UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-07831

FMI Funds, Inc.

(Exact name of registrant as specified in charter)

100 East Wisconsin Avenue

Suite 2200

Milwaukee, WI 53202

(Address of principal executive offices) (Zip code)

Ted D. Kellner

Fiduciary Management, Inc.

100 East Wisconsin Avenue

Suite 2200

Milwaukee, WI 53202

(Name and address of agent for service)

(414) 226-4555

(Registrant's telephone number, including area code)

Date of fiscal year end: September 30

Date of reporting period: September 30, 2014

Item 1. Reports to Stockholders.

ANNUAL REPORT

September 30, 2014

FMI Large Cap Fund

(FMIHX)

FMI Common Stock Fund

(FMIMX)

FMI International Fund

(FMIJX)

| |

| |

| |

| FMI Funds |

| Advised by Fiduciary Management, Inc. |

| www.fmifunds.com |

FMI Funds

TABLE OF CONTENTS

| FMI Large Cap Fund | | |

| | | |

| Shareholder Letter | | | 2 |

| | | | |

| Management’s Discussion of Fund Performance | | | 8 |

| | | | |

| Schedule of Investments | | | 9 |

| | | | |

| Industry Sectors | | | 10 |

| | | | |

| | | | |

| | | | |

| FMI Common Stock Fund | | | |

| | | | |

| Shareholder Letter | | | 11 |

| | | | |

| Management’s Discussion of Fund Performance | | | 17 |

| | | | |

| Schedule of Investments | | | 18 |

| | | | |

| Industry Sectors | | | 20 |

| | | | |

| | | | |

| FMI International Fund | | | |

| | | | |

| Shareholder Letter | | | 21 |

| | | | |

| Management’s Discussion of Fund Performance | | | 27 |

| | | | |

| Schedule of Investments | | | 28 |

| | | | |

| Schedule of Forward Currency Contracts | | | 30 |

| | | | |

| Industry Sectors | | | 30 |

| | | | |

| | | | |

| Financial Statements | | | |

| | | | |

| Statements of Assets and Liabilities | | | 31 |

| | | | |

| Statements of Operations | | | 32 |

| | | | |

| Statements of Changes in Net Assets | | | 33 |

| | | | |

| Financial Highlights | | | 34 |

| | | | |

| Notes to Financial Statements | | | 36 |

| | | | |

| | | | |

| Report of Independent Registered Public Accounting Firm | | | 40 |

| | | | |

| Additional Information | | | 40 |

| | | | |

| Expense Example | | | 41 |

| | | | |

| Directors and Officers | | | 42 |

| | | | |

| Disclosure Information | | | 43 |

| | | | |

| Tax Notice | | | 45 |

| | | | |

| Notice of Privacy Policy | | | 45 |

| | | | |

| Householding Notice | | | 45 |

FMI

Large Cap

Fund

September 30, 2014

Dear Fellow Shareholders:

The FMI Large Cap Fund declined 1.77% in the three months ended September 30 compared to a gain of 1.13% for the benchmark Standard & Poor’s 500 Index (S&P 500). Process Industries, Consumer Non-Durables and Electronic Technology all detracted from performance. Potash, Danone and TE Connectivity were all down in the period. Devon and Schlumberger, both energy-related stocks, declined along with the price of oil. GlaxoSmithKline, which has been a disappointing investment, was sold in the quarter, as our thesis that both the industry and the company had changed proved not to be the case. On the flip side, Consumer Services, Distribution Services and Producer Manufacturing were positive contributors. Time Warner, AmerisourceBergen and Berkshire Hathaway gained in the quarter. The bid by Twenty-First Century Fox for Time Warner gave us the opportunity to exit this stock. Despite a few tough days, the market overall has continued its remarkable and almost uninterrupted run, now exceeding 66 months. We haven’t been willing to pay up for stocks… at least not the ones the market favors today. Gilead, Amgen, and Facebook, all very expensive momentum stocks, were among the top ten contributors to the benchmark this quarter. Our research team continues to scour the landscape for good values but these remain fairly rare. We are finding a few special situations and relative values to tide us over until a deeper turbulence surfaces.

As this bull market stretches on, we are encountering some common questions from our shareholders, clients and consultants. Below we take our best shot at addressing them before reviewing a couple of investments.

At what rate should the stock market appreciate?

Before answering this, let’s look at what stocks have achieved over the long term. According to the most reliable data from Ibbotson Associates, from 1926-2013 large company stocks have had a compound annual return of approximately 10%, with price appreciation constituting roughly 6%, and 4% coming from the dividend yield.

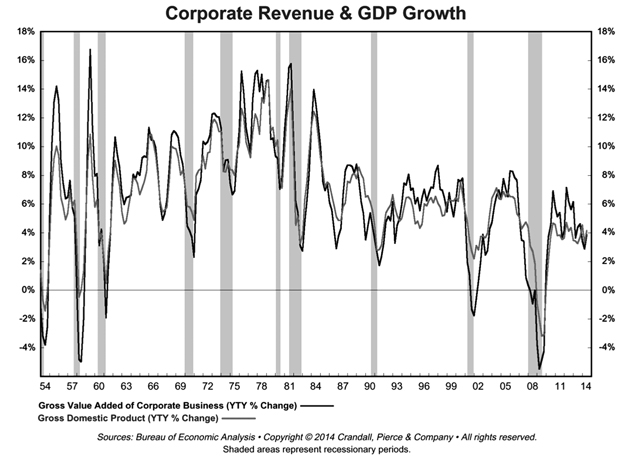

If one views the stock market as a proxy for the growth of corporations (sales and earnings), it is logical to expect the market to appreciate at roughly the rate of corporate sales and earnings growth. It just so happens that sales and earnings for the S&P 500 and broader measures of corporate earnings have, over long periods of time, grown at approximately the same rate of about 6%, although the figure is highly volatile over short time frames. Margins have also gone through years of expansion and contraction, which of course influences the growth rate of earnings compared to sales. In recent years margins have reached all-time highs so it wouldn’t be surprising to see them contract, causing earnings growth to lag sales growth.

Since the S&P 500 total sales typically make up about two-thirds of the economy’s gross domestic product (GDP), and Bureau of Economic Analysis (BEA) compiled corporate revenue figures are an even larger percentage of GDP, it is not surprising that the growth rates for both corporate sales and the economy, as measured by GDP, have been roughly similar over long periods of time. Nearby is a chart of corporate revenue compared to nominal GDP and it is easy to see the high correlation. From 1926 through June of 2014, the nominal GDP growth rate has been 6.1%, although recently it has been much less.

So, the logical or natural rate at which stock prices “should” appreciate appears to be about 6% (total return would include the dividend yield), but of course investors and speculators sometimes do not have long-term time horizons and also, perhaps do not have a deep appreciation of where we are on the valuation-growth rate spectrum. Investor perceptions, manifested in valuations, tend to dominate short-to-intermediate performance of the stock market. Interest rates, inflation, and a whole host of factors play into valuations. If we go back in time, we find some very interesting data. In some sense, we can look at the modern investment world in two phases, post WWII (we’ll start with 1947) up to 1982, and from that period through today. From June of 1947 through June of 1982 the S&P 500 had a total price change of 620%, or 5.8% compounded annually (the total return was 10.6% with dividends… those were the years of big dividends!). S&P 500 earnings grew 6.3% from 1947-1982. In that same period, nominal GDP gained 1238.5%, or 7.7% compounded annually. So, stock market price returns lagged both nominal GDP and corporate earnings.

In the second period, from June of 1982 through June of 2014, the S&P 500 had a total price change of 1688.4%, or 9.2% compounded annually (12.2% with dividends). The S&P 500 earnings grew at roughly the same rate as they did in the prior period. Nominal GDP, on the other hand, gained 417.5%, or just 5.3% compounded. Obviously, the stock market trounced both the economy and earnings in this time frame. Over the last five and a half years alone, the total price change of the S&P 500 was 191.5% (21.5% compounded) compared to nominal GDP growth of just 23.7%1 (3.9% compounded).

In summary, stocks should (over time) roughly match the underlying growth of the economy and the fundamentals of the corporations that constitute the economy. Historically this rate of growth has been approximately 6%. The last few years have been characterized by a significant increase in stock prices relative to the growth in the economy and the underlying performance of U.S. corporations. The result is a stock market that is very expensive. The Leuthold Group data of 48 different valuation measures (most series exceed 60 years) that we tally every quarter puts the average current market valuation in the 9th decile (10 being the most expensive).

_______________

| 1 | Nominal GDP estimated using 3% for the September 2014 quarter. |

Why can’t valuations remain high?

The simple answer is they can… for a while. And a “while” can be pretty long, as we have seen over the last several years. The Fed has had an “emergency” policy in place for six years and while we will spare the reader a rehashing of prior letters which articulate the damaging short- and long-term elements of this approach, it certainly has helped drive stocks higher and make valuations expensive. Each time reported data is weaker than expected it fuels the market to go higher as investors gain confidence that interest rate policies will remain loose. The prevailing sentiment today is that the “Fed has investors’ backs.” Thus, issues that would normally cause the stock market to correct remain at bay. Subpar economic growth, rather than being a negative, is actually the opposite in today’s market. Modest inflation and low interest rates are taken as a given for the future. It is ironic how opposite the sentiment is today from what it was in 1982. This was a period of very high interest and inflation rates and very low valuations. Sentiment was awful. Today, on the other hand, investors are presented with conditions that are essentially the opposite: low inflation, rock bottom interest rates and sky-high valuations. 1982 turned out to be one of the greatest buying opportunities of all time. Logically, how could 2014 also be a great buying opportunity? Yet that is the Wall Street pitch.�� It should come as no surprise that we do not believe it!

Valuations are unlikely to remain high forever. Aside from being tied to the fundamentals of the economy and the companies that make up the economy (and being completely out of sync there) they are tied to sentiment and emotion. Right now the sentiment is that nothing will derail the equity train. Our experience tells us something will. History suggests the same. The fact that so far this market has shrugged off massive destabilization in the Middle East; a new terrorist threat in ISIS (Islamic State in Iraq and Syria); a renewed Cold War; an economic U-turn in Europe, Japan, Brazil and Russia; the failure of Fed Policy; and the lack of any nod to business or free market principles in Washington, should worry rather than embolden investors. Deep down people know that things are not right. How can an economy be right if nearly 37% of the working-age citizens are not working? Real household incomes, except for those at the top, have been stagnant to declining for over a decade. More people than ever are living off the taxpayer. Companies are not investing enough in capital. The past ten years have seen one of the lowest capital investment relative to GDP since records have been kept. Companies are underinvesting in people. New healthcare mandates, higher taxes and a mountain of new regulations all thwart the effort. Instead, companies borrow at manipulated rates and buy back stock, lifting earnings per share (EPS) for Wall Street while fattening management and board paydays. CEOs make nearly ten times what they made 30 years ago relative to the average hourly worker. This income disparity is translated to great wealth disparity by the Fed’s interest rate policies, which make financial asset owners even wealthier. Will this fuel class animosity and a deepened political crisis? What will happen to stock multiples if labor unrest grows? Minorities, particularly African-Americans, have fallen further behind despite all the subsidies, food stamps and other government help. Our answer to this issue is to throw more money over the wall instead of addressing cause and effect. How will stock markets react to the next Ferguson, Missouri? The market sees through all of this until it doesn’t. We don’t have any idea when this will happen, and frankly, we wouldn’t be that worried about it (from a stock market perspective) were it not for the high valuation levels. Low valuations favor the optimist; high valuations favor the skeptic.

Why are cash levels elevated?

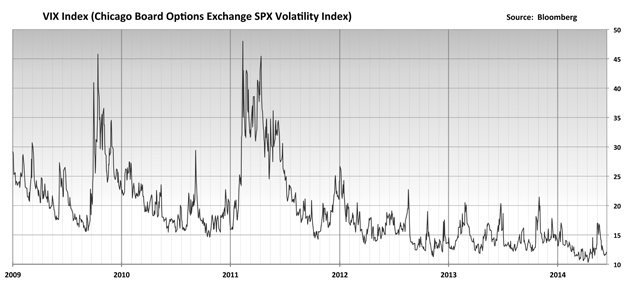

Cash levels are elevated because a number of stocks have reached full value and have been sold, and a number of others have been trimmed as they approach full value. The difference between today and other points in FMI’s history is that just about every sector of the market is elevated and very few companies are trading at significant discounts to fair value. This bull market has seen almost no corrections, and in recent years has not delivered the sort of industry or sector declines that are normal even in an overall rising market. This has prevented us from reloading and staying fully invested. Volatility has been below-average in recent years as can be seen by the nearby chart.

What would it take for you to have a stronger period of outperformance?

To expect stocks to appreciate at 15-20% when the “natural” growth rate of the economy and earnings is around 6% is completely unrealistic. When a market phase is extended (this bull run is now over 66 months old, making it one of the longest on record) people believe it is a new paradigm. But it never is, because humans will always be susceptible to the emotions of greed and fear. We are very confident that opportunities will eventually present themselves through a general market decline or increased sector volatility. In the meantime, we are relegated to special situations or relative value ideas. It is unlikely we would outperform in a market that continues to rise uninterruptedly. Historically, we have performed very well in choppy and down markets. Nobody cheers for poor markets, but these periods are inevitable and we would be surprised if they weren’t a source of outperformance. So, we need to be patient and avoid the temptation to play somebody else’s game.

Why not just invest in an index fund?

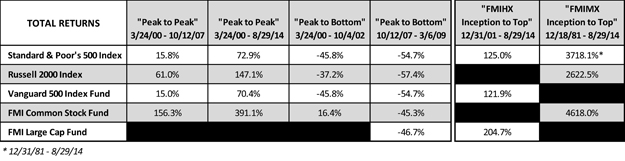

There are times and circumstances that may make sense for this approach. If you don’t have the time, mindset or wherewithal to identify truly talented active managers, then buying an index fund might be a reasonable approach. After a market has been crushed, when nearly all stocks are cheap, is often an advantageous time. There is a tendency, however, for investors to believe it is less risky to buy an index fund. As with any asset, an index fund can become overvalued when the underlying stocks become overvalued. These types of funds are particularly risky at cycle highs, which we believe we are near today. We remember like it was yesterday when John Bogle, Chairman and CEO of Vanguard and the unofficial spokesman for passive investing, stood on the proverbial mountaintop in 1999 telling everyone they should index. Let’s look at what that did for investors: From the peak in March of 2000 to the trough in October of 2002, the S&P 500 (and the Vanguard 500) declined approximately 45.8%. The Russell 2000 Index, a benchmark for smaller capitalization stocks, fell by 37.2%. The FMI Large Cap Fund had not yet begun in early 2000, but the FMI Common Stock Fund was well-established. The FMI Common Stock Fund gained 16.4% during this time frame. If we go “peak to peak” (March of 2000 to October of 2007) the S&P 500 gained 15.8% and the Russell 2000 advanced 61.0%. The FMI Common Stock Fund was up 156.3%. Below is a table looking at returns following peaks, as well as columns for the FMI Large Cap Fund and FMI Common Stock Fund since their respective inception dates.

As is our custom in September, we highlight a couple of investments.

Progressive Corporation (PGR)

(Analyst: Matthew Goetzinger)

Description

Progressive is one of the largest U.S. auto insurers with approximately 9% market share. The company writes personal auto insurance (90% of net premiums written) on both an agency and direct basis, and has consistently achieved an industry-leading low 90% combined ratio. The residual 10% of net premiums written is accounted for by the company’s small commercial auto book. A.M. Best gives Progressive an A+ rating.

Good Business

| | • | Progressive operates in a consolidated and rational market where the top five companies control over 50% of industry premiums. Consistent, time-proven pricing and reserving methodologies, as well as scale, enable the larger and more sophisticated industry players to grow faster than the broader market. |

| | • | Auto insurance is a mandatory consumer coverage which results in predictable and recurring premium volumes. Progressive achieves a solid customer retention rate given the company’s mix of business. |

| | • | Industry-leading policy growth and a low-cost distribution model outpace marketing and advertising spending to generate a high-teens underwriting return on investment (ROI). |

| | • | Progressive has one of the industry’s strongest balance sheets. The company has over $1 billion of excess capital and generates close to $2 billion of operating cash flow annually. The free cash flow yield is in excess of 10%. |

Valuation

| | • | Progressive’s normalized return on equity (ROE) should be in the 18-20% range, implying a target price-to-book multiple (P/B) of close to 3.0 times. On this basis, the stock’s fair value is approximately 50% higher than today’s price. |

| | • | Over the past five years, Progressive has held a median P/B of 2.2 times, ranging from a low of 1.8 times to a high of 2.6 times. Presently the shares trade at 2.0 times book value. |

| | • | The stock’s current price-to-earnings (P/E) multiple is slightly higher than the 5-year range, but earnings are relatively depressed. |

| | • | Excluding excess balance sheet capital, Progressive trades for less than 10.0 times normalized earnings. |

| | • | The 2011 acquisition of Esurance by Allstate, and the 1996 consolidation of GEICO by Berkshire Hathaway, both indicate a private market value of at least 2.5 times book value for Progressive. |

Management

| | • | Consistent with the overall conservative posture of the company, the executive team is incentivized by a sensible compensation plan. |

| | • | The company’s “Gainsharing” program measures performance of the underwriting business, and uses the same performance criteria for all employee bonuses as well as the company’s annual variable dividend. |

| | • | Progressive’s CEO, Glenn Renwick, has 25 years of experience at the company including a variety of operating and leadership roles such as President of a number of operating units, head of the consumer marketing group, and Chief Information Officer. Mr. Renwick has been CEO since 2000. |

Investment Thesis

Measured by underwriting profits, Progressive is the second largest U.S. auto insurer. The company is also a high-quality, technological innovator that has historically grown in a consistent manner. We expect this to continue due to significant scale, a low-cost direct business model, and tremendous pricing analytics which should enable Progressive to earn predictable underwriting profits. The stock is trading at a discount to its historical book multiple, and where it could trade, provided the business develops as we envision.

Honeywell International Inc. (HON)

(Analyst: Andy Ramer)

Description

Honeywell is a diversified global technology and manufacturing company organized into three strategic business groups: Aerospace (avionics, power, turbochargers) – 39% of sales and 43% of profit; Automation & Control Solutions (control products and services) – 44% and 38%; and Performance Materials & Technologies (catalysts, absorbents, refrigerants) – 17% and 19%.

Good Business

| | • | Honeywell has established market-leading positions due to their innovative technology and excellent support and service network. The company has consequently developed a large installed base of equipment. |

| | • | This installed base of equipment is mission-critical and creates the opportunity for follow-on sales in the aftermarket. Recurring revenue and revenues in backlog account for approximately 50% of sales. |

| | • | Honeywell’s return on invested capital (ROIC) is greater than 20%. |

| | • | The businesses are generally easy to understand. |

| | • | Operating and financial performance has been turned around by focusing on factors that they can control rather than relying on significant end market tailwinds or below-the-line items. |

| | • | The long-term debt-to-capital ratio net of cash is only 13% and the leverage ratio is a modest 0.4 times. The pension plan is fully funded. Honeywell is a strong cash generator. |

Valuation

| | • | This is an above-average business, with ROIC greater than that of the S&P 500, and net debt-to-capital less than that of the S&P 500. It trades at an average valuation in line with, or at a slight discount to, the S&P 500. |

| | • | Shares are valued at 16.8 times the fiscal year 1 earnings per share estimate, which is slightly above their 10-year average multiple of 15.8 times. Other high quality industrials like 3M, Danaher, Emerson, ITW, and Rockwell Automation trade for 19.0-20.0 times. |

| | • | The enterprise value-to-2014 (estimate) sales multiple is 1.9 times, relative to a forecast operating margin of 15.5%. Margins are several hundred basis points below peers, and should rise significantly. |

| | • | If Honeywell can grow earnings per share at a 12% compound annual rate over the next five years (which would be at the mid-point of their target range) and the market re-rates the company to 18.0 times, then the shares offer 14% compound annual appreciation potential. The dividend yields 1.9%. |

Management

| | • | Since joining Honeywell in July of 2002, Chairman & CEO Dave Cote has reinvigorated the new product pipeline, shed assets that he deemed were non-core, made acquisitions that strengthened the core, and addressed legacy liabilities. |

| | • | The company has a strong and deep management and an excellent corporate culture. They are conservatively managed from a business, accounting, and balance sheet perspective. |

| | • | Honeywell is an example of where behavior follows incentives. Compensation is tied to ROI, working capital turnover, free cash flow, margin expansion, and revenue. |

Investment Thesis

Honeywell’s product and service offerings are aligned with important global macro trends – energy efficiency, clean energy generation, safety and security, urbanization/High Growth Region development, and customer productivity. The portfolio is balanced between short, mid-range and long, when viewed from a business cycle standpoint. Successful execution should drive organic growth above the multi-industrial average and the valuation is reasonable in a very expensive market.

Thank you for your support of the FMI Large Cap Fund.

100 E. Wisconsin Ave., Suite 2200 • Milwaukee, WI 53202 • 414-226-4555

www.fmifunds.com

This shareholder letter is unaudited.

FMI Large Cap Fund

MANAGEMENT’S DISCUSSION OF FUND PERFORMANCE

During the fiscal year ended September 30, 2014, the FMI Large Cap Fund (the “Fund”) had a total return of 15.77%. The benchmark S&P 500 returned 19.73% in the same period. From a sector standpoint, Electronic Technology, Consumer Non-Durables and Transportation all hurt relative performance. The primary reason Electronic Technology underperformed was our underweighting. The lagging performance of the Consumer Non-Durable sector was largely due to stock selection, particularly Danone, which was down over the year. Expeditors International performed poorly over the past twelve months, hurting the Transportation sector. A higher-than-normal cash levels also hurt performance. Cash has been elevated due to the lack of attractive new ideas and this has been a significant drag on performance over the past two years. On the positive side, Consumer Services, Finance and Energy Minerals all aided relative results. Time Warner, benefitting from a bid by Twenty-First Century Fox, performed strongly for the Consumer Services sector. Bank of New York drove the outperformance in the Finance area. Strong performance by Devon and an underweighted position in Energy contributed to the positive sector results in Energy. Over the past twelve months a number of stocks were sold: Sysco, Willis Group, Wal-Mart, Covidien, Illinois Tool Works, Time Warner and GlaxoSmithKline. Sysco, Willis Group, Wal-Mart and GlaxoSmithKline were sold primarily because of a reassessment of the long term fundamentals. The others were due to valuation. Investments added in the period included Unilever, Progressive Corp., Ross Stores, Omnicom Group, Honeywell, Comcast Corp. and eBay. At September 30, 2014, significantly overweighted sectors included Producer Manufacturing, Commercial Services and Distribution Services. Heavily underweighted areas included Electronic Technology, Health Technology and Utilities.

Strong performance across a number of sectors but particularly in some of the more speculative technology and biotechnology areas helped drive another outstanding year in the S&P 500. The market has gone five and a half years without a meaningful correction. Valuations are near the upper end of historical parameters. Easy monetary policy appears to have been a significant driver of stock market performance in recent years. The economy seems to be somewhat better but has grown at less than half of its long term historical rate. The unemployment rate has also improved, but the labor participation rate remains at a very low level and an extraordinarily high number of citizens are dependent on government support. Companies have been restrained with respect to investing in both capital equipment and labor, which has resulted in less than satisfactory internal growth rates. The economies in Europe, China, Brazil, Japan and Russia have all weakened. Debt levels remain very high in all of these economies as well as in the United States. Geopolitical problems have escalated over the past year. This, combined with less than average growth and very high valuations makes us cautious on the stock market in the short run. We continue to believe, however, that stocks have the best chance to adjust to a dynamic environment over the long run. The Fund sells at a discount to the S&P 500 on most valuation measures.

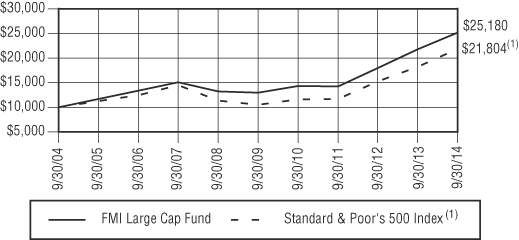

COMPARISON OF CHANGE IN VALUE OF $10,000 INVESTMENT IN

FMILARGE CAP FUND AND STANDARD & POOR’S 500 INDEX(1)

AVERAGE ANNUALIZED TOTAL RETURN

| | | | | Since |

| | | | | Inception |

| | 1-Year | 5-Year | 10-Year | 12/31/01 |

| FMI Large Cap Fund | 15.77% | 14.25% | 9.67% | 8.94% |

| S&P 500 Index | 19.73% | 15.70% | 8.11% | 6.45% |

The graph and the table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Performance data quoted represents past performance; past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of a Fund may be lower or higher than the performance quoted. The total returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Total return includes change in share prices and in each case includes reinvestments of any dividends, interest and capital gain distributions. Performance data current to the most recent month-end may be obtained by visiting www.fmifunds.com or by calling 1-800-811-5311.

| (1) | The Standard & Poor’s 500 Index consists of 500 selected common stocks, most of which are listed on the New York Stock Exchange. The Standard & Poor’s Ratings Group designates the stocks to be included in the Index on a statistical basis. A particular stock’s weighting in the Index is based on its relative total market value (i.e., its market price per share times the number of shares outstanding). Stocks may be added or deleted from the Index from time to time. |

An investment cannot be made directly into an index.

This page is unaudited.

FMI Large Cap Fund

SCHEDULE OF INVESTMENTS

| Shares | | | | Cost | | | Value | |

| | | | | | | | | |

| COMMON STOCKS — 91.6% (a) | | | | | | |

| | | | | | | |

| COMMERCIAL SERVICES SECTOR — 5.2% | | | | | | |

| | | Advertising/Marketing Services — 3.0% | | | | | | |

| | 3,966,000 | | Omnicom Group Inc. | | $ | 277,353,255 | | | $ | 273,098,760 | |

| | | | Miscellaneous Commercial Services — 2.2% | | | | | | | | |

| | 2,890,000 | | Cintas Corp. | | | 72,227,745 | | | | 204,005,100 | |

| | | | | | | | | |

| CONSUMER NON-DURABLES SECTOR — 9.7% | | | | | | | | |

| | | | Food: Major Diversified — 7.3% | | | | | | | | |

| | 27,475,000 | | Danone S.A. - SP-ADR | | | 388,621,919 | | | | 368,165,000 | |

| | 4,150,000 | | Nestle’ S.A. - SP-ADR | | | 222,649,146 | | | | 305,564,500 | |

| | | | | | | 611,271,065 | | | | 673,729,500 | |

| | | | Household/Personal Care — 2.4% | | | | | | | | |

| | 5,287,000 | | Unilever PLC - SP-ADR | | | 212,079,561 | | | | 221,525,300 | |

| | | | | | | | | |

| CONSUMER SERVICES SECTOR — 5.1% | | | | | | | | |

| | | | Cable/Satellite TV — 3.0% | | | | | | | | |

| | 5,200,000 | | Comcast Corp. - Class A | | | 284,589,282 | | | | 279,656,000 | |

| | | | Other Consumer Services - 2.1% | | | | | | | | |

| | 3,460,000 | | eBay Inc.* | | | 184,248,517 | | | | 195,939,800 | |

| | | | | | | | | |

| DISTRIBUTION SERVICES SECTOR — 4.0% | | | | | | | | |

| | | | Medical Distributors — 4.0% | | | | | | | | |

| | 4,815,000 | | AmerisourceBergen Corp. | | | 161,061,013 | | | | 372,199,500 | |

| | | | | | | | | |

| ELECTRONIC TECHNOLOGY SECTOR — 2.8% | | | | | | | | |

| | | | Electronic Components — 2.8% | | | | | | | | |

| | 4,705,000 | | TE Connectivity Ltd. | | | 107,496,842 | | | | 260,139,450 | |

| | | | | | | | | |

| ENERGY MINERALS SECTOR — 4.3% | | | | | | | | |

| | | | Oil & Gas Production — 4.3% | | | | | | | | |

| | 5,840,000 | | Devon Energy Corp. | | | 355,441,165 | | | | 398,171,200 | |

| | | | | | | | | |

| FINANCE SECTOR — 15.6% | | | | | | | | |

| | | | Financial Conglomerates — 3.7% | | | | | | | | |

| | 3,909,000 | | American Express Co. | | | 167,357,366 | | | | 342,193,860 | |

| | | | Major Banks — 8.9% | | | | | | | | |

| | 12,010,000 | | Bank of New York Mellon Corp. | | | 291,634,831 | | | | 465,147,300 | |

| | 7,010,000 | | Comerica Inc. | | | 216,460,410 | | | | 349,518,600 | |

| | | | | | | 508,095,241 | | | | 814,665,900 | |

| | | | Property/Casualty Insurance — 3.0% | | | | | | | | |

| | 10,830,000 | | Progressive Corp. | | | 269,585,441 | | | | 273,782,400 | |

| | | | | | | | | |

| HEALTH SERVICES SECTOR — 5.1% | | | | | | | | |

| | | | Managed Health Care — 5.1% | | | | | | | | |

| | 5,421,000 | | UnitedHealth Group Inc. | | | 395,782,179 | | | | 467,561,250 | |

| | | | | | | | | |

| INDUSTRIAL SERVICES SECTOR — 4.4% | | | | | | | | |

| | | | Oilfield Services/Equipment — 4.4% | | | | | | | | |

| | 3,950,000 | | Schlumberger | | | 260,767,543 | | | | 401,675,500 | |

| | | | | | | | | |

| PROCESS INDUSTRIES SECTOR — 5.9% | | | | | | | | |

| | | | Chemicals: Agricultural — 5.9% | | | | | | | | |

| | 15,640,000 | | Potash Corp. of Saskatchewan Inc. | | | 586,668,893 | | | | 540,518,400 | |

| | | | | | | | | |

| PRODUCER MANUFACTURING SECTOR — 15.1% | | | | | | | | |

| | | | Industrial Conglomerates — 12.2% | | | | | | | | |

| | 2,500,000 | | 3M Co. | | | 178,166,900 | | | | 354,200,000 | |

| | 3,402,000 | | Berkshire Hathaway Inc. - Cl B* | | | 243,591,013 | | | | 469,952,280 | |

| | 3,230,000 | | Honeywell International Inc. | | | 307,340,217 | | | | 300,777,600 | |

| | | | | | | 729,098,130 | | | | 1,124,929,880 | |

SCHEDULE OF INVESTMENTS (Continued)

| Shares or Principal Amount | | Cost | | | Value | |

| | | | | | | |

| COMMON STOCKS — 91.6% (a) (Continued) | | | | | | |

| | | Trucks/Construction/Farm Machinery — 2.9% | | | | | | |

| | 4,675,000 | | PACCAR Inc. | | $ | 213,920,376 | | | $ | 265,890,625 | |

| | | | | | | | | |

| RETAIL TRADE SECTOR — 2.8% | | | | | | | | |

| | | | Apparel/Footwear Retail — 2.8% | | | | | | | | |

| | 3,430,000 | | Ross Stores Inc. | | | 232,823,199 | | | | 259,239,400 | |

| | | | | | | | | |

| TECHNOLOGY SERVICES SECTOR — 8.9% | | | | | | | | |

| | | | Information Technology Services — 5.2% | | | | | | | | |

| | 5,870,000 | | Accenture PLC | | | 307,651,961 | | | | 477,348,400 | |

| | | | Packaged Software — 3.7% | | | | | | | | |

| | 7,430,000 | | Microsoft Corp. | | | 222,830,276 | | | | 344,454,800 | |

| | | | | | | | | |

| TRANSPORTATION SECTOR — 2.7% | | | | | | | | |

| | | | Air Freight/Couriers — 2.7% | | | | | | | | |

| | 6,150,000 | | Expeditors International of Washington Inc. | | | 231,833,459 | | | | 249,567,000 | |

| | | | Total common stocks | | | 6,392,182,509 | | | | 8,440,292,025 | |

| | | | | | | | | | | | |

| | | | | | | | | |

| SHORT-TERM INVESTMENTS — 8.3% (a) | | | | | | | | |

| | | | Commercial Paper — 8.3% | | | | | | | | |

| $ | 766,900,000 | | U.S. Bank N.A., 0.03%, due 10/01/14 | | | 766,900,000 | | | | 766,900,000 | |

| | | | Total investments — 99.9% | | $ | 7,159,082,509 | | | | 9,207,192,025 | |

| | | | Other assets, less liabilities — 0.1% (a) | | | | | | | 10,206,497 | |

| | | | TOTAL NET ASSETS — 100.0% | | | | | | $ | 9,217,398,522 | |

| * | Non-income producing security. |

| (a) | Percentages for the various classifications relate to net assets. |

PLC – Public Limited Company

SP-ADR – Sponsored American Depositary Receipt

The accompanying notes to financial statements are an integral part of this schedule.

INDUSTRY SECTORS

as of September 30, 2014 (Unaudited)

FMI

Common Stock

Fund

September 30, 2014

Dear Fellow Shareholders:

The FMI Common Stock Fund declined 4.90% in the three months ended September 30 compared to a fall of 7.36% for the benchmark Russell 2000 Index. Health Services, Process Industries, and Health Technology all detracted from performance. Hanger, H.B. Fuller, Lindsay and Valmont Industries were all down in the period. On the positive side, Industrial Services, Energy Minerals and Finance all aided relative performance, primarily because of our underweighting and stock selection. Individual securities that did relatively well in the period included Dresser–Rand Group, MKS Instruments and Dun & Bradstreet. Small cap stocks underperformed larger cap stocks in the quarter and while down, have yet to experience a significant correction. The market has continued its remarkable and almost uninterrupted run, now exceeding 66 months. We haven’t been willing to pay up for stocks… at least not the ones the market favors today. Puma Biotechology, InterMune, Inc., and Avanir Pharmaceuticals were the top three contributors to the benchmark this quarter. Each one has years of losses, a high cash burn rate and is not projected to make money any time soon. It is an indication of the speculative nature of this market. Our research team continues to scour the landscape for good values but these are still fairly rare. We are finding a few special situations and relative values to tide us over until turbulence resurfaces. Perhaps a continuation of the weakness present at the end of the quarter will give us more attractive opportunities.

The longer the market goes without a large correction, the more we encounter some common questions from our shareholders, clients and consultants. Below we take our best shot at addressing them before reviewing a couple of investments.

At what rate should the stock market appreciate?

Before answering this, let’s look at what stocks have achieved over the long term. According to the most reliable data from Ibbotson Associates, from 1926-2013 large company stocks have had a compound annual return of approximately 10%, with price appreciation constituting roughly 6%, and 4% coming from the dividend yield.

If one views the stock market as a proxy for the growth of corporations (sales and earnings), it is logical to expect the market to appreciate at roughly the rate of corporate sales and earnings growth. It just so happens that sales and earnings for the S&P 500 and broader measures of corporate earnings have, over long periods of time, grown at approximately the same rate of about 6%, although the figure is highly volatile over short time frames. Margins have also gone through years of expansion and contraction, which of course influences the growth rate of earnings compared to sales. In recent years margins have reached all-time highs so it wouldn’t be surprising to see them contract, causing earnings growth to lag sales growth.

Since the S&P 500 total sales typically make up about two-thirds of the economy’s gross domestic product (GDP), and Bureau of Economic Analysis (BEA) compiled corporate revenue figures are an even larger percentage of GDP, it is not surprising that the growth rates for both corporate sales and the economy, as measured by GDP, have been roughly similar over long periods of time. Nearby is a chart of corporate revenue compared to nominal GDP and it is easy to see the high correlation. From 1926 through June of 2014, the nominal GDP growth rate has been 6.1%, although recently it has been much less.

So, the logical or natural rate at which stock prices “should” appreciate appears to be about 6% (total return would include the dividend yield), but of course investors and speculators sometimes do not have long-term time horizons and also, perhaps do not have a deep appreciation of where we are on the valuation-growth rate spectrum. Investor perceptions, manifested in valuations, tend to dominate short-to-intermediate performance of the stock market. Interest rates, inflation, and a whole host of factors play into valuations. If we go back in time, we find some very interesting data. In some sense, we can look at the modern investment world in two phases, post WWII (we’ll start with 1947) up to 1982, and from that period through today. From June of 1947 through June of 1982 the S&P 500 had a total price change of 620%, or 5.8% compounded annually (the total return was 10.6% with dividends… those were the years of big dividends!). S&P 500 earnings grew 6.3% from 1947-1982. In that same period, nominal GDP gained 1238.5%, or 7.7% compounded annually. So, stock market price returns lagged both nominal GDP and corporate earnings.

In the second period, from June of 1982 through June of 2014, the S&P 500 had a total price change of 1688.4%, or 9.2% compounded annually (12.2% with dividends). The S&P 500 earnings grew at roughly the same rate as they did in the prior period. Nominal GDP, on the other hand, gained 417.5%, or just 5.3% compounded. Obviously, the stock market trounced both the economy and earnings in this time frame. Over the last five and a half years alone, the total price change of the S&P 500 was 191.5% (21.5% compounded) compared to nominal GDP growth of just 23.7%1 (3.9% compounded).

In summary, stocks should (over time) roughly match the underlying growth of the economy and the fundamentals of the corporations that constitute the economy. Historically this rate of growth has been approximately 6%. The last few years have been characterized by a significant increase in stock prices relative to the growth in the economy and the underlying performance of U.S. corporations. The result is a stock market that is very expensive. The Leuthold Group data of 48 different valuation measures (most series exceed 60 years) that we tally every quarter puts the average current market valuation in the 9th decile (10 being the most expensive).

_______________

| 1 | Nominal GDP estimated using 3% for the September 2014 quarter. |

Why can’t valuations remain high?

The simple answer is they can… for a while. And a “while” can be pretty long, as we have seen over the last several years. The Fed has had an “emergency” policy in place for six years and while we will spare the reader a rehashing of prior letters which articulate the damaging short- and long-term elements of this approach, it certainly has helped drive stocks higher and make valuations expensive. Each time reported data is weaker than expected it fuels the market to go higher as investors gain confidence that interest rate policies will remain loose. The prevailing sentiment today is that the “Fed has investors’ backs.” Thus, issues that would normally cause the stock market to correct remain at bay. Subpar economic growth, rather than being a negative, is actually the opposite in today’s market. Modest inflation and low interest rates are taken as a given for the future. It is ironic how opposite the sentiment is today from what it was in 1982. This was a period of very high interest and inflation rates and very low valuations. Sentiment was awful. Today, on the other hand, investors are presented with conditions that are essentially the opposite: low inflation, rock bottom interest rates and sky-high valuations. 1982 turned out to be one of the greatest buying opportunities of all time. Logically, how could 2014 also be a great buying opportunity? Yet that is the Wall Street pitch. It should come as no surprise that we do not believe it!

Valuations are unlikely to remain high forever. Aside from being tied to the fundamentals of the economy and the companies that make up the economy (and being completely out of sync there) they are tied to sentiment and emotion. Right now the sentiment is that nothing will derail the equity train. Our experience tells us something will. History suggests the same. The fact that so far this market has shrugged off massive destabilization in the Middle East; a new terrorist threat in ISIS (Islamic State in Iraq and Syria); a renewed Cold War; an economic U-turn in Europe, Japan, Brazil and Russia; the failure of Fed Policy; and the lack of any nod to business or free market principles in Washington, should worry rather than embolden investors. Deep down people know that things are not right. How can an economy be right if nearly 37% of the working-age citizens are not working? Real household incomes, except for those at the top, have been stagnant to declining for over a decade. More people than ever are living off the taxpayer. Companies are not investing enough in capital. The past ten years have seen the lowest capital investment relative to GDP since records have been kept. Companies are underinvesting in people. New healthcare mandates, higher taxes and a mountain of new regulations all thwart the effort. Instead, companies borrow at manipulated rates and buy back stock, lifting earnings per share (EPS) for Wall Street while fattening management and board paydays. CEOs make nearly ten times what they made 30 years ago relative to the average hourly worker. This income disparity is translated to great wealth disparity by the Fed’s interest rate policies, which make financial asset owners even wealthier. Will this fuel class animosity and a deepened political crisis? What will happen to stock multiples if labor unrest grows? Minorities, particularly African-Americans, have fallen further behind despite all the subsidies, food stamps and other government help. Our answer to this issue is to throw more money over the wall instead of addressing cause and effect. How will stock markets react to the next Ferguson, Missouri? The market sees through all of this until it doesn’t. We don’t have any idea when this will happen, and frankly, we wouldn’t be that worried about it (from a stock market perspective) were it not for the high valuation levels. Low valuations favor the optimist; high valuations favor the skeptic.

Why are cash levels elevated?

Cash levels are elevated because a number of stocks have reached full value and have been sold, and a number of others have been trimmed as they approach full value. The difference between today and other points in FMI’s history is that just about every sector of the market is elevated and very few companies are trading at significant discounts to fair value. This bull market has seen almost no corrections, and in recent years has not delivered the sort of industry or sector declines that are normal even in an overall rising market. This has prevented us from reloading and staying fully invested. Volatility has been below-average in recent years as can be seen by the nearby chart.

What would it take for you to have a stronger period of outperformance?

To expect stocks to appreciate at 15-20% when the “natural” growth rate of the economy and earnings is around 6% is completely unrealistic. When a market phase is extended (this bull run is now over 66 months old, making it one of the longest on record) people believe it is a new paradigm. But it never is, because humans will always be susceptible to the emotions of greed and fear. We are very confident that opportunities will eventually present themselves through a general market decline or increased sector volatility. In the meantime, we are relegated to special situations or relative value ideas. It is unlikely we would outperform in a market that continues to rise uninterruptedly. Historically, we have performed very well in choppy and down markets. Nobody cheers for poor markets, but these periods are inevitable and we would be surprised if they weren’t a source of outperformance. So, we need to be patient and avoid the temptation to play somebody else’s game.

Why not just invest in an index fund?

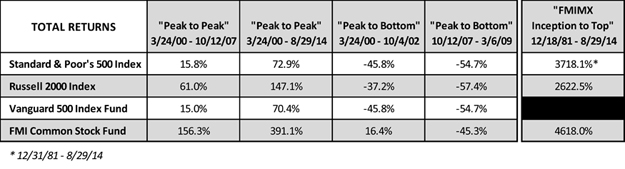

There are times and circumstances that may make sense for this approach. If you don’t have the time, mindset or wherewithal to identify truly talented active managers, then buying an index fund might be a reasonable approach. After a market has been crushed, when nearly all stocks are cheap, it is often an advantageous time. There is a tendency, however, for investors to believe it is less risky to buy an index fund. As with any asset, an index fund can become overvalued when the underlying stocks become overvalued. These types of funds are particularly risky at cycle highs, which we believe we are near today. We remember like it was yesterday when John Bogle, Chairman and CEO of Vanguard and the unofficial spokesman for passive investing, stood on the proverbial mountaintop in 1999 telling everyone they should index. Let’s look at what that did for investors: From the peak in March of 2000 to the trough in October of 2002, the S&P 500 (and the Vanguard 500) declined approximately 45.8%. The Russell 2000, a benchmark for smaller capitalization stocks, fell by 37.2%. The FMI Common Stock Fund gained 16.4% during this time frame. If we go “peak to peak” (March of 2000 to October of 2007) the S&P 500 gained 15.8% and the Russell 2000 advanced 61.0%. The FMI Common Stock Fund was up 156.3%. Below is a table looking at returns following peaks, as well as a column for the FMI Common Stock Fund since its inception.

As is our custom in September, we highlight a couple of investments.

UniFirst Corporation (UNF)

(Analyst: Rob Helf)

Description

Boston-based UniFirst is the third largest uniform rental provider in North America with approximately 8% of market share in a $16 billion market. The company’s primary business is to design, manufacture and market company uniforms for rental, and then clean, maintain and repair them on a weekly basis.

Good Business

| | • | The largest four participants control less than 50% of the industry; there is plenty of room for consolidation. UniFirst has demonstrated skill in making tuck-in acquisitions. |

| | • | The industry has historically grown faster than GDP. |

| | • | The revenue model is generally recurring, with 5-year contracts and price escalators. |

| | • | The company has no customers comprising greater than 1% of overall revenues. |

| | • | The economics of a rental program are profitable for both UniFirst and the customer when compared to an in-house uniform program. |

| | • | Over the past ten years, revenues and earnings per share (EPS) have grown at 8% and 14%, respectively. We expect approximately 9-10% earnings growth over the next five years. |

| | • | Excluding unneeded cash ($6.50 per share), UniFirst generates a low double-digit return on invested capital (ROIC). |

| | • | The company has historically generated free cash flow at 90% of net income. |

Valuation

| | • | UniFirst trades at 16.3 times and 15.0 times fiscal 2015 (August) and 2016 EPS estimates, respectively. Excluding excess cash, the multiple is about 6% cheaper. |

| | • | Historically, the company has traded at 15.0 times next 12 months earnings, in a range of 12.6 to 17.4 times. |

| | • | On an enterprise value-to-sales basis, the company is valued at 1.3 times, which is above its historical average of 1.1 times; however, it is attractive relative to the 13-14% margins it currently generates. |

| | • | UniFirst trades at a discount to its competitors. |

Management

| | • | Ron Croatti is Chairman, President and CEO. He has been part of UniFirst since 1965. He became CEO in 1991 and President in 1995. Ron’s family started the company in 1936 as an industrial laundry/delivery company. He and his family have a 25% ownership interest in the company. |

| | • | Steven Sintros has been VP and CFO since 2009. He has been with the company since February of 2004 and served as its Corporate Controller until January 13, 2009. He previously served as manager with Ernst & Young LLP and Arthur Andersen LLP. |

| | • | Bruce P. Boynton is Senior VP, Operations and is also COO of the Canadian operations. |

Investment Thesis

UniFirst is one of the most profitable participants in the uniform rental industry, primarily by focusing on the details of this simple but necessary business. Most companies that have a margin structure and growth profile like UniFirst trade at a significant premium to the company. The premium is nonexistent in UniFirst because it is unlikely to be bought out, given its high insider control. When interest rates and market sentiment changes, takeover premiums will fall and UniFirst should experience strong relative performance.

Genpact Ltd. (G)

(Analyst: Karl Poehls)

Description

Genpact is a global leader in business process management (BPM) and information technology (IT) outsourcing services. The company executes its strategy according to its proprietary Smart Enterprise Processes (SEP) framework. Genpact was spun off from General Electric (GE) in 2007 and continues to operate with an intense focus on Lean and Six Sigma. The company has broad exposure across a number of industry verticals, employs over 60,000 professionals around the globe, delivers services to more than 700 clients from a network of more than 70 delivery centers, and competes in 18 countries while supporting more than 30 languages.

Good Business

| | • | Genpact is a leading provider of BPM and IT outsourcing services with the majority of its revenues derived from Fortune Global 500 and Fortune 1000 companies. |

| | • | The company estimates that more than 80% of its revenues can be considered recurring in nature and organic growth has averaged 11% over the past five years. |

| | • | In 2012, customer satisfaction scores reached an all-time high. |

| | • | The company’s products and services provide customers with a tangible return on investment (ROI). |

| | • | Genpact has a strong balance sheet with net debt-to-earnings before interest taxes depreciation and amortization (EBITDA) and interest coverage ratios of 1.2 and 9.6 times, respectively. |

| | • | Over the past five years, the company’s return on invested capital (ROIC) has averaged 10.0%, which exceeds its cost of capital. We expect Genpact’s ROIC will approach 13.0-15.0% over the next few years. |

Valuation

| | • | Since the spin-off from GE in August of 2007, Genpact’s stock price has significantly underperformed the Standard & Poor’s 500 and Russell 2000 indices by 30% and 45%, respectively. |

| | • | The stock trades for 1.8 times revenue, which compares to an expected operating margin (EBIT) of 14.0% in 2014 and a trailing 5-year average of 15.3%. |

| | • | Genpact’s trailing price-to-earnings (P/E) multiple is 16.3 times. Over the trailing 5-year period, the company’s stock has traded for an average P/E of 17.5 times. |

| | • | Acquisitions of comparable companies in the IT services, business processing outsourcing (BPO), enterprise software, and financial processing industries typically occur at 10-16 times EBITDA. Genpact’s shares trade for approximately 11 times EBITDA. |

Management

| | • | Current CEO, N.V. “Tiger” Tyagarajan, has led the company since June of 2011. He is considered a pioneer of the BPO industry and has a deep knowledge of Lean and Six Sigma. Mr. Tyagarajan owns 450,000 shares of Genpact’s common stock. |

| | • | Bain Capital has approximately $1 billion invested in the company, which represents 27% of the outstanding shares. Further, representatives of Bain occupy four seats on Genpact’s board of directors. We believe this significant ownership interest will help to drive future shareholder value creation. |

Investment Thesis

In February, Genpact issued 2014 financial guidance that was below expectations and the stock sold off 17%. Management is taking the hard step of driving short-term profit margins down by investing in the business to accelerate future top-line growth. This appears to be the correct path for the long term and has given us the opportunity to invest in a relatively high-growth franchise, with a sticky customer base and strong balance sheet, at a reasonable price.

Thank you for your support of the FMI Common Stock Fund.

100 E. Wisconsin Ave., Suite 2200 • Milwaukee, WI 53202 • 414-226-4555

www.fmifunds.com

This shareholder letter is unaudited.

FMI Common Stock Fund

MANAGEMENT’S DISCUSSION OF FUND PERFORMANCE

During the fiscal year ended September 30, 2014, the FMI Common Stock Fund (the “Fund”) had a total return of 10.44%. The benchmark Russell 2000 returned 3.93% in the same period. Sectors that aided relative performance included Finance, Commercial Services and Distribution Services. The buyout of Protective Life along with strong performance in most of the other financial holdings accounted for the positive results in the Finance sector. Cintas and Robert Half International were the two primary drivers of the positive Commercial Services sector. Arrow was behind the good performance in Distribution Services. On the negative side, Health Services, Process Industries and Health Technology pulled down relative performance, along with higher-than-normal cash levels. Hanger was down significantly in the period, hurting the Health Services sector performance. Process Industries were affected by negative returns from H.B. Fuller. Our underweighted position in Health Technology accounted for the relative performance in that group. Selling fully priced stocks and the inability to replace them with good businesses at attractive valuations caused cash levels to rise. Stocks sold in the period included Kaydon, Molex, Owens & Minor, AptarGroup, A.J. Gallagher, World Fuel, Protective Life, Family Dollar and Dresser-Rand. Kaydon, Molex, Protective Life, Family Dollar and Dresser-Rand were all either taken over or were the subject of buy-out offers. AptarGroup and A.J. Gallagher were sold due to valuation and World Fuel and Owens & Minor were sold because of fundamental concerns. A number of new additions were made over the past twelve months, including Flir Systems, Lindsay Corp., MSC Industrial, Woodward, NVR Corp., Valmont, Genpact, Dresser-Rand, Progress Software, Hanger, Interpublic Group, UniFirst and Sturm, Ruger. At September 30, 2014, the Fund was significantly overweighted in Distribution Services, Commercial Services and Process Industries and meaningfully underweighted in Health Technology, Finance and Electronic Technology.

Good performance across a number of sectors but particularly in some of the more speculative technology and biotechnology areas helped drive positive results for the Russell 2000. While the last three months of the fiscal year exhibited moderately negative results, the market has gone five and a half years without a significant correction. Smaller capitalization stocks have recently underperformed larger capitalization issues. Valuations remain near the upper end of historical parameters. Easy monetary policy appears to have been a significant driver of stock market performance in recent years. The economy seems to be somewhat better but has grown at less than half of its long term historical rate. The unemployment rate has also improved, but the labor participation rate remains at a very low level and an extraordinarily high number of citizens are dependent on government support. Companies have been restrained with respect to investing in both capital equipment and labor, which has resulted in less than satisfactory internal growth rates. The economies in Europe, China, Brazil, Japan and Russia have all weakened. Debt levels remain very high in all of these economies as well as in the United States. Geopolitical problems have escalated over the past year. This, combined with less than average growth and very high valuations makes us cautious on the stock market in the short run. We continue to believe, however, that stocks have the best chance to adjust to a dynamic environment over the long run. The Fund sells at a discount to the Russell 2000 on most valuation measures.

COMPARISON OF CHANGE IN VALUE OF $10,000 INVESTMENT IN

FMI COMMON STOCK FUND AND THE RUSSELL 2000 INDEX(1)

AVERAGE ANNUALIZED TOTAL RETURN

| | | | | Since |

| | | | | Inception |

| | 1-Year | 5-Year | 10-Year | 12/18/81 |

| FMI Common | | | | |

| Stock Fund | 10.44% | 13.80% | 10.75% | 12.34% |

| Russell 2000 Index | 3.93% | 14.29% | 8.19% | 10.39% |

The graph and the table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Performance data quoted represents past performance; past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of a Fund may be lower or higher than the performance quoted. The total returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Total return includes change in share prices and in each case includes reinvestments of any dividends, interest and capital gain distributions. Performance data current to the most recent month-end may be obtained by visiting www.fmifunds.com or by calling 1-800-811-5311.

| (1) | The Russell 2000 Index measures the performance of the 2,000 smallest companies in the Russell 3000 Index, which comprises the 3,000 largest U.S. companies based on total market capitalization. |

An investment cannot be made directly into an index.

This page is unaudited.

FMI Common Stock Fund

SCHEDULE OF INVESTMENTS

| Shares | | | | Cost | | | Value | |

| | | | | | | |

| COMMON STOCKS — 86.5% (a) | | | | | | |

| | | | | | | |

| COMMERCIAL SERVICES SECTOR — 16.0% | | | | | | |

| | | Advertising/Marketing Services — 3.0% | | | | | | |

| | 2,305,000 | | Interpublic Group of Cos. Inc. | | $ | 41,246,565 | | | $ | 42,227,600 | |

| | | | Financial Publishing/Services — 2.3% | | | | | | | | |

| | 272,000 | | Dun & Bradstreet Corp. | | | 18,520,002 | | | | 31,951,840 | |

| | | | Miscellaneous Commercial Services — 9.2% | | | | | | | | |

| | 467,000 | | Cintas Corp. | | | 10,992,977 | | | | 32,965,530 | |

| | 3,182,000 | | Genpact Ltd.* | | | 54,527,385 | | | | 51,930,240 | |

| | 30,000 | | Graham Holdings Co. | | | 21,383,963 | | | | 20,987,700 | |

| | 1,708,000 | | RPX Corp.* | | | 28,639,896 | | | | 23,450,840 | |

| | | | | | | 115,544,221 | | | | 129,334,310 | |

| | | | Personnel Services — 1.5% | | | | | | | | |

| | 425,000 | | Robert Half International Inc. | | | 11,128,001 | | | | 20,825,000 | |

| | | | | | | | | |

| CONSUMER DURABLES SECTOR — 3.1% | | | | | | | | |

| | | | Homebuilding — 2.0% | | | | | | | | |

| | 25,000 | | NVR Inc.* | | | 25,402,257 | | | | 28,250,500 | |

| | | | Recreational Products — 1.1% | | | | | | | | |

| | 305,000 | | Sturm, Ruger & Co. Inc. | | | 15,271,532 | | | | 14,850,450 | |

| | | | | | | | | |

| CONSUMER SERVICES SECTOR — 1.0% | | | | | | | | |

| | | | Other Consumer Services — 1.0% | | | | | | | | |

| | 150,000 | | UniFirst Corp. | | | 15,331,988 | | | | 14,488,500 | |

| | | | | | | | | |

| DISTRIBUTION SERVICES SECTOR — 13.8% | | | | | | | | |

| | | | Electronics Distributors — 9.0% | | | | | | | | |

| | 503,000 | | Anixter International Inc. | | | 33,236,071 | | | | 42,674,520 | |

| | 987,000 | | Arrow Electronics Inc.* | | | 17,585,961 | | | | 54,630,450 | |

| | 857,000 | | ScanSource Inc.* | | | 22,062,384 | | | | 29,643,630 | |

| | | | | | | 72,884,416 | | | | 126,948,600 | |

| | | | Medical Distributors — 3.2% | | | | | | | | |

| | 1,078,000 | | Patterson Cos. Inc. | | | 23,705,261 | | | | 44,661,540 | |

| | | | Wholesale Distributors — 1.6% | | | | | | | | |

| | 258,000 | | MSC Industrial Direct Co. Inc. | | | 20,681,595 | | | | 22,048,680 | |

| | | | | | | | | |

| ELECTRONIC TECHNOLOGY SECTOR — 3.4% | | | | | | | | |

| | | | Aerospace & Defense — 1.5% | | | | | | | | |

| | 693,000 | | FLIR Systems Inc. | | | 20,964,815 | | | | 21,718,620 | |

| | | | Electronic Production Equipment — 1.9% | | | | | | | | |

| | 823,000 | | MKS Instruments Inc. | | | 22,350,717 | | | | 27,471,740 | |

| | | | | | | | | |

| ENERGY MINERALS SECTOR — 2.0% | | | | | | | | |

| | | | Oil & Gas Production — 2.0% | | | | | | | | |

| | 219,000 | | Cimarex Energy Co. | | | 11,689,715 | | | | 27,710,070 | |

| | | | | | | | | |

| FINANCE SECTOR — 11.4% | | | | | | | | |

| | | | Finance/Rental/Leasing — 2.1% | | | | | | | | |

| | 332,000 | | Ryder System Inc. | | | 13,831,912 | | | | 29,870,040 | |

| | | | Property/Casualty Insurance — 4.7% | | | | | | | | |

| | 804,000 | | Greenlight Capital Re Ltd.* | | | 19,808,449 | | | | 26,057,640 | |

| | 840,000 | | W.R. Berkley Corp. | | | 20,975,570 | | | | 40,152,000 | |

| | | | | | | 40,784,019 | | | | 66,209,640 | |

| | | | Regional Banks — 4.6% | | | | | | | | |

| | 590,000 | | Cullen/Frost Bankers Inc. | | | 34,252,169 | | | | 45,140,900 | |

| | 700,000 | | Zions Bancorporation | | | 16,735,687 | | | | 20,342,000 | |

| | | | | | | 50,987,856 | | | | 65,482,900 | |

FMI Common Stock Fund

SCHEDULE OF INVESTMENTS (Continued)

September 30, 2014

| Shares or Principal Amount | | Cost | | | Value | |

| | | | | | | |

| COMMON STOCKS — 86.5% (a) (Continued) | | | | | | |

| | | | | | | |

| HEALTH SERVICES SECTOR — 0.6% | | | | | | |

| | | Medical/Nursing Services — 0.6% | | | | | | |

| | 418,000 | | Hanger Inc.* | | $ | 14,191,926 | | | $ | 8,577,360 | |

| | | | | | | | | |

| HEALTH TECHNOLOGY SECTOR — 3.1% | | | | | | | | |

| | | | Medical Specialties — 3.1% | | | | | | | | |

| | 537,000 | | Varian Medical Systems Inc.* | | | 40,211,151 | | | | 43,024,440 | |

| | | | | | | | | |

| PROCESS INDUSTRIES SECTOR — 12.3% | | | | | | | | |

| | | | Chemicals: Agricultural — 2.7% | | | | | | | | |

| | 1,460,000 | | Sociedad Quimica y Minera de Chile SA - SP-ADR | | | 43,860,775 | | | | 38,164,400 | |

| | | | Chemicals: Specialty — 4.0% | | | | | | | | |

| | 380,000 | | Compass Minerals International Inc. | | | 27,626,318 | | | | 32,026,400 | |

| | 446,000 | | Innophos Holdings Inc. | | | 22,106,900 | | | | 24,570,140 | |

| | | | | | | 49,733,218 | | | | 56,596,540 | |

| | | | Containers/Packaging — 2.4% | | | | | | | | |

| | 756,000 | | Avery Dennison Corp. | | | 21,521,769 | | | | 33,755,400 | |

| | | | Industrial Specialties — 3.2% | | | | | | | | |

| | 1,133,700 | | H.B. Fuller Co. | | | 43,073,563 | | | | 45,007,890 | |

| | | | | | | | | |

| PRODUCER MANUFACTURING SECTOR — 10.1% | | | | | | | | |

| | | | Industrial Machinery — 4.2% | | | | | | | | |

| | 584,500 | | Kennametal Inc. | | | 22,649,686 | | | | 24,145,695 | |

| | 726,800 | | Woodward Inc. | | | 31,188,890 | | | | 34,610,216 | |

| | | | | | | 53,838,576 | | | | 58,755,911 | |

| | | | Miscellaneous Manufacturing — 4.1% | | | | | | | | |

| | 351,000 | | Carlisle Cos. Inc. | | | 8,802,944 | | | | 28,213,380 | |

| | 220,500 | | Valmont Industries Inc. | | | 32,862,955 | | | | 29,752,065 | |

| | | | | | | 41,665,899 | | | | 57,965,445 | |

| | | | Trucks/Construction/Farm Machinery — 1.8% | | | | | | | | |

| | 337,000 | | Lindsay Corp. | | | 27,007,889 | | | | 25,190,750 | |

| | | | | | | | | |

| TECHNOLOGY SERVICES SECTOR — 6.2% | | | | | | | | |

| | | | Data Processing Services — 4.6% | | | | | | | | |

| | 1,558,000 | | Broadridge Financial Solutions Inc. | | | 34,988,238 | | | | 64,859,540 | |

| | | | Internet Software/Services — 1.6% | | | | | | | | |

| | 955,000 | | Progress Software Corp.* | | | 21,329,244 | | | | 22,834,050 | |

| | | | | | | | | |

| TRANSPORTATION SECTOR — 3.5% | | | | | | | | |

| | | | Air Freight/Couriers — 1.1% | | | | | | | | |

| | 352,000 | | Forward Air Corp. | | | 11,267,415 | | | | 15,780,160 | |

| | | | Marine Shipping — 2.4% | | | | | | | | |

| | 283,000 | | Kirby Corp.* | | | 11,134,976 | | | | 33,351,550 | |

| | | | Total common stocks | | | 934,149,511 | | | | 1,217,913,466 | |

| | | | | | | | | |

| SHORT-TERM INVESTMENTS — 14.0% (a) | | | | | | | | |

| | | | Commercial Paper — 14.0% | | | | | | | | |

| $ | 196,600,000 | | U.S. Bank N.A., 0.03%, due 10/01/14 | | | 196,600,000 | | | | 196,600,000 | |

| | | | Total investments — 100.5% | | $ | 1,130,749,511 | | | | 1,414,513,466 | |

| | | | Liabilities, less other assets — (0.5%) (a) | | | | | | | (6,673,199 | ) |

| | | | TOTAL NET ASSETS — 100.0% | | | | | | $ | 1,407,840,267 | |

| * | Non-income producing security. |

| (a) | Percentages for the various classifications relate to net assets. |

SP-ADR – Sponsored American Depositary Receipt

The accompanying notes to financial statements are an integral part of this schedule.

FMI Common Stock Fund

INDUSTRY SECTORS

as of September 30, 2014 (Unaudited)

FMI

International

Fund

September 30, 2014

Dear Fellow Shareholders:

The third quarter of 2014 yielded mixed results for global equity markets, with stock indices in Japan and France advancing by 5.71% and 0.04%, respectively, while German and the U.K. stocks fell by 3.65% and 0.90%, respectively1, as weak economic data (including a 0.2% decline in Germany’s second quarter GDP2) weighed on investor sentiment. The FMI International Fund (FMIJX) fell by 1.38% in the period, which compares with an MSCI EAFE Index gain of 0.93% in local currency and a decline of 5.88% in U.S. Dollars (USD). The relative performance of FMIJX was aided by the Consumer Non-Durables, Retail Trade, and Energy Minerals sectors, while Electronic Technology, Health Technology and Finance sectors were a drag on results. Amorepacific Corp., LG Household & Health Care, and Taiwan Secom generated strong individual returns, while Electrocomponents, Admiral Group, and Adecco each fell in value. The USD strengthened by over 5% against the Japanese Yen, Euro and British Pound. As a reminder, we have chosen to hedge currency risk so that the Fund’s performance is predominantly driven by stock selection, not movements in foreign exchange rates.

To avoid sounding like a broken record, we will spare our readers the reiteration of our view that stock markets are expensive, growth is weak, macro risks abound, and fiscal and monetary policies are misguided and reckless (see our previous shareholder letters for reference). We thought a little change of pace might be refreshing, so instead we will share a few takeaways from our recent research trip to Asia, where two of our analysts visited Japan, South Korea, and Hong Kong. FMI met with over 60 companies, a handful of industry analysts, a Chinese economist, and a member of the Ministry of Finance in Japan. There were a number of interesting observations from the trip:

Japan: Perceptions & Reality

Consistent with our prior meetings in Japan, it remains clear that a vast majority of companies do not have a grasp of return on invested capital (ROIC). It’s all too common for businesses in Japan to fail to earn their cost of capital. During our recent travels, we often came across businesses with long-term (beyond 2020) aspirational targets for return on equity (ROE) that were at or below 10%… far from inspiring. Sometimes this can be a result of an inefficient balance sheet (i.e. hoarding cash and investments), and at other times, an outcome of a low-quality business, poor management, or a lack of focus on profitability (i.e. margins well below global peers). Some companies are slowly starting to talk more about returning additional cash to shareholders, with an increase in dividends and buybacks appearing to be a more realistic consideration. In terms of management quality, we do not expect this to improve overnight, as it will take a long time to change the business culture in Japan. In the meantime, we strive to find the exceptions to the rule, which we believe we have found in FMIJX’s existing Japanese holdings: SMC Corp., Secom, and Shin-Etsu Chemical. Each is a high-quality, dominant business with strong profitability and significant barriers to entry. Their balance sheet efficiency (flush with cash), on the other hand, still has room for improvement.

While we do not believe “Abenomics” will ultimately be successful in rescuing Japan from its mountain of debt, demographic headwinds, and weak economic growth, the policy does appear to be making some initial progress on the inflation front (we would note, however, that printing money is a dangerous game, as modest inflation can quickly turn into hyperinflation). After over fifteen years of deflation, Japan’s inflation rate is now over 1% (with a 2% target), and consumers and companies alike appear to be embracing the reality that prices can actually go up. Companies have long tried to creatively “raise prices” by offering new services and/or technologies, innovative new products, new packaging, reduced product count at the same price, etc. If inflation sticks, companies might actually look to change prices the old fashioned way – simply raise them. This could have a profound impact on a company such as Secom, which provides electronic security services to commercial and residential buildings (think ADT in the U.S., but with its own nationwide security force). Due to low penetration rates in Japan, Secom’s volume growth has been strong for many years, but pricing pressure has held back

_______________

| 1 | The following market indexes are being referred to above: Japan TOPIX, U.K. FTSE All-Share, France CAC-40, and Germany DAX. |

| 2 | Germany’s GDP (gross domestic product) declined 0.2% in the second quarter of 2014, on a quarter-over-quarter basis. |

topline growth. Pricing has started to stabilize in recent years, and our discussions with the company suggest there may be an opportunity to start increasing prices down the road. This could change the company’s growth profile dramatically, and potentially lead to a re-rating of the stock. Inflation in Japan was never baked into our original investment assumptions, but could end up being a positive catalyst nonetheless.

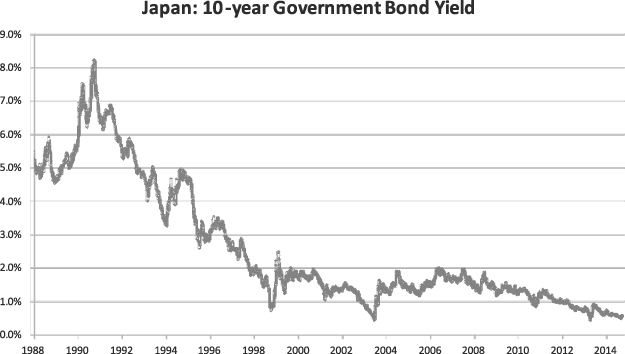

During our time in Japan, we also sat in on a presentation and Q&A session presented by the Ministry of Finance’s new investor relations (IR) department for Japanese Government Bonds (JGBs). The IR people will have their work cut out for them trying to drum up support for JGBs; why any rational international investor would be interested in buying 10-year bonds from the most indebted (not to mention economically-challenged) developed country in the world at a paltry yield of 0.53% is beyond our comprehension. As it stands today, Japan’s national debt service accounts for 24% of the 2014 annual budget and 46% of the tax revenues, despite unsustainably low financing costs. To calm investor fears that a rise in interest rates would cripple the country, IR presented a sensitivity table assuming interest rates could go as high as 4.4% by 2017 (our worst-case would be far higher). Under this scenario, debt service would increase to ¥37.5 trillion from ¥23.3 trillion today (+61%), held down by the duration of the existing portfolio. The further you go out, however, the worse the interest burden will become. According to the speaker, as long as their economic recovery continues (they assume 3% nominal growth), “everything will be okay.” When asked what would happen if rates rose but the economy went into a recession, there was basically no response. It appears there is a blind trust that the government will know just what to do. To our amazement, a comment was made that interest rates “never” really go up above 2%.3 The chart below (with a slightly longer memory) might beg to differ:

Source: Bloomberg

South Korea: Opportunities & Pitfalls

South Korea remains intriguing, as valuations are among the lowest in the developed world (we do not consider it an emerging market4), and a number of inefficiencies still remain, creating attractive investment opportunities. We were pleasantly surprised by a handful of our company meetings. While English filings and language skills can be limited in some cases, financial statements are often available in far more detail than is provided elsewhere in the world. A prime example of the inefficiencies in Korea is the discount placed on the preferred share class, a mispricing that is not economically justified. In Korea, preferred shares typically have the same economic interest as the common shares and pay a higher dividend, but are less liquid and do not have voting rights. As many of the companies are family-controlled, voting rights are of less

_______________

| 3 | “The Japanese Economy and Debt Management,” presentation published by Financial Bureau, Ministry of Finance, Japan, September 2014. |

| 4 | Please see shareholder letter from March 31, 2013 for an in-depth discussion. |

significance, so the discount is mainly attributed to liquidity. As recently as last year, preferred shares traded at discounts as wide as 60% to 80% versus the common shares, an anomaly that simply did not make sense. We have been able to exploit this opportunity through our investments in Amorepacific Corp. and LG Household & Health Care Ltd. (LG H&H), which were purchased at single-digit multiples of earnings — a significant margin of safety for the L’Oreal and Procter & Gamble equivalents of Korea. Over time, we had expected the discount to narrow, to be more in line with what we see in Europe where similar preferred shares trade much closer to par. This has started to play out, as AmorePacific and LG H&H’s preferred shares now trade at a 52% and 46% discount, respectively, from 67% and 70% at the time of purchase. Both stocks remain attractive from an absolute valuation perspective, which we view as far more important than the nominal spread.

The two biggest takeaways from our trip to Korea were the major pitfalls we need to avoid: government involvement and poor corporate governance. While we were already aware from prior research that the government can influence certain industries with a heavy hand, we were surprised to hear from as many companies as we did that they were being adversely affected. The government is a champion for the consumer, so industries that provide basic necessities appear to be the most at risk. The government’s influence is not always through official policy, and in some cases may be through direct communication with an industry and an expectation of compliance. For example, one of the country’s leading instant noodle makers had not been able to raise prices for years, as they were not permitted to by the government. One of the leading discount hypermarket chains was forced to close two days per month so that small- and medium-size enterprises would have a better chance at success. Wireless telecom providers are told one day to cut tariffs, and to cap subsidies another. The list goes on. When a company cannot control its own destiny, we will simply pass and move on to the next.