| | | Page |

| i |

| v |

| 1 |

| Item 1. | | 1 |

| Item 2. | | 1 |

| Item 3. | | 1 |

| Item 4. | | 55 |

| Item 4A. | | 119 |

| Item 5. | | 119 |

| Item 6. | | 154 |

| Item 7. | | 169 |

| Item 8. | | 175 |

| Item 9. | | 181 |

| Item 10. | | 184 |

| Item 11. | | 207 |

| Item 12. | | 211 |

| 212 |

| Item 13. | | 212 |

| Item 14. | | 212 |

| Item 15. | | 212 |

| Item 16. | | 213 |

| Item 16A. | | 213 |

| Item 16B. | | 213 |

| Item 16C. | | 213 |

| Item 16D. | | 214 |

| Item 16E. | | 214 |

| Item 16F. | | 217 |

| Item 16G. | | 217 |

| Item 16H. | | 219 |

| Item 16I. | | 219 |

| 220 |

| Item 17. | | 220 |

| Item 18. | | 220 |

| Item 19. | | 220 |

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

Certain Defined Terms

In this annual report on Form 20-F (“Annual Report”), unless otherwise indicated or the context requires otherwise: (i) references to “we,” “us,” “our” and the “Company” mean Transportadora de Gas del Sur S.A. (“TGS”) and its consolidated subsidiaries, Telcosur S.A. (“Telcosur”), TGSLatam Energía S.A. (“TGSLatam”) and CTG Energía S.A.U. (“CTG”), (ii) references to “Argentina” are to the Republic of Argentina, (iii) references to the “United States” or “U.S.” are to the United States of America, (iv) references to “pesos” or “Ps.” are to Argentine pesos, the legal currency of Argentina, (v) references to “U.S. dollars,” “dollars” or “U.S.$” are to United States dollars, the legal currency of the United States, (vi) a “billion” is a thousand million, (vii) references to “cf” are to cubic feet, (viii) references to “MMcf” are to millions of cubic feet, (ix) references to “Bcf” are to billions of cubic feet, (x) references to “m3” are to cubic meters, (xi) references to “d” are to days, and (xii) references to “HP” are to horsepower.

Financial Statements and Basis of Preparation

We maintain our financial books and records and publish our consolidated Financial Statements (as defined below) in pesos, which is our functional currency. This Annual Report includes our audited consolidated statements of financial position as of December 31, 2021 and 2020, and our audited consolidated statements of comprehensive income, changes in equity and cash flows, and the related explanatory notes for the years ended December 31, 2021, 2020 and 2019 (our “Financial Statements”). Our Financial Statements have been prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”) and as in effect on the date of preparation of the Financial Statements. IFRS have been adopted by the Federación Argentina de Consejos Profesionales de Ciencias Económicas (“FACPCE”) as its professional accounting standards and are required to be adopted by certain public companies in Argentina (entidades incluidas en el régimen de oferta pública de la Ley de Mercado de Capitales) pursuant to the rules of the Comisión Nacional de Valores (“CNV”), compiled under General Resolution No. 622/2013 (as amended by General Resolution No. 668/2016 and as further amended, the “CNV Rules”).

At our shareholders’ meeting held on April 26, 2017, as a result of a proposal by our controlling shareholder, Compañía de Inversiones de Energía S.A. (“CIESA”), our shareholders voted in favor of having a joint audit on our consolidated financial statements commencing with fiscal year ended December 31, 2017, even though there is currently no legal requirement in Argentina for a joint audit. As a result, our Financial Statements were jointly audited by Price Waterhouse & Co. S.R.L., Buenos Aires, Argentina (“PwC”), member firm of PricewaterhouseCoopers International Limited, and Pistrelli, Henry Martin y Asociados S.R.L. (“EY”), member firm of Ernst & Young Global Limited. The joint report of PwC and EY, dated April 26, 2022, is included elsewhere in this Annual Report. Each of PwC and EY is an independent registered public accounting firm, as stated in the joint report appearing herein.

International Accounting Standard 29 (“IAS 29”) “Financial reporting in hyperinflationary economies” requires that the financial statements of an entity whose functional currency is one of a hyperinflationary economy be expressed in terms of the current unit of measurement at the closing date of the reporting period, regardless of whether such financial statements are based on the historical cost method or the current cost method. This requirement also comprises the restatement of comparative information of the financial statements to be presented in the current currency as of December 31, 2021, without modifying the statutory decisions made based on the financial information corresponding to those fiscal years.

IAS 29 describes characteristics that may indicate that an economy is hyperinflationary. However, it states that it is a matter of judgement by management when restatement of financial statements becomes necessary. Among other factors, an economy is “hyperinflationary” in accordance with IAS 29 when it has a cumulative inflation rate over three years that approaches, or exceeds, 100%, also taking into consideration other qualitative factors related to the macroeconomic environment.

The IASB does not identify specific economies that satisfy the requirements to be deemed hyperinflationary. The International Practices Task Force (“IPTF”) of the Centre for Audit Quality monitors the status of “highly inflationary” countries. The criteria of IPTF for identifying such countries are similar to those for identifying “hyperinflationary economies” under IAS 29. From time to time, the IPTF issues reports of its discussions with the staff of the Securities and Exchange Commission (“SEC”) on the IPTF’s recommendations of which countries should be considered highly inflationary, and which countries are on the IPTF’s inflation “watch list.” The IPTF’s discussion document for its November 6, 2021 meeting states that in the view of the IPTF, Argentina had a three-year cumulative inflation rate exceeding 100%.

Inflation in Argentina significantly increased during 2021, 2020 and 2019, which resulted in an accumulated inflation rate for each of the three-year periods ended December 31, 2021, 2020 and 2019, in excess of 100%. In addition, the rest of the indicators do not contradict the conclusion that Argentina should be considered a hyperinflationary economy for accounting purposes. As a result, our management considers that there is sufficient evidence to conclude that Argentina is a hyperinflationary economy in terms of IAS 29, effective as from July 1, 2018.

The Financial Statements and the other financial information included in this Annual Report for all the periods reported are presented on the basis of constant pesos as of December 31, 2021 (“Current Currency”). Thus, our audited consolidated statements of financial position as of December 31, 2020, and our audited consolidated statements of comprehensive income, changes in equity and cash flows, and the related explanatory notes for each of the years ended December 31, 2020 and 2019, included elsewhere in this Annual Report have been restated in accordance with IAS 29 for comparative purposes from the original figures reported and supersede any previously disclosed consolidated financial statements relating to such periods.

In analyzing the provisions of IAS 29, our management used the inflation rates stated in the official statistics published by the Instituto Nacional de Estadística y Censos (“INDEC”), similar to the criteria adopted by the accounting profession and corporate regulatory bodies in Argentina. In order to restate the financial statements referred in the immediately preceding paragraph, the CNV has established that the series of indexes to be used for the application of IAS 29 is determined by the FACPCE. This series of indexes combines the National Consumer Price Index (“CPI”) as of January 2020 (base month December 2019) with the Domestic Wholesale Price Index (“WPI”), both published by INDEC until that date. According to information from FACPCE, inflation was 50.9%, 36.1% and 53.8% in the years ended December 31, 2021, 2020 and 2019, respectively.

For more information, see note 4(d) to the Financial Statements and “Item 5. Operating and Financial Review and Prospects—A. Operating Results—Factors Affecting Our Consolidated Results of Operation.” Also, see “Item 3. Key Information—D. Risk Factors—Risks Relating to Argentina—High levels of inflation could negatively affect our business, results of operations and financial condition, the value of our securities, and our ability to meet our financial obligations.”

Currency

Solely for the convenience of the reader, certain amounts presented in pesos in this Annual Report as of and for the year ended December 31, 2021, have been converted into U.S. dollars at specified exchange rates. Unless otherwise specified, all exchange rate information contained in this Annual Report has been derived from information published by Banco de la Nación Argentina (“Banco Nación”) on December 31, 2021, without any independent verification by us. As a result of fluctuations in the peso/U.S. dollar exchange rate, the exchange rate at such date may not be indicative of current or future exchange rates. Such fluctuations may affect the U.S. dollar equivalent of peso amounts included in this Annual Report. Consequently, these translations should not be construed as a representation that the peso amounts represent, or have been, or could be converted, into, U.S. dollars at that or any other rate.

Fluctuations in the exchange rate between pesos and U.S. dollars would affect the U.S. dollar equivalent of the peso price of our Class “B” shares, par value Ps.1 each (the “Class B Shares”), on the Buenos Aires Stock Exchange (Bolsas y Mercados Argentinos (“BYMA”)) and, as a result, the market price of our American Depositary Shares (“ADSs”) on the New York Stock Exchange (“NYSE”) as well.

Historically, Argentina has been subject to several restrictions imposed on the foreign exchange market. In the recent years, the Central Bank of the Republic of Argentina (Banco Central de la República Argentina or the “BCRA”) issued several communications which introduced several changes to the then existing foreign exchange control regime. For additional information, see “Item 10. Additional Information—D. Exchange Controls.”

The following table sets forth, for the periods indicated, high, low, average and period-end exchange rates between the peso and the U.S. dollar, as reported by Banco Nación. The Federal Reserve Bank of New York does not publish a buying rate for the peso. The average rate is calculated by using the average of Banco Nación reported exchange rates on each day during the relevant monthly period and on the last day of each month during the relevant annual period.

| | | | | |

| | | | | | | | | | | | | |

| Most recent six months: | | | | | | | | | | | | |

November 2021 | | | 100.9600 | | | | 84.7000 | | | | 95.1607 | | | | 102.7200 | |

December 2021 | | | 102.7200 | | | | 99.8100 | | | | 100.3124 | | | | 100.9600 | |

January 2022 | | | 105.0200 | | | | 101.0000 | | | | 101.8860 | | | | 102.7200 | |

February 2022 | | | 107.4500 | | | | 103.0000 | | | | 103.9881 | | | | 105.0200 | |

March 2022 | | | | | | 105.1200 | | | | 106.3047 | | | | 107.4500 | |

April 2022 (through April 25, 2022) | | | 114.6800 | | | | 111.1200 | | | | 112.8687 | | | | 114.6800 | |

| | | | | | | | | | | | | | | | | |

| Year ended December 31, | | | | | | | | | | | | | | | | |

2017 | | | 19.2000 | | | | 15.1900 | | | | 16.5717 | | | | 18.6490 | |

2018 | | | 41.2500 | | | | 18.4100 | | | | 28.1313 | | | | 37.7000 | |

2019 | | | 60.4000 | | | | 36.9000 | | | | 48.2340 | | | | 59.8900 | |

2020 | | | 84.1500 | | | | 59.8150 | | | | 70.7795 | | | | 84.1500 | |

2021 | | | 102.7200 | | | | 84.7000 | | | | 95.1607 | | | | 102.7200 | |

Our results of operations and financial condition are highly sensitive to changes in the peso-U.S. dollar exchange rate because a significant portion of our revenues (73% of our total consolidated revenues from sales for the year ended December 31, 2021), most of our capital expenditures, almost all of our debt obligations and the cost of natural gas used in our Liquids business are denominated in U.S. dollars, but substantially all of our assets are located in Argentina, and our functional currency is the peso.

Currency fluctuations would also affect the U.S. dollar amounts received by holders of our ADSs upon conversion (by us or by Citibank N.A. (the “Depositary”), pursuant to the deposit agreement for the issuance of the ADSs entered into between the Depositary and us (the “Deposit Agreement”)) of the cash dividends paid in pesos on the underlying Class “B” Shares.

Rounding

Certain figures included in this Annual Report have been rounded for ease of presentation. Percentage figures included in this Annual Report have not, in all cases, been calculated on the basis of such rounded figures but on the basis of such amounts prior to rounding. For this reason, percentage amounts in this Annual Report may vary from those obtained by performing the same calculations using the figures in our Financial Statements. Certain numerical figures shown as totals in some tables may not be an arithmetic aggregation of the figures that preceded them due to rounding.

Available Information

The SEC maintains an internet site (http://www.sec.gov) that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC. Our telephone number is (54-11) 4865-9050, and our principal executive offices are located at Don Bosco 3672, 5th Floor, C1206ABF City of Buenos Aires, Argentina. Our internet address is www.tgs.com.ar. This URL is intended to be an inactive textual reference only. It is not intended to be an active hyperlink to our website. The information included in our website or which may be accessed through our website is not part of this Annual Report, is not incorporated by reference herein or otherwise and should not be relied upon in determining whether to make an investment in any securities issued by us.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

Some of the information in this Annual Report, including information incorporated by reference herein, may constitute estimates and forward-looking statements within the meaning of Section 27A of the U.S. Securities Act of 1933 (the “Securities Act”) and Section 21E of the U.S. Securities Exchange Act of 1934, as amended (the “Exchange Act”). These estimates and forward-looking statements can be identified by the use of forward-looking terminology such as “anticipate,” “believe,” “can,” “continue,” “estimate,” “expect,” “goal,” “intend,” “may,” “plan” “potential,” “predict,” “projection,” “should,” “will,” “will likely result,” “would” or other similar words. These estimates and statements appear in a number of places in this Annual Report and include statements regarding our intent, belief or current expectations, and those of our officers, with respect to (among other things) our business, financial condition and results of operations. Although we believe that these estimates and forward-looking statements are based upon reasonable assumptions, they are subject to several risks and uncertainties and are based on information available to us as of the date of this Annual Report.

When considering forward-looking statements, you should keep in mind the factors described in “Item 3. Key Information—D. Risk Factors” and other cautionary statements appearing in “Item 5. Operating and Financial Review and Prospects.” These factors and statements, as well as other statements contained herein, describe circumstances that could cause actual results to differ materially from those expressed in or implied by any forward-looking statement.

Forward-looking statements include, but are not limited to, the following:

| • | statements regarding changes in general economic, business, political or other conditions in Argentina and globally, including changes from actions taken by the the Argentine government (the “Government”) and changes due to natural and human-induced disasters (including the COVID-19 virus (“COVID”) pandemic and the recent invasion of Ukraine by Russia), and the impact of the foregoing; |

| • | estimates relating to future energy demand (including demand for fossil fuels), tariffs and volumes for our natural gas transportation services and future prices and volumes for our natural gas liquid products such as propane and butane (also referred to as liquid petroleum gas or “LPG”), ethane and natural gasoline (collectively “Liquids”) and for products and services provided in the Other Services business segment; |

| • | statements regarding future political developments in Argentina and future developments regarding the license granted to us by Government to provide natural gas transportation services through the exclusive use of the southern natural gas transportation system in Argentina (“License”), the impact of the adoption of the new revised scheme of tariffs resulting from the renegotiation process of our License with the Government, regulatory actions by Ente Nacional Regulador del Gas (“ENARGAS”) and other agencies of the Government, the legal framework established by the Federal Energy Bureau and any other applicable governmental authority that may affect us and our business; |

| • | with our employees in Argentina; |

| • | statements and estimates regarding future pipeline expansion and other projects and the cost of, or return to us from, any such expansion or projects; |

| • | estimates of our future level of capital expenditures and delays in such capital expenditures, including those required by ENARGAS or other governmental authorities for the expansion of our pipeline system or other purposes, and unscheduled and unexpected expenditures for the repair and maintenance of our fixed or capital assets; |

| • | statements regarding the ability of companies engaged in the upstream business in the region where we operate to identify drilling locations and prospects for future drilling opportunities, and drill and develop such locations (such as the Vaca Muerta formation), as well as the Government’s regulations and policies affecting such companies and projects; and |

| • | the risk factors discussed under “Item 3. Key Information—D. Risk Factors.” |

Estimates and forward-looking statements speak only as of the date of this Annual Report and we do not undertake any obligation to update any forward-looking statement or other information contained in this Annual Report to reflect events or circumstances occurring after the date of this Annual Report or to reflect the occurrence of unanticipated events. Additional factors affecting our business emerge from time to time and it is not possible for us to predict all of those factors, nor can we assess the impact of all such factors on our business, operations or financial condition, or the extent to which any factors, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statement. Estimates and forward-looking statements involve risks and uncertainties and do not guarantee future performance, as actual results or developments may be substantially different from the expectations described in the forward-looking statements. In light of the risks and uncertainties described above, the events referred to in the estimates and forward-looking statements included in this Annual Report may or may not occur, and our business performance, financial condition and results of operations may differ materially from those expressed in our estimates and forward-looking statements, due to factors that include but are not limited to those mentioned above. Investors are warned not to place undue reliance on any estimates or forward-looking statements in making any investment decision.

| Item 1. | Identity of Directors, Senior Management and Advisers |

Not applicable.

| Item 2. | Offer Statistics and Expected Timetable |

Not applicable.

| B. | Capitalization and Indebtedness |

Not applicable.

| C. | Reasons for the Offer and Use of Proceeds |

Not applicable.

You should carefully consider the following risks and uncertainties, and any other information appearing elsewhere in this Annual Report. The risks and uncertainties described below are intended to highlight risks and uncertainties that are specific to us. Additional risks and uncertainties, including those generally affecting Argentina and the industry in which we operate, risks and uncertainties that we currently consider immaterial or risks and uncertainties generally applicable to similar companies in Argentina may also impair our business, results of operations, financial condition, the value of our securities and our ability to meet our financial obligations.

The information in this Risk Factors section includes forward-looking statements that involve risks and uncertainties. Our actual results could differ materially from those anticipated in these forward-looking statements as a result of numerous factors, including those described in “Cautionary Statement Regarding Forward-Looking Statements” above.

The following summarizes some, but not all, of the risks provided below. The following summary of material risk factors could materially and adversely affect our business, financial condition and results of operation, and our ability to meet our financial obligations. Consequently, such risk factors may cause historical results to differ materially from any results projected, forecasted, estimated or budgeted by us in our forward-looking statements. Please carefully consider all of the information discussed in this “Item 3. Key Information—D. Risk Factors” in this Annual Report for a more thorough description of these and other risks:

| • | Risks Relating to Our Business |

| ‒ | failure or delay in the implementation of tariff increases and our inability to obtain tariff adjustments reflecting the increase in operating cost; |

| ‒ | our operations are subject to extensive regulation; |

| ‒ | failure to maintain our relationships with labor unions; |

| ‒ | our ability to maintain our License for our regulated business; |

| ‒ | our creditors may not be able to enforce their claims against us in Argentina; |

| ‒ | the Government’s strategies, measures and programs with respect to the natural gas transportation industry; |

| ‒ | Government-mandated interruption of contracted firm transportation services; |

| ‒ | a significant portion of our revenues is generated under natural gas transportation contracts that must be renegotiated and/or extended periodically; |

| ‒ | our business may require substantial capital expenditures; |

| ‒ | our Liquids production depends on the natural gas that arrives at the Cerri Complex through three main pipelines from the Neuquina, Austral and San Jorge natural gas basins; |

| ‒ | measures taken by the Government on the supply of natural gas to the Cerri Complex; |

| ‒ | fluctuations in market prices and the enactment of new taxes or regulations limiting the sales price of LPG and natural gasoline; |

| ‒ | the continued spread of the COVID; |

| ‒ | our ethane sales depend on the capacity of PBB Polisur S.R.L. (“PBB”), as the sole purchaser of our ethane production; |

| ‒ | the delay in the collection of our sales receivables with customers and/or subsidies owed by the Government for the supply of LPG in the domestic market; |

| ‒ | our failure to renew firm transportation contracts; |

| ‒ | our Other Services business depends significantly on the need of Vaca Muerta fields gas producers to evacuate untreated natural gas; |

| ‒ | the affirmative and restrictive covenants in our currently outstanding indebtedness; |

| ‒ | our insurance policies may not fully cover damage or we may not be able to obtain insurance against certain risks; |

| ‒ | changes in the interpretation by the courts of labor laws that tend to favor employees; |

| ‒ | risks related to litigation and administrative proceedings; |

| ‒ | impact of environmental, occupational health and safety regulations; |

| ‒ | we may face competition; |

| ‒ | downgrades in our credit ratings; |

| ‒ | cyberattacks or other risks related to new technologies; |

| ‒ | mechanical or electrical failures and any resulting unavailability; |

| ‒ | risks arising from natural disasters, catastrophic accidents and terrorist attacks; |

| ‒ | failure to comply with anti-trust, anti-corruption, anti-bribery and anti-money laundering laws; and |

| ‒ | inability to retain our employees or attract other skilled employees or contractors. |

| • | Risks Relating to Argentina |

| ‒ | Argentina’s public debt may not be sustainable in the near future; |

| ‒ | Argentina’s fiscal situation could limit the country's access to the capital market and adversely affect the Argentine economy; |

| ‒ | Certain risks inherent to any investment in a company operating in an emerging market such as Argentina; |

| ‒ | economic volatility in Argentina; |

| ‒ | the ongoing political instability in Argentina; |

| ‒ | the impact of reforms and measures taken or to be taken by the Fernandez administration, including the Solidarity Law; |

| ‒ | high levels of inflation; |

| ‒ | restrictions on transfers of foreign currency; |

| ‒ | fluctuations in the value of the peso; |

| ‒ | the impossibility of addressing the actual and potential risks of institutional deterioration and corruption; |

| ‒ | Government intervention in the Argentine economy; |

| ‒ | Impact on the Argentine economy of economic developments in other markets; |

| ‒ | Argentina’s past default and litigation with holdout bondholders; |

| ‒ | a sustained deterioration in the terms of trade given a decline in the global prices for Argentina’s main commodity exports or an increase in the global prices for Argentina’s main commodity imports; |

| ‒ | further downgrades in the credit rating or rating outlook of Argentina; and |

| ‒ | the Argentine government may mandate salary increases for private sector employees; |

| | ‒ | Geopolitical uncertainty due to the ongoing military conflict between Russia and Ukraine. |

| • | Risks Relating to Our Shares and ADSs |

| ‒ | shareholders outside Argentina may face additional investment risk from currency exchange rate fluctuations in connection with their holding of our shares or ADSs represented by ADRs; |

| ‒ | our principal shareholders exercise significant control over matters affecting us, and may have interests that differ from those of our other shareholders; |

| ‒ | sales of a substantial number of shares could decrease the market prices of our shares and the ADRs; |

| ‒ | under Argentine law, shareholder rights may be fewer or less well defined than in other jurisdictions; |

| ‒ | as a foreign private issuer we are exempt from certain rules that apply to domestic U.S. issuers; |

| ‒ | changes in Argentine tax laws may adversely affect the tax treatment of our Class B Shares or ADSs; |

| ‒ | holders of ADRs may be unable to exercise voting rights with respect to our Class B Shares underlying the ADRs at our shareholders’ meetings; |

| ‒ | holders of ADRs may be unable to exercise preemptive, accretion or other rights with respect to the Class B shares underlying the ADSs; |

| ‒ | the NYSE and/or the BASE (by delegated authority of BYMA) may suspend trading and/or delist our ADSs and common shares, respectively; |

| ‒ | the price of our Class B Shares and the ADSs may fluctuate substantially; and |

| ‒ | the relative volatility and illiquidity of the Argentine securities markets. |

Risks Relating to Our Business

Failure or delay in the implementation of tariff increases could have a material adverse effect on our business, results of operations and financial condition, the value of our securities, and our ability to meet our financial obligations. In addition, our inability to obtain tariff adjustments reflecting the increase in operating cost could harm the development of our Natural Gas Transportation business segment.

All of our net revenues from the Natural Gas Transportation public service (which represented 27% of total net revenues during 2021) are attributable to contracts, which are subject to Government regulation. Prior to the enactment of the Public Emergency Law and Foreign Exchange System Reform Law No. 25,561 (the “Public Emergency Law”), our tariffs were stated in U.S. dollars, adjusted on a semiannual basis by reference to the U.S. Producer Price Index (“PPI”), and further adjusted every five years, based on the efficiency of, and investments in, our gas transportation business. The Public Emergency Law, however, eliminated tariff indexation, and public service tariffs were converted into pesos and fixed at an exchange rate of Ps.1.00 per U.S.$1.00, even though the peso was devaluating significantly against the U.S. dollar.

Sustained inflation in Argentina since 2002, without any corresponding increase in our natural gas transportation tariffs until recently, has adversely affected, and continued inflation would continue to adversely affect, our Natural Gas Transportation revenues, net revenues and financial condition.

On March 30, 2017, ENARGAS issued Resolution No. 4362/2017 (“Resolution 4362”), which approved a staged tariff increase which contemplates an aggregate transportation tariff increase of 214.2% and an aggregate access and use charge (“CAU”) increase of 37%. This staged increase is structured to provide the same economic benefits to us as if the increases had been fully effective on April 1, 2017. Pursuant to this resolution, we must also execute a capital expenditures program for a five-year period (from April 1, 2017, to March 31, 2022), which contemplates investments of Ps.6,786 million (in nominal value at December 31, 2016) to improve the operation and maintenance of the pipeline system (the “Five-Year Plan”). In addition, Resolution 4362 contemplates a non-automatic semiannual adjustment mechanism for the natural gas transportation tariff to reflect changes in WPI, which must be approved by ENARGAS evaluating the evolution of the economic circumstances.

On March 27, 2018, through Decree No. 250/2018 (“Decree 250”), the Executive Branch ratified the tariff structure under Resolution 4362, following the approval of several governmental authorities, including the Argentine Congress. Decree 250 concludes the renegotiation process of our License with the Government, which lasted more than 17 years.

On April 1, 2019, ENARGAS analyzed the evolution of the WPI adjustment index for the period August 2018–February 2019 in order to establish the biannual adjustments applicable to our tariffs.

As a consequence of Argentina’s economic condition, and together with other measures taken by the Government, on September 3, 2019, the Secretary of Hydrocarbon Resources (“SHR”) (formerly the Federal Energy Bureau) issued Resolution No. 521/2019 (“Resolution 521”), which defers the semiannual adjustment corresponding to October 1, 2019, to January 1, 2020. During 2019 and 2020, according to the RTI, we were entitled to receive two tariff increases, one each year, in order to compensate us for inflation, which affects our operating costs. We have only received a tariff increase in April 2019.

The tariff increases mentioned above were not granted to us within the framework of the Solidarity Law and the subsequent decrees issued by the Executive Branch that determined the freezing of our tariff schedule and the beginning of a new RTI process. In this context, and within the framework of Decree No. 1020, the Executive Branch started the renegotiation of the RTI (concluded in 2018), which may not exceed two years. Until then, the renegotiation agreements in force are suspended. Such renegotiation remains under control of ENARGAS and subject to confirmation by the Executive Branch.

In addition, Decree 1020 extends the tariff freeze for an additional period of 90 calendar days or until transitory tariffs are approved. On March 16, 2021, a public hearing was held to discuss the transitory tariff increases. After such hearing, TGS received a transitory tariff revision agreement, which we later rejected. On June 2, 2021, ENARGAS issued Resolution No. 149/2021 that provides a Transitional Tariff Regime, which, among other issues, does not grant a transitory tariff increase in our favor, but instead maintained the tariff in force since April 1, 2019.

Subsequently, a new public hearing was held in January, which resulted ENARGAS issuing Resolution 60/2022 on February 25, 2022, whereby a transitional tariff increase of 60% was provided. For additional information see “Item 4. Our Information—B. Business Overview—Natural Gas Transportation—Regulatory Framework—Tariff Situation.”

In the past, we have suffered from our inability to receive tariff increases, which meant the deterioration of our financial and economic condition. Also, we have received insufficient tariff increases to compensate for the increases in our operating costs due to inflation. For additional information about the prior integral tariff renegotiation (“RTI”) processes and failure by ENRAGAS to increase tariffs, and the status of the ongoing RTI see “Item 4. Our Information—B. Business Overview—Natural Gas Transportation—Regulatory Framework—Tariff Situation.”

We cannot assure you that the current negotiations with the Government will provide us with a tariff schedule that permits us to compensate the increases in our operating costs. Failure by the Government to timely comply with agreements resulting from the new RTI process could negatively affect our results of operations and financial condition.

Moreover, as of the date of this Annual Report, we are unable to predict which permanent measures will be taken by the Government in connection with the tariff system, or if such system will be amended, adversely affecting our financial situation and our results of operations.

Further, we cannot assure you that the current negotiations with the Government under the framework of the Solidarity Law will provide us with a tariff schedule that permits us to compensate the increases in our operating costs. Failure by the Government to timely comply with agreements resulting from the RTI process could negatively affect our results of operations and financial condition.

In addition, we cannot predict whether additional operating restrictions or mandatory investments could be imposed on us in the future nor the outcome from the renegotiation process of the current RTI stated by the Solidarity Law. If such outcome is adverse to us, our results of operations and financial condition could be negatively affected.

Our operations are subject to extensive regulation.

The Argentine oil and gas industry is subject to extensive government regulation and control. As a result, our business is to a large extent dependent upon regulatory and political conditions prevailing in Argentina and our business, results of operations and financial condition, the value of our securities, and our ability to meet our financial obligations may be adversely affected by regulatory and political changes in Argentina. Therefore, we face risks and challenges relating to government regulation and control of the energy sector, including those set forth below and elsewhere in these risk factors:

| • | limitations on our ability to increase prices or to reflect the effects of higher domestic taxes, increases in operating costs or increases in international prices of natural gas and other hydrocarbon fuels and exchange rate fluctuations on our domestic prices; |

| • | risks in connection with the former and current incentive programs established by the Government for the oil and gas industry, such as the natural gas additional injection stimulus program and cash collection of balances with the Government; |

| • | legislation and regulatory initiatives relating to hydraulic stimulation and other drilling activities for non-conventional oil and gas hydrocarbons, which could increase our cost of doing business or cause delays and adversely affect our operations; and |

| • | the implementation or imposition of stricter quality requirements for hydrocarbon products in Argentina. |

In recent years, the Government has made certain changes in regulations and policies governing the energy sector to give absolute priority to domestic supply at stable prices in order to sustain economic recovery. As a result of the above-mentioned changes, for example, on days during which a gas shortage occurs, exports of natural gas (which are also affected by other government curtailment orders) and the provision of gas supplies to industries, electricity generation plants and service stations selling compressed natural gas are interrupted to prioritize residential consumers at lower prices. The Expropriation Law of Argentina has declared the achievement of self-sufficiency in the supply of hydrocarbons, as well as in the exploitation, industrialization, transportation and sale of hydrocarbons, is in the national public interest and a priority for Argentina. In addition, its stated goal is to guarantee socially equitable economic development, the creation of jobs, the increase of the competitiveness of various economic sectors and the equitable and sustainable growth of the Argentine provinces and regions. We cannot assure you that these and other changes in applicable laws and regulations, or adverse judicial or administrative interpretations of such laws and regulations, will not adversely affect our business, results of operations, financial condition, the value of our securities and our ability to meet our financial obligations.

Failure to maintain our relationships with labor unions may have an adverse effect on our business, financial condition, results of operations and prospects.

A significant portion of our workforce is represented by labor unions, and the majority of our non-unionized employees have the same employment benefits as unionized employees. While we believe we have enjoyed satisfactory relationships with all of the labor organizations that represent our associates, and we believe our relationships with labor organizations will continue to be satisfactory, labor-related disputes may still arise. In particular, labor lawsuits are common in the energy sector in Argentina, and industry-wide organized actions by unionized employees in the industry, such as blockages in the access to facilities and route cuts have occurred in the past. We have suffered interruptions as a result of our employees joining such organized activities. We cannot assure you that future business interruptions resulting from strikes and other organized activities by our employees would not have a significant adverse effect on our business, financial condition, results of operations and prospects.

The collective bargaining agreements with our unions are valid for one year. Currently, we have a collective bargaining agreement in effect for the period from April 2022 to March 2023.

However, we cannot assure you that we will not suffer business interruptions or strikes in the future as a result of collective actions by our employees. We have insurance that covers terrorism and organized actions against our assets, among other items, for a total insured amount of U.S.$50,000,000 with a deductible per event of U.S.$500,000, but we cannot assure you that our insurance coverage will be sufficient to cover damages and losses caused by the organized actions of our employees.

In addition, in the past, the Government has enacted laws and regulations forcing private companies to maintain certain wage levels and to provide additional benefits to their employees. We cannot assure you that in the future the Government will not increase wages or require additional benefits for workers or employees or that unions will not pressure the Government to demand such measures. All wage increases, as well as any additional benefits, could result in increased costs and adversely affect our results of operations.

Our regulated business is dependent on our ability to maintain our License, which is subject to revocation under some circumstances.

We conduct our Natural Gas Transportation business pursuant to the License, which authorizes us to provide natural gas transportation services through the exclusive use of the southern natural gas transportation system in Argentina. Our License may be revoked in certain circumstances based on the recommendation of ENARGAS. Revocation of our license would require an administrative proceeding, which would be subject to judicial review. Reasons for which our License may be revoked include:

| • | repeated failure to comply with the obligations of our License and failure to remedy a significant breach of an obligation in accordance with specified procedures; |

| • | total or partial interruption of service for reasons attributable to us that affects transportation capacity during the periods stipulated in our License; |

| • | sale, assignment or transfer of our essential assets or the placing of encumbrances thereon without ENARGAS’s prior authorization, unless such encumbrances serve to finance extensions and improvements to the gas pipeline system; |

| • | our bankruptcy, dissolution or liquidation; |

| • | cessation and abandonment of the provision of the licensed service, an attempt to assign or unilaterally transfer our License in full or in part without the prior authorization of ENARGAS, or relinquishing our License, other than in the cases permitted therein; and |

| • | delegation of the functions granted in such License without the prior authorization of ENARGAS, or the termination of such License without regulatory approval of a license. |

If our License were revoked, we would be required to cease providing natural gas transportation services. The impact of a loss of our License on our business, financial condition and results of operations would be material and adverse. Additionally, certain changes to the License could result in a default under our outstanding debt instruments.

Our creditors may not be able to enforce their claims against us in Argentina.

We are a stock corporation with limited liability (sociedad anónima), incorporated and organized under the laws of Argentina. Substantially all of our assets are located in Argentina.

Under Argentine law, foreign judgments may be enforced by Argentine courts; provided that the requirements of Articles 517 through 519 of the Federal Code of Civil and Commercial Procedure are met. Foreign judgments cannot violate principles of public policy (orden público) of Argentine law, as determined by Argentine courts. It is possible that an Argentine court would deem the enforcement of foreign judgments ordering us to make a payment in a foreign currency outside of Argentina to be contrary to Argentine public policy if at that time there are legal restrictions prohibiting Argentine debtors from transferring foreign currency outside of Argentina. Although currently there are no legal restrictions prohibiting Argentine debtors from transferring foreign currency outside of Argentina to satisfy principal or interest payments on outstanding debt that has been previously reported to the BCRA, we cannot assure you that the Government or an Argentine court will not impose such restrictions in the future.

In addition, under Argentine law, attachment prior to execution and attachment in aid of execution will not be ordered by an Argentine court with respect to property located in Argentina and determined by such courts to be utilized for the provision of essential public services. A significant portion of our assets may be considered by Argentine courts to be dedicated to the provision of an essential public service. If an Argentine court were to make such a determination with respect to any of our assets, unless the Government ordered the release of such assets, such assets would not be subject to attachment, execution or other legal process as long as such determination stands, and the ability of any of our creditors to realize a judgment against such assets may be adversely affected.

The Government’s strategies, measures and programs with respect to the natural gas transportation industry could materially adversely affect our business, results of operations, financial condition, the value of our securities and our ability to meet our financial obligations.

Since 1992 and after the privatization of several state companies, until the economic crisis in 2002, the Government reduced its control over the natural gas transportation industry. After the economic crisis in 2002 the Government increased its role in the energy sector implementing strict regulations and increasing its intervention. Intervention primarily included the expansion of our pipeline through the creation of trust funds and the interruption and redirection of natural gas firm transportation services (including the diversification of natural gas supply from our liquids processing plant located at General Cerri Complex, in the Province of Buenos Aires (“Cerri Complex”)).

In the past, natural gas distribution companies, including us, were prohibited from passing through price increases to consumers. Producers of natural gas, therefore, had difficulty implementing wellhead natural gas price adjustments that would increase the costs of distribution companies, which caused such producers to suffer a sharp decline in their rate of return on investment activities. As a result, natural gas production was not sufficient to meet the increasing demand. Likewise, until 2016, the lack of tariff adjustments for natural gas transportation companies caused a decrease in the profitability of such companies.

In light of these events, the Government implemented a number of strategies, measures and programs aimed at mitigating the energy crisis and supporting the recovery of the Argentine economy generally. With respect to the natural gas industry, these strategies, measures and programs included, among others, the expansion of our pipeline through the creation of financial trust funds used as vehicles to facilitate financing of those investments (“Gas Trusts”). For more information on the pipeline expansions, please see “Item 4. Our Information—B. Business Overview—Natural Gas Transportation—Pipeline Operations—Pipeline Expansions.” Although the expansion projects described above have not adversely affected our results of operations or financial condition, we cannot assure you that future, or even present, expansion projects will not have such adverse effects.

Within the framework of the measures adopted as a result of the restrictions imposed to face the sanitary emergency arising from the COVID pandemic, the Argentinian Government took a series of measures to mitigate its impact on certain socioeconomic sectors. Within this framework, during 2020, service cuts to non-paying residential users were suspended, the “Plan Gas.Ar” was created with the purpose of promoting natural gas production and certain limitations to tariff increases were imposed to keep pace with the evolution of inflation and cost increases.

We cannot predict what other measures will be adopted by the Government to mitigate the impact of the COVID pandemic, nor the effect that such measures may have on our business, results of operations and financial condition, the value of our securities, and our ability to meet our financial obligations.

Government-mandated interruption of contracted firm transportation services could materially adversely affect our business, results of operations, financial condition, the value of our securities and our ability to meet our financial obligations.

In 2004, the Executive Branch issued Presidential Decree No. 181/04, directing the Federal Energy Bureau to have a system of priority pursuant to the demand of natural gas customers, regardless of whether those customers have contracted under a firm transportation contract or a firm natural gas supply contract. Pursuant to ENARGAS Resolution No. 1,410/2010, due to the lack of sufficient natural gas provision, natural gas transportation service (including to those with firm transportation contracts) may be interrupted and/or relocated in order to service priority demand customers.

On June 1, 2016, the former Ministry of Energy issued Resolution No. 89/2016, which required ENARGAS to develop a procedure to amend and supplement ENARGAS Resolution No. 1,410/2010 and establish daily operating conditions for the transportation and distribution systems. It also established a methodology to satisfy the demand for natural gas of those customers classified as “high-priority.”

On June 5, 2016, ENARGAS issued Resolution No. I/3833/2016, creating the “Supplementary Procedure for Gas Requests, Confirmations and Control.” According to this resolution, if any gas transportation and distribution company finds that the transportation capacity is not sufficient to supply priority demand customers, such company shall summon an emergency committee composed of company and ENARGAS representatives. This emergency committee shall determine adjustments to be made to the daily natural gas deliveries in order to address such shortage, considering the availability of natural gas and the demands of residential consumers and power plants.

On June 26, 2018, ENARGAS issued Resolution No. 124/2018, which replaced Resolution No. 716/1998 and incorporated content from the repealed Resolution No. 1,410/2010 and Resolution No. 3,833/2016. Additionally, this resolution established the Internal Rules of Dispatch Centers (Reglamento Interno de los Centros de Despacho).

Although neither our results of operations nor our financial condition have been materially adversely affected by transportation service interruptions in recent years, we cannot assure you that similar interruptions will not materially adversely affect our business, results of operations, financial condition, the value of our securities and our ability to meet our financial obligations. As of the date of this Annual Report there are some unresolved disputes with one of our clients (Profertil S.A.), in respect of service interruptions between 2007 and 2013. In that action, through Resolution No. 306/2009, ENARGAS ruled in our favor, finding that there was a shortage in the supply of natural gas. However, we cannot assure you that future interruptions of supply to our firm natural gas transportation clients will not lead to further legal action, which could have a significant adverse effect on our business, results of operations, financial condition, the value of our securities and our ability to meet our financial obligations.

Additionally, we cannot predict whether new measures requiring the interruption or relocation of the natural gas transportation service will be taken. If such measures are implemented, we could be subject to legal actions initiated by those affected by such measures.

A significant portion of our revenues is generated under natural gas transportation contracts that must be renegotiated and/or extended periodically.

In 2021, 78% of our average daily natural gas deliveries were made under long-term firm transportation contracts. As of December 31, 2021, our long-term firm natural gas transportation contracts had a remaining weighted average life of approximately 11 years; our long-term firm natural gas transportation contracts with our top five costumers had a remaining weighted average life of approximately eight years. We cannot assure you that we will be able to extend or replace these contracts when they expire or that the terms of any renegotiated contracts will be as favorable as the existing contracts. In particular, our ability to extend and/or replace contracts could be adversely affected by factors we cannot control, including:

| • | Argentine natural gas transportation regulations; |

| • | international oil and gas prices; |

| • | timing, volume and location of new market demand; |

| • | competition from alternative energy sources; |

| • | supply and price of natural gas in Argentina; |

| • | demand for natural gas in the markets we serve; and |

| • | availability and competitiveness of alternative gas transportation infrastructure in the markets we serve. |

Additionally, most of our transportation contracts include a clause allowing for the termination of the relevant contract before the expiration of its term by any of the parties, in case of (i) breach of the other party, or (ii) an extended event of force majeure.

For our Liquids Production and Commercialization business segment, we commercialize ethane through a long-term agreement renewed with PBB for a ten-year period. We have short-term contracts with international traders for LPG and natural gasoline sales.

Our business may require substantial capital expenditures for ongoing maintenance requirements and the expansion of our installed transportation capacity; we could be unable to make such expenditures due to the lack of financing.

Resolution No. 4362/2017 (“Resolution 4362”) issued by ENARGAS on March 30, 2017, stated that we should have executed capital expenditures of Ps.6,786 million (in nominal value at December 31, 2016, adjustable by WPI) for the five-year period (from April 1, 2017, to March 31, 2022), to improve the operation and maintenance of the pipeline system (the “Five-Year Plan”). As of the date of issuance of this Annual Report the Five-Year Plan is suspended as a consequence of the new RTI process.

As part of the measures adopted to reduce the impact of COVID and in order to adapt our business plan to the economic expectations of Argentina, we have implemented a reduction in the current investment plans, without compromising safety, which allows us to guarantee continuity in the development of our activities.

The natural gas transportation service is an activity involving significant amounts of capital expenditures in order to improve the operation and maintenance of the pipeline system. Incremental capital expenditures may be required to fund maintenance of our pipeline system. Furthermore, capital expenditures will be required to finance current and future expansions of our transportation capacity. If we are unable to finance any such capital expenditures in terms satisfactory to us or at all, our business, results of operations and financial condition, the value of our securities, and our ability to meet our financial obligations may be adversely affected. In addition, our financing ability may be limited by market restrictions on financing availability for Argentine companies. See “—Risks Relating to Argentina—Argentina’s past default and litigation with holdout bondholders may limit our ability to access international markets.”

In the past, expansion projects by the Government have not had adverse effects over our results of operations and financial condition. However, we cannot assure you that future expansion projects will not adversely affect our business.

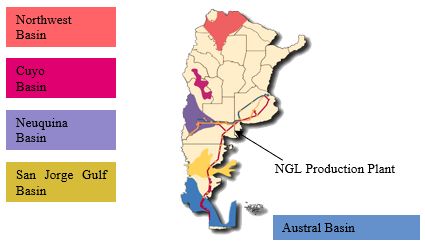

Our Liquids production depends on the natural gas that arrives at the Cerri Complex through three main pipelines from the Neuquina, Austral and San Jorge natural gas basins. The flow and heating value of this natural gas are subject to risks that could materially adversely affect our Liquids and midstream business segment.

Argentina relies heavily on natural gas. However, its natural gas reserves are declining. Despite the decline in 2015 and 2016, the volume of natural gas that has been produced from the Neuquina basin has increased. Although production volume increased in recent years, it had previously decreased between 2009 and 2013 and it is possible that natural gas production will again decrease in the future, which would adversely affect our Liquids business segment by reducing the amount of natural gas flowing to the Cerri Complex and, therefore, the amount of Liquids we produce. In addition, the reduction in the production of natural gas could affect the flow of natural gas provided for our midstream services.

Since 2009, the quality and volume of natural gas injected from the Neuquina basin has been lower (as a consequence of the reduction of natural gas production in this basin) and not appropriate for processing in the Cerri Complex, negatively impacting our level of output from this facility. As a consequence of this lower output of natural gas from the Neuquina basin, we have had to buy natural gas at higher prices, causing an increase in the cost of Liquids production and commercialization activities for our own account reducing our profit from these activities. In addition, competition might affect the volume and quality (i.e., gas with lower liquids content) of natural gas arriving at the Cerri Complex.

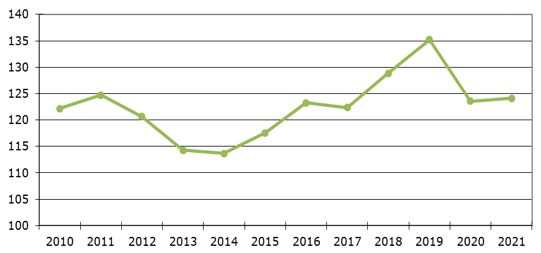

In 2009, nonconventional natural gas was discovered in the Vaca Muerta field of the Neuquina basin by YPF. Exploration and exploitation of this natural gas reserve involved high extraction costs. Argentina’s national natural gas production has steadily increased in the past three years, largely due to the increased production of shale from the Vaca Muerta formation. Because of the measures taken by the Government to ensure production levels throughout the country, during 2016 and 2015, natural gas production increased approximately 4.9% and 3.4%, respectively. However, in 2017 natural gas production slightly declined by 0.9% primarily as a result of the termination of certain incentive programs implemented. In 2018 natural gas production increased by 5.3% with respect to 2017, and on December 31, 2019 it reached its peak production compared to the last 10 years.

During 2020, Argentina’s natural gas production decreased (8.6%), interrupting the series of increases recorded during the last few years. This decline was due to the limiting effects of the preventive and mandatory lockdown measures, combined with a higher autumn temperature.

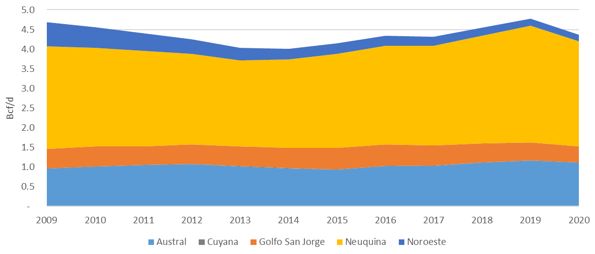

During 2021, Argentina’s natural gas production increased 0.4%. In 2021, 55% of the natural gas transported by our system originated in the Neuquina basin with the remainder primarily from the Austral basin. Conventional gas production (48% of the total) decreased 7.7% year-over-year. Non-conventional production increased 11.8% year-over-year. The Neuquén basin, with 52% of the national production, where most of the unconventional of non-conventional developments, explains the year-on-year increase. The rest of the basins decrease their production in the twelve-month accumulated measurements (with the exception of the Cuyana basin, which has a low representation in the national the Cuyana basin of low representativeness).

However, after the freezing of fuel prices and the current economic situation that Argentina is experiencing, there is uncertainty regarding the investments that natural gas producers can make in that area. The Plan Gas.Ar establishes the need to guarantee the supply of natural gas demand while establishing incentives to make immediate investments for the maintenance and/or growth of production in the productive basins, where the natural gas producers must commit themselves to achieve a production curve that guarantees the maintenance and/or increase of the current levels.

We cannot assure you, however, that this new natural gas resource at the Neuquina basin, or the Plan Gas.Ar, or any other measures taken by the Government to increase natural gas production and supply (including pipeline expansion projects and the construction of new pipelines such as the Tratayén-Salliqueló-San Jerónimo pipeline), will be successful in increasing Argentine natural gas reserves or production and, if unsuccessful, our midstream or Liquids Production and Commercialization businesses could be adversely affected.

Measures taken by the Government may have an adverse effect on the supply of natural gas to the Cerri Complex and the margins we are able to obtain from our Liquids business, which may adversely affect the results in our Liquids Production and Commercialization segment and, as a result, our overall business and results of operations.

Due to regulatory, economic and government policy factors, domestic gasoline, diesel, natural gas, propane and butane, and other fuel prices and related services have differed substantially from prevailing international and regional market prices for such products and services. Our ability to increase prices in connection with international price or domestic cost increases, including those resulting from the peso devaluation, has been limited from time to time. The prices that we are able to obtain for our products and services affect the viability of investments in expansion capacity and processing facilities and, as a result, the timing and amount of our capital expenditures for such purposes.

Although our Liquids production and commercialization activities are not subject to regulation by ENARGAS, with the aim to give priority to domestic supply, the Government has taken certain regulatory actions in recent years that have affected our Liquids business. For example, in April 2005, the Government enacted Law No. 26,020, which set the framework by which the SHR may establish regulations to cause LPG suppliers to guarantee sufficient supply of LPG in the domestic market at low prices. Law No. 26,020 creates a price regime pursuant to which the SHR periodically publishes reference prices for LPG sold in the local market. It also sets forth LPG volumes to be sold in the local market.

We participate in two programs created by the Government under this framework, which provide for the payment of compensation based on the difference between the price set by the Government and the export parity price. Over recent years, this compensation has been paid to us with significant delays. For further information, see “Item 4—Our Information—B—Business Overview—Competition—Liquids Production and Commercialization.”

On March 25, 2020, after COVID pandemic, the Executive Branch issued Decree No. 311/2020, which determines that the maximum reference price for LPG sold in the domestic market will remain at their values in force at such date for a 180-day period.

During 2021, prices of the products sold under these programs were slightly increased. In August 2021, within the framework of Plan Hogar, the Energy Secretariat through Res. No. 809/2021 provided financial assistance to butane producers. The assistance was effective from August to December 2021 inclusive.

Also, we cannot assure you that we will be able to maintain or increase the domestic prices of our products, and limitations on our ability to do so would adversely affect our business, results of operations and financial condition, the value of our securities, and our ability to meet our financial obligations. Similarly, we cannot assure you that LPG prices in Argentina will track increases or decreases in the international or regional markets.

Our Liquids business is highly dependent on the supply of natural gas to the Cerri Complex at reasonable prices that allow for reasonable profit margins.

Since 2017, the Government has taken a series of necessary measures to initiate a convergence between the local price of natural gas and the international price. However, during 2018, due to a combination of internal and external factors, the increase in natural gas and fuel prices was significant which meant that the intended liberalization was unsuccessful.

During 2018, the Government introduced several changes to the process by which the natural gas is acquired for the electric energy generators. Among them, modifications were introduced to the regulations through which Compañía Administradora del Mercado Mayorista Eléctrico S.A. (“CAMMESA”), a government-controlled company, had to provide this supply to the power plants. Finally, on November 6, 2018, the Secretary of Energy issued Resolution No. 70/2018, which returned to power generators the ability to purchase their own natural gas supply. Most of the power generators recovered the ability to do so, therefore, the price of natural gas purchased under the bidding processes decreased further because of the competition for demand in the low consumption season and in an environment with oversupply and economic recession.

Since December 2018, the government again decreased the natural gas price reference for power generation based on the supply basin of origin. As a result, during 2019, CAMMESA called for several bidding processes under the same conditions which resulted in even lower natural gas prices for generation.

The prices at which power plants or CAMMESA acquire natural gas can be considered a reference to determine the price of natural gas acquired as shrinkage gas (“RTP”) by us, which is why any additional increase in the costs of our Liquids Production and Commercialization segment may adversely affect our business, results of operations, financial condition, the value of our securities and our ability to meet our financial obligations.

As described above, actions taken by the Government during winter periods of recent years resulted in natural gas being redirected away from certain users, including the Cerri Complex, toward priority users, including residential customers. See “—The Government’s strategies, measures and programs with respect to the natural gas transportation industry could materially adversely affect our business, results of operations, financial condition, the value of our securities and our ability to meet our financial obligations.” To a lesser extent, during the winter of 2016 and 2017, processing at the Cerri Complex was interrupted because of continued governmental actions to ensure natural gas supply to the domestic market, but thanks to the development of the Vaca Muerta formation, during the five-year period ended December 31, 2021, we did not register any interruption in the supply of natural gas in the Cerri Complex.

Additionally, in view of the scarcity of natural gas supply, the national government has resorted to importing liquefied natural gas (“LGN”) (which is regasified in the ports located in the cities of Escobar and Bahía Blanca, in the province of Buenos Aires) and from Bolivia. The recent war between Ukraine and Russia resulted in a significant increase in natural gas prices. In view of the country’s fiscal situation, it is not possible to guarantee that Argentina will be able to acquire all the natural gas and LGNs necessary to meet demand. Likewise, this situation caused difficulties in the negotiations between Argentina and Bolivia to extend the agreement to import natural gas from Bolivia.

In the event that Argentina is unable to meet the demand, it is highly likely that there will be scheduled natural gas outages during the winter to certain non-priority users (among them the Cerri Complex).

In addition, regarding natural gas producers, the Government has recently introduced measures to moderate the impact of fuel prices in the economy. The prices that natural gas producers are able to obtain for oil and natural gas affect the viability of investments in new exploration, development and refining and, as a result, the timing and amount of our projected capital expenditures for such purposes. Any diversion of the supply of natural gas from the Cerri Complex may require us to purchase natural gas from third parties to supply our Liquids business, which may result in increased costs. If we are unable to purchase natural gas from other sources, the volume of our Liquids productions may decrease.

After the first award of volumes and prices carried out on December 3, 2020, under the framework of Plan Gas.Ar, an increase in the natural gas price at the Point of Entry to the Transportation System (the “PIST” after its acronym in Spanish) for thermal generation and for natural gas distributors was verified, which is highly likely to affect industrial users, which will ultimately impact the costs of natural gas consumed in the Cerri Complex, thus affecting our operating margins. However, such plan would allow the drop in production levels that has been recorded in recent periods to be reversed in order to sustain our gas processing business at the Cerri Complex.

It is uncertain whether in the future measures taken by the Government or other measures that could adversely affect our business, results of operations and ability to meet our financial obligations will be implemented. It is also uncertain the impact of the Solidarity Law, regulations to be issued under its framework or whether our regulatory obligations may be increased, which could result in higher taxes, amendments to the tariff structure, or any other obligations that could increase our costs and adversely affect our financial situation.

Fluctuations in market prices and the enactment of new taxes or regulations limiting the sales price of LPG and natural gasoline may affect our Liquids business.

We extract LPG and natural gasoline from natural gas delivered to the Cerri Complex and sell LPG and natural gasoline. As a result of the deterioration of our Natural Gas Transportation segment, operations relating to our Liquids production and commercialization have represented more than 50% of our total net revenues between 2004 and 2017 and during fiscal year 2021.

Over the last few years, the price of Liquids has experienced high levels of volatility. Factors affecting prices include weak demand levels from emerging markets, significant variations in production and storage levels, and climatic and geopolitical aspects.

During the first months of 2020 and as a result of the complex global scenario caused by COVID, the international reference prices of the products we export suffered sharp drops, which were later reduced as the global health and economic situation stabilized, with the exception of butane, which experienced a significant increase in the last days of the year due to a decrease in global stock levels.

The prices of the main energy commodities experienced a significant increase in 2021 compared to the previous year. In less than six months, natural gas liquids (“NGL”) prices went from record lows (due to the impact of COVID) to record highs. This was mainly due to the global economic recovery and greater restrictions on access to natural gas in European countries.

In recent years, the Government issued a series of measures, which significantly affected our Liquids Production and Commercialization segment. Since 2002, LPG and natural gasoline exports have been subject to a withholding tax on exports. After several regulatory modifications, in March 2008, the Government introduced a “sliding-scale” regime for LPG and natural gasoline, where the withholding tax rate applicable to exports of LPG and natural gasoline (as a percentage) would vary in the same proportion as the variation in the international reference prices.

At the beginning of 2015, to reduce the impact of the sharp decrease in the international reference prices for LPG and natural gasoline, the Government reduced to 1% the applicable rate of withholding tax for exports, maintaining the “sliding-scale” regime in case international prices were higher than a certain level set by the Federal Energy Bureau. This regime was in effect until January 7, 2017. Finally, on September 3, 2018, the Executive Branch issued Decree No. 793/2018, which set a new tax on exports framework.

For further information, see “Item 4. Our Information—B. Business Overview—Competition—Liquids Production and Commercialization.”

In addition, after the issuance of Resolutions Nos. 1,982/11 and 1,991/11 (the “Gas Charge Resolutions”), the natural gas processing charge created by Decree No. 2,067/08 (the “Natural Gas Processing Charge”) increased from Ps.0.049 to Ps.0.405 per cubic meter of natural gas effective from December 1, 2011, representing a significant increase in our variable costs of natural gas processing.

In order to avoid an adverse effect on our Liquids business, we initiated legal proceedings against Decree No. 2,067/08 and the Gas Charge Resolutions, including the Government, ENARGAS and the former Ministerio de Producción y de Planificación Federal, Inversión Pública y Servicios (the “MPFIPyS”) as defendants.

On March 28, 2016, the former Ministry of Energy issued Resolution No. 28 (“Resolution 28”), which instructs ENARGAS to take all the necessary measures to reduce to zero the Natural Gas Processing Charge starting April 1, 2016. Since that date, we have not been required to pay for the Natural Gas Processing Charge. However, Resolution 28 did not invalidate the Natural Gas Processing Charge or Gas Charge Resolutions for the period in which they were in force, for which reason the judicial action is still ongoing. On March 26, 2019, we were served notice of the first instance judgment rendered in the proceedings, which upholds the legal action filed by us and declares the unconstitutionality of Executive Decree No. 2,067/08, MPFIPyS Resolution No. 1451/08 and the Gas Charge Resolutions, and Section 53 and 54 of Act No. 26,784 (General budget of the National Public Administration for the fiscal year 2013), as well as of any other act aimed at enforcing Executive Decree No. 2,067/08, and therefore declares invalid said regulations. On March 29, 2019, the National Secretariat of Energy appealed the judgment, which appeal was granted on April 3, 2019. On December 1, 2020, the judge resolved to extend the injunction (medida cautelar) for six months, or until the award becomes final. On May 14, 2021, we were notified that such judgment (i) was revoked, and (ii) costs were imposed for both instances in the order caused. For additional information, see “Item 8. Financial Information—A. Consolidated Statements and Other Financial Information—Legal and Regulatory Proceedings—Tax Claims.”

Any new regulations regarding the cost and availability of the natural gas used in the production of Liquids and the effect of the continuing decline or volatility in international prices of LPG or natural gasoline could cause our operating margins to drop significantly and materially adversely affect our business, results of operations, financial condition, the value of our securities, and our ability to meet our financial obligations. In addition, the Government could modify the current taxes and export/import regulations in a manner that could adversely affect our financial condition and results of operations.

Our business, financial condition and results of operations have been, and may continue to be, adversely affected by the ongoing COVID pandemic or other similar outbreaks of contagious diseases.

Outbreaks of contagious diseases and other adverse public health developments affecting us and/or the third parties on which we rely, could have a material and adverse effect on our business, financial condition and results of operations. The recent COVID pandemic has introduced uncertainty in a number of areas of our business, including our operational, commercial and financial activities. The COVID pandemic has impacted, and is continuing to impact, many aspects of society, including the operation of healthcare systems, global travel, supply and labor markets and other business and economic activity worldwide. Argentina and countries around the world have, at times during the pandemic, issued and implemented quarantines, vaccine and masking mandates, executive orders and other similar government orders, restrictions and recommendations for their residents to help control the spread of COVID. Such orders, mandates, restrictions and/or recommendations have, at times during the pandemic, resulted in widespread interruptions and closures of businesses, including healthcare systems that serve people living with addiction and serious mental illness, work stoppages, slowdowns and/or delays, remote work policies and travel restrictions, among other effects.

COVID has also impacted negatively, and may continue to impact negatively, global economic activity, demand for energy including NGL and funds flows and sentiment in the global financial markets. It has also impacted our business. For example, pandemic and the related responses of governmental authorities and others to limit the spread of the virus significantly reduced global economic activity, which resulted in an unprecedented decline in the demand for commodities during 2020. This decline contributed to a swift and material deterioration in commodity prices in early 2020. Although commodity prices subsequently recovered, COVID or its variants may lead to similar protracted periods of depressed commodity prices, which in turn could have significant adverse consequences for our financial condition and liquidity. Moreover, the COVID pandemic has contributed to disruption and volatility in our supply chain, which has resulted, and may continue to result, in delays for performed maintenance works or to operate our Puerto Galván and Cerri Complex facilities. Also, in the Natural Gas Transportation business segment, during 2020, we suffered delays in the collections of our receivables.

The long-term effects to the global economy and the Company of the COVID pandemic are difficult to assess or predict, and may include a further decline in the market prices of our Shares and ADSs, risks to employee health and safety, risks for the deployment and logistic of our services and reduced sales mainly in the Liquids business segment. Our share price has recently declined significantly, due in part to the impact of the COVID.

The COVID pandemic has caused, and may continue to cause, varying degrees of disruption to our employees, our communities and our business operations. While we have continued to operate our facilities and to performed essential works in our facilities without interruption throughout the pandemic, any prolonged labor or supply chain shortages at our facilities could impact our ability to receive revenue in a timely matter.