Table of Contents

| OMB APPROVAL | ||

| OMB Number: 3235-0570 | ||

| Expires: April 30, 2008 | ||

| Estimated average burden hours per response...............19.4 | ||

SECURITIES AND EXCHANGE COMMISSION

MANAGEMENT INVESTMENT COMPANIES

| 7337 E. Doubletree Ranch Rd., Scottsdale, AZ | 85258 | |

| (Address of principal executive offices) | (Zip code) | |

Table of Contents

| Funds |

| Semi-Annual Report | |

| November 30, 2007 | |

| Classes A, B, C, I, O and Q | |

| Domestic Equity and Income Fund | |

| • ING Real Estate Fund | |

| Domestic Equity Growth Funds | |

| • ING Fundamental Research Fund | |

| • ING LargeCap Growth Fund | |

| • ING MidCap Opportunities Fund | |

| • ING Opportunistic LargeCap Fund | |

| • ING SmallCap Opportunities Fund | |

| Domestic Equity Value Funds | |

| • ING Financial Services Fund | |

| • ING LargeCap Value Fund | |

| • ING SmallCap Value Choice Fund |

| • | ING Value Choice Fund |

E-Delivery Sign-up – details inside E-Delivery Sign-up – details inside |

| This report is submitted for general information to shareholders of the ING Funds. It is not authorized for distribution to prospective shareholders unless accompanied or preceded by a prospectus which includes details regarding the funds’ investment objectives, risks, charges, expenses and other information. This information should be read carefully. |

| 1 | ||||||||

| 2 | ||||||||

| 4 | ||||||||

| 14 | ||||||||

| 19 | ||||||||

| 25 | ||||||||

| 28 | ||||||||

| 33 | ||||||||

| 59 | ||||||||

| 82 | ||||||||

| Advisory Contract Approval Discussion | 110 | |||||||

| EX-99.CERT | ||||||||

| EX-99.906CERT | ||||||||

| Go Paperless with E-Delivery! | ||

| Sign up now for on-line prospectuses, fund reports, and proxy statements. In less than five minutes, you can help reduce paper mail and lower fund costs. |

Just go to www.ingfunds.com, click on the E-Delivery icon from the home page, follow the directions and complete the quick 5 Steps to Enroll.

You will be notified by e-mail when these communications become available on the internet. Documents that are not available on the internet will continue to be sent by mail.

A description of the policies and procedures that the Funds use to determine how to vote proxies related to portfolio securities is available: (1) without charge, upon request, by calling Shareholder Services toll-free at (800) 992-0180; (2) on the Funds’ website at www.ingfunds.com; and (3) on the U.S. Securities and Exchange Commission (“SEC”) website at www.sec.gov. Information regarding how the Funds voted proxies related to portfolio securities during the most recent 12-month period ended June 30 is available without charge on the Funds’ website at www.ingfunds.com and on the SEC’s website at www.sec.gov.

The Funds file their complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. The Funds’ Forms N-Q are available on the SEC’s website at www.sec.gov. The Funds’ Forms N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC, and information on the operation of the Public Reference Room may be obtained by calling (800) SEC-0330; and is available upon request from the Funds by calling Shareholder Services toll-free at (800) 992-0180.

Table of Contents

(THIS PAGE INTENTIONALLY LEFT BLANK)

Table of Contents

Dear Shareholder,

It is impossible to discuss the current market climate without acknowledging the recent turmoil brought on by problems in the sub-prime mortgage market. Clearly the excesses in this sector of the market and other segments of collateralized debt have created challenges throughout credit markets worldwide.

Amidst the volatility, we at ING Funds remind our shareholders that the creditworthiness and quality of our funds’ holdings is our ultimate priority — whether those holdings are part of our money market funds, fixed income funds or equity funds. Market volatility is an often present component of investing and we believe the best way to manage through turbulent environments is to build a well-balanced, fully-diversified portfolio, which aligns with your goals and risk tolerance.

ING Funds remains committed to developing and offering a diverse array of mutual funds designed to meet the goals of most investors. We urge you to work with your investment professional to make sure you are invested appropriately. Together, you can select the funds that will help you achieve your financial goals. We thank you for choosing ING Funds and look forward to continuing to serve you.

Sincerely,

For more complete information, or to obtain a prospectus for any ING fund, please call your Investment Professional or ING Funds Distributor, LLC at (800) 992-0180 or log on to www.ingfunds.com. The prospectus should be read carefully before investing. Consider the fund’s investment objectives, risks, charges and expenses carefully before investing. The prospectus contains this information and other information about the fund. Check with your Investment Professional to determine which funds are available for sale within their firm. Not all funds are available for sale at all firms.

1

Table of Contents

We started our new fiscal year knowing that the last one would be a hard act to follow, with the equity indices for most of the major regions returning more than 20% in local currencies. Few, however, could have expected the tumult of the first half of the reporting period. After nervous optimism persisted into July 2007, a credit crisis sent investors fleeing stock markets and into Treasuries. The U.S. Federal Reserve Board (the “Fed”) rate cuts provided some solace, but by the end of November 2007, these were no longer enough. For the six-month period ended November 30, 2007, global equities in the form of the Morgan Stanley Capital International World IndexSM(1) (“MSCI World IndexSM”) measured in local currencies, including net reinvested dividends (“MSCI” for regions discussed below) fell 3.4%. In currencies, the view that European interest rates would stay firmer than those in the U.S., supported the pound and euro for most of the period, while the yen continued to be dragged down by the “carry trade”, in which speculators borrow in yen at low interest rates and buy higher yielding securities in other currencies. But in the flight from risk, these trades were unwound and the yen rebounded. For the six months ended November 30, 2007, the dollar fell 9.1%, 4.5% and 9.5% against the euro (repeatedly making new lows), pound and yen, respectively.

The recession in the housing market had taken a new disturbing turn by the summer, as lax lending standards especially in the sub-prime mortgage loan sector were sending foreclosure rates and default provisions soaring, and some lenders into bankruptcy. Furthermore, the huge volumes of securities backed by such loans were declining in value, if they could find a bid at all. Much of this exposure was held by hedge funds and structured investment vehicles, which financed their purchases with investors’ money and by issuing lower yielding short term commercial paper, a variant of the carry trade. In June 2007, the investment bank, Bear Stearns, had to step in to rescue two of its hedge funds in distress over holdings in mortgage bonds.

So far, few observers believed that the sub-prime mortgage problems might lead to recession. But from mid-July 2007, a series of shocks sent investors scurrying for cover. A large mortgage lender, Countrywide, reported that the sub-prime default crisis had spread to other classes of mortgage loans. Worse, by month-end, American Home Mortgage revealed that its creditors had initiated margin calls and that bankruptcy was a possibility. A week later it was fact.

Confirmation that the global asset-backed commercial paper market was close to atrophy came on August 9, 2007 from an unlikely source when French bank BNP Paribas announced similar problems with its own U.S. mortgage-backed structured investment vehicles. Banks were by now reluctant to lend to each other because no-one could be sure where the exposure to tainted securities ultimately lay.

Central banks responded by pouring billions into the inter-bank system. On August 17, 2007, the Fed cut the discount rate, (the rate it will lend to banks), by 50 basis points (0.50%), followed on September 18, 2007, by an unexpectedly soothing 50 basis points (0.50%) federal funds rate reduction and another 50 basis points (0.50%) cut in the discount rate. Finally, on October 31, 2007, the Federal Open Market Committee (“FOMC”) cut both rates by an additional 0.25%.

Yet, as November 2007 wore on, many wondered how much further the FOMC could go, with consumer price inflation above 2%, and even whether rate cutting was the answer to what seemed like a different set of problems. Bank lending standards to businesses and consumers were tightening. The asset-backed commercial paper market continued to shrink. Financial institutions were writing down mortgage backed securities in billions of dollars at a time. Home prices were still falling.

U.S. equities, represented by the Standard & Poor’s 500® Composite Stock Price Index(2) (“S&P 500® Index”) including dividends, had at last breached their March 2000 record in May 2007 and the S&P 500® Index proceeded fitfully to its best level yet on July 19, 2007, reassured by better than expected corporate profits. But the prospect of continued takeover activity, that other great pillar of stock market support worldwide, vanished with the liquidity required to fund it, as the events described above played out. This and general risk aversion took the S&P 500® Index down about 9.5% in the next 19 trading sessions. Recovery was swift after rate cut expectations set in, with a rise of nearly 3% in response to the pleasant surprise on September 18, 2007, and a new all time record close on October 9, 2007. It didn’t last. The financials sector led third quarter S&P 500 earnings lower by about 9% year over year and with growing doubts that any real progress out of the crisis was being made, the same sector dragged the S&P 500® Index down sharply in

2

Table of Contents

November 2007, leading to a return of (2.3)% for the six-month period ended November 30, 2007.

Internationally, the MSCI Japan® Index(3) fell 12.0% in the first half of the fiscal year. As the period started gross domestic product (“GDP”) was already contracting, while consumer prices and wages maintained a downward drift almost without interruption through November 2007. Additionally, the unwinding of carry trades boosted the yen and threatened exports. The MSCI Europe ex UK® Index(4) returned (4.9)% over the same period. A rally on continuing merger and acquisition activity and record low Eurozone unemployment, succumbed to nervousness in mid-July 2007, after another rate increase and turned into a rout as the sub-prime debacle unfolded. The MSCI UK® Index(5) retreated 2.1% after stocks initially surged into the summer, shrugging off a rate increase to a six-year high as a robust service sector and merger and acquisition activity bolstered sentiment. The August 2007 slide then was even more violent than in continental Europe.

(2) The S&P 500® Index is an unmanaged index that measures the performance of securities of approximately 500 of the largest companies in the United States.

(3) The MSCI Japan® Index is a free float-adjusted market capitalization index that is designed to measure developed market equity performance in Japan.

(4) The MSCI Europe ex UK® Index is a free float adjusted market capitalization index that is designed to measure developed market equity performance in Europe, excluding the UK.

(5) The MSCI UK® Index is a free float-adjusted market capitalization index that is designed to measure developed market equity performance in the UK.

All indices are unmanaged and investors cannot invest directly in an index.

Past performance does not guarantee future results. The performance quoted represents past performance. Investment return and principal value of an investment will fluctuate, and shares, when redeemed, may be worth more or less than their original cost. The Funds’ performance is subject to change since the period’s end and may be lower or higher than the performance data shown. Please call (800) 992-0180 or log on to www.ingfunds.com to obtain performance data current to the most recent month end.

Market Perspective reflects the views of ING’s Chief Investment Risk Officer only through the end of the period, and is subject to change based on market and other conditions.

3

Table of Contents

ING Real Estate Fund (the “Fund”) seeks total return consisting of long-term capital appreciation and current income. The Fund is managed by T. Ritson Ferguson, CFA and Joseph P. Smith, CFA, Portfolio Managers, both of ING Clarion Real Estate Securities L.P. — the Sub-Adviser.

Performance: For the six months ended November 30, 2007, the Fund’s Class A shares, excluding sales charges, provided a total return of (14.43)% compared to the Morgan Stanley Capital International U.S. REIT Index(1) (“MSCI U.S. REIT® Index”), which returned (15.02)%, for the same period.

Portfolio Specifics: The last six months have been a difficult period for real estate stocks as concerns regarding an economic slowdown have weighed heavily on the markets. Market angst regarding conditions in the U.S. housing market and the sub-prime lending market washed over to real estate stocks, which we believe to be unwarranted as commercial property fundamentals have remained solid and we continue to see earnings growth in 2008 to be at or above long-term sector averages.

The Fund outperformed its benchmark for the six-month period as the result of strong security selection. The Fund’s exposure to the industrial, mall, shopping center, hotel and healthcare sectors contributed to positive relative performance for the period. The Fund’s exposure to the office sector was the only relative detractor from performance during this period. The Fund maintained an average overweight to the mall, hotel and office sectors during the period and maintained an average underweight to the industrial, shopping center, healthcare, apartment and storage sectors. Allocations to the apartment and mall sectors added to relative performance, while allocations to the industrial and office sectors hindered relative performance. Current sector positioning, at November 30, 2007, is highlighted by overweights to the mall, healthcare, office and shopping center sectors and underweights to the industrial, apartment and storage sectors.

The top performing stock during the period was Hilton Hotels Corp., which appreciated sharply as a result of the announcement during the summer that it would be taken private by the Blackstone Group. Additionally, shopping center real estate investment trusts (“REITs”) Federal Realty and Tanger Factory Outlet Centers, Inc., healthcare REITs Ventas, Inc. and Nationwide Health Properties, Inc., as well as mall REIT Taubman Centers, Inc. were outperformers in a down market, contributing to relative performance. Office REITs SL Green Realty Corp. and Highwoods Properties, Inc., and apartment REIT Post Properties, Inc. were Fund holdings that underperformed during this period.

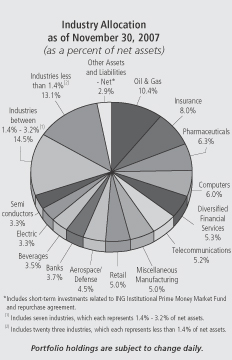

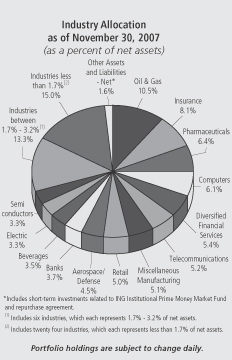

Industry Allocation

Current Strategy and Outlook: When recently assessing Fund strategy, we considered three scenarios which center on different outlooks for the U.S. economy and implications for real estate company performance in the coming months. The most pessimistic scenario assumed the U.S. falls into recession and the most optimistic scenario assumed only a minor slow down in U.S. economic growth, consistent with the prevailing consensus.

In assessing the real estate market environment, the scenario to which we ascribed the greatest probability (50%), sees U.S. gross domestic product (“GDP”) growth at 1.0% in 2008 and no recession. We believe the Federal Reserve will remain accommodative, with up to a further 50 basis point (0.5%) reduction in the federal funds rate over the coming year. From a bottom-up standpoint, we project growth in cash flow per share among the companies we cover and estimate a further rise in cap rates, with a resulting decrease in net asset values (“NAV”). The “good news” from a valuation standpoint is that our increase in cap rates is already reflected in current pricing. The “bad news” is that sentiment remains fragile amid macro-economic crosscurrents.

Fund strategy has seen a shift to a more defensive positioning in recent months, trimming exposure from more economically-sensitive sectors (hotels, apartments and storage) and adding exposure to less economically-sensitive sectors (healthcare, malls and shopping centers), given the current economic environment, our forward earnings outlook, and view of relative valuations.

The rationale for a listed property strategy remains very much intact, including diversification via low correlation to broad equities and bonds, continued strong property fundamentals, and attractive current dividend yields (4.7% average REIT dividend yield, versus a 4% 10-Year Treasury yield). More importantly, current valuations relative to private market real estate are quite favorable, as we estimate U.S. property companies are currently trading at an average 14% discount to their NAV.

The approximate 30% sell-off from February’s peak is reminiscent of the corrections in the early and late 90’s (August 1989 to October 1990 and January 1998 to November 1999), each of which saw a peak-to-trough decline in excess of -20%. Both of these previous corrections were followed by fairly sharp rebounds in the twelve months after the market bottom (36% in the first case and 22% in the second).

It is important to understand the differences between this and previous corrections. Today, the U.S. REIT universe consists primarily of companies that we believe to have strong balance sheets

Top Ten Holdings

| Simon Property Group, Inc. | 9.3% |

| Prologis | 6.9% |

| Boston Properties, Inc. | 6.0% |

| Vornado Realty Trust | 4.6% |

| Federal Realty Investment Trust | 4.4% |

| Regency Centers Corp. | 4.2% |

| General Growth Properties, Inc. | 4.1% |

| Ventas, Inc. | 4.1% |

| Host Hotels & Resorts, Inc. | 3.9% |

| SL Green Realty Corp. | 3.6% |

Portfolio holdings are subject to change daily.

and to have been prudent capital allocators — unlike the 1998-99 situation when many (if not most) REITs were in the midst of huge acquisition programs as part of the “pie-eating” philosophy prevailing at the time encouraging companies to take full advantage of the open equity window offered by Wall Street. In our view, today’s companies have been very sparing issuers of new equity and have had fairly modest acquisition programs, leaving very few in distressed situations.

In our opinion, the market has priced in a pessimistic scenario that is likely beyond what the actual experience will be in terms of economic slowdown and changes in commercial real estate valuations. While it is always possible to imagine scenarios that are even worse than expected, it now appears to us that much of the bad news is already built in to the stock prices and that this is looking like a buying opportunity to us, especially since nobody has the courage to step up and buy. It feels more like capitulation and panic than rational selling. An interesting arbitrage has opened up between public and private market real estate affording investors who are not faint-of-heart, given the high volatility of market prices, an opportunity to buy real estate now in the public market at very attractive relative valuations.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Fund may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

4

Table of Contents

ING Fundamental Research Fund (the “Fund”) seeks to maximize total return. The Fund is managed by Christopher Corapi, Portfolio Manager, of ING Investment Management Co. — the Sub-Adviser.

Performance: For the six months ended November 30, 2007, the Fund’s Class A shares, excluding sales charges, provided a total return of (2.12)% compared to Standard & Poor’s 500® Composite Stock Price Index(1) (“S&P 500® Index”), which returned (2.33)%, for the same period.

Portfolio Specifics: The Fund benefited the most from favorable sector allocation decisions, particularly by underweighting financials and consumer discretionary while overweighting technology. Stock selection in the financial, industrials and healthcare sectors was another contributor to performance. The Fund was hurt by stock selection in the consumer discretionary and consumer staples sectors.

Among the stocks that contributed most to return within financials were Assurant, Inc. and Principal Financial Group, Inc. Assurant, Inc., a niche insurance player, benefited from the turmoil in the sub-prime mortgage market. Their dominant position in the force-placed homeowners market expanded as credit worsened. Principal Financial Group, Inc. had strong fund flows in their 401(k) business. Additionally, their life and health insurance businesses improved dramatically from last quarter.

Within health care, Covance, Inc. and Merck & Co., Inc. contributed meaningfully to results. Pharmaceutical companies are outsourcing research to contract research organizations such as Covance, Inc. Covance, Inc., an industry leader in toxicology services in drug develop-

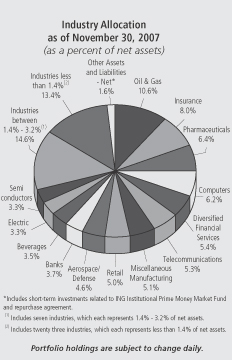

Industry Allocation

ment, is benefiting from this trend, especially as the demand for toxicology services is rising. Merck & Co., Inc. reported positive quarterly results beating Wall Street estimates. The firm has executed well on its pipeline development and gotten drug approvals at the FDA. In industrials, our investment in Foster Wheeler (sold) experienced strong growth abroad and was recently awarded new power contracts.

The stocks that detracted most from return in the consumer discretionary sector were Children’s Place, Liz Claiborne, Inc. and Macy’s, Inc. We exited our position in Children’s Place after the firm violated its newly re-signed contract with Disney. An accounting scandal also surfaced damaging the stock. We sold Macy’s, Inc. as the current credit crunch dampened our thesis that Macy’s, Inc. was a strong takeout candidate. Liz Claiborne, Inc. has suffered along with the entire retail group as fears of a macroeconomic slowdown and poor weather have weighed heavily on the company’s outlook. We believe the firm’s recent business divestures and reallocation of resources to its main brands are positive potential catalysts for the stock.

Within consumer staples, Fomento Economico Mexicano S.A.B. de C.V. (“Fomento”) (sold) was a drag on performance. The hurricanes in Mexico dampened demand for beer. To combat weaker beer sales, Fomento and their competitors aggressively dropped prices pressuring margins.

Current Strategy and Outlook: Currently, the Fund is positioned in companies that we believe have strong or improving competitive positions, robust end markets or superior capital allocation opportunities. We believe each stock possesses an attractive valuation and a clear catalyst to improve it.

Top holdings include XTO Energy, Inc., Google, Inc., Intel Corp., Microsoft Corp. and Merck & Co., Inc. (mentioned above). XTO Energy has consistently grown its reserve base. We believe this low cost producer will continue to generate enough cash to fund its own growth. Furthermore, we have high confidence in XTO’s management. We believe that the Google’s IT invest-

| ExxonMobil Corp. | 5.2% |

| Microsoft Corp. | 3.5% |

| Google, Inc. — Class A | 3.0% |

| AT&T, Inc. | 2.8% |

| Intel Corp. | 2.7% |

| Lehman Brothers Holdings, Inc. | 2.5% |

| Altria Group, Inc. | 2.5% |

| Merck & Co., Inc. | 2.3% |

| General Electric Co. | 2.2% |

| Johnson & Johnson | 2.1% |

| * | Excludes short-term investments related to ING Institutional Prime Money Market Fund. |

Portfolio holdings are subject to change daily.

ments in new product development such as its mobile phone initiatives as well as its online advertising business may help drive growth going forward. We expect the PC cycle to be longer and stronger than Wall Street expectations boosting Intel and Microsoft. Strong unit growth in PC shipments and emerging market growth are potential catalysts.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Fund may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

5

Table of Contents

ING LargeCap Growth Fund (the “Fund”) seeks long-term capital appreciation. The Fund is managed by Andrew J. Schilling, Portfolio Manager of Wellington Management Company, LLP — the Sub-Adviser.

Performance: For the six months ended November 30, 2007, the Fund’s Class A shares, excluding sales charges, provided a total return of 5.46% compared to the Russell 1000® Growth Index(1) and the Russell 1000® Index(2), which returned 2.24% and (2.56)%, respectively, for the same period.

Portfolio Specifics: The Fund’s outperformance was driven by security selection; sector allocation, a result of bottom-up stock selection, had a negligible effect on relative performance, as overweight positions in strong materials and information technology stocks and an underweight in lagging consumer discretionary stocks was largely offset by an overweight among trailing telecommunication services stocks. Selection was particularly strong in the industrials and materials sectors.

Top contributors to relative returns included Suntech Power Holdings Co., Ltd. (industrials), Transocean, Inc. (energy), Fluor (industrials), and Vale, previously known as Cia Vale do Rio Doce, (materials). Chinese solar manufacturer Suntech Power Holdings Co., Ltd. saw its shares gain after higher-than-expected quarterly earnings led to upward earnings revisions. Transocean, Inc., the world’s largest offshore drilling firm, is benefiting from high day rates, strong rig utilization, record backlog, and a strong financial position. We believe the company is well positioned in a strong industry cycle for international oil and gas services. Engineering and construction company Fluor reported solid earnings, led by strength in oil and gas, power generation, and infrastructure projects. Fluor

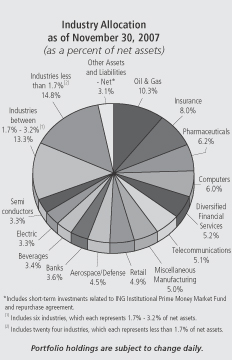

Industry Allocation

remains favorably positioned with a healthy project pipeline and a series of large contract wins. Brazilian metals and mining company Vale’s shares moved sharply higher on strength in iron ore prices. The firm is benefiting from solid iron ore fundamentals as strong Chinese demand sustains tight capacity and a favorable pricing environment. Top absolute contributors during the period included consumer electronics company Apple and search giant Google, Inc.

NII Holdings, Inc. (telecommunication services), Kohl’s Corp. (consumer discretionary), and Manpower, Inc. (industrials) were among the top detractors from relative and absolute performance during the period. NII Holdings, Inc. a wireless communications company primarily serving Latin America, saw its stock fall on concerns of rising push-to-talk competition in Mexico. We believe the market is underestimating subscriber growth trends and margin expansion potential. Specialty department store company Kohl’s Corp. saw its shares decline with disappointing same-store-sales trends and investor concerns about overall consumer spending. We believe that new store growth and margin expansion opportunities could benefit the shares going forward and maintain a position in the stock. Shares in staffing services company Manpower, Inc. moved lower due to concerns of a weaker outlook for U.S. business growth. We believe that the global professional staffing outlook remains favorable, particularly outside the U.S.

Current Strategy and Outlook: Our investment approach is very much a “bottom-up” process: we pick one stock at a time based upon the attractiveness of each company’s valuation and fundamentals. As a result of this bottom-up stock selection, we were most overweight industrials and information technology at the end of the period. Our industrials positions favor capital goods companies such as General Dynamics Corp. and Danaher Corp. Significant information technology holdings include software companies Google, Inc. and Electronic Arts, Inc. We remain broadly underweight consumer stocks amid concerns that consumer spending will be negatively impacted by housing market

| Google, Inc. — Class A | 3.6% |

| General Dynamics Corp. | 2.9% |

| Microsoft Corp. | 2.8% |

| Schering-Plough Corp. | 2.4% |

| Apple, Inc. | 2.3% |

| Oracle Corp. | 2.2% |

| Merck & Co., Inc. | 2.0% |

| Danaher Corp. | 2.0% |

| Apollo Group, Inc. — Class A | 2.0% |

| Fluor Corp. | 1.9% |

| * | Excludes short-term investments related to securities lending collateral and U.S. government agency obligation. |

Portfolio holdings are subject to change daily.

turmoil and a slowing economy. We are also underweight healthcare as we reduced our exposure to pharmaceutical firm Schering-Plough and eliminated our position in medical device company Medtronic, Inc.

(2) The Russell 1000® Index is an unmanaged, comprehensive large- cap index measuring the performance of the largest 1,000 U.S. incorporated companies.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Fund may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

6

Table of Contents

ING MidCap Opportunities Fund (the “Fund”) seeks long term capital appreciation. The Fund is managed by Richard Welsh and Jeff Bianchi, Portfolio Managers, both of ING Investment Management Co. — the Sub-Adviser.

Performance: For the six months ended November 30, 2007, the Fund’s Class A shares, excluding sales charges, provided a total return of 3.91% compared to the Russell Midcap® Growth Index(1) and the Russell Midcap® Index(2), which returned (1.60)% and (5.79)%, respectively, for the same period.

Portfolio Specifics: The market was adversely affected by ongoing sub-prime and credit problems and a spike in crude oil prices, which hovered near $100 a barrel by period-end. The extent of decline was limited by a 0.75% reduction in the federal funds rate, which occurred in two phases. Also helpful was the expectation that additional rate relief was coming, to forestall significant damage to the real economy from the credit crisis.

The telecommunication services and consumer discretionary sectors led the market lower, falling 15% and 11%, respectively. The decline in the telecommunication services sector was due in part to increased price competition and slower line growth overall. Consumer discretionary stocks started discounting slower consumer spending as a consequence of tighter credit standards, higher energy prices and lower confidence. Financials were led lower by overall credit issues and large write-downs of assets.

Rising crude oil prices provided a positive backdrop for the energy sector,

Industry Allocation

which gained the most at nearly 8%. The industrial and health care sectors had modest gains with help from construction and engineering and life sciences industries.

The Fund’s out performance was primarily due to stock selection, particularly in the consumer discretionary, industrials, healthcare and financial sectors. The Fund’s underweighting of the consumer discretionary sector also contributed to return. Growth factors utilized in our stock selection process, such as earnings momentum and price momentum, were effective prognosticators of stock performance.

Kyphon, Inc., Cameron International Corp., and McDermott International, Inc. made equivalent contributions to returns. Kyphon, Inc.’s shares benefited from a takeover by Medtronic, Inc. Cameron International Corp.’s shares reacted to robust demand for oil equipment as indicated by a record deep sea oil equipment order backlog. McDermott International, Inc. is also experiencing strong order backlogs for engineering and construction energy services. The company reported stronger than expected earnings for the second and third quarters.

Peabody Energy Corp. underperformed as mild summer weather hurt coal demand and caused an inventory build-up and pricing pressures. Phillips-Van Heusen shares were weak on concern that the outlook could be hurt by weakness in retail. Gartner performed poorly because earnings expectations were reduced to the low end of the projected range as a consequence of higher discretionary spending.

Current Strategy and Outlook: Following three months of gains, the equity market retreated in November as investors pondered the impact of financial dislocations on the outlook for real growth and profits. We anticipate profit

Top Ten Holdings*

| Hologic, Inc. | 2.7% |

| NRG Energy, Inc. | 2.6% |

| Hess Corp. | 2.3% |

| TJX Cos., Inc. | 2.2% |

| Fiserv, Inc. | 2.2% |

| St. Jude Medical, Inc. | 2.1% |

| Respironics, Inc. | 2.1% |

| Gildan Activewear, Inc. | 2.0% |

| Corrections Corp. of America | 1.9% |

| ITT Corp. | 1.8% |

| * | Excludes short-term investments related to securities lending collateral. |

Portfolio holdings are subject to change daily.

growth to slow into 2008 largely due to, in our opinion, the impact of reduced credit availability on personal spending gains. Despite this, the market, we believe should be supported by strong corporate balance sheets, global growth and rate reductions by central banks. As a result, companies that exhibit the strong business characteristics we find attractive should be rewarded with expanding, if not premium, valuations.

(2) The Russell Midcap® Index is an unmanaged index that measures the performance of the 800 smallest companies in the Russell 1000® Index, which represents approximately 26% of the total market capitalization of the Russell 1000® Index.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Fund may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

7

Table of Contents

ING Opportunistic LargeCap Fund (the “Fund”) seeks capital appreciation. The Fund is managed by Omar Aguilar, Ph.D., Portfolio Manager, and Vincent Costa, CFA both of ING Investment Management Co. — the Sub-Adviser.

Performance: For the six months ended November 30, 2007, the Fund’s Class A shares, excluding sales charges, provided a total return of (1.07)% compared to the Russell 1000® Growth Index(1), which returned 2.24%, for the same period.

Portfolio Specifics: The reporting period was difficult for ING quantitative equity, as most of our strategies underperformed their benchmarks.

The dislocation of quantitative funds was driven by changes in liquidity that impacted the risk and leverage of many quantitative managers. During the latter part of June and early July, we saw a clear transition in market leadership from value to growth and from small-cap to large-cap, in combination with a spike in volatility triggered by turmoil in the sub-prime mortgage market.

Quantitative managers with significant amounts of leverage were forced to unwind positions, which affected all our strategies during the first week of August. In fact, much of our negative

performance came from poorly ranked stocks that were underweighted in our funds, suggesting that quant hedge fund managers were willing to sell their highly ranked stocks to cover their short positions. After a tough summer, performance was bouncing back by the end of November, as we recalibrated factor weights in our quantitative model to adjust to the new “growth” market environment.

Sector positions that detracted from results for the period included underweight positions in the consumer staples and information technology sectors. These losses were partially offset by an underweight position in financials and an overweight position in the materials sector. Security selection detracted from performance in the information technology, healthcare and consumer staples sectors. These losses were partially offset by security selection in the telecommunication and materials sectors.

The most significant detractors for the period were in the healthcare sector, with names like WellCare Group (sold) which lost more than half its value in a day due to fraud investigations by the Securities and Exchange Commission and King Pharmaceuticals Inc. (sold) hurting performance the most. The top contributors included China Mobile Ltd. and Mosaic Co.

Current Strategy and Outlook: Our research builds structured funds of stock with fundamental characteristics that we believe will translate into performance advantage over the benchmark. Our analysis positions the Fund to capitalize on high quality companies with superior business momentum, strong earnings and attractive valuations.

Top Ten Holdings

| Humana, Inc. | 3.8% |

| Microsoft Corp. | 3.6% |

| Lockheed Martin Corp. | 3.4% |

| Amazon.com, Inc. | 3.2% |

| Aetna, Inc. | 3.2% |

| Apple, Inc. | 3.1% |

| Express Scripts, Inc. | 2.9% |

| Intel Corp. | 2.7% |

| Harris Corp. | 2.7% |

| Mosaic Co. | 2.6% |

Portfolio holdings are subject to change daily.

We are currently overweight in the materials and telecom services sectors and underweight in the financials, consumer staples and healthcare sectors.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Fund may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

8

Table of Contents

ING SmallCap Opportunities Fund (the “Fund”) seeks capital appreciation. The Fund is managed by Steve Salopek, Portfolio Manager of ING Investment Management Co. — the Sub-Adviser.

Performance: For the six months ended November 30, 2007, the Fund’s Class A shares, excluding sales charges, provided a total return of (2.83)% compared to the Russell 2000® Growth Index(1) and the Russell 2000® Index(2), which returned (3.25)% and (8.82)%, respectively, for the same period.

Portfolio Specifics: During the reporting period, concerns about credit and global growth hurt smaller U.S. stocks and resulted in increased market volatility. Concerns about credit availability affected banks and financial firms and began to spread into the consumer discretionary sector, including retailers and retail real estate investment trusts (“REITS”).

Utilities was the best performing sector for the period; followed by materials, which benefited from a weakening U.S. dollar and international growth. Telecommunication services and healthcare, which are perceived to be more stable businesses, also helped performance.

Stock selection was the main performance driver over the quarter. Selection within healthcare and financials contributed most to results; selection in consumer discretionary and consumer staples detracted the most.

Kyphon, Inc. and Alexion Pharmaceuticals contributed significantly to performance over the period. Kyphon, Inc. is a global medical device company specializing in the design, manufacture and marketing of medical devices to treat and restore spinal anatomy using minimally invasive technologies. During the reporting period, Kyphon, Inc. and

Industry Allocation

Medtronic, Inc. announced that Medtronic, Inc. will acquire all of the outstanding shares of Kyphon, Inc. for $71 per share, which represents a 34% premium to the stock price. We sold the Fund’s position.

Alexion Pharmaceuticals develops biopharmaceuticals for patients with serious and life-threatening medical conditions. The company’s first product, Soliris, for the treatment of PNH, received approval from the U.S. FDA and the European regulatory during the period. The stock performed well as initial results from the launch of Soliris exceeded market expectations.

Xyratex Ltd. and Pantry, Inc. were two of the largest detractors from performance over the period. Xyratex Ltd., which makes test equipment for disk drives, had a downturn in sales, as its largest customer, Seagate, has temporarily stopped placing orders. Seagate acquired Maxtor, which manufactured disk drives, and is utilizing Maxtor’s test equipment rather than placing new orders. We continue to hold a position in the company, as we believe that business will turn positive again once Seagate has worked through their excess capacity and resumes placing orders with Xyratex.

Pantry, Inc., which operates a convenience store chain in the southeastern United States, reported earnings below expectations due to problems with the level of gas margins they were able to achieve. The Fund continues to hold its position, as we believe the company’s valuation is compelling based on its unchanged longer-term fundamentals. What’s more, we believe the company will be able to achieve better gas margins.

Current Strategy and Outlook: We continue to focus on companies with strong balance sheets and cash flow generation capabilities. We believe the Fund is defensively positioned in the financials sector, with exposure to banks, diversified financials and insurance. We are underweight REITS, as we think the real estate market is overextended. Within healthcare, the Fund remains positioned to gain from strong demand for behavioral health

| FTI Consulting, Inc. | 1.4% |

| Hologic, Inc. | 1.3% |

| Psychiatric Solutions, Inc. | 1.2% |

| Moog, Inc. | 1.1% |

| Verigy Ltd. | 1.1% |

| Greif, Inc. | 1.1% |

| Vistaprint Ltd. | 1.1% |

| Semtech Corp. | 1.1% |

| Formfactor, Inc. | 1.1% |

| Digital Realty Trust, Inc. | 1.1% |

| * | Excludes short-term investments related to ING Institutional Prime Money Market Fund and securities lending collateral. |

providers, healthcare equipment suppliers with niche franchises and disease-management providers. We are underweight biotech stocks due to risk and valuation considerations, and we have no exposure to Medicaid managed-care providers due to the, in our opinion, deteriorating reimbursement environment. Our technology exposure is in software and services, hardware and equipment, and semiconductors.

(2) The Russell 2000® Index is an index that measures the performance of securities of small U.S. companies.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Fund may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

9

Table of Contents

ING Financial Services Fund (the “Fund”) seeks long-term capital appreciation. The Fund is managed by Robert M. Kloss and Steven L. Rayner, Portfolio Managers, of ING Investment Management Co. — the Sub-Adviser.

Performance: For the six months ended November 30, 2007, the Fund’s Class A shares, excluding sales charges, provided a total return of (13.42)% compared to Standard & Poor’s 500 Financials Index(1) (“S&P 500 Financials Index”) and the Standard & Poor’s 500® Composite Stock Price Index(2) (“S&P 500® Index”), which returned (16.79)% and (2.33)%, respectively, for the same period.

Portfolio Specifics: Financial stocks were hit hard during the six month period, as systemic liquidity and credit concerns emerged and snow-balled. Those financial stocks most directly exposed to housing and credit risk were among the worst performers. The Fund benefited from its significant overweight position in the insurance area, as these stocks generally held up well, largely by virtue of having less exposure to those risks. The Fund’s underweight position in the mortgage finance sub-sector also helped relative performance, as most of these stocks sold off with the declines in the housing and credit outlook.

The Fund’s outperformance arose from security selection. The Fund benefited from positions in life/health insurers AFLAC, Inc., Principal Financial Group and StanCorp Financial Group — these stocks were viewed as havens from the most troublesome areas of credit risk. The Fund also benefited from a position added during the period in niche insurer Assurant Inc., which derives a significant portion of its earnings from businesses that benefit from worsening housing credit conditions.

Among capital markets-oriented financial stocks, some stocks suffered while others, whose earnings streams were viewed as more insulated from direct effects of the crisis, performed well. Stocks fitting the latter description

included Deutsche Bourse AG, the European stock exchange and trading system provider; custodian/securities servicer State Street Corp.; and Lazard Ltd., an international investment banking advisor that takes little direct balance sheet risk compared to traditional investment banks. The Fund also benefited from its position in asset manager Nuveen (sold), which was acquired during the period.

The biggest individual detractor from performance this period was E*Trade Financial Corp. (sold), which declined as the company’s banking operations were forced to take significant asset write-downs and hopes of industry consolidation faded. The Fund’s position in bond guarantor MBIA, Inc. also hurt results as ratings downgrades of securities insured by the company raised questions about its own rating and capital adequacy.

Other individual names that hindered performance included smaller positions in office/industrial REIT Liberty Property Trust, bond insurer Security Capital Assurance, mortgage insurer MGIC and commercial lender CIT Group, the latter three of which we sold during the period.

Current Strategy and Outlook: During the summer and early fall we reduced our credit- and capital markets-exposed holdings in favor of stocks we believe will have defensive characteristics in a vulnerable market.

We remain cautious regarding companies that depend on a more benign credit environment or strong economic growth. Though further federal interest rate relief may be forthcoming, we continue to believe that the housing and credit-related downturn is more likely to worsen and spread to other parts of the economy.

Our primary issue is now this: to what extent has the market already discounted the bad news to come? We are still positioned defensively, but are evaluating the possibility that a combination of Federal Reserve actions, other government attempts to provide relief to the housing market, private equity capital infusions to prominent financial companies, more attractive valuations or improved liquidity in the financial system could combine to cause a turn in financial

| JPMorgan Chase & Co. | 5.8% |

| Wells Fargo & Co. | 5.3% |

| Bank of America Corp. | 5.0% |

| American International Group, Inc. | 4.9% |

| US Bancorp. | 4.5% |

| Citigroup, Inc. | 3.7% |

| Wachovia Corp. | 3.3% |

| PNC Financial Services Group, Inc. | 2.9% |

| State Street Corp. | 2.8% |

| Protective Life Corp. | 2.8% |

Portfolio holdings are subject to change daily.

stocks. Our current assessment is that it’s too early to massively bottom-fish — bad credit results make a tough headwind for financial stocks to overcome — but in the context of an extremely dynamic sector, this view could change at any point.

(2) The S&P 500® Index is an unmanaged index that measures the performance of securities of approximately 500 large-capitalization companies whose securities are traded on major U.S. stock markets.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Fund may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

10

Table of Contents

ING LargeCap Value Fund (the “Fund”) seeks long-term capital appreciation. The Fund is managed by Brandes Investment Partners, L.P. (“Brandes”), the Sub-Adviser. Brandes’ Large Cap Investment Committee is responsible for making day-to-day investment decisions for the Fund. The six voting members of the Large Cap Investment Committee are: Glenn Carlson, CFA, Chief Executive Officer, Brent Woods, CFA, Managing Director — Investments, Amelia Maccoun Morris, CFA, Director — Investments, Keith Colestock, CFA, Director — Investments, W. James Brown, CFA, Director — Investments, and Brent Fredberg, Senior Analyst.

Performance: For the six months ended November 30, 2007, the Fund’s Class A shares, excluding sales charges, provided a total return of (17.24)% compared to the Russell 1000® Value Index(1) and the Russell 1000® Index(2), which returned (7.33)% and (2.56)%, respectively, for the same period.

Portfolio Specifics: Price declines for the Fund’s holdings in the thrifts & mortgage finance industry weighed heaviest on performance during the six-month period. Countrywide Financial Corp., Federal Home Loan Mortgage Corp. (“Freddie Mac”), and Washington Mutual, Inc. were some of the positions from this industry enduring the greatest share price declines. Unfavorable results for securities in the media, commercial banking, and communications equipment industries also had a negative effect on returns. The largest detractors from these industries included Gannett Co., Inc. (media), Popular, Inc. (commercial banking), and Alcatel-Lucent (France — communications equipment). Fund holdings in the household durables, insurance, and IT services industries also tended to lose ground during the period.

Industry Allocation

While a number of the Fund’s holdings declined over the trailing six months, select positions posted gains. Advances for Intel Corp. (semiconductors & semiconductor equipment), Microsoft Corp. (software), and Johnson & Johnson (pharmaceuticals) helped to offset some of the Fund’s negative results.

On a relative basis, the Fund’s stock selection and allocation within the thrifts & mortgage industry weakened returns. The Fund’s lack of exposure to the oil, gas, & consumable fuels industry, coupled with poor relative performance for holdings in the media and communications equipment industries, proved unfavorable. Keep in mind that industry allocations are not top-down forecasts, but a residual of our company-by-company analysis.

During the period, we sold our positions in companies such as International Business Machines Corp. (computers & peripherals), Tribune Company (media), and Merck & Co., Inc. (pharmaceuticals), to pursue other investment opportunities. We used the proceeds from these sales to purchase shares of new holdings at prices that we consider attractive. During the period, we purchased Countrywide Financial Corp. (thrifts & mortgage finance), Federal Home Loan Mortgage Corp. (thrifts & mortgage finance), and Home Depot, Inc. (specialty retail) at what we believe to be discounts to their true value.

As a result of select buying and selling, as well as changes in the prices of holdings, many of the Fund’s industry exposures shifted. For example, exposure to the thrifts & mortgage finance industry increased as a result of new purchases, while exposure to the computers & peripherals and diversified telecommunication services industries declined amid select parebacks and sales. As of November 30, 2007, the Fund retained its greatest exposure to the pharmaceuticals industry.

Top Ten Holdings*

| Sara Lee Corp. | 4.3% |

| Pfizer, Inc. | 3.9% |

| Amgen, Inc. | 3.9% |

| Boston Scientific Corp. | 3.9% |

| Ford Motor Co. | 3.7% |

| H&R Block, Inc. | 3.7% |

| Safeway, Inc. | 3.6% |

| Micron Technology, Inc. | 3.3% |

| Gannett Co., Inc. | 3.2% |

| Whirlpool Corp. | 3.1% |

| * | Excludes short-term investments related to securities lending collateral. |

Portfolio holdings are subject to change daily.

Current Strategy and Outlook: Keep in mind that industry exposures are the direct result of purchase and sell decisions made on a bottom-up, company-by-company basis. While we continue to monitor short-term events in U.S. equity markets, our investment philosophy focuses on company-by-company analysis. We take a long-term perspective and believe that none or very little of the short-term “market news” provides useful information to investors. Instead, we remain focused on purchasing large-cap stocks at discounts to our estimates of their intrinsic values. We believe that this approach will provide patient investors with favorable returns over the long term.

(2) The Russell 1000® Index measures the performance of the largest 1,000 U.S. incorporated companies.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Fund may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

11

Table of Contents

ING SmallCap Value Choice Fund (the “Fund”) seeks maximum long term capital appreciation. The Fund is managed by Phyllis G. Thomas, CFA, Managing Director, of NWQ Investment Management Company, LLC (“NWQ”), Robert A. Schwarzkopf, CFA & Sandi L. Gleason, CFA both of Kayne Anderson Rudnick Investment Management, LLC (“Kayne”) and Omar Aguilar, Ph.D. & Vincent Costa, CFA both of ING Investment Management Co. (“ING IM”) — the Sub-Advisers.

Performance: For the six months ended November 30, 2007, the Fund’s Class A shares, excluding sales charges, provided a total return of (14.48)% compared to the Russell 2000® Value Index(1) and the Russell 2000® Index(2), which returned (14.38)% and (8.82)%, respectively, for the same period.

Portfolio Specifics: NWQ — The U.S. equity markets experienced significant turbulence during the six months ending November 30, 2007, as concerns over rising defaults within the sub-prime mortgage industry broadened adversely affecting the financial markets. After the extreme market instability in July and August, the stock market rallied strongly into October in anticipation of an additional interest rate cut by the U.S. Federal Reserve Board (the “Fed”). Growing problems in the banking system, however, triggered a renewal of the summer weakness in November as witnessed in the decline of the equity markets and the extreme day-to-day volatility.

The Fund underperformed the Russell 2000® Index and Russell 2000® Value Index over the reporting period. Investments in the financial sector, particularly in the mortgage industry, were the main detractors from performance during the period. The largest detractors included RAIT Financial Trust, Franklin Bank Corp. and Griffon Corp. Helping to partially offset these declines were several investments that posted strong gains, particularly in the energy and consumer discretionary sectors. The Fund’s top performers included Denbury Resources, Inc., Fossil, Inc., and WD-40 Co. Small and mid capitalization companies in general underperformed compared to large capitalization stocks, while growth stocks significantly outperformed value stocks.

Industry Allocation

Kayne — The sixth months ending November 30, 2007, were marked by a renewed focus on risk due to the widespread credit crunch that emerged with the failure of sub-prime mortgage securitizations, a declining housing market, and record high oil prices. The difficulties in the credit markets and economy worked to the advantage of high-quality stocks. Stocks with A rankings by Standard & Poor’s held up better in the market decline, as did those with strong credit ratings. Consumer discretionary and basic materials contributed the most to the Fund’s outperformance due to strong stock selection. Utilities detracted the most from performance due to the Fund’s underweight in this sector.

ING IM — The Fund’s underperformance was primarily due to its “deep value” approach, which fell out of favor during the reporting period. In the last several months, we have seen a rotation in style leadership from value to growth stocks. This rotation and the spike in volatility triggered by the sub-prime turmoil forced quantitative managers with significant amounts of leverage to unwind their positions, which hurt many of our strategies. After a tough summer, performance bounced back in the fourth quarter and the Fund had recovered slightly by the end of the reporting period.

Financials and information technology were the worst performing sectors for the period; the Fund’s underperformance in these sectors was primarily due to stock selection.

In the financials sector, overweight positions in real estate companies such as RAIT Financial Trust (sold) and Newcastle Investment Corp. were the greatest detractors from results, losing more than two-thirds and half of their value, respectively. Their losses were due to the downturn in the real estate market resulting from the sub-prime turmoil. Worst detractors in the information technology sector were overweight positions in CMGI, Inc. and Imation (sold), which slipped as they issued lower earnings guidance.

Current Strategy and Outlook: NWQ — We believe the markets appear to be torn between the positive scenario of additional Fed easing in December and the negative scenario of potential stagflation. Falling interest rates are of little benefit as falling home prices are leaving many homeowners with negative equity and thus an inability to refinance their adjustable rate mortgages. This phenomenon combined with sharply rising energy prices suggests a weakening consumer. The most likely outcome, in our opinion, is more aggressive Fed easing. In this more difficult economic environment, risk premiums have clearly been rising from very low levels this spring. We continue to stress test the valuations of our holdings for a more difficult market environment.

Kayne — Investors heightened their focus on credit risk for the first time in roughly five years. Credit spreads between 10-year high-yield bonds and 10-year Treasury bonds widened from 2.7% at the end of May to 5.0% at the end of November. The Fed lowered the federal funds rate two times during this time period, alleviating some market jitters.

We believe the debt markets have become more rational and investors will increasingly be focused on those companies that can grow in a weaker economy without reliance on cheap financing, much like the high quality businesses that comprise our portfolios. As

Top Ten Holdings

| WD-40 Co. | 3.5% |

| Wausau Paper Corp. | 2.7% |

| Lincoln Electric Holdings, Inc. | 2.6% |

| Warren Resources, Inc. | 2.5% |

| Sauer-Danfoss, Inc. | 2.4% |

| Albany International Corp. | 2.4% |

| Griffon Corp. | 2.4% |

| Community Health Systems, Inc. | 2.3% |

| Bob Evans Farms, Inc. | 2.3% |

| Casey’s General Stores, Inc. | 2.3% |

Portfolio holdings are subject to change daily.

always, we endeavor to manage the Fund with the highest quality businesses, outgrowing their markets, purchased at discount values.

ING IM — Our research builds structured funds of stocks with fundamental characteristics that we believe will translate into a performance advantage over the benchmark. Our analysis positions the Fund to capitalize on high-quality companies with superior business momentum, growing earnings and attractive valuations.

The Fund is currently overweight in the information technology and energy sectors and underweight in the financials, industrials and consumer discretionary sectors.

(1) The Russell 2000® Value Index measures the performance of those Russell 2000 companies with lower price-to-book ratios and lower forecasted growth values.

(2) The Russell 2000® Index is an unmanaged index that measures the performance of securities of small U.S. companies.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Fund may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

12

Table of Contents

ING Value Choice Fund (the “Fund”) seeks long-term capital appreciation. The Fund is managed by David B. Iben, CFA, Chief Investment Officer and Managing Director of Tradewinds Global Investors, LLC — the Sub-Adviser.

Performance: For the six months ended November 30, 2007, the Fund’s Class A shares, excluding sales charges, provided a total return of 1.44% compared to the Russell 3000 Value Index(1), Russell Midcap® Value Index(2) and the Russell Midcap® Index(3), which returned (7.92)%, (10.90)% and (5.79)%, respectively, for the same period.

Portfolio Specifics: The materials & processing sector, the Fund’s largest sector weighting, was the best performing sector during the period. Four of the top six performing portfolio holdings over the past six months were all gold mining companies: Newmont Mining Corp., AngloGold Ashanti Ltd. ADR, Newcrest Mining Corp. and Kinross Gold Corp. During the period, the price of gold reached its highest level in 27 years, and many of the gold producers benefited as a result.

The Fund’s best contributors to performance included holdings in the producer durables and energy sectors. AGCO Corp., a manufacturer and distributor of agricultural equipment and related replacement parts, has benefited from a global boom in the agricultural industry. Coal producer Peabody Energy Corp. also gained during the period upon expectations for higher coal prices and robust demand over the next several years. Demand from emerging market countries such as China and India continues and escalating gas prices may encourage users to turn to coal as a cheaper alternative.

The consumer staples sector was the Fund’s worst performing sector during the period, primarily a result of the performance of Tyson Foods Inc., a leading global producer, distributor and marketer of chicken, beef, pork, and

Industry Allocation

prepared foods. The stock was the Fund’s largest individual detractor from performance during the last six month period. The company announced more recently that it was scaling back beef production, as higher cattle prices have squeezed operating margins.

While the Fund outperformed its primary benchmark, other portfolio holdings detracted from performance. The stock price of Levitt Corp., a homebuilding and real estate development company in the Southeastern United States, surged at the end of January after BFC Financial Corp. said it would pay about $286 million for the homebuilder. These gains were more than erased after BFC announced in August that it terminated its merger agreement. New Mexico energy provider PNM Resources, Inc. also suffered due to restructuring costs, higher energy purchasing prices, and weak contributions from its wholesale business. Sanmina-SCI Corporation shares declined significantly in July after the electronics contract manufacturer provided a weak third quarter report and fourth quarter outlook. AbitibiBowater Incorporated was formed in late October as a result of a merger between Abitibi-Consolidated Incorporated and Bowater Incorporated. The company, a producer of coated and specialty papers and newsprint, was the largest among the few Materials & Processing sector holdings that did not perform well. The paper industry as a whole is suffering from poor supply/demand fundamentals.

Current Strategy and Outlook: As the end of the year approaches, we believe concerns caused by the U.S. sub-prime mortgage meltdown and softening housing conditions will continue to work themselves out, and as such, markets will continue to be volatile. Excess money from Federal Reserve and European Central Bank credit injections should find their way into investments with a scarcity of supply, such as oil, commodities and gold. As such, we continue to believe that the long-term supply and demand fundamentals for gold companies are compelling. While many metals and mining positions have shined -with gold prices reaching a 27-year high in September — in real terms, the price of gold is still less than 50 percent of its 1980

| Anglogold Ashanti Ltd. ADR | 5.6% |

| Newmont Mining Corp. | 4.8% |

| Tyson Foods, Inc. | 4.1% |

| Nippon Telegraph & Telephone Corp. ADR | 3.0% |

| Smithfield Foods, Inc. | 2.9% |

| PNM Resources, Inc. | 2.8% |

| Kinross Gold Corp. | 2.6% |

| Coeur d’Alene Mines Corp., 1.250%, due 01/15/24 | 2.6% |

| Allied Waste Industries, Inc. | 2.6% |

| Apex Silver Mines Ltd. | 2.5% |

| * | Excludes short-term investments related to securities lending collateral and U.S. government agency obligation. |

Portfolio holdings are subject to change daily.

high. We also continue to believe the Fund is well positioned worldwide in other strong business franchises — such as in food, agriculture, and basic materials companies — that have the potential to appreciate over the long-term.

(2) The Russell Midcap® Value Index is an unmanaged index that measures the performance of Russell MidCap companies with lower price-to-book ratios and lower forecasted growth values.

(3) The Russell Midcap® Index measures the performance of the 800 smallest companies in the Russell 1000® Index, which represents approximately 26% of the total market capitalization of the Russell 1000® Index.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Fund may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

13

Table of Contents

As a shareholder of a Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, redemption fees, and exchange fees; and (2) ongoing costs, including management fees, distribution and/or service (12b–1) fees, and other Fund expenses. These Examples are intended to help you understand your ongoing costs (in dollars) of investing in a Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Examples are based on an investment of $1,000 invested at the beginning of the period and held for the entire period from June 1, 2007 to November 30, 2007. The Funds’ expenses are shown without the imposition of any sales charges or fees. Expenses would have been higher if such charges were included.

Actual Expenses

The first section of the table shown, “Actual Fund Return,” provides information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second section of the table shown, “Hypothetical (5% return before expenses),” provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in each Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the hypothetical lines of the table are useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

14

Table of Contents

| Beginning | Ending | Expenses Paid | |||||||||||||||

| Account | Account | Annualized | During the | ||||||||||||||

| Value | Value | Expense | Period Ended | ||||||||||||||

| ING Real Estate Fund | June 1, 2007 | November 30, 2007 | Ratio | November 30, 2007* | |||||||||||||

| Actual Fund Return | |||||||||||||||||

| Class A | $ | 1,000.00 | $ | 855.70 | 1.27 | % | $ | 5.89 | |||||||||

| Class B | 1,000.00 | 852.30 | 2.02 | 9.35 | |||||||||||||

| Class C | 1,000.00 | 852.00 | 2.02 | 9.35 | |||||||||||||

| Class I | 1,000.00 | 856.70 | 0.97 | 4.50 | |||||||||||||

| Class O | 1,000.00 | 856.30 | 1.27 | 5.89 | |||||||||||||

| Class Q | 1,000.00 | 855.00 | 1.16 | 5.38 | |||||||||||||

| Hypothetical (5% return before expenses) | |||||||||||||||||

| Class A | $ | 1,000.00 | $ | 1,018.65 | 1.27 | % | $ | 6.41 | |||||||||

| Class B | 1,000.00 | 1,014.90 | 2.02 | 10.18 | |||||||||||||

| Class C | 1,000.00 | 1,014.90 | 2.02 | 10.18 | |||||||||||||

| Class I | 1,000.00 | 1,020.15 | 0.97 | 4.90 | |||||||||||||

| Class O | 1,000.00 | 1,018.65 | 1.27 | 6.41 | |||||||||||||

| Class Q | 1,000.00 | 1,019.20 | 1.16 | 5.86 | |||||||||||||

ING Fundamental Research Fund | |||||||||||||||||

| Actual Fund Return | |||||||||||||||||

| Class A | $ | 1,000.00 | $ | 978.80 | 1.25 | % | $ | 6.18 | |||||||||

| Class B | 1,000.00 | 975.20 | 2.00 | 9.88 | |||||||||||||

| Class C | 1,000.00 | 975.20 | 2.00 | 9.88 | |||||||||||||

| Class I | 1,000.00 | 980.40 | 1.00 | 4.95 | |||||||||||||

| Hypothetical (5% return before expenses) | |||||||||||||||||

| Class A | $ | 1,000.00 | $ | 1,018.75 | 1.25 | % | $ | 6.31 | |||||||||

| Class B | 1,000.00 | 1,015.00 | 2.00 | 10.08 | |||||||||||||

| Class C | 1,000.00 | 1,015.00 | 2.00 | 10.08 | |||||||||||||

| Class I | 1,000.00 | 1,020.00 | 1.00 | 5.05 | |||||||||||||

| * | Expenses are equal to each Fund’s respective annualized expense ratios multiplied by the average account value over the period, multiplied by 183/366 to reflect the most recent fiscal half-year. |

15

Table of Contents

| Beginning | Ending | Expenses Paid | |||||||||||||||

| Account | Account | Annualized | During the | ||||||||||||||

| Value | Value | Expense | Period Ended | ||||||||||||||

| ING LargeCap Growth Fund | June 1, 2007 | November 30, 2007 | Ratio | November 30, 2007* | |||||||||||||

| Actual Fund Return | |||||||||||||||||

| Class A | $ | 1,000.00 | $ | 1,054.60 | 1.45 | % | $ | 7.45 | |||||||||

| Class B | 1,000.00 | 1,051.20 | 2.10 | 10.77 | |||||||||||||

| Class C | 1,000.00 | 1,051.40 | 2.10 | 10.77 | |||||||||||||

| Class I | 1,000.00 | 1,056.70 | 0.99 | 5.09 | |||||||||||||

| Class Q | 1,000.00 | 1,055.60 | 1.23 | 6.32 | |||||||||||||

| Hypothetical (5% return before expenses) | |||||||||||||||||

| Class A | $ | 1,000.00 | $ | 1,017.75 | 1.45 | % | $ | 7.31 | |||||||||

| Class B | 1,000.00 | 1,014.50 | 2.10 | 10.58 | |||||||||||||

| Class C | 1,000.00 | 1,014.50 | 2.10 | 10.58 | |||||||||||||

| Class I | 1,000.00 | 1,020.05 | 0.99 | 5.00 | |||||||||||||

| Class Q | 1,000.00 | 1,018.85 | 1.23 | 6.21 | |||||||||||||

ING MidCap Opportunities Fund | |||||||||||||||||

| Actual Fund Return | |||||||||||||||||

| Class A | $ | 1,000.00 | $ | 1,039.10 | 1.25 | % | $ | 6.37 | |||||||||

| Class B | 1,000.00 | 1,035.70 | 2.00 | 10.18 | |||||||||||||

| Class C | 1,000.00 | 1,035.30 | 2.00 | 10.18 | |||||||||||||

| Class I | 1,000.00 | 1,041.60 | 0.80 | 4.08 | |||||||||||||

| Class Q | 1,000.00 | 1,040.20 | 1.05 | 5.36 | |||||||||||||

| Hypothetical (5% return before expenses) | |||||||||||||||||

| Class A | $ | 1,000.00 | $ | 1,018.75 | 1.25 | % | $ | 6.31 | |||||||||

| Class B | 1,000.00 | 1,015.00 | 2.00 | 10.08 | |||||||||||||

| Class C | 1,000.00 | 1,015.00 | 2.00 | 10.08 | |||||||||||||

| Class I | 1,000.00 | 1,021.00 | 0.80 | 4.04 | |||||||||||||

| Class Q | 1,000.00 | 1,019.75 | 1.05 | 5.30 | |||||||||||||

ING Opportunistic LargeCap Fund | |||||||||||||||||

| Actual Fund Return | |||||||||||||||||

| Class A | $ | 1,000.00 | $ | 989.30 | 1.25 | % | $ | 6.22 | |||||||||

| Class B | 1,000.00 | 984.30 | 2.00 | 9.92 | |||||||||||||

| Class C | 1,000.00 | 985.00 | 2.00 | 9.93 | |||||||||||||

| Class I | 1,000.00 | 989.30 | 1.00 | 4.97 | |||||||||||||

| Hypothetical (5% return before expenses) | |||||||||||||||||

| Class A | $ | 1,000.00 | $ | 1,018.75 | 1.25 | % | $ | 6.31 | |||||||||

| Class B | 1,000.00 | 1,015.00 | 2.00 | 10.08 | |||||||||||||

| Class C | 1,000.00 | 1,015.00 | 2.00 | 10.08 | |||||||||||||

| Class I | 1,000.00 | 1,020.00 | 1.00 | 5.05 | |||||||||||||

| * | Expenses are equal to each Fund’s respective annualized expense ratios multiplied by the average account value over the period, multiplied by 183/366 to reflect the most recent fiscal half-year. |

16

Table of Contents

| Beginning | Ending | Expenses Paid | |||||||||||||||

| Account | Account | Annualized | During the | ||||||||||||||

| Value | Value | Expense | Period Ended | ||||||||||||||

| ING SmallCap Opportunities Fund | June 1, 2007 | November 30, 2007 | Ratio | November 30, 2007* | |||||||||||||

| Actual Fund Return | |||||||||||||||||

| Class A | $ | 1,000.00 | $ | 971.70 | 1.50 | % | $ | 7.39 | |||||||||

| Class B | 1,000.00 | 968.00 | 2.25 | 11.07 | |||||||||||||

| Class C | 1,000.00 | 968.00 | 2.25 | 11.07 | |||||||||||||

| Class I | 1,000.00 | 973.80 | 1.07 | 5.28 | |||||||||||||

| Class Q | 1,000.00 | 972.60 | 1.32 | 6.51 | |||||||||||||

| Hypothetical (5% return before expenses) | |||||||||||||||||

| Class A | $ | 1,000.00 | $ | 1,017.50 | 1.50 | % | $ | 7.57 | |||||||||

| Class B | 1,000.00 | 1,013.75 | 2.25 | 11.33 | |||||||||||||

| Class C | 1,000.00 | 1,013.75 | 2.25 | 11.33 | |||||||||||||

| Class I | 1,000.00 | 1,019.65 | 1.07 | 5.40 | |||||||||||||

| Class Q | 1,000.00 | 1,018.40 | 1.32 | 6.66 | |||||||||||||

ING Financial Services Fund | |||||||||||||||||

| Actual Fund Return | |||||||||||||||||

| Class A | $ | 1,000.00 | $ | 865.80 | 1.27 | % | $ | 5.92 | |||||||||

| Class B | 1,000.00 | 862.50 | 2.02 | 9.41 | |||||||||||||

| Class C | 1,000.00 | 862.70 | 2.02 | 9.41 | |||||||||||||

| Class O | 1,000.00 | 865.80 | 1.27 | 5.92 | |||||||||||||

| Hypothetical (5% return before expenses) | |||||||||||||||||

| Class A | $ | 1,000.00 | $ | 1,018.65 | 1.27 | % | $ | 6.41 | |||||||||

| Class B | 1,000.00 | 1,014.90 | 2.02 | 10.18 | |||||||||||||

| Class C | 1,000.00 | 1,014.90 | 2.02 | 10.18 | |||||||||||||

| Class O | 1,000.00 | 1,018.65 | 1.27 | 6.41 | |||||||||||||

ING LargeCap Value Fund | |||||||||||||||||

| Actual Fund Return | |||||||||||||||||

| Class A | $ | 1,000.00 | $ | 827.60 | 1.45 | % | $ | 6.63 | |||||||||

| Class B | 1,000.00 | 824.60 | 2.20 | 10.04 | |||||||||||||

| Class C | 1,000.00 | 825.20 | 2.20 | 10.04 | |||||||||||||

| Class I | 1,000.00 | 828.90 | 1.11 | 5.08 | |||||||||||||

| Hypothetical (5% return before expenses) | |||||||||||||||||

| Class A | $ | 1,000.00 | $ | 1,017.75 | 1.45 | % | $ | 7.31 | |||||||||

| Class B | 1,000.00 | 1,014.00 | 2.20 | 11.08 | |||||||||||||

| Class C | 1,000.00 | 1,014.00 | 2.20 | 11.08 | |||||||||||||

| Class I | 1,000.00 | 1,019.45 | 1.11 | 5.60 | |||||||||||||

| * | Expenses are equal to each Fund’s respective annualized expense ratios multiplied by the average account value over the period, multiplied by 183/366 to reflect the most recent fiscal half-year. |

17

Table of Contents

| Expenses | |||||||||||||||||

| Ending | Paid | ||||||||||||||||

| Beginning | Account | During the | |||||||||||||||

| Account | Value | Annualized | Period Ended | ||||||||||||||

| Value | November 30, | Expense | November 30, | ||||||||||||||

| ING SmallCap Value Choice Fund | June 1, 2007 | 2007 | Ratio | 2007* | |||||||||||||

| Actual Fund Return | |||||||||||||||||

| Class A | $ | 1,000.00 | $ | 855.20 | 1.49 | % | $ | 6.91 | |||||||||

| Class B | 1,000.00 | 851.90 | 2.24 | 10.37 | |||||||||||||

| Class C | 1,000.00 | 852.00 | 2.24 | 10.37 | |||||||||||||

| Class I | 1,000.00 | 856.80 | 1.18 | 5.48 | |||||||||||||

| Hypothetical (5% return before expenses) | |||||||||||||||||

| Class A | $ | 1,000.00 | $ | 1,017.55 | 1.49 | % | $ | 7.52 | |||||||||

| Class B | 1,000.00 | 1,013.80 | 2.24 | 11.28 | |||||||||||||

| Class C | 1,000.00 | 1,013.80 | 2.24 | 11.28 | |||||||||||||

| Class I | 1,000.00 | 1,019.10 | 1.18 | 5.96 | |||||||||||||