UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-07257

SEI Institutional Investments Trust

(Exact name of registrant as specified in charter)

SEI Investments

One Freedom Valley Drive

Oaks, PA 19456

(Address of principal executive offices) (Zip code)

CT Corporation

101 Federal Street

Boston, MA 02110

(Name and address of agent for service)

Registrant’s telephone number, including area code: 1-800-342-5734

Date of fiscal year end: May 31, 2010

Date of reporting period: May 31, 2010

Item 1. Reports to Stockholders.

SEI Institutional Investments Trust

Annual Report as of May 31, 2010

Large Cap Fund

Large Cap Diversified Alpha Fund

Large Cap Disciplined Equity Fund

Large Cap Index Fund

Small Cap Fund

Small/Mid Cap Equity Fund

U.S. Managed Volatility Fund

International Equity Fund

World Equity Ex-US Fund

Screened World Equity Ex-US Fund

Enhanced LIBOR Opportunities Fund

Core Fixed Income Fund

High Yield Bond Fund

Long Duration Fund

Emerging Markets Debt Fund

Real Return Fund

TABLE OF CONTENTS

The Trust files its complete schedule of portfolio holdings with the Securities and Exchange Commission for the first and third quarters of each fiscal year on Form N-Q within sixty days after the end of the period. The Trust’s Forms N-Q are available on the Commission’s website at http://www.sec.gov, and may be reviewed and copied at the Commission’s Public Reference Room in Washington, DC. Information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

A description of the policies and procedures that the Trust uses to determine how to vote proxies relating to portfolio securities, as well as information relating to how a Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30, is available (i) without charge, upon request, by calling 1-800-DIAL-SEI; and (ii) on the Commission’s website at http://www.sec.gov.

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

SEI INSTITUTIONAL INVESTMENTS TRUST — MAY 31, 2010 (Unaudited)

Large Cap Fund

I. Objective:

The Large Cap Fund (the “Fund) seeks to provide long-term growth of capital and income.

II. Multi-Manager Approach Statement:

The Fund uses a multi-manager approach, relying on a number of sub-advisors with differing investment approaches to manage portions of the Fund’s portfolio under the general supervision of SEI Investments Management Corp. (SIMC). The Fund utilized the following sub-advisers as of May 31, 2010: Quantitative Management Associates, LLC, Legg Mason Capital Management Inc., Delaware Investments Company, Neuberger Berman Management LLC, Aronson + Johnson + Ortiz L.P. and LSV Asset Management. For the fiscal year ended May 31, 2010, Neuberger Berman Management LLC was added to the Fund, while Intech Investment Management, LLC and Goldman Sachs Asset Management were terminated.

III. Market Commentary:

The U.S. equity market, as measured by the Russell 1000 Index, gained 22.33% during the fiscal year ended May 31, 2010. After a historic fall in 2008, equity markets staged a strong rebound in 2009 off the heels of unprecedented global intervention by governments and central banks. Stocks and sectors that suffered the steepest declines in the year prior drove market returns in 2009. More specifically, smaller-cap and lower-quality names, most of which were assumed to be insolvent, posted significant gains.

For the fiscal year, value stocks outperformed their growth counterparts in the large-cap universe. All ten Global Industry Classification Standard (GICS) sectors posted positive performance during the period. A renewed confidence in economic recovery revived investors’ willingness for risk taking. The Consumer Discretionary sector was the best-performing sector, up 44%, followed by Industrials and Information Technology. Conversely, more defensive sectors, which performed well during the year before, lagged the broad market. Utilities, Consumer Staples and Healthcare names failed to keep pace with the market, as investors sought higher returns in riskier assets. Energy shares were a surprise during the fiscal year. Widely thought of as a cyclical sector, Energy was the worst-performing sector during the period. Exxon Mobil and Chevron, both significant constituents of the sector, trailed the benchmark. From a factor perspective, small-size and value factors, both traditional and relative, were the best-performing factors. Earnings and price momentum factors performed worst.

IV. Return vs. Benchmark:

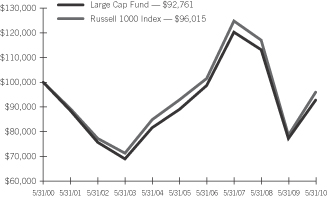

For the fiscal year ended May 31, 2010, the Fund underperformed the Russell 1000 Index, returning 20.05% versus the index return of 22.33%.

V. Fund Attribution:

Although it posted a strong absolute return, the Fund lagged its benchmark, mostly due to an underweight to Financials and poor stock selection in Information Technology. The sudden rebound in banks and real estate caught managers short-handed, as many had been focusing instead on the less risky industry of diversified financials, as these names were more insulated from the recent credit crisis. On the Technology side, many software and hardware names that did well in the early part of 2009 had a reversal during the subsequent rally and continued to lag in 2010. In general, the Fund’s managers hold higher-quality names and thus did not participate in the rebound experienced by stocks that were priced for bankruptcy. The Fund benefited from an underweight to one of the defensive sectors, Consumer Staples, which lagged during the fiscal year ended May 31, 2010. A similar story can be told for the Energy sector, which the Fund also underweighted and which has come down in valuation over the past year.

Large Cap Fund

AVERAGE ANNUAL TOTAL RETURN1

| | | | | | | | | | |

| | | One Year

Return | | Annualized

3 Year

Return | | Annualized

5 Year

Return | | Annualized

10 Year

Return | | Annualized

Inception

to Date |

| Large Cap Fund, Class A | | 20.05% | | (8.31)% | | 0.84% | | (0.75)% | | 5.34% |

Comparison of Change in the Value of a $100,000 Investment in the Large Cap Fund, versus the Russell 1000 Index

| | 1 | | For the period ended May 31, 2010. Past performance is not an indication of future performance. Class A shares were offered beginning 6/14/96. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower. |

| | |

| SEI Institutional Investments Trust / Annual Report / May 31, 2010 | | 1 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

SEI INSTITUTIONAL INVESTMENTS TRUST — MAY 31, 2010 (Unaudited)

Large Cap Diversified Alpha Fund

I. Objective:

The Large Cap Diversified Alpha Fund (the “Fund”) seeks to provide long-term growth of capital and income.

II. Multi-Manager Approach Statement:

The Fund uses a multi-manager approach, relying on a number of sub-advisors with differing investment approaches to manage portions of the Fund’s portfolio under the general supervision of SEI Investments Management Corp. (SIMC). The Fund utilized the following sub-advisers as of May 31, 2010: Quantitative Management Associates, LLC, Analytic Investors, LLC, Intech Investment Management, LLC, Legg Mason Capital Management, Inc., Delaware Management Company and Aronson + Johnson + Ortiz L.P. There were no changes to the portfolio in the fiscal year.

III. Market Commentary:

The U.S. equity market, as measured by the Russell 1000 Index, gained 22.33% during the fiscal year ended May 31, 2010. After a historic fall in 2008, equity markets staged a strong rebound in 2009 off the heels of unprecedented global intervention by governments and central banks. Stocks and sectors that suffered the steepest declines in the year prior drove market returns in 2009. More specifically, smaller-cap and lower-quality names, most of which were assumed to be insolvent, posted significant gains.

For the fiscal year, value stocks outperformed their growth counterparts in the large-cap universe. All ten Global Industry Classification Standard (GICS) sectors posted positive performance during the period. A renewed confidence in economic recovery revived investors’ willingness for risk taking. The Consumer Discretionary sector was the best-performing sector, up 44%, followed by Industrials and Information Technology. Conversely, more defensive sectors, which performed well during the year before, lagged the broad market. Utilities, Consumer Staples and Healthcare names failed to keep pace with the market, as investors sought higher returns in riskier assets. Energy shares were a surprise during the fiscal year. Widely thought of as a cyclical sector, Energy was the worst-performing sector during the period. Exxon Mobil and Chevron, both significant constituents of the sector, trailed the benchmark. From a factor perspective, small-size and value factors, both traditional and relative, were the best-performing factors. Earnings and price momentum factors performed worst.

IV. Return vs. Benchmark:

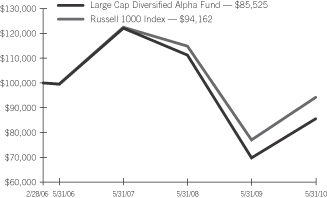

For the fiscal year ended May 31, 2010, the Fund outperformed the Russell 1000 Index, returning 22.61% versus the index return of 22.33%.

V. Fund Attribution:

The Fund delivered strong performance, with the LIBOR Plus portfolio and an allocation to Consumer Staples as major contributors. On the Technology side, many software and hardware names that did well in the early part of 2009 had a reversal during the subsequent rally and continued to lag in 2010. In general, the Fund’s managers hold higher-quality names and thus did not participate in the bounce experienced by many stocks that were priced for bankruptcy. Positioning in Financials also detracted from performance. The sudden rebound in real estate caught managers short-handed, as many had instead been focusing on the less risky industry of diversified financials, where companies were more insulated from the recent credit crisis. On the bright side, strong stock selection in the Healthcare sector boosted returns, especially once investors came back to the sector after decisions were finalized surrounding potential government regulation. In addition, the Fund benefited from an underweight to the Energy sector, which had come down in valuation over the past year.

Large Cap Diversified Alpha Fund

AVERAGE ANNUAL TOTAL RETURN1

| | | | | | |

| | | One Year

Return | | Annualized

3 Year

Return | | Annualized

Inception

to Date |

| Large Cap Diversified Alpha Fund, Class A | | 22.61% | | (11.18)% | | (3.61)% |

Comparison of Change in the Value of a $100,000 Investment in the Large Cap Diversified Alpha Fund, versus the Russell 1000 Index

| | 1 | | For the period ended May 31, 2010. Past performance is no indication of future performance. Class A shares were offered beginning 2/28/06. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower. |

| | |

| 2 | | SEI Institutional Investments Trust / Annual Report / May 31, 2010 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

SEI INSTITUTIONAL INVESTMENTS TRUST — MAY 31, 2010 (Unaudited)

Large Cap Disciplined Equity Fund

I. Objective:

The Large Cap Disciplined Equity Fund (the “Fund”) seeks to provide capital appreciation.

II. Multi-Manager Approach Statement:

The Fund uses a multi-manager approach, relying on a number of sub-advisors with differing investment approaches to manage portions of the Fund’s portfolio under the general supervision of SEI Investments Management Corp. (SIMC). The Fund utilized the following sub-advisers as of May 31, 2010: Quantitative Management Associates, LLC, Analytic Investors, Inc., INTECH Investment Management, LLC, Massachusetts Financial Services Company and Lazard Asset Management LLC. For the one-year period ending May 31,2010, Lazard Asset Management LLC was added to the Fund.

III. Market Commentary:

The U.S. equity market, as measured by the Russell 1000 Index, gained 22.33% during the fiscal year ending May 31, 2010. After a historic fall in 2008, equity markets staged a strong rebound in 2009 off the heels of unprecedented global intervention by governments and central banks. Stocks and sectors that suffered the steepest declines in the year prior drove market returns in 2009. More specifically, smaller-cap and lower-quality names, most of which were assumed to be insolvent, posted significant gains.

For the fiscal year, value stocks outperformed their growth counterparts in the large-cap universe. All ten Global Industry Classification Standard (GICS) sectors posted positive performance during the period. A renewed confidence in economic recovery revived investors’ willingness for risk taking. The Consumer Discretionary sector was the best-performing sector, up 44%, followed by Industrials and Information Technology. Conversely, more defensive sectors, which performed well during the year before, lagged the broad market. Telecommunications, Healthcare and Materials names failed to keep pace with the market, as investors sought higher returns in riskier assets. Energy shares were a surprise during the fiscal year. Widely thought of as a cyclical sector, Energy was the worst-performing sector during the period. Exxon Mobil and Chevron, both significant constituents of the sector, trailed the benchmark. From a factor perspective, small size and expected growth were the best-performing factors. Momentum factors for both earnings and prices were negative.

IV. Return vs. Benchmark:

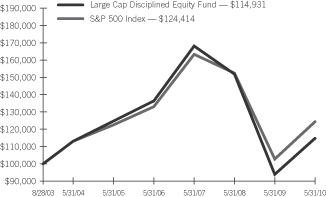

For the fiscal year ended May 31, 2010, the Fund outperformed the S&P 500 Index, returning 22.32% versus the index return of 20.99%.

V. Fund Attribution:

After a difficult time for quantitative managers, the tide turned during the past year for all but the factor rotation manager. The latter manager had a difficult time during the choppy markets, as its process relies on a trending market with a clear direction to add value. A decrease in the Chicago Board Options Exchange Volatility Index (VIX), a measure of implied volatility in S&P 500 Index options that is also known as the “fear index,” benefited the volatility capture manager for most of the period, as did the out-performance of smaller stocks, which the manager is typically biased towards. Investors began rewarding value factors once more—a boon to the traditional quantitative managers in the Fund—although this was dampened by the headwind from lower-quality names (usually underweighted by quantitative managers) outperforming during the market rally. The Fund’s hybrid manager did especially well, namely due to holdings in the Consumer Discretionary sector. The Libor Plus portfolio added significant alpha to the Fund as well, as credit spreads have continued to narrow.

Large Cap Disciplined Equity Fund

AVERAGE ANNUAL TOTAL RETURN1

| | | | | | | | |

| | | One Year

Return | | Annualized

3 Year

Return | | Annualized

5 Year

Return | | Annualized

Inception

to Date |

Large Cap Disciplined

Equity Fund, Class A | | 22.32% | | (11.90)% | | (1.64)% | | 2.08% |

Comparison of Change in the Value of a $100,000 Investment in the Large Cap Disciplined Equity Fund, versus the S&P 500 Index

| | 1 | | For the period ended May 31, 2010. Past performance is not an indication of future performance. Class A shares were offered beginning 8/28/03. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower. |

| | |

| SEI Institutional Investments Trust / Annual Report / May 31, 2010 | | 3 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

SEI INSTITUTIONAL INVESTMENTS TRUST — MAY 31, 2010 (Unaudited)

Large Cap Index Fund

I. Objective:

The Large Cap Index Fund (the “Fund”) seeks to provide investment results that correspond to the aggregate price and dividend performance of the securities in the Russell 1000 Index.

II. Manager Approach Statement:

The Fund uses a sub-advisor to manage the Fund under the supervision of SEI Investments Management Corporation (SIMC). Currently, the sub-advisor is State Street Global Advisors. There were no manager changes during the period.

III. Market Commentary:

The U.S. equity market, as measured by the Russell 1000 Index, gained 22.33% during the fiscal year ended May 31, 2010. After a historic fall in 2008, equity markets staged a strong rebound in 2009 off the heels of unprecedented global intervention by governments and central banks. Stocks and sectors that suffered the steepest declines in the year prior drove market returns in 2009. More specifically, smaller-cap and lower-quality names, most of which were assumed to be insolvent, posted significant gains.

For the fiscal year, value stocks outperformed their growth counterparts in the large-cap universe. All ten Global Industry Classification Standard (GICS) sectors posted positive performance during the period. A renewed confidence in economic recovery revived investors’ willingness for risk taking. The Consumer Discretionary sector was the best-performing sector, up 44%, followed by Industrials and Information Technology. Conversely, more defensive sectors, which performed well during the year before, lagged the broad market. Utilities, Consumer Staples and Healthcare names failed to keep pace with the market, as investors sought higher returns in riskier assets. Energy shares were a surprise during the fiscal year. Widely thought of as a cyclical sector, Energy was the worst-performing sector during the period. Exxon Mobil and Chevron, both significant constituents of the sector, trailed the benchmark. From a factor perspective, small-size and value factors, both traditional and relative, were the best-performing factors. Earnings and price momentum factors performed worst.

IV. Return vs. Benchmark:

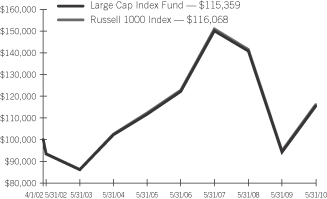

For the fiscal year ended May 31, 2010, the Fund outperformed the Russell 1000 Index, returning 22.34% versus the benchmark return of 22.33%.

V. Fund Attribution:

Incremental excess return was generated due to cash flows. As an index fund, performance is designed to track that of the index.

Large Cap Index Fund

AVERAGE ANNUAL TOTAL RETURN1

| | | | | | | | |

| | | One Year

Return | | Annualized

3 Year

Return | | Annualized

5 Year

Return | | Annualized

Inception

to Date |

| Large Cap Index Fund, Class A | | 22.34% | | (8.40)% | | 0.64% | | 1.77% |

Comparison of Change in the Value of a $100,000 Investment in the Large Cap Index Fund, versus the Russell 1000 Index

| | 1 | | For the period ended May 31, 2010. Past performance is not an indication of future performance. Class A shares were offered beginning 4/1/02. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower. |

| | |

| 4 | | SEI Institutional Investments Trust / Annual Report / May 31, 2010 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

SEI INSTITUTIONAL INVESTMENTS TRUST — MAY 31, 2010 (Unaudited)

Small Cap Fund

I. Objective:

The Small Cap Fund (the “Fund”) seeks to provide capital appreciation.

II. Multi-Manager Approach Statement:

The Fund uses a multi-manager approach, relying upon a number of sub-advisers with differing investment philosophies to manage portions of the Fund’s portfolio under the general supervision of SEI Investments Management Corporation (“SIMC”). The Fund utilized the following sub-advisers as of May 31, 2010: AQR Capital Management, LLC, Artisan Partners Limited Partnership, Janus Capital Management, Inc., Lee Munder Capital Group LLC, Los Angeles Capital Management & Equity Research, Inc., LSV Asset Management, Oppenheimer Capital, LC, Robeco Investment Management, Inc., Security Capital Research and Management, Inc. and Wellington Management Company, LLP.

For the fiscal year ended May 31, 2010, BlackRock Capital Management, Inc., McKinley Capital Management, Inc., Neuberger Berman Management, LLC, PanAgora Asset Management, Inc and Martingale Asset Management, L.P. were removed from the Fund. AQR Capital Management, LLC was added during the period.

III. Market Commentary:

The U.S. small-cap equity market, as measured by the Russell 2000 Index, gained over 33% during the fiscal year ended May 31, 2010. After small-cap stocks lost nearly half of their value in 2008 and early 2009, U.S. Small Cap stocks turned decisively positive in March 2009 as the extreme fear over the state of the U.S. and world financial systems subsided. An extended rally followed as investors discounted government intervention and became hopeful of an economic recovery, albeit a moderate one. From a factor perspective, price and earnings momentum performed very poorly for the fiscal year. Value, small market cap and low price were the best factors as the companies investors believed to be the most likely bankruptcy candidates during the downturn tended to lead the market during the rebound.

IV. Return vs. Benchmark:

For the fiscal year ended May 31, 2010, the Fund outperformed the Russell 2000 Index, returning 35.32% versus the index return of 33.62%.

V. Fund Attribution:

The majority of out-performance occurred in the third quarter of 2009, as the initial rally from the March 2009 low extended, and an underweight to the lagging banking industry added to performance. The Fund posted solid performance on a relative basis, principally due to stock selection within the Financials sector, particularly the real estate investment trust (REIT) industry. Strong stock selection in the Industrials sector contributed meaningfully as well. The core quantitative managers outperformed for the period, as factor returns began to trend and value factors saw positive returns. The value managers also contributed to performance, with a majority of them outperforming the Russell 2000 Value Index.

Small Cap Fund

AVERAGE ANNUAL TOTAL RETURN1

| | | | | | | | | | |

| | | One Year

Return | | Annualized

3 Year

Return | | Annualized

5 Year

Return | | Annualized

10 Year

Return | | Annualized

Inception

to Date |

| Small Cap Fund, Class A | | 35.32% | | (8.39)% | | 1.93% | | 4.54% | | 6.66% |

Comparison of Change in the Value of a $100,000 Investment in the Small Cap Fund, versus the Russell 2000 Index

| | 1 | | For the period ended May 31, 2010. Past performance is not an indication of future performance. Class A shares were offered beginning 6/14/96. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower. |

| | |

| SEI Institutional Investments Trust / Annual Report / May 31, 2010 | | 5 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

SEI INSTITUTIONAL INVESTMENTS TRUST — MAY 31, 2010 (Unaudited)

Small/Mid Cap Equity Fund

I. Objective:

The Small/Mid Cap Equity Fund (the “Fund”) seeks to provide long-term capital appreciation.

II. Multi-Manager Approach Statement:

The Fund uses a multi-manager approach, relying upon a number of sub-advisers with differing investment philosophies to manage portions of the Fund’s portfolio under the general supervision of SEI Investments Management Corporation (“SIMC”). The Fund utilized the following sub-advisers as of May 31, 2010: Integrity Asset Management, LLC, Janus Capital Management, Inc., Lee Munder Capital Group LLC, Los Angeles Capital Management & Equity Research, Inc., LSV Asset Management, PanAgora Asset Management, Inc., Security Capital Research and Management, Inc., Wellington Management Company, LLP and Wells Capital Management, Inc.

For the fiscal year ended May 31, 2010, BlackRock Capital Management, Inc. and Martingale Asset Management, L.P. were removed from the Fund. Wellington’s Small Cap Growth product was added during the period.

III. Market Commentary:

The U.S. small/mid cap equity market, as measured by the Russell 2500 Index, gained over 35% during the fiscal year ended May 31, 2010. After small- and mid-cap stocks lost nearly half of their value in 2008 and early 2009, these markets turned decisively positive in March 2009 as the extreme fear over the state of the U.S. and world financial systems subsided. An extended rally followed as investors discounted government intervention and became hopeful of an economic recovery, albeit a moderate one. From a factor perspective, price and earnings momentum performed very poorly for the fiscal year. Value, small market cap and low price were the best factors as the companies investors believed to be the most likely bankruptcy candidates during the downturn tended to lead the market during the rebound.

IV. Return vs. Benchmark:

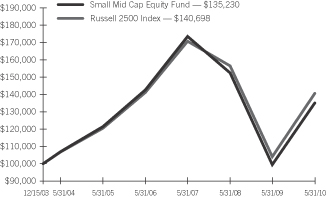

For the fiscal year ended May 31, 2010, the Fund outperformed the Russell 2500 Index, returning 35.79% versus the index return of 35.07%.

V. Fund Attribution:

The majority of out-performance occurred in the third quarter of 2009 as markets continued to rally off of March lows. The Fund posted solid performance on a relative basis, largely due to stock selection within the Financials sector, particularly the REIT industry. Strong stock selection in the Materials sector was also beneficial. From a style perspective, the Fund’s value managers contributed to performance, with each outperforming the Russell 2000 Value Index, and Wells Capital, added in 2008, contributed to performance as the best-performing growth manager over the period.

Small/Mid Cap Equity Fund

AVERAGE ANNUAL TOTAL RETURN1

| | | | | | | | |

| | | One Year

Return | | Annualized

3 Year

Return | | Annualized

5 Year

Return | | Annualized

Inception

to Date |

| Small/Mid Cap Equity Fund, Class A | | 35.79% | | (7.99)% | | 2.17% | | 4.78% |

Comparison of Change in the Value of a $100,000 Investment in the Small Mid Cap Equity Fund, versus the Russell 2500 Index

| | 1 | | For the period ended May 31, 2010. Past performance is not an indication of future performance. Class A shares were offered beginning 12/15/03. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower. |

| | |

| 6 | | SEI Institutional Investments Trust / Annual Report / May 31, 2010 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

SEI INSTITUTIONAL INVESTMENTS TRUST — MAY 31, 2010 (Unaudited)

U.S. Managed Volatility Fund

I. Objective:

The U.S. Managed Volatility Fund (the “Fund”) seeks to provide capital appreciation with less volatility than the broad U.S. equity markets.

II. Multi-Manager Approach Statement:

The Fund uses a multi-manager approach, relying on a number of Sub-Advisers with differing investment approaches to manage portions of the Fund’s portfolio under the general supervision of SIMC. The Fund utilized the following sub-advisors as of May 31, 2010: Aronson + Johnson + Ortiz, LP and Analytic Investors LLC. No manager changes were made during the period.

III. Market Commentary:

Economic recovery and excess liquidity prompted a sharp market rebound. Cyclical sectors, which previously experienced the heaviest declines, led the rally. Consumer Discretionary and Industrials posted the best returns, with the defensive Utilities and Telecommunications sectors lagging the broader market.

Companies that seemed to have a questionable chance for survival in 2008 were rewarded the most. These stocks generally had high levels of debt and a high beta, or more sensitivity to the movements in the broader market. High-beta names outperformed the low-beta ones overall.

May 2010 saw an increase in risk aversion compared to the last 12 months. Concerns over Southern European sovereign debt, an overheating Chinese property market and possibly the economy, as well as consequences of BP’s oil spill for the entire industry caused investors to seek refuge in the safer Consumer Staples, Telecommunications and Utilities sectors.

IV. Return vs. Benchmark:

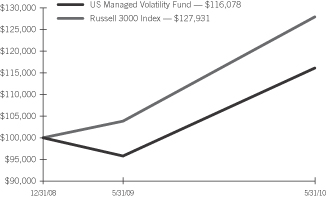

For the fiscal year ended May 31, 2010, the Fund underperformed the Russell 3000 Index, returning 21.12% versus the index return of 23.20%.

V. Fund Attribution:

The Fund’s underperformance was primarily driven by its defensive stance, which is required to achieve the primary objective of lowering volatility and providing downside protection to investors. In fact, the volatility reduction goal was comfortably achieved. For the fiscal year ended May 31, 2010, the Fund realized an annualized standard deviation of 14% (daily frequency) as compared to the benchmark’s results of 19%.

To achieve its intended low risk profile, the managers target lower-beta, lower-risk names with stable earnings streams and lower leverage ratios. In the early stages of market recovery, such positioning prevented the Fund from fully participating in the rally. As low-beta stocks lagged their high-beta counterparts by over 18%, this has had a major negative allocation effect. After adjusting for the beta positioning, stock selection was strong. From a more traditional sector perspective, the Fund’s overweight to the defensive Consumer Staples, Utilities, and Healthcare sectors detracted significantly.

U.S. Managed Volatility Fund

AVERAGE ANNUAL TOTAL RETURN1

| | | | |

| | | One Year

Return | | Annualized

Inception

to Date |

| U.S. Managed Volatility Fund | | 21.12% | | 11.08% |

Comparison of Change in the Value of a $100,000 Investment in the US Managed Volatility Fund, versus the Russell 3000 Index

| | 1 | | For the period ended May 31, 2010. Past performance is not an indication of future performance. Class A shares were offered beginning 12/31/08. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower. |

| | |

| SEI Institutional Investments Trust / Annual Report / May 31, 2010 | | 7 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

SEI INSTITUTIONAL INVESTMENTS TRUST — MAY 31, 2010 (Unaudited)

International Equity Fund

I. Objective:

The International Equity Fund (the “Fund”) seeks to provide capital appreciation.

II. Multi-Manager Approach Statement:

The Fund uses a multi-manager approach, relying upon a number of sub-advisors with differing investment philosophies to manage portions of the Fund’s portfolio under the general supervision of SEI Investments Management Corporation (“SIMC”). The Fund utilizes the following sub-advisers as of May 31, 2010: Acadian Asset Management, LLC, AXA Rosenberg Investment Management, LLC, Declaration Management and Research, LLC, INTECH Investment Management, LLC, Neuberger Berman Management, LLC, Quantitative Management Associates, LLC, and Schroder Investment Management North America, Inc.

For the fiscal year ended May 31, 2010, Neuberger Berman Management and Schroder Investment Management were added to the Fund; McKinley Capital Management, Principal Global Investors, and Wellington Management Company were terminated.

III. Market Commentary:

Global equity markets continued their tumble from 2008 well into the first quarter of 2009. However, hopeful signs emerged in March 2009 as global stimulus efforts began to take effect. Investors started to feel more confident about a global economic recovery and their appetite for risk returned, fueling a strong rally through the end of the year. Starting in March, stocks that had suffered the most during the credit crisis led the rally. This was reflected in the leadership by the cheapest stocks, particularly as measured by prices relative to book values (assets minus liabilities). Companies that had the highest levels of debt also outperformed the index. In the third quarter, earnings releases for many companies were better than expected, pushing prices higher. However, as the rally matured, investors began to favor companies with higher-quality balance sheets and opportunities to gain market share. In the first five months of 2010, global equity markets were down overall as macroeconomic events, which included the European sovereign debt crisis, a slowdown in Chinese growth, and the oil spill in the Gulf of Mexico, took center stage.

IV. Return vs. Benchmark:

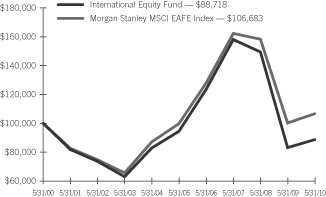

For the fiscal year ended May 31, 2010, the Fund outperformed the MSCI EAFE Index, returning 6.68% versus the index return of 6.38%.

V. Fund Attribution:

The Fund outperformed the benchmark, driven primarily by positive stock selection by the sub-advisors; however, allocation also contributed to performance. From a regional perspective, in addition to positive stock selection, the Fund’s underweight allocation to Europe ex-UK was beneficial as the region struggled with mounting

sovereign debt issues and fears of contagion. On the other hand, the Fund’s underweight allocation and stock selection in Pacific ex-Japan detracted from performance. Australia, the largest constituent in Pacific ex-Japan, was one of the hottest markets during the period and the Fund’s underweight allocation detracted. From a sector perspective, performance was diverse, favoring neither cyclical nor defensive sectors. Consumer Discretionary stocks performed the best, with automobile companies dominating positive performance. Industrial and Health Care detracted due to weak stock selection for the time period.

International Equity Fund

AVERAGE ANNUAL TOTAL RETURN1

| | | | | | | | | | |

| | | One Year

Return | | Annualized

3 Year

Return | | Annualized

5 Year

Return | | Annualized

10 Year

Return | | Annualized

Inception

to Date |

| International Equity Fund, Class A | | 6.68% | | (17.51)% | | (1.24)% | | (1.19)% | | 2.35% |

Comparison of Change in the Value of a $100,000 Investment in the International Equity Fund, versus the Morgan Stanley MSCI EAFE Index

| | 1 | | For the period ended May 31, 2010. Past performance is not an indication of future performance. Class A shares were offered beginning 6/14/96. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower. |

| | |

| 8 | | SEI Institutional Investments Trust / Annual Report / May 31, 2010 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

SEI INSTITUTIONAL INVESTMENTS TRUST — MAY 31, 2010 (Unaudited)

World Equity Ex-US Fund

I. Objective:

The objective of the World Equity Ex-US Fund (the “Fund”) is to provide capital appreciation.

II. Multi-Manager Approach Statement:

The Fund uses a multi-manager approach, relying upon a number of sub-advisors with differing investment philosophies to manage portions of the Fund’s portfolio under the general supervision of SEI Investments Management Corporation (“SIMC”). The Fund utilizes the following sub-advisors as of May 31, 2010: Acadian Asset Management, Inc., Artisan Partners Limited Partnership, Declaration Management & Research LLC, McKinley Capital Management, LLC, NFJ Investment Group LLC, Principal Global Investors, LLC, Quantitative Management Associates, LLC and Thornburg Investment Management LLC.

For the fiscal year ended May 31, 2010, NFJ Investment Group LLC and Thornburg Investment Management LLC were added to the Fund; Wellington Management Company, LLC, AXA Rosenberg Investment Management, LLC, INTECH Investment Management, LLC and Rexiter Capital Management Limited were terminated.

III. Market Commentary:

Global equity markets continued their tumble from 2008 well into the first quarter of 2009. However, hopeful signs emerged in March 2009 as global stimulus efforts began to take effect. Investors started to feel more confident about a global economic recovery and their appetite for risk returned, fueling a strong rally through the end of the year. Starting in March, stocks that had suffered the most during the credit crisis led the rally. This was reflected in the leadership by the cheapest stocks, particularly as measured by prices relative to book values (assets minus liabilities). Companies that had the highest levels of debt also outperformed the index. In the third quarter, earnings releases for many companies were better than expected, pushing prices higher. However, as the rally matured, investors began to favor companies with higher-quality balance sheets and opportunities to gain market share.

In the first five months of 2010, global equity markets were down overall as macroeconomic events, which included the European sovereign debt crisis, a slowdown in Chinese growth and the oil spill in the Gulf of Mexico, took center stage. For the time period, emerging markets outperformed developed markets and sector performance was mixed.

IV. Return vs. Benchmark:

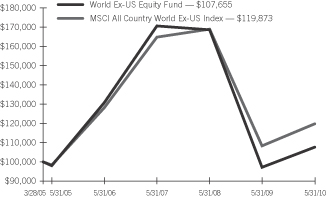

For the fiscal year ended May 31, 2010, the Fund outperformed the MSCI All Country World Ex-U.S. Index, returning 10.74% versus the index return of 10.63%.

V. Fund Attribution:

The Fund outperformed the benchmark, driven primarily by positive stock selection by the sub-advisors; however, allocation also contributed to performance. From a regional perspective, emerging markets outperformed developed markets, so the Fund’s overweight allocation to emerging markets benefitted performance. Brazilian and Mexican stocks were especially strong. The Fund’s underweight allocation to Europe Ex-U.K. was beneficial, as the region struggled with mounting sovereign debt issues and fears of contagion. On the other hand, the Fund’s underweight allocation and stock selection in Pacific Ex-Japan detracted from performance. Australia, the largest constituent in Pacific Ex-Japan, was one of the hottest performers among the developed markets, and the Fund’s underweight positioning detracted from performance.

From a sector perspective, performance was diverse, favoring neither cyclical nor defensive sectors. Consumer Discretionary stocks performed the best, with automobile companies dominating positive performance. Telecommunication Services was the largest detractor with wireless services stocks down the most.

World Equity Ex-US Fund

AVERAGE ANNUAL TOTAL RETURN1

| | | | | | | | |

| | | One Year

Return | | Annualized

3 Year

Return | | Annualized

5 Year

Return | | Annualized

Inception

to Date |

| World Equity Ex-US Fund, Class A | | 10.74% | | (14.24)% | | 1.88% | | 1.44% |

Comparison of Change in the Value of a $100,000 Investment in the World Ex-US Equity Fund, versus the MSCI All Country World Ex-US Index

| | 1 | | For the period ended May 31, 2010. Past performance is not an indication of future performance. Class A shares were offered beginning 3/28/05. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower. |

| | |

| SEI Institutional Investments Trust / Annual Report / May 31, 2010 | | 9 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

SEI INSTITUTIONAL INVESTMENTS TRUST — MAY 31, 2010 (Unaudited)

Screened World Equity Ex-US Fund

I. Objective:

The Screened World Equity Ex-US Fund (the “Fund”) seeks to provide capital appreciation.

II. Multi-Manager Approach Statement:

The Fund uses a multi-manager approach, relying upon a number of sub-advisors with differing investment philosophies to manage portions of the Fund’s portfolio under the general supervision of SEI Investments Management Corporation (“SIMC”). The Fund utilizes the following sub-advisers as of May 31, 2010: Acadian Asset Management LLC, McKinley Capital Management, LLC, Principal Global Investors, LLC, Quantitative Management Associates, LLC, and Thornburg Investment Management LLC.

For the fiscal year ended May 31, 2010, Acadian Asset Management and Thornburg Investment Management LLC were added to the Fund; AXA Rosenberg Investment Management, LLC was terminated.

III. Market Commentary:

Global equity markets continued their tumble from 2008 well into the first quarter of 2009. However, hopeful signs emerged in March 2009 as global stimulus efforts began to take effect. Investors started to feel more confident about a global economic recovery and their appetite for risk returned, fueling a strong rally through the end of the year. Starting in March, stocks that had suffered the most during the credit crisis led the rally. This was reflected by the leadership of the cheapest stocks, particularly as measured by prices relative to book values (assets minus liabilities). Companies that had the highest levels of debt also outperformed the index. In the third quarter, earnings releases for many companies were better than expected, pushing prices higher. However, as the rally matured, investors began to favor companies with higher-quality balance sheets and opportunities to gain market share.

In the first five months of 2010, global equity markets were down overall as macroeconomic events, which included the European sovereign debt crisis, a slowdown in Chinese growth, and the oil spill in the Gulf of Mexico, took center stage. For the time period, emerging markets outperformed developed markets and sector performance was diverse.

IV. Return vs. Benchmark:

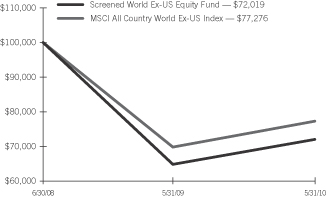

For the fiscal year ended May 31, 2010, the Fund outperformed the MSCI All Country World Ex-U.S. Index, returning 11.00% versus the index return of 10.63%.

V. Fund Attribution:

The Fund outperformed the benchmark, driven primarily by positive stock selection by the sub-advisors; however, allocation was slightly beneficial. From a regional perspective, stock selection was especially strong in Europe Ex-U.K. despite the region’s sovereign debt crisis. Stock selection in emerging markets was also positive, with Latin American stocks posting the largest returns. On the other hand, the Fund’s underweight allocation and stock selection in Pacific Ex-Japan detracted from performance. Australia, the largest constituent in Pacific Ex-Japan, was one of the hottest performers among the developed markets, and the Fund’s underweight positioning and stock selection detracted. From a sector perspective, performance was diverse across cyclical and defensive sectors. Industrials, Information Technology and Energy were the best performers, while Telecommunication Services and Materials lagged the index the most.

Screened World Equity Ex-US Fund

AVERAGE ANNUAL TOTAL RETURN1

| | | | |

| | | One Year

Return | | Annualized

Inception

to Date |

| Screened World Equity Ex-US Fund, Class A | | 11.00% | | (15.74)% |

Comparison of Change in the Value of a $100,000 Investment in the Screened World Ex-US Equity Fund, versus the MSCI All Country World Ex-US Index

| | 1 | | For the period ended May 31, 2010. Past performance is not an indication of future performance. Class A shares were offered beginning 6/30/08. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower. |

| | |

| 10 | | SEI Institutional Investments Trust / Annual Report / May 31, 2010 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

SEI INSTITUTIONAL INVESTMENTS TRUST — MAY 31, 2010 (Unaudited)

Enhanced LIBOR Opportunities Fund

I. Objective:

The Enhanced LIBOR Opportunities Fund (the “Fund”) seeks to provide capital appreciation and income.

II. Multi-Manager Approach Statement:

The Fund uses a multi-manager approach, relying on a number of sub-advisors with differing investment approaches to manage portions of the Fund’s portfolio under the general supervision of SEI Investments Management Corp. (SIMC). The Fund utilizes the following sub-advisors as of May 31, 2010: Declaration Management & Research LLC, UBS Global Asset Management (Americas), Inc., Wellington Management Company, LLP and Ares Management LLC. No changes were made to the Fund during the period.

III. Market Commentary:

Fixed-income market conditions for the fiscal year ended May 31, 2010 reflected a dramatic recovery from the crisis conditions of 2008, including the bankruptcy of Lehman Brothers. The period was characterized by an increased investor appetite for risk that drove powerful rallies in most of the non-Treasury sectors in the market. The catalyst for the market recovery was a series of government programs designed to improve credit availability, which included the Term Asset-Backed Securities Lending Facility (TALF), the Public-Private Investment Program (PPIP) and a $1.25 trillion purchase program of agency mortgage-backed securities (MBS) by the U.S. Federal Reserve (Fed). The Fed’s purchase program brought MBS spreads and mortgage rates to historic lows. The TALF and PPIP programs helped drive strong performance in the non-agency MBS market, including commercial MBS, and the asset-backed securities market. The corporate bond market was supported by stabilizing economic conditions, lower default rates and improved market liquidity. The senior bank loan market also saw stellar returns, as fundamental credit conditions continued to improve and the technical environment remained supportive of higher loan prices, with demand outpacing supply. The strong market recovery was interrupted in the spring of 2010, as the European sovereign credit crisis triggered a modest flight to quality that served to bring Treasury yields back to the lower end of their trading range. Despite the more recent caution displayed by market participants, the rallies in the non-Treasury sectors provided very strong performance for the fixed income markets for the twelve-month period.

IV. Return vs. Benchmark:

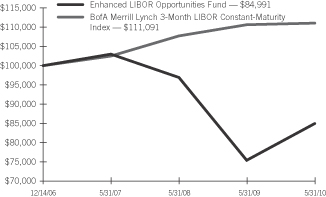

For the fiscal year ended May 31, 2010, the Fund outperformed the Bank of America (“BofA”) Merrill Lynch 3-Month London Interbank Offered Rate (LIBOR) Constant Maturity Index, returning 12.66% versus the index return of 0.39%.

V. Fund Attribution:

During the fiscal year ended May 31, 2010, the Fund’s large allocation to non-Treasury sectors outperformed—particularly the portfolio’s allocations to non-agency mortgage-backed securities, commercial mortgage-backed securities and senior bank loans.

Enhanced LIBOR Opportunities Fund

AVERAGE ANNUAL TOTAL RETURN1

| | | | | | |

| | | One Year

Return | | Annualized

3 Year

Return | | Annualized

Inception

to Date |

| Enhanced LIBOR Opportunities Fund, Class A | | 12.66% | | (6.21)% | | (4.59)% |

Comparison of Change in the Value of a $100,000 Investment in the Enhanced LIBOR Opportunities Fund, versus the BofA Merrill Lynch 3-Month LIBOR Constant-Maturity Index

| | 1 | | For the period ended May 31, 2010. Past performance is not an indication of future performance. Class A shares were offered beginning 12/14/06. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower. |

| | |

| SEI Institutional Investments Trust / Annual Report / May 31, 2010 | | 11 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

SEI INSTITUTIONAL INVESTMENTS TRUST — MAY 31, 2010 (Unaudited)

Core Fixed Income Fund

I. Objective:

The Core Fixed Income Fund (the “Fund”) seeks to provide current income consistent with the preservation of capital.

II. Multi-Manager Approach Statement:

The Fund uses a multi-manager approach, relying on a number of sub-advisors with differing investment approaches to manage portions of the Fund’s portfolio, under the general supervision of SEI Investments Management Corp. (SIMC). The Fund utilized the following sub-advisors as of May 31, 2010: Trust Company of the West (formerly Metropolitan West Asset Management), J.P. Morgan Investment Management, Inc., Western Asset Management Company, Wells Capital Management, Inc. and Jennison Associates LLC. During the fiscal year ended May 31, 2010, Jennison Associates LLC was added to the Fund.

III. Market Commentary:

Fixed-income market conditions for the fiscal year ended May 31, 2010 reflected a dramatic recovery from the crisis conditions of 2008 and the post-Lehman bankruptcy. The period was characterized by an increased investor appetite for risk that drove powerful rallies in most of the non-Treasury sectors of the market. The catalyst for the market recovery was a series of government programs designed to improve credit availability. These programs included the Term Asset-Backed Securities Loan Facility (TALF), the Public-Private Investment Program (PPIP) and a $1.25 trillion purchase program of agency mortgage-backed securities (MBS) by the U.S. Federal Reserve (Fed). The Fed’s purchase program brought MBS spreads and mortgage rates to historic lows. The TALF and PPIP programs helped drive strong performance in the non-agency MBS market (including commercial MBS) and the asset-backed securities market. The corporate market was supported by stabilizing economic conditions, lower default rates and improved market liquidity. The strong market recovery was interrupted in the spring of 2010, as the European sovereign credit crisis triggered a modest flight to quality that served to bring Treasury yields back to the lower end of their trading range. Despite this more recent market caution, the rallies in the non-Treasury sectors provided very strong performance for fixed-income markets during the twelve-month period.

IV. Return vs. Benchmark:

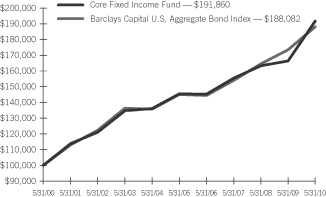

For the fiscal year ended May 31, 2010, the Fund outperformed the Barclays Capital U.S. Aggregate Bond Index, returning 15.34% versus the index return of 8.42%.

V. Fund Attribution:

The Fund’s overweight positions in corporate bonds, non-agency MBS and commercial MBS were the key drivers of performance. In addition, the Fund entered the year with a positive bias towards agency MBS due to the Federal Reserve’s purchase program, but as

prices relative to Treasuries continued to climb, managers moved to an increasingly underweight position. As the Fed discontinued these purchases, prices relative to Treasuries weakened modestly, and the Fund gradually added exposure toward the end of the measurement period. Duration exposure did not have a meaningful impact on performance, as managers chose to utilize their risk budgets on securities within the non-Treasury sectors.

Specifically, an overweight to corporate bonds, especially those issued by large-cap financial firms, generated significant out-performance relative to Treasuries. The steep yield curve combined with improved access to the capital markets allowed the largest of the U.S. banking institutions to repair their balance sheets and return to profitability throughout the year. Non-agency mortgages recovered dramatically as the forced selling resulting from ratings downgrades and the unwinding of large levered positions abated. The announcement and implementation of PPIP and TALF during the year restored confidence in the market, thereby allowing private capital to flow back into the securitized markets. Finally, the Fund’s overweight to commercial MBS contributed to performance, as these securities posted the largest out-performance versus Treasuries of any sector within the Barclays Capital U.S. Aggregate Bond Index.

Core Fixed Income Fund

AVERAGE ANNUAL TOTAL RETURN1

| | | | | | | | | | |

| | | One Year

Return | | Annualized

3 Year

Return | | Annualized

5 Year

Return | | Annualized

10 Year

Return | | Annualized

Inception

to Date |

| Core Fixed Income Fund, Class A | | 15.34% | | 7.28% | | 5.70% | | 6.73% | | 6.67% |

Comparison of Change in the Value of a $100,000 Investment in the Core Fixed Income Fund, versus the Barclays Capital U.S. Aggregate Bond Index

| | 1 | | For the period ended May 31, 2010. Past performance is not an indication of future performance. Class A shares were offered beginning 6/14/96. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower. |

| | |

| 12 | | SEI Institutional Investments Trust / Annual Report / May 31, 2010 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

SEI INSTITUTIONAL INVESTMENTS TRUST — MAY 31, 2010 (Unaudited)

High Yield Bond Fund

I. Objective:

The High Yield Bond Fund (the “Fund”) seeks to maximize total return.

II. Multi-Manager Approach Statement:

The Fund uses a multi-manager approach, relying on a number of sub-advisors with differing investment approaches to manage portions of the Fund’s portfolio under the general supervision of SEI Investments Management Corp. (SIMC). The Fund utilizes the following sub-advisers as of May 31, 2010: Ares Management, LLC, Brigade Capital Management, LLC, Delaware Management Company, Guggenheim Partners, LLC, J.P. Morgan Investment Management, Inc., and SEI Structured Credit. During the one-year period ended May 31, 2010, the Fund did not make any manager changes.

III. Market Commentary:

For the fiscal year ended May 31, 2010, the high-yield market, as measured by the Bank of America Merrill Lynch U.S. High Yield Master II Constrained Index, returned 29.91%. Credit quality spreads tightened 473 basis points (bps) to finish the period at 698 bps, down significantly from the peak of 2,168 basis points reached in December 2008. The Moody’s U.S. issuer-default rate fell from 10.86% to 7.91% over the fiscal year, after peaking at an all-time high of 14.51% in November 2009. Default rates are projected to continue their descent to 2.7% by the end of 2010. The significant amount of new issuance over the past 12 months, particularly for refinancing purposes, has improved the creditworthiness of many high-yield companies. Also putting downward pressure on the default rate is the fact that a large number of defaults occurred in the first half of 2009, therefore moving out of the 12-month window. Issuance in the primary market has been extremely robust over the period, with $247.5 billion coming to market, the second largest 12-month stretch on record (12 months ended April 30, 2010 saw the highest volume). The technical condition of the market was positive, as high-yield mutual funds saw $18.1 billion of inflows during the period, although May 2010 was a weak month due to European sovereign debt concerns; $3.5 billion exited funds, which reversed most of the YTD inflows. For the fiscal year, an increase in investor risk appetites and improved market

liquidity led to strong returns across all quality segments, but lower- quality credits outperformed, with CCCs up 60.72%, followed by Bs up 23.21%, and BBs up 23.15%.

The best-performing sectors were the higher-beta segments of the market, such as the Financial-related and Technology sectors. Insurance, Real Estate, Financial Services and Banking all outperformed the market, with the first three mentioned generating returns greater than twice the index gain. AIG, which has subsidiaries that operate in the Insurance and Financial Services sectors, had the largest impact on returns, while Realogy and iStar Financial boosted the performance in the Real Estate space. AIG was up on optimism about the insurer’s success in raising capital by selling off business units. AIG was scheduled to sell its Asian Life Unit to Prudential for $35.5B (Prudential pulled out of this deal in June, 2010), and to sell American Life Insurance Company (Alico) to MetLife for $15.5B, as they work to repay TARP money to the U.S. government. Technology companies did well over the year also, as investors moved into these high-growth companies as confidence in the economic recovery increased. Semiconductor firms were particularly strong, as many of these firms cut staff in 2008/2009, which has resulted in better earnings as chip sales for personal computers and cell phones, the biggest market drivers, are projected to grow in the low-to-mid-teens in 2010.

The Utilities and Telecommunications sectors lagged the overall high-yield market over the year, producing the lowest total returns among the sectors in the index. These sectors are both considered to be more defensive in nature and thus would be expected to under-perform in an environment where high-risk securities rally sharply. More specifically, electric generation companies within the Utilities sector were negatively impacted by numerous issues. Weak demand for power and natural gas hurt this sector, as well as unimpressive earnings results that reflected a poor operating environment and bleak future outlook for the sector. Uncertainty surrounding future environmental regulations and commodity prices remains. Within telecom, wireless companies have suffered from increased competition within the industry, which has created both pricing pressures and subscriber losses, two factors that have led to weaker earnings across many companies in the sector.

| | |

| SEI Institutional Investments Trust / Annual Report / May 31, 2010 | | 13 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

SEI INSTITUTIONAL INVESTMENTS TRUST — MAY 31, 2010 (Unaudited)

High Yield Bond Fund (Concluded)

IV. Return vs. Benchmark:

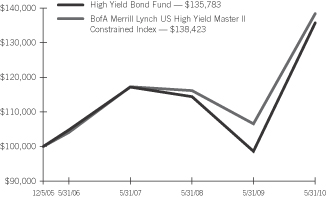

For the fiscal year ended May 31, 2010, the Fund outperformed the Bank of America (“BofA”) Merrill Lynch U.S. High Yield Master II Constrained Index, returning 37.60% versus the index return of 29.91%.

V. Fund Attribution:

The Fund’s allocation to CLOs and other structured investments outperformed the high-yield market, enhancing relative performance. The fundamental picture of the CLO marketplace has improved drastically due to the continued upturn in the high-yield loan and bond markets, the slowing pace of defaults/downgrades, and the ability of borrowers to successfully amend their credit agreements. Additionally, the technical picture has been a large driver of the rally, with the prospects for new issuance dim and a significant amount of money on the sidelines waiting to invest.

Another contributor to out-performance was the Fund’s underweight to and strong security selection within the Energy sector. An underweight to gas distribution companies’ debt boosted returns, since these firms were negatively impacted by low natural gas prices and a poor outlook for the industry. Security selection was strong within the integrated energy industry due to an overweight to ethanol producer Aventine Renewable Energy. Aventine emerged from Chapter 11 bankruptcy during the year and has also benefited from rumors that the EPA will boost the limit for blending ethanol with gasoline from 10% to 12-15%, which would increase demand for ethanol.

Security selection in the Media and Insurance sectors detracted from performance during the period. Poor security selection in the Media sector was largely impacted by an underweight to Clear Channel Communications, as the broadcasting company’s bonds benefited from improving financial results, the successful execution of several exchange offers for existing debt, and several new issues. These actions were taken to address immediate liquidity concerns and they dramatically improved the financial health of the company. Within the Insurance sector, an underweight to AIG hampered returns, as the company’s bonds rallied after it was able to raise a substantial amount of capital through both the new-issue market and asset sales, as mentioned above in the Market Commentary section.

High Yield Bond Fund

AVERAGE ANNUAL TOTAL RETURN1

| | | | | | |

| | | One Year

Return | | Annualized

3 Year

Return | | Annualized

Inception

to Date |

| High Yield Bond Fund, Class A | | 37.60% | | 5.02% | | 7.06% |

Comparison of Change in the Value of a $100,000 Investment in the High Yield Bond Fund, versus the BofA Merrill Lynch US High Yield Master II Constrained Index

| | 1 | | For the period ended May 31, 2010. Past performance is not an indication of future performance. Class A shares were offered beginning 12/05/05. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower. |

| | |

| 14 | | SEI Institutional Investments Trust / Annual Report / May 31, 2010 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

SEI INSTITUTIONAL INVESTMENTS TRUST — MAY 31, 2010 (Unaudited)

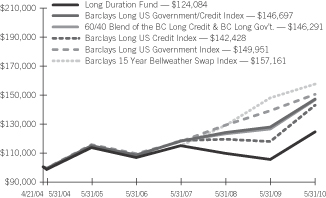

Long Duration Fund

I. Objective:

The Long Duration Fund (the “Fund”) seeks to provide return characteristics similar to those of high-quality corporate bonds with a duration range of 9 to 14 years.

II. Multi-Manager Approach Statement:

The Fund uses a multi-manager approach, relying on a number of sub-advisors with differing investment approaches to manage portions of the Fund’s portfolio under the general supervision of SEI Investments Management Corp. (SIMC). The Fund utilizes the following sub-advisors as of May 31, 2010: Trust Company of the West (formerly Metropolitan West Asset Management LLC), Jennison Associates LLC and Income Research & Management. For the fiscal year ended May 31, 2010, Jennison Associates LLC and Income Research & Management were added to the Fund.

III. Market Commentary:

Fixed-income market conditions for the fiscal year ended May 31, 2010 reflected a dramatic recovery from the crisis conditions of 2008, including the bankruptcy of Lehman Brothers. The period was characterized by an increased investor appetite for risk that drove powerful rallies in most of the non-Treasury sectors in the market. The catalyst for the market recovery was a series of government programs designed to improve credit availability, which included the Term Asset-Backed Securities Lending Facility (TALF), the Public-Private Investment Program (PPIP) and a $1.25 trillion purchase program of agency mortgage-backed securities (MBS) by the U.S. Federal Reserve (Fed). The Fed’s purchase program brought MBS spreads and mortgage rates to historic lows. The TALF and PPIP programs helped drive strong performance in the non-agency MBS market, including commercial MBS, and the asset-backed securities market. The corporate bond market was supported by stabilizing economic conditions, lower default rates and improved market liquidity. The strong market recovery was interrupted in the spring of 2010, as the European sovereign credit crisis triggered a modest flight to quality that served to bring Treasury yields back to the lower end of their trading range. Despite this more recent market caution, the rallies in the non-Treasury sectors provided very strong performance for the fixed-income markets for the one-year period.

IV. Return vs. Benchmark:

For the fiscal year ended May 31, 2010, the SIIT Long Duration Fund returned 18.11% compared to 15.11% for its benchmark, the Barclays Long U.S. Government/Credit Index.

V. Fund Attribution:

The Fund’s out-performance came from its overweight exposure to the corporate bond sector. The corporate overweight was focused on the Financials sector, which led the strong rally in the corporate market. The modest drop in intermediate- and longer-term Treasury yields served to support the very strong absolute return of the Fund.

Long Duration Fund

AVERAGE ANNUAL TOTAL RETURN1

| | | | | | | | |

| | | One Year

Return | | Annualized

3 Year

Return | | Annualized

5 Year

Return | | Annualized

Inception

to Date |

| Long Duration Fund, Class A | | 18.11% | | 2.72% | | 1.85% | | 3.60% |

Comparison of Change in the Value of a $100,000 Investment in the Long Duration Fund, versus the Barclays Long US Government/Credit Index2, the Barclays 15 Year Bellwether Swap Index2, 60/40 Blend of the Barclays Long Credit Index & Barclays Long Government Index, the Barclays Long US Credit Index, and the Barclays Long US Government Index

| | 1 | | For the period ended May 31, 2010. Past performance is not an indication of future performance. Class A shares were offered beginning 4/21/04. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower. |

| | 2 | | This table compares the Fund’s average annual total returns for Class A Shares to those of the Barclays Long U.S. Government/Credit Index. In prior years, the Fund’s return had been compared to the Barclays 15 Year Bellwether Swap Index. The Fund’s adviser believes that the Barclays Long U.S. Government/Credit Index better represents the Fund’s investment opportunities. |

| | |

| SEI Institutional Investments Trust / Annual Report / May 31, 2010 | | 15 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

SEI INSTITUTIONAL INVESTMENTS TRUST — MAY 31, 2010 (Unaudited)

Emerging Markets Debt Fund

I. Objective:

The Emerging Markets Debt Fund (the “Fund”) seeks to maximize total return.

II. Multi-Manager Approach Statement:

The Fund uses a multi-manager approach, relying on a number of sub-advisors with differing investment approaches to manage portions of the Fund’s portfolio under the general supervision of SEI Investments Management Corp. (SIMC). The Fund utilized the following sub-advisors as of May 31, 2010: Ashmore Investment Management Limited, ING Investment Management Advisors, B.V. and Stone Harbor Investment Partners L.P. For the fiscal year ended May 31, 2010, no sub-advisor changes were made in the Fund.

III. Market Commentary:

The credit crisis abated and risk appetite amongst investors returned very quickly, which led to emerging markets debt posting its strongest annual performance since 1996. The market returned 29% in 2009 and carried the momentum into 2010 with a 3.55% return through the end of May. Spreads began the fiscal year at 478 basis points and tightened by as much as 222 basis points over U.S. Treasuries before widening in April and May to 338 basis points on broader risk aversion emanating from the Greek and eurozone sovereign debt crisis.

The fundamentals of emerging-markets debt remain strong and are supported by various factors. Stable and rising commodity prices, rising foreign currency reserves, declining debt levels and less political turbulence all contribute to a favorable outlook for the asset class. These factors have contributed to a substantial increase in credit-rating upgrades, with only a handful of downgrades during the last 12 months. Positive surprises to economic growth across the broader emerging markets universe have been supportive, while election results and unorthodox policy changes (which have rattled emerging markets in the past) have been conducted in more democratic ways with less violence and protest.

In addition to solid fundamentals, technical factors greatly contributed to performance for the period. The ability of emerging markets to weather the credit crisis of 2008 better than other spread sectors caught the attention of both new and existing investors. As a result, inflows into the asset class amounted to $54 billion for the period. Inflows are rising and becoming increasingly diversified, especially with more instrument selection coming from the growing local and corporate sectors of the market. As investors poured historically high amounts of money into emerging-markets debt, emerging-market issuers took advantage of lower financing rates and issued record amounts of bonds to meet the rising demand for emerging-market debt assets. In 2009 alone, emerging-market issuers raised $210 billion via new external debt issuance and have sold $105 billion through the first five months of 2010. With another $90 billion still in the pipeline for the remainder of the year, technicals are still expected to remain a key driver of performance going forward. The proceeds of these sales will be used for deficit funding, refinancing and infrastructure & development projects.

Central banks and local governments have done their part to improve confidence amongst investors and market participants. Fiscal policy continues to improve, and although monetary policy has been accommodative and successful in implementing counter-cyclical measures during the last 12 months, policymakers will be challenged going forward as inflationary pressures, stimulus unwinding, financial reforms and the fiscal crisis in Europe pose potential risks that could hinder growth. The outlook for emerging markets is positive, and fundamentals have not yet been threatened by any potential risks. Emerging countries are expected to grow approximately 6.2% in 2010, while the developed world is expected to grow by less than 3%. Problems in Europe and the rest of the developed world should only benefit the asset class as investors look for alternative opportunities.

IV. Return vs. Benchmark:

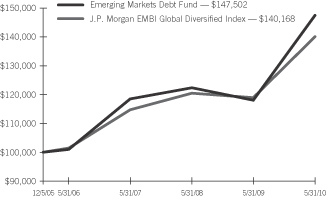

For the fiscal year ended May 31, 2010, the Fund outperformed the J.P. Morgan Emerging Markets Bond Index (EMBI) Global Diversified Index, returning 24.93% versus the index return of 17.85%.

| | |

| 16 | | SEI Institutional Investments Trust / Annual Report / May 31, 2010 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

SEI INSTITUTIONAL INVESTMENTS TRUST — MAY 31, 2010 (Unaudited)

Emerging Markets Debt Fund (Concluded)

V. Fund Attribution:

Security selection in Argentina contributed to positive relative performance for the period. The country had been plagued by political problems and fiscal concerns prior to and during the credit crisis that nearly led to a default. Fortunately, rising commodity prices led to strong export revenues, and the country’s endless commitment to comforting creditors and servicing debt was fulfilled via multiple debt swaps and an eventual decision to proceed with what the country hopes to be the final restructuring of past defaulted debt. Markets reacted favorably to the news and Argentina finished the period returning 69%, one of the top-performing countries in emerging-markets debt universe. An overweight to Russia added to out-performance, as rising oil prices helped support a country with one of the worst primary fiscal balances in emerging markets. Additionally, the government increased support to the struggling banking sector while inflation continued to slow, allowing rate cuts to follow and help revive the economy. Russia is better positioned to service its debt than its emerging-markets peers, and its rising level of foreign currency reserves has improved its financial flexibility. Allocations to local currency debt in Brazil also added to relative performance, as the country was marginally impacted by the credit crisis. The country’s diversified export base benefited from rising commodities, foreign currency reserves continued to rise, and loan growth and consumption helped drive its first-quarter 2010 gross domestic product growth to an annualized rate of 11.25%, one of the highest in the world.

The Fund’s underweight in Belize detracted from relative performance, as bonds returned 100% for the period. Belize makes up a very small portion of the index and generates most of its growth from agriculture and tourism. The country is a low-quality credit and rallied with other risky assets. An underweight in Ghana also detracted from performance. Similar to Belize, Ghana is a lower-quality country and also one of the smallest countries in the index. The country carries a higher beta than the index and outperformed the market on improved sentiment and a rally in commodity prices. Fund managers chose not to allocate to Belize or Ghana because the risk/reward opportunities were more attractive in more fiscally sound countries.

Emerging Markets Debt Fund

AVERAGE ANNUAL TOTAL RETURN1

| | | | | | |

| | | One Year

Return | | Annualized

3 Year

Return | | Annualized

Inception

to Date |

| Emerging Markets Debt Fund, Class A | | 24.93% | | 7.55% | | 9.05% |

Comparison of Change in the Value of a $100,000 Investment in the Emerging Markets Debt Fund, versus the J.P. Morgan EMBI Global Diversified Index

| | 1 | | For the period ended May 31, 2010. Past performance is not an indication of future performance. Class A shares were offered beginning 12/05/05. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower. |

| | |

| SEI Institutional Investments Trust / Annual Report / May 31, 2010 | | 17 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

SEI INSTITUTIONAL INVESTMENTS TRUST — MAY 31, 2010 (Unaudited)

Real Return Fund

I. Objective:

The Real Return Fund (the “Fund”) seeks to provide total return exceeding the rate of inflation.

II. Multi-Manager Approach Statement:

The Fund uses a sub-adviser to manage the Fund under the supervision of SEI Investments Management Corporation (SIMC). Currently, the sub-advisor is Wellington Management Company, LLC. There were no manager changes during the period.

III. Market Commentary:

Fixed-income market conditions for the fiscal year ended May 31, 2010 reflected a dramatic recovery from the crisis conditions of 2008, including the bankruptcy of Lehman Brothers. The period was characterized by an increased investor appetite for risk that drove powerful rallies in most of the non-Treasury sectors in the market. The catalyst for the market recovery was a series of government programs designed to improve credit availability, which included the Term Asset-Backed Securities Lending Facility (TALF), the Public-Private Investment Program (PPIP) and a $1.25 trillion purchase program of agency mortgage-backed securities (MBS) by the U.S. Federal Reserve (Fed). The Fed’s purchase program brought MBS spreads and mortgage rates to historic lows. The TALF and PPIP programs helped drive strong performance in the non-agency MBS market, including commercial MBS, and the asset-backed securities market. These actions helped stabilize economic conditions, which in turn supported the Treasury Inflation-Protected Securities (TIPS) market, as there were higher inflation expectations among investors and improved market liquidity. The strong market recovery was interrupted in the spring of 2010, as the European sovereign credit crisis triggered a modest flight to quality that served to bring Treasury yields back to the lower end of their trading range. Despite the more recent caution displayed by market participants, the rally in TIPS provided strong performance for the for the twelve month period.

IV. Return vs. Benchmark:

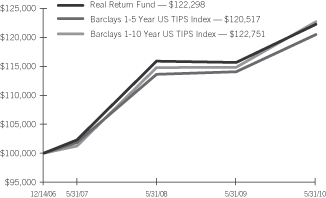

For the fiscal year ended May 31, 2010, the Fund returned 5.70% compared to 5.63% for its benchmark. The Fund’s adviser believes the Barclays 1-5 Year U.S. TIPS Index better represents the Fund’s investment opportunities.

V. Fund Attribution:

The Fund’s out-performance was a result of its tactical and timely allocation to nominal Treasuries. As Treasuries were the main beneficiaries of the recent flight to quality, this allocation helped the Fund outperform its benchmark. In addition, the modest drop in TIPS yields served to support the absolute return of the Fund.

Real Return Fund

AVERAGE ANNUAL TOTAL RETURN1

| | | | | | |

| | | One Year

Return | | Annualized

3 Year

Return | | Annualized

Inception

to Date |