Exhibit 99.4

FORWARD FOCUS

Cameco

2013 Business Overview

Focused on

RESULTS

2012 was an eventful year for our business and our industry – and another strong year for Cameco. We demonstrated resilience in 2012, exceeding our production target, delivering on our sales guidance, and achieving $2.3 billion in revenue, despite a challenging environment.

The economic malaise felt around the world, and the lingering effects of the events in Japan, overshadowed our industry, exerting significant downward pressure on uranium prices throughout the year. This resulted in many producers, including us, delaying or cancelling projects that had become uneconomic. We also decided to slow our growth plans and focus primarily on projects with the most certainty, while pursuing our other projects at a more measured pace. As a result, we plan to provide 36 million pounds of annual supply by 2018, while at the same time maintaining optionality in our project portfolio – what we call our ‘bullpen’ – to allow us to be the first to respond when the market signals new production is needed. This will let us spread out our capital spend over a longer period of time to improve near-term results, and also prepare for the longer term picture.

We were, however, able to find opportunity in the current market environment, acquiring the NUKEM trading group, as well as the Yeelirrie project in Australia and an increased portion of the Millennium project in Saskatchewan. These are world-class assets, and our decision to acquire them reflects our confidence in the nuclear industry and our commitment to be ready to supply new production when it is needed.

Ours is still a growth plan, to prepare for the strong long-term demand we see for uranium. There is strong reactor growth around the world

at a time when uranium supply is diminishing: the Russian Highly Enriched Uranium commercial agreement ends this year and, as I already mentioned, new uranium mining projects are being delayed and cancelled. Each day these projects don’t move forward, the larger the future supply-demand gap becomes.

At Cameco, we are maintaining a forward focus – continuing to move forward towards that increased long-term demand, but, as always, with an emphasis on achieving our growth plans safely, efficiently and profitably.

Tim Gitzel,

President and CEO

March 15, 2013

Focused on the

FUTURE

Around the world, demand for energy continues to expand and nuclear remains an important part of the energy mix. Cameco continues to move forward on the path towards increasing annual uranium supply to 36 M lbs by 2018 in order to meet future uranium demand.

A GOOD FORWARD-LOOKING

INVESTMENT TODAY

• Strong growth potential based on a sound business strategy – increasing production over the next 5 years

• Capable senior management team with deep knowledge of the industry

• Pure-play nuclear investment – proven track record

• An industry leader

URANIUM PRODUCTION

McArthur River/Key Lake

Northern Saskatchewan, Canada

Ownership: 70%, operator

OVERVIEW: McArthur River is the world’s largest, high-grade uranium mine, and Key Lake is the largest uranium mill in the world. Ore grades at the McArthur River mine are 100 times the world average, which means it can produce more than 18 million pounds per year by mining only 150 to 200 tonnes of ore per day. McArthur River is one of our three material uranium properties.

Rabbit Lake

Northern Saskatchewan, Canada

Ownership: 100%, operator

OVERVIEW: The Rabbit Lake operation, which opened in 1975, is the longest operating uranium production facility in North America, and the second largest uranium mill in the world. It has produced over 190 million pounds over the last three decades and currently has sufficient mineral reserves to continue production through to 2017.

Smith Ranch-Highland and North Butte

Wyoming, US

Crow Butte

Nebraska, US

Ownership: 100%, operator

OVERVIEW: Our US operations are long-established in situ recovery operations. We operate Smith Ranch and Highland as a combined operation. Each has its own processing facility, but the Smith Ranch central plant processes all the uranium. Together, they form the largest uranium production facility in the US.

Inkai

Kazakhstan

Ownership: 60%

OVERVIEW: Inkai is a joint venture that gives us access to a significant uranium deposit located in Kazakhstan. There are two production areas (blocks 1 and 2) and an exploration area (block 3). The operator is Joint Venture Inkai Limited Liability Partnership, which we jointly own (60%) with Kazatomprom (40%). Inkai is one of our three material uranium properties.

2012 PRODUCTION

13.6 million lbs (our share)

2013 TARGET

13.2 million lbs (our share)

2012 PRODUCTION

3.8 million lbs

2013 TARGET

4.2 million lbs

2012 PRODUCTION

1.9 million lbs

2013 TARGET

2.6 million lbs

2012 PRODUCTION

2.6 million lbs (our share)

2013 TARGET

2.9 million lbs (our share)

UPDATE: In 2012, McArthur River/ Key Lake continued its record of reliable production, beating its annual target. The Key Lake mill contributed to the success of the operation with record performance as a result of our mill revitalization program, which will continue in 2013. We will also continue working to develop zone 4 north to bring it into production for 2014, and to advance our expansion plans at McArthur River to increase production to 22 million lbs (100% basis) per year by 2018.

UPDATE: 2012 production at Rabbit Lake was slightly above plan, and we replaced key pieces of mill infrastructure. We also continued our underground drilling reserve replacement program, which returned promising results.

In 2013, we will progress with reserve replacement drilling. We also plan to expand the existing tailings management by the end of 2017 to have the capacity to process ore from other potential sources and to support the extension of Rabbit Lake’s mine life.

UPDATE: Production was lower than plan for 2012 due to the lengthened review process to obtain regulatory approvals. However, approval for one wellfield was received, which came into full production in August. We also started construction for the satellite plant and first wellfield at North Butte, and expect to begin production in 2013. We will continue the permitting process for the rest of our expansion plans throughout 2013.

UPDATE: 2012 production was in line with our target as we continued to bring on additional wellfields to maintain new, typically higher grade wellfields in the production mix. In 2013, we plan to continue to pursue government approval to implement production increases to 5.2 million lbs per year (100% basis) from blocks 1 and 2. At block 3, we plan to complete delineation drilling, complete construction of the test leach facility and test wellfields, and start operation of the test wellfields.

Cigar Lake

Northern Saskatchewan, Canada

Ownership: 50%, operator

OVERVIEW: Cigar Lake is the world’s second largest high-grade uranium deposit, with grades that are 100 times the world average. Currently under development, and expected to begin production this year, it is one of our three material uranium properties. We expect it will provide us with 9 million lbs of uranium per year once it is in full production.

Millennium

Northern Saskatchewan, Canada

Ownership: 70%, operator

OVERVIEW: Millennium is a uranium deposit in northern Saskatchewan that we expect will use our excess milling capacity.

Kintyre

Western Australia

Ownership: 70%, operator

OVERVIEW: Kintyre is an advanced uranium exploration project in Western Australia that is amenable to open pit mining techniques. We acquired the project in 2008 and are the operator.

Yeelirrie

Western Australia

Ownership: 100%, operator

OVERVIEW: Yeelirrie is a near-surface calcrete-style deposit that is amenable to open pit mining techniques and is one of Australia’s largest undeveloped uranium deposits. We acquired this project from BHP Billiton at the end of 2012.

2012 PRODUCTION

Under development

2013 TARGET

0.3 million lbs (our share)

2012 / 2013

Under evaluation

2012 / 2013

Under evaluation

2012 / 2013

Under evaluation

UPDATE: In 2012, we continued to progress toward first production, achieving a number of milestones such as completing the sinking of shaft 2 to its final depth and beginning infrastructure installation, completing the Seru Bay pipeline, and commissioning the jet boring mining system to begin underground testing. We expect to bring the mine into production in mid-2013 and produce the first packaged pounds from AREVA’s McClean Lake mill in Q4 of 2013.

UPDATE: In 2012, we acquired additional interest in the project, increasing our ownership to 70%. We also continued to work on the environmental assessment, completed a summer drilling program that increased our indicated and inferred mineral resource estimate, and carried out additional design work to advance the project. In 2013 we will continue to advance the project toward a development decision at a pace aligned with market opportunities.

UPDATE: In 2012, we completed the prefeasibility study and signed a mine development agreement with the Martu. We also carried out further exploration drilling to test for other potential satellite deposits, though no additional resources were identified. In 2012 Q3, we decided not to advance to a feasibility study until market conditions improve. In 2013 we will continue the value engineering and exploration drilling.

UPDATE: In 2013, we expect to conduct a full document review of Yeelirrie and complete a mineral resource estimate in accordance with NI 43-101. We will advance the development of this project at a pace aligned with market opportunities, using our stage gate process.

Focused on

PERFORMANCE

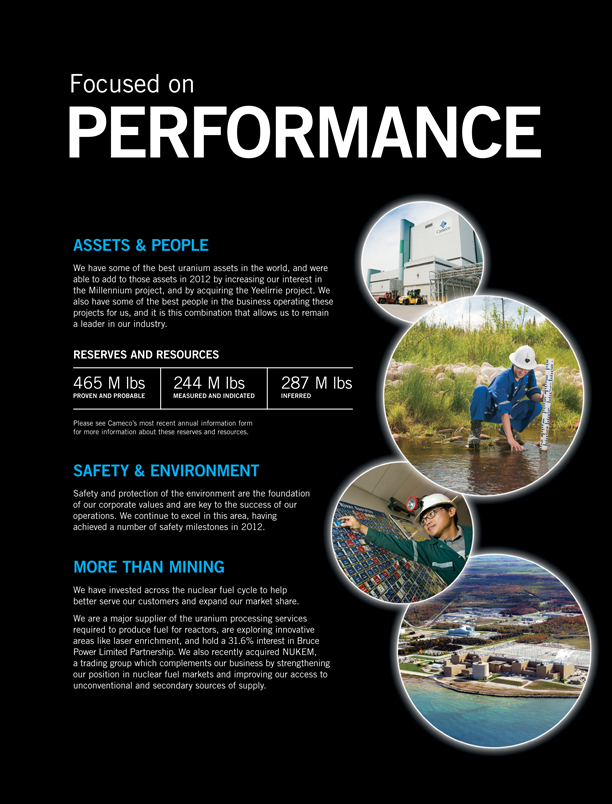

ASSETS & PEOPLE

We have some of the best uranium assets in the world, and were able to add to those assets in 2012 by increasing our interest in the Millennium project, and by acquiring the Yeelirrie project. We also have some of the best people in the business operating these projects for us, and it is this combination that allows us to remain a leader in our industry.

RESERVES AND RESOURCES

465 M lbs 244 M lbs 287 M lbs

PROVEN AND PROBABLE MEASURED AND INDICATED INFERRED

Please see Cameco’s most recent annual information form for more information about these reserves and resources.

SAFETY & ENVIRONMENT

Safety and protection of the environment are the foundation of our corporate values and are key to the success of our operations. We continue to excel in this area, having achieved a number of safety milestones in 2012.

MORE THAN MINING

We have invested across the nuclear fuel cycle to help better serve our customers and expand our market share. We are a major supplier of the uranium processing services required to produce fuel for reactors, are exploring innovative areas like laser enrichment, and hold a 31.6% interest in Bruce Power Limited Partnership. We also recently acquired NUKEM, a trading group which complements our business by strengthening our position in nuclear fuel markets and improving our access to unconventional and secondary sources of supply.

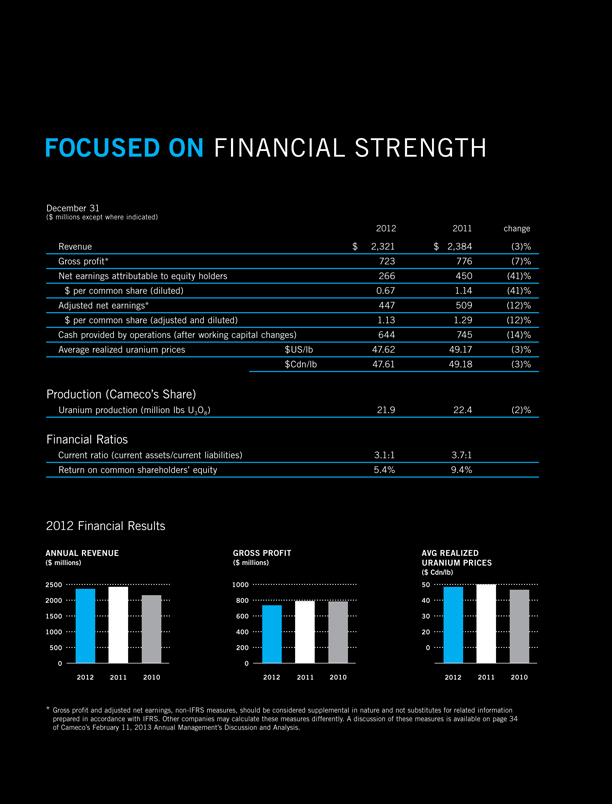

FOCUSED ON FINANCIAL STRENGTH

December 31

($ millions except where indicated)

2012 2011 change

Revenue $ 2,321 $ 2,384(3)%

Gross profit* 723 776(7)%

Net earnings attributable to equity holders 266 450(41)%

$ per common share (diluted) 0.67 1.14(41)%

Adjusted net earnings* 447 509(12)%

$ per common share (adjusted and diluted) 1.13 1.29(12)%

Cash provided by operations (after working capital changes) 644 745(14)%

Average realized uranium prices $ US/lb 47.62 49.17(3)%

$ Cdn/lb 47.61 49.18(3)%

Production (Cameco’s Share)

Uranium production (million lbs U3 O8 ) 21.9 22.4(2)%

Financial Ratios

Current ratio (current assets/current liabilities) 3.1:1 3.7:1

Return on common shareholders’ equity 5.4% 9.4%

2012 Financial Results

ANNUAL REVENUE GROSS PROFIT AVG REALIZED

($ millions) ($ millions) URANIUM PRICES

($ Cdn/lb)

2500 2000 1500 1000 500 0

2012 2011 2010

1000 800 600 400 200 0

2012 2011 2010

50 40 30 20 0

2012 2011 2010

* Gross profit and adjusted net earnings, non-IFRS measures, should be considered supplemental in nature and not substitutes for related information prepared in accordance with IFRS. Other companies may calculate these measures differently. A discussion of these measures is available on page 34 of Cameco’s February 11, 2013 Annual Management’s Discussion and Analysis.

INVESTOR INFORMATION

Common Shares

Toronto (CCO) | New York (CCJ)

Transfer Agents and Registrars

The registrar and transfer agent for Cameco’s common shares is CIBC Mellon Trust Company1. For information on common shareholdings, dividend cheques, lost share certificates and address changes, contact:

In Canada:

CIBC Mellon Trust Company c/o Canadian Stock Transfer Company Inc.

P.O. Box 700, Station B Montreal, Quebec H3B 3K3

In the United States:

American Stock Transfer

& Trust Company, LLC

Attention: General Counsel 6201 15th Avenue Brooklyn, NY

11219

Telephone:

1-800-387-0825 OR

1-416-682-3860 outside of North America www.canstockta.com

1 Canadian Stock Transfer Company Inc. acts as the Administrative Agent for CIBC Mellon Trust Company.

Annual Meeting

The annual meeting of shareholders of Cameco Corporation is scheduled to be held on Tuesday, May 14, 2013 at 1:30 p.m. at Cameco’s head office in Saskatoon, Saskatchewan.

Dividend Policy

The board of directors has established a policy of paying a quarterly dividend of $0.10 ($0.40 per year) per common share. This policy will be reviewed from time to time in light of the company’s cash flow, earnings, financial position and other relevant factors.

Inquiries

Cameco Corporation 2121 – 11th Street West

Saskatoon, Saskatchewan S7M 1J3 Phone: 306-956-6200 Fax: 306-956-6201

Caution about forward-looking information

We are making statements and providing information about our expectations for the future which are considered to be forward-looking information or forward-looking statements under Canadian and United States securities laws. These include our statements about: our plan to provide 36 million pounds of annual uranium supply by 2018, while at the same time maintaining optionality to allow us to be the first to respond when the market signals new production is needed; our ability to spread out our capital spend over a longer period of time to improve near-term results and also prepare for the longer term; the increasing future gap between uranium supply and demand; our ability to achieve our growth plans safely, efficiently and profitably; our expectations regarding future production at our projects and planned activities for 2013; and our expectation that our acquisition of NUKEM will strengthen our position in nuclear fuel markets and improve our access to unconventional and secondary sources of supply. They also include other statements using words such as plan, will, expect and continue, and statements described as goals or milestones. These statements represent our views as of March 15, 2013 and can change significantly. We are presenting this information to help you understand management’s current views of our future prospects, and it may not be appropriate for other purposes. We will not necessarily update this information unless we are required to by securities laws. This information is based on a number of material assumptions and is subject to a number of material risks which are discussed in our current annual MD&A under the heading “Caution about forward-looking information” and elsewhere, and you should refer to them. In particular, we have made assumptions about the demand for uranium, our expected production level and production costs, our expected level of uranium by-product supply, the reliability of our reserve and resource estimates, the geological, hydrological and other conditions at our mines and our ability to continue our operations without any significant disruptions due to accidents or other development or operating risks. The material risks that could prevent us from reaching our production targets and our uranium supply target for 2018 include the risks that actual sales volumes or market prices are lower than we expect; production costs are higher than planned, or necessary supplies are not available; our mineral reserve and resource estimates are not reliable, or we face unexpected or challenging conditions; we are unable to obtain the expected level of uranium by-product supply; or our operations are disrupted for any reason.

Qualified Persons

Information of a scientific and technical nature concerning Cigar Lake was prepared under the supervision of Grant Goddard, P. Eng., Cameco’s Vice-President, Saskatchewan Mining North, concerning McArthur River was prepared under the supervision of David Bronkhorst, P. Eng., Cameco’s Vice-President, Saskatchewan Mining South, and concerning Inkai was prepared under the supervision of Alain Mainville, Director, Mineral Resources Management. Each of these individuals is a qualified person for the purpose of NI 43-101.

For comprehensive financial information visit:

CAMECO.COM