| | OMB APPROVAL |

| | OMB Number: | 3235-0570 |

| | Expires: | October 31, 2006 |

| UNITED STATES | Estimated average burden hours per response. . . . . . . . . . . . . . . . .19.3 |

| SECURITIES AND EXCHANGE COMMISSION | |

| Washington, D.C. 20549 | |

| | | | |

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-07651 |

|

ING Variable Portfolios, Inc. |

(Exact name of registrant as specified in charter) |

|

7337 E. Doubletree Ranch Rd., Scottsdale, AZ | | 85258 |

(Address of principal executive offices) | | (Zip code) |

|

The Corporation Trust Incorporated, 300 E. Lombard Street, Baltimore, MD 21202 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | 1-800-992-0180 | |

|

Date of fiscal year end: | December 31 | |

|

Date of reporting period: | December 31, 2004 | |

| | | | | | | | |

Item 1. Reports to Stockholders.

The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Act (17 CFR 270.30e-1):

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

(Registrant): ING Variable Portfolios, Inc.

By | /s/ James M. Hennessy | |

| James M. Hennessy |

| President and Chief Executive Officer |

|

Date: | March 4, 2005 | |

| | | | | |

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, this report has been signed below by the following persons on behalf of the registrant and in the capacities and on the dates indicated.

1

By | /s/ James M. Hennessy | |

| James M. Hennessy |

| President and Chief Executive Officer |

|

Date: | March 4, 2005 | |

|

|

By | /s/ Michael J. Roland | |

| Michael J. Roland |

| Executive Vice President and Chief Financial Officer |

|

Date: | March 4, 2005 | |

| | | | | | | | | | |

2

Annual Report

December 31, 2004

Classes I and S

ING Variable Product Funds

Domestic Equity and Income Portfolios

§ ING VP Balanced Portfolio

§ ING VP Growth and Income Portfolio

Domestic Equity Growth Portfolios

§ ING VP Growth Portfolio

§ ING VP Small Company Portfolio

Domestic Equity Value Portfolio

§ ING VP Value Opportunity Portfolio

Fixed Income Portfolios

§ ING VP Intermediate Bond Portfolio

(formerly, ING VP Bond Portfolio)

§ ING VP Money Market Portfolio

Global and International Equity Portfolios

§ ING VP Global Science and Technology Portfolio

§ ING VP International Equity Portfolio

This report is submitted for general information to shareholders of the ING Funds. It is not authorized for distribution to prospective shareholders unless accompanied or preceded by a prospectus which includes details regarding the funds’ investment objectives, risks, charges, expenses and other information. This information should be read carefully. |

|

PROXY VOTING INFORMATION

A description of the policies and procedures that the Registrants use to determine how to vote proxies related to portfolio securities is available (1) without charge, upon request, by calling Shareholder Services toll-free at 800-992-0180; (2) on the Registrants’ website at www.ingfunds.com and (3) on the SEC’s website at www.sec.gov. Information regarding how the Registrants voted proxies related to portfolio securities during the most recent 12-month period ended June 30 is available without charge on the Registrants’ website at www.ingfunds.com and on the SEC’s website at www.sec.gov.

QUARTERLY PORTFOLIO HOLDINGS

The Registrants file their complete schedule of portfolio holdings with the Commission for the first and third quarters of each fiscal year on Form N-Q. The Registrants’ Forms N-Q are available on the SEC’s website at www.sec.gov. The Registrants’ Forms N-Q may be reviewed and copied at the Commission’s Public Reference Room in Washington, DC, and information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330; and is available upon request from the Registrants by calling Shareholder Services toll-free at 800-992-0180.

(THIS PAGE INTENTIONALLY LEFT BLANK)

| Dear Shareholder: |

|

The past year has brought about numerous changes in the mutual funds industry, including requests for additional disclosures. I would like to draw your attention to some additional information you will now see in the reports due, in part, to these new requirements: |

|

• You will see a new section entitled “Shareholder Expense Examples”. These examples are intended to illustrate for you the ongoing costs of investing in a mutual fund and to provide a method to compare those costs with the ongoing costs of investing in other mutual funds. |

|

• In addition to the normal performance tables included in the Portfolio Managers’ Reports, there are now additional graphical or tabular presentations, which illustrate the current holdings of the funds as of the period-end. |

• Each fund now also files its complete schedule of portfolio holdings with the Securities Exchange Commission (“SEC”) for the first and third quarters of each fiscal year on Form N-Q. These Forms are available for shareholders to view on the SEC’s website at www.sec.gov.

We welcome these changes and believe that they will provide valuable information to our shareholders. We hope you will find these additional disclosures beneficial and easy to understand.

On behalf of ING Funds, I thank you for your continued support and confidence and look forward to serving you in 2005 and beyond.

Sincerely,

James M. Hennessy

President

ING Funds

January 25, 2005

1

In our semi-annual report, we referred to sharp swings in sentiment as investors took stock after the handsome gains of 2003. By the middle of the year, the markets had not done much of anything; however, over the next six months sentiment would change twice more and in the end major asset classes posted respectable returns for the year, if not better.

Global equities gained 10.8% in the six months ended December 31, 2004, according to the Morgan Stanley Capital International (“MSCI”) World Index(1), including net reinvested dividends, and 14.7% for entire year. Nearly one quarter of the annual gain was due to dollar weakness, the main story in the currency markets. The dollar was ahead for most of the year, but by mid October had succumbed to continuing concern over the United States twin budget and trade deficits and whether overseas investors would continue to finance them, raising the nightmare of a disorderly slide in the dollar. In 2004, the euro gained 7.6%, a new record. The yen rose 4.5% to a level not seen since early 2000, while the pound stood 7.4% higher, at a remarkable 12-year peak.

Perhaps the most notable feature in investment grade U.S. fixed income markets in the second six months was the curious “curve flattening” trend. Short-term interest rates drifted up as the Federal Open Market Committee (“FOMC”) raised the Federal Funds rate four times, by 1% in all, while bond yields ignored this and fell in the face of weak economic data and continued foreign central bank purchases. Contrary to earlier fears, tame inflation was a backdrop throughout, while the influential employment reports were weak in July, August, October and December. On December 15, the spread between the yields on the 10-year Note and the 90-day Treasury Bill fell to a three-year low. For the six months, the yield on 10-year Treasury Notes fell by 40 basis points to 4.22%, but the yield on 13-week Treasury Bills soared 88 basis points to 2.18%. More broadly, the Lehman Brothers Aggregate Bond Index(2) gained 4.18% for the six months. For the whole year, the Index returned 4.34%, underscoring the dominance of the second half in driving market movement, and implying not much underlying price change over the year.

Prices rose on riskier asset classes, however, as investors chased more attractive returns than investment grade bonds were offering. The Lehman Brothers U.S. Corporate High Yield Bond Index(3) for example, returned a robust 9.64% in the six months through December and 11.13% for the year.

U.S. equities in the form of the Standard & Poor’s (“S&P”) 500 Index(4), rose 7.2% including dividends for the six months ended December 31, 2004, breaching and holding levels not seen since before September 11, 2001. By year end, the market was trading at a price to earnings level of just under 16½ times 2005 estimated earnings. For the entire year, the Index returned 10.88%. From the middle of the year, equity investors were disappointed by the weak employment reports referred to above and distracted by surging oil prices as well as bad news affecting individual stocks. The market reached its lowest point in mid-August. But after oil prices climbed over $56 per barrel on October 22, and then slumped, equities squeezed out a narrow gain for the month in the last few days. In November, oil prices continued their retreat and the market powered ahead, cheered by this, the clear presidential election result, perceived as business and shareholder friendly, and at last a powerful employment report. By month end, sentiment was further bolstered by an upward revision to third quarter gross domestic product (“GDP”) growth to 4%, which was doubtless encouraging. But the data released also showed that the engine of growth, the U.S. consumer, was only saving at the rate of 0.5% per annum, which many regard as unsustainable. In addition, the rate of corporate profits growth was already falling and in 2005 may not reach double digits. It is hard to see then what dynamic propelled the S&P 500 Index to another 3.5% gain in December. And while many commentators celebrated this break out and the fact that smaller-cap indices had by then scaled all-time high levels, others feared a reversal before 2005 was very old.

International markets had mixed returns in the second half, but all were inflated in dollar terms by the weakness of that currency. Nonetheless even in local currency terms, Europe’s markets regained mid-2002 levels. Japan equities rose 4.6% in dollar terms during the period, based on the MSCI Japan Index(5) plus net dividends, but fell 1.7% in yen. For the year, Japan returned 15.9% in dollars. First half optimism about

2

MARKET PERSPECTIVE: YEAR ENDED DECEMBER 31, 2004

GDP growth was dashed as growth collapsed or was revised down as the year wore on.

European excluding (“ex”) UK markets advanced 18.2% in the second half of 2004, according to the MSCI Europe ex UK Index(6) (in dollars including net dividends), about one third due to currency. For all of 2004, the region returned 21.6% in dollars. Profits did grow strongly and markets remain cheap, but given all the issues surrounding low domestic demand, unemployment at 8.9% for the last 20 months and inflexible labor markets, arguably they deserve to be.

The UK market returned 15.7% in the six months through December, based on the MSCI UK Index(7) including net dividends, about 40% due to currency. For the whole year, the UK rose 19.6% in dollars. Contrary to the rest of Europe, the Bank of England has been trying to cool consumer demand and a property boom with five interest rate increases in 12 months. They seem to be succeeding for the most part.

(1) The MSCI World Index measures the performance of over 1,400 securities listed on exchanges in the United States, Europe, Canada, Australia, New Zealand and the Far East.

(2) The Lehman Brothers Aggregate Bond Index is composed of securities from the Lehman Brothers Government/Corporate Bond Index, Mortgage-Backed Securities Index, and the Asset-Backed Securities Index. Total return comprises price appreciation/depreciation and income as a percentage of the original investment.

(3) The Lehman Brothers U.S. Corporate High Yield Bond Index is generally representative of corporate bonds rated below investment-grade.

(4) The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

(5) The MSCI Japan Index is a free float-adjusted market capitalization index that is designed to measure developed market equity performance in Japan.

(6) The MSCI Europe ex UK Index is a free float-adjusted market capitalization index that is designed to measure developed market equity performance in Europe, excluding the UK.

(7) The MSCI UK Index is a free float-adjusted market capitalization index that is designed to measure developed market equity performance in the UK.

All indices are unmanaged and investors cannot invest directly in an index.

Past performance does not guarantee future results. The performance quoted represents past performance. Investment return and principal value of an investment will fluctuate, and shares, when redeemed, may be worth more or less than their original cost. The Portfolio’s performance is subject to change since the period’s end and may be lower or higher than the performance data shown. Please call (800) 366-0066 or log on to www.ingfunds.com to obtain performance data current to the most recent month end.

Market Perspective reflects the views of the Chief Investment Risk Officer only through the end of the period, and is subject to change based on market and other conditions.

3

Investment Types*

as of December 31, 2004

(as a percent of net assets)

* Excludes other assets and liabilities of - -16.3% of net assets and 11.2%

of net assets for short-term investments related to securities lending.

Portolio holdings are subject to change daily.

The ING VP Balanced Portfolio (the “Portfolio”) seeks to maximize investment return consistent with reasonable safety of principal, by investing in a diversified portfolio of one or more of the following asset classes: stocks, bonds and cash equivalents. The Portfolio is managed by a team of equity investment specialists led by Hugh T.M. Whelan, Portfolio Manager, and James B. Kauffmann, Portfolio Manager, ING Investment Management Co. — the Sub-Adviser.

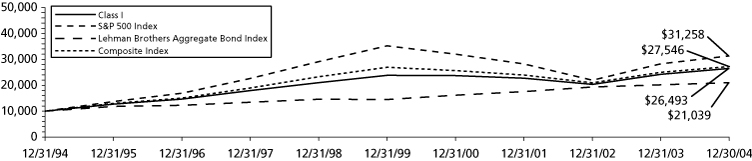

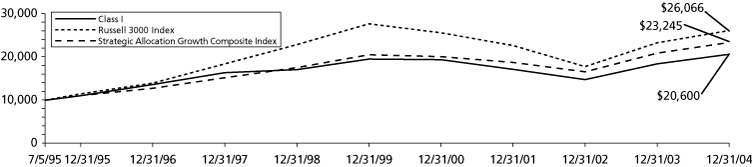

Performance: For the year ended December 31, 2004, the Portfolio’s Class I shares provided a total return of 9.42% compared to 10.88% for the Standard & Poor’s (“S&P”) 500 Index(1), 4.34% for the Lehman Brothers Aggregate Bond (“LBAB”) Index(2) and 8.30% for the Composite Index (60% S&P 500/40% LBAB).

Portfolio Specifics: The equity component of the Portfolio outperformed the S&P 500 Index due to security selection as well as our usual, modest exposure to small- and mid-cap stocks, which outperformed large-cap stocks as a group. Stock selection was strongest in the health care and technology sectors but was weaker in consumer staples and industrials. Sector allocation had a positive impact, with gains from overweights in energy and industrials and an underweight in consumer staples only partially offset by losses from an overweight in technology and an underweight in financials. The Portfolio benefited in particular from overweight positions in TXU Corp., Apple Computer, Inc. and Aetna, Inc., which returned 178%, 201%, and 85%, respectively, for the year. Securities that detracted from results were AT&T Wireless, which we did not own, rose 87%, and Walgreen Co. and Paychex, Inc., two stocks we overweighted and previously held that turned in disappointing results of 6% and -7%, respectively.

The fixed income component of the Portfolio outperformed its benchmark, the Lehman Brothers Aggregate Bond Index during the period as a short duration posture and yield curve exposure proved beneficial. For most of the year, we were well positioned for a rising rate environment in which the yields on shorter maturities rise more than those of longer maturities. Our underweight in five-year maturities was particularly helpful. Nevertheless, we brought the fixed income component back to a neutral duration stance as the year came to a close. Overweights in the outperforming securitized sectors — mortgage-backed securities, asset-backed securities, and commercial mortgage-backed securities — also enhanced performance. We maintained our increased allocation to credit, and this sector posted the highest excess returns during the period. Exposure to high yield and emerging markets debt were also significant sources of outperformance.

Current Strategy and Outlook: Our outlook for 2005 is positive for equities. We believe inflation should continue to be benign and oil prices should continue to moderate early in 2005. The Federal Reserve (“Fed”) is likely to continue to raise short-term interest rates, while leaving itself latitude to pause. Earnings are still rising, although at a slower pace in 2005. We expect to see job creation pick up after the impacts of higher oil prices percolate through the economy. Given all these economic factors, gross domestic product is likely to decelerate over the next few months to a trend-like growth rate in 2005. Despite increases to the Fed funds rate, longer-term fixed income issues have shown resilience through this period. Looking to 2005, however, we do project rising longer-term rates for the bond market.

The equity portfolio is overweight in the consumer discretionary and energy sectors and underweight in the information technology and financials sectors. However, our overall sector exposures are by design quite close to the S&P 500 Index so that nearly all of our relative performance is driven by individual stock selection.

Tactically, the fixed income portfolio was neutral duration as the year came to a close; however, we continue to believe that the improving domestic economy, signs of increasing inflation, and enduring dollar weakness point to higher rates in the near future. We are neutral home mortgages, overweight asset-backed and commercial mortgage-backed securities, and underweight the intermediate and front ends of the yield curve, which appear most vulnerable in a tightening cycle. We are also underweight agencies, which had witnessed intense regulatory criticism. While stretched valuations in investment-grade credit still warrant caution, credit continues to post positive excess returns, and we have moved closer to neutral credit on a contribution-to-duration basis. Exposures to emerging markets debt and crossover high yield remain intact.

Top Ten Industries*

as of December 31, 2004

(as a percent of net assets)

Federal National Mortgage Association | | 8.4 | % |

Whole Loan Collaterized Mortgage Obligation | | 7.3 | % |

Banks | | 6.3 | % |

Diversified Financial Services | | 5.7 | % |

Oil and Gas | | 5.5 | % |

Retail | | 4.8 | % |

Insurance | | 4.4 | % |

U.S. Treasury Bonds | | 4.1 | % |

Computers | | 3.4 | % |

Electric | | 3.1 | % |

* Excludes short-term investments related to securities lending.

Portfolio holdings are subject to change daily.

4

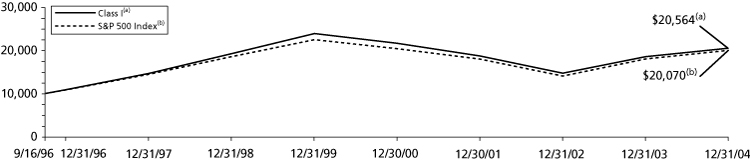

PORTFOLIO MANAGERS’ REPORT | ING VP BALANCED PORTFOLIO |

| Average Annual Total Returns for the Periods Ended December 31, 2004 | |

| | | 1 Year | | 5 Year | | 10 Year | | Since Inception

of Class S

May 29, 2003 | |

| Class I | | 9.42 | % | 2.13 | % | 10.22 | % | — | |

| Class S | | 9.06 | % | — | | — | | 12.42 | % |

| S&P 500 Index(1) | | 10.88 | % | (2.30 | )% | 12.07 | % | 17.61 | %(3) |

| Lehman Brothers Aggregate Bond Index(2) | | 4.34 | % | 7.71 | % | 7.72 | % | 2.70 | %(3) |

| Composite Index (60% S&P 500 Index/40% Lehman

Brothers Aggregate Bond Index) | | 8.30 | % | 1.98 | % | 10.66 | % | 11.54 | %(3) |

| | | | | | | | | | |

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING VP Balanced Portfolio against the S&P 500 Index, the Lehman Brothers Aggregate Bond Index and the Composite Index (60% S&P 500 Index, 40% Lehman Brothers Aggregate Bond Index). The Indices have no cash in their portfolios, impose no sales charges and incur no operating expenses. An investor cannot invest directly in an index. The Portfolio’s performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on portfolio distributions or the redemption of portfolio shares.

Total returns reflect that the Investment Manager may have waived or recouped fees and expenses otherwise payable by the Portfolio.

The performance update illustrates performance for a variable investment option available through a variable annuity contract. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. Please call (800) 366-0066 to get performance through the most recent month end.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Portfolio holdings are subject to change daily.

(1) The S&P 500 Index is an unmanaged index that measures the performance of securities of approximately 500 large-capitalization companies whose securities are traded on major U.S. stock markets.

(2) The Lehman Brothers Aggregate Bond Index is an unmanaged index composed of securities from the Lehman Brothers Government/Corporate Bond Index, Mortgage-Backed Securities Index and the Asset-Backed Securities Index.

(3) Since inception performance for the index is shown from June 1, 2003.

5

ING VP GROWTH AND INCOME PORTFOLIO | PORTFOLIO MANAGERS’ REPORT |

Industry Allocation*

as of December 31, 2004

(as a percent of net assets)

* Excludes other assets and liabilities of -6.5% of net assets and 6.2% of

net assets for short-term investments related to securities lending.

Portolio holdings are subject to change daily.

The ING VP Growth and Income Portfolio (the “Portfolio”) seeks to maximize total return through investments in a diversified portfolio of common stocks and securities convertible into common stock. The Portfolio is managed by a team of equity investment specialists led by Christopher F. Corapi, Portfolio Manager and Director of Fundamental Equity Research, and Scott Lewis, Portfolio Manager, ING Investment Management Co. — the Sub-Adviser.

Performance: For the year ended December 31, 2004, the Portfolio’s Class I shares provided a total return of 8.39% compared to the Standard & Poor’s (“S&P”) 500 Index(1), which returned 10.88% for the same period.

Portfolio Specifics: The Portfolio modestly underperformed the S&P 500 Index benchmark during 2004, but it should be noted that a new investment team took over the management of the Portfolio in May of 2004. While there were areas of both strength and weakness with respect to sector allocation and stock selection, poor stock selection in the technology sector was by far the most negative factor impacting full year performance. The Portfolio was slightly overweighted in the poorly performing technology sector during most of the year and relatively poor stock selection caused further negative impact. The stock positions that detracted from performance included Cisco Systems, Inc., Intel Corp., as well as previously held Hewlett Packard Co., Siebel Systems, Inc. and JDS Uniphase Corp. On the other hand, many stocks contributed to performance across many different sectors such as Aetna, Inc. and Countrywide Financial Corp. in the financial sector, Altria Group, Inc. in consumer staples, Exxon Mobil Corp. in energy and Motorola, Inc. in technology.

Entering 2005, the technology sector remains the most relatively overweighted sector while consumer staples remains the most relatively underweighted versus the benchmark. Overall, the Portfolio is positioned to benefit from those areas where we believe that valuation is attractive, above average earnings growth is forecast and our investment team has a high level of conviction with respect to future price performance. Presently, the three largest sector weightings in the Portfolio are the consumer discretionary, health care and technology sectors.

Current Strategy and Outlook: Despite the strong market advance during the final quarter of 2004, we continue to believe that the markets are moderately attractive. While we expect that interest rates and inflation will rise gradually as 2005 progresses, improving corporate profits, lower energy prices, and reasonable equity valuations all suggest that positive stock market returns are likely this year. During the past several years, value stocks have generally provided better returns than growth stocks, while small capitalization stocks have consistently outperformed their larger cap brethren. Looking ahead, we continue to believe that these areas should generate positive returns; however, we think that portfolios should be gradually tilted toward larger cap and growth oriented names.

Top Ten Holdings*

as of December 31, 2004

(as a percent of net assets)

General Electric Co. | | 4.1 | % |

Altria Group, Inc. | | 3.2 | % |

Microsoft Corp. | | 3.1 | % |

Citigroup, Inc. | | 3.0 | % |

Tyco International Ltd. | | 3.0 | % |

Johnson & Johnson | | 3.0 | % |

Wells Fargo & Co. | | 2.3 | % |

Intel Corp. | | 2.1 | % |

Exxon Mobil Corp. | | 1.9 | % |

PepsiCo, Inc. | | 1.7 | % |

* Excludes short-term investments related to securities lending.

Portfolio holdings are subject to change daily.

6

PORTFOLIO MANAGERS’ REPORT | ING VP GROWTH AND INCOME PORTFOLIO |

| Average Annual Total Returns for the Periods Ended December 31, 2004 | |

| | | 1 Year | | 5 Year | | 10Year | | Since Inception

of Class S

June 11, 2003 | |

| Class I | | 8.39 | % | (5.72 | )% | 7.90 | % | — | |

| Class S | | 8.10 | % | — | | — | | 12.98 | % |

| S&P 500 Index(1) | | 10.88 | % | (2.30 | )% | 12.07 | % | 17.61 | %(2) |

| | | | | | | | | | |

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING VP Growth and Income Portfolio against the S&P 500 Index. The Index has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Portfolio’s performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on portfolio distributions or the redemption of portfolio shares.

Total returns reflect that the Investment Manager may have waived or recouped fees and expenses otherwise payable by the Portfolio.

The performance update illustrates performance for a variable investment option available through a variable annuity contract. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. Please call (800) 366-0066 to get performance through the most recent month end.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

The views expressed in this report reflect those of the portfolio manager only through the end of the period as stated on the cover. The portfolio manager’s views are subject to change at any time based on market and other conditions.

Portfolio holdings are subject to change daily.

(1) The S&P 500 Index is an unmanaged index that measures the performance of securities of approximately 500 large-capitalization companies whose securities are traded on major U.S. stock markets.

(2) Since inception performance for the index is shown from June 1, 2003.

7

ING VP GROWTH PORTFOLIO | PORTFOLIO MANAGERS’ REPORT |

Industry Allocation*

as of December 31, 2004

(as a percent of net assets)

* Excludes other assets and liabilities of - -5.9% of net assets and 5.9%

of net assets for short-term investments related to securities lending.

Portfolio holdings are subject to change daily.

The ING VP Growth Portfolio (the “Portfolio”) seeks growth of capital through investment in a diversified portfolio consisting primarily of common stocks and securities convertible into common stocks believed to offer growth potential. The Portfolio is managed by a team of equity investment specialists led by Kenneth Bragdon, Portfolio Manager, ING Investment Management Co. — the Sub-Adviser.

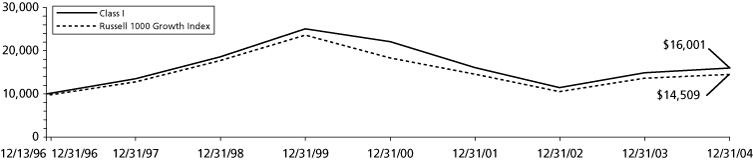

Performance: For the year ended December 31, 2004, the Portfolio’s Class I shares provided a total return of 7.19% compared to the Russell 1000 Growth Index(1), which returned 6.30% for the same period.

Portfolio Specifics: During the year ended December 31, 2004, the Portfolio benefited from strong stock selection in the “other” (multi-industry) and health care sectors. In addition, positive stock and sector selection due to an overweight position in the energy sector added to relative returns. In the multi-industry sector, Tyco Intl. Ltd. outperformed the market due to the global economic upturn. In addition, the company began to reap the benefits of the restructuring initiated by its new management. Within health care, Gilead Sciences, Inc. and DaVita, Inc. contributed most to relative returns. Gilead’s AIDS drug franchise grew quite strongly in 2004 aided by its new drug Truvada. DaVita gained after announcing their intention to purchase Gambro Healthcare’s dialysis assets. This pending announcement is expected to have material earnings accretion. In the energy sector, Halliburton Co. and Transocean, Inc. benefited from strong commodity prices and the increased demand for oil services and equipment.

The financial services and technology sectors detracted from relative returns. American Intl. Group, Inc. sold off following the widespread investigation into the selling and commission practices of the property and casualty insurance industry. This was partially offset by the absence of insurance brokerage holdings in the portfolio. Capital market sensitive companies, such as previously held Morgan Stanley and Merrill Lynch & Co., underperformed on weak trading results. The outlook for Countrywide Financial Corp., which was previously held, was disappointing following the release of third-quarter earnings due to a slowdown in mortgage activity. Within the technology sector, bellwether Cisco Systems, Inc. was the largest detractor from results. Weak pricing and rising inventories raised concerns that demand forecasts for the company were too optimistic. Similar factors lead to the negative contribution of Intel Corp and Sandisk Corp., which was held during the period.

Current Strategy and Outlook: The beginning of 2005 has seen lessened political and energy concerns in the U.S., which should allow the market to focus on other factors. We expect the expansion phase of the economic recovery to continue unabated in the near term. This should be accompanied by increased pricing power and corporate profit growth. Barring significantly higher inflation expectations, or a surprisingly weak dollar, large-capitalization growth stocks should perform relatively well, in our view. In addition, we would expect the performance gap between large- and small-capitalization stocks to narrow if not reverse at some point in the future. In that environment, we will continue to invest the portfolio in companies that are demonstrating positive underlying fundamentals at reasonable prices to seek positive results.

Top Ten Holdings*

as of December 31, 2004

(as a percent of net assets)

Microsoft Corp. | | 4.3 | % |

Johnson & Johnson | | 4.0 | % |

Monsanto Co. | | 3.4 | % |

International Business Machines Corp. | | 3.3 | % |

Dell, Inc. | | 2.8 | % |

Qualcomm, Inc. | | 2.8 | % |

Gilead Sciences, Inc. | | 2.8 | % |

Procter & Gamble Co. | | 2.6 | % |

General Electric Co. | | 2.6 | % |

Tyco Intl. Ltd. | | 2.5 | % |

* Excludes short-term investments related to securities lending.

Portfolio holdings are subject to change daily.

8

PORTFOLIO MANAGERS’ REPORT | ING VP GROWTH PORTFOLIO |

| Average Annual Total Returns for the Periods Ended December 31, 2004 | |

| | 1 Year | | 5 Year | | Since Inception

of Class I

December 13, 1996 | | Since Inception

of Class S

November 1, 2001 | |

| Class I | | 7.19 | % | (8.60 | )% | 6.01 | % | — | |

| Class S | | 6.98 | % | — | | — | | 1.12 | % |

| Russell 1000 Growth Index(1) | | 6.30 | % | (9.29 | )% | 4.71 | %(2) | 2.70 | % |

| | | | | | | | | | |

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING VP Growth Portfolio against the Russell 1000 Growth Index. The Index has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Portfolio’s performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on portfolio distributions or the redemption of portfolio shares.

Total returns reflect that the Investment Manager may have waived or recouped fees and expenses otherwise payable by the Portfolio.

The performance update illustrates performance for a variable investment option available through a variable annuity contract. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. Please call (800) 366-0066 to get performance through the most recent month end.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

The views expressed in this report reflect those of the portfolio manager only through the end of the period as stated on the cover. The portfolio manager’s views are subject to change at any time based on market and other conditions.

Portfolio holdings are subject to change daily.

(1) The Russell 1000 Growth Index measures the performance of the 1,000 largest companies in the Russell 3000 Index with higher price-to-book ratios and higher forecasted growth. The Russell 3000 Index is an unmanaged index that measures the performance of 3,000 U.S. companies based on total market capitalization.

(2) Since inception performance for the index is shown from December 1, 1996.

9

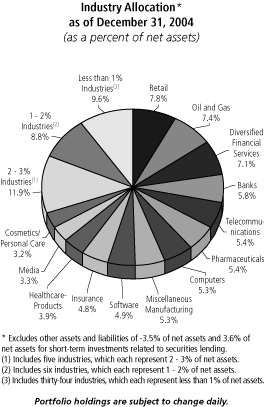

ING VP SMALL COMPANY PORTFOLIO | PORTFOLIO MANAGERS’ REPORT |

Industry Allocation*

as of December 31, 2004

(as a percent of net assets)

* Excludes other assets and liabilities of 0.4% of net assets.

(1) Includes eleven industries, which each represent 2 - 3% of net assets.

(2) Includes nine industries, which each represent 1 - 2% of net assets.

(3) Includes twelve industries, which each represent less than 1% of net assets.

Portfolio holdings are subject to change daily.

The ING VP Small Company Portfolio (the “Portfolio”) seeks growth of capital primarily through investment in a diversified portfolio of common stocks and securities convertible into common stocks of companies with smaller market capitalizations. The Portfolio is managed by a team of equity investment specialists led by Carolie Burroughs, Portfolio Manager, ING Investment Management Co. — the Sub-Adviser.

Performance: For the year ended December 31, 2004, the Portfolio’s Class I shares provided a total return of 14.39% compared to the Russell 2000 Index(1), which returned 18.33% for the same period.

Portfolio Specifics: Sector rotation prevailed in the market, as investors flocked to or fled from groups of stocks based on underlying macro trends — oil prices, commodity prices, and chip prices (semiconductors); dividend yields and cash flow yields; interest rates and cap rates; and even the outcome of the presidential election. Our stock selection in the producer durables and utilities sectors contributed positively to the Portfolio’s performance. Stock selection in the consumer staples and health care sectors contributed negatively. The largest individual positive contributors to performance during the period were Southwestern Energy Co., Louisiana Pacific Corp., and Terex Corp. The most disappointing holdings were Lexar Media, Inc., which was held during the period, Knight Trading Group, Inc., and Cumulus Media, Inc. Our underweight position in health care contributed positively to the Portfolio’s performance, while our 2 - 4% average cash position in a rising market was a drag on returns.

During the year, we moved from an underweight position in the autos and transportation sector to a slight overweight. We trimmed back to a market weight position at the end of the year as this sector rose almost 20% during the fourth quarter. In the energy and financial services sectors, we added stocks that are less impacted by the direction of oil prices and interest rates, respectively. We reduced our position in the technology sector by more than 200 basis points, effectively emphasizing the more defensive technology stocks. Toward the end of the period, we trimmed our exposure in producer durables, our best performing sector, as investors began to take profits. We continued to maintain the plus or minus 5% over- or underweighting limit for all of our sector weights and a style neutral position to mitigate harm caused by market swings.

Current Strategy and Outlook: We are encouraged by the economic data presented in 2004, and expect the U.S. economy to continue its gradual pace of expansion in 2005. Although we expect the U.S. equities market to finish 2005 in positive territory, we anticipate a rocky first half. We expect ongoing sector rotation, especially if the Federal Reserve voices greater concern over inflation. We also anticipate further shifts in asset allocation, which may cause the smaller capitalization benchmarks to underperform, despite improving fundamentals. However, this will likely set the stage for the second half of 2005, during which we expect the market to reward those stocks with stronger fundamentals.

We expect the small-cap cycle to complete its final phase. First of all, multiples of smaller capitalization stocks relative to large-cap stocks are still below historical averages, yet forward earnings expectations for large-cap stocks are only at a slight discount to those for small-cap stocks. Although productivity gains and a weak dollar have contributed to near-term profitability for large-cap stocks, in the long run, expectations for large-cap stocks are still too high. Second, access to capital for small-cap stocks has improved, particularly in the convertible debt and high yield markets. Growth in commercial lending by the banking industry benefits smaller companies. Finally, merger and acquisition activity remains strong. On a price-to-cash basis, large-cap companies still trump their smaller capitalization counterparts. We expect consolidation to continue with most deals continuing to occur in the small-cap space.

Looking forward, we are optimistic on the economic recovery and U.S. equities market. Whatever challenges the market presents in the short term, we continue to follow our discipline and focus on stocks that have the best fundamentals to outperform over the long run. We believe the Portfolio is well positioned to benefit as the small-cap cycle continues to move up the market cap spectrum and better quality stocks begin to consistently outperform.

Top Ten Holdings

as of December 31, 2004

(as a percent of net assets)

Avid Technology, Inc. | | 2.2 | % |

Terex Corp. | | 1.8 | % |

Corn Products Intl., Inc. | | 1.8 | % |

Select Medical Corp. | | 1.6 | % |

Southwestern Energy Co. | | 1.6 | % |

Kindred Healthcare, Inc. | | 1.6 | % |

Ametek, Inc. | | 1.6 | % |

Hudson United BanCorp | | 1.6 | % |

Denbury Resources, Inc. | | 1.5 | % |

Potlatch Corp. | | 1.5 | % |

Portfolio holdings are subject to change daily.

10

PORTFOLIO MANAGERS’ REPORT | ING VP SMALL COMPANY PORTFOLIO |

| Average Annual Total Returns for the Periods Ended December 31, 2004 | |

| | 1 Year | | 5 Year | | Since Inception

of Class I

December 27, 1996 | | Since Inception

of Class S

November 1, 2001 | |

| Class I | | 14.39 | % | 6.02 | % | 11.62 | % | — | |

| Class S | | 14.09 | % | — | | — | | 9.49 | % |

| Russell 2000 Index(1) | | 18.33 | % | 6.61 | % | 8.99 | %(2) | 15.65 | % |

| | | | | | | | | | |

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING VP Small Company Portfolio against the Russell 2000 Index. The Index has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Portfolio’s performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on portfolio distributions or the redemption of portfolio shares.

Total returns reflect that the Investment Manager may have waived or recouped fees and expenses otherwise payable by the Portfolio.

The performance update illustrates performance for a variable investment option available through a variable annuity contract. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. Please call (800) 366-0066 to get performance through the most recent month end.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

The views expressed in this report reflect those of the portfolio manager, only through the end of the period as stated on the cover. The portfolio manager’s views are subject to change at any time based on market and other conditions.

Portfolio holdings are subject to change daily.

(1) The Russell 2000 Index measures the performance of the 2,000 smallest companies in the Russell 3000 Index. The Russell 3000 Index is an unmanaged index that measures the performance of 3,000 U.S. companies based on total market capitalization.

(2) Since inception performance for the index is shown from January 1, 1997.

11

ING VP VALUE OPPORTUNITY PORTFOLIO | PORTFOLIO MANAGERS’ REPORT |

Industry Allocation

as of December 31, 2004

(as a percent of net assets)

Portfolio holdings are subject to change daily.

The ING VP Value Opportunity Portfolio (the “Portfolio”) seeks growth of capital primarily through investment in a diversified portfolio of common stocks and securities convertible into common stock. The Portfolio is managed by a team of equity investment specialists led by William F. Coughlin, Portfolio Manager, ING Investment Management Co. — the Sub-Adviser.

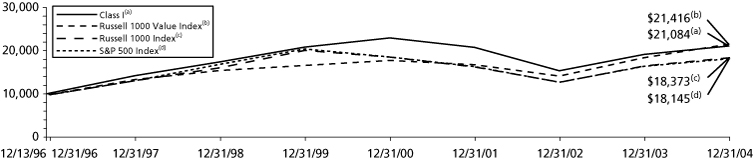

Performance: For the year ended December 31, 2004, the Portfolio’s Class I shares provided a total return of 10.15% compared to the Russell 1000 Value Index(1) and the Russell 1000 Index(2), which returned 16.49% and 11.40%, respectively, for the same period.

Portfolio Specifics: The investment team focuses on high quality companies selling at low price to earnings multiples. The Portfolio is well diversified, with exposure to all the major economic sectors and remains sensitive to the sector weighting of its Russell 1000 Value Index benchmark. During 2004, both sector allocation and stock selection combined to cause the Portfolio to underperform its benchmark. The Portfolio underperformed the benchmark’s return in all sectors. The worst performing stock was Koninklijke Philips Electronics NV. The Portfolio’s largest sector exposure was a 31.1% average weighting in financial services, somewhat below the 34.0% benchmark weighting. While this underweighting had a reasonably neutral allocation impact on results, the poor price performance of the Portfolio’s financial services positions, especially American Intl. Group, Inc. and Fannie Mae, had a decidedly more negative overall effect. The health care sector also negatively impacted overall results from both a sector allocation and stock selection perspective as overweighting this poorly performing sector severely reduced the sector allocation contribution, while several positions, including previously held Bristol-Myers Squibb Co. and Merck & Co., as well as Pfizer, Inc., all suffered price declines in 2004. This had a negative impact on Portfolio results. The strongest contribution from sector allocation was the result of overweighting the energy sector, but while the Portfolio’s stocks performed very well as a group (+26.0%), this was below the benchmark energy sector return of 30.6%. Several stocks in this sector were particularly strong, including Exxon Mobil Corp., ChevronTexaco Corp. and Halliburton Co. Overall, this sector was a positive contributor from a sector allocation perspective, but negative when considering specific stock selection.

Current Strategy and Outlook: Despite the strong market advance during the final quarter of 2004, we continue to believe that the markets are moderately attractive. While we expect that interest rates and inflation will rise gradually as 2005 progresses, improving corporate profits, lower energy prices, and reasonable equity valuations all suggest that positive stock market returns are likely this year. During the past several years, value stocks have generally provided better returns than growth stocks, while small capitalization has consistently outperformed larger cap stocks. Looking ahead, we continue to believe that these areas should generate positive returns; however, we think that portfolios should be gradually tilted toward larger cap, growth-oriented names.

Top Ten Holdings

as of December 31, 2004

(as a percent of net assets)

Bank of America Corp. | | 3.8 | % |

BP PLC ADR | | 3.6 | % |

ChevronTexaco Corp. | | 3.5 | % |

Washington Mutual, Inc. | | 3.4 | % |

Emerson Electric Co. | | 3.4 | % |

Nestle SA ADR | | 3.1 | % |

General Dynamics Corp. | | 3.1 | % |

Exxon Mobil Corp. | | 3.1 | % |

Wells Fargo & Co. | | 3.1 | % |

American Intl. Group, Inc. | | 3.1 | % |

Portfolio holdings are subject to change daily.

12

PORTFOLIO MANAGERS’ REPORT | ING VP VALUE OPPORTUNITY PORTFOLIO |

| Average Annual Total Returns for the Periods Ended December 31, 2004 | |

| | 1 Year | | 5 Year | | Since Inception

of Class I

December 13, 1996 | | Since Inception

of Class S

July 16, 2001 | |

| Class I | | 10.15 | % | 0.24 | % | 9.70 | % | — | |

| Class S | | 9.88 | % | — | | — | | (2.38 | )% |

| Russell 1000 Value Index(1) | | 16.49 | % | 5.27 | % | 9.88 | %(4) | 6.15 | %(5) |

| Russell 1000 Index(2) | | 11.40 | % | (1.76 | )% | 7.82 | %(4) | 2.35 | %(5) |

| S&P 500 Index(3) | | 10.88 | % | (2.30 | )% | 7.65 | %(4) | 1.72 | %(5) |

| | | | | | | | | | |

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING VP Value Opportunity Portfolio against the S&P 500 Index. The Index has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Portfolio’s performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on portfolio distributions or the redemption of portfolio shares.

Total returns reflect that the Investment Manager may have waived or recouped fees and expenses otherwise payable by the Portfolio.

The performance update illustrates performance for a variable investment option available through a variable annuity contract. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. Please call (800) 366-0066 to get performance through the most recent month end.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

The views expressed in this report reflect those of the portfolio manager, only through the end of the period as stated on the cover. The portfolio manager’s views are subject to change at any time based on market and other conditions.

Portfolio holdings are subject to change daily.

(1) The Russell 1000 Value Index is an unmanaged index that measures the performance of those Russell 1000 companies with lower price-to-book ratios and lower forecasted growth values, which more closely tracks the types of securities in which the Portfolio invests than the S&P 500 Index.

(2) The Russell 1000 Index is a comprehensive large-cap index measuring the performance of the largest 1,000 U.S. incorporated companies.

(3) The S&P 500 Index is an unmanaged index that measures the performance of securities of approximately 500 large-capitalization companies whose securities are traded on major U.S. stock markets.

(4) Since inception performance for the index is shown from December 1, 1996.

(5) Since inception performance for the index is shown from August 1, 2001.

13

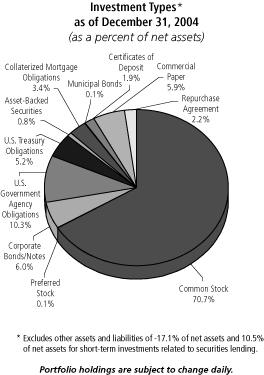

ING VP INTERMEDIATE BOND PORTFOLIO | PORTFOLIO MANAGERS’ REPORT |

Investment Types*

as of December 31, 2004

(as a percent of net assets)

* Excludes other assets and liabilities of -14.5% of net assets.

Portfolio holdings are subject to change daily.

The ING VP Intermediate Bond Portfolio (formerly, ING VP Bond Portfolio, the “Portfolio”) seeks to maximize total return consistent with reasonable risk by investing in investment-grade corporate bonds and debt securities issued or guaranteed by the U.S. Government, its agencies or instrumentalities. While the Portfolio invests in securities guaranteed by the U.S. Government as to timely payment of interest and principal, the Portfolio shares are not insured or guaranteed. The Portfolio is managed primarily by James B. Kauffmann, Portfolio Manager, ING Investment Management Co. — the Sub-Adviser.

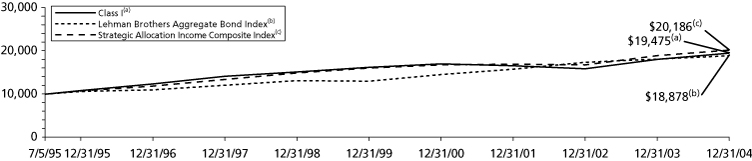

Performance: For the year ended December 31, 2004, the Portfolio’s Class I shares provided a total return of 4.88% compared to 4.34% for the Lehman Brothers Aggregate Bond (LBAB) Index(1).

Portfolio Specifics: Throughout the year ended December 31, 2004, the Federal Open Market Committee (“FOMC”) was true to its oft-stated “measured pace” guidance, with 25 basis points moves starting in June. The Committee continues to focus on developing economic releases, which will influence the timing and size of future tightenings. Yields on shorter-term Treasuries moved higher, while those of 10- and 30-year bonds dropped. In fact, the benchmark 10-year bond closed at 4.22%, despite being as high as 4.50%. The growth in employment lagged past recoveries even as domestic economic news brightened. The dollar dropped against most major currencies, and oil and gold headed higher. Concerns about the twin U. S. deficits continue to vex the currency markets, and the re-election of George Bush has done little to allay fears of the burgeoning costs of social security and Medicare.

Performance benefited during the period from a short duration posture and yield curve exposure. For most of the year, the Portfolio was well positioned for a rising rate environment in which yields on shorter maturities rise more than those of longer maturities. Our underweight in five-year maturities was particularly helpful. Nevertheless, we brought the Portfolio back to a neutral duration stance as the year came to a close. Overweights in the outperforming securitized sectors — mortgage-backed securities, asset-backed securities, and commercial mortgage-backed securities — also helped. We maintained our increased allocation to credit, and this sector posted the highest excess returns during the period. Exposure to high yield and emerging markets debt also contributed positively to performance.

Current Strategy and Outlook: While the bond market has renewed its focus on the improving economic releases, we do not believe that the yields on shorter maturity Treasuries fully reflect the pace of economic activity nor likely Federal Reserve tightenings. Some projections place a neutral overnight rate around 4% or 5%, indicating that monetary policy is still highly accommodative.

Tactically, the Portfolio was neutral duration as the year came to a close; however, we continue to believe that the improving domestic economy, signs of increasing inflation and enduring dollar weakness point to higher rates in the near future. We are neutral home mortgages, overweight asset-backed and commercial mortgage-backed securities, and underweight the intermediate and front ends of the yield curve, which appear most vulnerable in a tightening cycle. We are also underweight agencies, which have witnessed intense regulatory criticism. While stretched valuations in investment-grade credit still warrant caution, credit continues to post positive excess returns, and we have moved closer to neutral credit on a contribution-to-duration basis. Exposures to emerging markets debt and crossover high yield remain intact.

Top Ten Industries

as of December 31, 2004

(as a percent of net assets)

Federal National Mortgage Association | | 22.3 | % |

Whole Loan Collaterized Mortgage Obligation | | 19.9 | % |

U.S. Treasury Bonds | | 11.4 | % |

Banks | | 6.6 | % |

U.S. Treasury Notes | | 6.3 | % |

Federal Home Loan Mortgage Corporation | | 5.7 | % |

Commercial Mortgage-Backed | | 5.2 | % |

Diversified Financial Services | | 4.6 | % |

Home Equity Asset-Backed | | 3.8 | % |

Electric | | 3.5 | % |

Portfolio holdings are subject to change daily.

14

PORTFOLIO MANAGERS’ REPORT | ING VP INTERMEDIATE BOND PORTFOLIO |

| Average Annual Total Returns for the Periods Ended December 31, 2004 | |

| | 1 Year | | 5 Year | | 10 Year | | Since Inception

of Class S

May 3, 2002 | |

| Class I | | 4.88 | % | 7.56 | % | 7.44 | % | — | |

| Class S | | 4.58 | % | — | | — | | 6.80 | % |

| Lehman Brothers Aggregate Bond Index(1) | | 4.34 | % | 7.71 | % | 7.72 | % | 6.19 | %(2) |

| | | | | | | | | | |

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING VP Intermediate Bond Portfolio against the Lehman Brothers Aggregate Bond Index. The Index has has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Portfolio’s performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on portfolio distributions or the redemption of portfolio shares.

Total returns reflect that the Investment Manager may have waived or recouped fees and expenses otherwise payable by the Portfolio.

The performance update illustrates performance for a variable investment option available through a variable annuity contract. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. Please call (800) 366-0066 to get performance through the most recent month end.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Portfolio holdings are subject to change daily.

(1) The Lehman Brothers Aggregate Bond Index is an unmanaged index composed of securities from the Lehman Brothers Government/Corporate Bond Index, Mortgage-Backed Securities Index and the Asset-Backed Securities Index.

(2) Since inception performance for the index is shown from May 1, 2002.

15

ING VP MONEY MARKET PORTFOLIO | PORTFOLIO MANAGERS’ REPORT |

Investment Types*

as of December 31, 2004

(as a percent of net assets)

* Excludes other assets and liabilities of -0.2% of net assets.

Portfolio holdings are subject to change daily.

The ING VP Money Market Portfolio (the “Portfolio”) seeks to provide high current return, consistent with preservation of capital and liquidity, through investment in high-quality money market instruments. The Portfolio is managed by a team of fixed-income specialists led by David S. Yealy, Portfolio Manager, ING Investment Management Co. — the Sub-Adviser.

Portfolio Specifics: The market for money market securities as represented by the LIBOR (London InterBank Offered Rate) curve started the year pricing in very modest expectations for the Federal Open Market Committee (“FOMC”) to start raising the Federal Reserve (“Fed”) funds rate and discount rate in the later part of the year. Our strategy of maintaining a slightly long weighted average maturity and barbell structure early in the year enhanced the yield for the Portfolio.

The non-farm payroll numbers released in early April indicated an improving labor market. The improvement in the labor market was confirmed by the early May non-farm payroll data release. The markets quickly started to anticipate that the FOMC might act sooner and more aggressively than previously expected. The LIBOR one-month to twelve-month curve steepened to over 100 basis points by mid-June from only 34 basis points at the beginning of the year.

We restructured the Portfolio in May by reducing our holdings of longer maturity securities, shortening the weighted average maturity, eliminating the barbell, increasing our holding of interest sensitive floating rate securities and shifting new purchases to very short maturity securities. This strategy shift worked well during the second half of the year as the FOMC raised the Fed funds rate by 25 basis points five times starting at the end of June. The Fed funds rate ended the year at 2.25% up from 1.00% at the start of the year.

Current Strategy and Outlook: The market as of the end of December was building in significant additional rate increases for 2005. The consensus expectation is for the Fed funds rate to be at 3.50% at the end of 2005. Our strategy heading into 2005 is similar to that employed since May of 2004. We are continuing to focus new purchases to the next FOMC meeting, maintaining a high exposure to floating rate notes, and making selective purchases in the three-month and under maturity sector where yield levels fully price in 25 basis point increases at each of the Fed meetings in between the purchase date and the maturity date. To the extent that the markets start to price in a more aggressive Fed, we are prepared to extend the weighted average maturity of the Portfolio by purchasing longer maturity corporate securities in the nine-month to thirteen-month sector. We will maintain a weighted average maturity shorter than the majority of our competitors until that time.

16

PORTFOLIO MANAGERS’ REPORT | ING VP MONEY MARKET PORTFOLIO |

Principal Risk Factor(s): An investment in the Portfolio is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Although the Portfolio seeks to preserve the value of your investment, it is possible to lose money by investing in the Portfolio.

The views expressed in this report reflect those of the portfolio managers only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Portfolio holdings are subject to change daily.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

17

ING VP GLOBAL SCIENCE AND TECHNOLOGY PORTFOLIO | PORTFOLIO MANAGERS’ REPORT |

Industry Allocation*

as of December 31, 2004

(as a percent of net assets)

* Excludes other assets and liabilities of 2.6% of net assets.

Portfolio holdings are subject to change daily.

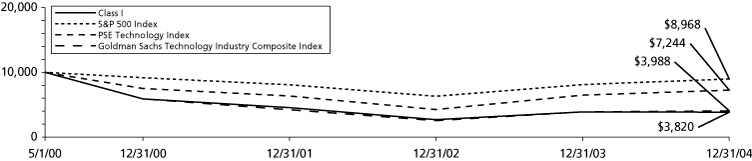

The ING VP Global Science and Technology Portfolio (the ‘‘Portfolio”) seeks long-term capital appreciation by investing primarily in equity securities issued by science and technology companies in all market capitalization ranges. The Portfolio is managed by Thomas P. Callan, CFA, Managing Director and Senior Portfolio Manager, and Daniel M. Rea, Vice President and Portfolio Manager, BlackRock Advisors, Inc. — the Sub-Adviser†.

Performance: During the year ended December 31, 2004, the Portfolio provided a total return of -1.29% compared to 10.88% for the Standard & Poor’s (“S&P”) 500 Index(1) and 12.09% for the Pacific Stock Exchange (“PSE”) Technology Index(2).

Portfolio Specifics: For the year ended December 31, 2004, the Portfolio underperformed its benchmark. During the first half of the year, investors became concerned about the sustainability of the recovery of capital spending on information technology. During the third quarter, negative earnings guidance from software companies fed these persistent concerns, and it appeared that excess inventories were building throughout the entire technology sector. Wall Street reaction to this news was negative, and analysts following these companies lowered their expectations. This trend temporarily reversed in the fourth quarter as investors took advantage of more reasonable valuations. Healthcare sector performance was generally driven by capital flows into companies with greater revenue and earnings visibility. As a result, medical device companies outperformed biotechnology companies. Overall, information technology and healthcare stocks were the two worst performing sectors of the S&P 500 Index during the period.

During the year, the Portfolio had less exposure to information technology and healthcare stocks than the benchmark while having heavier exposure to telecommunication services companies. When BlackRock took responsibility for the Portfolio at the beginning of the year, the prior Sub-adviser’s sector allocations tilted the Portfolio toward companies with cyclical earnings growth, especially semiconductor devices. This sub-industry encountered challenging supply/demand dynamics, and caused much of the Portfolio’s underperformance early in the period. Over time, we moderated this exposure as the Portfolio’s mandate evolved to include a broader group of investment opportunities.

The primary sources of underperformance during the year were an underweight in computer hardware combined with negative stock selection and an overweight position in semiconductor devices. In the computer hardware space, lack of exposure to Apple Computer, Inc. and NCR Corp. were the key detractors. In the semiconductors sector, a meaningful overweight to the relatively weak devices sub-industry and poor performance tied to company-specific inventory issues negatively impacted returns. In the healthcare sector, capitalization had a meaningful effect on relative performance as the larger-capitalization biotechnology companies in the benchmark outperformed the smaller companies held by the Portfolio.

On the positive side, relative value was added in wireless telecommunication services, systems software, and Internet retail stocks. Wireless telecom companies levered to improving economies in Russia, Turkey and Indonesia outperformed as subscriber growth and utilization remained robust. In the software group, opportunistic purchases of Veritas Software Corp. and BMC Software, Inc., added value. Finally, category-dominant Internet companies such as eBay, Inc, benefited from increasing on-line traffic and transaction volumes as well as an acceleration in on-line advertising and gained significantly during the period as a result.

Current Strategy and Outlook: Despite the prospects for rising short-term interest rates, we believe low interest rates and high corporate cash balances may support additional capital spending. As a result, we maintain a favorable outlook on the technology sector, despite the recent weakness. In fact, we believe this gives us the opportunity to increase our exposure to select segments of the market, as some valuations have become attractive.

† Subsequent to the period end, Erin Xie, Director and Portfolio Manager, replaced Daniel M. Rea.

Top Ten Holdings

as of December 31, 2004

(as a percent of net assets)

Microsoft Corp. | | 2.0 | % |

Oracle Corp. | | 1.7 | % |

International Business Machines Corp. | | 1.6 | % |

SAP AG ADR | | 1.6 | % |

Electronic Arts, Inc. | | 1.5 | % |

Boston Scientific Corp. | | 1.5 | % |

Samsung Electronics Co. Ltd. | | 1.5 | % |

Cisco Systems, Inc. | | 1.5 | % |

Genentech, Inc. | | 1.5 | % |

Agilent Technologies, Inc. | | 1.4 | % |

Portfolio holdings are subject to change daily.

18

PORTFOLIO MANAGERS’ REPORT | ING VP GLOBAL SCIENCE AND TECHNOLOGY PORTFOLIO |

| Average Annual Total Returns for the Periods Ended December 31, 2004 | |

| | 1 Year | | Since Inception

of Class I

May 1, 2000 | |

| Class I | | (1.29 | )% | (18.62 | )% |

| S&P 500 Index(1) | | 10.88 | % | (2.31 | )% |

| PSE Technology Index(2) | | 12.09 | % | (6.66 | )% |

| Goldman Sachs Technology Industry Composite Index(3) | | 2.91 | % | (17.87 | )% |

| | | | | | |

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING VP Global Science and Technology Portfolio against the S&P 500 Index, the PSE Technology Index and the Goldman Sachs Technology Industry Composite Index. The Indices have no cash in their portfolios, impose no sales charges and incur no operating expenses. An investor cannot invest directly in an index. The Portfolio’s performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on portfolio distributions or the redemption of portfolio shares.

Total returns reflect that the Investment Manager may have waived or recouped fees and expenses otherwise payable by the Portfolio.

The performance update illustrates performance for a variable investment option available through a variable annuity contract. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. Please call (800) 366-0066 to get performance through the most recent month end.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Portfolio holdings are subject to change daily.

(1) The S&P 500 Index is an unmanaged index that measures the performance of securities of approximately 500 large-capitalization companies whose securities are traded on major U.S. stock markets.

(2) The PSE Technology Index, an unmanaged index published by the Pacific Exchange, is comprised of 100 listed and over-the-counter stocks from 15 different industries including computer hardware, software, semiconductors, telecommunications, data storage and processing, electronics and biotechnology. This Index is included as an additional comparative index for Portfolio performance.

(3) The Goldman Sachs Technology Industry Composite Index is a widely recognized, unmanaged index of technology stocks.

19

ING VP INTERNATIONAL EQUITY PORTFOLIO | PORTFOLIO MANAGERS’ REPORT |

Country Allocation

as of December 31, 2004

(as a percent of net assets)

Portolio holdings are subject to change daily.

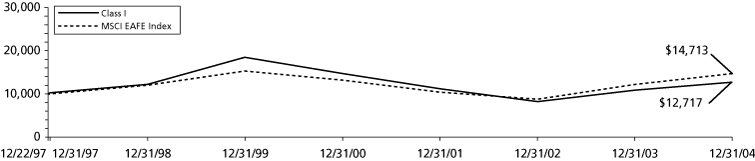

The ING VP International Equity Portfolio (the “Portfolio”) seeks long-term capital growth primarily through investment in a diversified portfolio of common stocks principally traded in countries outside of the United States. The Portfolio is managed by a team of equity investment specialists led by Martin Jansen, Portfolio Manager, ING Investment Management Co. — the Sub-Adviser.

Performance: For the year ended December 31, 2004, the Portfolio’s Class I shares provided a total return of 17.17% compared to the Morgan Stanley Capital International Europe, Australasia and Far East (“MSCI EAFE”) Index(1), which returned 20.70% for the same period.

Portfolio Specifics: In a continuation of the trends manifest in 2003, larger capitalization issues and the growth segment of the investment spectrum performed considerably weaker than the MSCI EAFE Index average. Our “growth at a reasonable price” investment philosophy, with its modest accent on growth and quality, consequently experienced a constant headwind during the year ended December 31, 2004. This was most prevalent in the period through mid-February, after which markets turned more cautious and were more inclined to focus on the integral growth/valuation relationship, which is the core of our investment process.

By design, our process allows for only modest regional over- or under-weightings. Within this context, our regional allocation result for the year was negative, due largely to our underweight in the strongly performing Developed Asia region and the opportunity cost of holding residual cash in a rising market. The bulk of the performance shortfall was attributable to stock selection in Europe and Developed Asia (excluding Japan). Sector positioning (excluding cash) added modest value, with the successful decisions to underweight a weak technology sector and overweight the strong energy sector. However, this was somewhat offset by an underweight position in consumer staples, which performed relatively strongly in the first part of the year.

Within sectors, stock selection proved most disappointing in the consumer discretionary, information technology, industrials and health care sectors. This was partly offset by positive contributions from our holdings in the materials, financials and telecommunication services sectors. At the security level, the worst performers were French technology services company Capgemini, which fell on substantially reduced earnings prospects, and Nokia Oyj, which had disappointing performance due to negative business trends. The most significant positive contribution came from our holdings in the Shell Transport & Trading Co. PLC and Japanese banks Mitsui Trust Holdings, Inc. and Sumitomo Trust & Banking Co., Ltd. The Portfolio also benefited from positions in Telecom Italia S.p.A. and France Telecom SA.

Current Strategy and Outlook: After strong recovery growth in 2003 and the first half of 2004, earnings growth in international markets is expected to decline to approximately 10% in 2005. With international markets in aggregate still undervalued, this would allow for further, albeit more modest, market gains. Given this expectation, our process indicates that stocks with relative earnings sustainability and visibility, which are trading at the low end of their historic premium range, are attractive. We maintain a modest positive exposure to Japan as we expect earnings growth here to exceed expectations, especially in the domestically oriented consumer discretionary sector. A small allocation was made to emerging market securities recently, as there are selective opportunities for above average growth trading at a discount to peers in the developed markets. Our largest active exposure remains the energy sector, which in our opinion remains undervalued. In the defensive growth segment, we prefer healthcare to consumer staples, which have less pricing power and increasing cost pressures. We are underweight in the information technology and industrial sectors.

Top Ten Industries

as of December 31, 2004

(as a percent of net assets)

Banks | | 21.4 | % |

Telecommunications | | 11.4 | % |

Oil and Gas | | 9.6 | % |

Pharmaceuticals | | 6.7 | % |

Insurance | | 6.0 | % |

Electric | | 5.3 | % |

Food | | 3.4 | % |

Home Furnishings | | 2.8 | % |

Retail | | 2.6 | % |

Electrical Components and Equipment | | 2.1 | % |

Portfolio holdings are subject to change daily.

20

PORTFOLIO MANAGERS’ REPORT | ING VP INTERNATIONAL EQUITY PORTFOLIO |

| Average Annual Total Returns for the Periods Ended December 31, 2004 | |

| | 1 Year | | 5 Year | | Since Inception

of Class I

December 22, 1997 | | Since Inception

of Class S

November 1, 2001 | |

| Class I | | 17.17 | % | (7.20 | )% | 3.48 | % | — | |

| Class S | | 16.87 | % | — | | — | | 5.74 | % |

| MSCI EAFE Index(1) | | 20.70 | % | (0.80 | )% | 5.67 | %(2) | 13.13 | % |

| | | | | | | | | | |

| | | | | | | | | | | |

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING VP International Equity Portfolio against the MSCI EAFE Index. The Index has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Portfolio’s performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on portfolio distributions or the redemption of portfolio shares.

Total returns reflect that the Investment Manager may have waived or recouped fees and expenses otherwise payable by the Portfolio.

The performance update illustrates performance for a variable investment option available through a variable annuity contract. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. Please call (800) 366-0066 to get performance through the most recent month end.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

The views expressed in this report reflect those of the portfolio manager only through the end of the period as stated on the cover. The portfolio manager’s views are subject to change at any time based on market and other conditions.

Portfolio holdings are subject to change daily.

(1) The MSCI EAFE Index is an unmanaged index that measures the performance of securities listed on exchanges in markets in Europe, Australasia and the Far East.

(2) Since inception performance for the index is shown from January 1, 1998.

21

As a shareholder of a Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution [and/or service] (12b–1) fees; and other Fund expenses. These Examples are intended to help you understand your ongoing costs (in dollars) of investing in a Fund and to compare these costs with the ongoing costs of investing in other mutual funds.