Massachusetts and Delaware revenue authorities for all taxable years beginning after September 30, 2004.

Distributions to shareholders from net investment income and net realized gains, if any, are recorded on the ex-dividend date. Such distributions are determined in conformity with income tax regulations, which may differ from generally accepted accounting principles.

Reclassifications have been made to the Fund’s components of net assets to reflect income and gains available for distribution (or available capital loss carryovers, as applicable) under income tax regulations. During the year ended September 30, 2008, the following amounts were reclassified:

Income, common expenses and realized and unrealized gains and losses are allocated to the classes based on the relative net assets of each class. Distribution fees, if any, are calculated daily at the class level based on the appropriate net assets of each class and the specific expense rates applicable to each class.

Evergreen Investment Management Company, LLC (“EIMC”), an indirect, wholly-owned subsidiary of Wachovia Corporation (“Wachovia”), is the investment advisor to the Fund and is paid an annual fee starting at 0.52% and declining to 0.41% as the aggregate average daily net assets of the Fund and its variable annuity counterpart, Evergreen VA Omega Fund, increase. For the year ended September 30, 2008, the advisory fee was equivalent to 0.52% of the Fund’s average daily net assets.

From time to time, EIMC may voluntarily or contractually waive its fee and/or reimburse expenses in order to limit operating expenses. During the year ended September 30, 2008, EIMC contractually waived its advisory fee in the amount of $383,980 and voluntarily reimbursed Distribution Plan expenses (see Note 4) relating to Class A shares in the amount of $122,410.

The Fund may invest in money market funds which are advised by EIMC. Income earned on these investments is included in income from affiliate on the Statement of Operations.

Effective January 1, 2008, EIMC replaced Evergreen Investment Services, Inc. (“EIS”), an indirect, wholly-owned subsidiary of Wachovia, as the administrator to the Fund upon the assignment of the Fund’s Administrative Services Agreement from EIS to EIMC. There were no changes to the services being provided or fees being paid by the Fund. The administrator provides the Fund with facilities, equipment and personnel and is paid an

NOTES TO FINANCIAL STATEMENTS continued

annual rate determined by applying percentage rates to the aggregate average daily net assets of the Evergreen funds (excluding money market funds) starting at 0.10% and declining to 0.05% as the aggregate average daily net assets of the Evergreen funds (excluding money market funds) increase. For the year ended September 30, 2008, the administrative services fee was equivalent to 0.10% of the Fund’s average daily net assets.

Evergreen Service Company, LLC (“ESC”), an indirect, wholly-owned subsidiary of Wachovia, is the transfer and dividend disbursing agent for the Fund. ESC receives account fees that vary based on the type of account held by the shareholders in the Fund. For the year ended September 30, 2008, the transfer agent fees were equivalent to an annual rate of 0.49% of the Fund’s average daily net assets.

Wachovia Bank NA, through its securities lending division of Wachovia Global Securities Lending, acts as the securities lending agent for the Fund.

The Fund has placed a portion of its portfolio transactions with brokerage firms that are affiliates of Wachovia. During the year ended September 30, 2008, the Fund paid brokerage commissions of $82,868 to Wachovia Securities, LLC.

4. DISTRIBUTION PLANS

EIS serves as distributor of the Fund’s shares. The Fund has adopted Distribution Plans, as allowed by Rule 12b-1 of the 1940 Act, for each class of shares, except Class I. Under the Distribution Plans, the Fund is permitted to pay distribution fees at an annual rate of up to 0.75% of the average daily net assets for Class A shares and up to 1.00% of the average daily net assets for each of Class B, Class C and Class R shares. However, currently the distribution fees for Class A shares are limited to 0.25% of the average daily net assets of the class and the distribution fees for Class R shares are limited to 0.50% of the average daily net assets of Class R shares. Prior to April 1, 2008, distribution fees were paid at an annual rate of 0.30% of the average daily net assets for Class A shares.

For the year ended September 30, 2008, EIS received $12,560 from the sale of Class A shares and $159, $227,584 and $902 in contingent deferred sales charges from redemptions of Class A, Class B and Class C shares, respectively.

5. INVESTMENT TRANSACTIONS

Cost of purchases and proceeds from sales of investment securities (excluding short-term securities) were $313,966,270 and $443,867,196, respectively, for the year ended September 30, 2008.

During the year ended September 30, 2008, the Fund loaned securities to certain brokers and earned $471,333 in affiliated income relating to securities lending activity which is included in income from affiliate on the Statement of Operations. At September 30, 2008, the value of securities on loan and the total value of collateral received for securities loaned amounted to $94,498,161 and $93,682,612, respectively. Any additional

28

NOTES TO FINANCIAL STATEMENTS continued

collateral required when the total value of collateral received is not sufficient to cover the value of the securities on loan due to market fluctuations is received the following business day.

On September 30, 2008, the aggregate cost of securities for federal income tax purposes was $701,398,733. The gross unrealized appreciation and depreciation on securities based on tax cost was $58,951,457 and $55,059,478, respectively, with a net unrealized appreciation of $3,891,979.

As of September 30, 2008 the Fund had $404,285,192 in capital loss carryovers for federal income tax purposes with $7,956,060 expiring in 2009, $196,908,105 expiring in 2010 and $199,421,027 expiring in 2011.

Certain portions of the capital loss carryovers of the Fund were assumed as a result of acquisitions. These losses are subject to certain limitations prescribed by the Internal Revenue Code.

6. INTERFUND LENDING

Pursuant to an Exemptive Order issued by the SEC, the Fund may participate in an interfund lending program with certain funds in the Evergreen fund family. This program allows the Fund to borrow from, or lend money to, other participating funds. During the year ended September 30, 2008, the Fund did not participate in the interfund lending program.

7. DISTRIBUTIONS TO SHAREHOLDERS

As of September 30, 2008 the components of distributable earnings on a tax basis were as follows:

Unrealized

Appreciation | | Capital Loss

Carryovers | | Temporary

Book/Tax

Differences |

|

|

|

|

|

$3,891,979 | | $404,285,192 | | $(43,410) |

|

|

|

|

|

The differences between the components of distributable earnings on a tax basis and the amounts reflected in the Statement of Assets and Liabilities are primarily due to wash sales. The temporary book/tax differences are a result of timing differences between book and tax recognition of income and/or expenses.

8. EXPENSE REDUCTIONS

Through expense offset arrangements with ESC and the Fund’s custodian, a portion of fund expenses has been reduced.

9. DEFERRED TRUSTEES’ FEES

Each Trustee of the Fund may defer any or all compensation related to performance of his or her duties as a Trustee. The Trustees’ deferred balances are allocated to deferral

29

NOTES TO FINANCIAL STATEMENTS continued

accounts, which are included in the accrued expenses for the Fund. The investment performance of the deferral accounts is based on the investment performance of certain Evergreen funds. Any gains earned or losses incurred in the deferral accounts are reported in the Fund’s Trustees’ fees and expenses. At the election of the Trustees, the deferral account will be paid either in one lump sum or in quarterly installments for up to ten years.

10. FINANCING AGREEMENT

The Fund and certain other Evergreen funds share in a $100 million unsecured revolving credit commitment for temporary and emergency purposes, including the funding of redemptions, as permitted by each participating fund’s borrowing restrictions. Borrowings under this facility bear interest at 0.50% per annum above the Federal Funds rate. All of the participating funds are charged an annual commitment fee of 0.09% on the unused balance, which is allocated pro rata. Prior to June 27, 2008, the annual commitment fee was 0.08%. During the year ended September 30, 2008, the Fund had no borrowings.

11. REGULATORY MATTERS AND LEGAL PROCEEDINGS

The Evergreen funds, EIMC and certain of EIMC’s affiliates are involved in various legal actions, including private litigation and class action lawsuits. In addition, the Evergreen funds, EIMC and certain of EIMC’s affiliates may be subject from time to time to regulatory inquiries and investigations. EIMC does not expect that any of the legal actions, inquiries or investigations currently pending or threatened will have a material adverse impact on the financial position or operations of any of the Evergreen funds or on EIMC’s ability to provide services to the Evergreen funds. There can be no assurance that these matters and any publicity surrounding or resulting from them will not result in reduced sales or increased redemptions of Evergreen fund shares, which could increase Evergreen fund transaction costs or operating expenses or have other adverse consequences on the Evergreen funds.

The SEC and the Secretary of the Commonwealth, Securities Division, of the Commonwealth of Massachusetts are conducting separate investigations of EIMC and EIS concerning alleged issues surrounding the drop in net asset value of the Evergreen Ultra Short Opportunities Fund (the “Ultra Short Fund”) in May and June 2008. In addition, various Evergreen entities are defendants in three purported class actions in U.S. District Court for the District of Massachusetts and related to the same events. The cases generally allege that investors in the Ultra Short Fund suffered losses as a result of (i) misleading statements in Ultra Short Fund’s prospectus, (ii) the failure to accurately price securities in the Ultra Short Fund at different points in time and (iii) the failure of the Ultra Short Fund’s risk disclosures and description of its investment strategy to inform investors adequately of the actual risks of the fund.

30

NOTES TO FINANCIAL STATEMENTS continued

12. NEW ACCOUNTING PRONOUNCEMENTS

In September 2006, FASB issued Statement of Financial Accounting Standards No. 157, Fair Value Measurements (“FAS 157”). FAS 157 establishes a single authoritative definition of fair value, establishes a framework for measuring fair value and expands disclosures about fair value measurements. FAS 157 applies to fair value measurements already required or permitted by existing standards. The change to current generally accepted accounting principles from the application of FAS 157 relates to the definition of fair value, the methods used to measure fair value, and the expanded disclosures about fair value measurements. Management of the Fund does not believe the adoption of FAS 157 will materially impact the financial statement amounts, however, additional disclosures will be required about the inputs used to develop the measurements and the effect of certain of the measurements on changes in net assets for the period. FAS 157 is effective for financial statements issued for fiscal years beginning after November 15, 2007 and interim periods within those fiscal years.

In March 2008, FASB issued Statement of Financial Accounting Standards No. 161, Disclosures about Derivative Instruments and Hedging Activities (“FAS 161”), an amendment of FASB Statement No. 133. FAS 161 requires enhanced disclosures about (a) how and why a fund uses derivative instruments, (b) how derivative instruments and hedging activities are accounted for, and (c) how derivative instruments and related hedging activities affect a fund’s financial position, financial performance, and cash flows. Management of the Fund does not believe the adoption of FAS 161 will materially impact the financial statement amounts, but will require additional disclosures. This will include qualitative and quantitative disclosures on derivative positions existing at period end and the effect of using derivatives during the reporting period. FAS 161 is effective for financial statements issued for fiscal years and interim periods beginning after November 15, 2008.

13. SUBSEQUENT EVENT

Wells Fargo & Company (“Wells Fargo”) and Wachovia announced on October 3, 2008 that Wells Fargo agreed to acquire Wachovia in a whole company transaction that will include all of Wachovia’s banking and other businesses. The transaction is expected to close during the fourth quarter of 2008, subject to receipt of regulatory approvals and Wachovia shareholder approval. In connection with this transaction, Wachovia has issued preferred shares representing approximately a 40% voting interest in Wachovia to Wells Fargo. Due to its ownership of preferred shares, Wells Fargo may be deemed to control EIMC.

If Wells Fargo is deemed to control EIMC, then the advisory agreement between the Fund and EIMC would have terminated automatically in connection with the issuance of preferred shares. To address this possibility, on October 20, 2008 the Board of Trustees approved an interim advisory agreement with EIMC which became effective upon the

31

NOTES TO FINANCIAL STATEMENTS continued

issuance of the preferred shares. The interim agreement will be in effect for a period of up to 150 days. EIMC’s receipt of the advisory fees under an interim advisory agreement is subject to the approval by shareholders of the Fund of a new advisory agreement with EIMC.

32

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

Board of Trustees and Shareholders

Evergreen Equity Trust

We have audited the accompanying statement of assets and liabilities, including the schedule of investments, of the Evergreen Omega Fund, a series of the Evergreen Equity Trust, as of September 30, 2008 and the related statement of operations for the year then ended, statements of changes in net assets for each of the years in the two-year period then ended and the financial highlights for each of the years or periods in the five-year period then ended. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of September 30, 2008 by correspondence with the custodian and brokers, or by other appropriate auditing procedures where replies from brokers were not received. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of the Evergreen Omega Fund as of September 30, 2008, the results of its operations, changes in its net assets and financial highlights for each of the years or periods described above, in conformity with U.S. generally accepted accounting principles.

Boston, Massachusetts

November 24, 2008

33

ADDITIONAL INFORMATION (unaudited)

INFORMATION ABOUT THE REVIEW AND APPROVAL OF THE FUND’S INVESTMENT ADVISORY AGREEMENT

Each year, the Fund’s Board of Trustees determines whether to approve the continuation of the Fund’s investment advisory agreements. In September 2008, the Trustees, including a majority of the Trustees who are not “interested persons” (as that term is defined in the 1940 Act) of the Fund or EIMC (the “independent Trustees”), approved the continuation of the Fund’s investment advisory agreements. (References below to the “Fund” are to Evergreen Omega Fund; references to the “funds” are to the Evergreen funds generally.)

At the same time, the Trustees considered the continuation of the investment advisory agreements for all of the funds. The description below refers in many cases to the Trustees’ process for considering, and conclusions regarding, all of the funds’ agreements. In all of its deliberations, the Board of Trustees and the independent Trustees were advised by independent counsel to the independent Trustees and counsel to the funds.

The review process. In connection with its review of the funds’ investment advisory agreements, the Board of Trustees requests and evaluates, and EIMC and any sub-advisors furnish, such information as the Trustees consider to be reasonably necessary in the circumstances. The Trustees began their 2008 review process at the time of the last advisory contract-renewal process in September 2007. In the course of their 2007 review, the Trustees identified a number of funds that had experienced either short-term or longer-term performance issues. During the 2008 review process, the Trustees monitored each of these funds in particular for changes in performance and for the results of any changes in a fund’s investment process or investment team. In addition, during the course of the year, the Trustees regularly reviewed information regarding the investment performance of all of the funds, paying particular attention to funds whose performance since September 2007 indicated short-term or longer-term performance issues.

In spring 2008, a committee of the Board of Trustees (the “Committee”), working with EIMC management, determined generally the types of information the Board would review as part of its 2008 review process and set a timeline detailing the information required and the dates for its delivery to the Trustees. The Board engaged the independent data provider Keil Fiduciary Strategies LLC (“Keil”) to provide fund-specific and industry-wide data containing information of a nature and in a format generally prescribed by the Committee, and the Committee worked with Keil and EIMC to develop appropriate groups of peer funds for each fund. The Committee also identified a number of expense, performance, and other issues and requested specific information as to those issues.

The Trustees reviewed, with the assistance of an independent industry consultant retained by the independent Trustees, the information that EIMC and Keil provided. The Trustees formed small groups to review individual funds in greater detail. In addition, the Trustees

34

ADDITIONAL INFORMATION (unaudited) continued

considered information regarding, among other things, brokerage practices of the funds, the use of derivatives by the funds, strategic planning for the funds, analyst and research support available to the portfolio management teams, and information regarding the various fall-out benefits received directly and indirectly by EIMC and its affiliates from the funds. The Trustees requested and received additional information following that review.

The Committee met several times by telephone during the 2008 review process to consider the information provided by EIMC. The Committee then met with representatives of EIMC. In addition, over the period of this review, the independent Trustees discussed the continuation of the funds’ advisory agreements with representatives of EIMC and in multiple private sessions with independent legal counsel at which no personnel of EIMC were present. At a meeting of the full Board of Trustees in September, the Committee reported the results of its discussions with EIMC, and the full Board met with representatives of EIMC and engaged in further review of the materials provided to it, and approved the continuation of each of the advisory and sub-advisory agreements.

In considering the continuation of the agreements, the Trustees did not identify any particular information or consideration that was all-important or controlling, and each Trustee attributed different weights to various factors. The Trustees evaluated information provided to them both in terms of the funds generally and with respect to each fund, including the Fund, specifically as they considered appropriate. Although the Trustees considered the continuation of the agreements as part of the larger process of considering the continuation of the advisory contracts for all of the funds, their determination to continue the advisory agreements for each of the funds was ultimately made on a fund-by-fund basis.

This summary describes a number of the most important, and not necessarily all, of the factors considered by the Board and the independent Trustees.

Information reviewed. The Board of Trustees and committees of the Board of Trustees meet periodically during the course of the year. At those meetings, EIMC presents a wide variety of information regarding the services it performs, the investment performance of the funds, and other aspects of the business and operations of the funds. At those meetings, and in the process of considering the continuation of the agreements, the Trustees considered information regarding, for example, the funds’ investment results; the portfolio management teams for the funds and the experience of the members of those teams, and any recent changes in the membership of the teams; portfolio trading practices; compliance by the funds and EIMC with applicable laws and regulations and with the funds’ and EIMC’s compliance policies and procedures; risk evaluation and oversight procedures at EIMC; services provided by affiliates of EIMC to the funds and shareholders of the funds; and other information relating to the nature, extent, and quality of

35

ADDITIONAL INFORMATION (unaudited) continued

services provided by EIMC. The Trustees considered a number of changes in portfolio management personnel at EIMC and its advisory affiliates in the year since September 2007. The Trustees also considered changes in personnel at the funds and EIMC, including the appointment of a new Chief Compliance Officer for the funds in June of 2007 and a new Chief Investment Officer at EIMC in August of 2008.

The Trustees considered the rates at which the funds pay investment advisory fees, and the efforts generally by EIMC and its affiliates as sponsors of the funds. The data provided by Keil showed the management fees paid by each fund in comparison to the management fees of other peer mutual funds, in addition to data regarding the investment performance of the funds in comparison to other peer mutual funds. The Trustees were assisted by an independent industry consultant in reviewing the information presented to them.

The Trustees noted that, in certain cases, EIMC and/or its affiliates provide advisory services to other clients that are comparable to the advisory services they provide to certain funds. The Trustees considered the information EIMC provided regarding the rates at which those other clients pay advisory fees to EIMC or its affiliates for such services. Fees charged to those other clients were generally lower than those charged to the respective funds. In respect of these other accounts, EIMC noted that the compliance, reporting, and other legal burdens of providing investment advice to mutual funds generally exceed those required to provide advisory services to non-mutual fund clients such as retirement or pension plans. The Trustees also considered the investment performance of those other accounts managed by EIMC and its affiliates, where applicable, and concluded that the performance of those accounts did not suggest any substantial difference in the quality of the service provided by EIMC and its affiliates to those accounts.

The Trustees considered the transfer agency fees paid by the funds to an affiliate of EIMC. They reviewed information presented to them showing that the transfer agency fees charged to the funds were generally consistent with industry norms.

The Trustees also considered that EIMC serves as administrator to the funds and receives a fee for its services as administrator. In their comparison of the advisory fee paid by the funds with those paid by other mutual funds, the Trustees considered administrative fees paid by the funds and those other mutual funds. The Board considered that EIS, an affiliate of EIMC, serves as distributor to the funds generally and receives fees from the funds for those services. They considered other so-called “fall-out” benefits to EIMC and its affiliates due to their other relationships with the funds, including, for example, soft-dollar services received by EIMC attributable to transactions entered into by EIMC for the benefit of the funds and brokerage commissions received by Wachovia Securities, LLC, an affiliate of EIMC, from transactions effected by it for the funds. The Trustees also noted that the funds pay sub-transfer agency fees to various financial institutions that hold fund shares in omnibus accounts, and that Wachovia Securities, LLC and its affiliates receive

36

ADDITIONAL INFORMATION (unaudited) continued

such payments from the funds in respect of client accounts they hold in omnibus arrangements, and that an affiliate of EIMC receives fees for administering the sub-transfer agency payment program. In reviewing the services provided by an affiliate of EIMC, the Trustees noted that an affiliate of EIMC had won recognition from Dalbar customer service each year since 1998, and also won recognition from National Quality Review for customer service and for accuracy in processing transactions in 2008. They also considered that Wachovia Securities, LLC and its affiliates receive distribution-related fees and shareholder servicing payments (including amounts derived from payments under the funds’ Rule 12b-1 plans) in respect of shares sold or held through it. The Trustees also noted that an affiliate of EIMC receives compensation for serving as a securities lending agent for a number of the funds.

In the period leading up to the Trustees’ approval of continuation of the investment advisory agreements, the Trustees were mindful of the financial condition of Wachovia Corporation (“Wachovia”), EIMC’s parent company. They considered the possibility that a significant adverse change in Wachovia’s financial condition could impair the ability of EIMC or its affiliates to perform services for the funds at the same level as in the past. The Trustees concluded that any change in Wachovia’s financial condition had not to date had any such effect, but determined to monitor EIMC’s and its affiliates’ performance, and financial conditions generally, going forward in order to identify any such impairment that may develop and to take appropriate action.

Nature and quality of the services provided. The Trustees considered that EIMC and its affiliates generally provide a comprehensive investment management service to the funds. They noted that EIMC formulates and implements an investment program for the Fund. They noted that EIMC makes its personnel available to serve as officers of the funds, and concluded that the reporting and management functions provided by EIMC with respect to the funds were generally satisfactory. The Trustees considered the investment philosophy of the Fund’s portfolio management team, and considered the in-house research capabilities of EIMC and its affiliates, as well as other resources available to EIMC, including research services available to it from third parties. The Board considered the managerial and financial resources available to EIMC and its affiliates, and the commitment that the Wachovia organization has made to the funds generally. On the basis of these factors, they determined that the nature and scope of the services provided by EIMC were consistent with their respective duties under the investment advisory agreements and appropriate and consistent with the investment programs and best interests of the funds.

The Trustees noted the resources EIMC and its affiliates have committed to the regulatory, compliance, accounting, tax and oversight of tax reporting, and shareholder servicing functions, and the number and quality of staff committed to those functions, which they

37

ADDITIONAL INFORMATION (unaudited) continued

concluded were appropriate and generally in line with EIMC’s responsibilities to the Fund and to the funds generally. The Board and the disinterested Trustees concluded, within the context of their overall conclusions regarding the funds’ advisory agreements, that they were generally satisfied with the nature, extent, and quality of the services provided by EIMC, including services provided by EIMC under its administrative services agreements with the funds.

Investment performance. The Trustees considered the investment performance of each fund, both by comparison to other comparable mutual funds and to broad market indices. Although the Trustees considered the performance of all share classes, the Trustees noted that, for the one- and three-year periods ended December 31, 2007, the Fund’s Class A shares had underperformed the Fund’s benchmark index, the Russell 1000 Growth Index, and performed in the fourth and fifth quintiles, respectively, of the mutual funds against which the Trustees compared the Fund’s performance for the same periods. The Trustees also noted that, for the five- and ten-year periods ended December 31, 2007, the Fund’s Class A shares had outperformed the Fund’s benchmark index, and performed in the fifth and fourth quintiles, respectively, of the mutual funds against which the Trustees compared the Fund’s performance for the same periods. The Trustees noted that they had previously discussed the performance of this Fund with EIMC, and that EIMC has taken steps intended to improve the Fund’s performance. They observed that the limited period of time that had elapsed since EIMC’s actions was insufficient for the Trustees to evaluate the success of these changes.

The Trustees discussed each fund’s performance with representatives of EIMC. In each instance where a fund experienced a substantial period of underperformance relative to its benchmark index and/or the non-Evergreen fund peers against which the Trustees compared the fund’s performance, the Trustees considered EIMC’s explanation of the reasons for the relative underperformance and the steps being taken to address the relative underperformance. The Trustees also noted that EIMC had appointed a new Chief Investment Officer in August of 2008 who had not yet had sufficient time to evaluate and direct remedial efforts with respect to funds that have experienced a substantial period of relative underperformance. The Trustees emphasized that the continuation of the investment advisory agreement for a fund should not be taken as any indication that the Trustees did not believe investment performance for any specific fund might not be improved, and they noted that they would continue to monitor closely the investment performance of the funds going forward.

Advisory and administrative fees. The Trustees recognized that EIMC does not seek to provide the lowest cost investment advisory service, but to provide a high quality, full-service investment management product at a reasonable price. They also noted that EIMC has in many cases sought to set its investment advisory fees at levels consistent with

38

ADDITIONAL INFORMATION (unaudited) continued

industry norms. The Trustees noted that, in certain cases, a fund’s management fees were higher than many or most other mutual funds in the same Keil peer group. However, in each case, the Trustees determined on the basis of the information presented that the level of management fees was not excessive. The Trustees noted that the Fund’s management fee was lower than the management fees paid by most of the other mutual funds against which the Trustees compared the Fund’s management fee, and that the level of profitability realized by EIMC in respect of the fee did not appear excessive.

Economies of scale. The Trustees noted the possibility that economies of scale would be achieved by EIMC in managing the funds as the funds grow. The Trustees noted that the Fund had implemented breakpoints in its advisory fee structure. The Trustees noted that they would continue to review the appropriate levels of breakpoints in the future, and concluded that the breakpoints as implemented appeared to be a reasonable step toward the realization of economies of scale by the Fund.

Profitability. The Trustees considered information provided to them regarding the profitability to the EIMC organization of the investment advisory, administration, and transfer agency (with respect to the open-end funds only) fees paid to EIMC and its affiliates by each of the funds. They considered that the information provided to them was necessarily estimated, and that the profitability information provided to them, especially on a fund-by-fund basis, did not necessarily provide a definitive tool for evaluating the appropriateness of each fund’s advisory fee. They noted that the levels of profitability of the funds to EIMC varied widely, depending on among other things the size and type of fund. They considered the profitability of the funds in light of such factors as, for example, the information they had received regarding the relation of the fees paid by the funds to those paid by other mutual funds, the investment performance of the funds, and the amount of revenues involved. In light of these factors, the Trustees concluded that the profitability of any of the funds, individually or in the aggregate, should not prevent the Trustees from approving the continuation of the agreements.

39

TRUSTEES AND OFFICERS

TRUSTEES1 | | |

Charles A. Austin III

Trustee

DOB: 10/23/1934

Term of office since: 1991

Other directorships: None | | Investment Counselor, Anchor Capital Advisors, LLC. (investment advice); Director, The Andover Companies (insurance); Trustee, Arthritis Foundation of New England; Former Director, The Francis Ouimet Society (scholarship program); Former Director, Executive Vice President and Treasurer, State Street Research & Management Company (investment advice) |

|

|

|

K. Dun Gifford

Trustee

DOB: 10/23/1938

Term of office since: 1974

Other directorships: None | | Chairman and President, Oldways Preservation and Exchange Trust (education); Trustee, Chairman of the Finance Committee, Member of the Executive Committee, and Former Treasurer, Cambridge College |

|

|

|

Dr. Leroy Keith, Jr.

Trustee

DOB: 2/14/1939

Term of office since: 1983

Other directorships: Trustee,

Phoenix Fund Complex

(consisting of 53 portfolios

as of 12/31/2007) | | Managing Director, Almanac Capital Management (commodities firm); Trustee, Phoenix Fund Complex; Director, Diversapack Co. (packaging company); Former Partner, Stonington Partners, Inc. (private equity fund); Former Director, Obagi Medical Products Co.; Former Director, Lincoln Educational Services |

|

|

|

Carol A. Kosel1

Trustee

DOB: 12/25/1963

Term of office since: 2008

Other directorships: None | | Former Consultant to the Evergreen Boards of Trustees; Former Vice President and Senior Vice President, Evergreen Investments, Inc.; Former Treasurer, Evergreen Funds; Former Treasurer, Vestaur Securities Fund |

|

|

|

Gerald M. McDonnell

Trustee

DOB: 7/14/1939

Term of office since: 1988

Other directorships: None | | Former Manager of Commercial Operations, CMC Steel (steel producer) |

|

|

|

Patricia B. Norris

Trustee

DOB: 4/9/1948

Term of office since: 2006

Other directorships: None | | President and Director of Buckleys of Kezar Lake, Inc. (real estate company); Former President and Director of Phillips Pond Homes Association (home community); Former Partner, PricewaterhouseCoopers, LLP (independent registered public accounting firm) |

|

|

|

William Walt Pettit

Trustee

DOB: 8/26/1955

Term of office since: 1988

Other directorships: None | | Partner and Vice President, Kellam & Pettit, P.A. (law firm); Director, Superior Packaging Corp. (packaging company); Member, Superior Land, LLC (real estate holding company), Member, K&P Development, LLC (real estate development); Former Director, National Kidney Foundation of North Carolina, Inc. (non-profit organization) |

|

|

|

David M. Richardson

Trustee

DOB: 9/19/1941

Term of office since: 1982

Other directorships: None | | President, Richardson, Runden LLC (executive recruitment advisory services); Director, J&M Cumming Paper Co. (paper merchandising); Trustee, NDI Technologies, LLP (communications); Former Consultant, AESC (The Association of Executive Search Consultants) |

|

|

|

Dr. Russell A. Salton III

Trustee

DOB: 6/2/1947

Term of office since: 1984

Other directorships: None | | President/CEO, AccessOne MedCard, Inc. |

|

|

|

40

TRUSTEES AND OFFICERS continued

Michael S. Scofield

Trustee

DOB: 2/20/1943

Term of office since: 1984

Other directorships: None | | Retired Attorney, Law Offices of Michael S. Scofield; Former Director and Chairman, Branded Media Corporation (multi-media branding company) |

|

|

|

Richard J. Shima

Trustee

DOB: 8/11/1939

Term of office since: 1993

Other directorships: None | | Independent Consultant; Director, Hartford Hospital; Trustee, Greater Hartford YMCA; Former Director,Trust Company of CT; Former Director, Old State House Association; Former Trustee, Saint Joseph College (CT) |

|

|

|

Richard K. Wagoner, CFA2

Trustee

DOB: 12/12/1937

Term of office since: 1999

Other directorships: None | | Member and Former President, North Carolina Securities Traders Association; Member, Financial Analysts Society |

|

|

|

OFFICERS

Dennis H. Ferro3

President

DOB: 6/20/1945

Term of office since: 2003 | |

Principal occupations: President and Chief Executive Officer, Evergreen Investment Company, Inc. and Executive Vice President, Wachovia Bank, N.A.; former Chief Investment Officer, Evergreen Investment Company, Inc.

|

|

|

|

Jeremy DePalma4

Treasurer

DOB: 2/5/1974

Term of office since: 2005 | | Principal occupations: Senior Vice President, Evergreen Investment Management Company, LLC; Former Vice President, Evergreen Investment Services, Inc.; Former Assistant Vice President, Evergreen Investment Services, Inc. |

|

|

|

Michael H. Koonce4

Secretary

DOB: 4/20/1960

Term of office since: 2000 | | Principal occupations: Senior Vice President and General Counsel, Evergreen Investment Services, Inc.; Secretary, Senior Vice President and General Counsel, Evergreen Investment Management Company, LLC and Evergreen Service Company, LLC; Senior Vice President and Assistant General Counsel, Wachovia Corporation |

|

|

|

Robert Guerin4

Chief Compliance Officer

DOB: 9/20/1965

Term of office since: 2007 | | Principal occupations: Chief Compliance Officer, Evergreen Funds and Senior Vice President of Evergreen Investments Co., Inc.; Former Managing Director and Senior Compliance Officer, Babson Capital Management LLC; Former Principal and Director, Compliance and Risk Management, State Street Global Advisors; Former Vice President and Manager, Sales Practice Compliance, Deutsche Asset Management |

|

|

|

1 | Each Trustee, except Mses. Kosel and Norris, serves until a successor is duly elected or qualified or until his or her death, resignation, retirement or removal from office. As new Trustees, Ms. Kosel’s and Ms. Norris’ initial terms end December 31, 2010 and June 30, 2009, respectively, at which times they may be re-elected by Trustees to serve until a successor is duly elected or qualified or until her death, resignation, retirement or removal from office by the Trustees. Each Trustee, except Ms. Kosel, oversaw 94 Evergreen funds as of December 31, 2007. Ms. Kosel became a Trustee on January 1, 2008. Correspondence for each Trustee may be sent to Evergreen Board of Trustees, P.O. Box 20083, Charlotte, NC 28202. |

2 | Mr. Wagoner is an “interested person” of the Fund because of his ownership of shares in Wachovia Corporation, the parent to the Fund’s investment advisor. |

3 | The address of the Officer is 401 S. Tryon Street, 20th Floor, Charlotte, NC 28288. |

4 | The address of the Officer is 200 Berkeley Street, Boston, MA 02116. |

Additional information about the Fund’s Board of Trustees and Officers can be found in the Statement of Additional Information (SAI) and is available upon request without charge by calling 800.343.2898.

41

563830 rv6 11/2008

Evergreen Small-Mid Growth Fund

| | table of contents |

1 | | LETTER TO SHAREHOLDERS |

4 | | FUND AT A GLANCE |

6 | | PORTFOLIO MANAGER COMMENTARY |

10 | | ABOUT YOUR FUND’S EXPENSES |

11 | | FINANCIAL HIGHLIGHTS |

13 | | SCHEDULE OF INVESTMENTS |

17 | | STATEMENT OF ASSETS AND LIABILITIES |

18 | | STATEMENT OF OPERATIONS |

19 | | STATEMENTS OF CHANGES IN NET ASSETS |

20 | | NOTES TO FINANCIAL STATEMENTS |

28 | | REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM |

29 | | ADDITIONAL INFORMATION |

36 | | TRUSTEES AND OFFICERS |

This annual report must be preceded or accompanied by a prospectus of the Evergreen fund contained herein. The prospectus contains more complete information, including fees and expenses, and should be read carefully before investing or sending money.

The fund will file its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. The fund’s Form N-Q will be available on the SEC’s Web site at http://www.sec.gov. In addition, the fund’s Form N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, D.C. Information on the operation of the Public Reference Room may be obtained by calling 800.SEC.0330.

A description of the fund’s proxy voting policies and procedures, as well as information regarding how the fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30, is available by visiting our Web site at EvergreenInvestments.com or by visiting the SEC’s Web site at http://www.sec.gov. The fund’s proxy voting policies and procedures are also available without charge, upon request, by calling 800.343.2898.

Mutual Funds:

| NOT FDIC INSURED | | MAY LOSE VALUE | | NOT BANK GUARANTEED |

Evergreen InvestmentsSM is a service mark of Evergreen Investment Management Company, LLC. Copyright 2008, Evergreen Investment Management Company, LLC.

Evergreen Investment Management Company, LLC is a subsidiary of Wachovia Corporation and is an affiliate of Wachovia Corporation’s other Broker Dealer subsidiaries.

Evergreen mutual funds are distributed by Evergreen Investment Services, Inc. 200 Berkeley Street, Boston, MA 02116

LETTER TO SHAREHOLDERS

November 2008

Dennis H. Ferro

President and Chief Executive Officer

Dear Shareholder:

We are pleased to provide the Annual Report for Evergreen Small-Mid Growth Fund for the twelve-month period ended September 30, 2008 (the “period”).

Investors encountered an extraordinary environment as the fiscal year came to a close. Market volatility intensified substantially in the final quarter of the period, particularly in September 2008, as spreading problems in the credit markets threatened to drag the global economy into a recession. Slowing economic activity and widening restrictions on credit availability undermined confidence in the leading financial institutions, both at home and abroad. Investors fled to the highest-quality securities available. U.S. Treasury securities proved to be the most noticeable beneficiary of the flight to quality. In contrast, the values of most stocks and corporate bonds dropped. Moreover, this turmoil in the capital markets only worsened in the first few weeks immediately after fiscal year end. Elsewhere, foreign equity markets also slumped as fears spread that economic weakening in the United States would prove contagious. In world bond markets, sovereign government securities in industrialized nations performed relatively well, but the values of emerging market debt and foreign high yield corporate bonds were pulled down as evidence mounted of a deceleration in global growth trends. Even the prices of oil and natural gas began to retreat on world markets after climbing to unprecedented heights in the summer of 2008.

After months of deterioration, the U.S. economy contracted in the third quarter of 2008. The U.S. Commerce Department reported in October 2008 that the nation’s real Gross Domestic Product fell by 0.3% from July 2008 through September 2008, with consumer spending recording its greatest drop in three decades. The report validated expectations that the economy had entered into a recession. Fears rose that the slowdown could persist at least through the first quarter of 2009. The news was hardly unexpected, as it followed the steady accumulation of reports documenting declining housing values, falling manufacturing activity, slowing consumer spending and rising unemployment levels. Perhaps the most dramatic news was the collapse or near-collapse of several venerable financial institutions both in the U.S. and in Europe. In response, the Federal Reserve Board (the “Fed”), the U.S. Treasury, the Federal Deposit Insurance Corporation and the Securities and Exchange Commission took a series of dramatic and innovative steps to help the economy and the financial markets emerge from this crisis. In October 2008, Congress rushed through a $700 billion rescue plan designed to address the capital inadequacy of banks. Meanwhile, in a further effort to re-stimulate lending activity, the Fed twice slashed the key fed funds rate in October 2008. The

1

LETTER TO SHAREHOLDERS continued

reductions brought the influential overnight lending rate to just 1.00%. It had been as high as 5.25% as recently as August 2007. Overseas, other major central banks also cut short-term rates to inject liquidity into the financial markets. At the same time, foreign governments took other measures to buttress financial institutions and forestall the possibility of a global recession.

During a volatile and challenging period in the capital markets, the investment managers of Evergreen’s growth-oriented equity funds focused on controlling risk and finding potential opportunities while maintaining the goal of seeking long-term capital appreciation. Managers of Evergreen Large Company Growth Fund and Evergreen Omega Fund focused on bottom-up, fundamental analysis in making individual stock selections. The management teams supervising Evergreen Mid Cap Growth Fund and Evergreen Small-Mid Growth Fund, meanwhile, sought out growing companies with strong fundamentals and reasonable valuations. At the same time, managers of Evergreen Growth Fund concentrated on opportunities among small cap growth companies with above-average earnings prospects and reasonable stock prices. The team supervising Evergreen Strategic Growth Fund, meanwhile, focused on large cap companies offering superior long-term growth potential.

As we look back over the extraordinary series of events during the period, we believe it is vitally important for all investors to keep perspective and remain focused on their long-term strategies. Most importantly, we continue to urge investors to pursue fully diversified strategies to participate in future market gains and limit the risks of potential losses. If they haven’t already done so, we encourage individual investors to work with their financial advisors to develop a diversified, long-term strategy and, most importantly, to adhere to it. Investors should keep in mind that the economy and the financial markets have had long and successful histories of adaptability, recovery, innovation and growth. Proper asset allocation decisions can have significant impacts on the returns of long-term portfolios.

Please visit us at EvergreenInvestments.com for more information about our funds and other investment products available to you. Thank you for your continued support of Evergreen Investments.

Sincerely,

Dennis H. Ferro

President and Chief Executive Officer

Evergreen Investment Company, Inc.

2

LETTER TO SHAREHOLDERS continued

Special Notices to Shareholders:

• | Dennis Ferro, President and Chief Executive Officer (CEO) of Evergreen Investments, will retire at the end of 2008 and Peter Cieszko, current President of Global Distribution, will succeed Mr. Ferro as President and CEO at that time. Additionally, David Germany has been named the new Chief Investment Officer (CIO). Please visit our Web site at EvergreenInvestments.com for additional information regarding these announcements. |

• | On October 3, 2008, Wachovia Corporation, parent company of Evergreen Investments, and Wells Fargo & Company announced a definitive agreement whereby Wells Fargo will acquire Wachovia in a stock-for-stock transaction. Please visit Wachovia.com for additional information regarding this announcement. |

3

FUND AT A GLANCE

as of September 30, 2008

MANAGEMENT TEAM

Investment Advisor:

Evergreen Investment Management Company, LLC

Portfolio Managers:

Kenneth J. Doerr; Robert C. Junkin, CPA; Lori S. Evans†; Julian J. Johnson†

†Effective May 7, 2008, Ms. Evans and Mr. Johnson became portfolio managers of the fund.

CURRENT INVESTMENT STYLE

Source: Morningstar, Inc.

Morningstar’s style box is based on a portfolio date as of 9/30/2008.

The Equity style box placement is based on 10 growth and valuation measures for each fund holding and the median size of the companies in which the fund invests.

PERFORMANCE AND RETURNS

Portfolio inception date: 10/11/2005

| | Class A | | Class I |

Class inception date | | 10/11/2005 | | 10/11/2005 |

|

|

|

|

|

Nasdaq symbol | | ESMGX | | ESMIX |

|

|

|

|

|

Average annual return* | | | | |

|

|

|

|

|

1-year with sales charge | | -24.61% | | N/A |

|

|

|

|

|

1-year w/o sales charge | | -20.01% | | -19.72% |

|

|

|

|

|

Since portfolio inception | | 3.59% | | 5.94% |

|

|

|

|

|

Maximum sales charge | | 5.75% | | N/A |

| | Front-end | | |

|

|

|

|

|

* | Adjusted for maximum applicable sales charge, unless noted. |

Past performance is no guarantee of future results. The performance quoted represents past performance and current performance may be lower or higher. The investment return and principal value of an investment will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. To obtain performance information current to the most recent month-end for Classes A or I, please go to EvergreenInvestments.com/fundperformance. The performance of each class may vary based on differences in loads, fees and expenses paid by the shareholders investing in each class. Performance includes the reinvestment of income dividends and capital gain distributions. Performance shown does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

The fund incurs a 12b-1 fee of 0.25% for Class A. Class I does not pay a 12b-1 fee.

The advisor is waiving a portion of its advisory fee. Had the fee not been waived, returns would have been lower. Returns reflect expense limits previously in effect for Class A, without which returns for Class A would have been lower.

Class I shares are only offered, subject to the minimum initial purchase requirements, in the following manner: (1) to investment advisory clients of EIMC (or its advisory affiliates), (2) to employer- or state-sponsored benefit plans, including but not limited to, retirement plans, defined benefit plans, deferred compensation plans, or savings plans, (3) to fee-based mutual fund wrap accounts, (4) through arrangements entered into on behalf of the Evergreen funds with certain financial services firms, (5) to certain institutional investors, and (6) to persons who owned Class Y shares in registered name in an Evergreen fund on or before December 31, 1994 or who owned shares of any SouthTrust fund in registered name as of March 18, 2005 or who owned shares of Vestaur Securities Fund as of May 20, 2005.

Class I shares are only available to institutional shareholders with a minimum of $1 million investment, which may be waived in certain situations.

4

FUND AT A GLANCE continued

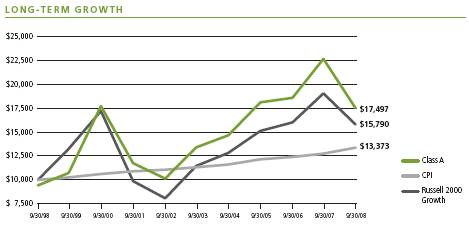

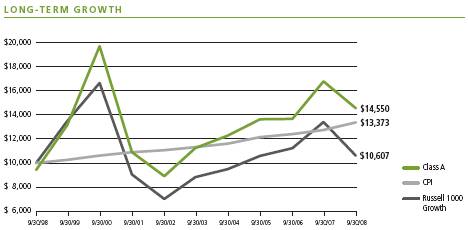

Comparison of a $10,000 investment in the Evergreen Small-Mid Growth Fund Class A shares versus a similar investment in the Russell 2500 Growth Index (Russell 2500 Growth) and the Consumer Price Index (CPI).

The Russell 2500 Growth is an unmanaged market index and does not include transaction costs associated with buying and selling securities, any mutual fund fees or expenses or any taxes. The CPI is a commonly used measure of inflation and does not represent an investment return. It is not possible to invest directly in an index.

The fund’s investment objective may be changed without a vote of the fund’s shareholders.

Small and mid cap securities may be subject to special risks associated with narrower product lines and limited financial resources compared to their large cap counterparts, and, as a result, small and mid cap securities may decline significantly in market downturns and may be more volatile than those of larger companies due to the higher risk of failure.

All data is as of September 30, 2008, and subject to change.

5

PORTFOLIO MANAGER COMMENTARY

The fund’s Class A shares returned -20.01% for the twelve-month period ended September 30, 2008, excluding any applicable sales charges. During the same period, the Russell 2500 Growth returned -20.70%.

The fund’s objective is to seek long-term capital growth.

Investment process

During the fiscal year ended September 30, 2008, market volatility as measured by the Chicago Board Options Exchange Volatility Index (VIX) rose to new highs not seen in the Index’s 15-year history. Equity markets worldwide retreated significantly. Investors were responding to the deepening global credit crisis and increased evidence that economic contraction in the United States would likely lead to substantial growth deceleration in both developed and developing markets. Energy and commodity prices had soared early in the period on expectations of continued emerging market growth and potential shortages causing speculative trading activity. Prices then dropped precipitously in the latter months of the period as growth expectations collapsed and traders were forced to unwind positions. The U.S. economy’s ability to approach normal functionality was impaired by bleak developments in the financial market. The government rescues of Fannie Mae and Freddie Mac, American International Group (AIG)’s close call and eventual bailout, Lehman Brothers’ bankruptcy filing, Washington Mutual’s seizure as the biggest U.S. bank failure in history, illiquid money market fund closings and a nearly frozen commercial paper market all stunned the capital markets. Industrial companies with exposure to emerging market growth saw their stock prices drop as investors lowered exposure to areas of higher perceived risk. Despite the negative environment, financial stocks proved to be some of the better performers during the summer months, recovering from a year-long slump.

During the year, we lowered exposure to Industrials, Information Technology and Consumer Discretionary while adding to the Consumer Staples, Health Care and Financials sectors. In Industrials, we eliminated Kaydon Corp. on weakening expectations for margins and earnings and trimmed Titan International on lowered growth in its end markets. Within the consumer area, we added Ralcorp Holdings and Warnaco in Consumer Staples. In Consumer Discretionary, the fund’s new position in quick-serve restaurant Buffalo Wild Wings proved a good addition. We eliminated most of our specialty retailers, including Zumiez and Polo Ralph Lauren, as well as the fund’s exposure to advertising through Lamar. Within Energy, we reduced the fund’s holdings in Atwood Oceanics and initiated a position in refiner Tesoro Corp. In poring over the Financials sector, we found several companies that we believe have attractive business models, balance sheets and opportunities for growth: Cash America, PrivateBancorp and NewAlliance Bancshares. Health Care equipment supplier ResMed was a new position, as was life science tools company Invitrogen. We believe these companies offer sustainable growth prospects at reasonable valuations. In Information Technology, we generally

6

PORTFOLIO MANAGER COMMENTARY continued

lowered exposure to Internet and communications equipment semiconductor companies by selling Akamai, SiRF, Acme Packet Intersil and Omniture.

Contributors to performance

Typically, the fund’s performance results from stock selection although occasionally we have benefited from sector allocation decisions. Positive contributions from allocation came from the fund’s underweight in Consumer Discretionary and Energy and the fund’s slightly higher-than-normal average cash position throughout the course of the year. Positive stock contributions came from Consumer Discretionary, Industrials, Energy and Consumer Staples. Post-secondary education provider Strayer Education and Buffalo Wild Wings were two stocks posting positive returns for the period. Strayer Education, a long-term holding, offered investors not only a perceived safe haven in the volatile market environment due to its sustainable growth characteristics and competitive advantages, but also strong revenue and earnings growth. Buffalo Wild Wings is a fast-growing quick serve restaurant whose stock appreciated after the company served up strong earnings and comparable store sales gains. Another relative contributor was priceline.com, a leader in Internet travel auctions. The company posted very strong gains in the early part of the period and the stock responded.

The Industrial sector, in which the fund had significant exposure for some time, outperformed the broader index slightly, and several of our stock selections in the area outperformed substantially. Many of these companies have benefited from global exposure, with strong growth in end markets in addition to the weak dollar. Two holdings in particular produced double-digit price gains: Watson Wyatt Worldwide and FTI Consulting. Watson Wyatt, a global consulting firm specializing in employee benefits and human resources, has reaped the benefits from pension law changes both in the United States and the U.K. FTI Consulting has seen a significant increase over the past year in demand for their specialties: restructuring and bankruptcy. Landstar, a truckload shipper benefiting from its asset-less business model, and machinery companies Kaydon Corp. and Titan International also produced strong gains. In Energy, our underweight allocation in the last several months of the fiscal year benefited the fund more than our strong stock performers, such as Southwest Energy, a beneficiary of rising natural gas prices and new production. Other strong stocks included FLIR Systems, a designer and manufacturer of infrared camera systems, which continued to see strong order growth. Ansys, an engineering simulation software company, beat earnings expectations, driving estimates—and the stock price—higher. In Materials, the fund’s fertilizer holding, CF Industries Holdings, continued to produce strong results and rose dramatically. Quality Systems, a Health Care information systems provider, bested estimates for earnings growth and installed a new CEO during the summer; its shares responded favorably. Several of our Health Care holdings proved solid performers, including cancer radiation treatment company Varian Medical Systems, biotech leader Cephalon and inpatient behavioral Health Care provider Psychiatric Solutions.

7

PORTFOLIO MANAGER COMMENTARY continued

Detractors from performance

The worst detractor from performance in the year was the fund’s underweight in Health Care stocks, followed closely by stock selection in Health Care and the fund’s overweight to Telecommunications. Materials stocks as well as several in Information Technology and Financials were prominent detractors. In the latter part of the period, Materials stocks were hit hard as commodity prices receded. In addition, as it became clear that the United States would likely tip into recession, followed by much of the global community, stocks fell further on the expectation that revenue and earnings growth estimates for 2009 would fall. Steel Dynamics, a U.S. steel manufacturer, was one of our worst performers. It gave up over half of its value, despite reporting much better-than-expected earnings early in the third calendar quarter and raising guidance for the remainder of the year. The key to the stock’s slide was investor perception that the growth driver for both the commodity and stock price over the preceding year—the worldwide steel shortage—had vanished in the wake of slowing global demand. We held the shares at year-end, believing the short-term selling was overdone.

In Health Care, some of the fund’s underperformance was due to lack of exposure to small biotech companies, many of which rose strongly in the last fiscal quarter. ArthroCare Corp. was a detractor, declining significantly early in the calendar year and then again in early summer after the company announced it would need to restate earnings for the previous two years. Other detractors in Health Care included Pediatrix Medical Group and device manufacturer Hologic. Nevertheless, we believe Hologic’s opportunity in the women’s health diagnostics market remains strong. Its revenue and earnings growth have been in line with our expectations and, despite a weakening hospital spending environment, we believe the company may offer significant technological innovation. Finally, our worst stock of the year was a semiconductor company called SiRF Technologies, which fell dramatically after announcing surprisingly disappointing earnings expectations for the first calendar quarter of 2008. The company was the leading manufacturer of semiconductors used in global positioning devices. In spite of healthy end market demand for personal navigation devices in the final months of 2007, the company experienced a sudden collapse in its margin structure due to competitive pressures. We sold the stock.

Portfolio management outlook

We believe the current economic environment both in the United States and overseas is more uncertain than at any other time in recent history. Global credit markets’ recent turmoil can be directly linked back to the U.S. subprime mortgage crisis in the summer of 2007. A year ago, liquidity was the issue; more recently, it has been availability of—and access to—credit for borrowers big and small. This has created a much deeper and more negative impact on the U.S. economy than the housing market decline of last year—and may prove much more difficult to resolve. Despite the negative returns year to date, there may still be difficult weeks and months to come as government and regulatory policy

8

PORTFOLIO MANAGER COMMENTARY continued

solutions are rolled out. There are bound to be surprises that no one today can anticipate, guard against or profit from. In the United States, the consumer has been facing increasingly strong headwinds as housing has continued to decline and unemployment has risen. Likewise, the government bailout of the financial sector will likely weigh on spending and taxation policies for some time.

Historically, some of the best long-term opportunities were created during periods of severe economic stress and uncertainty. Today, our research suggests that, amid the market turmoil, excellent valuation opportunities exist. We believe that several high-quality, profitable growth companies with solid balance sheets are priced well below our estimation of their intrinsic value. Although economic recovery may take time, we believe preconditions for fundamental improvement have begun to emerge: lower oil prices, lower commodity prices, attractive valuations, low real-interest rates and government initiatives to stabilize mortgage and housing markets. We believe that, in many cases, U.S. corporate balance sheets outside the Financial sector are strong, liquid and not overly leveraged.

We believe today’s environment has created attractive opportunities for the long-term investor, and we believe the fund is currently positioned to take advantage of them. On the more defensive side, we currently have increased the fund’s weight in Consumer Staples and Health Care stocks, focusing on companies with competitive advantages driving top and bottom line growth. The more cyclical areas—including Information Technology, Telecommunications and Industrials—have been hard hit in the past several quarters as investors expected growth to slow. We have been focusing our research on companies with strong franchise and global growth components as we believe there are bargains to be had. Valuations in the Energy and Materials sectors—both performance leaders for the past year—have slid dramatically, many to levels suggesting there may be no growth for the foreseeable future.

This commentary reflects the views and opinions of the fund’s portfolio manager(s) on the date indicated and may include statements that constitute “forward-looking statements” under the U.S. Securities laws. Forward-looking statements include, among other things, projections, estimates, and information about possible or future results related to the fund, markets, or regulatory developments. The views expressed above are not guarantees of future performance or economic results and involve certain risks, uncertainties, and assumptions that could cause actual outcomes and results to differ materially from the views expressed herein. The views expressed above are subject to change at any time based upon economic, market, or other conditions and Evergreen undertakes no obligation to update the views expressed herein. Any discussions of specific securities should not be considered a recommendation to buy or sell those securities. The views expressed herein (including any forward-looking statements) may not be relied upon as investment advice or as an indication of the fund’s trading intent.

You should carefully consider the fund’s investment objectives, policies, risks, charges and expenses before investing. To obtain a prospectus, which contains this and other important information visit www.EvergreenInvestments.com or call 1.800.847.5397.

Please read the prospectus carefully before investing.

9

ABOUT YOUR FUND’S EXPENSES

The Example below is intended to describe the fees and expenses borne by shareholders and the impact of those costs on your investment.

Example

As a shareholder of the fund, you incur two types of costs: (1) transaction costs, including sales charges (loads), redemption fees and exchange fees; and (2) ongoing costs, including management fees, distribution (12b-1) fees and other fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the fund and to compare these costs with the ongoing costs of investing in other mutual funds. The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from April 1, 2008 to September 30, 2008.

The example illustrates your fund’s costs in two ways:

The section in the table under the heading “Actual” provides information about actual account values and actual expenses. You may use the information in these columns, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the appropriate column for your share class, in the column entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

• Hypothetical example for comparison purposes |

The section in the table under the heading “Hypothetical (5% return before expenses)” provides information about hypothetical account values and hypothetical expenses based on the fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees or exchange fees. Therefore, the section in the table under the heading “Hypothetical (5% return before expenses)” is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | Beginning

Account Value

4/1/2008 | | Ending

Account Value

9/30/2008 | | Expenses Paid

During Period* |

|

|

|

|

|

|

|

Actual | | | | | | | | | | |

Class A | | $1,000.00 | | $ | 922.81 | | | $ | 5.72 | |

Class I | | $1,000.00 | | $ | 924.87 | | | $ | 4.43 | |

Hypothetical | | | | | | | | | | |

(5% return before expenses) | | | | | | | | | | |

Class A | | $1,000.00 | | $ | 1,019.05 | | | $ | 6.01 | |

Class I | | $1,000.00 | | $ | 1,020.40 | | | $ | 4.65 | |

|

|

|

|

|

|

|

|

|

|

|

* | For each class of the fund, expenses are equal to the annualized expense ratio of each class (1.19% for Class A and 0.92% for Class I), multiplied by the average account value over the period, multiplied by 183 / 366 days. |

10

FINANCIAL HIGHLIGHTS

(For a share outstanding throughout each period)

| | Year Ended September 30, |

| |

|

CLASS A | | | 2008 | | | 2007 | | | 20061 |

|

|

|

|

|

|

|

|

|

|

Net asset value, beginning of period | | $ | 14.73 | | $ | 11.53 | | $ | 10.00 |

|

|

|

|

|

|

|

|

|

|

Income from investment operations | | | | | | | | | |

Net investment income (loss) | | | (0.08) | | | (0.11)2 | | | (0.05) |

Net realized and unrealized gains or losses on investments | | | (2.59) | | | 3.31 | | | 1.58 |

| |

|

|

|

|

|

|

|

|

Total from investment operations | | | (2.67) | | | 3.20 | | | 1.53 |

|

|

|

|

|

|

|

|

|

|

Distributions to shareholders from | | | | | | | | | |

Net realized gains | | | (1.36) | | | 0 | | | 0 |

Tax basis return of capital | | | (0.06) | | | 0 | | | 0 |

| |

|

|

|

|

|

|

|

|

Total distributions to shareholders | | | (1.42) | | | 0 | | | 0 |

|

|

|

|

|

|

|

|

|

|

Net asset value, end of period | | $ | 10.64 | | $ | 14.73 | | $ | 11.53 |

|

|

|

|

|

|

|

|

|

|

Total return3 | | | (20.01)% | | | 27.75% | | | 15.30% |

|

|

|

|

|

|

|

|

|

|

Ratios and supplemental data | | | | | | | | | |

Net assets, end of period (thousands) | | $ | 26,497 | | $ | 45,706 | | $ | 3 |

Ratios to average net assets | | | | | | | | | |

Expenses including waivers/reimbursements but excluding expense reductions | | | 1.18% | | | 1.17% | | | 1.18%4,5 |

Expenses excluding waivers/reimbursements and expense reductions | | | 1.33% | | | 1.28% | | | 1.99%4 |

Net investment income (loss) | | | (0.48)% | | | (0.79)% | | | (0.66)%4 |

Portfolio turnover rate | | | 129% | | | 192% | | | 132% |

|

|

|

|

|

|

|

|

|

|

1 | For the period from October 11, 2005 (commencement of class operations), to September 30, 2006. |

2 | Net investment income (loss) per share is based on average shares outstanding during the period. |

3 | Excluding applicable sales charges |

5 | Including the expense reductions, the ratio would be 1.17%. |

See Notes to Financial Statements

11

FINANCIAL HIGHLIGHTS

(For a share outstanding throughout each period)

| | Year Ended September 30, |

| |

|

CLASS I | | | 2008 | | | 2007 | | | 20061 |

|

|

|

|

|

|

|

|

|

|

Net asset value, beginning of period | | $ | 14.77 | | $ | 11.54 | | $ | 10.00 |

|

|

|

|

|

|

|

|

|

|

Income from investment operations | | | | | | | | | |

Net investment income (loss) | | | (0.03)2 | | | (0.06)2 | | | (0.02) |

Net realized and unrealized gains or losses on investments | | | (2.61) | | | 3.30 | | | 1.56 |

| |

|

|

|

|

|

|

|

|

Total from investment operations | | | (2.64) | | | 3.24 | | | 1.54 |

|

|

|

|

|

|

|

|

|

|

Distributions to shareholders from | | | | | | | | | |

Net investment income | | | 0 | | | (0.01) | | | 0 |

Net realized gains | | | (1.36) | | | 0 | | | 0 |

Tax basis return of capital | | | (0.06) | | | 0 | | | 0 |

| |

|

|

|

|

|

|

|

|

Total distributions to shareholders | | | (1.42) | | | (0.01) | | | 0 |

|

|

|

|

|

|

|

|

|

|

Net asset value, end of period | | $ | 10.71 | | $ | 14.77 | | $ | 11.54 |

|

|

|

|

|

|

|

|

|

|

Total return | | | (19.72)% | | | 28.11% | | | 15.40% |

|

|

|

|

|

|

|

|

|

|

Ratios and supplemental data | | | | | | | | | |

Net assets, end of period (thousands) | | $ | 17,489 | | $ | 140,931 | | $ | 22,429 |

Ratios to average net assets | | | | | | | | | |

Expenses including waivers/reimbursements but excluding expense reductions | | | 0.92% | | | 0.92% | | | 0.93%3,4 |

Expenses excluding waivers/reimbursements and expense reductions | | | 1.04% | | | 0.98% | | | 1.74%3 |

Net investment income (loss) | | | (0.27)% | | | (0.42)% | | | (0.37)%3 |

Portfolio turnover rate | | | 129% | | | 192% | | | 132% |

|

|

|

|

|

|

|

|

|

|

1 | For the period from October 11, 2005 (commencement of class operations), to September 30, 2006. |

2 | Net investment income (loss) per share is based on average shares outstanding during the period. |

4 | Including the expense reductions, the ratio would be 0.92% |

See Notes to Financial Statements

12

SCHEDULE OF INVESTMENTS

September 30, 2008

| | Shares | | Value |

|

|

|

|

|

COMMON STOCKS 93.6% | | | | | | |

CONSUMER DISCRETIONARY 15.0% | | | | | | |

Diversified Consumer Services 4.0% | | | | | | |

Capella Education Co. * ρ | | | 18,157 | | $ | 778,209 |

Strayer Education, Inc. | | | 4,800 | | | 961,248 |

| | | | |

|

|

| | | | | | 1,739,457 |

| | | | |

|

|

Hotels, Restaurants & Leisure 3.7% | | | | | | |

Buffalo Wild Wings, Inc. * ρ | | | 25,548 | | | 1,028,052 |

Penn National Gaming, Inc. | | | 23,000 | | | 611,110 |

| | | | |

|

|

| | | | | | 1,639,162 |

| | | | |

|

|

Internet & Catalog Retail 0.8% | | | | | | |

priceline.com, Inc. * | | | 5,200 | | | 355,836 |

| | | | |

|

|

Specialty Retail 3.2% | | | | | | |

Aeropostale, Inc. * | | | 24,100 | | | 773,851 |

GameStop Corp., Class A * | | | 17,800 | | | 608,938 |

| | | | |

|

|

| | | | | | 1,382,789 |

| | | | |

|

|

Textiles, Apparel & Luxury Goods 3.3% | | | | | | |

Hanesbrands, Inc. * | | | 42,000 | | | 913,500 |

Warnaco Group, Inc. * | | | 12,300 | | | 557,067 |

| | | | |

|

|

| | | | | | 1,470,567 |

| | | | |

|

|

CONSUMER STAPLES 6.4% | | | | | | |

Food Products 4.2% | | | | | | |