UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-08495

GARTMORE MUTUAL FUNDS

|

| (Exact name of registrant as specified in charter) |

1200 RIVER ROAD, SUITE 1000, CONSHOHOCKEN, PENNSYLVANIA 19428

(Address of principal executive offices) (Zip code)

Eric Miller

1200 River Road

Suite 1000

Conshohocken, Pennsylvania 19428

|

| (Name and address of agent for service) |

Registrant’s telephone number, including area code: (484) 530-1300

Date of fiscal year end: October 31, 2005

Date of reporting period: October 31, 2005

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

| Item 1. | Reports to Stockholders. |

Include a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Act (17 CFR 270.30e-1).

Annual Report

| | |

| | |

| | October 31, 2005 |

Core Equity Series

Gartmore Large Cap Value Fund

Gartmore Mid Cap Growth Fund

Gartmore Small Cap Fund

Core Fixed Income Series

Gartmore Bond Fund

Gartmore Government Bond Fund

Gartmore Morley Enhanced Income Fund

Gartmore Short Duration Bond Fund

Gartmore Tax-Free Income Fund

www.gartmorefunds.com

Solutions.

| | | | |

| UNITED STATES | | UNITED KINGDOM | | JAPAN |

Based in greater metropolitan Philadelphia, Gartmore is the global asset management arm of Nationwide®. Gartmore’s affiliated advisers* collectively manage more than $82 billion1 in assets through its global investment platform encompassing more than 185 investment management professionals supported by an 800-person staff.

We provide core and specialty equity, fixed-income and alternative investment solutions through mutual funds, separate accounts, commingled portfolios and wrap accounts to individual and institutional clients around the world.

This wide range of investment opportunities is built on sound investment management processes designed to increase the probability of delivering enhanced risk-adjusted returns over the long term.

Our investment management teams incorporate fundamental stock selection with the application of technology to help control risk and add to returns. Insightful stock selection is a function of the efforts of talented alpha-driven managers and analysts, working in an entrepreneurial environment, who are specialists in their respective investment disciplines.

www.gartmore.com

*Gartmore’s Affiliated Advisers

The following 11 asset management affiliates of Nationwide do business under the trade name “Gartmore Group”: Gartmore Capital Management Ltd2, Gartmore Fund Managers Ltd2, Gartmore Global Partners2, 3, Gartmore Investment Ltd2, Gartmore Japan Ltd2, Gartmore Morley Capital Management, Inc.3, Gartmore Mutual Fund Capital Trust3, 4, Gartmore Riverview, LLC, Gartmore SA Capital Trust3, 4, Gartmore Separate Accounts LLC3, and NorthPointe Capital® LLC3

| 2. | | These advisers are subsidiaries of Gartmore Investment Management plc, which ultimately reports to Nationwide®. |

| 3. | | These are SEC-registered investment advisers based in the United States. Collectively, these advisers manage $43 billion as of Oct. 31, 2005. |

| 4. | | Together, these advisers do business as Gartmore Global Investments, Inc. |

Gartmore Global Investments is the investment adviser to Gartmore Funds. NorthPointe Capital is a federally registered service mark of Gartmore Global Investments, Inc. Nationwide is a federally registered service mark of Nationwide Mutual Insurance Company.

Gartmore Funds distributed by Gartmore Distribution Services, Inc., Member NASD. 1200 River Road, Suite 1000, Conshohocken, PA 19428.

© 2005 Gartmore Global Investments, Inc. All rights reserved.

Annual Report

| | |

| | |

| | October 31, 2005 |

Commentary provided by Gartmore Global Investments, investment adviser to Gartmore Funds. All opinions and estimates included in this report constitute Gartmore Global Investments’ judgment as of the date of this report and are subject to change without notice.

Statement Regarding Availability of Quarterly Portfolio Schedule.

The Gartmore Funds file complete schedules of portfolio holdings for each Fund with the Securities and Exchange Commission (the “Commission”) for the first and third quarters of each fiscal year on Form N-Q. The Funds’ Forms N-Q are available on the Commission’s website at http://www.sec.gov. The Funds’ Forms N-Q may be reviewed and copied at the Commission’s Public Reference Room in Washington, DC, and information on the operation of the Public Reference Room may be obtained by calling 800-SEC-0330; and the Funds make the information on Form N-Q available to shareholders on www.gartmorefunds.com or upon request without charge.

Statement Regarding Availability of Proxy Voting Record.

Information regarding how the Fund voted proxies relating to portfolio securities held during the most recent 12-month period ended October 31, 2005 is available without charge, upon request, by calling 800-848-0920, and on the Commission’s website at http://www.sec.gov.

Message to Shareholders

October 31, 2005

Dear Shareholders,

At times during the annual reporting period ended Oct. 31, 2005, it seemed as though a host of uncertain and unpredictable events coalesced into a “perfect storm” of market volatility.

Hurricane Katrina is one example. This Category 5 storm not only bore down on a major American city and its environs, it also had one of the country’s largest energy-Producing regions in its sights. If that weren’t enough, the storm occurred just as oil and natural gas prices were spiraling to record levels, concurrent with fears of a great strain on global supply and capacity.

On another front, the intent to better integrate the member nations of the European Union (EU) was dealt a blow by France’s repudiation of a proposed EU constitution, a move that called into question the EU’s long-term effectiveness. Within a matter of weeks, France itself was rocked by what initially appeared to be youthful unrest in one section of Paris. As riots spread across the country, however, the situation revealed a disturbing and broad-based economic condition; unemployment among France’s immigrant population is five times the national average, and the segment’s per capita income is 40% below the national average. The lingering sense is that a number of European countries will have to deal with a long-overlooked social and economic issue at a time when the EU is struggling to retain its authority.

These are just two examples illustrating that market volatility can be a function of unexpected, and sometimes unrelated, global events. The accompanying “Market Perspectives” commentary provides a more detailed analysis of the various economic and social factors that influenced the market during the past year. I’d like to focus on Gartmore’s view on how best to navigate uncertain domestic and global markets in the pursuit of acceptable investment returns.

Risk, regardless of its source, is part and parcel of investing. The challenge is to mitigate risk as much as possible through sound portfolio diversification. Gartmore is committed to offering a diverse range of equity, fixed-income and alternative investment solutions designed to capture global investment opportunities. The informed investment response to complex, volatile markets is to configure a series of diverse, uncorrelated, well-performingfunds into a dynamic portfolio. At Gartmore, we seek to provide the core and satellite investments needed to construct a broadly diversified investment portfolio.

Moreover, Gartmore believes that seasoned investment experts employing well-articulated and tested processes and aided by global research form the path to acceptable risk-adjusted returns. We hold a core belief that the ideas and insights of talented investment professionals can add quantifiable investment returns. In that regard, we are pleased to report that the returns of 30 of our 47 retail mutual funds (Class A at NAV) exceeded their respective benchmarks for the annual period ended Oct. 31, 2005.

The performance of a number of Gartmore’s funds from a variety of sectors and regions strengthens the case for holding uncorrelated investments. For example, the performance of the Gartmore Global Natural Resources Fund, which during the reporting period returned 65.51% (Class A at NAV) versus the Goldman Sachs Natural Resources Index return of 34.75%, was driven by escalating energy prices derived from increased global demand coupled with concerns about supply shortages. Within the energy sector, the Fund concentrated on smaller companies with higher capacity for growth. It is widely believed that energy will be in great demand for an extended period of time; therefore, the Fund will remain focused on the energy services sector companies that acquire, develop, and exploit oil and natural gas properties. The Wall Street Journal cited the Fund as a “Category King” in the Mutual Fund Monthly Review of Sept. 6, 2005.

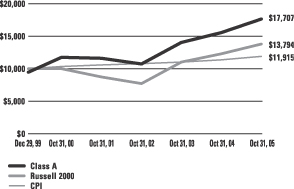

The Gartmore Small Cap Fund garnered above-average returns during the reporting period, posting a 31.51% return (Class A at NAV) versus the Russell 2000® Index return of 12.08%. Most of the Fund’s outperformance came from strong stock selection in the information technology and energy sectors, in addition to astute sector allocations. Shortly after the close of the period, the Fund was cited in The Wall Street Journal as a “Category King” and noted as the second-best-performing fund in its respective sector for October 2005.

In addition, during the reporting period, Gartmore’s small-cap investment team was enhanced by the hiring of senior portfolio manager Jayne Stevlingson, who has managed small-cap funds at both OppenheimerFunds, Inc. and Morgan Stanley.

The case for broad global diversification was made through the performance of several of our non-U.S. funds during the reporting period. In comparison to equity prices in Europe and Japan, those in the United States were more muted during the past year, reflecting stretched valuations and increasing uncertainty in the outlook for consumers. The emerging markets, however, outperformed all other regions. Though its performance slightly lagged that of its benchmark, the Gartmore Emerging Markets Fund posted very strong returns of 30.02% (Class A at NAV) for the reporting period. The Gartmore International Growth Fund, returning 26.13%

(Class A at NAV) versus the Morgan Stanley Capital International (MSCI) All Country World ex-U.S. Index return of 20.06%, also benefited from the impressive performance of emerging-market and Pacific Rim equities. In addition, Latin American securities delivered notably robust performance on the back of strong commodity prices.

The Gartmore Worldwide Leaders Fund, which returned 23.44% (Class A at NAV) versus 13.27% for the MSCI World IndexSM, benefited from both domestic and international developments. Overall, U.S. growth remained strong in the face of inflationary worries, while both Europe and Japan showed increasing signs of recovery. European export growth increased due to the weak euro at the same time that Japan experienced rising real incomes and increased capital expenditures. As a result, the Fund’s largest regional contributors were the United States, the United Kingdom and Japan. The Fund also benefited from strong stock selection within the technology, financial services, health-care and energy sectors.

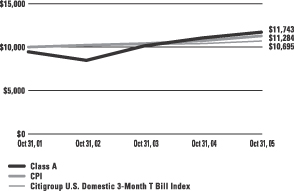

Despite considerable volatility in both the U.S. economy and the U.S. equity markets during the past year, the Gartmore U.S. Growth Leaders Fund handily outperformed the Standard & Poor’s (S&P) 500® Index return of 8.72% with a return of 17.31% (Class A at NAV). The Fund’s performance was almost exclusively driven by strong stock selection, particularly in the technology and consumer goods areas. Concurrently, the Gartmore U.S. Growth Leaders Long-Short Fund returned 6.09% (Class A at NAV) versus 2.68% for its benchmark, the Citigroup 3-Month T-Bill Index. Again, adept stock selection, coupled with strong sector allocations, drove the Fund’s outperformance.

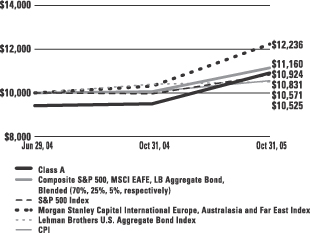

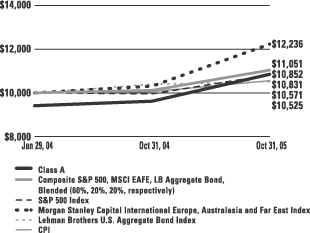

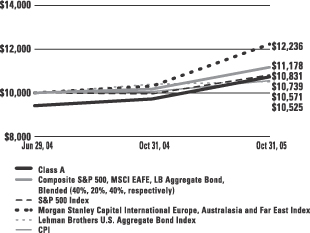

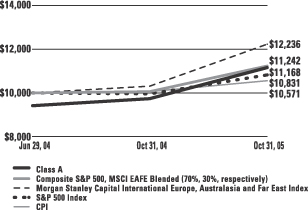

In addition to a suite of actively managed funds, Gartmore provides packaged asset allocation and diversification solutions. The Gartmore Optimal Allocations Funds, launched in June 2004, consist primarily of various proprietary Gartmore funds offered in four varieties, calibrated to different levels of risk: Moderate, Moderately Aggressive, Aggressive and Specialty. We are very pleased to report that each of these Funds, which serve as complements to actively managed holdings, outperformed their respective composite benchmarks for the reporting period.

| | | | | | |

| Fund Name | | Fund

Return* | | Benchmark Return | | Benchmark |

| Gartmore Optimal Allocations: Moderate | | 10.41% | | 7.56% | | S&P 500 (40%); MSCI EAFE (20%); Lehman Brothers U.S. Aggregate (40%) |

| Gartmore Optimal Allocations: Moderately Aggressive | | 12.77% | | 9.08% | | S&P 500 (60%); MSCI EAFE (20%); Lehman Brothers U.S. Aggregate (20%) |

| Gartmore Optimal Allocations: Aggressive | | 14.86% | | 10.67% | | S&P 500 (70%); MSCI EAFE (25%); Lehman Brothers U.S. Aggregate (5%) |

| Gartmore Optimal Allocations: Specialty | | 14.59% | | 11.50% | | S&P 500 (70%); MSCI EAFE (30%) |

| *All | Fund returns are Class A at NAV, as of Oct. 31, 2005. |

As we head into 2006, the only constant is uncertainty, which is a companion to opportunity. The informed and experienced investment manager, supported by broad-based research and analysis, can discern the investment opportunities associated with volatility. In today’s global investment landscape, a host of variables exist that impact investment returns, both positively and negatively. At Gartmore, we put all of our resources into our goal of achieving acceptable risk-adjusted returns on behalf of our investors. We measure our investment success by your performance standards. We appreciate the trust you have placed in us, and we will continue to strive to fulfill your investment objectives in the coming year.

Wishing you a very happy and prosperous 2006,

Young D. Chin

Co-Global Chief Investment Officer-Equities

President and CEO

Gartmore Global Investments

Market Perspectives

October 31, 2005

Market volatility continues, but with a positive trend

The one-year period ended Oct. 31, 2005, witnessed considerable quarter-to-quarter volatility. The past 12 months clearly have been rife with reasons to justify the wide swings in market pricing. Although the markets gave investors a bumpy ride, most of those who held on were rewarded, illustrated by the fact that, for the annual reporting period, the Morgan Stanley Capital International Europe, Australasia and Far East (MSCI EAFE®) Index returned 18.59% and the Standard & Poor’s (S&P) 500® Index was up 8.72%.

A broad rally in global equity markets took hold in the final two months of 2004. International stocks, as represented by the MSCI EAFE Index, advanced 11.55% during this period, while the S&P 500 Index, a broad measure of the U.S. equity market, gained 7.59%.

As 2005 began, however, concerns about slack economic growth, the onset of inflation, increasing interest rates and spiraling energy costs led to a far less favorable environment for stocks, leaving most markets on the defensive. To varying degrees, these concerns would continue to plague the equity markets for the remainder of the year. The overall global economy nonetheless proved resilient. In the United States, the economy grew at a faster pace during the fiscal third quarter than initially anticipated, signaling improving economic health. From July through September, gross domestic product, the broadest measure of U.S. economic activity, grew 4.3%.

The dominant topic in 2005, particularly during the latter half of the year, was the continued impact of rising energy costs. As Hurricane Katrina barreled down on the energy-intensive Louisiana coast, the futures price of crude oil rose to a high of $70 per barrel while natural gas prices doubled–a classic one-two economic punch. A confluence of increased global demand, particularly from China, and concerns about supply shortages also contributed to energy price hikes.

Meanwhile, the Federal Reserve Board continued its measured increases of short-term interest rates, despite speculation that the moves would halt amid spiking energy costs. Throughout the reporting period, the rate rose from 1.75% to 3.75% as a result of eight consecutive 0.25% increases. As September wound down, however, energy prices began to fall, though they still were far above their year-ago averages. Further, inflationary fears began to subside as the Fed displayed its confidence in the economy. Ben Bernanke was appointed the new Fed Chairman in October to replace Alan Greenspan, who retires at the end of his term in January 2006.

Toward the end of the reporting period, consumer sentiment began to lag. From August to September, the consumer confidence measure fell from 105.5 to 86.6. In August, wages and salaries increased by 6.6%, yet disposable income declined 0.1% along with personal spending, which fell 0.5%–the biggest drop in more than three years.

During the reporting period, energy and natural resource company profits surged alongside soaring energy costs and expanding global demand. In the telecommunications industry, on the other hand, the costs of consolidation muted returns. Domestically, within the S&P 500 Index for the entire reporting period, sector performance ranged from a high of 59% for health services (31% in the MSCI EAFE Index) to a low of –5% for consumer services (9% in the MSCI EAFE Index). Stocks in industrials, energy and distribution services delivered returns of 42%, 31% and 25% (43%, 24% and 46% in the MSCI EAFE Index), respectively, while stocks in consumer durables and communications delivered negative returns of –4% and –0.5% (14% and 5% in the MSCI EAFE Index), respectively.

Key trends for investors to watch

As we look toward the coming year, these are some of the key trends that we are paying particularly close attention to as we shape our investment strategies at Gartmore:

An aging population. During 2005, a landmark social milestone occurred when the leading edge of the baby boom generation reached 60 years of age. Since the early post-World War II years, the baby boomers, as one of the largest subsections of the U.S. population, have reshaped the social landscape in innumerable ways. This group’s retirement will continue the process. The country’s financial institutions, for example, will accelerate the re-engineering of their products and services toward wealth preservation, not just wealth generation. On the downside, though, the strain on many under-funded pension plans, in addition to the Social Security system, may reverberate through the markets in unexpected and unsettling ways.

Housing prices–up, down or sideways? The housing market remained strong during the reporting period, with 30-year fixed mortgage rates remaining below 6% for the

majority of the time. Confounding expectations amid Hurricanes Katrina and Rita and rising energy costs, existing home sales advanced to an all-time high of 2% in August. The robust housing market contributed much to the overall “wealth effect” for real estate investors. By the end of the reporting period, however, more pronounced signs of softening became evident.

One housing trend associated with the aging of the population: a wave of residential downsizing as retirees seek more practical, late-in-life living arrangements. Moreover, individuals are pulling back from the real estate speculation of the past few years as quick price appreciation has cooled in once-hot markets such as Las Vegas, Miami, Phoenix and San Diego.

The cost of socialization. During the past year, it has become even clearer that many corporations and countries must take a harder look at dealing with the burgeoning weight of socialization, which consists of, among other factors, health-care and retirement benefits. In fact, the future cost of socialization at both the corporate and country level will be of increasing concern in determining investment potential. Many longstanding business models and corporate policies will be revised in light of unsustainably heavy socialization costs.

France’s refusal to endorse the European Union (EU) constitution, for example, can be tied to the issue of socialization. Most observers believe that voters feared that a stronger EU would create an influx of cheap labor just as France was struggling to reduce high unemployment. In the United States, the issue of socialization was clearly evident in the United Auto Workers’ agreement with General Motors Corp. (GM) to cut health-care benefits for employees, retirees and their families. GM successfully argued that escalating pension and health-care benefits for a vast pool of retirees was forcing the enterprise into bankruptcy, which is a landmark shift in the auto industry’s historical model.

The international economic picture. In the latter part of 2005, the economies of Japan and Europe, including the United Kingdom, improved due to strong corporate profitability and expectations of higher levels of merger-and-acquisition activity. Europe was buoyed by export growth on the back of the weak euro. In Japan, meanwhile, rising real incomes and capital expenditure led to hopes of a sustainable recovery. Expectations rose when Prime Minister Junichiro Koizumi achieved a resounding victory in parliamentary elections, which gave his government a solid mandate for reform.

China’s economy grew rapidly during the reporting period. Despite ongoing criticism that governmental controls on the economy were overly rigid–particularly regarding commodity prices and imports/exports–China’s economy has largely stabilized and shows strong signs of continued growth. In fact, the government’s economic controls, once viewed as unduly prohibitive, are now credited with controlling what was becoming a dangerously overheated economy. For example, new factories were being developed in China at a rapid rate based on capital secured with minimal credit checks. Before long, some banks held portfolios with up to 45% nonperforming loans as a result of default. Government regulators subsequently mandated stricter credit rules and have even expressed a desire to improve China’s banks to such a degree that their credit quality would be attractive to foreign investors.

Throughout the first half of the year, the U.S. dollar continued its sustained, three-year decline versus benchmark currencies such as the euro. In mid-summer, however, the dollar reversed its multi-year trend. The dollar’s increase is due primarily to the strengthening U.S. economic outlook relative to the global platform and disappointment in European reform. In addition, two factors—the United Kingdom’s halting of interest-rate hikes and France’s vote against the EU constitution–have placed pressure on the euro, effectively bolstering the U.S. dollar.

The return of capital expenditures. As we look toward 2006, we are seeing a trend toward companies deploying large amounts of excess cash on their balance sheets. Since the 2000 market meltdown, many companies have relied on cash as their primary hedge against diminished revenues. Now, however, as the equity markets continue to recover, many of these firms are feeling the pressure either to put the money to work in various ways, such as toward acquisitions, or return the money to shareholders in the form of dividend payouts or share buybacks. The technology sector could be a notable beneficiary of this trend. Research and development as well as new product rollouts are key drivers in the technology industry, and both areas will be bolstered by increased spending.

Looking ahead

For the near term, investors will face a mixture of positive and negative factors. On the one hand, economic and corporate earnings growth is likely to slow in the coming months. Counterbalancing this slowdown could be positive sentiment surrounding the end of the Fed’s cycle of interest-rate hikes, which we anticipate will occur in the first half of 2006. If, as we expect, the peak in rates is accompanied by softening oil prices and a firm U.S. dollar, the investment environment should be favorable for equity markets.

Market Perspectives

Continued

PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS.

To obtain performance information current to the most recent month-end, which may be higher or lower than the performance shown above, please call 800-848-0920 or go to www.gartmorefunds.com

The opinions expressed herein are those of Gartmore Global Investments and may not come to pass.

Investing in mutual funds involves risk, including possible loss of principal. There is no assurance that the investment objective of any fund will be achieved.

The Gartmore Optimal Allocations Funds are designed to provide diversification and asset allocation across several types of investments and asset classes, primarily by investing in underlying Gartmore funds.

There is no assurance that a diversified portfolio will produce better results than a nondiversified one.

Each Fund is subject to different levels of risk, based on the size of its asset class allocations.

Index performance is provided for comparison purposes only; indexes are unmanaged and no fees or expenses are reflected. Individuals cannot invest directly in an index. Market index performance is provided by a third party source that Gartmore deems reliable.

The Gartmore Small Cap Fund may purchase securities in initial public offerings, which can be very volatile and carry high transaction costs.

Small-company stocks have higher risks than the stocks of larger, more established companies and have significant short-term price volatility.

Funds that concentrate on specific sectors or a relatively small number of securities may be subject to greater volatility than that of other mutual funds. International investing involves additional risks, including currency fluctuations, differences in accounting standards, political instability and foreign regulations, all of which are magnified in emerging markets.

In order to achieve the Gartmore U.S. Growth Leaders Long-Short Fund’s objective, the managers may use sophisticated investment strategies such as short selling, short-term trading and investing in smaller companies. These strategies may cause the Fund to have greater risk and volatility, and higher expenses, than those of other investments. The risks of investing in this Fund are more fully detailed within the Fund’s prospectus.

The Gartmore Optimal Allocations Fund: Aggressive benchmark consists of 70% S&P 500 Index, 25% MSCI EAFE Index and 5% Lehman Brothers U.S. Aggregate Index.

The Gartmore Optimal Allocations Fund: Moderately Aggressive benchmark consists of 60% S&P 500 Index, 20% MSCI EAFE Index and 20% Lehman Brothers U.S. Aggregate Index.

The Gartmore Optimal Allocations Fund: Moderate benchmark consists of 40% S&P 500 Index, 20% MSCI EAFE Index and 40% Lehman Brothers U.S. Aggregate Index.

The Gartmore Optimal Allocations Fund: Specialty benchmark consists of 70& S&P 500 Index and 30% MSCI EAFE Index.

Standard & Poor’s 500® (S&P 500) Index: An unmanaged, market capitalization-weighted index of 500 widely held stocks of large-cap U.S. companies that gives a broad look at how the stock prices of those companies have performed.

Lehman Brothers U.S. Aggregate Index: An unmanaged, market value-weighted index of investment-grade, fixed-rate debt issues (including government, corporate, asset-backed, and mortgage-backed securities with maturities of one year or more) that is generally representative of the bond market as a whole.

Morgan Stanley Capital International Europe, Australasia and Far East (MSCI EAFE®) Index: An unmanaged, free float-adjusted, market capitalization-weighted index that is designed to measure the performance of stocks in developed markets outside the United States and Canada.

Goldman Sachs Natural Resources Index: An unmanaged, modified market capitalization-weighted sector index of U.S.-traded natural resource-related stocks; includes companies in the categories of extractive industries, energy companies, owners and operators of timber tracts, forestry services, producers of pulp and paper, and owners of plantations.

Citigroup 3-Month T-Bill Index: An unmanaged index that is generally representative of 3-month Treasury bills; consists of an average of the last 3-month Treasury bill issues (excluding the current month-end bill).

Morgan Stanley Capital International Emerging Markets (MSCI EM) IndexSM: An unmanaged, free float-adjusted, market capitalization-weighted index that is designed to measure the performance of the stocks in emerging-country markets.

Morgan Stanley Capital International (MSCI) All Country World excluding U.S. Index: An unmanaged, free float-adjusted, market-capitalization weighted index that is designed to measure the performance of the stocks in companies in all countries except the United States.

Morgan Stanley Capital International (MSCI) World IndexSM: An unmanaged, free float-adjusted, market capitalization-weighted index that is designed to measure the performance of global developed-market equities.

Russell 2000® Index: An unmanaged index that measures the performance of the stocks of small-capitalization U.S. companies; includes the smallest 2,000 U.S. companies in the Russell 3000® Index, which measures the performance of the largest 3,000 U.S. companies, based on market capitalization.

Each Fund’s underlying funds may be subject to specific investment risks such as those associated with a concentrated number of securities (such as REITs), small companies, international stocks, initial public offerings, short selling, short-term trading, bonds and short-term instruments.

Investors should carefully consider a fund’s investment objectives, risks, fees, charges and expenses before investing any money. To obtain this and other information on Gartmore’s funds, please call 800-848-0920 to request a prospectus, or download a prospectus at www.gartmorefunds.com. Please read it carefully before investing any money.

Gartmore Funds distributed by Gartmore Distribution Services, Inc., Member NASD. 1200 River Road, Suite 1000, Conshohocken, PA 19428.

Lipper Analytical Services, Inc. is an industry research firm whose rankings are based on total return performance and do not reflect the effect of sales charges. Each fund is ranked within a universe of funds similar in investment objective as determined by Lipper.

Market Perspectives

Continued

International investing involves additional risks, including currency fluctuations, differences in accounting standards, political instability and foreign regulations, all of which are magnified in emerging markets.

The Gartmore Small Cap Fund may purchase securities in initial public offerings, which can be volatile and carry high transaction costs.

While the Gartmore Bond Fund, the Gartmore Government Bond Fund, the Gartmore Short Duration Bond Fund and the Gartmore Morley Enhanced Income Fund invest primarily in securities of the U.S. government and its agencies, these Funds’ value is not guaranteed by these entities.

An investment in a money market fund is not insured or guaranteed by the FDIC or any other government agency. Although a money market fund seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in the money market.

For some investors, income from the Gartmore Tax-Free Income Fund may be subject to state and local taxes, and the Federal Alternative Minimum Tax.

Investing in mutual funds involves risk, including possible loss of principal.

There is no assurance that the investment objective of any fund will be achieved.

Gartmore Global Investments, one of its affiliated advisers, or its employees, may have a position in the securities named in this report.

This report is for informational purposes only, and is not intended as an offer or recommendation with respect to the purchase or sale of any security, option, future or other derivatives in such securities.

A complete list of all transactions in the last 12-months is available upon request.

Although third party information has been obtained from and is based on sources the Firm believes to be reliable, the Firm does not guarantee the accuracy of the information, and it may be incomplete or condensed.

Commentary provided by Gartmore Global Investments, the investment adviser to Gartmore Funds. All opinions and estimates included in this report constitute Gartmore Global Investments’ judgment as of the date of this report and are subject to change without notice.

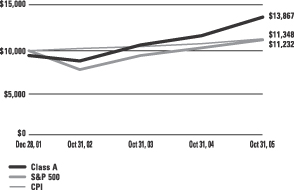

Gartmore Large Cap Value Fund

For the annual period ended Oct. 31, 2005, the Gartmore Large Cap Value Fund (Class A at NAV) returned 12.63% versus 11.86% for its benchmark, the Russell 1000® Value Index. For broader comparison, the average return for the Fund’s peer category of Large Cap-Value Funds was 9.75%.

The reporting period was strong for the U.S. large-cap equity market. As a result of several factors–lower oil prices, the conclusion of the U.S. presidential election, reasonably good economic and earnings news, reactions to the $32 billion Microsoft dividend and the beginning of the seasonally strong year-end period–the large-cap equity market experienced most of its gains for the reporting period in November and December of 2004. Large-cap value stocks, as measured by the Russell 1000® Value Index, outperformed large-cap growth stocks, as measured by the Russell 1000® Growth Index, returning 11.86% versus 8.81% respectively.

Our rigorous investment process helped us to deliver competitive investment returns. Stock selection continued to drive performance. Fund results were strongest in the energy, utilities and materials sectors. Among the Fund’s holdings in the energy sector, the overweighting of oil refining and marketing companies contributed to positive Fund performance. Monsanto Co., a leading provider of agricultural products and technology-based solutions to farmers, was the standout performer among the Fund’s materials holdings. Edison International and Texas Utilities (TXU Corp.) were the Fund’s stalwarts in the utilities sector.

Fund performance was challenged in the information technology, telecommunication, and consumer staples sectors. Lucent Technologies, Verizon Communications, and Sara Lee were three of the portfolio’s main detractors of performance.

The Fund is positioned to perform in a stock market that rewards investing in undervalued companies, those that are experiencing improving fundamentals. For the past 12 months, the market trend has been to reward individual issues whose fundamentals are improving more than expected. The best proxy for this trend in our process is our forecast earnings momentum factor. During the past fiscal year, this factor has been our strongest and most consistent model. As a result, we have begun to place more emphasis on estimate revisions in our investment process. It is our belief that a sound value investment philosophy coupled with a focus on earnings momentum should be the winning strategy in this environment.

We continue to focus on delivering competitive, active large-cap value performance through the consistent use of quantitative stock selection and portfolio construction techniques. Given the high-profile nature of large-cap value stocks, achieving outperformance can be a challenge. We believe that the best route to success is adherence to our investment decision making process.

Portfolio Manager:

Peter Cahill

| | |

Fund Performance | | Gartmore Large Cap Value Fund |

Average Annual Total Return

(For periods ended October 31, 2005)

| | | | | | | | |

| | | | | 1 Yr. | | 5 Yr. | | Inception1 |

| Class A | | w/o SC2 | | 12.63% | | 5.53% | | 5.65% |

| | | w/SC3 | | 6.15% | | 4.28% | | 4.76% |

| Class B | | w/o SC2 | | 11.97% | | 4.84% | | 4.87% |

| | | w/SC4 | | 6.97% | | 4.51% | | 4.87% |

| Class C5 | | w/o SC2 | | 11.98% | | 4.88% | | 4.90% |

| | | w/SC6 | | 10.98% | | 4.88% | | 4.90% |

| Class R7,8 | | | | 12.73% | | 5.09% | | 5.05% |

All figures showing the effect of a sales charge reflect the maximum charge possible, because it has the most dramatic effect on performance data.

| 1 | Fund commenced operations on November 2, 1998. |

| 2 | These returns do not reflect the effects of sales charges (SC). |

| 3 | A 5.75% front-end sales charge was deducted. |

| 4 | A 5.00% contingent deferred sales charge (CDSC) was deducted. The CDSC declines to 0% after 6 years. |

| 5 | These returns until the creation of Class C shares (3/1/01) include the performance of the Fund’s Class B shares. Excluding the effects of any fee waivers or reimbursements, such prior performance is substantially similar to what Class C shares would have produced because Class C shares invest in the same portfolio of securities as Class B shares and have the same expenses after fee waivers or reimbursements. For Class C shares returns with sales charges, these returns have been restated for the applicable sales charges. |

| 6 | A CDSC of 1.00% was deducted from the one year return because it is charged when you sell Class C shares within the first year after purchase. |

| 7 | These returns until the creation of Class R shares (10/1/03) include the performance of the Fund’s Class B shares. The returns have been adjusted for the fact that Class R shares do not have any applicable sales charges but have not been adjusted for the lower expenses applicable to Class R shares. Excluding the effect of any fee waivers or reimbursements, such prior performance is similar to what Class R shares would have produced because the Class R shares will invest in the same portfolio of securities as Class B shares. |

| 8 | Not subject to any sales charges. |

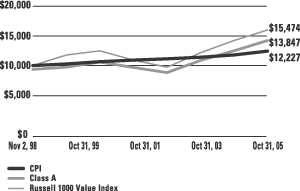

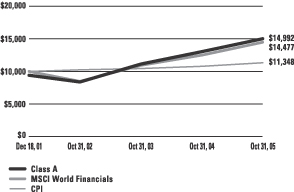

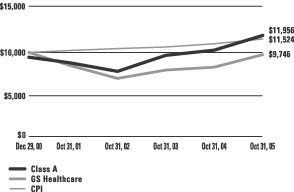

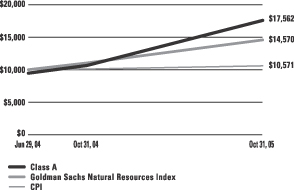

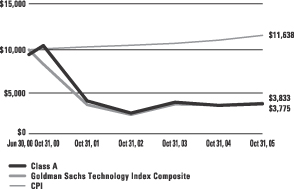

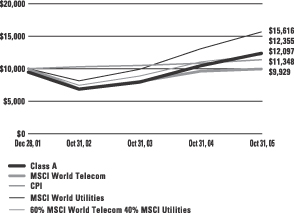

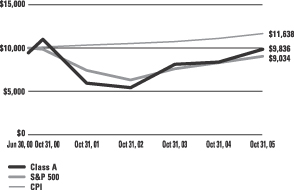

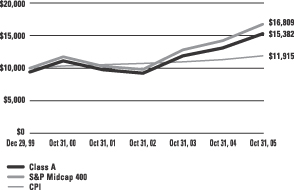

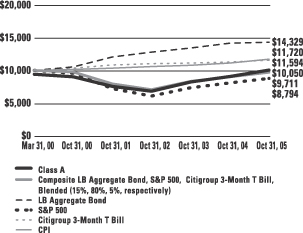

Performance of a $10,000 Investment

Investment return and principal value will fluctuate, and when redeemed, shares may be worth more or less than original cost. Past performance is no guarantee of future results and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Investing in mutual funds involves market risk, including loss of principal. Performance returns assume the reinvestment of all distributions.

Comparative performance of $10,000 invested in Class A shares of the Gartmore Large Cap Value Fund, the Russell 1000 Value Index (Russell 1000 Value)(a), and the Consumer Price Index (CPI)(b) since inception. Unlike the Fund, the returns for these unmanaged indexes do not reflect any fees, expenses, or sales charges. Investors cannot invest directly in market indexes.

| (a) | The Russell 1000 Value is an unmanaged index of large capitalization value securities of U.S. companies included in the Russel 1000 Value Index. |

| (b) | The CPI represents changes in prices of a basket of goods and services purchased for consumption by urban households. |

| | |

Shareholder Expense Example | | Gartmore Large Cap Value Fund |

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) paid on purchase payments and redemption fees; and (2) ongoing costs, including investment advisory fees, administration fees, distribution fees and other Fund expenses. The examples below are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. Per SEC requirements, the examples assume that you had a $1,000 investment in the Class at the beginning of the reporting period, May 1, 2005, and continued to hold your shares at the end of the reporting period, October 31, 2005.

Actual Expenses

For each Class of the Fund in the table below, the first line provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line of each Class under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during the period.

Hypothetical Example for Comparison Purposes

The second line of each Class in the table below provides information about hypothetical account values and hypothetical expenses based on the Class’ actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Class’ actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Class of the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transaction costs, such as sales charges (loads) or redemption fees. Therefore, the second line for each Class in the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher. The examples also assume all dividends and distributions have been reinvested.

Schedule of Shareholder Expenses

Expense Analysis of a $1,000 Investment

(October 31, 2005)

| | | | | | | | | | | | | | |

| Large Cap Value Fund | | | | | Beginning

Account Value,

May 1, 2005 | | Ending

Account Value,

October 31, 2005 | | Expenses Paid

During Period* | | Annualized

Expense Ratio* |

| Class A | | Actual | | | $ | 1,000.00 | | $ | 1,056.80 | | $ | 7.52 | | 1.45% |

| | | Hypothetical | 1 | | $ | 1,000.00 | | $ | 1,017.69 | | $ | 7.40 | | 1.45% |

| Class B | | Actual | | | $ | 1,000.00 | | $ | 1,054.50 | | $ | 10.67 | | 2.06% |

| | | Hypothetical | 1 | | $ | 1,000.00 | | $ | 1,014.62 | | $ | 10.51 | | 2.06% |

| Class C | | Actual | | | $ | 1,000.00 | | $ | 1,054.30 | | $ | 10.67 | | 2.06% |

| | | Hypothetical | 1 | | $ | 1,000.00 | | $ | 1,014.62 | | $ | 10.51 | | 2.06% |

| Class R | | Actual | | | $ | 1,000.00 | | $ | 1,058.10 | | $ | 6.95 | | 1.34% |

| | | Hypothetical | 1 | | $ | 1,000.00 | | $ | 1,018.24 | | $ | 6.84 | | 1.34% |

| * | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period multiplied by 184/365 (to reflect the one-half year period). The expense ratio presented represents a six month, annualized ratio in accordance with SEC guidelines. |

| 1 | Represents the hypothetical 5% return before expenses. |

| | |

Portfolio Summary | | Gartmore Large Cap Value Fund |

The SEC adopted a requirement that Funds present their portfolio holdings in a table, chart or graph format in their annual and semiannual reports to shareholders, whether or not a statement of investments is utilized. The following tables, which present portfolio holdings as a percentage of net assets, are provided in compliance with this requirement.

| | |

| Asset Allocation | | |

| Common Stocks | | 98.7% |

| Cash Equivalents | | 1.2% |

| Other Investments* | | 8.8% |

| Liabilities in excess of Other Assets** | | -8.7% |

| | |

|

| | | 100.0% |

| * | Includes value of collateral received from securities lending. |

| ** | Includes value of collateral owed from securities lending. |

| | |

| Top Industries | | |

| Oil & Gas | | 14.4% |

| Diversified Financials | | 13.3% |

| Banks | | 12.1% |

| Electric Utilities | | 6.6% |

| Insurance | | 6.2% |

| Diversified Telecommunication Services | | 5.4% |

| Pharmaceuticals | | 4.7% |

| Media | | 4.6% |

| Retail | | 3.1% |

| Real Estate | | 3.0% |

| Other Industries | | 26.6% |

| | |

|

| | | 100.0% |

| | |

| Top Holdings*** | | |

| Exxon Mobil Corp. | | 5.1% |

| Bank of America Corp. | | 4.5% |

| Citigroup, Inc. | | 4.5% |

| J.P. Morgan Chase & Co. | | 2.8% |

| ConocoPhillips | | 2.7% |

| ChevronTexaco Corp. | | 2.3% |

| Wachovia Corp. | | 2.1% |

| Wells Fargo Co. | | 2.1% |

| SBC Communications, Inc. | | 1.9% |

| Exelon Corp. | | 1.9% |

| Other Holdings | | 70.1% |

| | |

|

| | | 100.0% |

| *** | For purpose of listing top holdings, repurchase agreements are considered cash equivalents and are included as part of Other Holdings. |

Statement of Investments

October 31, 2005

Gartmore Large Cap Value Fund

| | | | | |

| | | Shares or

Principal Amount | | Value |

| | | | | | |

Aerospace & Defense (0.6%) | | | | | |

Northrop Grumman Corp. | | 4,100 | | $ | 219,965 |

| | | | |

|

|

Air Freight & Logistics (0.6%) | | | | | |

FedEx Corp. | | 2,400 | | | 220,632 |

| | | | |

|

|

Automobiles (0.5%) | | | | | |

Ford Motor Co. (c) | | 19,300 | | | 160,576 |

| | | | |

|

|

Banks (12.1%) | | | | | |

Bank of America Corp. | | 35,818 | | | 1,566,679 |

U.S. Bancorp | | 20,300 | | | 600,474 |

Wachovia Corp. | | 14,400 | | | 727,488 |

Washington Mutual, Inc. | | 14,748 | | | 584,003 |

Wells Fargo Co. | | 11,800 | | | 710,360 |

| | | | |

|

|

| | | | | | 4,189,004 |

| | | | |

|

|

Chemicals (2.1%) | | | | | |

Lyondell Chemical Co. | | 15,500 | | | 415,400 |

Monsanto Co. | | 5,000 | | | 315,050 |

| | | | |

|

|

| | | | | | 730,450 |

| | | | |

|

|

Communications Equipment (0.7%) | | | |

Lucent Technologies, Inc. (b) (c) | | 81,200 | | | 231,420 |

| | | | |

|

|

Computer Software & Services (0.6%) | | | |

Cognizant Technology Solutions Corp. (b) | | 4,600 | | | 202,308 |

| | | | |

|

|

Computers & Peripherals (2.0%) | | | |

Apple Computer, Inc. (b) | | 7,700 | | | 443,443 |

Hewlett-Packard Co. | | 8,700 | | | 243,948 |

| | | | |

|

|

| | | | | | 687,391 |

| | | | |

|

|

Diversified Financials (13.3%) | | | | | |

Citigroup, Inc. | | 33,960 | | | 1,554,689 |

Countrywide Credit Industries, Inc. | | 13,398 | | | 425,654 |

Fannie Mae | | 6,400 | | | 304,128 |

Goldman Sachs Group, Inc. | | 4,000 | | | 505,480 |

J.P. Morgan Chase & Co. | | 26,028 | | | 953,145 |

Merrill Lynch & Co., Inc. | | 7,500 | | | 485,550 |

Morgan Stanley Dean Witter & Co. | | 6,700 | | | 364,547 |

| | | | |

|

|

| | | | | | 4,593,193 |

| | | | |

|

|

Common Stocks (98.7%) Common Stocks (98.7%) |

| | | | | |

| | | Shares or

Principal Amount | | Value |

| | | | | | |

Diversified Telecommunication Services (5.4%) |

Bellsouth Corp. | | 23,500 | | $ | 611,470 |

SBC Communications, Inc. | | 28,100 | | | 670,185 |

Verizon Communications, Inc. | | 18,500 | | | 582,935 |

| | | | |

|

|

| | | | | | 1,864,590 |

| | | | |

|

|

Electric Utilities (6.6%) | | | | | |

Duke Power Co. (c) | | 8,000 | | | 211,840 |

Edison International | | 11,600 | | | 507,616 |

Emerson Electric Co. | | 2,700 | | | 187,785 |

Entergy Corp. | | 3,800 | | | 268,736 |

Exelon Corp. | | 12,600 | | | 655,578 |

TXU Corp. | | 4,400 | | | 443,300 |

| | | | |

|

|

| | | | | | 2,274,855 |

| | | | |

|

|

Electronics — Military (0.8%) | | | | | |

L-3 Communications Holdings,

Inc. (c) | | 3,600 | | | 280,152 |

| | | | |

|

|

Financial — Investment Banker/Broker (2.1%) | | | |

Lehman Brothers Holdings, Inc. | | 5,100 | | | 610,317 |

New Century Financial Corp. (c) | | 3,800 | | | 117,306 |

| | | | |

|

|

| | | | | | 727,623 |

| | | | |

|

|

Food & Beverages (2.7%) | | | | | |

Archer-Daniels-Midland Co. | | 16,500 | | | 402,105 |

Constellation Brands, Inc. (b) | | 16,700 | | | 393,118 |

Pilgrim’s Pride Corp. (c) | | 4,700 | | | 147,956 |

| | | | |

|

|

| | | | | | 943,179 |

| | | | |

|

|

Gas Utilities (1.0%) | | | | | |

Sempra Energy | | 7,900 | | | 349,970 |

| | | | |

|

|

Health Care Providers & Services (1.6%) | | | |

Aetna, Inc. | | 4,200 | | | 371,952 |

PacifiCare Health Systems, Inc. (b) | | 2,100 | | | 172,956 |

| | | | |

|

|

| | | | | | 544,908 |

| | | | |

|

|

Hotels & Motels (0.8%) | | | | | |

Marriott International, Inc., Class A | | 4,700 | | | 280,214 |

| | | | |

|

|

Household Products (0.6%) | | | | | |

Colgate-Palmolive Co. | | 3,600 | | | 190,656 |

| | | | |

|

|

Statement of Investments (Continued)

October 31, 2005

Gartmore Large Cap Value Fund (Continued)

| | Common Stocks (continued) |

| | | | | |

| | | Shares or

Principal Amount | | Value |

| | | | | | |

Insurance (6.2%) | | | | | |

Allstate Corp. (The) | | 7,900 | | $ | 417,041 |

American International Group, Inc. | | 5,250 | | | 340,200 |

Genworth Financial, Inc., Class A | | 6,600 | | | 209,154 |

Hartford Financial Services Group, Inc. | | 4,900 | | | 390,775 |

Prudential Financial, Inc. | | 4,700 | | | 342,113 |

St. Paul Travelers Cos., Inc. (The) | | 9,700 | | | 436,791 |

| | | | |

|

|

| | | | | | 2,136,074 |

| | | | |

|

|

Machinery (0.8%) | | | | | |

Paccar, Inc. | | 4,150 | | | 290,583 |

| | | | |

|

|

Media (4.6%) | | | | | |

Comcast Corp. (b) | | 19,600 | | | 545,468 |

Time Warner, Inc. | | 36,700 | | | 654,361 |

Walt Disney Co. (The) (c) | | 15,600 | | | 380,172 |

| | | | |

|

|

| | | | | | 1,580,001 |

| | | | |

|

|

Metals & Mining (0.5%) | | | | | |

United States Steel Corp. | | 5,000 | | | 182,650 |

| | | | |

|

|

Multi-Sector Companies (1.5%) | | | |

General Electric Co. | | 8,200 | | | 278,062 |

Textron, Inc. | | 3,300 | | | 237,732 |

| | | | |

|

|

| | | | | | 515,794 |

| | | | |

|

|

Oil & Gas (14.4%) | | | | | |

Anadarko Petroleum Corp. | | 3,600 | | | 326,556 |

ChevronTexaco Corp. | | 13,800 | | | 787,566 |

ConocoPhillips | | 14,200 | | | 928,396 |

Devon Energy Corp. | | 6,800 | | | 410,584 |

Exxon Mobil Corp. | | 31,600 | | | 1,774,025 |

Tesoro Petroleum Corp. | | 4,900 | | | 299,635 |

Valero Energy Corp. | | 4,000 | | | 420,960 |

| | | | |

|

|

| | | | | | 4,947,722 |

| | | | |

|

|

Packaging & Containers (0.4%) | | | |

Sonoco Products Co. (c) | | 5,200 | | | 147,160 |

| | | | |

|

|

Paper & Forest Products (1.0%) | | | |

Georgia Pacific Corp. | | 10,700 | | | 348,071 |

| | | | |

|

|

| | | | | |

| | | Shares or

Principal Amount | | Value |

| | | | | | |

Pharmaceuticals (4.7%) | | | | | |

Bristol-Myers Squibb Co. | | 8,300 | | $ | 175,711 |

Merck & Co., Inc. | | 12,200 | | | 344,284 |

Pfizer, Inc. | | 29,600 | | | 643,504 |

Wyeth | | 10,100 | | | 450,056 |

| | | | |

|

|

| | | | | | 1,613,555 |

| | | | |

|

|

Printing & Publishing (0.9%) | | | | | |

Donnelley (R.R.) & Sons Co. | | 8,600 | | | 301,172 |

| | | | |

|

|

Real Estate (3.0%) | | | | | |

General Growth Properties,

Inc. (c) | | 9,200 | | | 390,816 |

HRPT Properties Trust (c) | | 14,600 | | | 159,286 |

MDC Holdings, Inc. (c) | | 4,500 | | | 308,700 |

Vornado Realty Trust (c) | | 2,200 | | | 178,200 |

| | | | |

|

|

| | | | | | 1,037,002 |

| | | | |

|

|

Retail (3.1%) | | | | | |

Abercrombie & Fitch Co. | | 4,900 | | | 254,751 |

Costco Wholesale Corp. | | 7,500 | | | 362,700 |

Federated Department Stores, Inc. | | 4,000 | | | 245,480 |

V.F. Corp. | | 3,900 | | | 203,775 |

| | | | |

|

|

| | | | | | 1,066,706 |

| | | | |

|

|

Software (0.5%) | | | | | |

BEA Systems, Inc. (b) (c) | | 20,500 | | | 180,810 |

| | | | |

|

|

Telecommunications (0.4%) | | | | | |

Comverse Technology, Inc. (b) | | 5,500 | | | 138,050 |

| | | | |

|

|

Tobacco (1.5%) | | | | | |

Altria Group, Inc. | | 6,800 | | | 510,340 |

| | | | |

|

|

Transportation (1.1%) | | | | | |

Yellow Roadway Corp. (b) (c) | | 8,000 | | | 363,600 |

| | | | |

|

|

| | |

Total Common Stocks | | | | | 34,050,376 |

| | | | |

|

|

Cash Equivalents (1.2%)

| | | | | | |

| | | Shares or

Principal Amount | | Value |

| | | | | | | |

Investments in repurchase agreements (Collateralized by U.S. Government Agencies and U.S. Government Agency Mortgages, in a joint trading account at 3.90%, dated 10/31/05, due 11/01/05, repurchase price $397,007) | | $ | 396,964 | | $ | 396,964 |

| | | | | |

|

|

| | |

Total Cash Equivalents | | | | | | 396,964 |

| | | | | |

|

|

| |

Short-Term Securities Held as Collateral for Securities

Lending (8.8%)

| | | | | | | |

| | | Shares or

Principal Amount | | Value | |

Pool of short-term securities for Gartmore Mutual Funds —

note 2 (Securities Lending) | | $ | 3,026,092 | | $ | 3,026,092 | |

| | | | | |

|

|

|

| |

Total Short-Term Securities Held as Collateral for Securities Lending | | | 3,026,092 | |

| | | | | |

|

|

|

| |

Total Investments

(Cost $32,568,194) (a) — 108.7% | | | 37,473,432 | |

| |

Liabilities in excess of other assets — (8.7)% | | | (3,009,350 | ) |

| | | | | |

|

|

|

| |

NET ASSETS — 100.0% | | $ | 34,464,082 | |

| | | | | |

|

|

|

| | (a) | See notes to financial statements for tax unrealized appreciation (depreciation) of securities. |

| | (b) | Denotes a non-income producing security. |

| | (c) | All or part of the security was on loan as of October 31, 2005. |

See notes to financial statements.

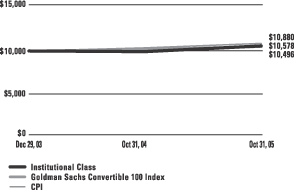

Gartmore Mid Cap Growth Fund

For the annual period ended Oct. 31, 2005, the Gartmore Mid Cap Growth Fund (Class A at NAV) returned 14.42% versus 15.91% for its benchmark, the Russell Midcap® Growth Index. For broader comparison, the average return for the Fund’s Lipper peer category of Mid-Cap Growth Funds was 14.07%.

The year started with the markets facing headwinds of higher energy prices and higher interest rates. But later in the year, the markets turned decidedly positive, driven by good macro economic data and declining energy prices. Encouraged by this backdrop, investors put new money to work in the stock market. Mid Cap Growth Funds benefited as investors rotated from Large Cap and Small Cap stocks into Mid Cap stocks. The ensuing rally propelled the group to new highs for 2005.

The Fund’s investment objective continues to be to seek price appreciation and consistent investment returns by selecting high-quality, industry-leading companies that display strong growth potential at a reasonable valuation. We define high-quality stocks as those with the following characteristics: above market earnings growth, low debt-to-equity ratio and double-digit return on equity. In our experience, companies that exhibit sustainable competitive advantages and consistent earnings streams tend to perform well throughout a complete market cycle.

The Fund underperformed its benchmark during the period. This underperformance was largely a result of the Fund’s holdings in the Technology sector. Specifically, certain companies held in the portfolio experienced adverse operating conditions which pressured their shares in the market. These holdings included: Infospace, Mercury Interactive and Tibco, which were sold during the period.

Strong stock selection in the energy and health-care sectors contributed positively to the Fund’s return. Our selections in these sectors stemmed directly from our disciplined investment approach and our bottom-up stock selection process. Positive contributors included: EOG Resources, Inc.; XTO Energy Inc.; and Express Scripts, Inc.

We maintain a discipline of finding high-quality growth stocks, regardless of the prevailing market conditions. As we expected, during the past year cyclical and lower-quality company stocks performed very well, a typical occurrence in the first stage of an economic recovery. Looking forward, we feel that we are entering the second phase of an earnings recovery in which higher-quality companies with sustainable earnings growth tend to outperform. We continue to believe that we are protected on the downside by our careful attention to stock selection. Our core philosophy has not changed; therefore, the Fund remains relatively sector-neutral to the benchmark, since we prefer to let stock selections drive performance. We remain focused on high-quality companies with sustainable competitive advantages, strong balance sheets and industry-leading returns trading at reasonable multiples. We feel confident that our strategy will be rewarded throughout the complete market cycle.

Portfolio Manager:

Robert D. Glise

| | |

Fund Performance | | Gartmore Mid Cap Growth Fund |

Average Annual Total Return

(For periods ended October 31, 2005)

| | | | | | |

| | | | | 1 Yr. | | Inception1 |

| Class A2 | | w/o SC3 | | 14.42% | | 18.10% |

| | | w/SC4 | | 7.82% | | 15.85% |

| Class B2 | | w/o SC3 | | 13.65% | | 17.57% |

| | | w/SC5 | | 8.65% | | 16.87% |

| Class C2 | | w/o SC3 | | 13.65% | | 17.57% |

| | | w/SC6 | | 12.65% | | 17.57% |

| Class R2,7 | | | | 14.38% | | 18.00% |

| Institutional Class7 | | | | 14.79% | | 18.38% |

All figures showing the effect of a sales charge reflect the maximum charge possible, because it has the most dramatic effect on performance data.

| 1 | Fund commenced operations on October 1, 2002. |

| 2 | These returns included performance based on the Fund’s Institutional Class shares, which was achieved prior to the creation of Class A shares (3/5/03), Class B and Class C shares (8/21/03), and Class R shares (10/1/03). Excluding the effects of any fee waivers or reimbursements, such prior performance is similar to what Class A, Class B, Class C and Class R shares would have produced because all classes of the Fund’s shares invest in the same portfolio of securities. The performance for these classes has been restated to reflect differences in sales charges (where applicable), but does not reflect the differing levels of other fees (primarily Rule 12b-1 and/or administrative services fees) applicable to such classes; if these fees were reflected, the performance for Class A, Class B, Class C and Class R would have been lower. |

| 3 | These returns do not reflect the effects of sales charges (SC). |

| 4 | A 5.75% front-end sales charge was deducted. |

| 5 | A 5.00% contingent deferred sales charge (CDSC) was deducted. The CDSC declines to 0% after 6 years. |

| 6 | A CDSC of 1.00% was deducted from the one year return because it is charged when you sell Class C shares within the first year after purchase. |

| 7 | Not subject to any sales charges. |

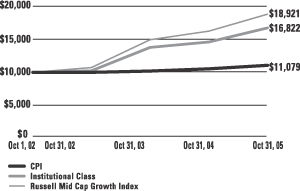

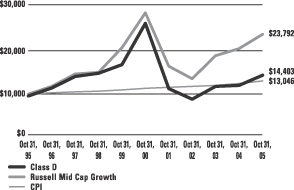

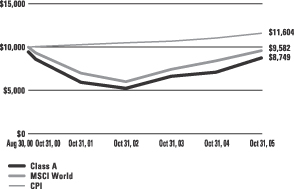

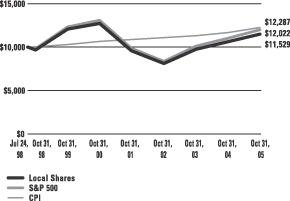

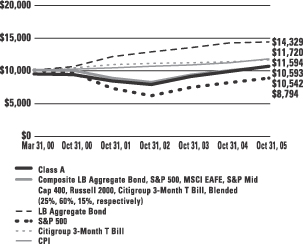

Performance of a $10,000 Investment

Investment return and principal value will fluctuate, and when redeemed, shares may be worth more or less than original cost. Past performance is no guarantee of future results and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Investing in mutual funds involves market risk, including loss of principal. Performance returns assume the reinvestment of all distributions.

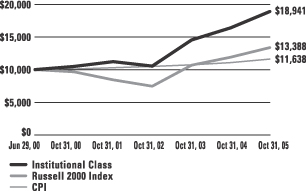

Comparative performance of $10,000 invested in the Institutional Class shares the Gartmore MidCap Growth Fund, Russell MidCap Growth Index (Russell MidCap Growth)(a), and the Consumer Price Index (CPI)(b) since inception. Unlike the Fund, the returns for these unmanaged indexes do not reflect any fees, expenses, or sales charges. Investors cannot invest directly in market indexes.

| (a) | The Russell MidCap Growth–an unmanaged index of the stock of medium-size U.S. companies with a capitalization range of $0.9 billion to $18.1 billion as of October 31, 2005, gives a broad look at how the stock price of medium-size U.S. companies have performed. |

| (b) | The CPI represents changes in prices of a basket of goods and services purchased for consumption by urban households. |

| | |

Shareholder Expense Example | | Gartmore Mid Cap Growth Fund |

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) paid on purchase payments and redemption fees; and (2) ongoing costs, including investment advisory fees, administration fees, distribution fees and other Fund expenses. The examples below are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. Per SEC requirements, the examples assume that you had a $1,000 investment in the Class at the beginning of the reporting period, May 1, 2005, and continued to hold your shares at the end of the reporting period, October 31, 2005.

Actual Expenses

For each Class of the Fund in the table below, the first line provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line of each Class under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during the period.

Hypothetical Example for Comparison Purposes

The second line of each Class in the table below provides information about hypothetical account values and hypothetical expenses based on the Class’ actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Class’ actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Class of the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transaction costs, such as sales charges (loads) or redemption fees. Therefore, the second line for each Class in the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher. The examples also assume all dividends and distributions have been reinvested.

Schedule of Shareholder Expenses

Expense Analysis of a $1,000 Investment

(October 31, 2005)

| | | | | | | | | | | | | |

| Mid Cap Growth Fund | | | | Beginning

Account Value,

May 1, 2005 | | Ending

Account Value,

October 31, 2005 | | Expenses Paid

During Period* | | Annualized

Expense Ratio* |

| Class A | | Actual | | $ | 1,000.00 | | $ | 1,113.90 | | $ | 7.62 | | 1.43% |

| | | Hypothetical1 | | $ | 1,000.00 | | $ | 1,017.79 | | $ | 7.30 | | 1.43% |

| Class B | | Actual | | $ | 1,000.00 | | $ | 1,110.10 | | $ | 11.44 | | 2.15% |

| | | Hypothetical1 | | $ | 1,000.00 | | $ | 1,014.16 | | $ | 10.97 | | 2.15% |

| Class C | | Actual | | $ | 1,000.00 | | $ | 1,110.10 | | $ | 11.44 | | 2.15% |

| | | Hypothetical1 | | $ | 1,000.00 | | $ | 1,014.16 | | $ | 10.97 | | 2.15% |

| Class R | | Actual | | $ | 1,000.00 | | $ | 1,113.40 | | $ | 7.78 | | 1.46% |

| | | Hypothetical1 | | $ | 1,000.00 | | $ | 1,017.64 | | $ | 7.45 | | 1.46% |

| Institutional Class | | Actual | | $ | 1,000.00 | | $ | 1,115.30 | | $ | 6.13 | | 1.15% |

| | | Hypothetical1 | | $ | 1,000.00 | | $ | 1,019.20 | | $ | 5.87 | | 1.15% |

| * | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period multiplied by 184/365 (to reflect the one-half year period). The expense ratio presented represents a six month, annualized ratio in accordance with SEC guidelines. |

| 1 | Represents the hypothetical 5% return before expenses. |

| | |

Portfolio Summary | | Gartmore Mid Cap Growth Fund |

The SEC adopted a requirement that Funds present their portfolio holdings in a table, chart or graph format in their annual and semiannual reports to shareholders, whether or not a statement of investments is utilized. The following tables, which present portfolio holdings as a percentage of net assets, are provided in compliance with this requirement.

| | |

| Asset Allocation | | |

| Common Stock | | 97.6% |

| Cash Equivalents | | 8.4% |

| Liabilities in excess of Other Assets | | -6.0% |

| | |

|

| | | 100.0% |

| | |

| Top Industries | | |

| Computer Software & Services | | 11.2% |

| Oil & Gas | | 8.8% |

| Retail | | 8.1% |

| Telecommunications | | 7.6% |

| Consumer Products | | 6.1% |

| Electronics | | 5.2% |

| Consumer & Commercial Services | | 4.6% |

| Medical Products & Services | | 4.6% |

| Financial Services | | 4.4% |

| Semiconductors | | 4.1% |

| Other Industries | | 35.3% |

| | |

|

| | | 100.0% |

| | |

| Top Holdings* | | |

| L-3 Communications Holdings, Inc. | | 3.0% |

| XTO Energy, Inc. | | 2.5% |

| Marvel Technology Group Ltd. | | 2.4% |

| Patterson-UTI Energy, Inc. | | 2.1% |

| Investors Financial Services Corp. | | 2.0% |

| Jarden Corp. | | 2.0% |

| Business Objectives S.A. ADR–FR | | 2.0% |

| Neustar, Inc. | | 1.9% |

| Penn National Gaming, Inc. | | 1.9% |

| EOG Resources, Inc. | | 1.9% |

| Other Holdings | | 78.3% |

| | |

|

| | | 100.0% |

| * | For purpose of listing top holdings, repurchase agreements are considered cash equivalents and are included as part of Other Holdings. |

Statement of Investments

October 31, 2005

Gartmore Mid Cap Growth Fund

| | | | | |

| | | Shares or

Principal Amount | | Value |

| | | | | | |

Aerospace & Defense (3.0%) | | | | | |

L-3 Communications Holdings, Inc. | | 1,750 | | $ | 136,185 |

| | | | |

|

|

Banks (3.8%) | | | | | |

City National Corp. | | 880 | | | 64,574 |

North Fork Bancorp, Inc. | | 1,910 | | | 48,399 |

Zions Bancorp | | 850 | | | 62,450 |

| | | | |

|

|

| | | | | | 175,423 |

| | | | |

|

|

Business Services (3.1%) | | | | | |

ChoicePoint, Inc. (b) | | 1,480 | | | 62,545 |

Corporate Executive Board Co. (The) | | 990 | | | 81,813 |

| | | | |

|

|

| | | | | | 144,358 |

| | | | |

|

|

Computer Software & Services (11.2%) |

Business Objectives S.A. ADR — FR (b) | | 2,650 | | | 90,815 |

eResearch Technology, Inc. (b) | | 2,900 | | | 41,557 |

Factset Research Systems, Inc. | | 1,740 | | | 61,022 |

Fiserv, Inc. (b) | | 1,490 | | | 65,083 |

Henry (Jack) & Associates, Inc. | | 2,320 | | | 41,714 |

Intuit, Inc. (b) | | 1,310 | | | 60,168 |

Mercury Interactive Corp. (b) | | 1,460 | | | 50,793 |

Navteq Corp. (b) | | 1,190 | | | 46,553 |

Network Appliance, Inc. (b) | | 2,120 | | | 58,003 |

| | | | |

|

|

| | | | | | 515,708 |

| | | | |

|

|

Construction (2.3%) | | | | | |

Centex Corp. | | 880 | | | 56,628 |

D.R. Horton, Inc. | | 1,683 | | | 51,651 |

| | | | |

|

|

| | | | | | 108,279 |

| | | | |

|

|

Consumer & Commercial Services (4.6%) |

Alliance Data Systems Corp. (b) | | 1,880 | | | 66,853 |

Heartland Payment Systems, Inc. (b) | | 1,570 | | | 38,025 |

Rollins, Inc. | | 3,090 | | | 58,772 |

Total System Services, Inc. | | 2,280 | | | 48,587 |

| | | | |

|

|

| | | | | | 212,237 |

| | | | |

|

|

Consumer Products (6.1%) | | | | | |

Ball Corp. | | 990 | | | 38,976 |

Church & Dwight, Inc. | | 1,140 | | | 39,957 |

Fortune Brands, Inc. | | 500 | | | 37,985 |

| | | | | |

| | | Shares or

Principal Amount | | Value |

| | | | | | |

Consumer Products (continued) | | | | | |

Gildan Activewear, Inc., Class A (b) | | 2,030 | | $ | 70,786 |

Jarden Corp. (b) | | 2,725 | | | 92,078 |

| | | | |

|

|

| | | | | | 279,782 |

| | | | |

|

|

Diagnostic Kits (1.2%) | | | | | |

Dade Behring Holdings, Inc. | | 1,590 | | | 57,256 |

| | | | |

|

|

Electronics (5.2%) | | | | | |

Amphenol Corp., Class A | | 1,600 | | | 63,952 |

Cabot Microelectronics Corp. (b) | | 1,440 | | | 42,336 |

Jabil Circuit, Inc. (b) | | 2,400 | | | 71,640 |

Microchip Technology, Inc. | | 2,080 | | | 62,754 |

| | | | |

|

|

| | | | | | 240,682 |

| | | | |

|

|

Energy (2.3%) | | | | | |

Headwaters, Inc. (b) | | 1,410 | | | 44,894 |

MDU Resources Group, Inc. | | 1,830 | | | 60,336 |

| | | | |

|

|

| | | | | | 105,230 |

| | | | |

|

|

Financial Services (4.4%) | | | | | |

Ameritrade Holdings Corp. (b) | | 2,200 | | | 46,266 |

BlackRock, Inc. | | 690 | | | 65,412 |

Investors Financial Services Corp. | | 2,420 | | | 92,396 |

| | | | |

|

|

| | | | | | 204,074 |

| | | | |

|

|

Gaming & Leisure (2.9%) | | | | | |

Penn National Gaming, Inc. (b) | | 3,030 | | | 89,537 |

Scientific Games Corp. (b) | | 1,440 | | | 43,142 |

| | | | |

|

|

| | | | | | 132,679 |

| | | | |

|

|

Healthcare (3.2%) | | | | | |

Express Scripts, Inc. (b) | | 910 | | | 68,623 |

St. Jude Medical, Inc. (b) | | 1,620 | | | 77,874 |

| | | | |

|

|

| | | | | | 146,497 |

| | | | |

|

|

Insurance (1.3%) | | | | | |

W.R. Berkley Corp. | | 1,350 | | | 58,995 |

| | | | |

|

|

Medical Products & Services (4.6%) |

Biomet, Inc. | | 1,110 | | | 38,661 |

Fisher Scientific International, Inc. (b) | | 930 | | | 52,545 |

Kinetic Concept, Inc. (b) | | 1,001 | | | 35,936 |

ResMed, Inc. (b) | | 2,180 | | | 83,124 |

| | | | |

|

|

| | | | | | 210,266 |

| | | | |

|

|

| | Common Stocks (continued) |

| | | | | |

| | | Shares or

Principal Amount | | Value |

| | | | | | |

Oil & Gas (8.8%) | | | | | |

EOG Resources, Inc. | | 1,300 | | $ | 88,114 |

Kinder Morgan, Inc. | | 660 | | | 59,994 |

Patterson-UTI Energy, Inc. | | 2,840 | | | 96,929 |

World Fuel Services Corp. | | 1,460 | | | 46,574 |

XTO Energy, Inc. | | 2,650 | | | 115,169 |

| | | | |

|

|

| | | | | | 406,780 |

| | | | |

|

|

Pharmaceuticals (2.7%) | | | | | |

Barr Pharmaceuticals, Inc. (b) | | 1,080 | | | 62,046 |

IVAX Corp. (b) | | 2 | | | 57 |

Kos Pharmaceuticals, Inc. (b) | | 1,010 | | | 60,600 |

| | | | |

|

|

| | | | | | 122,703 |

| | | | |

|

|

Retail (8.1%) | | | | | |

Bed, Bath & Beyond, Inc. (b) | | 1,370 | | | 55,512 |

Coach, Inc. (b) | | 2,230 | | | 71,761 |

Copart, Inc. (b) | | 1,970 | | | 46,078 |

Office Depot, Inc. (b) | | 2,430 | | | 66,898 |

Staples, Inc. | | 2,660 | | | 60,462 |

Williams Sonoma, Inc. (b) | | 1,850 | | | 72,354 |

| | | | |

|

|

| | | | | | 373,065 |

| | | | |

|

|

Schools (1.2%) | | | | | |

Education Management Corp. (b) | | 1,820 | | | 56,129 |

| | | | |

|

|

Scientific Instruments (0.7%) | | | | | |

Waters Corp. (b) | | 950 | | | 34,390 |

| | | | |

|

|

Security & Commodity Exchanges (1.4%) |

Chicago Mercantile Exchange | | 180 | | | 65,727 |

| | | | |

|

|

Semiconductors (4.1%) | | | | | |

KLA-Tencor Corp. | | 1,440 | | | 66,658 |

Marvel Technology Group Ltd. (b) | | 2,370 | | | 109,991 |

Tessera Technologies, Inc. (b) | | 450 | | | 12,555 |

| | | | |

|

|

| | | | | | 189,204 |

| | | | |

|

|

Telecommunications (7.6%) | | | | | |

ADC Telecommunications, Inc. (b) | | 2,820 | | | 49,209 |

Amdocs Ltd. ADR (b) | | 1,810 | | | 47,911 |

Comverse Technology, Inc. (b) | | 2,320 | | | 58,232 |

Flir Systems, Inc. (b) | | 1,430 | | | 29,973 |

Neustar, Inc. (b) | | 2,930 | | | 89,658 |

NII Holdings, Inc. (b) | | 910 | | | 75,457 |

| | | | |

|

|

| | | | | | 350,440 |

| | | | |

|

|

| | | | | | | |

| | | Shares or

Principal Amount | | Value | |

| | | | | | | | |

Transportation (2.3%) | | | | | | | |

Knight Transportation, Inc. | | | 1,970 | | $ | 53,604 | |

Oshkosh Truck Corp. | | | 1,180 | | | 51,401 | |

| | | | | |

|

|

|

| | | | | | | 105,005 | |

| | | | | |

|

|

|

Waste Disposal (1.5%) | | | | | | | |

Stericycle, Inc. (b) | | | 1,190 | | | 68,496 | |

| | | | | |

|

|

|

| | |

Total Common Stocks | | | | | | 4,499,590 | |

| | | | | |

|

|

|

|

Cash Equivalents (8.4%) | |

Investments in repurchase agreements (Collateralized by U.S. Government Agencies and U.S. Government Agency Mortgages, in a joint trading account at 3.90%, dated 10/31/05, due 11/01/05, repurchase price $388,912) | | $ | 388,870 | | | 388,870 | |

| | | | | |

|

|

|

| | |

Total Cash Equivalents | | | | | | 388,870 | |

| | | | | |

|

|

|

| |

Total Investments

(Cost $4,230,989) (a) — 106.0% | | | 4,888,460 | |

| |

Liabilities in excess of other assets — (6.0)% | | | (275,270 | ) |

| | | | | |

|

|

|

| |

NET ASSETS — 100.0% | | $ | 4,613,190 | |

| | | | | |

|

|

|

| | (a) | See notes to financial statements for tax unrealized appreciation (depreciation) of securities. |

| | (b) | Denotes a non-income producing security. |

| | ADR | American Depositary Receipt |

See notes to financial statements.

Gartmore Small Cap Fund

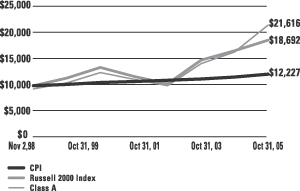

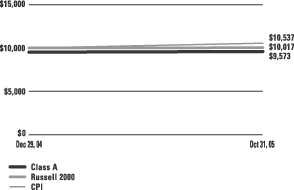

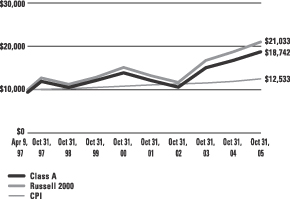

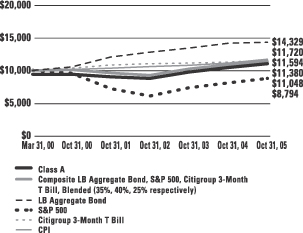

For the annual period ended Oct. 31, 2005, the Gartmore Small Cap Fund (Class A at NAV) returned 31.51% versus 12.08% for its benchmark, the Russell 2000® Index. For broader comparison, the average return for the Fund’s Lipper peer category of Small-Cap Core Funds was 13.22%.

Equity markets rallied in the last fiscal quarter of 2004 before slowing in early 2005, as investors took profits amid growing concerns that the Federal Reserve Board’s measured increases in interest rates might slow economic growth. Small-cap stocks experienced a period of difficulty, given the circumstances, and the mindset of many market analysts shifted toward large caps.