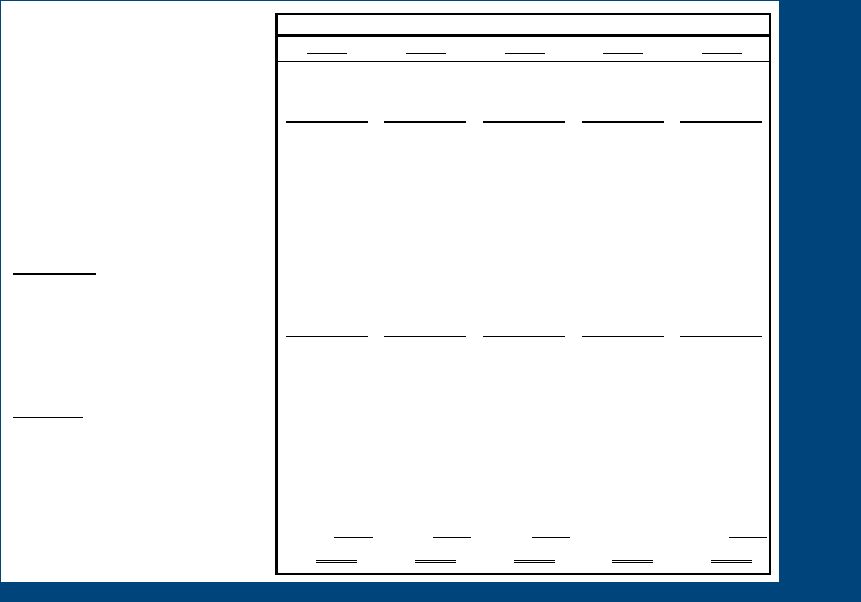

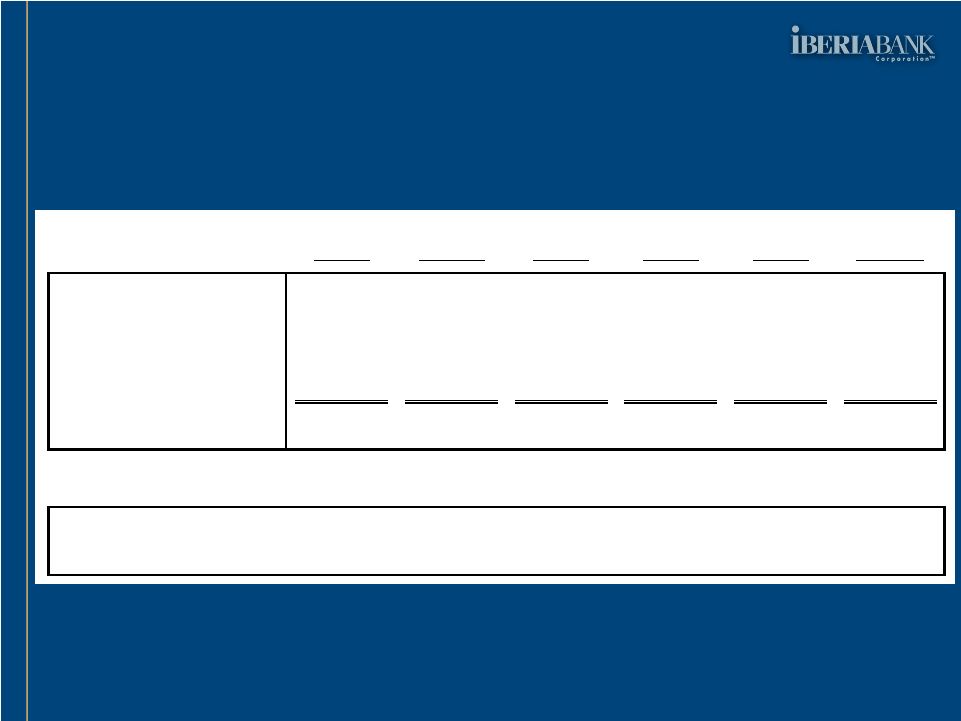

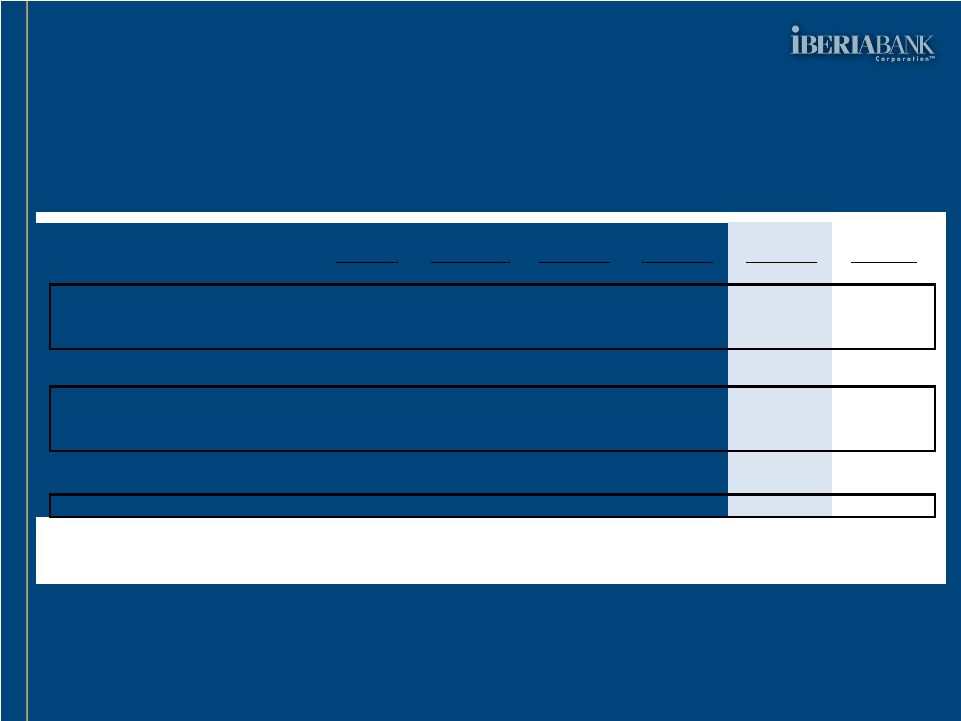

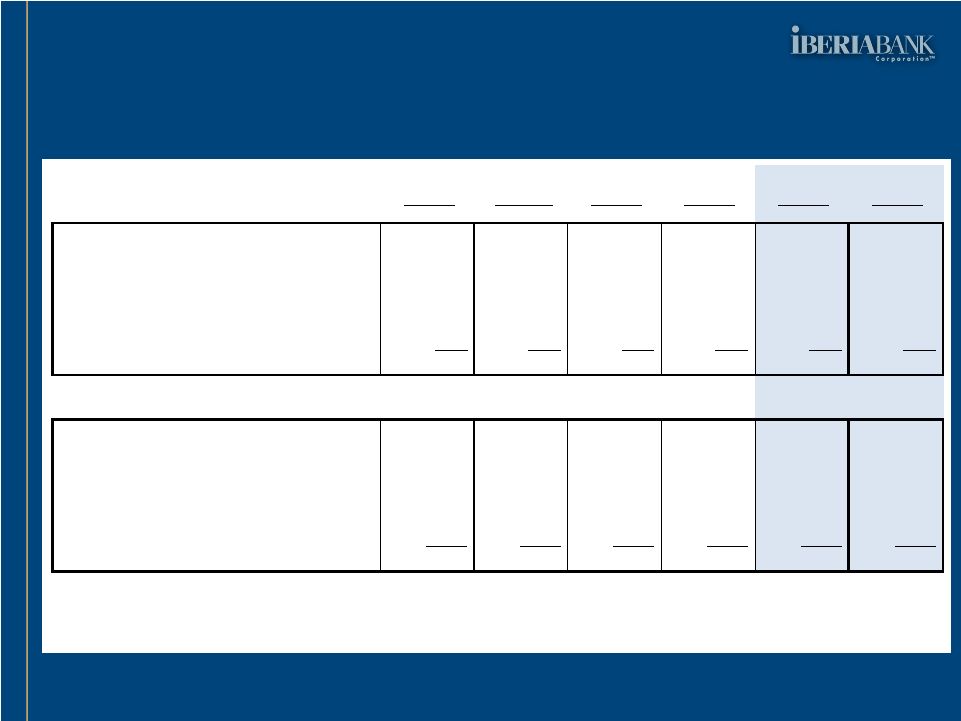

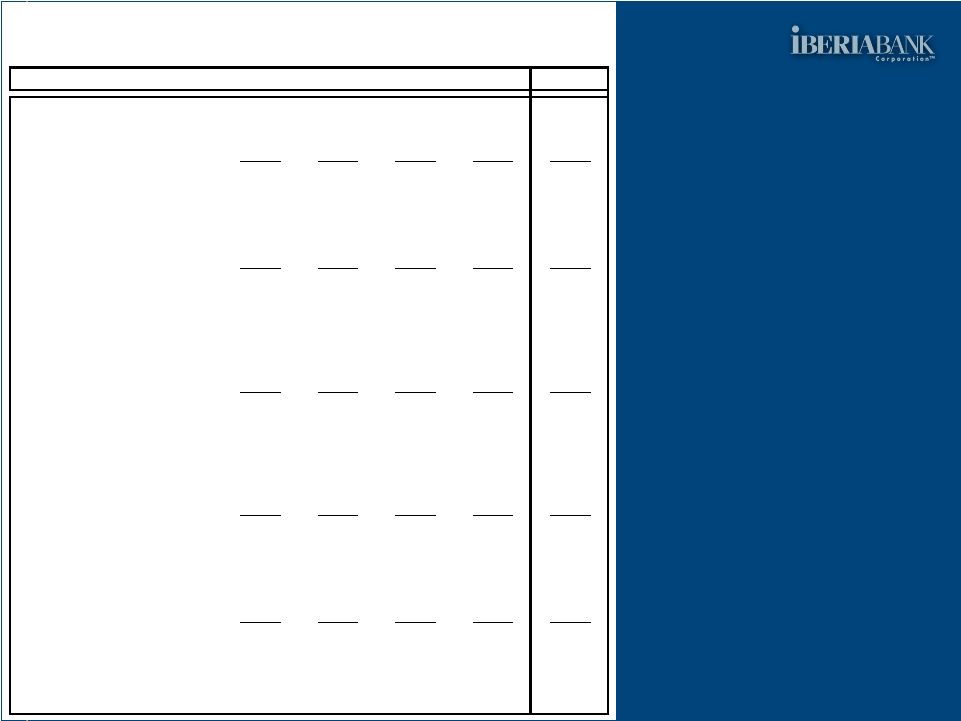

Loss Share Performance Covered Loan Portfolio Rollforward 40 Average Income / Expense Average Yield Average Income / Expense Average Yield Average Income / Expense Average Yield Average Income / Expense Average Yield Covered Loans 1,466,627 39,453 10.592% 1,545,551 54,118 14.049% 1,489,782 40,454 10.768% 1,421,784 28,201 7.819% Mortgage Loans 247,827 6,159 9.941% 253,360 6,865 10.839% 243,303 4,487 7.378% 229,678 5,209 9.072% Indirect Automobile - - 0.000% - - 0.000% - - 0.000% - - 0.000% Credit Card 1,154 20 6.934% 1,083 19 7.091% 1,026 17 6.721% 972 16 6.693% Consumer 213,082 3,225 6.005% 196,378 3,926 8.107% 189,022 (234) -0.497% 172,391 3,780 8.698% Line Of Credit-Consumer Loans 79,958 4,582 22.733% 79,580 7,391 37.664% 81,575 2,967 14.588% 80,650 2,372 11.669% Commercial & Business Banking 924,098 25,467 10.792% 1,015,204 35,917 14.155% 975,301 33,217 13.477% 938,554 16,824 7.018% Loans in Process 508 - 0.000% (54) - 0.000% (445) - 0.000% (460) - 0.000% Overdrafts 0 - 0.000% 0 - 0.000% 0 - 0.000% 0 - 0.000% FDIC Loss Share Receivable 899,558 (8,619) -3.749% 708,809 (21,913) -12.366% 666,159 (18,315) -10.877% 626,551 (2,602) -1.625% Net Covered Loan Portfolio 2,366,185 30,834 5.143% 2,254,360 32,205 5.744% 2,155,941 22,139 4.080% 2,048,335 25,599 4.930% Average Income / Expense Average Yield Average Income / Expense Average Yield Average Income / Expense Average Yield Average Income / Expense Average Yield Covered Loans 1,466,627 39,453 10.592% 1,545,551 54,118 14.049% 1,489,782 40,454 10.768% 1,421,784 28,201 7.819% CapitalSouth Bank 250,865 8,355 13.171% 251,762 10,188 16.262% 240,511 5,196 8.536% 227,549 (1,827) -3.080% Orion Bank 742,289 24,721 13.046% 823,081 32,651 16.025% 794,202 29,013 14.479% 759,860 24,875 12.861% Century Bank 332,360 3,878 4.610% 339,135 9,156 10.795% 323,681 4,105 5.072% 303,773 3,024 3.979% Sterling Bank 141,113 2,499 6.770% 131,574 2,123 6.472% 131,388 2,140 6.464% 130,602 2,130 6.405% FDIC Loss Share Receivable 899,558 (8,619) -3.749% 708,809 (21,913) -12.366% 666,159 (18,315) -10.877% 626,551 (2,602) -1.625% CapitalSouth Bank 79,553 (2,600) -12.788% 58,914 (1,877) -12.744% 58,676 (4,456) -30.041% 57,146 5,754 39.402% Orion Bank 555,610 (5,568) -3.921% 418,948 (18,861) -18.009% 392,880 (13,256) -13.348% 375,943 (11,021) -11.472% Century Bank 197,355 (593) -1.177% 163,829 (1,385) -3.383% 157,959 (756) -1.894% 145,807 2,505 6.723% Sterling Bank 67,040 142 0.830% 67,119 210 1.253% 56,644 152 1.065% 47,655 159 1.310% Net Covered Loan Portfolio 2,366,185 30,834 5.143% 2,254,360 32,205 5.744% 2,155,941 22,139 4.080% 2,048,335 25,599 4.930% CapitalSouth Bank 330,418 5,756 6.921% 310,676 8,311 10.762% 299,187 740 0.954% 284,696 3,927 5.448% Orion Bank 1,297,899 19,153 5.783% 1,242,029 13,790 4.546% 1,187,083 15,757 5.269% 1,135,803 13,853 4.807% Century Bank 529,715 3,285 2.457% 502,963 7,770 6.177% 481,639 3,349 2.787% 449,580 5,529 4.869% Sterling Bank 208,153 2,641 4.854% 198,692 2,333 4.709% 188,032 2,293 4.838% 178,257 2,290 5.043% 4Q2010 1Q2011 2Q2011 3Q2011 4Q2010 1Q2011 2Q2011 3Q2011 |