UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

Form 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2006

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number: 000-22283

VIRGINIA FINANCIAL GROUP, INC.

(Exact name of registrant as specified in its charter)

| VIRGINIA | 54-1829288 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

102 S. Main Street, Culpeper, Virginia 22701

(Address of principal executive offices, including zip code)

(540) 829-1633

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Securities registered pursuant to section 12 (g) of the Act:

None

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in the definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated file. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ¨ Accelerated Filer x Non-accelerated filer ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). ¨ Yes x No

The aggregate market value of the voting and non-voting stock held by non-affiliates of the registrant as of June 30, 2006 was $295,080,616.

There were 10,791,669 shares of common stock outstanding as of March 2, 2007.

Documents Incorporated by Reference:

Portions of Portions of the Proxy Statement for the Company’s Annual Meeting of Shareholders to be held on May 14, 2007 are incorporated by reference in Part III of this report.

VIRGINIA FINANCIAL GROUP, INC.

FORM 10-K

TABLE OF CONTENTS

| Page | ||||

| PART I | ||||

| Item 1. | Business | 1 | ||

| Item 1A. | Risk Factors | 4 | ||

| Item 1B. | Unresolved Staff Comments | 7 | ||

| Item 2. | Properties | 7 | ||

| Item 3. | Legal Proceedings | 8 | ||

| Item 4. | Submission of Matters to a Vote of Security Holders | 8 | ||

| PART II | ||||

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 10 | ||

| Item 6. | Selected Financial Data | 12 | ||

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 13 | ||

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 30 | ||

| Item 8. | Financial Statements and Supplementary Data | 32 | ||

| Item 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | 77 | ||

| Item 9A. | Controls and Procedures | 77 | ||

| Item 9B. | Other Information | 79 | ||

| PART III | ||||

| Item 10. | Directors and Executive Officers of the Registrant | 79 | ||

| Item 11. | Executive Compensation | 79 | ||

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 80 | ||

| Item 13. | Certain Relationships and Related Transactions | 80 | ||

| Item 14. | Principal Accountant Fees and Services | 80 | ||

| PART IV | ||||

| Item 15. | Exhibits and Financial Statement Schedules | 81 | ||

| Signatures | 83 | |||

PART I

| Item 1. | BUSINESS |

GENERAL

Virginia Financial Group, Inc. (VFG or the Company) is a bank holding company incorporated under the laws of the Commonwealth of Virginia. Currently, VFG is one of the largest independent bank holding companies headquartered in the Commonwealth of Virginia with total assets of approximately $1.6 billion. VFG’s trust affiliate, Virginia Commonwealth Trust Company, manages fee and commission based assets of approximately $597 million. Affiliates of the Company include: Planters Bank & Trust Company of Virginia—in Staunton, Second Bank & Trust—in Culpeper, Virginia Heartland Bank—in Fredericksburg, Virginia Commonwealth Trust Company—in Culpeper and VFG Limited Liability Trust. VFG, through its affiliates, also owns a 70% interest in VFG Title, LLC. VFG combined its Virginia Heartland Bank (Fredericksburg) into its Second Bank & Trust (Culpeper) affiliate on February 16, 2007. The two banks were geographically contiguous, shared increasingly similar market dynamics and offered the opportunity to create efficiencies and management depth. The organization has a network of forty branches serving a contiguous market throughout central, south central and southwest Virginia. Virginia Commonwealth Trust Corporation has offices in Culpeper, Fredericksburg, Harrisonburg and Staunton.

VFG’s affiliate banks are community-oriented and offer services customarily provided by full-service banks, including individual and commercial demand and time deposit accounts, commercial and consumer loans, residential mortgages, credit card services and deposit services. VFG’s affiliate banks offer internet banking access for banking services, and online bill payment for both consumers and commercial customers. Lending is focused on individuals and small and middle-market businesses in the local market of VFG’s affiliate banks. VFG’s trust affiliate provides a variety of wealth management and personal trust services including estate administration, employee benefit plan administration and planning specifically addressing the investment and financial management needs of its customers. Utilizing a “super-community” banking strategy, each affiliate is run autonomously, with the holding company providing common services such as corporate finance, information technology, marketing, human resources, compliance, audit and loan review.

EMPLOYEES

At December 31, 2006, VFG had 580 full time equivalent employees. No employees are represented by any collective bargaining unit. VFG considers relations with its employees to be good.

COMPETITION

VFG and its affiliates incur strong competition in each of its primary markets from large regional and national financial institutions, savings and loans, credit unions and other community banking organizations. In addition, consumer finance companies, asset managers and mortgage companies all provide competition. Out-of-state bank holding companies are providing increased competition through merger with and acquisition of Virginia banks.

VFG’s deposit market share at June 30, 2006 represented 1% of the total banking deposits in the Commonwealth of Virginia. Competition for deposits is influenced by rates paid, customer loyalty factors, product offerings and convenience of branch network.

The competition in the industry has also increased as a result of the passage of the Gramm-Leach-Bliley Act of 1999 (the “Act”), which drew new lines between the types of activities that are financial in nature and permitted for banking organizations, and those activities that are commercial in nature and not permitted. The Act imposes Community Reinvestment requirements on financial service organizations that seek to qualify for the expanded powers to engage in broader financial activities and affiliations with financial companies that are permitted.

The Act created a new form of financial organization called a financial holding company that may own banks, insurance companies and securities firms. A financial holding company is authorized to engage in any activity that is

1

financial in nature, incidental to an activity that is financial in nature, or is a complimentary activity. These activities may include insurance, securities transactions, and traditional banking related activities. The Act establishes a consultative and cooperative procedure between the Federal Reserve and the Secretary of the Treasury for purposes of determination as to the scope of activities permitted by the Act. VFG is not a financial holding company.

No material part of the business of the affiliate banks is dependent upon a single or a few customers and the loss of one or more customers would not have a materially adverse effect upon the business of the banks. Management is not aware of any indications that the business of the banks or material portion thereof is, or may be, seasonal.

REGULATION, SUPERVISION AND GOVERNMENT POLICY

Bank Holding Company

VFG is registered as a bank holding company under the Federal Bank Holding Corporation Act of 1956, as amended, and is subject to supervision and regulation by the Board of Governors of the Federal Reserve System (the “Federal Reserve Board”) and State Corporation Commission (“SCC”). As a bank holding company, VFG is required to furnish to the Federal Reserve Board an annual report of its operations at the end of each fiscal year and to furnish such additional information as the Federal Reserve Board may require pursuant to the Bank Holding Corporation Act. The Federal Reserve Board and SCC also may conduct examinations of VFG and its affiliates.

A bank holding company must satisfy special criteria to qualify for the expanded powers authorized by the Act, including the maintenance of a well-capitalized and well-managed status for all affiliate banks and a satisfactory community reinvestment rating.

Capital Requirements

The Company is subject to various regulatory capital requirements administered by the federal banking agencies. Failure to meet minimum capital requirements can initiate certain mandatory or possibly additional discretionary actions by regulators that, if undertaken, could have a direct material effect on the Company’s financial statements. Under capital adequacy guidelines and the regulatory framework for prompt corrective action, the Company must meet specific capital guidelines that involve quantitative measures of the Company’s assets, liabilities, and certain off-balance-sheet items as calculated under regulatory accounting practices. The Company’s capital amounts and classifications are also subject to qualitative judgments by the regulators about components, risk weightings, and other factors.

Quantitative measures established by regulation to ensure capital adequacy require the Company to maintain minimum amounts and ratios of total and Tier 1 capital (as defined in the regulations) to risk-weighted assets, and of Tier 1 capital to average assets. Management believes, as of December 31, 2006, that the Company and its affiliate banks meet all capital adequacy requirements to which it is subject.

As of December 31, 2006, the most recent notification from the Federal Reserve Bank of Richmond categorized the Company’s subsidiary banks as “well capitalized” under the regulatory framework for prompt corrective action under the Federal Deposit Insurance Act of 1991 (FDICIA). To be categorized as “well capitalized,” the Company must maintain minimum total risk-based, Tier 1 risk-based, and Tier 1 leverage ratios. There are no conditions or events since notification that management believes have changed the Company’s category.

Dividends

VFG is a separate operating entity from its affiliates, and thus has liquidity needs that are funded primarily from the income of its affiliates. The parent company’s cash outflows consist of dividends to shareholders and unallocated corporate expenses. The main sources of funding for the parent Company are the management fees and dividends it receives from its banking and trust affiliates. Under the current supervisory regulation, prior approval from such agencies is required if the community bank pays cash dividends that exceed certain levels as defined. During 2006, the

2

banking affiliates and the non-bank subsidiary paid $13.0 million in management fees to the Company, and $12.5 million in dividends were paid to the Company. As of January 1, 2007, the aggregate amount of additional unrestricted funds, which could be transferred from the banking affiliates to VFG without prior regulatory approval totaled $42.1 million or 27.9% of the consolidated net assets.

Sarbanes-Oxley Act of 2002

The Sarbanes-Oxley Act of 2002 (Sarbanes-Oxley), which was signed into law in July, 2002, impacts all companies with securities registered under the Securities Exchange Act of 1934, including the Company. Sarbanes-Oxley created new requirements in the areas of corporate governance and financial disclosure including, among other things, (i) increased responsibility for the Chief Executive Officers and Chief Financial Officers with respect to the content of filings with the SEC; (ii) enhanced requirements for audit committees, including independence and disclosure of expertise; (iii) enhanced requirements for auditor independence and the types of non-audit services that auditors can provide; (iv) accelerated filing requirements for SEC reports; (v) increased disclosure and reporting obligations for companies, their directors and executive officers; and (vi) new and increased civil and criminal penalties for violations of securities laws. Certifications of the Chief Executive Officer and Chief Financial Officer can be found in the “Exhibits” section of this document. Management’s “Statement of Management’s Responsibility” can be found in Item 9A of this report.

BANK REGULATION

Each of VFG’s affiliate banks are subject to supervision and regulation by the Federal Reserve Board and the SCC. The various laws and regulations administered by the regulatory agencies affect corporate practices, including business practices related to payment and charging of interest, documentation and disclosures, and affect the ability to open and close offices or purchase other affiliates.

USA Patriot Act.VFG’s affiliate banks are subject to the requirements of the USA Patriot Act, which provides for the facilitation of information sharing among governmental entities and financial institutions for the purpose of combating terrorism and money laundering. The Act places a significantly increased reporting responsibility and regulatory oversight on financial institutions to share information with the federal government concerning activities that may involve money laundering or terrorist activities. The USA Patriot Act is considered a significant banking law in terms of information disclosure regarding certain customer transactions. Certain provisions of the USA Patriot Act impose the obligation to establish anti-money laundering programs, including the development of a customer identification program, and the screening of all customers against any government lists of known or suspected terrorists. The Company is in compliance with both the requirements of the Act.

Insurance of Accounts.VFG’s affiliate banks have deposits which are insured by the Federal Deposit Insurance Corporation (FDIC), and the banks are subject to insurance premium assessments by the FDIC. The FDIC has developed a risk-based assessment system, under which the assessment rate for an insured depository institution varies according to its level of risk. An institution’s risk category is based upon whether the institution is well capitalized, adequately capitalized or undercapitalized and the institution’s “supervisory subgroups”: Subgroup A, B or C. Subgroup A institutions are financially sound institutions with a few minor weaknesses; Subgroup B institutions are institutions that demonstrate weaknesses which, if not corrected, could result in significant deterioration; and Subgroup C institutions are institutions for which there is a substantial probability that the FDIC will suffer a loss in connection with the institution unless effective action is taken to correct the areas of weakness. Based on its capital and supervisory subgroups, each DIF member institution is assigned an annual FDIC assessment rate per $100 of insured deposits varying between 0.05% per annum (for well capitalized Subgroup A institutions) and 0.43% per annum (for undercapitalized Subgroup C institutions). All of VFG’s subsidiary bank’s Subgroup for 2006 was A. Each of VFG’s affiliate banks expect to receive a one-time assessment credit to offset the cost of expected higher deposit insurance premiums for 2007.

Community Reinvestment Act.VFG’s affiliate banks are subject to the requirements of the Community Reinvestment Act of 1977 (CRA). The CRA imposes on financial institutions an affirmative and ongoing obligation to meet the needs of the local communities, including low and moderate income neighborhoods. If any of our bank affiliates receives a rating from the Federal Reserve of less than satisfactory under the CRA, restrictions on our operating activities would be imposed. Our bank’s currently meet the CRA requirements.

3

Privacy Legislation.Several new regulations issued by federal banking agencies also provide new protections against the transfer and use of customer information by financial institutions. A financial institution must provide to its customers information regarding its polices and procedures with respect to the handling of customers personal information. Each institution must conduct an internal risk assessment of its ability to protect customer information. These privacy provisions generally prohibit a financial institution from providing a customer’s personal financial information to unaffiliated parties without prior notice and approval from the customer.

Basel Committee.On February 28, 2007, the federal banking agencies released for comment the new Basel Capital Accord (“Basel II”), which proposes establishment of a new framework of capital adequacy for banking organizations; the Committee published the text of the framework on July 26, 2004. Despite the release of the Basel II framework, it is not clear at this time whether and in what manner the new accord will be adopted by bank regulators with respect to banking organizations that they supervise and regulate. Although the Committee’s stated intent is that Basel II will not change the amount of overall capital in the global banking system, adoption of the proposed new accord could require individual banking organizations, including the Company, to increase the minimum level of capital held. The Company will continue to closely monitor regulatory action on this matter and assess the potential impact to the Company.

Consumer Laws and Regulations. VFG’s affiliate banks are also subject to certain consumer laws and regulations that are designed to protect consumers in transactions with banks. While the list set forth herein is not exhaustive, these laws and regulations include the Truth in Lending Act, the Truth in Savings Act, the Electronic Funds Transfer Act, the Expedited Funds Availability Act, the Equal Credit Opportunity Act, Real Estate Settlement Procedures (RESPA), Home Mortgage Disclosure Act (HMDA), the Fair Credit Reporting Act and the Fair Housing Act, among others. These laws and regulations mandate certain disclosure requirements and regulate the manner in which financial institutions transact business with customers. VFG’s affiliate banks must comply with the applicable provisions of these consumer protection laws and regulations as part of its ongoing customer relations.

ACCESS TO FILINGS

The Company files annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and other filings with the Securities and Exchange Commission (“SEC”). The public may read and copy any documents the Company files at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The Company’s SEC filings can also be obtained on the SEC’s website on the internet at http://www.sec.gov. Also, annual reports on Form 10-K and quarterly reports on Form 10-Q are posted on the Company’s website at http://www.vfgi.net as soon as reasonably practical after filing electronically with the SEC.

| Item 1A. | RISK FACTORS |

This section highlights specific risks that could affect our business and us. Although we have tried to discuss key factors, please be aware that other risks may prove to be important in the future. New risks may emerge at any time and we cannot predict such risks or estimate the extent to which they may affect our financial performance. In addition to the factors discussed elsewhere in this report, among the other factors that could cause actual results to differ materially are the following:

Our profitability depends on interest rates generally.

Our profitability depends in substantial part on our net interest margin, which is the difference between the rates we receive on loans and investments and the rates we pay for deposits and other sources of funds. Our net interest margin depends on many factors that are partly or completely outside of our control, including competition, federal economic, monetary and fiscal policies, and economic conditions generally. Changes in interest rates will affect our operating performance and financial condition. We try to minimize our exposure to interest rate risk, but we are unable to completely eliminate this risk.

4

Our profitability depends significantly on local economic conditions.

Our success depends primarily on the general economic conditions of the markets in which we operate. Unlike larger banks that are more geographically diversified, we provide banking and financial services to customers primarily in Northern, Central and Western Virginia. The local economic conditions in these areas have a significant impact on our business, real estate and construction loans, the ability of the borrowers to repay these loans and the value of the collateral securing these loans. A significant decline in general economic conditions, caused by inflation, recession, acts of terrorism, an outbreak of hostilities or other international or domestic calamities, unemployment or other factors beyond our control, could impact these local economic conditions and could negatively affect the financial results of our banking operations.

Our affiliate banks’ ability to pay dividends is subject to regulatory limitations which, to the extent VFG requires such dividends in the future, may affect our ability to pay obligations and dividends.

VFG is a separate legal entity from the affiliate banks and independent trust company, and thus does not have significant revenue sources of its own. We currently depend on the affiliate banks’ cash and liquidity as well as dividends from our subsidiaries to pay our operating expenses and dividends to shareholders. No assurance can be made that in the future the affiliate banks will have the capacity to pay the necessary dividends and that VFG will not require dividends from the affiliate banks to satisfy VFG’s obligations. The availability of dividends from our affiliate banks is limited by various statutes and regulations. It is possible, depending upon the financial condition of VFG and other factors, that the Federal Reserve could assert that payment of dividends or other payments by the affiliate banks are an unsafe or unsound practice. In the event the affiliate banks are unable to pay dividends sufficient to satisfy the Company’s obligations and the affiliate banks are unable to pay dividends to the Company, VFG may not be able to service its obligations as they become due, or pay dividends on the Company’s common stock. Consequently, the inability to receive dividends from the affiliate banks could adversely affect our financial condition, results of operations and cash flows.

Our profitability may suffer because of rapid and unpredictable changes in the highly regulated environment in which we operate.

We are subject to extensive supervision by several governmental regulatory agencies at the federal and state levels. Recently enacted, proposed and future banking legislation and regulations have had, will continue to have, or may have a significant impact on the financial services industry. These regulations, which are intended to protect depositors and not our shareholders, and the interpretation and application of them by federal and state regulators, are beyond our control, may change rapidly and unpredictably and can be expected to influence our earnings and growth. Our success depends on our continued ability to maintain compliance with these regulations. Some of these regulations may increase our costs and thus place other financial institutions that are not subject to similar regulation in stronger, more favorable competitive positions.

If our allowance for loan losses becomes inadequate, our results of operations may be adversely affected.

We maintain an allowance for loan losses that we believe is adequate to absorb estimated incurred losses inherent in our loan portfolio. Through a periodic review and consideration of the loan portfolio, management determines the amount of the allowance for loan losses by considering current general market conditions, credit quality of the loan portfolio and performance of our customers relative to their financial obligations with us. The amount of future losses is susceptible to changes in economic, operating and other conditions, including changes in interest rates that may be beyond our control and these losses may cause our loan loss provision to vary widely from recent levels. Although we believe the allowance for loan losses is adequate to absorb probable incurred losses in our loan portfolio, it is an estimate subject to revision as losses are confirmed. Higher levels of loan losses in the future could have a material adverse impact on our financial performance. Federal and state regulators, as an integral part of their supervisory function, periodically review our allowance for loan losses. These regulatory agencies may require us to increase our

5

provision for loan losses or to recognize further loan charge offs based upon their judgments, which may be different from ours. Any increase in the allowance for loan losses required by these regulatory agencies could have a negative effect on our financial condition and results of operations.

Our concentration in loans secured by real estate may increase our loan losses, which would negatively affect our financial results.

We offer a variety of secured loans, including commercial lines of credit, commercial term loans, real estate, construction, home equity, consumer and other loans. Many of our loans are secured by real estate (both residential and commercial) in our market area. At December 31, 2006, approximately 47% and 41% of our $1.22 billion loans receivable portfolio were secured by commercial and residential real estate, respectively. A major change in the real estate market, such as deterioration in the value of this collateral, or in the local or national economy, could adversely affect our customers’ ability to pay these loans, which in turn could impact us. Risk of loan defaults and foreclosures are unavoidable in the banking industry, and we try to limit our exposure to this risk by monitoring our extensions of credit carefully. We cannot fully eliminate credit risk, and as a result credit losses may occur in the future.

Our future success is dependent on our ability to compete effectively in the highly competitive banking industry.

We face vigorous competition from other banks and other financial institutions, including savings and loan associations, savings banks, finance companies and credit unions for deposits, loans and other financial services in our market area. Many competitors offer products and services which we do not and many have substantially greater resources, name recognition and market presence that benefit them in attracting business. In addition, larger competitors may be able to price loans and deposits more aggressively than we do. Some of the financial services organizations with which we compete are not subject to the same degree of regulation as is imposed on bank holding companies and federally insured state-chartered banks, national banks and federal savings institutions. As a result, these nonbank competitors have certain advantages over us in accessing funding and in providing various services. The differences in resources and regulations may make it harder for us to compete profitably, reduce the rates that we can earn on loans and investments, increase the rates we must offer on deposits and other funds, and adversely affect our overall financial condition and earnings.

We depend on the services of our key personnel, and a loss of any of those personnel may disrupt our operations and result in reduced revenues.

Our success depends upon the continued service of our senior management team and upon our ability to attract and retain qualified financial services personnel. Competition for qualified employees is intense. In our experience, it can take a significant period of time to identify and hire personnel with the combination of skills and attributes required in carrying out our strategy. If we lose the services of our key personnel, or are unable to attract additional qualified personnel, our business, financial condition, results of operations and cash flows could be materially adversely affected.

We may identify a material weakness or a significant deficiency in our internal control over financial reporting that may adversely affect our ability to properly account for non-routine transactions.

As we have grown and expanded, we have acquired and added, and expect to continue to acquire and add, businesses and other activities that complement our core retail and commercial banking functions. Such acquisitions or additions frequently involve complex operational and financial reporting issues that can influence management’s internal control system. While we make every effort to thoroughly understand any new activity or acquired entity’s business processes, our planning for proper integration into our Company can give no assurance that we will not encounter operational and financial reporting difficulties impacting our controls over the Company.

If we need additional capital in the future to continue our growth, we may not be able to obtain it on terms that are favorable. This could negatively affect our performance and the value of our common stock.

Our business strategy calls for continued growth. We anticipate that we will be able to support this growth through the generation of additional deposits at new branch locations as well as investment opportunities. However, we may need

6

to raise additional capital in the future to support our continued growth and to maintain our capital levels. Our ability to raise capital through the sale of additional securities will depend primarily upon our financial condition and the condition of financial markets at that time. We may not be able to obtain additional capital in the amounts or on terms satisfactory to us. Our growth may be constrained if we are unable to raise additional capital as needed.

Because our mortgage banking revenue is sensitive to changes in economic conditions, decreased economic activity, a slowdown in the housing market or higher interest rates may reduce our profits.

Maintaining a high level of fees from this operation depends primarily on our ability to continue to originate mortgage loans. Production levels are sensitive to changes in economic conditions and can suffer from decreased economic activity, a slowdown in the housing market or higher interest rates. Generally, any sustained period of decreased economic activity or higher interest rates could adversely affect our mortgage originations and, consequently, reduce our income from mortgage banking activities. As a result, these conditions may adversely affect our net income.

| Item 1B. | UNRESOLVED STAFF COMMENTS |

None.

| Item 2. | PROPERTIES |

The Company’s headquarters is located at 102 S. Main Street in Culpeper, Virginia, and also maintains executive offices at 1807 Seminole Trail, Charlottesville, Virginia. The Company’s subsidiary banks operate forty branch locations. They own thirty-four branches and lease the remaining six. Two additional locations are owned by our bank affiliates to facilitate operations and loan production. Additional information regarding lease commitments can be found in Note 19 of the 2006 Consolidated Financial Statements.

7

As of December 31, 2006 the offices (including executive offices) of our subsidiaries were as follows:

Subsidiary | Location of Executive Office | Executive Office Owned/Leased | Location of Offices (including executive office) | |||

| Second Bank & Trust | 102 South Main Street Culpeper Virginia | Owned | 15 banking offices in Culpeper, Madision, Orange, Locust Grove, Albemarle, Spotsylvania, Caroline and Stafford Counties, Virginia; Charlottesville, Fredericksburg, and Bowling Green Cities, Virginia | |||

| 4700 Harrison Road Fredericksburg, Virginia | Leased | |||||

| Planters Bank & Trust Company of Virginia | 24 South Augusta Street Staunton, Virginia | Owned | 25 banking offices in Augusta, Rockbridge, Franklin, Prince Prince Edward, and Bedford Counties, Virginia; Grottoes, Woodstock, Rocky Mount, and Farmville Towns, Virginia; Waynesboro, Harrisonburg, Lynchburg, Buena Vista, Staunton, and Covington Cities, Virginia | |||

| Virginia Commonwealth Trust Company | 102 South Main Street Culpeper, Virginia | Owned | 5 trust offices in Albemarle, and Culpeper, Counties, Virginia; Fredericksburg, Staunton and Harrisonburg Cities, Virginia | |||

All of the Company’s properties are in good operating condition and are adequate for the Company’s present needs.

| Item 3. | LEGAL PROCEEDINGS |

There are no material proceedings to which the Company or any of our subsidiaries are a party or by which, to the Company’s knowledge, we, or any subsidiaries, are threatened. All legal proceedings presently pending or threatened against the Company or our subsidiaries involve routine litigation incidental to the business of the Company or the subsidiary involved and are not material in respect to the amount in controversy.

| Item 4. | SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS |

No matters were submitted during the fourth quarter of the fiscal year covered by this report to a vote of security holders of the Company through a solicitation of proxies or otherwise.

8

EXECUTIVE OFFICERS OF REGISTRANT

The executive officers of the Company are appointed each year at the organizational meeting of the Board of Directors, which follows the annual meeting of the shareholders, and at other Board of Directors meetings as appropriate. Each of the executive officers has been employed by the Company in the position or positions indicated in the list and pertinent notes below. Messrs. Barham and Farrar have been employed by the Company as executive officers for more than five years.

Name | Age | Current Position | ||

| O.R. Barham, Jr. | 56 | Mr. Barham has been President and Chief Executive Officer of the Company since 2002. Mr. Barham served as a director of the Company since 1996. Prior to January 2002, he served as President and Chief Executive Officer of Virginia Commonwealth Financial Corporation and its predecessor, Second National Financial Corporation. | ||

| Jeffrey W. Farrar | 46 | Mr. Farrar has been Executive Vice President and Chief Financial Officer of the Company since January 18, 2002. Mr. Farrar served as Executive Vice President and Chief Financial Officer of Virginia Commonwealth Financial Corporation and its predecessor, Second National Financial Corporation, since 1996. | ||

| Litz Van Dyke | 43 | Mr. Van Dyke is Executive Vice President and Chief Operating Officer of the Company. Mr. Van Dyke joined the Company in September 2004, and previously served in a similar capacity for FNB Corporation of Christiansburg, Virginia. | ||

| Richard L. Saunders | 53 | Mr. Saunders is Chief Credit Officer of the Company. Mr. Saunders joined the Company in May 2004 and previously served in a similar capacity for Guaranty Bank of Charlottesville, Virginia. | ||

| James T. Huerth | 45 | Mr. Huerth has been President & CEO of Planters Bank & Trust Company of Virginia since January 2005. Mr. Huerth served as an Area Commercial Executive for Branch Banking & Trust (BB&T) in Georgia’s northern market prior to joining the Company. |

9

PART II

| Item 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

The Company’s stock trades on the NASDAQ Global Select Market, and currently trades under the trading symbolVFGI. As of March 1, 2007, there were approximately 5,100 shareholders of record and the closing price of the Company’s common stock was $24.10. There were no repurchases of stock conducted during 2006. Listed below are the high and low prices for the common stock, as reported by NASDAQ, and dividends paid for each quarter in the two year period ended December 31, 2006. VFG anticipates the same level of dividend payment in the future. On September 6, 2006 the Company paid a three-for-two stock split in the form of a 50% stock dividend. The per share amounts below and throughout this document have been restated to reflect the three-for-two stock split for all periods presented.

| Sales Price | Dividends Per Share | |||||||||||||||||

| 2006 | 2005 | 2006 | 2005 | |||||||||||||||

| High | Low | High | Low | |||||||||||||||

1st Quarter | $ | 27.97 | $ | 23.70 | $ | 25.53 | $ | 21.01 | $ | 0.15 | $ | 0.13 | ||||||

2nd Quarter | 29.67 | 24.87 | 24.33 | 21.20 | 0.15 | 0.14 | ||||||||||||

3rd Quarter | 29.45 | 25.05 | 25.00 | 21.71 | 0.15 | 0.14 | ||||||||||||

4th Quarter | 28.94 | 26.17 | 26.20 | 22.13 | 0.16 | 0.15 | ||||||||||||

10

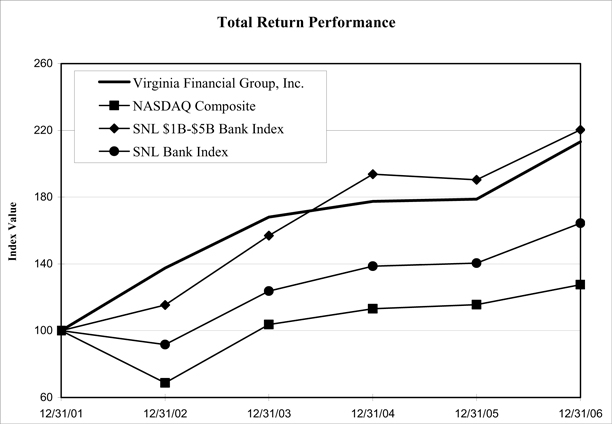

STOCK PERFORMANCE GRAPH

The following graph compares the Company’s annual percentage change in cumulative total return on common stock over the past five years with the cumulative total return of companies comprising the NASDAQ Composite Index, the SNL $1-$5 Billion Bank Index and SNL Composite Bank Index. The SNL indexes are indexes are published by SNL Financial, LC. The Bank indexes are, in the opinion of management, a more relevant standard by which to compare performance, whereas the peer groups are more similar in terms of size and business profiles.

This presentation assumes that $100 was invested in shares of the relevant issuers on December 31, 2001, and that dividend received were immediately invested in additional shares. The graph plots the value of the intial investment at one-year intervals for the fiscal years shown.

| Period Ending | ||||||||||||

Index | 12/31/01 | 12/31/02 | 12/31/03 | 12/31/04 | 12/31/05 | 12/31/06 | ||||||

Virginia Financial Group, Inc. | 100.00 | 137.53 | 168.07 | 177.51 | 178.79 | 213.14 | ||||||

NASDAQ Composite | 100.00 | 68.76 | 103.67 | 113.16 | 115.57 | 127.58 | ||||||

SNL $1B-$5B Bank Index | 100.00 | 115.44 | 156.98 | 193.74 | 190.43 | 220.36 | ||||||

SNL Bank Index | 100.00 | 91.69 | 123.69 | 138.61 | 140.50 | 164.35 | ||||||

On January 22, 2002, the Company’s common stock began trading on the NASDAQ National Market , and currently trades on the NASDAQ Global Select Market under the trading symbol VFGI.

There can be no assurance that the Company’s stock performance in the future will continue with the same or similar trends depicted in the graph above.

11

| Item 6. | SELECTED FINANCIAL DATA |

The following is selected financial data for the Company for the last five years.

| Years Ended December 31, | ||||||||||||||||||||

(In thousands, except per share data) | 2006 | 2005 | 2004 | 2003 | 2002 | |||||||||||||||

Statement of Operations Data: | ||||||||||||||||||||

Interest Income | $ | 95,627 | $ | 80,706 | $ | 70,402 | $ | 62,827 | $ | 63,723 | ||||||||||

Interest Expense | 35,482 | 23,861 | 19,628 | 19,357 | 23,101 | |||||||||||||||

Net Interest Income | 60,145 | 56,845 | 50,774 | 43,470 | 40,622 | |||||||||||||||

Provision for Loan Losses | 750 | 2,012 | 2,534 | 1,290 | 1,602 | |||||||||||||||

Total Noninterest Income | 15,485 | 15,443 | 14,544 | 15,227 | 12,721 | |||||||||||||||

Total Noninterest Expense | 46,918 | 43,702 | 41,016 | 38,866 | 35,030 | |||||||||||||||

Net Income | 19,497 | 18,216 | 15,203 | 13,492 | 12,335 | |||||||||||||||

Performance Ratios: | ||||||||||||||||||||

Return on Average Assets | 1.24 | % | 1.23 | % | 1.07 | % | 1.13 | % | 1.15 | % | ||||||||||

Return on Average Equity | 13.57 | % | 13.86 | % | 12.40 | % | 11.47 | % | 11.09 | % | ||||||||||

Net Interest Margin | 4.25 | % | 4.29 | % | 4.04 | % | 4.15 | % | 4.29 | % | ||||||||||

Efficiency Ratio (1) | 60.54 | % | 59.32 | % | 61.12 | % | 64.42 | % | 63.08 | % | ||||||||||

Per Share Data: | ||||||||||||||||||||

Net Income—Basic | $ | 1.81 | $ | 1.69 | $ | 1.42 | $ | 1.26 | $ | 1.13 | ||||||||||

Net Income—Diluted | 1.80 | 1.68 | 1.41 | 1.25 | 1.13 | |||||||||||||||

Cash Dividends | 0.61 | 0.56 | 0.52 | 0.50 | 0.48 | |||||||||||||||

Book Value | 13.97 | 12.66 | 11.83 | 11.17 | 10.63 | |||||||||||||||

Market Price Per Share | 27.99 | 24.02 | 24.44 | 23.68 | 19.87 | |||||||||||||||

Cash Dividend Payout Ratio | 34.03 | % | 33.07 | % | 36.76 | % | 39.81 | % | 42.65 | % | ||||||||||

Balance Sheet Data: | ||||||||||||||||||||

Assets | $ | 1,625,989 | $ | 1,505,184 | $ | 1,449,608 | $ | 1,387,211 | $ | 1,114,905 | ||||||||||

Loans | 1,217,632 | 1,143,076 | 1,061,575 | 922,689 | 700,979 | |||||||||||||||

Investment securities | 264,141 | 241,032 | 286,856 | 360,041 | 295,628 | |||||||||||||||

Deposits | 1,318,281 | 1,255,509 | 1,257,164 | 1,210,774 | 959,822 | |||||||||||||||

Total borrowings | 144,812 | 101,831 | 56,649 | 48,821 | 32,415 | |||||||||||||||

Stockholders’ Equity | 150,652 | 136,105 | 127,089 | 119,830 | 114,371 | |||||||||||||||

Capital Ratios: | ||||||||||||||||||||

Tier 1 Capital (to Average Assets) | 9.65 | % | 9.32 | % | 8.77 | % | 7.03 | % | 9.63 | % | ||||||||||

Total Capital (to Risk Weighted Assets) | 12.44 | % | 12.18 | % | 12.37 | % | 10.57 | % | 14.30 | % | ||||||||||

Asset Quality Ratios: | ||||||||||||||||||||

Total allowance for loan losses to total loans outstanding | 1.19 | % | 1.19 | % | 1.10 | % | 1.06 | % | 1.31 | % | ||||||||||

Non-performing assets to year-end loans and other property owned | 0.25 | % | 0.16 | % | 0.38 | % | 0.80 | % | 1.15 | % | ||||||||||

| (1) | Computed by dividing non-interest expense by the sum of net interest income and non-interest income, net of gains or losses on securities, fixed assets and foreclosed assets. This is a non-GAAP financial measure, which we believe provides investors with important information regarding our operational efficiency. Comparison of our efficiency ratio with those of other companies may not be possible, because other companies may calculate the efficiency ratio differently. |

12

| Item 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

VIRGINIA FINANCIAL GROUP, INC.

Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion provides management’s analysis of the consolidated financial results of operations, financial condition, liquidity and capital resources of Virginia Financial Group, Inc. and its affiliates (VFG). This discussion and analysis should be read in conjunction with the audited financial statements and footnotes appearing elsewhere in this report.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

In addition to historical information, Management’s Discussion and Analysis contains forward-looking statements. The forward-looking statements are subject to certain risks and uncertainties, which could cause actual results to differ materially from historical results, or those anticipated. When we use words such as “believes”, “expects”, “anticipates” or similar expressions, we are making forward-looking statements. Readers are cautioned not to place undue reliance on these forward-looking statements, which reflect management’s analysis only as of the date thereof. VFG wishes to caution the reader that factors, such as those listed below, in some cases have affected and could affect VFG’s actual results, causing actual results to differ materially from those in any forward looking statement. These factors include:

| • | Expected cost savings from VFG’s acquisitions and dispositions, |

| • | Competitive pressure in the banking industry or in VFG’s markets may increase significantly, |

| • | Changes in the interest rate environment may reduce margins, |

| • | General economic conditions, either nationally or regionally, may be less favorable than expected, resulting in, among other things, credit quality deterioration and reduced mortgage banking revenue, |

| • | Changes may occur in banking legislation and regulation, |

| • | Our concentration in loans secured by real estate could increase our loan losses, |

| • | Turnover in key personnel would disrupt our operations, |

| • | We may identify a material weakness or a significant deficiency in our internal control over financial reporting that may adversely affect our ability too properly account for non-routine transactions, |

| • | We may need additional capital in the future to continue our growth and may not be able to obtain it on terms that are favorable, |

| • | Changes may occur in general business conditions, and |

| • | Changes may occur in the securities markets. |

EXECUTIVE OVERVIEW

VFG’s earnings per diluted share grew 7.1% in 2006 versus 2005. Net revenue was $75.6 million for the year ended December 31, 2006 as compared to $72.3 million in 2005. VFG earned $19.5 million or $1.80 per diluted share, an increase of 7.0% over 2005 earnings of $18.2 million or $1.68 per diluted share. VFG generated approximately $22.3 million in cash flow from operating activities in 2006. It paid dividends to stockholders of $6.6 million, invested $10.8 million in capital expenditures and borrowed approximately $25 million in long term debt, net.

Despite adding four full-service financial centers, additional key management positions and an environment fostering margin compression during the year, VFG still managed to grow earnings a respectable 7% over 2005. Asset quality has remained strong despite soft real estate markets throughout many of the regions serviced by the Company. Net interest margin remained acceptable despite an inverted yield curve and competitive pressures encountered during the year. Continuing improvement in noninterest income related to retail banking, trust and brokerage services was observed, but must improve to counter the impact of anticipated net interest margin contraction in 2007.

VFG’s focus for 2007 will include loan portfolio diversification, standardization of loan and deposit pricing metrics, concentration on the current forty branch network for retail delivery optimization in a changing competitive landscape and improvement of revenue diversification through increased contribution of noninterest revenue streams. We will

13

likely slow de novo branch activity as we focus on the maturation of six branches opened during the past eighteen months. Another significant initiative will be aggressive focus on demand deposit penetration in our markets via a direct marketing program. All of our strategic efforts are intended to grow and diversify our revenue streams, support sustained profitability and better serve the customer.

NON-GAAP FINANCIAL MEASURES

This report refers to the efficiency ratio, which is computed by dividing noninterest expense by the sum of net interest income and noninterest income, net of gains or losses on securities, fixed assets and foreclosed assets. The efficiency ratio is not a recognized reporting measure under Accounting Principles Generally Accepted in the United States (USGAAP). We believe this measure provides investors with important information regarding our operational efficiency. Management believes such financial information is meaningful to the reader in understanding operating performance, but cautions that such information not be viewed as a substitute for USGAAP. VFG, in referring to its net income, is referring to income under Accounting Principles Generally Accepted in the United States. Comparison of our efficiency ratio with those of other companies may not be possible, because other companies may calculate the efficiency ratio differently.

CRITICAL ACCOUNTING POLICIES

General

The Company’s financial statements are prepared in accordance with accounting principles generally accepted in the United States (GAAP). The financial information contained within our statements is, to a significant extent, financial information that is based on measures and estimates of the financial effects of transactions and events that have already occurred. A variety of factors could affect the ultimate value that is obtained either when earning income, recognizing an expense, recovering an asset or relieving a liability. In addition, USGAAP itself may change from one previously acceptable method to another method. Although the economics of our transactions would be the same, the timing of events that would impact our transactions could change.

Allowance for Loan Losses

We use historical loss factors as one factor in determining the inherent loss that may be present in our loan portfolio. Actual losses could differ significantly from the historical factors that we use. The Company’s affiliate banks conduct an analysis of the loan portfolio on a regular basis. This analysis is used in assessing the sufficiency of the allowance for loan losses and in the determination of the necessary provision for loan losses. The review process generally begins with lenders identifying problem loans to be reviewed on an individual basis for impairment. When a loan has been identified as impaired, a specific reserve may be established based on the bank’s calculation of the loss embedded in the individual loan. In addition to impairment testing, the banks have an eight point grading system for each non-homogeneous loan in the portfolio. The loans meeting the criteria for impairment are segregated from performing loans within the portfolio. Loans are then grouped by loan type and, in the case of commercial loans, by risk rating. Each loan type is assigned an allowance factor based on historical loss experience, economic conditions, and overall portfolio quality including delinquency rates. This evaluation is inherently subjective as it requires estimates that are susceptible to significant revision as more information becomes available.

A loan is considered impaired when, based on current information and events, it is probable that the bank will be unable to collect the scheduled payments of principal or interest when due according to the contractual terms of the loan agreement. Factors considered by management in determining impairment include payment status, collateral value, and the probability of collecting scheduled principal and interest payments when due. Loans that experience insignificant payment delays and payment shortfalls generally are not classified as impaired. Management determines the significance of payment delays and payment shortfalls on a case-by-case basis, taking into consideration all of the circumstances surrounding the loan and the borrower, including the length of the delay, the reasons for the delay, the borrower’s prior payment record, and the amount of the shortfall in relation to the principal and interest owed. Impairment is measured on a loan-by-loan basis for commercial and construction loans by either the present value of expected future cash flows discounted at the loan’s effective interest rate, the loan’s obtainable market price, or the fair value of the collateral if the loan is collateral dependent. Larger groups of smaller balance homogeneous loans are collectively evaluated for impairment. Accordingly, the Company does not separately identify individual consumer and residential loans for impairment disclosures, unless such loans are subject to a restructuring agreement.

14

Goodwill

Goodwill is subject to impairment testing at least annually to determine whether write-downs of the recorded balances are necessary. In this testing, the Company employs general industry practices in accordance with USGAAP. A fair value is determined for each reporting unit using various market valuation methodologies. If the fair values of the reporting units exceed their book values, no write-down of recorded goodwill is necessary. If the fair value of a reporting unit is less, an expense may be required on the Company’s books to write down the related goodwill to the proper carrying value. The Company tests for impairment of goodwill in September each year, and again at any quarter-end if any material events occur during a quarter that may affect goodwill. Through its annual analysis as of September 30, 2006, the Company has not identified any impairment of its goodwill. No events occurred during the fourth quarter 2006 necessitating a re-test of goodwill impairment. No assurance can be given that future goodwill impairment tests will not result in a charge to earnings.

Income Taxes

Deferred income tax assets and liabilities are determined using the liability (or balance sheet) method. Under this method, the net deferred tax asset or liability is determined based on the tax effects of the temporary differences between the book and tax bases of the various balance sheet assets and liabilities and gives current recognition to changes in tax rates and laws.

Stock-Based Compensation

The Company has a stock-based employee compensation plan under which nonqualified stock options may be granted periodically to certain employees. The Company’s stock options typically have an exercise price equal to at least the fair value of the stock on the date of grant, and vest based on continued service with the Company for a specified period, generally five years. The Company adopted SFAS 123R effective January 1, 2006 using the modified prospective method and as such, results for prior periods have not been restated. Prior to January 1, 2006, the value of restricted stock awards was expensed by the Company over the restriction period, and no compensation expense was recognized for stock option grants as all such grants had an exercise price not less than fair market value on the date of grant.

SFAS 123R also requires that new awards to employees eligible for retirement prior to the award becoming fully vested be recognized as compensation cost over the period through the date that the employee first becomes eligible to retire and is no longer required to provide service to earn the award.

RESULTS OF OPERATIONS

NET INTEREST INCOME

The primary source of VFG’s traditional banking revenue is net interest income, which represents the difference between interest income on earning assets and interest expense on liabilities used to fund those assets. Earning assets include loans, securities, and federal funds sold. Interest bearing liabilities include deposits and borrowings. To compare the tax-exempt yields to taxable yields, amounts are adjusted to pretax equivalents based on a 35% federal corporate income tax rate.

Net interest income is affected by changes in interest rates, volume of interest bearing assets and liabilities, and the composition of those assets and liabilities. The “interest rate spread” and “net interest margin” are two common statistics related to changes in net interest income. The interest rate spread represents the difference between the yields earned on interest earning assets and the rates paid for interest bearing liabilities. The net interest margin is defined as the percentage of net interest income to average earning assets. Earning assets obtained through noninterest bearing sources of funds such as regular demand deposits and stockholders’ equity result in a net interest margin that is higher than the interest rate spread.

15

2006 Compared to 2005

Tax equivalent net interest income in 2006 was $62.1 million, an increase of $3.7 million or 6.3% compared to $58.5 million in 2005. Improvements in the growth and mix of average earning assets were primary contributors to this growth and outpaced the margin compression for the year. Average interest earning assets increased $95.9 million or 7.0% to $1.46 billion, while average loans increased $75.2 or 6.8% to $1.19 billion.

The average interest rate spread was 3.66% in 2006, down eighteen basis points from 3.84% in 2005. The net interest margin was 4.25% in 2006, down four basis points from 4.29% in 2005. The slight decrease in the Company’s net interest margin was a result of several factors, including a modestly liability sensitive position in a rising rate environment, additional wholesale funding costs and a more aggressive pricing of deposits with durations of nine months or less to minimize exposure to a potential downward cycle in short term rates, offset partially by the aforementioned changes in asset mix. The yield on average loans increased seventy-one basis points in 2006, reflecting the increase in short term rates during the year, while the yield on investment securities increased thirty-seven basis points for the period. Interest expense as a percentage of average earning assets increased to 2.44%, up sixty-nine basis points from 1.75% in 2005, reflecting a seventy-three basis point increase in average cost of retail deposits to 2.76%, and an eighty-three basis point increase in average total funding cost to 3.03%.

2005 Compared to 2004

Tax equivalent net interest income in 2005 was $58.5 million, an increase of $5.9 million or 11.2% compared to $52.6 million in 2004. Improvements in the growth and mix of average earning assets, coupled with net interest margin expansion, were primary contributors to this growth. Average interest earning assets increased $62.7 million or 4.8% to $1.36 billion, while average loans increased $121.3 or 12.2% to $1.11 billion.

The average interest rate spread was 3.84% in 2005, up thirteen basis points from 3.71% in 2004. The net interest margin was 4.29% in 2005, up twenty-five basis points from 4.04% in 2004. The increase in the Company’s net interest margin was a result of several factors, including changes in asset mix, a modestly asset sensitive position in a rising rate environment, offset partially by additional wholesale funding costs. The yield on average loans receivable increased forty-eight basis points in 2005, reflecting the increase in short term rates during the year, while the yield on investment securities increased nine basis points for the period. Interest expense as a percentage of average earning assets increased to 1.75%, up twenty-four basis points from 1.51% in 2004, reflecting a twenty-five basis point increase in average cost of retail deposits to 2.03%, and an increase in average total funding cost to 2.20%.

16

The following table presents net interest income on a fully taxable equivalent basis, interest rate spread and net interest margin for the years ending December 31, 2006, 2005 and 2004.

| 2006 | 2005 | 2004 | ||||||||||||||||||||||||||||

Dollars in thousands | Average Balance | Income/ Expense | Average Rate | Average Balance | Income/ Expense | Average Rate | Average Balance | Income/ Expense | Average Rate | |||||||||||||||||||||

ASSETS | ||||||||||||||||||||||||||||||

Loans receivable, net (1) (2) | $ | 1,188,388 | $ | 84,159 | 7.08 | % | $ | 1,113,206 | $ | 70,908 | 6.37 | % | $ | 991,911 | $ | 58,463 | 5.89 | % | ||||||||||||

Investment securities | ||||||||||||||||||||||||||||||

Taxable | 165,083 | 7,210 | 4.37 | % | 173,668 | 6,844 | 3.94 | % | 233,429 | 9,160 | 3.92 | % | ||||||||||||||||||

Tax exempt (2) | 85,020 | 5,247 | 6.17 | % | 63,029 | 4,069 | 6.46 | % | 66,610 | 4,403 | 6.61 | % | ||||||||||||||||||

Total investments | 250,103 | 12,457 | 4.98 | % | 236,697 | 10,913 | 4.61 | % | 300,039 | 13,563 | 4.52 | % | ||||||||||||||||||

Interest bearing deposits | 2,681 | 74 | 2.76 | % | 1,256 | 41 | 3.26 | % | 416 | 4 | 0.96 | % | ||||||||||||||||||

Federal funds sold | 18,805 | 930 | 4.95 | % | 12,968 | 464 | 3.58 | % | 9,044 | 152 | 1.68 | % | ||||||||||||||||||

Total interest earning assets | 1,459,977 | 97,620 | 6.69 | % | 1,364,127 | 82,326 | 6.04 | % | 1,301,410 | 72,182 | 5.55 | % | ||||||||||||||||||

Allowance for loan losses | (14,118 | ) | (12,644 | ) | (10,776 | ) | ||||||||||||||||||||||||

Total nonearning assets | 124,919 | 126,235 | 132,570 | |||||||||||||||||||||||||||

Total assets | $ | 1,570,778 | $ | 1,477,718 | $ | 1,423,204 | ||||||||||||||||||||||||

LIABLILITIES AND STOCKHOLDERS EQUITY |

| |||||||||||||||||||||||||||||

Interest-bearing deposits | ||||||||||||||||||||||||||||||

Interest checking | $ | 170,204 | $ | 765 | 0.45 | % | $ | 192,987 | $ | 807 | 0.42 | % | $ | 195,131 | $ | 950 | 0.49 | % | ||||||||||||

Money market | 170,892 | 3,734 | 2.19 | % | 176,606 | 2,325 | 1.32 | % | 176,386 | 1,649 | 0.94 | % | ||||||||||||||||||

Savings | 108,659 | 853 | 0.79 | % | 131,420 | 880 | 0.67 | % | 140,925 | 948 | 0.67 | % | ||||||||||||||||||

Time deposits: | ||||||||||||||||||||||||||||||

Less than $100,000 | 393,897 | 15,099 | 3.83 | % | 364,645 | 11,473 | 3.15 | % | 370,746 | 10,233 | 2.76 | % | ||||||||||||||||||

$100,000 and more | 189,353 | 8,045 | 4.25 | % | 137,197 | 4,923 | 3.59 | % | 121,135 | 4,079 | 3.37 | % | ||||||||||||||||||

Total interest-bearing deposits | 1,033,005 | 28,496 | 2.76 | % | 1,002,855 | 20,408 | 2.03 | % | 1,004,323 | 17,859 | 1.78 | % | ||||||||||||||||||

Federal funds purchased & repurchase agreements | 4,738 | 219 | 4.62 | % | 21,189 | 568 | 2.68 | % | 23,801 | 238 | 1.00 | % | ||||||||||||||||||

Federal Home Loan Bank advances | 61,612 | 2,834 | 4.60 | % | 33,056 | 1,351 | 4.09 | % | 12,960 | 801 | 6.18 | % | ||||||||||||||||||

Subordinated debt | 20,619 | 1,636 | 7.93 | % | 20,619 | 1,260 | 6.11 | % | 16,281 | 683 | 4.20 | % | ||||||||||||||||||

Commercial paper | 50,530 | 2,275 | 4.50 | % | 7,724 | 255 | 3.30 | % | ||||||||||||||||||||||

Other borrowings | 363 | 22 | 6.06 | % | 947 | 19 | 2.01 | % | 10,277 | 47 | 0.46 | % | ||||||||||||||||||

Total interest-bearing liabilities | 1,170,867 | 35,482 | 3.03 | % | 1,086,390 | 23,861 | 2.20 | % | 1,067,642 | 19,628 | 1.84 | % | ||||||||||||||||||

Demand deposits | 239,332 | 249,938 | 224,877 | |||||||||||||||||||||||||||

Other liabilities | 16,857 | 9,953 | 8,035 | |||||||||||||||||||||||||||

Total liabilities | 1,427,056 | 1,346,281 | 1,300,554 | |||||||||||||||||||||||||||

Stockholders’ equity | 143,722 | 131,437 | 122,650 | |||||||||||||||||||||||||||

Total liabilities and stockholders’ equity | $ | 1,570,778 | $ | 1,477,718 | $ | 1,423,204 | ||||||||||||||||||||||||

Net interest income (tax equivalent) (3) | $ | 62,138 | $ | 58,465 | $ | 52,554 | ||||||||||||||||||||||||

Average interest rate spread | 3.66 | % | 3.84 | % | 3.71 | % | ||||||||||||||||||||||||

Interest expense as a percent of average earning assets | 2.43 | % | 1.75 | % | 1.51 | % | ||||||||||||||||||||||||

Net interest margin | 4.25 | % | 4.29 | % | 4.04 | % | ||||||||||||||||||||||||

| (1) | Includes nonaccrual loans |

| (2) | Income and yields are reported on a taxable equivalent basis using a 35% tax rate. |

| (3) | The tax equivalent interest adjustments included in the yields presented above were $2.0, million, $1.6 million and $1.8 million for each of the three years ended December 31, 2006. |

17

The next table analyzes the changes in net interest income on a fully taxable equivalent basis for the periods broken down by their rate and volume components. The change in interest due to both rate and volume has been allocated proportionately to change due to volume versus change due to rate.

| Years Ended December 31, | ||||||||||||||||||||||||

2006 vs. 2005 Increase (Decrease) Due to changes in: | 2005 vs. 2004 Increase (Decrease) Due to changes in: | |||||||||||||||||||||||

(Dollars in thousands) | Volume | Rate | Total | Volume | Rate | Total | ||||||||||||||||||

Interest Income: | ||||||||||||||||||||||||

Loans | $ | 5,015 | $ | 8,236 | $ | 13,251 | $ | 7,451 | $ | 4,994 | $ | 12,445 | ||||||||||||

Securities, taxable | (355 | ) | 721 | 366 | (2,362 | ) | 46 | (2,316 | ) | |||||||||||||||

Securities, tax-exempt | 1,368 | (190 | ) | 1,178 | (236 | ) | (98 | ) | (334 | ) | ||||||||||||||

Interest-bearing deposits | 40 | (7 | ) | 33 | 17 | 20 | 37 | |||||||||||||||||

Federal funds sold | 252 | 214 | 466 | 86 | 226 | 312 | ||||||||||||||||||

Total Interest Earning Assets | $ | 6,320 | $ | 8,974 | $ | 15,294 | $ | 4,956 | $ | 5,188 | $ | 10,144 | ||||||||||||

Interest Expense: | ||||||||||||||||||||||||

Time and savings deposits: | ||||||||||||||||||||||||

Interest checking | $ | (97 | ) | $ | 55 | $ | (42 | ) | $ | (8 | ) | $ | (135 | ) | $ | (143 | ) | |||||||

Money market | (65 | ) | 1,474 | 1,409 | 2 | 674 | 676 | |||||||||||||||||

Savings | (171 | ) | 144 | (27 | ) | (68 | ) | — | (68 | ) | ||||||||||||||

Time deposits | ||||||||||||||||||||||||

Less than $100,000 | 1,001 | 2,625 | 3,626 | (185 | ) | 1,425 | 1,240 | |||||||||||||||||

$100,000 and more | 2,104 | 1,018 | 3,122 | 566 | 278 | 844 | ||||||||||||||||||

Total time and savings deposits | 2,772 | 5,316 | 8,088 | 307 | 2,242 | 2,549 | ||||||||||||||||||

Federal funds and repurchase agreements | (606 | ) | 257 | (349 | ) | (29 | ) | 359 | 330 | |||||||||||||||

Federal Home Loan Bank advances | 1,296 | 187 | 1,483 | 874 | (324 | ) | 550 | |||||||||||||||||

Subordinated debt | — | 376 | 376 | 215 | 362 | 577 | ||||||||||||||||||

Commercial paper | 1,896 | 124 | 2,020 | 255 | — | 255 | ||||||||||||||||||

Other borrowings | (17 | ) | 20 | 3 | (73 | ) | 45 | (28 | ) | |||||||||||||||

Total Interest Bearing Liabilities | 5,341 | 6,280 | 11,621 | 1,549 | 2,684 | 4,233 | ||||||||||||||||||

Net Interest Income | $ | 979 | $ | 2,694 | $ | 3,673 | $ | 3,407 | $ | 2,504 | $ | 5,911 | ||||||||||||

18

NONINTEREST INCOME

2006 Compared to 2005

Noninterest income increased to $15.5 million in 2006, an increase of $42 thousand or .3% compared to 2005. The 2006 results include a loss of $196 thousand on sale of securities available for sale. Included in the 2005 results were net gains on sales of securities available for sale of $296 thousand and a net gain of $421 thousand in connection with the sale of two branches located in Tazewell County. Retail banking fees increased to $7.0 million, an increase of $28 thousand or .4% from 2005. Increases in fees associated with new account generation and debit card activity were offset by decreases in the volume of overdrafts.

Gains on sales of mortgage loans from mortgage banking activities decreased to $2.9 million, a decrease of $222 thousand or 7.2%. Due to the higher mortgage rates and a cooling of real estate markets during 2006, the Company experienced a decline in mortgage originations in both purchase money and refinance mortgages when compared to the robust levels noted during 2005. VFG originated $134.1 million and sold $138.6 million of secondary mortgage loans during 2006, compared to $176.5 million originated and $176.1 million sold in 2005.

Commissions and fees from fiduciary and brokerage activities associated with our trust and wealth management activities increased to $3.9 million for 2006, an increase of $187 thousand or 5.1% over 2005. At December 31, 2006, VFG’s trust affiliate had assets under management and brokerage assets of $597 million, compared to $511 million at December 31, 2005.

Other operating income increased to $1.7 million in 2006 an increase of $587 thousand or 55.1% compared to 2005. The largest contributors to this increase were a $489 thousand in commission revenue generated by Virginia Financial Title Agency (VFTA) which opened during 2006 and $231 thousand of income related to bank owned life insurance (BOLI) offset by minor decreases in commissions from the sale of other banking products. Income produced by VFTA is aggregated into the income generated by our subsidiary banks and is considered an operating entity, but not a separate reporting entity or segment.

2005 Compared to 2004

Noninterest income increased to $15.4 million in 2005, an increase of $899 thousand or 6.2% compared to 2004. Retail banking fees decreased to $7.0 million, a decrease of $568 thousand or 7.6% from 2004. Decreased fees associated with overdraft charges accounted for most of this decrease.

Gains on sales of mortgage loans from mortgage banking activities increased to $3.1 million, an increase of $627 thousand or 25.4%. The Company experienced higher levels of mortgage originations in both purchase money and refinance mortgages during 2005. VFG originated $176.5 million and sold $176.1 million of secondary mortgage loans during 2005, compared to $148.2 million originated and $150.1 million sold in 2004.

Commissions and fees from fiduciary and brokerage activities associated with our trust and wealth management activities increased to $3.7 million for 2005, an increase of $210 thousand or 6.1% over 2004. At December 31, 2005, VFG’s trust affiliate had assets under management and brokerage assets of $511 million, compared to $515 million at December 31, 2004.

The Company realized a gain of $421 thousand during 2005 in conjunction with the sale of two branches located in Tazewell County, Virginia. The Company also realized a gain on sale of securities during 2005 of $296 thousand.

Other operating income amounted to $1.1 million in 2005, essentially flat with 2004.

19

NONINTEREST EXPENSE

The following table presents the components of noninterest expense and the variance or percentage change:

| 2006 vs. 2005 | 2005 vs. 2004 | |||||||||||||||||

In thousands) | 2006 | 2005 | % | 2005 | 2004 | % | ||||||||||||

Compensation and employee benefits | $ | 26,607 | $ | 25,284 | 5.2 | % | $ | 25,284 | $ | 22,669 | 11.5 | % | ||||||

Net occupancy expense | 3,147 | 2,888 | 9.0 | % | 2,888 | 2,721 | 6.1 | % | ||||||||||

Supplies and equipment expenses | 4,141 | 4,056 | 2.1 | % | 4,056 | 4,333 | -6.4 | % | ||||||||||

Amortization—intangible assets | 578 | 643 | -10.1 | % | 643 | 694 | -7.3 | % | ||||||||||

Marketing | 1,214 | 887 | 36.9 | % | 887 | 636 | 39.5 | % | ||||||||||

State franchise taxes | 973 | 870 | 11.8 | % | 870 | 599 | 45.2 | % | ||||||||||

Data processing | 1,389 | 1,389 | 0.0 | % | 1,389 | 1,464 | -5.1 | % | ||||||||||

Professional fees | 823 | 804 | 2.4 | % | 804 | 922 | -12.8 | % | ||||||||||

Telecommunications | 1,006 | 1,017 | -1.1 | % | 1,017 | 1,055 | -3.6 | % | ||||||||||

Other operating expense | 7,040 | 5,864 | 20.1 | % | 5,864 | 5,923 | -1.0 | % | ||||||||||

| $ | 46,918 | $ | 43,702 | 7.4 | % | $ | 43,702 | $ | 41,016 | 6.5 | % | |||||||

Noninterest expenses increased to $46.9 million in 2006, an increase of $3.2 million or 7.4% over 2005. This increase was mainly attributable to the following factors:

| • | Additional operating, compensation and occupancy costs arising from the opening of four additional full-service branches. |

| • | Compensation and benefits associated with merit increases and additional costs associated with employee benefit costs, particularly health and welfare plans. |

| • | Costs associated with marketing and branding initiatives. |

| • | Expenses related to strategic initiatives within our secondary mortgage division. |

| • | Increase in bank franchise taxes associated with increased capital levels coupled with decreased qualifying securities deductions. |

Noninterest expenses increased to $43.7 million in 2005, an increase of $2.7 million or 6.5% over 2004. This increase was mainly attributable to the following factors:

| • | Compensation and benefits associated with merit increases and additional costs associated with employee benefit costs, particularly health and welfare plans. |

| • | Compensation and benefits associated with a $1.7 million increase in incentive accruals. |

| • | Costs associated with marketing and branding initiatives. |

| • | General decreases in operational costs (data processing, professional fees, telecommunications) associated with improved operating efficiency and sale of Tazewell branches. |

| • | Increase in bank franchise taxes associated with increased capital levels coupled with decreased qualifying securities deductions. |

INCOME TAXES

For the year ended December 31, 2006, income taxes were $8.5 million, resulting in an effective tax rate of 30.2% compared to $8.4 million or 31.4% in 2005 and $6.6 million or 30.2% in 2004. The decrease in the effective tax rate for 2006 as compared to 2005 can be attributed to the tax free income generated by the investment in bank owned life insurance and investments in tax credits. The decrease in the effective tax rate for 2005 as compared to 2004 can be attributed to a higher proportion of earnings from tax-exempt assets, such as obligations of states and political subdivisions during those years.

20

ASSET QUALITY

The allowance for loan losses represents an estimate, in management’s judgment, of the amount needed to absorb losses incurred through the reporting date on existing loans in the portfolio. The following table represents VFG’s activity in its allowance for loan losses:

| December 31, | ||||||||||||||||||||

(In thousands) | 2006 | 2005 | 2004 | 2003 | 2002 | |||||||||||||||

Allowance for loan losses, January 1 | $ | 13,581 | $ | 11,706 | $ | 9,743 | $ | 9,180 | $ | 8,266 | ||||||||||

Loans Charged Off: | ||||||||||||||||||||

Real estate—construction | — | — | 48 | — | 6 | |||||||||||||||

Real estate—mortgage | 30 | 55 | 82 | 180 | 200 | |||||||||||||||

Non-farm, Non-residential | — | 38 | 30 | — | — | |||||||||||||||

Commercial, financial and agricultural | 88 | 41 | 124 | 191 | 330 | |||||||||||||||

Consumer loans | 284 | 318 | 518 | 585 | 427 | |||||||||||||||

All other loans | — | — | — | — | — | |||||||||||||||

Total Loans Charged Off | 402 | 452 | 802 | 956 | 963 | |||||||||||||||

Recoveries | ||||||||||||||||||||

Real estate—construction | — | 48 | — | — | — | |||||||||||||||

Real estate—mortgage | 24 | 4 | 4 | 1 | 89 | |||||||||||||||

Non-farm, Non-residential | — | 23 | — | — | — | |||||||||||||||

Commercial, financial and agricultural | 83 | 50 | 83 | 11 | 14 | |||||||||||||||

Consumer loans | 464 | 190 | 144 | 217 | 172 | |||||||||||||||

All other loans | — | — | — | — | — | |||||||||||||||

Total Recoveries | 571 | 315 | 231 | 229 | 275 | |||||||||||||||

Net (Recoveries) Charge-offs | (169 | ) | 137 | 571 | 727 | 688 | ||||||||||||||

Provision for Loan Losses | 750 | 2,012 | 2,534 | 1,290 | 1,602 | |||||||||||||||

Allowance for loan losses, December 31 | $ | 14,500 | $ | 13,581 | $ | 11,706 | $ | 9,743 | $ | 9,180 | ||||||||||

Ratio of allowance for loan losses to total loans outstanding at end of year | 1.19 | % | 1.19 | % | 1.10 | % | 1.06 | % | 1.31 | % | ||||||||||

Ratio of net charge offs (recoveries) to average loans outstanding during the year | (0.01 | )% | 0.01 | % | 0.06 | % | 0.09 | % | 0.10 | % | ||||||||||

The balance of the allowance for loan losses was $14.5 million as of December 31, 2006, compared to $13.6 million and $11.7 million as of December 31, 2005 and 2004, respectively. The allowance for loan losses was 1.19% of outstanding loans as of both December 31, 2006, and 2005 and 1.10% as of December 31, 2004. The allowance as a percentage of loans during 2006 and 2005 remained consistent and increased when compared to 2004 due to the following:

| • | An increase in commercial real estate concentration over the last several years. Including multifamily, nonresidential and junior liens, commercial real estate loans which remained stable in 2006 and grew $85.7 million in 2005, representing growth of and 16.9%. |

| • | A real estate market that remains soft.Commercial real estate activity experienced a significant decline in our markets during the second half of 2006. The number of building permits issued, median home sales prices, new homes in inventory, number of days on market, housing affordability and new mortgage originations indicate that a general cyclical decline in the residential real estate market is occurring as well. |

| • | The growing popularity of non-traditional mortgage products. While the Company’s affiliate banks do not originate non-traditional mortgages within their own portfolios, we do have the risk associated with borrowers who have them. The allowance analysis has considered this and other factors in the determination of soft factors. |

21