UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-07261 |

|

CREDIT SUISSE TRUST |

(Exact name of registrant as specified in charter) |

|

One Madison Avenue, New York, New York | | 10010 |

(Address of principal executive offices) | | (Zip code) |

|

John G. Popp Credit Suisse Trust One Madison Avenue New York, New York 10010 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | (212) 325-2000 | |

|

Date of fiscal year end: | December 31st | |

|

Date of reporting period: | January 1, 2017 to December 31, 2017 | |

| | | | | | | | |

Item 1. Reports to Stockholders.

CREDIT SUISSE FUNDS

Annual Report

December 31, 2017

n CREDIT SUISSE TRUST

COMMODITY RETURN STRATEGY PORTFOLIO

Credit Suisse Trust — Commodity Return Strategy Portfolio (the "Portfolio") shares are not available directly to individual investors, but may be offered only through certain insurance products and pension and retirement plans.

The Portfolio's investment objective, risks, charges and expenses (which should be considered carefully before investing), and more complete information about the Portfolio, are provided in the Prospectus, which should be read carefully before investing. You may obtain additional copies by calling 877-870-2874 or by visiting our website at www.credit-suisse.com/us/funds.

Credit Suisse Securities (USA) LLC, Distributor, is located at One Madison Avenue, New York, NY 10010. The Portfolio is advised by Credit Suisse Asset Management, LLC.

Portfolio shares are not deposits or other obligations of Credit Suisse Asset Management, LLC ("Credit Suisse") or any affiliate, are not FDIC-insured and are not guaranteed by Credit Suisse or any affiliate. Portfolio investments are subject to investment risks, including loss of your investment.

Credit Suisse Trust — Commodity Return Strategy Portfolio

Annual Investment Adviser's Report

December 31, 2017 (unaudited)

January 19, 2018

Dear Shareholder:

We are pleased to present this Annual Report covering the activities of the Credit Suisse Trust — Commodity Return Strategy Portfolio (the "Portfolio") for the 12 months ended December 31, 2017.

Performance Summary

01/01/17 – 12/31/17

Fund & Benchmark | | Performance | |

Credit Suisse Trust — Commodity Return Strategy

Portfolio1 | | | 1.52 | % | |

| Bloomberg Commodity Index Total Return2 | | | 1.70 | % | |

Market and Strategy Review:

Commodities were higher for the 12 months ended December 31, 2017. The Bloomberg Commodity Index Total Return (the "Benchmark") increased 1.70%, with 13 out of 22 index constituents trading higher.

For the 12 months ended December 31, 2017, the Portfolio outperformed the Benchmark before fees and fund expenses, but underperformed net of fees and expenses. Commodity strategies and underlying cash management both positively contributed to relative performance. The Portfolio held derivatives linked to futures contracts which expire on different dates than those held within the Benchmark; this forward curve positioning in all five Benchmark sectors had a positive impact on Portfolio performance relative to the Benchmark. Positioning within the Agriculture, Energy and Livestock sectors contributed the most to positive relative performance.

Industrial Metals was the best performing sector, increasing 29.35%, as economic growth improved globally. Countries increased infrastructure spending, particularly in China and India, which was supportive of base metals demand. A continuous stream of positive and expansionary economic readings, particularly in the manufacturing sector for major economies, also increased demand expectations as supplies continued to tighten across the sector. The top three performing Benchmark constituents were all Industrial Metals. Aluminum increased 31.18%. During the first quarter, the U.S. Department of Commerce began to investigate if China was selling aluminum foil in the U.S. at prices below market cost. By year end, the U.S. government decided to impose anti-dumping duties on Chinese imports, restricting supplies. China, one of the world's largest producers of the metal, also imposed various environmental controls to temper air pollution during the winter season, hampering aluminum

1

Credit Suisse Trust — Commodity Return Strategy Portfolio

Annual Investment Adviser's Report (continued)

December 31, 2017 (unaudited)

production within the country. This caused stockpiles in China and those tracked by the London Metal Exchange (the "LME") to shrink as demand increased. Zinc rose 29.71% as large zinc mines remained offline since late 2015. Reduced raw zinc supplies forced some Chinese smelters to shut down earlier than expected, causing refined output to reach a three-year low in July, according to China's National Bureau of Statistics. The reduced production of refined zinc led LME-tracked stockpiles to reach their lowest levels since 2008. Copper gained 29.17% as labor disputes at copper mines in Chile, Indonesia and Peru throughout the year reduced output. Upcoming wage negotiations between labor groups and mine owners in 2018, particularly in Chile, may further disrupt production.

Precious Metals increased 10.94%. The U.S. Dollar declined over the period, potentially due to expectations for increased fiscal stimulus, despite the U.S. Federal Reserve (the "Fed") raising short-term interest rates three times in 2017. Various geopolitical issues marked the calendar year, among them: threats of military action between the U.S. and North Korea, continued tensions in the Middle East, and further regional tensions within major European nations which increased unease within the European Union. These events increased the appeal of Gold and Silver as safe haven assets.

Livestock rose 6.36%, with both Live Cattle and Lean Hogs increasing, due to strong domestic and export demand for U.S. beef and pork throughout the year, as reported by the U.S. Department of Agriculture (the "USDA"). USDA trade data showed pork and beef monthly export levels reached new highs during the 2017 marketing year. Robust economic growth and higher employment levels potentially indicate a continuation of rising demand for U.S. meat products in 2018.

Energy decreased 4.31%. Natural Gas declined the most for the year, losing 36.37%. The U.S. started 2017 with particularly mild winter weather in key heating demand areas, leading to lower-than-expected demand and essentially ending the rally seen at the end of a chilly 2016. Temperatures largely remained near historical averages for a majority of the year across the continental U.S. Production growth in the U.S. Northeast towards year end ahead of the completion of key pipeline projects increased supplies and also sent prices lower. However, crude oil and petroleum products ended the year positively as global crude oil inventories moved closer to the five-year average. The Organization of the Petroleum Exporting Countries ("OPEC") and other nations remained disciplined in curtailing global supplies by agreeing to extend their crude oil production cuts twice in the year, with the agreement potentially extending through the end of 2018. Higher exports of crude oil from the U.S. to make up

2

Credit Suisse Trust — Commodity Return Strategy Portfolio

Annual Investment Adviser's Report (continued)

December 31, 2017 (unaudited)

for lower supplies elsewhere, along with various pipeline disruptions, provided additional support to crude oil and petroleum products.

Agriculture dropped 11.05%, as both softs and grains declined as supplies outweighed demand. Sugar declined 25.38%, falling precipitously in the first half of the year due to record output from Brazil and a growing global surplus, as reported by the Brazilian Sugarcane Industry Association, despite a trend for more sugarcane-based ethanol demand. Continued supportive weather during Brazil's sugar harvesting season further improved crop yields in the second half of the year. Coffee decreased 16.02%, also due to bountiful harvests in Brazil amid ideal growing and harvesting conditions. In its June Foreign Agricultural Service report, the USDA revised production levels upward for the 2016/2017 season and predicted a surplus for the next season. Producers also sold down their stockpiles to take advantage of a weaker Brazilian Real versus the U.S. Dollar during the second half of the year, adding additional downward pressure to both Sugar and Coffee.

Outlook:

In 2017, commodities as an asset class sustained some of the momentum it garnered during the previous year. With the help of increasing demand for crude oil, OPEC and its partners have slowly but successfully brought down global supplies closer to the five-year average through their coordinated production cuts. Their agreement to potentially extend the cuts through the end of 2018, and the possibility of including Libya and Nigeria in the agreement, may rein in the glut in supplies to a greater degree in the coming year. Markets will remain focused on compliance levels from parties to the agreement, including Russia, next year. In addition, the biggest question remains how much incremental oil production will be seen from U.S. shale as prices continue to climb. There have been signs of more restraint from major U.S. producers; however, this may change as prices continue to rise, possibly enabling smaller companies to grow production as well.

Environmental controls implemented by various governments in Asia contributed to reduced production for most industrial metals throughout the year as increasing demand, due to improving global economic growth, outpaced refined supplies. Environmental protections, a major focus in China, raised costs of production for base metals. For other commodities, disruptive weather events failed to materialize during key growing and harvesting seasons, allowing many agricultural commodities to remain oversupplied. More health-conscious diets and the increasing demand for protein-rich foods globally should continue to shape what farmers choose to grow. This has been exemplified in the U.S., where soybeans are now planted in farmland once dedicated to wheat. In addition,

3

Credit Suisse Trust — Commodity Return Strategy Portfolio

Annual Investment Adviser's Report (continued)

December 31, 2017 (unaudited)

U.S. pork and beef production has increased significantly compared to years past to meet rising demand.

Earlier in the year, the Organization for Economic Cooperation and Development (the "OECD") predicted the Gross Domestic Product ("GDP") of all 45 countries it monitors would grow in 2017, backed by low interest rates, lower unemployment and elevated consumer confidence. Some central banks, such as the Fed and the Bank of England, have already begun to tighten monetary policies, though largely accommodative stimulus measures remain for both and for the rest of the developed world. However, China may relax some credit controls in 2018 if it determines its central bank restricted liquidity too quickly in its effort to rein in some excesses and has jeopardized growth prospects.

Within the U.S., employment levels continued to improve and consumer confidence levels continued to increase, with more consumers taking on debt. This evidence of growing consumer buying power has led to some heightened inflation expectations, enough for the Fed to raise rates three times in 2017 alone. However, there is skepticism as to whether the Fed will raise rates at the same pace in 2018. As the tax overhaul plan was passed into law right before year end, the country may shift its focus to infrastructure and capital spending. There is much uncertainty on this point, but if anything major materializes following significant campaign promises, it may improve employment levels even further and serve as a boon for commodities demand.

The Credit Suisse Commodities Management Team

Nelson Louie

Christopher Burton

This Portfolio is non-diversified, which means it may invest a greater proportion of its assets in the securities of a smaller number of issuers than a diversified mutual fund and may therefore be subject to greater volatility. The Portfolio's investment in commodity-linked derivative instruments may subject the Portfolio to greater volatility than investments in traditional securities, particularly in investments involving leverage.

The use of derivatives such as commodity-linked structured notes, swaps and futures entails substantial risks, including risk of loss of a significant portion of their principal value, commodity exposure risk, correlation risk, derivatives risk, exposure risk, fixed income risk, focus risk, futures contract risk, leveraging risk, liquidity risk, interest rate risk, market risk, portfolio turnover risk, structured note risk, subsidiary risk, swap agreements risk, U.S. government securities risk, credit risk and tax risk. Gains and

4

Credit Suisse Trust — Commodity Return Strategy Portfolio

Annual Investment Adviser's Report (continued)

December 31, 2017 (unaudited)

losses from speculative positions in derivatives may be much greater than the derivative's cost. At any time, the risk of loss of any individual security held by the Portfolio could be significantly higher than 50% of the security's value. For a detailed discussion of these and other risks, please refer to the Portfolio's Prospectus, which should be read carefully before investing.

In addition to historical information, this report contains forward-looking statements, which may concern, among other things, domestic and foreign markets, industry and economic trends and developments and government regulation, and their potential impact on the Portfolio's investments. These statements are subject to risks and uncertainties and actual trends, developments and regulations in the future, and their impact on the Portfolio, could be materially different from those projected, anticipated or implied. The Portfolio has no obligation to update or revise forward-looking statements.

The views of the Portfolio's management are as of the date of this letter and the Portfolio holdings described in this document are as of December 31, 2017; these views and Portfolio holdings may have changed subsequent to these dates. Nothing in this document is a recommendation to purchase or sell securities.

5

Credit Suisse Trust — Commodity Return Strategy Portfolio

Annual Investment Adviser's Report (continued)

December 31, 2017 (unaudited)

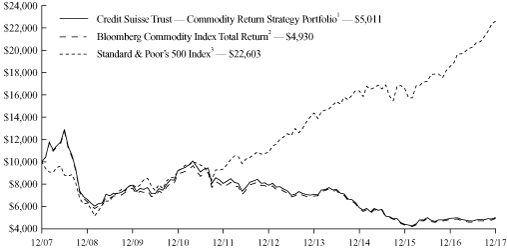

Comparison of Change in Value of $10,000 Investment in the

Credit Suisse Trust — Commodity Return Strategy Portfolio1, the

Bloomberg Commodity Index Total Return2 and the

Standard & Poor's 500 Index3 For Ten Years.

1 Fee waivers and/or expense reimbursements reduce expenses for the Portfolio, without which performance would be lower. The Portfolio entered into a written contract to limit expenses to 1.05% of the Portfolio's average daily net assets through at least May 1, 2019. This limit excludes certain expenses, as set forth in the Portfolio's Prospectus.

2 The Bloomberg Commodity Index Total Return is a broadly diversified futures index currently composed of futures contracts on 22 physical commodities. The index does not have transaction costs and investors may not invest directly in the index.

3 The Standard & Poor's 500 Index is an unmanaged index (with no defined investment objective) of common stocks, includes reinvestment of dividends, and is a registered trademark of The McGraw-Hill Companies, Inc. The index does not have transaction costs and investors may not invest directly in the index.

6

Credit Suisse Trust — Commodity Return Strategy Portfolio

Annual Investment Adviser's Report (continued)

December 31, 2017 (unaudited)

Average Annual Returns as of December 31, 20171

| 1 Year | | 5 Years | | 10 Years | |

| | 1.52 | % | | | (8.70 | )% | | | (6.68 | )% | |

Returns represent past performance and include change in share price and reinvestment of dividends and capital gain distributions, if any. Past performance cannot guarantee future results. The current performance of the Portfolio may be lower or higher than the figures shown. Returns and share price will fluctuate, and redemption value may be more or less than original cost. The performance results do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares. Performance information current to the most recent month end is available at www.credit-suisse.com/us/funds.

The annualized gross expense ratio is 1.11%. The annualized net expense ratio after fee waivers and/or expense reimbursements is 1.05%.

1 Fee waivers and/or expense reimbursements reduce expenses for the Portfolio, without which performance would be lower. The Portfolio entered into a written contract to limit expenses to 1.05% of the Portfolio's average daily net assets through at least May 1, 2019. This limit excludes certain expenses, as set forth in the Portfolio's Prospectus.

7

Credit Suisse Trust — Commodity Return Strategy Portfolio

Annual Investment Adviser's Report (continued)

December 31, 2017 (unaudited)

Information About Your Portfolio's Expenses

As an investor of the Portfolio, you incur two types of costs: ongoing expenses and transaction costs. Ongoing expenses include management fees, distribution and service (12b-1) fees and other Portfolio expenses. Examples of transaction costs include sales charges (loads), redemption fees and account maintenance fees, which are not shown in this section and which would result in higher total expenses. The following table is intended to help you understand your ongoing expenses of investing in the Portfolio and to help you compare these expenses with the ongoing expenses of investing in other mutual funds. The table is based on an investment of $1,000 made at the beginning of the six months ended December 31, 2017.

The table illustrates your Portfolio's expenses in two ways:

• Actual Portfolio Return. This helps you estimate the actual dollar amount of ongoing expenses paid on a $1,000 investment in the Portfolio using the Portfolio's actual return during the period. To estimate the expenses you paid over the period, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the "Expenses Paid per $1,000" line.

• Hypothetical 5% Portfolio Return. This helps you to compare the Portfolio's ongoing expenses with those of other mutual funds using the Portfolio's actual expense ratio and a hypothetical rate of return of 5% per year before expenses. Examples using a 5% hypothetical portfolio return may be found in the shareholder reports of other mutual funds. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period.

Please note that the expenses shown in these tables are meant to highlight your ongoing expenses only and do not reflect any transaction costs, such as sales charges (loads) or redemption fees. If these transaction costs had been included, your costs would have been higher. The "Expenses Paid per $1,000" line of the tables is useful in comparing ongoing expenses only and will not help you determine the relative total expenses of owning different funds.

8

Credit Suisse Trust — Commodity Return Strategy Portfolio

Annual Investment Adviser's Report (continued)

December 31, 2017 (unaudited)

Expenses and Value for a $1,000 Investment

for the six-month period ended December 31, 2017

Actual Portfolio Return | |

Beginning Account Value 07/01/17 | | $ | 1,000.00 | | |

Ending Account Value 12/31/17 | | $ | 1,066.10 | | |

Expenses Paid per $1,000* | | $ | 5.47 | | |

Hypothetical 5% Portfolio Return | |

Beginning Account Value 07/01/17 | | $ | 1,000.00 | | |

Ending Account Value 12/31/17 | | $ | 1,019.91 | | |

Expenses Paid per $1,000* | | $ | 5.35 | | |

Annualized Expense Ratio* | | | 1.05 | % | |

* Expenses are equal to the Portfolio's annualized expense ratio multiplied by the average account value over the period, multiplied by 184/365 to reflect the one-half year period.

The "Expenses Paid per $1,000" and the "Annualized Expense Ratio" in the tables are based on actual expenses paid by the Portfolio during the period, net of fee waivers and/or actual expense reimbursements, if applicable. If those fee waivers and/or expense reimbursements had not been in effect, the Portfolio's actual expenses would have been higher. Expenses do not reflect additional charges and expenses that are, or may be, imposed under the variable contracts or plans. Such charges and expenses are described in the prospectus of the insurance company separate account or in the plan documents or other informational materials supplied by plan sponsors. The Portfolio's expenses should be considered with these charges and expenses in evaluating the overall cost of investing in the separate account.

For more information, please refer to the Portfolio's Prospectus.

9

Credit Suisse Trust — Commodity Return Strategy Portfolio

Annual Investment Adviser's Report (continued)

December 31, 2017 (unaudited)

Portfolio Breakdown*

United States Agency Obligations | | | 71.71 | % | |

United States Treasury Obligations | | | 25.93 | | |

Short-Term Investment1 | | | 2.36 | | |

Total | | | 100.00 | % | |

* Expressed as a percentage of total investments (excluding securities lending collateral, if applicable) and may vary over time.

1 Primarily reflects cash invested in State Street Bank and Trust Co. Euro Time Deposit, for which the purchases of securities have been executed but not yet settled at December 31, 2017, if applicable.

10

Credit Suisse Trust — Commodity Return Strategy Portfolio

Consolidated Schedule of Investments

December 31, 2017

Par

(000) | | | | Ratings†

(S&P/Moody's) | | Maturity | | Rate% | | Value | |

| UNITED STATES AGENCY OBLIGATIONS (68.9%) | | | |

$ | 7,200 | | | Federal Farm Credit Banks,

LIBOR 1M + 0.175%(1) | | (AA+, Aaa) | | 02/25/19 | | | 1.727 | | | $ | 7,223,884 | | |

| | 8,400 | | | Federal Farm Credit Banks,

LIBOR 1M + 0.150%(1) | | (AA+, Aaa) | | 03/15/19 | | | 1.627 | | | | 8,423,719 | | |

| | 3,600 | | | Federal Farm Credit Banks,

USBMMY3M + 0.090%(1) | | (AA+, Aaa) | | 06/19/19 | | | 1.540 | | | | 3,605,229 | | |

| | 8,100 | | | Federal Farm Credit Banks,

LIBOR 1M + 0.190%(1) | | (AA+, Aaa) | | 08/19/19 | | | 1.685 | | | | 8,132,932 | | |

| | 3,600 | | | Federal Farm Credit Banks,

LIBOR 3M - 0.010%(1) | | (AA+, Aaa) | | 09/23/19 | | | 1.665 | | | | 3,605,762 | | |

| | 2,900 | | | Federal Farm Credit Banks,

LIBOR 1M + 0.180%(1) | | (AA+, Aaa) | | 10/11/19 | | | 1.612 | | | | 2,911,922 | | |

| | 5,200 | | | Federal Farm Credit Banks,

LIBOR 1M + 0.180%(1) | | (AA+, Aaa) | | 10/24/19 | | | 1.732 | | | | 5,221,631 | | |

| | 7,900 | | | Federal Farm Credit Banks,

LIBOR 3M - 0.060%(1) | | (AA+, Aaa) | | 10/25/19 | | | 1.307 | | | | 7,908,766 | | |

| | 11,700 | | | Federal Farm Credit Banks,

LIBOR 3M - 0.120%(1) | | (AA+, Aaa) | | 01/27/20 | | | 1.254 | | | | 11,707,898 | | |

| | 11,200 | | | Federal Farm Credit Banks,

LIBOR 1M + 0.050%(1) | | (AA+, Aaa) | | 02/21/20 | | | 1.561 | | | | 11,224,137 | | |

| | 1,800 | | | Federal Farm Credit Banks,

FCPR DLY - 3.010%(1) | | (AA+, Aaa) | | 07/21/20 | | | 1.490 | | | | 1,800,628 | | |

| | 4,700 | | | Federal Farm Credit Banks,

LIBOR 1M + 0.010%(1) | | (AA+, Aaa) | | 08/24/20 | | | 1.562 | | | | 4,700,945 | | |

| | 1,800 | | | Federal Farm Credit Banks,

FCPR DLY - 3.020%(1) | | (AA+, Aaa) | | 09/28/20 | | | 1.480 | | | | 1,799,758 | | |

| | 4,000 | | | Federal Farm Credit Banks,

LIBOR 1M + 0.200%(1) | | (AA+, Aaa) | | 10/26/20 | | | 1.752 | | | | 4,020,330 | | |

| | 8,200 | | | Federal Farm Credit Banks,

FCPR DLY - 2.980%(1) | | (AA+, Aaa) | | 11/12/20 | | | 1.520 | | | | 8,196,477 | | |

| | 4,100 | | | Federal Farm Credit Banks,

USBMMY3M + 0.130%(1) | | (AA+, Aaa) | | 11/12/20 | | | 1.580 | | | | 4,108,025 | | |

| | 4,000 | | | Federal Farm Credit Banks,

LIBOR 1M + 0.350%(1) | | (AA+, Aaa) | | 02/05/21 | | | 1.729 | | | | 4,035,420 | | |

| | 4,400 | | | Federal Farm Credit Banks,

LIBOR 1M + 0.260%(1) | | (AA+, Aaa) | | 11/23/21 | | | 1.812 | | | | 4,436,150 | | |

| | 800 | | | Federal Farm Credit Banks,

LIBOR 1M + 0.240%(1) | | (AA+, Aaa) | | 01/18/22 | | | 1.731 | | | | 805,875 | | |

| | 8,050 | | | Federal Farm Credit Banks,

LIBOR 1M + 0.400%(1) | | (AA+, Aaa) | | 12/08/23 | | | 1.807 | | | | 8,106,774 | | |

| | 5,700 | | | Federal Home Loan Banks,

LIBOR 3M - 0.120%(1) | | (AA+, Aaa) | | 09/20/18 | | | 1.505 | | | | 5,702,660 | | |

| | 6,500 | | | Federal Home Loan Banks,

LIBOR 1M - 0.085%(1) | | (AA+, Aaa) | | 03/13/19 | | | 1.375 | | | | 6,500,543 | | |

| | 9,250 | | | Federal Home Loan Banks,

LIBOR 1M - 0.090%(1) | | (AA+, Aaa) | | 06/21/19 | | | 1.421 | | | | 9,248,109 | | |

See Accompanying Notes to Consolidated Financial Statements.

11

Credit Suisse Trust — Commodity Return Strategy Portfolio

Consolidated Schedule of Investments (continued)

December 31, 2017

Par

(000) | | | | Ratings†

(S&P/Moody's) | | Maturity | | Rate% | | Value | |

| UNITED STATES AGENCY OBLIGATIONS (continued) | | | |

$ | 8,900 | | | Federal Home Loan Banks,

LIBOR 1M - 0.095%(1) | | (AA+, Aaa) | | 06/27/19 | | | 1.457 | | | $ | 8,897,379 | | |

| | 9,200 | | | Federal Home Loan Banks | | (AA+, Aaa) | | 08/28/19 | | | 1.550 | | | | 9,129,648 | | |

| | 10,000 | | | Federal Home Loan Banks,

LIBOR 1M - 0.055%(1) | | (AA+, Aaa) | | 12/16/19 | | | 1.422 | | | | 9,998,389 | | |

| | 5,400 | | | Federal Home Loan Banks,

LIBOR 1M - 0.065%(1) | | (AA+, Aaa) | | 12/26/19 | | | 1.487 | | | | 5,397,890 | | |

| | 4,300 | | | Federal Home Loan Banks,

LIBOR 1M - 0.070%(1) | | (AA+, Aaa) | | 12/27/19 | | | 1.482 | | | | 4,298,695 | | |

| | 6,000 | | | Federal Home Loan Banks,

LIBOR 3M + 0.125%(1) | | (AA+, Aaa) | | 07/01/20 | | | 1.820 | | | | 6,035,230 | | |

| | 7,600 | | | Federal Home Loan Banks,

LIBOR 1M + 0.150%(1) | | (AA+, Aaa) | | 09/28/20 | | | 1.714 | | | | 7,629,003 | | |

| | 6,000 | | | Federal Home Loan Banks | | (AA+, Aaa) | | 07/23/21 | | | 2.000 | | | | 5,965,188 | | |

| | 3,300 | | | Federal Home Loan Mortgage Corp.,

LIBOR 3M - 0.030%(1) | | (AA+, Aaa) | | 01/08/18 | | | 1.319 | | | | 3,300,114 | | |

| | 4,600 | | | Federal Home Loan Mortgage Corp.,

LIBOR 3M + 0.020%(1) | | (AA+, Aaa) | | 03/08/18 | | | 1.543 | | | | 4,601,262 | | |

| | 13,050 | | | Federal Home Loan Mortgage Corp. | | (AA+, Aaa) | | 07/26/19 | | | 1.600 | | | | 12,983,706 | | |

| | 2,600 | | | Federal Home Loan Mortgage Corp. | | (AA+, Aaa) | | 08/15/19 | | | 1.375 | | | | 2,578,100 | | |

| | 6,600 | | | Federal Home Loan Mortgage Corp. | | (AA+, Aaa) | | 09/27/19 | | | 1.500 | | | | 6,549,965 | | |

| | 3,500 | | | Federal Home Loan Mortgage Corp.

Discount Notes | | (AA+, Aaa) | | 02/02/18 | | | 1.100 | | | | 3,496,052 | | |

| | 5,000 | | | Federal Home Loan Mortgage Corp.

Discount Notes | | (AA+, Aaa) | | 02/05/18 | | | 1.080 | | | | 4,993,815 | | |

| | 3,400 | | | Federal National Mortgage Association | | (AA+, Aaa) | | 02/26/19 | | | 1.250 | | | | 3,375,826 | | |

| | 14,000 | | | Federal National Mortgage Association,

LIBOR 1M + 0.000%(1) | | (AA+, Aaa) | | 02/28/19 | | | 1.564 | | | | 14,015,767 | | |

| | 17,100 | | | Federal National Mortgage Association,

LIBOR 1M + 0.000%(1) | | (AA+, Aaa) | | 03/08/19 | | | 1.407 | | | | 17,113,957 | | |

| | 8,000 | | | Federal National Mortgage Association,

LIBOR 3M - 0.150%(1) | | (AA+, Aaa) | | 03/13/20 | | | 1.413 | | | | 8,004,298 | | |

| | 6,700 | | | Federal National Mortgage Association,

LIBOR 3M - 0.160%(1) | | (AA+, Aaa) | | 03/25/20 | | | 1.515 | | | | 6,700,732 | | |

| | 3,200 | | | Federal National Mortgage Association | | (AA+, Aaa) | | 04/27/20 | | | 1.800 | | | | 3,179,392 | | |

| TOTAL UNITED STATES AGENCY OBLIGATIONS (Cost $281,596,060) | | | 281,671,982 | | |

| UNITED STATES TREASURY OBLIGATIONS (24.9%) | | | |

| | 4,000 | | | United States Treasury Floating Rate Notes,

USBMMY3M + 0.174%(1) | | (AA+, Aaa) | | 07/31/18 | | | 1.624 | | | | 4,004,659 | | |

| | 8,000 | | | United States Treasury Floating Rate Notes,

USBMMY3M + 0.170%(1),(2) | | (AA+, Aaa) | | 10/31/18 | | | 1.620 | | | | 8,012,917 | | |

| | 10,500 | | | United States Treasury Floating Rate Notes,

USBMMY3M + 0.140%(1) | | (AA+, Aaa) | | 01/31/19 | | | 1.590 | | | | 10,517,931 | | |

| | 24,000 | | | United States Treasury Floating Rate Notes,

USBMMY3M + 0.070%(1),(2) | | (AA+, Aaa) | | 04/30/19 | | | 1.520 | | | | 24,023,586 | | |

See Accompanying Notes to Consolidated Financial Statements.

12

Credit Suisse Trust — Commodity Return Strategy Portfolio

Consolidated Schedule of Investments (continued)

December 31, 2017

Par

(000) | | | | Ratings†

(S&P/Moody's) | | Maturity | | Rate% | | Value | |

| UNITED STATES TREASURY OBLIGATIONS (continued) | | | |

$ | 20,100 | | | United States Treasury Floating Rate Notes,

USBMMY3M + 0.060%(1),(2),(3) | | (AA+, Aaa) | | 07/31/19 | | | 1.510 | | | $ | 20,115,560 | | |

| | 29,200 | | | United States Treasury Floating Rate Notes,

USBMMY3M + 0.048%(1),(2) | | (AA+, Aaa) | | 10/31/19 | | | 1.408 | | | | 29,209,133 | | |

| | 2,000 | | | United States Treasury Notes | | (AA+, Aaa) | | 03/31/18 | | | 0.750 | | | | 1,996,951 | | |

| | 3,000 | | | United States Treasury Notes | | (AA+, Aaa) | | 03/31/18 | | | 0.875 | | | | 2,996,327 | | |

| | 1,000 | | | United States Treasury Notes | | (AA+, Aaa) | | 07/15/18 | | | 0.875 | | | | 996,465 | | |

| TOTAL UNITED STATES TREASURY OBLIGATIONS (Cost $101,805,508) | | | 101,873,529 | | |

| SHORT-TERM INVESTMENT (2.3%) | | | |

| | 9,280 | | | State Street Bank and Trust Co. Euro Time Deposit

(Cost $9,280,159) | | | | 01/02/18 | | | 0.120 | | | | 9,280,159 | | |

| TOTAL INVESTMENTS AT VALUE (96.1%) (Cost $392,681,727) | | | 392,825,670 | | |

| OTHER ASSETS IN EXCESS OF LIABILITIES (3.9%) | | | 16,055,204 | | |

| NET ASSETS (100.0%) | | $ | 408,880,874 | | |

† Credit ratings given by the Standard & Poor's Division of the McGraw-Hill Companies, Inc. ("S&P") and Moody's Investors Service, Inc. ("Moody's") are unaudited.

(1) Variable rate obligation — The interest rate shown is the rate in effect as of December 31, 2017.

(2) At December 31, 2017, a portion of the value of these securities totaling $6,635,337 have been pledged as collateral for open swap contracts.

(3) At December 31, 2017, $2,602,002 in the value of this security has been pledged to cover initial margin requirements for open futures contracts.

INVESTMENT ABBREVIATIONS

1M = 1 Month

3M = 3 Month

DLY = Daily

FCPR = Federal Reserve Bank Prime Loan Rate U.S.

LIBOR = London Interbank Offered Rate

USBMMY3M = U.S. Treasury 3 Month Bill Money Market Yield

Futures Contracts

Contract Description | | Currency | | Expiration

Date | | Number of

Contracts | | Notional

Value | | Net Unrealized

Appreciation

(Depreciation) | |

Contracts to Purchase | |

Energy | |

Light Sweet Crude Oil Futures | | USD | | | | Dec 2018 | | | 119 | | | $ | 6,910,330 | | | $ | 663,822 | | |

Brent Crude Oil Futures | | USD | | | | Dec 2018 | | | 42 | | | | 2,672,880 | | | | 349,964 | | |

| | $ | 1,013,786 | | |

See Accompanying Notes to Consolidated Financial Statements.

13

Credit Suisse Trust — Commodity Return Strategy Portfolio

Consolidated Schedule of Investments (continued)

December 31, 2017

Futures Contracts (continued)

Contract Description | | Currency | | Expiration

Date | | Number of

Contracts | | Notional

Value | | Net Unrealized

Appreciation

(Depreciation) | |

Contracts to Sell | |

Energy | |

Brent Crude Oil Futures | | USD | | | | Mar 2018 | | | (42 | ) | | $ | (2,808,540 | ) | | $ | (441,427 | ) | |

Light Sweet Crude Oil Futures | | USD | | | | Mar 2018 | | | (80 | ) | | | (4,835,200 | ) | | | (502,739 | ) | |

Light Sweet Crude Oil Futures | | USD | | | | May 2018 | | | (39 | ) | | | (2,350,530 | ) | | | (85,449 | ) | |

| | $ | (1,029,615 | ) | |

Net unrealized appreciation (depreciation) | | $ | (15,829 | ) | |

Total Return Swap Contracts

Currency | | Notional

Amount | | Expiration

Date | | Counterparty | | Receive

Return of the

Reference

Index | | Pay | | Upfront

Premiums

Paid | | Upfront

Premiums

Received | | Net Unrealized

Appreciation

(Depreciation) | |

| | | | | | | | | | | Bloomberg Commodity | | | | | | | | | |

USD | | | | $ | 17,436,516 | | | 01/23/18 | | CIBC | | Index Total Return | | | 1.56 | % | | $ | — | | | $ | — | | | $ | 638,331 | | |

USD | | | | | 13,397,836 | | | 01/23/18 | | CIBC | | Bloomberg Commodity

Index 2 Month Forward

Total Return | | | 1.61 | % | | | — | | | | — | | | | 437,490 | | |

USD | | | | | 13,408,337 | | | 01/23/18 | | Citigroup | | Bloomberg Commodity

Index Total Return | | | 1.56 | % | | | — | | | | — | | | | 490,864 | | |

USD | | | | | 39,080,915 | | | 01/23/18 | | Citigroup | | Bloomberg Commodity

Index 2 Month Forward

Total Return | | | 1.61 | % | | | — | | | | — | | | | 1,276,140 | | |

USD | | | | | 13,946,839 | | | 01/23/18 | | JPMorgan Chase | | Bloomberg Commodity

Index Total Return | | | 1.54 | % | | | — | | | | — | | | | 510,647 | | |

USD | | | | | 17,387,661 | | | 01/23/18 | | JPMorgan Chase | | Bloomberg Commodity

Index 2 Month Forward

Total Return | | | 1.60 | % | | | — | | | | — | | | | 567,816 | | |

USD | | | | | 4,131,914 | | | 01/23/18 | | Macquarie | | Bloomberg Commodity

Index Total Return | | | 1.53 | % | | | — | | | | — | | | | 151,295 | | |

USD | | | | | 42,314,065 | | | 01/23/18 | | Macquarie | | Macquarie Commodity

Customized Product

112T Index | | | 1.70 | % | | | — | | | | — | | | | 1,487,909 | | |

USD | | | | | 7,914,315 | | | 01/23/18 | | Bank of America | | Bloomberg Commodity

Index Total Return | | | 1.54 | % | | | — | | | | — | | | | 289,773 | | |

USD | | | | | 13,042,298 | | | 01/23/18 | | Bank of America | | Bloomberg Commodity

Index 2 Month Forward

Total Return | | | 1.60 | % | | | — | | | | — | | | | 425,913 | | |

USD | | | | | 33,047,534 | | | 01/23/18 | | Bank of America | | Merrill Lynch

Commodity Index

Extra CS2T Total Return | | | 1.70 | % | | | — | | | | — | | | | 1,156,871 | | |

USD | | | | | 41,160,297 | | | 01/23/18 | | Morgan Stanley | | Bloomberg Commodity

Index 2 Month Forward

Total Return | | | 1.62 | % | | | — | | | | — | | | | 1,343,938 | | |

See Accompanying Notes to Consolidated Financial Statements.

14

Credit Suisse Trust — Commodity Return Strategy Portfolio

Consolidated Schedule of Investments (continued)

December 31, 2017

Total Return Swap Contracts (continued)

Currency | | Notional

Amount | | Expiration

Date | | Counterparty | | Receive

Return of the

Reference

Index | | Pay | | Upfront

Premiums

Paid | | Upfront

Premiums

Received | | Net Unrealized

Appreciation

(Depreciation) | |

USD | | | | $ | 5,177,418 | | | 01/23/18 | | RBC Capital | | Bloomberg Commodity

Index Total Return | | | 1.56 | % | | $ | — | | | $ | — | | | $ | 189,539 | | |

USD | | | | | 9,803,281 | | | 01/23/18 | | RBC Capital | | Bloomberg Commodity

Index 2 Month Forward

Total Return | | | 1.64 | % | | | — | | | | — | | | | 320,042 | | |

USD | | | | | 20,878,948 | | | 01/23/18 | | Societe Generale | | Bloomberg Commodity

Index Total Return | | | 1.56 | % | | | — | | | | — | | | | 764,355 | | |

USD | | | | | 25,626,100 | | | 01/23/18 | | Societe Generale | | Bloomberg Commodity

Index 2 Month Forward

Total Return | | | 1.64 | % | | | — | | | | — | | | | 836,600 | | |

USD | | | | | 36,192,625 | | | 01/23/18 | | Societe Generale | | Societe Generale P04

TR Index(a) | | | 1.70 | % | | | — | | | | — | | | | 1,271,779 | | |

USD | | | | | 23,165,401 | | | 01/23/18 | | UBS | | Bloomberg Commodity

Index Total Return | | | 1.55 | % | | | — | | | | — | | | | 848,117 | | |

USD | | | | | 17,026,819 | | | 01/23/18 | | UBS | | Bloomberg Commodity

Index 2 Month Forward

Total Return | | | 1.59 | % | | | — | | | | — | | | | 556,074 | | |

| | | $ | 13,563,493 | | |

(a) The index seeks to provide exposure to a diversified group of commodities, inclusive of energy, livestock and meat, agricultural and metals. The Portfolio has indirect exposure to all of the below underlying positions that make up the custom index. When applicable, the table is limited to the largest 50 positions (based on absolute market value) and any other position where the notional value for the position exceeds 1% of the notional value of the index.

Commodity Ticker | | Commodity Name | | Contract | | Weight | | 12/31 Price | |

NG | | Natural Gas | | NGH18 Comdty | | | 6.64 | % | | | 2.906 | | |

CL | | Crude Oil | | CLZ8 Comdty | | | 7.29 | % | | | 58.070 | | |

CO | | Brent Oil | | COZ8 Comdty | | | 8.36 | % | | | 63.640 | | |

XB | | Unleaded Gasoline | | XBH8 Comdty | | | 3.80 | % | | | 181.330 | | |

HO | | Heating Oil | | HOH8 Comdty | | | 4.24 | % | | | 204.380 | | |

W | | Wheat | | W K8 Comdty | | | 3.12 | % | | | 440.250 | | |

| KW | | Kansas Wheat | | KWK8 Comdty | | | 1.09 | % | | | 441.000 | | |

C | | Corn | | C H8 Comdty | | | 6.79 | % | | | 350.750 | | |

S | | Soybeans | | S H8 Comdty | | | 5.33 | % | | | 961.750 | | |

SB | | Sugar | | SBK8 Comdty | | | 2.34 | % | | | 15.020 | | |

CT | | Cotton | | CTH8 Comdty | | | 1.41 | % | | | 78.630 | | |

KC | | Coffee | | KCK8 Comdty | | | 1.96 | % | | | 128.550 | | |

BO | | Soybean Oil | | BOH8 Comdty | | | 2.49 | % | | | 33.260 | | |

SM | | Soybean Meal | | SMH8 Comdty | | | 2.80 | % | | | 316.800 | | |

LC | | Live Cattle | | LCG8 Comdty | | | 3.91 | % | | | 121.550 | | |

LH | | Lean Hogs | | LHG8 Comdty | | | 2.17 | % | | | 71.775 | | |

LA | | Aluminum | | LAH18 Comdty | | | 5.55 | % | | | 2,271.500 | | |

HG | | Copper | | HGH8 Comdty | | | 9.13 | % | | | 330.050 | | |

LX | | Zinc | | LXZ8 Comdty | | | 3.11 | % | | | 3,238.000 | | |

LN | | Nickel | | LNH8 Comdty | | | 2.94 | % | | | 12,760.000 | | |

GC | | Gold | | GCG8 Comdty | | | 11.56 | % | | | 1,309.300 | | |

SI | | Silver | | SIZ8 Comdty | | | 3.97 | % | | | 17.471 | | |

See Accompanying Notes to Consolidated Financial Statements.

15

Credit Suisse Trust — Commodity Return Strategy Portfolio

Consolidated Statement of Assets and Liabilities

December 31, 2017

Assets | |

Investments at value (Cost $392,681,727) (Note 2) | | $ | 392,825,670 | | |

Cash segregated at brokers for swap contracts (Note 2) | | | 5,441,020 | | |

Unrealized appreciation on open swap contracts (Note 2) | | | 13,563,493 | | |

Interest receivable | | | 708,322 | | |

Receivable for Portfolio shares sold | | | 220,233 | | |

Prepaid expenses and other assets | | | 4,986 | | |

Total assets | | | 412,763,724 | | |

Liabilities | |

Investment advisory fee payable (Note 3) | | | 158,567 | | |

Administrative services fee payable (Note 3) | | | 22,288 | | |

Shareholder servicing/Distribution fee payable (Note 3) | | | 83,506 | | |

Payable for Portfolio shares redeemed | | | 99,674 | | |

Variation margin payable on futures contracts (Note 2) | | | 32,501 | | |

Due to custodian | | | 3,180,000 | | |

Trustees' fee payable | | | 9,556 | | |

Accrued expenses | | | 296,758 | | |

Total liabilities | | | 3,882,850 | | |

Net Assets | |

Capital stock, $.001 par value (Note 6) | | | 101,343 | | |

Paid-in capital (Note 6) | | | 402,331,359 | | |

Undistributed net investment income | | | 7,879,048 | | |

Accumulated net realized loss on investments, futures contracts and swap contracts | | | (15,122,483 | ) | |

Net unrealized appreciation from investments, futures contracts and swap contracts | | | 13,691,607 | | |

Net assets | | $ | 408,880,874 | | |

Shares outstanding | | | 101,343,268 | | |

Net asset value, offering price and redemption price per share | | $ | 4.03 | | |

See Accompanying Notes to Consolidated Financial Statements.

16

Credit Suisse Trust — Commodity Return Strategy Portfolio

Consolidated Statement of Operations

For the Year Ended December 31, 2017

Investment Income | |

Interest | | $ | 4,128,512 | | |

Securities lending (Note 2) | | | 1,173 | | |

Total investment income | | | 4,129,685 | | |

Expenses | |

Investment advisory fees (Note 3) | | | 2,175,220 | | |

Administrative services fees (Note 3) | | | 64,921 | | |

Shareholder servicing/Distribution fees (Note 3) | | | 921,703 | | |

Transfer agent fees (Note 3) | | | 414,379 | | |

Printing fees | | | 269,265 | | |

Legal fees | | | 65,208 | | |

Audit and tax fees | | | 64,560 | | |

Trustees' fees | | | 51,228 | | |

Custodian fees | | | 31,177 | | |

Commitment fees (Note 4) | | | 10,441 | | |

Insurance expense | | | 8,403 | | |

Miscellaneous expense | | | 5,026 | | |

Total expenses | | | 4,081,531 | | |

Less: fees waived (Note 3) | | | (210,376 | ) | |

Net expenses | | | 3,871,155 | | |

Net investment income | | | 258,530 | | |

Net Realized and Unrealized Gain (Loss) from Investments, Futures Contracts and Swap Contracts | |

Net realized gain from investments | | | 2,128,284 | | |

Net realized loss from futures contracts | | | (82,045 | ) | |

Net realized loss from swap contracts | | | (1,877,305 | ) | |

Net change in unrealized appreciation (depreciation) from investments | | | (2,146,601 | ) | |

Net change in unrealized appreciation (depreciation) from futures contracts | | | 59,075 | | |

Net change in unrealized appreciation (depreciation) from swap contracts | | | 9,531,049 | | |

Net realized and unrealized gain from investments, futures contracts and swap contracts | | | 7,612,457 | | |

Net increase in net assets resulting from operations | | $ | 7,870,987 | | |

See Accompanying Notes to Consolidated Financial Statements.

17

Credit Suisse Trust — Commodity Return Strategy Portfolio

Consolidated Statement of Changes in Net Assets

| | | For the Year

Ended

December 31, 2017 | | For the Year

Ended

December 31, 2016 | |

From Operations | |

Net investment income (loss) | | $ | 258,530 | | | $ | (1,095,931 | ) | |

Net realized gain from investments, futures contracts and swap contracts | | | 168,934 | | | | 30,948,691 | | |

Net change in unrealized appreciation (depreciation)

from investments, futures contracts and swap contracts | | | 7,443,523 | | | | 5,958,497 | | |

Net increase in net assets resulting from operations | | | 7,870,987 | | | | 35,811,257 | | |

From Dividends | |

Dividends from net investment income | | | (33,847,314 | ) | | | — | | |

| From Capital Share Transactions (Note 6) | |

Proceeds from sale of shares | | | 66,298,696 | | | | 51,657,341 | | |

Reinvestment of dividends | | | 33,847,314 | | | | — | | |

Net asset value of shares redeemed | | | (12,406,829 | ) | | | (15,185,554 | ) | |

Net increase in net assets from capital share transactions | | | 87,739,181 | | | | 36,471,787 | | |

Net increase in net assets | | | 61,762,854 | | | | 72,283,044 | | |

Net Assets | |

Beginning of year | | | 347,118,020 | | | | 274,834,976 | | |

End of year | | $ | 408,880,874 | | | $ | 347,118,020 | | |

Undistributed net investment income | | $ | 7,879,048 | | | $ | 33,847,009 | | |

See Accompanying Notes to Consolidated Financial Statements.

18

Credit Suisse Trust — Commodity Return Strategy Portfolio

Consolidated Financial Highlights

(For a Share of the Portfolio Outstanding Throughout Each Year)

| | | For the Year Ended December 31, | |

| | | 2017 | | 2016 | | 2015 | | 2014 | | 2013 | |

Per share data | |

Net asset value, beginning of year | | $ | 4.38 | | | $ | 3.91 | | | $ | 5.22 | | | $ | 6.29 | | | $ | 7.01 | | |

INVESTMENT OPERATIONS | |

Net investment income (loss)1 | | | 0.002 | | | | (0.01 | ) | | | (0.03 | ) | | | (0.05 | ) | | | (0.05 | ) | |

Net gain (loss) from investments, futures contracts

and swap contracts (both realized and unrealized) | | | 0.04 | | | | 0.48 | | | | (1.28 | ) | | | (1.02 | ) | | | (0.67 | ) | |

Total from investment operations | | | 0.04 | | | | 0.47 | | | | (1.31 | ) | | | (1.07 | ) | | | (0.72 | ) | |

LESS DIVIDENDS | |

Dividends from net investment income | | | (0.39 | ) | | | — | | | | — | | | | — | | | | — | | |

Total dividends | | | (0.39 | ) | | | — | | | | — | | | | — | | | | — | | |

Net asset value, end of year | | $ | 4.03 | | | $ | 4.38 | | | $ | 3.91 | | | $ | 5.22 | | | $ | 6.29 | | |

Total return3 | | | 1.52 | % | | | 12.02 | % | | | (25.10 | )% | | | (17.01 | )% | | | (10.27 | )% | |

RATIOS AND SUPPLEMENTAL DATA | |

Net assets, end of year (000s omitted) | | $ | 408,881 | | | $ | 347,118 | | | $ | 274,835 | | | $ | 273,055 | | | $ | 257,040 | | |

Ratio of net expenses to average net assets | | | 1.05 | % | | | 1.05 | % | | | 1.05 | % | | | 1.05 | % | | | 1.05 | % | |

Ratio of net investment income (loss) to average

net assets | | | 0.07 | % | | | (0.35 | )% | | | (0.73 | )% | | | (0.83 | )% | | | (0.83 | )% | |

Decrease reflected in above operating expense

ratios due to waivers/reimbursements | | | 0.06 | % | | | 0.02 | % | | | 0.04 | % | | | 0.05 | % | | | 0.28 | % | |

Portfolio turnover rate | | | 94 | % | | | 113 | % | | | 113 | % | | | 96 | % | | | 41 | %4 | |

1 Per share information is calculated using the average shares outstanding method.

2 This amount represents less than $0.01 per share.

3 Total returns are historical and include change in share price and reinvestment of all dividends and distributions. Had certain expenses not been reduced during the years shown, total returns would have been lower. Total returns do not reflect charges and expenses attributable to any particular variable contract or plan.

4 Portfolio turnover calculation does not include $170,753,807 of in-kind subscriptions.

See Accompanying Notes to Consolidated Financial Statements.

19

Credit Suisse Trust — Commodity Return Strategy Portfolio

Notes to Consolidated Financial Statements

December 31, 2017

Credit Suisse Trust (the "Trust") is an open-end management investment company registered under the Investment Company Act of 1940, as amended (the "1940 Act"), which currently offers the Commodity Return Strategy Portfolio (the "Portfolio"). The Portfolio is a non-diversified, open-end management investment company that seeks total return that exceeds the return of its benchmark index, the Bloomberg Commodity Index Total Return (the "Benchmark"). Shares of the Portfolio are not available directly to individual investors but may be offered only through (a) variable annuity contracts and variable life insurance contracts offered by separate accounts of certain insurance companies and (b) tax qualified pension and retirement plans. The Portfolio may not be available in connection with a particular contract or plan. The Trust was organized under the laws of the Commonwealth of Massachusetts as a business trust on March 15, 1995.

Credit Suisse Asset Management, LLC ("Credit Suisse"), the investment adviser to the Portfolio, is registered as a Commodity Pool Operator with the Commodity Futures Trading Commission. The Portfolio intends to gain exposure to commodity derivatives through investing in a wholly-owned subsidiary, Credit Suisse Cayman Commodity Fund II, Ltd. (the "Subsidiary"), organized under the laws of the Cayman Islands. The Subsidiary invests in commodity-linked derivative instruments, such as swaps and futures. The Subsidiary may also invest in debt securities, some of which are intended to serve as margin or collateral for the Subsidiary's derivatives positions.

The Subsidiary is managed by the same portfolio managers that manage the Portfolio and the accompanying financial statements reflect the financial position of the Portfolio and the Subsidiary and the results of operations on a consolidated basis. The consolidated financial statements include portfolio holdings of the Portfolio and the Subsidiary and all intercompany transactions and balances have been eliminated. The Portfolio may invest up to 25% of its total assets in the Subsidiary. As of December 31, 2017, the Portfolio held $80,469,547 in the Subsidiary, representing 19.7% of the Portfolio's consolidated net assets. For the year ended December 31, 2017, the net realized loss on securities and other financial instruments held in the Subsidiary was $1,940,717.

Subsequent references to the Portfolio within the Notes to Consolidated Financial Statements collectively refer to the Portfolio and the Subsidiary.

Note 2. Significant Accounting Policies

The following is a summary of significant accounting policies followed by the Portfolio in the preparation of its consolidated financial statements. The

20

Credit Suisse Trust — Commodity Return Strategy Portfolio

Notes to Consolidated Financial Statements (continued)

December 31, 2017

Note 2. Significant Accounting Policies (continued)

policies are in accordance with generally accepted accounting principles in the United States of America ("GAAP"). The preparation of consolidated financial statements requires management to make estimates and assumptions that affect the reported amounts and disclosures in the consolidated financial statements. Actual results could differ from those estimates. The Portfolio is considered an investment company for financial reporting purposes under GAAP and follows Accounting Standards Codification ("ASC") Topic 946 — Financial Services — Investment Companies.

A) SECURITY VALUATION — The net asset value of the Portfolio is determined daily as of the close of regular trading on the New York Stock Exchange, Inc. (the "Exchange") on each day the Exchange is open for business. The valuations for fixed income securities (which may include, but are not limited to, corporate, government, municipal, mortgage-backed, collateralized mortgage obligations and asset-backed securities) and certain derivative instruments are typically the prices supplied by independent third party pricing services, which may use market prices or broker/dealer quotations or a variety of valuation techniques and methodologies. The independent third party pricing services use inputs that are observable such as issuer details, interest rates, yield curves, prepayment speeds, credit risks/spreads, default rates and quoted prices for similar securities. These pricing services generally price fixed income securities assuming orderly transactions of an institutional "round lot" size, but some trades occur in smaller "odd lot" sizes which may be effected at lower prices than institutional round lot trades. Structured note agreements are valued in accordance with a dealer-supplied valuation based on changes in the value of the underlying index. Futures contracts are valued daily at the settlement price established by the board of trade or exchange on which they are traded. Forward contracts are valued at the London closing spot rates and the London closing forward point rates on a daily basis. The currency forward contract pricing model derives the differential in point rates to the expiration date of the forward and calculates its present value. Equity securities for which market quotations are available are valued at the last reported sales price or official closing price on the primary market or exchange on which they trade. The Portfolio may utilize a service provided by an independent third party which has been approved by the Board of Trustees (the "Board") to fair value certain securities. When fair value pricing is employed, the prices of securities used by the Portfolio to calculate its net asset value may differ from quoted or published prices for the same securities. If independent third party pricing services are unable to supply prices for a portfolio investment, or if the prices supplied are deemed by the investment

21

Credit Suisse Trust — Commodity Return Strategy Portfolio

Notes to Consolidated Financial Statements (continued)

December 31, 2017

Note 2. Significant Accounting Policies (continued)

adviser to be unreliable, the market price may be determined by the investment adviser using quotations from one or more brokers/dealers or at the transaction price if the security has recently been purchased and no value has yet been obtained from a pricing service or pricing broker. When reliable prices are not readily available, such as when the value of a security has been significantly affected by events after the close of the exchange or market on which the security is principally traded, but before the Portfolio calculates its net asset value, the Portfolio values these securities as determined in accordance with procedures approved and established by the Board.

The Portfolio uses valuation techniques to measure fair value that are consistent with the market approach and/or income approach, depending on the type of security and the particular circumstance. The market approach uses prices and other relevant information generated by market transactions involving identical or comparable securities. The income approach uses valuation techniques to discount estimated future cash flows to present value.

GAAP established a disclosure hierarchy that categorizes the inputs to valuation techniques used to value assets and liabilities at each measurement date. These inputs are summarized in the three broad levels listed below:

• Level 1 – quoted prices in active markets for identical investments

• Level 2 – other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risk, etc.)

• Level 3 – significant unobservable inputs (including the Portfolio's own assumptions in determining the fair value of investments)

The inputs or methodologies used to value securities are not necessarily an indication of the risk associated with investing in those securities.

The following is a summary of the inputs used as of December 31, 2017 in valuing the Portfolio's assets and liabilities carried at fair value:

Assets | | Level 1 | | Level 2 | | Level 3 | | Total | |

Investments in Securities | |

United States Agency Obligations | | $ | — | | | $ | 281,671,982 | | | $ | — | | | $ | 281,671,982 | | |

United States Treasury Obligations | | | — | | | | 101,873,529 | | | | — | | | | 101,873,529 | | |

Short-Term Investment | | | — | | | | 9,280,159 | | | | — | | | | 9,280,159 | | |

| | | $ | — | | | $ | 392,825,670 | | | $ | — | | | $ | 392,825,670 | | |

Other Financial Instruments* | |

Futures Contracts | | $ | 1,013,786 | | | $ | — | | | $ | — | | | $ | 1,013,786 | | |

Swap Contracts** | | | — | | | | 13,563,493 | | | | — | | | | 13,563,493 | | |

22

Credit Suisse Trust — Commodity Return Strategy Portfolio

Notes to Consolidated Financial Statements (continued)

December 31, 2017

Note 2. Significant Accounting Policies (continued)

Liabilities | | Level 1 | | Level 2 | | Level 3 | | Total | |

Other Financial Instruments* | |

Futures Contracts | | $ | 1,029,615 | | | $ | — | | | $ | — | | | $ | 1,029,615 | | |

* Other financial instruments include unrealized appreciation (depreciation) on futures and swap contracts.

** Value includes any premium paid or received with respect to swap contracts, if applicable.

For the year ended December 31, 2017, there were no transfers among Level 1, Level 2 and Level 3. All transfers, if any, are assumed to occur at the end of the reporting period.

B) DERIVATIVE INSTRUMENTS AND HEDGING ACTIVITIES — The Portfolio follows authoritative guidance on disclosures about derivative instruments and hedging activities which require that a portfolio disclose (a) how and why an entity uses derivative instruments, (b) how derivative instruments and hedging activities are accounted for and (c) how derivative instruments and related hedging activities affect a portfolio's financial position, financial performance and cash flows. For the year ended December 31, 2017, the Portfolio's derivatives did not qualify for hedge accounting as they are held at fair value.

The following table presents the fair value and the location of derivatives within the Consolidated Statement of Assets and Liabilities at December 31, 2017 and the effect of these derivatives on the Consolidated Statement of Operations for the year ended December 31, 2017.

| Primary Underlying Risk | | Derivative

Assets | | Derivative

Liabilities | | Realized Gain

(Loss) | | Change in Unrealized

Appreciation (Depreciation) | |

Commodity price | |

Futures contracts | | $ | 1,013,786 | | | $ | 1,029,615 | | | $ | (82,045 | ) | | $ | 59,075 | | |

Total return swap contracts | | | 13,563,493 | | | | — | | | | (1,877,305 | ) | | | 9,531,049 | | |

| | $ | 14,577,279 | | | $ | 1,029,615 | | | $ | (1,959,350 | ) | | $ | 9,590,124 | | |

The notional amount of futures contracts and swap contracts at December 31, 2017 is reflected in the Consolidated Schedule of Investments. For the year ended December 31, 2017, the Portfolio held average monthly notional values on a net basis of $6,030,749, $6,145,671 and $364,800,678 in long futures contracts, short futures contracts and swap contracts, respectively.

The Portfolio is a party to International Swap and Derivatives Association, Inc. ("ISDA") Master Agreements ("Master Agreements") with certain counterparties that govern over-the-counter derivative (including Total Return, Credit Default and Interest Rate Swaps) and foreign exchange contracts entered into by the Portfolio. The Master Agreements may contain provisions

23

Credit Suisse Trust — Commodity Return Strategy Portfolio

Notes to Consolidated Financial Statements (continued)

December 31, 2017

Note 2. Significant Accounting Policies (continued)

regarding, among other things, the parties' general obligations, representations, agreements, collateral requirements, events of default and early termination. Termination events applicable to the Portfolio may occur upon a decline in the Portfolio's net assets below a specified threshold over a certain period of time.

The following table presents by counterparty the Portfolio's derivative assets, net of related collateral held by the Portfolio, at December 31, 2017:

Counterparty | | Gross Amount of

Assets Presented in

the Consolidated

Statement of Assets

and Liabilities(a) | | Financial

Instruments

and Derivatives

Available for Offset | | Non-Cash

Collateral

Received | | Cash

Collateral

Received | | Net Amount

of Derivative

Assets | |

Bank of America | | $ | 1,872,557 | | | $ | — | | | $ | — | | | $ | — | | | $ | 1,872,557 | | |

CIBC | | | 1,075,821 | | | | — | | | | — | | | | — | | | | 1,075,821 | | |

Citigroup | | | 1,767,004 | | | | — | | | | — | | | | — | | | | 1,767,004 | | |

JPMorgan Chase | | | 1,078,463 | | | | — | | | | — | | | | — | | | | 1,078,463 | | |

Macquarie | | | 1,639,204 | | | | — | | | | — | | | | — | | | | 1,639,204 | | |

Morgan Stanley | | | 1,343,938 | | | | — | | | | — | | | | — | | | | 1,343,938 | | |

RBC Capital | | | 509,581 | | | | — | | | | — | | | | — | | | | 509,581 | | |

Societe Generale | | | 2,872,734 | | | | — | | | | — | | | | — | | | | 2,872,734 | | |

UBS | | | 1,404,191 | | | | — | | | | — | | | | — | | | | 1,404,191 | | |

| | | $ | 13,563,493 | | | $ | — | | | $ | — | | | $ | — | | | $ | 13,563,493 | | |

(a) Swap contracts are included.

C) SECURITY TRANSACTIONS AND INVESTMENT INCOME/ EXPENSE — Security transactions are accounted for on a trade date basis. Interest income/expense is recorded on the accrual basis. The Portfolio amortizes premiums and accretes discounts using the effective interest method. Dividend income/expense is recorded on the ex-dividend date. The cost of investments sold is determined by use of the specific identification method for both financial reporting and income tax purposes. To the extent any issuer defaults or a credit event occurs that impacts the issuer, the Portfolio may halt any additional interest income accruals and consider the realizability of interest accrued up to the date of default or credit event.

D) DIVIDENDS AND DISTRIBUTIONS TO SHAREHOLDERS — Dividends from net investment income, if any, are declared and paid quarterly. Distributions of net realized capital gains, if any, are declared and paid at least annually. However, to the extent that a net realized capital gain can be reduced by a capital loss carryforward, such gain will not be distributed. Dividends and distributions to shareholders of the Portfolio are recorded on the

24

Credit Suisse Trust — Commodity Return Strategy Portfolio

Notes to Consolidated Financial Statements (continued)

December 31, 2017

Note 2. Significant Accounting Policies (continued)

ex-dividend date and are determined in accordance with federal income tax regulations, which may differ from GAAP.

E) FEDERAL AND OTHER TAXES — No provision is made for federal taxes as it is the Portfolio's intention to continue to qualify as a regulated investment company ("RIC") under the Internal Revenue Code of 1986, as amended (the "Code"), and to make the requisite distributions to its shareholders, which will be sufficient to relieve it from federal income and excise taxes.

In order to qualify as a RIC under the Code, the Portfolio must meet certain requirements regarding the source of its income, the diversification of its assets and the distribution of its income. One of these requirements is that the Portfolio derive at least 90% of its gross income for each taxable year from dividends, interest, payments with respect to certain securities loans, gains from the sale or other disposition of stock, securities or foreign currencies, other income derived with respect to its business of investing in such stock, securities or currencies or net income derived from interests in certain publicly-traded partnerships ("Qualifying Income"). The Portfolio may, through its investment in the Subsidiary, seek to track the performance of the Benchmark by the Subsidiary's investments in commodity-linked swaps and/or futures contracts. The Portfolio has obtained a private letter ruling from the Internal Revenue Service which confirms that its investment in the Subsidiary produces Qualifying Income.

If the Portfolio is unable to ensure continued qualification as a RIC, the Portfolio may be required to change its investment objective, policies or techniques, or may be liquidated. If the Portfolio fails to qualify as a RIC, the Portfolio will be subject to federal income tax on its net income and capital gains at regular corporate rates (without reduction for distributions to shareholders). If the Portfolio were to fail to qualify as a RIC and become subject to federal income tax, shareholders of the Portfolio would be subject to the risk of diminished returns.

The Portfolio adopted the authoritative guidance for uncertainty in income taxes and recognizes a tax benefit or liability from an uncertain position only if it is more likely than not that the position is sustainable based solely on its technical merits and consideration of the relevant taxing authority's widely understood administrative practices and procedures. The Portfolio has reviewed its current tax positions and has determined that no provision for income tax is required in the Portfolio's financial statements. The Portfolio's federal and state income tax returns for tax years for which the applicable

25

Credit Suisse Trust — Commodity Return Strategy Portfolio

Notes to Consolidated Financial Statements (continued)

December 31, 2017

Note 2. Significant Accounting Policies (continued)

statutes of limitations have not expired are subject to examination by the Internal Revenue Service and state departments of revenue.

F) SHORT-TERM INVESTMENTS — The Portfolio, together with other funds/portfolios advised by Credit Suisse, pools available cash into a short-term variable rate time deposit issued by State Street Bank and Trust Company ("SSB"), the Portfolio's custodian. The short-term time deposit issued by SSB is a variable rate account classified as a short-term investment.

G) FUTURES — The Portfolio may enter into futures contracts to the extent permitted by its investment policies and objectives. The Portfolio may use futures contracts to gain exposure to or hedge against changes in commodities. Upon entering into a futures contract, the Portfolio is required to deposit cash and/or pledge U.S. Government securities as initial margin with a Futures Commission Merchant ("FCM"). Subsequent payments, which are dependent on the daily fluctuations in the value of the underlying instrument, are made or received by the Portfolio each day (daily variation margin) and are recorded as unrealized gains or losses in the Consolidated Statement of Operations until the contracts are closed. When the contracts are closed, the Portfolio records a realized gain or loss equal to the difference between the proceeds from (or cost of) the closing transaction and the Portfolio's basis in the contract. Risks of entering into futures contracts for hedging purposes include the possibility that a change in the value of the contract may not correlate with the changes in the value of the underlying instruments. Futures have minimal counterparty credit risk because futures are exchange traded and the exchange's clearinghouse, as counterparty to all exchange-traded futures, guarantees the futures against default. In addition, the purchase of a futures contract involves the risk that the Portfolio could lose more than the original margin deposit and subsequent payments may be required for a futures transaction. The Portfolio's open futures contracts are disclosed in the Consolidated Schedule of Investments. At December 31, 2017, the amount of restricted cash held at brokers related to open futures contracts was $0.

The Commodity Exchange Act requires an FCM to segregate all customer transactions and assets from the FCM's proprietary activities. A customer's cash and other equity deposited with an FCM are considered commingled with all other customer funds subject to the FCM's segregation requirements. In the event of an FCM's insolvency, recovery may be limited to the Portfolio's pro-rata share of segregated customer funds available. It is possible that the recovery amount could be less than the total of cash and other equity deposited.

26

Credit Suisse Trust — Commodity Return Strategy Portfolio

Notes to Consolidated Financial Statements (continued)

December 31, 2017

Note 2. Significant Accounting Policies (continued)

H) SWAPS — The Portfolio may enter into commodity index swaps either for hedging purposes or to seek to increase total return. A swap contract is an agreement that obligates two parties to exchange a series of cash flows at specified intervals based upon or calculated by reference to changes in specified prices or rates for a specified amount of an underlying asset or notional principal amount. The Portfolio will enter into swap contracts only on a net basis, which means that the two payment streams are netted out, with the Portfolio receiving or paying, as the case may be, only the net amount of the two payments. Risks may arise as a result of the failure of the counterparty to the swap contract to comply with the terms of the swap contract. The extent of the Portfolio's exposure to credit and counterparty risks is the discounted net value of the cash flows to be received from the counterparty over the contract's remaining life, to the extent that the amount is positive. These risks are mitigated by having a master netting arrangement between the Portfolio and the counterparty and by the posting of collateral by the counterparty to the Portfolio to cover the Portfolio's exposure to the counterparty. Therefore, the Portfolio considers the creditworthiness of each counterparty as well as the amounts posted by the counterparty pursuant to the master netting agreement to a swap contract in evaluating potential credit risk. Additionally, risks may arise from unanticipated movements in interest rates or in the value of the underlying reference asset or index.

The Portfolio may enter into total return swap contracts, involving commitments to pay interest in exchange for a market-linked return, both based on notional amounts. The Portfolio may invest in total return swap contracts for hedging purposes or to seek to increase total return. To the extent the total return of the security or index underlying the transaction exceeds or falls short of the offsetting interest rate obligation, the Portfolio will receive a payment from or make a payment to the counterparty.

The Portfolio records unrealized gains or losses on a daily basis representing the value and the current net receivable or payable relating to open swap contracts. Net amounts received or paid on the swap contract are recorded as realized gains or losses. Fluctuations in the value of swap contracts are recorded for financial statement purposes as unrealized appreciation or depreciation from swap contracts. Realized gains and losses from terminated swaps are included in net realized gains/losses from swap contracts. The Portfolio's open swap contracts are disclosed in the Consolidated Schedule of Investments. At December 31, 2017, the amount of restricted cash held at brokers related to open swap contracts was $5,441,020.

27

Credit Suisse Trust — Commodity Return Strategy Portfolio

Notes to Consolidated Financial Statements (continued)

December 31, 2017

Note 2. Significant Accounting Policies (continued)

I) SECURITIES LENDING — The initial collateral received by the Portfolio is required to have a value of at least 102% of the market value of domestic securities on loan (including any accrued interest thereon) and 105% of the market value of foreign securities on loan (including any accrued interest thereon). The collateral is maintained thereafter at a value equal to at least 102% of the current market value of the securities on loan. The market value of loaned securities is determined at the close of each business day of the Portfolio and any additional required collateral is delivered to the Portfolio, or excess collateral returned by the Portfolio, on the next business day. Cash collateral received by the Portfolio in connection with securities lending activity may be pooled together with cash collateral for other funds/portfolios advised by Credit Suisse and may be invested in a variety of investments, including funds advised by SSB, the Portfolio's securities lending agent, or money market instruments. However, in the event of default or bankruptcy by the other party to the agreement, realization and/or retention of the collateral may be subject to legal proceedings.

SSB has been engaged by the Portfolio to act as the Portfolio's securities lending agent. The Portfolio's securities lending arrangement provides that the Portfolio and SSB will share the net income earned from securities lending activities. Securities lending income is accrued as earned. At December 31, 2017, there were no securities out on loan.

During the year ended December 31, 2017, total earnings from the Portfolio's investment in cash collateral received in connection with securities lending arrangements was $1,492, of which $0 was rebated to borrowers (brokers). The Portfolio retained $1,173 in income from the cash collateral investment, and SSB, as lending agent, was paid $319.

J) OTHER — In the normal course of business the Portfolio trades financial instruments and enters into financial transactions for which risk of potential loss exists due to changes in the market (market risk) or failure of the other party to a transaction to perform (credit risk). Similar to credit risk, the Portfolio may be exposed to counterparty risk, including securities lending, or the risk that an institution or other entity with which the Portfolio has unsettled or open transactions will default. The potential loss could exceed the value of the financial assets recorded in the consolidated financial statements. Financial assets, which potentially expose the Portfolio to credit risk, consist principally of cash due from counterparties and investments. The extent of the Portfolio's exposure to credit and counterparty risks in respect to these financial assets

28

Credit Suisse Trust — Commodity Return Strategy Portfolio

Notes to Consolidated Financial Statements (continued)

December 31, 2017

Note 2. Significant Accounting Policies (continued)

approximates their carrying value as recorded in the Portfolio's Consolidated Statement of Assets and Liabilities.

K) RECENT ACCOUNTING PRONOUNCEMENTS — In October 2016, the U.S. Securities and Exchange Commission adopted new rules and amended existing rules (together, "final rules") intended to modernize the reporting and disclosure of information by registered investment companies. In part, the final rules amend Regulation S-X and require standardized, enhanced disclosure about derivatives in investment company financial statements, as well as other amendments. The compliance date for the amendments to Regulation S-X is August 1, 2017. The Portfolio has adopted the amendments to Regulation S-X and upon evaluation, has concluded that the amendments do not materially impact the financial statements. However, as required, additional or enhanced disclosure has been included.

L) SUBSEQUENT EVENTS — In preparing the financial statements as of December 31, 2017, management considered the impact of subsequent events for potential recognition or disclosure in these financial statements through the date of release of this report. No such events requiring recognition or disclosure were identified through the date of the release of this report.

Note 3. Transactions with Affiliates and Related Parties

Credit Suisse serves as investment adviser and administrator for the Portfolio. For its investment advisory and administration services, Credit Suisse is entitled to receive a fee from the Portfolio at an annual rate of 0.59% of the Portfolio's average daily net assets. For the year ended December 31, 2017, investment advisory and administration fees earned and fees waived/expenses reimbursed by Credit Suisse were $2,175,220 and $210,376, respectively. Credit Suisse has contractually agreed to limit expenses so that the Portfolio's annual operating expenses do not exceed 1.05% of the Portfolio's average daily net assets. The Portfolio is authorized to reimburse Credit Suisse for management fees previously limited and/or for expenses previously reimbursed by Credit Suisse, provided, however, that any reimbursements must be paid at a date not more than three years after the end of the fiscal year during which such fees were limited or expenses were reimbursed by Credit Suisse and the reimbursements do not cause the Portfolio to exceed the applicable expense limitation in the contract at the time the fees are recouped. This contract may not be terminated before May 1, 2019.

29

Credit Suisse Trust — Commodity Return Strategy Portfolio

Notes to Consolidated Financial Statements (continued)

December 31, 2017

Note 3. Transactions with Affiliates and Related Parties (continued)

The amounts waived and reimbursed by Credit Suisse, which are available for potential future recoupment by Credit Suisse, and the expiration schedule at December 31, 2017 are as follows:

Fee waivers/ expense

reimbursements

subject to

recoupment | | Expires

December 31,

2018 | | Expires

December 31,

2019 | | Expires

December 31,

2020 | |

| $ | 385,539 | | | $ | 102,268 | | | $ | 72,895 | | | $ | 210,376 | | |

For its co-administrative services, SSB receive a fee, exclusive of out-of-pocket expenses, calculated in total for all the Credit Suisse funds/portfolios co-administered by SSB and allocated based upon the relative average net assets of each fund/portfolio, subject to an annual minimum fee. For the year ended December 31, 2017, co-administrative services fees earned by SSB (including out-of-picket expenses) with respect to the Portfolio were $64,921.