UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 20-F

(Mark One)

[ ] REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

[ X ] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year endedMay 31, 2012

OR

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

[ ] SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Date of event requiring this shell company report

For the transition period from _____________ to ___________________

Commission file number: 000-26296

Petaquilla Minerals Ltd.

(Exact name of Registrant as specified in its charter)

Not Applicable

(Translation of Registrant's name into English)

Province of British Columbia, Canada

(Jurisdiction of incorporation or organization)

Suite 1230, 777 Hornby Street, Vancouver, British Columbia, Canada V6Z 1S4

(Address of principal executive offices)

Mr. Ezequiel Sirotinsky, Chief Financial Officer

Telephone (604) 694-0021, facsimile (604) 694-0063, email: esirotinsky@petaquilla.com

Suite 1230, 777 Hornby Street, Vancouver, British Columbia, Canada V6Z 1S4

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

| |

| Form 20-F_Fiscal Year Ended 2012 May 31 | Page 1 |

Securities registered or to be registered pursuant to Section 12(b) of the Act.

| | |

Title of each class | None | Name of each exchange on which registered |

| | Not applicable | |

Securities registered or to be registered pursuant to Section 12(g) of the Act.

Common Shares without Par Value

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

Not Applicable

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

221,863,781 common shares, without par value, as at May 31, 2012

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

[ ] Yes [ X ] No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

[ ] Yes [ X ] No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

[ X ] Yes [ ] No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

[ X ] Yes [ ] No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

| | |

| Large accelerated filer [ ] | Accelerated filer [ X ] | Non-accelerated filer [ ] |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| | |

| U.S. GAAP [ ] | International Financial Reporting Standards as issued | Other [ ] |

| | By the International Accounting Standards Board [ X ] | |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

[ ] Item 17 [ ] Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

[ ] Yes [ X ] No

| |

| Form 20-F_Fiscal Year Ended 2012 May 31 | Page 2 |

| | |

| PETAQUILLA MINERALS LTD.

SECURITIES AND EXCHANGE COMMISSION

FORM 20-F

TABLE OF CONTENTS | Page No. |

| | |

| | GLOSSARY OF MINING TERMS | 8 |

| | CAUTIONARY NOTE REGARDING RESOURCE AND RESERVE ESTIMATES | 10 |

| | CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING INFORMATION | 10 |

| | CURRENCY PRESENTATION | 11 |

| | INTRODUCTION | 12 |

| | |

| PART I | | 12 |

| | |

| ITEM 1. | IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS | 12 |

| | |

| ITEM 2. | OFFER STATISTICS AND EXPECTED TIMETABLE | 12 |

| | |

| ITEM 3. | KEY INFORMATION | 12 |

| | |

| 3.A. | Selected Financial Data | 12 |

| 3.B. | Capitalization and Indebtedness | 14 |

| 3.C. | Reasons for the Offer and Use of Proceeds | 14 |

| 3.D. | Risk Factors | 14 |

| | Mining operations and projects are vulnerable to supply chain disruptions and ouroperations and development projects could be adversely affected by shortages of, as well aslead times to deliver, strategic spares, critical consumables, mining equipment ormetallurgical plant equipment. | 14 |

| | We face uncertainty and risks in our exploration and project evaluation activities. | 14 |

| | We face many risks related to the development of our mining projects that may adverselyaffect our results of operations and profitability. | 15 |

| | We may require additional funding in order to continue our operations. | 16 |

| | Our consolidated financial statements are prepared on a going concern basis. | 16 |

| | Our level of indebtedness could adversely affect our business. | 16 |

| | We face many risks related to our operations that may adversely affect our cash flows andoverall profitability. | 17 |

| | Mineral prices can fluctuate dramatically and have a material adverse effect on our resultsof operations. | 17 |

| | We face risks related to operations in foreign countries. | 18 |

| | The requirements of the Ley Petaquilla may have an adverse impact on us. | 18 |

| | Our operations are subject to environmental and other regulation. | 19 |

| | Our directors and officers may have conflicts of interest in connection with other mineralexploration and development companies. | 20 |

| | Environmental protestors are present in Panama. | 20 |

| | Our common shares are subject to penny stock rules, which could affect trading in ourshares. | 20 |

| |

| Form 20-F Fiscal Year Ended 2012 May 31 | Page 3 |

| | |

| | U.S. investors may not be able to enforce their civil liabilities against us or our directors,controlling persons and officers. | 20 |

| | If we have been or are characterized as a passive foreign investment company (“PFIC”) forU.S. federal income tax purposes, our U.S. Holders may be subject to adverse U.S. federalincome tax consequences. | 20 |

| | We face competition from companies with greater financial resources and operational capabilities. | 21 |

| | We may not pay dividends on our common shares in the foreseeable future. | 21 |

| | |

| ITEM 4. | INFORMATION ON THE COMPANY | 21 |

| | |

| 4.A. | History and Development of the Company | 21 |

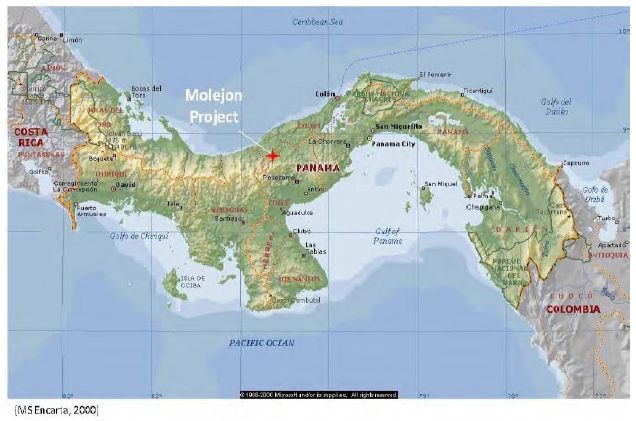

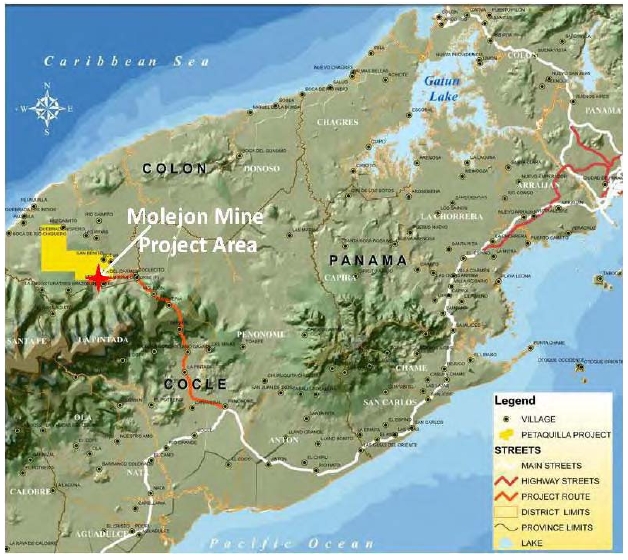

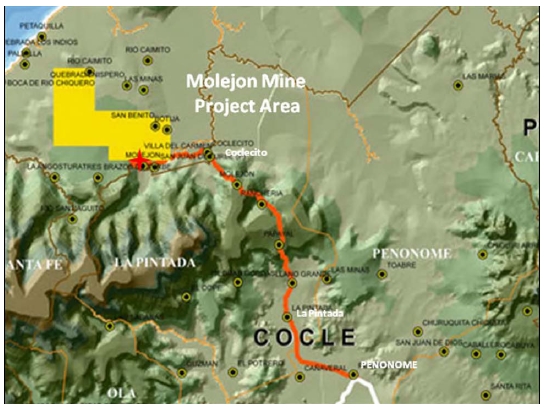

| | Molejon Property – Panama | 22 |

| | Principal Capital Expenditures and Divestitures Over Last Three Fiscal Years | 23 |

| | Current Principal Capital Expenditures and Divestitures | 23 |

| | Public Takeover Offers | 23 |

| | Lomero-Poyatos Property – Spain | 24 |

| 4.B. | Business Overview | 24 |

| | Molejon Property – Panama | 24 |

| | Lomero-Poyatos Property – Spain | 25 |

| 4.C. | Organizational Structure | 25 |

| 4.D. | Property, Plants and Equipment | 25 |

| | Mineral Concession Lands | 25 |

| | Introduction | 25 |

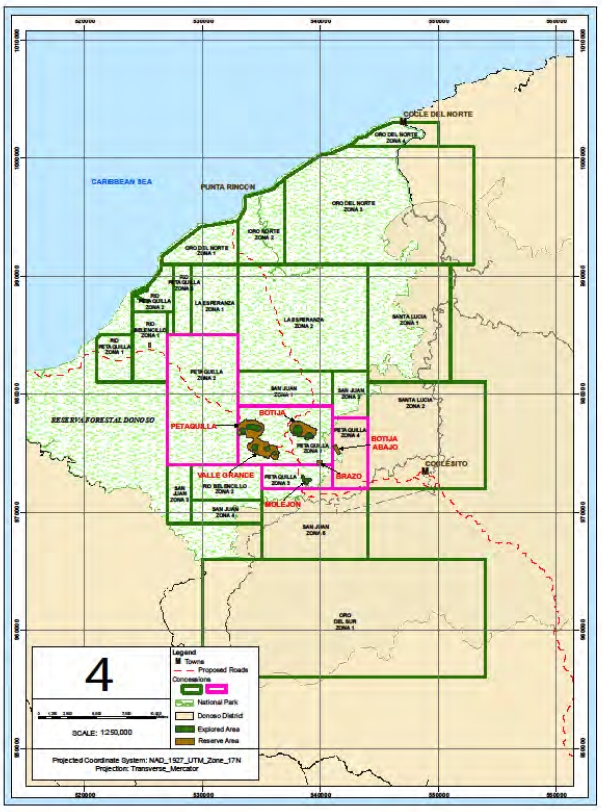

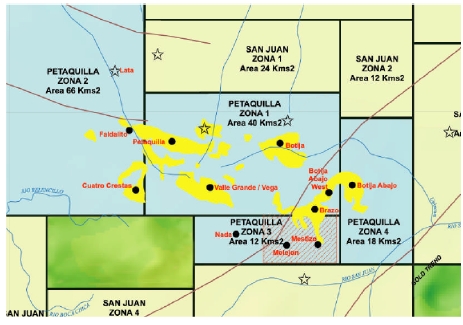

| | Property Location - Panama | 25 |

| | Location, Access & Physiography | 30 |

| | Plant and Equipment | 30 |

| | Mine Operations | 33 |

| | Mineral Recoveries | 33 |

| | Commodity Price | 34 |

| | Exploration and Advancement of the Molejon Property | 36 |

| | Title | 36 |

| | Cerro Petaquilla Concession – Panama | 36 |

| | Molejon Property – Panama | 36 |

| | Exploration History | 37 |

| | Summary of Exploration History and Ownership | 37 |

| | Resource and Reserve Estimates | 39 |

| | Regional and Local Geology | 41 |

| | Mineralization | 41 |

| | Doing Business in Panama | 42 |

| | Property Location - Spain | 44 |

| | Summary of Exploration History and Ownership | 46 |

| | Resource and Reserve Estimates | 46 |

| | Geology and Mineralization | 46 |

| | Outlook – 2013 | 47 |

| | |

| ITEM 4A. | UNRESOLVED STAFF COMMENTS | 47 |

| | |

| ITEM 5. | OPERATING AND FINANCIAL REVIEW AND PROSPECTS | 47 |

| |

| Form 20-F_Fiscal Year Ended 2012 May 31 | Page 4 |

| | |

| 5.A. | Operating Results | 47 |

| | Year Ended May 31, 2012, Compared to Year Ended May 31, 2011 (prepared in accordancewith IFRS) | 48 |

| | Year Ended May 31, 2011, Compared to Year Ended May 31, 2010 (both originallyprepared in accordance with generally accepted accounting principles in Canada) | 49 |

| | Year Ended May 31, 2010, Compared to Year Ended May 31, 2009 (both originallyprepared in accordance with generally accepted accounting principles in Canada) | 50 |

| 5.B | Liquidity and Capital Resources | 52 |

| | May 31, 2012, Compared with May 31, 2011 | 52 |

| | May 31, 2011, Compared with June 1, 2010 | 53 |

| 5.C. | Research and Development, Patents and Licenses, etc. | 53 |

| 5.D. | Trend Information | 53 |

| 5.E. | Off-Balance Sheet Arrangements | 54 |

| 5.F. | Tabular Disclosure of Contractual Obligations | 55 |

| | Commitments | 55 |

| | Long-Term Debt | 56 |

| | Bank Loans | 56 |

| | Finance Lease Obligations | 57 |

| | Convertible Loan | 57 |

| | Secured Notes | 58 |

| | Convertible Secured Notes | 58 |

| | Community Support Obligation | 59 |

| | Asset Retirement Obligation | 59 |

| 5.G. | Safe Harbour | 60 |

| | |

| ITEM 6. | DIRECTORS, SENIOR MANAGEMENT AND EMPLOYEES | 60 |

| | |

| 6.A. | Directors and Senior Management | 60 |

| 6.B. | Compensation | 62 |

| | Cash and Non-Cash Compensation – Directors and Officers | 62 |

| | Option Grants to Directors and Officers During Fiscal Year Ended May 31, 2012 | 63 |

| | Options Acquired Upon Acquisition of Iberian Resources Corp. During Fiscal Year EndedMay 31, 2012 | 63 |

| | Aggregated Option Exercises in Last Fiscal Year and Fiscal Year-End Option Values | 64 |

| | Defined Benefit or Actuarial Plan Disclosure | 65 |

| | Termination of Employment, Change in Responsibilities and Employment Contracts | 65 |

| | Directors | 65 |

| 6.C. | Board Practices | 65 |

| 6.D. | Employees | 66 |

| 6.E. | Share Ownership | 66 |

| | |

| ITEM 7. | MAJOR SHAREHOLDERS AND RELATED PARTY TRANSACTIONS | 68 |

| | |

| 7.A. | Major Shareholders | 68 |

| 7.B. | Related Party Transactions | 69 |

| 7.C. | Interests of Experts and Counsel | 70 |

| | |

| ITEM 8. | FINANCIAL INFORMATION | 70 |

| | |

| 8.A. | Consolidated Statements and Other Financial Information | 70 |

| |

| Form 20-F Fiscal Year Ended 2012 May 31 | Page 5 |

| | |

| 8.B. | Significant Changes | 70 |

| | |

| ITEM 9. | THE OFFER AND LISTING | 70 |

| | |

| 9.A. | Offer and Listing Details | 70 |

| 9.B. | Plan of Distribution | 72 |

| 9.C. | Markets | 73 |

| 9.D. | Selling Shareholders | 73 |

| 9.E. | Dilution | 73 |

| 9.F. | Expenses of the Issue | 73 |

| | |

| ITEM 10. | ADDITIONAL INFORMATION | 73 |

| | |

| 10.A. | Share Capital | 73 |

| 10.B. | Memorandum and Articles of Association | 73 |

| 10.C. | Material Contracts | 75 |

| 10.D. | Exchange Controls | 75 |

| 10.E. | Taxation | 77 |

| | Material Canadian Federal Income Tax Consequences | 77 |

| | Dividends | 77 |

| | Capital Gains | 77 |

| | Material United States Federal Income Tax Consequences | 78 |

| | U.S. Holders | 78 |

| | Distributions on our Common Shares | 79 |

| | Disposition of our Common Shares | 79 |

| | Passive Foreign Investment Company | 80 |

| | Foreign Tax Credit | 80 |

| | Information Reporting and Backup Withholding | 81 |

| 10.F. | Dividends and Paying Agents | 81 |

| 10.G. | Statements by Experts | 81 |

| 10.H. | Documents on Display | 81 |

| 10.I. | Subsidiary Information | 81 |

| | |

| ITEM 11. | QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | 81 |

| | |

| | Credit risk | 81 |

| | Liquidity risk | 82 |

| | Market risk | 82 |

| | Currency risk | 82 |

| | Interest rate risk | 82 |

| | Price risk | 82 |

| | Qualitative information about market risk | 82 |

| | |

| ITEM 12. | DESCRIPTION OF SECURITIES OTHER THAN EQUITY SECURITIES | 83 |

| | |

| PART II | | 83 |

| | |

| ITEM 13. | DEFAULTS, DIVIDEND ARREARAGES AND DELINQUENCIES | 83 |

| | |

| ITEM 14. | MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS | 83 |

| |

| Form 20-F_Fiscal Year Ended 2012 May 31 | Page 6 |

| | |

| ITEM 15. | CONTROLS AND PROCEDURES | 83 |

| | Management’s Annual Report on Internal Control over Financial Reporting | 84 |

| | Attestation Report of our External Auditor | 84 |

| | Changes in Internal Control over Financial Reporting | 84 |

| | Inherent Limitations on Effectiveness of Controls | 84 |

| | |

| ITEM 16. | [RESERVED] | 85 |

| | |

| 16.A. | AUDIT COMMITTEE FINANCIAL EXPERT | 85 |

| | |

| 16.B. | CODE OF ETHICS | 85 |

| | |

| 16.C. | PRINCIPAL ACCOUNTANT FEES AND SERVICES | 85 |

| | |

| 16.D. | EXEMPTIONS FROM THE LISTING STANDARDS FOR AUDIT COMMITTEES | 86 |

| | |

| 16.E. | PURCHASES OF EQUITY SECURITIES BY THE ISSUER AND AFFILIATED PURCHASERS | 86 |

| | |

| 16.F. | CHANGE IN REGISTRANT’S CERTIFYING ACCOUNTANT | 86 |

| | |

| 16.G. | CORPORATE GOVERNANCE | 86 |

| | |

| 16.H. | MINE SAFETY DISCLOSURE | 86 |

| | |

| PART III | | 87 |

| | |

| ITEM 17. | FINANCIAL STATEMENTS | 87 |

| | |

| ITEM 18. | FINANCIAL STATEMENTS | 152 |

| | |

| ITEM 19. | EXHIBITS | 152 |

| | |

| | SIGNATURES | 154 |

| |

| Form 20-F Fiscal Year Ended 2012 May 31 | Page 7 |

GLOSSARY OF MINING TERMS

The following is a glossary of some of the terms used in the mining industry and referenced herein:

| |

| cut-off grade | the deemed grade of mineralization, established by reference to economic factors, above which material is included in mineral deposit calculations and below which material is considered waste. May be either an external cut-off grade, which refers to the grade of mineralization used to control the external or design limits of an open pit based upon the expected economic parameters of the operation, or an internal cut-off grade, which refers to the minimum grade required for blocks of mineralization present within the confines of an open pit to be included in mineral deposit estimates |

| diamond drill | a machine designed to rotate under pressure an annular diamond-studded cutting tool to produce a more or less continuous solid sample (drill core) of the material that is drilled |

| epithermal | a term applied to those mineral deposits formed in and along fissures or other openings in rocks by deposition at shallow depths from ascending hot solutions |

| indicated mineral resource | that part of a Mineral Resource for which quantity, grade or quality, densities, shape and physical characteristics, can be estimated with a level of confidence sufficient to allow the appropriate application of technical and economic parameters, to support mine planning and evaluation of the economic viability of the deposit. The estimate is based on detailed and reliable exploration and testing information gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes that are spaced closely enough for geological and grade continuity to be reasonably assumed |

| inferred mineral resource | that part of a Mineral Resource for which quantity, grade or quality can be estimated on the basis of geological evidence and limited sampling and reasonably assumed, but not verified, geological and grade continuity. The estimate is based on limited information and sampling gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes |

| measured mineral resource | that part of a Mineral Resource for which quantity, grade or quality, densities, shape and physical characteristics are so well established that they can be estimated with confidence sufficient to allow the appropriate application of technical and economic parameters, to support production planning and evaluation of the economic viability of the deposit. The estimate is based on detailed and reliable exploration, sampling and testing information gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes that are spaced closely enough to confirm both geological and grade continuity |

| mineral deposit, deposit or mineralized material | a mineralized body which has been physically delineated by sufficient drilling, trenching and/or underground work and found to contain a sufficient average grade of metal or metals to warrant further exploration and/or development expenditures. Such a deposit does not qualify under standards of the Securities Exchange Commission as a commercially mineable ore body or as containing ore reserves, until final legal, technical and economic factors have been resolved |

| mineral reserve | the economically mineable part of a Measured or Indicated Mineral Resource demonstrated by at least a Preliminary Feasibility Study. This Study must include adequate information on mining, processing, metallurgical, economic and other relevant factors that demonstrate, at the time of reporting, that economic extraction can be justified. A Mineral Reserve includes diluting materials and allowances for losses that may occur when the material is mined |

| mineral resource | a concentration or occurrence of diamonds, natural solid inorganic material or natural solid fossilized organic material including base and precious metals, coal and industrial minerals in or on the Earth’s crust in such form and quantity and of such a grade or quality that it has reasonable prospects for economic extraction. The location, quantity, grade, geological characteristics and continuity of a Mineral |

| |

| Form 20-F_Fiscal Year Ended 2012 May 31 | Page 8 |

| |

| | Resource are known, estimated or interpreted from specific geological evidence and knowledge |

| open pit mining | the process of mining an ore body from the surface in progressively deeper steps. Sufficient waste rock adjacent to the ore body is removed to maintain mining access and to maintain the stability of the resulting pit |

| ore | a natural aggregate of one or more minerals which, at a specified time and place, may be mined and sold at a profit, or from which some part may be profitably separated |

| ounces | troy ounces |

| oz/tonne | troy ounces per metric tonne |

| ppb | parts per billion |

| ppm | parts per million |

| porphyry deposit | a disseminated mineral deposit often closely associated with porphyritic intrusive rocks; |

| preliminary feasibility study | a comprehensive study of the viability of a mineral project that has advanced to a stage where the mining method, in the case of underground mining, or the pit configuration, in the case of an open pit, has been established and an effective method of mineral processing has been determined, and includes a financial analysis based on reasonable assumptions of technical, engineering, legal, operating, economic, social and environmental factors and the evaluation of other relevant factors which are sufficient for a Qualified Person, acting reasonably, to determine if all or part of the Mineral Resource may be classified as a Mineral Reserve |

| probable mineral reserve | the economically mineable part of an Indicated mineral resource and, in some circumstances, a Measured Mineral Resource demonstrated by at least a Preliminary Feasibility Study. Such Study must include adequate information on mining, processing, metallurgical, economic and other relevant factors that demonstrate, at the time of reporting, that economic extraction can be justified |

| proven mineral reserve | the economically mineable part of a Measured Mineral Resource demonstrated by at least a Preliminary Feasibility Study. Such study must include adequate information on mining, processing, metallurgical, economic and other relevant factors that demonstrate, at the time of reporting, that economic extraction is justified |

| qualified person | an individual who is an engineer or geoscientist with at least five years of experience in mineral exploration, mine development or operation or mineral project assessment, or any combination of these; has experience relevant to the subject matter of the mineral project and the technical report; and is a member or licensee in good standing of a professional association |

| stockwork | a rock mass so interpenetrated by small veins of ore that the whole must be mined together. Stockworks are distinguished from tabular or sheet deposits, (i.e. veins or beds), which have a small degree of thickness in comparison with their extension in the main plane of the deposit |

| tonne | body, metric ton (2,204 pounds) |

| |

| Form 20-F_Fiscal Year Ended 2012 May 31 | Page 9 |

CAUTIONARY NOTE REGARDING RESOURCE AND RESERVE ESTIMATES

The terms “mineral reserve”, “proven mineral reserve” and “probable mineral reserve” are Canadian mining terms as defined in accordance with Canadian National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43-101”) and the Canadian Institute of Mining, Metallurgy and Petroleum (the “CIM”) - CIM Definition Standards on Mineral Resources and Mineral Reserves, adopted by the CIM Council, as amended. These definitions differ from the definitions in United States Securities and Exchange Commission (“SEC”) Industry Guide 7 under the United States Securities Act of 1993, as amended (the “Securities Act”). Under the United States Security and Exchange Commission (“SEC”) Industry Guide 7 standards, a “final” or “bankable” feasibility study is required to report reserves, the three-year historical average price is used in any reserve or cash flow analysis to designate reserves and the primary environmental analysis or report must be filed with the appropriate governmental authority.

In addition, the terms “mineral resource”, “measured mineral resource”, “indicated mineral resource” and “inferred mineral resource” are defined in and required to be disclosed by NI 43-101; however, these terms are not defined terms under SEC Industry Guide 7 and are normally not permitted to be used in reports and registration statements filed with the SEC. Investors are cautioned not to assume that any part or all of mineral deposits in these categories will ever be converted into reserves. “Inferred mineral resources” have a great amount of uncertainty as to their existence and great uncertainty as to their economic and legal feasibility. It cannot be assumed that all or any part of an inferred mineral resource will ever be upgraded to a higher category. Under Canadian rules, estimates of inferred mineral resources may not form the basis of feasibility or pre-feasibility studies, except in rare cases. Investors are cautioned not to assume that all or any part of an inferred mineral resource exists or is economically or legally mineable. Disclosure of “contained ounces” in a resource is permitted disclosure under Canadian regulations; however, the SEC normally only permits issuers to report mineralization that does not constitute “reserves” by SEC Industry Guide 7 standards as in place tonnage and grade without reference to unit measures.

Accordingly, information contained in this Annual Report contains descriptions of our mineral deposits that may not be comparable to similar information made public by U.S. companies subject to the reporting and disclosure requirements under the United States federal securities laws and the rules and regulations there under.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING INFORMATION

This Annual Report on Form 20-F contains forward-looking information and forward-looking statements as defined in applicable securities laws. These statements relate to future events or our future performance. All statements other than statements of historical fact are forward-looking statements.

Forward-looking statements include, but are not limited to, statements with respect to the future price of gold, silver and other minerals, the estimation of mineral reserves and resources, the realization of mineral reserve estimates, the timing and amount of estimated future production, costs of production, capital expenditures, costs and timing of the development of new deposits, success of exploration activities, permitting time lines, currency exchange rate fluctuations, requirements for additional capital, completion of a plant capacity expansion, government regulation of mining operations, government approval to commence mining at Lomero-Poyatos Mine, fiscal 2013 plans, combined ore on two leach pads, planned recovery rate, production through the on/off leach operation will progressively increase, throughput will increase beginning in the second quarter of fiscal 2013, additional tpd processing capacity, expectation on the spin-out of Panama Development and Infrastructure Ltd., environmental risks, unanticipated reclamation expenses, title disputes or claims, limitations on insurance coverage.

Generally, these forward-looking statements can be identified by the use of forward-looking terminology such as “plans”, “expects” or “does not expect”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates” or “does not anticipate” or “believes”, or variations of such words and phrases or state that certain actions, events or results “may”, “could”, “would”, “might” or “will be taken”, “occur” or “be achieved”.

Forward-looking statements are subject to known and unknown risks, uncertainties and other factors that may cause our actual results, level of activity, performance or achievements to be materially different from those expressed or implied by such forward-looking statements, including but not limited to: risks related to international operations; risks related to joint venture operations; actual results of current exploration activities; conclusions of economic evaluations; changes in project parameters as plans continue to be refined; future prices of gold and silver; possible

| |

| Form 20-F_Fiscal Year Ended 2012 May 31 | Page 10 |

variations in ore reserves, grade or recovery rates; failure of plant, equipment or processes to operate as anticipated; accidents, labor disputes and other risks of the mining industry; delays in obtaining governmental approvals or financing or in the completion of development or construction activities, as well as those factors discussed in the section entitled “Risk Factors” in this Annual Report on Form 20-F. Although we have attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements.

Statements in this Annual Report on Form 20-F regarding expected completion dates of feasibility studies, anticipated mining or metal production operations, projected quantities of future metal production and anticipated production rates, operating efficiencies, costs and expenditures are forward-looking statements. Actual results could differ materially depending upon the availability of materials, equipment, required permits or approvals and financing, the occurrence of unusual weather or operating conditions, the accuracy of reserve estimates, lower than expected ore grades or the failure of equipment or processes to operate in accordance with specifications. Additional information about these and other assumptions, risks and uncertainties that may affect our future financial performance are set out inItem 3.D. – Key Information – Risk Factors.

Forward-looking statements in this Annual Report on Form 20-F are as of September 11, 2012. We do not undertake to update any forward-looking statements that are incorporated by reference herein, except in accordance with applicable securities laws.

CURRENCY PRESENTATION

This Annual Report on Form 20-F contains references to United States dollars and Canadian dollars. Unless otherwise indicated, all dollar amounts referred to herein are expressed in United States dollars and all financial information presented has been prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”). Canadian dollars are referred to as “CAD$”.

| |

| Form 20-F_Fiscal Year Ended 2012 May 31 | Page 11 |

INTRODUCTION

Petaquilla Minerals Ltd. is organized under the British Columbia Business Corporations Act. As used in this Annual Report on Form 20-F (the “Annual Report”), the terms “Petaquilla”, “we”, “us” and “our” refer to Petaquilla Minerals Ltd. and our subsidiaries unless otherwise indicated or if the context otherwise requires.

Our principal corporate offices are located at Suite 1230, 777 Hornby Street, Vancouver, British Columbia, Canada V6Z 1S4. Our telephone number is 604-694-0021.

We file reports and other information with the SEC located at 100 F Street NE, Washington, D.C. 20549; you may obtain copies of our filings with the SEC by accessing its Electronic Data Gathering Analysis and Retrieval (“EDGAR”) System located at www.sec.gov. Further, we file reports under Canadian regulatory requirements on the System for Electronic Document Analysis and Retrieval of the Canadian Securities Administrators (“SEDAR”); you may access our reports filed on SEDAR by accessing the following website: www.sedar.com.

The information set forth in this Annual Report is as at August 29, 2012, unless an earlier or later date is indicated.

PART I

| |

| ITEM 1. | IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS |

This Form 20-F is being filed as an annual report under the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and as such, there is no requirement to provide information under this item.

| |

| ITEM 2. | OFFER STATISTICS AND EXPECTED TIMETABLE |

This Form 20-F is being filed as an annual report under the Exchange Act, and as such, there is no requirement to provide information under this item.

| |

| 3.A. | Selected Financial Data |

Our selected financial data for the fiscal years ended May 31, 2012, and 2011, was derived from our consolidated annual financial statements, prepared in accordance with IFRS as issued by the IASB.

The consolidated financial statements for the year ended May 31, 2012, and its comparative periods were prepared in accordance with IFRS as issued by the IASB, and audited by Ernst & Young, LLP, Chartered Accountants, as indicated in the audit report covering such periods included elsewhere in this Annual Report. Our selected financial data should be read in conjunction with the consolidated financial statements and other financial information included elsewhere in this Annual Report.

Subject to certain transition elections disclosed in Note 33 of the consolidated financial statements for the year ended May 31, 2012, we have consistently applied the same accounting policies in our opening IFRS statement of financial position at June 1, 2010, and throughout all periods presented, as if these policies had always been in effect. Note 33 of the consolidated financial statements further discloses the impact of the transition to IFRS on our reported financial position, financial performance and cash flows, including the nature and effect of significant changes in accounting policies from those used in our consolidated financial statements for the year ended May 31, 2011.

We have not declared any dividends on our common shares since incorporation and do not anticipate that we will do so in the foreseeable future. Our present policy is to retain future earnings for use in our operations and expansion of our business.

The following tables summarize our selected consolidated financial information for the periods indicated and is extracted from the more detailed consolidated financial statements and related notes included herein. The following tables should be ready in conjunction with “Item 5 – Operating and Financial Review and Prospects”, and the consolidated financial statements included in Item 17. Results for the periods presented are not necessarily indicative of results for future periods.

| |

| Form 20-F_Fiscal Year Ended 2012 May 31 | Page 12 |

SELECTED FINANCIAL DATA, DERIVED FROM OUR CONSOLIDATED ANNUAL FINANCIAL

STATEMENTS, PRESENTED IN ACCORDANCE WITH IFRS AS ISSUED BY THE IASB

| | | | |

| | | Year Ended | Year Ended | |

| | | May 31, 2012 | May 31, 2011 | |

| | | ($) | ($) | |

| | Total revenue | 94,297,396 | 71,708,685 | |

| | Net income (loss) | 22,419,634 | (3,843,516) | |

| | Basic and diluted earnings (loss) per share(1) | 0.10 | (0.01) | |

| | Total assets | 186,251,191 | 128,733,415 | |

| | Total long-term debt(2) | 10,443,250 | 14,689,811 | |

| | Shareholders’ equity | 55,929,263 | 10,398,510 | |

| | Cash dividends declared per share | n/a | n/a | |

| | Capital stock (number of issued and outstanding common shares) | 221,863,781 | 176,429,501 | |

| | | As at May 31, 2012 | As at May 31, 2011 | |

| | Cash and cash equivalents | 1,975,660 | 5,712,792 | |

| | Short term investments | 340,000 | 200,000 | |

| | Inventories | 29,523,783 | 13,886,081 | |

| | Working capital | (41,775,106) | (23,848,920) | |

| | Long-term debt(2) | 10,443,250 | 14,689,811 | |

| | Shareholders’ equity | 55,929,263 | 10,398,510 | |

| | Total assets | 186,251,191 | 128,733,415 | |

| | | As at June 1, 2010 | | |

| | Cash and cash equivalents | 4,625,649 | | |

| | Short term investments | - | | |

| | Inventories | 4,742,031 | | |

| | Working Capital | (89,616,869) | | |

| | Long-term debt(2) | 76,432,676 | | |

| | Shareholders’ equity (deficiency) | (25,246,279) | | |

| | Total assets | 90,258,202 | | |

(1) The effect of potential share issuances pursuant to the exercise of options and warrants would be anti-dilutive and, therefore, basic and diluted losses per share are the same.

(2) Includes bank loans, finance lease obligations, convertible loan, secured notes and convertible secured notes. See note 15 to our consolidated financial statements for year ended May 31, 2012.

| |

| Form 20-F_Fiscal Year Ended 2012 May 31 | Page 13 |

| |

| 3. B. | Capitalization and Indebtedness |

This Form 20-F is being filed as an annual report under Exchange Act, and as such, there is no requirement to provide information under this item.

| |

| 3. C. | Reasons for the Offer and Use of Proceeds |

This Form 20-F is being filed as an annual report under Exchange Act, and as such, there is no requirement to provide information under this item.

The following is a brief discussion of those distinctive or special characteristics of our operations and industry, which may have a material impact on, or constitute risk factors in respect of, our financial performance. However, there may be additional risks unknown to us and other risks, currently believed to be immaterial, that could turn out to be material. These risks, either individually or simultaneously, could significantly affect our business and financial results.

We operate in a dynamic and rapidly changing environment that involves numerous risks and uncertainties. Investors should carefully consider the risks described below before investing in our securities. The occurrence of any of the following events could harm us. If these events occur, the trading price of our common shares could decline, and investors may lose part or even all of their investment.

Mining operations and projects are vulnerable to supply chain disruptions and our operations and development projects could be adversely affected by shortages of, as well as lead times to deliver, strategic spares, critical consumables, mining equipment or metallurgical plant equipment.

Our operations and development projects could be adversely affected by shortages of, as well as lead times to deliver, strategic spares, critical consumables and processing equipment. In the past, we and other gold mining companies have experienced shortages in critical consumables, particularly as production capacity in the global mining industry has expanded in response to increased demand for commodities, and we have experienced increased delivery times for these items. These shortages have also resulted in unanticipated increases in the price of certain of these items. Shortages of strategic spares, critical consumables or mining equipment, which could occur in the future, could result in production delays and production shortfalls, and increases in prices result in an increase in both operating costs and the capital expenditure to maintain and develop mining operations. We and other gold mining companies, individually, have limited influence over manufacturers and suppliers of these items. In certain cases there are only limited suppliers for certain strategic spares, critical consumables and processing equipment and they command superior bargaining power relative to us, or we could at times face limited supply or increased lead time in the delivery of such items. If we experience shortages, or increased lead times in delivery of strategic spares, critical consumables or processing equipment our results of operations and our financial condition could be adversely affected.

We face uncertainty and risks in our exploration and project evaluation activities.

Exploration activities are speculative in nature and project evaluation activities necessary to determine whether a viable mining operation exists or can be developed are often unproductive. These activities also often require substantial expenditure to establish the presence, and to quantify the extent and grades (metal content), of mineralized material through exploration drilling. Once mineralization is discovered it can take several years to determine whether adequate ore reserves exist. During this time, the economic feasibility of production may change owing to fluctuations in factors that affect revenue, as well as cash and other operating costs, including:

future metal and other commodity prices;

anticipated tonnage, grades and metallurgical characteristics of the ore to be mined and processed;

anticipated recovery rates of gold from the ore; and

anticipated capital expenditure and cash operating costs.

These estimates depend upon the data available and the assumptions made at the time the relevant estimate is made.

| |

| Form 20-F_Fiscal Year Ended 2012 May 31 | Page 14 |

Resource estimates are not precise calculations and depend on the interpretation of limited information on the location, shape and continuity of the occurrence and on the available sampling results. Further exploration and studies can result in new data becoming available that may change previous resource estimates which will impact upon both the technical and economic viability of production of the relevant mining project. Changes in the forecast prices of commodities, exchange rates, production costs or recovery rates may change the economic status of resources resulting in revisions to previous resource estimates. These revisions could impact depreciation and amortization rates, asset-carrying values provisions for closedown, restoration and environmental clean-up costs. These estimates depend upon the data available and the assumptions made at the time the relevant estimate is made.

We undertake revisions to our resource estimates based upon actual exploration and production results, new information on geology and fluctuations in production, operating and other costs and which could adversely affect the life-of-mine plans and consequently the total value of our mining asset base. Resource restatements could negatively affect our results, financial condition and prospects, as well as our reputation. The increased demand for gold and other commodities, combined with a declining rate of discovery, has resulted in existing reserves being depleted at an accelerated rate in recent years. We, therefore, face intense competition for the acquisition of attractive mining properties.

From time to time, we evaluate the acquisition of exploration properties and operating mines, either as stand-alone assets or as part of companies. Our decisions to acquire these properties have historically been based on a variety of factors including estimates of and assumptions regarding the extent of resources, cash and other operating costs, gold prices and projected economic returns and evaluations of existing or potential liabilities associated with the relevant property and our operations and how these factors may change in the future. All of these factors are uncertain and could have an impact upon revenue, cash and other operating issues, as well as the uncertainties related to the process used to estimate resources.

As a result of these uncertainties, the exploration programs and acquisitions engaged in by us may not result in the expansion or replacement of the current production with new resources or operations. Our operating results and financial condition are directly related to the success of our exploration and acquisition efforts and our ability to replace or increase existing resources. If we are not able to maintain or increase our resources, our results of operations and our financial condition and prospects could be adversely affected.

We face many risks related to the development of our mining projects that may adversely affect our results of operations and profitability.

The profitability of mining companies depends, in part, on the actual costs of developing and operating mines, which may differ significantly from estimates determined at the time a relevant mining project was approved. The development of mining projects may also be subject to unexpected problems and delays that could increase the cost of development and the ultimate operating cost of the relevant project. Our decision to develop a mineral property is based on estimates made as to the expected or anticipated project economic returns. These estimates are based on assumptions regarding:

future gold prices;

anticipated tonnage, grades and metallurgical characteristics of ore to be mined and processed;

anticipated recovery rates of gold extracted from the ore; and

anticipated capital expenditure and cash operating costs.

Actual cash operating costs, production and economic returns may differ significantly from those anticipated by such estimates.

There are a number of uncertainties inherent in the development and construction of an extension to an existing mine, or in the development and construction of any new mine. In addition to those discussed above, these uncertainties include the:

timing and cost of the construction of mining and processing facilities, which can be considerable;

availability and cost of skilled labor, power, water and transportation facilities;

need to obtain necessary environmental and other governmental permits and the time to obtain such permits; and

availability of funds to finance construction and development activities.

| |

| Form 20-F_Fiscal Year Ended 2012 May 31 | Page 15 |

New mining operations could experience unexpected problems and delays during development, construction and mine start-up. In addition, delays in the commencement of mineral production could occur. Finally, operating cost and capital expenditure estimates could fluctuate considerably as a result of changes in the prices of commodities consumed in the construction and operation of mining projects. Accordingly, our future development activities may not result in the expansion or replacement of current production with new production, or one or more new production sites or facilities may be less profitable than currently anticipated or may not be profitable at all. Our operating results and financial conditions are directly related to the success of our project developments. A failure in our ability to develop and operate mining projects in accordance with, or in excess of, expectations could negatively affect our results of operations and our financial condition and prospects.

We may require additional funding in order to continue our operations.

We have been producing since January 8, 2010, when we achieved commercial production at the Molejon gold property. Considering our increase in cash margin, our improvements in throughput and production capacity at our Molejon gold processing plant, in addition to the initiation of our on/off leach operation during fiscal 2012, the risk of our requiring additional funding in order to continue our operations has been mitigated. In addition, our net income for the year ended May 31, 2012, reflects a positive trend in the finance and operational performance of our company. This positive trend will enable us to manage our cash flow from operations to comply with operational requirements and also with our planned exploration and development programs. Alternative sources of funding, depending on market conditions and the potential desire of investors to increase their participation in our company’s business or other projects, may become available and could be considered. However, there can be no assurance that funding from these sources will be sufficient in the future to satisfy our operational requirements, debt repayments and cash commitments. This is dependent on market expectations and on our performance, production and results.

We have an accumulated deficit as at May 31, 2012, of $122,969,497; however, during the year ended May 31, 2012, we obtained an operating margin of $34,932,034, which considered on an accumulated basis together with that obtained during fiscal 2011, we have accumulated a total of $54,973,287.

Our consolidated financial statements are prepared on a going concern basis.

Our consolidated financial statements for the year ended May 31, 2012, have been prepared on a going concern basis, which assumes that we will be able to realize our assets at the amounts recorded and discharge our liabilities in the normal course of business in the foreseeable future. Our management believes that based on our planned fiscal 2013 projections, we have sufficient cash flow to operate for the next twelve months.

Our level of indebtedness could adversely affect our business.

Although this risk could affect our financial situation, it has been managed appropriately and such management has enabled us to payout all of our Notes and Convertible Notes during the year ended May 31, 2012.

Due to new acquisitions and our growth strategy, we may incur additional indebtedness in the future. A significant increase in our debt levels may have important consequences for us, including, but not limited to the following:

Our ability to obtain additional financing for working capital, capital expenditures, general corporate and other purposes or to fund future operations may not be available on terms favorable to us or at all;

A significant amount of our operating cash flow is dedicated to the payment of interest and principal on our indebtedness, thereby diminishing funds that would otherwise be available for our operations and for other purposes;

Increasing our vulnerability to current and future adverse economic and industry conditions;

A substantial decrease in net operating cash flows or increase in our expenses could make it more difficult for us to meet our debt service requirements, which could force us to modify our operations;

Our leveraged capital structure may place us at a competitive disadvantage by hindering our ability to adjust rapidly to changing market conditions or by making us vulnerable to a downturn in our business or the economy in general;

| |

| Form 20-F_Fiscal Year Ended 2012 May 31 | Page 16 |

We may have to offer debt or equity securities on terms that may not be favorable to us or to our shareholders;

Limiting our flexibility in planning for, or reacting to, changes and opportunities in our business and our industry; and

Our level of indebtedness increases the possibility that we may be unable to generate cash sufficient to pay the principal or interest due in respect of our indebtedness.

We face many risks related to our operations that may adversely affect our cash flows and overall profitability.

Gold mining is susceptible to numerous events that may have an adverse impact on our mining business, our ability to produce gold and meet our production targets. These events include, but are not limited to:

environmental hazards, including discharge of metals, pollutants or hazardous chemicals;

industrial accidents;

fires;

labor disputes;

mechanical breakdowns;

electrical power interruptions;

encountering unexpected geological formations;

unanticipated ground conditions;

ingresses of water;

process water shortages;

failure of mining pit slopes, water dams, waste stockpiles and tailings dam walls;

legal and regulatory restrictions and changes to such restrictions;

safety-related stoppages;

other natural phenomena, such as floods, droughts or inclement weather conditions, potentially exacerbated by climate change.

Mineral prices can fluctuate dramatically and have a material adverse effect on our results of operations.

Our revenues are primarily derived from the sale of gold and the market price for gold fluctuates widely. These fluctuations are caused by numerous factors beyond our control including:

speculative positions taken by investors or traders in gold;

changes in the demand for gold as an investment;

changes in the demand for gold used in jewelery and for other industrial uses, including as a result of prevailing economic conditions;

changes in the supply of gold from production, disinvestment, scrap and hedging;

financial market expectations regarding the rate of inflation;

strength of the US dollar (the currency in which the gold price trades internationally) relative to other currencies;

changes in interest rates;

actual or expected sales or purchases of gold by central banks and the International Monetary Fund;

gold hedging and de-hedging by gold producers;

global or regional political or economic events; and

the cost of gold production in major gold producing countries.

On September 11, 2012, the afternoon fixing price of gold on the London Bullion Market was $1,737 per ounce. The price of gold is often subject to sharp, short-term changes resulting from speculative activities. While the overall supply of and demand for gold can affect its market price, because of the considerable size of above-ground stocks of the metal in comparison to other commodities, these factors typically do not affect the gold price in the same manner or degree that the supply of and demand for other commodities tends to affect their market price. In addition, the recent shift in gold demand from physical demand to investment and speculative demand may exacerbate the volatility of gold prices.

| |

| Form 20-F_Fiscal Year Ended 2012 May 31 | Page 17 |

A sustained period of significant gold price volatility may adversely affect our ability to evaluate the feasibility of undertaking new capital projects or continuing existing operations or to make other long-term strategic decisions. If revenue from gold sales falls below the cost of production for an extended period, we may experience losses and be forced to curtail or suspend some or all of our capital projects or existing operations. In addition, we would have to assess the economic impact of low gold prices on our ability to recover any losses that may be incurred during that period and on our ability to maintain adequate cash reserves.

We face risks related to operations in foreign countries.

Currently our properties are located in Panama, Spain and Portugal. Panama is a country with a developing mining sector but with no other commercially producing mines. Consequently, we are subject to, and our mineral exploration and mining activities may be affected in varying degrees by, certain risks associated with foreign ownership including inflation, political instability, political conditions and government regulations. Any changes in regulations or shifts in political conditions are beyond our control and may adversely affect our business. Operations may be affected by government regulations with respect to restrictions on production, restrictions on foreign exchange and repatriation, price controls, export controls, restriction of earnings distribution, taxation laws, expropriation of property, environmental legislation, water use, mine safety and renegotiation or nullification of existing concessions, licenses, permits, and contracts.

Failure to comply strictly with applicable laws, regulations and local practices relating to mineral rights applications and tenure could result in loss, reduction or expropriation of entitlements, or the imposition of additional local or foreign parties as joint venture partners with carried or other interests. The occurrence of these various factors and uncertainties cannot be accurately predicted and could have an adverse effect on our operations or profitability.

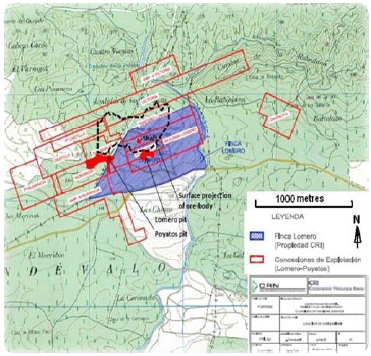

As part of our strategy to manage this kind of country risk, we are looking to diversify our project portfolio. During the first quarter of fiscal 2012, a majority of our shareholders approved the acquisition of Iberian Resources Corp. ("Iberian"). Iberian owns 100% of the Lomero-Poyatos Project through its wholly-owned Spanish affiliate, Corporacion de Recursos Iberia S.L. The Lomero-Poyatos Project is located about 85 kilometers northeast of Seville, in the northeast part of the Iberian Pyrite Belt. Iberian also owns several other exploration licenses in Iberia through its wholly-owned Spanish and Portuguese affiliates Sulfuros Complejos Andalucia Mining S.L. and Almada Mining S.A.

The requirements of the Ley Petaquilla may have an adverse impact on us.

Our operations in Panama are governed primarily by Law No. 9 of the Legislative Assembly of Panama (the “Ley Petaquilla”), a project-specific piece of legislation enacted in February 1997 to deal with the orderly development of the Cerro Petaquilla Concession.

The Ley Petaquilla granted a mineral exploration and exploitation concession to Minera Petaquilla, S.A. (formerly named Minera Petaquilla, S.A. (“MPSA”)), a Panamanian company formed in 1997 to hold the Cerro Petaquilla Concession covering approximately 136 square kilometers in north-central Panama. Although we no longer hold an interest in the copper deposits therein, we continue to hold the rights to the Molejon gold deposit and, as the Cerro Petaquilla Concession encompasses this deposit, the Ley Petaquilla governs our exploration activities.

The Ley Petaquilla contains fiscal and legal stability clauses necessary in order to obtain project financing and includes tax exemptions on income, dividends and imports. The Ley Petaquilla also provides for an increase in the annual available infrastructure tax credit, higher depreciation rates for depreciable assets which cannot be used in the infrastructure tax credit pool, and a favorable depletion allowance.

In order to maintain the Cerro Petaquilla Concession in good standing, MPSA must pay to the Government of Panama an annual rental fee of $1.00 per hectare during the first five years of the concession, $2.50 per hectare in the ninth to the tenth years of the concession and $3.50 per hectare thereafter. Initially the annual rental was approximately $13,600 payable by MPSA and funded pro rata by its shareholders. The current annual rental is approximately $34,000. The concession was granted for a 20 year term with up to two 20 year extensions permitted, subject to the requirement to begin mine development and to make a minimum investment of $400 million in the development of the Cerro Petaquilla Concession.

Under the Ley Petaquilla, MPSA was required to begin mine development by August 2001. However, MPSA was able to defer commencing development operations by one month for every month that the price of copper remained below $1.155 per pound for up to a further five years (i.e. until August 2006 at the latest). In September 2005, the multi-phase Petaquilla Mine Development Plan (the “Plan”) submitted to the Government of Panama by our Company and MPSA was approved by Ministerial Resolution. The Molejon gold mineral deposit forms part of the

| |

| Form 20-F_Fiscal Year Ended 2012 May 31 | Page 18 |

Cerro Petaquilla Concession and the first phase of the Plan focus on the advancement of the Molejon gold deposit by us as commenced in 2006. Subsequent phases of the Plan are the responsibility of MPSA.

The Ley Petaquilla also requires MPSA to (i) deliver an environmental report to the General Directorate of Mineral Resources of the Ministry of Commerce and Industries (“MICI”) for evaluation; (ii) submit, prior to extraction, an environmental feasibility study specific to the project area in which the respective extraction will take place; (iii) submit annually a work plan comprising the projections and approximate costs for the respective year to the MICI; (iv) post letters of credit in support of required compliance and environmental protection guarantees; (v) annually pay surface canons; (vi) annually pay royalties for extracted minerals; (vii) annually present to the MICI detailed reports covering operations and employment and training; (viii) create and participate in the administration of a scholarship fund to finance studies and training courses or professional training for the inhabitants of the communities neighboring the Cerro Petaquilla Concession in the provinces of Coclé and Colon; and (ix) maintain all mining and infrastructure works and services of the project, always complying with the standards and regulations of general application in force that pertain to occupational safety, health and construction.

For reference, a copy of Law No. 9, as passed by the Legislative Assembly of Panama on February 26, 1997, was provided with our Form 20-F for the fiscal year ended May 31, 2009, as Exhibit 4.V.

Our operations are subject to environmental and other regulation.

Our current or future operations, including development activities and commencement of production on our properties, require permits from various governmental authorities and such operations are and will be subject to laws and regulations governing prospecting, development, mining, production, exports, taxes, labor standards, occupational health, waste disposal, toxic substances, land use, environmental protection, mine safety, community services and other matters. Companies engaged in the development and operation of mines and related facilities generally experience increased costs and delays in production and other schedules as a result of the need to comply with applicable laws, regulations and permits. Other than the Molejon gold mine, there can be no assurance that approvals and permits required to commence production on our various properties will be obtained. Additional permits and studies, which may include environmental impact studies conducted before permits can be obtained, may be necessary prior to operation of the properties in which we have interests and there can be no assurance that we will be able to obtain or maintain all necessary permits that may be required to commence construction, development or operation of mining facilities at these properties on terms which enable operations to be conducted at economically justifiable costs.

Our potential mining and processing operations and exploration activities in Panama are subject to various federal and provincial laws governing land use, the protection of the environment, prospecting, development, production, exports, taxes, labor standards, occupational health, waste disposal, toxic substances, mine safety, community services and other matters. Such operations and exploration activities are also subject to substantial regulation under these laws by governmental agencies and may require that we obtain permits from various governmental agencies. We believe that we are in substantial compliance with all material laws and regulations that currently apply to corporate activities. There can be no assurance, however, that all permits which may be required for construction of mining facilities and conduct of mining operations will be obtainable on reasonable terms or that such laws and regulations would not have a material adverse effect on any mining project that we might undertake.

Failure to comply with applicable laws, regulations, and permitting requirements may result in enforcement actions there under, including orders issued by regulatory or judicial authorities causing operations to cease or be curtailed, and may include corrective measures requiring capital expenditures, installation of additional equipment, or remedial actions. Parties engaged in mining operations may be required to compensate those suffering loss or damage by reason of the mining activities and may have civil or criminal fines or penalties imposed for violations of applicable laws or regulations.

Amendments to current laws, regulations and permits governing operations and activities of mining companies, or more stringent implementation thereof, could have a material adverse impact on the Company and cause increases in capital expenditures or production costs or reductions in levels of production at producing properties or abandonment or delays in development of new mining properties. See Note 30 to the consolidated financial statements for the year ended May 31, 2012.

To the best of our knowledge, we are currently operating in compliance with all applicable environmental regulations except as to matters under mitigation as requested by the government of Panama.

| |

| Form 20-F_Fiscal Year Ended 2012 May 31 | Page 19 |

Our directors and officers may have conflicts of interest in connection with other mineral exploration and development companies.

Some of our directors and officers may also serve as directors and/or officers and/or shareholders of other companies involved in natural resource exploration and development. Consequently, it is possible that conflicts of interest may arise between these individuals’ duties as directors and officers of our company and their duties with respect to other corporations. For example, certain corporate opportunities may come to the attention of such individuals where such opportunities would be attractive to both our company and another corporation for which the individual serves as a director, officer or is a shareholder. Any decision made by any of such directors and officers involving our company should be made in accordance with their duties and obligations to deal fairly and in good faith with a view to the best interests of our company and its shareholders. In addition, each of the directors is required to declare and refrain from voting on any matter in which such directors may have a conflict of interest in accordance with the procedures set forth in the Business Corporations Act (British Columbia) and other applicable laws.

Environmental protestors are present in Panama.

Various independent environmental groups or individuals would like to prevent the operation of mining in Panama. Our operations could be significantly disrupted or suspended by activities such as protests or blockades that may be undertaken by such groups or individuals. Although these protests or blockades could happen, we have in place a contingency plan to ensure the continuity of our operations and activities at our Molejon mine.

Our common shares are subject to penny stock rules, which could affect trading in our shares.

Our common shares are classified as “penny stock” as defined in Rule 15g-9 promulgated under the Exchange Act. In response to perceived abuse in the penny stock market generally, the Exchange Act was amended in 1990 to add new requirements in connection with penny stocks. In connection with effecting any transaction in a penny stock, a broker or dealer must give the customer a written risk disclosure document that (a) describes the nature and level of risk in the market for penny stocks in both public offerings and secondary trading, (b) describes the broker's or dealer's duties to the customer and the rights and remedies available to such customer with respect to violations of such duties, (c) describes the dealer market, including “bid” and “ask” prices for penny stock and the significance of the spread between the bid and ask prices, (d) contains a toll-free telephone number for inquiries on disciplinary histories of brokers and dealers and (e) defines significant terms used in the disclosure document or the conduct of trading in penny stocks. In addition, the broker-dealer must provide to a penny stock customer a written monthly account statement that discloses the identity and number of shares of each penny stock held in the customer’s account and the estimated market value of such shares. The extensive disclosure and other broker-dealer compliance related to penny stocks may result in reducing the level of trading activity in the secondary market for our common shares, thus limiting the ability of our shareholders to sell their shares.

U.S. investors may not be able to enforce their civil liabilities against us or our directors, controlling persons and officers.

Our company, our officers and some of our directors are residents of countries other than the United States, and all of our assets are located outside the United States. As a result, it may not be possible for investors to effect service of process within the United States upon such persons or enforce in the United States against such persons judgments obtained in United States courts, including judgments predicated upon the civil liability provisions of United States federal securities laws or state securities laws.

We believe that a judgment of a United States court predicated solely upon civil liability under United States securities laws would probably be enforceable in Canada if the United States court in which the judgment was obtained has a basis for jurisdiction in the matter that was recognized by a Canadian court for such purposes. However, there is doubt whether an action could be brought in Canada in the first instance on the basis of liability predicated solely upon such laws.

If we have been or are characterized as a passive foreign investment company (“PFIC”) for U.S. federal income tax purposes, our U.S. Holders may be subject to adverse U.S. federal income tax consequences.

A non-U.S. corporation generally is considered a PFIC for U.S. federal income tax purposes for any tax year if either (1) at least 75% of its gross income is passive income or (2) at least 50% of the value of its assets (based on an average of the quarterly values of the assets during a taxable year) is attributable to assets that produce or are held for the production of passive income. We have not made a determination as to whether we are considered a PFIC for the current tax year or any prior tax years.

In general, if we are a PFIC in any tax year in which a U.S. Holder (as defined in “Item 10 – Additional

| |

| Form 20-F_Fiscal Year Ended 2012 May 31 | Page 20 |

Information—E. Taxation—Material United States Federal Income Tax Consequences”) owns our common shares, any gain recognized on a sale by such U.S. Holder of its common shares and any “excess distributions” (as specifically defined in the U.S. Internal Revenue Code of 1986, as amended) paid to such U.S. Holder on its common shares must be ratably allocated to each day in such U.S. taxpayer’s holding period for the common shares. The amount of any such gain or excess distribution allocated to prior years of such U.S. Holder’s holding period for the common shares generally will be subject to U.S. federal income tax at the highest tax applicable to ordinary income in each such prior year, and the U.S. taxpayer will be required to pay interest on the resulting tax liability for each such prior year, calculated as if such tax liability had been due in each such prior year. For more information, see “Item 10 – Additional Information—E. Taxation—Material United States Federal Income Tax Consequences—Passive Foreign Investment Company”.

We face competition from companies with greater financial resources and operational capabilities.

The mining industry is competitive in all of its phases. We face strong competition from other mining companies in connection with the acquisition of properties producing, or capable of producing, precious and base metals. Many of these companies have greater financial resources, operational experience and technical capabilities than our company. Other companies could outbid us for potential projects or produce minerals at lower costs, which would have a negative effect on our operations. As a result of this competition, we may be unable to maintain or acquire attractive mining properties on terms we consider acceptable or at all. Consequently, our revenues, operations and financial condition could be materially adversely affected.

We may not pay dividends on our common shares in the foreseeable future.

We have paid no dividends on our common shares since incorporation and do not anticipate paying dividends in the foreseeable future. Payment of any future dividends will be at the discretion of our company’s board of directors after taking into account many factors, including our operating results, financial condition and current and anticipated cash needs.

| |

| ITEM 4. | INFORMATION ON THE COMPANY |

| |

| 4. A. | History and Development of the Company |

We are a corporation organized under the laws of the Province of British Columbia, Canada. Our legal and commercial name is Petaquilla Minerals Ltd. We were incorporated on October 10, 1985, under the name Adrian Resources Ltd. by registration of our Memorandum and Articles of Association with the British Columbia Registrar of Companies pursuant to the Company Act (British Columbia) (the “BCCA”). The BCCA was replaced by the Business Corporations Act (British Columbia) (the “BCA) in March 2004 and we are now governed by the BCA. Our name was changed from Adrian Resources Ltd. to Petaquilla Minerals Ltd. on October 12, 2004.

Our principal office is located at Suite 1230, 777 Hornby Street, Vancouver, British Columbia, Canada, V6Z 1S4. The telephone number for our principal office is (604) 694-0021 and the facsimile number is (604) 694-0063.

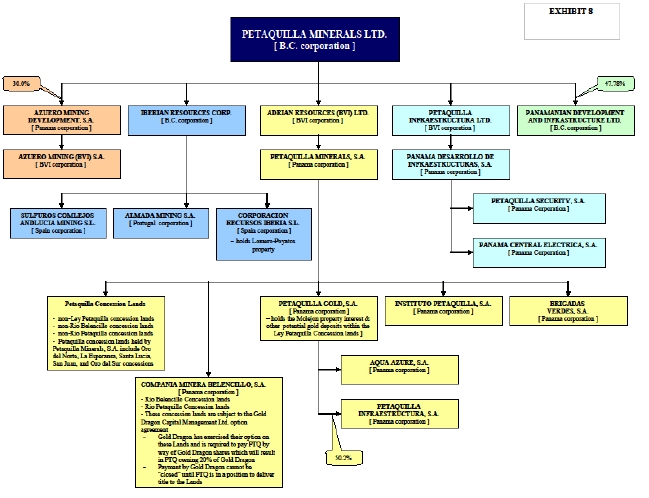

We have nineteen subsidiaries as detailed below:

| (i) | We own all of the issued shares of Adrian Resources (BVI) Ltd., which was incorporated in the British Virgin Islands on December 17, 1999. |

| |

| (ii) | Adrian Resources (BVI) Ltd. owns all of the issued shares of Petaquilla Minerals, S.A., which was incorporated in the Republic of Panama on April 28, 1992, and holds title to certain of our exploration concessions in the Republic of Panama. Although originally incorporated under the name Adrian Resources, S.A., the name of such subsidiary was changed to Petaquilla Minerals, S.A on February 3, 2005. |

| |

| (iii) | Petaquilla Minerals, S.A. owns all of the issued shares of Petaquilla Gold, S.A., a Panamanian corporation formed on August 11, 2005. Petaquilla Gold, S.A. holds the Molejon gold property interest and other potential gold deposits within the Cerro Petaquilla Concession lands. |

| |

| (iv) | Petaquilla Minerals, S.A. owns all of the issued shares of Instituto Petaquilla, S.A., a Panamanian corporation which was formed on April 23, 2007, to conduct training and education programs for our personnel. |

| |

| (v) | Petaquilla Minerals, S.A. owns all of the issued shares of Brigadas Verdes, S.A., a Panamanian corporation which was formed on March 27, 2007, to coordinate and manage reforestation activities. |

| |

| (vi) | Petaquilla Minerals, S.A. owns all of the issued shares of Compañìa Minera Belencillo, S.A., a Panamanian |

| |

| |

| Form 20-F_Fiscal Year Ended 2012 May 31 | Page 21 |

corporation formed on September 21, 2005, and which holds 100% interests in Zones 1 and 2 of the Rio Belencillo Concession. On May 7, 2005, we entered into an option agreement with Gold Dragon Capital Management Ltd. (“Gold Dragon”) whereby Gold Dragon could earn a 100% interest in the concession lands by the expenditure of $500,000 over two years on mutually agreed upon property expenditures. On March 8, 2012, we entered into an agreement with Madison Minerals Inc. and its Panamanian subsidiary, Madison Enterprises (Latin America) S.A. (collectively referred as “Madison”) to acquire Madison’s 31% interest in Compañía Minera Belencillo, S.A. (“Minera Belencillo”), an entity formed in Panamá to oversee and manage exploration projects within the Belencillo concession. We issued 175,438 common shares to Madison on March 8, 2012 and have committed to issue a further 250,000 common shares upon commencement of commercial production at the Belencillo concession. As a result of the additional 31% interest, Minera Belencillo became a 100% wholly-owned subsidiary of our Company.

| (vii) | Petaquilla Gold, S.A. owns 50.2% of the shares of Petaquilla Infraestructura, S.A. (formerly named Petaquilla Power & Water, S.A.), a Panamanian corporation formed on September 21, 2006, primarily for the purposes of (i) designing, constructing, operating, maintaining and installing equipment and networks for the generation, transmission and commercialization of electrical energy; and (ii) developing projects for the production, distribution and commercialization of potable water. |

| |

|

|

|

| (viii) | Petaquilla Gold, S.A. also owns all of the issued shares of Aqua Azure, S.A., a Panamanian corporation which was formed on October 10, 2006, to purchase, sell, lease, manage, commercialize and hold investment in various moveable goods. |

| |

|

| (ix) | We own all of the issued shares of Iberian Resources Corp., which is incorporated in British Columbia, Canada. Iberian Resources Corp. and its directly held subsidiaries of Sulfuros Complejos Andalucia Mining S.L., incorporated in Spain, Almada Mining S.A., incorporated in Portugal, and Corporacion Recursos Iberia S.L., incorporated in Spain, were acquired by us on September 1, 2011. |

| |

|

|

| (x) | We own 30% of the issued shares of Azuero Mining Development, S.A., incorporated in Panama. Azuero Mining Development, S.A., in turn, owns 100% of the issued shares of Azuero Mining (BVI) S.A.(formerly Vintage Mining (BVI) Ltd.), incorporated in the British Virgin Islands. |

| |

|

| (xi) | We own 47.78% of the issued shares of Panamanian Development and Infrastructure Ltd., formerly Petaquilla Infrastructure Ltd., incorporated in British Columbia, Canada, on May 29, 2009. |

| | |

| (xii) | We own all of the issued shares of Petaquilla Infraestructura Ltd., which was incorporated in the British Virgin Islands on February 21, 2008. |

| | |

| (xiii) | Petaquilla Infraestructura Ltd. owns all of the issued shares of Panama Desarrollo de Infraestructuras, S.A., formerly Petaquilla Hidro, S.A., a Panamanian corporation formed on October 10, 2008. |

| | |

| (xiv) | Panama Desarrollo de Infraestructuras, S.A. owns all of the issued shares of Petaquilla Security, S.A., a Panamamanian corporation formed on April 25, 2007. |

| | |

| (xv) | Panama Desarrollo de Infraestructuras, S.A. owns all of the issued shares of Panama Central Electrica, S.A., a Panamanian corporation formed on February 16, 2009. |

| | |