Exhibit 99.1

Earnings

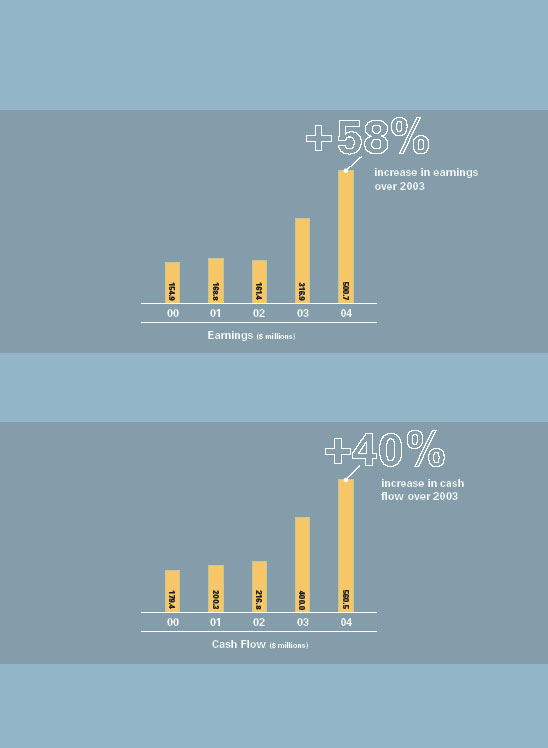

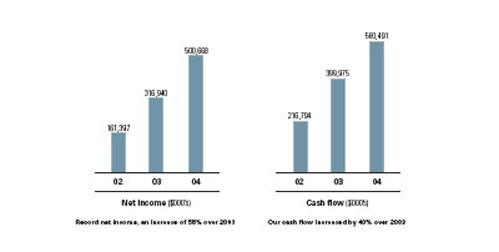

PetroKazakhstan generated record earnings of over $0.5 billion in 2004, an increase of 58% versus 2003.

Cash flow

PetroKazakhstan generated record cash flow of $0.56 billion in 2004, an increase of 40% versus 2003.

4 PetroKazakhstan Inc. |

| 5 |

2004 Highlights and Achievements |

Achievements

| 4 | Record financial results |

| 4 | Significant increase in oil reserves |

| 4 | Reserve recognition of substantial Natural Gas Liquids and natural gas |

| 4 | Exploration success in Kyzylkiya, Aryskum and Akshabulak |

| 4 | Introduction of a regular quarterly dividend policy |

| 4 | KAM pipeline and Dzhusaly rail loading terminal operating effectively |

| 4 | Completed construction and commissioned the Gas Utilization Project |

| 4 | Acquired additional exploration acreage |

| 4 | Increased shipments of crude oil to China |

| 4 | PetroKazakhstan’s common shares listed on the Kazakhstan Stock Exchange |

FINANCIAL AND OPERATING HIGHLIGHTS

EXPRESSED IN MILLIONS OF UNITED STATES DOLLARS (EXCEPT PER SHARE AMOUNTS)

| Years ended December 31 | 2004 | 2003 | 2002 | |||||||

FINANCIAL | ||||||||||

| Net Income | 500.7 | 316.9 | 161.4 | |||||||

Per share (basic) ($) | 6.40 | 4.06 | 2.00 | |||||||

| Cash Flow | 560.5 | 400.0 | 216.8 | |||||||

Per share (basic) ($) | 7.16 | 5.12 | 2.68 | |||||||

| EBITDA | 931.6 | 590.5 | 343.6 | |||||||

| Capital Expenditures | 166.0 | 203.2 | 140.1 | |||||||

| Total Assets | 1,269.1 | 1,041.5 | 709.7 | |||||||

| Shareholders’ Equity | 890.1 | 571.7 | 266.9 | |||||||

| Shares Outstanding at December 31 | 76,223,130 | 77,920,226 | 78,956,875 | |||||||

| Number of Employees at December 31 | 3,001 | 2,610 | 3,306 | |||||||

OPERATING | ||||||||||

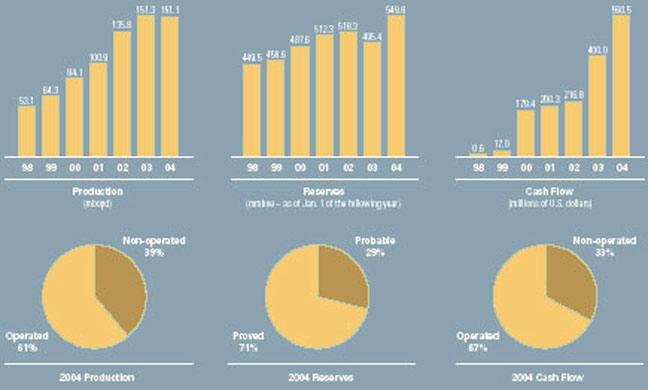

Production (bopd) | 151,102 | 151,349 | 135,842 | |||||||

Reserves (proved plus probable) (mmboes)* | 549.8 | 495.4 | 518.3 | |||||||

*As of January 1 of the following year

6 PetroKazakhstan Inc. |

Operating Achievements

| 4 | Replaced 180% of 2004 crude oil production |

| 4 | Five-year finding and development costs of $1.53/bbl based on proved reserves |

| 4 | Continuous operations of the 55 MW gas utilization plant |

| 4 | Exploration success in three fields |

| 4 | Yearly differential reduced by $1.49/bbl versus 2003 |

2005 Objectives

| 4 | Increase production by 12.5% |

| 4 | Reduce export differential |

| 4 | Develop asset base through further exploration and appraisal work |

| 4 | Continue to improve the yield of the Shymkent refinery |

| 4 | Commission a Liquified Petroleum Gas facility |

| 4 | Implement an Enhanced Oil Recovery project |

| 7 |

A Message from Mr. Bernard Isautier - President and Chief Executive Officer |

Our Company has continued to generate record financial results for 2004. This was achieved through strong commodity prices, a reduction in our differential and enhanced refinery contributions.

Going beyond boundaries summarizes what the Company has achieved in 2004 and the path it will continue to follow in the future. In 2004, PetroKazakhstan focused on proving exploration concepts resulting in new oil discoveries, further exploiting its asset base through new technologies, creating new refined products such as Vacuum Gas Oil (VGO), implementing new activities in the form of electrical power generation, identifying new markets for crude oil and refined products, developing new transportation routes, investing in logistics and adding new talents and professional disciplines to our organization. These initiatives contributed to the generation of record financial results. ASSET AND RESERVE GROWTH In 2004, the Company was successful in significantly increasing its exploration land position from the prior year. Due to these land acquisitions the Company initiated and completed a basin study. This study has led to the identification of an exploration inventory that includes 94 independent structures which will give us many years of drilling prospects. This increased focus on exploration led to the discovery of a new reservoir within the Aryskum field license and new channel sands on the Akshabulak license. It also proved the presence of a significant northern extension to the Kyzylkiya field and identified other highly prospective opportunities on new exploration land blocks. We plan to continue to aggressively prove up and identify other new structures and plays in 2005. As of January 1, 2005 PetroKazakhstan’s reserves were independently determined by the Canadian company McDaniel & Associates Consultants Ltd., to be 549.8 million barrels of | oil equivalent (mmboe) comprised of 502.9 million barrels (mmbbls) of crude oil, 31.2 mmboe of Natural Gas Liquids (NGLs) and 88.4 billion cubic feet (bcf) of gas on a proved plus probable basis. This represents a 197% replacement of 2004 production on a boe basis even though he more stringent Canadian standard of reserves definition and recognition as set out in National Instrument 51-101 (Standards of Disclosure for Oil and Natural Gas activities) was used. QUARTERLY DIVIDEND POLICY AND SHARE BUY-BACKS PetroKazakhstan introduced a regular quarterly dividend in early 2004. On December 13, 2004, the Company’s Board of Directors approved a 33% increase in its quarterly dividend from C$0.15 per share to C$0.20 per share. As an additional means of adding shareholder value, the Company has implemented, for a third year in a row, a share repurchase program approved by the Toronto Stock Exchange. This share repurchase program, called a Normal Course Issuer Bid (NCIB), allows the Company to repurchase up to 10% of its public float or 7,091,429 shares, for our most recent program, over a one year time period beginning August 13, 2004 and terminating no later than August 12, 2005. As of the end of 2004, the Company had repurchased and cancelled 1,257,500 shares. Subsequent to year end 2004, the Company has continued to repurchase and cancel shares. In 2004 PetroKazakhstan also implemented a Dutch auction substantial issuer bid share tender. This share tender ended on July 19, 2004 and resulted in the repurchase and cancellation of 3,999,975 shares at C$40.00 per share. |

8 PetroKazakhstan Inc. |

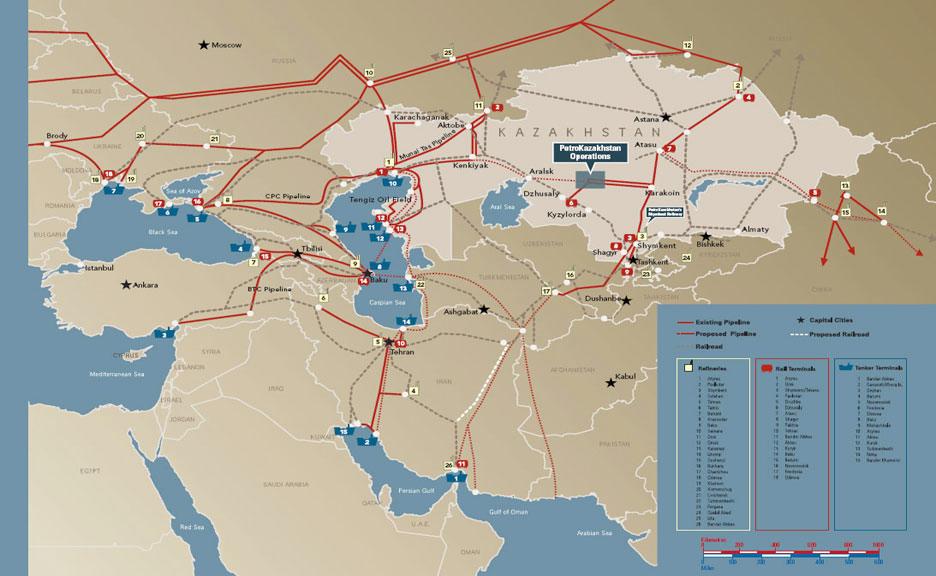

RECORD RESULTS Our Company has continued to generate record financial results for 2004. This was achieved through strong commodity prices, a reduction in our differential and enhanced refinery contributions. Some of the key financial results were: 4 Cash flow reached $560.5 million, an increase of 40% over 2003 4 Net income was $500.7 million, an increase of 58% over 2003 BROADER MARKET RECOGNITION PetroKazakhstan was successful in becoming the first foreign company to have its shares listed on the Kazakhstan Exchange as of December 27, 2004. This listing will allow all Kazakhstan institutions and citizens, including our own employees, to become PetroKazakhstan shareholders, to become more involved in the market activities of our Company and to more generally participate in the development of the market economy in Kazakhstan. TRANSPORTATION COSTS Transportation costs continued to be the Company’s largest operating expense and hence our largest opportunity for cost reduction throughout 2004. Effective use of our newly constructed 177 kilometer (km) Kyzylkiya, Aryskum and Maibulak (KAM) pipeline which became operational in June 2003 was key. The savings in rail transportation costs for crude oil exports, sent west to the Black Sea, has been approximately $2.00/barrel (bbl). Shipments of crude oil and refined products to China continued to increase in 2004. After many years of planning, the governments of Kazakhstan and China broke ground and began the | construction of a 1,000 km pipeline from Kazakhstan to the Chinese border. This pipeline, which is currently planned for construction completion by the end of 2005, with start-up in early 2006, will structurally change the movement and flow of oil within Kazakhstan. With an initial capacity of 200,000 bopd, expandable to 400,000 bopd and beyond, via additional construction phases, this pipeline will draw on Kazakhstan oil to feed the voracious Chinese appetite for oil. PetroKazakhstan believes it is well positioned to supply significant amounts of crude oil into this pipeline, given appropriate terms. In 2004, crude oil produced by Turgai Petroleum (Turgai), our joint venture with Lukoil, exported via the Caspian Pipeline Consortium (CPC) pipeline, was increased. Shipments in 2004 represented 92% of our CPC contractual maximum of 31,800 bopd gross (1.5 million tonnes per year). Shipments in 2005 are expected to be greater than that achieved in 2004. The construction of a 1,000,000 bopd pipeline originating in Azerbaijan, terminating at the Mediterranean Sea via Turkey, the Baku-Tbilisi-Ceyhan (BTC) pipeline will further lead to enhanced competition for crude oil and potential tariff cost reductions. This $4 billion pipeline, scheduled for start-up in mid 2005, will significantly increase the current take-away capacity for crude produced in the region. The Company has approached consortium partners and expressed its desire to ship crude through BTC, given the appropriate terms. Oil exports via China, Iran, CPC, BTC and Atyrau are expected to result in further transportation cost savings. To efficiently handle increased rail movement of exported crude, the Company expanded its fleet of controlled railcars from just over 2,000 cars at the end of 2003 to approximately 5,000 cars by year end 2004. |

| 9 |

UPSTREAM OPERATIONS The Company’s 2005 annual production plan is to produce 170,000 bopd. Achievement of this technical potential remains subject to timely receipt of various regulatory approvals and the absence of unforeseen marketing constraints. This projection represents a 12.5% increase in production versus 2004 and will be accomplished through further development of a number of our existing fields. Phase I of the Kumkol South Enhanced Oil Recovery (EOR) project will begin in 2005 as will the development of the East Kumkol field and the commissioning of the Akshabulak gas plant for Liquefied Petroleum Gas (LPG). These projects will increase our production and reserve base. From an exploration and production perspective, PetroKazakhstan now has land interests of approximately 3.4 million acres (13,760 km2) in the South Turgai basin, where we operate, with 3.2 million acres being exploratory in nature. The South Turgai basin has long been identified as having reserve potential in the billions of barrels. To date the Company has been successful in proving up additional new exploration concepts which have led to new field discoveries. In 2005 we will continue to aggressively drill exploration wells on our exploration acreage to find and prove up additional reserves. DOWNSTREAM OPERATIONS The downstream sector continues to be a very important aspect of our integrated business, not only from an opportunity driven basis, but also from a revenue generation perspective. Our focus has and continues to be, enhancing the product slate of the refinery and the implementation of ongoing process improvements. The startup of the Vacuum Distillation Unit (VDU) in 2004 has led to a lower yield of heavy fuel oil (mazut). Over the course of 2004, the mazut yield has been reduced by 29%, from an average of 32.5% in 2003 of crude feedstock to an average of 23.1% for 2004. With the startup of a newly constructed boiler which generates steam required in the operations of our refinery, we have been able to achieve energy efficiencies and therefore, cost savings. HEALTH, SAFETY AND ENVIRONMENT 2004 was the first year of continuous operations of the Company’s newly built 55-megawatt (MW) power plant located at the Kumkol field. This plant has reduced gas emissions by converting associated gas produced from the Kumkol fields into electricity. In 2005, a second natural gas project at the Company’s joint venture field at Akshabulak will be commissioned. | This project will further reduce gas emissions and will also provide natural gas to the Kyzylorda region. Improving safety is one of our primary focuses. In 2004, in our Upstream operations, we had one lost time accident and reported 10 accidents/incidents. We had no lost time accidents at our refinery for a second consecutive year, a record we are very proud of. In 2005, we will continue in our efforts to make our workplace as safe as possible. LOOKING FORWARD PetroKazakhstan’s key objectives for 2005 and beyond will be to focused on: 4Increasing production and reserves through development, exploration and acquisitions. 4Reducing the export differential. 4Continuing to improve the product yield of the Shymkent refinery. 4Increasing the value obtained for our refined products. 4Commissioning a new Liquefied Petroleum Gas facility. 4Implementing an Enhanced Oil Recovery project. PEOPLE GOING BEYOND BOUNDARIES As we continue to expand our businesses, we add new professional disciplines to deal with the new challenges which require much energy and commitment to resolve. I’m proud of the quality of our staff and the dedication shown by our staff in continuing to achieve excellent results for our Company. On behalf of the Board of Directors, thank-you to all of our employees. Respectfully submitted on behalf of the Board of Directors, (signed) BERNARD F. ISAUTIER President and Chief Executive Officer |

10 PetroKazakhstan Inc. |

President’s Questions and Answers |

Q & A

Q4 | Production for year 2004 was flat versus 2003 even though you projected production increases, why? |

A4 | Three unforeseen key operational factors arose in 2004 leading to this situation. Early in 2004, 19 Kumkol South wells were shut in while a mutually acceptable resolution on the operating conditions of wells located at the border between Kumkol South and Kumkol North was sought with the neighboring license holder, Turgai Petroleum. In June, all wells were back on production, although at a reduced rate from their potential. The net impact on the Company’s average annual rate of production was a decrease of 8,500 bopd. Unexpected failures of electrical submersible pumps in two prolific South Kumkol producers had a further impact of 4,500 bopd on the Company’s annual rate of production. During the fourth quarter of 2004, pumps were optimized and field production resumed at normal rates. The Company has increased the pump stock inventory to minimize individual well downtime when equipment failures occur. Lastly, a significant delay in the arrival of a drilling rig reduced the number of Aryskum development wells resulting in an additional impact of 2,300 bopd on the Company’s average annual production rate. Therefore, these three factors resulted in a total reduction of 15,300 bopd. |

Q4 | With these unforeseen operational factors, can you continue to increase production and grow your assets in 2005? |

A4 | Yes, we can. We own or operate 11 oilfields. Of these fields, a number of them are just in the initial phases of development. We have plans in place to increase production from these fields. With regard to reserves, two methods to increase them are through ongoing appraisal and extensions of existing fields and via EOR. |

| We estimate that the additional possible reserve potential from EOR is anywhere from 55 to 180 million barrels. We are also looking at recovering significant LPG reserves from our fields. As of January 1, 2005, our current reserves, on a proven and probable basis, are 549.8 million barrels of oil equivalent. Independent consultants have determined we have in excess of 250 million barrels of possible oil reserves that we intend to prove up in the future through additional drilling. With regard to exploration, the basin in which we operate is still at a very early phase of maturity. There has been limited exploration in this region over the last 10 years. Independent experts, the US Geological Survey, have estimated that the remaining undiscovered oil potential of the basin is 2.7 billion barrels. Our own portfolio of exploration prospects and leads has identified over 1.0 billion barrels of potential unrisked reserves. So in the years to come, we intend to carry out a very aggressive exploration program to find additional reserves. | |

Q4 | Are you still looking at acquisitions as another means of growth? |

A4 | Yes. Our philosophy is that acquisitions should add value for our shareholders. We are not driven by size for the sake of size. To this point we have been quite successful in acquiring exploration acreage. We have not yet made a large reserve acquisition because in the current high oil price environment, there is a gap between seller and buyer expectations. We are reviewing opportunities in Kazakhstan and in countries that are close to Kazakhstan, where the current operating environment may have some similarities. We are ready to move if the right opportunity materializes. Even without acquisitions, we are confident we can continue to deliver substantial internal growth to our shareholders. |

| 12 PetroKazakhstan Inc. |

Q4 | How important is Kazakhstan as an oil producer and where are the markets for its products at this point? What are your strategies and opportunities? |

A4 | Kazakhstan is a very important country supplying oil into the international market. Three years ago, a discovery was made in the Caspian Sea, the Kashagan discovery, which could have up to 40 billion barrels of oil in place. This is the largest oil discovery made in the world over the last 35 years. So Kazakhstan is the Kuwait of Central Asia, and all international companies are interested in investing in Kazakhstan. The Kashagan discovery is not unique; there are quite a large number of prospects still to be explored with a high likelihood of success. So the question is how do you bring these resources to the international markets? Kazakhstan is a landlocked country. However, the distances from the fields in Kazakhstan to export points are similar to other producing countries in the world. Kazakhstan has a number of options for the export of its oil, and intends to capitalize on all of them - selling crude oil through pipeline via Russia to the European markets; selling through pipeline via the Black Sea, the Bosphorus and then the Mediterranean Sea; shipping across the Caspian Sea then through pipeline, directly to the Mediterranean market; possibly shipping through Iran to the Persian Gulf; and also selling to China via pipeline, the construction of which started in the fall of 2004. As a company, we as well, are pursuing all these export options. |

Q4 | What is your priority regarding transportation costs and continuing to reduce your export differential in 2005? |

A4 | One of our priorities is to continue to lower transportation costs. Transportation is the single largest operating cost we have. Our main export markets are China, the Persian Gulf, the Mediterranean and Black Seas. Even though we have significantly reduced our transportation costs to these markets over the last few years, we continue to seek further cost reduction opportunities. This implies diversification, negotiation of better tariffs and enhanced competition between various routes. We are in an environment that is moving more and more to a free competitive international market. This will benefit us and will enhance the value of our assets. |

Q4 | Why was PetroKazakhstan’s common stock listed on the Kazakhstan Stock Exchange in 2004 given that you are already listed on four other major exchanges, namely Canada, the United States, the United Kingdom and Germany? |

A4 | Over the last few years we have worked hard to raise the profile of our Company in North America, with success. By listing on the Kazakhstan Stock Exchange we hope to be able to attract new shareholders and local investment. By doing so we will become more ingrained in the daily lives of the Kazakh investor, leading to increased confidence and support. |

Q4 | What will you do with the build up of cash that you are experiencing? |

A4 | We will continue to return excess cash to our shareholders through various means. We are buying back shares and paying out dividends on a quarterly basis and we continue to review the possibility of further increasing the amount we will pay out to investors. We have made special dividend distributions in the past and don’t rule out the possibility of doing it again. We will also look at other means of effectively and efficiently enhancing shareholder value. While doing so, we are careful to maintain the flexibility to finance an acquisition or unusual capital project. |

Q4 | How has the dismantling of Yukos in Russia and the current Russian political situation impacted PetroKazakhstan or Kazakhstan? |

A4 | The dismantling of Yukos has not impacted PetroKazakhstan’s operations. Needless to say, Kazakhstan is not Russia in any respect. However, the average investor has become more sensitive to the state of affairs in Russia and as a result, additional downward pressure has been exerted on the stock prices of companies who operate near Russia, including ourselves. By continuing to effectively communicate our opportunities and challenges to investors, we believe we can help alleviate that pressure. |

| 13 |

Q4 | Have the challenges or problems which you faced in 2004 changed and if so, how? |

A4 | No, not to any appreciable degree. The challenge of operating in Kazakhstan is that there are still many opportunities which are not being realized. Significant amounts of time are being spent in negotiations with officials at various levels to obtain the approvals and support needed to realize these opportunities. We are focused on this and are rising to the challenge. |

Q4 | What misperceptions do you still continue to face in the investment community today? |

A4 | The main communication challenge that we still face is the lack of familiarity with Kazakhstan. Not all investors are experts in geopolitics. Their lack of familiarity with Kazakhstan means that they attribute more “political risk” to Kazakhstan than we believe is appropriate. We feel that the risks are manageable. Kazakhstan is a country that is pro foreign investment, pro market economy and is growing rapidly. It is working on accession to the WTO. While we continue to make progress with familiarizing the investment community with Kazakhstan, we still have a long way to go. |

Q4 | Can you comment on your staff? |

A4 | We have built an outstanding team. An area where we have significantly invested in talents is marketing and transportation. We have assembled an outstanding team of traders, engineers, transportation specialists, market analysts and regulatory specialists to deal with the unique transportation issues. We also have something that many companies don’t have, a government relations and regulatory affairs group that monitors very closely the regulatory and energy policy developments in the region, not only in Kazakhstan, but in the countries where we sell our crude oil and products. These groups are supported by a team of analysts. We have the right talents to prepare professional submissions to government authorities, always advocating liberalization of the economy and for policies that promote economic development in the interest of all parties. Our Upstream team continues to deliver excellent results as new reserves have been found and developed. Our investor relations group has worked hard over the last five years to significantly increase our worldwide shareholder base. We have broadened our U.S. investor base, both institutional and retail. We have also expanded our European, Russian and emerging market shareholder base. It is most gratifying to see the skills and motivation of our executives and staff. |

Q4 | What are your goals with respect to being independent in an industry where there is consolidation and growth through merger and acquisition? |

A4 | We’d like to remain an independent company as we believe we can deliver superior value to our shareholders. The Board would not however, oppose or resist a takeover attempt if this was made on the basis of a fair assessment of our net asset value. But until this happens, we will continue to focus our work and efforts on the profitable growth of the Company. |

Q4 | Has your vision for PetroKazakhstan changed over the last year? |

A4 | No. PetroKazakhstan’s vision is to continue to be recognized as a leader in the international oil and gas industry within the Former Soviet Union; to be a leader recognized by its ability to create shareholder value, to operate in a professional manner and to be recognized in Kazakhstan as a model corporate citizen. |

Q4 | What changes should we expect to see in PetroKazakhstan over the next three years? |

A4 | We expect to be focused on further increases in production and reserves and cost reductions, especially transportation costs. We will continue to develop our Downstream operations and hope to have established another area of operation in or around Kazakhstan to support our further growth. |

Q4 | Why should someone invest in PetroKazakhstan today? |

A4 | We have an exceptional and proven track record of delivering growth. We offer a management team operating under western governance and reporting criteria. Our finding and development costs and operating costs are extremely low by world standards. We have been effective in reducing transportation costs and are delivering solid netbacks and returns to our investors. We continue to focus on value creation by buying back our shares and by paying a regular quarterly dividend. We have a history of growth in production, reserves and share price. For all these reasons, we believe PetroKazakhstan remains an outstanding investment opportunity. |

| 14 PetroKazakhstan Inc. |

Operations Overview |

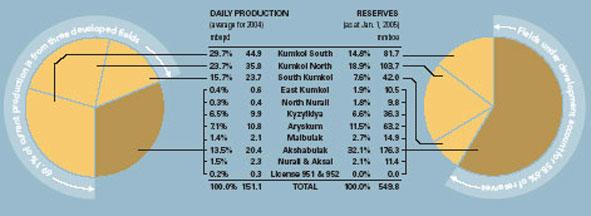

All of PetroKazakhstan’s exploration and production operations are located in the 80,000 km2 South Turgai basin in south central Kazakhstan. PetroKazakhstan holds working interests in four exploration licenses covering a total of over 3.4 million acres. This acreage is 10 times larger than our holdings two years ago. PetroKazakhstan has interests in eleven fields. Within the Kumkol Area there are three developed fields, Kumkol South, Kumkol North and South Kumkol. In close proximity are two new fields in the early stages of development, East Kumkol and North Nurali. To the west of the Kumkol area are the three KAM fields which are in development. Finally, to the south of Kumkol we have interests in three fields, Akshabulak, which is under development and Nurali and Aksai, on test production for appraisal. As of January 1, 2005, proved reserves were estimated at 392.0 mmboe. Proved plus probable reserves were 549.8 mmboe. During PetroKazakhstan’s tenure in Kazakhstan our reserve portfolio has grown by 204 mmbbls of oil in the proved plus probable category net of production of 302 mmbbls. This net production is twice the volume of proved reserves that were attributed to the Company at its inception. Average daily oil production in 2004 was 151,102 bopd. Our fields generally have productive zones at relatively shallow depths ranging from 760 m to 1,830 m with some of our newly drilled wells ranging from 2,300 m to 3,550 m. Most of our reservoirs have high porosity and permeability. Our reservoirs produce light, sweet crude at 37° to 44° American Petroleum Institute (API) gravity with a sulphur content of less than 0.4%. These favourable field and crude oil characteristics enable us to develop our fields and produce and refine our crude oil at a low cost. There are three main processing facilities. A Central Processing Facility (CPF) located in South Kumkol services all production from Kumkol South, South Kumkol and Kumkol North fields and has the capacity to handle 300,000 barrels of fluid per day (bfpd). Gas is gathered from these fields and used to feed a 55 MW power plant in Kumkol. Under construction at the Kyzylkiya and Aryskum fields are facilities that will be capable of processing all fluids from these two fields and that of the Maibulak field to the northwest. In addition, all gas produced from the KAM fields will be injected back into the Aryskum gas cap. | Akshabulak crude is treated at the field facilities, which are being expanded to handle 70,000 bopd. An LPG plant is under construction and a 124 km gas line has been laid from the field, and runs south to the city of Kyzylorda. Substantial unutilized capacity in the government controlled oil pipeline, which runs from our fields to our refinery at Shymkent, still exists. This combination of facilities and pipelines allows for continued production growth and the development of additional reserves without the need for new transportation infrastructure. In addition, the KAM pipeline, commissioned in June 2003, provides an alternative export transportation route directly to our Dzhusaly rail-loading terminal. Beginning in early 2002, our exploration program was primarily focused on accessing stratigraphic prospects, which had not been explored to any great extent in the basin. We have been successful in proving up these concepts in discovering the North Nurali field. The exploration program has also been successful in finding reserves within current production licenses at Kyzylkiya and Aryskum. One of our recent successes has been the discovery of previously unexplored channel sands below the Aryskum gas cap. The 3-year exploration and appraisal success ratio is 73%. The Company has increased its exploration acreage by a factor of ten over the past 2 years providing excellent opportunities for further discoveries from the estimated 94 leads and prospects held therein. As of January 1, 2005, our proved reserves are 392.0 mmboe. Proved and Probable reserves are now 549.8 mmboe which includes 15 mmboe or 88.4 bcf of gas, and 32.1 mmbbls of NGLs. As of January 1, 2005, our proved, probable and possible reserves as determined by our independent reservoir engineering consultants totaled in excess of 800 mmboe. We intend to focus on the complete reserve base and continue to develop and bring more reserves into the proved category. |

| 21 |

Upstream - Property Review |

14 | Kumkol South |

Working interest % | 100 | |||

Operator | PKKR | |||

Acreage (acres) | 18,604 | |||

2004 oil production (mbopd) | 44.9 | |||

2004 gas production (mboepd) | 0.6 | |||

Production wells | 158 | |||

Wells drilled in 2004 | 0 | |||

2005 target oil production (mbopd) | 39 .2 |

The Kumkol field was discovered in 1984 and has been producing since 1990. We are producing from six horizons, in the Cretaceous and Jurassic formations, located at depths less than 1,400 m. The crude oil is sweet and light, 42º API. The field is divided into two operating areas, Kumkol South and Kumkol North.

As the field has matured and water production has increased, significant modifications have been made to the process facilities and the water injection system. Production facilities now handle over 300,000 barrels fluid per day (bfpd) and some 200,000 barrels water per day (bwpd) are re-injected back into the reservoirs to provide pressure support.

PetroKazakhstan is evaluating the potential for EOR in all of its producing fields. A hydrocarbon miscible flood scheme utilizing excess produced gas has been developed for Kumkol South. Phase one of this EOR project is underway with injection expected to commence in the third quarter of 2005 into one of the Kumkol South reservoirs. Our independent reserve engineers have made a nominal addition of probable reserves associated with this project.

24 | South Kumkol |

Working interest % | 100 | |||

Operator | PKKR | |||

Acreage (acres) | 2,826 | |||

2004 oil production (mbopd) | 23.7 | |||

2004 gas production (mboepd) | 0.1 | |||

Production wells | 23 | |||

Wells drilled in 2004 | 0 | |||

2005 target oil production (mbopd) | 22.8 |

The South Kumkol field was discovered in 1992 and has been producing since 1997 from the Cretaceous and Jurassic sands from an average depth of 1200 m. South Kumkol crude is processed at the Kumkol CPF. Water injection is undertaken to maintain reservoir pressure and all wells make use of downhole pumps to maximize production and reserves exploitation. EOR is being evaluated for South Kumkol.

34 | Kyzylkiya |

Working interest % | 100 | |||

Operator | PKKR | |||

Acreage (acres) | 95,657 | |||

2004 oil production (mbopd) | 9.9 | |||

Production wells | 34 | |||

Wells drilled in 2004 | 15 | |||

2005 target oil production (mbopd) | 13.5 |

The Kyzylkiya field was discovered in 1988. Production, which commenced in August 2000, is from the Cretaceous and Jurassic formations at depths less than 1,600 m.

3D seismic has been acquired over the entire field. Development drilling continued in 2004 within the main field structure and to the north into our Kolzhan license area. 4 wells drilled in this area have confirmed the extension of the main Kyzylkiya field to the north. The Company was successful in acquiring additional acreage to the south of the field in which seismic and exploration drilling are planned in 2005.

An integrated oil and gas gathering system is being constructed to deliver produced fluids to Aryskum for crude shipment to our KAM pipeline with gas being re-injected into the Aryskum gas cap.

| 22 PetroKazakhstan Inc. |

44 | Aryskum |

Working interest % | 100 | |||

Operator | PKKR | |||

Acreage (acres) | 41,634 | |||

2004 oil production (mbopd) | 10.8 | |||

Production wells | 34 | |||

Wells drilled in 2004 | 19 | |||

2005 target oil production (mbopd) | 21.5 |

The Aryskum field was discovered in 1988 and was on test production for three years from Cretaceous horizons at 1,200 m. 3D seismic was acquired over the entire field in 2002. Full development is on-going as 34 production wells and 1 gas injection well have been drilled. Oil processing facilities are in place along with water injection and gas injection facilities. Gas injection commenced in 2004 as part of a field pressure maintenance and gas conservation program. Ultimately, gas from all the KAM fields and excess gas from the Kumkol fields will be injected into the Aryskum gas cap. The Company was successful in discovering oil in Jurassic channel sands below this gas cap. The sands, which are of excellent quality and exhibited well flowrates of up to 1,600 bopd, were not anticipated in the initial development plan and add to the reserve base for this field. The Company intends to continue its appraisal of further channel sands in the area.

54 | Maibulak |

Working interest % | 100 | |||

Operator | PKKR | |||

Acreage (acres) | 10,263 | |||

2004 oil production (mbopd) | 2.1 | |||

Production wells | 9 | |||

Wells drilled in 2004 | 0 | |||

2005 target oil production (mbopd) | 3.9 |

The Maibulak field was discovered in 1988 with four productive zones in the Jurassic formation identified at depths of less than 1,400 m. 3D seismic surveys have been conducted over the entire field. Test production crude has been trucked to Aryskum, some 40 km to the south east. Full development is underway where all produced fluids including gas will be piped to the Aryskum facilities. Water injection facilities are in place and operational.

64 | East Kumkol |

Working interest % ** | 80 | |||

Operator | PKKR | |||

Acreage (acres)* | 8,151 | |||

2004 oil production (mbopd) * | 0.6 | |||

Production wells * | 5 | |||

Wells drilled in 2004 * | 0 | |||

2005 target oil production (mbopd)* | 0.9 |

East Kumkol has been in an appraisal testing phase. 3D seismic survey acquired over the entire field confirmed that the field extends into the Kumkol North (Turgai) license area. PetroKazakhstan and Turgai have developed joint venture agreements, a joint development plan and production agreements for approval by the authorities. The field is currently not producing pending finalization of the development and production plan and necessary regulatory approvals.

74 | North Nurali |

Working interest % | 100 | |||

Operator | PKKR | |||

2004 oil production (mbopd) | 0.4 | |||

Production wells | 8 | |||

Wells drilled in 2004 | 3 | |||

2005 target oil production (mbopd) | 2.5 |

Just 5 kms west of the Kumkol field, North Nurali has proved to be a success in the Company’s exploration of new concept leads in the South Turgai Basin. A total of ten wells have been drilled by PetroKazakhstan in this field to depths ranging from 2,300 m to 3,550 m. Application is being made for an extended test production program with produced fluids being tied into the Kumkol facilities.

| 23 |

84 | Kumkol North |

Working interest % | 50 | |||

Operator | Turgai | |||

Acreage (acres)* | 40,655 | |||

2004 oil production (mbopd) * | 71.5 | |||

2004 gas production (mboepd) * | 2.9 | |||

Production wells * | 228 | |||

Wells drilled in 2004 * | 18 | |||

2005 target oil production (mbopd)* | 71.6 |

Turgai operates Kumkol North, which is owned equally between PetroKazakhstan and Lukoil Overseas Ltd. Production and ancillary support facilities are provided by PetroKazakhstan as the operator of Kumkol South on a fee basis. The crude is commingled after a metering station at the field’s border, and then processed at the CPF. Eighteen development wells were drilled in 2004.

94 | Akshabulak |

Working interest % | 50 | |||

Operator | Kazgermunai | |||

Acreage (acres) * | 64,118 | |||

2004 oil production (mbopd) * | 40.8 | |||

Production wells * | 20 | |||

Wells drilled in 2004 * | 4 | |||

2005 target oil production (mbopd)* | 55.0 |

Kazgermunai operates Akshabulak which is owned 50% by PetroKazakhstan, 25% by RWE, 17.5% by EEG and 7.5% by International Finance Corporation (IFC). The Akshabulak field was discovered in 1988 and production began in 1997. Production is currently being transported by pipeline to the Kumkol field where it ties into the Kumkol - - Karakoin pipeline. This in turn connects to the central pipeline that delivers oil to the Shymkent refinery. Kazgermunai sells all of its crude into the export market.

Full development of the field is still to be accomplished. It has been delayed by the German joint venture partners, pending assurances from the Government of Kazakhstan on marketing and transportation issues. However, full field development has progressed with the acquisition of 3D seismic and development drilling of eleven wells over the past two years. Facility expansion is ongoing which should enable production of up to 70,000 bopd by the end of 2005. An LPG plant will be commissioned in the third quarter of 2005 and dry gas will be exported to the city of Kyzylorda via a 10” pipeline.

104 | Nurali and Aksai |

Working interest % | 50 | |||

Operator | Kazgermunai | |||

Acreage (acres)* | 164,795 | |||

2004 oil production (mbopd) * | 4.6 | |||

Production wells * | 15 | |||

Wells drilled in 2004 * | 4 | |||

2005 target oil production (mbopd)* | 5.0 |

Nurali and Aksai have the same ownership structure as Akshabulak. The complex geology of the Nurali and Aksai fields has led to a new assessment of the appraisal and development plan. 3D seismic has been acquired and interpreted.

Four wells were drilled and selective wells were put on test production in 2004. The development will continue in 2005 with the drilling of up to five more wells during the year based on the interim production plan approved by the authorities.

* Items are at 100% or gross working interest. ** Subject to variation on settelment

| 24 PetroKazakhstan Inc. |

Exploration - - 260 D1 License

This 333,841 acre license surrounds the Kumkol field and continues to be one of our focus areas for our exploration efforts. The term of this license has been extended to June 2007. Leads that were originally identified in this license area from a comprehensive basin study resulted in the discovery of the North Nurali field.

The wells identified deeper target sands in stratigraphic traps, unexplored in the basin. Well depths for all the leads range from 2,300 m to 4,000 m. The North Nurali wells have validated the concept of producible hydrocarbons from deep stratigraphic traps. Extensive exploration and appraisal work has been conducted with the acquisition of 3D seismic over the North Nurali field itself and to the north where there exists the potential for a field extension in which a well will be drilled in 2005.

The exploration program will continue in 2005 with the acquisition of 3D seismic over the Karavanchy structure (east of the Kyzylkiya field) and over an area to the north of the Kumkol main reservoir in which an exploration well is planned.

Exploration - - License 952 (Kolzhan)

The acquisition of the 122,811 acre Kolzhan license, directly north of the Kyzylkiya field, was completed in the 4th quarter of 2003 and the license term has been extended to June 2007. Well KK34, drilled to 1,500 m produced light, sweet, oil at a rate of 1,000 bopd. Well evaluation results confirm that this accumulation is an extension of the main Kyzylkiya field. 3D seismic was acquired over the western half of the block enabling mapping of the main Kyzylkiya field extension. To date, 5 wells have been drilled with at least a further 4 wells planned in 2005 and the reprocessing of 2D seismic over the eastern half of the block. We had test production of 0.3 mbopd in 2004.

Exploration - - License 951-D

PetroKazakhstan has farmed-in to acquire operatorship and a 75% equity position in two separate blocks totaling over one million acres (4,290 km2) in a joint venture with Orient Petroleum. Two exploration wells on this license previously tested oil. The license is split into two blocks, Doshan to the north and Zhamansu to the south. Following the acquisition and interpretation of 714 kms of 2D seismic over the license, some 32 leads were identified in the Zhamansu block. Four wells were drilled in this block late in 2004, 2 wells encountered hydrocarbon sands but commercial production rates could not be attained. Two wells were dry.

Interpretation of data in the Doshan has identified a number of prospects and two exploration wells are planned for 2005.

Exploration - - Karaganda License

This large (1,876,508 acre) license, lies to the north of the 260 D1 and 952 Kolzhan licenses, and has been awarded to PetroKazakhstan. We are currently awaiting confirmation of the contract terms. The combination of large structural leads and evidence of oil migration into this area (the Company has drilled a well directly to the south of this license) elevates the prospectivity. The staged worked program will start with reprocessing of 400 km of 2D seismic and the acquisition of new 2D seismic in 2005.

| 25 |

GAS RESOURCE CONSERVATION AND EXPLOITATION

The Company has addressed the issue of utilizing associated produced gas in a number of ways.

| 4 | PetroKazakhstan has built a 55 MW power plant in the Kumkol field. This facility uses associated produced gas from the Kumkol South, South Kumkol and Kumkol North fields to produce electricity for field use and to minimize gas flaring. |

| 4 | As a joint venture partner in the Akshabulak fields, PetroKazakhstan is participating in a project to provide natural gas to the Kyzylorda region and to extract LPG. This plant will be operational in the third quarter of 2005. The gas pipeline has been built. |

| 4 | The Kumkol field’s EOR project with LPG injection will commence in the third quarter of 2005 and will use excess produced gas. |

| 4 | Aryskum gas is now re-injected back into the reservoir for gas conservation and pressure maintenance. Kyzylkiya and Maibulak produced gas will also be re-injected as part of the KAM field development program. |

| 4 | The Company has embarked on a complete gas gathering program through all its fields. NGLs will be extracted for sale, and dry gas will be re-injected back into reservoir gas caps for conservation and reservoir pressure maintenance. |

McDaniel and Associates Consultants Ltd., the Company’s independent reserve engineers, have acknowledged these programs through the recognition of reserves.

HEALTH, SAFETY AND ENVIRONMENT

PetroKazakhstan is committed to the continuous improvement of its Health, Safety and the Environment (HS&E) performance. During 2004, Upstream operations experienced only one lost time accident and reported 10 accidents/incidents. The Company has paid particular attention to its contractors’ performance through routine and operations specific safety meetings, the addition of contractual HS&E obligations and implementation of a contractor safety reporting program. Training is an integral part of our HS&E program and we employ experienced HS&E staff to assist all levels of the workforce in addressing issues. We routinely test and certify staff for work in critical and hazardous operations to ensure a high level of safe working practices.

We are conducting a program of upgrading all emergency response plans that will be complete in the second quarter of 2005.

We have reduced emissions through the continued use of our 55 MW power generation plant at Kumkol which uses, previously flared, produced associated gas. In addition, the Company has commissioned the Aryskum gas re-injection facility which reduces flared emissions in the Aryskum oilfield. PetroKazakhstan implemented several other capital projects such as bio-remediation, waste water treatment and improved handling of oilfield and domestic waste programs.

The Company continues to maintain a close working relationship with local authorities to ensure continuing compliance with the Republic of Kazakhstan’s laws and regulations.

| 26 PetroKazakhstan Inc. |

Reserves |

RESERVES RECONCILIATION BY FIELD

Proved plus probable (mmboe)

| Kumkol | Kumkol | South | East | North | |||||||||||||||||||||||||||||||||

| South | North | Kumkol | Kumkol | Nurali | Kyzylkiya | Aryskum | Maibulak | Akshabulak | Nurali | Aksai | Total | ||||||||||||||||||||||||||

| Reserves as of Jan 1, 2004 | 71.9 | 100.3 | 47.1 | 11.7 | 12.8 | 35.3 | 47.7 | 14.0 | 143.5 | 9.9 | 1.3 | 495.5 | |||||||||||||||||||||||||

| Revisions | 26.4 | 17.0 | 3.6 | (1.0 | ) | (2.9 | ) | 4.7 | 19.5 | 1.7 | 40.6 | 0.9 | (0.2 | ) | 110.3 | ||||||||||||||||||||||

| Production | (16.6 | ) | (13.6 | ) | (8.7 | ) | (0.2 | ) | (0.1 | ) | (3.7 | ) | (4.0 | ) | (0.8 | ) | (7.8 | ) | (0.5 | ) | (0.0 | ) | (56.0 | ) | |||||||||||||

Reserves as of Jan 1, 2005 | 81.7 | 103.7 | 42.0 | 10.5 | 9.8 | 36.3 | 63.2 | 14.9 | 176.3 | 10.3 | 1.1 | 549.8 | |||||||||||||||||||||||||

Total PetroKazakhstan interest by field. As at January 1, 2005. McDaniel & Associates Consultants Ltd.

| Proved + | |||||||||||||

Reserves (mmboe) | Proved | % | Probable | % | |||||||||

| Kumkol South | 60.4 | 15.4 | % | 81.7 | 14.9 | % | |||||||

| Kumkol North | 83.7 | 21.3 | % | 103.7 | 18.9 | % | |||||||

| South Kumkol | 34.6 | 8.8 | % | 42.0 | 7.6 | % | |||||||

| East Kumkol | 7.1 | 1.8 | % | 10.5 | 1.9 | % | |||||||

| North Nurali | 1.8 | 0.5 | % | 9.8 | 1.8 | % | |||||||

| Kyzylkiya | 21.9 | 5.6 | % | 36.3 | 6.6 | % | |||||||

| Aryskum | 47.4 | 12.1 | % | 63.2 | 11.5 | % | |||||||

| Maibulak | 7.2 | 1.8 | % | 14.9 | 2.7 | % | |||||||

| Akshabulak | 123.0 | 31.4 | % | 176.3 | 32.0 | % | |||||||

| Nurali | 4.9 | 1.3 | % | 10.3 | 1.9 | % | |||||||

| Aksai | 0.0 | 0.0 | % | 1.1 | 0.2 | % | |||||||

| Total | 392.0 | 100.0 | % | 549.8 | 100.0 | % | |||||||

RESERVE EVALUATION

Summary of remaining reserves.As at January 1, 2005. McDaniel & Associates Consultants Ltd.

| Crude Oil | Natural Gas | Natural Gas Liquids | Total Reserves | ||||||||||||||||||||||

(mmbbls) | (bcf) | (mmbbls) | (mmboe) | ||||||||||||||||||||||

| Property | Company | Property | Company | Property | Company | Property | Company | ||||||||||||||||||

| Gross | Gross* | Gross | Gross* | Gross | Gross* | Gross | Gross* | ||||||||||||||||||

| Proved developed producing | 342.8 | 224.4 | 49.3 | 31.6 | 0.0 | 0.0 | 351.0 | 229.7 | |||||||||||||||||

| Proved developed non-producing | 73.5 | 48.7 | 0.0 | 0.0 | 0.0 | 0.0 | 73.5 | 48.7 | |||||||||||||||||

| Proved undeveloped | 135.7 | 84.2 | 54.8 | 27.0 | 36.9 | 24.9 | 181.8 | 113.6 | |||||||||||||||||

| Total proved | 552.0 | 357.3 | 104.1 | 58.6 | 36.9 | 24.9 | 606.3 | 392.0 | |||||||||||||||||

| Probable | 219.2 | 145.6 | 53.2 | 29.8 | 10.7 | 7.2 | 238.7 | 157.8 | |||||||||||||||||

| Proved plus probable | 771.2 | 502.9 | 157.3 | 88.4 | 47.6 | 32.1 | 845.0 | 549.8 | |||||||||||||||||

| Possible | 389.1 | 254.8 | 389.1 | 254.8 | |||||||||||||||||||||

| Proved plus probable plus possible | 1,160.3 | 757.7 | 1,234.1 | 804.6 | |||||||||||||||||||||

* | Company gross reserves are before royalties. |

| 28 PetroKazakhstan Inc. |

Summary of remaining reserves and present values. As at January 1, 2005. McDaniel & Associates Consultants Ltd.

Escalating Price Assumptions

| Total Reserves | Net Present Worth Value Before Income Taxes - Unrisked | ||||||||||||||||||

(mmboe) | (thousands of U.S. dollars) | ||||||||||||||||||

| Company | |||||||||||||||||||

| Gross* | 0% | 5% | 10% | 15% | 20% | ||||||||||||||

| Proved developed producing | 229.7 | 3,793,089 | 3,310,873 | 2,951,983 | 2,674,373 | 2,452,976 | |||||||||||||

| Proved developed non-producing | 48.7 | 849,166 | 650,887 | 520,695 | 429,922 | 363,558 | |||||||||||||

| Proved undeveloped | 113.6 | 1,409,587 | 1,042,773 | 806,970 | 646,100 | 530,957 | |||||||||||||

| Total proved | 392.0 | 6,051,842 | 5,004,533 | 4,279,648 | 3,750,395 | 3,347,491 | |||||||||||||

| Probable | 157.8 | 2,591,473 | 1,837,721 | 1,376,159 | 1,075,414 | 869,004 | |||||||||||||

| Proved plus probable | 549.8 | 8,643,315 | 6,842,254 | 5,655,807 | 4,825,809 | 4,216,495 | |||||||||||||

| Possible | 254.8 | ||||||||||||||||||

| Proved plus probable plus possible | 804.6 | ||||||||||||||||||

* | Company gross reserves are before royalties. |

Summary of remaining reserves and present values. As at January 1, 2005. McDaniel & Associates Consultants Ltd.

Constant Price Assumptions

| Total Reserves | Net Present Worth Value Before Income Taxes - Unrisked | ||||||||||||||||||

(mmboe) | (thousands of U.S. dollars) | ||||||||||||||||||

| Company | |||||||||||||||||||

| Gross* | 0% | 5% | 10% | 15% | 20% | ||||||||||||||

| Proved developed producing | 229.7 | 4,727,816 | 4,044,562 | 3,545,453 | 3,166,130 | 2,868,555 | |||||||||||||

| Proved developed non-producing | 48.7 | 1,091,466 | 836,676 | 667,538 | 548,911 | 461,993 | |||||||||||||

| Proved undeveloped | 113.6 | 1,854,692 | 1,378,832 | 1,069,072 | 856,048 | 702,891 | |||||||||||||

| Total proved | 392.0 | 7,673,974 | 6,260,070 | 5,282,063 | 4,571,089 | 4,033,439 | |||||||||||||

| Probable | 157.8 | 3,281,302 | 2,344,077 | 1,760,493 | 1,375,554 | 1,109,133 | |||||||||||||

| Proved plus probable | 549.8 | 10,955,276 | 8,604,147 | 7,042,556 | 5,946,643 | 5,142,572 | |||||||||||||

| Possible | 254.8 | ||||||||||||||||||

| Proved plus probable plus possible | 804.6 | ||||||||||||||||||

* | Company gross reserves are before royalties. |

| 29 |

Downstream Review |

Our refinery at Shymkent continues to be the best performing refinery in Kazakhstan and further improvements are being made through process improvements.

BACKGROUND PetroKazakhstan exports crude oil from a variety of loading points through a number of pipeline systems, and rail and sea routes to different markets and customers. The flexibility provided through these alternative routes continues to allow us to improve our export and domestic sales netbacks and provides security in the event that one route is closed for some unforeseen operational reason. Our refinery at Shymkent continues to be the best performing refinery in Kazakhstan and further improvements are being made through process improvements. Our refinery is well located and designed to serve both the domestic and export markets. PetroKazakhstan refined products continue to be recognised in both the domestic and export markets as being of exceptional quality and offering excellent value. CRUDE OIL LOGISTICS PetroKazakhstan’s and Turgai Petroleum’s crude oil export shipments increased from 3.5 million tonnes (27.1 mmbbls) in 2003 to 3.9 million tonnes (30.2 mmbbls) in 2004, an increase in average daily shipments from 9,800 tonnes per day to 10,800 tonnes per day from 2003 to 2004. Seventy two percent of these shipments were loaded through our KAM pipeline and Dzhusaly Terminal which continues to generate the $2.00/bbl savings forecasted at the time the project was conceived. Shipments through the CPC pipeline accounted for around 36% of all shipments as volumes approached their maximum contractual limit. Deliveries to China accounted for 19% of the overall shipments. Eighty eight percent of all shipments to China were made via the state owned pipeline to Atasu, eliminating a significant rail journey and the associated costs. | Shipments to the Tehran refinery under the swap agreement with the National Iranian Oil Company grew steadily until June 2004, after which the Ministry of Energy and Mineral Resources (MEMR) of the Republic of Kazakhstan imposed export limits and finally blocked all exports on this route. The dialogue between PetroKazakhstan and MEMR is continuing and we are hopeful of a positive outcome. PetroKazakhstan’s position is that the imposition of quota restrictions on this route is unjustified as we provide all the necessary logistics, there are no physical constraints on this route and such restrictions are not in the best interest of the Republic of Kazakhstan or the neighbouring transit republics of Uzbekistan and Turkmenistan and is contrary to the policy wishes of the governments of Kazakhstan and Iran. As part of our on-going strategy to take control of and improve our logistics costs, crude oil exports on an FCA (Free Carrier) basis were completely eliminated during 2004. In support of this initiative the number of rail cars in the fleet dedicated to PetroKazakhstan grew to approximately 5,000 at the end of 2004 up significantly from 2,000 at the end of 2003. The enlarged fleet comprises a mix of owned and long and short-term leased rail cars to provide operational and financial flexibility. CRUDE OIL TRADING Throughout 2004, the international crude oil markets remained nervous about the lead up to the elections in Iraq, production interruptions, and the level of US inventories. At the same time strong demand from China and transportation capacity limits in Russia added further upward pressure to an already rising market. As a consequence, and due to an element of speculation by traders, international crude oil prices remained at extremely high levels with an enormous level of volatility. The highest recorded daily mean for Brent dated in 2004 was $52.03/bbl with a low of $29.12/bbl producing a price spread over the year of $22.90/bbl. |

| 31 |

In response to supply concerns OPEC increased their output of heavier sour crudes. While this addressed the overall supply demand balance it caused a distortion of the heavy sour/light sweet differentials. Crude grades such as Urals saw their discount against Brent rise from around $1.60/bbl at the beginning of 2004 to a high of $7.50/bbl by October 2004. This generated a strong incentive for European refineries to buy the cheaper heavier grades and consequently the Mediterranean market became long on sweet crude and prices for sweet crudes began to slide against Brent in November 2004. Grades like CPC Blend and Siberian Light fared the worst, recording a discount to Brent of up to $4.50/bbl. While Kumkol performed better, the premium against Brent which is typically between $0.50 to $0.80/bbl slipped to a discount of between $0.10 and $2.00/bbl during the last 6 weeks of 2004. Kumkol closed the year at a discount to Brent of $0.12/bbl. The improvement in our differentials to Brent recorded for the first three quarters of 2004 were as a result of the elimination of FCA contracts, the higher utilisation of better routes and the utilization of our KAM pipeline and Dzhusaly terminal. The fourth quarter of 2004 saw a deterioration of differentials reflecting the changes in the crude oil markets as mentioned above and the seasonal impact of night-time shipping restrictions in the Bosphorus Straits and some intermittent weather problems at Aktau. This situation is expected to continue for the first quarter of 2005. Nevertheless, the average differential for 2004 was a substantial improvement over 2003. REFINERY OPERATIONS AND REFINED PRODUCT SALES The ongoing continuous improvement program at our Shymkent refinery continues to yield significant value benefits. We measure the change in product yield value on a fixed crude and product price basis thus eliminating the variations of market prices. This measure indicates a steady trend of improvements over the last two years which has generated an improvement in refining margins in excess of $2.00/bbl. By the second quarter of 2004 the VDU was operating at maximum capacity and regular sales were being made through the Baltic port of Tallinn. During 2005 we expect to be able to increase the yield of VGO and to develop additional outlets for this product. Refinery per unit costs showed an increase from $0.58/bbl in 2003 to $0.80/bbl which is line with the equivalent figures for 2002. The reasons for the increase were lower throughput, the maintenance turnaround in 2004 and the additional operating costs associated with the start up of the VDU. | The average price of refined products improved by $7.84/bbl compared to 2003. These improvements were as a result of firmer market prices, the improved yield of higher value products, a greater proportion of refined product exports and improved pricing management keeping a balance between Kazakh prices and Russian competitor prices. Exports of refined products were on average around 75,000 tonnes per month (approximately 19,100 bpd) destined primarily for the neighbouring republics although some products such as VGO and fuel oil were sold on the international market in the Baltic and the Mediterranean. HEALTH, SAFETY AND ENVIRONMENT Preservation of the environment and the health and safety of our refinery employees and contractors continues to be a top management priority. Environmental and safety indicators demonstrate a continuing improvement. In 2003 and 2004, a zero Lost Time Incident rate amongst refinery employees was achieved versus five incidents in 2002. This performance is attributed to a focused effort in passing on responsibility for safety to the supervisory level. Emphasis is placed on meeting or improving on regulatory environmental limits and education of employees and contractors regarding occupational health issues. The oil and gas industry is a focal point for environmental performance and scrutiny by government authorities. The Republic of Kazakhstan is no exception. Our refinery faces increasingly stringent limits imposed by the Kazakh ministries. In 2004, with the exception of a minor spill from a waste water line which posed no environmental hazard, the refinery performance continued to improve. Waste water from the refinery to off-site treatment works has declined by 43% in the last two years. Since 2002, refinery emissions have consistently been at least 10% under license limits. We are well placed to meet future challenges. Areas of environmental focus in 2005 include projects to: 4 Reduce emissions from our refined fuels. 4 Further reduce Sulphur Dioxide and Nitrous Oxide emissions. 4 Improve water conservation and waste water quality. 4 Improve the oily waste processing facilities. 4 Rehabilitate soils. |

| 32 PetroKazakhstan Inc. |

Management’s Discussion and Analysis |

The following Management’s Discussion and Analysis (“MD&A”) of the financial condition and results of our operations should be read in conjunction with our consolidated financial statements and notes relating thereto that are included elsewhere in this report. Our financial statements have been prepared in accordance with Canadian generally accepted accounting principles (“GAAP”). This discussion and analysis contains forward-looking statements, which involve risks and uncertainties. Our actual results could differ materially from those anticipated in the forward-looking statements.

These forward-looking statements can generally be identified by the use of statements that include phrases such as “believe”, “expect”, “anticipate”, “intend”, “plan”, “likely”, “will” or similar words or phrases. Similarly, statements that describe our objectives, plans or goals are or may be forward-looking statements. These forward-looking statements are based on our current expectations and projections about future events. However, whether actual results and developments will conform with our expectations and projections is subject to a number of risks and uncertainties, including, among other things, the risks and uncertainties described under section “Risk Analysis” and the risk factors described in our Annual Information Form for the year ended December 31, 2004 under the heading “Risk Factors”. These are not necessarily all of the important factors that could cause actual results to differ materially from those expressed in any of our forward-looking statements. Other known or unpredictable factors could also harm our results. Consequently, there can be no assurance that the actual results or developments anticipated by us will be realized or, even if substantially realized, that they will have the expected consequences to, or affects on, us. Unless otherwise required by applicable securities law, we disclaim any intention or obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

In our MD&A we use certain terms, which are specific to the oil and gas industry, including “net return” and “cash flow”. These are non-GAAP terms defined within our MD&A.

Except as otherwise required by the context, reference in this MD&A to “our”, “we” or “us” refer to the combined business of PetroKazakhstan Inc. and all of its subsidiaries and joint ventures.

Additional information filed with Canadian securities commissions and the United States Securities and Exchange Commission, including our quarterly and annual reports and our Annual Information Form (AIF/40-F), are available on line at www.sedar.com and www.sec.gov.

All numbers are in U.S. Dollars unless otherwise indicated.

| 33 |

OVERVIEW AND STRATEGY

PetroKazakhstan Inc. is an integrated oil company that owns and operates oil and gas production and a refinery in Kazakhstan. We use the term “Upstream” to refer to the exploration for and production of oil and gas from our licenses in the South Turgai Basin, Kazakhstan. We use the term “Downstream” to refer to the operations of our refinery located in Shymkent, Kazakhstan and the marketing and transportation of refined products and the management of the marketing and transportation of crude oil for Upstream.

BUSINESS STRATEGY

PetroKazakhstan strives to be the leading integrated oil and gas company in the Former Soviet Union and an exemplary corporate citizen. Our goal is to create superior value for our shareholders and the Republic of Kazakhstan while protecting the health and safety of our people and the environment.

The primary elements of our strategy are to:

| 4 | Explore our undeveloped properties.We have approximately 3,400,000 acres of land that we intend to explore and develop. |

| 4 | Capitalize on development opportunities.We intend to bring our proved undeveloped reserves into production in a timely, efficient and profitable manner. |

| 4 | Fully exploit our reserves.We intend to focus on the complete reserve base and continue to develop and bring more reserves into the proved category. |

| 4 | Seek selective acquisition opportunities. As part of our strategy to increase reserves and production, we are pursuing opportunities to acquire additional reserves from third parties. Our acquisition strategy has focused on acreage and assets, both producing and of exploration potential, within the vicinity of our current oil fields and throughout Kazakhstan. |

| 4 | Open new transportation routes to international markets and reduce our transportation costs.In 2004, approximately 55% of crude oil sales went to export markets. Though we have been successful in reducing our transportation costs to these markets, they still remain our single largest cost of operations. |

| 4 | Improve the operational performance of our refinery. Since the acquisition of the refinery in 2000, we have been implementing projects designed to increase product quality and production yields and to improve the refinery’s product mix. |

| 4 | Control and reduce our overhead and operating costs.Overlaps in the operations of our principal operating subsidiaries, PKKR and PKOP, have been essentially eliminated by establishing a joint marketing and transportation team. We have divested non-core activities and continue to aim at reduction of our operating costs. |

| 4 | Manage our environmental and social responsibilities to ensure that we earn support from all stakeholders for PetroKazakhstan’s growth and operating plans.In late 2003 we commissioned our gas utilization project designed to reduce the flaring of gas produced from our Kumkol fields and the consequential release of pollutants into the environment. We also plan to complete the construction of a gas processing plant in our Akshabulak field in 2005, which will further reduce gas flaring. |

| 34 PetroKazakhstan Inc. |

HIGHLIGHTS

| Years ended December 31 | ||||||||||||||||

2004 | 2003 | |||||||||||||||

2004 | 2003 | 2002 | vs 2003 | vs 2002 | ||||||||||||

Net income ($000’s) | 500,668 | 316,940 | 161,397 | 58 | % | 96 | % | |||||||||

Cash flow($000’s)1 | 560,491 | 399,975 | 216,794 | 40 | % | 84 | % | |||||||||

| Basic net income per share | 6.40 | 4.06 | 2.00 | 58 | % | 103 | % | |||||||||

| Basic cash flow per share | 7.16 | 5.12 | 2.68 | 40 | % | 91 | % | |||||||||

Production, bopd2 | 151,102 | 151,349 | 135,842 | - | 11 | % | ||||||||||

| Capital expenditures | 165,952 | 203,213 | 140,102 | (18 | %) | 45 | % | |||||||||

| Total assets | 1,269,081 | 1,041,451 | 709,723 | 22 | % | 47 | % | |||||||||

| Long-term debt | 134,862 | 246,655 | 281,797 | (45 | %) | (12 | %) | |||||||||

| Cash dividends declared | 39,253 | - | - | 100 | % | - | ||||||||||

| Common shares outstanding | 76,223,130 | 77,920,226 | 78,956,875 | (2 | %) | (1 | %) | |||||||||

1 | Cash flow: We evaluate our operations based upon our net income and cash flow. Cash flow is a non-GAAP measure that represents cash generated from operating activities before changes in non-cash working capital. We consider this to be a key measure as we use this measure to evaluate our ability to generate cash to fund our growth through capital expenditures and our ability to repay debt. The comparable GAAP measure is cash flow from operating activities. The following table reconciles our non-GAAP measure cash flow to the comparable GAAP measure “Cash flow from operating activities”. Cash flow does not have any standardized meaning prescribed by Canadian GAAP and is, therefore, unlikely to be comparable to similar measures presented by other issuers. |

| Years ended December 31 | ||||||||||

($000’s) | 2004 | 2003 | 2002 | |||||||

| Cash flow | 560,491 | 399,975 | 216,794 | |||||||

| Changes in non-cash operating working capital items | (24,899 | ) | (60,625 | ) | (37,816 | ) | ||||

| Cash flow from operating activities | 535,592 | 339,350 | 178,978 | |||||||

2 | We report production before royalties as we measure our Upstream operations on this basis, which is consistent with industry practice in Canada. |

| 35 |

NET INCOME VARIANCES

| $ millions | ||||

| Net income for the year ended December 31, 2002: | 161 | |||

| Increase in the price of crude oil | 76 | |||

| Increase in net return at Kumkol for refined products | 72 | |||

| Increase in refined products sales volumes | 23 | |||

| Increase in crude oil export sales volumes | 16 | |||

| Increase in depletion and depreciation | (16 | ) | ||

| Other variances | (15 | ) | ||

| Net income for the year ended December 31, 2003: | 317 | |||

| Increase in the price of crude oil | 200 | |||

| Increase in net return at Kumkol for refined products | 92 | |||

| Improvement in differential | 32 | |||

| Increase in crude oil export sales volumes | 24 | |||

| Increase in prices for crude oil purchases | (38 | ) | ||

| Excess profit tax | (35 | ) | ||

| Hedging | (26 | ) | ||

| Decrease in refined products sales volumes | (22 | ) | ||

| Increase in depletion and depreciation | (16 | ) | ||

| Higher income tax rate for Kazgermunai | (12 | ) | ||

| Other variances | (15 | ) | ||

Net income for the year ended December 31, 2004: | 501 | |||

Higher prices for crude oil and refined products in 2003 and 2004 were the major reason for our record results. Our efforts to improve our differential in 2004 added an additional $32.0 million to our net income. These gains were partially offset by the foregone revenue from our hedging program and the increased prices paid for crude oil purchased from third parties. Lower throughput volumes and the refinery turnaround led to lower sales of refined products in 2004.

KEY PERFORMANCE INDICATORS

We measure the performance of our Upstream and Downstream operations using the following key performance indicators:

| Years ended December 31 | ||||||||||

2004 | 2003 | 2002 | ||||||||

| Production, bopd | 151,102 | 151,349 | 135,842 | |||||||

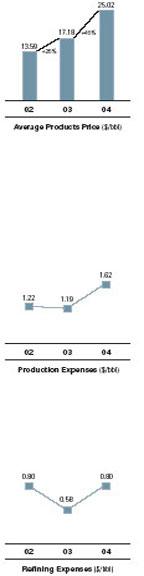

Differential ($/bbl) | 12.62 | 14.11 | 13.97 | |||||||

Average refined products price($/bbl) | 25.02 | 17.18 | 13.59 | |||||||

Production expense($/bbl) | 1.62 | 1.19 | 1.22 | |||||||

Refining cost($/bbl) | 0.80 | 0.58 | 0.80 | |||||||

General and administrative($/bbl) | 1.16 | 1.12 | 1.39 | |||||||

Effective income tax rate(%) | 37.5 | 32.8 | 38.0 | |||||||

Production. SeeVolumetrics for a discussion of our production.

| 36 PetroKazakhstan Inc. |

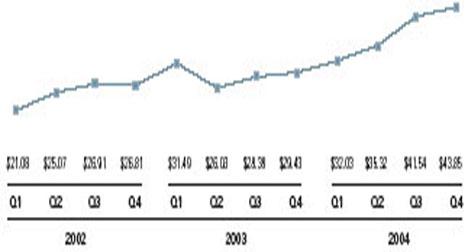

Strategy: Open new transportation routes to international markets and reduce our transportation costs

Differentials. The graph below shows the evolution of our differential.

* | Our differential is calculated as the difference between the average Brent price for crude oil export sales received by PKKR and Turgai, and our net return at Kumkol. Differential is a non-GAAP measure that is the sum of the costs and discounts incurred in order to transport and sell our crude oil to international markets. The sales revenue used in this measure differs from sales revenue in the statement of net income and the net return table for the following reasons: | |

4 | The differential does not include Kazgermunai sales over which we have limited control. Kazgermunai is excluded because the differential is used to measure the performance of our internal marketing group. | |

4 | The differential is calculated using finalized sales transactions. Our financial statements include estimates that may or may not reflect the finalized transactions. | |

The term “differential” does not have a standardized meaning prescribed by Canadian GAAP and is, therefore, unlikely to be comparable to similar measures presented by other companies. | ||

Our differential constitutes our single largest expenditure and the management of this cost is one of our primary objectives. To achieve this, we have a dedicated crude oil marketing and logistics team whose objective is to sell our crude oil to end users and to obtain a greater understanding and control over our export routes. To accomplish this, we have acquired a fleet of approximately 5,000 purchased and leased rail cars, obtained access to loading facilities and ports and we have opened new transportation routes.

We export crude oil in all geographical directions, north to Atyrau through our Dzhusaly terminal and then onward through the CPC pipeline, east to China via the Atasu terminal, south to Uzbekistan and Iran and west through Aktau to the port of Batumi and some onward shipments to ports in the Mediterranean.

| 37 |

We have made greater use of pipelines thereby reducing our rail costs. Specifically, our KAM pipeline and the KTO pipeline to Atasu with onward rail to China.

In the third quarter of 2004, the combination of different routes, increased utilisation of pipelines, having railcars under our control, and reduced discounts negotiated with buyers led to our overall crude differential reaching its lowest level in four years at $11.66/bbl.

In the fourth quarter of 2004 our differential increased by $0.79/bbl over the fourth quarter of 2003 and increased by $2.17/bbl over the third quarter of 2004.

Increased demand for sour crudes in the Mediterranean as a result of increases in the differential between sweet and sour crudes, changed the average premium of Kumkol over Brent of $0.68/bbl in the third quarter of 2004 to a discount of $0.38/bbl by the fourth quarter of 2004, an impact of $1.06/bbl.

Increased shipping rates and demurrage costs for vessels, a seasonal factor, were exacerbated by the hurricanes in the United States during the fall of 2004, which led to worldwide increased shipping rates charged by crude oil purchasers during the fourth quarter of 2004. For cargoes of approximately 80,000 metric tonnes average freight and demurrage rates increased from $1.06/bbl in the third quarter of 2004 to $3.37/bbl in the fourth quarter of 2004. Approximately 68% of completed sales during the fourth quarter of 2004 were affected by these rate increases.

To address this issue, we have chartered our own vessels on better terms than those obtained through our crude oil purchasers, and our cargoes are being delivered by us directly into the Mediterranean. We have also concentrated our efforts on selling into markets that are not affected by this increase in shipping rates, including Central Asia and China.

The Kumkol premium to Brent during the fourth quarter of 2003 was $0.37/bbl. The improved discounts we have negotiated on our sales and the impact of increased volumes on routes with better differentials were offset by the year over year $0.75/bbl change in the premium/discount of Kumkol crude oil to Brent, and our increased shipping and demurrage costs when comparing the fourth quarter of 2004 with 2003.

Outlook: Expectations going forward are that the differential will remain between $13.50/bbl and $14.00/bbl until the end of the first quarter of 2005, with a return to the $12.00/bbl mark for the second and third quarters of 2005. The seasonal factors discussed above will likely increase our fourth quarter differential in 2005, though it is difficult to predict by how much and we will take all possible steps to mitigate these factors.

| 38 PetroKazakhstan Inc. |

| Average refined products price Our average refined product price received in 2004 was $7.84 higher than the average price we received in 2003. This was due to improvements in our yield such that we obtain greater volumes of higher value products per each barrel of crude oil refined. In addition, international crude oil prices influence refined product prices, as does economic growth within Kazakhstan. The price of refined products in Russia has a significant impact on the market price in Kazakhstan as products from Russia move across the border with relative ease and if refined product prices rise above Russian prices the Kazakhstan market is oversupplied with refined products from Russia. Outlook: Refined product prices will be determined by market prices, including refined product prices in Russia and world oil prices. Strategy: Control and reduce our overhead and operation costs Production expenses Production expenses were higher in 2004 compared to 2003 due to a number of factors. We continued to use temporary power generators to operate single well batteries in the KAM fields pending construction of infrastructure. The water cut in a number of our fields including our joint venture Turgai continued to increase resulting in higher production expenses. The number of wells and facilities commissioned in 2004 was higher compared to 2003. During 2004, we drilled 54 new production wells, including 25 wells that were drilled by our joint ventures. Outlook: During 2005 we will be installing flowlines to tie in the single wells at the KAM fields to our main facilities and we are also planning to increase the capacity of existing facilities to handle the increasing water production. Our Upstream operations have embarked on a program focused on reducing production expenses. A number of initiatives have been identified and we are in the process of implementation. Refining cost Refining costs in 2004 reflected the impact of the first major turnaround since 2002. Major repairs were performed on the main crude processing units, visbreaker and storage facilities. Annual purchased energy costs were also marginally higher due to the operation of the Vacuum Distillation Unit (VDU) brought online in January 2004. Outlook: We do not plan to have a major turnaround in 2005. Refining costs should therefore be lower. |

| 39 |