UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number :811-08231

SPIRIT OF AMERICA INVESTMENT FUND, INC.

(Exact name of registrant as specified in charter)

477 Jericho Turnpike

P.O. Box 9006

Syosset, NY 11791-9006

(Address of principal executive offices) (Zip code)

Mr. David Lerner

David Lerner Associates

477 Jericho Turnpike

P.O. Box 9006

Syosset, NY 11791-9006

(Name and address of agent for service)

Registrant’s telephone number, including area code:1-516-390-5565

Date of fiscal year end:November 30

Date of reporting period:November 30, 2018

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

| |

ANNUAL REPORT

NOVEMBER 30, 2018 | |

Spirit of America Energy Fund | |

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Fund’s shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports from the Fund or from your financial intermediary, David Lerner Associates Inc. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

You may elect to receive all future reports in paper free of charge. You can inform the Fund that you wish to continue receiving paper copies of your shareholder reports by following the instructions included with this document or by calling Shareholder Services at (800) 452-4892. Your election to receive reports in paper will apply to all funds held within the fund family.

The Fund does not currently offer electronic delivery of its shareholder reports. Should the Fund begin to offer this method of delivery, however, we will notify you and you will be able to sign up for electronic delivery of the Fund’s shareholder reports at that time. Instructions will then be provided by the Fund or your financial intermediary, David Lerner Associates Inc.

MESSAGE TO OUR SHAREHOLDERS (UNAUDITED)

Dear Shareholder,

We would like to start off by thanking you, our clients, for investing in the Spirit of America Energy Fund. We believe that the future of energy is bright. The idea of energy independence in this country is one we find appealing and probable. We believe as American energy continues to assert itself on the world stage, the benefits could be substantial.

When we first began this fund in July of 2014 we believed that there has always been a strong and consistent demand for energy; that new sources of energy were creating investment opportunities; and that there was potential for long term growth in the energy sector. This vision is still firmly in place.

The Spirit of America Energy Fund’s investment philosophy moving into 2019 will be to continue to invest in the energy infrastructure of our country. We believe there is long term value to investing in companies that are involved in the midstream oil and gas sector. We are dedicated to diligently focusing on quality companies with the potential for long term growth.

At the end of the 2018 fiscal year, we are extremely proud to highlight that the Energy Fund has over $500 million in assets under management and over 18,000 investors.

We thank you for your support and look forward to a prosperous and successful 2019.

Sincerely,

|

David Lerner |

|

William Mason |

ENERGY FUND | | 1 |

MANAGEMENT DISCUSSION OF FUND PERFORMANCE (UNAUDITED)

Economic Summary

At the end of November, the U.S. Bureau of Economic Analysis released its second reading of the third quarter of 2018 gross domestic product (GDP) leaving the estimate unchanged from the previous reading 3.5% annual growth. This pace represents a slowdown in the pace of growth compared to the second quarter of 2018 when the economy grew at a 4.2% pace. The third quarter’s growth rate is still higher than first quarter’s 2.2% pace and the fourth quarter’s 2.0% pace. Growth is being driven by the White House’s $1.5 trillion tax cut package, which has given consumer spending a jolt and bolstered business investment.

The U.S. Bureau of Labor Statistics reported the U.S. economy added 155,000 nonfarm payroll jobs in November, falling short of economists’ expectations of 198,000 jobs. In addition to the November jobs report falling below expectations, October’s count was revised lower from an initially reported 250,000 to 237,000. September’s total was revised up slightly. The unemployment rate held steady at 3.7% in November, its lowest rate since 1969. Average hourly earnings, a closely watched sign of whether inflation pressures are building, rose at a 3.1% pace from a year ago. This report comes amid questions over whether the above-trend growth in 2018, the best since the recession ended in mid-2009, can continue as fiscal stimulus fades and interest rates rise. Financial markets have been skittish lately, posting aggressive gains and losses, and the major indexes have been in and out of correction territory.

Minutes from the November meeting of the Federal Open Market Committee (FOMC,) indicated a strong likelihood officials will raise interest rates another quarter-point at the upcoming December meeting. This would be the fourth rate hike of 2018. The fed funds rate is currently targeted at 2% - 2.25%. Of note, two items most frequently mentioned were tariffs and debt. The U.S. and its trading partners, notably China, have been engaged in a volley of tariffs this year. At the same time, corporations, particularly those with weaker balance sheets and lower credit ratings, continue to load up on debt making them more susceptible to a negative shock on economic activity.

Market Commentary

During the Fund’s fiscal year ended November 30, 2018, the S&P 500 provided a total return of 6.27%. The Alerian MLP Index, a leading gauge of energy MLPs, had a total return of 1.21% over the fiscal year. At the same time oil prices dropped 11.27% with U.S. crude oil closing at $50.93, up significantly from its low of $26.21 on February 11, 2016, but down pointedly from its high of the year of 76.41 on October 3rd 2018.

November closed with oil prices edging lower due to concerns of oversupply and a strong dollar but losses were limited by expectations that OPEC (Organization of the Petroleum Exporting Countries) and Russia would agree to some form of production cut over the coming week. The two benchmarks, North Sea Brent and U.S. crude had their weakest month in more than 10 years in November, losing more than 20% as global supply outpaced demand. Oil prices also came under pressure as the dollar rose against a basket of currencies as investors hoped that the United States and China would come to an agreement over trade talks.

Fund Summary

The Spirit of America Energy Fund, SOAEX (the “Fund”), remained diversified across many U.S. geographic areas, with a heavy focus on midstream MLPs. The Fund had a total return of (3.62)% (no load, gross of fees) for fiscal year ended November 30, 2018. This compares to the 6.27% returned by its benchmark, the S&P 500 Index, for the same period. The Fund’s underperformance relative to its benchmark was principally due to its focus solely on the energy segment of the market compared to the S&P 500 which is a broader perspective.

Over the same time period the Fund underperformed the Alerian MLP Index, which had a total return of 1.21%. The main factor in the Fund’s underperformance compared to the Alerian MLP Index was the weightings of a handful of positions in the Oil & Gas Storage & Transportation, or “midstream,” sector classified holdings. The majority of the Fund’s underperformance in the midstream sector was due to the size of the positon of Energy Transfer Partners LP, which had a total return of over 40% for the year. The Alerian held almost a 9% average weighting whereas the Fund held less than half of that position on average for the year. Additionally, stock selection in exploration and production, or “upstream,” classified holdings which generally move in accordance with the price of oil effected the Fund’s performance. Finally, the Fund did not hold any positions in the Coal & Consumable Fuels industry which performed well for the Alerian MLP Index over the year.

2 | | SPIRIT OF AMERICA |

MANAGEMENT DISCUSSION OF FUND PERFORMANCE (UNAUDITED) (CONT.)

The material factors that affected the Fund were market direction and stock selection. The holdings of the Fund were chosen based on consideration of several factors including market capitalization, stable balance sheets relative to peers, and companies with promising growth potential. The Fund did not rely on derivatives or leverage strategies, and focused on U.S. based energy companies.

Including sales charge and expenses, as of November 30, 2018 the Fund’s Class A Shares fiscal year return was (10.50)%.

Summary of Portfolio Holdings(Unaudited) As of November 30, 2018 | ||

Oil & Gas Storage & Transportation (MLP) | 69.09% | $358,676,954 |

Common Stocks (non-MLP) | 24.86% | 129,090,937 |

Oil & Gas Equipment & Services (MLP) | 2.01% | 10,452,541 |

Oil & Gas Refining & Marketing (MLP) | 1.00% | 5,175,311 |

Money Market Funds | 0.13% | 681,708 |

Oil & Gas Exploration & Production (MLP) | 2.09% | 10,857,316 |

Gas Utilities (MLP) | 0.82% | 4,281,575 |

Total Investments | 100.00% | $519,216,342 |

ENERGY FUND | | 3 |

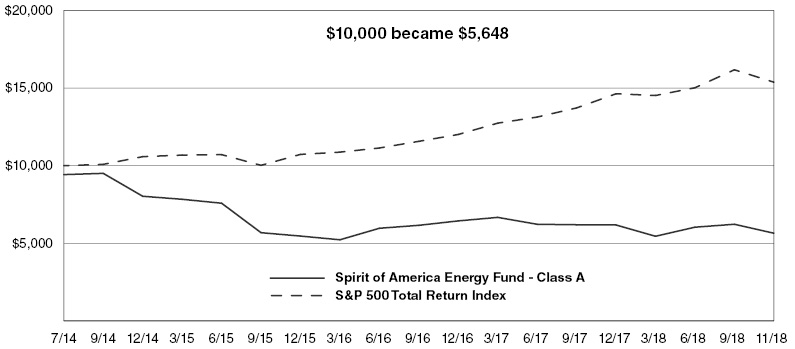

ILLUSTRATION OF INVESTMENT (UNAUDITED)

Average Annual Returns(Unaudited) For the periods ended November 30, 2018 | |||

1 Year | 3 Year | Since Inception | |

Class A Shares — no load | (4.95)% | (1.23)% | (11.01)% |

Class A Shares — with load | (10.50)% | (3.15)% | (12.20)% |

Class C Shares — no load1 | (5.60)% | (2.24)% | (11.84)% |

Class C Shares — with load1 | (6.40)% | (2.24)% | (11.84)% |

S&P 500 Index2 | 6.27% | 12.16% | 10.30% |

The Fund’s past performance does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Total returns, with load, include the 5.75% maximum sales charge for the Class A Shares or the 1.00% maximum deferred sales charge for the Class C Shares.

1 | Class C Shares commenced operations on March 15, 2016. Prior to March 15, 2016, performance is based on the performance of Class A Shares adjusted for the Class C Shares’ 12b-1 fees and contingent deferred sales charge. |

2 | S&P 500 Index is an unmanaged capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The performance of an index assumes no transaction costs, taxes, management fees or other expenses. A direct investment in an index is not possible. |

Fixed Distribution Policy(Unaudited)

The Board of Directors of the Fund has set a fixed distribution per share policy of $1.6875 per year payable in twelve payments of $0.140625; two payments in January and one payment in each of February through November. The per share distribution amounts have been adjusted for a 1:3 reverse stock split and a 25% reduction that occurred on April 20, 2018.

Shareholders should not draw any conclusions about the Fund’s investment performance from the amount of these distributions.

The Fund’s total return based on net asset value is presented in the table above as well as in the Financial Highlights tables.

4 | | SPIRIT OF AMERICA |

ILLUSTRATION OF INVESTMENT (UNAUDITED) (CONT.)

Growth of $10,000(Unaudited)

(includes one-time 5.75% maximum sales charge and reinvestment of all distributions)

The graph below compares the increase in value of a $10,000 investment in the Spirit of America Energy Fund Class A Shares with the performance of the S&P 500® Index. The values and returns for Spirit of America Energy Fund Class A Shares include reinvested dividends and the impact of the maximum sales charge of 5.75% placed on purchases. The returns shown do not reflect taxes that a shareholder would pay on fund distributions or on the redemption of fund shares.

* | Commenced operations on July 10, 2014. |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and net asset value will fluctuate so that an investor’s shares, when redeemed may be worth more or less than the original cost. To obtain performance information current to the most recent month-end, please call 1-800- 452-4892.

S&P 500 Index is an unmanaged capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The performance of an index assumes no transaction costs, taxes, management fees or other expenses. A direct investment in an index is not possible.

ENERGY FUND | | 5 |

SCHEDULE OF INVESTMENTS | NOVEMBER 30, 2018

Shares | Market Value | |||||||

Master Limited Partnership — Common Stocks 75.73% | ||||||||

Gas Utilities 0.83% | ||||||||

AmeriGas Partners LP | 115,220 | $ | 4,281,575 | |||||

Oil & Gas Equipment & Services 2.03% | ||||||||

USA Compression Partners LP | 722,859 | 10,452,541 | ||||||

Oil & Gas Exploration & Production 2.11% | ||||||||

Viper Energy Partners LP | 361,549 | 10,857,316 | ||||||

Oil & Gas Refining & Marketing 1.01% | ||||||||

EnLink Midstream Partners LP | 391,180 | 5,175,311 | ||||||

Oil & Gas Storage & Transportation 69.75% | ||||||||

Andeavor Logistics LP | 305,770 | 11,411,336 | ||||||

Antero Midstream GP LP | 80,050 | 1,185,541 | ||||||

Antero Midstream Partners LP | 733,684 | 20,293,699 | ||||||

BP Midstream Partners LP | 183,296 | 3,092,204 | ||||||

Buckeye Partners LP | 147,047 | 4,346,709 | ||||||

Cheniere Energy Partners LP | 632,384 | 23,828,229 | ||||||

CNX Midstream Partners LP | 786,353 | 14,232,989 | ||||||

Crestwood Equity Partners LP | 189,775 | 5,636,318 | ||||||

DCP Midstream LP | 248,000 | 8,451,840 | ||||||

Dominion Energy Midstream Partners LP | 271,241 | 5,039,658 | ||||||

Enable Midstream Partners LP | 714,308 | 9,528,869 | ||||||

Enbridge Energy Partners LP | 157,073 | 1,707,384 | ||||||

Energy Transfer Equity LP | 1,283,170 | 18,695,787 | ||||||

Enterprise Products Partners LP | 857,024 | 22,496,880 | ||||||

EQT GP Holdings LP | 201,361 | 4,031,247 | ||||||

EQT Midstream Partners LP | 325,253 | 15,501,558 | ||||||

Genesis Energy LP | 238,392 | 5,256,544 | ||||||

Global Partners LP | 110,797 | 1,914,572 | ||||||

Golar LNG Partners LP | 135,013 | 1,640,408 | ||||||

Hess Midstream Partners LP | 260,035 | 5,008,274 | ||||||

Holly Energy Partners LP | 420,075 | 11,816,710 | ||||||

Magellan Midstream Partners LP | 306,165 | 18,516,859 | ||||||

MPLX LP | 650,858 | 21,562,926 | ||||||

NGL Energy Partners LP | 154,568 | 1,434,391 | ||||||

Noble Midstream Partners LP | 294,419 | 9,754,101 | ||||||

PBF Logistics LP | 84,225 | 1,691,238 | ||||||

Phillips 66 Partners LP | 355,039 | 16,651,329 | ||||||

Plains All American Pipeline LP | 320,549 | 7,382,243 | ||||||

Shell Midstream Partners LP | 747,343 | 14,079,942 | ||||||

Spectra Energy Partners LP | 293,859 | 10,652,389 | ||||||

Sprague Resources LP | 220,282 | 3,925,425 | ||||||

Summit Midstream Partners LP | 157,364 | 1,934,004 | ||||||

Sunoco LP | 213,729 | 5,975,863 | ||||||

Tallgrass Energy LP | 287,587 | 6,142,858 | ||||||

TC PipeLines LP | 74,369 | 2,215,453 | ||||||

Teekay LNG Partners LP | 220,861 | 2,990,458 | ||||||

Valero Energy Partners LP | 413,740 | 17,406,042 | ||||||

See accompanying notes which are an integral part of these financial statements

6 | | SPIRIT OF AMERICA |

SCHEDULE OF INVESTMENTS (CONT.) | NOVEMBER 30, 2018

Shares | Market Value | |||||||

Oil & Gas Storage & Transportation (cont.) | ||||||||

Western Gas Equity Partners LP | 201,673 | $ | 5,844,484 | |||||

Western Gas Partners LP | 346,539 | 15,400,193 | ||||||

| 358,676,954 | ||||||||

Total Master Limited Partnership — Common Stocks | ||||||||

(Cost $397,495,186) | 389,443,697 | |||||||

Common Stocks 25.10% | ||||||||

Gas Utilities 1.36% | ||||||||

UGI Corporation | 122,000 | 7,008,900 | ||||||

Integrated Oil & Gas 3.00% | ||||||||

Chevron Corporation | 42,425 | 5,046,029 | ||||||

Exxon Mobil Corporation | 63,565 | 5,053,418 | ||||||

Occidental Petroleum Corporation | 76,300 | 5,361,601 | ||||||

| 15,461,048 | ||||||||

Mortgage REITs 0.27% | ||||||||

Hannon Armstrong Sustainable Infrastructure Capital, Inc. | 61,441 | 1,403,927 | ||||||

Oil & Gas Exploration & Production 0.89% | ||||||||

Marathon Oil Corporation | 116,300 | 1,941,047 | ||||||

Parsley Energy, Inc., Class A(a) | 129,650 | 2,609,854 | ||||||

| 4,550,901 | ||||||||

Oil & Gas Refining & Marketing 6.05% | ||||||||

Marathon Petroleum Corporation | 223,411 | 14,557,461 | ||||||

Phillips 66 | 81,887 | 7,658,072 | ||||||

Valero Energy Corporation | 111,314 | 8,893,989 | ||||||

| 31,109,522 | ||||||||

Oil & Gas Storage & Transportation 13.53% | ||||||||

Cheniere Energy, Inc.(a) | 28,420 | 1,737,030 | ||||||

Enbridge, Inc. | 105,436 | 3,450,920 | ||||||

EnLink Midstream, LLC | 355,450 | 4,062,794 | ||||||

Kinder Morgan, Inc. | 1,079,662 | 18,429,830 | ||||||

ONEOK, Inc. | 221,648 | 13,615,837 | ||||||

Targa Resources Corporation | 266,400 | 11,889,432 | ||||||

TransCanada Corporation | 27,550 | 1,127,346 | ||||||

Williams Companies, Inc. (The) | 602,032 | 15,243,450 | ||||||

| 69,556,639 | ||||||||

Total Common Stocks | ||||||||

(Cost $128,246,735) | 129,090,937 | |||||||

See accompanying notes which are an integral part of these financial statements

ENERGY FUND | | 7 |

SCHEDULE OF INVESTMENTS (CONT.) | NOVEMBER 30, 2018

Shares | Market Value | |||||||

Money Market Funds 0.13% | ||||||||

Morgan Stanley Institutional Liquidity Government Portfolio, Institutional Class, 2.09%(b) | 681,708 | $ | 681,708 | |||||

Total Money Market Funds | ||||||||

(Cost $681,708) | 681,708 | |||||||

Total Investments — 100.96% | ||||||||

(Cost $526,423,629) | 519,216,342 | |||||||

Liabilities in Excess of Other Assets — (0.96)% | (4,917,315 | ) | ||||||

NET ASSETS — 100.00% | $ | 514,299,027 | ||||||

(a) | Non-income producing security. |

(b) | Rate disclosed is the seven day effective yield as of November 30, 2018. |

The sectors shown on the schedule of investments are based on the Global Industry Classification Standard, or GICS® (“GICS”). The GICS was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC (“S&P”). GICS is a service mark of MSCI, Inc. and S&P and has been licensed for use by Ultimus Fund Solutions, LLC.

See accompanying notes which are an integral part of these financial statements

8 | | SPIRIT OF AMERICA |

STATEMENT OF ASSETS AND LIABILITIES | NOVEMBER 30, 2018

ASSETS | ||||

Investments in securities at value (cost $526,423,629) | $ | 519,216,342 | ||

Receivable for Fund shares sold | 191,802 | |||

Dividends and interest receivable | 413,275 | |||

Income tax receivable | 52,020 | |||

Prepaid expenses | 27,755 | |||

TOTAL ASSETS | 519,901,194 | |||

LIABILITIES | ||||

Payable for Fund shares redeemed | 757,815 | |||

Payable for distributions to shareholders | 4,109,997 | |||

Payable for investment advisory fees | 413,139 | |||

Payable for distribution (12b-1) fees | 112,357 | |||

Payable for accounting and administration fees | 23,049 | |||

Payable for transfer agent fees | 13,551 | |||

Franchise tax expense | 7,384 | |||

Other accrued expenses | 164,875 | |||

TOTAL LIABILITIES | 5,602,167 | |||

NET ASSETS | $ | 514,299,027 | ||

SOURCE OF NET ASSETS | ||||

As of November 30, 2018, net assets consisted of: | ||||

Paid-in capital | $ | 632,437,802 | ||

Accumulated earnings (deficit), net of deferred taxes | (118,138,775 | ) | ||

NET ASSETS | $ | 514,299,027 | ||

NET ASSETS: | ||||

Class A Shares | $ | 508,512,361 | ||

Class C Shares | $ | 5,786,666 | ||

SHARES OUTSTANDING ($0.001 par value, 500,000,000 authorized shares): | ||||

Class A Shares | 52,276,749 | |||

Class C Shares | 611,691 | |||

NET ASSET VALUE AND REDEMPTION PRICE PER SHARE | ||||

Class A Shares | $ | 9.73 | ||

Class C Shares | $ | 9.46 | ||

OFFERING PRICE PER SHARE (100%/(100%-maximum sales charge) of net asset value adjusted to the nearest cent) per share: | ||||

Class A Shares | $ | 10.32 | ||

MAXIMUM SALES CHARGE: | ||||

Class A Shares | 5.75 | % |

See accompanying notes which are an integral part of these financial statements

ENERGY FUND | | 9 |

STATEMENT OF OPERATIONS

For the Year Ended | ||||

INVESTMENT INCOME | ||||

MLP Distributions | $ | 35,667,843 | ||

Less Return of Capital | (35,667,843 | ) | ||

Dividends (net of foreign taxes withheld of $52,973) | 5,148,637 | |||

Interest | 50,353 | |||

TOTAL INVESTMENT INCOME | 5,198,990 | |||

EXPENSES | ||||

Investment advisory | 5,866,335 | |||

Distribution (12b-1) — Class A | 1,527,779 | |||

Accounting and Administration | 316,601 | |||

Sub transfer agent | 143,622 | |||

Transfer agent | 151,190 | |||

Printing | 104,904 | |||

Directors | 67,377 | |||

Distribution (12b-1) — Class C | 63,983 | |||

Legal | 51,370 | |||

Custodian | 41,920 | |||

Registration | 41,276 | |||

Auditing | 38,098 | |||

Insurance | 23,869 | |||

Chief Compliance Officer | 13,239 | |||

Interest | 8,136 | |||

Line of credit | 2,862 | |||

Other | 96,923 | |||

TOTAL EXPENSES | 8,559,484 | |||

NET INVESTMENT LOSS BEFORE TAXES | (3,360,494 | ) | ||

Current and deferred income tax expense/(benefit), net of valuation allowance | — | |||

NET INVESTMENT LOSS NET OF DEFERRED TAXES | (3,360,494 | ) | ||

REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS | ||||

Net realized loss from investment transactions | (31,274,131 | ) | ||

Net realized loss on foreign currency transactions | (2,808 | ) | ||

Current and deferred income tax expense/(benefit), net of valuation allowance | — | |||

Net realized loss, net of deferred taxes | (31,276,939 | ) | ||

Net change in unrealized appreciation of investments | 7,585,928 | |||

Current and deferred income tax expense/(benefit), net of valuation allowance | — | |||

NET REALIZED AND UNREALIZED LOSS ON INVESTMENTS | (23,691,011 | ) | ||

NET DECREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | (27,051,505 | ) | |

See accompanying notes which are an integral part of these financial statements

10 | | SPIRIT OF AMERICA |

STATEMENTS OF CHANGES IN NET ASSETS

For the Year Ended | For the Year Ended | |||||||

OPERATIONS | ||||||||

Net investment loss net of deferred taxes | $ | (3,360,494 | ) | $ | (5,355,530 | ) | ||

Net realized loss on investment transactions, net of deferred taxes | (31,276,939 | ) | (11,802,858 | ) | ||||

Net change in unrealized appreciation (depreciation) of investments, net of deferred taxes | 7,585,928 | (14,639,525 | ) | |||||

Net increase (decrease) in net assets resulting from operations | (27,051,505 | ) | (31,797,913 | ) | ||||

DISTRIBUTIONS TO SHAREHOLDERS | ||||||||

From return of capital: | ||||||||

Class A | (99,904,176 | ) | (107,701,525 | ) | ||||

Class C | (1,075,174 | ) | (883,178 | ) | ||||

Total distributions to shareholders | (100,979,350 | ) | (108,584,703 | ) | ||||

CAPITAL TRANSACTIONS | ||||||||

Class A Shares: | ||||||||

Shares sold | 78,395,936 | 238,396,408 | ||||||

Shares issued from reinvestment of distributions | 46,630,482 | 53,781,151 | ||||||

Shares redeemed | (136,495,008 | ) | (60,761,329 | ) | ||||

Total Class A Shares | (11,468,590 | ) | 231,416,230 | |||||

Class C Shares: | ||||||||

Shares sold | 1,469,882 | 5,050,350 | ||||||

Shares issued from reinvestment of distributions | 549,796 | 393,153 | ||||||

Shares redeemed | (1,128,082 | ) | (603,058 | ) | ||||

Total Class C Shares | 891,596 | 4,840,445 | ||||||

Increase in net assets derived from capital share transactions | (10,576,994 | ) | 236,256,675 | |||||

Total increase (decrease) in net assets | (138,607,849 | ) | 95,874,059 | |||||

NET ASSETS | ||||||||

Beginning of period | 652,906,876 | 557,032,817 | ||||||

End of period | $ | 514,299,027 | $ | 652,906,876 | ||||

SHARE TRANSACTIONS | ||||||||

Class A Shares (b): | ||||||||

Shares sold | 6,735,557 | 16,499,067 | ||||||

Shares issued from reinvestment of distributions | 4,156,468 | 3,891,994 | ||||||

Shares redeemed | (12,135,121 | ) | (4,495,090 | ) | ||||

Total Class A Shares | (1,243,096 | ) | 15,895,971 | |||||

Class C Shares (b): | ||||||||

Shares sold | 128,569 | 357,012 | ||||||

Shares issued from reinvestment of distributions | 50,346 | 29,290 | ||||||

Shares redeemed | (101,246 | ) | (47,182 | ) | ||||

Total Class C Shares | 77,669 | 339,120 | ||||||

Increase (decrease) in shares outstanding | (1,165,427 | ) | 16,235,091 | |||||

(a) | As of November 30, 2017, accumulated net investment loss was $12,001,187. |

(b) | Share amounts have been adjusted for 1:3 reverse stock split that occurred on April 20, 2018. |

See accompanying notes which are an integral part of these financial statements

ENERGY FUND | | 11 |

FINANCIAL HIGHLIGHTS — CLASS A

The table below sets forth financial data for one share of beneficial interest outstanding throughout each period presented. *

For the | For the | For the | For the | For the | ||||||||||||||||

Net Asset Value, Beginning of Period | $ | 12.09 | $ | 14.73 | $ | 16.35 | $ | 26.79 | $ | 30.00 | ||||||||||

Income from Investment Operations: | ||||||||||||||||||||

Net investment income (loss)(b) | (0.06 | ) | (0.12 | ) | (0.12 | ) | (0.27 | ) | (0.15 | ) | ||||||||||

Return of capital(b) | 0.64 | 0.75 | 0.90 | 1.53 | 0.78 | |||||||||||||||

Net realized and unrealized loss on investments | (1.06 | ) | (1.02 | ) | (0.15 | ) | (9.45 | ) | (3.09 | ) | ||||||||||

Total income from investment operations | (0.48 | ) | (0.39 | ) | 0.63 | (8.19 | ) | (2.46 | ) | |||||||||||

Less distributions: | ||||||||||||||||||||

Distributions from net investment income | — | — | — | — | (0.03 | ) | ||||||||||||||

From return of capital | (1.88 | ) | (2.25 | ) | (2.25 | ) | (2.25 | ) | (0.72 | ) | ||||||||||

Total distributions | (1.88 | ) | (2.25 | ) | (2.25 | ) | (2.25 | ) | (0.75 | ) | ||||||||||

| ||||||||||||||||||||

Net Asset Value, End of Period | $ | 9.73 | $ | 12.09 | $ | 14.73 | $ | 16.35 | $ | 26.79 | ||||||||||

Total Return(c) | (4.95 | )% | (3.62 | )% | 5.17 | % | (32.13 | )% | (8.35 | )%(d) | ||||||||||

Ratios/Supplemental Data: | ||||||||||||||||||||

Net assets, end of period (000) | $ | 508,512 | $ | 646,562 | $ | 554,182 | $ | 291,733 | $ | 121,211 | ||||||||||

Ratio of expenses to average net assets: | ||||||||||||||||||||

Before expense waivers or recoupment and deferred tax benefit | 1.38 | % | 1.38 | % | 1.43 | % | 1.49 | % | 1.86 | %(e) | ||||||||||

Net of expense waivers or recoupment and before deferred tax benefit | 1.38 | % | 1.38 | % | 1.43 | % | 1.52 | % | 1.55 | %(e) | ||||||||||

Deferred tax expense(f) | 0.00 | % | 0.00 | % | 0.00 | % | 0.02 | % | 0.00 | %(e) | ||||||||||

Total net expenses | 1.38 | % | 1.38 | % | 1.43 | % | 1.54 | % | 1.55 | %(e) | ||||||||||

Ratio of net investment income (loss) to average net assets: | ||||||||||||||||||||

Before expense waivers or recoupment and deferred tax benefit | (0.54 | )% | (0.79 | )% | (0.87 | )% | (1.12 | )% | (1.76 | )%(e) | ||||||||||

Net of expense waivers or recoupment and before deferred tax benefit | (0.54 | )% | (0.79 | )% | (0.87 | )% | (1.15 | )% | (1.45 | )%(e) | ||||||||||

Deferred tax benefit (loss)(g) | 0.00 | % | 0.00 | % | 0.00 | % | (0.06 | )% | 0.51 | %(e) | ||||||||||

Net investment loss | (0.54 | )% | (0.79 | )% | (0.87 | )% | (1.21 | )% | (0.94 | )%(e) | ||||||||||

Portfolio turnover | 19 | % | 11 | % | 18 | % | 15 | % | 12 | %(d) | ||||||||||

* | Share amounts have been adjusted for 1:3 reverse stock split that occurred on April 20, 2018. |

(a) | For the period July 10, 2014 (commencement of operations) to November 30, 2014. |

(b) | Calculated using average shares method. |

(c) | Calculation does not reflect sales load. |

(d) | Calculation is not annualized. |

(e) | Calculation is annualized. |

(f) | Deferred tax expense (benefit) estimate for the ratio calculation is derived from the net investment income (loss) and realized and unrealized gain (loss). |

(g) | Deferred tax benefit (expense) estimate for the ratio calculation is derived from the net investment income (loss) only. |

See accompanying notes which are an integral part of these financial statements

12 | | SPIRIT OF AMERICA |

FINANCIAL HIGHLIGHTS — CLASS C

The table below sets forth financial data for one share of beneficial interest outstanding throughout each period presented. *

For the | For the | For the | ||||||||||

Net Asset Value, Beginning of Period | $ | 11.88 | $ | 14.64 | $ | 13.41 | ||||||

Income from Investment Operations: | ||||||||||||

Net investment income (loss)(b) | (0.14 | ) | (0.21 | ) | (0.18 | ) | ||||||

Return of capital(b) | 0.62 | 0.75 | 0.72 | |||||||||

Net realized and unrealized gain on investments | (1.02 | ) | (1.05 | ) | 2.37 | |||||||

Total income from investment operations | (0.54 | ) | (0.51 | ) | 2.91 | |||||||

Less distributions: | ||||||||||||

From return of capital | (1.88 | ) | (2.25 | ) | (1.68 | ) | ||||||

Total distributions | (1.88 | ) | (2.25 | ) | (1.68 | ) | ||||||

| ||||||||||||

Net Asset Value, End of Period | $ | 9.46 | $ | 11.88 | $ | 14.64 | ||||||

Total Return(c) | (5.60 | )% | (4.52 | )% | 21.58 | %(d) | ||||||

Ratios/Supplemental Data: | ||||||||||||

Net assets, end of period (000) | $ | 5,787 | $ | 6,344 | $ | 2,851 | ||||||

Ratio of expenses to average net assets: | ||||||||||||

Before deferred tax benefit | 2.13 | % | 2.13 | % | 2.16 | %(e) | ||||||

Deferred tax expense(f) | 0.00 | % | 0.00 | % | 0.00 | %(e) | ||||||

Total net expenses | 2.13 | % | 2.13 | % | 2.16 | %(e) | ||||||

Ratio of net investment income (loss) to average net assets: | ||||||||||||

Before deferred tax benefit | (1.28 | )% | (1.49 | )% | (1.67 | )%(e) | ||||||

Deferred tax benefit (loss)(g) | 0.00 | % | 0.00 | % | 0.00 | %(e) | ||||||

Net investment loss | (1.28 | )% | (1.49 | )% | (1.67 | )%(e) | ||||||

Portfolio turnover | 19 | % | 11 | % | 18 | %(d) | ||||||

* | Share amounts have been adjusted for 1:3 reverse stock split that occurred on April 20, 2018. |

(a) | For the period March 15, 2016 (commencement of operations) to November 30, 2016. |

(b) | Calculated using average shares method. |

(c) | Calculation does not reflect contingent deferred sales charge. |

(d) | Calculation is not annualized. |

(e) | Calculation is annualized. |

(f) | Deferred tax expense (benefit) estimate for the ratio calculation is derived from the net investment income (loss) and realized and unrealized gain (loss). |

(g) | Deferred tax benefit (expense) estimate for the ratio calculation is derived from the net investment income (loss) only. |

See accompanying notes which are an integral part of these financial statements

ENERGY FUND | | 13 |

NOTES TO FINANCIAL STATEMENTS | NOVEMBER 30, 2018

Note 1 – Organization

Spirit of America Energy Fund (the “Fund”), a series of Spirit of America Investment Fund, Inc. (the “Company”), is an open-end mutual fund registered under the Investment Company Act of 1940, as amended (the “1940 Act”). The Company was incorporated under the laws of Maryland on May 15, 1997. The Fund commenced operations on July 10, 2014. The Fund seeks to provide shareholders with total return, which may consist of income dividends, distributions of long-term capital gains and/or return of capital, through diversified exposure to securities of companies principally engaged in activities in the energy industry, such as the exploration, production, and transmission of energy or energy fuels; the making and servicing of component products for such activities; energy research; and energy conservation.

The Fund currently offers Class A Shares and Class C Shares. Each class of shares for the Fund has identical rights and privileges except with respect to distribution (12b-1) and service fees, voting rights on matters affecting a single class of shares, exchange privileges of each class of shares and sales charges. The price at which the Fund will offer or redeem shares is the net asset value (“NAV”) per share next determined after the order is considered received, subject to any applicable front end or contingent deferred sales charges. Class A shares have a maximum sales charge on purchases of 5.75% as a percentage of the original purchase price. A Contingent Deferred Sales Charge (“CDSC”) of 1.00% may be imposed on redemptions of Class A shares that were purchased within one year of the redemption date where an indirect commission was paid. A CDSC of 1.00% on Class C Shares applies to shares sold within 13 months of purchase.

Effective April 20, 2018 the Fund underwent a 1-for-3 reverse share split. The effect of the reverse share split transactions was to divide the number of outstanding shares of the Fund by the reverse split factor, with a corresponding increase in the net asset value per share. These transactions did not change the net assets of the Fund or the value of a shareholder’s investment. The historical share transactions presented in the Statements of Changes in Net Assets and per share data presented in the Financial Highlights have been adjusted retroactively to give effect to the reverse share split.

Note 2 – Significant Accounting Policies

The Fund is an investment company and follows accounting and reporting guidance under Financial Accounting Standards Board Accounting Standards Codification (“ASC”) Topic 946, “Financial Services-Investment Companies”. The following is a summary of significant accounting policies consistently followed by the Fund in the preparation of its financial statements. These policies are in conformity with generally accepted accounting principles in the United States of America (“GAAP”) for investment companies.

A. Security Valuation: The offering price and net asset value (“NAV”) per share for the Fund are calculated as of the close of regular trading on the New York Stock Exchange (“NYSE”), currently 4:00 p.m., Eastern Time on each day the NYSE is open for trading. The Fund’s securities are valued at the official close or the last reported sales price on the principal exchange on which the security trades, or if no sales price is reported, the mean of the latest bid and asked prices is used. Securities traded over-the-counter are priced at the mean of the latest bid and asked prices. Unlisted securities traded in the over-the-counter market are valued using an evaluated quote provided by the independent pricing service, or, if an evaluated quote is unavailable, such securities are valued using prices received from dealers, provided that if the dealer supplies both bid and ask prices, the price to be used is the mean of the bid and asked prices. The independent pricing service derives an evaluated quote by obtaining dealer quotes, analyzing the listed markets, reviewing trade execution data and employing sensitivity analysis. Evaluated quotes may also reflect appropriate factors such as individual characteristics of the issue, communications with broker-dealers, and other market data. Fund securities for which market quotations are not readily available are valued at fair value as determined in good faith under procedures established by and under the supervision of the Board.

B. Fair Value Measurements: Various inputs are used in determining the fair value of investments which are as follows:

● | Level 1 – | Inputs that reflect unadjusted quoted prices in active markets for identical assets or liabilities that the Fund has the ability to access at the measurement date. |

● | Level 2 – | Observable inputs other than quoted prices included in level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument on an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data. |

14 | | SPIRIT OF AMERICA |

NOTES TO FINANCIAL STATEMENTS (CONT.) | NOVEMBER 30, 2018

● | Level 3 – | Unobservable inputs based on the best information available in the circumstances, to the extent observable inputs are not available (including the Fund’s own assumptions used in determining the fair value of investments). |

The summary of inputs used to value the Fund’s investments as of November 30, 2018 is as follows:

| Level 1 | Level 2 | Level 3 | Total | ||||||||||||

Investment Securities: | ||||||||||||||||

Master Limited Partnerships - Common Stocks | $ | 389,443,697 | $ | — | $ | — | $ | 389,443,697 | ||||||||

Common Stocks | 129,090,937 | — | — | 129,090,937 | ||||||||||||

Money Market Funds | 681,708 | — | — | 681,708 | ||||||||||||

Total Investment Securities | $ | 519,216,342 | $ | — | $ | — | $ | 519,216,342 | ||||||||

The Fund did not hold any investments at any time during the reporting period in which significant unobservable inputs were used in determining fair value; therefore, no reconciliation of Level 3 securities is included for this reporting period.

C. Investment Income and Securities Transactions: Security transactions are accounted for on the date the securities are purchased or sold (trade date) for financial reporting purposes. Cost is determined and gains and losses are based on the identified cost basis for both financial statement and federal income tax purposes.

Discounts and premiums on securities purchased are accreted and amortized over the lives of the respective securities. Dividend income and distributions to shareholders are reported on the ex-dividend date. Interest income and expenses are accrued daily.

D. Federal Income Taxes: The Fund is taxed as a regular C-corporation for federal income tax purposes. This differs from most investment companies, which elect to be treated as “regulated investment companies” under the Code in order to avoid paying entity level income taxes. Under current law, the Fund is not eligible to elect treatment as a regulated investment company due to its investments primarily in MLPs invested in energy assets. As a result, the Fund will be obligated to pay applicable federal and state corporate income taxes on its taxable income as opposed to most other investment companies which are not so obligated. The Fund expects that a portion of the distributions it receives from MLPs may be treated as a tax-deferred return of capital, thus reducing the Fund’s current tax liability. However, the amount of taxes currently paid by the Fund will vary depending on the amount of income and gains derived from investments and/or sales of MLP interests and such taxes will reduce your return from an investment in the Fund.

The Tax Cuts and Jobs Act (“Tax Reform Bill”) was signed into law on December 22, 2017. The Tax Reform Bill includes changes to the corporate income tax rate and alternative minimum tax (AMT) and modifications to the net operating loss (NOL) deduction. Prior to enactment, the highest marginal federal income tax rate was 35%. The Tax Reform Bill reduced the corporate rate to a flat income tax rate of 21%. The Fund may be subject to a 20% federal alternative minimum tax on its federal alternative taxable income to the extent that its alternative minimum tax exceeds its regular federal income tax. For tax years beginning after December 31, 2017 the Tax Reform Bill repealed the corporate AMT. The Tax Reform Bill eliminated the NOL carryback ability and replaced the 20 year carryforward period with an indefinite carryforward period for any NOLs arising in tax years ending after December 31, 2017. The Tax Reform Bill also established a limitation for any NOLs generated in tax years beginning after December 31, 2017 to the lesser of the aggregate of available NOLs or 80% of taxable income before any NOL utilization.

Cash distributions from MLPs to the Fund that exceed such Fund’s allocable share of such MLP’s net taxable income are considered a tax- deferred return of capital that will reduce the Fund’s adjusted tax basis in the equity securities of the MLP. These reductions in such Fund’s adjusted tax basis in the MLP equity securities will increase the amount of gain (or decrease the amount of loss) recognized by the Fund on a subsequent sale of the securities. The Fund will accrue deferred income taxes for any future tax liability associated with (i) that portion of MLP distributions considered to be a tax-deferred return of capital as well as (ii) capital appreciation of its investments. Upon the sale of an MLP security, the Fund may be liable for previously deferred taxes. The Fund will rely to some extent on information provided by the MLPs, which is not necessarily timely, to estimate deferred tax liability for purposes of financial statement reporting and determining the NAV. From time to time, Spirit of America Energy Fund will modify the estimates or assumptions related

ENERGY FUND | | 15 |

NOTES TO FINANCIAL STATEMENTS (CONT.) | NOVEMBER 30, 2018

to the Fund’s deferred tax liability as new information becomes available. The Fund will generally compute deferred income taxes based on the marginal regular federal income tax rate applicable to corporations and an assumed rate attributable to state taxes.

Since the Fund will be subject to taxation on its taxable income, the NAV of Fund shares will also be reduced by the accrual of any deferred tax liabilities. The Index, however, is calculated without any adjustments for taxes. As a result, the Fund’s after tax performance could differ significantly from the Index even if the pretax performance of the Fund and the performance of the Index are closely correlated.

The Fund’s income tax expense/(benefit) consists of the following:

November 30, 2018 | Current | Deferred | Total | |||||||||

Federal | $ | — | $ | 6,195,580 | $ | 6,195,580 | ||||||

State (net of federal) | — | (1,300,364 | ) | (1,300,364 | ) | |||||||

Valuation Allowance | — | (4,895,216 | ) | (4,895,216 | ) | |||||||

Total tax expense | $ | — | $ | — | $ | — | ||||||

Deferred income taxes reflect the net tax effect of temporary differences between the carrying amount of assets and liabilities for financial reporting and tax purposes.

Components of the Fund’s deferred tax assets and liabilities are as follows:

Deferred tax assets: | As of | |||

Net operating loss carryforward | $ | 21,515,386 | ||

Net capital loss carryforward | 18,220,582 | |||

Other | 17,700 | |||

Valuation Allowance | (29,610,578 | ) | ||

| $ | 10,143,090 | |||

Deferred tax liability: | ||||

Net unrealized gain (loss) on investment securities | $ | (10,143,090 | ) | |

Net Deferred Tax Asset/(Liability) | $ | — | ||

Net operating loss carryforwards are available to offset future taxable income. For net operating losses generated prior to December 31, 2017, net operating loss carryforwards can be carried forward for 20 years and, accordingly, would begin to expire as of November 30, 2035. For tax years after December 31, 2017, net operating losses generated by the Fund in the future are eligible to be carried forward indefinitely. The Fund has net operating loss carryforwards for federal income tax purposes as follows:

Year-Ended | Amount | Expiration | ||||||

November 30, 2015 | $ | 5,229,524 | November 30, 2035 | |||||

November 30, 2016 | 25,466,568 | November 30, 2036 | ||||||

November 30, 2017 | 40,373,794 | November 30, 2037 | ||||||

| November 30, 2018 | 18,131,548 | Indefinite | ||||||

16 | | SPIRIT OF AMERICA |

NOTES TO FINANCIAL STATEMENTS (CONT.) | NOVEMBER 30, 2018

Net capital loss carryforwards are available to offset future capital gains. Capital loss carryforwards can be carried forward for 5 years and, accordingly, would begin to expire as of November 30, 2020. The Fund has net capital loss carryforwards for federal income tax purposes as follows:

Year-Ended | Amount | Expiration | ||||||

November 30, 2015 | $ | 9,221,227 | November 30, 2020 | |||||

November 30, 2016 | 35,470,784 | November 30, 2021 | ||||||

November 30, 2017 | 6,587,134 | November 30, 2022 | ||||||

November 30, 2018 | 24,262,240 | November 30, 2023 | ||||||

The Fund reviews the recoverability of its deferred tax assets based upon the weight of available evidence. When assessing the recoverability of its deferred tax assets, significant weight was given to the effects of potential future realized and unrealized gains on investments and the period over which these deferred tax assets can be realized.

Based upon the Fund’s assessment, it has determined that is it more likely than not that a portion of its deferred tax assets will not be realized through future taxable income of the appropriate character. Accordingly, a valuation allowance has been established for the Fund’s deferred tax assets. The Fund will continue to assess the need for additional valuation allowance in the future. Significant changes in the fair value of its portfolio investments may change the Fund’s assessment of the recoverability of these assets and may impact the valuation allowances recorded against all or a portion of the Fund’s gross deferred tax assets.

Total income tax expense (current and deferred) differs from the amount computed by applying the federal statutory income tax rate of 21% to net investment and realized and unrealized gain/(losses) on investment before taxes as follows:

Year Ended | ||||

Income tax expense at statutory rate | $ | (5,680,816 | ) | |

State income taxes (net of federal effect) | (844,007 | ) | ||

Permanent differences, net | (555,430 | ) | ||

Change in estimated federal and state deferred rate | 11,741,550 | |||

Other | 233,919 | |||

Valuation Allowance | (4,895,216 | ) | ||

Net income tax expense | $ | — | ||

* | The tax rate change listed in the table above is reflective of the change in deferred tax assets and liabilities due to the federal corporate tax rate change enacted by the Tax Reform Bill as of December 22, 2017 (date of enactment). For tax years beginning after December 31, 2017, corporations will be taxed at a flat rate of 21%. |

The Fund recognizes interest accrued related to unrecognized tax benefits and penalties as income tax expense. For the year ended November 30, 2018, the Fund had no accrued penalties or interest.

The Fund recognizes the tax benefits of uncertain tax positions only where the position is “more likely than not” to be sustained assuming examination by tax authorities. Management has analyzed the Fund’s tax positions, and has concluded that no liability for unrecognized tax benefits should be recorded related to uncertain tax positions taken on U.S. tax returns and state tax returns filed since inception of the fund. No U.S. federal or state income tax returns are currently under examination. The tax periods ended, November 30, 2015, November 30, 2016 and November 30, 2017 remain subject to examination by tax authorities in the United States. Due to the nature of the Fund’s investments, the Fund may be required to file income tax returns in several states. The Fund is not aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits will change materially in the next 12 months.

ENERGY FUND | | 17 |

NOTES TO FINANCIAL STATEMENTS (CONT.) | NOVEMBER 30, 2018

The adjusted cost basis of investment and gross unrealized appreciation and depreciation of investments for federal income tax purposes were as follows:

Year Ended | ||||

Gross unrealized appreciation - investment securities | $ | 80,498,599 | ||

Gross unrealized depreciation - investment securities | (38,445,988 | ) | ||

Net unrealized appreciation - investment securities | $ | 42,052,611 | ||

Cost basis of investments | $ | 477,163,731 | ||

E. Use of Estimates: In preparing financial statements in conformity with GAAP, management makes estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements, as well as the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

F. Distributions to Shareholders: The Fund intends to declare and pay distributions monthly which are expected to be characterized as return of capital distributions generated from the Fund’s holdings. The Fund intends to declare and pay income dividends generated from the Fund’s earnings annually, however, the Fund may distribute such dividends more frequently. All such dividends and distributions are generally taxable to the shareholder whether received in cash or reinvested in shares. The final determination of the amount of the Fund’s return of capital distributions for the period will be made after the end of each calendar year. The Fund anticipates that a significant portion of its distributions to shareholders will consist of a tax-free return of capital with respect to an investor’s principal investment for U.S. federal income tax purposes.

G. Allocation of Income, Expenses, Gains and Losses: Income, expenses (other than those attributable to a specific class), gains and losses are allocated on a daily basis to each class of shares based upon the relative proportion of net assets represented by such class. Operating expenses directly attributable to a specific class are charged against the operations of that class.

Note 3 – Purchases and Sales of Securities

Purchases and proceeds from the sales of securities for the fiscal year ended November 30, 2018, excluding short-term investments, were $114,264,156 and $215,014,195, respectively.

Note 4 – Investment Management Fee and Other Transactions with Affiliates

Spirit of America Management Corp. (the “Adviser”) has been retained to act as the Company’s investment adviser pursuant to an Investment Advisory Agreement (the “Advisory Agreement”). The Adviser was incorporated in 1997 and is a registered investment adviser under the Investment Advisers Act of 1940, as amended. Under the Advisory Agreement, the Fund pays the Adviser a monthly fee of 1/12 of 0.95% of the Fund’s average daily net assets. Investment advisory fees for the fiscal year ended November 30, 2018 were $5,866,335.

The Adviser agreed to waive all or a portion of its fees and to reimburse certain expenses so that the total operating expenses of the Fund’s Class A Shares and Class C Shares until April 30, 2019 would not exceed 1.55% and 2.30% of the Fund’s average daily net assets, respectively. The waiver did not include front end or contingent deferred loads, taxes, interest, dividend expenses on short sales, brokerage commissions or expenses incurred in connection with any merger or reorganization or extraordinary expenses such as litigation. Any amounts waived or reimbursed by the Adviser were subject to reimbursement by the Fund within the following three years, provided the Fund is able to make such reimbursement and remain in compliance with the expense limitation as stated above. The Adviser did not waive any fees or reimburse expenses during the fiscal year ended November 30, 2018.

The Fund has adopted a Plan of Distribution (the “12b-1 Plan”) pursuant to Rule 12b-1 under the 1940 Act. The 12b-1 Plan permits the Fund or class, as applicable, to pay David Lerner Associates, Inc. (the “Distributor”) from its own assets for the Distributor’s services and expenses in distributing shares of the Fund (“12b-1 fees”) and providing personal services and/or maintaining shareholder accounts (“service fees”). The Energy Fund’s Class A Shares pay a 12b-1 fee at the annual rate of 0.25% of average daily net assets. With respect to Class C Shares, the fee paid to the Distributor by the Fund is 1.00% of the average daily net assets of the Class C Shares. Of this amount, 0.75% represents distribution fees and

18 | | SPIRIT OF AMERICA |

NOTES TO FINANCIAL STATEMENTS (CONT.) | NOVEMBER 30, 2018

0.25% represents shareholder servicing fees paid to institutions that have agreements with the Distributor to provide such services. Each class of shares of the Energy Fund has exclusive voting rights with respect to its 12b-1 Plan. Since 12b-1 fees are paid out of the assets of the respective share class of the Energy Fund on an on-going basis, over time these fees will increase the cost of your investment and may cost you more than paying other types of sales charges. For the fiscal year ended November 30, 2018, fees paid to the Distributor under the Plan were $1,591,762.

The Fund’s Class A Shares are subject to an initial sales charge imposed at the time of purchase, in accordance with the Fund’s current prospectus. For the fiscal year ended November 30, 2018, sales charges received by the Distributor were $328,826. CDSC fees collected for the fiscal year ended November 30, 2018 were $1,329 for Class A Shares and $3,102 for Class C Shares.

Certain Officers and Directors of the Company are “affiliated persons”, as that term is defined in the 1940 Act, of the Adviser or the Distributor. Each Director of the Company, who is not an affiliated person of the Adviser or Distributor, receives a quarterly retainer of $7,400, $1,500 for each Board meeting attended, and $500 for each committee meeting attended plus reimbursement for certain travel and other out-of-pocket expenses incurred in connection with attending Board meetings. The Company does not compensate the Officers directly for the services they provide. There are no Directors’ fees paid to affiliated Directors of the Company. For the fiscal year ended November 30, 2018, the Fund was allocated $13,239 of the Chief Compliance Officer’s salary.

Note 5 – Concentration and Other Risks

The Fund concentrates its investments in securities and other assets of energy and energy related companies. A fund that invests primarily in a particular sector could experience greater volatility than funds investing in a broader range of industries. Due to the fact that the Fund normally invests at least 80% of its assets in the securities of companies principally engaged in activities in the energy industry, the Fund’s performance largely depends on the overall condition of the energy industry. The energy industry could be adversely affected by energy prices, supply-and- demand for energy resources, and various political, regulatory, and economic factors. Investments in securities of MLPs involve risks that differ from investments in common stock, including risks related to limited control and limited rights to vote on matters affecting the MLP, risks related to potential conflicts of interest between the MLP and the MLP’s general partner, cash flow risks, dilution risks and risks related to the general partner’s right to require unit holders to sell their common units at an undesirable time or price.

Note 6 – Line of Credit

The Fund participates in a short-term credit agreement (“Line of Credit) with The Huntington National Bank, the custodian of the Fund’s investments expiring on May 22, 2019. Borrowing under this agreement bear interest at London Interbank Offered Rate (“LIBOR”) plus 1.500%. Maximum borrowings for the Fund is the lesser of $3,000,000 or 10% of the Fund’s daily market value. During the fiscal year ended November 30, 2018, the Fund’s borrowing activity was as follows:

Total bank line of credit as of November 30, 2018 | $ | 3,000,000 | ||

Average borrowings during period | $ | 361,143 | ||

Number of days outstanding* | 55 | |||

Average interest rate during period | 3.511 | % | ||

Highest balance drawn during period | $ | 2,024,323 | ||

Highest balance interest rate | 3.742 | % | ||

Interest expense incurred | $ | 8,136 | ||

Interest rate at November 30, 2018 | 3.837 | % |

* | Number of days outstanding represents the total days during the fiscal year ended November 30, 2018 that the Fund utilized the line of credit. |

ENERGY FUND | | 19 |

NOTES TO FINANCIAL STATEMENTS (CONT.) | NOVEMBER 30, 2018

Note 7 – Other Matters

In June 2011, several class action complaints were filed against DLA, the Fund’s principal underwriter and distributor, in connection with its role as managing dealer of several unaffiliated Real Estate Investment Trust offerings (“Apple REITs”). The complaints asserted federal and state securities law claims and various state common law claims against DLA. On April 3, 2013, the class action complaints were dismissed, with prejudice, in their entirety. On April 12, 2013, plaintiffs filed a notice of appeal of the class action dismissal. On April 23, 2014, the United States Court of Appeals for the Second Circuit substantially affirmed the April 3, 2013 decision of United States District Judge, Kiyo A. Matsumoto, dismissing with prejudice the class action complaint in In Re Apple REITs Litigation. The Second Circuit held that Judge Matsumoto correctly found that there were no material misrepresentations or omissions in the offering materials for Apple REITs. The appeals court upheld dismissal of ten of the thirteen claims in the case, including all federal and state securities law claims, and also upheld Judge Matsumoto’s refusal to allow plaintiffs to amend their complaint. The appeals court remanded three state common law claims to the District Court for the Eastern District of New York for further proceedings. On March 25, 2015, the District Court dismissed the remaining state common law claims against DLA, with prejudice. Plaintiffs did not file an appeal. Neither the Adviser nor the Fund were parties to these class action litigations.

In October 2013, a class action litigation, titled Lewis v. Delaware Charter Guarantee & Trust Company, et al., (the “Litigation”) was commenced in federal court in Nevada against DLA, the Fund’s principal underwriter and distributor, along with other defendants, alleging, inter alia, breach of fiduciary duty, aiding and abetting breach of fiduciary duty, negligence and misrepresentation. The plaintiffs, purportedly customers who maintained individual retirement accounts at DLA which contained non-traded Apple REIT securities, alleged, among other things, that the defendants failed to accurately provide annual fair market values for those REIT securities. The Litigation was transferred to the U.S. District Court for the Eastern District of New York. On March 30, 2015, the District Court dismissed all claims against DLA, with prejudice. Plaintiffs appealed the decision dismissing the claims. On April 14, 2016, the United States Court of Appeals for the Second Circuit unanimously affirmed judgement of the District Court dismissing the claims against DLA. Plaintiffs did not appeal that dismissal. Neither the Adviser nor the Fund were parties to this Litigation.

Note 8 – Recent Accounting Pronouncement

In August 2018, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (“ASU”) 2018-13, which changes the fair value measurement disclosure requirements of FASB Accounting Standards Codification Topic 820, Fair Value Measurement. The update to Topic 820 includes new, eliminated, and modified disclosure requirements. ASU 2018-13 is effective for fiscal years beginning after December 15, 2019, including interim periods, although early adoption is permitted. Management has evaluated the implications of certain provisions of ASU 2018-13 and has determined to early adopt all aspects related to the removal and modification of certain fair value measurement disclosures under the ASU effective immediately.

Note 9 – Subsequent Events

Management of the Fund has evaluated the need for disclosures resulting from subsequent events through the date these financial statements were issued. Management has determined that there were no items requiring additional disclosure.

20 | | SPIRIT OF AMERICA |

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Directors and Shareholders

Spirit of America Energy Fund

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities of Spirit of America Energy Fund (the “Fund”), a series of Spirit of America Investment Fund, Inc., including the schedule of investments, as of November 30, 2018, the related statement of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, financial highlights for each of the four years in the period then ended and for the period July 10, 2014 (commencement of operations) to November 30, 2014, and the related notes (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund as of November 30, 2018, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended, and the financial highlights for each of the four years in the period then ended and for the period July 10, 2014 (commencement of operations) to November 30, 2014, in conformity with accounting principles generally accepted in the United States of America.

Basis for Opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB. We have served as the Fund’s auditor since 1998.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Fund is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audits we are required to obtain an understanding of internal control over financial reporting, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. Our procedures included confirmation of securities owned as of November 30, 2018 by correspondence with the custodian. We believe that our audits provide a reasonable basis for our opinion.

| TAIT, WELLER & BAKER LLP |

Philadelphia, Pennsylvania

January 28, 2019

ENERGY FUND | | 21 |

DISCLOSURE OF FUND EXPENSES (UNAUDITED)

FOR THE SIX MONTH PERIOD JUNE 1, 2018 TO NOVEMBER 30, 2018

We believe it is important for you to understand the impact of fees regarding your investment. All mutual funds have operating expenses. As a shareholder of the Fund, you incur ongoing costs, which include costs for portfolio management, administrative services, and shareholder reports (like this one), among others. Operating expenses, which are deducted from the Fund’s gross income, directly reduce the investment return of the Fund.

The Fund’s expenses are expressed as a percentage of its average net assets. This figure is known as the expense ratio. The following examples are intended to help you understand the ongoing fees (in dollars) of investing in your Fund and to compare these costs with those of other mutual funds. The examples are based on an investment of $1,000 made at the beginning of the period shown and held for the six month period, June 1, 2018 to November 30, 2018.

Beginning | Ending | Expenses | Expenses | |

Class A Shares | ||||

Actual | $ 1,000.00 | $ 917.90 | 1.39% | $ 6.68 |

Hypothetical(2) | $ 1,000.00 | $ 1,018.10 | 1.39% | $ 7.03 |

Class C Shares | ||||

Actual | $ 1,000.00 | $ 914.20 | 2.14% | $ 10.27 |

Hypothetical(2) | $ 1,000.00 | $ 1,014.34 | 2.14% | $ 10.81 |

(1) | Expenses are equal to the Fund’s annualized expense ratios, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period). |

(2) | Assumes a 5% annual return before expenses. |

This table illustrates your Fund’s costs in two ways:

Actual Fund Return: This section helps you to estimate the actual expenses that you paid over the period. The “Ending Account Value” shown is derived from the Fund’s actual return, the third column shows the period’s annualized expense ratio, and the last column shows the dollar amount that would have been paid by an investor who started with $1,000 in the Fund at the beginning of the period. You may use the information here, together with your account value, to estimate the expenses that you paid over the period.

To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period.”

Hypothetical 5% Return: This section is intended to help you compare your Fund’s costs with those of other mutual funds. It assumes that the Fund had a return of 5% before expenses during the period shown, but that the expense ratio is unchanged. In this case, because the return used is not the Fund’s actual return, the results do not apply to your investment. You can assess your Fund’s costs by comparing this hypothetical example with the hypothetical examples that appear in shareholder reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs such as sales charges (loads), or redemption fees.

22 | | SPIRIT OF AMERICA |

MANAGEMENT OF THE COMPANY (UNAUDITED)

Information pertaining to the Directors and Officers of the Company is set forth below. The Statement of Additional Information includes additional information about the Directors and is available without charge, upon request, by calling 516-390-5565.

Name, (Age) and Address1 | Term of Office2 | Principal Occupation(s) | Number of | Other Directorships |

INTERESTED DIRECTORS | ||||

David Lerner3 (82) Director, Chairman of the Board, President | Since 1998 | Founder, David Lerner Associates, Inc., a registered broker-dealer and the Company’s Distributor; and President, Spirit of America Management Corp., the Company’s investment adviser. | 6 | President and a Director of Spirit of America Management Corp., the Company’s investment adviser. |

Daniel Lerner3 (57) Director | Since 1998 | Senior Vice President, Investment Counselor with David Lerner Associates, Inc., a registered broker-dealer and the Company’s Distributor, since September 2000. | 6 | Director of David Lerner Associates, Inc., a registered broker-dealer and the Company’s Distributor. |

INDEPENDENT DIRECTORS | ||||

Allen Kaufman (82) Director | Since 1998 | President and Chief Executive Officer of K.G.K. Agency, Inc., a property and casualty insurance agency, since 1963.4 | 6 | Director of K.G.K. Agency, Inc., a property and casualty insurance agency. |

Stanley S. Thune (82) Lead Director | Since 1998 | President and Chief Executive Officer, Freight Management Systems, Inc., a third party logistics management company, since 1994; private investor. | 6 | Director of Freight Management Systems, Inc. |

Richard Weinberger (82) Director | Since 2005 | Of Counsel to Ballon Stoll Bader & Nadler, P.C., a mid-sized law firm, since January 2005 to March 2011; Shareholder, Ballon Stoll Bader & Nadler, P.C., January 2000 to December 2004. | 6 | None. |

OFFICERS | ||||

David Lerner President (see biography above) | ||||

Alan P. Chodosh (65) Treasurer and Secretary | Since 2003 (Treasurer) Since 2005 (Secretary) | Senior Advisor at David Lerner Associates, Inc. since April 2016; Executive Vice President and Chief Financial Officer of David Lerner Associates, Inc. from June 1999, until April 2016. | N/A | N/A |

Joseph Pickard (58) Chief Compliance Officer | Since 2007 | Chief Compliance Officer of Spirit of America Investment Fund, Inc. and Spirit of America Management Corp. since July 2007; Counsel to the Interested Directors of Spirit of America Investment Fund, Inc. since July 2002; General Counsel of David Lerner Associates, Inc. since July 2002. | N/A | N/A |

1 | All addresses are in c/o Spirit of America Investment Fund, Inc., 477 Jericho Turnpike, Syosset, New York 11791. |

2 | Each Director serves for an indefinite term, until his successor is elected. |

3 | David Lerner is an “interested” Director, as defined in the 1940 Act, by reason of his positions with the Adviser, and Daniel Lerner is an “interested” Director by reason of his position with the Distributor. Daniel Lerner is the son of David Lerner. |

4 | K.G.K. Agency, Inc. provides insurance to David Lerner Associates, Inc. and affiliated entities. However, the Board has determined that Mr. Kaufman is not an “interested” Director because the insurance services are less than $120,000 in value. |

ENERGY FUND | | 23 |

APPROVAL OF THE INVESTMENT ADVISORY AGREEMENT (UNAUDITED)

The Investment Company Act of 1940, as amended (the “1940 Act”) requires that the continuance of a registered management investment company’s investment advisory agreement be approved annually by both the board of directors and also by a majority of its directors who are not parties to the investment advisory agreement or “interested persons” (as defined by the 1940 Act) of any such party (the “Independent Directors”). At a meeting held on November 7, 2018, the Board of Directors (the “Board” or “Directors”) of Spirit of America Investment Fund, Inc. (the “Company”) met in person (the “Meeting”) to, among other things, consider the approval of the Investment Advisory Agreement (the “Advisory Agreement”) by and between Spirit of America Management Corp. (the “Adviser”) and the Company, on behalf of the Spirit of America Energy Fund (the “Fund”). At the Meeting, the Board, including the Independent Directors voting separately, approved the Advisory Agreement after determining that the Adviser’s compensation, pursuant to the terms of the Advisory Agreement, would be fair and reasonable and concluded that the approval of the Advisory Agreement would be in the best interest of the Fund’s shareholders. The Board’s approval was based on consideration and evaluation of the information and material provided to the Board and a variety of specific factors discussed at the Meeting and at prior meetings of the Board, including the factors described below.

As part of the approval process and oversight of the advisory relationship, counsel to the Independent Directors (“Independent Counsel”) sent an information request letter to the Adviser seeking certain relevant information and the Directors received, for their review in advance of the Meeting, the Adviser’s responses. In addition, the Directors were provided with the opportunity to request additional materials. In advance of the Meeting, the Board including the Independent Directors, requested and received materials provided by the Adviser and Independent Counsel, including, among other things, the following: (i) Independent Counsel’s 15(c) questionnaire and the responses provided by the Adviser; (ii) comparative information on the investment performance of the Fund, relevant indices and Morningstar category peer funds as of September 30, 2018 in the form of reports generated by the Fund’s administrator; (iii) graphs of fee comparisons for the minimum fee, maximum fee, average fee and median fee in the form of reports generated by the Fund’s administrator; (iv) graphs of performance comparisons for the minimum performing fund, maximum performing fund, average performing fund and median performing fund for various time periods in the form of reports generated by the Fund’s administrator; (v) the allocation of the Fund’s brokerage commissions, (vi) the record of compliance with the Fund’s investment policies and restrictions and with the Fund’s Code of Ethics as well as the structure and responsibilities of the Adviser’s compliance departments; (vii) the profitability of the Fund’s investment advisory business to the Adviser taking into account both advisory fees and any other potential direct or indirect benefits; (viii) the Form ADV of the Adviser; and (ix) a memorandum from Independent Counsel regarding the responsibilities of the Independent Directors related to the approval of the Investment Advisory Agreement.

In evaluating the Investment Advisory Agreement, the Board, including the Independent Directors, requested, reviewed and considered materials furnished by the Adviser and questioned personnel of the Adviser, including the Fund’s portfolio manager, with respect to, among other things, personnel, the Fund’s performance, operations and financial condition of the Adviser. Among other information, the Board, including the Independent Directors, requested and was provided information regarding:

● | The Investment performance of the Fund over various time periods both by itself and in relation to relevant indices; |

● | The fees charged by the Adviser for investment advisory services, as well as the compensation received by the Adviser and its affiliates; |

● | The waivers of fees and reimbursements of expenses at times by the Adviser under the Operating Expenses Agreement; |

● | The investment performance, fees and total expenses of mutual funds with similar objectives and strategies managed by other investment advisers; |

● | The investment management staffing and the experience of the Adviser, as well as the Adviser’s administrative and other personnel providing services to the Fund and the historical quality of the services provided by the Adviser; and |

● | The profitability to the Adviser of managing and its affiliate of distributing the Fund, and the methodology in allocating expenses to the management of the Fund. |

24 | | SPIRIT OF AMERICA |

APPROVAL OF THE INVESTMENT ADVISORY AGREEMENT (UNAUDITED)