ANNUAL REPORT OCTOBER 31, 2011

| President’s Letter | 2 |

| Independent Chairman’s Letter | 3 |

| Market Perspective | 4 |

| Performance | 5 |

| Portfolio Commentary | 7 |

| Fund Characteristics | 9 |

| Shareholder Fee Example | 10 |

| Schedule of Investments | 12 |

| Statement of Assets and Liabilities | 15 |

| Statement of Operations | 16 |

| Statement of Changes in Net Assets | 17 |

| Notes to Financial Statements | 18 |

| Financial Highlights | 24 |

| Report of Independent Registered Public Accounting Firm | 26 |

| Management | 27 |

| Approval of Management Agreement | 30 |

| Additional Information | 35 |

Any opinions expressed in this report reflect those of the author as of the date of the report, and do not necessarily represent the opinions of American Century Investments® or any other person in the American Century Investments organization. Any such opinions are subject to change at any time based upon market or other conditions and American Century Investments disclaims any responsibility to update such opinions. These opinions may not be relied upon as investment advice and, because investment decisions made by American Century Investments funds are based on numerous factors, may not be relied upon as an indication of trading intent on behalf of any American Century Investments fund. Security examples are used for representational purposes only and are not intended as recommendations to purchase or sell securities. Performance information for comparative indices and securities is provided to American Century Investments by third party vendors. To the best of American Century Investments’ knowledge, such information is accurate at the time of printing.

Dear Investor:

Thank you for reviewing this annual report for the period ended October 31, 2011. Our report offers investment performance and portfolio information, presented with the expert perspective of our portfolio management team.

This report remains one of our most important vehicles for conveying information about investment performance, as well as market factors and strategies that affected fund returns. For additional, updated information, we encourage you to visit our website, americancentury.com. Click on the “Fund Performance” and “Insights & News” headings at the top of our Individual Investors site.

Volatile Period Produces Moderate U.S. Stock Returns

Broad U.S. stock market indices returned roughly 7–10% during the 12 months ended October 31, 2011. That’s a moderate level of equity performance compared with the shorter-term volatility we experienced during the period.

For example, from October 31, 2010, to April 29, 2011, the S&P 500 Index gained over 15%. That upturn was the latter part of an approximately 30% rally (extending back to late August 2010) that began in expectation of the Federal Reserve’s second round of quantitative easing (government securities purchases intended to stimulate economic growth and investment risk-taking), which started during the fourth quarter of 2010.

Economic optimism and increased risk-taking governed market performance from the third quarter of 2010 until the end of April 2011. That optimism eroded, however, and investors’ risk tolerance reversed as high fuel prices, further U.S. home value declines, elevated U.S. unemployment rates, natural disasters, a near-default on U.S. government debt, a U.S. debt rating downgrade, and a resurgence of the European sovereign debt crisis ebbed the economic tide.

In response, the S&P 500 Index declined over 15% from the end of April to early October 2011. And the roller coaster wasn’t over—the S&P 500 Index rebounded over 14% during a stretch in October on better economic news and European efforts to ease the debt crisis.

Unfortunately, further volatility appears likely in 2012 as the markets wrestle with uncertainties regarding European debt, economic strength, government budget deficits, and the U.S. presidential election. We believe strongly in adhering to a disciplined, diversified, long-term investment approach during volatile periods, and we appreciate your continued trust in us during these unsettled times.

Sincerely,

Jonathan Thomas

President and Chief Executive Officer

American Century Investments

Independent Chairman’s Letter |

Don Pratt

Dear Fellow Shareholders,

The board of directors of the fund was pleased at the announcement of a new strategic partner for the investment advisor to the American Century Investments funds. Canadian Imperial Bank of Commerce (CIBC), a leading Canadian financial institution, purchased the 41 percent economic interest in American Century Companies, the parent corporation of the advisor, previously held by JPMorgan Chase & Co. Based in Toronto, CIBC provides a full range of retail and wholesale banking services to almost 11 million clients through approximately 1,100 branches and offices in Canada, the U.S. and around the world. This transaction will benefit fund shareholders by bolstering the financial strength of the advisor and providing a strategic partner to help support its growth initiative to broaden non-U.S. distribution of its products and services.

The board also has been briefed throughout the year on the impact on fund performance of the European banking crisis, the U.S. deficit reduction debates, and the pace of economic growth. While the performance of all funds has been affected, the majority of American Century Investments funds overseen by the board are exceeding their benchmarks for the one-, three-, five-, and ten-year periods ended September 30, 2011. This is commendable performance, particularly in these challenging market conditions.

We are completing another year of board oversight on your behalf. We appreciate any comments you would like to share with the board. Send them to me at dhpratt@fundboardchair.com. Thank you for your continued investment in American Century Investments funds.

Best regards,

Don Pratt

By Greg Woodhams,

Chief Investment Officer,

U.S. Growth Equity—Large Cap

Stocks Advanced in a Volatile Year

U.S. equities managed positive returns during a volatile 12 months ended October 31, 2011. Action in stocks in some respects mirrored changes in the pace of economic growth—U.S. gross domestic product expanded at a 2.3% annual rate in the fourth quarter of 2010, but dipped to 0.4% and 1.3% in the first and second quarters of 2011, respectively, before returning to 2.0% growth in the third quarter of the year.

Similarly, stocks began the period with gains, buoyed by robust corporate earnings growth; the Federal Reserve’s second round of quantitative easing; and the extension of unemployment benefits and Bush-era tax cuts. But uncertainty generated by a series of events—including political unrest in the Middle East, the tragic earthquake and nuclear disaster in Japan, and concerns around the resolution of European sovereign debt and U.S. budgetary issues—served to compress price/earnings multiples. Equity markets finished the fiscal year with a sharp rebound in October after the economic data turned out to be not as bad as feared.

Growth Outperformed Value

In that environment, growth-oriented shares outperformed value across all capitalization ranges as measured by the various Russell indices (see accompanying returns table). In terms of returns by size, large-capitalization stocks did better than those of mid- and small-cap companies.

Looking at the major sectors in the Russell 1000 Growth Index, performance was widely dispersed, reflecting the volatile nature of the reporting period. For example, both consumer staples and consumer discretionary stocks were among the best-performing segments within the index. It was a similar story when looking at many economically sensitive sectors—energy was the top performer, while materials and industrials were among the lagging sectors. Financials also underperformed, partly as a result of worry about exposure to Europe and the slowing economy. Information technology stocks fared reasonably well overall, though performance varied widely within the sector.

| U.S. Stock Index Returns |

| For the 12 months ended October 31, 2011 |

| Russell 1000 Index (Large-Cap) | 8.01% | | Russell 2000 Index (Small-Cap) | 6.71% |

| Russell 1000 Growth Index | 9.92% | | Russell 2000 Growth Index | 9.84% |

| Russell 1000 Value Index | 6.16% | | Russell 2000 Value Index | 3.54% |

| Russell Midcap Index | 7.85% | | |

| Russell Midcap Growth Index | 10.08% | | | |

| Russell Midcap Value Index | 5.83% | | | |

| Total Returns as of October 31, 2011 |

| | | | Average Annual Returns | |

| | Ticker Symbol | 1 year | 5 years | 10 years | Since Inception | Inception Date |

| Investor Class | TWCUX | 10.59% | 3.37% | 3.03% | 10.97% | 11/2/81 |

| Russell 1000 Growth Index | — | 9.92% | 3.04% | 3.56% | 9.98%(1) | — |

| S&P 500 Index | — | 8.09% | 0.25% | 3.69% | 11.00%(1) | — |

| Institutional Class | TWUIX | 10.85% | 3.58% | 3.24% | 4.57% | 11/14/96 |

A Class(2) No sales charge* With sales charge* | TWUAX | 10.33% 3.98% | 3.11% 1.90% | 2.78% 2.17% | 4.35% 3.95% | 10/2/96 |

| C Class | TWCCX | 9.48% | 2.34% | 2.01% | 1.83% | 10/29/01 |

| R Class | AULRX | 10.03% | 2.85% | — | 3.29% | 8/29/03 |

| Sales charges include initial sales charges and contingent deferred sales charges (CDSCs), as applicable. A Class shares have a 5.75% maximum initial sales charge and may be subject to a maximum CDSC of 1.00%. C Class shares redeemed within 12 months of purchase are subject to a maximum CDSC of 1.00%. The SEC requires that mutual funds provide performance information net of maximum sales charges in all cases where charges could be applied. |

| (1) | Since 10/31/81, the date nearest the Investor Class’s inception for which data are available. |

| (2) | Prior to September 4, 2007, the A Class was referred to as the Advisor Class and did not have a front-end sales charge. Performance prior to that date has been adjusted to reflect this charge. |

Data presented reflect past performance. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance shown. Investment return and principal value will fluctuate, and redemption value may be more or less than original cost. To obtain performance data current to the most recent month end, please call 1-800-345-2021 or visit americancentury.com. International investing involves special risks, such as political instability and currency fluctuations.

Unless otherwise indicated, performance reflects Investor Class shares; performance for other share classes will vary due to differences in fee structure. For information about other share classes available, please consult the prospectus. Data assumes reinvestment of dividends and capital gains, and none of the charts reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for the indices are provided for comparison. The fund’s total returns include operating expenses (such as transaction costs and management fees) that reduce returns, while the total returns of the indices do not.

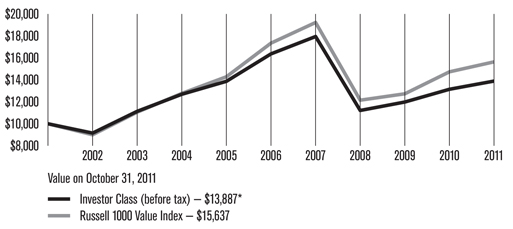

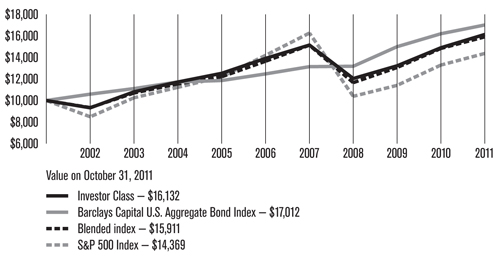

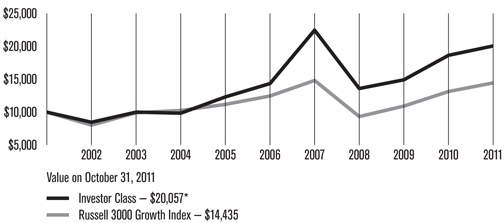

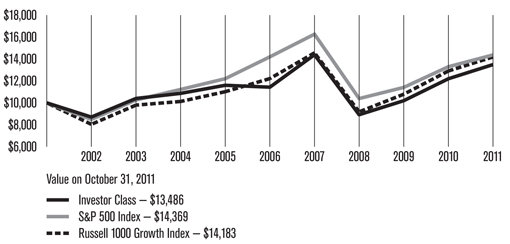

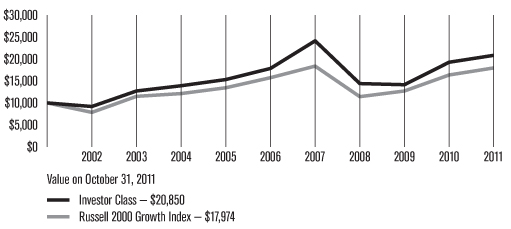

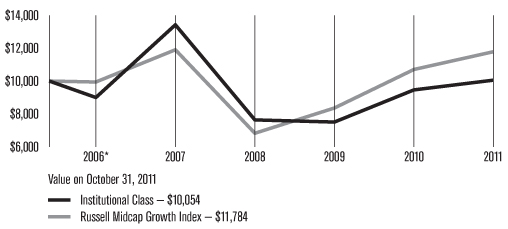

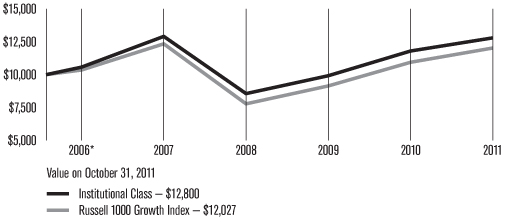

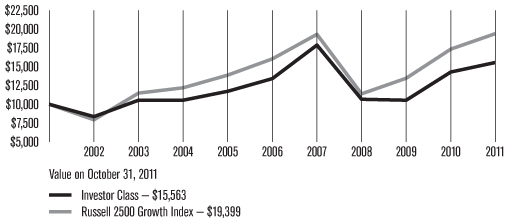

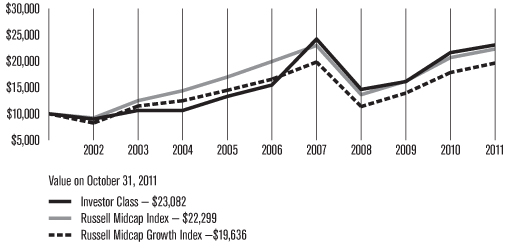

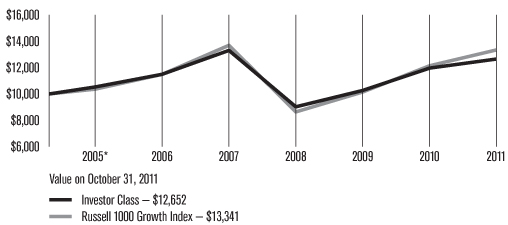

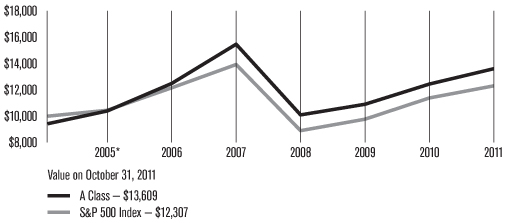

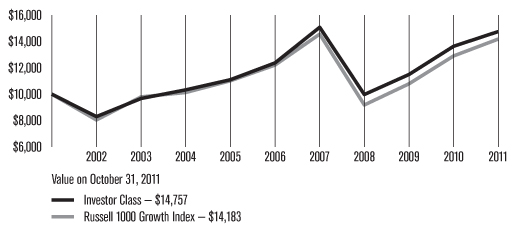

| Growth of $10,000 Over 10 Years |

| $10,000 investment made October 31, 2001 |

| Total Annual Fund Operating Expenses |

| Investor Class | Institutional Class | A Class | C Class | R Class |

| 1.00% | 0.80% | 1.25% | 2.00% | 1.50% |

The total annual fund operating expenses shown is as stated in the fund’s prospectus current as of the date of this report. The prospectus may vary from the expense ratio shown elsewhere in this report because it is based on a different time period, includes acquired fund fees and expenses, and, if applicable, does not include fee waivers or expense reimbursements.

Data presented reflect past performance. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance shown. Investment return and principal value will fluctuate, and redemption value may be more or less than original cost. To obtain performance data current to the most recent month end, please call 1-800-345-2021 or visit americancentury.com. International investing involves special risks, such as political instability and currency fluctuations.

Unless otherwise indicated, performance reflects Investor Class shares; performance for other share classes will vary due to differences in fee structure. For information about other share classes available, please consult the prospectus. Data assumes reinvestment of dividends and capital gains, and none of the charts reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for the indices are provided for comparison. The fund’s total returns include operating expenses (such as transaction costs and management fees) that reduce returns, while the total returns of the indices do not.

Portfolio Managers: Keith Lee and Michael Li

Performance Summary

Ultra returned 10.59%* for the 12 months ended October 31, 2011, compared with the 9.92% return of its benchmark, the Russell 1000 Growth Index, and the 8.09% return of the S&P 500 Index, a broader market measure.

As discussed in the Market Perspective on page 4, equity indices generally gained during the reporting period, although they struggled with the challenges of a weak global economic recovery, ongoing sovereign debt concerns in Europe, and Treasury debt downgrade. Although this created a challenging environment for growth and momentum oriented shares, Ultra delivered solid returns and outperformed its benchmark.

Within the portfolio, security selection in the information technology and health care sectors accounted for the bulk of Ultra’s outperformance relative to the benchmark. Stock selection in the materials, consumer discretionary, and consumer staples sectors also added to relative returns. Stock decisions in the energy and financials sectors detracted from relative results.

Information Technology, Health Care Led Gains

The information technology sector was a source of relative outperformance for Ultra. Within the computers and peripherals industry group, an underweight stake in Hewlett-Packard helped relative results as the stock underperformed in the benchmark. An overweight position in personal electronic device maker Apple also benefited relative performance. The company experienced acceleration in revenues and earnings, added new carriers, and gained penetration with existing carriers, while increasing market share.

Within the software industry group, the portfolio held an overweight position in video game publisher Electronic Arts. The company’s share price climbed amid rising sales of its core video games as well as growth of its newer digital business, which includes downloadable content for PCs, social networks, and mobile platforms. Effective stock decisions in the communications equipment and semiconductor groups also contributed to relative returns.

Also in the information technology sector, though, Ultra did not hold a position in IBM. This decision proved detrimental as the company’s stock benefited from being perceived as somewhat of a “safe haven” within the technology sector during the market downturn. The managers do not find IBM attractive based on the stock’s relative valuation and the company’s growth rate.

In the health care equipment group, an overweight stake in Intuitive Surgical added meaningfully to gains. The maker of robotic surgery systems experienced a sharp rise in earnings amid continued adoption of its technology and increased sales of its surgical system.

*All fund returns referenced in this commentary are for Investor Class shares.

Materials, Consumer Discretionary, Consumer Staples Helped

Within the materials sector, the portfolio’s overweight allocation to the chemicals industry included a stake in chemicals company Nalco Holding Co. The company experienced strong volume and price gains amid growing demand.

In the consumer discretionary sector, an overweight stake in Tiffany added meaningfully to relative results. The fine jewelry retailer delivered higher-than-expected earnings as sales levels climbed, driven largely by same-store sales growth in Asia, Europe, and the Americas.

However, not all holdings in the consumer discretionary sector helped performance. An overweight stake in Netflix represented the largest single detractor from relative returns. The company stumbled when it raised prices 60% for its mail order DVD rental service, and then announced that it would separate its video streaming business from its DVD offering. Both moves alienated customers, and, although the company lowered guidance for its subscriber base, subscription levels fell below that revised level. Although Netflix management handled the transition poorly, we believe that the company’s evolution from its legacy DVD business to the video streaming business is positive, as it will require lower overhead and offers more growth potential.

Within the consumer staples sector, an overweight position in Costco Wholesale contributed to relative returns. The membership discount retailer benefited from a focus on lower-end providers of consumer goods in the weak economic environment.

Energy, Financials, Lagged Benchmark

The energy sector detracted from relative returns. Within the sector, Ultra held several overweight stakes in the oil, gas, and consumable fuels group that underperformed, while maintaining underweight positions in some companies that outperformed in the benchmark.

The financials sector was also a source of underperformance relative to the benchmark. Here, Ultra held several positions in the diversified financial services group that lagged.

Starting Point for Next Reporting Period

The environment for growth- and momentum-oriented investment styles continued to be challenging during the reporting period. Nonetheless, Ultra delivered sound results for the period. Going forward, we remain confident in our investment beliefs that stocks which exhibit high-quality, accelerating fundamentals, positive relative strength, and attractive valuations will outperform in the long term.

| OCTOBER 31, 2011 | |

| Top Ten Holdings | % of net assets |

| Apple, Inc. | 7.2% |

| Google, Inc., Class A | 4.5% |

| Amazon.com, Inc. | 3.0% |

| Exxon Mobil Corp. | 2.6% |

| Gilead Sciences, Inc. | 2.4% |

| Philip Morris International, Inc. | 2.4% |

| Schlumberger Ltd. | 2.3% |

| Costco Wholesale Corp. | 2.2% |

| Oracle Corp. | 2.2% |

| QUALCOMM, Inc. | 2.2% |

| | |

| Top Five Industries | % of net assets |

| Computers and Peripherals | 8.7% |

| Software | 7.5% |

| Internet Software and Services | 6.4% |

| Oil, Gas and Consumable Fuels | 6.3% |

| Machinery | 5.9% |

| | |

| Types of Investments in Portfolio | % of net assets |

| Domestic Common Stocks | 92.5% |

| Foreign Common Stocks* | 7.1% |

| Total Common Stocks | 99.6% |

| Temporary Cash Investments | 0.5% |

| Other Assets and Liabilities | (0.1)% |

*Includes depositary shares, dual listed securities and foreign ordinary shares.

Fund shareholders may incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments and redemption/exchange fees; and (2) ongoing costs, including management fees; distribution and service (12b-1) fees; and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in your fund and to compare these costs with the ongoing cost of investing in other mutual funds.

The example is based on an investment of $1,000 made at the beginning of the period and held for the entire period from May 1, 2011 to October 31, 2011.

Actual Expenses

The table provides information about actual account values and actual expenses for each class. You may use the information, together with the amount you invested, to estimate the expenses that you paid over the period. First, identify the share class you own. Then simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

If you hold Investor Class shares of any American Century Investments fund, or Institutional Class shares of the American Century Diversified Bond Fund, in an American Century Investments account (i.e., not a financial intermediary or retirement plan account), American Century Investments may charge you a $12.50 semiannual account maintenance fee if the value of those shares is less than $10,000. We will redeem shares automatically in one of your accounts to pay the $12.50 fee. In determining your total eligible investment amount, we will include your investments in all personal accounts (including American Century Investments Brokerage accounts) registered under your Social Security number. Personal accounts include individual accounts, joint accounts, UGMA/UTMA accounts, personal trusts, Coverdell Education Savings Accounts and IRAs (including traditional, Roth, Rollover, SEP-, SARSEP- and SIMPLE-IRAs), and certain other retirement accounts. If you have only business, business retirement, employer-sponsored or American Century Investments Brokerage accounts, you are currently not subject to this fee. We will not charge the fee as long as you choose to manage your accounts exclusively online. If you are subject to the Account Maintenance Fee, your account value could be reduced by the fee amount.

Hypothetical Example for Comparison Purposes

The table also provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio of each class of your fund and an assumed rate of return of 5% per year before expenses, which is not the actual return of a fund’s share class. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in your fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) or redemption/exchange fees. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | Beginning Account Value 5/1/11 | Ending Account Value 10/31/11 | Expenses Paid During Period(1) 5/1/11 – 10/31/11 | Annualized Expense Ratio(1) |

| Actual | | | | |

| Investor Class | $1,000 | $950.90 | $4.87 | 0.99% |

| Institutional Class | $1,000 | $951.90 | $3.89 | 0.79% |

| A Class | $1,000 | $949.50 | $6.09 | 1.24% |

| C Class | $1,000 | $946.00 | $9.76 | 1.99% |

| R Class | $1,000 | $948.40 | $7.32 | 1.49% |

| Hypothetical | | | | |

| Investor Class | $1,000 | $1,020.22 | $5.04 | 0.99% |

| Institutional Class | $1,000 | $1,021.22 | $4.02 | 0.79% |

| A Class | $1,000 | $1,018.96 | $6.31 | 1.24% |

| C Class | $1,000 | $1,015.17 | $10.11 | 1.99% |

| R Class | $1,000 | $1,017.69 | $7.58 | 1.49% |

| (1) | Expenses are equal to the class’s annualized expense ratio listed in the table above, multiplied by the average account value over the period, multiplied by 184, the number of days in the most recent fiscal half-year, divided by 365, to reflect the one-half year period. |

| | Shares | Value |

| Common Stocks — 99.6% |

| AEROSPACE AND DEFENSE — 1.6% |

| General Dynamics Corp. | 1,539,583 | $ 98,825,833 |

| AUTO COMPONENTS — 0.5% |

| Gentex Corp. | 1,077,000 | 32,439,240 |

| BEVERAGES — 1.1% |

| Coca-Cola Co. (The) | 949,000 | 64,835,680 |

| BIOTECHNOLOGY — 4.4% |

Alexion Pharmaceuticals, Inc.(1) | 645,000 | 43,543,950 |

Celgene Corp.(1) | 1,202,000 | 77,925,660 |

Gilead Sciences, Inc.(1) | 3,522,000 | 146,726,520 |

| | | 268,196,130 |

| CHEMICALS — 4.3% |

| Monsanto Co. | 1,550,000 | 112,762,500 |

| Nalco Holding Co. | 1,570,000 | 59,204,700 |

| Potash Corp. of Saskatchewan, Inc. | 1,356,000 | 64,179,480 |

| RPM International, Inc. | 1,107,000 | 24,874,290 |

| | | 261,020,970 |

| COMMUNICATIONS EQUIPMENT — 2.5% |

| Cisco Systems, Inc. | 1,036,000 | 19,197,080 |

| QUALCOMM, Inc. | 2,538,000 | 130,960,800 |

| | | 150,157,880 |

| COMPUTERS AND PERIPHERALS — 8.7% |

Apple, Inc.(1) | 1,085,000 | 439,186,300 |

EMC Corp.(1) | 3,843,000 | 94,191,930 |

| | | 533,378,230 |

| CONSUMER FINANCE — 1.1% |

| American Express Co. | 1,341,000 | 67,881,420 |

| DIVERSIFIED FINANCIAL SERVICES — 2.0% |

| CME Group, Inc. | 270,000 | 74,401,200 |

| JPMorgan Chase & Co. | 1,372,000 | 47,690,720 |

| | | 122,091,920 |

| ELECTRICAL EQUIPMENT — 4.9% |

ABB Ltd.(1) | 1,756,000 | 33,105,449 |

ABB Ltd. ADR(1) | 2,431,000 | 45,727,110 |

| Cooper Industries plc | 1,317,000 | 69,089,820 |

| Emerson Electric Co. | 2,221,000 | 106,874,520 |

Polypore International, Inc.(1) | 858,673 | 45,037,399 |

| | | 299,834,298 |

| ENERGY EQUIPMENT AND SERVICES — 2.7% |

| Core Laboratories NV | 215,000 | 23,275,900 |

| Schlumberger Ltd. | 1,911,000 | 140,401,170 |

| | | 163,677,070 |

| FOOD AND STAPLES RETAILING — 2.2% |

| Costco Wholesale Corp. | 1,612,000 | 134,199,000 |

| FOOD PRODUCTS — 2.9% |

| Hershey Co. (The) | 994,000 | 56,886,620 |

| Mead Johnson Nutrition Co. | 731,000 | 52,522,350 |

| Nestle SA | 1,207,000 | 69,848,761 |

| | | 179,257,731 |

| HEALTH CARE EQUIPMENT AND SUPPLIES — 3.8% |

HeartWare International, Inc.(1) | 161,000 | 10,936,730 |

Intuitive Surgical, Inc.(1) | 275,000 | 119,311,500 |

| St. Jude Medical, Inc. | 1,492,000 | 58,188,000 |

Varian Medical Systems, Inc.(1) | 684,000 | 40,164,480 |

| | | 228,600,710 |

| HEALTH CARE PROVIDERS AND SERVICES — 3.4% |

Express Scripts, Inc.(1) | 2,643,000 | 120,864,390 |

Medco Health Solutions, Inc.(1) | 175,899 | 9,649,819 |

| UnitedHealth Group, Inc. | 1,600,000 | 76,784,000 |

| | | 207,298,209 |

| HOTELS, RESTAURANTS AND LEISURE — 4.0% |

Chipotle Mexican Grill, Inc.(1) | 91,000 | 30,586,920 |

| McDonald’s Corp. | 1,378,000 | 127,947,300 |

| Starbucks Corp. | 2,064,000 | 87,389,760 |

| | | 245,923,980 |

| INSURANCE — 1.1% |

| MetLife, Inc. | 1,841,000 | 64,729,560 |

| INTERNET AND CATALOG RETAIL — 3.7% |

Amazon.com, Inc.(1) | 846,000 | 180,629,460 |

Netflix, Inc.(1) | 524,000 | 43,009,920 |

| | | 223,639,380 |

| INTERNET SOFTWARE AND SERVICES — 6.4% |

Baidu, Inc. ADR(1) | 505,000 | 70,790,900 |

Google, Inc., Class A(1) | 469,000 | 277,948,160 |

| Tencent Holdings Ltd. | 1,835,000 | 42,030,653 |

| | | 390,769,713 |

| IT SERVICES — 2.4% |

| MasterCard, Inc., Class A | 301,000 | 104,519,240 |

Teradata Corp.(1) | 686,000 | 40,926,760 |

| | | 145,446,000 |

| LEISURE EQUIPMENT AND PRODUCTS — 0.9% |

| Hasbro, Inc. | 1,456,000 | 55,415,360 |

| MACHINERY — 5.9% |

| Cummins, Inc. | 575,000 | 57,172,250 |

| Donaldson Co., Inc. | 513,000 | 32,857,650 |

| Joy Global, Inc. | 1,253,000 | $ 109,261,600 |

| Parker Hannifin Corp. | 1,062,000 | 86,606,100 |

WABCO Holdings, Inc.(1) | 940,000 | 47,197,400 |

| Wabtec Corp. | 441,000 | 29,626,380 |

| | | 362,721,380 |

| METALS AND MINING — 1.7% |

| BHP Billiton Ltd. ADR | 479,000 | 37,400,320 |

| Freeport-McMoRan Copper & Gold, Inc. | 1,713,000 | 68,965,380 |

| | | 106,365,700 |

| OIL, GAS AND CONSUMABLE FUELS — 6.3% |

| Cimarex Energy Co. | 484,000 | 30,976,000 |

| EOG Resources, Inc. | 356,000 | 31,837,080 |

| Exxon Mobil Corp. | 2,060,000 | 160,865,400 |

Newfield Exploration Co.(1) | 723,000 | 29,107,980 |

| Occidental Petroleum Corp. | 1,071,000 | 99,538,740 |

Southwestern Energy Co.(1) | 796,000 | 33,463,840 |

| | | 385,789,040 |

| PERSONAL PRODUCTS — 1.1% |

| Estee Lauder Cos., Inc. (The), Class A | 695,000 | 68,422,750 |

| PHARMACEUTICALS — 0.7% |

| Teva Pharmaceutical Industries Ltd. ADR | 1,107,000 | 45,220,950 |

| SEMICONDUCTORS AND SEMICONDUCTOR EQUIPMENT — 3.5% |

| Altera Corp. | 1,905,000 | 72,237,600 |

| Linear Technology Corp. | 2,441,000 | 78,868,710 |

| Microchip Technology, Inc. | 1,721,000 | 62,231,360 |

| | | 213,337,670 |

| SOFTWARE — 7.5% |

Adobe Systems, Inc.(1) | 1,703,000 | 50,085,230 |

Electronic Arts, Inc.(1) | 4,408,000 | 102,926,800 |

| Microsoft Corp. | 994,000 | 26,470,220 |

NetSuite, Inc.(1) | 613,000 | 23,318,520 |

| Oracle Corp. | 4,052,000 | 132,784,040 |

Salesforce.com, Inc.(1) | 474,000 | 63,122,580 |

VMware, Inc., Class A(1) | 583,000 | 56,988,250 |

| | | 455,695,640 |

| SPECIALTY RETAIL — 4.3% |

O’Reilly Automotive, Inc.(1) | 763,000 | 58,026,150 |

| Tiffany & Co. | 1,455,000 | 116,007,150 |

| TJX Cos., Inc. (The) | 1,545,000 | 91,046,850 |

| | | 265,080,150 |

| TEXTILES, APPAREL AND LUXURY GOODS — 1.6% |

| NIKE, Inc., Class B | 1,010,000 | 97,313,500 |

| TOBACCO — 2.4% |

| Philip Morris International, Inc. | 2,055,000 | 143,582,850 |

TOTAL COMMON STOCKS(Cost $3,939,630,810) | 6,081,147,944 |

| Temporary Cash Investments — 0.5% |

Repurchase Agreement, Bank America Merrill Lynch, (collateralized by various U.S. Treasury obligations, 0.50%, 10/15/14, valued at $9,182,054), in a joint trading account at 0.06%, dated 10/31/11, due 11/1/11 (Delivery value $8,988,751) | 8,988,736 |

Repurchase Agreement, Credit Suisse First Boston, Inc., (collateralized by various U.S. Treasury obligations, 4.50%, 5/15/38, valued at $9,211,981), in a joint trading account at 0.03%, dated 10/31/11, due 11/1/11 (Delivery value $8,988,742) | 8,988,735 |

Repurchase Agreement, Goldman Sachs & Co., (collateralized by various U.S. Treasury obligations, 3.875%, 8/15/40, valued at $9,159,731), in a joint trading account at 0.04%, dated 10/31/11, due 11/1/11 (Delivery value $8,988,745) | 8,988,735 |

| SSgA U.S. Government Money Market Fund | 688,715 | 688,715 |

TOTAL TEMPORARY CASH INVESTMENTS (Cost $27,654,921) | 27,654,921 |

TOTAL INVESTMENT SECURITIES — 100.1% (Cost $3,967,285,731) | 6,108,802,865 |

| OTHER ASSETS AND LIABILITIES — (0.1)% | (3,924,879) |

| TOTAL NET ASSETS — 100.0% | $6,104,877,986 |

| Forward Foreign Currency Exchange Contracts |

| Contracts to Sell | Counterparty | Settlement Date | Value | Unrealized Gain (Loss) |

| 74,053,400 | CHF for USD | Credit Suisse AG | 11/30/11 | $84,396,597 | $(47,552) |

(Value on Settlement Date $84,349,045)

Notes to Schedule of Investments

ADR = American Depositary Receipt

CHF = Swiss Franc

USD = United States Dollar

| (1) | Non-income producing. |

See Notes to Financial Statements.

Statement of Assets and Liabilities |

| OCTOBER 31, 2011 | |

| Assets | |

| Investment securities, at value (cost of $3,967,285,731) | | | $6,108,802,865 | |

| Foreign currency holdings, at value (cost of $129,650) | | | 129,911 | |

| Receivable for capital shares sold | | | 1,380,666 | |

| Dividends and interest receivable | | | 3,695,383 | |

| | | | 6,114,008,825 | |

| | | | | |

| Liabilities | | | | |

| Payable for investments purchased | | | 812,824 | |

| Payable for capital shares redeemed | | | 3,317,312 | |

| Unrealized loss on forward foreign currency exchange contracts | | | 47,552 | |

| Accrued management fees | | | 4,937,343 | |

| Distribution and service fees payable | | | 15,808 | |

| | | | 9,130,839 | |

| | | | | |

| Net Assets | | | $6,104,877,986 | |

| | | | | |

| Net Assets Consist of: | | | | |

| Capital (par value and paid-in surplus) | | | $4,501,993,545 | |

| Undistributed net investment income | | | 47,552 | |

| Accumulated net realized loss | | | (538,815,412 | ) |

| Net unrealized appreciation | | | 2,141,652,301 | |

| | | | $6,104,877,986 | |

| | | Net assets | | Shares outstanding | | Net asset value per share |

| Investor Class, $0.01 Par Value | | | $5,984,971,737 | | | | 255,590,135 | | | | $23.42 | |

| Institutional Class, $0.01 Par Value | | | $52,751,124 | | | | 2,202,924 | | | | $23.95 | |

| A Class, $0.01 Par Value | | | $62,304,182 | | | | 2,738,838 | | | | $22.75 | * |

| C Class, $0.01 Par Value | | | $677,999 | | | | 32,255 | | | | $21.02 | |

| R Class, $0.01 Par Value | | | $4,172,944 | | | | 184,658 | | | | $22.60 | |

| * | Maximum offering price $24.14 (net asset value divided by 0.9425) |

See Notes to Financial Statements.

| YEAR ENDED OCTOBER 31, 2011 | |

| Investment Income (Loss) | |

| Income: | | | |

| Dividends (net of foreign taxes withheld of $517,960) | | | $72,688,495 | |

| Interest | | | 20,643 | |

| | | | 72,709,138 | |

| | | | | |

| Expenses: | | | | |

| Management fees | | | 62,300,410 | |

| Distribution and service fees: | | | | |

| A Class | | | 176,386 | |

| B Class | | | 1,020 | |

| C Class | | | 7,690 | |

| R Class | | | 18,623 | |

| Directors’ fees and expenses | | | 253,387 | |

| Other expenses | | | 2,847 | |

| | | | 62,760,363 | |

| | | | | |

| Net investment income (loss) | | | 9,948,775 | |

| | | | | |

| Realized and Unrealized Gain (Loss) | | | | |

| Net realized gain (loss) on: | | | | |

| Investment transactions | | | 302,986,483 | |

| Foreign currency transactions | | | (10,491,201 | ) |

| | | | 292,495,282 | |

| | | | | |

| Change in net unrealized appreciation (depreciation) on: | | | | |

| Investments | | | 328,812,884 | |

| Translation of assets and liabilities in foreign currencies | | | (225,211 | ) |

| | | | 328,587,673 | |

| | | | | |

| Net realized and unrealized gain (loss) | | | 621,082,955 | |

| | | | | |

| Net Increase (Decrease) in Net Assets Resulting from Operations | | | $631,031,730 | |

See Notes to Financial Statements.

Statement of Changes in Net Assets |

| YEARS ENDED OCTOBER 31, 2011 AND OCTOBER 31, 2010 | |

| Increase (Decrease) in Net Assets | | 2011 | | | 2010 | |

| Operations | |

| Net investment income (loss) | | | $9,948,775 | | | | $14,027,620 | |

| Net realized gain (loss) | | | 292,495,282 | | | | 188,141,888 | |

| Change in net unrealized appreciation (depreciation) | | | 328,587,673 | | | | 836,699,181 | |

| Net increase (decrease) in net assets resulting from operations | | | 631,031,730 | | | | 1,038,868,689 | |

| | | | | | | | | |

| Distributions to Shareholders | | | | | | | | |

| From net investment income: | | | | | | | | |

| Investor Class | | | (12,309,961 | ) | | | (26,725,188 | ) |

| Institutional Class | | | (189,254 | ) | | | (528,963 | ) |

| A Class | | | — | | | | (172,872 | ) |

| Decrease in net assets from distributions | | | (12,499,215 | ) | | | (27,427,023 | ) |

| | | | | | | | | |

| Capital Share Transactions | | | | | | | | |

| Net increase (decrease) in net assets from capital share transactions | | | (537,865,157 | ) | | | (577,726,077 | ) |

| | | | | | | | | |

| Net increase (decrease) in net assets | | | 80,667,358 | | | | 433,715,589 | |

| | | | | | | | | |

| Net Assets | | | | | | | | |

| Beginning of period | | | 6,024,210,628 | | | | 5,590,495,039 | |

| End of period | | | $6,104,877,986 | | | | $6,024,210,628 | |

| | | | | | | | | |

| Undistributed net investment income | | | $47,552 | | | | $12,243,093 | |

See Notes to Financial Statements.

Notes to Financial Statements |

OCTOBER 31, 2011

1. Organization

American Century Mutual Funds, Inc. (the corporation) is registered under the Investment Company Act of 1940, as amended (the 1940 Act), as an open-end management investment company and is organized as a Maryland corporation. Ultra Fund (the fund) is one fund in a series issued by the corporation. The fund is diversified as defined under the 1940 Act. The fund’s investment objective is to seek long-term capital growth. The fund pursues its objective by investing primarily in equity securities of large companies that management believes will increase in value over time.

The fund is authorized to issue the Investor Class, the Institutional Class, the A Class, the B Class, the C Class and the R Class. The A Class may incur an initial sales charge. The A Class, B Class and C Class may be subject to a contingent deferred sales charge. The share classes differ principally in their respective sales charges and distribution and shareholder servicing expenses and arrangements. The Institutional Class is made available to institutional shareholders or through financial intermediaries whose clients do not require the same level of shareholder and administrative services as shareholders of other classes. As a result, the Institutional Class is charged a lower unified management fee. On October 21, 2011, all outstanding B Class shares were converted to A Class shares and the fund discontinued issuance of the B Class.

2. Significant Accounting Policies

The following is a summary of significant accounting policies consistently followed by the fund in preparation of its financial statements. The financial statements are prepared in conformity with accounting principles generally accepted in the United States of America, which may require management to make certain estimates and assumptions at the date of the financial statements. Actual results could differ from these estimates.

Investment Valuations — The fund determines the fair value of its investments and computes its net asset value per share as of the close of regular trading (usually 4 p.m. Eastern time) on the New York Stock Exchange (NYSE) on each day the NYSE is open.

Equity securities that are listed or traded on a domestic securities exchange are valued at the last reported sales price or at the official closing price as provided by the exchange. Equity securities traded on foreign securities exchanges are typically valued at the closing price on the exchange where primarily traded or as of the close of the NYSE, if that is earlier. If no last sales price is reported, or if local convention or regulation so provides, the mean of the latest bid and asked prices is used. Depending on local convention or regulation, securities traded over-the-counter are valued at the mean of the latest bid and asked prices, the last sales price, or the official closing price. In its determination of fair value, the fund may review several factors including: market information specific to a security; news developments in U.S. and foreign markets; the performance of particular U.S. and foreign securities, indices, comparable securities, American Depositary Receipts, Exchange-Traded Funds, and other relevant market indicators.

Debt securities maturing within 60 days at the time of purchase may be valued at cost, plus or minus any amortized discount or premium or at the evaluated mean as provided by an independent pricing service. Evaluated mean prices are commonly derived through utilization of market models, which may consider, among other factors, trade data, quotations from dealers and active market makers, relevant yield curve and spread data, related sector levels, creditworthiness, and other relevant market information on the same or comparable securities.

Investments in open-end management investment companies are valued at the reported net asset value per share. Repurchase agreements are valued at cost. Forward foreign currency exchange contracts are valued at the mean of the latest bid and asked prices of the forward currency rates as provided by an independent pricing service.

The value of investments initially expressed in foreign currencies is translated into U.S. dollars at prevailing exchange rates.

If the fund determines that the market price for a portfolio security is not readily available or the valuation methods mentioned above do not reflect a security’s fair value, such security is valued as determined in good faith by the Board of Directors or its designee, in accordance with procedures adopted by the Board of Directors. Circumstances that may cause the fund to use these procedures to value a security include, but are not limited to: a security has been declared in default; trading in a security has been halted during the trading day; there is a foreign market holiday and no trading occurred; or an event occurred between the close of a foreign exchange and the NYSE that may affect the value of a security.

Security Transactions — Security transactions are accounted for as of the trade date. Net realized gains and losses are determined on the identified cost basis, which is also used for federal income tax purposes.

Investment Income — Dividend income less foreign taxes withheld, if any, is recorded as of the ex-dividend date. Distributions received on securities that represent a return a capital or capital gain are recorded as a reduction of cost of investments and/or as a realized gain. The fund estimates the components of distributions received that may be considered nontaxable distributions or capital gain distributions for income tax purposes. Interest income is recorded on the accrual basis and includes accretion of discounts and amortization of premiums.

Foreign Currency Translations — All assets and liabilities initially expressed in foreign currencies are translated into U.S. dollars at prevailing exchange rates at period end. The fund may enter into spot foreign currency exchange contracts to facilitate transactions denominated in a foreign currency. Purchases and sales of investment securities, dividend and interest income, spot foreign currency exchange contracts, and expenses are translated at the rates of exchange prevailing on the respective dates of such transactions. Net realized and unrealized foreign currency exchange gains or losses related to investment securities are a component of net realized gain (loss) on investment transactions and change in net unrealized appreciation (depreciation) on investments, respectively.

Repurchase Agreements — The fund may enter into repurchase agreements with institutions that American Century Investment Management, Inc. (ACIM) (the investment advisor) has determined are creditworthy pursuant to criteria adopted by the Board of Directors. The fund requires that the collateral, represented by securities, received in a repurchase transaction be transferred to the custodian in a manner sufficient to enable the fund to obtain those securities in the event of a default under the repurchase agreement. ACIM monitors, on a daily basis, the securities transferred to ensure the value, including accrued interest, of the securities under each repurchase agreement is equal to or greater than amounts owed to the fund under each repurchase agreement.

Joint Trading Account — Pursuant to an Exemptive Order issued by the Securities and Exchange Commission, the fund, along with certain other funds in the American Century Investments family of funds, may transfer uninvested cash balances into a joint trading account. These balances are invested in one or more repurchase agreements that are collateralized by U.S. Treasury or Agency obligations.

Income Tax Status — It is the fund’s policy to distribute substantially all net investment income and net realized gains to shareholders and to otherwise qualify as a regulated investment company under provisions of the Internal Revenue Code. The fund is no longer subject to examination by tax authorities for years prior to 2008. At this time, management believes there are no uncertain tax positions which, based on their technical merit, would not be sustained upon examination and for which it is reasonably possible that the total amounts of unrecognized tax benefits will significantly change in the next twelve months. Accordingly, no provision has been made for federal or state income taxes.

Multiple Class — All shares of the fund represent an equal pro rata interest in the net assets of the class to which such shares belong, and have identical voting, dividend, liquidation and other rights and the same terms and conditions, except for class specific expenses and exclusive rights to vote on matters affecting only individual classes. Income, non-class specific expenses, and realized and unrealized capital gains and losses of the fund are allocated to each class of shares based on their relative net assets.

Distributions to Shareholders — Distributions from net investment income and net realized gains, if any, are generally declared and paid annually.

Indemnifications — Under the corporation’s organizational documents, its officers and directors are indemnified against certain liabilities arising out of the performance of their duties to the fund. In addition, in the normal course of business, the fund enters into contracts that provide general indemnifications. The maximum exposure under these arrangements is unknown as this would involve future claims that may be made against a fund. The risk of material loss from such claims is considered by management to be remote.

3. Fees and Transactions with Related Parties

Management Fees — The corporation has entered into a management agreement with ACIM, under which ACIM provides the fund with investment advisory and management services in exchange for a single, unified management fee (the fee) per class. The agreement provides that all expenses of managing and operating the fund, except distribution and service fees, brokerage expenses, taxes, interest, fees and expenses of the independent directors (including legal counsel fees), and extraordinary expenses, will be paid by ACIM. The fee is computed and accrued daily based on each class’s daily net assets and paid monthly in arrears. The rate of the fee is determined by applying a fee rate calculation formula. This formula takes into account the fund’s assets as well as certain assets, if any, of other clients of the investment advisor outside the American Century Investments family of funds (such as subadvised funds and separate accounts) that have very similar investment teams and investment strategies (strategy assets). The annual management fee schedule ranges from 0.800% to 1.000% for the Investor Class, A Class, B Class, C Class and R Class. The Institutional Class is 0.200% less at each point within the range. The effective annual management fee for each class for the year ended October 31, 2011 was 0.99% for the Investor Class, A Class, C Class and R Class and 0.79% for the Institutional Class.

Distribution and Service Fees — The Board of Directors has adopted a separate Master Distribution and Individual Shareholder Services Plan for each of the A Class, B Class, C Class and R Class (collectively the plans), pursuant to Rule 12b-1 of the 1940 Act. The plans provide that the A Class will pay American Century Investment Services, Inc. (ACIS) an annual distribution and service fee of 0.25%. The plans provide that the B Class and C Class will each pay ACIS an annual distribution and service fee of 1.00%, of which 0.25% is paid for individual shareholder services and 0.75% is paid for distribution services. The plans provide that the R Class will pay ACIS an annual distribution and service fee of 0.50%. The fees are computed and accrued daily based on each class’s daily net assets and paid monthly in arrears. The fees are used to pay financial intermediaries for distribution and individual shareholder services. Fees incurred under the plans during the year ended October 31, 2011 are detailed in the Statement of Operations.

Related Parties — Certain officers and directors of the corporation are also officers and/or directors of American Century Companies, Inc. (ACC), the parent of the corporation’s investment advisor, ACIM, the distributor of the corporation, ACIS, and the corporation’s transfer agent, American Century Services, LLC.

The fund was eligible to invest in a money market fund for temporary purposes, which is managed by J.P. Morgan Investment Management, Inc. (JPMIM). The fund had a securities lending agreement with JPMorgan Chase Bank (JPMCB) and a mutual funds services agreement with J.P. Morgan Investor Services Co. (JPMIS). JPMCB was a custodian of the fund. JPMIM, JPMIS and JPMCB are wholly owned subsidiaries of JPMorgan Chase & Co. (JPM). Prior to August 31, 2011, JPM was an equity investor in ACC. The services provided to the fund by JPMIM, JPMIS and JPMCB terminated on July 31, 2011.

4. Investment Transactions

Purchases and sales of investment securities, excluding short-term investments, for the year ended October 31, 2011 were $800,364,554 and $1,333,203,776, respectively.

5. Capital Share Transactions

Transactions in shares of the fund were as follows:

| | | Year ended October 31, 2011 | | | Year ended October 31, 2010 | |

| | | Shares | | | Amount | | | Shares | | | Amount | |

| Investor Class/Shares Authorized | | | 3,500,000,000 | | | | | | | 3,500,000,000 | | | | |

| Sold | | | 7,967,748 | | | | $184,093,884 | | | | 8,040,692 | | | | $157,299,128 | |

| Issued in reinvestment of distributions | | | 529,802 | | | | 11,930,837 | | | | 1,335,312 | | | | 25,958,465 | |

| Redeemed | | | (31,294,147 | ) | | | (725,130,132 | ) | | | (35,922,123 | ) | | | (700,572,950 | ) |

| | | | (22,796,597 | ) | | | (529,105,411 | ) | | | (26,546,119 | ) | | | (517,315,357 | ) |

| Institutional Class/Shares Authorized | | | 200,000,000 | | | | | | | | 200,000,000 | | | | | |

| Sold | | | 651,707 | | | | 15,348,582 | | | | 729,074 | | | | 14,762,326 | |

| Issued in reinvestment of distributions | | | 8,231 | | | | 189,232 | | | | 25,921 | | | | 514,529 | |

| Redeemed | | | (567,827 | ) | | | (13,398,417 | ) | | | (2,701,567 | ) | | | (53,218,916 | ) |

| | | | 92,111 | | | | 2,139,397 | | | | (1,946,572 | ) | | | (37,942,061 | ) |

| A Class/Shares Authorized | | | 100,000,000 | | | | | | | | 100,000,000 | | | | | |

| Sold | | | 1,456,808 | | | | 33,705,237 | | | | 534,148 | | | | 10,123,675 | |

| Issued in reinvestment of distributions | | | — | | | | — | | | | 8,809 | | | | 166,840 | |

| Redeemed | | | (2,020,737 | ) | | | (44,830,105 | ) | | | (1,712,426 | ) | | | (32,190,650 | ) |

| | | | (563,929 | ) | | | (11,124,868 | ) | | | (1,169,469 | ) | | | (21,900,135 | ) |

| B Class/Shares Authorized | | | 50,000,000 | | | | | | | | 50,000,000 | | | | | |

| Sold | | | 929 | | | | 19,516 | | | | 6 | | | | 112 | |

| Redeemed | | | (5,900 | ) | | | (131,961 | ) | | | — | | | | — | |

| | | | (4,971 | ) | | | (112,445 | ) | | | 6 | | | | 112 | |

| C Class/Shares Authorized | | | 50,000,000 | | | | | | | | 50,000,000 | | | | | |

| Sold | | | 6,859 | | | | 146,359 | | | | 3,687 | | | | 64,700 | |

| Redeemed | | | (15,725 | ) | | | (324,172 | ) | | | (17,068 | ) | | | (301,317 | ) |

| | | | (8,866 | ) | | | (177,813 | ) | | | (13,381 | ) | | | (236,617 | ) |

| R Class/Shares Authorized | | | 50,000,000 | | | | | | | | 50,000,000 | | | | | |

| Sold | | | 78,707 | | | | 1,717,632 | | | | 41,073 | | | | 780,064 | |

| Redeemed | | | (52,771 | ) | | | (1,201,649 | ) | | | (59,405 | ) | | | (1,112,083 | ) |

| | | | 25,936 | | | | 515,983 | | | | (18,332 | ) | | | (332,019 | ) |

| Net increase (decrease) | | | (23,256,316 | ) | | | $(537,865,157 | ) | | | (29,693,867 | ) | | | $(577,726,077 | ) |

6. Fair Value Measurements

The fund’s securities valuation process is based on several considerations and may use multiple inputs to determine the fair value of the positions held by the fund. In conformity with accounting principles generally accepted in the United States of America, the inputs used to determine a valuation are classified into three broad levels as follows:

| • | Level 1 valuation inputs consist of unadjusted quoted prices in an active market for identical securities; |

| • | Level 2 valuation inputs consist of direct or indirect observable market data (including quoted prices for similar securities, evaluations of subsequent market events, interest rates, prepayment speeds, credit risk, etc.); or |

| • | Level 3 valuation inputs consist of unobservable data (including a fund’s own assumptions). |

The level classification is based on the lowest level input that is significant to the fair valuation measurement. The valuation inputs are not necessarily an indication of the risks associated with investing in these securities or other financial instruments.

The following is a summary of the level classifications as of period end. The Schedule of Investments provides additional information on the fund’s portfolio holdings.

| | | Level 1 | | Level 2 | | Level 3 |

| Investment Securities | | | | | | | | | |

| Domestic Common Stocks | | | $5,649,568,421 | | | | — | | | | — | |

| Foreign Common Stocks | | | 286,594,660 | | | | $144,984,863 | | | | — | |

| Temporary Cash Investments | | | 688,715 | | | | 26,966,206 | | | | — | |

| Total Value of Investment Securities | | | $5,936,851,796 | | | | $171,951,069 | | | | — | |

| | | | | | | | | | | | | |

| Other Financial Instruments | | | | | | | | | | | | |

Total Unrealized Gain (Loss) on Forward Foreign Currency Exchange Contracts | | | — | | | | $(47,552 | ) | | | — | |

7. Derivative Instruments

Foreign Currency Risk — The fund is subject to foreign currency exchange rate risk in the normal course of pursuing its investment objectives. The value of foreign investments held by a fund may be significantly affected by changes in foreign currency exchange rates. The dollar value of a foreign security generally decreases when the value of the dollar rises against the foreign currency in which the security is denominated and tends to increase when the value of the dollar declines against such foreign currency. A fund may enter into forward foreign currency exchange contracts to reduce a fund’s exposure to foreign currency exchange rate fluctuations. The net U.S. dollar value of foreign currency underlying all contractual commitments held by a fund and the resulting unrealized appreciation or depreciation are determined daily. Realized gain or loss is recorded upon the termination of the contract. Net realized and unrealized gains or losses occurring during the holding period of forward foreign currency exchange contracts are a component of net realized gain (loss) on foreign currency transactions and change in net unrealized appreciation (depreciation) on translation of assets and liabilities in foreign currencies, respectively. A fund bears the risk of an unfavorable change in the foreign currency exchange rate underlying the forward contract. Additionally, losses, up to the fair value, may arise if the counterparties do not perform under the contract terms. The risk of loss from non-performance by the counterparty may be reduced by the use of master netting agreements. The foreign currency risk derivative instruments held at period end as disclosed on the Schedule of Investments are indicative of the fund’s typical volume during the period.

The value of foreign currency risk derivative instruments as of October 31, 2011, is disclosed on the Statement of Assets and Liabilities as a liability of $47,552 in unrealized loss on forward foreign currency exchange contracts. For the year ended October 31, 2011, the effect of foreign currency risk derivative instruments on the Statement of Operations was $(11,183,109) in net realized gain (loss) on foreign currency transactions and $(281,636) in change in net unrealized appreciation (depreciation) on translation of assets and liabilities in foreign currencies.

8. Risk Factors

There are certain risks involved in investing in foreign securities. These risks include those resulting from future adverse political, social and economic developments, fluctuations in currency exchange rates, the possible imposition of exchange controls, and other foreign laws or restrictions.

9. Federal Tax Information

The tax character of distributions paid during the years ended October 31, 2011 and October 31, 2010 were as follows:

| | | 2011 | | 2010 |

| Distributions Paid From | | | | | | |

| Ordinary income | | | $12,499,215 | | | | $27,427,023 | |

| Long-term capital gains | | | — | | | | — | |

The book-basis character of distributions made during the year from net investment income or net realized gains may differ from their ultimate characterization for federal income tax purposes. These differences reflect the differing character of certain income items and net realized gains and losses for financial statement and tax purposes, and may result in reclassification among certain capital accounts on the financial statements.

As of October 31, 2011, the federal tax cost of investments and the components of distributable earnings on a tax-basis were as follows:

| Federal tax cost of investments | | | $4,022,866,028 | |

| Gross tax appreciation of investments | | | $2,201,322,486 | |

| Gross tax depreciation of investments | | | (115,385,649 | ) |

| Net tax appreciation (depreciation) of investments | | | $2,085,936,837 | |

Net tax appreciation (depreciation) on derivatives and translation of assets and liabilities in foreign currencies | | | $182,718 | |

| Net tax appreciation (depreciation) | | | $2,086,119,555 | |

| Undistributed ordinary income | | | — | |

| Accumulated capital losses | | | $(483,235,114 | ) |

The difference between book-basis and tax-basis cost and unrealized appreciation (depreciation) is attributable primarily to the tax deferral of losses on wash sales and the realization for tax purposes of unrealized gains (losses) on certain forward foreign currency exchange contracts.

The accumulated capital losses represent net capital loss carryovers that may be used to offset future realized capital gains for federal income tax purposes. Future capital loss carryover utilization in any given year may be subject to Internal Revenue Code limitations. Capital loss carryovers expire in 2017.

On December 22, 2010, the Regulated Investment Company Modernization Act of 2010 (the “Act”) was enacted, which changed various technical rules governing the tax treatment of regulated investment companies. The changes are generally effective for taxable years beginning after the date of enactment. Under the Act, the fund will be permitted to carry forward capital losses incurred in taxable years beginning after the date of enactment for an unlimited period. However, any losses incurred during those future taxable years will be required to be utilized prior to the losses incurred in pre-enactment taxable years, which carry an expiration date. As a result of this ordering rule, pre-enactment capital loss carryforwards may be more likely to expire unused.

| For a Share Outstanding Throughout the Years Ended October 31 (except as noted) | |

| Per-Share Data | Ratios and Supplemental Data | |

| | | Income From Investment Operations: | Distributions From: | | | Ratio to Average Net Assets of: | | | |

| | Net Asset Value, Beginning of Period | Net Investment Income (Loss)(1) | Net Realized and Unrealized Gain (Loss) | Total From Investment Operations | Net Investment Income | Net Realized Gains | Total Distributions | Net Asset Value, End of Period | Total Return(2) | Operating Expenses | Net Investment Income (Loss) | Portfolio Turnover Rate | Net Assets, End of Period (in thousands) |

| Investor Class | |

| 2011 | $21.22 | 0.04 | 2.20 | 2.24 | (0.04) | — | (0.04) | $23.42 | 10.59% | 0.99% | 0.16% | 13% | $5,984,972 | |

| 2010 | $17.82 | 0.05 | 3.44 | 3.49 | (0.09) | — | (0.09) | $21.22 | 19.63% | 1.00% | 0.25% | 24% | $5,906,158 | |

| 2009 | $15.67 | 0.11 | 2.12 | 2.23 | (0.08) | — | (0.08) | $17.82 | 14.35% | 1.00% | 0.69% | 53% | $5,435,051 | |

| 2008 | $33.48 | 0.08 | (9.95) | (9.87) | — | (7.94) | (7.94) | $15.67 | (38.02)% | 0.99% | 0.36% | 152% | $5,275,836 | |

| 2007 | $28.55 | (0.01) | 6.95 | 6.94 | — | (2.01) | (2.01) | $33.48 | 25.89% | 0.99% | (0.04)% | 93% | $10,065,759 | |

| Institutional Class | |

| 2011 | $21.69 | 0.08 | 2.27 | 2.35 | (0.09) | — | (0.09) | $23.95 | 10.85% | 0.79% | 0.36% | 13% | $52,751 | |

| 2010 | $18.22 | 0.09 | 3.51 | 3.60 | (0.13) | — | (0.13) | $21.69 | 19.81% | 0.80% | 0.45% | 24% | $45,791 | |

| 2009 | $16.02 | 0.14 | 2.17 | 2.31 | (0.11) | — | (0.11) | $18.22 | 14.58% | 0.80% | 0.89% | 53% | $73,933 | |

| 2008 | $33.98 | 0.15 | (10.17) | (10.02) | — | (7.94) | (7.94) | $16.02 | (37.89)% | 0.79% | 0.56% | 152% | $76,339 | |

| 2007 | $28.90 | 0.05 | 7.04 | 7.09 | — | (2.01) | (2.01) | $33.98 | 26.14% | 0.79% | 0.16% | 93% | $325,035 | |

A Class(3) | |

| 2011 | $20.62 | (0.02) | 2.15 | 2.13 | — | — | — | $22.75 | 10.33% | 1.24% | (0.09)% | 13% | $62,304 | |

| 2010 | $17.33 | —(4) | 3.33 | 3.33 | (0.04) | — | (0.04) | $20.62 | 19.24% | 1.25% | 0.00%(5) | 24% | $68,109 | |

| 2009 | $15.23 | 0.07 | 2.07 | 2.14 | (0.04) | — | (0.04) | $17.33 | 14.14% | 1.25% | 0.44% | 53% | $77,484 | |

| 2008 | $32.83 | 0.03 | (9.69) | (9.66) | — | (7.94) | (7.94) | $15.23 | (38.19)% | 1.24% | 0.11% | 152% | $85,723 | |

| 2007 | $28.11 | (0.08) | 6.81 | 6.73 | — | (2.01) | (2.01) | $32.83 | 25.56% | 1.24% | (0.29)% | 93% | $235,217 | |

| For a Share Outstanding Throughout the Years Ended October 31 (except as noted) | |

| Per-Share Data | Ratios and Supplemental Data | |

| | | Income From Investment Operations: | Distributions From: | | | Ratio to Average Net Assets of: | | | |

| | Net Asset Value, Beginning of Period | Net Investment Income (Loss)(1) | Net Realized and Unrealized Gain (Loss) | Total From Investment Operations | Net Investment Income | Net Realized Gains | Total Distributions | Net Asset Value, End of Period | Total Return(2) | Operating Expenses | Net Investment Income (Loss) | Portfolio Turnover Rate | Net Assets, End of Period (in thousands) |

| C Class | |

| 2011 | $19.20 | (0.17) | 1.99 | 1.82 | — | — | — | $21.02 | 9.48% | 1.99% | (0.84)% | 13% | $678 | |

| 2010 | $16.22 | (0.13) | 3.11 | 2.98 | — | — | — | $19.20 | 18.45% | 2.00% | (0.75)% | 24% | $789 | |

| 2009 | $14.32 | (0.04) | 1.94 | 1.90 | — | — | — | $16.22 | 13.20% | 2.00% | (0.31)% | 53% | $884 | |

| 2008 | $31.54 | (0.13) | (9.15) | (9.28) | — | (7.94) | (7.94) | $14.32 | (38.63)% | 1.99% | (0.64)% | 152% | $891 | |

| 2007 | $27.26 | (0.29) | 6.58 | 6.29 | — | (2.01) | (2.01) | $31.54 | 24.64% | 1.99% | (1.04)% | 93% | $2,129 | |

| R Class | |

| 2011 | $20.54 | (0.08) | 2.14 | 2.06 | — | — | — | $22.60 | 10.03% | 1.49% | (0.34)% | 13% | $4,173 | |

| 2010 | $17.26 | (0.05) | 3.33 | 3.28 | — | — | — | $20.54 | 19.00% | 1.50% | (0.25)% | 24% | $3,260 | |

| 2009 | $15.17 | 0.03 | 2.07 | 2.10 | (0.01) | — | (0.01) | $17.26 | 13.84% | 1.50% | 0.19% | 53% | $3,056 | |

| 2008 | $32.80 | (0.03) | (9.66) | (9.69) | — | (7.94) | (7.94) | $15.17 | (38.35)% | 1.49% | (0.14)% | 152% | $3,276 | |

| 2007 | $28.15 | (0.15) | 6.81 | 6.66 | — | (2.01) | (2.01) | $32.80 | 25.26% | 1.49% | (0.54)% | 93% | $5,971 | |

Notes to Financial Highlights

| (1) | Computed using average shares outstanding throughout the period. |

| (2) | Total returns are calculated based on the net asset value of the last business day and do not reflect applicable sales charges, if any. Total returns for periods less than one year are not annualized. |

| (3) | Prior to September 4, 2007, the A Class was referred to as the Advisor Class. |

| (4) | Per-share amount was less than $0.005. |

| (5) | Ratio was less than 0.005%. |

See Notes to Financial Statements.

Report of Independent Registered Public Accounting Firm |

The Board of Directors and Shareholders,

American Century Mutual Funds, Inc.:

We have audited the accompanying statement of assets and liabilities, including the schedule of investments, of Ultra Fund, one of the funds constituting American Century Mutual Funds, Inc. (the “Corporation”), as of October 31, 2011, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended. These financial statements and financial highlights are the responsibility of the Corporation’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. The Corporation is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Corporation’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of October 31, 2011, by correspondence with the custodian and brokers; where replies were not received from brokers, we performed other auditing procedures. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of Ultra Fund of American Century Mutual Funds, Inc., as of October 31, 2011, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America.

Deloitte & Touche LLP

Kansas City, Missouri

December 20, 2011

The Board of Directors

The individuals listed below serve as directors of the funds. Each director will continue to serve in this capacity until death, retirement, resignation or removal from office. The mandatory retirement age for directors who are not “interested persons,” as that term is defined in the Investment Company Act (independent directors), is 72. However, the mandatory retirement age for an individual director may be extended with the approval of the remaining independent directors.

Mr. Thomas is the only director who is an “interested person” because he currently serves as President and Chief Executive Officer of American Century Companies, Inc. (ACC), the parent company of American Century Investment Management, Inc. (ACIM or the advisor).

The other directors (more than three-fourths of the total number) are independent; that is, they have never been employees, directors or officers of, and have no financial interest in, ACC or any of its wholly owned, direct or indirect, subsidiaries, including ACIM, American Century Investment Services, Inc. (ACIS) and American Century Services, LLC (ACS). The directors serve in this capacity for seven (in the case of Mr. Thomas, 15) registered investment companies in the American Century Investments family of funds.

The following presents additional information about the directors. The mailing address for each director is 4500 Main Street, Kansas City, Missouri 64111.

Name (Year of Birth) | Position(s) Held with Funds | Length of Time Served | Principal Occupation(s) During Past 5 Years | Number of American Century Portfolios Overseen by Director | Other Directorships Held During Past 5 Years |

| Independent Directors |

Thomas A. Brown (1940) | Director | Since 1980 | Managing Member, Associated Investments, LLC (real estate investment company); Brown Cascade Properties, LLC (real estate investment company) (2001 to 2009) | 65 | None |

Andrea C. Hall (1945) | Director | Since 1997 | Retired as advisor to the President, Midwest Research Institute (not-for-profit research organization) (June 2006) | 65 | None |

Jan M. Lewis (1957) | Director | Since 2011 | President and Chief Executive Officer, Catholic Charities of Northeast Kansas (human services organization) (2006 to present); President, BUCON, Inc. (full-service design-build construction company) (2004 to 2006) | 65 | None |

James A. Olson (1942) | Director | Since 2007 | Member, Plaza Belmont LLC (private equity fund manager); Chief Financial Officer, Plaza Belmont LLC (September 1999 to September 2006) | 65 | Saia, Inc. and Entertainment Properties Trust |

| (Year of Birth) | Position(s) Held with Funds | Length of Time Served | Principal Occupation(s) During Past 5 Years | Number of American Century Portfolios Overseen by Director | Other Directorships Held During Past 5 Years |

| Independent Directors | | | | | |

Donald H. Pratt (1937) | Director and Chairman of the Board | Since 1995 (Chairman since 2005) | Chairman and Chief Executive Officer, Western Investments, Inc. (real estate company) | 65 | None |

M. Jeannine Strandjord (1945) | Director | Since 1994 | Retired | 65 | DST Systems Inc., Euronet Worldwide Inc., and Charming Shoppes, Inc. |

John R. Whitten (1946) | Director | Since 2008 | Project Consultant, Celanese Corp. (industrial chemical company) | 65 | Rudolph Technologies, Inc. |

Stephen E. Yates (1948) | Advisory Director | Since 2011 | Retired; Executive Vice President, Technology & Operations, KeyCorp. (computer services) (2004 to 2010) | 65 | Applied Industrial Technology (2001 to 2010) |

| |

| Interested Director |

Jonathan S. Thomas (1963) | Director and President | Since 2007 | President and Chief Executive Officer, ACC (March 2007 to present); Chief Administrative Officer, ACC (February 2006 to February 2007); Executive Vice President, ACC (November 2005 to February 2007). Also serves as: Chief Executive Officer and Manager, ACS; Executive Vice President, ACIM; Director, ACC, ACIM and other ACC subsidiaries | 106 | None |

Officers

The following table presents certain information about the executive officers of the funds. Each officer serves as an officer for each of the 15 investment companies in the American Century family of funds, unless otherwise noted. No officer is compensated for his or her service as an officer of the funds. The listed officers are interested persons of the funds and are appointed or re-appointed on an annual basis. The mailing address for each officer listed below is 4500 Main Street, Kansas City, Missouri 64111.

Name (Year of Birth) | | Offices with the Funds | Principal Occupation(s) During the Past Five Years |

Jonathan S. Thomas (1963) | | Director and President since 2007 | President and Chief Executive Officer, ACC (March 2007 to present); Chief Administrative Officer, ACC (February 2006 to February 2007); Executive Vice President, ACC (November 2005 to February 2007). Also serves as: Chief Executive Officer and Manager, ACS; Executive Vice President, ACIM; Director, ACC, ACIM and other ACC subsidiaries |

Barry Fink (1955) | | Executive Vice President since 2007 | Chief Operating Officer and Executive Vice President, ACC (September 2007 to present); President, ACS (October 2007 to present); Managing Director, Morgan Stanley (2000 to 2007); Global General Counsel, Morgan Stanley (2000 to 2006). Also serves as: Manager, ACS and Director, ACC and certain ACC subsidiaries |

Maryanne L. Roepke (1956) | | Chief Compliance Officer since 2006 and Senior Vice President since 2000 | Chief Compliance Officer, American Century funds, ACIM and ACS (August 2006 to present); Assistant Treasurer, ACC (January 1995 to August 2006); and Treasurer and Chief Financial Officer, various American Century funds (July 2000 to August 2006). Also serves as: Senior Vice President, ACS |

Charles A. Etherington (1957) | | General Counsel since 2007 and Senior Vice President since 2006 | Attorney, ACC (February 1994 to present); Vice President, ACC (November 2005 to present), General Counsel, ACC (March 2007 to present); Also serves as General Counsel, ACIM, ACS, ACIS and other ACC subsidiaries; and Senior Vice President, ACIM and ACS |

Robert J. Leach (1966) | | Vice President, Treasurer and Chief Financial Officer since 2006 | Vice President, ACS (February 2000 to present); and Controller, various American Century funds (1997 to September 2006) |

David H. Reinmiller (1963) | | Vice President since 2000 | Attorney, ACC (January 1994 to present); Associate General Counsel, ACC (January 2001 to present). Also serves as Vice President, ACIM and ACS |

Ward D. Stauffer (1960) | | Secretary since 2005 | Attorney, ACC (June 2003 to present) |

The Statement of Additional Information has additional information about the fund’s directors and is available without charge, upon request, by calling 1-800-345-2021.

Approval of Management Agreement |

At a meeting held on June 9, 2011, the Fund’s Board of Directors unanimously approved the renewal of the management agreement pursuant to which American Century Investment Management, Inc. (the “Advisor”) acts as the investment advisor for the Fund. Under Section 15(c) of the Investment Company Act, contracts for investment advisory services are required to be reviewed, evaluated, and approved by a majority of a fund’s independent directors (the “Directors”) each year.

As a part of the approval process, the Board requested and reviewed extensive data and information compiled by the Advisor and certain independent providers of evaluation data concerning the Fund and the services provided to the Fund by the Advisor. This review was in addition to the oversight and evaluation undertaken by the Board and its committees on a continuous basis throughout the year and included, but was not limited to the following:

| • | the nature, extent, and quality of investment management, shareholder services, and other services provided by the Advisor to the Fund; |

| • | the wide range of other programs and services the Advisor provides to the Fund and its shareholders on a routine and non-routine basis; |

| • | the investment performance of the fund, including data comparing the Fund’s performance to appropriate benchmarks and/or a peer group of other mutual funds with similar investment objectives and strategies; |

| • | data comparing the cost of owning the Fund to the cost of owning similar funds; |

| the Advisor’s compliance policies, procedures, and regulatory experience; |

| financial data showing the cost of services provided to the Fund, the profitability of the Fund to the Advisor, and the overall profitability of the Advisor; |

| data comparing services provided and charges to other investment management clients of the Advisor; and |

| consideration of collateral benefits derived by the Advisor from the management of the Fund and any potential economies of scale relating thereto. |

In keeping with its practice, the Board held two in-person meetings and one telephonic meeting to review and discuss the information provided. The Directors also had the benefit of the advice of independent counsel throughout the period.

Factors Considered

The Directors considered all of the information provided by the Advisor, the independent data providers, and independent counsel, and evaluated such information for the Fund. In connection with their review, the Directors did not identify any single factor as being all-important or controlling, and each Director may have attributed different levels of importance to different factors. In deciding to renew the management agreement, the Board based its decision on a number of factors, including the following:

Nature, Extent and Quality of Services — Generally. Under the management agreement, the Advisor is responsible for providing or arranging for all services necessary for the operation of the Fund. The Board noted that under the management agreement, the Advisor provides or arranges at its own expense a wide variety of services including:

| constructing and designing the Fund |

| portfolio research and security selection |

| initial capitalization/funding |

| daily valuation of the Fund’s portfolio |

| shareholder servicing and transfer agency, including shareholder confirmations, recordkeeping, and communications |

| regulatory and portfolio compliance |

| marketing and distribution |

The Board noted that many of these services have expanded over time both in terms of quantity and complexity in response to shareholder demands, competition in the industry, changing distribution channels, and the changing regulatory environment.