UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

| | |

| Investment Company Act file number: | | 811-08085 |

| |

| Exact name of registrant as specified in charter: | | Strategic Partners Mutual Funds, Inc. |

| |

| Address of principal executive offices: | | Gateway Center 3, 100 Mulberry Street, Newark, New Jersey 07102 |

| |

| Name and address of agent for service: | | Deborah A. Docs Gateway Center 3, 100 Mulberry Street, Newark, New Jersey 07102 |

| |

| Registrant’s telephone number, including area code: | | 973-367-7521 |

| |

| Date of fiscal year end: | | 10/31/2005 |

| |

| Date of reporting period: | | 10/31/2005 |

Item 1 – Reports to Stockholders – [ INSERT REPORT ]

ANNUAL REPORT

OCTOBER 31, 2005

STRATEGIC PARTNERS

MUTUAL FUNDS, INC.

This report is not authorized for distribution to prospective investors unless preceded or accompanied by a current prospectus.

The views expressed in this report and information about the Funds’ portfolio holdings are for the period covered by this report and are subject to change thereafter.

Strategic Partners Mutual Funds, Inc.

List of Subadvisers as of October 31, 2005

| | |

| STRATEGIC PARTNERS FUND NAME | | SUBADVISER |

| Strategic Partners International Growth Fund | | William Blair & Company, L.L.C. |

| Strategic Partners Small Cap Growth Fund | | Deutsche Asset Management, Inc.; RS Investment Management, L.P.; and Transamerica Asset Management LLC |

| Strategic Partners Mid Cap Growth Fund | | Goldman Sachs Asset Management, L.P. |

| Strategic Partners Mid Cap Value Fund | | Neuberger Berman Management, Inc. |

| Strategic Partners Technology Fund | | The Dreyfus Corporation |

| Strategic Partners Health Sciences Fund | | A I M Capital Management, Inc. |

| Strategic Partners Managed OTC Fund | | ProFund Advisors LLC |

| Strategic Partners Capital Growth Fund | | Marsico Capital Management, LLC |

| Strategic Partners Concentrated Growth Fund | | Goldman Sachs Asset Management, L.P. |

| Strategic Partners Core Value Fund | | Alliance Capital Management, L.P. |

| Strategic Partners Large Cap Core Fund | | Alliance Capital Management, L.P. |

| Strategic Partners Equity Income Fund | | Alliance Capital Management, L.P. and T. Rowe Price Associates, Inc. |

| Strategic Partners Balanced Fund | | American Century Investment Management, Inc. |

| Strategic Partners High Yield Bond Fund | | Goldman Sachs Asset Management, L.P. |

| Strategic Partners Money Market Fund | | Prudential Investment Management, Inc. |

Subadvisers are subject to change.

For more information about Strategic Partners Mutual Funds, Inc. see the prospectus. You should consider the Funds’ investment objectives, risks, charges, and expenses carefully before investing. The prospectus will contain this and other information about the investment company. Please read the prospectus carefully before investing.

Shares of Strategic Partners Mutual Funds, Inc. are distributed by Prudential Investment Management Services LLC (PIMS), Three Gateway Center, 14th Floor, Newark, NJ 07102-4077; and American Skandia Marketing, Incorporated (ASMI), One Corporate Drive, Shelton, CT 06484. Both are Prudential Financial companies and members Securities Investor Protection Corporation (SIPC).

December 15, 2005

Dear Shareholder:

We hope you find the annual report for Strategic Partners Mutual Funds, Inc. informative and useful. As a Strategic Partners mutual fund shareholder, you may be thinking about where you can find additional growth opportunities. You could invest in last year’s top-performing asset class and hope history repeats itself or you could stay in cash while waiting for the “right moment” to invest.

Instead, we believe it is better to take advantage of developing domestic and global investment opportunities through a diversified portfolio of stock and bond mutual funds. A diversified asset allocation offers two potential advantages. It helps you manage downside risk by not being overly exposed to any particular asset class, plus it gives you a better opportunity to have at least some of your assets in the right place at the right time. Your financial professional can help you create a diversified investment plan that may include mutual funds covering all the basic asset classes and that reflects your personal investment profile and tolerance for risk.

Strategic Partners Mutual Funds gives you a wide range of choices that can help you make progress toward your financial goals. Our funds feature leading asset managers not just from a single company but from the entire investment industry.

Thank you for choosing Strategic Partners Mutual Funds.

Sincerely,

Judy A. Rice President, Strategic Partners Mutual Funds, Inc.

Strategic Partners Mutual Funds

CUSIP Numbers and NASDAQ Symbols

| | | | | | |

| FUND | | CLASS | | CUSIP | | NASDAQ |

| International Growth Fund | | A | | 86277E492 | | N/A |

| | | B | | 86277E476 | | N/A |

| | | C | | 86277E450 | | WBCIX |

| | | L* | | 86277E484 | | WBAIX |

| | | M** | | 86277E468 | | WBBIX |

| | | X*** | | 86277E443 | | WBZIX |

| | | | | | |

| FUND | | CLASS | | CUSIP | | NASDAQ |

| Small Cap Growth Fund | | A | | 86277E831 | | N/A |

| | | B | | 86277E815 | | N/A |

| | | C | | 86277E781 | | PBHCX |

| | | L* | | 86277E823 | | PBSAX |

| | | M** | | 86277E799 | | PBSBX |

| | | X*** | | 86277E773 | | PBSZX |

| | | | | | |

| FUND | | CLASS | | CUSIP | | NASDAQ |

| Mid Cap Growth Fund | | A | | 86277C512 | | N/A |

| | | B | | 86277C488 | | N/A |

| | | C | | 86277C462 | | GCMGX |

| | | L* | | 86277C496 | | GAMGX |

| | | M** | | 86277C470 | | GBMGX |

| | | X*** | | 86277C454 | | N/A |

| | | | | | |

| FUND | | CLASS | | CUSIP | | NASDAQ |

| Mid Cap Value Fund | | A | | 86277E807 | | N/A |

| | | B | | 86277E872 | | N/A |

| | | C | | 86277E856 | | NCBVX |

| | | L* | | 86277E880 | | NABVX |

| | | M** | | 86277E864 | | NBBVX |

| | | X*** | | 86277E849 | | NBVZX |

| | | Z***** | | 86277E435 | | N/A |

| | | | | | |

| FUND | | CLASS | | CUSIP | | NASDAQ |

| Technology Fund | | A | | 86277C314 | | N/A |

| | | B | | 86277C280 | | N/A |

| | | C | | 86277C264 | | ICNVX |

| | | L* | | 86277C298 | | IANVX |

| | | M** | | 86277C272 | | IBNVX |

| | | X*** | | 86277C256 | | IXNZX |

| | | | | | |

| FUND | | CLASS | | CUSIP | | NASDAQ |

| Health Sciences Fund | | A | | 86277C371 | | N/A |

| | | B | | 86277C355 | | N/A |

| | | C | | 86277C330 | | INHCX |

| | | L* | | 86277C363 | | INHAX |

| | | M** | | 86277C348 | | IHSBX |

| | | X*** | | 86277C322 | | N/A |

| | | | | | |

| FUND | | CLASS | | CUSIP | | NASDAQ |

| Managed OTC Fund | | A | | 86277E690 | | N/A |

| | | B | | 86277E674 | | N/A |

| | | C | | 86277E658 | | PCMOX |

| | | L* | | 86277E682 | | PRMAX |

| | | M** | | 86277E666 | | PMOBX |

| | | X*** | | 86277E641 | | N/A |

| | | | | | |

| FUND | | CLASS | | CUSIP | | NASDAQ |

| Capital Growth Fund | | A | | 86277C249 | | N/A |

| | | B | | 86277C223 | | N/A |

| | | C | | 86277C199 | | MARCX |

| | | L* | | 86277C231 | | MARAX |

| | | M** | | 86277C215 | | MARBX |

| | | X*** | | 86277C181 | | MARZX |

| | | | | | |

| FUND | | CLASS | | CUSIP | | NASDAQ |

| Concentrated Growth Fund | | A | | 86277C579 | | N/A |

| | | B | | 86277C553 | | N/A |

| | | C | | 86277C538 | | CCGSX |

| | | L* | | 86277C561 | | CAGSX |

| | | M** | | 86277C546 | | CBGSX |

| | | X*** | | 86277C520 | | CZGSX |

| | | | | | |

| FUND | | CLASS | | CUSIP | | NASDAQ |

| Core Value Fund | | A | | 86277E633 | | N/A |

| | | B | | 86277E617 | | N/A |

| | | C | | 86277E583 | | SBVCX |

| | | L* | | 86277E625 | | SOVAX |

| | | M** | | 86277E591 | | SVCBX |

| | | X*** | | 86277E575 | | N/A |

| | | | | | |

| FUND | | CLASS | | CUSIP | | NASDAQ |

| Large Cap Core Fund | | A | | 86277E567 | | N/A |

| | | B | | 86277E542 | | N/A |

| | | C | | 86277E526 | | MCIFX |

| | | L* | | 86277E559 | | MAIFX |

| | | M** | | 86277E534 | | MBIFX |

| | | X*** | | 86277E518 | | MXIFX |

| | | | | | |

| FUND | | CLASS | | CUSIP | | NASDAQ |

| Equity Income Fund | | A | | 86277C108 | | N/A |

| | | B | | 86277C306 | | N/A |

| | | C | | 86277C504 | | AGOCX |

| | | L* | | 86277C207 | | AGOAX |

| | | M** | | 86277C405 | | AGOBX |

| | | X*** | | 86277C603 | | AXGOX |

| | | | | | |

| FUND | | CLASS | | CUSIP | | NASDAQ |

| Balanced Fund | | A | | 86277C702 | | N/A |

| | | B | | 86277C884 | | N/A |

| | | C | | 86277C868 | | ACBCX |

| | | L* | | 86277C801 | | AACBX |

| | | M** | | 86277C876 | | ACBBX |

| | | X*** | | 86277C850 | | ACBZX |

| | | | | | |

| FUND | | CLASS | | CUSIP | | NASDAQ |

| High Yield Bond Fund | | A | | 86277C710 | | N/A |

| | | B | | 86277C686 | | N/A |

| | | C | | 86277C660 | | FCHYX |

| | | L* | | 86277C694 | | FHYAX |

| | | M** | | 86277C678 | | FBHYX |

| | | X*** | | 86277C652 | | FHYZX |

| | | | | | |

| FUND | | CLASS | | CUSIP | | NASDAQ |

| Money Market Fund**** | | A | | 86277E104 | | N/A |

| | | C | | 86277E609 | | ASCXX |

| | | D | | 86277E302 | | N/A |

| | | L* | | 86277E203 | | AASXX |

| | | M** | | 86277E500 | | ABSXX |

| | | X*** | | 86277E708 | | ASXXX |

*Closed to most new purchases (with the exception of reinvested dividends and purchases by college savings plans) and available for limited exchanges only.

**Closed to new purchases (with the exception of reinvested dividends) and available for limited exchanges only.

***Closed to new purchases and available for limited exchanges only (with the exception of reinvested dividends).

****Available for limited exchanges only.

*****Inception date of 11/28/05.

STRATEGIC PARTNERS MUTUAL FUNDS, INC.

Table of Contents

Summary of Definitions

The following pages present information on the investment performance of each Fund that has been in operation for at least 12 months as of October 31, 2005, including comparisons with relevant market indexes.

Definitions for Broad Market Indexes

Investors cannot invest directly in an index. Returns for the Indexes on the following pages would be lower if they included the effects of sales charges, operating expenses of a mutual fund, or taxes.

Blended Index—The Blended Index is calculated by weighting the S&P 500 Index at 60% and the Lehman Brothers Government/Corporate Bond Index at 40%. The Lehman Brothers Government/Corporate Bond Index is an unmanaged index composed of intermediate- and long-term government and investment-grade corporate debt securities.

Lehman Brothers U.S. Aggregate Bond Index—The Lehman Brothers U.S. Aggregate Bond Index is an unmanaged, market-weighted index that tracks the daily price, coupon pay-downs, and total return performance of fixed-rate, publicly placed, dollar-denominated, and nonconvertible investment-grade debt issues without at least $100 million par amount outstanding and with at least one year to final maturity.

Lehman Brothers U.S. Corporate High Yield Index—The Lehman Brothers U.S. Corporate High Yield Index is an unmanaged index that is generally representative of corporate bonds rated below investment grade. It comprises issues that meet the following criteria: at least $150 million par value outstanding, maximum credit rating of Ba1 or BB+ (including defaulted issues), and at least one year to maturity.

ML High Yield Master II Index—The Merrill Lynch (ML) High Yield Master II Index is an unmanaged index of publicly traded, nonconvertible U.S. bonds rated below investment grade.

MSCI EAFE® Index—The Morgan Stanley Capital International Europe, Australasia, Far East Index (MSCI EAFE® Index) is an unmanaged, weighted index of performance that reflects stock price movements in Europe, Australasia, and the Far East.

NASDAQ-100 Index—The NASDAQ-100 Index is an unmanaged, modified, capitalization-weighted index of the 100 largest and most active nonfinancial domestic and international issues listed on the NASDAQ.

Russell 2000 Index—The Russell 2000 Index is an unmanaged, weighted index that comprises the smallest 2,000 stocks among the largest 3,000 equity-capitalized U.S. corporations and represents approximately 10% of their aggregate market value.

S&P MidCap 400 Index—The Standard & Poor’s MidCap 400 Stock Index (S&P MidCap 400 Index) is an unmanaged index of 400 domestic stocks chosen for market size, liquidity, and industry group representation. It gives a broad look at how U.S. mid-cap stock prices have performed.

S&P 500 Index—The Standard & Poor’s 500 Composite Stock Price Index (S&P 500 Index) is an unmanaged index of 500 stocks of large U.S. public companies. It gives a broad look at how U.S. stock prices have performed.

Definitions for Lipper Averages

Lipper Averages are the average returns of all funds in the specified Lipper comparison group. The Lipper Averages on the following pages reflect the deduction of operating expenses, but not sales charges or taxes.

Lipper Balanced Funds Average—Funds in the Lipper Balanced Funds Average have primary objectives to conserve principal by maintaining at all times a balanced portfolio of both stocks and bonds. Typically, the stock:bond ratio ranges around 60%:40%.

Lipper Corporate Debt Funds A-Rated Average—Funds in the Lipper Corporate Debt Funds A-Rated Average invest primarily in corporate debt issues rated “A” or better, or government issues.

Lipper Equity Income Funds Average—Funds in the Lipper Equity Income Funds Average seek relatively high current income and growth of income through investing 60% or more of its portfolio in equities.

Lipper Health/Biotechnology Funds Average—Funds in the Lipper Health/Biotechnology Funds Average invest primarily in shares of companies engaged in healthcare, medicine, and biotechnology.

Lipper High Current Yield Funds Average—Funds in the Lipper High Current Yield Funds Average aim at high (relative) current yield from fixed income securities, have no quality or maturity restrictions, and tend to invest in lower-grade debt issues.

Lipper International Multi-Cap Growth Funds Average—Funds in the Lipper International Multi-Cap Growth Funds Average invest in a variety of market-capitalization ranges without concentrating 75% of their equity assets in any one market-capitalization range over an extended period of time. Multi-cap funds typically have 25% to 75% of their assets invested in companies strictly outside of the United States with market capitalizations (on a three-year weighted basis) greater than the 250th largest company in the S&P/Citigroup World ex-U.S. Broad Market Index. Multi-cap growth funds typically have an above-average price-to-cash flow ratio, price-to-book ratio, and three-year sales-per-share growth value compared with the S&P/Citigroup World ex-U.S. BMI.

Lipper Large-Cap Core Funds Average—Funds in the Lipper Large-Cap Core Funds Average, by portfolio practice, invest at least 75% of their equity assets in companies with market capitalizations (on a three-year weighted basis) greater than 300% of the dollar-weighted median market capitalization of the middle 1,000 securities of the S&P SuperComposite 1500 Index. Large-cap core funds have more latitude in the companies in which they invest. These funds typically have an average price-to-earnings ratio, price-to-book ratio, and three-year sales-per-share growth value compared with the S&P 500 Index.

Lipper Large-Cap Growth Funds Average—Funds in the Lipper Large-Cap Growth Funds Average, by portfolio practice, invest at least 75% of their equity assets in companies with market capitalizations (on a three-year weighted basis) greater than 300% of the dollar-weighted median market capitalization of the middle 1,000 securities of the S&P SuperComposite 1500 Index. Large-cap growth funds typically have an above-average price-to-earnings ratio, price-to-book ratio, and three-year sales-per-share growth value compared with the S&P 500 Index.

Lipper Large-Cap Value Funds Average—Funds in the Lipper Large-Cap Value Funds Average, by portfolio practice, invest at least 75% of their equity assets in companies with market capitalizations (on a three-year weighted basis) greater than 300% of the dollar-weighted median market capitalization of the middle 1,000 securities of the S&P SuperComposite 1500 Index. Large-cap value funds typically have a below-average price-to-earnings ratio, price-to-book ratio, and three-year sales-per-share growth value compared with the S&P 500 Index.

Lipper Mid-Cap Core Funds Average—Funds in the Lipper Mid-Cap Core Funds Average, by portfolio practice, invest at least 75% of their equity assets in companies with market capitalizations (on a three-year weighted basis) less than 300% of the dollar-weighted median market capitalization of the middle 1,000 securities of the S&P SuperComposite 1500 Index. Mid-cap core funds have more latitude in the companies in which they invest. These funds typically have an average price-to-earnings ratio, price-to-book ratio, and three-year sales-per-share growth value compared with the S&P MidCap 400 Index.

Lipper Mid-Cap Value Funds Average—Funds in the Lipper Mid-Cap Value Funds Average, by portfolio practice, invest at least 75% of their equity assets in companies with market capitalizations (on a three-year weighted basis) less than

300% of the dollar-weighted median market capitalization of the middle 1,000 securities of the S&P SuperComposite 1500 Index. Mid-cap value funds typically have a below-average price-to-earnings ratio, price-to-book ratio, and three-year sales-per-share growth value compared with the S&P MidCap 400 Index.

Lipper Money Market Instrument Funds Average—Funds in the Lipper Money Market Instrument Funds invest in high-quality financial instruments rated in top two grades with dollar-weighted average maturities of less than 90 days. These funds typically intend to keep a constant net asset value.

Lipper Multi-Cap Growth Funds Average—Funds in the Lipper Multi-Cap Growth Funds Average invest in a variety of market-capitalization ranges without concentrating 75% of their equity assets in any one market-capitalization range over an extended period of time. Multi-cap funds typically have between 25% and 75% of their assets invested in companies with market capitalizations (on a three-year weighted basis) above 300% of the dollar-weighted median market capitalization of the middle 1,000 securities of the S&P SuperComposite 1500 Index. Multi-cap growth funds typically have an above-average price-to-earnings ratio, price-to-book ratio, and three-year sales-per-share growth value compared with the S&P SuperComposite 1500 Index.

Lipper Multi-Cap Value Funds Average—Funds in the Lipper Multi-Cap Value Funds Average, by portfolio practice, invest in a variety of market-capitalization ranges without concentrating 75% of their equity assets in any one market-capitalization range over an extended period of time. Multi-cap funds typically have between 25% and 75% of their assets invested in companies with market capitalizations (on a three-year weighted basis) above 300% of the dollar-weighted median market capitalization of the middle 1,000 securities of the S&P SuperComposite 1500 Index. Multi-cap value funds have a below-average price-to-earnings ratio, price-to-book ratio, and three-year sales-per-share growth value compared with the S&P SuperComposite 1500 Index.

Lipper Science & Technology Funds Average—Funds in the Lipper Science & Technology Funds Average invest primarily in science and technology stocks.

Lipper Small-Cap Core Funds Average—Funds in the Lipper Small-Cap Core Funds Average, by portfolio practice, invest at least 75% of their equity assets in companies with market capitalizations (on a three-year weighted basis) less than 250% of the dollar-weighted median of the smallest 500 of the middle 1,000 securities of the S&P SuperComposite 1500 Index. Small-cap core funds have more latitude in the companies in which they invest. These funds typically have an average price-to-earnings ratio, price-to-book ratio, and three-year sales-per-share growth value compared with the S&P SmallCap 600 Index.

Lipper Small-Cap Growth Funds Average—Funds in the Lipper Small-Cap Growth Funds Average, by portfolio practice, invest at least 75% of their equity assets in companies with market capitalizations (on a three-year weighted basis) less than 250% of the dollar-weighted median of the smallest 500 of the middle 1,000 securities of the S&P SuperComposite 1500 Index. Small-cap growth funds typically have an above-average price-to-earnings ratio, price-to-book ratio, and three-year sales-per-share growth value compared with the S&P SmallCap 600 Index.

The Investing Environment

Broad-based stock and bond indexes were positive over the 12 months ended October 31, 2005, and the return for the U.S. stock market overall (as measured by the Russell 3000 Index) was slightly above its 10-year average. However, the performance of individual securities was very uneven. Share prices fell in many industries, particularly in the consumer discretionary and telecommunication services sectors.

World GDP growth moderated from a 3.8% pace to 3.1% as the United States and Asian countries slowed from above-average growth while Europe remained sluggish. Late in the period, the U.S. Gulf coast was hit by hurricanes Katrina and Rita. Investors responded by focusing on the potential long-term impact of higher energy prices, bringing the markets down sharply in September and the first half of October. On the other hand, analysts raised earnings growth estimates for 2006, taking into account the planned $200 billion rebuilding effort.

In our view, the hurricanes exacerbated existing supply concerns in the energy and housing markets. They are likely to raise the cost of doing business for energy-dependent industries and for agricultural industries that use the Mississippi River for transportation. Industries selling to consumers also may be more vulnerable. Nonetheless, we don’t think the impacts are enough to derail the current economic expansion.

Economic and earnings growth remained strong in 2005. However, investors looking ahead were concerned about the slowing of earnings growth from its very rapid rate in 2004, the impact of energy prices on consumer demand for other goods, and rising interest rates. Within the U.S. equity market, mid-cap stocks outpaced large-cap and small-cap stocks. Indeed, the Russell Midcap Index was substantially above its 10-year average, while shares of the very largest corporations lagged both the overall market and their 10-year average return. We think that these are the firms best positioned to benefit from globalization, and their underperformance has generated a buying opportunity.

Value stocks both domestically and internationally performed best through most of the period, but growth outperformed in the third quarter of 2005. After a long period when companies improved their profits primarily by cutting costs, future growth will be more dependent on raising revenues. Currently, investors are paying little or no premium for revenue growth, and we think that is likely to change at some point, driving the prices of growth stocks higher.

The energy sector had extraordinary gains as oil prices rose above $70/barrel in the wake of the hurricanes. Utilities, which are typically value-style investments, also produced strong returns over the period. The industrials, materials, and health care sectors had modest overall returns. Most health care industry groups were among the market’s leaders, but the sector return was pulled down by several very large drug companies’ steep share-price declines. The negative return of the consumer discretionary sector was concentrated in automobile-related and media industries and in the Internet retail stock eBay, while tobacco and housing stocks were strong.

International stock market returns were significantly higher than those in the United States. China took the first step toward an independent monetary policy by loosening the link of its currency to the U.S. dollar. This contributed to global stability by reducing the threat of a rapid economic slowdown triggered by the growing financial imbalances between China and the United States. Japanese voters handed Prime Minister Koizumi a strong mandate to proceed with economic restructuring. This bolsters our confidence that the world’s second largest economy will indeed emerge from 15 years of stagnation—a clear plus for the global economy. Although investment results for U.S. dollar-based investors were reduced somewhat by the steep rise of the dollar in the latter part of the reporting period, international markets generally outperformed U.S. markets even after currency adjustments.

U.S. investment-grade bonds generated very modest returns over the period. Short-term yields rose as the Federal Reserve continued to make incremental rate increases to cool the U.S. economy and keep inflation low. Longer-term yields were more stable, with 30-year yields actually falling to reflect a benign inflation picture. As a result, longer-term bond investors had better returns for the year. Investors reaching for higher yielding alternatives helped high yield corporate (“junk”) and emerging market bonds become the best performing fixed income sectors. Strong U.S. economic growth and solid corporate fundamentals supported junk bonds while high commodity prices and continued fiscal improvement helped the bonds of many key emerging market countries.

This Page Intentionally Left Blank

Your Fund’s Performance

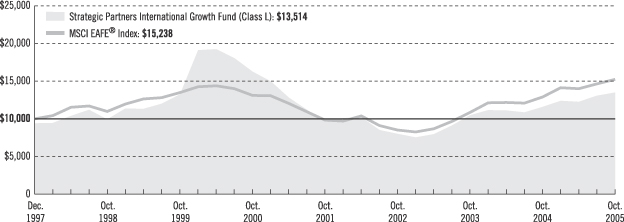

Strategic Partners International Growth Fund

Fund objective

The investment objective of the Strategic Partners International Growth Fund is to seek long-term growth of capital. There can be no assurance that the Fund will achieve its investment objective.

Performance data quoted represent past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate, so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the past performance data quoted. An investor may obtain performance data as of the most recent month-end by visiting our website at www.strategicpartners.com or by calling (800) 225-1852. Class A and Class L shares have a maximum initial sales charge of 5.50% and 5.75% respectively. Class L shares are closed to most new purchases (with the exception of reinvested dividends and purchases by certain college savings plans).

| | | | | | | | | |

| Cumulative Total Returns1 as of 10/31/05 | | | | | | | | | |

| | | One Year | | | Five Years | | | Since Inception2 | |

Class A3 | | 16.76 | % | | N/A | | | 14.32 | % |

Class B4 | | 15.87 | | | N/A | | | 12.93 | |

Class C | | 15.93 | | | –19.05 | % | | 38.10 | |

Class L3 | | 16.52 | | | –16.97 | | | 43.38 | |

Class M4 | | 15.87 | | | –19.10 | | | 37.78 | |

Class X | | 15.96 | | | –19.04 | | | 37.88 | |

MSCI EAFE® Index5 | | 18.09 | | | 16.15 | | | * | |

Lipper International Multi-Cap Growth Funds Avg.5 | | 17.54 | | | 2.22 | | | ** | |

| | | | | | | | | | |

| Average Annual Total Returns1 as of 9/30/05 | | | | | | | | | |

| | | One Year | | | Five Years | | | Since Inception2 | |

Class A3 | | 18.39 | % | | N/A | | | 8.13 | % |

Class B4 | | 19.40 | | | N/A | | | 8.89 | |

Class C | | 23.33 | | | –4.63 | % | | 4.64 | |

Class L3 | | 17.68 | | | –5.09 | | | 4.47 | |

Class M4 | | 18.40 | | | –4.83 | | | 4.74 | |

Class X | | 18.29 | | | –5.01 | | | 4.65 | |

MSCI EAFE® Index5 | | 25.79 | | | 3.16 | | | * | |

Lipper International Multi-Cap Growth Funds Avg.5 | | 25.12 | | | –0.46 | | | ** | |

The cumulative total returns do not reflect the deduction of applicable sales charges. If reflected, the applicable sales charges would reduce the cumulative total return performance quoted. Class A and Class L shares are subject to a maximum front-end sales charge of 5.50% and 5.75% respectively. Class L shares are closed to most new purchases (with the exception of reinvested dividends and purchases by certain college savings plans). Class M shares are also closed to most new purchases (with the exception of reinvested dividends). Class L, Class M, and Class X shares are only exchangeable with Class L, Class M, and Class X shares, respectively, offered by the other Strategic Partners Funds. Under certain circumstances, Class A and Class L shares may be subject to a contingent deferred sales charge (CDSC) of 1%. Class B, Class C, Class M, and Class X shares are subject to a maximum CDSC of 5%, 1%, 6%, and 6% respectively.

1Source: Prudential Investments LLC and Lipper Inc. The average annual total returns do take into account applicable sales charges. The returns in the tables do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or following the redemption of Fund shares. During certain periods shown, fee waivers and/or expense reimbursements were in effect. Without such fee waivers and/or expense reimbursements, the returns for the share classes would have been lower. Without a distribution and service (12b-1) fee waiver of 0.05% for Class A shares, the returns would have been lower. Class A shares are subject to a 12b-1 fee of up to 0.30% annually. Class B, Class C, Class M, and Class X shares are subject to a 12b-1 fee of 1.00%. Class L shares are subject to a 12b-1 fee of 0.50%.

2Inception dates: Class A and Class B, 4/12/04; Class C, Class L, Class M, and Class X, 12/31/97.

3Prior to April 12, 2004, Class L shares were known as Class A shares. On April 12, 2004, Class A shares were redesignated as Class L shares and a new Class A was opened.

4Prior to April 12, 2004, Class M shares were known as Class B shares. On April 12, 2004, Class B shares were redesignated as Class M shares and a new Class B was opened.

5See page 1 for a summary of definitions for the Fund’s benchmarks.

*MSCI EAFE® Index Closest Month-End to Inception cumulative total returns as of 10/31/05 are 22.04% for Class A and Class B; and 52.39% for Class C, Class L, Class M, and Class X. MSCI EAFE® Index Closest Month-End to Inception average annual total returns as of 9/30/05 are 16.48% for Class A and Class B; and 5.99% for Class C, Class L, Class M, and Class X.

**Lipper International Equity Funds Average Closest Month-End to Inception cumulative total returns as of 10/31/05 are 17.79% for Class A and Class B; and 50.54% for Class C, Class L, Class M, and Class X. Lipper International Equity Funds Average Closest Month-End to Inception average annual total returns as of 9/30/05 are 13.88% for Class A and Class B; and 5.53% for Class C, Class L, Class M, and Class X.

| | | |

| Five Largest Holdings expressed as a percentage of net assets as of 10/31/05 | | | |

Roche Holding AG, Pharmaceuticals | | 3.3 | % |

Mitsubishi UFG Financial Group, Inc., Financial Bank & Trust | | 3.1 | |

BG Group PLC, Oil & Gas | | 3.0 | |

SAP AG, Computer Services & Software | | 2.8 | |

ORIX Corp., Real Estate | | 2.6 | |

Holdings reflect only long-term investments and are subject to change.

Fund Manager’s Report

For the fiscal year ended October 31, 2005, the Strategic Partners International Growth Fund was subadvised by William Blair & Company, L.L.C. Its Class A shares had a total return of 16.76% compared with the 18.09% return of the MSCI EAFE Index. The Fund trailed the Lipper International Multi-Cap Growth Funds Average (+17.54%).

Strength in the benchmark MSCI EAFE Index was broad, with all sectors posting positive returns and weakness concentrated in the information technology and telecommunication services industries. The strongest sectors were those reflecting broad economic development such as industrials and financials. Sectors where there also were limitations on supply—energy and materials—were the market leaders with substantially higher returns than the others.

The Fund’s bottom-up stock selection process resulted in an overweight in the technology sector and underweight in materials. These emphases hurt its performance. An overweight in the consumer discretionary sector had a somewhat smaller negative impact.

Relative performance was helped by the Fund’s exposure to developing markets, which are not represented in the MSCI EAFE Index, particularly to Brazil, India, Mexico, and South Korea. An emphasis on mid-cap stocks also contributed to relative performance as these stocks outperformed the shares of the largest companies.

The Fund’s stock selection was strong within the energy sector where positions in BG Group (a U.K. natural gas and oil producer) and Statoil ASA (Norway) were among the largest contributors to its return. Holdings in the financials sector also performed well. The Australian firm Macquarie Bank made a particularly large contribution as its share price benefited from rising demand for investment funds it manages. Holdings in the telecommunication services sector also outperformed comparable stocks in the MSCI EAFE Index.

The Fund’s stock selection was relatively weak in the industrials sector, although no single position stood out.

Your Fund’s Performance

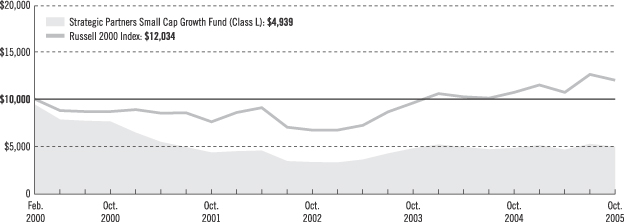

Strategic Partners Small Cap Growth Fund

Fund objective

The investment objective of the Strategic Partners Small Cap Growth Fund is to seek capital growth. There can be no assurance that the Fund will achieve its investment objective.

Performance data quoted represent past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate, so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the past performance data quoted. An investor may obtain performance data as of the most recent month-end by visiting our website at www.strategicpartners.com or by calling (800) 225-1852. Class A and Class L shares have a maximum initial sales charge of 5.50% and 5.75% respectively. Class L shares are closed to most new purchases (with the exception of reinvested dividends and purchases by certain college savings plans).

| | | | | | | | | |

| Cumulative Total Returns1 as of 10/31/05 | | | | | | | | | |

| | | One Year | | | Five Years | | | Since Inception2 | |

Class A3 | | 3.13 | % | | N/A | | | –5.21 | % |

Class B4 | | 2.43 | | | N/A | | | –7.34 | |

Class C | | 2.41 | | | –36.69 | % | | –49.10 | |

Class L3 | | 2.95 | | | –35.15 | | | –47.60 | |

Class M4 | | 2.41 | | | –36.69 | | | –49.10 | |

Class X | | 2.41 | | | –36.68 | | | –49.03 | |

Russell 2000 Index5 | | 12.08 | | | 38.60 | | | | * |

Lipper Small-Cap Growth Funds Avg.5 | | 11.79 | | | –3.32 | | | ** | |

| | | | | | | | | | |

| Average Annual Total Returns1 as of 9/30/05 | | | | | | | | | |

| | | One Year | | | Five Years | | | Since Inception2 | |

Class A3 | | 2.81 | % | | N/A | | | –4.79 | % |

Class B4 | | 3.03 | | | N/A | | | –5.18 | |

Class C | | 6.96 | | | –9.57 | % | | –10.78 | |

Class L3 | | 2.26 | | | –10.21 | | | –11.28 | |

Class M4 | | 1.98 | | | –9.97 | | | –11.13 | |

Class X | | 1.96 | | | –10.14 | | | –11.10 | |

Russell 2000 Index5 | | 17.95 | | | 6.45 | | | * | |

Lipper Small-Cap Growth Funds Avg.5 | | 18.57 | | | –2.45 | | | ** | |

The cumulative total returns do not reflect the deduction of applicable sales charges. If reflected, the applicable sales charges would reduce the cumulative total return performance quoted. Class A and Class L shares are subject to a maximum front-end sales charge of 5.50% and 5.75% respectively. Class L shares are closed to most new purchases (with the exception of reinvested dividends and purchases by certain college savings plans). Class M shares are also closed to most new purchases (with the exception of reinvested dividends). Class L, Class M, and Class X shares are only exchangeable with Class L, Class M, and Class X shares, respectively, offered by the other Strategic Partners Funds. Under certain circumstances, Class A and Class L shares may be subject to a contingent deferred sales charge (CDSC) of 1%. Class B, Class C, Class M, and Class X shares are subject to a maximum CDSC of 5%, 1%, 6%, and 6% respectively.

1Source: Prudential Investments LLC and Lipper Inc. The average annual total returns do take into account applicable sales charges. The returns in the tables do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or following the redemption of Fund shares. During certain periods shown, fee waivers and/or expense reimbursements were in effect. Without such fee waivers and/or expense reimbursements, the returns for the share classes would have been lower. Without a distribution and service (12b-1) fee waiver of 0.05% for Class A shares, the returns would have been lower. Class A shares are subject to a 12b-1 fee of up to 0.30% annually. Class B, Class C, Class M, and Class X shares are subject to a 12b-1 fee of 1.00%. Class L shares are subject to a 12b-1 fee of 0.50%.

2Inception dates: Class A and Class B, 4/12/04; Class C, Class L, Class M, and Class X, 7/28/97.

3Prior to April 12, 2004, Class L shares were known as Class A shares. On April 12, 2004, Class A shares were redesignated as Class L shares and a new Class A was opened.

4Prior to April 12, 2004, Class M shares were known as Class B shares. On April 12, 2004, Class B shares were redesignated as Class M shares and a new Class B was opened.

5See page 1 for a summary of definitions for the Fund’s benchmarks.

*Russell 2000 Index Closest Month-End to Inception cumulative total returns as of 10/31/05 are 11.55% for Class A and Class B; and 20.32% for Class C, Class L, Class M, and Class X. Russell 2000 Index Closest Month-End to Inception average annual total returns as of 9/30/05 are 9.84% for Class A and Class B; and 3.95% for Class C, Class L, Class M, and Class X.

**Lipper Small-Cap Growth Funds Average Closest Month-End to Inception cumulative total returns as of 10/31/05 are 7.36% for Class A and Class B; and –13.65% for Class C, Class L, Class M, and Class X. Lipper Small-Cap Growth Funds Average Closest Month-End to Inception average annual total returns as of 9/30/05 are 7.15% for Class A and Class B; and –3.86% for Class C, Class L, Class M, and Class X.

| | | |

| Five Largest Holdings expressed as a percentage of net assets as of 10/31/05 | | | |

Cal Dive International, Inc., Oil & Gas | | 1.3 | % |

DRS Technologies, Inc., Aerospace | | 1.2 | |

Valueclick, Inc., Financial Services | | 1.2 | |

St. Mary Land & Exploration Co., Oil & Gas | | 0.9 | |

Chemed Corp., Commercial Services | | 0.9 | |

Holdings reflect only long-term investments and are subject to change.

Fund Manager’s Report

For the fiscal year ended October 31, 2005, the Strategic Partners Small-Cap Growth Fund was subadvised by Deutsche Asset Management, Inc. Its Class A shares had a total return of 3.13% compared with returns of 12.08% for the Russell 2000 Index and 10.91% for the Russell 2000 Growth Index. It trailed the Lipper Small-Cap Growth Funds Average (+11.79%).

During the reporting period, the small-cap market generally favored less risk-averse strategies rather than the Fund’s more conservative growth style. The Fund’s strategy is based upon quantitative stock-selection methods and controlling the size of risk exposures (deviations from the security allocations of the Russell 2000 Growth Index). Risk exposures are generally limited at the sector level, but within the financials, information technology, and healthcare sectors the Fund’s stock selection and industry emphases hurt its relative performance. There were deep losses on holdings in the thrifts & mortgages and consumer finance industry groups in the financials sector, and on biotechnology and pharmaceuticals in the healthcare sector.

An overweight of the pharmaceutical industry compared with the Russell 2000 Growth Index and an underweight of real estate detracted substantially from performance. However, these impacts were more than offset by the advantages of overweights in the oil & gas and machinery industries. Overall, the Fund’s exposures to various industries improved its relative performance. It benefited as well from its style’s inherent underweighting of stocks that are relatively low priced and have high dividend yields, a characteristic that was not rewarded by the market.

Your Fund’s Performance

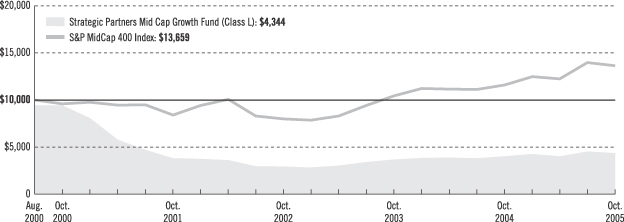

Strategic Partners Mid Cap Growth Fund

Fund objective

The investment objective of the Strategic Partners Mid Cap Growth Fund is to seek long-term growth of capital. There can be no assurance that the Fund will achieve its investment objective.

Performance data quoted represent past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate, so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the past performance data quoted. An investor may obtain performance data as of the most recent month-end by visiting our website at www.strategicpartners.com or by calling (800) 225-1852. Class A and Class L shares have a maximum initial sales charge of 5.50% and 5.75% respectively. Class L shares are closed to most new purchases (with the exception of reinvested dividends and purchases by certain college savings plans).

| | | | | | | | | |

| Cumulative Total Returns1 as of 10/31/05 | | | | | | | | | |

| | | One Year | | | Five Years | | | Since Inception2 | |

Class A3 | | 8.18 | % | | N/A | | | 9.20 | % |

Class B4 | | 7.38 | | | N/A | | | 7.90 | |

Class C | | 7.42 | | | –55.13 | % | | –55.08 | |

Class L3 | | 7.98 | | | –53.96 | | | –53.91 | |

Class M4 | | 7.40 | | | –54.98 | | | –54.98 | |

Class X | | 7.42 | | | –55.08 | | | –55.08 | |

S&P MidCap 400 Index5 | | 17.65 | | | 42.38 | | | * | |

Lipper Mid-Cap Growth Funds Avg.5 | | 14.07 | | | –14.17 | | | ** | |

| | | | | | | | | | |

| Average Annual Total Returns1 as of 9/30/05 | | | | | | | | | |

| | | One Year | | | Five Years | | | Since Inception2 | |

Class A3 | | 8.88 | % | | N/A | | | 4.35 | % |

Class B4 | | 9.22 | | | N/A | | | 5.03 | |

Class C | | 13.57 | | | –14.60 | % | | –14.09 | |

Class L3 | | 8.45 | | | –15.18 | | | –14.67 | |

Class M4 | | 8.53 | | | –14.91 | | | –14.40 | |

Class X | | 8.57 | | | –15.12 | | | –14.44 | |

S&P MidCap 400 Index5 | | 22.16 | | | 7.05 | | | * | |

Lipper Mid-Cap Growth Funds Avg.5 | | 20.63 | | | –4.70 | | | ** | |

The cumulative total returns do not reflect the deduction of applicable sales charges. If reflected, the applicable sales charges would reduce the cumulative total return performance quoted. Class A and Class L shares are subject to a maximum front-end sales charge of 5.50% and 5.75% respectively. Class L shares are closed to most new purchases (with the exception of reinvested dividends and purchases by certain college savings plans). Class M shares are also closed to most new purchases (with the exception of reinvested dividends). Class L, Class M, and Class X shares are only exchangeable with Class L, Class M, and Class X shares, respectively, offered by the other Strategic Partners Funds. Under certain circumstances, Class A and Class L shares may be subject to a contingent deferred sales charge (CDSC) of 1%. Class B, Class C, Class M, and Class X shares are subject to a maximum CDSC of 5%, 1%, 6%, and 6% respectively.

1Source: Prudential Investments LLC and Lipper Inc. The average annual total returns do take into account applicable sales charges. The returns in the tables do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or following the redemption of Fund shares. During certain periods shown, fee waivers and/or expense reimbursements were in effect. Without such fee waivers and/or expense reimbursements, the returns for the share classes would have been lower. Without a distribution and service (12b-1) fee waiver of 0.05% for Class A shares, the returns would have been lower. Class A shares are subject to a 12b-1 fee of up to 0.30% annually. Class B, Class C, Class M, and Class X shares are subject to a 12b-1 fee of 1.00%. Class L shares are subject to a 12b-1 fee of 0.50%.

2Inception dates: Class A and Class B, 4/12/04; Class C, Class L, Class M, and Class X, 9/11/00.

3Prior to April 12, 2004, Class L shares were known as Class A shares. On April 12, 2004, Class A shares were redesignated as Class L shares and a new Class A was opened.

4Prior to April 12, 2004, Class M shares were known as Class B shares. On April 12, 2004, Class B shares were redesignated as Class M shares and a new Class B was opened.

5See page 1 for a summary of definitions for the Fund’s benchmarks.

*S&P MidCap 400 Index Closest Month-End to Inception cumulative total returns as of 10/31/05 are 18.16% for Class A and Class B; and 36.61% for Class C, Class L, Class M, and Class X. S&P MidCap 400 Index Closest Month-End to Inception average annual total returns as of 9/30/05 are 13.40% for Class A and Class B; and 6.78% for Class C, Class L, Class M, and Class X.

**Lipper Mid-Cap Growth Funds Average Closest Month-End to Inception cumulative total returns as of 10/31/05 are 12.39% for Class A and Class B; and –21.12% for Class C, Class L, Class M, and Class X. Lipper Mid-Cap Growth Funds Average Closest Month-End to Inception average annual total returns as of 9/30/05 are 10.11% for Class A and Class B; and –5.12% for Class C, Class L, Class M, and Class X.

| | | |

| Five Largest Holdings expressed as a percentage of net assets as of 10/31/05 | | | |

Grainger, (W.W), Inc., Producer Goods | | 2.3 | % |

Biomet, Inc., Supplies & Equipment | | 2.2 | |

Zebra Technologies Corp., Computer Hardware | | 2.2 | |

Smith International, Inc., Oil Well Services & Equipment | | 2.2 | |

Fortune Brands, Inc., Consumer Products & Services | | 2.1 | |

Holdings reflect only long-term investments and are subject to change.

Fund Manager’s Report

For the fiscal year ended October 31, 2005, the Strategic Partners Mid Cap Growth Fund was subadvised by Goldman Sachs Asset Management, L.P. Its Class A shares had a total return of 8.18% compared with a return of 15.91% for the Russell Midcap Growth Index. It trailed the Lipper Mid-Cap Growth Funds Average (+14.07%).

The Fund’s underperformance was attributable to inopportune sector emphases and poor stock selection within sectors. Its overweight in consumer services, primarily in media stocks, and underweight in energy and basic materials stocks were the main detractors from its relative performance. During this period, energy and basic materials stocks provided much of the market’s strength in this asset class, while consumer services stocks continued to trail well into 2005. The Fund’s manager historically has tended to emphasize the media and leisure industries, which were among the market’s worst performers during this reporting period. Moreover, stock selection in other sectors didn’t help the Fund’s return. Several holdings in the financials, consumer services, and information technology sectors proved unprofitable.

The Fund’s portfolio was more sensitive, overall, to broad market movements than its benchmark, which helped its performance during this strong period for mid-cap growth stocks. This exposure was particularly beneficial in May through July 2005 when the market climbed steeply. Other portfolio risk exposures generally offset one another in impact.

Your Fund’s Performance

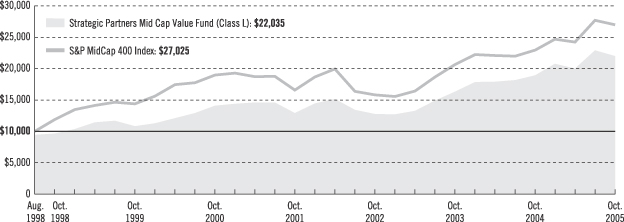

Strategic Partners Mid Cap Value Fund***

Fund objective

The investment objective of the Strategic Partners Mid Cap Value Fund is to seek capital growth. There can be no assurance that the Fund will achieve its investment objective.

Performance data quoted represent past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate, so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the past performance data quoted. An investor may obtain performance data as of the most recent month-end by visiting our website at www.strategicpartners.com or by calling (800) 225-1852. Class A and Class L shares have a maximum initial sales charge of 5.50% and 5.75% respectively. Class L shares are closed to most new purchases (with the exception of reinvested dividends and purchases by certain college savings plans).

| | | | | | | | | |

| Cumulative Total Returns1 as of 10/31/05 | | | | | | | | | |

| | | One Year | | | Five Years | | | Since Inception2 | |

Class A3 | | 16.74 | % | | N/A | | | 19.78 | % |

Class B4 | | 15.85 | | | N/A | | | 18.24 | |

Class C | | 15.75 | | | 52.45 | % | | 125.74 | |

Class L3 | | 16.29 | | | 56.32 | | | 133.79 | |

Class M4 | | 15.75 | | | 52.45 | | | 125.75 | |

Class X | | 15.67 | | | 52.35 | | | 125.13 | |

S&P MidCap 400 Index5 | | 17.65 | | | 42.38 | | | * | |

Lipper Mid-Cap Value Funds Avg.5 | | 14.51 | | | 67.32 | | | ** | |

| | | | | | | | | | |

| Average Annual Total Returns1 as of 9/30/05 | | | | | | | | | |

| | | One Year | | | Five Years | | | Since Inception2 | |

Class A3 | | 17.51 | % | | N/A | | | 13.11 | % |

Class B4 | | 18.29 | | | N/A | | | 13.98 | |

Class C | | 22.26 | | | 9.99 | % | | 12.88 | |

Class L3 | | 16.74 | | | 9.47 | | | 12.65 | |

Class M4 | | 17.26 | | | 9.95 | | | 13.04 | |

Class X | | 17.20 | | | 9.80 | | | 12.94 | |

S&P MidCap 400 Index5 | | 22.16 | | | 7.05 | | | * | |

Lipper Mid-Cap Value Funds Avg.5 | | 20.19 | | | 11.73 | | | ** | |

The cumulative total returns do not reflect the deduction of applicable sales charges. If reflected, the applicable sales charges would reduce the cumulative total return performance quoted. Class A and Class L shares are subject to a maximum front-end sales charge of 5.50% and 5.75% respectively. Class L shares are closed to most new purchases (with the exception of reinvested dividends and purchases by certain college savings plans). Class M shares are also closed to most new purchases (with the exception of reinvested dividends). Class L, Class M, and Class X shares are only exchangeable with Class L, Class M, and Class X shares, respectively, offered by the other Strategic Partners Funds. Under certain circumstances, Class A and Class L shares may be subject to a contingent deferred sales charge (CDSC) of 1%. Class B, Class C, Class M, and Class X shares are subject to a maximum CDSC of 5%, 1%, 6%, and 6% respectively.

1Source: Prudential Investments LLC and Lipper Inc. The average annual total returns do take into account applicable sales charges. The returns in the tables do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or following the redemption of Fund shares. During certain periods shown, fee waivers and/or expense reimbursements were in effect. Without such fee waivers and/or expense reimbursements, the returns for the share classes would have been lower. Without a distribution and service (12b-1) fee waiver of 0.05% for Class A shares, the returns would have been lower. Class A shares are subject to a 12b-1 fee of up to 0.30% annually. Class B, Class C, Class M, and Class X shares are subject to a 12b-1 fee of 1.00%. Class L shares are subject to a 12b-1 fee of 0.50%.

2Inception dates: Class A and Class B, 4/12/04; Class C, Class L, Class M, Class X, 8/19/98, and Class Z, 11/28/05. Returns for Class Z are not shown since the share class had not existed prior to 10/31/05.

3Prior to April 12, 2004, Class L shares were known as Class A shares. On April 12, 2004, Class A shares were redesignated as Class L shares and a new Class A was opened.

4Prior to April 12, 2004, Class M shares were known as Class B shares. On April 12, 2004, Class B shares were redesignated as Class M shares and a new Class B was opened.

5See page 1 for a summary of definitions for the Fund’s benchmarks.

*S&P MidCap 400 Index Closest Month-End to Inception cumulative total returns as of 10/31/05 are 18.16% for Class A and Class B; and 170.30% for Class C, Class L, Class M, and Class X. S&P MidCap 400 Index Closest Month-End to Inception average annual total returns as of 9/30/05 are 13.40% for Class A and Class B; and 15.42% for Class C, Class L, Class M, and Class X.

**Lipper Mid-Cap Value Funds Average Closest Month-End to Inception cumulative total returns as of 10/31/05 are 17.37% for Class A and Class B; and 150.39% for Class C, Class L, Class M, and Class X. Lipper Mid-Cap Value Funds Average Closest Month-End to Inception average annual total returns as of 9/30/05 are 13.83% for Class A and Class B; and 14.14% for Class C, Class L, Class M, and Class X.

***Prior to November 28, 2005, the Strategic Partners Mid Cap Value Fund was known as the Strategic Partners Relative Value Fund.

| | | |

| Five Largest Holdings expressed as a percentage of net assets as of 10/31/05 | | | |

Arch Coal, Inc., Metals & Mining | | 3.1 | % |

XTO Energy, Inc., Oil & Gas | | 2.8 | |

TXU Corp., Utilities | | 2.6 | |

Canadian Natural Resources Ltd., Oil & Gas | | 2.4 | |

Lennar Corp. (Class A Stock), Construction | | 2.3 | |

Holdings reflect only long-term investments and are subject to change.

Fund Manager’s Report

For the fiscal year ended October 31, 2005, the Strategic Partners Mid Cap Value Fund was subadvised by Neuberger Berman Management, Inc. Its Class A shares had a total return of 16.74% compared with returns of 17.65% for the S&P MidCap 400 Index and 19.50% for the Russell Midcap Value Index. It outperformed the Lipper Mid-Cap Value Funds Average (+14.51%).

During this reporting period, there were significant management changes at the Fund. Its portfolio managers left Neuberger Berman Management in June 2005 and their responsibilities were assumed by another Neuberger Berman portfolio manager. The change didn’t appear to hurt the Fund, whose strongest performance relative to both the S&P MidCap 400 and Russell Midcap Value Indexes came in August.

The Fund trailed the style-appropriate Russell Midcap Value Index primarily because of stock selection, particularly among retailers and insurers. The largest detractors from its relative performance included the automobile parts supplier Lear Corporation (which was sold from the portfolio by period-end), the computer printer company Lexmark International, and the nutritional supplement firm NBTY (whose brand names include Nature’s Bounty and Sundown). The Fund is managed in a bottom-up style, which means that any exposure to various risk factors is the result of decisions made about individual securities. We normally expect stock selection to be the primary driver of the Fund’s relative performance.

The Fund’s holdings performed better than the Russell MidCap Value Index in the healthcare and consumer staples sectors. In addition, it had a greater-than-Index weighting in the healthcare sector, which had an above-average return, and a below-Index weighting in the underperforming basic materials sector. These beneficial sector emphases were partially offset by the Fund’s substantial overweighting in the poor-performing consumer cyclical sector and underweightings in the better-performing utility and financials sectors.

Your Fund’s Performance

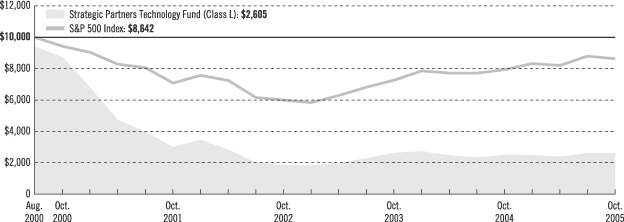

Strategic Partners Technology Fund

Fund objective

The investment objective of the Strategic Partners Technology Fund is to seek capital growth by investing primarily in the equity securities of companies engaged in technology-related industries. There can be no assurance that the Fund will achieve its investment objective.

Performance data quoted represent past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate, so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the past performance data quoted. An investor may obtain performance data as of the most recent month-end by visiting our website at www.strategicpartners.com or by calling (800) 225-1852. Class A and Class L shares have a maximum initial sales charge of 5.50% and 5.75% respectively. Class L shares are closed to most new purchases (with the exception of reinvested dividends and purchases by certain college savings plans).

| | | | | | | | | |

| Cumulative Total Returns1 as of 10/31/05 | | | | | | | | | |

| | | One Year | | | Five Years | | | Since Inception2 | |

Class A3 | | 4.14 | % | | N/A | | | –4.48 | % |

Class B4 | | 3.10 | | | N/A | | | –5.67 | |

Class C | | 3.48 | | | –71.06 | % | | –73.20 | |

Class L3 | | 3.76 | | | –70.18 | | | –72.36 | |

Class M4 | | 3.49 | | | –71.14 | | | –73.30 | |

Class X | | 3.08 | | | –71.03 | | | –73.20 | |

S&P 500 Index5 | | 8.72 | | | –8.38 | | | * | |

Lipper Science & Technology Funds Avg.5 | | 8.47 | | | –54.26 | | | ** | |

| | | | | | | | | | |

| Average Annual Total Returns1 as of 9/30/05 | | | | | | | | | |

| | | One Year | | | Five Years | | | Since Inception2 | |

Class A3 | | 4.51 | % | | N/A | | | –6.52 | % |

Class B4 | | 4.88 | | | N/A | | | –6.28 | |

Class C | | 8.84 | | | –23.32 | % | | –22.94 | |

Class L3 | | 4.15 | | | –23.77 | | | –23.37 | |

Class M4 | | 3.88 | | | –23.69 | | | –23.31 | |

Class X | | 3.80 | | | –23.73 | | | –23.20 | |

S&P 500 Index5 | | 12.25 | | | –1.49 | | | * | |

Lipper Science & Technology Funds Avg.5 | | 17.40 | | | –17.17 | | | ** | |

The cumulative total returns do not reflect the deduction of applicable sales charges. If reflected, the applicable sales charges would reduce the cumulative total return performance quoted. Class A and Class L shares are subject to a maximum front-end sales charge of 5.50% and 5.75% respectively. Class L shares are closed to most new purchases (with the exception of reinvested dividends and purchases by certain college savings plans). Class M shares are also closed to most new purchases (with the exception of reinvested dividends). Class L, Class M, and Class X shares are only exchangeable with Class L, Class M, and Class X shares, respectively, offered by the other Strategic Partners Funds. Under certain circumstances, Class A and Class L shares may be subject to a contingent deferred sales charge (CDSC) of 1%. Class B, Class C, Class M, and Class X shares are subject to a maximum CDSC of 5%, 1%, 6%, and 6% respectively.

1Source: Prudential Investments LLC and Lipper Inc. The average annual total returns do take into account applicable sales charges. The returns in the tables do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or following the redemption of Fund shares. During certain periods shown, fee waivers and/or expense reimbursements were in effect. Without such fee waivers and/or expense reimbursements, the returns for the share classes would have been lower. Without a distribution and service (12b-1) fee waiver of 0.05% for Class A shares, the returns would have been lower. Class A shares are subject to a 12b-1 fee of up to 0.30% annually. Class B, Class C, Class M, and Class X shares are subject to a 12b-1 fee of 1.00%. Class L shares are subject to a 12b-1 fee of 0.50%.

2Inception dates: Class A and Class B, 4/12/04; Class C, Class L, Class M, and Class X, 9/11/00.

3Prior to April 12, 2004, Class L shares were known as Class A shares. On April 12, 2004, Class A shares were redesignated as Class L shares and a new Class A was opened.

4Prior to April 12, 2004, Class M shares were known as Class B shares. On April 12, 2004, Class B shares were redesignated as Class M shares and a new Class B was opened.

5See page 1 for a summary of definitions for the Fund’s benchmarks.

*S&P 500 Index Closest Month-End to Inception cumulative total returns as of 10/31/05 are 10.17% for Class A and Class B; and –13.58% for Class C, Class L, Class M, and Class X. S&P 500 Index Closest Month-End to Inception average annual total returns as of 9/30/05 are 7.88% for Class A and Class B; and –2.51% for Class C, Class L, Class M, and Class X.

**Lipper Science & Technology Funds Average Closest Month-End to Inception cumulative total returns as of 10/31/05 are 2.21% for Class A and Class B; and –62.75% for Class C, Class L, Class M, and Class X. Lipper Science & Technology Funds Average Closest Month-End to Inception average annual total returns as of 9/30/05 are 2.79% for Class A and Class B; and –18.76% for Class C, Class L, Class M, and Class X.

| | | |

| Five Largest Holdings expressed as a percentage of net assets as of 10/31/05 | | | |

Google, Inc. (Class A Shares), Internet Services | | 4.3 | % |

Apple Computer, Inc., Computer Hardware | | 3.9 | |

Adobe Systems, Inc., Computer Services & Software | | 3.8 | |

Yahoo!, Inc., Internet Services | | 3.4 | |

Motorola, Inc., Telecommunications | | 3.4 | |

Holdings reflect only long-term investments and are subject to change.

Fund Manager’s Report

For the fiscal year ended October 31, 2005, the Strategic Partners Technology Fund was subadvised by The Dreyfus Corporation. Its Class A shares had a total return of 4.14% compared with the 8.72% return of the S&P 500 Index and 6.1% for the S&P SuperComposite Information Technology Index. It trailed the Lipper Science & Technology funds Average (+8.47%).

The Fund’s underperformance of the sector-appropriate S&P SuperComposite Information Technology Index during this period was primarily attributable to poor stock selection within the information technology sector, where its relative performance was hurt by a decision not to hold Hewlett-Packard or Apple Computer. These stocks performed extremely well. Overweights compared to the S&P Supercomposite Information Technology Index in Anaya and Xilinx also detracted significantly. On the positive side, overweights in Corning and Marvell Technology Group were among the Fund’s strongest performers, and the Fund also benefited from not having a position in International Business Machines, whose stock declined.

The Fund typically invests a significant amount in technology-oriented firms that are classified in other sectors, such as the consumer discretionary stocks eBay (Internet retail) and Apollo Group (education, including on-line and technical training). The consumer discretionary positions significantly detracted from the Fund’s performance. Overall, however, the Fund’s holdings outside the information technology sector, particularly in healthcare technology, helped its performance. Positions in Amgen, Genentech, and Teva Pharmaceutical Industries performed strongly.

Your Fund’s Performance

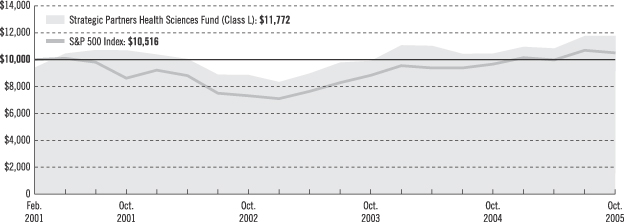

Strategic Partners Health Sciences Fund

Fund objective

The investment objective of the Strategic Partners Health Sciences Fund is to seek growth. There can be no assurance that the Fund will achieve its investment objective.

Performance data quoted represent past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate, so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the past performance data quoted. An investor may obtain performance data as of the most recent month-end by visiting our website at www.strategicpartners.com or by calling (800) 225-1852. Class A and Class L shares have a maximum initial sales charge of 5.50% and 5.75% respectively. Class L shares are closed to most new purchases (with the exception of reinvested dividends and purchases by certain college savings plans).

| | | | | | |

| Cumulative Total Returns1 as of 10/31/05 | | | | | | |

| | | One Year | | | Since Inception2 | |

Class A3 | | 13.04 | % | | 4.92 | % |

Class B4 | | 12.23 | | | 3.56 | |

Class C | | 12.10 | | | 22.30 | |

Class L3 | | 12.62 | | | 24.90 | |

Class M4 | | 12.12 | | | 22.10 | |

Class X | | 12.09 | | | 22.40 | |

S&P 500 Index5 | | 8.72 | | | * | |

Lipper Health/Biotechnology Funds Avg.5 | | 15.03 | | | ** | |

| | | | | | |

| | | | | | | |

| Average Annual Total Returns1 as of 9/30/05 | | | | | | |

| | | One Year | | | Since Inception2 | |

Class A3 | | 8.07 | % | | 0.96 | % |

Class B4 | | 8.43 | | | 1.37 | |

Class C | | 12.39 | | | 4.82 | |

Class L3 | | 7.30 | | | 4.16 | |

Class M4 | | 7.33 | | | 4.62 | |

Class X | | 7.29 | | | 4.49 | |

S&P 500 Index5 | | 12.25 | | | * | |

Lipper Health/Biotechnology Funds Avg.5 | | 15.79 | | | ** | |

The cumulative total returns do not reflect the deduction of applicable sales charges. If reflected, the applicable sales charges would reduce the cumulative total return performance quoted. Class A and Class L shares are subject to a maximum front-end sales charge of 5.50% and 5.75% respectively. Class L shares are closed to most new purchases (with the exception of reinvested dividends and purchases by certain college savings plans). Class M shares are also closed to most new purchases (with the exception of reinvested dividends). Class L, Class M, and Class X shares are only exchangeable with Class L, Class M, and Class X shares, respectively, offered by the other Strategic Partners Funds. Under certain circumstances, Class A and Class L shares may be subject to a contingent deferred sales charge (CDSC) of 1%. Class B, Class C, Class M, and Class X shares are subject to a maximum CDSC of 5%, 1%, 6%, and 6% respectively.

1Source: Prudential Investments LLC and Lipper Inc. The average annual total returns do take into account applicable sales charges. The returns in the tables do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or following the redemption of Fund shares. During certain periods shown, fee waivers and/or expense reimbursements were in effect. Without such fee waivers and/or expense reimbursements, the returns for the share classes would have been lower. Without a distribution and service (12b-1) fee waiver of 0.05% for Class A shares, the returns would have been lower. Class A shares are subject to a 12b-1 fee of up to 0.30% annually. Class B, Class C, Class M, and Class X shares are subject to a 12b-1 fee of 1.00%. Class L shares are subject to a 12b-1 fee of 0.50%.

2Inception dates: Class A and Class B, 4/12/04; Class C, Class L, Class M, and Class X, 3/1/01.

3Prior to April 12, 2004, Class L shares were known as Class A shares. On April 12, 2004, Class A shares were redesignated as Class L shares and a new Class A was opened.

4Prior to April 12, 2004, Class M shares were known as Class B shares. On April 12, 2004, Class B shares were redesignated as Class M shares and a new Class B was opened.

5See page 1 for a summary of definitions for the Fund’s benchmarks.

*S&P 500 Index Closest Month-End to Inception cumulative total returns as of 10/31/05 are 10.17% for Class A and Class B; and 5.17% for Class C, Class L, Class M, and Class X. S&P 500 Index Closest Month-End to Inception average annual total returns as of 9/30/05 are 12.04% for Class A and Class B; and 6.95% for Class C, Class L, Class M, and Class X.

**Lipper Health/Biotechnology Funds Average Closest Month-End to Inception cumulative total returns as of 10/31/05 are 9.58% for Class A and Class B; and 10.68% for Class C, Class L, Class M, and Class X. Lipper Health/Biotechnology Funds Average Closest Month-End to Inception average annual total returns as of 9/30/05 are 7.97% for Class A and Class B; and 2.16% for Class C, Class L, Class M, and Class X.

| | | |

| Five Largest Holdings expressed as a percentage of net assets as of 10/31/05 | | | |

Roche Holding AG, Pharmaceuticals | | 8.0 | % |

Protein Design Labs, Inc., Biotechnology Healthcare | | 4.3 | |

St. Jude Medical, Inc., Medical Equipment & Devices | | 3.7 | |

Amgen, Inc., Biotechnology Healthcare | | 3.7 | |

Eisai Co. Ltd., Medical Supplies & Equipment | | 3.3 | |

Holdings reflect only long-term investments and are subject to change.

Fund Manager’s Report

For the fiscal year ended October 31, 2005, the Strategic Partners Health Sciences Fund was subadvised by INVESCO Institutional (N.A.), Inc. Its Class A shares had a total return of 13.04% compared with the 8.72% return of the S&P 500 Index and 12.23% return of the S&P SuperComposite Health Care Index. The Fund trailed the Lipper Health/Biotechnology Funds Average (+15.03%).

The Fund outperformed the sector-appropriate S&P SuperComposite Health Care Index primarily because of good stock selection. In particular, in the pharmaceutical industry, the Fund had substantial underexposure to the large drug companies Merck (–5.16%) and Pfizer (–24.51%), which were hurt by drug recalls, product liability problems, and other negative factors. Its largest holding at period-end was Roche (+45.81%). The Fund also had significant positions in Eisai (+35.14%) and Amgen (+35.84%).

However, it was a position in health services company PacifiCare Health Systems (+131.09%) that made the largest contribution to the Fund’s total return. In fact, the health services industry generally performed very strongly over this reporting period. Although the Fund’s holdings in the sector also did well, the fact that it did not emphasize the sector limited the benefit of the rally.

The Fund’s mix of established and less-established but more rapidly growing firms generally worked well. Some of the top contributors to its performance were biotechnology and medical device companies, but positions in more established firms also helped results.

Your Fund’s Performance

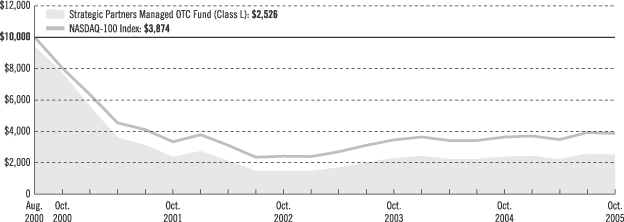

Strategic Partners Managed OTC Fund

Fund objective

The investment objective of the Strategic Partners Managed OTC Fund is to provide investment results that correlate to the performance of a benchmark for securities that are traded in the over-the-counter market. The Fund’s current benchmark is a multiple of the NASDAQ-100 Index. There can be no assurance that the Fund will achieve its investment objective.

Performance data quoted represent past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate, so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the past performance data quoted. An investor may obtain performance data as of the most recent month-end by visiting our website at www.strategicpartners.com or by calling (800) 225-1852. Class A and Class L shares have a maximum initial sales charge of 5.50% and 5.75% respectively. Class L shares are closed to most new purchases (with the exception of reinvested dividends and purchases by certain college savings plans).

| | | | | | | | | |

| Cumulative Total Returns1 as of 10/31/05 | | | | | | | | | |

| | | One Year | | | Five Years | | | Since Inception2 | |

Class A3 | | 5.47 | % | | N/A | | | 4.65 | % |

Class B4 | | 4.80 | | | N/A | | | 2.75 | |

Class C | | 4.80 | | | –68.09 | % | | –73.80 | |

Class L3 | | 5.10 | | | –67.40 | | | –73.20 | |

Class M4 | | 4.78 | | | –68.01 | | | –73.70 | |

Class X | | 4.78 | | | –67.97 | | | –73.70 | |

NASDAQ-100 Index5 | | 6.22 | | | –51.89 | | | * | |

Lipper Multi-Cap Growth Funds Avg.5 | | 12.95 | | | –26.01 | | | ** | |

| | | | | | | | | | |

| Average Annual Total Returns1 as of 9/30/05 | | | | | | | | | |

| | | One Year | | | Five Years | | | Since Inception2 | |

Class A3 | | 8.66 | % | | N/A | | | 0.75 | % |

Class B4 | | 8.56 | | | N/A | | | 0.75 | |

Class C | | 12.56 | | | –22.52 | % | | –22.94 | |

Class L3 | | 7.87 | | | –23.10 | | | –23.51 | |

Class M4 | | 7.98 | | | –22.79 | | | –23.20 | |

Class X | | 7.98 | | | –22.94 | | | –23.20 | |

NASDAQ-100 Index5 | | 13.37 | | | –14.81 | | | * | |

Lipper Multi-Cap Growth Funds Avg.5 | | 17.74 | | | –7.89 | | | ** | |

The cumulative total returns do not reflect the deduction of applicable sales charges. If reflected, the applicable sales charges would reduce the cumulative total return performance quoted. Class A and Class L shares are subject to a maximum front-end sales charge of 5.50% and 5.75% respectively. Class L shares are closed to most new purchases (with the exception of reinvested dividends and purchases by certain college savings plans). Class M shares are also closed to most new purchases (with the exception of reinvested dividends). Class L, Class M, and Class X shares are only exchangeable with Class L, Class M, and Class X shares, respectively, offered by the other Strategic Partners Funds. Under certain circumstances, Class A and Class L shares may be subject to a contingent deferred sales charge (CDSC) of 1%. Class B, Class C, Class M, and Class X shares are subject to a maximum CDSC of 5%, 1%, 6%, and 6% respectively.

1Source: Prudential Investments LLC and Lipper Inc. The average annual total returns do take into account applicable sales charges. The returns in the tables do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or following the redemption of Fund shares. During certain periods shown, fee waivers and/or expense reimbursements were in effect. Without such fee waivers and/or expense reimbursements, the returns for the share classes would have been lower. Without a distribution and service (12b-1) fee waiver of 0.05% for Class A shares, the returns would have been lower. Class A shares are subject to a 12b-1 fee of up to 0.30% annually. Class B, Class C, Class M, and Class X shares are subject to a 12b-1 fee of 1.00%. Class L shares are subject to a 12b-1 fee of 0.50%.

2Inception dates: Class A and Class B, 4/12/04; Class C, Class L, Class M, and Class X, 9/11/00.

3Prior to April 12, 2004, Class L shares were known as Class A shares. On April 12, 2004, Class A shares were redesignated as Class L shares and a new Class A was opened.

4Prior to April 12, 2004, Class M shares were known as Class B shares. On April 12, 2004, Class B shares were redesignated as Class M shares and a new Class B was opened.

5See page 1 for a summary of definitions for the Fund’s benchmarks.

*NASDAQ-100 Index Closest Month-End to Inception cumulative total returns as of 10/31/05 are 9.79% for Class A and Class B; and –61.27% for Class C, Class L, Class M, and Class X. NASDAQ–100 Index Closest Month-End to Inception average annual total returns as of 9/30/05 are 7.43% for Class A and Class B; and –16.79% for Class C, Class L, Class M, and Class X.

**Lipper Multi-Cap Growth Funds Average Closest Month-End to Inception cumulative total returns as of 10/31/05 are 11.38% for Class A and Class B; and –33.51% for Class C, Class L, Class M, and Class X. Lipper Multi-Cap Growth Funds Average Closest Month-End to Inception average annual total returns as of 9/30/05 are 8.61% for Class A and Class B; and –8.59% for Class C, Class L, Class M, and Class X.

| | | |

| Five Largest Holdings expressed as a percentage of net assets as of 10/31/05 | | | |

Microsoft Corp., Software | | 6.9 | % |

QUALCOMM Inc., Telecommunications | | 5.7 | |

Apple Computer, Inc., Computer | | 4.8 | |

Intel Corp., Semiconductors | | 3.6 | |

Cisco Systems, Inc., Telecommunications | | 2.9 | |

Holdings reflect only long-term investments and are subject to change.

Fund Manager’s Report

For the fiscal year ended October 31, 2005, the Strategic Partners Managed OTC Fund was subadvised by ProFund Advisors LLC. Its Class A shares had a total return of 5.47% compared with a return of 6.22% for the NASDAQ-100 Index. It trailed the Lipper Multi-Cap Growth Funds Average (+12.95%).

The NASDAQ-100 Index is an unmanaged index that includes 100 of the largest (based on market capitalization) and most active non-financial domestic and international companies listed on the NASDAQ Stock Market. It includes major industry groups such as computer hardware and software, telecommunications, retail/wholesale trade, and biotechnology. It does not contain financial companies, including investment companies. The Fund is managed with a passive approach, not speculating on the future direction of the overall NASDAQ-100 Index or of any of the companies included in it. Leveraged investment techniques (investing borrowed money) give the Fund approximately 125% exposure to the Index every day.

The Fund benefited from a favorable market environment in November and December 2004, helped by its inherent leveraged exposure. During these months gains were led by the diversified consumer services, hotels, and Internet services industries. However, when the NASDAQ-100 Index performed poorly, primarily in January through April 2005, the Fund trailed the Index. The decline was concentrated in the same industries that had led during the rally. The Fund underperformed the NASDAQ-100 because the Index rose rapidly for only a short period compared with a longer period of decline.