UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-08846

First Focus Funds, Inc.

(Exact name of registrant as specified in charter)

First National Bank

1620 Dodge Street

Omaha, Nebraska 68197

(Address of principal executive offices)

Daniel W. Koors

Jackson Fund Services

225 West Wacker Drive, Suite 1200

Chicago, Illinois 60606

(Name and address of agent for service)

Registrant's telephone number, including area code: (800) 662-4203

Date of Fiscal Year End: March 31

Date of Reporting Period: March 31, 2010

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. §3507.

Item 1. Report to Shareholders.

Annual Report

| Short-Intermediate Bond Fund |

| Income Fund |

| Balanced Fund |

| Core Equity Fund |

| Large Cap Growth Fund |

| Growth Opportunities Fund |

| Small Company Fund |

| International Equity Fund |

Value. Stability. Service.

Notice to Investors

Shares of First Focus Funds:

• Are Not FDIC Insured • May Lose Value • Have No Bank Guarantee

Investors should carefully consider the investment objectives, risks, charges and expenses of the First Focus Funds. Mutual funds involve risk including loss of principal. This and other important information about the Funds is contained in the prospectus, which can be obtained by calling 1-800-662-4203. The prospectus should be read carefully before investing. The First Focus Funds are distributed by Northern Lights Distributors, LLC member FINRA/SIPC.

Table of Contents

| Shareholder Letter | 1 |

| Management Discussion and Analysis | 2 |

| Schedules of Portfolio Investments | 18 |

| Statements of Assets & Liabilities | 34 |

| Statements of Operations | 36 |

| Statements of Changes in Net Assets | 38 |

| Financial Highlights | 42 |

| Notes to Financial Statements | 44 |

| Report of Independent Registered Public Accounting Firm | 54 |

| Additional Fund Information | 55 |

| Review and Approval of the Funds’ Advisory and Sub-Advisory Agreements | 58 |

| Directors and Officers | 65 |

Dear Shareholder,

The last 10 years have been one of the most challenging decades of modern times for the investing class. No need to rehash all of the reasons why, we are all painfully aware. However, it is appropriate, now more than ever, to understand where you have your money invested and with whom. Sadly, many investors have been devastated by “trusting” their advisers, only to wake up one morning to learn on the news that this person or entity has not been a great steward of their assets as they once thought.

Your First Focus Funds are affiliated with the largest privately owned bank holding company in North America, First National Nebraska, Inc (“FNNI”). FNNI’s independent roots can be traced back to 1855. The fifth and sixth generations of the founding family continue to be involved in the day-to-day operations of the company. This type of long-term focus not only permeates the philosophy of the holding company, but also that of your First Focus Funds. Our research attempts to differentiate between the volatility associated with following momentum and “hot” trends and the discipline it takes to do a tremendous amount of research before committing our Fund holders’ resources, and then having the courage and patience it takes to stick with this discipline in good times an d bad. We are particularly focused on principal preservation and seek to outperform when things get especially difficult.

Starting in 2000, the First Focus Funds Board of Directors set out a 10 year plan to have competitive offerings in all of it’s the First Focus Funds’ strategies. This involved the replacement of some fund managers, the shedding of certain non-competitive offerings and the addition of certain key asset classes to the complex, for which the Funds have hired independent third party managers. We worked diligently to create a well rounded product offering to meet the needs of our First Focus Fund shareholders.

I’m pleased to report that as of April 1, 2010, of our Funds rated by Morningstar, 42% have an overall rating of 3 stars, 42% are rated 4 star and 14% have achieved the coveted 5 star rating. Of the funds with 10 year ratings, 40% are rated 4 stars and 60% 5 stars!

For the fiscal year ended March 31st, we have also had strong growth in assets. We have seen growth from both the addition of new channels and strong growth in our existing channels. A number of channels that we previously were unable to gain access to, have invited us to be a part of their platforms – largely due to customer requests, growth in our complex size and our performance. By increasing the ways customers can purchase the First Focus Funds we are making investing in our funds more convenient for you!

We are currently in the process of re-calibrating our course for the next 10 years and like what we see. We feel we have built a fundamentally strong fund complex, one with strong overall performance based on solid long-term thinking. In the coming months, we will be working on a strategic plan that, if executed correctly, should allow us to achieve the type of scope and scale critical to our long-term growth. As much as the last 10 years has been about strengthening the offerings and broadening the scope of those offerings, we hope the next 10 years will be about distribution. We hope to have exciting news before we close out 2010, including success in opening new distribution channels for your Funds.

Stephen Frantz

Chief Investment Officer

sfrantz@fnni.com

Comments are provided as a general market overview and should not be considered investment advice or predictive of any future market performance.

Morningstar calculates a Morningstar RatingTM based on a Morningstar Risk-Adjusted Return measure that accounts for variation in a fund’s monthly performance (including the effects of sales charges, loads and redemption fees), placing more emphasis on downward variations and rewarding consistent performance. The top 10% of the funds in each category receive 5 stars, the next 22.5% receive 4 stars, the next 35% receive 3 stars, the next 22.5% receive 2 stars and the bottom 10% receive 1 star.

Investors should carefully consider the investment objectives, risks, charges and expenses of the First Focus Funds. Mutual funds involve risk including possible risk of principal. The First Focus Funds are distributed by Northern Lights Distributors, LLC member FINRA.

0748-NLD-5/26/2010

1

FIRST FOCUS SHORT-INTERMEDIATE BOND FUND

Investment Objective

The First Focus Short-Intermediate Bond Fund seeks to maximize total returns in a manner consistent with generation of current income, preservation of capital and reduce price volatility.

Manager Commentary

A little over a year ago, the financial markets were in disarray and the real economy was in the midst of a terrible recession; the future of our financial system and dynamic economy was very much in doubt. The government attempted various measures to prop up the markets and instill confidence in the system, but with limited success.

As often happens during crises, however, the “animal spirits” of the financial markets became abruptly more positive by the end of March 2009. Perhaps driven by the mandated “stress test” applied to the largest financial institutions, or growing confidence that the U.S. Federal Reserve’s (the “Fed”) myriad actions would finally halt the decline in risky assets, investors slowly began to remove the “systemic collapse” premium that had been priced into almost all financial markets. Over the ensuing months we witnessed a dramatic and swift rally in stock and bond markets (with the lone exception of U.S. Treasuries). The volatility of the past two years is truly amazing; high-yield corporate bonds returned -22% for the year ended March 2009, but followed that with a 62% annual return through March 2010. All non-U.S. Treasury sectors of the bond market posted positive results for the past twelve months, although not as dramatic. Investment-grade corporate bonds returned 25%, agency-guaranteed mortgage-backed securities (“MBS”), 5%, and commercial mortgage-backed securities (“CMBS”), 43%. As noted previously, the only disappointing sector in the bond market was U.S. Treasuries, which returned -1.2% for the year ended March 2010.

On the heels of rapidly improving financial markets, the real economy began to slowly pull out of its downward trajectory. Monthly job losses moderated as the year progressed, and industrial activity picked up sharply as companies began to re-stock depleted inventories. Gross Domestic Product (“GDP”) growth bottomed in Q109, posting a -6.4% annualized drop, but recovered steadily, culminating with an annualized 5.6% increase in the fourth quarter. Despite this macro improvement, the large amount of slack in the labor and physical capital markets (capacity utilization fell to decade lows in Q209) kept the Fed on the sidelines. The Fed maintained its effective zero target on the Fed Funds rate and continued to clearly communicate its intent to maintain this level for the foreseeable future.

Over the past year, the First Focus Short-Intermediate Fund returned 7.18% on a net basis. This compares to a 5.31% return for the Barclays Capital U.S. Government/Credit 1-5 Year Index.

The primary driver of the outperformance was the significant return generated by the non-U.S. Treasury sectors of the Fund. We began the fiscal year with an overweight position in the agency MBS, CMBS and private-label MBS sectors, and notably increased our allocation to corporate bonds during the year. The Fund’s larger allocation to “spread sectors” provided two benefits relative to the index—an increase in principal value as yield spreads fell rapidly, and a substantial coupon (yield) advantage. The Fund also benefited from our shorter duration exposure versus the index, as risk-free yields rose throughout the year.

As of March 31, 2010, the portfolio’s composition was 21% U.S. Treasury securities, 6% U.S. Government agency MBS, 40% corporate bonds, 10% agencies, 18% mortgage related, 1% municipals, and 4% cash equivalents. The overall weighted average maturity of the portfolio was 2.51 years.1

The striking improvement in risk appetite over the past year has driven down yield spreads to levels more in-line with historical norms; indeed some pockets of the corporate bond market carry yields that we believe don’t adequately compensate investors for assumed risk. That said, we expect that corporate and asset-backed securities as a group will continue to outperform risk-free sectors of the market as the Fed remains accommodative and the economy slowly improves. Our long-term focus and rigorous credit and structural analysis should serve our investors well through this more difficult environment in the fixed income market.

1 Disclosures

Portfolio composition is as of March 31, 2010 and is subject to change.

2

FIRST FOCUS SHORT-INTERMEDIATE BOND FUND

Return of a $10,000 Investment as of March 31, 2010

Portfolio Composition as of March 31, 2010

% Based on Total Value of Investments

(Portfolio composition is subject to change)

Portfolio Analysis as of March 31, 2010

(Portfolio composition is subject to change)

Weighted Average Maturity: 2.51 years

| Average Annual Total Return for the Year Ended March 31, 2010* | |||

| 1 Year | 5 Year | 10 Year | |

| First Focus Short- | |||

| Intermediate Bond Fund | 7.18% | 4.24% | 4.66% |

| Barclays Capital U.S. | |||

| Government/Credit | |||

| 1-5 Year Index | 5.31% | 4.90% | 5.35% |

| Prospectus Expense Ratio (Gross/Net)† | 1.20%/0.91% | ||

| Expense Ratio for the Year Ended | |||

| March 31, 2010 (Gross/Net) | 1.17%/0.86% | ||

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. Total return figures include change in share price, reinvestment of dividends and capital gains. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit our website at www.firstfocusfunds.com.

(†)The above expense ratios are from the Fund’s prospectus dated August 1, 2009. Net expense ratio is net of contractual waivers which are in effect from August 1, 2009 through July 31, 2010.

(*) Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower.

The line chart assumes an initial investment of $10,000 made on March 31, 2000. Total return is based on net change in net asset value (“NAV”) assuming reinvestment of distributions. Returns shown include the reinvestment of all dividends and other distributions.

The Barclays Capital U.S. Government/Credit 1-5 Year Index measures the performance of U.S. Treasury and agency securities, and corporate bonds with 1-5 year maturities.

The above referenced index is unmanaged and does not reflect the deduction of fees or taxes associated with a mutual fund, such as investment management and fund accounting fees. Investors cannot invest directly in an index.

3

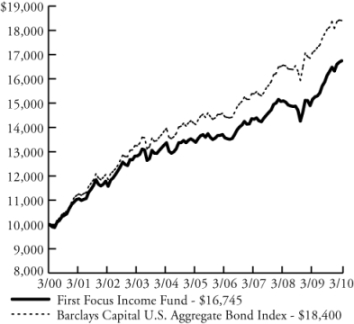

FIRST FOCUS INCOME FUND

Investment Objective

The First Focus Income Fund seeks to maximize total returns in a manner consistent with generation of current income and the preservation of capital.

Manager Commentary

A little over a year ago, the financial markets were in disarray and the real economy was in the midst of a terrible recession; the future of our financial system and dynamic economy was very much in doubt. The government attempted various measures to prop up the markets and instill confidence in the system, but with limited success.

As often happens during crises, however, the “animal spirits” of the financial markets became abruptly more positive by the end of March 2009. Perhaps driven by the mandated “stress test” applied to the largest financial institutions, or growing confidence that the U.S. Federal Reserve’s (the “Fed”) myriad actions would finally halt the decline in risky assets, investors slowly began to remove the “systemic collapse” premium that had been priced into almost all financial markets. Over the ensuing months we witnessed a dramatic and swift rally in stock and bond markets (with the lone exception of U.S. Treasuries). The volatility of the past two years is truly amazing; high-yield corporate bonds returned -22% for the year ended March 2009, but followed that with a 62% annual return through March 2010. All non-U.S. Treasury sectors of the bond market posted positive results for the past twelve months, although not as dramatic. Investment-grade corporate bonds returned 25%, agency-guaranteed mortgage-backed securities (“MBS”), 5%, and commercial mortgage-backed securities (“CMBS”), 43%. As noted previously, the only disappointing sector in the bond market was U.S. Treasuries, which returned -1.2% for the year ended March 2010.

On the heels of rapidly improving financial markets, the real economy began to slowly pull out of its downward trajectory. Monthly job losses moderated as the year progressed, and industrial activity picked up sharply as companies began to re-stock depleted inventories. Gross Domestic Product (“GDP”) growth bottomed in Q109, posting a -6.4% annualized drop, but recovered steadily, culminating with an annualized 5.6% increase in the fourth quarter. Despite this macro improvement, the large amount of slack in the labor and physical capital markets (capacity utilization fell to decade lows in Q209) kept the Fed on the sidelines. The Fed maintained its effective zero target on the Fed Funds rate and continued to clearly communicate its intent to maintain this level for the foreseeable future.

Over the past year, the First Focus Income Fund returned 10.49% on a net basis. This compares to a 7.69% return for the Barclays Capital U.S. Aggregate Bond Index.

The primary driver of the outperformance was the significant return generated by the non-Treasury sectors of the Fund. We began the fiscal year with an overweight position in the CMBS and private-label MBS sectors, and notably increased our allocation to corporate bonds during the year. The Fund’s larger allocation to “spread sectors” provided two benefits relative to the index—an increase in principal value as yield spreads fell rapidly, and a substantial coupon (yield) advantage. We maintained an underweight to agency MBS given the distortion caused by the Fed’s purchase program, which modestly detracted from performance as spreads in that sector continued to compress.

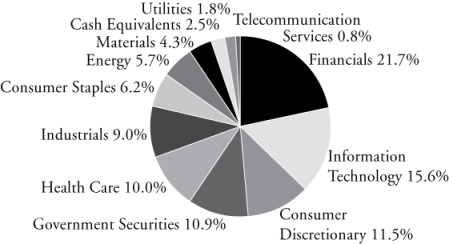

As of March 31, 2010, the portfolio’s composition was 13% U.S. Treasury securities, 25% U.S. government agency mortgage-backed securities, 29% corporate bonds, 2% agencies, 26% mortgage related, 2% municipals, and 3% cash equivalents. The overall weighted average maturity of the portfolio was 6.70 years.1

The striking improvement in risk appetite over the past year has driven down yield spreads to levels more in-line with historical norms; indeed some pockets of the corporate bond market carry yields that we believe don’t adequately compensate investors for assumed risk. That said, we expect that corporate and asset-backed securities as a group will continue to outperform risk-free sectors of the market as the Fed remains accommodative and the economy slowly improves. Our long-term focus and rigorous credit and structural analysis should serve our investors well through this more difficult environment in the fixed income market.

1 Disclosures

Portfolio composition is as of March 31, 2010 and is subject to change.

4

FIRST FOCUS INCOME FUND

Return of a $10,000 Investment as of March 31, 2010

Portfolio Composition as of March 31, 2010

% Based on Total Value of Investments

(Portfolio composition is subject to change)

Portfolio Analysis as of March 31, 2010

(Portfolio composition is subject to change)

Weighted Average Maturity: 6.70 years

| Average Annual Total Return for the Year Ended March 31, 2010* | ||||

| 1 Year | 5 Year | 10 Year | ||

| First Focus Income Fund | 10.49% | 4.58% | 5.29% | |

| Barclays Capital U.S. | ||||

| Aggregate Bond Index | 7.69% | 5.44% | 6.29% | |

| Prospectus Expense Ratio (Gross/Net)† | 1.33%/0.86% | |||

| Expense Ratio for the Year Ended | ||||

| March 31, 2010 (Gross/Net) | 1.27%/0.77% | |||

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. Total return figures include change in share price, reinvestment of dividends and capital gains. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit our website at www.firstfocusfunds.com.

(†)The above expense ratios are from the Fund’s prospectus dated August 1, 2009. Net expense ratio is net of contractual waivers which are in effect from August 1, 2009 through July 31, 2010.

(*) For periods prior to March 9, 2001, when the Fund began operating, the performance quoted reflects performance of the Adviser’s similarly managed collective investment fund, adjusted to reflect the Fund’s fees and expenses. The collective investment fund was not a registered mutual fund and therefore was not subject to certain investment and tax restrictions, which may have adversely affected performance. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower.

The line chart assumes an initial investment of $10,000 made on March 31, 2000. Total return is based on net change in net asset value (“NAV”) assuming reinvestment of distributions. Returns shown include the reinvestment of all dividends and other distributions.

The Barclays Capital U.S. Aggregate Bond Index is a market value-weighted index which covers the USD-denominated, investment-grade, fixed-rate, taxable bond market of SEC-registered securities. The index includes bonds from the Treasury, Government-Related, Corporate, MSB (agency fixed-rate and hybrid ARM passthroughs), ABS, and CMBS sectors.

The above referenced index is unmanaged and does not reflect the deduction of fees or taxes associated with a mutual fund, such as investment management and fund accounting fees. Investors cannot invest directly in an index.

5

FIRST FOCUS BALANCED FUND

Investment Objective

The First Focus Balanced Fund seeks capital appreciation and current income.

Manager Commentary

A year ago on these pages, as the economy tumbled and the markets collapsed, the case was made that the worst was past and a recovery would come before the end of the year. At the time it was difficult to know how the financial collapse was going to be contained and resolved, but as the year progressed, confidence began to return, and the financial markets began to recuperate. By the end of the year it was becoming clear that the economy was also on the path to recovery, providing the fundamental underpinnings to a sustained market advance.

Asset allocation is the largest factor determining if the First Focus Balanced Fund will perform better or worse than its peer group. An emphasis on stocks and corporate bonds allowed the Fund to consistently outperform the Lipper® Balanced Fund Index through the past year, finishing with a total return of 45.17% versus 31.57% for the Lipper Balanced Fund Index. With regard to the Fund’s benchmark, the segment of the Fund allocated to stocks performed better than the S&P 500 Index’s return of 49.77%, while the segment of the Fund allocated to fixed income performed better than the Barclays Capital U.S. Government/Credit Index’s return of 7.51%. Consistency has been a hallmark of your First Focus Balanced Fund, earning t he Fund a Five Star rating overall and Five Stars for last ten years from Morningstar®.1

As noted above the emphasis on stocks over bonds was the single largest contributor to excess returns this year. Also generating a positive contribution to relative returns was an emphasis on corporate and Build America bonds in the fixed income segment of the Fund. In the equity segment of the Fund an emphasis on economically sensitive areas like manufacturing, industrial and material stocks all contributed to performance. A significant underweighting in financial stocks, particularly banks, which performed strongly during the year, was the most significant drag on returns.1

With each passing month the economy moves further down the path toward self-sustaining economic expansion. While the economy and financial markets still face many vulnerabilities, the year ahead is looking better.

1 Disclosures

Portfolio composition is as of March 31, 2010 and is subject to change.

Lipper® Balanced Fund Index is an unmanaged index of thirty selected balanced funds.

Morningstar Inc. All Rights Reserved. The information, data, analysis and opinions contained herein (1) include the confidential and proprietary information of Morningstar, (2) may not be copied or redistributed, (3) do not constitute investment advice offered by Morningstar, (4) are provided solely for the informational purposes and therefore are not an offer to buy or sell a security, and (5) are not warranted to be correct, complete or accurate. Except as otherwise required by law, Morningstar shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, this information, data, analysis or opinions or their use. For each fund with at least a three-year history, Morningstar calculates a Morningstar RatingTM based on a Mornin gstar Risk-Adjusted Return measure that accounts for variation in a fund’s monthly performance (including the effects of sales charges, loads and redemption fees), placing more emphasis on downward variations and rewarding consistent performance. The top 10% of the funds in each category receive 5 stars, the next 22.5% receive 4 stars, the next 35% receive 3 stars, the next 22.5% receive 2 stars and the bottom 10% receive 1 star. (Each share class is counted as a fraction of one fund within the scale and rated separately, which may cause slight variations in the distribution percentages).

6

FIRST FOCUS BALANCED FUND

Return of a $10,000 Investment as of March 31, 2010

Portfolio Composition as of March 31, 2010

% Based on Total Value of Investments

(Portfolio composition is subject to change)

| Average Annual Total Return for the Year Ended March 31, 2010* | ||||

| 1 Year | 5 Year | 10 Year | ||

| First Focus Balanced Fund | 45.17% | 4.96% | 6.30% | |

| Barclays Capital U.S. | ||||

| Government/Credit Index | 7.51% | 5.17% | 6.22% | |

| S&P 500 Index | 49.77% | 1.92% | -0.65% | |

| Composite Index | 31.57% | 3.54% | 2.40% | |

| Prospectus Expense Ratio (Gross/Net)† | 1.55%/1.40% | |||

| Expense Ratio for the Year Ended | ||||

| March 31, 2010 (Gross/Net) | 1.53%/1.37% | |||

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. Total return figures include change in share price, reinvestment of dividends and capital gains. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit our website at www.firstfocusfunds.com.

(†)The above expense ratios are from the Fund’s prospectus dated August 1, 2009. Net expense ratio is net of contractual waivers which are in effect from August 1, 2009 through July 31, 2010.

(*) Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower.

The line chart assumes an initial investment of $10,000 made on March 31, 2000. Total return is based on net change in net asset value (“NAV”) assuming reinvestment of distributions. Returns shown include the reinvestment of all dividends and other distributions.

The Barclays Capital U.S. Government/Credit Index is the non-securitized component of the U.S. Aggregate Index and includes Treasuries (i.e, public obligations of the U.S. Treasury that have remaining maturities of more than one year), Government-Related issues (i.e, agency, sovereign, supranational, and local authority debt), and USD Corporates.

The S&P 500 Index is an index of 500 selected common stocks most of which are listed on the New York Stock Exchange. The index is heavily weighted toward stocks with large market capitalizations and represents approximately two-thirds of the total market value of all domestic common stocks.

The Composite Index is a combined index of 60% of the S&P 500 Index and 40% of the Barclays Capital U.S. Government/Credit Index. The Composite Index is intended to provide a single benchmark that more accurately reflects the composition of securities held by the Balanced Fund. The individual performance of each index that comprises the Composite Index is detailed in the chart above.

The above referenced indices are unmanaged and do not reflect the deduction of fees or taxes associated with a mutual fund, such as investment management and fund accounting fees. Investors cannot invest directly in an index.

7

FIRST FOCUS CORE EQUITY FUND

Investment Objective

The First Focus Core Equity Fund seeks long-term capital appreciation.

Manager Commentary

For the year ended March 31, 2010, the First Focus Core Equity Fund had a total return of 44.10% compared to a total return of 49.77% for the S&P 500 Index and 53.56% for the Russell 1000® Value Index. We were pleased with the strong absolute return for the Fund during this period, after the challenging market in 2008. However, we were not satisfied with the Fund’s relative performance, which was adversely affected by modest cash holdings and your portfolio managers’ preference for more defensive, high-quality companies. As it turned out, many of the same portfolio strategies that enabled the Fund to significantly outperform during the bear market in 2008, caused it to lag relative to indexes during the past year.

After a tortuous decline during 2008 and the first two months of 2009, the U.S. equity markets rallied from the low on March 9, 2009 and sustained strong positive returns in each of the next four quarters. Investor sentiment shifted 180 degrees from extreme uncertainty at the end of 2008 when many feared that numerous large financial institutions were on the verge of collapse, to euphoria that the crisis had passed. Swift action by the U.S. Federal Reserve (the “Fed”) and the Bush and Obama administrations (along with similar actions taken by other countries) stabilized the credit environment and enabled the economy to begin recovering during the second half on 2009.

However, the recovery has not been evenly distributed. The developing countries such as China, India and Brazil have experienced strong economic growth, while the U.S., Europe, and Japan realized relatively modest growth compared to past economic recoveries.

The strongest S&P 500 Index sectors during the 12-month period ended March 31, 2009 were Financials, Industrials and Consumer Discretionary, which had gains of 82%, 72% and 69%, respectively. The Fund’s largest gains were in the same sectors. The weakest S&P 500 Index sectors during this period were Telecommunications, Utilities and Energy with total returns of 12%, 21% and 30%, respectively. This rally was also led by smaller-capitalization and lower-quality companies (e.g. companies with weaker financial positions, lower returns on equity and more cyclical earnings).1

The difference between your Fund’s return and that of the S&P 500 Index and the Russell 1000 Value Index can be explained primarily by three reasons. First, despite being relatively fully invested with average cash balances of 4.4% of total assets, the holding of cash reduced the Fund’s relative return by over 280 basis points (2.80 percentage points). Second, your portfolio managers underweighted the Fund’s allocation to Consumer Discretionary stocks and chose to hold primarily defensive consumer companies, due to our belief that U.S. consumer spending would recover slowly during 2009. However, despite restrained consumer spending, the more aggressive cyclical consumer stocks performed the best during this period, which caused the Fund to under-perform by over 100 basis points (1.00 percentage point). Finally, our stock se lection in the Technology sector under-performed the S&P 500 Index’s Technology sector by over 125 basis points (1.25 percentage point). On the positive side, our security selections in Health Care, Industrials, Consumer Staples, and Energy outperformed their sector benchmarks and the sector allocation (excluding cash) was a positive contributor.1

The outlook for 2010 and beyond looks better than it did a year ago, but it will be largely influenced by government policies, which makes forecasting very uncertain. The Fed has kept short-term interest rates at near zero and had been a ready purchaser of mortgage-backed securities, which kept mortgage rates at historically low levels. The Fed will need to reverse these policies or risk the encouragement of new speculative bubbles and higher inflation in the future. The U.S. Federal Government has and is spending billions on various stimulus plans including “cash for clunkers” and home purchase tax credits. The federal deficit has ballooned to over $1.4 trillion and there is no clear plan to address future deficits, which will be exacerbated by the demographically-challenged federal health care and social security programs. In addit ion, the Bush tax cuts are set to expire in 2010, which will increase tax rates in the future. Finally, the U.S. consumer is facing more limited access to credit, the need to further delever (household debt as a percent of income is still nearly double the average of the last 20 years), and a significant loss of net worth just as the baby boomers are starting to retire. We think it is a good bet that the U.S. personal savings rate will remain high for the foreseeable future.

The good news is that much of the developing world is in relatively good financial shape. China, India, Brazil and a host of smaller developing countries are experiencing solid economic growth. In 2009, China succeeded the U.S. as the largest car market in the world and the BRIC countries (Brazil, Russia, India and China), in total, imported more goods than the U.S. This trend is not lost on U.S. corporations, which have been steadily expanding into foreign markets over the past ten years. In fact, revenues from foreign sources now represent over 45% of total revenues from the 500 companies in the Standard & Poor’s Index. The Fund owns many of these large global companies, which are well-positioned to succeed in a less U.S.-centric world.

1 Disclosures

Portfolio composition is as of March 31, 2010 and is subject to change.

8

FIRST FOCUS CORE EQUITY FUND

Return of a $10,000 Investment as of March 31, 2010

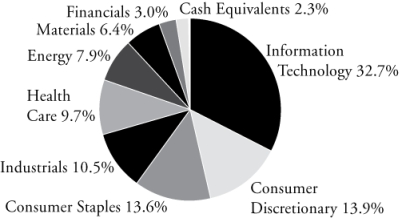

Portfolio Composition as of March 31, 2010

% Based on Total Value of Investments

(Portfolio composition is subject to change)

| Average Annual Total Return for the Year Ended March 31, 2010* | ||||

| 1 Year | 5 Year | 10 Year | ||

| First Focus Core Equity Fund | 44.10% | 2.89% | 4.01% | |

| S&P 500 Index | 49.77% | 1.92% | -0.65% | |

| Russell 1000 Value Index | 53.56% | 1.05% | 3.10% | |

| Prospectus Expense Ratio (Gross/Net)† | 1.43%/1.28% | |||

| Expense Ratio for the Year Ended | ||||

| March 31, 2010 (Gross/Net) | 1.34%/1.18% | |||

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. Total return figures include change in share price, reinvestment of dividends and capital gains. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit our website at www.firstfocusfunds.com.

(†)The above expense ratios are from the Fund’s prospectus dated August 1, 2009. Net expense ratio is net of contractual waivers which are in effect from August 1, 2009 through July 31, 2010.

(*) Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower.

The line chart assumes an initial investment of $10,000 made on March 31, 2000. Total return is based on net change in net asset value (“NAV”) assuming reinvestment of distributions. Returns shown include the reinvestment of all dividends and other distributions.

The S&P 500 Index is an index of 500 selected common stocks, most of which are listed on the New York Stock Exchange. The index is heavily weighted toward stocks with large market capitalizations and represents approximately two-thirds of the total market value of all domestic common stocks.

The Russell 1000 Value Index measures the performance of the large-cap value segment of the U.S. equity universe. It includes those Russell 1000 companies with lower price-to-book-value ratios and lower expected growth values.

The above referenced indices are unmangaged and do not reflect the deduction of fees or taxes associated with a mutual fund, such as investment management and fund accounting fees. Investors cannot invest directly in an index.

9

FIRST FOCUS LARGE CAP GROWTH FUND

Investment Objective

The First Focus Large Cap Growth Fund seeks long-term capital appreciation.

Manager Commentary

For the year ended March 31, 2010, the First Focus Large Cap Growth Fund returned 46.40% versus the Russell 1000® Growth Index return of 49.75%. As has been the case in recent years, much angst accompanied these positive returns.

March 9, 2009 marked an inflection point whereby major indices rebounded from multi-year lows to advance over 50%. Enormous fiscal and monetary stimuli served to provide investors some short-term confidence that the economy will stabilize. Corporate profits, benefiting from cost reduction measures coupled with modest investor expectations, pleasantly surprised. In the end, this year positively concluded what proved to be an otherwise challenging decade for equity investors.

Generally speaking, those stocks and sectors that struggled most in the year prior performed best in this last year. Companies possessing the greatest amount of economic sensitivity bounced back the most as investors anticipated an economic rebound. Top performing sectors included the Information Technology, Financials and Consumer Discretionary sectors.

Once again, this past year illustrates the perils of allowing emotions to drive investment decisions. Many market participants capitulated in January and February of 2009 by selling their equity holdings as demonstrated by mutual fund outflows. They opted for cash, U.S. Treasuries, and other relatively safe instruments offering little risk of loss. As a result, these investors collectively missed one of the more historic stock market rallies.

Following two remarkable years in the equity markets, the year ahead promises to be equally intriguing. While it is unlikely that we will realize either the depths of the 2008 market or the inspiring returns of 2009, investors are facing a pivotal point in time.

The ability of the markets to climb the proverbial “wall of worry” will likely determine whether our current market rally will sustain. During the year, the markets demonstrated an impressive level of resiliency to shrug off macro worries to post solid advances. While the current backdrop is somewhat favorable for equities, continued resilience will be helpful to continue our current market rally.

Unlike the past several quarters, it is easier today to paint an attractive backdrop for markets. The domestic economy is showing signs of sustenance with respect to growth. Inflation remains tame while growth is returning. The employment picture, while still bleak, is showing early signs of improvement.

Reported corporate profits continued to impress and most expect the strong reports to endure for the remainder of the year. Against the backdrop of heightened investor expectations, we will be looking for companies to report respectable revenue growth in addition to attractive profits.

Corporate balance sheets also demonstrate strength. According to the Wall Street Journal, undistributed corporate profits recently hit an all-time high of $527 billion. This cash will likely be used to increase dividend payouts and for increased merger-and-acquisition activity. Both actions are generally viewed as favorable to the equity markets.

While one can paint an optimistic equity picture, we are not suggesting that potential storm clouds do not exist. Countries, including the U.S. and China, will be gradually removing some of the stimulative measures deployed to combat the 2008 financial crisis. Domestically, the U.S. Federal Reserve has signaled that it will likely end its easing policy and could, depending on economic conditions, ultimately reverse this policy.

Continue to expect further sovereign debt scrutiny. Several European countries, including Greece, Portugal, Spain, and Ireland are in difficult fiscal positions. Many questions remain concerning how long the U.S. can continue to finance massive budget deficits.

Lastly, businesses of all sizes face increased regulation and likely tax increases from Washington D.C. The cost of conducting business in the U.S. will likely rise over the next several years. Several pieces of legislation are already proposed to increase the regulation authority of the federal government. The recently passed health care legislation also promises to increase the cost of doing business.

Regardless of our current opinion on the economic climate, we continue to position the portfolio with companies able to build their earnings power regardless of the economic backdrop. To the greatest extent possible, we invest in companies that are not dependent upon short-term economic vitality to grow their businesses.1

1 Disclosures

Portfolio composition is as of March 31, 2010 and is subject to change.

10

FIRST FOCUS LARGE CAP GROWTH FUND

Return of a $10,000 Investment as of March 31, 2010

Portfolio Composition as of March 31, 2010

% Based on Total Value of Investments

(Portfolio composition is subject to change)

| Average Annual Total Return for the Year Ended March 31, 2010* | ||

| 1 Year | Since Inception† | |

| First Focus Large Cap Growth Fund | 46.40% | -4.48% |

| Russell 1000 Growth Index | 49.75% | -3.87% |

| Prospectus Expense Ratio (Gross/Net)†† | 1.57%/1.37% | |

| Expense Ratio for the Year Ended | ||

| March 31, 2010 (Gross/Net) | 1.53%/1.22% | |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. Total return figures include change in share price, reinvestment of dividends and capital gains. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit our website at www.firstfocusfunds.com.

(††)The above expense ratios are from the Fund’s prospectus dated August 1, 2009. Net expense ratio is net of contractual waivers which are in effect from August 1, 2009 through July 31, 2010.

(†) Since July 5, 2007. The First Focus Large Cap Growth Fund was initially offered on July 2, 2007, however, no shareholder activity occurred until July 5, 2007, which is the commencement of operations.

(*) Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower.

The line chart assumes an initial investment of $10,000 made on July 5, 2007. Total return is based on net change in net asset value (“NAV”) assuming reinvestment of distributions. Returns shown include the reinvestment of all dividends and other distributions.

The Russell 1000 Growth Index measures the performance of the large-cap growth segment of the U.S. equity universe. It includes those Russell 1000 companies with higher price-to-book-values ratios and higher forecasted growth values.

The above referenced index is unmanaged and does not reflect the deduction of fees or taxes associated with a mutual fund, such as investment management and fund accounting fees. Investors cannot invest directly in an index.

11

FIRST FOCUS GROWTH OPPORTUNITIES FUND

Investment Objective

The First Focus Growth Opportunities Fund seeks long-term capital appreciation.

Manager Commentary

A year ago on these pages, as the economy tumbled and the markets collapsed, the case was made that the worst was past and a recovery would come before the end of the year. At the time it was difficult to know how the financial collapse was going to be contained and resolved, but as the year progressed, confidence began to return, and the markets began to recuperate. By the end of the year it was becoming clear that the economy was also on the path to recovery, providing the fundamental underpinnings to a sustained market advance.

The First Focus Growth Opportunities Fund was positioned too defensively during the first half of the past year, quickly falling behind its benchmark, the Russell Midcap® Growth Index. As our confidence in an economic recovery grew, and we positioned the Fund in a more economically sensitive fashion, performance improved, and the First Focus Growth Opportunities Fund began outperforming the benchmark in the second half of the year. For the year as a whole the Fund had a 56.25% return versus 63.00% for the Russell Midcap Growth Index. The S&P 500 Index returned 49.77% for the year. While the First Focus Growth Opportunities Fund finished near the middle of the pack for the past year, consistently strong relative perf ormance over the years has earned the Fund a Five Star rating from Morningstar® for the last ten years.1

The First Focus Growth Opportunities Fund is managed with a focus on fundamental factors like sales and earnings that can support the current valuation of a company’s stock. We will continue to focus on reasonably valued companies with superior growth characteristics, with sound financial strength.1

With each passing month the economy moves further down the path toward self-sustaining economic expansion. While the economy and financial markets still face many vulnerabilities, the year ahead is looking better.

1 Disclosures

Portfolio composition is as of March 31, 2010 and is subject to change.

Morningstar Inc. All Rights Reserved. The information, data, analysis and opinions contained herein (1) include the confidential and proprietary information of Morningstar, (2) may not be copied or redistributed, (3) do not constitute investment advice offered by Morningstar, (4) are provided solely for the informational purposes and therefore are not an offer to buy or sell a security, and (5) are not warranted to be correct, complete or accurate. Except as otherwise required by law, Morningstar shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, this information, data, analysis or opinions or their use. For each fund with at least a three-year history, Morningstar calculates a Morningstar RatingTM based on a Mornin gstar Risk-Adjusted Return measure that accounts for variation in a fund’s monthly performance (including the effects of sales charges, loads and redemption fees), placing more emphasis on downward variations and rewarding consistent performance. The top 10% of the funds in each category receive 5 stars, the next 22.5% receive 4 stars, the next 35% receive 3 stars, the next 22.5% receive 2 stars and the bottom 10% receive 1 star. (Each share class is counted as a fraction of one fund within the scale and rated separately, which may cause slight variations in the distribution percentages).

12

FIRST FOCUS GROWTH OPPORTUNITIES FUND

Return of a $10,000 Investment as of March 31, 2010

Portfolio Composition as of March 31, 2010

% Based on Total Value of Investments

(Portfolio composition is subject to change)

| Average Annual Total Return for the Year Ended March 31, 2010* | |||

| 1 Year | 5 Year | 10 Year | |

| First Focus Growth | |||

| Growth Opportunities Fund | 56.25% | 4.28% | 5.06% |

| Russell Midcap Growth Index | 63.00% | 4.27% | -1.69% |

| S&P 500 Index | 49.77% | 1.92% | -0.65% |

| Prospectus Expense Ratio (Gross/Net)† | 1.48%/1.33% | ||

| Expense Ratio for the Year Ended | |||

| March 31, 2010 (Gross/Net) | 1.35%/1.18% | ||

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. Total return figures include change in share price, reinvestment of dividends and capital gains. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit our website at www.firstfocusfunds.com.

(†)The above expense ratios are from the Fund’s prospectus dated August 1, 2009. Net expense ratio is net of contractual waivers which are in effect from August 1, 2009 through July 31, 2010.

(*) Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower.

The line chart assumes an initial investment of $10,000 made on March 31, 2000. Total return is based on net change in net asset value (“NAV”) assuming reinvestment of distributions. Returns shown include the reinvestment of all dividends and other distributions.

The Russell Midcap Growth Index measures the performance of the mid-cap growth segment of the U.S. equity universe. It includes those Russell Midcap Index companies with higher price-to-book-value ratios and higher forecasted growth values.

The Fund’s primary index is the Russell Midcap Growth Index, however to provide a broader market comparative we have also listed an additional index.

The S&P 500 Index is an index of 500 selected common stocks, most of which are listed on the New York Stock Exchange. The index is heavily weighted toward stocks with large market capitalizations and represents approximately two-thirds of the total market value of all domestic common stocks.

The above referenced indices are unmanaged and do not reflect the deduction of fees or taxes associated with a mutual fund, such as investment management and fund accounting fees. Investors cannot invest directly in an index.

13

FIRST FOCUS SMALL COMPANY FUND

Investment Objective

The First Focus Small Company Fund seeks long-term capital appreciation.

Manager Commentary

For the year ended March 31, 2010, the First Focus Small Company Fund returned 68.04%, versus 62.76% for the Russell 2000® Index and 65.07% for the Russell 2000® Value Index.

In 2008, investors were concerned about sub-prime loan issues, declining residential real estate prices, a failing banking system, falling corporate earnings and U.S. Government bailouts and rescue plans for financial services companies and the auto industry. The strong returns witnessed over the last year were likely a result of investors assuming that the worst of the financial crisis has passed.

Taking a look at the source of returns over the last year in the small cap market, several trends emerged. Generally, smaller capitalization companies outperformed larger capitalization companies, lower valuations (price-to-earnings ratio and price-to-book ratio) outperformed higher valuations, companies with higher price volatility (beta) outperformed companies with lower price volatility and companies with lower profitability (return on equity and return on assets) outperformed higher profitability companies. The top three performing sectors in the Russell 2000 Index during the trailing twelve months were Consumer Discretionary (+99%), Materials (+97%) and Energy (+89%). The three weakest performing sectors in the Russell 2000 Index during the last twelve months were Utilities (+28%), Financials (+47%) and Cons umer Staples (+49%).

We are very pleased with the Fund’s performance in such a strong market over the last year. Typically, a market favoring higher beta and lower profitability companies would not benefit our investment style. However, we were able to overcome these trends through positive individual stock selection. On an economic sector basis, the Fund outperformed in seven of the ten sectors that we track and our strongest outperformance was from companies in the Financials, Industrials and Energy sectors.1

As of March 31, 2010 the portfolio held shares of 64 companies diversified across the major sectors of the market. Eleven new companies were introduced into the Fund in the past twelve months, eight positions were eliminated and three companies were acquired.1

While many economic statistics in the U.S. continue to look anemic on an absolute basis, their trends have changed for the better. Unemployment, while still high at 9.7% at the end of March 2010, is down from a peak of 10.1% in late 2009. U.S. housing starts appear to have bottomed and are slowly beginning to increase while the S&P/Case-Shiller Home Price Index is showing flat year-over-year home prices versus declines of nearly 20% year-over-year at the beginning of 2009.1

U.S. household net worth has been recovering the last three quarters ended in December 2009 after having bottomed in March 2009. Retail sales have seen positive year-over-year increases beginning in November 2009 through February 2010. Lastly, Gross Domestic Product (“GDP”) in the U.S. had finally broken into positive territory at the end of September 2009 and followed that up with a stronger positive reading in December of 2009. While there certainly has been improvement in some economic indicators, many investors are debating whether the market has moved too far, too fast.

There are still several concerns that could derail the current stock market recovery. Unemployment remains very high in some areas of the country. The U.S. fiscal deficit has risen dramatically as the U.S. Government has propped up the economy via stimulus programs and bailouts. Eventually, this spending will cease and the economy will have to support itself. In addition, all the money being borrowed and/or printed by the U.S. Government has some investors worried about future inflation. Lastly, there is some concern that the next shoe to drop in the U.S. will come from the commercial real estate market as loans in this segment turn sour.

Whatever path the economy takes going forward, we will continue to stay true to our investment philosophy and process. Our approach to investing identifies quality companies that we believe are temporarily priced below their long-term intrinsic value. Purchases are made primarily on the merits of each individual company, maintaining a diversified portfolio across the various economic sectors. Over the long-term, we believe that our philosophy of owning higher quality businesses at reasonable prices will provide Fund shareholders an appropriate rate of return for the level of risk taken.1

1 Disclosures

Portfolio composition is as of March 31, 2010 and is subject to change.

The S&P/Case-Schiller Home Price Indices measures the residential housing market, tracking changes in the value of the residential real estate market in 20 metropolitan regions across the U.S.

14

FIRST FOCUS SMALL COMPANY FUND

Return of a $10,000 Investment as of March 31, 2010

Portfolio Composition as of March 31, 2010

% Based on Total Value of Investments

(Portfolio composition is subject to change)

| Average Annual Total Return for the Year Ended March 31, 2010* | |||

| 1 Year | 5 Year | 10 Year | |

| First Focus | |||

| Small Company Fund | 68.04% | 6.26% | 9.24% |

| Russell 2000 Index | 62.76% | 3.36% | 3.68% |

| Russell 2000 Value Index | 65.07% | 2.75% | 8.90% |

| Prospectus Expense Ratio (Gross/Net)† | 1.62%/1.47% | ||

| Expense Ratio for the Year Ended | |||

| March 31, 2010 (Gross/Net) | 1.50%/1.34% | ||

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. Total return figures include change in share price, reinvestment of dividends and capital gains. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit our website at www.firstfocusfunds.com.

(†)The above expense ratios are from the Fund’s prospectus dated August 1, 2009. Net expense ratio is net of contractual waivers which are in effect from August 1, 2009 through July 31, 2010.

(*) Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower.

The line chart assumes an initial investment of $10,000 made on March 31, 2000. Total return is based on net change in net asset value (“NAV”) assuming reinvestment of distributions. Returns shown include the reinvestment of all dividends and other distributions.

The Russell 2000 Index measures the performance of the small-cap segment of the U.S. equity universe. The Russell 2000 Index is a subset of the Russell 3000® Index representing approximately 10% of the total market capitalization of that index. It includes approximately 2000 of the smallest securities based on a combination of their market cap and current index membership.

The Russell 2000 Value Index measures the performance of small-cap value segment of the U.S. equity universe. It includes those Russell 2000 companies with lower price-to-book-value ratios and lower forecasted growth values.

The above referenced indices are unmanaged and do not reflect the deduction of fees or taxes associated with a mutual fund, such as investment management and fund accounting fees. Investors cannot invest directly in an index.

15

FIRST FOCUS INTERNATIONAL EQUITY FUND

Investment Objective

The First Focus International Equity Fund seeks long-term capital appreciation.

Manager Commentary

For the year ended March 31, 2010, the First Focus International Equity Fund returned 62.63% while the Fund’s benchmark, the MSCI EAFE Index, returned 55.20% (both in US Dollar terms).

International investment markets saw significant gains during the 12 months ended March 2010. Following the bear market lows in March 2009, investor sentiment improved dramatically over the course of the following months, driven at the outset by relief at the avoidance of a global depression. However, as 2009 progressed, the global economy began to emerge from recession and continued its recovery path into the initial months of 2010.

The portfolio was well positioned to take advantage of the recovery benefiting from an allocation to companies active in Emerging Markets, where a lack of indebtedness and better performance during the global financial crisis has filtered through into stronger equity returns. This inevitably boosted the relative return of the Fund against the benchmark MSCI EAFE Index as did the Fund’s underweight position in the Japanese market where performance lagged during 2009 with continued concerns over deflation in the economy setting it apart from the more general global economic recovery.1

In the final months of 2009, we looked to reduce the volatility of the Fund and re-positioned our sector and regional positions versus the MSCI EAFE Index. Our stock picking has firmly shifted towards companies with strong balance sheets, consistent earnings and good dividend growth. Some of the Fund’s current key positions include ENI, GlaxoSmithKline and RSA Insurance Group. All three stocks exhibit strong balance sheet characteristics with sustainable, strong dividend yields and high payout ratios. These are the type of companies we believe will reward investors in the current environment.1

It is our belief that the easy money has now been made and from here markets are likely to grind upwards. The economic recovery appears to be on a sustainable recovery path, with “double-dip” risks relatively minimal. Economic releases in recent months have been consistent with recovery and corporate profits in particular continue to be ahead of expectations. However, as we go through the next number of months, equity markets are likely to be vulnerable to a setback. To date we have been in a “sweet spot” where extremely low interest rates, attractive valuations and a recovery in economic growth and profits have been positive for risk assets. Perhaps paradoxically, the more assured the recovery becomes over the coming months, the higher the probability that central banks will start to tighten interest rates again. Therefo re good or strong economic news may not necessarily translate into good news for the markets.

Nevertheless, we remain comfortable that the economic recovery will continue and expect the gradual move to the “new normal” world that is less exuberant than the world that entered the recession. A subdued, though solid, economic recovery means that interest rates will not be raised aggressively. In such an environment, we expect equity returns to be more moderate and furthermore that investors can expect these more moderate returns from equities to continue for a sustained period of time. The process of normalizing interest rate policy and removing the emergency liquidity measures will pan out over a number of years. In addition, the next few years will see a significant de-leveraging process as the developed world has to cope with too much debt. This in itself wi ll moderate economic growth levels. In our view this has significant implications for the income component of equity returns. When the potential for capital appreciation is constrained and the expected level of equity returns modest, then the contribution that reinvested income makes to the total return achievable is at its highest. This has already fed through into our stock selection process.1

1 Disclosures

Portfolio composition is as of March 31, 2010 and is subject to change.

16

FIRST FOCUS INTERNATIONAL EQUITY FUND

Return of a $10,000 Investment as of March 31, 2010

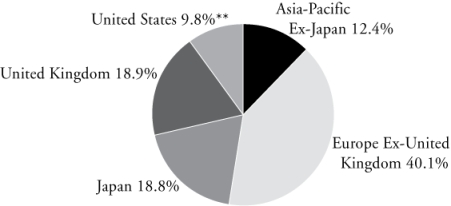

Country Weightings as of March 31, 2010

% Based on Total Value of Investments

(Portfolio composition is subject to change)

| Return of a $10,000 Investment for the Year Ended March 31, 2010* | |||||

| 1 Year | 5 Year | Since Inception† | |||

| First Focus International | |||||

| Equity Fund | 62.63% | 3.82% | 5.01% | ||

| MSCI EAFE Index | 55.20% | 4.23% | 6.97% | ||

| Prospectus Expense Ratio (Gross/Net)†† | 1.90%/1.75% | ||||

| Expense Ratio for Year Ended | |||||

| March 31, 2010 (Gross/Net) | 1.66%/1.45% | ||||

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. Total return figures include change in share price, reinvestment of dividends and capital gains. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit our website at www.firstfocusfunds.com.

(††)The above expense ratios are from the Fund’s prospectus dated August 1, 2009. Net expense ratio is net of contractual waivers which are in effect from August 1, 2009 through July 31, 2010.

(†) Commencement date is May 30, 2002.

(*) Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower.

The line chart assumes an initial investment of $10,000 made on May 30, 2002. Total return is based on net change in net asset value (“NAV”) assuming reinvestment of distributions. Returns shown include the reinvestment of all dividends and other distributions.

The Morgan Stanley Capital International Europe, Australasia and Far East (“MSCI EAFE”) Index is an arithmetic, market value-weighted average of the performance of over 900 securities listed on the stock exchanges of countries in Europe, Australia, and the Far East.

The above referenced index is unmanaged and does not reflect the deduction of fees or taxes associated with a mutual fund, such as investment management and fund accounting fees. Investors cannot invest directly in an index.

(**) 9.5% of this category is comprised of Exchange Traded Funds which provide international equity exposure.

17

SCHEDULES OF PORTFOLIO INVESTMENTS

March 31, 2010

SHORT-INTERMEDIATE BOND FUND

| Principal Amount | Security Description | Value |

| Non-U.S. Government Agency Asset-Backed | ||||

| Securities - 17.8% | ||||

| $ 706,252 | AmeriCredit Automobile Receivables | |||

| Trust (insured by FSA Assurance), | ||||

| 5.64%, 09/06/13 | $ 725,159 | |||

| 600,000 | Banc of America Commercial Mortgage | |||

| Inc., 7.38%, 09/15/32 (a) | 602,268 | |||

| 541,066 | Banc of America Commercial Mortgage | |||

| Inc., 5.00%, 10/10/45 | 544,594 | |||

| 315,000 | Bayview Financial Acquisition Trust, | |||

| 6.21%, 05/28/37 (a) | 296,718 | |||

| 890,000 | Bear Stearns Commercial Mortgage | |||

| Securities, 5.53%, 09/11/41 | 942,467 | |||

| 512,999 | Citimortgage Alternative Loan Trust, | |||

| 5.25%, 03/25/21 | 480,200 | |||

| 523,036 | Countrywide Alternative Loan Trust, | |||

| 6.06%, 08/25/36 (a) | 515,581 | |||

| 858,000 | Countrywide Asset-Backed Certificates, | |||

| 1.50%, 05/25/37 (a) | 42,472 | |||

| 443,991 | Credit Suisse First Boston Mortgage | |||

| Securities Corp., 5.00%, 08/25/20 | 410,869 | |||

| 775,000 | First Union National Bank Commercial | |||

| Mortgage, 7.80%, 10/15/32 (a) (e) | 787,024 | |||

| 580,000 | First Union National Bank Commercial | |||

| Mortgage, 6.67%, 12/12/33 | 584,231 | |||

| 372,062 | Home Equity Asset Trust, | |||

| 0.36%, 07/25/37 (a) | 357,876 | |||

| 671,000 | LB-UBS Commercial Mortgage Trust, | |||

| 6.37%, 12/15/28 | 700,886 | |||

| 850,000 | LB-UBS Commercial Mortgage Trust, | |||

| 6.30%, 11/15/33 | 884,305 | |||

| 678,236 | MASTR Asset Securitization Trust, | |||

| 5.25%, 11/25/35 | 618,778 | |||

| 600,200 | Nationstar Home Equity Loan Trust | |||

| REMIC, 0.31%, 06/25/37 (a) | 582,403 | |||

| 405,088 | Nomura Asset Acceptance Corp., | |||

| 6.00%, 03/25/47 (a) | 242,674 | |||

| 611,308 | Preferred Term Securities XXIV Ltd., | |||

| 0.56%, 03/22/37 (a) (e) (f) | 372,898 | |||

| 533,913 | Residential Accredit Loans Inc., | |||

| 5.50%, 01/25/34 | 524,739 | |||

| 148,296 | Residential Accredit Loans Inc., | |||

| 6.00%, 10/25/34 | 136,756 | |||

| 471,947 | Residential Accredit Loans Inc., | |||

| 5.50%, 02/25/35 | 395,709 | |||

| 758,620 | Residential Asset Mortgage Products Inc. | |||

| (insured by AMBAC Assurance Corp.), | ||||

| 4.02%, 03/25/33 | 590,350 | |||

| 390,821 | Structured Asset Securities Corp., | |||

| 5.50%, 07/25/33 | 390,826 | |||

| 467,927 | Triad Auto Receivables Owner Trust | |||

| (insured by AMBAC Assurance Corp.), | ||||

| 5.31%, 05/13/13 | 486,438 | |||

| 542,000 | Wells Fargo Home Equity Trust, | |||

| 0.39%, 07/25/36 (a) | 479,157 | |||

| Total Non-U.S. Government Agency Asset-Backed | ||||

| Securities (cost $13,445,231) | 12,695,378 | |||

| Corporate Bonds - 39.6% | ||||

| Consumer Discretionary - 1.6% | ||||

| 175,000 | Stanford University, 3.63%, 05/01/14 | 181,818 | ||

| 505,000 | Comcast Corp., 6.50%, 01/15/15 | 568,453 | ||

| 375,000 | Mohawk Industries Inc., | |||

| 6.88%, 01/15/16 | 387,188 | |||

| 1,137,459 | ||||

| Consumer Staples - 3.1% | ||||

| 423,000 | Bottling Group LLC, 4.63%, 11/15/12 | 454,126 | ||

| 448,000 | Kellogg Co., 5.13%, 12/03/12 | 485,190 | ||

| 500,000 | Kimberly-Clark Corp., 5.00%, 08/15/13 | 543,539 | ||

| 335,000 | SUPERVALU Inc., 8.00%, 05/01/16 | 339,187 | ||

| 375,000 | Wal-Mart Stores Inc., 5.00%, 04/05/12 | 402,214 | ||

| 2,224,256 | ||||

| Energy - 3.0% | ||||

| 615,000 | ConocoPhillips, 4.60%, 01/15/15 | 659,580 | ||

| 460,000 | Enterprise Products Operating LLC, | |||

| 9.75%, 01/31/14 | 558,576 | |||

| 579,000 | Occidental Petroleum Corp., | |||

| 7.00%, 11/01/13 | 670,682 | |||

| 220,000 | Transocean Inc., 1.50%, 12/15/37 | 214,774 | ||

| 2,103,612 | ||||

| Financials - 19.4% | ||||

| 540,000 | ACE INA Holdings Inc., 5.60%, 05/15/15 | 589,597 | ||

| 585,000 | American Express Credit Corp., | |||

| 7.30%, 08/20/13 | 656,612 | |||

| 450,000 | American Honda Finance Corp., | |||

| 2.64%, 06/29/11 (a) (e) | 458,803 | |||

| 890,000 | Bank of New York Mellon, | |||

| 6.38%, 04/01/12 | 969,594 | |||

| 600,000 | Berkshire Hathaway Finance Corp., | |||

| 5.00%, 08/15/13 | 655,247 | |||

| 615,000 | Citigroup Inc., 6.50%, 08/19/13 | 662,977 | ||

| 720,000 | General Electric Capital Corp., | |||

| 0.52%, 09/15/14 (a) | 684,336 | |||

| 620,000 | Goldman Sachs Group Inc., | |||

| 6.00%, 05/01/14 | 678,890 | |||

See accompanying notes to financial statements.

18

SCHEDULES OF PORTFOLIO INVESTMENTS

March 31, 2010

SHORT-INTERMEDIATE BOND FUND (CONTINUED)

| Principal Amount | Security Description | Value |

| $ 280,000 | Hartford Financial Services Group Inc., | |||

| 4.00%, 03/30/15 | $ 277,386 | |||

| 610,000 | JPMorgan Chase & Co., | |||

| 5.75%, 01/02/13 | 662,015 | |||

| 525,000 | KeyBank NA, 3.20%, 06/15/12 | 545,228 | ||

| 415,000 | KeyBank NA, 5.80%, 07/01/14 | 424,438 | ||

| 410,000 | Merrill Lynch & Co. Inc., | |||

| 5.45%, 02/05/13 | 433,784 | |||

| 620,000 | Metropolitan Life Global Funding I, | |||

| 5.13%, 04/10/13 (e) | 665,630 | |||

| 655,000 | Morgan Stanley, 4.75%, 04/01/14 | 668,805 | ||

| 250,000 | National City Corp., 4.00%, 02/01/11 | 254,375 | ||

| 650,000 | PNC Funding Corp., 0.45%, 01/31/14 (a) | 624,347 | ||

| 615,000 | Pricoa Global Funding I, | |||

| 5.45%, 06/11/14 (e) | 659,945 | |||

| 950,000 | Regions Bank, 3.25%, 12/09/11 | 985,337 | ||

| 570,000 | Regions Financial Corp., 7.25%, 11/10/14 | 599,720 | ||

| 650,000 | State Street Bank & Trust Co., | |||

| 0.45%, 12/08/15 (a) | 611,286 | |||

| 550,000 | USB Capital IX, 6.19% | |||

| (callable at 100 beginning 04/15/11) (b) | 470,250 | |||

| 650,000 | Wells Fargo Bank NA, 0.46%, 05/16/16 (a) | 593,768 | ||

| 13,832,370 | ||||

| Health Care - 0.8% | ||||

| 580,000 | Medtronic Inc., 1.50%, 04/15/11 | 589,425 | ||

| Industrials - 1.2% | ||||

| 475,000 | Textron Inc., 6.20%, 03/15/15 | 503,103 | ||

| 350,000 | United Technologies Corp., | |||

| 6.10%, 05/15/12 | 382,768 | |||

| 885,871 | ||||

| Information Technology - 3.6% | ||||

| 525,000 | CA Inc., 6.13%,12/01/14 (e) | 572,835 | ||

| 825,000 | Cisco Systems Inc., 5.25%, 02/22/11 | 858,588 | ||

| 300,000 | Hewlett-Packard Co., 2.00%, 02/24/11 (a) | 304,740 | ||

| 250,000 | Hewlett-Packard Co., 2.95%, 08/15/12 | 258,201 | ||

| 520,000 | International Business Machines Corp., | |||

| 6.50%, 10/15/13 | 596,883 | |||

| 2,591,247 | ||||

| Materials - 2.8% | ||||

| 495,000 | Dow Chemical Co., 7.60%, 05/15/14 | 565,088 | ||

| 335,000 | Nalco Co., 8.25%, 05/15/17 (e) | 355,938 | ||

| 480,000 | Praxair Inc., 3.95%, 06/01/13 | 504,877 | ||

| 475,000 | Rio Tinto Finance USA Ltd., | |||

| 8.95%, 05/01/14 | 572,376 | |||

| 1,998,279 | ||||

| Telecommunication Services - 0.9% | ||||

| 595,000 | AT&T Inc., 7.30%, 11/15/11 | 650,384 | ||

| Utilities - 3.2% | ||||

| 400,000 | Dayton Power & Light Co., | |||

| 5.13%, 10/01/13 | 432,356 | |||

| 416,000 | PacifiCorp, 5.45%, 09/15/13 | 456,093 | ||

| 370,000 | Public Service Co. of Colorado, | |||

| 7.88%, 10/01/12 | 423,687 | |||

| 575,000 | South Carolina Electric & Gas Co., | |||

| 6.70%, 02/01/11 | 602,221 | |||

| 380,000 | Wisconsin Energy Corp., 6.50%, 04/01/11 | 400,635 | ||

| 2,314,992 | ||||

| Total Corporate Bonds (cost $27,133,661) | 28,327,895 | |||

| Government And Agency Obligations - 37.9% | ||||

| GOVERNMENT SECURITIES - 31.7% | ||||

| Federal Home Loan Bank - 5.9% | ||||

| 1,700,000 | Federal Home Loan Bank, | |||

| 4.88%, 05/14/10 (g) | 1,709,379 | |||

| 1,600,000 | Federal Home Loan Bank, | |||

| 3.50%, 07/16/10 (g) | 1,615,384 | |||

| 830,000 | Federal Home Loan Bank, | |||

| 4.50%, 09/16/13 (g) | 897,521 | |||

| 4,222,284 | ||||

| Federal Home Loan Mortgage Corp. - 3.7% | ||||

| 1,500,000 | Federal Home Loan Mortgage Corp., | |||

| 6.88%, 09/15/10 (g) | 1,546,227 | |||

| 1,000,000 | Federal Home Loan Mortgage Corp., | |||

| 4.50%, 07/15/13 (g) | 1,081,449 | |||

| 2,627,676 | ||||

| Municipals - 1.3% | ||||

| 205,000 | Lincoln Nebraska Tax Allocation, | |||

| Perot Systems Redevelopment Project, | ||||

| 3.25%, 11/01/12 | 208,237 | |||

| 165,000 | Lincoln Nebraska Tax Allocation, | |||

| Perot Systems Redevelopment Project, | ||||

| 4.25%, 11/01/14 | 166,607 | |||

| 550,000 | Nebraska Public Power District, Revenue, | |||

| Series B, 4.14%, 01/01/13 | 582,005 | |||

| 956,849 | ||||

| Treasury Inflation Index Securities - 2.9% | ||||

| 964,128 | U.S. Treasury Inflation Indexed Note, | |||

| 3.00%, 07/15/12 (d) | 1,038,547 | |||

| 1,021,329 | U.S. Treasury Inflation Indexed Note, | |||

| 1.63%, 01/15/15 (d) | 1,066,970 | |||

| 2,105,517 | ||||

| U.S. Treasury Securities - 17.9% | ||||

| 3,800,000 | U.S. Treasury Bill, 0.14%, 06/24/10 | 3,798,803 | ||

| 7,215,000 | U.S. Treasury Note, 1.75%, 11/15/11 | 7,323,788 | ||

See accompanying notes to financial statements.

19

SCHEDULES OF PORTFOLIO INVESTMENTS

March 31, 2010

SHORT-INTERMEDIATE BOND FUND (CONTINUED)

| Shares or | ||||

| Principal Amount | Security Description | Value |

| $ 1,600,000 | U.S. Treasury Note, 2.75%, 10/31/13 | $ 1,646,374 | ||

| 12,768,965 | ||||

| U.S. GOVERNMENT AGENCY MORTGAGE | ||||

| BACKED SECURITIES - 6.2% | ||||

| Federal Home Loan Mortgage Corp. - 2.2% | ||||

| 1,532,300 | Federal Home Loan Mortgage Corp. | |||

| REMIC, 4.50%, 12/15/17 | 1,593,973 | |||

| Federal National Mortgage Association - 4.0% | ||||

| 1,256,456 | Federal National Mortgage Association | |||

| REMIC, 4.00%, 09/25/10 | 1,266,394 | |||

| 1,515,227 | Federal National Mortgage Association | |||

| REMIC, 5.50%, 11/25/34 | 1,587,419 | |||

| 2,853,813 | ||||

| Total Government and Agency | ||||

| Obligations (cost $26,724,674) | 27,129,077 | |||

| Investment Companies - 3.9% | ||||

| Mutual Funds - 3.9% | ||||

| 88,140 | Federated Institutional High-Yield Bond | |||

| Fund | 854,955 | |||

| 1,942,630 | Goldman Sachs Financial Square Funds, | |||

| Treasury Obligations Fund, 0.04% (c) | 1,942,630 | |||

| Total Investment Companies (cost $2,692,630) | 2,797,585 | |||

| Total Investments - 99.2% (cost $69,996,196) | 70,949,935 | |||

| Other assets in excess of liabilities - 0.8% | 553,153 | |||

| NET ASSETS - 100% | $ 71,503,088 | |||

| (a) | Variable rate security. The rate reflected is the rate in | |||

| effect at March 31, 2010. | ||||

| (b) | Perpetual maturity security. Interest rate is fixed until | |||

| the first call date and variable thereafter. | ||||

| (c) | Dividend yield changes daily to reflect current market | |||

| conditions. Rate was the quoted yield as of | ||||

| March 31, 2010. | ||||

| (d) | U.S. Treasury inflation indexed note, par amount | |||

| adjusted for inflation. | ||||

| (e) | Security is exempt from registration under Rule144A of | |||

| the Securities Act of 1933. The security may be resold | ||||

| in transactions exempt from registration, normally to | ||||

| qualified buyers. This security has been deemed liquid | ||||

| by the Fund’s investment adviser based on procedures | ||||