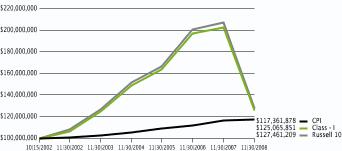

OMB APPROVAL |

OMB Number: 3235-0570

Expires: September 30, 2007

Estimated average burden hours per response: 19.4 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSRS

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-08413

Evergreen Equity Trust

_____________________________________________________________

(Exact name of registrant as specified in charter)

200 Berkeley Street

Boston, Massachusetts 02116

_____________________________________________________________

(Address of principal executive offices) (Zip code)

Michael H. Koonce, Esq.

200 Berkeley Street

Boston, Massachusetts 02116

____________________________________________________________

(Name and address of agent for service)

Registrant's telephone number, including area code: (617) 210-3200

Date of fiscal year end: Registrant is making a semi-annual filing for three of its series, Evergreen Market Index Fund, Evergreen Market Index Growth Fund and Evergreen Market Index Value Fund, for the six months ended November 30, 2008. These series have May 31 fiscal year end.

Date of reporting period: November 30, 2008

Item 1 - Reports to Stockholders.

Semiannual Report

as of November 30, 2008

|

This semiannual report must be preceded or accompanied by a prospectus of the Evergreen funds contained herein. The prospectus contains more complete information, including fees and expenses, and should be read carefully before investing or sending money. Each fund will file its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q.

Each fund's Form N-Q will be available on the SEC's Web site at http://www.sec.gov. In addition, each fund's Form N-Q may be reviewed and copied at the SEC's Public Reference Room in Washington, D.C. Information on the operation of the Public Reference Room may be obtained by calling 800.SEC.0330.

A description of each fund's proxy voting policies and procedures, as well as information regarding how each fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30, is available by visiting our Web site at EvergreenInvestments.com or by visiting the SEC's Web site at http://www.sec.gov. Each fund's proxy voting policies and procedures are also available without charge, upon request, by calling 800.343.2898.

Mutual Funds:

| NOT FDIC INSURED | MAY LOSE VALUE | NOT BANK GUARUANTEED |

Evergreen InvestmentsSM is a service mark of Evergreen Investment Management Company, LLC. Copyright 2008, Evergreen Investment Management Company, LLC.

Evergreen Investment Management Company, LLC is a subsidiary of Wachovia Corporation and is an affiliate of Wachovia Corporation's other Broker Dealer subsidiaries.

Evergreen mutual funds are distributed by Evergreen Investment Services, Inc. 200 Berkeley Street, Boston, MA 02116

| 1 | | LETTER TO SHAREHOLDERS |

MARKET INDEX FUND |

| 4 | | FUND AT A GLANCE |

| 6 | | ABOUT YOUR FUND'S EXPENSES |

| 7 | | FINANCIAL HIGHLIGHTS |

| 8 | | SCHEDULE OF INVESTMENTS |

| 23 | | STATEMENT OF ASSETS AND LIABILITIES |

| 24 | | STATEMENT OF OPERATIONS |

| 25 | | STATEMENTS OF CHANGES IN NET ASSETS |

MARKET INDEX GROWTH FUND |

| 26 | | FUND AT A GLANCE |

| 28 | | ABOUT YOUR FUND'S EXPENSES |

| 29 | | FINANCIAL HIGHLIGHTS |

| 30 | | SCHEDULE OF INVESTMENTS |

| 48 | | STATEMENT OF ASSETS AND LIABILITIES |

| 49 | | STATEMENT OF OPERATIONS |

| 50 | | STATEMENTS OF CHANGES IN NET ASSETS |

MARKET INDEX VALUE FUND |

| 51 | | FUND AT A GLANCE |

| 53 | | ABOUT YOUR FUND'S EXPENSES |

| 54 | | FINANCIAL HIGHLIGHTS |

| 55 | | SCHEDULE OF INVESTMENTS |

| 73 | | STATEMENT OF ASSETS AND LIABILITIES |

| 74 | | STATEMENT OF OPERATIONS |

| 75 | | STATEMENTS OF CHANGES IN NET ASSETS |

CLOSING PAGE |

| 76 | | COMBINED NOTES TO FINANCIAL STATEMENTS |

| 84 | | ADDITIONAL INFORMATION |

| 111 | | TRUSTEES AND OFFICERS |

Dear Shareholder:

W. Douglas Munn

President and Chief Executive Officer

We are pleased to provide the Semiannual Report for the Evergreen Market Index Funds for the six-month period ended November 30, 2008 (the "period").

Growing concerns about a weakening economy, deteriorating corporate profitability and an uncertain future for the auto industry combined to cause domestic equity prices to plummet during the period. Few stocks escaped the damage that affected shares of growth companies, value companies and corporations of all sizes and industry groups. Well-recognized benchmarks for the general stock market as well as for specific subgroups typically fell by 30% or more during the period. In the bond markets, investors sought out quality and tried to minimize risk. Treasuries and higher quality short-term debt securities held up well, while corporate bond prices fell victim to the same forces undermining equity valuations. As sentiment in the fixed income markets moved from worries about inflation to concerns about deflation, investors appeared willing to accept virtually nothing for short-term loans to the federal government. The domestic trends extended to capital markets beyond the United States. Foreign sovereign government debt of industrialized nations held up relatively well, but equity prices and virtually all other asset classes suffered declines. Further signs of a global recession also pulled commodity and oil prices lower, while the market for gold strengthened.

Economic news seemed only to get worse during the period. After months of deceleration, the U.S. economy finally contracted in the third quarter of 2008. Real Gross Domestic Product ("GDP") fell by 0.5%, with consumer spending recording its greatest drop in three decades. Economists believed GDP for the fourth quarter of 2008 could drop by more and that the nation's unemployment rate could climb above 8% in 2009. The National Bureau of Economic Research announced that the domestic economy was officially in recession. Meanwhile, reports of slumping manufacturing production and weakening economic activity appeared throughout the world, signaling a global slowdown. The European Union's economic analysis bureau reported that GDP for the 15-nation Eurozone fell by 0.2% during the third quarter of 2008. The economic deceleration extended to China, where the central government announced a major fiscal program to stimulate growth while the central bank cut interest rates by one-half of a percentage point. Faced with widening evidence of economic deterioration, the central banks in the U.S. and other major industrialized nations injected added liquidity into the markets. These efforts continued into December 2008, after the fiscal period ended, when the U.S. Federal Reserve dropped official interest rates to an historically low range, slashing the target fed funds rate to a range of zero to 0.25%. Meanwhile, Congress and officials of both the outgoing and incoming administrations considered new spending plans to revive the economy and, perhaps, rescue the staggering domestic auto industry.

During a volatile and challenging period in the capital markets, the portfolio manager of Evergreen's market index funds continued to implement quantitative-based methodologies intended to produce results consistent with underlying stock market indexes of each portfolio. Evergreen Market Index Fund, for example, is designed to reflect the results of the Standard & Poor's 500 Index, a benchmark for the overall stock market. Evergreen Market Index Growth Fund, meanwhile, is designed to reflect the performance of the Russell 1000 Growth Index, a standard for large cap growth stocks, while the portfolio of Evergreen Market Index Value Fund is structured to be consistent with the Russell 1000 Value Index, which reflects the performance of large cap value stocks.

As we look back over the extraordinary series of events during the period, we believe it is vitally important for all investors to keep perspective and remain focused on their long-term strategies. Most importantly, we continue to urge investors to pursue fully diversified strategies to participate in future market gains and limit the risks of potential losses. If they haven't already done so, we encourage individual investors to work with their financial advisors to develop a diversified, long-term strategy and, most importantly, to adhere to it. Investors should keep in mind that the economy and the financial markets have had long and successful histories of adaptability, recovery, innovation and growth. Proper asset allocation decisions can have significant impacts on the returns of long-term portfolios.

Please visit us at EvergreenInvestments.com for more information about our funds and other investment products available to you. Thank you for your continued support of Evergreen Investments.

Sincerely,

W. Douglas Munn

President and Chief Executive Officer

Evergreen Funds

Notices to Shareholders:

- On December 31, 2008, Wachovia Corporation merged with and into Wells Fargo & Company ("Wells Fargo"). As a result of the merger, Evergreen Investment Management Company, LLC ("EIMC"), Tattersall Advisory Group, Inc., J.L. Kaplan Associates, LLC, First International Advisors, LLC, Metropolitan West Capital Management, LLC, Evergreen Investment Services, Inc. and Evergreen Service Company, LLC, are subsidiaries of Wells Fargo.

After the merger, new interim advisory agreements between the Evergreen Funds and EIMC went into effect, as did new interim sub-advisory agreements with each sub-advisor to the Evergreen Funds. These interim agreements will be in effect until no later than March 19, 2009. Shareholders of the Evergreen Funds will meet on or around February 12, 2009 to consider definitive advisory and sub-advisory agreements for the Evergreen Funds, which would replace the interim agreements.

- Effective January 1, 2009, W. Douglas Munn became President and Chief Executive Officer of the Evergreen Funds.

Market Index Fund

FUND AT A GLANCE |

Management Team

| Investment Advisor: |

| Evergreen Investment Management Company, LLC |

|

| Portfolio Manager: |

| William E. Zieff |

CURRENT INVESTMENT STYLE

| Source: Morningstar, Inc. Morningstar's style box is based on a portfolio date as of 9/30/2008. The Equity style box placement is based on 10 growth and valuation measures for each fund holding and the median size of the companies in which the fund invests. |

PERFORMANCE AND RETURNS

| Portfolio inception date: 10/15/2002 |

| Class I |

| Class inception date | 10/15/2002 |

| 6-month return | -35.16 | % |

| Average annual return |

| 1-year | -38.06 | % |

| 5-year | -1.41 | % |

| Since portfolio inception | 2.19 | % |

| Past performance is no guarantee of future results. The performance quoted represents past performance and current performance may be lower or higher. The investment return and principal value of an investment will fluctuate so that investors' shares, when redeemed, may be worth more or less than their original cost. Performance includes the reinvestment of income dividends and capital gain distributions. |

| The advisor is waiving its advisory fee and reimbursing the fund for a portion of other expenses. Had the fee not been waived and expenses not reimbursed, returns would have been lower. |

| The fund is only offered to certain pension plans having at least $100 million. Class I are sold without a front-end or deferred sales charge. The minimum initial investment for the fund is $100 million, which may be waived in certain situations. There is no minimum required for subsequent purchases. |

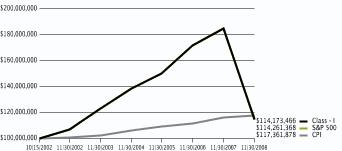

LONG-TERM GROWTH

| Comparison of a $100,000,000 investment in the Evergreen Market Index Fund Class I shares versus a similar investment in the S&P 500 Index (S&P) and the Consumer Price Index (CPI). |

| The S&P 500 is an unmanaged market index and does not include transaction costs associated with buying and selling securities, any mutual fund fees or expenses or any taxes. The CPI is a commonly used measure of inflation and does not represent an investment return. It is not possible to invest directly in an index. |

| The fund's investment objective may be changed without a vote of the fund's shareholders. |

| "Standard & Poor's," "S&P," "S&P 500," "Standard & Poor's 500" and "500" are trademarks of The McGraw-Hill Companies, Inc. and have been licensed for use by Evergreen Investments. The product is not sponsored, endorsed, sold or promoted by Standard & Poor's and Standard & Poor's makes no representation regarding the advisability of investing in the product. |

| All data is as of November 30, 2008, and subject to change. |

Market Index Fund ABOUT YOUR FUND'S EXPENSES |

The Example below is intended to describe the fees and expenses borne by shareholders and the impact of those costs on your investment.

Example

As a shareholder of the fund, you incur two types of costs: (1) transaction costs, including sales charges (loads), redemption fees and exchange fees; and (2) ongoing costs, including management fees, distribution (12b-1) fees and other fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the fund and to compare these costs with the ongoing costs of investing in other mutual funds. The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from June 1, 2008 to November 30, 2008.

The example illustrates your fund's costs in two ways:

- Actual expenses

The section in the table under the heading "Actual" provides information about actual account values and actual expenses. You may use the information in these columns, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the appropriate column for your share class, in the column entitled "Expenses Paid During Period" to estimate the expenses you paid on your account during this period. - Hypothetical example for comparison purposes

The section in the table under the heading "Hypothetical (5% return before expenses)" provides information about hypothetical account values and hypothetical expenses based on the fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees or exchange fees. Therefore, the section in the table under the heading "Hypothetical (5% return before expenses)" is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would havebeen higher.

| Beginning

Account Value

6/1/2008 | Ending

Account Value

11/30/2008 | Expenses Paid

During Period* |

| Actual | | | | | | |

| Class I | $1,000.00 | | $648.36 | | $0.08 | |

| Hypothetical (5% return before expenses) | | | | | | |

| Class I | $1,000.00 | | $1,024.97 | | $0.10 | |

| *Expenses are equal to the fund's annualized expense ratio (0.02% for Class I), multiplied by the average account value over the period, multiplied by 183/365 days. |

Market Index Fund FINANCIAL HIGHLIGHTS |

(For a share outstanding throughout each period) |

| | Six Months Ended November 30, 2008 | | Year Ended May 31, |

| Class I | (unaudited) | 2008 | 2007 | 2006 | 2005 | 2004 |

| Net asset value, beginning of period | $ | 13.11 | | $ | 14.48 | | $ | 14.50 | | $ | 13.81 | | $ | 12.97 | | $ | 11.02 | |

| Income from investment operations | | | | | | | | | | | | | | | | | | |

| Net investment income (loss) | | 0.14 | | | 0.28 | 1 | | 0.27 | 1 | | 0.27 | 1 | | 0.30 | | | 0.18 | |

| Net realized and unrealized gains or losses on investments | | (4.75 | ) | | (1.24 | ) | | 2.76 | | | 0.91 | | | 0.76 | | | 1.83 | |

| Total from investment operations | | (4.61 | ) | | (0.96 | ) | | 3.03 | | | 1.18 | | | 1.06 | | | 2.01 | |

| Distributions to shareholders from | | | | | | | | | | | | | | | | | | |

| Net investment income | | 0 | | | (0.23 | ) | | (0.30 | ) | | (0.32 | ) | | (0.20 | ) | | (0.06 | ) |

| Net realized gains | | 0 | | | (0.18 | ) | | (2.75 | ) | | (0.17 | ) | | (0.02 | ) | | 0 | |

| Total distributions to shareholders | | 0 | | | (0.41 | ) | | (3.05 | ) | | (0.49 | ) | | (0.22 | ) | | (0.06 | ) |

| Net asset value, end of period | $ | 8.50 | | $ | 13.11 | | $ | 14.48 | | $ | 14.50 | | $ | 13.81 | | $ | 12.97 | |

| Total return | | (35.16 | )% | | (6.71 | )% | | 22.78 | % | | 8.56 | % | | 8.24 | % | | 18.25 | % |

| Ratios and supplemental data | | | | | | | | | | | | | | | | | | |

| Net assets, end of period (thousands) | $ | 227,730 | | $ | 351,138 | | $ | 558,366 | | $ | 406,581 | | $ | 722,863 | | $ | 716,998 | |

| Ratios to average net assets | | | | | | | | | | | | | | | | | | |

| Expenses including waivers/reimbursements but excluding expense reductions | | 0.02 | %2 | | 0.03 | % | | 0.03 | % | | 0.03 | % | | 0.03 | % | | 0.02 | % |

| Expenses excluding waivers/reimbursements and expense reductions | | 0.46 | %2 | | 0.46 | % | | 0.46 | % | | 0.46 | % | | 0.46 | % | | 0.45 | % |

| Net investment income (loss) | | 2.55 | %2 | | 2.01 | % | | 1.93 | % | | 1.90 | % | | 2.08 | % | | 1.70 | % |

| Portfolio turnover rate | | 2 | % | | 7 | % | | 5 | % | | 6 | % | | 6 | % | | 2 | % |

| 1 | Net investment income (loss) per share is based on average shares outstanding during the period. |

| 2 | Annualized |

See Combined Notes to Financial Statements Market Index Fund SCHEDULE OF INVESTMENTS |

November 30, 2008 (unaudited) |

| | Shares | | | Value | |

| COMMON STOCKS 99.5% | | | | | | |

| CONSUMER DISCRETIONARY 8.0% | | | | | | |

| Auto Components 0.1% | | | | | | |

| Goodyear Tire & Rubber Co. * | | 6,978 | | $ | 44,868 | |

| Johnson Controls, Inc. | | 17,183 | | | 303,452 | |

| | | | | 348,320 | |

| Automobiles 0.2% | | | | | | |

| Ford Motor Co. * Þ | | 65,440 | | | 176,034 | |

| General Motors Corp. Þ | | 17,666 | | | 92,570 | |

| Harley-Davidson, Inc. Þ | | 6,810 | | | 115,838 | |

| | | | | 384,442 | |

| Distributors 0.1% | | | | | | |

| Genuine Parts Co. | | 4,682 | | | 183,300 | |

| | | | | | |

| Diversified Consumer Services 0.2% | | | | | | |

| Apollo Group, Inc., Class A * | | 3,073 | | | 236,129 | |

| H&R Block, Inc. Þ | | 9,494 | | | 181,620 | |

| | | | | 417,749 | |

| Hotels, Restaurants & Leisure 1.4% | | | | | | |

| Carnival Corp. Þ | | 12,645 | | | 265,545 | |

| Darden Restaurants, Inc. Þ | | 4,064 | | | 74,331 | |

| International Game Technology | | 8,959 | | | 95,951 | |

| Marriott International, Inc., Class A Þ | | 8,552 | | | 143,588 | |

| McDonald's Corp. | | 32,546 | | | 1,912,077 | |

| Starbucks Corp. * | | 21,142 | | | 188,798 | |

| Starwood Hotels & Resorts Worldwide, Inc. Þ | | 5,403 | | | 91,095 | |

| Wyndham Worldwide Corp. | | 5,136 | | | 24,550 | |

| Wynn Resorts, Ltd. Þ | | 1,779 | | | 70,840 | |

| Yum! Brands, Inc. | | 13,564 | | | 365,414 | |

| | | | | 3,232,189 | |

| Household Durables 0.4% | | | | | | |

| Black & Decker Corp. Þ | | 1,735 | | | 73,633 | |

| Centex Corp. Þ | | 3,576 | | | 32,756 | |

| D.R. Horton, Inc. Þ | | 7,971 | | | 54,761 | |

| Fortune Brands, Inc. | | 4,338 | | | 163,976 | |

| Harman International Industries, Inc. Þ | | 1,694 | | | 25,495 | |

| KB Home Þ | | 2,178 | | | 25,330 | |

| Leggett & Platt, Inc. | | 4,652 | | | 67,919 | |

| Lennar Corp., Class A Þ | | 4,091 | | | 29,087 | |

| Newell Rubbermaid, Inc. | | 8,019 | | | 107,134 | |

| Pulte Homes, Inc. Þ | | 6,183 | | | 65,849 | |

| Snap-On, Inc. Þ | | 1,662 | | | 59,915 | |

| Stanley Works | | 2,274 | | | 72,291 | |

| Whirlpool Corp. Þ | | 2,154 | | | 84,825 | |

| | | | | 862,971 | |

| Internet & Catalog Retail 0.2% | | | | | | |

| Amazon.com, Inc. * Þ | | 9,244 | | | 394,719 | |

| Expedia, Inc. * | | 6,056 | | | 50,870 | |

| | | | | 445,589 | |

| Leisure Equipment & Products 0.1% | | | | | | |

| Eastman Kodak Co. Þ | | 7,769 | | | 58,811 | |

| Hasbro, Inc. Þ | | 3,633 | | | 97,365 | |

| | Shares | | | Value | |

| COMMON STOCKS continued | | | | | | |

| CONSUMER DISCRETIONARY continued | | | | | | |

| Leisure Equipment & Products continued | | | | | | |

| Mattel, Inc. | | 10,433 | | $ | 142,619 | |

| | | | | 298,795 | |

| Media 2.5% | | | | | | |

| CBS Corp., Class B Þ | | 19,676 | | | 131,042 | |

| Comcast Corp., Class A | | 84,448 | | | 1,464,328 | |

| DIRECTV Group, Inc. * Þ | | 15,805 | | | 347,868 | |

| Gannett Co., Inc. Þ | | 6,601 | | | 57,495 | |

| Interpublic Group of Cos. * Þ | | 13,788 | | | 56,393 | |

| McGraw-Hill Cos. Þ | | 9,191 | | | 229,775 | |

| Meredith Corp. Þ | | 1,048 | | | 16,915 | |

| New York Times Co., Class A Þ | | 3,370 | | | 25,410 | |

| News Corp., Class A | | 66,442 | | | 524,892 | |

| Omnicom Group, Inc. | | 9,226 | | | 261,003 | |

| Scripps Networks Interactive, Inc., Class A Þ | | 2,601 | | | 72,282 | |

| Time Warner, Inc. Þ | | 103,681 | | | 938,313 | |

| Viacom, Inc., Class B * | | 17,968 | | | 286,051 | |

| Walt Disney Co. Þ | | 54,301 | | | 1,222,858 | |

| Washington Post Co., Class B Þ | | 173 | | | 68,491 | |

| | | | | 5,703,116 | |

| Multiline Retail 0.7% | | | | | | |

| Big Lots, Inc. * Þ | | 2,374 | | | 41,592 | |

| Family Dollar Stores, Inc. Þ | | 4,043 | | | 112,314 | |

| J.C. Penney Co., Inc. | | 6,427 | | | 122,049 | |

| Kohl's Corp. * Þ | | 8,813 | | | 287,833 | |

| Macy's, Inc. Þ | | 12,170 | | | 90,301 | |

| Nordstrom, Inc. Þ | | 4,615 | | | 52,473 | |

| Sears Holdings Corp. * Þ | | 1,646 | | | 59,667 | |

| Target Corp. | | 21,839 | | | 737,285 | |

| | | | | 1,503,514 | |

| Specialty Retail 1.7% | | | | | | |

| Abercrombie & Fitch Co., Class A Þ | | 2,519 | | | 48,692 | |

| AutoNation, Inc. * Þ | | 3,118 | | | 26,628 | |

| AutoZone, Inc. * Þ | | 1,107 | | | 120,907 | |

| Bed Bath & Beyond, Inc. * Þ | | 7,536 | | | 152,906 | |

| Best Buy Co., Inc. Þ | | 9,775 | | | 202,440 | |

| GameStop Corp., Class A * Þ | | 4,727 | | | 103,285 | |

| Gap, Inc. Þ | | 13,588 | | | 176,916 | |

| Home Depot, Inc. Þ | | 49,151 | | | 1,135,880 | |

| Limited Brands, Inc. | | 8,259 | | | 76,891 | |

| Lowe's Cos. | | 42,415 | | | 876,294 | |

| Office Depot, Inc. * | | 7,958 | | | 15,677 | |

| RadioShack Corp. Þ | | 3,795 | | | 37,381 | |

| Sherwin-Williams Co. Þ | | 2,855 | | | 168,245 | |

| Staples, Inc. | | 20,576 | | | 357,199 | |

| Tiffany & Co. Þ | | 3,589 | | | 71,026 | |

| TJX Cos. | | 12,137 | | | 276,966 | |

| | | | | 3,847,333 | |

| | Shares | | | Value | |

| COMMON STOCKS continued | | | | | | |

| CONSUMER DISCRETIONARY continued | | | | | | |

| Textiles, Apparel & Luxury Goods 0.4% | | | | | | |

| Coach, Inc. * | | 9,749 | | $ | 174,507 | |

| Jones Apparel Group, Inc. | | 2,414 | | | 12,384 | |

| Liz Claiborne, Inc. Þ | | 2,743 | | | 7,818 | |

| Nike, Inc., Class B Þ | | 11,353 | | | 604,547 | |

| Polo Ralph Lauren Corp. Þ | | 1,645 | | | 71,064 | |

| VF Corp. Þ | | 2,521 | | | 131,823 | |

| | | | | 1,002,143 | |

| CONSUMER STAPLES 13.0% | | | | | | |

| Beverages 2.6% | | | | | | |

| Brown-Forman Corp., Class B | | 2,838 | | | 124,560 | |

| Coca-Cola Co. | | 57,526 | | | 2,696,243 | |

| Coca-Cola Enterprises, Inc. | | 9,176 | | | 84,235 | |

| Constellation Brands, Inc., Class A * | | 5,609 | | | 71,571 | |

| Dr. Pepper Snapple Group, Inc. * | | 7,341 | | | 118,484 | |

| Molson Coors Brewing Co., Class B | | 4,359 | | | 193,845 | |

| Pepsi Bottling Group, Inc. | | 3,952 | | | 71,492 | |

| PepsiCo, Inc. | | 45,304 | | | 2,568,737 | |

| | | | | 5,929,167 | |

| Food & Staples Retailing 3.3% | | | | | | |

| Costco Wholesale Corp. | | 12,582 | | | 647,596 | |

| CVS Caremark Corp. | | 41,532 | | | 1,201,521 | |

| Kroger Co. | | 18,952 | | | 524,212 | |

| Safeway, Inc. | | 12,600 | | | 274,680 | |

| SUPERVALU, Inc. | | 6,147 | | | 73,211 | |

| Sysco Corp. | | 17,421 | | | 408,522 | |

| Wal-Mart Stores, Inc. | | 64,891 | | | 3,626,109 | |

| Walgreen Co. Þ | | 28,646 | | | 708,702 | |

| Whole Foods Market, Inc. Þ | | 4,060 | | | 42,955 | |

| | | | | 7,507,508 | |

| Food Products 1.8% | | | | | | |

| Archer Daniels Midland Co. | | 18,644 | | | 510,473 | |

| Campbell Soup Co. Þ | | 6,128 | | | 196,402 | |

| ConAgra Foods, Inc. | | 13,109 | | | 193,358 | |

| Dean Foods Co. * | | 4,409 | | | 64,195 | |

| General Mills, Inc. | | 9,729 | | | 614,581 | |

| H.J. Heinz Co. Þ | | 9,038 | | | 351,036 | |

| Hershey Co. Þ | | 4,796 | | | 172,656 | |

| J.M. Smucker Co. | | 3,414 | | | 154,893 | |

| Kellogg Co. | | 7,246 | | | 314,694 | |

| Kraft Foods, Inc., Class A | | 43,932 | | | 1,195,390 | |

| McCormick & Co., Inc. | | 3,732 | | | 111,101 | |

| Sara Lee Corp. | | 20,442 | | | 187,657 | |

| Tyson Foods, Inc., Class A | | 8,683 | | | 58,263 | |

| | | | | 4,124,699 | |

| Household Products 3.3% | | | | | | |

| Clorox Co. Þ | | 3,996 | | | 236,403 | |

| Colgate-Palmolive Co. | | 14,635 | | | 952,299 | |

| | Shares | | | Value | |

| COMMON STOCKS continued | | | | | | |

| CONSUMER STAPLES continued | | | | | | |

| Household Products continued | | | | | | |

| Kimberly-Clark Corp. | | 12,016 | | $ | 694,405 | |

| Procter & Gamble Co. Þ | | 86,690 | | | 5,578,502 | |

| | | | | 7,461,609 | |

| Personal Products 0.1% | | | | | | |

| Avon Products, Inc. | | 12,319 | | | 259,931 | |

| Estee Lauder Cos., Class A Þ | | 3,323 | | | 92,712 | |

| | | | | 352,643 | |

| Tobacco 1.9% | | | | | | |

| Altria Group, Inc. | | 59,605 | | | 958,448 | |

| Lorillard, Inc. Þ | | 5,033 | | | 304,144 | |

| Philip Morris International, Inc. | | 59,648 | | | 2,514,760 | |

| Reynolds American, Inc. Þ | | 4,919 | | | 202,073 | |

| UST, Inc. | | 4,270 | | | 293,562 | |

| | | | | 4,272,987 | |

| ENERGY 14.2% | | | | | | |

| Energy Equipment & Services 2.0% | | | | | | |

| Baker Hughes, Inc. | | 8,920 | | | 310,684 | |

| BJ Services Co. | | 8,512 | | | 102,059 | |

| Cameron International Corp. * Þ | | 6,299 | | | 132,909 | |

| ENSCO International, Inc. | | 4,147 | | | 134,404 | |

| Halliburton Co. | | 25,375 | | | 446,600 | |

| Nabors Industries, Ltd. * Þ | | 8,107 | | | 117,551 | |

| National Oilwell Varco, Inc. * | | 12,078 | | | 341,687 | |

| Noble Corp. Þ | | 7,788 | | | 208,641 | |

| Rowan Companies, Inc. | | 3,270 | | | 56,734 | |

| Schlumberger, Ltd. Þ | | 34,715 | | | 1,761,439 | |

| Smith International, Inc. | | 6,251 | | | 182,779 | |

| Transocean, Inc. | | 9,232 | | | 617,436 | |

| Weatherford International, Ltd. * | | 19,697 | | | 251,531 | |

| | | | | 4,664,454 | |

| Oil, Gas & Consumable Fuels 12.2% | | | | | | |

| Anadarko Petroleum Corp. Þ | | 13,557 | | | 556,515 | |

| Apache Corp. | | 9,679 | | | 748,187 | |

| Cabot Oil & Gas Corp. | | 2,991 | | | 89,640 | |

| Chesapeake Energy Corp. | | 15,084 | | | 259,143 | |

| Chevron Corp. | | 59,453 | | | 4,697,382 | |

| ConocoPhillips Þ | | 43,981 | | | 2,309,882 | |

| Consol Energy, Inc. | | 5,301 | | | 153,570 | |

| Devon Energy Corp. | | 12,785 | | | 924,867 | |

| El Paso Corp. Þ | | 20,292 | | | 149,958 | |

| EOG Resources, Inc. | | 7,200 | | | 612,144 | |

| Exxon Mobil Corp. | | 150,307 | | | 12,047,106 | |

| Hess Corp. | | 8,191 | | | 442,642 | |

| Marathon Oil Corp. | | 20,418 | | | 534,543 | |

| Massey Energy Co. | | 2,447 | | | 38,222 | |

| Murphy Oil Corp. | | 5,511 | | | 242,760 | |

| Noble Energy, Inc. | | 4,998 | | | 261,295 | |

| Occidental Petroleum Corp. | | 23,645 | | | 1,280,140 | |

| | Shares | | | Value | |

| COMMON STOCKS continued | | | | | | |

| ENERGY continued | | | | | | |

| Oil, Gas & Consumable Fuels continued | | | | | | |

| Peabody Energy Corp. | | 7,870 | | $ | 184,394 | |

| Pioneer Natural Resources Co. Þ | | 3,463 | | | 69,537 | |

| Range Resources Corp. | | 4,488 | | | 186,117 | |

| Southwestern Energy Co. * | | 9,931 | | | 341,328 | |

| Spectra Energy Corp. | | 17,792 | | | 289,298 | |

| Sunoco, Inc. Þ | | 3,382 | | | 134,401 | |

| Tesoro Corp. Þ | | 3,990 | | | 36,668 | |

| Valero Energy Corp. | | 15,139 | | | 277,801 | |

| Williams Cos. Þ | | 16,676 | | | 270,485 | |

| XTO Energy, Inc. | | 15,897 | | | 607,901 | |

| | | | | 27,745,926 | |

| FINANCIALS 13.4% | | | | | | |

| Capital Markets 2.4% | | | | | | |

| American Capital, Ltd. Þ | | 5,990 | | | 25,398 | |

| Ameriprise Financial, Inc. | | 6,278 | | | 115,892 | |

| Bank of New York Mellon Corp. | | 33,166 | | | 1,001,945 | |

| Charles Schwab Corp. Þ | | 26,996 | | | 494,837 | |

| E*TRADE Financial Corp. * Þ | | 15,547 | | | 20,988 | |

| Federated Investors, Inc., Class B | | 2,543 | | | 50,479 | |

| Franklin Resources, Inc. Þ | | 4,406 | | | 267,664 | |

| Goldman Sachs Group, Inc. | | 12,572 | | | 993,062 | |

| INVESCO, Ltd. Þ | | 11,192 | | | 140,460 | |

| Janus Capital Group, Inc. Þ | | 4,625 | | | 37,694 | |

| Legg Mason, Inc. Þ | | 4,102 | | | 73,918 | |

| Merrill Lynch & Co., Inc. | | 44,318 | | | 585,884 | |

| Morgan Stanley | | 32,093 | | | 473,372 | |

| Northern Trust Corp. | | 6,397 | | | 293,558 | |

| State Street Corp. | | 12,494 | | | 526,122 | |

| T. Rowe Price Group, Inc. Þ | | 7,488 | | | 256,164 | |

| | | | | 5,357,437 | |

| Commercial Banks 3.2% | | | | | | |

| BB&T Corp. Þ | | 15,901 | | | 476,553 | |

| Comerica, Inc. Þ | | 4,354 | | | 98,183 | |

| Fifth Third Bancorp Þ | | 16,713 | | | 159,776 | |

| First Horizon National Corp. Þ | | 5,838 | | | 62,408 | |

| Huntington Bancshares, Inc. Þ | | 10,596 | | | 84,768 | |

| KeyCorp. Þ | | 14,315 | | | 134,275 | |

| M&T Bank Corp. Þ | | 2,232 | | | 143,406 | |

| Marshall & Ilsley Corp. Þ | | 7,508 | | | 115,998 | |

| National City Corp. Þ | | 60,567 | | | 121,740 | |

| PNC Financial Services Group, Inc. | | 10,027 | | | 529,125 | |

| Regions Financial Corp. Þ | | 20,106 | | | 204,880 | |

| SunTrust Banks, Inc. | | 10,235 | | | 324,756 | |

| U.S. Bancorp | | 50,412 | | | 1,360,116 | |

| Wachovia Corp. ° | | 62,474 | | | 351,104 | |

| Wells Fargo & Co. Þ ° | | 107,549 | | | 3,107,091 | |

| Zions Bancorp Þ | | 3,318 | | | 105,811 | |

| | | | | 7,379,990 | |

| | | | | | |

| | Shares | | | Value | |

| COMMON STOCKS continued | | | | | | |

| FINANCIALS continued | | | | | | |

| Consumer Finance 0.8% | | | | | | |

| American Express Co. | | 33,551 | | $ | 782,074 | |

| Capital One Financial Corp. Þ | | 10,873 | | | 374,140 | |

| Discover Financial Services Þ | | 13,872 | | | 141,910 | |

| MasterCard, Inc., Class A Þ | | 2,093 | | | 304,113 | |

| SLM Corp. * Þ | | 13,523 | | | 124,547 | |

| | | | | 1,726,784 | |

| Diversified Financial Services 3.6% | | | | | | |

| Bank of America Corp. Þ | | 145,130 | | | 2,358,362 | |

| CIT Group, Inc. Þ | | 8,258 | | | 27,582 | |

| Citigroup, Inc. | | 157,581 | | | 1,306,346 | |

| CME Group, Inc., Class A Þ | | 1,942 | | | 411,607 | |

| IntercontinentalExchange, Inc. * Þ | | 2,181 | | | 160,522 | |

| JPMorgan Chase & Co. | | 106,608 | | | 3,375,209 | |

| Leucadia National Corp. Þ | | 5,121 | | | 100,116 | |

| Moody's Corp. Þ | | 5,712 | | | 124,008 | |

| NASDAQ OMX Group, Inc. * Þ | | 3,934 | | | 84,581 | |

| NYSE Euronext Þ | | 7,698 | | | 183,289 | |

| | | | | 8,131,622 | |

| Insurance 2.4% | | | | | | |

| AFLAC, Inc. | | 13,781 | | | 638,060 | |

| Allstate Corp. | | 15,671 | | | 398,670 | |

| American International Group, Inc. Þ | | 77,811 | | | 156,400 | |

| AON Corp. | | 8,035 | | | 363,986 | |

| Assurant, Inc. | | 3,432 | | | 74,715 | |

| Chubb Corp. | | 10,434 | | | 535,890 | |

| Cincinnati Financial Corp. Þ | | 4,699 | | | 137,399 | |

| Genworth Financial, Inc., Class A | | 12,532 | | | 18,171 | |

| Hartford Financial Services Group, Inc. Þ | | 8,719 | | | 73,676 | |

| Lincoln National Corp. | | 7,432 | | | 102,041 | |

| Loews Corp. | | 10,479 | | | 287,020 | |

| Marsh & McLennan Cos. | | 14,843 | | | 378,496 | |

| MBIA, Inc. Þ | | 5,658 | | | 33,099 | |

| MetLife, Inc. Þ | | 22,042 | | | 633,928 | |

| Principal Financial Group, Inc. | | 7,500 | | | 103,575 | |

| Progressive Corp. Þ | | 19,549 | | | 293,626 | |

| Prudential Financial, Inc. | | 12,357 | | | 268,147 | |

| Torchmark Corp. Þ | | 2,524 | | | 91,243 | |

| Travelers Companies, Inc. | | 17,097 | | | 746,284 | |

| UnumProvident Corp. | | 9,998 | | | 148,970 | |

| XL Capital, Ltd., Class A Þ | | 9,572 | | | 48,147 | |

| | | | | 5,531,543 | |

| Real Estate Investment Trusts (REITs) 0.8% | | | | | | |

| Apartment Investment & Management Co., Class A Þ | | 2,478 | | | 28,423 | |

| AvalonBay Communities, Inc. Þ | | 2,230 | | | 135,294 | |

| Boston Properties, Inc. Þ | | 3,467 | | | 185,138 | |

| Developers Diversified Realty Corp. Þ | | 3,480 | | | 16,704 | |

| Equity Residential Þ | | 7,840 | | | 238,571 | |

| HCP, Inc. | | 7,282 | | | 150,519 | |

| | Shares | | | Value | |

| COMMON STOCKS continued | | | | | | |

| FINANCIALS continued | | | | | | |

| Real Estate Investment Trusts (REITs) continued | | | | | | |

| Host Hotels & Resorts, Inc. Þ | | 15,033 | | $ | 113,048 | |

| Kimco Realty Corp. Þ | | 6,571 | | | 92,980 | |

| Plum Creek Timber Co., Inc. Þ | | 4,952 | | | 176,242 | |

| ProLogis Þ | | 7,596 | | | 29,093 | |

| Public Storage, Inc. Þ | | 3,624 | | | 253,281 | |

| Simon Property Group, Inc. Þ | | 6,512 | | | 309,320 | |

| Vornado Realty Trust Þ | | 3,963 | | | 211,822 | |

| | | | | 1,940,435 | |

| Real Estate Management & Development 0.0% | | | | | | |

| CB Richard Ellis Group, Inc., Class A * Þ | | 6,207 | | | 28,304 | |

| | | | | | |

| Thrifts & Mortgage Finance 0.2% | | | | | | |

| Hudson City Bancorp, Inc. Þ | | 15,039 | | | 251,301 | |

| People's United Financial, Inc. Þ | | 10,039 | | | 191,444 | |

| Sovereign Bancorp, Inc. Þ | | 15,727 | | | 38,846 | |

| | | | | 481,591 | |

| HEALTH CARE 14.0% | | | | | | |

| Biotechnology 2.0% | | | | | | |

| Amgen, Inc. * | | 30,618 | | | 1,700,524 | |

| Biogen Idec, Inc. * | | 8,400 | | | 355,404 | |

| Celgene Corp. * | | 13,164 | | | 685,844 | |

| Cephalon, Inc. Þ | | 1,967 | | | 144,535 | |

| Genzyme Corp. * | | 7,774 | | | 497,691 | |

| Gilead Sciences, Inc. * | | 26,621 | | | 1,192,355 | |

| | | | | 4,576,353 | |

| Health Care Equipment & Supplies 2.1% | | | | | | |

| Baxter International, Inc. | | 18,164 | | | 960,876 | |

| Becton, Dickinson & Co. | | 7,048 | | | 447,759 | |

| Boston Scientific Corp. * | | 43,426 | | | 267,938 | |

| C.R. Bard, Inc. Þ | | 2,875 | | | 235,836 | |

| Covidien, Ltd. | | 14,522 | | | 535,136 | |

| Dentsply International, Inc. | | 4,302 | | | 112,196 | |

| Hospira, Inc. * | | 4,614 | | | 138,558 | |

| Intuitive Surgical, Inc. * Þ | | 1,124 | | | 148,964 | |

| Medtronic, Inc. | | 32,651 | | | 996,509 | |

| St. Jude Medical, Inc. * | | 9,891 | | | 277,245 | |

| Stryker Corp. | | 7,159 | | | 278,628 | |

| Varian Medical Systems, Inc. * Þ | | 3,613 | | | 145,821 | |

| Zimmer Holdings, Inc. * | | 6,518 | | | 243,252 | |

| | | | | 4,788,718 | |

| Health Care Providers & Services 1.9% | | | | | | |

| Aetna, Inc. | | 13,647 | | | 297,778 | |

| AmerisourceBergen Corp. | | 4,586 | | | 143,771 | |

| Cardinal Health, Inc. | | 10,393 | | | 337,980 | |

| CIGNA Corp. | | 7,954 | | | 96,323 | |

| Coventry Health Care, Inc. * | | 4,286 | | | 53,446 | |

| DaVita, Inc. * | | 3,021 | | | 151,805 | |

| Express Scripts, Inc. * Þ | | 7,137 | | | 410,449 | |

| Humana, Inc. * | | 4,887 | | | 147,734 | |

| | Shares | | | Value | |

| COMMON STOCKS continued | | | | | | |

| HEALTH CARE continued | | | | | | |

| Health Care Providers & Services continued | | | | | | |

| Laboratory Corp. of America Holdings * Þ | | 3,218 | | $ | 203,893 | |

| McKesson Corp. | | 7,984 | | | 278,961 | |

| Medco Health Solutions, Inc. * | | 14,634 | | | 614,628 | |

| Patterson Companies, Inc. * Þ | | 2,636 | | | 49,610 | |

| Quest Diagnostics, Inc. | | 4,574 | | | 213,011 | |

| Tenet Healthcare Corp. * Þ | | 12,004 | | | 14,525 | |

| UnitedHealth Group, Inc. | | 35,237 | | | 740,329 | |

| WellPoint, Inc. * | | 14,797 | | | 526,773 | |

| | | | | 4,281,016 | |

| Health Care Technology 0.0% | | | | | | |

| IMS Health, Inc. | | 5,263 | | | 69,208 | |

| | | | | | |

| Life Sciences Tools & Services 0.4% | | | | | | |

| Life Technologies Corp. Þ | | 4,992 | | | 130,303 | |

| Millipore Corp. * Þ | | 1,597 | | | 80,904 | |

| PerkinElmer, Inc. | | 3,458 | | | 62,451 | |

| Thermo Fisher Scientific, Inc. * Þ | | 12,126 | | | 432,656 | |

| Waters Corp. * Þ | | 2,864 | | | 118,083 | |

| | | | | 824,397 | |

| Pharmaceuticals 7.6% | | | | | | |

| Abbott Laboratories Þ | | 44,610 | | | 2,337,118 | |

| Allergan, Inc. | | 8,899 | | | 335,314 | |

| Barr Pharmaceuticals, Inc. * | | 3,149 | | | 205,913 | |

| Bristol-Myers Squibb Co. | | 57,287 | | | 1,185,841 | |

| Eli Lilly & Co. | | 28,953 | | | 988,745 | |

| Forest Laboratories, Inc. * | | 8,822 | | | 213,316 | |

| Johnson & Johnson | | 80,868 | | | 4,737,247 | |

| King Pharmaceuticals, Inc. * Þ | | 7,133 | | | 68,548 | |

| Merck & Co., Inc. | | 62,000 | | | 1,656,640 | |

| Mylan Laboratories, Inc. * Þ | | 8,811 | | | 82,912 | |

| Pfizer, Inc. | | 195,074 | | | 3,205,066 | |

| Schering-Plough Corp. | | 47,042 | | | 790,776 | |

| Watson Pharmaceuticals, Inc. * | | 3,023 | | | 71,796 | |

| Wyeth | | 38,588 | | | 1,389,554 | |

| | | | | 17,268,786 | |

| INDUSTRIALS 11.0% | | | | | | |

| Aerospace & Defense 2.6% | | | | | | |

| Boeing Co. | | 21,422 | | | 913,220 | |

| General Dynamics Corp. | | 11,496 | | | 593,998 | |

| Goodrich Corp. | | 3,620 | | | 121,813 | |

| Honeywell International, Inc. | | 21,543 | | | 600,188 | |

| L-3 Communications Holdings, Inc. | | 3,514 | | | 236,035 | |

| Lockheed Martin Corp. | | 9,635 | | | 742,955 | |

| Northrop Grumman Corp. | | 9,768 | | | 400,000 | |

| Precision Castparts Corp. | | 4,033 | | | 252,869 | |

| Raytheon Co. Þ | | 12,065 | | | 588,772 | |

| Rockwell Collins Corp. Þ | | 4,613 | | | 157,211 | |

| United Technologies Corp. | | 27,907 | | | 1,354,327 | |

| | | | | 5,961,388 | |

| | | | | | |

| | Shares | | | Value | |

| COMMON STOCKS continued | | | | | | |

| INDUSTRIALS continued | | | | | | |

| Air Freight & Logistics 1.2% | | | | | | |

| C.H. Robinson Worldwide, Inc. Þ | | 4,920 | | $ | 251,314 | |

| Expeditors International of Washington, Inc. Þ | | 6,165 | | | 206,096 | |

| FedEx Corp. Þ | | 9,005 | | | 636,203 | |

| United Parcel Service, Inc., Class B Þ | | 29,175 | | | 1,680,480 | |

| | | | | 2,774,093 | |

| Airlines 0.1% | | | | | | |

| Southwest Airlines Co. | | 21,239 | | | 183,717 | |

| | | | | | |

| Building Products 0.0% | | | | | | |

| Masco Corp. Þ | | 10,418 | | | 99,804 | |

| | | | | | |

| Commercial Services & Supplies 0.5% | | | | | | |

| Allied Waste Industries, Inc. * | | 9,807 | | | 105,327 | |

| Avery Dennison Corp. Þ | | 3,082 | | | 95,850 | |

| Cintas Corp. Þ | | 3,825 | | | 91,876 | |

| Pitney Bowes, Inc. | | 6,013 | | | 148,581 | |

| R.R. Donnelley & Sons Co. | | 6,077 | | | 77,543 | |

| Stericycle, Inc. | | 2,472 | | | 141,646 | |

| Waste Management, Inc. | | 14,193 | | | 414,436 | |

| | | | | 1,075,259 | |

| Construction & Engineering 0.2% | | | | | | |

| Fluor Corp. | | 5,180 | | | 235,897 | |

| Jacobs Engineering Group, Inc. * | | 3,543 | | | 158,620 | |

| | | | | 394,517 | |

| Electrical Equipment 0.5% | | | | | | |

| Cooper Industries, Inc. | | 5,035 | | | 121,545 | |

| Emerson Electric Co. | | 22,455 | | | 805,910 | |

| Rockwell Automation, Inc. | | 4,213 | | | 131,235 | |

| | | | | 1,058,690 | |

| Industrial Conglomerates 3.1% | | | | | | |

| 3M Co. Þ | | 20,228 | | | 1,353,860 | |

| General Electric Co. | | 303,734 | | | 5,215,113 | |

| Textron, Inc. Þ | | 7,192 | | | 109,534 | |

| Tyco International, Ltd. | | 13,741 | | | 287,187 | |

| | | | | 6,965,694 | |

| Machinery 1.6% | | | | | | |

| Caterpillar, Inc. | | 17,615 | | | 722,039 | |

| Cummins, Inc. | | 5,866 | | | 150,052 | |

| Danaher Corp. Þ | | 7,384 | | | 410,846 | |

| Deere & Co. | | 12,357 | | | 430,147 | |

| Dover Corp. | | 5,436 | | | 162,156 | |

| Eaton Corp. | | 4,810 | | | 222,895 | |

| Flowserve Corp. | | 1,660 | | | 83,548 | |

| Illinois Tool Works, Inc. Þ | | 11,573 | | | 394,871 | |

| Ingersoll-Rand Co., Ltd., Class A | | 9,218 | | | 144,538 | |

| ITT Corp. | | 5,259 | | | 220,142 | |

| Manitowoc Co. | | 3,770 | | | 29,708 | |

| Paccar, Inc. Þ | | 10,515 | | | 293,053 | |

| | Shares | | | Value | |

| COMMON STOCKS continued | | | | | | |

| INDUSTRIALS continued | | | | | | |

| Machinery continued | | | | | | |

| Pall Corp. | | 3,469 | | $ | 95,432 | |

| Parker Hannifin Corp. | | 4,851 | | | 199,279 | |

| | | | | 3,558,706 | |

| Professional Services 0.1% | | | | | | |

| Equifax, Inc. Þ | | 3,711 | | | 94,445 | |

| Monster Worldwide, Inc. * Þ | | 3,588 | | | 41,154 | |

| Robert Half International, Inc. Þ | | 4,512 | | | 94,256 | |

| | | | | 229,855 | |

| Road & Rail 1.0% | | | | | | |

| Burlington Northern Santa Fe Corp. | | 8,173 | | | 626,134 | |

| CSX Corp. | | 11,797 | | | 439,320 | |

| Norfolk Southern Corp. Þ | | 10,858 | | | 537,145 | |

| Ryder System, Inc. Þ | | 1,634 | | | 58,677 | |

| Union Pacific Corp. | | 14,735 | | | 737,339 | |

| | | | | 2,398,615 | |

| Trading Companies & Distributors 0.1% | | | | | | |

| Fastenal Co. Þ | | 3,739 | | | 143,989 | |

| W.W. Grainger, Inc. Þ | | 1,875 | | | 132,319 | |

| | | | | 276,308 | |

| INFORMATION TECHNOLOGY 14.9% | | | | | | |

| Communications Equipment 2.5% | | | | | | |

| Ciena Corp. * Þ | | 2,614 | | | 19,343 | |

| Cisco Systems, Inc. * | | 170,944 | | | 2,827,414 | |

| Corning, Inc. | | 45,663 | | | 411,424 | |

| Harris Corp. | | 3,883 | | | 135,439 | |

| JDS Uniphase Corp. * | | 6,204 | | | 16,875 | |

| Juniper Networks, Inc. * Þ | | 15,729 | | | 273,370 | |

| Motorola, Inc. Þ | | 65,557 | | | 282,551 | |

| QUALCOMM, Inc. | | 47,487 | | | 1,594,138 | |

| Tellabs, Inc. * Þ | | 11,505 | | | 47,976 | |

| | | | | 5,608,530 | |

| Computers & Peripherals 4.3% | | | | | | |

| Apple, Inc. * Þ | | 25,636 | | | 2,375,688 | |

| Dell, Inc. * | | 50,438 | | | 563,393 | |

| EMC Corp. * | | 59,918 | | | 633,333 | |

| Hewlett-Packard Co. Þ | | 70,873 | | | 2,500,400 | |

| International Business Machines Corp. | | 39,207 | | | 3,199,291 | |

| Lexmark International, Inc., Class A * Þ | | 2,269 | | | 59,402 | |

| NetApp, Inc. * Þ | | 9,474 | | | 127,899 | |

| QLogic Corp. * Þ | | 3,796 | | | 40,314 | |

| SanDisk Corp. * Þ | | 6,511 | | | 52,088 | |

| Sun Microsystems, Inc. * | | 21,789 | | | 69,071 | |

| Teradata Corp. * | | 5,166 | | | 69,379 | |

| | | | | 9,690,258 | |

| Electronic Equipment & Instruments 0.3% | | | | | | |

| Agilent Technologies, Inc. * | | 10,347 | | | 194,834 | |

| Amphenol Corp., Class A | | 5,116 | | | 118,793 | |

| Jabil Circuit, Inc. | | 6,078 | | | 39,993 | |

| | Shares | | | Value | |

| COMMON STOCKS continued | | | | | | |

| INFORMATION TECHNOLOGY continued | | | | | | |

| Electronic Equipment & Instruments continued | | | | | | |

| Molex, Inc. Þ | | 4,128 | | $ | 56,141 | |

| Tyco Electronics, Ltd. | | 13,668 | | | 225,249 | |

| | | | | 635,010 | |

| Internet Software & Services 1.3% | | | | | | |

| Akamai Technologies, Inc. * | | 4,894 | | | 60,049 | |

| eBay, Inc. * Þ | | 31,615 | | | 415,105 | |

| Google, Inc., Class A * | | 6,916 | | | 2,026,111 | |

| VeriSign, Inc. * | | 5,591 | | | 120,710 | |

| Yahoo!, Inc. * Þ | | 40,103 | | | 461,586 | |

| | | | | 3,083,561 | |

| IT Services 0.8% | | | | | | |

| Affiliated Computer Services, Inc., Class A * | | 2,815 | | | 113,867 | |

| Automatic Data Processing, Inc. | | 14,726 | | | 604,649 | |

| Cognizant Technology Solutions Corp., Class A * | | 8,439 | | | 162,029 | |

| Computer Sciences Corp. * | | 4,380 | | | 122,027 | |

| Convergys Corp. * | | 3,525 | | | 22,172 | |

| Fidelity National Information Services, Inc. | | 5,490 | | | 94,318 | |

| Fiserv, Inc. * | | 4,747 | | | 162,063 | |

| Paychex, Inc. | | 9,285 | | | 262,394 | |

| Total System Services, Inc. | | 5,721 | | | 81,639 | |

| Western Union Co. | | 21,100 | | | 279,997 | |

| | | | | 1,905,155 | |

| Office Electronics 0.1% | | | | | | |

| Xerox Corp. | | 25,241 | | | 176,434 | |

| | | | | | |

| Semiconductors & Semiconductor Equipment 2.0% | | | | | | |

| Advanced Micro Devices, Inc. * Þ | | 17,571 | | | 41,468 | |

| Altera Corp. Þ | | 8,705 | | | 128,051 | |

| Analog Devices, Inc. Þ | | 8,405 | | | 143,725 | |

| Applied Materials, Inc. | | 38,826 | | | 371,953 | |

| Broadcom Corp., Class A * | | 12,772 | | | 195,539 | |

| Intel Corp. Þ | | 162,692 | | | 2,245,150 | |

| KLA-Tencor Corp. Þ | | 5,013 | | | 94,294 | |

| Linear Technology Corp. Þ | | 6,411 | | | 127,899 | |

| LSI Corp. * Þ | | 18,625 | | | 49,915 | |

| MEMC Electronic Materials, Inc. * | | 6,537 | | | 98,186 | |

| Microchip Technology, Inc. Þ | | 5,328 | | | 98,568 | |

| Micron Technology, Inc. * Þ | | 22,023 | | | 60,343 | |

| National Semiconductor Corp. | | 5,642 | | | 62,062 | |

| Novellus Systems, Inc. * Þ | | 2,869 | | | 35,547 | |

| NVIDIA Corp. * | | 16,107 | | | 120,319 | |

| Teradyne, Inc. * | | 4,887 | | | 18,522 | |

| Texas Instruments, Inc. | | 37,935 | | | 590,648 | |

| Xilinx, Inc. | | 8,000 | | | 130,880 | |

| | | | | 4,613,069 | |

| Software 3.6% | | | | | | |

| Adobe Systems, Inc. * | | 15,351 | | | 355,529 | |

| Autodesk, Inc. * Þ | | 6,510 | | | 108,001 | |

| BMC Software, Inc. * | | 5,499 | | | 137,255 | |

| | Shares | | | Value | |

| COMMON STOCKS continued | | | | | | |

| INFORMATION TECHNOLOGY continued | | | | | | |

| Software continued | | | | | | |

| CA, Inc. | | 11,398 | | $ | 191,942 | |

| Citrix Systems, Inc. * | | 5,278 | | | 140,712 | |

| Compuware Corp. * | | 7,376 | | | 46,838 | |

| Electronic Arts, Inc. * | | 9,226 | | | 175,848 | |

| Intuit, Inc. * | | 9,289 | | | 205,844 | |

| Microsoft Corp. | | 227,226 | | | 4,594,510 | |

| Novell, Inc. * | | 9,991 | | | 45,459 | |

| Oracle Corp. * | | 113,394 | | | 1,824,509 | |

| Salesforce.com, Inc. * Þ | | 3,011 | | | 86,175 | |

| Symantec Corp. * Þ | | 24,282 | | | 292,112 | |

| | | | | 8,204,734 | |

| MATERIALS 3.0% | | | | | | |

| Chemicals 1.9% | | | | | | |

| Air Products & Chemicals, Inc. Þ | | 6,130 | | | 292,769 | |

| CF Industries Holdings, Inc. | | 1,635 | | | 86,050 | |

| Dow Chemical Co. Þ | | 26,767 | | | 496,528 | |

| E.I. DuPont de Nemours & Co. | | 26,107 | | | 654,241 | |

| Eastman Chemical Co. Þ | | 2,099 | | | 69,057 | |

| Ecolab, Inc. Þ | | 5,080 | | | 195,021 | |

| International Flavors & Fragrances, Inc. | | 2,273 | | | 69,417 | |

| Monsanto Co. | | 15,916 | | | 1,260,547 | |

| PPG Industries, Inc. | | 4,749 | | | 208,576 | |

| Praxair, Inc. Þ | | 9,115 | | | 538,241 | |

| Rohm & Haas Co. | | 3,584 | | | 245,182 | |

| Sigma-Aldrich Corp. Þ | | 3,645 | | | 157,136 | |

| | | | | 4,272,765 | |

| Construction Materials 0.1% | | | | | | |

| Vulcan Materials Co. Þ | | 3,178 | | | 190,617 | |

| | | | | | |

| Containers & Packaging 0.1% | | | | | | |

| Ball Corp. | | 2,798 | | | 101,987 | |

| Bemis Co., Inc. | | 2,884 | | | 77,926 | |

| Pactiv Corp. * | | 3,789 | | | 94,687 | |

| Sealed Air Corp. | | 4,575 | | | 72,422 | |

| | | | | 347,022 | |

| Metals & Mining 0.7% | | | | | | |

| AK Steel Holding Corp. Þ | | 3,247 | | | 25,586 | |

| Alcoa, Inc. Þ | | 23,538 | | | 253,269 | |

| Allegheny Technologies, Inc. Þ | | 2,902 | | | 66,601 | |

| Freeport-McMoRan Copper & Gold, Inc. Þ | | 11,111 | | | 266,553 | |

| Newmont Mining Corp. Þ | | 13,216 | | | 444,718 | |

| NuCor Corp. Þ | | 9,161 | | | 326,865 | |

| Titanium Metals Corp. Þ | | 2,463 | | | 20,812 | |

| United States Steel Corp. Þ | | 3,400 | | | 103,360 | |

| | | | | 1,507,764 | |

| Paper & Forest Products 0.2% | | | | | | |

| International Paper Co. Þ | | 12,373 | | | 154,044 | |

| | Shares | | | Value | |

| COMMON STOCKS continued | | | | | | |

| MATERIALS continued | | | | | | |

| Paper & Forest Products continued | | | | | | |

| MeadWestvaco Corp. Þ | | 4,943 | | $ | 57,635 | |

| Weyerhaeuser Co. Þ | | 6,114 | | | 230,009 | |

| | | | | 441,688 | |

| TELECOMMUNICATION SERVICES 3.8% | | | | | | |

| Diversified Telecommunication Services 3.6% | | | | | | |

| AT&T, Inc. Þ | | 170,534 | | | 4,870,451 | |

| CenturyTel, Inc. Þ | | 2,962 | | | 78,671 | |

| Embarq Corp. | | 4,124 | | | 134,607 | |

| Frontier Communications Corp. Þ | | 9,143 | | | 79,727 | |

| Qwest Communications International, Inc. Þ | | 42,954 | | | 137,453 | |

| Verizon Communications, Inc. | | 82,409 | | | 2,690,654 | |

| Windstream Corp. Þ | | 12,722 | | | 112,717 | |

| | | | | 8,104,280 | |

| Wireless Telecommunication Services 0.2% | | | | | | |

| American Tower Corp., Class A * | | 11,400 | | | 310,536 | |

| Sprint Nextel Corp. | | 82,596 | | | 230,443 | |

| | | | | 540,979 | |

| UTILITIES 4.2% | | | | | | |

| Electric Utilities 2.7% | | | | | | |

| Allegheny Energy, Inc. | | 4,887 | | | 172,267 | |

| American Electric Power Co., Inc. Þ | | 11,641 | | | 364,247 | |

| Consolidated Edison, Inc. Þ | | 7,906 | | | 319,323 | |

| Duke Energy Corp. | | 36,604 | | | 569,558 | |

| Edison International | | 9,428 | | | 314,895 | |

| Entergy Corp. | | 5,544 | | | 471,794 | |

| Exelon Corp. | | 19,022 | | | 1,069,227 | |

| FirstEnergy Corp. | | 8,821 | | | 516,734 | |

| FPL Group, Inc. Þ | | 11,821 | | | 576,392 | |

| Pepco Holdings, Inc. | | 6,244 | | | 112,330 | |

| Pinnacle West Capital Corp. | | 2,915 | | | 88,616 | |

| PPL Corp. Þ | | 10,837 | | | 367,266 | |

| Progress Energy, Inc. Þ | | 7,582 | | | 300,930 | |

| Southern Co. Þ | | 22,288 | | | 809,500 | |

| | | | | 6,053,079 | |

| Gas Utilities 0.1% | | | | | | |

| Nicor, Inc. Þ | | 1,307 | | | 53,300 | |

| Questar Corp. | | 5,017 | | | 161,497 | |

| | | | | 214,797 | |

| Independent Power Producers & Energy Traders 0.1% | | | | | | |

| AES Corp. * | | 19,468 | | | 149,709 | |

| Constellation Energy Group, Inc. | | 5,161 | | | 126,289 | |

| Dynegy, Inc., Class A * Þ | | 14,630 | | | 32,625 | |

| | | | | 308,623 | |

| Multi-Utilities 1.3% | | | | | | |

| Ameren Corp. Þ | | 6,083 | | | 216,433 | |

| CenterPoint Energy, Inc. | | 9,892 | | | 127,904 | |

| CMS Energy Corp. Þ | | 6,519 | | | 66,233 | |

| Dominion Resources, Inc. Þ | | 16,783 | | | 617,950 | |

| | Shares | | | Value | |

| COMMON STOCKS continued | | | | | | |

| UTILITIES continued | | | | | | |

| Multi-Utilities continued | | | | | | |

| DTE Energy Co. | | 4,720 | | $ | 175,537 | |

| Integrys Energy Group, Inc. | | 2,212 | | | 97,726 | |

| NiSource, Inc. | | 7,936 | | | 95,629 | |

| PG&E Corp. | | 10,376 | | | 394,703 | |

| Public Service Enterprise Group, Inc. | | 14,715 | | | 454,693 | |

| Sempra Energy | | 7,130 | | | 332,757 | |

| TECO Energy, Inc. Þ | | 6,156 | | | 80,028 | |

| Wisconsin Energy Corp. Þ | | 3,383 | | | 147,025 | |

| Xcel Energy, Inc. Þ | | 12,907 | | | 242,781 | |

| | | | | 3,049,399 | |

| Total Common Stocks (cost $228,675,496) | | | | | 226,599,048 | |

| | | | | | |

| | Principal Amount | | | Value | |

| SHORT-TERM INVESTMENTS 23.4% | | | | | | |

| U.S. TREASURY OBLIGATION 0.1% | | | | | | |

| U.S. Treasury Bill, 0.85%, 12/04/2008 ƒ ß | $ | 150,000 | | | 150,000 | |

| | Shares | | | Value | |

| MUTUAL FUND SHARES 23.3% | | | | | | |

| Evergreen Institutional Money Market Fund, Class I, 2.09% q ø | | 109,810 | | | 109,810 | |

| State Street Navigator Securities Lending Prime Portfolio, 1.99% § ÞÞ | | 53,090,268 | | | 53,090,268 | |

| | | | | 53,200,078 | |

| Total Short-Term Investments (cost $53,350,057) | | | | | 53,350,078 | |

| Total Investments (cost $282,025,553) 122.9% | | | | | 279,949,126 | |

| Other Assets and Liabilities (22.9%) | | | | | (52,218,914 | ) |

| Net Assets 100.0% | | | | $ | 227,730,212 | |

| * | Non-income producing security |

| Þ | All or a portion of this security is on loan. |

| ° | Investment in non-controlled affiliate. At November 30, 2008, the Fund owned shares of Wachovia Corporation with a cost basis of $6,066,590 and shares of Wells Fargo & Co. with a cost basis of $2,739,122. The Fund earned $6,188 of income from Wachovia Corporation for the six months ended November 30, 2008 and $32,412 of income from Wells Fargo & Co. for the period from October 3, 2008 to November 30, 2008, which is included in income from affiliates. |

| ƒ | All or a portion of this security was pledged to cover initial margin requirements for open futures contracts. |

| ß | Rate shown represents the yield to maturity at date of purchase. |

| q | Rate shown is the 7-day annualized yield at period end. |

| ÞÞ | All or a portion of this security represents investment of cash collateral received from securities on loan. |

| ø | Evergreen Investment Management Company, LLC is the investment advisor to both the Fund and the money market fund. |

| § | Rate shown is the 1-day annualized yield at period end. |

The following table shows the percent of total long-term investments by sector as of November 30, 2008:

| Information Technology | 15.0 | % | | | |

| Energy | 14.3 | % | | | |

| Health Care | 14.1 | % | | | |

| Financials | 13.5 | % | | | |

| Consumer Staples | 13.1 | % | | | |

| Industrials | 11.0 | % | | | |

| Consumer Discretionary | 8.0 | % | | | |

| Utilities | 4.2 | % | | | |

| Telecommunication Services | 3.8 | % | | | |

| Materials | 3.0 | % | | | |

| 100.0 | % | | | |

Market Index Fund STATEMENT OF ASSETS AND LIABILITIES |

November 30, 2008 (unaudited) |

| Assets | | | |

| Investments in securities, at value (cost $273,110,031) including $52,503,676 of securities loaned | $ | 276,381,121 | |

| Investments in affiliates, at value (cost $8,915,522) | | 3,568,005 | |

| Total investments | | 279,949,126 | |

| Receivable for securities sold | | 146,387 | |

| Dividends receivable | | 746,475 | |

| Receivable for daily variation margin on open futures contracts | | 10,465 | |

| Receivable for securities lending income | | 44,682 | |

| Receivable from investment advisor | | 2,336 | |

| Total assets | | 280,899,471 | |

| Liabilities | | | |

| Payable for securities purchased | | 46,226 | |

| Payable for securities on loan | | 53,090,268 | |

| Due to related parties | | 1,973 | |

| Trustees' fees and expenses payable | | 15,426 | |

| Custodian and accounting fees payable | | 5,655 | |

| Accrued expenses and other liabilities | | 9,711 | |

| Total liabilities | | 53,169,259 | |

| Net assets | $ | 227,730,212 | |

| Net assets represented by | | | |

| Paid-in capital | $ | 186,453,399 | |

| Undistributed net investment income | | 12,953,446 | |

| Accumulated net realized gains on investments | | 30,404,806 | |

| Net unrealized losses on investments | | (2,081,439 | ) |

| Total net assets | $ | 227,730,212 | |

| Shares outstanding (unlimited number of shares authorized) | | | |

| Class I | | 26,789,084 | |

| Net asset value per share | | | |

| Class I | $ | 8.50 | |

Market Index Fund STATEMENT OF OPERATIONS |

Six Months Ended November 30, 2008 (unaudited) |

| Investment income | | | |

| Dividends | $ | 3,521,734 | |

| Securities lending | | 180,906 | |

| Income from affiliates | | 50,583 | |

| Interest | | 1,365 | |

| Total investment income | | 3,754,588 | |

| Expenses | | | |

| Advisory fee | | 466,984 | |

| Administrative services fee | | 145,933 | |

| Transfer agent fees | | 31 | |

| Trustees' fees and expenses | | 2,977 | |

| Printing and postage expenses | | 4,899 | |

| Custodian and accounting fees | | 36,620 | |

| Registration and filing fees | | 941 | |

| Professional fees | | 17,051 | |

| Other | | 7,727 | |

| Total expenses | | 683,163 | |

| Less: Expense reductions | | (632 | ) |

| Fee waivers and expense reimbursements | | (646,778 | ) |

| Net expenses | | 35,753 | |

| Net investment income | | 3,718,835 | |

| Net realized and unrealized gains or losses on investments | | | |

| Net realized losses on: | | | |

| Securities | | (3,941,556 | ) |

| Futures contracts | | (402,706 | ) |

| Net realized losses on investments | | (4,344,262 | ) |

| Net change in unrealized gains or losses on investments | | (122,782,636 | ) |

| Net realized and unrealized gains or losses on investments | | (127,126,898 | ) |

| Net decrease in net assets resulting from operations | $ | (123,408,063 | ) |

Market Index Fund STATEMENTS OF CHANGES IN NET ASSETS |

| Six Months Ended

November 30, 2008

(unaudited) | Year Ended

May 31, 2008 |

| Operations | | | | | | | | | | |

| Net investment income | | | $ | 3,718,835 | | | | $ | 9,425,929 | |

| Net realized gains or losses on investments | | | | (4,344,262 | ) | | | | 35,363,590 | |

| Net change in unrealized gains or losses on investments | | | | (122,782,636 | ) | | | | (82,016,910 | ) |

| Net decrease in net assets resulting from operations | | | | (123,408,063 | ) | | | | (37,227,391 | ) |

| Distributions to shareholders from | | | | | | | | | | |

| Net investment income | | | | 0 | | | | | (9,035,174 | ) |

| Net realized gains | | | | 0 | | | | | (7,122,511 | ) |

| Total distributions to shareholders | | | | 0 | | | | | (16,157,685 | ) |

| Shares | | | | | Shares | | | | |

| Capital share transactions | | | | | | | | | | |

| Net asset value of shares issued in reinvestment of distributions | 0 | | | 0 | | 1,172,071 | | | 16,157,685 | |

| Payment for shares redeemed | 0 | | | 0 | | (12,945,583 | ) | | (170,000,000 | ) |

| Net increase (decrease) in net assets resulting from capital share transactions | | | | 0 | | | | | (153,842,315 | ) |

| Total decrease in net assets | | | | (123,408,063 | ) | | | | (207,227,391 | ) |

| Net assets | | | | | | | | | | |

| Beginning of period | | | | 351,138,275 | | | | | 558,365,666 | |

| End of period | | | $ | 227,730,212 | | | | $ | 351,138,275 | |

| Undistributed net investment income | | | $ | 12,953,446 | | | | $ | 9,234,611 | |

Market Index Growth Fund FUND AT A GLANCE |

Management Team

| Investment Advisor: |

| Evergreen Investment Management Company, LLC |

|

| Portfolio Manager: |

| William E. Zieff |

CURRENT INVESTMENT STYLE

| Source: Morningstar, Inc. Morningstar's style box is based on a portfolio date as of 9/30/2008. The Equity style box placement is based on 10 growth and valuation measures for each fund holding and the median size of the companies in which the fund invests. |

PERFORMANCE AND RETURNS

| Portfolio inception date: 10/15/2002 |

| Class I |

| Class inception date | 10/15/2002 |

| 6-month return | -38.24 | % |

| Average annual return |

| 1-year | -39.70 | % |

| 5-year | -3.10 | % |

| Since portfolio inception | 0.71 | % |

| Past performance is no guarantee of future results. The performance quoted represents past performance and current performance may be lower or higher. The investment return and principal value of an investment will fluctuate so that investors' shares, when redeemed, may be worth more or less than their original cost. Performance includes the reinvestment of income dividends and capital gain distributions. |

| The advisor is waiving its advisory fee and reimbursing the fund for a portion of other expenses. Had the fee not been waived and expenses not reimbursed, returns would have been lower. |

| The fund is only offered to certain pension plans having at least $100 million. Class I shares are sold without a front-end or deferred sales charge. The minimum initial investment for the fund is $100 million, which may be waived in certain situations. There is no minimum amount required for subsequent purchases. |

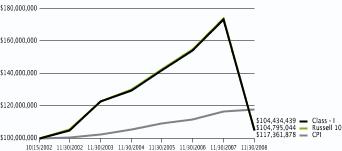

LONG-TERM GROWTH

| Comparison of a $100,000,000 investment in the Evergreen Market Index Growth Fund Class I shares versus a similar investment in the Russell 1000 Growth Index (Russell 1000 Growth) and the Consumer Price Index (CPI). |

The Russell 1000 Growth is an unmanaged market index and does not include transaction costs associated with buying and selling securities, any mutual fund fees or expenses or any taxes. . The CPI is a commonly used measure of inflation and does not represent an investment return. It is not possible to invest directly in an index. |

| The Fund's investment objective may be charged without a vote of the fund's shareholders. |

| "Russell 1000 Growth Index" is a trademark and service mark of Frank Russell Company (FRC) and has been licensed for use by Evergreen Investments. The product is not sponsored, endorsed, sold or promoted by FRC and FRC makes no representation regarding the advisability of investing in the product. |

| All data is as of November 30, 2008, and subject to change. |

Market Index Growth Fund ABOUT YOUR FUND'S EXPENSES |

The Example below is intended to describe the fees and expenses borne by shareholders and the impact of those costs on your investment.

Example

As a shareholder of the fund, you incur two types of costs: (1) transaction costs, including sales charges (loads), redemption fees and exchange fees; and (2) ongoing costs, including management fees, distribution (12b-1) fees and other fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the fund and to compare these costs with the ongoing costs of investing in other mutual funds. The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from June 1, 2008 to November 30, 2008.

The example illustrates your fund's costs in two ways:

- Actual expenses

The section in the table under the heading "Actual" provides information about actual account values and actual expenses. You may use the information in these columns, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the appropriate column for your share class, in the column entitled "Expenses Paid During Period" to estimate the expenses you paid on your account during this period. - Hypothetical example for comparison purposes

The section in the table under the heading "Hypothetical (5% return before expenses)" provides information about hypothetical account values and hypothetical expenses based on the fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees or exchange fees. Therefore, the section in the table under the heading "Hypothetical (5% return before expenses)" is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would havebeen higher.

| Beginning

Account Value

6/1/2008 | Ending

Account Value

11/30/2008 | Expenses Paid

During Period* |

| Actual | | | | | | |

| Class I | $1,000.00 | | $617.59 | | $0.12 | |

| Hypothetical (5% return before expenses) | | | | | | |

| Class I | $1,000.00 | | $1,024.92 | | $0.15 | |

| *Expenses are equal to the fund's annualized expense ratio (0.03% for Class I), multiplied by the average account value over the period, multiplied by 183/365 days. |

Market Index Growth Fund FINANCIAL HIGHLIGHTS |

(For a share outstanding throughout each period) |

| | Six Months Ended November 30, 2008 | | Year Ended May 31, |

| Class I | (unaudited) | 2008 | 2007 | 2006 | 2005 | 2004 |

| Net asset value, beginning of period | $ | 15.01 | | $ | 15.36 | | $ | 13.44 | | $ | 12.99 | | $ | 12.77 | | $ | 10.86 | |

| Income from investment operations | | | | | | | | | | | | | | | | | | |

| Net investment income (loss) | | 0.11 | | | 0.22 | | | 0.14 | | | 0.18 | | | 0.15 | | | 0.12 | |

| Net realized and unrealized gains or losses on investments | | (5.85 | ) | | (0.23 | ) | | 2.53 | | | 0.62 | | | 0.27 | | | 1.83 | |

| Total from investment operations | | (5.74 | ) | | (0.01 | ) | | 2.67 | | | 0.80 | | | 0.42 | | | 1.95 | |

| Distributions to shareholders from | | | | | | | | | | | | | | | | | | |

| Net investment income | | 0 | | | (0.17 | ) | | (0.16 | ) | | (0.15 | ) | | (0.12 | ) | | (0.04 | ) |

| Net realized gains | | 0 | | | (0.17 | ) | | (0.59 | ) | | (0.20 | ) | | (0.08 | ) | | 0 | |

| Total distributions to shareholders | | 0 | | | (0.34 | ) | | (0.75 | ) | | (0.35 | ) | | (0.20 | ) | | (0.04 | ) |

| Net asset value, end of period | $ | 9.27 | | $ | 15.01 | | $ | 15.36 | | $ | 13.44 | | $ | 12.99 | | $ | 12.77 | |

| Total return | | (38.24 | )% | | (0.14 | )% | | 20.34 | % | | 6.11 | % | | 3.28 | % | | 17.97 | % |

| Ratios and supplemental data | | | | | | | | | | | | | | | | | | |

| Net assets, end of period (thousands) | $ | 432,533 | | $ | 729,526 | | $ | 945,116 | | $ | 721,771 | | $ | 854,566 | | $ | 678,560 | |

| Ratios to average net assets | | | | | | | | | | | | | | | | | | |

| Expenses including waivers/reimbursements but excluding expense reductions | | 0.03 | %1 | | 0.03 | % | | 0.03 | % | | 0.03 | % | | 0.03 | % | | 0.02 | % |

| Expenses excluding waivers/reimbursements and expense reductions | | 0.46 | %1 | | 0.46 | % | | 0.46 | % | | 0.46 | % | | 0.46 | % | | 0.45 | % |

| Net investment income (loss) | | 1.56 | %1 | | 1.21 | % | | 1.23 | % | | 1.12 | % | | 1.45 | % | | 1.03 | % |

| Portfolio turnover rate | | 20 | % | | 24 | % | | 18 | % | | 25 | % | | 15 | % | | 9 | % |

See Combined Notes to Financial Statements

Market Index Growth Fund SCHEDULE OF INVESTMENTS |

November 30, 2008 (unaudited) |

| | Shares | | | Value | |

| COMMON STOCKS 98.8% | | | | | | |

| CONSUMER DISCRETIONARY 9.1% | | | | | | |

| Auto Components 0.2% | | | | | | |

| BorgWarner, Inc. Þ | | 9,910 | | $ | 234,471 | |

| Gentex Corp. Þ | | 13,962 | | | 122,447 | |

| Goodyear Tire & Rubber Co. * | | 15,124 | | | 97,247 | |

| Johnson Controls, Inc. | | 8,819 | | | 155,743 | |

| Wabco Holdings, Inc. | | 6,413 | | | 95,297 | |

| | | | | 705,205 | |

| Automobiles 0.1% | | | | | | |

| Harley-Davidson, Inc. Þ | | 20,538 | | | 349,351 | |

| Thor Industries, Inc. Þ | | 1,028 | | | 16,078 | |

| | | | | 365,429 | |

| Distributors 0.0% | | | | | | |

| LKQ Corp. Þ * | | 13,245 | | | 138,013 | |

| | | | | | |

| Diversified Consumer Services 0.7% | | | | | | |

| Apollo Group, Inc., Class A * | | 12,460 | | | 957,426 | |

| Brink's Home Security Holdings, Inc. * | | 3,967 | | | 79,340 | |

| DeVry, Inc. Þ | | 5,990 | | | 344,305 | |

| H&R Block, Inc. Þ | | 31,812 | | | 608,564 | |

| Hillenbrand, Inc. | | 6,104 | | | 97,176 | |

| ITT Educational Services, Inc. Þ * | | 3,796 | | | 341,944 | |

| Strayer Education, Inc. Þ | | 1,390 | | | 333,058 | |

| Weight Watchers International, Inc. | | 2,995 | | | 84,758 | |

| | | | | 2,846,571 | |

| Hotels, Restaurants & Leisure 2.5% | | | | | | |

| Boyd Gaming Corp. Þ | | 678 | | | 2,983 | |

| Brinker International, Inc. | | 9,900 | | | 65,736 | |

| Burger King Holdings, Inc. Þ | | 7,842 | | | 168,681 | |

| Carnival Corp. | | 8,699 | | | 182,679 | |

| Chipotle Mexican Grill, Inc., Class A Þ * | | 3,224 | | | 159,846 | |

| Choice Hotels International, Inc. Þ | | 1,027 | | | 25,788 | |

| Darden Restaurants, Inc. | | 13,693 | | | 250,445 | |

| International Game Technology | | 30,270 | | | 324,192 | |

| Interval Leisure Group, Inc. * | | 465 | | | 2,464 | |

| Las Vegas Sands Corp. Þ * | | 10,321 | | | 53,360 | |

| Marriott International, Inc., Class A | | 28,897 | | | 485,181 | |

| McDonald's Corp. | | 100,520 | | | 5,905,550 | |

| MGM MIRAGE Þ * | | 11,413 | | | 136,728 | |

| Orient Express Hotels, Ltd. Þ | | 3,526 | | | 24,153 | |

| Panera Bread Co., Class A Þ * | | 2,593 | | | 115,233 | |

| Penn National Gaming, Inc. Þ | | 7,251 | | | 153,721 | |

| Scientific Games Corp., Class A * Þ | | 6,311 | | | 94,728 | |

| Starbucks Corp. * | | 71,178 | | | 635,619 | |

| Starwood Hotels & Resorts Worldwide, Inc. Þ | | 18,253 | | | 307,746 | |

| Tim Hortons, Inc. Þ | | 18,059 | | | 449,488 | |

| Wynn Resorts, Ltd. Þ | | 5,589 | | | 222,554 | |

| Yum! Brands, Inc. | | 46,317 | | | 1,247,780 | |

| | | | | 11,014,655 | |

| | | | | | |

| | Shares | | | Value | |

| COMMON STOCKS continued | | | | | | |

| CONSUMER DISCRETIONARY continued | | | | | | |

| Household Durables 0.1% | | | | | | |

| Garmin, Ltd. Þ * | | 12,525 | | $ | 213,927 | |

| Harman International Industries, Inc. | | 4,244 | | | 63,872 | |

| NVR, Inc. * Þ | | 32 | | | 13,896 | |

| Pulte Homes, Inc. Þ | | 4,837 | | | 51,514 | |

| | | | | 343,209 | |

| Internet & Catalog Retail 0.4% | | | | | | |

| Amazon.com, Inc. * Þ | | 30,791 | | | 1,314,776 | |

| HSN, Inc. * Þ | | 465 | | | 1,739 | |

| IAC/InteractiveCorp. Þ | | 1,163 | | | 17,201 | |

| priceline.com, Inc. * Þ | | 3,766 | | | 259,854 | |

| Ticketmaster Entertainment, Inc. * | | 465 | | | 1,855 | |

| | | | | 1,595,425 | |

| Leisure Equipment & Products 0.0% | | | | | | |

| Hasbro, Inc. Þ | | 5,049 | | | 135,313 | |

| | | | | | |

| Media 1.9% | | | | | | |

| Central European Media Enterprises, Ltd., Class A * Þ | | 3,521 | | | 54,118 | |

| Clear Channel Outdoor Holdings, Inc. Þ * | | 3,092 | | | 22,633 | |

| Comcast Corp., Class A | | 80,052 | | | 1,388,102 | |

| CTC Media, Inc. Þ * | | 5,147 | | | 21,875 | |

| DIRECTV Group, Inc. Þ * | | 58,256 | | | 1,282,215 | |

| DISH Network Corp., Class A Þ | | 19,942 | | | 220,957 | |

| DreamWorks Animation SKG, Inc., Class A * | | 7,812 | | | 180,457 | |

| Interpublic Group of Cos. Þ * | | 39,498 | | | 161,547 | |

| John Wiley & Sons, Inc., Class A Þ | | 3,938 | | | 141,610 | |

| Lamar Advertising Co., Class A Þ * | | 7,523 | | | 111,867 | |

| Liberty Global, Inc., Class A Þ * | | 15,331 | | | 222,146 | |

| Liberty Media Corp. - Liberty Entertainment, Ser. A * | | 50,516 | | | 599,625 | |

| McGraw-Hill Cos. Þ | | 15,644 | | | 391,100 | |

| Morningstar, Inc. * Þ | | 1,578 | | | 50,812 | |

| News Corp., Class A | | 90,578 | | | 715,566 | |

| Omnicom Group, Inc. | | 28,968 | | | 819,505 | |

| Sirius XM Radio, Inc. * Þ | | 290,284 | | | 60,466 | |

| Time Warner Cable, Inc. * | | 7,563 | | | 153,529 | |

| Time Warner, Inc. Þ | | 38,834 | | | 351,448 | |

| Viacom, Inc., Class B * | | 51,355 | | | 817,572 | |

| Walt Disney Co. Þ | | 21,608 | | | 486,612 | |

| Warner Music Group Corp. Þ | | 1,378 | | | 4,106 | |

| | | | | 8,257,868 | |

| Multiline Retail 0.9% | | | | | | |

| Big Lots, Inc. * Þ | | 7,956 | | | 139,389 | |

| Dollar Tree Stores, Inc. Þ * | | 8,798 | | | 372,683 | |

| Family Dollar Stores, Inc. Þ | | 1,065 | | | 29,586 | |

| Kohl's Corp. Þ * | | 23,015 | | | 751,670 | |

| Nordstrom, Inc. Þ | | 17,792 | | | 202,295 | |

| Target Corp. Þ | | 71,397 | | | 2,410,363 | |

| | | | | 3,905,986 | |

| | | | | | |

| | Shares | | | Value | |

| COMMON STOCKS continued | | | | | | |

| CONSUMER DISCRETIONARY continued | | | | | | |

| Specialty Retail 1.6% | | | | | | |

| Abercrombie & Fitch Co., Class A Þ | | 8,452 | | $ | 163,377 | |

| Advance Auto Parts, Inc. | | 9,316 | | | 282,834 | |

| American Eagle Outfitters, Inc. | | 11,829 | | | 113,558 | |

| AnnTaylor Stores Corp. * | | 2,130 | | | 9,564 | |

| AutoZone, Inc. * Þ | | 3,788 | | | 413,725 | |

| Bed Bath & Beyond, Inc. * Þ | | 20,835 | | | 422,742 | |

| Best Buy Co., Inc. Þ | | 32,653 | | | 676,244 | |

| CarMax, Inc. Þ * | | 21,381 | | | 162,710 | |

| Dick's Sporting Goods, Inc. * Þ | | 8,257 | | | 104,121 | |

| GameStop Corp., Class A Þ * | | 15,962 | | | 348,770 | |

| Gap, Inc. | | 23,512 | | | 306,126 | |

| Guess?, Inc. | | 5,897 | | | 78,017 | |

| Limited Brands, Inc. Þ | | 18,214 | | | 169,572 | |

| Lowe's Cos. | | 7,147 | | | 147,657 | |

| O'Reilly Automotive, Inc. * Þ | | 4,781 | | | 124,641 | |

| PETsMART, Inc. | | 12,448 | | | 218,462 | |

| Ross Stores, Inc. Þ | | 13,031 | | | 345,322 | |

| Sherwin-Williams Co. Þ | | 9,839 | | | 579,812 | |

| Staples, Inc. | | 58,350 | | | 1,012,956 | |

| Tiffany & Co. Þ | | 12,328 | | | 243,971 | |

| TJX Cos. | | 41,524 | | | 947,578 | |

| Urban Outfitters, Inc. * Þ | | 11,101 | | | 201,705 | |

| Williams-Sonoma, Inc. Þ | | 1,398 | | | 9,800 | |

| | | | | 7,083,264 | |

| Textiles, Apparel & Luxury Goods 0.7% | | | | | | |

| Coach, Inc. * | | 33,369 | | | 597,305 | |

| Hanesbrands, Inc. Þ * | | 9,197 | | | 118,825 | |

| Nike, Inc., Class B | | 34,588 | | | 1,841,811 | |

| Phillips-Van Heusen Corp. | | 4,400 | | | 76,736 | |

| Polo Ralph Lauren Corp. Þ | | 5,482 | | | 236,823 | |

| | | | | 2,871,500 | |