Use these links to rapidly review the document

TABLE OF CONTENTS

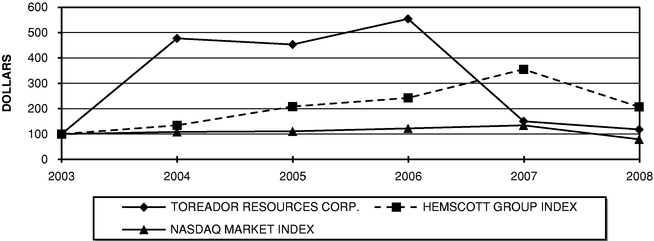

Item 8. Financial Statements

Table of Contents

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington D.C. 20549

Form 10-K

| | |

| ý | | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

|

For the fiscal year ended: December 31, 2008 |

OR |

o |

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number: 0-02517

Toreador Resources Corporation

(Exact name of Registrant as specified in its charter)

| | |

| Delaware | | 75-0991164 |

(State or other jurisdiction

of incorporation) | | (I.R.S. Employer

Identification Number) |

13760 Noel Road #1100

Dallas, Texas

(Address of principal executive office) |

|

75240

(Zip Code) |

Registrant's telephone number, including area code: (214) 559-3933

Securities registered pursuant to Section 12(b) of the Exchange Act:

| | |

Title of each Class: | | Name of each exchange on which registered: |

|---|

COMMON STOCK, PAR VALUE

$.15625 PER SHARE | | NASDAQ GLOBAL MARKET |

Securities registered pursuant to Section 12(g) of the Exchange Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer or a smaller reporting company. See definitions of "large accelerated filer," "accelerated filer," and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| | | | | | |

| Large accelerated filer o | | Accelerated filer ý | | Non-accelerated filer o

(Do Not Check if a Smaller

Reporting Company) | | Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined by Rule 12b-2 of the Exchange Act). Yes o No ý

The aggregate market value of the voting and non-voting common equity of the registrant held by non-affiliates, computed by reference to the closing sales price of such stock, as of June 30, 2008 was $115,162,327. (For purposes of determination of the aggregate market value, only directors, executive officers and 10% or greater stockholders have been deemed affiliates.)

The number of shares outstanding of the registrant's common stock, par value $.15625, as of March 10, 2009 was 20,264,333 shares.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant's Proxy Statement for the 2009 Annual Meeting of Stockholders, expected to be filed on or before April 30, 2009, are incorporated by reference into Part III of this Form 10-K

Table of Contents

TABLE OF CONTENTS

Table of Contents

PART I

Items 1 and 2. Business and Properties

Toreador Resources Corporation, a Delaware corporation (together with its direct and indirect subsidiaries, "Toreador," "we," "us," "our," or the "Company"), is an independent international energy company engaged in oil and natural gas exploration, development, production and acquisition activities. We are primarily focused on our core areas in France and Hungary. Our international operations are all located in European Union or European Union candidate countries that we believe have stable governments, have existing transportation infrastructure, have attractive fiscal policies and are net importers of oil and natural gas.

We currently hold interests in permits granting us the right to explore and develop oil and natural gas properties in offshore and onshore Turkey, Hungary, Romania and France. At December 31, 2008, we held interests in approximately 5.9 million gross acres and approximately 4.2 million net acres, of which 99.4% is undeveloped. At December 31, 2008, our estimated net proved reserves were 7.6 million barrels of oil equivalent (MMBOE).

Historically, our operations have been concentrated in the Paris Basin in France and in south central onshore Turkey and offshore Turkey in the Black Sea. These two regions accounted for 98% of our total proved reserves as of December 31, 2008 and approximately 90.4% of our total production for the year ended December 31, 2008.

Incorporated in 1951, we were formerly known as Toreador Royalty Corporation.

See the "Glossary of Selected Oil and Natural Gas Terms" at the end of Item 1 for the definition of certain terms in this annual report.

Recent Developments

On January 23, 2009 the Company and Nanes Balkany Partners I LP ("Nanes Balkany"), one of its largest stockholders, announced that they had entered into a settlement agreement (the "Agreement") pursuant to which the Company appointed Julien Balkany, Peter Hill, non-executive Chairman, and Craig McKenzie to its Board of Directors, Nigel J. Lovett resigned as Chief Executive Officer, President and a director of the Company, and John M. McLaughlin resigned as a non-executive Chairman and a director. The Company also appointed Craig McKenzie interim Chief Executive Officer while a search for a permanent Chief Executive Officer is completed. The Company has also agreed to redeem its Stockholder Rights Plan announced November 20, 2008 after obtaining the requisite approvals from its lender.

On February 3, 2009, the Company announced that it had agreed to revised terms for the sale to Petrol Ofisi of a 26.75% interest in the South Akcakoca Sub-Basin project and associated licenses located in the Black Sea offshore Turkey in the amount of US $55 million. Following the closing Toreador will retain a 10% interest in the SASB.

On February 23, 2009 the Company announced a cohesive plan to turn around the Company that includes cutting overhead, divesting non-core assets, reducing debt and improving its core operations in France and Hungary. The plan includes closing the corporate headquarters in Dallas, Texas and moving it to Paris, France and exiting Turkey by the end of 2009.

On March 3, 2009, the sale to Petrol Ofisi of 26.75% out of a 36.75% working interest in the South Akcakoca Sub-Basin for $55 million was closed. Upon closing the Company received cash proceeds of $50 million and the additional $5 million is due on September 1, 2009.

Upon funding of the sale to Petrol Ofisi, the Company retired the outstanding amount due under the facilities with the International Finance Corporation. The total amount paid was $36.4 million which was comprised of $30 million in principal, $5.9 million in additional compensation, as defined in the Loan and

1

Table of Contents

Guarantee Agreement among Toreador Resources Corporation and the International Finance Corporation dated December 28, 2006, and $500,000 in accrued interest and fees.

Update on current operations

On February 6, 2009, the Balotaszallas-E-1 ("THL Ba-E-1") well was spudded. This is a deep Kiskunhalas well in the Tompa Block. The well is being drilled in an updip location to evaluate a deep gas play that was first identified by two wells drilled in the late 1980's by OKGT (the former Hungarian state oil company) and the U.S. Geological Survey. The wells produced gas in drill stem tests from a conglomerate encountered below 3,200m depth in the northwestern corner of the Tompa block. The terms of the joint venture for drilling the THL Ba-E-1 well are for the partner to drill, case and test a well projected to cost up to $21 million in return for a 75% interest in the Tompa block. Toreador is being carried for the first well and retains a 25% working interest in the block.

In the fourth quarter of 2008 and during the first quarter of 2009, Toreador farmed out all of its working interest in Romania to three different companies and has closed its office. The terms of each farmout are as follows:

A joint venture agreement with Stratum Energy Company Limited, a private Texas-based exploration and production company was entered into in the third quarter of 2008. The terms of the agreement call for Stratum to either re-enter a well and drill two new wells or drill three new wells to earn a 70% interest and operatorship in the Moinesti block. In January 2009, Toreador farmed out its remaining 30% interest to a Romanian oil and gas company for a 15% gross overriding royalty interest.

In January 2009, Toreador sold its interest to Lotus Petrol SRL, a Romanian oil and gas company, in consideration of i) a 12.5% gross overriding royalty interest; ii) an agreement to drill a 3,000 meter obligation well in 2009; iii) the assumption of all environmental liabilities in the field, both past and future and iv) the assumption of all liabilities related to any and all service contracts.

In February 2009, we entered into a Farmout Agreement with Amromco Energy L.L.C., whereby we farmed out 100% of our interest in this block in exchange for a 10% gross overriding royalty interest and the agreement to drill a 1,500 meter well in the next two years.

Strategy

The Company is in the process of formulating a new long-term strategy that will be presented to shareholders by the planned Annual Shareholder Meeting set for June 2009. In the interim, the Company has developed a platform that is in direct response to the current crisis in the credit and equity markets and sharply reduced commodity prices. The Company is facing significant debt obligations and current commodity prices are less than half that of peak 2008 levels.

Under the new corporate platform the Company has taken the following proactive steps:

- •

- The $55 million sale of a 26.75% interest in the South Akcakoca Sub-Basin ("SASB") to Petrol Ofisi was closed and $50 million was funded on March 3, 2009;

2

Table of Contents

- •

- The Company has retained Stellar Energy Advisors, based in London, UK, to manage an open bid process to sell its remaining 10% interest in the SASB, in addition to its onshore production and 2.7 million net acres in exploration licenses that are currently held;

- •

- Per the covenants of the International Finance Corporation facilities, a portion of the net proceeds of the Petrol Ofisi sale have been used to fully repay and retire the facility;

- •

- A share buyback program has been adopted by the Board of Directors for the repurchase of up to 1 million common shares of Toreador that may be repurchased in the open market at any time over the next 12 months;

- •

- The Company intends to repurchase a portion of the Convertible Senior Notes;

- •

- Notwithstanding that the Company is incorporated in Delaware and listed on the NASDAQ, its operations are located in Europe. With its current headquarters in Dallas costing over $7 million a year in overhead, there is considerable room to improve efficiency and integrate activities across the Company. The Company expects to have completed moving its headquarters to its Paris office by July 2009, reducing its presence in the United States to focus only on securities exchange requirements and investor relations;

- •

- The Company plans to continue with its efforts to establish a strong presence in Hungary and is currently drilling an exploration well on the Tompa Block in Hungary, the results of which are expected by early second quarter 2009;

- •

- The Paris Basin will remain the Company's core asset with current production of approximately 1,000 net barrels per day coming from low-decline, long-life assets. A comprehensive portfolio review of our fields and 461,000 net acres held pursuant to licenses is now underway. The results of the study will be launched as part of the three year strategic plan at the Annual Stockholders Meeting in June 2009.

The Corporate Platform focuses on the following four areas:

Due to the Company's operations being in Europe we will relocate the corporate headquarters to our Paris, France office and we have retained Stellar Energy Advisors to assist in selling our remaining interest in Turkey. The relocation and the sale will result in a significant savings in general and administrative costs specifically that should be accomplished through a consolidation of job functions and success based compensation for employees.

In 2009 and 2010 the Company's primary use of cash will be for the reduction of debt, purchasing up to 1 million shares of Toreador common stock and funding our 2009 capital expenditure program.

Since we retired the facilities with the International Finance Corporation in March 2009, our focus will be on the repurchasing outstanding Convertible Senior Notes to reduce further our debt.

Our capital expenditure program is limited to those costs that must be incurred in order to retain our interest in the licenses. We estimate that our 2009 capital expenditure program will be approximately $7.2 million, which could possibly be reduced further if we sell our remaining interest in Turkey. We will continue to farmout all seismic and exploration drilling. We will attempt to secure partners to pay for all seismic and drilling costs up to casing point. Our plan is for industry partners to pay for 100% of all exploratory costs in order to earn a 50%-75% working interest.

3

Table of Contents

The Company believes that stockholder value can best be achieved by focusing on those areas that offer the best chance of success and have a proven infrastructure for the oil and natural gas industry. We believe that our current acreage positions in France and Hungary can serve as the platform for growth and offer the Company the best opportunity to create stockholder value. Therefore, we have farmed out our interest in Romania, retaining an override in the permits, and we plan to monetize our remaining interest in Turkey prior to the end of 2009.

The Board and management are committed to the best practices in corporate governance and will continually be reviewing and where necessary revising the procedures used to operate the Company. We intend to use third party expertise to review and challenge our procedures and methodologies, both operationally and administratively. Also, performance management actions followed by positive results will become a driving principle in operating the Company.

Our Properties

We hold a 100% working interest and operate the production permit covering the Charmottes Field, which currently has 7 producing oil wells. The field is producing from two separate reservoirs, one at 1,500m (4,500 feet) in a fractured limestone from the Dogger formation and the second reservoir from the Triassic sandstones at 2,500m (7,500 feet) in the Donnemarie formation. Production is approximately 140 BOPD from both reservoirs.

We operate and hold a 100% working interest in the two permits covering the Neocomian Fields, which consist of a group of four oil fields. The complex currently has 80 producing oil wells and production is approximately 850 BOPD.

An exploration prospect has been identified in the Dogger objective located 500 meters below the Neocomian producing reservoirs. This prospect is based upon oil shows found in 1957 in the Dogger section of the discovery well CR01 for the Chateaurenard field. A structural updip of 10 meters to the CR1 well has been identified from the seismic 500 meters north of the well.

We hold a 100% working interest and are the operator of this permit which covers approximately 93,157 net acres located east of the Neocomian Fields. A Dogger prospect called Les Colins was defined in 2008. Oil shows in the Dogger were encountered in 1984 in the Cudot 1 well drilled by Sun Oil on the flank of the structure in a downdip position. We propose to drill a well (Les Colins) to reach the top of the structure with a 20 meter updip to the Cudot 1 well. This prospect is analogous to the CR76 Dogger prospect on the Neocomian concession

We hold a 50% working interest in this permit covering approximately 23,635 net acres which is operated by Lundin Petroleum AB.

4

Table of Contents

We hold a 100% working interest and operate this permit covering approximately 33,111 acres. After drilling the Ichy 1D dry hole in May 2007, the seismic lines have been entirely reprocessed and are being re-interpreted now for delineating new attractive prospects at the Dogger objective. We anticipate that drilling activities will resume in 2010 on this acreage.

We hold a 100% working interest and operate this permit covering approximately 65,976 acres. The existing seismic lines representing around 900 km. have been interpreted to identify drillable Dogger prospects in the Jurassic section, analogous to the Itteville field sitting immediately north of our permit. It is anticipated that drilling will take place in 2010 to test our best Dogger prospect on this acreage.

We hold a 100% working interest and operate this permit covering approximately 82,779 acres. The existing seismic lines representing around 1000 km. were reprocessed and interpreted in 2008. Several Dogger prospects have been identified and mapped. We are anticipating drilling the Dogger La Garenne prospect in early 2010. This prospect is an analogous structure to the Saint Martin de Bossenay field located 15 km north which has produced 9 MMBbl. Two wells drilled by Total in the 1980's on the prospect had oil shows and some production. These wells were drilled downdip on the flank of the structure.

We hold a 100% working interest and operate this permit covering approximately 33,100 acres. Seismic interpretation is underway on the acreage to delineate prospects in the Portlandian limestone where significant oil shows and production occurred in the 1960's.

The Nogent sur Seine exploration permit was granted 100% to Toreador on September 23, 2008. This permit covers approximately 65,729 acres. All of the existing seismic coverage representing around 1,012 km has been purchased and seismic reprocessing will take place in 2009 to identify Dogger and Triassic prospects over this block, located in the heart of the oil kitchen of the Paris Basin.

The Leudon en Brie permit was granted 100% to Toreador on September 23, 2008 for an initial first four year period. This permit covers approximately 26,193 acres. The 655 km. grid of existing seismic recently purchased in 2008 will be reprocessed in 2009 and interpreted for identifying Dogger and Triassic prospects.

We established our initial position in Hungary in June 2005 through the acquisition of Pogo Hungary Ltd., from Pogo Producing Company for $9 million. We currently hold an interest in one exploration permit covering two blocks aggregating approximately 127,000 net acres.

Two new applications with a combined gross area of 405,000 acres have been submitted and are under consideration by the Hungarian Mining Authority. Both application areas have upside potential given their proximity to existing production and recent discoveries.

5

Table of Contents

As part of the farm-out that was concluded in late 2007, two exploration wells were drilled and a 133 sq. km 3D seismic program (Kunszentmárton program) was acquired in the southern portion of the Szolnok block. The exploration program was funded by four joint venture partners, who agreed to pay 100% of the program's cost to earn an aggregate of 75% working interest. Initially, we retained a 25% working interest in the joint venture and were the operator. The joint venture partners include three independent oil and gas exploration companies, one of which presently operates in Hungary, and a private investment company.

The Tik-1 well was drilled to the primary objective encountering approximately 40 net meters of reservoir quality, gas-filled sand in the lower Pannonian sequence, but analysis of the reservoir gas revealed that it was mainly composed of inert gases with only traces of methane. The well was subsequently suspended pending further analysis.

The second well in the program, Nko-Ny-1, which was drilled to the primary objective failed to encounter commercial hydrocarbons and was declared a dry hole.

In July 2008 one of the joint venture partners increased its participating interest to 59.5% leaving us as the operator with 15% of the Szolnok block. The remaining parties to the agreement reduced their interest in the block accordingly in return for future financial considerations.

A second 3D seismic campaign totaling 145sq. km. was carried out in October 2008 in the Endrod / Mezotur area. The acquisition focused on an area adjacent to several existing producing fields and to a number of discoveries made in the late 1970's by the previous state oil company, OKGT. Preliminary interpretation of the processed data has yielded positive indications however given the time remaining under the current license and the option to establish a production license over a considerable portion of the seismic acquisition area drilling within this area shall be deferred to the development phase which is expected in late 2009 or early 2010.

Interpretation of the Kunszentmárton seismic campaign has yielded a number of leads and prospects, one of which is scheduled to be drilled in the first quarter of 2009.

Two gas wells were drilled by the previous operator in the Szolnok Block, each of which initially tested at over 4 Mmcf per day. These stranded reserves are uneconomic to produce under current market conditions and therefore a call for bids shall be extended to a number of interested parties in 2009.

The farm-out to a private European energy fund was completed in March of 2008. A well of approximately 3,800m (12,470 feet) targeting deep, high-pressure gas up-dip of two wells drilled in the 1980's shall be drilled, cased, fraced and tested at a projected cost of $21 million in return for a 75% interest in any unconventional hydrocarbon resources discovered by the joint venture in the Kiskunhalas Trough area located in the northwest corner of Toreador's Tompa block. Toreador is being carried for its 25% interest in the well. The location was constructed in November and December of 2008 and the well was spudded on February 6, 2009.

A gas sales and technical agreement with a major European gas wholesaler in relation to the Kiha-15 production well is expected to be executed in early 2009. Permitting and planning for the pipeline route are well advanced and production is expected in 2009. Long lead items have been procured and delivery of such items is expected in the first half of 2009.

A 1 km. pipeline connecting the deep Kiskunhalas well and the Kiha-15 location is a component of the Kiha-15 pipeline plans, which once constructed should permit long term production and gas sales from the deep well in 2009.

6

Table of Contents

On March 3, 2009, the sale to Petrol Ofisi of 26.75% out of a 36.75% working interest in the South Akcakoca Sub-Basin for $55 million was closed. Upon closing the Company received proceeds of $50 million and the additional $5 million is due on September 1, 2009.

The Company has retained Stellar Energy Advisors, based in London, UK, to manage an open bid process to sell its remaining 10% interest in the SASB, in addition to its onshore production, and 2.2 million net acres in exploration licenses that are currently held;

We established our initial position in Turkey at the end of 2001 through the acquisition of Madison Oil Company. In Turkey we currently hold interests in 38 exploration and two exploitation permits covering approximately 2.2 million net acres. Our exploration and development program focuses on the following areas:

The Turkish national oil company, TPAO, currently is the operator, and after the sale to Petrol Ofisi, we hold a 10% working interest in the Western Black Sea permits, which cover approximately 961,550 gross acres.

The South Akcakoca sub-basin is an area of approximately 50,000 acres located in the Western Black Sea, offshore Turkey. We discovered gas in September 2004 with the Ayazli-1 well and since that time have drilled 18 additional successful delineation wells. The first phase of infrastructure development included: setting up three production platforms; laying a sub-sea pipeline; constructing the onshore processing facility for the entire sub-basin development; and constructing the onshore pipeline to tie into the national pipeline operated by the Turkish national gas utility. The Second Phase of the development to build a production platform over the Akcakoca 3 and 4 wells and tie the platform to the existing sub sea pipeline network is now in progress. First gas from the Phase II Development is expected to be completed mid 2010. Operator TPAO has proposed at least one deeper water exploration well during 2009.

The Eregli sub-basin is an area of approximately 75,000 acres located in the Western Black Sea, offshore Turkey. Approximately 1225 km of high resolution 2D marine seismic survey on the permit has been acquired in preparation for future exploration.

A joint venture agreement for exploration in the 844,382 gross acre Thrace Black Sea permit area in Turkish waters between the Bulgarian border and the Bosporus has been finalized with a Canadian oil and gas company which agreed to spend approximately $10.7 million in exploration expenses to earn a 42% interest in the seven permit blocks in the area. We have retained a 25% working interest and our prior partner HEMA retained a 33% interest.

Toreador has formed a joint venture with Thrace Basin Natural Gas Corporation and Pinnacle Turkey Inc. to explore six blocks in the northwest area of the Sea of Marmara adjacent to natural gas production onshore in the Thrace area of Turkey and to the immediate west of the offshore Kuzey Marmara Field. A 1,070 km 2D seismic survey and 1,014 km Gravity-Magnetic survey has been completed in the shallow water part of the licenses. The new seismic data is now being processed.

7

Table of Contents

The three permits cover approximately 329,204 acres. We hold a 100% working interest and negotiation is ongoing in the entire block with a potential partner that has already paid a portion of the costs for re-processing of existing 2D seismic data.

We have an exploration permit on three blocks in the Eastern Black Sea offshore Turkey in the coastal waters to the west-northwest of the city of Trabzon. The three blocks total approximately 357,062 acres. We are the operator and hold 100% working interest in this permit.

The Van permit area is in Eastern Turkey and covers approximately 964,629 acres. We have been gathering geological and geophysical data to define prospective structures. We have initiated the re-processing of existing 2D seismic data. We are the operator and hold a 100% working interest.

The Adiyaman permit, in which we hold a 100% working interest, covers approximately 39,450 acres located in southeast Turkey. We have completed interpretation of existing 2D seismic data in the permit area and negotiations are ongoing in the block with a potential farmout partner.

The area is on trend with oil fields in Turkey and Syria and is prospective for both natural gas and oil. Toreador has entered into a joint venture agreement with AKSA Enerji Uretim A.S., a division of the Kazanci Group of Companies, to evaluate the hydrocarbon potential in the 95,897 acre exploration permit area. We have completed the re-processing of all 2D seismic data which were acquired by the previous operator.

In the fourth quarter of 2008 and during the first quarter of 2009, Toreador farmed out all of its working interest in Romania to three different companies and has closed its office. The terms of each farmout are as follows:

A joint venture agreement with Stratum Energy Company Limited, a private Texas-based exploration and production company, was entered into in the third quarter of 2008. The terms of the agreement call for Stratum to either re-enter a well and drill two new wells or drill three new wells to earn a 70% interest and operatorship in the Moinesti block. In January 2009, we farmed out the remaining 30% interest to a Romanian oil and gas company for a 15% gross overriding royalty interest.

In January 2009, we sold our interest to Lotus Petrol SRL, a Romanian oil and gas company, for i) a 12.5% gross overriding royalty interest; ii) an agreement to drill a 3,000 meter well in 2009; iii) the assumption of all environmental liabilities in the field, both past and future, and iv) the assumption of all liabilities related to any and all service contracts.

8

Table of Contents

A farmout agreement was completed and signed in February 2009, with Amromco Energy L.L.C., whereby we farmed out 100% of our interest in exchange for a 10% gross overriding royalty interest in the block and an agreement to drill a 1,500m well in the next two years.

Title to Oil and Natural Gas Properties

We do not hold title to any of our properties, but we have been granted permits by the applicable government entities that allow us to engage in exploration, exploitation and production.

We hold nine French exploration permits: Aufferville, Nemours, Courtenay, Rigny, Joigny, Malesherbes, Mairy, Nogent sur Seine and Leudon en Brie. The French exploration permits have minimum financial requirements that we expect to meet during their terms. If such obligations are not met, the permits could be subject to forfeiture.

Under French mining law, exploitation permits can be extended by successive prolongations, with each prolongation not to exceed 25 years and such extensions are not subject to competitive bidding or public inquiry. Although the French government has no obligation to renew exploitation permits, based on conversations with the French mining authority, we believe it will renew such exploitation permits so long as we, the permit holder, demonstrate financial and technical capabilities and establish the studies used in defining the work schedule.

There is a long and clear track record of extending permits in France. Our subsidiaries have been operating in France since 1993 and have never been denied any exploration or exploitation permit for which they have applied or been denied any extension for which they have applied since 2001. However, there can be no assurance that we will be able to renew our exploitation permits.

The French exploitation permits that cover five producing oil fields in the Paris Basin are:

| | | | | | | | | | | | | |

| |

| | At December 31, 2008 | |

|---|

Property | | Permit

Expiration

Year | | Total Proved

Reserves

(MBbl) | | Post-Expiration

Proved Reserves

(MBbl) | | Percent of Proved

Reserves

Post-Expiration | |

|---|

Neocomian Fields | | | 2011 | | | 4,677 | | | 3,816 | | | 81.61 | % |

Charmottes Field | | | 2013 | | | 238 | | | 105 | | | 44.12 | % |

We have one exploration license that expires in March 2009. Several mining plots "production licenses" shall be applied for in both the Szolnok and Tompa blocks either prior to or post license expiration in March 2009. Development programs shall be implemented once the license has been awarded.

Our Hungarian proved reserves are as follows:

| | | | | | | | | | | | | | | | | | | |

| |

| | At December 31, 2008 | |

|---|

| |

| | Total Proved

Reserves | | Post-Expiration

Proved

Reserves | |

| |

|---|

| |

| | Percent of

Proved

Reserves

Post-Expiration | |

|---|

| | Permit

Expiration

Year | |

|---|

Property | | (MBbl) | | (MMCF) | | (MBbl) | | (MMCF) | |

|---|

Szolnok | | | 2009 | | | 1 | | | 950 | | | .572 | | | 806 | | | 84.86 | % |

In the opinion of Toreador's Hungarian counsel, PRK Partners/Bellak Law office under Hungarian mining law, if we provide the Hungarian mining authority with a closing report accounting for the results of

9

Table of Contents

our exploration on the exploration permit area and such closing report is approved, for one year after March 2009, we will have the exclusive right to apply for a mining plot designation in respect of that area.

If upon timely application for a mining plot designation, we meet the requirements of Hungarian mining law for a mining plot designation, the Hungarian mining authority must grant us the mining plot. We anticipate applying for a mining plot covering the relevant area within the exploration permit within the one year exclusivity period beginning in March 2009 and providing the Hungarian mining authority with the required information to obtain the mining plot designation for the relevant area.

There is a long and clear track record of exploration permits being converted into mining plot designations. Based on information provided by the Hungarian Mining Bureau, since 1991 when MOL (MOL Hungarian Oil and Gas Public Limited Company), formerly the Hungarian state oil company, became a private company, there have been at least 72 mining plots requested, all of which were granted except for eight due to non-compliance to the request for additional information, the lack of a final exploration report, the lack of an environmental license or due to regional incompatibility with the mining rights of another entity. There can be no assurance that we will be able to convert our exploration permit into a mining plot designation.

We have 38 exploration permits covering seven Petroleum Districts. The Western Black Sea permits have been extended through November 2010. The Bakuk permit and the Eastern Black Sea permits expire in September 2009, and we anticipate renewing them for an additional two year term. The Thrace Black Sea licenses expire in June 2009 and will be extended by an additional two years. The Central Black Sea license will be extended from the first quarter of 2009 for an additional two years. The Van and Adiyaman permits expire in May and July, 2010, respectively, and the Sea of Marmara permit expires in late 2011.

Onshore exploration permits are granted for four-year terms and may be extended for two additional two-year terms, and offshore exploration permits are granted for six-year terms and may be extended for two additional three-year terms, provided that drilling obligations stipulated under Turkish law are satisfied. Under Turkish law, exploitation permits are generally granted for a period of 20 years and may be renewed upon application for two additional 10-year periods. If an exploration permit is extended for development as an exploitation permit, the period of the exploration permit is counted toward the 20-year exploitation permit. In the opinion of Toreador's Turkish counsel, Kaya-Aksoy, a holder of an exploration permit that has had a discovery made on such exploration permit area and who applies for an exploitation permit in accordance with Turkish petroleum law shall be granted an exploitation permit for any area or areas covered by the exploration permit up to one-half of the exploration permit area. Therefore, in the opinion of Kaya-Aksoy, upon application for an exploitation permit, the exploration permit covering the area of the South Akcakoca Sub-Basin in which the gas discovery was made will be converted into an exploitation permit with an initial period of 20 years.

In addition, the Cendere exploitation permits are in their initial 20 year period and are eligible for renewal for up to two periods of 10 years each. In the opinion of Kaya-Aksoy, renewal applications for exploitation permits will be granted to those holders who have production of economical quantities of petroleum and comply fully with the obligations under the Turkish petroleum law. There is a long and clear track record of extending exploitation permits since 1998, there have been at least 48 renewals of exploitation permits with a majority of those renewals occurring since 2001, and as of March 2009, an application for renewal of an exploitation permit has never been denied and at least 70 conversions of exploration permits to exploitation permits have been granted and a conversion to an exploitation permit has never been denied. However, there can be no assurance that our exploration permit will be converted into exploitation permits or that our exploitation permits will be renewed.

10

Table of Contents

Our Turkish proved reserves at December 31, 2008 were as follows:

| | | | | | | | | | | | | | | | | | | |

| |

| | At December 31, 2008 | |

|---|

| |

| | Total Proved

Reserves | | Post-Expiration

Proved

Reserves | |

| |

|---|

| |

| | Percent of

Proved

Reserves

Post-Expiration | |

|---|

| | Permit

Expiration

Year | |

|---|

Property | | (MBbl) | | (MMCF) | | (MBbl) | | (MMCF) | |

|---|

Cendere (2 permits) | | | 2012 | (1) | | 740 | | | — | | | 423 | | | — | | | 57.15 | % |

S Akcakoca Sub-Basin | | | 2010 | (2) | | — | | | 10,477 | | | — | | | 8,440 | | | 80.56 | % |

Pro forma proved reserves reflecting the sale to Petrol Ofisi of 26.75% of our 36.75% interest in the South Akcakoca Sub-Basin are:

| | | | | | | | | | | | | | | | | | | |

| |

| | Pro Forma at December 31, 2008 | |

|---|

| |

| | Total Proved

Reserves | | Post-Expiration

Proved

Reserves | |

| |

|---|

| |

| | Percent of

Proved

Reserves

Post-Expiration | |

|---|

| | Permit

Expiration

Year | |

|---|

Property | | (MBbl) | | (MMCF) | | (MBbl) | | (MMCF) | |

|---|

Cendere (2 permits) | | | 2012 | (1) | | 740 | | | — | | | 423 | | | — | | | 57.15 | % |

S Akcakoca Sub-Basin | | | 2010 | (2) | | — | | | 2,851 | | | — | | | 2,297 | | | 80.56 | % |

- (1)

- Exploitation Permit

- (2)

- Exploration Permit

The Moinesti and Viperesti permits will expire in 2009 and the Fauresti rehabilitation permit will expire in 2015. If, prior to the expiration of our Romanian permits, we have not completed the minimum exploration program required by the permits, we must pay the estimated costs of such exploration program to the Romanian government. The Company does not expect to make such required payments to the Romanian government as the drilling obligations were assumed as part of the farmout agreements entered into with our partners. We have not yet established proved reserves on the Moinesti and Viperesti permits.

The following is information relating to our Romanian proved reserves at December 31, 2008, all of which relate to the pre-expiration period of the Fauresti Rehabilitation permit:

| | | | | | | | | | |

| |

| | At December 31, 2008 | |

|---|

Property | | Permit

Expiration

Year | | Oil

(MBbl) | | Gas

(MMcf) | |

|---|

Fauresti | | | 2015 | | | 1 | | | 86 | |

By the end of February 2009, we had either sold or farmed out all of our working interests in all Romanian permits while retaining an overriding royalty interest. See "Properties — Romania" for terms of each permit. Therefore we do not have any proved reserves in Romania.

Oil and Natural Gas Reserves

The following table sets forth information about our estimated net proved reserves at December 31, 2008 and December 31, 2007 for our properties. LaRoche Petroleum Consultants, Ltd., an independent petroleum engineering firm in Dallas, Texas, prepared the estimates of proved developed (PD) reserves, proved undeveloped (PUD) reserves and discounted present value (pretax). We prepared the estimate of standardized measure of proved reserves in accordance with Financial Accounting Standards Board Statement of Financial Accounting Standards No. 69,Disclosures about Oil and Gas Producing Activities. No reserve reports have been provided to any governmental agencies.

11

Table of Contents

The major changes affecting proved developed and undeveloped reserves when comparing December 31, 2008 to December 31, 2007 are summarized below:

- 1)

- Pertaining to France:

- a)

- A decrease in economic life of proved developed wells due to a decline in the oil price at December 31, 2008, to $34.72, as opposed to $96.65 at December 31, 2007. This resulted in a net decrease of 1,682 MBbl.

- b)

- Removing 12 proved undeveloped locations caused a net decrease 1,889 MBbl.

- c)

- Negative proved developed reserve revisions resulted in a decrease in reserves of 405 MBbl.

- d)

- Fourteen proved developed wells were shut-in resulting in a decrease of 401 MBbl.

- e)

- Three drilled locations in prior years resulted in one producing well which is non-commercial at December 31, 2008 causing a net decrease of 280 MBbl of proved developed reserves.

- f)

- One well was lost during 2008 workover operations causing a net decrease of 37 MBbl in proved developed reserves.

- 2)

- Total company production for 2008 was 805 MBOE.

- 3)

- In Hungary, we secured a gas contract which increased reserves by 159 MBOE.

- 4)

- In Romania, the poor operational performance of the wells resulted in a decrease of 54 MBOE in proved developed reserves. Additionally, effective January 1, 2009, we had sold our interest in the proved reserves associated with Romania.

- 5)

- In Turkey, a decrease in economic life of proved developed wells resulted in a net decrease of 390 MBOE.

The above changes also had a negative impact on the standardized measure of proved reserves. Additionally, in 2008 the operator of the offshore Turkey natural gas project finalized the budget for Phase II and increased the capital cost from $15.8 million (net) to $61.7 million (net). This $45.9 million increase resulted in almost a dollar-for-dollar reduction in the standardized measure value, since it is

12

Table of Contents

expected to be incurred in 2009 and 2010. The above referenced dollar amounts do not reflect the sale to Petrol Ofisi of 26.75% of 36.75% interest in SASB.

| | | | | | | |

| | December 31, | |

|---|

| | 2008 | | 2007 | |

|---|

TURKEY(1) | | | | | | | |

Proved developed: | | | | | | | |

Oil (MBbl) | | | 500 | | | 808 | |

Gas (MMcf) | | | 2,437 | | | 4,248 | |

Total (MBOE) | | | 906 | | | 1,516 | |

Proved undeveloped: | | | | | | | |

Oil (MBbl) | | | 240 | | | 241 | |

Gas (MMcf) | | | 8,040 | | | 8,691 | |

Total (MBOE) | | | 1,580 | | | 1,689 | |

Discounted present value at 10% (pretax) (in thousands)(2) | | $ | 27,047 | | $ | 89,376 | |

Standardized measure of proved reserves (in thousands) | | $ | 27,048 | | $ | 84,048 | |

HUNGARY | | | | | | | |

Proved developed: | | | | | | | |

Oil (MBbl) | | | 1 | | | — | |

Gas (MMcf) | | | 950 | | | — | |

Total (MBOE) | | | 159 | | | — | |

Discounted present value at 10% (pretax) (in thousands)(2) | | $ | 9,286 | | $ | — | |

Standardized measure of proved reserves (in thousands) | | $ | 9,278 | | $ | — | |

ROMANIA | | | | | | | |

Proved developed: | | | | | | | |

Oil (MBbl) | | | 1 | | | 6 | |

Gas (MMcf) | | | 86 | | | 772 | |

Total (MBOE) | | | 15 | | | 134 | |

Discounted present value at 10% (pretax) (in thousands)(2)(3) | | $ | (119 | ) | $ | 1,110 | |

Standardized measure of proved reserves (in thousands)(3) | | $ | (121 | ) | $ | 1,110 | |

FRANCE | | | | | | | |

Proved developed: | | | | | | | |

Oil (MBbl) | | | 4,385 | | | 7,170 | |

Proved undeveloped: | | | | | | | |

Oil (MBbl) | | | 530 | | | 2,798 | |

Discounted present value at 10% (pretax) (in thousands)(2) | | $ | 25,107 | | $ | 262,605 | |

Standardized measure of proved reserves (in thousands) | | $ | 18,563 | | $ | 174,211 | |

COMBINED(1) | | | | | | | |

Proved developed: | | | | | | | |

Oil (MBbl) | | | 4,887 | | | 7,984 | |

Gas (MMcf) | | | 3,473 | | | 5,020 | |

Total (MBOE) | | | 5,466 | | | 8,822 | |

Proved undeveloped: | | | | | | | |

Oil (MBbl) | | | 770 | | | 3,039 | |

Gas (MMcf) | | | 8,040 | | | 8,691 | |

Total (MBOE) | | | 2,110 | | | 4,488 | |

Total proved: | | | | | | | |

Oil (MBbl) | | | 5,657 | | | 11,023 | |

Gas (MMcf) | | | 11,513 | | | 13,711 | |

Total (MBOE) | | | 7,576 | | | 13,308 | |

Discounted present value at 10% (pretax) (in thousands)(2) | | $ | 61,321 | | $ | 353,091 | |

Standardized measure of proved reserves (in thousands) | | $ | 54,768 | | $ | 259,369 | |

- (1)

- Pro forma the sale to Petrol Ofisi of 26.75% of our 36.75% interest in the South Akcakoca Sub-Basin our December 31, 2008, Turkish proved developed gas reserves would be 663 MMcf and proved undeveloped reserves would be 2,188 MMcf. Total Turkey discounted present value at 10% would be $11,189 and standardized measure of proved reserves would be $11,189. Total Company proved reserves on a BOE basis would be 5,686 MBOE, discounted present value at 10% would be $47,075 and standardized measure of proved reserves would be $38,806.

- (2)

- The discounted present value represents the discounted future cash flows attributable to our proved oil and natural gas reserves before income tax, discounted at 10%. Although it is a non-GAAP measure, we believe that the presentation of the discounted present value is relevant and useful to our investors because it presents the discounted future net cash flows attributable to our proved reserves prior to taking into account corporate future income taxes and our current tax structure. We use this measure when assessing the potential return on investment related to our oil and natural gas properties. The standardized measure of discounted future net cash flows represents the present value of future cash flows attributable to our proved oil and natural gas reserves after income tax, discounted at 10%.

- (3)

- The negative values are due to plugging and abandonment costs incurred in the final year.

13

Table of Contents

Reserves were estimated using oil and natural gas prices and production and development costs in effect on December 31, 2008 and 2007, without escalation. The reserves were determined using both volumetric and production performance methods. Proved reserves are those estimated quantities of crude oil, natural gas and natural gas liquids that geological and engineering data demonstrate with reasonable certainty to be recoverable in future years from known reservoirs under existing economic and operating conditions.THE VALUES REPORTED MAY NOT NECESSARILY REFLECT THE FAIR MARKET VALUE OF THE RESERVES.

Approximately 27.9% of our proved reserves are classified as proved undeveloped (PUD) as determined by the LaRoche 2008 reserve report. These reserves were identified from 13 (PUD) locations as part of LaRoche's geological and reservoir engineering studies of our hydrocarbon producing assets.

The first 6 PUD locations are direct offsets to our existing French production in the Paris basin. Fault blocks have been mapped containing recoverable hydrocarbons that because of a lack of wellbores have typically underperformed from the existing waterflood. Additional wellbores may be drilled starting in 2009 to improve the recovery efficiency of the trapped hydrocarbons in these fault blocks.

Three other PUD locations were identified from our non-operated, onshore Cendere field in Turkey. Since we are not the operator of the Cendere field, we have no control of the timing or the success of any field operations.

The remaining PUD locations were identified from our 2007 drilling program in the Western Black Sea offshore Turkey. The company intends to commence recompletion operations in late 2009 as part of a Phase II development plan for the Akcakoca area.

The successful conversion of these PUD reserves into proved developed reserves is dependent upon the following:

- •

- Our ability to secure related oilfield equipment and services on a timely and competitive basis. Presently, there is great demand for and often extensive delays in securing oilfield equipment and services at any price. No assurance can be given that the requisite oilfield equipment and services can be secured in a timely and competitive manner.

- •

- Projections for proved undeveloped reserves are largely based on their analogy to similar producing properties and to volumetric calculations. Reserves projections based on analogy are subject to change due to subsequent changes in the analogous properties.

Productive Wells

The following table shows our gross and net interests in productive oil and natural gas wells as of December 31, 2008. Productive wells include wells currently producing or capable of production.

| | | | | | | | | | | | | | | | | | | |

| | Gross(1) | | Net(2) | |

|---|

| | Oil | | Gas | | Total | | Oil | | Gas | | Total | |

|---|

Turkey | | | 15 | | | 7 | | | 22 | | | 2.65 | | | 2.57 | | | 5.22 | |

Romania | | | — | | | 5 | | | 5 | | | — | | | 5.00 | | | 5.00 | |

France | | | 131 | | | — | | | 131 | | | 130.50 | | | — | | | 130.50 | |

Hungary | | | — | | | 1 | | | 1 | | | — | | | 1.00 | | | 1.00 | |

14

Table of Contents

Pro forma productive wells reflecting the sale of 26.75% of our 36.75% interest in the South Akcakoca Sub-Basin are as follows:

| | | | | | | | | | | | | | | | | | | |

| | Gross(1) | | Net(2) | |

|---|

| | Oil | | Gas | | Total | | Oil | | Gas | | Total | |

|---|

Turkey | | | 15 | | | 7 | | | 22 | | | 2.65 | | | 0.70 | | | 3.35 | |

- (1)

- "Gross" refers to wells in which we have a working interest.

- (2)

- "Net" refers to the aggregate of our percentage working interest in gross wells before royalties, before or after payout, as appropriate.

Acreage

The following table shows the developed and undeveloped acreage attributable to our ownership as of December 31, 2008.

| | | | | | | | | | | | | | | | | | | |

| | Developed Acreage | | Undeveloped Acreage | | Total Acreage | |

|---|

| | Gross | | Net | | Gross | | Net | | Gross | | Net | |

|---|

France | | | 24,260 | | | 24,260 | | | 555,236 | | | 454,800 | | | 579,496 | | | 479,060 | |

Turkey | | | 7,858 | | | 1,554 | | | 3,956,590 | | | 2,929,240 | | | 3,964,448 | | | 2,930,794 | |

Romania | | | 1,325 | | | 1,325 | | | 624,000 | | | 624,000 | | | 625,325 | | | 625,325 | |

Hungary | | | 494 | | | 494 | | | 763,743 | | | 126,282 | | | 764,237 | | | 126,776 | |

| | | | | | | | | | | | | | |

Total | | | 33,937 | | | 27,633 | | | 5,899,569 | | | 4,134,322 | | | 5,933,506 | | | 4,161,955 | |

| | | | | | | | | | | | | | |

Pro forma developed and undeveloped acreage reflecting the sale of 26.75% of our 36.75% interest in the South Akcakoca Sub-Basin would be:

| | | | | | | | | | | | | | | | | | | |

| | Developed Acreage | | Undeveloped Acreage | | Total Acreage | |

|---|

| | Gross | | Net | | Gross | | Net | | Gross | | Net | |

|---|

France | | | 24,260 | | | 24,260 | | | 555,236 | | | 454,800 | | | 579,496 | | | 479,060 | |

Turkey | | | 7,858 | | | 1,554 | | | 3,956,590 | | | 2,659,045 | | | 3,964,448 | | | 2,660,599 | |

Romania | | | 1,325 | | | 1,325 | | | 624,000 | | | 624,000 | | | 625,325 | | | 625,325 | |

Hungary | | | 494 | | | 494 | | | 763,743 | | | 126,270 | | | 764,237 | | | 126,764 | |

| | | | | | | | | | | | | | |

Total | | | 33,937 | | | 27,633 | | | 5,899,569 | | | 3,864,115 | | | 5,933,506 | | | 3,891,748 | |

| | | | | | | | | | | | | | |

Undeveloped acreage includes only those acres on which wells have not been drilled or completed to permit the production of commercial quantities of oil and natural gas regardless of whether or not the acreage contains proved reserves.

15

Table of Contents

Drilling Activity

The following table shows our drilling activities on a gross and net basis for the years ended 2008, 2007 and 2006.

| | | | | | | | | | | | | | | | | | | | | |

| | Year ended December 31, | |

|---|

| | 2008 | | 2007 | | 2006 | |

|---|

| | Gross(1) | | Net(2) | | Gross(1) | | Net(2) | | Gross(1) | | Net(2) | |

|---|

TURKEY | | | | | | | | | | | | | | | | | | | |

Development: | | | | | | | | | | | | | | | | | | | |

| | Gas(3) | | | — | | | — | | | — | | | — | | | 7 | | | 2.57 | |

| | Abandoned(4) | | | — | | | — | | | — | | | — | | | 2 | | | 0.56 | |

| | | | | | | | | | | | | | |

| | | Total | | | — | | | — | | | — | | | — | | | 9 | | | 3.13 | |

| | | | | | | | | | | | | | |

Exploratory | | | | | | | | | | | | | | | | | | | |

| | Gas(5) | | | — | | | — | | | 3 | | | 1.00 | | | — | | | — | |

| | Abandoned(4) | | | — | | | — | | | 1 | | | .50 | | | — | | | — | |

| | | | | | | | | | | | | | |

| | | Total | | | — | | | — | | | 4 | | | 1.50 | | | — | | | — | |

| | | | | | | | | | | | | | |

HUNGARY | | | | | | | | | | | | | | | | | | | |

Exploratory | | | | | | | | | | | | | | | | | | | |

| | | Abandoned(4) | | | 2 | | | .30 | | | 2 | | | 2.00 | | | 1 | | | 1.00 | |

ROMANIA | | | | | | | | | | | | | | | | | | | |

Exploratory | | | | | | | | | | | | | | | | | | | |

| | Abandoned(4) | | | — | | | — | | | 3 | | | 3.00 | | | — | | | — | |

FRANCE | | | | | | | | | | | | | | | | | | | |

Exploratory: | | | | | | | | | | | | | | | | | | | |

| | Abandoned(4) | | | — | | | — | | | 2 | | | 2.00 | | | — | | | — | |

- (1)

- "Gross" is the number of wells in which we have a working interest.

- (2)

- "Net" is the aggregate obtained by multiplying each gross well by our after payout percentage working interest.

- (3)

- "Gas" means natural gas wells that are either currently producing or are capable of production.

- (4)

- "Abandoned" means wells that were dry when drilled and were abandoned without production casing being run.

- (5)

- "Gas" means gas flow was tested and temporarily suspended awaiting further work.

16

Table of Contents

Net Production, Unit Prices and Costs

The following table summarizes our oil, natural gas and natural gas liquids production, net of royalties, for the periods indicated for France, Turkey and Romania. It also summarizes calculations of our total average unit sales prices and unit costs.

| | | | | | | | | | | | | |

| | France | | Turkey | | Romania | | Total | |

|---|

Year Ended December 31, 2008 | | | | | | | | | | | | | |

Production: | | | | | | | | | | | | | |

Oil (Bbls) | | | 365,361 | | | 55,417 | | | 3,262 | | | 424,040 | |

Daily average (Bbls/Day) | | | 1,001 | | | 152 | | | 9 | | | 1,162 | |

Gas (Mcf) | | | — | | | 1,840,420 | | | 445,606 | | | 2,286,026 | |

Daily average (Mcf/Day) | | | — | | | 5,042 | | | 1,221 | | | 6,263 | |

Daily average (BOE/Day) | | | 1,001 | | | 992 | | | 212 | | | 2,205 | |

Unit prices: | | | | | | | | | | | | | |

Average oil price ($/Bbl) | | $ | 93.32 | | $ | 93.21 | | $ | 57.97 | | $ | 93.04 | |

Average gas price ($/Mcf) | | | — | | | 11.14 | | | 5.32 | | | 10.00 | |

Average equivalent price ($/BOE) | | | 93.32 | | | 70.88 | | | 32.99 | | | 77.41 | |

Unit costs ($/BOE): | | | | | | | | | | | | | |

Lease operating | | $ | 25.35 | | $ | 9.60 | | $ | 57.58 | | $ | 21.38 | (1) |

Exploration and acquisition | | | 0.39 | | | 7.33 | | | 6.84 | | | 7.21 | (1) |

Depreciation, depletion and amortization | | | 12.83 | | | 75.01 | | | 11.48 | | | 41.17 | (1) |

Impairment of oil and natural gas properties | | | — | | | 227.36 | | | 7.88 | | | 105.88 | (1) |

General and administrative | | | 3.55 | | | 5.57 | | | — | | | 19.24 | (1) |

| | | | | | | | | | |

Total | | $ | 42.12 | | $ | 324.87 | | $ | 83.78 | | $ | 194.88 | |

| | | | | | | | | | |

Year Ended December 31, 2007 | | | | | | | | | | | | | |

Production: | | | | | | | | | | | | | |

Oil (Bbls) | | | 383,341 | | | 65,686 | | | 9,594 | | | 458,621 | |

Daily average (Bbls/Day) | | | 1,050 | | | 180 | | | 26 | | | 1,256 | |

Gas (Mcf) | | | — | | | 904,927 | | | 689,290 | | | 1,594,217 | |

Daily average (Mcf/Day) | | | — | | | 2,479 | | | 1,888 | | | 4,367 | |

Daily average (BOE/Day) | | | 1,050 | | | 593 | | | 341 | | | 1,984 | |

Unit prices: | | | | | | | | | | | | | |

Average oil price ($/Bbl) | | $ | 67.49 | | $ | 61.98 | | $ | 57.59 | | $ | 66.50 | |

Average gas price ($/Mcf) | | | — | | | 8.60 | | | 4.90 | | | 7.00 | |

Average equivalent price ($/BOE) | | | 67.49 | | | 54.77 | | | 31.55 | | | 57.51 | |

Unit costs ($/BOE): | | | | | | | | | | | | | |

Lease operating | | $ | 19.17 | | $ | 12.18 | | $ | 21.42 | | $ | 17.46 | (1) |

Exploration and acquisition | | | 2.23 | | | 11.83 | | | 51.83 | | | 20.36 | (1) |

Depreciation, depletion and amortization | | | 10.80 | | | 46.49 | | | 54.05 | | | 29.36 | (1) |

Dry hole cost and impairment of oil and natural gas properties | | | 10.04 | | | 20.74 | | | 189.16 | | | 48.74 | (1) |

General and administrative | | | 7.39 | | | 17.18 | | | 4.32 | | | 23.91 | (1) |

| | | | | | | | | | |

Total | | $ | 49.63 | | $ | 108.42 | | $ | 320.78 | | $ | 139.83 | |

| | | | | | | | | | |

17

Table of Contents

| | | | | | | | | | | | | |

| | France | | Turkey | | Romania | | Total | |

|---|

Year Ended December 31, 2006 | | | | | | | | | | | | | |

Production: | | | | | | | | | | | | | |

Oil (Bbls) | | | 441,759 | | | 68,342 | | | 7,728 | | | 517,829 | |

Daily average (Bbls/Day) | | | 1,210 | | | 187 | | | 21 | | | 1,418 | |

Gas (Mcf) | | | — | | | — | | | 502,192 | | | 502,192 | |

Daily average (Mcf/Day) | | | — | | | — | | | 1,376 | | | 1,376 | |

Daily average (BOE/Day) | | | 1,210 | | | 199 | | | 250 | | | 1,659 | |

Unit prices: | | | | | | | | | | | | | |

Average oil price ($/Bbl) | | $ | 61.74 | | $ | 56.10 | | $ | 52.71 | | $ | 60.86 | |

Average gas price ($/Mcf) | | | — | | | — | | | 3.57 | | | 3.57 | |

Average equivalent price ($/BOE) | | | 61.74 | | | 56.10 | | | 24.06 | | | 55.37 | |

Unit costs ($/BOE): | | | | | | | | | | | | | |

Lease operating | | $ | 16.36 | | $ | 11.60 | | $ | 7.86 | | $ | 14.52 | (1) |

Exploration and acquisition | | | 0.98 | | | 11.69 | | | 7.09 | | | 6.55 | (1) |

Depreciation, depletion and amortization | | | 7.06 | | | 10.94 | | | 22.85 | | | 10.43 | (1) |

Dry hole cost and impairment of oil and natural gas properties | | | — | | | — | | | — | | | 2.83 | (1) |

General and administrative | | | 4.31 | | | 11.81 | | | 6.09 | | | 15.78 | (1) |

| | | | | | | | | | |

Total | | $ | 28.71 | | $ | 46.04 | | $ | 43.89 | | $ | 50.11 | |

| | | | | | | | | | |

- (1)

- Total amounts include costs related to operations in the US and Hungary.

Office Lease

We occupy 23,297 square feet of office space at 13760 Noel Rd., Suite 1100, Dallas, Texas 75240. The lease for this space became effective on October 1, 2007 and is for seven years, and the average monthly rental is $33,005 per month for the term of the lease. We also occupy 3,218 square feet of office space in Paris, France, approximately 9,000 square feet of office in Ankara, Turkey, 3,767 square feet in Bucharest, Romania and 2,896 square feet of office space in Budapest, Hungary. Total rental expense for 2008 was approximately $953,000.

Markets and Competition

In France, we currently sell all of our oil production to Elf Antar France S.A., the largest purchaser in the area. This production is shipped by truck to a nearby Elf refinery. The oil also can be transported to refineries on the north coast of France via pipeline. Oil production in Turkey is sold to refineries in the southern part of the country. Our Turkish gas is sold through the national pipeline.

The oil and natural gas industry is highly competitive. We encounter strong competition from other independent operators and from major oil companies in acquiring properties, contracting for drilling equipment and securing trained personnel. Many of these competitors have financial and technical resources and staffs substantially larger than those available to us. As a result, our competitors may be able to pay more for desirable leases, and they may pay more to evaluate, bid for and purchase a greater number of properties or prospects than our financial or personnel resources permit us to do.

We also are affected by competition for drilling rigs and the availability of tubular goods and certain other equipment. While the oil and natural gas industry has experienced shortages of drilling rigs and equipment, pipe and personnel in the past, we are not presently experiencing any shortages and do not

18

Table of Contents

foresee any such shortages in the near future; however, we are unable to predict how long current market conditions will continue.

Competition for attractive oil and natural gas producing properties, undeveloped leases and drilling rights is also strong, and we can give no assurance we will be able to compete satisfactorily in acquiring properties. Since many major oil companies have publicly indicated their decision to focus on overseas activities, we cannot ensure we will be successful in acquiring any such properties.

Government Regulation

Our current exploration activities are conducted in Turkey, Hungary and France. Such activities are affected in varying degrees by political stability and government regulations relating to foreign investment and the oil and natural gas industry. Changes in these regulations or shifts in political attitudes are beyond our control and may adversely affect our business. Operations may be affected in varying degrees by government regulations with respect to restrictions on production, price controls, export controls, income taxes, expropriation of property, environmental legislation and mine safety.

Our current or future operations, including exploration and development activities on our properties, require permits from various governmental authorities, and such operations are and will be governed by laws and regulations governing prospecting, development, production, exports, taxes, labor standards, occupational health, waste disposal, toxic substances, land use, environmental protection and other matters. Compliance with these requirements may prove to be difficult and expensive. See "Risk Factors" for further information regarding international government regulation.

In order to carry out exploration and development of mineral interests or to place these into commercial production, we may require certain licenses and permits from various governmental authorities. There can be no guarantee that we will be able to obtain all necessary licenses and permits that may be required. In addition, such licenses and permits are subject to change and there can be no assurances that any application to renew any existing licenses or permits will be approved. See "Risk Factors" for further information regarding our foreign permits and licenses.

Currently, there are no restrictions on the repatriation of earnings or capital to foreign entities from France, Turkey, Romania or Hungary. However, there can be no assurance that any such restrictions on repatriation of earnings or capital from the aforementioned countries or any other country where we may invest will not be imposed in the future.

The oil and natural gas industry is subject to extensive and varying environmental regulations in each of the jurisdictions in which we may operate. Environmental regulations establish standards respecting health, safety and environmental matters and place restrictions and prohibitions on emissions of various substances produced concurrently with oil and natural gas. These regulations can have an impact on the selection of drilling locations and facilities, potentially resulting in increased capital expenditures. In addition, environmental legislation may require those wells and production facilities to be abandoned and sites reclaimed to the satisfaction of local authorities. We are committed to complying with environmental and operation legislation wherever we operate.

19

Table of Contents

Employees

As of March 10, 2009, we employed 81 full-time employees. None of our employees are represented by unions or covered by collective bargaining agreements. To date, we have not experienced any strikes or work stoppages due to labor problems, and we believe that we have good relations with our employees. As needed, we also utilize the services of independent consultants on a contract basis.

Segment Reporting

See Note 15 in the Notes to Consolidated Financial Statements for financial information by segment.

Internet Address/Availability of Reports

Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 are made available free of charge on our website athttp://www.toreador.net as soon as reasonably practicable after we electronically file such material with, or otherwise furnish it to, the Securities and Exchange Commission.

Glossary of Selected Oil and Natural Gas Terms

"2D" or"2D SEISMIC." An exploration method of sending energy waves or sound waves into the earth and recording the wave reflections to indicate the type, size, shape, and depth of subsurface rock formations. 2D seismic provides a two dimensional representation along the profile of the line as it was shot. 2D surveys are measured in kilometers or miles.

"3D" or"3D SEISMIC." An exploration method of sending energy waves or sound waves into the earth and recording the wave reflections to indicate the type, size, shape, and depth of subsurface rock formations. 3D seismic lines are shot very close together. This allows for the ability for computers to generate seismic profiles in any direction and form 3D surfaces. 3D surveys are measured in square kilometers or square miles.

"Bbl." One stock tank barrel, or 42 U.S. gallons liquid volume, used herein in reference to crude oil or other liquid hydrocarbons.

"BOE." Barrels of oil equivalent. BTU equivalent of six thousand cubic feet (Mcf) of natural gas which is equal to the BTU equivalent of one barrel of oil.

"BOPD" Barrels of oil per day.

"BTU." British Thermal Unit.

"DEVELOPMENT WELL" A well drilled within the proved boundaries of an oil or natural gas reservoir with the intention of completing the stratigraphic horizon known to be productive.

"DISCOUNTED PRESENT VALUE." The present value of proved reserves is an estimate of the discounted future net cash flows from each property at the specified date, or as otherwise indicated. Net cash flow is defined as net revenues, after deducting production and ad valorem taxes, less future capital costs and operating expenses, but before deducting federal income taxes. The future net cash flows have been discounted at an annual rate of 10% to determine their "present value." The present value is shown to indicate the effect of time on the value of the revenue stream and should not be construed as being the fair market value of the properties. In accordance with Securities and Exchange Commission rules, estimates have been made using constant oil and natural gas prices and operating costs at the specified date, or as otherwise indicated.

"DRY HOLE." A development or exploratory well found to be incapable of producing either oil or natural gas in sufficient quantities to justify completion as an oil or natural gas well.

20

Table of Contents

"EXPLORATORY WELL" A well drilled to find and produce oil or natural gas in an unproved area, to find a new reservoir in a field previously found to be productive of oil or natural gas in another reservoir, or to extend a known reservoir.

"GROSS ACRES" or"GROSS WELLS." The total number of acres or wells, as the case may be, in which a working or any type of royalty interest is owned.

"KM." One kilometer.

"MBbl." One thousand Bbls.

"MMBbl" One million Bbls.

"MBOE." One thousand BOE.

"MMBOE." One million BOE.

"Mcf." One thousand cubic feet of natural gas.

"MMcf" One million cubic feet of natural gas.

"NET ACRES." The sum of the fractional working or any type of royalty interests owned in gross acres.

"PERMIT." An area onshore or offshore that comprises a contiguous acreage, or leasehold, position on which an operator drills exploratory and/or development wells. Sometimes designated as a "lease" or "block."

"PRODUCING WELL" or"PRODUCTIVE WELL."A well that is capable of producing oil or natural gas in economic quantities.

"PROVED DEVELOPED RESERVES." The oil and natural gas reserves that can be expected to be recovered through existing wells with existing equipment and operating methods. Additional oil and natural gas expected to be obtained through the application of fluid injection or other improved recovery techniques for supplementing the natural forces and mechanisms of primary recovery should be included as "proved developed reserves" only after testing by a pilot project or after the operation of an installed program has confirmed through production response that increased recovery will be achieved.

"PROVED RESERVES." The estimated quantities of crude oil, natural gas and natural gas liquids that geological and engineering data demonstrate with reasonable certainty to be recoverable in future years from known reservoirs under existing economic and operating conditions.

"PROVED UNDEVELOPED RESERVES." The oil and natural gas reserves that are expected to be recovered from new wells on undrilled acreage or from existing wells where a relatively major expenditure is required for recompletion. Reserves on undrilled acreage are limited to those drilling units offsetting productive units that are reasonably certain of production when drilled. Proved reserves for other undrilled units can be claimed only where it can be demonstrated with certainty that there is continuity of production from the existing productive formation. Under no circumstances should estimates for proved undeveloped reserves be attributable to any acreage for which an application of fluid injection or other improved recovery techniques is contemplated, unless such techniques have been proved effective by actual tests in the area and in the same reservoir.

"ROYALTY INTEREST." An interest in an oil and natural gas property entitling the owner to a share of oil and natural gas production free of production costs.

"STANDARDIZED MEASURE." Under the Standardized Measure, future cash flows are estimated by applying year-end prices, adjusted for fixed and determinable changes, to the estimated future production of year-end proved reserves. Future cash inflows are reduced by estimated future production and development costs based on period-end costs to determine pretax cash inflows. Future income taxes

21

Table of Contents

are computed by applying the statutory tax rate to the excess inflows over a company's tax basis in the associated properties.

Tax credits, net operating loss carryforwards and permanent differences also are considered in the future tax calculation. Future net cash inflows after income taxes are discounted using a 10% annual discount rate to arrive at the Standardized Measure.

"UNDEVELOPED ACREAGE." Lease acreage on which wells have not been drilled or completed to a point that would permit the production of commercial quantities of oil and natural gas regardless of whether such acreage contains proved reserves.

"WORKING INTEREST." The operating interest (not necessarily as operator) that gives the owner the right to drill, produce and conduct operating activities on the property and a share of production, subject to all royalties, overriding royalties and other burdens, and to all exploration, development and operational costs including all risks in connection therewith.

Item 1A. Risk Factors

Risks Related To Our Company

Our growth depends on our ability to obtain additional capital and we may not be able to obtain sufficient additional capital to grow our business.

Effectuation of our business strategy will require substantial capital expenditures. In order to fund our future growth we will need to obtain additional capital. The amount and timing of our future capital requirements will depend upon a number of factors, including:

- •

- drilling results and costs;

- •

- transportation costs;

- •

- equipment costs and availability;

- •

- marketing expenses;

- •

- oil and natural gas prices;

- •

- requirements and commitments under existing permits;

- •

- staffing levels and competitive conditions; and

- •

- any purchases or dispositions of assets.

Our ability to raise additional capital will depend on the results of our operations and the status of various capital and industry markets at the time we seek such capital. Our failure or inability to obtain any required additional financing on favorable terms could materially and adversely affect our growth, cash flow and earnings, including our ability to meet our capital expenditures budgets.

Although we retired the facilities with the International Finance Corporation in March 2009, we have outstanding $80.3 million of Convertible Senior Notes due October 2025 and plan to attempt to enter into another credit facility.

Given the current state of the credit market, no assurance can be given that we will be able to enter into a new credit facility on acceptable terms; therefore there can be no assurances that we will have the needed additional capital to fund our future growth.

In addition, to the extent that we are not able to obtain additional capital by the incurrence of additional debt, we may need to issue additional equity which may be difficult in light of the current equity market. Any such issuance of equity could be materially dilutive to our outstanding equity and equity holders.

22

Table of Contents

If we enter into a new credit facility, our debt to equity ratio may limit our ability to obtain additional indebtedness. Additionally any new credit facility may restrict our ability to incur additional indebtedness because of financial ratios we must meet.

Thus, we may not be able to obtain sufficient capital to grow our business, effectuate our business strategy and may lose opportunities to acquire interests in oil and natural gas properties or related businesses because of our inability to fund such growth.

Our ability to comply with the restrictions and covenants of any future credit facility is uncertain and will be affected by the levels of cash flow from our operations and events or circumstances beyond our control. Our failure to comply with any of the restrictions and covenants could result in a default, which could permit the lender to accelerate repayments and foreclose on the collateral securing the indebtedness.

We currently have operations involving the U.S. dollar, Euro, New Turkish Lira, Forint and Romanian Lei. We are subject to fluctuations in the value of the U.S. dollar as compared to the Euro, New Turkish Lira, Forint and Romanian Lei respectively. These fluctuations, including the recent fluctuations, may adversely affect our results of operations.

On a consistent basis, we evaluate and, where appropriate, pursue acquisition opportunities on terms we consider favorable. In particular, we pursue acquisitions of businesses or interests that will complement and allow us to expand our exploration activities; however, currently, we have no binding commitments related to any acquisitions. The successful acquisition of interests in oil and natural gas properties requires an assessment of:

- •

- recoverable reserves;

- •

- exploration potential;

- •

- future oil and natural gas prices;

- •

- operating costs;

- •

- potential environmental and other liabilities and other factors; and

- •

- permitting and other environmental authorizations required for our operations.

In connection with such an assessment, we would expect to perform a review of the subject properties that we believe to be generally consistent with industry practices. Nonetheless, the resulting conclusions are necessarily inexact and their accuracy inherently uncertain and such an assessment may not reveal all existing or potential problems, nor will it necessarily permit us to become sufficiently familiar with the properties to fully assess their merits and deficiencies. Inspections may not always be performed on every platform or well, and structural and environmental problems are not necessarily observable even when an inspection is undertaken. As a result, acquired properties may prove to be worth less than we pay for them.

Future acquisitions could pose numerous additional risks to our operations and financial results, including:

- •

- problems integrating the purchased operations, personnel or technologies;

- •

- unanticipated costs;

- •

- diversion of resources and management attention from our core business;

- •