UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| Investment Company Act file number | 811-00816 | |||||

| AMERICAN CENTURY MUTUAL FUNDS, INC. | ||||||

| (Exact name of registrant as specified in charter) | ||||||

| 4500 MAIN STREET, KANSAS CITY, MISSOURI | 64111 | |||||

| (Address of principal executive offices) | (Zip Code) | |||||

CHARLES A. ETHERINGTON 4500 MAIN STREET, KANSAS CITY, MISSOURI 64111 | ||||||

| (Name and address of agent for service) | ||||||

| Registrant’s telephone number, including area code: | 816-531-5575 | |||||

| Date of fiscal year end: | 10-31 | |||||

| Date of reporting period: | 10-31-2012 | |||||

ITEM 1. REPORTS TO STOCKHOLDERS.

ANNUAL REPORT OCTOBER 31, 2012

| All Cap Growth Fund |

| President’s Letter | 2 |

| Independent Chairman’s Letter | 3 |

| Market Perspective | 4 |

| Performance | 5 |

| Portfolio Commentary | 7 |

| Fund Characteristics | 9 |

| Shareholder Fee Example | 10 |

| Schedule of Investments | 12 |

| Statement of Assets and Liabilities | 15 |

| Statement of Operations | 16 |

| Statement of Changes in Net Assets | 17 |

| Notes to Financial Statements | 18 |

| Financial Highlights | 24 |

| Report of Independent Registered Public Accounting Firm | 26 |

| Management | 27 |

| Approval of Management Agreement | 30 |

| Additional Information | 35 |

Any opinions expressed in this report reflect those of the author as of the date of the report, and do not necessarily represent the opinions of American Century Investments® or any other person in the American Century Investments organization. Any such opinions are subject to change at any time based upon market or other conditions and American Century Investments disclaims any responsibility to update such opinions. These opinions may not be relied upon as investment advice and, because investment decisions made by American Century Investments funds are based on numerous factors, may not be relied upon as an indication of trading intent on behalf of any American Century Investments fund. Security examples are used for representational purposes only and are not intended as recommendations to purchase or sell securities. Performance information for comparative indices and securities is provided to American Century Investments by third party vendors. To the best of American Century Investments’ knowledge, such information is accurate at the time of printing.

Dear Investor:

Thank you for reviewing this annual report for the 12 months ended October 31, 2012. Our report offers investment performance, market analysis, and portfolio information, presented with the expert perspective of our portfolio management team.

This report remains one of our most important vehicles for conveying information about fund returns, including key factors that affected fund performance. For additional, updated insights, we encourage you to visit our website, americancentury.com.

Favorable Fiscal-Year Returns for Most U.S. Stock and Bond Benchmarks

In a period fraught with concerns about factors such as the global economic recovery, European financial system stability, and the U.S. political picture, the 12-month returns for U.S. investors were generally favorable.

Both U.S. stocks and bonds rallied for much of the period, with U.S. equities generally outperforming their non-U.S. counterparts. The S&P 500 Index advanced 15.21%, compared with 4.61% for the MSCI EAFE (Europe, Australasia, Far East) Index. The Barclays U.S. Aggregate Bond Index returned 5.25%, and the 10-year U.S. Treasury note returned 7.47%, according to Barclays.

As it turned out, the overseas setbacks and the coordinated monetary policy response provided by prominent central banks around the world ultimately proved beneficial to the U.S. capital markets. Both U.S. stocks and bonds generally benefited from global investors’ trust in the U.S. financial system and from declining interest rates, helped by central bank purchases of government securities. The 10-year U.S. Treasury yield fell to a record low during the period, finishing at 1.69%.

The U.S. economy showed signs of improvement during the fiscal year, particularly the long-depressed housing market. However, the outlook for 2013 remains guarded, as the fragile recovery remains vulnerable to fiscal and financial factors that could trigger further slowdowns and market volatility.

Under these conditions, we continue to believe in a disciplined, diversified, long-term investment approach, using both stocks and bonds—as appropriate—for meeting financial goals. We appreciate your continued trust in us in this challenging environment.

Sincerely,

Jonathan Thomas

President and Chief Executive Officer

American Century Investments

2

Dear Fellow Shareholders,

The board has once again completed its annual review of the advisory contract between the American Century Investments mutual funds overseen by the board and the funds’ advisor, American Century Investment Management, Inc. This process, often referred to as the 15(c) review, involves the independent directors considering all of the material monitored throughout the year and evaluating a wide range of factors to determine whether the management fee paid by each fund to the advisor is reasonable.

The independent directors’ rationale for this decision is provided in detail in this, or in a previous, report. However, there are several highlights that should be of interest to all shareholders.

| • | Fund performance and client service continue to be rated among the industry’s best. |

| • | Target date and other asset allocation products continue to successfully gather assets and industry acclaim. |

| • | Compliance programs continue to function successfully with no issues impacting shareholder interests. |

| • | Fees were found to be within an acceptable competitive range, with minor fee waivers being negotiated on five funds. |

Knowing that most shareholders are long term investors, the board was particularly pleased with our succession planning review. Talented professionals are being added within portfolio management and experienced managers have been added to the senior management team.

Overall it was a very positive review for the American Century Investments mutual funds during a challenging market environment.

Best personal regards,

Don Pratt

3

Stocks Gained Amid Volatility

The U.S. stock market generated positive results for the 12-month period ended October 31, 2012, although it endured significant volatility along the way. As the reporting period began, stocks were in the midst of a rebound. Investors grew optimistic as signs of improving economic activity quashed recession fears; in particular, job growth began to exceed expectations, driving the unemployment rate to its lowest level in three years by February 2012. Another positive factor was promising news out of Europe, as the European Central Bank provided favorable long-term financing to the debt markets and support for the Continent’s banking sector.

The optimism proved to be short-lived, as headwinds returned to the equity market. Evidence of slowing economic activity in the U.S. and adverse developments in Europe—including political turmoil in Greece and troubled banks in Spain—weighed on investor confidence, sending stocks down sharply.

Late in the period, stocks reversed course once again. The Federal Reserve announced a third round of quantitative easing measures, as well as an extension of its near-zero interest rate policy until 2015. The European Central Bank, meanwhile, announced a plan under which it would purchase bonds to support financially troubled debt markets in Europe. These measures, as well as others taken by central banks around the world, helped to restore investor confidence and drive markets upward, despite some concerns about slowing corporate profits and the looming U.S. fiscal cliff.

As the table below illustrates, large-cap issues generated the strongest returns for the reporting period, outpacing mid- and small-cap shares. Value stocks outpaced growth shares across the market capitalization spectrum.

From a sector perspective, all sectors within the Russell 3000 Index delivered positive results; the telecommunication services sector fared the best. Health care, financials, consumer discretionary, and consumer staples all finished ahead of the Russell 3000 Index. On the other side, the energy and information technology sectors achieved more moderate gains.

| U.S. Stock Index Returns | ||||

| For the 12 months ended October 31, 2012 | ||||

| Russell 1000 Index (Large-Cap) | 14.97% | Russell 2000 Index (Small-Cap) | 12.08% | |

| Russell 1000 Growth Index | 13.02% | Russell 2000 Growth Index | 9.70% | |

| Russell 1000 Value Index | 16.89% | Russell 2000 Value Index | 14.47% | |

| Russell Midcap Index | 12.15% | |||

| Russell Midcap Growth Index | 9.09% | |||

| Russell Midcap Value Index | 14.99% | |||

4

| Total Returns as of October 31, 2012 | ||||||

| Average Annual Returns | ||||||

Ticker Symbol | 1 year | 5 years | 10 years | Since Inception | Inception Date | |

| Investor Class | TWGTX | 11.40% | -0.10% | 10.19%(1) | 11.15% | 11/25/83 |

| Russell 3000 Growth Index | — | 12.76% | 1.90% | 7.32% | 9.19%(2) | — |

| Institutional Class | ACAJX | 11.62% | — | — | 21.59% | 9/30/11 |

A Class No sales charge* With sales charge* | ACAQX | 11.15% 4.76% | — — | — — | 21.08% 14.69% | 9/30/11 |

| C Class | ACAHX | 10.32% | — | — | 20.17% | 9/30/11 |

| R Class | ACAWX | 10.86% | — | — | 20.76% | 9/30/11 |

| * | Sales charges include initial sales charges and contingent deferred sales charges (CDSCs), as applicable. A Class shares have a 5.75% maximum initial sales charge and may be subject to a maximum CDSC of 1.00%. C Class shares redeemed within 12 months of purchase are subject to a maximum CDSC of 1.00%. The SEC requires that mutual funds provide performance information net of maximum sales charges in all cases where charges could be applied. |

| (1) | Returns would have been lower if a portion of the management fee had not been waived. |

| (2) | Since 11/30/83, the date nearest the Investor Class’s inception for which data are available. |

Data presented reflect past performance. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance shown. Investment return and principal value will fluctuate, and redemption value may be more or less than original cost. To obtain performance data current to the most recent month end, please call 1-800-345-2021 or visit americancentury.com. International investing involves special risks, such as political instability and currency fluctuations.

Unless otherwise indicated, performance reflects Investor Class shares; performance for other share classes will vary due to differences in fee structure. For information about other share classes available, please consult the prospectus. Data assumes reinvestment of dividends and capital gains, and none of the charts reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for the index are provided for comparison. The fund’s total returns include operating expenses (such as transaction costs and management fees) that reduce returns, while the total returns of the index do not.

5

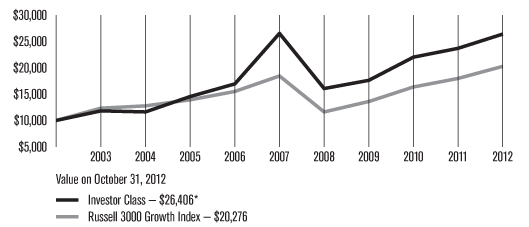

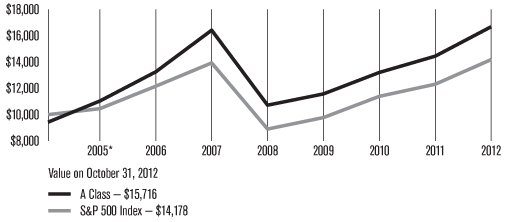

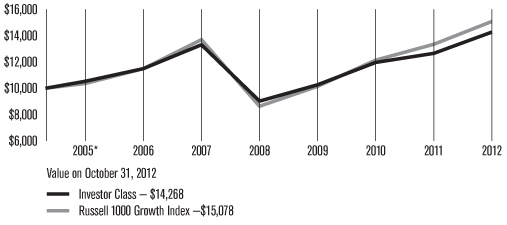

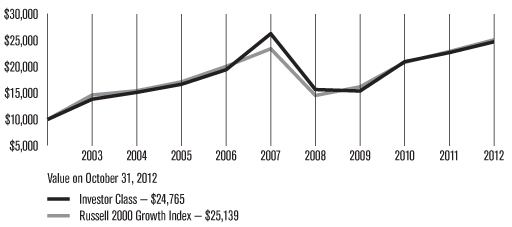

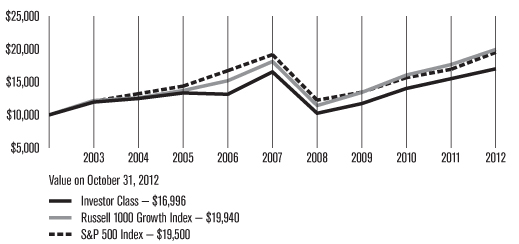

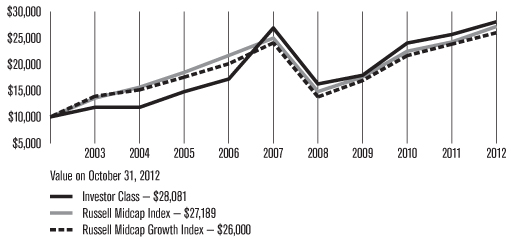

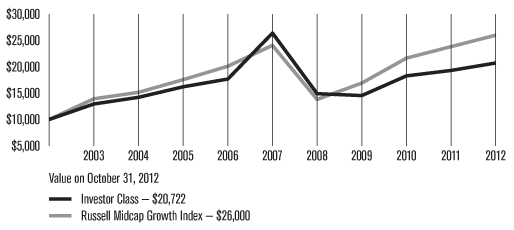

| Growth of $10,000 Over 10 Years |

| $10,000 investment made October 31, 2002 |

*Ending value would have been lower if a portion of the management fee had not been waived.

| Total Annual Fund Operating Expenses | ||||

| Investor Class | Institutional Class | A Class | C Class | R Class |

| 1.00% | 0.80% | 1.25% | 2.00% | 1.50% |

The total annual fund operating expenses shown is as stated in the fund’s prospectus current as of the date of this report. The prospectus may vary from the expense ratio shown elsewhere in this report because it is based on a different time period, includes acquired fund fees and expenses, and, if applicable, does not include fee waivers or expense reimbursements.

Data presented reflect past performance. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance shown. Investment return and principal value will fluctuate, and redemption value may be more or less than original cost. To obtain performance data current to the most recent month end, please call 1-800-345-2021 or visit americancentury.com. International investing involves special risks, such as political instability and currency fluctuations.

Unless otherwise indicated, performance reflects Investor Class shares; performance for other share classes will vary due to differences in fee structure. For information about other share classes available, please consult the prospectus. Data assumes reinvestment of dividends and capital gains, and none of the charts reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for the index are provided for comparison. The fund’s total returns include operating expenses (such as transaction costs and management fees) that reduce returns, while the total returns of the index do not.

6

Portfolio Managers: David Hollond, Michael Orndorff, and Marcus Scott.

Marcus Scott became a Portfolio Manager on the All Cap Growth team in February 2012.

Performance Summary

All Cap Growth returned 11.40%* for the 12 months ended October 31, 2012, lagging the 12.76% return of the portfolio’s benchmark, the Russell 3000 Growth Index.

As discussed in the Market Perspective on page 4, equity indices generally gained during the reporting period, although they struggled with the challenges of a tepid global economic recovery and continued sovereign debt concerns in Europe. Price momentum and acceleration, two factors that the All Cap Growth team looks for in portfolio holdings, were not rewarded consistently during the reporting period.

Within the portfolio, stock decisions in the consumer discretionary and industrials sectors accounted for the bulk of underperformance versus the benchmark. Stock selection in the health care, information technology, and financials sectors partially offset those relative losses.

Consumer Discretionary, Industrials Lagged

In the consumer discretionary sector, an underweight allocation to the media industry hurt relative results. As optimism grew about the economic environment, advertising spending grew, helping companies in the industry group. Detrimental holdings in the media industry included China-based Focus Media Holding Ltd., which sold off sharply due to a third party research report. Stock decisions in the hotels, restaurants, and leisure group, as well as the diversified consumer services group, trimmed relative returns.

Elsewhere in the sector, however, it helped to own high-growth international retailer Michael Kors. The stock outperformed during the fiscal year following its initial public offering thanks to brand strength and exposure to luxury spending.

The industrials sector was a meaningful source of underperformance versus the benchmark. In the machinery industry, mining equipment manufacturer Joy Global was one of several overweight positions that trimmed relative performance. The mining equipment company underperformed along with lower metals prices and slowing economic growth.

In the electrical equipment industry group, Polypore, which manufactures separators for batteries used in automobiles and consumer electronic devices, was hurt by slower than expected demand. Commercial services overweight Clean Harbors also detracted. The hazardous waste disposal company suffered from concerns about pricing pressure in their energy service business as natural gas prices fell.

Health Care, Financials Gained

The health care sector was the largest source of relative gains, attributable largely to stock decisions among health care providers. The top individual contributor in the portfolio by far was pharmacy benefit manager SXC Health Solutions, which

*All fund returns referenced in this commentary are for Investor Class shares.

7

acquired Catalyst Health Solutions during the reporting period. The portfolio held overweight positions in both companies, and they each posted strong returns. The merger provides the combined entity (renamed Catamaran Corp.) increased scale to go after larger potential clients.

Spanish health care company Grifols also contributed, as its acquisition of U.S. based Talecris drove gains in net revenues and net income.

In the financials sector, a position in consumer finance company Discover helped relative returns. Discover benefitted from reports of improving consumer credit quality and an alliance with PayPal, which will use Discover’s network for mobile payment transactions.

Information Technology Contributed, but Some Positions Detracted

The information technology sector was the second-largest source of relative outperformance. Here, an overweight position in Apple added significantly to results, as the company unveiled its much-anticipated iPhone 5 in September, selling more than five million units in its debut weekend. Apple also won a patent lawsuit against Samsung, its major rival in the smart phone market. Also in the sector, the portfolio underweighted the semiconductor group, an allocation decision that helped results versus the benchmark.

Some positions in the sector, though, detracted significantly from relative performance. A stake in China’s dominant internet search engine, Baidu was the largest individual detractor from relative returns. The company reported strong results, but underperformed after guiding future growth lower. Investor concerns about slowing economic growth in China also weighed on the company’s share price.

Information security software company Check Point Software Technologies detracted. Check Point underperformed after announcing slower-than-expected license revenue growth, which the company attributed to a pause in orders ahead of a new operating system launch.

Outlook

All Cap Growth’s investment process focuses on companies of all sizes with accelerating revenue and earnings growth rates, which are also exhibiting share-price strength. We believe that active investing in such companies will generate attractive absolute and relative investment performance over time. This process, which has historically added value, has faced unprecedented headwinds in recent reporting periods. Despite this challenge, All Cap Growth provided solid absolute returns during the reporting period. The team believes such a portfolio can outperform All Cap Growth’s peers and its benchmark, the Russell 3000 Growth Index, over time.

8

| OCTOBER 31, 2012 | |

| Top Ten Holdings | % of net assets |

| Apple, Inc. | 9.8% |

| Philip Morris International, Inc. | 3.5% |

| Express Scripts Holding Co. | 3.2% |

| QUALCOMM, Inc. | 2.9% |

| Costco Wholesale Corp. | 2.8% |

| Precision Castparts Corp. | 2.6% |

| Microsoft Corp. | 2.5% |

| Catamaran Corp. | 2.3% |

| Whole Foods Market, Inc. | 2.2% |

| Google, Inc. Class A | 2.1% |

| Top Five Industries | % of net assets |

| Computers and Peripherals | 10.8% |

| Food and Staples Retailing | 6.4% |

| Specialty Retail | 6.1% |

| IT Services | 5.5% |

| Health Care Providers and Services | 5.5% |

| Types of Investments in Portfolio | % of net assets |

| Domestic Common Stocks | 93.1% |

| Foreign Common Stocks* | 6.0% |

| Total Common Stocks | 99.1% |

| Temporary Cash Investments | 1.0% |

| Other Assets and Liabilities | (0.1)% |

| *Includes depositary shares, dual listed securities and foreign ordinary shares. | |

9

Fund shareholders may incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments and redemption/exchange fees; and (2) ongoing costs, including management fees; distribution and service (12b-1) fees; and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in your fund and to compare these costs with the ongoing cost of investing in other mutual funds.

The example is based on an investment of $1,000 made at the beginning of the period and held for the entire period from May 1, 2012 to October 31, 2012.

Actual Expenses

The table provides information about actual account values and actual expenses for each class. You may use the information, together with the amount you invested, to estimate the expenses that you paid over the period. First, identify the share class you own. Then simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

If you hold Investor Class shares of any American Century Investments fund, or Institutional Class shares of the American Century Diversified Bond Fund, in an American Century Investments account (i.e., not a financial intermediary or retirement plan account), American Century Investments may charge you a $12.50 semiannual account maintenance fee if the value of those shares is less than $10,000. We will redeem shares automatically in one of your accounts to pay the $12.50 fee. In determining your total eligible investment amount, we will include your investments in all personal accounts (including American Century Investments Brokerage accounts) registered under your Social Security number. Personal accounts include individual accounts, joint accounts, UGMA/UTMA accounts, personal trusts, Coverdell Education Savings Accounts and IRAs (including traditional, Roth, Rollover, SEP-, SARSEP- and SIMPLE-IRAs), and certain other retirement accounts. If you have only business, business retirement, employer-sponsored or American Century Investments Brokerage accounts, you are currently not subject to this fee. If you are subject to the Account Maintenance Fee, your account value could be reduced by the fee amount.

Hypothetical Example for Comparison Purposes

The table also provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio of each class of your fund and an assumed rate of return of 5% per year before expenses, which is not the actual return of a fund’s share class. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in your fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

10

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) or redemption/exchange fees. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

Beginning Account Value 5/1/12 | Ending Account Value 10/31/12 | Expenses Paid During Period(1) 5/1/12 – 10/31/12 | Annualized Expense Ratio(1) | |

| Actual | ||||

| Investor Class | $1,000 | $966.00 | $4.94 | 1.00% |

| Institutional Class | $1,000 | $967.00 | $3.96 | 0.80% |

| A Class | $1,000 | $965.00 | $6.17 | 1.25% |

| C Class | $1,000 | $961.40 | $9.86 | 2.00% |

| R Class | $1,000 | $963.40 | $7.40 | 1.50% |

| Hypothetical | ||||

| Investor Class | $1,000 | $1,020.11 | $5.08 | 1.00% |

| Institutional Class | $1,000 | $1,021.12 | $4.06 | 0.80% |

| A Class | $1,000 | $1,018.85 | $6.34 | 1.25% |

| C Class | $1,000 | $1,015.08 | $10.13 | 2.00% |

| R Class | $1,000 | $1,017.60 | $7.61 | 1.50% |

| (1) | Expenses are equal to the class’s annualized expense ratio listed in the table above, multiplied by the average account value over the period, multiplied by 184, the number of days in the most recent fiscal half-year, divided by 366, to reflect the one-half year period. |

11

| Shares | Value | |||||||

| Common Stocks — 99.1% | ||||||||

| AEROSPACE AND DEFENSE — 3.2% | ||||||||

| Precision Castparts Corp. | 144,599 | $25,025,749 | ||||||

| TransDigm Group, Inc. | 46,354 | 6,174,816 | ||||||

| 31,200,565 | ||||||||

| AUTOMOBILES — 1.3% | ||||||||

| Harley-Davidson, Inc. | 101,037 | 4,724,490 | ||||||

| Hyundai Motor Co. | 36,662 | 7,546,873 | ||||||

| 12,271,363 | ||||||||

| BEVERAGES — 1.9% | ||||||||

| Beam, Inc. | 38,651 | 2,147,450 | ||||||

| Coca-Cola Co. (The) | 419,030 | 15,579,535 | ||||||

Monster Beverage Corp.(1) | 17,245 | 770,334 | ||||||

| 18,497,319 | ||||||||

| BIOTECHNOLOGY — 2.7% | ||||||||

Alexion Pharmaceuticals, Inc.(1) | 92,876 | 8,394,133 | ||||||

Biogen Idec, Inc.(1) | 6,369 | 880,323 | ||||||

Gilead Sciences, Inc.(1) | 105,872 | 7,110,364 | ||||||

Grifols SA(1) | 217,005 | 7,526,809 | ||||||

Onyx Pharmaceuticals, Inc.(1) | 37,478 | 2,936,776 | ||||||

| 26,848,405 | ||||||||

| CAPITAL MARKETS — 0.5% | ||||||||

| Lazard Ltd., Class A | 157,675 | 4,645,106 | ||||||

| CHEMICALS — 3.3% | ||||||||

| American Vanguard Corp. | 96,873 | 3,461,272 | ||||||

| Cytec Industries, Inc. | 43,837 | 3,016,862 | ||||||

| FMC Corp. | 89,150 | 4,771,308 | ||||||

| Monsanto Co. | 226,005 | 19,452,251 | ||||||

| Sherwin-Williams Co. (The) | 10,406 | 1,483,688 | ||||||

| 32,185,381 | ||||||||

| COMMERCIAL BANKS — 0.7% | ||||||||

| East West Bancorp., Inc. | 137,927 | 2,936,466 | ||||||

SVB Financial Group(1) | 66,851 | 3,783,098 | ||||||

| 6,719,564 | ||||||||

| COMMERCIAL SERVICES AND SUPPLIES — 0.4% | ||||||||

| Cintas Corp. | 89,884 | 3,758,050 | ||||||

| COMMUNICATIONS EQUIPMENT — 4.6% | ||||||||

| Cisco Systems, Inc. | 673,547 | 11,544,596 | ||||||

Palo Alto Networks, Inc.(1) | 87,734 | 4,823,615 | ||||||

| QUALCOMM, Inc. | 482,184 | 28,243,928 | ||||||

| 44,612,139 | ||||||||

| COMPUTERS AND PERIPHERALS — 10.8% | ||||||||

| Apple, Inc. | 160,075 | 95,260,632 | ||||||

EMC Corp.(1) | 424,178 | 10,358,427 | ||||||

| 105,619,059 | ||||||||

| CONSTRUCTION AND ENGINEERING — 1.0% | ||||||||

| Chicago Bridge & Iron Co. NV New York Shares | 100,128 | 3,759,806 | ||||||

Quanta Services, Inc.(1) | 248,014 | 6,431,003 | ||||||

| 10,190,809 | ||||||||

| CONSUMER FINANCE — 2.4% | ||||||||

| American Express Co. | 61,865 | 3,462,584 | ||||||

| Discover Financial Services | 478,484 | 19,617,844 | ||||||

| 23,080,428 | ||||||||

| DIVERSIFIED TELECOMMUNICATION SERVICES — 1.7% | ||||||||

| Verizon Communications, Inc. | 366,371 | 16,354,801 | ||||||

| ELECTRONIC EQUIPMENT, INSTRUMENTS AND COMPONENTS — 0.5% | ||||||||

| Jabil Circuit, Inc. | 28,117 | 487,549 | ||||||

Trimble Navigation Ltd.(1) | 87,313 | 4,119,427 | ||||||

| 4,606,976 | ||||||||

| ENERGY EQUIPMENT AND SERVICES — 2.3% | ||||||||

Cameron International Corp.(1) | 111,493 | 5,646,005 | ||||||

| National Oilwell Varco, Inc. | 227,311 | 16,752,821 | ||||||

| 22,398,826 | ||||||||

| FOOD AND STAPLES RETAILING — 6.4% | ||||||||

| Costco Wholesale Corp. | 279,447 | 27,505,968 | ||||||

Natural Grocers by Vitamin Cottage, Inc.(1) | 86,046 | 1,745,013 | ||||||

| PriceSmart, Inc. | 46,272 | 3,840,113 | ||||||

| Wal-Mart Stores, Inc. | 106,633 | 7,999,608 | ||||||

| Whole Foods Market, Inc. | 225,452 | 21,357,068 | ||||||

| 62,447,770 | ||||||||

| FOOD PRODUCTS — 0.6% | ||||||||

| Mead Johnson Nutrition Co. | 100,926 | 6,223,097 | ||||||

| HEALTH CARE EQUIPMENT AND SUPPLIES — 2.8% | ||||||||

| Baxter International, Inc. | 197,938 | 12,396,857 | ||||||

| Cooper Cos., Inc. (The) | 39,189 | 3,761,360 | ||||||

| Covidien plc | 139,604 | 7,671,240 | ||||||

IDEXX Laboratories, Inc.(1) | 38,611 | 3,714,378 | ||||||

| 27,543,835 | ||||||||

| HEALTH CARE PROVIDERS AND SERVICES — 5.5% | ||||||||

Catamaran Corp.(1) | 483,969 | 22,823,978 | ||||||

Express Scripts Holding Co.(1) | 504,369 | 31,038,868 | ||||||

| 53,862,846 | ||||||||

| HEALTH CARE TECHNOLOGY — 0.8% | ||||||||

Cerner Corp.(1) | 105,659 | 8,050,159 | ||||||

12

| Shares | Value | |||||||

| HOTELS, RESTAURANTS AND LEISURE — 3.1% | ||||||||

Penn National Gaming, Inc.(1) | 81,035 | $3,276,245 | ||||||

| Starbucks Corp. | 302,878 | 13,902,100 | ||||||

| Yum! Brands, Inc. | 186,175 | 13,052,730 | ||||||

| 30,231,075 | ||||||||

| HOUSEHOLD DURABLES — 0.3% | ||||||||

Toll Brothers, Inc.(1) | 102,301 | 3,376,956 | ||||||

| INTERNET AND CATALOG RETAIL — 3.0% | ||||||||

Amazon.com, Inc.(1) | 47,250 | 11,000,745 | ||||||

Blue Nile, Inc.(1) | 41,344 | 1,561,563 | ||||||

| Expedia, Inc. | 52,957 | 3,132,407 | ||||||

priceline.com, Inc.(1) | 23,477 | 13,470,398 | ||||||

| 29,165,113 | ||||||||

| INTERNET SOFTWARE AND SERVICES — 4.9% | ||||||||

eBay, Inc.(1) | 150,358 | 7,260,788 | ||||||

Facebook, Inc. Class A(1) | 481,159 | 10,159,672 | ||||||

Google, Inc. Class A(1) | 30,652 | 20,836,310 | ||||||

LinkedIn Corp., Class A(1) | 46,441 | 4,965,936 | ||||||

Rackspace Hosting, Inc.(1) | 68,046 | 4,333,850 | ||||||

| 47,556,556 | ||||||||

| IT SERVICES — 5.5% | ||||||||

| Accenture plc, Class A | 163,551 | 11,024,973 | ||||||

Alliance Data Systems Corp.(1) | 116,390 | 16,649,590 | ||||||

Cognizant Technology Solutions Corp., Class A(1) | 81,613 | 5,439,506 | ||||||

| MasterCard, Inc., Class A | 27,808 | 12,817,541 | ||||||

Teradata Corp.(1) | 117,048 | 7,995,549 | ||||||

| 53,927,159 | ||||||||

| MACHINERY — 2.1% | ||||||||

| Caterpillar, Inc. | 41,350 | 3,506,893 | ||||||

Chart Industries, Inc.(1) | 57,778 | 4,090,105 | ||||||

| Flowserve Corp. | 29,370 | 3,979,341 | ||||||

| Trinity Industries, Inc. | 130,877 | 4,093,833 | ||||||

| Valmont Industries, Inc. | 39,483 | 5,334,153 | ||||||

| 21,004,325 | ||||||||

| MEDIA — 0.5% | ||||||||

| CBS Corp., Class B | 160,262 | 5,192,489 | ||||||

| METALS AND MINING — 1.7% | ||||||||

| Carpenter Technology Corp. | 146,933 | 7,142,413 | ||||||

| Freeport-McMoRan Copper & Gold, Inc. | 249,943 | 9,717,784 | ||||||

| 16,860,197 | ||||||||

| MULTILINE RETAIL — 0.5% | ||||||||

| Family Dollar Stores, Inc. | 69,598 | 4,590,684 | ||||||

| OIL, GAS AND CONSUMABLE FUELS — 0.7% | ||||||||

Concho Resources, Inc.(1) | 40,802 | $3,513,868 | ||||||

| Linn Energy LLC | 77,398 | 3,260,004 | ||||||

| 6,773,872 | ||||||||

| PHARMACEUTICALS — 3.4% | ||||||||

| Allergan, Inc. | 196,631 | 17,681,060 | ||||||

| Perrigo Co. | 91,314 | 10,502,023 | ||||||

Watson Pharmaceuticals, Inc.(1) | 58,596 | 5,036,326 | ||||||

| 33,219,409 | ||||||||

| ROAD AND RAIL — 2.4% | ||||||||

| Canadian Pacific Railway Ltd. | 58,585 | 5,393,335 | ||||||

| Kansas City Southern | 218,633 | 17,591,211 | ||||||

| 22,984,546 | ||||||||

| SOFTWARE — 5.5% | ||||||||

Citrix Systems, Inc.(1) | 51,551 | 3,186,367 | ||||||

CommVault Systems, Inc.(1) | 61,533 | 3,843,966 | ||||||

| Microsoft Corp. | 855,813 | 24,420,624 | ||||||

NetSuite, Inc.(1) | 138,264 | 8,781,147 | ||||||

Nuance Communications, Inc.(1) | 150,329 | 3,346,324 | ||||||

Salesforce.com, Inc.(1) | 52,057 | 7,599,281 | ||||||

Splunk, Inc.(1) | 90,604 | 2,541,442 | ||||||

| 53,719,151 | ||||||||

| SPECIALTY RETAIL — 6.1% | ||||||||

ANN, Inc.(1) | 71,552 | 2,515,768 | ||||||

Cabela’s, Inc.(1) | 107,780 | 4,829,622 | ||||||

| GNC Holdings, Inc. Class A | 165,497 | 6,399,769 | ||||||

| Home Depot, Inc. (The) | 196,250 | 12,045,825 | ||||||

Lumber Liquidators Holdings, Inc.(1) | 60,147 | 3,357,406 | ||||||

| PetSmart, Inc. | 173,229 | 11,500,673 | ||||||

| TJX Cos., Inc. (The) | 303,681 | 12,642,240 | ||||||

| Ulta Salon Cosmetics & Fragrance, Inc. | 63,014 | 5,811,151 | ||||||

| 59,102,454 | ||||||||

| TEXTILES, APPAREL AND LUXURY GOODS — 1.8% | ||||||||

| Coach, Inc. | 71,649 | 4,015,927 | ||||||

Lululemon Athletica, Inc.(1) | 46,964 | 3,240,986 | ||||||

Michael Kors Holdings Ltd.(1) | 145,889 | 7,978,669 | ||||||

Vera Bradley, Inc.(1) | 68,383 | 2,038,497 | ||||||

| 17,274,079 | ||||||||

| TOBACCO — 4.2% | ||||||||

| Altria Group, Inc. | 204,021 | 6,487,868 | ||||||

| Philip Morris International, Inc. | 390,375 | 34,571,610 | ||||||

| 41,059,478 | ||||||||

TOTAL COMMON STOCKS (Cost $692,941,190) | 967,154,041 | |||||||

13

| Shares | Value | |||||||

| Temporary Cash Investments — 1.0% | ||||||||

Repurchase Agreement, Bank of America Merrill Lynch, (collateralized by various U.S. Treasury obligations, 1.50% - 2.00%, 1/31/16 - 6/30/16, valued at $3,879,539), in a joint trading account at 0.23%, dated 10/31/12, due 11/1/12 (Delivery value $3,801,363) | $3,801,339 | |||||||

Repurchase Agreement, Credit Suisse First Boston, Inc., (collateralized by various U.S. Treasury obligations, 3.125% - 3.75%, 8/15/41 - 2/15/42, valued at $3,888,558), in a joint trading account at 0.20%, dated 10/31/12, due 11/1/12 (Delivery value $3,801,360) | 3,801,339 | |||||||

Repurchase Agreement, Goldman Sachs & Co., (collateralized by various U.S. Treasury obligations, 4.625%, 2/15/40, valued at $1,614,781), in a joint trading account at 0.16%, dated 10/31/12, due 11/1/12 (Delivery value $1,583,392) | $1,583,385 | |||||||

| SSgA U.S. Government Money Market Fund | 25,908 | 25,908 | ||||||

TOTAL TEMPORARY CASH INVESTMENTS (Cost $9,211,971) | 9,211,971 | |||||||

TOTAL INVESTMENT SECURITIES — 100.1% (Cost $702,153,161) | 976,366,012 | |||||||

| OTHER ASSETS AND LIABILITIES — (0.1)% | (551,852 | ) | ||||||

| TOTAL NET ASSETS — 100.0% | $975,814,160 | |||||||

| Forward Foreign Currency Exchange Contracts | |||||

| Contracts to Sell | Counterparty | Settlement Date | Value | Unrealized Gain (Loss) | |

| 4,253,569 | EUR for USD | UBS AG | 11/30/12 | $5,514,606 | $(9,381) |

(Value on Settlement Date $5,505,225)

Notes to Schedule of Investments

EUR = Euro

USD = United States Dollar

(1) Non-income producing.

See Notes to Financial Statements.

14

| OCTOBER 31, 2012 | ||||

| Assets | ||||

| Investment securities, at value (cost of $702,153,161) | $976,366,012 | |||

| Receivable for investments sold | 8,080,109 | |||

| Receivable for capital shares sold | 425,714 | |||

| Dividends and interest receivable | 1,162,150 | |||

| 986,033,985 | ||||

| Liabilities | ||||

| Payable for investments purchased | 8,331,087 | |||

| Payable for capital shares redeemed | 1,023,926 | |||

| Unrealized loss on forward foreign currency exchange contracts | 9,381 | |||

| Accrued management fees | 851,090 | |||

| Distribution and service fees payable | 4,341 | |||

| 10,219,825 | ||||

| Net Assets | $975,814,160 | |||

| Net Assets Consist of: | ||||

| Capital (par value and paid-in surplus) | $637,339,216 | |||

| Accumulated net investment loss | (200,949 | ) | ||

| Undistributed net realized gain | 64,472,423 | |||

| Net unrealized appreciation | 274,203,470 | |||

| $975,814,160 | ||||

| Net assets | Shares outstanding | Net asset value per share | |

| Investor Class, $0.01 Par Value | $961,562,056 | 31,588,991 | $30.44 |

| Institutional Class, $0.01 Par Value | $61,452 | 2,015 | $30.50 |

| A Class, $0.01 Par Value | $11,333,944 | 373,364 | $30.36* |

| C Class, $0.01 Par Value | $1,992,567 | 66,187 | $30.11 |

| R Class, $0.01 Par Value | $864,141 | 28,545 | $30.27 |

*Maximum offering price $32.21 (net asset value divided by 0.9425).

See Notes to Financial Statements.

15

| YEAR ENDED OCTOBER 31, 2012 | ||||

| Investment Income (Loss) | ||||

| Income: | ||||

| Dividends (net of foreign taxes withheld of $14,978) | $10,216,291 | |||

| Interest | 12,700 | |||

| 10,228,991 | ||||

| Expenses: | ||||

| Management fees | 9,796,331 | |||

| Distribution and service fees: | ||||

| A Class | 11,601 | |||

| C Class | 7,946 | |||

| R Class | 905 | |||

| Directors’ fees and expenses | 35,889 | |||

| 9,852,672 | ||||

| Net investment income (loss) | 376,319 | |||

| Realized and Unrealized Gain (Loss) | ||||

| Net realized gain (loss) on: | ||||

| Investment transactions | 66,894,843 | |||

| Foreign currency transactions | 240,950 | |||

| 67,135,793 | ||||

| Change in net unrealized appreciation (depreciation) on: | ||||

| Investments | 35,910,577 | |||

| Translation of assets and liabilities in foreign currencies | 16,234 | |||

| 35,926,811 | ||||

| Net realized and unrealized gain (loss) | 103,062,604 | |||

| Net Increase (Decrease) in Net Assets Resulting from Operations | $103,438,923 | |||

See Notes to Financial Statements.

16

| YEARS ENDED OCTOBER 31, 2012 AND OCTOBER 31, 2011 | ||||||||

| Increase (Decrease) in Net Assets | October 31, 2012 | October 31, 2011 | ||||||

| Operations | ||||||||

| Net investment income (loss) | $376,319 | $(846,286 | ) | |||||

| Net realized gain (loss) | 67,135,793 | 126,248,283 | ||||||

| Change in net unrealized appreciation (depreciation) | 35,926,811 | (49,826,959 | ) | |||||

| Net increase (decrease) in net assets resulting from operations | 103,438,923 | 75,575,038 | ||||||

| Distributions to Shareholders | ||||||||

| From net realized gains: | ||||||||

| Investor Class | (23,595,114 | ) | — | |||||

| Institutional Class | (705 | ) | — | |||||

| A Class | (705 | ) | — | |||||

| C Class | (1,880 | ) | — | |||||

| R Class | (705 | ) | — | |||||

| Decrease in net assets from distributions | (23,599,109 | ) | — | |||||

| Capital Share Transactions | ||||||||

| Net increase (decrease) in net assets from capital share transactions | (39,887,723 | ) | (99,159,677 | ) | ||||

| Net increase (decrease) in net assets | 39,952,091 | (23,584,639 | ) | |||||

| Net Assets | ||||||||

| Beginning of period | 935,862,069 | 959,446,708 | ||||||

| End of period | $975,814,160 | $935,862,069 | ||||||

| Accumulated undistributed net investment income (loss) | $(200,949 | ) | $26,069 | |||||

See Notes to Financial Statements.

17

1. Organization

American Century Mutual Funds, Inc. (the corporation) is registered under the Investment Company Act of 1940, as amended (the 1940 Act), as an open-end management investment company and is organized as a Maryland corporation. All Cap Growth Fund (the fund) is one fund in a series issued by the corporation. The fund is diversified as defined under the 1940 Act. The fund’s investment objective is to seek long-term capital growth. The fund pursues its objective by investing in stocks of companies of all sizes that management believes will increase in value over time.

The fund offers the Investor Class, the Institutional Class, the A Class, the C Class and the R Class. The A Class may incur an initial sales charge. The A Class and C Class may be subject to a contingent deferred sales charge. The share classes differ principally in their respective sales charges and distribution and shareholder servicing expenses and arrangements. The Institutional Class is made available to institutional shareholders or through financial intermediaries whose clients do not require the same level of shareholder and administrative services as shareholders of other classes. As a result, the Institutional Class is charged a lower unified management fee. Sale of the Institutional Class, A Class, C Class and R Class commenced on September 30, 2011.

2. Significant Accounting Policies

The following is a summary of significant accounting policies consistently followed by the fund in preparation of its financial statements. The financial statements are prepared in conformity with accounting principles generally accepted in the United States of America, which may require management to make certain estimates and assumptions at the date of the financial statements. Actual results could differ from these estimates.

Investment Valuations — The fund determines the fair value of its investments and computes its net asset value per share as of the close of regular trading (usually 4 p.m. Eastern time) on the New York Stock Exchange (NYSE) on each day the NYSE is open.

Equity securities that are listed or traded on a domestic securities exchange are valued at the last reported sales price or at the official closing price as provided by the exchange. Equity securities traded on foreign securities exchanges are typically valued at the closing price on the exchange where primarily traded or as of the close of the NYSE, if that is earlier. If no last sales price is reported, or if local convention or regulation so provides, the mean of the latest bid and asked prices is used. Depending on local convention or regulation, securities traded over-the-counter are valued at the mean of the latest bid and asked prices, the last sales price, or the official closing price. In its determination of fair value, the fund may review several factors including: market information specific to a security; news developments in U.S. and foreign markets; the performance of particular U.S. and foreign securities, indices, comparable securities, American Depositary Receipts, Exchange-Traded Funds, and other relevant market indicators.

Debt securities maturing within 60 days at the time of purchase may be valued at cost, plus or minus any amortized discount or premium or at the evaluated mean as provided by an independent pricing service. Evaluated mean prices are commonly derived through utilization of market models, which may consider, among other factors, trade data, quotations from dealers and active market makers, relevant yield curve and spread data, related sector levels, creditworthiness, and other relevant market information on the same or comparable securities.

Investments in open-end management investment companies are valued at the reported net asset value per share. Repurchase agreements are valued at cost. Forward foreign currency exchange contracts are valued at the mean of the latest bid and asked prices of the forward currency rates as provided by an independent pricing service.

The value of investments initially expressed in foreign currencies is translated into U.S. dollars at prevailing exchange rates.

18

If the fund determines that the market price for a portfolio security is not readily available or the valuation methods mentioned above do not reflect a security’s fair value, such security is valued as determined in good faith by the Board of Directors or its designee, in accordance with procedures adopted by the Board of Directors. Circumstances that may cause the fund to use these procedures to value a security include, but are not limited to: a security has been declared in default; trading in a security has been halted during the trading day; there is a foreign market holiday and no trading occurred; or an event occurred between the close of a foreign exchange and the NYSE that may affect the value of a security.

Security Transactions — Security transactions are accounted for as of the trade date. Net realized gains and losses are determined on the identified cost basis, which is also used for federal income tax purposes.

Investment Income — Dividend income less foreign taxes withheld, if any, is recorded as of the ex-dividend date. Distributions received on securities that represent a return of capital or capital gain are recorded as a reduction of cost of investments and/or as a realized gain. The fund estimates the components of distributions received that may be considered nontaxable distributions or capital gain distributions for income tax purposes. Interest income is recorded on the accrual basis and includes accretion of discounts and amortization of premiums.

Foreign Currency Translations — All assets and liabilities initially expressed in foreign currencies are translated into U.S. dollars at prevailing exchange rates at period end. The fund may enter into spot foreign currency exchange contracts to facilitate transactions denominated in a foreign currency. Purchases and sales of investment securities, dividend and interest income, spot foreign currency exchange contracts, and expenses are translated at the rates of exchange prevailing on the respective dates of such transactions. Net realized and unrealized foreign currency exchange gains or losses related to investment securities are a component of net realized gain (loss) on investment transactions and change in net unrealized appreciation (depreciation) on investments, respectively.

Repurchase Agreements — The fund may enter into repurchase agreements with institutions that American Century Investment Management, Inc. (ACIM) (the investment advisor) has determined are creditworthy pursuant to criteria adopted by the Board of Directors. The fund requires that the collateral, represented by securities, received in a repurchase transaction be transferred to the custodian in a manner sufficient to enable the fund to obtain those securities in the event of a default under the repurchase agreement. ACIM monitors, on a daily basis, the securities transferred to ensure the value, including accrued interest, of the securities under each repurchase agreement is equal to or greater than amounts owed to the fund under each repurchase agreement.

Joint Trading Account — Pursuant to an Exemptive Order issued by the Securities and Exchange Commission, the fund, along with certain other funds in the American Century Investments family of funds, may transfer uninvested cash balances into a joint trading account. These balances are invested in one or more repurchase agreements that are collateralized by U.S. Treasury or Agency obligations.

Income Tax Status — It is the fund’s policy to distribute substantially all net investment income and net realized gains to shareholders and to otherwise qualify as a regulated investment company under provisions of the Internal Revenue Code. The fund is no longer subject to examination by tax authorities for years prior to 2009. Additionally, non-U.S. tax returns filed by the fund due to investments in certain foreign securities remain subject to examination by the relevant taxing authority for seven years from the date of filing. At this time, management believes there are no uncertain tax positions which, based on their technical merit, would not be sustained upon examination and for which it is reasonably possible that the total amounts of unrecognized tax benefits will significantly change in the next twelve months. Accordingly, no provision has been made for federal or state income taxes.

19

Multiple Class — All shares of the fund represent an equal pro rata interest in the net assets of the class to which such shares belong, and have identical voting, dividend, liquidation and other rights and the same terms and conditions, except for class specific expenses and exclusive rights to vote on matters affecting only individual classes. Income, non-class specific expenses, and realized and unrealized capital gains and losses of the fund are allocated to each class of shares based on their relative net assets.

Distributions to Shareholders — Distributions from net investment income and net realized gains, if any, are generally declared and paid annually.

Indemnifications — Under the corporation’s organizational documents, its officers and directors are indemnified against certain liabilities arising out of the performance of their duties to the fund. In addition, in the normal course of business, the fund enters into contracts that provide general indemnifications. The maximum exposure under these arrangements is unknown as this would involve future claims that may be made against a fund. The risk of material loss from such claims is considered by management to be remote.

3. Fees and Transactions with Related Parties

Management Fees — The corporation has entered into a management agreement with ACIM, under which ACIM provides the fund with investment advisory and management services in exchange for a single, unified management fee (the fee) per class. The agreement provides that all expenses of managing and operating the fund, except distribution and service fees, brokerage expenses, taxes, interest, fees and expenses of the independent directors (including legal counsel fees), and extraordinary expenses, will be paid by ACIM. The fee is computed and accrued daily based on each class’s daily net assets and paid monthly in arrears. The annual management fee is 1.00% for the Investor Class, A Class, C Class and R Class and 0.80% for the Institutional Class.

Distribution and Service Fees — The Board of Directors has adopted a separate Master Distribution and Individual Shareholder Services Plan for each of the A Class, C Class and R Class (collectively the plans), pursuant to Rule 12b-1 of the 1940 Act. The plans provide that the A Class will pay American Century Investment Services, Inc. (ACIS) an annual distribution and service fee of 0.25%. The plans provide that the C Class will pay ACIS an annual distribution and service fee of 1.00%, of which 0.25% is paid for individual shareholder services and 0.75% is paid for distribution services. The plans provide that the R Class will pay ACIS an annual distribution and service fee of 0.50%. The fees are computed and accrued daily based on each class’s daily net assets and paid monthly in arrears. The fees are used to pay financial intermediaries for distribution and individual shareholder services. Fees incurred under the plans during the year ended October 31, 2012 are detailed in the Statement of Operations.

Related Parties — Certain officers and directors of the corporation are also officers and/or directors of American Century Companies, Inc., the parent of the corporation’s investment advisor, ACIM, the distributor of the corporation, ACIS, and the corporation’s transfer agent, American Century Services, LLC.

4. Investment Transactions

Purchases and sales of investment securities, excluding short-term investments, for the year ended October 31, 2012 were $533,433,401 and $599,893,274, respectively.

20

5. Capital Share Transactions

Transactions in shares of the fund were as follows:

| Year ended October 31, 2012 | Year ended October 31, 2011(1) | |||||||||||||||

| Shares | Amount | Shares | Amount | |||||||||||||

| Investor Class/Shares Authorized | 200,000,000 | 200,000,000 | ||||||||||||||

| Sold | 1,442,712 | $43,890,074 | 229,937 | $6,555,442 | ||||||||||||

| Issued in reinvestment of distributions | 873,776 | 23,207,496 | — | — | ||||||||||||

| Redeemed | (4,078,501 | ) | (121,343,490 | ) | (3,675,174 | ) | (105,815,119 | ) | ||||||||

| (1,762,013 | ) | (54,245,920 | ) | (3,445,237 | ) | (99,259,677 | ) | |||||||||

| Institutional Class/Shares Authorized | 25,000,000 | 25,000,000 | ||||||||||||||

| Sold | 1,317 | 40,379 | 987 | 25,000 | ||||||||||||

| Issued in reinvestment of distributions | 27 | 705 | — | — | ||||||||||||

| Redeemed | (316 | ) | (9,915 | ) | — | — | ||||||||||

| 1,028 | 31,169 | 987 | 25,000 | |||||||||||||

| A Class/Shares Authorized | 25,000,000 | 25,000,000 | ||||||||||||||

| Sold | 396,764 | 12,260,804 | 987 | 25,000 | ||||||||||||

| Issued in reinvestment of distributions | 27 | 705 | — | — | ||||||||||||

| Redeemed | (24,414 | ) | (751,345 | ) | — | — | ||||||||||

| 372,377 | 11,510,164 | 987 | 25,000 | |||||||||||||

| C Class/Shares Authorized | 25,000,000 | 25,000,000 | ||||||||||||||

| Sold | 68,891 | 2,084,611 | 987 | 25,000 | ||||||||||||

| Issued in reinvestment of distributions | 71 | 1,880 | — | — | ||||||||||||

| Redeemed | (3,762 | ) | (115,245 | ) | — | — | ||||||||||

| 65,200 | 1,971,246 | 987 | 25,000 | |||||||||||||

| R Class/Shares Authorized | 25,000,000 | 25,000,000 | ||||||||||||||

| Sold | 32,043 | 986,202 | 987 | 25,000 | ||||||||||||

| Issued in reinvestment of distributions | 27 | 705 | — | — | ||||||||||||

| Redeemed | (4,512 | ) | (141,289 | ) | — | — | ||||||||||

| 27,558 | 845,618 | 987 | 25,000 | |||||||||||||

| Net increase (decrease) | (1,295,850 | ) | $(39,887,723 | ) | (3,441,289 | ) | $(99,159,677 | ) | ||||||||

| (1) | September 30, 2011 (commencement of sale) through October 31, 2011 for the Institutional Class, A Class, C Class and R Class. |

6. Fair Value Measurements

The fund’s securities valuation process is based on several considerations and may use multiple inputs to determine the fair value of the positions held by the fund. In conformity with accounting principles generally accepted in the United States of America, the inputs used to determine a valuation are classified into three broad levels as follows:

| • | Level 1 valuation inputs consist of unadjusted quoted prices in an active market for identical securities; |

| • | Level 2 valuation inputs consist of direct or indirect observable market data (including quoted prices for similar securities, evaluations of subsequent market events, interest rates, prepayment speeds, credit risk, etc.); or |

| • | Level 3 valuation inputs consist of unobservable data (including a fund’s own assumptions). |

The level classification is based on the lowest level input that is significant to the fair valuation measurement. The valuation inputs are not necessarily an indication of the risks associated with investing in these securities or other financial instruments.

21

The following is a summary of the level classifications as of period end. The Schedule of Investments provides additional information on the fund’s portfolio holdings.

| Level 1 | Level 2 | Level 3 | ||||||||||

| Investment Securities | ||||||||||||

| Domestic Common Stocks | $908,366,244 | — | — | |||||||||

| Foreign Common Stocks | 43,714,115 | $15,073,682 | — | |||||||||

| Temporary Cash Investments | 25,908 | 9,186,063 | — | |||||||||

| Total Value of Investment Securities | $952,106,267 | $24,259,745 | — | |||||||||

| Other Financial Instruments | ||||||||||||

Total Unrealized Gain (Loss) on Forward Foreign Currency Exchange Contracts | — | $(9,381 | ) | — | ||||||||

7. Derivative Instruments

Foreign Currency Risk — The fund is subject to foreign currency exchange rate risk in the normal course of pursuing its investment objectives. The value of foreign investments held by a fund may be significantly affected by changes in foreign currency exchange rates. The dollar value of a foreign security generally decreases when the value of the dollar rises against the foreign currency in which the security is denominated and tends to increase when the value of the dollar declines against such foreign currency. A fund may enter into forward foreign currency exchange contracts to reduce a fund’s exposure to foreign currency exchange rate fluctuations. The net U.S. dollar value of foreign currency underlying all contractual commitments held by a fund and the resulting unrealized appreciation or depreciation are determined daily. Realized gain or loss is recorded upon the termination of the contract. Net realized and unrealized gains or losses occurring during the holding period of forward foreign currency exchange contracts are a component of net realized gain (loss) on foreign currency transactions and change in net unrealized appreciation (depreciation) on translation of assets and liabilities in foreign currencies, respectively. A fund bears the risk of an unfavorable change in the foreign currency exchange rate underlying the forward contract. Additionally, losses, up to the fair value, may arise if the counterparties do not perform under the contract terms. The foreign currency risk derivative instruments held at period end as disclosed on the Schedule of Investments are indicative of the fund’s typical volume during the period.

The value of foreign currency risk derivative instruments as of October 31, 2012, is disclosed on the Statement of Assets and Liabilities as a liability of $9,381 in unrealized loss on forward foreign currency exchange contracts. For the year ended October 31, 2012, the effect of foreign currency risk derivative instruments on the Statement of Operations was $270,463 in net realized gain (loss) on foreign currency transactions and $16,688 in change in net unrealized appreciation (depreciation) on translation of assets and liabilities in foreign currencies.

8. Risk Factors

There are certain risks involved in investing in foreign securities. These risks include those resulting from future adverse political, social and economic developments, fluctuations in currency exchange rates, the possible imposition of exchange controls, and other foreign laws or restrictions.

22

9. Federal Tax Information

The tax character of distributions paid during the years ended October 31, 2012 and October 31, 2011 were as follows:

| 2012 | 2011 | |

| Distributions Paid From | ||

| Ordinary income | — | — |

| Long-term capital gains | $23,599,109 | — |

The book-basis character of distributions made during the year from net investment income or net realized gains may differ from their ultimate characterization for federal income tax purposes. These differences reflect the differing character of certain income items and net realized gains and losses for financial statement and tax purposes, and may result in reclassification among certain capital accounts on the financial statements.

As of October 31, 2012, the federal tax cost of investments and the components of distributable earnings on a tax-basis were as follows:

| Federal tax cost of investments | $702,929,376 | |||

| Gross tax appreciation of investments | $284,207,497 | |||

| Gross tax depreciation of investments | (10,770,861 | ) | ||

| Net tax appreciation (depreciation) of investments | $273,436,636 | |||

| Undistributed ordinary income | — | |||

| Accumulated long-term gains | $65,248,637 | |||

| Late-year ordinary loss deferral | $(210,329 | ) |

The difference between book-basis and tax-basis cost and unrealized appreciation (depreciation) is attributable primarily to the tax deferral of losses on wash sales.

Loss deferrals represent certain qualified losses that the fund has elected to treat as having been incurred in the following fiscal year for federal income tax purposes.

23

| For a Share Outstanding Throughout the Years Ended October 31 (except as noted) | |||||||||||||||||||||||||||||||||||||

| Per-Share Data | Ratios and Supplemental Data | ||||||||||||||||||||||||||||||||||||

| Income From Investment Operations: | Distributions From: | Ratio to Average Net Assets of: | |||||||||||||||||||||||||||||||||||

Net Asset Value, Beginning of Period | Net Investment Income (Loss)(1) | Net Realized and Unrealized Gain (Loss) | Total From Investment Operations | Net Investment Income | Net Realized Gains | Total Distributions | Net Asset Value, End of Period | Total Return(2) | Operating Expenses | Net Investment Income (Loss) | Portfolio Turnover Rate | Net Assets, End of Period (in thousands) | |||||||||||||||||||||||||

| Investor Class | |||||||||||||||||||||||||||||||||||||

| 2012 | $28.06 | 0.01 | 3.08 | 3.09 | — | (0.71 | ) | (0.71 | ) | $30.44 | 11.40 | % | 1.00 | % | 0.04 | % | 55 | % | $961,562 | ||||||||||||||||||

| 2011 | $26.07 | (0.02 | ) | 2.01 | 1.99 | — | — | — | $28.06 | 7.63 | % | 1.00 | % | (0.08 | )% | 75 | % | $935,751 | |||||||||||||||||||

| 2010 | $20.86 | (0.05 | ) | 5.26 | 5.21 | — | — | — | $26.07 | 24.98 | % | 1.01 | % | (0.22 | )% | 88 | % | $959,447 | |||||||||||||||||||

| 2009 | $19.08 | 0.03 | 1.81 | 1.84 | (0.06 | ) | — | (0.06 | ) | $20.86 | 9.72 | % | 1.00 | % | 0.19 | % | 167 | % | $837,839 | ||||||||||||||||||

| 2008 | $31.53 | (0.13 | ) | (12.32 | ) | (12.45 | ) | — | — | — | $19.08 | (39.49 | )% | 1.00 | % | (0.48 | )% | 171 | % | $803,771 | |||||||||||||||||

| Institutional Class | |||||||||||||||||||||||||||||||||||||

| 2012 | $28.06 | 0.09 | 3.06 | �� | 3.15 | — | (0.71 | ) | (0.71 | ) | $30.50 | 11.62 | % | 0.80 | % | 0.24 | % | 55 | % | $61 | |||||||||||||||||

2011(3) | $25.32 | (0.01 | ) | 2.75 | 2.74 | — | — | — | $28.06 | 10.82 | % | 0.80 | %(4) | (0.28 | )%(4) | 75 | %(5) | $28 | |||||||||||||||||||

| A Class | |||||||||||||||||||||||||||||||||||||

| 2012 | $28.05 | (0.02 | ) | 3.04 | 3.02 | — | (0.71 | ) | (0.71 | ) | $30.36 | 11.15 | % | 1.25 | % | (0.21 | )% | 55 | % | $11,334 | |||||||||||||||||

2011(3) | $25.32 | (0.02 | ) | 2.75 | 2.73 | — | — | — | $28.05 | 10.78 | % | 1.25 | %(4) | (0.73 | )%(4) | 75 | %(5) | $28 | |||||||||||||||||||

| C Class | |||||||||||||||||||||||||||||||||||||

| 2012 | $28.03 | (0.25 | ) | 3.04 | 2.79 | — | (0.71 | ) | (0.71 | ) | $30.11 | 10.32 | % | 2.00 | % | (0.96 | )% | 55 | % | $1,993 | |||||||||||||||||

2011(3) | $25.32 | (0.03 | ) | 2.74 | 2.71 | — | — | — | $28.03 | 10.70 | % | 2.00 | %(4) | (1.48 | )%(4) | 75 | %(5) | $28 | |||||||||||||||||||

| R Class | |||||||||||||||||||||||||||||||||||||

| 2012 | $28.04 | (0.08 | ) | 3.02 | 2.94 | — | (0.71 | ) | (0.71 | ) | $30.27 | 10.86 | % | 1.50 | % | (0.46 | )% | 55 | % | $864 | |||||||||||||||||

2011(3) | $25.32 | (0.02 | ) | 2.74 | 2.72 | — | — | — | $28.04 | 10.74 | % | 1.50 | %(4) | (0.98 | )%(4) | 75 | %(5) | $28 | |||||||||||||||||||

24

Notes to Financial Highlights

| (1) | Computed using average shares outstanding throughout the period. |

| (2) | Total returns are calculated based on the net asset value of the last business day and do not reflect applicable sales charges, if any. Total returns for periods less than one year are not annualized. |

| (3) | September 30, 2011 (commencement of sale) through October 31, 2011. |

| (4) | Annualized. |

| (5) | Portfolio turnover is calculated at the fund level. Percentage indicated was calculated for the year ended October 31, 2011. |

See Notes to Financial Statements.

25

The Board of Directors and Shareholders of

American Century Mutual Funds, Inc.:

We have audited the accompanying statement of assets and liabilities, including the schedule of investments, of All Cap Growth Fund, one of the funds constituting American Century Mutual Funds, Inc. (the “Corporation”) as of October 31, 2012, and the related statement of operations for the year then ended, the statement of changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the periods presented. These financial statements and financial highlights are the responsibility of the Corporation’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. The Corporation is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Corporation’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of October 31, 2012, by correspondence with the custodian and brokers; where replies were not received from brokers, we performed other auditing procedures. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of All Cap Growth Fund of American Century Mutual Funds, Inc., as of October 31, 2012, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended, and the financial highlights for each of the periods presented, in conformity with accounting principles generally accepted in the United States of America.

Deloitte & Touche LLP

Kansas City, Missouri

December 19, 2012

26

The Board of Directors

The individuals listed below serve as directors of the funds. Each director will continue to serve in this capacity until death, retirement, resignation or removal from office. The mandatory retirement age for directors who are not “interested persons,” as that term is defined in the Investment Company Act (independent directors), is 72. However, the mandatory retirement age for an individual director may be extended with the approval of the remaining independent directors.

Mr. Thomas is an “interested person” because he currently serves as President and Chief Executive Officer of American Century Companies, Inc. (ACC), the parent company of American Century Investment Management, Inc. (ACIM or the advisor). Mr. Fink is an “interested person” because he currently serves as Executive Vice President of ACC.

The other directors (more than three-fourths of the total number) are independent; that is, they have never been employees, directors or officers of, and have no financial interest in, ACC or any of its wholly owned, direct or indirect, subsidiaries, including ACIM, American Century Investment Services, Inc. (ACIS) and American Century Services, LLC (ACS). The directors serve in this capacity for seven (in the case of Mr. Thomas, 15) registered investment companies in the American Century Investments family of funds.

The following table presents additional information about the directors. The mailing address for each director is 4500 Main Street, Kansas City, Missouri 64111.

Name (Year of Birth) | Position(s) Held with Funds | Length of Time Served | Principal Occupation(s) During Past 5 Years | Number of American Century Portfolios Overseen by Director | Other Directorships Held During Past 5 Years | |||||

| Independent Directors | ||||||||||

Thomas A. Brown (1940) | Director | Since 1980 | Managing Member, Associated Investments, LLC (real estate investment company); Brown Cascade Properties, LLC (real estate investment company) (2001 to 2009) | 66 | None | |||||

Andrea C. Hall (1945) | Director | Since 1997 | Retired | 66 | None | |||||

Jan M. Lewis (1957) | Director | Since 2011 | President and Chief Executive Officer, Catholic Charities of Northeast Kansas (human services organization) | 66 | None | |||||

James A. Olson (1942) | Director | Since 2007 | Member, Plaza Belmont LLC (private equity fund manager) | 66 | Saia, Inc. (2002 to 2012) and Entertainment Properties Trust | |||||

Donald H. Pratt (1937) | Director and Chairman of the Board | Since 1995 (Chairman since 2005) | Chairman and Chief Executive Officer, Western Investments, Inc. (real estate company) | 66 | None | |||||

27

Name (Year of Birth) | Position(s) Held with Funds | Length of Time Served | Principal Occupation(s) During Past 5 Years | Number of American Century Portfolios Overseen by Director | Other Directorships Held During Past 5 Years | |||||

| Independent Directors | ||||||||||

M. Jeannine Strandjord (1945) | Director | Since 1994 | Retired | 66 | Euronet Worldwide Inc.; Charming Shoppes, Inc. (2006 to 2010); and DST Systems Inc. (1996 to 2012) | |||||

John R. Whitten (1946) | Director | Since 2008 | Retired | 66 | Rudolph Technologies, Inc. | |||||

Stephen E. Yates (1948) | Director | Since 2012 | Retired; Executive Vice President, Technology & Operations, KeyCorp. (computer services)(2004 to 2010) | 66 | Applied Industrial Technologies, Inc. (2001 to 2010) | |||||

| Interested Directors | ||||||||||

Barry Fink (1955) | Director and Executive Vice President | Since 2012 (Executive Vice President since 2007) | Executive Vice President, ACC (September 2007 to present); President, ACS (October 2007 to present); Chief Operating Officer, ACC (September 2007 to November 2012). Also serves as Manager, ACS | 66 | None | |||||

Jonathan S. Thomas (1963) | Director and President | Since 2007 | President and Chief Executive Officer, ACC (March 2007 to present). Also serves as Chief Executive Officer and Manager, ACS; Executive Vice President, ACIM; Director, ACC, ACIM and other ACC subsidiaries | 108 | None | |||||

28

Officers

The following table presents certain information about the executive officers of the funds. Each officer serves as an officer for each of the 15 investment companies in the American Century family of funds, unless otherwise noted. No officer is compensated for his or her service as an officer of the funds. The listed officers are interested persons of the funds and are appointed or re-appointed on an annual basis. The mailing address for each officer listed below is 4500 Main Street, Kansas City, Missouri 64111.

Name (Year of Birth) | Offices with the Funds | Principal Occupation(s) During the Past Five Years | ||

Jonathan S. Thomas (1963) | Director and President since 2007 | President and Chief Executive Officer, ACC (March 2007 to present). Also serves as Chief Executive Officer and Manager, ACS; Executive Vice President, ACIM; Director, ACC, ACIM and other ACC subsidiaries | ||

Barry Fink (1955) | Director since 2012 and Executive Vice President since 2007 | Executive Vice President, ACC (September 2007 to present); President, ACS (October 2007 to present); Chief Operating Officer, ACC (September 2007 to November 2012). Also serves as Manager, ACS | ||

Maryanne L. Roepke (1956) | Chief Compliance Officer since 2006 and Senior Vice President since 2000 | Chief Compliance Officer, American Century funds, ACIM and ACS (August 2006 to present). Also serves as Senior Vice President, ACS | ||

Charles A. Etherington (1957) | General Counsel since 2007 and Senior Vice President since 2006 | Attorney, ACC (February 1994 to present); Vice President, ACC (November 2005 to present), General Counsel, ACC (March 2007 to present). Also serves as General Counsel, ACIM, ACS, ACIS and other ACC subsidiaries; and Senior Vice President, ACIM and ACS | ||

C. Jean Wade (1964) | Vice President, Treasurer and Chief Financial Officer since 2012 | Vice President, ACS (February 2000 to present) | ||

Robert J. Leach (1966) | Vice President since 2006 and Assistant Treasurer since 2012 | Vice President, ACS (February 2000 to present) | ||

David H. Reinmiller (1963) | Vice President since 2000 | Attorney, ACC (January 1994 to present); Associate General Counsel, ACC (January 2001 to present). Also serves as Vice President, ACIM and ACS | ||

Ward D. Stauffer (1960) | Secretary since 2005 | Attorney, ACC (June 2003 to present) |

The Statement of Additional Information has additional information about the fund’s directors and is available without charge, upon request, by calling 1-800-345-2021.

29

At a meeting held on June 21, 2012, the Fund’s Board of Directors unanimously approved the renewal of the management agreement pursuant to which American Century Investment Management, Inc. (the “Advisor”) acts as the investment advisor for the Fund. Under Section 15(c) of the Investment Company Act, contracts for investment advisory services are required to be reviewed, evaluated, and approved by a majority of a fund’s independent directors (the “Directors”) each year.

As a part of the approval process, the Board requested and reviewed extensive data and information compiled by the Advisor and certain independent providers of evaluation data concerning the Fund and the services provided to the Fund by the Advisor. This review was in addition to the oversight and evaluation undertaken by the Board and its committees on a continuous basis throughout the year and included, but was not limited to the following:

| • | the nature, extent, and quality of investment management, shareholder services, and other services provided by the Advisor to the Fund; |

| • | the wide range of other programs and services the Advisor provides to the Fund and its shareholders on a routine and non-routine basis; |

| • | the investment performance of the fund, including data comparing the Fund’s performance to appropriate benchmarks and/or a peer group of other mutual funds with similar investment objectives and strategies; |

| • | data comparing the cost of owning the Fund to the cost of owning similar funds; |

| • | the Advisor’s compliance policies, procedures, and regulatory experience; |

| • | financial data showing the cost of services provided to the Fund, the profitability of the Fund to the Advisor, and the overall profitability of the Advisor; |

| • | data comparing services provided and charges to other investment management clients of the Advisor; and |

| • | consideration of collateral benefits derived by the Advisor from the management of the Fund and any potential economies of scale relating thereto. |

In keeping with its practice, the Board held two in-person meetings and one telephonic meeting to review and discuss the information provided. The Directors also had the benefit of the advice of independent counsel throughout the period.

Factors Considered

The Directors considered all of the information provided by the Advisor, the independent data providers, and independent counsel, and evaluated such information for the Fund. In connection with their review, the Directors did not identify any single factor as being all-important or controlling, and each Director may have attributed different levels of importance to different factors. In deciding to renew the management agreement, the Board based its decision on a number of factors, including the following:

30

Nature, Extent and Quality of Services — Generally. Under the management agreement, the Advisor is responsible for providing or arranging for all services necessary for the operation of the Fund. The Board noted that under the management agreement, the Advisor provides or arranges at its own expense a wide variety of services including:

| • | constructing and designing the Fund |

| • | portfolio research and security selection |

| • | initial capitalization/funding |

| • | securities trading |

| • | Fund administration |

| • | custody of Fund assets |

| • | daily valuation of the Fund’s portfolio |

| • | shareholder servicing and transfer agency, including shareholder confirmations, recordkeeping, and communications |

| • | legal services |

| • | regulatory and portfolio compliance |

| • | financial reporting |

| • | marketing and distribution |

The Board noted that many of these services have expanded over time both in terms of quantity and complexity in response to shareholder demands, competition in the industry, changing distribution channels, and the changing regulatory environment.

Investment Management Services. The nature of the investment management services provided to the Fund is quite complex and allows Fund shareholders access to professional money management, instant diversification of their investments within an asset class, the opportunity to easily diversify among asset classes by investing in or exchanging among various American Century Investments funds, and liquidity. In evaluating investment performance, the Board expects the Advisor to manage the Fund in accordance with its investment objectives and approved strategies. Further, the Directors recognize that the Advisor has an obligation to monitor trading activities, and in particular to seek the best execution of fund trades, and to evaluate the use of and payment for research. In providing these services, the Advisor utilizes teams of investment professionals (portfolio managers, analysts, research assistants, and securities traders) who require extensive information technology, research, training, compliance and other systems to conduct their business. The Board, directly and through its Fund Performance Review Committee, regularly reviews investment performance information for the Fund, together with comparative information for appropriate benchmarks and/or peer groups of similarly-managed funds, over different time horizons. The

31