UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-9082 |

|

M Fund, Inc. |

(Exact name of registrant as specified in charter) |

|

M Financial Plaza 1125 NW Couch Street, Suite 900 Portland, Oregon | | 97209 |

(Address of principal executive offices) | | (Zip code) |

|

Bridget McNamara-Fenesy, President, M Fund, Inc. M Financial Plaza, 1125 NW Couch Street, Suite 900 Portland, Oregon 97209 |

(Name and address of agent for service) |

|

with a Copy to: Cynthia Beyea Eversheds Sutherland LLP 700 Sixth Street, N.W. Washington, D.C. 20001-3980 |

|

Registrant’s telephone number, including area code: | (503) 232-6960 | |

|

Date of fiscal year end: | 12/31 | |

|

Date of reporting period: | 12/31/2018 | |

| | | | | | | | |

Item 1. Reports to Stockholders.

The annual report for the period January 1, 2018 through December 31, 2018 is filed herewith.

M FUND, INC.

M International Equity Fund

M Large Cap Growth Fund

M Capital Appreciation Fund

M Large Cap Value Fund

Annual Report

December 31, 2018

Beginning in February 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Funds' shareholder reports like this one will no longer be sent by mail, unless you specifically request paper copies of the reports from the Funds or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Funds electronically by calling your insurance company. If you own these shares through a financial intermediary, you may contact your financial intermediary.

You may elect to receive all future reports in paper free of charge. You can inform the Funds that you wish to continue receiving paper copies of your shareholder reports by sending a request in writing to your insurance company or to your financial intermediary. Your election to receive reports in paper will apply to all funds held with the fund complex.

M Fund, Inc.

PRESIDENT'S LETTER

Dear Contract Owners:

We are pleased to share the financial condition of M Fund, Inc. (the "Corporation") as presented in the following Annual Report dated December 31, 2018. Total assets under management at year end 2018 were $579.6 million.

Sub-Advisers to the portfolios, under the direction of M Financial Investment Advisers, Inc., the investment adviser to the Corporation, have prepared the attached discussion of results for each portfolio of the Corporation for the year ended December 31, 2018.

Sub-Advisers to the portfolios of the Corporation are: Dimensional Fund Advisors LP for the M International Equity Fund, DSM Capital Partners LLC for the M Large Cap Growth Fund, Frontier Capital Management Company, LLC for the M Capital Appreciation Fund and AJO, LP for the M Large Cap Value Fund.

On behalf of the Corporation's Board of Directors, M Financial Investment Advisers, Inc. and the Corporation's participating insurance carriers, we thank you for your business and remain committed to providing opportunities that add value to our investors in the upcoming year.

Sincerely,

BRIDGET MCNAMARA-FENESY

President

M Fund, Inc.

M INTERNATIONAL EQUITY FUND

As of December 12, 2018, Dimensional Fund Advisors LP became the sub-adviser to the M International Equity Fund. Because of their late-year involvement in managing the Fund, the commentary below is provided by M Financial Investment Advisers ("MFIA"), the Adviser to the M International Equity Fund.

Performance

For the twelve months ended December 31, 2018, the M International Equity Fund had a return of (20.57)% (net of management fees) versus a total return (including reinvestment of dividends) of (14.20)% for its benchmark, the MSCI ACWI (All Country World Index) ex US Index1.

Fund Review/Current Positioning

The M International Equity Fund trailed its benchmark in 2018 by 6.37%. MFIA describes the reasons the Fund was behind its benchmark throughout each of the four quarters below:

• Within sectors, stock selection drove underperformance, notably within the Consumer Discretionary, Health Care, Consumer Staples, and Industrials sectors. Stock selection aided relative performance within Information Technology and Financials sectors.

• Sector allocation aided relative performance, especially with an overweight allocation to Health Care and an underweight allocation to Financials. An overweight allocation to Consumer Discretionary detracted from relative performance.

• Within countries, stock selection drove underperformance, notably within the US, Columbia, and France. Stock selection added aided relative performance within Germany, the UK, and China.

• Country allocation aided relative performance, especially with an overweight allocation to France and underweight allocations to China and South Korea. Underweight allocations to Australia and Taiwan and an overweight allocation to Germany aided relative performance

• First quarter top contributors to relative performance were Las Vegas Sands and Wynn Resorts, while bottom contributors were AXA, Bayer, and The Linde Group

• Second quarter top contributors to relative performance were Teva Pharmaceuticals and Las Vegas Sands, while bottom contributors were Fanuc Corporation and Schlumberger

• Third quarter top contributors to relative performance were Reckitt Benckiser and Sony Corporation, while bottom contributors were Las Vegas Sands and Wynn Resorts

• Fourth Quarter top contributors to relative performance were Philip Morris International, Alibaba and Hoya and a maintained overweight in Colombia following underperformance in Q3 helped. Overall stock selection in the Eurozone slightly helped in the quarter. Bottom contributors were Schlumberger, Wynn Resorts and Olympus Corp Stock selection in the UK stock market was also a factor.

M Financial Investment Advisors

Investment Adviser to the M International Equity Fund

Performance represented is net of management fees. The Fund returns listed include fund level fees and expenses, reinvestment of dividends, and distributions. Returns do not reflect product level charges of the applicable separate accounts and variable products, all of which vary to a considerable extent and are described in your

2

product prospectus. Policy level returns would be lower after all policy fees and expenses are deducted. The foregoing reflects the thoughts and opinions of MFIA exclusively and is subject to change without notice. The information provided in this material should not be considered a recommendation to purchase or sell any particular security. It should not be assumed that any security transactions, holdings, or sectors discussed were or will be profitable, or that the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance discussed herein. Strategies discussed are subject to change at any time by the investment manager in its discretion due to market conditions or opportunities. Market conditions may impact performance. The performance results presented were achieved in particular market conditions which may not be repeated. Moreover, the current market volatility and uncertain regulatory environment may have a negative impact on future performance. Portfolio characteristics are as of December 31, 2018. Please note that all indices are unmanaged and are not available for direct investment.

This commentary may include statements that constitute "forward looking statements" under the U.S. securities laws. Forward-looking statements include, among other things, projections, estimates, and information about possible or future results related to the Fund, market or regulatory developments. The views expressed above are not guarantees of future performance or economic results and involve certain risks, uncertainties and assumptions that could cause actual outcomes and results to differ materially from the views expressed herein. The views expressed above are subject to change at any time based upon economic, market, or other conditions and the subadvisory firm undertakes no obligation to update the views expressed herein. Any discussions of specific securities should not be considered a recommendation to buy or sell those securities. The views expressed above (including any forward-looking statement) may not be relied upon as investment advice or as an indication of the Fund's trading intent. Information about the Fund's holdings, asset allocation or country diversification is historical and is not an indication of future Fund composition, which may vary. Investors cannot invest directly in an Index. The performance of any index mentioned in this commentary has not been adjusted for ongoing management, distribution and operating expenses, and sales charges applicable to mutual fund investments. In addition, the returns do not reflect additional fees charged by separate accounts or variable insurance contracts that an investor in the Fund may pay. If these additional fees were reflected, performance would have been lower.

3

COMPARISON OF CHANGE IN VALUE OF $10,000 INVESTMENT IN

THE M INTERNATIONAL EQUITY FUND, MSCI AC WORLD ex USA

The M International Equity Fund's total return is calculated net of Investment Advisory Fees and operating expenses. Performance figures represent past performance and are not indicative of future performance of the M International Equity Fund or Index. Share value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than the original investment. Please note that all indices are unmanaged, do not incur expenses, and are not available for direct investment. Persons who invest in the M International Equity Fund through a variable annuity or variable life insurance contract should note this graph does not reflect separate account expenses deducted by the insurance company.

* 12/31/08 to 12/31/18

+ MSCI EAFE—Effective May 1, 2014, the Fund changed its benchmark index from the MSCI EAFE Index to the MSCI AC World ex US Index. The MSCI AC World ex US Index is more representative of the Fund's investment portfolio than its previous index.

MSCI ACWI (ALL COUNTRY WORLD INDEX) ex US INDEX

1 The MSCI ACWI (All Country World Index) ex US Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets excluding the US.

4

M LARGE CAP GROWTH FUND

Performance

For the twelve months ended December 31, 2018, the M Large Cap Growth Fund had a return of (4.95)% (net of management fees) versus a total return (including reinvestment of dividends) of (1.51)% for its benchmark, the Russell 1000 Growth Index1.

Market Environment/Conditions

In 2018, despite earnings growth approaching 30%, the M Large Cap Growth Fund portfolio underperformed due to various macro concerns, including fears of rising interest rates, a US-China trade war, slowing global economic growth, and political turmoil in the EU due to Brexit, protests in Paris and political problems in Italy. The portfolio's earnings growth and valuation entering 2019 closely mirror those of early 2017 when the portfolio appreciated nearly 39%.

Importantly, by DSM's calculation, the market's valuation is just 15.7x trailing earnings of $163 which is approximately the long-term market average P/E since WWII. During periods of low inflation the market typically sells at 18x to 22x trailing earnings. In certain periods of time the market's valuation has exceeded 22x while in others, typically in periods of distressed investor psychology, valuation has dipped to 15x trailing earnings as it is today. Historically the market has not remained at compressed valuation levels of 15x for very long.

DSM has projected for many years that the current global economic expansion would last longer than the majority of previous economic growth periods, and continues to believe that a global economic recession is not likely to occur until 2021 or later. While DSM's expectations of global GDP growth in excess of 3% in 2019 may prove a bit too optimistic, they continue to believe that the economic impact of the trade war, European political disarray and the partial American government shutdown will be relatively limited. DSM sees the current global economic cycle being driven by low inflation and low, albeit rising, interest rates. That said, the reductions to corporate tax rates in the United States are quite substantial, and DSM believes they will have a sustained positive impact on GDP growth which is being underestimated by many analysts. Recently reported strength in US employment was broad-based across most economic sectors, perhaps indicating that the trade war is having limited impact thus far. Interestingly, late last month Chairman Powell of the Federal Reserve indicated that future rate hikes may be delayed during this period of economic uncertainty, characterized by lower inflation and the resulting reduction in longer term interest rates.

DSM believes the market will rebound during 2019 and the portfolio's performance should rebound significantly as well. In DSM's view earnings growth will continue to be solid going forward, while concerns of a trade war gradually dissipate causing the global economic outlook to brighten.

Fund Review/Current Positioning

The Fund's portfolio remains focused on unique businesses that have been identified and continuously subject to analysis by DSM's investment team. The portfolio holdings remain characterized by very strong balance sheets and significant free cash flow. The majority of the Fund is invested in the technology, health care, communication services and consumer discretionary sectors, with smaller weightings in the financials, consumer staples and industrials sectors.

For the year ended December 31, 2018, the M Large Cap Growth Fund underperformed the benchmark primarily as a result of stock selection in the consumer discretionary sector. DSM's stock selections in technology and health

5

care benefitted performance versus the benchmark. By security, the top five contributors to the Fund's performance for the year included Adobe Systems, Abbott Laboratories, Zoetis, Visa and Microsoft. The five positions which contributed the least were Facebook, Alibaba Group, Tencent Holdings, Monster Beverage and Charles Schwab.

DSM remains focused on earnings because they believe that strong and growing earnings, when combined with reasonable valuations, drive stock prices higher. DSM expects earnings to continue to grow at a mid-to-high-teens rate through 2022, while the Fund portfolio is valued at approximately 20.6x next twelve months of earnings through December of 2019. The positive scenario of ongoing and perhaps improving global economic growth, moderate global inflation, low albeit rising interest rates, healthy global corporate earnings, continues to form the foundation of an upwardly driven global equity market. DSM believes 2018's earnings growth combined with last year's market decline have created market valuations that are very attractive given the current global economy.

DSM Capital Partners LLC

Investment Sub-Adviser to the M Large Cap Growth Fund

Performance represented is net of fees. The foregoing reflects the thoughts and opinions of DSM Capital Partners LLC exclusively and is subject to change without notice. The information provided in this material should not be considered a recommendation to purchase or sell any particular security. It should not be assumed that any security transactions, holdings, or sectors discussed were or will be profitable, or that the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance discussed herein. Strategies discussed are subject to change at any time by the investment manager in its discretion due to market conditions or opportunities. Market conditions may impact performance. The performance results presented were achieved in particular market conditions which may not be repeated. Moreover, the current market volatility and uncertain regulatory environment may have a negative impact on future performance. Portfolio characteristics are as of December 31, 2018. Please note that all indices are unmanaged and are not available for direct investment.

This commentary may include statements that constitute "forward looking statements" under the U.S. securities laws. Forward-looking statements include, among other things, projections, estimates, and information about possible or future results related to the Fund, market or regulatory developments. The views expressed above are not guarantees of future performance or economic results and involve certain risks, uncertainties and assumptions that could cause actual outcomes and results to differ materially from the views expressed herein. The views expressed above are subject to change at any time based upon economic, market, or other conditions and the subadvisory firm undertakes no obligation to update the views expressed herein. Any discussions of specific securities should not be considered a recommendation to buy or sell those securities. The views expressed above (including any forward-looking statement) may not be relied upon as investment advice or as an indication of the Fund's trading intent. Information about the Fund's holdings, asset allocation or country diversification is historical and is not an indication of future Fund composition, which may vary. Direct investment in any index is not possible. The performance of any index mentioned in this commentary has not been adjusted for ongoing management, distribution and operating expenses, and sales charges applicable to mutual fund investments. In addition, the returns do not reflect additional fees charged by separate accounts or variable insurance contracts that an investor in the Fund may pay. If these additional fees were reflected, performance would have been lower.

6

COMPARISON OF CHANGE IN VALUE OF $10,000 INVESTMENT IN

THE M LARGE CAP GROWTH FUND AND THE RUSSELL 1000 GROWTH INDEX (Unaudited)

The M Large Cap Growth Fund's total return is calculated net of Investment Advisory Fees and operating expenses. Performance figures represent past performance and are not indicative of future performance of the M Large Cap Growth Fund or Index. Share value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than the original investment. Please note that all indices are unmanaged, do not incur expenses, and are not available for direct investment. Persons who invest in the M Large Cap Growth Fund through a variable annuity or variable life insurance contract should note this graph does not reflect separate account expenses deducted by the insurance company.

* 12/31/08 to 12/31/18

RUSSELL 1000 GROWTH INDEX

1 The Russell 1000 Growth Total Return Index includes dividends reinvested in the Russell 1000 Growth Index as reported by the Russell Company. The Russell 1000 Growth Index is a capitalization weighted index containing over 600 widely held securities with growth characteristics. DSM uses the Russell 1000 Growth Index as a benchmark because its average market capitalization is similar to that of the M Large Cap Growth Fund, and it is an industry standard. Characteristics of any benchmark may differ materially from accounts managed by DSM. Investors cannot invest directly in an Index.

7

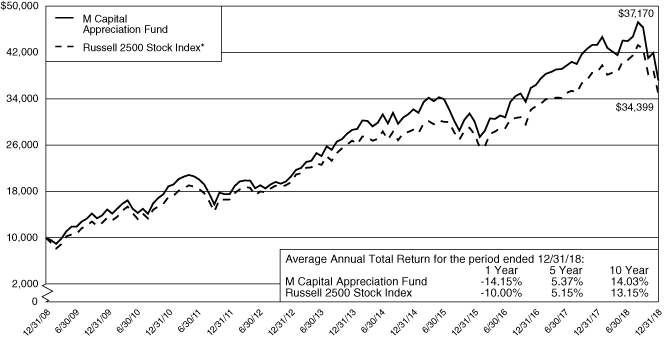

M CAPITAL APPRECIATION FUND

Performance

For the twelve months ended December 31, 2018, the M Capital Appreciation Fund had a return of (14.15)% (net of management fees) versus a total return (including reinvestment of dividends) of (10.00)% for its benchmark, the Russell 2500® Index1.

Market Environment/Conditions

2018 was a tale of two markets, with very low volatility and healthy returns through the first three quarters of the year, followed by a sharp correction in the fourth quarter. Investor enthusiasm flourished with GDP growth accelerating to 4.2% in the second quarter, the fastest pace in nearly four years, and unemployment declining to 3.7% in September, the lowest level in 48 years. Signs of coordinated global growth emerged with economic improvement in Europe, Brazil and other parts of the world. These factors drove a 10.4% return in the Russell 2500® for the first nine months of the year. The continued investor preference for high growth stocks was also notable in this time period, with the Russell 2500® Growth returning 15.8% by comparison as valuations stretched for high-growth, momentum stocks. In fact, the number of companies trading at over ten-times revenue in the overall market reached the highest level since the internet bubble, approaching 10% of the Russell 3000® holdings.

In the fourth quarter, equities experienced a sharp correction, with the Russell 2500® declining 18.5%, driven by multiple investor concerns. Attention shifted to forecasts of slowing U.S. economic growth, with GDP predicted to slow to 2.0% by the fourth quarter of 2019 as fiscal stimulus fades. Other geographies including Europe, Japan and China demonstrated signs of economic deceleration, with Japan and Germany GDP actually shrinking in the third quarter. Meanwhile, a trade war has erupted between the U.S. and China with both sides levying meaningful tariffs. Corporate earnings for the S&P 500® are now forecasted to slow from 20% growth in 2018 to 8% in 2019. Movements in interest rates raised concerns and exacerbated volatility, as the 10-year treasury yield spiked to 3.2% in early October and investors grew wary of a nearly flat yield curve, a potential harbinger of recession. Valuations compressed meaningfully and investors grew particularly valuation sensitive towards stocks with cyclical exposure. While some sectors of the economy, such as housing and autos have demonstrated softness, overall economic activity has remained solid.

Looking forward, the probable lower economic growth rate and uncertainty regarding tariffs, monetary policy and global economic growth is likely to continue to drive volatility into the new year. Historically, we have successfully taken advantage of opportunities that a volatile market provides. In this environment, we are able to initiate positions in new holdings that previously did not meet our valuation hurdle. In addition, we are able to add to existing holdings with compelling risk reward characteristics.

A common theme in the 2018 market was to sell economically sensitive stocks and buy expensive, rapidly growing companies perceived to be immune from economic weakness. We do not believe a recession is imminent simply because our economy has been recovering for approximately a decade. The recovery has been modest by historical standards and has only recently approached historic peak production levels. There are few signs of recession on the horizon as unemployment, interest rates and inflation all remain low while consumer confidence remains high. At a price earnings ratio of 13x and a projected five-year EPS growth rate of 18%2, our strategy has rarely been more attractive. In summary, the Fund last year took the pain from a recession that may or may not happen. As such, we believe the risk reward equation is now strongly in our favor.

8

Fund Review/Current Positioning

From a thematic standpoint, stocks with accelerated organic revenue growth largely outperformed the market with little regard for valuation. Furthermore, stocks with material cyclical exposure tended to lag the market materially and in some cases approached valuations we believe to be more indicative of a recession scenario. Given Capital Appreciation's underlying valuation discipline and exposure to economically sensitive companies, this combination proved to be a burden on results. This bifurcation of the market is quite pronounced when you observe price performance isolated and ranked by valuation at the beginning of the year. On both a price-to-sales basis and a price-to-earnings basis, those stocks that were ranked as most expensive at the beginning of the year materially outperformed for the year as a whole: for example, the top quintile ranked by price-to-earnings was essentially flat for the year while the bottom quartile decreased by over 16%. In short, investors were rewarded for simply selecting the most expensive stocks. This behavior is indicative of a momentum market where investors will pay almost anything for growth while ignoring traditional valuation metrics, which is very different than our Growth at a Reasonable Price (GARP) discipline. We have been through a few similar periods in the history of the fund, and would expect Capital Appreciation to lag in such a market. Fortunately, it also has been our experience that the equity market ultimately returns to a focus on fundamentals which should be very good for the Fund as it stands today.

At the Fund level, sector allocation accounted for approximately one-third of the underperformance primarily the result of our overweight in materials & processing. The remaining sector allocations were largely immaterial to performance. Negative stock selection in the technology, materials & processing and consumer discretionary sectors were partially offset by very strong returns in the Fund's health care holdings.

The largest detractor in technology was Rogers Corporation. After roughly doubling in 2017, Rogers traded down 39% in 2018 as a combination of factors pressured both near-term earnings and forward expectations for the stock. Historically Rogers has been susceptible to the underlying cycles of demand from industrial companies and China infrastructure spend, both of which had investors concerned this past year. A pause in telecommunications spending in China and a slower-than-expected ramp in global 5G wireless infrastructure spend led to a reset in earnings expectations while near-term profit pressures from higher raw material costs and manufacturing inefficiencies caused reported earnings to lag. We continue to be bullish as Rogers maintains dominant market share, is well positioned in anticipation of secular growth trends such as electric vehicle penetration and wireless communications spend, and has internal profit targets that should drive material EPS upside. Putting near-term volatility aside, Rogers is progressing to becoming a solid mid cap specialty materials company with double digit revenue growth, strong margins and high returns on capital. It has been a long-term holding of the fund and remains a top position.

In the materials & processing sector, Ferroglobe (-90%) and Kraton Corporation (-55%) were the largest detractors. Ferroglobe faced an abrupt reversal in fortune as pricing for silicon metals fell out of balance following an unexpected ruling that eliminated tariffs against countries that had been dumping product on the U.S. market. The stock had traded up over 45% in 2017 largely in anticipation of these tariffs being enacted. Furthermore, weaker global demand for silicon products and ensuing excess supply caused Ferroglobe's projected EBITDA to fall well short of internal expectations. The company has shuttered some capacity in an effort to restore global supply dynamics. We continue to hold the stock following what we believe to be an excessively negative response to near-term fundamentals. Kraton, a producer of specialty polymers used in a wide range of applications, declined on a confluence of what we believe are one-time, temporary issues. These included a damaged plant from Hurricane Michael, a chemical fire at another facility and the dismissal of the CFO for non-business reasons. In addition, historically low water levels on the Rhine River prevented key materials from reaching one of their major plants in Germany resulting in lower guidance for 2018. These factors will keep financial leverage levels elevated for longer

9

than anticipated. We continue to own the stock as we believe in Kraton's ability to overcome these transitory setbacks and grow earnings over time while simultaneously improving their balance sheet.

Health care was a bright spot for the Fund as five of the top ten largest contributing stocks resided in this sector. Within this group, three holdings with exposure to treating the diabetes epidemic continued to drive performance, Tandem Diabetes (+1,509%), Dexcom (+109%) and Insulet (+15%). Tandem Diabetes was the clear standout, accounting for roughly half of the total contribution in health care as the stock rallied from a low of roughly $2 in February 2018 to a high of over $52 in September before retracting and ending the year at $38. Capital Appreciation had taken an initial position in Tandem in 2015 on the basis of promising pump technology that positioned the company for considerable market share gain; however, it had remained a small position until we bought aggressively near the lows on a secondary offering that secured adequate financing to remain a going concern. With financial risk largely behind the company investors began to focus on the underlying fundamental merits of their technology which showed increasing momentum throughout the year. In the most recent quarter, for example, Tandem posted 91% growth in pump sales and materially exceeded estimates. We expect the company to continue to post accelerated growth given the quality of their product portfolio and relatively limited position.

Frontier Capital Management Co., LLC

Investment Sub-Adviser to the M Capital Appreciation Fund

Performance represented is net of fees. The foregoing reflects the thoughts and opinions of Frontier exclusively and is subject to change without notice. The information provided in this material should not be considered a recommendation to purchase or sell any particular security. It should not be assumed that any security transactions, holdings, or sectors discussed were or will be profitable, or that the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance discussed herein. Strategies discussed are subject to change at any time by the investment manager in its discretion due to market conditions or opportunities. Market conditions may impact performance. The performance results presented were achieved in particular market conditions which may not be repeated. Moreover, the current market volatility and uncertain regulatory environment may have a negative impact on future performance. Portfolio characteristics are as of December 31, 2018. Please note that all indices are unmanaged and are not available for direct investment.

This commentary may include statements that constitute "forward looking statements" under the U.S. securities laws. Forward-looking statements include, among other things, projections, estimates, and information about possible or future results related to the Fund, market or regulatory developments. The views expressed above are not guarantees of future performance or economic results and involve certain risks, uncertainties and assumptions that could cause actual outcomes and results to differ materially from the views expressed herein. The views expressed above are subject to change at any time based upon economic, market, or other conditions and the subadvisory firm undertakes no obligation to update the views expressed herein. Any discussions of specific securities should not be considered a recommendation to buy or sell those securities. The views expressed above (including any forward-looking statement) may not be relied upon as investment advice or as an indication of the Fund's trading intent. Information about the Fund's holdings, asset allocation or country diversification is historical and is not an indication of future Fund composition, which may vary. Direct investment in any index is not possible. The performance of any index mentioned in this commentary has not been adjusted for ongoing management, distribution and operating expenses, and sales charges applicable to mutual fund investments. In addition, the returns do not reflect additional fees charged by separate accounts or variable insurance contracts that an investor in the Fund may pay. If these additional fees were reflected, performance would have been lower.

10

COMPARISON OF CHANGE IN VALUE OF $10,000 INVESTMENT IN

THE M CAPITAL APPRECIATION FUND AND RUSSELL 2500 STOCK INDEX (Unaudited)

The M Capital Appreciation Fund's total return is calculated net of Investment Advisory Fees and operating expenses. Performance figures represent past performance and are not indicative of future performance of the M Capital Appreciation Fund or Index. Share value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than the original investment. Please note that all indices are unmanaged, do not incur expenses, and are not available for direct investment. Persons who invest in the M Capital Appreciation Fund through a variable annuity or variable life insurance contract should note this graph does not reflect separate account expenses deducted by the insurance company.

* 12/31/08 to 12/31/2018

RUSSELL 2500 INDEX

1 The Russell 2500® Index measures the performance of the small to mid-cap segment of the U.S. equity universe, commonly referred to as "smid" cap. The Russell 2500® Index is a subset of the Russell 3000® Index. It includes approximately 2500 of the smallest securities based on a combination of their market cap and current index membership.

2 Source: FactSet

11

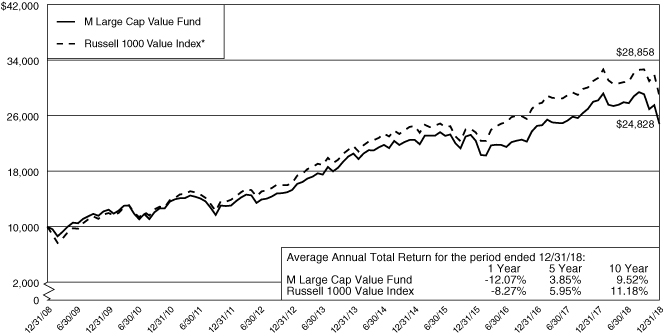

M LARGE CAP VALUE FUND

Performance

For the twelve months ended December 31, 2018, the M Large Cap Value Fund had a return of (12.07)% (net of management fees) versus a total return (including reinvestment of dividends) of (8.27)% for its benchmark, the Russell 1000 Value Index1.

Market Environment/Conditions

2018 was a bust in terms of absolute returns, as just about every equity market segment posted negative results. U.S. losses were modest compared to international results, especially among emerging markets. Across the size and style spectrum, top caps outperformed small caps threefold, and growth continued to trounce value. A glimmer of hope was found toward the end of the year among low-volatility stocks.

Fund Review/Current Positioning

The Fund is fully invested in U.S. equities with no broad sector bets, and only modest industry-level and stock specific bets. The goal is to outperform the benchmark, the Russell 1000 Value Index, with incremental gains across many holdings. Using bottom-up, quantitatively-driven stock selection, AJO evaluates companies relative to their industry peers using four broad categories of measures: value, management, momentum, and sentiment. Value means the somewhat traditional ratios of price to fundamental value; management means evidence that a company's executive team has and will continue to emphasize earning power; momentum indicates when stocks might begin to rise toward full valuation; and sentiment captures the buying and selling behavior of key investor segments in various markets. When considering new investments, AJO, LP strongly focuses on minimizing transaction costs, which helps maximize profits for the Fund.

The Fund trailed its benchmark in 2018 by 3.80%. AJO describes the reasons behind relative returns using the framework of their investment process described above:

• AJO's stock selection drove the Fund's underperformance, notably within consumer discretionary, financials, and industrials sectors.

• Value and sentiment trends were inconsistent throughout the year, while management and momentum factors—quality and stability—were reliable contributors.

• On the risk front, AJO's bottom-up stock selection led to industry and size bets that ultimately disappointed.

• While the Fund remained sector-neutral to its Russell 1000 Value benchmark, it can (and does) emphasize industries with the most attractive valuation (and avoid the contrary)—a result of its bottom-up stock picking. Industry bets distracted this year, primarily a result of bets within the consumer discretionary sector (emphasizing motor vehicles and consumer durables and avoiding consumer services companies). That said, industry bets within the information technology sector (betting for software companies and against semiconductors stocks) proved helpful.

• Successful stock picks include ExxonMobil, Philip Morris, and Verisign.

• The Fund was negatively impacted from holding Ingredion, Masco, and Lincoln National.

12

AJO strongly believes that superior results can be achieved through a consistent, systematic approach that focuses on low-priced companies with proven management, earnings power, and favorable sentiment.

AJO, LP

Investment Sub-Adviser to M Large Cap Value Fund

Performance represented is net of fees. The foregoing reflects the thoughts and opinions of AJO exclusively and is subject to change without notice. The information provided in this material should not be considered a recommendation to purchase or sell any particular security. It should not be assumed that any security transactions, holdings, or sectors discussed were or will be profitable, or that the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance discussed herein. Strategies discussed are subject to change at any time by the investment manager in its discretion due to market conditions or opportunities. Market conditions may impact performance. The performance results presented were achieved in particular market conditions which may not be repeated. Moreover, the current market volatility and uncertain regulatory environment may have a negative impact on future performance. Portfolio characteristics are as of December 31, 2018. Please note that all indices are unmanaged and are not available for direct investment.

This commentary may include statements that constitute "forward looking statements" under the U.S. securities laws. Forward-looking statements include, among other things, projections, estimates, and information about possible or future results related to the Fund, market or regulatory developments. The views expressed above are not guarantees of future performance or economic results and involve certain risks, uncertainties and assumptions that could cause actual outcomes and results to differ materially from the views expressed herein. The views expressed above are subject to change at any time based upon economic, market, or other conditions and the subadvisory firm undertakes no obligation to update the views expressed herein. Any discussions of specific securities should not be considered a recommendation to buy or sell those securities. The views expressed above (including any forward-looking statement) may not be relied upon as investment advice or as an indication of the Fund's trading intent. Information about the Fund's holdings, asset allocation or country diversification is historical and is not an indication of future Fund composition, which may vary. Direct investment in any index is not possible. The performance of any index mentioned in this commentary has not been adjusted for ongoing management, distribution and operating expenses, and sales charges applicable to mutual fund investments. In addition, the returns do not reflect additional fees charged by separate accounts or variable insurance contracts that an investor in the Fund may pay. If these additional fees were reflected, performance would have been lower.

13

COMPARISON OF CHANGE IN VALUE OF $10,000 INVESTMENT IN

THE M LARGE CAP VALUE FUND AND THE RUSSELL 1000 VALUE INDEX (Unaudited)

The M Large Cap Value Fund's total return is calculated net of Investment Advisory Fees and operating expenses. Performance figures represent past performance and are not indicative of future performance of the M Large Cap Value Fund or Index. Share value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than the original investment. Please note that all indices are unmanaged, do not incur expenses, and are not available for direct investment. Persons who invest in the M Large Cap Value Fund through a variable annuity or variable life insurance contract should note this graph does not reflect separate account expenses deducted by the insurance company.

* 12/13/08 to 12/31/18

RUSSELL 1000 VALUE INDEX

4 The Russell 1000® Value Index is a market capitalization-weighted index that measures the performance of those Russell 1000 companies with lower price-to-book ratios and lower forecasted growth.

14

M International Equity Fund

SCHEDULE OF INVESTMENTS

December 31, 2018

Shares | |

| | Value

(Note 1) | |

| | | COMMON STOCKS—74.7% | |

| | | Australia—3.7% | |

| | 3,702 | | | AGL Energy, Ltd. | | $ | 53,715 | | |

| | 8,035 | | | ALS, Ltd. | | | 38,371 | | |

| | 1,335 | | | Altium, Ltd. | | | 20,405 | | |

| | 9,599 | | | Amcor, Ltd. | | | 89,584 | | |

| | 12,594 | | | AMP, Ltd. | | | 21,733 | | |

| | 1,231 | | | Ansell, Ltd. | | | 19,110 | | |

| | 4,576 | | | Aristocrat Leisure, Ltd. | | | 70,393 | | |

| | 487 | | | ASX, Ltd. | | | 20,561 | | |

| | 4,297 | | | Atlas Arteria, Ltd. | | | 18,946 | | |

| | 27,196 | | | Aurizon Holdings, Ltd. | | | 81,986 | | |

| | 12,821 | | | Ausdrill, Ltd. | | | 10,746 | | |

| | 16,565 | | | Australia & New Zealand Banking

Group, Ltd. | | | 285,388 | | |

| | 1,660 | | | Bank of Queensland, Ltd. | | | 11,341 | | |

| | 19,836 | | | Beach Energy, Ltd. | | | 18,792 | | |

| | 2,901 | | | Bendigo & Adelaide Bank, Ltd. | | | 22,047 | | |

| | 28,363 | | | BHP Group, Ltd. | | | 683,829 | | |

| | 6,586 | | | BlueScope Steel, Ltd. | | | 50,842 | | |

| | 8,539 | | | Boral, Ltd. | | | 29,711 | | |

| | 9,097 | | | Brambles, Ltd. | | | 65,036 | | |

| | 1,732 | | | Caltex Australia, Ltd. | | | 31,084 | | |

| | 2,491 | | | carsales.com, Ltd. | | | 19,300 | | |

| | 5,928 | | | Challenger, Ltd. | | | 39,624 | | |

| | 16,096 | | | Cleanaway Waste

Management, Ltd. | | | 18,876 | | |

| | 6,210 | | | Coca-Cola Amatil, Ltd. | | | 35,823 | | |

| | 400 | | | Cochlear, Ltd. | | | 48,902 | | |

| | 8,123 | | | Coles Group, Ltd.* | | | 67,170 | | |

| | 13,861 | | | Commonwealth Bank of Australia | | | 706,743 | | |

| | 3,340 | | | Computershare, Ltd. | | | 40,440 | | |

| | 3,820 | | | Costa Group Holdings, Ltd. | | | 19,964 | | |

| | 2,419 | | | Crown Resorts, Ltd. | | | 20,207 | | |

| | 3,245 | | | CSL, Ltd. | | | 423,205 | | |

| | 4,400 | | | Downer EDI, Ltd. | | | 20,950 | | |

| | 4,297 | | | DuluxGroup, Ltd. | | | 19,854 | | |

| | 4,311 | | | Elders, Ltd. | | | 21,437 | | |

| | 13,141 | | | Evolution Mining, Ltd. | | | 34,154 | | |

| | 669 | | | Flight Centre Travel Group, Ltd. | | | 20,224 | | |

| | 24,562 | | | Fortescue Metals Group, Ltd. | | | 72,488 | | |

| | 9,317 | | | GWA Group, Ltd. | | | 18,244 | | |

| | 9,170 | | | Incitec Pivot, Ltd. | | | 21,185 | | |

| | 7,352 | | | Independence Group NL | | | 19,781 | | |

| | 14,639 | | | Insurance Australia Group Ltd. | | | 72,177 | | |

| | 2,408 | | | JB Hi-Fi, Ltd. | | | 37,551 | | |

Shares | |

| | Value

(Note 1) | |

| | | Australia (Continued) | |

| | 2,512 | | | LendLease Group | | $ | 20,577 | | |

| | 4,284 | | | Link Administration Holdings, Ltd. | | | 20,428 | | |

| | 2,349 | | | Macquarie Group, Ltd. | | | 179,763 | | |

| | 1,171 | | | Magellan Financial Group, Ltd. | | | 19,416 | | |

| | 22,423 | | | Mayne Pharma Group, Ltd.* | | | 12,240 | | |

| | 12,504 | | | Metcash, Ltd. | | | 21,578 | | |

| | 1,851 | | | Mineral Resources, Ltd. | | | 20,169 | | |

| | 19,807 | | | National Australia Bank, Ltd. | | | 335,802 | | |

| | 2,235 | | | Newcrest Mining, Ltd. | | | 34,318 | | |

| | 5,029 | | | NEXTDC, Ltd.* | | | 21,643 | | |

| | 5,984 | | | nib holdings, Ltd. | | | 21,917 | | |

| | 7,157 | | | Northern Star Resources, Ltd. | | | 46,579 | | |

| | 11,110 | | | NRW Holdings, Ltd. | | | 12,638 | | |

| | 4,065 | | | Oil Search, Ltd. | | | 20,500 | | |

| | 4,936 | | | oOh!media, Ltd. | | | 11,890 | | |

| | 1,697 | | | Orica, Ltd. | | | 20,619 | | |

| | 10,538 | | | Origin Energy, Ltd.* | | | 48,023 | | |

| | 9,118 | | | Orora, Ltd. | | | 19,716 | | |

| | 3,315 | | | OZ Minerals, Ltd. | | | 20,547 | | |

| | 3,547 | | | Pendal Group, Ltd. | | | 19,912 | | |

| | 2,030 | | | Premier Investments, Ltd. | | | 21,033 | | |

| | 10,651 | | | Qantas Airways, Ltd. | | | 43,437 | | |

| | 7,304 | | | QBE Insurance Group, Ltd. | | | 51,960 | | |

| | 1,072 | | | Ramsay Health Care, Ltd. | | | 43,590 | | |

| | 6,758 | | | Regis Resources, Ltd. | | | 22,991 | | |

| | 3,594 | | | Rio Tinto, Ltd. | | | 198,642 | | |

| | 4,596 | | | Sandfire Resources NL | | | 21,624 | | |

| | 10,594 | | | Santos, Ltd. | | | 40,891 | | |

| | 10,376 | | | Saracen Mineral Holdings, Ltd.* | | | 21,413 | | |

| | 3,349 | | | SEEK, Ltd. | | | 39,912 | | |

| | 2,601 | | | Sonic Healthcare, Ltd. | | | 40,506 | | |

| | 9,838 | | | South32, Ltd. | | | 23,214 | | |

| | 10,287 | | | Southern Cross Media

Group, Ltd. | | | 7,282 | | |

| | 12,721 | | | Spark Infrastructure Group | | | 19,802 | | |

| | 6,758 | | | St Barbara, Ltd. | | | 22,372 | | |

| | 4,658 | | | Star Entertainment

Grp, Ltd. (The) | | | 14,961 | | |

| | 11,105 | | | Steadfast Group, Ltd. | | | 21,510 | | |

| | 3,030 | | | Suncorp Group, Ltd. | | | 26,955 | | |

| | 4,226 | | | Super Retail Group, Ltd. | | | 20,925 | | |

| | 4,242 | | | Sydney Airport | | | 20,108 | | |

| | 6,942 | | | Tabcorp Holdings, Ltd. | | | 20,976 | | |

| | 32,411 | | | Telstra Corp., Ltd. | | | 65,062 | | |

| | 16,090 | | | Transurban Group | | | 132,029 | | |

| | 1,963 | | | Treasury Wine Estates, Ltd. | | | 20,463 | | |

The accompanying notes are an integral part of these financial statements.

15

M International Equity Fund

SCHEDULE OF INVESTMENTS (Continued)

December 31, 2018

Shares | |

| | Value

(Note 1) | |

| | | Australia (Continued) | |

| | 12,616 | | | Vocus Group, Ltd.* | | $ | 28,435 | | |

| | 8,107 | | | Wesfarmers, Ltd. | | | 183,982 | | |

| | 25,089 | | | Westpac Banking Corp. | | | 442,493 | | |

| | 6,375 | | | Whitehaven Coal, Ltd. | | | 19,398 | | |

| | 3,888 | | | Woodside Petroleum, Ltd. | | | 85,770 | | |

| | 7,616 | | | Woolworths Group, Ltd. | | | 157,819 | | |

| | 2,336 | | | WorleyParsons, Ltd. | | | 18,790 | | |

| | | | 6,268,539 | | |

| | | Austria—0.2% | |

| | 984 | | | ANDRITZ AG | | | 45,232 | | |

| | 658 | | | CA Immobilien Anlagen AG | | | 20,823 | | |

| | 133 | | | DO & Co. AG | | | 12,313 | | |

| | 2,245 | | | Erste Group Bank AG* | | | 74,722 | | |

| | 1,377 | | | FACC AG | | | 20,889 | | |

| | 1,233 | | | IMMOFINANZ AG* | | | 29,525 | | |

| | 211 | | | Lenzing AG | | | 19,207 | | |

| | 1,814 | | | OMV AG | | | 79,498 | | |

| | 3,082 | | | Raiffeisen Bank International AG | | | 78,393 | | |

| | 1,874 | | | Telekom Austria AG* | | | 14,257 | | |

| | 1,734 | | | UNIQA Insurance Group AG | | | 15,616 | | |

| | | | 410,475 | | |

| | | Belgium—0.7% | |

| | 219 | | | Ackermans & van Haaren NV | | | 33,071 | | |

| | 2,424 | | | Ageas | | | 109,148 | | |

| | 5,568 | | | AGFA-Gevaert NV* | | | 21,244 | | |

| | 7,147 | | | Anheuser-Busch InBev SA/NV | | | 472,486 | | |

| | 609 | | | Colruyt SA | | | 43,429 | | |

| | 258 | | | D'ieteren SA/NV | | | 9,731 | | |

| | 175 | | | Elia System Operator SA/NV | | | 11,690 | | |

| | 1,410 | | | Euronav NV | | | 10,048 | | |

| | 548 | | | EVS Broadcast Equipment SA | | | 14,567 | | |

| | 202 | | | Galapagos NV* | | | 18,645 | | |

| | 197 | | | Gimv NV | | | 10,586 | | |

| | 1,847 | | | KBC Group NV | | | 119,946 | | |

| | 796 | | | Ontex Group NV | | | 16,325 | | |

| | 1,637 | | | Proximus SADP | | | 44,302 | | |

| | 214 | | | Sipef NV | | | 11,965 | | |

| | 449 | | | Solvay SA | | | 44,921 | | |

| | 449 | | | Telenet Group Holding NV | | | 20,886 | | |

| | 1,442 | | | UCB SA | | | 117,800 | | |

| | 523 | | | Umicore SA | | | 20,889 | | |

| | | | 1,151,679 | | |

Shares | |

| | Value

(Note 1) | |

| | | Canada—8.2% | |

| | 1,800 | | | Absolute Software Corp. | | $ | 10,205 | | |

| | 1,679 | | | Aecon Group, Inc. | | | 21,658 | | |

| | 607 | | | Ag Growth International, Inc. | | | 20,808 | | |

| | 1,389 | | | Agnico Eagle Mines, Ltd. | | | 56,061 | | |

| | 1,100 | | | Air Canada* | | | 20,917 | | |

| | 3,318 | | | Alamos Gold, Inc., Class A | | | 11,933 | | |

| | 4,334 | | | Algonquin Power & Utilities Corp. | | | 43,588 | | |

| | 3,403 | | | Alimentation Couche-Tard, Inc.,

Class B | | | 169,278 | | |

| | 1,185 | | | Altus Group, Ltd. | | | 20,546 | | |

| | 9,937 | | | ARC Resources, Ltd. | | | 58,958 | | |

| | 989 | | | Aritzia, Inc.* | | | 11,881 | | |

| | 700 | | | Atco, Ltd., Class I | | | 19,797 | | |

| | 1,849 | | | ATS Automation Tooling

Systems, Inc.* | | | 19,490 | | |

| | 5,109 | | | Aurora Cannabis, Inc.* | | | 25,373 | | |

| | 29,347 | | | B2Gold Corp.* | | | 85,771 | | |

| | 8,595 | | | Bank of Montreal | | | 561,521 | | |

| | 9,700 | | | Bank of Nova Scotia (The) | | | 483,508 | | |

| | 16,126 | | | Barrick Gold Corp. | | | 217,699 | | |

| | 4,271 | | | Bausch Health Cos., Inc.* | | | 78,994 | | |

| | 1,608 | | | BCE, Inc. | | | 63,521 | | |

| | 9,500 | | | Birchcliff Energy, Ltd. | | | 21,154 | | |

| | 7,292 | | | BlackBerry, Ltd.* | | | 51,864 | | |

| | 16,000 | | | Bonavista Energy Corp. | | | 14,064 | | |

| | 2,062 | | | Boralex, Inc., Class A | | | 25,435 | | |

| | 5,600 | | | Brookfield Asset Management,

Inc., Class A | | | 214,615 | | |

| | 785 | | | BRP, Inc. | | | 20,321 | | |

| | 3,678 | | | CAE, Inc. | | | 67,595 | | |

| | 6,709 | | | Cameco Corp. | | | 76,073 | | |

| | 4,900 | | | Canaccord Genuity Group, Inc. | | | 20,710 | | |

| | 400 | | | Canada Goose Holdings, Inc.* | | | 17,486 | | |

| | 3,635 | | | Canadian Imperial Bank of

Commerce | | | 270,735 | | |

| | 5,715 | | | Canadian National Railway Co. | | | 423,267 | | |

| | 19,631 | | | Canadian Natural Resources, Ltd. | | | 473,663 | | |

| | 1,117 | | | Canadian Pacific Railway, Ltd. | | | 198,200 | | |

| | 995 | | | Canadian Tire Corp., Ltd., Class A | | | 104,033 | | |

| | 500 | | | Canadian Utilities, Ltd., Class A | | | 11,471 | | |

| | 2,480 | | | Canadian Western Bank | | | 47,304 | | |

| | 1,876 | | | Canfor Corp.* | | | 22,715 | | |

| | 2,194 | | | Capital Power Corp. | | | 42,733 | | |

| | 2,300 | | | Cascades, Inc. | | | 17,235 | | |

| | 1,637 | | | CCL Industries, Inc., Class I | | | 60,027 | | |

The accompanying notes are an integral part of these financial statements.

16

M International Equity Fund

SCHEDULE OF INVESTMENTS (Continued)

December 31, 2018

Shares | |

| | Value

(Note 1) | |

| | | Canada (Continued) | |

| | 2,566 | | | Celestica, Inc.* | | $ | 22,480 | | |

| | 9,834 | | | Cenovus Energy, Inc. | | | 69,152 | | |

| | 5,235 | | | Centerra Gold, Inc.* | | | 22,471 | | |

| | 9,000 | | | CES Energy Solutions Corp. | | | 20,766 | | |

| | 1,621 | | | CGI Group, Inc., Class A* | | | 99,146 | | |

| | 4,339 | | | CI Financial Corp. | | | 54,921 | | |

| | 2,372 | | | Cineplex, Inc. | | | 44,201 | | |

| | 490 | | | Cogeco Communications, Inc. | | | 23,610 | | |

| | 300 | | | Cogeco, Inc. | | | 12,798 | | |

| | 825 | | | Colliers International Group, Inc. | | | 45,498 | | |

| | 217 | | | Constellation Software, Inc. | | | 138,901 | | |

| | 2,837 | | | Cott Corp. | | | 39,504 | | |

| | 3,330 | | | CRH Medical Corp.* | | | 10,196 | | |

| | 4,912 | | | Detour Gold Corp.* | | | 41,485 | | |

| | 500 | | | Dollarama, Inc. | | | 11,892 | | |

| | 1,821 | | | Dorel Industries, Inc., Class B | | | 23,529 | | |

| | 2,200 | | | DREAM Unlimited Corp., Class A* | | | 11,023 | | |

| | 6,100 | | | Dundee Precious Metals, Inc.* | | | 16,086 | | |

| | 4,100 | | | ECN Capital Corp. | | | 10,361 | | |

| | 12,077 | | | Element Fleet Management Corp. | | | 61,128 | | |

| | 663 | | | Emera, Inc. | | | 21,227 | | |

| | 12,600 | | | Enbridge, Inc. | | | 391,420 | | |

| | 7,600 | | | Encana Corp. | | | 43,868 | | |

| | 2,494 | | | Enerflex, Ltd. | | | 29,193 | | |

| | 7,134 | | | Enerplus Corp. | | | 55,496 | | |

| | 441 | | | Enghouse Systems, Ltd. | | | 21,452 | | |

| | 4,100 | | | Ensign Energy Services, Inc. | | | 14,385 | | |

| | 4,400 | | | Extendicare, Inc. | | | 20,466 | | |

| | 391 | | | Fairfax Financial Holdings, Ltd. | | | 172,124 | | |

| | 2,600 | | | Fiera Capital Corp. | | | 21,502 | | |

| | 3,098 | | | Finning International, Inc. | | | 54,008 | | |

| | 2,677 | | | First Capital Realty, Inc. | | | 36,963 | | |

| | 4,882 | | | First Majestic Silver Corp.* | | | 28,680 | | |

| | 3,400 | | | First Quantum Minerals, Ltd. | | | 27,495 | | |

| | 547 | | | FirstService Corp. | | | 37,539 | | |

| | 3,902 | | | Fortis, Inc. | | | 130,076 | | |

| | 1,030 | | | Franco-Nevada Corp. | | | 72,225 | | |

| | 787 | | | Genworth MI Canada, Inc. | | | 23,174 | | |

| | 1,045 | | | George Weston, Ltd. | | | 68,929 | | |

| | 1,500 | | | Gibson Energy, Inc. | | | 20,524 | | |

| | 1,871 | | | Gildan Activewear, Inc. | | | 56,793 | | |

| | 2,859 | | | Gluskin Sheff + Associates, Inc. | | | 21,842 | | |

| | 8,185 | | | Goldcorp, Inc. | | | 80,159 | | |

| | 5,700 | | | Gran Tierra Energy, Inc.* | | | 12,442 | | |

| | 1,337 | | | Great Canadian Gaming Corp.* | | | 46,881 | | |

Shares | |

| | Value

(Note 1) | |

| | | Canada (Continued) | |

| | 806 | | | Great-West Lifeco, Inc. | | $ | 16,637 | | |

| | 1,700 | | | Home Capital Group, Inc.* | | | 17,931 | | |

| | 7,321 | | | Hudbay Minerals, Inc. | | | 34,642 | | |

| | 8,282 | | | Husky Energy, Inc. | | | 85,598 | | |

| | 2,998 | | | Hydro One, Ltd.# | | | 44,469 | | |

| | 3,400 | | | IAMGOLD Corp.* | | | 12,477 | | |

| | 800 | | | Imperial Oil, Ltd. | | | 20,270 | | |

| | 2,161 | | | Industrial Alliance Insurance &

Financial Services, Inc. | | | 68,968 | | |

| | 2,417 | | | Innergex Renewable Energy, Inc. | | | 22,201 | | |

| | 795 | | | Intact Financial Corp. | | | 57,762 | | |

| | 5,565 | | | Inter Pipeline, Ltd. | | | 78,836 | | |

| | 2,045 | | | Interfor Corp.* | | | 21,600 | | |

| | 2,087 | | | Intertape Polymer Group, Inc. | | | 25,866 | | |

| | 1,600 | | | Invesque, Inc. | | | 11,408 | | |

| | 19,814 | | | Ivanhoe Mines, Ltd., Class A* | | | 34,397 | | |

| | 700 | | | Jamieson Wellness, Inc. | | | 10,937 | | |

| | 500 | | | K-Bro Linen, Inc. | | | 12,247 | | |

| | 7,152 | | | Kelt Exploration, Ltd.* | | | 24,308 | | |

| | 3,848 | | | Keyera Corp. | | | 72,749 | | |

| | 1,864 | | | Kinder Morgan Canada, Ltd.# | | | 21,750 | | |

| | 24,613 | | | Kinross Gold Corp.* | | | 79,327 | | |

| | 2,070 | | | Kirkland Lake Gold, Ltd. | | | 53,979 | | |

| | 1,199 | | | Labrador Iron Ore Royalty Corp. | | | 21,289 | | |

| | 800 | | | Laurentian Bank of Canada | | | 22,309 | | |

| | 1,289 | | | Linamar Corp. | | | 42,772 | | |

| | 1,322 | | | Loblaw Cos., Ltd. | | | 59,176 | | |

| | 8,900 | | | Lucara Diamond Corp. | | | 9,648 | | |

| | 13,050 | | | Lundin Mining Corp. | | | 53,913 | | |

| | 8,872 | | | Magna International, Inc. | | | 402,723 | | |

| | 4,800 | | | Major Drilling Group

International, Inc.* | | | 16,173 | | |

| | 10,673 | | | Manulife Financial Corp. | | | 151,433 | | |

| | 1,530 | | | Maple Leaf Foods, Inc. | | | 30,629 | | |

| | 2,600 | | | Martinrea International, Inc. | | | 20,683 | | |

| | 1,895 | | | Medical Facilities Corp. | | | 20,877 | | |

| | 1,388 | | | Methanex Corp. | | | 66,757 | | |

| | 1,982 | | | Metro, Inc. | | | 68,728 | | |

| | 1,162 | | | Morneau Shepell, Inc. | | | 21,313 | | |

| | 470 | | | MTY Food Group, Inc. | | | 20,877 | | |

| | 2,700 | | | Mullen Group, Ltd. | | | 24,148 | | |

| | 6,167 | | | National Bank of Canada | | | 253,194 | | |

| | 1,740 | | | NFI Group, Inc. | | | 43,385 | | |

| | 1,156 | | | Norbord, Inc. | | | 30,737 | | |

| | 1,126 | | | North West Co., Inc. (The) | | | 25,915 | | |

The accompanying notes are an integral part of these financial statements.

17

M International Equity Fund

SCHEDULE OF INVESTMENTS (Continued)

December 31, 2018

Shares | |

| | Value

(Note 1) | |

| | | Canada (Continued) | |

| | 2,067 | | | Northland Power, Inc. | | $ | 32,855 | | |

| | 3,318 | | | Nutrien, Ltd. | | | 155,838 | | |

| | 11,800 | | | OceanaGold Corp. | | | 43,044 | | |

| | 393 | | | Onex Corp. | | | 21,403 | | |

| | 3,650 | | | Open Text Corp. | | | 118,975 | | |

| | 3,287 | | | Osisko Gold Royalties, Ltd. | | | 28,820 | | |

| | 4,296 | | | Pan American Silver Corp. | | | 62,716 | | |

| | 4,549 | | | Parex Resources, Inc.* | | | 54,480 | | |

| | 700 | | | Park Lawn Corp. | | | 11,824 | | |

| | 2,607 | | | Parkland Fuel Corp. | | | 67,486 | | |

| | 1,760 | | | Pason Systems, Inc. | | | 23,579 | | |

| | 1,770 | | | Pembina Pipeline Corp. | | | 52,522 | | |

| | 4,630 | | | Peyto Exploration &

Development Corp. | | | 24,011 | | |

| | 11,600 | | | Precision Drilling Corp.* | | | 20,138 | | |

| | 300 | | | Premium Brands Holdings Corp. | | | 16,450 | | |

| | 1,000 | | | Quebecor, Inc., Class B | | | 21,052 | | |

| | 700 | | | Recipe Unlimited Corp. | | | 13,419 | | |

| | 1,500 | | | Restaurant Brands

International, Inc. | | | 78,362 | | |

| | 1,345 | | | Richelieu Hardware, Ltd. | | | 22,354 | | |

| | 1,489 | | | Ritchie Bros Auctioneers, Inc. | | | 48,710 | | |

| | 2,834 | | | Rogers Communications, Inc.,

Class B | | | 145,229 | | |

| | 5,300 | | | Rogers Sugar, Inc. | | | 21,119 | | |

| | 12,600 | | | Royal Bank of Canada | | | 862,397 | | |

| | 1,740 | | | Russel Metals, Inc. | | | 27,186 | | |

| | 1,898 | | | Saputo, Inc. | | | 54,485 | | |

| | 4,547 | | | Secure Energy Services, Inc. | | | 23,348 | | |

| | 11,834 | | | SEMAFO, Inc.* | | | 25,572 | | |

| | 2,897 | | | Seven Generations Energy, Ltd.* | | | 23,639 | | |

| | 7,519 | | | Shaw Communications, Inc.,

Class B | | | 136,093 | | |

| | 1,968 | | | ShawCor, Ltd. | | | 23,901 | | |

| | 200 | | | Shopify, Inc., Class A* | | | 27,657 | | |

| | 1,794 | | | Sienna Senior Living, Inc. | | | 20,684 | | |

| | 1,359 | | | Sleep Country Canada

Holdings, Inc.# | | | 19,879 | | |

| | 1,519 | | | SNC-Lavalin Group, Inc. | | | 51,093 | | |

| | 737 | | | Spin Master Corp.#, * | | | 20,725 | | |

| | 3,369 | | | SSR Mining, Inc.* | | | 40,718 | | |

| | 1,600 | | | Stantec, Inc. | | | 35,054 | | |

| | 400 | | | Stella-Jones, Inc. | | | 11,606 | | |

| | 3,244 | | | Sun Life Financial, Inc. | | | 107,618 | | |

| | 22,526 | | | Suncor Energy, Inc. | | | 629,151 | | |

Shares | |

| | Value

(Note 1) | |

| | | Canada (Continued) | |

| | 3,579 | | | Superior Plus Corp. | | $ | 25,377 | | |

| | 12,012 | | | Teck Resources, Ltd. | | | 258,594 | | |

| | 3,900 | | | Teranga Gold Corp.* | | | 11,513 | | |

| | 1,944 | | | TFI International, Inc. | | | 50,266 | | |

| | 1,433 | | | Thomson Reuters Corp. | | | 69,204 | | |

| | 3,200 | | | Timbercreek Financial Corp. | | | 20,510 | | |

| | 801 | | | TMX Group, Ltd. | | | 41,499 | | |

| | 6,950 | | | TORC Oil & Gas, Ltd. | | | 22,247 | | |

| | 1,339 | | | Toromont Industries, Ltd. | | | 53,219 | | |

| | 14,500 | | | Toronto-Dominion Bank (The) | | | 720,752 | | |

| | 5,111 | | | Tourmaline Oil Corp. | | | 63,569 | | |

| | 7,036 | | | TransAlta Corp. | | | 28,810 | | |

| | 2,812 | | | TransAlta Renewables, Inc. | | | 21,360 | | |

| | 2,700 | | | TransCanada Corp. | | | 96,414 | | |

| | 3,001 | | | Tricon Capital Group, Inc. | | | 21,301 | | |

| | 15,700 | | | Turquoise Hill Resources, Ltd.* | | | 25,875 | | |

| | 1,000 | | | Uni-Select, Inc. | | | 14,218 | | |

| | 1,200 | | | Valener, Inc. | | | 17,000 | | |

| | 3,227 | | | Vermilion Energy, Inc. | | | 67,982 | | |

| | 1,800 | | | Wajax Corp. | | | 21,861 | | |

| | 800 | | | Waste Connections, Inc. | | | 59,379 | | |

| | 1,290 | | | West Fraser Timber Co., Ltd. | | | 63,725 | | |

| | 12,500 | | | Western Forest Products, Inc. | | | 17,305 | | |

| | 1,324 | | | Wheaton Precious Metals Corp. | | | 25,858 | | |

| | 1,500 | | | Wheaton Precious Metals Corp. | | | 29,281 | | |

| | 4,700 | | | Whitecap Resources, Inc. | | | 14,976 | | |

| | 400 | | | Winpak, Ltd. | | | 13,991 | | |

| | 863 | | | WSP Global, Inc. | | | 37,088 | | |

| | 25,721 | | | Yamana Gold, Inc. | | | 60,478 | | |

| | | | 13,924,100 | | |

| | | Colombia—1.6% | |

| | 376,157 | | | Grupo Argos SA | | | 1,957,522 | | |

| | 73,115 | | | Grupo de Inversiones

Suramericana SA | | | 723,158 | | |

| | | | 2,680,680 | | |

| | | Denmark—1.1% | |

| | 11 | | | AP Moller - Maersk A/S, Class A | | | 12,998 | | |

| | 23 | | | AP Moller - Maersk A/S, Class B | | | 28,885 | | |

| | 907 | | | Bang & Olufsen A/S* | | | 12,374 | | |

| | 641 | | | Carlsberg A/S, Class B | | | 68,128 | | |

| | 555 | | | Chr Hansen Holding A/S | | | 49,108 | | |

| | 568 | | | Coloplast A/S, Class B | | | 52,734 | | |

| | 1,040 | | | Danske Bank A/S | | | 20,572 | | |

The accompanying notes are an integral part of these financial statements.

18

M International Equity Fund

SCHEDULE OF INVESTMENTS (Continued)

December 31, 2018

Shares | |

| | Value

(Note 1) | |

| | | Denmark (Continued) | |

| | 2,005 | | | DSV A/S | | $ | 132,057 | | |

| | 316 | | | FLSmidth & Co. A/S | | | 14,213 | | |

| | 261 | | | Genmab A/S* | | | 42,756 | | |

| | 1,611 | | | GN Store Nord A/S | | | 60,148 | | |

| | 818 | | | H+H International A/S, Class B* | | | 11,925 | | |

| | 3,142 | | | ISS A/S | | | 87,777 | | |

| | 593 | | | Jyske Bank A/S | | | 21,403 | | |

| | 1,970 | | | Matas A/S | | | 17,534 | | |

| | 266 | | | Nilfisk Holding A/S* | | | 9,409 | | |

| | 362 | | | NNIT A/S# | | | 10,177 | | |

| | 12,082 | | | Novo Nordisk A/S, Class B | | | 552,325 | | |

| | 2,254 | | | Novozymes A/S, Class B | | | 100,620 | | |

| | 1,030 | | | Orsted A/S# | | | 68,867 | | |

| | 614 | | | Pandora A/S | | | 24,997 | | |

| | 376 | | | Per Aarsleff Holding A/S | | | 11,482 | | |

| | 402 | | | Ringkjoebing Landbobank A/S | | | 20,974 | | |

| | 44 | | | Rockwool International A/S,

Class A | | | 10,094 | | |

| | 186 | | | Rockwool International A/S,

Class B | | | 48,523 | | |

| | 1,104 | | | Royal Unibrew A/S | | | 76,068 | | |

| | 836 | | | Scandinavian Tobacco Group A/S# | | | 10,064 | | |

| | 198 | | | Schouw & Co. A/S | | | 14,755 | | |

| | 638 | | | SimCorp A/S | | | 43,627 | | |

| | 1,256 | | | Spar Nord Bank A/S | | | 10,080 | | |

| | 555 | | | Sydbank A/S | | | 13,210 | | |

| | 676 | | | Topdanmark A/S | | | 31,432 | | |

| | 837 | | | Tryg A/S | | | 21,052 | | |

| | 2,306 | | | Vestas Wind Systems A/S | | | 174,140 | | |

| | 1,375 | | | William Demant Holding A/S* | | | 39,014 | | |

| | | | 1,923,522 | | |

| | | Finland—0.9% | |

| | 631 | | | Cramo OYJ | | | 10,787 | | |

| | 2,156 | | | Elisa OYJ | | | 89,126 | | |

| | 5,712 | | | Fortum OYJ | | | 125,000 | | |

| | 1,730 | | | Huhtamaki OYJ | | | 53,657 | | |

| | 934 | | | Kemira OYJ | | | 10,541 | | |

| | 239 | | | Kesko OYJ, Class A | | | 11,939 | | |

| | 373 | | | Kesko OYJ, Class B | | | 20,129 | | |

| | 2,212 | | | Kone OYJ, Class B | | | 105,532 | | |

| | 1,119 | | | Konecranes OYJ | | | 33,834 | | |

| | 1,568 | | | Metso OYJ | | | 41,141 | | |

| | 1,091 | | | Neste Oyj | | | 84,201 | | |

| | 22,938 | | | Nokia OYJ | | | 132,195 | | |

Shares | |

| | Value

(Note 1) | |

| | | Finland (Continued) | |

| | 1,922 | | | Nokian Renkaat OYJ | | $ | 59,061 | | |

| | 281 | | | Olvi OYJ, Class A | | | 10,142 | | |

| | 7,100 | | | Oriola OYJ, Class B | | | 16,107 | | |

| | 727 | | | Orion OYJ, Class A | | | 25,239 | | |

| | 1,558 | | | Orion OYJ, Class B | | | 54,052 | | |

| | 5,228 | | | Outokumpu OYJ | | | 19,138 | | |

| | 7,476 | | | Raisio OYJ | | | 20,086 | | |

| | 873 | | | Revenio Group OYJ | | | 12,563 | | |

| | 3,993 | | | Sampo OYJ, Class A | | | 175,725 | | |

| | 8,204 | | | Stora Enso OYJ | | | 94,796 | | |

| | 390 | | | Tieto OYJ | | | 10,537 | | |

| | 1,160 | | | Tikkurila OYJ | | | 15,975 | | |

| | 2,646 | | | Tokmanni Group Corp. | | | 21,767 | | |

| | 8,944 | | | UPM-Kymmene OYJ | | | 226,984 | | |

| | 559 | | | Vaisala OYJ | | | 10,568 | | |

| | 2,116 | | | Valmet OYJ | | | 43,518 | | |

| | 5,634 | | | Wartsila OYJ Abp | | | 89,694 | | |

| | 1,665 | | | YIT OYJ | | | 9,739 | | |

| | | | 1,633,773 | | |

| | | France—6.8% | |

| | 969 | | | Accor SA | | | 41,201 | | |

| | 292 | | | Aeroports de Paris | | | 55,369 | | |

| | 3,912 | | | Air France-KLM* | | | 42,491 | | |

| | 3,707 | | | Air Liquide SA | | | 460,619 | | |

| | 4,542 | | | Airbus SE | | | 436,927 | | |

| | 966 | | | Alstom SA | | | 39,037 | | |

| | 476 | | | Alten SA | | | 39,649 | | |

| | 272 | | | Amundi SA# | | | 14,385 | | |

| | 1,401 | | | Arkema SA | | | 120,325 | | |

| | 286 | | | Atos SE | | | 23,423 | | |

| | 368 | | | Aubay | | | 11,869 | | |

| | 10,652 | | | AXA SA | | | 230,153 | | |

| | 570 | | | BioMerieux | | | 37,552 | | |

| | 5,629 | | | BNP Paribas SA | | | 254,591 | | |

| | 5,062 | | | Bollore SA | | | 20,299 | | |

| | 3,865 | | | Bouygues SA | | | 138,784 | | |

| | 2,992 | | | Bureau Veritas SA | | | 61,003 | | |

| | 1,394 | | | Capgemini SE | | | 138,635 | | |

| | 5,158 | | | Carrefour SA | | | 88,115 | | |

| | 6,743 | | | Cie de St-Gobain | | | 225,323 | | |

| | 3,063 | | | Cie Generale des Etablissements

Michelin SCA | | | 304,268 | | |

| | 961 | | | CNP Assurances | | | 20,392 | | |

| | 4,370 | | | Credit Agricole SA | | | 47,215 | | |

The accompanying notes are an integral part of these financial statements.

19

M International Equity Fund

SCHEDULE OF INVESTMENTS (Continued)

December 31, 2018

Shares | |

| | Value

(Note 1) | |

| | | France (Continued) | |

| | 5,283 | | | Danone SA | | $ | 372,320 | | |

| | 368 | | | Dassault Systemes SE | | | 43,724 | | |

| | 5,436 | | | Derichebourg SA | | | 24,901 | | |

| | 106 | | | Devoteam SA | | | 10,019 | | |

| | 2,880 | | | Edenred | | | 105,955 | | |

| | 1,777 | | | Eiffage SA | | | 148,546 | | |

| | 6,771 | | | Electricite de France SA | | | 107,059 | | |

| | 1,532 | | | Elior Group SA# | | | 22,924 | | |

| | 4,742 | | | Elis SA | | | 79,052 | | |

| | 9,816 | | | Engie SA | | | 140,865 | | |

| | 722 | | | EssilorLuxottica SA | | | 91,368 | | |

| | 155 | | | Eurofins Scientific SE | | | 57,895 | | |

| | 993 | | | Euronext NV# | | | 57,228 | | |

| | 1,237 | | | Europcar Mobility Group# | | | 11,147 | | |

| | 4,666 | | | Eutelsat Communications SA | | | 91,979 | | |

| | 178 | | | Fnac Darty SA* | | | 11,645 | | |

| | 180 | | | Gaztransport Et Technigaz SA | | | 13,849 | | |

| | 218 | | | Hermes International | | | 121,090 | | |

| | 77 | | | ID Logistics Group* | | | 10,146 | | |

| | 454 | | | Iliad SA | | | 63,799 | | |

| | 410 | | | Imerys SA | | | 19,720 | | |

| | 812 | | | Ingenico Group SA | | | 46,089 | | |

| | 308 | | | Ipsen SA | | | 39,824 | | |

| | 614 | | | JCDecaux SA | | | 17,249 | | |

| | 637 | | | Kaufman & Broad SA | | | 24,377 | | |

| | 569 | | | Kering SA | | | 268,335 | | |

| | 913 | | | Korian SA | | | 32,512 | | |

| | 1,281 | | | L'Oreal SA | | | 295,302 | | |

| | 1,721 | | | Lagardere SCA | | | 43,420 | | |

| | 1,064 | | | Lectra | | | 22,163 | | |

| | 3,569 | | | Legrand SA | | | 201,597 | | |

| | 2,967 | | | LVMH Moet Hennessy Louis

Vuitton SA | | | 877,735 | | |

| | 444 | | | Mersen SA | | | 11,955 | | |

| | 8,152 | | | Natixis SA | | | 38,472 | | |

| | 993 | | | Neopost SA | | | 27,101 | | |

| | 683 | | | Nexity SA | | | 30,832 | | |

| | 31,311 | | | Orange SA | | | 507,804 | | |

| | 525 | | | Orpea | | | 53,667 | | |

| | 583 | | | Pernod-Ricard SA | | | 95,720 | | |

| | 13,186 | | | Peugeot SA | | | 281,686 | | |

| | 3,769 | | | Publicis Groupe SA | | | 216,262 | | |

| | 179 | | | Remy Cointreau SA | | | 20,293 | | |

| | 2,261 | | | Renault SA | | | 141,314 | | |

| | 5,791 | | | Rexel SA | | | 61,706 | | |

Shares | |

| | Value

(Note 1) | |

| | | France (Continued) | |

| | 611 | | | Rothschild & Co. | | $ | 21,597 | | |

| | 873 | | | Rubis SCA | | | 46,891 | | |

| | 2,096 | | | Safran SA | | | 253,117 | | |

| | 5,900 | | | Sanofi | | | 511,456 | | |

| | 174 | | | Sartorius Stedim Biotech | | | 17,414 | | |

| | 4,165 | | | Schneider Electric SE | | | 284,987 | | |

| | 2,540 | | | SCOR SE | | | 114,662 | | |

| | 393 | | | SEB SA | | | 50,791 | | |

| | 6,297 | | | SES SA, ADR | | | 120,559 | | |

| | 411 | | | Societe BIC SA | | | 41,981 | | |

| | 3,636 | | | Societe Generale SA | | | 115,897 | | |

| | 1,401 | | | Sodexo SA | | | 143,665 | | |

| | 1,621 | | | SPIE SA | | | 21,526 | | |

| | 5,033 | | | STMicroelectronics NV | | | 71,995 | | |

| | 3,853 | | | Suez | | | 50,900 | | |

| | 606 | | | Teleperformance | | | 96,928 | | |

| | 943 | | | Thales SA | | | 110,205 | | |

| | 19,482 | | | Total SA | | | 1,030,807 | | |

| | 1,226 | | | Ubisoft Entertainment SA* | | | 99,002 | | |

| | 3,814 | | | Veolia Environnement SA | | | 78,461 | | |

| | 224 | | | Vicat SA | | | 10,641 | | |

| | 4,958 | | | Vinci SA | | | 409,119 | | |

| | 95 | | | Virbac SA* | | | 12,387 | | |

| | 4,303 | | | Vivendi SA | | | 104,914 | | |

| | 214 | | | Worldline SA/France#,* | | | 10,347 | | |

| | | | 11,642,520 | | |

| | | Germany—6.0% | |

| | 1,211 | | | Aareal Bank AG | | | 37,449 | | |

| | 1,377 | | | adidas AG | | | 287,772 | | |

| | 210 | | | ADO Properties SA# | | | 10,952 | | |

| | 2,638 | | | Allianz SE, Registered | | | 529,358 | | |

| | 136 | | | Amadeus Fire AG | | | 12,699 | | |

| | 8,773 | | | Aroundtown SA | | | 72,573 | | |

| | 735 | | | Axel Springer SE | | | 41,584 | | |

| | 12,319 | | | BASF SE | | | 852,515 | | |

| | 3,864 | | | Bayer AG, Registered | | | 268,110 | | |

| | 4,607 | | | Bayerische Motoren Werke AG | | | 373,188 | | |

| | 474 | | | BayWa AG | | | 11,188 | | |

| | 261 | | | Bechtle AG | | | 20,290 | | |

| | 196 | | | Beiersdorf AG | | | 20,472 | | |

| | 456 | | | Bilfinger SE | | | 13,312 | | |

| | 1,357 | | | Borussia Dortmund GmbH & Co.

KGaA | | | 12,384 | | |

| | 2,718 | | | Brenntag AG | | | 117,403 | | |

The accompanying notes are an integral part of these financial statements.

20

M International Equity Fund

SCHEDULE OF INVESTMENTS (Continued)

December 31, 2018

Shares | |

| | Value

(Note 1) | |

| | | Germany (Continued) | |

| | 603 | | | CANCOM SE | | $ | 19,801 | | |

| | 159 | | | Cewe Stiftung & Co. KGAA | | | 11,313 | | |

| | 6,421 | | | Commerzbank AG* | | | 42,545 | | |

| | 1,367 | | | Continental AG | | | 189,123 | | |

| | 1,506 | | | Covestro AG# | | | 74,507 | | |

| | 1,019 | | | CTS Eventim AG & Co. KGaA | | | 38,038 | | |

| | 12,083 | | | Daimler AG, Registered | | | 635,582 | | |

| | 17,813 | | | Deutsche Bank AG, Registered | | | 142,191 | | |

| | 584 | | | Deutsche Beteiligungs AG | | | 22,449 | | |

| | 1,312 | | | Deutsche Boerse AG | | | 157,763 | | |

| | 696 | | | Deutsche EuroShop AG | | | 20,207 | | |

| | 5,519 | | | Deutsche Lufthansa AG | | | 124,571 | | |

| | 1,962 | | | Deutsche Pfandbriefbank AG# | | | 19,647 | | |

| | 10,000 | | | Deutsche Post AG, Registered | | | 273,949 | | |

| | 35,313 | | | Deutsche Telekom AG, Registered | | | 599,615 | | |

| | 2,787 | | | Deutsche Wohnen SE | | | 127,728 | | |

| | 3,473 | | | Deutz AG | | | 20,473 | | |

| | 821 | | | Dialog Semiconductor Plc* | | | 21,202 | | |

| | 507 | | | Duerr AG | | | 17,735 | | |

| | 33,931 | | | E.ON SE | | | 335,387 | | |

| | 298 | | | Eckert & Ziegler AG | | | 21,066 | | |

| | 601 | | | Elmos Semiconductor AG | | | 13,331 | | |

| | 2,150 | | | Evonik Industries AG | | | 53,701 | | |

| | 1,986 | | | Evotec AG* | | | 39,513 | | |

| | 334 | | | Fielmann AG | | | 20,665 | | |

| | 479 | | | Fraport AG Frankfurt Airport

Services Worldwide | | | 34,279 | | |

| | 2,143 | | | Freenet AG | | | 41,606 | | |

| | 3,621 | | | Fresenius Medical Care AG &

Co. KGaA | | | 234,986 | | |

| | 2,593 | | | Fresenius SE & Co. KGaA | | | 125,908 | | |

| | 305 | | | FUCHS PETROLUB SE | | | 12,231 | | |

| | 2,497 | | | GEA Group AG | | | 64,371 | | |

| | 620 | | | Gerresheimer AG | | | 40,668 | | |

| | 287 | | | Gesco AG | | | 7,169 | | |

| | 1,432 | | | Grand City Properties SA | | | 31,092 | | |

| | 499 | | | Hannover Rueck SE | | | 67,293 | | |

| | 1,015 | | | HeidelbergCement AG | | | 62,078 | | |

| | 524 | | | Hella GmbH & Co. KGaA | | | 20,893 | | |

| | 443 | | | Henkel AG & Co. KGaA | | | 43,524 | | |

| | 963 | | | Henkel AG & Co. KGaA | | | 105,260 | | |

| | 160 | | | HOCHTIEF AG | | | 21,577 | | |

| | 461 | | | Hornbach Holding AG &

Co. KGaA | | | 21,761 | | |

| | 1,048 | | | HUGO BOSS AG | | | 64,744 | | |

Shares | |

| | Value

(Note 1) | |

| | | Germany (Continued) | |

| | 14,412 | | | Infineon Technologies AG | | $ | 286,740 | | |

| | 3,678 | | | K+S AG | | | 66,245 | | |

| | 578 | | | KION Group AG | | | 29,357 | | |

| | 2,961 | | | Kloeckner & Co. SE | | | 20,559 | | |

| | 529 | | | LANXESS AG | | | 24,365 | | |

| | 874 | | | LEG Immobilien AG | | | 91,246 | | |

| | 746 | | | Merck KGaA | | | 76,909 | | |

| | 4,159 | | | METRO AG | | | 63,830 | | |

| | 456 | | | MTU Aero Engines AG | | | 82,758 | | |

| | 714 | | | Muenchener Rueckversicherungs-

Gesellschaft AG in Muenchen | | | 155,882 | | |

| | 361 | | | Nemetschek SE | | | 39,604 | | |

| | 397 | | | Norma Group SE | | | 19,641 | | |

| | 390 | | | OHB SE | | | 13,807 | | |

| | 1,631 | | | OSRAM Licht AG | | | 70,862 | | |

| | 40 | | | Puma SE | | | 19,569 | | |

| | 1,192 | | | QIAGEN NV* | | | 40,535 | | |

| | 19 | | | Rational AG | | | 10,798 | | |

| | 1,056 | | | Rheinmetall AG | | | 93,357 | | |

| | 863 | | | Rocket Internet SE#,* | | | 19,954 | | |

| | 641 | | | RTL Group SA | | | 34,298 | | |

| | 4,660 | | | RWE AG | | | 101,258 | | |

| | 1,686 | | | SAF-Holland SA | | | 21,635 | | |

| | 523 | | | Salzgitter AG | | | 15,322 | | |

| | 3,258 | | | SAP SE | | | 324,497 | | |

| | 963 | | | Scout24 AG# | | | 44,311 | | |

| | 2,778 | | | Siemens AG | | | 309,950 | | |

| | 185 | | | Sixt SE | | | 14,668 | | |

| | 435 | | | Software AG | | | 15,744 | | |

| | 286 | | | STRATEC SE | | | 16,483 | | |

| | 324 | | | Stroeer SE & Co. KGaA | | | 15,658 | | |

| | 1,073 | | | Symrise AG | | | 79,296 | | |

| | 1,795 | | | TAG Immobilien AG | | | 40,947 | | |

| | 1,202 | | | Takkt AG | | | 18,785 | | |

| | 315 | | | Talanx AG* | | | 10,755 | | |

| | 420 | | | Technotrans SE | | | 11,790 | | |

| | 5,253 | | | Telefonica Deutschland Holding AG | | | 20,572 | | |

| | 2,041 | | | thyssenkrupp AG | | | 35,030 | | |

| | 1,100 | | | TLG Immobilien AG | | | 30,525 | | |

| | 1,644 | | | Uniper SE | | | 42,570 | | |

| | 2,405 | | | United Internet AG | | | 105,261 | | |

| | 542 | | | Volkswagen AG | | | 86,381 | | |

| | 3,099 | | | Volkswagen AG (Preference) | | | 493,260 | | |

| | 4,022 | | | Vonovia SE | | | 182,439 | | |