SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

Report of Foreign Private Issuer

Pursuant to Rule 13a-16 or 15d-16 of the

Securities Exchange Act of 1934

For the month of May 2008

CREDICORP LTD.

(Exact name of registrant as specified in its charter)

Clarendon House

Church Street

Hamilton HM 11 Bermuda

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover Form 20-F or Form 40-F.

Form 20-F x Form 40-F o

Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.

Yes o No x

| ||||

CREDICORP Ltd. Reports First Quarter 2008 Earnings Lima, Peru, May 7, 2008 - Credicorp (NYSE:BAP) announced today its unaudited results for the first quarter of 2008. These results are reported on a consolidated basis in accordance with IFRS in nominal U.S. Dollars. HIGHLIGHTS | ||||

| · | Following a period of strong currency volatility and BCR intervention, Credicorp reported an extraordinary increase of its net income of 89% QoQ and 125% YoY, totaling unprecedented net earnings for the quarter of US$ 178 million. | |||

| · | Such unexpectedly high income includes a significant currency translation gain of US$ 68.7 million which resulted from the accelerated appreciation of the local currency vs. the US Dollar during this 1Q08 combined with a controlled management of Credicorp’s Soles/Dollar positions geared to take advantage of such currency volatility. | |||

| · | Even excluding such translation gain, Credicorp’s results show 43% QoQ earnings growth to US$ 109 million, reflecting the continuing strong growth and income generation of Credicorp’s core businesses. | |||

| · | Loan growth reported by its banking business continued strong, though somewhat inflated by the revaluation of its Soles denominated loans (32% of the loan book), revealing an 8.1% QoQ loan portfolio growth. | |||

| · | Interest income followed this trend with a robust 9.9% QoQ growth. | |||

| · | NIM however, drops slightly from 5.2% to 5.1% and reflects herewith a continued stronger growth of our corporate -thus tighter in margins- dollar loan portfolio on the back of strong investment activity; higher funding costs after the BCR’s intervention to control inflation and currency volatility; and a significantly increased investment portfolio which is very attractive given the tax advantages it generates, but contributes only with tighter nominal margins to NIM calculation. | |||

| · | Non financial income grows a strong 24.6% QoQ, though it includes also a significant extraordinary income from the sale of the group’s VISA shares of close to US$ 13 million on an after tax basis. Still, fee income grows a robust 12.4% QoQ and 34% YoY, revealing the increasing transactional income generation. | |||

| · | Loan portfolio quality continues strong, reaching a PDL/Loans ratio of only 0.8%. Net provisioning increased however 62.7% QoQ to US$ 16.1 million as a result of a change towards a more conservative provisioning policy for our retail portfolio. | |||

| · | BCP’s consolidated numbers reflect a very healthy and dynamic banking environment with core revenues up 7.3% QoQ and 37.8% for the year. Such improved income combined with less than projected operating expenses and the important positive translation effect mentioned above, led to a completely extraordinary 92.3% QoQ higher net income for BCP for 1Q08 which reached US$ 165.8 million, and translates into a contribution to Credicorp of US$ 161.4 million for this 1Q08. | |||

| · | BCP Bolivia, which is consolidated in BCP, continues its consistent growth and reports a contribution 4% higher QoQ and 118% higher YoY, reaching US$ 10.5 million for 1Q08. | |||

| · | ASHC remains a stable and growing business in line with the increasing wealth in the country and reports a contribution improvement of 14% QoQ at US$ 5.7 million. | |||

| · | PPS, though still troubled by its property and casualty business, reports this quarter recovered contribution to Credicorp of US$ 2.34 million, helped by its financial management which generated also an important translation gain. | |||

| · | Finally, Prima AFP reports a significantly higher contribution of US$ 9 million following expected improved business results, but also an extraordinary income from the treatment of deferred tax liabilities which led to the recognition of US$ 2.3 million earnings from previous periods in this 1Q08. | |||

I. Credicorp Ltd.

Overview

Following a period of strong currency volatility (8.41% revaluation of the Sol) and BCR intervention (interest rate and reserve requirement changes), Credicorp reported an extraordinary increase of its net income of 89% QoQ and 125% YoY, totaling unprecedented net earnings for the quarter of US$ 178 million, and resulting in an improved ROAE of 40% for the quarter.

Such unexpectedly high income includes a significant currency translation gain of US$ 68.7 million which resulted from the accelerated appreciation of the local currency vs. the US Dollar during this 1Q08. Such currency fluctuation generated a gain through the impact on the net Soles position on our books (i.e. appreciation of the Soles loan book which represents 32% of the portfolio, and investment portfolio vs. soles denominated liabilities). However, a significant portion of such gain was also generated by the management of such positions at BCP and the different subsidiaries, where our US Dollar position was intentionally diminished in light of the US Dollar devaluation expectations, generating additional translation gains in our IFRS US Dollar accounting. Thus, significantly different results were reported in local currency accounting, where the devaluation of the dollar generated a loss instead. In both cases, the calculated management of the currency position either increased gains or minimized losses. Nevertheless, we should keep in mind the volatile source and nature of these gains, which can be equally reverted with changing market conditions given such a highly volatile moment.

Thus, when excluding such translation gain, Credicorp’s results show 43% QoQ earnings growth, with earnings after minorities for the quarter of US$ 109.3 million, a number closer to our optimistic projections, and thus reflecting the continuing strong growth and income generation of Credicorp’s businesses. However, such 1Q08 income also includes an additional one-off gain generated by the VISA shares IPO which resulted in a bottom line after tax addition of around US$ 13 million.

Aside from these one-off’s, Credicorp’s core banking business reported a strong performance, with total loan growth this last quarter reaching 8.1% QoQ. Though slightly overstated by the revaluation of the Soles loan portfolio, loan growth was fueled, not only by the already expected strong retail segment, but also a continuing strong investment activity which led to high quarterly growth of the corporate US Dollar loan book.

Credicorp Ltd. | Quarter | Change % | ||||||||||||||

| US$ thousands | 1Q08 | 4Q07 | 1Q07 | 1Q08/1Q07 | 1Q08/4Q07 | |||||||||||

| Net interest income | 192,090 | 174,756 | 138,859 | 38.3 | % | 9.9 | % | |||||||||

| Total provisions, net of recoveries | (16,148 | ) | (9,926 | ) | (4,418 | ) | 265.5 | % | 62.7 | % | ||||||

| Non financial income | 152,048 | 122,043 | 111,194 | 36.7 | % | 24.6 | % | |||||||||

| Insurance premiums and claims | 12,298 | 12,222 | 17,363 | -29.2 | % | 0.6 | % | |||||||||

| Operating expenses | (185,532 | ) | (193,327 | ) | (149,810 | ) | 23.8 | % | -4.0 | % | ||||||

Net income before working profit sharing & IT | 154,757 | 105,768 | 113,188 | 36.7 | % | 46.3 | % | |||||||||

| Worker's profit sharing and income taxes | (38,726 | ) | (24,606 | ) | (27,924 | ) | 38.7 | % | 57.4 | % | ||||||

Net income before minority interest &translation result | 116,031 | 81,163 | 85,264 | 36.1 | % | 43.0 | % | |||||||||

| Minority interest | (6,728 | ) | (4,590 | ) | (7,897 | ) | -14.8 | % | 46.6 | % | ||||||

Net income before translation result | 109,303 | 76,573 | 77,368 | 41.3 | % | 42.7 | % | |||||||||

| Translation results | 68,695 | 17,442 | 1,645 | 4075.4 | % | 293.8 | % | |||||||||

Net income attributed to Credicorp | 177,998 | 94,016 | 79,013 | 125.3 | % | 89.3 | % | |||||||||

| Net income/share (US$) | 2.23 | 1.18 | 0.99 | 125.3 | % | 89.3 | % | |||||||||

Total loans | 8,919,841 | 8,250,819 | 6,239,870 | 42.9 | % | 8.1 | % | |||||||||

Deposits and Obligations | 12,929,288 | 11,401,275 | 9,336,519 | 38.5 | % | 13.4 | % | |||||||||

Net Shareholders' Equity | 1,850,680 | 1,676,009 | 1,420,716 | 30.3 | % | 10.4 | % | |||||||||

| Net interest margin | 5.1 | % | 5.2 | % | 5.2 | % | ||||||||||

| Efficiency ratio | 40.2 | % | 46.2 | % | 42.5 | % | ||||||||||

| Return on average shareholders' equity | 40.4 | % | 22.9 | % | 23.5 | % | ||||||||||

| PDL/Total loans | 0.8 | % | 0.7 | % | 1.2 | % | ||||||||||

| Coverage ratio of PDLs | 310.0 | % | 343.7 | % | 251.4 | % | ||||||||||

| Employees | 17,348 | 16,160 | 14,757 | |||||||||||||

NII followed this robust loan growth and reached 9.9% QoQ despite the persistent competition and pressure on rates.

Net interest margin however, drops slightly from 5.2% to 5.1% and reflects herewith (1) a continued stronger growth of our corporate -thus tighter in margins- dollar loan portfolio on the back of strong investment activity, (2) higher funding costs after the BCR’s intervention to control inflation and currency volatility, and (3) a significantly increased investment portfolio of BCR CD’s which became very attractive given their tax advantages, but contributed only tighter nominal margins to this calculation. These developments had an impact not only on our loan book mix, but on our interest earning assets mix, which have developed differently than projected but according to the market opportunities, leading to the extraordinary earnings results reported.

Non Financial income reported 24.6% QoQ growth. However, this number includes the above mentioned significant gain in the sale of Credicorp’s VISA shares (within the Visa IPO) of about US$ 18 million before tax. Nevertheless, a strong fee income growth of 12.4% QoQ reveals further increases in bank transactional activity and fee expansion at the pension fund business.

Though the insurance business reports a good quarterly net premiums growth of 9%, claims in the property and casualty sector remain high this quarter due to the “El Niño” weather phenomenon, which though mild, is however affecting the northern areas of the country with torrential rains. Thus, operating income remained flat and was mainly generated by the more profitable life and health insurance businesses. Furthermore, a timely financial management of its currency positions also contributed some additional currency translation gains helping the overall bottom line and contribution to Credicorp.

On the cost side, total operating costs were down by 4% QoQ resulting in an improved efficiency ratio of 40.2% vs. 46.2% the previous quarter, contrary to expectations. Such development is a reflection of the seasonality in costs, since in 4Q07 these had a significant year-end related increase and thus set a high comparison base for this quarter. Furthermore, projected expense levels for this quarter were not reached due to an expansion process which is not as linear as were projections; and despite the negative (inflating) effect of Soles denominated costs in our US Dollar accounting following the significant revaluation of the Sol. Thus, the YoY growth of 23.8% appears moderate in light of the expansion being experienced by the loan book and income sides of the equation. Having said this, we would like to point out that the expansion plans do continue full speed ahead and are a core part of Credicorp’s business strategy.

2

Another positive development is the continuing strength of portfolio quality, which remains healthy with a PDL/Loans ratio of only 0.8% this 1Q08. Total provisions net of recoveries of US$ 16.1 million (up 62.7%) however, reveal an increase in provisions at BCP in line with loan growth and with a more conservative provisioning policy for our retail portfolio, increasing the internal minimum provisioning requirements in line with a more sophisticated risk assessment methodology. This decision was taken based on a conservative prudent approach and does not follow any deterioration of portfolio quality indicators, which to date remain very healthy.

These developments resulted in improved ratios for the quarter, with ROAE climbing to 40.4% from 22.9% the previous quarter.

Credicorp - the Sum of its Parts

Going through a period of significant volatility can impact results in many different ways. Therefore, we are very pleased to have managed the strong currency volatility of the 1Q08 in favor of Credicorp’s results. It took a series of timely financial decisions regarding our currency positions and investments in the different subsidiaries that led to the strong financial gains related to the currency translation. However, these are the result of the high currency and interest rates volatility and can quickly change according to market conditions.

In fact, BCP reported extraordinarily high income contribution this 1Q08 of US$ 161.4 million, which included an approximate US$ 57 million translation gain, though revealing at the same time significant core business expansion even excluding such translation income and other one-off contributions, confirming this way its expanding earnings generation capacity.

Such income reflected an obviously one time high 57% ROAE for the quarter.

| (US$ Thousands) | 1Q08 | 4Q07 | 1Q07 | 1Q08/1Q07 | 1Q08/4Q07 | 1Q08 | 1Q07 | 1Q08/1Q07 | |||||||||||||||||

| Banco de Crédito BCP(1) | 161,353 | 83,869 | 70,649 | 128 | % | 92 | % | 161,353 | 70,649 | 128 | % | ||||||||||||||

| BCB | 10,476 | 10,065 | 4,804 | 118 | % | 4 | % | 10,476 | 4,804 | 118 | % | ||||||||||||||

| Atlantic | 5,673 | 4,988 | 4,969 | 14 | % | 14 | % | 5,673 | 4,969 | 14 | % | ||||||||||||||

| PPS | 2,342 | 645 | 6,616 | -65 | % | 263 | % | 2,342 | 6,616 | -65 | % | ||||||||||||||

| Grupo Crédito (2) | 9,807 | 3,242 | 1,202 | 716 | % | 202 | % | 9,807 | 1,202 | 716 | % | ||||||||||||||

| Prima | 9,015 | 2,307 | 178 | 4972 | % | 291 | % | 9,015 | 178 | 4972 | % | ||||||||||||||

| Others | 792 | 935 | 1,024 | -23 | % | -15 | % | 792 | 1,024 | -23 | % | ||||||||||||||

| Credicorp and Others (3) | (1,178 | ) | 1,272 | (4,422 | ) | -73 | % | -193 | % | (1,178 | ) | (4,422 | ) | -73 | % | ||||||||||

| Credicorp Ltd. | (1,724 | ) | 787 | (4,678 | ) | -63 | % | -319 | % | (1,724 | ) | (4,678 | ) | -63 | % | ||||||||||

| Otras | 546 | 485 | 256 | 1.13 | 13 | % | 546 | 256 | 113 | % | |||||||||||||||

Net income attributable to Credicorp | 177,998 | 94,016 | 79,013 | 125 | % | 89 | % | 177,998 | 79,013 | 125 | % | ||||||||||||||

| (1) Includes Banco de Crédito de Bolivia. | ||||||||

| (2) Includes Grupo Crédito, Servicorp and Prima AFP | ||||||||

| (3) Includes taxes on BCP's and PPS's dividends, and other expenses at the holding company level. |

BCP Bolivia, which is consolidated within BCP, reported a contribution of US$ 10.5 million for 1Q08, maintaining its high level despite a significant stagnation of investment activity in the country, which will eventually generate a notorious slowdown.

3

ASHC reports a contribution improvement of 14% QoQ reaching US$ 5.7 million for the 1Q08. ASHC’s business is constantly expanding as a result also of the increasing wealth generation in the country, and represents a stable, no-risk investment, for which its ROEA of 16.2% is more than satisfactory.

As explained before, though the insurance business reports a good quarterly net premiums growth of 9%, claims in the property and casualty sector remain high this quarter due to the mild Niño affecting the northern areas of the country with torrential rains. Thus, with the Life and Health businesses doing very well and offering good returns, turning the P&C business into a profitable operation continues being PPS’s main focus, though it is proving to be troublesome. Following this objective, significant efforts are being made to develop the more massive and better predictable retail business and limit exposure to the wholesale insurance P&C business, as well as to improve the financial investment management to achieve better returns overall. This process will take more time than expected. Nevertheless, such positive financial management results which benefited also from translation gains, contributed to improve PPS’s bottom line results despite the casualties of the P&C sector, leading to a US$ 2.34 million contribution to Credicorp, which represented a ROAE of about 11.2%.

Finally, Prima’s business results were better than expected with total quarterly earnings of US$ 9 million. This improved results followed a change in treatments of deferred tax liabilities which had been generating overstated deferred liabilities and consequently understated income, leading to US$ 2.3 million income recognition from periods prior to December 2007, in this 1Q08. Thus, this totally unexpected high earnings contribution to Credicorp represented a ROAE of over 27%, which is certainly not sustainable at such high level given the one-off income recognition from previous periods. Nevertheless, Prima’s business results are better than expected following the cost reduction efforts of last year and business plan. Prima has established a dominant position in the market, capturing important market shares (31.4% of AuM, 33.7% of collections and 47.2% of voluntary contributions to the funds).

II. Banco de Crédito - BCP Consolidated

Overview 1Q08

The earnings evolution seen at Credicorp stems mainly from BCP’s performance which reveals extraordinary and historically unprecedented net earnings for the 1Q08 of US$ 165.8 million. This earnings number includes US$ 57 million of translation gains which resulted, as explained before when discussing Credicorp, from the high currency volatility and careful management of BCP’s US Dollar/Soles positions when reporting under IFRS US Dollar accounting. It is therefore important to keep the volatile source and nature of this income in mind. Excluding this extraordinary income, net earnings for 1Q08 was US$ 108.5 million, still a very strong 53% earnings growth QoQ.

Another boost to BCP earnings results for the quarter was the sale of Visa Inc. shares, which generated additional pre-tax extraordinary income of US$ 17.8 million on a consolidated basis with BCP Bolivia.

4

Core Earnings

Core Revenues | Quarter | Change | ||||||||||||||

US$ 000 | 1Q08 | 4Q07 | 1Q07 | 1Q08/1Q07 | 1Q08/4Q07 | |||||||||||

| Net interest and dividend income | 172,611 | 155,565 | 123,289 | 40.0 | % | 11.0 | % | |||||||||

| Fee income, net | 79,747 | 76,708 | 62,470 | 27.7 | % | 4.0 | % | |||||||||

| Net gain on foreign exchange transactions | 19,971 | 21,497 | 11,937 | 67.3 | % | -7.1 | % | |||||||||

Core Revenues | 272,329 | 253,770 | 197,696 | 37.8 | % | 7.3 | % | |||||||||

Nevertheless, BCP’s business performance, excluding such significant extraordinary and non recurrent income remains as strong as in the previous quarters. In fact, net interest income increased 11% QoQ following a robust loan book growth of 7.5% when looking at quarter end book balances. Fee income also followed the trend of previous quarters showing a 4% quarterly growth, compensating a drop in FX-transaction and resulting in Core Earnings growth of 7.3%. While on the cost side, operating costs dropped 8.9% despite the inflating effect of our Soles costs due to the revaluation in US Dollar accounting for two reasons: (1) the seasonality reflected by the year-end related expense hike of the last 4Q07 which set a high comparison base, and (2) the evolution of BCP’s expansion costs, which are in reality not as linear as projections. Furthermore, such strong income generation also allowed for 53% higher provisions as our provisioning policy was revised and higher provisioning levels set for our growing retail business.

Looking at total loan growth measured by the average daily balances for the quarter (and including the effect of the local currency revaluation which inflates US Dollar results slightly for our local currency book which amounts to 32% of our portfolio) reached a strong 9.8% QoQ growth. But even excluding the revaluation effect, such growth would still be strong at about 8% for the quarter. Contrary to expectations, however, the strongest growing sector contributing to such high 9.8% quarterly loan growth was again this 1Q08 the corporate business fueled by the impressively strong longer term investment activity. Such corporate business reported a 12.2% QoQ loan growth in average balances (approx. 10.5% clean of the revaluation effect), while the retail sector, our typically most dynamic sector reached 11.1% QoQ growth (or 8.5% clean of revaluation effect), with SME, consumer and credit card loans maintaining their strong growth in that order.

But net interest income growth was a result not only of such loan portfolio evolution, but also a very strong increase in the volume of BCP’s investment portfolio, which was up by 45.9% QoQ. Such growth was to an important extent a result of the revaluation in our US Dollar reporting of our mainly Soles denominated investment portfolio, though aslo fueled by the strong inflow of US Dollar into the system lured by the large speculative earnings opportunities offered by investments in Soles through the revaluation of the Soles and interest rate differentials generated by the BCR’s monetary policy. The soles liquidity generated this way in the local financial system was again captured by BCR CD’s, resulting in very attractive investment for financial institutions given their tax shelter. This evolution and revaluation generated a recomposition of our interest earning assets with investment with lower nominal returns (though higher real returns through tax advantages) reporting a greater expansion than our loan portfolio. This impacted our net interest margin (NIM), as did as well our stronger growth of our corporate and less profitable portfolio vis-à-vis our retail book. The result was a contraction of NIM from 5.2% in 4Q07 to 5.1% in 1Q08. Furthermore, the evolution of the funding side contributed to the contraction in NIM, since interest rates on deposits in general increased and the higher reserve requirements and lower remuneration of these impacted our funding cost.

Though slightly higher as of the end of the 1Q08, PDL/ total loans continues at an extremely healthy level of 0.79%, showing no identifiable real signs of any deterioration. Coverage remains strong at 313.2% (though down from 351%).

5

Banco de Crédito and Subsidiaries | Quarter | Change | ||||||||||||||

| US$ 000 | 1Q08 | 4Q07 | 1Q07 | 1Q08/1Q07 | 1Q08/4Q07 | |||||||||||

| Net Financial income | 172,611 | 155,565 | 123,289 | 40.0 | % | 11.0 | % | |||||||||

| Total provisions, net of recoveries | (16,951 | ) | (11,089 | ) | (5,859 | ) | 189.3 | % | 52.9 | % | ||||||

| Non financial income | 124,563 | 103,458 | 86,255 | 44.4 | % | 20.4 | % | |||||||||

| Operating expenses | (138,335 | ) | (151,867 | ) | (108,218 | ) | 27.8 | % | -8.9 | % | ||||||

Net income before Workers' profit sharing and IT | 141,888 | 96,068 | 95,467 | 48.6 | % | 47.7 | % | |||||||||

| Worker's profit sharing and income taxes | (33,365 | ) | (25,123 | ) | (24,121 | ) | 38.3 | % | 32.8 | % | ||||||

Net income before translation result | 108,523 | 70,945 | 71,346 | 52.1 | % | 53.0 | % | |||||||||

| Tranlation results | 57,249 | 15,253 | 1,310 | 4270.2 | % | 275.3 | % | |||||||||

Net income | 165,773 | 86,198 | 72,657 | 128.2 | % | 92.3 | % | |||||||||

| Net income/ share (US$) | 0.129 | 0.067 | 0.057 | 128.1 | % | 92.4 | % | |||||||||

| Total loans | 8,837,689 | 8,224,613 | 6,182,300 | 43.0 | % | 7.5 | % | |||||||||

| Deposits and obligations | 12,938,927 | 11,249,104 | 8,842,654 | 46.3 | % | 15.0 | % | |||||||||

| Shareholders equity | 1,195,587 | 1,132,564 | 881,485 | 35.6 | % | 5.6 | % | |||||||||

| Net financial margin | 5.1 | % | 5.2 | % | 5.2 | % | ||||||||||

| Efficiency ratio | 47.5 | % | 56.9 | % | 49.8 | % | ||||||||||

| Return on average equity | 57.0 | % | 31.7 | % | 31.5 | % | ||||||||||

| PDL/ Total loans | 0.8 | % | 0.7 | % | 1.2 | % | ||||||||||

| Coverage ratio of PDLs | 313.2 | % | 351.8 | % | 252.1 | % | ||||||||||

| Branches | 277 | 273 | 245 | |||||||||||||

| ATMs | 778 | 748 | 691 | |||||||||||||

| Employees | 13,540 | 12,667 | 10,934 | |||||||||||||

Net provisions increased 53% to US$ 16.9 million in 1Q08. This is the result of higher gross provisions due to a more conservative provisioning policy implemented this year, increasing the provision requirements for the retail business. Thus, gross provisions reached US$ 25.9 million, while recoveries were still strong at US$ 8.9 million. The latter includes the recoveries related to a very old problem loan which was finally settled.

The 4.0% fee income growth stems from higher account maintenance fees, transactional fees, credit card fees and operational charges. Though higher fee income was reported, a drop in the average number of monthly transactions from 33.3 million to 32.3 million QoQ is explained by the seasonal all-year high recorded every 4Q of the year due to the holiday season.

FX-transactions gains were 7.1% lower QoQ, mainly because of the high transactional level of the year end in 2007 which set a high base of comparison and despite the currency fluctuation this 1Q08.

Gains on the sale of securities, on the other hand, reported a jump from US$2.7 million in 4Q07 to US$22.7 million. The Visa Inc. IPO explains completely this jump since it resulted in gains for BCP and BCP Bolivia, which reached US$17.9 million.

On the cost side, operating costs dropped 8.9% despite the inflating effect of our Soles denominated costs due to the revaluation in US Dollar accounting for two reasons: (1) the seasonality reflected by the year-end related expense hike of the last 4Q07 which set a high comparison base, and (2) the evolution of BCP’s expansion costs, which are in reality not as linear as projections. Thus, personnel costs and administrative costs dropped 6.1% and 18.1% respectively in the 1Q08, despite, as said before, the revaluation effect of the soles denominated costs.

Finally, as indicated at the beginning, translation results were significantly higher this quarter given the strong revaluation of the Nuevo Sol vis-a-vis the US Dollar which went from S/.2.996 in December 2007 to S/.2.744 by the end of March 2008, i.e. a devaluation of the US Dollar of 8.41%. Furthermore, such devaluation expectations fueled by the monetary policy of the BCR which increased the Soles interest rates and the speculative trade opportunities generated by this evolution, which also attracted significant foreign capital, led to a change in BCP’s decisions related to its US Dollar / Soles positions. Thus, BCP intentionally reduced its US Dollar position significantly, generating an even large gain in US Dollar NIIF accounting.

Month | US$ Averag. net asset position | Nuevos Soles Averag. net asset | Exchange rate | Monthly devaluation | Calculated translation | Translation registered on P&L | |||||||||||||

| Jan-08 | 245,207 | 529,751 | 2.934 | -2.1 | % | 11,194 | 8,145 | ||||||||||||

| Feb-08 | 187,982 | 625,179 | 2.886 | -1.6 | % | 10,398 | 11,055 | ||||||||||||

| Mar-08 | 137,347 | 725,057 | 2.744 | -4.9 | % | 37,521 | 38,049 | ||||||||||||

Translation 1Q08 | 59,114 | 57,249 | |||||||||||||||||

As a consequence of all the above, quarterly ratios for BCP are extremely good at: 47.5% efficiency ratio explained by the lower operating costs reported while income increased, 0.8% PDL/Total loans reflecting excellent portfolio quality with a 313.2% coverage ratio, and an unusual ROAE of 57.0% which includes the translation gains.

6

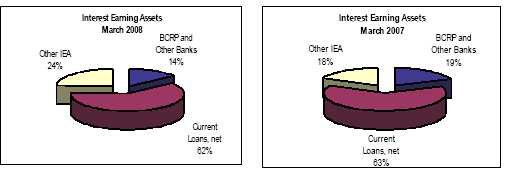

II.1 Interest Earning Assets

Market evolution leads to a change in interest earning assets mix with BCP’s investment portfolio driving growth.

Interest Earning Assets | Quarter | Change | ||||||||||||||

| US$ 000 | 1Q08 | 4Q07 | 1Q07 | 1Q08/1Q07 | 1Q08/4Q07 | |||||||||||

| BCRP and Other Banks | 2,077,660 | 2,255,572 | 1,828,663 | 13.6 | % | -7.9 | % | |||||||||

| Interbank funds | 1,469 | 5,000 | 4,542 | -67.7 | % | -70.6 | % | |||||||||

| Trading Securities | 38,538 | 102,316 | 54,505 | -29.3 | % | -62.3 | % | |||||||||

| Available For Sale Securities | 3,449,781 | 2,364,084 | 1,641,157 | 110.2 | % | 45.9 | % | |||||||||

| Current Loans, net | 8,767,674 | 8,164,334 | 6,109,064 | 43.5 | % | 7.4 | % | |||||||||

Total interest earning assets | 14,335,123 | 12,891,306 | 9,637,930 | 48.7 | % | 11.2 | % | |||||||||

Growth of IEA this first quarter of 2008 reflects an unexpected market evolution resulting from the combination of the BCR monetary policy to control inflation through an increase of the Soles reference rates, the weakness of the US Dollar, the speculative strong inflow of funds into the Peruvian financial system to benefit from such market opportunity and the intervention of the Central Bank in the FX market to control the fall of the US Dollar exchange rate. The result of these forces result in large soles deposits in the system which excess after loan growth was channeled to CB CD’s which provide a very attractive after tax yield (given their tax shelter). Thus, BCP experienced a strong asset expansion of 11.2% as a result of this evolution, but also to a large extent as a result of the revaluation in US Dollar reporting of its already large Soles denominated investment portfolio. Thus, the significant increase of its investment portfolio of over US$1.1 billion, while its net loan growth for the quarter reached about US$600 million resulted in a charge of its interest earnings asset mix.

Loan Portfolio

Loan portfolio continues its expanding trend reaching total net loans of US$ 8,768 million as of the end of the March 2008, revealing a 7.4% QoQ and 43.5% YoY growth. Measured by average daily balances for each quarter, which give a better reflection of reality, similar growth rates are reported reaching 9.8% QoQ and 45.2% YoY. This growth numbers, however, do conceal the revaluation impact on the local currency portfolio, which represents a significant 32% of total loan portfolio. We have calculated an approximate “clean” growth number to estimate the potential distortion generated by such currency fluctuations and reached an approximate 8% QoQ growth of average daily balances for the total portfolio, still a robust quarterly growth.

What is however an unexpected evolution, is the continuation of a very strong investment activity in the corporate market which has turned this sector in the fastest growing for the second consecutive quarter, reaching 12.2% QoQ growth (measuring average balances). The growth within the corporate sector reveals some interesting features: US Dollar loans grew stronger than Soles denominated loans which actually stagnated during this first quarter, a relatively logical evolution given the currency and interest rates development. Further, longer term loans grew significantly more than short term loans, giving again a clear indication of the investment activity in the back of this growth. Though this is certainly good news, given the large volumes involved (US$ 3.2 billion portfolio) in the corporate sector, it impacts our loan mix contrary to our expectations and designed strategy to grow the retail segment more, and thus our strategy to protect our NIM. On the other hand, we are certainly reinforcing our dominant position in this market which allows BCP to capture and/or participate in almost every important investment and has resulted in a further consolidation of its market dominance despite the presence of aggressive international players.

7

The Middle Market portfolio (US$ 1,8 billion), though last in the growth ranking after the corporate and retail sectors, still reached good quarterly growth numbers at 7.1% QoQ growth.

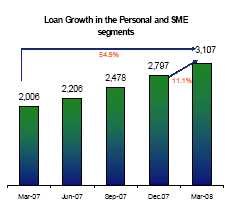

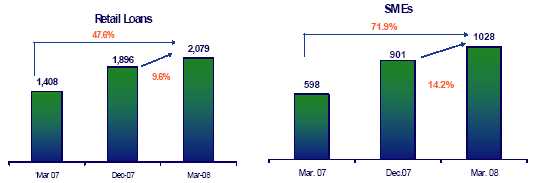

Though the corporate sector outperformed all other again this 1Q08, the retail sector continues being the strong performer on a consistent way. Thus, its portfolio reached US$ 3.1 billion in average monthly balances, reporting consistently outstanding quarterly growth of 11.1% this quarter vs. 12.9% the previous quarter. Star performers within the retail segment continue being Consumer loans and SME lending, which reported 14.4% and 14.2% QoQ growth respectively, while Credit Card loans increased by 11.9% QoQ. Mortgages reported the lowest growth rates within the retail segment, but were still extremely good at 7% QoQ growth.

8

Given the distortion generated by the currency fluctuations and the fact that BCP’s loan portfolio is in both currencies but reported in US Dollars, it is helpful to look at the evolution of the different loan portfolios by currency to see the real growth in each portfolio. The following chart intends to shed some light over such loan growth analysis…

Domestic Currency Loans | Foreign Currency Loans | ||||||||||||||||||||||||||||||

(Nuevos Soles million) | (US$ million) | ||||||||||||||||||||||||||||||

| 1Q07 | 4Q07 | 1Q08 | YoY | QoQ | 1Q07 | 4Q07 | 1Q08 | YoY | QoQ | ||||||||||||||||||||||

| Corporate | 2,059.2 | 2,506.5 | 2,783.7 | 35.2 | % | 11.1 | % | 1,383.4 | 2,002.7 | 2,208.8 | 59.7 | % | 10.3 | % | |||||||||||||||||

| Middle Market | 694.4 | 861.4 | 946.6 | 36.3 | % | 9.9 | % | 1,158.4 | 1,439.5 | 1,518.1 | 31.0 | % | 5.5 | % | |||||||||||||||||

| Retail | 2,218.7 | 3,555.6 | 4,015.6 | 81.0 | % | 12.9 | % | 1,310.3 | 1,610.6 | 1,697.7 | 29.6 | % | 5.4 | % | |||||||||||||||||

SME | 935.0 | 1,270.9 | 1,393.8 | 49.1 | % | 9.7 | % | 304.9 | 476.7 | 539.2 | 76.9 | % | 13.1 | % | |||||||||||||||||

Mortgages | 320.5 | 735.5 | 891.9 | 178.3 | % | 21.3 | % | 792.7 | 866.5 | 876.7 | 10.6 | % | 1.2 | % | |||||||||||||||||

Consumer | 310.4 | 722.3 | 836.7 | 169.5 | % | 15.8 | % | 169.9 | 212.6 | 225.1 | 32.5 | % | 5.9 | % | |||||||||||||||||

Credit Cards | 652.8 | 826.9 | 893.3 | 36.8 | % | 8.0 | % | 42.8 | 54.8 | 56.8 | 32.8 | % | 3.7 | % | |||||||||||||||||

| Consolidated total | 4,993.0 | 6,950.2 | 7,764.2 | 55.5 | % | 11.7 | % | 4,441.9 | 5,625.5 | 5,997.1 | 35.0 | % | 6.6 | % | |||||||||||||||||

* Includes work out unit, other banking and BCP Bolivia | |||||||||||

*Average daily balances for the quarter |

… revealing the following:

| · | The corporate sector grows a strong 10.3% its USD portfolio which represents 60% of its total portfolio. The reported 11.1% growth of its Soles portfolio hides minimal growth in the 1Q08, and a very strong growth of its Soles portfolio within the 4Q07, which when comparing averages led to such number. |

| · | The middle market segment, which has 82% of its portfolio in USD, reports a moderate 5.5% growth of its loan book, which is in line with projections. |

| · | The retail segment in turn, has half its portfolio in each currency and shows a stronger growth in its Soles loan book of 12.9%, while its USD loan book grows at a more moderate 5.4%. |

9

Market Share

BCP’s market share continues leading the market despite the strong competition, characterized by the incursion of new foreign players and the already stronghold position it has. Thus, BCP’s market share of loans placed reached 31.9% as of March 2008, showing a slight decrease in comparison to December 2007 (32.2%). However, there was an increase of 0.4 percentage points in comparison to the second best competitor.

Furthermore, market shares for the corporate and middle market sectors continue revealing BCP’s solid positioning, reaching 48% and 35%, respectively, as of February 2008. These reflect a minor growth in the corporate market and a stable position in the middle market compared to the previous quarter.

Market shares in the retail market had mixed results during this quarter. Consumer loans were down by 0.2% reaching 17.1%, while Credit Cards and SME decreased 0.2% pps and 0.3% pps, respectively, reaching 18.7% and 18.5%. However, mortgages increased 0.4% pps to 40.1% consolidating its strong position.

Dollarization

The de-dollarization process of BCP’s assets this 1Q08 continued with respect to the previous quarter. Thus, in 1Q08 Nuevos Soles conformed 32.5% of total loan portfolio, which represent a slight increase of 0.5% with respect to 4Q07. In addition, the system continues experiencing further de-dollarization of its loans and deposits, reaching a high 41% of loans in Nuevos Soles and 59% in US Dollar as of March 2008. The de-dollarization process is more intense in deposits specially because the local currency appreciation during this quarter. Thus, the share of deposits in nuevos soles was 51% (vs. 39% for Mar. 2007).

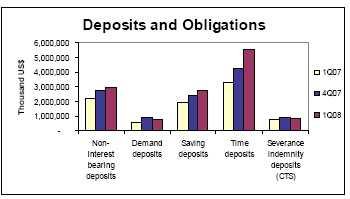

II.2 Deposits and Mutual Funds

Deposits grew 15% QoQ and 46% YoY, remaining as main funding source to support the strong loan growth

Deposits and Obligations | Quarter ended | Change | ||||||||||||||

| US$ (000) | 1Q08 | 4Q07 | 1Q07 | 1Q08/1Q07 | 1Q08/4Q07 | |||||||||||

| Non-interest bearing deposits | 2,965,756 | 2,729,860 | 2,194,439 | 35.1 | % | 8.6 | % | |||||||||

| Demand deposits | 761,123 | 926,817 | 604,445 | 25.9 | % | -17.9 | % | |||||||||

| Saving deposits | 2,749,983 | 2,381,012 | 1,966,838 | 39.8 | % | 15.5 | % | |||||||||

| Time deposits | 5,543,993 | 4,268,233 | 3,293,110 | 68.4 | % | 29.9 | % | |||||||||

| Severance indemnity deposits (CTS) | 859,630 | 896,283 | 747,065 | 15.1 | % | -4.1 | % | |||||||||

| Interest payable | 58,442 | 46,899 | 36,759 | 59.0 | % | 24.6 | % | |||||||||

Total customer deposits | 12,938,927 | 11,249,104 | 8,842,655 | 46.3 | % | 15.0 | % | |||||||||

| Mutual funds in Perú | 2,088,039 | 1,955,547 | 1,432,924 | 45.7 | % | 6.8 | % | |||||||||

| Mutual funds in Bolivia | 83,890 | 70,919 | 60,201 | 39.3 | % | 18.3 | % | |||||||||

Total customer funds | 12,938,927 | 11,249,104 | 8,842,655 | 46.3 | % | 15.0 | % | |||||||||

The evolution in deposits, especially Nuevos Soles deposits, reflects as well the market environment and significant inflow of capital into the local financial system lured by the speculative opportunity offered by higher Soles rates and US Dollar weakness. This explains the Soles denominated deposits aslo contributed to the high reported deposits growth figures, reaching an overall high 15% deposits’ growth for the quarter.

10

While saving deposits continue expanding at a good rate, demand and CTS deposits, which drop in volumes, reflect the tighter competition for deposits in the market and growing sensitivity of our clients to interest rates earned on their funds. Nevertheless, deposits continue being the prime source of low cost funding since 57% of deposits are either low cost or interest free deposits. The retail segment is also of significant importance since 45% of deposits are generated by BCP’s retail clients.

Market Share

Despite the strong competition for deposits, BCP increased further its market share of deposits to 39.6% by the end of this 1Q08 from 38.8% as of December 2007.

BCP’s leadership is evident in all deposits, being our CTS market share the strongest with 52%, way above our next competitor with 19.6%. In demand deposits BCP holds 48.4% in local currency and 39.7% in US Dollars, while savings deposits reached 36.2% y 42.5% respectively. Finally, in time deposits BCP’s market share reached 25.6% y 39.6% in local and foreign currency.

Through Credifondo, BCP maintains its leadership in the mutual funds’ business with a total of US$ 2,088 million administered funds, up 6.8% QoQ and 45.7% YoY. This represents a market share of 43.7% for the end of March 2008. This increase in market share is noteworthy since it has become a more competitive and sophisticated market.

Another important evolution is the accelerated de-dollarization of deposits, with US Dollar deposits dropping to 61% of the total portfolio, fueled by dollar weakness and higher rates of the Nuevo Sol.

11

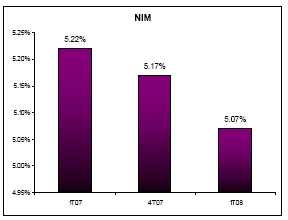

II.3 Net Interest Income

Despite an 11.0% QoQ net interest income growth, the re-composition of interest earning assets and loan portfolio impacted negatively on NIM, dropping to 5.07% for 1Q08.

Net interest income | Quarter | Change | ||||||||||||||

US$ 000 | 1Q08 | 4Q07 | 1Q07 | 1Q08/1Q07 | 1Q08/4Q07 | |||||||||||

Interest income | 296,660 | 272,204 | 195,388 | 51.8 | % | 9.0 | % | |||||||||

| Interest on loans | 213,932 | 201,414 | 148,943 | 43.6 | % | 6.2 | % | |||||||||

| Interest and dividends on investments | 1 | 139 | 8 | -87.5 | % | 100 | ||||||||||

| Interest on deposits with banks | 16,924 | 17,901 | 16,250 | 4.1 | % | -5.5 | % | |||||||||

| Interest on trading securities | 54,527 | 47,069 | 28,545 | 91.0 | % | 15.8 | % | |||||||||

| Other interest income | 11,276 | 5,681 | 1,642 | 586.7 | % | 98.5 | % | |||||||||

Interest expense | 124,049 | 116,640 | 72,099 | 72.1 | % | 6.4 | % | |||||||||

| Interest on deposits | 90,233 | 83,039 | 54,694 | 65.0 | % | 8.7 | % | |||||||||

| Interest on borrowed funds | 15,545 | 14,670 | 5,632 | 176.0 | % | 6.0 | % | |||||||||

| Interest on bonds and subordinated notes | 11,480 | 11,782 | 7,853 | 46.2 | % | -2.6 | % | |||||||||

| Other interest expense | 6,791 | 7,149 | 3,920 | 73.2 | % | -5.0 | % | |||||||||

Net interest income | 172,611 | 155,564 | 123,289 | 40.0 | % | 11.0 | % | |||||||||

| Average interest earning assets | 13,613,215 | 12,031,956 | 9,444,029 | 44.1 | % | 13.1 | % | |||||||||

Net interest margin* | 5.07 | % | 5.17 | % | 5.22 | % | ||||||||||

Interest income increased by a very significant 9% QoQ, as a result of not only the strong loan portfolio growth which generated 6.2% more interest income, but also the significantly larger investment portfolio leading to a 15.8% higher interest income for the quarter. This, combined with a lower interest expense expansion of 6.4% resulted in a total and impressive 11% net interest income quarterly growth.

This is no doubt the result of an unexpected market evolution, since the speculative inflow of large amounts of funds looking to benefit from higher Soles interest rates and the US Dollar weakness together with the revaluation effect on existing assets resulted in the change in BCP's interest earning assets mix that made possible this interest income growth. Excess liquidity was channeled to CBCD’s, which despite carrying a low nominal yield, are extremely attractive on an after tax yield basis given the tax shelter they provide. However, with BCP’s investment portfolio with a lower nominal yield growing significantly more in US Dollar terms (up 45.9%) than its loan portfolio (up 7.4%), and at the same time, its loan portfolio mix also growing more in the corporate sector than in the retail sector as seen before, a drop in a net interest margin (NIM) was unavoidable.

Quarterly growth of interest earning assets | Balance as of | Change | ||||||||||||||||||||

| US$ 000 | Mar 08 | Dec 07 | Sept 07 | Mar 07 | ´Dec 06 | Mar 08/ Mar 07 | Mar 08/ Dec 07 | |||||||||||||||

| BCRP and Other Banks | 2,077,660 | 2,255,572 | 1,740,636 | 1,828,663 | 2,031,936 | 13.6 | % | -7.9 | % | |||||||||||||

| Interbank funds | 1,469 | 5,000 | 1,000 | 4,542 | 25,079 | -67.7 | % | -70.6 | % | |||||||||||||

| Trading Securities | 38,538 | 102,316 | 49,465 | 54,505 | 37,475 | -29.30 | % | -62.3 | % | |||||||||||||

| Available For Sale Securities | 3,449,781 | 2,364,084 | 1,998,309 | 1,641,157 | 1,359,847 | 110.2 | % | 45.9 | % | |||||||||||||

| Current Loans, net | 8,767,674 | 8,164,334 | 7,383,196 | 6,109,064 | 5,795,790 | 43.5 | % | 7.4 | % | |||||||||||||

Total interest earning assets | 14,335,123 | 12,891,306 | 9,637,930 | 9,637,930 | 9,250,127 | 48.7 | % | 11.2 | % | |||||||||||||

| Total average interest earning assets | 13,613,215 | 12,031,956 | 10,970,685 | 9,444,029 | 8,854,003 | |||||||||||||||||

Furthermore, interest rates increases and the impact of the higher reserve requirements on funding costs contributed also to such drop. As a result, NIM fell from 5.17% in 4Q07 to 5.07% in 1Q08.

12

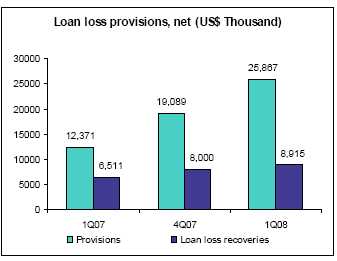

II.4 Loan provisions

Provisions grow following more conservative provisioning policies for the retail portfolio. Portfolio quality ratios remain at excellent levels.

Provisión for loan losses | Quarter ended | Change | ||||||||||||||

| US$ 000 | 1Q08 | 4Q07 | 1Q07 | 1Q08/1Q07 | 1Q08/4Q07 | |||||||||||

| Provisions | (25,867 | ) | (19,089 | ) | (12,371 | ) | 109.1 | % | 35.5 | % | ||||||

| Loan loss recoveries | 8,915 | 8,000 | 6,511 | 36.9 | % | 11.4 | % | |||||||||

Total provisions, net of recoveries | (16,951 | ) | (11,089 | ) | (5,859 | ) | 189.3 | % | 52.9 | % | ||||||

Total loans | 8,837,689 | 8,224,613 | 6,182,300 | 43.0 | % | 7.5 | % | |||||||||

Reserve for loan losses (RLL) | 219,295 | 212,060 | 184,627 | 18.8 | % | 3.4 | % | |||||||||

Bcp's Charge-Off amount | 9,281 | 12,034 | 10,507 | -11.7 | % | -22.9 | % | |||||||||

Past due loans (PDL) | 70,015 | 60,279 | 73,237 | -4.4 | % | 16.2 | % | |||||||||

| PDL/Total loans | 0.79 | % | 0.73 | % | 1.18 | % | ||||||||||

| Coverage | 313.21 | % | 351.80 | % | 252.10 | % | ||||||||||

Gross provisions reached US$ 25.9 million in 1Q08, 35.5% higher QoQ, reflecting not only the increase in the loan book, but also a change in provisioning policy for our retail portfolio, raising the minimum provisions for each of the retail products to levels calculated applying a more sophisticated risk assessment methodology.

Recoveries, on the other hand increased also a strong 11.4% due to the sale of a large and old troubled loan. This transaction represented income from recovery of US$ 1.7 million.

Past due loans in absolute terms reflect an increase of US$ 10 million, though such relatively small movements compared to the loan portfolio size are not unusual and are not an indicator of any portfolio quality deterioration. Thus, PDL/total loans ratio of 0.79% continues being an excellent ratio, as is the 313% coverage ratio for 1Q08.

13

II.5 Non Financial Income

During 1Q08, non financial income was boosted by the extraordinary income generated for financial institutions members of Visa by the Visa IPO.

Non financial income | Quarter | Change | ||||||||||||||

| US$ 000 | 1Q08 | 4Q07 | 1Q07 | 1Q08/1Q07 | 1Q08/4Q07 | |||||||||||

| Fee income | 79,747 | 76,708 | 62,470 | 27.7 | % | 4.0 | % | |||||||||

| Net gain on foreign exchange transactions | 19,971 | 21,497 | 11,937 | 67.3 | % | -7.1 | % | |||||||||

| Net gain on sales of securities | 22,655 | 2,661 | 9,210 | 146.0 | % | 751.4 | % | |||||||||

| Other income | 2,190 | 2,592 | 2,638 | -17.0 | % | -15.5 | % | |||||||||

Total non financial income | 124,563 | 103,458 | 86,255 | 44.4 | % | 20.4 | % | |||||||||

Fee income growth of 4% QoQ comes from increased income from account maintenance fees, credit card fees, transactional fees and charges.

Net gain in FX transactions dropped 7.1% QoQ after having had a significantly higher FX gain in the 4Q07 due to the strong year end activity.

Net gain in the sale of securities reflects an extraordinary jump from US$2.7 million to US$22.7 million this quarter. This responds to the sale of the Visa shares through the IPO of Visa Inc. which resulted in income of US$17.9 million in 1Q08 and thus accounts for most of the income increase.

Even though commissions for banking transactions grow, the average number of monthly transactions drops from 33.3 million to 32.3 million, reflecting a drop of 2.9% QoQ. This is a normal seasonal evolution with transaction volume always peeking during the 4Q of every year.

14

Quarter | Change | |||||||||||||||

N° of Transactions per Channel | Average 1Q08 | Average 4Q07 | Average 1Q07 | 1Q08/ 1Q07 | 1Q08/ 4Q07 | |||||||||||

| Teller | 9,091,066 | 9,371,270 | 8,310,053 | 9.4 | % | -3.0 | % | |||||||||

| ATMS ViaBCP | 5373782 | 5,540,733 | 4,191,183 | 28.2 | % | -3.0 | % | |||||||||

| Balance Inquiries | 2,249,668 | 2,468,491 | 2,022,884 | 11.2 | % | -8.9 | % | |||||||||

| Telephone Banking | 1,108,666 | 1,203,838 | 943,356 | 17.5 | % | -7.9 | % | |||||||||

| Internet Banking ViaBCP | 7,448,052 | 7,284,113 | 5,891,783 | 26.4 | % | 2.3 | % | |||||||||

| Agente BCP | 1,248,203 | 1,092,778 | 497,603 | 150.8 | % | 14.2 | % | |||||||||

| Telecrédito | 2,884,387 | 3,374,932 | 2,532,613 | 13.9 | % | -14.5 | % | |||||||||

| Direct Debit | 341,265 | 346,710 | 281,029 | 21.4 | % | -1.6 | % | |||||||||

| P.O.S. | 2,466,764 | 2,489,588 | 1,983,368 | 24.4 | % | -0.9 | % | |||||||||

| Other ATM network | 173,343 | 168,839 | 139,280 | 24.5 | % | 2.7 | % | |||||||||

| Total transactions | 32,385,197 | 33,341,293 | 26,793,154 | 20.9 | % | -2.9 | % | |||||||||

From the chart above, the evolution of the number of transactions done through the “Agente BCP” is truly noteworthy, reflecting its significance; as well as the evolution of electronic channels vis-à-vis the traditional teller transactions.

Quarter | Change | |||||||||||||||||||||

| Mar-08 | Dec-07 | Sep-07 | Mar-07 | Dec-06 | Mar. 08/ Dec. 07 | Mar. 08/ Mar. 07 | ||||||||||||||||

| Branches | 277 | 273 | 254 | 245 | 237 | 1 | % | 13 | % | |||||||||||||

| ATMs | 778 | 748 | 724 | 691 | 655 | 4 | % | 13 | % | |||||||||||||

| Agentes BCP | 1,358 | 1,221 | 1,017 | 703 | 551 | 11 | % | 93 | % | |||||||||||||

| Total | 2,413 | 2,242 | 1,995 | 1,639 | 1,443 | 8 | % | 47 | % | |||||||||||||

II.6 Operating Costs and Efficiency

The efficiency ratio improved this 1Q08 to 47.5%, with operating expenses dropping 8.9% QoQ after the high year end related cost increase reported in 4Q07 and despite the negative impact of the revaluation of Soles denominated costs.

Operating expenses | Quarter | Change | ||||||||||||||

| US$ 000 | 1Q08 | 4Q07 | 1Q07 | 1Q08/1Q07 | 1Q08/4Q07 | |||||||||||

| Salaries and employees benefits | 70,553 | 75,147 | 51,302 | 37.5 | % | -6.1 | % | |||||||||

| Administrative, general and tax expenses | 48,520 | 59,234 | 37,755 | 28.5 | % | -18.1 | % | |||||||||

| Depreciation and amortizacion | 10,364 | 10,000 | 9,423 | 10.0 | % | 3.6 | % | |||||||||

| Other expenses | 8,898 | 7,485 | 9,738 | -8.6 | % | 18.9 | % | |||||||||

Total operating expenses | 138,335 | 151,867 | 108,218 | 27.8 | % | -8.9 | % | |||||||||

Efficiency Ratio | 47.53 | % | 56.89 | % | 49.81 | % | ||||||||||

Though fixed Soles denominated salaries expense increased approximately 19% this quarter as the number of employees increased to 13,540 from 12,667 by the end of last year driven by the network expansion plans, on a comparative base with the previous quarter, a drop of 6.1% is reported due to the high comparison base set by the seasonally higher year end costs (related to performance compensation) and the unusual provisions for the retirement of a few members of senior management in the 4Q07. The differential between quarters in personnel expenses was in fact stronger than reported since the revaluation effect of the Soles works exacerbating in dollar terms the increased nominal soles payroll. This is more evident in a YoY comparison where a 37.5% growth is observed, which is certainly exacerbated by the Soles revaluation. Nevertheless, despite the 19% nominal payroll increase, this was below expectations and explained by a non linear progression in expenses related to the network expansion, which resulted in less expense growth for the beginning of the year than projected.

15

Administrative expenses on the other side, also reported a significant drop of 18.1% from the previous quarter. Once again, the year end strong increases in expenses in 4Q07, in all sectors such as marketing, systems support, consultancy jobs and transportation, set a high expense level for last quarter, and given the normalized level of expenses and also the mentioned non linear distribution of such, helps explains the drop reported. In fact marketing expenses dropped 58.7% QoQ and systems support expenses were down 24.4%. We would however like to point out, that the network expansion plan and systems support investments are going full speed ahead and will result in expense increases along the year.

Such administrative expense expansion is thus better reflected by the yearly growth reported of a total of 28.5%.

Administrative expenses | Quarter | Change | |||||||||||||||||||||||

| US$ 000 | 1Q08 | % | 4Q07 | % | 1Q07 | % | 1Q08/1Q07 | 1Q08/4Q07 | |||||||||||||||||

| Marketing | 5,032 | 10 | % | 12,180 | 21 | % | 3,785 | 10 | % | 32.9 | % | -58.7 | % | ||||||||||||

| Systems | 6,892 | 14 | % | 9,121 | 15 | % | 6,967 | 18 | % | -1.1 | % | -24.4 | % | ||||||||||||

| Transportation | 4,458 | 9 | % | 4,864 | 8 | % | 3,528 | 9 | % | 26.4 | % | -8.3 | % | ||||||||||||

| Maintenance | 2,444 | 5 | % | 2,319 | 4 | % | 1,605 | 4 | % | 52.3 | % | 5.4 | % | ||||||||||||

| Communications | 2,497 | 5 | % | 2,217 | 4 | % | 1,938 | 5 | % | 28.9 | % | 12.6 | % | ||||||||||||

| Consulting | 2,207 | 5 | % | 3,174 | 5 | % | 1,747 | 5 | % | 26.3 | % | -30.5 | % | ||||||||||||

| Other expenses | 14,195 | 29 | % | 16,483 | 28 | % | 10,057 | 27 | % | 41.2 | % | -13.9 | % | ||||||||||||

| Porperty taxes and others | 5,487 | 11 | % | 4,897 | 8 | % | 4,097 | 11 | % | 33.9 | % | 12.0 | % | ||||||||||||

| Other subsidiaries and eliminations, net | 5,308 | 11 | % | 3,979 | 7 | % | 4,031 | 11 | % | 31.7 | % | 33.4 | % | ||||||||||||

Total administrative expenses | 48,520 | 100 | % | 59,234 | 100 | % | 37,755 | 100 | % | 28.5 | % | -18.1 | % | ||||||||||||

Other expenses increased 18.9% QoQ and are explained by the volatility experienced by our own stock during 1Q08 which was reflected in the coverage levels and provisions related to the Stock Appreciation Rights program.

Thus, a drop in operating costs (excluding others) of 10.4%, while operating income improved 7.3% resulted in a significant recovery of BCP’s efficiency ratio from 56.9% in 4Q07 to 47.5% this 1Q08.

II.7 Shareholders’ Equity and Regulatory Capital

Shareholders' equity | Quarter | Change | ||||||||||||||

| US$ 000 | 1Q08 | 4Q07 | 1Q07 | 1Q08/1Q07 | 1Q08/4Q07 | |||||||||||

| Capital stock | 364,706 | 364,706 | 364,706 | 0.0 | % | 0.0 | % | |||||||||

| Reserves | 388,062 | 282,189 | 282,189 | 37.5 | % | 37.5 | % | |||||||||

| Unrealized Gains and Losses | 90,285 | 57,771 | 65,449 | 37.9 | % | 56.3 | % | |||||||||

| Retained Earnings | 186,761 | 96,245 | 96,484 | 93.6 | % | 94.0 | % | |||||||||

| Income for the year | 165,772 | 331,652 | 72,657 | 128.2 | % | -50.0 | % | |||||||||

Total shareholders' equity | 1,195,587 | 1,132,564 | 881,485 | 35.6 | % | 5.6 | % | |||||||||

| Return on average equity (ROAE) | 56.96 | % | 31.67 | % | 31.50 | % | ||||||||||

Total shareholders’ equity reached US$ 1,195 million as of March 2008, i.e. up 5.6% QoQ. ROAE however, reached un unprecedented level of 56.96% boosted by the impact of the sudden and strong revaluation of the local currency throughout the results of the bank, leading to the extremely high translation gain of over US$ 57 million..

16

At the end of March 2008, the capital adequacy ratio for BCP unconsolidated reached 13.8% (7.3 times), higher than 11.8% (8.4 times) for 4Q07. Therefore, this indicator outperforms the one established by the system (9.1%) and our more conservative internal ratio of 11.5%.

The improved BIS ratio responds to the capitalization of retained earnings for US$ 106 million and the reduction of capital requirements as the risk adjusted capital improved as a result of the reduction of BCP’s US Dollar position and consequent reduction of exposure and risk to currency fluctuations.

On the other hand, Tier I reached US$ 951.9 million. Risk adjusted assets include a significantly reduced US$ 97.9 million market risk, which requires US$ 8.9 million of equity. Total regulatory capital includes US$ 307 million subordinated debt. In addition, US$ 80.8 million of capitalized earnings are included in the present period.

Regulatory Capital and Capital Adequacy Ratios | Quarter ended | Change | ||||||||||||||

| US$ 000 | 1Q08 | 4Q07 | 1Q07 | 1Q08/1Q07 | 1Q08/4Q07 | |||||||||||

| Capital Stock, net | 468,851 | 429,415 | 404,187 | 16.0 | % | 9.2 | % | |||||||||

| Legal and Other capital reserves | 484,105 | 346,418 | 326,066 | 48.5 | % | 39.7 | % | |||||||||

| Generic Contingency loss reserves | 91,469 | 85,005 | 61,130 | 49.6 | % | 7.6 | % | |||||||||

| Subordinated Debt | 307,422 | 294,648 | 137,610 | 123.4 | % | 4.3 | % | |||||||||

| Net income capitalized | 80,816 | 74,019 | - | - | 9.2 | % | ||||||||||

Total | 1,432,663 | 1,229,505 | 928,993 | 54.2 | % | 16.5 | % | |||||||||

| Less: Investment in multilateral organization and banks | (158,279 | ) | (175,762 | ) | (136,336 | ) | 16.1 | % | -9.9 | % | ||||||

Total regulatory capital | 1,274,385 | 1,053,743 | 792,657 | 60.8 | % | 20.9 | % | |||||||||

| Risk-weighted assets (Credit risk) | 9,168,514 | 8,603,291 | 6,218,204 | 47.4 | % | 6.6 | % | |||||||||

Market Risk | 8,893 | 26,714 | 43,093 | -79.4 | % | -66.7 | % | |||||||||

Capital Ratios: | ||||||||||||||||

| Regulatory capital as a percentage of risk-weighted assets | 13.75 | % | 11.84 | % | 11.84 | % | ||||||||||

| Ratio of risk-weihted assets to regularoy capital | 7.27 | 8.44 | 8.44 | |||||||||||||

17

III. Banco de Crédito de Bolivia

Bolivian Financial System

Bolivian Financial System reached US$ 4,719 million in deposits as of March 2008, 32% higher than the US$ 3,585 million registered in the previous year. Total loan volume reached US$ 3,258.2 as of March 2008, +16.6% YoY. In addition, PDL ratio of the loan portfolio reached 5.7% as of March 2008 vs. 5.6% as of December 2007 and 8.8% as of March 2007; while the coverage ratio was 112.2%.

The politically uncertain scenario presented by the country today has resulted in very low levels of investments, which might eventually lead to a downturn in the economy.

Results

In 1Q08, BCP Bolivia reached a net income of US$ 10.4 million, showing a growth of 7.4% QoQ and 116.7% YoY, mainly as a result of increased interest income (11% QoQ and 39.1% YoY), and higher non financial income (24.6% QoQ and 49.8% YoY).

Higher net interest income was a result of higher volumes of loans and investments and higher interest rates on loans. Non financial income increased mainly as a result of higher profits from the sale of securities (694.7% QoQ and 3,220.8% YoY). It is important to mention that this growth was led by the sale of VISA’s shares during March, which represented US$ 1.9 million boosting significantly the gains on sales of securities in the first quarter 2008.

Excluding the extraordinary gains from the sale of this investment, BCB’s net income would have been US$8.5 million for the 1Q08.

A conservative credit risk management strategy led to a PDL ratio of 1.7% (1.7% in 4Q07 and 3.6% in 1Q07) and a coverage ratio of 227.8% (240.1% in 4Q07 and 161.1% in 1Q07). BCP Bolivia’s ROAE was 56.1%, 37.3% higher than December 2007. Thus, these figures show that BCP Bolivia had one of the best loan quality ratios within the Bolivian banking system, which reported ratios of 5.7% and 109.6%, respectively.

Assets and liabilities

As of march 2008, total loans reached US$ 467.6 million, 0.8% higher than US$ 463.8 million as of December 2007 and 20.3% greater YoY. The smaller quarterly growth is the result of the reduction in economic activity, due to political uncertainty in the country. The political evolution and the low economic activity generated an uncertain situation and discourages businessmen from carrying out greater investments. This has been translated into the stagnation of the Bolivian economy, and therefore in a smaller growth of our loan portfolio QoQ.

During 1Q08, Retail Banking revealed the highest growth (8.4% TaT and 25.5% AaA), which has an important impact in BCB’s results, given that it represents 46.4% of BCB’s loan portfolio and generates greater margins, while Corporate and Middle Market Banking represents 48.4%. Both segments represent 94.8% of total loans.

Within the Retail Banking segment, Personal loans and SME grew 9.2% and 8.2%, respectively. Both segments represented 28.4% of total retail loans and showed the greatest QoQ growth. In addition, the mortgage segment, which represented 52.8% of total retail portfolio, grew 0.9% TaT and 6.1% AaA.

18

In terms of liabilities, BCP Bolivia showed an increase in deposits of 5.6% QoQ and 28.3% YoY. Demand deposits grew 7.3% QoQ and 27.2% YoY, saving deposits, 5.5% QoQ and 45.6% YoY, and time deposits increased 4.1% QoQ and 12.6% YoY.

Shareholders’ equity decreased 10.9% QoQ due to dividends distribution. Nevertheless, this reduction was compensated by net income of the quarter. The net shareholders’ equity grew 21.1% YoY.

Finally, BCP Bolivia holds market shares of 14.0% and 14.6% of loans and deposits, respectively, which represent the third place in the Bolivian Banking System.

Banco de Crédito de Bolivia | Quarter | Change % | ||||||||||||||

| US$ millon | 1Q08 | 4Q07 | 1Q07 | 1Q08/1Q07 | 1Q08/4Q07 | |||||||||||

| Total loans | 467.6 | 463.8 | 388.8 | 20.3 | % | 0.8 | % | |||||||||

| Past due loans | 7.9 | 7.8 | 13.7 | -42.3 | % | 2.3 | % | |||||||||

| Loan loss reserves | (18.1 | ) | (18.6 | ) | (22.2 | ) | -18.4 | % | -3.0 | % | ||||||

| Total Assets | 845.0 | 821.9 | 675.3 | 25.1 | % | 2.8 | % | |||||||||

| Deposits | 701.0 | 663.9 | 546.3 | 28.3 | % | 5.6 | % | |||||||||

| Shareholders net equity | 75.8 | 85.1 | 62.6 | 21.1 | % | -10.9 | % | |||||||||

Net income | 10.4 | 9.7 | 4.8 | 116.7 | % | 7.4 | % | |||||||||

| PDL/ Total loans | 1.7 | % | 1.7 | % | 3.6 | % | ||||||||||

| Coveage ratio of PDLs | 227.8 | % | 240.1 | % | 161.1 | % | ||||||||||

| ROAE | 56.1 | % | 37.3 | % | 27.6 | % | ||||||||||

| Branches | 61 | 61 | 57 | |||||||||||||

| ATMs | 167 | 157 | 143 | |||||||||||||

| Employees | 1503 | 1441 | 1178 | |||||||||||||

19

IV. Atlantic Security Holding Corporation

ASHC | Quarter | Change % | ||||||||||||||

(US$ Million) | 1Q 2008 | 4Q 2007 | 1Q 2007 | 1Q08 / 1Q07 | 1Q08 / 4Q07 | |||||||||||

| Net interest income | 5.7 | 4.9 | 4.3 | 34.2 | 16.3 | |||||||||||

| Dividend income | 0.0 | 0.2 | 19.1 | -99.7 | -79.1 | |||||||||||

| Fees and commissions from services | 2.1 | 2.2 | 2.0 | 9.3 | -2.1 | |||||||||||

| Net gains on foreign exchange transactions | 0.6 | 0.8 | 0.0 | 4,906.9 | -23.2 | |||||||||||

Core Revenues | 8.5 | 8.2 | 25.3 | -66.3 | 4.7 | |||||||||||

| Total provisions, net of recoveries | -2.0 | -3.1 | -0.3 | -535.5 | 35.7 | |||||||||||

| Net gains from sale of securities | 0.7 | 2.4 | 0.6 | 24.7 | -70.0 | |||||||||||

| Other income | 0.5 | 0.4 | 0.3 | 95.1 | 29.1 | |||||||||||

| Operating expenses | -2.2 | -2.9 | -1.9 | 13.3 | -26.1 | |||||||||||

Net income | 5.7 | 5.0 | 24.0 | -76.3 | 13.7 | |||||||||||

| Net income/share | 0.1 | 0.1 | 0.4 | -76.3 | 13.7 | |||||||||||

| Total loans | 146.4 | 130.1 | 125.4 | 16.8 | 12.5 | |||||||||||

| Total investments available for sale | 824.3 | 853.7 | 801.9 | 2.8 | -3.4 | |||||||||||

| Total asset | 1,490.7 | 1,615.3 | 1,432.2 | 4.1 | -7.7 | |||||||||||

| Total deposits | 1,227.9 | 1,382.9 | 1,197.8 | 2.5 | -11.2 | |||||||||||

| Shareholder's equity | 208.5 | 214.1 | 217.6 | -4.2 | -2.6 | |||||||||||

| Net interest margin | 1.66 | % | 1.34 | % | 1.34 | % | ||||||||||

| Efficiency ratio | 22.0 | % | 26.6 | % | 7.3 | % | ||||||||||

| Return on average equity* | 16.3 | % | 16.5 | % | 17.1 | % | ||||||||||

| PDL / Total loans | 0.00 | 0.00 | 0.00 | |||||||||||||

| Cover ratio | 0.9 | % | 1.0 | % | 1.9 | % | ||||||||||

| BIS ratio | 14.93 | % | 15.07 | % | 16.68 | % | ||||||||||

*Figures of ASB | ||||||||||||||||

Net income for Atlantic Security Holding Corporation (ASHC) of USD 5.7 million reflects an important QoQ increase of 13.7%, though on a yearly comparison a distortion is obvious given that the 1Q07 included the Credicorp dividend, which is being paid this year in April. Excluding that distortion, a yearly growth would also be reported.

Core revenues were up 4.7% for the quarter, and net of the Credicorp dividend, also 16.3% for the year. The driver of this growth is net interest income, which increased 16.3%. This increase in net interest income is reported in the midst of a declining interest rate environment, which led the bank to react with an active management of its cost of funds, through periodical adjustments to interest rates paid on deposits and careful management of its maturity structure, therefore generating wider margins.

Commissions and fees income remain stable, and net gains on foreign exchange transactions reflect gains from the appreciation against the US Dollar of foreign currency positions maintained by the bank, mainly Peruvian Nuevos Soles.

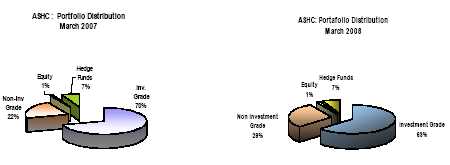

Net provisions reported in 1Q08 of US$ 2.0 million were lower in 35.7% when compared to those reported in 4Q07. These respond to the necessary recognition of an adverse market effect on the Bank’s proprietary investment portfolio; triggered by the current financial markets’ turmoil. Nevertheless, the investment portfolio maintains a significant concentration of 63% in investment grade securities indicating a high credit quality exposure. We estimate that reserves will remain within the same levels reported for 1QT08 in the following quarter.

Realized gains on the sale of securities show a volatile performance, though we estimate these will remain constant or below current 1Q08 figures for the following months.

20

Net interest margin presents an increase from 1.34% to 1.66% during this 1Q08 mainly due to a reduction of interests on deposits, which were aligned to the reductions observed in the LIBOR rate.

Efficiency ratio presented a slight reduction from 26.6% in 4Q07 to 22.0% this 1Q08. This improvement is a result of the slightly increased net income. The 1Q07 efficiency ratio reported of 7.3% is totally distorted again by the extraordinary Cerdicorp dividend income in that period. Net of that distortion, the ratio is 26%, i.e. similar to ratios reported during the last quarters.

Total asset levels decreased by 7.7% on QoQ due to outgoing customers’ deposits and their migration to structured products managed off-balance sheet for customers motivated by higher yields.

Interest Earning Assets

Interest earning assets reached US$ 1.358 MM, as shown in the table below. This figure dropped 8.1% on a QoQ basis, while an increase of 6.1% YoY is observed. This follows the migration mentioned above of deposits to off-balance sheet investment opportunities and outgoing funds from customers’ accounts during this 1QT08.

The share of investment-grade securities in the investment portfolio is 63%, emphasizing ASB’s prudent investment policy of concentrating its portfolio in high credit quality, high liquidity securities.

INTEREST EARNING ASSETS* | Quarter | % Change | ||||||||||||||

(US$ Million) | 1Q 2008 | 4Q 2007 | 1Q 2007 | 1Q08/ 1Q07 | 1Q08/ 4Q07 | |||||||||||

| Due from banks | 437 | 548 | 402 | 8.7 | % | -20.2 | % | |||||||||

| Loans | 146 | 130 | 125 | 16.8 | % | 12.5 | % | |||||||||

| Investments | 774 | 799 | 752 | 2.9 | % | -3.2 | % | |||||||||

Total interest-earning assets | 1,358 | 1,478 | 1,280 | 6.1 | % | -8.1 | % | |||||||||

| (*) Excludes investments in equities and mutual funds. |

21

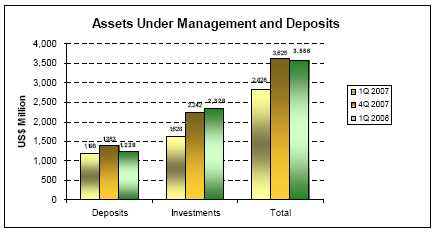

Asset Management Business

In the Asset Management business we include customers’ deposits, and investments such as proprietary mutual funds and securities custody. The total of these funds dropped by 1.9% QoQ and 25.9% YoY. Such drop is basically explained by the market valuation of the portfolio, since the outgoing funds from our deposits were completely captured by our asset management products. Thus, total funds under management shows a valuation of 3,556 million vs. US$3,625 million in 4Q07. The management of third party funds in off-balance sheet accounts continues to be the focus of our new business development of ASHC.

22

V. PRIMA AFP

Market Developments

During 1Q08, competition in the Private Pension Fund System slightly decreased in comparison to the previous quarter. Thus, the level of transfers dropped to an average of 24 thousand per month in 1Q08 from an average of 27 thousand per month in 4Q07. Reduction in sales force has not affected significantly new affiliations, which increased from an average level of 18 thousand to 21 thousand during 1Q08.

In terms of funds under management (FuM), there was an increase with respect to December 2007 of 9.3%, mainly due to the strong domestic currency appreciation, reaching a total of US$ 22.3 billion. Market behavior affected voluntary contributions, which showed a decreasing trend.

Financially, companies have shown a positive evolution in terms of earnings and expenses, supported by the strong local currency appreciation. It is important to mention that this development took place despite the double accrued earnings effect in the first month of the year.

Private Pension Fund System: Main Indicators

At the end of period: | 1Q08 | 4Q07 | 1Q07 | |||||||

| Affiliates (thousand) | 4,156 | 4,101 | 3,939 | |||||||

| % Change (1) | 1.3 | % | 1.3 | % | 1.5 | % | ||||

| Sales force | 2,031 | 2,340 | 5,179 | |||||||

| Assets under management (US$ mm) | 22,279 | 20,371 | 16,763 | |||||||

| % Change (1) | 9.4 | % | 0.4 | % | 16.5 | % | ||||

| Income (US$ mm) | 68.0 | 51.4 | 51.5 | |||||||

| Operating Expenses (US$ mm) | 44.1 | 43.9 | 44.5 | |||||||

| Operating income (US$ mm) | 23.9 | 7.5 | 7.0 | |||||||

| Net Income (US$ mm) | 15.7 | -0.5 | 22.0 | |||||||

(1) Quarter variation.

In local Peruvian accounting, legal reserves are included in the income statement as opposed to the IFRS.

There is no information for results adjusted to international financial reporting standards for the Total System.

The first and third quarter include double collection

Prima AFP

During 1Q08, Prima AFP maintained a good performance in terms of commercial and investment activities. In commercial terms, Prima AFP reduced the number of affiliates as a consequence of more transfers to other pension funds, potentially a consequence of being the leader in the reduction of the sale force. However, despite the reduced sale force, Prima AFP continued increasing its volumes of funds as a result of its increased sales force productivity and the quality of its contributors’ portfolio.

Prima AFP maintained its leadership in the market in terms of collections and voluntary contributions. Likewise, in comparison to the previous quarter position, Prima’s market share was superior despite the reduction in volume of voluntary contributions as a consequence of the market volatility.

23

PRIMA 1Q08 | System 1Q08 | % Share 1Q08 | PRIMA 4Q07 | % Share 4Q07 | ||||||||||||

| Affiliates (1) | 1,029,814 | 4,156,077 | 24.8 | % | 1,023,482 | 25.0 | % | |||||||||

| New affiliations (2) | 11,130 | 62,583 | 17.8 | % | 10,707 | 19.8 | % | |||||||||

| Funds under management US$ mm (1) | 6,989 | 22,279 | 31.4 | % | 6,403 | 31.4 | % | |||||||||

| Collections US$ mm (3) | 153 | 443 | 34.4 | % | 124 | 33.7 | % | |||||||||

| Voluntary contributions US$ mm (4) | 163 | 339 | 48.1 | % | 168 | 47.2 | % | |||||||||

| RAM US$ mm (5) | 352 | 1,080 | 32.6 | % | 308 | 32.1 | % | |||||||||

(1) Source: Superintendencia de Banca y Seguros

(2) At the end of period.

(3) Accumulated to the Quarter. Include voluntary contributions

(4) Stock level at the end of period

(5)Monthly remuneration retained, earnings base calculation estimated by PRIMA on average earnings during the last 4 months excluding double collection effect, special collections and voluntary contributions fees.

Commercial Results

During 1Q08, Prima AFP developed its business in a relatively stable competition framework.

The client base increased by near 14,000 in-coming transfers and 11,000 new affiliations, which compensated 17,000 transfers away, and resulted in a positive net effect in the period. In addition, Prima’s sales force productivity is higher than the system’s in terms of average funds transferred to the company.

Prima’s funds under management reached US$ 6,989 million, which represented 31.4% of the system as of March 2008, similar to level shown in December 2007.

Investments

In terms of investments, international market volatility, mainly characterized by the uncertainty of the United States economy, affected domestic market and the corresponding profitability of funds under management, during this first quarter. Nonetheless, thanks to profitability achieved in previous quarters, during the period March 2008/ March 2007 Prima AFP obtained good performance levels of 6.70%, 12.16% and 17.86%, for funds number 1, 2, and 3, respectively. Thus, Prima reached position N°2 in funds number 1 and 3 and the third position in fund number 2. However, it is important to mention that results in a 24 month basis were 31.18%, 56.8% and 139.96% in funds N°1, 2 and 3, respectively, showing a leadership in all these funds and consistency and solid results in a long term basis.

Mar-08 | % | Dec-07 | % | ||||||||||

| Fund 1 | 349 | 5.0 | % | 277 | 4.3 | % | |||||||

| Fund 2 | 4,519 | 64.7 | % | 4,154 | 64.9 | % | |||||||

| Fund 3 | 2,121 | 30.4 | % | 1,973 | 30.8 | % | |||||||

| Total | 6,989 | 100.0 | % | 6,403 | 100.0 | % | |||||||

Source: Superintendencia de Banca y Seguros

According to the PF rules, the Central Reserve Bank of Peru raised the limit to foreign investment to 20%; while the Superintendencia de Banca Seguros listed new investment securities allowing more investment opportunities for the pension fund system.

Financial Results

During the 1Q08, Prima AFP recalculated the total amount of its deferred income tax and working profit sharing liability, resulting in a favorable adjustment of US$ 2.3 million corresponding to the year 2007. Excluding such adjustment from 2008, the real net income for Prima in 1Q08 is US$6.7 million.

24

Income:

During the first quarter of 2008, the total earnings of the company reached US$ 19.1 million, a figure higher than that expected as a result of higher income base and the domestic currency appreciation effect.

According to estimates based on income and administration fees for every company, during the first quarter, Prima AFP had the highest average income base of the system (32.6%).

PRIMA 1Q07 | Total System 1Q08 | PRIMA % Share | ||||||||

| Income (1) | 6.11 | 22.04 | 27.7 | % | ||||||

| Administration Fees | 1.5 | % | n.a. | |||||||

| RAM estimated base (2) | 352 | 1,080 | 32.6 | % | ||||||

Prima AFP estimates. in accordance to local public information, (CONASEV)

(1) Income excluding special management for collections from voluntary payments

(2) RAM: Monthly Accumulated Salary

Expenses:

In terms of expenses, the exchange rate effect was partially offset by a permanent cost control effort. Thus, sales personnel expenses were below budget and partially compensated extraordinary incentives adjustments related to administrative personnel, resulting in a higher operating margin than expected. Operating expenses were higher when compared to the previous quarter (US$ 11.6 million vs. US$ 9.9 million), mainly as a result of extraordinary incentives to administrative personnel and since in 4Q07 higher variable deferred expenses related to portfolio transfers, according to IFRS, were registered.

Likewise, financial results include expenses related to the amortization of assets identified in the merger operation. Including the amortization and depreciation for investments in properties and systems, total expense in D&A was US$ 2.1 million for the period.

The “other income and expenses” line, includes the extraordinary result explained by the gains obtained from exchange rate differences and the reduction of financial expenses after prepayments of banking debt.

Thus, following such changes in income, expenses and charges mentioned above, Prima reported net income of US$ 9.0 million (includes deferred adjustment of US$2.2 million in 2007), 300% higher than its budget.

Total assets level remains relatively stable reaching US$ 254.3 million, as well as liabilities (US$ 116.5 million) and equity (US$ 137.7 million).

PRIMA AFP: Main financial indicators (US$ Thousand)

1Q08 | 4Q07 | Change % | ||||||||

| Income | 19,053 | 14,413 | 32 | % | ||||||

| General Expenses | (10,038 | ) | (12,105 | ) | -17 | % | ||||

| Net Income / Loss | 9,015 | 2,308 | 291 | % | ||||||

| Total Assets | 254,311 | 246,095 | 3 | % | ||||||

| Total Liabilities | 116,534 | 116,485 | 0 | % | ||||||

| Equity | 137,777 | 129,610 | 6 | % | ||||||

IFRS

25

VI. EL PACIFICO PERUANO SUIZA Y SUBSIDIARIAS

VI.1 PACIFICO GRUPO

Results for the quarter