UNITED STATES |

SECURITIES AND EXCHANGE COMMISSION |

Washington, D.C. 20549 |

| |

FORM 10-Q |

| |

(Mark One) | |

[ü] QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF |

THE SECURITIES EXCHANGE ACT OF 1934 |

| |

| For the Quarterly Period Ended September 30, 2005 |

| |

OR |

| |

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF |

THE SECURITIES EXCHANGE ACT OF 1934 |

| |

| For the transition period from to |

| |

| Commission File Number 1-14174 |

| |

AGL RESOURCES INC. |

| (Exact name of registrant as specified in its charter) |

| |

Georgia | 58-2210952 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| |

Ten Peachtree Place NE, Atlanta, Georgia 30309 |

| (Address and zip code of principal executive offices) |

| |

404-584-4000 |

| (Registrant's telephone number, including area code) |

| |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to the filing requirements for at least the past 90 days. Yes ü No |

| |

Indicate by check mark whether the registrant is an accelerated filer (as defined in Rule 12b-2 of the Exchange Act). Yes ü No |

| |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes No ü |

| |

| Indicate the number of shares outstanding of each of the issuer's classes of common stock, as of the latest practicable date. |

| |

Class | Outstanding as of October 20, 2005 |

| Common Stock, $5.00 Par Value | 77,651,829 |

AGL RESOURCES INC.

Form 10-Q

For the Quarterly Period Ended September 30, 2005

Item Number | | Page(s) |

| | | |

| | PART I - FINANCIAL INFORMATION | 3-50 |

| | | |

| 1 | Condensed Consolidated Financial Statements (Unaudited) | 3-22 |

| | Condensed Consolidated Balance Sheets | 3 |

| | Condensed Consolidated Statements of Income | 4 |

| | Condensed Consolidated Statements of Common Shareholders’ Equity | 5 |

| | Condensed Consolidated Statements of Cash Flows | 6 |

| | Notes to Condensed Consolidated Financial Statements | 7 |

| | Note 1 - Accounting Policies and Methods of Application | 7-9 |

| | Note 2 - NUI Corporation Acquisition Update | 9 |

| | Note 3 - Recent Accounting Pronouncements | 9-10 |

| | Note 4 - Risk Management | 10-12 |

| | Note 5 - Regulatory Assets and Liabilities | 13-15 |

| | Note 6 - Pension and Other Post-retirement Benefits | 15-16 |

| | Note 7 - Compensation Plans | 16 |

| | Note 8 - Financing | 17 |

| | Note 9 - Commitments and Contingencies | 18 |

| | Note 10 - Segment Information | 18-22 |

| 2 | Management's Discussion and Analysis of Financial Condition and Results of Operation | 23-50 |

| | Cautionary Statement Regarding Forward-Looking Information | 23 |

| | Overview | 23-27 |

| | Results of Operations | 27-43 |

| | AGL Resources | 27-30 |

| | Distribution Operations | 30-34 |

| | Retail Energy Operations | 34-35 |

| | Wholesale Services | 36-40 |

| | Energy Investments | 40-41 |

| | Corporate | 42-43 |

| | Liquidity and Capital Resources | 44-47 |

| | Critical Accounting Policies and Estimates | 47-48 |

| | Accounting Developments | 48 |

| 3 | Quantitative and Qualitative Disclosures About Market Risk | 48-50 |

| 4 | Controls and Procedures | 50 |

| | | |

| | PART II - OTHER INFORMATION | 50-51 |

| | | |

| 1 | Legal Proceedings | 50-51 |

| 2 | Unregistered Sales of Equity Securities and Use of Proceeds | 51 |

| 6 | Exhibits | 51 |

| | | |

| | SIGNATURE | 52 |

PART I - Financial Information Item 1. Condensed Consolidated Financial Statements (Unaudited) | |

| | |

| |

CONDENSED CONSOLIDATED BALANCE SHEETS | |

(UNAUDITED) | |

| | | | | | | | |

In millions, except shares and par value | | Sept. 30, 2005 | | Dec. 31, 2004 | | Sept. 30, 2004 | |

Current assets | | | | | | | |

| Cash and cash equivalents | | $ | 57 | | $ | 49 | | $ | 44 | |

| Receivables (less allowance for uncollectible accounts of $13 at Sept. 30, 2005, $15 at Dec. 31, 2004 and $12 at Sept. 30, 2004) | | | 781 | | | 737 | | | 328 | |

| Inventories | | | 518 | | | 332 | | | 340 | |

| Energy marketing and risk management assets | | | 161 | | | 38 | | | 33 | |

| Unbilled revenues | | | 58 | | | 152 | | | 34 | |

| Recoverable environmental remediation costs | | | 29 | | | 27 | | | 26 | |

| Recoverable pipeline replacement program costs | | | 24 | | | 24 | | | 24 | |

| Other | | | 190 | | | 98 | | | 19 | |

| Total current assets | | | 1,818 | | | 1,457 | | | 848 | |

Property, plant and equipment | | | | | | | | | | |

| Property, plant and equipment | | | 4,727 | | | 4,615 | | | 3,509 | |

| Less accumulated depreciation | | | 1,487 | | | 1,437 | | | 1,072 | |

| Property, plant and equipment-net | | | 3,240 | | | 3,178 | | | 2,437 | |

Deferred debits and other assets | | | | | | | | | | |

| Goodwill | | | 405 | | | 354 | | | 177 | |

| Recoverable pipeline replacement program costs | | | 331 | | | 337 | | | 358 | |

| Recoverable environmental remediation costs | | | 180 | | | 173 | | | 147 | |

| Other | | | 112 | | | 141 | | | 67 | |

| Total deferred debits and other assets | | | 1,028 | | | 1,005 | | | 749 | |

Total assets | | $ | 6,086 | | $ | 5,640 | | $ | 4,034 | |

Current liabilities | | | | | | | | | | |

| Payables | | $ | 819 | | $ | 728 | | $ | 423 | |

| Short-term debt | | | 344 | | | 334 | | | 51 | |

| Energy marketing and risk management liabilities | | | 278 | | | 15 | | | 26 | |

| Accrued expenses | | | 118 | | | 65 | | | 38 | |

| Accrued pipeline replacement program costs | | | 47 | | | 85 | | | 88 | |

| Other | | | 152 | | | 250 | | | 157 | |

| Total current liabilities | | | 1,758 | | | 1,477 | | | 783 | |

Accumulated deferred income taxes | | | 412 | | | 437 | | | 433 | |

Long-term liabilities | | | | | | | | | | |

| Accrued pipeline replacement program costs | | | 270 | | | 242 | | | 264 | |

| Deferred credits | | | 168 | | | 73 | | | 70 | |

| Accumulated removal costs | | | 92 | | | 94 | | | 93 | |

| Accrued environmental remediation costs | | | 90 | | | 63 | | | 36 | |

| Accrued pension obligations | | | 87 | | | 84 | | | 28 | |

| Accrued postretirement benefit costs | | | 54 | | | 58 | | | 48 | |

| Other | | | 57 | | | 68 | | | 10 | |

| Total long-term liabilities | | | 818 | | | 682 | | | 549 | |

Commitments and contingencies (Note 9) | | | | | | | | | | |

Minority interest | | | 31 | | | 36 | | | 30 | |

Capitalization | | | | | | | | | | |

| Long-term debt | | | 1,616 | | | 1,623 | | | 1,216 | |

| Shareholders’ equity (Common stock, $5 par value, 750 million shares authorized; 77.6 million shares issued and outstanding at September 30, 2005; 76.7 million shares issued and outstanding at December 31, 2004; 64.9 million shares issued and outstanding at September 30, 2004) | | | 1,451 | | | 1,385 | | | 1,023 | |

| Total capitalization | | | 3,067 | | | 3,008 | | | 2,239 | |

Total liabilities and capitalization | | $ | 6,086 | | $ | 5,640 | | $ | 4,034 | |

See Notes to Condensed Consolidated Financial Statements (Unaudited)

AGL RESOURCES INC. AND SUBSIDIARIES | |

CONDENSED CONSOLIDATED STATEMENTS OF INCOME | |

(UNAUDITED) | |

| | | | | | | | | | |

| | | Three months ended September 30, | | Nine months ended September 30, | |

| | 2005 | | 2004 | | 2005 | | 2004 | |

| Operating revenues | | $ | 393 | | $ | 262 | | $ | 1,736 | | $ | 1,206 | |

| Operating expenses | | | | | | | | | | | | | |

| Cost of gas | | | 191 | | | 105 | | | 972 | | | 626 | |

| Operation and maintenance | | | 106 | | | 83 | | | 334 | | | 257 | |

| Depreciation and amortization | | | 33 | | | 23 | | | 99 | | | 71 | |

| Taxes other than income | | | 9 | | | 5 | | | 30 | | | 20 | |

| Total operating expenses | | | 339 | | | 216 | | | 1,435 | | | 974 | |

| Operating income | | | 54 | | | 46 | | | 301 | | | 232 | |

| Other income | | | - | | | - | | | 2 | | | 2 | |

| Interest expense | | | (27 | ) | | (17 | ) | | (79 | ) | | (49 | ) |

| Minority interest | | | (2 | ) | | - | | | (18 | ) | | (14 | ) |

| Earnings before income taxes | | | 25 | | | 29 | | | 206 | | | 171 | |

| Income taxes | | | 10 | | | 9 | | | 79 | | | 64 | |

| Net income | | $ | 15 | | $ | 20 | | $ | 127 | | $ | 107 | |

| | | | | | | | | | | | | | |

| Basic earnings per common share | | $ | 0.19 | | $ | 0.31 | | $ | 1.64 | | $ | 1.66 | |

| Diluted earnings per common share | | $ | 0.19 | | $ | 0.31 | | $ | 1.62 | | $ | 1.64 | |

| Weighted-average number of common shares outstanding | | | | | | | | | | | | | |

| Basic | | | 77.5 | | | 65.1 | | | 77.2 | | | 64.8 | |

| Diluted | | | 78.1 | | | 65.8 | | | 77.8 | | | 65.5 | |

See Notes to Condensed Consolidated Financial Statements (Unaudited)

AGL RESOURCES INC. AND SUBSIDIARIES | |

CONDENSED CONSOLIDATED STATEMENTS OF COMMON SHAREHOLDERS’ EQUITY | |

(UNAUDITED) | |

| | | | | | | | | | | | | | |

| | | | | | | Premium on | | | | Other | | | |

| | | Common stock | | common | | Earnings | | comprehensive | | | |

In millions, except per share amount | | Shares | | Amount | | shares | | reinvested | | income | | Total | |

| Balance as of December 31, 2004 | | | 76.7 | | $ | 384 | | $ | 632 | | $ | 415 | | $ | (46 | ) | $ | 1,385 | |

| Comprehensive income: | | | | | | | | | | | | | | | | | | | |

| Net income | | | - | | | - | | | - | | | 127 | | | - | | | 127 | |

| Net unrealized loss from hedging activities (net of taxes) | | | - | | | - | | | - | | | - | | | (8 | ) | | (8 | ) |

| Total comprehensive income | | | | | | | | | | | | | | | | | | 119 | |

| Dividends on common shares ($0.93 per share) | | | - | | | - | | | - | | | (72 | ) | | - | | | (72 | ) |

| Stock compensation, dividend reinvestment and share purchase plans | | | 0.9 | | | 4 | | | 15 | | | - | | | - | | | 19 | |

| Balance as of September 30, 2005 | | | 77.6 | | $ | 388 | | $ | 647 | | $ | 470 | | $ | (54 | ) | $ | 1,451 | |

See Notes to Condensed Consolidated Financial Statements (Unaudited)

| |

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS | |

(UNAUDITED) | |

| | | | |

| | | Nine months ended | |

| | | September 30, | |

In millions | | 2005 | | 2004 | |

Cash flows from operating activities | | | | | |

| Net income | | $ | 127 | | $ | 107 | |

| Adjustments to reconcile net income to net cash flow provided by operating activities | | | | | | | |

| Depreciation and amortization | | | 99 | | | 71 | |

| Deferred income taxes | | | (25 | ) | | 57 | |

| Changes in certain assets and liabilities | | | | | | | |

| Payables | | | 93 | | | (38 | ) |

| Receivables | | | 43 | | | 200 | |

| Inventories | | | (187 | ) | | (102 | ) |

| Other | | | 37 | | | (40 | ) |

| Net cash flow provided by operating activities | | | 187 | | | 255 | |

Cash flows from investing activities | | | | | | | |

| Property, plant and equipment expenditures | | | (194 | ) | | (168 | ) |

| Sale of ownership interest in Saltville Gas Storage Company, LLC | | | 66 | | | - | |

| Sale of ownership interest in US Propane, LP | | | - | | | 31 | |

| Other | | | 8 | | | 13 | |

| Net cash flow used in investing activities | | | (120 | ) | | (124 | ) |

Cash flows from financing activities | | | | | | | |

| Payments and borrowings of short-term debt | | | 11 | | | (261 | ) |

| Payments of medium-term notes | | | - | | | (49 | ) |

| Dividends paid on common shares | | | (72 | ) | | (56 | ) |

| Borrowings from senior notes | | | - | | | 250 | |

| Distribution to minority interest | | | (19 | ) | | (14 | ) |

| Other | | | 21 | | | 26 | |

| Net cash flow used in financing activities | | | (59 | ) | | (104 | ) |

| Net increase in cash and cash equivalents | | | 8 | | | 27 | |

| Cash and cash equivalents at beginning of period | | | 49 | | | 17 | |

| Cash and cash equivalents at end of period | | $ | 57 | | $ | 44 | |

Cash paid during the period for | | | | | | | |

| Interest (net of allowance for funds used during construction of $1 million for the nine months ended September 30, 2005 and $2 million for the nine months ended September 30, 2004) | | $ | 62 | | $ | 36 | |

| Income taxes | | $ | 48 | | $ | 27 | |

See Notes to Condensed Consolidated Financial Statements (Unaudited)

AGL RESOURCES INC. AND SUBSIDIARIES NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED)

Note 1

Accounting Policies and Methods of Application

General

AGL Resources Inc. is an energy services holding company that conducts substantially all of its operations through its subsidiaries. Unless the context requires otherwise, references to “we,”“us,”“our” or the “company” are intended to mean consolidated AGL Resources Inc. and its subsidiaries (AGL Resources).

We have prepared the accompanying unaudited condensed consolidated financial statements under the rules of the Securities and Exchange Commission (SEC). Under such rules and regulations, we have condensed or omitted certain information and notes normally included in financial statements prepared in conformity with accounting principles generally accepted in the United States of America (GAAP). However, the condensed consolidated financial statements reflect all adjustments that are, in the opinion of management, necessary for a fair presentation of our financial results for the interim periods. You should read these condensed consolidated financial statements in conjunction with our consolidated financial statements and related notes included in our Annual Report on Form 10-K for the year ended December 31, 2004, filed with the SEC on February 15, 2005, as updated in our Current Report on Form 8-K filed with the SEC on July 28, 2005. All subsequent references to our Form 8-K filed with the SEC on July 28, 2005 herein should also be considered with reference to our Form 10-K as filed on February 15, 2005.

Due to the seasonal nature of our business, our results of operations for the three and nine months ended September 30, 2005 and 2004, and our financial position as of December 31, 2004 and September 30, 2005 and 2004, are not necessarily indicative of the results of operations and financial condition to be expected for any other period or as of any other date.

Basis of Presentation

Our condensed consolidated financial statements as of and for the period ended September 30, 2005 include our accounts, the accounts of our majority-owned and controlled subsidiaries and the accounts of variable interest entities for which we are the primary beneficiary. All significant intercompany items have been eliminated in consolidation. The December 31, 2004 balance sheet amounts are derived from our audited balance sheet as of December 31, 2004.

On January 1, 2004, we adopted the provisions of Financial Accounting Standards Board (FASB) Interpretation No. 46, “Consolidation of Variable Interest Entities” (FIN 46) as revised in December 2003 (FIN 46R). Upon adoption, we consolidated with our subsidiaries’ accounts all the accounts of SouthStar Energy Services LLC (SouthStar), a variable interest entity of which we currently own a noncontrolling 70% financial interest but have a 75% interest in the earnings and a 50% voting interest. We eliminated all intercompany balances in the consolidation. We recorded the portion of SouthStar’s earnings that are attributable to our joint venture partner, Piedmont Natural Gas Company, Inc. (Piedmont), as a minority interest in our condensed consolidated statements of income, and we recorded Piedmont’s portion of SouthStar’s capital as a minority interest in our condensed consolidated balance sheets. We determined that SouthStar is a variable interest entity as defined in FIN 46R because:

| · | Our equal voting rights with Piedmont are not proportional to our economic obligation to absorb 75% of any losses or residual returns from SouthStar, and |

| · | SouthStar obtains substantially all its transportation capacity for delivery of natural gas through our wholly-owned subsidiary, Atlanta Gas Light Company (Atlanta Gas Light). |

Prior to the sale of Saltville Gas Storage Company, LLC (Saltville) in August 2005, we utilized the equity method to account for and report our 50% interest in Saltville. We utilized the equity method because we exercised significant influence over but did not control the entity and because we were not the primary beneficiary as defined by FIN 46R.

Comprehensive Income

Our comprehensive income includes net income plus other comprehensive income (OCI), which includes other gains and losses affecting shareholders’ equity that GAAP excludes from net income. Such items consist primarily of unrealized gains and losses on certain derivatives designated as cash flow hedges and minimum pension liability adjustments. The following table illustrates our OCI acitivity for the nine months ended September 30, 2005:

In millions | | | |

| Change in cash flow hedges: | | | | |

| Net derivative losses arising during the period (net of $1 tax) | | $ | (2 | ) |

| Less reclassification adjustment of gains included in income (net of $3 in tax) | | | (6 | ) |

| Total | | $ | (8 | ) |

Stock-based Compensation

We have several stock-based employee compensation plans, and we account for these plans under the recognition and measurement principles of Accounting Principles Board Opinion No. 25, “Accounting for Stock Issued to Employees” (APB 25) and Statement of Financial Accounting Standards (SFAS) No. 123, “Accounting for Stock-Based Compensation” (SFAS 123). For our stock option plans, we generally do not reflect stock-based employee compensation cost in net income, as options granted under those plans have an exercise price equal to the market value of the underlying common stock on the date of grant. The following table illustrates the effect on our net income and earnings per share as if we had applied the optional fair value recognition provisions of SFAS 123:

| | | Three months ended September 30, | |

In millions, except per share amounts | | 2005 | | 2004 | |

| Net income, as reported | | $ | 15 | | $ | 20 | |

| Deduct stock-based employee compensation expense determined under fair value-based method for all awards, net of related tax effect | | | 1 | | | - | |

| Pro-forma net income | | $ | 14 | | $ | 20 | |

| | | | | | | | |

| Earnings per share: | | | | | | | |

| Basic - as reported | | $ | 0.19 | | $ | 0.31 | |

| Basic - pro-forma | | $ | 0.18 | | $ | 0.30 | |

| | | | | | | | |

| Fully diluted - as reported | | $ | 0.19 | | $ | 0.31 | |

| Fully diluted - pro-forma | | $ | 0.18 | | $ | 0.30 | |

| | | Nine months ended September 30, | |

In millions, except per share amounts | | 2005 | | 2004 | |

| Net income, as reported | | $ | 127 | | $ | 107 | |

| Deduct stock-based employee compensation expense determined under fair value-based method for all awards, net of related tax effect | | | 2 | | | 1 | |

| Pro-forma net income | | $ | 125 | | $ | 106 | |

| | | | | | | | |

| Earnings per share: | | | | | | | |

| Basic - as reported | | $ | 1.64 | | $ | 1.66 | |

| Basic - pro-forma | | $ | 1.62 | | $ | 1.64 | |

| | | | | | | | |

| Fully diluted - as reported | | $ | 1.63 | | $ | 1.64 | |

| Fully diluted - pro-forma | | $ | 1.60 | | $ | 1.63 | |

Earnings per Common Share

We compute basic earnings per common share by dividing our net income available to common shareholders by the weighted average number of common shares outstanding daily. Diluted earnings per common stock reflect the potential reduction in earnings per common share that could occur when potential dilutive common shares are added to common shares outstanding.

We derive our potential dilutive common shares by calculating the number of shares issuable under restricted share units and stock options. The outstanding issuance of shares underlying the restricted stock units depends on the satisfaction of certain performance criteria. The pre-established issuance of shares underlying stock options depends upon whether the exercise prices of the stock options are less than the average market price of the common shares for the respective periods. The following tables show the calculation of our diluted shares, assuming that outstanding restricted stock units ultimately vest and stock options currently exercisable with exercise prices below the average market prices are exercised. Our weighted average shares outstanding increased by 12 million in the first nine months of 2005 as compared to the same period last year, primarily as a result of our 11 million share equity offering completed in November 2004.

| | | Three months ended September 30, | |

In millions | | 2005 | | 2004 | |

| Denominator for basic earnings per share (1) | | | 77.5 | | | 65.1 | |

| Assumed vesting of restricted stock units and exercise of stock options | | | 0.6 | | | 0.7 | |

| Denominator for diluted earnings per share | | | 78.1 | | | 65.8 | |

| | | Nine months ended September 30, | |

In millions | | 2005 | | 2004 | |

| Denominator for basic earnings per share (1) | | | 77.2 | | | 64.8 | |

| Assumed vesting of restricted stock units and exercise of stock options | | | 0.6 | | | 0.7 | |

| Denominator for diluted earnings per share | | | 77.8 | | | 65.5 | |

| (1) | Daily weighted average shares outstanding |

NUI Corporation Acquisition Update

On November 30, 2004, we acquired NUI Corporation (NUI) for approximately $825 million, including the assumption of $709 million in debt. During the nine months ended September 30, 2005, we adjusted our purchase price allocation by $51 million for additional known items, including adjustments related to pension obligations; severance; lease obligations related to NUI’s former corporate offices; environmental remediation liabilities; and asset sales; however, there were no material adjustments for the three months ended September 30, 2005. As of September 30, 2005, goodwill related to the NUI acquisition was $209 million. We are currently evaluating other open items, including environmental remediation liabilities and tax adjustments. We will complete our allocation by November 30, 2005, but do not expect these open items to result in a material adjustment to our balance sheet during the fourth quarter of 2005.

Sale of Saltville On August 10, 2005, we completed the sale of our 50% interest in Saltville and associated subsidiaries (Virginia Gas Pipeline and Virginia Gas Storage) to a subsidiary of Duke Energy Corporation, the other 50% partner in the Saltville joint venture. We acquired these assets as part of our purchase of NUI in November 2004. We received $66 million in cash at closing, which included $4 million in working capital adjustments, and used the proceeds to repay debt and for other general corporate purposes. The transaction was reflected as a decrease of $5 million in goodwill associated with the NUI acquisition.

Sale of Other NUI Assets On September 15, 2005, we completed the sale of an appliance business in Florida for approximately $7 million, which increased goodwill associated with the NUI acquisition by approximately $3 million. We are marketing certain other NUI entities for sale, with buyers being actively solicited. The assets, liabilities, revenues and expenses of these entities are not considered to be material to our financial statements.

Note 3

Recent Accounting Pronouncements

Issued But Not Yet Adopted

SFAS 123(R) In December 2004, the FASB issued SFAS No 123(R), “Accounting for Stock Based Compensation” (SFAS 123R). SFAS 123R revises the guidance in SFAS No. 123 and supersedes APB 25 and its related implementation guidance. SFAS 123R focuses primarily on the accounting for share-based payments to employees in exchange for services, and it requires a public entity to measure and recognize compensation cost for these payments. Our share-based payments are typically in the form of stock option and performance unit awards. The primary change in accounting under SFAS 123R is related to the requirement to recognize compensation cost for stock option awards that was not recognized under APB 25. SFAS 123R requires compensation cost to be measured based on the fair value of the equity or liability instruments issued. For stock option awards, fair value would be estimated using an option pricing model such as the Black-Scholes model. In April 2005, the SEC voted to delay the effective date of SFAS 123R from June 30, 2005 to January 1, 2006. See Note 1, “Accounting Policies and Methods of Application,” for additional information related to the pro-forma effects on our earnings of recognizing compensation expense related to our stock option awards.

SFAS 123R is effective for equity compensation expense in fiscal years beginning after December 15, 2005, and we will adopt it prospectively on January 1, 2006. We are currently assessing the impact it will have on our financial statements.

SFAS 154 In June 2005, the FASB issued SFAS No. 154, “Accounting Changes and Error Corrections,” a replacement of APB Opinion No. 20 and FASB Statement No. 3. SFAS 154 requires retrospective application to prior periods’ financial statements of a voluntary change in accounting principle, unless it is impractical. Opinion No. 20 previously required that most voluntary changes in accounting principle be recognized by including, in net income for the period of the change, the cumulative effect of changing to the newly adopted accounting principle. SFAS 154 also requires that a change in the method of depreciation, amortization, or depletion for long-lived, non-financial assets be accounted for as a change in accounting estimate that is effected by a change in accounting principle. Opinion No. 20 previously required that such a change be reported as a change in accounting principle. SFAS 154 also requires that any errors in the financial statements of a prior period shall be reported as a prior-period adjustment by restating the prior period financial statements. SFAS 154 is effective for accounting changes and corrections of errors made in fiscal years beginning after December 15, 2005. We do not currently expect this statement to will have an impact on our financial statements.

| · | more consistent recognition of liabilities relating to AROs among companies; |

| · | more information about expected future cash outflows associated with those obligations stemming from the retirement of the asset(s); and |

| · | more information about investments in long-lived assets because additional asset retirement costs will be recognized by increasing the carrying amounts of the assets identified to be retired. |

FIN 47 is effective for fiscal years ending after December 15, 2005. We will adopt it prospectively in the first quarter 2006, but we have not yet determined whether the interpretation will have a significant impact on our financial statements.

Note 4

Risk Management

Our enterprise risk management activities are monitored by our Risk Management Committee (RMC). The RMC is, among other things, charged with the review and enforcement of risk management policies that place limitations on our use of derivative financial instruments and physical transactions. We use the following derivative financial instruments and physical transactions to manage commodity price risks:

| · | Storage and transportation capacity transactions |

Interest Rate Swaps

To maintain an effective capital structure, it is our policy to borrow funds using a mix of fixed-rate and variable-rate debt. We have entered into interest rate swap agreements through our wholly-owned subsidiary, AGL Capital Corporation (AGL Capital), for the purpose of managing the interest rate risk associated with our fixed-rate and variable-rate debt obligations. We designated these interest rate swaps as fair value hedges and accounted for them using the “shortcut” method prescribed by SFAS No. 133, “Accounting for Derivative Instruments and Hedging Activities” (SFAS 133), which allows us to designate derivatives that hedge exposure to changes in the fair value of a recognized asset or liability. We record the gain or loss on fair value hedges in earnings in the period of change, together with the offsetting loss or gain on the hedged item attributable to the risk being hedged.

We adjust the carrying value of each interest rate swap to its fair value at the end of each period, with an offsetting and equal adjustment to the carrying value of the debt securities whose fair value is being hedged. Consequently, our earnings are not affected negatively or positively by changes in fair value of the interest swaps each quarter. As of September 30, 2005, a notional principal amount of $100 million of these interest rate swap agreements effectively converted the interest expense associated with a portion of our senior notes from fixed rates to variable rates based on an interest rate equal to the London Interbank Offered Rate (LIBOR), plus a spread determined at the swap date. The floating rate swap range for our interest rate swaps for the three months ended September 30, 2005 was 4.58% to 7.21% and the floating rate swap range for the nine months ended September 30, 2005 was 3.61% to 7.21%.

On September 7, 2005, we terminated interest rate swap agreements associated with our note payable to AGL Capital Trust II in the principal amount of $75 million. We received a payment of $1 million related to this termination, which included accrued interest and the fair value of these interest rate swap agreements at the termination date.

On September 9, 2005, we executed five treasury-lock agreements totaling $125 million to hedge the interest rate risk associated with an anticipated 2006 financing. The agreements will result in a 4.11% interest rate on the 10-year United States Treasury bond and were designated as cash flow hedges against the future interest payments on the anticipated financing. The fair value of this agreement was $3 million at September 30, 2005, with the increase in the fair value included as a credit to OCI.

Commodity-Related Derivative Instruments

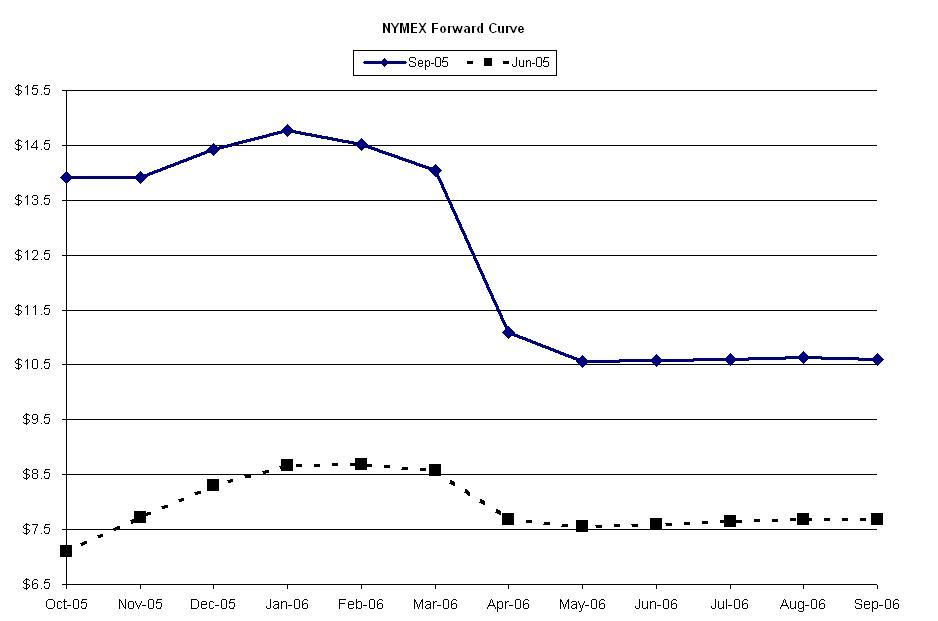

Elizabethtown Gas A program mandated by the New Jersey Board of Public Utilities requires Elizabethtown Gas to utilize certain derivatives to hedge the impact of market fluctuations of natural gas prices. Pursuant to SFAS 133, such derivative products are marked-to-market each reporting period. In accordance with regulatory requirements, realized gains and losses related to these derivatives are reflected in purchased gas costs and ultimately included in billings to customers. Unrealized gains and losses are reflected as a regulatory asset (loss) or liability (gain), as appropriate, on our condensed consolidated balance sheets. As of September 30, 2005, Elizabethtown Gas had entered into New York Mercantile Exchange (NYMEX) futures contracts to purchase approximately 8.7 billion cubic feet (Bcf) of natural gas. Approximately 80% of these contracts have duration of one year or less, and none of these contracts extends beyond February 2007.

Sequent We are exposed to risks associated with changes in the market price of natural gas. Our wholly owned energy trading and marketing subsidiary, Sequent Energy Management, L.P. (Sequent), uses derivative financial instruments to reduce our exposure to the risk of changes in the prices of natural gas. The fair value of these derivative financial instruments reflects the estimated amounts that we would receive or pay to terminate or close the contracts at the reporting date, taking into account the current unrealized gains or losses on open contracts. We use external market quotes and indices to value substantially all of the financial instruments we use.

We mitigate substantially all of the commodity price risk associated with Sequent’s natural gas portfolio by locking in the economic margin at the time we enter into natural gas purchase transactions for our stored natural gas. We purchase natural gas for storage when the difference in the current market price we pay to buy and transport natural gas plus the cost to store the natural gas is less than the market price we can receive in the future, resulting in a positive net profit margin. We use NYMEX futures contracts and other over-the-counter derivatives to sell natural gas at that future price to substantially lock in the profit margin we will ultimately realize when the stored gas is actually sold. These futures contracts meet the definition of derivatives under SFAS 133 and are recorded at fair value and marked-to-market in our condensed consolidated balance sheets, with changes in fair value recorded in earnings in the period of change. The purchase, transportation, storage and sale of natural gas are accounted for on a weighted average basis rather than on the mark-to-market basis we utilize for the derivatives used to mitigate the commodity price risk associated with our storage portfolio. This difference in accounting can result in volatility in our reported net income, even though the economic margin is essentially unchanged from the date the transactions were consummated.

At September 30, 2005, Sequent’s commodity-related derivative financial instruments, which exclude interest rate swaps, represented purchases (long) of 467 Bcf with maximum maturities less than 2 years. In addition, Sequent’s financial instruments included sales (short) of 523 Bcf with approximately 99% of these scheduled to mature in less than 2 years and the remaining 1% in 3-9 years. Sequent’s unrealized losses were $116 million for the three months ended September 30, 2005 and $10 million for the same period last year. Sequent’s unrealized losses were $125 million for the nine months ended September 30, 2005, and its unrealized gains were $5 million for the nine months ended September 30, 2004.

SouthStar The commodity-related derivative financial instruments (futures, options and swaps) used by SouthStar manage exposures arising from changing commodity prices, as such exposure would relate to the relative economics of inventory versus flowing gas supply. SouthStar’s objective for holding these derivatives is to utilize the most effective method to reduce or eliminate the impacts of this exposure. A portion of SouthStar’s derivative transactions are designated as cash flow hedges under SFAS 133. Derivative gains or losses arising from cash flow hedges are recorded in OCI and are reclassified into earnings in the same period as the settlement of the underlying hedged item. Any hedge ineffectiveness, defined as when the gains or losses on the hedging instrument do not perfectly offset the losses or gains on the hedged item, is recorded in cost of gas on our condensed consolidated income statement in the period in which it occurs. SouthStar currently has minimal hedge ineffectiveness. The remainder of SouthStar’s derivative instruments is not designated as hedges under SFAS 133 and, accordingly, changes in their fair value are recorded in earnings in the period of change.

At September 30, 2005, the fair values of these SouthStar derivatives were reflected in our condensed consolidated balance sheets as an asset of $30 million and a liability of $43 million. The maximum maturity of open positions is 1 year and represents purchases of 11.4 Bcf and sales of 9.6 Bcf.

Concentration of Credit Risk

Wholesale Services Sequent has a concentration of credit risk for services it provides to marketers and to utility and industrial customers. This credit risk is measured by 30-day receivable exposure plus forward exposure, which is generally concentrated in 20 of its customers. Sequent evaluates the credit risk of its customers using a Standard & Poor’s Rating Services (S&P) equivalent credit rating, which is determined by a process of converting the lower of the S&P or Moody’s Investor Service (Moody’s) rating to an internal rating ranging from 9.00 to 1.00, with 9.00 being equivalent to AAA/Aaa by S&P and Moody’s and 1.00 being equivalent to D or Default by S&P and Moody’s. A customer that does not have an external rating is assigned an internal rating based on Sequent’s analysis of the strength of its financial ratios. At September 30, 2005, Sequent’s top 20 customers represented approximately 65% of the total credit exposure of $507 million, derived by adding the top 20 customers’ exposures and dividing by the total of Sequent’s exposures. Sequent’s customers or the customers’ guarantors had a weighted average S&P equivalent rating of A- at September 30, 2005.

The weighted average credit rating is obtained by multiplying each customer’s assigned internal rating by its credit exposure and then adding the individual results for all counterparties. That total is divided by the aggregate total exposure. This numeric value is converted to an S&P equivalent.

Sequent has established credit policies to determine and monitor the creditworthiness of counterparties as well as the quality of pledged collateral. When Sequent is engaged in more than one outstanding derivative transaction with the same counterparty and it also has a legally enforceable netting agreement with that counterparty, the “net” mark-to-market exposure represents the netting of the positive and negative exposures with that counterparty and a reasonable measure of Sequent’s credit risk. Sequent also uses other netting agreements with certain counterparties with which it conducts significant transactions.

Note 5

Regulatory Assets and Liabilities

We record regulatory assets and liabilities in our consolidated balance sheets in accordance with the requirements of SFAS No. 71, “Accounting for the Effects of Certain Types of Regulation.” Our regulatory assets and liabilities, as well as the liabilities associated with our recoverable pipeline replacement program (PRP) costs and recoverable environmental remediation costs (ERC), are summarized in the table below:

In millions | | Sept. 30, 2005 | | Dec. 31, 2004 | | Sept. 30, 2004 | |

Regulatory assets | | | | | | | |

| Recoverable PRP costs | | $ | 355 | | $ | 361 | | $ | 382 | |

| Recoverable ERC | | | 209 | | | 200 | | | 173 | |

| Unrecovered postretirement benefit costs | | | 14 | | | 14 | | | 9 | |

| Unrecovered seasonal rates | | | 10 | | | 11 | | | 10 | |

| Unamortized purchased gas adjustment | | | 3 | | | 5 | | | - | |

| Regulatory tax asset | | | 1 | | | 2 | | | 3 | |

| Other | | | 8 | | | 20 | | | 6 | |

| Total regulatory assets | | $ | 600 | | $ | 613 | | $ | 583 | |

Regulatory liabilities | | | | | | | | | | |

| Accumulated removal costs | | $ | 92 | | $ | 94 | | $ | 93 | |

| Unamortized investment tax credit | | | 19 | | | 20 | | | 18 | |

| Deferred purchased gas adjustment | | | 37 | | | 37 | | | 34 | |

| Regulatory tax liability | | | 9 | | | 14 | | | 14 | |

| Other | | | 1 | | | 18 | | | 2 | |

| Total regulatory liabilities | | | 158 | | | 183 | | | 161 | |

Associated liabilities | | | | | | | | | | |

| PRP costs | | | 317 | | | 327 | | | 352 | |

| ERC | | | 98 | | | 90 | | | 61 | |

| Total associated liabilities | | | 415 | | | 417 | | | 413 | |

| Total regulatory and associated liabilities | | $ | 573 | | $ | 600 | | $ | 574 | |

| | | | | | | | | | | |

Our regulatory assets and liabilities are described in Note 5 to our Consolidated Financial Statements in our 2004 Annual Report on Form 10-K, as updated in our Current Report on Form 8-K filed with the SEC on July 28, 2005. The following represent significant changes to our regulatory assets and liabilities during the nine months ended September 30, 2005:

Pipeline Replacement Program

The PRP, ordered by the Georgia Public Service Commission (Georgia Commission), required that Atlanta Gas Light replace all bare steel and cast iron pipe in its system within a 10-year period that began October 1, 1998. October 1, 2005 marked the beginning of the eighth year of the original 10-year PRP.

On June 10, 2005, Atlanta Gas Light and the Georgia Commission entered into a Settlement Agreement that, among other things, extends Atlanta Gas Light’s PRP by five years to require that all replacements be completed by December 2013, with the timing of such replacements to be subsequently determined through ongoing discussions with Georgia Commission staff. Under the Settlement Agreement, rates charged to customers will remain unchanged through April 30, 2010, but Atlanta Gas Light will recognize reduced base rate revenues of $5 million on an annual basis through April 30, 2010. The five-year total reduction in recognized base rate revenues of $25 million will be applied to the amount of costs incurred to replace pipe, reducing the amount recovered from customers under the PRP rider.

The Settlement Agreement also allowed Atlanta Gas Light to recover through the PRP $4 million of the $32 million capital costs associated with its purchase of 250 miles of pipeline in central Georgia from Southern Natural Gas, a subsidiary of El Paso Corporation. The remaining capital costs are included in Atlanta Gas Light’s rate base and collected through base rates.

Environmental Remediation Costs

We are subject to federal, state and local laws and regulations governing environmental quality and pollution control. These laws and regulations require us to remove or remedy the effect on the environment of the disposal or release of specified substances at current and former operating sites.

Atlanta Gas Light The presence of coal tar and certain other by-products of a natural gas manufacturing process used to produce natural gas prior to the 1950s has been identified at or near 10 former Atlanta Gas Light operating sites in Georgia and at three sites of predecessor companies in Florida. Atlanta Gas Light has active environmental remediation or monitoring programs in effect at 10 of these sites. Two sites in Florida are currently in the investigation or preliminary engineering design phase, and one Georgia site has been deemed compliant with state standards, subject to approval of a continuing action plan. The required soil remediation at our remaining Georgia sites is substantially complete, although actions on groundwater impacts continue. As of September 30, 2005, Atlanta Gas Light’s remediation program was approximately 96% complete with respect to its Georgia sites.

Atlanta Gas Light has customarily reported estimates of future remediation costs for these former sites based on probabilistic models of potential costs. These estimates are reported on an undiscounted basis. As cleanup options and plans mature and cleanup contracts are entered into, Atlanta Gas Light is able to provide conventional engineering estimates of the likely costs of remediation at its former sites. These estimates contain various engineering uncertainties, but Atlanta Gas Light continuously attempts to refine and update these engineering estimates.

Atlanta Gas Light’s current engineering estimate projects costs to be $20 million for completion of Georgia site remediation, excluding monitoring. This is a reduction of $10 million from September 2004’s estimate resulting primarily from program expenditures.

The current estimate for the remaining cost of future actions at these former operating sites is $15 million, which may change depending on whether future measures for groundwater will be required. Atlanta Gas Light estimates certain other costs related to administering the remediation program, including administrative costs, to be $2 million.

For those Florida sites currently in the investigation phase, Atlanta Gas Light’s estimate for remediation is a range from $5 million to $12 million. This estimate is based on preliminary data received during 2004 and 2005 with respect to the existence of contamination at those sites.

These liabilities do not include other potential expenses, such as unasserted property damage claims, personal injury or natural resource damage claims, unbudgeted legal expenses or other costs for which Atlanta Gas Light may be held liable but with respect to which it cannot reasonably estimate an amount. As of September 30, 2005, the remediation expenditures expected to be incurred over the next 12 months are reflected as a current liability of $8 million.

The ERC liability is included in a corresponding regulatory asset, which is a combination of accrued ERC and unrecovered cash expenditures for investigation and cleanup costs. Atlanta Gas Light has three ways of recovering investigation and cleanup costs. First, the Georgia Commission has approved an ERC recovery rider. The ERC recovery mechanism allows for recovery of expenditures over a five-year period subsequent to the period in which the expenditures are incurred. Atlanta Gas Light expects to collect $29 million in revenues over the next 12 months under the ERC recovery rider, which is reflected as a current asset.

The second way to recover costs is by exercising the legal rights Atlanta Gas Light believes it has to recover a share of its costs from other potentially responsible parties, typically former owners or operators of these sites. The third way to recover costs is from the receipt of net profits from the sale of remediated property. There were no material recoveries from potentially responsible parties or remediated property sales during the nine months ended September 30, 2005.

Elizabethtown Gas In New Jersey, Elizabethtown Gas is currently conducting remedial activities with oversight from the New Jersey Department of Environmental Protection. Although the actual total cost of future environmental investigation and remediation efforts cannot be estimated with precision, based on probabilistic models similar to those used at Atlanta Gas Light’s former operating sites, the range of reasonably probable costs is $57 million to $109 million. As of September 30, 2005, no value within this range is a better estimate than any other value, so we have recorded a liability equal to the low end of that range, or $57 million.

Prudently incurred remediation costs for the New Jersey properties have been authorized by the New Jersey Board of Public Utilities to be recoverable in rates through a remediation adjustment clause. As a result, Elizabethtown Gas has recorded a regulatory asset of approximately $64 million, inclusive of interest, as of September 30, 2005, reflecting the future recovery of both incurred costs and accrued carrying charges. Elizabethtown Gas has also been successful in recovering a portion of remediation costs incurred in New Jersey from its insurance carriers and continues to pursue additional recovery.

Sites in North Carolina We also own a former NUI remediation site in Elizabeth City, North Carolina, which is subject to a remediation order by the North Carolina Department of Energy and Natural Resources. We currently have only limited information regarding environmental impacts at the Elizabeth City site, and therefore we can make quantitative cost estimates only for limited components of a site cleanup, such as investigative efforts. However, experience at other similar sites suggests that costs for remediation of this site will likely range from $4 million to $19 million. As of September 30, 2005, we have recorded a liability of $4 million related to this site.

There is one other site in North Carolina where investigation and remediation is probable, although no remediation order exists and we do not believe costs associated with this site can be reasonably estimated. In addition, there are as many as six other sites with which NUI had some association, although no basis for liability has been asserted, and accordingly we have not accrued any remediation liability. There are currently no cost recovery mechanisms for the environmental remediation sites in North Carolina. As a result, any change in estimate occurring after our purchase price allocation period which ends in November 2005 could affect our environmental costs and, hence, reported earnings in future periods.

We are continuing to evaluate the estimates at Elizabethtown Gas and at NUI’s other former remediation sites. The differences between our current estimates and new estimates identified within one year of the acquisition of NUI could affect the amount ultimately recorded as part of our purchase price of NUI.

Note 6

Pension and Other Post-retirement Benefits

Pension Benefits We sponsor two defined benefit post-retirement plans for our eligible employees: the AGL Resources Inc. Retirement Plan and the NUI Corporation Retirement Plan. A defined benefit plan specifies the amount of benefits an eligible participant will receive following retirement using information about the participant. We contributed $5 million in August 2005 to the AGL Resources Inc. Retirement Plan. The following are the cost components of our two pension plans for the periods indicated:

| | | Three months ended | |

| | | September 30, | |

In millions | | 2005 | | 2004 | |

| Service cost | | $ | 2 | | $ | 1 | |

| Interest cost | | | 7 | | | 5 | |

| Expected return on plan assets | | | (8 | ) | | (6 | ) |

| Net amortization | | | - | | | - | |

| Recognized actuarial loss | | | 2 | | | 2 | |

| Net annual cost | | $ | 3 | | $ | 2 | |

| | | Nine months ended | |

| | | September 30, | |

In millions | | 2005 | | 2004 | |

| Service cost | | $ | 7 | | $ | 4 | |

| Interest cost | | | 20 | | | 14 | |

| Expected return on plan assets | | | (24 | ) | | (17 | ) |

| Net amortization | | | (1 | ) | | (1 | ) |

| Recognized actuarial loss | | | 5 | | | 3 | |

| Net annual cost | | $ | 7 | | $ | 3 | |

Post-retirement Health Care Benefits We sponsor two defined benefit post-retirement health care plans for our eligible employees: the AGL Resources Inc. Postretirement Health Care Plan and the Employers’ Retirement Plan of NUI Corporation. Eligibility for these benefits is based on age and years of service. The following are the cost components of these two post-retirement benefit plans for the periods indicated:

| | | Three months ended | |

| | | September 30, | |

In millions | | 2005 | | 2004 | |

| Service cost | | $ | - | | $ | - | |

| Interest cost | | | 1 | | | 1 | |

| Expected return on plan assets | | | (1 | ) | | - | |

| Net amortization | | | (1 | ) | | (1 | ) |

| Recognized actuarial loss | | | - | | | - | |

| Net annual cost | | $ | (1 | ) | $ | - | |

| | | Nine months ended | |

| | | September 30, | |

In millions | | 2005 | | 2004 | |

| Service cost | | $ | 1 | | $ | 1 | |

| Interest cost | | | 4 | | | 5 | |

| Expected return on plan assets | | | (3 | ) | | (2 | ) |

| Net amortization | | | (3 | ) | | (1 | ) |

| Recognized actuarial loss | | | 1 | | | 1 | |

| Net annual cost | | $ | - | | $ | 4 | |

Note 7

Compensation Plans

Restricted Stock Units In general, a restricted stock unit is an award that represents the opportunity to receive a specified number of shares of our common stock, subject to the achievement of certain pre-established performance criteria.

In January 2005, we granted to a group of officers a total of 85,900 restricted stock units. As of September 30, 2005, only 77,100 of these units were outstanding. The awards were made pursuant to our Amended and Restated Long-Term Incentive Plan (1999) (Incentive Plan), as amended.

The restricted stock units have a twelve-month performance measurement period. If the performance goals set forth in the restricted stock unit agreement are achieved, the performance units are converted to an equal number of shares of our common stock and thereafter are subject to the vesting schedule set forth in the restricted stock unit agreement. If the performance goals set forth in the agreement are not attained, the restricted units will be forfeited and returned to us. The performance goals are related to management’s success in integrating its acquisitions and generating improvement in earnings from these acquired businesses.

Performance Cash Units In general, a performance cash unit award is an award that represents the opportunity to receive an incentive payment, in cash, subject to the achievement of certain pre-established performance criteria.

In January 2005, we granted performance cash units to a select group of officers pursuant to our Incentive Plan. The performance cash units represent a maximum aggregate payout of $5 million. The performance cash units have a performance measurement period that ranges from 12 to 36 months. The performance criteria relate to our internal measure of total shareholder return. Based on our anticipated performance and the related vesting schedules, as of September 30, 2005, we had recorded a liability of $2 million for these performance cash units.

Note 8

Financing

Our financing consists of short and long-term debt as indicated in the following table. There have been no significant changes to our financing as described in Note 8 to our Consolidated Financial Statements in our 2004 Annual Report on Form 10-K, as updated in our Current Report on Form 8-K filed with the SEC on July 28, 2005, other than the information described below.

| | | | | | | Outstanding as of: | |

Dollars in millions | | Year(s) due (1) | | Int. rate (1) | | Sept. 30, 2005 | | Dec. 31, 2004 | | Sept. 30, 2004 | |

Short-term debt | | | | | | | | | | | |

| Commercial paper | | | 2005 | | | 3.8%(2 | ) | $ | 318 | | $ | 314 | | $ | 51 | |

| Current portion of long-term debt | | | - | | | - | | | - | | | - | | | 34 | |

| Sequent lines of credit | | | 2005 | | | 4.4(3 | ) | | 25 | | | 18 | | | - | |

| Current portion of capital leases | | | 2005 | | | 4.9 | | | 1 | | | 2 | | | - | |

Total short-term debt | | | | | | 3.9%(4 | ) | $ | 344 | | $ | 334 | | $ | 85 | |

Long-term debt - net of current portion | | | | | | | | | | | | | | | | |

| Medium-term notes | | | 2012-2027 | | | 6.6 - 9.1 | % | $ | 208 | | $ | 208 | | $ | 208 | |

| Senior notes | | | 2011-2034 | | | 4.5 - 7.1 | % | | 975 | | | 975 | | | 775 | |

| Gas facility revenue bonds, net of unamortized issuance costs | | | 2022-2033 | | | 2.5 - 5.7 | % | | 199 | | | 199 | | | - | |

| Notes payable to trusts | | | 2037-2041 | | | 8.0 - 8.2 | % | | 232 | | | 232 | | | 232 | |

| Capital leases | | | 2013 | | | 4.9 | % | | 7 | | | 8 | | | - | |

| Interest rate swaps | | | 2011 | | | 7.2 | % | | (5 | ) | | 1 | | | 1 | |

Total long-term debt | | | | | | 6.1%(4 | ) | $ | 1,616 | | $ | 1,623 | | $ | 1,216 | |

| | | | | | | | | | | | | | | | | |

Total short-term and long-term debt | | | | | | 5.7%(4 | ) | $ | 1,960 | | $ | 1,957 | | $ | 1,301 | |

| (1) | As of September 30, 2005. |

| (2) | The daily weighted average rate was 3.1% for the nine months ended September 30, 2005. |

| (3) | The daily weighted average rate was 3.7% for the nine months ended September 30, 2005. |

| (4) | Weighted average interest rate, including interest rate swaps if applicable and excluding debt issuance and other financing related costs. |

Commercial Paper On August 30, 2005 we amended our credit facility that supports our commercial paper program. Under the terms of the amendment, the aggregate principal amount available under the credit facility has been increased from $750 million to $850 million and we have the option to increase the aggregate principal amount available for borrowing to $1.1 billion on not more than three occasions during each calendar year. The amended credit facility expires on August 31, 2010.

Sequent Line of Credit In June 2005, Sequent’s existing $25 million unsecured line of credit was extended to July 2006. In September 2005, Sequent entered into an additional $20 million unsecured line of credit scheduled to expire in September 2006. These unsecured lines of credit, which total $45 million, are used solely for the posting of exercise deposits and are unconditionally guaranteed by AGL Resources.

Gas Facility Revenue Bonds In April 2005, we refinanced $20 million of our Gas Facility Revenue Bonds due October 1, 2024. The original bonds had a fixed interest rate of 6.4% per year and were refunded with $20 million of adjustable rate Gas Facility Revenue Bonds. The maturity date of these bonds remains October 1, 2024. The new bonds were issued at an initial annual interest rate of 2.8% and initially have a 35-day auction period where the interest rate will adjust every 35 days. The interest rate at September 30, 2005 was 2.5%.

In May 2005, we refinanced an additional $47 million in Gas Facility Revenue Bonds due October 1, 2022 and bearing interest at an annual fixed rate of 6.35%. The new bonds were issued at an initial annual interest rate of 2.9% and initially have a 35-day auction period where the interest rate will adjust every 35 days. The maturity date remains October 1, 2022. The interest rate at September 30, 2005 was 2.5%.

Commitments and Contingencies

Contractual Obligations and Commitments We have incurred various contractual obligations and financial commitments in the normal course of our operations and financing activities. Contractual obligations include future cash payments required under existing contractual arrangements, such as debt and lease agreements. These obligations may result from both general financing activities and from commercial arrangements that are directly supported by related revenue-producing activities.

SouthStar has natural gas purchase commitments related to the supply of minimum natural gas volumes to its customers. These commitments are priced on both a fixed basis and an index plus premium basis. At September 30, 2005, SouthStar had obligations under these arrangements for 6.9 Bcf through December 31, 2005.

We have also incurred various contingent financial commitments in the normal course of business. The following table sets forth, as of September 30, 2005, the maximum potential amount of our expected contingent financial commitments representing obligations that become payable only if certain pre-defined events occur.

| | | | | Commitments due before Dec. 31, | |

| | | | | | | 2006 & | |

In millions | | Total | | 2005 | | thereafter | |

| Standby letters of credit, performance / surety bonds | | $ | 20 | | $ | 20 | | $ | - | |

Litigation We are involved in litigation arising in the normal course of business, and we believe the ultimate resolution of such litigation will not have a material adverse effect on our consolidated financial position, results of operations or cash flows. There has been no significant change in the litigation which was described in Note 10 to our Consolidated Financial Statements in our 2004 Annual Report on Form 10-K, as updated in our Current Report on Form 8-K filed with the SEC on July 28, 2005.

Segment Information

Prior to 2005, our business was organized into three operating segments based on similarities in economic characteristics, products and services, types of customers, methods of distribution and regulatory environments as well as the manner in which we manage these segments and our internal management information flows.

Beginning in 2005, we added an additional segment, retail energy operations, which consists of the operations of SouthStar, our retail gas marketing subsidiary that conducts business primarily in Georgia. We added this segment as a result of the way management views its operations in consideration of the impact of our acquisitions of NUI and Pivotal Jefferson Island Storage & Hub, LLC (Pivotal Jefferson Island) in the fourth quarter of 2004. The addition of this segment also is consistent with our desire to provide transparency and visibility to SouthStar on a stand-alone basis and to provide additional visibility to the remaining businesses in the energy investments segment, principally Pivotal Jefferson Island and Pivotal Propane of Virginia, Inc. (Pivotal Propane), which are more closely related in structure and operation.

We have recast the segment information for the three and nine months ended September 30, 2004 in accordance with the guidance set forth in SFAS 131 as shown in the tables below. Additionally, we have recast the segment information for the years ended December 31, 2004, 2003 and 2002 in our Current Report on Form 8-K filed with the SEC on July 28, 2005.

Our four operating segments are now as follows:

| · | Distribution operations consists primarily of: |

| o | Chattanooga Gas Company |

| o | Virginia Natural Gas, Inc. |

| · | Retail energy operations consists of SouthStar |

| · | Wholesale services consists of Sequent |

| · | Energy investments consists primarily of: |

| o | Pivotal Jefferson Island |

We treat corporate, our fifth segment, as a non-operating business segment, and it includes AGL Resources Inc., AGL Services Company, Pivotal Energy Development, nonregulated financing subsidiaries and the effect of intercompany eliminations. We eliminated intersegment sales for the three and nine months ended September 30, 2005 and 2004 from our condensed consolidated statements of income.

We evaluate segment performance based on earnings before interest and taxes (EBIT), which includes the effects of corporate expense allocations. EBIT is a non-GAAP measure that includes operating income, other income, minority interest and gain on sales of assets. Items that are not included in EBIT are: financing costs; including interest and debt expense; income taxes; and the cumulative effect of changes in accounting principles, each of which is evaluated at the consolidated level. Management believes EBIT is useful to investors as a measurement of our operating segments’ performance because it can be used to evaluate the effectiveness of our businesses from an operational perspective, exclusive of the costs to finance those activities and exclusive of income taxes, neither of which is directly relevant to the efficiency of those operations.

You should not consider EBIT as an alternative to, or a more meaningful indicator of our operating performance than, operating income or net income as determined in accordance with GAAP. In addition, our EBIT may not be comparable to a similarly-titled measure of another company. The reconciliations of EBIT to operating income and net income for the three and nine months ended September 30, 2005 and 2004 are presented in the following table.

| | | Three months ended September 30, | |

In millions | | 2005 | | 2004 | |

| Operating revenues | | $ | 393 | | $ | 262 | |

| Operating expenses | | | 339 | | | 216 | |

| Operating income | | | 54 | | | 46 | |

| Other income | | | - | | | - | |

| Minority interest | | | (2 | ) | | - | |

| EBIT | | | 52 | | | 46 | |

| Interest expense | | | 27 | | | 17 | |

| Earnings before income taxes | | | 25 | | | 29 | |

| Income taxes | | | 10 | | | 9 | |

| Net income | | $ | 15 | | $ | 20 | |

| | | Nine months ended September 30, | |

In millions | | 2005 | | 2004 | |

| Operating revenues | | $ | 1,736 | | $ | 1,206 | |

| Operating expenses | | | 1,435 | | | 974 | |

| Operating income | | | 301 | | | 232 | |

| Other income | | | 2 | | | 2 | |

| Minority interest | | | (18 | ) | | (14 | ) |

| EBIT | | | 285 | | | 220 | |

| Interest expense | | | 79 | | | 49 | |

| Earnings before income taxes | | | 206 | | | 171 | |

| Income taxes | | | 79 | | | 64 | |

| Net income | | $ | 127 | | $ | 107 | |

Summarized income statement information and capital expenditures by segment for the periods indicated are shown in the following tables:

| | | | | | |

Three months ended September 30, 2005 | | | | | | | |

In millions | | Distribution operations | | Retail energy operations | | Wholesale services | | Energy investments | | Corporate and intersegment eliminations | | Consolidated AGL Resources | |

| Operating revenues from external parties | | $ | 225 | | $ | 153 | | $ | 1 | | $ | 14 | | $ | - | | $ | 393 | |

| Intersegment revenues (1) | | | 38 | | | - | | | - | | | - | | | (38 | ) | | - | |

| Total revenues | | | 263 | | | 153 | | | 1 | | | 14 | | | (38 | ) | | 393 | |

| Operating expenses | | | | | | | | | | | | | | | | | | | |

| Cost of gas | | | 95 | | | 129 | | | - | | | 4 | | | (37 | ) | | 191 | |

| Operation and maintenance | | | 85 | | | 13 | | | 6 | | | 4 | | | (2 | ) | | 106 | |

| Depreciation and amortization | | | 28 | | | 1 | | | 1 | | | 1 | | | 2 | | | 33 | |

| Taxes other than income taxes | | | 7 | | | 1 | | | - | | | - | | | 1 | | | 9 | |

| Total operating expenses | | | 215 | | | 144 | | | 7 | | | 9 | | | (36 | ) | | 339 | |

| Operating income (loss) | | | 48 | | | 9 | | | (6 | ) | | 5 | | | (2 | ) | | 54 | |

| Other income | | | 1 | | | - | | | - | | | - | | | (1 | ) | | - | |

| Minority interest | | | - | | | (2 | ) | | - | | | - | | | - | | | (2 | ) |

| EBIT | | $ | 49 | | $ | 7 | | $ | (6 | ) | $ | 5 | | $ | (3 | ) | $ | 52 | |

| | | | | | | | | | | | | | | | | | | | |

| Capital expenditures | | $ | 51 | | $ | - | | $ | - | | $ | 1 | | $ | 12 | | $ | 64 | |

Three months ended September 30, 2004 | | | | | | | |

In millions | | Distribution operations | | Retail energy operations | | Wholesale services | | Energy investments | | Corporate and intersegment eliminations | | Consolidated AGL Resources | |

| Operating revenues from external parties | | $ | 129 | | $ | 128 | | $ | 3 | | $ | 2 | | $ | - | | $ | 262 | |

| Intersegment revenues (1) | | | 37 | | | - | | | - | | | - | | | (37 | ) | | - | |

| Total revenues | | | 166 | | | 128 | | | 3 | | | 2 | | | (37 | ) | | 262 | |

| Operating expenses | | | | | | | | | | | | | | | | | | | |

| Cost of gas | | | 31 | | | 110 | | | - | | | 1 | | | (37 | ) | | 105 | |

| Operation and maintenance | | | 63 | | | 16 | | | 4 | | | 1 | | | (1 | ) | | 83 | |

| Depreciation and amortization | | | 20 | | | 1 | | | - | | | - | | | 2 | | | 23 | |

| Taxes other than income taxes | | | 4 | | | (1 | ) | | - | | | 1 | | | 1 | | | 5 | |

| Total operating expenses | | | 118 | | | 126 | | | 4 | | | 3 | | | (35 | ) | | 216 | |

| Operating income (loss) | | | 48 | | | 2 | | | (1 | ) | | (1 | ) | | (2 | ) | | 46 | |

| Other income | | | - | | | - | | | - | | | - | | | - | | | - | |

| Minority interest | | | - | | | - | | | - | | | - | | | - | | | - | |

| EBIT | | $ | 48 | | $ | 2 | | $ | (1 | ) | $ | (1 | ) | $ | (2 | ) | $ | 46 | |

| | | | | | | | | | | | | | | | | | | | |

| Capital expenditures | | $ | 49 | | $ | 2 | | $ | 2 | | $ | 6 | | $ | 5 | | $ | 64 | |

Nine months ended September 30, 2005 | | | | | | | |

In millions | | Distribution operations | | Retail energy operations | | Wholesale services | | Energy investments | | Corporate and intersegment eliminations | | Consolidated AGL Resources | |

| Operating revenues from external parties | | $ | 1,045 | | $ | 627 | | $ | 21 | | $ | 43 | | $ | - | | $ | 1,736 | |

| Intersegment revenues (1) | | | 145 | | | - | | | - | | | - | | | (145 | ) | | - | |

| Total revenues | | | 1,190 | | | 627 | | | 21 | | | 43 | | | (145 | ) | | 1,736 | |

| Operating expenses | | | | | | | | | | | | | | | | | | | |

| Cost of gas | | | 590 | | | 513 | | | - | | | 12 | | | (143 | ) | | 972 | |

| Operation and maintenance | | | 269 | | | 40 | | | 19 | | | 12 | | | (6 | ) | | 334 | |

| Depreciation and amortization | | | 85 | | | 2 | | | 2 | | | 4 | | | 6 | | | 99 | |

| Taxes other than income taxes | | | 24 | | | 1 | | | - | | | 1 | | | 4 | | | 30 | |

| Total operating expenses | | | 968 | | | 556 | | | 21 | | | 29 | | | (139 | ) | | 1,435 | |

| Operating income (loss) | | | 222 | | | 71 | | | - | | | 14 | | | (6 | ) | | 301 | |

| Other income | | | 2 | | | - | | | - | | | 1 | | | (1 | ) | | 2 | |

| Minority interest | | | - | | | (18 | ) | | - | | | - | | | - | | | (18 | ) |

| EBIT | | $ | 224 | | $ | 53 | | $ | - | | $ | 15 | | $ | (7 | ) | $ | 285 | |

| | | | | | | | | | | | | | | | | | | | |

| Capital expenditures | | $ | 160 | | $ | 2 | | $ | 1 | | $ | 7 | | $ | 24 | | $ | 194 | |

Nine months ended September 30, 2004 | | | | | | | |

In millions | | Distribution operations | | Retail energy operations | | Wholesale services | | Energy investments | | Corporate and intersegment eliminations | | Consolidated AGL Resources | |

| Operating revenues from external parties | | $ | 595 | | $ | 583 | | $ | 23 | | $ | 5 | | $ | - | | $ | 1,206 | |

| Intersegment revenues (1) | | | 144 | | | - | | | - | | | - | | | (144 | ) | | - | |

| Total revenues | | | 739 | | | 583 | | | 23 | | | 5 | | | (144 | ) | | 1,206 | |

| Operating expenses | | | | | | | | | | | | | | | | | | | |

| Cost of gas | | | 284 | | | 485 | | | - | | | 1 | | | (144 | ) | | 626 | |

| Operation and maintenance | | | 199 | | | 42 | | | 17 | | | 3 | | | (4 | ) | | 257 | |

| Depreciation and amortization | | | 62 | | | 1 | | | - | | | 1 | | | 7 | | | 71 | |

| Taxes other than income taxes | | | 16 | | | - | | | - | | | 1 | | | 3 | | | 20 | |

| Total operating expenses | | | 561 | | | 528 | | | 17 | | | 6 | | | (138 | ) | | 974 | |

| Operating income (loss) | | | 178 | | | 55 | | | 6 | | | (1 | ) | | (6 | ) | | 232 | |

| Other income | | | 1 | | | - | | | - | | | 2 | | | (1 | ) | | 2 | |

| Minority interest | | | - | | | (14 | ) | | - | | | - | | | - | | | (14 | ) |

| EBIT | | $ | 179 | | $ | 41 | | $ | 6 | | $ | 1 | | $ | (7 | ) | $ | 220 | |

| | | | | | | | | | | | | | | | | | | | |

| Capital expenditures | | $ | 134 | | $ | 4 | | $ | 7 | | $ | 17 | | $ | 6 | | $ | 168 | |

| (1) | Intersegment revenues - Wholesale services records its energy marketing and risk management revenues net of its cost of gas. The following table provides information regarding wholesale services’ gross revenues from distribution operations and total gross revenues: |

| | | Three months ended September 30, | | Nine months ended September 30, | |

In millions | | 2005 | | 2004 | | 2005 | | 2004 | |

| Third-party gross revenues | | $ | 1,663 | | $ | 1,007 | | $ | 4,133 | | $ | 3,069 | |

| Intersegment revenues | | | 201 | | | 88 | | | 450 | | | 279 | |

| Total gross revenues | | $ | 1,864 | | $ | 1,095 | | $ | 4,583 | | $ | 3,348 | |

Balance sheet information at September 30, 2005 and 2004 and December 31, 2004 by segment is shown in the following tables:

As of September 30, 2005 | | | | | | | | | | | | | |

In millions | | Distribution operations | | Retail energy operations | | Wholesale services | | Energy investments | | Corporate and intersegment eliminations (2) | | Consolidated AGL Resources | |

| | | | | | | | | | | | | | |

| Goodwill | | $ | 390 | | $ | 1 | | $ | - | | $ | 14 | | $ | - | | $ | 405 | |

| Identifiable assets (1) | | $ | 4,597 | | $ | 226 | | $ | 1,108 | | $ | 348 | | $ | (193 | ) | $ | 6,086 | |

| Investment in joint ventures | | | - | | | - | | | - | | | - | | | - | | | - | |

| Total assets | | $ | 4,597 | | $ | 226 | | $ | 1,108 | | $ | 348 | | $ | (193 | ) | $ | 6,086 | |

As of December 31, 2004 | | | | | | | | | | | | | |

In millions | | Distribution operations | | Retail energy operations | | Wholesale services | | Energy investments | | Corporate and intersegment eliminations (2) | | Consolidated AGL Resources | |

| Goodwill | | $ | 340 | | $ | - | | $ | - | | $ | 14 | | $ | - | | $ | 354 | |

| Identifiable assets (1) | | $ | 4,386 | | $ | 244 | | $ | 696 | | $ | 386 | | $ | (86 | ) | $ | 5,626 | |

| Investment in joint ventures | | | - | | | - | | | - | | | 235 | | | (221 | ) | | 14 | |

| Total assets | | $ | 4,386 | | $ | 244 | | $ | 696 | | $ | 621 | | $ | (307 | ) | $ | 5,640 | |

As of September 30, 2004 | | | | | | | | | | | | | |

In millions | | Distribution operations | | Retail energy operations | | Wholesale services | | Energy investments | | Corporate and intersegment eliminations (2) | | Consolidated AGL Resources | |

| Goodwill | | $ | 177 | | $ | - | | $ | - | | $ | - | | $ | - | | $ | 177 | |

| Identifiable assets (1) | | $ | 3,360 | | $ | 162 | | $ | 458 | | $ | 135 | | $ | (81 | ) | $ | 4,034 | |

| Investment in joint ventures | | | - | | | - | | | - | | | - | | | - | | | - | |

| Total assets | | $ | 3,360 | | $ | 162 | | $ | 458 | | $ | 135 | | $ | (81 | ) | $ | 4,034 | |

| (1) | Identifiable assets are those assets used in each segment’s operations. |

| (2) | Our corporate segment’s assets consist primarily of intercompany eliminations, cash and cash equivalents and property, plant and equipment. |

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING INFORMATION

Certain expectations and projections regarding our future performance referenced in this “Management’s Discussion and Analysis of Financial Condition and Results of Operation” section and elsewhere in this report, as well as in other reports and proxy statements we file with the Securities and Exchange Commission (SEC) are forward-looking statements. Officers and other key employees may also make verbal statements to analysts, investors, regulators, the media and others that are forward-looking.

Forward-looking statements involve matters that are not historical facts, and because these statements involve anticipated events or conditions, forward-looking statements often include words such as "anticipate," "assume," "can," "could," "estimate," "expect," "forecast," "future," "indicate," "intend," "may," "plan," "predict," "project, "seek," "should," "target," "will," "would," or similar expressions. Our expectations are not guarantees and are based on currently available competitive, financial and economic data along with our operating plans. While we believe that our expectations are reasonable in view of the currently available information, our expectations are subject to future events, risks and uncertainties, and there are several factors - many beyond our control - that could cause results to differ significantly from our expectations. Such events, risks and uncertainties include, but are not limited to, changes in price, supply and demand for natural gas and related products, impact of changes in state and federal legislation and regulation, actions taken by government agencies on rates and other matters, concentration of credit risk, utility and energy industry consolidation, impact of acquisitions and divestitures, direct or indirect effects on AGL Resources' business, financial condition or liquidity resulting from a change in our credit ratings or the credit ratings of our counterparties or competitors, interest rate fluctuations, financial market conditions and general economic conditions, uncertainties about environmental issues and the related impact of such issues, impacts of changes in weather upon the temperature-sensitive portions of the business, impacts of natural disasters such as hurricanes upon the supply and price of natural gas, acts of war or terrorism, and other factors contained in our filings with the SEC.

We caution readers that, in addition to the important factors described elsewhere in this report, the factors set forth in our 2004 Annual Report on Form 10-K, as updated in our Current Report on Form 8-K filed with the SEC on July 28, 2005 (2004 Form 10-K), under “Management’s Discussion and Analysis of Financial Condition and Results of Operations” under the caption “Risk Factors,” among others, could cause our business, results of operations or financial condition in 2005 and thereafter to differ significantly from those expressed in any forward-looking statements. There also may be other factors not described in these reports that could cause results to differ significantly from our expectations.

Forward-looking statements are only as of the date they are made, and we do not undertake any obligation to update these statements to reflect subsequent changes.

We are a Fortune 1000 energy services holding company whose principal business is the distribution of natural gas in six states - Florida, Georgia, Maryland, New Jersey, Tennessee and Virginia. Our six utilities serve more than 2.3 million end-use customers, making us the largest distributor of natural gas in the Southeast and mid-Atlantic regions of the United States based on customer count. We also are involved in various related businesses, including retail natural gas marketing to end-use customers, primarily in Georgia; natural gas asset management and related logistics activities for our own utilities as well as for other non-affiliated companies; natural gas storage arbitrage and related activities; operation of high-deliverability underground natural gas storage assets; and construction and operation of telecommunications conduit and fiber infrastructure within selected metropolitan areas. We manage these businesses through four operating segments - distribution operations, retail energy operations, wholesale services and energy investments - and a non-operating corporate segment.