UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-08932

Artisan Funds, Inc.

(Exact name of registrant as specified in charter)

875 East Wisconsin Avenue, Suite 800

Milwaukee, WI 53202

(Address of principal executive offices) (Zip Code)

| | |

| Janet D. Olsen | | Alyssa Albertelli |

| Artisan Funds, Inc. | | Ropes & Gray LLP |

| 875 East Wisconsin Avenue, Suite 800 | | One Metro Center |

| Milwaukee, Wisconsin 53202 | | 700 12th Street, N.W., Suite 900 |

| | Washington, D.C. 20005-3948 |

(Name and address of agents for service)

Registrant’s telephone number, including area code: (414) 390-6100

Date of fiscal year end: 9/30/09

Date of reporting period: 3/31/09

| Item 1. | Reports to Shareholders. |

SEMIANNUAL

R E P O R T

March 31, 2009

ARTISAN GLOBAL VALUE FUND

ARTISAN INTERNATIONAL FUND

ARTISAN INTERNATIONAL SMALL CAP FUND

ARTISAN INTERNATIONAL VALUE FUND

ARTISAN MID CAP FUND

ARTISAN MID CAP VALUE FUND

ARTISAN OPPORTUNISTIC GROWTH FUND

ARTISAN OPPORTUNISTIC VALUE FUND

ARTISAN SMALL CAP FUND

ARTISAN SMALL CAP VALUE FUND

ARTISAN

ARTISAN FUNDS, INC.

INVESTOR SHARES

ARTISAN FUNDS

P.O. BOX 8412

BOSTON, MA 02266-8412

This report and the unaudited financial statements contained herein are provided for the general information of the shareholders of Artisan Funds. Before investing, investors should consider carefully each Fund’s investment objective, risks and charges and expenses. For a prospectus, which contains that information and more information about each Fund, please call 800.344.1770 or visit our website at www.artisanfunds.com. Read it carefully before you invest or send money.

Company discussions are for illustration only and are not intended as recommendations of individual stocks. The discussions present information about the companies believed to be accurate, and the views of the portfolio managers, as of March 31, 2009. That information and those views may change, and the Funds disclaim any obligation to advise shareholders of any such changes. Artisan Emerging Markets Fund, Artisan International Fund, Artisan International Value Fund and Artisan Mid Cap Fund offer other classes of shares. A report on each of the other classes is available under separate cover.

Artisan Funds offered through Artisan Distributors LLC, member FINRA.

TABLE OF CONTENTS

ARTISAN GLOBAL VALUE FUND (ARTGX)

INVESTMENT PROCESS HIGHLIGHTS

Artisan Global Value Fund employs a bottom-up investment process to construct a diversified portfolio of securities of undervalued U.S. and non-U.S. companies. The Fund’s investment process is focused on identifying what the investment team considers to be high quality, undervalued businesses that offer the potential for superior risk/reward outcomes. The team’s in-depth research process focuses on four key investment characteristics:

Undervaluation. Determining the intrinsic value of the business is the heart of the team’s research process. The team believes that intrinsic value represents the amount that a buyer would pay to own a company’s future cash flows. The team seeks to invest at a significant discount to the team’s estimate of the intrinsic value of a business.

Business quality. The team seeks to invest in companies with histories of generating strong free cash flow, improving returns on capital and strong competitive positions in their industries.

Financial strength. The team believes that investing in companies with strong balance sheets helps to reduce the potential for capital risk and provides company management the ability to build value when attractive opportunities are available.

Shareholder-oriented management. The team’s research process attempts to identify management teams with a history of building value for shareholders.

The Fund primarily invests in common stocks and other equity securities, both within and outside the U.S., with market capitalizations of at least $2 billion at the time of initial purchase.

PERFORMANCE HISTORY

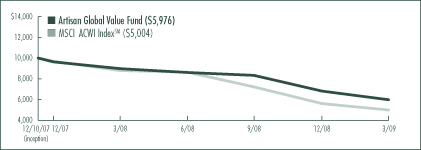

GROWTH OF AN ASSUMED $10,000 INVESTMENT (12/10/2007 to 3/31/2009)

AVERAGE ANNUAL TOTAL RETURNS (as of 3/31/2009)

| | | | | | |

| Fund / Index | | 1-Year | | | Since

Inception | |

Artisan Global Value Fund | | -33.45 | % | | -32.56 | % |

MSCI ACWI (All Country World Index) IndexSM | | -43.10 | | | -41.12 | |

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate, so that an investor’s shares in the Fund, when redeemed, may be worth more or less than their original cost. The Fund’s return may vary greatly over short periods, and current performance may be materially lower or higher than the performance data quoted. For current to most recent month-end performance information, visit www.artisanfunds.com or call 800.344.1770. The graph and table above do not reflect the deduction of taxes that a shareholder would pay on distributions or sale of Fund shares. The performance shown does not reflect the deduction of a 2% redemption fee on shares held by an investor for 90 days or less and, if reflected, the fee would reduce the performance quoted. The Fund’s performance information reflects Artisan Partners’ voluntary undertaking to limit the Fund’s expenses to no more than 1.50%, which may be terminated at any time, has been in effect since the Fund’s inception and has had a material impact on the Fund’s performance, which would have been lower in its absence. In addition, the outside directors of Artisan Funds waived that portion of their fees allocable to the Fund through September 30, 2008. Absent that expense waiver, the Fund’s performance would have been lower. See page 92 for a description of each index.

2

INVESTING ENVIRONMENT

Global equities suffered additional losses during the six-month period ended March 31, 2009. Governments adopted an increasingly activist role in order to stem the decline and restore confidence, but investors remained concerned about declining economic conditions and continued instability in the world’s financial systems. Market weakness centered largely on financials, but every market sector ended the period with double-digit losses. Returns were similar on a regional basis as all major developed and emerging markets declined.

SECTOR DIVERSIFICATION

| | | | | | |

| Sector | | 9/30/08 | | | 3/31/09 | |

Consumer Discretionary | | 26.7 | % | | 14.6 | % |

Consumer Staples | | 10.4 | | | 15.3 | |

Energy | | — | | | 2.7 | |

Financials | | 19.4 | | | 22.8 | |

Healthcare | | 15.6 | | | 11.0 | |

Industrials | | 11.0 | | | 15.0 | |

Information Technology | | 11.1 | | | 12.3 | |

Telecommunication Services | | 1.8 | | | 2.2 | |

Other assets less liabilities | | 4.0 | | | 4.1 | |

Total | | 100.0 | % | | 100.0 | % |

As a percentage of total net assets.

PERFORMANCE DISCUSSION

Artisan Global Value Fund declined - -28.17% during the period, holding up better than the MSCI All Country World IndexSM, which decreased -30.68% over the same period.

We remained focused on the intersection of balance sheet strength, business quality and valuation.

Performance of the following stocks had a positive impact on the portfolio during the six-month period: Google Inc., a search engine provider; Publicis Groupe, a French advertising services company; and Arch Capital Group Ltd., a provider of reinsurance and insurance products. Our worst performers included: Mohawk Industries, Inc., a provider of floor coverings in the U.S.; American Express Company, a credit card and business services company; Marsh & McLennan Companies, Inc., an insurance broker; Tyco Electronics Ltd., a U.S. electronic components manufacturer; and International Speedway Corporation, a promoter of motorsports activities in the U.S.

REGION ALLOCATION

| | | | | | |

| Region | | 9/30/08 | | | 3/31/09 | |

Americas | | 47.3 | % | | 49.4 | % |

Europe | | 38.5 | | | 35.4 | |

Pacific Basin | | 7.2 | | | 6.9 | |

Emerging Markets | | 3.0 | | | 4.2 | |

As a percentage of total net assets.

FUND CHANGES

During the period, we found several valuation opportunities. We continued to invest in certain holdings as their valuations fell and made new investments where we believed the risk/reward balance was more favorable than it was for those companies already in the portfolio. New purchases included previously mentioned Google Inc. and Publicis Groupe. We also added The Procter & Gamble Company, a consumer products manufacturer; 3M Company, a diversified global manufacturer; Daiwa Securities Group Inc., a Japanese financial services firm; and European integrated oil companies Total SA and Royal Dutch Shell PLC.

We exited a number of positions during the period, including Sekisui House, Ltd., Mattel, Inc., Neopost SA, Sanofi-Aventis, International Speedway Corporation, Nokia Corporation and Sodexo.

3

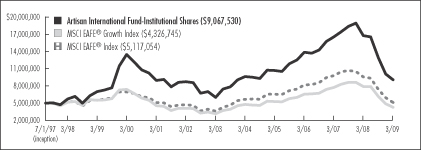

ARTISAN INTERNATIONAL FUND (ARTIX)

INVESTMENT PROCESS HIGHLIGHTS

Artisan International Fund employs a fundamental stock selection process focused on identifying long-term growth opportunities.

Themes. The investment team’s thematic approach identifies catalysts for change and develops investment themes with the objective of capitalizing on them globally. Changing demographics, developing technology, privatization of economic resources and outsourcing are among the long-term catalysts for change that currently form the basis for the team’s investment themes. The team incorporates these catalysts along with sector and regional fundamentals into a long-term global framework for investment analysis and decision-making.

Sustainable Growth. The team applies a fundamental approach to identifying the long term, sustainable growth characteristics of potential investments. The team seeks high quality companies that are well managed, have a dominant or improving market position and competitive advantages compared to industry and regional peers.

Valuation. The team assesses the relationship between its estimate of a company’s sustainable growth prospects and the company’s stock price. The team uses multiple valuation metrics to establish price targets.

The Fund primarily invests in non-U.S. growth companies of all market capitalizations in developed markets and emerging and less developed markets.

PERFORMANCE HISTORY

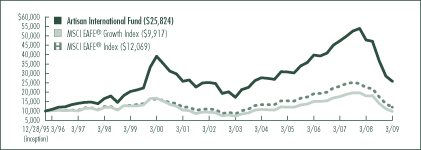

GROWTH OF AN ASSUMED $10,000 INVESTMENT (12/28/1995 to 3/31/2009)

AVERAGE ANNUAL TOTAL RETURNS (as of 3/31/2009)

| | | | | | | | | | | | | | | |

| Fund / Index | | 1-Year | | | 3-Year | | | 5-Year | | | 10-Year | | | Since

Inception | |

Artisan International Fund | | -46.09 | % | | -13.40 | % | | -1.50 | % | | 2.37 | % | | 7.42 | % |

MSCI EAFE® Growth Index | | -45.36 | | | -13.12 | | | -1.99 | | | -2.46 | | | -0.06 | |

MSCI EAFE® Index | | -46.51 | | | -14.47 | | | -2.18 | | | -0.84 | | | 1.43 | |

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate, so that an investor’s shares in the Fund, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For current to most recent month-end performance information, visit www.artisanfunds.com or call 800.344.1770. The graph and table above do not reflect the deduction of taxes that a shareholder would pay on distributions or sale of Fund shares. The performance shown does not reflect the deduction of a 2% redemption fee on shares held by an investor for 90 days or less and, if reflected, the fee would reduce the performance quoted. See page 92 for a description of each index.

4

INVESTING ENVIRONMENT

Save for short-term rallies in December and March, international equities generally trended lower throughout the six months ended March 31, 2009. Economic and corporate reports continued to disappoint and the battle between the effects of fiscal and monetary stimulus endured. Emerging markets fared better than developed markets on the back of huge stimulus spending and continued economic growth. For this semiannual reporting period, the MSCI EAFE® Index returned -31.11% and every sector suffered double digit losses. The financial sector was hit hardest, declining more than -45%. Losses were similarly broad on a regional basis. Every country in the Index experienced meaningful declines, with many falling by more than -30%.

SECTOR DIVERSIFICATION

| | | | | | |

| Sector | | 9/30/08 | | | 3/31/09 | |

Consumer Discretionary | | 11.2 | % | | 12.4 | % |

Consumer Staples | | 9.8 | | | 18.8 | |

Energy | | 9.1 | | | 4.6 | |

Financials | | 14.2 | | | 14.0 | |

Healthcare | | 7.9 | | | 7.4 | |

Industrials | | 17.4 | | | 12.7 | |

Information Technology | | 4.7 | | | 9.0 | |

Materials | | 7.4 | | | 6.5 | |

Telecommunication Services | | 3.1 | | | 5.9 | |

Utilities | | 9.4 | | | 4.4 | |

Other assets less liabilities | | 5.8 | | | 4.3 | |

Total | | 100.0 | % | | 100.0 | % |

As a percentage of total net assets.

PERFORMANCE DISCUSSION

Artisan International Fund held up better than the MSCI EAFE® Index with a return of -29.79% for the six months ended March 31, 2009. We benefited from the relative outperformance of our financial holdings as well as our underweight position in the beaten up sector. Strong security selection in the technology sector also aided relative returns. Our Chinese companies, China Resources Land Limited, China Construction Bank and China Life Insurance Co., Limited, held up better than peers. Semiconductor manufacturing equipment producer ASML Holding N.V., credit and debit card transaction processor Redecard SA and integrated circuit manufacturer Taiwan Semiconductor Manufacturing Company Ltd. drove our relative outperformance in the technology sector. Anheuser-Busch InBev NV, Delhaize Group and Carrefour SA, holdings in the consumer staples sector, were other top contributors.

Relative returns were held back by weaknesses among our energy, utilities and materials holdings. SeaDrill Ltd., Gazprom, Fortum Oyj, National Grid PLC, Holcim Ltd. and Wacker Chemie AG were some of our biggest detractors in these sectors. Our underweight position in the relatively strong energy sector also worked against us.

FUND CHANGES

Throughout the turbulence, we have remained committed to our thematic and fundamental investment process. We seek to invest in companies with sustainable growth characteristics, trading at reasonable valuations with exposure to the secular themes we have identified. New purchases during the period included telecommunications services provider France Telecom SA, brewer Anheuser-Busch InBev NV, tobacco products producer Philip Morris International Inc., financial services provider Muenchener Rueckversicherungs-Gesellschaft AG, grocery chain operator Carrefour SA and oil services company Schlumberger Limited.

Our sales during the period included Electricite de France, SeaDrill Ltd., Mitsui & Co., Ltd., Lloyds TSB Group plc and Orkla ASA.

REGION ALLOCATION

| | | | | | |

| Region | | 9/30/08 | | | 3/31/09 | |

Europe | | 61.0 | % | | 62.7 | % |

Emerging Markets | | 15.5 | | | 15.8 | |

Pacific Basin | | 15.0 | | | 11.9 | |

Americas | | 2.2 | | | 5.3 | |

Middle East | | 0.5 | | | — | |

As a percentage of total net assets.

5

ARTISAN INTERNATIONAL SMALL CAP FUND (ARTJX)

INVESTMENT PROCESS HIGHLIGHTS

Artisan International Small Cap Fund employs a fundamental stock selection process focused on identifying long-term growth opportunities among small non-U.S. companies.

Themes. The investment team’s thematic approach identifies catalysts for change and develops investment themes with the objective of capitalizing on them globally. Changing demographics, developing technology, privatization of economic resources and outsourcing are among the long-term catalysts for change that currently form the basis for the team’s investment themes. The team incorporates these catalysts along with sector and regional fundamentals into a long-term global framework for investment analysis and decision-making.

Sustainable Growth. The team applies a fundamental approach to identifying the long term, sustainable growth characteristics of potential investments. The team seeks high quality companies that are well managed, have a dominant or improving market position and competitive advantages compared to industry and regional peers.

Valuation. The team assesses the relationship between its estimate of a company’s sustainable growth prospects and the company’s stock price. The team uses multiple valuation metrics to establish price targets.

The Fund primarily invests in non-U.S. small-cap growth companies in developed and emerging markets with market capitalizations less than $3 billion at the time of investment.

PERFORMANCE HISTORY

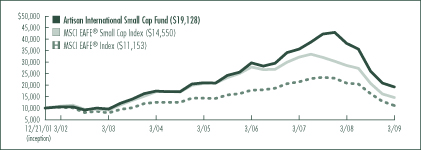

GROWTH OF AN ASSUMED $10,000 INVESTMENT (12/21/2001 to 3/31/2009)

AVERAGE ANNUAL TOTAL RETURNS (as of 3/31/2009)

| | | | | | | | | | | | |

| Fund / Index | | 1-Year | | | 3-Year | | | 5-Year | | | Since

Inception | |

Artisan International Small Cap Fund | | -49.70 | % | | -13.54 | % | | 1.97 | % | | 9.33 | % |

MSCI EAFE® Small Cap Index | | -48.89 | | | -19.35 | | | -3.17 | | | 5.29 | |

MSCI EAFE® Index | | -46.51 | | | -14.47 | | | -2.18 | | | 1.51 | |

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate, so that an investor’s shares in the Fund, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For current to most recent month-end performance information, visit www.artisanfunds.com or call 800.344.1770. The graph and table above do not reflect the deduction of taxes that a shareholder would pay on distributions or sale of Fund shares. The performance shown does not reflect the deduction of a 2% redemption fee on shares held by an investor for 90 days or less and, if reflected, the fee would reduce the performance quoted. The Fund’s investments in initial public offerings (IPOs) made a material contribution to the Fund’s performance. IPO investments are not an integral component of the Fund’s investment process and may not be available in the future. See page 92 for a description of each index.

6

INVESTING ENVIRONMENT

Save for short-term rallies in December and March, international small-cap equities generally trended lower throughout the six months ended March 31, 2009. Economic and corporate reports continued to disappoint and the battle between the effects of fiscal and monetary stimulus endured. Emerging markets fared better than developed markets on the back of huge stimulus spending and continued economic growth. For this semiannual reporting period, the MSCI EAFE® Small Cap Index returned -29.58% and every sector suffered double digit losses. Losses were similarly broad on a regional basis. Every country in the Index experienced meaningful declines, with many falling by more than -30%.

SECTOR DIVERSIFICATION

| | | | | | |

| Sector | | 9/30/08 | | | 3/31/09 | |

Consumer Discretionary | | 8.5 | % | | 10.7 | % |

Consumer Staples | | 15.8 | | | 18.2 | |

Energy | | 6.1 | | | — | |

Financials | | 22.4 | | | 14.9 | |

Healthcare | | 1.6 | | | 2.9 | |

Industrials | | 21.3 | | | 24.3 | |

Information Technology | | 9.9 | | | 14.2 | |

Materials | | 2.6 | | | 2.4 | |

Other assets less liabilities | | 11.8 | | | 12.4 | |

Total | | 100.0 | % | | 100.0 | % |

As a percentage of total net assets.

PERFORMANCE DISCUSSION

Artisan International Small Cap Fund held up better than the MSCI EAFE® Small Cap Index with a return of -26.24%. The outperformance of our industrials holdings was the primary driver of our relative strength. Rail and mass transport systems supplier Ansaldo STS SpA and Vossloh AG, a leader in rail infrastructure, were our top contributors in the sector. Schindler Holding AG, China Everbright International Limited and Intertek Group PLC also held up better than peers. Additionally, strong security selection in consumer staples and technology aided relative returns. Hengan International Group Company Limited and KWS Saat AG drove our relative outperformance in the consumer staples sector, while Wirecard AG was our top contributor in the technology sector.

Relative returns were held back by weaknesses among our financial and energy holdings. Two stocks, industrial real estate company Spazio Investment NV and Bank Sarasin & Cie AG, a leading private Swiss bank, were responsible for the vast majority of our relative underperformance in the financial sector. We sold a number of holdings in both sectors.

REGION ALLOCATION

| | | | | | |

| Region | | 9/30/08 | | | 3/31/09 | |

Europe | | 50.0 | % | | 53.9 | % |

Emerging Markets | | 24.8 | | | 25.7 | |

Pacific Basin | | 12.3 | | | 8.0 | |

Americas | | 1.1 | | | — | |

As a percentage of total net assets.

FUND CHANGES

Throughout the turbulence, we have remained committed to our thematic and fundamental investment process. We seek to invest in companies with sustainable growth characteristics, trading at reasonable valuations with exposure to the secular themes we have identified. During the period, we added three new names – global hotel operator InterContinental Hotels Group PLC, dental implants producer Nobel Biocare Holding AG and Domino’s Pizza Enterprises Limited, owner of the master franchise agreement for Domino’s Pizza® restaurants in Australia and New Zealand.

We completely sold out of our energy names during the period with the sales of SeaDrill Ltd., Sibir Energy PLC, SBM Offshore NV, Socotherm S.p.A. and C.A.T. oil AG. The sales we made in the financial sector included Hong Kong Exchanges & Clearing Limited, Hellenic Exchanges S.A., Tian An China Investments Company Limited and Bursa Malaysia Bhd.

7

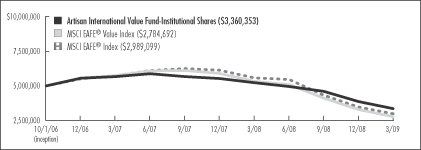

ARTISAN INTERNATIONAL VALUE FUND (ARTKX)

INVESTMENT PROCESS HIGHLIGHTS

Artisan International Value Fund employs a bottom-up investment process to construct a diversified portfolio of stocks of undervalued non-U.S. companies. The Fund’s investment process is focused on identifying what the investment team believes are high quality, undervalued businesses that offer the potential for superior risk/reward outcomes. The team’s in-depth research process focuses on four key investment characteristics:

Undervaluation. Determining the intrinsic value of the business is the heart of the team’s research process. The team believes that intrinsic value represents the amount that a buyer would pay to own a company’s future cash flows. The team seeks to invest at a significant discount to its estimate of the intrinsic value of a business.

Business quality. The team seeks to invest in companies with histories of generating strong free cash flow, improving returns on capital and strong competitive positions in their industries.

Financial strength. The team believes that investing in companies with strong balance sheets helps to reduce the potential for capital risk and provides company management the ability to build value when attractive opportunities are available.

Shareholder-oriented management. The team’s research process attempts to identify management teams with a history of building value for shareholders.

The Fund primarily invests in common stocks and other equity securities of non-U.S. companies of all market capitalizations in developed and emerging markets.

PERFORMANCE HISTORY

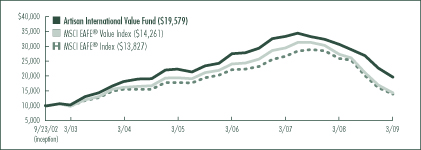

GROWTH OF AN ASSUMED $10,000 INVESTMENT (9/23/2002 to 3/31/2009)

AVERAGE ANNUAL TOTAL RETURNS (as of 3/31/2009)

| | | | | | | | | | | | |

| Fund / Index | | 1-Year | | | 3-Year | | | 5-Year | | | Since

Inception | |

Artisan International Value Fund | | -35.96 | % | | -10.69 | % | | 1.61 | % | | 10.86 | % |

MSCI EAFE® Value Index | | -47.72 | | | -15.92 | | | -2.49 | | | 5.60 | |

MSCI EAFE® Index | | -46.51 | | | -14.47 | | | -2.18 | | | 5.10 | |

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate, so that an investor’s shares in the Fund, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For current to most recent month-end performance information, visit www.artisanfunds.com or call 800.344.1770. The graph and table above do not reflect the deduction of taxes that a shareholder would pay on distributions or sale of Fund shares. The performance shown does not reflect the deduction of a 2% redemption fee on shares held by an investor for 90 days or less and, if reflected, the fee would reduce the performance quoted. See page 92 for a description of each index.

8

INVESTING ENVIRONMENT

International equities suffered additional losses during the six-month period ended March 31, 2009. Governments adopted an increasingly activist role in order to stem the decline and restore confidence, but investors remained concerned about declining economic conditions and continued instability in the world’s financial systems. Market weakness centered largely on financials, but every market sector ended the period with double-digit losses. Returns were similar on a regional basis as all major developed and emerging markets declined.

SECTOR DIVERSIFICATION

| | | | | | |

| Sector | | 9/30/08 | | | 3/31/09 | |

Consumer Discretionary | | 22.3 | % | | 20.1 | % |

Consumer Staples | | 13.0 | | | 12.5 | |

Energy | | — | | | 2.9 | |

Financials | | 19.0 | | | 18.7 | |

Healthcare | | 13.5 | | | 9.3 | |

Industrials | | 15.1 | | | 15.9 | |

Information Technology | | 8.3 | | | 7.9 | |

Materials | | 2.2 | | | 2.6 | |

Telecommunication Services | | 1.6 | | | 1.8 | |

Other assets less liabilities | | 5.0 | | | 8.3 | |

Total | | 100.0 | % | | 100.0 | % |

As a percentage of total net assets.

PERFORMANCE DISCUSSION

Artisan International Value Fund declined -26.98% during the period, holding up better than the MSCI EAFE® Index, which decreased -31.11% over the same period.

We remained focused on the intersection of balance sheet strength, business quality and valuation.

Performance of the following stocks had a positive impact on the portfolio during the six-month period: Lancashire Holdings Ltd, a U.K. specialty insurance provider; Publicis Groupe, a French advertising services company; and IGM Financial, Inc., a Canadian asset manager. Experian PLC, a U.K. credit-checking company, was our largest holding at the end of the period. The company’s share price recorded a single- digit loss, but it held up considerably better than the overall market in a challenging period for equities. Notable detractors included Societe Television Francaise 1, a French television channel owner; Covidien Limited, a U.S. medical products maker; Tyco Electronics Ltd., a U.S. electronic components manufacturer; MEITEC CORPORATION, a Japanese provider of outsourcing services primarily in the engineering industry; and Signet Jewelers Ltd., a jewelry retailer in the U.S. and U.K.

FUND CHANGES

During the period, we found several valuation opportunities. We continued to invest in certain holdings as their valuations fell and made new investments where we believed the risk/reward balance was more favorable than those companies already in the portfolio. New purchases included previously mentioned Publicis Groupe and IGM Financial, Inc. We also added Daiwa Securities Group Inc., a Japanese financial services firm; Nobel Biocare Holding AG, a Swiss dental implant maker; L’Oreal SA, a French cosmetics company; and European integrated oil companies Total SA and Royal Dutch Shell PLC.

We exited a number of positions during the period. Benfield Group Ltd, Kimberly-Clark de Mexico, S.A.B. de C.V., UNICHARM CORPORATION, Pfeiffer Vacuum Technology AG, Neopost SA, Nokia Corporation, Sanofi-Aventis, Sekisui House, Ltd., and Willis Group Holdings Limited were all sold.

REGION ALLOCATION

| | | | | | |

| Region | | 9/30/08 | | | 3/31/09 | |

Europe | | 63.8 | % | | 60.5 | % |

Americas | | 10.7 | | | 11.8 | |

Pacific Basin | | 14.2 | | | 11.8 | |

Emerging Markets | | 6.3 | | | 7.6 | |

As a percentage of total net assets.

9

ARTISAN MID CAP FUND (ARTMX)

INVESTMENT PROCESS HIGHLIGHTS

Artisan Mid Cap Fund employs a bottom-up investment process to construct a diversified portfolio of primarily U.S. mid-cap growth companies. The Fund’s investment process focuses on two distinct areas – security selection and capital allocation.

The Fund’s investment team attempts to identify companies that possess franchise characteristics that are selling at attractive valuations and benefiting from an accelerating profit cycle.

Franchise characteristics. These are characteristics that the team believes help to protect a company’s stream of cash flow from the effects of competition. The team looks for companies with at least two of the following characteristics: low cost production capability, possession of a proprietary asset, dominant market share or a defensible brand name.

Attractive valuations. Through its own fundamental research, the team estimates the amount a buyer would pay to buy the entire company (the company’s “intrinsic value” or “private market value”) and considers whether to purchase a stock if it sells at a discount to that estimate.

Accelerating profit cycle. The team tries to invest in companies that are well positioned for long-term growth, at an early enough stage in their profit cycle to benefit from the increased cash flows produced by the profit cycle.

Based on the investment team’s fundamental analysis of a company’s profit cycle, portfolio holdings develop through three stages. GardenSM investments are small positions in the early part of their profit cycle that will warrant a more sizeable allocation once their profit cycle accelerates. CropSM investments are positions that are being increased to a full weight because they are moving through the strongest part of their profit cycle. HarvestSM investments are positions that are being reduced as they near the team’s estimate of full valuation or their profit cycle begins to decelerate.

PERFORMANCE HISTORY

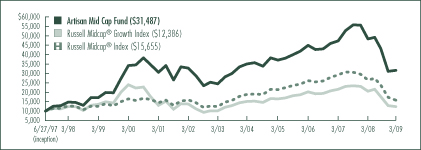

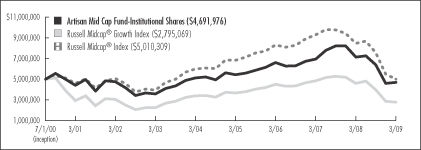

GROWTH OF AN ASSUMED $10,000 INVESTMENT (6/27/1997 to 3/31/2009)

AVERAGE ANNUAL TOTAL RETURNS (as of 3/31/2009)

| | | | | | | | | | | | | | | |

| Fund / Index | | 1-Year | | | 3-Year | | | 5-Year | | | 10-Year | | | Since

Inception | |

Artisan Mid Cap Fund | | -34.54 | % | | -11.01 | % | | -2.05 | % | | 6.26 | % | | 10.25 | % |

Russell Midcap® Growth Index | | -39.58 | | | -14.89 | | | -3.91 | | | -0.86 | | | 1.84 | |

Russell Midcap® Index | | -40.81 | | | -15.53 | | | -3.53 | | | 2.27 | | | 3.89 | |

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate, so that an investor’s shares in the Fund, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For current to most recent month-end performance information, visit www.artisanfunds.com or call 800.344.1770. The graph and table above do not reflect the deduction of taxes that a shareholder would pay on distributions or sale of Fund shares. See page 92 for a description of each index.

10

INVESTING ENVIRONMENT

During the semiannual reporting period ended March 31, 2009, mid-cap stocks sank along with the broader market amid worsening economic conditions and turmoil in the financial sector. The Russell Midcap® Index declined -33.80%. Growth stocks held up better than value names as the Russell Midcap® Growth Index fell -29.81%, while its value counterpart tumbled -37.87%. Within the growth index, all sectors closed lower, with financial and energy stocks down the most.

SECTOR DIVERSIFICATION

| | | | | | |

| Sector | | 9/30/08 | | | 3/31/09 | |

Consumer Discretionary | | 7.7 | % | | 14.0 | % |

Consumer Staples | | 4.8 | | | 3.0 | |

Energy | | 4.0 | | | 4.6 | |

Financials | | 8.0 | | | 6.5 | |

Healthcare | | 25.4 | | | 22.7 | |

Industrials | | 14.9 | | | 14.0 | |

Information Technology | | 28.5 | | | 31.8 | |

Materials | | 1.6 | | | 1.5 | |

Telecommunication Services | | 0.4 | | | 0.6 | |

Utilities | | 2.0 | | | — | |

Other assets less liabilities | | 2.7 | | | 1.3 | |

Total | | 100.0 | % | | 100.0 | % |

As a percentage of total net assets.

PERFORMANCE DISCUSSION

Artisan Mid Cap Fund returned -26.82% during the period, outperforming the Russell Midcap® and Russell Midcap® Growth indices. Relative to the benchmarks, the Fund benefited from strong security selection, particularly among our healthcare and industrials holdings, although our leading performers came from a variety of sectors. Sector positioning was also helpful, due in part to our low weighting in the energy sector. In the health care sector, CropSM holdings Cerner Corporation, a health care information technology company, specialty pharmaceuticals company Allergan, Inc. and C. R. Bard, Inc., a medical devices maker, were key to our strong relative performance. In the industrials sector, Roper Industries, Inc., an industrial products manufacturer, and contracting services company Quanta Services, Inc. were two companies that held up relatively well. Other standout performers included Hansen Natural Corporation, Broadcom Corporation and Best Buy Co., Inc.

Compared to the Russell Midcap® Growth Index, the greatest sources of weakness included our relatively low weight in consumer discretionary stocks and underperformance in the financials and utilities sectors. The St. Joe Company, a real estate operating company, and credit card issuer Discover Financial Services were among our worst performing financial holdings. Our underperformance in the utilities sector was driven by independent power producers Calpine Corporation and Dynegy Inc.

FUND CHANGES

The most notable changes to the portfolio during the period were increased exposures to the consumer discretionary and information technology sectors. In the consumer discretionary sector, we purchased several new holdings, including YUM! Brands, Inc., Dick’s Sporting Goods, Inc. and CarMax, Inc. In the information technology sector, new purchases included VMware, Inc., Citrix Systems, Inc. and Quality Systems, Inc., among others.

We funded our new purchases in part with sales from a broad range of sectors. Celgene Corporation, AGCO Corporation, Calpine Corporation and Varian Medical Systems, Inc. were all CropSM positions that were sold during the period. We also sold ImClone Systems Incorporated, a GardenSM position, after it received a premium takeout offer from Eli Lilly and Company.

11

ARTISAN MID CAP VALUE FUND (ARTQX)

INVESTMENT PROCESS HIGHLIGHTS

Artisan Mid Cap Value Fund employs a bottom-up investment process to construct a diversified portfolio of stocks of medium-sized U.S. companies that the investment team believes are undervalued, in solid financial condition and have attractive business economics. The team believes companies with these characteristics are less likely to experience eroding values over the long term.

Attractive valuation. The team values a business using what it believes are reasonable expectations for the long-term earnings power and capitalization rates of that business. This results in a range of values for the company that the team believes would be reasonable. The team generally will purchase a security if the stock price falls below or toward the lower end of that range.

Sound financial condition. The team favors companies with an acceptable level of debt and positive cash flow. At a minimum, the team tries to avoid companies that have so much debt that management may be unable to make decisions that would be in the best interests of the companies’ shareholders.

Attractive business economics. The team favors cash-producing businesses that it believes are capable of earning acceptable returns on capital over the company’s business cycle.

The Fund generally will not initiate a position in a company unless it has a market capitalization between $2 billion and $15 billion.

PERFORMANCE HISTORY

GROWTH OF AN ASSUMED $10,000 INVESTMENT (3/28/2001 to 3/31/2009)

AVERAGE ANNUAL TOTAL RETURNS (as of 3/31/2009)

| | | | | | | | | | | | |

| Fund / Index | | 1-Year | | | 3-Year | | | 5-Year | | | Since

Inception | |

Artisan Mid Cap Value Fund | | -31.16 | % | | -9.77 | % | | 1.01 | % | | 5.95 | % |

Russell Midcap® Value Index | | -42.51 | | | -16.68 | | | -3.81 | | | 1.92 | |

Russell Midcap® Index | | -40.81 | | | -15.53 | | | -3.53 | | | 1.17 | |

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate, so that an investor’s shares in the Fund, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For current to most recent month-end performance information, visit www.artisanfunds.com or call 800.344.1770. The graph and table above do not reflect the deduction of taxes that a shareholder would pay on distributions or sale of Fund shares. See page 92 for a description of each index.

12

INVESTING ENVIRONMENT

For the six-month period ended March 31, 2009, the Russell Midcap® Value and Russell Midcap® indices returned -37.87% and

-33.80%, respectively. It was a challenging period for equity investors as the economic slowdown continued to take its toll. In the Russell Midcap® Value Index, all sectors suffered double-digit declines and, in general, the more cyclical sectors were the weakest. The financials, energy, consumer discretionary, industrials and materials sectors all declined more than -40%. The traditionally defensive utilities and consumer staples sectors were more resilient.

SECTOR DIVERSIFICATION

| | | | | | |

| Sector | | 9/30/08 | | | 3/31/09 | |

Consumer Discretionary | | 18.3 | % | | 15.9 | % |

Consumer Staples | | 0.8 | | | 2.9 | |

Energy | | 4.4 | | | 8.1 | |

Financials | | 19.4 | | | 18.0 | |

Healthcare | | 2.0 | | | 3.7 | |

Industrials | | 27.6 | | | 24.2 | |

Information Technology | | 20.5 | | | 21.0 | |

Utilities | | 0.8 | | | 0.7 | |

Other assets less liabilities | | 6.2 | | | 5.5 | |

Total | | 100.0 | % | | 100.0 | % |

As a percentage of total net assets.

PERFORMANCE DISCUSSION

Artisan Mid Cap Value Fund returned - -28.93% during the six-month period ended March 31, 2009. Our holdings in the industrials and consumer discretionary sectors were among our worst absolute performers. However, our stocks in those sectors held up considerably better than those in the Russell Midcap® Value Index and contributed to our relative outperformance. We experienced a similar trend in the financials and technology sectors where our losses were less severe than the Index’s. We also benefited from our minimal investment in the REIT industry and our lack of investment in banks, both of which were particularly hard hit. Our minimal investment in the utilities and consumer staples sectors hurt our relative performance as those areas were more resilient than most. From an individual stock perspective, our leading performers included title insurer Fidelity National Financial, Inc., LCD glass manufacturer Corning Incorporated, auto parts and accessories retailer AutoZone, Inc., drafting and design software developer Autodesk, Inc. and mortgage REIT Annaly Capital Management, Inc. Our biggest decliners during the period included insurance provider White Mountains Insurance Group, Ltd., floor coverings manufacturer Mohawk Industries, Inc., land drilling contractor Nabors Industries Ltd., lighting fixtures manufacturer Acuity Brands, Inc., and trucking companies Con-way Inc. and Ryder System, Inc.

FUND CHANGES

One positive outcome of the weak environment was the emergence of new investment opportunities. During the period, we added the following companies to the portfolio: powertrain components manufacturer BorgWarner Inc., diversified defense company General Dynamics Corporation, drafting and design software developer Autodesk Inc., pharmaceutical distributor Cardinal Health, Inc., consumer credit information provider Equifax Inc., oil and gas company EOG Resources, Inc. and cruise line operator Carnival Corporation.

On the sale side, we trimmed or exited several of our retail names due to increased concern about industry fundamentals as a whole. During the period, we reduced our positions in AutoZone Inc., Kohl’s Corporation and Bed Bath & Beyond Inc., and we completely sold our positions in Limited Brands, Inc., Rent-A-Center, Inc. and Williams-Sonoma, Inc. Other sales during the period included Holly Corporation, BJ Services Company, Smithfield Foods, Inc. and SAIC, Inc.

13

ARTISAN OPPORTUNISTIC GROWTH FUND (ARTRX)

INVESTMENT PROCESS HIGHLIGHTS

Artisan Opportunistic Growth Fund employs a bottom-up investment process to construct a diversified portfolio of growth companies across a broad capitalization range. The Fund’s investment process focuses on two distinct areas – security selection and capital allocation.

The Fund’s investment team attempts to identify companies that possess franchise characteristics that are selling at attractive valuations and benefiting from an accelerating profit cycle.

Franchise characteristics. These are characteristics that the team believes help to protect a company’s stream of cash flow from the effects of competition. The team looks for companies with at least two of the following characteristics: low cost production capability, possession of a proprietary asset, dominant market share or a defensible brand name.

Attractive valuations. Through its own fundamental research, the team estimates the amount a buyer would pay to buy the entire company (the company’s “intrinsic value” or “private market value”) and considers whether to purchase a stock if it sells at a discount to that estimate.

Accelerating profit cycle. The team tries to invest in companies that are well positioned for long-term growth, at an early enough stage in their profit cycle to benefit from the increased cash flows produced by the profit cycle.

Based on the investment team’s fundamental analysis of a company’s profit cycle, portfolio holdings develop through three stages. GardenSM investments are small positions in the early part of their profit cycle that will warrant a more sizeable allocation once their profit cycle accelerates. CropSM investments are positions that are being increased to a full weight because they are moving through the strongest part of their profit cycle. HarvestSM investments are positions that are being reduced as they near the team’s estimate of full valuation or their profit cycle begins to decelerate.

PERFORMANCE HISTORY

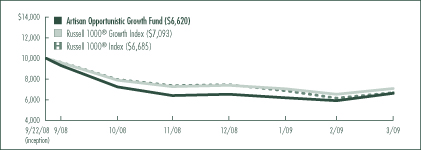

GROWTH OF AN ASSUMED $10,000 INVESTMENT (9/22/2008 to 3/31/2009)

TOTAL RETURNS (as of 3/31/2009)

| | | |

| Fund / Index | | Since

Inception(1) | |

Artisan Opportunistic Growth Fund | | -33.80 | % |

Russell 1000® Growth Index | | -29.07 | |

Russell 1000® Index | | -33.15 | |

(1) | For the period from commencement of operations (September 22, 2008) through March 31, 2009; not annualized. |

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate, so that an investor’s shares in the Fund, when redeemed, may be worth more or less than their original cost. The Fund’s return may vary greatly over short periods, and current performance may be materially lower or higher than the performance data quoted. For current to most recent month-end performance information, visit www.artisanfunds.com or call 800.344.1770. The table above does not reflect the deduction of taxes that a shareholder would pay on distributions or sale of Fund shares. The Fund’s performance information reflects Artisan Partners’ voluntary undertaking to limit the Fund’s expenses to no more than 1.50%, which may be terminated at any time, has been in effect since the Fund’s inception and has had a material impact on the Fund’s performance, which would have been lower in its absence. In addition, the outside directors of Artisan Funds have waived that portion of their fees allocable to the Fund until September 30, 2009. Absent that expense waiver, the Fund’s performance would have been lower. See page 92 for a description of each index.

14

INVESTING ENVIRONMENT

During the semiannual reporting period ended March 31, 2009, stocks sank amid worsening economic conditions and turmoil in the financial sector. The Russell 1000® Index declined -30.59% as of the end of the period. Growth stocks held up better than value names as the Russell 1000® Growth Index fell -25.97%, while its value counterpart tumbled -35.22%. Within the Russell 1000® Index, all sectors closed lower, although there was a fair amount of dispersion in returns. The financials sector, which has been at the center of the credit crisis, dropped by more than 50%. The telecommunication services and health care sectors held up best.

PERFORMANCE DISCUSSION

Artisan Opportunistic Growth Fund utilizes a bottom-up investment process to construct a diversified portfolio of growth companies across a broad capitalization range without regard for the sector composition of the benchmark. Because our sector weights and market cap characteristics vary quite widely from those of the index, discussing performance relative to a benchmark over the short-term will typically not provide meaningful insight about the portfolio. Instead, we expect that over the long term our security selection will be the primary driver of portfolio returns. For the six-month period ended March 31, 2009, the Fund returned -28.97%. Our top performers were Brazilian energy company Petroleo Brasileiro S.A., specialty coffee retailer Starbucks Corporation, consumer electronics retailer Best Buy Co., Inc., semiconductor company Broadcom Corporation, and online retailer Amazon.com, Inc. The Fund’s largest decliners were video game publisher Electronic Arts Inc., credit card issuer Discover Financial Services, money transfer company The Western Union Company, Spanish wind-turbine maker Gamesa Corporacion Tecnologica, S.A., and scientific equipment and consumables provider Thermo Fisher Scientific, Inc.

SECTOR DIVERSIFICATION

| | | | | | |

| Sector | | 9/30/08 | | | 3/31/09 | |

Consumer Discretionary | | 6.4 | % | | 17.3 | % |

Consumer Staples | | 10.2 | | | 6.5 | |

Energy | | 2.0 | | | 5.2 | |

Financials | | 12.2 | | | 13.3 | |

Healthcare | | 19.2 | | | 16.7 | |

Industrials | | 10.2 | | | 5.9 | |

Information Technology | | 31.3 | | | 26.4 | |

Materials | | 1.9 | | | 3.1 | |

Telecommunication Services | | 1.1 | | | — | |

Other assets less liabilities | | 5.5 | | | 5.6 | |

Total | | 100.0 | % | | 100.0 | % |

As a percentage of total net assets.

FUND CHANGES

The six-month period ended March 31, 2009 was the first full reporting period since inception of the Fund. The Fund typically holds between 30 and 50 stocks. The number of holdings increased from 36 to 44 during the period. Our list of purchases included Starbucks Corporation, JPMorgan Chase & Co., Apple Inc., Juniper Networks, Inc., and EMC Corporation. The investment team attempts to identify companies that possess franchise characteristics that are selling at attractive valuations and benefiting from an accelerating profit cycle.

These purchases were partially funded with sales of AGCO Corporation, Analog Devices, Inc., Celgene Corporation, Avon Products, Inc. and Cisco Systems, Inc., among others.

REGION ALLOCATION

| | | | | | |

| Region | | 9/30/08 | | | 3/31/09 | |

Americas | | 89.5 | % | | 88.9 | % |

Europe | | 3.9 | | | 2.8 | |

Emerging Markets | | 1.1 | | | 2.7 | |

As a percentage of total net assets.

15

ARTISAN OPPORTUNISTIC VALUE FUND (ARTLX)

INVESTMENT PROCESS HIGHLIGHTS

Artisan Opportunistic Value Fund employs a bottom-up investment process to construct a diversified portfolio of stocks that the team believes are undervalued, in solid financial condition with attractive business economics. The team believes companies with these characteristics are less likely to experience eroding values over the long term.

Attractive valuation. The team values a business using what it believes are reasonable expectations for the long-term earnings power and capitalization rates of that business. This results in a range of values for the company that the team believes would be reasonable. The team generally will purchase a security if the stock price falls below or toward the lower end of that range.

Sound financial condition. The team favors companies with an acceptable level of debt and positive cash flow. At a minimum, the team tries to avoid companies that have so much debt that management may be unable to make decisions that would be in the best interest of the companies’ shareholders.

Attractive business economics. The team favors cash-producing businesses that it believes are capable of earning acceptable returns on capital over the company’s business cycle.

The Fund will invest in U.S. companies with market capitalizations of at least $2 billion at the time of initial purchase, and may invest up to 25% of its net assets at market value at the time of purchase in non-U.S. securities.

PERFORMANCE HISTORY

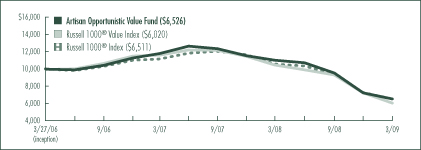

GROWTH OF AN ASSUMED $10,000 INVESTMENT (3/27/2006 to 3/31/2009)

AVERAGE ANNUAL TOTAL RETURNS (as of 3/31/2009)

| | | | | | | | | |

| Fund / Index | | 1-Year | | | 3-Year | | | Since

Inception | |

Artisan Opportunistic Value Fund | | -40.69 | % | | -13.20 | % | | -13.22 | % |

Russell 1000® Value Index | | -42.42 | | | -15.40 | | | -15.51 | |

Russell 1000® Index | | -38.27 | | | -13.24 | | | -13.28 | |

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate, so that an investor’s shares in the Fund, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For current to most recent month-end performance information, visit www.artisanfunds.com or call 800.344.1770. The graph and table above do not reflect the deduction of taxes that a shareholder would pay on distributions or sale of Fund shares. See page 92 for a description of each index.

16

INVESTING ENVIRONMENT

Stocks of all sizes suffered losses during the six-month period ended March 31, 2009, as the economic slowdown continued to take its toll. The Russell 1000® and Russell 1000® Value indices returned -30.59% and -35.22%, respectively, during the period. Weakness in the market was broad across sectors, though the more cyclical businesses, such as financials, industrials and materials, fared the worst. The traditionally defensive utilities, consumer staples and healthcare sectors were more resilient.

SECTOR DIVERSIFICATION

| | | | | | |

Sector | | 9/30/08 | | | 3/31/09 | |

Consumer Discretionary | | 11.9 | % | | 12.6 | % |

Consumer Staples | | 0.8 | | | 4.8 | |

Energy | | 4.7 | | | 7.5 | |

Financials | | 18.0 | | | 15.0 | |

Healthcare | | 2.6 | | | 8.0 | |

Industrials | | 13.8 | | | 14.5 | |

Information Technology | | 44.0 | | | 33.0 | |

Other assets less liabilities | | 4.2 | | | 4.6 | |

Total | | 100.0 | % | | 100.0 | % |

As a percentage of total net assets.

PERFORMANCE DISCUSSION

Artisan Opportunistic Value Fund is constructed from the bottom up without concern for the characteristics of a benchmark, so we expect security selection to be the primary driver of portfolio returns. For the six-month period ended March 31, 2009, the Fund returned -31.50%. Our strongest positive contributors to performance on a relative basis, were concentrated in the financials sector. They included title insurer Fidelity National Financial, Inc., mortgage REIT Annaly Capital Management, Inc. and specialty insurance and reinsurance provider Allied World Assurance Company Holdings, Ltd. We also benefited from strength in computer components manufacturer Intel Corporation. The Fund’s largest decliners during the period included floor coverings manufacturer Mohawk Industries, Inc., insurance company The Allstate Corporation, land drilling contractor Nabors Industries Ltd., investment management firm AllianceBernstein Holding L.P. and mobile phone operator Nokia Corporation.

FUND CHANGES

One positive outcome of the weak environment was the emergence of new investment opportunities. During the period, we added the following companies to the portfolio: oil and gas exploration and production company Apache Corporation, tobacco company Philip Morris International Inc., diversified defense company General Dynamics Corporation and entertainment company The Walt Disney Company.

We exited our positions in pork producer Smithfield Foods, Inc. and investment management firm AllianceBernstein Holding L.P. due to deteriorating fundamentals. We also sold integrated circuits manufacturer Taiwan Semiconductor Manufacturing Company Ltd. and electronics components distributor Arrow Electronics, Inc. in favor of other investment opportunities.

REGION ALLOCATION

| | | | | | |

| Region | | 9/30/08 | | | 3/31/09 | |

Americas | | 88.5 | % | | 89.6 | % |

Europe | | 4.4 | | | 5.8 | |

Emerging Markets | | 2.9 | | | — | |

As a percentage of total net assets.

17

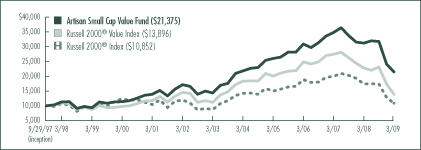

ARTISAN SMALL CAP FUND (ARTSX)

INVESTMENT PROCESS HIGHLIGHTS

Artisan Small Cap Fund employs a bottom-up investment process to construct a diversified portfolio of U.S. small-cap growth companies.

Competitive advantages. A sustainable competitive advantage is critical to producing above-average growth and profitability. Identifying the source of a company’s competitive advantage lends confidence to the team’s assessment of intrinsic value.

Return on invested capital. The team believes that, over time, a company with improving returns on its invested capital will be rewarded with a higher valuation. The team determines how much capital investment is needed to achieve a company’s continued growth and analyzes management’s ability to use that capital in the most effective way to support that growth.

Intrinsic value. The team estimates a company’s intrinsic value—the value it thinks a buyer would pay to buy the entire company. The team bases its buy and sell targets for a company’s stock on its intrinsic value estimates.

The Fund will not initiate a position in a company unless it has a market capitalization of less than $2.5 billion and meets the team’s standards for earnings growth and sustainable growth prospects.

PERFORMANCE HISTORY

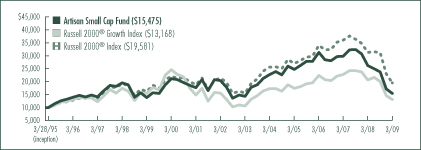

GROWTH OF AN ASSUMED $10,000 INVESTMENT (3/28/1995 to 3/31/2009)

AVERAGE ANNUAL TOTAL RETURNS (as of 3/31/2009)

| | | | | | | | | | | | | | | |

| Fund / Index | | 1-Year | | | 3-Year | | | 5-Year | | | 10-Year | | | Since

Inception | |

Artisan Small Cap Fund | | -41.08 | % | | -20.97 | % | | -7.44 | % | | 1.09 | % | | 3.17 | % |

Russell 2000® Growth Index | | -36.36 | | | -16.20 | | | -5.37 | | | -1.60 | | | 1.98 | |

Russell 2000® Index | | -37.50 | | | -16.80 | | | -5.24 | | | 1.93 | | | 4.91 | |

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate, so that an investor’s shares in the Fund, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For current to most recent month-end performance information, visit www.artisanfunds.com or call 800.344.1770. The graph and table above do not reflect the deduction of taxes that a shareholder would pay on distributions or sale of Fund shares. See page 92 for a description of each index.

18

INVESTING ENVIRONMENT

The six months ended March 31, 2009 was a challenging period for small-cap stocks and the broader market in general, owing to distressed credit markets and deterioration in the economy. Small-cap stocks suffered severe declines with the Russell 2000® and Russell 2000® Growth indices plunging - -37.17% and -34.51%, respectively. Within the Russell 2000® Growth Index, all sectors dropped by double-digit percentages. The most severe decline occurred in the energy sector as the price of oil lost over half its value, after starting the period priced at over $100 per barrel. Telecommunication services and consumer staples stocks held up best.

SECTOR DIVERSIFICATION

| | | | | | |

| Sector | | 9/30/08 | | | 3/31/09 | |

Consumer Discretionary | | 10.6 | % | | 11.0 | % |

Consumer Staples | | 2.7 | | | 2.9 | |

Energy | | 7.1 | | | 8.3 | |

Financials | | 5.4 | | | 6.2 | |

Healthcare | | 18.0 | | | 15.0 | |

Industrials | | 25.8 | | | 21.7 | |

Information Technology | | 23.6 | | | 27.4 | |

Materials | | 0.6 | | | 1.6 | |

Telecommunication Services | | 0.7 | | | — | |

Utilities | | 1.2 | | | 1.8 | |

Other assets less liabilities | | 4.3 | | | 4.1 | |

Total | | 100.0 | % | | 100.0 | % |

As a percentage of total net assets.

PERFORMANCE DISCUSSION

Artisan Small Cap Fund returned - -35.07% during the period, outperforming the Russell 2000® Index, but falling short of the Russell 2000® Growth Index. Compared with the Russell 2000® Growth Index, the Fund benefited from strong security selection in the industrials sector and an overweight position in the technology sector. Stocks that helped our relative performance in the industrials sector included ship refueling services company Aegean Marine Petroleum Network Inc., less-than-truckload provider Old Dominion Freight Line, Inc. and multi-discipline consulting firm FTI Consulting, Inc. Other leading performers on a relative basis during the period were sporting goods retailer Hibbett Sports, Inc., content-protection company Macrovision Corporation, and pet supplies retailer PETsMART, Inc.

The healthcare sector was the primary area of relative weakness. The Fund’s underperformance was driven in part by our underweight in the biotechnology industry, which held up better than the other industries in the sector. Also detracting from our performance in the sector were ICON PLC, a global clinical research services contractor, Psychiatric Solutions, Inc., a behavioral health services provider, and Wright Medical Group, Inc., an orthopedic device company. Other major detractors to performance were oil services contractor Hercules Offshore, Inc., oil and gas producer Carrizo Oil & Gas, Inc. and commodity risk management company FCStone Group, Inc.

FUND CHANGES

Record levels of volatility in the period created many new purchase opportunities. The biggest shifts occurred in the information technology and industrials sectors, which increased and decreased in weight, respectively. In the technology sector, we added Internet exchange services provider Equinix, Inc., information technology national security company ManTech International Corporation and design software company ANSYS, Inc. Other stocks that met our security selection criteria were chemicals producer Albemarle Corporation, previously mentioned FTI Consulting, Inc., and contract drilling company Atwood Oceanics, Inc.

Our exposure to the industrials sector declined due in part to reduced positions in Interline Brands, Inc. and AAR CORP. and sales of Healthcare Services Group, Inc., Innerworkings, Inc. and Ladish Co., Inc.

19

ARTISAN SMALL CAP VALUE FUND (ARTVX)

INVESTMENT PROCESS HIGHLIGHTS

Artisan Small Cap Value Fund employs a bottom-up investment process to construct a diversified portfolio of small-cap U.S. companies that the team believes are undervalued, in solid financial condition and have attractive business economics. The team believes companies with these characteristics are less likely to experience eroding values over the long term.

Attractive valuation. The team values a business using what it believes are reasonable expectations for the long-term earnings power and capitalization rates of that business. This results in a range of values for the company that the team believes would be reasonable. The team generally will purchase a security if the stock price falls below or toward the lower end of that range.

Sound financial condition. The team favors companies with an acceptable level of debt and positive cash flow. At a minimum, the team tries to avoid companies that have so much debt that management may be unable to make decisions that would be in the best interest of the companies’ shareholders.

Attractive business economics. The team favors cash-producing businesses that it believes are capable of earning acceptable returns on capital over the company’s business cycle.

The Fund will not initiate a position in a company unless it has a market capitalization below $2 billion.

PERFORMANCE HISTORY

GROWTH OF AN ASSUMED $10,000 INVESTMENT (9/29/1997 to 3/31/2009)

AVERAGE ANNUAL TOTAL RETURNS (as of 3/31/2009)

| | | | | | | | | | | | | | | |

| Fund / Index | | 1-Year | | | 3-Year | | | 5-Year | | | 10-Year | | | Since

Inception | |

Artisan Small Cap Value Fund | | -31.50 | % | | -11.54 | % | | -0.32 | % | | 8.71 | % | | 6.83 | % |

Russell 2000® Value Index | | -38.89 | | | -17.54 | | | -5.30 | | | 4.87 | | | 2.90 | |

Russell 2000® Index | | -37.50 | | | -16.80 | | | -5.24 | | | 1.93 | | | 0.71 | |

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate, so that an investor’s shares in the Fund, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For current to most recent month-end performance information, visit www.artisanfunds.com or call 800.344.1770. The graph and table above do not reflect the deduction of taxes that a shareholder would pay on distributions or sale of Fund shares. See page 92 for a description of each index.

20

INVESTING ENVIRONMENT

The six-month period ended March 31, 2009 proved to be a challenging time for small-cap equity investors. Economic reports painted a gloomy picture and consumer confidence sunk to historic lows. For this semiannual reporting period, the Russell 2000® Value and Russell 2000® indices returned - -39.64% and -37.17%, respectively. Every sector in the Russell 2000® Value Index suffered a double-digit decline. The traditionally defensive utilities, consumer staples and health care sectors held up best. The energy sector was hit hardest, losing more than -60%, and the consumer discretionary sector lost almost -50%.

SECTOR DIVERSIFICATION

| | | | | | |

| Sector | | 9/30/08 | | | 3/31/09 | |

Consumer Discretionary | | 13.1 | % | | 10.1 | % |

Consumer Staples | | 3.1 | | | 3.3 | |

Energy | | 6.3 | | | 7.9 | |

Financials | | 11.8 | | | 9.9 | |

Healthcare | | 5.6 | | | 3.7 | |

Industrials | | 20.3 | | | 25.9 | |

Information Technology | | 28.1 | | | 30.4 | |

Materials | | 2.3 | | | 5.1 | |

Utilities | | 3.2 | | | 0.8 | |

Other assets less liabilities | | 6.2 | | | 2.9 | |

Total | | 100.0 | % | | 100.0 | % |

As a percentage of total net assets.

PERFORMANCE DISCUSSION

Artisan Small Cap Value Fund held up better than the Russell 2000® Value Index with a return of -32.58%. We benefited from our security selection as our holdings in most sectors outperformed those in the benchmark. Our outsized position in the relatively strong technology sector also aided relative returns. Our biggest gainers this period included civil construction and transportation contractor Granite Construction Incorporated, energy services company McDermott International, Inc., steel scrap recycler Schnitzer Steel Industries, Inc., chicken producer Sanderson Farms, Inc. and program management and consulting services provider MAXIMUS, Inc.

Our investments in the health care and utilities sectors held back results relative to the benchmark. AMN Healthcare Services, Inc., Cross Country Healthcare, Inc. and HealthSpring, Inc. were among our biggest detractors in the health care sector. Although our utilities holdings did not keep pace with those in the benchmark, our underweight position in the sector was a bigger negative. Ethan Allen Interiors Inc., Quanex Building Products Corporation, Cousins Properties Incorporated, Acuity Brands, Inc. and AnnTaylor Stores Corp. were among our weakest performers.

FUND CHANGES

One positive outcome of the weak environment was the emergence of new investment opportunities. Some of our largest purchases included McDermott International, Inc., semiconductor processing equipment company Varian Semiconductor Equipment Associates, Inc., computer products distributor Arrow Electronics, Inc., inland tank barge operator Kirby Corporation, construction materials manufacturer Eagle Materials Inc., specialty chemicals producer OM Group, Inc. and metal products manufacturer Mueller Industries, Inc.

We had a handful of takeouts that were completed during the period. Hilb Rogal & Hobbs Company was acquired by Willis Group Holdings Limited, Grey Wolf, Inc. was bought by Precision Drilling Trust and SI International Inc. was acquired by Serco Group plc. We also sold ALLETE, Inc., The Men’s Wearhouse, Inc., AnnTaylor Stores Corporation and UIL Holdings Corporation in favor of other opportunities.

21

ARTISAN GLOBAL VALUE FUND

Schedule of Investments – March 31, 2009 (Unaudited)

| | | | | |

| | | Shares

Held | | Value |

| | | | | |

| COMMON AND PREFERRED STOCKS - 95.9% | | | | | |

| | | | | |

| FRANCE - 5.2% | | | | | |

Publicis Groupe(1) | | 16,210 | | $ | 415,034 |

Societe Television Francaise 1(1) | | 29,828 | | | 233,461 |

Total SA(1) | | 4,694 | | | 232,803 |

| | | | | |

| | | | | 881,298 |

| HONG KONG - 2.7% | | | | | |

Guoco Group Limited(1) | | 82,250 | | | 456,681 |

| | | | | |

| JAPAN - 4.2% | | | | | |

Credit Saison Co., Ltd.(1) | | 25,500 | | | 251,276 |

Daiwa Securities Group Inc.(1) | | 52,596 | | | 232,802 |

SANKYO CO., LTD.(1) | | 5,548 | | | 240,141 |

| | | | | |

| | | | | 724,219 |

| KOREA - 2.2% | | | | | |

SK Telecom Co., Ltd. (DR) | | 23,928 | | | 369,688 |

| | | | | |

| MEXICO - 2.0% | | | | | |

Grupo Modelo, S.A. de C.V., Series C | | 112,336 | | | 340,220 |

| | | | | |

| NETHERLANDS - 1.4% | | | | | |

Wolters Kluwer NV(1) | | 14,705 | | | 238,736 |

| | | | | |

| SWITZERLAND - 10.2% | | | | | |

Adecco SA(1) | | 13,709 | | | 428,893 |

Novartis AG(1) | | 13,999 | | | 528,375 |

Panalpina Welttransport Holding AG(1) | | 5,853 | | | 287,607 |

Pargesa Holding SA(1) | | 9,141 | | | 485,472 |

| | | | | |

| | | | | 1,730,347 |

| UNITED KINGDOM - 18.6% | | | | | |

Cadbury PLC(1) | | 20,363 | | | 153,792 |

Cadbury PLC (DR) | | 2,825 | | | 85,598 |

Diageo plc(1) | | 47,119 | | | 532,043 |

Experian PLC(1) | | 134,438 | | | 842,198 |

Home Retail Group plc(1) | | 114,727 | | | 367,266 |

Royal Dutch Shell PLC, Class A(1) | | 10,304 | | | 231,195 |

Signet Jewelers Ltd. | | 46,331 | | | 530,490 |

Unilever PLC (DR) | | 23,028 | | | 435,920 |

| | | | | |

| | | | | 3,178,502 |

| UNITED STATES - 49.4% | | | | | |

3M Company | | 10,061 | | | 500,233 |

American Express Company | | 33,566 | | | 457,505 |

Arch Capital Group Ltd., Series A Preferred, 8.00% | | 5,904 | | | 117,194 |

| | | | | | | |

| | | Shares

Held | | Value | |

| | | | | | | |

| UNITED STATES (CONTINUED) | | | | | | | |

Arch Capital Group Ltd., Series B Preferred, 7.875% | | | 15,930 | | $ | 296,935 | |

The Bank of New York Mellon Corporation | | | 24,924 | | | 704,103 | |

Cintas Corporation | | | 20,140 | | | 497,861 | |

Dell Inc.(2) | | | 43,205 | | | 409,583 | |

Google Inc., Class A(2) | | | 1,704 | | | 593,094 | |

Johnson & Johnson | | | 16,209 | | | 852,593 | |

Marsh & McLennan Companies, Inc. | | | 43,842 | | | 887,801 | |

Microsoft Corporation | | | 40,895 | | | 751,241 | |

Mohawk Industries, Inc.(2) | | | 7,053 | | | 210,673 | |

The Procter & Gamble Company | | | 12,144 | | | 571,861 | |

The Sherwin-Williams Company | | | 4,974 | | | 258,499 | |

Tyco Electronics Ltd. | | | 30,555 | | | 337,327 | |

Wal-Mart Stores, Inc. | | | 9,199 | | | 479,268 | |

WellPoint Inc.(2) | | | 13,155 | | | 499,495 | |

| | | | | | | |

| | | | | | 8,425,266 | |

| | | | | | | |

Total common and preferred stocks

(Cost $19,349,787) | | | | | | 16,344,957 | |

| | |

| | | Par

Amount | | | |

SHORT-TERM INVESTMENTS

(CASH EQUIVALENTS) - 4.9% | | | | | | | |

Repurchase agreement with Fixed Income Clearing Corporation, 0.11%, dated 3/31/09, due 4/1/09, maturity value $830,003(3)

(Cost $830,000) | | $ | 830,000 | | | 830,000 | |

| | | | | | | |

| | | | | | | |

Total investments - 100.8%

(Cost $20,179,787) | | | | | | 17,174,957 | |

| | | | | | | |

Other assets less liabilities - (0.8%) | | | | | | (132,396 | ) |

| | | | | | | |

| | | | | | | |

Total net assets - 100.0%(4) | | | | | $ | 17,042,561 | |

| | | | | | | |

(1) | Valued at a fair value in accordance with procedures established by the board of directors of Artisan Funds, Inc. In total, securities valued at a fair value were $6,157,775 or 36.1% of total net assets. |

(2) | Non-income producing security. |

| | | | | | | | |

Issuer | | Rate | | | Maturity | | Value |

U.S. Treasury Bond | | 7.50 | % | | 11/15/2024 | | $ | 848,484 |

(4) | Percentages for the various classifications relate to total net assets. |

22

| | | | | | | |

| PORTFOLIO DIVERSIFICATION - March 31, 2009 (Unaudited) | |

| | | Value | | | Percentage

of Total

Net Assets | |

Consumer Discretionary | | $ | 2,494,300 | | | 14.6 | % |

Consumer Staples | | | 2,598,702 | | | 15.3 | |

Energy | | | 463,998 | | | 2.7 | |

Financials | | | 3,889,769 | | | 22.8 | |

Healthcare | | | 1,880,463 | | | 11.0 | |

Industrials | | | 2,556,792 | | | 15.0 | |

Information Technology | | | 2,091,245 | | | 12.3 | |

Telecommunication Services | | | 369,688 | | | 2.2 | |

| | | | | | | |

Total common and preferred stocks | | | 16,344,957 | | | 95.9 | |

Short-term investments | | | 830,000 | | | 4.9 | |

| | | | | | | |

Total investments | | | 17,174,957 | | | 100.8 | |

Other assets less liabilities | | | (132,396 | ) | | (0.8 | ) |

| | | | | | | |

Total net assets | | $ | 17,042,561 | | | 100.0 | % |

| | | | | | | |

| | | | | | |

| CURRENCY EXPOSURE - March 31, 2009 (Unaudited) | |

| | | Value | | Percentage

of Total

Investments | |

British pound | | $ | 1,895,299 | | 11.0 | % |

Euro | | | 1,351,229 | | 7 .9 | |

Hong Kong dollar | | | 456,681 | | 2 .6 | |

Japanese yen | | | 724,219 | | 4 .2 | |

Mexican peso | | | 340,220 | | 2 .0 | |

Swiss franc | | | 1,730,347 | | 10.1 | |

US dollar | | | 10,676,962 | | 62.2 | |

| | | | | | |

Total investments | | $ | 17,174,957 | | 100.0 | % |

| | | | | | |

| | | | | |

| TOP TEN HOLDINGS - March 31, 2009 (Unaudited) | |

Company Name | | Country | | Percentage

of Total

Net Assets | |

Marsh & McLennan Companies, Inc. | | United States | | 5.2 | % |

Johnson & Johnson | | United States | | 5.0 | |

Experian PLC | | United Kingdom | | 4.9 | |

Microsoft Corporation | | United States | | 4.4 | |

The Bank of New York Mellon Corporation | | United States | | 4.1 | |

Google Inc. | | United States | | 3.5 | |

The Procter & Gamble Company | | United States | | 3.4 | |

Diageo plc | | United Kingdom | | 3.1 | |

Signet Jewelers Ltd. | | United Kingdom | | 3.1 | |

Novartis AG | | Switzerland | | 3.1 | |

| | | | | |

Total | | | | 39.8 | % |

| | | | | |

For the purpose of determining the Fund’s top ten holdings, securities of the same issuer are aggregated to determine the weight in the Fund.

Company names are as reported by a data service provider and in some cases are translations; a company’s legal name may be different.

(DR) Depository Receipt, voting rights may vary.

The accompanying notes are an integral part of the financial statements.

23

ARTISAN INTERNATIONAL FUND

Schedule of Investments – March 31, 2009 (Unaudited)

| | | | | |

| | | Shares

Held | | Value |

| | | | | |

| COMMON AND PREFERRED STOCKS AND EQUITY-LINKED SECURITIES - 95.7% | | | | | |

| | | | | |

| BELGIUM - 2.7% | | | | | |

Anheuser-Busch InBev NV(1) | | 4,427,502 | | $ | 122,258,266 |

Delhaize Group(1) | | 1,198,546 | | | 77,733,249 |

| | | | | |

| | | | | 199,991,515 |

| BRAZIL - 2.7% | | | | | |

Petroleo Brasileiro S.A., Preferred (DR) | | 3,921,249 | | | 96,070,601 |

Redecard SA | | 8,367,560 | | | 101,179,031 |

| | | | | |

| | | | | 197,249,632 |

| CANADA - 2.5% | | | | | |

Canadian Pacific Railway Limited | | 6,105,810 | | | 180,915,150 |

| | | | | |

| CHINA - 7.2% | | | | | |

China Construction Bank, H Shares(1) | | 209,744,100 | | | 119,113,330 |

China Life Insurance Co., Limited, H Shares(1) | | 53,517,900 | | | 176,074,519 |

China Merchants Holdings International Company Limited(1) | | 29,090,900 | | | 68,756,417 |

China Resources Land Limited(1) | | 81,290,631 | | | 127,245,303 |

Guangzhou R&F Properties Company Limited, H Shares(1) | | 6,318,400 | | | 7,328,504 |

Ping An Insurance (Group) Company of China Limited, H Shares(1) | | 4,855,300 | | | 29,081,376 |

| | | | | |

| | | | | 527,599,449 |

| FINLAND - 1.6% | | | | | |

Fortum Oyj(1) | | 6,093,763 | | | 115,992,799 |

| | | | | |

| FRANCE - 13.8% | | | | | |

Accor SA(1) | | 107,358 | | | 3,731,122 |

Alstom(1) | | 1,719,145 | | | 89,002,694 |

BNP Paribas(1) | | 1,357,207 | | | 55,939,426 |

Bouygues SA(1) | | 4,342,228 | | | 154,915,632 |

Carrefour SA(1) | | 1,853,105 | | | 72,219,089 |

France Telecom SA(1) | | 6,175,278 | | | 140,431,784 |

LVMH Moet Hennessy Louis Vuitton SA(1) | | 2,576,248 | | | 161,499,512 |

Technip SA(1) | | 588,562 | | | 20,742,710 |

Unibail-Rodamco(1) | | 282,163 | | | 40,146,687 |

Vinci SA(1) | | 7,181,150 | | | 265,985,179 |

| | | | | |

| | | | | 1,004,613,835 |

| GERMANY - 13.7% | | | | | |

Allianz SE(1) | | 846,656 | | | 71,325,038 |

| | | | | |

| | | Shares

Held | | Value |

| | | | | |

| GERMANY (CONTINUED) | | | | | |

Bayer AG(1) | | 5,389,022 | | $ | 258,168,458 |

Daimler AG(1) | | 5,831,509 | | | 148,233,749 |

Deutsche Post AG(1) | | 1,204,068 | | | 12,964,179 |

Fraport AG(1) | | 2,205,066 | | | 70,942,630 |

Linde AG(1) | | 2,858,072 | | | 194,210,886 |

Muenchener Rueckversicherungs-Gesellschaft AG(1) | | 808,141 | | | 98,708,223 |

Wacker Chemie AG(1) | | 1,775,435 | | | 147,781,347 |

| | | | | |

| | | | | 1,002,334,510 |

| HONG KONG - 2.4% | | | | | |

The Bank of East Asia, Ltd.(1) | | 23,730,840 | | | 45,885,174 |

Hutchison Whampoa Limited(1) | | 7,521,906 | | | 37,036,985 |

Li & Fung Limited(1) | | 12,632,000 | | | 29,801,762 |

NWS Holdings Limited(1) | | 34,876,746 | | | 47,555,284 |

Sun Hung Kai Properties Limited(1) | | 2,004,234 | | | 17,992,203 |

| | | | | |

| | | | | 178,271,408 |

| INDIA - 1.2% | | | | | |

Housing Development Finance Corporation Ltd.(1) | | 1,248,822 | | | 34,937,483 |

ICICI Bank Limited(1) | | 2,180,220 | | | 14,489,638 |

ICICI Bank Limited (DR) | | 3,052,424 | | | 40,566,715 |

| | | | | |

| | | | | 89,993,836 |

| ITALY - 1.0% | | | | | |

Intesa Sanpaolo(1) | | 26,345,861 | | | 72,453,323 |

| | | | | |

| JAPAN - 9.5% | | | | | |

CANON INC.(1) | | 2,258,200 | | | 65,870,984 |

DENSO CORPORATION(1) | | 5,416,600 | | | 109,434,389 |

JAPAN TOBACCO INC.(1) | | 83,074 | | | 221,859,579 |

Mitsubishi UFJ Financial Group, Inc.(1) | | 7,800,145 | | | 38,319,502 |

Mizuho Financial Group, Inc.(1) | | 16,436,343 | | | 31,995,704 |

SUZUKI MOTOR CORPORATION(1) | | 8,848,650 | | | 148,070,056 |