UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

[ x ] QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended September 30, 2009

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _________ to _________

Commission file number: 000-32409

UNITED MORTGAGE TRUST

(Exact name of registrant as specified in its charter)

| Maryland | 75-6493585 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

1301 Municipal Way, Suite 220

Grapevine, Texas 76051

(Address of principal executive offices)(Zip Code)

(214) 237-9305

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes X No ___

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act

Large accelerated filer___ Accelerated filer____ Non-accelerated filer (Do not check if a smaller reporting company)

X Smaller Reporting Company

Indicate by check mark whether the registrant has submitted electronically and posted to its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes[X] No [_]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act) Yes No X

The number of shares outstanding of the Registrant’s shares of beneficial interest, par value $0.01 per share, as of the close of business on November 12, 2009 was 6,423,566.

UNITED MORTGAGE TRUST

INDEX

PART I - FINANCIAL INFORMATION

| | | Page |

| ITEM 1. | Financial Statements | |

| | | |

| | Consolidated Balance Sheets as of September 30, 2009 (unaudited) and December 31, 2008 | 3 |

| | Consolidated Statements of Income for the three months and nine months ended September 30, 2009 and September 30, 2008 (unaudited) | 4 |

| | Consolidated Statements of Cash Flows for the nine months ended September 30, 2009 and September 30, 2008 (unaudited) | 5 |

| | Notes to Consolidated Financial Statements (unaudited) | 6 |

| | | |

| ITEM 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 14 |

| ITEM 3. | Quantitative and Qualitative Disclosures about Market Risk | 27 |

| ITEM 4. | Controls and Procedures | 28 |

| |

| PART II - OTHER INFORMATION |

| | | |

| ITEM 1. | Legal Proceedings | 28 |

| ITEM 2. | Unregistered Sales of Equity Securities and Use of Proceeds | 28 |

| ITEM 3. | Defaults Upon Senior Securities | 29 |

| ITEM 4. | Submission of Matters to a Vote of Security Holders | 29 |

| ITEM 5. | Other Information | 30 |

| ITEM 6. | Exhibits | 31 |

| | Signatures | 32 |

UNITED MORTGAGE TRUST

CONSOLIDATED BALANCE SHEETS

| | | | | | |

| | | | | | |

| | | | | |

Cash and cash equivalents | $ | | $ | | |

| | | | | | |

| | | | | |

Investment in trust receivable | | | | | |

Interim mortgages, affiliates | | | | | |

| | | | | |

Allowance for loan losses | | | ) | | |

Total mortgage investments | | | | | |

| | | | | | |

Line of credit receivable, affiliate | | | | | |

Line of credit receivable, non-affiliate | | | | | |

Accrued interest receivable | | | | | |

Accrued interest receivable, affiliate | | | | | |

Recourse obligations, affiliates | | | | | |

Residential mortgages and contracts for deed foreclosed | | | | | |

Interim mortgages foreclosed | | | | | |

| | | | | |

Deficiency note, affiliate | | | | | |

Allowance for loan losses – deficiency notes | | | ) | | ) |

| | | | | |

| $ | | $ | | |

| | | | | | |

Liabilities and Shareholders’ Equity | | | | | |

| | | | | |

Accounts payable and accrued liabilities | $ | | $ | | |

| | | | | |

| | | | | |

Participation payable, affiliate | | | | | |

| | | | | |

| | | | | | |

Commitments and contingencies | | | | | |

| | | | | | |

| | | | | |

Shares of beneficial interest; $0.01 par value; 100,000,000 shares authorized; 8,255,523 and 8,218,591 shares issued in 2009 and 2008, respectively; and 6,420,409 and 6,436,569 outstanding in 2009 and 2008, respectively | | | | | |

Additional paid-in capital | | | | | |

| | | | | |

Cumulative distributions in excess of earnings | | | | | |

| | | | | | |

Less treasury stock of 1,835,114 and 1,782,022 shares in 2009 and 2008, respectively, at cost | | | ) | | ) |

Total shareholders' equity | | | | | |

Total liabilities and shareholders' equity | $ | | $ | | |

See accompanying notes to consolidated financial statements.

UNITED MORTGAGE TRUST

CONSOLIDATED STATEMENTS OF INCOME

(unaudited)

| | | Three Months Ended September 30, | | Nine Months Ended September 30, |

| | | | | | | | | |

| | | | | |

Interest income, affiliates | | | | | | | | | |

Interest income, non-affiliates | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | |

| | | | | | | | | |

| | | | | | | | | |

General and administrative | | | | | | | | | |

Provision for loan losses | | | | | | | | | |

| | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | |

| | | | | | | | | | |

Net income per share of beneficial interest | | | | | | | | | |

| | | | | | | | | | |

Weighted average shares outstanding | | | | | | | | | |

| | | | | | | | | | |

Distributions per weighted share outstanding | | | | | | | | | |

See accompanying notes to consolidated financial statements.

UNITED MORTGAGE TRUST

CONSOLIDATED STATEMENTS OF CASH FLOWS

(unaudited)

| | | Nine Months Ended September 30, | |

| | | 2009 | | 2008 | |

| | | | | |

| $ | | $ | | |

Adjustments to reconcile net income to net cash provided | | | | | |

| | | | | |

Provision for loan losses | | | | | |

Depreciation and amortization | | | | | |

Changes in assets and liabilities: | | | | | |

Accrued interest receivable | | | ) | | ) |

| | | ) | | |

Accounts payable and accrued liabilities | | | ) | | ) |

Net cash provided by operating activities | | | | | |

| | | | | | |

| | | | | |

Investment in trust receivable | | | ) | | ) |

Principal receipts on trust receivable | | | | | |

Investment in interim mortgages | | | ) | | ) |

Principal receipts on interim mortgages | | | | | |

Investments in interim mortgages, affiliates | | | ) | | ) |

Principal receipts on interim mortgages, affiliates | | | | | |

Principal receipts on residential mortgages and contracts for deed, net | | | | | |

Principal receipts (investments in) line of credit receivable, affiliate, net | | | ) | | |

Investments in line of credit receivable, non-affiliate, net | | | ) | | |

Principal receipts (investments in) recourse obligations, net | | | | | ) |

Net cash provided by (used in) investing activities | | | ) | | |

| | | | | | |

| | | | | |

Proceeds from issuance of shares of beneficial interest | | | | | |

Purchase of treasury stock | | | ) | | ) |

Draws on line of credit, net | | | | | |

| | | ) | | ) |

Net cash used in financing activities | | | ) | | ) |

| | | | | | |

Net increase (decrease) in cash and cash equivalents | | | ) | | |

Cash and cash equivalents at beginning of period | | | | | |

Cash and cash equivalents at end of period | $ | | $ | | |

| | | | | | |

Supplemental Disclosure of Cash Flow Information | | | | | |

Cash paid during the period for interest | | | | | |

| | | | | |

Transfers of affiliate and non-affiliate loans to foreclosed properties or recourse obligations | | | | | |

Participation receivable, affiliate | | | ) | | ) |

Participation payable, affiliate | | | | | |

Participation accrued interest receivable, affiliate | | | | | ) |

Participation accrued interest payable, affiliate | | | ) | | |

See accompanying notes to consolidated financial statements.

UNITED MORTGAGE TRUST

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

United Mortgage Trust (the “Company” and “UMT”) is a Maryland real estate investment trust that qualifies as a real estate investment trust (a “REIT”) under federal income tax laws. The Company’s principal investment objectives are to invest proceeds from its dividend reinvestment plan, financing proceeds, capital transaction proceeds and retained earnings in the following types of investments: (i) first lien secured interim mortgage loans with initial terms of 12 months or less for the acquisition and renovation of single-family homes, which we refer to as “Interim Loans”; (ii) secured, line of credit to UMTH Lending Company, L.P. for origination of Interim Loans; (iii) lines of credit and secured loans for the acquisition and development of single-family home lots, referred to as “Land Development Loans”; (iv) lines of credit and loans secured by developed single-family lots, referred to as “Finished Lot Loans”; (v) lines of credit and loans secured by completed model homes, referred to as “Model Home Loans”; (vi) loans provided to entities that have recently filed for bankruptcy protection under Chapter 11 of the U.S. bankruptcy code, secured by a priority lien over pre-bankruptcy secured creditors, referred to as “Debtor in Possession Loans”, (vii) lines of credit and loans, with terms of 18 months or less, secured by single family lots and homes constructed thereon, referred to as “Construction Loans”; (viii) first lien secured mortgage loans with terms of 12 to 360 months for the acquisition of single-family homes, referred to as “Residential Mortgages”, and, (ix) discounted cash flows secured by assessments on real property. We collectively refer to the above listed loans as “Mortgage Investments”. Additionally, our portfolio includes obligations of affiliates of our Advisor, which we refer to as “recourse loans.”

The Company has no employees. The Company pays a monthly trust administration fee to UMTH General Services, L.P. (“UMTHGS” or “Advisor”), a subsidiary of UMT Holdings, L.P. (“UMTH”), a Delaware real estate finance company and affiliate, for the services relating to its daily operations. The Company’s offices are located in Grapevine, Texas.

The consolidated financial statements include the accounts of the Company and certain wholly-owned subsidiaries and all significant intercompany accounts and transactions have been eliminated. In the opinion of management, all adjustments (consisting of normal recurring adjustments) considered necessary for a fair presentation have been included. These consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United States (“GAAP”) for interim financial information and with the instructions for Form 10-Q and Article 10 of Regulation S-X adopted by the Securities and Exchange Commission (“SEC”). Accordingly, the financial statements do not include all of the information and footnotes required by GAAP for complete financial statements and should be read in conjunction with our consolidated financial statements, and notes thereto, for the year ended December 31, 2008, included in our Annual Report on Form 10-K filed with the SEC on March 31, 2009. Operating results for the nine months ended September 30, 2009, are not necessarily indicative of the results that may be expected for the year ended December 31, 2009. Certain prior period amounts have been reclassified to conform to current period presentation.

| 3. | Impact of Recently Issued Accounting Standards |

On July 1, 2009, the Financial Accounting Standards Board (FASB) issued FASB Statement of Financial Accounting Standards No. 168, “FASB Accounting Standards Codification and the Hierarchy of Generally Accepted Accounting Principles,” which is included in FASB Accounting Standards Codification (ASC) 105 “Generally Accepted Accounting Principles.” This new guidance approved the FASB ASC as the single source of authoritative nongovernmental GAAP. The FASB ASC is effective for interim or annual periods ending after September 15, 2009. All existing accounting standards have been superseded and all other accounting literature not included in the FASB ASC will be considered nonauthoritative. The ASC is a restructuring of GAAP designed to simplify access to all authoritative literature by providing a topically organized structure. The adoption of FASB ASC did not impact the Company’s financial condition or results of operations. Technical references to GAAP included in these notes to the Consolidated Financial Statements are provided under the new FASB ASC structure.

In September 2006, the Financial Accounting Standards Board (“FASB”) issued SFAS No. 157, Fair Value Measurements (“SFAS 157”) which amends FASB ASC 820, “Fair Value Measurement and Disclosure.” SFAS 157 defines fair value, establishes a market-based framework or hierarchy for measuring fair value, and expands disclosures about fair value measurements. SFAS 157 is applicable whenever another accounting pronouncement requires or permits assets and liabilities to be measured at fair value. SFAS 157 does not expand or require any new fair value measures; however the application of this statement may change current practice. The requirements of SFAS 157 are first effective for the Company for the fiscal year beginning January 1, 2008. However, in February 2008, the FASB issued FASB Staff Position (“FSP”) 157-2, Effective Date of FASB Statement No. 157 (“FSP 157-2”). FSP 157-2 delays the effective date of SFAS 157 for all nonfinancial assets and nonfinancial liabilities, except for items that are recognized or disclosed at fair value in the financial statements on a recurring basis (at least annually), until the beginning of the first quarter 2009. Accordingly, the Company’s adoption of this standard on January 1, 2008 was limited to financial assets and liabilities. The Company’s adoption of SFAS 157 as of January 1, 2009, has not had a material impact on the Company’s financial condition or results of operations.

In February 2007, FASB issued SFAS No. 159, “The Fair Value Option for Financial Assets and Financial Liabilities Including an Amendment of FASB Statement No. 115,” which amends FASB ASC 825, “Financial Instruments.” The fair value option permits entities to choose to measure eligible financial instruments at fair value at specified election dates. The entity will report unrealized gains and losses on the items on which it has elected the fair value option in earnings. SFAS 159 is effective beginning in fiscal year 2008. The adoption of FAS 159 did not have a material impact on the Company’s financial position or results of operations.

On October 10, 2008, the FASB issued FSP 157-3 (“FSP 157-3”), Determining the Fair Value of a Financial Asset When the Market for that Asset Is Not Active, which amends FASB ASC 820, “Fair Value Measurements and Disclosure.” FSP 157-3 clarifies the application of Statement 157 in a market that is not active and provides an example to illustrate key considerations in determining the fair value of a financial asset when the market for the financial asset is not active. FSP 157-3 was effective upon issuance, including prior periods for which financial statements have not been issued. The adoption of FSP 157-3 did not have a material impact on the Company’s financial position or results of operations.

4. Deficiency Notes – Affiliate and Non-Affiliate

The Company has made loans in the normal course of business to affiliates and non-affiliates, the proceeds from which have been used to originate underlying loans that are pledged to the Company as security for such obligations. When principal and interest on an underlying loan is due in full, at maturity or otherwise, the corresponding obligation owed by the originating company to the Company is also due in full. If the borrower or the Company foreclosed on property securing an underlying loan, or if the Company foreclosed on property securing a purchased loan, and the proceeds from the sale were insufficient to pay the loan in full, the originating company had the option of (1) repaying the outstanding balance owed to the Company associated with the underlying loan or purchased loan, as the case may be, or (2) delivering to the Company an unsecured deficiency note in the amount of the deficiency.

As of September 30, 2009 and December 31, 2008, the Company had two deficiency notes with non-affiliates in the amount of approximately $7,189,000 and $6,981,000, respectively. The Company has recorded reserves of $4,344,128 and $3,131,155 against these notes as of September 30, 2009 and December 31, 2008 respectively. These notes do not accrue interest as the underlying collateral value approximates the note balance, net of reserves.

As of December 31, 2007, UMTH Lending Company, L.P.(“UMTHLC”) issued to the Company a variable amount promissory note in the original amount of $5,100,000 to evidence its deficiency obligations to the Company. The initial principal amount of the note was approximately $1,848,000. The principal balance will fluctuate from time to time based on the underlying loan activity and the amount of deficiencies realized by the affiliate. The note bears interest at a rate of 10%, and requires monthly principal and interest payments based on a ten-year amortization for the outstanding principal balance. The note is secured by a limited guaranty by UMTHGS, the Advisor, equal to a monthly amount not to exceed 33% of the advisory fee received by UMTHGS under the terms of its advisory agreement with the Company. This note had a balance of approximately $7,335,000 and $5,332,000 at September 30, 2009 and December 31, 2008, respectively. Per the terms of the Secured Notes, the unpaid principal balance may be greater or less than the initial principal amount of the note and is not considered an event of default. As of September 30, 2009 no reserves have been recognized on this loan based on management’s assertion.

5. Related Party Transactions

1) UMTH is a Delaware limited partnership which is in the real estate finance business. UMTH holds a 99.9% limited partnership interest in UMTH Lending Company, L.P., which originates interim loans that the Company is assigned, UMTH Land Development, L.P. ("UMTHLD"), which holds a 50% profit interest in United Development Funding, L.P. (“UDF”) and acts as UDF's asset manager, and Prospect Service Corp. (“PSC”), which services the Company’s residential mortgages and contracts for deed and manages the Company’s REO. In addition, UMTH has a limited guarantee of the obligations of Capital Reserve Group (“CRG”), Ready America Funding Corp (“RAFC”), and South Central Mortgage, Incorporated (“SCMI”), a Texas corporation that sold mortgage investments to the Company, under the Secured Notes. United Development Funding III, L.P., (“UDF III”) which is managed by UMTH Land Development, L.P., has previously provided a limited guarantee of the UDF line of credit and has purchased an economic participation in a revolving credit facility we have provided to UDF.

2) UMTHLC is a Delaware limited partnership, and subsidiary of UMTH. The Company loans money to UMTHLC so it can make loans to its borrowers. The loans are collaterally assigned to the Company, as security for the promissory note between UMTHLC and the Company. The unpaid principal balance of the loans at September 30, 2009 and December 31, 2008 was approximately $17,726,000 and $18,195,000, respectively.

On March 26, 2009, the Company executed a secured line of credit promissory note with UMTH Lending, Company, L.P. in the amount of $8,000,000. The note bears interest at 12.50% per annum, matures on March 26, 2012 and is secured by first lien mortgage interests in single family residential properties. At September 30, 2009, the outstanding balance on this line of credit was approximately $6,951,000.

See Note 4 above for discussion of additional related party transactions with UMTHLC.

3) RAFC is a Texas corporation that is 50% owned by SCMI, which is owned by Todd Etter. RAFC is in the business of financing interim loans for the purchase of land and the construction of modular and manufactured single-family homes placed on the land by real estate investors. The Company continues to directly fund obligations under one existing RAFC loan, which was collaterally assigned to the Company, but does not fund new originations. The unpaid principal balance of the loans at September 30, 2009 and December 31, 2008 was approximately $24,079,000 and $23,380,000, respectively.

4) Wonder Funding, LP (“Wonder”) is a Delaware limited partnership that is owned by Ready Mortgage Corp. (“RMC”). RMC is beneficially owned by Craig Pettit, a partner of UMTH and the sole proprietor of two companies that own 50% of RAFC. Wonder is in the business of financing interim loans for the purchase of land and the construction of single family homes. The Company has ceased funding any new originations. As of September 30, 2009 and December 31, 2008, respectively, all remaining obligations owed by Wonder to the Company are included in the recourse obligations discussed below.

5) Recourse Obligations. The Company has made recourse loans to (a) CRG, which is owned by Todd Etter and William Lowe, (b) RAFC, which is owned by SCMI and two companies owned by Craig Pettit, Eastern Intercorp, Inc. and Ready Mortgage Corp. (“RMC”), and (c) SCMI, which is owned by Todd Etter, (these companies are referred to as the "originating companies"). In addition to the originating companies discussed above, the Company made loans with recourse to Wonder. Each of these entities used the proceeds from such loans to originate loans, that are referred to as "underlying loans," that are pledged to the Company as security for such originating company's obligations to the Company. When principal and interest on an underlying loan are due in full, at maturity or otherwise, the corresponding obligation owed by the originating company to the Company is also due in full.

In addition, some of the originating companies have sold loans to the Company, referred to as the "purchased loans," and entered into recourse agreements under which the originating company agreed to repay certain losses the Company incurred with respect to purchased loans.

If the originating company forecloses on property securing an underlying loan, or the Company forecloses on property securing a purchased loan, and the proceeds from the sale are insufficient to pay the loan in full, the originating company has the option of (1) repaying the outstanding balance owed to the Company associated with the underlying loan or purchased loan, as the case may be, or (2) delivering an unsecured deficiency note in the amount of the deficiency to the Company.

On March 30, 2006, but effective December 31, 2005, the Company and each originating company agreed to consolidate (1) all outstanding amounts owed by such originating company to the Company under the loans made by the Company to the originating company and under the deficiency notes described above and (2) the estimated maximum future liability to the Company under the recourse arrangements described above, into secured promissory notes. Each originating company issued to the Company a secured variable amount promissory note dated December 31, 2005 (the “Secured Notes”) in the principal amounts shown below, which amounts represent all principal and accrued interest owed as of such date. The initial principal amounts are subject to increase if the Company incurs losses upon the foreclosure of loans covered by recourse arrangements with the originating company. The Secured Notes (including related guaranties discussed below) are secured by an assignment of the distributions on the Class C units, Class D units and Class EIA units of limited partnership interest of UMT Holdings held by each originating company.

| Name | Initial principal amount | Balance at September 30, 2009 | Promissory Note principal amount (2) | | Units pledged as security | C Units distributed in 2009 | Units remaining | Nominal Collateral Value (3) |

| | | | | 4,984 Class C and 2,710 Class D | | 3,548 Class C and 2,710 Class D | |

| | | | | 11,165 Class C and 6,659 Class D and 1,066 Class EIA | | 9,233 Class C, 6,659 Class D and 1,066 EIA | |

| | | | | 4,545 Class and 3,000 Class D | | 2,919 Class C and 3,000 Class D | |

| | | | | | | | |

Wonder Indemnification (1) | | | | | | | | |

| | | | | | | | |

| | (1) Wonder is collateralized by an indemnification agreement from UMTH in the amount of $1,134,000, and is secured by the pledge of 3,870 C Units from RMC. 2,213 of the pledged C Units also cross-collateralize the RAFC obligation. |

| | (2) The CRG and Wonder balances at September 30, 2009 exceeded the stated principal amount per their variable Secured Notes by approximately $131,000 and $561,000, respectively. Per the terms of the Secured Notes, the unpaid principal balance may be greater or less than the initial principal amount of the note and is not considered an event of default. The rapid rate of liquidation of the remaining portfolio of properties caused a more rapid increase in the Unpaid Principal Balance (“UPB”) than originally anticipated and outpaced the minimum principal reductions scheduled for the loans. |

| | (3) Nominal collateral value does not reflect pledge of D units of limited partnership interest of UMTH held by WLL, Ltd., RAFC and KLA, Ltd. UMTH D units represent equity interests in UMT Holdings, LP. Pledge of the UMTH D units entitles the beneficiary to a pro-rata share of UMTH partnership D unit cash distributions. |

Through September 2007, the Secured Notes incurred interest at a rate of 10% per annum. The CRG, RAFC and RAF/Wonder Secured Notes amortize over 15 years and mature on December 31, 2020. The SCMI Secured Note amortizes over approximately 22 years and matures on December 31, 2027, which was the initial amortization of the deficiency notes from SCMI that were consolidated. The Secured Notes required the originating company to make monthly payments equal to the greater of (1) principal and interest amortized over 180 months and 264 months, respectively, or (2) the amount of any distributions paid to the originating company with respect to the pledged Class C and EIA units. Effective, October, 2007, the recourse loans were modified to accommodate the anticipated increases in principal balances throughout the remaining liquidation periods of the underlying assets, suspended the principal component of the amortized loans for the period of July 2007 through June 2009, and reduced the interest rate from 10% to 6%. Effective, July 2009, the above modifications were extended through December 31, 2009. Management has not recognized any reserves on these loans as the underlying collateral value exceeds the outstanding loan amounts.

The Secured Notes have also been guaranteed by the following entities under the arrangements described below, all of which are dated effective December 31, 2005:

| - | UMT Holdings. This guaranty is limited to a maximum of $10,582,336 due under all of the Secured Notes and is unsecured. |

| - | WLL, Ltd., an affiliate of CRG. This guaranty is of all amounts due under Secured Note from CRG is non-recourse and is secured by an assignment of 2,492 Class C Units and 1,355 Class D units of limited partnership interest of UMT Holdings held by WLL, Ltd. |

| - | RMC. This guaranty is non-recourse, is limited to 50% of all amounts due under the Secured Note from RAFC and is secured by an assignment of 3,870 Class C units of limited partnership interest of UMT Holdings |

| - | Wonder. Wonder Funding obligations are evidenced by a note from RAFC (“RAFC Wonder Note”) and are secured by a pledge of a certain Indemnification Agreement given by UMTH to RAFC and assigned to UMT in the amount of $1,134,000, which amount is included in the UMTH limited guarantee referenced above. |

In addition, WLL, Ltd. has obligations to UMT Holdings under an indemnification agreement between UMT Holdings, WLL, Ltd. and William Lowe, under which UMT Holdings is indemnified for certain losses on loans and advances made to William Lowe by UMT Holdings. That indemnification agreement allows UMT Holdings to offset any amounts subject to indemnification against distributions made to WLL, Ltd., with respect to the Class C and Class D units of limited partnership interest held by WLL, Ltd. Because WLL, Ltd. has pledged these Class C and Class D units to the Company to secure its guaranty of Capital Reserve Corp.'s obligations under its Secured Note, UMT Holdings and the Company entered into an Intercreditor and Subordination Agreement under which UMT Holdings has agreed to subordinate its rights to offset amounts owed to it by WLL, Ltd. to the Company’s lien on such units.

6) On June 20, 2006, the Company entered into a Second Amended and Restated Secured Line of Credit Promissory Note (the "Amendment") with UDF, a Nevada limited partnership that is affiliated with the Company's Advisor, UMTHGS. The Amendment increased an existing revolving line of credit facility ("Loan") to $45 million. The Loan matures on December 31, 2009. The purpose of the Loan is to finance UDF's loans and investments in real estate development projects. On July 29, 2009, our trustees approved an amendment to increase of the revolving line of credit facility to an amount not to exceed $60,000,000.

The Loan is secured by the pledge of all of UDF's land development loans and equity investments. Those UDF loans may be first lien loans or subordinate loans.

The Loan interest rate is the lower of 15% or the highest rate allowed by law, further adjusted with the addition of a credit enhancement to a minimum of 14%.

UDF may use the Loan proceeds to finance indebtedness associated with the acquisition of any assets to seek income that qualifies under the Real Estate Investment Trust provisions of the Internal Revenue Code to the extent such indebtedness, including indebtedness financed by funds advanced under the Loan and indebtedness financed by funds advanced from any other source, including Senior Debt, is no more than 85% of 80% (68%) of the appraised value of all subordinate loans and equity interests for land development and/or land acquisition owned by UDF and 75% for first lien secured loans for land development and/or acquisitions owned by UDF.

As a condition of the Amendment, UDF III, a public limited partnership that is affiliated with UDF and with the Company’s Advisor, had provided a guarantee of payment and performance of the Loan up to $30 million. The Company released the UDF III Guarantee January 1, 2008.

On September 19, 2008, UMT entered into an Economic Interest Participation Agreement with UDF III pursuant to which UDF III purchased (i) an economic interest in the $45,000,000 revolving credit facility (“Loan”) from UMT to UDF I and (ii) a purchase option to acquire a full ownership participation interest in the Loan (the “Option”). On July 29, 2009 our trustees approved an amendment to increase of the revolving line of credit facility to an amount not to exceed $60,000,000.

The Loan is the $60,000,000 revolving line of credit facility evidenced by a Second Amended and Restated Secured Line of Credit Promissory Note dated as of June 20, 2006, as modified by amendments effective September 1, 2006 and June 29, 2009 (as amended, the “Amendment”). The UMT Loan is secured by a security interest in the assets of UDF including UDF's land development loans and equity investments pursuant to the First Amended and Restated Security Agreement dated as of September 30, 2004, executed by UDF in favor of UMT (the “Security Agreement”).

Pursuant to the Economic Interest Agreement, each time UDF requests an advance of principal under the UMT Loan, UDF III will fund the required amount to UMT and UDF III’s economic interest in the UMT Loan increases proportionately. UDF III’s economic interest in the UMT Loan gives UDF III the right to receive payment from UMT of principal and accrued interest relating to amounts funded by UDF III to UMT which are applied towards UMT’s funding obligations to UDF under the UMT Loan. UDF III may abate its funding obligations under the Economic Participation Agreement at any time for a period of up to twelve months by giving UMT notice of the abatement.

The Option gives UDF III the right to convert its economic interest into a full ownership participation interest in the UMT Loan at any time by giving written notice to UMT and paying an exercise price of $100. The participation interest includes all rights incidental to ownership of the UMT Loan and the Security Agreement, including participation in the management and control of the UMT Loan. UMT will continue to manage and control the UMT Loan while UDF III owns an economic interest in the UMT Loan. If UDF III exercises its Option and acquires a participation interest in the UMT Loan, UMT will serve as the loan administrator but both UDF III and UMT will participate in the control and management of the UMT Loan. The UMT Loan matures on December 31, 2009. At September 30, 2009, UDF III had funded approximately $51,545,000 to UDF under this agreement. On July 29, 2009 our trustees approved an amendment to increase of the revolving line of credit facility to an amount not to exceed $60,000,000.

The UMT Loan is subordinate to UDF Senior Debt, which includes a line of credit provided by Textron Financial Corporation in the amount of $30,000,000, and all other indebtedness of UDF to any national or state chartered banking association or other institutional lender that is approved by UMT in writing. On June 14, 2009, the Textron loan agreement matured and became due and payable in full. The loan is in default and as of September 30, 2009, the outstanding balance owing to Textron under the Textron loan agreement was approximately $27,732,000. Effective August 15, 2009, Textron and UDF entered into a Forbearance Agreement pursuant to which Textron agreed to forbear in exercising its rights and remedies under their loan agreement until November 15, 2009; provided, that the forbearance period will end earlier if UDF otherwise defaults under the Forbearance Agreement. Textron and UDF I are currently engaged in discussions which management believes will result in an agreement between UDF I and Textron to extend the current Forbearance Agreement for an additional forbearance period. Management understands that UDF intends to continue to make payments on the Textron loan and does not believe that the repayment of the Textron debt will have a material adverse effect on UDF III’s participation in the Company’s subordinate line of credit to UDF.

7) Loans are made to certain affiliates of the Advisor. Below is a table of the aggregate principal amount of mortgages funded during the quarters ended September 30, 2009 and September 30, 2008, respectively, from the companies affiliated with the Advisor, and named in the table and aggregate amount of draws made by UDF under the line of credit, during the two quarters indicated:

8) As of August 1, 2006, (now subject to an Advisory Agreement effective January 1, 2009) the Company entered into an Advisory Agreement with UMTHGS. Under the terms of the agreement, UMTHGS is paid a monthly trust administration fee. The fee is calculated monthly depending on the Company’s annual distribution rate, ranging from 1/12th of 1% up to 1/12th of 2% of the amount of average invested assets per month. During the three months ended September 30, 2009 and September 30, 2008, the net fees paid to the Company’s Advisors were approximately $260,000 and $266,000, respectively. During the nine months ended September 30, 2009 and September 30, 2008, the net fees paid to the Company’s Advisors were approximately $774,000 and $812,000, respectively.

The agreement also provides for a subordinated incentive fee equal to 25% of the amount by which the Company’s net income for a year exceeds a 10% per annum non-compounded cumulative return on its adjusted contributions. No incentive fee was paid during 2009 or 2008. In addition, for each year in which it receives a subordinated incentive fee, the Advisor will receive a 5-year option to purchase 10,000 shares at a price of $20.00 per share (not to exceed 50,000 shares). As of September 30, 2009, the Advisor has not received options to purchase shares under this arrangement.

The Advisor and its affiliates are also entitled to reimbursement of costs of materials and services obtained from unaffiliated third parties for the Company’s benefit, except for note servicing and for travel and expenses incurred in connection with efforts to acquire investments for the Company or to dispose of any of its investments. During each of the three months ended September 30, 2009 and September 30, 2008, the Company paid the Advisor approximately $19,000 as reimbursement for costs associated with providing shareholder relations activities. During each of the nine months ended September 30, 2009 and September 30, 2008, the Company paid the Advisor approximately $57,000 as reimbursement for costs associated with providing shareholder relations activities.

The Advisory Agreement provides for the Advisor to pay all of the Company’s expenses and for the Company to reimburse the Advisor for any third-party expenses that should have been paid by the Company but which were instead paid by the Advisor. However, the Advisor remains obligated to pay: (1) the employment expenses of its employees, (2) its rent, utilities and other office expenses and (3) the cost of other items that are part of the Advisor's overhead that is directly related to the performance of services for which it otherwise receives fees from the Company.

The Advisor Agreement also provides for the Company to pay to the Advisor a debt placement fee. The Company may engage the Advisor, or an Affiliate of the Advisor, to negotiate lines of credit on behalf of the Company. UMT shall pay a negotiated fee, not to exceed 1% of the amount of the line of credit secured, upon successful placement of the line of credit. The Company paid a debt placement fee of $50,000 to an affiliate of the Advisor in September 2009. This fee is amortized monthly, as an adjustment to interest expense, over the term of the credit facility agreement described in Note 7.

9) The Company pays loan servicing fees to PSC, a subsidiary of UMTH, under the terms of a Mortgage Servicing Agreement. During the three months ended September 30, 2009 and September 30, 2008, the Company paid loan servicing fees of approximately $3,000 and $1,400, respectively. During the nine months ended September 30, 2009 and September 30, 2008, the Company paid loan servicing fees of approximately $7,000 and $4,200, respectively.

10) The Company paid the first of three annual credit enhancement fees of $50,000 to UDF III, L.P. in September 2009. This fee is due annually on the anniversary date of the loan and amortized over 12 months as an adjustment to interest expense.

6. Fair Value of Financial Instruments

In accordance with the reporting requirements of SFAS No. 107, Disclosures About Fair Value of Financial Instruments, the Company calculates the fair value of its assets and liabilities that qualify as financial instruments under this statement and includes additional information in notes to the Company’s consolidated financial statements when the fair value is different than the carrying value of those financial instruments. The estimated fair value of cash equivalents, accrued interest receivable, receivable from affiliate, accounts payable and accrued liabilities approximate the carrying value due to the relatively short maturity of these instruments. The carrying value of residential mortgages and contracts for deed, interim loans, lines of credit, recourse obligations from affiliates, deficiency notes and the Company’s line of credit payable also approximate fair value since these instruments bear market rates of interest. None of these instruments are held for trading purposes.

7. Long Term Debt

During August 2009, the Company entered into a new revolving line of credit facility with a bank for $5,000,000. The line of credit bears interest at prime plus one percent, with a floor of 5.50%, and requires monthly interest payments. Principal and all unpaid interest will be due at maturity, which is August 2012. The line is collateralized by a first lien security interest in the underlying real estate financed by the line of credit. The outstanding balance on this line of credit was $3,575,000 at September 30, 2009.

8. Subsequent Events

On October 28, 2008, the Company executed two construction loan agreements with a homebuilder. Each loan agreement has a maximum commitment of up to $15,000,000 to a total maximum commitment of up to $30,000,000 and a termination date of October 28, 2009. Advances are made at the base rate of 13.0% and are secured by first liens on the projects under construction. The loan agreements limit advances to no more than 85% of the projected sale price of the finished home (85% LTV) and limits are also in place regarding the number of speculation and model homes allowed in each approved subdivision. Effective October 28, 2009, these loans were renewed with similar terms through October 2010.

We have evaluated subsequent events for potential recognition and/or disclosure through November 13, 2009, the date the consolidated financial statements were issued.

| | ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

| | Cautionary Statement Regarding Forward-Looking Statements |

This Form 10-Q contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Such statements involve known and unknown risks, uncertainties, and other factors which may cause our actual results, performance, or achievements to be materially different from future results, performance or achievements expressed or implied by such forward-looking statements. Such factors include, but are not limited to, our ability to find suitable mortgage investments, the difficulties of the real estate industry generally in response to the “sub-prime crisis” and the “credit crisis,” changes in the overall economic environment and the requirement to maintain qualification as a real estate investment trust. Although we believe that the assumptions underlying the forward-looking statements contained herein are reasonable, any of the assumptions could be inaccurate, and therefore we cannot give assurance that such statements included in this Form 10-Q will prove to be accurate. In light of the significant uncertainties inherent in the forward-looking statements included herein, the inclusion of such information should not be regarded as a representation by us or by any other person that the results or conditions described in such statements or in our objectives and plans will be realized. Readers should carefully review our financial statements and the notes thereto contained in our Annual Report on Form 10-K for the year ended December 31, 2008, as well as those statements contained in this report, and in our other filings with the Securities and Exchange Commission.

In light of these risks, uncertainties and assumptions, the forward-looking events discussed in this Form 10-Q may not occur. We undertake no obligation to update or revise our forward-looking statements, whether as a result of new information, future events or otherwise.

RESULTS OF OPERATIONS FOR THE THREE AND NINE MONTHS ENDED SEPTEMBER 30, 2009 AND SEPTEMBER 30, 2008

General Investment Information

United Mortgage Trust (the “Company”) is a Maryland real estate investment trust that qualifies as a real estate investment trust (a “REIT”) under federal income tax laws. Our principal investment objectives are to invest proceeds from our dividend reinvestment plan, financing proceeds, capital transaction proceeds and retained earnings in following types of investments:

| (i) | first lien secured interim mortgage loans with initial terms of 12 months or less for the acquisition and renovation of single-family homes, which we refer to as “Interim Loans”; |

| (ii) | secured, subordinate line of credit to UMTH Lending Company, L.P. for origination of Interim Loans; |

| | (iii) | lines of credit and secured loans for the acquisition and development of single-family home lots, referred to as “Land Development Loans”; |

| | (iv) | lines of credit and loans secured by entitled and developed single-family lots, referred to as “Finished Lot Loans”; and, |

| | (v) | lines of credit and loans secured by completed model homes, referred to as “Model Home Loans”; and, |

| | (vi) | loans provided to entities that have recently filed for bankruptcy protection under Chapter 11 of the U.S. bankruptcy code, secured by a priority lien over pre-bankruptcy secured creditors, referred to as “Debtor in Possession Loans” and, |

| | (vii) | lines of credit and loans, with terms of 18 months or less, secured by single family lots and homes constructed thereon, referred to as “Construction Loans,, |

| | (viii) | first lien secured mortgage loans with terms of 12 to 360 months for the acquisition of single-family homes, referred to as “Residential Mortgages”, and, |

| | (ix) | discounted cash flows secured by assessments levied on real property. |

We collectively refer to the above listed loans as “Mortgage Investments”. Additionally, our portfolio includes obligations of affiliates of our Advisor, which we refer to as “recourse loans.” Loans are originated by others to the Company’s specifications or to specifications approved by the Company. Most, if not all, of such loans are not insured or guaranteed by a federally owned or guaranteed mortgage agency.

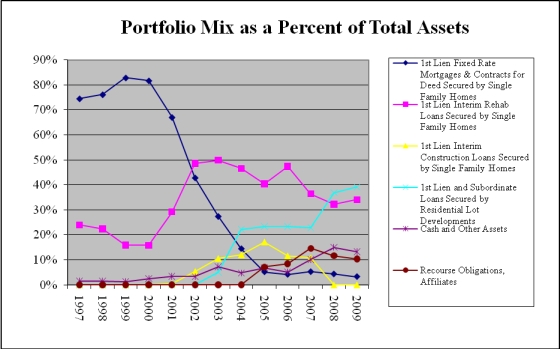

The following table illustrates the percentage of our mortgage portfolio dedicated to each mortgage loan category as of September 30, 2009 and December 31, 2008:

| | |

| | |

First lien secured interim mortgages 12 months or less and residential mortgages and contracts for deed | | |

Secured interim mortgages and LOC to UMTH Lending Co., L.P. | | |

| | |

| | |

The following table summarizes mortgage loans by type and original loan size held by United Mortgage Trust at September 30, 2009.

| | | | | | Face amount of Mortgage (1) | Carrying amount of Mortgage (2) | |

Single family residential 1st mortgages and interim loans (5): | | | | | | | | |

Original balance > $100,000 | | | | | | | | |

Original balance $50,000 - $99,999 | | | | | | | | |

Original balance $20,000 - $49,999 | | | | | | | | |

Original balance under $20,000 | | | | | | | | |

| | | | | | | | | |

First Lien secured interim mortgages | | | | | | | | |

Ready America Funding (4) | | | | | | | | |

Howe Note Consolidation (5) | | | | | | | | |

| | | | | | | | | |

Secured, subordinate LOC to UMTH Lending Co., L.P. (4), (5) | | | | | | | | |

| | | | | | | | | |

| | | | | | | | |

UDF III Economic Interest Participation | | | | | | | | |

UDF III Bear Creek Participation | | | | | | | | |

| | | | | | | | | |

| | | | | | | | |

| | | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| (1) | Current book value of loans. |

| (2) | Net of allowance for loan losses on mortgage loans of $610,896 at September 30, 2009. |

| (3) | Principal amounts greater than thirty (30) days past due. |

| (4) | Lines of credit with Ready America Funding and UMTH Lending Co., L.P. are collateralized by 17 and 162 loans, respectively. Principal amounts due upon disposition of assets. |

| (5) | No specific maturity date as UMT has first lien collateral position in these loans funded by the originator. |

Below is a reconciliation and walk forward of mortgage loans, net of allowance for loan losses, for the nine months ended September 30 2009.

Balance at beginning of period | |

| |

| |

Other –UDF III participation | |

| | |

Deductions during period: | |

| |

Other decreases in principal- | |

| |

| |

| |

Balance at close of period | |

Material Trends Affecting Our Business

We are a real estate investment trust and derive a substantial portion of our income from loans secured by single-family homes (both finished homes and homes under construction), single-family home lots, and entitled land under development into single-family home lots. We intend to concentrate our lending activities in the southeast and southwest sections of the United States, particularly in Texas. We believe these areas continue to experience demand for new construction of single-family homes; however, the U.S. housing market has suffered declines over the past three years, particularly in geographic areas that had experienced rapid growth, steep increases in property values and speculation. Additionally, we intend to concentrate our lending activities with national and regional homebuilders and developers who sell single-family residential home lots to such national and regional homebuilders. National and regional homebuilders have responded to this decline by reducing the number of new homes constructed in 2009 as compared to 2008 and 2007. However, we expect to see continued healthy demand for our products as the supply of finished new homes and land is once again aligned with our market demand.

Generally, demand for new homes continued to deteriorate throughout 2008, accelerating with the cascading events in credit and equity markets in September and October, and bottoming in early 2009. Since then, we have seen the consumer confidence index rise from the record low to which it fell in early 2009, but the index still remains generally depressed, hovering near 50 – historically a number only reached in recession. Confidence remains particularly depressed in consumers’ assessment of current conditions – an assessment likely affected by a rising national unemployment rate and the persistent high foreclosure rate in many markets across the country. However, while job security and economic stability continue to weigh on consumers’ concerns, we believe that demand for new homes is slowly returning. Though sales remain low relative to historical standards, we believe that consumers are cautiously re-entering the marketplace, encouraged by tax credits, low mortgage rates, and near-record-high home affordability, and that the residential real estate market is beginning a tentative recovery.

Nationally, new single-family home sales and new home inventory continued to improve in the third quarter. According to estimates released jointly by the U.S. Census Bureau and the Department of Housing and Urban Development, the sales of new single-family residential homes in September 2009 were at a seasonally adjusted annual rate of 402,000 units – a continued improvement from the second quarter figure of 399,000 and up significantly (22.2%) from their bottom in January 2009 of 329,000. Still, sales remain approximately 7.8% below the September 2008 estimate of 436,000. The seasonally adjusted estimate of new houses for sale at the end of September 2009 was 251,000, which represents a supply of 7.5 months at the current sales rate – a reduction of nearly 30,000 homes from the second quarter supply of 8.4 months. We believe that the drop in the number of new single family homes for sale by approximately 144,000 units year-over-year reflects the homebuilding industry’s extensive – and largely successful – efforts to bring the new home market back to equilibrium by reducing new housing starts and selling existing new home inventory. According to the same sources identified above, permits and starts were steadily reduced month-over-month through 2008, nationally, as a result and in anticipation of an elevated supply of and decreased demand for new single-family residential homes. Since the beginning of 2009, however, permits and starts have risen from their bottoms by 31.6% and 40.3%, respectively, in response to increasing demand. Single-family homes authorized by building permits in September 2009 were at a seasonally adjusted annual rate of 450,000 units, though this is still 14.9% below the September 2008 estimate of 529,000 units. Single-family home starts for September 2009 were at a seasonally adjusted annual rate of 501,000 units. This is 8.7% below the September 2008 estimate of 549,000 units. We believe that, as a result of such reductions, new home inventory levels are approaching equilibrium even at relatively low levels of demand. As we have stated for several quarters, we believe that what is necessary to regain prosperity in housing markets is the return of healthy levels of demand.

The primary factors affecting new home sales are housing prices, home affordability, and housing demand. Housing supply may affect both new home prices and demand for new homes. When new home supplies exceed new home demand, new home prices may generally be expected to decline. Declining new home prices may result in diminished new home demand as people postpone a new home purchase until such time as they are comfortable that stable price levels have been reached.

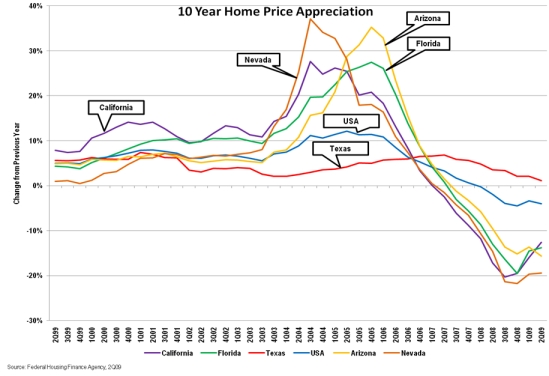

Generally, housing markets are improving but remain challenged across the country. Prices continue to decline on a national basis with those declines and difficulties most pronounced in markets that had previously experienced rapid growth, steep increases in property values, and speculation, such as in California, Florida, Arizona, and Nevada. However, a few markets, such as Texas, though weakened from its high in 2007, continue to remain fairly healthy relative to national trends. The graph below illustrates the declines in national home price and prices in Arizona, California, Nevada, and Florida, though recently, price declines have begun to moderate in those states, and certain markets in California, Arizona, and Florida have even experienced small, month-over-month price increases, based on the S&P Case-Shiller Home Price Indices. Further, the chart illustrates how Texas has maintained price stability and avoided such pronounced declines.

The Federal Housing Finance Agency (“FHFA”) analyzes the combined mortgage records of Fannie Mae and Freddie Mac, which form the nation’s largest database of conventional, conforming mortgage transactions, and produces an all-transactions house price index that tracks average house price changes in repeat sales or refinancings of the same single-family properties. The index is based on data obtained from Fannie Mae and Freddie Mac for mortgages originated over the past 35 years.

The Second Quarter 2009 all-transactions house price index reports that over the past twelve months, home prices have risen 1.12% on average in Texas while, nationally, home prices have fallen 3.99% over that same period. According to that same source, only 8 states have seen home prices increase over the past 12 months, while 42 states and the District of Columbia have seen home prices fall. Furthermore, only three states, Texas, North Dakota, and South Dakota, have seen home prices rise by more than 1.0% over the past 12 months while four states, Arizona, Florida, Nevada, and California, have seen home prices fall by more than 12.0% over that period. Home prices in the states of Arizona, Florida, California, and Nevada fell 15.62%, 13.84%, 12.58%, and 19.42%, respectively.

As of September 30, 2009, a great majority of our assets are secured by assets located in Texas. While housing woes beleaguer the national economy, Texas housing markets have held up as some of the best in the country, even as housing woes continue to beleaguer the national economy. We believe the Texas markets have remained relatively healthy due to continued strong population growth, diverse economies, affordable housing, and home building and development discipline on the part of home builders and developers operating in Texas markets. Though recent job growth has ceased due to the current economic climate, the Texas Comptroller of Public Accounts reports that Texas has added nearly three quarters of a million new jobs over the past five years, and we believe that long term employment fundamentals in Texas remain sound.

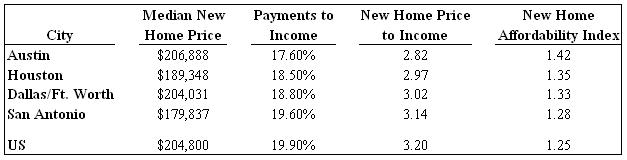

According to numbers publicly released by Residential Strategies, Inc. or Metrostudy, leading providers of primary and secondary market information, the median new home prices for September 2009 in the metropolitan areas of Austin, Houston, Dallas, and San Antonio are $206,888, $189,348, $204,031 and $179,837, respectively. These amounts are at par with or slightly below the September 2009 national median sales price of new homes sold of $204,800, according to estimates released jointly by the U.S. Census Bureau and the Department of Housing and Urban Development.

Using the Department of Housing and Urban Development’s estimated 2009 median family income for the respective metropolitan areas of Austin, Houston, Dallas, and San Antonio, the median income earner in those areas has 1.42 times, 1.35 times, 1.33 times, and 1.28 times the income required to qualify for a mortgage to purchase the median priced new home in the respective metropolitan area. These numbers illustrate the high affordability of Texas homes. Our measurement of housing affordability, as referenced above, is determined as the ratio of median family income to the income required to qualify for a 90 percent, 30-year fixed-rate mortgage to purchase the median-priced new home, assuming an annual mortgage insurance premium of 50 basis points for private mortgage insurance and a cost that includes estimated property taxes and insurance for the home.

Using the U.S. Census Bureau’s 2009 income data to project an estimated median income for the United States of $64,000 and the September 2009 national median sales prices of new homes sold of $204,800, we conclude that the national median income earner has 1.25 times the income required to qualify for a mortgage loan to purchase the median-priced new home in the United States. This estimation reflects the increase in home affordability in housing markets outside of Texas over the past 24 months, as new home prices in housing markets outside of Texas generally have fallen. Indeed, the national median new home price of $204,800 has fallen by 9.06% from the September 2008 median new home sales price of $225,200, according to the Department of Housing and Urban Development. As a result of these falling home prices, we believe that affordability has been restored to the national housing market.

Additional indicators that provide insight into the extent of new home affordability are the ratio of new home prices to median income and the percentage of income required for new home payments. Historically, the ratio of new home prices to median income in stable markets is between 3 and 4, and the average percentage of monthly income needed to service a conforming mortgage has been between 19% and 25%, between 29% and 37% for a first-time home purchase. By each of these historical measures, new home prices are very affordable both nationally and within the four major Texas markets.

Sources: Residential Strategies, MetroStudy, Federal Housing Finance Board, U.S. Census Bureau, United Development Funding

The Third Quarter 2009 U.S. Market Risk Index, a study prepared by PMI Mortgage Insurance Co., the U.S. subsidiary of The PMI Group, Inc., which ranks the nation’s 50 largest metropolitan areas through the second quarter of 2009 according to the likelihood that home prices will be lower in two years, reported that Texas cities are among the nation’s best for home price stability. This index analyzes housing price trends, the impact of foreclosure rates, and the consequence of excess housing supply on home prices. The quarterly report projects that there is less than a 20% chance that the Dallas/Fort Worth-area and Houston-area home prices will fall during the next two years; a 9.4% chance that San Antonio-area home prices will fall during the next two years; and a 39.6% chance that Austin-area home prices will fall during the next two years. Except for the Austin area, all Texas metropolitan areas included in the report are in the Top 10 least-likely areas to experience a decline in home prices in two years. The Austin area is ranked the sixteenth least-likely area to experience a decline. Dallas-Plano-Irving, Texas is the nation’s fifth least-likely metropolitan area, Fort Worth-Arlington, Texas is seventh least-likely, Houston-Sugar Land-Baytown, Texas is ninth least-likely, and San Antonio, Texas is second least-likely.

The FHFA all-transaction price index reports that Texas had a healthy existing home price appreciation between the second quarter of 2009 and the second quarter of 2008 of 1.12%. That report provides that existing home price appreciation between the second quarter of 2009 and the second quarter of 2008 for (a) Austin was 0.09%; (b) Houston was 2.42%; (c) Dallas was 1.13%; (d) Fort Worth was 1.63%; (e) San Antonio was 0.67%; and (f) Lubbock was 2.27%. The FHFA tracks average house price changes in repeat sales or refinancings of the same single-family properties utilizing conventional, conforming mortgage transactions.

We also believe that changes in population and employment affect new home demand. The United States Census Bureau reported in its 2008 Estimate of Population Change July 1, 2007 to July 1, 2008 that Texas led the country in population growth during that period. The estimate concluded that Texas grew by 483,542 people, or 2.00% – a number that was 1.28 times greater in terms of raw population growth than the next closest state, California, and more than 2.67 times the second closest state, North Carolina. According to the same source, Texas also led the country in population growth during the previous year of July 1, 2006 to July 1, 2007 with an estimated population growth of 496,751 people, or 2.12%. The United States Census Bureau also reported that Texas had the most counties of any state among the 100 fastest-growing counties in the nation with 19 counties and that Texas had the most counties that added the greatest number of residents between July 1, 2007 and July 1, 2008. Six of the top 15 counties were in Texas: Harris (Houston), Tarrant (Fort Worth), Bexar (San Antonio), Collin (North Dallas), Dallas (Dallas) and Travis (Austin). Additionally, the United States Census Bureau reported that four out of Texas’ five major cities – Austin, Houston, Dallas and Fort Worth – were among the top ten in the nation for population growth from 2007 to 2008 for metropolitan statistical areas with a population estimate exceeding 1 million. Dallas-Fort Worth-Arlington led the nation in numerical population growth with an estimated population increase of 146,532, with Dallas-Plano-Irving showing an estimated increase of 97,036 and Fort Worth-Arlington showing an estimated increase of 49,496. Houston-Sugarland-Baytown was second in the nation in numerical population growth with an estimated increase of 130,185. Austin-Round Rock had an estimated population growth of 60,012. San Antonio ranked fifteenth with an estimated population growth of 46,524 over this same period. The percentage increase in population for these major Texas cities ranged from 2.34% to 3.77%.

As stated earlier, the Texas economy has added a net of nearly three quarters of a million new jobs over the past five years. However, due to the national and global recession, the Texas economy has begun to slow, beginning in the fourth quarter of 2008 and continuing through the first three quarters of 2009. Over the twelve month period ending September 2009, the United States Department of Labor reported that Texas lost approximately 303,700 jobs and the unemployment rate is 8.2%, up from 5.1% in September 2008. However, the same source states that, nationally, the United States lost approximately 5,785,000 jobs over that same period, and the unemployment rate rose to 9.8% from 6.2% in September 2008.

The Texas Workforce Commission reports that as of September 2009, the unemployment rate for Austin-Round Rock, Texas was 7.2%, up from 4.6% in September 2008; Dallas-Fort Worth-Arlington, Texas was 8.3%, up from 5.2%; Houston-Sugar Land-Baytown, Texas was 8.5%, up from 5.1%; and San Antonio, Texas was 7.1%, up from 4.9%. In the most recent quarter, Austin experienced a net loss of 5,500 jobs year-over-year for the twelve month period ending September 30, 2009. During those same 12 months, Houston, Dallas-Fort Worth, and San Antonio experienced net losses of 76,700, 64,500, and 9,200 jobs, respectively. However, these cities have added an estimated net total of 617,000 jobs over the past five years. Austin added 103,700; Dallas-Fort Worth added 209,800; Houston added 221,800; and San Antonio added 81,700.

Due to the national and global recession, we believe that Texas will likely suffer a net loss of jobs in 2009. The National Bureau of Economic Research has concluded that the U.S. economy entered into a recession in December 2007, ending an economic expansion that began in November 2001. We believe that the transition from month-over-month and year-over-year job gains in Texas, to year-over-year and month-over-month job losses indicates that the Texas economy has slowed significantly, beginning in the fourth quarter of 2008 when we believe Texas followed the nation into recession. However, we also believe that the Texas economy will continue to outperform the national economy. According to the Texas Workforce Commission, Texas tends to enter into recessions after the national economy has entered a recession and usually leads among states in the economic recovery. In the current downturn, Texas’ recession trailed the national recession by nearly a year, and the state economy now looks poised for recovery. Dallas Federal Reserve’s Index of Texas leading indicators has steadily improved since reaching a low in March 2009 and independent reports and forecasts are now predicting that Texas MSAs will be among the first to recover based on employment figures, gross metropolitan product, and home prices.

In sharp contrast to the conditions of many homebuilding markets in the country where unsold housing inventory remains a challenge, new home sales are greater than new home starts in Texas markets, indicating that home builders in Texas are focused on preserving a balance between new home demand and new home supply. Home builders and developers in Texas have remained disciplined on new home construction and project development. New home starts have been declining year-over-year and are outpaced by new home sales in all of our Texas markets where such data is available. Inventories of finished new homes and total new housing (finished vacant, under construction, and model homes) remain at generally healthy and balanced levels in all four major Texas markets, Austin, Dallas-Fort Worth, Houston, and San Antonio. Each major Texas market is experiencing a rise in the number of months of finished lot inventories as homebuilders continue to reduce the number of new home starts, with each major Texas market reaching elevated levels. Houston has an estimated inventory of finished lots of approximately 44.6 months, Austin has an estimated inventory of finished lots of approximately 49.4 months, San Antonio has an estimated inventory of finished lots of approximately 61.9 months, and Dallas-Fort Worth has an estimated inventory of finished lots of approximately 81.0 months. A 24-28 month supply is considered equilibrium for finished lot supplies.

The recent rise in month’s supply of finished lot inventory in Texas markets owes itself principally to the decrease in the pace of annual starts rather than an increase in the raw number of developed lots. Indeed, the number of finished lots dropped by more than 1,200 lots in Austin and San Antonio, more than 2,000 in Houston, and by more than 3,500 lots in Dallas-Fort Worth in the third quarter of 2009. Annual starts in each of the Austin, San Antonio, Houston, and Dallas-Fort Worth markets continue to outpace lot deliveries. With the discipline evident in these markets, we expect to see a continued decline in raw numbers of finished lot inventories in coming quarters as new projects have been significantly reduced.

Texas markets continue to be some of the strongest homebuilding markets in the country, though home building in Texas has weakened over the past year. While the decline in housing starts has caused vacant lot inventory to become elevated from its previously balanced position, it has also maintained a balance in the housing inventory. Annual new home sales in Austin outpace starts 8,107 versus 6,888, with annual new home sales declining year-over-year by approximately 31.60%. Finished housing inventory and total new housing inventory (finished vacant, under construction and model homes) rose to elevated levels of 2.7 months and 7.3 months, respectively. The generally accepted equilibrium levels for finished housing inventory and total new housing inventory are a 2-to-2.5 month supply and a 6.0 month supply, respectively. Like Austin, San Antonio is also a healthy homebuilding market. Annual new home sales in San Antonio outpace starts 8,486 versus 7,408, with annual new home sales declining year-over-year by approximately 19.56%. Finished housing inventory remained at a healthy level with a 2.3 month supply – within the considered equilibrium level. Total new housing inventory rose to a slightly elevated 6.4 month supply. Houston, too, is a relatively healthy homebuilding market. Annual new home sales there outpace starts 23,116 versus 18,458, with annual new home sales declining year-over-year by approximately 33.08%. Finished housing inventory and total new housing inventory are slightly above equilibrium at a 3.24 month supply and a 7.2 month supply, respectively. Dallas-Fort Worth is a healthy homebuilding market as well. Annual new home sales in Dallas-Fort Worth outpace starts 18,055 versus 13,107, with annual new home sales declining year-over-year by approximately 33.35%. Finished housing inventory declined slightly to a 3.1 month supply while total new housing inventory rose to a 6.9 month supply, respectively, each measurement slightly above the considered equilibrium level. All numbers are as publicly released by Residential Strategies, Inc. or Metrostudy, leading providers of primary and secondary market information.

The Real Estate Center at Texas A&M University has reported that the sales of existing homes remain relatively healthy in our Texas markets, as well. Though the year-over-year sales pace has fallen between 11% and 16% in each of the four largest Texas markets, inventory levels have generally remained stable. In September, the number of months of home inventory for sale in Austin, Houston, Dallas, Fort Worth, and Lubbock was 6.4 months, 6.5 months, 6.3 months, 6.7 months, and 5.5 months, respectively. San Antonio’s inventory is more elevated with an 8.1 month supply of homes for sale. A 6-month supply of inventory is considered a balanced market with more than 6 months of inventory generally being considered a buyer’s market and less than 6 months of inventory generally being considered a seller’s market. Through September 2009, the number of existing homes sold year-to-date in (a) Austin is 15,651, down 15% year-over-year; (b) San Antonio is 13,889, down 11% year-over-year; (c) Houston is 44,561, down 14% year-over-year, (d) Dallas is 34,285, down 16% year-over-year, (e) Fort Worth is 6,288, down 20% year-over-year, and (f) Lubbock is 2,508, down 7% year-over-year.

In managing and understanding the markets and submarkets in which we make loans, we monitor the fundamentals of supply and demand. We track the economic fundamentals in each of the respective markets, analyzing demographics, household formation, population growth, employment, migration, immigration, and housing affordability. We also watch movements in home prices and the presence of market disruption activity, such as investor or speculator activity that can create a false impression of demand and result in an oversupply of homes in a market. Further, we study new home starts, new home closings, finished home inventories, finished lot inventories, existing home sales, existing home prices, foreclosures, absorption, prices with respect to new and existing home sales, finished lots and land, and the presence of sales incentives, discounts, or both, in a market.

Generally, the residential homebuilding industry is cyclical and highly sensitive to changes in broader economic conditions, such as levels of employment, consumer confidence, income, availability of financing for acquisition, construction, and permanent mortgages, interest rate levels, and demand for housing. The condition of the resale market for used homes, including foreclosed homes, also has an impact on new home sales. In general, housing demand is adversely affected by increases in interest rates, housing costs, and unemployment and by decreases in the availability of mortgage financing or in consumer confidence, which can occur for numerous reasons, including increases in energy costs, interest rates, housing costs, and unemployment.

We face a risk of loss resulting from deterioration in the value of the land purchased by the developer with the proceeds of loans from us, a diminution of the site improvement and similar reimbursements used to repay loans made by us, and a decrease in the sales price of the single-family residential lots developed with the proceeds of loans from us. Deterioration in the value of the land, a diminution of the site improvement and similar reimbursements, and a decrease in the sales price of the residential lots can occur in cases where the developer pays too much for the land to be developed, the developer is unable or unwilling to develop the land in accordance with the assumptions required to generate sufficient income to repay the loans made by us, or is unable to sell the residential lots to homebuilders at a price that allows the developer to generate sufficient income to repay the loans made by us. Our Advisor actively monitors the markets and submarkets in which we make loans, including mortgage markets, homebuilding economies, the supply and demand for homes, finished lots, and land and housing affordability to mitigate such risks. Our Advisor also actively manages our loan portfolio in the context of events occurring with respect to the loan and in the market and submarket in which we made the loan. We anticipate that there may be defaults on development loans made by us and that we will take action with respect to such defaults at any such time that we determine it prudent to do so, including such time as we determine it prudent to maintain and protect the value of the collateral securing a loan by originating another development loan to another developer with respect to the same project to maintain and protect the value of the collateral securing our initial loan.

We face a risk of loss resulting from adverse changes in interest rates. Changes in interest rates may affect both demand for our real estate finance products and the rate of interest on the loans we make. In most instances, the loans we make will be junior in the right of repayment to senior lenders, who will provide loans representing 70% to 80% of total project costs. As senior lender interest rates available to our borrowers increase, demand for our mortgage loans may decrease, and vice versa.

Developers to whom we make mortgage loans use the proceeds of such loans to develop raw real estate into residential home lots. The developers obtain the money to repay these development loans by selling the residential home lots to home builders or individuals who will build single-family residences on the lots, receiving qualifying site improvement reimbursements, and by obtaining replacement financing from other lenders. If interest rates increase, the demand for single-family residences may decrease. Also, if mortgage financing underwriting criteria become stricter, demand for single-family residences may decrease. In such an interest rate and/or mortgage financing climate, developers may be unable to generate sufficient income from the resale of single-family residential lots to repay loans from us, and developers’ costs of funds obtained from lenders in addition to us may increase as well. If credit markets deteriorate, developers may not be able to obtain replacement financing from other lenders. Accordingly, increases in single-family mortgage interest rates, decreases in the availability of mortgage financing, or decreases in the availability of replacement financing could increase the number of defaults on development loans made by us.