Filed Pursuant to Rule 433

Registration Statement No. 333-228614

| CAPPED NOTES WITH ABSOLUTE RETURN BUFFER (Capped Notes) |

Capped Notes with Absolute Return Buffer Linked to the S&P 500® Index | |

| Issuer | The Bank of Nova Scotia (“BNS”) |

| Principal Amount | $10.00 per unit |

| Term | Approximately 2 years |

| Market Measure | The S&P 500® Index (Bloomberg symbol: “SPX”) |

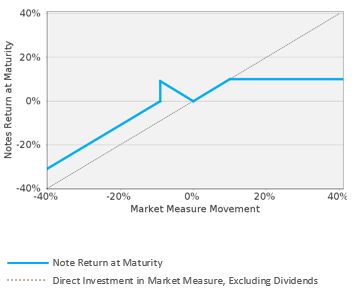

| Payout Profile at Maturity | • 1-to-1 upside exposure to increases in the Market Measure, subject to the Capped Value • A positive return equal to the absolute value of the percentage decline in the level of the Market Measure only if the Market Measure does not decline by more than [7.00% to 11.00%] (e.g., if the negative return of the Market Measure is -5.00%, you will receive a positive return of +5.00%) • 1-to-1 downside exposure to decreases in the Market Measure beyond a [7.00% to 11.00%] decline, with up to [93.00% to 89.00%] of your principal at risk |

| Capped Value | $11.00 per unit, a 10.00% return over the principal amount. |

| Threshold Value | [93.00% to 89.00%] of the Starting Value of the Market Measure, to be determined on the pricing date. |

| Investment Considerations | This investment is designed for investors who anticipate that the Market Measure will either increase moderately over the term of the notes or decrease to a level which is not below the Threshold Value and are willing to accept a capped return, take downside risk below a threshold and forgo interim interest payments. |

| Preliminary Offering Documents | |

| Exchange Listing | No |

You should read the relevant Preliminary Offering Documents before you invest. Click on the Preliminary Offering Documents hyperlink above or call your Financial Advisor for a hard copy.

Risk factors

Please see the Preliminary Offering Documents for a description of certain risks related to this investment, including, but not limited to, the following:

• | Depending on the performance of the Market Measure as measured shortly before the maturity date, your investment may result in a loss; there is no guaranteed return of principal. |

• | Payments on the notes are subject to the credit risk of BNS, and actual or perceived changes in the creditworthiness of BNS are expected to affect the value of the notes. If BNS becomes insolvent or is unable to pay its obligations, you may lose your entire investment. |

• | Your potential for a positive return based on the depreciation of the Market Measure is limited and may be less than that of a comparable investment that takes a short position directly in the Market Measure (or the stocks included in the Market Measure). The absolute value return feature applies only if the Ending Value is less than the Starting Value but greater than or equal to the Threshold Value. Because the Threshold Value is [93.00% to 89.00%] of the Starting Value, any positive return due to the depreciation of the Market Measure is limited to [7.00% to 11.00%] (the actual Threshold Value, and by extension, the cap on the positive return due to the depreciation of the Market Measure, will be determined on the pricing date). Any decline in the Ending Value from the Starting Value by more than [7.00% to 11.00%] will result in a loss, rather than a positive return, on the notes. In contrast, for example, a short position in the Market Measure (or the stocks included in the Market Measure) would allow you to receive the full benefit of any decrease in the level of the Market Measure (or the stocks included in the Market Measure). |

• | Your investment return based on any increase in the level of the Market Measure limited to the return represented by the Capped Value and may be less than a comparable investment directly in the stocks included in the Market Measure. |

• | The initial estimated value of the notes on the pricing date will be less than their public offering price. |

• | If you attempt to sell the notes prior to maturity, their market value may be lower than both the public offering price and the initial estimated value of the notes on the pricing date. |

• | You will have no rights of a holder of the securities represented by the Market Measure, and you will not be entitled to receive securities or dividends or other distributions by the issuers of those securities. |

• | The COVID-19 virus may have an adverse impact on BNS. |

Final terms will be set on the pricing date within the given range for the specified Market-Linked Investment. Please see the Preliminary Offering Documents for complete product disclosure, including related risks and tax disclosure.

The graph above and the table below reflect the hypothetical return on the notes, based on the terms contained in the table to the left (using the mid-point for any range(s)). The graph and table have been prepared for purposes of illustration only and do not take into account any tax consequences from investing in the notes.

| Hypothetical Percentage Change from the Starting Value to the Ending Value | Hypothetical Redemption Amount per Unit | Hypothetical Total Rate of Return on the Notes |

| -100.00% | $0.90 | -91.00% |

| -50.00% | $5.90 | -41.00% |

| -30.00% | $7.90 | -21.00% |

| -20.00% | $8.90 | -11.00% |

| -10.00% | $9.90 | -1.00% |

-9.00%(1) | $10.90 | 9.00% |

| -5.00% | $10.50 | 5.00% |

| -3.00% | $10.30 | 3.00% |

| 0.00% | $10.00 | 0.00% |

| 2.00% | $10.20 | 2.00% |

| 5.00% | $10.50 | 5.00% |

| 10.00% | $11.00(2) | 10.00% |

| 20.00% | $11.00 | 10.00% |

| 30.00% | $11.00 | 10.00% |

| 40.00% | $11.00 | 10.00% |

| 50.00% | $11.00 | 10.00% |

| 60.00% | $11.00 | 10.00% |

(1) | This hypothetical percentage change corresponds to the Threshold Value. |

(2) | Any positive return based on the appreciation of the Market Measure cannot exceed the Capped Value. |

The Bank of Nova Scotia (“BNS”) has filed a registration statement (which includes a prospectus) with the U.S. Securities and Exchange Commission (SEC) for the notes that are described in this Guidebook. Before you invest, you should carefully read the prospectus in that registration statement and other documents that BNS has filed with the SEC for more complete information about BNS and any offering described in this Guidebook. You may obtain these documents without cost by visiting EDGAR on the SEC Website at www.sec.gov. BNS’s Central Index Key, or CIK, on the SEC website is 9631. Alternatively, Merrill Lynch will arrange to send you the prospectus and other documents relating to any offering described in this document if you so request by calling toll-free 1-800-294-1322. BNS faces risks that are specific to its business, and we encourage you to carefully consider these risks before making an investment in its securities.