| | |

| UNITED STATES

SECURITIES AND EXCHANGE COMMISSION |

| | |

| CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

|

| | |

| Investment Company Act file number: | (811- 07237) |

| | |

| Exact name of registrant as specified in charter: | Putnam Investment Funds |

| | |

| Address of principal executive offices: | One Post Office Square, Boston, Massachusetts 02109 |

| | |

| Name and address of agent for service: | Robert T. Burns, Vice President

One Post Office Square

Boston, Massachusetts 02109 |

| | |

| Copy to: | John W. Gerstmayr, Esq.

Ropes & Gray LLP

800 Boylston Street

Boston, Massachusetts 02199-3600 |

| | |

| Registrant’s telephone number, including area code: | (617) 292-1000 |

| | |

| Date of fiscal year end: | August 31, 2013 |

| | |

| Date of reporting period: | September 1, 2012 — February 28, 2013 |

| | |

|

Item 1. Report to Stockholders: | |

| | |

| The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940: | |

Putnam

International Capital

Opportunities Fund

Semiannual report

2 | 28 | 13

| | | |

| Message from the Trustees | 1 | | |

| | |

| About the fund | 2 | | |

| | |

| Performance snapshot | 4 | | |

| | |

| Interview with your fund’s portfolio manager | 5 | | |

| | |

| Your fund’s performance | 11 | | |

| | |

| Your fund’s expenses | 13 | | |

| | |

| Terms and definitions | 15 | | |

| | |

| Other information for shareholders | 16 | | |

| | |

| Financial statements | 17 | | |

| | |

Consider these risks before investing: International investing involves certain risks, such as currency fluctuations, economic instability, and political developments. Additional risks may be associated with emerging-market securities, including illiquidity and volatility. Investments in small and/or midsize companies increase the risk of greater price fluctuations. Derivatives also involve the risk of increasing investment exposure or, in the case of many over-the-counter instruments, of the potential inability to terminate or sell derivatives positions and the potential failure of the other party to the instrument to meet its obligations. Growth stocks may be more susceptible to earnings disappointments, and value stocks may fail to rebound. The prices of stocks in the fund’s portfolio may fall or fail to rise over extended periods of time for a variety of reasons, including both general financial market conditions and factors related to a specific company or industry. You can lose money by investing in the fund.

Message from the Trustees

Dear Fellow Shareholder:

The U.S. stock market has set record highs recently, thanks to steadily improving housing and employment data and the Federal Reserve’s pledge to continue to add stimulus until it believes the economy has meaningfully improved. The federal budget battle continues among Washington lawmakers, but investors appear to believe that a resolution will eventually take place.

The by-now familiar risks that have buffeted markets for a few years have not gone away entirely, but they appear to be steadily abating. Europe, while having slumped further into recession, is slowly addressing its sovereign debt problem; China’s economy appears to be improving; and here in the United States economic recovery is underway.

Times like these require a measured, balanced approach to investing. At Putnam, our investment team is actively focused on managing risk while pursuing returns. The guidance of your financial advisor is also important in helping to ensure that your portfolio remains in line with your individual goals and tolerance for risk.

We would like to extend a welcome to new shareholders of the fund and to thank all of our investors for your continued confidence in Putnam.

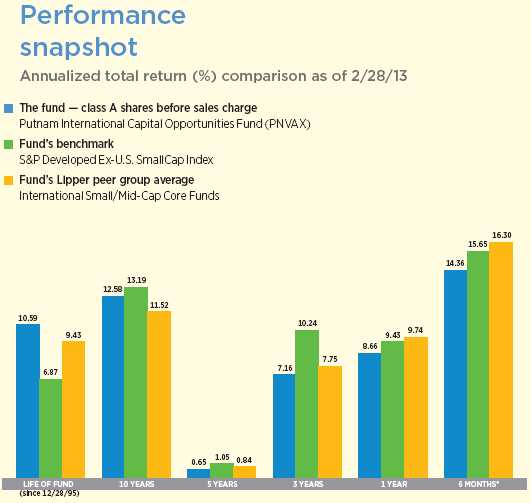

Current performance may be lower or higher than the quoted past performance, which cannot guarantee future results. Share price, principal value, and return will fluctuate, and you may have a gain or a loss when you sell your shares. Performance of class A shares assumes reinvestment of distributions and does not account for taxes. Fund returns in the bar chart do not reflect a sales charge of 5.75%; had they, returns would have been lower. See pages 5 and 11–13 for additional performance information. For a portion of the periods, the fund had expense limitations, without which returns would have been lower. A short-term trading fee of 1% may apply to redemptions or exchanges from certain funds within the time period specified in the fund’s prospectus. To obtain the most recent month-end performance, visit putnam.com.

* Returns for the six-month period are not annualized, but cumulative.

| |

| 4 | International Capital Opportunities Fund |

Interview with your fund’s portfolio manager

Putnam International Capital Opportunities Fund delivered a strong absolute return during the period, but the fund performed just below its benchmark’s 15.65% return. What key factors drove this result?

Stock selection was the most important contributor to the fund’s overall return. The fund did slightly lag its benchmark, though, because of volatility experienced by some of the portfolio holdings. In the course of the period, we took steps to lower the portfolio’s volatility, and we are optimistic that this could help with results relative to the benchmark in the months ahead.

How would you describe the investment environment for small- and mid-cap international stocks during the period?

It was generally a strong investment environment, which took its cue from the U.S. economy’s continuing recovery. For its part, the U.S. economy seemed to gain its direction from signs of health in the housing market. We suspect that the U.S. consumer is feeling the wealth effect of rebounding home equity values. For one thing, U.S. consumers in aggregate have not appeared to wilt in the face of the new year’s higher payroll or other income taxes. To us, this suggests that housing is once again playing a positive psychological role for the average consumer — and consumer spending is a

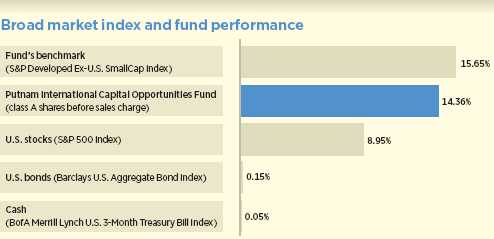

This comparison shows your fund’s performance in the context of broad market indexes for the six months ended 2/28/13. See pages 4 and 11–13 for additional fund performance information. Index descriptions can be found on page 15.

| |

| International Capital Opportunities Fund | 5 |

critical component of U.S. economic growth. With U.S. trends setting a positive tone, international markets, particularly in the small- and mid-cap space, were largely led upward. We see this trajectory continuing in the months ahead — and we anticipate even more upside potential in international relative to U.S. stocks.

Does your anticipation of an upward trajectory include the European economy and markets?

We see Europe in a stabilization phase, but its stock markets, in our view, have room to run. Some of the biggest risks that beset Europe with varying degrees of urgency in 2012 — such as a potential breakup of the European Union and a failure of the euro currency — appear to have been severely curtailed by the efforts of eurozone policymakers. Consequently, we wouldn’t be surprised to see healthy economic growth emerge from Europe sometime in the next 12 to 24 months. As of the end of the reporting period, however, European stocks appeared to be priced for a long, slow recovery, so we generally have an easy time finding what we consider attractive opportunities — companies with strong balance sheets and steady cash flows. These are companies that have the kind of staying power that we believe will help them thrive once the European economy is more fully on track.

Japanese stocks solidly ran up during the period, partly as a result of the yen trending steeply downward. How do these developments affect your outlook for Japanese equities?

The large decline in the value of the yen relative to other major currencies has helped make some Japanese companies more competitive relative to their counterparts in other countries. If the currency continues to depreciate, this could have an important

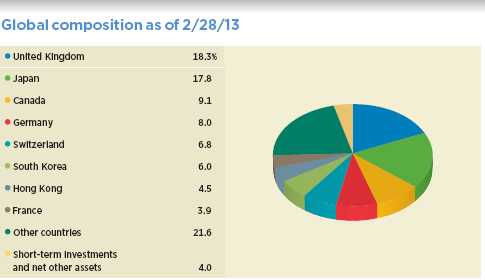

Country allocations are represented as a percentage of the fund’s net assets. Summary information may differ from the information in the portfolio schedule notes included in the financial statements due to the inclusion of derivative securities, any interest accruals, the exclusion of as-of trades, if any, and the use of different classifications of securities for presentation purposes. Holdings and allocations may vary over time.

| |

| 6 | International Capital Opportunities Fund |

effect on Japanese equities over a longer time frame, which could be an important catalyst for renewed economic health in Japan.

Having said that, Japanese stocks moved up very quickly at the end of 2012 and into the early months of 2013. As many investors began chasing Japanese equity returns, Japanese stocks that we formerly would have called relatively cheap became far less attractively priced in just a matter of weeks. In the portfolio, we held on to the stocks we already owned, which was beneficial for the fund’s returns in an absolute sense, but we did not make any substantive changes to the fund’s allocation to Japanese stocks.

Did you make any large changes in sector allocations during the period?

We made a couple of shifts worth noting. Specifically, we reduced consumer discretionary, health-care, and information technology weightings and redeployed the proceeds from these stock sales into consumer staples and financials. Among the latter, we increased the portfolio’s exposure to insurance companies, but we continue to be underweight in real estate investment trusts, which appear in general to be fully valued.

Which stocks contributed most to the fund’s performance during the period?

A Canada-based mining company, Inmet, was the largest contributor to the fund’s return. The company’s share price rose when another mining company, First Quantum, made an offer to acquire Inmet. We sold the stock after the bid was announced, locking in profits for the fund.

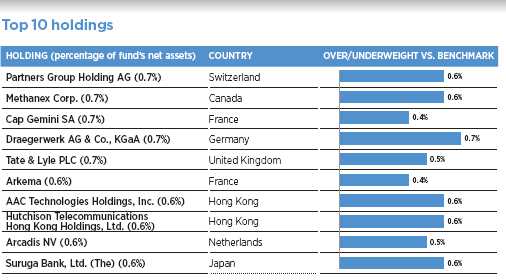

This table shows the fund’s top 10 holdings by percentage of the fund’s net assets as of 2/28/13. Summary information may differ from the portfolio schedule included in the financial statements due to the inclusion of derivative securities, any interest accruals, the exclusion of as-of trades, if any, and the use of different classifications of securities for presentation purposes. Holdings will vary over time.

| |

| International Capital Opportunities Fund | 7 |

The second-largest contributor to the fund’s performance was GS Home Shopping, a South Korean version of the U.S.-based Home Shopping Network. Formerly, the company emphasized home appliances, which was a relatively low-margin business. Management initiated an important shift in focus, however, as the company began selling more low-priced apparel — a higher-margin business that gained traction with the downturn-weary South Korean consumer. The company also continued its expansion into a variety of other countries, including India and Thailand — moves that should help maintain the company’s long-term performance potential.

Another top contributor was Japan-based Suruga Bank, which performed well as the Japanese real estate market improved. Suruga’s net interest income increased as a result of its ability to make more mortgage loans. In addition, the company has an arrangement with the Japan Post Bank — one of the world’s largest savings banks in terms of consumer assets — whereby the Post Bank refers banking business to Suruga. This was an additional source of growth for the company.

Which stocks detracted the most from the fund’s return during the period?

The largest detractor from returns was Royal Imtech, a Netherlands-based technical services provider that offers a wide range of businesses in electrical services, energy distribution, and information and communication technology. Unfortunately, the company reported issues related to receivable collections during the period that made us reconsider the position and ultimately led us to sell it.

The second-largest detractor was SmarTone, a mobile phone operator based in Hong Kong. The company’s operating expenses

This chart shows the fund’s largest allocation shifts, by percentage, over the past six months. Allocations are represented as a percentage of the fund’s net assets. Current period summary information may differ from the portfolio schedule included in the financial statements due to the inclusion of derivative securities, any interest accruals, the exclusion of as-of trades, if any, and the use of different classifications of securities for presentation purposes. Holdings and allocations may vary over time.

| |

| 8 | International Capital Opportunities Fund |

rose during the period as it transitioned more of its customers to its 4G network. The company is also getting reduced revenue from roaming charges due to price competition. We continue to like the stock, however, because the company has not stopped paying out close to 100% of its free cash flow to shareholders. Also, we think the 4G transition poses merely a short-term cost setback for the company. In our estimation, it should gradually gain scale as more customers move on to the new network.

The next-largest detractors were the South Korea-based mobile gaming companies, Daum and NHN, each of which have segments devoted to the mobile social gaming market. Concerns flared up in the period over the expectation that government regulation was slated to become more restrictive for this aspect of Daum’s and NHN’s businesses, and the share prices of both companies lagged. By period-end, we sold our position in NHN but continued to hold Daum with confidence in its longer-term potential.

From your perspective, what are the key developments to watch for in international equity markets in the months ahead?

For the past year, international small- and mid-cap stocks have been much more attractive from a valuation standpoint than their U.S. counterparts. Despite the fact that international markets have had a good run, we are still able to find what we consider cheap stocks. In the U.S. equity space, by contrast, it is relatively more difficult to find cheaply valued stocks. While we cannot say how long this difference will persist, the comparison is rather stark in our analysis, which makes us that much more optimistic about international equity investing in 2013.

Lastly, I would say the market all too frequently assumes that acquiring attractively valued stocks requires that one must compromise on quality. We disagree with this assumption, and feel we are able to locate both attributes — good value and high quality — quite frequently among international stocks today. This is nowhere more true, in our opinion, than in Europe, where we believe strong security-selection ability can help us establish compelling positions in stocks with attractive risk/ reward characteristics.

Thank you, Joe, for this update on the fund.

The views expressed in this report are exclusively those of Putnam Management and are subject to change. They are not meant as investment advice.

Please note that the holdings discussed in this report may not have been held by the fund for the entire period. Portfolio composition is subject to review in accordance with the fund’s investment strategy and may vary in the future. Current and future portfolio holdings are subject to risk.

Portfolio Manager Joseph P. Joseph has an M.B.A. from the Stern School of Business at New York University and a B.A. from Loyola College. He joined Putnam in 1994 and has been in the investment industry since 1987.

In addition to Joe, your fund’s portfolio managers are Randy J. Farina, CFA, and John McLanahan, CFA.

| |

| International Capital Opportunities Fund | 9 |

IN THE NEWS

The global economy continues to expand, but the rate of expansion slowed recently. Manufacturing production and services activity worldwide both eased in February, according to data compiled by JPMorgan and Market Economics. Economic growth was led by the United States, followed by China, Germany, the United Kingdom, Brazil, India, Russia, and Ireland. The rate of increase, however, dropped in most of those countries, with the United States and Russia being the exceptions. Japan’s economic output, meanwhile, was stagnant. In the still-troubled eurozone, conditions weakened substantially in France, Italy, and Spain, with output contracting sharply in these countries’ manufacturing and services sectors. While the global economic deceleration was considered slight by most observers, the expansion rate hit a four-month low in February. As the employment picture improves in the United States and around the world, economists hope that jobs growth will spur further demand.

| |

| 10 | International Capital Opportunities Fund |

Your fund’s performance

This section shows your fund’s performance, price, and distribution information for periods ended February 28, 2013, the end of the first half of its current fiscal year. In accordance with regulatory requirements for mutual funds, we also include performance information as of the most recent calendar quarter-end and expense information taken from the fund’s current prospectus. Performance should always be considered in light of a fund’s investment strategy. Data represent past performance. Past performance does not guarantee future results. More recent returns may be less or more than those shown. Investment return and principal value will fluctuate, and you may have a gain or a loss when you sell your shares. Performance information does not reflect any deduction for taxes a shareholder may owe on fund distributions or on the redemption of fund shares. For the most recent month-end performance, please visit the Individual Investors section at putnam.com or call Putnam at 1-800-225-1581. Class R and class Y shares are not available to all investors. See the Terms and Definitions section in this report for definitions of the share classes offered by your fund.

Fund performance Total return for periods ended 2/28/13

| | | | | | | | | | |

| | Class A | Class B | Class C | Class M | Class R | Class Y |

| (inception dates) | (12/28/95) | (10/30/96) | (7/26/99) | (10/30/96) | (1/21/03) | (2/1/00) |

|

| | Before | After | | | | | Before | After | Net | Net |

| | sales | sales | Before | After | Before | After | sales | sales | asset | asset |

| | charge | charge | CDSC | CDSC | CDSC | CDSC | charge | charge | value | value |

|

| Annual average | | | | | | | | | | |

| (life of fund) | 10.59% | 10.21% | 9.76% | 9.76% | 9.76% | 9.76% | 10.03% | 9.81% | 10.33% | 10.80% |

|

| 10 years | 226.98 | 208.18 | 203.51 | 203.51 | 203.39 | 203.39 | 211.27 | 200.37 | 219.97 | 235.55 |

| Annual average | 12.58 | 11.91 | 11.74 | 11.74 | 11.74 | 11.74 | 12.02 | 11.63 | 12.33 | 12.87 |

|

| 5 years | 3.29 | –2.65 | –0.52 | –2.46 | –0.50 | –0.50 | 0.78 | –2.75 | 2.06 | 4.60 |

| Annual average | 0.65 | –0.54 | –0.10 | –0.50 | –0.10 | –0.10 | 0.16 | –0.56 | 0.41 | 0.90 |

|

| 3 years | 23.05 | 15.97 | 20.31 | 17.31 | 20.27 | 20.27 | 21.23 | 16.99 | 22.17 | 23.99 |

| Annual average | 7.16 | 5.06 | 6.36 | 5.46 | 6.35 | 6.35 | 6.63 | 5.37 | 6.90 | 7.43 |

|

| 1 year | 8.66 | 2.41 | 7.86 | 2.86 | 7.86 | 6.86 | 8.13 | 4.35 | 8.39 | 8.94 |

|

| 6 months | 14.36 | 7.78 | 13.92 | 8.92 | 13.92 | 12.92 | 14.09 | 10.10 | 14.21 | 14.50 |

|

Current performance may be lower or higher than the quoted past performance, which cannot guarantee future results. After-sales-charge returns for class A and M shares reflect the deduction of the maximum 5.75% and 3.50% sales charge, respectively, levied at the time of purchase. Class B share returns after contingent deferred sales charge (CDSC) reflect the applicable CDSC, which is 5% in the first year, declining over time to 1% in the sixth year, and is eliminated thereafter. Class C share returns after CDSC reflect a 1% CDSC for the first year that is eliminated thereafter. Class R and Y shares have no initial sales charge or CDSC. Performance for class B, C, M, R, and Y shares before their inception is derived from the historical performance of class A shares, adjusted for the applicable sales charge (or CDSC) and the higher operating expenses for such shares, except for class Y shares, for which 12b-1 fees are not applicable.

Recent performance may have benefited from one or more legal settlements.

For a portion of the periods, the fund had expense limitations, without which returns would have been lower.

Class B share performance does not reflect conversion to class A shares.

A short-term trading fee of 1% may apply to redemptions or exchanges from certain funds within the time period specified in the fund’s prospectus.

| |

| International Capital Opportunities Fund | 11 |

Comparative index returns For periods ended 2/28/13

| | |

| | | Lipper International Small/ |

| | S&P Developed | Mid-Cap Core Funds |

| | Ex-U.S. SmallCap Index | category average* |

|

| Annual average (life of fund) | 6.87% | 9.43% |

|

| 10 years | 245.25 | 201.33 |

| Annual average | 13.19 | 11.52 |

|

| 5 years | 5.34 | 4.78 |

| Annual average | 1.05 | 0.84 |

|

| 3 years | 33.96 | 25.70 |

| Annual average | 10.24 | 7.75 |

|

| 1 year | 9.43 | 9.74 |

|

| 6 months | 15.65 | 16.30 |

|

Index and Lipper results should be compared with fund performance before sales charge, before CDSC, or at net asset value.

* Over the 6-month, 1-year, 3-year, 5-year, 10-year, and life-of-fund periods ended 2/28/13, there were 52, 50, 40, 33, 23, and 8 funds, respectively, in this Lipper category.

Fund price and distribution information For the six-month period ended 2/28/13

| | | | | | |

| Distributions | Class A | Class B | Class C | Class M | Class R | Class Y |

|

| Number | 1 | 1 | 1 | 1 | 1 | 1 |

|

| Income | $0.387 | $0.113 | $0.129 | $0.226 | $0.253 | $0.472 |

|

| Capital gains | — | — | — | — | — | — |

|

| Total | $0.387 | $0.113 | $0.129 | $0.226 | $0.253 | $0.472 |

|

| | Before | After | Net | Net | Before | After | Net | Net |

| | sales | sales | asset | asset | sales | sales | asset | asset |

| Share value | charge | charge | value | value | charge | charge | value | value |

|

| 8/31/12 | $30.33 | $32.18 | $30.09 | $30.07 | $30.14 | $31.23 | $29.81 | $30.37 |

|

| 2/28/13 | 34.28 | 36.37 | 34.16 | 34.12 | 34.15 | 35.39 | 33.78 | 34.28 |

|

The classification of distributions, if any, is an estimate. Before-sales-charge share value and current dividend rate for class A and M shares, if applicable, do not take into account any sales charge levied at the time of purchase. After-sales-charge share value, current dividend rate, and current 30-day SEC yield, if applicable, are calculated assuming that the maximum sales charge (5.75% for class A shares and 3.50% for class M shares) was levied at the time of purchase. Final distribution information will appear on your year-end tax forms.

| |

| 12 | International Capital Opportunities Fund |

Fund performance as of most recent calendar quarter

Total return for periods ended 3/31/13

| | | | | | | | | | |

| | Class A | Class B | Class C | Class M | Class R | Class Y |

| (inception dates) | (12/28/95) | (10/30/96) | (7/26/99) | (10/30/96) | (1/21/03) | (2/1/00) |

|

| | Before | After | | | | | Before | After | Net | Net |

| | sales | sales | Before | After | Before | After | sales | sales | asset | asset |

| | charge | charge | CDSC | CDSC | CDSC | CDSC | charge | charge | value | value |

|

| Annual average | | | | | | | | | | |

| (life of fund) | 10.65% | 10.27% | 9.82% | 9.82% | 9.82% | 9.82% | 10.09% | 9.87% | 10.39% | 10.86% |

|

| 10 years | 238.23 | 218.78 | 213.55 | 213.55 | 213.64 | 213.64 | 221.78 | 210.52 | 230.62 | 246.82 |

| Annual average | 12.96 | 12.29 | 12.11 | 12.11 | 12.11 | 12.11 | 12.40 | 12.00 | 12.70 | 13.24 |

|

| 5 years | 5.63 | –0.45 | 1.72 | –0.27 | 1.71 | 1.71 | 3.02 | –0.59 | 4.35 | 6.94 |

| Annual average | 1.10 | –0.09 | 0.34 | –0.05 | 0.34 | 0.34 | 0.60 | –0.12 | 0.85 | 1.35 |

|

| 3 years | 15.50 | 8.86 | 12.94 | 9.94 | 12.89 | 12.89 | 13.77 | 9.79 | 14.66 | 16.36 |

| Annual average | 4.92 | 2.87 | 4.14 | 3.21 | 4.12 | 4.12 | 4.39 | 3.16 | 4.66 | 5.18 |

|

| 1 year | 10.14 | 3.80 | 9.30 | 4.30 | 9.30 | 8.30 | 9.58 | 5.74 | 9.85 | 10.38 |

|

| 6 months | 11.35 | 4.95 | 10.94 | 5.94 | 10.93 | 9.93 | 11.07 | 7.19 | 11.22 | 11.50 |

|

See the discussion following the Fund performance table on page 11 for information about the calculation of fund performance.

Your fund’s expenses

As a mutual fund investor, you pay ongoing expenses, such as management fees, distribution fees (12b-1 fees), and other expenses. Using the following information, you can estimate how these expenses affect your investment and compare them with the expenses of other funds. You may also pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial representative.

Expense ratios

| | | | | | |

| | Class A | Class B | Class C | Class M | Class R | Class Y |

|

| Total annual operating expenses | | | | | | |

| for the fiscal year ended 8/31/12 | 1.41% | 2.16% | 2.16% | 1.91% | 1.66% | 1.16% |

|

| Annualized expense ratio for | | | | | | |

| the six-month period ended | | | | | | |

| 2/28/13* | 1.43% | 2.18% | 2.18% | 1.93% | 1.68% | 1.18% |

|

Fiscal-year expense information in this table is taken from the most recent prospectus, is subject to change, and may differ from that shown for the annualized expense ratio and in the financial highlights of this report. Expenses are shown as a percentage of average net assets.

* Includes an increase of 0.11% from annualizing the performance fee adjustment for the six months ended 2/28/13.

| |

| International Capital Opportunities Fund | 13 |

Expenses per $1,000

The following table shows the expenses you would have paid on a $1,000 investment in the fund from September 1, 2012, to February 28, 2013. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

| | | | | | |

| | Class A | Class B | Class C | Class M | Class R | Class Y |

|

| Expenses paid per $1,000*† | $7.60 | $11.56 | $11.56 | $10.24 | $8.92 | $6.28 |

|

| Ending value (after expenses) | $1,143.60 | $1,139.20 | $1,139.20 | $1,140.90 | $1,142.10 | $1,145.00 |

|

* Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of average net assets for the six months ended 2/28/13. The expense ratio may differ for each share class.

† Expenses are calculated by multiplying the expense ratio by the average account value for the period; then multiplying the result by the number of days in the period; and then dividing that result by the number of days in the year.

Estimate the expenses you paid

To estimate the ongoing expenses you paid for the six months ended February 28, 2013, use the following calculation method. To find the value of your investment on September 1, 2012, call Putnam at 1-800-225-1581.

Compare expenses using the SEC’s method

The Securities and Exchange Commission (SEC) has established guidelines to help investors assess fund expenses. Per these guidelines, the following table shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total costs) of investing in the fund with those of other funds. All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

| | | | | | |

| | Class A | Class B | Class C | Class M | Class R | Class Y |

|

| Expenses paid per $1,000*† | $7.15 | $10.89 | $10.89 | $9.64 | $8.40 | $5.91 |

|

| Ending value (after expenses) | $1,017.70 | $1,013.98 | $1,013.98 | $1,015.22 | $1,016.46 | $1,018.94 |

|

* Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of average net assets for the six months ended 2/28/13. The expense ratio may differ for each share class.

† Expenses are calculated by multiplying the expense ratio by the average account value for the period; then multiplying the result by the number of days in the period; and then dividing that result by the number of days in the year.

| |

| 14 | International Capital Opportunities Fund |

Terms and definitions

Important terms

Total return shows how the value of the fund’s shares changed over time, assuming you held the shares through the entire period and reinvested all distributions in the fund.

Before sales charge, or net asset value, is the price, or value, of one share of a mutual fund, without a sales charge. Before-sales-charge figures fluctuate with market conditions, and are calculated by dividing the net assets of each class of shares by the number of outstanding shares in the class.

After sales charge is the price of a mutual fund share plus the maximum sales charge levied at the time of purchase. After-sales-charge performance figures shown here assume the 5.75% maximum sales charge for class A shares and 3.50% for class M shares.

Contingent deferred sales charge (CDSC) is generally a charge applied at the time of the redemption of class B or C shares and assumes redemption at the end of the period. Your fund’s class B CDSC declines over time from a 5% maximum during the first year to 1% during the sixth year. After the sixth year, the CDSC no longer applies. The CDSC for class C shares is 1% for one year after purchase.

Share classes

Class A shares are generally subject to an initial sales charge and no CDSC (except on certain redemptions of shares bought without an initial sales charge).

Class B shares are not subject to an initial sales charge. They may be subject to a CDSC.

Class C shares are not subject to an initial sales charge and are subject to a CDSC only if the shares are redeemed during the first year.

Class M shares have a lower initial sales charge and a higher 12b-1 fee than class A shares and no CDSC (except on certain redemptions of shares bought without an initial sales charge).

Class R shares are not subject to an initial sales charge or CDSC and are available only to certain defined contribution plans.

Class Y shares are not subject to an initial sales charge or CDSC, and carry no 12b-1 fee. They are generally only available to corporate and institutional clients and clients in other approved programs.

Comparative indexes

Barclays U.S. Aggregate Bond Index is an unmanaged index of U.S. investment-grade fixed-income securities.

BofA (Bank of America) Merrill Lynch U.S. 3-Month Treasury Bill Index is an unmanaged index that seeks to measure the performance of U.S. Treasury bills available in the marketplace.

S&P 500 Index is an unmanaged index of common stock performance.

S&P Developed Ex-U.S. SmallCap Index is an unmanaged index of small-cap stocks from developed countries, excluding the United States.

Indexes assume reinvestment of all distributions and do not account for fees. Securities and performance of a fund and an index will differ. You cannot invest directly in an index.

Lipper is a third-party industry-ranking entity that ranks mutual funds. Its rankings do not reflect sales charges. Lipper rankings are based on total return at net asset value relative to other funds that have similar current investment styles or objectives as determined by Lipper. Lipper may change a fund’s category assignment at its discretion. Lipper category averages reflect performance trends for funds within a category.

| |

| International Capital Opportunities Fund | 15 |

Other information for shareholders

Important notice regarding delivery of shareholder documents

In accordance with Securities and Exchange Commission (SEC) regulations, Putnam sends a single copy of annual and semiannual shareholder reports, prospectuses, and proxy statements to Putnam shareholders who share the same address, unless a shareholder requests otherwise. If you prefer to receive your own copy of these documents, please call Putnam at 1-800-225-1581, and Putnam will begin sending individual copies within 30 days.

Proxy voting

Putnam is committed to managing our mutual funds in the best interests of our shareholders. The Putnam funds’ proxy voting guidelines and procedures, as well as information regarding how your fund voted proxies relating to portfolio securities during the 12-month period ended June 30, 2012, are available in the Individual Investors section of putnam.com, and on the SEC’s website, www.sec.gov. If you have questions about finding forms on the SEC’s website, you may call the SEC at 1-800-SEC-0330. You may also obtain the Putnam funds’ proxy voting guidelines and procedures at no charge by calling Putnam’s Shareholder Services at 1-800-225-1581.

Fund portfolio holdings

The fund will file a complete schedule of its portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. Shareholders may obtain the fund’s Forms N-Q on the SEC’s website at www.sec.gov. In addition, the fund’s Forms N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, D.C. You may call the SEC at 1-800-SEC-0330 for information about the SEC’s website or the operation of the Public Reference Room.

Trustee and employee fund ownership

Putnam employees and members of the Board of Trustees place their faith, confidence, and, most importantly, investment dollars in Putnam mutual funds. As of February 28, 2013, Putnam employees had approximately $366,000,000 and the Trustees had approximately $87,000,000 invested in Putnam mutual funds. These amounts include investments by the Trustees’ and employees’ immediate family members as well as investments through retirement and deferred compensation plans.

| |

| 16 | International Capital Opportunities Fund |

Financial statements

A guide to financial statements

These sections of the report, as well as the accompanying Notes, constitute the fund’s financial statements.

The fund’s portfolio lists all the fund’s investments and their values as of the last day of the reporting period. Holdings are organized by asset type and industry sector, country, or state to show areas of concentration and diversification.

Statement of assets and liabilities shows how the fund’s net assets and share price are determined. All investment and non-investment assets are added together. Any unpaid expenses and other liabilities are subtracted from this total. The result is divided by the number of shares to determine the net asset value per share, which is calculated separately for each class of shares. (For funds with preferred shares, the amount subtracted from total assets includes the liquidation preference of preferred shares.)

Statement of operations shows the fund’s net investment gain or loss. This is done by first adding up all the fund’s earnings — from dividends and interest income — and subtracting its operating expenses to determine net investment income (or loss). Then, any net gain or loss the fund realized on the sales of its holdings — as well as any unrealized gains or losses over the period — is added to or subtracted from the net investment result to determine the fund’s net gain or loss for the fiscal period.

Statement of changes in net assets shows how the fund’s net assets were affected by the fund’s net investment gain or loss, by distributions to shareholders, and by changes in the number of the fund’s shares. It lists distributions and their sources (net investment income or realized capital gains) over the current reporting period and the most recent fiscal year-end. The distributions listed here may not match the sources listed in the Statement of operations because the distributions are determined on a tax basis and may be paid in a different period from the one in which they were earned. Dividend sources are estimated at the time of declaration. Actual results may vary. Any non-taxable return of capital cannot be determined until final tax calculations are completed after the end of the fund’s fiscal year.

Financial highlights provide an overview of the fund’s investment results, per-share distributions, expense ratios, net investment income ratios, and portfolio turnover in one summary table, reflecting the five most recent reporting periods. In a semiannual report, the highlights table also includes the current reporting period.

| |

| International Capital Opportunities Fund | 17 |

The fund’s portfolio 2/28/13 (Unaudited)

| | |

| COMMON STOCKS (96.1%)* | Shares | Value |

|

| Australia (3.4%) | | |

| Abacus Property Group R | 1,893,764 | $4,277,069 |

|

| Cardno, Ltd. S | 568,769 | 4,157,652 |

|

| Flight Centre, Ltd. S | 161,774 | 5,371,401 |

|

| Lend Lease Group | 306,514 | 3,329,048 |

|

| Medusa Mining, Ltd. S | 580,223 | 2,527,869 |

|

| Monadelphous Group, Ltd. S | 194,955 | 4,945,250 |

|

| Wotif.com Holdings, Ltd. S | 862,251 | 4,324,312 |

|

| | | 28,932,601 |

| Austria (0.9%) | | |

| Andritz AG | 78,347 | 5,520,240 |

|

| Bank Austria Creditanstalt AG (acquired 8/7/08, cost $—) FΔΔ | 471 | — |

|

| EVN AG S | 129,468 | 1,852,553 |

|

| | | 7,372,793 |

| Canada (9.6%) | | |

| AuRico Gold, Inc. † | 565,600 | 3,537,572 |

|

| Calfrac Well Services, Ltd. | 181,895 | 4,303,746 |

|

| Canaccord Financial, Inc. | 564,643 | 4,090,069 |

|

| Canadian Real Estate Investment Trust R | 66,700 | 3,040,550 |

|

| Centerra Gold, Inc. | 554,100 | 3,599,971 |

|

| Corus Entertainment, Inc. Class B S | 184,300 | 4,542,939 |

|

| Dollarama, Inc. | 92,800 | 5,453,265 |

|

| Domtar Corp. | 63,309 | 4,720,319 |

|

| Ensign Energy Services, Inc. S | 298,724 | 4,964,974 |

|

| Industrial Alliance Insurance and Financial Services, Inc. | 90,000 | 3,229,091 |

|

| InnVest Real Estate Investment Trust R | 713,600 | 3,093,132 |

|

| Lululemon Athletica, Inc. † | 65,399 | 4,383,398 |

|

| Lundin Mining Corp. † | 921,348 | 4,172,310 |

|

| MacDonald Dettwiler & Associates, Ltd. | 62,500 | 4,318,182 |

|

| Methanex Corp. S | 165,996 | 6,076,460 |

|

| Metro, Inc. S | 76,200 | 4,772,614 |

|

| Mullen Group, Ltd. | 207,100 | 4,400,059 |

|

| Open Text Corp. † | 90,774 | 4,997,081 |

|

| Peyto Exploration and Development Corp. S | 208,907 | 5,098,850 |

|

| | | 82,794,582 |

| China (1.2%) | | |

| AAC Technologies Holdings, Inc. | 1,306,000 | 5,559,500 |

|

| China BlueChemical, Ltd. | 6,950,000 | 4,455,914 |

|

| | | 10,015,414 |

| Denmark (2.2%) | | |

| D/S Norden | 107,994 | 3,432,626 |

|

| DSV A/S | 131,380 | 3,222,458 |

|

| H. Lundbeck A/S | 206,456 | 3,499,694 |

|

| Sydbank A/S † | 200,653 | 4,071,647 |

|

| Topdanmark A/S † | 20,099 | 4,623,743 |

|

| | | 18,850,168 |

| France (3.9%) | | |

| Arkema | 55,140 | 5,583,737 |

|

| Cap Gemini SA | 117,199 | 5,757,729 |

|

| Ingenico S | 88,611 | 5,353,248 |

|

| |

| 18 | International Capital Opportunities Fund |

| | |

| COMMON STOCKS (96.1%)* cont. | Shares | Value |

|

| France cont. | | |

| M6-Metropole Television | 191,833 | $3,147,477 |

|

| Publicis Group SA | 77,583 | 5,128,354 |

|

| SEB SA | 49,957 | 3,714,010 |

|

| Teleperformance | 125,498 | 5,166,384 |

|

| | | 33,850,939 |

| Germany (8.0%) | | |

| Aurubis AG S | 71,739 | 5,033,456 |

|

| Bertrandt AG S | 34,123 | 3,781,431 |

|

| Bilfinger SE | 47,147 | 4,949,718 |

|

| Carl Zeiss Meditec AG S | 122,190 | 3,826,010 |

|

| Celesio AG | 129,783 | 2,346,620 |

|

| Draegerwerk AG & Co., KGaA (Preference) S | 44,305 | 5,664,567 |

|

| Gerry Weber International AG | 107,117 | 4,844,684 |

|

| Gildemeister AG | 216,114 | 5,356,590 |

|

| Hugo Boss AG | 44,287 | 5,134,427 |

|

| Krones AG | 26,955 | 1,754,865 |

|

| Lanxess AG | 56,811 | 4,810,245 |

|

| Leoni AG | 114,888 | 5,179,559 |

|

| MTU Aero Engines Holding AG | 54,476 | 5,066,097 |

|

| Software AG | 120,144 | 4,737,452 |

|

| Stada Arzneimittel AG | 83,539 | 3,265,414 |

|

| Vossloh AG | 28,624 | 3,006,379 |

|

| | | 68,757,514 |

| Hong Kong (3.3%) | | |

| China New Town Development Co., Ltd. † | 1 | — |

|

| Dah Sing Financial Holdings | 751,600 | 4,042,248 |

|

| Hutchison Telecommunications Hong Kong Holdings, Ltd. | 11,266,000 | 5,536,127 |

|

| SmarTone Telecommunications Holdings, Ltd. | 2,516,000 | 4,598,300 |

|

| Techtronic Industries Co. | 2,231,000 | 4,445,684 |

|

| Television Broadcasts, Ltd. | 672,000 | 5,122,439 |

|

| Wing Hang Bank, Ltd. | 448,500 | 4,978,794 |

|

| | | 28,723,592 |

| Ireland (2.4%) | | |

| C&C Group PLC | 765,410 | 4,890,920 |

|

| Kerry Group PLC Class A | 97,801 | 5,480,002 |

|

| Kingspan Group PLC | 439,973 | 5,090,481 |

|

| United Drug PLC | 1,113,383 | 4,829,863 |

|

| | | 20,291,266 |

| Italy (2.3%) | | |

| Ansaldo STS SpA | 511,142 | 4,929,091 |

|

| Danieli & Co. SpA S | 167,342 | 4,469,860 |

|

| De’Longhi SpA | 323,387 | 4,962,471 |

|

| Recordati SpA | 501,928 | 4,975,396 |

|

| | | 19,336,818 |

| Japan (17.8%) | | |

| ABC-Mart, Inc. S | 83,600 | 2,916,300 |

|

| Advance Residence Investment Corp. R | 2,261 | 4,798,451 |

|

| Aeon Credit Service Co., Ltd. | 137,700 | 3,204,880 |

|

| Asics Corp. | 338,000 | 5,315,635 |

|

| Capcom Co., Ltd. | 238,300 | 3,657,508 |

|

| |

| International Capital Opportunities Fund | 19 |

| | |

| COMMON STOCKS (96.1%)* cont. | Shares | Value |

|

| Japan cont. | | |

| Century Tokyo Leasing Corp. | 139,500 | $3,249,061 |

|

| Dainippon Sumitomo Pharma Co., Ltd. | 335,200 | 4,840,688 |

|

| Disco Corp. | 80,200 | 4,591,972 |

|

| Fuyo General Lease Co., Ltd. | 96,100 | 3,425,232 |

|

| Gunma Bank, Ltd. (The) | 880,000 | 4,783,236 |

|

| Horiba, Ltd. | 151,200 | 4,719,967 |

|

| Itochu Techno-Solutions Corp. | 97,500 | 4,258,733 |

|

| Japan Petroleum Exploration Co. | 64,700 | 2,452,549 |

|

| Japan Real Estate Investment Corp. R | 485 | 5,320,506 |

|

| JSR Corp. | 241,800 | 4,927,684 |

|

| Kakaku.com, Inc. | 121,700 | 4,726,076 |

|

| Kobayashi Pharmaceutical Co., Ltd. | 58,400 | 2,768,927 |

|

| Kurita Water Industries, Ltd. | 213,400 | 4,262,572 |

|

| Kuroda Electric Co., Ltd. | 245,300 | 2,809,305 |

|

| Mandom Corp. | 124,300 | 3,876,152 |

|

| Misumi Group, Inc. | 174,200 | 4,442,398 |

|

| Mitsubishi Tanabe Pharma Corp. | 250,700 | 3,556,148 |

|

| Moshi Moshi Hotline, Inc. | 347,000 | 4,903,731 |

|

| Musashino Bank, Ltd. (The) | 82,900 | 2,928,002 |

|

| Nihon Kohden Corp. | 138,600 | 4,814,200 |

|

| Nippo Corp. | 263,000 | 3,454,368 |

|

| Nitto Denko Corp. | 90,100 | 5,294,555 |

|

| NTT Urban Development Corp. | 3,317 | 3,376,606 |

|

| Ono Pharmaceutical Co., Ltd. | 67,300 | 3,568,401 |

|

| Park24 Co., Ltd. | 197,000 | 3,599,773 |

|

| Rinnai Corp. | 59,900 | 4,300,531 |

|

| Sanwa Holdings Corp. | 908,000 | 4,641,431 |

|

| Shimamura Co., Ltd. | 41,200 | 4,208,619 |

|

| Suruga Bank, Ltd. (The) | 376,000 | 5,522,997 |

|

| Suzuken Co., Ltd. | 81,300 | 2,827,775 |

|

| Taikisha, Ltd. | 232,000 | 5,066,754 |

|

| Toridoll.corp S | 152,900 | 1,522,477 |

|

| Unipres Corp. | 204,700 | 4,564,983 |

|

| | | 153,499,183 |

| Mexico (0.6%) | | |

| Grupo Financiero Banorte SAB de CV | 724,600 | 5,358,766 |

|

| | | 5,358,766 |

| Netherlands (1.8%) | | |

| Aalberts Industries NV | 224,434 | 4,968,084 |

|

| Arcadis NV | 197,745 | 5,523,562 |

|

| Koninklijke Boskalis Westminster NV | 115,897 | 4,953,729 |

|

| | | 15,445,375 |

| Norway (2.4%) | | |

| DNO International ASA † | 1,113,863 | 1,998,368 |

|

| Fred Olsen Energy ASA | 97,400 | 4,229,499 |

|

| SpareBank 1 SR-Bank ASA | 615,119 | 4,945,429 |

|

| Subsea 7 SA | 192,353 | 4,547,558 |

|

| TGS-NOPEC Geophysical Co. ASA | 136,879 | 5,164,357 |

|

| | | 20,885,211 |

| |

| 20 | International Capital Opportunities Fund |

| | |

| COMMON STOCKS (96.1%)* cont. | Shares | Value |

|

| Russia (0.4%) | | |

| Oriflame Cosmetics SA SDR S | 90,329 | $3,117,360 |

|

| | | 3,117,360 |

| Singapore (1.0%) | | |

| Great Eastern Holdings, Ltd. | 219,000 | 3,180,580 |

|

| M1, Ltd. | 2,261,000 | 5,110,141 |

|

| | | 8,290,721 |

| South Korea (6.0%) | | |

| BS Financial Group, Inc. | 309,870 | 4,477,174 |

|

| Daelim Industrial Co., Ltd. | 40,484 | 3,593,932 |

|

| Daum Communications Corp. | 52,380 | 4,608,345 |

|

| DGB Financial Group, Inc. | 322,930 | 4,840,476 |

|

| Dong-A Pharmaceutical Co., Ltd. | 46,073 | 5,301,809 |

|

| Dongbu Insurance Co., Ltd. | 100,980 | 4,421,036 |

|

| GS Home Shopping, Inc. | 29,324 | 5,258,271 |

|

| Hyundai Marine & Fire Insurance Co., Ltd. | 142,870 | 4,144,971 |

|

| Hyundai Mipo Dockyard | 25,887 | 2,802,961 |

|

| LIG Insurance Co., Ltd. | 126,380 | 2,722,924 |

|

| S1 Corp. | 78,398 | 4,985,032 |

|

| Seah Besteel Corp. | 160,564 | 4,938,756 |

|

| | | 52,095,687 |

| Spain (0.5%) | | |

| Prosegur Compania de Securidad SA | 679,914 | 3,994,396 |

|

| | | 3,994,396 |

| Sweden (2.1%) | | |

| AF AB Class B | 176,081 | 5,047,648 |

|

| Boliden AB | 265,009 | 4,477,092 |

|

| Intrum Justita AB | 260,723 | 4,676,791 |

|

| JM AB S | 184,004 | 4,202,132 |

|

| | | 18,403,663 |

| Switzerland (6.8%) | | |

| Actelion, Ltd. | 100,064 | 5,151,068 |

|

| Aryzta AG | 90,604 | 5,207,335 |

|

| Baloise Holding AG | 48,296 | 4,328,297 |

|

| Banque Cantonale Vaudoise (BCV) | 7,736 | 4,403,576 |

|

| Barry Callebaut AG | 5,074 | 4,955,460 |

|

| Bucher Industries AG | 22,990 | 5,034,519 |

|

| Burckhardt Compression Holding AG | 12,103 | 4,364,533 |

|

| Dufry AG † | 33,987 | 4,633,031 |

|

| Forbo Holding AG | 6,703 | 4,399,470 |

|

| Georg Fischer AG | 11,517 | 5,205,204 |

|

| Partners Group Holding AG | 26,499 | 6,116,501 |

|

| Sika AG | 1,999 | 4,953,309 |

|

| | | 58,752,303 |

| Taiwan (0.7%) | | |

| Radiant Opto-Electronics Corp. | 666,543 | 2,407,502 |

|

| TSRC Corp. | 1,839,200 | 3,788,607 |

|

| | | 6,196,109 |

| Turkmenistan (0.5%) | | |

| Dragon Oil PLC | 501,544 | 4,691,648 |

|

| | | 4,691,648 |

| |

| International Capital Opportunities Fund | 21 |

| | |

| COMMON STOCKS (96.1%)* cont. | Shares | Value |

|

| United Kingdom (17.2%) | | |

| Aberdeen Asset Management PLC | 746,310 | $4,856,550 |

|

| Amlin PLC | 629,060 | 4,065,695 |

|

| Ashmore Group PLC | 796,845 | 4,331,561 |

|

| Aveva Group PLC | 126,315 | 4,414,397 |

|

| Barratt Developments PLC † | 1,370,007 | 4,978,746 |

|

| Berkeley Group Holdings PLC † | 171,421 | 4,943,338 |

|

| Bunzl PLC | 273,832 | 5,231,277 |

|

| Burberry Group PLC | 209,110 | 4,365,980 |

|

| Cape PLC | 821,156 | 2,894,937 |

|

| Close Brothers Group PLC | 295,213 | 4,675,968 |

|

| DS Smith PLC | 1,503,683 | 5,490,227 |

|

| Halma PLC | 579,575 | 4,328,160 |

|

| IMI PLC | 270,899 | 5,011,178 |

|

| Inchcape PLC | 611,468 | 4,690,943 |

|

| Interserve PLC | 728,372 | 5,449,831 |

|

| Intertek Group PLC | 96,632 | 4,895,766 |

|

| Meggitt PLC | 722,078 | 4,982,013 |

|

| Mitie Group PLC | 1,134,578 | 4,939,499 |

|

| Morgan Sindall Group PLC | 258,246 | 2,114,899 |

|

| Next PLC | 83,910 | 5,338,079 |

|

| Persimmon PLC | 327,253 | 4,530,701 |

|

| Provident Financial PLC | 133,948 | 2,971,336 |

|

| Rathbone Brothers PLC | 145,989 | 3,115,722 |

|

| Rotork PLC | 123,449 | 5,342,566 |

|

| Savills PLC | 675,657 | 5,430,979 |

|

| Schroders PLC | 164,453 | 4,971,494 |

|

| Spectris PLC | 142,721 | 5,143,365 |

|

| Speedy Hire PLC | 5,365,898 | 3,398,501 |

|

| Tate & Lyle PLC | 457,664 | 5,635,968 |

|

| UBM PLC | 418,242 | 4,912,845 |

|

| Ultra Electronics Holdings PLC | 103,917 | 2,662,722 |

|

| Whitbread PLC | 125,551 | 4,806,630 |

|

| William Hill PLC | 565,528 | 3,463,241 |

|

| | | 148,385,114 |

| United States (1.1%) | | |

| Amdocs, Ltd. | 134,692 | 4,912,217 |

|

| Aspen Insurance Holdings, Ltd. | 137,514 | 4,931,252 |

|

| | | 9,843,469 |

| | | |

| Total common stocks (cost $687,009,604) | | $827,884,692 |

|

| |

| U.S. TREASURY OBLIGATIONS (0.1%)* | Principal amount | Value |

|

| U.S. Treasury Notes 1/4s, April 30, 2014 i | $440,000 | $440,629 |

|

| U.S. Treasury Notes 1/4s, May 31, 2014 i | 220,000 | 220,262 |

|

| Total U.S. treasury obligations (cost $660,891) | | $660,891 |

| |

| 22 | International Capital Opportunities Fund |

| | | | |

| WARRANTS (—%)*† | Expiration | Strike | | |

| | date | price | Warrants | Value |

|

| Nieuwe Steen Investments NV (Netherlands) F | 4/1/13 | EUR 0.01 | 126,921 | $166 |

|

| Total warrants (cost $—) | | | | $166 |

| | |

| SHORT-TERM INVESTMENTS (11.9%)* | Principal amount/shares | Value |

|

| Putnam Cash Collateral Pool, LLC 0.21% d | 66,554,366 | $66,554,366 |

|

| Putnam Short Term Investment Fund 0.10% L | 32,967,027 | 32,967,027 |

|

| SSgA Prime Money Market Fund 0.08% P | 760,000 | 760,000 |

|

| U.S. Treasury Bills with an effective yield of 0.172%, | | |

| May 30, 2013 Δ | $491,000 | 490,871 |

|

| U.S. Treasury Bills with effective yields ranging from 0.182% | | |

| to 0.189%, May 2, 2013 Δ | 1,195,000 | 1,194,804 |

|

| U.S. Treasury Bills with effective yields ranging from 0.140% | | |

| to 0.147%, February 6, 2014 Δ | 613,000 | 612,113 |

|

| Total short-term investments (cost $102,578,954) | | $102,579,181 |

|

| |

| TOTAL INVESTMENTS | | |

|

| Total investments (cost $790,249,449) | | $931,124,930 |

| |

| Key to holding’s currency abbreviations |

| |

| EUR | Euro |

| |

| Key to holding’s abbreviations |

| |

| SDR | Swedish Depository Receipts: represents ownership of foreign securities on deposit with a custodian bank |

| | |

Notes to the fund’s portfolio

Unless noted otherwise, the notes to the fund’s portfolio are for the close of the fund’s reporting period, which ran from September 1, 2012 through February 28, 2013 (the reporting period). Within the following notes to the portfolio, references to “ASC 820” represent Accounting Standards Codification ASC 820 Fair Value Measurements and Disclosures and references to “OTC”, if any, represent over-the-counter.

* Percentages indicated are based on net assets of $861,125,318.

† Non-income-producing security.

Δ This security, in part or in entirety, was pledged and segregated with the custodian for collateral on certain derivative contracts at the close of the reporting period.

ΔΔ Security is restricted with regard to public resale. The total market value of this security and any other restricted securities (excluding 144A securities), if any, held at the close of the reporting period was less than $1, or less than 0.1% of net assets.

d Affiliated company. See Note 1 to the financial statements regarding securities lending. The rate quoted in the security description is the annualized 7-day yield of the fund at the close of the reporting period.

F Is valued at fair value following procedures approved by the Trustees. Securities may be classified as Level 2 or Level 3 for ASC 820 based on the securities’ valuation inputs. At the close of the reporting period, fair value pricing was also used for certain foreign securities in the portfolio (Note 1).

i Security was pledged, or purchased with cash that was pledged, to the fund for collateral on certain derivative contracts (Note 1).

L Affiliated company (Note 6). The rate quoted in the security description is the annualized 7-day yield of the fund at the close of the reporting period.

P Security was pledged, or purchased with cash that was pledged, to the fund for collateral on certain derivatives contracts. The rate quoted in the security description is the annualized 7-day yield of the fund at the close of the reporting period (Note 1).

| |

| International Capital Opportunities Fund | 23 |

R Real Estate Investment Trust.

S Security on loan, in part or in entirety, at the close of the reporting period (Note 1).

At the close of the reporting period, the fund maintained liquid assets totaling $2,561,511 to cover certain derivatives contracts.

Debt obligations are considered secured unless otherwise indicated.

The dates shown on debt obligations are the original maturity dates.

The fund had the following sector concentrations greater than 10% at the close of the reporting period (as a percentage of net assets):

| |

| Industrials | 23.2% |

| Financials | 19.0 |

| Consumer discretionary | 17.3 |

FORWARD CURRENCY CONTRACTS at 2/28/13 (aggregate face value $204,974,298) (Unaudited)

| | | | | | |

| | | | | | Unrealized |

| | Contract | Delivery | | Aggregate | appreciation/ |

| Counterparty | Currency | type | date | Value | face value | (depreciation) |

|

| Bank of America N.A. | | | | | | |

|

| | Australian Dollar | Buy | 4/17/13 | $2,117,226 | $2,154,632 | $(37,406) |

|

| | Euro | Buy | 3/20/13 | 3,567,954 | 3,731,352 | (163,398) |

|

| Barclays Bank PLC | | | | | | |

|

| | British Pound | Buy | 3/20/13 | 2,559,037 | 2,659,690 | (100,653) |

|

| | Canadian Dollar | Sell | 4/17/13 | 1,320,234 | 1,362,736 | 42,502 |

|

| | Euro | Buy | 3/20/13 | 8,138,815 | 8,507,956 | (369,141) |

|

| | Hong Kong Dollar | Sell | 5/15/13 | 9,456,187 | 9,459,975 | 3,788 |

|

| | Japanese Yen | Buy | 5/15/13 | 3,724,459 | 3,732,726 | (8,267) |

|

| | Singapore Dollar | Buy | 5/15/13 | 1,596,895 | 1,596,835 | 60 |

|

| | Swedish Krona | Buy | 3/20/13 | 11,793 | 12,073 | (280) |

|

| | Swiss Franc | Buy | 3/20/13 | 1,380,591 | 1,429,597 | (49,006) |

|

| Citibank, N.A. | | | | | | |

|

| | Australian Dollar | Buy | 4/17/13 | 4,123,179 | 4,196,106 | (72,927) |

|

| | British Pound | Buy | 3/20/13 | 506,802 | 526,592 | (19,790) |

|

| | Danish Krone | Sell | 3/20/13 | 9,334,105 | 9,713,373 | 379,268 |

|

| | Euro | Buy | 3/20/13 | 12,560,957 | 13,133,361 | (572,404) |

|

| | Singapore Dollar | Buy | 5/15/13 | 5,752,731 | 5,754,939 | (2,208) |

|

| Credit Suisse International | | | | | | |

|

| | Australian Dollar | Buy | 4/17/13 | 3,367,281 | 3,426,508 | (59,227) |

|

| | British Pound | Buy | 3/20/13 | 5,634,129 | 5,856,142 | (222,013) |

|

| | Canadian Dollar | Sell | 4/17/13 | 698,816 | 722,676 | 23,860 |

|

| | Euro | Buy | 3/20/13 | 8,810,466 | 9,209,733 | (399,267) |

|

| | Japanese Yen | Buy | 5/15/13 | 5,054,927 | 5,067,026 | (12,099) |

|

| | New Zealand Dollar | Buy | 4/17/13 | 1,560,502 | 1,594,823 | (34,321) |

|

| | Norwegian Krone | Sell | 3/20/13 | 5,220,574 | 5,472,802 | 252,228 |

|

| Deutsche Bank AG | | | | | | |

|

| | Australian Dollar | Buy | 4/17/13 | 3,297,342 | 3,355,274 | (57,932) |

|

| Euro | Buy | 3/20/13 | 16,065,975 | 16,728,002 | (662,027) |

|

| HSBC Bank USA, National Association | | | | | |

|

| Australian Dollar | Buy | 4/17/13 | 2,892,262 | 2,943,816 | (51,554) |

|

| Euro | Sell | 3/20/13 | 9,610,860 | 10,045,847 | 434,987 |

|

| Norwegian Krone | Sell | 3/20/13 | 6,397,769 | 6,706,689 | 308,920 |

|

| |

| 24 | International Capital Opportunities Fund |

FORWARD CURRENCY CONTRACTS at 2/28/13 (aggregate face value $204,974,298) (Unaudited) cont.

| | | | | | |

| | | | | | | Unrealized |

| | | Contract | Delivery | | Aggregate | appreciation/ |

| Counterparty | Currency | type | date | Value | face value | (depreciation) |

|

| JPMorgan Chase Bank N.A. | | | | | |

|

| | Australian Dollar | Buy | 4/17/13 | $1,807,537 | $1,839,507 | $(31,970) |

|

| | British Pound | Buy | 3/20/13 | 2,843,307 | 2,953,511 | (110,204) |

|

| | Euro | Buy | 3/20/13 | 33,034 | 34,523 | (1,489) |

|

| | Japanese Yen | Buy | 5/15/13 | 1,579,667 | 1,583,688 | (4,021) |

|

| State Street Bank and Trust Co. | | | | | |

|

| | Australian Dollar | Buy | 4/17/13 | 5,265,119 | 5,358,140 | (93,021) |

|

| | Canadian Dollar | Sell | 4/17/13 | 316,376 | 326,541 | 10,165 |

|

| | Euro | Buy | 3/20/13 | 6,535,416 | 6,831,233 | (295,817) |

|

| | Israeli Shekel | Buy | 4/17/13 | 4,536,957 | 4,553,942 | (16,985) |

|

| | Norwegian Krone | Sell | 3/20/13 | 3,333,954 | 3,495,420 | 161,466 |

|

| | Swedish Krona | Buy | 3/20/13 | 8,767,242 | 8,972,421 | (205,179) |

|

| UBS AG | | | | | | |

|

| | Australian Dollar | Buy | 4/17/13 | 4,262,244 | 4,336,919 | (74,675) |

|

| | British Pound | Buy | 3/20/13 | 2,770,799 | 2,879,487 | (108,688) |

|

| | Canadian Dollar | Sell | 4/17/13 | 2,996,462 | 3,038,668 | 42,206 |

|

| | Euro | Sell | 3/20/13 | 10,118,124 | 10,578,758 | 460,634 |

|

| | Norwegian Krone | Buy | 3/20/13 | 196,272 | 205,802 | (9,530) |

|

| WestPac Banking Corp. | | | | | |

|

| | Australian Dollar | Buy | 4/17/13 | 3,618,127 | 3,681,926 | (63,799) |

|

| | British Pound | Buy | 3/20/13 | 1,543,310 | 1,603,728 | (60,418) |

|

| | Euro | Sell | 3/20/13 | 3,441,562 | 3,598,803 | 157,241 |

|

| Total | | | | | | $(1,692,391) |

| |

| International Capital Opportunities Fund | 25 |

ASC 820 establishes a three-level hierarchy for disclosure of fair value measurements. The valuation hierarchy is based upon the transparency of inputs to the valuation of the fund’s investments. The three levels are defined as follows:

Level 1: Valuations based on quoted prices for identical securities in active markets.

Level 2: Valuations based on quoted prices in markets that are not active or for which all significant inputs are observable, either directly or indirectly.

Level 3: Valuations based on inputs that are unobservable and significant to the fair value measurement.

The following is a summary of the inputs used to value the fund’s net assets as of the close of the reporting period:

| | | |

| | | Valuation inputs | |

|

| Investments in securities: | Level 1 | Level 2 | Level 3 |

|

| Common stocks: | | | |

|

| Australia | $— | $28,932,601 | $— |

|

| Austria | — | 7,372,793 | — |

|

| Canada | 82,794,582 | — | — |

|

| China | — | 10,015,414 | — |

|

| Denmark | — | 18,850,168 | — |

|

| France | — | 33,850,939 | — |

|

| Germany | — | 68,757,514 | — |

|

| Hong Kong | — | 28,723,592 | — |

|

| Ireland | — | 20,291,266 | — |

|

| Italy | — | 19,336,818 | — |

|

| Japan | — | 153,499,183 | — |

|

| Mexico | 5,358,766 | — | — |

|

| Netherlands | — | 15,445,375 | — |

|

| Norway | — | 20,885,211 | — |

|

| Russia | — | 3,117,360 | — |

|

| Singapore | — | 8,290,721 | — |

|

| South Korea | — | 52,095,687 | — |

|

| Spain | — | 3,994,396 | — |

|

| Sweden | — | 18,403,663 | — |

|

| Switzerland | — | 58,752,303 | — |

|

| Taiwan | — | 6,196,109 | — |

|

| Turkmenistan | — | 4,691,648 | — |

|

| United Kingdom | — | 148,385,114 | — |

|

| United States | 9,843,469 | — | — |

|

| Total common stocks | 97,996,817 | 729,887,875 | — |

| | | | |

| Warrants | — | — | 166 |

|

| U.S. treasury obligations | — | 660,891 | — |

|

| Short-term investments | 33,727,027 | 68,852,154 | — |

|

| Totals by level | $131,723,844 | $799,400,920 | $166 |

| | | | | |

| | | Valuation inputs | |

|

| Other financial instruments: | Level 1 | Level 2 | Level 3 |

|

| Forward currency contracts | $— | $(1,692,391) | $— |

|

| Totals by level | $— | $(1,692,391) | $— |

At the start and close of the reporting period, Level 3 investments in securities were not considered a significant portion of the fund’s portfolio.

The accompanying notes are an integral part of these financial statements.

| |

| 26 | International Capital Opportunities Fund |

Statement of assets and liabilities 2/28/13 (Unaudited)

| |

| ASSETS | |

|

| Investment in securities, at value, including $59,913,545 of securities on loan (Note 1): | |

| Unaffiliated issuers (identified cost $690,728,056) | $831,603,537 |

| Affiliated issuers (identified cost $99,521,393) (Notes 1 and 6) | 99,521,393 |

|

| Cash | 687 |

|

| Foreign currency (cost $211,849) (Note 1) | 211,674 |

|

| Dividends, interest and other receivables | 989,360 |

|

| Foreign Tax reclaim | 292,344 |

|

| Receivable for shares of the fund sold | 651,900 |

|

| Receivable for investments sold | 1,407,171 |

|

| Unrealized appreciation on forward currency contracts (Note 1) | 2,277,325 |

|

| Total assets | 936,955,391 |

| |

| LIABILITIES | |

|

| Payable for shares of the fund repurchased | 2,095,961 |

|

| Payable for compensation of Manager (Note 2) | 538,919 |

|

| Payable for custodian fees (Note 2) | 81,602 |

|

| Payable for investor servicing fees (Note 2) | 403,476 |

|

| Payable for Trustee compensation and expenses (Note 2) | 225,275 |

|

| Payable for administrative services (Note 2) | 10,104 |

|

| Payable for distribution fees (Note 2) | 353,754 |

|

| Unrealized depreciation on forward currency contracts (Note 1) | 3,969,716 |

|

| Collateral on securities loaned, at value (Note 1) | 66,554,366 |

|

| Collateral on certain derivative contracts, at value (Note 1) | 1,420,891 |

|

| Other accrued expenses | 176,009 |

|

| Total liabilities | 75,830,073 |

| | |

| Net assets | $861,125,318 |

|

| |

| REPRESENTED BY | |

|

| Paid-in capital (Unlimited shares authorized) (Notes 1 and 4) | $912,129,611 |

|

| Undistributed net investment income (Note 1) | 618,732 |

|

| Accumulated net realized loss on investments and foreign currency transactions (Note 1) | (190,783,641) |

|

| Net unrealized appreciation of investments and assets and liabilities in foreign currencies | 139,160,616 |

|

| Total — Representing net assets applicable to capital shares outstanding | $861,125,318 |

(Continued on next page)

| |

| International Capital Opportunities Fund | 27 |

Statement of assets and liabilities (Continued)

| |

| COMPUTATION OF NET ASSET VALUE AND OFFERING PRICE | |

|

| Net asset value and redemption price per class A share | |

| ($603,468,651 divided by 17,603,157 shares) | $34.28 |

|

| Offering price per class A share (100/94.25 of $34.28)* | $36.37 |

|

| Net asset value and offering price per class B share ($20,392,181 divided by 596,979 shares)** | $34.16 |

|

| Net asset value and offering price per class C share ($40,314,432 divided by 1,181,440 shares)** | $34.12 |

|

| Net asset value and redemption price per class M share ($7,925,361 divided by 232,099 shares) | $34.15 |

|

| Offering price per class M share (100/96.50 of $34.15)* | $35.39 |

|

| Net asset value, offering price and redemption price per class R share | |

| ($67,467,546 divided by 1,997,362 shares) | $33.78 |

|

| Net asset value, offering price and redemption price per class Y share | |

| ($121,557,147 divided by 3,546,213 shares) | $34.28 |

|

* On single retail sales of less than $50,000. On sales of $50,000 or more the offering price is reduced.

** Redemption price per share is equal to net asset value less any applicable contingent deferred sales charge.

The accompanying notes are an integral part of these financial statements.

| |

| 28 | International Capital Opportunities Fund |

Statement of operations Six months ended 2/28/13 (Unaudited)

| |

| INVESTMENT INCOME | |

|

| Dividends (net of foreign tax of $612,816) | $6,371,943 |

|

| Interest (including interest income of $15,416 from investments in affiliated issuers) (Note 6) | 15,701 |

|

| Securities lending (Note 1) | 197,919 |

|

| Total investment income | 6,585,563 |

| |

| EXPENSES | |

|

| Compensation of Manager (Note 2) | 3,539,632 |

|

| Investor servicing fees (Note 2) | 1,211,386 |

|

| Custodian fees (Note 2) | 81,388 |

|

| Trustee compensation and expenses (Note 2) | 42,951 |

|

| Distribution fees (Note 2) | 1,266,221 |

|

| Administrative services (Note 2) | 14,475 |

|

| Other | 167,900 |

|

| Total expenses | 6,323,953 |

| | |

| Expense reduction (Note 2) | (741) |

|

| Net expenses | 6,323,212 |

| | |

| Net investment income | 262,351 |

|

| |

| Net realized gain on investments (Notes 1 and 3) | 52,099,093 |

|

| Net realized loss on foreign currency transactions (Note 1) | (1,096,057) |

|

| Net unrealized depreciation of assets and liabilities in foreign currencies during the period | (1,100,207) |

|

| Net unrealized appreciation of investments during the period | 64,967,192 |

|

| Net gain on investments | 114,870,021 |

| | |

| Net increase in net assets resulting from operations | $115,132,372 |

|

The accompanying notes are an integral part of these financial statements.

| |

| International Capital Opportunities Fund | 29 |

Statement of changes in net assets

| | |

| INCREASE (DECREASE) IN NET ASSETS | Six months ended 2/28/13* | Year ended 8/31/12 |

|

| Operations: | | |

| Net investment income | $262,351 | $13,889,231 |

|

| Net realized gain (loss) on investments | | |

| and foreign currency transactions | 51,003,036 | (30,508,623) |

|

| Net unrealized appreciation (depreciation) of investments | | |

| and assets and liabilities in foreign currencies | 63,866,985 | (28,199,676) |

|

| Net increase (decrease) in net assets resulting | | |

| from operations | 115,132,372 | (44,819,068) |

|

| Distributions to shareholders (Note 1): | | |

| From ordinary income | | |

| Net investment income | | |

|

| Class A | (6,926,613) | (19,036,576) |

|

| Class B | (69,775) | (475,307) |

|

| Class C | (154,638) | (917,269) |

|

| Class M | (53,011) | (184,024) |

|

| Class R | (583,768) | (3,324,589) |

|

| Class Y | (1,687,227) | (3,309,906) |

|

| Increase in capital from settlement payments | — | 238,808 |

|

| Redemption fees (Note 1) | 7,214 | 43,529 |

|

| Decrease from capital share transactions (Note 4) | (92,040,763) | (152,697,470) |

|

| Total increase (decrease) in net assets | 13,623,791 | (224,481,872) |

| |

| NET ASSETS | | |

|

| Beginning of period | 847,501,527 | 1,071,983,399 |

|

| End of period (including undistributed net investment | | |

| income of $618,732 and $9,831,413, respectively) | $861,125,318 | $847,501,527 |

|

* Unaudited

The accompanying notes are an integral part of these financial statements.

| |

| 30 | International Capital Opportunities Fund |

|

| This page left blank intentionally. |

| |

| International Capital Opportunities Fund | 31 |

Financial highlights (For a common share outstanding throughout the period)

| | | | | | | | | | | | | | | |

| INVESTMENT OPERATIONS: | | LESS DISTRIBUTIONS: | | RATIOS AND SUPPLEMENTAL DATA: |

|

| | | | | | | | | | | | | | | Ratio | |

| | Net asset | | Net realized | | | | | | | | | | Ratio | of net investment | |

| | value, | | and unrealized | Total from | From | From | | | | | Total return | Net assets, | of expenses | income (loss) | |

| | beginning | Net investment | gain (loss) | investment | net investment | net realized gain | Total | Redemption | Non-recurring | Net asset value, | at net asset | end of period | to average | to average | Portfolio |

| Period ended | of period | income (loss) a | on investments | operations | income | on investments | distributions | fees b | reimbursements | end of period | value (%) c | (in thousands) | net assets (%) d | net assets (%) | turnover (%) |

|

| Class A | | | | | | | | | | | | | | | |

| February 28, 2013** | $30.33 | .02 | 4.32 | 4.34 | (.39) | — | (.39) | — | — | $34.28 | 14.36* | $603,469 | .71* | .05* | 24* |

| August 31, 2012 | 32.47 | .47 | (1.75) | (1.28) | (.87) | — | (.87) | — | .01 e | 30.33 | (3.57) | 578,024 | 1.41 | 1.58 | 34 |

| August 31, 2011 | 28.17 | .33 | 4.14 | 4.47 | (.30) | — | (.30) | — | .13 f,g | 32.47 | 16.26 | 754,251 | 1.47 | .95 | 23 |

| August 31, 2010 | 28.69 | .20 | (.61) | (.41) | (.12) | — | (.12) | — | .01 h | 28.17 | (1.43) | 793,406 | 1.64 i | .66 | 27 |

| August 31, 2009 | 32.09 | .39 | (3.35) | (2.96) | (.47) | — | (.47) | — | .03 j,k | 28.69 | (8.33) | 874,265 | 1.64 i,l | 1.78 l | 84 |

| August 31, 2008 | 41.54 | .63 | (8.27) | (7.64) | (1.50) | (.31) | (1.81) | — | — | 32.09 | (19.01) | 1,259,641 | 1.47 l | 1.68 l | 41 |

|

| Class B | | | | | | | | | | | | | | | |

| February 28, 2013** | $30.09 | (.10) | 4.28 | 4.18 | (.11) | — | (.11) | — | — | $34.16 | 13.92* | $20,392 | 1.08* | (.32)* | 24* |

| August 31, 2012 | 32.08 | .24 | (1.68) | (1.44) | (.56) | — | (.56) | — | .01 e | 30.09 | (4.27) | 20,546 | 2.16 | .81 | 34 |

| August 31, 2011 | 27.80 | .05 | 4.10 | 4.15 | — | — | — | — | .13 f,g | 32.08 | 15.40 | 30,517 | 2.22 | .15 | 23 |

| August 31, 2010 | 28.42 | (.06) | (.57) | (.63) | — | — | — | — | .01 h | 27.80 | (2.18) | 41,441 | 2.39 i | (.19) | 27 |

| August 31, 2009 | 31.30 | .22 | (3.10) | (2.88) | (.03) | — | (.03) | — | .03 j,k | 28.42 | (9.04) | 72,873 | 2.39 i,l | 1.04 l | 84 |

| August 31, 2008 | 40.45 | .27 | (7.99) | (7.72) | (1.12) | (.31) | (1.43) | — | — | 31.30 | (19.61) | 166,262 | 2.22 l | .74 l | 41 |

|

| Class C | | | | | | | | | | | | | | | |

| February 28, 2013** | $30.07 | (.10) | 4.28 | 4.18 | (.13) | — | (.13) | — | — | $34.12 | 13.92* | $40,314 | 1.08* | (.32)* | 24* |

| August 31, 2012 | 32.11 | .24 | (1.70) | (1.46) | (.59) | — | (.59) | — | .01 e | 30.07 | (4.30) | 38,301 | 2.16 | .81 | 34 |

| August 31, 2011 | 27.87 | .07 | 4.09 | 4.16 | (.05) | — | (.05) | — | .13 f,g | 32.11 | 15.38 | 53,823 | 2.22 | .20 | 23 |

| August 31, 2010 | 28.48 | (.03) | (.59) | (.62) | — | — | — | — | .01 h | 27.87 | (2.14) | 55,847 | 2.39 i | (.10) | 27 |

| August 31, 2009 | 31.61 | .22 | (3.20) | (2.98) | (.18) | — | (.18) | — | .03 j,k | 28.48 | (9.02) | 62,683 | 2.39 i,l | 1.02 l | 84 |

| August 31, 2008 | 40.96 | .33 | (8.14) | (7.81) | (1.23) | (.31) | (1.54) | — | — | 31.61 | (19.63) | 99,261 | 2.22 l | .89 l | 41 |

|

| Class M | | | | | | | | | | | | | | | |

| February 28, 2013** | $30.14 | (.06) | 4.30 | 4.24 | (.23) | — | (.23) | — | — | $34.15 | 14.09* | $7,925 | .96* | (.20)* | 24* |

| August 31, 2012 | 32.22 | .32 | (1.72) | (1.40) | (.69) | — | (.69) | — | .01 e | 30.14 | (4.06) | 7,397 | 1.91 | 1.09 | 34 |

| August 31, 2011 | 27.95 | .16 | 4.11 | 4.27 | (.13) | — | (.13) | — | .13 f,g | 32.22 | 15.71 | 9,013 | 1.97 | .46 | 23 |

| August 31, 2010 | 28.50 | .04 | (.60) | (.56) | — | — | — | — | .01 h | 27.95 | (1.93) | 9,345 | 2.14 i | .15 | 27 |

| August 31, 2009 | 31.66 | .28 | (3.23) | (2.95) | (.24) | — | (.24) | — | .03 j,k | 28.50 | (8.79) | 10,957 | 2.14 i,l | 1.28 l | 84 |

| August 31, 2008 | 40.97 | .40 | (8.12) | (7.72) | (1.28) | (.31) | (1.59) | — | — | 31.66 | (19.40) | 17,334 | 1.97 l | 1.08 l | 41 |

|

| Class R | | | | | | | | | | | | | | | |

| February 28, 2013** | $29.81 | (.01) | 4.23 | 4.22 | (.25) | — | (.25) | — | — | $33.78 | 14.21* | $67,468 | .83* | (.02)* | 24* |

| August 31, 2012 | 31.95 | .38 | (1.70) | (1.32) | (.83) | — | (.83) | — | .01 e | 29.81 | (3.78) | 98,121 | 1.66 | 1.30 | 34 |

| August 31, 2011 | 27.73 | .26 | 4.06 | 4.32 | (.23) | — | (.23) | — | .13 f,g | 31.95 | 15.99 | 107,047 | 1.72 | .76 | 23 |

| August 31, 2010 | 28.29 | .15 | (.63) | (.48) | (.09) | — | (.09) | — | .01 h | 27.73 | (1.67) | 85,829 | 1.89 i | .51 | 27 |

| August 31, 2009 | 31.72 | .31 | (3.31) | (3.00) | (.46) | — | (.46) | — | .03 j,k | 28.29 | (8.55) | 58,878 | 1.89 i,l | 1.42 l | 84 |

| August 31, 2008 | 41.17 | .58 | (8.23) | (7.65) | (1.49) | (.31) | (1.80) | — | — | 31.72 | (19.21) | 23,843 | 1.72 l | 1.59 l | 41 |

|

| Class Y | | | | | | | | | | | | | | | |

| February 28, 2013** | $30.37 | .05 | 4.33 | 4.38 | (.47) | — | (.47) | — | — | $34.28 | 14.50* | $121,557 | .59* | .16* | 24* |

| August 31, 2012 | 32.54 | .55 | (1.76) | (1.21) | (.97) | — | (.97) | — | .01 e | 30.37 | (3.33) | 105,113 | 1.16 | 1.84 | 34 |

| August 31, 2011 | 28.22 | .44 | 4.13 | 4.57 | (.38) | — | (.38) | — | .13 f,g | 32.54 | 16.58 | 117,332 | 1.22 | 1.27 | 23 |

| August 31, 2010 | 28.73 | .29 | (.63) | (.34) | (.18) | — | (.18) | — | .01 h | 28.22 | (1.19) | 117,828 | 1.39 i | .97 | 27 |

| August 31, 2009 | 32.21 | .43 | (3.38) | (2.95) | (.56) | — | (.56) | — | .03 j,k | 28.73 | (8.11) | 105,588 | 1.39 i,l | 2.00 l | 84 |

| August 31, 2008 | 41.69 | .72 | (8.30) | (7.58) | (1.59) | (.31) | (1.90) | — | — | 32.21 | (18.82) | 117,703 | 1.22 l | 1.93 l | 41 |

|

See notes to financial highlights at the end of this section.

The accompanying notes are an integral part of these financial statements.

| | | |

| 32 | International Capital Opportunities Fund | International Capital Opportunities Fund | 33 |

Financial highlights (Continued)

* Not annualized.

** Unaudited.

a Per share net investment income (loss) has been determined on the basis of the weighted average number of shares outstanding during the period.

b Amount represents less than $0.01 per share.

c Total return assumes dividend reinvestment and does not reflect the effect of sales charges.