UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-07751

Nuveen Multistate Trust IV

(Exact name of registrant as specified in charter)

Nuveen Investments

333 West Wacker Drive Chicago, IL 60606

(Address of principal executive offices) (Zip code)

Kevin J. McCarthy

Nuveen Investments

333 West Wacker Drive Chicago, IL 60606

(Name and address of agent for service)

Registrant’s telephone number, including area code: (312) 917-7700

Date of fiscal year end: May 31

Date of reporting period: November 30, 2007

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policy making roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss.3507.

Item 1. Reports to Stockholders.

NUVEEN INVESTMENTS MUTUAL FUNDS

Semi-Annual Report dated November 30, 2007 | Dependable, tax-free income because it’s not what you earn, it’s what you keep.® | |

Nuveen Investments

Municipal Bond Funds

Nuveen Kansas Municipal Bond Fund

Nuveen Kentucky Municipal Bond Fund

Nuveen Michigan Municipal Bond Fund

Nuveen Missouri Municipal Bond Fund

Nuveen Ohio Municipal Bond Fund

Nuveen Wisconsin Municipal Bond Fund

NOW YOU CAN RECEIVE YOUR

NUVEEN INVESTMENTS FUND REPORTS FASTER.

NO MORE WAITING.

SIGN UP TODAY TO RECEIVE NUVEEN INVESTMENTS FUND INFORMATION BY E-MAIL.

It only takes a minute to sign up for E-Reports. Once enrolled, you’ll receive an e-mail as soon as your Nuveen Investments Fund information is ready — no more waiting for delivery by regular mail. Just click on the link within the e-mail to see the report, and save it on your computer if your wish.

IT’S FAST, EASY & FREE:

www.investordelivery.com

if you get your Nuveen Investments Fund dividends and statements from your financial advisor or brokerage account.

(Be sure to have the address sheet that accompanied this report handy. You’ll need it to complete the enrollment process.)

OR

www.nuveen.com/accountaccess

if you get your Nuveen Investments Fund dividends and statements directly from Nuveen Investments.

| Must be preceded by or accompanied by a prospectus. | NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE |

Dear Shareholder,

Once again, I am pleased to report that during the six-month period covered by this report your Fund provided tax-free income and solid performance from a carefully selected portfolio of municipal bonds. Detailed information on your Fund’s performance can be found in the Portfolio Managers’ Comments and Fund Spotlight sections of this report.

As we begin a new year, no one knows for certain what the future will bring. But one thing we do know is that a well-balanced portfolio – often including municipal bonds – can provide diversification that can reduce overall investment risk. To learn more about the potential benefits of portfolio diversification, we encourage you to consult a trusted financial advisor. He or she should be able to help you understand how a municipal bond investment like your Nuveen Fund can be an important building block in a portfolio crafted to perform well through a variety of market conditions.

I also wanted to update you on some important news about Nuveen Investments. The firm recently was acquired by a group led by Madison Dearborn Partners, LLC. While this affected the corporate structure of Nuveen Investments, it has no impact on the investment objectives, portfolio management strategies or dividend policy of your Fund.

Since 1898, Nuveen Investments has offered financial products and solutions that incorporate careful research, diversification, and the application of conservative risk-management principles. We are grateful that you have chosen us as a partner as you pursue your financial goals. We look forward to continuing to earn your trust in the months and years ahead.

Sincerely,

Timothy R. Schwertfeger

Chairman of the Board

January 15, 2008

[PHOTO] Timothy R. Schwertfeger

“But one thing we do know is that a well-balanced portfolio – often including municipal bonds – can provide diversification that can reduce overall investment risk.”

Semi-Annual Report Page 1

Portfolio Managers’ Comments for the Nuveen Kansas,

Kentucky, Michigan, Missouri, Ohio and Wisconsin Municipal Bond Funds

Portfolio managers Scott Romans and Daniel Close examine key investment strategies and the performance of the Nuveen Kansas, Kentucky, Michigan, Missouri, Ohio and Wisconsin Municipal Bond Funds. Scott, who has 7 years of investment experience, began managing the Kansas, Missouri and Wisconsin Funds in 2003. Dan has 6 years of investment experience and began managing the Kentucky, Ohio and Michigan Funds in March 2007.

How did the Funds perform during the six-month period ended November 30, 2007?

The table on page three provides total return performance information for the six Funds discussed in this report for the six-month, one-year, five-year, and ten-year periods ended November 30, 2007. Each Fund’s performance is compared with its respective state-specific Lehman Brothers Indexes, the national Lehman Brothers Municipal Bond Index, and its Lipper peer fund category average. The factors determining the performance of each Fund are discussed later in this report.

Over this six-month reporting period, all six Funds’ Class A shares total return at net asset value outperformed their respective Lipper peer group averages while lagging both their state-specific and the national Lehman Brothers Index to varying degrees.

What strategies were used to manage the Funds during the period? How did these strategies influence performance?

Our management strategies were consistent across all six Funds, although our ability to implement those strategies depended on the individual characteristics of each portfolio as well as market conditions within each state. Below we provide more specific information about the performance and management of the Funds.

During the first half of the six-month reporting period, the municipal bond market was relatively subdued. Yields moved slightly upward, while bond prices fell modestly (bond yields and prices move in opposite directions). In August, however, market conditions changed dramatically. The subprime mortgage crisis left investors worried about potential exposure to bad debts. As these worries grew, the municipal market became less liquid, and credit spreads – the premium paid to investors for taking on added credit risk – widened considerably, causing lower-rated bonds to underperform higher-rated securities.

Nuveen Kansas Municipal Bond Fund

Favorable credit-quality positioning proved to be helpful for the Kansas Fund’s recent performance. Specifically, the Fund benefited from its relatively sizeable allocation to higher-quality bonds and its relative underexposure to lower-quality bonds – both of which were beneficial given the risk-averse market environment of the period. Duration positioning also contributed to performance, with an underweighting in longer-duration bonds and an overweighting in the better-performing short-duration segment of the yield curve both having a favorable influence on the portfolio’s returns.

On the negative side, the Fund’s weakest performers tended to be lower-rated bonds, which suffered as the municipal market environment became more challenging beginning in August. As credit spreads widened, the underperformance in the municipal market occurred in some surprising places – for example, insured bonds backed by Radian Asset Assurance, whose parent company disclosed some exposure to subprime debt. Although the subsidiary had no subprime exposure of its own, the market’s concern caused Radian-insured bonds to substantially lag the rest of the insured municipal market to levels close to what one would expect from uninsured bonds from the underlying municipal issuers. The Kansas portfolio had some exposure to these Radian-insured bonds, which detracted from the Fund’s performance.

Discussions of specific investments are for illustration only and are not intended as recommendations of individual investments. The views expressed herein represent those of the portfolio managers as of the date of this report and are subject to change at any time, based on market conditions and other factors. The Funds disclaim any obligation to advise shareholders of such changes.

Semi-Annual Report Page 2

Class A Shares—

Average Annual Total Returns

as of 11/30/07

| 6-Month | 1-Year | 5-Year | 10-Year | |||||

Nuveen Kansas Municipal Bond Fund | 2.12% -2.21% | 2.38% -1.88% | 4.45% 3.56% | 4.59% 4.14% | ||||

Lipper Kansas Municipal Debt Funds Category Average1 | 1.51% | 1.67% | 3.66% | 4.13% | ||||

Lehman Brothers Kansas Municipal Bond Index2 | 2.81% | 3.18% | 4.35% | 5.10% | ||||

Lehman Brothers Municipal Bond Index3 | 2.40% | 2.71% | 4.68% | 5.30% | ||||

Nuveen Kentucky Municipal Bond Fund | 2.21% -2.08% | 2.25% -2.04% | 4.66% 3.76% | 4.62% 4.17% | ||||

Lipper Kentucky Municipal Debt Funds Category Average1 | 1.75% | 1.63% | 3.73% | 4.20% | ||||

Lehman Brothers Kentucky Municipal Bond Index2 | 2.88% | 3.22% | 4.50% | 5.09% | ||||

Lehman Brothers Municipal Bond Index3 | 2.40% | 2.71% | 4.68% | 5.30% | ||||

Nuveen Michigan Municipal Bond Fund | 2.02% -2.26% | 2.16% -2.10% | 4.50% 3.62% | 4.72% 4.26% | ||||

Lipper Michigan Municipal Debt Funds Category Average1 | 1.08% | 1.15% | 3.76% | 4.30% | ||||

Lehman Brothers Michigan Municipal Bond Index2 | 2.75% | 3.00% | 4.64% | 5.33% | ||||

Lehman Brothers Municipal Bond Index3 | 2.40% | 2.71% | 4.68% | 5.30% | ||||

Nuveen Missouri Municipal Bond Fund | 1.61% -2.63% | 1.72% -2.53% | 4.67% 3.77% | 4.69% 4.24% | ||||

Lipper Missouri Municipal Debt Funds Category Average1 | 1.19% | 1.07% | 3.92% | 4.44% |

| 6-Month | 1-Year | 5-Year | 10-Year | |||||

Lehman Brothers Missouri Municipal Bond Index2 | 2.79% | 2.86% | 4.74% | 5.24% | ||||

Lehman Brothers Municipal Bond Index3 | 2.40% | 2.71% | 4.68% | 5.30% | ||||

Nuveen Ohio Municipal Bond Fund | 1.98% -2.27% | 1.95% -2.37% | 4.58% 3.70% | 4.58% 4.14% | ||||

Lipper Ohio Municipal Debt Funds Category Average1 | 1.52% | 1.48% | 3.81% | 4.24% | ||||

Lehman Brothers Ohio Municipal Bond Index2 | 2.36% | 2.64% | 4.40% | 5.10% | ||||

Lehman Brothers Municipal Bond Index3 | 2.40% | 2.71% | 4.68% | 5.30% | ||||

Nuveen Wisconsin Municipal Bond Fund | 1.73% -2.55% | 1.60% -2.68% | 4.24% 3.34% | 4.55% 4.11% | ||||

Lipper Other States Municipal Debt Funds Category Average1 | 1.44% | 1.51% | 3.66% | 4.12% | ||||

Lehman Brothers Wisconsin Municipal Bond Index2 | 2.34% | 2.99% | 4.91% | 5.34% | ||||

Lehman Brothers Municipal Bond Index3 | 2.40% | 2.71% | 4.68% | 5.30% |

Returns quoted represent past performance, which is no guarantee of future results. Returns less than one year are cumulative. Returns at NAV would be lower if the sales charge were included. Current performance may be higher or lower than the performance shown. Investment returns and principal value will fluctuate so that when shares are redeemed, they may be worth more or less than their original cost. Class A shares have a 4.2 percent maximum sales charge. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares. For the most recent month-end performance, visit www.nuveen.com or call (800) 257-8787.

Please see each Fund’s Spotlight Page later in this report for more complete performance data and expense ratios.

| 1 | The Lipper category averages shown represent the average annualized total return for all reporting funds in the respective categories. The Lipper Kansas Municipal Debt Funds Category Average contained 11, 10, 9 and 8 funds, the Lipper Kentucky Municipal Debt Funds Category Average had 18, 18, 17 and 11 funds, the Lipper Michigan Municipal Debt Funds Category Average had 32, 32, 27 and 24 funds, the Lipper Missouri Municipal Debt Funds Category Average had 18, 18, 17 and 15 funds, the Lipper Ohio Municipal Debt Funds Category Average had 46, 46, 41 and 34 funds, and the Lipper Other States Municipal Debt Funds Category Average had 76, 76, 70 and 54 funds for the six-month, one-year, five-year and ten-year periods ended November 30, 2007, respectively. The returns account for the effects of management fees and assume reinvestment of dividends, but do not reflect any applicable sales charges. You cannot invest directly in a Lipper Category. |

| 2 | The Lehman Brothers Kansas Municipal Bond Index is an unmanaged index comprised of investment grade, tax-exempt Kansas bonds with maturities of two years or greater. The Lehman Brothers Kentucky Municipal Bond Index is an unmanaged index comprised of investment grade, tax-exempt Kentucky bonds with maturities of two years or greater. The Lehman Brothers Michigan Municipal Bond Index is an unmanaged index comprised of investment grade, tax-exempt Michigan bonds with maturities of two years or greater. The Lehman Brothers Missouri Municipal Bond Index is an unmanaged index comprised of investment grade, tax-exempt Missouri bonds with maturities of two years or greater. The Lehman Brothers Ohio Municipal Bond Index is an unmanaged index comprised of investment grade, tax-exempt Ohio bonds with maturities of two years or greater. The Lehman Brothers Wisconsin Municipal Bond Index is an unmanaged index comprised of investment grade, tax-exempt Wisconsin bonds with maturities of two years or greater. The indexes do not reflect any initial or ongoing expenses and are not available for direct investment. |

| 3 | The Lehman Brothers Municipal Bond Index is an unmanaged index composed of a broad range of investment-grade municipal bonds and does not reflect any initial or ongoing expenses. An index is not available for direct investment. |

Semi-Annual Report Page 3

Changes to the portfolio were relatively modest, with only three new purchases made during the period. In each case, we took advantage of market conditions to invest in opportunities that we believed provided our shareholders with unusual levels of value. One of these purchases was of a lower-rated hospital bond issue, while the two others were insured by AMBAC, another municipal bond insurer that recently disclosed exposure to subprime loans. These AMBAC-insured bonds were offering nearly a half-percentage point of additional yield compared to the benchmark AAA-rated Municipal Market Data (MMD) curve – a very rare situation. After careful research, we remained confident in these securities’ underlying financial strength and believed they provided excellent future total return potential for shareholders.

To fund these purchases, most of our selling activity during the period focused on high-quality bonds purchased during the much-lower market-rate environment of the past several years. By selling these bonds, we could replace them with newer bonds offering more favorable yields.

Nuveen Kentucky Municipal Bond Fund

Overall, duration positioning helped the Kentucky Fund’s performance. During the period, we were overweighted in the intermediate part of the yield curve, which generally performed well. A relative underweighting in the market’s longest-duration bonds also proved beneficial, although an underweighting in the positive-performing shortest portion of the yield curve was a corresponding negative.

The Fund was modestly overweighted in AAA-rated bonds. This allocation proved helpful as cautious investors preferred higher-quality issues during the last half of the reporting period. Another noteworthy positive was the Fund’s derivative position, which we had implemented to help maintain the portfolio’s duration within target levels. We had invested small portions of the Fund in forward interest-rate swaps tied to two common interest rates: LIBOR (London Inter-bank Offered Rate) and the Securities Industry and Financial Markets (SIFM) Municipal Swap Index (previously known as BMA). With these derivative positions, we were able to reduce the portfolio’s volatility and manage its duration without being forced to sell positions in the portfolios that we believed were attractive. These derivative securities outperformed the municipal market generally and added to the Fund’s total returns.

Not surprisingly, given the challenging market environment of the period, the Fund’s exposure to lower-credit-quality bonds detracted from overall performance. For example, lower-rated health care positions as well as a modest holding in Puerto Rico–issued tobacco-backed bonds provided a negative influence.

Portfolio activity was relatively modest. Recent purchases focused on essential service bonds offering maturities between 20 to 30 years. When selling bonds, we primarily sold shorter-dated bonds. As these securities gained in value, we took advantage of market conditions to sell them at favorable prices. In addition, we were actively selling some of our bonds whose income is subject to the alternative minimum tax, taking advantage of opportunities to sell these positions at what we believed were attractive prices.

Nuveen Michigan Municipal Bond Fund

The Michigan Fund was helped by our duration positioning, with an overweighting in intermediate-maturity bonds adding to results. An underweighting in longer-duration issues was also a relative positive. However, as with the Kentucky Fund, our relative underexposure to very-short-maturity bonds detracted from performance, as these securities benefited the most from investors’ growing risk aversion. That risk aversion also boosted the market’s highest-quality bonds, in which the Fund was overweighted. Nevertheless, the Fund would have benefited from having greater exposure to pre-refunded1 bonds and general obligation/tax-supported debt.

Another source of positive results came from a modest derivative position, which outperformed the municipal market as a whole during the period. As in the Kentucky Fund, this derivative exposure allowed us to limit the portfolio’s volatility as well as keep its duration within target levels.

The Fund’s worst performers overall were lower-quality bonds, which suffered the most as investors engaged in a flight to quality. In particular, we

| 1 | Advance refundings, also known as pre-refundings or refinancings, occur when an issuer sells new bonds and uses the proceeds to fund principal and interest payments of older existing bonds. This process often results in lower borrowing costs for bond issuers. |

Semi-Annual Report Page 4

owned a number of lower-quality hospital bonds – health care issuance represents a significant portion of the Michigan municipal market – many of which performed relatively poorly during the past six months. Our lower-rated industrial development revenue bonds were generally disappointing performers as well.

As municipal investor sentiment weakened, we found periodic opportunities to buy lower-rated bonds at particularly compelling yields. In the health care sector, for example, we took advantage of several BBB-rated hospital bond issues offering what we believed were excellent values. Otherwise, the rest of our purchases were focused on higher-quality essential service general obligation and tax-backed bonds. These included a variety of school district issues with maturities ranging from 2025 to 2037, as well as a water/sewer issue with a 2023 maturity date.

Our sales were primarily of short-dated pre-refunded securities, for which we were able to get what we believed was a good price in return. These sales enabled us to reinvest in longer-dated and higher-rated paper, thus allowing us to accomplish our credit and duration-management objectives.

Nuveen Missouri Municipal Bond Fund

In the Missouri Fund, we saw ample opportunities to add new lower-rated positions to the portfolio. Many of these were in the health care sector. At various points, we were able to buy new uninsured hospital bonds at wider spreads to AAA-rated bonds than we had become used to seeing in recent years. Unfortunately, in August, when credit concerns led to significant municipal market underperformance, our lower-rated bonds – including some that we had added in an earlier round of spread widening prior to the start of the period – were significant overall detractors from the Fund’s return.

The Fund did benefit modestly from its duration positioning. An underweighting in the most interest-rate-sensitive bonds added to results, as these holdings tended to be the worst performers along the yield curve. An additional favorable performance impact came from our pre-refunded bonds which tended to have shorter-dated maturities and thus held their value better as interest rates rose in the second half of the period.

Most of our purchases during the period were of bonds with 20- to 30-year maturities, enabling us to maintain the Fund's duration at desired levels. Bond sales during the period were primarily shorter bonds, as well as longer-dated bonds that had been issued in recent years during substantially lower interest rate environments. We took advantage of the widening of credit spreads in August to add new lower-rated positions when we believed in their underlying financial strength and saw exceptional value opportunities. We also took advantage of market conditions to sell certain underperforming lower-rated holdings, exchanging these bonds for similar ones offering comparable levels of risk but better embedded yields – thus improving the portfolio's income characteristics.

Nuveen Ohio Municipal Bond Fund

The primary positive influence on the Ohio Fund’s performance was favorable security selection, with a number of our higher-rated and shorter-maturity positions enjoying strong results. On the negative side, we were modestly underweighted in the highest-quality segments of the market, which fared relatively well. In addition, we were overweighed in both industrial development revenue bonds and housing bonds – two sectors that underperformed.

We made a number of new purchases. For example, we added four new general obligation or tax-backed bond positions offering maturities ranging from 2028 to 2034. The majority of our purchases had maturities in the 25- to 30-year range – enabling us to keep the Fund’s duration in line with our target. Other purchases included several longer-dated Ginnie Mae housing bond issues that we believed offered attractive value.

In addition, throughout the period, but especially in August following the municipal market’s downturn, we took advantage of available opportunities to add lower-rated bonds providing what we felt were unusually good values. This included a health care bond issue rated BBB- as well as a water/sewer bond issue. Another recent opportunity was to buy Ohio tobacco settlement backed bonds, part of a multibillion dollar issue that took place in October. Because the issuance was during a fairly weak period for tobacco debt, we were able to purchase these securities at attractive prices and provide good future value potential for our shareholders.

Semi-Annual Report Page 5

Nuveen Wisconsin Municipal Bond Fund

Management activity in the Wisconsin Fund was quite limited during the past six months. This is not unusual, in our experience, because the unique tax laws in Wisconsin limit the type of municipal entities which can issue fully-tax-exempt bonds. As a result, we made only two new purchases during the past six months both of which were of Puerto Rico bond issues which led to a modest increase in the portfolio’s allocation to U.S. territorial issues. In a state such as Wisconsin, where appropriate in-state paper can sometimes be difficult to come by, territorial bonds can be extremely useful investment alternatives, as they are generally fully tax-exempt in all 50 states.

Our duration positioning helped the Fund’s performance. The portfolio was significantly exposed to the intermediate part of the yield curve, which outperformed longer-duration bonds. The Fund’s exposure to higher-rated bonds also proved to be beneficial in the risk-averse investment environment. On the negative side, the Fund’s Puerto Rico exposure tended to be both relatively long in duration and offer credit ratings at the lower end of the investment-grade credit spectrum – two factors that detracted from results.

Recent Market Events

Many of the municipal bonds in the portfolios are covered by policies of insurance, issued by one of several municipal bond insurers, under which the insurer guarantees the timely payment of interest and principal on the bonds. Certain of those insurers, including AMBAC, MBIA and FGIC, historically rated AAA (the highest grade), also insure investment vehicles representing interests in subprime mortgages, which suffered severe credit deterioration during the semi-annual period covered by this report. The defaults and/or credit deterioration of the subprime mortgage investments they insured have caused losses to the insurers, which has reduced the insurers’ capital and called into question the insurers’ continued ability to pay interest and principal on insured bonds for the life of those bonds. One rating agency has already reduced the rating for AMBAC-insured bonds to AA, and other rating agencies may follow, and this rating may fall even further. While the major rating agencies continue to give the other affected insurers their highest rating, as of the date this report was written one or more rating agencies have placed each of these insurers on “negative credit watch”, which may presage one or more rating reductions in the future. The value of the insurance associated with bonds held by the Funds in this report (a component of the value of the bond/insurance combination) generally declined during and after the reporting period, and further credit deterioration or rating downgrades of the insurers could cause further declines in the value of the insurance component of an insured bond, although it has not and should not affect the creditworthiness of the municipal issuer of, and the uninsured value of, the underlying bond.

Dividend Information

Throughout the six-month period, all share classes of the Kansas Fund saw a November increase to its monthly tax-free dividend, while the Class C shares of the Kentucky Fund experienced a dividend increase in August. All share classes of the Ohio Fund saw a dividend reduction in August. The Michigan, Missouri, and Wisconsin Funds saw no dividend changes during the past six months.

Each Fund seeks to pay dividends at a rate that reflects the past and projected performance of the Fund. To permit a Fund to maintain a more stable monthly dividend, the Fund may pay dividends at a rate that may be more or less than the amount of net investment income actually earned by the Fund during the period. If the Fund has cumulatively earned more than it has paid in dividends, it will hold the excess in reserve as undistributed net investment income (UNII) as part of the Fund’s net asset value. Conversely, if the Fund has cumulatively paid in dividends more than it has earned, the excess will constitute a negative UNII that will likewise be reflected in the Fund’s net asset value. Each Fund will, over time, pay all its net investment income as dividends to shareholders.

As of November 30, 2007, the Kentucky, Michigan, Missouri, Ohio, and Wisconsin Funds had negative UNII balances for financial statement purposes and positive UNII balances, based upon our best estimate, for tax purposes. The Kansas Fund had a positive UNII balance for financial statement purposes and a positive UNII balance, based upon our best estimate, for tax purposes.

Semi-Annual Report Page 6

Fund Spotlight as of 11/30/07 Nuveen Kansas Municipal Bond Fund

| Quick Facts | ||||||||

| A Shares | B Shares | C Shares | R Shares | |||||

NAV | $10.41 | $10.32 | $10.41 | $10.45 | ||||

Latest Monthly Dividend1 | $0.0355 | $0.0290 | $0.0310 | $0.0375 | ||||

Inception Date | 1/09/92 | 2/19/97 | 2/11/97 | 2/25/97 |

Returns quoted represent past performance which is no guarantee of future results. Returns without sales charges would be lower if the sales charge were included. Current performance may be higher or lower than the performance shown. Investment returns and principal value will fluctuate so that when shares are redeemed, they may be worth more or less than their original cost. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares. Income is generally exempt from regular federal income taxes. Some income may be subject to state and local taxes and to the federal alternative minimum tax. Capital gains, if any, are subject to tax. For the most recent month-end performance visit www.nuveen.com or call (800) 257-8787.

Returns reflect differences in sales charges and expenses, which are primarily differences in distribution and service fees. Class A shares have a 4.2% maximum sales charge. Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within 18 months of purchase. Class B shares have a CDSC that begins at 5% for redemptions during the first year and declines periodically to 0% over the following five years. Class B shares automatically convert to Class A shares eight years after purchase. Class C shares have a 1% CDSC for redemptions within less than one year, which is not reflected in the one-year total return. Class R shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors. Returns reflect an expense limitation by the Fund’s investment adviser.

| Average Annual Total Returns as of 11/30/07 | ||||

| A Shares | NAV | Offer | ||

1-Year | 2.38% | -1.88% | ||

5-Year | 4.45% | 3.56% | ||

10-Year | 4.59% | 4.14% | ||

| B Shares | w/o CDSC | w/CDSC | ||

1-Year | 1.54% | -2.39% | ||

5-Year | 3.67% | 3.49% | ||

10-Year | 3.97% | 3.97% | ||

| C Shares | NAV | |||

1-Year | 1.76% | |||

5-Year | 3.87% | |||

10-Year | 4.03% | |||

| R Shares | NAV | |||

1-Year | 2.51% | |||

5-Year | �� | 4.65% | ||

10-Year | 4.80% | |||

| Tax-Free Yields | ||||

| A Shares | NAV | Offer | ||

Dividend Yield2 | 4.09% | 3.92% | ||

30-Day Yield2 | 3.68% | — | ||

SEC 30-Day Yield2,3 | — | 3.53% | ||

Taxable-Equivalent Yield3,4 | 5.46% | 5.24% | ||

| B Shares | NAV | |||

Dividend Yield2 | 3.37% | |||

30-Day Yield2 | 2.93% | |||

Taxable-Equivalent Yield4 | 4.35% | |||

| C Shares | NAV | |||

Dividend Yield2 | 3.57% | |||

30-Day Yield2 | 3.13% | |||

Taxable-Equivalent Yield4 | 4.64% | |||

| R Shares | NAV | |||

Dividend Yield2 | 4.31% | |||

SEC 30-Day Yield2 | 3.88% | |||

Taxable-Equivalent Yield4 | 5.76% | |||

Average Annual Total Returns as of 12/31/07

| ||||

| A Shares | NAV | Offer | ||

1-Year | 2.63% | -1.68% | ||

5-Year | 3.93% | 3.04% | ||

10-Year | 4.42% | 3.98% | ||

| B Shares | w/o CDSC | w/CDSC | ||

1-Year | 1.88% | -2.06% | ||

5-Year | 3.19% | 3.01% | ||

10-Year | 3.79% | 3.79% | ||

| C Shares | NAV | |||

1-Year | 2.00% | |||

5-Year | 3.37% | |||

10-Year | 3.85% | |||

| R Shares | NAV | |||

1-Year | 2.85% | |||

5-Year | 4.17% | |||

10-Year | 4.63% | |||

| Portfolio Statistics | ||

Net Assets ($000) | $124,262 | |

Average Effective Maturity on Securities (Years) | 18.27 | |

Average Duration | 5.80 |

| Expense Ratios | ||||||

| Share Class | Gross Expense Ratios | Net Expense Ratios | As of Date | |||

Class A | 0.85% | 0.84% | 5/31/07 | |||

Class B | 1.61% | 1.59% | 5/31/07 | |||

Class C | 1.40% | 1.39% | 5/31/07 | |||

Class R | 0.65% | 0.63% | 5/31/07 | |||

The expense ratios shown factor in Annual Fund Operating Expenses including management fees and other fees and expenses. The Net Expense Ratios reflect a custodian fee credit from the custodian bank whereby certain fees and expenses are reduced by credits earned on the Fund’s cash on deposit with the bank. There is no guarantee that the Fund will earn such credits in the future. Absent the credit, the Net Expense Ratios would be higher and total returns would be less. These expense ratios may vary from the expense ratios shown elsewhere in this report.

| 1 | Paid December 3, 2007. This is the latest monthly tax-exempt dividend declared during the period ended November 30, 2007. |

| 2 | Dividend Yield is the most recent dividend per share (annualized) divided by the appropriate price per share. The SEC 30-Day Yield is computed under an SEC standardized formula and is based on the maximum offer price per share. The 30-Day Yield is computed under the same formula but is based on the Net Asset Value (NAV) per share. The Dividend Yield may differ from the SEC 30-Day Yield because the Fund may be paying out more or less than it is earning and it may not include the effect of amortization of bond premium. |

| 3 | The SEC 30-Day Yield and Taxable-Equivalent Yield on A Shares at NAV applies only to A Shares purchased at no-load pursuant to the Fund’s policy permitting waiver of the A Share load in certain specified circumstances. |

| 4 | The Taxable-Equivalent Yield represents the yield that must be earned on a fully taxable investment in order to equal the yield of the Fund on an after-tax basis at a specified tax rate. With respect to investments that generate qualified dividend income that is taxable at a maximum rate of 15%, the Taxable-Equivalent Yield is lower. The Taxable-Equivalent Yield is based on the Fund’s 30-Day Yield on the indicated date and a combined federal and state income tax rate of 32.6%. |

Semi-Annual Report Page 7

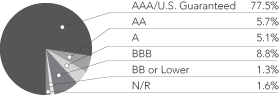

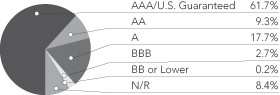

Fund Spotlight as of 11/30/07 Nuveen Kansas Municipal Bond Fund

Bond Credit Quality1,2

Industries2

Tax Obligation/Limited | 27.2% | |

Health Care | 22.3% | |

Housing/Single Family | 18.9% | |

Tax Obligation/General | 10.8% | |

Water and Sewer | 6.6% | |

Other | 14.2% |

| 1 | The percentage of AAA ratings shown in the foregoing chart reflects the AAA ratings on certain bonds insured by AMBAC, FGIC or MBIA as of November 30, 2007. As explained earlier in the Portfolio Managers’ Comments section of this report, one rating agency has reduced the rating for AMBAC to AA, and one or more rating agencies have placed each of these insurers on “negative credit watch”, which may presage one or more rating reductions for such insurer or insurers in the future. If one or more insurers’ ratings are reduced below AAA by these rating agencies, it would likely reduce the effective rating of many of the bonds insured by that insurer or insurers, and thereby reduce the percentage of the portfolio rated AAA from the percentage shown in the foregoing chart. |

| 2 | As a percentage of total investments as of November 30, 2007. Holdings are subject to change. |

Expense Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including front and back end sales charges (loads) or redemption fees, where applicable; and (2) ongoing costs, including management fees; distribution and service (12b-1) fees, where applicable; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example below is based on an investment of $1,000 invested at the beginning of the period and held for the period.

The information under “Actual Performance,” together with the amount you invested, allows you to estimate actual expenses incurred over the reporting period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.60) and multiply the result by the cost shown for your share class, in the row entitled “Expenses Incurred During Period” to estimate the expenses incurred on your account during this period.

The information under “Hypothetical Performance,” provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expense you incurred for the period. You may use this information to compare the ongoing costs of investing in the Fund and other Funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as front and back end sales charges (loads) or redemption fees, where applicable. Therefore, the hypothetical information is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds or share classes. In addition, if these transactional costs were included, your costs would have been higher.

| Hypothetical Performance | ||||||||||||||||||||||||

| Actual Performance | (5% annualized return before expenses) | |||||||||||||||||||||||

| A Shares | B Shares | C Shares | R Shares | A Shares | B Shares | C Shares | R Shares | |||||||||||||||||

Beginning Account Value (6/01/07) | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | ||||||||

Ending Account Value (11/30/07) | $ | 1,021.20 | $ | 1,017.50 | $ | 1,018.60 | $ | 1,021.30 | $ | 1,020.76 | $ | 1,017.00 | $ | 1,018.00 | $ | 1,021.76 | ||||||||

Expenses Incurred During Period | $ | 4.36 | $ | 8.14 | $ | 7.14 | $ | 3.34 | $ | 4.36 | $ | 8.14 | $ | 7.13 | $ | 3.35 | ||||||||

For each class of the Fund, expenses are equal to the Fund’s annualized net expense ratio of .86%, 1.61%, 1.41% and ..66% for Classes A, B, C and R, respectively, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period).

Semi-Annual Report Page 8

Fund Spotlight as of 11/30/07 Nuveen Kentucky Municipal Bond Fund

| Quick Facts | ||||||||

| A Shares | B Shares | C Shares | R Shares | |||||

NAV | $10.98 | $10.99 | $10.98 | $10.98 | ||||

Latest Monthly Dividend1 | $0.0365 | $0.0295 | $0.0315 | $0.0380 | ||||

Latest Capital Gain Distribution2 | $0.0223 | $0.0223 | $0.0223 | $0.0223 | ||||

Inception Date | 5/04/87 | 2/05/97 | 10/04/93 | 2/07/97 |

Returns quoted represent past performance which is no guarantee of future results. Returns without sales charges would be lower if the sales charge were included. Current performance may be higher or lower than the performance shown. Investment returns and principal value will fluctuate so that when shares are redeemed, they may be worth more or less than their original cost. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares. Income is generally exempt from regular federal income taxes. Some income may be subject to state and local taxes and to the federal alternative minimum tax. Capital gains, if any, are subject to tax. For the most recent month-end performance visit www.nuveen.com or call (800) 257-8787.

Returns reflect differences in sales charges and expenses, which are primarily differences in distribution and service fees. Class A shares have a 4.2% maximum sales charge. Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within 18 months of purchase. Class B shares have a CDSC that begins at 5% for redemptions during the first year and declines periodically to 0% over the following five years. Class B shares automatically convert to Class A shares eight years after purchase. Class C shares have a 1% CDSC for redemptions within less than one year, which is not reflected in the one-year total return. Class R shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors. Returns reflect an expense limitation by the Fund’s investment adviser.

| Average Annual Total Returns as of 11/30/07 | ||||

| A Shares | NAV | Offer | ||

1-Year | 2.25% | -2.04% | ||

5-Year | 4.66% | 3.76% | ||

10-Year | 4.62% | 4.17% | ||

| B Shares | w/o CDSC | w/CDSC | ||

1-Year | 1.56% | -2.36% | ||

5-Year | 3.89% | 3.71% | ||

10-Year | 3.98% | 3.98% | ||

| C Shares | NAV | |||

1-Year | 1.66% | |||

5-Year | 4.08% | |||

10-Year | 4.04% | |||

| R Shares | NAV | |||

1-Year | 2.51% | |||

5-Year | 4.87% | |||

10-Year | 4.82% | |||

| Tax-Free Yields | ||||

| A Shares | NAV | Offer | ||

Dividend Yield3 | 3.99% | 3.82% | ||

30-Day Yield3 | 3.32% | — | ||

SEC 30-Day Yield3,4 | — | 3.18% | ||

Taxable-Equivalent Yield4,5 | 4.90% | 4.70% | ||

| B Shares | NAV | |||

Dividend Yield3 | 3.22% | |||

30-Day Yield3 | 2.57% | |||

Taxable-Equivalent Yield5 | 3.80% | |||

| C Shares | NAV | |||

Dividend Yield3 | 3.44% | |||

30-Day Yield3 | 2.77% | |||

Taxable-Equivalent Yield5 | 4.09% | |||

| R Shares | NAV | |||

Dividend Yield3 | 4.15% | |||

SEC 30-Day Yield3 | 3.52% | |||

Taxable-Equivalent Yield5 | 5.20% | |||

| Average Annual Total Returns as of 12/31/07 | ||||

| A Shares | NAV | Offer | ||

1-Year | 2.62% | -1.72% | ||

5-Year | 4.26% | 3.36% | ||

10-Year | 4.47% | 4.02% | ||

| B Shares | w/o CDSC | w/CDSC | ||

1-Year | 1.93% | -2.01% | ||

5-Year | 3.49% | 3.32% | ||

10-Year | 3.86% | 3.86% | ||

| C Shares | NAV | |||

1-Year | 2.12% | |||

5-Year | 3.69% | |||

10-Year | 3.90% | |||

| R Shares | NAV | |||

1-Year | 2.88% | |||

5-Year | 4.47% | |||

10-Year | 4.68% | |||

| Portfolio Statistics | ||

Net Assets ($000) | $436,932 | |

Average Effective Maturity on Securities (Years) | 13.86 | |

Average Duration | 5.46 |

| Expense Ratios | ||||||

| Share Class | Gross Expense Ratios | Net Expense Ratios | As of Date | |||

Class A | 0.90% | 0.89% | 5/31/07 | |||

Class B | 1.65% | 1.65% | 5/31/07 | |||

Class C | 1.45% | 1.44% | 5/31/07 | |||

Class R | 0.70% | 0.69% | 5/31/07 | |||

The expense ratios shown factor in Annual Fund Operating Expenses including management fees and other fees and expenses. The Net Expense Ratios reflect a custodian fee credit from the custodian bank whereby certain fees and expenses are reduced by credits earned on the Fund’s cash on deposit with the bank. There is no guarantee that the Fund will earn such credits in the future. Absent the credit, the Net Expense Ratios would be higher and total returns would be less. These expense ratios may vary from the expense ratios shown elsewhere in this report.

| 1 | Paid December 3, 2007. This is the latest monthly tax-exempt dividend declared during the period ended November 30, 2007. |

| 2 | Paid December 5, 2006. Capital gains are subject to federal taxation. |

| 3 | Dividend Yield is the most recent dividend per share (annualized) divided by the appropriate price per share. The SEC 30-Day Yield is computed under an SEC standardized formula and is based on the maximum offer price per share. The 30-Day Yield is computed under the same formula but is based on the Net Asset Value (NAV) per share. The Dividend Yield may differ from the SEC 30-Day Yield because the Fund may be paying out more or less than it is earning and it may not include the effect of amortization of bond premium. |

| 4 | The SEC 30-Day Yield and Taxable-Equivalent Yield on A Shares at NAV applies only to A Shares purchased at no-load pursuant to the Fund’s policy permitting waiver of the A Share load in certain specified circumstances. |

| 5 | The Taxable-Equivalent Yield represents the yield that must be earned on a fully taxable investment in order to equal the yield of the Fund on an after-tax basis at a specified tax rate. With respect to investments that generate qualified dividend income that is taxable at a maximum rate of 15%, the Taxable-Equivalent Yield is lower. The Taxable-Equivalent Yield is based on the Fund’s 30-Day Yield on the indicated date and a combined federal and state income tax rate of 32.3%. |

Semi-Annual Report Page 9

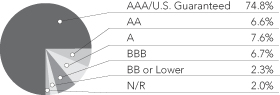

Fund Spotlight as of 11/30/07 Nuveen Kentucky Municipal Bond Fund

Bond Credit Quality1,2

Industries2

Tax Obligation/Limited | 24.5% | |

U.S. Guaranteed | 18.5% | |

Water and Sewer | 11.5% | |

Health Care | 11.0% | |

Utilities | 10.6% | |

Tax Obligation/General | 7.6% | |

Transportation | 4.8% | |

Other | 11.5% |

| 1 | The percentage of AAA ratings shown in the foregoing chart reflects the AAA ratings on certain bonds insured by AMBAC, FGIC or MBIA as of November 30, 2007. As explained earlier in the Portfolio Managers’ Comments section of this report, one rating agency has reduced the rating for AMBAC to AA, and one or more rating agencies have placed each of these insurers on “negative credit watch”, which may presage one or more rating reductions for such insurer or insurers in the future. If one or more insurers’ ratings are reduced below AAA by these rating agencies, it would likely reduce the effective rating of many of the bonds insured by that insurer or insurers, and thereby reduce the percentage of the portfolio rated AAA from the percentage shown in the foregoing chart. |

| 2 | As a percentage of total investments as of November 30, 2007. Holdings are subject to change. |

Expense Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including front and back end sales charges (loads) or redemption fees, where applicable; and (2) ongoing costs, including management fees; distribution and service (12b-1) fees, where applicable; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example below is based on an investment of $1,000 invested at the beginning of the period and held for the period.

The information under “Actual Performance,” together with the amount you invested, allows you to estimate actual expenses incurred over the reporting period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.60) and multiply the result by the cost shown for your share class, in the row entitled “Expenses Incurred During Period” to estimate the expenses incurred on your account during this period.

The information under “Hypothetical Performance,” provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expense you incurred for the period. You may use this information to compare the ongoing costs of investing in the Fund and other Funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as front and back end sales charges (loads) or redemption fees, where applicable. Therefore, the hypothetical information is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds or share classes. In addition, if these transactional costs were included, your costs would have been higher.

| Hypothetical Performance | ||||||||||||||||||||||||

| Actual Performance | (5% annualized return before expenses) | |||||||||||||||||||||||

| A Shares | B Shares | C Shares | R Shares | A Shares | B Shares | C Shares | R Shares | |||||||||||||||||

Beginning Account Value (6/01/07) | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | ||||||||

Ending Account Value (11/30/07) | $ | 1,022.10 | $ | 1,018.20 | $ | 1,019.20 | $ | 1,022.90 | $ | 1,020.46 | $ | 1,016.75 | $ | 1,017.70 | $ | 1,021.51 | ||||||||

Expenses Incurred During Period | $ | 4.66 | $ | 8.40 | $ | 7.44 | $ | 3.60 | $ | 4.66 | $ | 8.39 | $ | 7.44 | $ | 3.60 | ||||||||

For each class of the Fund, expenses are equal to the Fund’s annualized net expense ratio of .92%, 1.66%, 1.47% and ..71% for Classes A, B, C and R, respectively, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period).

Semi-Annual Report Page 10

Fund Spotlight as of 11/30/07 Nuveen Michigan Municipal Bond Fund

| Quick Facts | ||||||||

| A Shares | B Shares | C Shares | R Shares | |||||

NAV | $11.40 | $11.42 | $11.39 | $11.40 | ||||

Latest Monthly Dividend1 | $0.0395 | $0.0325 | $0.0340 | $0.0415 | ||||

Latest Capital Gain and Ordinary Income Distribution2 | $0.0993 | $0.0993 | $0.0993 | $0.0993 | ||||

Inception Date | 6/27/85 | 2/03/97 | 6/22/93 | 2/03/97 |

Returns quoted represent past performance which is no guarantee of future results. Returns without sales charges would be lower if the sales charge were included. Current performance may be higher or lower than the performance shown. Investment returns and principal value will fluctuate so that when shares are redeemed, they may be worth more or less than their original cost. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares. Income is generally exempt from regular federal income taxes. Some income may be subject to state and local taxes and to the federal alternative minimum tax. Capital gains, if any, are subject to tax. For the most recent month-end performance visit www.nuveen.com or call (800) 257-8787.

Returns reflect differences in sales charges and expenses, which are primarily differences in distribution and service fees. Class A shares have a 4.2% maximum sales charge. Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within 18 months of purchase. Class B shares have a CDSC that begins at 5% for redemptions during the first year and declines periodically to 0% over the following five years. Class B shares automatically convert to Class A shares eight years after purchase. Class C shares have a 1% CDSC for redemptions within less than one year, which is not reflected in the one-year total return. Class R shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors. Returns reflect an expense limitation by the Fund’s investment adviser.

| Average Annual Total Returns as of 11/30/07 | ||||

| A Shares | NAV | Offer | ||

1-Year | 2.16% | -2.10% | ||

5-Year | 4.50% | 3.62% | ||

10-Year | 4.72% | 4.26% | ||

| B Shares | w/o CDSC | w/CDSC | ||

1-Year | 1.32% | -2.56% | ||

5-Year | 3.73% | 3.56% | ||

10-Year | 4.10% | 4.10% | ||

| C Shares | NAV | |||

1-Year | 1.49% | |||

5-Year | 3.94% | |||

10-Year | 4.14% | |||

| R Shares | NAV | |||

1-Year | 2.29% | |||

5-Year | 4.72% | |||

10-Year | 4.92% | |||

| Tax-Free Yields | ||||

| A Shares | NAV | Offer | ||

Dividend Yield3 | 4.16% | 3.98% | ||

30-Day Yield3 | 3.51% | — | ||

SEC 30-Day Yield3,4 | — | 3.36% | ||

Taxable-Equivalent Yield4,5 | 5.07% | 4.86% | ||

| B Shares | NAV | |||

Dividend Yield3 | 3.42% | |||

30-Day Yield3 | 2.77% | |||

Taxable-Equivalent Yield5 | 4.00% | |||

| C Shares | NAV | |||

Dividend Yield3 | 3.58% | |||

30-Day Yield3 | 2.96% | |||

Taxable-Equivalent Yield5 | 4.28% | |||

| R Shares | NAV | |||

Dividend Yield3 | 4.37% | |||

SEC 30-Day Yield3 | 3.71% | |||

Taxable-Equivalent Yield5 | 5.36% | |||

| Average Annual Total Returns as of 12/31/07 | ||||

| A Shares | NAV | Offer | ||

1-Year | 2.45% | -1.88% | ||

5-Year | 4.04% | 3.16% | ||

10-Year | 4.57% | 4.12% | ||

| B Shares | w/o CDSC | w/CDSC | ||

1-Year | 1.70% | -2.22% | ||

5-Year | 3.27% | 3.10% | ||

10-Year | 3.95% | 3.95% | ||

| C Shares | NAV | |||

1-Year | 1.86% | |||

5-Year | 3.46% | |||

10-Year | 4.00% | |||

| R Shares | NAV | |||

1-Year | 2.67% | |||

5-Year | 4.25% | |||

10-Year | 4.77% | |||

| Portfolio Statistics | ||

Net Assets ($000) | $225,125 | |

Average Effective Maturity on Securities (Years) | 15.01 | |

Average Duration | 5.69 |

| Expense Ratios | ||||||

| Share Class | Gross Expense Ratios | Net Expense Ratios | As of Date | |||

Class A | 0.91% | 0.90% | 5/31/07 | |||

Class B | 1.67% | 1.65% | 5/31/07 | |||

Class C | 1.46% | 1.45% | 5/31/07 | |||

Class R | 0.71% | 0.70% | 5/31/07 | |||

The expense ratios shown factor in Annual Fund Operating Expenses including management fees and other fees and expenses. The Net Expense Ratios reflect a custodian fee credit from the custodian bank whereby certain fees and expenses are reduced by credits earned on the Fund’s cash on deposit with the bank. There is no guarantee that the Fund will earn such credits in the future. Absent the credit, the Net Expense Ratios would be higher and total returns would be less. These expense ratios may vary from the expense ratios shown elsewhere in this report.

| 1 | Paid December 3, 2007. This is the latest monthly tax-exempt dividend declared during the period ended November 30, 2007. |

| 2 | Paid December 5, 2006. Capital gains and/or ordinary income are subject to federal taxation. |

| 3 | Dividend Yield is the most recent dividend per share (annualized) divided by the appropriate price per share. The SEC 30-Day Yield is computed under an SEC standardized formula and is based on the maximum offer price per share. The 30-Day Yield is computed under the same formula but is based on the Net Asset Value (NAV) per share. The Dividend Yield may differ from the SEC 30-Day Yield because the Fund may be paying out more or less than it is earning and it may not include the effect of amortization of bond premium. |

| 4 | The SEC 30-Day Yield and Taxable-Equivalent Yield on A Shares at NAV applies only to A Shares purchased at no-load pursuant to the Fund’s policy permitting waiver of the A Share load in certain specified circumstances. |

| 5 | The Taxable-Equivalent Yield represents the yield that must be earned on a fully taxable investment in order to equal the yield of the Fund on an after-tax basis at a specified tax rate. With respect to investments that generate qualified dividend income that is taxable at a maximum rate of 15%, the Taxable-Equivalent Yield is lower. The Taxable-Equivalent Yield is based on the Fund’s 30-Day Yield on the indicated date and a combined federal and state income tax rate of 30.8%. |

Semi-Annual Report Page 11

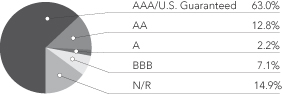

Fund Spotlight as of 11/30/07 Nuveen Michigan Municipal Bond Fund

Bond Credit Quality1,2

Industries2

Tax Obligation/General | 35.9% | |

Tax Obligation/Limited | 13.6% | |

U.S. Guaranteed | 12.9% | |

Water and Sewer | 11.7% | |

Health Care | 10.6% | |

Education and Civic Organizations | 4.6% | |

Other | 10.7% |

| 1 | The percentage of AAA ratings shown in the foregoing chart reflects the AAA ratings on certain bonds insured by AMBAC, FGIC or MBIA as of November 30, 2007. As explained earlier in the Portfolio Managers’ Comments section of this report, one rating agency has reduced the rating for AMBAC to AA, and one or more rating agencies have placed each of these insurers on “negative credit watch”, which may presage one or more rating reductions for such insurer or insurers in the future. If one or more insurers’ ratings are reduced below AAA by these rating agencies, it would likely reduce the effective rating of many of the bonds insured by that insurer or insurers, and thereby reduce the percentage of the portfolio rated AAA from the percentage shown in the foregoing chart. |

| 2 | As a percentage of total investments as of November 30 , 2007. Holdings are subject to change. |

Expense Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including front and back end sales charges (loads) or redemption fees, where applicable; and (2) ongoing costs, including management fees; distribution and service (12b-1) fees, where applicable; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example below is based on an investment of $1,000 invested at the beginning of the period and held for the period.

The information under “Actual Performance,” together with the amount you invested, allows you to estimate actual expenses incurred over the reporting period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.60) and multiply the result by the cost shown for your share class, in the row entitled “Expenses Incurred During Period” to estimate the expenses incurred on your account during this period.

The information under “Hypothetical Performance,” provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expense you incurred for the period. You may use this information to compare the ongoing costs of investing in the Fund and other Funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as front and back end sales charges (loads) or redemption fees, where applicable. Therefore, the hypothetical information is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds or share classes. In addition, if these transactional costs were included, your costs would have been higher.

| Hypothetical Performance | ||||||||||||||||||||||||

| Actual Performance | (5% annualized return before expenses) | |||||||||||||||||||||||

| A Shares | B Shares | C Shares | R Shares | A Shares | B Shares | C Shares | R Shares | |||||||||||||||||

Beginning Account Value (6/01/07) | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | ||||||||

Ending Account Value (11/30/07) | $ | 1,020.20 | $ | 1,016.40 | $ | 1,017.20 | $ | 1,021.30 | $ | 1,020.86 | $ | 1,017.10 | $ | 1,018.10 | $ | 1,021.81 | ||||||||

Expenses Incurred During Period | $ | 4.25 | $ | 8.04 | $ | 7.03 | $ | 3.29 | $ | 4.26 | $ | 8.04 | $ | 7.03 | $ | 3.29 | ||||||||

For each class of the Fund, expenses are equal to the Fund’s annualized net expense ratio of .84%, 1.59%, 1.39% and ..65% for Classes A, B, C and R, respectively, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period).

Semi-Annual Report Page 12

Fund Spotlight as of 11/30/07 Nuveen Missouri Municipal Bond Fund

| Quick Facts | ||||||||

| A Shares | B Shares | C Shares | R Shares | |||||

NAV | $10.98 | $10.99 | $10.97 | $10.99 | ||||

Latest Monthly Dividend1 | $0.0375 | $0.0305 | $0.0325 | $0.0395 | ||||

Latest Capital Gain Distribution2 | $0.0068 | $0.0068 | $0.0068 | $0.0068 | ||||

Inception Date | 8/03/87 | 2/06/97 | 2/02/94 | 2/19/97 |

Returns quoted represent past performance which is no guarantee of future results. Returns without sales charges would be lower if the sales charge were included. Current performance may be higher or lower than the performance shown. Investment returns and principal value will fluctuate so that when shares are redeemed, they may be worth more or less than their original cost. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares. Income is generally exempt from regular federal income taxes. Some income may be subject to state and local taxes and to the federal alternative minimum tax. Capital gains, if any, are subject to tax. For the most recent month-end performance visit www.nuveen.com or call (800) 257-8787.

Returns reflect differences in sales charges and expenses, which are primarily differences in distribution and service fees. Class A shares have a 4.2% maximum sales charge. Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within 18 months of purchase. Class B shares have a CDSC that begins at 5% for redemptions during the first year and declines periodically to 0% over the following five years. Class B shares automatically convert to Class A shares eight years after purchase. Class C shares have a 1% CDSC for redemptions within less than one year, which is not reflected in the one-year total return. Class R shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors. Returns reflect an expense limitation by the Fund’s investment adviser.

| Average Annual Total Returns as of 11/30/07 | ||||

| A Shares | NAV | Offer | ||

1-Year | 1.72% | -2.53% | ||

5-Year | 4.67% | 3.77% | ||

10-Year | 4.69% | 4.24% | ||

| B Shares | w/o CDSC | w/CDSC | ||

1-Year | 0.95% | -2.96% | ||

5-Year | 3.88% | 3.71% | ||

10-Year | 4.07% | 4.07% | ||

| C Shares | NAV | |||

1-Year | 1.17% | |||

5-Year | 4.09% | |||

10-Year | 4.12% | |||

| R Shares | NAV | |||

1-Year | 1.94% | |||

5-Year | 4.88% | |||

10-Year | 4.90% | |||

| Tax-Free Yields | ||||

| A Shares | NAV | Offer | ||

Dividend Yield3 | 4.10% | 3.93% | ||

30-Day Yield3 | 4.00% | — | ||

SEC 30-Day Yield3,4 | — | 3.83% | ||

Taxable-Equivalent Yield4,5 | 5.91% | 5.66% | ||

| B Shares | NAV | |||

Dividend Yield3 | 3.33% | |||

30-Day Yield3 | 3.25% | |||

Taxable-Equivalent Yield5 | 4.80% | |||

| C Shares | NAV | |||

Dividend Yield3 | 3.56% | |||

30-Day Yield3 | 3.45% | |||

Taxable-Equivalent Yield5 | 5.10% | |||

| R Shares | NAV | |||

Dividend Yield3 | 4.31% | |||

SEC 30-Day Yield3 | 4.19% | |||

Taxable-Equivalent Yield5 | 6.19% | |||

Average Annual Total Returns as of 12/31/07

| ||||

| A Shares | NAV | Offer | ||

1-Year | 1.73% | -2.54% | ||

5-Year | 4.14% | 3.26% | ||

10-Year | 4.49% | 4.04% | ||

| B Shares | w/o CDSC | w/CDSC | ||

1-Year | 0.96% | -2.94% | ||

5-Year | 3.37% | 3.20% | ||

10-Year | 3.88% | 3.88% | ||

| C Shares | NAV | |||

1-Year | 1.18% | |||

5-Year | 3.58% | |||

10-Year | 3.92% | |||

| R Shares | NAV | |||

1-Year | 1.95% | |||

5-Year | 4.35% | |||

10-Year | 4.71% | |||

| Portfolio Statistics | ||

Net Assets ($000) | $247,911 | |

Average Effective Maturity on Securities (Years) | 16.17 | |

Average Duration | 6.66 |

| Expense Ratios | ||||||

| Share Class | Gross Expense Ratios | Net Expense Ratios | As of Date | |||

Class A | 0.88% | 0.87% | 5/31/07 | |||

Class B | 1.63% | 1.61% | 5/31/07 | |||

Class C | 1.43% | 1.42% | 5/31/07 | |||

Class R | 0.68% | 0.67% | 5/31/07 | |||

The expense ratios shown factor in Annual Fund Operating Expenses including management fees and other fees and expenses. The Net Expense Ratios reflect a custodian fee credit from the custodian bank whereby certain fees and expenses are reduced by credits earned on the Fund’s cash on deposit with the bank. There is no guarantee that the Fund will earn such credits in the future. Absent the credit, the Net Expense Ratios would be higher and total returns would be less. These expense ratios may vary from the expense ratios shown elsewhere in this report.

| 1 | Paid December 3, 2007. This is the latest monthly tax-exempt dividend declared during the period ended November 30, 2007. |

| 2 | Paid December 5, 2006. Capital gains are subject to federal taxation. |

| 3 | Dividend Yield is the most recent dividend per share (annualized) divided by the appropriate price per share. The SEC 30-Day Yield is computed under an SEC standardized formula and is based on the maximum offer price per share. The 30-Day Yield is computed under the same formula but is based on the Net Asset Value (NAV) per share. The Dividend Yield may differ from the SEC 30-Day Yield and Taxable-Equivalent Yield because the Fund may be paying out more or less than it is earning and it may not include the effect of amortization of bond premium. |

| 4 | The SEC 30-Day Yield and Taxable-Equivalent Yield on A Shares at NAV applies only to A Shares purchased at no-load pursuant to the Fund’s policy permitting waiver of the A Share load in certain specified circumstances. |

| 5 | The Taxable-Equivalent Yield represents the yield that must be earned on a fully taxable investment in order to equal the yield of the Fund on an after-tax basis at a specified tax rate. With respect to investments that generate qualified dividend income that is taxable at a maximum rate of 15%, the Taxable-Equivalent Yield is lower. The Taxable-Equivalent Yield is based on the Fund’s 30-Day Yield on the indicated date and a combined federal and state income tax rate of 32.3%. |

Semi-Annual Report Page 13

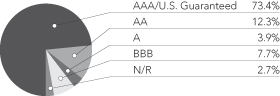

Fund Spotlight as of 11/30/07 Nuveen Missouri Municipal Bond Fund

Bond Credit Quality1,2

Industries2

Tax Obligation/Limited | 19.9% | |

Tax Obligation/General | 16.2% | |

Health Care | 12.2% | |

U.S. Guaranteed | 11.3% | |

Water and Sewer | 6.8% | |

Education and Civic Organizations | 5.6% | |

Long-Term Care | 5.6% | |

Housing/Single Family | 5.3% | |

Consumer Staples | 4.9% | |

Other | 12.2% |

| 1 | The percentage of AAA ratings shown in the foregoing chart reflects the AAA ratings on certain bonds insured by AMBAC, FGIC or MBIA as of November 30, 2007. As explained earlier in the Portfolio Managers’ Comments section of this report, one rating agency has reduced the rating for AMBAC to AA, and one or more rating agencies have placed each of these insurers on “negative credit watch”, which may presage one or more rating reductions for such insurer or insurers in the future. If one or more insurers’ ratings are reduced below AAA by these rating agencies, it would likely reduce the effective rating of many of the bonds insured by that insurer or insurers, and thereby reduce the percentage of the portfolio rated AAA from the percentage shown in the foregoing chart. |

| 2 | As a percentage of total investments as of November 30, 2007. Holdings are subject to change. |

Expense Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including front and back end sales charges (loads) or redemption fees, where applicable; and (2) ongoing costs, including management fees; distribution and service (12b-1) fees, where applicable; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example below is based on an investment of $1,000 invested at the beginning of the period and held for the period.

The information under “Actual Performance,” together with the amount you invested, allows you to estimate actual expenses incurred over the reporting period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.60) and multiply the result by the cost shown for your share class, in the row entitled “Expenses Incurred During Period” to estimate the expenses incurred on your account during this period.

The information under “Hypothetical Performance,” provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expense you incurred for the period. You may use this information to compare the ongoing costs of investing in the Fund and other Funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as front and back end sales charges (loads) or redemption fees, where applicable. Therefore, the hypothetical information is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds or share classes. In addition, if these transactional costs were included, your costs would have been higher.

| Hypothetical Performance | ||||||||||||||||||||||||

| Actual Performance | (5% annualized return before expenses) | |||||||||||||||||||||||

| A Shares | B Shares | C Shares | R Shares | A Shares | B Shares | C Shares | R Shares | |||||||||||||||||

Beginning Account Value (6/01/07) | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | ||||||||

Ending Account Value (11/30/07) | $ | 1,016.10 | $ | 1,012.20 | $ | 1,013.30 | $ | 1,018.10 | $ | 1,020.81 | $ | 1,017.05 | $ | 1,018.05 | $ | 1,021.81 | ||||||||

Expenses Incurred During Period | $ | 4.30 | $ | 8.07 | $ | 7.07 | $ | 3.29 | $ | 4.31 | $ | 8.09 | $ | 7.08 | $ | 3.29 | ||||||||

For each class of the Fund, expenses are equal to the Fund’s annualized net expense ratio of .85%, 1.60%, 1.40% and ..65% for Classes A, B, C and R, respectively, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period).

Semi-Annual Report Page 14

Fund Spotlight as of 11/30/07 Nuveen Ohio Municipal Bond Fund

| Quick Facts | ||||||||

| A Shares | B Shares | C Shares | R Shares | |||||

NAV | $11.24 | $11.22 | $11.21 | $11.22 | ||||

Latest Monthly Dividend1 | $0.0380 | $0.0310 | $0.0330 | $0.0400 | ||||

Latest Capital Gain Distribution2 | $0.0325 | $0.0325 | $0.0325 | $0.0325 | ||||

Inception Date | 6/27/85 | 2/03/97 | 8/03/93 | 2/03/97 |

Returns quoted represent past performance which is no guarantee of future results. Returns without sales charges would be lower if the sales charge were included. Current performance may be higher or lower than the performance shown. Investment returns and principal value will fluctuate so that when shares are redeemed, they may be worth more or less than their original cost. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares. Income is generally exempt from regular federal income taxes. Some income may be subject to state and local taxes and to the federal alternative minimum tax. Capital gains, if any, are subject to tax. For the most recent month-end performance visit www.nuveen.com or call (800) 257-8787.

Returns reflect differences in sales charges and expenses, which are primarily differences in distribution and service fees. Class A shares have a 4.2% maximum sales charge. Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within 18 months of purchase. Class B shares have a CDSC that begins at 5% for redemptions during the first year and declines periodically to 0% over the following five years. Class B shares automatically convert to Class A shares eight years after purchase. Class C shares have a 1% CDSC for redemptions within less than one year, which is not reflected in the one-year total return. Class R shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors. Returns reflect an expense limitation by the Fund’s investment adviser.

| Average Annual Total Returns as of 11/30/07 | ||||

| A Shares | NAV | Offer | ||

1-Year | 1.95% | -2.37% | ||

5-Year | 4.58% | 3.70% | ||

10-Year | 4.58% | 4.14% | ||

| B Shares | w/o CDSC | w/CDSC | ||

1-Year | 1.11% | -2.79% | ||

5-Year | 3.83% | 3.65% | ||

10-Year | 3.96% | 3.96% | ||

| C Shares | NAV | |||

1-Year | 1.42% | |||

5-Year | 4.03% | |||

10-Year | 4.01% | |||

| R Shares | NAV | |||

1-Year | 2.08% | |||

5-Year | 4.79% | |||

10-Year | 4.79% | |||

| Tax-Free Yields | ||||

| A Shares | NAV | Offer | ||

Dividend Yield3 | 4.06% | 3.89% | ||

30-Day Yield3 | 3.59% | — | ||

SEC 30-Day Yield3,4 | — | 3.44% | ||

Taxable-Equivalent Yield4,5 | 5.30% | 5.08% | ||

| B Shares | NAV | |||

Dividend Yield3 | 3.32% | |||

30-Day Yield3 | 2.84% | |||

Taxable-Equivalent Yield5 | 4.19% | |||

| C Shares | NAV | |||

Dividend Yield3 | 3.53% | |||

30-Day Yield3 | 3.04% | |||

Taxable-Equivalent Yield5 | 4.49% | |||

| R Shares | NAV | |||

Dividend Yield3 | 4.28% | |||

SEC 30-Day Yield3 | 3.79% | |||

Taxable-Equivalent Yield5 | 5.60% | |||

| Average Annual Total Returns as of 12/31/07 | ||||

| A Shares | NAV | Offer | ||

1-Year | 2.30% | -1.99% | ||

5-Year | 4.08% | 3.20% | ||

10-Year | 4.42% | 3.98% | ||

| B Shares | w/o CDSC | w/CDSC | ||

1-Year | 1.55% | -2.35% | ||

5-Year | 3.33% | 3.15% | ||

10-Year | 3.81% | 3.81% | ||

| C Shares | NAV | |||

1-Year | 1.77% | |||

5-Year | 3.53% | |||

10-Year | 3.85% | |||

| R Shares | NAV | |||

1-Year | 2.53% | |||

5-Year | 4.29% | |||

10-Year | 4.63% | |||

| Portfolio Statistics | ||

Net Assets ($000) | $525,223 | |

Average Effective Maturity on Securities (Years) | 15.18 | |

Average Duration | 6.47 |

| Expense Ratios | ||||||

| Share Class | Gross Expense Ratios | Net Expense Ratios | As of Date | |||

Class A | 0.98% | 0.98% | 5/31/07 | |||

Class B | 1.73% | 1.73% | 5/31/07 | |||

Class C | 1.53% | 1.53% | 5/31/07 | |||

Class R | 0.78% | 0.78% | 5/31/07 | |||

The expense ratios shown factor in Annual Fund Operating Expenses including management fees and other fees and expenses. These expense ratios may vary from the expense ratios shown elsewhere in this report.

| 1 | Paid December 3, 2007. This is the latest monthly tax-exempt dividend declared during the period ended November 30, 2007. |

| 2 | Paid December 5, 2006. Capital gains are subject to federal taxation. |

| 3 | Dividend Yield is the most recent dividend per share (annualized) divided by the appropriate price per share. The SEC 30-Day Yield is computed under an SEC standardized formula and is based on the maximum offer price per share. The 30-Day Yield is computed under the same formula but is based on the Net Asset Value (NAV) per share. The Dividend Yield may differ from the SEC 30-Day Yield because the Fund may be paying out more or less than it is earning and it may not include the effect of amortization of bond premium. |

| 4 | The SEC 30-Day Yield and Taxable-Equivalent Yield on A Shares at NAV applies only to A Shares purchased at no-load pursuant to the Fund’s policy permitting waiver of the A Share load in certain specified circumstances. |