SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

(Exact name of registrant as specified in charter)

| (a) | Annual Report |

ANNUAL REPORT

September 30, 2022

FMI Large Cap Fund

Investor Class (Ticker Symbol: FMIHX)

Institutional Class (Ticker Symbol: FMIQX)

FMI Common Stock Fund

Investor Class (Ticker Symbol: FMIMX)

Institutional Class (Ticker Symbol: FMIUX)

FMI International Fund

Investor Class (Ticker Symbol: FMIJX)

Institutional Class (Ticker Symbol: FMIYX)

FMI International Fund II – Currency Unhedged

Investor Class (Not Available For Sale)

Institutional Class (Ticker Symbol: FMIFX)

| FMI Funds, Inc. Advised by Fiduciary Management, Inc. www.fmifunds.com |

FMI Funds, Inc.

TABLE OF CONTENTS

Large Cap

Fund

| (unaudited) | September 30, 2022 |

The FMI Large Cap Fund (“Fund”) declined 6.43%1 in the September quarter compared to a 4.88% decline in the S&P 500 Index and a 5.56% decline in the iShares Russell 1000 Value ETF2. Relative to the S&P 500 Index, sectors that helped included Producer Manufacturing, Finance, and Process Industries. Underperforming sectors included Electronic Technology, Health Services, and Retail Trade. Carlisle Cos. Inc., The Charles Schwab Corp., and Avery Dennison Corp. aided performance while Fresenius Medical Care AG & Co. KGaA-SP-ADR (Fresenius), Koninklijke Philips N.V.-SP-ADR (Philips), and Sony Group Corp.-SP-ADR all detracted. Both stocks and bonds entered bear market territory this year on multiple concerns, some of which will be addressed shortly.

While the markets have been difficult, the team has not been this optimistic about future performance in many years, perhaps not since the Great Financial Crisis. There are several factors that give us optimism:

| ● | Valuations are attractive on both an absolute and relative basis. |

| ● | The sentiment of the market is negative, which is a contrarian’s delight. |

| ● | The strength and durability of the current portfolio has rarely been stronger. |

| ● | The full cycle return on invested capital of the constituents is very good. |

| ● | Many current holdings are significantly depressed, and we view them as coiled springs. |

| ● | The era of ultra-low interest rates appears to be over. This should favor our approach. |

Many of the worrisome issues and themes we have discussed in recent years are coming to pass. Rates have escalated rapidly. Reckless, and even feckless, monetary policies have been revealed. The bond market has suffered steep declines. Stocks are in disarray. The private equity and leverage bubbles have started to burst. Inflation is much higher. A “black swan” geopolitical event (Russia’s war on Ukraine) has transpired. Many of the risk items that sky-high valuations suggested would not occur are now happening. But the time to be “negative” has passed. These worries are out in the open and recognized, and now fear is the prevailing sentiment. History suggests this is the time to be more constructive. We are positive about the future and feel the set up for stocks is the best it has been in years.

We will delve into this theme shortly. Before that, we want to address some issues that have held back the performance in recent periods. Although the FMI Large Cap Fund has a greater percentage of its holdings’ revenue in the U.S. than the S&P 500, about 15% of the Fund, on average, in recent years has been in American Depositary Receipts (ADRs). We felt these franchises were better values than their U.S. counterparts, as depicted in the nearby table.

| 1 | The FMI Large Cap Fund Investor Class (FMIHX) and the FMI Large Cap Fund Institutional Class (FMIQX) had a return of -6.43% and -6.44%, respectively, for the third quarter of 2022. |

| 2 | Source: Bloomberg – returns do not reflect management fees, transaction costs or expenses. Performance is based on market price returns. Beginning 8/10/2020, market price returns are calculated using closing price. Prior to 8/10/2020, market price returns were calculated using midpoint bid/ask spread at 4:00 PM ET. |

| Sponsored ADR’s | EV/EBITDA NTM | U.S. Stock | EV/EBITDA NTM | Discount |

| SAP SE | 11.1x | Salesforce Inc. Workday Inc. | 13.6x 20.4x | -18% -46% |

| Unilever PLC | 12.4x | Procter & Gamble Co. Colgate-Palmolive Co. | 15.2x 14.7x | -18% -16% |

| Sony Group Corp. | 6.6x | Electronic Arts Inc. Warner Music Group Corp. | 10.8x 12.8x | -39% -48% |

| Smith & Nephew PLC | 9.3x | Stryker Corp. Zimmer Biomet Holdings Inc. | 17.4x 11.5x | -47% -19% |

| Koninklijke Philips N.V. | 7.0x | Boston Scientific Corp. Medtronic PLC | 16.4x 12.6x | -57% -44% |

| Fresenius Medical Care AG & Co. KGaA | 7.0x | Da Vita Inc. | 8.6x | -19% |

| Source: FactSet - EV/EBITDA NTM as of 9/30/2022 | ||||

Unfortunately, the unprecedented strength of the U.S. Dollar (USD) has hurt performance of these shares (which can easily reverse), but significant idiosyncratic factors have been more impactful. Philips, for example, has declined dramatically in response to issues surrounding their respiratory business, including a product recall and FDA letter. While this is less than 10% of Philip’s revenue and earnings, the impact on the market capitalization has been severe. Fear of a large legal settlement and negative news flow has, in our opinion, far exceeded the likely outcome. Fresenius, which provides dialysis care, was hurt by excess mortality during COVID. Post-COVID inflation has taken a much greater-than-expected bite out of earnings (and the stock price). Smith & Nephew PLC-SP-ADR has suffered disproportionately from COVID (deferred elective procedures), supply chain problems, and mismanagement in their orthopedic franchise. We probably should have anticipated the inflation issue at Fresenius, and we could have better understood the management issues at Smith & Nephew, but when we re-underwrote these investments, we felt the stock’s long-term upside potential was high. The decline in SAP SE-SP-ADR is related to market fears about the success of their efforts to transition the software business from a site license model to a cloud-based recurring revenue construct. Based on our research, we believe the company is on a positive cloud development path and that better stock performance is likely. Finally, the Fund has been hurt by very little exposure to energy and commodity related businesses. We feel these types of companies can periodically be great “trading” stocks, but over long periods of time, they generally underperform due to their low business quality attributes.

The team’s optimism starts with valuations. The portfolio trades at a modest 14.0 times projected 2023 earnings, 2.1 times the latest twelve month’s revenue and 12.9 times the trailing year’s EV/EBITDA. On these metrics that is about a 34% discount to the iShares S&P 500 ETF, as illustrated by the nearby table. The Fund also trades at a discount to the large cap value benchmark.

| September 30, 2022 Weighted Average | FMI Large Cap Fund | iShares S&P 500 | Discount to S&P 500 |

| P/E (1 Year Trailing) | 21.1x | 29.3x | 28% |

| FY2 P/E | 14.0x | 19.4x | 28% |

| P/S | 2.1x | 4.5x | 53% |

| EV/EBITDA | 12.9x | 18.1x | 29% |

| Average Discount | 34% | ||

| *Estimated valuations for FMI and the iShares are weighted average valuation calculations, not reweighted to exclude cash, and financial companies are excluded from the EV/EBITDA calculation. Valuations for both the portfolio and the ETF are modified based on criteria identified by FMI. For more detailed information regarding these valuations, please contact FMI. | |||

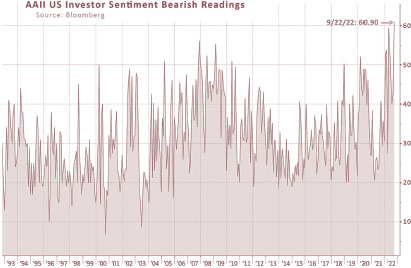

Bearish sentiment indicators (see chart below) are high. We view this as a positive. It is very difficult to avoid dwelling on “losses,” but there is nothing we can do about the past. If the business is sound and the balance sheet is solid, then the stock is likely to recover. Unfortunately, most investors react to the past rather than looking forward. The current Fund constituents are characterized by good balance sheets, solid return structures, and competitive strengths. Strong companies on sale for reasonable prices are a source of optimism, not pessimism.

Financial markets are apoplectic about interest rates. The overwhelming consensus opinion is that higher rates will crush the economy for an extended period. We think the fear that has been fanned by the rate move may indeed result in a temporary hit to the economy or a recession, but at FMI, we like to turn our analysis 180 degrees. Did the move from “normal” interest rates, prior to the Great Financial Crisis, to zero percent rates for years afterwards cause the economy to boom? No! Economic growth was historically weak over the past 15 years. Abnormally low rates boosted asset prices and set the mergers and acquisitions (M&A) and private equity markets aflame, but it did very little for organic economic growth. We had a boom in financial engineering. So why will economic growth be terrible when the reverse conditions prevail? We think economic growth will be much better over the next decade than it has been over the last. Price to earnings (P/E) multiples, however, will likely be lower. Inflation is obviously very elevated but appears to finally be on a downward path. We don’t know if the inflation rate will get back to 2% anytime soon but feel it will be significantly lower than it has been over the past year. Earning an outsized spread over inflation in stocks, like we have seen for many years, is probably not in the cards, but we believe quality, value-oriented equities, especially our stocks, have the best chance of beating inflation over a three-to-five-year time horizon.

Before delving into a couple of portfolio companies in greater detail, we want to illustrate what’s happened since our January investment in CarMax Inc., a stock highlighted in the March letter. It illustrates our investment approach. CarMax is currently out-of-favor, yet it has a winning business model, and a leading share of the used car market. With just 4% of a $270 billion market, it has a long runway for growth. Over the past few years, the bears believed that Carvana Co. and other “online” car resellers were going to take the used car market by storm, leaving CarMax in the dust. Carvana’s stock was a rocket and at one point carried a market valuation in excess of $40 billion, despite the company losing money hand over fist. Our research indicated that customers wanted multiple ways to purchase used cars (not just online like Carvana) and that CarMax offered not only the more traditional car lot sale, but also a full online and delivered-to-the-home model. CarMax was (and remains) profitable and has a good balance sheet. Carvana was chewing through cash and relied on capital markets to fund its growth-at-all-cost approach. Carvana’s stock is down roughly 90% year-to-date; they’ve had to raise equity, and some question their viability. CarMax is also down significantly, reflecting recession fears, higher borrowing rates, and tough earnings comparisons, which we discussed in March. So, while the stock has been difficult, we feel CarMax is actually stronger from a competitive standpoint. It looks like we will have to wait out a downturn, but from today’s valuation, we feel the next several years hold a lot of promise for the stock.

Below are two more examples of good business franchises trading at attractive values.

Avery Dennison Corp. (AVY)

Analyst: Ben Karek

Description

Avery Dennison is a vertically integrated manufacturer of pressure sensitive labels and assorted tickets and tags. Pressure sensitive labels are used on products such as beverages, shampoo, shipping packages, pharmaceuticals, etc. Avery reports in three segments: Pressure Sensitive Materials (65% of sales), Retail Branding & Information Solutions (26%), and Industrial & Healthcare Materials (9%). Avery primarily manufactures locally and operates 200 manufacturing and distribution facilities in over 50 countries.

Good Business

| ● | Avery is the global leader in its main product lines and is 2.5 times larger than its next largest competitor in pressure sensitive labels. This confers scale benefits that allow it to earn best-in-class margins while still leading on innovation. |

| ● | Avery is minimally cyclical. Fast turning product lines, including consumer goods, retail, and logistics/shipping account for ~80% of sales. Avery has proven adept at cost management in periods of lower demand. |

| ● | Avery’s product usage is not impacted by the shift to private label and/or start up brands, a perennial challenge in home and personal care/consumer packaged goods categories. |

| ● | Avery’s products are low-cost relative to the total product, yet they convey high value information to the consumer (brand image, product quality, etc.). |

| ● | Avery has 50%+ market share in ultra-high frequency radio frequency identification (UHF RFID) tags, which are undergoing secular growth in the +15-20% range. |

| ● | Avery’s historical and incremental returns on capital are high. ROIC was 18% in 2021, up from 9% in 2012, driven by both capital discipline and operating profit growth. |

| ● | Avery’s balance sheet is appropriately levered. |

Valuation

| ● | With high-single-digit long term earnings growth expectations and a 20% return on invested capital, 16 times forward earnings and 11.4 times forward EBITDA are reasonable absolute multiples. |

| ● | Prior to this period of raw material inflation and a potential macro slow down, Avery traded at 25 times forward earnings and 16 times forward EBITDA. The P/E is below the 5-year average and EV/EBITDA is equal to the 5-year average. |

| ● | RFID is 8% of sales and continues to grow well above the company average. We believe that this could structurally increase Avery’s trading multiple in the next 3-5 years. |

Management

| ● | CEO Mitch Butier was a chief architect of Avery’s Economic Value Added (EVA) strategy. He has previously served as COO and CFO for Avery Dennison. His track record since becoming CEO in 2016 is very strong. Mitch owns 270 thousand shares, worth $50 million at today’s prices. |

| ● | Avery’s incentives are aligned with shareholders. Short term incentives are based on organic sales, adjusted earnings per share (EPS), and free cash flow. Long term incentives are driven by total shareholder return and EVA. |

Investment Thesis

Avery has two key drivers that allow them to grow organic revenue above GDP: high value categories and emerging markets. 60% of sales are now exposed to one or both categories. Of note within high value products, Avery is by far the market leader in UHF RFID tags used in end markets like apparel, aviation, and food. This business is growing 15-20% and has a long runway in both existing and yet to be tapped end markets. These factors allow for long run volume growth in the 4% range. This story is simple to understand and, in more benign times, generates a lot of interest from investors. Combined with a long running cost efficiency program and share buybacks, we expect a reasonably stable high single digit percentage earnings growth profile. This is particularly valuable as Avery is run on EVA and thus consistently balances growth, margins, and returns on capital (i.e. they are not growing for growth’s sake). Avery has run into a few headwinds that are giving us an opportunity to invest. First, Avery’s commodity raw materials are derived from paper and oil, both of which have seen significant spikes driven by supply and demand factors. This has put pressure on Avery’s margins as it takes one to two quarters to catch up to cost inflation. Given the magnitude and duration of the inflation, there is concern around when they will recapture price/cost neutrality. Second, inflation combined with other macro challenges (like the war in Ukraine), have led to concerns about a global recession. Although Avery is much less cyclical than average, it is more cyclical than some other packaging companies and thus is sold quickly when macro fears emerge. We believe all these factors to be transitory, and thus believe that the valuation is attractive.

Ferguson PLC (FERG)

Analyst: Jordan Teschendorf

Description

Ferguson is the world’s largest distributor of plumbing and heating products to trade professionals with sales and trading profit of $22.8 billion and $2.1 billion, respectively. Following disposals of lower quality international businesses over more than a decade, concluding with the recent sale of the UK business in January 2021, Ferguson’s operations are now entirely focused on the attractive North American market. Ferguson’s sales exposure by end market is split Residential (54%), Commercial (32%), Civil/Infrastructure (7%), and Industrial (7%), with sales further split 60%/40% remodel, maintenance, and improvement (RMI) versus new construction. Ferguson’s U.S. headquarters is in Newport News, Virginia.

Good Business

| ● | Ferguson has exited many unprofitable or low-returning businesses over the last decade and reoriented towards organic growth and selective bolt-on acquisitions, driving improved margins and returns on capital. |

| ● | The business is easy to understand, occupies a critical role between fragmented suppliers (over 37 thousand) and customers (over 1 million), and consistently grows 3-4% ahead of the end markets that it serves. |

| ● | The company’s scale, branch density, and distribution footprint provide it with a competitive advantage in terms of purchasing, fulfillment, contractor relationships, and superior service levels versus its fragmented competition. |

| ● | In 2021, approximately 60% of Ferguson’s sales were related to RMI work, which is less cyclical and typically carries higher margins than sales to the new build market. This mix compares favorably with the group’s 31% RMI exposure in 2008. |

| ● | Ferguson’s U.S. business has a terrific long-term track record, with operating profit growing in the double-digits over the trailing 10, 20, and 30-year periods. We believe the customer value proposition and franchise continue to strengthen with scale, which should flow through to improving economics for shareowners. |

Ferguson maintains a solid balance sheet, and is a strong free cash flow generator, with total cash returns exceeding $9.0 billion over the last decade.

Valuation

| ● | The stock trades at 11.3 times forward EPS estimates, approximately two standard deviations below its long-term average and a double-digit discount to its closest U.S. peers. |

| ● | The below average valuation does not adequately reflect the company’s increasingly attractive business mix as well as the continued strengthening of Ferguson’s competitive positioning. |

| ● | Ferguson pays regular and special dividends and recently restarted its share repurchase program (repurchased more than $500 million in the third quarter of fiscal year 2022 alone). |

Management

| ● | Over the last decade, management has focused on organic growth and returns, strengthening its already market leading U.S. business and divesting operations in several less attractive geographies. |

| ● | Kevin Murphy was elevated to group CEO in 2019, previously serving as CEO of Ferguson (U.S.A.) and COO. He has built a solid track record of profitable and disciplined growth through prioritizing data/analytics, digital capability, and talent management to position Ferguson closer to its trade customers. He joined Ferguson decades ago through the acquisition of his family’s business. |

| ● | Operating profit/EPS growth and cash conversion are components of the compensation plan, capturing the essence of value creation for a physical distribution business. |

| ● | We believe Ferguson has a strong corporate culture. |

Investment Thesis

Ferguson provides the Fund exposure to the building, repair, and replacement of critical components, touching virtually every modern physical structure and piece of infrastructure in North America. Given its advantages, including its scale, branch density, distribution footprint, and technology and service superiority, we expect Ferguson will continue to take share in its markets over time. Concerns over rising interest rates, consumer confidence, and normalizing demand patterns in residential end markets (~55% of sales) have recently weighed on sentiment. We acknowledge these concerns, but note the company’s track record of managing through cycles, stronger outlook in several non-residential markets, and significantly improved business mix this cycle (U.S. pure play, higher repair & replacement, network density, etc.). Assuming reasonably supportive end markets and continued strong execution, Ferguson should be capable of growing underlying EPS at a double-digit annual rate through the cycle while maintaining 20%+ returns on capital and balance sheet strength. The stock is attractively valued on an absolute and relative basis. Additionally, we think it is likely that Ferguson will be added to S&P 500 and other U.S. indices within the next year.

Thank you for your confidence in The FMI Large Cap Fund.

This shareholder letter is unaudited.

FMI Large Cap Fund

MANAGEMENT’S DISCUSSION OF FUND PERFORMANCE (Unaudited)

During the fiscal year ended September 30, 2022, the FMI Large Cap Fund (“Fund”) had a total return of minus 15.86%1. The benchmark S&P 500 Index returned minus 15.47% in the same period. The trailing 12-month return for the iShares Russell 1000 Value ETF2 was minus 11.40%. Relative to the S&P 500, sectors that aided performance included Finance, Retail Trade, and Producer Manufacturing. Progressive Corp., The Charles Schwab Corp., Arch Capital Group Ltd., and Chubb Ltd. drove the results in the Finance sector, as all continued to grow earnings and benefit from higher interest rates or solid underwriting. In Retail Trade, Dollar Tree Inc. and Dollar General Corp. gained significantly in the period, with the former benefitting from a new management team and the latter from efficient execution. In Producer Manufacturing, Carlisle Cos. Inc. had strong results as the commercial roofing business grew significantly. On the negative side of sector performance, Health Technology, Health Services, and Electronic Technology all detracted. Koninklijke Philips N.V.-SP-ADR continued to decline due to ongoing fallout from a product recall in the sleep apnea area and an FDA letter. Smith & Nephew PLC-SP-ADR also underperformed, as missteps in the orthopedic area combined with supply chain problems derailed the earnings recovery from COVID related trading conditions. Fresenius Medical Care AG & Co. KGaA-SP-ADR, which has suffered from excess mortality related to COVID, also missed earnings expectations because of their inability to quickly pass on inflationary costs. In all three of these health care related stocks, the Fund managers believe the problems are fixable and short-term in nature. In the Electronic Technology sector, Micron Technology Inc. dropped significantly in the second half of the fiscal year as a downturn beset the memory market. Sony Group Corp.-SP-ADR also hurt performance, primarily due to supply chain issues and currency. The Fund managers believe the problems at Micron and Sony are temporary. The Fund managers seek to own high quality, value-oriented stocks. Sometimes the market wants stocks in areas that we believe are lower quality in nature, such as energy and commodities. The Fund had no direct exposure to Energy Minerals, which significantly detracted from the relative results compared to both the S&P 500 and the iShares Russell 1000 Value ETF.

Other stocks that helped performance included Berkshire Hathaway Inc. – Cl B, PACCAR Inc., and The TJX Cos. Inc. Berkshire benefitted from solid underwriting results and good performance in the operating units. PACCAR and TJX managed their respective businesses well in the face of choppy end markets. Other detractors included Meta Platforms Inc. – Cl A, Alphabet Inc. – Cl A, and SAP SE-SP-ADR. Meta and Alphabet experienced a slowdown in their digital advertising businesses. Additionally, Meta faced stronger competition from TikTok. The market has been skeptical of SAP’s transition from a software site license business to a cloud-based revenue model. New additions to the Fund over the past twelve months included SAP, CarMax Inc., Carlisle, CDW Corp., Avery Dennison Corp., Ferguson PLC, and BlackRock Inc. Stocks sold during the year included Expeditors International of Washington Inc., Emerson Electric Co., Quest Diagnostics Inc., PPG Industries Inc., Dover Corp., Chubb Ltd., and Comcast Corp. – Cl A. As of September 30, 2022, the Fund was significantly overweighted in Producer Manufacturing, Retail Trade, and Finance. The Fund was meaningfully underweighted in Technology Services, Electronic Technology, and Health Technology.

The S&P 500 entered a traditionally defined bear market in fiscal 2022 (down 20%). Earnings growth has remained relatively robust over the year, so valuations have come down significantly. Worries about high inflation, rising interest rates, and an economic slowdown permeate the landscape. Geopolitical issues, particularly the Russian war with Ukraine and the saber rattling by China over Taiwan, have further spooked investors.

| 1 | The FMI Large Cap Fund Investor Class (FMIHX) and the FMI Large Cap Fund Institutional Class (FMIQX) had a return of -15.86% and -15.73%, respectively, for the fiscal year ended 09/30/2022. |

| 2 | Source: Bloomberg – returns do not reflect management fees, transaction costs or expenses. Performance is based on market price returns. Beginning 8/10/2020, market price returns are calculated using closing price. Prior to 8/10/2020, market price returns were calculated using midpoint bid/ask spread at 4:00 PM ET. |

FMI Large Cap Fund

MANAGEMENT’S DISCUSSION OF FUND PERFORMANCE (Unaudited) (Continued)

The Fund managers have become more optimistic about future performance now that many potential worries have become visible realities. The Federal Reserve is no longer printing money, but instead is engaging in quantitative tightening. This should help control inflation and engender a more normal interest rate environment. A realistic cost of capital helps move the economy from one driven by financial engineering to one driven by fundamental investment. Companies with solid balance sheets that make money stand a better chance of outperforming compared to the previous environment, where more speculative businesses outperformed. The Fund trades at a meaningful discount to the S&P 500, and the managers believe the quality of the underlying companies is better than the benchmark.

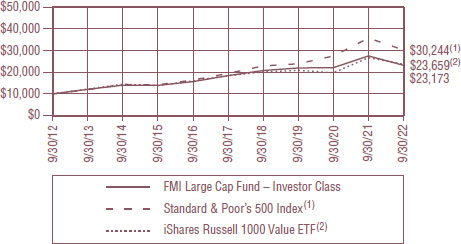

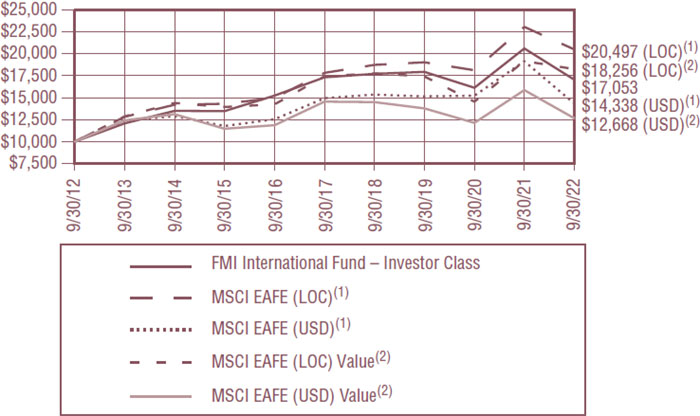

COMPARISON OF CHANGE IN VALUE OF $10,000 INVESTMENT IN

FMI LARGE CAP FUND – INVESTOR CLASS — STANDARD & POOR’S 500 INDEX(1)

AND THE ISHARES RUSSELL 1000 VALUE ETF(2)

Source: Bloomberg – returns do not reflect management fees, transaction costs or expenses. Performance is based on market price returns. Beginning 8/10/2020, market price returns are calculated using closing price. Prior to 8/10/2020, market price returns were calculated using midpoint bid/ask spread at 4:00 PM ET.

AVERAGE ANNUALIZED TOTAL RETURN

| Inception Date | 1-Year | 5-Year | 10-Year | Inception through 9/30/2022 | |

| FMI Large Cap Fund – Investor Class | 12/31/01 | -15.86% | 4.67% | 8.77% | 7.99% |

| FMI Large Cap Fund – Institutional Class | 10/31/16 | -15.73% | 4.82% | N/A | 7.43% |

| Standard & Poor’s 500 Index(1)* | -15.47% | 9.24% | 11.70% | 7.74% | |

| iShares Russell 1000 Value ETF(2)* | -11.40% | 5.15% | 8.99% | 6.85% |

The graph and the table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Performance data quoted represents past performance; past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of a Fund may be lower or higher than the performance quoted. The total returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Total return includes change in share prices and in each case includes reinvestments of any dividends, interest and capital gain distributions. Performance data current to the most recent month-end may be obtained by visiting www.fmifunds.com or by calling 1-800-811-5311.

FMI Large Cap Fund

MANAGEMENT’S DISCUSSION OF FUND PERFORMANCE (Unaudited) (Continued)

| (1) | The Standard & Poor’s 500 Index consists of 500 selected common stocks, most of which are listed on the New York Stock Exchange. The Standard & Poor’s Ratings Group designates the stocks to be included in the Index on a statistical basis. A particular stock’s weighting in the Index is based on its relative total market value (i.e., its market price per share times the number of shares outstanding). Stocks may be added or deleted from the Index from time to time. |

| (2) | The iShares Russell 1000 Value ETF seeks to track investment results of an index composed of large- and mid-capitalization U.S. equities that exhibit value characteristics. Performance is compared to the iShares Russell 1000 Value (“ETF”) for illustrative purposes only. The metrics regarding the comparative ETF have been obtained from Bloomberg and the returns do not reflect management fees, transaction costs or expenses. Performance is based on market price returns. Beginning 8/10/2020, market price returns are calculated using closing price. Prior to 8/10/2020, market price returns were calculated using midpoint bid/ask spread at 4:00 PM ET. The ETF is not subject to the same fees or expenses as the Fund. The Fund is not restricted to investing in those securities which comprise the ETF. The Fund’s performance may or may not correlate to the ETF, and it should not be considered a proxy for the ETF. |

| * | The benchmark since inception returns are calculated since inception of the Investor Class, December 31, 2001 to September 30, 2022. |

An investment cannot be made directly into an index.

FMI Large Cap Fund

September 30, 2022

| Shares | Cost | Value | ||||||||||

| COMMON STOCKS — 99.0% (a) | ||||||||||||

| COMMERCIAL SERVICES SECTOR — 2.9% | ||||||||||||

| Advertising/Marketing Services — 2.9% | ||||||||||||

| 935,000 | Omnicom Group Inc. | $ | 62,185,448 | $ | 58,989,150 | |||||||

| CONSUMER NON-DURABLES SECTOR — 3.7% | ||||||||||||

| Household/Personal Care — 3.7% | ||||||||||||

| 1,755,000 | Unilever PLC — SP-ADR | 69,516,156 | 76,939,200 | |||||||||

| CONSUMER SERVICES SECTOR — 3.7% | ||||||||||||

| Other Consumer Services — 3.7% | ||||||||||||

| 47,000 | Booking Holdings Inc.* | 81,939,448 | 77,230,870 | |||||||||

| DISTRIBUTION SERVICES SECTOR — 2.9% | ||||||||||||

| Wholesale Distributors — 2.9% | ||||||||||||

| 580,000 | Ferguson PLC | 74,726,132 | 59,699,400 | |||||||||

| ELECTRONIC TECHNOLOGY SECTOR — 6.5% | ||||||||||||

| Computer Processing Hardware — 3.3% | ||||||||||||

| 1,060,000 | Sony Group Corp. — SP-ADR | 66,875,744 | 67,893,000 | |||||||||

| Semiconductors — 3.2% | ||||||||||||

| 1,330,000 | Micron Technology Inc. | 69,772,589 | 66,633,000 | |||||||||

| FINANCE SECTOR — 23.2% | ||||||||||||

| Investment Banks/Brokers — 5.5% | ||||||||||||

| 1,565,000 | The Charles Schwab Corp. | 64,239,804 | 112,476,550 | |||||||||

| Investment Managers — 1.7% | ||||||||||||

| 65,000 | BlackRock Inc. | 38,281,392 | 35,768,200 | |||||||||

| Major Banks — 2.2% | ||||||||||||

| 435,000 | JPMorgan Chase & Co. | 27,689,577 | 45,457,500 | |||||||||

| Multi-Line Insurance — 8.5% | ||||||||||||

| 1,210,000 | Arch Capital Group Ltd.* | 44,658,577 | 55,103,400 | |||||||||

| 450,000 | Berkshire Hathaway Inc. — Cl B* | 22,426,305 | 120,159,000 | |||||||||

| 67,084,882 | 175,262,400 | |||||||||||

| Property/Casualty Insurance — 2.0% | ||||||||||||

| 360,000 | Progressive Corp. | 26,875,563 | 41,835,600 | |||||||||

| Regional Banks — 3.3% | ||||||||||||

| 805,000 | Northern Trust Corp. | 69,526,301 | 68,875,800 | |||||||||

| HEALTH SERVICES SECTOR — 5.7% | ||||||||||||

| Managed Health Care — 4.4% | ||||||||||||

| 180,000 | UnitedHealth Group Inc. | 12,853,494 | 90,907,200 | |||||||||

| Medical/Nursing Services — 1.3% | ||||||||||||

| 1,955,000 | Fresenius Medical Care | |||||||||||

| AG & Co. KGaA — SP-ADR | 78,587,312 | 27,448,200 | ||||||||||

The accompanying notes to financial statements are an integral part of this schedule.

FMI Large Cap Fund

SCHEDULE OF INVESTMENTS (Continued)

September 30, 2022

| Shares | Cost | Value | ||||||||||

| COMMON STOCKS — 99.0% (a) (Continued) | ||||||||||||

| HEALTH TECHNOLOGY SECTOR — 4.0% | ||||||||||||

| Medical Specialties — 4.0% | ||||||||||||

| 2,135,000 | Koninklijke Philips N.V. — SP-ADR | $ | 95,584,258 | $ | 32,857,650 | |||||||

| 2,165,000 | Smith & Nephew PLC — SP-ADR | 78,055,967 | 50,271,300 | |||||||||

| 173,640,225 | 83,128,950 | |||||||||||

| INDUSTRIAL SERVICES SECTOR — 1.6% | ||||||||||||

| Oilfield Services/Equipment — 1.6% | ||||||||||||

| 945,000 | Schlumberger Ltd. | 18,181,044 | 33,925,500 | |||||||||

| PROCESS INDUSTRIES SECTOR — 3.3% | ||||||||||||

| Containers/Packaging — 3.3% | ||||||||||||

| 420,000 | Avery Dennison Corp. | 72,915,271 | 68,334,000 | |||||||||

| PRODUCER MANUFACTURING SECTOR — 13.8% | ||||||||||||

| Building Products — 7.6% | ||||||||||||

| 266,000 | Carlisle Cos. Inc. | 64,210,810 | 74,589,060 | |||||||||

| 1,785,000 | Masco Corp. | 58,390,770 | 83,341,650 | |||||||||

| 122,601,580 | 157,930,710 | |||||||||||

| Electrical Products — 2.4% | ||||||||||||

| 375,000 | Eaton Corp. PLC | 35,556,027 | 50,010,000 | |||||||||

| Trucks/Construction/Farm Machinery — 3.8% | ||||||||||||

| 945,000 | PACCAR Inc. | 44,973,544 | 79,087,050 | |||||||||

| RETAIL TRADE SECTOR — 15.8% | ||||||||||||

| Apparel/Footwear Retail — 2.5% | ||||||||||||

| 835,000 | The TJX Cos. Inc. | 33,029,932 | 51,870,200 | |||||||||

| Discount Stores — 10.8% | ||||||||||||

| 560,000 | Dollar General Corp. | 39,984,997 | 134,321,600 | |||||||||

| 655,000 | Dollar Tree Inc.* | 56,883,492 | 89,145,500 | |||||||||

| 96,868,489 | 223,467,100 | |||||||||||

| Specialty Stores — 2.5% | ||||||||||||

| 770,000 | CarMax Inc.* | 79,041,953 | 50,835,400 | |||||||||

| TECHNOLOGY SERVICES SECTOR — 11.9% | ||||||||||||

| Information Technology Services — 3.8% | ||||||||||||

| 500,000 | CDW Corp. | 88,032,215 | 78,040,000 | |||||||||

| Internet Software/Services — 5.3% | ||||||||||||

| 865,000 | Alphabet Inc. — Cl A* | 100,993,814 | 82,737,250 | |||||||||

| 205,000 | Meta Platforms Inc. — Cl A | |||||||||||

| (formerly Facebook Inc.)* | 64,934,226 | 27,814,400 | ||||||||||

| 165,928,040 | 110,551,650 | |||||||||||

| Packaged Software — 2.8% | ||||||||||||

| 725,000 | SAP SE — SP-ADR | 86,680,260 | 58,906,250 | |||||||||

| Total common stocks | 1,827,602,422 | 2,051,502,880 | ||||||||||

The accompanying notes to financial statements are an integral part of this schedule.

FMI Large Cap Fund

SCHEDULE OF INVESTMENTS (Continued)

September 30, 2022

| Principal Amount | Cost | Value | ||||||||||

| SHORT-TERM INVESTMENTS — 0.9% (a) | ||||||||||||

| Bank Deposit Account — 0.9% | ||||||||||||

| $ | 19,135,997 | U.S. Bank N.A., 2.65%^ | $ | 19,135,997 | $ | 19,135,997 | ||||||

| Total short-term investments | 19,135,997 | 19,135,997 | ||||||||||

| Total investments — 99.9% | $ | 1,846,738,419 | 2,070,638,877 | |||||||||

| Other assets, less liabilities — 0.1% (a) | 1,534,469 | |||||||||||

| TOTAL NET ASSETS — 100.0% | $ | 2,072,173,346 | ||||||||||

| * | Non-income producing security. |

| ^ | The rate shown is as of September 30, 2022. |

| (a) | Percentages for the various classifications relate to total net assets. |

| PLC | Public Limited Company |

| SP-ADR | Sponsored American Depositary Receipt |

The accompanying notes to financial statements are an integral part of this schedule.

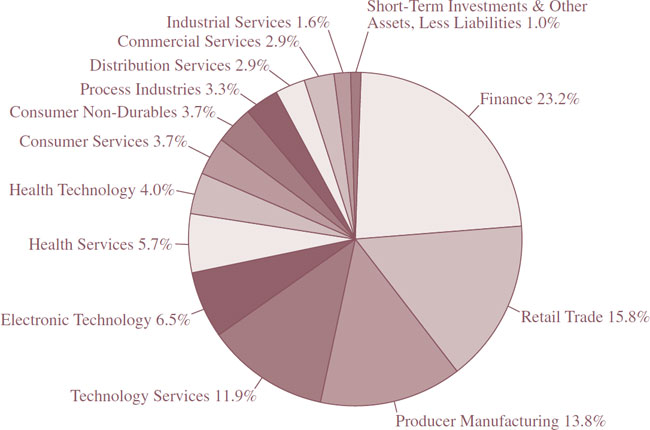

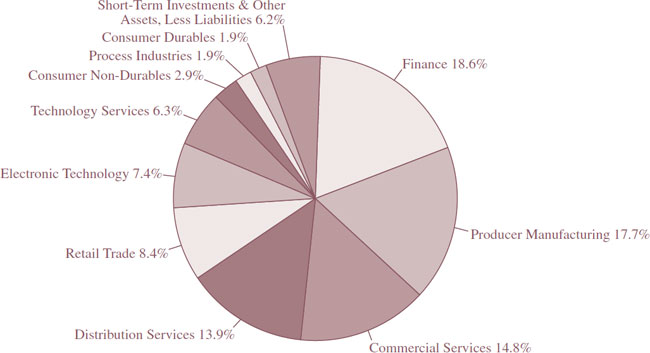

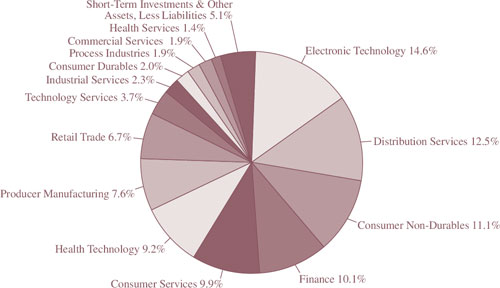

INDUSTRY SECTORS as a percentage of net assets

as of September 30, 2022 (Unaudited)

| FMI | ||

| Common Stock | ||

| Fund | ||

| (unaudited) | September 30, 2022 |

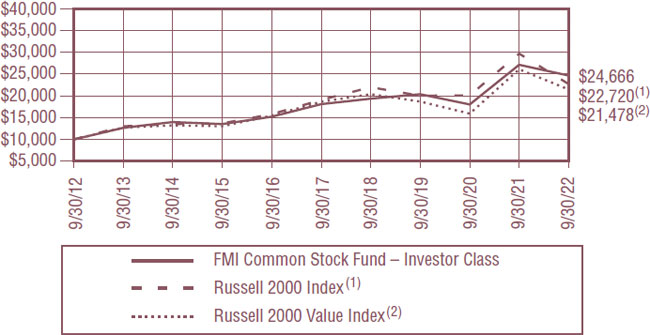

The FMI Common Stock Fund (“Fund”) declined 1.22%1 in the September quarter compared to a 2.19% decline in the Russell 2000 Index (“Russell 2000”) and a 4.61% loss in the Russell 2000 Value Index (“Russell 2000 Value”). Relative to the Russell 2000, sectors that helped included Retail Trade, Finance, and Electronic Technology. Underperforming sectors included Health Technology, Distribution Services, and Commercial Services. BJ’s Wholesale Club Holdings Inc., FirstCash Holdings Inc., and Plexus Corp. aided performance while Simpson Manufacturing Co. Inc., Arrow Electronics Inc., and Concentrix Corp. all detracted. Both stocks and bonds entered bear market territory this year on multiple concerns, some of which will be addressed shortly.

While the markets have been difficult, the team has not been this optimistic about future performance in many years, perhaps not since the Great Financial Crisis. There are several factors that give us optimism:

| ● | Valuations are attractive on both an absolute and relative basis. |

| ● | The sentiment of the market is negative, which is a contrarian’s delight. |

| ● | The strength and durability of the current portfolio has rarely been stronger. |

| ● | The full cycle return on invested capital of the constituents is very good. |

| ● | Many current holdings are significantly depressed, and we view them as coiled springs. |

| ● | The era of ultra-low interest rates appears to be over. This should favor our approach. |

Many of the worrisome issues and themes we have discussed in recent years are coming to pass. Rates have escalated rapidly. Reckless, and even feckless, monetary policies have been revealed. The bond market has suffered steep declines. Stocks are in disarray. The private equity and leverage bubbles have started to burst. Inflation is much higher. A “black swan” geopolitical event (Russia’s war on Ukraine) has transpired. Many of the risk items that sky-high valuations suggested would not occur are now happening. But the time to be “negative” has passed. These worries are out in the open and recognized and now fear is the prevailing sentiment. History suggests this is the time to be more constructive. We are positive about the future and feel the set up for stocks is the best it has been in years.

We will delve into this theme shortly. Before that, we want to address some stocks that have lagged recently and why we have decided to stick with them or cut them loose. Arrow Electronics has been a long-term holding for the Fund. The stock is much more volatile than the underlying fundamentals. Arrow distributes semiconductors and technology hardware, and those end markets are in a cyclical downturn, taking the stock with them. Arrow has proven its ability to adjust to the cycles and ultimately thrive, and with the valuation low, our current plan is to stick with it. Henry Schein Inc., like Arrow, is a distributor, primarily in the dental arena, but also in medical supplies. Fears about slowing dental markets and tough comparisons have hurt the stock in the short run. We do not think Henry Schein’s competitive position has diminished. With a reasonable valuation for a high-quality defensive company, we’ve increased our investment. On the flipside, we exited Phibro Animal Health Corp. – Cl A, the animal health products producer. Inconsistent execution doomed this idea. It was a small holding that was proving more trouble than it was worth. Concentrix, which had been a good stock initially, fell significantly since the last quarter. The market was spooked by a modest slowing of growth. We were more concerned about a ramping up of the mergers and acquisitions (M&A) rhetoric and decided to move to the sidelines.

| 1 | The FMI Common Stock Fund Investor Class (FMIMX) and the FMI Common Stock Fund Institutional Class (FMIUX) had a return of -1.22% and -1.22%, respectively, for the third quarter of 2022. |

The team’s optimism starts with valuations. The Fund trades at a modest 12.9 times projected 2023 earnings, 1.3 times the latest twelve month’s revenue and 10.3 times the trailing year’s EV/EBITDA. On these metrics that is about a 54% discount to the iShares Russell 2000 ETF, as illustrated by the nearby table. The Fund also trades at a discount to the small cap value benchmark.

| September 30, 2022 Weighted Average | FMI Common Stock Fund | iShares Russell 2000 | Discount to Russell 2000 |

| P/E (1Year Trailing) | 15.9x | 29.4x | 46% |

| FY2 P/E | 12.9x | 23.5x | 45% |

| P/S | 1.3x | 5.3x | 75% |

| EV/EBITDA | 10.3x | 20.6x | 50% |

| Average Discount | 54% | ||

| *Estimated valuations for FMI and the iShares are weighted average valuation calculations, not reweighted to exclude cash, and financial companies are excluded from the EV/EBITDA calculation. Valuations for both the portfolio and the ETF are modified based on criteria identified by FMI. For more detailed information regarding these valuations, please contact FMI. | |||

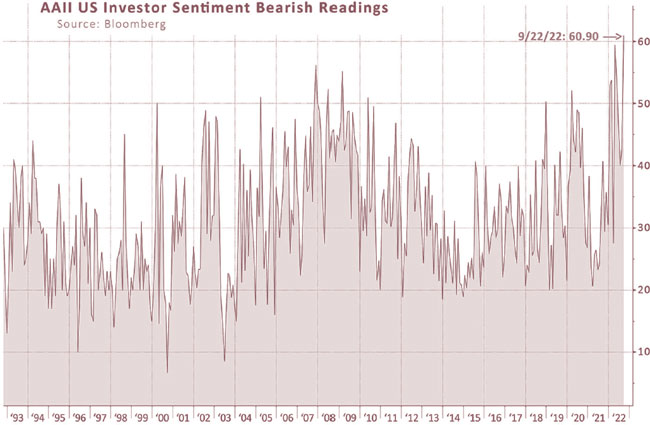

Bearish sentiment indicators (see chart below) are high. We view this as a positive. It is very difficult to avoid dwelling on “losses,” but there is nothing anyone can do about the past. If the business is sound and the balance sheet is solid, then the stock is likely to recover. Unfortunately, most investors react to the past rather than look forward. The current Fund constituents are characterized by good balance sheets, solid return structures, and competitive strengths. Strong companies on sale for reasonable prices are a source of optimism, not pessimism.

Financial markets are apoplectic about interest rates. The overwhelming consensus opinion is that higher rates will crush the economy for an extended period. We think the fear that has been fanned by the rate move may indeed result in a temporary hit to the economy or a recession, but at FMI, we like to turn our analysis 180 degrees. Did the move from “normal” interest rates prior to the Great Financial Crisis, to zero percent rates for years afterwards cause the economy to boom? No! Economic growth was historically weak over the past 15 years. Abnormally low rates boosted asset prices and set the mergers and acquisitions (M&A) and private equity markets aflame, but it did very little for organic economic growth. We had a boom in financial engineering. So why will economic growth be terrible when the reverse conditions prevail? We think economic growth will be better over the next decade than it has been over the last. Price to earnings (P/E) multiples, however, will likely be lower. Inflation is obviously very elevated but appears to finally be on a downward path. We don’t know if the inflation rate will get back to 2% anytime soon, but feel it will be significantly lower than it has been over the past year. Earning an outsized spread over inflation in stocks, like we have seen for many years, is probably not in the cards, but we believe quality, value-oriented equities, especially our stocks, have the best chance of beating inflation over a three-to-five-year time horizon.

Before delving into a couple of portfolio companies in greater detail, we want to discuss what’s happened since our late 2021 investment in Skechers U.S.A. Inc. – Cl A, a stock highlighted in the March letter. It illustrates our investment approach. Skechers has performed about in line with the small cap benchmarks since purchase but is down approximately 30% in absolute terms. Earnings estimates for 2022 are only down about 11% since we bought it. China lockdown issues and European exposure have been cited as factors. We expect some of these pressures to continue for a few months or quarters, but the franchise remains strong, and we’ve added to the stock. Management has performed admirably for decades at Skechers and we think the odds favor the stock at today’s attractive valuation.

Below are two more examples of good business franchises trading at attractive values.

Simpson Manufacturing Co. Inc. (SSD)

Analyst: Rob Helf

Description

Simpson Manufacturing Co. Inc., designs, engineers, and manufactures wood and concrete construction products. These include connectors, truss plates, and fasteners/fastening systems, as well as concrete construction products (adhesives, specialty chemicals, mechanical anchors, powder actuated tools, and reinforcing fiber materials). Structural connectors are typically steel devices used to strengthen, support, and connect load-bearing elements within a building. We estimate that wood connector products are 80% of both revenue and gross profits for the company. Importantly, most of the wood products are for new home construction (50%), with the balance being multi-family construction and repair and remodel (30%).

Good Business

| ● | Simpson is a leader in structural connector manufacturing with a solid track record of organic growth and profitability. Management estimates that the company has over 75% of market share in the connector industry. |

| ● | The company’s competitive advantages are built on the Strong-Tie brand, engineering excellence, and superior customer service. This has led to strong pricing power and increasing profitability and cash flow. Simpson maintains significant scale as it manufactures over 15,000 wood products and 1,000 concrete products. |

| ● | Simpson’s products enhance structural integrity in the event of natural disasters (hurricanes, earthquakes, fires). The company actively works with state and local code writers to improve construction practices, which leads to mandating the use of structural connectors. |

| ● | Much of the country’s population growth is occurring in the Western and Southern regions, which have home building codes that often require greater use of structural connectors in construction. |

| ● | The company generates mid-to-high teens margins and returns on invested capital (ROIC). Since 2018, ROIC has become an important part of management compensation. |

| ● | Free cash flow has approximated 90% of net income over the past 6 years. |

| ● | Simpson has $275 million of net cash and anticipates deploying about 50% of operating cash flow towards dividends and share repurchases. |

Valuation

| ● | Simpson trades for 11.4 times trailing twelve-month earnings per share (EPS) and 12 times 2023 estimated EPS. Historically, Simpson has traded between 21-34 times trailing EPS and 20-30 times projected earnings. |

| ● | In the last 5 years, the company has focused the business on profitability and ROIC. We argue that this should result in a higher multiple going forward. |

| ● | The shares traded at 11 times forward EPS in 2009, the worst housing crisis in recent times. |

Management

| ● | Karen Colonias is the current CEO and has been with Simpson since 2004. She will retire as CEO on December 31, 2022. |

| ● | Michael Olosky has been President and COO since 2020 and will replace Colonias as CEO at the end of the year. Prior to Simpson, Olosky spent 22 years in numerous leadership positions at Henkel, most recently as Regional President North America/Head of the Electronics and Industrial Division. Olosky has a BS in Mechanical Engineering from Michigan Tech and an MBA from Michigan State. |

| ● | Brian Magstadt has served as CFO since 2012. Magstadt has served in numerous financial positions at Simpson since 2004. He is a CPA and has an MBA from Santa Clara University. |

| ● | Since 2018, a significant portion of executive compensation has been tied to ROIC. |

Investment Thesis

Simpson is a leading producer in a very good, but cyclical business. The company’s highly engineered and patented Strong-Tie connectors provide robust architectural integrity for a modest price and are the industry standard. The high-margin products are specified and mandated in the design of new homes, especially in the South and West where natural disasters have increased the importance of the products. The recent share performance reflects a market that is focused on short-term new housing activity. Additionally, earnings comparisons are difficult as the company raised prices last year ahead of higher steel costs. Management has been transparent with this price/cost dynamic. We believe these concerns are embedded in the valuation which is near all-time lows. This is a high-quality company trading at a low valuation due to near-term macro worries and tough comparisons.

Genpact Ltd. (G)

Analyst: Julia Ramon

Description

Genpact is a global business process management and outsourcing provider that works with clients to help them design, transform, and run business-critical operations. Genpact reports under two segments: Data-Tech-AI (~45% of revenue) and Digital Operations (~55% of revenue). Data-Tech-AI consists of client projects where Genpact is designing, building, and transforming businesses using technology. Digital Operations consists of more traditional business process outsourcing work such as operating and streamlining workflows and processes. The company has broad exposure across a number of industry verticals, employs over 114,000 professionals around the globe, and operates in over 30 countries.

Good Business

| ● | Genpact is an industry-leading provider of business process outsourcing and digital transformational services and has experience running thousands of processes for hundreds of Fortune Global 500 clients. Its process excellence and proprietary methodologies of delivery have been developed and fine-tuned over its two decades+ of operations. |

| ● | The company estimates that more than 80% of its revenues are somewhat recurring in nature, with average deal length around 3 years and annual client retention in the high-90 percentage range. |

| ● | Over the trailing 3, 5, and 10-year periods, Genpact has grown revenue at an average rate of 10.1%, 9.5%, and 9.6%, respectively. The company expects organic growth to exceed 10% per year over the next several years, along with accelerated margin expansion through scale efficiencies. |

| ● | Genpact’s solutions provide customers with a tangible return on investment primarily by helping customers decrease costs, drive growth, and reduce risks. |

| ● | The company estimates its current total addressable market opportunity is approximately $750 billion and growing in the high single digit percent range annually. |

| ● | Over the trailing 5-year period, the company’s ROIC has averaged approximately 12%, which exceeds its cost of capital. |

| ● | Genpact has a good balance sheet with a net debt-to-EBITDA ratio of 1.7 times. |

Valuation

| ● | Genpact trades (on a GAAP basis) at a forward price-to-earnings multiple of 17.4 times and a price-to-sales multiple of 1.9 times, both of which are roughly a standard deviation below the 10-year average. |

| ● | Our expectation for accelerating organic growth and margin expansion over the next several years supports a valuation multiple above the company’s historical average. |

| ● | The stock trades at a significant discount to the Russell 2000, despite having above-average business quality and a higher expected EPS growth rate. |

Management

| ● | Current CEO, N.V. “Tiger” Tyagarajan, has led the company since June 2011. He is considered a pioneer of the industry and has a deep knowledge of Lean and Six Sigma. He beneficially owns 3.05 million shares. |

| ● | Genpact has an experienced management team, and its average named executive officer tenure is greater than 10 years. |

Investment Thesis

Genpact is a global leader in the business process outsourcing industry. Over the past decade, Genpact has significantly diversified its client base away from its former parent company (General Electric Company) by aggressively growing other client revenue and winning new customers. General Electric is now just ~9% of revenue. Additionally, over the last several years, management has invested significantly to add vertical expertise, enhance its brand image, and grow its digital transformation offerings. As a result, Genpact is winning large new deals with blue-chip companies and continues to gain share in a market that is already secularly growing. We think Genpact is well positioned for 10%+ organic sales growth with margin expansion over the next 3-5 years and expect the business to perform well in most economic environments (revenue and operating income grew at double-digit rates through the Great Financial Crisis). Overall, we think Genpact’s strong growth profile, defensive business aspects, solid balance sheet, and attractive valuation make for a good outlook.

Thank you for your confidence in The FMI Common Stock Fund.

This shareholder letter is unaudited.

FMI Common Stock Fund

MANAGEMENT’S DISCUSSION OF FUND PERFORMANCE (Unaudited)

During the fiscal year ended September 30, 2022, the FMI Common Stock Fund (“Fund”) had a total return of minus 9.10%1. The benchmark Russell 2000 Index (“Russell 2000”) returned minus 23.50% in the same period. The trailing 12-month return for the Russell 2000 Value Index (“Russell 2000 Value”) was minus 17.69%. Relative to the Russell 2000, sectors that aided relative performance included Technology Services, Producer Manufacturing, and Retail Trade. CDK Global Inc., KBR Inc., and Insight Enterprises Inc. drove the results in the Technology Services sector, as all three continued to grow earnings and CDK was bought out. In Producer Manufacturing, Carlisle Cos. Inc. had strong results as the commercial roofing business grew significantly. In Retail Trade, BJ’s Wholesale Club Holdings Inc. performed strongly as consumers sought better values for food. On the negative side of sector performance, Energy Minerals, Utilities, and Industrial Services detracted. The Fund managers seek to own high quality, value-oriented stocks. Sometimes the market wants stocks in areas that we believe are lower quality in nature, such as energy and commodities. The Fund had no direct exposures to these three sectors that outperformed. Stocks that detracted from performance included Concentrix Corp., Gates Industrial Corp. PLC, ManpowerGroup Inc., Herbalife Nutrition Ltd., Dentsply Sirona Inc., LGI Homes Inc., and Skechers U.S.A. Inc. – Cl A. Nearly all of these companies experienced a slowdown in demand. Better opportunities surfaced and the Fund managers removed Concentrix, Herbalife, and Dentsply Sirona.

Other stocks that helped performance included FTI Consulting Inc., Beacon Roofing Supply Inc., and nVent Electric PLC. FTI experienced solid underlying demand and efficient execution. Beacon’s business is somewhat weather driven, which helped, but there is also underlying secular demand growth. nVent has benefited from secular growth in electric products and electricity management. New additions to the Fund over the past twelve months included Skechers, Gates Industrial, Triton International Ltd., Five Below Inc., AptarGroup Inc., and The AZEK Co. Inc. Stocks sold during the year included Ryder Systems Inc., EnPro Industries Inc., Trinity Industries Inc., A.O. Smith Corp., Huntington Ingalls Industries Inc., Phibro Animal Health Corp. – Cl A, Flowserve Corp., Dentsply Sirona, Herbalife Nutrition, Brady Corp. – Cl A, CDK Global, and Concentrix. As of September 30, 2022, the Fund was significantly overweighted in Producer Manufacturing, Distribution Services, and Commercial Services. The Fund was meaningfully underweighted in Finance, Health Technology, and Energy Minerals.

The Russell 2000 entered a traditionally defined bear market in fiscal 2022 (down 20%). Earnings growth has remained relatively robust over the year, so valuations have come down significantly. Worries about high inflation, rising interest rates, and an economic slowdown permeate the landscape. Geopolitical issues, particularly the Russian war with Ukraine and the saber rattling by China over Taiwan, have further spooked investors.

The Fund managers have become more optimistic about future performance now that many potential worries have become visible realities. The Federal Reserve is no longer printing money, but instead is engaging in quantitative tightening. This should help control inflation and engender a more normal interest rate environment. A realistic cost of capital helps move the economy from one driven by financial engineering to one driven by fundamental investment. Companies with solid balance sheets that make money stand a better chance of outperforming compared to the previous environment, where more speculative businesses outperformed. The Fund trades at a meaningful discount to the Russell 2000, and the managers believe the quality of the underlying companies is better than the benchmark.

| 1 | The FMI Common Stock Fund Investor Class (FMIMX) and the FMI Common Stock Fund Institutional Class (FMIUX) had a return of -9.10% and -8.99%, respectively, for the fiscal year ended 09/30/2022. |

FMI Common Stock Fund

MANAGEMENT’S DISCUSSION OF FUND PERFORMANCE (Unaudited) (Continued)

COMPARISON OF CHANGE IN VALUE OF $10,000 INVESTMENT IN FMI COMMON STOCK FUND – INVESTOR CLASS — THE RUSSELL 2000© INDEX(1) AND THE RUSSELL 2000© VALUE INDEX(2)

AVERAGE ANNUALIZED TOTAL RETURN

| Inception | ||||||||||||||||||

| through | ||||||||||||||||||

| Inception Date | 1-Year | 5-Year | 10-Year | 9/30/2022 | ||||||||||||||

| FMI Common Stock Fund – | ||||||||||||||||||

| Investor Class | 12/18/81 | -9.10% | 6.39% | 9.45% | 11.34% | |||||||||||||

| FMI Common Stock Fund – | ||||||||||||||||||

| Institutional Class | 10/31/16 | -8.99% | 6.51% | N/A | 9.14% | |||||||||||||

| Russell 2000 Index(1)* | -23.50% | 3.55% | 8.55% | 9.66% | ||||||||||||||

| Russell 2000 Value Index(2)* | -17.69% | 2.87% | 7.94% | 11.06% | ||||||||||||||

The graph and the table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Performance data quoted represents past performance; past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of a Fund may be lower or higher than the performance quoted. The total returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Total return includes change in share prices and in each case includes reinvestments of any dividends, interest and capital gain distributions. Performance data current to the most recent month-end may be obtained by visiting www.fmifunds.com or by calling 1-800-811-5311.

| (1) | The Russell 2000 Index measures the performance of the 2,000 smallest companies in the Russell 3000 Index, which comprises the 3,000 largest U.S. companies based on total market capitalization. |

| (2) | The Russell 2000 Value Index includes equities that exhibit value characteristics and the Russell 2000 Growth Index includes equities that exhibit growth characteristics. |

| * | The benchmark since inception returns are calculated since inception of the Investor Class, December 18, 1981 to September 30, 2022. |

An investment cannot be made directly into an index.

FMI Common Stock Fund

September 30, 2022

| Shares | Cost | Value | ||||||||||

| COMMON STOCKS — 93.8% (a) | ||||||||||||

| COMMERCIAL SERVICES SECTOR — 14.8% | ||||||||||||

| Advertising/Marketing Services — 4.0% | ||||||||||||

| 1,498,000 | Interpublic Group of Cos. Inc. | $ | 30,126,593 | $ | 38,348,800 | |||||||

| Miscellaneous Commercial Services — 6.0% | ||||||||||||

| 52,000 | FTI Consulting Inc.* | 5,764,039 | 8,616,920 | |||||||||

| 1,098,000 | Genpact Ltd. | 24,384,380 | 48,059,460 | |||||||||

| 30,148,419 | 56,676,380 | |||||||||||

| Personnel Services — 4.8% | ||||||||||||

| 164,000 | ManpowerGroup Inc. | 10,836,641 | 10,609,160 | |||||||||

| 450,000 | Robert Half International Inc. | 23,718,963 | 34,425,000 | |||||||||

| 34,555,604 | 45,034,160 | |||||||||||

| CONSUMER DURABLES SECTOR — 1.9% | ||||||||||||

| Homebuilding — 1.9% | ||||||||||||

| 219,000 | LGI Homes Inc.* | 26,779,990 | 17,820,030 | |||||||||

| CONSUMER NON-DURABLES SECTOR — 2.9% | ||||||||||||

| Apparel/Footwear — 2.9% | ||||||||||||

| 863,000 | Skechers U.S.A. Inc. — Cl A* | 38,551,158 | 27,374,360 | |||||||||

| DISTRIBUTION SERVICES SECTOR — 13.9% | ||||||||||||

| Electronics Distributors — 2.5% | ||||||||||||

| 255,000 | Arrow Electronics Inc.* | 8,631,673 | 23,508,450 | |||||||||

| Medical Distributors — 4.9% | ||||||||||||

| 707,000 | Henry Schein Inc.* | 45,894,406 | 46,499,390 | |||||||||

| Wholesale Distributors — 6.5% | ||||||||||||

| 246,000 | Applied Industrial Technologies Inc. | 16,206,081 | 25,283,880 | |||||||||

| 664,000 | Beacon Roofing Supply Inc.* | 36,010,377 | 36,334,080 | |||||||||

| 52,216,458 | 61,617,960 | |||||||||||

| ELECTRONIC TECHNOLOGY SECTOR — 7.4% | ||||||||||||

| Electronic Components — 3.5% | ||||||||||||

| 1,044,000 | nVent Electric PLC | 23,635,972 | 33,000,840 | |||||||||

| Electronic Production Equipment — 3.9% | ||||||||||||

| 424,000 | Plexus Corp.* | 32,624,637 | 37,125,440 | |||||||||

| FINANCE SECTOR — 18.6% | ||||||||||||

| Finance/Rental/Leasing — 5.2% | ||||||||||||

| 533,000 | FirstCash Holdings Inc. | 24,856,958 | 39,095,550 | |||||||||

| 188,000 | Triton International Ltd. | 11,759,611 | 10,289,240 | |||||||||

| 36,616,569 | 49,384,790 | |||||||||||

| Investment Banks/Brokers — 2.8% | ||||||||||||

| 348,000 | Houlihan Lokey Inc. — Cl A | 17,591,157 | 26,232,240 | |||||||||

| Life/Health Insurance — 3.3% | ||||||||||||

| 251,000 | Primerica Inc. | 33,827,635 | 30,985,950 | |||||||||

The accompanying notes to financial statements are an integral part of this schedule.

FMI Common Stock Fund

SCHEDULE OF INVESTMENTS (Continued)

September 30, 2022

| Shares | Cost | Value | ||||||||||

| COMMON STOCKS — 93.8% (a) (Continued) | ||||||||||||

| FINANCE SECTOR — 18.6% (Continued) | ||||||||||||

| Multi-Line Insurance — 1.8% | ||||||||||||

| 13,000 | White Mountains Insurance Group Ltd. | $ | 11,806,982 | $ | 16,939,260 | |||||||

| Real Estate Development — 2.4% | ||||||||||||

| 82,930 | The Howard Hughes Corp.* | 4,440,207 | 4,593,493 | |||||||||

| 1,203,000 | Kennedy-Wilson Holdings Inc. | 21,324,408 | 18,598,380 | |||||||||

| 25,764,615 | 23,191,873 | |||||||||||

| Regional Banks — 3.1% | ||||||||||||

| 586,000 | Zions Bancorporation N.A | 17,456,925 | 29,803,960 | |||||||||

| PROCESS INDUSTRIES SECTOR — 1.9% | ||||||||||||

| Containers/Packaging — 1.9% | ||||||||||||

| 194,000 | AptarGroup Inc. | 20,138,347 | 18,435,820 | |||||||||

| PRODUCER MANUFACTURING SECTOR — 17.7% | ||||||||||||

| Auto Parts: OEM — 3.2% | ||||||||||||

| 610,000 | Donaldson Co. Inc. | 28,541,421 | 29,896,100 | |||||||||

| Building Products — 7.6% | ||||||||||||

| 541,000 | The AZEK Co. Inc.* | 9,864,261 | 8,991,420 | |||||||||

| 132,000 | Carlisle Cos. Inc. | 5,740,764 | 37,014,120 | |||||||||

| 335,000 | Simpson Manufacturing Co. Inc. | 35,161,477 | 26,264,000 | |||||||||

| 50,766,502 | 72,269,540 | |||||||||||

| Industrial Machinery — 2.0% | ||||||||||||

| 1,062,000 | Gates Industrial Corp. PLC* | 16,347,995 | 10,365,120 | |||||||||

| 112,000 | Woodward Inc. | 4,866,634 | 8,989,120 | |||||||||

| 21,214,629 | 19,354,240 | |||||||||||

| Miscellaneous Manufacturing — 4.9% | ||||||||||||

| 176,000 | LCI Industries | 24,111,382 | 17,856,960 | |||||||||

| 1,126,000 | TriMas Corp. | 26,149,035 | 28,228,820 | |||||||||

| 50,260,417 | 46,085,780 | |||||||||||

| RETAIL TRADE SECTOR — 8.4% | ||||||||||||

| Discount Stores — 2.9% | ||||||||||||

| 197,000 | Five Below Inc.* | 25,641,331 | 27,120,990 | |||||||||

| Specialty Stores — 5.5% | ||||||||||||

| 714,000 | BJ’s Wholesale Club Holdings Inc.* | 41,256,609 | 51,986,340 | |||||||||

| TECHNOLOGY SERVICES SECTOR — 6.3% | ||||||||||||

| Information Technology Services — 6.3% | ||||||||||||

| 446,000 | Insight Enterprises Inc.* | 32,283,044 | 36,754,860 | |||||||||

| 521,000 | KBR Inc. | 20,610,805 | 22,517,620 | |||||||||

| 52,893,849 | 59,272,480 | |||||||||||

| Total common stocks | 756,941,898 | 887,965,173 | ||||||||||

The accompanying notes to financial statements are an integral part of this schedule.

FMI Common Stock Fund

SCHEDULE OF INVESTMENTS (Continued)

September 30, 2022

| Principal Amount | Cost | Value | ||||||||||

| SHORT-TERM INVESTMENTS — 6.2% (a) | ||||||||||||

| Bank Deposit Account — 6.2% | ||||||||||||

| $ | 58,652,586 | U.S. Bank N.A., 2.65%^ | $ | 58,652,586 | $ | 58,652,586 | ||||||

| Total short-term investments | 58,652,586 | 58,652,586 | ||||||||||

| Total investments — 100.0% | $ | 815,594,484 | 946,617,759 | |||||||||

| Other assets, less liabilities — 0.0% (a) | 324,847 | |||||||||||

| TOTAL NET ASSETS — 100.0% | $ | 946,942,606 | ||||||||||

| * | Non-income producing security. |

| ^ | The rate shown is as of September 30, 2022. |

| (a) | Percentages for the various classifications relate to total net assets. |

| PLC | Public Limited Company |

The accompanying notes to financial statements are an integral part of this schedule.

INDUSTRY SECTORS as a percentage of net assets

as of September 30, 2022 (Unaudited)

and

FMI International Fund II – Currency Unhedged

| (unaudited) | September 30, 2022 |

International stock markets continued their descent in the September quarter, with the Ukraine war weighing on economic growth and fueling inflation, particularly in food and energy. World GDP growth is slowing, and most major central banks are tightening monetary policy to stem the persistent upward pressure on prices. Economic indicators point to an outlook that may get worse before it gets better, and several stock and bond markets are in bear market territory. Amidst the carnage lies opportunities.

For the quarter, the FMI International Funds (“Funds”) fell by 5.04%1 on a currency hedged basis and 10.53%2 currency unhedged, compared with the MSCI EAFE Index’s decline of 3.59% in local currency (LOC) and 9.36% in U.S. Dollars (USD). The MSCI EAFE Value Index dropped 4.23% (LOC) and 10.21% (USD). FMI’s currency hedged performance benefited from a very strong USD. The Consumer Services, Producer Manufacturing, and Distribution Services sectors were additive to performance, while Retail Trade, Health Services, and Electronic Technology detracted. Sodexo S.A., DBS Group Holdings Ltd., and Unilever PLC performed well individually, as Fresenius Medical Care AG & Co. KGaA, B&M European Value Retail S.A., and Koninklijke Philips N.V. each lagged the market. The Funds’ UK consumer exposure has weighed on our relative performance, but we remain constructive over the long-term which we will discuss below.

While global stock markets have been challenging, we are as optimistic about our future performance as we have been in years, for several reasons: valuations are attractive, both on an absolute and relative basis. The sentiment of the market is overwhelmingly negative, which can create exciting prospects for those that are contrarian. The strength and durability of our companies are robust, yet many of our stocks are depressed; we believe we own several coiled springs. Lastly, the era of ultra-low interest rates appears to be ending (Japan is still holding out), which should bode well for our investment approach. We see brighter days ahead for the portfolios and will continue to stay the course during these tough times.

| 1 | The FMI International Fund [currency hedged] Investor Class (FMIJX) and the FMI International Fund [currency hedged] Institutional Class (FMIYX) had a return of -5.04% and -4.96%, respectively, for the third quarter of 2022. |

| 2 | The FMI International Fund [currency unhedged] Investor Class (FMIFX) had a return of -10.53% for the third quarter of 2022. |

Long in the Tooth?

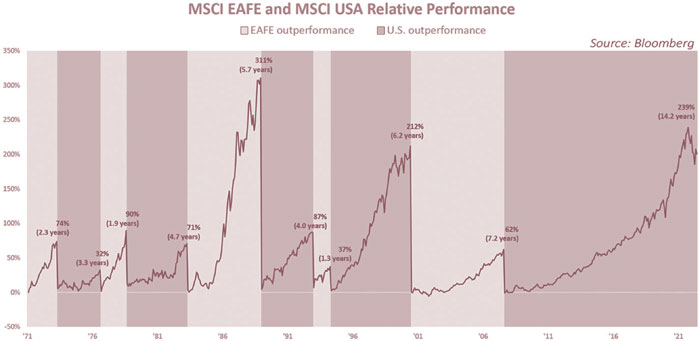

Stock markets move in cycles, and today we are in an especially painful one for international investors. As illustrated in the chart on the following page, we are in the throes of the longest (14.2 years) and widest period of underperformance (239%) for developed international markets versus the U.S. in over 50 years:

Several headwinds have impacted overseas markets during the period, including the European sovereign debt crisis, Brexit, Europe’s proximity to the Ukraine war (and resulting energy crisis), and USD strength, to name a few. Additionally, international stock markets have had more exposure to the financial sector, while U.S. markets are over-indexed to big tech, which has not helped the comparison. Today, Europe is in the eye of the storm, facing higher inflation and weaker economic growth than the U.S., in addition to being well behind the curve in terms of tightening monetary policy. Headline inflation is expected to soon peak in most major economies, but to date has remained stubbornly high. Meanwhile, Japan is still playing with fire, continuing to embrace negative interest rates and quantitative easing, while intervening to prop up the Yen for the first time since 1998.3 There is no shortage of macro risks.

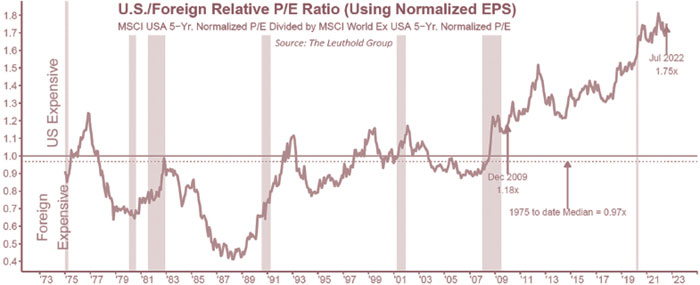

That said, valuations finally appear to be incorporating a lot of bad news, which is consistent with stock market history. In times of excess fear, investors predictably take the prevailing sentiment to the extreme, selling individual stocks to levels far below their intrinsic value. This is the nature of bear markets, and we find ourselves in one today. The opposite is certainly true during periods of market exuberance. Encouragingly, the normalized valuation spread between U.S. and foreign stocks is near an all-time high, as depicted below. This may create an attractive relative opportunity for those investing internationally, as a simple reversion to the mean could work wonders over time.

| 3 | Kana Inagaki and Leo Lewis. “Japan intervenes to prop up yen for first time since 1998.” Financial Times, September 22, 2022. |

When markets fall indiscriminately, stock picking becomes paramount. The FMI International portfolios are discerning. Not only does FMI focus on high-quality businesses (compounders) with strong balance sheets, but we remain disciplined on valuation, looking for companies being sold at significant discounts. Today, the portfolios’ valuation is compelling, trading at less than 12 times consensus estimates for 2023 earnings, approximately a 25% discount to the iShares MSCI EAFE ETF. The set-up appears attractive. While it is easy to dwell on recent mark-to-market “losses” in the portfolios, if the businesses and balance sheets are sound, the stocks are likely to recover. When companies with strong competitive positions temporarily go on sale, it is reason to be optimistic.

House on Fire

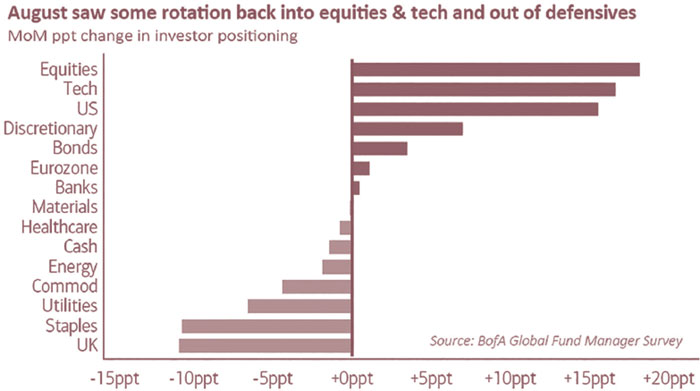

Investors are vacating the UK in droves, as depicted by the Bank of America chart below, pulled from their recent “Global Fund Manager Survey.”4 Consumer-related stocks, in particular, have been left for dead. Among the 56 European macro themes that Goldman Sachs tracks, UK Consumption ranks second-to-last in terms of year-to-date stock performance, with the representative basket of stocks down ~54%. For comparison, the EU Consumption basket is down ~29%.5 Are the prospects in the UK that much worse? We have our doubts, and at the very least, believe there are diamonds in the rough.

According to OECD economic forecasts from just last week, the UK economy is expected to outperform the Eurozone this year (3.4% versus 3.1%), but lag by a similar amount in 2023 (0% verus 0.3%).6 Inflation in the UK was running a bit higher than the Eurozone in August, at 9.9% versus 9.1%. The official statistics at the end of the first quarter showed government debt-to-GDP (UK: 99.6%, Eurozone: 95.6%) and deficit levels (2.6%, 2.3%) within striking distance of one another.7 So why such an extreme stock price divergence?

| 4 | Michael Hartnett and Myung-Jee Jung. “Global Fund Manager Survey: Bulls Wanted.” BofA Global Research, August 16, 2022. |

| 5 | Source: Bloomberg. |

| 6 | Mathias Cormann and Alvaro Santos Pereira. “OECD Economic Outlook: Paying the Price of War.” September 26, 2022. |

| 7 | https://www.ons.gov.uk/ |

https://ec.europa.eu/eurostat

New UK Prime Minister, Liz Truss, played a role by spooking markets with a sweeping fiscal proposal of tax cuts (household and corporate), reduced regulations, and emergency energy subsidies, among other measures. The fiscal package would be largely funded with debt. UK stock and bond markets came under intense selling pressure, as did the pound, which touched a record low versus the USD. The Bank of England intervened in the long-dated bond market to ensure stability. Critics voiced concerns around fueling inflation, an increasing government debt burden, and the need to raise rates significantly, while supporters touted improved economic growth prospects and debt falling as a percentage of GDP over the medium term.8 While the plethora of macro crosscurrents is nearly impossible to predict, we have a more favorable viewpoint than the naysayers. In the early 1980s, after a period of high inflation, many believed that U.S. tax cuts would be catastrophic – yet an economic revival ensued. Lower taxes and regulations have a long history of being quite good for business activity.

We are also skeptical about the fear factor around higher interest rates, given we remain well below historical levels. As we explain in our domestic shareholder letters (and it applies to the UK as well): “Financial markets are apoplectic about interest rates. The overwhelming consensus opinion is that higher rates will crush the economy for an extended period. We think the fear that has been fanned by the rate move may indeed result in a temporary hit to the economy or a recession, but at FMI we like to turn our analysis 180 degrees. Did the move from ”normal“ interest rates prior to the Great Financial Crisis to zero percent rates for years afterwards cause the economy to boom? No! Economic growth was historically weak over the past 15 years. Abnormally low rates boosted asset prices and set the mergers and acquisitions (M&A) and private equity markets aflame, but it did very little for organic economic growth. We had a boom in financial engineering. So why will economic growth be terrible when the reverse conditions prevail? We think economic growth will be much better over the next decade than it has been over the last.”

Furthermore, if higher rates and inflation are sustained, we believe the portfolios are well-positioned. Our quality businesses have inherent pricing power given their competitive advantages and barriers to entry, their balance sheets are built for difficult times, and the valuations embed a significant margin of safety. The portfolios have not benefited from ultra-low interest rates like many of the high-flying growth stocks.

As UK consumer stocks have come under extreme pressure, we have been leaning into the wind, adding to each of our related holdings: Greggs PLC (featured in the March shareholder letter), B&M Value European Retail, and Howden Joinery Group PLC (both featured on the following pages). We believe their respective stock moves are overblown, as these are strong, durable franchises that will be able to weather the storm. We do not view the sell-off as a permanent impairment of capital. Quite the opposite: we see tremendous upside potential and a very attractive risk/reward from current depressed levels. This is what we have been trained to do ... go against the grain and take advantage of mispricing in the market. This is the essence of value investing.

----

FMI will continue to hold true to our core principles, as we believe wholeheartedly in our investment process. Investors can take comfort knowing that our team “eats our own cooking,” and is invested right alongside our shareholders in each of our strategies. Our net worth is tied to the very same stocks our shareholders own.

| 8 | Philip Aldrick. “UK’s Biggest Tax Cuts Since 1972 Trigger Crash in Pound, Bonds” Bloomberg, September 23, 2022. |

As promised, a summary of the aforementioned investments is provided below:

B&M European Value Retail S.A. (BME LN)

Analyst: Jordan Teschendorf

Description

B&M European Value Retail is the largest general merchandise discount retailer in the UK, operating 1,119 stores under the B&M (701 stores; 91% EBITDA) and Heron Foods (311 stores; 4% EBITDA) banners (fiscal year 2022), primarily outside of Southeastern England. The company operates 107 stores in France under the Babou banner (5% EBITDA) and recently sold its German operations (Jawoll). It’s core B&M franchise operates low-cost store formats, offering a variety of branded consumables (grocery and fast-moving consumer goods products) and private label general merchandise at “everyday low prices” (typically 20-30% cheaper).

Good Business

| ● | B&M stores perform well in a variety of economic environments, evidenced by consistently growing same store sales over the last decade. B&M generated positive comparisons through the financial crisis (+10.4% average on fiscal years 2008-2010). |