As filed with the Securities and Exchange Commission on March 20, 2006.

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

| |  | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE | | | |

| | | SECURITIES EXCHANGE ACT OF 1934 | | | |

| | | | | | |

| | | or | | | |

| | | | | | |

| |  | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE | | | |

| | | SECURITIES EXCHANGE ACT OF 1934 for the fiscal year ended December 31, 2005 | | | |

| | | | | | |

| | | or | | | |

| | | | | | |

| | | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE | | | |

| | | SECURITIES EXCHANGE ACT OF 1934 | | | |

| | | | | | |

| | | or | | | |

| | | | | | |

| | | SHELL COMPANY REPORT PURSUANT TO SECTION 14 OR 15(d) OF THE | | | |

| | | SECURITIES EXCHANGE ACT OF 1934 | | | |

For the transition period from N/A to N/A

Commission file number: 1-14930

HSBC Holdings plc

(Exact name of Registrant as specified in its charter)

| N/A | United Kingdom |

| (Translation of Registrant’s name into English) | (Jurisdiction of incorporation or organization) |

8 Canada Square

London E14 5HQ

United Kingdom

(Address of principal executive offices)

Securities registered or to be registered pursuant to Section 12(b) of the Securities Exchange Act of 1934:

| Title of each class | Name of each exchange on which registered |

| |

| Ordinary Shares, nominal value US$0.50 each. | London Stock Exchange

Hong Kong Stock Exchange

Euronext Paris

Bermuda Stock Exchange

New York Stock Exchange* |

| | |

American Depository Shares, each representing 5 Ordinary

Shares of nominal value US$0.50 each. | New York Stock Exchange

|

| | |

| 6.20% Non-Cumulative Dollar Preference Shares, Series A | New York Stock Exchange* |

| | |

| American Depository Shares, each representing one-fortieth of a Share of 6.20% Non-Cumulative Dollar Preference Shares, Series A | New York Stock Exchange |

Securities registered or to be registered pursuant to Section 12(g) of the Securities Exchange Act of 1934: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Securities Exchange Act of 1934: None

The number of outstanding shares of each of the issuer’s classes of capital or common stock as of December 31, 2005 was:

| Ordinary Shares, nominal value US$0.50 each | 11,172,075,550 |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act:

| Yes | No |

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934:

| Yes | No |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes | No |

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act:

| Large accelerated filer | Accelerated filer | Non-accelerated filer |

Indicate by check mark which financial statements Item the registrant has elected to follow:

| Item 17 | Item 18 |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act):

| Yes | No |

* Not for trading, but only in connection with the registration of American Depositary Shares.

H S B C H O L D I N G S P L C

Table ofContents

Certain Defined Terms

| | | |

| | | |

| Unless the context requires otherwise, ‘HSBC Holdings’ means HSBC Holdings plc and ‘HSBC’ or the ‘Group’ means HSBC Holdings together with its subsidiaries and associates. Within this document the Hong Kong Special Administrative Region of the | | People’s Republic of China is referred to as ‘Hong Kong’. When used in the terms ‘shareholders’ equity’ and ‘total shareholders’ equity’, ‘shareholders’ means holders of HSBC Holdings ordinary and preference shares. |

Back to Contents

| H S B C H O L D I N G S P L C |

| |

| |

| Financial Highlights |

| | |

| | |

HSBC’s Financial Statements and Notes thereon, as set out on pages 236 to 402, are prepared in accordance with International Financial Reporting Standards (‘IFRSs’) as endorsed by the EU and effective for HSBC’s reporting for the year ended 31 December 2005. There is no difference between IFRSs currently in effect and EU-endorsed IFRSs as they apply to the Group. This is the first time HSBC’s annual financial statements have been prepared under IFRSs. Moving to IFRSs has necessarily involved the application of a number of available transition exemptions which means that prior year figures are not fully comparable with those presented in respect of 2005. Details of HSBC’s transition to IFRSs are set out on page 332. HSBC previously reported under United Kingdom Generally Accepted Accounting Principles (‘UK GAAP’).

In July 2005, HSBC published2004 IFRS Comparative Financial Information, summarising the principal effects of IFRSs on the financial information previously reported in respect of 2004 and including a reconciliation between data previously reported in respect of 2004 under UK GAAP and under IFRSs. HSBC’s opening balance sheet at 1 January 2005 differs from the closing balance sheet at 31 December 2004 as the former reflects first-time adoption of International Accounting Standard 32 ‘Financial Instruments: Presentation’ (‘IAS 32’), IAS 39 ‘Financial Instruments: Recognition and Measurement’ (‘IAS 39’) and IFRS 4 ‘Insurance Contracts’ (‘IFRS 4’).

Certain information for years prior to 2004 has been prepared under UK GAAP, which is not comparable with IFRSs.

HSBC uses the US dollar as its presentation currency because the US dollar and currencies linked to it form the major currency bloc in which HSBC transacts its business. Unless otherwise stated, the accounting information presented in this document has been prepared in accordance with IFRSs.

| | 2005 | | 2004 | |

| | US$m | | US$m | |

| For the year | | | | |

| Total operating income | 61,704 | | 55,988 | |

| Profit before tax | 20,966 | | 18,943 | |

| Profit attributable to shareholders of the parent company | 15,081 | | 12,918 | |

| Dividends | 7,750 | | 6,932 | |

| | | | | |

| At the year-end | | | | |

| Total equity | 98,226 | | 99,197 | |

| Total shareholders’ equity | 92,432 | | 85,522 | |

| Capital resources | 105,449 | | 90,780 | |

| Customer accounts and deposits by banks | 809,146 | | 777,127 | |

| Total assets | 1,501,970 | | 1,279,974 | |

| Risk-weighted assets | 827,164 | | 759,210 | |

| | | | | |

| | US$ | | US$ | |

| Per ordinary share | | | | |

| Basic earnings | 1.36 | | 1.18 | |

| Diluted earnings | 1.35 | | 1.17 | |

| Dividends | 0.69 | | 0.63 | |

| Net asset value at the year-end | 8.16 | | 7.66 | |

| | At | | At | |

| | 31 December | | 31 December | |

| | 2005 | | 2004 | |

| Share information | | | | |

| US$0.50 ordinary shares in issue (million) | 11,334 | | 11,172 | |

| Market capitalisation (billion) | US$182 | | US$190 | |

| Closing market price per ordinary share: | | | | |

| – London | £9.33 | | £8.79 | |

| – Hong Kong | HK$124.50 | | HK$133.00 | |

| Closing market price per American Depositary Share (‘ADS’)1 | US$80.47 | | US$85.14 | |

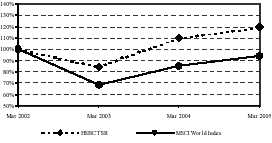

| | Over 1 year | | Over 3 years | | Over 5 years | |

| HSBC total shareholder return (‘TSR’) to 31 December 20052 | 111.3 | | 158.8 | | 121.2 | |

| Benchmarks: | | | | | | |

| – FTSE 1003 | 120.8 | | 158.4 | | 105.9 | |

| – MSCI World4 | 123.1 | | 159.1 | | 99.1 | |

For footnotes, see page 4.

1

Back to Contents

| H S B C H O L D I N G S P L C |

| |

| |

| Financial Highlights (continued) |

| | |

| | |

Capital and performance ratios

| | 2005 | | 2004 | |

| | % | | % | |

| Capital ratios | | | | |

| Tier 1 capital | 9.0 | | 8.9 | |

| Total capital | 12.8 | | 12.0 | |

| | | | | |

| Performance ratios | | | | |

| Return on average invested capital5 | 15.9 | | 15.0 | |

| Return on average total shareholders’ equity6 | 16.8 | | 16.3 | |

| Post-tax return on average total assets | 1.06 | | 1.14 | |

| Post-tax return on average risk-weighted assets | 2.01 | | 2.13 | |

| | | | | |

| Credit coverage ratios | | | | |

| Loan impairment charges as a percentage of total operating income | 12.74 | | 11.06 | |

| Loan impairment charges as a percentage of average gross customer advances | 1.16 | | 1.04 | |

| Total outstanding allowances against loan impairment as a percentage of non-performing loans at the year end | 99.1 | | 100.9 | |

| | | | | |

| Efficiency and revenue mix ratios | | | | |

| Cost efficiency ratio7 | 51.2 | | 51.6 | |

| – constant currency basis | 51.2 | | 52.4 | |

| As a percentage of total operating income: | | | | |

| – net interest income | 50.8 | | 55.5 | |

| – net fee income | 23.4 | | 23.1 | |

| – trading income | 9.5 | | 5.0 | |

Constant currency

Constant currency comparatives in respect of 2004 used in the 2005 commentaries are computed by retranslating into US dollars:

| • | the income statements for 2004 of non-US dollar branches, subsidiaries, joint ventures and associates at the average rates of exchange for 2005; and |

| | |

| • | the balance sheets at 31 December 2004 for non-US dollar branches, subsidiaries, joint ventures and associates at the prevailing rates of exchange on 31 December 2005. |

| | |

No adjustment is made to the exchange rates used to translate foreign currency denominated assets and liabilities into the functional currency of any HSBC branch, subsidiary, joint venture or associate.

| | 2005 compared with 2004 | |

| |

| |

| | As | | Constant | |

| reported | currency on |

| | an underlying |

| | basis |

| % | % |

| Operating income and cost growth | | | | |

| Total operating income | 10 | | 10 | |

| Net operating income before loan impairment charges and other credit risk provisions | 12 | | 12 | |

| Total operating expenses | 11 | | 9 | |

For details of the underlying constant currency basis, see ‘Comparison of financial information’ on page4.

For footnotes, see page 4.

2

Back to Contents

Five-year comparison

| 2005 | | 2004 | | | 2003 | | 2002 | | 2001 | |

| US$m | | US$m | | | US$m | | US$m | | US$m | |

| | | | | For the year | | | | | | |

| 31,334 | | 31,099 | | Net interest income | 25,598 | | 15,460 | | 14,725 | |

| 30,370 | | 24,889 | | Other operating income | 15,474 | | 11,135 | | 11,163 | |

| (7,801 | ) | (6,191 | ) | Loan impairment charges and other credit risk provisions | – | | – | | – | |

| – | | – | | Provisions for bad and doubtful debts | (6,093 | ) | (1,321 | ) | (2,037 | ) |

| (29,514 | ) | (26,487 | ) | Total operating expenses | (22,532 | ) | (15,808 | ) | (15,404 | ) |

| 20,966 | | 18,943 | | Profit before tax | 12,816 | | 9,650 | | 8,000 | |

| 15,081 | | 12,918 | | Profit attributable to shareholders of the parent company | 8,774 | | 6,239 | | 4,992 | |

| 7,750 | | 6,932 | | Dividends | 6,532 | | 5,001 | | 4,467 | |

| | | | | | | | | | | |

| | | | | At the year-end | | | | | | |

| 5,667 | | 5,587 | | Called up share capital | 5,481 | | 4,741 | | 4,678 | |

| 92,432 | | 85,522 | | Total shareholders’ equity | – | | – | | – | |

| – | | – | | Shareholders’ funds | 74,473 | | 51,765 | | 45,688 | |

| 105,449 | | 90,780 | | Capital resources10 | 74,042 | | 57,430 | | 50,854 | |

| 739,419 | | 693,072 | | Customer accounts | 573,130 | | 495,438 | | 449,991 | |

| 3,474 | | 3,686 | | Undated subordinated loan capital | 3,617 | | 3,540 | | 3,479 | |

| 35,856 | | 32,914 | | Dated subordinated loan capital | 17,580 | | 14,831 | | 12,001 | |

| 740,002 | | 672,891 | | Loans and advances to customers11,12 | 528,977 | | 352,344 | | 308,649 | |

| 1,501,970 | | 1,279,974 | | Total assets | 1,034,216 | | 758,605 | | 695,545 | |

| | | | | | | | | | | |

| US$ | | US$ | | | US$ | | US$ | | US$ | |

| | | | | Per ordinary share | | | | | | |

| 1.36 | | 1.18 | | Basic earnings | 0.84 | | 0.67 | | 0.54 | |

| 1.35 | | 1.17 | | Diluted earnings | 0.83 | | 0.66 | | 0.53 | |

| 0.69 | | 0.63 | | Dividends | 0.60 | | 0.53 | | 0.48 | |

| 8.16 | | 7.66 | | Net asset value at year-end | 6.79 | | 5.46 | | 4.88 | |

| | | | | | | | | | | |

| | | | | Share information | | | | | | |

| 11,334 | | 11,172 | | US$0.50 ordinary shares in issue (millions) | 10,960 | | 9,481 | | 9,355 | | |

| | | | | | | | | | | |

| % | | % | | | % | | % | | % | |

| | | | | Financial ratios | | | | | | |

| 50.7 | | 53.4 | | Dividend payout ratio13 | 60.6 | | 69.7 | | 76.2 | |

| 1.06 | | 1.14 | | Post-tax return on average total assets | 1.01 | | 0.97 | | 0.86 | |

| 16.8 | | 16.3 | | Return on average total shareholders’ equity | – | | – | | – | |

| – | | – | | Return on average shareholders’ funds | 13.0 | | 12.4 | | 10.6 | |

| 5.96 | | 6.35 | | Average total shareholders’ equity to average total assets | – | | – | | – | |

| – | | – | | Average shareholders’ funds to average total assets | 7.06 | | 6.91 | | 6.87 | |

| | | | | | | | | | | |

| | | | | Capital ratios | | | | | | |

| 9.0 | | 8.9 | | Tier 1 capital | 8.9 | | 9.0 | | 9.0 | |

| 12.8 | | 12.0 | | Total capital | 12.0 | | 13.3 | | 13.0 | |

| | | | | | | | | | | |

| | | | | Foreign exchange translation rates toUS$ | | | | | | |

| 0.581 | | 0.517 | | Closing – £:US$1 | 0.560 | | 0.620 | | 0.690 | |

| 0.847 | | 0.733 | | – €:US$1 | 0.793 | | 0.953 | | 1.130 | |

| 0.550 | | 0.546 | | Average – £:US$1 | 0.612 | | 0.666 | | 0.695 | |

| 0.805 | | 0.805 | | – €:US$1 | 0.885 | | 1.061 | | 1.117 | |

For footnotes, see page 4.

3

Back to Contents

| H S B C H O L D I N G S P L C |

| |

| |

| Financial Highlights (continued) |

| | |

| | |

Five-year comparison(continued)

Amounts in accordance with US GAAP

| | 2005 | | 2004 | | 2003 | | 2002 | | 2001 | |

| | US$m | | US$m | | US$m | | US$m | | US$m | |

| Income statement for the year | | | | | | | | | | |

| Net income available for ordinary shareholders | 14,703 | | 12,506 | | 7,231 | | 4,900 | | 4,911 | |

| Other comprehensive income | (7,271 | ) | 983 | | 7,401 | | 5,502 | | (1,439 | ) |

| Dividends | 7,750 | | 6,932 | | 6,974 | | 4,632 | | 4,394 | |

| | | | | | | | | | | |

| Balance sheet at 31 December | | | | | | | | | | |

| Total assets | 1,406,944 | | 1,266,365 | | 1,012,023 | | 763,565 | | 698,312 | |

| Shareholders’ funds | 93,524 | | 90,082 | | 80,251 | | 55,831 | | 48,444 | |

| | | | | | | | | | | |

| | US$ | | US$ | | US$ | | US$ | | US$ | |

| Per ordinary share | | | | | | | | | | |

| Basic earnings | 1.33 | | 1.15 | | 0.69 | | 0.52 | | 0.53 | |

| Diluted earnings | 1.32 | | 1.13 | | 0.69 | | 0.52 | | 0.53 | |

| Dividends | 0.69 | | 0.63 | | 0.685 | | 0.495 | | 0.48 | |

| Net asset value at year end | 8.25 | | 8.06 | | 7.32 | | 5.89 | | 5.18 | |

Comparison of financial information

When reference to ‘constant currency’ or ‘constant exchange rates’ is made, comparative data reported in the functional currencies of HSBC’s operations have been translated at the appropriate exchange rates applied in the current period in respect of the income statement or the balance sheet. When reference to ‘underlying basis’ is made, comparative information has been expressed at constant currency and adjusted for the effect of acquisitions and the change in presentation of non-equity minority issues.

As the transition to IFRSs affects the comparability of the financial information presented in this document (see Note 1 on the Financial Statements), the commentary that follows specifies the impact when this is material to a reader’s understanding of the underlying business trends.

Footnotes to ‘Financial Highlights’

| | |

| 1 | Each ADS represents five ordinary shares. |

| 2 | Total shareholder return (‘TSR’) is defined on page 220. |

| 3 | The Financial Times-Stock Exchange 100 Index. |

| 4 | The Morgan Stanley Capital International World Index. |

| 5 | The definition of return on average invested capital and a reconciliation to the equivalent GAAP measures are set out on page 43. |

| 6 | The return on average total shareholders’ equity is defined as profit attributable to shareholders of the parent company divided by average total shareholders’ equity. |

| 7 | The cost efficiency ratio is defined as total operating expenses divided by net operating income before loan impairment charges and other credit risk provisions. |

| 8 | Comparative data for 2004 excludes the provisions of IAS 32, IAS 39 and IFRS 4, which were adopted for the first time with effect from 1 January 2005. |

| 9 | The periods 2001-2003 were prepared in accordance with UK GAAP. The principal adjustments necessary to conform these periods with IFRSs are described in Note 46 on the Financial Statements on page 332. HSBC’s accounting policies under UK GAAP are stated in Note 2 on the Financial Statements in the2004 Annual Report and Accounts. |

| 10 | Capital resources are defined on page 173. A detailed computation for 2005 and 2004 is provided on page 176. |

| 11 | Net of suspended interest and provisions for bad and doubtful debts (UKGAAP). |

| 12 | Net of impairment allowances against customers (IFRSs). |

| 13 | Dividends per share expressed as a percentage of earnings per share (2001 to 2003: excluding goodwill amortisation). |

4

Back to Contents

| H S B C H O L D I N G S P L C |

| |

| |

| Cautionary Statement regarding Forward-Looking Statements |

| | |

| | |

ThisAnnual Report contains certain forward-looking statements with respect to the financial condition, results of operations and business of HSBC.

Statements that are not historical facts, including statements about HSBC’s beliefs and expectations, are forward-looking statements. Words such as ‘expects’, ‘anticipates’, ‘intends’, ‘plans’, ‘believes’, ‘seeks’, ‘estimates’, ‘potential’ and ‘reasonably possible’, variations of these words and similar expressions are intended to identify forward-looking statements. These statements are based on current plans, estimates and projections, and therefore undue reliance should not be placed on them. Forward-looking statements speak only as of the date they are made, and it should not be assumed that they have been revised or updated in the light of new information or future events.

Written and/or oral forward-looking statements may also be made in the periodic reports to the United States Securities and Exchange Commission, summary financial statements to shareholders, proxy statements, offering circulars and prospectuses, press releases and other written materials, and in oral statements made by HSBC’s Directors, officers or employees to third parties, including financial analysts.

Forward-looking statements involve inherent risks and uncertainties. Readers are cautioned that a number of factors could cause actual results to differ, in some instances materially, from those anticipated or implied in any forward-looking statement. These factors include, among others:

| • | changes in general economic conditions in the markets in which HSBC operates, such as: |

| | | |

| | – | changes in foreign exchange rates, in both market exchange rates (for example, between the US dollar and the pound sterling) and government-established exchange rates (for example, between the Hong Kong dollar and the US dollar); |

| | | |

| | – | volatility in interest rates; |

| | | |

| | – | volatility in equity markets, including in the smaller and less liquid trading markets in Asia and South America; |

| | | |

| | – | lack of liquidity in wholesale funding markets in periods of economic or political crisis; |

| | | |

| | – | illiquidity and downward price pressure in national real estate markets, particularly consumer-owned real estate markets; |

| | | – | the impact of lower than expected investment returns on the burden of funding private and public sector defined benefit pensions; |

| |

| | | – | the effect of unexpected changes in actuarial assumptions on longevity which would influence the funding of private and public sector defined benefit pensions; |

| |

| | | – | continuing or deepening recessions and employment fluctuations; and |

| |

| | | – | consumer perception as to the continuing availability of credit, and price competition in the market segments served by HSBC. |

| |

| | • | changes in governmental policy and regulation, including: |

| | | | |

| | | – | the monetary, interest rate and other policies of central banks and bank and other regulatory authorities, including the United Kingdom Financial Services Authority, the Bank of England, the Hong Kong Monetary Authority, the United States Federal Reserve, the US Office of the Comptroller of the Currency, the European Central Bank, the People’s Bank of China and the central banks of other leading economies and markets where HSBC operates; |

| |

| | | – | expropriation, nationalisation, confiscation of assets and changes in legislation relating to foreign ownership; |

| |

| | | – | initiatives by local, state and national regulatory agencies or legislative bodies to revise the practices, pricing or responsibilities of financial institutions serving their consumer markets; |

| |

| | | – | changes in bankruptcy legislation in the principal markets in which HSBC operates and the consequences thereof; |

| |

| | | – | general changes in governmental policy that may significantly influence investor decisions in particular markets in which HSBC operates; |

| |

| | | – | other unfavourable political or diplomatic developments producing social instability or legal uncertainty which in turn may affect demand for HSBC’s products and services; |

| |

| | | – | the costs, effects and outcomes of regulatory reviews, actions or litigation, including any additional compliance requirements; and |

5

Back to Contents

| H S B C H O L D I N G S P L C |

| |

| |

| Cautionary Statement regarding Forward-Looking Statements (continued) |

| | |

| | |

| | – | the effects of competition in the markets where HSBC operates including increased competition from non-bank financial services companies, including securities firms. |

| | | |

| • | factors specific to HSBC: |

| | | |

| | – | the success of HSBC in adequately identifying the risks it faces, such as the |

| | | incidence of loan losses or delinquency, and managing those risks (through account management, hedging and other techniques). Effective risk management depends on, among other things, HSBC’s ability through stress testing and other techniques to prepare for events that cannot be captured by the statistical models it uses. |

| | | |

| |

| Information about the Enforceability of Judgements made in the United States |

| | |

| | |

HSBC Holdings is a public limited company incorporated in England and Wales. Most of HSBC Holdings’ Directors and executive officers live outside the US. As a result, it may not be possible to serve process on such persons or HSBC Holdings in the US or to enforce judgements obtained in US courts against them or HSBC Holdings based on civil liability provisions of the securities laws of the US. There is doubt as to whether English courts would enforce:

| • | certain civil liabilities under US securities laws in original actions; or |

| | |

| • | judgements of US courts based upon these civil liability provisions. |

In addition, awards of punitive damages in actions brought in the US or elsewhere may be unenforceable in the UK. The enforceability of any judgement in the UK will depend on the particular facts of the case as well as the laws and treaties in effect at the time

| |

| Exchange Controls and Other Limitations affecting Equity Security Holders |

| | |

| | |

There are currently no UK laws, decrees or regulations which would prevent the import or export of capital or remittance of distributable profits by way of dividends and other payments to holders of HSBC Holdings’ equity securities who are not residents of the UK. There are also no

restrictions under the laws of the UK or the terms of the Memorandum and Articles of Association of HSBC Holdings concerning the right of non-resident or foreign owners to hold HSBC Holdings’ equity securities or, when entitled to vote, to do so.

6

Back to Contents

H S B C H O L D I N G S P L C

Description of Business

HSBC is one of the largest banking and financial services organisations in the world, with a market capitalisation of US$182 billion at 31 December 2005.

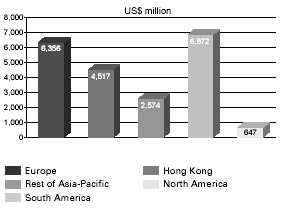

Headquartered in London, HSBC operates through long-established businesses and has an international network of over 9,800 properties in 76 countries and territories in five geographical regions: Europe; Hong Kong; Rest of Asia-Pacific, including the Middle East and Africa; North America and South America. Within these regions, a comprehensive range of financial services is offered to personal, commercial, corporate, institutional, investment and private banking clients. Services are delivered primarily by domestic banks, typically with large retail deposit bases, and consumer finance operations.

HSBC manages its business through four customer groups: Personal Financial Services; Commercial Banking; Corporate, Investment Banking and Markets; and Private Banking. Personal Financial Services incorporates the Group’s consumer finance businesses, reflecting their increasing integration within mainstream financial services around the world. The largest of these is HSBC Finance Corporation, one of the leading consumer finance companies in the US.

The establishment in 1999 of HSBC as a uniform, international brand name ensured that the Group’s hexagon corporate symbol has become an increasingly familiar sight across the world.

The founding member of HSBC, The Hongkong and Shanghai Banking Corporation Limited (‘The Hongkong and Shanghai Banking Corporation’), was established in both Hong Kong and Shanghai in 1865. The bank expanded rapidly, with an emphasis on building up representation in mainland China and throughout the rest of Asia, while also establishing a presence in the major financial and trading centres in Europe and America.

In the mid-1950s, The Hongkong and Shanghai Banking Corporation embarked on a strategy of pursuing profitable growth through acquisition as well as organic development – a combination that has remained a key feature of HSBC’s approach ever since.

With each acquisition, HSBC focused on integrating its newly acquired operations with its existing businesses with the aim of maximising the

synergy between the various components. Key to this integration process is the blending of local and international expertise.

The most significant developments are described below. Other acquisitions in 2005 are discussed in the ‘Financial Review’ on pages 26 to 177.

The Hongkong and Shanghai BankingCorporation purchased The Mercantile Bank of India Limited and The British Bank of the Middle East, now HSBC Bank Middle East Limited (‘HSBC Bank Middle East’) in 1959. In 1965, it acquired a 51 per cent interest (subsequently increased to 62.14 per cent) in Hang Seng Bank Limited (‘Hang Seng Bank’), consolidating its leadership position in Hong Kong. Hang Seng Bank is the third-largest listed bank in Hong Kong by market capitalisation.

The Hongkong and Shanghai Banking Corporation entered the US market in 1980 by acquiring a 51 per cent interest in Marine Midland Banks, Inc., now HSBC USA, Inc. The remaining interest was acquired in 1987.

In 1981, The Hongkong and Shanghai Banking Corporation incorporated its then existing Canadian operations. HSBC Bank Canada has since made numerous acquisitions, expanding rapidly to become the largest foreign-owned bank in Canada and the seventh-largest overall at 31 December 2005.

From the early 1980s, The Hongkong and Shanghai Banking Corporation began to focus its acquisition strategy on the UK. In 1987, it purchased a 14.9 per cent interest in Midland Bank plc, now HSBC Bank plc (‘HSBC Bank’), one of the UK’s principal clearing banks. In 1991, HSBC Holdings plc was established as the parent company of the HSBC Group and, in 1992, it purchased the remaining interest in HSBC Bank. As a consequence of this acquisition, HSBC’s head office was transferred from Hong Kong to London in January 1993.

In 1997, HSBC assumed selected assets, liabilities and subsidiaries of Banco Bamerindus do Brasil S.A., now HSBC Bank Brasil S.A.-Banco Múltiplo (‘HSBC Bank Brazil’), following the intervention of the Central Bank of Brazil, and in Argentina completed the acquisition of Grupo Roberts, now part of HSBC Bank Argentina S.A. (‘HSBC Bank Argentina’).

In December 1999, HSBC acquired Republic New York Corporation, subsequently merged with HSBC USA, Inc., and Safra Republic Holdings S.A. In July 2004, HSBC Bank USA, Inc. merged with

7

Back to Contents

H S B C H O L D I N G S P L C

Description of Business(continued)

HSBC Bank & Trust (Delaware) N.A. to form HSBC Bank USA, N.A. (‘HSBC Bank USA’).

To expand its base in the euro zone, in 2000 HSBC completed its acquisition of 99.99 per cent of the issued share capital of Crédit Commercial de France S.A., subsequently CCF S.A. (‘CCF’) and now HSBC France, a major French banking group.

In 2002, HSBC took further steps in expanding its presence in the Americas, completing the acquisition of 99.59 per cent of Grupo Financiero Bital, S.A. de C.V., the holding company of what is now HSBC México, S.A. (‘HSBC Mexico’), the fourth-largest banking group in Mexico measured by assets and the third by customer deposits.

Mainland China remains a key long-term growth area for the Group. In 2002, HSBC completed the acquisition of a 10 per cent equity stake in Ping An Insurance Company of China Limited (‘Ping An Insurance’), reducing its holding to 9.99 per cent following an initial public offering (‘IPO’) in 2004. In August 2005, HSBC acquired a further 9.91 per cent of Ping An Insurance at a cost of US$1,039 million, increasing its investment to 19.9 per cent. Ping An Insurance is the second-largest life insurer and the third-largest property and casualty insurer in mainland China.

In 2003, HSBC acquired HouseholdInternational, Inc., now HSBC Finance Corporation (‘HSBC Finance’). HSBC Finance brought to the Group national coverage in the US for consumer lending, credit cards and credit insurance through multiple distribution channels, as well as expertise in consumer finance for HSBC to roll out internationally.

Also in 2003, HSBC expanded in Brazil, acquiring Banco Lloyds TSB S.A.-Banco Múltiplo and the country’s leading consumer finance company, Losango Promotora de Vendas Limitada (‘Losango’).

In 2004, the acquisition of The Bank of Bermuda Limited (‘Bank of Bermuda’) was completed.

In the same year, HSBC acquired Marks and Spencer Retail Financial Services Holdings Limited, which trades as Marks and Spencer Money (‘M&S Money’) in the UK.

In mainland China in 2004, HSBC acquired 19.9 per cent of Bank of Communications Limited (‘Bank of Communications’), mainland China’s fifth largest bank by total assets. In the same year, Hang Seng Bank acquired 15.98 per cent of Industrial Bank Co.

Limited (‘Industrial Bank’), one of only 13 national joint-stock banks.

In December 2005, HSBC Finance completed the acquisition of Metris Companies Inc. (‘Metris’) for US$1.6 billion. HSBC is now the 5th largest issuer of MasterCard® and Visa® cards1 in the US.

In the near term, the outlook is encouraging. The world economy continues to grow steadily. The US economy is strong, the UK resilient, Japan and Germany are recovering and the emerging markets are buoyant.

Longer term prospects are more uncertain. Apart from the possibility, albeit remote, of a sudden shock to the world’s financial system, HSBC remains concerned about the unprecedented level of trade imbalances. Similarly, the implications of demographic change and of ageing populations for financial markets and businesses will be profound. It is inevitable that at some stage a process of adjustment will begin, but the timing is open to question. So far, the financial markets are taking a benign view of these potential sources of instability.

Progressively, globalisation is forcing countries and businesses operating within them to re-evaluate their comparative advantages and to adjust to a world in which emerging markets compete not only in terms of cost but also in skills and technology. The globalisation of the services industry, spurred on by new technologies and the rapid fall in communication costs, will afford huge opportunities but also pose significant challenges to many areas of economic activity, including financial services. Incipient protectionism, resulting from a reluctance to face up to the new competitive realities, remains a threat to the continuing growth of the world economy.

In certain mature markets, under-funded pension schemes threaten to become a drain on companies’ resources. Combined with the rising cost of long-term health care, they pose a considerable challenge to policy makers. Continuing productivity growth is, therefore, increasingly important. Only if it is achieved will financial markets be able to offer returns with a meaningful premium to the risk-free rate embodied in government debt. Without such productivity gains and associated financial returns, the affordability of pension and health care promises

| 1 | Visa is a registered trademark of VISA USA, Inc.and MasterCard is a registered trademark of MasterCard International, Incorporated. |

8

Back to Contents

will become increasingly burdensome. The challenge to society of managing the equitable distribution of wealth created between competing generations may well become one of the most pressing of the next decade.

In this environment HSBC, with its unique international footprint, is determined to continue to deliver profitable growth and value to its various constituencies. Success ensures that the Group can offer good employment prospects to an ever more diverse workforce. It means that HSBC can afford to continue to invest in expanding the platforms by which it delivers services to its customers. It enables the Group to contribute to the savings and retirement needs of those who invest in HSBC directly, or indirectly through pension plans and investment funds.

Building on its achievements, HSBC’s priority for the rest of 2006 is to continue to implement its Managing for Growth strategy. It will achieve this by being distinctive, reinforcing its brand values of trust and integrity in all its dealings with customers. The Group will make itself even more relevant by broadening the product, channel and geographical coverage it offers. Furthermore, HSBC will ensure that the scale and complexity needed to compete successfully will be seamless from the perspective of its customers and manageable from that of its employees.

HSBC’s businesses in Asia, Turkey, Mexico, Brazil and the Middle East see strong opportunities for growth on the back of investments already made. The Group also sees opportunities to strengthen its position in its franchises in the UK, Hong Kong, North America and France. HSBC believes there is growing momentum from the development of its new business streams within Corporate, Investment Banking and Markets businesses. Overall, HSBC is well positioned for further growth.

At the end of 2003, HSBC launched ‘Managing for Growth’, a strategic plan that provides HSBC with a blueprint for growth and development during the period to 2008. The strategy is evolutionary, not revolutionary. It builds on HSBC’s strengths and it addresses the areas where further improvement is considered both desirable and attainable.

Management’s vision for the Group remains consistent: HSBC aims to be the world’s leading financial services company. In this context, ‘leading’ means preferred, admired and dynamic, and being recognised for giving the customer a fair deal. HSBC

will strive to secure and maintain a leading position within each of its customer groups in selected markets.

HSBC will concentrate on growing earnings over the long term at a rate which will place it favourably when compared with its peer group. It will also focus on investing in its delivery platforms, its technology, its people and its brand to support the future value of HSBC as reflected in its comparative stock market rating and TSR. HSBC remains committed to benchmarking its performance both absolutely and by comparison with a peer group. For full details of the peer group benchmark, see page 220.

HSBC’s core values are integral to its strategy, and communicating them to customers, shareholders and employees is intrinsic to the plan. These values comprise an emphasis on long-term, ethical client relationships; high productivity through teamwork; a confident and ambitious sense of excellence; being international in outlook and character; prudence; creativity and customer-focused marketing.

The plan also reaffirms HSBC’s recognition of its corporate social responsibility (‘CSR’). HSBC has always aspired to the highest standards of conduct, recognises its wider obligations to society and believes there is a strong link between CSR, long-term success and value creation. Moreover, changing public expectations across a wide spectrum of social, ethical and environmental issues require continuing attention to this area. The strategy therefore calls for a renewed emphasis on CSR and for increased external communication of the Group’s CSR policies and performance, particularly on education and the environment, which will remain the principal beneficiaries of HSBC’s philanthropic activities.

HSBC’s growth ambitions centre on its four customer groups: Personal Financial Services; Commercial Banking; Corporate, Investment Banking and Markets; and Private Banking; and specific strategies are being implemented for each of them. HSBC believes that by organising its internal and external reporting around customer groups, it reinforces to all its employees the Group’s customer focus.

Within Personal Financial Services, the increasing integration, skills sharing and transfer of technology with the consumer finance business has augmented and enhanced existing activities. In addition, the introduction of skills and practices from the world’s leading retailing businesses is shaping HSBC’s competitive positioning.

9

Back to Contents

H S B C H O L D I N G S P L C

Description of Business(continued)

Key elements in achieving HSBC’s objectives for its customer groups will be accelerating the rate of growth of revenue; developing the brand strategy further; improving productivity; and maintaining the Group’s prudent risk management and strong financial position. Developing the skills of HSBC’s staff will also be critical and it will be necessary to ensure that all employees understand how they can contribute to the successful achievement of the Group’s objectives. Employees who do make such a contribution will be rewarded accordingly.

Operational management will continue to be organised geographically under four regional intermediate head offices, with business activities concentrated in locations where growth and critical mass are to be found.

| | The plan contains eight strategic imperatives: |

| | |

| • | Brand: make HSBC and its hexagon symbol one of the world’s leading brands for customer experience and corporate social responsibility; |

| | |

| • | Personal Financial Services: drive growth in key markets and through appropriate channels to make HSBC the strongest global player in personal financial services; |

| | |

| • | Consumer Finance: extend the reach of this business to existing customers through a wider product range and penetrate new markets; |

| | |

| • | Commercial Banking: make the most of HSBC’s international customer base through effective relationship management and improved product offerings in all the Group’s markets; |

| | |

| • | Corporate, Investment Banking and Markets: accelerate growth by enhancing capital markets and advisory capabilities focused on client service in defined sectors where HSBC has critical relevance and strength; |

| | |

| • | Private Banking: serve the Group’s highest value personal clients around the world; |

| | |

| • | People: attract, develop and motivate HSBC’s people, rewarding success and rejecting mediocrity; and |

| | |

| • | TSR: fulfil HSBC’s TSR target by achieving strong competitive performances in earnings per share growth and efficiency. |

At 31 December 2005, HSBC’s customers were served by 284,000 employees (including part-time employees) worldwide, compared with 253,000 at 31 December 2004 and 232,000 at 31 December 2003. The main centres of employment are the UK

with 55,000 employees, the US 49,000, Brazil 28,000, Hong Kong 26,000, Mexico 22,000, India 20,000 and France 14,000. HSBC negotiates with recognised unions, and estimates that approximately 40 per cent of its employees are unionised. The highest concentrations of union membership are in Brazil, France, India, Malaysia, Malta, Mexico, the Philippines, Singapore and the UK. As a result of well-developed communications and consultation programmes, HSBC has not experienced any material disruptions to its operations from labour disputes during the past five years.

In support of its strategy, HSBC focuses on attracting, developing and motivating the very best individuals and on encouraging talent internally. Emphasis is placed on performance management; differentiated rewards; succession planning; diversity; and learning and development, with priority accorded to enhancing sales and relationship management skills. HSBC continues to endeavour to ensure that employees’ engagement with the business is maximised as this is beneficial to shareholders, colleagues and customers alike.

HSBC recruits from a broad cross-section of society and encourages the sharing of individual perspectives and ideas through collective training and global secondments. HSBC’s diverse workforce represents a significant competitive advantage. The broad cultural mix and increasing cross-border mobility of its employees enables HSBC to resource operations with individuals who have detailed knowledge of local markets and of HSBC globally. This strengthens international networks and facilitates the sharing of best practices. In addition, a continuing focus on policies that encourage an inclusive working environment and the availability of career opportunities for all is critical to HSBC being an employer of choice. HSBC seeks to maintain an employee profile that reflects its customer base.

HSBC operates in a highly competitive and international business environment. Through its network of international operations, it has the advantage of being able to respond to the availability of talented employees wherever they are, in order to enhance customer service and improve productivity. As education levels improve globally and as investments in technology and telecommunications facilitate access at competitive cost to hitherto untapped resources, the balance of employment continues to change, resulting in global resource centres of excellence. Job losses may arise in some countries, but HSBC has a good record of communicating openly and sensitively in these circumstances, and of reassigning employees and

10

Back to Contents

minimising compulsory redundancies wherever possible.

HSBC seeks to promote and recruit the most able people and attaches great importance to cultivating its own talent. Resources have been set aside to ensure a supply of talented individuals to meet business succession needs, with support provided for these employees in the form of career enhancement and personal development programmes. In addition, HSBC recognises that there are lessons to be learned from other successful businesses, and will recruit from non-banking industries where appropriate.

| Customer groups |

|

| Profit before tax by customer group |

| |

| Year ended 31 December 2005 |

Total assets1 by customer group

As at 31 December 2005

| 1 | Excluding Hong Kong Government certificates of indebtedness. |

Personal Financial Services

Personal Financial Services provides some 120 million individual and self-employed customers with a wide range of banking and related financial services. The precise nature of the products and services provided is, to some extent, driven by local regulations, market practices and the market positioning of HSBC’s local businesses. Typically, products provided include

current and savings accounts, mortgages and personal loans, credit cards, and local and international payments services.

Personal customers prefer to conduct their financial business at times convenient to them, using a range of delivery channels. This demand for flexibility is met through the increased provision of direct channels such as the internet and self-service terminals, in addition to traditional and automated branches and service centres accessed by telephone.

Delivering the right products and services for particular target markets is a fundamental requirement in any retail service business, and market research and customer analysis is key to developing an in-depth understanding of significant customer segments and their needs. This understanding of the customer ensures that Customer Relationship Management (‘CRM’) systems are effectively used to identify and fulfil sales opportunities, and to manage the sales process.

HSBCPremieris a premium banking service providing personalised relationship management, 24-hour priority telephone access, global travel assistance and cheque encashment facilities. There are now over 1.3 million HSBCPremier customers, who can use more than 250 specially designatedPremierbranches and centres in 35 countries and territories, either when visiting, or on a more permanent basis if they require a banking relationship in more than one country.

Insurance and investment products play an important part in meeting the needs of customers. Insurance products sold and distributed by HSBC through its direct channels and branch networks include loan protection, life, property and health insurance, and pensions. Acting as both broker and underwriter, HSBC sees continuing opportunities to deliver insurance products to its personal customer base.

HSBC also makes available a wide range of investment products. A choice of third party and proprietary funds is offered, including traditional ‘long only’ equity and bond funds; structured funds that provide capital security and opportunities for an enhanced return; and ‘fund of funds’ products which offer customers the ability to diversify their investments across a range of best-in-class fund managers chosen after a rigorous and objective selection process. Comprehensive financial planning services covering customers’ investment, retirement, personal and asset protection needs are offered through specialist financial planning managers.

11

Back to Contents

H S B C H O L D I N G S P L CDescription of Business(continued)

High net worth individuals and their families who choose the differentiated services offered within Private Banking are not included in this customer group.

Consumer FinanceWithin Personal Financial Services, HSBC Finance’s operations in the US, the UK and Canada make credit available to customer groups not well catered for by traditional banking operations, facilitate point-of-sale credit in support of retail purchases and support major affiliate credit card programmes. At 31 December 2005 HSBC Finance had over 60 million customers with total gross advances of US$142.1 billion. Consumer Finance products are offered through the following businesses of HSBC Finance:

Theconsumer lendingbusiness is one of the largest sub-prime home equity originators in the US, marketed under the HFC and Beneficial brand names through a network of nearly 1,400 branches in 45 states, direct mail, telemarketing, strategic alliances and the internet. Consumer lending also acquires sub-prime loans on the secondary market. ‘Sub-prime’ is a category used in the US which describes customers who have limited credit histories, modest incomes, high debt-to-income ratios, high loan-to-value ratios (for real estate secured products) or have experienced credit problems caused by occasional delinquencies, prior charge-offs, bankruptcy or other credit-related actions. Consumer lending products include secured and unsecured loans such as first and second lien closed-end mortgages, open-ended home equity loans, personal loans, loans secured on motor vehicles and retail finance contracts. Consumer lending also offers a near-prime mortgage product which was first introduced in 2003 to broaden the range of customers to which its products are relevant.

The mortgage servicesbusiness purchases first and second lien residential mortgage loans, including open-end home equity loans, from a network of over 280 unaffiliated third-party lenders in the US. Purchases are primarily of pools of loans (‘bulk acquisitions’), but also include individual loan portfolios (‘flow acquisitions’), made under predetermined underwriting guidelines. Forward commitments are offered to selected correspondents to strengthen relationships and create a sustainable growth channel for this business. HSBC Finance, through its subsidiary, Decision One Mortgage Company (‘Decision One’), also originates mortgage loans referred by mortgage brokers.

Theretail servicesbusiness is one of the

largest providers of third party private label credit cards (or store cards) in the US based on receivables outstanding, with over 70 merchant relationships and 15.8 million active customer accounts.

In addition to originating and refinancing motor vehicle loans, HSBC Finance’smotor vehicle financebusiness purchases retail instalment contracts of US customers who do not have access to traditional prime-based lending sources. The loans are largely sourced from a network of approximately 10,000 motor dealers.

Thecredit card services business is the fifth largest issuer of MasterCard® and Visa®credit cards in the US, and also includes affiliation programmes such as the GM Card® and the AFL-CIO Union Plus® credit card. Also, credit cards issued in the name of Household Bank, Orchard Bank and Direct Merchants Bank brands are offered to customers under-served by traditional providers, or are marketed primarily through merchant relationships established by the retail services business.

A wide range ofinsurance services is offered by HSBC Finance to customers in the US, the UK and Canada who are typically not well-served by traditional sources.

Thetaxpayer financial services business accelerates access to funds for US taxpayers who are entitled to tax refunds and offers financial services through more than 25,000 tax return preparers in the US. The business is seasonal with most revenues generated in the first three months of the year.

HSBC Finance’s business in the UK (‘HFC Bank’) provides mid-market consumers with mortgages, secured and unsecured loans, insurance products, credit cards and retail finance products. It concentrates on customer service through its 187 HFC Bank and Beneficial branches, and finances consumer electronic goods through its retail finance operations. Its credit card business was sold to HSBC Bank in December 2005. In Canada, similar products are offered through trust operations of HSBC Finance’s subsidiary there.

Commercial BankingHSBC is one of the world’s leading, and most international, banks in the provision of financial services and products to small, medium-sized and middle market businesses, with over 2.5 million customers including sole proprietors, partnerships, clubs and associations, incorporated businesses and publicly quoted companies.

12

Back to Contents

At 31 December 2005, HSBC had total commercial customer account balances of US$148.1 billion and total commercial customer loans and advances, net of loan impairment allowances, of US$142.0 billion.

Commercial Banking places particular emphasis on multi-disciplinary and geographical collaboration in meeting its commercial customers’ needs, thereby differentiating, broadening and enhancing its offering. The range of products includes:

Payments and cash management: HSBC is a leading provider of payments, collections, liquidity management and account services worldwide, enabling commercial customers to manage their cash efficiently on a global basis. HSBC’s extensive network of offices and strong domestic capabilities in many countries, including direct access to local clearing systems, enhances its ability to provide high-quality competitive cash management services.

Treasury and capital markets: Commercial Banking customers have long been volume users of the Group’s foreign exchange capabilities. These are now being supplemented with more sophisticated currency and interest rate options.

Investment banking: A small number of Commercial Banking customers need occasional investment banking advisory support. Co-operation with Corporate, Investment Banking and Markets ensures that in most key markets such requirements are serviced internally.

Wealth management services: These include advice and products related to savings and investments. They are provided to Commercial Banking customers and their employees through HSBC’s worldwide network of branches and business banking centres.

Insurance: HSBC offers insurance protection, employee benefits programmes and pension schemes designed to meet the needs of businesses and their employees, and to help fulfil the applicable statutory obligations of client companies. These products are provided by HSBC either as an intermediary (broker, agent or consultant) or as a supplier of in-house or third party offerings. Products and services include a full range of commercial insurance, including pension schemes; healthcare schemes; ‘key man’ life insurance; car fleet; goods in transit; trade credit protection; risk management and insurance due diligence reviews; and actuarial/employee benefit consultancy.

Trade services: HSBC has more than 140 years of experience in trade services. A complete range of traditional documentary credit, collections and

financing products is offered, as well as specialised services such as insured export finance, international factoring and forfaiting. HSBC’s expertise is supported by highly automated systems.

Leasing, finance and factoring: HSBC has established specialised divisions to provide leasing and instalment finance for vehicles, plant and equipment, machinery and materials handling, and large complex leases. HSBC also provides domestic and international factoring and receivables finance services through a network of 11 businesses worldwide.

Credit cards: HSBC offers commercial credit card services in 18 countries. Commercial card issuing provides small to middle market businesses with services, including corporate and purchasing cards, which variously enhance cash management, improve cost control and streamline purchasing processes. Commercial card acquiring enables merchants to accept credit card payments either in-store or on the internet.

Corporate, Investment Banking and Markets

HSBC’s Corporate, Investment Banking and Markets business provides tailored financial solutions to major government, corporate and institutional clients worldwide. Managed as a global business, this customer group operates a long-term relationship management approach to build a full understanding of clients’ financial requirements. Sectoral client service teams comprising relationship managers and product specialists develop financial solutions to meet individual client needs. With dedicated offices in over 60 countries and with access to HSBC’s worldwide presence and capabilities, this business serves subsidiaries and offices of its clients on a global basis.

Products and services offered include:

Global MarketsHSBC’s operations in Global Markets consist of treasury and capital markets services for supranationals, central banks, corporations, institutional and private investors, financial institutions and other market participants. Products include:

| • | foreign exchange; |

| | |

| • | currency, interest rate, bond, credit, equity and other specialised derivatives; |

| | |

| • | government and non-government fixed income and money market instruments; |

| | |

| • | precious metals and exchange traded futures; |

13

Back to Contents

H S B C H O L D I N G S P L CDescription of Business(continued)

| • | equity services, including research, sales and trading for institutional, corporate and private clients and asset management services, including global investment advisory and fund management services; and |

| | |

| • | distribution of capital markets instruments, including debt, equity and structured products, utilising links with HSBC’s global networks. |

Corporate and Investment Banking

Global Investment Banking comprises:

| • | capital raising, both publicly and privately, including debt and equity capital, structured finance and syndicated finance; |

| | |

| • | corporate finance and advisory services for mergers and acquisitions, asset disposals, stock exchange listings, privatisations and capital restructurings; and |

| | |

| • | project and export finance services providing non-recourse finance to exporters, importers and financial institutions, and working closely with all major export credit agencies. |

Corporate and Institutional Banking includes:

| • | direct lending, including structured finance for complex investment facilities; |

| | |

| • | leasing finance with an emphasis on ‘large ticket’ transactions; and |

| | |

| • | deposit-taking. |

Global Transaction Banking includes international, regional and ‘in-country’ payments and cash management services; trade services, particularly the specialised ‘supply chain’ product; and securities services, where HSBC is one of the world’s leading custodians providing custody and clearing services and funds administration to both domestic and cross-border investors. Factoring and banknotes services are also provided by specialist units.

Private Equitycomprises HSBC’s captive private equity fund management activities, strategic relationships with certain third party private equity managers together with direct listed and unlisted equity investments and fund commitments.

Group Investment Businesses

These comprise asset management products and services for institutional investors, intermediaries and individual investors and their advisers.

Management structure

During February 2006, the management structure of Global Markets and Corporate and Investment Banking was restructured. Under the new structure, there are three principal business lines: Global Banking, Global Markets and Global Transaction Banking. This new structure will allow Corporate, Investment Banking and Markets to focus on the relationships and sectors that best fit the Group’s footprint and ensure seamless delivery of HSBC’s enhanced product capabilities to clients.

Private BankingHSBC’s presence in all the major wealth-creating regions has enabled it to build one of the world’s leading private banking groups, providing financial services to high net worth individuals and their families in 74 locations in 35 countries, with total assets under management of US$282 billion at 31 December 2005. HSBC Private Bank is the principal marketing name of the HSBC Group’s international private banking business which, together with HSBC Guyerzeller and HSBC Trinkaus & Burkhardt, provides private banking services.

Utilising the most suitable products from the marketplace, Private Banking works with its clients to offer both traditional and innovative ways to manage and preserve wealth whilst optimising returns. Products and services offered include:

Investment services: These comprise both advisory and discretionary investment services. A wide range of investment vehicles is covered, including bonds, equities, derivatives, options, futures, structured products and alternative products, mutual funds, hedge funds and fund of funds. Supported by six major advisory centres in Hong Kong, Singapore, Geneva, New York, Paris and London, Private Banking seeks to select the most suitable investments for clients’ needs and investment strategies.

Global wealth solutions: These comprise inheritance planning, trustee and other fiduciary services designed to protect existing wealth and create tailored structures to preserve wealth for future generations. Areas of expertise include trusts, foundation and company administration, charitable trusts and foundations, insurance and offshore structures.

Specialist advisory services: Private Banking offers expertise in several specialist areas of wealth management including tax advisory and financial planning, family office advisory, corporate finance,

14

Back to Contents

consolidated reporting, industry services such as charities and foundations, media, shipping, diamond and jewellery, and real estate planning. Specialist advisers are available to deliver products and services that are tailored to meet the full range of high net worth clients’ individual financial needs.

General banking services: These comprise treasury and foreign exchange, offshore and onshore deposits, credit and specialised lending, tailor-made loans and internet banking. Private Banking works to ensure its clients have full access to relevant skills and products available throughout HSBC, such as corporate banking, investment banking and insurance.

Profit before tax split by geographical region

Year ended 31 December 2005

Total assets1 split by geographical region

As at 31 December 2005

| 1 | Excluding Hong Kong Government certificates of indebtedness. |

Additional information regarding business developments in 2005 may be found in the ‘Financial Review’ on pages 26 to 177.

Europe

HSBC’s principal banking operations in Europe are HSBC Bank in the UK, HSBC France, HSBC Bank

A.S. in Turkey, HSBC Bank Malta, HSBC Private Bank (Suisse), HSBC Trinkaus & Burkhardt KGaA and HSBC Guyerzeller Bank AG. Through these operations HSBC provides a wide range of banking, treasury and financial services to personal, commercial and corporate customers across Europe.

Hong Kong

HSBC’s principal banking subsidiaries in Hong Kong are The Hongkong and Shanghai Banking Corporation and Hang Seng Bank. The former is the largest bank incorporated in Hong Kong and is HSBC’s flagship bank in the Asia-Pacific region. It is one of Hong Kong’s three note-issuing banks, accounting for more than 65 per cent by value of banknotes in circulation in 2005.

Rest of Asia-Pacific (including the Middle East)

The Hongkong and Shanghai Banking Corporation offers personal, commercial, corporate and investment banking and markets services in mainland China. The bank’s network spans 12 major cities, comprising 12 branches and eight sub-branches. Hang Seng Bank offers personal and commercial banking services and operates six branches, four sub-branches, and two representative offices in eight cities in mainland China. HSBC also participates indirectly in mainland China through its three associates, Bank of Communications (19.9 per cent owned), Ping An Insurance (19.9 per cent) and Industrial Bank (15.98 per cent).

Outside Hong Kong and mainland China, the HSBC Group conducts business in the Asia-Pacific region primarily through branches and subsidiaries of The Hongkong and Shanghai Banking Corporation in 22 countries, with particularly strong coverage in India, Indonesia, South Korea, Singapore and Taiwan. HSBC’s presence in the Middle East is led by HSBC Bank Middle East in a network of branches and subsidiaries with the widest coverage in the region; in Australia by HSBC Bank Australia Limited; and in Malaysia by HSBC Bank Malaysia Berhad, which has the second largest presence of any foreign-owned bank in the country. HSBC’s associate in Saudi Arabia, The Saudi British Bank (40 per cent owned), is the Kingdom’s sixth largest bank.

North America

HSBC’s North American businesses cover the US, Canada, Mexico, Bermuda and Panama. Operations in the US are primarily conducted through HSBC Bank USA, N.A. which is concentrated in New York State, and HSBC Finance, a national consumer

15

Back to Contents

H S B C H O L D I N G S P L CDescription of Business(continued)

finance company based in Chicago. HSBC’s businesses in Mexico and Panama are run through HSBC Mexico, with HSBC Bank Canada and Bank of Bermuda responsible for operations in their respective countries.

South AmericaHSBC’s operations in South America principally comprise HSBC Bank Brazil and HSBC Bank Argentina, although HSBC is also represented in Venezuela, Chile and Uruguay. In addition to banking services, HSBC operates large insurance businesses in Argentina and Brazil. In Argentina, HSBC’s main insurance business is HSBC La Buenos Aires and, through Máxima and HSBC New York Life, HSBC offers pensions and life assurance products. In Brazil, HSBC also offers consumer finance products through its subsidiary, Losango.

HSBC believes that open and competitive markets are good for both local economies and their participants, and the Group faces very strong competition in the markets it serves. In personal and commercial banking, it competes with a wide range of institutions including commercial banks, consumer finance companies, retail financial service companies, savings and loan associations, credit unions, general retailers, brokerage firms and investment companies. In investment banking, HSBC faces competition from specialist providers and the investment banking operations of other commercial banks.

Regulators routinely monitor and investigate the competitiveness of the financial services industry (of which HSBC is a part) in a number of areas, particularly in the UK and Europe.

Global factorsConsolidation in the banking industry

Over the past few decades there has been a trend towards consolidation in banking and financial services, both nationally and internationally. This development has created a large and growing number of institutions which are capable of competing with HSBC across a wide range of services.

Limited market growth

The majority of HSBC’s business is conducted in the US, the UK and Hong Kong. Penetration of standard banking services in these markets is nearing saturation, with little scope for further market

growth. Greater potential for expansion lies in the provision of a wider range of financial services, including consumer finance, to new and existing customers. HSBC has also identified emerging economies in Asia-Pacific, Mexico, the Middle East, Turkey and Latin America as a source of current and future growth.

Advances in technology

Over the last decade, new technologies such as the internet and related innovations have matured, and financial institutions have not been alone in recognising the potential of these developments. Financial services and other market participants can now deliver a large and expanding range of products and services through these channels and competition is, as a result, fierce. However, with competition come opportunities. HSBC will continue to offer a full range of services via the channels preferred by its customers. These currently include the internet, interactive TV, mobile phone, WAP and telephone banking as well as the traditional branch network.

Regional factors

Europe

The European Commission has commenced inquiries into retail banking and business insurance across all member states. All HSBC entities affected have responded to the initial questionnaires.

The 65 member banks of the European Payments Council have signed an agreement to create a Single European Payments Area by 2008 which aims to harmonise transfers, banker’s orders and cards transactions. This should offer strong growth opportunities for some banks but will also lead to more competition.

UKAfter several very positive years, UK growth slowed in 2005. Although corporate earnings rose and the UK stock market was healthy, strong commodity and oil prices adversely affected several sectors.Retailers are suffering from declining levels of consumer confidence and disposable income, mainly caused by high levels of indebtedness and rising tax and utility burdens.

A stable interest rate environment, strong employment levels and a solid housing market helped to keep demand for consumer finance strong but could not prevent a rise in default and arrears rates in all forms of unsecured personal lending.

16

Back to Contents

Despite these developments, competition in the retail banking sector for the best customers remained intense, with pressure on credit products, interest margins and, in particular, deposit rates.

The high level of personal indebtedness and strong competition within the retail banking and consumer finance sectors led regulatory authorities to continue to monitor closely the financial services sector.

In December, the UK Competition Commission released its provisional remedies to improve competition following its investigation into the US$8.3 billion store card industry. HSBC continues to co-operate with the Commission as the inquiry draws to a conclusion.

Also in 2005, the Office of Fair Trading (‘OFT’) continued with its inquiry into credit card terms under the Unfair Terms in Consumer Contracts regulations. HSBC has made various submissions to the OFT and discussions continue.

The OFT also published its decision on the multilateral interchange agreement between MasterCard members in October. MasterCard has appealed against the decision to the Competition Appeals Tribunal. Visa is also subject to investigation but the case is suspended pending resolution of the MasterCard case.

In November, the Financial Services Authority published the results of its themed review of the sale of Payment Protection Insurance. It has expressed concerns regarding some practices which were common within the industry. HSBC has not received a negative response in respect of its own procedures, but will be considering its products and sales practices in the light of the findings. The OFT will be undertaking a market investigation into Payment Protection Insurance following a super-complaint from the Citizens’ Advice Bureau.

Throughout 2005, a Payments Task Force chaired by the OFT has brought together representatives of the banking industry, consumer bodies and business with the Bank of England and HM Treasury to look at various aspects of the payments system. Its first report recommended that the payment industry implement a faster means of making low cost electronic payments. HSBC agrees that this is in the consumer’s interest and favours its early implementation.

The Consumer Credit Bill, currently in its second reading in Parliament, updates existing consumer legislation in order to provide better consumer protection, and is likely to come into force during 2006.

HSBC’s policy is to co-operate and work positively with all its regulators, inputting data and perspective on those issues which affect all financial service providers via industry bodies.

FranceStable interest rates in the euro zone contributed to a strong growth in real estate investment in France. Competition between French banks was concentrated on the promotion of real estate mortgage loans, which are the principal means by which new customers in France are acquired. Market activity increased and consumers enjoyed improved pricing to the detriment of bank margins throughout 2005.

The payment of interest on sight deposits, which has only been permitted since the beginning of 2005, was introduced by one major mutual French bank. This move did not provoke a widespread reaction in the domestic market and, to date, no other leading French bank has followed suit.

In December 2005, Banque Postale (a subsidiary of the French Postal service) received the necessary regulatory approvals and with effect from January 2006 will be able to offer real estate mortgages and financial services, including the sale of investment products manufactured by third party providers. Given the scale of Banque Postale’s geographical coverage, this will increase competition in an already competitive market.

The French government has reformed tax law for 2006/2007 with two measures which will increase disposable income for high income individuals: a tax exemption on capital gains on equities held for more than eight years, which brings the French taxation regime into line with practices in many other European countries, and a cap on total household taxes at 60 per cent of income. This will boost one of the market segments on which HSBC France focuses.

At the end of December, French banks were granted approval, as in the UK, to provide equity release mortgages. This will assist customers to invest in real estate and finance consumption.

Hong KongWhile fierce competition in traditional core banking products remained evident in Hong Kong, the rising cost of funds in the second half of 2005 from increasing interbank rates made banks with smaller deposit bases more cautious in price competition. A decline in property loan demand also added pressure on banks to look for new outlets for lending. Personal loans, including credit card advances, attracted

17

Back to Contents

H S B C H O L D I N G S P L C

Description of Business(continued)

banks’ attention as consumer spending revived strongly.

The Chinese currency regime was reformed in July 2005 and the second phase of Hong Kong’s renminbi business introduced late in the year. While developments in these areas remain at an early stage, they are expected, along with the benefits flowing from the liberalisation of China’s financial sector under the World Trade Organisation agreement, to be a continued source of growth in the future.

Rest of Asia-Pacific

(including the Middle East)

The competitive environment in the Rest of Asia-Pacific continues to intensify as international banks focus on targeted sectors in emerging markets in pursuit of higher returns. Local banks are also actively expanding their reach and business, both within countries and across borders. Competition remains intense throughout the region in all the customer groups served by HSBC. However, in many countries the growing sophistication of the relatively young population and increasing affluence of the middle class continue to provide HSBC with further opportunities for growth.

Banks and non-banks, both local and international, are rapidly building consumer finance and direct banking businesses in a number of countries in the region.

North AmericaIn an already highly competitive US financial services industry, institutions involved in a broad range of financial products and services continued to consolidate. Within the banking sector, consolidation continued into 2006, with a greater focus on national networks and retail branch banking.

The Group’s principal US subsidiaries, HSBC Bank USA and HSBC Finance, face vigorous competition from a wide array of financial institutions. These include banks, thrifts, insurance companies, credit unions, mortgage lenders and brokers, and non-bank suppliers of consumer credit and other financial services. Many of these institutions are not subject to US banking industry regulation, unlike HSBC. This gives some of them cost and product advantages and will further increase competitive pressures. HSBC competes by expanding its customer base through portfolio acquisitions or alliances, co-branding opportunities and direct sales channels, by offering a very wide variety of consumer loan products and by maintaining a strong service orientation.

The five largest banks in Canada dominate the country’s financial services industry. Despite this, the market remains very competitive with comparable financial products and services offered by other banks, insurance companies and other institutions. Merger activity among the largest banks in Canada remains possible, but without such consolidation major financial institutions will continue to look elsewhere for growth.