ANNUAL

REPORT

NEEDHAM FUNDS

Seeking to build wealth for long-term investors

December 31, 2022

Needham Growth Fund

Needham Aggressive Growth Fund

Needham Small Cap Growth Fund

www.needhamfunds.com

250 Park Avenue, 10th Floor

New York, New York 10177

1-800-625-7071

www.needhamfunds.com

Annual Report

December 31, 2022

CONTENTS

| Letter from the Adviser | 1 |

| Portfolio Characteristics (Unaudited) | |

| Needham Growth Fund | 5 |

| Needham Aggressive Growth Fund | 6 |

| Needham Small Cap Growth Fund | 7 |

| Disclosure of Fund Expenses | 9 |

| Schedules of Investments | |

| Needham Growth Fund | 11 |

| Needham Aggressive Growth Fund | 14 |

| Needham Small Cap Growth Fund | 18 |

| Statements of Assets and Liabilities | 20 |

| Statements of Operations | 21 |

| Statements of Changes in Net Assets | 22 |

| Financial Highlights | |

| Needham Growth Fund | 25 |

| Needham Aggressive Growth Fund | 27 |

| Needham Small Cap Growth Fund | 29 |

| Notes to Financial Statements | 31 |

| Report of Independent Registered Public Accounting Firm | 37 |

| Information about Directors and Officers | 38 |

| Supplementary Information | 40 |

This report is authorized for distribution to prospective investors only when preceded or accompanied by a current prospectus.

The prospectus contains more complete information, including investment objectives, risks, expenses and charges and should be

read carefully before investing or sending any money. To obtain a prospectus or summary prospectus, please call 1-800-625-7071.

Portfolios of The Needham Funds, Inc., like all mutual funds:

| | • | Are NOT FDIC insured |

| | • | Have no bank guarantee |

| | • | May lose value |

The Needham Funds, Inc. are distributed by Needham & Company, LLC.

Annual Report 2022

| 250 Park Avenue, 10th Floor New York, New York 10177 (800) 625-7071 www.needhamfunds.com |

| |

| |

| |

February 2023

Dear Shareholders, Friends of Needham, and Prospective Shareholders,

We report Needham Funds’ results for the year ending December 31, 2022. Our mission is to create wealth for long-term investors, and 2022 was a step backward.

MARKET OVERVIEW/MACRO OBSERVATIONS

2022 was one of the worst years for investors in modern history. The S&P 500 had its worst first half since 1970 and ended the year down 18.11%. The Russell 2000 Growth Index fell 26.36% in 2022. By some measures, bonds had their worst year since 1754.1 It was all about inflation. In June, year-over-year inflation as measured by the Consumer Price Index peaked at 9.1%, and the price of gasoline increased 59.9% year-over-year. By November, year-over-year inflation remained high, but had fallen to 7.1%. In an effort to rein in inflation, the Federal Reserve aggressively raised interest rates, starting from 0.00% to 0.25% in March, and ending the year at 4.25% to 4.50%. The March increase was the first since 2015. As the Fed reaches the end of its rate hike cycle, markets could respond positively in 2023.

In March 2022, Russia began its attack on Ukraine. All year, we saw atrocities from the Russian assault on civilians, and it laid bare our assumptions about geopolitical stability and international economic cooperation. The war has reinforced the vulnerability of Europe’s reliance on Russian natural gas, and the need for increased defense spending. Combined with supply chain disruptions from the pandemic, the war underscores the need for countries and regions to shorten supply chains and become self-sufficient in energy and manufacturing.

The reshoring of U.S. manufacturing should create investment opportunities across life sciences, chemicals, oil and gas, alternative energy, and other industrial sectors. The Titanium Economy: How Industrial Technology Can Create a Better, Faster, Stronger America, written by several McKinsey partners, describes how industrial technology companies are important to the United States’ economic future.2 Clean Harbors, Inc. (CLH), a holding of Needham Growth Fund and Needham Aggressive Growth Fund, is one of the companies featured in the book. We have long focused our investments on companies supplying technology for manufacturing and R&D, but see even greater opportunities now.

NEEDHAM SMALL CAP GROWTH FUND – CHRIS RETZLER, PORTFOLIO MANAGER

For the year ended December 31, 2022, the Fund’s Institutional (NESIX) and Retail classes (NESGX) returned -29.82% and -30.33%, respectively, underperforming the Russell 2000 Growth Index’s -26.36%.

In 2022, the Fund benefitted from its concentrated investments in Intevac, Inc. (IVAC), Photronics, Inc. (PLAB), KVH Industries, Inc. (KVHI), TTM Technologies, Inc. (TTMI) and Edgio, Inc. (EGIO). The Fund’s top detractors in 2022 were Standard BioTools, Inc. (LAB), Telos Corporation (TLS), Sientra, Inc. (SIEN), 8x8, Inc. (EGHT), and nLight, Inc. (LASR).

In November 2022, the Fund’s long-term holding Benefitfocus (BNFT) announced its acquisition by Voya Financial. This is a perfect example of a management team that was improving operations, but realized that it is more prudent to consolidate based on economic circumstances and higher costs of capital. We expect more transactions like this one in 2023.

Throughout the second half of the year, the Fund increased its investment in Aspen Aerogels, Inc. (ASPN), a long-time portfolio holding. We are excited about the future of its aerogel insulation within the electric vehicle industry and its proposed expansion plans to supply accelerating customer demand.

The market volatility and multiples compression we experienced in the first half of 2022 began to abate in the last few months of the year. After the Fed surprised the markets in January 2022 with its faster-than-expected removal of monetary accommodation and numerous projected interest rate hikes, the markets reacted quickly and sold off. The interest rate yield curve remains steeply inverted as the Federal Reserve fights inflation and slows economic activity. Inflation is proving difficult to tame due to a variety of reasons, including supply constraints, component shortages, government regulations, energy supplies, food production costs, and transportation and logistics complications. We expect inflation to substantially decline in 2023.

As an asset class, small cap growth stocks experienced continued selling pressure in 2022. Wage pressures, logistics and transportation complications, higher commodity prices, and supply chain constraints continued to hamper earnings and forward guidance for many companies. These trends hurt smaller companies that lack the buying power and operational flexibility of larger companies. Overall, supply chain interruptions negatively impacted 2022 global growth and simultaneously supported persistently high inflation.

____________

1 | https://www.cnbc.com/2022/06/30/the-markets-worst-first-half-in-50-years-has-all-come-down-to-one-thing.html |

2 | https://www.mckinsey.com/featured-insights/mckinsey-on-books/the-titanium-economy |

Needham Funds

Widespread semiconductor shortages had negative implications for many end markets, including automotive, medical, industrial, and defense. However, supply chains have been recalibrated and disruptions have improved somewhat.

In August 2022, Congress passed the CHIPS and Science Act, which includes substantial funding and tax credits for domestic semiconductor production. The funding will help accelerate semiconductor development within the U.S., which has lagged over the past decade and will have enormous geopolitical benefits.

We continue to like the semiconductor capital equipment industry, including portfolio holdings Photronics, Inc., FormFactor, Inc. (FORM), and Veeco Instruments, Inc. (VECO). We like semiconductor manufacturers that are exposed to automotive, industrial, 5G and overall wireless infrastructure, such as portfolio holdings Sensata Technologies plc (ST), Marvell Technology, Inc. (MRVL) and Akoustis Technologies, Inc. (AKTS).

We also continue to like medical capital equipment and devices, and we expect to see growth as elective procedures increase. An example in our portfolio is ViewRay, Inc. (VRAY), a radiation oncology company. ViewRay is working on novel approaches to treating cancer, and it is experiencing acceleration in systems sales and placements.

We believe technology remains a great area to invest for the long term, and there are major secular trends firmly in place to support the technology sector’s continued growth. Areas of long-term investment that we like are mobile electrification, communications infrastructure, artificial intelligence, cloud computing, 5G devices and wireless connectivity, software and security, and specialty material manufacturing. We also see opportunities in military modernization and advancements in healthcare technologies.

As we enter 2023, we expect volatility to remain elevated as investors digest data from a slowing economy. However, we believe a lot of the damage to the equity markets was done in 2022. Improved global growth and accelerating revenue prospects should provide companies with leverage and drive improved earnings and cash flow. We expect the 2022 selloff to provide long-term investors with opportunities to buy high-quality growth stocks at reasonable prices in 2023. We will continue our strategy of patiently investing in small cap growth companies with good management teams, strong balance sheets, and the ability to generate cash flow and profits.

NEEDHAM GROWTH FUND – JOHN BARR AND CHRIS RETZLER, CO-PORTFOLIO MANAGERS

For the year ended December 31, 2022, the Fund’s Institutional (NEEIX) and Retail classes (NEEGX) returned -33.34% and -33.66%, underperforming the S&P 500’s -18.11% and the Russell 2000’s -20.44%.

Super Micro Computer, Inc. (SMCI) was the Fund’s leading contributor in 2022. Super Micro designs and manufactures servers. It grew throughout the year, sustained by large internet companies that operate their own data centers. These customers are investing in the computing power needed for the rapid growth of artificial intelligence applications. Super Micro is followed by just 4 Wall Street analysts who estimate 30% revenue growth in fiscal year 2023. Super Micro is valued at just 7x estimated earnings for the fiscal year ending June 30, 2023.

Parsons Corporation (PSN) was the Fund’s second leading contributor. Parsons does planning, construction, design, and implementation for infrastructure and government security programs. It builds airports, bridges, tunnels, roads, and railways. Its Federal Systems business does high-speed data and signal processing, network visualization, RF spectrum collection, geospatial collection systems, on-demand 3-D processing, missile defense, and counter hypersonics. We see Parsons as a beneficiary of the “Titanium Economy.”

Aspen Aerogels was the leading detractor in 2022, after being the largest contributor in 2021. The company supplies aerogel insulation used to insulate pipelines and refinery pipes. Aspen’s aerogel prevents thermal runaway in lithium-ion batteries, a major cause of fires in electric vehicles (EVs). Aspen has agreements with General Motors Company (GM), Toyota Motor Corp. ADRs (TM) and other EV makers to supply its PyroThinTM thermal barriers for use in EV batteries. We believe every EV maker has a similar need and that Aspen’s near-20 years of experience with aerogels puts it far ahead of any competitor. The EV battery market has the potential to increase Aspen’s revenues from $100 million to over $1 billion. However, Aspen needs to build a plant to meet this potential increase in demand. The plant in Statesboro, GA is making progress with the first products expected off the production lines in 2024. In November, Aspen completed a financing at $9.50 per share for most of its funding needs for the new plant. The Funds bought additional shares on this offering.

Entegris, Inc. (ENTG) was the second leading detractor in 2022, after being the Fund’s second leading contributor for 2021. Entegris supplies filters and chemicals used in advanced semiconductor manufacturing processes. We believe semiconductors will continue to increase as a percentage of industrial output, and that Entegris’ filtration and specialty materials products will grow faster than the semiconductor industry.3

____________

3 | https://www.regions.com/-/media/pdfs/AssetManagement-The-Semiconductor-Cycle.pdf?revision=1da76437-de80-4ebd-96f3-dc8ab8257328&la=en&hash=414BE463A90E72789127F9AB4D334AAA |

In 2022, Entegris acquired CMC Materials (formerly CCMP) for $6.5 billion. CMC produces specialty chemicals used to manufacture semiconductors. The acquisition is expected to be EPS accretive in the first year. Financed with debt and equity, it increased Entegris’ leverage ratio to over 4x adjusted EBITDA. We believe Entegris stock was down on concern over the leverage taken on for the acquisition, the difficulties in the semiconductor market, and the United States’ trade restrictions on China.

The Fund’s largest new positions in 2022 included Analog Devices, Inc. (ADI), ASM Holding NV ADR (ASML), and nLight Inc. (LASR). The Fund’s largest additions to existing positions were Laboratory Corporation of America (LH), Photronics, and Veeco.

The Fund’s largest position exits were IPG Photonics Corporation (IPGP) and Everbridge, Inc. (EVBG). The Fund reduced positions in some of the longer-term, larger holdings, including Gilead Sciences Inc. (GILD, Super Micro Computer, Comcast Corp. (CMSCA), and Thermo Fisher Scientific Inc. (TMO).

Morningstar categorizes the Fund as Mid-Cap Growth. Lipper categorizes it as Multi-Cap Core. When you hold companies for 10-15 years, and they succeed, they grow to larger market capitalization categories. Our mission is to find companies that may be compounders over many years, independent of industry or market cap.

NEEDHAM AGGRESSIVE GROWTH FUND – JOHN BARR, PORTFOLIO MANAGER

For the year ended December 31, 2022, the Fund’s Institutional (NEAIX) and Retail classes (NEAGX) returned -27.02%% and -27.53%, slightly underperforming the Russell 2000’s -26.36%.

Like the Needham Growth Fund, the Fund’s top contributors for 2022 were Super Micro Computer and Parsons. Other top contributors in 2022 were Vishay Precision Group Inc. (VPG), KVH Industries, Sharps Compliance Corp. (formerly SMED), and CRA International Inc. (CRAI).

In 2022, the top detractors to the Fund’s performance were Aspen Aerogels and Vicor Corporation (VICR). Many artificial intelligence and machine learning applications require sophisticated power conversion, and Vicor is uniquely positioned to meet these needs. Vicor was supply-constrained throughout 2022, and the stock suffered due to these supply constraints followed by slower orders in the second half. It opened a new manufacturing facility in May 2022 in Andover, MA.

Other major detractors were Entegris, Nova, Ltd. (NVMI), and Smith-Midland Corporation. (SMID). These stocks were top contributors in 2021.

NEEDHAM AGGRESSIVE GROWTH FUND – 2022 PORTFOLIO CHANGES

We believe 2022 was a good year to invest - time will tell. We took advantage of the market weakness throughout the year to invest the Fund’s cash position, which was 22.5% of assets on March 31 due to inflows, and ended the year at 6.7%. Many of these investments could benefit from the reshoring of U.S. manufacturing. We highlight the Fund’s most significant new positions below:

| | – | Adams Resources and Energy, Inc. (AE) was founded by Bud Adams, the founding owner of the Houston Oilers (now Tennessee Titans) football team. The $100 million market cap company transports liquid chemicals, pressurized gases, asphalt and dry bulk around the southern U.S. with a fleet of 300 trucks. It also markets, stores and transports crude oil via truck and pipeline connecting the Eagle Ford and other shale fields to the Gulf of Mexico. The company is an astute acquirer of complementary businesses. In November, it bought out the Adams heirs’ 44% ownership. We estimate Adams is valued at just 3-4x EBITDA. |

| | | |

| | – | Mativ Holdings, Inc. (MATV) was formed in July by the merger of Neenah, Inc. (formerly NP) and Schweitzer-Maudit International (formerly SWM). Mativ is a specialty materials company making filtration media and fine paper and packaged products for industrial and consumer markets. Mativ’s stock and its earnings suffered early in 2022 from a lag in passing through cost increases. |

| | | |

| | – | Bright Horizons Family Solutions, Inc. (BFAM) is a leading provider of child care centers. It suffered due to COVID-19, limited staff availability, and a slow return to the office. |

The most significant additions to existing positions in the portfolio were:

| | – | Vishay Precision Group, a specialty sensors and instruments company. |

| | | |

| | – | Photronics, a long-time portfolio company that manufactures photomasks used to manufacture semiconductors and LCD displays. Photronics reported disappointing earnings in August. |

| | | |

| | – | LabCorp- we believe there is hidden value in LabCorp’s contract research organization business. |

| | | |

| | – | Unisys Corporation (UIS), the new version of the old-line computer company. Unisys provides digital workplace solutions, cloud & infrastructure, and enterprise computing. We believe the profitability of its legacy operating system business alone is worth multiples of the current stock price. |

| | | |

| | – | Clean Harbors, an environmental services and used oil reprocessing company serving the energy and industrial markets. We believe the current stock price reflects little more than the replacement value of their incinerators and landfills. |

In 2022, the Fund exited Neophotonics Corporation (formerly NPTN), ChannelAdvisor Corporation (formerly ECOM) and Sharp Compliance Corp., on takeovers. We exited IPG Photonics because of its significant operations in Russia. The Fund reduced its position in Apple, Inc. (AAPL) to manage its position size.

CLOSING

We believe the U.S. remains the best place in the world to be investing, and we continue to see an opportunity to invest in small- and mid-cap stocks. Most importantly, we see a revolution happening in technology that has created and continues to create investment opportunities. We believe the reshoring of manufacturing in the U.S. will create investment opportunities. We see opportunity in our strategy of investing in companies that we know well and that we believe are positioned with secular growth drivers.

We welcome our new investors and thank all of our investors for their continued support. If you have any questions, thoughts or concerns, please contact us at (800) 625-7071 or jbarr@needhamco.com and cretzler@needhamco.com. For information about the Needham Funds, please visit our website at www.needhamfunds.com.

Sincerely,

|  |

| Chris Retzler, | John O. Barr, |

| Portfolio Manager | Portfolio Manager |

The information presented in this commentary is not intended as personalized investment advice and does not constitute a recommendation to buy or sell a particular security or other investments. Past performance is no guarantee of future results. The views of Needham Investment Management L.L.C., the Funds’ investment adviser (the “Adviser”), and the securities described in this report are as of December 31, 2022; these views and portfolio holdings may have changed subsequent to this date. The specific securities discussed may, in aggregate, represent only a small percentage of a Fund’s holdings. If a specific security discussed is not found in a Fund’s Schedule of Investments, it may have been held by the Fund during the period. It should not be assumed that securities identified and discussed were, or will be, profitable, or that the investment decisions made in the future will be profitable, or equal the investment performance of the securities discussed herein. There can be no guarantee as to the accuracy of any outlooks for markets, sectors and securities as discussed herein.

This message is not an offer of the Needham Growth Fund, the Needham Aggressive Growth Fund or the Needham Small Cap Growth Fund. Shares are sold only through the currently effective prospectus. Please read the prospectus or summary prospectus carefully and consider the investment objectives, risks and charges and expenses of the Funds carefully before you invest. The prospectus and summary prospectus contain this and other information about the Funds and can be obtained on our website, www.needhamfunds.com or by contacting the Funds’ transfer agent U.S. Bancorp Fund Services LLC doing business as U.S. Bank Global Fund Services (“Fund Services”) at 1-800-625-7071.

Investment returns and principal value will fluctuate, and when redeemed, shares may be worth more or less than their original cost. Performance data quoted represents past performance, and does not guarantee future results. Current performance may be higher or lower than these results. Performance current to the most recent month-end may be obtained by calling our transfer agent at 1-800-625-7071. Total return figures include reinvestment of all dividends and capital gains.

All three of the Needham Funds have substantial exposure to small and micro capitalized companies. Funds holding smaller capitalized companies are subject to greater price fluctuation than those of larger companies. The coronavirus disease 2019 (COVID-19) global pandemic and the aggressive responses taken by many governments or voluntarily imposed by private parties, including closing borders, restricting travel and imposing prolonged quarantines or similar restrictions, as well as the closure of, or operational changes to, many retail and other businesses, have had negative impacts, and in many cases severe negative impacts, on markets worldwide. It is not known how long such impacts, or any future impacts of other significant events described above, will or would last, but there could be a prolonged period of global economic slowdown, which may impact your Fund investment. Needham & Company, LLC, member FINRA/SIPC, is the distributor of The Needham Funds, Inc.

The Russell 2000 Index is a broad unmanaged index composed of the smallest 2,000 companies in the Russell 3000 Index. The Russell 3000 Index is a market-capitalization-weighted equity index that provides exposure to the entire U.S. stock market. The Russell 3000 Index tracks the performance of the 3,000 largest U.S.-traded stocks. The Russell 2000 Growth Index measures the performance of the small cap growth segment of the U.S. equity universe. It includes those Russell 2000 companies with relatively higher price-to-value ratios and higher forecasted growth values. Please see the disclaimer regarding these indexes under “Supplementary Information—Index Disclaimer” on page 41 of this report.

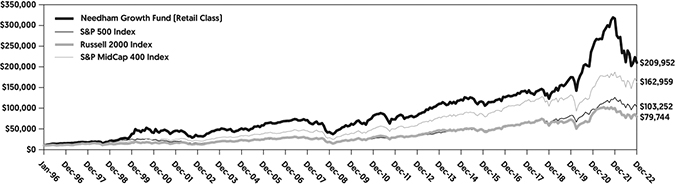

| NEEDHAM GROWTH FUND | Retail Class |

| Portfolio Characteristics (Unaudited) | Ticker Symbol: NEEGX |

| | Institutional Class |

| | Ticker Symbol: NEEIX |

COMPARISON OF CHANGE IN VALUE OF A $10,000 INVESTMENT

The chart above assumes an initial gross investment of $10,000 made on January 1, 1996.

COMPARATIVE PERFORMANCE STATISTICS AS OF DECEMBER 31, 2022

| | 1 | 5 | 10 | Since |

| | Year | Years | Years | Inception |

Needham Growth Fund Retail Class(1)(2) | -33.66% | 8.90% | 9.84% | 11.94% |

Needham Growth Fund Institutional Class(1)(3) | -33.34% | 9.42% | n/a | 9.33% |

S&P 500 Index(4)(5) | -18.11% | 9.42% | 12.56% | 9.03%(9) |

S&P MidCap 400 Index(4)(6) | -13.06% | 6.71% | 10.78% | 10.89%(9) |

Russell 2000 Index(4)(7) | -20.44% | 4.13% | 9.01% | 7.99%(9) |

Top Ten Holdings*

(as a % of total investments, as of December 31, 2022)

| | | % of Total |

Security | | Investments |

| Thermo Fisher Scientific, Inc. | TMO | 8.68% |

| PDF Solutions, Inc. | PDFS | 8.02% |

| Entegris, Inc. | ENTG | 5.39% |

| KVH Industries, Inc. | KVHI | 4.24% |

| Super Micro Computer, Inc. | SMCI | 3.92% |

| Aspen Aerogels, Inc. | ASPN | 3.91% |

| Becton Dickinson & Co. | BDX | 3.90% |

| Vicor Corp. | VICR | 3.57% |

| CarMax, Inc. | KMX | 3.46% |

| Nova, Ltd. | NVMI | 3.05% |

| | | |

Top Ten Holdings = 48.14% of Total Investments† | | |

Sector Weightings*

(as a % of net investments, as of December 31, 2022)

Sector(10) | Long(11) | (Short) | Total(12) |

| Cash | 4.6% | — | 4.6% |

| Communication Services | 4.4% | — | 4.4% |

| Consumer Discretionary | 4.1% | — | 4.1% |

| Energy | 0.9% | — | 0.9% |

| Health Care | 19.7% | — | 19.7% |

| Industrials | 8.4% | — | 8.4% |

| Information Technology | 53.5% | — | 53.5% |

| Materials | 3.9% | — | 3.9% |

| Real Estate | 0.4% | — | 0.4% |

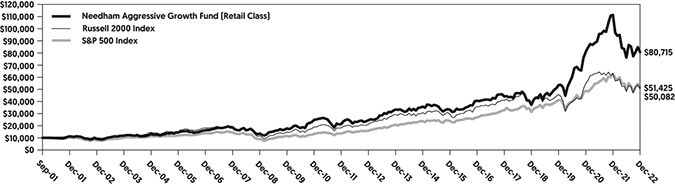

| NEEDHAM AGGRESSIVE GROWTH FUND | Retail Class |

| Portfolio Characteristics (Unaudited) | Ticker Symbol: NEAGX |

| | Institutional Class |

| | Ticker Symbol: NEAIX |

COMPARISON OF CHANGE IN VALUE OF A $10,000 INVESTMENT

The chart above assumes an initial gross investment of $10,000 made on September 4, 2001.

COMPARATIVE PERFORMANCE STATISTICS AS OF DECEMBER 31, 2022

| | 1 | 5 | 10 | Since |

| | Year | Years | Years | Inception |

Needham Aggressive Growth Fund Retail Class(1)(2) | -27.53% | 12.83% | 12.67% | 10.29% |

Needham Aggressive Growth Fund Institutional Class(1)(3) | -27.02% | 13.53% | n/a | 12.82% |

S&P 500 Index(4)(5) | -18.11% | 9.42% | 12.56% | 9.03%(9) |

Russell 2000 Index(4)(7) | -20.44% | 4.13% | 9.01% | 7.85%(9) |

Russell 2000 Growth Index(4)(8) | -26.36% | 3.51% | 9.20% | 7.39%(9) |

Top Ten Holdings*

(as a % of total investments, as of December 31, 2022)

| | | % of Total |

Security | | Investments |

| PDF Solutions, Inc. | PDFS | 7.33% |

| KVH Industries, Inc. | KVHI | 5.02% |

| Vicor Corp. | VICR | 4.51% |

| Super Micro Computer, Inc. | SMCI | 3.98% |

| Vishay Precision Group, Inc. | VPG | 3.90% |

| Nova, Ltd. | NVMI | 3.65% |

| Aspen Aerogels, Inc. | ASPN | 3.14% |

| Entegris, Inc. | ENTG | 3.05% |

| Photronics, Inc. | PLAB | 2.82% |

| Apple, Inc. | AAPL | 2.69% |

| | | |

Top Ten Holdings = 40.09% of Total Investments† | | |

Sector Weightings*

(as a % of net investments, as of December 31, 2022)

Sector(10) | Long(11) | (Short) | Total(12) |

| Cash | 6.7% | — | 6.7% |

| Communication Services | 0.6% | — | 0.6% |

| Consumer Discretionary | 5.4% | — | 5.4% |

| Consumer Staples | 1.1% | — | 1.1% |

| Energy | 2.6% | — | 2.6% |

| Financials | 1.5% | — | 1.5% |

| Health Care | 6.1% | — | 6.1% |

| Industrials | 18.3% | — | 18.3% |

| Information Technology | 48.9% | — | 48.9% |

| Materials | 7.4% | — | 7.4% |

| Real Estate | 1.4% | — | 1.4% |

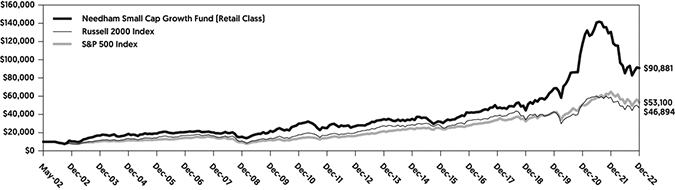

| NEEDHAM SMALL CAP GROWTH FUND | Retail Class |

| Portfolio Characteristics (Unaudited) | Ticker Symbol: NESGX |

| | Institutional Class |

| | Ticker Symbol: NESIX |

COMPARISON OF CHANGE IN VALUE OF A $10,000 INVESTMENT

The chart above assumes an initial gross investment of $10,000 made on May 22, 2002.

COMPARATIVE PERFORMANCE STATISTICS AS OF DECEMBER 31, 2022

| | 1 | 5 | 10 | Since |

| | Year | Years | Years | Inception |

Needham Small Cap Growth Fund Retail Class(1)(2) | -30.33% | 14.19% | 12.84% | 11.30% |

Needham Small Cap Growth Fund Institutional Class(1)(3) | -29.82% | 14.93% | n/a | 14.51% |

S&P 500 Index(4)(5) | -18.11% | 9.42% | 12.56% | 8.44%(9) |

Russell 2000 Index(4)(7) | -20.44% | 4.13% | 9.01% | 7.79%(9) |

Russell 2000 Growth Index(4)(8) | -26.36% | 3.51% | 9.20% | 7.75%(9) |

Top Ten Holdings*

(as a % of total investments, as of December 31, 2022)

| | | % of Total |

Security | | Investments |

| Intevac, Inc. | IVAC | 5.16% |

| nLight, Inc. | LASR | 5.03% |

| ViewRay, Inc. | VRAY | 4.92% |

| Photronics, Inc. | PLAB | 4.59% |

| Sumo Logic, Inc. | SUMO | 4.02% |

| Aspen Aerogels, Inc. | ASPN | 3.77% |

| Cambium Networks Corp. | CMBM | 3.76% |

| Infinera Corp. | INFN | 3.68% |

| Yext, Inc. | YEXT | 3.56% |

| 8x8, Inc. | EGHT | 3.43% |

| | | |

Top Ten Holdings = 41.92% of Total Investments† | | |

Sector Weightings*

(as a % of net investments, as of December 31, 2022)

\Sector(10) | Long(11) | (Short) | Total(12) |

| Cash | 17.7% | — | 17.7% |

| Consumer Discretionary | 0.3% | — | 0.3% |

| Health Care | 7.1% | — | 7.1% |

| Industrials | 5.1% | — | 5.1% |

| Information Technology | 66.0% | — | 66.0% |

| Materials | 3.8% | — | 3.8% |

Each Fund’s performance figures are for the years ended December 31, 2022. The performance data quoted is historical. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance data quoted. The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. To obtain performance information current to the most recent month-end, please visit www.needhamfunds.com or call 1-800-625-7071. The returns shown above are net of expenses. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemptions of Fund shares. In the absence of fee waivers and expense reimbursements, when they are necessary to keep the Fund’s total annual operating expenses at the expense cap currently in effect, total return would be reduced. Performance figures for periods greater than one year are annualized. For information about each index shown above, please see the notes below. The Global Industry Classification Standard (“GICS”) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor Financial Services LLC (“S&P”). GICS is a service mark of MSCI and S&P and has been licensed for use by U.S. Bancorp Fund Services, LLC, doing business as U.S. Bank Global Fund Services (“Fund Services”).

| (1) | Investment results calculated after reinvestment of dividends. |

| (2) | The inception date of the Retail Class of each Fund was as follows: Needham Growth Fund – 1/1/96; Needham Aggressive Growth Fund – 9/4/01; and Needham Small Cap Growth Fund – 5/22/02. |

| (3) | The inception date of the Institutional Class of each Fund was 12/30/16. |

| (4) | It is not possible to invest directly in an index. The performance of the index does not include the deduction of expenses associated with a mutual fund, such as investment management fees. |

| (5) | The S&P 500 Index focuses on the large-cap sector of the market; however, since it includes a significant portion of the total value of the market, it also is considered representative of the market. Companies in the S&P 500 are considered leading companies in leading industries. |

| (6) | The S&P MidCap 400 Index provides investors with a benchmark for mid-sized companies. The index seeks to remain an accurate measure of mid-sized companies, reflecting the risk and return characteristics of the broader mid-cap universe on an on-going basis. |

| (7) | The Russell 2000 Index measures the performance of the small-cap segment of the U.S. equity universe. The Russell 2000 Index is a subset of the Russell 3000 Index representing approximately 8% of the total market capitalization of that index. The Russell 2000 Index includes approximately 2,000 of the smallest securities based on a combination of their market cap and current index membership. |

| (8) | The Russell 2000 Growth Index is constructed to provide a comprehensive and unbiased barometer for the small-cap growth segment. The index is completely reconstituted annually to ensure new and growing equities are included and that the represented companies continue to reflect growth characteristics. |

| (9) | The return shown for the index is from the inception date of the Retail Class. The returns for the S&P 500 Index, S&P MidCap 400 Index, Russell 2000 Growth, and the Russell 2000 Index from the inception date of the Institutional Class are 11.40%, 8.24%, 6.40%, and 5.81%, respectively. |

| (10) | These categories represent broad market sectors. Refer to the Schedule of Investments for a more detailed categorization by industry. |

| (11) | Percentage of total investments includes all stocks, plus cash. |

| (12) | Net exposure represents the difference between the long exposure and the short exposure, which produces the net investment exposure. |

| * | Current portfolio holdings may not be indicative of future portfolio holdings. |

| † | Percentage of total investments. |

Disclosure of Fund Expenses (Unaudited)

The following expense table is shown so that you can understand the impact of fees on your investment. All mutual funds have operating expenses. As a shareholder of a Portfolio, you incur transactional costs and ongoing costs, which include costs for portfolio management, administrative services, and shareholder reports, among others. A Portfolio’s expenses are expressed as a percentage of its average net assets. This figure is known as the expense ratio. The following examples are intended to help you understand the ongoing costs (in dollars) of investing in each Portfolio and to compare these costs with those of other mutual funds. The examples are based on an investment of $1,000 made at the beginning of a six-month period and held for the entire period. The expense example table below illustrates your fund’s cost in two ways:

| • | Actual Expenses. This section helps you to estimate the actual expenses after fee waivers that you paid over the period. The “Ending Account Value” shown is derived from the Portfolio’s actual return, and “Expenses Paid During Period” shows the dollar amount that would have been paid by an investor who started with $1,000 in the Portfolio. You may use the information here, together with the amount you invested, to estimate the expenses that you paid over the period. To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for your Portfolio under the heading entitled “Expenses Paid During Period”. |

| | |

| • | Hypothetical Expenses on a 5% Return. This section is intended to help you compare your Portfolio’s costs with those of other mutual funds. It assumes that the Portfolio had a return of 5% before expenses during the period shown, but that the expense ratio is unchanged. In this case, because the return used is not the Portfolio’s actual return, the results do not apply to your investment. The example is useful in making comparisons because the Securities and Exchange Commission requires all mutual funds to calculate expenses based on a 5% return. You can assess your Portfolio’s cost by comparing this hypothetical example with the hypothetical examples that appear in shareholders reports of other funds. |

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

For the Period July 1, 2022 to December 31, 2022

Expense Example Table (Unaudited)

| | Beginning | Ending | Expenses Paid | Expense Ratio |

| | Account Value | Account Value | During Period* | During Period* |

| | 7/1/22 | 12/31/22 | 7/1/22 – 12/31/22 | 7/1/22 – 12/31/22 |

| Needham Growth Fund | | | | |

| Retail Class Actual Expenses | $1,000.00 | $ 993.80 | $9.19 | 1.83% |

| Retail Class Hypothetical | | | | |

| Example for Comparison Purposes | | | | |

| (5% return before expenses) | $1,000.00 | $1,015.99 | $9.29 | 1.83% |

| Institutional Class Actual Expenses | $1,000.00 | $ 996.20 | $7.04 | 1.40% |

| Institutional Class Hypothetical | | | | |

| Example for Comparison Purposes | | | | |

| (5% return before expenses) | $1,000.00 | $1,018.15 | $7.12 | 1.40% |

| | | | | |

| Needham Aggressive Growth Fund | | | | |

| Retail Class Actual Expenses | $1,000.00 | $1,058.70 | $9.60 | 1.85% |

| Retail Class Hypothetical | | | | |

| Example for Comparison Purposes | | | | |

| (5% return before expenses) | $1,000.00 | $1,015.88 | $9.40 | 1.85% |

| Institutional Class Actual Expenses | $1,000.00 | $1,062.60 | $6.13 | 1.18% |

| Institutional Class Hypothetical | | | | |

| Example for Comparison Purposes | | | | |

| (5% return before expenses) | $1,000.00 | $1,019.26 | $6.01 | 1.18% |

| | | | | |

| Needham Small Cap Growth Fund | | | | |

| Retail Class Actual Expenses | $1,000.00 | $1,066.40 | $9.64 | 1.85% |

| Retail Class Hypothetical | | | | |

| Example for Comparison Purposes | | | | |

| (5% return before expenses) | $1,000.00 | $1,015.88 | $9.40 | 1.85% |

| Institutional Class Actual Expenses | $1,000.00 | $1,070.70 | $6.16 | 1.18% |

| Institutional Class Hypothetical | | | | |

| Example for Comparison Purposes | | | | |

| (5% return before expenses) | $1,000.00 | $1,019.26 | $6.01 | 1.18% |

| * | Expenses are equal to the average account value times the Portfolio’s annualized expense ratio multiplied 184/365 (to reflect the one-half-year period). |

Needham Growth Fund

Schedule of Investments

December 31, 2022

| | | Shares | | | Fair Value | |

| Common Stocks (95.3%) | | | | | | |

| | | | | | | |

| Aerospace & Defense (3.0%) | | | | | | |

| Parsons Corp. (a) | | | 77,500 | | | $ | 3,584,375 | |

| | | | | | | | | |

| Biotechnology (1.4%) | | | | | | | | |

| G1 Therapeutics, Inc. (a) | | | 64,000 | | | | 347,520 | |

| Gilead Sciences, Inc. | | | 15,000 | | | | 1,287,750 | |

| | | | | | | | 1,635,270 | |

| Chemicals (3.9%) | | | | | | | | |

| Aspen Aerogels, Inc. (a) | | | 400,000 | | | | 4,716,000 | |

| | | | | | | | | |

| Commercial Services & Supplies (1.1%) | | | | | | | | |

| Clean Harbors, Inc. (a) | | | 11,900 | | | | 1,358,028 | |

| | | | | | | | | |

| Communications Equipment (8.1%) | | | | | | | | |

| ADTRAN Holdings, Inc. | | | 125,000 | | | | 2,348,750 | |

| Cambium Networks Corp. (a) | | | 94,250 | | | | 2,042,398 | |

| KVH Industries, Inc. (a) | | | 500,000 | | | | 5,110,000 | |

| ViaSat, Inc. (a)(c) | | | 10,000 | | | | 316,500 | |

| | | | | | | | 9,817,648 | |

| Diversified Consumer Services (0.4%) | | | | | | | | |

| Bright Horizons Family Solutions, Inc. (a) | | | 8,000 | | | | 504,800 | |

| | | | | | | | | |

| Electrical Equipment (3.6%) | | | | | | | | |

| Vicor Corp. (a) | | | 80,000 | | | | 4,300,000 | |

| | | | | | | | | |

| Electronic Equipment, Instruments & Components (3.9%) | | | | | | | | |

| Coherent Corp. (a) | | | 18,500 | | | | 649,350 | |

| Corning, Inc. | | | 37,500 | | | | 1,197,750 | |

| nLight, Inc. (a) | | | 135,850 | | | | 1,377,519 | |

| Vishay Intertechnology, Inc. | | | 55,000 | | | | 1,186,350 | |

| Vishay Precision Group, Inc. (a) | | | 8,000 | | | | 309,200 | |

| | | | | | | | 4,720,169 | |

| Health Care Equipment & Supplies (5.7%) | | | | | | | | |

| Becton Dickinson & Co. | | | 18,500 | | | | 4,704,550 | |

| Medtronic PLC | | | 20,000 | | | | 1,554,400 | |

| ViewRay, Inc. (a) | | | 144,780 | | | | 648,614 | |

| | | | | | | | 6,907,564 | |

| Health Care Providers & Services (2.9%) | | | | | | | | |

| Laboratory Corp. of America Holdings | | | 11,000 | | | | 2,590,280 | |

| Quest Diagnostics, Inc. | | | 5,500 | | | | 860,420 | |

| | | | | | | | 3,450,700 | |

| Hotels, Restaurants & Leisure (0.2%) | | | | | | | | |

| Vacasa, Inc. – Class A (a) | | | 214,150 | | | | 269,829 | |

| | | | | | | | | |

| Industrial Conglomerates (0.5%) | | | | | | | | |

| Honeywell International, Inc. – ADR | | | 2,500 | | | | 535,750 | |

| | | | | | | | | |

| Interactive Media & Services (0.4%) | | | | | | | | |

| Alphabet, Inc. – Class A (a) | | | 5,000 | | | | 441,150 | |

See accompanying notes to financial statements.

Needham Growth Fund

Schedule of Investments (Continued)

December 31, 2022

| | | Shares | | | Fair Value | |

| Common Stocks – Continued | | | | | | |

| | | | | | | |

| IT Services (2.5%) | | | | | | |

| Akamai Technologies, Inc. (a)(c) | | | 33,000 | | | $ | 2,781,900 | |

| BigCommerce Holdings, Inc. (a) | | | 30,000 | | | | 262,200 | |

| | | | | | | | 3,044,100 | |

| Life Sciences Tools & Services (9.7%) | | | | | | | | |

| Bruker Corp. | | | 7,500 | | | | 512,625 | |

| CryoPort, Inc. (a) | | | 43,500 | | | | 754,725 | |

| Thermo Fisher Scientific, Inc. | | | 19,000 | | | | 10,463,110 | |

| | | | | | | | 11,730,460 | |

| Media (4.1%) | | | | | | | | |

| The Trade Desk, Inc. – Class A (a) | | | 47,000 | | | | 2,107,010 | |

| Comcast Corp. – Class A | | | 80,000 | | | | 2,797,600 | |

| | | | | | | | 4,904,610 | |

| Oil, Gas & Consumable Fuels (0.9%) | | | | | | | | |

| Chevron Corp. | | | 5,000 | | | | 897,450 | |

| Navigator Holdings, Ltd. (a) | | | 20,000 | | | | 239,200 | |

| | | | | | | | 1,136,650 | |

| Real Estate Investment Trusts (REITs) (0.4%) | | | | | | | | |

| American Tower Corp. | | | 2,500 | | | | 529,650 | |

| | | | | | | | | |

| Semiconductors & Semiconductor Equipment (30.9%) (d) | | | | | | | | |

| Analog Devices, Inc. | | | 10,000 | | | | 1,640,300 | |

| Applied Materials, Inc. | | | 9,000 | | | | 876,420 | |

| ASML Holding NV (Netherlands) | | | 2,250 | | | | 1,229,400 | |

| AXT, Inc. (a) | | | 335,450 | | | | 1,469,271 | |

| Entegris, Inc. | | | 99,000 | | | | 6,493,410 | |

| FormFactor, Inc. (a) | | | 119,500 | | | | 2,656,485 | |

| Lam Research Corp. | | | 2,500 | | | | 1,050,750 | |

| Marvell Technology, Inc. | | | 15,000 | | | | 555,600 | |

| MKS Instruments, Inc. | | | 23,000 | | | | 1,948,790 | |

| Nova, Ltd. (Israel)(a) | | | 45,000 | | | | 3,675,600 | |

| PDF Solutions, Inc. (a) | | | 338,990 | | | | 9,667,995 | |

| Photronics, Inc. (a) | | | 185,000 | | | | 3,113,550 | |

| SiTime Corp. (a) | | | 12,500 | | | | 1,270,250 | |

| Teradyne, Inc. | | | 2,500 | | | | 218,375 | |

| Veeco Instruments, Inc. (a) | | | 75,000 | | | | 1,393,500 | |

| | | | | | | | 37,259,696 | |

| Software (1.9%) | | | | | | | | |

| Alteryx, Inc. – Class A (a) | | | 23,500 | | | | 1,190,745 | |

| Q2 Holdings, Inc. (a) | | | 16,500 | | | | 443,355 | |

| Telos Corp. (a) | | | 120,000 | | | | 610,800 | |

| | | | | | | | 2,244,900 | |

| Specialty Retail (3.5%) | | | | | | | | |

| CarMax, Inc. (a) | | | 68,500 | | | | 4,170,965 | |

See accompanying notes to financial statements.

Needham Growth Fund

Schedule of Investments (Continued)

December 31, 2022

| | | Shares | | | Fair Value | |

| Common Stocks – Continued | | | | | | |

| | | | | | | |

| Technology Hardware, Storage & Peripherals (6.1%) | | | | | | |

| Apple, Inc. | | | 8,500 | | | $ | 1,104,405 | |

| Hewlett Packard Enterprise Co. | | | 17,500 | | | | 279,300 | |

| Intevac, Inc. (a) | | | 200,000 | | | | 1,294,000 | |

| Super Micro Computer, Inc. (a) | | | 57,500 | | | | 4,720,750 | |

| | | | | | | | 7,398,455 | |

| Trading Companies & Distributors (0.2%) | | | | | | | | |

| Air Lease Corp. | | | 7,500 | | | | 288,150 | |

| Total Common Stocks | | | | | | | | |

| (Cost $55,611,915) | | | | | | $ | 114,948,919 | |

| | | | | | | | | |

| Short-Term Investments (4.6%) | | | | | | | | |

| | | | | | | | | |

| Money Market Fund (4.6%) | | | | | | | | |

| Dreyfus Treasury Securities Cash Management – Institutional Class, 3.93% (b) | | | | | | | | |

| Total Short-Term Investments | | | | | | | | |

| (Cost $5,532,105) | | | 5,532,105 | | | $ | 5,532,105 | |

| Total Investments (99.9%) | | | | | | | | |

| (Cost $61,144,020) | | | | | | | 120,481,024 | |

| Other Assets in Excess of Liabilities (0.1%) | | | | | | | 78,581 | |

| Net Assets (100.0%) | | | | | | $ | 120,559,605 | |

| | Percentages are stated as a percent of net assets. |

| | Industry classifications may be different than those used for compliance monitoring purposes. |

| (a) | Non-income producing security. |

| (b) | Rate shown is the seven day yield as of December 31, 2022. |

| (c) | Security position is either entirely or partially held in a segregated account as collateral for securities sold short, aggregating a total market value of $1,122,525. |

| (d) | As of December 31, 2022, the Fund had a significant portion of its assets invested in the Semiconductors & Semiconductor Equipment industry. |

| | |

| ADR | American Depositary Receipt |

The Global Industry Classification Standard (“GICS”) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC (“S&P”). GICS is a service mark of MSCI and S&P and has been licensed for use by U.S. Bancorp Fund Services, LLC.

Distribution of investments by country or territory of incorporation, as a percentage of Total Investments, is as follows (Unaudited):

| Country | | Long | |

| United States^ | | | 95.9 | % | |

| Israel | | | 3.1 | % | |

| Netherlands | | | 1.0 | % | |

| Total | | | 100.0 | % | |

| ^ | United States allocation includes Short-Term Investment-Money Market Fund of 4.6% |

See accompanying notes to financial statements.

Needham Aggressive Growth Fund

Schedule of Investments

December 31, 2022

| | | Shares | | | Fair Value | |

| Common Stocks (92.8%) | | | | | | |

| | | | | | | |

| Aerospace & Defense (2.7%) | | | | | | |

| Parsons Corp. (a) | | | 77,500 | | | $ | 3,584,375 | |

| | | | | | | | | |

| Biotechnology (0.3%) | | | | | | | | |

| Avrobio, Inc. (a) | | | 24,513 | | | | 17,475 | |

| G1 Therapeutics, Inc. (a) | | | 70,000 | | | | 380,100 | |

| | | | | | | | 397,575 | |

| Building Products (0.7%) | | | | | | | | |

| Alpha Pro Tech, Ltd. (a) | | | 220,000 | | | | 884,400 | |

| Jewett-Cameron Trading Co., Ltd. (a) | | | 7,500 | | | | 43,275 | |

| | | | | | | | 927,675 | |

| Chemicals (5.1%) | | | | | | | | |

| Aspen Aerogels, Inc. (a) | | | 357,000 | | | | 4,209,030 | |

| Mativ Holdings, Inc. | | | 130,000 | | | | 2,717,000 | |

| | | | | | | | 6,926,030 | |

| Commercial Services & Supplies (2.7%) | | | | | | | | |

| ACV Auctions, Inc. – Class A (a) | | | 86,500 | | | | 710,165 | |

| Clean Harbors, Inc. (a) | | | 26,000 | | | | 2,967,120 | |

| | | | | | | | 3,677,285 | |

| Communications Equipment (7.1%) | | | | | | | | |

| ADTRAN Holdings, Inc. | | | 70,000 | | | | 1,315,300 | |

| Cambium Networks Corp. (a) | | | 71,400 | | | | 1,547,238 | |

| KVH Industries, Inc. (a) | | | 658,750 | | | | 6,732,425 | |

| | | | | | | | 9,594,963 | |

| Construction & Engineering (0.7%) | | | | | | | | |

| Matrix Service Co. (a) | | | 150,000 | | | | 933,000 | |

| | | | | | | | | |

| Construction Materials (2.2%) | | | | | | | | |

| Smith-Midland Corp. (a) | | | 146,100 | | | | 2,995,050 | |

| | | | | | | | | |

| Distributors (0.9%) | | | | | | | | |

| Educational Development Corp. | | | 400,000 | | | | 1,264,000 | |

| | | | | | | | | |

| Diversified Consumer Services (1.5%) | | | | | | | | |

| Bright Horizons Family Solutions, Inc. (a) | | | 32,500 | | | | 2,050,750 | |

| | | | | | | | | |

| Electrical Equipment (8.5%) | | | | | | | | |

| Thermon Group Holdings, Inc. (a) | | | 117,500 | | | | 2,359,400 | |

| Vertiv Holdings Co. | | | 220,000 | | | | 3,005,200 | |

| Vicor Corp. (a) | | | 112,500 | | | | 6,046,875 | |

| | | | | | | | 11,411,475 | |

| Electronic Equipment, Instruments & Components (5.3%) | | | | | | | | |

| Arlo Technologies, Inc. (a) | | | 45,000 | | | | 157,950 | |

| nLight, Inc. (a) | | | 148,800 | | | | 1,508,832 | |

| VIA Optronics AG (Germany) – ADR (a) | | | 130,000 | | | | 207,506 | |

| Vishay Precision Group, Inc. (a) | | | 135,500 | | | | 5,237,075 | |

| | | | | | | | 7,111,363 | |

See accompanying notes to financial statements.

Needham Aggressive Growth Fund

Schedule of Investments (Continued)

December 31, 2022

| | | Shares | | | Fair Value | |

| Common Stocks – Continued | | | | | | |

| | | | | | | |

| Entertainment (0.1%) | | | | | | |

| World Wrestling Entertainment, Inc. – Class A | | | 2,250 | | | $ | 154,170 | |

| | | | | | | | | |

| Health Care Equipment & Supplies (1.7%) | | | | | | | | |

| LeMaitre Vascular, Inc. | | | 20,500 | | | | 943,410 | |

| Omnicell, Inc. (a) | | | 2,900 | | | | 146,218 | |

| Precision Optics Corp., Inc. (a) | | | 198,500 | | | | 1,117,555 | |

| Sientra, Inc. (a) | | | 20,000 | | | | 4,058 | |

| ViewRay, Inc. (a) | | | 4,300 | | | | 19,264 | |

| | | | | | | | 2,230,505 | |

| Health Care Providers & Services (2.5%) | | | | | | | | |

| Laboratory Corp. of America Holdings | | | 12,300 | | | | 2,896,404 | |

| Quest Diagnostics, Inc. | | | 3,000 | | | | 469,320 | |

| | | | | | | | 3,365,724 | |

| Hotels, Restaurants & Leisure (1.2%) | | | | | | | | |

| Vacasa, Inc. – Class A (a) | | | 1,250,000 | | | | 1,575,000 | |

| | | | | | | | | |

| Household Products (1.1%) | | | | | | | | |

| Oil-Dri Corp. of America | | | 45,000 | | | | 1,509,300 | |

| | | | | | | | | |

| Insurance (1.5%) | | | | | | | | |

| Markel Corp. (a) | | | 1,500 | | | | 1,976,235 | |

| | | | | | | | | |

| Interactive Media & Services (0.1%) | | | | | | | | |

| AcuityAds Holdings, Inc. (Canada) (a) | | | 50,000 | | | | 77,500 | |

| | | | | | | | | |

| Internet & Direct Marketing Retail (0.7%) | | | | | | | | |

| ThredUp, Inc. – Class A (a) | | | 700,000 | | | | 917,000 | |

| | | | | | | | | |

| IT Services (2.9%) | | | | | | | | |

| Akamai Technologies, Inc. (a)(b) | | | 14,500 | | | | 1,222,350 | |

| BigCommerce Holdings, Inc. (a) | | | 7,500 | | | | 65,550 | |

| Research Solutions, Inc. (a) | | | 480,000 | | | | 926,400 | |

| Unisys Corp. (a) | | | 325,000 | | | | 1,660,750 | |

| | | | | | | | 3,875,050 | |

| Life Sciences Tools & Services (1.6%) | | | | | | | | |

| Bruker Corp. | | | 22,500 | | | | 1,537,875 | |

| CryoPort, Inc. (a) | | | 37,500 | | | | 650,625 | |

| Standard BioTools, Inc. (a) | | | 25,000 | | | | 29,250 | |

| | | | | | | | 2,217,750 | |

| Machinery (0.2%) | | | | | | | | |

| Westinghouse Air Brake Technologies Corp. | | | 3,000 | | | | 299,430 | |

| | | | | | | | | |

| Media (0.4%) | | | | | | | | |

| The Trade Desk, Inc. – Class A (a) | | | 12,000 | | | | 537,960 | |

| | | | | | | | | |

| Oil, Gas & Consumable Fuels (2.6%) | | | | | | | | |

| Adams Resources & Energy, Inc. | | | 90,500 | | | | 3,522,260 | |

| | | | | | | | | |

| Professional Services (1.8%) | | | | | | | | |

| CRA International, Inc. | | | 20,000 | | | | 2,448,600 | |

See accompanying notes to financial statements.

Needham Aggressive Growth Fund

Schedule of Investments (Continued)

December 31, 2022

| | | Shares | | | Fair Value | |

| Common Stocks – Continued | | | | | | |

| | | | | | | |

| Real Estate Investment Trusts (REITs) (1.4%) | | | | | | |

| American Tower Corp. | | | 2,250 | | | $ | 476,685 | |

| Equinix, Inc. | | | 2,100 | | | | 1,375,563 | |

| | | | | | | | 1,852,248 | |

| Semiconductors & Semiconductor Equipment (21.9%) | | | | | | | | |

| ASML Holding NV (Netherlands) | | | 2,500 | | | | 1,366,000 | |

| AXT, Inc. (a) | | | 125,000 | | | | 547,500 | |

| Entegris, Inc. | | | 62,500 | | | | 4,099,375 | |

| FormFactor, Inc. (a) | | | 30,000 | | | | 666,900 | |

| MKS Instruments, Inc. | | | 22,000 | | | | 1,864,060 | |

| Nova, Ltd. (Israel) (a) | | | 60,000 | | | | 4,900,800 | |

| PDF Solutions, Inc. (a)(b) | | | 345,000 | | | | 9,839,400 | |

| Photronics, Inc. (a) | | | 225,000 | | | | 3,786,750 | |

| Pivotal Systems Corp. (a) | | | 1,082,494 | | | | 39,430 | |

| SiTime Corp. (a) | | | 5,000 | | | | 508,100 | |

| SkyWater Technology, Inc. (a) | | | 7,500 | | | | 53,325 | |

| Teradyne, Inc. | | | 5,000 | | | | 436,750 | |

| Veeco Instruments, Inc. (a) | | | 75,000 | | | | 1,393,500 | |

| | | | | | | | 29,501,890 | |

| Software (4.5%) | | | | | | | | |

| Altair Engineering, Inc. – Class A (a) | | | 26,000 | | | | 1,182,220 | |

| Copperleaf Technologies, Inc. (Canada) (a) | | | 75,000 | | | | 317,947 | |

| ESI Group (France) (a) | | | 35,000 | | | | 2,764,962 | |

| GSE Systems, Inc. (a)(d) | | | 1,500,000 | | | | 1,080,000 | |

| Q2 Holdings, Inc. (a) | | | 8,000 | | | | 214,960 | |

| Telos Corp. (a) | | | 100,000 | | | | 509,000 | |

| | | | | | | | 6,069,089 | |

| Specialty Retail (0.9%) | | | | | | | | |

| CarMax, Inc. (a) | | | 20,500 | | | | 1,248,245 | |

| | | | | | | | | |

| Technology Hardware, Storage & Peripherals (7.0%) | | | | | | | | |

| Apple, Inc. (b) | | | 27,800 | | | | 3,612,054 | |

| Intevac, Inc. (a) | | | 85,000 | | | | 549,950 | |

| Super Micro Computer, Inc. (a) | | | 65,000 | | | | 5,336,500 | |

| | | | | | | | 9,498,504 | |

| Textiles, Apparel & Luxury Goods (0.1%) | | | | | | | | |

| Allbirds, Inc. (a) | | | 75,000 | | | | 181,500 | |

| | | | | | | | | |

| Trading Companies & Distributors (0.9%) | | | | | | | | |

| Transcat, Inc. (a) | | | 17,500 | | | | 1,240,225 | |

| Total Common Stocks | | | | | | | | |

| (Cost $98,908,881) | | | | | | $ | 125,171,726 | |

See accompanying notes to financial statements.

Needham Aggressive Growth Fund

Schedule of Investments (Continued)

December 31, 2022

| | | Shares | | | Fair Value | |

| Short-Term Investments (6.7%) | | | | | | |

| | | | | | | |

| Money Market Fund (6.7%) | | | | | | |

| Dreyfus Treasury Securities Cash Management – Institutional Class, 3.93% (c) | | | | | | |

| Total Short-Term Investments | | | | | | |

| (Cost $9,027,317) | | | 9,027,317 | | | $ | 9,027,317 | |

| Total Investments (99.5%) | | | | | | | | |

| (Cost $107,936,197) | | | | | | | 134,199,043 | |

| Other Assets in Excess of Liabilities (0.5%) | | | | | | | 720,261 | |

| Net Assets (100.0%) | | | | | | $ | 134,919,304 | |

| | Percentages are stated as a percent of net assets. |

| | Industry classifications may be different than those used for compliance monitoring purposes. |

| (a) | Non-income producing security. |

| (b) | Security position is either entirely or partially held in a segregated account as collateral for securities sold short, aggregating a total market value of $1,185,535. |

| (c) | Rate shown is the seven day yield as of December 31, 2022. |

| (d) | Affiliated security. Please refer to Note 11 of the Financial Statements. |

| | |

| ADR | American Depositary Receipt |

The Global Industry Classification Standard (“GICS”) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC (“S&P”).

Distribution of investments by country or territory of incorporation, as a percentage of Total Investments, is as follows:

| Country | | Long | |

| United States^ | | | 92.8 | % | |

| Israel | | | 3.7 | % | |

| France | | | 2.1 | % | |

| Netherlands | | | 1.0 | % | |

| Canada | | | 0.2 | % | |

| Germany | | | 0.2 | % | |

| Total | | | 100.0 | % | |

| ^ | United States allocation includes Short-Term Investment-Money Market Fund of 6.7% |

See accompanying notes to financial statements.

Needham Small Cap Growth Fund

Schedule of Investments

December 31, 2022

| | | Shares | | | Fair Value | |

| Common Stocks (84.4%) | | | | | | |

| | | | | | | |

| Chemicals (3.9%) | | | | | | |

| Aspen Aerogels, Inc. (a)(b) | | | 644,734 | | | $ | 7,601,414 | |

| | | | | | | | | |

| Communications Equipment (16.8%) | | | | | | | | |

| ADTRAN Holdings, Inc. | | | 300,000 | | | | 5,637,000 | |

| Cambium Networks Corp. (a) | | | 350,000 | | | | 7,584,500 | |

| Infinera Corp. (a) | | | 1,100,000 | | | | 7,414,000 | |

| KVH Industries, Inc. (a) | | | 492,500 | | | | 5,033,350 | |

| Lumentum Holdings, Inc. (a) | | | 100,000 | | | | 5,217,000 | |

| ViaSat, Inc. (a) | | | 70,000 | | | | 2,215,500 | |

| | | | | | | | 33,101,350 | |

| Electrical Equipment (3.6%) | | | | | | | | |

| Sensata Technologies Holding PLC | | | 75,000 | | | | 3,028,500 | |

| Vicor Corp. (a) | | | 75,000 | | | | 4,031,250 | |

| | | | | | | | 7,059,750 | |

| Electronic Equipment, Instruments & Components (11.5%) | | | | | | | | |

| Akoustis Technologies, Inc. (a) | | | 1,092,500 | | | | 3,080,850 | |

| Coherent Corp. (a) | | | 100,000 | | | | 3,510,000 | |

| Frequency Electronics, Inc. (a)(d) | | | 570,000 | | | | 4,018,500 | |

| nLight, Inc. (a) | | | 1,000,000 | | | | 10,140,000 | |

| Rogers Corp. (a) | | | 15,000 | | | | 1,790,100 | |

| Vishay Precision Group, Inc. (a) | | | 4,000 | | | | 154,600 | |

| | | | | | | | 22,694,050 | |

| Health Care Equipment & Supplies (5.1%) | | | | | | | | |

| Sientra, Inc. (a) | | | 700,000 | | | | 142,030 | |

| ViewRay, Inc. (a) | | | 2,215,000 | | | | 9,923,200 | |

| | | | | | | | 10,065,230 | |

| IT Services (2.1%) | | | | �� | | | | |

| BigCommerce Holdings, Inc. (a) | | | 380,000 | | | | 3,321,200 | |

| Edgio, Inc. (a) | | | 700,000 | | | | 791,000 | |

| | | | | | | | 4,112,200 | |

| Life Sciences Tools & Services (2.2%) | | | | | | | | |

| Standard BioTools, Inc. (a) | | | 3,647,157 | | | | 4,267,174 | |

| | | | | | | | | |

| Machinery (1.6%) | | | | | | | | |

| Chart Industries, Inc. (a) | | | 27,500 | | | | 3,168,825 | |

| | | | | | | | | |

| Semiconductors & Semiconductor Equipment (12.5%) | | | | | | | | |

| AXT, Inc. (a) | | | 1,000,000 | | | | 4,380,000 | |

| FormFactor, Inc. (a)(b) | | | 180,000 | | | | 4,001,400 | |

| MaxLinear, Inc. (a) | | | 25,000 | | | | 848,750 | |

| MKS Instruments, Inc. | | | 44,500 | | | | 3,770,485 | |

| Photronics, Inc. (a)(b) | | | 550,000 | | | | 9,256,500 | |

| Veeco Instruments, Inc. (a) | | | 120,000 | | | | 2,229,600 | |

| | | | | | | | 24,486,735 | |

See accompanying notes to financial statements.

Needham Small Cap Growth Fund

Schedule of Investments (Continued)

December 31, 2022

| | | Shares | | | Fair Value | |

| Common Stocks – Continued | | | | | | |

| | | | | | | |

| Software (19.5%) | | | | | | |

| 8x8, Inc. (a) | | | 1,600,000 | | | $ | 6,912,000 | |

| Alteryx, Inc. – Class A (a) | | | 30,000 | | | | 1,520,100 | |

| Sumo Logic, Inc. (a) | | | 1,000,000 | | | | 8,100,000 | |

| Telos Corp. (a) | | | 1,200,000 | | | | 6,108,000 | |

| Upland Software, Inc. (a) | | | 542,500 | | | | 3,868,025 | |

| Yext, Inc. (a) | | | 1,100,612 | | | | 7,186,996 | |

| Zuora, Inc. – Class A (a) | | | 727,488 | | | | 4,626,823 | |

| | | | | | | | 38,321,944 | |

| Specialty Retail (0.3%) | | | | | | | | |

| CarMax, Inc. (a) | | | 10,000 | | | | 608,900 | |

| | | | | | | | | |

| Technology Hardware, Storage & Peripherals (5.3%) | | | | | | | | |

| Intevac, Inc. (a)(d) | | | 1,608,550 | | | | 10,407,319 | |

| Total Common Stocks | | | | | | | | |

| (Cost $209,684,812) | | | | | | $ | 165,894,891 | |

| | | | | | | | | |

| Warrants (0.0%) | | | | | | | | |

| Agile Therapeutics, Inc. 0.34% (a) | | | 4,375 | | | | 345 | |

| Total Warrants | | | | | | | | |

| (Cost $1,750) | | | | | | | 345 | |

| | | | | | | | | |

| Short-Term Investments (18.2%) | | | | | | | | |

| | | | | | | | | |

| Money Market Fund (18.2%) | | | | | | | | |

| Dreyfus Treasury Securities Cash Management – Institutional Class, 3.93% (c) | | | | | | | | |

| Total Short-Term Investments | | | | | | | | |

| (Cost $35,794,583) | | | 35,794,583 | | | $ | 35,794,583 | |

| Total Investments (102.6%) | | | | | | | | |

| (Cost $245,481,145) | | | | | | | 201,689,819 | |

| Liabilities in Excess of Other Assets (-2.6%) | | | | | | | (5,057,138 | ) |

| Net Assets (100.0%) | | | | | | $ | 196,632,681 | |

| | Percentages are stated as a percent of net assets. |

| | Industry classifications may be different than those used for compliance purposes. |

| (a) | Non-income producing security. |

| (b) | Security position is either entirely or partially held in a segregated account as collateral for securities sold short, aggregating a total market value of $1,284,750. |

| (c) | Rate shown is the seven day yield as of December 31, 2022. |

| (d) | Affiliated security. Please refer to Note 11 of the Financial Statements. |

The Global Industry Classification Standard (“GICS”) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC (“S&P”).

Distribution of investments by country or territory of incorporation, as a percentage of Total Investments, is as follows (Unaudited):

| Country | | Long | |

| United States^ | | | 100.0 | % | |

| Total | | | 100.0 | % | |

| ^ | United States allocation includes Short-Term Investment-Money Market Fund of 18.2% |

See accompanying notes to financial statements.

Statements of Assets and Liabilities

December 31, 2022

| | | | | | Needham | | | Needham | |

| | | Needham | | | Aggressive | | | Small Cap | |

| | | Growth Fund | | | Growth Fund | | | Growth Fund | |

| Assets | | | | | | | | | |

| Investments, at Value | | | | | | | | | |

| Unaffiliated Securities (Cost $61,144,020, $105,325,932, $231,022,813) | | $ | 120,481,024 | | | $ | 133,119,043 | | | $ | 187,264,000 | |

| Affiliated Securities, (Cost $—, $2,610,265, $14,458,332) | | | — | | | | 1,080,000 | | | | 14,425,819 | |

| Foreign Currency, (Cost $—, $9, $—) | | | — | | | | 10 | | | | — | |

| Cash | | | 32,655 | | | | — | | | | 321,999 | |

| Receivables: | | | | | | | | | | | | |

| Deposit with Broker for Securities Sold Short | | | 2,059 | | | | — | | | | — | |

| Dividends and Interest | | | 50,502 | | | | 34,054 | | | | 182,978 | |

| Fund Shares Sold | | | 121,078 | | | | 492,674 | | | | 536,663 | |

| Investment Securities Sold | | | 936,573 | | | | 564,722 | | | | — | |

| Prepaid Expenses | | | 24,250 | | | | 40,976 | | | | 59,075 | |

| Total Assets | | | 121,648,141 | | | | 135,331,479 | | | | 202,790,534 | |

| | | | | | | | | | | | | |

| Liabilities | | | | | | | | | | | | |

| Payables: | | | | | | | | | | | | |

| Investment Securities Purchased | | | 303,314 | | | | 130,150 | | | | 3,026,851 | |

| Fund Shares Redeemed | | | 525,875 | | | | 75,694 | | | | 2,716,801 | |

| Due to Adviser, net | | | 133,596 | | | | 110,220 | | | | 231,105 | |

| Distribution Fees | | | 13,954 | | | | 12,041 | | | | 9,963 | |

| Administration and Accounting Fees | | | 26,072 | | | | 27,450 | | | | 33,689 | |

| Transfer Agent Fees | | | 8,734 | | | | 14,069 | | | | 26,751 | |

| Audit and Tax Fees | | | 42,263 | | | | 26,867 | | | | 64,129 | |

| Directors’ Fees | | | 3,537 | | | | 5,190 | | | | 6,600 | |

| Accrued Expenses and Other Liabilities | | | 31,191 | | | | 10,494 | | | | 41,964 | |

| Total Liabilities | | | 1,088,536 | | | | 412,175 | | | | 6,157,853 | |

| Net Assets | | $ | 120,559,605 | | | $ | 134,919,304 | | | $ | 196,632,681 | |

| | | | | | | | | | | | | |

| Retail Class Shares | | | | | | | | | | | | |

| Net Assets | | | 62,117,974 | | | | 55,027,842 | | | | 59,054,176 | |

| Shares Issued and Outstanding $0.001 Par Value | | | | | | | | | | | | |

| (Authorized 800,000,000,100,000,000 and 100,000,000 respectively) | | | 1,423,712 | | | | 1,871,668 | | | | 3,810,407 | |

| Net Asset Value and Offering Price Per Share | | $ | 43.63 | | | $ | 29.40 | | | $ | 15.50 | |

| | | | | | | | | | | | | |

| Institutional Class Shares | | | | | | | | | | | | |

| Net Assets | | | 58,441,631 | | | | 79,891,462 | | | | 137,578,505 | |

| Shares Issued and Outstanding $0.001 Par Value | | | | | | | | | | | | |

| (Authorized 800,000,000,100,000,000 and 100,000,000 respectively) | | | 1,291,010 | | | | 2,600,002 | | | | 8,388,897 | |

| Net Asset Value and Offering Price Per Share | | $ | 45.27 | | | $ | 30.73 | | | $ | 16.40 | |

| | | | | | | | | | | | | |

| Components of Net Assets | | | | | | | | | | | | |

| Paid-in Capital | | | 61,853,166 | | | | 108,659,960 | | | | 279,162,720 | |

| Distributable Earnings | | | 58,706,439 | | | | 26,259,344 | | | | (82,530,039 | ) |

| Total Net Assets | | $ | 120,559,605 | | | $ | 134,919,304 | | | $ | 196,632,681 | |

See accompanying notes to financial statements.

Statements of Operations

For the year ended December 31, 2022

| | | | | | Needham | | | Needham | |

| | | Needham | | | Aggressive | | | Small Cap | |

| | | Growth Fund | | | Growth Fund | | | Growth Fund | |

| Investment Income | | | | | | | | | |

| Dividend Income from unaffiliated securities | | $ | 661,140 | | | $ | 436,696 | | | $ | 143,595 | |

| (net of foreign withholding tax of $4,963, $5,038, $—) | | | | | | | | | | | | |

| Interest Income | | | 63,455 | | | | 227,063 | | | | 690,411 | |

| Total Investment Income | | | 724,595 | | | | 663,759 | | | | 834,006 | |

| | | | | | | | | | | | | |

| Expenses | | | | | | | | | | | | |

| Investment Advisory Fees | | | 1,802,550 | | | | 1,755,716 | | | | 2,591,993 | |

| Distribution Fees | | | 183,081 | | | | 144,812 | | | | 182,305 | |

| Administration and Accounting Fees | | | 172,696 | | | | 166,696 | | | | 230,646 | |

| Audit Fees | | | 56,230 | | | | 40,848 | | | | 95,351 | |

| Chief Compliance Officer Fees | | | 11,004 | | | | 10,615 | | | | 15,749 | |

| Custodian Fees | | | 14,521 | | | | 16,224 | | | | 15,764 | |

| Directors’ Fees | | | 9,810 | | | | 12,433 | | | | 25,798 | |

| Filing Fees | | | 71,550 | | | | 58,156 | | | | 78,997 | |

| Legal Fees | | | 48,534 | | | | 29,603 | | | | 120,203 | |

| Printing Fees | | | 9,527 | | | | 14,285 | | | | 42,896 | |

| Transfer Agent Fees | | | 53,718 | | | | 66,755 | | | | 134,681 | |

| Other Expenses | | | 40,878 | | | | 19,935 | | | | 963 | |

| Total Expenses | | | 2,474,099 | | | | 2,336,078 | | | | 3,535,346 | |

| Fees Waived by Investment Adviser | | | (163,006 | ) | | | (371,424 | ) | | | (724,898 | ) |

| Fees Recouped by Investment Adviser | | | 36,285 | | | | 80,996 | | | | 125,549 | |

| Net Expenses | | | 2,347,378 | | | | 2,045,650 | | | | 2,935,997 | |

| Net Investment Loss | | | (1,622,783 | ) | | | (1,381,891 | ) | | | (2,101,991 | ) |

| | | | | | | | | | | | | |

| Net Realized / Change in Unrealized Gain (Loss) from Investments, | | | | | | | | | | | | |

| Securities Sold Short, Foreign Currency Transactions and Currency | | | | | | | | | | | | |

| Net Realized Gain (Loss) from Unaffiliated Securities | | | (625,056 | ) | | | 1,207,400 | | | | (38,412,252 | ) |

| Net Realized Loss from Affiliated Securities | | | — | | | | — | | | | (123,086 | ) |

| Net Realized Gain from Securities Sold Short | | | 63,370 | | | | 43,149 | | | | 385,614 | |

| Net Realized Gain from Foreign Currency Transactions and Currency | | | — | | | | 1,578 | | | | — | |

| Change in Unrealized Depreciation on Investments and Securities Sold Short | | | (65,440,863 | ) | | | (45,962,634 | ) | | | (44,675,487 | ) |

| Change in Unrealized Appreciation (Depreciation) on Affiliated Investments | | | — | | | | (1,456,987 | ) | | | 1,441,780 | |

| Change in Unrealized Appreciation on Foreign Currency Transactions and Currency | | | — | | | | 1,654 | | | | — | |

| Net Realized / Change in Unrealized Gain from Investments, | | | | | | | | | | | | |

| Securities Sold Short, Foreign Currency Transactions and Currency | | | (66,002,549 | ) | | | (46,165,840 | ) | | | (81,383,431 | ) |

| Change in Net Assets Resulting from Operations | | $ | (67,625,332 | ) | | $ | (47,547,731 | ) | | $ | (83,485,422 | ) |

See accompanying notes to financial statements.

Needham Growth Fund

Statements of Changes in Net Assets

| | | Year Ended | | | Year Ended | |

| | | December 31, 2022 | | | December 31, 2021 | |

| Change in Net Assets | | | | | | |

| Operations: | | | | | | |

| Net Investment Loss | | $ | (1,622,783 | ) | | $ | (2,057,039 | ) |

| Net Realized Gain (Loss) from Investments, Securities Sold Short, | | | | | | | | |

| Foreign Currency Transactions, and Currency | | | (561,686 | ) | | | 11,831,914 | |

| Net Change in Unrealized Appreciation (Depreciation) on Investments, | | | | | | | | |

| Securities Sold Short, Foreign Currency Translations | | | (65,440,863 | ) | | | 30,202,068 | |

| Change in Net Assets Resulting from Operations | | | (67,625,332 | ) | | | 39,976,943 | |

| | | | | | | | | |

| Distributable Earnings: | | | | | | | | |

| Retail Class | | | (1,112,516 | ) | | | (6,609,791 | ) |

| Institutional Class | | | (1,008,195 | ) | | | (6,714,291 | ) |

| Total Distributable Earnings | | | (2,120,711 | ) | | | (13,324,082 | ) |

| | | | | | | | | |

| Capital Transactions: | | | | | | | | |

| Retail Class: | | | | | | | | |

| Shares Issued | | | 3,103,586 | | | | 10,831,860 | |

| Shares Issued in Reinvestment of Distribution | | | 1,046,663 | | | | 6,263,875 | |

| Shares Exchanged for Institutional Class Shares | | | (329,331 | ) | | | (766,301 | ) |

| Shares Redeemed | | | (8,542,497 | ) | | | (12,784,502 | ) |

| Institutional Class: | | | | | | | | |

| Shares Issued | | | 12,533,645 | | | | 43,574,350 | |

| Shares Issued in Reinvestment of Distribution | | | 975,002 | | | | 6,484,070 | |

| Shares Issued in Exchange for Retail Class Shares | | | 329,331 | | | | 766,302 | |

| Shares Redeemed | | | (35,719,878 | ) | | | (4,786,939 | ) |

| Total Change in Net Assets from Capital Transactions | | | (26,603,479 | ) | | | 49,582,715 | |

| | | | | | | | | |

| Change in Net Assets | | | (96,349,522 | ) | | | 76,235,576 | |

| | | | | | | | | |

| Total Net Assets | | | | | | | | |

| Beginning of Year | | | 216,909,127 | | | | 140,673,551 | |

| End of Year | | $ | 120,559,605 | | | $ | 216,909,127 | |

| | | | | | | | | |

| Share Transaction: | | | | | | | | |

| Retail Class: | | | | | | | | |

| Number of Shares Issued | | | 57,289 | | | | 160,422 | |

| Number of Shares Reinvested | | | 23,584 | | | | 90,245 | |

| Number of Shares Exchanged for Institutional Class Shares | | | (6,573 | ) | | | (11,849 | ) |

| Number of Shares Redeemed | | | (165,817 | ) | | | (202,111 | ) |

| Change in Retail Class Shares | | | (91,517 | ) | | | 36,707 | |

| Institutional Class: | | | | | | | | |

| Number of Shares Issued | | | 228,548 | | | | 629,968 | |

| Number of Shares Reinvested | | | 21,182 | | | | 90,547 | |

| Number of Shares Issued in Exchange for Retail Class Shares | | | 6,351 | | | | 11,515 | |

| Number of Shares Redeemed | | | (638,226 | ) | | | (70,897 | ) |

| Change in Institutional Class Shares | | | (382,145 | ) | | | 661,133 | |

| Total Change in Shares | | | (473,662 | ) | | | 697,840 | |

See accompanying notes to financial statements.

Needham Aggressive Growth Fund

Statements of Changes in Net Assets

| | | Year Ended | | | Year Ended | |

| | | December 31, 2022 | | | December 31, 2021 | |

| Change in Net Assets | | | | | | |

| Operations: | | | | | | |

| Net Investment Loss | | $ | (1,381,891 | ) | | $ | (1,185,089 | ) |

| Net Realized Gain from Investments, Securities Sold Short, | | | | | | | | |

| Foreign Currency Transactions, and Currency | | | 1,252,127 | | | | 7,541,822 | |

| Net Change in Unrealized Appreciation (Depreciation) on Investments, | | | | | | | | |

| Securities Sold Short, Foreign Currency Translations | | | (47,417,967 | ) | | | 23,112,286 | |

| Change in Net Assets Resulting from Operations | | | (47,547,731 | ) | | | 29,469,019 | |

| | | | | | | | | |

| Distributable Earnings: | | | | | | | | |

| Retail Class | | | — | | | | (3,505,617 | ) |

| Institutional Class | | | — | | | | (3,738,621 | ) |

| Total Distributable Earnings | | | — | | | | (7,244,238 | ) |

| | | | | | | | | |

| Capital Transactions: | | | | | | | | |

| Retail Class: | | | | | | | | |

| Shares Issued | | | 32,589,452 | | | | 17,590,552 | |

| Shares Issued in Reinvestment of Distribution | | | — | | | | 3,443,051 | |

| Shares Exchanged for Institutional Class Shares | | | (738,424 | ) | | | (2,770,037 | ) |

| Shares Redeemed | | | (19,962,515 | ) | | | (6,070,119 | ) |

| Institutional Class: | | | | | | | | |

| Shares Issued | | | 75,218,012 | | | | 33,454,969 | |

| Shares Issued in Reinvestment of Distribution | | | — | | | | 3,737,661 | |

| Shares Issued in Exchange for Retail Class Shares | | | 738,424 | | | | 2,770,037 | |

| Shares Redeemed | | | (45,755,366 | ) | | | (8,393,730 | ) |

| Total Change in Net Assets from Capital Transactions | | | 42,089,583 | | | | 43,762,384 | |

| | | | | | | | | |

| Change in Net Assets | | | (5,458,148 | ) | | | 65,987,165 | |

| | | | | | | | | |

| Total Net Assets | | | | | | | | |

| Beginning of Year | | | 140,377,452 | | | | 74,390,287 | |

| End of Year | | $ | 134,919,304 | | | $ | 140,377,452 | |

| | | | | | | | | |

| Share Transaction: | | | | | | | | |

| Retail Class: | | | | | | | | |

| Number of Shares Issued | | | 962,894 | | | | 446,334 | |

| Number of Shares Reinvested | | | — | | | | 84,430 | |

| Number of Shares Exchanged for Institutional Class Shares | | | (23,793 | ) | | | (73,582 | ) |

| Number of Shares Redeemed | | | (635,372 | ) | | | (164,073 | ) |

| Change in Retail Class Shares | | | 303,729 | | | | 293,109 | |

| Institutional Class: | | | | | | | | |

| Number of Shares Issued | | | 2,160,212 | | | | 824,655 | |

| Number of Shares Reinvested | | | — | | | | 88,361 | |

| Number of Shares Issued in Exchange for Retail Class Shares | | | 22,856 | | | | 71,151 | |

| Number of Shares Redeemed | | | (1,406,449 | ) | | | (211,402 | ) |

| Change in Institutional Class Shares | | | 776,619 | | | | 772,765 | |

| Total Change in Shares | | | 1,080,348 | | | | 1,065,874 | |

See accompanying notes to financial statements.

Needham Small Cap Growth Fund

Statements of Changes in Net Assets

| | | Year Ended | | | Year Ended | |

| | | December 31, 2022 | | | December 31, 2021 | |

| Change in Net Assets | | | | | | |

| Operations: | | | | | | |

| Net Investment Loss | | $ | (2,101,991 | ) | | $ | (3,645,056 | ) |

| Net Realized Gain (Loss) from Investments, Securities Sold Short, | | | | | | | | |

| Foreign Currency Transactions, and Currency | | | (38,149,724 | ) | | | 60,836,434 | |

| Net Change in Unrealized Depreciation on Investments, | | | | | | | | |

| Securities Sold Short, Foreign Currency Translations | | | (43,233,707 | ) | | | (41,922,251 | ) |

| Change in Net Assets Resulting from Operations | | | (83,485,422 | ) | | | 15,269,127 | |

| | | | | | | | | |

| Distributable Earnings: | | | | | | | | |

| Retail Class | | | (2,436,435 | ) | | | (24,383,677 | ) |

| Institutional Class | | | (5,043,317 | ) | | | (34,026,765 | ) |

| Total Distributable Earnings | | | (7,479,752 | ) | | | (58,410,442 | ) |

| | | | | | | | | |

| Capital Transactions: | | | | | | | | |

| Retail Class: | | | | | | | | |

| Shares Issued | | | 23,274,194 | | | | 105,261,275 | |

| Shares Issued in Reinvestment of Distribution | | | 2,249,936 | | | | 22,837,418 | |

| Shares Exchanged for Institutional Class Shares | | | (355,490 | ) | | | (5,552,115 | ) |

| Shares Redeemed | | | (44,181,952 | ) | | | (81,878,650 | ) |

| Institutional Class: | | | | | | | | |

| Shares Issued | | | 89,867,190 | | | | 181,275,931 | |

| Shares Issued in Reinvestment of Distribution | | | 4,912,810 | | | | 31,653,377 | |

| Shares Issued in Exchange for Retail Class Shares | | | 355,490 | | | | 5,552,115 | |

| Shares Redeemed | | | (75,209,316 | ) | | | (146,472,526 | ) |

| Total Change in Net Assets from Capital Transactions | | | 912,862 | | | | 112,676,825 | |

| | | | | | | | | |

| Change in Net Assets | | | (90,052,312 | ) | | | 69,535,510 | |