| | |

| UNITED STATES |

| SECURITIES AND EXCHANGE COMMISSION |

| Washington, D.C. 20549 |

| |

| FORM N-CSR |

|

| CERTIFIED SHAREHOLDER REPORT OF REGISTERED |

| MANAGEMENT INVESTMENT COMPANIES |

| | |

| Investment Company Act file number | 811-00816 |

| |

| AMERICAN CENTURY MUTUAL FUNDS, INC. |

| (Exact name of registrant as specified in charter) |

| |

| 4500 MAIN STREET, KANSAS CITY, MISSOURI | 64111 |

| (Address of principal executive offices) | | (Zip Code) |

| |

| CHARLES A. ETHERINGTON |

| 4500 MAIN STREET, KANSAS CITY, MISSOURI 64111 |

| (Name and address of agent for service) |

| |

| Registrant’s telephone number, including area code: | 816-531-5575 |

| |

| Date of fiscal year end: | 10-31 |

| |

| Date of reporting period: | 10-31-2009 |

ITEM 1. REPORTS TO STOCKHOLDERS. |

|

| Annual Report |

| October 31, 2009 |

|

| American Century Investments |

Ultra® Fund

| |

| President’s Letter | 2 |

| Independent Chairman’s Letter | 3 |

| Market Perspective | 4 |

| U.S. Stock Index Returns | 4 |

| |

| Ultra | |

| |

| Performance | 5 |

| Portfolio Commentary | 7 |

| Top Ten Holdings | 9 |

| Top Five Industries | 9 |

| Types of Investments in Portfolio | 9 |

| |

| Shareholder Fee Example | 10 |

| |

| Financial Statements | |

| |

| Schedule of Investments | 12 |

| Statement of Assets and Liabilities | 15 |

| Statement of Operations | 17 |

| Statement of Changes in Net Assets | 18 |

| Notes to Financial Statements | 19 |

| Financial Highlights | 26 |

| Report of Independent Registered Public Accounting Firm | 32 |

| |

| Other Information | |

| |

| Management | 33 |

| Approval of Management Agreement | 36 |

| Additional Information | 41 |

| Index Definitions | 42 |

The opinions expressed in the Market Perspective and the Portfolio Commentary reflect those of the portfolio management team as of the date of the report, and do not necessarily represent the opinions of American Century Investments or any other person in the American Century Investments organization. Any such opinions are subject to change at any time based upon market or other conditions and American Century Investments disclaims any responsibility to update such opinions. These opinions may not be relied upon as investment advice and, because investment decisions made by American Century Investments funds are based on numerous factors, may not be relied upon as an indication of trading intent on behalf of any American Century Investments fund. Security examples are used for representational purposes only and are not intended as recommendations to purchase or sell securities. Performance information for comparative i ndices and securities is provided to American Century Investments by third party vendors. To the best of American Century Investments’ knowledge, such information is accurate at the time of printing.

Dear Investor:

Thank you for taking time to review the following pages, which provide the performance of your investment along with the perspectives of our experienced portfolio management team for the financial reporting period ended October 31, 2009. We appreciate your trust in American Century Investments® at this volatile, transitional time in the economy and investment markets.

As the upheavals associated with the “Great Recession” gradually subside, our senior management team has put considerable thought into how the investment environment has changed and what new challenges and opportunities await us. Critical factors that we are anticipating in the coming year include marked shifts in investment and spending behavior, along with consolidation in our industry.

Most importantly, we think the economic recovery will be slow and extended. The economy and capital markets have come a long way since Lehman Brothers collapsed in the third quarter of 2008, but 2010 will likely bring continuing challenges. The stock market’s rebound since last March and the third-quarter economic surge in 2009 were fueled largely by corporate cost-cutting and unprecedented monetary and fiscal stimulus, including some key programs that have since expired or been scaled back.

Meanwhile, the resilient but struggling consumer sector still faces double-digit unemployment, heavy debt burdens, tight credit conditions, and a housing market that is starting to stabilize, but remains vulnerable. Much of our investment positioning in 2009 cautiously reflected these still unstable economic fundamentals, leading to underperformance, in some cases, versus market benchmarks buoyed by the rally of riskier assets. We still support our fundamentally based positioning because we believe strongly that some markets—driven more by technical factors than fundamentals—have advanced further than underlying economic conditions warrant, and remain susceptible to the possibility of more volatility ahead.

Thank you for your continued confidence in us.

Sincerely,

Jonathan Thomas

President and Chief Executive Officer

American Century Investments

2

|

| Independent Chairman’s Letter |

In my first letter to shareholders of the American Century Investments funds, I invited you to contact me with your questions. I have been gratified with your response. Most shareholder inquiries to date have related to specific fund performance issues. As I noted in my individual responses, your board through the Fund Performance Committee continues to stress improved performance in our quarterly meetings with chief investment officers and fund managers.

An important part of our fund performance review process is a face-to-face meeting with portfolio managers. The board traveled during the second quarter to the American Century Investments office in Mountain View, California to meet with the fund of funds and asset allocation portfolio management teams. These meetings validated the importance of thorough reviews of investment opportunities by the credit management personnel resident in that office. As a result of their efforts, American Century Investments funds were able to avoid the “toxic assets” that plagued many other fund families in 2008.

From April through June 2009, the board conducted its annual review of the advisory contracts between American Century Investments and each fund. Our efforts involved a review of fund information, including assets under management; total expense ratio compared to peers; economies of scale; fee breakpoints that reduce shareholder costs as assets increase; performance compared to peers and benchmarks; and the quality of services provided to fund shareholders. A detailed discussion of board considerations in connection with advisory contract renewal is included annually in each fund’s shareholder reports. During this review, the board focuses on a detailed comparison of the competitive position of each fund and has negotiated more than 60 breakpoints or fee reductions in the past five years.

The board looks forward to another year of work on your behalf and your comments are appreciated. You are invited to email me at dhpratt@fundboardchair.com.

Don Pratt

3

By Greg Woodhams, Chief Investment Officer, U.S. Growth Equity—Large Cap

Signs of Economic Recovery Boosted Stocks

The year ended October 31, 2009, was a period of extremes for the U.S. stock market. The market began the period in the midst of a historically steep decline, then finished the period with one of its strongest rallies since the 1930s. The market’s dramatic swings resulted from rapidly shifting expectations regarding the economic and financial environment.

Stocks fell sharply in late 2008 and early 2009 as investors grew increasingly concerned about a deep economic downturn and a lack of liquidity in the credit markets. In response, the federal government took unprecedented actions to shore up the credit sector, support the housing market, and revive the stalled economy.

These efforts began to bear fruit in the spring of 2009 as signs of economic stabilization emerged. Although the unemployment rate continued to climb, reaching a 26-year high of 10.2% by October, the broader economy showed evidence of improvement, producing real growth in the third quarter of 2009—the first positive quarterly growth in more than a year. In addition, cost-management efforts at many companies helped generate better-than-expected earnings in the second and third quarters.

As a result, the equity market reached a multi-year low on March 9 and then reversed course, rising steadily throughout the last seven months of the period. The rally helped erase the market’s earlier losses, enabling the major stock indexes to produce gains of approximately 10% overall. Growth stocks outperformed value shares by a wide margin (see the table below) across all market capitalizations, though they lagged modestly over the last six months.

Economic Challenges Remain

Although recent economic trends have been encouraging, the recovery will likely be gradual until there is sustained improvement in the delinquency levels of consumer debt and the unemployment rate. Thus far, the U.S. consumer has been conspicuously absent from the recovery, and given the weakness in the U.S. dollar and improving economic conditions elsewhere in the world, we may see an export-led recovery until the consumer gets back on firmer footing.

| | | | |

| U.S. Stock Index Returns | | | | |

| For the 12 months ended October 31, 2009 | | | |

| Russell 1000 Index (Large-Cap) | 11.20% | | Russell 2000 Index (Small-Cap) | 6.46% |

| Russell 1000 Growth Index | 17.51% | | Russell 2000 Growth Index | 11.34% |

| Russell 1000 Value Index | 4.78% | | Russell 2000 Value Index | 1.96% |

| Russell Midcap Index | 18.75% | | | |

| Russell Midcap Growth Index | 22.48% | | | |

| Russell Midcap Value Index | 14.52% | | | |

4

| | | | | | |

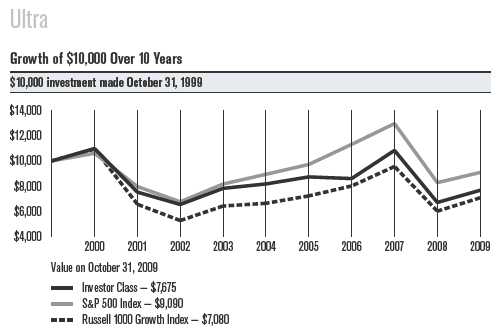

| Ultra | | | | | |

| |

| Total Returns as of October 31, 2009 | | | | |

| | | | Average Annual Returns | |

| | | | | | Since | Inception |

| | | 1 year | 5 years | 10 years | Inception | Date |

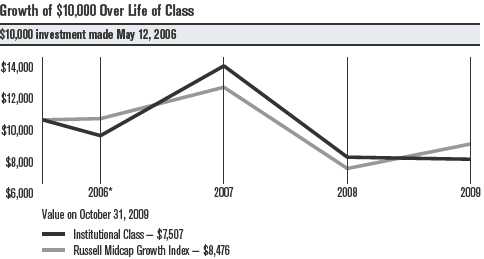

| Investor Class | 14.35% | -1.26% | -2.61% | 10.69% | 11/2/81 |

| Russell 1000 Growth Index(1) | 17.51% | 1.27% | -3.39% | 9.65%(2) | — |

| S&P 500 Index(1) | 9.80% | 0.33% | -0.95% | 10.92%(2) | — |

| Institutional Class | 14.58% | -1.06% | -2.42% | 3.01% | 11/14/96 |

| A Class(3) | | | | | 10/2/96 |

| No sales charge* | 14.14% | -1.49% | -2.84% | 2.86% | |

| With sales charge* | 7.58% | -2.66% | -3.42% | 2.39% | |

| B Class | | | | | 9/28/07 |

| No sales charge* | 13.23% | — | — | -13.69% | |

| With sales charge* | 9.23% | — | — | -15.39% | |

| C Class | 13.20% | -2.24% | — | -0.97% | 10/29/01 |

| R Class | 13.84% | -1.74% | — | -0.08% | 8/29/03 |

| *Sales charges include initial sales charges and contingent deferred sales charges (CDSCs), as applicable. A Class shares have a 5.75% |

| maximum initial sales charge for equity funds and may be subject to a maximum CDSC of 1.00%. B Class shares redeemed within six |

| years of purchase are subject to a CDSC that declines from 5.00% during the first year after purchase to 0.00% the sixth year after |

| purchase. C Class shares redeemed within 12 months of purchase are subject to a maximum CDSC of 1.00%. The SEC requires that |

| mutual funds provide performance information net of maximum sales charges in all cases where charges could be applied. |

| |

| (1) | Data provided by Lipper Inc. — A Reuters Company. © 2009 Reuters. All rights reserved. Any copying, republication or redistribution of Lipper |

| | content, including by caching, framing or similar means, is expressly prohibited without the prior written consent of Lipper. Lipper shall not be |

| | liable for any errors or delays in the content, or for any actions taken in reliance thereon. | | | |

| | The data contained herein has been obtained from company reports, financial reporting services, periodicals and other resources believed to be |

| | reliable. Although carefully verified, data on compilations is not guaranteed by Lipper and may be incomplete. No offer or solicitations to buy or |

| | sell any of the securities herein is being made by Lipper. | | | | |

| (2) | Since 10/31/81, the date nearest the Investor Class’s inception for which data are available. | | |

| (3) | Prior to September 4, 2007, the A Class was referred to as the Advisor Class. Performance, with sales charge, prior to that date has been |

| | adjusted to reflect the A Class’s current sales charge. | | | | |

Data presented reflect past performance. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance shown. Investment return and principal value will fluctuate, and redemption value may be more or less than original cost. To obtain performance data current to the most recent month end, please call 1-800-345-2021 or visit americancentury.com. International investing involves special risks, such as political instability and currency fluctuations.

Unless otherwise indicated, performance reflects Investor Class shares; performance for other share classes will vary due to differences in fee structure. For information about other share classes available, please consult the prospectus. Data assumes reinvestment of dividends and capital gains, and none of the charts reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for the indices are provided for comparison. The fund’s total returns include operating expenses (such as transaction costs and management fees) that reduce returns, while the total returns of the indices do not.

5

| | | | | | | | | | |

| One-Year Returns Over 10 Years | | | | | | | |

| Periods ended October 31 | | | | | | | | | |

| | 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 |

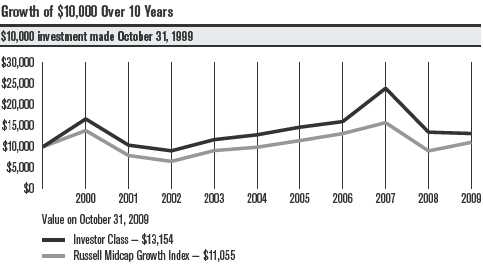

| Investor Class | 9.81% | -31.44% | -12.99% | 19.50% | 4.46% | 6.81% | -1.51% | 25.89% | -38.02% | 14.35% |

| Russell 1000 | | | | | | | | | | |

| Growth Index | 9.33% | -39.95% | -19.62% | 21.81% | 3.38% | 8.81% | 10.84% | 19.23% | -36.95% | 17.51% |

| S&P 500 Index | 6.09% | -24.90% | -15.11% | 20.80% | 9.42% | 8.72% | 16.34% | 14.56% | -36.10% | 9.80% |

| | | | | | | | | | | |

| Total Annual Fund Operating Expenses | | | | | | |

| | Institutional | | | | | | | | |

| Investor Class | Class | A Class | B Class | C Class | R Class |

| 0.99% | 0.79% | 1.24% | 1.99% | 1.99% | 1.49% |

The total annual fund operating expenses shown is as stated in the fund’s prospectus current as of the date of this report. The prospectus may vary from the expense ratio shown elsewhere in this report because it is based on a different time period, includes acquired fund fees and expenses, and, if applicable, does not include fee waivers or expense reimbursements.

Data presented reflect past performance. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance shown. Investment return and principal value will fluctuate, and redemption value may be more or less than original cost. To obtain performance data current to the most recent month end, please call 1-800-345-2021 or visit americancentury.com. International investing involves special risks, such as political instability and currency fluctu ations.

Unless otherwise indicated, performance reflects Investor Class shares; performance for other share classes will vary due to differences in fee structure. For information about other share classes available, please consult the prospectus. Data assumes reinvestment of dividends and capital gains, and none of the charts reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for the indices are provided for comparison. The fund’s total returns include operating expenses (such as transaction costs and management fees) that reduce returns, while the total returns of the indices do not.

6

Ultra

Portfolio Managers: Keith Lee and Michael Li

Performance Summary

Ultra returned 14.35%* for the fiscal year ended October 31, 2009, trailing the 17.51% return of the fund’s benchmark, the Russell 1000 Growth Index, but outpacing the 9.80% return of the broad S&P 500 Index.

The 12-month period was one of the most volatile in the history of the U.S. stock market, featuring a plunge of approximately 30%, followed by a sharp rally of more than 55%. The volatility reflected an extraordinary swing in market sentiment resulting from a sudden change in perception about the direction of the U.S. economy. The initial market decline was driven by rampant pessimism in the face of a recession, a financial sector on the verge of collapse, and a deep freeze in the credit markets. But when signs of economic stabilization began to appear, along with improving financial and credit conditions, confidence and optimism returned to the equity market, producing a dramatic rebound in stock prices.

Given that backdrop, Ultra posted a double-digit gain for the 12-month period and outperformed the broad stock market indices. However, the fund underperformed its growth-oriented benchmark index as price momentum and accelerating growth—key factors in Ultra’s investment process—were out of favor for much of the period, creating significant performance headwinds. In addition, the rally during the last seven months of the period was led by lower-quality stocks, whereas we emphasize higher-quality companies in the Ultra portfolio.

Despite these challenges, we remained committed to our long-term investment philosophy, and the positive impact of our stock selection process helped mitigate the overall underperformance versus the benchmark.

Health Care Lagged

The fund’s health care holdings had the biggest negative impact on performance versus the Russell 1000 Growth Index. Stock selection among biotechnology firms and an underweight position in pharmaceutical companies contributed the lion’s share of the underperformance in this sector.

The portfolio’s biggest individual detractor was biotech company Genzyme, which makes “orphan” medications that treat rare genetic diseases. The company has a strong product lineup and favorable market position, but the stock was hurt by poor execution—Genzyme faced FDA approval delays on one of its new products and was forced to temporarily shutter a production facility because of viral contamination. These issues weighed on the company’s earnings and cast doubts on its quality-control practices.

*All fund returns referenced in this commentary are for Investor Class shares.

7

Ultra

Other notable detractors in the health care sector included cancer treatment developer Celgene, which reported disappointing sales of its core drug Revlimid in early 2009, and health services provider UnitedHealth Group, whose stock has been negatively impacted by uncertainty related to health care reform.

Materials and Consumer Staples Detracted

The portfolio’s materials and consumer staples holdings also underper-formed their counterparts in the benchmark index. Virtually all of the underperformance in the materials sector resulted from stock selection and an overweight position in chemicals companies. The most significant detractor was agricultural products maker Monsanto, which slumped as increased price competition from a generic version of its Roundup herbicide in China weighed on earnings. Beyond this short-term issue, however, we believe Monsanto’s patent seed business will drive robust long-term growth for the company in a global environment of diminishing resources and arable land.

In the consumer staples sector, a heavy weighting in discount retailer Wal-Mart—the fund’s largest holding on average during the 12-month period—detracted the most. Wal-Mart held up well during the market decline in late 2008 and early 2009 but has underperformed during the recent rally as investors flocked to more cyclical stocks.

Technology and Consumer Discretionary Outperformed

On the positive side, the fund’s information technology and consumer discretionary holdings were the best absolute performers and also added value versus the Russell 1000 Growth Index. The outperformance in the technology sector was driven largely by strong results among Internet companies. Online search and advertising firm Baidu—one of the best-positioned Chinese companies—posted healthy revenue growth and gained market share in China, where e-commerce penetration is relatively low. Chinese Internet portal Tencent Holdings also fared well, benefiting from strength in online gaming. These two stocks were among several foreign holdings that contributed meaningfully to both absolute and relative performance.

Internet retailer Amazon.com was the big winner in the consumer discretionary sector and the portfolio’s top contributor. Amazon delivered consistently strong revenue growth and reinforced its competitive position by adding more products and categories. Other top performers included department store chain Kohl’s, which benefited from rising sales of private-label brands, and comic book publisher Marvel Entertainment, which was acquired by Disney.

A Look Ahead

The U.S. economy appears to be on the road to recovery as we move into 2010, but the pace of this recovery remains uncertain. Our emphasis will remain on executing our disciplined investment process, which seeks high-quality stocks exhibiting price momentum, accelerating growth, positive relative strength, and attractive valuations.

8

| | | |

| Ultra | | |

| |

| Top Ten Holdings as of October 31, 2009 | | |

| | | % of net assets | % of net assets |

| | | as of 10/31/09 | as of 4/30/09 |

| Google, Inc., Class A | 4.1% | 3.2% |

| Apple, Inc. | 3.9% | 3.0% |

| Microsoft Corp. | 2.8% | 2.8% |

| Wal-Mart Stores, Inc. | 2.8% | 3.0% |

| Cisco Systems, Inc. | 2.7% | 2.8% |

| Hewlett-Packard Co. | 2.6% | 2.3% |

| Express Scripts, Inc. | 2.5% | 2.3% |

| Amazon.com, Inc. | 2.5% | 1.0% |

| Coca-Cola Co. (The) | 2.5% | 1.7% |

| QUALCOMM, Inc. | 2.2% | 2.4% |

| |

| Top Five Industries as of October 31, 2009 | | |

| | | % of net assets | % of net assets |

| | | as of 10/31/09 | as of 4/30/09 |

| Computers & Peripherals | 7.8% | 6.3% |

| Software | 7.5% | 7.0% |

| Internet Software & Services | 5.6% | 4.3% |

| Communications Equipment | 4.9% | 5.2% |

| Food & Staples Retailing | 4.2% | 4.1% |

| |

| Types of Investments in Portfolio | | |

| | | % of net assets | % of net assets |

| | | as of 10/31/09 | as of 4/30/09 |

| Domestic Common Stocks | 91.9% | 94.2% |

| Foreign Common Stocks(1) | 7.7% | 5.4% |

| Total Common Stocks | 99.6% | 99.6% |

| Temporary Cash Investments | 0.4% | 0.8% |

| Other Assets and Liabilities | —(2) | (0.4)% |

| (1) | Includes depositary shares, dual listed securities and foreign ordinary shares. | | |

| (2) | Category is less than 0.05% of total net assets. | | |

9

|

| Shareholder Fee Example (Unaudited) |

Fund shareholders may incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments and redemption/ exchange fees; and (2) ongoing costs, including management fees; distribution and service (12b-1) fees; and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in your fund and to compare these costs with the ongoing cost of investing in other mutual funds.

The example is based on an investment of $1,000 made at the beginning of the period and held for the entire period from May 1, 2009 to October 31, 2009.

Actual Expenses

The table provides information about actual account values and actual expenses for each class. You may use the information, together with the amount you invested, to estimate the expenses that you paid over the period. First, identify the share class you own. Then simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

If you hold Investor Class shares of any American Century Investments fund, or Institutional Class shares of the American Century Diversified Bond Fund, in an American Century Investments account (i.e., not a financial intermediary or retirement plan account), American Century Investments may charge you a $12.50 semiannual account maintenance fee if the value of those shares is less than $10,000. We will redeem shares automatically in one of your accounts to pay the $12.50 fee. In determining your total eligible investment amount, we will include your investments in all personal accounts (including American Century Investments Brokerage accounts) registered under your Social Security number. Personal accounts include individual accounts, joint accounts, UGMA/UTMA accounts, personal trusts, Coverdell Education Savings Accounts and IRAs (including traditional, Roth, Rollover, SEP-, SARSEP- and SIMPLE-IRAs), and certain other retirement accounts. If you have only business, business retirement, employer-sponsored or American Century Investments Brokerage accounts, you are currently not subject to this fee. We will not charge the fee as long as you choose to manage your accounts exclusively online. If you are subject to the Account Maintenance Fee, your account value could be reduced by the fee amount.

Hypothetical Example for Comparison Purposes

The table also provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio of each class of your fund and an assumed rate of return of 5% per year before expenses, which is not the actual return of a fund’s share class. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in your fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

10

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) or redemption/exchange fees. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | | |

| | Beginning | Ending | Expenses Paid | |

| | Account Value | Account Value | During Period* | Annualized |

| | 5/1/09 | 10/31/09 | 5/1/09 – 10/31/09 | Expense Ratio* |

| Actual | | | | |

| Investor Class | $1,000 | $1,183.30 | $5.50 | 1.00% |

| Institutional Class | $1,000 | $1,184.70 | $4.41 | 0.80% |

| A Class | $1,000 | $1,182.10 | $6.88 | 1.25% |

| B Class | $1,000 | $1,177.20 | $10.98 | 2.00% |

| C Class | $1,000 | $1,177.20 | $10.98 | 2.00% |

| R Class | $1,000 | $1,180.60 | $8.24 | 1.50% |

| Hypothetical | | | | |

| Investor Class | $1,000 | $1,020.16 | $5.09 | 1.00% |

| Institutional Class | $1,000 | $1,021.17 | $4.08 | 0.80% |

| A Class | $1,000 | $1,018.90 | $6.36 | 1.25% |

| B Class | $1,000 | $1,015.12 | $10.16 | 2.00% |

| C Class | $1,000 | $1,015.12 | $10.16 | 2.00% |

| R Class | $1,000 | $1,017.64 | $7.63 | 1.50% |

| *Expenses are equal to the class’s annualized expense ratio listed in the table above, multiplied by the average account value over the period, |

| multiplied by 184, the number of days in the most recent fiscal half-year, divided by 365, to reflect the one-half year period. |

11

|

| Schedule of Investments |

| Ultra |

| | | | | | |

| OCTOBER 31, 2009 | | | | | | |

| |

| | Shares | Value | | | Shares | Value |

| Common Stocks — 99.6% | | | ELECTRICAL EQUIPMENT — 3.7% | |

| | | | | ABB Ltd.(1) | 1,285,000 | $ 23,938,378 |

| AEROSPACE & DEFENSE — 1.7% | | | | | |

| General Dynamics Corp. | 1,530,000 | $ 95,931,000 | | ABB Ltd. ADR(1) | 2,130,000 | 39,468,900 |

| BEVERAGES — 2.9% | | | | Cooper Industries plc, | | |

| | | | | Class A | 1,461,000 | 56,526,090 |

| Coca-Cola Co. (The) | 2,577,000 | 137,379,870 | | | | |

| | | | | Emerson Electric Co. | 2,353,000 | 88,825,750 |

| PepsiCo, Inc. | 437,000 | 26,460,350 | | | | |

| | | | | | | 208,759,118 |

| | | 163,840,220 | | | | |

| | | | | ENERGY EQUIPMENT & SERVICES — 1.8% | |

| BIOTECHNOLOGY — 4.1% | | | | | | |

| | | | | Oceaneering | | |

| Alexion | | | | International, Inc.(1) | 297,000 | 15,176,700 |

| Pharmaceuticals, Inc.(1) | 795,000 | 35,305,950 | | | | |

| | | | | Schlumberger Ltd. | 1,342,000 | 83,472,400 |

| Celgene Corp.(1) | 1,270,000 | 64,833,500 | | | | |

| | | | | | | 98,649,100 |

| Genzyme Corp.(1) | 390,000 | 19,734,000 | | | | |

| | | | | FOOD & STAPLES RETAILING — 4.2% | |

| Gilead Sciences, Inc.(1) | 2,565,000 | 109,140,750 | | | | |

| | | | | Costco Wholesale Corp. | 1,347,000 | 76,576,950 |

| | | 229,014,200 | | Wal-Mart Stores, Inc. | 3,154,000 | 156,690,720 |

| CAPITAL MARKETS — 3.4% | | | | | | 233,267,670 |

| BlackRock, Inc. | 223,000 | 48,277,270 | | FOOD PRODUCTS — 2.4% | | |

| Charles Schwab Corp. (The) | 4,051,000 | 70,244,340 | | General Mills, Inc. | 1,094,000 | 72,116,480 |

| Goldman Sachs | | | | Nestle SA | 1,353,000 | 62,894,221 |

| Group, Inc. (The) | 410,000 | 69,769,700 | | | | |

| | | 188,291,310 | | | | 135,010,701 |

| CHEMICALS — 3.1% | | | | HEALTH CARE EQUIPMENT & SUPPLIES — 3.0% |

| Monsanto Co. | 1,338,000 | 89,886,840 | | Baxter International, Inc. | 1,356,000 | 73,305,360 |

| | | | | Gen-Probe, Inc.(1) | 443,000 | 18,481,960 |

| Mosaic Co. (The) | 1,062,000 | 49,627,260 | | | | |

| | | | | Intuitive Surgical, Inc.(1) | 98,000 | 24,142,300 |

| Nalco Holding Co. | 1,489,000 | 31,492,350 | | | | |

| | | 171,006,450 | | NuVasive, Inc.(1) | 501,000 | 18,181,290 |

| COMMUNICATIONS EQUIPMENT — 4.9% | | | Varian Medical | | |

| | | | | Systems, Inc.(1) | 780,000 | 31,964,400 |

| Cisco Systems, Inc.(1) | 6,656,000 | 152,089,600 | | | | |

| | | | | | | 166,075,310 |

| QUALCOMM, Inc. | 2,899,000 | 120,047,590 | | HEALTH CARE PROVIDERS & SERVICES — 4.1% |

| | | 272,137,190 | | Express Scripts, Inc.(1) | 1,759,000 | 140,579,280 |

| COMPUTERS & PERIPHERALS — 7.8% | | | | | |

| | | | | Medco Health | | |

| Apple, Inc.(1) | 1,167,000 | 219,979,500 | | Solutions, Inc.(1) | 206,000 | 11,560,720 |

| EMC Corp.(1) | 4,315,000 | 71,068,050 | | UnitedHealth Group, Inc. | 2,902,000 | 75,306,900 |

| Hewlett-Packard Co. | 3,105,000 | 147,363,300 | | | | 227,446,900 |

| | | 438,410,850 | | HOTELS, RESTAURANTS & LEISURE — 2.6% | |

| CONSTRUCTION & ENGINEERING — 0.2% | | | Intercontinental Hotels | | |

| Fluor Corp. | 306,000 | 13,592,520 | | Group plc | 1,749,462 | 22,403,307 |

| CONSUMER FINANCE — 0.6% | | | | McDonald’s Corp. | 1,696,000 | 99,402,560 |

| American Express Co. | 1,025,000 | 35,711,000 | | Yum! Brands, Inc. | 641,000 | 21,120,950 |

| DIVERSIFIED FINANCIAL SERVICES — 2.6% | | | | | 142,926,817 |

| CME Group, Inc. | 269,000 | 81,402,090 | | HOUSEHOLD PRODUCTS — 1.8% | |

| JPMorgan Chase & Co. | 1,561,000 | 65,202,970 | | Colgate-Palmolive Co. | 1,263,000 | 99,309,690 |

| | | 146,605,060 | | INSURANCE — 1.4% | | |

| | | | | MetLife, Inc. | 2,256,000 | 76,771,680 |

12

| | | | | | |

| Ultra | | | | | | |

| |

| | Shares | Value | | | Shares | Value |

| INTERNET & CATALOG RETAIL — 2.5% | | | ASML Holding NV | 1,748,000 | $ 47,059,443 |

| Amazon.com, Inc.(1) | 1,175,000 | $ 139,601,750 | | Linear Technology Corp. | 1,722,000 | 44,565,360 |

| INTERNET SOFTWARE & SERVICES — 5.6% | | | Microchip Technology, Inc. | 1,695,000 | 40,612,200 |

| Baidu, Inc. ADR(1) | 124,000 | 46,862,080 | | | | 231,325,483 |

| Google, Inc., Class A(1) | 428,000 | 229,459,360 | | SOFTWARE — 7.5% | | |

| Tencent Holdings Ltd. | 2,090,000 | 36,475,104 | | Adobe Systems, Inc.(1) | 3,216,000 | 105,935,040 |

| | | 312,796,544 | | Electronic Arts, Inc.(1) | 1,977,000 | 36,060,480 |

| IT SERVICES — 3.5% | | | | Microsoft Corp. | 5,663,000 | 157,034,990 |

| International Business | | | | Oracle Corp. | 4,194,000 | 88,493,400 |

| Machines Corp. | 186,000 | 22,433,460 | | VMware, Inc., Class A(1) | 854,000 | 32,819,220 |

| MasterCard, Inc., Class A | 471,000 | 103,158,420 | | | | 420,343,130 |

| Visa, Inc., Class A | 941,000 | 71,290,160 | | SPECIALTY RETAIL — 3.2% | | |

| | | 196,882,040 | | Lowe’s Cos., Inc. | 3,214,000 | 62,897,980 |

| LEISURE EQUIPMENT & PRODUCTS — 0.7% | | Staples, Inc. | 2,541,000 | 55,139,700 |

| Hasbro, Inc. | 1,436,000 | 39,159,720 | | TJX Cos., Inc. (The) | 1,633,000 | 60,992,550 |

| LIFE SCIENCES TOOLS & SERVICES — 0.3% | | | | | 179,030,230 |

| Thermo Fisher | | | | TEXTILES, APPAREL & LUXURY GOODS — 1.1% |

| Scientific, Inc.(1) | 342,609 | 15,417,405 | | | | |

| | | | | NIKE, Inc., Class B | 1,010,000 | 62,801,800 |

| MACHINERY — 2.7% | | | | TOBACCO — 2.1% | | |

| Cummins, Inc. | 769,000 | 33,113,140 | | Philip Morris | | |

| Joy Global, Inc. | 1,000,000 | 50,410,000 | | International, Inc. | 2,503,000 | 118,542,080 |

| Parker-Hannifin Corp. | 1,259,000 | 66,676,640 | | TRADING COMPANIES & DISTRIBUTORS — 0.4% |

| | | 150,199,780 | | W.W. Grainger, Inc. | 225,000 | 21,089,250 |

| METALS & MINING — 1.8% | | | | TOTAL COMMON STOCKS | | |

| BHP Billiton Ltd. ADR | 1,039,000 | 68,137,620 | | (Cost $4,591,536,135) | | 5,567,606,198 |

| Nucor Corp. | 831,000 | 33,115,350 | | Temporary Cash Investments — 0.4% |

| | | 101,252,970 | | JPMorgan U.S. Treasury | | |

| MULTILINE RETAIL — 1.3% | | | | Plus Money Market Fund | | |

| Kohl’s Corp.(1) | 1,258,000 | 71,982,760 | | Agency Shares | 70,843 | 70,843 |

| OIL, GAS & CONSUMABLE FUELS — 2.7% | | | Repurchase Agreement, Deutsche Bank | |

| EOG Resources, Inc. | 703,000 | 57,406,980 | | Securities, Inc., (collateralized by various | |

| | | | | U.S. Treasury obligations, 1.25%, 5/12/12, | |

| Occidental Petroleum Corp. | 800,000 | 60,704,000 | | valued at $21,222,692), in a joint trading | |

| Southwestern Energy Co.(1) | 813,000 | 35,430,540 | | account at 0.04%, dated 10/30/09, due | |

| | | 153,541,520 | | 11/2/09 (Delivery value $20,800,069) | 20,800,000 |

| PHARMACEUTICALS — 3.8% | | | | TOTAL TEMPORARY | | |

| | | | | CASH INVESTMENTS | | |

| Abbott Laboratories | 2,183,000 | 110,394,310 | | (Cost $20,870,843) | | 20,870,843 |

| Bristol-Myers Squibb Co. | 724,000 | 15,783,200 | | TOTAL INVESTMENT | | |

| Teva Pharmaceutical | | | | SECURITIES — 100.0% | | |

| Industries Ltd. ADR | 1,678,000 | 84,705,440 | | (Cost $4,612,406,978) | | 5,588,477,041 |

| | | 210,882,950 | | OTHER ASSETS | | |

| SEMICONDUCTORS & | | | | AND LIABILITIES(2) | | 2,017,998 |

| SEMICONDUCTOR EQUIPMENT — 4.1% | | | TOTAL NET ASSETS — 100.0% | | $5,590,495,039 |

| Altera Corp. | 2,612,000 | 51,691,480 | | | | |

| Applied Materials, Inc. | 3,885,000 | 47,397,000 | | | | |

13

| | | | | |

| Ultra | | | | |

| |

| Forward Foreign Currency Exchange Contracts | | |

| Contracts to Sell | Settlement Date | Value | Unrealized Gain (Loss) |

| | 44,054,135 | CHF for USD | 11/30/09 | $42,949,475 | $169,500 |

| | 16,107,820 | EUR for USD | 11/30/09 | 23,703,624 | 116,442 |

| | 6,971,606 | GBP for USD | 11/30/09 | 11,440,266 | (17,152) |

| | | | | $78,093,365 | $268,790 |

| (Value on Settlement Date $78,362,155) | | | |

| |

| Notes to Schedule of Investments | | |

| ADR = American Depositary Receipt | | | |

| CHF = Swiss Franc | | | | |

| EUR = Euro | | | | |

| GBP = British Pound | | | | |

| USD = United States Dollar | | | |

| (1) | Non-income producing. | | | |

| (2) | Category is less than 0.05% of total net assets. | | | |

Industry classifications are unaudited.

See Notes to Financial Statements.

14

|

| Statement of Assets and Liabilities |

| |

| OCTOBER 31, 2009 | |

| Assets | |

| Investment securities, at value (cost of $4,612,406,978) | $5,588,477,041 |

| Cash | 78,050 |

| Foreign currency holdings, at value (cost of $652,936) | 658,135 |

| Receivable for investments sold | 20,495,757 |

| Receivable for capital shares sold | 1,501,101 |

| Receivable for forward foreign currency exchange contracts | 285,942 |

| Dividends and interest receivable | 5,524,716 |

| | 5,617,020,742 |

| |

| Liabilities | |

| Payable for investments purchased | 18,149,493 |

| Payable for capital shares redeemed | 3,499,211 |

| Payable for forward foreign currency exchange contracts | 17,152 |

| Accrued management fees | 4,840,648 |

| Service fees (and distribution fees — A Class and R Class) payable | 18,565 |

| Distribution fees payable | 634 |

| | 26,525,703 |

| |

| Net Assets | $5,590,495,039 |

| |

| |

| See Notes to Financial Statements. | |

15

| |

| OCTOBER 31, 2009 | |

| Net Assets Consist of: | |

| Capital (par value and paid-in surplus) | $ 5,620,528,613 |

| Undistributed net investment income | 27,142,625 |

| Accumulated net realized loss on investment and foreign currency transactions | (1,033,541,646) |

| Net unrealized appreciation on investments and translation of assets and liabilities in foreign currencies | 976,365,447 |

| | $ 5,590,495,039 |

| | |

| Investor Class, $0.01 Par Value | |

| Net assets | $5,435,051,104 |

| Shares outstanding | 304,932,851 |

| Net asset value per share | $17.82 |

| | |

| Institutional Class, $0.01 Par Value | |

| Net assets | $73,932,659 |

| Shares outstanding | 4,057,385 |

| Net asset value per share | $18.22 |

| | |

| A Class, $0.01 Par Value | |

| Net assets | $77,484,381 |

| Shares outstanding | 4,472,236 |

| Net asset value per share | $17.33 |

| Maximum offering price (net asset value divided by 0.9425) | $18.39 |

| | |

| B Class, $0.01 Par Value | |

| Net assets | $87,110 |

| Shares outstanding | 4,965 |

| Net asset value per share | $17.54 |

| | |

| C Class, $0.01 Par Value | |

| Net assets | $883,795 |

| Shares outstanding | 54,502 |

| Net asset value per share | $16.22 |

| | |

| R Class, $0.01 Par Value | |

| Net assets | $3,055,990 |

| Shares outstanding | 177,054 |

| Net asset value per share | $17.26 |

| |

| |

| See Notes to Financial Statements. | |

16

| |

| YEAR ENDED OCTOBER 31, 2009 | |

| Investment Income (Loss) | |

| Income: | |

| Dividends (net of foreign taxes withheld of $241,388) | $ 85,368,409 |

| Interest | 46,391 |

| | 85,414,800 |

| | |

| Expenses: | |

| Management fees | 50,306,192 |

| Distribution fees: | |

| B Class | 425 |

| C Class | 5,959 |

| Service fees: | |

| B Class | 142 |

| C Class | 1,986 |

| Distribution and service fees: | |

| A Class | 182,901 |

| R Class | 15,625 |

| Directors’ fees and expenses | 201,297 |

| Other expenses | 7,447 |

| | 50,721,974 |

| | |

| Net investment income (loss) | 34,692,826 |

| | |

| Realized and Unrealized Gain (Loss) | |

| Net realized gain (loss) on: | |

| Investment transactions | (658,029,675) |

| Foreign currency transactions | (6,934,078) |

| | (664,963,753) |

| | |

| Change in net unrealized appreciation (depreciation) on: | |

| Investments | 1,318,769,128 |

| Translation of assets and liabilities in foreign currencies | (101,392) |

| | 1,318,667,736 |

| | |

| Net realized and unrealized gain (loss) | 653,703,983 |

| | |

| Net Increase (Decrease) in Net Assets Resulting from Operations | $ 688,396,809 |

| |

| |

| See Notes to Financial Statements. | |

17

|

| Statement of Changes in Net Assets |

| | |

| YEARS ENDED OCTOBER 31, 2009 AND OCTOBER 31, 2008 | | |

| Increase (Decrease) in Net Assets | 2009 | 2008 |

| Operations | | |

| Net investment income (loss) | $ 34,692,826 | $ 29,064,990 |

| Net realized gain (loss) | (664,963,753) | (368,571,720) |

| Change in net unrealized appreciation (depreciation) | 1,318,667,736 | (3,217,056,037) |

| Net increase (decrease) in net assets resulting from operations | 688,396,809 | (3,556,562,767) |

| | | |

| Distributions to Shareholders | | |

| From net investment income: | | |

| Investor Class | (25,630,818) | — |

| Institutional Class | (491,887) | — |

| A Class | (226,924) | — |

| R Class | (1,496) | — |

| From net realized gains: | | |

| Investor Class | — | (2,312,270,157) |

| Institutional Class | — | (65,091,994) |

| A Class | — | (50,919,711) |

| B Class | — | (11,669) |

| C Class | — | (533,319) |

| R Class | — | (1,501,522) |

| Decrease in net assets from distributions | (26,351,125) | (2,430,328,372) |

| | | |

| Capital Share Transactions | | |

| Net increase (decrease) in net assets from capital share transactions | (513,655,552) | 794,859,566 |

| | | |

| Net increase (decrease) in net assets | 148,390,132 | (5,192,031,573) |

| | | |

| Net Assets | | |

| Beginning of period | 5,442,104,907 | 10,634,136,480 |

| End of period | $5,590,495,039 | $ 5,442,104,907 |

| | | |

| Undistributed net investment income | $27,142,625 | $25,735,002 |

| |

| |

| See Notes to Financial Statements. | | |

18

|

| Notes to Financial Statements |

OCTOBER 31, 2009

1. Organization and Summary of Significant Accounting Policies

Organization — American Century Mutual Funds, Inc. (the corporation) is registered under the Investment Company Act of 1940 (the 1940 Act) as an open-end management investment company. Ultra Fund (the fund) is one fund in a series issued by the corporation. The fund is diversified under the 1940 Act. The fund’s investment objective is to seek long-term capital growth. The fund pursues this objective by investing primarily in equity securities of large companies, but may invest in companies of any size. The following is a summary of the fund’s significant accounting policies.

Multiple Class — The fund is authorized to issue the Investor Class, the Institutional Class, the A Class, the B Class, the C Class and the R Class. The A Class may incur an initial sales charge. The A Class, the B Class, and the C Class may be subject to a contingent deferred sales charge. The share classes differ principally in their respective sales charges and distribution and shareholder servicing expenses and arrangements. All shares of the fund represent an equal pro rata interest in the net assets of the class to which such shares belong, and have identical voting, dividend, liquidation and other rights and the same terms and conditions, except for class specific expenses and exclusive rights to vote on matters affecting only individual classes. Income, non-class specific expenses, and realized and unrealized capital gains and loss es of the fund are allocated to each class of shares based on their relative net assets.

Security Valuations — Securities traded primarily on a principal securities exchange are valued at the last reported sales price, or at the mean of the latest bid and asked prices where no last sales price is available. Depending on local convention or regulation, securities traded over-the-counter are valued at the mean of the latest bid and asked prices, the last sales price, or the official close price. Investments in open-end management investment companies are valued at the reported net asset value. Debt securities not traded on a principal securities exchange are valued through a commercial pricing service or at the mean of the most recent bid and asked prices. Discount notes may be valued through a commercial pricing service or at amortized cost, which approximates fair value. Securities traded on foreign securities exchanges and ov er-the-counter markets are normally completed before the close of business on days that the New York Stock Exchange (the Exchange) is open and may also take place on days when the Exchange is not open. If an event occurs after the value of a security was established but before the net asset value per share was determined that was likely to materially change the net asset value, that security would be valued as determined in accordance with procedures adopted by the Board of Directors. If the fund determines that the market price of a portfolio security is not readily available, or that the valuation methods mentioned above do not reflect the security’s fair value, such security is valued as determined by the Board of Directors or its designee, in accordance with procedures adopted by the Board of Directors, if such determination would materially impact a fund’s net asset value. Certain other circumstances may cause the fund to use alternative procedures to value a security such as: a security has b een declared in default; trading in a security has been halted during the trading day; or there is a foreign market holiday and no trading will commence.

Security Transactions — For financial reporting purposes, security transactions are accounted for as of the trade date. Net realized gains and losses are determined on the identified cost basis, which is also used for federal income tax purposes.

Investment Income — Dividend income less foreign taxes withheld, if any, is recorded as of the ex-dividend date. Interest income is recorded on the accrual basis and includes accretion of discounts and amortization of premiums.

Foreign Currency Translations — All assets and liabilities initially expressed in foreign currencies are translated into U.S. dollars at prevailing exchange rates at period end. The fund may enter into spot foreign currency exchange contracts to facilitate transactions denominated in a foreign currency. Purchases and sales of investment securities, dividend and interest income, spot foreign currency exchange contracts, and certain expenses are translated at the rates of exchange prevailing on the respective dates of such transactions.

19

For assets and liabilities, other than investments in securities, net realized and unrealized gains and losses from foreign currency translations arise from changes in currency exchange rates.

Net realized and unrealized foreign currency exchange gains or losses occurring during the holding period of investment securities are a component of net realized gain (loss) on investment transactions and net unrealized appreciation (depreciation) on investments, respectively. Certain countries may impose taxes on the contract amount of purchases and sales of foreign currency contracts in their currency. The fund records the foreign tax expense, if any, as a reduction to the net realized gain (loss) on foreign currency transactions.

Repurchase Agreements — The fund may enter into repurchase agreements with institutions that American Century Investment Management, Inc. (ACIM) (the investment advisor) has determined are creditworthy pursuant to criteria adopted by the Board of Directors. Each repurchase agreement is recorded at cost. The fund requires that the collateral, represented by securities, received in a repurchase transaction be transferred to the custodian in a manner sufficient to enable the fund to obtain those securities in the event of a default under the repurchase agreement. ACIM monitors, on a daily basis, the securities transferred to ensure the value, including accrued interest, of the securities under each repurchase agreement is equal to or greater than amounts owed to the fund under each repurchase agreement.

Joint Trading Account — Pursuant to an Exemptive Order issued by the Securities and Exchange Commission, the fund, along with certain other funds in the American Century Investments family of funds, may transfer uninvested cash balances into a joint trading account. These balances are invested in one or more repurchase agreements that are collateralized by U.S. Treasury or Agency obligations.

Income Tax Status — It is the fund’s policy to distribute substantially all net investment income and net realized gains to shareholders and to otherwise qualify as a regulated investment company under provisions of the Internal Revenue Code. The fund is no longer subject to examination by tax authorities for years prior to 2006. At this time, management believes there are no uncertain tax positions which, based on their technical merit, would not be sustained upon examination and for which it is reasonably possible that the total amounts of unrecognized tax benefits will significantly change in the next twelve months. Accordingly, no provision has been made for federal or state income taxes. Interest and penalties associated with any federal or state income tax obligations, if any, are recorded as interest expense.

Distributions to Shareholders — Distributions to shareholders are recorded on the ex-dividend date. Distributions from net investment income and net realized gains, if any, are generally declared and paid annually.

Indemnifications — Under the corporation‘s organizational documents, its officers and directors are indemnified against certain liabilities arising out of the performance of their duties to the fund. In addition, in the normal course of business, the fund enters into contracts that provide general indemnifications. The maximum exposure under these arrangements is unknown as this would involve future claims that may be made against a fund. The risk of material loss from such claims is considered by management to be remote.

Use of Estimates — The financial statements are prepared in conformity with accounting principles generally accepted in the United States of America, which may require management to make certain estimates and assumptions at the date of the financial statements. Actual results could differ from these estimates.

Subsequent Events — Management has evaluated events or transactions that may have occurred since October 31, 2009, that would merit recognition or disclosure in the financial statements. This evaluation was completed through December 28, 2009, the date the financial statements were issued.

20

2. Fees and Transactions with Related Parties

Management Fees — The corporation has entered into a Management Agreement with ACIM, under which ACIM provides the fund with investment advisory and management services in exchange for a single, unified management fee (the fee) per class. The Agreement provides that all expenses of the fund, except brokerage commissions, taxes, interest, fees and expenses of those directors who are not considered “interested persons” as defined in the 1940 Act (including counsel fees) and extraordinary expenses, will be paid by ACIM. The fee is computed and accrued daily based on the daily net assets of each specific class of shares of the fund and paid monthly in arrears. For funds with a stepped fee schedule, the rate of the fee is determined by applying a fee rate calculation formula. This formula takes into account each fund’s asset s as well as certain assets, if any, of other clients of the investment advisor outside the American Century Investments family of funds (such as subadvised funds and separate accounts) that have very similar investment teams and investment strategies (strategy assets). The annual management fee schedule ranges from 0.800% to 1.000% for the Investor Class, A Class, B Class, C Class and R Class. The Institutional Class is 0.200% less at each point within the range. The effective annual management fee for each class of the fund for the year ended October 31, 2009 was 1.00% for the Investor Class, A Class, B Class, C Class and R Class, and 0.80% for the Institutional Class.

Distribution and Service Fees — The Board of Directors has adopted a separate Master Distribution and Individual Shareholder Services Plan for each of the A Class, B Class, C Class and R Class (collectively the plans), pursuant to Rule 12b-1 of the 1940 Act. The plans provide that the A Class will pay American Century Investment Services, Inc. (ACIS) an annual distribution and service fee of 0.25%. The plans provide that the B Class and the C Class will each pay ACIS an annual distribution fee of 0.75% and service fee of 0.25%. The plans provide that the R Class will pay ACIS an annual distribution and service fee of 0.50%. The fees are computed and accrued daily based on each class’s daily net assets and paid monthly in arrears. The fees are used to pay financial intermediaries for distribution and individual shareholder service s. Fees incurred under the plans during the year ended October 31, 2009, are detailed in the Statement of Operations.

Related Parties — Certain officers and directors of the corporation are also officers and/or directors, and, as a group, controlling stockholders of American Century Companies, Inc. (ACC), the parent of the corporation’s investment advisor, ACIM, the distributor of the corporation, ACIS, and the corporation’s transfer agent, American Century Services, LLC.

The fund is eligible to invest in a money market fund for temporary purposes, which is managed by J.P. Morgan Investment Management, Inc. (JPMIM). The fund has a Mutual Funds Services Agreement with J.P. Morgan Investor Services Co. (JPMIS) and a securities lending agreement with JPMorgan Chase Bank (JPMCB). JPMCB is a custodian of the fund. JPMIM, JPMIS and JPMCB are wholly owned subsidiaries of JPMorgan Chase & Co. (JPM). JPM is an equity investor in ACC.

3. Investment Transactions

Purchases and sales of investment securities, excluding short-term investments, for the year ended October 31, 2009, were $2,680,376,654 and $3,078,532,540, respectively.

21

| | | | |

| 4. Capital Share Transactions | | | | |

| |

| Transactions in shares of the fund were as follows: | | |

| |

| | Year ended October 31, 2009 | Year ended October 31, 2008 |

| | Shares | Amount | Shares | Amount |

| Investor Class/Shares Authorized | 3,500,000,000 | | 3,500,000,000 | |

| Sold | 10,713,688 | $ 162,466,559 | 15,047,819 | $ 349,727,360 |

| Issued in reinvestment of distributions | 1,792,590 | 24,916,998 | 91,021,431 | 2,229,114,850 |

| Redeemed | (44,276,980) | (673,015,336) | (70,022,806) | (1,625,259,696) |

| | (31,770,702) | (485,631,779) | 36,046,444 | 953,582,514 |

| Institutional Class/Shares Authorized | 200,000,000 | | 200,000,000 | |

| Sold | 616,942 | 9,517,688 | 1,768,195 | 41,370,627 |

| Issued in reinvestment of distributions | 33,797 | 479,581 | 2,567,071 | 64,151,093 |

| Redeemed | (1,359,616) | (20,634,403) | (9,133,416) | (232,001,615) |

| | (708,877) | (10,637,134) | (4,798,150) | (126,479,895) |

| A Class/Shares Authorized | 100,000,000 | | 100,000,000 | |

| Sold | 761,220 | 11,227,185 | 1,495,972 | 34,046,242 |

| Issued in reinvestment of distributions | 16,176 | 219,026 | 2,076,111 | 49,536,018 |

| Redeemed | (1,933,030) | (28,089,270) | (5,107,987) | (116,870,252) |

| | (1,155,634) | (16,643,059) | (1,535,904) | (33,287,992) |

| B Class/Shares Authorized | 50,000,000 | | 50,000,000 | |

| Sold | 2,779 | 44,188 | 1,429 | 39,247 |

| Issued in reinvestment of distributions | — | — | 478 | 11,669 |

| Redeemed | (429) | (7,449) | (82) | (1,808) |

| | 2,350 | 36,739 | 1,825 | 49,108 |

| C Class/Shares Authorized | 50,000,000 | | 50,000,000 | |

| Sold | 11,640 | 167,046 | 18,798 | 403,824 |

| Issued in reinvestment of distributions | — | — | 22,734 | 513,343 |

| Redeemed | (19,376) | (267,383) | (46,798) | (965,829) |

| | (7,736) | (100,337) | (5,266) | (48,662) |

| R Class/Shares Authorized | 50,000,000 | | 50,000,000 | |

| Sold | 73,819 | 1,103,287 | 104,389 | 2,462,123 |

| Issued in reinvestment of distributions | 95 | 1,278 | 56,879 | 1,354,849 |

| Redeemed | (112,765) | (1,784,547) | (127,380) | (2,772,479) |

| | (38,851) | (679,982) | 33,888 | 1,044,493 |

| Net increase (decrease) | (33,679,450) | $(513,655,552) | 29,742,837 | $ 794,859,566 |

22

5. Fair Value Measurements

The fund’s securities valuation process is based on several considerations and may use multiple inputs to determine the fair value of the positions held by the fund. In conformity with accounting principles generally accepted in the United States of America, the inputs used to determine a valuation are classified into three broad levels as follows:

• Level 1 valuation inputs consist of actual quoted prices in an active market for identical securities;

• Level 2 valuation inputs consist of significant direct or indirect observable market data (including quoted prices for similar securities, evaluations of subsequent market events, interest rates, prepayment speeds, credit risk, etc.); or

• Level 3 valuation inputs consist of significant unobservable inputs (including a fund’s own assumptions.)

The level classification is based on the lowest level input that is significant to the fair valuation measurement. The valuation inputs are not an indication of the risks associated with investing in these securities or other financial instruments.

The following is a summary of the valuation inputs used to determine the fair value of the fund’s securities and other financial instruments as of October 31, 2009:

| | | |

| | Level 1 | Level 2 | Level 3 |

| Investment Securities | | | |

| Domestic Common Stocks | $5,135,661,705 | — | — |

| Foreign Common Stocks | 239,174,040 | $192,770,453 | — |

| Temporary Cash Investments | 70,843 | 20,800,000 | — |

| Total Value of Investment Securities | $5,374,906,588 | $213,570,453 | — |

| | | | |

| Other Financial Instruments | | | |

| Total Unrealized Gain (Loss) on Forward Foreign | | | |

| Currency Exchange Contracts | — | $268,790 | — |

6. Derivative Instruments

Foreign Currency Risk — The fund is subject to foreign currency exchange rate risk in the normal course of pursuing its investment objectives. The value of foreign investments held by a fund may be significantly affected by changes in foreign currency exchange rates. The dollar value of a foreign security generally decreases when the value of the dollar rises against the foreign currency in which the security is denominated and tends to increase when the value of the dollar declines against such foreign currency. A fund may enter into forward foreign currency exchange contracts to reduce a fund’s exposure to foreign currency exchange rate fluctuations. The net U.S. dollar value of foreign currency underlying all contractual commitments held by a fund and the resulting unrealized appreciation or depreciation are determined daily using prevailing exchange rates. Realized gain or loss is recorded upon the termination of the contract. Net realized and unrealized gains or losses occurring during the holding period of forward foreign currency exchange contracts are a component of net realized gain (loss) on foreign currency transactions and change in net unrealized appreciation (depreciation) on translation of assets and liabilities in foreign currencies, respectively. A fund bears the risk of an unfavorable change in the foreign currency exchange rate underlying the forward contract. Additionally, losses, up to the fair value, may arise if the counterparties do not perform under the contract terms. The risk of loss from non-performance by the counterparty may be reduced by the use of master netting agreements. During the year ended October 31, 2009, the fund participated in forward foreign currency exchange contracts.

23

The value of foreign currency risk derivatives as of October 31, 2009, is disclosed on the Statement of Assets and Liabilities as an asset of $285,942 in receivable for forward foreign currency exchange contracts and a liability of $17,152 in payable for forward foreign currency exchange contracts. For the year ended October 31, 2009, the effect of foreign currency risk derivatives on the Statement of Operations was $(6,906,793) in net realized gain (loss) on foreign currency transactions and $(301,472) in change in net unrealized appreciation (depreciation) on translation of assets and liabilities in foreign currencies.

The derivative instruments at period end as disclosed on the Schedule of Investments are indicative of the fund’s typical volume.

7. Risk Factors

There are certain risks involved in investing in foreign securities. These risks include those resulting from future adverse political, social, and economic developments, fluctuations in currency exchange rates, the possible imposition of exchange controls, and other foreign laws or restrictions.

8. Bank Line of Credit

The fund, along with certain other funds in the American Century Investments family of funds, had a $500,000,000 unsecured bank line of credit agreement with Bank of America, N.A. The line expired December 10, 2008, and was not renewed. The agreement allowed the fund to borrow money for temporary or emergency purposes to fund shareholder redemptions. Borrowings under the agreement were subject to interest at the Federal Funds rate plus 0.40%. The fund did not borrow from the line during the year ended October 31, 2009.

9. Interfund Lending

The fund, along with certain other funds in the American Century Investments family of funds, may participate in an interfund lending program, pursuant to an Exemptive Order issued by the Securities and Exchange Commission (SEC). This program provides an alternative credit facility allowing the fund to borrow from or lend to other funds in the American Century Investments family of funds that permit such transactions. Interfund lending transactions are subject to each fund’s investment policies and borrowing and lending limits. The interfund loan rate earned/paid on interfund lending transactions is determined daily based on the average of certain current market rates. Interfund lending transactions normally extend only overnight, but can have a maximum duration of seven days. The program is subject to annual approval by the Board of Directors. During the year ended October 31, 2009, the fund did not utilize the program.

10. Federal Tax Information

The tax character of distributions paid during the years ended October 31, 2009 and October 31, 2008 were as follows:

| | |

| | 2009 | 2008 |

| Distributions Paid From | | |

| Ordinary income | $26,351,125 | — |

| Long-term capital gains | — | $2,430,328,372 |

The book-basis character of distributions made during the year from net investment income or net realized gains may differ from their ultimate characterization for federal income tax purposes. These differences reflect the differing character of certain income items and net realized gains and losses for financial statement and tax purposes, and may result in reclassification among certain capital accounts on the financial statements.

24

As of October 31, 2009, the federal tax cost of investments and the components of distributable earnings on a tax-basis were as follows:

| |

| Federal tax cost of investments | $4,698,205,177 |

| Gross tax appreciation of investments | $1,055,224,421 |

| Gross tax depreciation of investments | (164,952,557) |

| Net tax appreciation (depreciation) of investments | $ 890,271,864 |

| Net tax appreciation (depreciation) of derivatives and translation of assets | |

| and liabilities in foreign currencies | $ 26,594 |

| Net tax appreciation (depreciation) | $890,298,458 |

| Undistributed ordinary income | $27,411,415 |

| Accumulated capital losses | $(947,743,447) |

The difference between book-basis and tax-basis cost and unrealized appreciation (depreciation) is attributable primarily to the tax deferral of losses on wash sales and the realization for tax purposes of unrealized gains on certain forward foreign currency exchange contracts.

The accumulated capital losses listed above represent net capital loss carryovers that may be used to offset future realized capital gains for federal income tax purposes. Future capital loss carryover utilization in any given year may be subject to Internal Revenue Code limitations. The capital loss carryovers of $(201,210,564) and $(746,532,883) expire in 2016 and 2017, respectively.

11. Recently Issued Accounting Standards

The Financial Accounting Standards Board (FASB) issued Accounting Standards Codification (ASC) Section 820-10 (formerly Statement of Financial Accounting Standards No. 157, “Fair Value Measurements”), in September 2006, which is effective for fiscal years beginning after November 15, 2007. ASC Section 820-10 defines fair value, establishes a framework for measuring fair value and expands the required financial statement disclosures about fair value measurements. The adoption of ASC Section 820-10 did not materially impact the determination of fair value.

In March 2008, the FASB issued ASC Section 815-10 (formerly Statement of Financial Accounting Standards No. 161, “Disclosures about Derivative Instruments and Hedging Activities — an amendment of FASB Statement No. 133”). ASC Section 815-10 is effective for interim periods beginning after November 15, 2008 and has been adopted by the fund. ASC Section 815-10 amends and expands disclosures about derivative instruments and hedging activities. ASC Section 815-10 requires qualitative disclosures about the objectives and strategies of derivative instruments, quantitative disclosures about the fair value amounts of and gains and losses on derivative instruments, and disclosures of credit-risk-related contingent features in hedging activities.

12. Other Tax Information (Unaudited)

The following information is provided pursuant to provisions of the Internal Revenue Code.

The fund hereby designates up to the maximum amount allowable as qualified dividend income for the fiscal year ended October 31, 2009.

For corporate taxpayers, the fund hereby designates $26,351,125, or up to the maximum amount allowable, of ordinary income distributions paid during the fiscal year ended October 31, 2009 as qualified for the corporate dividends received deduction.

25

| | | | | | |

| Ultra | | | | | |

| |

| Investor Class | | | | | |

| For a Share Outstanding Throughout the Years Ended October 31 | | | |

| | | 2009 | 2008 | 2007 | 2006 | 2005 |

| Per-Share Data | | | | | |

| Net Asset Value, Beginning of Period | $15.67 | $33.48 | $28.55 | $29.02 | $27.17 |

| Income From Investment Operations | | | | | |

| Net Investment Income (Loss)(1) | 0.11 | 0.08 | (0.01) | (0.06) | 0.02 |

| Net Realized and Unrealized Gain (Loss) | 2.12 | (9.95) | 6.95 | (0.37) | 1.83 |

| Total From Investment Operations | 2.23 | (9.87) | 6.94 | (0.43) | 1.85 |

| Distributions | | | | | |

| From Net Investment Income | (0.08) | — | — | (0.04) | — |

| From Net Realized Gains | — | (7.94) | (2.01) | — | — |

| Total Distributions | (0.08) | (7.94) | (2.01) | (0.04) | — |

| Net Asset Value, End of Period | $17.82 | $15.67 | $33.48 | $28.55 | $29.02 |

| |

| Total Return(2) | 14.35% | (38.02)% | 25.89% | (1.51)% | 6.81% |

| |

| Ratios/Supplemental Data | | | | | |

| Ratio of Operating Expenses | | | | | |

| to Average Net Assets | 1.00% | 0.99% | 0.99% | 0.99% | 0.99% |

| Ratio of Net Investment Income (Loss) | | | | | |

| to Average Net Assets | 0.69% | 0.36% | (0.04)% | (0.15)% | 0.09% |

| Portfolio Turnover Rate | 53% | 152% | 93% | 62% | 33% |

| Net Assets, End of Period (in millions) | $5,435 | $5,276 | $10,066 | $13,482 | $18,904 |

| (1) | Computed using average shares outstanding throughout the period. | | | | |

| (2) | Total return assumes reinvestment of net investment income and capital gains distributions, if any. The total return of the classes may not |

| | precisely reflect the class expense differences because of the impact of calculating the net asset value to two decimal places. If net asset values |

| | were calculated to three decimal places, the total return differences would more closely reflect the class expense differences. The calculation of |

| | net asset values to two decimal places is made in accordance with SEC guidelines and does not result in any gain or loss of value between one |

| | class and another. | | | | | |

| |

| |

| See Notes to Financial Statements. | | | | | |

26

| | | | | | |

| Ultra | | | | | |

| |

| Institutional Class | | | | | |

| For a Share Outstanding Throughout the Years Ended October 31 | | | |

| | | 2009 | 2008 | 2007 | 2006 | 2005 |

| Per-Share Data | | | | | |

| Net Asset Value, Beginning of Period | $16.02 | $33.98 | $28.90 | $29.38 | $27.44 |

| Income From Investment Operations | | | | | |

| Net Investment Income (Loss)(1) | 0.14 | 0.15 | 0.05 | —(2) | 0.07 |

| Net Realized and Unrealized Gain (Loss) | 2.17 | (10.17) | 7.04 | (0.38) | 1.87 |

| Total From Investment Operations | 2.31 | (10.02) | 7.09 | (0.38) | 1.94 |

| Distributions | | | | | |

| From Net Investment Income | (0.11) | — | — | (0.10) | — |

| From Net Realized Gains | — | (7.94) | (2.01) | — | — |

| Total Distributions | (0.11) | (7.94) | (2.01) | (0.10) | — |

| Net Asset Value, End of Period | $18.22 | $16.02 | $33.98 | $28.90 | $29.38 |

| |

| Total Return(3) | 14.58% | (37.89)% | 26.14% | (1.33)% | 7.07% |

| |

| Ratios/Supplemental Data | | | | | |

| Ratio of Operating Expenses | | | | | |

| to Average Net Assets | 0.80% | 0.79% | 0.79% | 0.79% | 0.79% |

| Ratio of Net Investment Income (Loss) | | | | | |

| to Average Net Assets | 0.89% | 0.56% | 0.16% | 0.05% | 0.29% |

| Portfolio Turnover Rate | 53% | 152% | 93% | 62% | 33% |

| Net Assets, End of Period (in thousands) | $73,933 | $76,339 | $325,035 | $1,073,767 | $1,460,343 |

| (1) | Computed using average shares outstanding throughout the period. | | | | |

| (2) | Per-share amount was less than $0.005. | | | | | |

| (3) | Total return assumes reinvestment of net investment income and capital gains distributions, if any. The total return of the classes may not |

| | precisely reflect the class expense differences because of the impact of calculating the net asset value to two decimal places. If net asset values |

| | were calculated to three decimal places, the total return differences would more closely reflect the class expense differences. The calculation of |

| | net asset values to two decimal places is made in accordance with SEC guidelines and does not result in any gain or loss of value between one |

| | class and another. | | | | | |

| |

| |

| See Notes to Financial Statements. | | | | | |

27

| | | | | | |

| Ultra | | | | | |

| |

| A Class(1) | | | | | |

| For a Share Outstanding Throughout the Years Ended October 31 | | | |

| | | 2009 | 2008 | 2007 | 2006 | 2005 |

| Per-Share Data | | | | | |

| Net Asset Value, Beginning of Period | $15.23 | $32.83 | $28.11 | $28.61 | $26.85 |

| Income From Investment Operations | | | | | |

| Net Investment Income (Loss)(2) | 0.07 | 0.03 | (0.08) | (0.13) | (0.05) |

| Net Realized and Unrealized Gain (Loss) | 2.07 | (9.69) | 6.81 | (0.37) | 1.81 |

| Total From Investment Operations | 2.14 | (9.66) | 6.73 | (0.50) | 1.76 |

| Distributions | | | | | |

| From Net Investment Income | (0.04) | — | — | — | — |

| From Net Realized Gains | — | (7.94) | (2.01) | — | — |

| Total Distributions | (0.04) | (7.94) | (2.01) | — | — |

| Net Asset Value, End of Period | $17.33 | $15.23 | $32.83 | $28.11 | $28.61 |

| |

| Total Return(3) | 14.14% | (38.19)% | 25.56% | (1.75)% | 6.55% |

| |

| Ratios/Supplemental Data | | | | | |

| Ratio of Operating Expenses | | | | | |

| to Average Net Assets | 1.25% | 1.24% | 1.24% | 1.24% | 1.24% |

| Ratio of Net Investment Income (Loss) | | | | | |

| to Average Net Assets | 0.44% | 0.11% | (0.29)% | (0.40)% | (0.16)% |

| Portfolio Turnover Rate | 53% | 152% | 93% | 62% | 33% |

| Net Assets, End of Period (in thousands) | $77,484 | $85,723 | $235,217 | $405,173 | $639,792 |

| (1) | Prior to September 4, 2007, the A Class was referred to as the Advisor Class. | | | |

| (2) | Computed using average shares outstanding throughout the period. | | | | |

| (3) | Total return assumes reinvestment of net investment income and capital gains distributions, if any, and does not reflect applicable sales charges. |

| | The total return of the classes may not precisely reflect the class expense differences because of the impact of calculating the net asset value to |

| | two decimal places. If net asset values were calculated to three decimal places, the total return differences would more closely reflect the class |

| | expense differences. The calculation of net asset values to two decimal places is made in accordance with SEC guidelines and does not result in |

| | any gain or loss of value between one class and another. | | | | |

| |

| |

| See Notes to Financial Statements. | | | | | |

28

| | | | |

| Ultra | | | |

| |

| B Class | | | |

| For a Share Outstanding Throughout the Years Ended October 31 (except as noted) | | |

| | | 2009 | 2008 | 2007(1) |

| Per-Share Data | | | |

| Net Asset Value, Beginning of Period | $15.49 | $33.45 | $31.63 |

| Income From Investment Operations | | | |

| Net Investment Income (Loss)(2) | (0.06) | (0.16) | (0.04) |

| Net Realized and Unrealized Gain (Loss) | 2.11 | (9.86) | 1.86 |

| Total From Investment Operations | 2.05 | (10.02) | 1.82 |

| Distributions | | | |

| From Net Realized Gains | — | (7.94) | — |

| Net Asset Value, End of Period | $17.54 | $15.49 | $33.45 |

| |

| Total Return(3) | 13.23% | (38.64)% | 5.75% |

| |

| Ratios/Supplemental Data | | | |

| Ratio of Operating Expenses to Average Net Assets | 2.00% | 1.99% | 1.99%(4) |

| Ratio of Net Investment Income (Loss) to Average Net Assets | (0.31)% | (0.64)% | (1.53)%(4) |

| Portfolio Turnover Rate | 53% | 152% | 93%(5) |

| Net Assets, End of Period (in thousands) | $87 | $41 | $26 |

| (1) | September 28, 2007 (commencement of sale) through October 31, 2007. | | | |

| (2) | Computed using average shares outstanding throughout the period. | | | |

| (3) | Total return assumes reinvestment of net investment income and capital gains distributions, if any, and does not reflect applicable sales charges. |

| | Total returns for periods less than one year are not annualized. The total return of the classes may not precisely reflect the class expense |

| | differences because of the impact of calculating the net asset value to two decimal places. If net asset values were calculated to three decimal |

| | places, the total return differences would more closely reflect the class expense differences. The calculation of net asset values to two decimal |

| | places is made in accordance with SEC guidelines and does not result in any gain or loss of value between one class and another. | |

| (4) | Annualized. | | | |

| (5) | Portfolio turnover is calculated at the fund level. Percentage indicated was calculated for the year ended October 31, 2007. | |

| |

| |

| See Notes to Financial Statements. | | | |

29

| | | | | | |

| Ultra | | | | | |

| |

| C Class | | | | | |

| For a Share Outstanding Throughout the Years Ended October 31 | | | |

| | | 2009 | 2008 | 2007 | 2006 | 2005 |

| Per-Share Data | | | | | |

| Net Asset Value, Beginning of Period | $14.32 | $31.54 | $27.26 | $27.96 | $26.44 |

| Income From Investment Operations | | | | | |

| Net Investment Income (Loss)(1) | (0.04) | (0.13) | (0.29) | (0.34) | (0.26) |

| Net Realized and Unrealized Gain (Loss) | 1.94 | (9.15) | 6.58 | (0.36) | 1.78 |

| Total From Investment Operations | 1.90 | (9.28) | 6.29 | (0.70) | 1.52 |

| Distributions | | | | | |

| From Net Realized Gains | — | (7.94) | (2.01) | — | — |

| Net Asset Value, End of Period | $16.22 | $14.32 | $31.54 | $27.26 | $27.96 |

| |

| Total Return(2) | 13.20% | (38.63)% | 24.64% | (2.50)% | 5.75% |

| |

| Ratios/Supplemental Data | | | | | |

| Ratio of Operating Expenses | | | | | |

| to Average Net Assets | 2.00% | 1.99% | 1.99% | 1.99% | 1.99% |

| Ratio of Net Investment Income (Loss) | | | | | |