UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ý ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE FISCAL YEAR ENDED DECEMBER 31, 2013.

or

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE TRANSITION PERIOD FROM TO

Commission File Number 1-13053

STILLWATER MINING COMPANY

(Exact name of registrant as specified in its charter)

|

| | |

| Delaware | | 81-0480654 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

1321 Discovery Drive, Billings, Montana 59102

(Address of principal executive offices and zip code)

(Registrant’s telephone number, including area code) (406) 373-8700

Securities registered pursuant to Section 12(b) of the Act:

|

| | |

| Title of each class | | Name of each exchange on which registered |

| Common Stock, $0.01 par value | | The New York Stock Exchange/Toronto Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ý YES ¨ NO

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ¨ YES ý NO

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ý YES ¨ NO

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Date File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). ý YES ¨ NO

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

| | | | | | |

Large Accelerated Filer ý | | Accelerated File ¨ | | Non-Accelerated Filer ¨ | | Smaller reporting company ¨ |

| | | | |

Indicate by check mark whether the registrant is a shell company (as defined in Exchange Act Rule 12b-2). ¨ YES ý NO

At June 28, 2013, the aggregate market value of the registrant's voting and non-voting common equity held by non-affiliates of the registrant was approximately $1.3 billion based on the closing sale price as reported on the New York Stock Exchange. There were 119,629,040 shares of common stock, par value $0.01 per share, outstanding on February 25, 2014.

DOCUMENTS INCORPORATED BY REFERENCE

Certain information required in Part III of this Annual Report on Form 10-K is incorporated herein by reference to the Registrant’s Proxy Statement for its 2014 Annual Meeting of Stockholders.

TABLE OF CONTENTS

|

| | |

| GLOSSARY OF SELECTED MINING TERMS | |

| | | |

| |

| ITEM 1A | | |

| ITEM 3 | | |

| ITEM 4 | | |

| | | |

| ITEM 5 | | |

| ITEM 6 | | |

| ITEM 7 | | |

| ITEM 7A | | |

| ITEM 8 | | |

| ITEM 9A | | |

| | | |

| ITEM 10 | | |

| ITEM 11 | | |

| ITEM 12 | | |

| ITEM 13 | | |

| ITEM 14 | | |

| | | |

| ITEM 15 | | |

| | | |

GLOSSARY OF SELECTED MINING TERMS

The following is a glossary of selected mining terms used in the United States and Canada and referenced in the Form 10-K that may be technical in nature:

|

| | |

| | |

| Concentrate | | A mineral processing product that generally describes the material that is produced after crushing and grinding ore, effecting significant separation of gangue (waste) minerals from the metal and / or metal minerals, and discarding the waste and minor amounts of metal and / or metal minerals. The resulting “concentrate” of metal and/or metal minerals typically has an order of magnitude higher content of metal and / or metal minerals than the beginning ore material. |

| | |

| Cut-off grade | | The lowest grade of mineralized material that qualifies as ore in a given deposit. The grade above which minerals are considered economically mineable considering the following parameters: estimates over the relevant period of mining costs, ore treatment costs, smelting and refining costs, process and refining recovery rates, royalty expenses, by-product credits, general and administrative costs, and PGM prices. |

| | |

| Dilution | | An estimate of the amount of waste or low-grade mineralized rock which will be mined with the ore as part of normal mining practices in extracting an ore body. |

| | |

| Developed state | | The portion of proven and probable ore reserves that are fully accessible and ready to mine at any point in time. |

| | | |

| Exploration stage | | Costs incurred in connection with acquisition of rights to explore, investigate, examine and evaluate an area for mineralization. Exploration may be conducted before or after the acquisition of mineral rights. |

| | |

| Grade | | The average metal content, as determined by assay of a volume of ore. For precious metals, grade is normally expressed as troy ounces per ton of ore or as grams per metric tonne of ore. (1 troy ounce per short ton is equivalent to about 34.3 grams per tonne.) |

| | |

| Mill | | A processing plant that produces a concentrate of the valuable minerals or metals contained in an ore. The concentrate must then be treated in some other type of plant, such as a smelter, to effect recovery of the pure metal. Term used interchangeably with concentrator. |

| | |

| Mineral deposit | | Geologic term measuring an aggregate of a mineral or metal in an unusually high concentration. The term deposit does not distinguish whether the mineral can be extracted economically. |

| | |

| Mineralization | | The concentration of metals and their compounds in rocks, and the processes involved therein. |

| | | |

| Mineralized material | | A mineralized body which has been delineated by appropriately spaced drilling and / or underground sampling to support a general estimate of available tonnage and average grade of metals. Such a deposit does not qualify as a reserve until a comprehensive evaluation based upon unit cost, grade, recoveries, and other material factors conclude legal and economic feasibility. |

| | |

| Ore | | That part of a mineral deposit which could be economically and legally extracted or produced at the time of reserve determination. |

| | |

| PGM | | The platinum group metals collectively and in any combination of palladium, platinum, rhodium, ruthenium, osmium, and iridium. Reference to PGM grades for the Company’s mine operations include measured quantities of palladium and platinum only. References to PGM grades associated with recycle materials typically include palladium, platinum and rhodium. |

| | |

| PGM-rich matte | | Matte is an intermediate product of smelting, an impure metallic sulfide mixture made by melting sulfide ore concentrates. PGM-rich matte is a matte with an elevated level of platinum group metals. |

| | |

Probable reserves | | Reserves for which quantity and grade and / or quality are computed from information similar to that used for proven reserves, but the sites for inspection, sampling, and measurement are farther apart or are otherwise less adequately spaced. The degree of assurance, although lower than that for proven reserves, is high enough to assume continuity between points of observation. |

| | |

| Proven reserves | | Reserves for which (a) quantity is computed from dimensions revealed in outcrops, trenches, workings or drill holes; grade and / or quality are computed from the results of detailed sampling; and (b) the sites for inspection, sampling and measurement are spaced so closely and the geologic character is so well defined that size, shape, depth and mineral content of reserves are well established. |

| | |

| Recovery | | The percentage of contained metal actually extracted from ore in the course of processing such ore. |

| | | |

|

| | |

| Reef | | A layer precipitated within the Stillwater Layered Igneous Complex enriched in platinum group metal-bearing minerals, chalcopyrite, pyrrhotite, pentlandite, and other sulfide materials. The J-M Reef, which the Company mines, occurs at a regular stratigraphic position within the Stillwater Complex. Note: this use of “reef” is uncommon and originated in South Africa where it is used to describe the PGM-bearing Merensky, UG2, and other similar layers in the Bushveld Complex. |

| | |

| Refining | | The final stage of metal production in which residual impurities are removed from the metal. |

| | |

| Reserves | | That part of a mineral deposit which could be economically and legally extracted or produced at the time of the reserve determination. |

| | |

| Stope | | A localized area of underground excavation from which ore is extracted. |

| | | |

| Tailings | | The portion of the mined material that remains after the valuable minerals have been extracted. |

| | |

| TBRC | | A “top-blown rotary converter,” a rotating furnace vessel which processes PGM-rich matte received from the smelter furnace, removing iron from the molten material by injecting a stream of oxygen. This process converts iron sulfides into an iron oxide slag which floats to the surface for separation. |

CAUTIONARY INFORMATION REGARDING FORWARD-LOOKING STATEMENTS

Some statements contained in this report are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (Securities Act), and Section 21E of the Securities Exchange Act of 1934, as amended (Exchange Act), and, therefore, involve uncertainties or risks that could cause actual results to differ materially. These statements may contain words such as “believes,” “anticipates,” “plans,” “expects,” “intends,” “estimates” or similar expressions. Such statements also include, but are not limited to, comments regarding expansion plans, costs, grade, production and recovery rates; permitting; financing needs and the terms of future credit facilities; exchange rates; capital expenditures; increases in processing capacity; cost reduction measures; safety; timing for engineering studies; environmental permitting and compliance; litigating; labor matters; and the palladium, platinum, copper and gold market. The forward-looking statements in this report are based on assumptions and analyses made by us in light of our experience and our perception of historical trends, current conditions, expected future developments, and other factors that we believe are appropriate under the circumstances. These statements are not guarantees of the Company’s future performance and are subject to risks, uncertainties and other important factors that could cause its actual performance or achievements to differ materially from those expressed or implied by these forward-looking statements. Some of these risks are described in "Item 1A - Risk Factors" section of this Form 10-K, and include such factors as:

| |

| • | Volatility in the supply and demand and as a result, the prices of the PGM group metals the Company produces and sells. |

| |

| • | Limits on access to capital markets or other sources of liquidity. |

| |

| • | The Company’s sales contracts do not include guaranteed floor prices and can subject the Company to fixed delivery commitments. |

| |

| • | If the Company is unable, or chooses not to secure sales agreements covering all of its production, it must sell its production on the spot market, which may be unpredictable. |

| |

| • | The Company is reliant on third party agreements to provide recyclable catalyst materials for its recycling business, and is subject to risk associated with advances made to such third party suppliers. |

| |

| • | There are interdependencies between the mining and recycling activities that may create risks for the recycling business. |

| |

| • | The Company may be competitively disadvantaged as a primary PGM producer with a preponderance of palladium and with a U.S. dollar-based cost structure. |

| |

| • | Achievement of the Company’s production goals is subject to uncertainties. |

| |

| • | Capital costs for new mine developments are difficult to estimate and may change over time. |

| |

| • | Ore reserves are very difficult to estimate and ore reserve estimates may require adjustment in the future; changes in ore grades, mining practices and economic factors could materially affect the Company’s production and reported results. |

| |

| • | An extended period of low PGM prices could result in a reduction of ore reserves and potential asset impairment charge. |

| |

| • | The Company’s business is subject to significant risks that may not be covered by insurance. |

| |

| • | Hedging and sales agreements could limit the realization of higher metal prices. |

| |

| • | Compliance with existing regulations and future changes in regulations could affect production, increase costs and cause delays. |

| |

| • | The Company is required to obtain and renew governmental permits in order to conduct mining operations, a process which is often costly and time-consuming. |

| |

| • | Limited availability of additional mining personnel and uncertainty of labor relations may affect the Company’s ability to achieve its production targets. |

| |

| • | Uncertainty of title to properties - the validity of unpatented mining claims is subject to title risk. |

| |

| • | The Company is subject to income taxes in various jurisdictions; income tax structures are subject to changes that could increase the Company’s effective tax rate. |

| |

| • | The Marathon and Peregrine acquisitions have created significant new uncertainties as to the Company’s future performance and commitments. |

The Company intends that the forward-looking statements contained herein be subject to the above-mentioned statutory safe harbors. Investors are cautioned that forward-looking statements are not guarantees of future performance and that actual results of performance may be materially different from those expressed or implied in the forward looking statements. Investors should not to rely on forward-looking statements. The forward-looking statements in this report speak as of the filing date of this report. Although the Company may from time to time voluntarily update its prior forward-looking statements, we disclaim any obligation to update forward-looking statements except as required by securities laws.

PART I

ITEMS 1 AND 2

BUSINESS AND PROPERTIES

INTRODUCTION

Stillwater Mining Company (the Company) is engaged in the development, extraction, processing, smelting and refining of palladium, platinum and associated metals (platinum group metals or PGMs) produced from a geological formation in south-central Montana known as the J-M Reef and from the recycling of spent catalytic converters. The Company is also engaged in expanding its mining operations on the J-M Reef, and holds the Marathon PGM-copper property adjacent to Lake Superior in northern Ontario, Canada and the Altar copper-gold property in the province of San Juan, Argentina.

The J-M Reef is the only known significant primary source of PGMs within the United States and one of the more significant resources outside South Africa and the Russian Federation. The J-M Reef is a narrow but extensive mineralized zone containing PGMs, which has been traced over a strike length of approximately 28 miles. In addition to PGMs, the Company's operations produce associated by-product metals including nickel, copper and minor amounts of gold, silver and rhodium.

PGMs are rare precious metals with unique physical properties that are used in diverse industrial applications and in jewelry. Currently, the most significant application for PGMs is in the automotive industry, in which PGMs are a necessary component in the production of catalytic converters that reduce harmful automobile emissions. Besides being used in automotive applications; palladium is used in jewelry, in the production of electronic components for personal computers, cellular telephones and facsimile machines, in dental applications and in petroleum and industrial catalysts. Industrial uses for platinum, in addition to automobile and industrial catalysts, include the manufacturing of data storage disks, fiberglass, paints, nitric acid, anti-cancer drugs, fiber optic cables, fertilizers, unleaded and high-octane gasoline and fuel cells. Rhodium, produced in the Company’s recycling operations and to a limited extent as a by-product from mining, is used in automotive catalytic converters to reduce nitrogen oxides, in laboratory equipment, in aircraft turbine engine parts and in jewelry as a plating agent to provide brightness.

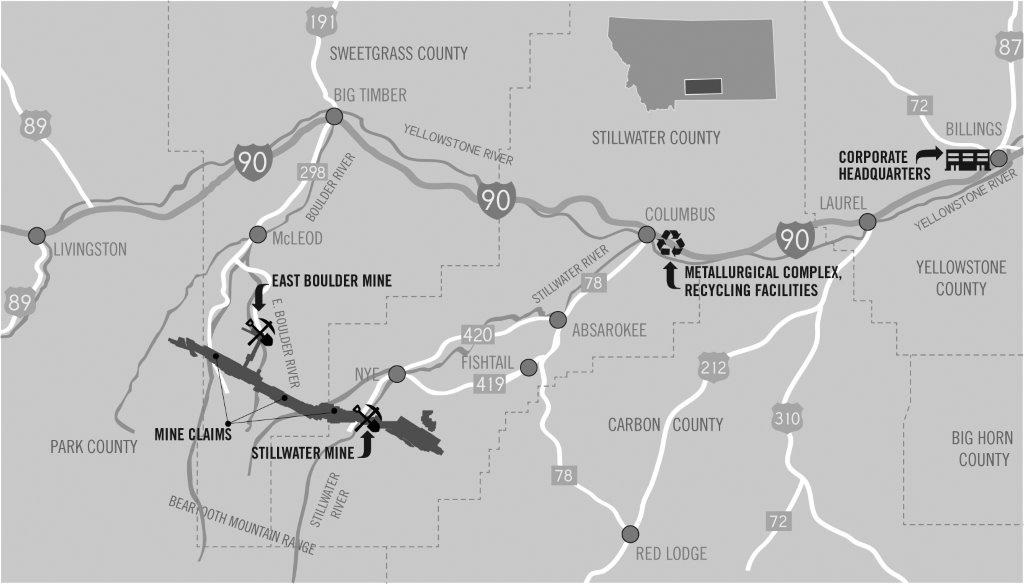

The Company conducts mining operations at its Stillwater Mine near Nye, Montana and at its East Boulder Mine south of Big Timber, Montana. Ore extraction at both mines takes place within the J-M Reef. A mill at each of the mining operations upgrades the mined production into a concentrated form. The Company operates a smelter and base metal refinery in Columbus, Montana which further upgrades the mined concentrates into a PGM-rich filter cake. The filter cake is then shipped to third-party refiners for final refining before the PGMs are sold to third-parties.

Besides processing mine concentrates, the Company also recycles spent catalyst material acquired from third-parties at its smelter and base metal refinery facilities to recover the contained PGMs, which consist mainly of palladium, platinum and rhodium. The Company currently has catalyst sourcing arrangements with various suppliers who deliver spent catalysts to the Company for processing. The Company smelts and refines the spent catalysts within the same process stream as the concentrates from its mining operations. The Company purchases recycling materials for its own account and also processes recycling materials on behalf of others for a fee.

The Company is currently in the midst of developing three new mining blocks adjacent to its current operations along the J-M Reef, consisting of the Graham Creek expansion at the East Boulder Mine and the Blitz and Lower Far West developments at the Stillwater Mine. Development of Graham Creek, which extends the East Boulder Mine underground infrastructure about 8,800 feet to the west, is now essentially complete and is expected to begin contributing incremental PGM production in late 2014 or early 2015. Blitz, which will extend underground development to the east of the Stillwater Mine, is similar to the Graham Creek development but considerably more significant in size.

Blitz consists of driving two parallel underground development drifts eastward from the Stillwater Mine on different levels that ultimately will each extend about 23,400 feet. A new surface portal for ventilation and emergency egress will be constructed at the far end of these two drifts. While much of Blitz will provide access to areas along the J-M Reef that are not yet well delineated geologically, there is evidence from the surface of ore continuity in this area. As the development progresses, the Company will have the opportunity to drill and evaluate the mineralization from underground to confirm the surface delineation results. Although it is difficult to provide specific guidance as to future production rates from the Blitz area, the Company expects that production from Blitz in the future will replace declining production from depleted mining areas within the Stillwater Mine, and may provide some growth in annual production rates as well.

The Company also expects that development of the Lower Far West area within the Stillwater Mine should provide some growth in annual production at the Stillwater Mine beginning in mid-2016. The Lower Far West area is located within the current boundaries of the Stillwater Mine, and is therefore increasingly being regarded as one of several active development areas ongoing within the mine, as opposed to a stand-alone development or expansion project.

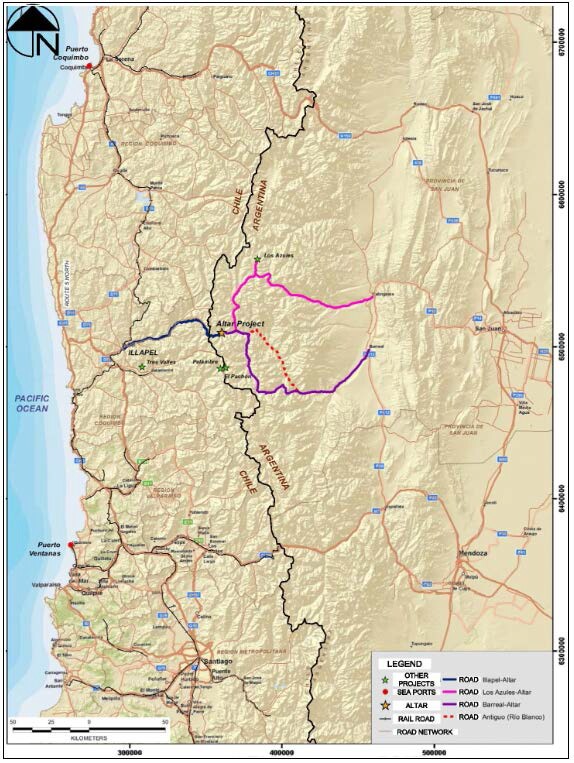

In addition to its Montana properties, the Company also holds interests in two undeveloped, exploration-stage projects, consisting of the Marathon project in Canada (Marathon) and the Peregrine project in Argentina, which is also referred to as Altar in reference to the single largest property in the project.

The Marathon project, in which the Company holds a 75% interest, consists of an undeveloped PGM-copper resource located near the north shore of Lake Superior in northern Ontario, Canada. The Company’s 25% partner in the Marathon project is Mitsubishi Corporation. In March 2012, the Company and Mitsubishi Corporation entered into an agreement through which Mitsubishi acquired a 25% interest in the Marathon project for approximately US $81.25 million. Including Mitsubishi's share of the venture's first cash call of $13.6 million, Mitsubishi has contributed cash totaling $94.9 million to the Marathon project. Mitsubishi is responsible for funding its 25% share of all future cash calls and exploration and operating expenditures on the Marathon properties. Under a related supply agreement, Mitsubishi will have an option to purchase up to 100% of the project's future PGM production at a small discount to the then prevailing market price.

Since Marathon was acquired in 2010, the Company has been working to advance both an updated feasibility study and the environmental assessment process for a future Marathon development. Substantial progress has been made on both fronts. The Company began the updated feasibility study in late 2011 to reconfirm the Marathon ore reserve work that had been completed prior to the acquisition. As the updated feasibility study progressed, it was determined that the initial ore reserve work contained an error, resulting in an overstatement of the palladium grades in portions of the ore reserve. Subsequent work has suggested that this error alone probably would not render development of the project uneconomical. However, as required by the definitions of proven and probable ore reserves set forth in the SEC's Industry Guide No. 7 (Description of Property by Issuers or to be Engaged in Significant Mining Operations), the previously reported ore reserves for the Marathon project could not be updated until the updated feasibility study and resulting project economics were finalized, which included completion of updated engineering design work in order to determine the project economics.

As the Company continues updating the Marathon feasibility study it has become clear that at current PGM and copper prices the project as currently conceived will not provide an acceptable economic rate of return. This is not because of the overstatement of palladium grades in the ore reserve discussed above, which the Company believes would not render the project uneconomical. Instead, the updated study is indicating that the Marathon project would have too short a mine life to adequately recover the initial capital required to construct it, and that prospective concentrate grades on average are lower than in the original study, reducing the net smelter return from third-party processing. As a result the Company and its partner are examining various potential options to modify the project to enhance returns. However, at this time there can be no assurance that these options, whether individually or in combination, will improve the project economics to the point where development of the project is viable. Several of these changes, if implemented, could necessitate changes to the project scope that are not contemplated in the current environmental assessment and permit approval process. Consequently, the Company recently agreed with the joint environmental review panel reviewing the Marathon project that the review process should be suspended until the Company has further clarity on the direction the project will take.

In light of the weak project economics emerging from the Marathon feasibility study, the Company concluded that at December 31, 2013 cash flows were not sufficient to recover the Company's investment in Marathon. The Company engaged SRK Consulting, a third-party valuation expert, to determine the fair market value of the property. The Company concluded that the fair value of the Marathon properties (and related mine development and depreciable fixed assets) is less than their carrying value on the Company’s books and consequently has written down the carrying value by $171.4 million. Additionally, in the absence of acceptable economics to support development of the project and eventual production of resources, beginning in this report the Company will no longer report proven and probable ore reserves at Marathon. The project is also being reclassified as an exploration-stage project rather than a development-stage project, and the Company will cease to capitalize future project expenditures incurred in connection with Marathon.

In October 2011, the Company completed the acquisition of Peregrine Metals Ltd., a Canadian exploration company (Peregrine). Peregrine's principal asset is the Altar copper-gold property, located in the San Juan province of Argentina. The Company paid a total of $166.4 million (net of cash acquired) in cash and issued 12.03 million common shares of the Company in consideration for Peregrine. Altar is an exploration-stage property at which initial drilling completed prior to the Company’s acquisition indicated the presence of a large copper-gold porphyry deposit. Subsequently, two additional seasons of exploration drilling conducted by the Company at Altar have significantly expanded the known boundaries of the resource in both area and depth. Despite the successful exploration efforts, in the third quarter of 2013, the Company concluded that due to the current difficult political environment in Argentina, coupled with a weakening market for exploration properties generally, the $392.4 million carrying value for Altar on the Company’s books was excessive. Consequently, after consultation with third-party valuation experts, the Company wrote down the carrying value of Altar to $102.0 million. The Company has determined to scale back its activities at Altar while it determines how best to realize value out of the property going forward.

Although the Company has significant liquidity available ($496.0 million in cash and cash equivalents plus highly liquid investments, as well as $75.6 million in available borrowing capacity under its revolving credit lines as of December 31, 2013), it relies on this liquidity together with cash flow from its PGM activities to fund its Montana mine expansion initiatives, sustain ongoing operations, complete the feasibility study and evaluation work at Marathon and maintain the Company's rights to the mineral concessions in Altar. The Company also attempts to maintain sufficient liquidity to protect against severe drops in PGM prices which occur periodically.

As of December 31, 2013, the Company reported proven and probable ore reserves at its Montana operations of approximately 48.5 million tons with an average combined in situ palladium and platinum grade of 0.45 ounces per ton of ore (0.35 ounces of palladium and 0.10 ounces of platinum per ton of ore). This is equivalent to approximately 22.1 million in-situ proven and probable ounces of palladium and platinum at a ratio of about 3.59 parts palladium to one part platinum, or approximately 17.3 million ounces of palladium and 4.8 million ounces of platinum.

2013 – YEAR IN REVIEW:

The Company reported a consolidated net loss attributable to common stockholders of $270.2 million, or $2.28 per share, for the year ended December 31, 2013, compared to consolidated net income attributable to common stockholders of $55.0 million, or $0.46 per diluted share, for the year ended December 31, 2012. The decline in net income in 2013 compared to 2012 was in large part due to the $290.4 million ($226.5 million, after-tax) impairment of the Peregrine property in Argentina and the $171.4 million, ($123.6 million, after-tax) impairment of the Marathon properties that the Company recorded in the fourth quarter of 2013. Mine Production segment revenues were $478.9 million, an increase of 5.2% from the $455.4 million in 2012 as a result of increased PGM prices and sales volume. PGM Recycling segment revenues increased by 62.6% during 2013 to $560.6 million from $344.8 million in 2012, a result of increased PGM prices and an increase in total volumes processed and sold. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Year Ended December 31, 2013 Compared to Year Ended December 31, 2012.”

The Company's mining operations produced a total of 523,900 ounces of palladium and platinum in 2013, an increase of 2.0% from the 513,700 ounces produced in 2012. Total consolidated cash cost per ounce, net of by-product and recycling credits, (a non-GAAP measure of extraction efficiency further defined in Part II, Item 6 of this Form 10-K) averaged $496 in 2013, compared with $484 per ounce in 2012. Higher cash costs in 2013 were a result of higher labor costs, general inflation on materials and supplies and the increase in mine production. Higher labor costs in 2013 were in part due to increases in contractual wage and benefit rates and an increase in the hiring rate for the Company's new-miner training program. The Company’s total revenues for 2013, 2012 and 2011 totaled $1.04 billion, $800.2 million and $906.0 million, respectively.

The following table sets forth the Company's revenues and sales volumes in 2013, 2012 and 2011, respectively: |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Year ended December 31, (In thousands) | | Sales Revenues | | Troy Ounces Sold |

| | Palladium | | Platinum | | Rhodium | | Other (1) | | Total | | Palladium | | Platinum | | Rhodium | | Other (3) | | Total |

| 2013 | | | | | | | | | | | | | | | | | | | | |

| Mine Production | | $ | 287,167 |

| | $ | 164,666 |

| | $ | 3,402 |

| | $ | 23,683 |

| | $ | 478,918 |

| | 398 |

| | 111 |

| | 3 |

| | 14 |

| | 526 |

|

| PGM Recycling | | 218,190 |

| | 292,818 |

| | 47,803 |

| | 1,777 |

| | 560,588 |

| | 306 |

| | 192 |

| | 44 |

| | — |

| | 542 |

|

| Total | | $ | 505,357 |

| | $ | 457,484 |

| | $ | 51,205 |

| | $ | 25,460 |

| | $ | 1,039,506 |

| | 704 |

| | 303 |

| | 47 |

| | 14 |

| | 1,068 |

|

| 2012 | | | | | | | | | | | | | | | | | | | | |

| Mine Production | | $ | 247,847 |

| | $ | 176,937 |

| | $ | 4,877 |

| | $ | 25,765 |

| | $ | 455,426 |

| | 386 |

| | 114 |

| | 4 |

| | 15 |

| | 519 |

|

| PGM Recycling | | 123,876 |

| | 183,719 |

| | 34,817 |

| | 2,406 |

| | 344,818 |

| | 192 |

| | 119 |

| | 25 |

| | — |

| | 336 |

|

| Total | | $ | 371,723 |

| | $ | 360,656 |

| | $ | 39,694 |

| | $ | 28,171 |

| | $ | 800,244 |

| | 578 |

| | 233 |

| | 29 |

| | 15 |

| | 855 |

|

| 2011 | | | | | | | | | | | | | | | | | | | �� | |

| Mine Production | | $ | 297,251 |

| | $ | 194,794 |

| | $ | 7,213 |

| | $ | 28,749 |

| | $ | 528,007 |

| | 402 |

| | 114 |

| | 5 |

| | 15 |

| | 536 |

|

| PGM Recycling | | 124,267 |

| | 201,195 |

| | 47,326 |

| | 4,032 |

| | 376,820 |

| | 169 |

| | 114 |

| | 23 |

| | — |

| | 306 |

|

Other (2) | | 7 |

| | 954 |

| | 181 |

| | — |

| | 1,142 |

| | — |

| | 1 |

| | — |

| | — |

| | 1 |

|

| Total | | $ | 421,525 |

| | $ | 396,943 |

| | $ | 54,720 |

| | $ | 32,781 |

| | $ | 905,969 |

| | 571 |

| | 229 |

| | 28 |

| | 15 |

| | 843 |

|

| |

| (1) | “Other” column includes gold, silver, nickel and copper by-product sales from mine production and revenue from processing recycling materials on a toll basis. |

| |

| (2) | “Other” row includes sales of metal purchased in the open market. |

| |

| (3) | “Other” column includes gold and silver by-product ounces and recycled ounces sold. Not reflected in the “other” ounce column in the table above are approximately 1.4 million pounds, 1.1 million pounds and 1.3 million pounds of nickel sold in 2013, 2012 and 2011, respectively, and approximately 0.9 million pounds, 0.7 million pounds and 0.8 million pounds of copper sold in 2013, 2012 and 2011, respectively. |

PGM Recycling segment revenues increased by 62.6% during 2013 to $560.6 million from $344.8 million in 2012, a result of increased PGM prices and an increase in total volumes processed and sold. A total of 541,800 ounces of PGMs were produced and sold from recycling materials purchased for the Company's own account in 2013, an increase of 61.0% over the 336,500 ounces sold in 2012. The Company’s combined average realization on recycling sales (which include sales of palladium, platinum and rhodium) increased to $1,031 per ounce in 2013 from $1,018 per ounce in 2012, reflecting slightly higher market prices for palladium and platinum. In addition to processing material purchased for its own account, the Company processed and returned 65,400 ounces of PGMs on a tolling basis in 2013, down from 98,800 returned toll ounces in 2012. Recycled volumes fed to the smelter totaled 616,700 ounces of PGMs in 2013, an increase of 38.5% from the 445,200 ounces fed in 2012, driven by increased availability of recycling materials in the market during 2013. Working capital associated with recycling activities in the form of inventories and advances was $76.1 million, $87.8 million and $64.5 million at December 31, 2013, 2012 and 2011, respectively. Included in these totals are outstanding procurement advances to recycling suppliers totaling $6.9 million, $10.2 million and $2.6 million at December 31, 2013, 2012 and 2011, respectively, representing cash advanced to suppliers for material in transit.

The Company currently has a one-year market-based platinum supply agreement in place with Tiffany & Co. that expires at the end of 2014. At the present, the Company sells the remainder of the PGMs it produces either in the spot market or under mutually agreed short-term extensions of prior supply agreements. The Company is reassessing its marketing strategy in light of increasing demand from consumers for PGMs sourced from jurisdictions with secure and stable operating environments. Until this reassessment is completed, management believes it should have no difficulty selling PGMs month to month on a spot basis.

The Company’s 2013 capital expenditures totaled $129.0 million which represents an increase of 15.1% from the $116.6 million of capital spending in 2012 that is largely the result of increased spending on the Company's Montana mine expansion initiatives. Capital outlay in 2013 included $108.5 million in development and infrastructure work at the Montana mines (including $13.9 million for Blitz development and $8.7 million for the Graham Creek development), $8.0 million in facilities and equipment and $12.4 million of project outlay at Marathon. Capital commitments in 2012 included $81.3 million for development and infrastructure work at the Montana mines (including $19.4 million for Blitz development and $3.5 million for the Graham Creek development), $26.7 million in facilities and equipment, and $8.6 million of capital outlay at Marathon.

The Company’s exploration expenditures during 2013 totaled $11.2 million, of which $8.0 million was spent on drilling at the Altar property in Argentina and $3.2 million was spent on the Marathon properties in Canada, primarily in connection with the ongoing update of the project feasibility study. Exploration expenditures during 2012 totaled $15.0 million, of which $14.2 million was spent on drilling at the Altar property and $0.8 million on the Marathon properties in Canada. Exploration outlay in 2011 totaled about $2.5 million, of which $2.0 million was spent on drilling at the Altar property and $0.5 million on the Marathon properties in Canada. The Company expenses exploration costs as incurred.

For the year ended December 31, 2013, capital, exploration and cash overhead costs for Stillwater Canada Inc (primarily the Marathon activities) totaled about $14.9 million, of which $9.2 million was capitalized as development costs of the Marathon project and $5.7 million was expensed as incurred. Exploration and cash overhead costs for the Peregrine properties (primarily Altar) totaled $10.7 million in the year ended December 31, 2013, and have been expensed as incurred.

As of December 31, 2013, the Company had balance sheet debt and capital lease obligations totaling $310.7 million. This debt is comprised of (i) $274.0 million (face amount of 396.75 million) of highly discounted 1.75% convertible debentures, first redeemable at the option of the holders on October 15, 2019; (ii) $2.2 million of 1.875% convertible debentures, next redeemable at the option of the holders on March 15, 2018; (iii) $29.6 million (face amount of $30.0 million) of discounted State of Montana Revenue Bonds maturing on July 1, 2020; and (iv) various minor secured obligations totaling $4.9 million with maturities over the next three years. Annual cash interest cost on the Company’s debt obligations is expected to be about $9.6 million in 2014. In addition to this balance sheet debt, the Company also has outstanding undrawn letters of credit under its revolving line of credit, mostly in support of long-term reclamation obligations, totaling $17.5 million as of December 31, 2013. Interest is charged on these letters of credit and on the unused portion of the revolving credit facility at rates determined based on the percent of the total line that is in use in any period. At the rates prevailing on December 31, 2013, the Company would expect to pay cash interest of about $1.0 million on its revolving credit facility during 2014.

SAFETY

Mining operations at the Stillwater Mine and at the East Boulder Mine are labor intensive, and involve the use of heavy machinery and unique drilling and blasting techniques specific to a narrow-vein underground working environment, which make these operations inherently dangerous and the focus of the Company’s extensive workplace safety program. In addition, the Company’s Metallurgical Complex in Columbus, Montana conducts complex smelting and refining processes that require constant focus and safety awareness. To partially mitigate the dangers posed by working in these environments, the Company's safety and health management system focuses on accident prevention through risk management, continually seeking safer methods of mining and processing, and increased employee awareness and training. Areas of specific focus include enhanced work place examinations, on-going education in hazard recognition, safety audits with a focus of continual improvement and sustaining of best practices, consistent safety standards adherence, accident / incidence investigations, near miss reporting and analysis, and use of focus teams who are part of the mining workforce. Salary and hourly focus teams have been successful in proactively resolving many safety related challenges. In recent years, the Company began implementing changes and enhancements to its successful "G.E.T. (Guide, Educate and Train) Safe" Safety and Health Management System (SHMS), including incorporating the CORESafety - Safety and Health Management System, which is a U.S. mining industry-wide safety initiative endorsed in April 2012 by the National Mining Association's executive Board.

Under the CORESafety system, the Company and its mining industry peers are working together toward a collective five-year goal of eliminating fatal accidents and sharply reducing the frequency and severity of on-the-job injuries within the mining industry. The CORESafety system is based on principles and programs such as creating an industry-wide safety forum to share knowledge regarding safety issues, providing the tools to continuously improve safety and health performance and joining with peers in sharing best practices. The CORESafety system is comprised of a series of 20 modules, which can be prioritized to address specific gaps in safety and health performance based on the Company's own "gap analysis." In 2013 the Company began integrating eight of these modules into its existing G.E.T. Safe SHMS and has identified an additional eight modules that it will begin implementing in 2014. The Company views the implementation of the CORESafety system as a significant opportunity to enhance the already successful G.E.T Safe SHMS and continue its pursuit of safety excellence.

The Company continues to use focus teams to address specific safety and health related issues as identified by the Mine Safety and Health Administration (MSHA) and the Occupational Safety and Health Administration (OSHA). MSHA identified powered haulage as the leading cause of fatalities in the U.S. mining industry during 2012 and the need for ongoing training for miners at all levels of experience. In response, in 2013 the Company began to build upon its task training program related to power haulage within its mines, and will continue these efforts in 2014. Additionally, the Company's smelter, base metal refinery and analytical laboratory added employee-led proactive task risk assessments and task safety observations in 2013 as part of a continuous improvement initiative to provide additional opportunities for employee participation and involvement in workplace safety.

For the year ended December 31, 2013, none of the Company’s mines received any written notices from MSHA of (i) a flagrant violation under section 110(b)(2) of the Mine Act; (ii) a pattern of violations of mandatory health or safety standards that are of such nature as could have significantly and substantially contributed to the cause and effect of other mine health or safety hazards under section 104(e) of the Mine Act; or (iii) the potential to have such a pattern. In addition, the Company's Metallurgical Complex did not receive any OSHA violations in 2013. The Metallurgical Complex is recognized by the Montana Department of Labor and Occupational Safety and Health Administration as a leader in workplace safety.

At year-end 2013 the Company's overall reportable incidence rate (measured as reportable incidents per 200,000 man hours worked) increased 7.7% from the Company's 2012 incidence rate. The 2013 results do however represent a 72.9% reduction in incidence rates for Company employees and contractors since the inception of the “G.E.T. Safe” Safety and Health Management Systems in 2001.

2014 – LOOKING FORWARD

Pricing Background and Outlook

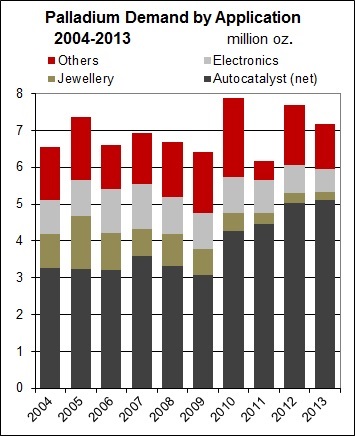

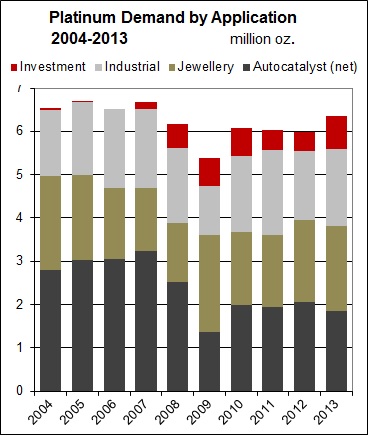

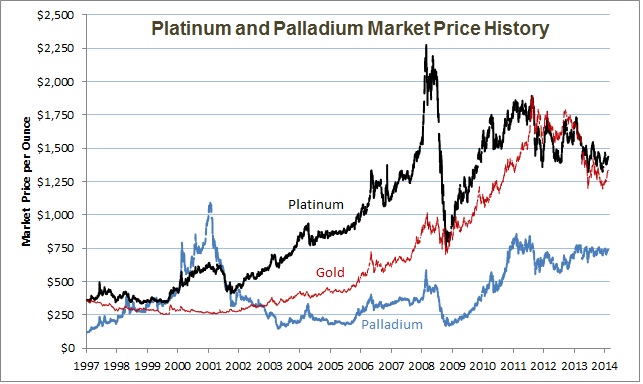

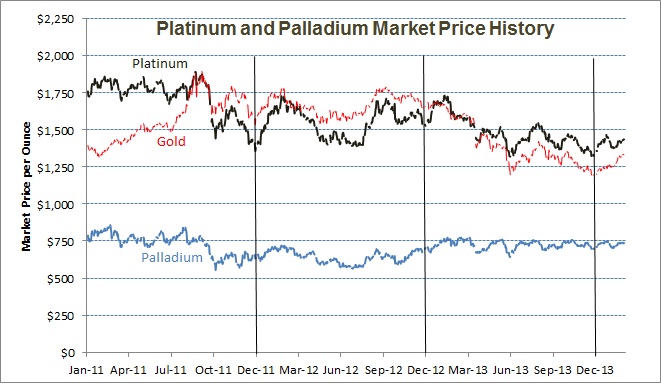

Following the economic recession in late 2008 and early 2009, market prices for palladium and platinum recovered fairly steadily until September of 2011, as the European sovereign debt crisis and restrictive credit policies in China took their toll on the markets. The price of palladium, which had traded as low as $164 per ounce in December 2008, was quoted at prices above $800 per ounce as recently as August 2011; since then, palladium has traded in a fairly narrow range, between about $600 and $700 per ounce in 2012, and between $650 and $750 per ounce in 2013. Platinum also saw some price recovery following the recession, but it has continued to be burdened by weak automotive demand in Europe. The European auto market is roughly 50% diesel, which utilizes disproportionate amounts of platinum in its autocatalysts. Consequently, with continuing European economic weakness, the market for platinum has been slow to return to full health.

During 2013, this dichotomous behavior between platinum and palladium continued in force. As the euro-zone currency woes subsided and the likelihood of the U.S. Federal Reserve slowing its bond purchases increased, precious metals markets declined in 2012 and 2013, led by weakness in the gold price. Platinum and silver both followed gold down, although platinum outperformed gold for the year. On the other hand, palladium, with its industrial character, was buoyed by strengthening auto markets in North America and China during 2013, and did not track the declines in other precious metals, but again traded in a fairly narrow range. Late in 2013, signs finally began to emerge of some recovery in the European auto market. Coupled with labor issues in South Africa that could constrain supply, platinum ended 2013 on a modest upswing.

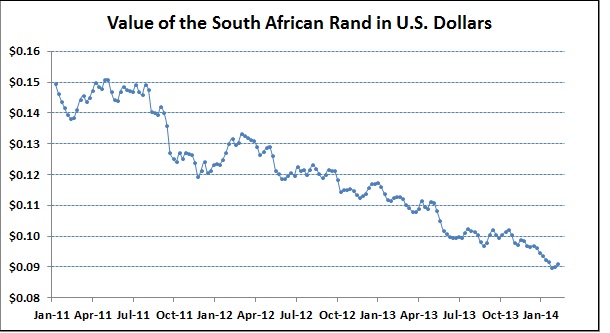

The outlook for PGM pricing in 2014 is encouraging, but may be constrained by one or two specific issues. Overall, automotive demand worldwide looks fairly strong, with the recovery in the European markets apparently continuing and demand in both North America and China still growing. As automotive demand is the largest use for both platinum and palladium, this suggests demand for both metals should be healthy in 2014. Jewelry demand for platinum in China also appears to be strong, helping to absorb some of the excess inventory that otherwise has accumulated as a result of the weak European economy. On the supply side, strike activity in South Africa seems likely to keep primary supply fairly tight, although the weakening of the rand has been favorable to the South African cost structure. Most analysts are projecting both platinum and palladium to be in deficit for 2014, suggesting that supply shortfalls will have to be met out of inventory liquidation. The inventory picture is the first of the specific issues that may affect 2014 prices. It is generally agreed that the Russian state inventories of palladium are nearing depletion, it is not clear whether there are other official or private inventory stockpiles available elsewhere in the world that may blunt the effect of stronger demand. The other uncertainty, as always, is the direction of the world economy as 2014 progresses - if world economic conditions deteriorate, demand for PGMs could falter.

The Company's financial performance is closely linked to the price of palladium and, to a lesser extent, platinum. The Company's earnings and cash flow are fairly sensitive to changes in PGM prices - based on 2013 revenues and costs, a 1% (or just under $9 per ounce) change in the Company's average combined realized price for palladium and platinum would result in approximately a 5.5% change to before-tax net income (measured before the 2013 impairment charges) and a 2.8% change to cash flow from operations.

While changes in the PGM market prices directly affect the Company's profitability, another important competitive consideration for the Company is the relative level of and relationship between the price of palladium and platinum. The Company’s mines generally produce about 3.4 times as much saleable palladium as platinum, while its South African competitors in many cases produce nearly twice as much platinum as palladium. Consequently, the Company benefits competitively relative to these producers whenever the spread between the palladium price and the platinum price narrows. The price ratio of palladium to platinum averaged between 20% and 25% between 2003 through the first half of 2010, but subsequently has increased to about 50%, a shift that has benefited the Company significantly. It is difficult to predict how this relationship might evolve during 2014 as the palladium market has been firmer than the platinum market during 2013, but the emerging resurgence in the European auto market could lift platinum demand disproportionately during 2014.

One other important element of PGM markets is the relationship between various key currencies. Virtually all PGM sales transactions worldwide (with the possible exception of retail sales of platinum jewelry) are denominated in U.S. dollars. However, mining costs are typically incurred mostly in the local currencies of the country in which the mine is located. Recent weakening of the South African rand relative to the U.S. dollar has served to increase the competitiveness of the South African PGM producers, as their costs in U.S. dollar terms have declined (or their revenues in rand terms have increased, depending on the perspective). In general, PGM prices tend to rise when the U.S. dollar weakens against the euro, and PGM prices decline when the U.S. dollar strengthens. The U.S. Federal Reserve has announced that it will continue tapering down its purchases of longer-dated securities during 2014, which has created a general expectation that the dollar will strengthen over the course of the year, which could put downward pressure on PGM prices.

Operational and Development Outlook

From an operating perspective, the Company’s ability to increase its mine production in response to higher PGM prices is very limited, as is generally the case throughout the PGM industry. Production is constrained primarily by the developed state of the mines (i.e., the number and quality of working faces available for mining) and by limits on the availability of skilled manpower and equipment. Removing these constraints, whether through accessing new working faces or bringing on line additional manpower and equipment, typically requires significant capital expenditure and lead time to implement, making it difficult or impossible for the Company to significantly increase production for a short period of time.

Capital spending in 2014 is budgeted at approximately $161 million, which anticipates higher spending on equipment replacement and mine development, plus completion of improvements at the smelter in Columbus, ongoing development spending for the Blitz, Far West, and Graham Creek development areas along the J-M Reef in Montana, and continuing feasibility work at the Company’s Marathon project in Canada. The Company expects to continue with some engineering work on the Marathon project, and will maintain baseline environmental monitoring at Marathon and Altar, but that work will all be expensed-as-incurred in 2014 and is not included in the capital expenditure budget.

As noted previously, the Company is involved in three mine expansion initiatives at its Montana mines along the J-M Reef. Blitz, adjacent to the existing Stillwater Mine operations, will ultimately add a total of 23,400 feet of new development to the east of the current mine works on two levels. The new portal and decline from surface will be permitted and installed about four miles to the east of the existing Stillwater Mine surface facilities, intersecting the two new drifts and providing ventilation and emergency egress for the Blitz area. As now contemplated, Blitz is estimated to cost about $195.8 million (of which about $56.8 million has already been incurred through the end of 2013) and will take about five more years to complete.

Graham Creek, located adjacent to and west of the East Boulder Mine, is nearing completion. A program of definitional drilling during 2014 will better define attractive mining areas along the 8,800 feet of new development. Production from Graham Creek is expected to begin later in 2014, ramping up to around 30,000 PGM ounces per year by 2015. Capital spending at Graham Creek for 2014 is expected to be about $1.0 million, which would bring the total cost of the project to around $13.4 million, which is in line with the project's original budget.

The Lower Far West development effort is situated within the Stillwater Mine, underneath the well-developed Upper West mining area, which has been in production for many years. Because Lower Far West is below the 5000 level primary Upper West haulage level, its development was delayed until the completion of the 3500 level rail haulage, which allows for the mechanized removal of ore from that part of the mine. This effort represents an acceleration of development in the Lower Far West area and a pulling forward of capital expenditures that would otherwise have occurred in later years. The development at Lower Far West will cost an incremental $28 million in total over about three years, and once it is fully operational it should increase the Stillwater Mine's annual PGM production by about 45,000 ounces. Production from the Lower Far West area is expected to start coming on line in the second half of 2015. Through the end of 2013, the Company has spent about $3.9 million on the Lower Far West development.

During 2014 the Company expects to continue advancing the Marathon project in Canada, but on a more limited scale than in prior years. The Company's focus is on completing the detailed, updated feasibility study and on exploring various options and opportunities to improve the project economics. The Company believes that such changes and enhancements, some of which could alter the scope of the Marathon development, will be required to make development of the Marathon project economically viable at recently prevailing and anticipated PGM prices. Because the scope of the project and resulting project design could be significantly modified, in early 2014 the Company recently agreed with the Canadian federal and provincial Joint Review Panel charged with completing an environmental assessment of the project to suspend its review process until the Company determines how the project is going to proceed.

With regard to the Altar project in Argentina, no proven or probable ore reserves have yet been defined at Altar. In view of the present political environment in Argentina and the anticipated very large scale of any ultimate development of the Altar resource, the Company has concluded that, although the project appears to be a significant copper-gold porphyry deposit, is a poor strategic fit for the Company. Consequently, the Company expects to scale back its spending at Altar during 2014. The camp at Altar will be opened for a brief period of time in 2014 to conduct requisite background environmental work, but no new drilling or other exploration work is planned during 2014.

SUMMARY OF THE COMPANY

Stillwater Mining Company (the Company) is engaged in the development, extraction, processing, smelting and refining of palladium, platinum and associated metals (platinum group metals or PGMs) from a geological formation in south-central Montana known as the J-M Reef and from the recycling of spent catalytic converters. The Company is also engaged in expanding its mining operations on the J-M Reef, and holds the Marathon PGM-copper property adjacent to Lake Superior in northern Ontario, Canada and the Altar copper-gold property in the province of San Juan, Argentina.

The J-M Reef is the only known significant primary source of PGMs inside the United States and one of the significant resources outside South Africa and the Russian Federation. Associated by-product metals at the Company's operations include significant amounts of nickel and copper and minor amounts of gold, silver and rhodium. The J-M Reef is a narrow but extensive mineralized zone containing PGMs, which has been traced over a strike length of approximately 28 miles.

THE STILLWATER COMPLEX AND J-M REEF

LOCATION

The Stillwater Layered Igneous Complex, or Stillwater Complex, in which the J-M Reef ore deposit is found, is located in the Beartooth Mountains in south-central Montana. It is situated along the northern edge of the Beartooth Uplift and Plateau, which rise to elevations in excess of 10,000 feet above sea level. The plateau and Stillwater Complex are deeply incised by the major drainages and tributaries of the Stillwater and Boulder Rivers down to elevations at the valley floor of approximately 5,000 feet above sea level.

GEOLOGY OF THE J-M REEF

Geologically, the Stillwater Complex is composed of a succession of ultramafic to mafic rocks derived from a large complex magma body emplaced deep in the Earth’s crust an estimated 2.7 billion years ago. The molten mass was sufficiently large and fluid at the time of emplacement to allow its chemical constituents to crystallize slowly and sequentially, with the heavier mafic minerals settling more rapidly toward the base of the cooling complex. The lighter, more siliceous suites crystallized more slowly and also settled into layered successions of norite, gabbroic and anorthosite suites. This systematic process resulted in mineral segregations being deposited into extensive and relatively uniform layers of varied mineral concentrations.

The J-M Reef package has been traced at its predictable geologic position and with unusual overall uniformity over considerable distances within the uplifted portion of the Stillwater Complex. The surface outcrops of the reef have been mapped and sampled for approximately 28 miles along its east-southeasterly course and over a known expression of over 8,200 feet vertically. The predictability and continuity of the J-M Reef has been further confirmed in subsurface mine workings of the Stillwater and East Boulder Mines and by over 38,000 drill hole penetrations.

The PGMs in the J-M Reef consist primarily of palladium, platinum and a minor amount of rhodium. The reef also contains significant amounts of nickel and copper and trace amounts of gold and silver. Five-year production figures from the Company’s mining operations on the J-M Reef are summarized in Part II, Item 6, “Selected Financial Data.”

The Company’s original long-term development strategy and certain elements of its current planning and mining practices on the J-M Reef ore deposit were based on initial feasibility and engineering studies conducted in the 1980s. Initial mine designs and practices were established in response to available technologies and the particular characteristics and challenges of the J-M Reef ore deposit. The Company’s current development plans, mining methods and ore extraction schedules are designed to provide systematic access to, and development of, the ore deposit within the framework of current and forecasted economic, regulatory and technological considerations as well as the specific characteristics of the J-M Reef ore deposit. Some of the challenges inherent in the development of the J-M Reef include:

| |

| • | Surface access limitations as a result of private property ownership and environmental sensitivity; |

| |

| • | Topographic and climatic extremes involving rugged mountainous terrain and substantial elevation differences; |

| |

| • | The specific configuration of the mineralized zone (narrow – average width 5 feet, depth – up to 1.5 miles of vertical extent, and long – approximately 28 miles in length), dipping downward at an angle varying from near vertical to 38 degrees; |

| |

| • | A deposit which extends both laterally and to depth from available mine openings, with travel distances underground from portal to working face of up to six miles; and |

| |

| • | Proven and probable ore reserves extending for a lateral distance of approximately 32,000 feet at the Stillwater Mine and approximately 12,500 feet at the East Boulder Mine – a combined extent underground of approximately 8.4 miles, with active underground travelways and ramps on multiple levels totaling more than 100 miles in extent that must be maintained and supported logistically. |

ORE RESERVE DETERMINATION METHODOLOGY

The Company utilizes statistical methodologies to calculate ore reserves based on interpolation between and projection beyond sample points. Interpolation and projection are limited by certain modifying factors including geologic boundaries, economic considerations and constraints imposed by safe mining practices. Sample points consist of variably spaced drill core intervals through the J-M Reef obtained from drill sites located on the surface and in underground development workings. Results from all sample points within the ore reserve area are evaluated and applied in determining the ore reserve.

For proven ore reserves, distances between samples range from 25 to 100 feet but are typically spaced at 50 foot intervals both horizontally and vertically. The sample data for proven ore reserves consists of survey data, lithologic data and assay results. Quality Assurance / Quality Control (QA / QC) protocols are in place at both mine sites to test the sampling and analysis procedures. To test assay accuracy and reproducibility, pulps from core samples are resubmitted and compared. To test for sample label errors or cross-contamination, blank core (waste core) samples are submitted with the mineralized sample lots and compared. The QA / QC protocols are practiced on both resource delineation and development and production samples. The resulting data is entered into a 3-dimensional modeling software package and is analyzed to produce a 3-dimensional solid block model of the resource. The assay values are further analyzed by a geostatistical modeling technique (kriging) to establish a grade distribution within the 3-dimensional block model. Dilution is then applied to the model and a diluted tonnage and grade are calculated for each block. Ore and waste tons, contained ounces and grade are then calculated and summed for all blocks. A percent mineable factor based on historic geologic unit values is applied and the final proven reserve tons and grade are calculated.

Two types of cut-off grades are recognized for the J-M Reef, a geologic cut-off grade and an economic cut-off grade. The geologic cut-off grade for both the Stillwater and East Boulder Mines falls in the range of 0.2 to 0.3 troy ounces of palladium plus platinum (Pd+Pt) per ton. The economic cut-off grade is lower than the geologic cut-off and can vary between the mines based on cost and efficiency factors. The determination of the economic cut-off grade is completed on a round by round basis and is driven primarily by excess mill capacity and geologic character encountered at the mining face. See “Business and Properties – Proven and Probable Ore Reserves – Discussion” for discussion of reserve sensitivity to changes in PGM pricing.

Probable ore reserve estimations are based on longer projections than proven reserves, and projections up to a maximum radius of 1,000 feet beyond the limit of existing drill hole sample intercepts of the J-M Reef are acceptable. Statistical modeling and the established continuity of the J-M Reef, as determined from results of 27 years of mining activity to date, support the Company’s technical confidence in estimates of tonnage and grade over this projection distance. Where appropriate, projections for the probable ore reserve determination are constrained by any known or anticipated restrictive geologic features.

The Company reviews its methodology for calculating ore reserves on an annual basis. Conversion, an indicator of the success in upgrading probable ore reserves to proven ore reserves, is evaluated annually as part of the reserve process. The annual review examines the effect of new geologic information, changes implemented or planned in mining practices and mine economics on the measures used for the estimation of probable ore reserves. The review includes an evaluation of the Company’s rate of conversion of probable reserves to proven reserves.

The proven and probable ore reserves are then modeled as a long-term mine plan and additional factors including mining methods, process recoveries, metal prices, mine operating productivities and costs and capital estimates are applied to determine the overall economics of the ore reserves. The Company has made available on its website (www.stillwatermining.com) in the Investor Relations section a report entitled “Technical Report for the Mining Operations at Stillwater Mining Company”, dated as of March 2011 and furnished to the United States Securities and Exchange Commission (SEC) on Form 8-K on June 23, 2011, that discusses the Company’s ore reserve methodology in greater detail. The information contained on the Company's website or connected to its website is not incorporated by reference into this Annual Report on Form 10-K and should not be considered part of this report.

SEC ORE RESERVE GUIDELINES

The SEC has established guidelines contained in Industry Guide No. 7: to assist registered companies as they estimate ore reserves. These guidelines set forth technical, legal, and economic criteria for determining whether the Company’s ore reserves can be classified as proven and probable.

The SEC’s economic guidelines historically have not constrained the Company’s ore reserves, and did not constrain the Company's ore reserves at December 31, 2013. Under these guidelines, ore may be classified as proven or probable if extraction and sale result in positive cumulative undiscounted cash flow. The Company utilizes the historical trailing twelve-quarter average combined PGM market price in ascertaining these cumulative undiscounted cash flows.

The Company believes that it is appropriate to use a long-term average price for measuring ore reserves; as such a price better matches the period over which the reserves will ultimately be mined. However, should metal prices decline substantially from their present level for an extended period, the twelve-quarter trailing average price might also decline and could result in a reduction of the Company’s reported ore reserves.

The Company’s Technical and Ore Reserve Committee, a committee of the Board, met six times during 2013 with management and third-party independent outside experts to review ore reserve methodology, to identify best practices in the industry and to receive reports on the progress and results of the Company’s mine development efforts. The Committee has reviewed the Company’s ore reserves as reported at December 31, 2013, and has met with management and with the Company’s independent consultant on ore reserves to discuss the finding of such review.

RESULTS

The December 31, 2013, ore reserves for the Montana operations were reviewed by Behre Dolbear & Company, Inc. (Behre Dolbear), third-party independent consultants, who are experts in mining, geology and ore reserve determination. The Company has utilized Behre Dolbear to carry out independent reviews and inventories of the Company’s ore reserves since 1990. Behre Dolbear has consented to be a named expert herein. See “Risk Factors – Ore reserves are very difficult to estimate and ore reserve estimates may require adjustment in the future, and changes in ore grades, mining practices and economic factors could materially affect the Company’s production and reported results.”

PROVEN AND PROBABLE ORE RESERVES

The Company’s proven ore reserves are generally expected to be extracted utilizing existing mine infrastructure. However, additional infrastructure development will be required to extract the Company’s probable ore reserves. Based on the 2014 mining plans at each mine, the year-end 2013 proven ore reserves of 3.2 million tons at the Stillwater Mine and 2.9 million tons at the East Boulder Mine represent an adequate level of proven ore reserves to support planned mining activities.

The grade of the Company’s J-M Reef ore reserves, measured in combined palladium and platinum ounces per ton, is a composite average of samples in all reserve areas. As is common in underground mines, the grade mined and the recovery rate achieved varies depending on the area being mined. In particular, mill head grade varies significantly between the Stillwater and East Boulder Mines, as well as within different areas of each mine. During 2013, 2012 and 2011, the average mill head grade for all tons processed from the Stillwater Mine was 0.50, 0.58 and 0.53 PGM ounces per ton of ore, respectively. During 2013 the average mill head grade for all tons processed from the East Boulder Mine was about 0.37 PGM ounces per ton of ore compared to an average mill head grade of 0.35 PGM ounces per ton of ore in 2012 and 2011. Concentrator feeds at both mines typically include, along with the ore, some PGM-bearing material that is below the cut-off grade for reserves (reef waste) but that is economic to process so long as there is capacity available in the concentrator.

As of December 31, 2013, 2012 and 2011 the Company’s proven and probable ore reserves in the J-M Reef were as follows: |

| | | | | | | | | | | | |

| STILLWATER MINE |

| | | ORE TONS (000’s) | | AVERAGE GRADE (OZ/TON) | | CONTAINED OUNCES (000’S) | | SALEABLE OUNCES (000’S) |

| As of December 31, 2013 | | | | | | | | |

| Proven Reserves | | 3,246 |

| | 0.57 |

| | 1,856 |

| | 1,545 |

|

| Palladium | | | | 0.45 |

| | 1,449 |

| | 1,199 |

|

| Platinum | | | | 0.12 |

| | 407 |

| | 346 |

|

| Probable Reserves | | 12,314 |

| | 0.57 |

| | 6,989 |

| | 5,818 |

|

| Palladium | | | | 0.44 |

| | 5,457 |

| | 4,516 |

|

| Platinum | | | | 0.13 |

| | 1,532 |

| | 1,302 |

|

| Total Proven and Probable Reserves (1) | | 15,560 |

| | 0.57 |

| | 8,845 |

| | 7,363 |

|

| Palladium | | | | 0.44 |

| | 6,906 |

| | 5,715 |

|

| Platinum | | | | 0.13 |

| | 1,939 |

| | 1,648 |

|

| As of December 31, 2012 | | | | | | | | |

| Proven Reserves | | 3,333 |

| | 0.59 |

| | 1,952 |

| | 1,639 |

|

| Palladium | | | | 0.46 |

| | 1,524 |

| | 1,272 |

|

| Platinum | | | | 0.13 |

| | 428 |

| | 367 |

|

| Probable Reserves | | 12,149 |

| | 0.59 |

| | 7,189 |

| | 6,035 |

|

| Palladium | | | | 0.46 |

| | 5,612 |

| | 4,684 |

|

| Platinum | | | | 0.13 |

| | 1,577 |

| | 1,351 |

|

| Total Proven and Probable Reserves (1) | | 15,482 |

| | 0.59 |

| | 9,141 |

| | 7,674 |

|

| Palladium | | | | 0.46 |

| | 7,136 |

| | 5,956 |

|

| Platinum | | | | 0.13 |

| | 2,005 |

| | 1,718 |

|

| As of December 31, 2011 | | | | | | | | |

| Proven Reserves | | 2,782 |

| | 0.62 |

| | 1,711 |

| | 1,401 |

|

| Palladium | | | | 0.48 |

| | 1,335 |

| | 1,087 |

|

| Platinum | | | | 0.14 |

| | 376 |

| | 314 |

|

| Probable Reserves | | 12,262 |

| | 0.60 |

| | 7,374 |

| | 6,039 |

|

| Palladium | | | | 0.47 |

| | 5,753 |

| | 4,684 |

|

| Platinum | | | | 0.13 |

| | 1,621 |

| | 1,355 |

|

| Total Proven and Probable Reserves (1) | | 15,044 |

| | 0.60 |

| | 9,085 |

| | 7,440 |

|

| Palladium | | | | 0.47 |

| | 7,087 |

| | 5,770 |

|

| Platinum | | | | 0.13 |

| | 1,997 |

| | 1,669 |

|

|

| | | | | | | | | | | | |

| EAST BOULDER MINE |

| | | ORE TONS (000’s) | | AVERAGE GRADE (OZ/TON) | | CONTAINED OUNCES (000’S) | | SALEABLE OUNCES (000’S) |

| As of December 31, 2013 | | | | | | | | |

| Proven Reserves | | 2,852 |

| | 0.41 |

| | 1,181 |

| | 1,002 |

|

| Palladium | | | | 0.32 |

| | 924 |

| | 779 |

|

| Platinum | | | | 0.09 |

| | 257 |

| | 223 |

|

| Probable Reserves | | 30,097 |

| | 0.40 |

| | 12,038 |

| | 10,212 |

|

| Palladium | | | | 0.31 |

| | 9,422 |

| | 7,937 |

|

| Platinum | | | | 0.09 |

| | 2,616 |

| | 2,275 |

|

| Total Proven and Probable Reserves (1) | | 32,949 |

| | 0.40 |

| | 13,219 |

| | 11,214 |

|

| Palladium | | | | 0.31 |

| | 10,346 |

| | 8,716 |

|

| Platinum | | | | 0.09 |

| �� | 2,873 |

| | 2,498 |

|

| As of December 31, 2012 | | | | | | | | |

| Proven Reserves | | 2,690 |

| | 0.42 |

| | 1,126 |

| | 951 |

|

| Palladium | | | | 0.33 |

| | 881 |

| | 739 |

|

| Platinum | | | | 0.09 |

| | 245 |

| | 212 |

|

| Probable Reserves | | 27,970 |

| | 0.40 |

| | 11,188 |

| | 9,456 |

|

| Palladium | | | | 0.31 |

| | 8,756 |

| | 7,349 |

|

| Platinum | | | | 0.09 |

| | 2,432 |

| | 2,107 |

|

| Total Proven and Probable Reserves (1) | | 30,660 |

| | 0.40 |

| | 12,314 |

| | 10,407 |

|

| Palladium | | | | 0.31 |

| | 9,638 |

| | 8,088 |

|

| Platinum | | | | 0.09 |

| | 2,676 |

| | 2,319 |

|

| As of December 31, 2011 | | | | | | | | |

| Proven Reserves | | 2,228 |

| | 0.41 |

| | 907 |

| | 767 |

|

| Palladium | | | | 0.32 |

| | 710 |

| | 595 |

|

| Platinum | | | | 0.09 |

| | 197 |

| | 172 |

|

| Probable Reserves | | 25,207 |

| | 0.40 |

| | 9,988 |

| | 8,449 |

|

| Palladium | | | | 0.31 |

| | 7,817 |

| | 6,551 |

|

| Platinum | | | | 0.09 |

| | 2,171 |

| | 1,898 |

|

| Total Proven and Probable Reserves (1) | | 27,435 |

| | 0.40 |

| | 10,895 |

| | 9,216 |

|

| Palladium | | | | 0.31 |

| | 8,527 |

| | 7,146 |

|

| Platinum | | | | 0.09 |

| | 2,368 |

| | 2,070 |

|

|

| | | | | | | | | | | | |

| TOTAL MONTANA MINES |

| | | ORE TONS (000’s) | | AVERAGE GRADE (OZ/TON) | | CONTAINED OUNCES (000’S) | | SALEABLE OUNCES (000’S) |

| As of December 31, 2013 | | | | | | | | |

| Proven Reserves | | 6,098 |

| | 0.50 |

| | 3,037 |

| | 2,547 |

|

| Probable Reserves | | 42,411 |

| | 0.45 |

| | 19,027 |

| | 16,030 |

|

| Total Proven and Probable Reserves (1) | | 48,509 |

| | 0.45 |

| | 22,064 |

| | 18,577 |

|

| As of December 31, 2012 | | | | | | | | |

| Proven Reserves | | 6,023 |

| | 0.51 |

| | 3,078 |

| | 2,590 |

|

| Probable Reserves | | 40,119 |

| | 0.46 |

| | 18,377 |

| | 15,491 |

|

| Total Proven and Probable Reserves (1) | | 46,142 |

| | 0.46 |

| | 21,455 |

| | 18,081 |

|

| As of December 31, 2011 | | | | | | | | |

| Proven Reserves | | 5,010 |

| | 0.51 |

| | 2,618 |

| | 2,168 |

|

| Probable Reserves | | 37,469 |

| | 0.46 |

| | 17,362 |

| | 14,488 |

|

| Total Proven and Probable Reserves (1) | | 42,479 |

| | 0.47 |

| | 19,980 |

| | 16,656 |

|

(1) Reserves are defined as that part of a mineral deposit that could be economically and legally extracted or produced at the time of the reserve determination. Proven ore reserves are defined as ore reserves for which (a) quantity is computed from dimensions revealed in outcrops, trenches, workings or drill holes; grade and / or quality are computed from the results of detailed sampling and (b) the sites for inspection, sampling and measurement are spaced so closely and the geologic character is so well defined that size, shape, depth and mineral content of ore reserves are well-established. Probable ore reserves are defined as ore reserves for which quantity and grade and / or quality are computed from information similar to that used for proven ore reserves, but the sites for inspection, sampling, and measurement are farther apart or are otherwise less adequately spaced. The degree of assurance, although lower than that for proven ore reserves, is high enough to assume continuity between points of observation. The proven and probable ore reserves reflect variations in the PGM content and structural impacts on the J-M Reef. These variations are the result of localized depositional and structural influences on the distributions of economic PGM mineralization. Geologic domains within the reserve boundaries of the two mines include areas where as little as 0% and up to 100% of the J-M Reef is economically mineable. The ore reserve estimate gives effect to these assumptions. See “Risk Factors” and “Cautionary Information Regarding Forward-Looking Statements.”

DISCUSSION