UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-07831

FMI Funds, Inc.

(Exact name of registrant as specified in charter)

(Exact name of registrant as specified in charter)

790 North Water Street, Suite 2100

Milwaukee, WI 53202

(Address of principal executive offices) (Zip code)

John S. Brandser

Fiduciary Management, Inc.

790 North Water Street

Suite 2100

Milwaukee, WI 53202

(Name and address of agent for service)

(414) 226-4545

Registrant's telephone number, including area code

Date of fiscal year end: September 30

Date of reporting period: September 30, 2023

Item 1. Reports to Stockholders.

| (a) |

ANNUAL REPORT

September 30, 2023

FMI Common Stock Fund

Investor Class (Ticker Symbol: FMIMX)

Institutional Class (Ticker Symbol: FMIUX)

FMI Large Cap Fund

Investor Class (Ticker Symbol: FMIHX)

Institutional Class (Ticker Symbol: FMIQX)

FMI International Fund

Investor Class (Ticker Symbol: FMIJX)

Institutional Class (Ticker Symbol: FMIYX)

FMI International Fund II – Currency Unhedged

Investor Class (Not Available For Purchase)

Institutional Class (Ticker Symbol: FMIFX)

| |

| FMI Funds, Inc. | |

| Advised by Fiduciary Management, Inc. | |

| www.fmifunds.com | |

FMI Funds, Inc.

TABLE OF CONTENTS

| Shareholder Letter | 1 | ||

| FMI Common Stock Fund | |||

| Management’s Discussion of Fund Performance | 8 | ||

| Schedule of Investments | 11 | ||

| Industry Sectors | 13 | ||

| FMI Large Cap Fund | |||

| Management’s Discussion of Fund Performance | 14 | ||

| Schedule of Investments | 18 | ||

| Industry Sectors | 20 | ||

| FMI International Fund and FMI International Fund II – Currency Unhedged | |||

| Management’s Discussion of Fund Performance | 21 | ||

| FMI International Fund | |||

| Schedule of Investments | 27 | ||

| Schedule of Forward Currency Contracts | 30 | ||

| Industry Sectors | 31 | ||

| FMI International Fund II – Currency Unhedged | |||

| Schedule of Investments | 32 | ||

| Industry Sectors | 35 | ||

| Financial Statements | |||

| Statements of Assets and Liabilities | 36 | ||

| Statements of Operations | 38 | ||

| Statements of Changes in Net Assets | 40 | ||

| Financial Highlights | 44 | ||

| Notes to Financial Statements | 51 | ||

Report of Independent Registered Public Accounting Firm | 63 | ||

| Expense Example | 64 | ||

| Directors and Officers | 66 | ||

| Liquidity Risk Management Program | 68 | ||

| Disclosure Information | 69 | ||

| Additional Information | 72 | ||

| Tax Notice | 72 | ||

| Notice of Privacy Policy | 73 | ||

| Householding Notice | 73 |

FMI Funds, Inc.

Shareholder Letter

(Unaudited)

September 30, 2023

Dear Fellow Shareholders:

After a strong start to the year, global equity markets gave up some ground in the September quarter. Fortunately, the speculative appetite we saw from investors in the first two quarters started to lose some steam. Value benchmarks began clawing back some relative performance, which was encouraging. Stock valuations are stretched and continue to prove more favorable in the U.S. Small Cap and International arenas. U.S. Large Caps remain exceedingly top-heavy with performance being dominated by a handful of mega-cap companies that trade at significant premiums. Across geographies, cyclical stocks have been outperforming their more defensive counterparts; we are finding incremental opportunities in the latter.

While economic growth in the U.S. has been resilient, both Europe and China have come under mounting pressure. Inflation has been falling but remains elevated. Debt levels and borrowing costs have increased, which combined with higher labor and input costs, have weighed on corporate margins and earnings. Over the long-term, we remain optimistic and are excited to see a more normal interest rate environment. This should bode well for organic growth, stock picking, and value investing. With global value stocks trading near a historically wide discount to growth, the current set-up looks attractive from here. Any reversion to the mean would result in brighter days for those with a value orientation. We’ve got our sunglasses ready.

To that end, each of the FMI Funds gained on their respective primary benchmark in the period. The third quarter performance commentary is outlined below:

FMI Common Stock Fund: Performance

The FMI Common Stock Fund (“Common Stock Fund”) declined 1.91%1, compared to a fall of 5.13% and 2.96% in the Russell 2000 Index (“Russell 2000”) and Russell 2000 Value Index (“Russell 2000 Value”), respectively. Relative to the Russell 2000, sectors that contributed to the performance included Finance, Electronic Technology, and Retail Trade, while Commercial Services, Consumer Durables, and Distribution Services lagged. Not having exposure to Health Technology—which is littered with money-losing bio-technology companies—was also additive in the period. Some top individual performers included BJ’s Wholesale Club Holdings Inc., Zions Bancorporation N.A., and Houlihan Lokey Inc. Cl A, while Interpublic Group of Cos. Inc., LGI Homes Inc., and Fortune Brands Innovations Inc. weighed. Over 40% of the companies in the Russell 2000 and Russell 2000 Value lose money…not an area we typically look to invest. Our business quality focus has been a key to our outperformance in recent years.

FMI Large Cap Fund: Performance

The FMI Large Cap Fund (“Large Cap Fund”) dropped 2.60%2, compared to a decrease of 3.27% and 3.19% in the S&P 500 Index (“S&P 500”) and iShares Russell 1000 Value ETF3,

_______________

1 | The FMI Common Stock Fund Investor Class (FMIMX) and the FMI Common Stock Fund Institutional Class (FMIUX) had a return of -1.91% and -1.88%, respectively, for the third quarter of 2023. |

2 | The FMI Large Cap Fund Investor Class (FMIHX) and the FMI Large Cap Fund Institutional Class (FMIQX) had a return of -2.60% and -2.54%, respectively, for the third quarter of 2023. |

3 | Source: Bloomberg – returns do not reflect management fees, transaction costs or expenses. Performance is based on market price returns. Beginning 8/10/20, market price returns are calculated using closing price. Prior to 8/10/20, market price returns were calculated using midpoint bid/ask spread at 4:00 PM ET. |

1

respectively. Relative to the S&P 500, our Electronic Technology, Consumer Services, and Finance sector exposures boosted our performance, while Retail Trade, Commercial Services, and Health Technology lagged. Booking Holdings Inc., CDW Corp., and Micron Technology Inc. outperformed, while Dollar General Corp., Dollar Tree Inc., and Omnicom Group Inc. detracted. Year-to-date (YTD), the Large Cap Fund’s performance has fallen squarely between the S&P 500 and iShares Russell 1000 Value ETF. As each day passes, the S&P 500 looks progressively more like a concentrated growth index (additional color to follow). The S&P 500 Equal Weight index has lagged the S&P 500 by over 11% YTD, as the S&P 500 returns are being driven by a select few stocks. Despite higher interest rates, the Russell 1000 Value has underperformed the Russell 1000 Growth Index by ~23% YTD, an extreme gap by historical standards; we don’t think the market’s lurch back to growth this year will persist.

FMI International Fund & FMI International Fund II – Currency Unhedged: Performance

The FMI International Funds (“International Funds”) fell 1.09%4 on a currency hedged basis and 4.08%5 currency unhedged, compared with the MSCI EAFE Index’s decline of 1.27% in local currency (LOC) and 4.11% in U.S. Dollars (USD). The MSCI EAFE Value Index gained 3.64% in LOC and 0.59% in USD. Relative to the MSCI EAFE Index, top contributing sectors included Producer Manufacturing, Consumer Services, and Industrial Services, while Health Technology, Finance, and a lack of exposure to Energy Minerals weighed. Strong individual contributions came from Schlumberger Ltd., Booking Holdings Inc., and Howden Joinery Group PLC, while Smith & Nephew PLC, Samsung Electronics Co. Ltd. Preferred, and Barry Callebaut AG gave up some ground. The MSCI EAFE Value outperformed significantly in the period, with the “deeper value” Energy and Finance sectors leading the way. FMI is typically under-weight these sectors due to business quality and balance sheet concerns. A strong USD was a tailwind for FMI’s currency hedged portfolio in the quarter.

The Bigger You Are The Harder You Fall

As illustrated in the chart below, the last five years have created a windfall for investors in the S&P 500 (U.S. Large Cap stocks), as it has trounced other asset class benchmarks, including the Russell 2000 (U.S. Small Cap stocks) and the MSCI EAFE (International Large Cap stocks). The performance gap has blown out again in 2023, and now stands at approximately 48% and 43%, respectively, over the full five-year period.

_______________

4 | The FMI International Fund [currency hedged] Investor Class (FMIJX) and the FMI International Fund [currency hedged] Institutional Class (FMIYX) had a return of -1.09% and -1.02%, respectively, for the third quarter of 2023. |

5 | The FMI International Fund [currency unhedged] Institutional Class (FMIFX) had a return of -4.08% for the third quarter of 2023. |

2

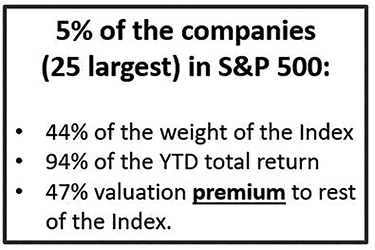

With this divergence comes risk. The concentration in the S&P 500 is truly extraordinary. The top 5% of the companies (25 largest) account for around 44% of the weight of the index, 94% of the YTD total return, and trade at an average valuation premium of 47%6 to the rest of the index. Expectations remain high for those chosen few. As illustrated in last quarter’s letter, leaders rise and fall, and this is consistent across business cycles (only one of the top ten companies in the S&P 500 in 2000 was in the top ten in 2020). Today’s exuberance has some earmarks of the “Nifty Fifty” in the 1970s, where investors crowded like lemmings into 50 indisputable companies, pushing valuations to extremes. The speculative fever eventually broke between 1973-74, when the Dow fell ~42%, while the “Nifty Fifty” dropped ~59%! Unfortunately, investors appear to have very short memories, and most were not alive through this painful experience. While market cycles are never identical, from the top they do have a long history of transitioning from overvalued to undervalued, as human nature doesn’t change (fear and greed). As we highlighted last quarter, the lion’s share of the top performing themes in the U.S. fell in the speculative camp, and for that we feel that caution is warranted today.

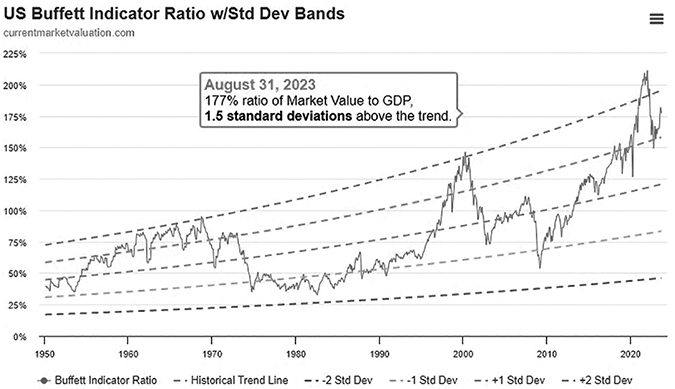

Valuations in the U.S. have ballooned, with numerous warning signals now flashing red. Through The Leuthold Group, we track 46 different valuation metrics, dating as far back as 1926. On a median basis, we are currently in the 10th decile of historical valuation – one of the most expensive stock markets in U.S. history. The widely referenced Buffett Indicator, measuring market value to GDP, tells a similar story of overvaluation (see chart on the following page). JPMorgan writes, “Equities are up YTD on multiple expansion while real rates and cost of capital are moving deeper into restrictive territory. History suggests this relationship is becoming increasingly unsustainable, with the S&P 500 multiple over-valued by 3-4x vs. real rates, posing risk to valuations, especially since earnings expectations already face a high hurdle for 2024.”

_______________

6 | Estimated Valuations are for the iShares S&P 500 ETF, calculations are based on the average discount to the average valuations as of September 30, 2023 for the trailing 1-year Price-to-Earnings Ratio, Fiscal Year One Price-to-Earnings Ratio, Fiscal Year Two Price-to-Earnings Ratio, Price-to-Sales Ratio, and Price-to-Book Ratio. Valuations for the ETF are scrubbed and adjusted based on criteria identified by FMI. For more detailed information regarding these valuations, please contact FMI. |

3

Fortunately, there are attractive relative values outside of the mega-cap companies in the S&P 500. As we pointed out last quarter, the discount for U.S. Small Caps vs. U.S. Large Caps is near an all-time high, as are European valuations vs. domestic. All of FMI’s portfolios trade at a significant discount to the core benchmarks, and we invest in above-average businesses with strong balance sheets. We see compelling opportunities across our holdings, with a collection of all-weather vehicles that can withstand these tough and unpredictable times.

China’s House of Cards

The macro environment features numerous headwinds, including waning global growth, record debt levels, elevated inflation, rising interest rates, and heightened geopolitical risks. On the growth front, the U.S. has been the most robust developed economy, with a strong labor market and a resilient consumer. That said, the Organisation for Economic Co-operation and Development (“OECD”) expects U.S. real GDP to slow to a “soft landing” from 2.2% in 2023 to 1.3% in 2024. European growth has already hit the skids, falling to 0.6% in 2023 with 1.1% expected in 2024. High food and energy inflation has weighed, business activity and bank lending has slowed, and a higher cost of borrowing is impacting investment, among other factors.

China, which just months ago was expected to account for almost 35% of global growth this year, has run into significant challenges. The property sector, which we have long described as a dangerous and a speculative bubble, has finally popped. In recent years, housing accounted for as much as 25% of China’s GDP. The property sector, which holds 70% of China’s households’ wealth, is ailing. Property sales are down nearly 40% from their 2021 peak, housing starts have fallen 60%, and prices have dropped 33%. Developer defaults and business losses are commonplace, and more strain may be on the horizon. Leverage in China is up dramatically, with total credit up 8.5 times since 2008, even as GDP is up less than half that (3.9 times).

China’s problems don’t end there. Their demographics are poor, with a working age population in decline since 2011 and a total population that started to shrink in 2022. Productivity growth is slowing, exports are weak, youth unemployment is high, and tensions with the West are rising. The glory days for the world’s second largest economy may be behind them. Unfortunately, additional weakness in China would be felt worldwide. Risks abound.

4

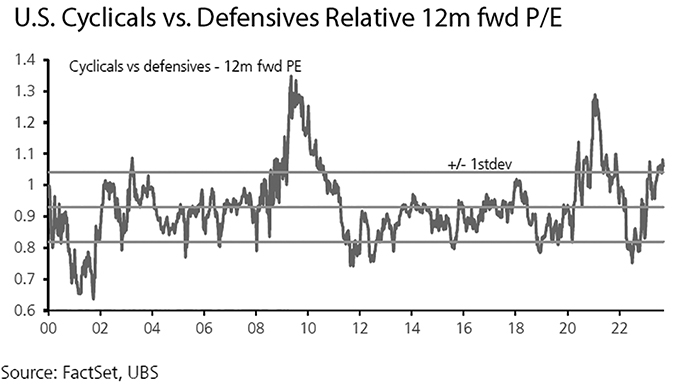

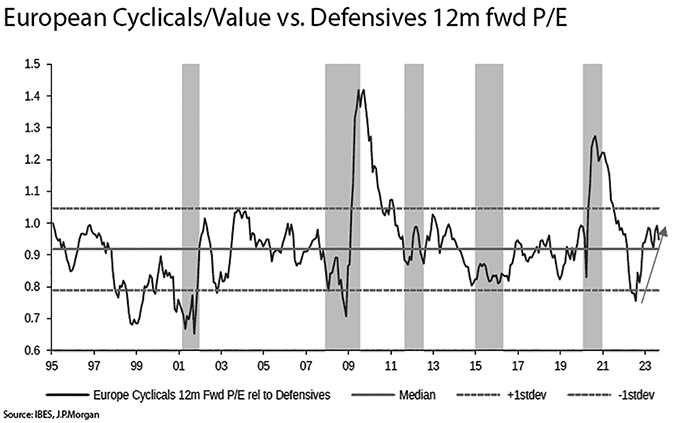

Not So Expensive Defensives

Despite the weakening economic backdrop described above, cyclical stocks have surprisingly outperformed “defensives” (steady, less-cyclical businesses) in both the U.S. and Europe over the past year. As illustrated below, valuations are looking more attractive on the defensive side of the equation. In the U.S., cyclicals are trading around a standard deviation above historical levels from a relative price-to-earnings standpoint, while in Europe they are trading above the historical median, but are not quite as extended.

5

We have found some interesting opportunities among the defensives that have been left behind. In the third quarter, we added a new position to each of our portfolios which fit the description. The idiosyncratic investment case for these new purchases is outlined below:

Valvoline Inc. (VVV) – FMI Common Stock Fund

After a long history of underinvestment under Ashland and a messy seven years as a standalone public company, Valvoline is finally a pure-play quick lube retailer, having sold their motor oil business earlier this year. We like the business model for its stability, growth potential, pricing power, and high returns on capital. The business offers customers a better oil change experience relative to the alternatives. Going forward, the story will be simpler to understand, the analyst coverage will be uniform, and it should get reclassified as retail. In the current environment, Valvoline has the added benefit of having a tight store-level culture that helps minimize labor turnover, and has effectively no shrink, which is currently a major thorn in the side of retailers. Given Valvoline’s choppy history (thanks to the divested motor oil business), we believe investors are in a wait and see mode as the company proves out its standalone financial results and accelerates its organic store expansion. Increased penetration in a fragmented market, expanded usage of synthetic oils, and a consistent experience as consumers continue to shift to do-it-for-me, should drive strong earnings per share growth at high incremental returns. Although we believe we can get an attractive return from just the growth, there is the chance for a higher valuation as Valvoline puts up its first year of (nearly) clean financials in Fiscal Year 2024. We also believe the short- to medium-term threat of electric vehicles is manageable. If our growth expectations are achieved, the downside is modest even if the multiple compresses meaningfully over our five-year investment horizon. We hope investors will increasingly appreciate Valvoline’s simple, high return model after a long period of being obfuscated by inferior businesses.

Sysco Corp. (SYY) – FMI Large Cap Fund

Sysco Corp. is the largest global distributor of food and related products to the foodservice or food-away-from-home industry. Sales in the U.S. account for approximately 82% of the company’s consolidated revenue, with the remainder mainly coming from Canada, Latin America, and Europe (18%). The company provides products and related services from thousands of suppliers to over 725,000 customer locations including restaurants (~62% of sales), education and government facilities (~8%), travel and leisure establishments (~8%), healthcare facilities (~7%), and other foodservice customers (15%). Sysco possesses many business characteristics that FMI finds attractive. The company has a dominant market position in a large, growing, resilient industry. They sell necessary, consumable products. Economies of scale allow Sysco to provide a better offering than peers while also allowing them to operate with higher margins. These advantages have helped Sysco take market share over time and earn a return on capital that consistently exceeds its cost of capital. We believe that Sysco will continue to grow its market share in the large and fragmented foodservice distribution market and should be able to generate mid-single-digit EBIT growth over time. When combined with share repurchases and dividend yield, the company should generate a high-single-digit to low-double-digit total return to investors without multiple expansion. The shares are trading at a depressed valuation relative to the S&P 500 and relative to the company’s history, which we believe provides us downside protection and could generate additional upside should it revert to the historical levels.

Coca-Cola Europacific Partners PLC (CCEP) – FMI International Funds

Coca-Cola Europacific Partners (CCEP) is the largest Coca-Cola bottling franchise, accounting for an estimated one-third of Coca-Cola System profits. CCEP sells whatever it deems to be the optimal mix of The Coca-Cola Company’s (TCCC) 200+ brands in its 30 countries (from its owned bottling plants and coolers) and CCEP sets all prices. Over the last decade plus, alignment has been structurally enhanced between TCCC and the top bottling groups through incidence-based pricing

6

(sales value rather than volume) and through direct ownership. Bottlers are increasingly benefiting from TCCC’s innovation and overall “total beverage” strategy (including TCCC’s acquired and licensed brands in energy drinks and ready-to-drink coffee, alcohol, and more). By year-end 2023, CCEP should also generate 28% of sales from the faster growing Asia-Pacific region (with no sales in China). CCEP is inexpensive compared to other global staples, with nearly 2x the average free cash flow yield. Compared to its own seven-year history, it trades at a significant discount on a price-to-earnings basis. It offers attractive defensive growth potential and predictable capital allocation.

Thank you for your continued support of FMI Funds, Inc.

Please see page 69 for important disclosures.

This shareholder letter is unaudited.

7

FMI Common Stock Fund

MANAGEMENT’S DISCUSSION OF FUND PERFORMANCE (Unaudited)

During the fiscal year ended September 30, 2023, the FMI Common Stock Fund (“Fund”) had a total return of 25.08%1. The benchmark Russell 2000 Index (“Russell 2000”) returned 8.93% in the same period. The trailing 12-month return for the Russell 2000 Value Index (“Russell 2000 Value”) was 7.84%.

Relative to the Russell 2000, sectors that aided relative performance included Finance, Technology Services, and Distribution Services. Primerica Inc., Houlihan Lokey Inc. – Cl A, FirstCash Holdings Inc., and Triton International Ltd. – Cl A, drove the results in the Finance sector. Triton International was acquired at a premium, while the others demonstrated strong business fundamentals. In Technology Services, Insight Enterprises Inc. outperformed, as investors were nervous about the impacts of a slowing macro environment, but the company’s fundamentals have thus far proved to be fairly resilient. In Distribution Services, despite a softening housing outlook, Beacon Roofing Supply Inc.’s ~80% replacement-centric business had a stronger-than-expected outlook, while Applied Industrial Technologies Inc. executed well as demand remained strong. Other stocks that helped performance included nVent Electric PLC, Skechers U.S.A. Inc. – Cl A, and Five Below Inc. nVent’s margin performance has been outstanding, and excitement over their fast-growing data solutions offerings, which benefits from AI adoption, has driven multiple expansion. Last year, Skechers’ fundamentals were negatively impacted by supply chain challenges and COVID-19 related lockdowns in China. Those headwinds have improved so far this year and the market has responded by re-rating the shares higher. Five Below performed strong fundamentally, but we sold the shares after the valuation no longer demonstrated a discount to our estimate of intrinsic value.

On the negative side of sector performance, Industrial Services, Energy Minerals, and Commercial Services detracted. The Fund had no direct exposures to the first two sectors that outperformed, as business quality concerns typically limits our investments in energy and commodities. In Commercial Services, Genpact Ltd. lagged, as negative sentiment around generative artificial intelligence (AI) has impacted the stock, but is believed to be significantly overblown. Additional stocks that detracted from performance included Zions Bancorporation N.A., BJ’s Wholesale Club Holdings Inc., and Robert Half International Inc. Zions got caught up in the first quarter 2023 contagion fear around Silicon Valley Bank’s collapse due to some optical similarities between their balance sheets (namely bonds carried at mark-to-market losses), and Zions being a West Coast regional bank. We believe the similarities largely end there. Softening consumer spending, particularly for higher margin discretionary merchandise, and lower year-over-year gas gross profits have caused analysts to anticipate a down earnings year for BJ’s Wholesale. Robert Half experienced a cyclical slowdown which was worse than expected.

New additions to the Fund over the past twelve months included Core & Main Inc. – Cl A, Timken Co., Valvoline Inc., Fabrinet, CTS Corp., ITT Inc., and Fortune Brands Innovations Inc. Stocks sold during the year included ManpowerGroup Inc., KBR Inc., Woodward Inc., Five Below Inc., AZEK Co. Inc. – Cl A, Kennedy-Wilson Holdings Inc., and FTI Consulting Inc.

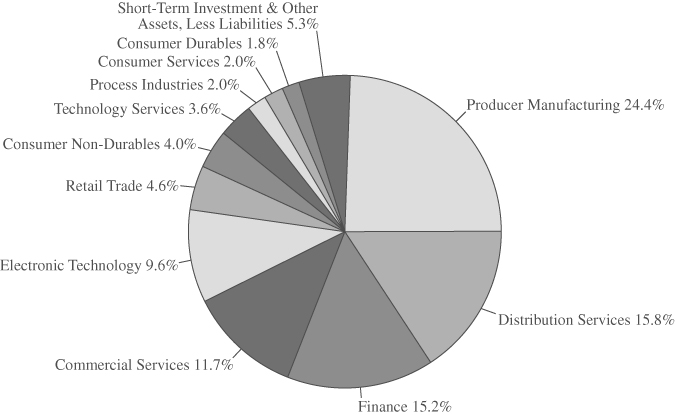

As of September 30, 2023, the Fund was significantly overweight in Producer Manufacturing, Distribution Services, and Commercial Services sectors. The Fund was meaningfully underweight in Health Technology, Technology Services, Energy Minerals and Finance sectors.

After a tough fiscal year 2022, U.S. stocks rebounded strongly in fiscal year 2023, despite concerns around a regional banking crisis, waning global growth, record debt levels, elevated inflation, rising interest rates, and heightened geopolitical risks. Furthermore, corporate earnings growth in the U.S. has slowed, as higher borrowing, labor and input costs have weighed. Growth stocks outperformed value stocks in the period, but much more significantly in the U.S. Large Cap arena, which remains exceedingly top-heavy with performance being dominated by a handful of mega-cap companies that trade at significant valuation premiums (see recent shareholder letters for further discussion). Speculation appears to be plentiful. Stock valuations in the U.S. have ballooned, as the market is currently trading in the 10th decile of historical valuation – one of the most expensive stock markets in U.S. history (on a median basis, tracking 46 different valuation metrics dating as far back as 1926). There are attractive relative values outside many of the anointed mega-cap companies in the S&P 500. For example, profitable U.S. Small Caps are now trading near an all-time high discount vs. U.S. Large Caps.

_______________

1 | The FMI Common Stock Fund Investor Class (FMIMX) and the FMI Common Stock Fund Institutional Class (FMIUX) had a return of 25.08% and 25.22%, respectively, for the fiscal year ending September 30, 2023. |

8

FMI Common Stock Fund

MANAGEMENT’S DISCUSSION OF FUND PERFORMANCE (Unaudited)

(Continued)

Given the backdrop, the Fund portfolio managers were pleased to outperform the Russell 2000 and Russell 2000 Value by a wide margin during the current fiscal year. Over 40% of the companies in the Russell 2000 and Russell 2000 Value lose money…not an area they typically look to invest. The managers business quality focus has been a key to outperformance in recent years. Over the long-term, they are optimistic and excited to see a more normal interest rate environment. This should bode well for organic growth, stock picking, and value investing. With global value stocks trading near a historically wide discount to growth, the current set-up looks attractive from here. Any reversion to the mean should result in brighter days for those with a value orientation. The Fund trades at a significant discount to the Russell 2000, the businesses have strong balance sheets, and management believes the companies are above average. Management sees opportunities across the Fund, with what they feel is a collection of all-weather vehicles that can withstand tough and unpredictable times.

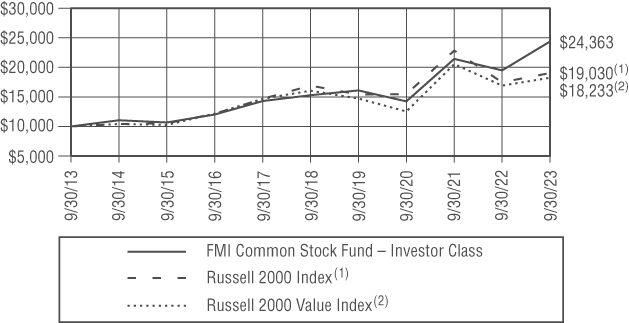

COMPARISON OF CHANGE IN VALUE OF $10,000 INVESTMENT IN FMI COMMON STOCK FUND –

INVESTOR CLASS — THE RUSSELL 2000© INDEX(1) AND THE RUSSELL 2000© VALUE INDEX(2)

AVERAGE ANNUALIZED TOTAL RETURN

| Inception | |||||

| through | |||||

| Inception Date | 1-Year | 5-Year | 10-Year | 9/30/2023 | |

FMI Common Stock Fund – | |||||

Investor Class | 12/18/81 | 25.08% | 9.78% | 9.31% | 11.65% |

FMI Common Stock Fund – | |||||

Institutional Class | 10/31/16 | 25.22% | 9.90% | N/A | 11.33% |

Russell 2000 Index(1)* | 8.93% | 2.40% | 6.65% | 9.64% | |

Russell 2000 Value Index(2)* | 7.84% | 2.59% | 6.19% | 10.98% |

The graph and the table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Performance data quoted represents past performance; past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of a Fund may be lower or higher than the performance quoted. The total returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Total return includes change in share prices and in each case includes reinvestments of any dividends, interest and capital gain distributions. Performance data current to the most recent month-end may be obtained by visiting www.fmifunds.com or by calling 1-800-811-5311.

9

FMI Common Stock Fund

MANAGEMENT’S DISCUSSION OF FUND PERFORMANCE (Unaudited)

(Continued)

| (1) | The Russell 2000 Index measures the performance of the 2,000 smallest companies in the Russell 3000 Index, which comprises the 3,000 largest U.S. companies based on total market capitalization. |

| (2) | The Russell 2000 Value Index includes equities that exhibit value characteristics and the Russell 2000 Growth Index includes equities that exhibit growth characteristics. |

| * | The benchmark since inception returns are calculated since inception of the Investor Class, December 18, 1981 to September 30, 2023. |

An investment cannot be made directly into an index.

10

FMI Common Stock Fund

SCHEDULE OF INVESTMENTS

September 30, 2023

| Shares | Cost | Value | |||||||||

COMMON STOCKS — 94.7%(1) | |||||||||||

COMMERCIAL SERVICES SECTOR — 11.7% | |||||||||||

| Advertising/Marketing Services — 3.3% | |||||||||||

1,660,000 | Interpublic Group of Cos. Inc. | $ | 35,407,016 | $ | 47,575,600 | ||||||

| Miscellaneous Commercial Services — 4.3% | |||||||||||

1,730,000 | Genpact Ltd. | 48,941,893 | 62,626,000 | ||||||||

| Personnel Services — 4.1% | |||||||||||

810,000 | Robert Half International Inc. | 50,876,453 | 59,356,800 | ||||||||

CONSUMER DURABLES SECTOR — 1.8% | |||||||||||

| Homebuilding — 1.8% | |||||||||||

267,000 | LGI Homes Inc.(2) | 32,458,963 | 26,563,830 | ||||||||

CONSUMER NON-DURABLES SECTOR — 4.0% | |||||||||||

| Apparel/Footwear — 4.0% | |||||||||||

1,183,000 | Skechers U.S.A. Inc. — Cl A(2) | 51,328,336 | 57,907,850 | ||||||||

CONSUMER SERVICES SECTOR — 2.0% | |||||||||||

| Other Consumer Services — 2.0% | |||||||||||

925,000 | Valvoline Inc. | 29,882,920 | 29,822,000 | ||||||||

DISTRIBUTION SERVICES SECTOR — 15.8% | |||||||||||

| Electronics Distributors — 2.6% | |||||||||||

309,000 | Arrow Electronics Inc.(2) | 15,554,791 | 38,699,160 | ||||||||

| Medical Distributors — 4.4% | |||||||||||

868,000 | Henry Schein Inc.(2) | 58,568,643 | 64,449,000 | ||||||||

| Wholesale Distributors — 8.8% | |||||||||||

235,000 | Applied Industrial Technologies Inc. | 15,033,348 | 36,333,350 | ||||||||

805,000 | Beacon Roofing Supply Inc.(2) | 45,952,730 | 62,121,850 | ||||||||

1,035,000 | Core & Main Inc. — Cl A(2) | 29,674,788 | 29,859,750 | ||||||||

90,660,866 | 128,314,950 | ||||||||||

ELECTRONIC TECHNOLOGY SECTOR — 9.6% | |||||||||||

| Electronic Components — 3.0% | |||||||||||

815,000 | nVent Electric PLC | 16,132,830 | 43,186,850 | ||||||||

| Electronic Production Equipment — 4.9% | |||||||||||

530,000 | CTS Corp. | 23,419,856 | 22,122,200 | ||||||||

523,000 | Plexus Corp.(2) | 42,104,151 | 48,628,540 | ||||||||

65,524,007 | 70,750,740 | ||||||||||

| Semiconductors — 1.7% | |||||||||||

145,000 | Fabrinet(2) | 13,771,658 | 24,159,900 | ||||||||

FINANCE SECTOR — 15.2% | |||||||||||

| Finance/Rental/Leasing — 3.7% | |||||||||||

533,000 | FirstCash Holdings Inc. | 26,908,468 | 53,502,540 | ||||||||

| Investment Banks/Brokers — 3.7% | |||||||||||

500,000 | Houlihan Lokey Inc. — Cl A | 31,228,156 | 53,560,000 | ||||||||

The accompanying notes to financial statements are an integral part of this schedule.

11

FMI Common Stock Fund

SCHEDULE OF INVESTMENTS (Continued)

September 30, 2023

| Shares | Cost | Value | |||||||||

COMMON STOCKS — 94.7%(1) (Continued) | |||||||||||

FINANCE SECTOR — 15.2% (Continued) | |||||||||||

| Life/Health Insurance — 3.8% | |||||||||||

282,874 | Primerica Inc. | $ | 39,281,082 | $ | 54,880,385 | ||||||

| Major Banks — 2.4% | |||||||||||

1,005,000 | Zions Bancorporation N.A. | 34,857,723 | 35,064,450 | ||||||||

| Multi-Line Insurance — 1.6% | |||||||||||

16,000 | White Mountains Insurance Group Ltd. | 16,123,980 | 23,931,040 | ||||||||

PROCESS INDUSTRIES SECTOR — 2.0% | |||||||||||

| Containers/Packaging — 2.0% | |||||||||||

237,000 | AptarGroup Inc. | 25,254,240 | 29,634,480 | ||||||||

PRODUCER MANUFACTURING SECTOR — 24.4% | |||||||||||

| Auto Parts: OEM — 3.1% | |||||||||||

765,000 | Donaldson Co. Inc. | 37,298,150 | 45,624,600 | ||||||||

| Building Products — 11.9% | |||||||||||

251,000 | Carlisle Cos. Inc. | 32,713,079 | 65,074,260 | ||||||||

770,000 | Fortune Brands Innovations Inc. | 45,401,719 | 47,863,200 | ||||||||

406,000 | Simpson Manufacturing Co. Inc. | 44,384,951 | 60,822,860 | ||||||||

122,499,749 | 173,760,320 | ||||||||||

| Industrial Machinery — 5.4% | |||||||||||

2,480,000 | Gates Industrial Corp. PLC(2) | 33,542,797 | 28,792,800 | ||||||||

330,000 | ITT Inc. | 27,234,245 | 32,310,300 | ||||||||

236,751 | Timken Co. | 17,247,965 | 17,398,831 | ||||||||

78,025,007 | 78,501,931 | ||||||||||

| Miscellaneous Manufacturing — 4.0% | |||||||||||

215,000 | LCI Industries | 28,646,678 | 25,245,300 | ||||||||

1,365,000 | TriMas Corp. | 32,750,235 | 33,797,400 | ||||||||

61,396,913 | 59,042,700 | ||||||||||

RETAIL TRADE SECTOR — 4.6% | |||||||||||

| Specialty Stores — 4.6% | |||||||||||

930,000 | BJ’s Wholesale Club Holdings Inc.(2) | 57,006,070 | 66,374,100 | ||||||||

TECHNOLOGY SERVICES SECTOR — 3.6% | |||||||||||

| Information Technology Services — 3.6% | |||||||||||

360,000 | Insight Enterprises Inc.(2) | 23,482,552 | 52,380,000 | ||||||||

Total common stocks | 1,062,470,466 | 1,379,669,226 | |||||||||

The accompanying notes to financial statements are an integral part of this schedule.

12

FMI Common Stock Fund

SCHEDULE OF INVESTMENTS (Continued)

September 30, 2023

| Shares | Cost | Value | |||||||||

SHORT-TERM INVESTMENT — 3.1%(1) | |||||||||||

| Money Market Fund — 3.1% | |||||||||||

44,431,688 | First American Treasury | ||||||||||

Obligations Fund, Cl X, 5.264%(3) | $ | 44,431,688 | $ | 44,431,688 | |||||||

Total short-term investment | 44,431,688 | 44,431,688 | |||||||||

Total investments — 97.8% | $ | 1,106,902,154 | 1,424,100,914 | ||||||||

Other assets, less liabilities — 2.2%(1) | 32,280,118 | ||||||||||

| TOTAL NET ASSETS — 100.0% | $ | 1,456,381,032 | |||||||||

| (1) | Percentages for the various classifications relate to total net assets. |

| (2) | Non-Income producing security. |

| (3) | The rate quoted is the annualized 7-day yield as of September 30, 2023. |

| PLC | Public Limited Company |

The accompanying notes to financial statements are an integral part of this schedule.

INDUSTRY SECTORS as a percentage of net assets

as of September 30, 2023 (Unaudited)

13

FMI Large Cap Fund

MANAGEMENT’S DISCUSSION OF FUND PERFORMANCE (Unaudited)

During the fiscal year ended September 30, 2023, the FMI Large Cap Fund (“Fund”) had a total return of 19.95%1. The benchmark Standard & Poor’s 500 Index returned 21.62% in the same period. The trailing 12-month return for the iShares Russell 1000 Value ETF2 was 14.13%.

Relative to the S&P 500, sectors that aided performance included Consumer Services, Health Technology, and Distribution Services. Booking Holdings Inc. drove the results in the Consumer Services sector, as travel continues to recover, with particular improvement in Europe, and Booking is taking market share from competitors. In Health Technology, Koninklijke Philips N.V.-SP-ADR recovered from a tough 2022, as business fundamentals improved. Ferguson PLC aided the relative performance in Distribution Services, as the business outperformed its respective end-markets which were challenging. Other stocks that helped performance included Arch Capital Group Ltd., SAP SE-SP-ADR, and Eaton Corp. PLC. Arch Capital has executed well, while benefiting from a hardening of the property catastrophic reinsurance and property and casualty insurance markets. SAP has been performing resiliently and tracking ahead of schedule on their cloud transition despite a tougher macro backdrop. Eaton has re-rated after strong execution and a successful portfolio transformation. The company is poised to benefit from big secular growth drivers including electrification and energy transition.

On the negative side of sector performance, Retail Trade, Electronic Technology, and Technology Services all detracted. In Retail Trade, Dollar General Corp. and Dollar Tree Inc. both underperformed. Macro conditions, such as persistent inflation, lower tax refunds, a reduction in SNAP benefits, high shrink, and a decline in spending on more profitable discretionary merchandise, have slowed Dollar General’s same store sales growth and negatively impacted gross margins. In addition, competitive pressures have ramped up and the company’s new management team has made some uncharacteristic operational missteps that now require re-investment in price, labor, and processes to correct. At Dollar Tree, while the top-line performance has been encouraging, the turnaround is proving to be larger and more costly than initially expected. In Technology Services and Electronic Technology, our under-weight exposure to mega-cap tech hurt significantly given their relative outperformance. Meta Platforms Inc. – Cl A hurt, as we sold the position at a loss after losing confidence in management and the Metaverse expense trajectory. Other detractors included The Charles Schwab Corp., Northern Trust Corp., and Carlisle Cos. Inc. Charles Schwab is seeing yield-seeking deposits move from the bank to money market funds. They’re staying within Schwab, but they’ll be monetized at a lower rate and are requiring some higher cost funding to temporarily replace them. This “cash sorting” was expected and happens every cycle, although the pace and magnitude of the rate increases were worse than initially expected. Northern Trust’s expense and net interest income guidance disappointed, but they are starting to focus more on expenses. Destocking and margin normalization has weighed on Carlisle.

New additions to the Fund over the past twelve months included Sysco Corp. and Carrier Global Corp. Stocks sold during the year included PACCAR Inc., JPMorgan Chase & Co., and Meta Platforms Inc. Cl A.

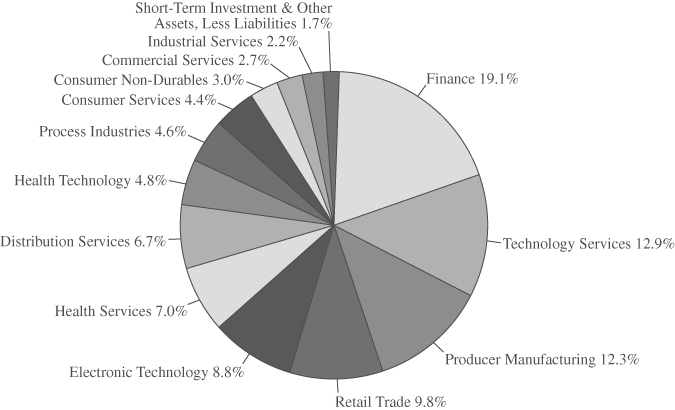

As of September 30, 2023, the Fund was significantly overweight in Producer Manufacturing, Finance, and Distribution Services. The Fund was meaningfully underweight in Technology Services, Electronic Technology, and Health Technology.

After a tough fiscal year 2022, U.S. stocks rebounded strongly in fiscal year 2023, despite concerns around a regional banking crisis, waning global growth, record debt levels, elevated inflation, rising interest rates, and heightened geopolitical risks. Furthermore, corporate earnings growth in the U.S. has slowed, as higher borrowing, labor and input costs have weighed. Growth stocks outperformed value stocks in the period, but much more significantly in the U.S. Large Cap arena, which remains exceedingly top-heavy with performance being dominated by a handful of mega-cap companies that trade at significant valuation premiums (see recent shareholder letters for further discussion). Speculation appears to be plentiful. Stock valuations in the U.S. have

_______________

1 | The Large Cap Fund Investor Class (FMIHX) and the FMI Large Cap Fund Institutional Class (FMIQX) had a return of 19.95% and 20.07%, respectively, for the fiscal year ending September 30, 2023. |

2 | Source: Bloomberg – returns do not reflect management fees, transaction costs or expenses. Performance is based on market price returns. Beginning 8/10/20, market price returns are calculated using closing price. Prior to 8/10/20, market price returns were calculated using midpoint bid/ask spread at 4:00 PM ET. |

14

FMI Large Cap Fund

MANAGEMENT’S DISCUSSION OF FUND PERFORMANCE (Unaudited)

(Continued)

ballooned, as the market is currently trading in the 10th decile of historical valuation – one of the most expensive stock markets in U.S. history (on a median basis, tracking 46 different valuation metrics dating as far back as 1926). There are attractive relative values outside many of the anointed mega-cap companies in the S&P 500.

Given the backdrop, the Fund portfolio managers were pleased to capture most of the upside of the S&P 500 during the current fiscal year, while outperforming the iShares Russell 1000 Value ETF by a wide margin. Over the long-term, they are optimistic and are excited to see a more normal interest rate environment. This should bode well for organic growth, stock picking, and value investing. With global value stocks trading near a historically wide discount to growth, the current set-up looks attractive from here. Any reversion to the mean should result in brighter days for those with a value orientation. The Fund trades at a significant discount to the S&P 500, the businesses have strong balance sheets, and management believes the companies are above average. Management sees opportunities across the Fund, with what they feel is a collection of all-weather vehicles that can withstand tough and unpredictable times.

15

FMI Large Cap Fund

MANAGEMENT’S DISCUSSION OF FUND PERFORMANCE (Unaudited)

(Continued)

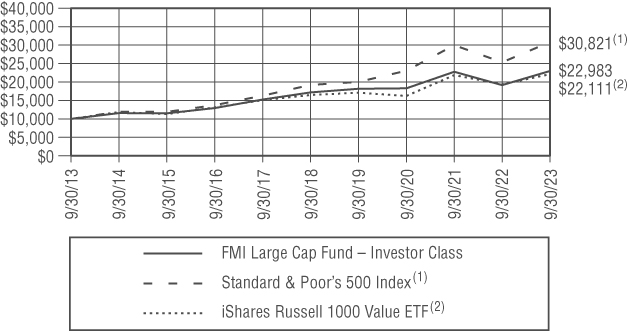

COMPARISON OF CHANGE IN VALUE OF $10,000 INVESTMENT IN

FMI LARGE CAP FUND – INVESTOR CLASS — STANDARD & POOR’S 500 INDEX(1)

AND THE ISHARES RUSSELL 1000 VALUE ETF(2)

AVERAGE ANNUALIZED TOTAL RETURN

| Inception | |||||

| through | |||||

| Inception Date | 1-Year | 5-Year | 10-Year | 9/30/2023 | |

FMI Large Cap Fund – Investor Class | 12/31/01 | 19.95% | 5.99% | 8.68% | 8.52% |

FMI Large Cap Fund – Institutional Class | 10/31/16 | 20.07% | 6.13% | N/A | 9.17% |

Standard & Poor’s 500 Index(1)* | 21.62% | 9.92% | 11.91% | 8.34% | |

iShares Russell 1000 Value ETF(2)* | 14.13% | 6.06% | 8.26% | 7.18% |

The graph and the table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Performance data quoted represents past performance; past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of a Fund may be lower or higher than the performance quoted. The total returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Total return includes change in share prices and in each case includes reinvestments of any dividends, interest and capital gain distributions. Performance data current to the most recent month-end may be obtained by visiting www.fmifunds.com or by calling 1-800-811-5311.

| (1) | The Standard & Poor’s 500 Index consists of 500 selected common stocks, most of which are listed on the New York Stock Exchange. The Standard & Poor’s Ratings Group designates the stocks to be included in the Index on a statistical basis. A particular stock’s weighting in the Index is based on its relative total market value (i.e., its market price per share times the number of shares outstanding). Stocks may be added or deleted from the Index from time to time. |

| (2) | The iShares Russell 1000 Value ETF seeks to track investment results of an index composed of large- and mid-capitalization U.S. equities that exhibit value characteristics. Performance is compared to the iShares Russell 1000 Value ETF (“ETF”) for illustrative purposes only. The metrics regarding the comparative ETF have been obtained from Bloomberg and the returns do not reflect management fees, transaction costs or |

16

FMI Large Cap Fund

MANAGEMENT’S DISCUSSION OF FUND PERFORMANCE (Unaudited)

(Continued)

| expenses. Performance is based on market price returns. Beginning 8/10/2020, market price returns are calculated using closing price. Prior to 8/10/2020, market price returns were calculated using midpoint bid/ask spread at 4:00 PM ET. The ETF is not subject to the same fees or expenses as the Fund. The Fund is not restricted to investing in those securities which comprise the ETF. The Fund’s performance may or may not correlate to the ETF, and it should not be considered a proxy for the ETF. | |

| * | The benchmark since inception returns are calculated since inception of the Investor Class, December 31, 2001 to September 30, 2023. |

An investment cannot be made directly into an index.

17

FMI Large Cap Fund

SCHEDULE OF INVESTMENTS

September 30, 2023

| Shares | Cost | Value | |||||||||

COMMON STOCKS — 98.3%(1) | |||||||||||

COMMERCIAL SERVICES SECTOR — 2.7% | |||||||||||

| Advertising/Marketing Services — 2.7% | |||||||||||

595,000 | Omnicom Group Inc. | $ | 39,572,557 | $ | 44,315,600 | ||||||

CONSUMER NON-DURABLES SECTOR — 3.0% | |||||||||||

| Household/Personal Care — 3.0% | |||||||||||

975,000 | Unilever PLC — SP-ADR | 38,480,544 | 48,165,000 | ||||||||

CONSUMER SERVICES SECTOR — 4.4% | |||||||||||

| Other Consumer Services — 4.4% | |||||||||||

23,000 | Booking Holdings Inc.(2) | 39,082,089 | 70,930,850 | ||||||||

DISTRIBUTION SERVICES SECTOR — 6.7% | |||||||||||

| Food Distributors — 1.4% | |||||||||||

350,000 | Sysco Corp. | 24,310,111 | 23,117,500 | ||||||||

| Wholesale Distributors — 5.3% | |||||||||||

520,000 | Ferguson PLC | 63,831,481 | 85,524,400 | ||||||||

ELECTRONIC TECHNOLOGY SECTOR — 8.8% | |||||||||||

| Computer Processing Hardware — 4.6% | |||||||||||

895,000 | Sony Group Corp. — SP-ADR | 55,884,978 | 73,756,950 | ||||||||

| Semiconductors — 4.2% | |||||||||||

1,005,000 | Micron Technology Inc. | 48,491,332 | 68,370,150 | ||||||||

FINANCE SECTOR — 19.1% | |||||||||||

| Investment Banks/Brokers — 4.3% | |||||||||||

1,275,000 | The Charles Schwab Corp. | 48,781,741 | 69,997,500 | ||||||||

| Investment Managers — 4.6% | |||||||||||

50,000 | BlackRock Inc. | 29,447,225 | 32,324,500 | ||||||||

615,000 | Northern Trust Corp. | 52,294,960 | 42,730,200 | ||||||||

81,742,185 | 75,054,700 | ||||||||||

| Multi-Line Insurance — 5.1% | |||||||||||

500,000 | Arch Capital Group Ltd.(2) | 18,047,650 | 39,855,000 | ||||||||

310,000 | Progressive Corp. | 25,601,757 | 43,183,000 | ||||||||

43,649,407 | 83,038,000 | ||||||||||

| Property/Casualty Insurance — 5.1% | |||||||||||

235,000 | Berkshire Hathaway Inc. Cl B(2) | 11,176,060 | 82,320,500 | ||||||||

HEALTH SERVICES SECTOR — 7.0% | |||||||||||

| Managed Health Care — 4.8% | |||||||||||

155,000 | UnitedHealth Group Inc. | 19,074,375 | 78,149,450 | ||||||||

| Medical/Nursing Services — 2.2% | |||||||||||

1,680,000 | Fresenius Medical | ||||||||||

Care AG & Co. KGaA — SP-ADR | 60,898,713 | 36,187,200 | |||||||||

The accompanying notes to financial statements are an integral part of this schedule.

18

FMI Large Cap Fund

SCHEDULE OF INVESTMENTS (Continued)

September 30, 2023

| Shares | Cost | Value | |||||||||

COMMON STOCKS — 98.3%(1) (Continued) | |||||||||||

HEALTH TECHNOLOGY SECTOR — 4.8% | |||||||||||

| Medical Specialties — 4.8% | |||||||||||

2,090,000 | Koninklijke Philips N.V. — SP-ADR(2) | $ | 74,431,031 | $ | 41,674,600 | ||||||

1,435,000 | Smith & Nephew PLC — SP-ADR | 50,892,058 | 35,544,950 | ||||||||

125,323,089 | 77,219,550 | ||||||||||

INDUSTRIAL SERVICES SECTOR — 2.2% | |||||||||||

| Contract Drilling — 2.2% | |||||||||||

605,000 | Schlumberger Ltd. | 11,639,716 | 35,271,500 | ||||||||

PROCESS INDUSTRIES SECTOR — 4.6% | |||||||||||

| Containers/Packaging — 4.6% | |||||||||||

405,000 | Avery Dennison Corp. | 69,607,906 | 73,981,350 | ||||||||

PRODUCER MANUFACTURING SECTOR — 12.3% | |||||||||||

| Building Products — 7.1% | |||||||||||

210,000 | Carlisle Cos. Inc. | 49,379,260 | 54,444,600 | ||||||||

1,145,000 | Masco Corp. | 35,821,692 | 61,200,250 | ||||||||

85,200,952 | 115,644,850 | ||||||||||

| Electrical Products — 1.4% | |||||||||||

106,000 | Eaton Corp. PLC | 9,606,292 | 22,607,680 | ||||||||

| Industrial Machinery — 3.8% | |||||||||||

1,110,000 | Carrier Global Corp. | 49,210,177 | 61,272,000 | ||||||||

RETAIL TRADE SECTOR — 9.8% | |||||||||||

| Apparel/Footwear Retail — 1.4% | |||||||||||

250,000 | The TJX Cos. Inc. | 8,458,463 | 22,220,000 | ||||||||

| Discount Stores — 5.2% | |||||||||||

415,000 | Dollar General Corp. | 38,033,546 | 43,907,000 | ||||||||

380,000 | Dollar Tree Inc.(2) | 32,487,797 | 40,451,000 | ||||||||

70,521,343 | 84,358,000 | ||||||||||

| Specialty Stores — 3.2% | |||||||||||

730,000 | CarMax Inc.(2) | 63,044,613 | 51,632,900 | ||||||||

TECHNOLOGY SERVICES SECTOR — 12.9% | |||||||||||

| Information Technology Services — 4.1% | |||||||||||

325,000 | CDW Corp. | 56,455,379 | 65,572,000 | ||||||||

| Internet Software/Services — 5.6% | |||||||||||

690,000 | Alphabet Inc. — Cl A(2) | 76,097,068 | 90,293,400 | ||||||||

| Packaged Software — 3.2% | |||||||||||

395,000 | SAP SE — SP-ADR | 42,748,166 | 51,081,400 | ||||||||

Total common stocks | 1,242,888,737 | 1,590,082,430 | |||||||||

The accompanying notes to financial statements are an integral part of this schedule.

19

FMI Large Cap Fund

SCHEDULE OF INVESTMENTS (Continued)

September 30, 2023

| Shares | Cost | Value | |||||||||

SHORT-TERM INVESTMENT — 1.6%(1) | |||||||||||

| Money Market Fund — 1.6% | |||||||||||

26,580,969 | First American Treasury | ||||||||||

Obligations Fund, Cl X, 5.264%(3) | $ | 26,580,969 | $ | 26,580,969 | |||||||

Total short-term investment | 26,580,969 | 26,580,969 | |||||||||

Total investments — 99.9% | $ | 1,269,469,706 | 1,616,663,399 | ||||||||

Other assets, less liabilities — 0.1%(1) | 1,741,757 | ||||||||||

| TOTAL NET ASSETS — 100.0% | $ | 1,618,405,156 | |||||||||

| (1) | Percentages for the various classifications relate to total net assets. |

| (2) | Non-Income producing security. |

| (3) | The rate quoted is the annualized 7-day yield as of September 30, 2023. |

| PLC | Public Limited Company |

| SP-ADR | Sponsored American Depositary Receipt |

The accompanying notes to financial statements are an integral part of this schedule.

INDUSTRY SECTORS as a percentage of net assets

as of September 30, 2023 (Unaudited)

20

FMI International Fund and FMI International Fund II – Currency Unhedged

MANAGEMENT’S DISCUSSION OF FUND PERFORMANCE (Unaudited)

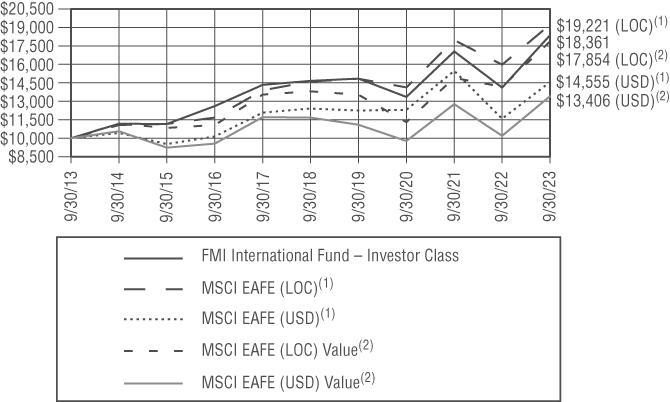

During the fiscal year ended September 30, 2023, the FMI International Funds gained 30.14%1 (“currency hedged”) and 33.78%2 (“currency unhedged”). Over the same period, the MSCI EAFE Index (“Index”) increased 20.32% in local currency (LOC) and 25.65% in U.S. Dollars (USD), while the MSCI EAFE Value Index (“Value Index”) added 25.89% in LOC and 31.51% in USD. FMI’s currency hedged performance was negatively impacted by a weak USD.

The Funds’ relative performance was aided by the Retail Trade, Consumer Services and Electronic Technology sectors. B&M European Value Retail S.A. drove the Retail Trade performance after a tough 2022 when UK consumer stocks were under extreme pressure. The stock recovered in 2023 as the business model proved resilient. Consumer Services was led by Booking Holdings Inc., as travel continues to recover, with particular improvement in Europe, and Booking is taking market share from competitors. In Electronic Technology, Safran S.A. performed well as they benefitted from rebounding global air travel while successfully navigating supply chain challenges and inflation, leading to an outlook for multiyear double-digit earnings growth. Additional stocks that performed well included Arch Capital Group Ltd., Ferguson PLC, and SAP SE. Arch Capital has executed well, while benefiting from a hardening of the property catastrophic reinsurance and property and casualty insurance markets. Ferguson’s business has outperformed its respective end-markets which were challenging. SAP has been performing resiliently and tracking ahead of schedule on their cloud transition despite a tougher macro backdrop.

Conversely, the Health Technology, Commercial Services, and Producer Manufacturing sectors all weighed on the Funds’ relative performance. In Health Technology, Roche Holdings AG declined, as an Alzheimer’s pipeline drug failure in late 2022 and weaker than expected 2023 guidance disappointed. In Commercial Services, Genpact Ltd. lagged, as negative sentiment around generative artificial intelligence (AI) has impacted the stock, but is believed to be significantly overblown. In Producer Manufacturing, Nabtesco Corp. lagged as cyclical pressure and operational execution weighed on the stock. Additional stocks that detracted from performance included DKSH Holdings AG, Barry Callebaut AG, and Smith & Nephew PLC. DKSH underperformed, as a sluggish recovery coming out of COVID-19 in China and other Asian countries has weighed on topline growth. For Barry Callebaut, rising chocolate prices and slowing economic growth have hurt global chocolate consumption this year. Additionally, last year’s Salmonella outbreak in one of Barry Callebaut’s plants is proving to be more impactful than initially expected. With Smith & Nephew, improving sales growth in Orthopedics did not yet translate into improving margins, which disappointed (despite margin targets being reiterated for 2023 and 2025).

New additions to the Fund over the past twelve months included Ryanair Holdings PLC-SP-ADR, Coca-Cola Europacific Partners PLC, Weir Group PLC, Barry Callebaut AG, Diageo PLC, Genpact Ltd. and Ashtead Group PLC. Stocks sold during the year included WPP PLC, CK Hutchison Holdings Ltd., Nabtesco Corp., Vivendi, Henkel AG & Co. KGaA, LG Household & Health Care Ltd. Pfd., and Amorepacific Corp. Pfd.

As of September 30, 2023, the Funds were significantly overweight in Distribution Services, Electronic Technology, and Consumer Services versus the Index, and underweight in Finance, Health Technology, and Energy Minerals. In terms of geographic revenue exposure, the Funds are overweight the United Kingdom and United States and underweight Japan and China.

After a tough fiscal year 2022, international stock markets rebounded strongly in fiscal year 2023, despite concerns around waning global growth, record debt levels, elevated inflation, rising interest rates, and heightened geopolitical risks. In the international arena, value stocks outperformed growth stocks in the period, with the “deeper value” Energy and Finance sectors performing strongly. FMI is typically under-weight these sectors due to business quality and balance sheet concerns. International stocks currently trade near an all-time high

_______________

1 | The FMI International Fund [currency hedged] Investor Class (FMIJX) and the FMI International Fund [currency hedged] Institutional Class (FMIYX) had a return of 30.14% and 30.30%, respectively, for the fiscal year ending September 30, 2023. |

2 | The FMI International Fund [currency unhedged] Institutional Class (FMIFX) had a return of 33.78% for the fiscal year ending September 30, 2023. |

21

FMI International Fund and FMI International Fund II – Currency Unhedged

MANAGEMENT’S DISCUSSION OF FUND PERFORMANCE (Unaudited)

(Continued)

discount to the U.S., which should provide some margin of safety. Some of the discount is warranted, as Europe is facing high food and energy inflation, business activity and bank lending has slowed, and a higher cost of borrowing is impacting investment. In China, the property sector, which we have long described as a dangerous and a speculative bubble, has finally popped. Furthermore, China’s demographics are poor, productivity growth is slowing, exports are weak, youth unemployment is high, and tensions with the West are rising.

Given the challenging backdrop, the Fund portfolio managers were pleased to outperform both the Index and Value Index in a rapidly rising stock market. Over the long-term, they remain optimistic and are excited to see a more normal interest rate environment. This should bode well for organic growth, stock picking, and value investing. With global value stocks currently trading near a historically wide discount to growth, the current set-up looks attractive from here. Any reversion to the mean should result in brighter days for those with a value orientation. The Funds trade at a significant discount to the Index, the businesses have strong balance sheets, and management believes the companies are above average. Management sees compelling opportunities across the Funds, with what they feel is a collection of all-weather vehicles that can withstand tough and unpredictable times.

22

FMI International Fund and FMI International Fund II – Currency Unhedged

MANAGEMENT’S DISCUSSION OF FUND PERFORMANCE (Unaudited)

(Continued)

COMPARISON OF CHANGE IN VALUE OF $10,000 INVESTMENT IN

FMI INTERNATIONAL FUND – INVESTOR CLASS — MSCI EAFE(1) AND MSCI EAFE VALUE(2)

AVERAGE ANNUALIZED TOTAL RETURN

| Inception | |||||

| through | |||||

| Inception Date | 1-Year | 5-Year | 10-Year | 9/30/2023 | |

FMI International Fund – Investor Class | 12/31/10 | 30.14% | 4.61% | 6.27% | 7.37% |

FMI International Fund – Institutional Class | 10/31/16 | 30.30% | 4.76% | N/A | 5.88% |

MSCI EAFE Net (LOC)(1)* | 20.32% | 5.65% | 6.75% | 6.98% | |

MSCI EAFE Net (LOC) Value(2)* | 25.89% | 5.27% | 5.97% | 6.35% | |

MSCI EAFE Net (USD)(1)* | 25.65% | 3.24% | 3.82% | 4.45% | |

MSCI EAFE Net (USD) Value(2)* | 31.51% | 2.81% | 2.97% | 3.77% |

The graph and the table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Performance data quoted represents past performance; past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of a Fund may be lower or higher than the performance quoted. The total returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Total return includes change in share prices and in each case includes reinvestments of any dividends, interest and capital gain distributions. Performance data current to the most recent month-end may be obtained by visiting www.fmifunds.com or by calling 1-800-811-5311.

| (1) | The MSCI EAFE Index (Europe, Australasia, Far East) is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the U.S. and Canada. The MSCI EAFE Index consists of the following 21 developed market country indices: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New |

23

FMI International Fund and FMI International Fund II – Currency Unhedged

MANAGEMENT’S DISCUSSION OF FUND PERFORMANCE (Unaudited)

(Continued)

| Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland and the United Kingdom. The MSCI EAFE Index is unmanaged and investors cannot invest directly in the Index. Index results are inclusive of dividends and net of foreign withholding taxes. The reported figures include reinvestment of dividends and capital gains distributions and do not reflect any fees or expenses. | |

| (2) | The MSCI EAFE Value Index captures large and mid cap securities exhibiting overall value style characteristics across Developed Markets countries around the world, excluding the U.S. and Canada. The value Investment style characteristics for index construction are defined using three variables: book value to price, 12-month forward earnings to price and dividend yield. |

| The MSCI EAFE and MSCI EAFE Value Index are calculated in local currency (LOC) as well as in U.S. dollars (USD). The concept of a LOC calculation excludes the impact of currency fluctuations. All currencies of listing are considered in the Index calculation in LOC where current prices (t) and previous day prices (t-1) are converted into USD using the same exchange rate (exchange rate t-1) in the numerator and denominator. As a consequence, the FX factor drops out of the equation. The USD calculation includes exchange rates at t and t-1. Therefore, the LOC calculation only represents the price appreciation or depreciation of the securities, whereas the USD calculation also accounts for the performance of the currency (or currencies) relative to the USD. MSCI EAFE is a service mark of MSCI Barra. | |

| * | The benchmark since inception returns are calculated since inception of the Investor Class, December 31, 2010 to September 30, 2023. |

An investment cannot be made directly into an index.

24

FMI International Fund and FMI International Fund II – Currency Unhedged

MANAGEMENT’S DISCUSSION OF FUND PERFORMANCE (Unaudited)

(Continued)

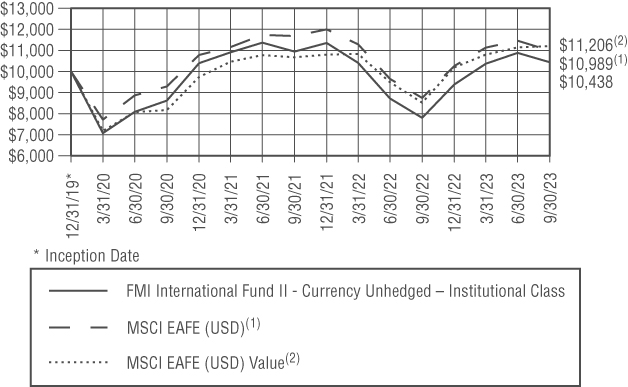

COMPARISON OF CHANGE IN VALUE OF $10,000 INVESTMENT IN

FMI INTERNATIONAL FUND II — CURRENCY UNHEDGED –

INSTITUTIONAL CLASS AND MSCI EAFE(1) AND MSCI EAFE VALUE(2)

AVERAGE ANNUALIZED TOTAL RETURN

| Inception | ||||

| through | ||||

| Inception Date | 1-Year | 3-Year | 9/30/2023 | |

FMI International Fund II – Currency Unhedged – | ||||

Institutional Class | 12/31/19 | 33.78% | 6.59% | 1.15% |

MSCI EAFE Net (USD)(1)* | 25.65% | 5.75% | 2.55% | |

MSCI EAFE Net (USD) Value(2)* | 31.51% | 11.11% | 3.08% |

The graph and the table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Performance data quoted represents past performance; past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of a Fund may be lower or higher than the performance quoted. The total returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Total return includes change in share prices and in each case includes reinvestments of any dividends, interest and capital gain distributions. Performance data current to the most recent month-end may be obtained by visiting www.fmifunds.com or by calling 1-800-811-5311.

| (1) | The MSCI EAFE Index (Europe, Australasia, Far East) is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the U.S. and Canada. The MSCI EAFE Index consists of the following 21 developed market country indices: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland and the United Kingdom. The MSCI EAFE |

25

FMI International Fund and FMI International Fund II – Currency Unhedged

MANAGEMENT’S DISCUSSION OF FUND PERFORMANCE (Unaudited)

(Continued)

| Index is unmanaged and investors cannot invest directly in the Index. Index results are inclusive of dividends and net of foreign withholding taxes. The reported figures include reinvestment of dividends and capital gains distributions and do not reflect any fees or expenses. | |

| (2) | The MSCI EAFE Value Index captures large and mid cap securities exhibiting overall value style characteristics across Developed Markets countries around the world, excluding the U.S. and Canada. The value Investment style characteristics for index construction are defined using three variables: book value to price, 12-month forward earnings to price and dividend yield. MSCI EAFE is a service mark of MSCI Barra. |

| * | The benchmark since inception returns are calculated since inception of the Institutional Class, December 31, 2019 to September 30, 2023. |

An investment cannot be made directly into an index.

26

FMI International Fund

SCHEDULE OF INVESTMENTS

September 30, 2023

| Shares | Cost | Value | |||||||||

LONG-TERM INVESTMENTS — 92.3%(1) | |||||||||||

COMMON STOCKS — 88.2%(1) | |||||||||||

COMMERCIAL SERVICES SECTOR — 2.9% | |||||||||||

| Miscellaneous Commercial Services — 2.9% | |||||||||||

3,325,000 | Genpact Ltd. (Bermuda) | $ | 140,202,262 | $ | 120,365,000 | ||||||

CONSUMER DURABLES SECTOR — 2.3% | |||||||||||

| Electronics/Appliances — 2.3% | |||||||||||

10,340,000 | Howden Joinery Group PLC (Britain)(4) | 76,308,220 | 92,518,147 | ||||||||

CONSUMER NON-DURABLES SECTOR — 12.1% | |||||||||||

| Beverages: Alcoholic — 2.1% | |||||||||||

2,320,000 | Diageo PLC (Britain)(4) | 100,448,240 | 85,534,562 | ||||||||

| Beverages: Non-Alcoholic — 2.1% | |||||||||||

1,385,000 | Coca-Cola Europacific Partners PLC (Britain) | 87,198,706 | 86,534,800 | ||||||||

| Food: Specialty/Candy — 4.7% | |||||||||||

38,000 | Barry Callebaut AG (Switzerland)(4) | 82,668,815 | 60,429,255 | ||||||||

4,425,000 | Greggs PLC (Britain)(4) | 119,945,004 | 131,736,110 | ||||||||

202,613,819 | 192,165,365 | ||||||||||

| Household/Personal Care — 3.2% | |||||||||||

2,625,000 | Unilever PLC (Britain)(4) | 112,240,154 | 129,851,140 | ||||||||

CONSUMER SERVICES SECTOR — 8.8% | |||||||||||

| Other Consumer Services — 3.9% | |||||||||||

52,000 | Booking Holdings Inc. (United States)(2) | 89,513,766 | 160,365,400 | ||||||||

| Restaurants — 4.9% | |||||||||||

1,935,000 | Sodexo S.A. (France)(4) | 157,266,344 | 199,203,548 | ||||||||

DISTRIBUTION SERVICES SECTOR — 12.1% | |||||||||||

| Medical Distributors — 2.2% | |||||||||||

1,325,000 | DKSH Holding AG (Switzerland)(4) | 75,162,258 | 89,625,755 | ||||||||

| Wholesale Distributors — 9.9% | |||||||||||

1,620,000 | Ferguson PLC (Jersey)(4) | 101,715,903 | 266,605,299 | ||||||||

6,115,000 | Rexel S.A. (France)(4) | 113,118,225 | 137,012,547 | ||||||||

214,834,128 | 403,617,846 | ||||||||||

ELECTRONIC TECHNOLOGY SECTOR — 10.4% | |||||||||||

| Aerospace & Defense — 4.5% | |||||||||||

1,175,000 | Safran S.A. (France)(4) | 123,160,730 | 184,133,359 | ||||||||

| Computer Processing Hardware — 4.3% | |||||||||||

2,130,000 | Sony Group Corp. (Japan)(4) | 134,755,032 | 174,181,994 | ||||||||

| Electronic Equipment/Instruments — 1.6% | |||||||||||

3,340,000 | Yokogawa Electric Corp. (Japan)(4) | 59,113,396 | 64,464,378 | ||||||||

FINANCE SECTOR — 8.3% | |||||||||||

| Finance/Rental/Leasing — 1.9% | |||||||||||

1,300,000 | Ashtead Group PLC (Britain)(4) | 63,126,241 | 78,835,892 | ||||||||

The accompanying notes to financial statements are an integral part of this schedule.

27

FMI International Fund

SCHEDULE OF INVESTMENTS (Continued)

September 30, 2023

| Shares | Cost | Value | |||||||||

LONG-TERM INVESTMENTS — 92.3%(1) (Continued) | |||||||||||

COMMON STOCKS — 88.2%(1) (Continued) | |||||||||||

FINANCE SECTOR — 8.3% (Continued) | |||||||||||

| Major Banks — 4.2% | |||||||||||

3,790,000 | DBS Group Holdings Ltd. (Singapore)(4) | $ | 84,316,013 | $ | 93,081,086 | ||||||

148,400,000 | Lloyds Banking Group PLC (Britain)(4) | 73,863,493 | 79,749,790 | ||||||||

158,179,506 | 172,830,876 | ||||||||||

| Multi-Line Insurance — 2.2% | |||||||||||

1,110,000 | Arch Capital Group Ltd. (Bermuda)(2) | 45,974,299 | 88,478,100 | ||||||||

HEALTH SERVICES SECTOR — 2.0% | |||||||||||

| Medical/Nursing Services — 2.0% | |||||||||||

| 1,885,000 | Fresenius Medical Care | ||||||||||

AG & Co. KGaA (Germany)(4) | 129,797,693 | 81,039,880 | |||||||||

HEALTH TECHNOLOGY SECTOR — 8.0% | |||||||||||

| Medical Specialties — 4.5% | |||||||||||

4,694,999 | Koninklijke Philips N.V. (Netherlands)(2)(4) | 151,535,337 | 93,675,820 | ||||||||

7,190,000 | Smith & Nephew PLC (Britain)(4) | 126,451,258 | 89,232,576 | ||||||||

277,986,595 | 182,908,396 | ||||||||||

| Pharmaceuticals: Major — 3.5% | |||||||||||

530,000 | Roche Holding AG (Switzerland)(4) | 180,660,334 | 144,690,592 | ||||||||

INDUSTRIAL SERVICES SECTOR — 2.6% | |||||||||||

| Contract Drilling — 2.6% | |||||||||||

1,845,000 | Schlumberger Ltd. (Curacao) | 68,316,952 | 107,563,500 | ||||||||

PROCESS INDUSTRIES SECTOR — 1.4% | |||||||||||

| Chemicals: Specialty — 1.4% | |||||||||||

1,415,000 | NOF Corp. (Japan)(4) | 74,286,266 | 56,489,256 | ||||||||

PRODUCER MANUFACTURING SECTOR — 6.1% | |||||||||||

| Building Products — 1.4% | |||||||||||

4,400,000 | Sanwa Holdings Corp. (Japan)(4) | 54,508,279 | 58,397,253 | ||||||||

| Electrical Products — 1.3% | |||||||||||

2,650,000 | Smiths Group PLC (Britain)(4) | 39,232,605 | 52,173,443 | ||||||||

| Industrial Conglomerates — 1.3% | |||||||||||

1,155,000 | Jardine Matheson Holdings Ltd. (Bermuda)(4) | 74,573,963 | 53,524,442 | ||||||||

| Trucks/Construction/Farm Machinery — 2.1% | |||||||||||

3,650,000 | Weir Group PLC (Britain)(4) | 82,013,006 | 84,333,766 | ||||||||

RETAIL TRADE SECTOR — 6.1% | |||||||||||

| Discount Stores — 6.1% | |||||||||||

35,000,000 | B&M European Value | ||||||||||

Retail S.A. (Luxembourg)(4) | 138,493,167 | 249,650,695 | |||||||||

The accompanying notes to financial statements are an integral part of this schedule.

28

FMI International Fund

SCHEDULE OF INVESTMENTS (Continued)

September 30, 2023

| Shares | Cost | Value | |||||||||

LONG-TERM INVESTMENTS — 92.3%(1) (Continued) | |||||||||||

COMMON STOCKS — 88.2%(1) (Continued) | |||||||||||

TECHNOLOGY SERVICES SECTOR — 3.5% | |||||||||||

| Packaged Software — 3.5% | |||||||||||

1,110,000 | SAP SE (Germany)(4) | $ | 119,105,141 | $ | 143,680,659 | ||||||

TRANSPORTATION SECTOR — 1.6% | |||||||||||

| Airlines — 1.6% | |||||||||||

655,000 | Ryanair Holdings PLC — SP-ADR (Ireland)(2) | 65,231,864 | 63,672,550 | ||||||||

Total common stocks | 3,144,302,966 | 3,600,830,594 | |||||||||

PREFERRED STOCK — 4.1%(1) | |||||||||||

ELECTRONIC TECHNOLOGY SECTOR — 4.1% | |||||||||||

| Telecommunications Equipment — 4.1% | |||||||||||

4,170,000 | Samsung Electronics Co. Ltd. (South Korea)(4) | 106,839,392 | 167,994,578 | ||||||||

Total preferred stock | 106,839,392 | 167,994,578 | |||||||||

Total long-term investments | 3,251,142,358 | 3,768,825,172 | |||||||||

SHORT-TERM INVESTMENTS — 2.7%(1) | |||||||||||

| Money Market Fund — 2.7% | |||||||||||

111,310,355 | First American Treasury | ||||||||||

Obligations Fund, Cl X, 5.264%(3) | 111,310,355 | 111,310,355 | |||||||||

Principal Amount | |||||||||||

| Bank Deposit Account — 0.0% | |||||||||||

$ | 144,349 | U.S. Bank N.A., 5.200%(5)(6) | 144,349 | 144,349 | |||||||

Total short-term investments | 111,454,704 | 111,454,704 | |||||||||

Total investments — 95.0% | $ | 3,362,597,062 | 3,880,279,876 | ||||||||

Other assets, less liabilities — 5.0%(1) | 205,289,584 | ||||||||||

| TOTAL NET ASSETS — 100.0% | $ | 4,085,569,460 | |||||||||

| (1) | Percentages for the various classifications relate to total net assets. |

| (2) | Non-Income producing security. |

| (3) | The rate quoted is the annualized 7-day yield as of September 30, 2023. |

| (4) | Security does not trade during New York Stock Exchange hours, provided that certain foreign exchanges may trade during a portion of the New York Stock Exchange hours, and has been valued in accordance with the Funds pricing procedures discussed in Note 2(a) to the financial statements and has been classified as level 2. As of September 30, 2023 the aggregate value of these securities was $3,141,845,822. |

| (5) | The rate shown is as of September 30, 2023. |

| (6) | This $144,349 security is held as collateral for certain forward currency contracts. |

| PLC | Public Limited Company |

| SP-ADR | Sponsored American Depositary Receipt |

The accompanying notes to financial statements are an integral part of this schedule.

29

FMI International Fund

SCHEDULE OF FORWARD CURRENCY CONTRACTS

September 30, 2023

| U.S. $Value on | U.S. $Value on | ||||||||||||||||||||

| September 30, | September 30, | ||||||||||||||||||||

| 2023 | 2023 | Unrealized | |||||||||||||||||||

| Settlement | Currency to | of Currency to | Currency to | of Currency to | Appreciation | ||||||||||||||||

| Date | Counterparty | be Delivered | be Delivered | be Received | be Received | (Depreciation) | |||||||||||||||

| 10/20/23 | State Street Bank | 1,050,000,000 | $ | 1,281,278,583 | 1,354,494,750 | $ | 1,354,494,750 | $ | 73,216,167 | ||||||||||||

| and Trust Co. | British Pound | U.S. Dollar | |||||||||||||||||||

| 10/20/23 | The Bank of | 760,000,000 | 804,220,964 | 856,390,800 | 856,390,800 | 52,169,836 | |||||||||||||||

| New York Mellon | Euro | U.S. Dollar | |||||||||||||||||||

| 10/20/23 | JPMorgan Chase | 585,000,000 | 74,739,759 | 75,007,308 | 75,007,308 | 267,549 | |||||||||||||||

| Bank, N.A. | Hong Kong Dollar | U.S. Dollar | |||||||||||||||||||

| 10/20/23 | The Bank of | 51,000,000,000 | 342,551,612 | 370,249,374 | 370,249,374 | 27,697,762 | |||||||||||||||

| New York Mellon | Japanese Yen | U.S. Dollar | |||||||||||||||||||

| 10/20/23 | JPMorgan Chase | 115,000,000 | 84,205,379 | 87,025,616 | 87,025,616 | 2,820,237 | |||||||||||||||

| Bank, N.A. | Singapore Dollar | U.S. Dollar | |||||||||||||||||||

| 10/20/23 | State Street Bank | 225,000,000,000 | 166,934,407 | 178,076,771 | 178,076,771 | 11,142,364 | |||||||||||||||

| and Trust Co. | South Korea Won | U.S. Dollar | |||||||||||||||||||

| 10/20/23 | JPMorgan Chase | 270,000,000 | 295,643,965 | 317,664,138 | 317,664,138 | 22,020,173 | |||||||||||||||

| Bank, N.A. | Swiss Franc | U.S. Dollar | |||||||||||||||||||

$ | 3,049,574,669 | $ | 3,238,908,757 | 189,334,088 | |||||||||||||||||

| 10/20/23 | JPMorgan Chase | 74,788,100 | $ | 74,788,100 | 585,000,000 | $ | 74,739,758 | $ | (48,342 | ) | |||||||||||

| Bank, N.A. | U.S. Dollar | Hong Kong Dollar | |||||||||||||||||||

$ | 74,788,100 | $ | 74,739,758 | $ | (48,342 | ) | |||||||||||||||

$ | 3,124,362,769 | $ | 3,313,648,515 | $ | 189,285,746 | ||||||||||||||||

The accompanying notes to financial statements are an integral part of this schedule.

30

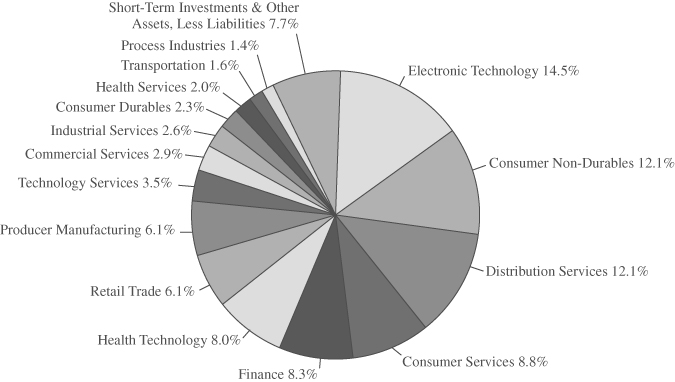

FMI International Fund

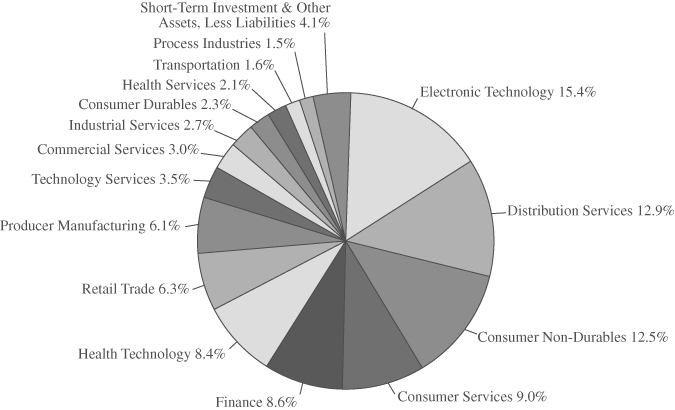

INDUSTRY SECTORS as a percentage of net assets

as of September 30, 2023 (Unaudited)

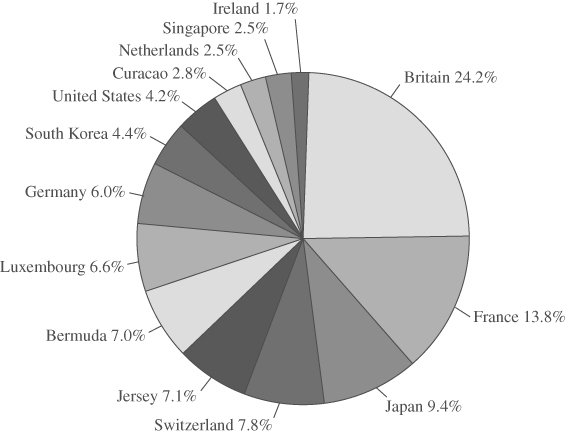

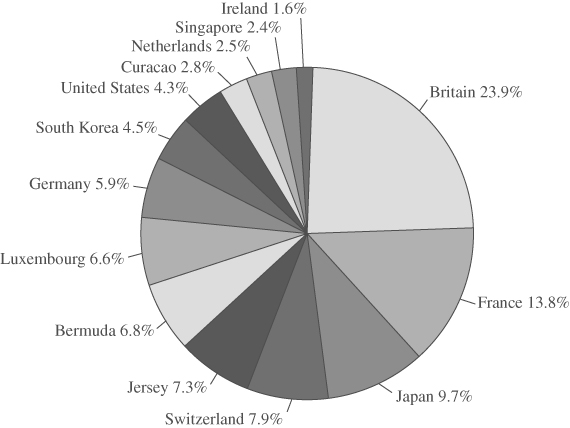

CONCENTRATION BY COUNTRY based on domicile of issuer as

a percentage of long-term investments only

as of September 30, 2023 (Unaudited)

31

FMI International Fund II – Currency Unhedged

SCHEDULE OF INVESTMENTS

September 30, 2023

| Shares | Cost | Value | |||||||||

LONG-TERM INVESTMENTS — 95.9%(1) | |||||||||||

COMMON STOCKS — 91.6%(1) | |||||||||||

COMMERCIAL SERVICES SECTOR — 3.0% | |||||||||||

| Miscellaneous Commercial Services — 3.0% | |||||||||||

58,100 | Genpact Ltd. (Bermuda) | $ | 2,455,443 | $ | 2,103,220 | ||||||

CONSUMER DURABLES SECTOR — 2.3% | |||||||||||

| Electronics/Appliances — 2.3% | |||||||||||

182,700 | Howden Joinery Group PLC (Britain)(4) | 1,436,350 | 1,634,726 | ||||||||

CONSUMER NON-DURABLES SECTOR — 12.5% | |||||||||||

| Beverages: Alcoholic — 2.2% | |||||||||||

41,750 | Diageo PLC (Britain)(4) | 1,806,230 | 1,539,253 | ||||||||

| Beverages: Non-Alcoholic — 2.1% | |||||||||||

24,000 | Coca-Cola Europacific Partners PLC (Britain) | 1,511,066 | 1,499,520 | ||||||||

| Food: Specialty/Candy — 4.9% | |||||||||||

675 | Barry Callebaut AG (Switzerland)(4) | 1,459,800 | 1,073,414 | ||||||||

81,000 | Greggs PLC (Britain)(4) | 2,232,684 | 2,411,441 | ||||||||

3,692,484 | 3,484,855 | ||||||||||

| Household/Personal Care — 3.3% | |||||||||||

48,100 | Unilever PLC (Britain)(4) | 2,620,042 | 2,379,368 | ||||||||

CONSUMER SERVICES SECTOR — 9.0% | |||||||||||

| Other Consumer Services — 4.1% | |||||||||||

950 | Booking Holdings Inc. (United States)(2) | 1,656,672 | 2,929,753 | ||||||||

| Restaurants — 4.9% | |||||||||||

34,000 | Sodexo S.A. (France)(4) | 2,840,854 | 3,500,217 | ||||||||

DISTRIBUTION SERVICES SECTOR — 12.9% | |||||||||||

| Medical Distributors — 2.3% | |||||||||||

24,150 | DKSH Holding AG (Switzerland)(4) | 1,463,052 | 1,633,556 | ||||||||

| Wholesale Distributors — 10.6% | |||||||||||

30,475 | Ferguson PLC (Jersey)(4) | 2,929,829 | 5,015,307 | ||||||||

111,950 | Rexel S.A. (France)(4) | 2,131,918 | 2,508,349 | ||||||||

5,061,747 | 7,523,656 | ||||||||||

ELECTRONIC TECHNOLOGY SECTOR — 11.1% | |||||||||||

| Aerospace & Defense — 4.8% | |||||||||||

21,625 | Safran S.A. (France)(4) | 2,326,250 | 3,388,837 | ||||||||

| Computer Processing Hardware — 4.7% | |||||||||||

40,700 | Sony Group Corp. (Japan)(4) | 3,070,730 | 3,328,266 | ||||||||

| Electronic Equipment/Instruments — 1.6% | |||||||||||