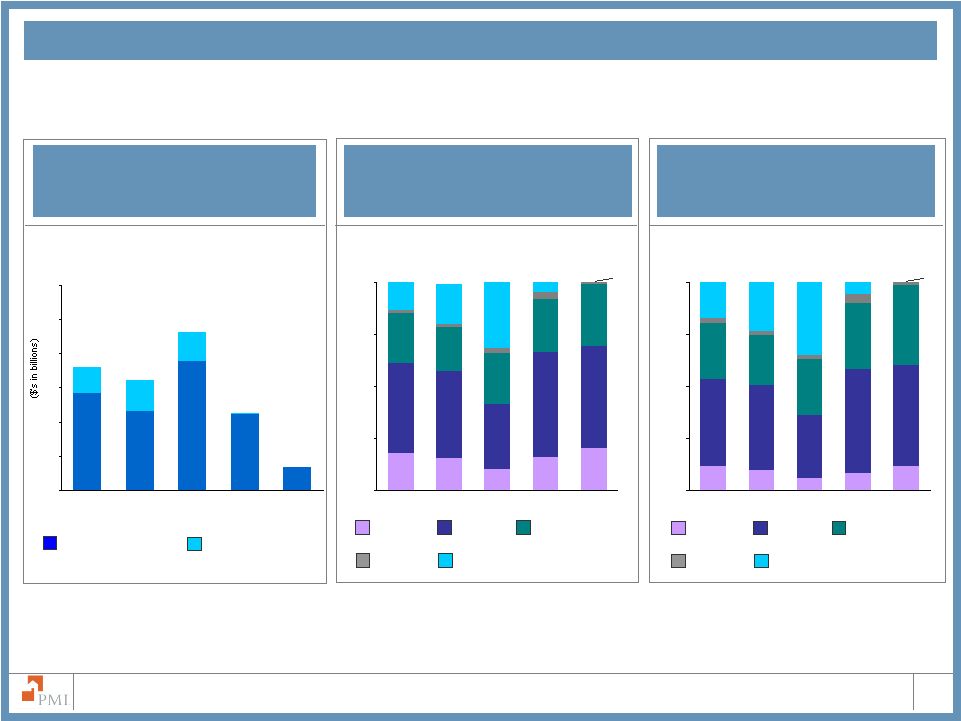

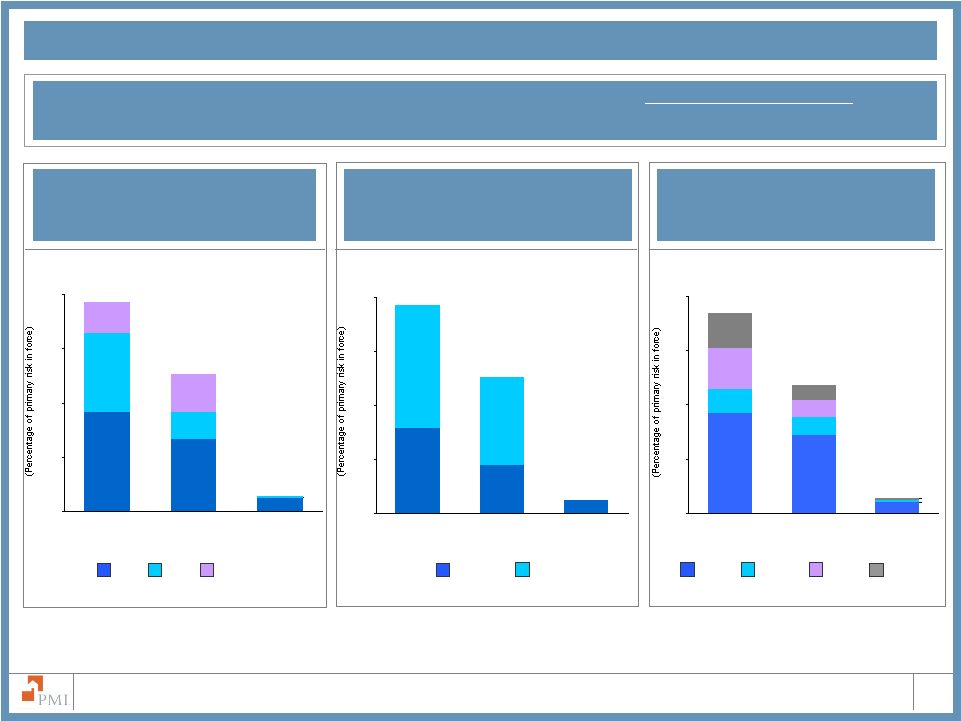

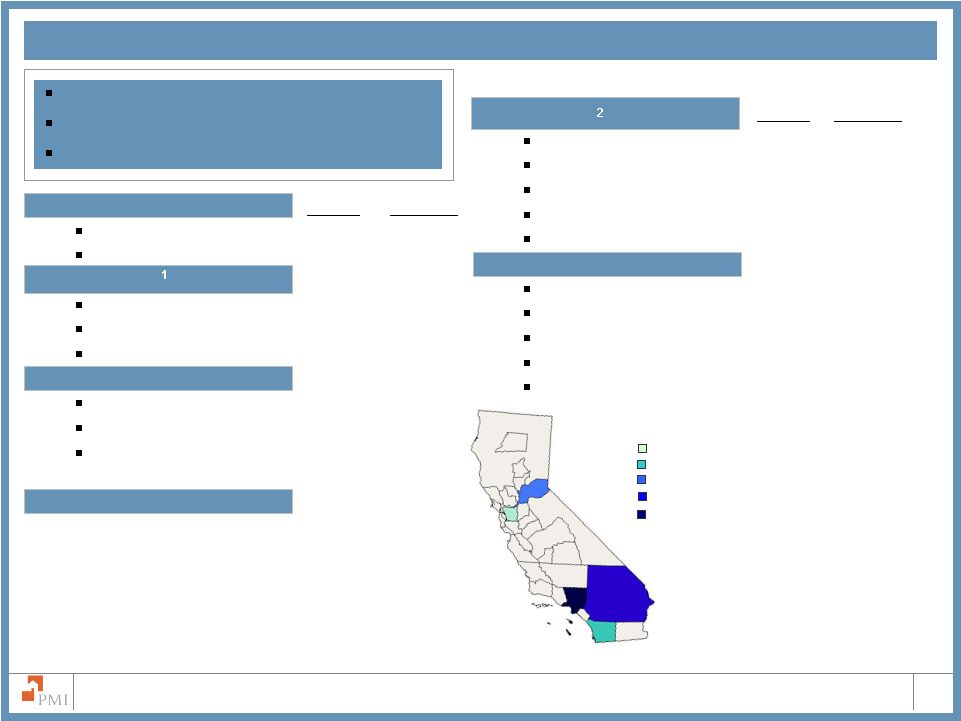

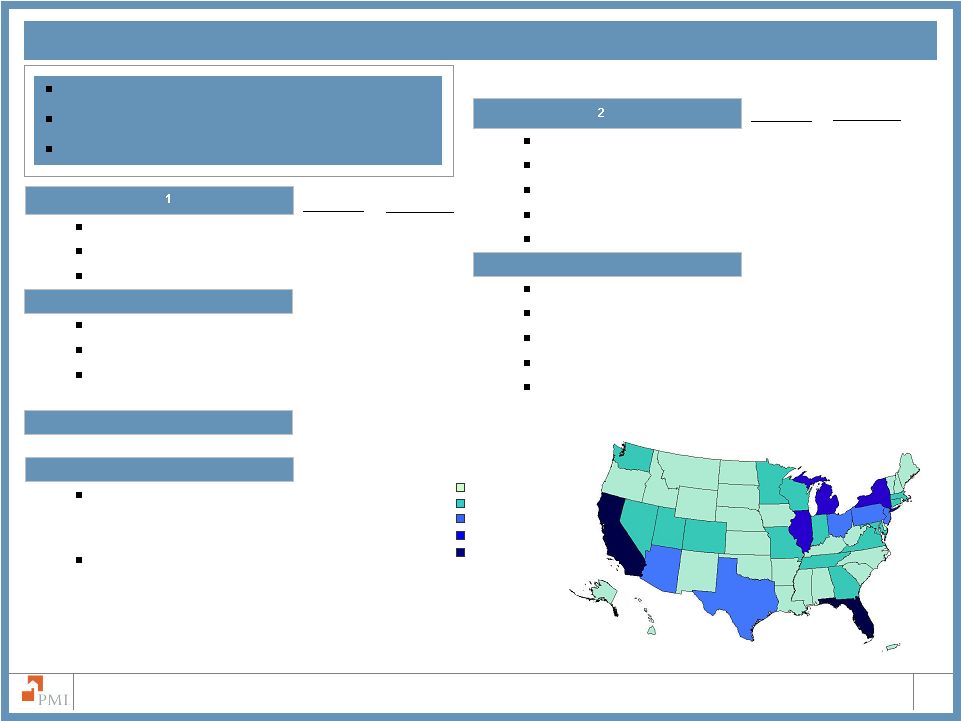

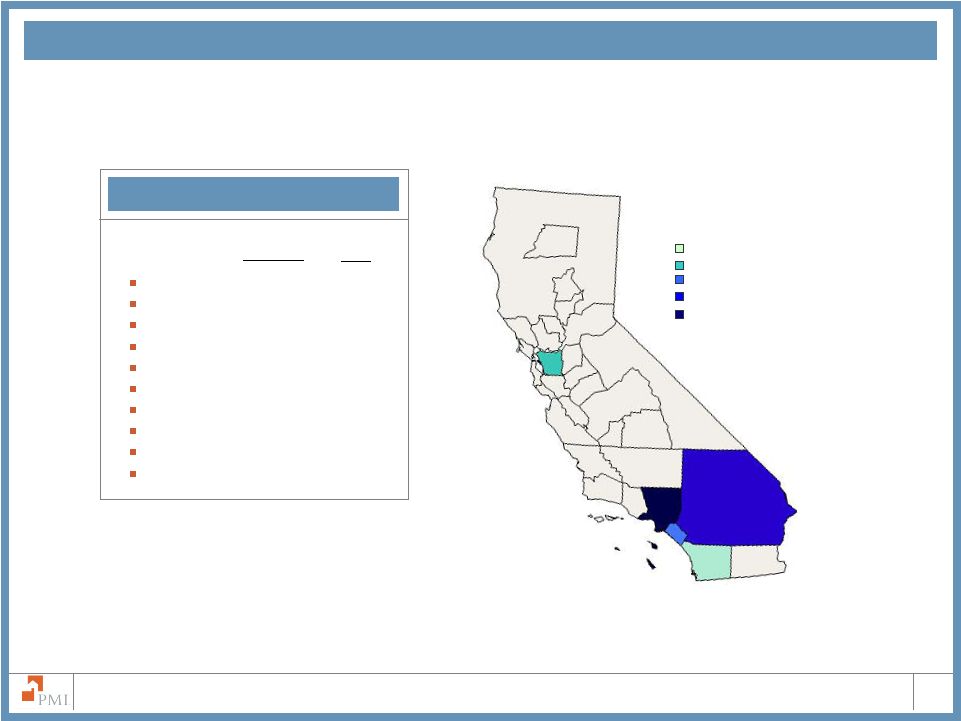

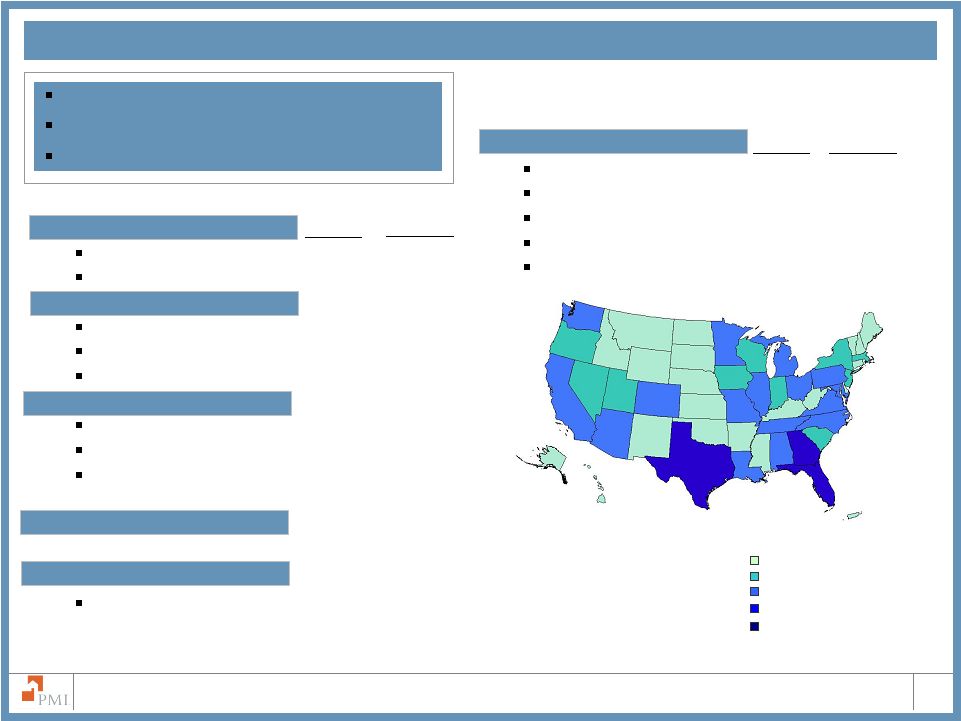

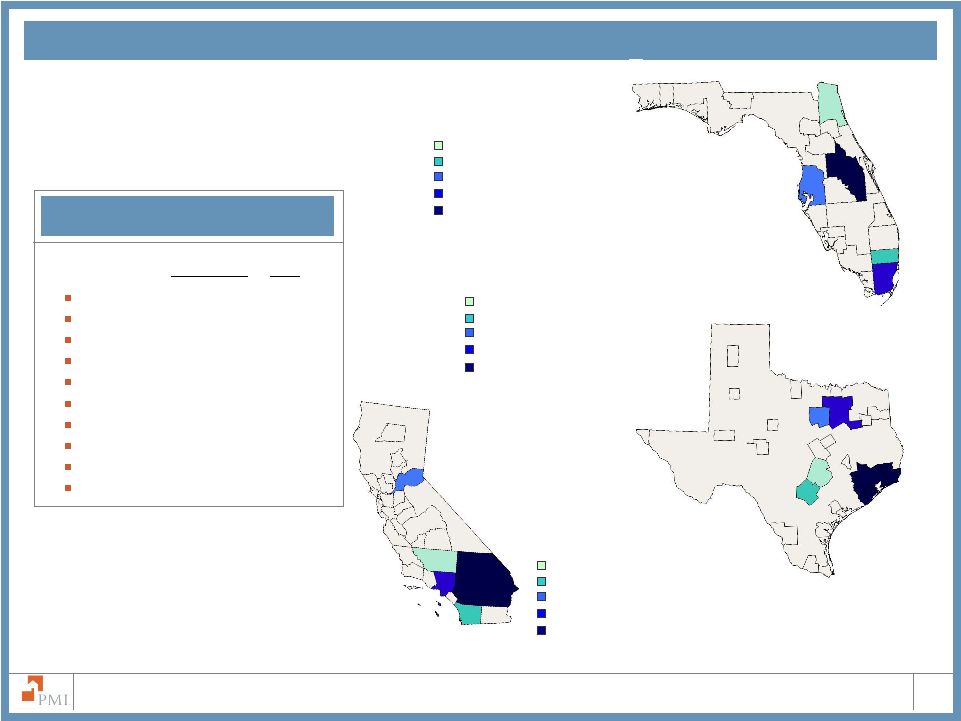

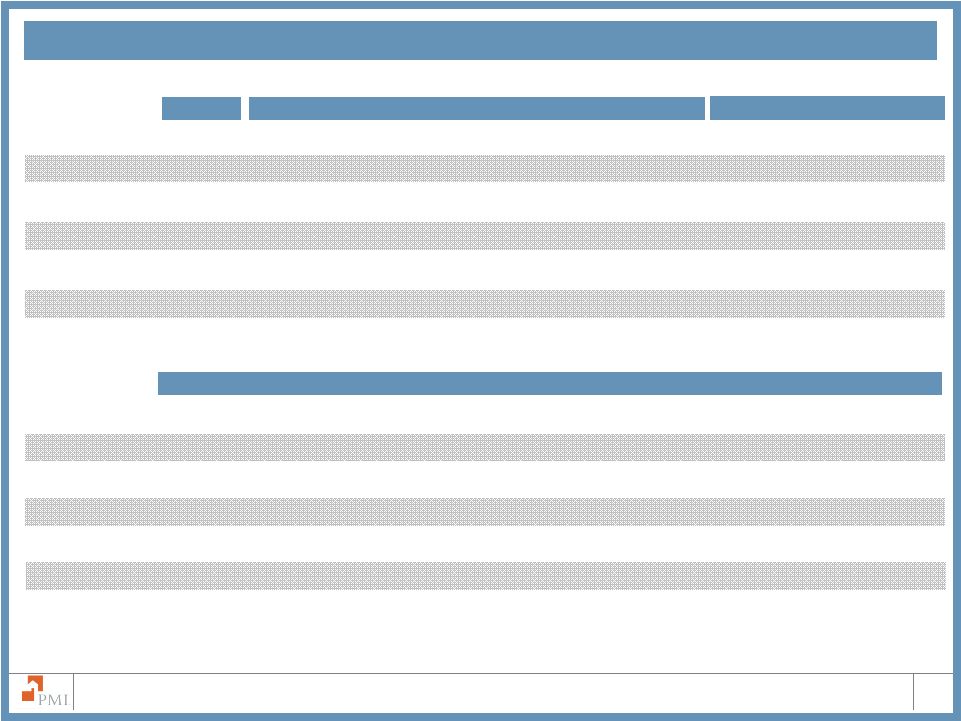

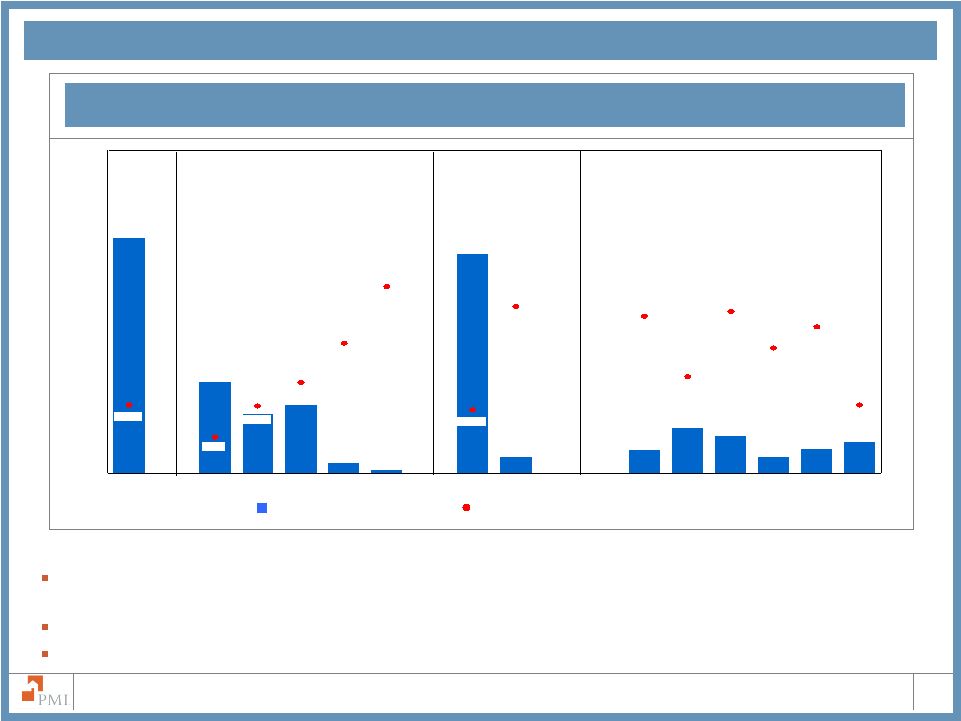

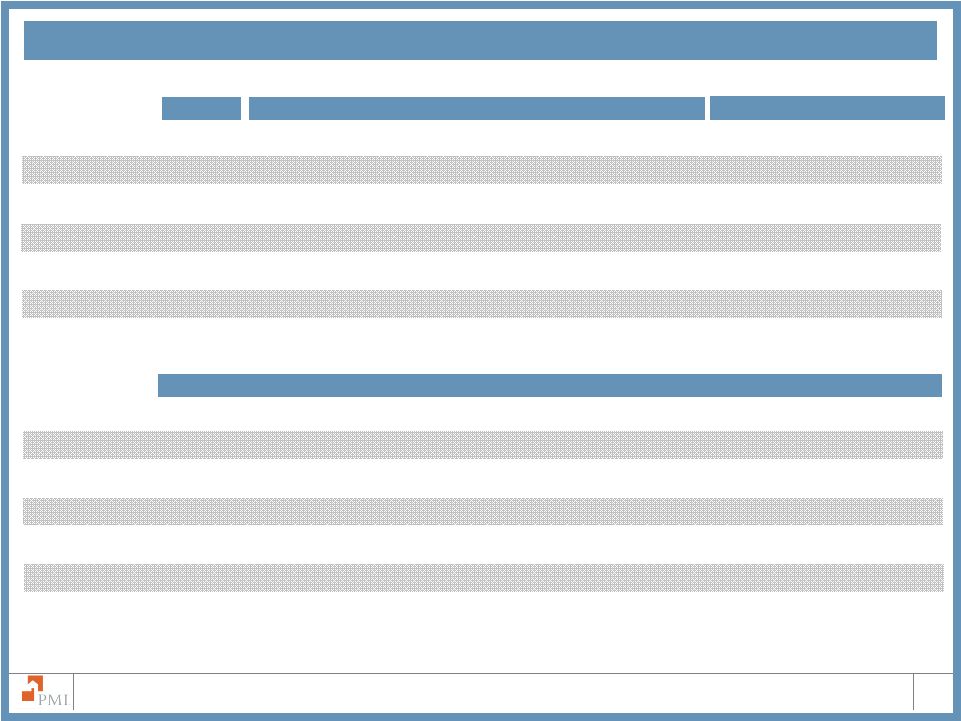

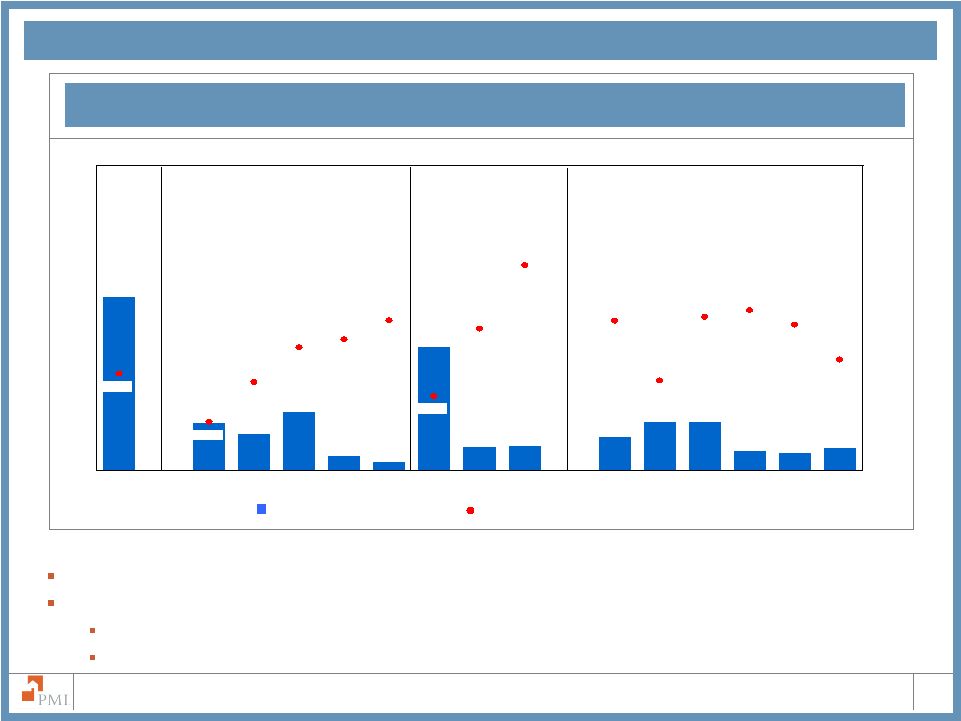

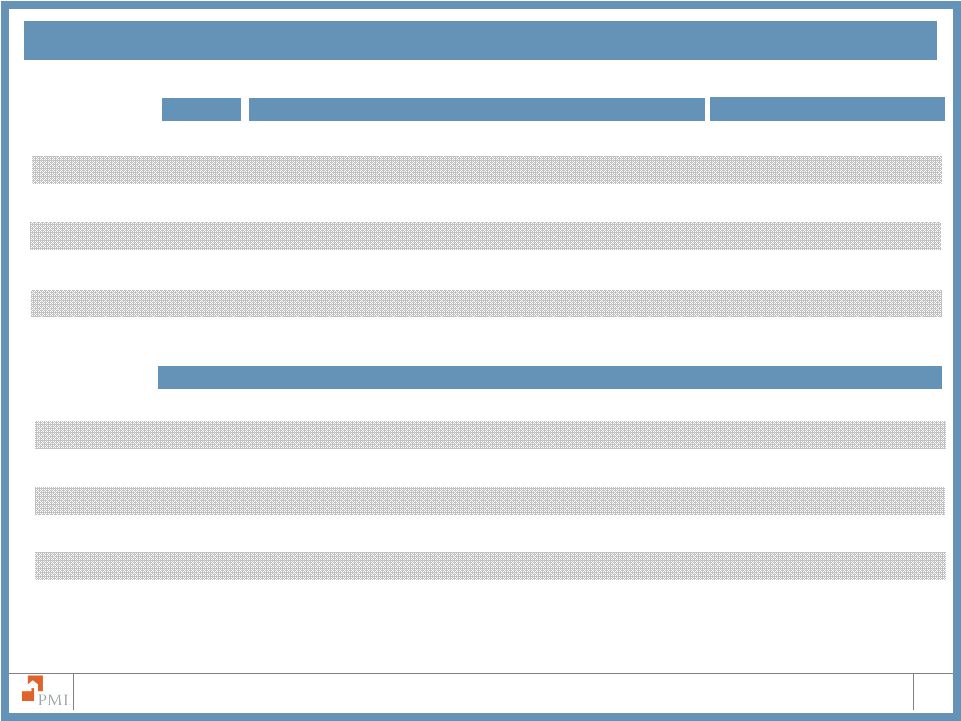

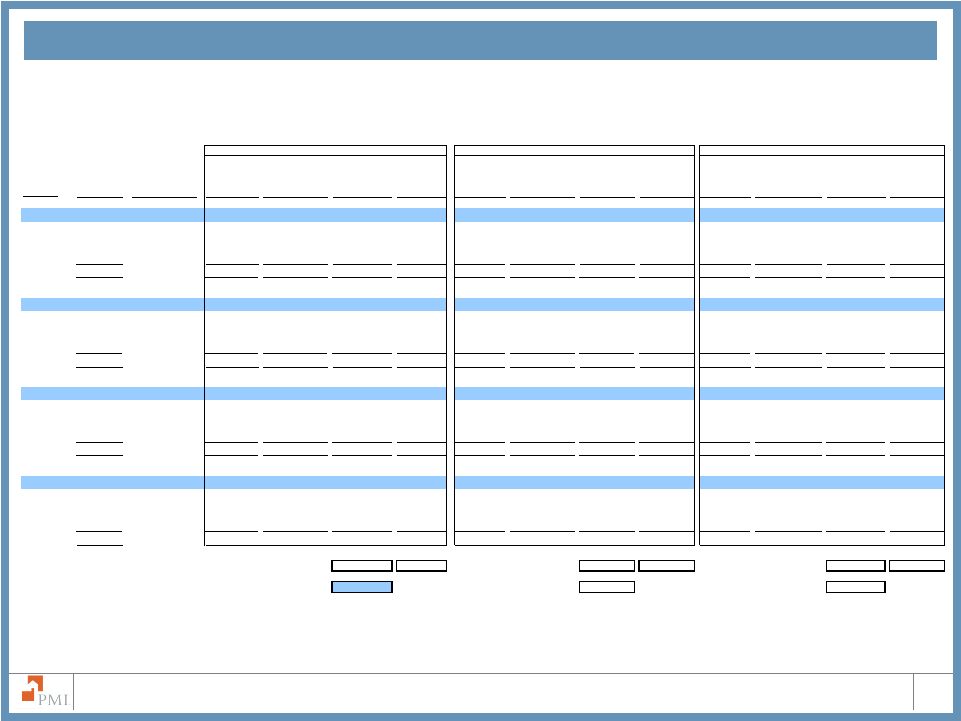

The PMI Group, Inc. Interest Only LTV > 97% Alt-A California Florida Auto States Avg Loan Size Avg LTV Avg FICO 35 Modified Pool Portfolio Characteristics Modified Pool IIF as of June 30, 2009 1 Excludes unreported FICO scores 2 Excludes Balloon, Buy Down, and Other 3 At origination Note: PMI did not insure any modified pool contracts with deductible in 2008 or 2009 and did not insure any modified pool contracts without deductible in 2007, 2008 or 2009 Categories are not mutually exclusive except for Credit Score and Loan Type. Vintage refers to the year the insurance was issued. All $ in Millions, except for Average Loan Size Specific Portfolio Characteristics Specific Portfolio Characteristics Credit Score Loan Type Credit Score Loan Type Total Total Fixed Rate ARM 2/28s Fixed Rate ARM 2/28s Deductible Non Deductible Less than 575 575 - 619 620 - 679 680 - 719 720 and above Less than 575 575 - 619 620 - 679 680 - 719 720 and above Interest Only LTV > 97% Alt-A California Florida Auto States Avg Loan Size Avg LTV Avg FICO Total Portfolio $32,267 $329 $818 $10,200 $9,924 $10,990 $30,386 $1,867 $2 2007 Vintage $7,370 $130 $301 $2,581 $2,484 $1,873 $6,912 $457 $0 2006 Vintage $12,602 $64 $144 $4,811 $4,226 $3,357 $12,432 $168 $2 2005 Vintage $6,396 $5 $54 $1,589 $2,022 $2,724 $5,301 $1,093 $1 2004 Vintage and Prior $5,899 $130 $320 $1,218 $1,192 $3,036 $5,742 $148 $0 Total Portfolio $10,915 $804 $20,916 $5,529 $3,493 $3,234 $173,681 78 699 2007 Vintage $3,140 $697 $4,855 $1,437 $739 $674 $203,973 82 686 2006 Vintage $4,680 $48 $9,097 $2,068 $1,532 $1,191 $187,439 79 693 2005 Vintage $2,399 $36 $4,449 $1,147 $844 $605 $173,310 79 708 2004 Vintage and Prior $697 $24 $2,515 $877 $378 $764 $129,610 72 710 Total Portfolio $7,918 $356 $801 $2,935 $1,874 $1,757 $4,957 $2,892 $16 2006 Vintage $4,334 $345 $759 $1,897 $867 $466 $1,641 $2,677 $16 2005 Vintage $1,322 $0 $5 $273 $391 $637 $1,301 $20 $0 2004 Vintage and Prior $2,262 $11 $37 $765 $617 $654 $2,015 $195 $0 Total Portfolio $1,061 $1,608 $2,946 $1,274 $723 $898 $150,389 86 673 2006 Vintage $306 $1,540 $341 $512 $450 $695 $156,337 93 650 2005 Vintage $604 $1 $939 $290 $100 $57 $195,187 76 718 2004 Vintage and Prior $152 $67 $1,666 $472 $172 $146 $124,599 78 693 |