As filed with the Securities and Exchange Commission on March 10, 2009.

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

| | |

| REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | |

| | or |

| | |

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2008 |

| | |

| | or |

| | |

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | |

| | or |

| SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | Date of event requiring this shell company report . . . . . . . . . . . . . . . |

For the transition period from N/A to N/A

Commission file number: 1-14930

HSBC Holdings plc

(Exact name of Registrant as specified in its charter)

| N/A | United Kingdom |

| (Translation of Registrant’s name into English) | (Jurisdiction of incorporation or organisation) |

8 Canada Square

London E14 5HQ

United Kingdom

(Address of principal executive offices)

Russell C Picot

8 Canada Square

London E14 5HQ

United Kingdom

Tel +44 (0) 20 7991 8888

Fax +44 (0) 20 7992 4880

(Name, Telephone, Email and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Securities Exchange Act of 1934:

| Title of each class | Name of each exchange on which registered |

| | |

| Ordinary Shares, nominal value US$0.50 each. | London Stock Exchange

Hong Kong Stock Exchange

Euronext Paris

Bermuda Stock Exchange

New York Stock Exchange* |

American Depository Shares, each representing 5 Ordinary

Shares of nominal value US$0.50 each. | New York Stock Exchange |

| 6.20% Non-Cumulative Dollar Preference Shares, Series A | New York Stock Exchange* |

| American Depositary Shares, each representing one-fortieth of a Share of 6.20% | |

| Non-Cumulative Dollar Preference Shares, Series A | New York Stock Exchange |

| 5.25% Subordinated Notes 2012 | New York Stock Exchange |

| 6.5% Subordinated Notes 2036 | New York Stock Exchange |

| 6.5% Subordinated Notes 2037 | New York Stock Exchange |

| 6.8% Subordinated Notes Due 2038 | New York Stock Exchange |

8.125% Perpetual Subordinated Capital Securities

Exchangeable at the Issuer’s Option into

Non-Cumulative Dollar Preference Shares | New York Stock Exchange |

| | |

Securities registered or to be registered pursuant to Section 12(g) of the Securities Exchange Act of 1934: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Securities Exchange Act of 1934: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the period covered by the annual report:

| Ordinary Shares, nominal value US$0.50 each | 12,105,265,082 |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

| Yes | No |

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

| Yes | No. |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

| Yes | No |

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filter | Accelerated filter | Non-accelerated filter |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP | International Financial Reporting Standards as issued by the

International Accounting Standards Board | Other |

If “Other” has been checked in response to the previous question indicate by check mark which financial statement item the registrant has elected to follow.

| Item 17 | Item 18 |

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

| Yes | No |

* Not for trading, but only in connection with the registration of American Depositary Shares.

Back to Contents

| H S B C H O L D I N G S P L C |

| |

| Annual Report and Accounts 2008 |

| | |

| | |

| | |

Headquartered in London, HSBC is one of the largest banking and financial services organisations in the world. Its international network comprises some 10,000 properties in 86 countries and territories in Europe; Hong Kong; Rest of Asia-Pacific, including the Middle East and Africa; North America and Latin America.

With listings on the London, Hong Kong, New York, Paris and Bermuda stock exchanges, shares in HSBC Holdings plc are held by over 210,000 shareholders in 120 countries and territories. The shares are traded on the New York Stock Exchange in the form of American Depositary Shares.

HSBC provides a comprehensive range of financial services to more than 100 million customers through four customer groups and global businesses: Personal Financial Services (including consumer finance); Commercial Banking; Global Banking and Markets; and Private Banking.

Certain defined terms

| | | |

| | | |

| Unless the context requires otherwise, ‘HSBC Holdings’ means HSBC Holdings plc and ‘HSBC’ or the ‘Group’ means HSBC Holdings together with its subsidiaries. Within this document the Hong Kong Special Administrative Region of the | | People’s Republic of China is referred to as ‘Hong Kong’. When used in the terms ‘shareholders’ equity’ and ‘total shareholders’ equity’, ‘shareholders’ means holders of HSBC Holdings ordinary shares and those preference shares classified as equity. |

Back to Contents

| H S B C H O L D I N G S P L C |

| |

| Contents |

| | |

| | |

| | |

1

Back to Contents

| H S B C H O L D I N G S P L C |

| |

| Financial Highlights |

| | |

| | |

| Highlights / Ratios |

| For the year |

| | |

| • | Total operating income up by 1 per cent to US$88,571 million (2007: US$87,601 million). |

| | |

| • | Net operating income before loan impairment charges up by 3 per cent to US$81,682 million (2007:US$78,993 million). |

| | |

| • | Group pre-tax profit down by 62 per cent to US$9,307 million (2007: US$24,212 million). |

| | |

| • | Profit attributable to shareholders of the parent company down by 70 per cent to US$5,728 million (2007:US$19,133 million). |

| | |

| • | Return on average shareholders’ equity of 4.7 per cent (2007: 15.9 per cent). |

| | |

| • | Earnings per ordinary share down by 72 per cent to US$0.47 (2007: US$1.65). |

| | |

| At the year-end1 |

| | |

| • | Total equity down by 26 per cent to US$100,229 million (2007: US$135,416 million). |

| | |

| • | Customer accounts and deposits by banks up by 1 per cent to US$1,245,411 million (2007:US$1,228,321 million). |

| | |

| • | Risk-weighted assets up by 2 per cent to US$1,147,974 million (2007: US$1,123,782 million). |

| | |

| Dividends and capital position1 |

| | |

| • | Total dividends declared in respect of 2008 of US$0.64 per share, a decrease of 28.9 per cent over dividends for2007; fourth interim dividend for 2008 of US$0.10 per share, a decrease of 74.4 per cent. |

| | |

| • | Tier 1 ratio of 8.3 per cent and total capital ratio of 11.4 per cent. |

| | Dividends per share2

(US dollars) | | Return on average invested capital

(per cent) | |

| |  | |  | |

| | | | | |

| | Earnings per share

(US dollars) | | Cost efficiency ratio

(per cent) | |

| |  | |  | |

For footnotes, see page 5.

2

Back to Contents

| Capital and performance ratios | | | | |

| | | | | |

| | 2008 | | 2007 | |

| | % | | % | |

| Capital ratios1 | | | | |

| Tier 1 ratio | 8.3 | | 9.3 | |

| Total capital ratio | 11.4 | | 13.6 | |

| | | | | |

| Performance ratios | | | | |

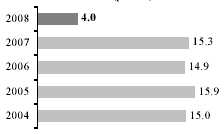

| Return on average invested capital3 | 4.0 | | 15.3 | |

| Return on average total shareholders’ equity4 | 4.7 | | 15.9 | |

| Post-tax return on average total assets | 0.26 | | 0.97 | |

| Post-tax return on average risk-weighted assets | 0.55 | | 1.95 | |

| | | | | |

| Credit coverage ratios | | | | |

| Loan impairment charges as a percentage of total operating income | 27.24 | | 19.61 | |

| Loan impairment charges as a percentage of average gross customer advances | 2.46 | | 1.97 | |

| Total impairment allowances outstanding as a percentage of impaired loans at the year-end | 94.3 | | 98.1 | |

| | | | | |

| Efficiency and revenue mix ratios | | | | |

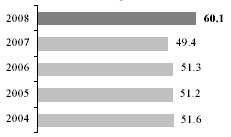

| Cost efficiency ratio5 | 60.1 | | 49.4 | |

| As a percentage of total operating income: | | | | |

| – net interest income | 48.1 | | 43.1 | |

| – net fee income | 22.6 | | 25.1 | |

| – net trading income | 7.4 | | 11.2 | |

| | | | | |

| Financial ratios | | | | |

| Loans and advances to customers as a percentage of customer accounts | 83.6 | | 89.5 | |

| Average total shareholders’ equity to average total assets | 4.87 | | 5.69 | |

| | | | | |

| Share information at the year-end | | | | |

| | | | | |

| | 2008 | | 2007 | |

| US$0.50 ordinary shares in issue (million) | 12,105 | | 11,829 | |

| Market capitalisation (billion) | US$114 | | US$198 | |

| Closing market price per ordinary share: | | | | |

| – London | £6.62 | | £8.42 | |

| – Hong Kong | HK$73.70 | | HK$131.70 | |

| Closing market price per American Depositary Share7 | US$48.67 | | US$83.71 | |

| | | | | | | |

| | Over 1 year | | Over 3 years | | Over 5 years | |

| HSBC total shareholder return to 31 December 20088 | 84.5 | | 84.5 | | 98.5 | |

| Benchmarks: | | | | | | |

| – FTSE 1009 | 71.7 | | 88.1 | | 118.3 | |

| – MSCI World10 | 81.8 | | 93.6 | | 123.7 | |

| – MSCI Banks11 | 63.0 | | 60.8 | | 82.7 | |

| For footnotes, see page 5. | | | | | | |

3

Back to Contents

| H S B C H O L D I N G S P L C |

| |

| Financial Highlights(continued) |

| | |

| | |

| 5-year comparison |

| Five-year comparison | | | | | | | | | | |

| | 2008 | | 2007 | | 2006 | | 2005 | | 200412 | |

| | US$m | | US$m | | US$m | | US$m | | US$m | |

| For the year | | | | | | | | | | |

| Net interest income | 42,563 | | 37,795 | | 34,486 | | 31,334 | | 31,099 | |

| Other operating income | 46,008 | | 49,806 | | 35,584 | | 30,370 | | 24,889 | |

| Loan impairment charges and other credit risk provisions | (24,937 | ) | (17,242 | ) | (10,573 | ) | (7,801 | ) | (6,191 | ) |

| Total operating expenses | (49,099 | ) | (39,042 | ) | (33,553 | ) | (29,514 | ) | (26,487 | ) |

| Profit before tax | 9,307 | | 24,212 | | 22,086 | | 20,966 | | 18,943 | |

| Profit attributable to shareholders of the parent company | 5,728 | | 19,133 | | 15,789 | | 15,081 | | 12,918 | |

| Dividends2 | 11,301 | | 10,241 | | 8,769 | | 7,750 | | 6,932 | |

| | | | | | | | | | | |

| At the year-end | | | | | | | | | | |

| Called up share capital | 6,053 | | 5,915 | | 5,786 | | 5,667 | | 5,587 | |

| Total shareholders’ equity | 93,591 | | 128,160 | | 108,352 | | 92,432 | | 85,522 | |

| Capital resources1,13 | 131,460 | | 152,640 | | 127,074 | | 105,449 | | 90,780 | |

| Customer accounts | 1,115,327 | | 1,096,140 | | 896,834 | | 739,419 | | 693,072 | |

| Undated subordinated loan capital | 2,843 | | 2,922 | | 3,219 | | 3,474 | | 3,686 | |

| Preferred securities and dated subordinated loan capital14 | 50,307 | | 49,472 | | 42,642 | | 35,856 | | 32,914 | |

| Loans and advances to customers15 | 932,868 | | 981,548 | | 868,133 | | 740,002 | | 672,891 | |

| Total assets | 2,527,465 | | 2,354,266 | | 1,860,758 | | 1,501,970 | | 1,279,974 | |

| | | | | | | | | | | |

| | US$ | | US$ | | US$ | | US$ | | US$ | |

| Per ordinary share | | | | | | | | | | |

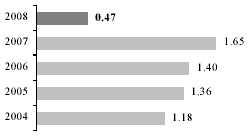

| Basic earnings | 0.47 | | 1.65 | | 1.40 | | 1.36 | | 1.18 | |

| Diluted earnings | 0.47 | | 1.63 | | 1.39 | | 1.35 | | 1.17 | |

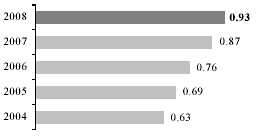

| Dividends | 0.93 | | 0.87 | | 0.76 | | 0.69 | | 0.63 | |

| Net asset value at year-end16 | 7.44 | | 10.72 | | 9.24 | | 8.03 | | 7.66 | |

| | | | | | | | | | | |

| Share information | | | | | | | | | | |

| US$0.50 ordinary shares in issue (millions) | 12,105 | | 11,829 | | 11,572 | | 11,334 | | 11,172 | |

| | | | | | | | | | | |

| | % | | % | | % | | % | | % | |

| Financial ratios | | | | | | | | | | |

| Dividend payout ratio17 | 197.9 | | 52.7 | | 54.3 | | 50.7 | | 53.4 | |

| Post-tax return on average total assets | 0.26 | | 0.97 | | 1.00 | | 1.06 | | 1.14 | |

| Return on average total shareholders’ equity | 4.7 | | 15.9 | | 15.7 | | 16.8 | | 16.3 | |

| Loans and advances to customers as a percentage of customer accounts | 83.6 | | 89.5 | | 96.8 | | 100.1 | | 97.1 | |

| | | | | | | | | | | |

| Average total shareholders’ equity to average total assets | 4.87 | | 5.69 | | 5.97 | | 5.96 | | 6.35 | |

| | | | | | | | | | | |

| Capital ratios1 | | | | | | | | | | |

| Tier 1 ratio | 8.3 | | 9.3 | | 9.4 | | 9.0 | | 8.9 | |

| Total capital ratio | 11.4 | | 13.6 | | 13.5 | | 12.8 | | 12.0 | |

| | | | | | | | | | | |

| Foreign exchange translation rates to US$ | | | | | | | | | | |

| Closing | – £:US$1 | 0.686 | | 0.498 | | 0.509 | | 0.581 | | 0.517 | |

| | – €:US$1 | 0.717 | | 0.679 | | 0.759 | | 0.847 | | 0.733 | |

| Average | – £:US$1 | 0.545 | | 0.500 | | 0.543 | | 0.550 | | 0.546 | |

| | – €:US$1 | 0.684 | | 0.731 | | 0.797 | | 0.805 | | 0.805 | |

| | | | | | | | | | | |

| For footnotes, see page 5. | | | | | | | | | | |

4

Back to Contents

| Consolidated Financial Statements |

The consolidated financial statements of HSBC and the separate financial statements of HSBC Holdings have been prepared in accordance with International Financial Reporting Standards (‘IFRSs’) as issued by the International Accounting Standards Board (‘IASB’) and as endorsed by the European Union (‘EU’). EU-endorsed IFRSs may differ from IFRSs as issued by the IASB if, at any point in time, new or amended IFRSs have not been endorsed by the EU. At 31 December 2008, there were no unendorsed standards effective for the year ended 31 December 2008 affecting these consolidated and separate financial statements, and there was no difference between IFRSs endorsed by the EU and IFRSs issued by the IASB in terms of their application to HSBC. Accordingly, HSBC’s financial statements for the year ended 31 December 2008 are prepared in accordance with IFRSs as issued by the IASB.

HSBC uses the US dollar as its presentation currency because the US dollar and currencies linked to it form the major currency bloc in which HSBC transacts its business. Unless otherwise stated, the information presented in this document has been prepared in accordance with IFRSs.

When reference to ‘underlying’ or ‘underlying basis’ is made in tables or commentaries, comparative information has been expressed at constant currency (see page 23) and adjusted for the effects of acquisitions and disposals. A reconciliation of reported and underlying profit before tax is presented on page 22.

| Footnotes to ‘Financial Highlights’ |

| | |

| 1 | The calculation of capital resources, capital ratios and risk-weighted assets for 31 December 2008 is on a Basel II basis. Comparatives are on a Basel I basis. |

| 2 | Dividends recorded in the financial statements are dividends per ordinary share declared in a year and are not dividends in respect of, or for, that year. First, second and third interim dividends for 2008, each of US$0.18 per ordinary share, were paid on 9 July 2008, 8 October 2008 and 14 January 2009, respectively. Note 12 on the Financial Statements provides more information on the dividends declared in 2008. On 2 March 2009 the Directors declared a fourth interim dividend for 2008 of US$0.10 per ordinary share in lieu of a final dividend, which will be payable to ordinary shareholders on 6 May 2009 in cash in US dollars, or in pounds sterling or Hong Kong dollars at exchange rates to be determined on 27 April 2009, with a scrip dividend alternative. The reserves available for distribution at 31 December 2008 were US$18,838 million. |

| |

| |

| | Quarterly dividends of US$15.50 per 6.20 per cent non-cumulative Series A US dollar preference share, equivalent to a dividend of US$0.3875 per Series A ADS, each of which represents one-fortieth of a Series A dollar preference share, were paid on 17 March 2008, 16 June 2008, 15 September 2008 and 15 December 2008. |

| | Quarterly coupons per 8.125 per cent capital securities of US$0.541 and US$0.508 were paid on 15 July 2008 and 15 October 2008 respectively. |

| 3 | The definition of return on average invested capital and a reconciliation to the equivalent GAAP measures are set out on page 19. |

| 4 | The return on average total shareholders’ equity is defined as profit attributable to shareholders of the parent company divided by average total shareholders’ equity. |

| 5 | The cost efficiency ratio is defined as total operating expenses divided by net operating income before loan impairment charges and other credit risk provisions. |

| 6 | This footnote is intentionally left blank. |

| 7 | Each American Depositary Share (‘ADS’) represents five ordinary shares. |

| 8 | Total shareholder return is defined on page 19. |

| 9 | The Financial Times Stock Exchange 100 Index. |

| 10 | The Morgan Stanley Capital International World Index. |

| 11 | The Morgan Stanley Capital International World Bank Index |

| 12 | Data for 2004 exclude the provisions of IAS 32, IAS 39 and IFRS 4, which were adopted with effect from 1 January 2005. |

| 13 | Capital resources are total regulatory capital, the calculation of which is set out on page 278. |

| 14 | Includes perpetual preferred securities, details of which can found in Note 32 on the Financial Statements. |

| 15 | Net of impairment allowances. |

| 16 | The definition of net asset value per share is total shareholders’ equity, less non-cumulative preference shares and capital securities, divided by the number of ordinary shares in issue. |

| 17 | Dividends per share expressed as a percentage of earnings per share. |

5

Back to Contents

| H S B C H O L D I N G S P L C |

| |

| Cautionary Statement Regarding Forward-Looking Statements |

| | |

| | |

| Cautionary Statement |

| | TheAnnual Reportand Accounts 2008 contains certain forward-looking statements with respect to the financial condition, results of operations and business of HSBC. |

| | | | |

| | Statements that are not historical facts, including statements about HSBC’s beliefs and expectations, are forward-looking statements. Words such as ‘expects’, ‘anticipates’, ‘intends’, ‘plans’, ‘believes’, ‘seeks’, ‘estimates’, ‘potential’ and ‘reasonably possible’, variations of these words and similar expressions are intended to identify forward-looking statements. These statements are based on current plans, estimates and projections, and therefore undue reliance should not be placed on them. Forward-looking statements speak only as of the date they are made, and it should not be assumed that they have been revised or updated in the light of new information or future events. |

| | | | |

| | Written and/or oral forward-looking statements may also be made in the periodic reports to the United States Securities and Exchange Commission, summary financial statements to shareholders, proxy statements, offering circulars and prospectuses, press releases and other written materials, and in oral statements made by HSBC’s Directors, officers or employees to third parties, including financial analysts. |

| | | | |

| | Forward-looking statements involve inherent risks and uncertainties. Readers are cautioned that a number of factors could cause actual results to differ, in some instances materially, from those anticipated or implied in any forward-looking statement. These factors include, among others: |

| | | | |

| | • | changes in general economic conditions in the markets in which HSBC operates, such as: |

| | | | |

| | | – | continuing or deepening recessions and fluctuations in employment; |

| | | | |

| | | – | changes in foreign exchange rates, in both market exchange rates (for example, between the US dollar and pound sterling) and government-established exchange rates (for example, between the Hong Kong dollar and US dollar); |

| | | | |

| | | – | volatility in interest rates; |

| | | | |

| | | – | volatility in equity markets, including in the smaller and less liquid trading markets in Asia and Latin America; |

| | | | |

| | | – | lack of liquidity in wholesale funding markets; |

| | | – | illiquidity and downward price pressure in national real estate markets, particularly consumer-owned real estate markets; |

| | | | |

| | | – | the length and severity of current market turmoil; |

| | | | |

| | | – | the impact of lower than expected investment returns on the funding of private and public sector defined benefit pensions; |

| | | | |

| | | – | the effect of unexpected changes in actuarial assumptions on longevity which would influence the funding of private and public sector defined benefit pensions; and |

| | | | |

| | | – | consumer perception as to the continuing availability of credit, and price competition in the market segments served by HSBC. |

| | | | |

| | • | changes in government policy and regulation, including: |

| | | | |

| | | – | the monetary, interest rate and other policies of central banks and other regulatory authorities, including the UK Financial Services Authority, the Bank of England, the Hong Kong Monetary Authority, the US Federal Reserve, the US Securities and Exchange Commission, the US Office of the Comptroller of the Currency, the European Central Bank, the People’s Bank of China and the central banks of other leading economies and markets where HSBC operates; |

| | | | |

| | | – | expropriation, nationalisation, confiscation of assets and changes in legislation relating to foreign ownership; |

| | | | |

| | | – | initiatives by local, state and national regulatory agencies or legislative bodies to revise the practices, pricing or responsibilities of financial institutions serving their consumer markets; |

| | | | |

| | | – | changes in bankruptcy legislation in the principal markets in which HSBC operates and the consequences thereof; |

| | | | |

| | | – | general changes in government policy that may significantly influence investor decisions, in particular in markets in which HSBC operates, including financial institutions newly taken into state ownership on a full or partial basis; |

| | | | |

| | | – | extraordinary government actions as a result of current market turmoil; |

6

Back to Contents

| | – | other unfavourable political or diplomaticdevelopments producing social instability orlegal uncertainty which in turn may affectdemand for HSBC’s products and services; |

| | | |

| | – | the costs, effects and outcomes of regulatoryreviews, actions or litigation, including anyadditional compliance requirements; and |

| | | |

| | – | the effects of competition in the marketswhere HSBC operates including increasedcompetition from non-bank financialservices companies, including securitiesfirms. |

| | • | | factors specific to HSBC: |

| | | | |

| | | – | the success of HSBC in adequately identifying the risks it faces, such as the incidence of loan losses or delinquency, and managing those risks (through account management, hedging and other techniques). Effective risk management depends on, among other things, HSBC’s ability through stress testing and other techniques to prepare for events that cannot be captured by the statistical models it uses. |

| | | | |

| | | – | the success of HSBC in addressing operational, legal and regulatory and litigation challenges. |

7

Back to Contents

| H S B C H O L D I N G S P L C |

| |

| Group Chairman’s Statement |

| | |

| | |

| Group Chairman’s Statement |

2008 was the most extraordinary year for the global economy and financial services in well over half a century. It marked the first crisis of the era of globalised securitisation. And it also marked the first crisis of the just-in-time global economy as the impact of the financial crisis fed rapidly straight into the performance of the real economy.

Causes of the crisis

|

| | |

| The causes of the crisis are complex and interrelated. But we can clearly see that a number of different factors contributed: |

| | |

| • | First, the global financial imbalances that arosefrom the accelerating global economic shifttowards emerging markets. The rapid growth ofemerging economies created a macro-economictriangle, made up of: the major consumermarkets, in particular the US but also a numberof other Western economies; major producernations – notably a number of fast-growingemerging markets which have beenmanufacturing a vast range of goods forconsumption in the West; and resource providerswhose wealth of hydrocarbons and othercommodities have helped power the producereconomies and have thus commanded such highprices until recently. This macro-economictriangle delivered high rates of growth, but alsocreated major financial imbalances as producernations and resource providers accumulatedmassive reserves whilst the US and otherconsumer markets ran significant and growingdeficits. |

| | |

| • | Second, cheap credit. A large proportion of theaccumulated savings of the producers andresource providers was invested in the world’sreserve currency, the US dollar, keeping rates low. This cheap money fuelled a consumer |

| | boom and rising house prices. It encouragedincreased borrowing by banks and by theircustomers, fuelling asset price bubblesparticularly in housing markets. Loose monetaryconditions in the US and in much of theemerging world gave added strength to thisalready potent cocktail. |

| | |

| • | Third, securitisation based on overly complexproduct structures. The complexity and opacityof certain financial instruments reached a pointwhere even senior and experienced bankers andprofessional investors had trouble understandingthem. This meant that people were selling andbuying assets whose risks they had not properlyassessed. |

| | |

| • | And finally, excessive gearing. Many banksbecame overgeared and too dependent onwholesale funding, which they assumed,incorrectly, would never dry up. Assets werecreated on the back of ever higher leverage, bothdirect and indirect. And when the securitisationmarket began to collapse, banks foundthemselves with assets that they could neithersell nor fund, so forcing large losses on the assetside and a funding challenge on the liability sidefor which they were entirely unprepared. |

| | |

| The result has been unprecedented stress in the financial system, and it has led to a major breakdown in trust. In many countries, huge support from taxpayers has been required in order to stabilise the system. |

| | |

| Failings in the banking industry |

| | |

| The industry has done many things wrong. It is important to remember that many ordinary bankers have always sought to provide good service to their customers; but we must also recognise that there have been too many who have profoundly damaged the industry’s reputation. |

| | |

| Inappropriate products were sold inappropriately by many. Compensation practices ran out of control and perverse incentives led to dangerous outcomes. There is genuine and widespread anger that the contributors to the crisis were in some cases amongst the biggest beneficiaries of the system. |

| | |

| Underlying all these events is a question about the culture and ethics of the industry. It is as if, too often, people had given up asking whether something was the right thing to do, and focused only whether it was legal and complied with the rules. The industry needs to recover a sense of what is right and suitable as a key impulse for doing business. |

8

Back to Contents

HSBC strategy intact

We at HSBC were not immune from the crisis. But we have built our business on very strong foundations and are able to report results which demonstrate our ability to withstand the storm.

Our strategy has been tested and remains intact. We will continue to build our business by focusing on faster-growing markets around the world and on businesses where international connectivity is important – all from a position of financial strength. If anything, the current crisis validates our renewed focus over the last few years on fast-growing economies, since it will accelerate the shift in the world’s centre of economic gravity from west to east.

Our robust balance sheet and liquidity means that we have continued to lend. In 2008, we grew our lending to commercial customers by 10 per cent on an underlying basis. Lending to personal customers increased in all regions except North America. And our brand strength continues to underpin our performance. It was noticeable that, at times of stress in many markets, HSBC was a beneficiary of funds flowing in. Recently, the HSBC brand was recognised as the number one brand in banking by Brand Finance.

Profitable from a broad-based earnings platform

Excluding the goodwill impairment on our North America Personal Financial Services business, HSBC reported a pre-tax profit for 2008 of US$19.9 billion, a decline of 18 per cent. On a reported basis, pre-tax profit was US$9.3 billion, down 62 per cent. Within this were some strong regional and business line performances. However, there is one area on which I would like to comment.

For North America, we reported a loss of US$15.5 billion including the goodwill impairment charge of US$10.6 billion in Personal Financial Services. The significant deterioration in US employment and economic outlook in the fourth quarter of 2008 were the primary factors in causing us to write off all the remaining goodwill carried on our balance sheet in respect of our Personal Financial Services business in North America.

The management team has worked tirelessly to address this problem acquisition in the US and we have considered all viable options. We saw the disruption in sub-prime lending as early as 2006 and sharply scaled back in 2007 while others continued

to grow. We also devoted considerable resources to helping our customers. Virtually no one then foresaw the subsequent scale of the deterioration in the US economy and financial markets. It is now clear that models of direct personal lending that depend on wholesale markets for funding are no longer viable. In light of this, we have taken the difficult decision that, with the exception of credit cards, we will write no further consumer finance business through the HFC and Beneficial brands in the US and close the majority of the network. Thus, in terms of new business, we are drawing a line and we will run off our existing business, providing all necessary support to HSBC Finance to enable it to do so in a measured way and meet all its commitments.

HSBC has a reputation for telling it as it is. With the benefit of hindsight, this is an acquisition we wish we had not undertaken.

The US remains the world’s largest economy and HSBC remains committed to the US, which we see as a core market for HSBC. HSBC Bank in the US is not affected by the restructure. In the immediate future we will focus on those businesses and customers for whom our global connectivity gives us advantage – primarily in corporate and commercial business, and in Private and Premier banking.

Performance overview and strategic activity

In this difficult environment, we missed our profitability targets. We hit our capital target with our tier 1 ratio at 8.3 per cent. We maintained a very conservative advances-to-deposits ratio at 84 per cent. We grew lending in each region outside North America on an underlying basis. And we constrained costs, with the cost efficiency ratio improving to 47.2 per cent, excluding the goodwill impairment mentioned above. We also continued implementation of OneHSBC, our programme to enhance customer experience and improve cost efficiency through standardising products, processes and technology around the world.

We also acquired businesses in strategic areas – we acquired the assets, liabilities and operations of The Chinese Bank in Taiwan in March; IL&FS Investsmart, a retail brokerage in India in May; and, in October, the acquisition of Bank Ekonomi in Indonesia was announced. The first two are complete and being integrated, the last is expected to be completed in the second quarter. The most notable disposal was the sale of our regional bank network in France for a consideration of US$3.2 billion.

9

Back to Contents

| H S B C H O L D I N G S P L C |

| |

| Group Chairman’s Statement(continued) |

| | |

| | |

| Group Chairman's Statement |

Thank you to our people

This was an extraordinary year and made extraordinary demands on many of our people. I want to express my sincere thanks for all their efforts and achievements. Our industry has rightly been under considerable public scrutiny and banks have been indiscriminately bunched together. It is through our staff that HSBC’s distinctive character stands out for our customers and it is they who ensure that not all banks are the same.

Dividend declaration and progressive dividend policy

The Directors have declared a fourth interim dividend for 2008 of US$0.10 per ordinary share (in lieu of a final dividend) which, together with the first three interim dividends for 2008 of US$0.18 already paid, will make a total distribution in respect of the year of US$0.64 per ordinary share. The payments in total represent a decrease of 29 per cent in US dollar terms compared with 2007 and of 15 per cent in sterling terms. The dividend will be payable on 6 May 2009 to shareholders on the register at the close of business on 20 March 2009.

After 15 years of double-digit dividend growth, we did not make the decision to lower the dividend lightly. Very careful consideration was given to the current operating environment and the increased uncertainty over both the supply of capital required in an increasingly volatile financial world and a pro-cyclical regulatory capital framework.

For 2009, HSBC has rebased the envisaged dividend per share for the first three interim dividends to US$0.08 to reflect the impact of the enlarged ordinary share capital following the Rights Issue we are announcing today, prevailing business conditions and capital requirements. The dividend payments remain substantial and reflect management’s long-term confidence in the business. HSBC will continue to aim to pay progressive dividends in line with the long-term growth of the business.

Maintaining HSBC’s financial strength

The logic of maintaining HSBC’s distinctive financial strength which we have applied to our dividend also applies to our capital position. We have announced today a Rights Issue to strengthen further our capital ratios. We propose to raise, on a fully underwritten basis, approximately US$17.7 billion of equity which will increase our capital ratios by 150 basis points, strengthening the core equity tier 1 ratio to 8.5 per cent and the tier 1 ratio to 9.8 per cent, both on a pro forma basis as at

31 December 2008. I shall be writing to all shareholders with full details.

Over the past 12 months, many of our competitors have received significant government capital injections – something we said we could not envisage – or have raised capital from shareholders and other investors. Higher regulatory capital requirements, in part from the effect of the economic downturn on capital requirements under the Basel II regime, as well as changing market sentiment on appropriate levels of leverage, have also raised expectations regarding capital levels. We are determined that HSBC should maintain its signature financial strength and we are now raising the top of our target range for the tier 1 ratio so that the range will be from 7.5 per cent to 10 per cent.

Planned internal capital generation remains strong and this capital raising will enhance our ability to deal with the impact of an uncertain economic environment and to respond to unforeseen events. Importantly, it will also give us options with respect to opportunities which we believe will present themselves to those with superior financial strength. These may involve organic investment in the continued taking of market share from more capital constrained competitors. There may also be opportunities to grow through targeted acquisitions by taking advantage of attractive valuations where the opportunities in question align with our strategy and the risks are understood.

Culture and compensation

We believe in the profound importance of culture and ethics in business. HSBC’s longstanding traditions of financial strength, long-term customer relationships and conservative management are as important today as ever. They have not always been fashionable and we have not always been perfect. One of the consequences of the crisis – and rightly – is that we are going to see a fundamental re-evaluation of the rules and regulations that govern our business. But we should remember that no amount of rules and regulations will be sufficient if the culture does not encourage people to do the right thing. It is the responsibility of Boards to supervise and management to embed a sustainable culture into the very fibre of the organisation. For HSBC, there is nothing more important.

We also intend to play our part in rebuilding public trust in our industry. This means we must be willing to take part in and shape the debate on how our industry should evolve in the coming years, based on the lessons which must be learnt from this crisis. In particular, we strongly believe that the

10

Back to Contents

industry must respond to the requirement for a more sober and reasonable approach to compensation. At HSBC, we are committed to the principle of sensible market-related pay, structured to align executive actions with long-term shareholder interests. A small number of individuals in a market system will inevitably receive compensation that is high in absolute terms, but this must be genuinely linked to long-term shareholder interests. It is clear that the banking industry got it wrong in the go-go years: we will play our part in helping the industry respond appropriately to the new realities.

It is right therefore that in HSBC’s case, I outline our present position. As Chairman I elected in 2007 to no longer receive any cash bonus award; any variable compensation would be delivered through performance share awards – which would only vest if performance hurdles are met. And no performance share awards will be made in the Group in respect of 2008. Mike Geoghegan, Group Chief Executive, and Stuart Gulliver, Chief Executive Global Banking and Markets, and Douglas Flint, Group Finance Director, have asked the Remuneration Committee not to consider them for any bonus award for 2008. No cash bonus award will be made to any Executive Director for 2008. Full details on Directors’ remuneration can be found in theAnnual Report.

Learning the lessons

We are living through a genuinely global crisis; it cannot be solved by one nation alone. Governments need to work together with our industry to tackle the root causes of the crisis, while maintaining the open, globalised markets that have helped spread prosperity in the last two decades. Protectionism, both in trade and in capital flows, is a threat and in all its forms must be resisted.

We must also urgently improve governance and regulation to create a more stable financial framework. The globalisation of financial markets contrasts sharply with the domestic agenda of the regulatory regimes that underpin it. We support intergovernmental efforts to enhance the coordination of regulatory oversight, since we believe that this is essential to the stable development of the international capital markets for the benefit of the common good.

Continued economic strain

The coming twelve months will be difficult. We expect parts of Asia, the Middle East and Latin America to continue to outperform Western economies, but to be constrained by the global downturn.

We see unemployment rising through 2009 into 2010 in both the US and the UK, together with continuing declines in housing markets. We should remember that the US is the driver of the global economy and global growth depends on the US recovery.

We remain confident that HSBC is well-placed in today’s environment and that our strength leads to opportunity. Our strategy has served HSBC well and positions it for long-term growth with attractive returns. HSBC continues to combine its position as the world’s leading emerging markets bank with an extensive international network across both developed and faster growing markets. At the same time, as the financial system exhibits stress, our competitive position is improving as the capacity and capabilities of financial institutions are constrained by lack of capital and funding; many of them are also focusing more on their domestic markets.

Further strengthening our capital base will enhance our ability to deal with the impact of an uncertain economic environment and to respond to unforeseen events, as well as giving us options regarding opportunities which will undoubtedly present themselves to those with superior financial strength.

S K Green,Group Chairman

2 March 2009

11

Back to Contents

| H S B C H O L D I N G S P L C |

| |

| Report of the Directors: Operating and Financial Review |

| | |

| | |

| Principal activities / Strategic direction / Challenges and uncertainties |

HSBC is one of the largest banking and financial services organisations in the world, with a market capitalisation of US$114 billion at 31 December 2008.

Through its subsidiaries and associates, HSBC provides a comprehensive range of banking and related financial services. Headquartered in London, HSBC operates through long-established businesses and has an international network of some 10,000 properties in 86 countries and territories in five geographical regions: Europe; Hong Kong; Rest of Asia-Pacific, including the Middle East and Africa; North America and Latin America. Within these regions, a comprehensive range of financial services is offered to personal, commercial, corporate, institutional, investment and private banking clients. Services are delivered primarily by domestic banks, typically with large retail deposit bases, and consumer finance operations. Taken together, the five largest customers of HSBC do not account for more than one per cent of HSBC’s income.

There were no significant acquisitions during the year (for details of acquisitions see page 418). HSBC disposed of its seven French regional banks for US$3.2 billion in July 2008 (see pages 418 and 458).

HSBC’s strategic direction reflects its position as ‘The world’s local bank’, combining the largest global emerging markets banking business and a uniquely cosmopolitan customer base with an extensive international network and substantial financial strength.

The Group’s strategy is aligned with key trends which are shaping the global economy. In particular, HSBC recognises that, over the long term, developing markets are growing faster than the mature economies, world trade is expanding at a greater rate than gross domestic product and life expectancy is lengthening virtually everywhere. Against this backdrop, HSBC’s strategy is focused on delivering superior growth and earnings over time by building on the Group’s heritage and skills. Its origins in trade in Asia have had a considerable influence over the development of the Group and, as a consequence, HSBC has an established and longstanding presence in many countries. The combination of local knowledge and international breadth is supported by a substantial financial capability founded on balance sheet strength, largely attributable to the scale of the Group’s retail deposit bases.

HSBC is, therefore, continuing to invest primarily in the faster growing markets and, in the more developed markets, by focusing on businesses which have international connectivity. Central to these reshaping activities is a policy of maintaining HSBC’s capital strength and strong liquidity position.

The Group has identified three main business models for its customer groups and global businesses that embody HSBC’s areas of natural advantage:

| | • | businesses with international customers forwhom developing markets connectivity iscrucial – Global Banking and Markets, PrivateBanking, the large business segment ofCommercial Banking and the mass affluentsegment of Personal Financial Services; |

| | | |

| | • | businesses with local customers whereefficiency can be enhanced through global scale– the small business segment of CommercialBanking and the mass market segment ofPersonal Financial Services; and |

| | | |

| | • | products where global scale is possible throughbuilding efficiency, expertise and brand – globalproduct platforms such as global transactionbanking. |

The means of executing the strategy, and further utilising the linkages within the Group, are clear:

| • | the HSBC brand and global networks will beleveraged to reach new customers and offerfurther services to existing clients; |

| | |

| • | efficiency will be enhanced by taking fulladvantage of local, regional and globaleconomies of scale, in particular by adoptinga common systems architecture whereverpossible; and |

| | |

| • | objectives and incentives will be aligned tomotivate and reward staff for being fullyengaged in delivering the strategy. |

| Challenges and uncertainties |

|

Current economic and market conditions may adversely affect HSBC’s results.

The global economy has entered the most severe downturn for 80 years, with the financial services industry facing extraordinary turbulence. A shortage of liquidity, lack of funding, pressure on capital and extreme price volatility across a wide range of asset classes are putting financial institutions under considerable pressure. This is leading governments and central banks to undertake unprecedented intervention designed to stabilise the global and

12

Back to Contents

domestic financial systems, to stimulate new lending and to support systemically important institutions at risk of failing. Many developed economies have entered recession and growth has slowed in many emerging countries, with serious adverse consequences for asset values, employment, consumer confidence and levels of economic activity. Commodity prices have significantly retrenched, in many cases from recent historical highs, interest rate yield curves have flattened, interest rates have fallen in absolute terms and trade flows have contracted. Global equity markets have experienced severe declines and various currencies, including sterling, have depreciated significantly against the US dollar. Emerging markets have suffered as portfolio investments have been repatriated and cross-border inter-bank funding has been withdrawn. Numerous governments and central banks have responded by proposing programmes to make substantial funds and guarantees available to boost liquidity and confidence in their financial systems, as well as cutting taxes and lowering interest rates. It is not known whether these responses will be effective in addressing the severe economic and market conditions or whether recently proposed measures will be implemented as initially proposed.

HSBC’s earnings are affected by global and local economic and market conditions. Dramatic declines in 2007 and 2008 in the housing markets in the US, the UK and elsewhere have combined with increasing unemployment to affect negatively the credit performance of real estate-related exposures, resulting in significant write-downs of asset values by financial institutions, including HSBC. These write-downs, initially of asset-backed securities but spreading to other securities and loans, have caused many financial institutions to seek additional capital, to reduce or eliminate dividends, to merge with larger and stronger competitors or, in some cases, to fail.

A worsening of these conditions may exacerbate the impact of these difficult market conditions on HSBC and other financial institutions and could have an adverse effect on HSBC’s operating results. In particular, the Group may face the following challenges in connection with these events:

| • | HSBC’s ability to assess the creditworthiness ofits customers or to estimate the values of itsassets may be impaired if the models andtechniques it uses become less accurate in theirpredictions of future behaviour, valuations orestimates. The process HSBC uses to estimatelosses inherent in its credit exposure or assessthe value of certain assets requires difficult, |

| | subjective and complex judgements. Theseinclude forecasts of economic conditions andhow predicted economic scenarios might impairthe ability of HSBC’s borrowers to repay theirloans or might affect the value of assets. As aconsequence, this process may be less capableof making accurate estimates which, in turn,may undermine the reliability of the process. |

| | |

| • | The demand for borrowing from creditworthycustomers may diminish as economic activityslows. |

| | |

| • | Lower interest rates will reduce net interestincome earned by HSBC on its excess deposits. |

| | |

| • | HSBC’s ability to borrow from other financialinstitutions or to engage in funding transactionson favourable terms, or at all, could beadversely affected by further disruption in thecapital markets or deteriorating investorsentiment. |

| | |

| • | Market developments may affect consumerconfidence and may cause declines in creditcard usage and adverse changes in paymentpatterns, leading to increases in delinquenciesand default rates, write-offs and loanimpairment charges beyond HSBC’sexpectations. |

| | |

| • | Loan impairment allowances and write-offs arelikely to rise as a result of a deterioration inpayment patterns and increased delinquenciesand default rates caused by weakeningconsumer confidence and increased businessfailures. A worsening of these economic factorsmay exacerbate the adverse effects of thesedifficult market conditions on HSBC and othersin the financial services industry. |

| | |

| • | HSBC expects to face increased regulation andsupervision of the financial services industry,following new or proposed regulatory measuresin countries in which it operates. |

| | |

| • | Trade and capital flows may further contract asa result of protectionist measures beingintroduced in certain markets. |

| | |

| • | Increased government ownership andcontrol over financial institutions and furtherconsolidation in the financial industry, whichcould significantly alter the competitivelandscape. |

As a worldwide financial institution, HSBC is exposed to these developments across all its businesses, both directly and through their impact on its customers and clients. Local variations exist, however, reflecting regional circumstances and

13

Back to Contents

| H S B C H O L D I N G S P L C |

| |

| Report of the Directors: Operating and Financial Review(continued) |

| | |

| | |

| Challenges and uncertainties |

presenting challenges to HSBC which are specific to those areas.

Europe

In the UK, the economy has entered recession and the currency has fallen in value against the US dollar, the yen and the euro. Changes in the marketplace are emerging following the part-nationalisation of some major financial institutions, and political interaction with the regulatory environment is becoming more frequent as the government seeks to stimulate lending to preserve economic activity. A period of low interest rates will reduce deposit spreads and HSBC’s retail business model will be more dependent on transactional fees and lending margin. Pension funding requirements, in particular for UK defined benefit schemes, will place increased financing demands on corporates, which may lead to unfunded commitments being drawn down, adding to pressure on system liquidity. The recent deterioration in credit quality is expected to continue as the economy contracts, with loan impairment charges rising as a result. Market volatility is also expected to continue.

In France, changes in the marketplace are slowly emerging following government measures to stimulate lending and preserve economic activity. A period of low interest rates will not adversely impact spreads in the short-term but will have an adverse effect in later years. HSBC’s retail business model is dependent on banking fees to maintain profitability and a recovery in financial markets is necessary in order to enhance brokerage and management fees and stimulate fund management activities. Deterioration in credit quality is expected to continue as the economy contracts, with commercial loan impairment charges rising as a result. Personal loan impairment charges are expected to remain at around current levels unless there is a very deep recession.

Conditions are likely to remain difficult in a number of markets in which HSBC currently trades and volatility is expected to continue.

Hong Kong and Rest of Asia-Pacific

In Asia-Pacific, a prolonged period of low interest rates is expected which will put pressure on HSBC’s net interest income from its strong deposit base. With capital market and currency volatility endemic, customers are likely to seek capital protection and become increasingly rate and risk sensitive, seeking out products which offer deposit insurance and government guarantees. Regulatory reforms in the areas of wealth management product complexity,

sales requirements and liquidity and reserve ratios are likely, and these will lead to a higher cost of compliance, greater standardisation and slower product approvals. International trade is expected to continue to contract, affecting import and export volumes and reducing HSBC’s earnings from trade financing. The quality of the asset book will deteriorate if economic factors beyond HSBC’s control do not improve, reducing customer credit ratings and, as a consequence, increasing risk- weighted asset allocations and capital requirements. This could be exacerbated if capital continues to be repatriated from emerging markets to more developed economies to take advantage of lower asset prices, adversely affecting emerging markets’ balance of payments and foreign exchange reserves. However, Asia is expected to adapt quickly to secure recovery from the global recession, led by mainland China and India.

The fall in global demand for oil products and related prices, and the contraction in financial surpluses held by key oil-producing countries following the declines in capital markets, will reduce the ability of some countries in the Middle East to maintain spending, borrowing and investment domestically and internationally. This will result in the cancellation or postponement of infrastructure projects which, together with weakening property prices, is expected to reduce both credit cover and revenue streams for financial institutions. The availability of economically priced, long-term funding is likely to contract. Business activity and private investment will also slow as consumer confidence declines. These factors will combine to place pressure on net revenues and on capital requirements.

North America

In the US, the steep decline in the housing market, with falling home prices and increasing foreclosures, and rising unemployment have resulted in significant write-downs of loans and advances and mortgage-backed securities. The effect of these write-downs subsequently spread to other capital market activities, leading many financial institutions to seek additional capital, merge with larger and stronger institutions and, in some cases, fail. Many lenders reduced or stopped providing funding to borrowers, including to other financial institutions. This market turmoil and resultant tightening of credit have led to an increased level of delinquencies, a fall in consumer confidence, increased market volatility and a widespread reduction in business activity in general. To date, various government intervention measures designed to stabilise the markets, including

14

Back to Contents

the decision of the Federal Reserve to reduce interest rates to unprecedentedly low levels, appear to be having an impact on the trading of both guaranteed and non-guaranteed debt in early 2009. A prolonged period of low Federal funds rates will put pressure on deposit spreads earned on HSBC’s deposit base. It is likely that these conditions will continue to adversely affect the Group’s results into 2010, the degree to which remains uncertain.

Latin America

Markets in Latin America are expected to be affected by recession in the developed world, particularly in the US. Output will fall as a decline in the demand for exports will adversely affect the export sector, and these factors are likely to combine with currency volatility to weaken the balance sheets of financial institutions. This may lead to a further contraction in the availability of credit, increasing the likelihood of bankruptcies and unemployment and reducing economic activity and consumption. Lower commodity prices and reduced remittance inflows are likely to affect economies in the region, particularly in Mexico and Central America. Exchange rates are likely to remain under pressure as growth stalls, and inflation may rise. The possibility of a combined credit crunch and stagflation in Latin America cannot be ruled out. The authorities may react with stricter prudential regulation and price controls. Public finances will come under strain if oil and other commodity prices remain low, restricting the authorities’ room for manoeuvre.

Risks associated with liquidity and funding, which are inherent in HSBC’s business, have been greatly increased by the current global market conditions

HSBC’s business model depends upon its ability to access financial resources whenever required to meet its obligations. To this end, HSBC seeks to maintain a diversified and stable funding base comprising core retail and corporate customer deposits and institutional balances and to augment this with wholesale funding and portfolios of highly liquid assets diversified by currency and maturity which are held to enable HSBC to respond to unforeseen liquidity requirements. HSBC’s earnings are affected by its ability to properly value financial instruments. In certain illiquid markets, determining the value at which financial instruments can be realised is highly subjective, and processes to ascertain value and estimates of value, both of which require substantial elements of judgement, assumptions and estimates (which may change over time), are required. Increased illiquidity adds to

uncertainty over the accessibility of financial resources and may reduce capital resources as valuations decline. Rating agencies, which determine HSBC’s own credit ratings and thereby influence the Group’s cost of funds, take into consideration management effectiveness and the success with which HSBC’s liquidity risk factors are managed. Actions by third parties and independent market participants, such as rating agency downgrades of instruments to which HSBC has exposure, can result in reduced liquidity and valuations of those instruments. HSBC’s liquidity could also be constrained by an inability to access the debt capital markets due to a variety of unforeseen market dislocations or interruptions.

The extreme market conditions facing the financial services industry have been reflected in shortages of liquidity, lack of funding, pressure on capital and extreme price volatility across a wide range of asset classes. Illiquidity of these assets has prevented the realisation of existing asset positions and has constrained risk distribution in ongoing banking activities. The extreme market conditions, which have highlighted the importance of a strong diversified core deposit base, have also lead to increased competition for such deposits and the risk of deposit migration. HSBC’s Global Banking and Markets business operates in the markets affected by illiquidity and extreme price volatility, either directly or indirectly, through exposures to securities, loans, derivatives and other commitments, and HSBC has made substantial write-downs and impairments on illiquid legacy credit and structured credit positions. While it is difficult to predict how long the conditions described above will exist and which of HSBC’s markets, products and other businesses will be affected, continuation of these factors could have an adverse effect on the Group’s results.

HSBC has significant exposure to counterparty risk

HSBC’s ability to engage in routine transactions to fund its operations and manage its risks could be adversely affected by the actions and commercial soundness of other financial services institutions. Financial institutions are extremely interdependent because of trading, clearing, counterparty or other relationships. As a consequence, a default by, or decline in market confidence in, individual institutions, or anxiety about the financial services industry generally, can lead to further individual and/or systemic difficulties, defaults and losses. HSBC has exposure to virtually all major industries and counterparties, and it routinely executes

15

Back to Contents

| H S B C H O L D I N G S P L C |

| |

| Report of the Directors: Operating and Financial Review (continued) |

| | |

| | |

| Challenges and uncertainties / KPIs |

transactions with counterparties in financial services, including brokers and dealers, commercial banks, investment banks, mutual and hedge funds, and other institutional clients. Many of these transactions expose HSBC to credit risk in the event of default by its counterparty or client. Where counterparty risk has been mitigated by taking collateral, HSBC’s credit risk may be exacerbated if the collateral it holds cannot be realised or has to be liquidated at prices which are insufficient to recover the full amount of its loan or derivative exposure. The failure of one of HSBC’s counterparties could have an adverse effect on its results.

HSBC operates in a highly competitive environment, and competition could intensify as a result of current global market conditions

Consolidation in the financial services industry is increasingly concentrating activity in companies that are capable of offering a wide array of financial products at competitive prices, with globalisation exposing HSBC to competition in capital markets and financial services at global and local levels alike. In addition, technological advances, the growth of e-commerce, regulatory developments and public sector participation or guarantees have made it possible for non-depository institutions to offer products and services that traditionally were the preserve of banks. The prominence in recent years of sovereign wealth funds, private equity and hedge funds as alternative sources of funding – which has increased competition for traditional financial institutions – may ease as investors seek safer, more traditional alternatives. Competition mayfurther intensifyor the competitive landscape may change as the consolidation of financial services companies continues and others are brought into part or full public ownership in response to the current market conditions. HSBC’s ability to grow its businesses, and therefore its earnings, is affected by these competitive pressures and is dependent on HSBC’s ability to attract and retain talented and dedicated employees.

HSBC is subject to political and economic risks in the countries in which it operates

HSBC operates through an international network of subsidiaries and affiliates in 86 countries and territories around the world. Its results are therefore subject to the risk of loss from unfavourable political developments, currency fluctuations, social instability and change in government policies on such matters as expropriation, authorisations, international ownership, interest-rate caps, limits

on dividend flows and tax in the jurisdictions in which it operates. These factors may also negatively affect revenues from the trading of securities and investment in securities, the effect being accentuated through certain international trading markets, particularly those in emerging market countries, being typically smaller, less liquid and more volatile than developed trading markets. HSBC’s subsidiaries’ and affiliates’ ability to pay dividends could be restricted by changes to official banking measures, exchange controls and other requirements. Because HSBC prepares its accounts in US dollars, while a substantial part of its assets, liabilities, assets under management, revenues and expenses are denominated in other currencies, changes in foreign exchange rates have an effect on its reported income and shareholders’ equity. For a detailed discussion of global and regional factors that impact the results of HSBC’s operations, see page 12.

Operational risks are inherent in HSBC’s business

HSBC is exposed to many types of operational risk, including fraudulent and other criminal activities (both internal and external), breakdowns in processes or procedures and systems failure or non-availability. HSBC is also subject to the risk of disruption of its business arising from events that are wholly or partially beyond its control (for example natural disasters, acts of terrorism, epidemics and transport or utility failures) which may give rise to losses in service to customers and/or economic loss to HSBC. All of these risks are also applicable where HSBC relies on outside suppliers or vendors to provide services to it and its customers.

HSBC is subject to legal risks, which have an adverse effect on the Group’s reputation

The risks to HSBC’s reputation arise from a variety of sources with the potential to cause harm to the Group and its ability to operate. These issues require the Group to deal appropriately with potential conflicts of interest; legal and regulatory requirements; ethical issues; anti-money laundering laws or regulations; privacy laws; information security policies; sales and trading practices; and the conduct of companies with which it is associated. Failure to address these issues appropriately may give rise to additional legal and compliance risk to HSBC, with an increase in the number of litigation claims and the amount of damages asserted against HSBC, or subject HSBC to regulatory enforcement actions, fines or penalties.

16

Back to Contents

Increased regulation of the financial services industry could have an adverse effect on HSBC’s operations

HSBC, its subsidiaries and its affiliates are subject to extensive and increasing regulation, accounting standards and interpretations thereof and legislation in the various countries in which the Group operates. From time to time, new laws are introduced, including tax, consumer protection, privacy and other legislation, which affect the operating environment in which the Group operates. As aresult ofthe recent interventions by governments in response to global economic conditions, it is widely expected that there will be a substantial increase in government regulation and supervision of the financial services industry, including the imposition of higher capital requirements and restrictions on certain types of transaction structure. If enacted, such new regulations could require additional capital to be injected into HSBC’s subsidiaries and affiliates, require HSBC to enter into business transactions that are not otherwise part of its current Group strategy, prevent HSBC from continuing current lines of operations, restrict the type or volume of transactions HSBC may enter into, limit HSBC’s subsidiaries’ and affiliates’ ability to declare dividends to HSBC, or set limits on or require the modification of rates or fees that HSBC charges on certain loan or other products. HSBC may also face increased compliance costs and limitations on its ability to pursue business opportunities. Separately, the Basel II Accord’s requirement for financial institutions to increase their capital in response to deteriorating market conditions may have secondary effects on lending, which could exacerbate the current market downturn. These measures, alone or in combination, could have an adverse effect on HSBC’s operations.

In the UK for example, the Banking Act 2009 includes a ‘Special Resolutions Regime’ which gives wide powers in respect of UK banks and their parent companies to the UK Treasury, the FSA and the Bank of England in circumstances where any such UK bank has encountered, or is likely to encounter, financial difficulties.

HSBC is subject to tax-related risks in the countries in which it operates, which could have an adverse effect on its operating results

HSBC is subject to the substance and interpretation of tax laws in all countries in which it operates.

A number of double taxation agreements entered into between countries also affect the taxation of the Group. Tax risk is the risk associated with changes in tax law or in the interpretation of tax law. It also includes the risk of changes in tax rates and the risk of consequences arising from failure to comply with procedures required by tax authorities. Failure to manage tax risks could lead to increased tax charges, including financial or operating penalties, for not complying as required with tax laws.

| Key performance indicators |

|

The Board of Directors and the Group Management Board monitor HSBC’s progress against its strategic objectives. Progress is assessed by comparison with the Group’s strategy, its operating plan targets and its historical performance using both financial and non-financial measures.

As a prerequisite for the vesting of Performance Shares, the Remuneration Committee must satisfy itself that HSBC Holdings’ financial performance has shown a sustained improvement in the period since the award date. In determining this, the Remuneration Committee will take account of all relevant factors but in particular comparisons against the total shareholder return (‘TSR’) comparator group with regard to the financial key performance indicators (‘KPIs’) described below.

Financial KPIs

To support the Group’s strategy and ensure that HSBC’s performance can be monitored, management utilises a number of financial KPIs. The table below presents these KPIs for the period from 2004 to 2008. At a business level, the KPIs are complemented by a range of benchmarks which are relevant to the planning process and to reviewing business performance.

HSBC has published a number of key targets against which future performance can be measured. Financial targets have been set as follows: the return on average total shareholders’ equity over the medium term has been set at 15-19 per cent; the cost efficiency ratio has been set in the range of 48-52 per cent; and the TSR in the top half of that achieved by peers. The cost efficiency ratio has been set as a range within which the business is expected to remain in order to accommodate the need for continued investment in support of future business growth.

17

Back to Contents

| H S B C H O L D I N G S P L C |

| |

| Report of the Directors: Operating and Financial Review (continued) |

| | |

| | |

| KPIs |

Financial KPIs – trend analysis

| | 2008 | | | 2007 | | | 2006 | | | 2005 | | | 2004 | | |

| | % | | | % | | | % | | | % | | | % | | |

| | | | | | | | | | | | | | | | |

| Revenue growth1 | 3.4 | | | 20.8 | | | 13.4 | | | 12.2 | | | – | | |

| Revenue mix2 | | | | | | | | | | | | | | | |

| Net interest income | 52.1 | | | 47.8 | | | 52.8 | | | 54.4 | | | 60.6 | | |

| Net fee income | 24.5 | | | 27.9 | | | 26.3 | | | 25.1 | | | 25.2 | | |

| Other income3 | 23.4 | | | 24.3 | | | 20.9 | | | 20.5 | | | 14.2 | | |

| Cost efficiency4 | 60.1 | | | 49.4 | | | 51.3 | | | 51.2 | | | 51.6 | | |

| Credit performance as measured by risk adjusted margin5 | 4.8 | | | 6.0 | | | 6.3 | | | 6.3 | | | 6.8 | | |

| Return on average invested capital6 | 4.0 | | | 15.3 | | | 14.9 | | | 15.9 | | | 15.0 | | |

| Dividends per share growth7 | (28.9 | ) | | 11.1 | | | 11.0 | | | 10.6 | | | 10.0 | | |

| Basic earnings per ordinary share8(US$) | 0.47 | | | 1.65 | | | 1.40 | | | 1.36 | | | 1.18 | | |

| Return on average total shareholders’ equity9 | 4.7 | | | 15.9 | | | 15.7 | | | 16.8 | | | 16.3 | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | Over | | | Over | | | Over | | | | | | | | |

| | 1 year | | | 3 years | | | 5 years | | | | | | | | |

| Total shareholder return | | | | | | | | | | | | | | | |

| HSBC TSR | 84.5 | | | 84.5 | | | 98.5 | | | | | | | | |

| Benchmarks: | | | | | | | | | | | | | | | |

| – FTSE 100 | 71.7 | | | 88.1 | | | 118.3 | | | | | | | | |

| – MSCI World | 81.8 | | | 93.6 | | | 123.7 | | | | | | | | |

| – MSCI Banks | 63.0 | | | 60.8 | | | 82.7 | | | | | | | | |

| | |

| 1 | The percentage increase in net operating income before loan impairment and other credit risk charges since the previous year. |

| 2 | As a percentage of net operating income before loan impairment charges and other credit risk provisions. |

| 3 | Other income comprises net operating income before loan impairment charges and other credit risk provisions less net interest income and net fee income. |

| 4 | Total operating expenses divided by net operating income before loan impairment and other credit risk charges. |

| 5 | Net operating income divided by average risk-weighted assets. |

| 6 | Profit attributable to ordinary shareholders divided by average invested capital. |

| 7 | The percentage increase in dividends per share since the previous year, based on the dividends paid in respect of the year to which the dividend relates. |

| 8 | Basic earnings per ordinary share is defined in Note 13 on the Financial Statements. |

| 9 | The return on average total shareholders’ equity is defined as profit attributable to shareholders of the parent company divided by the average total shareholders’ equity. |

Revenue growth provides an important guide to the Group’s success in generating business. In 2008, total revenue grew by 3.4 per cent to US$81.7 billion, 2.1 per cent on an underlying basis, reflecting the resilience of HSBC’s income generating capabilities in these exceptionally difficult economic circumstances.

Revenue mix represents the relative distribution of revenue streams between net interest income, net fee income and other revenue. It is used to understand how changing economic factors affect the Group, to highlight dependence on balance sheet utilisation for income generation and to indicate success in cross-selling fee-based services to customers with loan facilities. This understanding assists management in making business investment decisions. Comparison of the revenue mix between 2005 and 2007 shows a trend of net fee income increasing at a faster rate than net interest income. This trend has been reversed in 2008 as net fee income’s contribution fell by 3.4 percentage points mainly due to lower fees on cards and equity-related products.

Cost efficiency is a relative measure that indicates the consumption of resources in generating revenue. Management uses this to assess the success of technology utilisation and, more generally, the productivity of the Group’s distribution platforms and sales forces. The cost efficiency ratio for 2008 deteriorated by 10.7 percentage points to 60.1 per cent. This included writing off goodwill in the US.

Credit performance as measured by risk-adjusted margin is an important gauge for assessing whether credit is correctly priced so that the returns available after recognising impairment charges meet the Group’s required return parameters. The ratio for 2008 was 4.8 per cent, showing a decline of 1.2 percentage points over 2007, as loan impairment charges rose at a faster rate than income on higher average risk-weighted assets.

18

Back to Contents