Wisconsin Electric Power Company PFD 6% (WELPM)

Filed: 28 Mar 14, 12:00am

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14C

Information Statement Pursuant to Section 14(c)

of the Securities Exchange Act of 1934 (Amendment No. )

Check the appropriate box: | ||||

| ¨ | Preliminary Information Statement | |||

| ¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14c-5(d)(2)) | |||

| x | Definitive Information Statement | |||

| Wisconsin Electric Power Company | ||||

| (Name of Registrant As Specified In Charter) | ||||

Payment of Filing Fee (Check the appropriate box): | ||||

| x | No fee required | |||

| ¨ | Fee computed on table below per Exchange Act Rules 14c-5(g) and 0-11. | |||

| (1) | Title of each class of securities to which transaction applies: | |||

| ||||

| (2) | Aggregate number of securities to which transaction applies: | |||

| ||||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (Set forth the amount on which the filing fee is calculated and state how it was determined): | |||

| ||||

| (4) | Proposed maximum aggregate value of transaction: | |||

| ||||

| (5) | Total fee paid: | |||

| ||||

| ¨ | Fee paid previously with preliminary materials. | |||

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing | |||

| (1) | Amount Previously Paid: | |||

| ||||

| (2) | Form, Schedule or Registration Statement No.: | |||

| ||||

| (3) | Filing Party: | |||

| ||||

| (4) | Date Filed: | |||

| ||||

| Gale E. Klappa Chairman, President and Chief Executive Officer 231 W Michigan Street Milwaukee, WI 53203 |

March 28, 2014

Dear Preferred Stockholder:

Wisconsin Electric Power Company, which does business under the trade name of We Energies, will hold its Annual Meeting of Stockholders on Thursday, April 24, 2014, at 10:00 a.m., in the Resource Center on the first floor of the Public Service Building, 231 West Michigan Street, Milwaukee, Wisconsin 53203.

We are not soliciting proxies for this meeting, as more than 99% of the voting stock is owned, and will be voted, by Wisconsin Electric Power Company’s parent, Wisconsin Energy Corporation. If you wish, you may vote your shares of preferred stock in person at the meeting; however, the business session will be very brief.

As an alternative, you might consider attending Wisconsin Energy Corporation’s Annual Meeting of Stockholders to be held Friday, May 2, 2014, at 10:00 a.m., Central time, at Concordia University Wisconsin in the R. John Buuck Field House located at 12800 North Lake Shore Drive, Mequon, Wisconsin 53097.

By attending this meeting, you would have the opportunity to meet many of the Wisconsin Electric Power Company officers and directors. Although you cannot vote your shares of Wisconsin Electric Power Company preferred stock at the Wisconsin Energy Corporation meeting, you may find the activities worthwhile.

You must pre-register and present photo identification at the door to attend Wisconsin Energy Corporation’s Annual Meeting. To pre-register for the meeting, please contact Wisconsin Energy Corporation’s Stockholder Services, 231 West Michigan Street, P.O. Box 1331, Milwaukee, Wisconsin 53201, or simply call 800-881-5882 or emailWEC.Stockholder-Services.Contact@wisconsinenergy.comand provide proof of your ownership of preferred stock, including a bank or brokerage firm account statement or a letter from the broker, trustee, bank or nominee holding your shares.

The annual report of Wisconsin Electric is attached as Appendix A to this information statement. If you have any questions or would like a copy of the Wisconsin Energy Corporation annual report, please call our toll-free stockholder hotline at 800-881-5882.

Thank you for your support.

Sincerely,

|

NOTICE OF ANNUAL MEETING OF STOCKHOLDERS

March 28, 2014

To the Stockholders of Wisconsin Electric Power Company:

The 2014 Annual Meeting of Stockholders of Wisconsin Electric Power Company will be held on Thursday, April 24, 2014, at 10:00 a.m., Central time, in the Resource Center on the first floor of the Public Service Building, 231 West Michigan Street, Milwaukee, Wisconsin 53203, for the following purposes:

| 1. | To elect the nine members of the Board of Directors to hold office until the 2015 Annual Meeting of Stockholders; and |

| 2. | To consider any other matters that may properly come before the meeting. |

Stockholders of record at the close of business on February 21, 2014, are entitled to vote. The following pages provide additional details about the meeting as well as other useful information.

Important Notice Regarding the Availability of Materials Related to the Stockholder Meeting to Be Held on April 24, 2014 – The Information Statement and 2013 Annual Report to Stockholders are available at:

www.wisconsinelectric.com

| By Order of the Board of Directors, |

|

| Susan H. Martin |

| Executive Vice President, General Counsel and Corporate Secretary |

| We Energies 231 West Michigan Street Milwaukee, Wisconsin 53203 |

INFORMATION STATEMENT

This information statement is being furnished to stockholders beginning on or about March 28, 2014, in connection with the annual meeting of stockholders of Wisconsin Electric Power Company (“WE” or the “Company”) to be held on Thursday, April 24, 2014 (the “Meeting”), at 10:00 a.m., Central time, in the Resource Center on the first floor of the Public Service Building, 231 West Michigan Street, Milwaukee, Wisconsin 53203, and all adjournments or postponements of the Meeting, for the purposes listed in the preceding Notice of Annual Meeting of Stockholders. If you need directions to the Meeting, please call our toll-free stockholder hotline at 800-881-5882. The WE annual report to stockholders is attached as Appendix A to this information statement.

We are not asking you for a proxy and you are requested not to send us a proxy.However, you may vote your shares of preferred stock at the Meeting.

VOTING SECURITIES

As of February 21, 2014, WE had outstanding 44,498 shares of $100 par value Six Per Cent. Preferred Stock; 260,000 shares of $100 par value 3.60% Serial Preferred Stock; and 33,289,327 shares of common stock. Each outstanding share of each class is entitled to one vote. Stockholders of record at the close of business on February 21, 2014 will be entitled to vote at the Meeting. In order to conduct the Meeting, a majority of the outstanding shares entitled to vote must be represented at the Meeting. This is known as a “quorum.” All of WE’s outstanding common stock, representing more than 99% of its voting securities, is owned by its parent company, Wisconsin Energy Corporation (“WEC”), and will be represented at the Meeting. The principal business address of WEC is 231 West Michigan Street, Milwaukee, Wisconsin 53203. A list of stockholders of record entitled to vote at the Meeting will be available for inspection by stockholders at WE’s principal business office at 231 West Michigan Street, Milwaukee, Wisconsin 53203, prior to and at the Meeting.

INTERNET AVAILABILITY OF INFORMATION

The following documents can be found atwww.wisconsinelectric.com:

| • | Notice of Annual Meeting; |

| • | Information Statement; and |

| • | 2013 Annual Report to Stockholders. |

ELECTION OF DIRECTORS

At the Meeting, there will be an election of nine directors. Based upon the recommendation of the Corporate Governance Committee of WEC’s Board of Directors, the individuals named below have been nominated by the WE Board of Directors (the “Board”) to serve a one-year term expiring at the 2015 Annual Meeting of Stockholders and until they are re-elected or until their respective successors are duly elected and qualified. Currently, directors of WEC also serve as the directors of WE.

Directors will be elected by a plurality of the votes cast by the shares entitled to vote, as long as a quorum is present. “Plurality” means that the individuals who receive the largest number of votes are elected as directors up to the maximum number of directors to be chosen. Therefore, shares not voted, whether by withheld authority or otherwise, have no effect in the election of directors.

Each nominee has consented to being nominated and to serve if elected. In the unlikely event that any nominee becomes unable to serve for any reason, the WE Board will select a substitute nominee based upon the recommendation of the Corporate Governance Committee of WEC’s Board of Directors.

| 1 | WE 2014 Annual Meeting Information Statement |

Director Nominees.

WEC’s Corporate Governance Committee evaluates each individual director nominee in the context of the WEC and WE Boards as a whole with the goal of recommending nominees with diverse backgrounds and experience that, together, can best perpetuate the success of WEC’s and WE’s businesses and represent shareholder interests. In addition to the specific experiences and skills identified for each individual director nominee below, the WEC Corporate Governance Committee believes that all of the director nominees should generally possess certain characteristics and skills.

Criteria and Processes Used to Evaluate Nominees.WE relies on WEC’s Corporate Governance Committee to identify and evaluate director nominees. WEC’s Corporate Governance Committee has established criteria for evaluating all director candidates, which are reviewed annually. As set forth in WEC’s Corporate Governance Guidelines, these include: proven integrity; mature and independent judgment; vision and imagination; ability to objectively appraise problems; ability to evaluate strategic options and risks; sound business experience and acumen; relevant technological, political, economic or social/cultural expertise; social consciousness; achievement of prominence in career; familiarity with national and international issues affecting WEC’s and the Company’s businesses; contribution to the Board’s desired diversity; and balance and, in the case of new directors, availability to serve for five years before reaching the directors’ retirement age of 72.

The Committee does not have a specific policy with regards to the consideration of diversity in identifying director nominees. However, WEC’s Corporate Governance Committee strives to recommend candidates who each bring a unique perspective to the Board in order to contribute to the collective diversity of the Board. As part of its process in connection with the nomination of new directors to the Board, the Committee considers several factors to ensure the entire Board collectively embraces a wide variety of characteristics, including professional background, experience, skills and knowledge as well as the criteria listed above. Each candidate will generally exhibit different and varying degrees of these characteristics.

In evaluating director candidates, WEC’s Corporate Governance Committee reviews potential conflicts of interest, including interlocking directorships and substantial business, civic and/or social relationships with other members of the Board that could impair the prospective Board member’s ability to act independently from the other Board members and management.

Once a person has been identified by WEC’s Corporate Governance Committee as a potential candidate, the Committee may collect and review publicly available information regarding the person to assess whether that person should be considered further. If the Committee determines that the candidate warrants further consideration, the chair or another member of the Board of Directors contacts the person. Generally, if the person expresses a willingness to be considered and to serve on the Board, the Committee requests additional information from the candidate, reviews the person’s accomplishments and qualifications and conducts one or more interviews with the candidate. In certain instances, Committee members may contact one or more references provided by the candidate or may contact other members of the business community or other persons who may have greater firsthand knowledge of the candidate’s accomplishments.

WEC’s Corporate Governance Committee evaluates all candidates, including those proposed by stockholders, using the criteria and process described above. The process is designed to provide the Board with a diversity of experience and stability to allow it to effectively meet the many challenges WE and WEC face in today’s challenging economic environment.

| 2 | WE 2014 Annual Meeting Information Statement |

Nominees for Election to the Board of Directors. Biographical information regarding each nominee is shown below. WE and Wisconsin Gas LLC (WG) do business as We Energies and are subsidiaries of WEC. Ages and biographical information are as of March 1, 2014.

John F. Bergstrom. Age 67.

| • | Bergstrom Corporation – Chairman and Chief Executive Officer since 1982. Bergstrom Corporation owns and operates numerous automobile sales and leasing companies. |

| • | Director of Advance Auto Parts Inc. since 2008; Director of Associated Banc-Corp since 2010; and Director of Kimberly-Clark Corporation since 1987. |

| • | Director of Midwest Air Group, Inc. from 1993 to 2009. |

| • | Director of Wisconsin Energy Corporation since 1987, Wisconsin Electric Power Company since 1985, and Wisconsin Gas LLC since 2000. |

Mr. Bergstrom has over 30 years of experience as CEO of Bergstrom Corporation, one of the top 50 automotive dealership groups in America, with dealerships across eastern Wisconsin, including several in We Energies’ utility service territories. Therefore, Mr. Bergstrom provides the Board experience and insight with respect to understanding the needs of the Company’s retail customers, as well as Wisconsin’s business environment. As the CEO of a large, diverse retailer, Mr. Bergstrom has a deep understanding of executive compensation issues and challenges and is well qualified to provide perspective on customer focus and satisfaction which continues to be a primary focus of the Company. Mr. Bergstrom also provides the Board with insight gained from his over 28 years of service as a director on the Company’s and its affiliates’ Boards, over 50 years of combined experience as a director on the boards of several other publicly traded U.S. corporations, and past or present directorships on the boards of several regional non-profit entities, including the Green Bay Packers, Inc.

Barbara L. Bowles. Age 66.

| • | Profit Investment Management – Retired Vice Chair. Served as Vice Chair from January 2006 until retirement in December 2007. Profit Investment Management is an investment advisory firm. |

| • | The Kenwood Group, Inc. – Retired Chairman. Served as Chairman from 2000 until 2006 when The Kenwood Group, Inc. merged into Profit Investment Management. Chief Executive Officer from 1989 to 2005. |

| • | Director of Hospira, Inc. since 2008. |

| • | Director of Black & Decker Corporation from 1993 to 2010. |

| • | Director of Wisconsin Energy Corporation and Wisconsin Electric Power Company since 1998, and Wisconsin Gas LLC since 2000. |

As founder, president and CEO of The Kenwood Group, Inc., a Chicago-based investment advisory firm that managed pension funds for corporations, public institutions and endowments, Ms. Bowles has over 19 years of investment advisory experience. Before founding The Kenwood Group, Ms. Bowles, who is a Chartered Financial Analyst, was a chief investor relations officer for two Fortune 50 companies. Prior to that, she served as a portfolio manager and utility analyst for more than 10 years. With this combined experience, Ms. Bowles is well qualified to provide perspective to the Board as to what issues are important to large investors, particularly what is important to analysts covering the Company’s industry. Ms. Bowles also served as chief compliance officer for the mid-cap portfolios following The Kenwood Group’s merger with Profit Investment Management, through which she gained a deep understanding of corporate governance issues and concerns. This experience is invaluable for Ms. Bowles’ positions as chair of the WEC Corporate Governance Committee and presiding independent director. Ms. Bowles’ past and present service as a director of other public companies, including service on several audit and finance committees, provides a resource to the Board in discussions of issues facing the Company.

Patricia W. Chadwick.Age 65.

| • | Ravengate Partners, LLC – President since 1999. Ravengate Partners, LLC provides businesses and not-for-profit institutions with advice about the financial markets, business management and global economics. |

| • | Director of AMICA Mutual Insurance Company since 1992; Director of ING Mutual Funds since 2006; and Director of The Royce Funds since 2009. |

| • | Director of Wisconsin Energy Corporation, Wisconsin Electric Power Company, and Wisconsin Gas LLC since 2006. |

Ms. Chadwick, who is a Chartered Financial Analyst, was an investment professional/portfolio manager or principal for 30 years, and served as a director of research for four of those years. Since 1999, Ms. Chadwick has been president of Ravengate Partners, LLC, a firm that provides businesses and not-for-profit institutions with advice about the economy and the financial markets. As indicated above, Ms. Chadwick currently serves as a director on the boards of two registered investment companies. She has served as the Chair of multiple committees at AMICA Mutual Insurance Company, including the Audit Committee and Nominating and Governance Committee (which she currently chairs). She is also the Chair of the Domestic Investment Review Committee at ING Mutual Funds and serves on the Audit Committees for AMICA Mutual Insurance Company and The Royce Funds, as well as the Finance Committee for AMICA. Ms. Chadwick’s career and experience allow her to provide needed advice and insight to the Board on the capital

| 3 | WE 2014 Annual Meeting Information Statement |

markets. This perspective is valuable to the Company and its affiliates, which operate in a capital-intensive industry and must consistently access the capital markets. In addition, Ms. Chadwick’s service on the Board of AMICA, including presently serving as lead director, has provided her with experience in dealing with insurance risk management issues.

Curt S. Culver. Age 61.

| • | MGIC Investment Corporation – Chairman since 2005, Chief Executive Officer since 2000, and President from 1999 to 2006. MGIC Investment Corporation is the parent of Mortgage Guaranty Insurance Corporation. |

| • | Mortgage Guaranty Insurance Corporation – Chairman since 2005, Chief Executive Officer since 1999, and President from 1996 to 2006. Mortgage Guaranty Insurance Corporation is a private mortgage insurance company. |

| • | Director of MGIC Investment Corporation since 1999. |

| • | Director of Wisconsin Energy Corporation, Wisconsin Electric Power Company, and Wisconsin Gas LLC since 2004. |

Mr. Culver’s experience as Chairman and CEO of MGIC, which is headquartered in Milwaukee, Wisconsin, not only provides the Board with expertise in the financial markets and risk assessment and management, but also knowledge of the challenges and issues facing a public company headquartered in the same city as the Company. In addition, with his experience in the insurance industry, Mr. Culver is in a position to advise the Finance Committee on the Company’s insurance program and its effect on overall risk management. Mr. Culver also has past and present experience serving on the boards of numerous Milwaukee-area non-profit and two private, regional for-profit entities.

Thomas J. Fischer.Age 66.

| • | Fischer Financial Consulting LLC – Principal since 2002. Fischer Financial Consulting LLC provides consulting on corporate financial, accounting and governance matters. |

| • | Arthur Andersen LLP – Retired as Managing Partner of the Milwaukee office and Deputy Managing Partner for the Great Plains Region in 2002. Served as Managing Partner from 1993 and as Partner from 1980. Arthur Andersen LLP was an independent public accounting firm. |

| • | Director of Actuant Corporation since 2003; Director of Badger Meter, Inc. since 2003; and Director of Regal-Beloit Corporation since 2004. |

| • | Director of Wisconsin Energy Corporation, Wisconsin Electric Power Company, and Wisconsin Gas LLC since 2005. |

As Principal of Fischer Financial Consulting LLC, Mr. Fischer has provided consulting services to companies in the areas of corporate financial, accounting and governance matters since 2002. Prior to this, Mr. Fischer, who is a Certified Public Accountant, worked for Arthur Andersen, which was a large, international independent public accounting firm, for 33 years, the last 22 as a partner responsible for services provided to large, complex public and private companies and several public utility audits. Combined with Mr. Fischer’s service as a director and member of the audit committee of three other Wisconsin-based public companies, Mr. Fischer provides the Board with a deep understanding of corporate governance issues, accounting and auditing matters, including financial reporting and regulatory compliance, and risk assessment and management. In light of this extensive experience, he is chair of the Audit and Oversight Committee for each of WEC and the Company.

Gale E. Klappa. Age 63.

| • | Wisconsin Energy Corporation – Chairman of the Board and Chief Executive Officer since 2004, and President from 2003 to July 2013. |

| • | Wisconsin Electric Power Company – Chairman of the Board since 2004. President and Chief Executive Officer since 2003. |

| • | Wisconsin Gas LLC – Chairman of the Board since 2004. President and Chief Executive Officer since 2003. |

| • | Director of Badger Meter, Inc. since 2010; and Director of Joy Global Inc. since 2006. |

| • | Director of Wisconsin Energy Corporation, Wisconsin Electric Power Company, and Wisconsin Gas LLC since 2003. |

As Chief Executive Officer of WEC, WE and WG, Mr. Klappa represents and communicates management’s perspective to the Board. Mr. Klappa provides the Board with an understanding of the day-to-day operations of the Company, and, in turn, communicates the Board’s vision and direction for the Company to the other officers and management. Mr. Klappa has more than 39 years of experience working in the public utility industry, the last 21 at a senior executive level. Immediately prior to joining WEC in 2003, Mr. Klappa served as Executive Vice President and Chief Financial Officer of The Southern Company, a public utility holding company serving the southeastern United States. Mr. Klappa also served in various other leadership positions during his tenure at Southern, including Chief Strategic Officer and Chief Executive of the company’s subsidiary in the United Kingdom. Mr. Klappa currently serves on the boards of Edison Electric Institute, an association of U.S. shareholder-owned electric companies, and Electric Power Research Institute, an independent, non-profit research company performing research, development and demonstration in the electricity sector.

| 4 | WE 2014 Annual Meeting Information Statement |

Henry W. Knueppel. Age 65.

| • | Regal Beloit Corporation – Retired Chairman of the Board and Chief Executive Officer. Served as Chief Executive Officer from 2005 to 2011 and as Chairman from 2006 to 2011. Regal Beloit Corporation is a leading manufacturer of electric motors, mechanical and electrical motion controls, and power generation products. |

| • | Harsco Corporation – Independent, Non-Executive Chairman of the Board since September 2012. Served as Interim Chairman and Chief Executive Officer from February 2012 to September 2012. Harsco Corporation is a diversified, worldwide industrial services company. |

| • | Director of Regal Beloit Corporation since 1985; Director of Harsco Corporation since 2008; and Director of Snap-on Incorporated since 2011. |

| • | Director of Wisconsin Energy Corporation, Wisconsin Electric Power Company, and Wisconsin Gas LLC since 2013. |

Prior to serving as Chief Executive Officer and Chairman of the Board, Mr. Knueppel held several leadership positions at Regal Beloit Corporation and has more than 30 years of senior management experience at the company. Mr. Knueppel’s years of service with Regal Beloit Corporation, a Wisconsin-based manufacturer of electrical motors, mechanical and electrical motion controls, and power generation products, provides him with knowledge of equipment used in the Company’s business. Mr. Knueppel continues to serve on Regal Beloit Corporation’s Board of Directors, as well as on the Boards of Directors of Harsco Corporation and Snap-On Incorporated, both large publicly-traded industrial companies. With his combined experience, Mr. Knueppel is well qualified to provide perspective on the issues facing the Company’s large commercial and industrial customers. Mr. Knueppel’s position as independent, non-executive Chairman of the Board at Harsco Corporation also provides him with insight into the latest corporate governance trends — experience Mr. Knueppel is able to bring to the Board.

Ulice Payne, Jr.Age 58.

| • | Addison-Clifton, LLC – Managing Member since 2004. Addison-Clifton, LLC provides global trade compliance advisory services. |

| • | Director of Manpower Group. since 2007; and Trustee of The Northwestern Mutual Life Insurance Company since 2005. |

| • | Director of Badger Meter, Inc. from 2000 to 2010; and Director of Midwest Air Group, Inc. from 1998 to 2008. |

| • | Director of Wisconsin Energy Corporation, Wisconsin Electric Power Company, and Wisconsin Gas LLC since 2003. |

Mr. Payne has extensive leadership experience within the local community and the state of Wisconsin, previously serving as president and CEO of the Milwaukee Brewers Baseball Club, Inc., as managing partner of the Milwaukee office of Foley & Lardner, a Milwaukee-based law firm, and as Securities Commissioner for the state of Wisconsin. In addition, Mr. Payne is and has been involved in numerous Milwaukee-area non-profit entities, including serving as past chair of the Bradley Center Sports and Entertainment Corporation. Therefore, Mr. Payne is well positioned to provide the Board with perspective on the issues and challenges affecting the Milwaukee region as well as a broad spectrum of the Company’s customers. Mr. Payne presently advises on global trade compliance as Managing Member of Addison-Clifton, LLC, where Mr. Payne consistently deals with public policy and compliance matters, experience he brings to the Board. In addition, Mr. Payne’s past and present directorship experience on the Boards of several public corporations includes service as a member of either the audit or finance committee at each of these companies, which is beneficial to the Board.

Mary Ellen Stanek.Age 57.

| • | Baird Financial Group – Managing Director and Director of Asset Management since 2000; Baird Advisors – Chief Investment Officer since 2000; Baird Funds, Inc. – President since 2000. Baird Financial Group provides wealth management, capital markets, private equity and asset management services to clients worldwide. Baird Advisors is an institutional fixed income investment advisor. Baird Funds, Inc. is a publicly registered investment company. |

| • | Director of Journal Communications Inc. (and its predecessor company) since 2002; and Trustee of The Northwestern Mutual Life Insurance Company since 2009. |

| • | Director of Wisconsin Energy Corporation, Wisconsin Electric Power Company, and Wisconsin Gas LLC since 2012. |

Ms. Stanek, who is a Chartered Financial Analyst, has over 34 years of investment management experience and is currently responsible for the development and portfolio management of all proprietary asset management services for Baird Financial Group. Ms. Stanek also co-manages several fixed income mutual funds as well as a number of taxable and tax-exempt portfolios. In addition to her positions set forth above, Ms. Stanek is also a director of Baird Financial Group, Baird Holding Company and Baird Financial Corp. Because of her career and experience, Ms. Stanek brings significant knowledge of, and financial expertise in, the financial markets to the Board and Finance Committee. In particular, Ms. Stanek’s focus on fixed income investments is valuable as the Company and its affiliates customarily issue debt securities as a means of raising capital. In addition, Ms. Stanek brings experience in dealing with insurance risk management issues through her service as a director of West Bend Mutual Insurance Company since 1999. Ms. Stanek’s past and present experience serving on the boards of numerous Milwaukee-area non-profit institutions provides her with a good understanding of the issues and challenges that impact the Milwaukee region.

| 5 | WE 2014 Annual Meeting Information Statement |

COMMITTEES OF THE BOARD OF DIRECTORS

Members | Principal Responsibilities; Meetings | |

Audit and Oversight Thomas J. Fischer, Chair John F. Bergstrom Barbara L. Bowles Patricia W. Chadwick Henry W. Knueppel | • Oversee the integrity of the financial statements. | |

• Oversee management compliance with legal and regulatory requirements. | ||

• Review, approve and evaluate the independent auditors’ services. | ||

• Oversee the performance of the internal audit function and independent auditors. • Review the Company’s risk exposure in such areas as compliance, environmental, legal/litigation and ethical conduct. | ||

• Prepare the report required by the SEC for inclusion in the information statement. | ||

• Establish procedures for the submission of complaints and concerns regarding WE’s accounting or auditing matters. | ||

• The Committee conducted six meetings in 2013. | ||

Compensation John F. Bergstrom, Chair Thomas J. Fischer Ulice Payne, Jr. | • Identify through succession planning potential executive officers. | |

• Provide a competitive, performance-based executive and director compensation program. | ||

• Set goals for the CEO, annually evaluate the CEO’s performance against such goals and determine compensation adjustments based on whether these goals have been achieved. | ||

• Prepare the report required by the SEC for inclusion in the information statement. | ||

• The Committee conducted five meetings in 2013, including one joint meeting with WEC’s Corporate Governance Committee. | ||

Finance Curt S. Culver, Chair Patricia W. Chadwick Ulice Payne, Jr. Mary Ellen Stanek | • Review and monitor the Company’s current and long-range financial policies and strategies, including its capital structure and dividend policy. | |

• Authorize the issuance of corporate debt within limits set by the Board. | ||

• Discuss policies with respect to risk assessment and risk management. | ||

• Review, approve and monitor the Company’s financial plan, including the capital budget. | ||

• The Committee conducted three meetings in 2013. | ||

Wisconsin Electric relies on WEC’s Corporate Governance Committee for identifying and evaluating director nominees. WEC’s Corporate Governance Committee is also responsible for establishing and reviewing the WEC Corporate Governance Guidelines which are followed by the Board. The members of WEC’s Corporate Governance Committee are Barbara L. Bowles (Chair), Curt S. Culver and Henry W. Knueppel. WEC’s Corporate Governance Committee conducted three meetings in 2013, including one joint meeting with the Company’s Compensation Committee.

The Board also has an Executive Committee which may exercise all powers vested in the Board except action regarding dividends or other distributions to stockholders, filling Board vacancies and other powers which by law may not be delegated to a committee or actions reserved for a committee comprised of independent directors. The members of the Executive Committee are Gale E. Klappa (Chair), John F. Bergstrom, Barbara L. Bowles, Thomas J. Fischer and Ulice Payne, Jr. The Executive Committee did not meet in 2013.

In addition to the number of committee meetings listed in the preceding table, the Board met six times in 2013 and executed one signed, written unanimous consent. The average meeting attendance during the year was 95.4%. No director attended fewer than 78.6% of the total number of meetings of the Board and Board committees on which he or she served.

| 6 | WE 2014 Annual Meeting Information Statement |

DIRECTOR COMPENSATION

The following table summarizes total compensation awarded to, earned by or paid to each of the Company’s non-employee directors during 2013. The amounts in the table are WEC consolidated compensation data.

(a) | (b) | (c) | (d) | (e) | (f) | (g) | (h) | |||||||||||||||||||||

Name | Fees Earned or Paid In Cash ($) | Stock Awards (2)(3) ($) | Option Awards ($) | Non-Equity Incentive Plan Compensation ($) | Change in Pension Value and Nonqualified Deferred Compensation Earnings(5) ($) | All Other Compensation (6) ($) | Total ($) | |||||||||||||||||||||

John F. Bergstrom | 87,000 | 80,000 | — | — | — | 24,244 | 191,244 | |||||||||||||||||||||

Barbara L. Bowles | 85,000 | 80,000 | — | — | — | 22,335 | 187,335 | |||||||||||||||||||||

Patricia W. Chadwick | 75,000 | 80,000 | — | — | — | 24,878 | 179,878 | |||||||||||||||||||||

Robert A. Cornog(1) | 75,000 | 403,116 | (4) | — | — | 4,758 | 24,893 | 507,767 | ||||||||||||||||||||

Curt S. Culver | 85,000 | 80,000 | — | — | — | 17,362 | 182,362 | |||||||||||||||||||||

Thomas J. Fischer | 90,000 | 80,000 | — | — | — | 28,428 | 198,428 | |||||||||||||||||||||

Henry W. Knueppel | 75,000 | 80,000 | — | — | — | — | 155,000 | |||||||||||||||||||||

Ulice Payne, Jr. | 75,000 | 80,000 | — | — | — | 12,537 | 167,537 | |||||||||||||||||||||

Mary Ellen Stanek | 75,000 | 80,000 | — | — | — | — | 155,000 | |||||||||||||||||||||

| (1) | Mr. Cornog did not stand for re-election at the Company’s Annual Meeting of Stockholders on April 25, 2013. |

| (2) | The amounts reported reflect the aggregate grant date fair value, as computed in accordance with FASB ASC Topic 718, of WEC restricted stock awards made to the directors in 2013. Each restricted stock award vests in full on the third anniversary of the grant date. |

| (3) | Other than Mr. Knueppel (2,185 shares) and Ms. Stanek (4,727 shares), each current director held 7,493 shares of WEC restricted stock as of December 31, 2013. |

| (4) | In connection with Mr. Cornog not standing for re-election to the Board, and in consideration of his exemplary service and contribution to the Board of Directors, the Compensation Committee accelerated the vesting of 7,293.8203 shares of WEC restricted stock previously awarded to Mr. Cornog. The incremental fair value associated with the acceleration was $323,116, which is included in the reported amount. |

| (5) | Reported amounts reflect above-market earnings on amounts deferred by the directors into the Prime Rate Fund under WEC’s Directors’ Deferred Compensation Plan. Above-market earnings represent the difference between the interest rate used to calculate earnings under the plan and 120% of the federal long-term rate prescribed by the Internal Revenue Code. |

| (6) | All amounts represent costs for the WEC Directors’ Charitable Awards Program. See “Compensation of the Board of Directors” below for additional information regarding this program. |

Compensation of the Board of Directors

During 2013, each non-employee director received an annual retainer fee of $75,000. Non-employee chairs of the Finance Committee and the WEC Corporate Governance Committee received a quarterly retainer of $2,500, the chair of the Compensation Committee received a quarterly retainer of $3,000 and the chair of the Audit and Oversight Committee received a quarterly retainer of $3,750. The Company reimbursed non-employee directors for all out-of-pocket travel expenses (which reimbursed amounts are not reflected in the table above). Each non-employee director also received on January 2, 2013, the 2013 annual stock compensation award in the form of WEC restricted stock equal to a value of $80,000, with all shares vesting three years from the grant date. Employee directors do not receive these fees. Insurance is also provided for director liability coverage, fiduciary and employee benefit liability coverage and travel accident coverage for director travel on Company business. The premiums paid for this insurance are not included in the amounts reported in the table above.

| 7 | WE 2014 Annual Meeting Information Statement |

Non-employee directors may defer all or a portion of director fees pursuant to the WEC Directors’ Deferred Compensation Plan. Deferred amounts can be credited to any of ten measurement funds, including a WEC phantom stock account. The value of these accounts will appreciate or depreciate based on market performance, as well as through the accumulation of reinvested dividends. Deferral amounts are credited to accounts in the name of each participating director on the books of WEC, are unsecured and are payable only in cash following termination of the director’s service to WEC and its subsidiaries, including the Company. The deferred amounts will be paid out of general corporate assets or the assets of the WEC Amended Non-Qualified Trust discussed later in this information statement.

Although Wisconsin Electric directors also serve on the Wisconsin Energy and Wisconsin Gas boards and their committees, a single annual retainer fee and quarterly committee chair retainer were paid. Fees were allocated among Wisconsin Energy, Wisconsin Electric and Wisconsin Gas based on services rendered.

WEC has a Directors’ Charitable Awards Program under which it intends to contribute up to $100,000 per year for 10 years to one or more charitable organizations chosen by each director, including employee directors, following the director’s death. Directors are provided with one charitable award benefit for serving on the boards of WEC and its subsidiaries, including the Company. Charitable donations under the program will be paid out of general corporate assets. Directors derive no financial benefit from the program, and all income tax deductions accrue solely to WEC. The tax deductibility of these charitable donations mitigates the net cost to WEC. The Directors’ Charitable Awards Program has been eliminated for any new directors elected after January 1, 2007. Directors already participating as of that date, which includes all of the current directors except Mr. Knueppel and Ms. Stanek, were grandfathered.

In December 2013, the Compensation Committee conducted its annual review of non-employee director compensation and determined that the total directors’ compensation package was slightly below the market median. In order to continue to place more emphasis on the stock component of the directors’ pay package than the cash retainer, the committee determined that it was appropriate to increase the annual WEC restricted stock award by $10,000. As a result, effective January 1, 2014, upon the recommendation of the committee, the Board of Directors increased the annual restricted stock award from $80,000 to $90,000.

OTHER MATTERS

The Board of Directors is not aware of any other matters that may properly come before the Meeting. The WE Bylaws set forth the requirements that must be followed should a stockholder wish to propose any floor nominations for director or floor proposals at annual or special meetings of stockholders. In the case of annual meetings, the Bylaws state, among other things, that notice and certain other documentation must be provided to WE at least 70 days and not more than 100 days before the scheduled date of the annual meeting. No such notices have been received by WE.

CORPORATE GOVERNANCE – FREQUENTLY ASKED QUESTIONS

| Does WE have Corporate Governance Guidelines? | The WE Board of Directors follows WEC’s Corporate Governance Guidelines that WEC has maintained since 1996. These Guidelines provide a framework under which the Board conducts its business. WEC’s Corporate Governance Committee reviews the Guidelines annually to ensure that the Board is providing effective governance over the affairs of the Company. The Guidelines are available in the “Governance” section of WEC’s Website atwww.wisconsinenergy.com and are available in print to any stockholder who requests them in writing from the Corporate Secretary. | |

| How are directors determined to be independent? | No director qualifies as independent unless the Board affirmatively determines that the director has no material relationship with the Company. WEC’s Corporate Governance Guidelines provide that the WEC Board should consist of at least a two-thirds majority of independent directors and currently, the directors of WEC also serve as the directors of WE. | |

| What are the Board’s standards of independence? | The guidelines the Board uses in determining director independence are located in Appendix A of WEC’s Corporate Governance Guidelines. These standards of independence, which are summarized below, include those established by the New York Stock Exchange as well as a series of standards that are more comprehensive than New York Stock Exchange requirements. A director will be considered independent by the Board if the director:

| |

• has not been an employee of the Company for the last five years; | ||

• has not received, in the past three years, more than $120,000 per year in direct compensation from the Company, other than director fees or deferred compensation for prior service; | ||

• is not a current partner or employee of a firm that is the Company’s internal or external auditor, was not within the last three years a partner or employee of such a firm and personally worked | ||

| 8 | WE 2014 Annual Meeting Information Statement |

on the Company’s audit within that time, has no immediate family member who is a current partner of such a firm, or has no immediate family member who is a current employee of such a firm and personally works on the Company’s audit; | ||

• has not been an executive officer, in the past three years, of another company where any of the Company’s present executives at the same time serves or served on that other company’s compensation committee; | ||

• in the past three years, has not been an employee of a company that makes payments to, or receives payments from, the Company for property or services in an amount which in any single fiscal year is the greater of $1 million or 2% of such other company’s consolidated gross revenues; | ||

• has not received, during the current calendar year or the immediately preceding calendar year, remuneration, other thande minimus remuneration, as a result of services as, or being affiliated with an entity that serves as, an advisor, consultant, or legal counsel to the Company or to a member of the Company’s senior management, or a significant supplier of the Company; | ||

• has no personal service contract(s) with the Company or any member of the Company’s senior management; | ||

• is not an employee or officer with a not-for profit entity that receives 5% or more of its total annual charitable awards from the Company; | ||

• is not employed by a public company at which an executive officer of the Company serves as a director; and | ||

• does not have any beneficial ownership interest of 5% or more in an entity that has received remuneration, other thande minimus remuneration, from the Company, its subsidiaries or affiliates. | ||

| The Board also considers whether a director’s immediate family members meet the above criteria, as well as whether a director has any relationships with the Company’s affiliates for certain of the above criteria, when determining the director’s independence. For purposes of the above discussion, “Company” refers to WEC and its subsidiaries, including WE. | ||

| Who are the independent directors? | The Board has affirmatively determined that Directors Bergstrom, Bowles, Chadwick, Culver, Fischer, Knueppel, Payne, and Stanek have no relationships described in the Board’s standards of independence noted above and otherwise have no material relationships with WE or WEC and are independent. This represents 89% of the current Board. Director Klappa is not independent due to his present employment with WEC and its affiliates. | |

| Since 2005, WEC has engaged Baird Financial Group primarily to provide consulting services for investments held in its various benefit plan trusts. The Board reviewed the terms of this engagement, including the approximately $386,850 in fees paid to Baird in 2013 (which are less than one-tenth of 1% of Baird’s total revenue), and Ms. Stanek’s position at Baird, and concluded that such engagement is not material and did not impact Ms. Stanek’s independence. | ||

| What are the committees of the Board? | The Board of Directors of WE has the following committees: Audit and Oversight, Compensation, Finance, and Executive. | |

| All committees, except the Executive Committee, operate under a charter approved by the Board. A copy of each committee charter is posted in the “Governance” section of WEC’s Website atwww.wisconsinenergy.com and is available in print to any stockholder who requests it in writing from the Corporate Secretary. | ||

| Are the Audit and Oversight and Compensation Committees comprised solely of independent directors? | Yes, these committees are comprised solely of independent directors, as determined under New York Stock Exchange rules and WEC’s Corporate Governance Guidelines.

In addition, the Board has determined that each member of the Audit and Oversight Committee and the Compensation Committee is independent under the rules of the New York Stock Exchange applicable to audit committee and compensation committee members, respectively. The Audit and Oversight Committee is a separately designated committee established in accordance with Section 3(a)(58)(A) of the Securities Exchange Act of 1934, as amended. | |

| 9 | WE 2014 Annual Meeting Information Statement |

| Is the office of CEO combined with the office of Chairman of the Board? | Yes, the office of CEO is combined with the office of Chairman of the Board. Consistent with WE’s Bylaws and WEC’s Corporate Governance Guidelines, the Board retains the right to exercise its discretion in combining or separating the offices of Chief Executive Officer and Chairman of the Board. Given the complexity of the Company’s industry, operations and regulatory environment, the Board believes that having a combined CEO and Chairman is the appropriate structure for the Company at this time. | |

| The Board currently does not appoint a lead independent director; however, Director Bowles, the chair of WEC’s Corporate Governance Committee, acts as presiding director when the independent directors meet in executive session without management present. The Board believes that such leadership evolves naturally and may vary depending upon the issue under consideration. Therefore, the Board does not believe that the appointment of a designated lead independent director is necessary at this time. | ||

| Do the non-management directors meet separately from management? | Yes, at every regularly scheduled Board meeting non-management (non-employee) directors meet in executive session without any management present. All non-management directors are independent. Director Bowles currently presides at these sessions. | |

| What is the Board’s role in risk oversight? | The Board oversees our risk environment and has delegated specific risk monitoring responsibilities to the Audit and Oversight Committee and the Finance Committee as described in each committee’s charter. Both of these committees routinely report back to the Board. The Board and its committees also periodically receive briefings from management on specific areas of risk as well as emerging risks to the enterprise. The Board’s role in risk oversight had no effect on the Board’s decision to keep the roles of Chairman and CEO combined. | |

| Over the course of the year, the Audit and Oversight Committee hears reports from management on the Company’s major risk exposures in such areas as compliance, environmental, legal/litigation and ethical conduct and steps taken to monitor and control such exposures. The Finance Committee discusses the Company’s risk assessment and risk management policies, and provides oversight of insurance matters to ensure that its risk management program is functioning properly. Both committees have direct access to, and meet as needed with, Company representatives without other management present to discuss matters related to risk management. | ||

| The CEO, who is ultimately responsible for managing risk, routinely reports to the Board on risk-related matters. As part of this process, the business unit leaders identify existing, new or emerging issues or changes within their business area that could have enterprise implications and report them to senior management. Management is tasked with ensuring that these risks and opportunities are appropriately addressed. In addition, the Company, along with WEC, has established a Compliance Risk Steering Committee, comprised of senior level management employees, whose purpose is to foster an enterprise-wide approach to managing compliance. The results of each of these risk-management efforts are reported to the CEO and to the Board or its appropriate committee. | ||

| How can interested parties contact the members of the Board? | Correspondence may be sent to the directors, including the non-management directors, in care of the Corporate Secretary, Susan H. Martin, at the Company’s principal business office, 231 West Michigan Street, P.O. Box 2046, Milwaukee, Wisconsin 53201. | |

| All communication received as set forth above will be opened by the Corporate Secretary for the sole purpose of confirming the contents represent a message to the Company’s directors. Pursuant to instructions from the Board of Directors, all communication, other than advertising, promotion of a product or service, or patently offensive material, will be forwarded promptly to the addressee. | ||

| Does the Company have a written code of ethics? | Yes, all WE and WEC directors, executive officers and employees, including the principal executive, financial and accounting officers, have a responsibility to comply with WEC’s Code of Business Conduct, to seek advice in doubtful situations and to report suspected violations.

WEC’s Code of Business Conduct addresses, among other things: conflicts of interest; confidentiality; fair dealing; protection and proper use of Company assets; and compliance with laws, rules and regulations (including insider trading laws). The Company has not provided any waiver to the Code for any director, executive officer or other employee. | |

| 10 | WE 2014 Annual Meeting Information Statement |

| The Code of Business Conduct is posted in the “Governance” section of WEC’s Website atwww.wisconsinenergy.com. It is also available in print to any stockholder upon request in writing to the Corporate Secretary. | ||

| The Company has several ways employees can raise questions concerning WEC’s Code of Business Conduct and other Company policies. As one reporting mechanism, the Company has contracted with an independent service for employees to confidentially and anonymously report suspected violations of WEC’s Code of Business Conduct or other concerns, including those regarding accounting, internal accounting controls or auditing matters. | ||

| Does the Company have policies and procedures in place to review and approve related party transactions? | All employees of the Company, including executive officers, and members of the Board are required to comply with WEC’s Code of Business Conduct. The Code addresses, among other things, what actions are required when potential conflicts of interest may arise, including those from related party transactions. Specifically, executive officers and members of the Board are required to obtain approval of the Audit and Oversight Committee chair (1) before obtaining any financial interest in or participating in any business relationship with any company, individual or concern doing business with WEC or any of its subsidiaries, including WE, (2) before participating in any joint venture, partnership or other business relationship with WEC or any of its subsidiaries, including WE, and (3) before serving as an officer or member of the board of any substantial outside for-profit organization (except the Chief Executive Officer must obtain the approval of the full Board before doing so and members of the Board of Directors must obtain the prior approval of WEC’s Corporate Governance Committee). Executive officers must obtain the prior approval of the Chief Executive Officer before accepting a position with a substantial non-profit organization; members of the Board must notify the Compliance Officer when joining the board of a substantial non-profit organization, but do not need to obtain prior approval. | |

| In addition, WEC’s Code of Business Conduct requires employees and directors to notify the Compliance Officer of situations where family members are a supplier or significant customer of WEC or the Company or employed by one. To the extent the Compliance Officer deems it appropriate, she will consult with the Audit and Oversight Committee chair in situations involving executive officers and members of the Board. | ||

| Does the Board evaluate CEO performance? | Yes, the Compensation Committee, on behalf of the Board, annually evaluates the performance of the CEO and reports the results to the Board. As part of this practice, the Compensation Committee obtains from each non-employee director his or her input on the CEO’s performance. | |

| The CEO is evaluated in a number of areas including leadership, vision, financial stewardship, strategy development, management development, effective communication with constituencies, demonstrated integrity and effective representation of the Company in community and industry affairs. The chair of the Compensation Committee shares the evaluation results with the CEO. The process is also used by the Committee to determine appropriate compensation for the CEO. This procedure allows the Board to evaluate the CEO and to communicate the Board’s expectations. | ||

| Does the Board evaluate its own performance? | Yes, the Board annually evaluates its own collective performance. Each director is asked to consider the performance of the Board on such things as: the establishment of appropriate corporate governance practices; providing appropriate oversight for key affairs of the Company (including its strategic plans, long-range goals, financial and operating performance, risks to the enterprise and customer satisfaction initiatives); communicating the Board’s expectations and concerns to the CEO; overseeing opportunities critical to the Company; and operating in a manner that ensures open communication, candid and constructive dialogue as well as critical questioning. WEC’s Corporate Governance Committee uses the results of this process as part of its annual review of the Corporate Governance Guidelines and to foster continuous improvement of the Board’s activities. | |

| Is Board committee performance evaluated? | Yes, each committee, except the Executive Committee, conducts an annual performance evaluation of its own activities and reports the results to the Board. The evaluation compares the performance of each committee with the requirements of its charter. The results of the annual evaluations are used by each committee to identify both its strengths and areas where its governance practices can be improved. Each committee may adjust its charter, with Board approval, based on the evaluation results. | |

| 11 | WE 2014 Annual Meeting Information Statement |

| Are all the members of the Audit Committee financially literate and does the committee have an “audit committee financial expert”? | Yes, the Board has determined that all of the members of the Audit and Oversight Committee are financially literate as required by New York Stock Exchange rules and qualify as audit committee financial experts within the meaning of Securities and Exchange Commission rules. Director Fischer serves on the audit committee of three other public companies. The Board determined that his service on these other audit committees will not impair Director Fischer’s ability to effectively serve on the Audit and Oversight Committee. No other member of the Audit and Oversight Committee serves as an audit committee member of more than three public companies. For this purpose, the Company considers service on the audit committees of Wisconsin Electric Power Company and Wisconsin Energy Corporation to be service on the audit committee of one public company because of the commonality of the issues considered by those committees. | |

| What are the principal processes and procedures used by the Compensation Committee to determine executive and director compensation? | One of the principal responsibilities of the Compensation Committee is to provide a competitive, performance-based executive and director compensation program. This includes: (1) determining and periodically reviewing the Committee’s compensation philosophy; (2) determining and reviewing the compensation paid to executive officers (including base salaries, incentive compensation and benefits); (3) overseeing the compensation and benefits to be paid to other officers and key employees; (4) establishing and administering the Chief Executive Officer compensation package; and (5) reviewing the results of WEC’s most recent stockholder advisory vote on compensation of the named executive officers. The Compensation Committee is also charged with administering the compensation package of the non-employee directors. The Compensation Committee meets with WEC’s Corporate Governance Committee annually to review the compensation package of WEC’s non-employee directors and to determine the appropriate amount of such compensation. Although it has not chosen to do so, the Committee may delegate all or a portion of its duties and responsibilities to a subcommittee of the Committee. | |

| The Company engaged (outside of the Compensation Committee) Towers Watson, a compensation consulting firm, to provide the Compensation Committee and Chief Executive Officer with compensation data surveys regarding general industry and the energy services industry prepared annually by Towers Watson. Although the Compensation Committee relies on this compensation data, Towers Watson does not recommend the amount or form of executive or director compensation. While Towers Watson was not engaged directly by the Compensation Committee, the Committee has unrestricted access to Towers Watson and may retain its own compensation consultant at its discretion. | ||

| The Chief Executive Officer, after reviewing the compensation data compiled by Towers Watson and each executive officer’s individual experience, performance, responsibility and contribution to the results of the Company’s operations, makes compensation recommendations to the Committee for all executive officers other than himself. The Compensation Committee is free to make adjustments to such recommendations as it deems appropriate. For more information regarding our executive compensation processes and procedures, please refer to the “Compensation Discussion and Analysis” later in this information statement. | ||

| Does the Board have a nominating committee? | WE does not have a nominating committee. WE relies on WEC’s Corporate Governance Committee for, among other things, identifying and evaluating director nominees. The chair of the Committee coordinates this effort. The WEC Board has determined that all members of the WEC Corporate Governance Committee are independent under New York Stock Exchange rules applicable to nominating committee members. | |

| The WEC Corporate Governance Committee operates under a charter approved by the WEC Board, a copy of which is posted in the “Governance” section of WEC’s Website atwww.wisconsinenergy.com. It is also available in print to any stockholder upon request in writing to the Corporate Secretary. | ||

| 12 | WE 2014 Annual Meeting Information Statement |

| What is the process used to identify director nominees and how do I recommend a nominee to WEC’s Corporate Governance Committee? | Candidates for director nomination may be proposed by stockholders, WEC’s Corporate Governance Committee and other members of the Board. The Committee may pay a third party to identify qualified candidates; however, no such firm was engaged with respect to the nominees listed in this information statement. No stockholder nominations or recommendations for director candidates were received from holders of either series of the Company’s preferred stock. | |

| Stockholders wishing to propose director candidates for consideration and recommendation by WEC’s Corporate Governance Committee for election at the Company’s 2015 Annual Meeting of Stockholders must submit the candidates’ names and qualifications to WEC’s Corporate Governance Committee no later than November 1, 2014, via the Corporate Secretary, Susan H. Martin, at WEC’s principal business office, 231 West Michigan Street, P.O. Box 1331, Milwaukee, Wisconsin 53201. | ||

| What is WE’s policy regarding director attendance at annual meetings? | Directors are not expected to attend the Company’s annual meetings of stockholders, as they are only short business meetings. Generally, all directors are expected to attend WEC’s annual meetings of stockholders. All directors attended WEC’s 2013 Annual Meeting, except for Mr. Bergstrom. | |

| 13 | WE 2014 Annual Meeting Information Statement |

INDEPENDENT AUDITORS’ FEES AND SERVICES

Deloitte & Touche LLP served as the independent auditors for the Company for the last twelve fiscal years beginning with the fiscal year ended December 31, 2002. They have been selected by the Audit and Oversight Committee as independent auditors for the Company for the fiscal year ending December 31, 2014, subject to ratification by the stockholders of Wisconsin Energy Corporation at WEC’s Annual Meeting of Stockholders on May 2, 2014.

Representatives of Deloitte & Touche LLP are not expected to be present at the Meeting, but are expected to attend WEC’s Annual Meeting of Stockholders on May 2, 2014. They will have an opportunity to make a statement at WEC’s Annual Meeting, if they so desire, and are expected to respond to appropriate questions that may be directed to them.

Pre-Approval Policy. The Audit and Oversight Committee has a formal policy delineating its responsibilities for reviewing and approving, in advance, all audit, audit-related, tax and other services of the independent auditors. The Committee is committed to ensuring the independence of the auditors, both in appearance as well as in fact.

Under the pre-approval policy, before engagement of the independent auditors for the next year’s audit, the independent auditors will submit a description of services anticipated to be rendered for the Committee to approve. Annual pre-approval will be deemed effective for a period of twelve months from the date of pre-approval, unless the Committee specifically provides for a different period. A fee level will be established for all permissible non-audit services. Any proposed non-audit services exceeding this level will require additional approval by the Committee.

The Audit and Oversight Committee delegated pre-approval authority to the Committee’s Chair. The Committee Chair is required to report any pre-approval decisions at the next scheduled Committee meeting. Under the pre-approval policy, the Committee may not delegate to management its responsibilities to pre-approve services performed by the independent auditors.

Under the pre-approval policy, prohibited non-audit services are services prohibited by the Securities and Exchange Commission or by the Public Company Accounting Oversight Board to be performed by the Company’s independent auditors. These services include bookkeeping or other services related to the accounting records or financial statements of the Company, financial information systems design and implementation, appraisal or valuation services, fairness opinions or contribution-in-kind reports, actuarial services, internal audit outsourcing services, management functions or human resources, broker-dealer, investment advisor or investment banking services, legal services and expert services unrelated to the audit, services provided for a contingent fee or commission and services related to planning, marketing or opining in favor of the tax treatment of a confidential transaction or an aggressive tax position transaction that was initially recommended, directly or indirectly, by the independent auditors. In addition, the Committee has determined that the independent auditors may not provide any services, including personal financial counseling and tax services, to any officer or other employee of the Company who serves in a financial reporting oversight role or to the chair of the Audit and Oversight Committee or to an immediate family member of these individuals, including spouses, spousal equivalents and dependents.

Fee Table.The following table shows the fees, all of which were pre-approved by the Audit and Oversight Committee, for professional audit services provided by Deloitte & Touche LLP for the audit of the Company’s annual financial statements for fiscal years 2013 and 2012 and fees for other services rendered during those periods. No fees were paid to Deloitte & Touche LLP pursuant to the “de minimus” exception to the pre-approval policy permitted under the Securities Exchange Act of 1934, as amended.

| 2013 | 2012 | |||||||

Audit Fees(1) | $ | 1,464,740 | 1,429,620 | |||||

Audit-Related Fees(2) | — | 36,000 | ||||||

Tax Fees | — | — | ||||||

All Other Fees(3) | 4,950 | — | ||||||

|

|

|

| |||||

Total | $ | 1,469,690 | $ | 1,465,620 | ||||

|

|

|

| |||||

| (1) | Audit Fees consist of fees for professional services rendered in connection with the audits of the Company’s annual financial statements, reviews of financial statements included in Form 10-Q filings of WE and services normally provided in connection with statutory and regulatory filings or engagements. |

| (2) | Audit-Related Fees consist of fees for professional services that are reasonably related to the performance of the audit or review of the Company’s financial statements and are not reported under “Audit Fees.” These services normally include consultations regarding implementation of accounting transactions or standards. |

| (3) | All Other Fees consist of costs for certain employees to attend accounting/tax seminars hosted by Deloitte & Touche LLP. |

| 14 | WE 2014 Annual Meeting Information Statement |

AUDIT AND OVERSIGHT COMMITTEE REPORT

The Audit and Oversight Committee, which is comprised solely of independent directors, oversees the integrity of the financial reporting process on behalf of the Board of Directors of Wisconsin Electric Power Company. In addition, the Committee oversees compliance with legal and regulatory requirements. The Committee operates under a written charter approved by the Board of Directors, which can be found in the “Governance” section of Wisconsin Energy Corporation’s Website atwww.wisconsinenergy.com.

The Committee is also responsible for the appointment, compensation, retention and oversight of the Company’s independent auditors, as well as the oversight of the Company’s internal audit function. The Committee selected Deloitte & Touche LLP to remain as the Company’s independent auditors for 2014, subject to ratification by Wisconsin Energy Corporation’s stockholders.

Management is responsible for the Company’s financial reporting process, the preparation of consolidated financial statements in accordance with generally accepted accounting principles and the system of internal controls and procedures designed to provide reasonable assurance regarding compliance with accounting standards and applicable laws and regulations. The Company’s independent auditors are responsible for performing an independent audit of the Company’s consolidated financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States) and issuing a report thereon.

The Committee held six meetings during 2013. Meetings are designed to facilitate and encourage open communication among the members of the Committee, management, the internal auditors and the Company’s independent auditors, Deloitte & Touche LLP. During these meetings, we reviewed and discussed with management, among other items, the Company’s unaudited quarterly and audited annual financial statements and the system of internal controls designed to provide reasonable assurance regarding compliance with accounting standards and applicable laws.

We have reviewed and discussed with management and the Company’s independent auditors the Company’s audited consolidated financial statements and related footnotes for the fiscal year ended December 31, 2013, and the independent auditor’s report on those financial statements. Management represented to us that the Company’s financial statements were prepared in accordance with generally accepted accounting principles. Deloitte & Touche LLP presented the matters required to be discussed with the Audit and Oversight Committee by PCAOB Auditing Standard No. 16,Communications with Audit Committees. This review included a discussion with management and the independent auditors about the quality of the Company’s accounting principles, the reasonableness of significant estimates and judgments and the disclosures in the Company’s financial statements, as well as the disclosures relating to critical accounting policies.

In addition, we received the written disclosures and the letter relative to the auditors’ independence from Deloitte & Touche LLP, as required by applicable requirements of the Public Company Accounting Oversight Board regarding Deloitte & Touche LLP’s communications with the Committee concerning independence. The Committee discussed with Deloitte & Touche LLP its independence and also considered the compatibility of non-audit services provided by Deloitte & Touche LLP with maintaining its independence.

Based on these reviews and discussions, the Audit and Oversight Committee recommended to the Board of Directors that the audited financial statements be included in Wisconsin Electric Power Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2013 and filed with the Securities and Exchange Commission.

Respectfully submitted to Wisconsin Electric Power Company’s stockholders by the Audit and Oversight Committee of the Board of Directors.

Thomas J. Fischer, Committee Chair |

John F. Bergstrom |

Barbara L. Bowles |

Patricia W. Chadwick |

Henry W. Knueppel |

| 15 | WE 2014 Annual Meeting Information Statement |

COMPENSATION DISCUSSION AND ANALYSIS

The following discussion provides an overview and analysis of our executive compensation program, including the role of the Compensation Committee, the elements of our executive compensation program, the purposes and objectives of these elements and the manner in which we established the compensation of our named executive officers for fiscal year 2013.

References to “we”, “us”, “our” and the “Company” in this discussion and analysis mean Wisconsin Electric Power Company and its management, as applicable, and references to “WEC” mean Wisconsin Energy Corporation.

The Compensation Committee of the Company is comprised of the same individuals who are members of the Compensation Committee of the Board of Directors of Wisconsin Energy Corporation (the “WEC Compensation Committee” and, together with the Company’s Compensation Committee, the “Compensation Committee”). The named executive officers of the Company are the same as the named executive officers of WEC, and the WEC Compensation Committee and the Company’s Compensation Committee each have responsibility for making compensation decisions regarding these executive officers.

Executive Summary. From a sluggish economy to a stock market where utilities lagged behind the broader indices, 2013 had its share of challenges. Despite these challenges, 2013 proved to be another exceptional year for WEC and the Company. In 2013, WEC saw an increase in its premium valuation against its peers as compared to 2012. In addition, WEC achieved industry leading total shareholder returns.

Returns for periods ending December 31, 2013 | ||||||||||||||||

| One Year | Three Year | Five Year | Ten Year | |||||||||||||

Wisconsin Energy | 16.1 | % | 55.5 | % | 131.8 | % | 227.1 | % | ||||||||

S&P Utilities Index | 13.2 | % | 37.5 | % | 62.3 | % | 141.8 | % | ||||||||

S&P Electric Index | 7.8 | % | 29.7 | % | 38.7 | % | 132.4 | % | ||||||||

Philadelphia Utility Index | 11.0 | % | 31.6 | % | 53.0 | % | 137.1 | % | ||||||||

Dow Jones Utilities Average | 12.7 | % | 37.1 | % | 64.2 | % | 170.5 | % | ||||||||

Source: Bloomberg; assumes all dividends are reinvested and returns are compounded daily.

The Company achieved strong financial results which contributed to WEC delivering solid earnings growth, generating strong cash flow and making significant progress toward a dividend payout that is more competitive with its peers. Not only did WEC increase its dividend significantly in 2013, but in January 2014 WEC again increased its quarterly dividend. The new quarterly rate is $0.39 per share, which is equivalent to an annual rate of $1.56 per share. The Company also achieved milestones in customer satisfaction and reliability during 2013. More specifically, WEC and the Company achieved the following:

| • | Financial performance |

| • | WEC earnings per share of $2.51, highest in WEC’s history. |

| • | Increased the WEC dividend by a total of 27.5% during 2013. |

| • | Returned more than $450 million to WEC stockholders during 2013 through dividends and repurchases under the share repurchase program approved by WEC’s Board of Directors in 2011. |

| • | WEC’s Board of Directors approved a new four year $300 million share repurchase program effective January 1, 2014. |

| • | WEC common stock traded at an all-time high of $45.00 per share on April 30, 2013. |

| • | Operational excellence |

| • | Named the most reliable utility in America for 2013. |

| • | Named the most reliable utility in the Midwest for the ninth time in the past 12 years. |

| • | Continued improvements in customer satisfaction based on customer surveys. Data from 2013 indicated that the Company and Wisconsin Gas LLC (WG) achieved their best customer satisfaction ratings since their operations merged in 2000. |

| • | Completed the new biomass facility in Rothschild, Wisconsin, on time and on budget. |

| • | Passed the cyber security and operational audits mandated by the National Electric Reliability Corporation. |

| • | WEC was named one of the 100 best corporate citizens in the United States by Corporate Responsibility magazine for the sixth consecutive year. |

| 16 | WE 2014 Annual Meeting Information Statement |

Compensation for 2013 reflected WEC‘s outstanding performance for its stockholders. Total WEC stockholder return for the three-year performance period ended December 31, 2013 was at the 73rd percentile of the peer group established by the Compensation Committee.

The primary objective of our executive compensation program is to provide a competitive, performance-based plan that enables the Company to attract and retain key individuals and to reward them for achieving both the Company’s short-term and long-term goals. Our program has been designed to provide a level of compensation that is strongly dependent upon the achievement of short-term and long-term goals that are aligned with the interests of WEC’s stockholders and our customers. To that end, a substantial portion of pay is at risk and generally, the value will only be realized upon strong corporate performance.

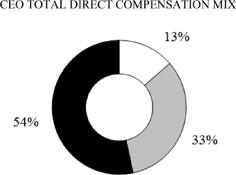

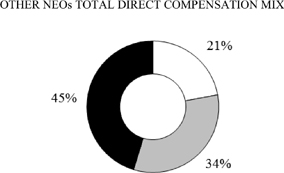

We have three primary elements of total direct compensation: (1) base salary; (2) annual incentive awards; and (3) long-term incentive awards consisting of a mix of WEC performance units, WEC stock options and WEC restricted stock. As shown in the charts below, 87% of Mr. Klappa’s total direct compensation as CEO and an average of 79% of the other named executive officers total direct compensation is tied to WEC performance and not guaranteed. The percentages shown are based on WEC consolidated compensation data.

|  |

In addition to the components of total direct compensation identified above, WEC’s retirement programs are another important component of the compensation program. We analyze market data provided by Towers Watson, a compensation consulting firm retained by management, to help determine the appropriate levels of compensation for each named executive officer. This Compensation Discussion and Analysis contains a more detailed discussion of each of these components and the extent to which we analyzed market data in establishing each individual component in 2013.

To the extent feasible, we believe it is important that the compensation program not dilute the interests of WEC’s current stockholders. Therefore, WEC currently uses open market purchases rather than new issue or treasury shares to satisfy its benefit plan obligations, including the exercise of WEC stock options and vesting of WEC restricted stock.