UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

[ x ] QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended March 31, 2010

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _________ to _________

Commission file number: 000-32409

UNITED MORTGAGE TRUST

(Exact name of registrant as specified in its charter)

| Maryland | 75-6493585 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

1301 Municipal Way, Suite 220

Grapevine, Texas 76051

(Address of principal executive offices)(Zip Code)

(214) 237-9305

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes X No ___

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act

Large accelerated filer___ Accelerated filer____ Non-accelerated filer (Do not check if a smaller reporting company)

X Smaller Reporting Company

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes[X] No [_]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act) Yes No X

The number of shares outstanding of the Registrant’s shares of beneficial interest, par value $0.01 per share, as of the close of business on May 14, 2010 was 6,418,998.

UNITED MORTGAGE TRUST

INDEX

PART I - FINANCIAL INFORMATION

| | | Page |

| ITEM 1. | Financial Statements | |

| | | |

| | Consolidated Balance Sheets as of March 31, 2010 (unaudited) and December 31, 2009 | 3 |

| | Consolidated Statements of Income for the three months March 31, 2010 and March 31, 2009 (unaudited) | 4 |

| | Consolidated Statements of Cash Flows for the three months ended March 31, 2010 and March 31, 2009 (unaudited) | 5 |

| | Notes to Consolidated Financial Statements (unaudited) | 7 |

| | | |

| ITEM 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 14 |

| ITEM 3. | Quantitative and Qualitative Disclosures about Market Risk | 28 |

| ITEM 4T. | Controls and Procedures | 29 |

| |

| PART II - OTHER INFORMATION |

| | | |

| ITEM 1. | Legal Proceedings | 29 |

| ITEM 2. | Unregistered Sales of Equity Securities and Use of Proceeds | 29 |

| ITEM 3. | Defaults Upon Senior Securities | 30 |

| ITEM 4. | (Removed and Reserved) | 30 |

| ITEM 5. | Other Information | 30 |

| ITEM 6. | Exhibits | 31 |

| | Signatures | 32 |

UNITED MORTGAGE TRUST

CONSOLIDATED BALANCE SHEETS

| | | | | | | |

| | | | | | | |

| | | | | | |

Cash and cash equivalents | | $ | 130,540 | | | $ | 338,336 | |

| | | | | | | | | |

| | | | | | | | |

Investment in trust receivable | | | 1,778,271 | | | | 2,023,327 | |

Investment in residential mortgages | | | 4,896,118 | | | | 5,005,413 | |

Interim mortgages, affiliates | | | 33,732,522 | | | | 34,249,793 | |

| | | 294,600 | | | | 294,600 | |

Allowance for loan losses | | | (307,213 | ) | | | (222,463 | ) |

Total mortgage investments | | | 40,394,298 | | | | 41,350,670 | |

| | | | | | | | | |

Line of credit receivable, affiliates | | | 61,036,491 | | | | 63,303,613 | |

Line of credit receivable, non-affiliate | | | 8,530,483 | | | | 8,202,706 | |

Accrued interest receivable, net | | | 442,383 | | | | 320,195 | |

Accrued interest receivable, affiliates, net | | | 12,002,293 | | | | 9,448,192 | |

Recourse obligations, affiliates | | | 16,644,957 | | | | 16,449,734 | |

| | | 9,503,001 | | | | 9,426,875 | |

| | | 7,277,280 | | | | 7,189,311 | |

Deficiency note, affiliates | | | 10,962,908 | | | | 10,315,478 | |

Allowance for loan losses – deficiency notes | | | (4,421,753 | ) | | | (4,314,128 | ) |

| | | 335,593 | | | | 504,617 | |

| | $ | 162,838,474 | | | $ | 162,535,599 | |

| | | | | | | | | |

Liabilities and Shareholders’ Equity | | | | | | | | |

| | | | | | | | |

| | $ | 310,000 | | | $ | 310,000 | |

| | | 4,437,342 | | | | 3,788,477 | |

Accounts payable and accrued liabilities | | | 533,271 | | | | 793,775 | |

Accounts payable and accrued liabilities, affiliates | | | 4,000,628 | | | | 1,990,108 | |

Participation payable, affiliate | | | 51,205,086 | | | | 53,768,482 | |

| | | 168,987 | | | | - | |

| | | 60,655,314 | | | | 60,650,842 | |

| | | | | | | | | |

Commitments and contingencies | | | | | | | | |

| | | | | | | | | |

| | | | | | | | |

Shares of beneficial interest; $0.01 par value; 100,000,000 shares authorized; 8,273,633 and 8,264,616 shares issued in 2010 and 2009, respectively; and 6,424,212 and 6,422,883 outstanding in 2010 and 2009, respectively | | | 82,736 | | | | 82,646 | |

Additional paid-in capital | | | 146,403,182 | | | | 146,259,724 | |

Cumulative distributions in excess of earnings | | | (8,429,918 | ) | | | (8,731,773 | ) |

| | | | 138,056,000 | | | | 137,610,597 | |

Less treasury stock of 1,849,421 and 1,841,733 shares in 2010 and 2009, respectively, at cost | | | (35,872,840 | ) | | | (35,725,840 | ) |

Total shareholders' equity | | | 102,183,160 | | | | 101,884,757 | |

Total liabilities and shareholders' equity | | $ | 162,838,474 | | | $ | 162,535,599 | |

See accompanying notes to consolidated financial statements.

UNITED MORTGAGE TRUST

CONSOLIDATED STATEMENTS OF INCOME

(unaudited)

| | | Three Months Ended March 31, |

| | | | | | | |

| | | | | | |

Interest income, affiliates | | | | | | | | |

| | | | | | | | |

| | | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

General and administrative | | | | | | | | |

Provision for loan losses | | | | | | | | |

| | | | | | | | |

| | | | | | | | | |

| | | | | | | | | |

| | | | | | | | |

| | | | | | | | | |

Net income per share of beneficial interest | | | | | | | | |

| | | | | | | | | |

Weighted average shares outstanding | | | | | | | | |

| | | | | | | | | |

Distributions per weighted share outstanding | | | | | | | | |

See accompanying notes to consolidated financial statements.

UNITED MORTGAGE TRUST

CONSOLIDATED STATEMENTS OF CASH FLOWS

(unaudited)

| | | Three Months Ended March 31, | |

| | | 2010 | | 2009 | |

| | | | | |

| $ | | $ | | |

Adjustments to reconcile net income to net cash provided | | | | | |

| | | | | |

Provision for loan losses | | | | | |

Depreciation and amortization | | | | | |

Changes in assets and liabilities: | | | | | |

Accrued interest receivable, net | | | ) | | ) |

Accrued interest receivable, affiliates, net | | | ) | | ) |

| | | | | |

Accounts payable and accrued liabilities | | | ) | | ) |

Accounts payable and accrued liabilities, affiliates | | | | | |

Net cash provided by operating activities | | | | | |

| | | | | | |

| | | | | |

Investment in trust receivables | | | | | ) |

Principal receipts on trust receivables | | | | | |

Investments in residential mortgages | | | ) | | |

Principal receipts on residential mortgages | | | | | |

Investment in interim mortgages and deficiency notes | | | ) | | ) |

Principal receipts on interim mortgages and deficiency notes | | | | | |

Investments in interim mortgages, affiliates | | | ) | | ) |

Principal receipts on interim mortgages, affiliates | | | | | |

Investments in recourse obligations, affiliates | | | ) | | ) |

Principal receipts from recourse obligations, affiliates | | | | | |

Principal receipts from (investments in) lines of credit receivable, affiliates | | | | | |

Principal receipts from (investments in) lines of credit receivable, non-affiliates | | | ) | | ) |

Investments in real estate owned | | | ) | | |

Principal receipts from real estate owned | | | | | |

Net cash used in investing activities | | | ) | | ) |

| | | | | | |

| | | | | |

Proceeds from issuance of shares of beneficial interest | | | | | |

Net borrowings on line of credit payable | | | | | |

Proceeds from notes payable | | | | | |

Purchase of treasury stock | | | ) | | ) |

| | | ) | | ) |

Net cash used in financing activities | | | ) | | ) |

| | | | | | |

Net decrease in cash and cash equivalents | | | ) | | ) |

Cash and cash equivalents at beginning of period | | | | | |

Cash and cash equivalents at end of period | $ | | $ | | |

| | | | | | |

See accompanying notes to consolidated financial statements.

UNITED MORTGAGE TRUST

CONSOLIDATED STATEMENTS OF CASH FLOWS (continued)

(unaudited)

| | | Three Months Ended March 31, | |

| | | | | | |

Supplemental Disclosure of Cash Flow Information | | | | | |

Cash paid during the period for interest | | | | | |

| | | | | |

Transfers of affiliate and non-affiliate loans to foreclosed properties or recourse obligations | | | | | |

Participation receivable, affiliate | | | | | ) |

Participation payable, affiliate | | | | | |

Participation accrued interest receivable, affiliate | | | ) | | ) |

Participation accrued interest payable, affiliate | | | | | |

See accompanying notes to consolidated financial statements.

UNITED MORTGAGE TRUST

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

United Mortgage Trust (the “Company” and “UMT”) is a Maryland real estate investment trust that qualifies as a real estate investment trust (a “REIT”) under federal income tax laws. The Company’s principal investment objectives are to invest proceeds from its dividend reinvestment plan, financing proceeds, capital transaction proceeds and retained earnings in the following types of investments: (i) secured, subordinate line of credit to UMTH Lending Company, L.P. for origination of Interim Loans; (ii) lines of credit and secured loans for the acquisition and development of single-family home lots, referred to as “Land Development Loans”; (iii) lines of credi t and loans secured by entitled and developed single-family lots, referred to as “Finished Lot Loans”; and,(iv) lines of credit and loans secured by completed model homes, referred to as “Model Home Loans”; and, (v) loans provided to entities that have recently filed for bankruptcy protection under Chapter 11 of the US bankruptcy code, secured by a priority lien over pre-bankruptcy secured creditors, referred to as “Debtor in Possession Loans” and, (vi) lines of credit and loans, with terms of 18 months or less, secured by single family lots and homes constructed thereon, referred to as “Construction Loans”; and, (vii) first lien secured mortgage loans with terms of 12 to 360 months for the acquisition of single-family homes, referred to as “Residential Mortgages”; and, (viii) discounted cash flows secured by assessments levied on real property. We collectively refer to the above listed loans as “Mortgage Investments”. Addit ionally, our portfolio includes obligations of affiliates of our Advisor, which we refer to as “recourse loans,” and deficiency notes.

The Company has no employees. The Company pays a monthly trust administration fee to UMTH General Services, L.P. (“UMTHGS” or “Advisor”), a subsidiary of UMT Holdings, L.P. (“UMTH”), a Delaware real estate finance company and affiliate, for the services relating to its daily operations. The Company’s offices are located in Grapevine, Texas.

The consolidated financial statements include the accounts of the Company and certain wholly-owned subsidiaries and all significant intercompany accounts and transactions have been eliminated. In the opinion of management, all adjustments (consisting of normal recurring adjustments) considered necessary for a fair presentation have been included. These consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United States (“GAAP”) for interim financial information and with the instructions for Form 10-Q and Article 10 of Regulation S-X adopted by the Securities and Exchange Commission (“SEC”). Accordingly, the financial statements do not include all of the information and footnotes required by GAAP for complete financial stateme nts and should be read in conjunction with our consolidated financial statements, and notes thereto, for the year ended December 31, 2009, included in our Annual Report on Form 10-K filed with the SEC on March 31, 2010. Operating results for the three months ended March 31, 2010, are not necessarily indicative of the results that may be expected for the year ended December 31, 2010. Certain prior period amounts have been reclassified to conform to current period presentation.

3. Deficiency Notes – Affiliate and Non-Affiliate

The Company has made loans in the normal course of business to affiliates and non-affiliates, the proceeds from which have been used to originate underlying loans that are pledged to the Company as security for such obligations. When principal and interest on an underlying loan is due in full, at maturity or otherwise, the corresponding obligation owed by the originating company to the Company is also due in full. If the borrower or the Company foreclosed on property securing an underlying loan, or if the Company foreclosed on property securing a purchased loan, and the proceeds from the sale were insufficient to pay the loan in full, the originating company had the option of (1) repaying the outstanding balance owed to the Company associated with the underlying loan or purchased loan, as the case may be, or (2) delivering to the Compa ny an unsecured deficiency note in the amount of the deficiency.

As of March 31, 2010 and December 31, 2009, the Company had two deficiency notes with non-affiliates in the amount of approximately $7,277,000 and $7,189,000, respectively. The Company has recorded reserves of approximately $4,422,000 and $4,314,000 against these notes as of March 31, 2010 and December 31, 2009 respectively. These notes do not accrue interest as the underlying collateral value approximates the note balance, net of reserves.

As of December 31, 2007, UMTH Lending Company, L.P.(“UMTHLC”) issued to the Company a variable amount promissory note in the original amount of $5,100,000 to evidence its deficiency obligations to the Company. The initial principal amount of the note was approximately $1,848,000. The principal balance will fluctuate from time to time based on the underlying loan activity and the amount of deficiencies realized by the affiliate. The note bears interest at a rate of 10%, and requires monthly principal and interest payments based on a ten-year amortization for the outstanding principal balance. The note is secured by a limited guaranty by UMTHGS, the Advisor, equal to a monthly amount not to exceed 33% of the advisory fee received by UMTHGS under the terms of its advisory agreement with the Com pany. This note had a balance of approximately $10,963,000 and $10,315,000 at March 31, 2010 and December 31, 2009, respectively. Per the terms of the Secured Notes, the unpaid principal balance may be greater or less than the initial principal amount of the note and is not considered an event of default.

4. Related Party Transactions

1) UMT Holdings, L.P. (“UMTH”) is a Delaware limited partnership which is in the real estate finance business. UMTH holds a 99.9% limited partnership interest in UMTH Lending Company, L.P., which originates interim loans that the Company is assigned, UMTH Land Development, L.P., which holds a 50% profit interest in UDF and acts as UDF's asset manager, and Prospect Service Corp. (“PSC”), which services the Company’s residential mortgages and contracts for deed and manages the Company’s real estate owned (“REO”). In addition, UMTH has a limited guarantee of the obligations of Capital Reserve Group (“CRG”), Ready America Funding Corp (“RAFC”), and South Central Mortgage, Incorporated (“SCMI”), a Texas corporation that sold mortgage investments to the Company, under the Secured Notes. United Development Funding III, L.P., (“UDF III”) which is managed by UMTH Land Development, L.P., has previously provided a limited guarantee of the UDF line of credit and has purchased an economic participation in a revolving credit facility we have provided to UDF.

2) UMTHLC is a Delaware limited partnership, and subsidiary of UMTH. The Company has loaned money to UMTHLC so it can make loans to its borrowers. The loans are collaterally assigned to the Company, as security for the promissory note between UMTHLC and the Company. The unpaid principal balance of the loans at March 31, 2010 and December 31, 2009 was approximately $16,776,000 and $16,842,000, respectively.

On March 26, 2009, the Company executed a secured line of credit promissory note with UMTH Lending, Company, L.P. in the amount of $8,000,000. The note bears interest at 12.50% per annum, matures on March 26, 2012 and is secured by first lien mortgage interests in single family residential properties. The outstanding balance on this line of credit at March 31, 2010 and December 31, 2009 was approximately $6,808,000 and $6,194,000 respectively.

See Note 3 above for discussion of additional related party transactions with UMTHLC.

3) Ready America Funding Corporation (“RAFC”) is a Texas corporation that is 50% owned by SCMI, which is owned by Todd Etter. RAFC is in the business of financing interim loans for the purchase of land and the construction of modular and manufactured single-family homes placed on the land by real estate investors. The Company continues to directly fund obligations under one existing RAFC loan, which was collaterally assigned to the Company, but does not fund new originations. The unpaid principal balance of the loans at March 31, 2010 and December 31, 2009 was approximately $23,764,000 and $23,602,000, respectively.

4) Wonder Funding, LP (“Wonder”) is a Delaware limited partnership that is owned by Ready Mortgage Corp. (“RMC”). RMC is beneficially owned by Craig Pettit, a partner of UMTH and the sole proprietor of two companies that own 50% of RAFC. Wonder is in the business of financing interim loans for the purchase of land and the construction of single family homes and the purchase and renovation of single family homes. The Company has ceased funding any new originations. As of March 31, 2010 and December 31, 2009, respectively, all remaining obligations owed by Wonder to the Company are included in the recourse obligations discussed below.

5) Recourse Obligations. The Company has made recourse loans to (a) Capital Reserve Group, Inc. (“CRG”), which is a Texas corporation that is 50% owned by Todd Etter and William Lowe, partners of UMTH, which owns the Advisor, (b) RAFC, which is owned by SCMI and two companies owned by Craig Pettit, Eastern Intercorp, Inc. and Ready Mortgage Corp. (“RMC”), and (c) SCMI, which is owned by Todd Etter, (these companies are referred to as the "originating companies"). In addition to the originating companies discussed above, the Company made loans with recourse to Wonder. Each of these entities used the proceeds from such loans to originate loans, that are referred to as "underlying loans," that are pledged to the Company as security for such originating company's obligations to the Company. Whe n principal and interest on an underlying loan are due in full, at maturity or otherwise, the corresponding obligation owed by the originating company to the Company is also due in full.

In addition, some of the originating companies have sold loans to the Company, referred to as the "purchased loans," and entered into recourse agreements under which the originating company agreed to repay certain losses the Company incurred with respect to purchased loans.

If the originating company forecloses on property securing an underlying loan, or the Company forecloses on property securing a purchased loan, and the proceeds from the sale are insufficient to pay the loan in full, the originating company has the option of (1) repaying the outstanding balance owed to the Company associated with the underlying loan or purchased loan, as the case may be, or (2) delivering an unsecured deficiency note in the amount of the deficiency to the Company.

On March 30, 2006, but effective December 31, 2005, the Company and each originating company agreed to consolidate (1) all outstanding amounts owed by such originating company to the Company under the loans made by the Company to the originating company and under the deficiency notes described above and (2) the estimated maximum future liability to the Company under the recourse arrangements described above, into secured promissory notes. Each originating company issued to the Company a secured variable amount promissory note dated December 31, 2005 (the “Secured Notes”) in the principal amounts shown below, which amounts represent all principal and accrued interest owed as of such date. The initial principal amounts are subject to increase if the Company incurs losses upon the foreclosure of loans covered by recourse arran gements with the originating company. The Secured Notes (including related guaranties discussed below) are secured by an assignment of the distributions on the Class C units, Class D units and Class EIA units of limited partnership interest of UMT Holdings held by each originating company.

| Name | Initial principal amount | Balance at March 31, 2010 | Promissory Note principal amount (2) | | Units pledged as security | Units remaining | Nominal Collateral Value (3) |

| | | | | 4,984 Class C and 2,710 Class D | 3,479 Class C and 2,710 Class D | |

| | | | | 11,165 Class C and 6,659 Class D and 1,066 Class EIA | 9,132 Class C, 6,659 Class D and 1,066 EIA | |

| | | | | 4,545 Class and 3,000 Class D | 2,865 Class C and 3,000 Class D | |

| | | | | | | |

Wonder Indemnification (1) | | | | | | | |

| | | | | | | |

| | (1) Wonder is collateralized by an indemnification agreement from UMTH in the amount of $1,134,000, and is secured by the pledge of 3,870 C Units from RMC. 2,213 of the pledged C Units also cross-collateralize the RAFC obligation. |

| | (2) The CRG and Wonder balances at March 31, 2010, exceeded the stated principal amount per their variable Secured Notes by approximately $137,000 and $561,000, respectively. Per the terms of the Secured Notes, the unpaid principal balance may be greater or less than the initial principal amount of the note and is not considered an event of default. The rapid rate of liquidation of the remaining portfolio of properties caused a more rapid increase in the Unpaid Principal Balance (“UPB”) than originally anticipated and outpaced the minimum principal reductions scheduled for the loans. |

| | (3) Nominal collateral value does not reflect pledge of D units of limited partnership interest of UMTH held by WLL, Ltd., RAFC and KLA, Ltd. UMTH D units represent equity interests in UMT Holdings, LP. Pledge of the UMTH D units entitles the beneficiary to a pro-rata share of UMTH partnership D unit cash distributions. |

Through September 2007, the Secured Notes incurred interest at a rate of 10% per annum. The CRG, RAFC and RAF/Wonder Secured Notes amortize over 15 years and mature on December 31, 2020. The SCMI Secured Note amortizes over approximately 22 years and matures on December 31, 2027, which was the initial amortization of the deficiency notes from SCMI that were consolidated. The Secured Notes required the originating company to make monthly payments equal to the greater of (1) principal and interest amortized over 180 months and 264 months, respectively, or (2) the amount of any distributions paid to the originating company with respect to the pledged Class C and EIA units. Effective, October, 2007, the recourse loans were modified to accommodate the anticipated increases in principal balances throughout the remaining liquidation periods o f the underlying assets, suspended the principal component of the amortized loans for the period of July 2007 through June 2009, and reduced the interest rate from 10% to 6%. The above modifications have been extended through June 30, 2010. These loans were reviewed by management and no reserves are deemed necessary at March 31, 2010.

The Secured Notes have also been guaranteed by the following entities under the arrangements described below, all of which are dated effective December 31, 2005:

| - | UMT Holdings. This guaranty is limited to a maximum of $10,582,336 due under all of the Secured Notes and is unsecured. |

| - | WLL, Ltd., an affiliate of CRG. This guaranty is of all amounts due under Secured Note from CRG is non-recourse and is secured by an assignment of 2,492 Class C Units and 1,355 Class D units of limited partnership interest of UMT Holdings held by WLL, Ltd. |

| - | RMC. This guaranty is non-recourse, is limited to 50% of all amounts due under the Secured Note from RAFC and is secured by an assignment of 3,870 Class C units of limited partnership interest of UMT Holdings |

| - | Wonder. Wonder Funding obligations are evidenced by a note from RAFC (“RAFC Wonder Note”) and are secured by a pledge of a certain Indemnification Agreement given by UMTH to RAFC and assigned to UMT in the amount of $1,134,000, which amount is included in the UMTH limited guarantee referenced above. |

In addition, WLL, Ltd. has obligations to UMT Holdings under an indemnification agreement between UMT Holdings, WLL, Ltd. and William Lowe, under which UMT Holdings is indemnified for certain losses on loans and advances made to William Lowe by UMT Holdings. That indemnification agreement allows UMT Holdings to offset any amounts subject to indemnification against distributions made to WLL, Ltd., with respect to the Class C and Class D units of limited partnership interest held by WLL, Ltd. Because WLL, Ltd. has pledged these Class C and Class D units to the Company to secure its guaranty of Capital Reserve Corp.'s obligations under its Secured Note, UMT Holdings and the Company entered into an Intercreditor and Subordination Agreement under which UMT Holdings has agreed to subordinate its rights to offset amounts owed to it by WLL, Lt d. to the Company’s lien on such units.

6) On June 20, 2006, the Company entered into a Second Amended and Restated Secured Line of Credit Promissory Note (the "Amendment") with UDF, L.P. (“UDF”), a Nevada limited partnership that is affiliated with the Company's Advisor, UMTHGS. The Amendment increased an existing revolving line of credit facility ("Loan") to $45,000,000. The purpose of the Loan is to finance UDF's loans and investments in real estate development projects. On July 29, 2009, our trustees approved an amendment to increase the revolving line of credit facility to an amount not to exceed $60,000,000. Effective December 31, 2009, the loan was extended for a period of one year and matures on December 31, 2010.

The Loan is secured by the pledge of all of UDF's land development loans and equity investments pursuant to the First Amended and Restated Security Agreement dated as of September 30, 2004, executed by UDF in favor of UMT (the “Security Agreement”). Those UDF loans may be first lien loans or subordinate loans.

The Loan interest rate is the lower of 15% or the highest rate allowed by law, further adjusted with the addition of a credit enhancement to a minimum of 14%.

UDF may use the Loan proceeds to finance indebtedness associated with the acquisition of any assets to seek income that qualifies under the Real Estate Investment Trust provisions of the Internal Revenue Code to the extent such indebtedness, including indebtedness financed by funds advanced under the Loan and indebtedness financed by funds advanced from any other source, including Senior Debt, is no more than 85% of 80% (68%) of the appraised value of all subordinate loans and equity interests for land development and/or land acquisition owned by UDF and 75% for first lien secured loans for land development and/or acquisitions owned by UDF.

On September 19, 2008, UMT entered into an Economic Interest Participation Agreement with UDF III pursuant to which UDF III purchased (i) an economic interest in the $45,000,000 revolving credit facility (“Loan”) from UMT to UDF and (ii) a purchase option to acquire a full ownership participation interest in the Loan (the “Option”). On July 29, 2009 our trustees approved an amendment to increase of the revolving line of credit facility to an amount not to exceed $60,000,000.

Pursuant to the Economic Interest Agreement, each time UDF requests an advance of principal under the UMT Loan, UDF III will fund the required amount to UMT and UDF III’s economic interest in the UMT Loan increases proportionately. UDF III’s economic interest in the UMT Loan gives UDF III the right to receive payment from UMT of principal and accrued interest relating to amounts funded by UDF III to UMT which are applied towards UMT’s funding obligations to UDF under the UMT Loan. UDF III may abate its funding obligations under the Economic Participation Agreement at any time for a period of up to twelve months by giving UMT notice of the abatement.

The Option gives UDF III the right to convert its economic interest into a full ownership participation interest in the UMT Loan at any time by giving written notice to UMT and paying an exercise price of $100. The participation interest includes all rights incidental to ownership of the UMT Loan and the Security Agreement, including participation in the management and control of the UMT Loan. UMT will continue to manage and control the UMT Loan while UDF III owns an economic interest in the UMT Loan. If UDF III exercises its Option and acquires a participation interest in the UMT Loan, UMT will serve as the loan administrator but both UDF III and UMT will participate in the control and management of the UMT Loan. The UMT Loan matures on December 31, 2010. At March 31, 2010 and December 31, 2009, UDF III had funded approxima tely $54,228,000 and $53,768,000, respectively, to UDF under this agreement. On July 29, 2009 the Company's trustees approved an amendment to increase of the revolving line of credit facility to an amount not to exceed $60,000,000.

The UMT Loan is subordinate to UDF Senior Debt, which includes a line of credit provided by Textron Financial Corporation in the amount of $30,000,000, and all other indebtedness of UDF to any national or state chartered banking association or other institutional lender that is approved by UMT in writing. On June 14, 2009, the Textron loan agreement matured and became due and payable in full. Effective August 15, 2009, Textron and UDF entered into a Forbearance Agreement pursuant to which Textron agreed to forbear in exercising its rights and remedies under their loan agreement until November 15, 2009. Pursuant to a second amendment to the Forbearance Agreement, effective March 1, 2010, the forbearance period has been extended to June 30, 2010; provided, that the forbearance period will end earlier if U DF otherwise defaults under the Forbearance Agreement. Management understands that UDF intends to continue to make payments on the Textron loan and does not believe that the repayment of the Textron debt will have a material adverse effect on UDF III’s participation in the Company’s subordinate line of credit to UDF.

7) Loans are made to certain affiliates of the Advisor. Below is a table of the aggregate principal amount of mortgages funded during the quarters ended March 31, 2010 and March 31, 2009, respectively, from the companies affiliated with the Advisor, and named in the table and aggregate amount of draws made by UDF under the line of credit, during the two quarters indicated:

8) As of August 1, 2006, (now subject to an Advisory Agreement effective January 1, 2009) the Company entered into an Advisory Agreement with UMTHGS. Under the terms of the agreement, UMTHGS is paid a monthly trust administration fee. The fee is calculated monthly depending on the Company’s annual distribution rate, ranging from 1/12th of 1% up to 1/12th of 2% of the amount of average invested assets per month. During the three months ended March 31, 2010 and March 31, 2009, the net fees paid to the Company’s Advisors were approximately $274,000 and $257,000, respectively.

The agreement also provides for a subordinated incentive fee equal to 25% of the amount by which the Company’s net income for a year exceeds a 10% per annum non-compounded cumulative return on its adjusted contributions. No incentive fee was paid during 2010 or 2009. In addition, for each year in which it receives a subordinated incentive fee, the Advisor will receive a 5-year option to purchase 10,000 shares at a price of $20.00 per share (not to exceed 50,000 shares). As of March 31, 2010, the Advisor has not received options to purchase shares under this arrangement.

The Advisor and its affiliates are also entitled to reimbursement of costs of materials and services obtained from unaffiliated third parties for the Company’s benefit. During each of the three months ended March 31, 2010 and March 31, 2009, the Company paid the Advisor approximately $19,000 as reimbursement for costs associated with providing shareholder relations activities.

The Advisory Agreement provides for the Advisor to pay all of the Company’s expenses and for the Company to reimburse the Advisor for any third-party expenses that should have been paid by the Company but which were instead paid by the Advisor. However, the Advisor remains obligated to pay: (1) the employment expenses of its employees, (2) its rent, utilities and other office expenses and (3) the cost of other items that are part of the Advisor's overhead that is directly related to the performance of services for which it otherwise receives fees from the Company.

The Advisor Agreement also provides for the Company to pay to the Advisor a debt placement fee. The Company may engage the Advisor, or an Affiliate of the Advisor, to negotiate lines of credit on behalf of the Company. UMT shall pay a negotiated fee, not to exceed 1% of the amount of the line of credit secured, upon successful placement of the line of credit. The Company paid a debt placement fee of $50,000 to an affiliate of the Advisor in September 2009. This fee is amortized monthly, as an adjustment to interest expense, over the term of the credit facility agreement described in Note 6.

9) The Company pays loan servicing fees to PSC, a subsidiary of UMTH, under the terms of a Mortgage Servicing Agreement. During the three months ended March 31, 2010 and March 31, 2009, the Company paid loan servicing fees of approximately $4,000 and $2,200, respectively.

10) The Company paid the first of three annual credit enhancement fees of $50,000 to UDF III, L.P. in September 2009. This fee is due annually on the anniversary date of the loan and amortized over 12 months as an adjustment to interest expense.

5. Fair Value of Financial Instruments

In accordance with the reporting requirements of Accounting Standards Codification (“ASC”) 825, Disclosures About Fair Value of Financial Instruments, the Company calculates the fair value of its assets and liabilities that qualify as financial instruments under this statement and includes additional information in notes to the Company’s consolidated financial statements when the fair value is different than the carrying value of those financial instruments. The estimated fair value of cash equivalents, accrued interest receivable, accrued interest receivable affiliates, accounts payable and accrued liabilities (including affiliates) approximate the carrying value due to the relatively short maturity of these instruments. The carrying value of investments in res idential mortgages, interim mortgages (including affiliates), lines of credit (including affiliates), recourse obligations from affiliates, notes payable, deficiency notes (including affiliates) and the Company’s line of credit payable also approximate fair value since these instruments bear market rates of interest. None of these instruments are held for trading purposes.

6. Long Term Debt

During August 2009, the Company entered into a revolving line of credit facility with a bank for $5,000,000. The line of credit bears interest at prime plus one percent, with a floor of 5.50%, and requires monthly interest payments. Principal and all unpaid interest will be due at maturity, which is August 2012. The line is collateralized by a first lien security interest in the underlying real estate financed by the line of credit. The outstanding balance on this line of credit at March 31, 2010 and December 31, 2009 was approximately $4,437,000 and $3,788,000, respectively.

7. Subsequent Events

On April 21, 2010, the Company entered into a new term loan credit facility with a bank for $1,600,000. The loan bears interest at prime plus one percent, with a floor of 7.0%, and requires monthly interest payments. Principal and all unpaid interest will be due at maturity which is October 21, 2011. The loan is collateralized by a first lien security interest in the underlying real estate financed by the loan.

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | |

| Cautionary Statement Regarding Forward-Looking Statements | |

In light of these risks, uncertainties and assumptions, the forward-looking events discussed in this Form 10-Q may not occur. We undertake no obligation to update or revise our forward-looking statements, whether as a result of new information, future events or otherwise.

RESULTS OF OPERATIONS FOR THE THREE MONTHS ENDED MARCH 31, 2010 AND MARCH 31, 2009

General Investment Information

United Mortgage Trust (the “Company”) is a Maryland real estate investment trust that qualifies as a real estate investment trust (a “REIT”) under federal income tax laws. Our principal investment objectives are to invest proceeds from our dividend reinvestment plan, financing proceeds, capital transaction proceeds and retained earnings in following types of investments:

| (i) | secured, subordinate line of credit to UMTH Lending Company, L.P. for origination of Interim Loans; |

| (ii) | lines of credit and secured loans for the acquisition and development of single-family home lots, referred to as “Land Development Loans”; |

| (iii) | lines of credit and loans secured by entitled and developed single-family lots, referred to as “Finished Lot Loans”; and, |

| (iv) | lines of credit and loans secured by completed model homes, referred to as “Model Home Loans”; and, |

| (v) | loans provided to entities that have recently filed for bankruptcy protection under Chapter 11 of the US bankruptcy code, secured by a priority lien over pre-bankruptcy secured creditors, referred to as “Debtor in Possession Loans” and, |

| (vi) | lines of credit and loans, with terms of 18 months or less, secured by single family lots and homes constructed thereon, referred to as “Construction Loans”; and, |

| (vii) | first lien secured mortgage loans with terms of 12 to 360 months for the acquisition of single-family homes, referred to as “Residential Mortgages”; and, |

| (viii) | discounted cash flows secured by assessments levied on real property. |

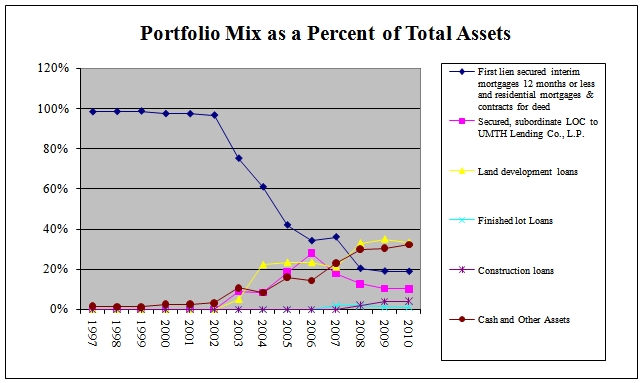

The following table illustrates the percentage of our mortgage portfolio dedicated to each mortgage loan category as of March 31, 2010 and December 31, 2009:

| | |

First lien secured interim mortgages 12 months or less and residential mortgages and contracts for deed | | |

Secured interim mortgages and line of credit to UMTHLC | | |

| | |

| | |

| | |

The following table summarizes mortgage loans by type and original loan amount held by United Mortgage Trust at March 31, 2010.

| | | | | | Face amount of Mortgage (1) | Carrying amount of Mortgage (2) | |

Single family residential 1st mortgages and interim loans (5): | | | | | | | | |

Original balance > $100,000 | | | | | | | | |

Original balance $50,000 - $99,999 | | | | | | | | |

Original balance $20,000 - $49,999 | | | | | | | | |

Original balance under $20,000 | | | | | | | | |

| | | | | | | | | |

First Lien secured interim mortgages | | | | | | | | |

Ready America Funding (4) | | | | | | | | |

Howe Note Consolidation (5) | | | | | | | | |

| | | | | | | | | |

Secured, subordinate LOC to UMTH Lending Co., L.P. (4), (5) | | | | | | | | |

| | | | | | | | | |

| | | | | | | | |

UDF III Economic Interest Participation | | | | | | | | |

| | | | | | | | | |

| | | | | | | | |

| | | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| (1) | Current book value of loans. |

| (2) | Net of allowance for loan losses on mortgage loans of $307,213 at March 31, 2010. |

| (3) | Principal amounts greater than thirty (30) days past due. |

| (4) | Lines of credit with Ready America Funding and UMTH Lending Co., L.P. are collateralized by 16 and 95 loans, respectively. Principal amounts due upon disposition of assets. |

| (5) | No specific maturity date as UMT has first lien collateral position in these loans funded by the originator. |

| (6) | Loan was paid in full on April 19, 2010. |

Below is a reconciliation and walk forward of mortgage loans, net of allowance for loan losses, for the three months ended March 31, 2010.

Balance at beginning of period | |

| |

Increase in mortgage loans | |

Deductions during period: | |

| |

Other – UDF III participation | |

Other (net change in allowance for loan loss) | |

Balance at close of period | |

Material Trends Affecting Our Business

We are a real estate investment trust and derive a substantial portion of our income from loans secured by single-family homes (both finished homes and homes under construction), single-family home lots, and entitled land under development into single-family home lots. We continue to concentrate our lending activities in the southwest sections of the United States, particularly in Texas. We believe these areas continue to experience demand for new construction of single-family homes; however, the U.S. housing market has suffered declines over the past three years, particularly in geographic areas that had experienced rapid growth, steep increases in property values and speculation. National and regional homebuilders responded to this decline by reducing the number of new homes constructed in 2009 as com pared to 2008 and 2007. However, we expect to see continued healthy demand for our products as the supply of finished new homes and land is once again aligned with our market demand.

We believe that the housing market, in Texas, has reached a bottom in its four-year decline and has begun to recover. New single-family home permits, starts, and sales have all risen from their respective lows, reflecting a slow return of demand for new homes. However, the shape and scope of the broader economic recovery is not yet clear. The consumer confidence index, which fell to record lows during the downturn, has begun a cautious recovery, though unemployment remains high and the availability of conventional bank financing remains limited. These concerns may pose obstacles to a robust recovery.

Ongoing credit constriction and disruption of mortgage markets and price correction have made potential new home purchasers and real estate lenders cautious. As a result of these factors, the national housing market experienced a protracted decline, and the time necessary to correct the market may mean a corresponding slow recovery for the housing industry.

Capital constraints at the heart of the credit crisis have reduced the number of real estate lenders able or willing to finance development, construction and the purchase of homes and have increased the number of undercapitalized or failed builders and developers. With credit less available and stricter underwriting standards, mortgages to purchase homes have become harder to obtain. The number of new homes developed also has decreased, which may result in a shortage of new homes and developed lots in select real estate markets in 2010 and more broadly in 2011. Further, the liquidity provided in the secondary market by Fannie Mae and Freddie Mac (“Government Sponsored Enterprises” or “GSEs”) to the mortgage industry is very important to the housing market and has been constricted as these entities have suffered significant losses as a result of depressed housing and credit market conditions. These losses have reduced their equity and prompted the U.S. government to guarantee the backing of all losses suffered by the GSEs. To further support the secondary residential mortgage market, the Federal Reserve began an unprecedented program to purchase approximately $1.25 trillion of residential mortgage backed securities between January 5, 2009 and March 31, 2010. This program ended on March 31, 2010, as scheduled by the Federal Reserve. As of the date of this quarterly report, the 30-year fixed-rate single family residential mortgage interest rate is below the rate that was available at the conclusion of the period of Federal Reserve purchases, which, we believe, indicates that the secondary residential mortgage market is operating smoothly independent of the support previously provided by the Federal Reserve. Notwithstanding the foregoing, limitations or restrictions on the availability of financing or on the liquidity provided by the GSEs could adversely affect interest rates and mortgage availability and could cause the number of homebuyers to decrease, which would increase the likelihood of defaults on our loans and, consequently, reduce our ability to pay distributions to our shareholders.

In the midst of the credit crisis, the federal government passed the Economic Stabilization Act of 2008, which was intended to inject emergency capital into financial institutions, ease accounting rules that require such institutions to show the deflated value of assets on their balance sheets, and ultimately help restore a measure of public confidence to enable financial institutions to raise capital. With the necessary capital, lenders will again be able to lend money for the development, construction and purchase of homes.

Nationally, new single-family home inventory continued to improve in the first quarter of 2010 from the fourth quarter of 2009 while new home sales rebounded significantly from the previous quarter. The U.S. Census Bureau reports that the sales of new single-family residential homes in March 2010 were at a seasonally adjusted annual rate of 411,000 units. This number is up significantly from the fourth quarter figure of 353,000 and up approximately 23.8% year over year from the March 2009 estimate of 332,000. The seasonally adjusted estimate of new houses for sale at the end of March 2010 was 228,000 – a supply of 6.7 months at the current sales rate – which is a reduction of approximately 3,000 homes from the fourth quarter supply of 231,000. Since 2006, homebuilders have reduced their starts and focused on selling existing new home inventory. In the past year, from March 2009 to March 2010, the number of new homes for sale has fallen by approximately 85,000 units. However, from January 2010 to March 2010, new home inventory was reduced by just 3,000 units. We believe that, with such reductions and the relative leveling of inventory over the most recent quarter, the new home market has been restored to equilibrium in most markets, even at low levels of demand. Further, we believe that what is necessary now to regain prosperity in housing markets is the return of healthy levels of demand.

According to the source identified above, new single-family residential home permits and starts fell nationally from 2006 through 2008, as a result and in anticipation of an elevated supply of and decreased demand for new single-family residential homes in that period. Since early 2009, however, single-family permits and starts have risen significantly. Single-family homes authorized by building permits in March 2010 were at a seasonally adjusted annual rate of 543,000 units. This is a 50.8% year-over-year increase from the March 2009 estimate of 360,000 units. Single-family home starts for March 2010 were at a seasonally adjusted annual rate of 531,000 units. This is 47.1% higher than the March 2009 estimate of 361,000 units. Such increases strongly suggest t o us that the homebuilding industry now anticipates greater demand for new homes in coming months relative to the demand evident in 2009. The primary factors affecting new home sales are housing prices, home affordability, and housing demand. Housing supply may affect both new home prices and demand for new homes. When new home supplies exceed new home demand, new home prices may generally be expected to decline. Declining new home prices may result in diminished new home demand as people postpone a new home purchase until such time as they are comfortable that stable price levels have been reached. The converse point is also true and equally important. When new home demand exceeds new home supply, new home prices may generally be expected to increase; and rising new home prices, particularly at or near the bottom of the housing market, may result in increased new� 0; home demand as people accelerate their timing of a new home purchase.

Long-term demand will be fueled by a growing population, household formation, population migration, immigration and job growth. The U.S. Census Bureau forecasts that California, Florida and Texas will account for nearly one-half of the total U.S. population growth between 2000 and 2030 and that the total population of Arizona and Nevada will double during that period. The U.S. Census Bureau projects that between 2000 and 2030 the total populations of Arizona and Nevada will grow from approximately 5,000,000 to more than 10,700,000 and from approximately 2,000,000 to nearly 4,300,000, respectively; Florida’s population will grow nearly 80% between 2000 and 2030, from nearly 16,000,000 to nearly 28,700,000; Texas’ population will increase 60% between 2000 and 2030 from nearly 21,000,000 to approximately 33,300,000; and Califo rnia’s population will grow 37% between 2000 and 2030, from approximately 34,000,000 to nearly 46,500,000.

The Harvard Joint Center for Housing Studies forecasts that an average of approximately 1.25 million new households will be formed per year over the next ten years. Likewise, The Homeownership Alliance, a joint project undertaken by the chief economists of Fannie Mae, Freddie Mac, the Independent Community Bankers of America, the National Association of Home Builders, and the National Association of Realtors, has projected that 1.3 million new households will be formed per year over the next decade and a similar number of single family homes should be started to meet such new demand.

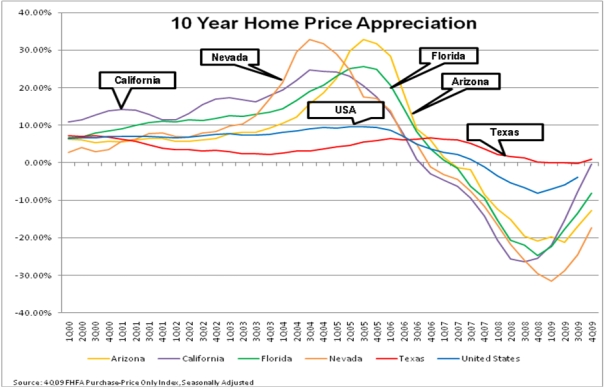

While housing woes have beleaguered the national economy, Texas housing markets have held up as some of the best in the country. We intend to focus much of our investment portfolio in Texas as we believe Texas markets, though weakened from their highs in 2007, have remained fairly healthy due to strong demographics and economies and high housing affordability ratios. Further, Texas did not experience the dramatic price appreciation (and subsequent depreciation) that states such as California, Florida, Arizona, and Nevada experienced. The following graph, created with data from the Federal Housing Finance Agency’s (“FHFA”) Purchase Only Price Index, illustrates the recent declines in home prices nationally, as well as in California, Florida, Arizona, and Nevada, though price declines have begun to moderate in those states too. Further, the graph illustrates how Texas has maintained home price stability and not experienced such pronounced declines.

According to numbers publicly released by Residential Strategies, Inc. or Metrostudy, leading providers of primary and secondary market information, the median new home prices for March 2010 in the metropolitan areas of Austin, Houston, Dallas, and San Antonio are $197,553, $198,399, $198,714 and $181,237, respectively. These amounts are all below the March 2010 national median sales price of new homes sold of $214,000, according to estimates released jointly by the U.S. Census Bureau and the Department of Housing and Urban Development.

Using the Department of Housing and Urban Development’s estimated 2009 median family income for the respective metropolitan areas of Austin, Houston, Dallas, and San Antonio, the median income earner in those areas has 1.48 times, 1.28 times, 1.36 times, and 1.26 times the income required to qualify for a mortgage to purchase the median priced new home in the respective metropolitan area. These numbers illustrate the high affordability of Texas homes. Our measurement of housing affordability, as referenced above, is determined as the ratio of median family income to the income required to qualify for a 90 percent, 30-year fixed-rate mortgage to purchase the median-priced new home, based on the average interest rate for March and assuming an annual mortgage insurance premium of 60 basis points for private mor tgage insurance, plus a cost that includes estimated property taxes and insurance for the home. Using the U.S. Census Bureau’s 2009 income data to project an estimated median income for the United States of $64,000 and the March 2010 national median sales prices of new homes sold of $214,000, we conclude that the national median income earner has 1.19 times the income required to qualify for a mortgage loan to purchase the median-priced new home in the United States. This estimation reflects the increase in home affordability in housing markets outside of Texas over the past 36 months, as new home prices in housing markets outside of Texas generally have fallen. Recently, however, such price declines have begun to stabilize. Indeed, the March 2010 national median new home price of $214,000 increased by approximately 4.3% year over year from the March 2009 median new home sales price of $205,100, according to the Department of Housing and Urban Development. We believe that su ch price stabilization indicates that new home affordability has been restored to the national housing market.

Due to the national and global recession, the Texas employment market slowed in the fourth quarter of 2008 through the first three quarters of 2009 until beginning to add jobs again in the fourth quarter of 2009. Texas continued this employment growth in the first quarter of 2010 by adding approximately 25,400 jobs in the first three months of 2010. Over the twelve month period ended March 2010, the United States Department of Labor reported that Texas lost approximately 160,800 jobs and the unemployment rate increased to 8.2% from 7.0% in March 2009. However, the same source states that, nationally, the United States lost approximately 2,199,000 jobs, and the unemployment rate rose to 9.7% from 8.6% in March 2009. In spite of year-over year job losses, we believe that the long term employmen t fundamentals are sound in Texas. The Texas Workforce Commission reports that Texas has added more than half a million new jobs over the past five years, and the Federal Reserve Bank of Dallas has forecasted that Texas may add between 100,000 and 200,000 jobs in 2010.

The Texas Workforce Commission reports that as of March 2010, the unemployment rate for Austin-Round Rock, Texas was 7.1%, up from 6.6% in March 2009; Dallas-Fort Worth-Arlington, Texas was 8.3%, up from 7.3%; Houston-Sugar Land-Baytown, Texas was 8.5%, up from 6.8%; and San Antonio, Texas was 7.3%, up from 6.3%. Austin experienced a net loss of 3,100 jobs year-over-year from March 2009 to March 2010. During those same 12 months, Houston, Dallas-Fort Worth, and San Antonio experienced net losses of 57,600, 42,700, and 15,700 jobs, respectively. However, these cities have added an estimated net total of 424,500 jobs over the past five years: Austin added 75,000 jobs; Dallas-Fort Worth added 114,300 jobs; Houston added 183,400 jobs; and San Antonio added 51,800 jobs.

As stated above, the Texas economy slowed and suffered a net loss of jobs over the past 12 months due to the national and global recession. The National Bureau of Economic Research has concluded that the U.S. economy entered into a recession in December 2007, ending an economic expansion that began in November 2001. We believe that the transition from month-over-month and year-over-year job gains in Texas, to year-over-year and month-over-month job losses indicates that the Texas economy slowed significantly and followed the nation into recession in the fourth quarter of 2008. However, we also believe that the Texas economy will continue to outperform the national economy. According to the Texas Workforce Comm ission, Texas tends to enter into recessions after the national economy has entered a recession and usually leads among states in the economic recovery. In the current downturn, Texas’ recession trailed the national recession by nearly a year, and the state’s economy now appears to be in the early stages of recovery. Dallas Federal Reserve’s Index of Texas leading indicators has steadily improved since reaching a low in March 2009 and now stands at its highest measurement since October 2008; the Texas Comptroller of Public Accounts projects that the Texas economy will grow by 2.6% in 2010; and we believe that Texas cities will be among the first to recover based on employment figures, consumer confidence, gross metropolitan product, and new home demand.

The United States Census Bureau reported in its 2009 Estimate of Population Change July 1, 2008 to July 1, 2009 that Texas led the country in population growth during that period. The estimate concluded that Texas grew by 478,012 people, or 2.00%, a number which was 1.25 times greater than the next closest state in terms of raw population growth, California, and more than 3.57 times the second closest state in terms of raw population growth, North Carolina. The United States Census Bureau also reported that among the 15 counties that added the largest number of residents between July 1, 2008 and July 1, 2009, six were in Texas: Harris (Houston), Tarrant (Fort Worth), Bexar (San Antonio), Collin (North Dallas), Dallas (Dallas) and Travis (Austin). In March 2010, the United States Census Bureau reported that Texas’ four major metro areas – Austin, Houston, San Antonio and Dallas-Fort Worth – were among the top 20 in the nation for population growth from 2008 to 2009. Dallas-Fort Worth-Arlington led the nation in numerical population growth with a combined estimated population increase of 146,530. Houston-Sugarland-Baytown was second in the nation with a population increase of 140,784 from July 1, 2008 to July 1, 2009. Austin-Round Rock had an estimated population growth of 50,975 and San Antonio had an estimated population growth of 41,437 over the same period. The percentage increase in population for each of these major Texas cities ranged from 2.0% to 3.1%.

The Fourth Quarter 2009 U.S. Market Risk Index, a study prepared by PMI Mortgage Insurance Co., the U.S. subsidiary of The PMI Group, Inc., which ranks the nation’s 50 largest metropolitan areas through the fourth quarter of 2009 according to the likelihood that home prices will be lower in two years, reported that Texas cities are among the nation’s best for home price stability. This index analyzes housing price trends, the impact of foreclosure rates, and the consequence of excess housing supply on home prices. The quarterly report projects that there is less than a 36% chance that Dallas/Fort Worth-area home prices will fall during the next two years; a 42.2% chance that Houston-area home prices will fall during the next two years; a 14.8% chance that San Antonio-area home prices will fall during t he next two years; and a 62.1% chance that Austin-area home prices will fall during the next two years. Except for the Austin area, all Texas metropolitan areas included in the report are among the nation’s top twenty least-likely areas to experience a decline in home prices in two years. The Austin area is ranked the twenty-second least-likely area to experience a decline. Dallas-Plano-Irving, Texas is the nation’s tenth least-likely metropolitan area, Fort Worth-Arlington, Texas is seventh least-likely, Houston-Sugar Land-Baytown, Texas is thirteenth least-likely, and San Antonio, Texas is third least-likely.

In their fourth quarter Purchase Only Price Index, the FHFA reports that Texas had a home price appreciation of 0.83% between the fourth quarter of 2008 and the fourth quarter of 2009. The FHFA’s all-transaction price index report provides that existing home price appreciation between the fourth quarter of 2008 and the fourth quarter of 2009 for (a) Austin was -1.66%; (b) Houston was 0.44%; (c) Dallas was -1.27%; (d) Fort Worth was -1.05%; (e) San Antonio was -0.72%; and (f) Lubbock was 1.38%. However, each city remains well above the national average in the same index, which was -4.66% between the fourth quarter of 2008 and the fourth quarter 2009. Besides sales prices, the all-transaction price index report also tracks average house price changes in refinancings of the same single-family pr operties utilizing conventional, conforming mortgage transactions.

The Texas Comptroller of Public Accounts notes that the rate of foreclosures and defaults in Texas has remained generally stable for the past three years and is currently well below the national average. Likewise, the Federal Reserve Bank of Dallas anticipates, in its economic letter for the fourth quarter of 2009, the Texas foreclosure rate will continue to remain below the national average in 2010. Homebuilding and residential construction employment are likely to remain generally weak for some time, but Texas again will likely continue to outperform the national standards. We believe that Texas’ housing sector is healthier, the cost of living and doing business is lower, and its economy is more dynamic and diverse than the national average.

In contrast to the conditions of many homebuilding markets in the country, new home sales are greater than new home starts in Texas markets, indicating that home builders in Texas continue to focus on preserving a balance between new home demand and new home supply. We believe that home builders and developers in Texas have remained disciplined on new home construction and project development. New home starts have been declining year-over-year and are outpaced by new home sales in all four major Texas markets where such data is available. Inventories of finished new homes and total new housing (finished vacant, under construction, and model homes) remain at healthy and balanced levels in all four major Texas markets: Austin, Dallas-Fort Worth, Houston, and San Antonio. Each m ajor Texas market has experienced a rise in the number of months of finished lot inventories as homebuilders reduced the number of new home starts in 2008, causing each major Texas market to reach elevated levels. Houston has an estimated inventory of finished lots of approximately 36.3 months, Austin has an estimated inventory of finished lots of approximately 44.8 months, San Antonio has an estimated inventory of finished lots of approximately 56.3 months, and Dallas-Fort Worth has an estimated inventory of finished lots of approximately 63.6 months. A 24-28 month supply is considered equilibrium for finished lot supplies.

The elevation in month’s supply of finished lot inventory in Texas markets owes itself principally to the decrease in the pace of annual starts rather than an increase in the raw number of developed lots. Indeed, the number of finished lots dropped by more than 550 lots in Austin, nearly 1,300 lots in San Antonio, more than 2,600 lots in Houston, and nearly 3,900 lots in Dallas-Fort Worth in the fourth quarter of 2009. Annual starts in each of the Austin, San Antonio, Houston, and Dallas-Fort Worth markets are outpacing lot deliveries. With the discipline evident in these markets, we expect to see a continued decline in raw numbers of finished lot inventories in coming quarters as new projects have been significantly reduced.

Texas markets continue to be some of the strongest homebuilding markets in the country, though home building in Texas has weakened over the past year as a result of the national economic downturn. While the decline in housing starts has caused the month supply of vacant lot inventory to become elevated from its previously balanced position, it has also preserved a balance in housing inventory. Annual new home sales in Austin slightly outpace starts 7,389 versus 7,158, with annual new home sales declining year-over-year by approximately 25.98%. Finished housing inventory fell to a slightly elevated level of 3.0 months, while total new housing inventory (finished vacant, under construction and model homes) rose to a slightly elevated 6.7 months. The generally accepted equilibrium levels for fin ished housing inventory and total new housing inventory are a 2-to-2.5 month supply and a 6.0 month supply, respectively. Like Austin, San Antonio is also a relatively healthy homebuilding market. Annual new home sales in San Antonio run slightly ahead of starts 7,789 versus 7,647, with annual new home sales declining year-over-year by approximately 21.37%. Finished housing inventory remained at a generally healthy level with a 2.8 month supply. Total new housing inventory rose to a slightly elevated 6.7 month supply. Houston, too, is a relatively healthy homebuilding market. Annual new home sales there outpace starts 22,148 versus 20,531, with annual new home sales declining year-over-year by approximately 21.31%. Finished housing inventory and total new housing inventory are slightly elevated at a 3.1 month supply and a 6.8 month supply, respectively. Dallas-Fort Worth is a relatively healthy homebuilding market as well. � 0;Annual new home sales in Dallas-Fort Worth outpace starts 16,513 versus 15,254, with annual new home sales declining year-over-year by approximately 27.29%. Finished housing inventory rose slightly to a 3.2 month supply, while total new housing inventory rose to a 7.3 month supply, respectively, each measurement above the considered equilibrium level. All numbers are as released by Residential Strategies, Inc. or Metrostudy, leading providers of primary and secondary market information.

The Real Estate Center at Texas A&M University has reported that inventory levels and sales of existing homes remain relatively healthy in Texas markets, as well. With the exception of the Dallas market, the year-over-year sales pace has increased between 2% and 17% in each of the four largest Texas markets, though inventory levels have also increased, most likely because residents in these markets are finally comfortable putting their homes up for sale. In March 2010, the number of months of home inventory for sale in Austin, Houston, Dallas, Fort Worth, and Lubbock was 6.6 months, 6.9 months, 6.3 months, 6.6 months, and 5.7 months, respectively. San Antonio’s inventory is more elevated with an 8.1 month supply of homes for sale. Like new home inventory, a 6-month supply of invento ry is considered a balanced market with more than 6 months of inventory generally being considered a buyer’s market and less than 6 months of inventory generally being considered a seller’s market. In March 2010, the number of existing homes sold to date in (a) Austin was 4,221, up 17% year-over-year; (b) San Antonio was 3,812, up 13% year-over-year; (c) Houston was 11,858, up 2% year-over-year, (d) Dallas was 8,830, down 1% year-over-year, (e) Fort Worth was 1,737, up 5% year-over-year, and (f) Lubbock was 611, up 3% year-over-year.

In managing and understanding the markets and submarkets in which we make and purchase loans, we monitor the fundamentals of supply and demand. We track the economic fundamentals in each of the respective markets, analyzing demographics, household formation, population growth, employment, migration, immigration, and housing affordability. We also watch movements in home prices and the presence of market disruption activity, such as investor or speculator activity that can create a false impression of demand and result in an oversupply of homes in a market. Further, we study new home starts, new home closings, finished home inventories, finished lot inventories, existing home sales, existing home prices, foreclosures, absorption, prices with respect to new and existing home sales, finished lots and land, and the presence of sales incentives, discounts, or both, in a market.

Generally, the residential homebuilding industry is cyclical and highly sensitive to changes in broader economic conditions, such as levels of employment, consumer confidence, income, availability of financing for acquisition, construction, and permanent mortgages, interest rate levels, and demand for housing. The condition of the resale market for used homes, including foreclosed homes, also has an impact on new home sales. In general, housing demand is adversely affected by increases in interest rates, housing costs, and unemployment and by decreases in the availability of mortgage financing or in consumer confidence, which can occur for numerous reasons, including increases in energy costs, interest rates, housing costs, and unemployment.

We face a risk of loss resulting from deterioration in the value of the land purchased by the developer with the proceeds of loans from us or loans purchased by us, a diminution of the site improvement and similar reimbursements used to repay loans made or purchased by us, and a decrease in the sales price of the single-family residential lots developed with the proceeds of loans from us or purchased by us. Deterioration in the value of the land, a diminution of the site improvement and similar reimbursements, and a decrease in the sales price of the residential lots can occur in cases where the developer pays too much for the land to be developed, the developer is unable or unwilling to develop the land in accordance with the assumptions required to generate sufficient income to repay the loans made or purchased b y us, or is unable to sell the residential lots to homebuilders at a price that allows the developer to generate sufficient income to repay the loans made or purchased by us. Our Advisor actively monitors the markets and submarkets in which we make and purchase loans, including mortgage markets, homebuilding economies, the supply and demand for homes, finished lots, and land and housing affordability to mitigate such risks. Our Advisor also actively manages our loan portfolio in the context of events occurring with respect to the loan and in the market and submarket in which we made or purchased the loan. We anticipate that there may be defaults on development loans made or purchased by us and that we will take action with respect to such defaults at any such time that we determine it prudent to do so, including such time as we determine it prudent to maintain and protect the value of the collateral securing a loan by originating another development loan to another developer with respect to the same project to maintain and protect the value of the collateral securing our initial loan.

We face a risk of loss resulting from adverse changes in interest rates. Changes in interest rates may affect both demand for our real estate finance products and the rate of interest on the loans we make or purchase. In most instances, the loans we make or purchase will be junior in the right of repayment to senior lenders, who will provide loans representing 60% to 75% of total project costs. As senior lender interest rates available to our borrowers increase, demand for our mortgage loans may decrease, and vice versa.

Developers to whom we make mortgage loans or whose loans we purchase use the proceeds of such loans to develop raw real estate into residential home lots. The developers obtain the money to repay these development loans by selling the residential home lots to home builders or individuals who will build single-family residences on the lots, receiving qualifying site improvement reimbursements, and by obtaining replacement financing from other lenders. If interest rates increase, the demand for single-family residences may decrease. Also, if mortgage financing underwriting criteria become stricter, demand for single-family residences may decrease. In such an interest rate and/or mortgage financing climate, developers may be unable to generate sufficient income from the resale of single-family r esidential lots to repay loans owned by us, and developers’ costs of funds obtained from lenders in addition to us may increase as well. If credit markets deteriorate, developers may not be able to obtain replacement financing from other lenders. Accordingly, increases in single-family mortgage interest rates, decreases in the availability of mortgage financing, or decreases in the availability of replacement financing could increase the number of defaults on development loans made or purchased by us.

We are not aware of any material trends or uncertainties, favorable or unfavorable, other than national economic conditions affecting real estate and interest rates generally, that we reasonably anticipate to have a material impact on either the income to be derived from our investments in mortgage loans or entities that make mortgage loans, other than those referred to in this Quarterly Report on Form 10-Q. The disruption of mortgage markets, in combination with a significant amount of negative national press discussing constriction in mortgage markets and the poor condition of the national housing industry, including declining home prices, have made potential new home purchasers and real estate lenders very cautious. The economic downturn, the failure of highly respected financial institutions, significant decli ne in equity markets around the world, unprecedented administrative and legislative actions in the United States, and actions taken by central banks around the globe to stabilize the economy have further caused many prospective home purchasers to postpone their purchases.

Outlook

In summary, we believe there is a general lack of urgency to purchase homes in these times of economic uncertainty. We believe that this has further slowed the sales of new homes and expect that this will result in a slowing of the sales of finished lots developed by our borrowers in certain markets; however, we continue to believe that the prices of those lots should not change materially. We also anticipate that the decrease in the availability of replacement financing may increase the number of defaults on development loans we invest in or extend the time period anticipated for the repayment of loans. We believe that United Mortgage Trust has been active in monitoring current market conditions and in implementing various measures to manage our risk and protect our return on our investments by shiftin g our portfolio to investments that are less directly sensitive to the adverse market conditions and that produce higher yields and by aggressively liquidating non-performing loans. Based on that assessment, we do not anticipate a significant disruption to our normal business operations. Nevertheless, our assessments inherently involve predicting future events and we cannot be sure of the length or extent of the current credit crisis and if it continues over an extended period of time, or if its severity increases, its impact on the economy as a whole and on the housing and mortgage lending market could cause us to suffer a higher level of delinquencies and losses than we are currently predicting and result in a material adverse impact on our business.

Interim Loan Portfolio Overview

The deterioration in the residential mortgage market, specifically the discontinuation of sub-prime and Alt – A products, referred to herein as the sub-prime credit crisis, and the continued slowdown in new home sales are directly and indirectly affecting the ability of our interim loan borrowers to sell the assets securing their loans, pay interest due us and repay the interim loans when due. New and existing home financing solutions are being introduced by both the private and public sectors. Housing inventories are slowly beginning to reduce to sustainable levels. However, consumer confidence remains low. Industry-wide lenders are reevaluating and restructuring credits affected by residential mortgage markets as housing sales decline. Overall recovery of the single f amily housing industry is likely to be prolonged. We believe that a pragmatic and pro-active approach to managing our interim loan credits will allow us to maximize repayments and properly report asset values. In consideration of the above, we are:

| | · | ceasing the origination of, and reducing our investment in interim loans dependent on sub-prime and Alt-A mortgage products for repayment of our loan. |

| | · | accepting a secured note from UMTHLC for shortfalls from foreclosed properties to enable UMTHLC to efficiently manage past due and foreclosed accounts throughout the duration of the credit crisis. |

| | · | increasing loss reserves for certain deficiency loans where full collection of the indebtedness is not assured. |