UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

Certified Shareholder Report of

Registered Management Investment Companies

Investment Company Act File Number: 811-00604

Washington Mutual Investors Fund

(Exact Name of Registrant as Specified in Charter)

6455 Irvine Center Drive

Irvine, California 92618

(Address of Principal Executive Offices)

Registrant's telephone number, including area code: (213) 486-9200

Date of fiscal year end: April 30

Date of reporting period: April 30, 2016

Jennifer L. Butler

Washington Mutual Investors Fund

333 South Hope Street

Los Angeles, California 90071

(Name and Address of Agent for Service)

ITEM 1 – Reports to Stockholders

Our quest for value focuses

on income and quality.

Special feature page 6

| Washington Mutual

Investors FundSM |

| |

Annual report

for the year ended

April 30, 2016 |

Washington Mutual Investors Fund seeks to produce income and to provide an opportunity for growth of principal consistent with sound common stock investing.

This fund is one of more than 40 offered by one of the nation’s largest mutual fund families, American Funds, from Capital Group. For 85 years, Capital has invested with a long-term focus based on thorough research and attention to risk.

Fund results shown in this report, unless otherwise indicated, are for Class A shares at net asset value. If a sales charge (maximum 5.75%) had been deducted, the results would have been lower. Results are for past periods and are not predictive of results for future periods. Current and future results may be lower or higher than those shown. Share prices and returns will vary, so investors may lose money. Investing for short periods makes losses more likely. Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value. For current information and month-end results, visit americanfunds.com.

Here are the average annual total returns on a $1,000 investment with all distributions reinvested for periods ended March 31, 2016 (the most recent calendar quarter-end):

| Class A shares | | 1 year | | 5 years | | 10 years |

| | | | | | | |

| Reflecting 5.75% maximum sales charge | | –4.40% | | 9.76% | | 6.02% |

For other share class results, visit americanfunds.com and americanfundsretirement.com.

The total annual fund operating expense ratio is 0.58% for Class A shares as of the prospectus dated July 1, 2016 (unaudited).

Investment results assume all distributions are reinvested and reflect applicable fees and expenses. When applicable, investment results reflect fee waivers, without which results would have been lower. Visit americanfunds.com for more information.

The fund’s 30-day yield for Class A shares as of May 31, 2016, reflecting the 5.75% maximum sales charge and calculated in accordance with the U.S. Securities and Exchange Commission formula, was 1.81%.

Refer to the fund prospectus and the Risk Factors section of this report for more information on risks associated with investing in the fund.

Fellow investors:

For the 12 months ended April 30, 2016, Washington Mutual Investors Fund reported a total return of 1.62%, compared with the 1.21% gain of the unmanaged Standard & Poor’s 500 Composite Index and the 2.46% decline of the Lipper Growth & Income Funds Index.

Over the past fiscal year, the fund paid four regular dividends, totaling 75 cents per share, and one special dividend of 7 cents. The fund also made a capital gain distribution of $1.59 per share in December 2015.

We’re pleased that the fund’s three-, five-and 10-year average annual total returns outpaced the Lipper Growth & Income Funds Index. Additionally, over its nearly 64-year lifetime, the fund’s average annual return has led the S&P 500.

Economic and market overview

In 2016, stocks of U.S. companies suffered one of the worst starts to a year in decades, held back by slowing growth in China and unstable oil prices. Following a 22-month low set in mid-February, however, stocks rallied through the end of April, indicating that prices may have stabilized.

As a result, the S&P 500 ended the first quarter of calendar-year 2016 with a modest gain, and in mid-April the Dow Jones Industrial Average crossed over 18,000 for the first time since July of 2015.

Economic data was mixed in the first half of the fund’s fiscal year. The U.S. economy, as represented by gross domestic product (GDP), grew by 3.9% in the second quarter of 2015 and then spiraled down from there — GDP expanded by 2.0% in the third quarter, 1.4% in the fourth quarter and just 0.5% (seasonally adjusted) in the first quarter of 2016. The decline was largely driven by less consumer spending and nonresidential investment, a strong dollar and weak global demand for exports.

Results at a glance

Average annual total returns for periods ended April 30, 2016, with all distributions reinvested.

| | | | | | | | | | | Lifetime |

| | | 1 year | | 3 years | | 5 years | | 10 years | | (since 7/31/52) |

| | | | | | | | | | | |

| Washington Mutual Investors Fund (Class A shares) | | | 1.62 | % | | | 10.10 | % | | | 10.62 | % | | | 6.57 | % | | | 11.77 | % |

| Standard & Poor’s 500 Composite Index* | | | 1.21 | | | | 11.26 | | | | 11.02 | | | | 6.91 | | | | 10.64 | |

| Lipper Growth & Income Funds Index | | | –2.46 | | | | 7.50 | | | | 7.61 | | | | 5.01 | | | | — | † |

| | | | | | | | | | | | | | | | | | | | | |

| * | The market index is unmanaged and, therefore, has no expenses. Investors cannot invest directly in an index. |

| † | This index was not in existence as of the date the fund’s Class A shares became available; therefore, lifetime results are not shown. |

| | |

| Washington Mutual Investors Fund | 1 |

Employment continued to strengthen. Almost 700,000 jobs were added through the three months to February, and the unemployment rate fell to an eight-year low of 4.9%. However, even though lower fuel costs boosted spending power, consumer spending remained sluggish. Inflation, as measured by core consumer prices, rose to a four-year high of 2.3%.

After raising rates for the first time in almost a decade in December, the U.S. Federal Reserve opted to keep interest rates unchanged through the first quarter of 2016. It also scaled back its interest-rate forecasts to two quarter-point rises this year, bringing them more in line with market expectations. Fed chair Janet Yellen indicated that proceeding cautiously would allow the central bank “to verify the labor market is continuing to strengthen, despite the risks from abroad.”

Sector overview

Over the 12-month period ended April 30, 2016, the utilities sector delivered strong returns, as did companies in the consumer staples and telecommunications sectors. Investors sought safe havens amid market volatility and against an uncertain long-term backdrop.

Consumer discretionary and industrial companies turned in better-than-average returns over the period. And although rebounding somewhat over the past couple of months, energy companies fell sharply over the past 12-month period, caught in the firm grip of a seven-year low of below $40 a barrel and a decline that started nearly two years ago as a result of a global oversupply of oil.

The highly cyclical basic materials sector lost ground over the period. Financial companies paid the price, which resulted in a decline over the period, as investors grew concerned about banks’ exposure to rising default rates among energy companies. Health care companies also retreated amid concerns over drug pricing.

Inside the portfolio

As of April 30, 2016, the fund’s 10 largest holdings were Microsoft (5.0%), Home Depot (4.4%), Verizon Communications (3.2%), Boeing (3.1%), Coca-Cola (2.9%), Comcast (2.7%), Lockheed Martin (2.6%), Merck (2.4%), JPMorgan Chase (2.1%) and Schlumberger (2.1%).

Shareholders benefited from stock selection in the information technology and health care sectors. Companies that helped lift relative fund results included Home Depot, Lockheed Martin, Coca-Cola and Microsoft.

On a relative basis, energy, utilities, materials and consumer staples sectors were the leading fund detractors.

Detracting companies on a relative basis included ConocoPhillips, Google and Union Pacific.

Looking ahead

It’s important to note that despite current market volatility, we continue to focus on delivering consistent income and competitive results, and with less volatility over the long term.

We invite you to read the special feature, which starts on page 6, for further discussion of our investment approach and culture, and why they’ve been so successful over time.

We thank our current investors for the confidence they’ve shown in American Funds and Washington Mutual Investors Fund and look forward to reporting to you again in six months.

Cordially,

Alan N. Berro

Vice Chairman and President

Washington Mutual Investors Fund

June 9, 2016

For current information about the fund, visit americanfunds.com.

| 2 | Washington Mutual Investors Fund |

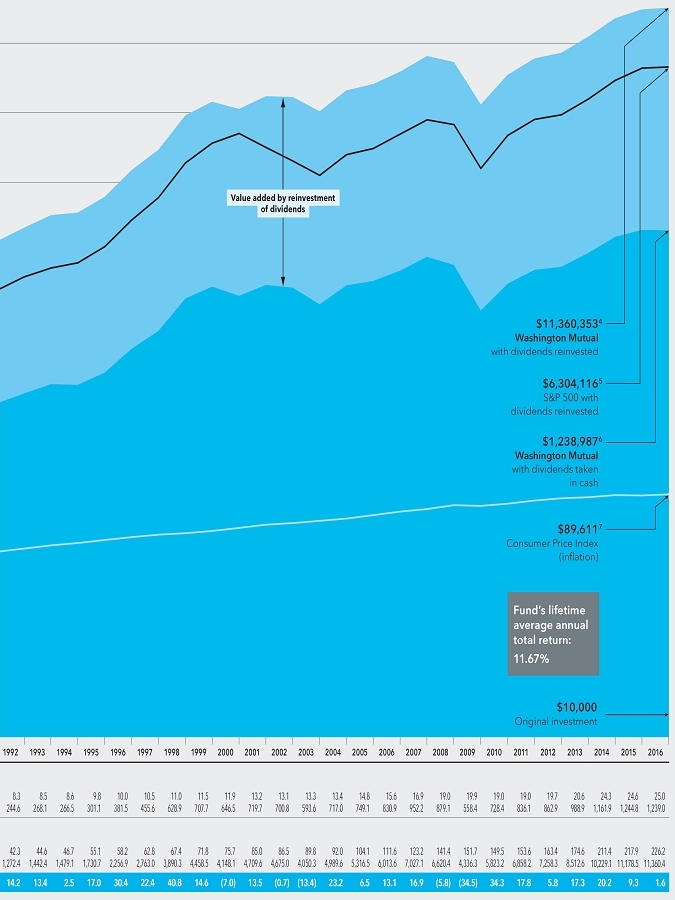

The value of a long-term perspective

Fund results shown are for Class A shares and reflect deduction of the maximum sales charge of 5.75% on the $10,000 investment.¹ Thus, the net amount invested was $9,425.² Results are for past periods and are not predictive of results for future periods. Current and future results may be lower or higher than those shown. Share prices and returns will vary, so investors may lose money. For current information and month-end results, visit americanfunds.com.

The results shown are before taxes on fund distributions and sale of fund shares.

| 1 | As outlined in the prospectus, the sales charge is reduced for accounts (and aggregated investments) of $25,000 or more and is eliminated for purchases of $1 million or more. There is no sales charge on dividends or capital gain distributions that are reinvested in additional shares. |

| 2 | The maximum initial sales charge was 8.50% prior to July 1, 1988. |

| 3 | For the period July 31, 1952 (when the fund began operations), through April 30, 1953. |

| 4 | Total value includes reinvested dividends of $3,163,268 and reinvested capital gain distributions of $3,895,792. |

| 5 | The market index is unmanaged and, therefore, has no expenses. Investors cannot invest directly in an index. |

| 6 | Capital value includes reinvested capital gain distributions of $592,900 but does not reflect income dividends of $488,168 taken in cash. |

| 7 | Computed from data supplied by the U.S. Department of Labor, Bureau of Labor Statistics. |

| Washington Mutual Investors Fund | 3 |

How a $10,000 investment has grown

While notable for their volatility in recent years, financial markets have tended to reward investors over the long term. Active management — bolstered by experience and careful research — can add even more value. As the chart shows, over its lifetime, Washington Mutual Investors Fund has done demonstrably better than its relevant benchmark.

| Washington Mutual Investors Fund | 5 |

Research and relationships

power our quest.

| 6 | Washington Mutual Investors Fund |

“It comes down to boots on the ground. We survey the investment landscape, turning over every stone to find something of value, something to make money for our shareholders.”

Alan Berro

Portfolio manager

By trade, George Washington first served the Colonies as a land surveyor. Our first president pursued this vocation throughout his life, starting with the documentation of settlement and agricultural boundaries along Virginia’s western frontier.

The benefits of such a career were myriad. He accrued first-hand knowledge of the land, and put that knowledge to use when deciding which parcels to purchase for his own estate, which ultimately grew to more than 70,000 prime acres between the Potomac and Ohio rivers.

It’s been said that success is where preparation and opportunity meet. Washington lived in that nexus — partly by chance, given the brave new world in which he lived, and partly by design, given the knowledge he gathered by hacking and backpacking his way through thousands of tangled acres of raw colonial land.

Washington’s situated expertise may be an apt model for the diverse group of portfolio managers and analysts who toil on behalf of the American Funds shareholders. One might even suggest that these investment professionals are modern-day surveyors, measuring and marking the changing investment landscape as they search for only those companies that meet the high standards of Washington Mutual Investors Fund.

And few do it as well or as thoroughly as American Funds investment professionals. To cite just one important statistic, from May 2015 to April 2016 the American Funds investment group participated in nearly 14,000 meetings and conference calls with companies in 48 countries.

“At American Funds,” says Alan Berro, vice chairman and president of Washington Mutual Investors Fund, “it comes down to boots on the ground. We survey the investment landscape, turning over every stone to find something of value, something to make money for our shareholders.”

So Alan himself draws the parallel to professional surveying: The fund’s success is founded on a detailed search for high-quality companies with superior business characteristics that pay dividends.

“If we do this well,” says fund portfolio manager Eric Stern, “we’ll be doing what we can to protect investors when the market declines.”

In this feature article, we’ll examine three of the fund’s largest holdings to demonstrate how American Funds investment professionals have helped Washington Mutual Investors Fund shareholders pursue long-term investment success since 1952.

Transformation takes longer than a quarter

Fund investment analyst Anne-Marie Peterson tries to determine what a company’s underlying earnings power will look like in three to five years or more, and if that level is sustainable.

“A company could earn much more than some people think,” says Anne-Marie, “and the potential for growth of earnings might be sustained for much longer than the market expects.”

One reason for this is that the market all too often defines the long term as a single year or even a single quarter. Anne-Marie defines long term as at least five years.

“That’s how you can find value,” she adds. “If something transformational is happening at a company, it often doesn’t play out in quarters. Rather, it plays out in years. Our job as long-term investors is to go deep, to see what others don’t or can’t see.”

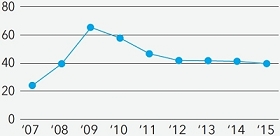

Anne-Marie cites The Home Depot as a good example of this.

Based on her research and relationship with company management, she became convinced in 2007 that the company’s stock was undervalued. Conventional wisdom held that the company had lost its way and outgrown its scale, failing to overhaul an overwhelmed supply chain and technology. Even with a newly appointed CEO, the market missed the key signals. The stock price continued to drift down, led by a weak housing market.

Anne-Marie, however, believed in that new CEO and the company.

“Structurally,” Anne-Marie recalls, “The Home Depot was a good, competitive business with high earnings. The basic

| Washington Mutual Investors Fund | 7 |

|  |  |

| | | |

| Eric Stern | Anne-Marie Peterson | Paul Benjamin |

| Portfolio manager | Investment analyst | Investment analyst |

fundamentals were sound. The problem had been management and significant cyclical housing market headwinds. For me, the primary questions were: Can the new CEO fix it? And if he fixes it, what is the real earnings power?”

After talking to former vendors, supply chain people and former employees, and participating in meetings with members of the management team, Anne-Marie concluded that the team — just by adjusting the business — would be able to successfully execute and, ultimately, unleash the company’s earnings power — with or without a housing industry recovery.

Shortly after, the new management team started to centralize The Home Depot’s supply chain, upgrade its technology, reinvigorate its culture and simplify supply and sales processes. Not only were these fixes able to reaffirm the company’s relationship with its do-it-yourself and do-it-for-me customer base, the adjustments also gave the company the tools and capacity to become more engaged with professional customers, the bulk-buying builders and contractors.

“Surprise, surprise,” says Anne-Marie, “it got better. Capital expenditures were coming down, and cash flow and dividends were suddenly growing and quickly.”

She adds that American Funds has this deep advantage that leads to discerning key relationships. “We understand that every investment is a combination of business and people; it’s that simple. When you buy the stock, you’re buying both,” she adds.

“There’s nuance in what we do, an art to investing. What on paper looks so obvious is easy to dismiss. It’s our job to go deeper and question those assumptions and study a thousand little details that go into figuring it all out.”

A market misunderstanding

Fund investment analyst Paul Benjamin has his own example of a company the market incorrectly undervalued, and from which fund shareholders benefited.

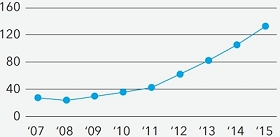

“Around the time we had decided to invest in Microsoft for the fund,” says Paul, “the market was coming to the realization that cloud computing would be the next information technology (IT) generation.” This refers to the growing trend of using a network of remote servers hosted on the internet to store, manage and process data, rather than a local server or a personal computer.

Generally, common wisdom held that those companies focused on the then-current IT generation — legacy or on-premises computing — would be in trouble. The proof was in cloud

The Home Depot

Dividend payout ratio (%)

Stock price ($)

Sales ($) (in billions)

Source: FactSet.

Microsoft

Dividend payout ratio (%)

Stock price ($)

Sales ($) (in billions)

Source: FactSet.

| 8 | Washington Mutual Investors Fund |

companies trading at premium stock prices, while legacy companies were trading at much lower prices.

“There was a massive divergence in valuation between the cloud companies and the on-premise companies,” recalls Paul. “I was convinced the market misunderstood the quality of Microsoft’s cloud assets.”

“We were already very familiar with the new management team and thought very highly of them. We also had done deep analysis of their nascent cloud products and been very impressed with their rate of progress. In spite of this, Microsoft was trading as if it were a legacy IT company, which made it very affordable,” says Paul.

Paul was bullish on Microsoft for several reasons. He was convinced that only two, or at most, three players would lead the cloud infrastructure business, while the consensus believed that there were many more players and that the public cloud would be a low-margin business. Amazon was the clear leader, Google was coming on strong, and a number of other vendors such as VMware, Rackspace and Hewlett-Packard were viewed as having strong offerings. Paul, however, believed that Microsoft would end up a strong number two, thanks to its public cloud product, Azure.

He was also convinced that Microsoft Office, which appeared to be threatened by Google Applications, was actually transforming into the Office 365 cloud computing application.

Microsoft’s on-premise database business was also in flux.

The New Geography of Investing®

Where a company does business can be more important than where it’s located. Here’s a look at Washington Mutual Investors Fund’s portfolio in terms of where its equity holdings earn their revenue. The charts below show the countries and regions in which the fund’s equity investments are located, and where the revenue comes from.

Equity portion breakdown by domicile (%)

| | | Region | | Fund |

| ■ | | United States | | | 95 | % |

| ■ | | Canada | | | 2 | |

| ■ | | Europe | | | 3 | |

| ■ | | Japan | | | — | |

| ■ | | Asia-Pacific ex. Japan | | | — | |

| ■ | | Emerging markets | | | — | |

| | | Total | | | 100 | % |

Equity portion breakdown by revenue (%)

| | | Region | | Fund |

| ■ | | United States | | | 64 | % |

| ■ | | Canada | | | 3 | |

| ■ | | Europe | | | 11 | |

| ■ | | Japan | | | 2 | |

| ■ | | Asia-Pacific ex. Japan | | | 1 | |

| ■ | | Emerging markets | | | 19 | |

| | | Total | | | 100 | % |

Source: Capital Group (as of March 31, 2016).

Pie charts indicate the percentage of net fund assets in each geographical area.

All figures, based on Capital Group data, include convertible securities.

| Washington Mutual Investors Fund | 9 |

High standards seek to raise the investment bar

The Washington Mutual Investors Fund Investment Standards are based on criteria originally established after the Great Depression by the U.S. District Court for the District of Columbia. The fund continues to embrace those founding principles, which require a thorough and rigorous investment-screening process to arrive at a list of eligible stocks, from which fund holdings can be chosen. Currently, the fund:

| • | | Can invest only in companies that meet the fund’s strict Investment Standards. |

| • | | Seeks to be 95% invested in equities (stocks) at all times. |

| • | | May invest only up to 10% of its assets in companies based outside the United States. |

| • | | Can invest no more than 5% of the fund’s total assets in stock of non-dividend-paying companies; however, those non-dividend-paying companies must meet additional, more stringent requirements. |

| • | | May not invest in companies that derive the majority of their revenues from alcohol or tobacco products. |

Many are called, few are chosen

As of December 31, 2015:

A focus on dividend-paying companies

Of the 163 stocks held by the fund, as of December 31, 2015, the following companies paid uninterrupted dividends over the periods cited:

“Microsoft was the number two or three player behind Oracle,” Paul says. “But the current CEO, who at the time was running that division, reassigned the database R&D work to Microsoft’s cloud group. The result is that Microsoft’s database in the cloud was able to simultaneously operate on hundreds or thousands of servers. Oracle’s database platform was only concurrently serving about 50 nodes.

“After Microsoft built that capability into the cloud,” Paul says, “the cloud team ported the technology back to its on-premise product. Proof is that Microsoft has been growing its database business at 10% to 15% for several years, while Oracle’s business has been flat.”

Some companies can rise to the challenge

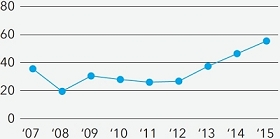

“In the case of Comcast,” says investment analyst Andrei Muresianu, “we believed that the market had overreacted to threats posed by changing trends. After all, just because trends are changing, doesn’t mean a company has to be any less profitable.”

Andrei’s deep research, which was supplemented by interviews with company management, clearly indicated that Comcast had an immense ability to grow across many channels and adapt to those changing trends.

The company already sold broadband services to more than half of the cable customers in America, was increasing market share among small- and medium-business telecommunication services, and was in the early stages of a turnaround of its NBCUniversal division.

| 10 | Washington Mutual Investors Fund |

“I think about powerful upside opportunities like Comcast, but first I think about conservation.”

Andrei Muresianu

Investment analyst

But Wall Street had doubts about whether Comcast could successfully navigate through the trend away from large, expensive cable-channel bundles and toward a more curated bundle, including on-demand and pay-per-view services.

Today its core cable and broadband businesses are delivering record cash flow and NBCUniversal has never been stronger, with park profits at record highs, and Universal Studios coming off one of the most successful years ever for a movie studio.

Comcast

Dividend payout ratio (%)

Stock price ($)

Sales ($) (in billions)

Source: FactSet.

Andrei believed that even if the world moved away from big cable bundles, NBC’s assets, which are heavy in sports and broadcast television, would remain a core offering even for smaller bundles.

“Even if no one pays for traditional television,” he says, “Comcast offers a broadband product that could be exceptionally profitable and offset any losses from TV cash flow.

“I think about powerful upside opportunities like Comcast,” says Andrei, “but first I think about conservation. I seek stocks that have the potential to protect shareholders and beat the market in a market decline. And while we love stocks that have the potential to outpace the index in a rising market, my first priority is to conserve capital while generating income. That only comes from very high-quality business models and safe balance sheets.”

It’s not all blockbusters and confetti

Most of the decisions to buy or sell are less dramatic than the ones we’ve spotlighted in this feature. More typically, each portfolio manager and investment analyst makes decisions that, taken independently, move the return needle only slightly. Collectively, however, those decisions can make a significant positive difference.

“Usually, the gap between what we believe and what the market believes is not massive,” says Eric Stern. “Our mission is simply to buy and stick with companies that we believe can compound value over time and deliver the dividend we expect from them.”

He cautions that it’s not always or necessarily about finding a company that has been left for dead and that American Funds believes can be nursed back to health.

When Eric looks over his top 10 holdings in the fund, he sees very different types of companies that all well suit the fund.

“I believe that they are high-quality companies with superior franchises,” he says, “that I think will be similarly positioned three and five years down the road and beyond. That’s one of the benefits of Washington Mutual,” he says. “It enables us to invest in a diverse set of companies across multiple industries and across capital-return policies.”

“Every fund manager in our business picks stocks,” Alan says. “And when you pick one, you don’t know if it will be a home run. Sometimes you get lucky, and it is. Our approach is to attempt to hit a lot of singles and doubles.”

American Funds, he adds, seeks to identify companies with strong underlying qualities that are misvalued by the market. Often, Alan notes, what the market finds fault with can be fixed with the right management team by, for example, focusing on the right core business issues, improving morale or upgrading systems.

That creates a virtuous cycle that can lead to rising stock prices, earnings, cash flow and margins. “However,” Alan adds, “for most companies it’s just a day-in and day-out effort, getting it done and trying to do it a little better. That’s what American Funds tries to do also.” ■

| Washington Mutual Investors Fund | 11 |

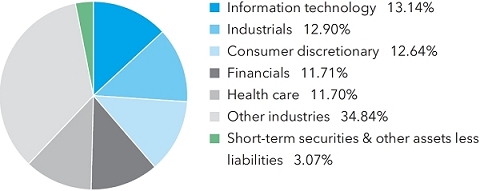

Summary investment portfolio April 30, 2016

| Industry sector diversification | Percent of net assets |

| Largest equity holdings | | Percent of net assets |

| Microsoft | | | 5.02 | % |

| Home Depot | | | 4.40 | |

| Verizon Communications | | | 3.22 | |

| Boeing | | | 3.06 | |

| Coca-Cola | | | 2.87 | |

| Comcast | | | 2.65 | |

| Lockheed Martin | | | 2.56 | |

| Merck | | | 2.35 | |

| JPMorgan Chase | | | 2.14 | |

| Schlumberger | | | 2.14 | |

| Common stocks 96.93% | | Shares | | | Value

(000) | |

| Energy 11.04% | | | | | | | | |

| Chevron Corp. | | | 12,554,300 | | | $ | 1,282,798 | |

| ConocoPhillips | | | 22,200,100 | | | | 1,060,943 | |

| Enbridge Inc. | | | 28,659,479 | | | | 1,190,515 | |

| Exxon Mobil Corp. | | | 6,578,200 | | | | 581,513 | |

| Pioneer Natural Resources Co. | | | 5,334,323 | | | | 886,031 | |

| Royal Dutch Shell PLC, Class B (ADR) | | | 22,600,000 | | | | 1,205,710 | |

| Schlumberger Ltd. | | | 20,869,300 | | | | 1,676,639 | |

| Other securities | | | | | | | 780,483 | |

| | | | | | | | 8,664,632 | |

| | | | | | | | | |

| Materials 5.49% | | | | | | | | |

| Dow Chemical Co. | | | 9,455,752 | | | | 497,467 | |

| E.I. du Pont de Nemours and Co. | | | 23,181,534 | | | | 1,527,895 | |

| Praxair, Inc. | | | 9,468,300 | | | | 1,112,146 | |

| Other securities | | | | | | | 1,171,159 | |

| | | | | | | | 4,308,667 | |

| | | | | | | | | |

| Industrials 12.90% | | | | | | | | |

| Boeing Co. | | | 17,822,700 | | | | 2,402,500 | |

| General Electric Co. | | | 25,018,000 | | | | 769,303 | |

| Lockheed Martin Corp. | | | 8,639,300 | | | | 2,007,601 | |

| Northrop Grumman Corp. | | | 4,557,700 | | | | 940,071 | |

| Union Pacific Corp. | | | 6,526,000 | | | | 569,263 | |

| Waste Management, Inc. | | | 14,964,400 | | | | 879,757 | |

| Other securities | | | | | | | 2,552,100 | |

| | | | | | | | 10,120,595 | |

| | | | | | | | | |

| Consumer discretionary 12.64% | | | | | | | | |

| Comcast Corp., Class A | | | 34,225,739 | | | | 2,079,556 | |

| Home Depot, Inc. | | | 25,775,600 | | | | 3,451,095 | |

| McDonald’s Corp. | | | 4,775,000 | | | | 603,990 | |

| VF Corp. | | | 11,230,200 | | | | 708,064 | |

| Other securities | | | | | | | 3,071,032 | |

| | | | | | | | 9,913,737 | |

| | | | | | | | | |

| Consumer staples 9.97% | | | | | | | | |

| Coca-Cola Co. | | | 50,298,000 | | | | 2,253,350 | |

| Costco Wholesale Corp. | | | 3,855,700 | | | | 571,145 | |

| CVS Health Corp. | | | 8,725,000 | | | | 876,863 | |

| Kraft Heinz Co. | | | 8,805,000 | | | | 687,406 | |

| Procter & Gamble Co. | | | 17,095,700 | | | | 1,369,708 | |

| Other securities | | | | | | | 2,060,959 | |

| | | | | | | | 7,819,431 | |

| 12 | Washington Mutual Investors Fund |

| | | | | | Value | |

| | | Shares | | | (000) | |

| Health care 11.70% | | | | | | | | |

| Aetna Inc. | | | 5,323,300 | | | $ | 597,647 | |

| Bristol-Myers Squibb Co. | | | 9,432,800 | | | | 680,859 | |

| Humana Inc.1 | | | 7,620,000 | | | | 1,349,273 | |

| Johnson & Johnson | | | 11,365,000 | | | | 1,273,789 | |

| Medtronic PLC | | | 10,961,700 | | | | 867,619 | |

| Merck & Co., Inc. | | | 33,683,000 | | | | 1,847,176 | |

| Pfizer Inc. | | | 30,256,000 | | | | 989,674 | |

| UnitedHealth Group Inc. | | | 3,667,300 | | | | 482,910 | |

| Other securities | | | | | | | 1,093,713 | |

| | | | | | | | 9,182,660 | |

| | | | | | | | | |

| Financials 11.71% | | | | | | | | |

| Chubb Corp. | | | 7,302,200 | | | | 860,637 | |

| CME Group Inc., Class A | | | 9,988,404 | | | | 918,034 | |

| JPMorgan Chase & Co. | | | 26,660,500 | | | | 1,684,944 | |

| Marsh & McLennan Companies, Inc. | | | 8,409,300 | | | | 531,047 | |

| PNC Financial Services Group, Inc. | | | 6,271,000 | | | | 550,468 | |

| Wells Fargo & Co. | | | 32,502,200 | | | | 1,624,460 | |

| Other securities | | | | | | | 3,018,188 | |

| | | | | | | | 9,187,778 | |

| | | | | | | | | |

| Information technology 13.14% | | | | | | | | |

| Alphabet Inc., Class A2 | | | 694,200 | | | | 491,410 | |

| Alphabet Inc., Class C2 | | | 228,750 | | | | 158,526 | |

| Intel Corp. | | | 31,549,000 | | | | 955,304 | |

| Intuit Inc. | | | 7,195,000 | | | | 725,903 | |

| Microsoft Corp. | | | 79,023,800 | | | | 3,940,917 | |

| Texas Instruments Inc. | | | 20,473,800 | | | | 1,167,826 | |

| Visa Inc., Class A | | | 7,301,100 | | | | 563,937 | |

| Other securities | | | | | | | 2,301,138 | |

| | | | | | | | 10,304,961 | |

| | | | | | | | | |

| Telecommunication services 3.87% | | | | | | | | |

| AT&T Inc. | | | 13,003,525 | | | | 504,797 | |

| Verizon Communications Inc. | | | 49,657,201 | | | | 2,529,538 | |

| | | | | | | | 3,034,335 | |

| | | | | | | | | |

| Utilities 2.82% | | | | | | | | |

| Dominion Resources, Inc. | | | 10,267,000 | | | | 733,782 | |

| PG&E Corp. | | | 8,698,500 | | | | 506,253 | |

| Other securities | | | | | | | 972,890 | |

| | | | | | | | 2,212,925 | |

| | | | | | | | | |

| Miscellaneous 1.65% | | | | | | | | |

| Other common stocks in initial period of acquisition | | | | | | | 1,292,998 | |

| | | | | | | | | |

| Total common stocks (cost: $52,724,366,000) | | | | | | | 76,042,719 | |

| Washington Mutual Investors Fund | 13 |

| Short-term securities 2.96% | Principal amount

(000) | | | Value

(000) | |

| Federal Home Loan Bank 0.30%–0.59% due 5/6/2016–9/2/2016 | | $ | 1,257,000 | | | $ | 1,256,569 | |

| General Electric Co. 0.31% due 5/2/2016 | | | 100,600 | | | | 100,597 | |

| Pfizer Inc. 0.49% due 5/6/20163 | | | 50,000 | | | | 49,997 | |

| Other securities | | | | | | | 911,808 | |

| | | | | | | | | |

| Total short-term securities (cost: $2,318,478,000) | | | | | | | 2,318,971 | |

| Total investment securities 99.89% (cost: $55,042,844,000) | | | | | | | 78,361,690 | |

| Other assets less liabilities 0.11% | | | | | | | 84,543 | |

| | | | | | | | | |

| Net assets 100.00% | | | | | | $ | 78,446,233 | |

This summary investment portfolio is designed to streamline the report and help investors better focus on the fund’s principal holdings. See the inside back cover for details on how to obtain a complete schedule of portfolio holdings.

As permitted by U.S. Securities and Exchange Commission regulations, “Miscellaneous” securities include holdings in their first year of acquisition that have not previously been publicly disclosed.

“Other securities” includes all issues that are not disclosed separately in the summary investment portfolio.

Investments in affiliates

A company is an affiliate of the fund under the Investment Company Act of 1940 if the fund’s holdings in that company represent 5% or more of the outstanding voting shares. The value of the fund’s affiliated-company holdings is either shown in the summary investment portfolio or included in the value of “Other securities” under the respective industry sectors. Further details on such holdings and related transactions during the year ended April 30, 2016, appear below.

| | | | | | | | | | | | | | | | | | Value of | |

| | | | | | | | | | | | | | | Dividend | | | affiliates at | |

| | | Beginning | | | | | | | | | Ending | | | income | | | 4/30/2016 | |

| | | shares | | | Additions | | | Reductions | | | shares | | | (000) | | | (000) | |

| Humana Inc. | | | 7,620,000 | | | | — | | | | — | | | | 7,620,000 | | | $ | 8,839 | | | $ | 1,349,273 | |

| KLA-Tencor Corp.4 | | | 8,038,000 | | | | — | | | | 6,867,000 | | | | 1,171,000 | | | | 1,941 | | | | — | |

| | | | | | | | | | | | | | | | | | | $ | 10,780 | | | $ | 1,349,273 | |

| 1 | Represents an affiliated company as defined under the Investment Company Act of 1940. |

| 2 | Security did not produce income during the last 12 months. |

| 3 | Acquired in a transaction exempt from registration under Section 4(2) of the Securities Act of 1933. May be resold in the U.S. in transactions exempt from registration, normally to qualified institutional buyers. The total value of all such securities, including those in “Other securities,” was $332,264,000, which represented .42% of the net assets of the fund. |

| 4 | Unaffiliated issuer at 4/30/2016. |

Key to abbreviation

ADR = American Depositary Receipts

See Notes to Financial Statements

| 14 | Washington Mutual Investors Fund |

Financial statements

Statement of assets and liabilities

| at April 30, 2016 | (dollars in thousands) |

| Assets: | | | | | | | | |

| Investment securities, at value: | | | | | | | | |

| Unaffiliated issuers (cost: $54,489,818) | | $ | 77,012,417 | | | | | |

| Affiliated issuers (cost: $553,026) | | | 1,349,273 | | | $ | 78,361,690 | |

| Cash | | | | | | | 130 | |

| Receivables for: | | | | | | | | |

| Sales of investments | | | 138,793 | | | | | |

| Sales of fund’s shares | | | 136,089 | | | | | |

| Dividends and interest | | | 108,394 | | | | 383,276 | |

| | | | | | | | 78,745,096 | |

| Liabilities: | | | | | | | | |

| Payables for: | | | | | | | | |

| Purchases of investments | | | 118,383 | | | | | |

| Repurchases of fund’s shares | | | 135,258 | | | | | |

| Investment advisory services | | | 15,170 | | | | | |

| Services provided by related parties | | | 21,644 | | | | | |

| Board members’ deferred compensation | | | 6,597 | | | | | |

| Other | | | 1,811 | | | | 298,863 | |

| Net assets at April 30, 2016 | | | | | | $ | 78,446,233 | |

| | | | | | | | | |

| Net assets consist of: | | | | | | | | |

| Capital paid in on shares of beneficial interest | | | | | | $ | 52,357,362 | |

| Undistributed net investment income | | | | | | | 138,349 | |

| Undistributed net realized gain | | | | | | | 2,631,676 | |

| Net unrealized appreciation | | | | | | | 23,318,846 | |

| Net assets at April 30, 2016 | | | | | | $ | 78,446,233 | |

(dollars and shares in thousands, except per-share amounts)

Shares of beneficial interest issued and outstanding (no stated par value) —

unlimited shares authorized (1,993,928 total shares outstanding)

| | | | | | Shares | | | Net asset value | |

| | | Net assets | | | outstanding | | | per share | |

| Class A | | $ | 50,716,657 | | | | 1,287,963 | | | $ | 39.38 | |

| Class B | | | 63,297 | | | | 1,615 | | | | 39.19 | |

| Class C | | | 1,587,599 | | | | 40,791 | | | | 38.92 | |

| Class F-1 | | | 2,897,372 | | | | 73,818 | | | | 39.25 | |

| Class F-2 | | | 6,097,224 | | | | 154,922 | | | | 39.36 | |

| Class 529-A | | | 1,787,918 | | | | 45,491 | | | | 39.30 | |

| Class 529-B | | | 11,061 | | | | 282 | | | | 39.23 | |

| Class 529-C | | | 442,398 | | | | 11,335 | | | | 39.03 | |

| Class 529-E | | | 91,869 | | | | 2,349 | | | | 39.10 | |

| Class 529-F-1 | | | 109,481 | | | | 2,791 | | | | 39.23 | |

| Class R-1 | | | 92,534 | | | | 2,373 | | | | 39.00 | |

| Class R-2 | | | 717,714 | | | | 18,460 | | | | 38.88 | |

| Class R-2E | | | 8,249 | | | | 210 | | | | 39.26 | |

| Class R-3 | | | 1,767,336 | | | | 45,221 | | | | 39.08 | |

| Class R-4 | | | 2,306,392 | | | | 58,832 | | | | 39.20 | |

| Class R-5E | | | 10 | | | | — | * | | | 39.36 | |

| Class R-5 | | | 1,948,987 | | | | 49,507 | | | | 39.37 | |

| Class R-6 | | | 7,800,135 | | | | 197,968 | | | | 39.40 | |

*Amount less than one thousand.

See Notes to Financial Statements

| Washington Mutual Investors Fund | 15 |

Statement of operations

| for the year ended April 30, 2016 | (dollars in thousands) |

| Investment income: | | | | | | | | |

| Income: | | | | | | | | |

| Dividends (net of non-U.S. taxes of $11,098; | | | | | | | | |

| also includes $10,780 from affiliates) | | $ | 1,970,711 | | | | | |

| Interest | | | 5,838 | | | $ | 1,976,549 | |

| Fees and expenses*: | | | | | | | | |

| Investment advisory services | | | 179,872 | | | | | |

| Distribution services | | | 170,695 | | | | | |

| Transfer agent services | | | 66,393 | | | | | |

| Administrative services | | | 17,890 | | | | | |

| Reports to shareholders | | | 2,507 | | | | | |

| Registration statement and prospectus | | | 1,289 | | | | | |

| Board members’ compensation | | | 1,331 | | | | | |

| Auditing and legal | | | 606 | | | | | |

| Custodian | | | 835 | | | | | |

| Other | | | 2,344 | | | | 443,762 | |

| Net investment income | | | | | | | 1,532,787 | |

| | | | | | | | | |

| Net realized gain and unrealized depreciation: | | | | | | | | |

| Net realized gain (loss) on: | | | | | | | | |

| Investments (includes $41,140 net loss from affiliates) | | | 3,042,194 | | | | | |

| Currency transactions | | | (213 | ) | | | 3,041,981 | |

| Net unrealized depreciation on investments | | | | | | | (3,338,626 | ) |

| Net realized gain and unrealized depreciation | | | | | | | (296,645 | ) |

| Net increase in net assets resulting from operations | | | | | | $ | 1,236,142 | |

*Additional information related to class-specific fees and expenses is included in the Notes to Financial Statements.

See Notes to Financial Statements

| 16 | Washington Mutual Investors Fund |

Statements of changes in net assets

(dollars in thousands)

| | | Year ended April 30 | |

| | | 2016 | | | 2015 | |

| Operations: | | | | | | | | |

| Net investment income | | $ | 1,532,787 | | | $ | 1,504,121 | |

| Net realized gain | | | 3,041,981 | | | | 4,641,236 | |

| Net unrealized (depreciation) appreciation | | | (3,338,626 | ) | | | 514,063 | |

| Net increase in net assets resulting from operations | | | 1,236,142 | | | | 6,659,420 | |

| Dividends and distributions paid to shareholders: | | | | | | | | |

| Dividends from net investment income | | | (1,569,346 | ) | | | (1,515,914 | ) |

| Distributions from net realized gain on investments | | | (3,006,010 | ) | | | (3,650,990 | ) |

| Total dividends and distributions paid to shareholders | | | (4,575,356 | ) | | | (5,166,904 | ) |

| Net capital share transactions | | | 3,175,152 | | | | 4,789,178 | |

| | | | | | | | | |

| Total (decrease) increase in net assets | | | (164,062 | ) | | | 6,281,694 | |

| | | | | | | | | |

| Net assets: | | | | | | | | |

| Beginning of year | | | 78,610,295 | | | | 72,328,601 | |

| End of year (including undistributed net investment income: $138,349 and $175,093, respectively) | | $ | 78,446,233 | | | $ | 78,610,295 | |

See Notes to Financial Statements

| Washington Mutual Investors Fund | 17 |

Notes to financial statements

1. Organization

Washington Mutual Investors Fund (the “fund”) is registered under the Investment Company Act of 1940 as an open-end, diversified management investment company. The fund’s investment objective is to produce income and to provide an opportunity for growth of principal consistent with sound common stock investing.

The fund has 18 share classes consisting of five retail share classes (Classes A, B and C, as well as two F share classes, F-1 and F-2), five 529 college savings plan share classes (Classes 529-A, 529-B, 529-C, 529-E and 529-F-1) and eight retirement plan share classes (Classes R-1, R-2, R-2E, R-3, R-4, R-5E, R-5 and R-6). The 529 college savings plan share classes can be used to save for college education. The retirement plan share classes are generally offered only through eligible employer-sponsored retirement plans. The fund’s share classes are described further in the following table:

| Share class | | Initial sales charge | | Contingent deferred sales charge upon

redemption | | Conversion feature |

| Classes A and 529-A | | Up to 5.75% | | None (except 1% for certain redemptions within one year of purchase without an initial sales charge) | | None |

| Classes B and 529-B* | | None | | Declines from 5% to 0% for redemptions within six years of purchase | | Classes B and 529-B convert to Classes A and 529-A, respectively, after eight years |

| Class C | | None | | 1% for redemptions within one year of purchase | | Class C converts to Class F-1 after 10 years |

| Class 529-C | | None | | 1% for redemptions within one year of purchase | | None |

| Class 529-E | | None | | None | | None |

| Classes F-1, F-2 and 529-F-1 | | None | | None | | None |

| Classes R-1, R-2, R-2E, R-3, R-4, R-5E, R-5 and R-6 | | None | | None | | None |

*Class B and 529-B shares of the fund are not available for purchase.

On November 20, 2015, the fund made an additional retirement plan share class (Class R-5E) available for sale pursuant to an amendment to its registration statement filed with the U.S. Securities and Exchange Commission. Refer to the fund’s prospectus for more details.

Holders of all share classes have equal pro rata rights to the assets, dividends and liquidation proceeds of the fund. Each share class has identical voting rights, except for the exclusive right to vote on matters affecting only its class. Share classes have different fees and expenses (“class-specific fees and expenses”), primarily due to different arrangements for distribution, transfer agent and administrative services. Differences in class-specific fees and expenses will result in differences in net investment income and, therefore, the payment of different per-share dividends by each share class.

2. Significant accounting policies

The fund is an investment company that applies the accounting and reporting guidance issued in Topic 946 by the U.S. Financial Board. The fund’s financial statements have been prepared to comply with U.S. generally accepted accounting principles (“U.S. GAAP”). These principles require the fund’s investment adviser to make estimates and assumptions that affect reported amounts and disclosures. Actual results could differ from those estimates. Subsequent events, if any, have been evaluated through the date of issuance in the preparation of the financial statements. The fund follows the significant accounting policies described in this section, as well as the valuation policies described in the next section on valuation.

Security transactions and related investment income — Security transactions are recorded by the fund as of the date the trades are executed with brokers. Realized gains and losses from security transactions are determined based on the specific identified cost of the securities. In the event a security is purchased with a delayed payment date, the fund will segregate liquid assets sufficient to meet its payment obligations. Dividend income is recognized on the ex-dividend date and interest income is recognized on an accrual basis. Market discounts, premiums and original issue discounts on fixed-income securities are amortized daily over the expected life of the security.

| 18 | Washington Mutual Investors Fund |

Class allocations — Income, fees and expenses (other than class-specific fees and expenses) and realized and unrealized gains and losses are allocated daily among the various share classes based on their relative net assets. Class-specific fees and expenses, such as distribution, transfer agent and administrative services, are charged directly to the respective share class.

Dividends and distributions to shareholders — Dividends and distributions to shareholders are recorded on the ex-dividend date.

3. Valuation

Capital Research and Management Company (“CRMC”), the fund’s investment adviser, values the fund’s investments at fair value as defined by U.S. GAAP. The net asset value of each share class of the fund is generally determined as of approximately 4:00 p.m. New York time each day the New York Stock Exchange is open.

Methods and inputs — The fund’s investment adviser uses the following methods and inputs to establish the fair value of the fund’s assets and liabilities. Use of particular methods and inputs may vary over time based on availability and relevance as market and economic conditions evolve.

Equity securities are generally valued at the official closing price of, or the last reported sale price on, the exchange or market on which such securities are traded, as of the close of business on the day the securities are being valued or, lacking any sales, at the last available bid price. Prices for each security are taken from the principal exchange or market on which the security trades.

Fixed-income securities, including short-term securities, are generally valued at prices obtained from one or more pricing vendors. Vendors value such securities based on one or more of the following inputs: benchmark yields, transactions, bids, offers, quotations from dealers and trading systems, new issues, spreads, interest rate volatilities, and other relationships observed in the markets among comparable securities; and proprietary pricing models such as yield measures calculated using factors such as cash flows, financial or collateral performance and other reference data.

When the fund’s investment adviser deems it appropriate to do so (such as when vendor prices are unavailable or deemed to be not representative), fixed-income securities will be valued in good faith at the mean quoted bid and ask prices that are reasonably and timely available (or bid prices, if ask prices are not available) or at prices for securities of comparable maturity, quality and type.

Securities with both fixed-income and equity characteristics, or equity securities traded principally among fixed-income dealers, are generally valued in the manner described for either equity or fixed-income securities, depending on which method is deemed most appropriate by the fund’s investment adviser.

Securities and other assets for which representative market quotations are not readily available or are considered unreliable by the fund’s investment adviser are fair valued as determined in good faith under fair valuation guidelines adopted by authority of the fund’s board of trustees as further described. The investment adviser follows fair valuation guidelines, consistent with U.S. Securities and Exchange Commission rules and guidance, to consider relevant principles and factors when making fair value determinations. The investment adviser considers relevant indications of value that are reasonably and timely available to it in determining the fair value to be assigned to a particular security, such as the type and cost of the security; contractual or legal restrictions on resale of the security; relevant financial or business developments of the issuer; actively traded similar or related securities; conversion or exchange rights on the security; related corporate actions; significant events occurring after the close of trading in the security; and changes in overall market conditions. In addition, the closing prices of equity securities that trade in markets outside U.S. time zones may be adjusted to reflect significant events that occur after the close of local trading but before the net asset value of each share class of the fund is determined. Fair valuations and valuations of investments that are not actively trading involve judgment and may differ materially from valuations that would have been used had greater market activity occurred.

Processes and structure — The fund’s board of trustees has delegated authority to the fund’s investment adviser to make fair value determinations, subject to board oversight. The investment adviser has established a Joint Fair Valuation Committee (the “Fair Valuation Committee”) to administer, implement and oversee the fair valuation process, and to make fair value decisions. The Fair Valuation Committee regularly reviews its own fair value decisions, as well as decisions made under its standing instructions to the investment adviser’s valuation teams. The Fair Valuation Committee reviews changes in fair value measurements from period to period and may, as deemed appropriate, update the fair valuation guidelines to better reflect the results of back testing and address new or evolving issues. The Fair Valuation Committee reports any changes to the fair valuation guidelines to the board of trustees with supplemental information to support the changes. The fund’s board and audit committee also regularly review reports that describe fair value determinations and methods.

| Washington Mutual Investors Fund | 19 |

The fund’s investment adviser has also established a Fixed-Income Pricing Review Group to administer and oversee the fixed-income valuation process, including the use of fixed-income pricing vendors. This group regularly reviews pricing vendor information and market data. Pricing decisions, processes and controls over security valuation are also subject to additional internal reviews, including an annual control self-evaluation program facilitated by the investment adviser’s compliance group.

Classifications — The fund’s investment adviser classifies the fund’s assets and liabilities into three levels based on the inputs used to value the assets or liabilities. Level 1 values are based on quoted prices in active markets for identical securities. Level 2 values are based on significant observable market inputs, such as quoted prices for similar securities and quoted prices in inactive markets. Certain securities trading outside the U.S. may transfer between Level 1 and Level 2 due to valuation adjustments resulting from significant market movements following the close of local trading. Level 3 values are based on significant unobservable inputs that reflect the investment adviser’s determination of assumptions that market participants might reasonably use in valuing the securities. The valuation levels are not necessarily an indication of the risk or liquidity associated with the underlying investment. For example, U.S. government securities are reflected as Level 2 because the inputs used to determine fair value may not always be quoted prices in an active market. The following table presents the fund’s valuation levels as of April 30, 2016 (dollars in thousands):

| | | Investment securities |

| | | Level 1 | | Level 2 | | Level 3 | | Total |

| Assets: | | | | | | | | | | | | | | | | |

| Common stocks: | | | | | | | | | | | | | | | | |

| Energy | | $ | 8,664,632 | | | $ | — | | | $ | — | | | $ | 8,664,632 | |

| Materials | | | 4,308,667 | | | | — | | | | — | | | | 4,308,667 | |

| Industrials | | | 10,120,595 | | | | — | | | | — | | | | 10,120,595 | |

| Consumer discretionary | | | 9,913,737 | | | | — | | | | — | | | | 9,913,737 | |

| Consumer staples | | | 7,819,431 | | | | — | | | | — | | | | 7,819,431 | |

| Health care | | | 9,182,660 | | | | — | | | | — | | | | 9,182,660 | |

| Financials | | | 9,187,778 | | | | — | | | | — | | | | 9,187,778 | |

| Information technology | | | 10,304,961 | | | | — | | | | — | | | | 10,304,961 | |

| Telecommunication services | | | 3,034,335 | | | | — | | | | — | | | | 3,034,335 | |

| Utilities | | | 2,212,925 | | | | — | | | | — | | | | 2,212,925 | |

| Miscellaneous | | | 1,292,998 | | | | — | | | | — | | | | 1,292,998 | |

| Short-term securities | | | — | | | | 2,318,971 | | | | — | | | | 2,318,971 | |

| Total | | $ | 76,042,719 | | | $ | 2,318,971 | | | $ | — | | | $ | 78,361,690 | |

4. Risk factors

Investing in the fund may involve certain risks including, but not limited to, those described below.

Market conditions — The prices of, and the income generated by, the common stocks and other securities held by the fund may decline — sometimes rapidly or unpredictably — due to various factors, including events or conditions affecting the general economy or particular industries; overall market changes; local, regional or global political, social or economic instability; governmental or governmental agency responses to economic conditions; and currency exchange rate, interest rate and commodity price fluctuations.

Issuer risks — The prices of, and the income generated by, securities held by the fund may decline in response to various factors directly related to the issuers of such securities, including reduced demand for an issuer’s goods or services, poor management performance and strategic initiatives such as mergers, acquisitions or dispositions and the market response to any such initiatives.

Investing in income-oriented stocks — Income provided by the fund may be reduced by changes in the dividend policies of, and the capital resources available for dividend payments at, the companies in which the fund invests.

Investing in growth-oriented stocks — Growth-oriented common stocks and other equity-type securities (such as preferred stocks, convertible preferred stocks and convertible bonds) may involve larger price swings and greater potential for loss than other types of investments.

Management — The investment adviser to the fund actively manages the fund’s investments. Consequently, the fund is subject to the risk that the methods and analyses employed by the investment adviser in this process may not produce the desired results. This could cause the fund to lose value or its investment results to lag relevant benchmarks or other funds with similar objectives.

| 20 | Washington Mutual Investors Fund |

5. Taxation and distributions

Federal income taxation — The fund complies with the requirements under Subchapter M of the Internal Revenue Code applicable to mutual funds and intends to distribute substantially all of its net taxable income and net capital gains each year. The fund is not subject to income taxes to the extent such distributions are made. Therefore, no federal income tax provision is required.

As of and during the period ended April 30, 2016, the fund did not have a liability for any unrecognized tax benefits. The fund recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the statement of operations. During the period, the fund did not incur any interest or penalties.

The fund is not subject to examination by U.S. federal and state tax authorities for tax years before 2012.

Non-U.S. taxation — Dividend and interest income are recorded net of non-U.S. taxes paid. The fund may file withholding tax reclaims in certain jurisdictions to recover a portion of amounts previously withheld. As a result of rulings from European courts, the fund filed for additional reclaims related to prior years. These reclaims are recorded when the amount is known and there are no significant uncertainties on collectability.

Distributions — Distributions paid to shareholders are based on net investment income and net realized gains determined on a tax basis, which may differ from net investment income and net realized gains for financial reporting purposes. These differences are due primarily to different treatment for items such as currency gains and losses; short-term capital gains and losses; capital losses related to sales of certain securities within 30 days of purchase; and deferred expenses. The fiscal year in which amounts are distributed may differ from the year in which the net investment income and net realized gains are recorded by the fund for financial reporting purposes. The fund may also designate a portion of the amount paid to redeeming shareholders as a distribution for tax purposes.

During the year ended April 30, 2016, the fund reclassified $122,000 from undistributed net investment income to undistributed net realized gain; and reclassified $63,000 from undistributed net investment income and $137,558,000 from undistributed net realized gain to capital paid in on shares of beneficial interest to align financial reporting with tax reporting.

As of April 30, 2016, the tax basis components of distributable earnings, unrealized appreciation (depreciation) and cost of investment securities were as follows (dollars in thousands):

| Undistributed ordinary income | | $ | 144,946 | |

| Undistributed long-term capital gains | | | 2,669,172 | |

| Gross unrealized appreciation on investment securities | | | 23,852,961 | |

| Gross unrealized depreciation on investment securities | | | (571,610 | ) |

| Net unrealized appreciation on investment securities | | | 23,281,351 | |

| Cost of investment securities | | | 55,080,339 | |

| Washington Mutual Investors Fund | 21 |

The tax character of distributions paid to shareholders was as follows (dollars in thousands):

| | | Year ended April 30, 2016 | | Year ended April 30, 2015 |

| Share class | | Ordinary

income | | Long-term

capital gains | | Total

dividends and

distributions

paid | | Ordinary

income | | Long-term

capital gains | | Total

dividends and

distributions

paid |

| Class A | | $ | 1,034,924 | | | $ | 1,974,246 | | | $ | 3,009,170 | | | $ | 1,048,522 | | | $ | 2,501,694 | | | $ | 3,550,216 | |

| Class B | | | 1,186 | | | | 3,597 | | | | 4,783 | | | | 2,267 | | | | 8,647 | | | | 10,914 | |

| Class C | | | 20,317 | | | | 62,909 | | | | 83,226 | | | | 21,539 | | | | 83,744 | | | | 105,283 | |

| Class F-1 | | | 55,906 | | | | 110,943 | | | | 166,849 | | | | 56,691 | | | | 137,660 | | | | 194,351 | |

| Class F-2 | | | 123,745 | | | | 221,315 | | | | 345,060 | | | | 83,206 | | | | 188,247 | | | | 271,453 | |

| Class 529-A | | | 34,505 | | | | 68,984 | | | | 103,489 | | | | 34,611 | | | | 86,336 | | | | 120,947 | |

| Class 529-B | | | 177 | | | | 602 | | | | 779 | | | | 350 | | | | 1,482 | | | | 1,832 | |

| Class 529-C | | | 5,292 | | | | 17,375 | | | | 22,667 | | | | 5,385 | | | | 22,176 | | | | 27,561 | |

| Class 529-E | | | 1,572 | | | | 3,599 | | | | 5,171 | | | | 1,585 | | | | 4,524 | | | | 6,109 | |

| Class 529-F-1 | | | 2,288 | | | | 4,111 | | | | 6,399 | | | | 2,258 | | | | 5,017 | | | | 7,275 | |

| Class R-1 | | | 1,194 | | | | 3,682 | | | | 4,876 | | | | 1,270 | | | | 4,863 | | | | 6,133 | |

| Class R-2 | | | 9,642 | | | | 29,004 | | | | 38,646 | | | | 10,478 | | | | 39,399 | | | | 49,877 | |

| Class R-2E1 | | | 43 | | | | 105 | | | | 148 | | | | — | 2 | | | 1 | | | | 1 | |

| Class R-3 | | | 30,965 | | | | 71,847 | | | | 102,812 | | | | 32,217 | | | | 92,148 | | | | 124,365 | |

| Class R-4 | | | 44,264 | | | | 87,910 | | | | 132,174 | | | | 45,018 | | | | 110,813 | | | | 155,831 | |

| Class R-5E3 | | | — | 2 | | | — | 2 | | | — | 2 | | | | | | | | | | | | |

| Class R-5 | | | 43,448 | | | | 73,597 | | | | 117,045 | | | | 42,052 | | | | 90,297 | | | | 132,349 | |

| Class R-6 | | | 159,878 | | | | 272,184 | | | | 432,062 | | | | 128,465 | | | | 273,942 | | | | 402,407 | |

| Total | | $ | 1,569,346 | | | $ | 3,006,010 | | | $ | 4,575,356 | | | $ | 1,515,914 | | | $ | 3,650,990 | | | $ | 5,166,904 | |

| 1 | Class R-2E shares were offered beginning August 29, 2014. |

| 2 | Amount less than one thousand. |

| 3 | Class R-5E shares were offered beginning November 20, 2015. |

6. Fees and transactions with related parties

CRMC, the fund’s investment adviser, is the parent company of American Funds Distributors,® Inc. (“AFD”), the principal underwriter of the fund’s shares, and American Funds Service Company® (“AFS”), the fund’s transfer agent. CRMC, AFD and AFS are considered related parties to the fund.

Investment advisory services — The fund has an investment advisory and service agreement with CRMC that provides for monthly fees accrued daily. These fees are based on a series of decreasing annual rates beginning with 0.342% on the first $3 billion of daily net assets and decreasing to 0.2115% on such assets in excess of $116 billion. For the year ended April 30, 2016, the investment advisory services fee was $179,872,000, which was equivalent to an annualized rate of 0.237% of average daily net assets.

Class-specific fees and expenses — Expenses that are specific to individual share classes are accrued directly to the respective share class. The principal class-specific fees and expenses are further described below:

Distribution services — The fund has plans of distribution for all share classes, except Class F-2, R-5E, R-5 and R-6 shares. Under the plans, the board of trustees approves certain categories of expenses that are used to finance activities primarily intended to sell fund shares and service existing accounts. The plans provide for payments, based on an annualized percentage of average daily net assets, ranging from 0.25% to 1.00% as noted in this section. In some cases, the board of trustees has limited the amounts that may be paid to less than the maximum allowed by the plans. All share classes with a plan may use up to 0.25% of average daily net assets to pay service fees, or to compensate AFD for paying service fees, to firms that have entered into agreements with AFD to provide certain shareholder services. The remaining amounts available to be paid under each plan are paid to dealers to compensate them for their sales activities.

For Class A and 529-A shares, distribution-related expenses include the reimbursement of dealer and wholesaler commissions paid by AFD for certain shares sold without a sales charge. These share classes reimburse AFD for amounts billed within the prior

| 22 | Washington Mutual Investors Fund |

15 months but only to the extent that the overall annual expense limit of 0.25% is not exceeded. As of April 30, 2016, there were no unreimbursed expenses subject to reimbursement for Class A or 529-A shares.

| | Share class | | Currently approved limits | | Plan limits |

| | Class A | | | 0.25 | % | | | 0.25 | % |

| | Class 529-A | | | 0.25 | | | | 0.50 | |

| | Classes B and 529-B | | | 1.00 | | | | 1.00 | |

| | Classes C, 529-C and R-1 | | | 1.00 | | | | 1.00 | |

| | Class R-2 | | | 0.75 | | | | 1.00 | |

| | Class R-2E | | | 0.60 | | | | 0.85 | |

| | Classes 529-E and R-3 | | | 0.50 | | | | 0.75 | |

| | Classes F-1, 529-F-1 and R-4 | | | 0.25 | | | | 0.50 | |

Transfer agent services — The fund has a shareholder services agreement with AFS under which the fund compensates AFS for providing transfer agent services to each of the fund’s share classes. These services include recordkeeping, shareholder communications and transaction processing. In addition, the fund reimburses AFS for amounts paid to third parties for performing transfer agent services on behalf of fund shareholders.

Administrative services — The fund has an administrative services agreement with CRMC under which the fund compensates CRMC for providing administrative services to Class A, C, F, 529 and R shares. These services include, but are not limited to, coordinating, monitoring, assisting and overseeing third parties that provide services to fund shareholders. Under the agreement, Class A shares pay an annual fee of 0.01% and Class C, F, 529 and R shares pay an annual fee of 0.05% of their respective average daily net assets.

529 plan services — Each 529 share class is subject to service fees to compensate the Virginia College Savings Plan (“Virginia529”) for its oversight and administration of the 529 college savings plan. The quarterly fee is based on a series of decreasing annual rates beginning with 0.10% on the first $30 billion of the net assets invested in Class 529 shares of the American Funds and decreasing to 0.05% on such assets in excess of $70 billion. The fee for any given calendar quarter is accrued and calculated on the basis of the average net assets of Class 529 shares of the American Funds for the last month of the prior calendar quarter. The fee is included in other expenses in the fund’s statement of operations. Virginia529 is not considered a related party to the fund.

For the year ended April 30, 2016, class-specific expenses under the agreements were as follows (dollars in thousands):

| | | | Distribution | | | Transfer agent | | | Administrative | | 529 plan |

| | Share class | | | services | | | services | | | services | | services |

| | Class A | | | $117,172 | | | | $45,385 | | | | $5,004 | | | Not applicable |

| | Class B | | | 992 | | | | 94 | | | | Not applicable | | | Not applicable |

| | Class C | | | 15,790 | | | | 1,404 | | | | 793 | | | Not applicable |

| | Class F-1 | | | 6,992 | | | | 3,245 | | | | 1,399 | | | Not applicable |

| | Class F-2 | | | Not applicable | | | | 6,126 | | | | 2,745 | | | Not applicable |

| | Class 529-A | | | 3,867 | | | | 1,299 | | | | 876 | | | $1,549 |

| | Class 529-B | | | 169 | | | | 16 | | | | 9 | | | 15 |

| | Class 529-C | | | 4,333 | | | | 349 | | | | 219 | | | 388 |

| | Class 529-E | | | 447 | | | | 40 | | | | 45 | | | 80 |

| | Class 529-F-1 | | | — | | | | 77 | | | | 52 | | | 92 |

| | Class R-1 | | | 938 | | | | 98 | | | | 47 | | | Not applicable |

| | Class R-2 | | | 5,462 | | | | 2,321 | | | | 367 | | | Not applicable |

| | Class R-2E | | | 13 | | | | 2 | | | | 1 | | | Not applicable |

| | Class R-3 | | | 9,021 | | | | 2,759 | | | | 904 | | | Not applicable |

| | Class R-4 | | | 5,499 | | | | 2,203 | | | | 1,101 | | | Not applicable |

| | Class R-5E* | | | Not applicable | | | | — | † | | | — | † | | Not applicable |

| | Class R-5 | | | Not applicable | | | | 948 | | | | 947 | | | Not applicable |

| | Class R-6 | | | Not applicable | | | | 27 | | | | 3,381 | | | Not applicable |

| | Total class-specific expenses | | | $170,695 | | | | $66,393 | | | | $17,890 | | | $2,124 |

| | * | Class R-5E shares were offered beginning November 20, 2015. |

| † | Amount less than one thousand. |

Board members’ deferred compensation — Board members who are unaffiliated with CRMC may elect to defer the cash payment of part or all of their compensation. These deferred amounts, which remain as liabilities of the fund, are treated as if invested in shares of the fund or other American Funds. These amounts represent general, unsecured liabilities of the fund and vary according to the total returns of the selected funds. Board members’ compensation of $1,331,000 in the fund’s statement of operations reflects $1,387,000 in current fees (either paid in cash or deferred) and a net decrease of $56,000 in the value of the deferred amounts.

| Washington Mutual Investors Fund | 23 |

Affiliated officers and trustees — Officers and certain trustees of the fund are or may be considered to be affiliated with CRMC, AFD and AFS. No affiliated officers or trustees received any compensation directly from the fund.

7. Capital share transactions

Capital share transactions in the fund were as follows (dollars and shares in thousands):

| | | Sales1 | | Reinvestments of

dividends and distributions | | Repurchases1 | | Net increase

(decrease) |

| Share class | | Amount | | | Shares | | | Amount | | | Shares | | | Amount | | | Shares | | | Amount | | | Shares | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Year ended April 30, 2016 | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Class A | | $ | 3,065,605 | | | | 78,555 | | | $ | 2,938,274 | | | | 77,218 | | | $ | (5,582,343 | ) | | | (142,345 | ) | | $ | 421,536 | | | | 13,428 | |

| Class B | | | 1,290 | | | | 33 | | | | 4,749 | | | | 126 | | | | (77,004 | ) | | | (1,976 | ) | | | (70,965 | ) | | | (1,817 | ) |

| Class C | | | 258,731 | | | | 6,705 | | | | 82,025 | | | | 2,185 | | | | (386,720 | ) | | | (9,986 | ) | | | (45,964 | ) | | | (1,096 | ) |

| Class F-1 | | | 524,963 | | | | 13,493 | | | | 163,622 | | | | 4,315 | | | | (577,054 | ) | | | (14,731 | ) | | | 111,531 | | | | 3,077 | |

| Class F-2 | | | 1,720,604 | | | | 44,066 | | | | 335,004 | | | | 8,809 | | | | (1,085,666 | ) | | | (27,823 | ) | | | 969,942 | | | | 25,052 | |

| Class 529-A | | | 152,175 | | | | 3,893 | | | | 103,462 | | | | 2,725 | | | | (228,677 | ) | | | (5,817 | ) | | | 26,960 | | | | 801 | |

| Class 529-B | | | 295 | | | | 8 | | | | 779 | | | | 20 | | | | (14,082 | ) | | | (359 | ) | | | (13,008 | ) | | | (331 | ) |

| Class 529-C | | | 39,959 | | �� | | 1,031 | | | | 22,661 | | | | 602 | | | | (64,306 | ) | | | (1,651 | ) | | | (1,686 | ) | | | (18 | ) |

| Class 529-E | | | 7,842 | | | | 203 | | | | 5,169 | | | | 137 | | | | (12,035 | ) | | | (309 | ) | | | 976 | | | | 31 | |

| Class 529-F-1 | | | 17,551 | | | | 451 | | | | 6,399 | | | | 169 | | | | (17,916 | ) | | | (455 | ) | | | 6,034 | | | | 165 | |

| Class R-1 | | | 16,827 | | | | 435 | | | | 4,875 | | | | 130 | | | | (25,829 | ) | | | (665 | ) | | | (4,127 | ) | | | (100 | ) |

| Class R-2 | | | 140,196 | | | | 3,630 | | | | 38,616 | | | | 1,030 | | | | (228,844 | ) | | | (5,907 | ) | | | (50,032 | ) | | | (1,247 | ) |

| Class R-2E | | | 8,516 | | | | 219 | | | | 147 | | | | 4 | | | | (511 | ) | | | (13 | ) | | | 8,152 | | | | 210 | |

| Class R-3 | | | 372,731 | | | | 9,575 | | | | 102,664 | | | | 2,721 | | | | (559,656 | ) | | | (14,406 | ) | | | (84,261 | ) | | | (2,110 | ) |

| Class R-4 | | | 558,013 | | | | 14,307 | | | | 132,148 | | | | 3,489 | | | | (568,282 | ) | | | (14,575 | ) | | | 121,879 | | | | 3,221 | |

| Class R-5E2 | | | 10 | | | | — | 3 | | | — | | | | — | | | | — | | | | — | | | | 10 | | | | — | 3 |

| Class R-5 | | | 342,492 | | | | 8,735 | | | | 116,951 | | | | 3,072 | | | | (425,516 | ) | | | (10,784 | ) | | | 33,927 | | | | 1,023 | |

| Class R-6 | | | 2,131,499 | | | | 54,833 | | | | 431,579 | | | | 11,334 | | | | (818,830 | ) | | | (20,945 | ) | | | 1,744,248 | | | | 45,222 | |

| Total net increase (decrease) | | $ | 9,359,299 | | | | 240,172 | | | $ | 4,489,124 | | | | 118,086 | | | $ | (10,673,271 | ) | | | (272,747 | ) | | $ | 3,175,152 | | | | 85,511 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Year ended April 30, 2015 | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Class A | | $ | 3,267,503 | | | | 78,831 | | | $ | 3,466,906 | | | | 84,024 | | | $ | (5,860,110 | ) | | | (141,380 | ) | | $ | 874,299 | | | | 21,475 | |

| Class B | | | 3,355 | | | | 82 | | | | 10,838 | | | | 264 | | | | (114,527 | ) | | | (2,786 | ) | | | (100,334 | ) | | | (2,440 | ) |

| Class C | | | 268,954 | | | | 6,562 | | | | 103,499 | | | | 2,538 | | | | (470,884 | ) | | | (11,497 | ) | | | (98,431 | ) | | | (2,397 | ) |

| Class F-1 | | | 644,726 | | | | 15,636 | | | | 190,773 | | | | 4,637 | | | | (1,841,177 | ) | | | (44,642 | ) | | | (1,005,678 | ) | | | (24,369 | ) |

| Class F-2 | | | 3,618,211 | | | | 87,651 | | | | 260,669 | | | | 6,320 | | | | (644,454 | ) | | | (15,532 | ) | | | 3,234,426 | | | | 78,439 | |

| Class 529-A | | | 167,905 | | | | 4,064 | | | | 120,920 | | | | 2,936 | | | | (216,781 | ) | | | (5,232 | ) | | | 72,044 | | | | 1,768 | |

| Class 529-B | | | 885 | | | | 21 | | | | 1,831 | | | | 45 | | | | (19,638 | ) | | | (477 | ) | | | (16,922 | ) | | | (411 | ) |

| Class 529-C | | | 44,775 | | | | 1,090 | | | | 27,546 | | | | 674 | | | | (63,992 | ) | | | (1,554 | ) | | | 8,329 | | | | 210 | |

| Class 529-E | | | 9,041 | | | | 219 | | | | 6,105 | | | | 149 | | | | (12,692 | ) | | | (307 | ) | | | 2,454 | | | | 61 | |

| Class 529-F-1 | | | 18,346 | | | | 443 | | | | 7,273 | | | | 177 | | | | (19,939 | ) | | | (482 | ) | | | 5,680 | | | | 138 | |

| Class R-1 | | | 18,942 | | | | 462 | | | | 6,124 | | | | 149 | | | | (26,557 | ) | | | (644 | ) | | | (1,491 | ) | | | (33 | ) |

| Class R-2 | | | 158,057 | | | | 3,859 | | | | 49,832 | | | | 1,223 | | | | (229,386 | ) | | | (5,602 | ) | | | (21,497 | ) | | | (520 | ) |

| Class R-2E4 | | | 15 | | | | — | 3 | | | — | 3 | | | — | 3 | | | — | | | | — | | | | 15 | | | | — | 3 |

| Class R-3 | | | 400,565 | | | | 9,751 | | | | 124,239 | | | | 3,033 | | | | (482,490 | ) | | | (11,712 | ) | | | 42,314 | | | | 1,072 | |

| Class R-4 | | | 554,917 | | | | 13,420 | | | | 155,751 | | | | 3,791 | | | | (609,688 | ) | | | (14,740 | ) | | | 100,980 | | | | 2,471 | |

| Class R-5 | | | 427,437 | | | | 10,325 | | | | 132,249 | | | | 3,205 | | | | (489,943 | ) | | | (11,912 | ) | | | 69,743 | | | | 1,618 | |

| Class R-6 | | | 1,973,800 | | | | 47,859 | | | | 402,111 | | | | 9,740 | | | | (752,664 | ) | | | (18,187 | ) | | | 1,623,247 | | | | 39,412 | |

| Total net increase (decrease) | | $ | 11,577,434 | | | | 280,275 | | | $ | 5,066,666 | | | | 122,905 | | | $ | (11,854,922 | ) | | | (286,686 | ) | | $ | 4,789,178 | | | | 116,494 | |

| 1 | Includes exchanges between share classes of the fund. |

| 2 | Class R-5E shares were offered beginning November 20, 2015. |

| 3 | Amount less than one thousand. |

| 4 | Class R-2E shares were offered beginning August 29, 2014. |

8. Investment transactions

The fund made purchases and sales of investment securities, excluding short-term securities and U.S. government obligations, if any, of $22,263,915,000 and $22,007,095,000, respectively, during the year ended April 30, 2016.

| 24 | Washington Mutual Investors Fund |

Financial highlights

| | | | | | Income from

investment operations1 | | | Dividends and distributions | | | | | | | | | | | | | | | | |

| | | Net asset

value,

beginning

of period | | | Net

investment

income | | | Net (losses)

gains on

securities (both

realized and

unrealized) | | | Total from

investment

operations | | | Dividends

(from net

investment

income) | | | Distributions

(from capital

gains) | | | Total

dividends

and

distributions | | | Net asset

value,

end

of period | | | Total

return2 | | | Net assets,

end of period

(in millions) | | | Ratio of

expenses to

average

net assets | | | Ratio of

net income

to average

net assets | |

| Class A: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |