UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

X Quarterly report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the quarterly period ended September 30, 2008

____ Transition report pursuant to Section 13 or 15(d) of the Exchange Act of 1934 For the transition period from _____________ to ___________

Commission file number: 0-26003

ALASKA PACIFIC BANCSHARES, INC.

(Exact name of registrant as specified in its charter)

| Alaska | | 92-0167101 |

| (State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

2094 Jordan Avenue, Juneau, Alaska 99801

(Address of Principal Executive Offices)

(907) 789-4844

(Registrant’s telephone number, including area code)

NA

(Former name, former address and former fiscal year,

if changed since last report)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirementsfor the past 90 days. Yes __X No _____

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company’ in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | | Accelerated filer | | |

| Non-accelerated filer | | Smaller reporting company | | __X___ |

| (do not check if a smaller reporting company) | | | | |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of theExchange Act). Yes _____ No __X _

State the number of shares outstanding of each of the issuer's classes of common equity as of the latest practicable date:

654,486 shares outstanding on November 1, 2008

| PART I. FINANCIAL INFORMATION | | | | | | | | | | |

| Item 1. Financial Statements | | | | | | | | | | |

| |

| Alaska Pacific Bancshares, Inc. and Subsidiary |

| Consolidated Balance Sheets |

| (Unaudited) |

| | | | | | | |

| September 30, | | | | | December 31, | |

| (dollars in thousands) | | | | 2008 | | | | | 2007 | |

|

| Assets | | | | | | | | | | |

| Cash and due from banks | | $ | | 8,151 | | | $ | | 7,110 | |

| Interest-earning deposits in banks | | | | 14,364 | | | | | 1,990 | |

|

| Total cash and cash equivalents | | | | 22,515 | | | | | 9,100 | |

| Investment securities available for sale, at fair value (amortized cost: | | | | | | | | | | |

| September 30, 2008 - $3,323; December 31, 2007 - $3,928) | | | | 3,316 | | | | | 3,913 | |

| Federal Home Loan Bank stock | | | | 1,784 | | | | | 1,784 | |

| Loans held for sale | | | | 1,608 | | | | | 2,920 | |

| Loans | | | | 174,380 | | | | | 165,506 | |

| Less allowance for loan losses | | | | (4,746 | ) | | | | (1,783 | ) |

|

| Loans, net | | | | 169,634 | | | | | 163,723 | |

| Accrued interest receivable | | | | 905 | | | | | 978 | |

| Premises and equipment, net | | | | 3,249 | | | | | 3,436 | |

| Repossessed assets | | | | 362 | | | | | - | |

| Other assets | | | | 3,063 | | | | | 1,628 | |

|

| Total Assets | | $ | | 206,436 | | | $ | | 187,482 | |

|

| |

| Liabilities and Shareholders’ Equity | | | | | | | | | | |

| Deposits: | | | | | | | | | | |

| Noninterest-bearing demand | | $ | | 34,419 | | | $ | | 29,019 | |

| Interest-bearing demand | | | | 33,731 | | | | | 29,784 | |

| Money market | | | | 31,934 | | | | | 25,648 | |

| Savings | | | | 18,730 | | | | | 17,192 | |

| Certificates of deposit | | | | 58,506 | | | | | 47,724 | |

|

| Total deposits | | | | 177,320 | | | | | 149,367 | |

| Federal Home Loan Bank advances | | | | 10,391 | | | | | 17,076 | |

| Advances from borrowers for taxes and insurance | | | | 276 | | | | | 731 | |

| Accounts payable and accrued expenses | | | | 502 | | | | | 534 | |

| Accrued interest payable | | | | 604 | | | | | 668 | |

| Other liabilities | | | | 108 | | | | | 437 | |

|

| Total liabilities | | | | 189,201 | | | | | 168,813 | |

| Shareholders’ Equity: | | | | | | | | | | |

| Preferred stock ($0.01 par value; 1,000,000 shares authorized; no | | | | | | | | | | |

| shares issued and outstanding at September 30, 2008) | | | | - | | | | | - | |

| Common stock ($0.01 par value; 20,000,000 shares authorized; | | | | | | | | | | |

| 655,415 shares issued; 654,486 shares outstanding at September 30, | | | | | | | | | | |

| 2008 and 653,009 shares outstanding at December 31, 2007) | | | | 7 | | | | | 7 | |

| Additional paid-in capital | | | | 6,085 | | | | | 6,067 | |

| Treasury stock | | | | (11 | ) | | | | (30 | ) |

| Unearned Employee Stock Ownership Plan (“ESOP”) shares | | | | (41 | ) | | | | (41 | ) |

| Retained earnings | | | | 11,199 | | | | | 12,675 | |

| Accumulated other comprehensive loss | | | | (4 | ) | | | | (9 | ) |

|

| Total shareholders’ equity | | | | 17,235 | | | | | 18,669 | |

|

| Total Liabilities and Shareholders’ Equity | | $ | | 206,436 | | | $ | | 187,482 | |

|

| |

| See selected notes to condensed consolidated interim financial statements. | | | | | | | | | | |

1

| Alaska Pacific Bancshares, Inc. and Subsidiary | | | | | |

| Consolidated Statements of Operations | | | | | | | | | |

| | | | | (Unaudited) | | | | | | | | | | | | | | | | | | |

| |

| | | | | Three Months Ended | | | | | | | | Nine Months Ended |

| | | | | September 30, | | | | | | | | September 30, |

|

| (in thousands, except per share data) | | | | 2008 | | | | | 2007 | | | | | | | | 2008 | | | | | 2007 |

|

| Interest Income | | | | | | | | | | | | | | | | | | | | | | |

| Loans | | $ | | 2,997 | | | $ | | 3,267 | | | | | | $ | | 9,092 | | | $ | | 9,547 |

| Investment securities | | | | 48 | | | | | 62 | | | | | | | | 158 | | | | | 199 |

| Interest-bearing deposits with banks | | | | 19 | | | | | 24 | | | | | | | | 36 | | | | | 47 |

|

| Total interest income | | | | 3,064 | | | | | 3,353 | | | | | | | | 9,286 | | | | | 9,793 |

| Interest Expense | | | | | | | | | | | | | | | | | | | | | | |

| Deposits | | | | 639 | | | | | 811 | | | | | | | | 2,028 | | | | | 2,345 |

| Federal Home Loan Bank advances | | | | 159 | | | | | 181 | | | | | | | | 582 | | | | | 669 |

|

| Total interest expense | | | | 798 | | | | | 992 | | | | | | | | 2,610 | | | | | 3,014 |

|

| Net Interest Income | | | | 2,266 | | | | | 2,361 | | | | | | | | 6,676 | | | | | 6,779 |

| Provision for loan losses | | | | 1,426 | | | | | 45 | | | | | | | | 3,206 | | | | | 135 |

|

| Net interest income after provision for | | | | 840 | | | | | 2,316 | | | | | | | | 3,470 | | | | | 6,644 |

| loan losses | | | | | | | | | | | | | | | | | | | | | | |

| Noninterest Income | | | | | | | | | | | | | | | | | | | | | | |

| Mortgage servicing income | | | | 40 | | | | | 29 | | | | | | | | 125 | | | | | 112 |

| Service charges on deposit accounts | | | | 182 | | | | | 166 | | | | | | | | 538 | | | | | 487 |

| Other service charges and fees | | | | 46 | | | | | 72 | | | | | | | | 138 | | | | | 163 |

| Mortgage banking income | | | | 46 | | | | | 92 | | | | | | | | 211 | | | | | 260 |

| Other noninterest income | | | | - | | | | | - | | | | | | | | 56 | | | | | - |

|

| Total noninterest income | | | | 314 | | | | | 359 | | | | | | | | 1,068 | | | | | 1,022 |

| Noninterest Expense | | | | | | | | | | | | | | | | | | | | | | |

| Compensation and benefits | | | | 1,208 | | | | | 1,319 | | | | | | | | 3,750 | | | | | 3,800 |

| Occupancy and equipment | | | | 368 | | | | | 353 | | | | | | | | 1,105 | | | | | 1,073 |

| Data processing | | | | 56 | | | | | 64 | | | | | | | | 196 | | | | | 189 |

| Professional and consulting fees | | | | 144 | | | | | 75 | | | | | | | | 358 | | | | | 206 |

| Marketing and public relations | | | | 77 | | | | | 75 | | | | | | | | 258 | | | | | 226 |

| Repossessed property | | | | 88 | | | | | - | | | | | | | | 88 | | | | | - |

| Other | | | | 293 | | | | | 388 | | | | | | | | 833 | | | | | 986 |

|

| Total noninterest expense | | | | 2,234 | | | | | 2,274 | | | | | | | | 6,588 | | | | | 6,480 |

|

| Income (loss) before income tax | | | | (1,080 | ) | | | | 401 | | | | | | | | (2,050 | ) | | | | 1,186 |

| Income tax expense (benefit) | | | | (408 | ) | | | | 152 | | | | | | | | (771 | ) | | | | 451 |

|

| Net Income (loss) | | $ | | (672 | ) | | $ | | 249 | | $ | | (1,279 | ) | | $ | | 735 |

|

|

|

| |

| Earnings (Loss) per share: | | | | | | | | | | | | | | | | | | | | | | |

| Basic | | $ | | (1.03 | ) | | $ | | .39 | | | | | | $ | | (1.97 | ) | | $ | | 1.16 |

| Diluted | | | | (1.03 | ) | | | | .38 | | | | | | | | (1.97 | ) | | | | 1.11 |

| Cash dividends per share | | | | - | | | | | .10 | | | | | | | | .20 | | | | | .29 |

|

|

|

See selected notes to condensed consolidated interim financial statements.

2

| Alaska Pacific Bancshares, Inc. and Subsidiary | | | | | | |

| Consolidated Statements of Cash Flows | | | | | | |

| (Unaudited) | | | | | | |

| | | | | | | | | | |

| | | | | | | | | Nine Months Ended | |

| | | | | | | | | September 30, | |

| |

|

| (in thousands) | | | | | | | | 2008 | | | | | 2007 | |

|

| Operating Activities | | | | | | | | | | | | | | |

| Net income (loss) | | $ | | (1,279 | ) | | $ | | 735 | |

| Adjustments to reconcile net income (loss) to net cash provided by (used in) | | | | | | | | | | | | | | |

| operating activities: | | | | | | | | | | | | | | |

| Provision for loan losses | | | | | | | | 3,206 | | | | | 135 | |

| Depreciation and amortization | | | | | | | | 296 | | | | | 296 | |

| Amortization of fees, discounts, and premiums, net | | | | | | | | (283 | ) | | | | (242 | ) |

| Deferred income tax expense | | | | | | | | - | | | | | 47 | |

| Stock compensation expense | | | | | | | | 22 | | | | | - | |

| Cash provided by (used in) changes in operating assets and liabilities: | | | | | | | | | | | | | | |

| Loans held for sale | | | | | | | | 1,312 | | | | | (871 | ) |

| Accrued interest receivable | | | | | | | | 73 | | | | | (43 | ) |

| Other assets | | | | | | | | (1,438 | ) | | | | (1,040 | ) |

| Advances from borrowers for taxes and insurance | | | | | | | | (455 | ) | | | | (531 | ) |

| Accrued interest payable | | | | | | | | (64 | ) | | | | 220 | |

| Accounts payable and accrued expenses | | | | | | | | (32 | ) | | | | 73 | |

| Other liabilities | | | | | | | | (329 | ) | | | | (49 | ) |

|

| Net cash provided by (used in) operating activities | | | | | | | | 1,029 | | | | | (1,270 | ) |

| Investing Activities | | | | | | | | | | | | | | |

| Maturities and principal repayments of investment securities available for sale | | | | | | | | 594 | | | | | 1,180 | |

| Loan originations, net of principal repayments | | | | | | | | (9,185 | ) | | | | (2,018 | ) |

| Purchase of premises and equipment | | | | | | | | (109 | ) | | | | (270 | ) |

|

| Net cash used in investing activities | | | | | | | | (8,700 | ) | | | | (1,108 | ) |

| Financing Activities | | | | | | | | | | | | | | |

| Proceeds from exercise of stock options | | | | | | | | 15 | | | | | 27 | |

| Net increase (decrease) in Federal Home Loan Bank advances | | | | | | | | (6,685 | ) | | | | (3,164 | ) |

| Net increase (decrease) in demand and savings deposits | | | | | | | | 17,171 | | | | | 5,094 | |

| Net increase (decrease) in certificates of deposit | | | | | | | | 10,782 | | | | | 4,034 | |

| Cash dividends paid | | | | | | | | (197 | ) | | | | (186 | ) |

|

| Net cash provided by financing activities | | | | | | | | 21,086 | | | | | 5,805 | |

|

| Increase in cash and cash equivalents | | | | | | | | 13,415 | | | | | 3,427 | |

| Cash and cash equivalents at beginning of period | | | | | | | | 9,100 | | | | | 8,579 | |

|

| Cash and cash equivalents at end of period | | | | | | $ | | 22,515 | | | $ | | 12,006 | |

|

| |

| Supplemental information: | | | | | | | | | | | | | | |

| Cash paid for interest | | | | | | $ | | 2,674 | | | $ | | 2,794 | |

| Net cash paid for income taxes | | | | | | | | 332 | | | | | 950 | |

| Loans foreclosed and transferred to repossessed assets | | | | | | | | 362 | | | | | - | |

| Net change in unrealized loss on securities available for sale, net of tax | | | | | | | | 5 | | | | | (3 | ) |

See selected notes to condensed consolidated interim financial statements. | | | | | | | | | | | | | | |

3

Alaska Pacific Bancshares, Inc. and Subsidiary

Selected Notes to Condensed Consolidated Interim Financial Statements

(Unaudited)

Note 1 - Basis of Presentation

The accompanying unaudited condensed consolidated financial statements include the accounts of Alaska Pacific Bancshares, Inc. (the “Company”) and its wholly owned subsidiary, Alaska Pacific Bank (the “Bank”), and have been prepared in accordance with generally accepted accounting principles for interim financial information. Accordingly, they do not include all of the information and footnotes required by accounting principles generally accepted in the United States for complete financial statements. They should be read in conjunction with the audited consolidated financial statements included in the Form 10-KSB for the year ended December 31, 2007. In the opinion of management, all adjustments (consisting of normal recurring accruals) considered necessary for fair presentation have been included. The results of operations for the interim periods ended September 30, 2008 and 2007, are not necessarily indicative of the results which may be expected for an entire year or any other period.

Certain amounts in prior-period financial statements have been reclassified to conform to the current-period presentation. These reclassifications had no effect on net income.

Note 2 - Fair Value Measurements – Adoption of SFAS 157 and SFAS 159

On January 1, 2008, the Company adopted the provisions of FASB Statement 159, The Fair Value Option for Financial Assets and Liabilities (“FAS 159”). In accordance with FAS 159, the Company, at its option, can value assets and liabilities at fair value on an instrument-by-instrument basis with changes in the fair value recorded in earnings. The Company elected not to value any additional assets or liabilities at fair value in accordance with FAS 159.

The Company adopted Statement of Financial Accounting Standards (“SFAS” or “Statement”) No. 157,Fair Value Measurements (SFAS 157), effective January 1, 2008. SFAS 157 defines fair value, establishes a consistent framework for measuring fair value and expands disclosures about fair value measurements. SFAS 157 has been applied prospectively as of January 1, 2008 .

SFAS 157 defines fair value as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. SFAS 157 requires the Company to maximize the use of observable inputs and minimize the use of unobservable inputs when measuring fair value. Observable inputs reflect market data obtained from independent sources, while unobservable inputs reflect the Company’s market assumptions. These two types of inputs create the following fair value hierarchy:

Level 1 - Unadjusted quoted prices for identical instruments in active markets;

Level 2 - Quoted prices for similar instruments in active markets; quoted prices for identical orsimilar instruments in markets that are not active; and model-derived valuations whose inputs are observable or whose significant value drivers are observable; and

4

Level 3 - Instruments whose significant value drivers are unobservable.

A financial instrument’s level within the fair value hierarchy is based on the lowest level of input that is significant to the fair value measurement.

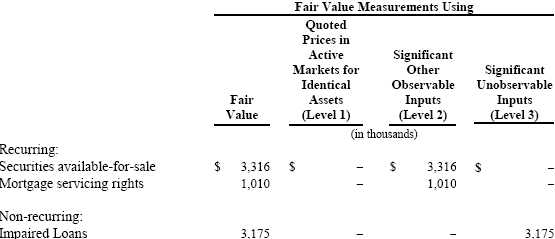

The following table sets for the Company’s financial assets by level within the fair value hierarchy that were measured at fair value basis during the third quarter of 2008.

FASB Staff Position No. FAS 157-2 delayed the effective date of Statement 157 for all nonfinancial assets and nonfinancial liabilities, except those that are recognized or disclosed at fair value on a recurring basis to fiscal years beginning after November 15, 2008. As a result, certain assets and liabilities, such as other real estate owned, that may be recognized or disclosed at fair value have been omitted from the above disclosures.

Securities available-for-sale are recorded at fair value on a recurring basis. Fair values are based on quoted market prices, where available. If quoted market prices are not available, fair values are estimated based on quoted market prices of comparable instruments with similar characteristics or discounted cash flows. Changes in fair market value are recorded in other comprehensive income, as the securities are available for sale.

Mortgage servicing rights (MSR) are measured at fair value on a recurring basis. These assets are classified as Level 2 as quoted prices are not available and the Company uses a model derived valuation methodology to estimate the fair value of MSR obtained from an independent broker on an annual basis. The model pools loans into buckets of homogeneous characteristics and performs a present value analysis of the future cash flows. The buckets are created by individual loan characteristics such as note rate, product type, and the remittance schedule.

5

Current market rates are utilized for discounting the future cash flows. Significant assumptions used in the valuation of MSR include discount rates, projected prepayment speeds, escrow calculations, ancillary income, delinquencies and option adjusted spreads. These assets are recorded at amortized cost.

Impaired loans are measured at fair value on a non-recurring basis. These assets are classified as Level 3 where significant value drivers are unobservable. The fair value of impaired loans are determined using the fair value of each loan’s collateral for collateral-dependent loans as determined, when possible, by an appraisal of the property, less estimated costs related to liquidation of the collateral. The appraisal amount may also be adjusted for current market conditions. Impaired loans were $14.6 million at September 30, 2008 with estimated reserves for impairment of $3.2 million.

Note 3 - Capital Compliance

At September 30, 2008, the Bank exceeded each of the three current minimum quantitative regulatory capital requirements and was categorized as “well capitalized” under the “prompt corrective action” regulatory framework. The following table summarizes the Bank's regulatory capital position and minimum requirements at September 30, 2008:

| (dollars in thousands) | | | | | | | |

|

| Tangible Capital: | | | | | | | |

| Actual | | $ | | 17,035 | | 8.29 | % |

| Required | | | | 3,083 | | 1.50 | |

|

| Excess | | $ | | 13,952 | | 6.79 | % |

|

|

|

| |

| Core Capital: | | | | | | | |

| Actual | | $ | | 17,035 | | 8.29 | % |

| Required | | | | 8,222 | | 4.00 | |

|

| Excess | | $ | | 8,813 | | 4.29 | % |

|

|

|

| |

| Total Risk-Based Capital: | | | | | | | |

| Actual | | $ | | 18,564 | | 11.53 | % |

| Required | | | | 12,880 | | 8.00 | |

|

| Excess | | $ | | 5,684 | | 3.53 | % |

|

6

Note 4 – Earnings Per Share

Basic earnings (loss) per share (“EPS”) is computed by dividing net income (loss) by the weighted-average number of common shares outstanding during the period less treasury stock and unallocated and not yet committed to be released ESOP shares (“unearned ESOP shares”). Diluted EPS is calculated by dividing net income (loss) by the weighted-average number of common shares used to compute basic EPS plus the incremental amount of potential common stock from stock options, determined by the treasury stock method.

| Three Months | | | | | | | | | | | | | | | | | | | | | | | | |

| Ended September 30, | | | | | | | 2008 | | | | | | | | | | | | 2007 | | | | | |

|

| | | | | | | | | | | | | Loss | | | | | | | | | | | | Earnings |

| | | | | Net | | | Average | | | | | Per | | | | | Net | | Average | | | | | Per |

| | | | | Loss | | | Shares | | | | | Share | | | | | Income | | Shares | | | | | Share |

|

| Net income | | | | | | | | | | | | | | | | | | | | | | | | |

| (loss)/average | | | | | | | | | | | | | | | | | | | | | | | | |

| shares issued | | $ | | (672,000 | ) | | 655,415 | | | | | | | | $ | | 249,000 | | 655,415 | | | | | |

| Treasury stock | | | | | | | (929 | ) | | | | | | | | | | | (13,306 | ) | | | | |

| Unearned ESOP | | | | | | | | | | | | | | | | | | | | | | | | |

| shares | | | | | | | (4,058 | ) | | | | | | | | | | | (8,412 | ) | | | | |

|

| Basic EPS | | | | (672,000 | ) | | 650,428 | | | $ | | (1.03 | ) | | | | 249,000 | | 633,697 | | | $ | | 0.39 |

| Incremental shares | | | | | | | | | | | | | | | | | | | | | | | | |

| under stock option | | | | | | | | | | | | | | | | | | | | | | | | |

| plan | | | | | | | - | | | | | | | | | | | | 27,619 | | | | | |

|

| Diluted EPS | | $ | | (672,000 | ) | | 650,428 | | | $ | | (1.03 | ) | | $ | | 249,000 | | 661,316 | | | $ | | 0.38 |

|

|

|

| |

| |

| |

| |

| Nine Months | | | | | | | | | | | | | | | | | | | | | | | | |

| Ended September 30, | | | | | | | 2008 | | | | | | | | | | | | 2007 | | | | | |

|

| | | | | | | | | | | | | Loss | | | | | | | | | | | | Earnings |

| | | | | Net | | | Average | | | | | Per | | | | | Net | | Average | | | | | Per |

| | | | | Loss | | | Shares | | | | | Share | | | | | Income | | Shares | | | | | Share |

|

| Net income | | | | | | | | | | | | | | | | | | | | | | | | |

| (loss)/average | | | | | | | | | | | | | | | | | | | | | | | | |

| shares issued | | $ | | (1,279,000 | ) | | 655,415 | | | | | | | | $ | | 735,000 | | 655,415 | | | | | |

| Treasury stock | | | | | | | (1,175 | ) | | | | | | | | | | | (13,939 | ) | | | | |

| Unearned ESOP | | | | | | | | | | | | | | | | | | | | | | | | |

| shares | | | | | | | (4,058 | ) | | | | | | | | | | | (8,412 | ) | | | | |

|

| Basic EPS | | | | (1,279,000 | ) | | 650,059 | | | $ | | (1.97 | ) | | | | 735,000 | | 633,064 | | | $ | | 1.16 |

| Incremental shares | | | | | | | | | | | | | | | | | | | | | | | | |

| under stock | | | | | | | | | | | | | | | | | | | | | | | | |

| option plan | | | | | | | - | | | | | | | | | | | | 27,737 | | | | | |

|

| Diluted EPS | | $ | | (1,279,000 | ) | | 650,059 | | | $ | | (1.97 | ) | | $ | | 735,000 | | 660,801 | | | $ | | 1.11 |

|

7

Note 5 – Comprehensive Income (Loss)

The Company’s only item of “other comprehensive income” is net unrealized gains or losses on investment securities available for sale. Comprehensive income (loss) is calculated in the following table:

| | | | | Three Months | | | | Nine Months | |

| | | | Ended | | | | Ended | |

| | | | | September 30, | | | | September 30, | |

|

| (in thousands) | | | | 2008 | | | | | 2007 | | | | 2008 | | | | | 2007 | |

|

| |

| Net income (loss) | | $ | | (672 | ) | | $ | | 249 | | $ | | (1,279 | ) | | $ | | 735 | |

| Other comprehensive income (loss) | | | | 16 | | | | | 15 | | | | 5 | | | | | (3 | ) |

|

| |

| Comprehensive income (loss) | | $ | | (656 | ) | | $ | | 264 | | $ | | (1,274 | ) | | $ | | 732 | |

|

|

|

Note 6 – Impaired Loans

Impaired loans were $14.6 million and $7.5 million at September 30, 2008 and December 31, 2007, respectively. Estimated specific reserves for impairment of $3.2 million and $556,000, respectively, were recognized on these loans in assessing the adequacy of the allowance for loan losses at September 30, 2008 and December 31, 2007.

Note 7 – Commitments

Commitments to extend credit, including lines of credit, totaled $10.7 million and $9.7 million at September 30, 2008 and December 31, 2007, respectively. Commitments to extend credit are arrangements to lend to a customer as long as there is no violation of any condition established in the contract. Commitments generally have fixed expiration dates (of less than one year) or other termination clauses and may require payment of a fee by the customer. Since many of the commitments are expected to expire without being drawn upon, the total commitment amounts do not necessarily represent future cash requirements. The Bank evaluates creditworthiness for commitments on an individual customer basis.

Undisbursed loan proceeds, primarily for real estate construction loans, totaled $2.7 million and $6.4 million at September 30, 2008 and December 31, 2007, respectively. These amounts are excluded from loan balances.

8

ITEM 2. Management's Discussion and Analysis of Financial Condition and Results of Operations

Forward-Looking Statements

This discussion contains forward-looking statements which are based on assumptions and describe future plans, strategies and expectations of the Company. These forward-looking statements are generally identified by use of the word “believe,” “expect,” “intend,” anticipate,” “estimate,” “project,” or similar words. The Company’s ability to predict results or the actual effect of future plans or strategies is uncertain. The Company’s actual results, performance, or achievements may differ materially from those suggested, expressed, or implied by forward-looking statements as a result of a wide variety or range of factors including, but not limited to, the credit risk of lending activities, including changes in the level and trend of loan delinquencies and write-offs; results of examinations by our banking regulators; interest rate fluctuations; economic conditions in the Compa ny’s primary market area and other market areas where it has loans and loan participations; demand for residential, commercial real estate, consumer, and other types of loans; success of new products; competitive conditions between banks and non-bank financial service providers; regulatory and accounting changes; technological factors affecting operations; pricing of products and services; and other risks detailed in the Company’s reports filed with the Securities and Exchange Commission, including its Annual Report on Form 10-KSB for the fiscal year ended December 31, 2007. You should consider these risks and uncertainties in evaluating forward-looking statements and you should not rely too much on these statements.

Recent Developments

Legislative Developments

Recent events in the U.S. and global financial markets, including the deterioration of the worldwide credit markets, have created significant challenges for financial institutions. Dramatic declines in the housing market during the past year, marked by falling home prices and increasing levels of mortgage foreclosures, have resulted in significant write-downs of asset values by many financial institutions, including government-sponsored entities and major commercial and investment banks. In addition, many lenders and institutional investors have reduced, and in some cases, ceased to provide funding to borrowers, including other financial institutions, as a result of concern about the stability of the financial markets and the strength of counterparties.

In response to the crises affecting the U.S. banking system and financial markets and attempt to bolster the distressed economy and improve consumer confidence in the financial system, on October 3, 2008, the U.S. Congress passed, and the President signed into law, the Emergency Economic Stabilization Act of 2008 (the “Stabilization Act”). The Stabilization Act authorizes the Secretary of the U.S. Treasury and the Federal Deposit Insurance Corporation (the “FDIC”) to implement various temporary emergency programs designed to strengthen the capital positions of financial institutions and stimulate the availability of credit within the U.S. financial system. Pursuant to the Stabilization Act, the U.S. Treasury will have the authority to, among other things, purchase up to $700 billion of mortgages, mortgage-backed securities and certain other financial instrum ents from financial institutions for the purpose of stabilizing and providing liquidity to the U.S. financial markets.

9

On October 14, 2008, the U.S. Treasury announced that it will purchase equity stakes in eligible financial institutions that wish to participate. This program, known as the Capital Purchase Program, allocates $250 billion from the $700 billion authorized by the Stabilization Act to the U.S. Treasury for the purchase of senior preferred shares from qualifying financial institutions. Eligible institutions will be able to sell equity interests to the U.S. Treasury in amounts equal to between 1% and 3% of the institution’s risk-weighted assets. In conjunction with the purchase of preferred stock, the U.S. Treasury will receive warrants to purchase common stock from the participating institutions with an aggregate market price equal to 15% of the preferred investment. Participating financial institutions will be required to adopt the U.S. Treasury’s standards for executive compensation and corporate governance for the period during w hich the U.S. Treasury holds equity issued under the Capital Purchase Program.

Also on October 14, 2008, using the systemic risk exception to the FDIC Improvement Act of 1991, the U.S. Treasury authorized the FDIC to provide a 100% guarantee of newly-issued senior unsecured debt and deposits in non-interest bearing accounts at FDIC insured institutions. Initially, all eligible financial institutions will automatically be covered under this program, known as the Temporary Liquidity Guarantee Program, without incurring any fees for a period of 30 days. Coverage under the Temporary Liquidity Guarantee Program after the initial 30-day period is available to insured financial institutions at a cost of 75 basis points per annum for senior unsecured debt and 10 basis points per annum for non-interest bearing deposits. After the initial 30-day period, institutions will continue to be covered under the Temporary Liquidity Guarantee Program unless they inform the FDIC that they have decided to opt out of the program. We have determined that we will participate in the insurance program covering the non-interest bearing deposits. Neither the Company nor the Bank has unsecured senior debt.

Under the Troubled Asset Auction Program, another initiative based on the authority granted by the Stabilization Act, the U.S. Treasury, through a newly-created Office of Financial Stability, will purchase certain troubled mortgage-related assets from financial institutions in a reverse-auction format. Troubled assets eligible for purchase by the Office of Financial Stability include residential and commercial mortgages originated on or before March 14, 2008, securities or obligations that are based on such mortgages, and any other financial instrument that the Secretary of the U.S. Treasury determines, after consultation with the Chairman of the Board of Governors of the Federal Reserve System, is necessary to promote financial market stability. The U.S. Treasury has not issued any definitive guidance regarding this program and we have not determined whether or not we will participate.

Under the Stabilization Act, the U.S. Treasury is also required to establish a program that will guarantee principal of, and interest on, troubled assets originated or issued prior to March 14, 2008, including mortgage-backed securities. The program may take any form and may vary by asset class, but it must be voluntary and self-funding. The U.S. Treasury has the authority to set premiums to reflect the credit risk characteristics of the insured assets.

10

The U.S. Treasury has solicited requests for comments on how the program should be structured but no program has been implemented to date. The Stabilization Act also temporarily increases the amount of insurance coverage of deposit accounts held at FDIC-insured depository institutions, including the Bank, from $100,000 to $250,000. The increased coverage is effective during the period from October 3, 2008 until December 31, 2009.

It is not clear at this time what impact the Stabilization Act, the Capital Purchase Program, the Temporary Liquidity Guarantee Program, the Troubled Asset Auction Program, other liquidity and funding initiatives of the Federal Reserve and other agencies that have been previously announced, and any additional programs that may be initiated in the future will have on our future financial condition and results of operations.

The preceding is a summary of recently enacted laws and regulations that could materially impact our results of operations or financial condition. This discussion is qualified in its entirety by reference to such laws and regulations and should be read in conjunction with the “Regulation” discussion contained in the Company’s 2007 Annual Report on Form 10-KSB.

Developments Relating to the Bank

In light of the current challenging operating environment, along with the Bank’s elevated level of non-performing assets, delinquencies, and adversely classified assets, the Bank may be subject to increased regulatory scrutiny, regulatory restrictions, and potential enforcement actions. Such enforcement actions could place limitations on our business and adversely affect our ability to implement our business plans. Even though the Bank remains well-capitalized in terms of its capital ratios, the regulatory agencies have the authority to restrict the Bank’s operations to those consistent with adequately capitalized institutions. For example, if the regulatory agencies were to implement such a restriction, we would likely have limitations on our lending activities and be limited in our ability to utilize brokered funds as a funding source, an area that has been a source of funds for the Bank in recent years. In addition, the regul atory agencies have the power to limit the rates paid by the Bank to attract retail deposits in its local markets. In addition, we may be required to provide notice to the OTS regarding any additions or changes to directors or senior executive officers and we would not be able to pay certain severance and other forms of compensation without regulatory approval. If any of these or similar restrictions are placed on the Bank, it would limit the resources currently available as a well-capitalized institution. No assurances can be made that the regulatory agencies will continue to consider the Bank well-capitalized. In addition, the Bank may be subject to higher regulatory assessments and FDIC deposit insurance premiums than those prevailing in prior periods.

11

Critical Accounting Policies

The discussion and analysis of the Company’s financial condition and results of operations are based upon the Company’s consolidated financial statements, which have been prepared in accordance with accounting principles generally accepted in the United States of America. The preparation of these financial statements requires management to make estimates and judgments that affect the reported amounts of assets and liabilities, revenues and expenses, and related disclosures of contingent assets and liabilities at the date of the financial statements. Actual results may differ from these estimates under different assumptions or conditions.

Accounting for the allowance for loan losses involves significant judgment and assumptions by management, which has a material impact on the carrying value of net loans. Management considers this accounting policy to be a critical accounting policy. The allowance is based on two principles of accounting: (i) Statement of Financial Accounting Standards (“SFAS” or “Statement”) No. 5,Accounting for Contingencies, which requires that losses be accrued when they are probable of occurring and can be estimated; and (ii) SFAS No. 114,Accounting by Creditors for Impairment of a Loan, as amended by SFAS No. 118,Accounting by Creditors for Impairment of a Loan-Income Recognition and Disclosures, which requires that losses be accrued based on the differences between the value of collateral, present value of future cash flows or values that are observable in the secondary market and the loan balance. The allowance has three components: (i) a formula allowance for groups of homogeneous loans, (ii) a specific valuation allowance for identified problem loans and (iii) an unallocated allowance. Each of these components is based upon estimates that can change over time. The formula allowance is based primarily on historical experience and as a result can differ from actual losses incurred in the future. The history is reviewed at least quarterly and adjustments are made as needed. Various techniques are used to arrive at specific loss estimates, including historical loss information, discounted cash flows and fair market value of collateral. The use of these techniques is inherently subjective and the actual losses could be greater or less than the estimates. For further details, see “Results of Operations - Provision for Loan Losses” included in this Form 10-Q.

The allowance for loan losses represents management's best estimate of incurred credit losses inherent in the Company's loan portfolio as of the balance sheet date. The estimate of the allowance is based on a variety of factors, including past loan loss experience, the current credit profile of borrowers, adverse situations that have occurred that may affect a borrower's ability to meet his financial obligations, the estimated value of underlying collateral, general economic conditions, and the impact that changes in interest rates and employment conditions have on a borrower's ability to repay adjustable-rate loans.

The fair value of impaired loans are determined using the fair value of each loan’s collateral for collateral-dependent loans as determined, when possible, by an appraisal of the property, less estimated costs related to liquidation of the collateral. The appraisal amount may also be adjusted for current marked conditions. Adjustments to reflect the fair value of collateral-dependent loans are a component in determining our best estimate of the allowance for loan losses.

12

Interest is generally not accrued on any loan when its contractual payments are more than 90 days delinquent unless collection of interest is considered probable. In addition, interest is not recognized on any loan where management has determined that collection is not reasonably assured. A nonaccrual loan may be restored to accrual status when delinquent principal and interest payments are brought current and future monthly principal and interest payments are expected to be collected.

Financial Condition

Total assets of the Company at September 30, 2008 were $206.4 million, an increase of $18.9 million, or 10.1%, from $187.5 million at December 31, 2007. The increase is primarily the result of an increase in interest earning deposits in banks associated with the receipt of annual permanent fund dividends and energy rebate deposits from the State of Alaska to every qualified resident in the State.

Loans (excluding loans held for sale) were $174.4 million at September 30, 2008, a $8.9 million, or 5.4%, increase from $165.5 million at December 31, 2007. Growth in the first three quarters of 2008 was primarily in permanent commercial nonresidential loans ($11.3 million, or 25.1%), partially offset by a decrease in construction one-to-four family loans ($4.0 million, or 34.4%) .

13

| Loans are summarized by category in the following table: | | | | | | | | |

| |

| | | | | September 30, | | | | December 31, |

| (in thousands) | | | | 2008 | | | | 2007 |

|

| Real estate: | | | | | | | | |

| Permanent: | | | | | | | | |

| One-to-four-family | | $ | | 39,239 | | $ | | 41,275 |

| Multifamily | | | | 1,876 | | | | 1,043 |

| Commercial nonresidential | | | | 56,387 | | | | 45,067 |

| Land | | | | 9,191 | | | | 6,321 |

|

| Total permanent real estate | | | | 106,693 | | | | 93,706 |

| Construction: | | | | | | | | |

| One-to-four-family | | | | 7,646 | | | | 11,648 |

| Multifamily | | | | 710 | | | | 719 |

| Commercial nonresidential | | | | 7,989 | | | | 11,564 |

|

| Total construction | | | | 16,345 | | | | 23,931 |

| Commercial business | | | | 26,314 | | | | 22,872 |

| Consumer: | | | | | | | | |

| Home equity | | | | 18,982 | | | | 19,128 |

| Boat | | | | 4,148 | | | | 3,974 |

| Automobile | | | | 1,060 | | | | 1,006 |

| Other | | | | 838 | | | | 889 |

|

| Total consumer | | | | 25,028 | | | | 24,997 |

|

| Loans | | $ | | 174,380 | | $ | | 165,506 |

|

| |

| Loans held for sale | | $ | | 1,608 | | $ | | 2,920 |

|

Deposits increased $27.9 million, or 18.7%, to $177.3 million at September 30, 2008, compared with $149.4 million at December 31, 2007. Growth in the first three quarters of 2008 was primarily in certificates of deposit ($10.8 million, or 22.6%) and money market accounts ($6.3 million, or 24.5%) .

The Bank began using CDARS deposits in 2005 as an alternative source of funds in addition to advances from the Federal Home Loan Bank of Seattle (“FHLB”). These are insured time deposits obtained through the nationwideCertificate of Deposit Account Registry Service. They range in maturities from one month to three years, and are generally priced higher than locally obtained deposits but are generally less expensive than other brokered deposits. Included in certificates of deposit were CDARS brokered deposits of $5.4 million at September 30, 2008 and $6.6 million at December 31, 2007.

14

The growth in certificates of deposit (CDs) in the first three quarters of 2008 is attributable to deposits made by a public entity under a CD program for qualified Alaskan financial institutions. In accordance with the program guidelines, the CD rates are based on an index rate and are generally less expensive than brokered deposits. These program CDs are secured by irrevocable standby letters of credit issued by the Federal Home Loan Bank and the total amount of CDs are limited to 100% of the Bank’s capital. Total CDs under this program amounted to $15 million, approximately 87% of the Bank’s capital, at September 30, 2008. There were no CDs under this program at December 31, 2007.

Results of Operations

Net Income (Loss). Net loss for the third quarter of 2008 was $672,000, or ($1.03 per diluted share) compared with net income of $249,000 ($0.38 per diluted share) for the third quarter of 2007. For the first three quarters of 2008, net income decreased $2.0 million, to a net loss of $1.3 million compared with net income of $735,000 for the first three quarters of 2007. The decrease in income for the nine months ended September 30, 2008 was due primarily to an increase of $3.1 million in provision for loan losses.

For purposes of comparison, income can be separated into major components as follows:

| | | | | Three Months Ended | | | | | Nine Months Ended | |

| | | | | September 30, | | | | | September 30, | |

| |

|

| | | | | | | | | | | | | | | Income | | | | | | | | | | | | | | | Income | |

| | | | | | | | | | | | | | | Incr. | | | | | | | | | | | | | | | Incr. | |

| (in thousands) | | | | 2008 | | | | | 2007 | | | | | (Decr.) | | | | | 2008 | | | | | 2007 | | | | | (Decr.) | |

|

| |

| Net interest income | | $ | | 2,266 | | | $ | | 2,361 | | | $ | | (95 | ) | | $ | | 6,676 | | | $ | | 6,779 | | | $ | | (103 | ) |

| Noninterest income, | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| excluding mortgage | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| banking income | | | | 268 | | | | | 267 | | | | | 1 | | | | | 857 | | | | | 762 | | | | | 95 | |

| Mortgage banking | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| income | | | | 46 | | | | | 92 | | | | | (46 | ) | | | | 211 | | | | | 260 | | | | | (49 | ) |

| Provision for loan losses | | | | (1,426 | ) | | | | (45 | ) | | | | (1,381 | ) | | | | (3,206 | ) | | | | (135 | ) | | | | (3,071 | ) |

| Noninterest expense | | | | (2,234 | ) | | | | (2,274 | ) | | | | 40 | | | | | (6,588 | ) | | | | (6,480 | ) | | | | (108 | ) |

|

| Income (loss) before | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| income tax | | | | (1,080 | ) | | | | 401 | | | | | (1,481 | ) | | | | (2,050 | ) | | | | 1,186 | | | | | (3,236 | ) |

| Income tax benefit | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (expense) | | | | 408 | | | | | (152 | ) | | | | 560 | | | | | 771 | | | | | (451 | ) | | | | 1,222 | |

|

| Net income (loss) | | $ | | (672 | ) | | $ | | 249 | | | $ | | (921 | ) | | $ | | (1,279 | ) | | $ | | 735 | | | $ | | (2,014 | ) |

|

|

|

Net Interest Income. Net interest income for the third quarter of 2008 decreased $95,000 (4.0%) compared with the third quarter of 2007. For the first three quarters of 2008, net interest income decreased $103,000 (1.5%) compared with the first three quarters of 2007. The net interest margin on average interest-earning assets for the third quarter and first three quarters of 2008 was 4.81% and 4.88%, respectively, compared with 5.46% and 5.32%, respectively, in the comparable periods in 2007.

15

The decrease in net interest income was primarily attributable to lost interest on non-accrual loans. Average loans increased $13.7 million (8.3%) for the third quarter of 2008 compared with the third quarter of 2007. At the same time, the overall yield on average earning assets decreased 125 basis points (“bp”) for the third quarter to 6.50% compared with the third quarter of 2007. For loans, the largest component of earning assets, the yield decreased 121 bp to 6.71% compared with third quarter of 2007. While higher-cost certificates of deposit and money market deposits increased, overnight borrowing balances decreased and the cost of average interest bearing liabilities declined 80bp to 2.21% for the third quarter of 2008 compared with the third quarter of 2007. The interest rate spread, which is the difference between the yield on average interest-earning assets and the average cost of interest-bearing liabilities, decreased 46 bp to 4.29% for the third quarter compared to the third quarter of 2007.

Provision for Loan Losses.The provisions for loan losses increased to $1.4 million for the third quarter of 2008 and $3.2 million for the first three quarters of 2008, compared with $45,000 and $135,000 for the third quarter and first three months of 2007, respectively. The increase in the Bank’s loan loss provision and allowance for loan losses was in response to the increase in nonaccrual and impaired loans. The provisions in both periods reflect management’s assessment of asset quality, overall risk, and estimated loan impairments and were considered appropriate in order to maintain the allowance for loan losses at a level that represents management’s best estimate of the probable credit losses inherent in the loan portfolio. Net loan charge offs (recoveries) were $244,000 for the third quarter of 2008 and $243,000 for the first three quarters o f 2008, compared with $49,000 and $66,000, respectively, during the comparable periods in 2007.

Noninterest Income.Noninterest income declined $45,000 (12.5%) for the third quarter of 2008 compared to the comparable period of 2007. Excluding mortgage banking income, noninterest income for the third quarter of 2008 increased $1,000 (0.40%) to $268,000 compared with $267,000 for the third quarter of 2007, and increased $95,000 to $857,000 in the first three quarters of 2008, each in comparison with 2007. The increase is primarily in service charges on deposit accounts associated with increases in service charge fee rates and additional types of service charge fees. Additionally, non-recurring income of $56,000 was recognized from the cash proceeds received on shares redeemed associated with the Company’s ownership in VISA and VISA’s initial public offering and business combination.

Mortgage banking income decreased $46,000 to $46,000 in the third quarter of 2008 and decreased $49,000 to $211,000 in the first three quarters of 2008, each compared with the comparable periods in 2007. The decrease is associated with a decrease in mortgage loans originated and sold and a decrease in mortgage loans sold with servicing rights retained.

16

Noninterest Expense.Noninterest expense for the third quarter of 2008 decreased $40,000 (1.8%) and for the first three quarters of 2008 increased $108,000 (1.7%) each in comparison with the comparable periods of 2007. The increase is primarily related to an increase in professional service fees and expense associated with repossessed assets.

Asset Quality

Nonaccrual loans were $7.1 million at September 30, 2008, compared with $323,000 at December 31, 2007. The $6.8 million increase in nonaccrual loans relates to the addition of four participation loans that totaled $6.6 million and two commercial business loans that total $443,000 offset with the resolution of one mortgage loan for $300,000.

At September 30, 2008 and December 31, 2007, the Bank had impaired loans of $14.6 million and $1.2 million, respectively. A specific allowance for estimated impairments of $3.2 million and $556,000, respectively, was established for these loans. The $13.4 million increase in impaired loans relates to one land loan, permanent one-to-four family loan, three one-to-four family construction loan, three permanent commercial nonresidential loans, two construction commercial non-residential loans and seven commercial business loans. At September 30, 2008 and December 31, 2007, the Bank had non-performing assets of $7.4 million and $323,000, respectively.

The $3.2 million increase in specific allowance for estimated impairments relates to three participation loans that are not performing as agreed, one commercial business loan and an increase in impaired loan balance associated with three commercial business loans to one borrower.

The commercial business loan is not performing as agreed and is secured by boats. Based on estimated value of “as is” collateral and other considerations, management has established a specific allowance for estimated impairment of $50,000 on this loan.

The impaired loan balance associated with the commercial loans to one borrower was $1.4 million and $1.2 million at September 30, 2008 and December 31, 2007, respectively. While the commercial loans are performing as agreed, because of financial difficulties that the borrower has encountered, management has established a specific allowance for estimated impairment of $550,000 and $547,000 at September 30, 2008 and December 31, 2007, respectively, based on a deficiency in collateral value.

The three participation loans total $4.8 million and are located outside of Alaska. Management is in the process of evaluating these loans along with the other participating banks. The largest of the three participation loans is a loan between 42 community banks for a multi-use commercial/residential condominium project located in Orem, Utah, of which the Bank’s portion is $2.5 million. Construction on the project has ceased, the loan is not performing as agreed and based on estimated value of “as is” collateral and other considerations, management has established a specific allowance for estimated impairment of $1.9 million on this loan.

17

A second participation loan of $530,000 is for a residential/non-commercial condominium marina project in Portland, Oregon. Construction on the project has ceased, the loan is not performing as agreed and based on estimated value of “as is” collateral and other considerations, management has established a specific allowance for estimated impairment of $317,700 on this loan. The third participation loan of $1.7 million is for a residential lot subdivision development project in Vancouver, Washington. The loan is not performing as agreed and based on estimated value of collateral and other considerations, management has established a specific allowance for estimated impairment of $400,000 on this loan.

The Bank had $362,000 of repossessed assets at September 30, 2008, compared with none at September 30, 2007. The addition consists of road building heavy equipment repossessed from a construction company. The Bank had no real estate owned at September 30, 2007 and 2008.

Liquidity and Capital Resources

The Company's primary sources of funds are deposits, borrowings, and principal and interest payments on loans. While maturities and scheduled amortization of loans are a predictable source of funds, deposit flows and loan prepayments are greatly influenced by general interest rates, economic conditions, and competition. The Company's primary investing activity is loan originations. The Company maintains liquidity levels believed to be adequate to fund loan commitments, investment opportunities, deposit withdrawals and other financial commitments. In addition, the Bank has available from the FHLB a line of credit generally equal to 25% of the Bank’s total assets, or approximately $52 million at September 30, 2008. The line is secured by a blanket pledge of the Company’s assets. At September 30, 2008, there was $10.4 million outstanding on the line and an additional $15.1 million of the borrowing line was committed to secure publi c deposits.

As disclosed in our Consolidated Statements of Cash Flows in Item 1 of this report on Form 10-Q, cash and cash equivalents increased by $13.4 million to $22.5 million as of September 30, 2008, from $9.1 million as of December 31, 2007. Net cash provided by operating activities was $1.0 million for the first nine months of 2008. Net cash of $8.7 million used in investing activities during the nine months ended September 30, 2008 consisted principally of a net increase in loan originations, net of principal pay downs of $9.2 million. The $21.1 million of cash provided by financing activities during the nine months ended September 30, 2008 primarily consisted of $28.0 million net increase in deposits, offset by a $6.7 million decrease in borrowed funds.

At September 30, 2008, management had no knowledge of any trends, events or uncertainties that may have material effects on the liquidity, capital resources, or operations of the Company.

18

The Company is not subject to any regulatory capital requirements separate from its banking subsidiary. The Bank exceeded all of its regulatory capital requirements at September 30, 2008. See Note 3 of the Selected Notes to Condensed Consolidated Interim Financial Statements contained herein for information regarding the Bank's regulatory capital position at September 30, 2008.

Recent Accounting Pronouncements

In December 2007, the FASB issued SFAS 141(R), "Business Combinations"and SFAS 160, “Noncontrolling Interests in Consolidated Financial Statements." SFAS 141(R) and SFAS 160 provide new guidance on accounting for business combinations and noncontrolling interests. The Statements will require more assets acquired and liabilities assumed to be measured at fair value as of the acquisition date and acquisition-related costs, such as legal and due diligence costs, to be expensed when incurred. Noncontrolling interests in subsidiaries are required to initially be valued at fair value and classified as a separate component of equity. The Statemen ts are effective for fiscal years beginning on or after December 15, 2008, with early adoption prohibited. SFAS 141(R) and SFAS 160 are not expected to have a material impact on the Company’s consolidated financial statements.

On December 21, 2007, the SEC staff issued SAB No. 110, which amends and replaces Question 6 of Section D2 of SAB Topic 14,Share-Based Payment-Certain Assumptions Used in Valuation Methods-Expected Term(SAB 107). In this release, the SEC staff document its views regarding the use of a "simplified" method in developing an estimate of expected term of "plain vanilla" share options in accordance with SFAS No. 123 (Revised 2004),Share-Based Payment. The guidance in this release is effective January 1, 2008. SAB No. 110 eliminates the scheduled date of December 31, 2007, after which the Staff would no longer accept use of the simplified method for esti mating the term of plain vanilla options.

19

Item 3. Quantitative and Qualitative Disclosures About Market Risk

Not Applicable

Item 4T. Controls and Procedures

(a)Evaluation of Disclosure Controls and Procedures: An evaluation of the registrant’s disclosure controls and procedures (as defined in Rule 13(a)-15(e) of the Securities Exchange Act of 1934 (the “Act”)) was carried out under the supervision and with the participation of the registrant’s Chief Executive Officer, Chief Financial Officer and other members of the registrant’s senior management. The registrant’s Chief Executive Officer and Chief Financial Officer concluded that, as of September 30, 2008, the registrant’s disclosure controls and procedures were effective in ensuring that the information required to be disclosed by the registrant in the reports it files or submits under the Act is (i) accumulated and communicated to the registrant’s management (includin g the Chief Executive Officer and Chief Financial Officer) in a timely manner, and (ii) recorded, processed, summarized and reported within the time periods specified in the SEC’s rules and forms.

The Company does not expect that its disclosures and procedures will prevent all error and all fraud. A control procedure, no matter how well conceived and operated, can provide only reasonable, not absolute, assurance that the objectives of the control procedure are met. Because of the inherent limitations in all control procedures, no evaluation of controls can provide absolute assurance that all control issues and instances of fraud, if any, within the Company have been detected. These inherent limitations include the realities that judgments in decision-making can be faulty, and that breakdowns can occur because of a simple error or mistake. Additionally, controls can be circumvented by the individual acts of some persons, by collusion of two or more people, or by management override of the control. The design of any control procedure also is based in part upon certain assumptions about the likelihood of future events, and there can b e no assurance that any design will succeed in achieving its stated goals under all potential future conditions; over time, controls may become inadequate because of changes in conditions, or the degree of compliance with the policies or procedures may deteriorate. Because of the inherent limitations in a cost-effective control procedure, misstatements due to error or fraud may occur and not be detected.

Section 404 of the Sarbanes-Oxley Act of 2002 requires that companies evaluate and annually report on their systems of internal control over financial reporting. Under the supervision and with the participation of the Company's management, including the Company's Chief Executive Officer and Chief Financial Officer, the Company conducted an assessment of the effectiveness of the Company's internal control over financial reporting based on the framework established in Internal Control-Integrated Framework issued by the Committee of Sponsoring Organizations of the Treadway Commission. As reported in the 10-KSB, based on this assessment, management determined that the Company's internal control over financial reporting as of December 31, 2007 is effective.

20

In addition, our independent accountants, beginning with our annual report on Form 10-K for the fiscal year ending December 31, 2009, must report on management's evaluation of its internal control over financial reporting. As a result of the ongoing evaluation and testing of our internal controls, there can be no assurance that if any control deficiencies are identified they will be remediated before the end of the 2008 fiscal year, or that there may not be significant deficiencies or material weaknesses that would be required to be reported. In addition, we expect the evaluation process and any required remediation, if applicable, to increase our accounting, legal and other costs and divert management resources from core business operations.

(b)Changes in Internal Controls: In the quarter ended September 30, 2008, the Company did not make any significant changes in, nor take any corrective actions regarding, its internal controls or other factors that could significantly affect these controls.

Item 4(T).Controls and Procedures

Information regarding internal control over financial reporting has been set forth in Item 4. This quarterly report does not include an attestation report of the Company’s registered public accounting firm regarding internal control over financial reporting. Management’s report was not subject to attestation by the Company’s registered public accounting firm pursuant to temporary rules of the Securities and Exchange Commission that permit the Company to provide only management’s report in this quarterly report.

PART II. OTHER INFORMATION

Item 1.Legal Proceedings

From time to time, the Company and its subsidiary may be a party to various legal proceedings incident to its or their business. At September 30, 2008, there were no legal proceedings to which the Company or any subsidiary was a party, or to which any of their property was subject, which were expected by management to result in a material loss.

Item 1A.Risk Factors

Not Applicable

Item 2.Unregistered Sales of Equity Securities and Use of Proceeds

None

Item 3.Defaults Upon Senior Securities

None

21

Item 4.Submission of Matters to a Vote of Security Holders

None

Item 5.Other Information

None

Item 6.Exhibits

| 3.1 | Articles of Incorporation of Alaska Pacific Bancshares, Inc. (1) |

| | |

| 3.2 | Bylaws of Alaska Pacific Bancshares, Inc. (2) |

| |

| 10.1 | Employment Agreement with Craig E. Dahl (3) |

| |

| 10.2 | Severance Agreement with Julie M. Pierce (8) |

| |

| 10.3 | Severance Agreement with Thomas C. Sullivan (3) |

| |

| 10.4 | Severance Agreement with Tammi L. Knight (3) |

| |

| 10.5 | Severance Agreement with John E. Robertson (5) |

| |

| 10.6 | Severance Agreement with Leslie D. Dahl (8) |

| |

| 10.7 | Severance Agreement with Christopher P. Bourque (8) |

| |

| 10.8 | Alaska Federal Savings Bank 401(k) Plan (1) |

| |

| 10.9 | Alaska Pacific Bancshares, Inc. Employee Stock Ownership Plan (3) |

| |

| 10.10 | Alaska Pacific Bancshares, Inc. Employee Severance Compensation Plan (3) |

| |

| 10.11 | Alaska Pacific Bancshares, Inc. 2000 Stock Option Plan (4) |

| |

| 10.12 | Alaska Pacific Bancshares, Inc. 2000 Management Recognition Plan (4) |

| |

| 10.13 | Alaska Pacific Bancshares, Inc. 2003 Stock Option Plan (6) |

| |

| 14 | Code of Ethics (7) | |

| |

| 31.1 | Certification of Chief Executive Officer pursuant to Section 302 of the Sarbanes-Oxley Act of 2002 | |

| |

| 31.2 | Certification of Chief Financial Officer pursuant to Section 302 of the Sarbanes-Oxley Act of 2002 | |

| |

| 32.1 | Certification of Chief Executive Officer pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 | |

| |

| 32.2 | Certification of Chief Financial Officer pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 | |

| | | |

________________

| (1) | Incorporated by reference to the registrant’s Registration Statement on Form SB-2 (333- 74827). |

| |

22

| (2) | Incorporated by reference to the registrant’s Registration Statement on Form SB-2 (333- 74827), except for amended Article III, Section 2, which was incorporated by reference to the registrant’s quarterly report on Form 10-QSB for the quarterly period ended March 31, 2004. |

| |

| (3) | Incorporated by reference to the registrant’s Annual Report on Form 10-KSB for the year ended December 31, 1999. |

| |

| (4) | Incorporated by reference to the registrant’s annual meeting proxy statement dated May 5, 2000. |

| |

| (5) | Incorporated by reference to the registrant’s quarterly report on Form 10-QSB for the quarterly period ended March 31, 2004. |

| |

| (6) | Incorporated by reference to the registrant’s annual meeting proxy statement dated April 10, 2004. |

| |

| (7) | Incorporated by reference to the registrant’s Annual Report on Form 10-KSB for the year ended December 31, 2005 |

| |

| (8) | Incorporated by reference to the registrant’s quarterly report on Form 10-QSB for the quarterly period ended September 30, 2007. |

| |

23

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned thereunto duly authorized.

Alaska Pacific Bancshares, Inc.

| November 12, 2008 | | /s/Craig E. Dahl |

| Date | | Craig E. Dahl |

| | | President and |

| | | Chief Executive Officer |

| November 12, 2008 | | /s/Julie M. Pierce |

| Date | | Julie M. Pierce |

| | | Senior Vice President and |

| | | Chief Financial Officer |

24

EXHIBIT INDEX

| 31.1 | Certification of Chief Executive Officer pursuant to Section 302 of the Sarbanes-Oxley Act of 2002 |

| |

| 31.2 | Certification of Chief Financial Officer pursuant to Section 302 of the Sarbanes-Oxley Act of 2002 |

| |

| 32.1 | Certification of Chief Executive Officer pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 |

| |

| 32.2 | Certification of Chief Financial Officer pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 |

| |

25

Exhibit 31.1

CERTIFICATION OF CHIEF EXECUTIVE OFFICER

PURSUANT TO SECTION 302 OF THE SARBANES-OXLEY ACT OF 2002

I, Craig E. Dahl, President and Chief Executive Officer, certify that:

| 1. | I have reviewed this Quarterly Report on Form 10-Q of Alaska Pacific Bancshares, Inc.; |

| |

| 2. | Based on my knowledge, this report does not contain any untrue statement of a material fact or omit to state amaterial fact necessary to make the statements made, in light of the circumstances under which suchstatements were made, not misleading with respect to the period covered by this report; |

| |

| 3. | Based on my knowledge, the financial statements, and other financial information included in this report, fairly present in all material respects the financial condition, results of operations and cash flows of the registrant as of, and for, the periods presented in this report; |

| |

| 4. | The registrant’s other certifying officer(s) and I are responsible for establishing and maintaining disclosure controls and procedures (as defined in Exchange Act Rules 13a-15(e) and 15d-15(e)) for the registrant and have: |

| |

| | (a) Designed such disclosure controls and procedures, or caused such disclosure controls and proceduresto be designed under our supervision, to ensure that material information relating to the registrant, including its consolidated subsidiaries, is made known to us by others within those entities, particularly during the period in which this report is being prepared; |

| |

| | (b) Evaluated the effectiveness of the registrant’s disclosure controls and procedures and presented in thisreport our conclusions about the effectiveness of the disclosure controls and procedures, as of the end of the period covered by this report based on such evaluation; and |

| |

| | (c) Disclosed in this report any change in the registrant’s internal control over financial reporting thatoccurred during the registrant’s most recent fiscal quarter (the registrant’s fourth fiscal quarter in the case of an annual report) that has materially affected, or is reasonably likely to materially affect, the registrant’s internal control over financial reporting; and |

| |

| 5. | The registrant’s other certifying officer(s) and I have disclosed, based on our most recent evaluation of internal control over financial reporting, to the registrant’s auditors and the audit committee of the registrant’s board of directors (or persons performing the equivalent functions): |

| |

| | (a) All significant deficiencies and material weaknesses in the design or operation of internal control overfinancial reporting which are reasonably likely to adversely affect the registrant’s ability to record, process, summarize and report financial information; and |

| |

| | (b) Any fraud, whether or not material, that involves management or other employees who have a significantrole in the registrant’s internal control over financial reporting. |

| | | |

| |

| Date: | | November 12, 2008 | | /s/Craig E. Dahl |

| | | | | Craig E. Dahl |

| | | | | President and |

| | | | | Chief Executive Officer |

26

Exhibit 31.2

CERTIFICATION CHIEF FINANCIAL OFFICER

PURSUANT TO SECTION 302 OF THE SARBANES-OXLEY ACT OF 2002

I, Julie M. Pierce, Senior Vice President and Chief Financial Officer, certify that:

| 1. | I have reviewed this Quarterly Report on Form 10-Q of Alaska Pacific Bancshares, Inc.; |

| |

| 2. | Based on my knowledge, this report does not contain any untrue statement of a material fact or omit to state a material fact necessary to make the statements made, in light of the circumstances under which such statements were made, not misleading with respect to the period covered by this report; |

| |

| 3. | Based on my knowledge, the financial statements, and other financial information included in this report, fairly present in all material respects the financial condition, results of operations and cash flows of the registrant as of, and for, the periods presented in this report; |

| |

| 4. | The registrant’s other certifying officer(s) and I are responsible for establishing and maintaining disclosure controls and procedures (as defined in Exchange Act Rules 13a-15(e) and 15d-15(e)) for the registrant and have: |

| |

| | (a) Designed such disclosure controls and procedures, or caused such disclosure controls and proceduresto be designed under our supervision, to ensure that material information relating to the registrant, including its consolidated subsidiaries, is made known to us by others within those entities, particularly during the period in which this report is being prepared; |

| |

| | (b) Evaluated the effectiveness of the registrant’s disclosure controls and procedures and presented in thisreport our conclusions about the effectiveness of the disclosure controls and procedures, as of the end of the period covered by this report based on such evaluation; and |

| |

| | (c) Disclosed in this report any change in the registrant’s internal control over financial reporting thatoccurred during the registrant’s most recent fiscal quarter (the registrant’s fourth fiscal quarter in the case of an annual report) that has materially affected, or is reasonably likely to materially affect, the registrant’s internal control over financial reporting; and |

| |

| 5. | The registrant’s other certifying officer(s) and I have disclosed, based on our most recent evaluation of internal control over financial reporting, to the registrant’s auditors and the audit committee of the registrant’s board of directors (or persons performing the equivalent functions): |

| |

| | (a) All significant deficiencies and material weaknesses in the design or operation of internal control overfinancial reporting which are reasonably likely to adversely affect the registrant’s ability to record, process, summarize and report financial information; and |

| |

| | (b) Any fraud, whether or not material, that involves management or other employees who have asignificant role in the registrant’s internal control over financial reporting. |

| |

| | | |

| Date: | | November 12, 2008 | | /s/Julie M. Pierce |

| | | | | Julie M. Pierce |

| | | | | Senior Vice President and |

| | | | | Chief Financial Officer |

27

Exhibit 32.1

CERTIFICATION OF CHIEF EXECUTIVE OFFICER OF ALASKA PACIFIC BANCSHARES, INC.

PURSUANT TO SECTION 906 OF THE SARBANES-OXLEY ACT OF 2002

Pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 (18 U.S.C. 1350), and in connection with the accompanying Quarterly Report on Form 10-Q, I hereby certify in my capacity as an officer of Alaska Pacific Bancshares, Inc. (“Company”) the Company’s Quarterly Report on Form 10-Q for the quarter ended September 30, 2008 that:

- The Report fully complies with the requirements of Sections 13(a) and 15(d) of the SecuritiesExchange Act of 1934, as amended, and

- The information contained in the Report fairly presents, in all material respects, the Company’sfinancial condition and results of operations as of the dates and for the periods presented in thefinancial statements included in the Report.

November 12, 2008

Date | /s/Craig E. Dahl

Craig E. Dahl President

and Chief Executive Officer |

28

Exhibit 32.2

CERTIFICATION OF CHIEF FINANCIAL OFFICER OF ALASKA PACIFIC BANCSHARES, INC.

PURSUANT TO SECTION 906 OF THE SARBANES-OXLEY ACT OF 2002

Pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 (18 U.S.C. 1350), and in connection with the accompanying Quarterly Report on Form 10-Q, I hereby certify in my capacity as an officer of Alaska Pacific Bancshares, Inc. (“Company”) the Company’s Quarterly Report on Form 10-Q for the quarter ended September 30, 2008 that:

- The Report fully complies with the requirements of Sections 13(a) and 15(d) of the SecuritiesExchange Act of 1934, as amended, and

- The information contained in the Report fairly presents, in all material respects, the Company’sfinancial condition and results of operations as of the dates and for the periods presented in thefinancial statements included in the Report.

November 12, 2008

Date | /s/Julie M. Pierce

Julie M. Pierce

Senior Vice President

and Chief Financial Officer |

29