Index. Due to the use of representative sampling, the Fund may or may not hold all of the securities that are included in the Index. For the 12-month period ended August 31, 2009 (the “reporting period”), the total return for the Fund was (20.59)%, while the total return for the Index was (20.01)%.

MARKET OVERVIEW AND DISCUSSION OF PERFORMANCE

A slowing global economic environment and ongoing credit crisis weighed on stock markets around the world during much of the reporting period. Early in the reporting period, the credit crisis that had begun with problems within the U.S. mortgage industry spurred extreme turmoil in the global financial sector, leading to a series of bankruptcies and takeovers among several major financial institutions in late 2008. The events impacted markets worldwide, pushing major indices downward and sapping strength from already weak economies. Unemployment rates climbed in most major economies as industrial output declined and levels of imports and exports fell. In an effort to stabilize markets, key central banks around the world took decisive steps, initiating debt purchase programs and easing monetary policy. In the U.S., the Federal Reserve Board cut the federal funds rate to an unprecedented range of 0.00% - 0.25% during the course of the reporting period. The European Central Bank echoed these actions, lowering its key lending rate from 4.25% to a historically low 1.00%.

After dipping to multi-year lows in early March 2009, most international markets rebounded strongly, as many investors appeared confident that the threats surrounding financial markets were beginning to recede. European markets followed these trends. Market strength continued through the end of the reporting period as early, yet uneven, signs of economic recovery emerged in key European markets. Germany and the U.K. experienced increases in industrial output, while consumer spending increased in France. In Switzerland, the KOF broad measure of economic activity reported large jumps in July and August.

Although the Netherlands’ equity market rebounded strongly in the final months of the reporting period, this was not sufficient to fully offset the substantial decline experienced in the first half of the period. Because the Dutch economy is based heavily on export trade, it is sensitive to the economic health of its trading partners. Neighboring European countries, in particular, account for roughly 75% of the Netherlands’ export market. During the reporting period, the economic sluggishness experienced across key European countries appears to have resulted in decreased demand for Dutch products. This, in turn, dampened economic growth for the country. Industrial production contracted throughout the period as export levels generally declined. Economic activity, as measured by GDP, dropped by an annualized 0.7% for the fourth quarter of 2008, and by a more severe 4.5% in the first quarter of 2009. The U.S dollar depreciated against the euro in the final months of the reporting period, benefiting dollar-denominated performance returns.

Eight of the ten largest Fund holdings as of August 31, 2009 delivered negative returns for the reporting period. Financial companies ING Groep NV and Aegon NV were the largest decliners. Express delivery service company TNT NV and Koninklijke Philips Electronics NV also posted double-digit declines. Beer maker Heineken NV experienced a moderate decline. On the positive side, ASML Holding NV and the Fund’s largest holding, consumer products company Unilever NV, posted positive returns for the reporting period.

| MANAGEMENT’S DISCUSSIONSOF FUND PERFORMANCE | 19 |

Table of Contents

Management’s Discussion of Fund Performance (Continued)

iSHARES® MSCI NETHERLANDS INVESTABLE MARKET INDEX FUND

Performance as of August 31, 2009

| Average Annual Total Returns | ||||||||||||||||

| Year Ended 8/31/09 | Five Years Ended 8/31/09 | Ten Years Ended 8/31/09 | ||||||||||||||

| NAV | MARKET | INDEX | NAV | MARKET | INDEX | NAV | MARKET | INDEX | ||||||||

| (20.59)% | (19.93)% | (20.01)% | 6.78% | 6.78% | 7.41% | (0.05)% | (0.04)% | 1.02% | ||||||||

| Cumulative Total Returns | ||||||||||||||||

| Year Ended 8/31/09 | Five Years Ended 8/31/09 | Ten Years Ended 8/31/09 | ||||||||||||||

| NAV | MARKET | INDEX | NAV | MARKET | INDEX | NAV | MARKET | INDEX | ||||||||

| (20.59)% | (19.93)% | (20.01)% | 38.81% | 38.83% | 42.96% | (0.54)% | (0.43)% | 10.68% | ||||||||

“Average Annual Total Returns” represent the average annual change in value of an investment over the period(s) indicated. “Cumulative Total Returns” represent the total change in value of an investment over the period(s) indicated.

The Fund’s per share net asset value or “NAV” is the value of one share of the Fund as calculated in accordance with the standard formula for valuing mutual fund shares. The NAV return is based on the NAV of the Fund and the market return is based on the market price per share of the Fund. The price used to calculate market return (“Market Price”) is determined by using the midpoint between the highest bid and the lowest offer on the primary stock exchange on which the shares of the Fund are listed for trading, as of the time that the Fund’s NAV is calculated. Market and NAV returns assume that dividends and capital gain distributions have been reinvested in the Fund at Market Price and NAV, respectively.

An index is a statistical composite that tracks a specified financial market or sector. Unlike the Fund, an index does not actually hold a portfolio of securities and therefore does not incur the expenses incurred by the Fund. These expenses negatively impact the performance of the Fund. Also, market returns do not include brokerage commissions that may be payable on secondary market transactions. If brokerage commissions were included, market returns would be lower. The performance shown in the table(s) and chart(s) above assumes reinvestment of all dividends and capital gain distributions and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption or sale of fund shares. The investment return and principal value of shares of the Fund will vary with changes in market conditions. Shares of the Fund may be worth more or less than their original cost when they are redeemed or sold in the market. The Fund’s past performance is no guarantee of future results.

| 20 | 2009 iSHARES ANNUAL REPORTTO SHAREHOLDERS |

Table of Contents

Management’s Discussion of Fund Performance (Continued)

iSHARES® MSCI NETHERLANDS INVESTABLE MARKET INDEX FUND

PORTFOLIO ALLOCATION As of 8/31/09 | |||

| Sector | Percentage of Net Assets | ||

Consumer Non-Cyclical | 31.81 | % | |

Financial | 19.81 | ||

Industrial | 15.78 | ||

Communications | 15.35 | ||

Basic Materials | 7.20 | ||

Technology | 6.15 | ||

Energy | 2.52 | ||

Diversified | 0.76 | ||

Consumer Cyclical | 0.31 | ||

Short-Term and Other Net Assets | 0.31 | ||

TOTAL | 100.00 | % | |

TEN LARGEST FUND HOLDINGS As of 8/31/09 | |||

| Security | Percentage of Net Assets | ||

Unilever NV | 16.80 | % | |

ING Groep NV | 11.00 | ||

Koninklijke KPN NV | 9.50 | ||

Koninklijke Philips Electronics NV | 7.45 | ||

Koninklijke Ahold NV | 4.85 | ||

Akzo Nobel NV | 4.80 | ||

ASML Holding NV | 4.75 | ||

Aegon NV | 4.37 | ||

TNT NV | 3.97 | ||

Heineken NV | 3.79 | ||

TOTAL | 71.28 | % | |

| MANAGEMENT’S DISCUSSIONOF FUND PERFORMANCE | 21 |

Table of Contents

Management’s Discussion of Fund Performance

iSHARES® MSCI SPAIN INDEX FUND

(TICKER: EWP)

INVESTMENT OBJECTIVE

The iShares MSCI Spain Index Fund (the “Fund”) seeks to provide investment results that correspond generally to the price and yield performance, before fees and expenses, of publicly traded securities in the aggregate in the Spanish market, as measured by the MSCI Spain IndexSM (the “Index”). The Fund invests in a representative sample of securities included in the Index that collectively has an investment profile similar to the Index. Due to the use of representative sampling, the Fund may or may not hold all of the securities that are included in the Index. For the 12-month period ended August 31, 2009 (the “reporting period”), the total return for the Fund was 0.64%, while the total return for the Index was 0.71%.

MARKET OVERVIEW AND DISCUSSION OF PERFORMANCE

A slowing global economic environment and ongoing credit crisis weighed on stock markets around the world during much of the reporting period. Early in the reporting period, the credit crisis that had begun with problems within the U.S. mortgage industry spurred extreme turmoil in the global financial sector, leading to a series of bankruptcies and takeovers among several major financial institutions in late 2008. The events impacted markets worldwide, pushing major indices downward and sapping strength from already weak economies. Unemployment rates climbed in most major economies as industrial output declined and levels of imports and exports fell. In an effort to stabilize markets, key central banks around the world took decisive steps, initiating debt purchase programs and easing monetary policy. In the U.S., the Federal Reserve Board cut the federal funds rate to an unprecedented range of 0.00% - 0.25% during the course of the reporting period. The European Central Bank echoed these actions, lowering its key lending rate from 4.25% to a historically low 1.00%.

After dipping to multi-year lows in early March 2009, most international markets rebounded strongly, as many investors appeared confident that the threats surrounding financial markets were beginning to recede. European markets followed these trends. Market strength continued through the end of the reporting period as early, yet uneven, signs of economic recovery emerged in key European markets. Germany and the U.K. experienced increases in industrial output, while consumer spending increased in France. In Switzerland, the KOF broad measure of economic activity reported large jumps in July and August.

Although the Spanish equity market declined sharply in the first half of the reporting period, it rebounded soundly in the final months and finished the period with a positive return. Because Spain’s neighboring European countries account for the vast majority of its exports, the country was hurt by the tumultuous economic environments in major European countries during the reporting period. Export trade slowed throughout the reporting period, but climbed in the final months of the period. Economic activity, as measured by GDP, contracted for the third and fourth quarters of 2008 and for the first two quarters of 2009. In the second quarter of 2009, annualized GDP declined 1.06%. As the country struggled with recession, unemployment levels rose. For the second quarter of 2009, the unemployment rate reached 18%, the highest level of all European countries. The U.S dollar depreciated against the euro in the final months of the reporting period, benefiting dollar-denominated performance returns.

Performance among the ten largest holdings as of August 31, 2009 was mostly positive for the reporting period. Among the ten largest holdings, infrastructure construction company Actividades de Construccion y Servicios SA delivered the largest gains, followed by clothing retailer Industria de Diseno Textil SA. Four financial companies posted positive returns, including Banco Bilbao Vizcaya Argentaria SA and the Fund’s largest holding, Banco Santander SA. The Fund’s second largest holding, Telefonica SA, also contributed meaningfully to Fund performance. On the negative side, electric utility company Iberdrola SA and oil and gas company Repsol YPF SA both declined for the reporting period.

| 22 | 2009 iSHARES ANNUAL REPORTTO SHAREHOLDERS |

Table of Contents

Management’s Discussion of Fund Performance (Continued)

iSHARES® MSCI SPAIN INDEX FUND

Performance as of August 31, 2009

| Average Annual Total Returns | ||||||||||||||||

| Year Ended 8/31/09 | Five Years Ended 8/31/09 | Ten Years Ended 8/31/09 | ||||||||||||||

| NAV | MARKET | INDEX | NAV | MARKET | INDEX | NAV | MARKET | INDEX | ||||||||

| 0.64% | 1.35% | 0.71% | 14.88% | 14.75% | 15.04% | 8.67% | 8.70% | 8.57% | ||||||||

| Cumulative Total Returns | ||||||||||||||||

| Year Ended 8/31/09 | Five Years Ended 8/31/09 | Ten Years Ended 8/31/09 | ||||||||||||||

| NAV | MARKET | INDEX | NAV | MARKET | INDEX | NAV | MARKET | INDEX | ||||||||

| 0.64% | 1.35% | 0.71% | 100.12% | 98.95% | 101.49% | 129.66% | 130.37% | 127.56% | ||||||||

“Average Annual Total Returns” represent the average annual change in value of an investment over the period(s) indicated. “Cumulative Total Returns” represent the total change in value of an investment over the period(s) indicated.

The Fund’s per share net asset value or ”NAV” is the value of one share of the Fund as calculated in accordance with the standard formula for valuing mutual fund shares. The NAV return is based on the NAV of the Fund and the market return is based on the market price per share of the Fund. The price used to calculate market return (“Market Price”) is determined by using the midpoint between the highest bid and the lowest offer on the primary stock exchange on which the shares of the Fund are listed for trading, as of the time that the Fund’s NAV is calculated. Market and NAV returns assume that dividends and capital gain distributions have been reinvested in the Fund at Market Price and NAV, respectively.

An index is a statistical composite that tracks a specified financial market or sector. Unlike the Fund, an index does not actually hold a portfolio of securities and therefore does not incur the expenses incurred by the Fund. These expenses negatively impact the performance of the Fund. Also, market returns do not include brokerage commissions that may be payable on secondary market transactions. If brokerage commissions were included, market returns would be lower. The performance shown in the table(s) and chart(s) above assumes reinvestment of all dividends and capital gain distributions and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption or sale of fund shares. The investment return and principal value of shares of the Fund will vary with changes in market conditions. Shares of the Fund may be worth more or less than their original cost when they are redeemed or sold in the market. The Fund’s past performance is no guarantee of future results.

| MANAGEMENT’S DISCUSSIONSOF FUND PERFORMANCE | 23 |

Table of Contents

Management’s Discussion of Fund Performance (Continued)

iSHARES® MSCI SPAIN INDEX FUND

PORTFOLIO ALLOCATION As of 8/31/09 | |||

| Sector | Percentage of Net Assets | ||

Financial | 46.17 | % | |

Communications | 19.50 | ||

Utilities | 10.27 | ||

Industrial | 6.64 | ||

Energy | 5.64 | ||

Consumer Cyclical | 4.96 | ||

Consumer Non-Cyclical | 4.52 | ||

Technology | 1.61 | ||

Basic Materials | 0.53 | ||

Short-Term and Other Net Assets | 0.16 | ||

TOTAL | 100.00 | % | |

TEN LARGEST FUND HOLDINGS As of 8/31/09 | |||

| Security | Percentage of Net Assets | ||

Banco Santander SA | 23.18 | % | |

Telefonica SA | 18.80 | ||

Banco Bilbao Vizcaya Argentaria SA | 7.43 | ||

Iberdrola SA | 4.86 | ||

Repsol YPF SA | 4.64 | ||

Industria de Diseno Textil SA | 4.58 | ||

Banco Popular Espanol SA | 3.44 | ||

Banco de Sabadell SA | 3.39 | ||

Abertis Infraestructuras SA | 3.16 | ||

Actividades de Construcciones y Servicios SA | 2.95 | ||

TOTAL | 76.43 | % | |

| 24 | 2009 iSHARES ANNUAL REPORTTO SHAREHOLDERS |

Table of Contents

Management’s Discussion of Fund Performance

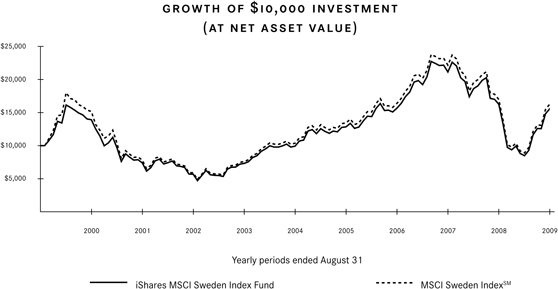

iSHARES® MSCI SWEDEN INDEX FUND

(TICKER: EWD)

INVESTMENT OBJECTIVE

The iShares MSCI Sweden Index Fund (the “Fund”) seeks to provide investment results that correspond generally to the price and yield performance, before fees and expenses, of publicly traded securities in the aggregate in the Swedish market, as measured by the MSCI Sweden IndexSM (the “Index”). The Fund invests in a representative sample of securities included in the Index that collectively has an investment profile similar to the Index. Due to the use of representative sampling, the Fund may or may not hold all of the securities that are included in the Index. For the 12-month period ended August 31, 2009 (the “reporting period”), the total return for the Fund was (4.04)%, while the total return for the Index was (4.16)%.

MARKET OVERVIEW AND DISCUSSION OF PERFORMANCE

A slowing global economic environment and ongoing credit crisis weighed on stock markets around the world during much of the reporting period. Early in the reporting period, the credit crisis that had begun with problems within the U.S. mortgage industry spurred extreme turmoil in the global financial sector, leading to a series of bankruptcies and takeovers among several major financial institutions in late 2008. The events impacted markets worldwide, pushing major indices downward and sapping strength from already weak economies. Unemployment rates climbed in most major economies as industrial output declined and levels of imports and exports fell. In an effort to stabilize markets, key central banks around the world took decisive steps, initiating debt purchase programs and easing monetary policy. In the U.S., the Federal Reserve Board cut the federal funds rate to an unprecedented range of 0.00% - 0.25% during the course of the reporting period. The European Central Bank echoed these actions, lowering its key lending rate from 4.25% to a historically low 1.00%.

After dipping to multi-year lows in early March 2009, most international markets rebounded strongly, as many investors appeared confident that the threats surrounding financial markets were beginning to recede. European markets followed these trends. Market strength continued through the end of the reporting period as early, yet uneven, signs of economic recovery emerged in key European markets. Germany and the U.K. experienced increases in industrial output, while consumer spending increased in France. In Switzerland, the KOF broad measure of economic activity reported large jumps in July and August.

Although it rebounded strongly in the final months of the reporting period, Sweden’s equity market declined modestly for the reporting period. Sweden’s economy relies heavily on exports, and it is sensitive to the economic health of its export partners. During the reporting period, the economic slowdown in neighboring European countries and in the U.S. appears to have resulted in reduced export levels for Sweden, which in turn translated into slowing economic conditions during the reporting period. For the fourth quarter of 2008 and first two quarters of 2009, annualized GDP contracted, declining 5.1%, 5.6%, and 6.1%, respectively. Unemployment levels escalated, topping 9% by July 2009. Consistent with central banks around the world, Sweden’s Riksbank lowered its key interest rate from 4.50% to 0.25% during the course of the reporting period in an effort to stimulate economic activity.

Seven of the Fund’s ten largest holdings delivered negative returns for the reporting period. Among the ten largest holdings, financial company Skandinaviska Enskilda Banken AB logged the largest decline. Machinery company Sandvik AB and car maker Volvo AB also experienced double-digit declines, as did the mobile phone maker Telefonaktiebolaget LM Ericsson. On the positive side, the clothing retailer Hennes & Mauritz AB contributed positively to Fund performance. Banks Svenska Handelsbanken AB and the Fund’s largest holding, Nordea Bank AB, both posted gains for the reporting period.

| MANAGEMENT’S DISCUSSIONSOF FUND PERFORMANCE | 25 |

Table of Contents

Management’s Discussion of Fund Performance (Continued)

iSHARES® MSCI SWEDEN INDEX FUND

Performance as of August 31, 2009

| Average Annual Total Returns | ||||||||||||||||

| Year Ended 8/31/09 | Five Years Ended 8/31/09 | Ten Years Ended 8/31/09 | ||||||||||||||

| NAV | MARKET | INDEX | NAV | MARKET | INDEX | NAV | MARKET | INDEX | ||||||||

| (4.04)% | (3.30)% | (4.16)% | 9.46% | 9.37% | 9.45% | 4.54% | 4.58% | 4.99% | ||||||||

| Cumulative Total Returns | ||||||||||||||||

| Year Ended 8/31/09 | Five Years Ended 8/31/09 | Ten Years Ended 8/31/09 | ||||||||||||||

| NAV | MARKET | INDEX | NAV | MARKET | INDEX | NAV | MARKET | INDEX | ||||||||

| (4.04)% | (3.30)% | (4.16)% | 57.13% | 56.47% | 57.06% | 55.83% | 56.45% | 62.73% | ||||||||

“Average Annual Total Returns” represent the average annual change in value of an investment over the period(s) indicated. “Cumulative Total Returns” represent the total change in value of an investment over the period(s) indicated.

The Fund’s per share net asset value or ”NAV” is the value of one share of the Fund as calculated in accordance with the standard formula for valuing mutual fund shares. The NAV return is based on the NAV of the Fund and the market return is based on the market price per share of the Fund. The price used to calculate market return (“Market Price”) is determined by using the midpoint between the highest bid and the lowest offer on the primary stock exchange on which the shares of the Fund are listed for trading, as of the time that the Fund’s NAV is calculated. Market and NAV returns assume that dividends and capital gain distributions have been reinvested in the Fund at Market Price and NAV, respectively.

An index is a statistical composite that tracks a specified financial market or sector. Unlike the Fund, an index does not actually hold a portfolio of securities and therefore does not incur the expenses incurred by the Fund. These expenses negatively impact the performance of the Fund. Also, market returns do not include brokerage commissions that may be payable on secondary market transactions. If brokerage commissions were included, market returns would be lower. The performance shown in the table(s) and chart(s) above assumes reinvestment of all dividends and capital gain distributions and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption or sale of fund shares. The investment return and principal value of shares of the Fund will vary with changes in market conditions. Shares of the Fund may be worth more or less than their original cost when they are redeemed or sold in the market. The Fund’s past performance is no guarantee of future results.

| 26 | 2009 iSHARES ANNUAL REPORTTO SHAREHOLDERS |

Table of Contents

Management’s Discussion of Fund Performance (Continued)

iSHARES® MSCI SWEDEN INDEX FUND

PORTFOLIO ALLOCATION As of 8/31/09 | |||

| Sector | Percentage of Net Assets | ||

Financial | 28.11 | % | |

Industrial | 22.97 | ||

Communications | 21.46 | ||

Consumer Cyclical | 15.34 | ||

Consumer Non-Cyclical | 5.90 | ||

Basic Materials | 5.22 | ||

Energy | 0.82 | ||

Short-Term and Other Net Assets | 0.18 | ||

TOTAL | 100.00 | % | |

TEN LARGEST FUND HOLDINGS As of 8/31/09 | |||

| Security | Percentage of Net Assets | ||

Nordea Bank AB | 13.86 | % | |

Hennes & Mauritz AB Class B | 11.63 | ||

Telefonaktiebolaget LM Ericsson AB Class B | 11.60 | ||

TeliaSonera AB | 5.97 | ||

Svenska Handelsbanken AB Class A | 4.84 | ||

Skandinaviska Enskilda Banken AB Class A | 4.38 | ||

Sandvik AB | 4.20 | ||

Volvo AB Class B | 3.92 | ||

Investor AB Class B | 3.59 | ||

Atlas Copco AB Class A | 3.18 | ||

TOTAL | 67.17 | % | |

| MANAGEMENT’S DISCUSSIONSOF FUND PERFORMANCE | 27 |

Table of Contents

Management’s Discussion of Fund Performance

iSHARES® MSCI SWITZERLAND INDEX FUND

(TICKER: EWL)

INVESTMENT OBJECTIVE

The iShares MSCI Switzerland Index Fund (the “Fund”) seeks to provide investment results that correspond generally to the price and yield performance, before fees and expenses, of publicly traded securities in the aggregate in the Swiss market, as measured by the MSCI Switzerland IndexSM (the “Index”). The Fund invests in a representative sample of securities included in the Index that collectively has an investment profile similar to the Index. Due to the use of representative sampling, the Fund may or may not hold all of the securities that are included in the Index. For the 12-month period ended August 31, 2009 (the “reporting period”), the total return for the Fund was (8.63)%, while the total return for the Index was (9.30)%.

MARKET OVERVIEW AND DISCUSSION OF PERFORMANCE