Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number 811-09025

New Covenant Funds

(Exact name of registrant as specified in charter)

SEI Investments

One Freedom Valley Drive

Oaks, PA 19456

(Address of principal executive offices) (Zip code)

The Corporation Trust Company

Corporation Trust Center

1209 Orange Street

Wilmington, Delaware 19801

(Name and address of agent for service)

Registrant’s telephone number, including area code: 1-877-835-4531

Date of fiscal year end: June 30, 2013

Date of reporting period: June 30, 2013

Table of Contents

Item 1. Reports to Stockholders.

Table of Contents

June 30, 2013

ANNUAL REPORT

New Covenant Funds

† New Covenant Growth Fund

† New Covenant Income Fund

† New Covenant Balanced Growth Fund

† New Covenant Balanced Income Fund

Table of Contents

| 1 | ||||

| 9 | ||||

| 34 | ||||

| 35 | ||||

| 36 | ||||

| 38 | ||||

| 42 | ||||

| 51 | ||||

| 52 | ||||

| 55 | ||||

| 56 | ||||

The Trust files its complete schedule of portfolio holdings with the Securities and Exchange Commission (the “Commission”) for the first and third quarters of each fiscal year on Form N-Q within sixty days after the end of the period. The Trust’s Forms N-Q are available on the Commission’s website at http://www.sec.gov, and may be reviewed and copied at the Commission’s Public Reference Room in Washington, DC. Information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

A description of the policies and procedures that the Trust uses to determine how to vote proxies relating to portfolio securities, as well as information relating to how a Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30, is available (i) without charge, upon request, by calling 1-877-835-4531; and (ii) on the Commission’s website at http://www.sec.gov.

Table of Contents

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

NEW COVENANT FUNDS — JUNE 30, 2013

New Covenant Growth Fund

I. Objective:

The New Covenant Growth Fund (the “Fund”) seeks to provide long-term capital appreciation.

II. Multi-Manager Approach Statement:

The Fund uses a multi-manager approach, relying on a number of sub-advisers with differing investment approaches to manage portions of the Fund’s portfolio under the general supervision of SEI Investments Management Corp. (SIMC). The Fund utilized the following sub-advisers as of June 30, 2013: Baillie Gifford Overseas Limited, Sustainable Growth Advisors, LP, Parametric Portfolio Associates, Tocqueville Asset Management L.P., WestEnd Advisors LLC and Waddell & Reed Investment Management Company. There were no sub-advisor changes made during the year.

III. Return vs. Benchmark:

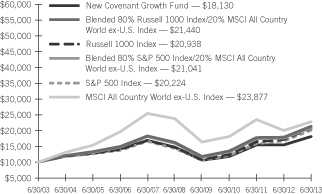

For the year ended June 30, 2013, the Fund returned 17.11%, while the Russell 1000 Index returned 21.24% and the blended benchmark of 80% Russell 1000 Index and 20% MSCI All Country World ex-U.S. Index advanced 19.74%.

IV. Market Commentary:

Domestic and international stock markets experienced a strong rally despite continued uncertainty among investors. The expanded central bank intervention in the U.S. and the promise of action within the eurozone bolstered investor confidence. European Central Bank (ECB) President Mario Draghi’s promise to do “whatever it takes” to preserve the euro, the outright monetary transactions program (to prop up banks through unlimited purchases of sovereign bonds on the secondary market), and the €500 billion European Stability Mechanism, were all designed to provide financial assistance to struggling members of the eurozone. Within the U.S., the re-election of President Obama and the last-minute resolution of the fiscal cliff paved the way for a strong start to 2013, despite the expiration of the payroll tax holiday. Abroad, we saw the election of Shinzo Abe in Japan and the introduction of “Abenomics”—a multi-step plan to boost Japan’s ailing economy through devaluation of the yen and domestic stimulus measures to shift the country from an environment of deflation to one of inflation. These announcements boosted investor

sentiment toward Japan and sparked a broad uptrend in Japanese equity markets. However, markets in Japan corrected in May 2013 after a few strong months, as investors became somewhat tentative of the long-term efficacy of Abe’s pledged actions. Near the end of the period under review, the potential scaling back of bond purchases by the Federal Reserve in the U.S., or “tapering‘” became a focus, as concerns cropped up that a slowdown in the world’s largest economy could have a carry-on effect on global markets. Overall, Europe and the Middle East ex-U.K. was the top-performing regional benchmark in the period, with the remaining developed regions performing roughly equally. Emerging markets lagged.

V. Fund Attribution:

The Fund underperformed as both sector allocation and stock selection each detracted. An underweight to Financials, one of the best-performing sectors during the year, was the largest detractor. Stock selection within Consumer Staples and Energy also proved challenging during the year. On the positive side, an underweight to Utilities helped, as investors sought riskier issues. Strong stock selection within Materials contributed as well, though this was partially offset by an overweight to the sector. From a regional perspective, the majority of underperformance stemmed from North America, while emerging markets within Europe, the Middle East and Africa were positive. From a market-cap perspective, the Fund was challenged across the capitalization spectrum with the exception of mega caps.

| New Covenant Funds / Annual Report / June 30, 2013 | 1 |

Table of Contents

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

NEW COVENANT FUNDS — JUNE 30, 2013

New Covenant Growth Fund (Concluded)

New Covenant Growth Fund

AVERAGE ANNUAL TOTAL RETURN1,2

| One Year Return | Annualized 3-Year Return | Annualized 5-Year Return | Annualized 10-Year Return | Annualized Inception to Date | ||||||||||||||||

| New Covenant Growth Fund | 17.11% | 15.14% | 4.12% | 6.13% | 5.28% | |||||||||||||||

| Russell 1000 Index3 | 21.24% | 18.63% | 7.12% | 7.67% | 9.12% | |||||||||||||||

| S&P 500 Index3 | 20.60% | 18.45% | 7.01% | 7.30% | 8.95% | |||||||||||||||

| Blended 80% Russell 1000 Index/20% MSCI All Country World ex-U.S. Index3 | 19.74% | 16.49% | 5.57% | 7.93% | 8.35% | |||||||||||||||

| Blended 80% S&P 500 Index/20% MSCI All Country World ex-U.S. Index3 | 19.34% | 16.46% | 5.58% | 7.72% | 8.29% | |||||||||||||||

Comparison of Change in the Value of a $10,000 Investment in the New Covenant Growth Fund, versus the Blended 80% Russell 1000 Index/20% MSCI All Country World ex-U.S. Index, Russell 1000 Index, Blended 80% S&P 500 Index/20% MSCI All Country World ex-U.S. Index, S&P 500 Index and MSCI All Country World ex-U.S. Index.

| 1 | For the years ended June 30, 2013. Past performance is not an indication of future performance. Fund Shares were offered beginning 7/1/99. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that year; absent fee waivers and reimbursements, performance would have been lower. |

| 2 | This table compares the Fund’s average annual total returns to those of a broad-based index and the Fund’s 80/20 Blended Benchmark, which consists of the Russell 1000 Index and the MSCI All Country World ex-U.S. Index. The Fund’s Blended Benchmark is designed to provide a useful comparison to the Fund’s overall performance and more accurately reflects the Fund’s investment strategy than the broad-based index. |

| 3 | The Fund has changed its primary benchmark from the S&P 500 Index to the Russell 1000 Index because the Adviser and Sub-Advisers believe that the Russell 1000 Index is more representative of the type of securities in which the Fund invests. |

| 2 | New Covenant Funds / Annual Report / June 30, 2013 |

Table of Contents

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

NEW COVENANT FUNDS — JUNE 30, 2013

New Covenant Income Fund

I. Objective:

The New Covenant Income Fund’s (the “Fund”) investment objective is a high level of current income with preservation of capital.

II. Multi-Manager Approach Statement:

The Fund uses a multi-manager approach, relying on a number of sub-advisers with differing investment approaches to manage portions of the Fund’s portfolio under the general supervision of SEI Investments Management Corp. (SIMC). The Fund utilized the following sub-advisers as of June 30, 2013: Western Asset Management Company, Western Asset Management Company Limited and J.P. Morgan Investment Management Inc.

III. Return vs. Benchmark:

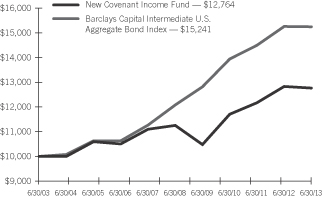

For the year ended June 30, 2013, the Fund returned -0.55%, compared to -0.12% for the benchmark, the Barclays Capital Intermediate U.S. Aggregate Bond Index.

IV. Market Commentary:

For the twelve-month period ending June 30, 2013, non-Treasuries generally outperformed duration-neutral Treasuries, thanks to global central banks’ accommodative policies. In 2012, the European Central Bank launched two rounds of long-term refinancing operations, which helped alleviate short-term funding pressure in the eurozone. In the U.S., the Federal Reserve (Fed) continued Operation Twist until December 2012, and started a third quantitative-easing program (QE3) to purchase $85 billion of agency mortgage-backed and long-term Treasury securities every month. In addition, economic and corporate fundamentals continued to improve, while inflation in the U.S. remained benign. The housing market experienced a strong recovery, with the S&P/Case-Shiller home-price index up double digits from a year ago. The non-agency mortgage-backed securities (MBS) market saw strong price appreciation over the year, helped by improving credit fundamentals and attractive valuations. Corporations, especially financial companies, have much stronger balance sheets and solid earnings after a few years of de-leveraging. Primary issuance was robust and has been met with strong demand from investors.

However, the market turned a corner at the beginning of May 2013, as fear of the Fed tapering QE3 caused interest rates to surge and

triggered a broad market selloff. The 10-year Treasury yield rose by 82 basis points and the 30-year Treasury yield increased by 62 basis points from beginning of May to the end of June. Credit spreads widened across sectors, and fixed-income funds witnessed the largest cash outflow since beginning of the year. Liquidity was hammered and dealer balance sheets were constrained by new financial regulations. Agency MBS were hit especially hard, as the sharp rise in Treasury yields resulted in significant extension risk and the QE3 uncertainty caused selling from real-estate investment trusts and overseas investors.

V. Fund Attribution:

The Fund’s flattening yield-curve position (Western) detracted from performance, as the curve significantly steepened. This was partially offset by the short-duration position (J.P. Morgan, Western), as Treasury yields rose sharply. The Fund’s allocation to non-agency MBS (J.P. Morgan, Western) was a big contributor, as the sector continued to be supported by improving housing fundamentals, strong technicals and still-attractive valuations. Lastly, security selection within agency MBS (J.P. Morgan, Western) added to performance. This was particularly true in collateralized mortgage obligations, which are less prepayment sensitive. During the year, the Fund utilized Treasury futures, euro-dollar futures and options on futures to manage the duration and yield-curve exposure.

| New Covenant Funds / Annual Report / June 30, 2013 | 3 |

Table of Contents

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

NEW COVENANT FUNDS — JUNE 30, 2013

New Covenant Income Fund (Concluded)

New Covenant Income Fund

AVERAGE ANNUAL TOTAL RETURN1

| One Year Return | Annualized 3-Year Return | Annualized 5-Year Return | Annualized 10-Year Return | Annualized Inception to Date | ||||||||||||||||

| New Covenant Income Fund | (0.55)% | 2.93% | 2.55% | 2.47% | 2.76% | |||||||||||||||

| Barclays Capital Intermediate U.S. Aggregate Bond Index | (0.12)% | 3.03% | 4.76% | 4.30% | 6.63% | |||||||||||||||

Comparison of Change in the Value of a $10,000 Investment in the New Covenant Income Fund, versus the Barclays Capital Intermediate U.S. Aggregate Bond Index

| 1 | For the years ended June 30, 2013. Past performance is not an indication of future performance. Fund Shares were offered beginning 7/1/99. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that year; absent fee waivers and reimbursements, performance would have been lower. |

| 4 | New Covenant Funds / Annual Report / June 30, 2013 |

Table of Contents

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

NEW COVENANT FUNDS — JUNE 30, 2013

New Covenant Balanced Growth Fund

I. Objective:

The New Covenant Balanced Growth Fund (the “Fund”) seeks to produce capital appreciation with less risk than would be present in a portfolio of only common stocks.

II. Multi-Manager Approach Statement:

The Fund invests 60% in the New Covenant Growth Fund and 40% in the New Covenant Income Fund. Each underlying Fund uses a multi-manager approach, relying on a number of sub-advisers with differing investment approaches to manage portions of the portfolios under the general supervision of SEI Investments Management Corp. (SIMC). The New Covenant Growth Fund utilized the following sub-advisers as of June 30, 2013: Baillie Gifford Overseas Limited, Sustainable Growth Advisors, LP, Parametric Portfolio Associates, Tocqueville Asset Management L.P., WestEnd Advisors LLC and Waddell & Reed Investment Management Company. The New Covenant Income Fund used the following sub-advisers as of June 30, 2013: Western Asset Management Company, Western Asset Management Company Limited and J.P. Morgan Investment Management Inc. There were no sub-advisor changes made during the year.

III. Return vs. Benchmark:

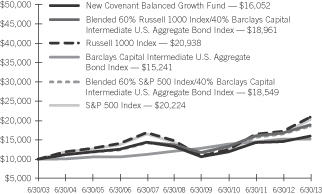

For the year ended June 30, 2013, the Fund returned 9.77%, while the blended benchmark of 60% Russell 1000 Index and 40% Barclays Capital Intermediate U.S. Aggregate Bond Index returned 12.30% and the blended reporting benchmark of 48% Russell 1000 Index, 12% MSCI All Country World ex-U.S. Index and 40% Barclays Capital Intermediate U.S. Aggregate Index advanced 11.38%.

IV. Market Commentary:

Domestic and international stock markets experienced a strong rally despite continued uncertainty among investors. The expanded central bank intervention in the U.S. and the promise of action within the eurozone bolstered investor confidence. European Central Bank (ECB) President Mario Draghi’s promise to do “whatever it takes” to preserve the euro, the outright monetary transactions program (to prop up banks through unlimited purchases of sovereign bonds on the secondary market), and the €500 billion European Stability Mechanism, were all designed to provide financial assistance to

struggling members of the eurozone. Within the U.S., the re-election of President Obama and the last-minute resolution of the fiscal cliff paved the way for a strong start to 2013, despite the expiration of the payroll tax holiday. Abroad, we saw the election of Shinzo Abe in Japan and the introduction of “Abenomics” — a multi-step plan to boost Japan’s ailing economy through devaluation of the yen and domestic stimulus measures to shift the country from an environment of deflation to one of inflation. These announcements boosted investor sentiment toward Japan and sparked a broad uptrend in Japanese equity markets. However, markets in Japan corrected in May 2013 after a few strong months, as investors became somewhat tentative of the long-term efficacy of Abe’s pledged actions. Near the end of the period under review, the potential scaling back of bond purchases by the Federal Reserve in the U.S., or “tapering‘” became a focus, as concerns cropped up that a slowdown in the world’s largest economy could have a carry-on effect on global markets.

Overall, Europe and the Middle East ex-U.K. was the top-performing regional benchmark in the period, with the remaining developed regions performing roughly equally. Emerging markets lagged.

Within fixed-income markets, non-Treasuries generally outperformed duration-neutral Treasuries, thanks to global central banks’ accommodative policies. In 2012, the ECB launched two rounds of long-term refinancing operations, which helped alleviate short-term funding pressure in the eurozone. In the U.S., the Federal Reserve (Fed) continued Operation Twist until December 2012, and started a third quantitative-easing program (QE3) to purchase $85 billion of agency mortgage-backed and long-term Treasury securities every month. In addition, economic and corporate fundamentals continued to improve, while inflation in the U.S. remained benign. The housing market experienced a strong recovery, with the S&P/Case-Shiller home-price index up double digits from a year ago. The non-agency mortgage-backed securities (MBS) market saw strong price appreciation over the year, helped by improving credit fundamentals and attractive valuations. Corporations, especially financial companies, have much stronger balance sheets and solid earnings after a few years of de-leveraging. Primary issuance was robust and has been met with strong demand from investors. However, the market turned a corner at the beginning of May 2013, as fear of the Fed tapering QE3 caused interest rates to surge and triggered a broad

| New Covenant Funds / Annual Report / June 30, 2013 | 5 |

Table of Contents

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

NEW COVENANT FUNDS — JUNE 30, 2013

New Covenant Balanced Growth Fund (Concluded)

market selloff. The 10-year Treasury yield rose by 82 basis points and the 30-year Treasury yield increased by 62 basis points from beginning of May to the end of June. Credit spreads widened across sectors, and fixed-income funds witnessed the largest cash outflow since beginning of the year. Liquidity was hammered and dealer balance sheets were constrained by new financial regulations. Agency MBS were hit especially hard, as the sharp rise in Treasury yields resulted in significant extension risk and the QE3 uncertainty caused selling from real-estate investment trusts and overseas investors.

V. Fund Attribution:

The Fund underperformed overall. For equities, both sector allocation and stock selection detracted. An underweight to Financials, one of the best-performing sectors during the year, was the largest detractor. Stock selection within Consumer Staples and Energy also proved challenging. On the positive side, an underweight to Utilities helped, as investors sought riskier issues. Strong stock selection within Materials contributed as well, though this was partially offset by an overweight to the sector. From a regional perspective, the majority of underperformance stemmed from North America, while emerging markets within Europe, the Middle East and Africa were positive. From a market-cap perspective, the Fund was challenged across the capitalization spectrum, with the exception of mega caps.

Within fixed income, the Fund’s flattening yield-curve position (Western) detracted from performance, as the curve significantly steepened. This was partially offset by the short-duration position (J.P. Morgan, Western), as Treasury yields rose sharply. The Fund’s allocation to non-agency MBS (J.P. Morgan, Western) was a big contributor, as the sector continued to be supported by improving housing fundamentals, strong technicals and still-attractive valuations. Lastly, security selection within agency MBS (J.P. Morgan, Western) added to performance. This was particularly true in collateralized mortgage obligations, which are less prepayment sensitive. During the year, the Fund utilized Treasury futures, euro-dollar futures and options on futures to manage the duration and yield-curve exposure.

New Covenant Balanced Growth Fund

AVERAGE ANNUAL TOTAL RETURN1,2

| One Year Return | Annualized 3-Year Return | Annualized 5-Year Return | Annualized 10-Year Return | Annualized Inception to Date | ||||||||||||||||

| New Covenant Balanced Growth Fund | 9.77% | 10.37% | 3.70% | 4.85% | 4.72% | |||||||||||||||

| Russell 1000 Index3 | 21.24% | 18.63% | 7.12% | 7.67% | 9.12% | |||||||||||||||

| S&P 500 Index3 | 20.60% | 18.45% | 7.01% | 7.30% | 8.95% | |||||||||||||||

| Barclays Capital Intermediate U.S. Aggregate Bond Index | (0.12)% | 3.03% | 4.76% | 4.30% | 6.63% | |||||||||||||||

| Blended 60% Russell 1000 Index/40% Barclays Capital Intermediate U.S. Aggregate Bond Index3 | 12.30% | 12.41% | 6.62% | 6.61% | 8.80% | |||||||||||||||

| Blended 60% S&P 500 Index/40% Barclays Capital Intermediate U.S. Aggregate Bond Index3 | 11.94% | 12.29% | 6.54% | 6.37% | 8.70% | |||||||||||||||

Comparison of Change in the Value of a $10,000 Investment in the New Covenant Balanced Growth Fund, versus the Blended 60% Russell 1000 Index/40% Barclays Capital Intermediate U.S. Aggregate Bond Index, Russell 1000 Index, Barclays Capital Intermediate U.S. Aggregate Bond Index, Blended 60% S&P 500 Index/40% Barclays Capital Intermediate U.S. Aggregate Bond Index and S&P 500 Index.

| 1 | For the years ended June 30, 2013. Past performance is not an indication of future performance. Fund Shares were offered beginning 7/1/99. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that year; absent fee waivers and reimbursements, performance would have been lower. |

| 2 | This table compares the Fund’s average annual total returns to those of a broad-based index and the Fund’s 60/40 Blended Benchmark, which consists of the Russell 1000 Index and the Barclays Capital Intermediate U.S. Aggregate Bond Index. The Fund’s Blended Benchmark is designed to provide a useful comparison to the Fund’s overall performance and more accurately reflects the Fund’s investment strategy than the broad-based index. |

| 3 | The Fund has changed one of its primary benchmarks from the S&P 500 Index to the Russell 1000 Index in connection with the corresponding change to the Growth Fund’s benchmark. |

| 6 | New Covenant Funds / Annual Report / June 30, 2013 |

Table of Contents

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

NEW COVENANT FUNDS — JUNE 30, 2013

New Covenant Balanced Income Fund

I. Objective:

The New Covenant Balanced Income Fund (the “Fund”) seeks to produce current income and long-term growth of capital.

II. Multi-Manager Approach Statement:

The Fund invests 60% in the New Covenant Income Fund and 40% in the New Covenant Growth Fund. Each underlying Fund uses a multi-manager approach, relying on a number of sub-advisers with differing investment approaches to manage portions of the portfolios under the general supervision of SEI Investments Management Corp. (SIMC). The New Covenant Income Fund used the following sub-advisers as of June 30, 2013: Western Asset Management Company, Western Asset Management Company Limited and J.P. Morgan Investment Management Inc. The New Covenant Growth Fund utilized the following sub-advisers as of June 30, 2013: Baillie Gifford Overseas Limited, Sustainable Growth Advisers, LP, Parametric Portfolio Associates, Tocqueville Asset Management L.P., WestEnd Advisors LLC and Waddell & Reed Investment Management Company. There were no sub-adviser changes made during the year.

III. Return vs. Benchmark:

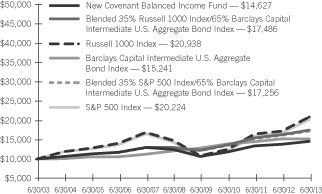

For the year ended June 30, 2013, the Fund returned 5.34%, while the blended benchmark of 35% Russell 1000 Index and 35% Barclays Capital Intermediate U.S. Aggregate Bond Index returned 6.98% and the blended reporting benchmark of 28% Russell 1000 Index, 7% MSCI All Country World ex-U.S. Index and 65% Barclays Capital Intermediate U.S. Aggregate Index advanced 6.47%.

IV. Market Commentary:

Domestic and international stock markets experienced a strong rally despite continued uncertainty among investors. The expanded central bank intervention in the U.S. and the promise of action within the eurozone bolstered investor confidence. European Central Bank (ECB) President Mario Draghi’s promise to do “whatever it takes” to preserve the euro, the outright monetary transactions program (to prop up banks through unlimited purchases of sovereign bonds on the secondary market), and the €500 billion European Stability Mechanism, were all designed to provide financial assistance to struggling members of the eurozone. Within the U.S., the re-election

of President Obama and the last-minute resolution of the fiscal cliff paved the way for a strong start to 2013, despite the expiration of the payroll tax holiday. Abroad, we saw the election of Shinzo Abe in Japan and the introduction of “Abenomics” — a multi-step plan to boost Japan’s ailing economy through devaluation of the yen and domestic stimulus measures to shift the country from an environment of deflation to one of inflation. These announcements boosted investor sentiment toward Japan and sparked a broad uptrend in Japanese equity markets. However, markets in Japan corrected in May 2013 after a few strong months, as investors became somewhat tentative of the long-term efficacy of Abe’s pledged actions. Near the end of the period under review, the potential scaling back of bond purchases by the Federal Reserve in the U.S., or “tapering‘” became a focus, as concerns cropped up that a slowdown in the world’s largest economy could have a carry-on effect on global markets.

Overall, Europe and the Middle East ex-U.K. was the top-performing regional benchmark in the period, with the remaining developed regions performing roughly equally. Emerging markets lagged.

Within fixed-income markets, non-Treasuries generally outperformed duration-neutral Treasuries, thanks to global central banks’ accommodative policies. In 2012, the ECB launched two rounds of long-term refinancing operations, which helped alleviate short-term funding pressure in the eurozone. In the U.S., the Federal Reserve (Fed) continued Operation Twist until December 2012, and started a third quantitative-easing program (QE3) to purchase $85 billion of agency mortgage-backed and long-term Treasury securities every month. In addition, economic and corporate fundamentals continued to improve, while inflation in the U.S. remained benign. The housing market experienced a strong recovery, with the S&P/Case-Shiller home-price index up double digits from a year ago. The non-agency mortgage-backed securities (MBS) market saw strong price appreciation over the year, helped by improving credit fundamentals and attractive valuations. Corporations, especially financial companies, have much stronger balance sheets and solid earnings after a few years of de-leveraging. Primary issuance was robust and has been met with strong demand from investors. However, the market turned a corner at the beginning of May 2013, as fear of the Fed tapering QE3 caused interest rates to surge and triggered a broad market selloff. The 10-year Treasury yield rose by 82 basis points and

| New Covenant Funds / Annual Report / June 30, 2013 | 7 |

Table of Contents

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

NEW COVENANT FUNDS — JUNE 30, 2013

New Covenant Balanced Income Fund (Concluded)

the 30-year Treasury yield increased by 62 basis points from beginning of May to the end of June. Credit spreads widened across sectors, and fixed-income funds witnessed the largest cash outflow since beginning of the year. Liquidity was hammered and dealer balance sheets were constrained by new financial regulations. Agency MBS were hit especially hard, as the sharp rise in Treasury yields resulted in significant extension risk and the QE3 uncertainty caused selling from real-estate investment trusts and overseas investors.

V. Fund Attribution:

The Fund underperformed overall. Within fixed income, the Fund’s flattening yield-curve position (Western) detracted from performance, as the curve significantly steepened. This was partially offset by the short-duration position (J.P. Morgan, Western), as Treasury yields rose sharply. The Fund’s allocation to non-agency MBS (J.P. Morgan, Western) was a big contributor, as the sector continued to be supported by improving housing fundamentals, strong technicals and still-attractive valuations. Lastly, security selection within agency MBS (J.P. Morgan, Western) added to performance. This was particularly true in collateralized mortgage obligations, which are less prepayment sensitive. During the year, the Fund utilized Treasury futures, euro-dollar futures and options on futures to manage the duration and yield-curve exposure.

For equities, both sector allocation and stock selection detracted. An underweight to Financials, one of the best-performing sectors during the year, was the largest detractor. Stock selection within Consumer Staples and Energy also proved challenging. On the positive side, an underweight to Utilities helped, as investors sought riskier issues. Strong stock selection within Materials contributed as well, although this was partially offset by an overweight to the sector. From a regional perspective, the majority of underperformance stemmed from North America, while emerging markets within Europe, the Middle East and Africa were positive. From a market-cap perspective, the Fund was challenged across the capitalization spectrum, with the exception of mega caps.

New Covenant Balanced Income Fund

AVERAGE ANNUAL TOTAL RETURN1,2

| One Year Return | Annualized 3-Year Return | Annualized 5-Year Return | Annualized 10-Year Return | Annualized Inception to Date | ||||||||||||||||

| New Covenant Balanced Income Fund | 5.34% | 7.20% | �� | 3.21% | 3.88% | 3.77% | ||||||||||||||

| Russell 1000 Index3 | 21.24% | 18.63% | 7.12% | 7.67% | 9.12% | |||||||||||||||

| S&P 500 Index3 | 20.60% | 18.45% | 7.01% | 7.30% | 8.95% | |||||||||||||||

| Barclays Capital Intermediate U.S. Aggregate Bond Index | (0.12)% | 3.03% | 4.76% | 4.30% | 6.63% | |||||||||||||||

| Blended 35% Russell 1000 Index/65% Barclays Capital Intermediate U.S. Aggregate Bond Index3 | 6.98% | 8.50% | 6.00% | 5.75% | 7.65% | |||||||||||||||

| Blended 35% S&P 500 Index/65% Barclays Capital Intermediate U.S. Aggregate Bond Index3 | 6.78% | 8.43% | 5.95% | 5.61% | 7.58% | |||||||||||||||

Comparison of Change in the Value of a $10,000 Investment in the New Covenant Balanced Income Fund, versus the Blended 35% Russell 1000 Index/65% Barclays Capital Intermediate U.S. Aggregate Bond Index, Russell 1000 Index, Barclays Capital Intermediate U.S. Aggregate Bond Index, Blended 35% S&P 500 Index/65% Barclays Capital Intermediate U.S. Aggregate Bond Index and S&P 500 Index.

| 1 | For the years ended June 30, 2013. Past performance is not an indication of future performance. Fund Shares were offered beginning 7/1/99. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that year; absent fee waivers and reimbursements, performance would have been lower. |

| 2 | This table compares the Fund’s average annual total returns to those of a broad-based index and the Fund’s 35/65 Blended Benchmark, which consists of the Russell 1000 Index and the Barclays Capital Intermediate U.S. Aggregate Bond Index. The Fund’s Blended Benchmark is designed to provide a useful comparison to the Fund’s overall performance and more accurately reflects the Fund’s investment strategy than the broad-based index. |

| 3 | The Fund has changed one of its primary benchmarks from the S&P 500 Index to the Russell 1000 Index in connection with the corresponding change to the Growth Fund’s primary benchmark. |

| 8 | New Covenant Funds / Annual Report / June 30, 2013 |

Table of Contents

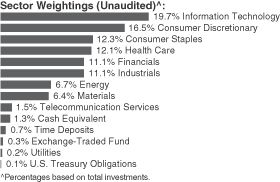

New Covenant Growth Fund

June 30, 2013

| Description | Shares | Market Value ($ Thousands) | ||||||

COMMON STOCK — 97.6% | ||||||||

Argentina — 0.3% | ||||||||

MercadoLibre | 11,500 | $ | 1,239 | |||||

|

| |||||||

Australia — 0.8% | ||||||||

Brambles (A) | 101,481 | 865 | ||||||

Cochlear (A) | 10,089 | 567 | ||||||

Diana Shipping* | 75,986 | 763 | ||||||

Woolworths (A) | 23,136 | 693 | ||||||

|

| |||||||

| 2,888 | ||||||||

|

| |||||||

Belgium — 0.1% | ||||||||

Groupe Bruxelles Lambert (A) | 7,239 | 544 | ||||||

|

| |||||||

Brazil — 0.2% | ||||||||

Embraer ADR | 11,236 | 414 | ||||||

Itau Unibanco Holding ADR | 36,677 | 474 | ||||||

|

| |||||||

| 888 | ||||||||

|

| |||||||

Canada — 1.5% | ||||||||

Cameco | 28,879 | 597 | ||||||

Canadian Pacific Railway | 18,895 | 2,293 | ||||||

Catamaran | 1,804 | 88 | ||||||

Cenovus Energy | 14,102 | 401 | ||||||

Fairfax Financial Holdings | 3,138 | 1,230 | ||||||

Ritchie Bros Auctioneers | 23,399 | 447 | ||||||

Thomson Reuters | 3,958 | 129 | ||||||

Westport Innovations* | 11,830 | 398 | ||||||

|

| |||||||

| 5,583 | ||||||||

|

| |||||||

China — 0.6% | ||||||||

Baidu ADR* | 9,368 | 886 | ||||||

China Shenhua Energy, Cl H (A) | 231,000 | 587 | ||||||

Want Want China Holdings (A) | 599,000 | 839 | ||||||

|

| |||||||

| 2,312 | ||||||||

|

| |||||||

Denmark — 0.7% | ||||||||

DSV (A) | 32,012 | 779 | ||||||

| Description | Shares | Market Value ($ Thousands) | ||||||

Novo Nordisk ADR | 8,025 | $ | 1,243 | |||||

Novozymes, Cl B (A) | 19,317 | 618 | ||||||

|

| |||||||

| 2,640 | ||||||||

|

| |||||||

Finland — 0.7% | ||||||||

Kone, Cl B (A) | 18,464 | 1,463 | ||||||

Sampo, Cl A (A) | 25,922 | 1,008 | ||||||

|

| |||||||

| 2,471 | ||||||||

|

| |||||||

France — 1.0% | ||||||||

Danone ADR | 60,030 | 900 | ||||||

Edenred (A) | 25,451 | 778 | ||||||

Essilor International (A) | 11,365 | 1,209 | ||||||

Lafarge (A) | 12,467 | 765 | ||||||

|

| |||||||

| 3,652 | ||||||||

|

| |||||||

Germany — 1.5% | ||||||||

Brenntag (A) | 4,412 | 670 | ||||||

Continental (A) | 6,066 | 807 | ||||||

Deutsche Boerse (A) | 13,408 | 880 | ||||||

SAP ADR | 31,822 | 2,318 | ||||||

SKY Deutschland (A) | 110,734 | 768 | ||||||

|

| |||||||

| 5,443 | ||||||||

|

| |||||||

Hong Kong — 0.9% | ||||||||

China Mobile (A) | 67,000 | 694 | ||||||

Hang Seng Bank (A) | 39,600 | 583 | ||||||

Hong Kong Exchanges and Clearing (A) | 72,400 | 1,087 | ||||||

Kunlun Energy (A) | 580,000 | 1,024 | ||||||

|

| |||||||

| 3,388 | ||||||||

|

| |||||||

Ireland — 1.8% | ||||||||

Accenture, Cl A | 781 | 56 | ||||||

Covidien | 521 | 33 | ||||||

CRH (A) | 33,302 | 674 | ||||||

Eaton | 2,465 | 162 | ||||||

Experian (A) | 64,403 | 1,116 | ||||||

Ingersoll-Rand | 14,112 | 784 | ||||||

Ryanair Holdings ADR | 22,504 | 1,160 | ||||||

Shire ADR | 15,121 | 1,438 | ||||||

Willis Group Holdings | 25,512 | 1,040 | ||||||

|

| |||||||

| 6,463 | ||||||||

|

| |||||||

Israel — 0.3% | ||||||||

Check Point Software Technologies | 22,211 | 1,103 | ||||||

|

| |||||||

Japan — 2.0% | ||||||||

FANUC (A) | 4,600 | 664 | ||||||

Fast Retailing (A) | 2,700 | 910 | ||||||

Mitsui (A) | 35,300 | 442 | ||||||

Olympus (A) | 30,200 | 916 | ||||||

Rakuten (A) | 97,200 | 1,148 | ||||||

Shimano (A) | 8,500 | 723 | ||||||

| New Covenant Funds / Annual Report / June 30, 2013 | 9 |

Table of Contents

SCHEDULE OF INVESTMENTS

New Covenant Growth Fund (Continued)

June 30, 2013

| Description | Shares | Market Value ($ Thousands) | ||||||

SMC (A) | 4,800 | $ | 961 | |||||

Tokyo Electron (A) | 10,400 | 525 | ||||||

Toyota Tsusho (A) | 22,100 | 567 | ||||||

Trend Micro (A) | 20,500 | 651 | ||||||

|

| |||||||

| 7,507 | ||||||||

|

| |||||||

Netherlands — 0.5% | ||||||||

Chicago Bridge & Iron | 509 | 31 | ||||||

CNH Global | 2,142 | 89 | ||||||

James Hardie Industries (A) | 72,273 | 621 | ||||||

QIAGEN | 1,417 | 28 | ||||||

Unilever (A) | 28,714 | 1,129 | ||||||

|

| |||||||

| 1,898 | ||||||||

|

| |||||||

Norway — 0.3% | ||||||||

Aker Solutions (A) | 36,344 | 494 | ||||||

Seadrill (A) | 13,177 | 528 | ||||||

|

| |||||||

| 1,022 | ||||||||

|

| |||||||

Portugal — 0.1% | ||||||||

Galp Energia, Cl B (A) | 24,181 | 358 | ||||||

|

| |||||||

Russia — 0.5% | ||||||||

Magnit GDR (A) | 19,728 | 1,126 | ||||||

Sberbank of Russia ADR (A) | 46,618 | 529 | ||||||

|

| |||||||

| 1,655 | ||||||||

|

| |||||||

Singapore — 0.4% | ||||||||

Avago Technologies, Cl A | 4,239 | 159 | ||||||

United Overseas Bank (A) | 75,552 | 1,179 | ||||||

|

| |||||||

| 1,338 | ||||||||

|

| |||||||

South Africa — 0.7% | ||||||||

Massmart Holdings | 29,394 | 531 | ||||||

Naspers, N Shares (A) | 26,735 | 1,965 | ||||||

|

| |||||||

| 2,496 | ||||||||

|

| |||||||

South Korea — 0.8% | ||||||||

Hyundai Mobis (A) | 2,276 | 542 | ||||||

NHN (A) | 2,005 | 509 | ||||||

Samsung Electronics GDR (A) | 3,200 | 1,860 | ||||||

|

| |||||||

| 2,911 | ||||||||

|

| |||||||

Spain — 0.3% | ||||||||

Inditex (A) | 8,508 | 1,048 | ||||||

|

| |||||||

Sweden — 1.0% | ||||||||

Allied World Assurance Holdings | 34 | 3 | ||||||

Atlas Copco, B Shares (A) | 64,927 | 1,381 | ||||||

Svenska Handelsbanken, A Shares (A) | 37,873 | 1,507 | ||||||

Volvo, Cl B (A) | 53,034 | 703 | ||||||

|

| |||||||

| 3,594 | ||||||||

|

| |||||||

| Description | Shares | Market Value ($ Thousands) | ||||||

Switzerland — 1.3% | ||||||||

Garmin | 3,446 | $ | 125 | |||||

Nestle (A) | 31,433 | 2,059 | ||||||

Pentair | 43,228 | 2,494 | ||||||

|

| |||||||

| 4,678 | ||||||||

|

| |||||||

Taiwan — 0.7% | ||||||||

Hon Hai Precision Industry GDR (A) | 101,826 | 494 | ||||||

Taiwan Semiconductor Manufacturing ADR | 117,993 | 2,162 | ||||||

|

| |||||||

| 2,656 | ||||||||

|

| |||||||

Turkey — 0.3% | ||||||||

BIM Birlesik Magazalar (A) | 29,202 | 633 | ||||||

Turkiye Garanti Bankasi ADR | 123,460 | 531 | ||||||

|

| |||||||

| 1,164 | ||||||||

|

| |||||||

United Kingdom — 3.2% | ||||||||

Amlin (A) | 121,563 | 725 | ||||||

Antofagasta (A) | 39,786 | 481 | ||||||

Aon | 440 | 28 | ||||||

ARM Holdings (A) | 97,000 | 1,170 | ||||||

BG Group (A) | 40,125 | 680 | ||||||

BHP Billiton (A) | 24,018 | 610 | ||||||

Burberry Group (A) | 16,285 | 334 | ||||||

Capita (A) | 67,879 | 995 | ||||||

Hargreaves Lansdown (A) | 37,885 | 510 | ||||||

Liberty Global, Cl A* | 93 | 7 | ||||||

Petrofac (A) | 30,000 | 545 | ||||||

Premier Farnell (A) | 124,129 | 380 | ||||||

Prudential (A) | 64,394 | 1,048 | ||||||

Rio Tinto (A) | 34,521 | 1,400 | ||||||

St. James’s Place (A) | 52,499 | 430 | ||||||

Standard Chartered (A) | 28,252 | 612 | ||||||

Tullow Oil (A) | 70,124 | 1,065 | ||||||

Wolseley (A) | 21,035 | 968 | ||||||

|

| |||||||

| 11,988 | ||||||||

|

| |||||||

United States — 75.1% | ||||||||

Consumer Discretionary — 14.4% | ||||||||

Aeropostale* | 64,213 | 886 | ||||||

Amazon.com | 873 | 242 | ||||||

Ascena Retail Group | 72,513 | 1,265 | ||||||

Cablevision Systems, Cl A | 5,421 | 91 | ||||||

CBS, Cl B | 49,234 | 2,406 | ||||||

Charter Communications, Cl A | 9,323 | 1,155 | ||||||

Chipotle Mexican Grill, Cl A | 3,815 | 1,390 | ||||||

Coach | 62,207 | 3,551 | ||||||

Comcast, Cl A | 6,120 | 256 | ||||||

Delphi Automotive | 2,133 | 108 | ||||||

DIRECTV* | 1,202 | 74 | ||||||

Expedia | 662 | 40 | ||||||

| 10 | New Covenant Funds / Annual Report / June 30, 2013 |

Table of Contents

| Description | Shares | Market Value ($ Thousands) | ||||||

Ford Motor | 4,525 | $ | 70 | |||||

Gannett | 313 | 8 | ||||||

General Motors | 4,000 | 133 | ||||||

Gentex | 172 | 4 | ||||||

Genuine Parts | 256 | 20 | ||||||

Harley-Davidson | 42,181 | 2,313 | ||||||

Home Depot | 23,561 | 1,825 | ||||||

Jarden* | 3,272 | 143 | ||||||

Johnson Controls | 857 | 31 | ||||||

L Brands | 445 | 22 | ||||||

Lennar, Cl A | 1,057 | 38 | ||||||

Liberty Interactive, Cl A* | 1,140 | 26 | ||||||

Liberty Media, Cl A* | 249 | 31 | ||||||

Lowe’s | 67,438 | 2,758 | ||||||

Macy’s | 19 | 1 | ||||||

Marriott International, Cl A | 213 | 8 | ||||||

Mattel | 2,653 | 120 | ||||||

McDonald’s | 2,429 | 240 | ||||||

McGraw Hill Financial | 16,914 | 900 | ||||||

Michael Kors Holdings | 492 | 31 | ||||||

Mohawk Industries | 490 | 55 | ||||||

Morningstar | 2,128 | 165 | ||||||

News, Cl A | 6,756 | 220 | ||||||

News, Cl B | 72,975 | 2,395 | ||||||

NIKE, Cl B | 58,611 | 3,732 | ||||||

Nordstrom | 57,434 | 3,443 | ||||||

Panera Bread, Cl A | 6,028 | 1,121 | ||||||

Polaris Industries | 76 | 7 | ||||||

priceline.com* | 60 | 50 | ||||||

PulteGroup | 443 | 9 | ||||||

Ralph Lauren, Cl A | 9,894 | 1,719 | ||||||

Ross Stores | 363 | 24 | ||||||

Signet Jewelers | 454 | 31 | ||||||

Staples | 81,579 | 1,294 | ||||||

Starbucks | 44,998 | 2,947 | ||||||

Starwood Hotels & Resorts Worldwide | 32,738 | 2,069 | ||||||

Target | 53,225 | 3,665 | ||||||

Tiffany | 8,101 | 590 | ||||||

Time Warner | 1,084 | 63 | ||||||

Time Warner Cable | 14,779 | 1,662 | ||||||

TJX | 2,126 | 106 | ||||||

Tupperware Brands | 1,523 | 118 | ||||||

Walt Disney | 56,845 | 3,590 | ||||||

Yum! Brands | 54,827 | 3,802 | ||||||

|

| |||||||

| 53,063 | ||||||||

|

| |||||||

Consumer Staples — 10.1% | ||||||||

Archer-Daniels-Midland | 3,910 | 133 | ||||||

Avon Products | 6,123 | 129 | ||||||

Bunge | 1,900 | 135 | ||||||

Campbell Soup | 19,827 | 888 | ||||||

Church & Dwight | 2,343 | 145 | ||||||

Clorox | 1,706 | 142 | ||||||

Coca-Cola | 69,208 | 2,776 | ||||||

| Description | Shares | Market Value ($ Thousands) | ||||||

Coca-Cola Enterprises | 3,360 | $ | 118 | |||||

Colgate-Palmolive | 63,700 | 3,649 | ||||||

ConAgra Foods | 4,128 | 144 | ||||||

Costco Wholesale | 46,839 | 5,179 | ||||||

CVS Caremark | 61,575 | 3,521 | ||||||

Dean Foods* | 6,848 | 69 | ||||||

Dr. Pepper Snapple Group | 2,621 | 120 | ||||||

Energizer Holdings | 1,290 | 130 | ||||||

Estee Lauder, Cl A | 69,468 | 4,569 | ||||||

Flowers Foods | 5,820 | 128 | ||||||

Fresh Market* | 2,766 | 138 | ||||||

General Mills | 3,656 | 177 | ||||||

Green Mountain Coffee Roasters* | 2,240 | 168 | ||||||

Hershey | 1,759 | 157 | ||||||

Hillshire Brands | 4,379 | 145 | ||||||

Hormel Foods | 3,334 | 129 | ||||||

Ingredion | 2,197 | 144 | ||||||

JM Smucker | 1,311 | 135 | ||||||

Kellogg | 2,537 | 163 | ||||||

Kimberly-Clark | 1,854 | 180 | ||||||

Kraft Foods Group | 3,280 | 183 | ||||||

Kroger | 4,206 | 145 | ||||||

McCormick | 1,682 | 118 | ||||||

Mead Johnson Nutrition, Cl A | 19,326 | 1,531 | ||||||

Mondelez International, Cl A | 123,243 | 3,516 | ||||||

Monster Beverage | 2,325 | 141 | ||||||

Nu Skin Enterprises, Cl A | 2,571 | 157 | ||||||

PepsiCo | 19,690 | 1,611 | ||||||

Pricesmart | 5,528 | 484 | ||||||

Procter & Gamble | 4,469 | 344 | ||||||

Safeway | 5,985 | 142 | ||||||

Smithfield Foods | 527 | 17 | ||||||

Sysco | 4,724 | 161 | ||||||

Tyson Foods, Cl A | 5,401 | 139 | ||||||

Wal-Mart Stores | 19,983 | 1,489 | ||||||

WhiteWave Foods, Cl A | 8,038 | 131 | ||||||

Whole Foods Market | 70,810 | 3,645 | ||||||

|

| |||||||

| 37,465 | ||||||||

|

| |||||||

Energy — 4.8% | ||||||||

Anadarko Petroleum | 2,042 | 175 | ||||||

Apache | 18,794 | 1,575 | ||||||

Baker Hughes | 25,364 | 1,170 | ||||||

Cameron International | 235 | 14 | ||||||

Chevron | 2,929 | 347 | ||||||

ConocoPhillips | 1,362 | 82 | ||||||

EOG Resources | 1,217 | 160 | ||||||

Exxon Mobil | 18,684 | 1,688 | ||||||

Kinder Morgan | 853 | 33 | ||||||

Murphy Oil | 14,281 | 870 | ||||||

National Oilwell Varco | 59,282 | 4,085 | ||||||

Noble Energy | 28,674 | 1,722 | ||||||

Occidental Petroleum | 12,057 | 1,076 | ||||||

Phillips 66 | 19,332 | 1,139 | ||||||

| New Covenant Funds / Annual Report / June 30, 2013 | 11 |

Table of Contents

SCHEDULE OF INVESTMENTS

New Covenant Growth Fund (Continued)

June 30, 2013

| Description | Shares | Market Value ($ Thousands) | ||||||

Schlumberger | 49,757 | $ | 3,566 | |||||

Spectra Energy | 845 | 29 | ||||||

Williams | 764 | 25 | ||||||

|

| |||||||

| 17,756 | ||||||||

|

| |||||||

Financials — 7.4% | ||||||||

Aflac | 11,210 | 652 | ||||||

American Express | 49,511 | 3,701 | ||||||

American International Group* | 69,822 | 3,121 | ||||||

Ameriprise Financial | 295 | 24 | ||||||

Arch Capital Group | 558 | 29 | ||||||

Ares Capital | 1,320 | 23 | ||||||

Axis Capital Holdings | 3,078 | 141 | ||||||

Bank of America | 12,876 | 166 | ||||||

Bank of New York Mellon | 1,615 | 45 | ||||||

BB&T | 906 | 31 | ||||||

Berkshire Hathaway, Cl B | 2,551 | 285 | ||||||

BlackRock, Cl A | 504 | 129 | ||||||

Boston Properties‡ | 97 | 10 | ||||||

Capital One Financial | 36,155 | 2,271 | ||||||

CBRE Group, Cl A | 31,725 | 741 | ||||||

Charles Schwab | 54,249 | 1,152 | ||||||

Chubb | 1,345 | 114 | ||||||

Citigroup | 45,120 | 2,164 | ||||||

Credicorp | 5,555 | 711 | ||||||

Discover Financial Services | 435 | 21 | ||||||

Equity Residential‡ | 2,092 | 121 | ||||||

Erie Indemnity, Cl A | 25 | 2 | ||||||

Everest Re Group | 226 | 29 | ||||||

Fidelity National Financial, Cl A | 247 | 6 | ||||||

Forest City Enterprises, Cl A* | 179 | 3 | ||||||

General Growth Properties‡ | 246 | 5 | ||||||

Goldman Sachs Group | 673 | 102 | ||||||

HCP‡ | 2,081 | 95 | ||||||

JPMorgan Chase | 42,116 | 2,223 | ||||||

Lazard, Cl A | 37,338 | 1,200 | ||||||

Leucadia National | 4,980 | 131 | ||||||

Loews | 544 | 24 | ||||||

Marsh & McLennan | 713 | 28 | ||||||

MetLife | 32,440 | 1,484 | ||||||

Morgan Stanley | 1,152 | 28 | ||||||

MSCI, Cl A* | 29,276 | 974 | ||||||

Northern Trust | 204 | 12 | ||||||

PartnerRe | 316 | 29 | ||||||

Plum Creek Timber‡ | 149 | 7 | ||||||

PNC Financial Services Group | 684 | 50 | ||||||

ProLogis‡ | 596 | 23 | ||||||

Prudential Financial | 632 | 46 | ||||||

Simon Property Group‡ | 1,047 | 165 | ||||||

SLM | 686 | 16 | ||||||

State Street | 46,432 | 3,028 | ||||||

US Bancorp | 2,716 | 98 | ||||||

Vornado Realty Trust‡ | 1,113 | 92 | ||||||

Wells Fargo | 7,955 | 328 | ||||||

| Description | Shares | Market Value ($ Thousands) | ||||||

Weyerhaeuser‡ | 43,789 | $ | 1,248 | |||||

White Mountains Insurance Group | 41 | 24 | ||||||

|

| |||||||

| 27,152 | ||||||||

|

| |||||||

Health Care — 10.4% | ||||||||

Abbott Laboratories | 1,908 | 66 | ||||||

AbbVie | 1,789 | 74 | ||||||

Agilent Technologies | 24,576 | 1,051 | ||||||

Alexion Pharmaceuticals* | 11,051 | 1,019 | ||||||

Allergan | 1,959 | 165 | ||||||

Amgen | 18,570 | 1,832 | ||||||

Baxter International | 881 | 61 | ||||||

Biogen Idec | 12,420 | 2,673 | ||||||

Bristol-Myers Squibb | 36,344 | 1,624 | ||||||

Celgene* | 14,352 | 1,678 | ||||||

Cerner | 20,832 | 2,002 | ||||||

DENTSPLY International | 183 | 7 | ||||||

Eli Lilly | 1,831 | 90 | ||||||

Express Scripts Holding* | 56,018 | 3,456 | ||||||

Forest Laboratories | 35,483 | 1,455 | ||||||

Gilead Sciences | 36,387 | 1,863 | ||||||

HCA Holdings | 1,295 | 46 | ||||||

Hologic | 52,776 | 1,019 | ||||||

IDEXX Laboratories | 7,826 | 703 | ||||||

Intuitive Surgical | 3,680 | 1,864 | ||||||

Johnson & Johnson | 58,886 | 5,056 | ||||||

Life Technologies | 232 | 17 | ||||||

Medtronic | 561 | 29 | ||||||

Merck | 5,629 | 261 | ||||||

Mettler-Toledo International | 42 | 9 | ||||||

Mylan* | 480 | 15 | ||||||

Perrigo | 17,034 | 2,061 | ||||||

Pfizer | 138,292 | 3,874 | ||||||

Regeneron Pharmaceuticals | 5,467 | 1,230 | ||||||

St. Jude Medical | 27,871 | 1,272 | ||||||

Teleflex | 11,338 | 879 | ||||||

Thermo Fisher Scientific | 1,016 | 86 | ||||||

UnitedHealth Group | 13,942 | 913 | ||||||

WellPoint | 452 | 37 | ||||||

|

| |||||||

| 38,487 | ||||||||

|

| |||||||

Industrials — 5.3% | ||||||||

3M | 1,695 | 186 | ||||||

ADT | 195 | 8 | ||||||

Alliant Techsystems | 1,840 | 152 | ||||||

AMETEK | 314 | 13 | ||||||

Armstrong World Industries | 462 | 22 | ||||||

BE Aerospace | 1,593 | 100 | ||||||

Caterpillar | 1,716 | 141 | ||||||

Cintas | 551 | 25 | ||||||

Copa Holdings, Cl A | 869 | 114 | ||||||

Crane | 2,252 | 135 | ||||||

CSX | 1,434 | 33 | ||||||

Cummins | 17,894 | 1,941 | ||||||

| 12 | New Covenant Funds / Annual Report / June 30, 2013 |

Table of Contents

| Description | Shares | Market Value ($ Thousands) | ||||||

Danaher | 2,292 | $ | 145 | |||||

Deere | 1,846 | 150 | ||||||

Delta Air Lines | 2,350 | 44 | ||||||

Dover | 243 | 19 | ||||||

Emerson Electric | 23,899 | 1,303 | ||||||

Exelis | 72,788 | 1,004 | ||||||

Fastenal | 37,800 | 1,733 | ||||||

FedEx | 224 | 22 | ||||||

General Electric | 77,714 | 1,802 | ||||||

GrafTech International | 110,526 | 805 | ||||||

Honeywell International | 2,483 | 197 | ||||||

Huntington Ingalls Industries | 2,320 | 131 | ||||||

IHS, Cl A | 64 | 7 | ||||||

Illinois Tool Works | 17,517 | 1,212 | ||||||

Kansas City Southern | 13,663 | 1,448 | ||||||

Masco | 4,598 | 90 | ||||||

Nielsen Holdings | 3,499 | 117 | ||||||

Norfolk Southern | 429 | 31 | ||||||

PACCAR | 497 | 27 | ||||||

Pall | 34,548 | 2,295 | ||||||

Parker Hannifin | 1,607 | 153 | ||||||

Precision Castparts | 217 | 49 | ||||||

Republic Services, Cl A | 692 | 23 | ||||||

Southwest Airlines | 2,246 | 29 | ||||||

Stanley Black & Decker | 1,500 | 116 | ||||||

Textron | 4,669 | 122 | ||||||

Timken | 2,717 | 153 | ||||||

Toro | 1,239 | 56 | ||||||

Towers Watson, Cl A | 74 | 6 | ||||||

TransDigm Group | 918 | 144 | ||||||

Triumph Group | 119 | 9 | ||||||

Union Pacific | 16,327 | 2,519 | ||||||

United Continental Holdings | 1,868 | 58 | ||||||

United Parcel Service, Cl B | 2,448 | 212 | ||||||

United Technologies | 2,323 | 216 | ||||||

URS | 102 | 5 | ||||||

Waste Management | 3,917 | 158 | ||||||

Xylem | 232 | 6 | ||||||

|

| |||||||

| 19,486 | ||||||||

|

| |||||||

Information Technology — 16.0% | ||||||||

Activision Blizzard | 1,707 | 24 | ||||||

Adobe Systems* | 83,462 | 3,802 | ||||||

Alliance Data Systems* | 67 | 12 | ||||||

Altera | 25,900 | 854 | ||||||

Amdocs | 3,848 | 143 | ||||||

Amphenol, Cl A | 366 | 28 | ||||||

Analog Devices | 25,447 | 1,147 | ||||||

ANSYS | 120 | 9 | ||||||

Apple | 10,527 | 4,170 | ||||||

Applied Materials | 127,266 | 1,898 | ||||||

Automatic Data Processing | 59,092 | 4,069 | ||||||

BMC Software | 214 | 10 | ||||||

Broadcom, Cl A | 697 | 24 | ||||||

| Description | Shares | Market Value ($ Thousands) | ||||||

CA | 799 | $ | 23 | |||||

Cisco Systems | 95,531 | 2,322 | ||||||

Citrix Systems | 245 | 15 | ||||||

Cognizant Technology Solutions, Cl A* | 248 | 16 | ||||||

Corning | 2,041 | 29 | ||||||

Cree | 139 | 9 | ||||||

Dell | 3,957 | 53 | ||||||

eBay* | 61,559 | 3,184 | ||||||

EMC | 145,618 | 3,439 | ||||||

F5 Networks* | 173 | 12 | ||||||

Facebook, Cl A* | 33,136 | 824 | ||||||

Freescale Semiconductor* | 6,600 | 89 | ||||||

Gartner* | 127 | 7 | ||||||

Genpact | 1,342 | 26 | ||||||

Google, Cl A* | 3,563 | 3,137 | ||||||

Hewlett-Packard | 2,215 | 55 | ||||||

Intel | 11,456 | 277 | ||||||

International Business Machines | 19,095 | 3,649 | ||||||

Intuit | 314 | 19 | ||||||

Juniper Networks | 693 | 13 | ||||||

LSI* | 117,887 | 842 | ||||||

Marvell Technology Group | 1,401 | 16 | ||||||

Mastercard, Cl A | 4,825 | 2,772 | ||||||

Maxim Integrated Products | 2,676 | 74 | ||||||

Microchip Technology | 234 | 9 | ||||||

MICROS Systems | 105 | 5 | ||||||

Microsoft | 61,073 | 2,109 | ||||||

Molex | 5,187 | 152 | ||||||

Motorola Solutions | 2,038 | 118 | ||||||

NetApp | 456 | 17 | ||||||

Oracle | 107,979 | 3,317 | ||||||

Paychex | 615 | 22 | ||||||

QUALCOMM | 100,303 | 6,127 | ||||||

Red Hat | 213 | 10 | ||||||

Riverbed Technology | 78,780 | 1,226 | ||||||

Salesforce.com* | 37,536 | 1,433 | ||||||

SanDisk | 310 | 19 | ||||||

Skyworks Solutions | 246 | 5 | ||||||

Solera Holdings | 92 | 5 | ||||||

Symantec | 982 | 22 | ||||||

Teradata | 35,867 | 1,802 | ||||||

Texas Instruments | 49,839 | 1,738 | ||||||

Total System Services | 6,302 | 154 | ||||||

Trimble Navigation | 3,253 | 85 | ||||||

VeriSign | 857 | 38 | ||||||

Visa, Cl A | 17,304 | 3,162 | ||||||

Xerox | 34,580 | 314 | ||||||

Yahoo! | 1,578 | 39 | ||||||

Zebra Technologies, Cl A | 1,845 | 80 | ||||||

|

| |||||||

| 59,100 | ||||||||

|

| |||||||

Materials — 5.2% | ||||||||

Air Products & Chemicals | 274 | 25 | ||||||

Ball | 3,167 | 132 | ||||||

| New Covenant Funds / Annual Report / June 30, 2013 | 13 |

Table of Contents

SCHEDULE OF INVESTMENTS

New Covenant Growth Fund (Concluded)

June 30, 2013

| Description | Shares | Market Value ($ Thousands) | ||||||

Crown Holdings | 2,386 | $ | 98 | |||||

Dow Chemical | 70,051 | 2,254 | ||||||

Ecolab | 32,943 | 2,806 | ||||||

E.I. du Pont de Nemours | 28,070 | 1,474 | ||||||

International Paper | 1,686 | 75 | ||||||

LyondellBasell Industries, Cl A | 13,269 | 879 | ||||||

MeadWestvaco | 694 | 23 | ||||||

Monsanto | 49,728 | 4,913 | ||||||

Newmont Mining | 24,630 | 738 | ||||||

Owens-Illinois | 34,827 | 968 | ||||||

Packaging Corp of America | 50 | 2 | ||||||

Praxair | 17,611 | 2,028 | ||||||

Sealed Air | 57,215 | 1,370 | ||||||

Sherwin-Williams | 97 | 17 | ||||||

Sonoco Products | 320 | 11 | ||||||

Southern Copper | 699 | 19 | ||||||

Vulcan Materials | 947 | 46 | ||||||

WR Grace* | 13,689 | 1,151 | ||||||

|

| |||||||

| 19,029 | ||||||||

|

| |||||||

Telecommunication Services — 1.3% |

| |||||||

AT&T | 8,653 | 306 | ||||||

CenturyLink* | 554 | 20 | ||||||

Crown Castle International | 50,530 | 3,658 | ||||||

SBA Communications, Cl A | 8,424 | 624 | ||||||

Verizon Communications | 5,444 | 274 | ||||||

Windstream | 1,862 | 14 | ||||||

|

| |||||||

| 4,896 | ||||||||

|

| |||||||

Utilities — 0.2% | ||||||||

Dominion Resources | 2,840 | 161 | ||||||

Duke Energy | 2,553 | 172 | ||||||

Entergy | 232 | 16 | ||||||

Exelon | 3,536 | 109 | ||||||

FirstEnergy | 225 | 9 | ||||||

NextEra Energy | 541 | 44 | ||||||

Northeast Utilities | 406 | 17 | ||||||

PG&E | 1,643 | 75 | ||||||

Southern | 3,498 | 155 | ||||||

Xcel Energy | 243 | 7 | ||||||

|

| |||||||

| 765 | ||||||||

|

| |||||||

| 277,199 | ||||||||

|

| |||||||

Total Common Stock | 360,126 | |||||||

|

| |||||||

| Description | Shares/Face Amount (Thousands) (1) | Market Value ($ Thousands) | ||||||||||

EXCHANGE-TRADED FUND — 0.3% |

| |||||||||||

SPDR Gold Trust | 9,170 | $ | 1,093 | |||||||||

|

| |||||||||||

Total Exchange-Traded Fund |

| 1,093 | ||||||||||

|

| |||||||||||

CASH EQUIVALENT — 1.2% |

| |||||||||||

SEI Daily Income Trust, Prime Obligation Fund, Cl A 0.010%†** |

| 4,660,971 | 4,661 | |||||||||

|

| |||||||||||

Total Cash Equivalent |

| 4,661 | ||||||||||

|

| |||||||||||

TIME DEPOSITS — 0.7% |

| |||||||||||

Brown Brothers Harriman | ||||||||||||

0.265%, 07/01/2013 | CAD | 3 | 2 | |||||||||

0.030%, 07/01/2013 | 2,540 | 2,540 | ||||||||||

0.005%, 07/01/2013 | JPY | 357 | 4 | |||||||||

|

| |||||||||||

Total Time Deposits | 2,546 | |||||||||||

|

| |||||||||||

U.S. TREASURY OBLIGATIONS — 0.1% |

| |||||||||||

U.S. Treasury Bills (B)(C) | ||||||||||||

0.091%, 02/06/2014 | $ | 91 | 91 | |||||||||

0.020%, 07/25/2013 | 200 | 200 | ||||||||||

|

| |||||||||||

Total U.S. Treasury Obligations |

| 291 | ||||||||||

|

| |||||||||||

Total Investments — 99.9% |

| $ | 368,717 | |||||||||

|

| |||||||||||

The open futures contracts held by the Fund at June 30, 2013 are as follows:

| Type of Contract | Number Of Contracts Long | Expiration Date | Unrealized Appreciation (Depreciation) ($ Thousands) | |||||||||

DJ Euro Stoxx 50 Index | 8 | Sep-2013 | $ | (10 | ) | |||||||

FTSE 100 Index | 2 | Sep-2013 | (1 | ) | ||||||||

S&P 500 Index EMINI | 50 | Sep-2013 | (11 | ) | ||||||||

S&P TSE 60 Index | 1 | Sep-2013 | (2 | ) | ||||||||

SPI 200 Index | 1 | Sep-2013 | (1 | ) | ||||||||

Topix Index | 2 | Sep-2013 | 3 | |||||||||

|

| |||||||||||

| $ | (22 | ) | ||||||||||

|

| |||||||||||

For the year ended June 30, 2013, the total amount of all open futures contracts, as presented in the table above, are representative of the volume of activity for the derivative type during the year.

The futures contracts are considered to have equity risk associated with them.

Percentages are based on a Net Assets of $369,133 ($ Thousands).

| * | Non-income producing security. |

| ** | The rate reported is the 7-day effective yield as of June 30, 2013. |

| † | Investment in Affiliated Security (see Note 3). |

| ‡ | Real Estate Investment Trust. |

| (1) | In U.S. Dollars unless otherwise indicated. |

| 14 | New Covenant Funds / Annual Report / June 30, 2013 |

Table of Contents

| (A) | Security fair valued using methods determined in good faith by the Valuation Committee of the Board of Trustees. The total market value of such securities as of June 30, 2013 was $57,143 ($ Thousands) and represented 15.5% of Net Assets. |

| (B) | The rate reported is the effective yield at time of purchase. |

| (C) | Security, or portion thereof, has been pledged as collateral on open futures contracts. |

ADR — American Depositary Receipt

CAD — Canadian Dollar

Cl — Class

DJ — Dow Jones

FTSE — Financial Times and the London Stock Exchange

GDR — Global Depositary Receipt

JPY — Japanese Yen

S&P — Standard & Poor’s

SPDR — Standard & Poor’s Depositary Receipt

SPI — Share Price Index

Topix — Tokyo Stock Price Index

TSE — Toronto Stock Exchange

The following is a list of the inputs used as of June 30, 2013 in valuing the Fund’s investments and other financial instruments carried at value ($ Thousands):

| Investments in Securities | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Common Stock | $ | 302,983 | $ | 57,143 | $ | — | $ | 360,126 | ||||||||

Exchange-Traded Fund | 1,093 | — | — | 1,093 | ||||||||||||

Cash Equivalent | 4,661 | — | — | 4,661 | ||||||||||||

Time Deposits | 2,546 | — | — | 2,546 | ||||||||||||

U.S. Treasury Obligations | — | 291 | — | 291 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Total Investments in Securities | $ | 311,283 | $ | 57,434 | $ | — | $ | 368,717 | ||||||||

|

|

|

|

|

|

|

| |||||||||

Other Financial Instruments | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Futures Contracts* | $ | (22 | ) | $ | — | $ | — | $ | (22 | ) | ||||||

|

|

|

|

|

|

|

| |||||||||

| * | Futures contracts are valued at the unrealized appreciation (depreciation) on the instrument. |

For the year ended June 30, 2013, there were transfers between Level 1 and Level 2 assets and liabilities. The primary reason for changes in the classifications between Levels 1 and 2 occurs when the foreign equity securities are fair valued using other observable market-based inputs in place of the closing exchange price due to events occurring after the close of the exchange or market on which the investment is principally traded.

For the year ended June 30, 2013, there were no transfers between Level 2 and Level 3 assets and liabilities.

For more information on valuation inputs, see Note 2 — Significant Accounting Policies in Note to Financial Statements.

The accompanying notes are an integral part of the financial statements.

| New Covenant Funds / Annual Report / June 30, 2013 | 15 |

Table of Contents

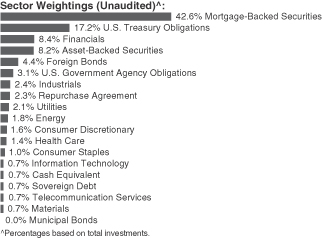

SCHEDULE OF INVESTMENTS

New Covenant Income Fund

June 30, 2013

| Description | Face Amount ($ Thousands) | Market Value ($ Thousands) | ||||||

MORTGAGE-BACKED SECURITIES — 46.3% |

| |||||||

Agency Mortgage-Backed Obligations — 41.1% |

| |||||||

FHLMC | ||||||||

5.500%, 12/01/2036 | $ | 313 | $ | 337 | ||||

5.500%, 08/01/2038 | 237 | 254 | ||||||

5.500%, 11/01/2038 | 142 | 153 | ||||||

5.500%, 12/01/2038 | 1,021 | 1,106 | ||||||

5.000%, 12/01/2020 | 509 | 545 | ||||||

5.000%, 05/01/2022 | 229 | 245 | ||||||

5.000%, 04/01/2024 | 207 | 222 | ||||||

5.000%, 08/01/2038 | 67 | 72 | ||||||

5.000%, 03/01/2039 | 40 | 42 | ||||||

5.000%, 02/01/2040 | 749 | 809 | ||||||

4.500%, 11/01/2039 | 763 | 804 | ||||||

4.500%, 08/01/2040 | 2,516 | 2,651 | ||||||

4.500%, 08/01/2040 | 2,156 | 2,272 | ||||||

4.000%, 09/01/2040 | 178 | 185 | ||||||

4.000%, 06/01/2043 | 100 | 105 | ||||||

4.000%, 06/01/2043 | 100 | 105 | ||||||

4.000%, 07/01/2043 | 100 | 105 | ||||||

4.000%, 07/01/2043 | 100 | 106 | ||||||

3.990%, 07/01/2040 (A) | 558 | 592 | ||||||

3.500%, 11/01/2042 | 396 | 397 | ||||||

3.500%, 01/01/2043 | 198 | 199 | ||||||

3.500%, 02/01/2043 | 99 | 100 | ||||||

3.500%, 04/01/2043 | 99 | 100 | ||||||

3.500%, 05/01/2043 | 396 | 403 | ||||||

3.500%, 05/01/2043 | 999 | 1,002 | ||||||

3.500%, 06/01/2043 | 998 | 1,001 | ||||||

FHLMC CMO, | ||||||||

Ser 2007-3349, Cl AS, IO | ||||||||

6.308%, 07/15/2037 (A) | 1,595 | 242 | ||||||

FHLMC CMO, | ||||||||

Ser 2011-3947, Cl SG, IO | ||||||||

5.758%, 10/15/2041 (A) | 909 | 227 | ||||||

FHLMC CMO, Ser 2012-274, Cl F1 | ||||||||

0.693%, 08/15/2042 (A) | 487 | 490 | ||||||

| Description | Face Amount ($ Thousands) | Market Value ($ Thousands) | ||||||

FHLMC CMO, Ser 2012-279, Cl F6 | ||||||||

0.643%, 09/15/2042 (A) | $ | 486 | $ | 489 | ||||

FHLMC CMO, | ||||||||

Ser 2012-4013, Cl AI, IO | ||||||||

4.000%, 02/15/2039 | 652 | 127 | ||||||

FHLMC CMO, | ||||||||

Ser 2012-4057, Cl SA, IO | ||||||||

5.858%, 04/15/2039 (A) | 592 | 121 | ||||||

FHLMC CMO, | ||||||||

Ser 2012-4057, Cl UI, IO | ||||||||

3.000%, 05/15/2027 | 545 | 59 | ||||||

FHLMC CMO, | ||||||||

Ser 2012-4068, Cl DS, IO | ||||||||

5.808%, 06/15/2042 (A) | 95 | 22 | ||||||

FHLMC CMO, | ||||||||

Ser 2012-4085, Cl IO, IO | ||||||||

3.000%, 06/15/2027 | 1,193 | 165 | ||||||

FHLMC CMO, | ||||||||

Ser 2012-4092, Cl AI, IO | ||||||||

3.000%, 09/15/2031 | 1,485 | 188 | ||||||

FHLMC CMO, | ||||||||

Ser 2012-4097, Cl ES, IO | ||||||||

5.908%, 08/15/2042 (A) | 189 | 44 | ||||||

FHLMC CMO, | ||||||||

Ser 2012-4097, Cl ST, IO | ||||||||

5.858%, 08/15/2042 (A) | 95 | 22 | ||||||

FHLMC CMO, | ||||||||

Ser 2012-4116, Cl LS, IO | ||||||||

6.008%, 10/15/2042 (A) | 562 | 122 | ||||||

FHLMC CMO, | ||||||||

Ser 2012-4120, Cl SV, IO | ||||||||

5.958%, 10/15/2042 (A) | 484 | 105 | ||||||

FHLMC CMO, | ||||||||

Ser 2012-4136, Cl SW, IO | ||||||||

5.958%, 11/15/2042 (A) | 97 | 25 | ||||||

FHLMC CMO, | ||||||||

Ser 2012-4147, Cl CS, IO | ||||||||

5.908%, 12/15/2042 (A) | 98 | 26 | ||||||

FHLMC CMO, | ||||||||

Ser 2013-4150, Cl SP, IO | ||||||||

5.958%, 01/15/2043 (A) | 195 | 44 | ||||||

FHLMC CMO, | ||||||||

Ser 2013-4199, Cl CS, IO | ||||||||

5.958%, 05/15/2043 (A) | 199 | 53 | ||||||

FHLMC CMO, | ||||||||

Ser 2013-4199, Cl SB, IO | ||||||||

6.008%, 05/15/2040 (A) | 199 | 48 | ||||||

FHLMC CMO, | ||||||||

Ser 2013-4203, Cl PS, IO | ||||||||

6.058%, 09/15/2042 (A) | 497 | 102 | ||||||

FHLMC CMO, | ||||||||

Ser 2013-4219, Cl JA | ||||||||

3.500%, 08/15/2039 | 1,000 | 1,057 | ||||||

| 16 | New Covenant Funds / Annual Report / June 30, 2013 |

Table of Contents

| Description | Face Amount ($ Thousands) | Market Value ($ Thousands) | ||||||

FHLMC Multifamily Structured | ||||||||

1.646%, 06/25/2022 (A) | $ | 559 | $ | 57 | ||||

FHLMC Multifamily Structured | ||||||||

1.026%, 09/25/2022 (A) | 279 | 18 | ||||||

FHLMC TBA | ||||||||

3.500%, 07/15/2041 | 1,400 | 1,418 | ||||||

2.500%, 07/15/2027 | 1,000 | 1,005 | ||||||

FNMA | ||||||||

7.000%, 11/01/2037 | 11 | 13 | ||||||

7.000%, 11/01/2037 | 5 | 6 | ||||||

7.000%, 12/01/2037 | 12 | 14 | ||||||

7.000%, 02/01/2038 | 14 | 16 | ||||||

7.000%, 09/01/2038 | 4 | 4 | ||||||

7.000%, 11/01/2038 | 15 | 18 | ||||||

7.000%, 11/01/2038 | 22 | 26 | ||||||

7.000%, 11/01/2038 | 10 | 11 | ||||||

7.000%, 11/01/2038 | 91 | 106 | ||||||

6.500%, 08/01/2017 | 158 | 171 | ||||||

6.000%, 12/01/2035 | 110 | 117 | ||||||

6.000%, 07/01/2037 | 246 | 267 | ||||||

6.000%, 09/01/2037 | 291 | 316 | ||||||

6.000%, 11/01/2038 | 376 | 409 | ||||||

5.500%, 09/01/2034 | 1,061 | 1,163 | ||||||

5.500%, 02/01/2035 | 636 | 697 | ||||||

5.000%, 01/01/2021 | 441 | 471 | ||||||

5.000%, 11/01/2025 | 296 | 322 | ||||||

5.000%, 06/01/2035 | 318 | 344 | ||||||

5.000%, 07/01/2035 | 1,612 | 1,740 | ||||||

5.000%, 02/01/2036 | 556 | 600 | ||||||

5.000%, 03/01/2036 | 788 | 849 | ||||||

5.000%, 03/01/2040 | 350 | 377 | ||||||

5.000%, 06/01/2040 | 859 | 933 | ||||||

5.000%, 06/01/2040 | 626 | 679 | ||||||

5.000%, 06/01/2040 | 80 | 86 | ||||||

4.601%, 04/01/2020 | 1,367 | 1,518 | ||||||

4.530%, 12/01/2019 | 997 | 1,130 | ||||||

4.501%, 01/01/2020 | 757 | 847 | ||||||

4.500%, 07/01/2037 | 1,700 | 1,799 | ||||||

4.377%, 11/01/2019 | 520 | 578 | ||||||

4.000%, 06/01/2025 | 549 | 579 | ||||||

4.000%, 07/13/2039 | 1,900 | 1,979 | ||||||

4.000%, 02/01/2041 | 1,934 | 2,022 | ||||||

4.000%, 09/01/2041 | 803 | 838 | ||||||

4.000%, 04/01/2042 | 5,522 | 5,781 | ||||||

4.000%, 07/01/2042 | 966 | 997 | ||||||

4.000%, 05/01/2043 | 199 | 209 | ||||||

4.000%, 06/01/2043 | 100 | 105 | ||||||

4.000%, 06/01/2043 | 100 | 105 | ||||||

4.000%, 06/01/2043 | 100 | 105 | ||||||

4.000%, 06/01/2043 | 100 | 105 | ||||||

4.000%, 06/01/2043 | 199 | 210 | ||||||

| Description | Face Amount ($ Thousands) | Market Value ($ Thousands) | ||||||

4.000%, 07/01/2043 | $ | 200 | $ | 210 | ||||

4.000%, 07/01/2043 | 100 | 105 | ||||||

4.000%, 07/01/2043 | 200 | 210 | ||||||

3.686%, 01/01/2021 | 1,470 | 1,556 | ||||||

3.500%, 05/01/2033 | 498 | 505 | ||||||

3.500%, 03/01/2041 | 947 | 963 | ||||||

3.500%, 10/01/2042 | 98 | 98 | ||||||

3.500%, 12/01/2042 | 198 | 199 | ||||||

3.500%, 12/01/2042 | 197 | 197 | ||||||

3.500%, 12/01/2042 | 98 | 98 | ||||||

3.500%, 03/01/2043 | 1,189 | 1,192 | ||||||

3.500%, 04/01/2043 | 696 | 698 | ||||||

3.500%, 06/01/2043 | 998 | 1,003 | ||||||

3.030%, 12/01/2021 | 732 | 737 | ||||||

3.000%, 07/01/2042 | 5,600 | 5,471 | ||||||

2.575%, 03/01/2036 (A) | 136 | 145 | ||||||

2.500%, 10/01/2042 | 1,068 | 994 | ||||||

2.500%, 07/25/2043 | 400 | 372 | ||||||

2.400%, 12/01/2022 | 250 | 239 | ||||||

1.940%, 07/01/2019 | 400 | 403 | ||||||

1.880%, 05/01/2043 (A) | 2,447 | 2,454 | ||||||

0.648%, 01/01/2023 (A) | 496 | 497 | ||||||

0.558%, 01/01/2023 (A) | 496 | 497 | ||||||

0.548%, 01/01/2023 (A) | 496 | 497 | ||||||

0.538%, 01/01/2023 (A) | 500 | 501 | ||||||

0.538%, 01/01/2023 (A) | 400 | 401 | ||||||

FNMA CMO, Ser 1992-1, Cl F | ||||||||

1.019%, 01/25/2022 (A) | 247 | 249 | ||||||

FNMA CMO, Ser 2003-W2, Cl 2A9 | ||||||||

5.900%, 07/25/2042 | 1,012 | 1,144 | ||||||

FNMA CMO, Ser 2004-90, Cl LH | ||||||||

5.000%, 04/25/2034 | 1,509 | 1,582 | ||||||

FNMA CMO, Ser 2005-22, Cl DA | ||||||||

5.500%, 12/25/2034 | 915 | 1,010 | ||||||

FNMA CMO, Ser 2009-86, Cl CA | ||||||||

4.500%, 09/25/2024 | 88 | 89 | ||||||

FNMA CMO, Ser 2010-100, Cl CS, IO | ||||||||

6.457%, 09/25/2040 (A) | 1,647 | 265 | ||||||

FNMA CMO, Ser 2012-108, Cl F | ||||||||

0.693%, 10/25/2042 (A) | 486 | 490 | ||||||

FNMA CMO, Ser 2012-111, Cl JS, IO | ||||||||

5.907%, 07/25/2040 (A) | 677 | 153 | ||||||

FNMA CMO, Ser 2012-111, Cl SB, IO | ||||||||

6.407%, 10/25/2042 (A) | 193 | 49 | ||||||

FNMA CMO, Ser 2012-128, Cl SL, IO | ||||||||

5.957%, 11/25/2042 (A) | 98 | 25 | ||||||

FNMA CMO, Ser 2012-128, Cl SQ, IO | ||||||||

5.957%, 11/25/2042 (A) | 97 | 25 | ||||||

FNMA CMO, Ser 2012-134, Cl SC, IO | ||||||||

5.957%, 12/25/2042 (A) | 194 | 46 | ||||||

FNMA CMO, Ser 2012-134, Cl SK, IO | ||||||||

5.957%, 12/25/2042 (A) | 97 | 23 | ||||||

FNMA CMO, Ser 2012-74, Cl AI, IO | ||||||||

3.000%, 07/25/2027 | 1,960 | 251 | ||||||

| New Covenant Funds / Annual Report / June 30, 2013 | 17 |

Table of Contents

SCHEDULE OF INVESTMENTS

New Covenant Income Fund (Continued)

June 30, 2013

| Description | Face Amount ($ Thousands) | Market Value ($ Thousands) | ||||||

FNMA CMO, Ser 2012-89, Cl AS, IO | ||||||||

5.857%, 05/25/2039 (A) | $ | 857 | $ | 162 | ||||

FNMA CMO, Ser 2012-93, Cl SG, IO | ||||||||

5.907%, 09/25/2042 (A) | 381 | 80 | ||||||

FNMA CMO, Ser 2012-93, Cl SM, IO | ||||||||

5.907%, 09/25/2042 (A) | 382 | 86 | ||||||

FNMA CMO, Ser 2012-93, Cl UI, IO | ||||||||

3.000%, 09/25/2027 | 1,515 | 194 | ||||||

FNMA CMO, Ser 2012-98, Cl SA, IO | ||||||||

5.857%, 05/25/2039 (A) | 95 | 20 | ||||||

FNMA CMO, Ser 2012-M11, Cl FA | ||||||||

0.723%, 08/25/2019 (A) | 432 | 433 | ||||||

FNMA CMO, Ser 2013-19, Cl SK, IO | ||||||||

5.957%, 03/25/2043 (A) | 99 | 25 | ||||||

FNMA CMO, Ser 2013-9, Cl SG, IO | ||||||||

6.007%, 03/25/2039 (A) | 99 | 23 | ||||||

FNMA CMO, Ser 2013-M7, Cl A2 | ||||||||

2.280%, 12/27/2022 | 219 | 204 | ||||||

FNMA TBA | ||||||||

5.481%, 06/01/2017 | 2,123 | 2,415 | ||||||

3.500%, 07/01/2041 | 4,700 | 4,771 | ||||||

2.500%, 07/01/2027 | 4,000 | 4,023 | ||||||

GNMA | ||||||||

5.500%, 02/20/2037 | 307 | 336 | ||||||

5.500%, 07/20/2038 | 177 | 194 | ||||||

5.500%, 01/15/2039 | 410 | 447 | ||||||

5.000%, 12/20/2038 | 144 | 149 | ||||||

5.000%, 03/15/2039 | 399 | 432 | ||||||

5.000%, 03/20/2039 | 289 | 304 | ||||||

5.000%, 07/20/2040 | 3,095 | 3,413 | ||||||

4.863%, 06/20/2061 | 1,676 | 1,851 | ||||||

4.826%, 06/20/2061 | 1,442 | 1,596 | ||||||

4.697%, 09/20/2061 | 1,392 | 1,536 | ||||||

4.650%, 12/20/2060 | 1,384 | 1,517 | ||||||

4.626%, 07/20/2061 | 1,509 | 1,646 | ||||||

4.500%, 07/20/2038 | 309 | 328 | ||||||

4.500%, 05/20/2040 | 1,738 | 1,871 | ||||||

4.500%, 07/20/2040 | 2,709 | 2,905 | ||||||

4.500%, 01/20/2041 | 951 | 1,025 | ||||||

4.500%, 07/20/2041 | 374 | 401 | ||||||

4.295%, 07/20/2061 | 1,330 | 1,457 | ||||||

3.500%, 07/01/2042 | 1,100 | 1,128 | ||||||

2.500%, 02/20/2027 | 2,595 | 2,623 | ||||||

GNMA CMO, Ser 2004-10, Cl C | ||||||||

4.666%, 07/16/2031 | 182 | 183 | ||||||

GNMA CMO, Ser 2004-108, Cl AB | ||||||||

4.397%, 12/16/2032 (A) | 148 | 151 | ||||||

GNMA CMO, Ser 2009-108, Cl WG | ||||||||

4.000%, 09/20/2038 | 827 | 888 | ||||||

GNMA CMO, Ser 2009-31, Cl MA | ||||||||

4.500%, 08/20/2033 | 137 | 140 | ||||||

GNMA CMO, Ser 2009-86, Cl A | ||||||||

3.536%, 09/16/2035 | 251 | 255 | ||||||

GNMA CMO, Ser 2010-48, Cl AC | ||||||||

4.229%, 02/16/2040 | 203 | 207 | ||||||

| Description | Face Amount ($ Thousands) | Market Value ($ Thousands) | ||||||

GNMA CMO, Ser 2010-71, Cl AD | ||||||||

3.489%, 03/16/2039 | $ | 711 | $ | 728 | ||||

GNMA CMO, Ser 2011-147, Cl A | ||||||||

2.174%, 07/16/2038 | 1,433 | 1,457 | ||||||

GNMA CMO, Ser 2012-22, Cl AB | ||||||||

1.661%, 03/16/2033 | 1,341 | 1,351 | ||||||

GNMA CMO, Ser 2012-H18, Cl NA | ||||||||

0.718%, 08/20/2062 (A) | 384 | 383 | ||||||

GNMA CMO, Ser 2012-66, Cl CI, IO | ||||||||

3.500%, 02/20/2038 | 279 | 44 | ||||||

GNMA CMO, Ser 2012-77, Cl KI, IO | ||||||||

7.500%, 04/20/2031 | 286 | 67 | ||||||

GNMA TBA | ||||||||

3.500%, 07/15/2041 | 1,100 | 1,129 | ||||||

NCUA Guaranteed Notes Trust, | ||||||||

2.900%, 10/29/2020 | 350 | 365 | ||||||

NCUA Guaranteed Notes Trust, | ||||||||

2.650%, 10/29/2020 | 362 | 376 | ||||||

|

| |||||||

| 119,812 | ||||||||

|

| |||||||

Non-Agency Mortgage-Backed Obligations — 5.2% |

| |||||||

American Home Mortgage Investment Trust, Ser 2004-4, Cl 1A1 | ||||||||

0.533%, 02/25/2045 (A) | 381 | 350 | ||||||

American Home Mortgage Investment Trust, Ser 2005-1, Cl 7A1 | ||||||||

2.414%, 06/25/2045 (A) | 388 | 387 | ||||||

Banc of America Commercial Mortgage Trust, Ser 2006-2, Cl AM | ||||||||

5.954%, 05/10/2045 (A) | 100 | 109 | ||||||

Banc of America Funding, | ||||||||

3.000%, 10/26/2039 (B)(C) | 185 | 185 | ||||||

Banc of America Merrill Lynch | ||||||||

5.743%, 06/10/2039 (A) | 382 | 393 | ||||||

Banc of America Mortgage Trust, | ||||||||

5.500%, 04/25/2034 | 124 | 127 | ||||||

Banc of America Mortgage Trust, | ||||||||

6.500%, 09/25/2032 | 155 | 163 | ||||||

BCAP Trust, Ser 2012-RR10, Cl 3A1 | ||||||||

0.383%, 05/26/2036 (A)(B) | 411 | 382 | ||||||

Bear Stearns ALT-A Trust, | ||||||||

0.833%, 07/25/2034 (A) | 132 | 125 | ||||||

Bear Stearns Commercial Mortgage Securities, Ser 2005-PWR9, Cl A4A | ||||||||

4.871%, 09/11/2042 | 328 | 350 | ||||||

| 18 | New Covenant Funds / Annual Report / June 30, 2013 |

Table of Contents

| Description | Face Amount ($ Thousands) | Market Value ($ Thousands) | ||||||

Bear Stearns Commercial Mortgage Securities, Ser 2007-PW16, Cl A4 | ||||||||

5.905%, 06/11/2040 (A) | $ | 550 | $ | 621 | ||||